GOLD PRICE CLOSED DOWN $4.60TO $2328.50

SILVER PRICE UP $0.11TO $27.32

Gold ACCESS CLOSED $2322.75

Silver ACCESS CLOSED: $27,33

The defense of $2300 gold is now upon us and surpassed. Next up $2400 gold//Silver’s next line is $28.42. Then $34.76

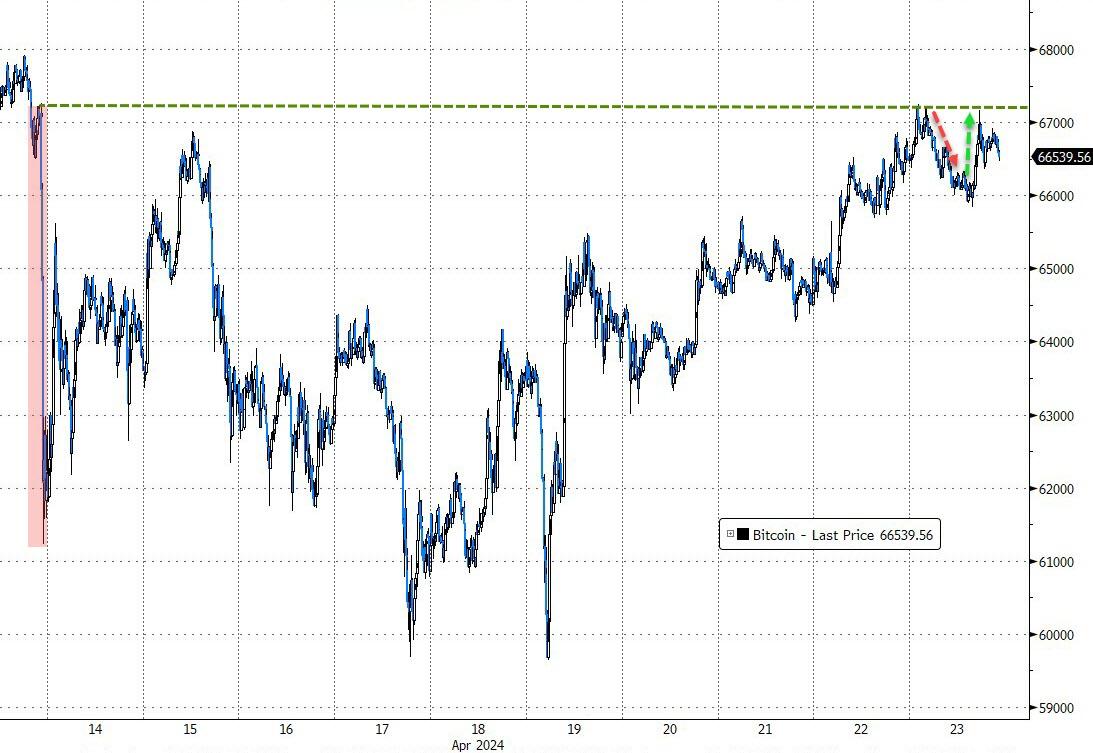

Bitcoin morning price:$66,094 DOWN 356 DOLLARS.

Bitcoin: afternoon price: $66,660 DOWN 912 dollars

Platinum price closing DOWN $9.10TO $914.65

Palladium price; UP $4.45 AT $1025.60

END

SHANGHAI GOLD PREMIUM 70 DOLLARS/COMEX GOLD

SHANGHAI GOLD…

…from the CME….

“As of Monday, April 1, 2024, CME Group settlement data is no longer accessible through ftp.cmegroup.com and has a delayed publication time of 12:00 a.m. CT on all cmegroup.com web pages. Learn about alternate ways to access the data in our FAQ.”

Now I retrieve the data after 1 am

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $3173.71DOWN 23.97 CDN dollars per oz( * NEW ALL TIME HIGH 3,301.52 CDN DOLLARS PER OZ//APRIL 16 2024)

*BRITISH GOLD: 1865,79DOWN 23.82pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2170.30DOWN 20.20uros per oz //* (ALL TIME CLOSING HIGH: 2248.89 EUROS PER OZ//APRIL 16.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: APRIL 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,332.200000000 USD

INTENT DATE: 04/22/2024 DELIVERY DATE: 04/24/2024

FIRM ORG FIRM NAME ISSUED STOPPED

435 H SCOTIA CAPITAL 1

661 C JP MORGAN 10

732 C RBC CAP MARKETS 1

737 C ADVANTAGE 18 2

905 C ADM 14

991 H CME 20

TOTAL: 33 33

JPMORGAN STOPPED (RECEIVED) 0/33CONTRACTS

FOR APRIL/2024

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2024. CONTRACT: 33 NOTICES FOR 3300 OZ or 0.1026 TONNES

total notices so far: 16,213contracts for 1,621300 Oz (50.429 tonnes)

FOR APRIL:

SILVER NOTICES: 0 NOTICE(S) FILED FOR 5,000 OZ/

total number of notices filed so far this month : 1626 for 8,130,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $4.60

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

NO CHANGES IN GOLD INVENTORY AT THE GLD:

/ /INVENTORY RESTS AT 831..91 TONNES

INVENTORY RESTS AT 831.91 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER UP $0.11 AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 10.97 MILLION OZ INTO THE SLV/

// INVENTORY INCREASES T0 427,346 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 427.346MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A MEGA HUMONGOUS SIZED 5628 CONTRACTS TO 174,134 BUT STILL RAPIDLY CLOSING IN ON THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, DESPITE THE RAID AND THIS HUMONGOUS SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR LOSS IN PRICE OF $1.51 IN SILVER PRICING AT THE COMEX ON MONDAY. WE HAD HUGE LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN PANICKING SHORT COVERING BY OUR SPECS WITH THE HUGE PRICE LOSS IN PRICE. WE HAD A HUGE SIZED 1523 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 1523 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $1.51), AND WERE SUCCESSFUL IN KNOCKING MANY SILVER LONGS AS WE HAD A MEGA GIGANTIC SIZED LOSS OF 4286 CONTRACTS ON OUR TWO EXCHANGES WITH THE FALL IN PRICE OF $1.51

WE MUST HAVE HAD:

A HUGE SIZED 875 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 2.465 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S NIL OZ QUEUE JUMP //NEW STANDING REMAINS AT 8.185 MILLION OZ//

//NEW STANDING FOR SILVER IS THUS 8.185 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI LOSS/ HUGE SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1523CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED A STRONG 278 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL

TOTAL CONTRACTS for 17 DAYS, total 26,812 contracts: OR 134.06 MILLION OZ (1577 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 134.06 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 134.06 MILLION OZ (THIS MONTH WILL PROBABLY BE A WHOPPER OF ISSUANCE OF EFPS)

RESULT: WE HAD A HUMONGOUS SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 5628 CONTRACTS WITH OUR LOSS IN PRICE OF SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A HUMONGOUS EFP ISSUANCE CONTRACTS: 875 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL. OF 2.465 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAYS’ 0 OZ QUEUE JUMP

//NEW TOTAL STANDING REMAINS AT 8.185 MILLION OZ

WE HAVE A MEGA GIGANTIC SIZED LOSS OF 4286 OI CONTRACTS ON THE TWO EXCHANGES WITH THE LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 875 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS

THE NEW TAS ISSUANCE MONDAY NIGHT (875 WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 0 NOTICE(S) FILED TODAY FOR nil OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 5454 OI CONTRACTS TO 514,937 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 897 CONTRACTS

WE HAD A GOOD SIZED DECREASE IN COMEX OI (4557 CONTRACTS) WITH OUR HUGE $59.90 LOSS IN PRICE//MONDAY. THE FRBNY SUPPLIEDTHE NECESSARY SHORT PAPER TO WHACK GOLD’S PRICE. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR APRIL. AT 44.8615 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S TINY E.F.P JUMP TO LONDON OF 100OZ.(0.003TONNES)

NEW STANDING 50.637 TONNES// ALL OF THIS HAPPENED WITH OUR $59.90 LOSS IN PRICE WITH RESPECT TO MONDAY’S TRADING. WE HAD A FAIR SIZED LOSS OF 2235 OI CONTRACTS (6.951 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 3219 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 514,937

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2235 CONTRACTS WITH 5454 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 3219 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 2235 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 2000 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3219 CONTRACTS) ACCOMPANYING THE GOOD SIZED LOSS IN COMEX OI (5454 //TOTAL LOSS FOR OUR THE TWO EXCHANGES: 2235 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 44.8615 TONNES FOLLOWED BY TODAY’S TINY 0.003TONNES EFP JUMP

//NEW STANDING 50.637 TONNES.

/ 3) HUGE LONG LIQUIDATION WITH THE LOSS IN PRICE.

// 4) GOOD SIZED COMEX OPEN INTEREST LOSS/ 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: FAIR T.A.S. ISSUANCE: 2000 CONTRACTS/ HUGE SHORT COVERING BY OUR WRONG FOOTED SPECS WITH THE FED’S CONTINUAL RAID ON THE COMEX GOLD.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

APRIL

REPORT THIS AD

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL. :

TOTAL EFP CONTRACTS ISSUED: 67,470CONTRACTS OR 6, 747,000 OZ OR 209.86TONNES IN 17 TRADING DAY(S) AND THUS AVERAGING: 3968 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17TRADING DAY(S) IN TONNES 209.86TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 209.86/3550 x 100% TONNES 5.91% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 209.86 TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A MEGA-HUGE SIZED 5628 CONTRACTS OI TO 174,601 AND FURTHER FROM THE COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 875 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 875 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 875 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 5161 CONTRACTS AND ADD TO THE 875 E.FP. ISSUED

WE OBTAIN A MEGA HUMONGOUS SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 4753 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 21.430 MILLION OZ

OCCURRED WITH OUR $1.51 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED DOWN 22.62 PTS OR 0.74% //Hang Seng CLOSED UP 317,24PTS OR 1.92% / Nikkei CLOSED UP 113.55PTS OR 0.36% //Australia’s all ordinaries CLOSED UP0.45%///Chinese yuan (ONSHORE) closed DOWN 7.2468//OFFSHORE CHINESE YUAN CLOSED DOWN TO 7.2663 /Oil DOWN TO 81.50dollars per barrel for WTI and BRENT UP AT 86.54/ Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 5454 CONTRACTS TO 514,937 WITH OUR HUGE LOSS IN PRICE OF $59.90 WITH RESPECT TO MONDAY TRADING. WE HAD HUMONGOUS TA.S. LIQUIDATION AS WELL AS SHORTS, DESPERATELY TRYING TO GET OUT OF THEIR NAKED SHORTS.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF APRIL..… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG 3219 EFP CONTRACTS WERE ISSUED: : JUNE 3219 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3219 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2235 CONTRACTS IN THAT 3219 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A GOOD SIZED LOSS OF 5454 COMEX CONTRACTS..AND THIS FAIR LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR HUGE LOSS IN PRICE OF $59.90 FRIDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT WAS A GOOD SIZED 2000 CONTRACTS. WE HAD 0 EX FOR RISK ISSUANCE. MOST OF THE TRADING AND SUPPLY OF CONTRACTS ON MONDAY WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: APRIL (50.637 TONNES) ( ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 50.637TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $59.90 //// AND WERE SUCCESSFUL IN KNOCKING MANY SPECULATOR LONGS AS WE HAD A FAIR SIZED LOSS OF 2235 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH OUR LOSSS IN PRICE 0F $59,90

WE HAD A HUMONGOUS T.A.S. LIQUIDATION ON THE FRONT END OF MONDAY’S TRADING ALONG. THE T.A.S. ISSUED ON MONDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE LOST A TOTAL OI OF 4.1617 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL. (44.8615 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S TINY E.F.P.JUMP TO LONDONOF 100 OZ (0.003TONNES)//NEW STANDING; 50.637TONNES

NEW STANDING: 50.637TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $59.90

WE HAD REMOVED 897 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET LOSS ON THE TWO EXCHANGES 2235 CONTRACTS OR 223,500 OZ (6.951 TONNES)

confirmed volume MONDAY 279,533contracts//STRONG

//speculators have left the gold arena

APRIL 23/ INITIAL APRIL GOLD

/ /// THE APRIL 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | oz NIL . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | 15,506.780 oz HSBC |

| No of oz served (contracts) today | 33 notice(s) 3300 OZ 0.1026 TONNES |

| No of oz to be served (notices) | 67 contracts 6700 OZ 0.2084ONNES |

| Total monthly oz gold served (contracts) so far this month | 16,213 notices 1,621300 oz 50.429 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: nil oz

total customer withdrawals: 0

i

we had total deposit of nil oz

NIL

Adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL.

For the front month of APRIL we have an oi of 100 contracts having LOST 71 contracts. We had 70 contracts served on MONDAY, so we LOST 1 contracts or an additional 100oz (0.003 tonnes) will OT stand at the comex as they were EFP’d over to London to take delivery on that side of the pond.

MAY GAINED 39 CONTRACTS TO STAND AT 2159

JUNE DECREASED ITS OI BY 7283 CONTRACTS DOWN TO 408,971CONTRACTS.

JULY INCREASED ITS OI BY 1351 CONTRACTS UP 1351.

We had 33 contracts filed for today representing 3300 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 33 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the APRIL. /2024. contract month, we take the total number of notices filed so far for the month (16,180 x 100 oz ), to which we add the difference between the open interest for the front month of APRIL. (100 CONTRACTS) minus the number of notices served upon today (33x 100 oz per contract( equals 1,628,1000 OZ OR 50.637 TONNES.

thus the INITIAL standings for gold for the APRIL. contract month: No of notices filed so far (16,213) x 100 oz + (100 {OI for the front month} minus the number of notices served upon today (33 x 100 oz which equals 1,628100 oz (50.637TONNES)

TOTAL COMEX GOLD STANDING FOR APRIL: 50.637 TONNES WHICH IS HUGE FOR THIS ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,599,812.623 49.76 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,585,422.823OZ

TOTAL REGISTERED GOLD 7,521,055.666 (233,93 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,066,367.153OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 5,921,234 oz (REG GOLD- PLEDGED GOLD) 184.175 tonnes/dropping like a stone

END

SILVER/COMEX

APRIL 23

INITIAL

//2024// THE APRIL 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 840,781,337oz cnt Delaware HSBC . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,197,105.800z ASAHI CNT |

| No of oz served today (contracts) | 0 CONTRACT(S) (nil OZ) |

| No of oz to be served (notices) | 11 contracts (55,000 oz) |

| Total monthly oz silver served (contracts) | 1626 Contracts (8,130,000oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit :nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 deposits customer account:

i) Into CNT 601,230,600oz

ii) Into ASAHI 595,875,200oz

total customer deposits 1,197,105.800oz

JPMorgan has a total silver weight: 130.170 million oz/292.775million or 44.52%

adjustment: 0

Comex withdrawals: 3

ii) Out of CNT 755,826.923oz

ii) Out of Delaware 4946.900 oz

iii) Out of HSBC 80,007.514 oz

total withdrawal 840,781.337 oz

TOTAL REGISTERED SILVER: 47.196MILLION OZ//.TOTAL REG + ELIGIBLE. 291.775million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF APRIL /2023 OI: 11 CONTRACTS HAVING LOST 1 CONTRACT(S).

WE HAD 1 CONTRACTSSERVED ON MONDAY, SO WE GAINED 0 CONTRACTS OR ADDITIONAL NIL OZ WILL STAND AT THE COMEX

.

MAY SAW A LOSS OF 13,848 CONTRACTS UP TO 52,475

JUNE SAW A LOSS OF 36 CONTRACTS FALLING TO 688

JULY SAW A GAIN OF 8185 CONTRACTS UP TO 97,729

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0for NIL oz

confirmed volume Friday: 114,158

CONFIRMED volume; ON MONDAY 151,085//HUGE

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 1626x 5,000 oz = 8,130,000 oz

to which we add the difference between the open interest for the front month of APRIL (11) and the number of notices served upon today 0x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL/2024 contract month: 1626 (notices served so far) x 5000 oz + OI for the front month of APRIL. (11 number of notices served upon today (0)x 500 oz of silver standing for the APRIL contract month equates to 8.185 MILLION OZ.

New total standing: 8.185 million oz.

There are 47.196 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

APRIL 23 WITH GOLD DOWN $4.60 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD / INVENTORY RISES AT 831.91 TONNES

APRIL 19 WITH GOLD UP $15.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 4.32 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 831.91 TONNES

APRIL 18 WITH GOLD UP $11.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE WITHDRAWAL OF 2.59 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 827.59 TONNES

APRIL 17 WITH GOLD DOWN $17.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 830;18 TONNES

APRIL 16 WITH GOLD UP $23.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 828.45 TONNES

APRIL 15 WITH GOLD UP $9.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE WITHDRAWAL OF 4.03 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 826.72 TONNES

APRIL 12 WITH GOLD UP $2.80 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD/ INVENTORY RISESS AT 830.75 TONN

APRIL 10 WITH GOLD DOWN $14.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 828.71 TONNES

APRIL 9 WITH GOLD UP $11.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 827,85 TONNES

APRIL 8 WITH GOLD UP $7.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A WITHDRAWAL OF 6.02 TONNES OF GOLD INTO THE GLD/ INVENTORY REMAINS AT 826.41 TONNES

APRIL 5 WITH GOLD UP $38.65 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/ INVENTORY REMAINS AT 832.45 TONNES

APRIL 4 WITH GOLD DOWN $3.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD/ INVENTORY REMAINS AT 830.73 TONNES

APRIL 3 WITH GOLD UP $33,85 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD // INVENTORY REMAINS AT 829.00 TONNES

APRIL 2 WITH GOLD UP $23.90 TODAY; HUG CHANGES IN GOLD INVENTORY AT THE GLD A WITH DRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD.:// INVENTORY REMAINS AT 829.00 TONNES

APRIL 1 WITH GOLD UP $18.70 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:// INVENTORY REMAINS AT 830.15 TONNES

MARCH 28 WITH GOLD UP $26.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:// INVENTORY REMAINS AT 830.15 TONNES

MARCH 27 WITH GOLD UP $15.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// INVENTORY FALLS TO 830.15 TONNES

MARCH 26 WITH GOLD UP $1.40 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 835.33 TONNES

MARCH 25 WITH GOLD UP $17.05 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 838.50 TONNES

MARCH 22 WITH GOLD DOWN $23.75 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 838.50 TONNES

GLD INVENTORY: 831.91 TONNES,

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 23/WITH SILVER UP $0.11TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.194 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 22/WITH SILVER DOWN $1.51 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.194 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 19/WITH SILVER UP 42 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.657 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 418.570 MILLION OZ

APRIL 18/WITH SILVER DOWN $.04TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.977 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 422.227 MILLION OZ

APRIL 17/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF .868 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 426/204 MILLION OZ

APRIL 16/WITH SILVER DOWN $0.46 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF NON EXISTENT SILVER// :SLV INVENTORY RESTS AT 427.072 MILLION OZ

APRIL 15/WITH SILVER UP $0.46 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 12/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 4.069 MILLION OZ FROM THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 11/WITH SILVER UP $0.23 TODAY: STRANGE INDEED! HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.931 MILLION OZ :SLV INVENTORY RESTS AT 437.998 MILLION OZ

APRIL 10/WITH SILVER UP $0.04 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:SLV INVENTORY RESTS AT 441.929 MILLION OZ

APRIL 9/WITH SILVER UP $0.15 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.549 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 441.929 MILLION OZ

APRIL 8/WITH SILVER UP $0.33 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.320 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 441.328 MILLION OZ

APRIL 5/WITH SILVER UP $0.61 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.748 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 441.060 MILLION OZ

APRIL 4/WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.671 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 437.312 MILLION OZ

APRIL 3/WITH SILVER UP $1.14 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.835 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 433.641 MILLION OZ

APRIL 2/WITH SILVER UP 84 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6.721 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 430.806 MILLION OZ

APRIL 1/WITH SILVER UP 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// SLV INVENTORY RESTS AT 424.085 MILLION OZ

MARCH 28/WITH SILVER UP 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.005 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 424.085 MILLION OZ

MARCH 27/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A A DEPOSIT OF 1.691 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 423.079 MILLION OZ

MARCH 26/WITH SILVER DOWN 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A A DEPOSIT OF 0.366 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 421.388 MILLION OZ

MARCH 25/WITH SILVER UP 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 3.887 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 421.022 MILLION OZ

MARCH 22/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE DEPOSIT OF 1.1899 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 424.909 MILLION OZ

CLOSING INVENTORY 416.376MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

PETER SCHIFF/SCHIFFGOLD/MIKE MAHARRAY

END

2.Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens/…

END

3. CHRIS POWELL//

Brien Lundin: Noise amid the signal

Submitted by admin on Mon, 2024-04-22 16:28 Section: Daily Dispatches

By Brien Lundin

Gold Newsletter / Golden Opportunities

Metairie, Louisiana

Monday, April 22, 2024

Anyone waiting on the sidelines for gold to go on sale is getting just what they asked for today.

Gold began diving right as trading opened overseas last evening, and the plunge gained steam in New York trading today.

As I write, gold is down nearly $60 (2.5%) and has yet to show any significant resistance to the selling pressure.

In fact, the price has reached lows not seen since … (checks notes) … last week.

The longer-term (one-month) chart above puts today’s selling in some needed perspective. A chart going way back to the March 1 beginning of the uptrend would show even less impact from today’s move.

That said, I don’t want to minimize this correction. This is an important test of the buying demand that has driven the price of gold nearly $400 higher since the end of February.

It’s still too early to determine precisely who’s selling (we may never know) and how low the price will go, but here’s what I’ve been able to glean so far….

… For the remainder of the analysis:

END

* * *

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS live from the vault

https://kinesis.money/live-from-the-vault

5 a. IMPORTANT COMMENTARIES ON COMMODITIES/

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.2469

OFFSHORE YUAN: UP TO 7.2663

SHANGHAI CLOSED DOWN 22.62PTS OR 0.74%

HANG SENG CLOSED UP 317.24PTS OR 1.92%

2. Nikkei closed UP 113.55OR 0.30%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 105.86 EURO RISES TO 1.0669 UP 15 BASIS PTS

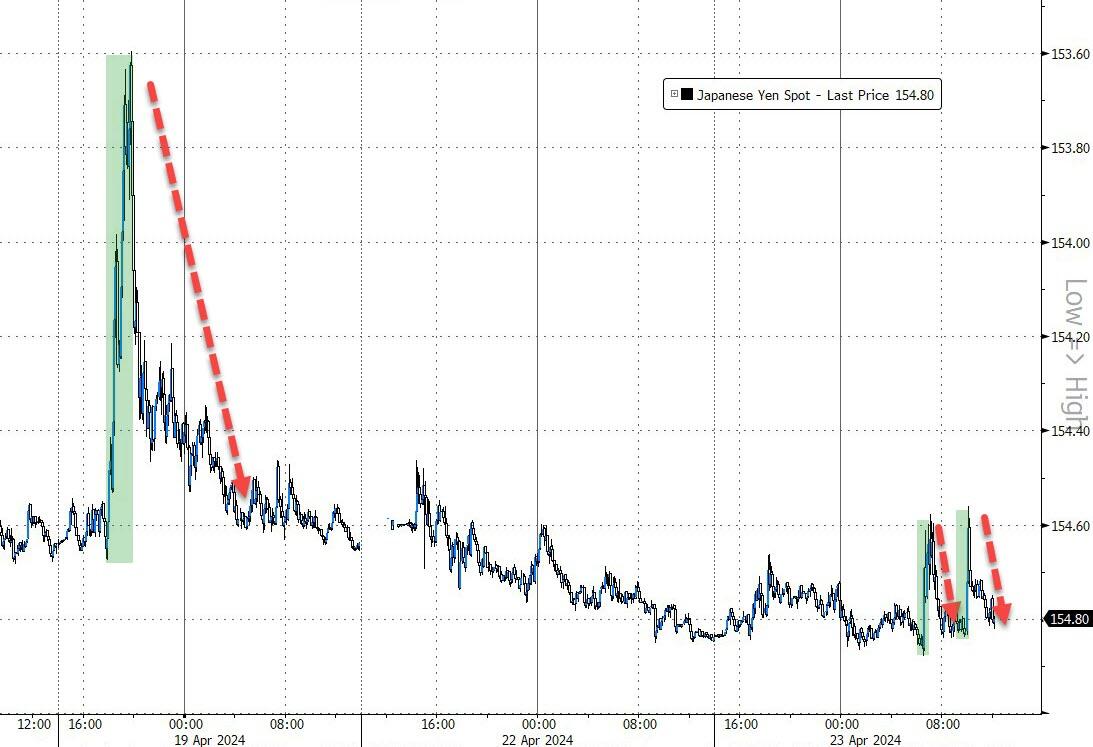

3b Japan 10 YR bond yield: RISES TO. +.885Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 154.78 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN:DOWN/ OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWNTO +2.4980**/Italian 10 Yr bond yield DOWN to 3.823/SPAIN 10 YR BOND YIELD DOWN TO 3.261*

3i Greek 10 year bond yield DOWN TO 3.420

3j Gold at $2302,35silver at: 26.96 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 23 /100 roubles/dollar; ROUBLE AT 93.23//

3m oil into the 81 dollar handle for WTI and 86 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 154.78/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.885% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9113 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.97024well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

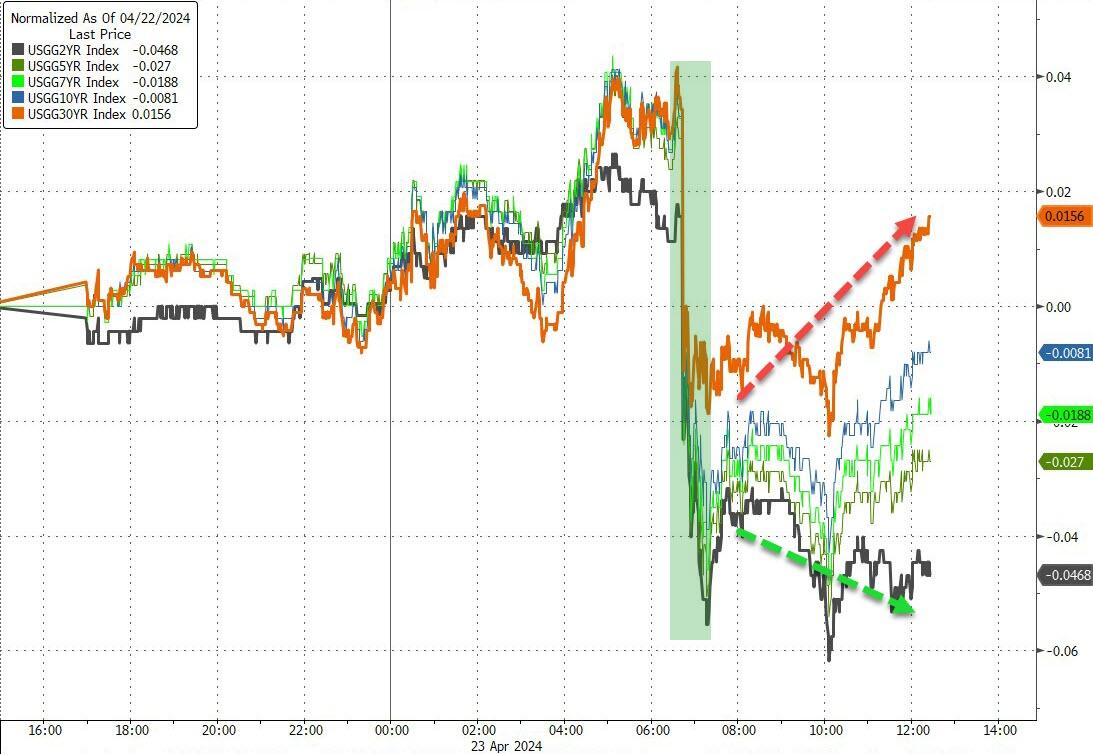

USA 10 YR BOND YIELD: 4.634 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.734 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.996UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.58…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 3 BASIS PTS AT 4.2865

end

2.a Overnight: Newsquawk and Zero hedge

Futures Extend Rebound Into Second Day Ahead Of Tesla Earnings Despite Rising Yields

BY TYLER DURDEN

TUESDAY, APR 23, 2024 – 08:19 AM

US equity futures are higher for the second day, even as small-caps underperform after bond yields rise about +4bps and trade near session highs. As of 7:40am S&P and Nasdaq futures were 0.3% higher after Wall Street’s rebound from a $2 trillion selloff; European stocks also rose on broad-based strength, with only commodity-related sectors in the red; the UK’s FTSE 100 index hit a record high as a rebound that took hold on Monday gathered momentum. Ahead of Tesla’s earnings today, the Mag7 are mixed with semis higher pre-mkt after the recent rout. Commodities are stronger led by Ags and Energy with a flat USD. The macro data focus is on Flash PMIs, Home Sales, Regional Mfg Activity indicators; earnings are skewed towards the Industrials sector with TSLA the first Mag7 stock set to report. We will see if the last few trading sessions sufficiently squared positions and if realized stock moves can match the implied moves, expected to be the largest in 1.5 years.

Early results Tuesday were mostly positive, with shares of United Parcel Service and General Motors rising in premarket trading after earnings beats. PepsiCo slipped after reporting falling volumes in North America. But the main event will be the “Magnificent Seven” cohort of tech megacaps, with Tesla set to be the first to report after today’s market close. Next up is Meta Platforms on Wednesday, followed by Microsoft and Alphabet on Thursday. Here are some other notable premarket movers:

- Abeona Therapeutics shares slumped 48.1% after the biotechnology company’s drug for a rare connective tissue disorder failed to win approval from the US Food and Drug Administration.

- Cadence Design shares drop 5.8% after the maker of semiconductor design software’s revenue and adjusted earnings per share forecast for 2Q fell short of average analyst estimates. Additionally, the company reported 1Q product and maintenance revenue that missed expectations.

- JD Sports shares gained after the British sportswear and sneakers retailer agreed to buy Hibbett (HIBB US) for about $1.1 billion to speed up its US expansion, in a deal expected to be accretive in the first full year of ownership. Hibbett gained 19%.

- Roblox shares rose 4.2% after the game maker was upgraded to overweight from neutral at JPMorgan, which said it sees a “compelling” entry point for a company that has bookings growth of around 20%, exiting a heavy investment cycle and ramping new revenue streams in advertising as well as commerce.

- Sunnova Energy shares fell 2.4% after the renewable energy company is cut to sector weight from overweight by KeyBanc Capital Markets. The downgrade reflects a cautious industry-wide stance, despite Sunnova’s “undemanding valuation,” analyst Sophie Karp writes in a note.

Earnings will stay front and center of investors’ minds this week with about 180 companies — over 40% of the S&P 500 market value — report results. The focus on corporate profits comes after a rout fueled by geopolitical fears and signals the Federal Reserve will be in no rush to lower rates. “Whether markets see further consolidation from here is likely to hinge on the assessment of the sustainability of AI demand ahead following the earnings releases,” said Eddie Cheung, a senior strategist at Credit Agricole CIB.

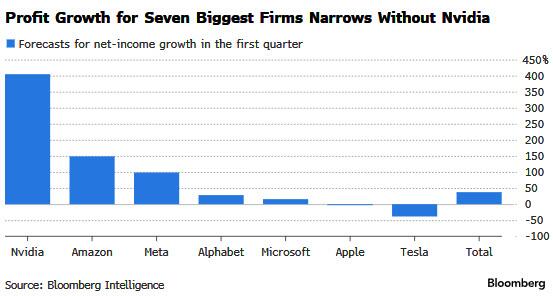

The challenge to S&P 500 returns is that companies will have to produce earnings, and outlooks, that support the already elevated multiples. Profits for the Magnificent Seven are forecast to rise 38% in the first quarter from a year ago, dwarfing the overall S&P 500’s 2.4% anticipated year-over-year earnings growth, according to Bloomberg Intelligence. But excluding Nvidia, the leading chipmaker for AI technology, expected net income growth for the group falls to 23%. Nvidia, which Goldman Sachs Group’s trading desk dubbed “the most important stock on planet Earth,” doesn’t report its earnings for another month.

“We remain focused on the current earnings season, which could re-focus investor attention on solid underlying fundamentals,” Citigroup Inc. strategists Mihir Tirodkar and Beata Manthey wrote in a note. “We would view the recent pullback as a buying opportunity.”

Meanwhile, Investor positioning on megacap growth and tech stocks continues to be cut, down from the 97th percentile in early March to the 77th percentile now, according to Deutsche Bank strategists. The group is still the only sector where positioning is above historical average, even if no longer extreme, the strategists wrote, countering the self-serving and incorrect observations by JPM’s Marko Kolanovic.

In Europe, the Stoxx 600 index climbed 1%, with technology and retail shares leading gains, while the mining sector lagged. SAP SE jumped more than 4% as a boom in demand for artificial intelligence fueled the German software company’s growth. Drugmaker Novartis AG added as much as 5% after lifting full-year guidance. Here are some other notable premarket movers:

- JD Sports shares gain as much as 7.5% after the British sportswear and sneakers retailer agreed to buy Hibbett for about $1.1 billion to speed up its US expansion

- Novartis shares advance as much as 5%, the most in more than 9 months, after the Swiss drugmaker reported results for the first quarter that impressed analysts

- Nordnet rises as much as 9.7%, the most since October, after the digital bank reported its first-quarter results. Both Citi and Morgan Stanley highlight the company’s higher-than-expected brokerage income

- SAP shares jump as much as 4.4% in Frankfurt after the software company reported quarter-over-quarter acceleration in the growth rate of current cloud backlog, a key indicator of cloud revenue to be booked within next 12 months

- Akzo Nobel shares fall as much as 6.6%, to the lowest since November, after the coatings maker failed to raise its profit forecast for the year. The stock had risen in five of the six sessions leading up to Tuesday’s earnings report

- DNB falls as much as 3.9%, the most since October, after the Norwegian lender reported a net interest income miss for the third quarter in a row, with analysts also flagging a low-quality profit beat due to it being attributable to provision income

- Anglo American falls as much as 3.9% in London after the miner reported first-quarter earnings. Analysts noted that sales were behind production in copper and iron ore, leading to temporary inventory builds

- Kuehne + Nagel shares drop as much as 3.9% after reporting first-quarter earnings in which pricing and cost performance were offset by lower volumes, according to Citigroup

- Boliden declines as much as 5.9% after its first-quarter results, with analysts flagging that headline operating profit missed, but underlying operations performed reasonably well

- OVH shares slide as much as 17%, the biggest drop since March 2023, as weaker-than-expected 2Q growth led the IT services provider to lower its forecast for growth and capex for the year

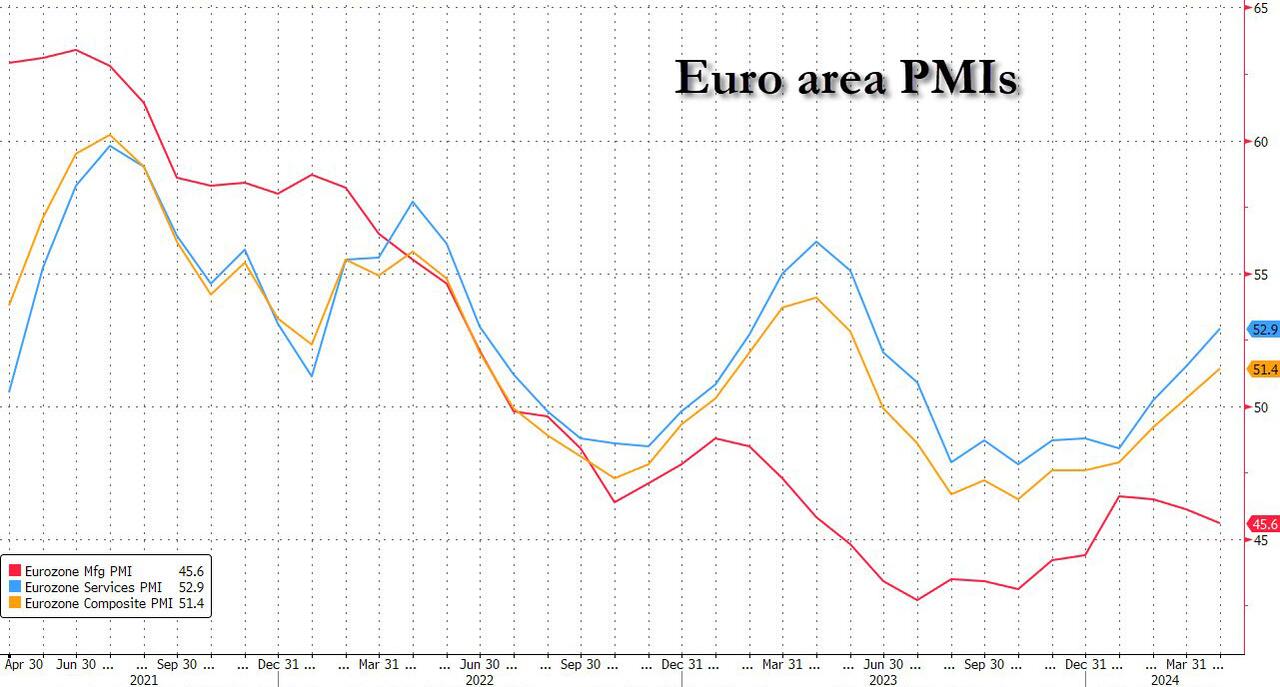

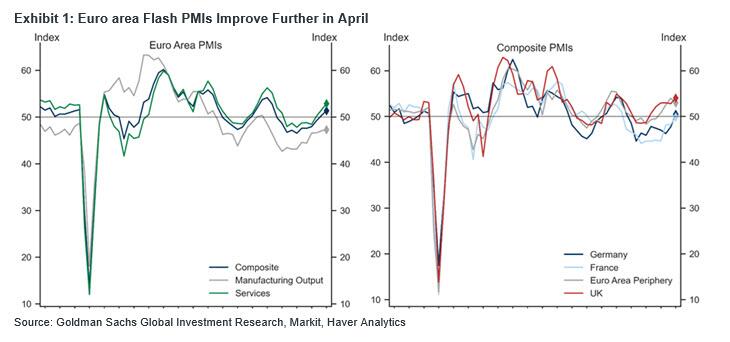

PMI data on Tuesday reinforced the positive mood in Europe. Private-sector activity advanced to the highest level in almost a year, driven by a buoyant services sector and Germany’s return to growth. And yet, barring any economic surprises, a rate cut in June is a “fait accompli,” European Central Bank Vice President Luis de Guindos said.

Earlier in the session, Asian stocks also rose for a second day as sentiment toward China continued to improve, with easing fears of a wider Middle East conflict offering additional support. The MSCI Asia Pacific Index rose as much as 0.8%, with TSMC and Tencent among the biggest boosts. Most regional markets advanced, though mainland China stocks fell for a third day and Japanese shares trimmed gains as the yen strengthened after Finance Minister Shunichi Suzuki’s comments on possible intervention. Hong Kong stocks led the region’s gains after UBS upgraded Chinese stocks to overweight, citing resilient earnings and a growing focus on shareholder returns. Investors are turning more upbeat on the nation’s assets thanks to green shoots in the economy as well as signs of improving corporate performance.

- Hang Seng and Shanghai Comp. were mixed with outperformance in Hong Kong due to tech strength, while the mainland lagged amid the PBoC’s continued tepid liquidity operations and with the US drafting sanctions that threaten to cut some Chinese banks off from the global financial system for aiding the Russian war effort.

- Nikkei 225 traded indecisively and on both sides of 37,500 after briefly wiping out all of its opening gains.

- ASX 200 was led by strength in real estate and tech, while the latest flash PMIs from Australia were varied.

“What makes us more positive now on earnings are the early signs of a pick-up in consumption,” UBS strategists including Sunil Tirumalai wrote in a note. “Any rebound in consumer confidence for us means the possibility of household savings flowing into consumption” and eventually markets.

In rates, treasuries are under modest pressure with front-end yields higher by ~2bp before a flurry of bond auctions that will test investors’ appetite after yields hit the highest in 2024: the latest weekly supply cycle (2-, 5- and 7-year auctions) is set to kick off with record $69b 2-year later today. US 10-year yields around 4.645%, higher by nearly 4bps on the day. In Europe, gilts underperform their German counterparts after the UK raised its planned gilt issuance for the fiscal year more than expected, as the government’s budget shortfall overshot forecasts; the belly of gilts curve cheapened after DMO announcement, with 5-year UK yields higher by around 2bp. Treasury coupon auctions resume at 1pm New York time with $69b 2-year, followed by 5- and 7-year notes Wednesday and Thursday. The WI 2-year yield at around 4.965% is ~37bp cheaper than last month’s, which tailed by 0.5bp

In commodities, oil prices advance, with WTI rising 0.4% to trade near $82.20. Gold extends Monday’s drop, down 1% on the day; Monday’s 2.7% drop was biggest in nearly two years. Bitcoin is modestly softer and holds around the USD 66k mark.

Looking at today’s calendar, US economic data slate includes April Philadelphia Fed non-manufacturing activity (8:30am), S&P manufacturing and services PMIs (9:45am), March new home sales and April Richmond Fed manufacturing index (10am). From central banks, we’ll hear from the ECB’s Panetta and Nagel, and the BoE’s Haskel and Pill as Fed members have entered quiet period ahead of May 1 policy announcement. Finally, today’s earnings releases include Visa, Tesla, PepsiCo, General Electric, UPS and General Motors.

Market Snapshot

- S&P 500 futures up 0.1% to 5,052.75

- STOXX Europe 600 up 0.6% to 505.15

- MXAP up 0.6% to 170.25

- MXAPJ up 0.9% to 524.40

- Nikkei up 0.3% to 37,552.16

- Topix up 0.1% to 2,666.23

- Hang Seng Index up 1.9% to 16,828.93

- Shanghai Composite down 0.7% to 3,021.98

- Sensex up 0.3% to 73,852.66

- Australia S&P/ASX 200 up 0.4% to 7,683.51

- Kospi down 0.2% to 2,623.02

- Brent Futures up 1.0% to $87.85/bbl

- Gold spot down 0.9% to $2,305.32

- US Dollar Index down 0.14% to 105.93

- German 10Y yield little changed at 2.50%

- Euro up 0.2% to $1.0680

Top Overnight News

- The U.S. is drafting sanctions that threaten to cut some Chinese banks off from the global financial system, arming Washington’s top envoy with diplomatic leverage that officials hope will stop Beijing’s commercial support of Russia’s military production, according to people familiar with the matter. WSJ

- Chinese universities and research institutes recently obtained high-end Nvidia artificial intelligence chips through resellers, despite the U.S. widening a ban last year on the sale of such technology to China. RTRS

- China QE drumbeat grows louder as the country’s finance minister expresses support for the PBOC to resume trading gov’t bonds (although many doubt this would lead to Fed/ECB-style QE). WSJ

- AAPL’s iPhone sales in China fell 19% during the March quarter, according to data from an independent research firm that marked the gadget’s worst performance there since Covid struck around 2020. BBG

- Japanese Finance Minister Shunichi Suzuki said last week’s meeting with his U.S. and South Korean counterparts has laid the groundwork for Tokyo to act against excessive yen moves, issuing the strongest warning to date on the chance of intervention. RTRS

- ECB’s Luis De Guindos says a June cut is all but guaranteed, but what happens beyond that could depend on the actions of the Fed. WSJ

- Europe’s flash PMIs for April point to firmer growth (and inflation), with the slump in manufacturing showing signs of easing while services rose to 52.9 (up from 51.5 in Mar and above the Street’s 51.8 forecast), and overall price pressures intensified slightly. S&P

- Tesla headlines today’s earnings after seven straight days of declines. Margins, its robotaxi and the fate of its lower-cost EV will be the focus. The company is also being sued in California by a former employee who claims it failed to provide required notice for layoffs. BBG

- MSFT launches smaller AI models that provide “good enough” capabilities for many, but at a fraction of the cost (the models don’t need high-end Nvidia chips to function). NYT

Earnings

- Nucor Corp (NUE) Q1 2024 (USD): EPS 3.46 (exp. 3.66), Revenue 8.14bln (exp. 8.26bln). Expects earnings to decrease in Q2 vs Q1 due to decreased earnings in the steel mills segment. Average scrap and scrap substitute cost per gross ton USD 421 (exp. 399.58). Sales tons to outside customers 6.22mln (exp. 6.41mln).

- SAP (SAP GY) Q1 24 (EUR): Adj. EPS 0.81 (exp. 0.89), adj. revenue 8.04bln (exp. 8.03bln). Adj. cloud and software revenue EUR 6.96bln (exp. 6.93bln). Adj. cloud revenue EUR 3.93bln (exp. 3.94bln). Adj. cloud revenue in constant currencies +25% (exp. +24.5%). Adj. operating profit EUR 1.53bln (exp. 1.7bln). GUIDANCE: Cloud revenue view between 17.0-17.3bln (prev. 13.66bln in 2023). Cloud and software revenue view at EUR 29.0-29.5bln (prev. 26.92bln in 2023) Adj. Operating profit view EUR 7.6-7.9bln (prev. 6.51bln in 2023). Raises 2023 dividend 7% to EUR 2.20/shr vs 2022 dividend. (Newswires) SAP ADR (SAP) rose 2.1% in the US after-hours. Index Weightings: DAX 40 (10.9% – largest), Euro Stoxx 50 (5% – third largest), Stoxx 600 (1.3%).

- Renault (RNO FP) Q1 (EUR): Revenue 11.71bln (exp. 11.7bln). Sales +2.6% Y/Y. Strong order book in Europe, reflecting a very good start to the year. Co. is progressing well toward its target of cost reduction to lower EV costs by 40%. The EV market is a bit slower than had expected a few years ago. Talks with Geely and Aramco on the ICE powertrain JV are at an advanced stage.

- Novartis (NOVN SW) Q1 (USD): Revenue 11.8bln (exp. 11.5bln). Core EPS 1.80 (exp. 1.73); Raises FY24 Net Sales and Core Operating Income guidance. Strong sales momentum in Entresto (+36% cc), Cosentyx (+25% cc), Kesimpta (+66% cc), Kisqali (+54% cc), Pluvicto (+47% cc) and Leqvio (+139% cc). Free cash flow 2.0bln (-24%) – declined due to a prior-year one-timer and timing of payments. Novartis proposes Dr. Giovanni Caforio as Chair of the Board of Directors at AGM 2025. Index Weightings: SMI (15.9% – second largest), Stoxx 600 (2%). Net Sales are expected to grow high-single to low double-digit digits. Core operating income is expected to grow low double-digit to mid-teens.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded with a mild positive bias after the tech-led rebound stateside. ASX 200 was led by strength in real estate and tech, while the latest flash PMIs from Australia were varied. Nikkei 225 traded indecisively and on both sides of 37,500 after briefly wiping out all of its opening gains. Hang Seng and Shanghai Comp. were mixed with outperformance in Hong Kong due to tech strength, while the mainland lagged amid the PBoC’s continued tepid liquidity operations and with the US drafting sanctions that threaten to cut some Chinese banks off from the global financial system for aiding the Russian war effort.

Top Asian News

- US is reportedly drafting sanctions that threaten to cut some Chinese banks off from the global financial system as it hopes to stop Beijing’s commercial support of Russia’s military production, according to WSJ.

- BoJ Governor Ueda reiterated that monetary policy will be data dependent and will depend on the economy and inflation, while he said they don’t have any pre-set idea on the timing and pace of future rate hikes and if trend inflation accelerates in line with their forecast, they will adjust the degree of monetary support through an interest rate hike. Ueda also stated if their price forecast changes, that will also be a reason to change policy but noted it is hard to say beforehand how long the BoJ should wait in gathering enough data to change policy and would like to leave some scope for adjustment by not pre-committing to a certain policy too much.

- Japanese Finance Minister Suzuki said the government is ready to respond appropriately to excessive FX moves and is closely watching FX moves with a high sense of urgency, while they won’t rule out any option and will deal appropriately with excessive FX moves. Suzuki also said he closely communicated with the US and South Korea on forex in Washington and won’t deny that last week’s discussions in Washington have laid the groundwork for Japan to take appropriate FX action.

- Senior Japanese ruling party official said recent JPY falls are excessive and out of line with fundamentals; said Japanese authorities could intervene to prop up the JPY at any time

- Japan Business Lobby Keidanren Chair Tokura said he think Government will make appropriate decision on intervention, via Kyodo

European bourses, Stoxx600 (+0.6%) began the session on a strong footing, and has remained at elevated (albeit contained) levels throughout the European morning. There was little reaction to the EZ Flash PMI data. European sectors hold a positive tilt; Tech takes the top spot, benefiting from US tech gains in the prior session, and post-earning strength in SAP (+3.9%). Basic Resources is found at the foot of the pile, amid broader weakness in metals prices. US Equity Futures (ES +0.1%, NQ +0.2%, RTY U/C) are tentative ahead of a busy earnings slate and the key US PMI data.

Top European News

- ECB’s de Guindos said a June rate cut looks like a set deal, if there are no surprises; end of inflation fight is in sight; largest remaining threat stems from services inflation. There’s a clear slowdown in wage dynamics. Inclined to be very cautious what happens after June. Need to take into account what’s happening in the US. What the Fed decides is crucial for the global economy. Beed to take impact of FX movements into account. Indicators point toward modest H2 Euro-area recovery.

- BoE’s Haskel said UK food price inflation is “unusually high”; UK labour market is is “extremely tight”, via Bloomberg. Inflation will stay high unless the job market weakens.

- Kantar UK Supermarket update (Apr): Grocery price inflation has fallen to 3.2% over the four weeks to 14 April, marking the fourteenth monthly drop in a row

FX

- DXY softer having briefly dipped under 106 amid gains in the EUR. Ultimately though, the index is in consolidation mode ahead of GDP and PCE metrics later this week and FOMC on May 1st. For now, the next downside target comes via last week’s low at 105.74.

- EUR is boosted by PMI metrics which saw strong services and composite PMIs overshadow a soft outturn for the manufacturing sector. EUR/USD as high as 1.0695 with the 1.07 level not breached since 12th April; 1.0729 was the high that day.

- GBP: After a soft session yesterday which dragged the pair to a low of 1.23, Cable is on the front foot thanks to a strong showing for services PMI. 1.2388 is the high watermark thus far.

- JPY is steady vs. the USD but made another multi-decade high at 154.85. The closer the pair moves to 155, the louder the calls for intervention will get. For now, jawboning is providing minimal help for JPY.

- Antipodeans are varied the USD with slight outperformance in Aussie after AUD/NZD extended above 1.0900. AUD/USD saw little follow-through from PMI data overnight with the pair lingering around yesterday’s best levels after printing a YTD low on Friday.

- PBoC set USD/CNY mid-point at 7.1059 vs exp. 7.2437 (prev. 7.1043).

Fixed Income

- USTs initially remained in overnight ranges, though succumbed to selling pressure, sparked by EZ-PMIs, which dragged EGBs lower. USTs matched yesterday’s 107.31 high earlier in the session before pulling back to circa 107.25, and further downside could bring Monday’s 107.17 low into view.

- Bunds looked as if they wanted to venture higher in early trade in an extension of yesterday’s gains and with de Guindos labelling June as a done deal. However, EZ-wide and regional PMIs acted as a drag thereafter with a strong showing for the services sector, helping composite metrics to beat expectations. 131.47 was the peak before prices made a low at 130.98.

- Gilts started the session on the back foot thanks to an unwind of yesterday’s Ramsden-induced gains and higher-than-expected public borrowing figures which saw the UK DMO revise higher its 2024/25 Gilt issuance remit. Gilts down as low as 96.90 with yesterday’s trough at 96.71.

- UK DMO revises higher its 2024/25 Gilt issuance remit to GBP 277.7bln (prev. GBP 265.3bln)

- Italy sell EUR 2.5bln vs exp. EUR 2-2.5bln 3.20% 2026 BTP Short Term and EUR 2.5bln vs exp. EUR 2-2.5bln 1.50% 2029 & 1.80% 2036 BTPei:

- Germany sells EUR vs exp. EUR 5bln 2.90% 2026 Schatz: b/c 2.7x (prev. 2.31x) & avg. yield 2.91% (prev. 2.84%) and retention 18.6% (prev. 17.7%)

Commodities

- Upside across the crude complex underpinned by the Flash PMIs from Europe which (although manufacturing fell short of expectations) pointed to a services-led recovery; however, prices have pulled back from best levels in recent trade. Brent June meanwhile trades in a USD 86.97-97.95/bbl range.

- Softer trade across precious metals despite the softer Dollar as the geopolitical unwind from yesterday continues, with relatively broad-based losses seen across spot gold, silver and palladium; XAU fell under USD 2,300/oz to find current intraday support around USD 2,291/oz.

- Base metals are lower across the board with sizeable intraday losses despite the softer Dollar and risk-on tone across the rest of the market. There has been no obvious catalyst for this pullback but some desks cite Asian investors being cautious of the recent rally driven, in part, by speculative trading.

- Anglo American (AAL LN) Q1 Copper Production 198k tonnes (exp. 191.3k tonnes)

Geopolitics: Middle East

- Israeli occupation forces reportedly stormed the city of Jericho in the eastern West Bank, while it was also reported that Israeli gunboats targeted the seashores in the city of Khan Younis in the southern Gaza Strip. In relevant news, sirens sounded in the town of Metulla and the Kiryat Shmona area in northern Israel on suspicion of rocket fire, according to Al Jazeera.

- Hezbollah fired dozens of rockets into northern Israel on Monday which drew retaliatory strikes, while it said its attack was in response to recent Israeli strikes on towns and villages in southern Lebanon, according to Associated Press.

- Israeli raids were reported on the town of Yaroun in southern Lebanon, according to Al Jazeera.

- Hamas said it condemns the statements of US Secretary of State Blinken and his attempt to hold the group responsible for obstructing reaching an agreement, according to Sky News Arabia. Hamas said Blinken’s statements contradict the fact that the movement has provided flexibility more than once to facilitate an agreement, while it added that the movement’s demands are a permanent ceasefire, the withdrawal of the occupation and the return of the displaced to their homes in all areas of the Gaza Strip.

- US defence official said the Al-Asad airbase in Iraq came under attack from an Iranian proxy group today which is the second attack on a US base in two days, according to Fox.

Geopolitics: Other

- UK PM Sunak is to unveil an extra GBP 500mln of military funding to Ukraine and announce the largest supply of munitions to Kyiv on Tuesday as he travels to Poland and Germany, according to FT.

- North Korean state media reported that leader Kim guided the first nuclear counterstrike drills, while it stated that the drills are a clear warning sign to enemies.

US Event calendar

- 08:30: April Philadelphia Fed Non-Manufactu, prior -18.3

- 09:45: April S&P Global US Composite PMI, est. 52.0, prior 52.1

- 09:45: April S&P Global US Services PMI, est. 52.0, prior 51.7

- 09:45: April S&P Global US Manufacturing PM, est. 52.0, prior 51.9

- 10:00: Revisions: Retail Sales

- 10:00: April Richmond Fed Business Conditio, prior -8

- 10:00: April Richmond Fed Index, est. -8, prior -11

- 10:00: March New Home Sales MoM, est. 1.1%, prior -0.3%

- 10:00: March New Home Sales, est. 669,000, prior 662,000

DB’s Jim Reid concludes the overnight wrap

It may not be saying a lot, but markets had their best performance in some time yesterday, as investors became a bit more optimistic about the near-term outlook. Equities recovered, and the S&P 500 (+0.87%) finally managed to advance after a run of 6 consecutive declines. Adding to the positive sentiment were growing hopes that a further escalation in the Middle East would be avoided, and Brent crude oil prices (-0.33%) fell back to their lowest level so far this month, at $87.00/bbl. So there were several pieces of better news for investors, but there’ll be no let-up on the calendar today, as we’ve got lots of earnings reports, including Tesla after the US close. While the Magnificent 7 were up +0.94% yesterday, Tesla was down -3.40%, extending its decline this year to -42.8% and having halved since last July. It’s maybe a slight warning for the darlings of the current AI boom that things can change quickly if profits don’t follow very high expectations as new technologies grow. Talking of which Nvidia bounced back from their -10.0% decline on Friday and rose +4.35% yesterday.

On top of earnings today, we’ll get an initial indication about how the global economy has performed in Q2, as the April flash PMIs are coming out for the major economies. These will be of particular interest for assessing the nascent recovery in the euro area economy. In March the composite PMI rose above the 50 level for the first time in 10 months. There will also be attention on the price components within the PMIs, especially in the US, where the composite output price index posted a 10-month high of its own last month.

We’ll have to see how those events pan out, but before all that, risk assets managed to post a strong recovery on both sides of the Atlantic. That made a change after three weeks of losses for global equities, with the major indices including the S&P 500 (+0.87%), the NASDAQ (+1.11%) and the STOXX 600 (+0.60%) all advancing. Information technology (+1.28%) and financials (+1.20%) outperformed within the S&P 500. Alongside that, the VIX index of volatility (-1.8pts) fell to 16.94pts, which is its lowest level since Iran launched their recent missile strike on Israel . And here in the UK, the FTSE 100 (+1.62%) even closed at an all-time high, aided by the weakness in sterling (-0.19%), which hit its weakest level against the US Dollar since November.

Henry did a piece yesterday (link here) looking at what happens next after the S&P 500 has seen 6 consecutive declines as we saw before last night’s positive close. The subsequent 1-month and 6-month performances have mostly been positive in recent history. Moreover, if the S&P had posted a 7th consecutive decline yesterday, that would have taken us into unusual territory, as it’s something we haven’t seen since February 2020 as Covid-19 spread globally. Indeed, the examples of 7 consecutive losses for the S&P 500 (in the 21st century at least) have either been during a crisis (GFC, US debt ceiling crisis, Euro Crisis, Covid-19) or in anticipation of a pivotal event with significant uncertainty (2016 US election).

As discussed at the top, sentiment was bolstered by the lack of any further escalation in the Middle East. Indeed, yesterday saw Iran’s foreign ministry spokesman say that Israel had received the “necessary response at this stage”. The apparent easing in tensions helped oil prices fall back, and there was also a sharp move lower in gold (-2.59%), which had its biggest daily decline since June 2021. It’s down another -0.90% this morning.

The more positive tone was evident across sovereign bonds too. They were supported by the drop in oil prices, which added to hopes that any spike in inflation would prove temporary, and the 1yr US inflation swap (-1.2bps) fell back for a 4th session to 2.71%. In turn, that meant investors grew a bit more hopeful about the prospect of rate cuts, and the amount of Fed rate cuts priced by the December meeting (+1.2bps) inched up to 40bps. Similarly at the ECB, the number of rate cuts priced by December’s meeting (+4.2bps) rose to 78bps.

With more rate cuts being priced in, that helped to push down yields, with those on 10yr bunds (-1.4bps), OATs (-2.7bps) and BTPs (-8.7bps) all moving lower. Admittedly, there was a decent intraday turnaround, as the 10yr bund yield had risen to 2.55% at one point, its highest level since November, before reversing course and ending the day lower at 2.48%. Meanwhile in the US, there was a decline in the 2yr Treasury yield (-1.5bps) to 4.97%, whilst the 10yr Treasury yield (-1.2bps) fell to 4.61%, as it also pared back its earlier losses, having still being above at 4.66% as Europe finished lunch.

In Asia the Hang Seng (+1.64%) is leading gains on a broker upgrade, with the Nikkei (+0.27%), the KOSPI (+0.20%) and the S&P/ASX 200 (+0.41%) seeing minor gains. Chinese stocks are the worst performers with the CSI (-0.56%) and the Shanghai Composite (-0.41%) both trading lower. US stock futures are broadly flat as I type.

Early morning data showed that key gauges of Japan’s manufacturing and service activity improved in April to its highest levels in nearly a year. The au Jibun Bank flash manufacturing PMI rose to 49.9 in April, as against a level of 48.2 in March. The services PMI advanced to 54.6 in April up from 54.1 in March indicating that the service sector continues to remain the primary driver of growth.

Elsewhere, Australia’s Judo Bank PMI data for April showed the manufacturing PMI rising to 49.9 from 47.3. Meanwhile, the service sector PMI came off slightly from 54.4 to 54.2, though still registering a decent growth environment. The composite PMI hit a 24-month high of 53.6 in April, an improvement from the previous month’s 53.3.

To the day ahead now, and the main data highlight will be the April flash PMIs from Europe and the US. Elsewhere, we’ll get US new home sales for March, UK public finances for March, and the Richmond Fed’s manufacturing index for April. From central banks, we’ll hear from the ECB’s Panetta and Nagel, and the BoE’s Haskel and Pill. Finally, today’s earnings releases include Visa, Tesla, PepsiCo, General Electric, UPS and General Motors.

2 B) NOW NEWSQUAWK (EUROPE/REPORT)

US equity futures tentative ahead of a busy earnings slate, Bonds flat but were pressured post EZ PMIs, XAU dips; US PMIs due – Newsquawk US Market Open

TUESDAY, APR 23, 2024 – 05:43 AM

- European equities are entirely in the green; US equity futures trade modestly on either side of the unchanged mark.

- Dollar is slightly softer, EUR incrementally firmer post-EZ PMI; USD/JPY hits multi-decade highs once again.

- USTs initially remained in overnight ranges but succumbed to modest selling pressure following EZ PMIs.

- Crude is marginally firmer, underpinned by EZ PMIs; XAU continues to decline and base metals slip.

- Apple (AAPL) iPhone sales in China -19% in Q1 and down 24% Y/Y in the first six weeks of the year, according to Bloomberg citing Counterpoint Research.

- Looking ahead, US PMIs, US Richmond Fed Index, Comments from BoE’s Pill & ECB’s Nagel, Supply from the US, Earnings from Spotify, General Motors, Philip Morris, PepsiCo, RTX, Fiserv, UPS, Visa, Lockheed Martin & Tesla

EUROPEAN TRADE

EQUITIES

- European bourses, Stoxx600 (+0.6%) began the session on a strong footing, and has remained at elevated (albeit contained) levels throughout the European morning. There was little reaction to the EZ Flash PMI data.

- European sectors hold a positive tilt; Tech takes the top spot, benefiting from US tech gains in the prior session, and post-earning strength in SAP (+3.9%). Basic Resources is found at the foot of the pile, amid broader weakness in metals prices.

- US Equity Futures (ES +0.1%, NQ +0.2%, RTY U/C) are tentative ahead of a busy earnings slate and the key US PMI data.

- Click here and here for the sessions European pre-market equity newsflow.

- Click here for more details.

FX

- DXY softer having briefly dipped under 106 amid gains in the EUR. Ultimately though, the index is in consolidation mode ahead of GDP and PCE metrics later this week and FOMC on May 1st. For now, the next downside target comes via last week’s low at 105.74.

- EUR is boosted by PMI metrics which saw strong services and composite PMIs overshadow a soft outturn for the manufacturing sector. EUR/USD as high as 1.0695 with the 1.07 level not breached since 12th April; 1.0729 was the high that day.

- GBP: After a soft session yesterday which dragged the pair to a low of 1.23, Cable is on the front foot thanks to a strong showing for services PMI. 1.2388 is the high watermark thus far.

- JPY is steady vs. the USD but made another multi-decade high at 154.85. The closer the pair moves to 155, the louder the calls for intervention will get. For now, jawboning is providing minimal help for JPY.

- Antipodeans are varied the USD with slight outperformance in Aussie after AUD/NZD extended above 1.0900. AUD/USD saw little follow-through from PMI data overnight with the pair lingering around yesterday’s best levels after printing a YTD low on Friday.

- PBoC set USD/CNY mid-point at 7.1059 vs exp. 7.2437 (prev. 7.1043).

- Click here for more details.

- Click here for NY Option Expiry details.

FIXED INCOME

- USTs initially remained in overnight ranges, though succumbed to selling pressure, sparked by EZ-PMIs, which dragged EGBs lower. USTs matched yesterday’s 107.31 high earlier in the session before pulling back to circa 107.25, and further downside could bring Monday’s 107.17 low into view.

- Bunds looked as if they wanted to venture higher in early trade in an extension of yesterday’s gains and with de Guindos labelling June as a done deal. However, EZ-wide and regional PMIs acted as a drag thereafter with a strong showing for the services sector, helping composite metrics to beat expectations. 131.47 was the peak before prices made a low at 130.98.

- Gilts started the session on the back foot thanks to an unwind of yesterday’s Ramsden-induced gains and higher-than-expected public borrowing figures which saw the UK DMO revise higher its 2024/25 Gilt issuance remit. Gilts down as low as 96.90 with yesterday’s trough at 96.71.

- UK DMO revises higher its 2024/25 Gilt issuance remit to GBP 277.7bln (prev. GBP 265.3bln)

- Italy sell EUR 2.5bln vs exp. EUR 2-2.5bln 3.20% 2026 BTP Short Term and EUR 2.5bln vs exp. EUR 2-2.5bln 1.50% 2029 & 1.80% 2036 BTPei:

- Germany sells EUR vs exp. EUR 5bln 2.90% 2026 Schatz: b/c 2.7x (prev. 2.31x) & avg. yield 2.91% (prev. 2.84%) and retention 18.6% (prev. 17.7%)

- Click here for more details.

COMMODITIES

- Upside across the crude complex underpinned by the Flash PMIs from Europe which (although manufacturing fell short of expectations) pointed to a services-led recovery; however, prices have pulled back from best levels in recent trade. Brent June meanwhile trades in a USD 86.97-97.95/bbl range.