APRIL 30/FIRST DAY NOTICE MAY CONTRACT//GOLD CLOSED DOWN $53.75 TO $2292.40/SILVER WAS DOWN 99 CENTS TO $26.45//PLATINUM WAS DOWN $19.45 TO $936.40 WHILE PALLADIUM WAS DOWN $957.70 TO $XXX//GOLD COMMENTARIES TONIGHT FROM PETER SCHIFF AND EGON VON GREYERZ//CHINA CONTINUES TO PURCHASE MOUNTAINS OF GOLD//GERMAN PROTESTERS DEMAND AN ISLAMIC STATE IN GERMANY//ISRAEL AWAITS HAMAS DECISION RE HOSTAGE RELEASE//HOUTHIS FIRE ON 4 SHIPS IN RED SEA //COVID UPDATES//VACCINE INJURIES/DR PAUL ALEXANDER//SLAY NEWS// USA DATA: CHICAGO PMI SERVICE DATA SCREAMS OF STAGFLATION//VICTOR DAVIS HANSON//SWAMP STORIES FOR YOU TONIGHT//

118 C MACQUARIE FUT 318 190 H BMO CAPITAL 105 323 C HSBC 640 363 H WELLS FARGO SEC 52 435 H SCOTIA CAPITAL 198 657 C MORGAN STANLEY 14

DLV615-T CME CLEARING BUSINESS DATE: 04/29/2024 DAILY DELIVERY NOTICES RUN DATE: 04/29/2024 PRODUCT GROUP: METALS RUN TIME: 20:46:04 661 C JP MORGAN 410 230 690 C ABN AMRO 16 737 C ADVANTAGE 90 880 C CITIGROUP 796 905 C ADM 1

TOTAL: 1,435 1,435

JPMorgan stopped 0/1439

FOR MAY2024

GOLD: NUMBER OF NOTICES FILED FOR MAY/2024. CONTRACT: 1439 NOTICES FOR 143,900 OZ or 4,4758 TONNES

total notices so far: 1439 contracts for 143,900 Oz (4,4758 tonnes)

FOR MAY:

SILVER NOTICES: 2514NOTICE(S) FILED FOR 12,570,000OZ/

total number of notices filed so far this month : 2514 for 12.570 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $53.75

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

NO CHANGES IN GOLD INVENTORY AT THE GLD:

/ /INVENTORY RESTS AT 832.19 TONNES

INVENTORY RESTS AT 832.19 TONNES

SLV//

WITH NO SILVER AROUND AND

SILVER DOWN $.99 AT THE SLV//

SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OT ,457 MILLION OZ

// INVENTORY INCREASES T0 429.174MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 429,174MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 645 CONTRACTS TO 169,739 AND STILL RAPIDLY CLOSING IN ON THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, DESPITE THE RAID AND THIS SMALL SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR SMALL GAIN OF $0,13 N SILVER PRICING AT THE COMEX ON MONDAY. WE HAD ZERO LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN PANICKING SHORT COVERING BY OUR SPECS WITH THE SMALL PRICE GAIN IN PRICE. WE HAD A SMALL SIZED 374 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 374 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUNUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.13, AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A HUGE SIZED GAIN OF 2012 CONTRACTS ON OUR TWO EXCHANGES WITH THE GAIN IN PRICE OF $0.13

WE MUST HAVE HAD:

A HUMONGOUS SIZED 1367 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 28.130MILLION OZ (FIRST DAY NOTICE)

//NEW STANDING FOR SILVER//MAY IS THUS 28.130 MILLION OZ

WE HAD:

/ STRONG SIZED COMEX OI GAIN/ HUGE SIZED EFP ISSUANCE/ VI) FAIR SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 374 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED A STRONG 177CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF APRIL

TOTAL CONTRACTS for 22DAYS, total 32,354 contracts: OR 161.770 MILLION OZ (1470CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 194.124 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770MILLION OZ (THIS MONTH WILL PROBABLY BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 645 CONTRACTS WITH OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG EFP ISSUANCE CONTRACTS: 1367 IISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAY OF 28.130 MILLION OZ ON FIRST DAY NOTICE F

//NEW TOTAL STANDING AT 28.130 MILLION OZ

WE HAVE A HUGE SIZED GAIN OF 2012 OI CONTRACTS ON THE TWO EXCHANGES WITH THE GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A FAIR SIZED 374 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS

THE NEW TAS ISSUANCE MONDAY NIGHT (733 WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 2514 NOTICE(S) FILED TODAY FOR 12.570 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 3535 OI CONTRACTS TO 524,852 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 764 CONTRACTS

WE HAD A STRONG SIZED INCREASE IN COMEX OI (4299 CONTRACTS) WITH OUR $10.55 GAIN IN PRICE//FRIDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER TO WHACK GOLD’S PRICE. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 4.684 TONNES ON FIRST DAY NOTICE

NEW STANDING 4.684TONNES// ALL OF THIS HAPPENED WITH OUR $10.55 GAIN IN PRICE WITH RESPECT TO MONDAY’S TRADING. WE HAD A STRONG SIZED GAIN OF 7971 OI CONTRACTS (24.793 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A VERY STRONG SIZED 4436 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 524,852

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7971 CONTRACTS WITH 3535 CONTRACTS INCREASED AT THE COMEX// AND A STRONG SIZED 4436 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 7971 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED 2729 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4436 CONTRACTS) ACCOMPANYING THE GOOD SIZED GAIN IN COMEX OI 3535 TOTAL GAIN FOR OUR THE TWO EXCHANGES: 7971 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 4.684TONNES

//NEW STANDING /MAY 4.684TONNES.

/ 3) ZERO LONG LIQUIDATION WITH THE GAIN IN PRICE.

// 4) GOOD SIZED COMEX OPEN INTEREST GAIN/ 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: STRONG T.A.S. ISSUANCE: 2729CONTRACTS/ HUGE SHORT COVERING BY OUR WRONG FOOTED SPECS WITH THE FED’S CONTINUAL RAID ON THE COMEX GOLD.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF APRIL. :

TOTAL EFP CONTRACTS ISSUED: 85,857CONTRACTS OR 8,585,700OZ OR 267.05 TONNES IN 22TRADING DAY(S) AND THUS AVERAGING: 3902 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 22TRADING DAY(S) IN TONNES 229.60 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 267.05 DIVIDED BY 3550 x 100% TONNES = 7.52% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER ROSE BY A STRONG SIZED 645 CONTRACTS OI TO 169,739 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1367 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1367 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1600 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 645 CONTRACTS AND ADD TO THE 1367 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2012 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 10.06MILLION OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

REPORT THIS AD

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING/MONDAY NIGHT

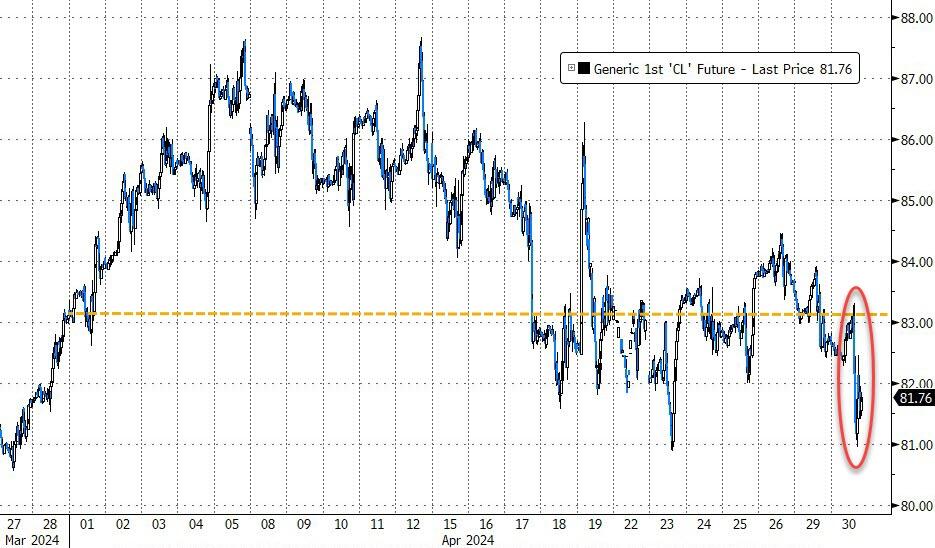

SHANGHAI CLOSED DOWN 8.22 PTS OR 0.28% //Hang Seng CLOSED UP 16.12 PTS OR 0.09% / Nikkei CLOSED UP 420.90 PT OR 1.24% //Australia’s all ordinaries CLOSED UP 0.32%///Chinese yuan (ONSHORE) closed UP 7.2410//OFFSHORE CHINESE YUAN CLOSED UP TO 7.2493 Oil DOWN TO 83.13dollars per barrel for WTI and BRENT UP AT 87.66 Stocks in Europe OPENED MOSTLY RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 3535 CONTRACTS TO 524,852 WITH OUR GAIN IN PRICE OF $10.55 WITH RESPECT TO MONDAY TRADING. WE HAD CONSIDERABLE A.S. LIQUIDATION AS WELL AS SHORTS, DESPERATELY TRYING TO GET OUT OF THEIR NAKED SHORTS.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAY.… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A HUGE 4436 EFP CONTRACTS WERE ISSUED: : JUNE4936& ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE:4036 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 7971 CONTRACTS IN THAT 4436 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A FAIR SIZED GAIN OF 3535 COMEX CONTRACTS..AND THIS STRONG GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $10.55 MONDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR FRIDAY NIGHT WAS A FAIR SIZED 2087 CONTRACTS. WE HAD 0 EX FOR RISK ISSUANCE. MOST OF THE TRADING AND SUPPLY OF CONTRACTS ON MONDAY WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (4.684TONNES) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

REPORT THIS AD

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2023 4.684 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE $10.55 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG SIZED GAIN OF7971 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN IN PRICE 0F $10.55

WE HAD A FAIR T.A.S. LIQUIDATION ON THE FRONT END OF MONDAY’S TRADING. THE T.A.S. ISSUED ON MONDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 24.793 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY (4.684 TONNES) ON FIRST DAY NOTICE

NEW STANDING: 50.650ONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $10.55

WE HAD REMOVED 301 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET GAIN ON THE TWO EXCHANGES 7971 CONTRACTS OR 797,100(24.793 TONNES)

Total monthly oz gold served (contracts) so far this month

1439notices 143,900 0oz 4.4758 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

1 dealer deposits:

i) Into ASAHI: 32,212.140 oz

total dealer deposits: 32,212.140oz

we have 2 customer deposits:

i)Into ASAHI 297,801

II) Into Brinks 1806.43 oz

total deposit 2104.23 oz

total customer withdrawals: 2

i) Out of HSBC 3182,949 oz

ii) Out of Delaware 346.567 oz

Adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL.

For the front month of MAY we have an oi of 1506contracts having LOST 171 contracts.

Thus be definition, the initial amount of gold standing in this non active delivery month of May is as follows:

1596 notices x 100 oz per notice = 150,600oz or 4.684tonnes.

JUNE INCREASED ITS OI BY 63 CONTRACTS UP TO 405,354CONTRACTS.

We had 1439 contracts filed for today representing 143,900 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1439 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the MAY /2024. contract month, we take the total number of notices filed so far for the month (1439 100 oz ), to which we add the difference between the open interest for the front month of MAY (1506CONTRACTS) minus the number of notices served upon today (1439x 100 oz per contract( equals 150,600 OZ OR 4.684 TONNES.

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (1439 x 100 oz + (1506 )OI for the front month} minus the number of notices served upon today (1439 x 100 oz which equals 150,600 oz (4.684TONNES)

TOTAL COMEX GOLD STANDING FOR MAY: 4.684 TONNES WHICH IS HUGE FOR THIS A NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,653,319.791OZ

TOTAL REGISTERED GOLD 7,531,878.894 (234.273 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,214,440.900OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 5,949,358 oz (REG GOLD- PLEDGED GOLD)

185.05 tonnes/dropping like a stone

END

SILVER/COMEX

APRIL 30

INITIAL

//2024// THE MAY 2025 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

12,130.320oz

CNT

.

Deposits to the Dealer Inventory

611,575.900 OZ ASAHI

Deposits to the Customer Inventory

741,644.121 oz

Brinks Delaware

No of oz served today (contracts)

2514CONTRACT(S) (12.570 OZ)

No of oz to be served (notices)

3112 contracts (15,.560 oz)

Total monthly oz silver served (contracts)

2514 Contracts (12,570,000oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 1 dealer deposit

i) Into ASAHI: 611,575.900 oz

total dealer deposit :611,575.900 oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 deposits customer account:

i) Into Brinks 601,257.681 oz

ii) Into Delaware 140,386,440 oz

total customer deposits 741,644.121oz

JPMorgan has a total silver weight: 129,598million oz/294.609million or 44.06%

adjustment: 4 all customer to dealer

ASAHI 2,049.700

Brinks 4,117,662.460 oz

CNT 1,612,505.780 0z

HSBC: 4959,974,280 oz

total 10.692 million oz

Comex withdrawals: 3

i) CNT 12,130.320

total withdrawal 12,130.320 oz

TOTAL REGISTERED SILVER: 62.660 MILLION OZ//.TOTAL REG + ELIGIBLE. 294.609million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF MAY/2024 OI: 35626 CONTRACTS HAVING LOST 5075 CONTRACT(S).

.

Thus by definition the initial amount of silver standing for delivery in this active delivery month of May is as follows:

5626 notices x 5,000 oz per notice = 28.130 million oz

JUNE SAW A GAIN OF 492 CONTRACTS RISING TO 1541

JULY SAW A GAIN OF 5058 CONTRACTS UP TO 137,364

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 2514for 12.570 million oz

CONFIRMED volume; ON MONDAY 77,929 very strong

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 2514 5,000 oz = 12,570,000oz

to which we add the difference between the open interest for the front month of MAY (5626and the number of notices served upon today 2514x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2024 contract month: 2514notices served so far) x 5000 oz + OI for the front month of MAY(5626number of notices served upon today (2514x 500 oz of silver standing for the APRIL contract month equates to 28.130 MILLION OZ.

New total standing: 28.130 million oz.

There are 62.660million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

APRIL 30 WITH GOLD DOWN $53.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNE

APRIL 29WITH GOLD UP $10,55TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNES

APRIL 26WITH GOLD UP $5.40TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.54 TONNES FROM THE GLD /INVENTORY RISES AT 832.19 TONNES

APRIL 25WITH GOLD UP $5.05 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD /INVENTORY RISES AT 833,63 TONNES

APRIL 19 WITH GOLD UP $15.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 4.32 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 831.91 TONNES

APRIL 18 WITH GOLD UP $11.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE WITHDRAWAL OF 2.59 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 827.59 TONNES

APRIL 17 WITH GOLD DOWN $17.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 830;18 TONNES

REPORT

APRIL 16 WITH GOLD UP $23.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 828.45 TONNES

REPORT THIS AD

APRIL 15 WITH GOLD UP $9.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE WITHDRAWAL OF 4.03 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 826.72 TONNES

APRIL 12 WITH GOLD UP $2.80 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD/ INVENTORY RISESS AT 830.75 TONN

APRIL 10 WITH GOLD DOWN $14.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 828.71 TONNES

APRIL 9 WITH GOLD UP $11.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 827,85 TONNES

APRIL 8 WITH GOLD UP $7.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A WITHDRAWAL OF 6.02 TONNES OF GOLD INTO THE GLD/ INVENTORY REMAINS AT 826.41 TONNES

APRIL 5 WITH GOLD UP $38.65 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/ INVENTORY REMAINS AT 832.45 TONNES

APRIL 4 WITH GOLD DOWN $3.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD/ INVENTORY REMAINS AT 830.73 TONNES

APRIL 3 WITH GOLD UP $33,85 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD // INVENTORY REMAINS AT 829.00 TONNES

APRIL 2 WITH GOLD UP $23.90 TODAY; HUG CHANGES IN GOLD INVENTORY AT THE GLD A WITH DRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD.:// INVENTORY REMAINS AT 829.00 TONNES

APRIL 1 WITH GOLD UP $18.70 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:// INVENTORY REMAINS AT 830.15 TONNES

MARCH 28 WITH GOLD UP $26.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:// INVENTORY REMAINS AT 830.15 TONNES

MARCH 27 WITH GOLD UP $15.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// INVENTORY FALLS TO 830.15 TONNES

MARCH 26 WITH GOLD UP $1.40 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 835.33 TONNES

MARCH 25 WITH GOLD UP $17.05 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 838.50 TONNES

MARCH 22 WITH GOLD DOWN $23.75 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 838.50 TONNES

GLD INVENTORY: 832.19TONNES,

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

APRIL 30WITH SILVER DOWN $0.99 TODAY: SMALLCHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF ,457 MILLION OZ INTO THE SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 29WITH SILVER UP $0.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 26WITH SILVER DOWN 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.097 MILLION OF SILVER INTO THE SLV// :SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 25WITH SILVER UP $.05 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 1.534 MILLION OF SILVER OUT OF THE SLV// :SLV INVENTORY RESTS AT 428.717 MILLION OZ

APRIL 24/WITH SILVER DOWN $.05 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 11.904MILLION OF SILVER INTO THE SLV// :SLV INVENTORY RESTS AT 428.280 MILLION OZ

APRIL 23/WITH SILVER UP $0.11TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV / :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 22/WITH SILVER DOWN $1.51 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.194 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 19/WITH SILVER UP 42 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.657 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 418.570 MILLION OZ

APRIL 18/WITH SILVER DOWN $.04TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.977 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 422.227 MILLION OZ

APRIL 17/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF .868 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 426/204 MILLION OZ

APRIL 16/WITH SILVER DOWN $0.46 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF NON EXISTENT SILVER// :SLV INVENTORY RESTS AT 427.072 MILLION OZ

APRIL 15/WITH SILVER UP $0.46 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 12/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 4.069 MILLION OZ FROM THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 11/WITH SILVER UP $0.23 TODAY: STRANGE INDEED! HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.931 MILLION OZ :SLV INVENTORY RESTS AT 437.998 MILLION OZ

APRIL 10/WITH SILVER UP $0.04 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:SLV INVENTORY RESTS AT 441.929 MILLION OZ

APRIL 9/WITH SILVER UP $0.15 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.549 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 441.929 MILLION OZ

APRIL 8/WITH SILVER UP $0.33 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.320 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 441.328 MILLION OZ

APRIL 5/WITH SILVER UP $0.61 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.748 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 441.060 MILLION OZ

APRIL 4/WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.671 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 437.312 MILLION OZ

APRIL 3/WITH SILVER UP $1.14 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.835 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 433.641 MILLION OZ

APRIL 2/WITH SILVER UP 84 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6.721 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 430.806 MILLION OZ

APRIL 1/WITH SILVER UP 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// SLV INVENTORY RESTS AT 424.085 MILLION OZ

MARCH 28/WITH SILVER UP 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.005 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 424.085 MILLION OZ

MARCH 27/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A A DEPOSIT OF 1.691 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 423.079 MILLION OZ

MARCH 26/WITH SILVER DOWN 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A A DEPOSIT OF 0.366 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 421.388 MILLION OZ

MARCH 25/WITH SILVER UP 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 3.887 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 421.022 MILLION OZ

MARCH 22/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE DEPOSIT OF 1.1899 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 424.909 MILLION OZ

In this week’s episode, Peter covers the dismal figures released Thursday and Friday, horrible tax policies, and the appalling lack of transparency in our government.

Peter has been predicting stagflation for a while, and now that it’s here, he sees mining stocks as an opportunity:

“That’s one of the reasons I’m so over-weighted in mining stocks, apart from the valuation, is if there is stagflation, you don’t have a better economic environment. Because you have inflation that the Fed can’t fight, because you have a weak economy. So the Fed is reluctant to raise rates, because it’ll weaken the economy further. … Plus, the weak economy widens the budget deficits. And that means a weaker dollar, more money printing, more inflation. So the best possible economic scenario for gold stocks is stagflation, which of course is the worst economic scenario for the economy.”

High consumer spending is especially alarming, considering these figures are probably conservative and underestimate the true extent of inflation in the economy:

“Why are people spending more? Well, because things cost more. That’s why they’re spending more. They’re not buying more. And even though these numbers are supposed to be adjusted for inflation, they’re not because you know the government numbers don’t accurately capture how much inflation there actually is.”

The savings rate also dipped from last month, dropping from 3.6% to 3.2%. Saving is a great economic indicator, as Peter explains:

“This is the lowest savings rate I think in a couple of years. So this is not good news— that Americans are having to deplete their savings. This is bad news. When the economy is good, you save more. That’s when you add to your rainy day fund. You have to tap into it when times are tough and you’re struggling. And that’s exactly what Americans are doing. They’re struggling, and they’re tapping into their savings in order to do it.”

Instead of addressing the Fed’s disastrous monetary policy, the Biden administration is trying to raise taxes on wealthy Americans, which means raising taxes on everyone eventually:

“They’re promising just to tax the rich, right? The millionaires and billionaires. Of course, that’s what they always say. That’s what they said in 1916 when they got the income tax or 16th amendment. It was just to tax Carnegie, Rockefeller, Vanderbilt. They were going to lower taxes on the middle class, right? If we just allow this 4% tiny little tax, that was the maximum bracket. … Next thing you knew that 4% rate was like 70, 80%. And then by the Second World War, they had the withholding tax and pretty much everybody was paying the income tax.”

“It would be very destructive to the economy, to wealth creation, to production, to employment. So it would be a complete economic disaster as well as being unconstitutional. So I mean, the good news is these are just talking points for the election. So it’s not going to actually happen. Now, it might happen if Biden won the election and the Democrats got the House and the Senate. Then it actually might happen. But as of now, it just shows you where they stand, and they’re throwing red meat to their base, which is basically socialist.”

At the end of this episode, Peter updates us on his FOIA request for the closing of his bank in Puerto Rico. After the government essentially refused to disclose all relevant information for his case, Peter explains how corrupt and shady this whole affair is:

“I have a right to see this information, but they don’t want me to see it. I think because it reveals the commission of a crime. And so, you know, the IRS can commit a crime and then they can cover it up. Because they’re the government, right? They prosecute the citizens for committing crimes, but then they get away with murder. They commit crimes all they want because they’re the cops, right? And they make the rules.”

Be sure to check out Peter’s recent interview with Anthony Crudele, in which they discuss the traditional value of gold, Bitcoin’s role in the economy, and the perpetual inflation that defines today’s economy.

END

2.Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens/…

Von Greyerz: The Real Move In Gold & Silver Is Yet To Start

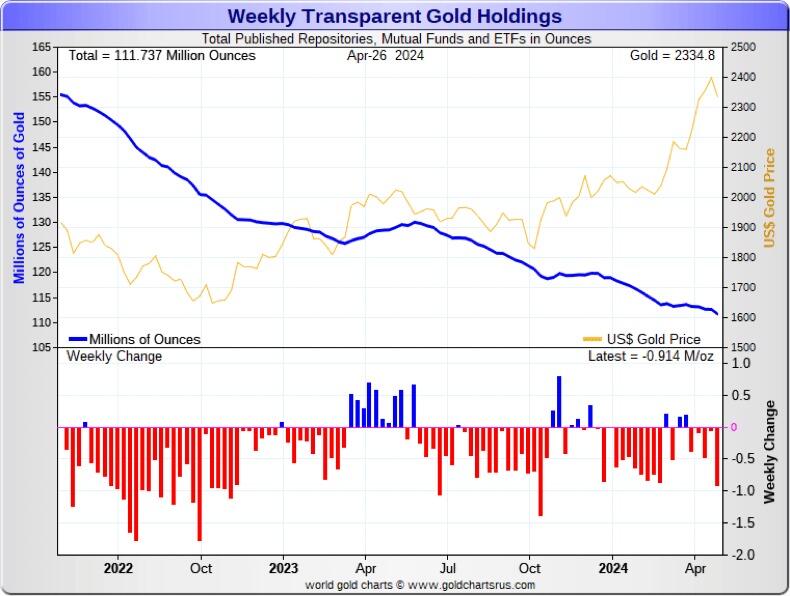

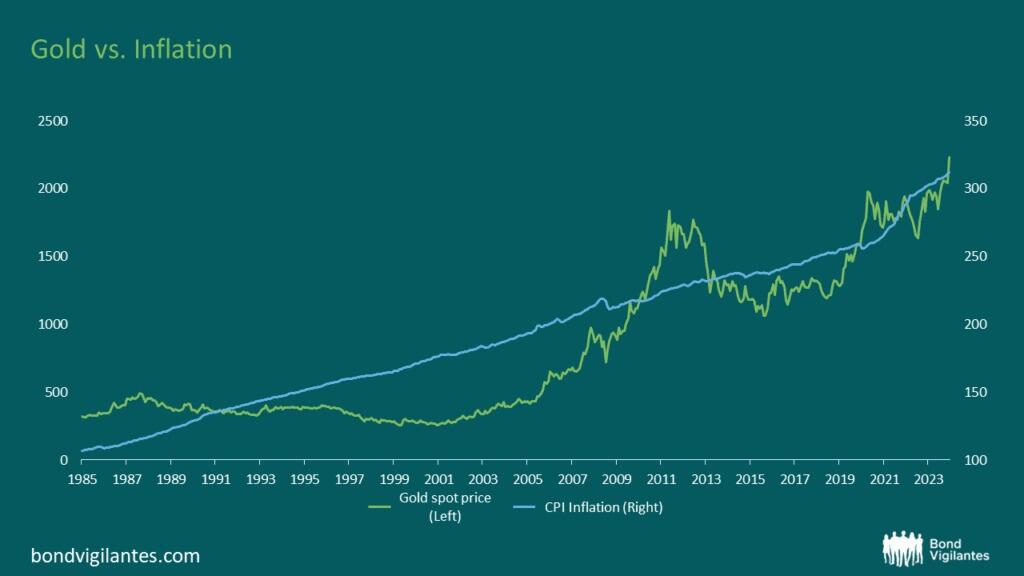

Gold Depositories, Gold Funds and Gold ETFs have lost just under 1,400 tonnes of their gold holdings in the last 2 years since May 2022.

But not only gold funds are seeing weak buying but also mints such as the Perth Mint and the US Mint with its coin sales down 96% year on year.

Clearly gold knows something that the market hasn’t discovered yet.

RATES MUCH HIGHER

For the last few years I have been clear that there will be no lasting interest rate cuts.

As the chart shows below, the 40 year down trend in US rates bottomed in 2020 and since then rates are in a secular uptrend.

I have discussed this in many articles as well as in for example this interview from 2022 when I stated that rates will exceed 10% and potentially much higher in the coming inflationary environment, fuelled by escalating deficits and debt explosion.

“But the Fed will keep rates down” I hear all the experts call out!

Finally the “experts” are changing their mind and believe that cuts will no longer happen.

No central bank can control interest rates when its government recklessly issues unlimited debt and the only buyer is the central bank itself.

PONZI SCHEME WORTHY OF A BANANA REPUBLIC

This is a Ponzi scheme only worthy of a Banana Republic. And this is where the US is heading.

So strongly rising long rates will pull short rates up.

And that’s when the fun panic starts.

As Niall Ferguson stated in a recent article:

“Any great power that spends more on debt service (interest payments on the national debt) than on defence will not stay great for very long. True of Habsburg Spain, true of ancien régime France, true of the Ottoman Empire, true of the British Empire”.

So based on the CBO (Congressional Budget Office), the US will spend more on interest than defence already at the end of 2024 as this chart shows:

But as often is the case, the CBO prefers not to tell uncomfortable truths.

The CBO forecasts interest costs to reach $1.6 trillion by 2034. But if we extrapolate the trends of the deficit and apply current interest rate, the annualised interest cost will reach $1.6 trillion at the end of 2024 rather than in 2034.

Just look at the steepness of the interest cost curve above. It is clearly EXPONENTIAL.

Total Federal debt was below $1 trillion in 1980. Now, interest on the debt is $1.6 trillion.

Debt today $35 trillion rising to $100 trillion by 2034.

The same with the US Federal Debt. Extrapolating the trend since 1980, the debt will be $100 trillion by 2036 and that is probably conservative.

With the interest trend up as explained above, a 10% rate in 2036 or before is not unrealistic. Remember rates back in the 1970s and early 1980s were well above 10% with a much lower debt and deficit.

US BONDS – BUY THEM AT YOUR PERIL

Let us analyse the current and future of a US treasury debt (and most sovereign debt):

Issuance will accelerate exponentially

It will never be repaid. At best only deferred or more probably defaulted on

The value of the currency will fall precipitously

HYPERINFLATION COMING

So where are we heading?

Most probably we are facing an inflationary period leading to probable hyperinflation

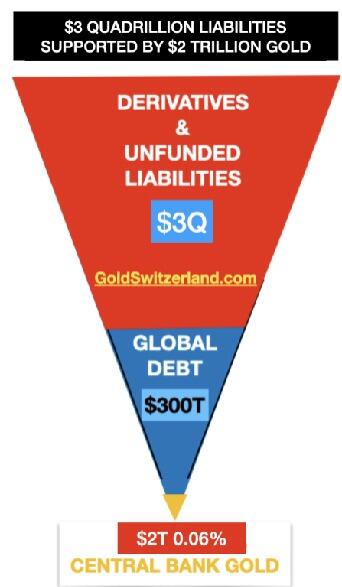

With global debt already up over 4x this century from $80 trillion to $350 trillion. Add to that a Derivative mountain of over $2 quadrillion plus unfunded liabilities and the total will exceed $3 quadrillion.

As central banks frenetically try to save the financial system, most of the 3 quadrillion will become debt as counterparties fail and banks will need to be saved with unlimited money printing.

But neither a bank nor a sovereign state can be saved by issuing worthless pieces of paper or digital money.

In March 2023, four US banks collapsed within a matter of days. And soon thereafter Credit Suisse was in trouble and had to be rescued.

The problems in the banking system have just started. Falling bond prices and collapsing values of property loans are just the beginning.

This week Republic First Bancorp had to be saved.

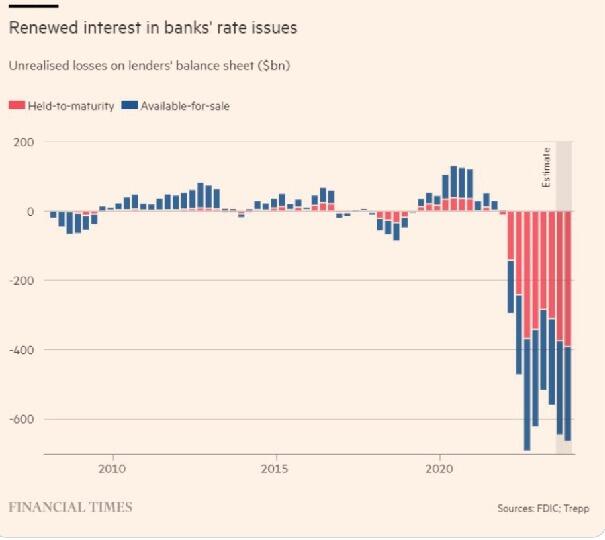

Just look at US banks’ unrealised losses on their bond portfolios in the graph below.

Unrealised losses on bonds held to maturity are $400 billion.

And losses on bonds available for sale are $250 billion. So the US banking system is sitting on identified losses of $650 billion just on their bond portfolios. As interest rates go up, these losses will increase.

Add to that, losses on loans against collapsing commercial property values and much more.

EXPONENTIAL MOVES

So we will see debt grow exponentially as it has already started to do. Exponential moves start gradually and then suddenly whether we talk about debt, inflation or population growth.

The stadium analogy below shows how it all develops:

It takes 50 minutes to fill a stadium with water, starting with one drop and doubling every minute – 1, 2, 4, 8 drops etc. After 45 minutes the stadium is only 7% full and the last 5 minutes it goes form 7% to 100%.

THE LAST 5 MINUTES OF THE FINANCIAL SYSTEM

So the world is most probably now in the last 5 minutes of our current financial system.

The coming final phase is likely to go very fast as all exponential moves do, just like in the Weimar Republic in 1923. In January 1923 one ounce of gold cost 372,000 marks and at the end of November in 1923 the price was 87 trillion marks!

The consequences of a collapse of the financial system and the global economy, especially in the West can take many decades to recover from. It will involve a debt and asset implosion plus a massive contraction of the economy and trade.

The East and South and especially the countries with major commodity reserves will recover much faster. Russia for example has $85 trillion in commodity reserves, the biggest in the world.

As US issuance of treasuries accelerate, the potential buyers will decline until there is only one bidder which is the Fed.

Even today no sane sovereign state would buy US treasuries. Actually no sane investor would buy US treasuries.

Here we have an already insolvent debtor that has no means of repaying his debt except for issuing more of the same rubbish which in future would only be good for toilet paper. But electronic paper is not even good for that.

This is a sign in a Zimbabwe toilet:

Let us analyse the current and future of a US treasury debt (and most sovereign debt):

Issuance will accelerate exponentially

It will never be repaid. At best only deferred or more probably defaulted on

The value of the currency will fall precipitously

That’s all there is to it. Thus anyone who buys US treasuries or other sovereign bonds has a 99.9% guarantee of not getting his money back.

So Bonds are no longer an asset of value but just a liability for the borrower that will or can not be repaid.

What about stocks or corporate bonds. Many companies won’t survive or experience a major decline in the stock price together with major cash flow pressures.

As I have discussed in many articles, we are entering the era of commodities and especially precious metals.

The coming era is not for speculation but for trying to keep as much of what you have as possible. For the investor who doesn’t protect himself, there will be a wealth destruction of an unprecedented magnitude.

There will no longer be a question what return you can get on your investment.

Instead it is a matter of losing as little as possible.

Holding stocks, bonds or property – all the bubble assets – are likely to lead to massive wealth erosion as we go into the “Everything Collapse”.

THE NEW ERA OF GOLD AND SILVER

For soon 25 years I have been urging investors to hold gold to preserve their wealth. Since the beginning of this century gold has outperformed most asset classes.

Between 2000 and today, the S&P, including reinvested dividends, has returned 7.7% per annum whilst gold has returned 9.2% per year or 8X.

In the next few years, all the factors discussed in this article will lead to major gains in the precious metals and falls in most conventional assets.

There are many other positive factors for gold.

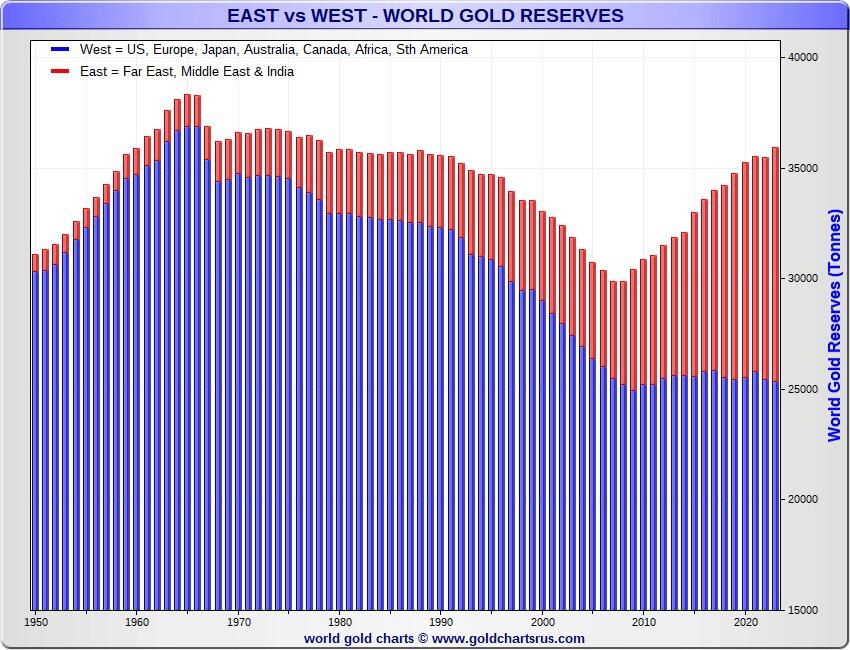

As the chart below shows, the West has reduced its gold reserves since the late 1960s, whilst the East is growing its gold reserves strongly. And we have just seen the beginning of this trend.

The US and EU sanctioning of Russia and the freezing/confiscation of the Russian assets in foreign banks are very beneficial for gold.

No sovereign states will hold their reserves in US dollars any more. Instead we will see central bank reserves move to gold. That shift has already started and is one of the reasons for gold’s rise.

In addition, gradually the BRICS countries are moving away from the dollar to trading in their local currencies. For commodity rich countries, gold will be an important part of their trading.

Thus there are major forces behind the gold move which has just started and will reach further both in price and time than anyone can imagine.

HOW TO OWN GOLD

But remember for investors, holding gold is for financial survival and protection of assets.

Therefore gold must be held in physical form outside the banking system with direct access for the investor.

Also gold must be held in safe jurisdictions with a long history of rule of law and stable government.

The cost of storing gold should not be the primary consideration for choosing a custodian. When you buy life insurance you mustn’t buy the cheapest but the best.

First consideration must be the owners and management. What is their reputation, background and previous history.

Thereafter secure servers, security, liquidity, location and insurance are very important.

Also, high level of personal service is paramount. Many vaults fail in this area.

Preferably gold should not be held in the country where you are resident, especially not in the US with its fragile financial system.

Neither gold nor silver has started the real move yet. Any major correction is likely to come from much higher levels.

Gold and silver are in a hurry so it is not too late to jump on the gold wagon.

Since the October 2023 gold low of just over $1,600 gold is up but is anyone buying?

Well no, certainly none of the normal playe

END

3. CHRIS POWELL//GATA DISPATCHES

Chinese public is buying more than twice as much gold as the nation mines

Submitted by admin on Mon, 2024-04-29 13:29 Section: Daily Dispatches

China’s consumers seek security in gold, ‘the only safe asset’

By Mia Nulimalmaiti South China Morning Post, Hong Kong Monday, April 29, 2024

Chinese consumers are increasing their appetite for gold, seeking to protect their assets amid a volatile stock market, a depreciating yuan, and property doldrums, which analysts said would continue to boost international gold prices coupled with geopolitical uncertainties.

Consumers in China bought 308.9 tonnes (10.9 million ounces) of gold in the first quarter, representing a 5.9 per cent increase compared with the same period in 2023, according to data released by the China Gold Association on Friday

Purchases of gold bars and coins, which largely reflect investment and hedging demand, surged by 26.8% year on year to 106.3 tonnes, while gold jewellery sales declined by 3% from a year earlier to 183.9 tonnes.

But China’s domestic gold production rose by 21.2% to only 139.184 tonnes in the first three months of the year, with 53.2 tonnes produced with imported ores or materials, indicating an overreliance on overseas suppliers. …

This year we will adjust investment proportions by reducing assets that could be affected by war and increasing investments in alternative assets such as gold and oil, which help to mitigate risk,” he said.

Gold and oil account for about 5% of the fund’s portfolio. …

Trump allies draw plans to reduce Fed’s independence

Submitted by admin on Sat, 2024-04-27 13:27 Section: Daily Dispatches

By Andrew Restuccia, Nick Timiraos, and Alex Leary The Wall Street Journal Friday, April 26, 2024

WASHINGTON — Donald Trump’s allies are quietly drafting proposals that would attempt to erode the Federal Reserve’s independence if the former president wins a second term, in the midst of a deepening divide among his advisers over how aggressively to challenge the central bank’s authority.

Former Trump administration officials and other supporters of the presumptive Republican nominee have in recent months discussed a range of proposals, from incremental policy changes to a long-shot assertion that the president himself should play a role in setting interest rates

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS

end

5 a. IMPORTANT COMMENTARIES ON COMMODITIES/

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP 7.2410

OFFSHORE YUAN: UP TO 7.2493

SHANGHAI CLOSED DOWN 8.22 PTS OR 0.28%

HANG SENG CLOSED UP 16.12PTS OR 0.09%

2. Nikkei closed UP 420.90 PTS OR 1.24%

3. Europe stocks SO FAR: ALL MOSTLY RED

USA dollar INDEX DOWN TO 105.84 EURO RISES TO 1.0723 UP 8 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.869 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 156.99JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN/ OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UPTO +2.5495/Italian 10 Yr bond yield DOWN to 3.832 SPAIN 10 YR BOND YIELD DOWN TO 3.315

3i Greek 10 year bond yield DOWNTO 3.420

3j Gold at $2310.30 //Silver at: 26.45 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 32/100 roubles/dollar; ROUBLE AT 93.32/

3m oil into the 83 dollar handle for WTI and 87 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 156.99/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.869% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9126 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9786 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

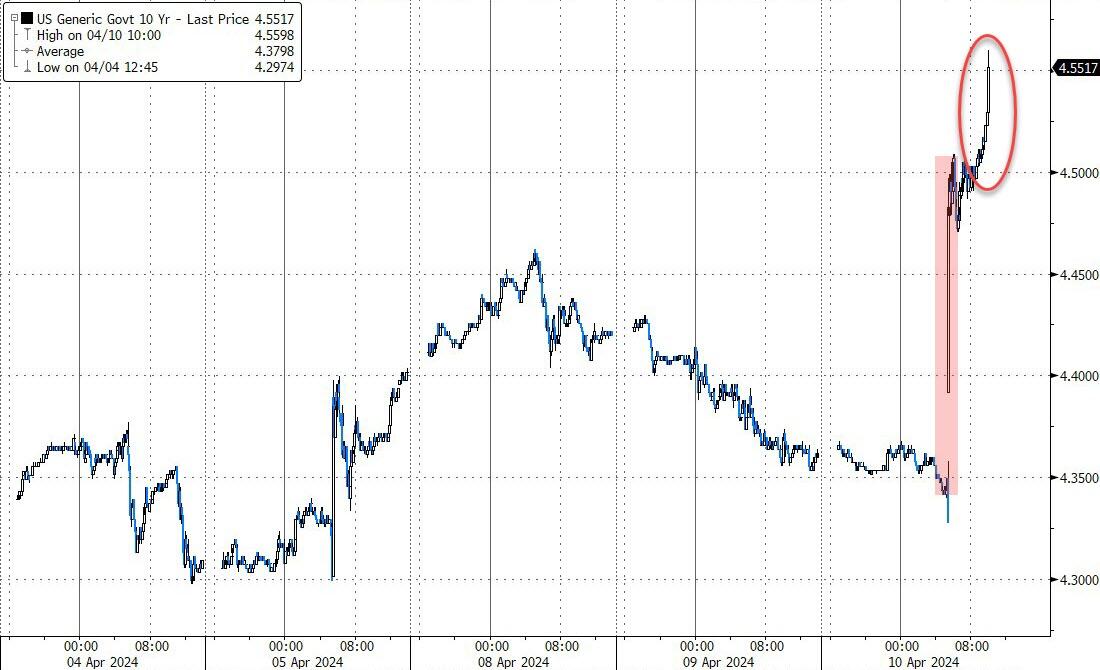

USA 10 YR BOND YIELD: 4.618 DOWN 0 BASIS PTS…

USA 30 YR BOND YIELD: 4.736 DOWN 0 BASIS PTS/

USA 2 YR BOND YIELD: 4.970 DOWN 0 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.38…(TURKEY)

10 YR UK BOND YIELD: 4.3490 UP 6 PTS

2a New York OPENING REPORT

US Futures Dip On Last Day Of April, First Down Month Of 2024

TUESDAY, APR 30, 2024 – 08:15 AM

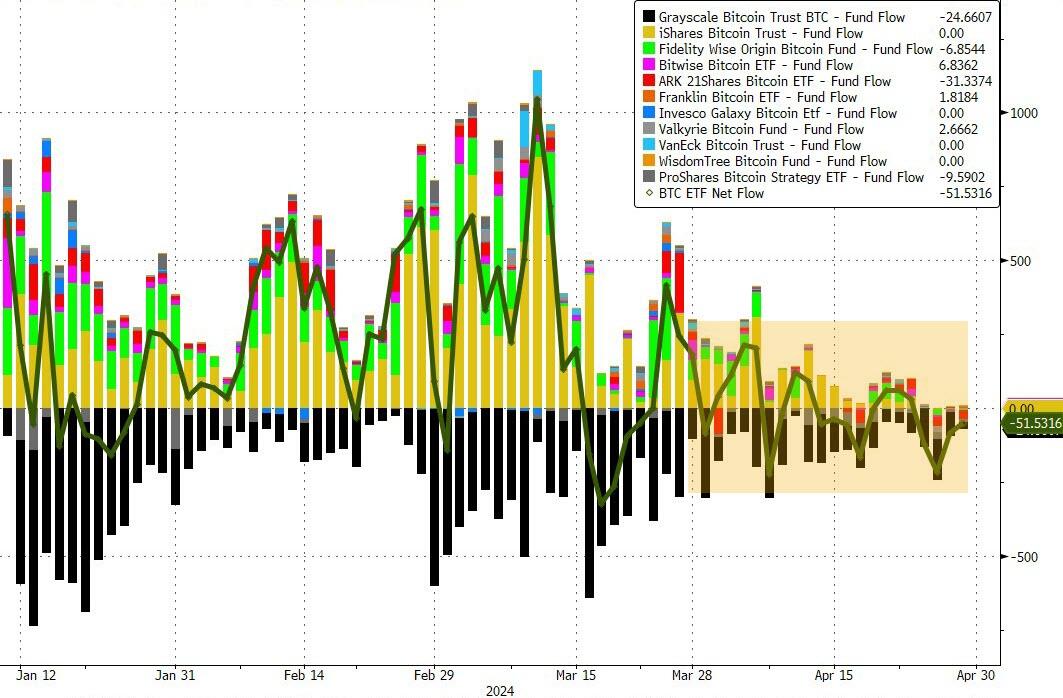

US equity futures dropped, and European markets were mixed on the last day of the month amid concerns the Fed may stick to its hawkish messaging at its meeting on Wednesday. As of 7:40am, S&P 500 and Nasdaq futures were down 0.1% while Europe’s Stoxx 600 index retreated 0.4%, while Asian stocks gained on Japan’s return from holiday. The Bloomberg Dollar Spot Index climbed and 10-year Treasury yields were steady at 4.62%. The yen resumed its decline even as a Bloomberg analysis found that Japan almost certainly conducted its first currency intervention since 2022 to prop up the yen on Monday. Commodities were mixed with metals down and oil rebounding from its biggest drop in almost two weeks amid discussions on a possible cease-fire in the Middle East. Macro data today includes Q1 employment cost index, Case Shiller home prices, April MNI Chicago PMI, consumer confidence and Dallas Fed services activity. Bitcoin tumbled after activity on Hong Kong’s new crypto ETFs came in far below expectations.

In premarket trading, HSBC Holdings climbed more than 3% after solid earnings and the surprise departure of CEO Noel Quinn, which some analysts said could pave the way for the next stage in the bank’s growth plans. Chegg shares fell 13% after the online educational platform company forecast total net revenue for the second quarter that missed the average estimate. Here are some other notable premarket movers:

Blend Labs shares jump 20% after it reported a $150 million investment by Haveli Investments in the form of convertible preferred stock with a zero percent coupon.

Coursera’s shares drop 14%, putting them on track for a one-year low, after the online educational firm cut full-year revenue and adjusted-Ebitda forecasts, prompting analysts to lower their price targets on the stock.

NXP Semiconductors shares rose 3.6% after the chipmaker reported better-than-expected 1Q adjusted earnings per share and forecast 2Q adjusted EPS and revenue largely above average analyst expectations.

Paramount Global analysts note that investors are more focused on the Skydance deal rather than results this quarter. The media company replaced CEO Bob Bakish as the board negotiates a possible change in control of the company. Shares in the company fell about 0.4% in premarket trading.

US stocks are on the edge of closing out the first monthly retreat of 2024, with the S&P 500 down 2.6% in April. Amazon.com, McDonald’s and Coca-Cola are due to report later today, but all eyes are on Fed Chair Powell who will likely bolster expectations interest rates will stay higher for longer after Wednesday’s rates announcement.

“Sentiment is positive but reserved,” said Peter Rosenstreich, head of investment products at Swissquote. “There has been plenty of hype around rates, earnings and the macro environment — now markets want to see the results.”

Meanwhile, as we reported first last night, Goldman’s desk calculated that momentum traders are modeled to buy equities over the next week, regardless of market direction. Commodity trading advisers — funds that use systematic strategies to trade futures contracts — are exposed to about $106 billion in long positions after the drawdown in April, Cullen Morgan, an equity derivatives and flows specialist at the bank, wrote in a note. That’s set to support a bounce in global equities after a rough month.

European stocks also fall, led by declines in autos as Volkswagen and Mercedes Benz shares fall post-earnings which offset better-than-expected European economic data. Here are the biggest movers Tuesday:

Logitech shares soar as much as 10%, the most in six months, after the Swiss maker of computer accessories reported better-than-expected FY25 sales guidance

Cargotec jumps as much as 17% to a fresh high after the Finnish crane and cargo-handling equipment firm reports “record” first-quarter earnings boosted by its Marine division

HSBC shares advanced as much as 3.6% after the lender announced a larger buyback than expected and reported earnings that analysts saw as solid

OMV shares jump as much as 5.3%, largest intraday rise since November, after Austrian refiner reported 1Q clean CCS operating profit beat

Clariant shares gain as much as 4.8%, to the highest level in more than six months after the Swiss specialty chemicals firm’s margins beat consensus despite some challenges

Rotork shares rise 3.9% after the valve manufacturer reported a solid start to the year. Sales and orders both grew, while its book-to-bill ratio also improved

European automakers shares fall as 1Q numbers from Stellantis, Volkswagen and Mercedes disappointed the market, making the SXAP auto index the worst performing subsector

Straumann shares drop as much as 10%, the most since Oct. 26, after a soft performance in North America overshadowed the Swiss dental equipment company’s 1Q revenue beat

SES depositary receipts drop as much as 12% after the satellite firm agreed to buy Intelsat for $3.1 billion, in a deal to be funded by cash on hand and new debt

Air France-KLM falls as much as 4.7% after carrier reports a wider operating loss than expected in the first quarter. Bernstein says one-off costs weighed on profitability

Santander shares drop as much as 2.9% after forecast-beating net interest income and fees in the first quarter were offset by a cost surge at the Spanish lender

Adidas shares fell as much as 1.6% as 1Q results broadly confirmed a recent pre-release, and the sportswear maker’s guidance was seen by some as conservative

Earlier in the session, Asian stocks advanced for a third day, led by a rally in Japanese shares as the yen stabilized following wild swings in the previous session. The MSCI Asia Pacific Index rose as much as 1.1%, led by industrial shares such as Hitachi and Toyota Motor. Japan’s Topix Index jumped more than 2% as the market reopened from a holiday. Traders remain on alert for sharp yen moves after the currency’s rebound from a 34-year low sparked speculation of intervention.

“While we remain constructive on the Japan equity market over the medium term, we also believe that near-term FX movement is likely to see some profit taking from investors in the broad Japanese equity market,” said Ricky Tang, head of client portfolio management at Value Partners Group.

In FX, the dollar gained against all its major peers on expectation of a hawkish message from the Federal Reserve on Wednesday. The euro outperformed and the region’s government bonds fell after data showed the largest economies of the bloc were stronger than expected in the first quarter. The yen weakens towards 157 against the dollar. The Aussie underperforms, falling 0.5% after retail sales missed estimates.

In rates, treasuries are slightly cheaper across the curve, paring a portion of Monday’s gains, amid steeper declines for bunds after first estimate of 1Q euro-zone growth rate topped estimates. US yields cheaper by 0.5bp to 1.5bp across the curve with losses led by intermediates, steepening 2s10s spread by 1bp on the day; 10-year yields around 4.63% with bunds underperforming by 1.5bp in the sector. Also during London morning, an array of regional inflation readings lifted intermediate German yields by ~3bp. Bunds are in the red, with German 10-year yields rising 2bps to 2.55%. S&P 500 futures are down 0.1%.

In commodities, oil prices advanced, with WTI rising 0.2% to trade near $82.80. Spot gold falls 0.8%.

Looking at today’s calendar, we have the 1Q employment cost index (8:30am), February FHFA house price index, S&P CoreLogic home prices (9am), April MNI Chicago PMI (9:45am, 3 minutes earlier for subscribers), consumer confidence (10am) and Dallas Fed services activity (10:30am). Fed members are in self-imposed quiet period ahead of May 1 policy announcement.

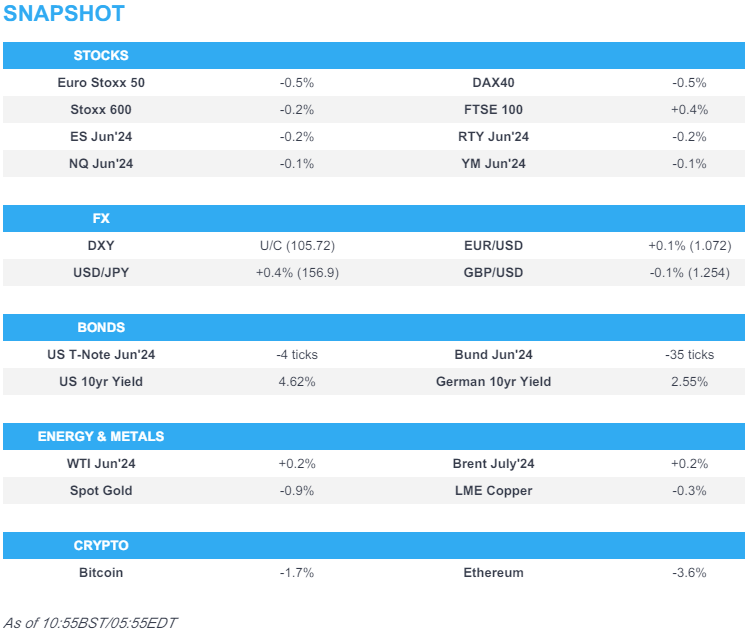

Market Snapshot

S&P 500 futures down 0.1% to 5,139.50

STOXX Europe 600 down 0.2% to 507.25

MXAP up 0.7% to 174.73

MXAPJ little changed at 540.41

Nikkei up 1.2% to 38,405.66

Topix up 2.1% to 2,743.17

Hang Seng Index little changed at 17,763.03

Shanghai Composite down 0.3% to 3,104.82

Sensex up 0.5% to 75,063.11

Australia S&P/ASX 200 up 0.3% to 7,664.08

Kospi up 0.2% to 2,692.06

German 10Y yield little changed at 2.54%

Euro down 0.2% to $1.0700

Brent Futures little changed at $88.47/bbl

Gold spot down 0.9% to $2,314.21

US Dollar Index up 0.31% to 105.90

Top Overnight News

China’s NBS PMIs for April are mixed, with manufacturing about inline at 50.4 (vs. the Street 50.3 and down from 50.8 in Mar) while non-manufacturing fell short at 51.2 (vs. the Street 52.3 and down from 53 in Mar). China’s Caixin manufacturing PMI came in at 51.4, slightly ahead of the Street’s 51 forecast. WSJ

China’s ruling Communist Party vowed to explore new measures to tackle a protracted housing crisis, which remains the biggest drag on the nation’s economy, and hinted at possible rate cuts ahead. BBG

HSBC’s chief executive Noel Quinn is to retire unexpectedly after five years, setting off a hunt for a successor at the UK-based bank. Quinn, 62, has overhauled the lender since taking charge in 2019, selling off parts of its global operations to increase its focus on Asia, where it makes the lion’s share of its profits. FT

BOJ accounts suggest Japan probably intervened in the FX market yesterday, buying around 5.5 trillion yen. Officials have declined to say whether they stepped in. BBG

The chief executive of Ericsson said a focus on regulation was “driving Europe to irrelevance” as he warned that the region’s competitiveness was being undermined and called for changes to antitrust policy. FT

EU’s Apr CPI was inline with the Street on a headline basis at +2.4% (unchanged vs. Mar) and a bit firmer on core (+2.7% vs. the Street +2.6% and vs. +2.9% in Mar). BBG

ECB’s Knot says it is “realistic” to anticipate a cut in June and expresses confidence in inflation coming back to 2%, although he doesn’t envision rates returning to their pandemic/pre-pandemic lows. Nikkei

Tensions grow between Trump and Lake in Arizona race for Senate. The former president fears that GOP candidate Kari Lake might not win and will drag down his own prospects in the battleground state. WaPo

Apple has poached dozens of artificial intelligence experts from Google and has created a secretive European laboratory in Zurich, as the tech giant builds a team to battle rivals in developing new AI models and products. FT

Caterpillar Caterpillar announced a voluntary delisting from Euronext Paris and the Six Swiss Exchange; cites low trading volumes and high administrative costs. CAT will solely trade on NYSE thereafter. (Newswires)

Tesla (TSLA) CEO Musk is reportedly planning more layoffs as two senior executives depart, while roughly 500 people will be laid off in supercharger group, according to The Information. (The Information)

WSJ’s Timiraos article “Fed to Signal It Has Stomach to Keep Rates High for Longer” & “Firmer price pressures could lead longer-term rates to rise as investors continue paring back expectations of cuts”

Earnings

NXP Semiconductors NV (NXPI) Shares climb 3.4% pre-market on top- and bottom-line beats, and guidance. Q1 adj. EPS 3.24 (exp. 3.16), Q1 revenue USD 3.13bln (exp. 3.13bln). Q1 gross margin 58.2% (exp. 58%), Q1 operating margin 34.5% (exp. 34%). Auto revenue -1% Y/Y, Industrial/IoT +14%, Mobile +34%, Communications Infrastructure -25% Y/Y. Exec said early views into H2 underpin a cautious optimism. Sees Q2 revenue of 3.125bln (exp. 3.11bln), Q2 EPS of 3.20 (exp. 3.12).

Paramount Global (PARA) Q1 Adj. EPS 0.62 (exp. 0.36), Q1 revenue USD 7.69bln (exp. 7.73bln); Q1 Paramount+ net additions +3.7mln (exp. +2.2mln); Q1 EBITDA USD 0.987bln (exp. 0.756bln), Q1 FCF USD 209mln (exp. -62mln). President and CEO Bob Bakish stepped down, as many press reports suggested he would do over the weekend. Establishes a management committee; George Cheeks, Chris McCarthy, and Brian Robbins will work with CFO Naveen Chopra to accelerate growth, streamline operations, and optimise streaming strategy; Chair Shari Redstone (of National Amusements) has expressed confidence in their leadership.

Adidas (ADS GY) Q1 (EUR): Revenue 5.45bln (exp. 5.46bln, prev. 5.27bln Y/Y). Currency-neutral sales +8% driven by growth in all regions except in North America, where revenue fell by 4% to 1.12bln. Europe: +14%.

Stellantis (STLAM IM/STLAP FP) Q1 (EUR): Revenue 41.7bln (exp. 43.92bln), -12% Y/Y due to “volume, mix and foreign exchange headwinds, partly offset by firm net pricing”.

HSBC (5 HK/ HSBA LN) Q1 (USD): Revenue 20.75bln (exp. 21.03bln). Pretax profit 12.65bln (exp. 12.61bln). CET1 ratio 15.2% (exp. 15.4%). CEO Quinn is unexpectedly retiring.

A more detailed look at markets courtesy of Newsquawk

APAC stocks were mostly higher but with gains capped heading into month-end amid a slew of data and earnings. ASX 200 was led by strength in the mining sector but with upside limited after a surprise contraction in Retail Sales. Nikkei 225 outperformed on return from the long weekend and as participants digested a slew of earnings releases. Hang Seng and Shanghai Comp. were varied in which the former made another brief foray into bull market territory, while the mainland lagged ahead of the Labour Day holidays and as participants reflected on mixed Chinese PMI data in which the official NBS Manufacturing and Caixin Manufacturing PMIs topped forecasts but Non-Manufacturing PMI disappointed despite remaining in expansion territory.

Top Asian News

PBoC injected CNY 440bln via 7-day reverse repos with the rate at 1.80%.

PBoC reportedly wants to halt the bond-buying spree and not join in on it, with the central bank concerned about bond market bubbles and economic gloom, according to Bloomberg.

Japan’s top currency diplomat Kanda said no comment on FX intervention and noted that a weak yen has positive and negative impacts, while he added the currency has a bigger impact on import prices now and that excessive FX moves could impact daily lives. Kanda said they need to take appropriate actions on FX and reiterated they are ready to take action 24 hours a day and will continue taking appropriate actions when needed.

BoJ keep monthly bond purchases plan for May unchanged from April

China’s Communist Party Central Committee is to hold a 3rd plenum during July, via State Media; Politburo undertook a meeting on Tuesday.

Former Japanese top FX diplomat Furusawa says it is highly likely the Japanese government intervened on Monday to prop up the JPY

European bourses, Stoxx600 (-0.3%) are mixed, with a slight negative bias. Indices initially opened around flat, though tilted lower as the morning progressed, with little driving the shift in sentiment. European sectors hold little bias, with the breadth of the market fairly narrow, with the exception of Autos, dragged down by poor results from Mercedes (-3.4%), Stellantis (-2.4%) and Volkswagen (-2.1%). Real Estate tops the pile, propped up by post-earning gains in Vonovia (+5.5%). US Equity Futures (ES -0.2%, NQ -0.2%, RTY -0.3%) are modestly softer, in fitting with the broader price action seen in European trade. Earnings include: McDonald’s, AMD, Amazon and Starbucks.

Top European News

ECB’s Knot said he is increasingly confident inflation is falling towards the 2% target but the ECB must be cautious beyond a June rate cut.

FX

USD is attempting to claw back some of yesterday’s JPY-induced losses which sent the index down to a low of 105.46. For now, the DXY has topped out at 105.96 and unable to reclaim 106 status, 106.18 was the high from yesterday. Recent EUR strength in the wake of the EZ data has led the index back down to the unchanged mark.

EUR is slightly firmer vs. the broadly flat USD in the wake of a slew of EZ data with EUR being propped up by firmer than expected growth metrics. Inflation data was in-line on a headline basis and mixed from a core perspective.

JPY is softer vs. the USD after yesterday’s wild (touted intervention led) session which saw USD/JPY swing from a 160.20 peak to a 154.51 low; currently trades towards the top end of a 156.08-99 range.

Antipodeans are giving back yesterday’s gains and then some as the USD regains some poise. AUD/USD had advanced to a peak of 0.6586 yesterday (highest since April 12th) before pulling back as low as 0.6514 with soft retail sales also acting as a drag.

Fixed Income

Bunds began on the backfoot after hotter than expected French inflation and a sticky Services metric, with additional pressure coming from better-than-forecast GDP prints by France & Germany ahead of the EZ figures. EZ HICP headline Y/Y was in-line with the core metrics mixed against expected, which led to a hawkish reaction; Bunds currently sit at session lows around 130.40 given the strong GDP numbers and potentially mixed core.

USTs are moving in tandem with EGBs which leaves the benchmark a touch softer but some way from Monday’s 107-18+ base. Specifics light thus far into Wednesday’s FOMC and Quarterly Refunding.

Gilts are once again following EGB/UST impetus. A narrative that is unlikely to change significantly in the near-term given a sparse UK docket before next week’s BoE; though, we are attentive to anything from the EZ/US, particularly around the Fed, which provides insight into the Central Bank divergence narrative.

UK sells GBP 4bln 4.125% 2029 Gilt: b/c 3.21x, average yield 4.251%, tail 0.8bps.

Commodities

Crude futures are choppy and now in modest positive territory after earlier subdued trade. Prices are on standby ahead of key macro risk events including the FOMC and US jobs data on Friday; Brent July similarly found an intraday base at USD 86.64/bbl.

Softer trade across precious metals amid yesterday’s geopolitical unwind coupled with a rebound in the Dollar today. Spot silver sits as the laggard after yesterday’s outperformance; XAU fell under yesterday’s low (USD 2,319.84/oz) to a current base at USD 2,310.96/oz.

Losses seen across base metals amid the aforementioned Dollar rebound coupled with a pullback in sentiment. 3M LME copper topped USD 10,200/t earlier to reach a USD 10,217.00/t intraday peak.

Geopolitics

“IDF finalizes Rafah plans, invasion possible if no deal in 72 hours”, according to Times of Israel.

“Israeli delegation will not head to Cairo until Hamas gives its response, according to Israeli official”, according to Walla’s Elster.

Hamas is expected to respond to the exchange deal proposal “tomorrow evening”, Al Arabiya reports

Hamas delegation left Cairo and will return with a written response to the ceasefire proposal, according to Egypt’s Al Qahera News.

An Israeli delegation plans to travel to Cairo to resume ceasefire talks if Hamas agrees to attend, according to NYT.

Israeli PM Netanyahu asked US President Biden to help prevent the ICC from issuing arrest warrants against Israeli officials, according to Axios.

Yemen’s Houthis said they targeted the ‘Cyclades’ vessel and two US destroyers in the Red Sea, while it also targeted ‘Israeli ship MSC Orion’ in the Indian Ocean, according to Reuters. US CENTCOM later confirmed that Iranian-backed Houthis fired three anti-ship ballistic missiles and three UAVs from Yemen into the Red Sea towards MV Cyclades but added there were no injuries or damages reported by US, coalition or merchant vessels.

Chinese Coast Guard expelled a Philippines Coast Guard ship and vessels from waters adjacent to the Scarborough Shoal.

Shanghai Maritime Safety Administration said military activities will be carried out in a part of the East China Sea from 07:00 AM on May 1st to 09:00 AM on May 9th local time and vessels unrelated to the activity are prohibited from entering the area.

US Event Calendar

08:30: 1Q Employment Cost Index, est. 1.0%, prior 0.9%

09:00: Feb. FHFA House Price Index MoM, est. 0.2%, prior -0.1%

09:00: Feb. S&P CS Composite-20 YoY, est. 6.70%, prior 6.59%

Feb. S&P/CS 20 City MoM SA, est. 0.10%, prior 0.14%

Feb. S&P/Case-Shiller US HPI YoY, est. 6.38%, prior 6.03%

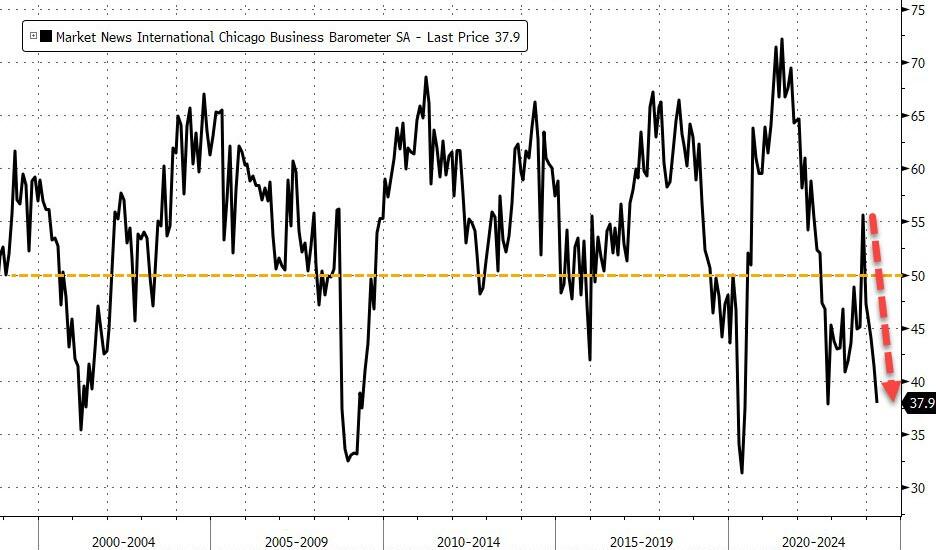

09:45: April MNI Chicago PMI, est. 45.0, prior 41.4

10:00: April Conf. Board Consumer Confidenc, est. 104.0, prior 104.7

April Conf. Board Present Situation, prior 151.0

April Conf. Board Expectations, prior 73.8

10:30: April Dallas Fed Services Activity, prior -5.5

DB’s Jim Reid concludes the overnight wrap

Markets got the week off to a decent start yesterday, with the S&P 500 (+0.32%) building on last week’s advance as we await the Fed’s decision tomorrow and an array of earnings releases. Several factors helped to boost sentiment, including a remarkable advance for Tesla (+15.31%) as outlets including Bloomberg and the Wall Street Journal reported that Chinese government officials had given the firm in-principle approval for its driver-assistance system. In addition, investors were reassured after there was nothing alarming in the flash CPI releases from several European countries, which cemented expectations that the ECB would deliver a rate cut in June. And alongside that, concern about a geopolitical escalation continued to ebb, with Brent crude oil prices down -1.23% to $88.40/bbl. So there were several positive catalysts helping to boost sentiment. The Yen’s range of around 160.25 – 154.5 was a constant side show all day, with heavy speculation that the government had intervened in very thin holiday trading. As we type this morning the Yen is trading down slightly at 156.75 from 156.35 as the US closed last night, which continues to leave it as the worst performing G10 currency year-to-date, down -10% against the US dollar. The intervention hasn’t been officially confirmed but top currency official Kanda has commented that the authorities are watching the Yen 24 hours a day and suggested they were looking more for the size of moves rather than specific levels.

Staying in Asia, China’s factory activity remained in expansion territory for the second consecutive month in April but the pace of expansion slowed slightly as the official manufacturing PMI came in at 50.4 (v/s 50.3 expected) as against a reading of 50.8 in March. Meanwhile, the decline in non-manufacturing activity was more pronounced as the official PMI moderated to 51.2 (v/s 52.3 expected) down from a reading of 53.0. At the same time, the Caixin manufacturing PMI advanced to 51.4 in April (v/s 51.0 expected), marking the fastest pace since February 2023 and compared to an expansion of 51.1 seen in March. Our Chinese economist reviews the details within today’s PMIs in a note just out here.