GOLD PRICE CLOSED DOWN $3.75TO $2324.75

SILVER PRICE DOWN $0.05 TO $27.27

Gold ACCESS CLOSED $2314,65

Silver ACCESS CLOSED: $27,16

The defense of $2300 gold is now upon us and surpassed. Next up $2400 gold//Silver’s next line is $28.42. Then $34.76

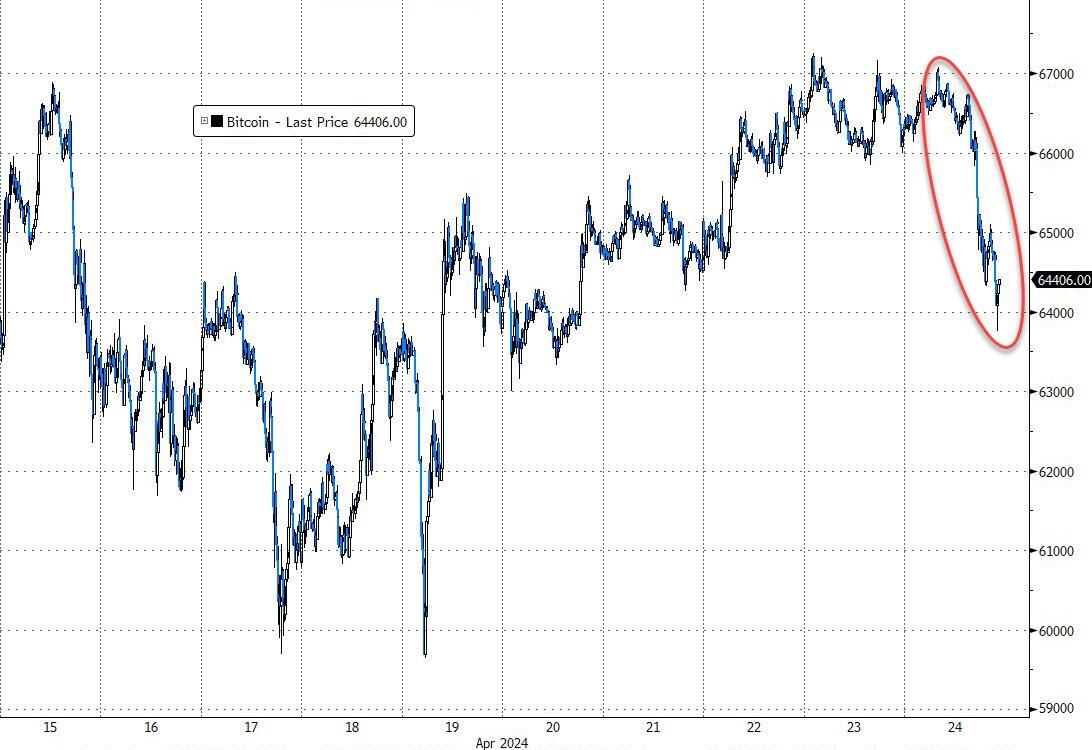

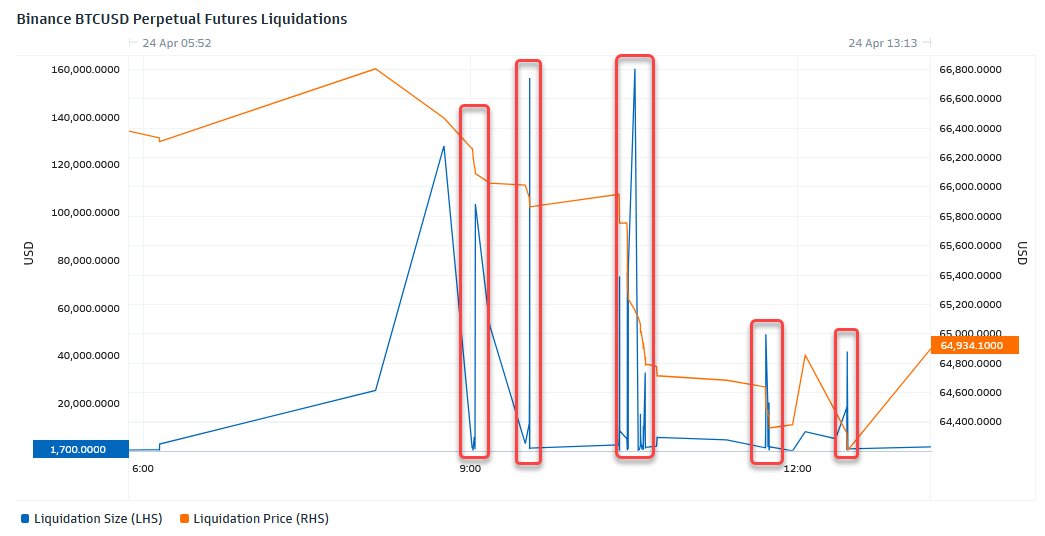

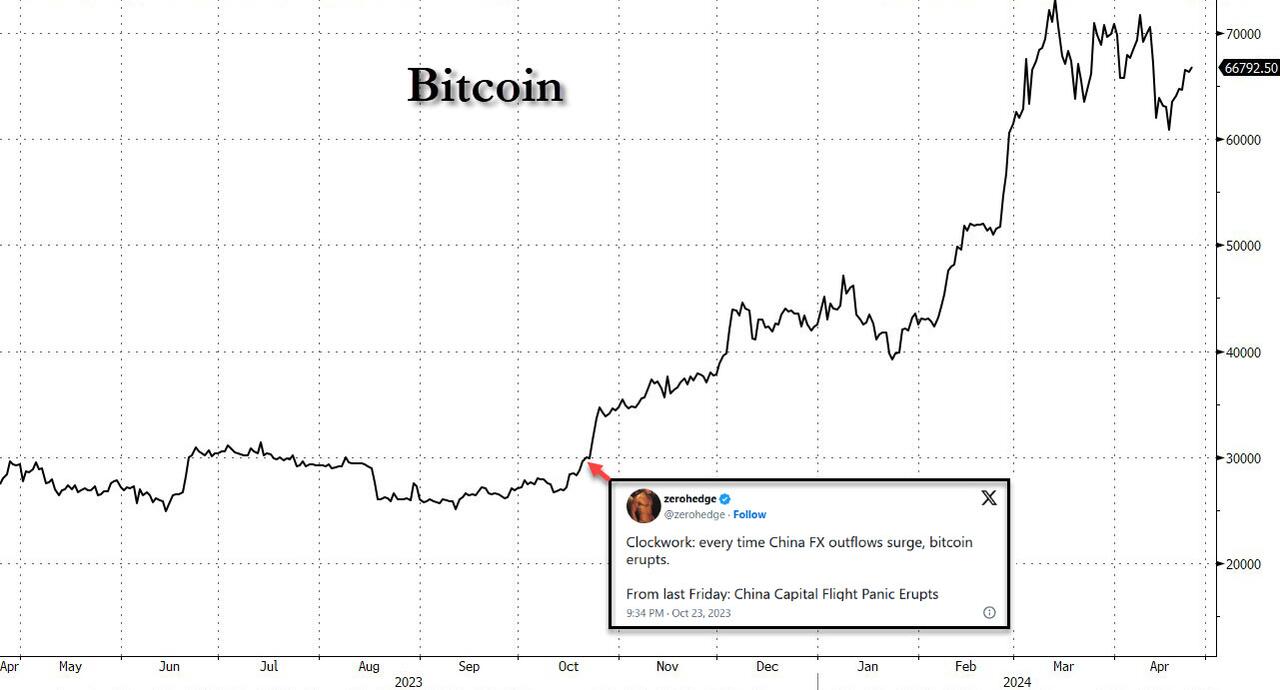

Bitcoin morning price:$66,390 DOWN 270 DOLLARS.

Bitcoin: afternoon price: $63,959 DOWN 3709 dollars

Platinum price closing DOWN $5.85TO $908,80

Palladium price; DOWN $19.55 AT $1006,05

END

SHANGHAI GOLD PREMIUM 38 DOLLARS/COMEX GOLD

SHANGHAI GOLD…

SHANGHAI GOLD (USD) FUTURES – QUOTES

Last Updated 24 Apr 2024 10:28:15 AM CT.

Market data is delayed by at least 10 minutes.

…from the CME….

“As of Monday, April 1, 2024, CME Group settlement data is no longer accessible through ftp.cmegroup.com and has a delayed publication time of 12:00 a.m. CT on all cmegroup.com web pages. Learn about alternate ways to access the data in our FAQ.”

Now I retrieve the data after 1 am

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $3171.69 DOWN 2.43CDN dollars per oz( * NEW ALL TIME HIGH 3,301.52 CDN DOLLARS PER OZ//APRIL 16 2024)

*BRITISH GOLD: 1857,18DOWN 8.10 pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2163.50 DOWN 713uros per oz //* (ALL TIME CLOSING HIGH: 2248.89 EUROS PER OZ//APRIL 16.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE: COMEX

XCHANGE: COMEX

CONTRACT: APRIL 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,327.700000000 USD

INTENT DATE: 04/23/2024 DELIVERY DATE: 04/25/2024

FIRM ORG FIRM NAME ISSUED STOPPED

132 C SG AMERICAS 14

435 H SCOTIA CAPITAL 7

657 C MORGAN STANLEY 5

737 C ADVANTAGE 2 1

905 C ADM 3

991 H CME 14

TOTAL: 23 23

JPMORGAN STOPPED (RECEIVED) 0/23 CONTRACTS

FOR APRIL/2024

GOLD: NUMBER OF NOTICES FILED FOR APRIL/2024. CONTRACT: 23 NOTICES FOR 2300 OZ or 0.0715 TONNES

total notices so far: 16,236contracts for 1,623600 Oz (50.500 tonnes)

FOR APRIL:

SILVER NOTICES: 8NOTICE(S) FILED FOR 40,000 OZ/

total number of notices filed so far this month : 1634 for 8,170,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $3.75

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD

/ /INVENTORY RESTS AT 833.63 TONNES

INVENTORY RESTS AT 833,63TONNES

SLV//

WITH NO SILVER AROUND AND SILVER UP $0.11 AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A MASSIVE DEPOSIT OF 11.904 MILLION OZ INTO THE SLV/

// INVENTORY INCREASES T0 428.280 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 428.280MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A MEGA HUMONGOUS SIZED 1606 CONTRACTS TO 175,740 AND STILL RAPIDLY CLOSING IN ON THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, DESPITE THE RAID AND THIS HUMONGOUS SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR SMALL GAIN OF $0,11 IN SILVER PRICING AT THE COMEX ON TUESDAY. WE HAD ZERO LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN PANICKING SHORT COVERING BY OUR SPECS WITH THE HUGE PRICE LOSS IN PRICE. WE HAD A HUGE SIZED 1417 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 1417 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUNUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.11, AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A GIGANTIC SIZED GAIN OF 2406 CONTRACTS ON OUR TWO EXCHANGES WITH THE GAIN IN PRICE OF $0.11

WE MUST HAVE HAD:

A HUGE SIZED 800 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 2.465 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S NIL OZ QUEUE JUMP //NEW STANDING REMAINS AT 8.225 MILLION OZ//

//NEW STANDING FOR SILVER IS THUS 8.225 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI GAIN/ HUGE SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1417 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED A STRONG 1121 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS FEB. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL

TOTAL CONTRACTS for 18 DAYS, total 27,612 contracts: OR 138,06 MILLION OZ (1534 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 138.06 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 138.06 MILLION OZ (THIS MONTH WILL PROBABLY BE A WHOPPER OF ISSUANCE OF EFPS)

RESULT: WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1606 CONTRACTS WITH OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUMONGOUS EFP ISSUANCE CONTRACTS: 800 ISSUED FOR MAY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR APRIL. OF 2.465 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAYS’ 0 OZ QUEUE JUMP

//NEW TOTAL STANDING REMAINS AT 8.225 MILLION OZ

WE HAVE A MEGA GIGANTIC SIZED GAIN OF 2406 OI CONTRACTS ON THE TWO EXCHANGES WITH THE GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 1417 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS

THE NEW TAS ISSUANCE TUESDAY NIGHT (875 WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 8 NOTICE(S) FILED TODAY FOR 40,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 1312 OI CONTRACTS TO 516,249 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 2022 CONTRACTS

WE HAD A FAIR SIZED INCREASE IN COMEX OI (1312 CONTRACTS) DESPITE OUR $4.60 LOSS IN PRICE//TUESSDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER TO WHACK GOLD’S PRICE. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR APRIL. AT 44.8615 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S TINY QUEUE JUMP OF 90OZ.(0.0279TONNES)

NEW STANDING 50.650 TONNES// ALL OF THIS HAPPENED WITH OUR $4.60 LOSS IN PRICE WITH RESPECT TO TUESDAY’S TRADING. WE HAD A STRONG SIZED GAIN OF 5469 OI CONTRACTS (23,30 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONGSIZED 4157 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 516,249

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5469 CONTRACTS WITH 1312 CONTRACTS INCREASED AT THE COMEX// AND A STRONG SIZED 4157 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 5469 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 1118 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4157 CONTRACTS) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI (1312 //TOTAL GAIN FOR OUR THE TWO EXCHANGES: 5469 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR APRIL. AT 44.8615 TONNES FOLLOWED BY TODAY’S TINY 0.0279TONNES QUEUE JUMP

//NEW STANDING 50.650TONNES.

/ 3) ZERO LONG LIQUIDATION DESPITE THE LOSS IN PRICE.

// 4) FAIR SIZED COMEX OPEN INTEREST LOSS/ 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: STRONG T.A.S. ISSUANCE: 4157 CONTRACTS/ HUGE SHORT COVERING BY OUR WRONG FOOTED SPECS WITH THE FED’S CONTINUAL RAID ON THE COMEX GOLD.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL. :

TOTAL EFP CONTRACTS ISSUED: 71,627 CONTRACTS OR 7,162,700 OZ OR 222.79TONNES IN 188TRADING DAY(S) AND THUS AVERAGING: 3968 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18TRADING DAY(S) IN TONNES 209.86TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 222.79 DIVIDED BY 3550 x 100% TONNES = 6.28% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 222.79 TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A MEGA-HUGE SIZED 1606 CONTRACTS OI TO 175,740 AND CLOSER TO THE COMEX HIGH RECORD //244,710(SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 800 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAY 800 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 800 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1312CONTRACTS AND ADD TO THE 800 E.FP. ISSUED

WE OBTAIN A MEGA HUMONGOUS SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2406 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 12.030 MILLION OZ

OCCURRED WITH OUR $0.11 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING/TUESDAY NIGHT

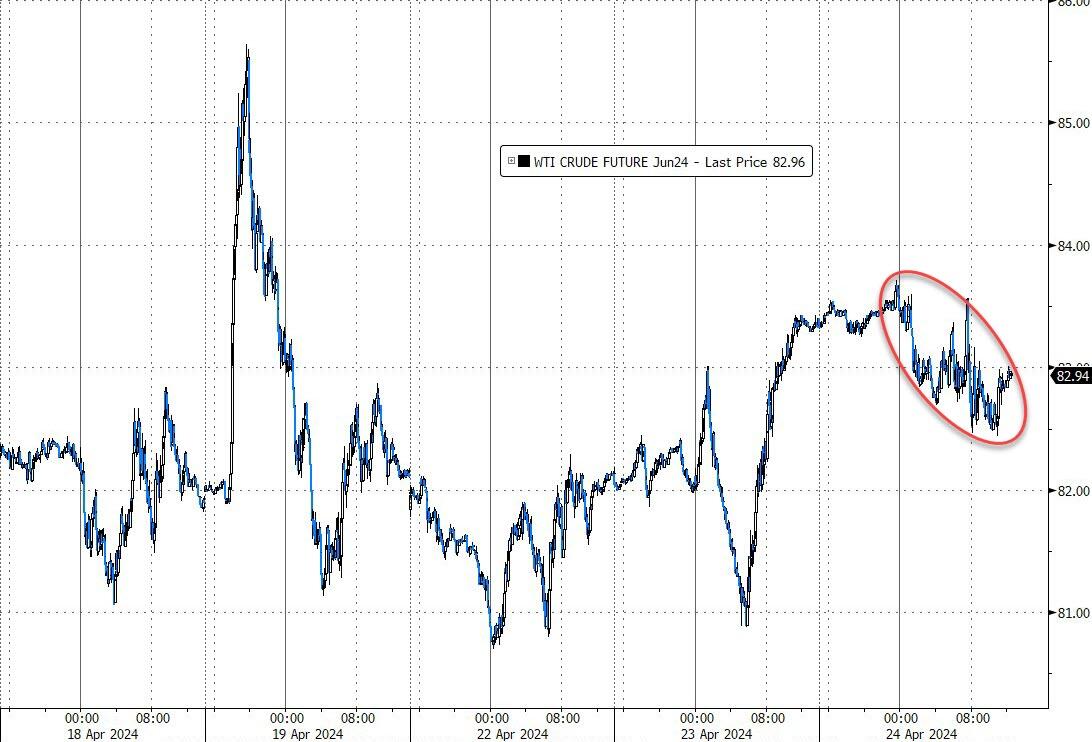

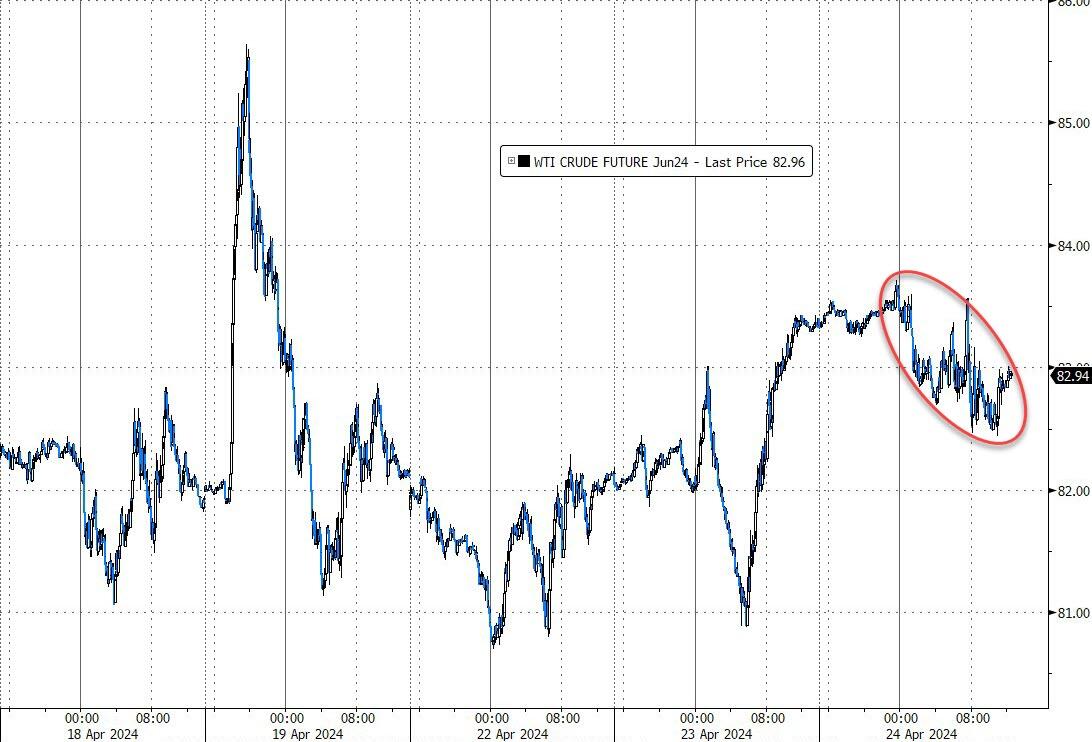

SHANGHAI CLOSED UP 22.84 PTS OR 0.76% //Hang Seng CLOSED UP 372.34PTS OR 2.21% / Nikkei CLOSED UP 907.92 PTS OR 2.42% //Australia’s all ordinaries CLOSED DOWN 0.43%///Chinese yuan (ONSHORE) closed DOWN 7.2460//OFFSHORE CHINESE YUAN CLOSED DOWN TO 7.2678/Oil UP TO 82.72dollars per barrel for WTI and BRENT UP AT 87.92 Stocks in Europe OPENED ALL MOSTLY GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 1312CONTRACTS TO 516,249 DESPITE OUR LOSS IN PRICE OF $4.60 WITH RESPECT TO TUESDAY TRADING. WE HAD CONSIDERABLE A.S. LIQUIDATION AS WELL AS SHORTS, DESPERATELY TRYING TO GET OUT OF THEIR NAKED SHORTS.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF APRIL..… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG 4157 EFP CONTRACTS WERE ISSUED: : JUNE 4157 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4157 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 7491 CONTRACTS IN THAT 4157 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A FAIR SIZED GAIN OF 1312 COMEX CONTRACTS..AND THIS STRONG GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $4.60 TUESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A STRONG SIZED 4157 CONTRACTS. WE HAD 0 EX FOR RISK ISSUANCE. MOST OF THE TRADING AND SUPPLY OF CONTRACTS ON TUESDAY WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: APRIL (50.650 TONNES) ( ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY: 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 50.650TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL $4.60 //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG SIZED GAIN OF 7491 TOTAL CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR LOSS IN PRICE 0F $4.60

WE HAD A STRONGT.A.S. LIQUIDATION ON THE FRONT END OF TUESDAY’S TRADING ALONG. THE T.A.S. ISSUED ON TUESDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 23.31 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR APRIL. (44.8615 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S SMALL QUEUE.JUMP OF 900 OZ (0.003TONNES)//NEW STANDING; 50.650TONNES

NEW STANDING: 50.650ONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $4.60

WE HAD REMOVED 2022 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET GAIN ON THE TWO EXCHANGES 5469 CONTRACTS OR 546,900 OZ (17.01TONNES)

confirmed volume TUESDAY 286,813 contracts//STRONG

//speculators have left the gold arena

APRIL 24/ INITIAL APRIL GOLD

/ /// THE APRIL 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | oz NIL . |

| Deposit to the Dealer Inventory in oz | nil oz |

| Deposits to the Customer Inventory, in oz | 4.999.770 oz HSBC |

| No of oz served (contracts) today | 23 notice(s) 2300 OZ 0.0715TONNES |

| No of oz to be served (notices) | 53 contracts 5300 OZ 0.1648ONNES |

| Total monthly oz gold served (contracts) so far this month | 16,236notices 1,623,600 oz 50.500 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: nil oz

total customer withdrawals: 0

DEPOSITS:

i) Into HSBC: 4999.770 oz

we had total deposit of 4999.770 oz

Adjustments: 1

adjustment: 9645.300 oz customer to dealer jpmorgan 300 kilobars

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL.

For the front month of APRIL we have an oi of 76 contracts having LOST 24 contracts. We had 33 contracts served on TUESDAY, so we GAINED 9 contracts or an additional 900 oz (0.02799 tonnes) will stand at the comex

MAY LOST 26 CONTRACTS TO STAND AT 2133

JUNE INREASED ITS OI BY 8 CONTRACTS UP TO 408,979 CONTRACTS.

We had 33 contracts filed for today representing 3300 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 23 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the APRIL. /2024. contract month, we take the total number of notices filed so far for the month (16,236 x 100 oz ), to which we add the difference between the open interest for the front month of APRIL. (76 CONTRACTS) minus the number of notices served upon today (23x 100 oz per contract( equals 1,628,1000 OZ OR 50.637 TONNES.

thus the INITIAL standings for gold for the APRIL. contract month: No of notices filed so far (16,234) x 100 oz + (76 {OI for the front month} minus the number of notices served upon today (23 x 100 oz which equals 1,628400 oz (50.650TONNES)

TOTAL COMEX GOLD STANDING FOR APRIL: 50.650 TONNES WHICH IS HUGE FOR THIS ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,609,457.923 50.060tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,596,433.593 OZ

TOTAL REGISTERED GOLD 7,530,700.966(234.236 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,659,721.627OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 5,921,243 oz (REG GOLD- PLEDGED GOLD) 184.175 tonnes/dropping like a stone

END

SILVER/COMEX

APRIL 24

INITIAL

//2024// THE APRIL 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 00oz . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1198,906.120 Brinks HSBC |

| No of oz served today (contracts) | 8 CONTRACT(S) (40,000 OZ) |

| No of oz to be served (notices) | 11 contracts (55,000 oz) |

| Total monthly oz silver served (contracts) | 1634 Contracts (8,170,000oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit :nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 deposits customer account:

i) Into Brinks 598,923.390 oz

ii) Into HSBC 598,982.780 oz

total customer deposits 1,198,906.120oz

JPMorgan has a total silver weight: 130.170 million oz/293.974million or 44.52%

adjustment: 0

Comex withdrawals: 0

i

total withdrawal nil oz

TOTAL REGISTERED SILVER: 47.196MILLION OZ//.TOTAL REG + ELIGIBLE. 293.974million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF APRIL /2023 OI: 11 CONTRACTS HAVING LOST 0 CONTRACT(S).

WE HAD 0CONTRACTSSERVED ON TUESDAY, SO WE GAINED 0 CONTRACTS OR ADDITIONAL NIL OZ WILL STAND AT THE COMEX

.

MAY SAW A LOSS OF 7952 CONTRACTS DOWNTO 44,523

JUNE SAW A GAIN OF 10 CONTRACTS RISING TO 698

JULY SAW A GAIN OF 9135 CONTRACTS UP TO 106,759

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 8 for 40,000 oz

CONFIRMED volume; ON MONDAY 153,364 /HUGE

To calculate the number of silver ounces that will stand for delivery in APRIL. we take the total number of notices filed for the month so far at 1634x 5,000 oz = 8,170,000 oz

to which we add the difference between the open interest for the front month of APRIL (11 and the number of notices served upon today 8x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the APRIL/2024 contract month: 1634(notices served so far) x 5000 oz + OI for the front month of APRIL. (11)number of notices served upon today (8)x 500 oz of silver standing for the APRIL contract month equates to 8.225 MILLION OZ.

New total standing: 8.225 million oz.

There are 47.196 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

APRIL 234WITH GOLD DOWN $4.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD / A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLDINVENTORY RISES AT 833,63 TONNES

APRIL 19 WITH GOLD UP $15.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 4.32 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 831.91 TONNES

APRIL 18 WITH GOLD UP $11.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE WITHDRAWAL OF 2.59 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 827.59 TONNES

APRIL 17 WITH GOLD DOWN $17.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 830;18 TONNES

APRIL 16 WITH GOLD UP $23.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 828.45 TONNES

APRIL 15 WITH GOLD UP $9.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE WITHDRAWAL OF 4.03 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 826.72 TONNES

APRIL 12 WITH GOLD UP $2.80 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD/ INVENTORY RISESS AT 830.75 TONN

APRIL 10 WITH GOLD DOWN $14.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 828.71 TONNES

APRIL 9 WITH GOLD UP $11.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 827,85 TONNES

APRIL 8 WITH GOLD UP $7.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A WITHDRAWAL OF 6.02 TONNES OF GOLD INTO THE GLD/ INVENTORY REMAINS AT 826.41 TONNES

APRIL 5 WITH GOLD UP $38.65 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/ INVENTORY REMAINS AT 832.45 TONNES

APRIL 4 WITH GOLD DOWN $3.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD/ INVENTORY REMAINS AT 830.73 TONNES

APRIL 3 WITH GOLD UP $33,85 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD // INVENTORY REMAINS AT 829.00 TONNES

APRIL 2 WITH GOLD UP $23.90 TODAY; HUG CHANGES IN GOLD INVENTORY AT THE GLD A WITH DRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD.:// INVENTORY REMAINS AT 829.00 TONNES

APRIL 1 WITH GOLD UP $18.70 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:// INVENTORY REMAINS AT 830.15 TONNES

MARCH 28 WITH GOLD UP $26.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:// INVENTORY REMAINS AT 830.15 TONNES

MARCH 27 WITH GOLD UP $15.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// INVENTORY FALLS TO 830.15 TONNES

MARCH 26 WITH GOLD UP $1.40 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 835.33 TONNES

MARCH 25 WITH GOLD UP $17.05 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 838.50 TONNES

MARCH 22 WITH GOLD DOWN $23.75 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 838.50 TONNES

GLD INVENTORY: 833,63 TONNES,

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 24/WITH SILVER DOWN $.05 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 11.904MILLION OF SILVER INTO THE SLV// :SLV INVENTORY RESTS AT 428.280 MILLION OZ

APRIL 23/WITH SILVER UP $0.11TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV / :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 22/WITH SILVER DOWN $1.51 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.194 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 19/WITH SILVER UP 42 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.657 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 418.570 MILLION OZ

APRIL 18/WITH SILVER DOWN $.04TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.977 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 422.227 MILLION OZ

APRIL 17/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF .868 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 426/204 MILLION OZ

APRIL 16/WITH SILVER DOWN $0.46 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF NON EXISTENT SILVER// :SLV INVENTORY RESTS AT 427.072 MILLION OZ

APRIL 15/WITH SILVER UP $0.46 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 12/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 4.069 MILLION OZ FROM THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 11/WITH SILVER UP $0.23 TODAY: STRANGE INDEED! HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.931 MILLION OZ :SLV INVENTORY RESTS AT 437.998 MILLION OZ

APRIL 10/WITH SILVER UP $0.04 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:SLV INVENTORY RESTS AT 441.929 MILLION OZ

APRIL 9/WITH SILVER UP $0.15 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.549 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 441.929 MILLION OZ

APRIL 8/WITH SILVER UP $0.33 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.320 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 441.328 MILLION OZ

APRIL 5/WITH SILVER UP $0.61 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.748 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 441.060 MILLION OZ

APRIL 4/WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.671 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 437.312 MILLION OZ

APRIL 3/WITH SILVER UP $1.14 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.835 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 433.641 MILLION OZ

APRIL 2/WITH SILVER UP 84 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6.721 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 430.806 MILLION OZ

APRIL 1/WITH SILVER UP 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// SLV INVENTORY RESTS AT 424.085 MILLION OZ

MARCH 28/WITH SILVER UP 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.005 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 424.085 MILLION OZ

MARCH 27/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A A DEPOSIT OF 1.691 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 423.079 MILLION OZ

MARCH 26/WITH SILVER DOWN 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A A DEPOSIT OF 0.366 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 421.388 MILLION OZ

MARCH 25/WITH SILVER UP 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 3.887 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 421.022 MILLION OZ

MARCH 22/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE DEPOSIT OF 1.1899 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 424.909 MILLION OZ

CLOSING INVENTORY 416.376MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

PETER SCHIFF/SCHIFFGOLD/MIKE MAHARRAY

END

2.Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens/…

END

3. CHRIS POWELL//GATA DISPATCHES

CPM Group’s Jeff Christian battles straw men to distract from the big issues of gold

Submitted by admin on Tue, 2024-04-23 22:04 Section: Daily Dispatches

10:22p ET Tuesday, April 23, 2024

Dear Friend of GATA and Gold:

Jeffrey Christian, managing director of metals consultancy CPM Group, today spent 16 minutes on YouTube raising and knocking down some straw men to give his viewers the misleading impression that there is nothing to be doubted about the U.S. government’s involvement with the gold market.

Christian challenged long-made but usually anonymous assertions that the U.S. gold reserve at Fort Knox, Kentucky, is gone or missing in large part. He notes that there are official audits asserting that all the gold is where it should be. Those who cast doubt on the integrity of the audits, Christian says, are “scum.”

But contrary to Christian’s suggestion, the big question about U.S. gold reserve is not the narrow one of whether there’s still metal at Fort Knox but whether the U.S. government has foreign gold obligations and whether these obligations are so large that U.S. gold reserves at Fort Knox and elsewhere are potentially impaired by multiple claims of ownership.

In this respect the curiosity of a more candid and honest analyst might be piqued by the recent refusal of the Federal Reserve to answer even for a member of Congress whether foreign nations have been repatriating their gold that nominally has been vaulted at the Federal Reserve Bank of New York:

The amount of foreign gold vaulted at the New York Fed used to be reported publicly by the Fed at various intervals. Why is it apparently a top secret matter now? Christian doesn’t seem to mind.

A more candid and honest analyst also might wonder aloud why the U.S. Commodity Futures Trading Commission repeatedly has refused to answer, even for a member of Congress, whether the commission has jurisdiction over manipulative trading in gold and other commodities undertaken by or at the behest of the U.S. government, or whether surreptitious futures market manipulation is considered legal when the government arranges it:

https://www.gata.org/node/23054

A more candid and honest analyst also might inquire publicly about the uses of the Central Bank Incentive Program run by the Chicago Mercantile Exchange, operator of all the major futures markets in the United States:

The program extends volume trading discounts to governments and central banks for their surreptitious trading in all CME futures contracts. A more candid and honest analyst might wonder whether the program would exist if it is never used. He also might wonder exactly how it is being used.

A more candid and honest analyst might be openly suspicious of the gold swaps long reported on a monthly basis by the Bank for International Settlements, transactions that confirm surreptitious intervention in the gold market by central banks, the operators of the BIS:

https://www.gata.org/node/23064

These transactions might strike a more candid and honest analyst as suspicious insofar as the BIS refuses to explain them — their objectives and participants.

A more candid and honest analyst might pursue the proclaimation by a top BIS official, speaking to an assembly of dozens of central bank representatives and academics in 2005, that a primary purpose of central bank cooperation is “to influence asset prices — especially gold and foreign exchange — in circumstances where this might be thought useful”:

https://www.gata.org/node/4279

A more candid and honest analyst might ask: What are those circumstances? Do they endure? Or are the gold and currency markets now all calm, sweetness, and light, as Christian seems to want people to think?

Christian implies that all doubts about U.S. government involvement in the gold market are resolved by the Fort Knox audits he cites. But true or false, the audits say nothing about the big issues of government intervention in gold. For Christian the audits are just convenient instruments of distraction with which he may ingratiate himself with CPM Group’s central bank clients.

Christian’s battle with the straw men can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Silver Bullion TV reviews the success of the Sound Money Defense League

Submitted by admin on Tue, 2024-04-23 22:43 Section: Daily Dispatches

10:42p ET Tuesday, April 23, 2024

Dear Friend of GATA and Gold:

Interviewed this week by Patrick Vierra of Silver Bullion TV in Singapore, Money Metals Exchange CEO Stefan Gleason explains the work of the Sound Money Defense League in the United States. The league lately has assisted passage of legislation in 45 of the 50 states to exempt monetary metals coin and bullion from sales taxes.

The league also has been encouraging states to hold some of their cash reserves in monetary metal to hedge their exposure to the U.S. dollar.

The interview is 40 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS

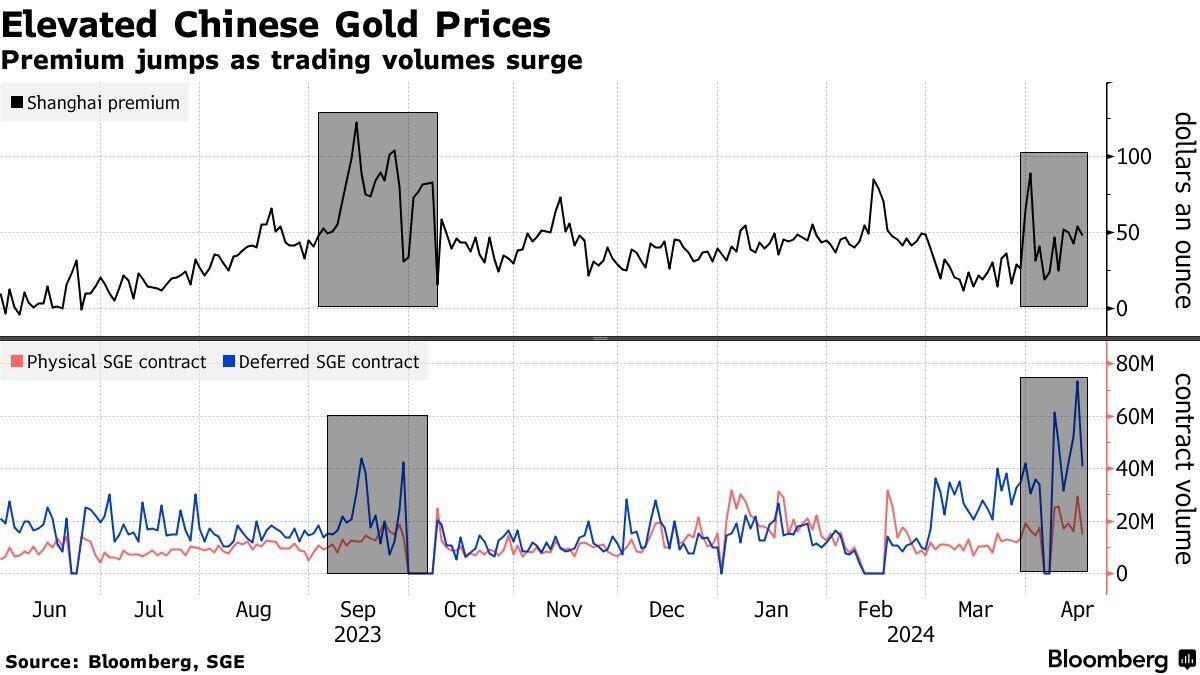

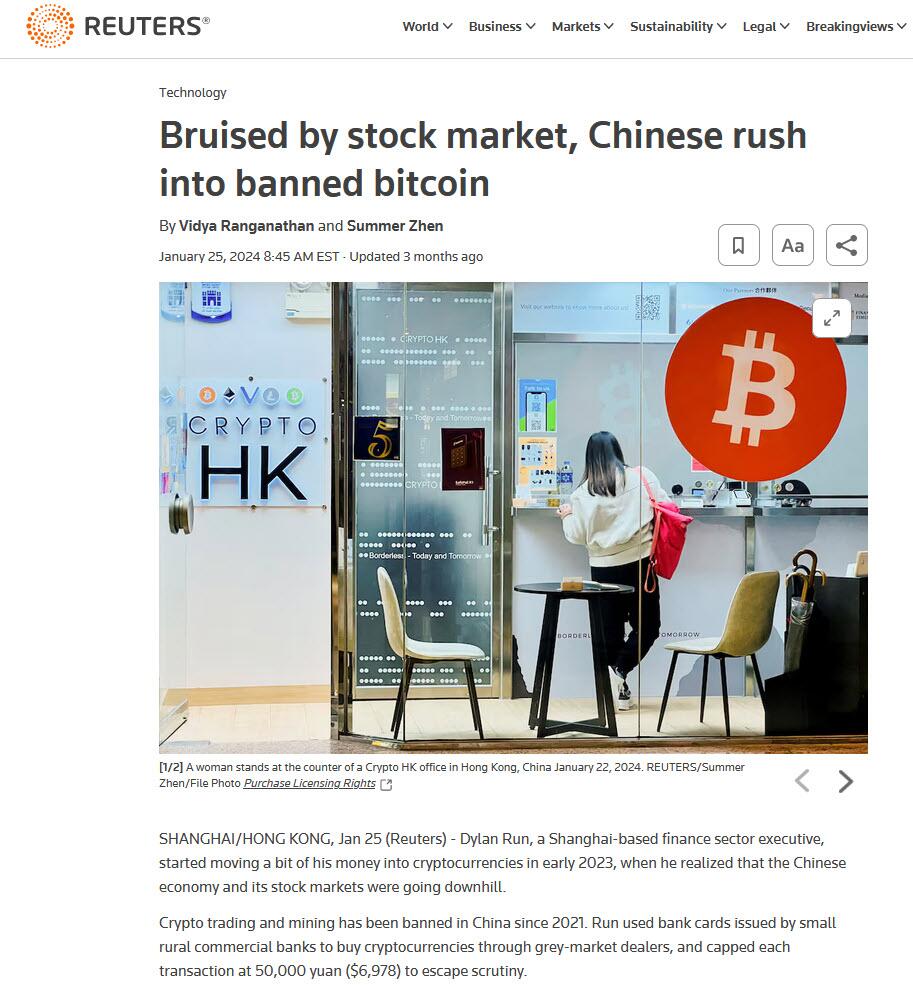

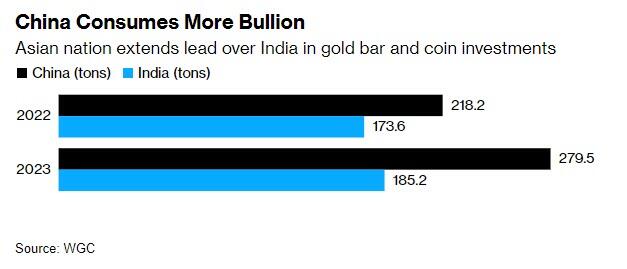

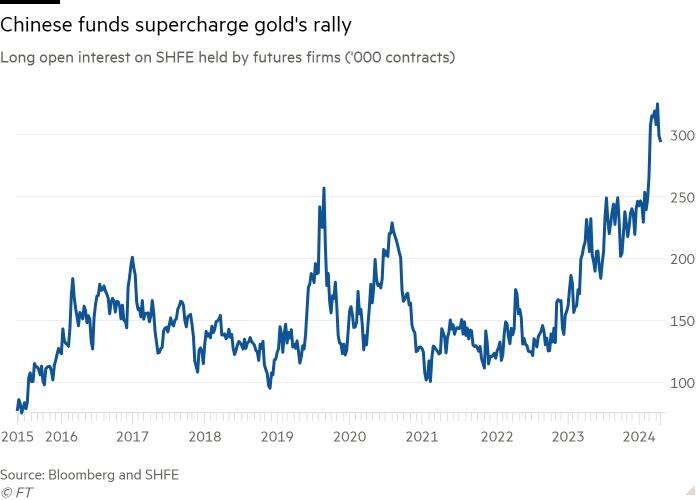

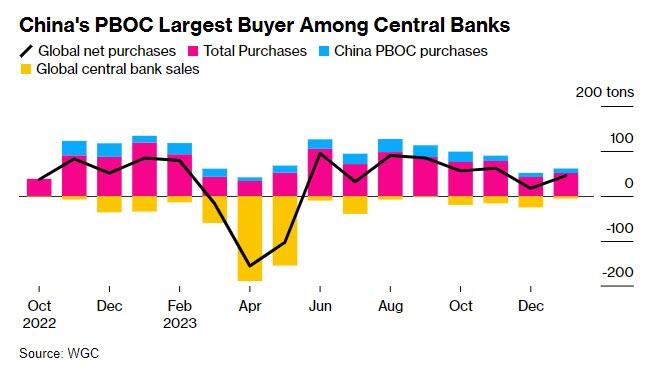

China is grabbing gold hand over first!

(zerohedge)

Chinese Have “Grabbed Gold By The Throat” As Capital Flight Accelerates

WEDNESDAY, APR 24, 2024 – 11:05 AM

“Chinese speculators have really grabbed gold by the throat…”

That is how John Reade, chief market strategist at the World Gold Council, describes the scramble in the communist nation among investors looking to move money anywhere but in the yuan or Chinese assets.

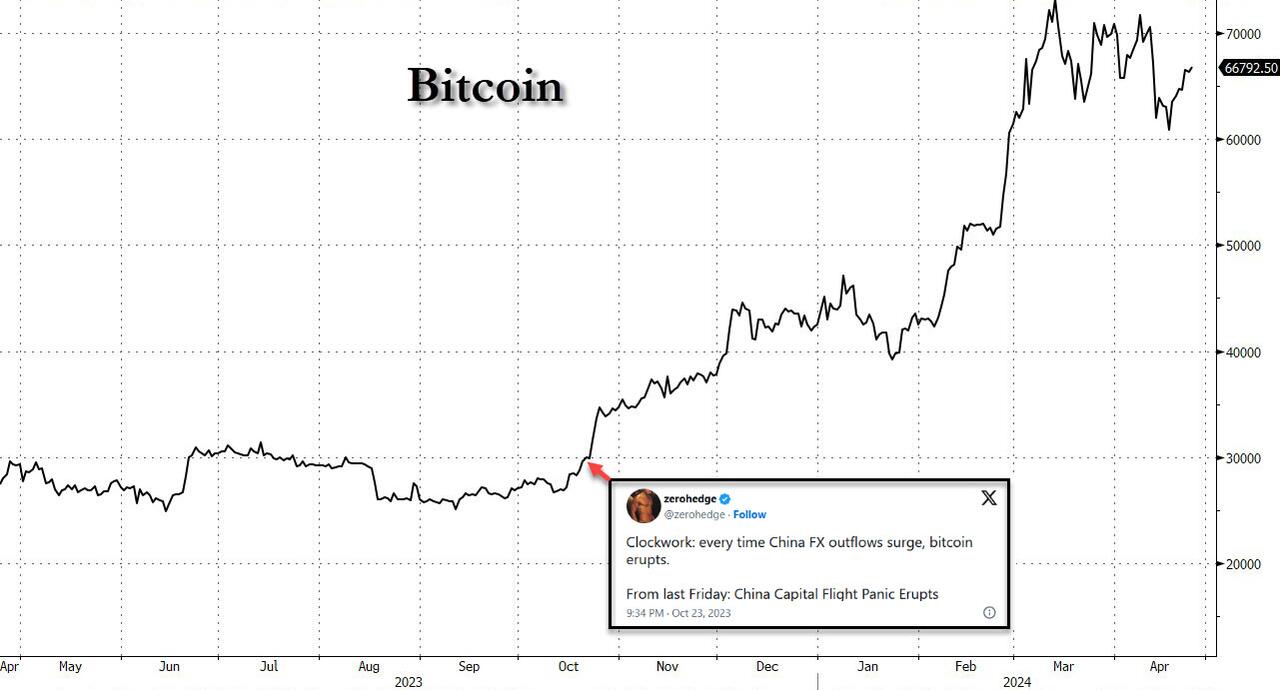

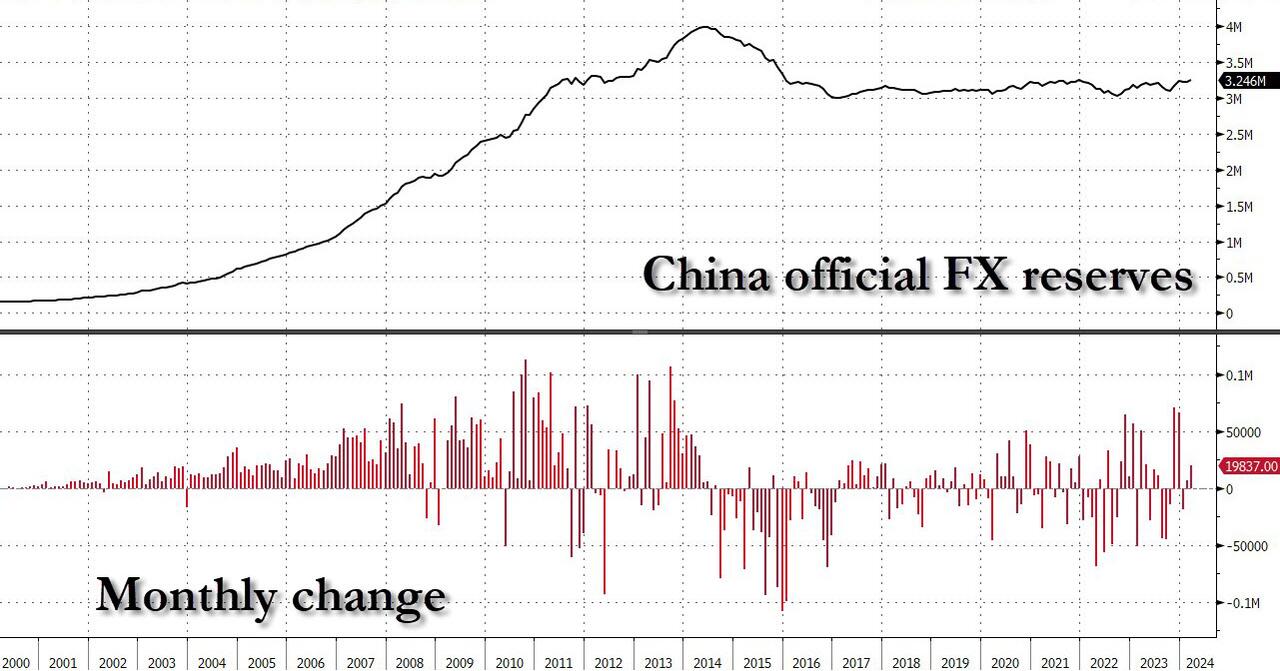

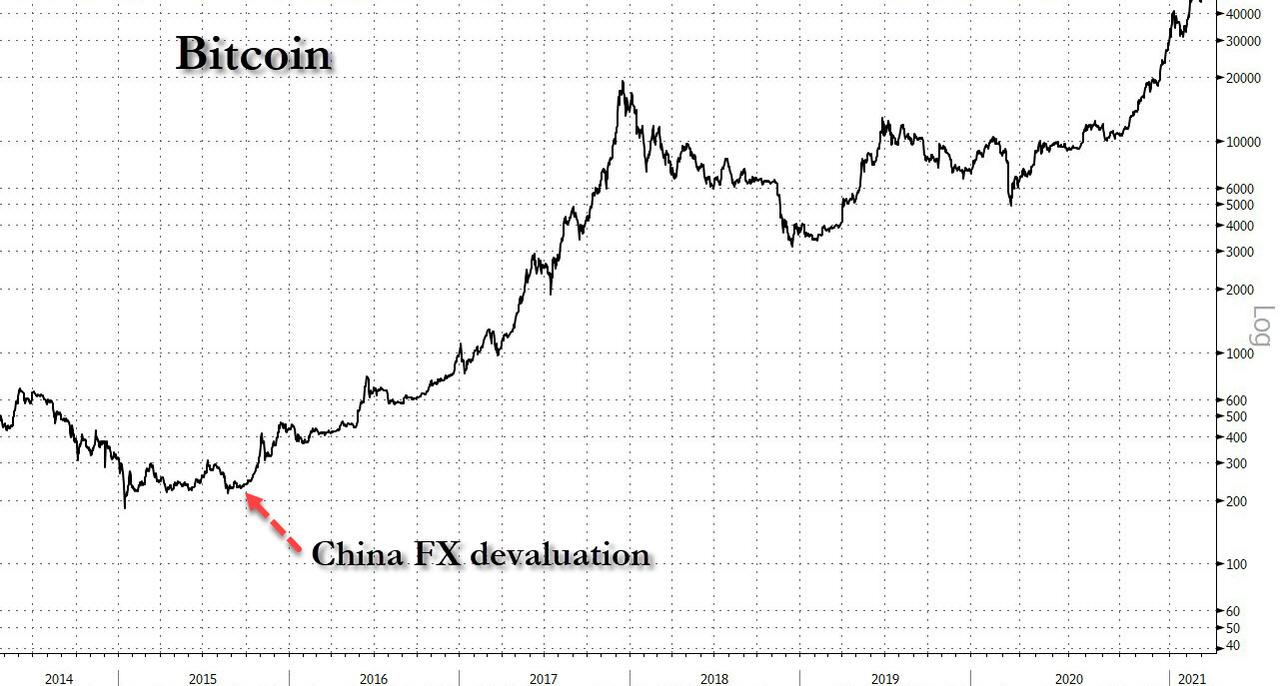

As evidenced by soaring Chinese FX outflows, the recent surges in ‘alternate currencies’ such as bitcoin and gold strongly suggest where the Chinese are seeking safety.

Of course, worsening geopolitical tensions, unprecedented fiscal profligacy by the Biden administration that shows no signs of slowing, and a Fed that seemed willing to support that spending with rate-cuts that were wholly un-necessary based on the ‘data’ they are so ‘dependent’ on (prompting fears of a policy error) are all factors driving precious metals higher, but, as Bloomberg reports, juicing the rally is unrelenting Chinese demand, as retail shoppers, fund investors, futures traders and even the central bank look to bullion as a store of value in uncertain times.

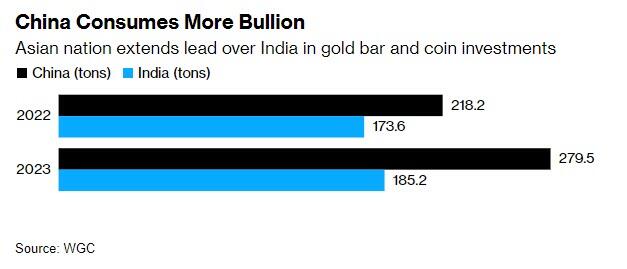

China and India have typically vied over the title of world’s biggest buyer. But that shifted last year as Chinese consumption of jewelry, bars and coins swelled to record levels. China’s gold jewelry demand rose 10% while India’s fell 6%. Chinese bar and coin investments, meanwhile, surged 28%.

And there’s still room for demand to grow, said Philip Klapwijk, managing director of Hong Kong-based consultant Precious Metals Insights Ltd. Amid limited investment options in China, the protracted crisis in its property sector, volatile stock markets and a weakening yuan are all driving money to assets that are perceived to be safer.

“The weight of money available under these circumstances for an asset like gold – and actually for new buyers to come in – is pretty considerable,” he said.

“There isn’t much alternative in China. With exchange controls and capital controls, you can’t just look at other markets to put your money into.”

But, there is another side to the Chinese demand for gold – speculators.

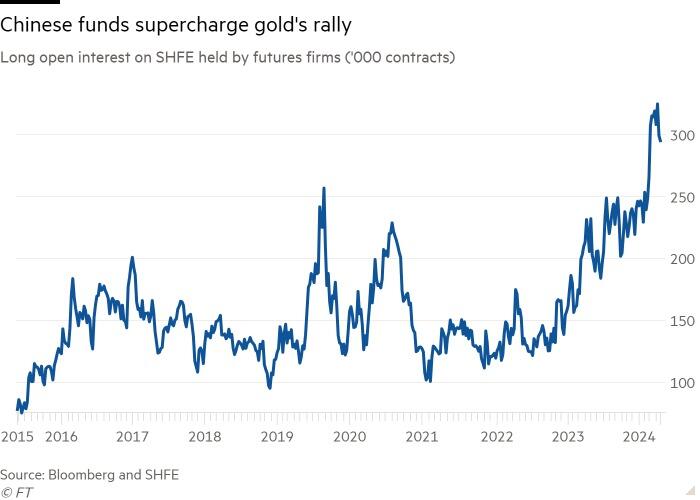

Long gold positions held by futures traders on the Shanghai Futures Exchange (SHFE) climbed to 295,233 contracts, equivalent to 295 tonnes of gold.

That marks a rise of almost 50 per cent since late September before geopolitical tensions flared up in the Middle East.

A record bullish position of 324,857 contracts was hit earlier this month, according to Bloomberg data going back to 2015.

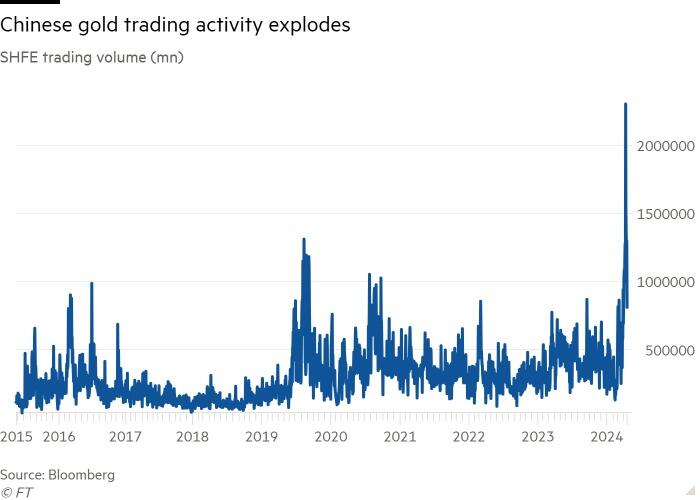

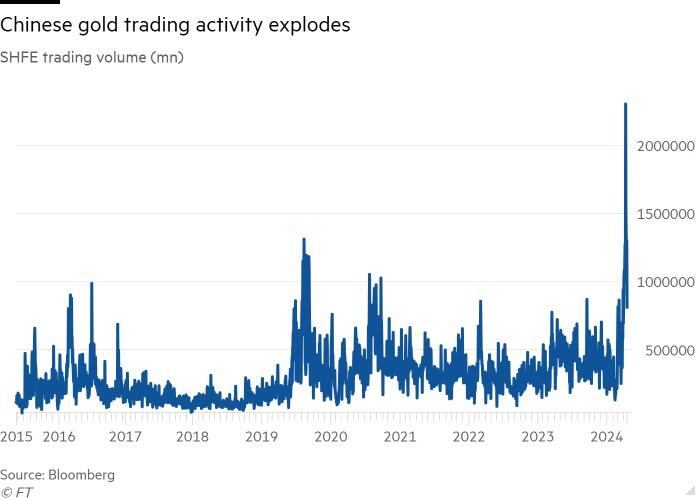

While the scale of gold’s rally has surprised many analysts, The FT points out that some point to activity on SHFE and the Shanghai Gold Exchange – where trading volumes on a key contract have doubled in March and April relative to last year – as a big driver of the rally, as Chinese investors aim to diversify from their crisis-ridden property sector and sagging stock market…

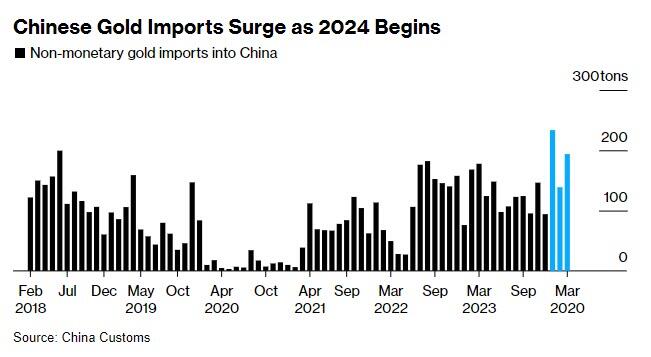

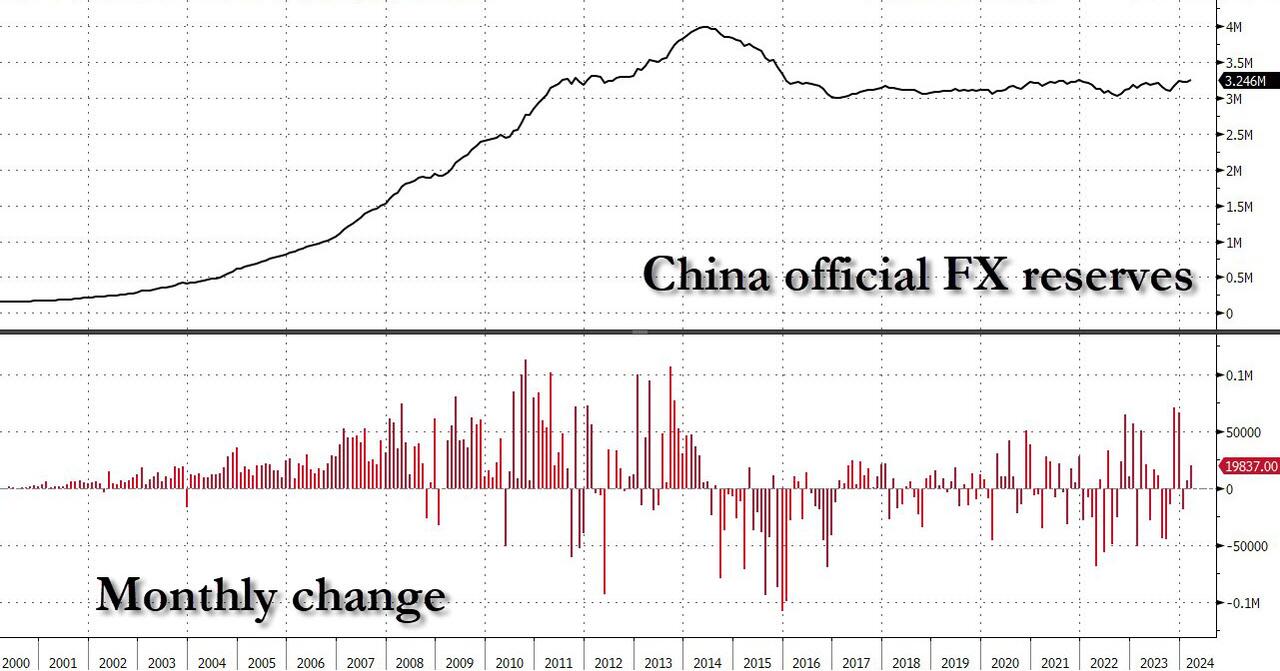

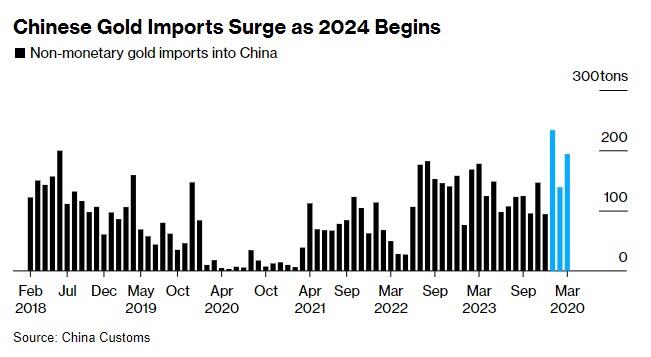

Additionally, Bloomberg reports that although China mines more gold than any other country, it still needs to import a lot and the quantities are getting larger.

In the last two years, overseas purchases totaled over 2,800 tons — more than all of the metal that backs exchange-traded funds around the world, or about a third of the stockpiles held by the US Federal Reserve.

Even so, the pace of shipments has accelerated lately. Imports surged in the run-up to China’s Lunar New Year, a peak season for gifts, and over the first three months of the year are 34% higher than they were in 2023.

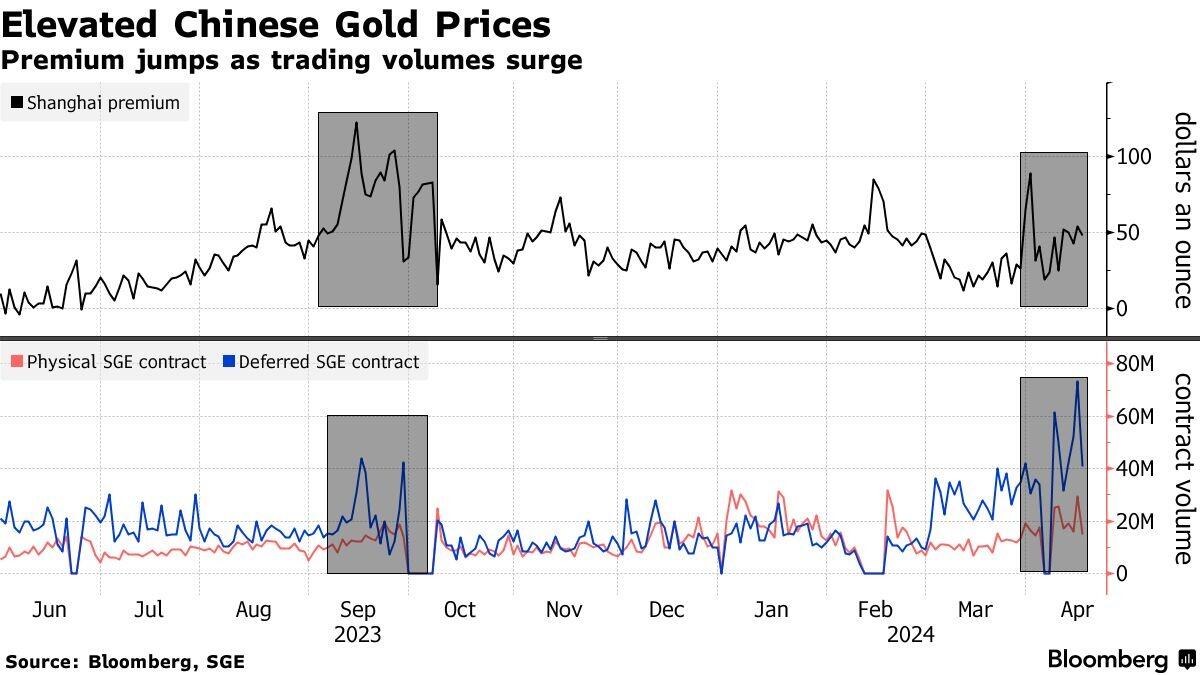

And finally, as evidence of Chinese demand (or the scale of the capital flight), the premium being paid for the precious metal over western prices is soaring…

Of course, China’s authorities, which can be quite hostile to market speculation and extremely hostile to capital flight, have warned, via their state media mouthpieces, that investors should be cautious in chasing the rally in gold.

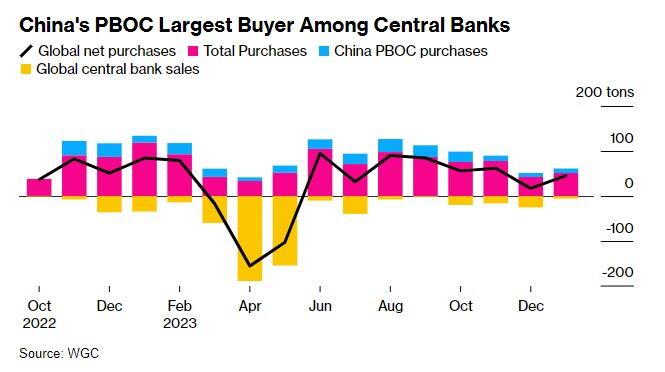

But, this is made all the more ironic given the fact that it is the Chinese central bank that is among the most prolific buyer of bullion in recent months…

Do as we say, not as we do… or maybe investors should ask ‘what does Beijing know?’

https://kinesis.money/live-from-the-vault

end

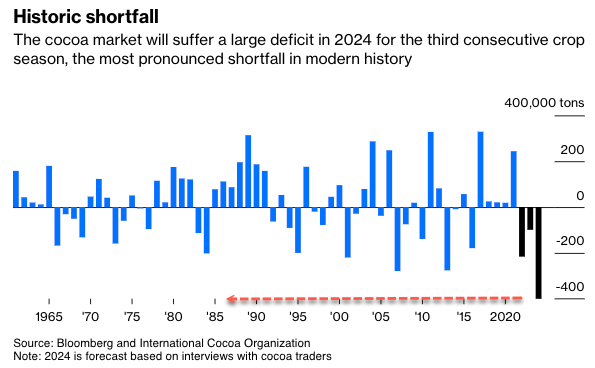

5 a. IMPORTANT COMMENTARIES ON COMMODITIES/COCOA

Cocoa Drops Most Since April 2009, Some Losses Recovered In Muti-Day Volatility Rollercoaster

Cocoa futures in London on Tuesday plunged the most since April 2009, tumbling as much as 8.1%, while prices slid as much as 7.7% in New York. Prices recovered some losses on Wednesday morning. It appears the downdraft was caused by fast-money traders taking profits after a record high of $12,250 per ton was recorded in New York on Friday.

Cocoa prices faded record highs as “opportunistic fast traders” exit positions to take profits after bearish signals flashed in recent sessions, Tristan Fletcher, chief executive officer at ChAI, a platform that uses AI to analyze commodity markets, told Bloomberg.

Last week’s catalyst for record-high prices came after data about grindings—where cocoa transforms into butter and powder used in candy—showed that demand destruction has not materialized despite soaring prices.

Here’s the cocoa grindings data from last week that served as fuel for bulls (via Barchart):

Cocoa also has support on signs that global cocoa demand remains resilient despite record-high prices. Last Thursday, the National Confectioners Association reported that North American Q1 cocoa grindings rose +9.3% q/q and +3.7 % y/y to 113,683 MT. Also, last Thursday, the Cocoa Association of Asia reported that Q1 Asia cocoa grindings rose +5.1% q/q, although they fell -0.2% y/y to 221,530 MT. In addition, the European Cocoa Association reported that Q1 European cocoa grindings rose +4.7% q/q, although they fell -2.2% y/y to 367,287 MT.

Paul Joules, an analyst at Rabobank, wrote in a note that grindings figures are “an indication that for now demand is holding up despite current pricing,” adding that “demand destruction will come, but clearly it’s taking longer to filter into grind data than the market was anticipating.”

Famed commodity trader Pierre Andurand told Bloomberg via an emailed interview, “We will finish the year with the lowest stocks-to-grinding ratio ever, and potentially run out of inventories late in the year.” He added that cocoa prices “could break $20,000 later this year” based on the thesis of worsening drought and disease ravaging the world’s largest cocoa farms in West Africa.

Paul Torres, a London-based trading and agricultural consultant, said, “I do not foresee prices falling significantly,” adding that prices could range between $8,000 to $10,000.

Torres noted: “There could be just some easing of the frenetic moves we’ve seen.”

Meanwhile, analysts from JPMorgan recently told clients that cocoa prices in New York could come down to around $6,000 a ton in the medium term, while Citi analysts said a bear market could begin in early 2025.

There is some good news for cocoa supply: Bloomberg quoted Marijn Moesbergen, sourcing lead at Cargill, at the World Cocoa Conference in Brussels on Wednesday as saying cocoa production is expected to bounce back next year as the El Nino effect won’t be in play.

“The current prices are maybe a bit overshooting. The question indeed is what will be the new equilibrium between this supply issues versus what will be the demand impact going forward,” adding, “That question will be answered in the coming period.”

The combination of a worsening global supply deficit plus bullish grindings data might only suggest prices have to head higher.

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN 7.2460

OFFSHORE YUAN: UP TO 7.2678

SHANGHAI CLOSED UP 22.84PTS OR 0.76%

HANG SENG CLOSED UP 372.34 PTS OR 2.21%

2. Nikkei closed UP 907.92 OR 2.21%

3. Europe stocks SO FAR: ALL MOSTLY GREEN

USA dollar INDEX UP TO 105.71 EURO RFALL TO 1.0686 D0WN16 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.887Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 154.93 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN:DOWN/ OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UPTO +2.5590*/Italian 10 Yr bond yield UP to 3.886SPAIN 10 YR BOND YIELD UP TO 3.333

3i Greek 10 year bond yield UP TO 3.484

3j Gold at $2315.60silver at: 27.12 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 67 /100 roubles/dollar; ROUBLE AT 92.46/

3m oil into the 82dollar handle for WTI and 86 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 154.93/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.887% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9145as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9774well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

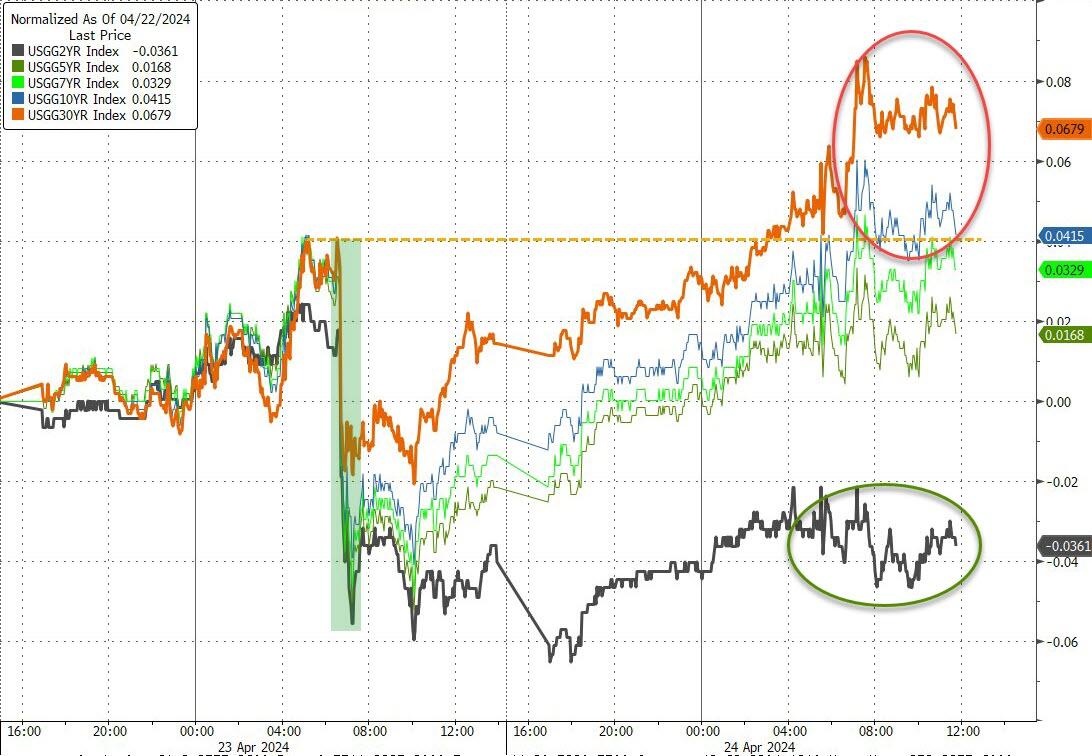

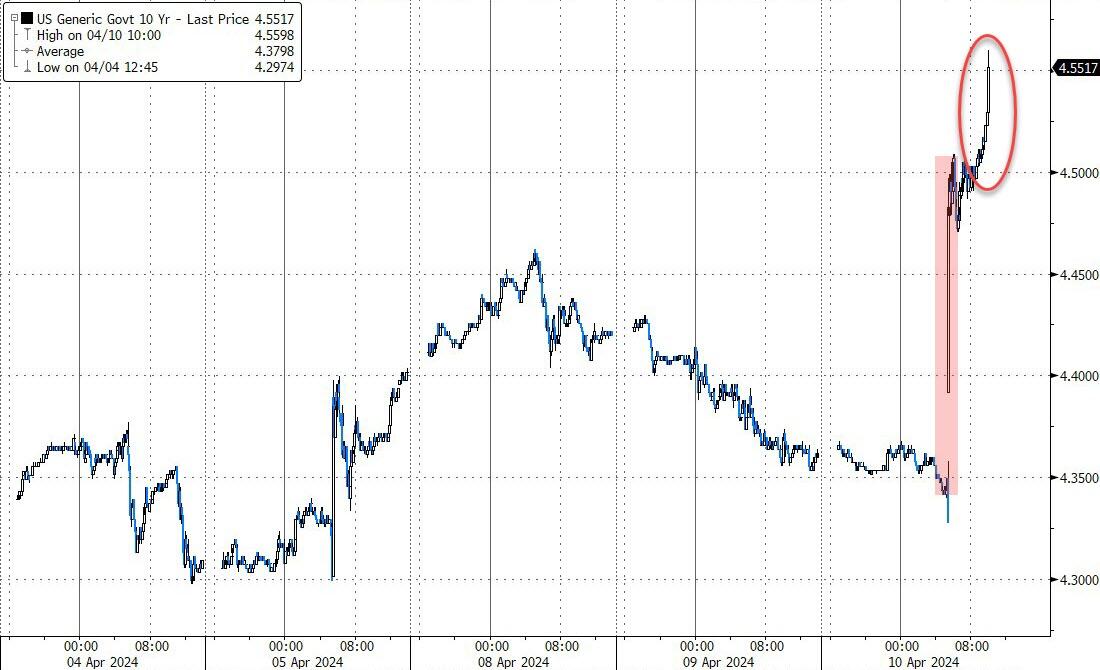

USA 10 YR BOND YIELD: 4.649UP 5BASIS PTS…

USA 30 YR BOND YIELD: 4.767 UP 4 BASIS PTS/

USA 2 YR BOND YIELD: 4.952 UP 35BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.52…(TURKEY SET TO BLOW UP FINANCIALLY)

GREAT BRITAIN/10 YEAR YIELD: UP 11 BASIS PTS AT 4.3569

end

2.a Overnight: Newsquawk and Zero hedge

Futures Rise For Third Day As Tesla, Texas Instruments Surge Boosts Tech Stocks

WEDNESDAY, APR 24, 2024 – 08:13 AM

Equity futures rose for the third day in a row – last week’s brutal drubbing a distant memory – with tech outperforming as Tesla soars premarket after Elon Musk vowed to launch less-expensive vehicles as soon as late this year while Texas Instruments jumped 7% after it forecast revenue above the average analyst estimate. The tech rally has kept stocks afloat after disappointing earnings in the European banking and luxury sectors. Technology shares stood out in the US, with contracts on the Nasdaq 100 rising 0.6% compared with a 0.3% gain for S&P 500 futures. Bond yields are 1-3bps higher, helping to boost the USD. Commodities are lower though base metals are positive. The macro data focus is on Durable/Cap Goods with META headlining today’s earnings releases. Keep an eye on macro read throughs from F, HAS, NSC, ODFL, SYF, WHR earnings, among others.

In premarket trading, Tesla soared 12% with analysts saying first-quarter results were not as bad as feared. The electric-vehicle maker is accelerating the launch of less-expensive cars in a bid to revive cooling demand. TXN jumped 7.3% following earnings while META +2.1% (which reports after the close), NVDA +1.8%, with the balance of Mag7 are all higher. Copper mining giant FCX is also +1.5% pre-mkt, and may point to investors looking at the broadening AI trade again.

TikTok to Fight Back as US Pushes for App’s Sale or Ban

https://imasdk.googleapis.com/js/core/bridge3.636.0_en.html#goog_879480185

- Enphase Energy shares drop 7.9% after the solar-equipment manufacturer reported first-quarter adjusted earnings per share and revenue that missed expectations. Additionally, the company issued a second-quarter revenue forecast that disappointed.

- MSCI shares rise 2.2% after the investment support company was upgraded to buy from hold by Deutsche Bank.

- Semiconductor stocks gain after Texas Instruments forecast revenue for the current quarter above the average analyst estimate, signaling a possible pickup in demand for industrial and auto components. Texas Instruments (TXN US) +7.0%, Luminar Technologies (LAZR US) +4.1%, ON Semiconductor (ON US) +5.1%, ARM Holdings (ARM US) +4.0%, Super Micro Computer (SMCI US) +3.3%, Analog Devices (ADI US) +3.2%, Wolfspeed (WOLF US) +2.8%

- Sirius XM (SIRI US) shares climb 3.8% after Citi raised its recommendation on the stock to neutral from sell.

- Travere Therapeutics (TVTX US) shares rise 6.8% after the biopharmaceutical company said the European Commission has granted conditional marketing authorization for Filspari (sparsentan) for the treatment of IgA nephropathy.

- VinFast (VFS US) shares trade 4.1% higher after the EV manufacturer signed agreements with 12 US dealers, bringing its total number of dealers in the US to 18.

- Visa (V US) shares rise 2.8% after the credit card company reported first quarter earnings that beat estimates, surprising analysts.

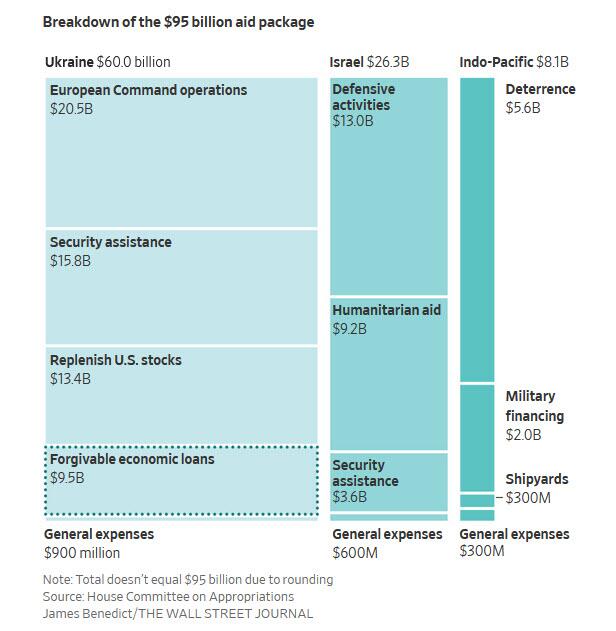

Overnight, the Senate passed a long-delayed $95 billion emergency aid package for Ukraine and other allies, clearing the way for resumed arms shipments to Kyiv within days. It also voted to ban TikTok’s ownership by Chinese parent Bytedance. Looking ahead, Meta Platforms is due to report after the bell.

After a strong performance by US tech giants on Tuesday, attention will be on Meta as the next of the so-called Magnificent Seven group of companies to report. International Business Machines Corp. and Boeing Co. are also due to release results.

“There are high hopes for big US tech,” said Alexandre Hezez, chief investment officer at Paris-based asset manager Group Richelieu. “Inflation and valuation levels don’t seem to be a concern at the moment.”

European stocks edged higher, with the Stoxx Europe 600 rising 0.2% as a surge in the shares of ASM International NV was offset by declines for Lloyds Banking Group Plc. Luxury names dropped as Kering SA tumbled after warning that profit will plunge on slowing sales at Gucci, its biggest brand. Here are the biggest movers Wednesday:

- ASM International soars as much as 14% the most since July 2022 after the chip-equipment maker reported stronger-than-expected quarterly order intake, boosted by demand from chipmakers aiming for next-generation gate-all-around transistors and high bandwidth memory

- Kone rises as much as 5.5% after reporting first-quarter results that largely met expectations and reassured investors with specified revenue and margin targets, according to an Alphavalue analyst

- Ipsen advance rise as much as 3.7% to the highest in almost six months, after the French drugmaker reported sales for the first quarter that beat the average analyst estimate

- Kering slumps as much as 10% to a six-year low after the luxury goods maker warned that first-half recurring operating income would decline 40% to 45% in an update that analysts said was worse than expected

- Air Liquide shares fell as much as 1.9% after the French industrial gas group reported revenue for the first quarter that missed expectations in terms of organic growth

- Volvo Car falls as much as 8.8%, the most in five months, after the Swedish carmaker reported first quarter results which missed analyst estimates. DNB expects some consensus downgrades

- Eurofins Scientific declines as much as 6.2% after disappointing with a first quarter miss in revenue and softer unadjusted organic growth, according to Jefferies analysts

- DSV slides as much as 5.7% to the lowest since October as its adjusted net income missed expectations for the first quarter

- Croda shares fell as much as 4.7%, reversing earlier gains, as traders tried to make sense of the chemicals group’s first-quarter sales

- Orange slips as much as 2.7% after the French telecom operator’s results showed pressure in its home market, with the firm continuing to lose broadband customers while more mobile customers chose not to renew contracts

- Allfunds shares fall as much as 11% after the firm abandoned discussions over a potential sale of the European fund distribution platform, Bloomberg News reported

In FX, the Bloomberg Dollar Spot Index rose 0.1% while the Australian dollar tops the G-10 FX pile, rising 0.3% versus the greenback after inflation topped estimates. Elsewhere, the yen remained a whisker away from the key 155 level to the dollar, with a former top Japanese foreign exchange official warning the country is on the brink of currency intervention.

In rates, treasuries were cheaper across the curve amid bigger losses in bunds and gilts after German 10-year auction and strong business sentiment gauge. Selloff began during Asia session when Australia’s bond market slumped on hot inflation data, its 3-year yield jumping as much as 19bps. US yields are cheaper by 3bp to 4bp across the curve with 10-year around 4.64%. Bunds and gilts lag by additional 1.5bp and 2.5bp in the sector. Australia’s 10-year closed almost 14bp cheaper on the day, its 2-year more than 18bp. Treasury coupon auctions resume at 1pm New York time with $70b 5-year notes, following strong 2-year note sale Tuesday. WI 5-year yield at around 4.655% is ~42bp cheaper than last month’s, which stopped through by 1bp in a solid sale. The week’s auction cycle concludes Thursday with $44b 7-year note sale

In commodities, oil prices decline, with WTI falling 0.5% to trade near $83. Spot gold falls 0.3%. Iron ore rises to a seven-week high.

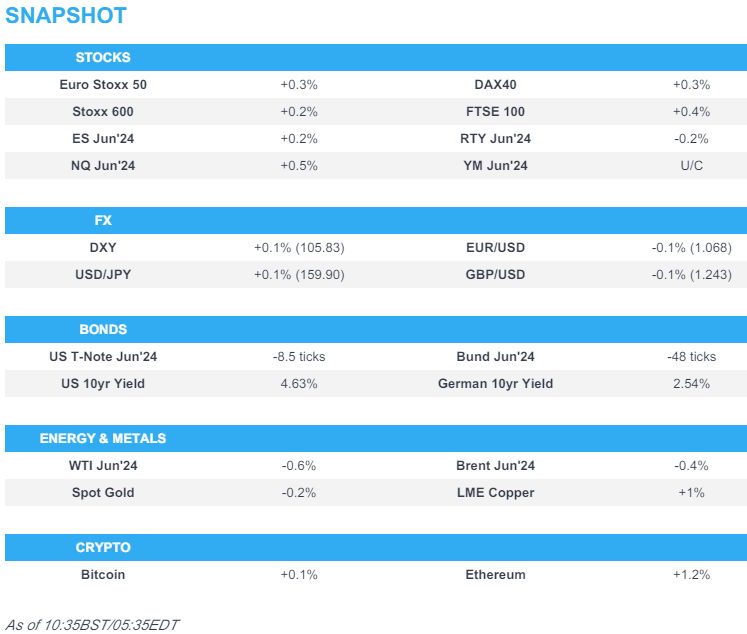

Bitcoin was flat and sits just above USD 66k, whilst Ethereum posted incremental gains and above USD 3.2k.

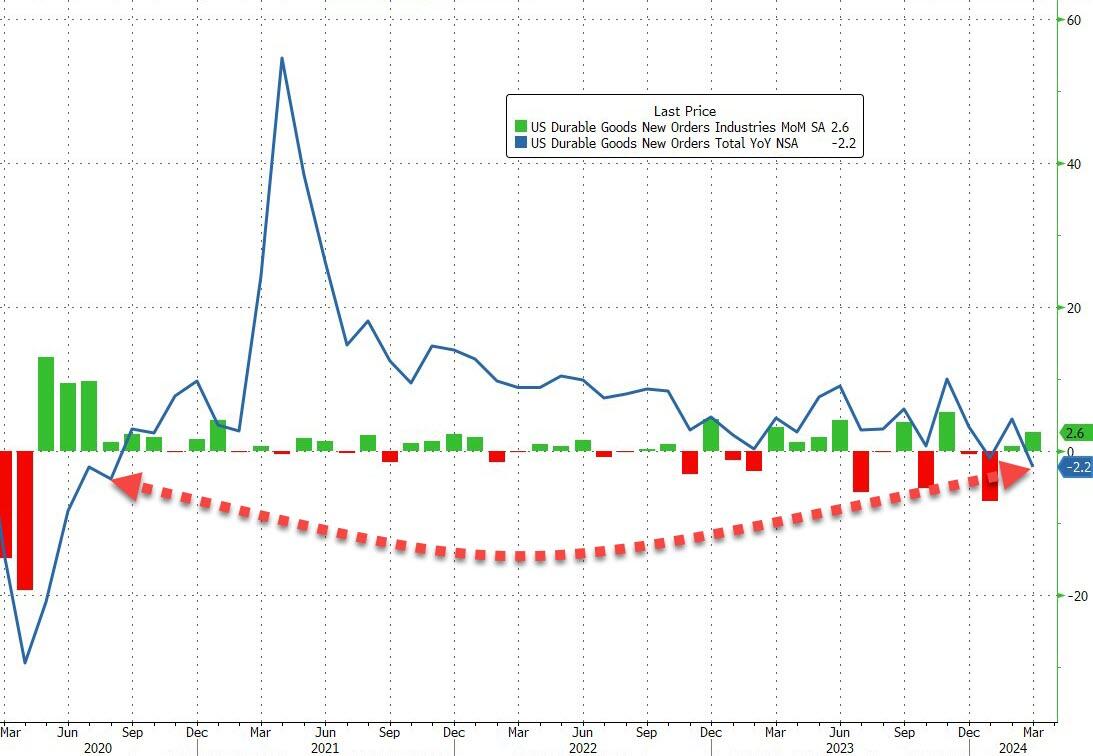

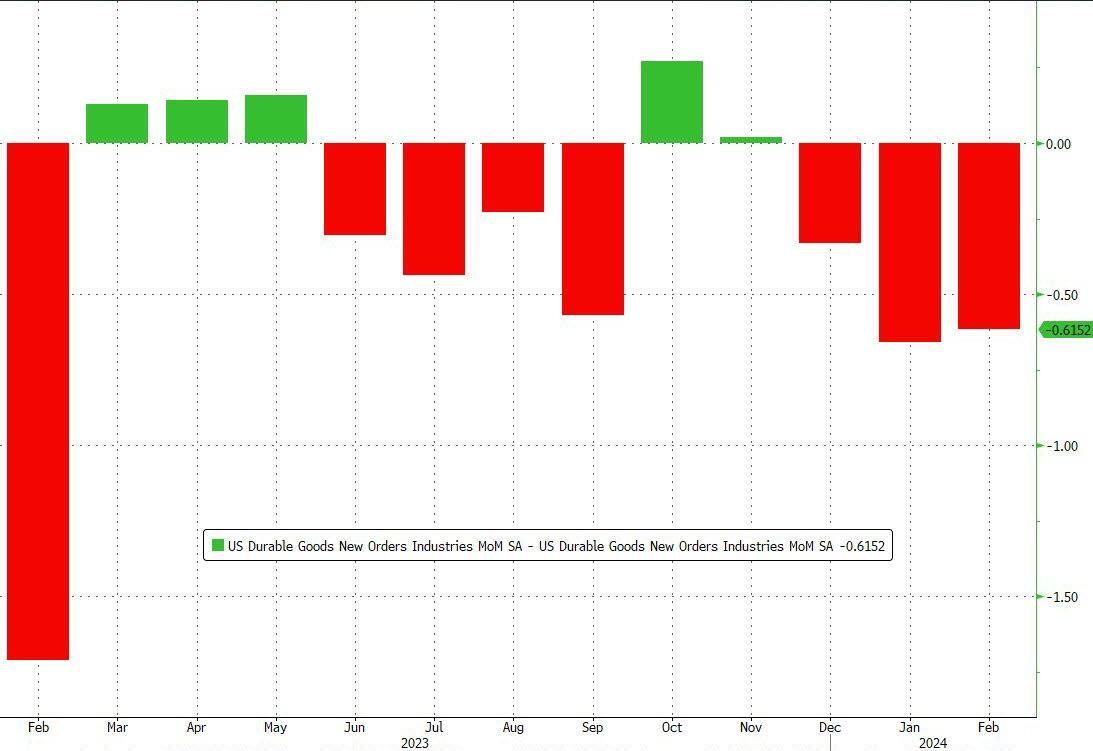

Looking at today’s calendar, US economic data slate includes March durable goods order at 8:30am. There are no speeches from Fed members who entered quiet period ahead of May 1 policy announcement.

Market Snapshot

- S&P 500 futures up 0.2% to 5,116.75

- STOXX Europe 600 up 0.2% to 508.58

- MXAP up 1.7% to 173.35

- MXAPJ up 1.7% to 533.79

- Nikkei up 2.4% to 38,460.08

- Topix up 1.7% to 2,710.73

- Hang Seng Index up 2.2% to 17,201.27

- Shanghai Composite up 0.8% to 3,044.82

- Sensex up 0.3% to 73,996.06

- Australia S&P/ASX 200 little changed at 7,683.00

- Kospi up 2.0% to 2,675.75

- German 10Y yield little changed at 2.53%

- Euro down 0.2% to $1.0683

- Brent Futures down 0.4% to $88.08/bbl

- Brent Futures down 0.4% to $88.08/bbl

- Gold spot down 0.2% to $2,318.21

- US Dollar Index up 0.20% to 105.88

Top Overnight News

- China’s central bank has again reiterated its cautious approach to monetary easing, reinforcing views that it’s unlikely to deliver a big liquidity boost via bond trading. WSJ

- The United States has preliminarily discussed sanctions on some Chinese banks but does not yet have a plan to implement such measures, a U.S. official told Reuters on Tuesday, as Washington seeks ways to curb Beijing’s support for Russia. RTRS

- Australian CPI remained strong in the latest quarter, illustrating the challenge the country’s central bank faces in bringing inflation back to target and adding uncertainty around the timing of interest-rate cuts. CPI rose by 3.6% in the March quarter from a year earlier, meaning the annual inflation rate is now more than half of its peak at the end of 2022. Still, CPI rose by 1.0% on a quarterly basis, accelerating from the 0.6% increase recorded for the three months through December. WSJ

- Indonesia surprises markets with a rate hike (most assumed policy would stay unchanged) as the central bank looks to bolster the tumbling rupiah. WSJ

- UBS Chairman Colm Kelleher said the bank is “seriously concerned” about proposed Swiss capital reforms. “Additional capital is the wrong remedy,” he told the AGM. BBG

- US crude inventories fell by 3.23 million barrels last week, API data is said to show. That would be the first drop in five weeks if confirmed by the EIA. Stockpiles at Cushing, as well as gasoline supplies declined. BBG

- The long-delayed $95 billion emergency aid package for Ukraine and other besieged allies passed the Senate. It included tacked-on legislation requiring TikTok’s Chinese owners to divest or face a US ban. Joe Biden plans to sign the bill today — beginning a 270-day countdown for Bytedance and a hefty legal fight. BBG

- Trump won the Pennsylvania primary, but Haley still captured the support of more than 155K voters despite being out of the race for more than a month, underscoring the existing rift within the GOP. NYT

- Tesla +12% premarket as investors cheered its pledge to speed up the launch of more affordable models to as soon as this year, even as profit and sales missed. Big Tech focus now turns to Meta’s earnings, due after the bell. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks gained as the region took impetus from the rally on Wall St where soft PMI data spurred a dovish reaction across asset classes. ASX 200 was led by gold miners after several quarterly production updates but with the advances in the index capped by firmer-than-expected CPI data. Nikkei 225 outperformed its peers and rose above the 38,000 level amid tech strength. Hang Seng and Shanghai Comp. conformed to the broad upbeat sentiment seen across the region amid tech strength in Hong Kong as SenseTime shares surged over 30% following the unveiling of its latest AI model. However, gains in the mainland were capped after the US Senate passed the Ukraine, Israel and Taiwan aid package which includes the threat to ban TikTok in the US.

Top Asian News

- EU opened a probe into China’s procurement of medical devices, according to Bloomberg.

- BoJ is to discuss the impact of the yen’s rapid slide at this week’s policy meeting and a further rate hike is seen as unlikely on Friday as the Bank keeps a close eye on inflation, according to Nikkei. BoJ is closely watching core inflation as it weighs the timing of additional hikes and rather than rushing further tweaks, the BoJ aims to carefully monitor moves by smaller businesses to raise pay and pass along increased costs to customers. Furthermore, a BoJ source said they want to confirm that the cycle between wage and price growth is strengthening and many at the BoJ believe that the weak Yen is not currently adding to inflation, while the increase in long-term interest rates is helping to keep the yen from weakening further.

- Indonesian Lending Facility Rate (Apr) 7.0% vs. Exp. 6.75% (Prev. 6.75%); Deposit Facility Rate (Apr) 5.5% vs. Exp. 5.25% (Prev. 5.25%); 7-Day Reverse Repo (Apr) 6.25% vs. Exp. 6.0% (Prev. 6.0%).

- SK Hynix (000660 KS) announces investment in new DRAM chip production base in South Korea; will invest KRW 20tln

European bourses, Stoxx 600 (+0.2%) are mostly firmer; price action today has been contained within tight ranges, although bourses remained at session highs throughout the morning. European sectors are mixed; Tech is the clear outperformer, following significant post-earnings strength in ASM International (+10.5%). Basic Resources benefits from broader strength in base metals prices. Banks are found towards the bottom of the pile, after Lloyds (-0.9%) reported softer NII metrics. US Equity Futures (ES +0.2%, NQ +0.6%, RTY -0.2%) are mixed, with clear outperformance in the NQ, whilst the RTY lags. The former benefits from Tech-led gains, after Texas Instruments (+7%) reported strong results. Additionally, Tesla (+10.5%) benefits pre-market, despite missing on top and bottom lines, as traders focus on plans for affordable models.

Top European News

- ECB’s Nagel said June rate cut is not necessarily followed by a series of rate cuts; not fully convinced that inflation will actually return to target in a timely sustained manner, services inflation remains high, driven by continued strong wage growth.

- ECB’s Cipollone “Innovation, integration and independence: taking the Single Euro Payments Area to the next level”; text release not on monetary policy.

FX

- Dollar is showing mixed performance vs. peers but higher on an index basis following yesterday’s PMI-induced losses. Currently towards the upper end of today’s 105.59-88 range, and still yet to test its 10DMA at 105.96.

- EUR is a touch softer vs. the USD and back below the 1.07 mark after diverging PMI metrics yesterday helped prop up the pair. ECB speakers continue to talk up a June cut and as such attention is turning towards what happens beyond that meeting. Notable Opex for the pair: 1.0600-10 (1.5BLN), 1.0650 (1.06BLN), 1.0685-90 (426M), 1.0700-10 (3.07BLN), 1.0715-25 (1.3BLN), 1.0730 (260M), 1.0750 (230M).

- GBP is on the backfoot after a session of hefty gains yesterday thanks to PMI data and comments from BoE’s Pill. Cable managed to top yesterday’s best and print a peak at 1.2464 before trimming gains.

- Another day, another multi-decade high for the JPY with 154.96 the peak thus far. As the pair moves ever-closer to 155, focus is firmly placed on intervention watch. However, comments from a Japanese lawmaker earlier suggested that 160 could be the new “line in the sand” for officials.

- Antipodeans are underpinned by the risk environment and with outperformance in AUD due to firmer-than-expected inflation data. AUD/USD is back above the 0.65 mark with the pair topping out around its 200DMA at 0.6528.

- PBoC set USD/CNY mid-point at 7.1048 vs exp. 7.2336 (prev. 7.1059).

Fixed Income

- USTs pulling back after yesterday’s PMI-induced gains which sent the 10yr benchmark to a 108.08 peak. Today’s calendar sees US durables, however, greater focus may fall on the USD 70bln 5yr note auction given the well-received 2yr offering yesterday.

- Bunds are following suit to the selling pressure in global peers with traders also mindful of better-than-expected German IFO data. Bunds remains at session lows with focus on a potential test of the 130.52 YTD trough.

- Gilts remain pressured in an extension of yesterday’s Pill-induced price action which saw traders re-evaluate the dovish price action prompted by Ramsden last Friday. The 96.40 low today is the lowest since 17th April with 96.01 thereafter.

- Orders for UK 4.375% 2054 Gilt exceed GBP 75bln (prev. GBP 57bln); price guidance 1.75bps (prev. 1.75-2bps), via bookrunner

Commodities

- Crude was initially propped up, benefiting from the post-US PMI Dollar weakness; though the complex has since succumbed to selling pressure amid the recent resurgence in the Dollar. Brent June currently holds around USD 88/bbl.

- Subdued trade across precious metals with spot gold and silver on a marginally softer footing, in fitting with the modest gains in the USD. XAU/USD sits in a tight range within USD 2,315.84-2,331.37/oz.

- Base metals are firmer across the board despite the stronger Dollar, but amidst a positive risk tone across global markets, with Chinese markets showcasing a strong performance underpinned by its tech and property sectors.

- China Coal Industry Group said cement industry capacity utilisation down to 50% (prev. 80% Y/Y), negatively impacting coal demand. Current domestic coal price of around CNH 800/metric ton seem as price floor for this year.

Geopolitics

- US Senate voted (79-18) to pass the USD 95bln bill with aid for Ukraine, Israel and Taiwan which also includes the threat to ban TikTok, while US President Biden said he will sign it into law on Wednesday.

- China’s Taiwan Affairs Office said it resolutely opposes the inclusion of Taiwan-related content in the relevant bill of the US Congress, while it urged the US to fulfill its commitment not to support ‘Taiwan independence’ with concrete actions and stop arming Taiwan in any way.

- North Korean leader Kim’s sister said North Korea will continue to build overwhelming military power to protect sovereignty and that the regional security environment is spiralling into turmoil because of US military manoeuvres, according to KCNA.

- Ambrey is aware of an incident Southwest of Aden, Yemen; “Yemeni sources: Houthis launch a ballistic missile towards the sea from in central Yemen”, according to Sky News Arabia; details light.

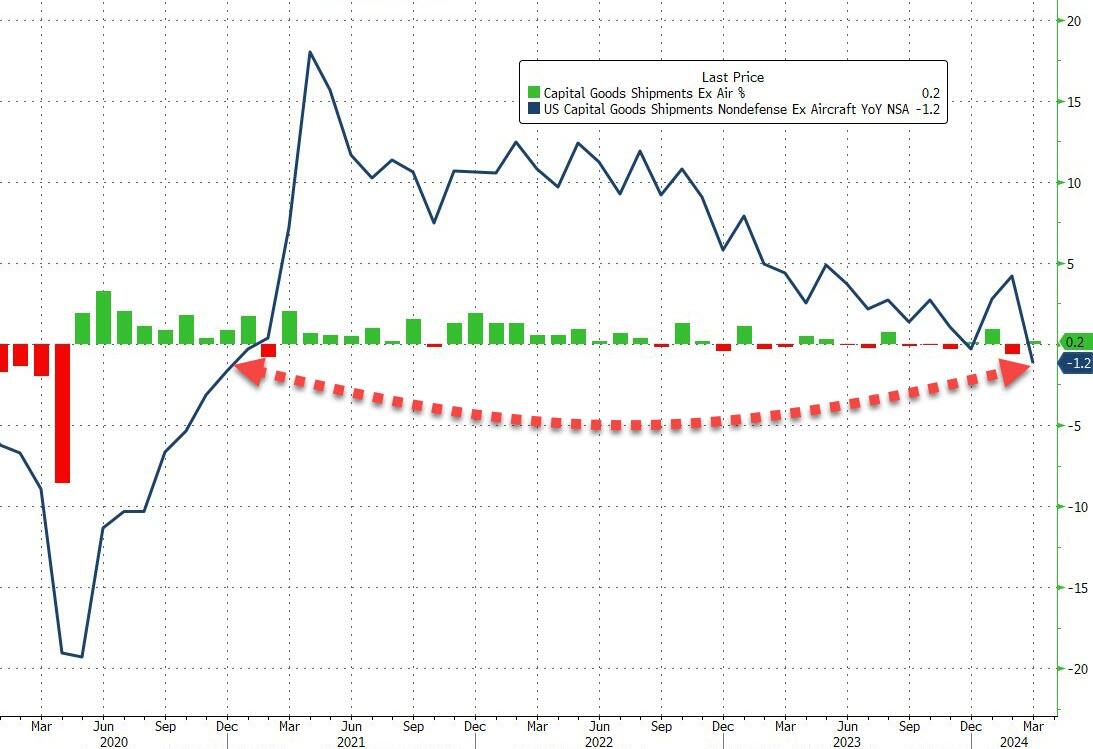

US Event Calendar

- 07:00: April MBA Mortgage Applications, prior 3.3%

- 08:30: March Durable Goods Orders, est. 2.5%, prior 1.3%

- 08:30: March Durables-Less Transportation, est. 0.2%, prior 0.3%

- 08:30: March Cap Goods Ship Nondef Ex Air, est. 0.2%, prior -0.6%

- 08:30: March Cap Goods Orders Nondef Ex Air, est. 0.2%, prior 0.7%

DB’s Jim Reid concludes the overnight wrap

A very big happy 50th birthday to DB’s logo for tomorrow. It came into being on April 25th 1974. The slanting line within a box is at exactly 53 degrees which ahead of my own 50th in less than 2 months time is about the same angle as my back as I get out of bed every morning.

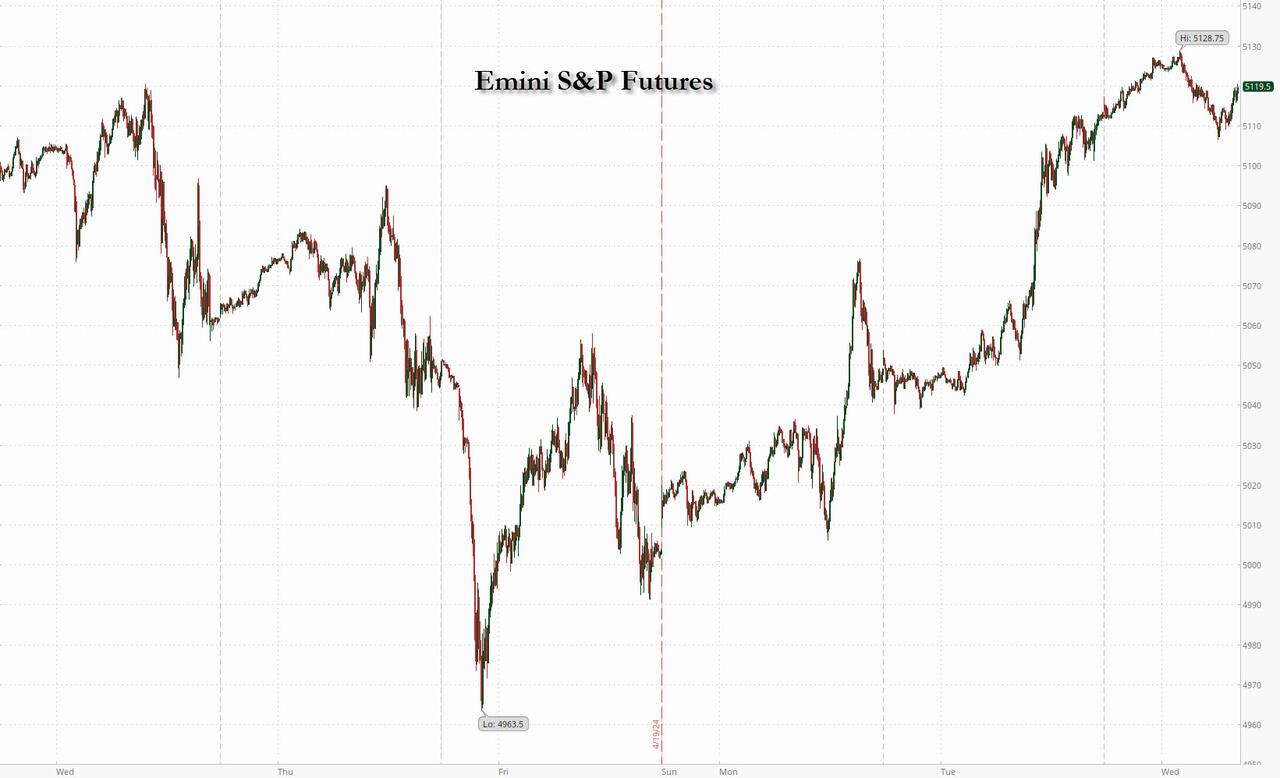

Markets went up at a similar angle yesterday, meaning that the S&P 500 (+1.20%) has now posted its strongest 2-day performance since February. Several factors helped to drive this, but perhaps the most important was actually the disappointing flash PMIs in the US, which added to hopes that rate cuts would still happen this year. That supported a rally in US Treasuries as well, with the 10yr yield (-0.9bps) falling back for a third consecutive day.

That rally yesterday was led by the M agnificent 7 (+1.96%), and after the close, we then received results from Tesla . These saw a headline miss on revenue ($21.3bn vs $22.3bn expected) and earnings estimates for Q1, with the company noting that “vehicle volume growth rate may be notably lower” in 2024 than in 2023. However, investors made a more upbeat take on the company’s strategy going forward, with a focus on “accelerating” the rollout of new cheaper models. This sent Tesla shares as much as +13% higher in after-market trading, so a sizeable degree of relief after the -42% decline the stock has seen so far this year up to the close (+1.80% yesterday). US equity futures are trading +0.36% higher for the S&P 500 and +0.72% for NASDAQ overnight on the back of this. I did a CoTD yesterday here showing that at its peak 2.5 years ago Tesla was worth the same amount as the next 12 largest global auto companies. It’s still the largest but was “only” around $83bn larger than Toyota in second place at the close yesterday. So it’s come back to the pack. It’s been a heavily shorted stock of late so the rebound in after hours probably also has something to do with that.

Earnings season will continue apace today, as we’ll hear from Meta after the US close later. Before the Tesla results, the weakness in the US PMIs helped to set the tone, with Treasury yields seeing a sharp intraday decline after they came out. In terms of the details, the composite PMI was down to 50.9 in April (vs. 52.0 expected), which is the lowest in 4 months. And there wasn’t much relief from the subcomponents, as new orders were down to a 7-month low of 48.4, whilst the employment index fell to 48.0, which is its lowest since May 2020 at the height of the pandemic. In sectoral terms, services fell to a 5-month low of 50.9 (vs. 52.0 expected), and manufacturing was at a 4-month low of 49.9 (vs. 52.0 expected).

The release led investors to dial up their expectations for Fed rate cuts this year, and the chance of a cut by the July meeting moved up from 46% to 52% by the close. In turn, that sparked a rally for US Treasuries, with the 2yr yield down by -3.9bps on the day to 4.93%, having been as high as 4.998% at its intraday peak. 2yr yields had troughed shortly after a solid 2yr auction that saw $69bn of notes issued at 4.898%, -0.6bps below the pre-sale yield. Further out the curve, the 10yr yield (-0.9bps) fell back marginally to 4.60%, having been just shy of 4.65% before the US PMIs. With rates moving lower, the broad dollar index (-0.38%) saw its weakest day in nearly three weeks. This morning in Asia, yields on the 10yr USTs (+1.7bps) have edged back higher to 4.617% as we go to print.

The rates rally helped to spur a fresh advance for equities, with the S&P 500 closing up +1.20%. That was its best performance in two months, and it was aided by a strong performance for the Magnificent 7 (+1.96%). In addition, the advance was a broad-based one, and the small-cap Russell 2000 (+1.79%) had its best performance so far this month. Meanwhile in Europe, the STOXX 600 (+1.09%) also saw a sharp rise, and the UK’s FTSE 100 (+0.26%) edged up to a fresh record high.

Whilst European equities were advancing, and US rates rallying, it was a different story for European sovereign bonds, as the flash PMIs showed a further improvement in April. In particular, the Euro Area composite PMI hit an 11-month high of 51.4 (vs. 50.7 expected), and the services PMI was up to 52.9 (vs. 51.8 expected). The only notable weak spot was in manufacturing, where the Euro Area PMI hit a 4-month low of 45.6 (vs. 46.5 expected). And here in the UK, the composite PMI was up to 54.0 (vs. 52.6).

With that in mind, yields on 10yr bunds (+1.7bps), OATs (+1.6bps) and gilts (+3.6bps) all moved higher on the day. The move was particularly pronounced for gilts, as we also heard from BoE Chief Economist Pill, who struck a somewhat hawkish tone on the prospect of rate cuts. He said in a speech that “there are greater risks associated with easing too early should inflation persist rather than easing too late should inflation abate”. Along with the upside surprise in the PMIs, that led investors to dial back the chances of a cut by the June meeting, which came down from 64% the previous day to 48% by the close. However, at the ECB, there was a continued convergence on the idea of a June cut with market pricing for June “only” down just a touch from 87% to 85% after the decent composite PMI. Bundesbank President Nagel, once of the more hawkish voices, said that “ If the favourable inflation outlook from March is confirmed in the June forecast and the incoming data supports this forecast, we can consider lowering interest rates.”

Shifting perceptions over risks in the Middle East led to a volatile day for oil prices. Brent crude fell from $87 to $86/bbl early on in the US session, but was up to $88.42 by the close (+1.63%) amid lingering uncertainty over new US sanctions against Iran as well as reports that American Petroleum Institute data showed a decline in US crude inventories last week. Easing geopolitical fears also saw gold fall to below $2300/oz intra-day for the first time in over two weeks, but it was virtually unchanged by the close (+0.02% to $2,330/oz).

In Asia markets are rallying hard this morning with the Nikkei (+2.07%) sharply higher and leading gains across the region with the KOSPI (+1.91%) and the Hang Seng (+1.53%) also climbing. China stocks are lagging with the Shanghai Composite (+0.31%) seeing softer gains.