GOLD PRICE CLOSED UP $7.60TO $2300.60

SILVER PRICE UP $0.99 TO $26.47

Gold ACCESS CLOSED $2315.30

Silver ACCESS CLOSED: $26.63

The defense of $2300 gold is now upon us and surpassed. Next up $2400 gold//Silver’s next line is $28.42. Then $34.76 …

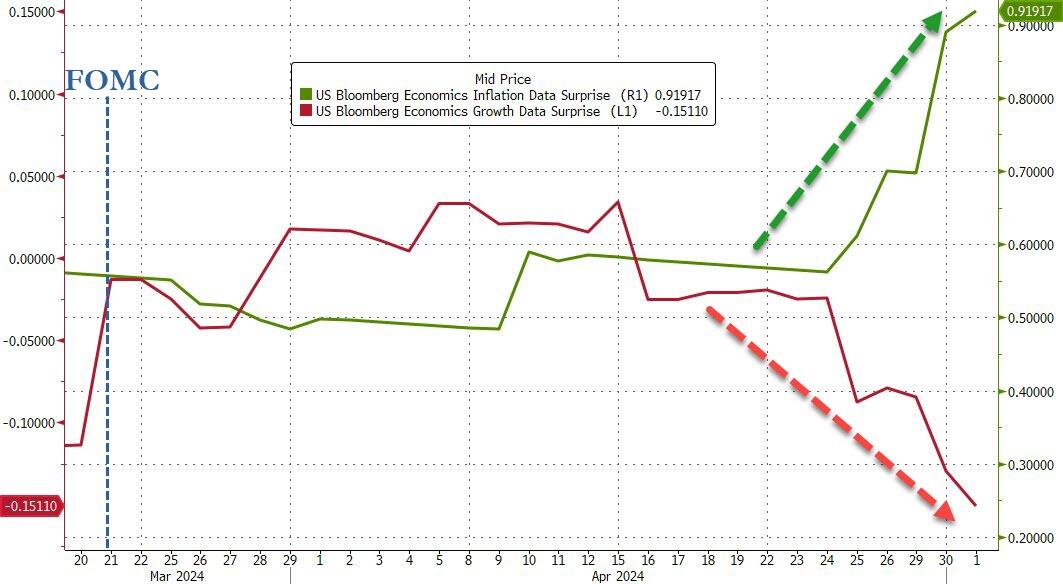

Today the Fed basically stated that interest rates are too high and that they must somehow lower them, However inflation is not cooling. We are heading for stagflation and gold/silver will be huge winners

Bitcoin morning price:$57,565 DOWN 2653 DOLLARS.

Bitcoin: afternoon price: $58,031 DOWN 2187dollars

Platinum price closing UP $10.00TO $946,40

Palladium price; DOWN $12.00 AT $945.15

END

SHANGHAI GOLD PREMIUM 55 DOLLARS/COMEX GOLD

SHANGHAI GOLD…

SHANGHAI GOLD (USD) FUTURES – QUOTES

Last Updated 01 May 2024 12:36:26 PM CT.

Market data is delayed by at least 10 minutes.

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $3183.20 UP 36.50 CDN dollars per oz( * NEW ALL TIME HIGH 3,301.52 CDN DOLLARS PER OZ//APRIL 16 2024)

*BRITISH GOLD: 1851.28 UP 21.20 pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2164.30 UP 18.20 Euros per oz //* (ALL TIME CLOSING HIGH: 2248.89 EUROS PER OZ//APRIL 16.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCGE: COMEX

XCHANGE: COMEX

CONTRACT: MAY 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,291.400000000 USD

INTENT DATE: 04/30/2024 DELIVERY DATE: 05/02/2024

FIRM ORG FIRM NAME ISSUED STOPPED

190 H BMO CAPITAL 4

435 H SCOTIA CAPITAL 19

624 H BOFA SECURITIES 36

657 C MORGAN STANLEY 1

661 C JP MORGAN 11

690 C ABN AMRO 16

737 C ADVANTAGE 90 11

880 C CITIGROUP 24

TOTAL: 106 106

JPMorgan stopped 11/106

FOR MAY2024

GOLD: NUMBER OF NOTICES FILED FOR MAY/2024. CONTRACT: 106 NOTICES FOR 10600 OZ or 0.3297 TONNES

total notices so far: 1541 contracts for 154,100 Oz (4,7932 tonnes)

FOR MAY:

SILVER NOTICES: 1563 NOTICE(S) FILED FOR 7,815,000 OZ/

total number of notices filed so far this month : 4077 for 20.385 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $7.60

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

NO CHANGES IN GOLD INVENTORY AT THE GLD:

/ /INVENTORY RESTS AT 832.19 TONNES

INVENTORY RESTS AT 832.19 TONNES

SLV//

WITH NO SILVER AROUND AND

SILVER UP 9 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 2.098 MILLION OZ

// INVENTORY INCREASES T0 427.072 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 429,174MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUMONGOUS SIZED 3143 CONTRACTS TO 166,596 BUT STALLS ON CLOSING IN ON THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUMONGOUS SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR HUGE LOSS OF $0,99 IN SILVER PRICING AT THE COMEX ON TUESDAY. WE HAD HUGE LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN SHORT COVERING BY OUR SPECS WITH THE HUGE PRICE LOSS IN PRICE. WE HAD A GIGANTIC SIZED 1427 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 1427 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.99 AND WERE SUCCESSFUL IN KNOCKING CONSIDERABLE SILVER LONGS AS WE HAD A HUGE SIZED LOSS OF 1343 CONTRACTS ON OUR TWO EXCHANGES WITH THE LOSS IN PRICE OF $0.99

WE MUST HAVE HAD:

A HUMONGOUS SIZED 1800 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 28.130MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S HUGE E,F,P, JUMP TO LONDON OF 2,105,000 OZ

//NEW STANDING FOR SILVER//MAY IS THUS 26.035 MILLION OZ

WE HAD:

/ HUMONGOUS SIZED COMEX OI LOSS HUGE SIZED EFP ISSUANCE/ VI) HUMONGOUS SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1427 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED A STRONG 281 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY

TOTAL CONTRACTS for 1 DAYS, total 1800 contracts: OR 9.0 MILLION OZ (1800CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 9.000 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770MILLION OZ (THIS MONTH WILL PROBABLY BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 9.00 MILLIONOZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3424 CONTRACTS WITH OUR LOSS IN PRICE OF SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUMONGOUS EFP ISSUANCE CONTRACTS: 1800 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAY OF 28.130 MILLION OZ ON FIRST DAY NOTICE FOLLOED BY TODAYS HUGE 2,105,000 OZ E,F,P, JUMP TO LONDON AS NO SILVER COULD BE FOUND BY OUR BANKERS OVER HERE

//NEW TOTAL STANDING AT 26.035 MILLION OZ

WE HAVE A HUGE SIZED LOSS OF 1624 OI CONTRACTS ON THE TWO EXCHANGES WITH THE LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 1427 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS

THE NEW TAS ISSUANCE TUESDAY NIGHT (1427 WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 1563 NOTICE(S) FILED TODAY FOR 7.815 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 5061 OI CONTRACTS TO 519,791 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED 35 CONTRACTS

WE HAD A STRONG SIZED DECREASE IN COMEX OI (5061 CONTRACTS) WITH OUR $53.75 LOSS IN PRICE//TUESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER TO WHACK GOLD’S PRICE. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 4.684 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY;S 10,600 OZ QUEUE JUMP//NEW STANDING 5,.001 TONNES

NEW STANDING 5.001 TONNES// ALL OF THIS HAPPENED DESPITE OUR $53.75 LOSS IN PRICE WITH RESPECT TO TUESDAY’S TRADING. WE HAD A FAIR SIZED LOSS OF 1624 OI CONTRACTS (5.237 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 3377 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 519,791

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1684 CONTRACTS WITH 5061 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 3377 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 1684 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED 2655 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3377 CONTRACTS) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI 5061TOTAL LOSS FOR OUR THE TWO EXCHANGES: 1684 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 4.684TONNES FOLLOWED BY TODAY;S 10,600 OZ QUEUE JUMP

//NEW STANDING /MAY 5.001 TONNES.

/ 3) CONSIDERABLE LONG LIQUIDATION WITH THE LOSS IN PRICE.

// 4) STRONG SIZED COMEX OPEN INTEREST LOSS/ 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: STRONG T.A.S. ISSUANCE: 2655 CONTRACTS/ HUGE SHORT COVERING BY OUR WRONG FOOTED SPECS WITH THE FED’S CONTINUAL RAID ON THE COMEX GOLD.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

APRIL

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY. :

TOTAL EFP CONTRACTS ISSUED: 3377CONTRACTS OR 337,700OZ OR 10.503 TONNES IN 1TRADING DAY(S) AND THUS AVERAGING: 3902 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAY(S) IN TONNES 10.503 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 10.503 DIVIDED BY 3550 x 100% TONNES = 0.295% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 10.503 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.Today, we had the open interest at the comex, in SILVER FELL BY A HUMONGOUS SIZED 3424 CONTRACTS OI TO 166,596 AND FURTHER FRIM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1800 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1800 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1800 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 3143CONTRACTS AND ADD TO THE 1800 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1624 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 8.120MILLION OZ

OCCURRED WITH OUR $0.99 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

REPORT

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED //Hang Seng CLOSED// Nikkei CLOSED DOWN 181.61PT OR 0.34% //Australia’s all ordinaries CLOSED DOWN 0.34%///Chinese yuan (ONSHORE) closed UP 7.2411//OFFSHORE CHINESE YUAN CLOSED UP TO 7.2470//Oil DOWN TO 80.79dollars per barrel for WTI and BRENT UP AT 85.17 Stocks in Europe OPENED MOSTLY RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 5061 CONTRACTS TO 519,791 WITH OUR HUGE LOSS IN PRICE OF $53.75 WITH RESPECT TO TUESDAY TRADING. WE HAD CONSIDERABLE T.A.S. LIQUIDATION AS WELL AS SHORTS, DESPERATELY TRYING TO GET OUT OF THEIR NAKED SHORTS.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAY.… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A HUGE 33377 EFP CONTRACTS WERE ISSUED: : JUNE 3373 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE:3373 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 1624 CONTRACTS IN THAT 3377 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 5061 COMEX CONTRACTS..AND THIS STRONG LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSSIN PRICE OF $53.75 TUESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A FAIR SIZED 2655 CONTRACTS. WE HAD 0 EX FOR RISK ISSUANCE. MOST OF THE TRADING AND SUPPLY OF CONTRACTS ON TUESDAY WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (5.001 TONNES) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

REPORT THIS AD

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2023 5.001TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL A HUGE $53.75 //// AND WERE SUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD ONLY A FAIR SIZED LOSS OF 1684 TOTAL CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR MAMMOTH LOSS IN PRICE 0F $53.75

WE HAD A FAIR T.A.S. LIQUIDATION ON THE FRONT END OF TUESDAY’S TRADING. THE T.A.S. ISSUED ON TUESDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE LOST A TOTAL OI OF 5.237 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY (4.684 TONNES) ON FIRST DAY NOTICE FOLLWED BY TODAY’S QUEUE JUMP OF 106 CONTRACTS OR 10600 OZ ( .3217BTONNES)

NEW STANDING: 5.001 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $53.75

WE HAD ADDED 35 CONTRACTS TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)

NET LOSS ON THE TWO EXCHANGES 1684 CONTRACTS OR 168400 (5.237 TONNES)

confirmed volume TUESDAY 247,763contracts//fair

//speculators have left the gold arena

MAY 1// MAY GOLD

/ /// THE MAY 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | nil . |

| Deposit to the Dealer Inventory in oz | 1736.154 oz Brinks enhanced |

| Deposits to the Customer Inventory, in oz | 65,826.694oz int. Delaware HSBC includes 17 kilobars |

| No of oz served (contracts) today | 106 notice(s) 10600OZ 0.3297TONNES |

| No of oz to be served (notices) | 67 contracts 6700 OZ 0.2083ONNES |

| Total monthly oz gold served (contracts) so far this month | 1541notices 154,100 oz 4.7932TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

1 dealer deposits:

i) Into Brinks enhanced: 1,736,154 oz

total dealer deposits: 1736.154 oz

we have 2 customer deposits:

i)Into HSBC: 65,280.127 oz

ii) Into Int Delaware 546,567 oz 17 kilobars

total deposit 65,826.694 oz

total customer withdrawals: 0

Adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR APRIL.

For the front month of MAY we have an oi of 173contracts having LOST 1333 contracts.

We had 1439 contracts served on Tuesday, so we immediately gained 106 contracts or 10,600 oz (,3217 tonnes). Thus the raid on gold only caused more gold to be sought over on this side of the pond.

JUNE DECREASED ITS OI BY 6682 CONTRACTS DOWN TO 398,672 CONTRACTS.

JULY GAINED 131 CONTRACTS TO STAND AT 131

We had 106 contracts filed for today representing 10,600 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 106contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 11 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the MAY /2024. contract month, we take the total number of notices filed so far for the month (1541 100 oz ), to which we add the difference between the open interest for the front month of MAY ( 173 CONTRACTS) minus the number of notices served upon today (106x 100 oz per contract( equals 160,800OZ OR 5.001 TONNES.

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (1541 x 100 oz + (173 )OI for the front month} minus the number of notices served upon today (106 x 100 oz which equals 160,800oz (5.001TONNES)

TOTAL COMEX GOLD STANDING FOR MAY: 5.001 TONNES WHICH IS HUGE FOR THIS A NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX84XXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,582,520,883 49.223tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,720,683.679 OZ

TOTAL REGISTERED GOLD 7,533,615.645( 234.327 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,187,767.594 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 5,951,095 oz (REG GOLD- PLEDGED GOLD)

185.10 tonnes/dropping like a stone

END

SILVER/COMEX

MAY 1

INITIAL

//2024// THE MAY 2025 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 707,773.791oz CNT ASAHI Delaware . |

| Deposits to the Dealer Inventory | 00OZ |

| Deposits to the Customer Inventory | 1069,123.160 oz Brinks |

| No of oz served today (contracts) | 1563 CONTRACT(S) (7.815 OZ) |

| No of oz to be served (notices) | 1130 contracts (5650 oz) |

| Total monthly oz silver served (contracts) | 4077 Contracts (20.385 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit :nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i) Into Brinks 1069,123.160 oz

total customer deposits 1069,123.160 oz

JPMorgan has a total silver weight: 129,598million oz/294.970million or 43.87%

adjustment: 2

customer to dealer Brinks 370,128.940 oz

dealer to customer Delaware 9718,327 oz

Comex withdrawals: 3

i) CNT 89,707.690 oz

ii) ASAHI 602m450,670 oz

iii) Delaware 15,615.431 oz

total withdrawal 707,773,791 oz

TOTAL REGISTERED SILVER: 62.6249MILLION OZ//.TOTAL REG + ELIGIBLE. 294.970million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF MAY/2024 OI: 2693 CONTRACTS HAVING LOST 2935 CONTRACT(S).

.

We had 2514 notices served on Tuesday so we lost an enormous 421 contracts or 2.105,000 oz were EFP’d to London to take immediate delivery over there as no silver could be found over here,

JUNE SAW A GAIN OF 289 CONTRACTS RISING TO 1838

JULY SAW A LOSS OF 1635 CONTRACTS DOWNTO 135,729

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 1563 for 7.815 million oz

CONFIRMED volume; ON TUESDAY 96,035 huge

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 4077 5,000 oz = 20,385 MILLION oz

to which we add the difference between the open interest for the front month of MAY (2693 and the number of notices served upon today 1563x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2024 contract month: 4077 notices served so far) x 5000 oz + OI for the front month of MAY (2693 number of notices served upon today (1563x 500 oz of silver standing for the APRIL contract month equates to 26.035 MILLION OZ.

New total standing: 26.035 million oz.

There are 62.299 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

MAY 1 WITH GOLD UP $7.80 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNE

APRIL 29WITH GOLD UP $10,55TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNES

APRIL 26WITH GOLD UP $5.40TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.54 TONNES FROM THE GLD /INVENTORY RISES AT 832.19 TONNES

APRIL 25WITH GOLD UP $5.05 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD /INVENTORY RISES AT 833,63 TONNES

APRIL 19 WITH GOLD UP $15.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 4.32 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 831.91 TONNES

APRIL 18 WITH GOLD UP $11.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE WITHDRAWAL OF 2.59 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 827.59 TONNES

APRIL 17 WITH GOLD DOWN $17.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 830;18 TONNES

REPORT

APRIL 16 WITH GOLD UP $23.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 828.45 TONNES

REPORT THIS AD

APRIL 15 WITH GOLD UP $9.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE WITHDRAWAL OF 4.03 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 826.72 TONNES

APRIL 12 WITH GOLD UP $2.80 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD/ INVENTORY RISESS AT 830.75 TONN

APRIL 10 WITH GOLD DOWN $14.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 828.71 TONNES

APRIL 9 WITH GOLD UP $11.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 827,85 TONNES

APRIL 8 WITH GOLD UP $7.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A WITHDRAWAL OF 6.02 TONNES OF GOLD INTO THE GLD/ INVENTORY REMAINS AT 826.41 TONNES

APRIL 5 WITH GOLD UP $38.65 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/ INVENTORY REMAINS AT 832.45 TONNES

APRIL 4 WITH GOLD DOWN $3.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD/ INVENTORY REMAINS AT 830.73 TONNES

APRIL 3 WITH GOLD UP $33,85 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD // INVENTORY REMAINS AT 829.00 TONNES

APRIL 2 WITH GOLD UP $23.90 TODAY; HUG CHANGES IN GOLD INVENTORY AT THE GLD A WITH DRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD.:// INVENTORY REMAINS AT 829.00 TONNES

APRIL 1 WITH GOLD UP $18.70 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:// INVENTORY REMAINS AT 830.15 TONNES

MARCH 28 WITH GOLD UP $26.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:// INVENTORY REMAINS AT 830.15 TONNES

MARCH 27 WITH GOLD UP $15.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// INVENTORY FALLS TO 830.15 TONNES

MARCH 26 WITH GOLD UP $1.40 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 835.33 TONNES

MARCH 25 WITH GOLD UP $17.05 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 838.50 TONNES

MARCH 22 WITH GOLD DOWN $23.75 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 838.50 TONNES

GLD INVENTORY: 832.19TONNES,

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 1 WITH SILVER UP 0.09 TODAY: SMALLCHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF ,457 MILLION OZ INTO THE SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 29WITH SILVER UP $0.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 26WITH SILVER DOWN 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.097 MILLION OF SILVER INTO THE SLV// :SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 25WITH SILVER UP $.05 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 1.534 MILLION OF SILVER OUT OF THE SLV// :SLV INVENTORY RESTS AT 428.717 MILLION OZ

APRIL 24/WITH SILVER DOWN $.05 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 11.904MILLION OF SILVER INTO THE SLV// :SLV INVENTORY RESTS AT 428.280 MILLION OZ

APRIL 23/WITH SILVER UP $0.11TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV / :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 22/WITH SILVER DOWN $1.51 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.194 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 19/WITH SILVER UP 42 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.657 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 418.570 MILLION OZ

APRIL 18/WITH SILVER DOWN $.04TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.977 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 422.227 MILLION OZ

APRIL 17/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF .868 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 426/204 MILLION OZ

APRIL 16/WITH SILVER DOWN $0.46 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF NON EXISTENT SILVER// :SLV INVENTORY RESTS AT 427.072 MILLION OZ

APRIL 15/WITH SILVER UP $0.46 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 12/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 4.069 MILLION OZ FROM THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 11/WITH SILVER UP $0.23 TODAY: STRANGE INDEED! HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.931 MILLION OZ :SLV INVENTORY RESTS AT 437.998 MILLION OZ

APRIL 10/WITH SILVER UP $0.04 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:SLV INVENTORY RESTS AT 441.929 MILLION OZ

APRIL 9/WITH SILVER UP $0.15 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.549 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 441.929 MILLION OZ

APRIL 8/WITH SILVER UP $0.33 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.320 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 441.328 MILLION OZ

APRIL 5/WITH SILVER UP $0.61 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.748 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 441.060 MILLION OZ

APRIL 4/WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.671 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 437.312 MILLION OZ

APRIL 3/WITH SILVER UP $1.14 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.835 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 433.641 MILLION OZ

APRIL 2/WITH SILVER UP 84 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6.721 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 430.806 MILLION OZ

APRIL 1/WITH SILVER UP 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// SLV INVENTORY RESTS AT 424.085 MILLION OZ

MARCH 28/WITH SILVER UP 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.005 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 424.085 MILLION OZ

MARCH 27/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A A DEPOSIT OF 1.691 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 423.079 MILLION OZ

MARCH 26/WITH SILVER DOWN 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A A DEPOSIT OF 0.366 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 421.388 MILLION OZ

MARCH 25/WITH SILVER UP 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 3.887 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 421.022 MILLION OZ

MARCH 22/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE DEPOSIT OF 1.1899 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 424.909 MILLION OZ

CLOSING INVENTORY 429.174MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

PETER SCHIFF/SCHIFFGOLD/MIKE MAHARRAY

3. CHRIS POWELL//GATA DISPATCHES

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS

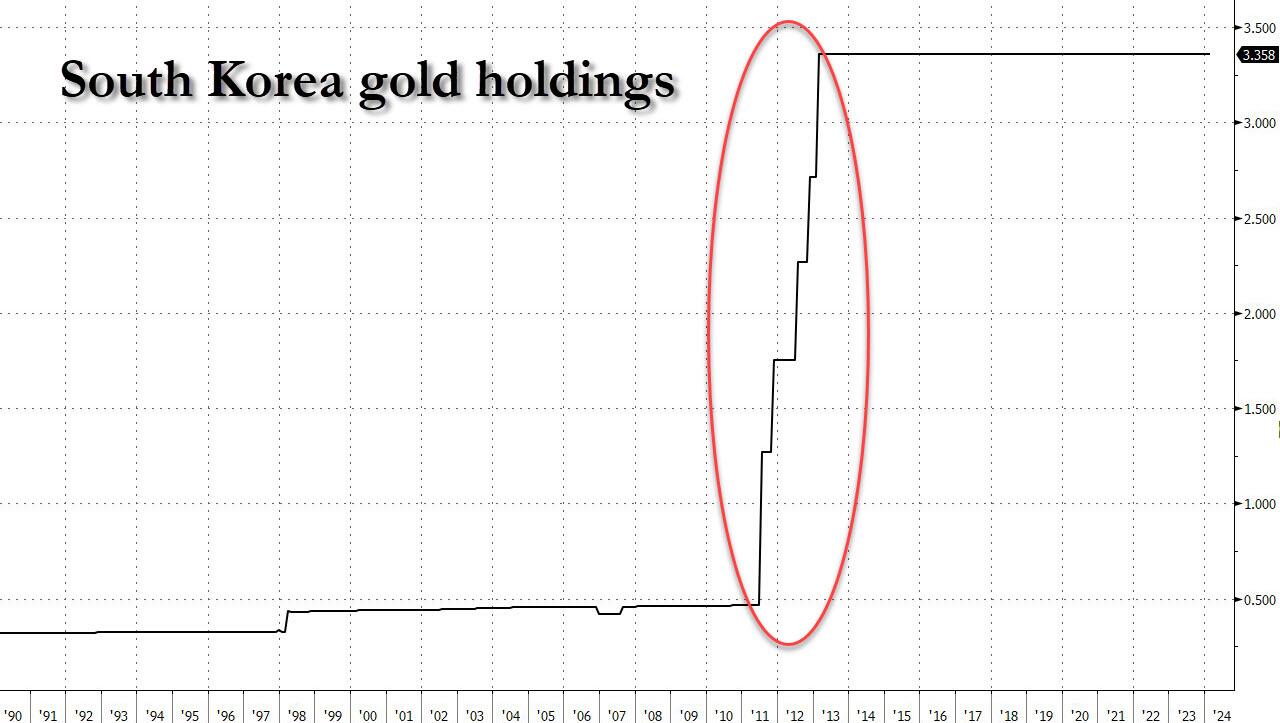

South Korea’s Central Bank Says May Buy Gold In The Mid To Long-Term

TUESDAY, APR 30, 2024 – 07:20 PM

Back in 2011, around the time gold hits its previous cycle high, South Korea surprised the fiat world when it revealed that it had spent more than a billion dollars in its first gold purchase in more than a decade, as uncertainty about global growth and sovereign debt push central banks around the world to diversify foreign reserves. It then proceeds to buy a lot more gold (relatively speaking) for the next year and a half before halting purchases indefinitely once again in 2013. It now holds 104.4 tonnes of gold in its foreign exchange reserves, or $4.8 billion, accounting for 1.1% of its total $419.3 billion in reserves at the end of March.

That may change soon, however, because with gold hitting a new all time high in recent weeks, South Korea’s central bank may consider buying more gold in the mid- to long-term, even if it is not thinking of immediately buying more after a recent surge in prices of the precious metal, a bank official said on Tuesday.

The bank’s rare comments come after this month’s record high of $2,431.29 an ounce in spot gold as growing Middle East tension drove investors to seek safe-haven assets. The metal has risen 13% this year, building on a gain of 13% in 2023.

“We don’t have any immediate plans to buy gold now,” Kwon Min-soo, head of the Bank of Korea’s reserve management group told Reuters, adding that numerous factors needed to be weighed to ensure the right circumstances for such purchases.

“Foreign exchange reserves must be on a sufficiently increasing trend, and the foreign exchange market must be stable in order to ‘consider’ purchasing additional gold as an asset, which is why we would consider them only in the mid- to long-term,” he said.

Translation: South Korea will buy more gold, but only after spot prices have jumped another several hundred dollars.

In a blog post earlier, the bank’s Reserve Management Group said it needed to be cautious when investing in gold, but advantages offered by the precious metal included its role as a hedge against inflation and an alternative to the US dollar.

Recent gains in gold prices were due mostly to purchases by central banks of countries such as China, Russia and Turkey, which are trying to become less dependent on the US currency or guard against war, the bank said.

The thaw in sentiment toward gold is a reversal from the BOK’s June 2023 position when the central bank said it was more desirable to maintain dollar liquidity than boost its gold holdings, after its first inspection of gold holdings at the Bank of England.

end

5 a. IMPORTANT COMMENTARIES ON COMMODITIES/

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

REPORT THIS AD

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP 7.2411

OFFSHORE YUAN: UP TO 7.2470

SHANGHAI CLOSED

HANG SENG CLOSED

2. Nikkei closed DOWN 181,61 PTS OR 0.34%

3. Europe stocks SO FAR: ALL MOSTLY RED

USA dollar INDEX UP TO 106.18 EURO RISES TO 1.0672 UP 86BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.888 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 157.89 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP/ OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UPTO +2.5825/Italian 10 Yr bond yield UP to 3.878SPAIN 10 YR BOND YIELD UP TO 3.348

3i Greek 10 year bond yield DOWNTO 3.454

3j Gold at $2295.00 //Silver at: 26.48 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 0 100 roubles/dollar; ROUBLE AT 93.05/

3m oil into the 80 dollar handle for WTI and 85 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 157.89/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.889% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9205 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9923well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

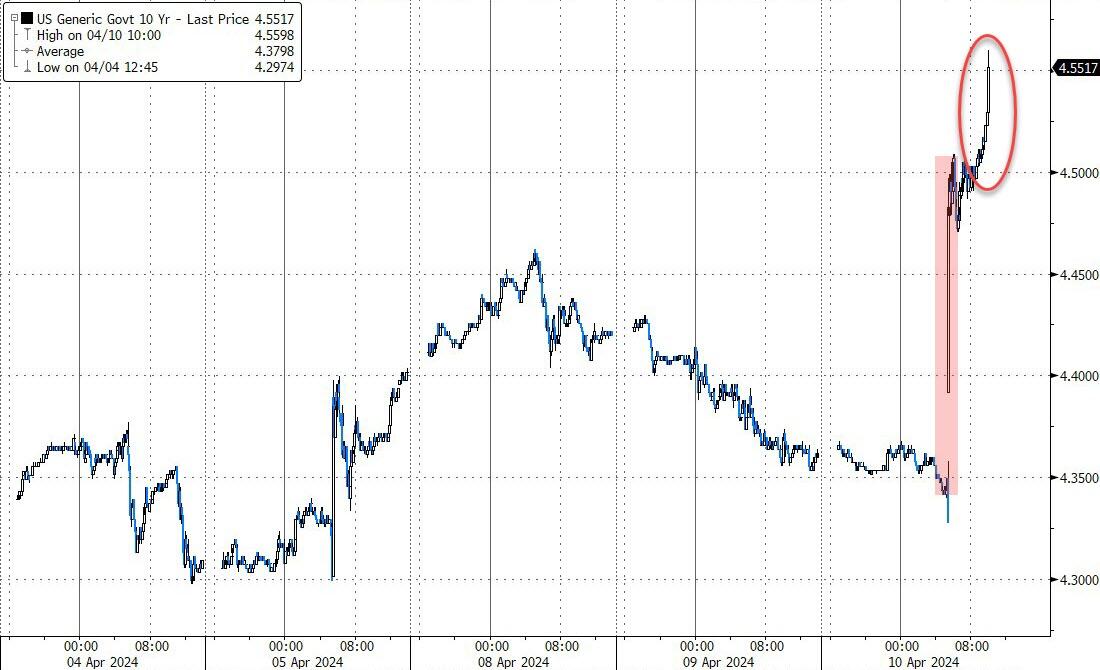

USA 10 YR BOND YIELD: 4.682 DOWN 1BASIS PTS…

USA 30 YR BOND YIELD: 4.784 DOWN 1BASIS PTS/

USA 2 YR BOND YIELD: 5.035 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.46…(TURKEY)

10 YR UK BOND YIELD: 4.4270 UP 8 PTS

2a New York OPENING REPORT

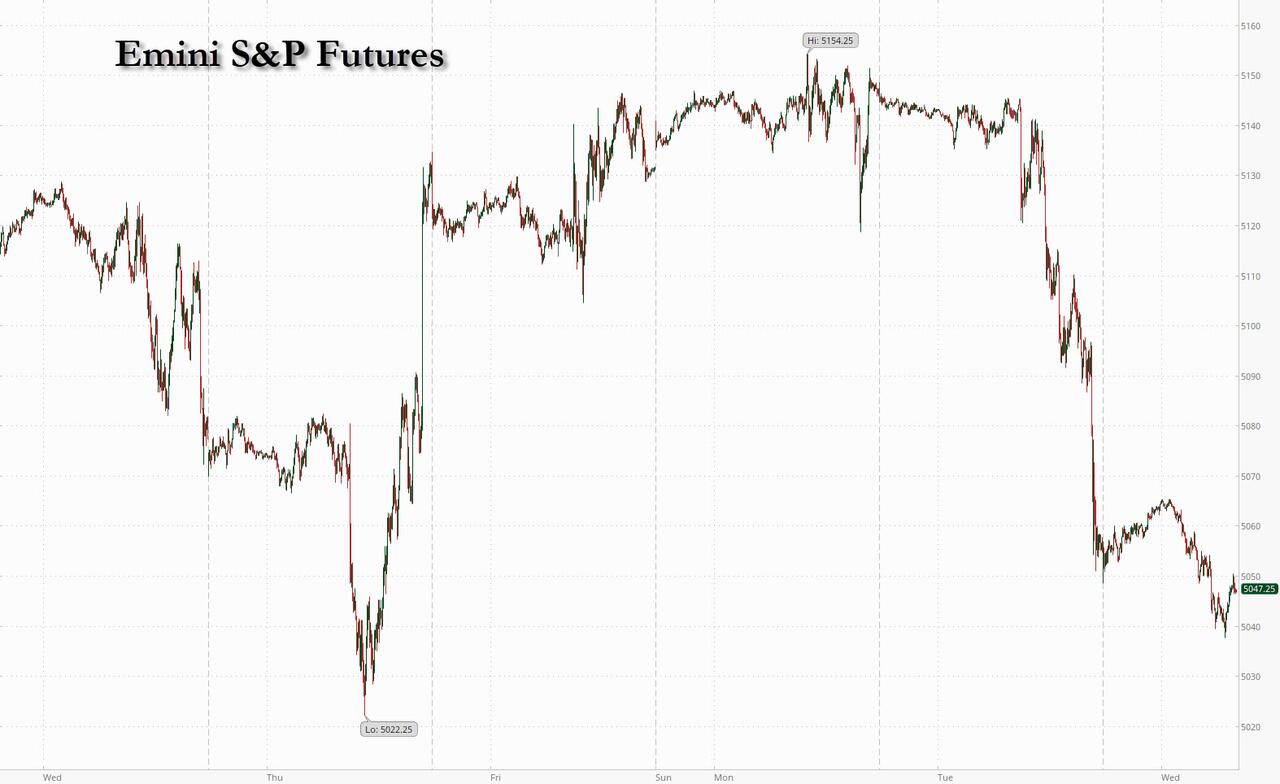

Future Slide In Damp Start To New Month As Fed Decision Looms

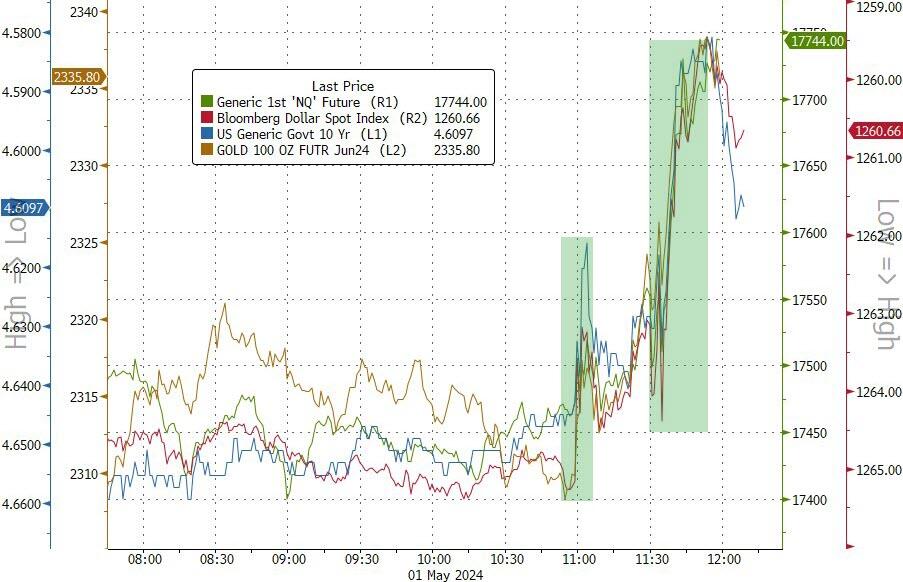

WEDNESDAY, MAY 01, 2024 – 08:13 AM

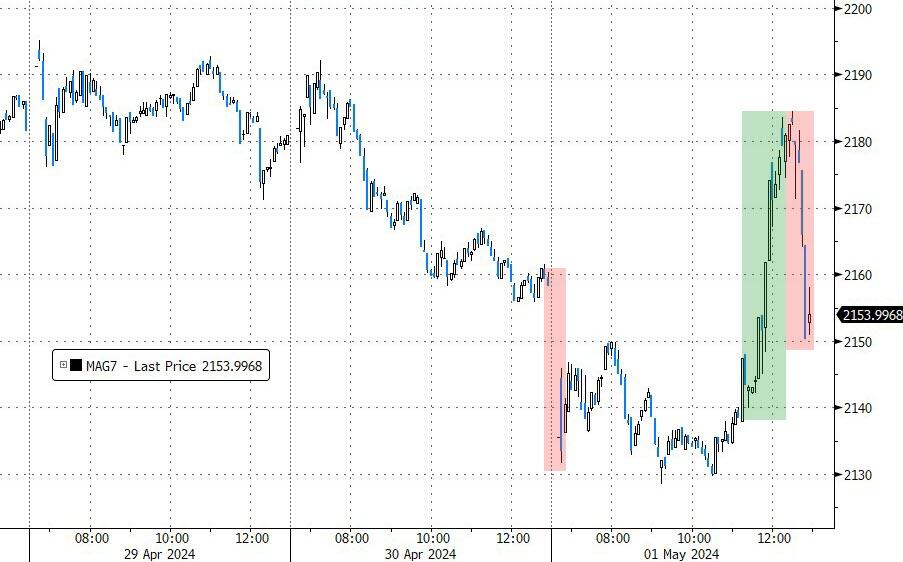

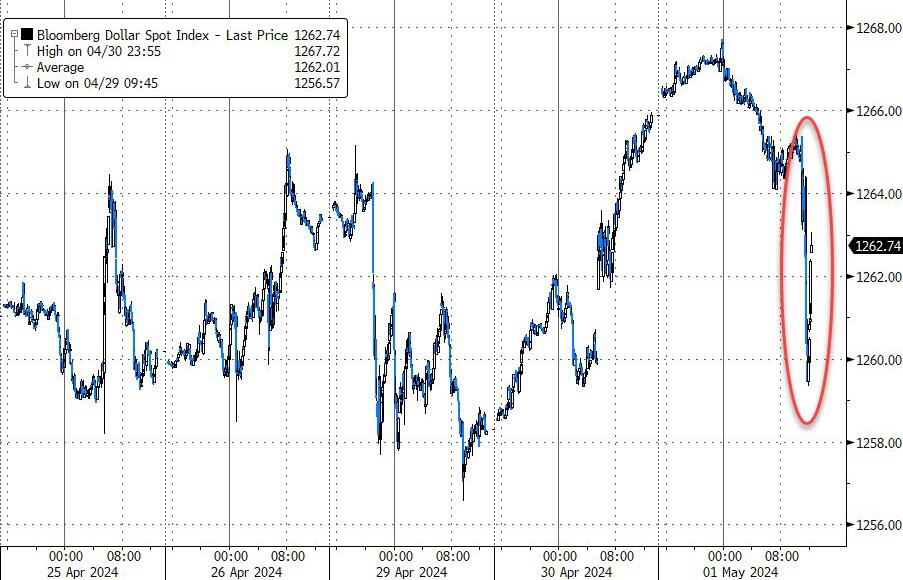

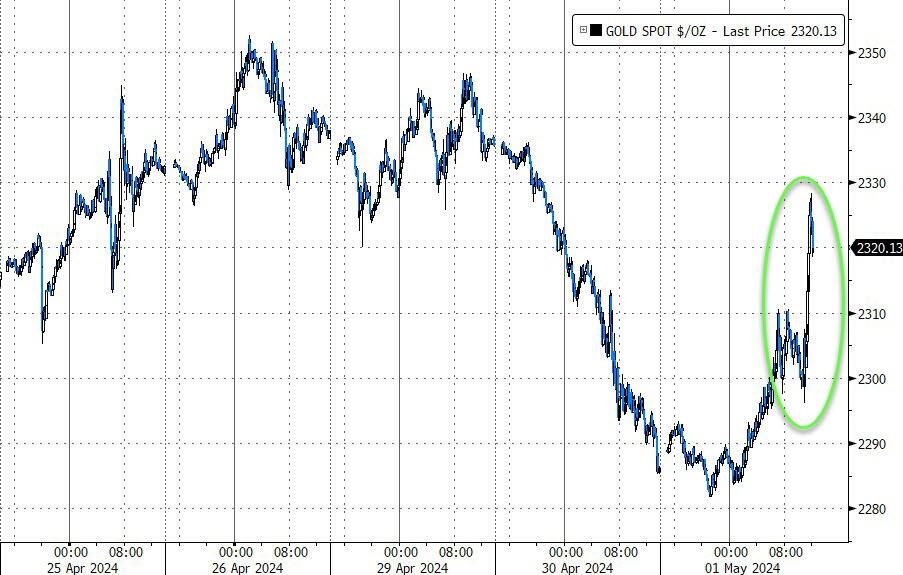

US equities were set for a second day of losses, as investors weighed disappointing tech earnings and braced for today’s Quarterly Refunding Announcement and Fed rate decision and Powell press conference where the Fed chair is expected to signal a delay to rate cuts. S&P 500 futures slid 0.4%, while Nasdaq 100 contracts dropped 0.8% as of 7:40 a.m. in New York, extending losses from Tuesday with markets digesting the surge the employment cost index, a measure of wages and benefits, driven by soaring union and government wages as well as the drop in US consumer confidence to its lowest since level 2022. Europe’s Stoxx 600 gauge edged lower in holiday-thinned trading. The Bloomberg dollar index was little changed, while the two-year Treasury yield held near a six-month high. Gold rebounded from yesterday’s rout but bitcoin did not and instead tumbled deeper below $60,000 driven by European selling. It’s a busy calendar and besides the FOMC, we also get the April ADP employment change (8:15am), April US manufacturing PMI (9:45am), March construction spending and JOLTS job openings and April ISM manufacturing (10am).

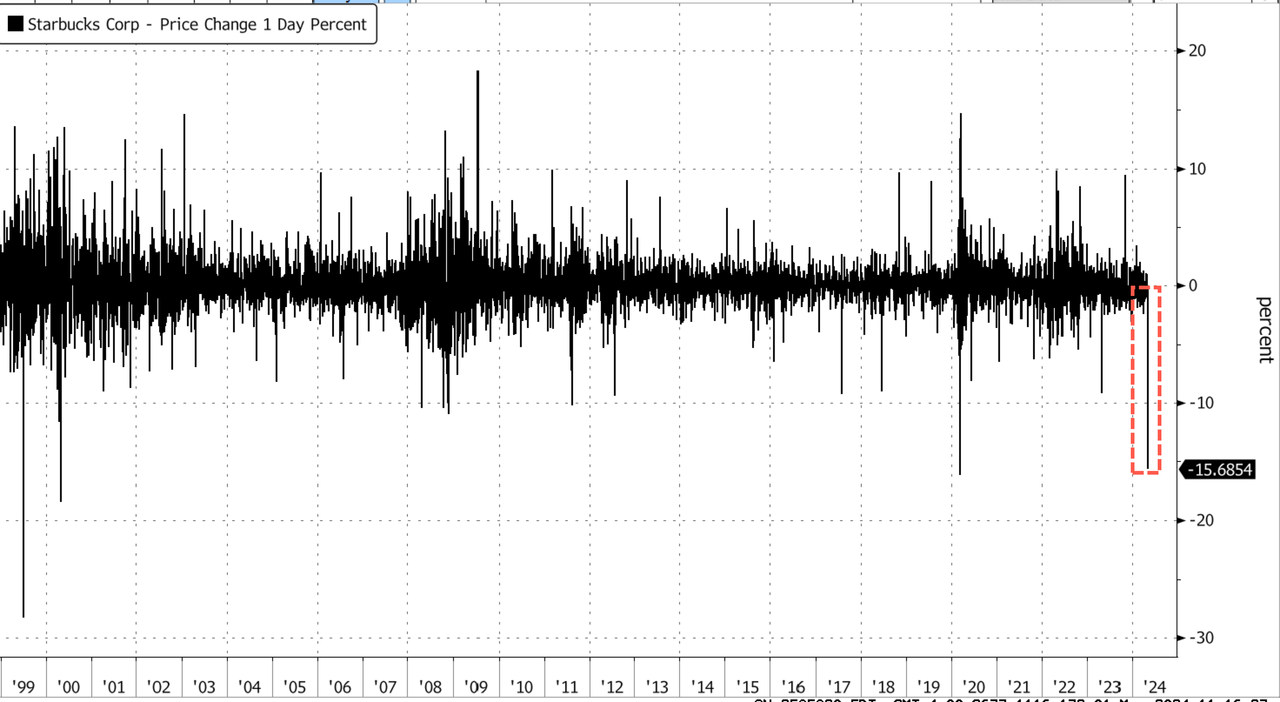

In premarket trading, AMD shares slipped after the chipmaker issued a disappointing forecast for artificial intelligence processors as it attempts to make inroads into the lucrative market dominated by Nvidia. Super Micro Computer also dropped despite beating forecasts. Starbucks slumped after quarterly sales fell for the first time since 2020. In contrast, Amazon.com shares rose in premarket trading after the e-commerce and cloud computing company reported first-quarter results that beat expectations. Pinterest jumped after the social media company’s better-than-expected results and outlook prompted analysts to raise their price targets on the stock. Here are the biggest premarket movers:

2 B) NOW NEWSQUAWK (EUROPE/REPORT)

US equity futures in the red, USD flat ahead of key US data & FOMC, Crude sinks lower – Newsquawk US Market Open

- dvanced Micro Devices shares slip 6.8% after the chipmaker issued a disappointing forecast for artificial intelligence processors as it attempts to make inroads into the lucrative market dominated by Nvidia.

- Amazon shares are up 2.2% after the e-commerce and cloud computing company reported first-quarter results that beat expectations.

- Cryptocurrency-linked stocks fall as the prospect of higher-for-longer interest rates is weighing on the sector and Bitcoin extends losses for a third consecutive session. Coinbase Global (COIN US) -3.9%, Marathon Digital (MARA US) -4.7%, Riot Platforms (RIOT US) -4.1%, Hut 8 Mining (HUT US) -6.9%, Cleanspark (CLSK US) -4.5%, MicroStrategy (MSTR US) -4.2%, Cipher Mining (CIFR US) -5.9%, Bitdeer Technologies (BTDR US) -2%

- Inari Medical shares rise 12% in premarket trading after the medical device firm reported a firm sales beat and boosted its year sales view.

- Leggett & Platt shares drop 13% after the furniture component maker slashed its dividend after over 50 years of reliable growth.

- Lemonade shares gain 8.1% after the company, which offers renters and homeowners insurance, raised its revenue forecast for the full year.

- Nio ADRs rise 2.1% after the Chinese EV maker reported a 32% jump in vehicle deliveries in April compared with the previous month.

- Pinterest shares gain 17% after the social media company’s better-than-expected results and outlook prompted analysts to raise their price targets on the stock.

- Polestar ADRs fall 7.9% after the electric vehicle maker postponed its fourth-quarter and full-year earnings report and identified accounting errors made in previous years.

- Root shares 28% after the car insurance company reported first-quarter total revenue that beat the average analyst estimate.

- Sirius XM shares rise 1.7% after Goldman Sachs lifts its rating on the satellite radio company to neutral from sell, citing a period of underperformance by the stock.

- Skyworks Solutions shares slump 14% after the semiconductor device company issued weaker-than-expected forecasts for revenue and profit in the current quarter, spurring analysts to cut their ratings and price targets on the stock.

- Starbucks shares slide 12% as a fall in the coffee chain’s second-quarter comparable sales bucked consensus estimates for a 1.5% increase. William Blair downgraded their recommendation on the stock.

- Super Micro Computer shares fall 9.9% after estimate-topping forecasts for adjusted EPS and net sales in the fourth quarter weren’t enough to impress investors. JPMorgan flags concern over capital needs.

- TransMedics shares gain 14% after sales beat expectations thanks to greater usage of organ transportation technologies, and the company boosted its 2024 revenue guidance.

Here are the biggest large cap (>$20BN) movers this morning:

- Pinterest (PINS US) +18.1%

- Amazon (AMZN US) +2.4%

- 3M Co (MMM US) +1.4%

- GE Healthcare (GEHC US) +1.2%

- Datadog (DDOG US) +1.2%

- Tesla (TSLA US) -2.5%

- Coinbase (COIN US) -3.0%

- AMD (AMD US) -6.2%

- Super Micro Computer (SMCI US) -9.2%

- Starbucks (SBUX US) -12.2%

“The main catalyst for the selloff yesterday came from the Employment Cost Index for the first quarter, which is an important one since the Fed view it as a high-quality indicator,” said Deutsche Bank AG strategist Jim Reid. “Moreover, it adds to the collection of readings which suggest that inflation is remaining stubbornly above target, and if anything might even be re-accelerating.”

US stocks had their first negative month since October, as volatility rose amid a more hawkish tone from Fed officials, pushing back against the timing for rate cuts. Bond markets are currently expecting just one rate cut by the end of the year, compared with almost seven in January.

Traders are bracing for big market moves and bonds are turning more bearish ahead of what many expect will be a hawkish tilt from Powell. After positioning at the start of the year for multiple reductions in 2024, investors are now pricing in just one full quarter-point cut.

With all eyes on the Fed today and Powell’s presser, a hawkish pivot is all but priced in and any dovish signalling could send stocks soaring (more in our preview here). The last time Powell spoke, he pointed to the lack of progress in bringing inflation down. The most recent signals on prices and the economy. along with expectations for a robust employment report on Friday, mean the chances of a a change in tune are low. Some are even pricing in higher odds of a rate hike than a rate cut in the immediate future, but not Goldman: this is what the bank wrote in its FOMC preview:

We continue to think that rate hikes are quite unlikely because there are no signs of genuine reheating at the moment, and the funds rate is already quite elevated. It would probably take either a serious global supply shock or very inflationary policy shocks for rate hikes to become realistic again. And even then, the FOMC might prefer to hold the funds rate steady at a high level unless the shocks seemed likely to spark a broader and more persistent inflation problem

Still, WSJ’s Timiraos wrote on X that “It’s another wait-and-see meeting for the Fed, but this time, the questions are likely to be tilted in the direction of filling out the Fed’s reaction function for upside risks on inflation and wages rather than downside risks or benign inflation.”

Others expect nothing major to be unveiled today: “We are unlikely to hear anything dovish from the Fed today,” said Lilian Chovin, head of asset allocation at Coutts. “The higher-for-longer narrative is not easy for markets to navigate.”

Still, the market isn’t taking any chances, and the options market is flagging a bigger move in the S&P 500 Index than at any point in the past 11 months. Meanwhile, data for the week leading up to April 23 showed hedge funds building short positions in bond futures. Commodity trading advisors, or CTAs, are now sitting at near “max short duration,” according to Bank of America strategists.

Ahead of the Fed meeting, traders face a slew of US economic releases including job openings and manufacturing data. They will also be on the watch for the Treasury’s quarterly plan of long-term debt sales, which are expected to remain steady, and the exact date for a Treasury program to buy back existing debt.

Elsewhere, global investors are unwinding bets on local-currency bonds in emerging markets as some central banks come under pressure to raise interest rates. A Bloomberg gauge of the asset class fell 1.3% in April, the the biggest monthly decline since September.

Most markets are closed in Europe and in Asia for the May day holiday. UK stocks held steady, with health care, banks and miners on the rise. The FTSE 100 rises 0.1%.

In FX, the Bloomberg Dollar Spot Index is little changed amid thin volumes, with some markets closed due to a public holidaySpot volumes run at 60%-70% of recent averages in the euro and the pound, a Europe-based trader says; DTCC data show options flows at 75% of average Options traders have added topside bets in the dollar versus its major peers; one-month risk reversals in BBDXY at 48 basis points, versus 34 basis points on April 24. USDJPY was hovering just below 158 as the market faded much of Japan’s intervention gains.

In rates, treasuries edged lower ahead of the Fed decision later on Wednesday. Treasuries were narrowly mixed with yields less than 1bp from Tuesday’s closing levels. Most US yields slightly higher on the day with 10-year around 4.68%; gilts lag by 3bp in the sector. European rates see wider losses, with gilts lagging after 10-year bond sale. Data-heavy US session includes April ADP employment change and manufacturing gauges and March JOLTS job openings before attention turns to Fed policy announcement.

The Fed rate decision expected at 2pm New York time, Chair Powell’s news conference thirty minutes later. Bond market positioning appears to lean short ahead of the meeting, anticipating a hawkish pivot

In commodities, oil prices decline, with WTI falling 1.8% to trade near $80.50. Bitcoin drops 4% to around $57,000.

Bitcoin (-4.3%) sank briefly below $57k after hefty selling pressure; currently holds just above the aforementioned level.

Looking at the day ahead, at 8:30am Treasury quarterly refunding announcement of next week’s auction sizes and projections for the May-to-July period is expected to deliver on January guidance of no further increases to nominals. US economic data slate includes April ADP employment change (8:15am), April final S&P Global US manufacturing PMI (9:45am), March construction spending and JOLTS job openings and April ISM manufacturing (10am). Finally, today’s earnings releases include Mastercard, Pfizer, and Qualcomm.

Market Snapshot

- S&P 500 futures down 0.3% to 5,053.75

- STOXX Europe 600 little changed at 504.61

- MXAP down 0.5% to 173.42

- MXAPJ down 0.3% to 537.53

- Nikkei down 0.3% to 38,274.05

- Topix down 0.5% to 2,729.40

- Hang Seng Index little changed at 17,763.03

- Shanghai Composite down 0.3% to 3,104.82

- Sensex down 0.3% to 74,482.78

- Australia S&P/ASX 200 down 1.2% to 7,569.95

- Kospi up 0.2% to 2,692.06

- German 10Y yield little changed at 2.58%

- Euro little changed at $1.0669

- Brent Futures down 1.1% to $85.42/bbl

- Gold spot up 0.0% to $2,286.31

- US Dollar Index little changed at 106.32

Earnings

- Amazon (AMZN) Q1 EPS 0.98 (exp. 0.83), Q1 revenue USD 143.31bln (exp. 142.5bln); North America net sales USD 86.34bln (exp. 85.55bln), International net sales USD 31.94bln (exp. 32.47bln); Q1 AWS net sales ex-FX +17% (exp. +14.5%); Q1 operating margin 10.7% (exp. 7.63%); Q1 North American retail operating margin 5.8% (exp. 5%). Sees Q2 net sales between USD 144-149bln (exp. 150.13bln), sees Q2 operating income of USD 12bln (exp. 12.7bln). Shares +2.4% pre-market

- Starbucks (SBUX) Q2 adj. EPS 0.68 (exp. 0.79), Q2 revenue USD 8.56bln (exp. 9.13bln); Q2 comp. sales -4% (exp. +1.46%), North America comps -3% (exp. +2.05%), US comps -3% (exp. +2.31%), International comps -6% (exp. +1.36%), China comps -11% (exp. -1.62%) Shares -12.1% pre-market

- Super Micro (SMCI) Q3 adj. EPS of 6.65 (exp. 5.78), Q3 revenue of USD 3.85bln (exp. 3.95bln); Q3 gross margin 15.6% (exp. 15.34%) Shares -9% pre-market

- Advanced Micro Devices (AMD) Q1 adj. EPS 0.62 (exp. 0.61), Q1 revenue USD 5.47bln (exp. 5.46bln). Sees Q2 revenue between USD 5.4-6bln (exp. 5.72bln), sees Q2 adj. gross margin of about 53% (exp. 53%), and sees AI chips sales of about USD 4bln (prev. saw USD 3.5bln). Shares -6.3% pre-market

- GSK (GSK LN) Q1 (GBP): Revenue 7.363bln (exp. 7.067bln). EPS 0.431 (exp. 0.360). Adj. Operating Profit 2.443bln (exp 2.096bln). Sees FY adj. EPS +8-10% (prev. +6-9%) and sees Adj. FY operating profit +9-11% (prev. +7-10%). Shares +1.6% in European trade

Top Overnight News

- Beijing is preparing for a second Trump term and bracing for the turmoil that would bring in US-China relations (China thinks a second Trump term would be a net negative for it). WSJ

- Starbucks missed a very low bar, with a significant miss on EPS (68c vs. the Street 80c) and sales (comps -4% vs. the Street +1.5%). Comps were weighed down by soft transactions (-6%, a huge swing from +3% in the prior quarter) and a China pressure (comps in China slumped 11%). Op. margins contracted 150bp to 12.8%, a large miss vs. the consensus. RTRS

- Aston Martin shares lower after the company reported a shortfall on Q1 revenue (-10% to GBP267.7MM vs. the Street GBP290MM) and EBITDA (-34% to GBP19.9MM vs. the Street GBP29.4MM). RTRS

- AMD reported Q1 inline and the Q2 guide was largely consistent w/expectations, but the new AI accelerator chip sales guidance of ~$4B for ’24 didn’t get increased by as much as hoped. RTRS

- US crude stockpiles increased 4.9 million barrels last week, the API is said to have reported. That would be the fifth expansion in six weeks if confirmed by the EIA today. Supplies at Cushing jumped, while those of gasoline and distillate dipped. BBG

- Amazon gained premarket after its AWS unit posted strong sales growth, making up for the company’s lower-than-expected current-quarter sales forecast. Its livestreaming site Twitch launched a short-form video platform that may rival TikTok. BBG

- We continue to think that rate hikes are quite unlikely because there are no signs of genuine reheating at the moment, and the funds rate is already quite elevated. It would probably take either a serious global supply shock or very inflationary policy shocks for rate hikes to become realistic again. And even then, the FOMC might prefer to hold the funds rate steady at a high level unless the shocks seemed likely to spark a broader and more persistent inflation problem. GIR

- New York City police stormed Columbia University’s campus on Tuesday night, arresting dozens of pro-Palestinian protesters in an attempt to quash unrest that has spread to campuses across the nation and inflamed US divisions over the war in Gaza. FT

- Pfizer is developing an online platform for patients to order medicine including anti-Covid drug Paxlovid and a migraine nasal spray, according to people familiar with the matter, in the latest push by drugmakers to cut out industry middlemen and sell straight to consumers. FT

A more detailed look at global markets courtesy of Newsquawk

APAC stocks took their cues from the losses on Wall St amid a hawkish impulse owing to the firmer-than-expected Employment Cost data heading into today’s FOMC and with trade mired by mass holiday closures. ASX 200 was pressured as gold miners led the declines after the precious metal slid beneath the USD 2,300/oz level, with underperformance also seen in rate-sensitive sectors. Nikkei 225 slipped at the open but held on to 38,000 status and briefly clawed back all of its losses with the downside cushioned by a weaker currency and as participants digested another batch of earnings releases, while it was also reported that Japan could provide tax breaks for companies repatriating foreign profits into the JPY.

Top Asian News

- NDRC said China will promote the development and growth of leading companies in the NEV industry, as well as accelerate the exit of lagging enterprises and capacities. Furthermore, China will lift foreign investment access restrictions in the manufacturing industry and it welcomes global automotive companies to deeply integrate into China’s market and industrial chain system.

- Japan may introduce measures to provide tax breaks for companies repatriating foreign profits into the JPY and include it in the government’s annual mid-year policy blueprint, according to Sankei.

- RBNZ Financial Stability Report stated New Zealand’s financial system remains strong and rising nominal incomes are helping many households navigate the transition onto higher interest rates, while it added some are doing it tough and reducing their spending or extending their repayment timelines. RBNZ also stated that although non-performing loans to businesses have increased, they remain low by historical standards and there remains a risk that new or persistent inflation pressures could mean global interest rates remain restrictive for longer.

- RBNZ Deputy Governor Hawkesby said New Zealand’s employment data is confirmation of the trend they were expecting to see and higher interest rates will involve a cooling of the labour market.

- Japan’s Government is considering laws and regulations for AI development and obligatory reporting to large-scale business, via Nikkei

European bourses are closed for Labour Day, with the exception of the UK’s FTSE 100 and Denmark’s Nasdaq Copenhagen. The FTSE 100 (+0.1%) is incrementally firmer, though has come under slight selling pressure in recent trade. GSK (+1.9%) gains post-earnings after beating on top/bottom lines, and raising guidance. US Equity Futures (ES -0.3%, NQ -0.6%, RTY -0.3%) are entirely in the red, with clear underperformance in the NQ, hampered by chip-led weakness. Amazon (+2.3%) firmer pre-market on its results, whilst dire Starbucks (-12.1%) earnings have led to pre-market pressure.

Top European News

- UK House Prices Fall Again After Mortgage Rates Creep Higher

- Bitcoin Hits Two-Month Low After Worst Stretch Since FTX Crash

- It’s the Weather, Stupid!: The London Rush

- GSK Expects Higher Profits Boosted By Vaccines, Asthma Drugs

- Ireland’s Listed Companies Now Have Zero Female CEOs

- Aston Martin Slumps; First Quarter a ‘Big Miss,’ Jefferies Says

- UAE Snubs London’s Lord Mayor as Row Over Sudan Role Deepens

FX

- USD is steady vs. peers after yesterday’s buying momentum followed through into the early stages of today’s trading with the index topping out just shy of the YTD peak at 106.51. A slew of US data and the FOMC thereafter will decide direction.

- EUR is flat vs. the USD with European markets closed for Labour Day. EUR/USD did drift as low as 1.0650 before staging a marginal pick up.

- JPY is trivially softer vs. the USD (compared to recent moves) with the pair briefly eclipsing the 158 mark. Focus is on today’s busy US data/FOMC docket and whether a hawkish outturn could see a revisit to 160.

- Antipodeans are both relatively steady vs. the USD after yesterday’s pronounced selling. AUD/USD marginally extended on yesterday’s low with the session trough at 0.6466 before picking up a touch.

Fixed Income

- USTs are flat ahead of a packed US session, holding at 107-14 which is 10 ticks above the contract low from last week. Alongside this, Quarterly refunding is due after Monday’s estimates were above exp., though coupon sizes seen unch. Q/Q with the extra need to be filled by bills.

- Gilts are softer as the benchmark catches up to the continued late-doors downside in benchmarks on Tuesday. Catalysts light thus far given the mass-European market closure for Labour Day. Gilt auction was incrementally softer than the prior but still solid overall with a few fleeting downticks to a 95.44 base.

Commodities

- A downbeat session for the crude complex thus far amid the broader risk aversion in APAC hours coupled with the surprise large build in crude stockpiles and the “positive” atmosphere in efforts to reach an Israel-Hamas ceasefire. Brent July slipped from a USD 85.88/bbl high to a trough at USD 85.22/bbl.

- A flat session for spot gold but mixed for the overall complex with spot silver posting mild gains and spot palladium in the red. Price action in the yellow metal has been minimal thus far amid the aforementioned mass closures and upcoming risk events state-side; Spot gold is currently confined to a USD 2,281-2,293.oz.

- Base metals are lower across the board amid the negative APAC sone coupled with low demand amid mass market closures. On that note, Chinese markets will remain closed for the rest of the week.

- US Energy Inventory Data (bbls): Crude +4.9mln (exp. -1.1mln), Gasoline -1.5mln (exp. -1.1mln), Distillate -2.2mln (exp. -0.2mln), Cushing +1.5mln.

- US and Philippines reportedly eye a partnership to cut China’s nickel dominance, according to Bloomberg.

Geopolitics

- Walla’s Elster citing a senior Egyptian source who told local media that efforts to reach a truce agreement continue in a “positive atmosphere”

- Hamas official says the group still studying recent ceasefire offer

- Philippines Coast Guard official said China’s Coast Guard has elevated the tension and level of aggression, while the official added the Chinese Coast Guard’s use of a water cannon is still not an armed attack but is using higher water pressure, according to Reuters.

US Event Calendar

- 07:00: April MBA Mortgage Applications -2.3%, prior -2.7%

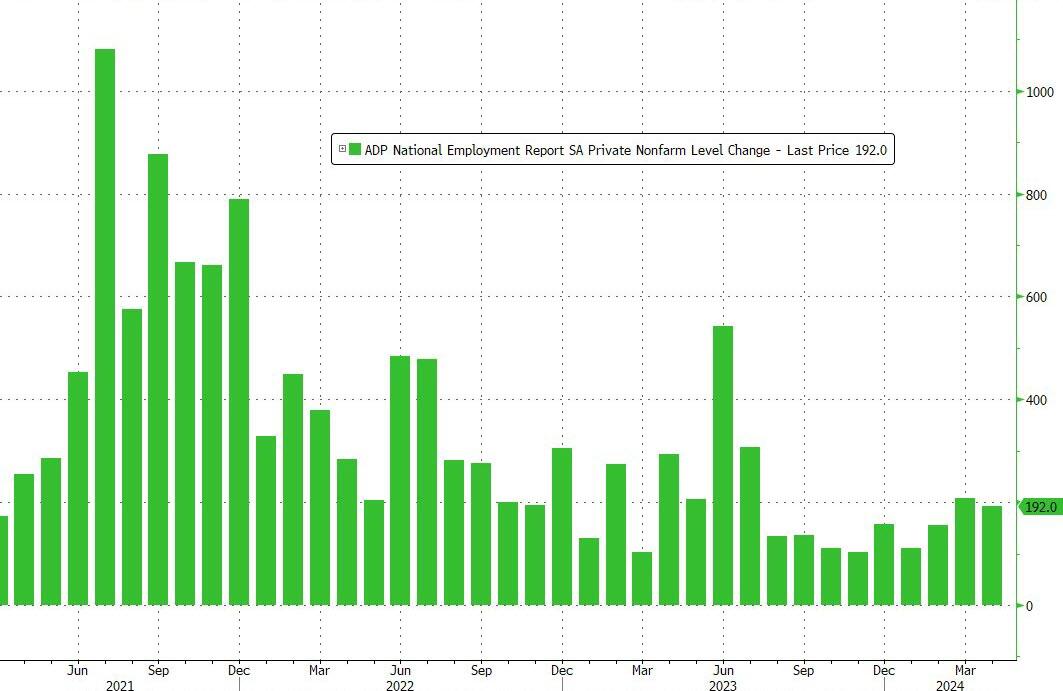

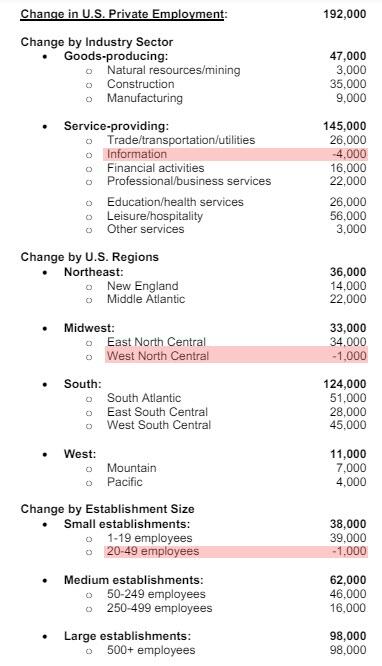

- 08:15: April ADP Employment Change, est. 180,000, prior 184,000

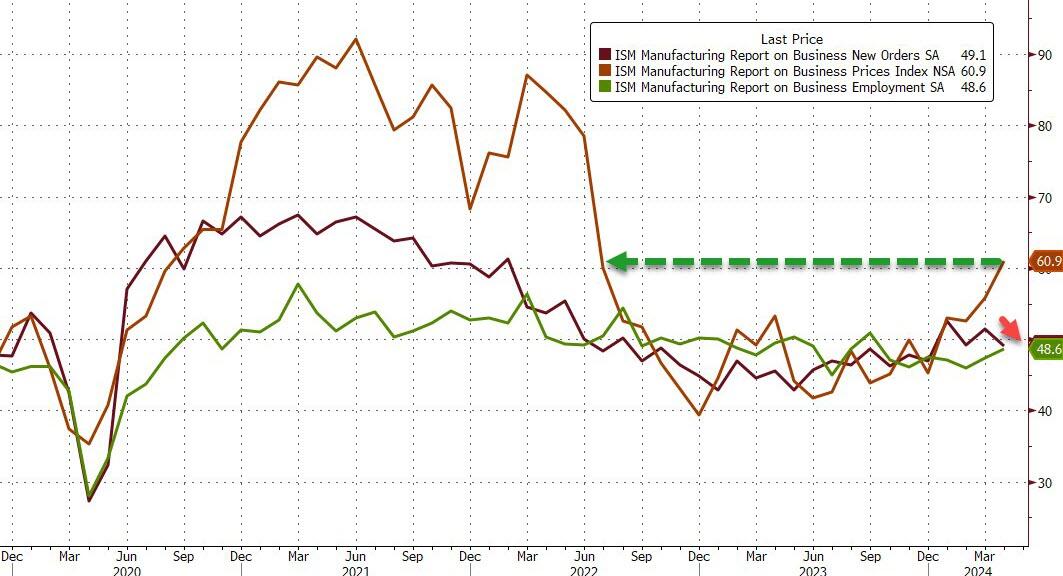

- 09:45: April S&P Global US Manufacturing PM, est. 49.9, prior 49.9

- 10:00: March JOLTs Job Openings, est. 8.69m, prior 8.76m

- 10:00: March Construction Spending MoM, est. 0.3%, prior -0.3%

- 10:00: April ISM Manufacturing, est. 50.0, prior 50.3

- 14:00: May FOMC Rate Decision

DB’s Jim Reid concludes the overnight wrap

Since it’s the start of the month, Henry will shortly be releasing our usual performance review for the month just gone. Overall, April marked a change in tone from the positivity of Q1, as investors’ concern grew about sticky US inflation and geopolitical tensions in the Middle East. Although that helped haven assets like gold and the US Dollar, it also meant the S&P 500 fell back (-4.16%) after 5 consecutive monthly gains, whilst 10yr Treasury yields (up +48bps) saw their biggest increase since September 2022. See the full report in your inboxes shortly. May will start with a holiday today across much of Europe and some of Asia but it won’t be quiet later on with the latest FOMC set to be fascinating in terms of what Powell says about inflation and rates. A full preview follows below.

Those April themes we discussed above were very evident on the last day of the month yesterday, as US data pointed to stubborn inflation and weak consumer confidence, which meant bonds and equities both lost substantial ground. That’s certainly a big part of our “what keeps us awake at night” pack. The main catalyst for the selloff yesterday came from the Employment Cost Index for Q1, which is an important one since the Fed view it as a high-quality indicator. That rose by +1.2% in Q1 (vs. +1.0% expected), which is the strongest reading in a year. Moreover, it adds to the collection of readings which suggest that inflation is remaining stubbornly above target, and if anything might even be re-accelerating. 90 minutes later, any remaining positive sentiment took a further hit after the Conference Board’s consumer confidence indicator fell back to 97.0 in April (vs. 104.0 expected). Maybe falling equities, rising yields, and higher oil earlier in the month played a part. That was its lowest reading since July 2022, back when there were heightened fears of a recession after the Fed had begun hiking by 75bps and global energy prices were surging. Elsewhere the Chicago PMI saw a very surprising slump to 37.9 vs. 45.0 expected, only one tenth off being the worst print since the early months of the pandemic and lower than anything seen between the GFC and the pandemic. This was once a bellwether but has lost a lot of its lead indicator sheen in recent months.

Given we’ve got the Fed’s latest decision tonight and Chair Powell’s press conference, we should soon find out how they’re thinking about all this data. But in the meantime, the ECI data led investors to price out the chance of cuts this year, and they now see just 28bps of cuts by the December meeting, which is the fewest so far. If that profile is realised, it would also mean that the Fed funds rate stays above 5% for the entirety of 2024, so depending how you define “higher for longer”, this is clearly moving in that direction. In turn, that led to a fresh selloff for US Treasuries, and the 2yr yield (+5.8bps) closed at 5.04%, marking the first time since November that it’s closed above 5%. The 10yr yield was also up +6.6bps to 4.68%, although it remains beneath its peak levels from last week. They are a basis point lower in Asia this morning.

In terms of the Fed’s decision, it’s widely expected that they’ll leave rates unchanged today. But given the recent inflation data, our US economists think there’ll be a more hawkish-leaning message, echoing Chair Powell’s view that it will take longer to gain confidence about disinflation. One thing to look out for will be if we hear anything about a potential slowing of QT, although our economists believe this is likely to wait until June, as the FOMC will want to avoid a dovish misinterpretation that could ease financial conditions inadvertently. In the press conference, they think Chair Powell will emphasise that there’s no urgency to reduce rates given the resilient economy. See their full preview here for more details. One possible saving grace for bond investors going into the Fed is that yields have tended to decline around Fed meetings, an empirical observation that our US team took a deep dive into in a report here on Monday. We also have the latest QRA today with our preview here. Our US rates strategists see the main focus as likely to be on details of the Treasury’s new buyback program.

With investors pricing in higher rates for longer, equities had a challenging month end on both sides of the Atlantic. The S&P 500 fell -1.57% yesterday, its worst decline since January, with an already bad day made worse by a -0.5% slump in the final 10 minutes of month-end trading. That means that the index was down by -4.16% over April as a whole, ending a run of 5 consecutive monthly gains. And as it happens, it was actually the index’s second-worst monthly performance since December 2022, around the time the S&P had seen a peak-to-trough decline of -25%. Only September 2023 has been worst since. In terms of yesterday’s moves, the Magnificent 7 (-2.55%) helped to drive the declines, with Tesla (-5.55%) falling back after its surge on Monday. But equities also struggled more broadly, with the small-cap Russell 2000 (-2.09%), the NASDAQ (-2.04%) and the Dow Jones (-1.49%) all posting large declines. Meanwhile in Europe, the STOXX 600 (-0.68%) fell back more modestly, though Spain’s IBEX 35 (-2.22%) had its worst daily performance in over a year.

After the US close, we had results from Amazon. These beat Q1 revenue and earnings estimates thanks to stronger cloud computing growth, but the positive read through was limited by softer-than-expected sales guidance for Q2. Amazon shares were up slightly over +1% in after-hours trading after falling -3.29% yesterday. The negative sentiment from the US equity close has continued overnight, with S&P (-0.09%) and NASDAQ (-0.27%) futures trading slightly lower as I type.

Earlier in the day, the European data had actually come in pretty strongly, as Euro Area GDP growth came in at +0.3% in Q1 (vs. +0.1% expected). Moreover, the flash CPI release was in line with expectations at +2.4%, even if core CPI was a touch higher than expected at +2.7% (vs. +2.6% expected). Nevertheless, that was still the lowest core CPI in over two years, and the GDP growth was the strongest since Q3 2022. So it adds to the signals that Euro Area growth is turning higher, and it didn’t provide anything to really shift expectations for an ECB rate cut in June either, with market pricing still pointing to an 87% chance of a move. That said, the combination of solid European data and the reaction to the US ECI release saw the amount of ECB rate cuts priced by December fall -6.5bps to 66bps yesterday, its lowest so far this cycle. With this backdrop, yields on 10yr bunds (+5.1bps), OATs (+4.9bps) and BTPs (+6.1bps) all moved higher.

Asian equity markets are lower this morning in holiday thinned trading. The Nikkei (-0.56%) is seeing further losses after its worst month since December 2022 while the S&P/ASX 200 (-0.97%) is trading notably lower. Otherwise most Asian markets are closed due to the Labor day holiday.

In terms of yesterday’s other data, German unemployment was up by +10k in April (vs. +8k expected), and German GDP was up by +0.2% in Q1 (vs. +0.1% expected). Here in the UK, mortgage approvals were up to an 18-month high in March of 61.3k (vs. 61.5k expected). And in the US, the FHFA house price index for February was up +1.2% (vs. +0.2% expected).

To the day ahead now, and the Federal Reserve decision and Chair Powell’s subsequent press conference will be the main highlight. Otherwise, US data releases include the ISM manufacturing for April, the ADP’s report of private payrolls for April, and the JOLTS report for March. From central banks, we’ll also hear from the ECB’s De Cos. Finally, today’s earnings releases include Mastercard, Pfizer, and Qualcomm.

WEDNESDAY, MAY 01, 2024 – 05:54 AM

- European bourses are closed for Labour Day, with the exception of the UK’s FTSE 100, which is incrementally firmer; US equity futures are entirely in the red

- Dollar is flat with G10 peers also holding pattern awaiting a slew of US data and the FOMC

- USTs are unchanged ahead of today’s key events, with QRA also in focus; Gilts subdued

- Crude sinks lower, XAU is incrementally firmer and base metals are lower across the board

- Looking ahead, US Manufacturing PMI, ISM, US ADP, JOLTS, FOMC Announcement, Treasury QRA, Fed Chair Powell, BoC’s Macklem & Rogers. Earnings from CVS, Qualcomm, MetLife, Pfizer, ADP, Marriott, Estee Lauder, Mastercard & eBay

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE – All major European markets (ex-UK) are closed for Labour Day

EQUITIES

- European bourses are closed for Labour Day, with the exception of the UK’s FTSE 100 and Denmark’s Nasdaq Copenhagen.

- The FTSE 100 (+0.1%) is incrementally firmer, though has come under slight selling pressure in recent trade. GSK (+1.9%) gains post-earnings after beating on top/bottom lines, and raising guidance.

- US Equity Futures (ES -0.3%, NQ -0.6%, RTY -0.3%) are entirely in the red, with clear underperformance in the NQ, hampered by chip-led weakness. Amazon (+2.3%) firmer pre-market on its results, whilst dire Starbucks (-12.1%) earnings have led to pre-market pressure.

- Click here and here for the sessions European pre-market equity newsflow, including notable earnings/updates from: GSK, Haleon & Aston Martin

- Click here for more details.

FX

- USD is steady vs. peers after yesterday’s buying momentum followed through into the early stages of today’s trading with the index topping out just shy of the YTD peak at 106.51. A slew of US data and the FOMC thereafter will decide direction.

- EUR is flat vs. the USD with European markets closed for Labour Day. EUR/USD did drift as low as 1.0650 before staging a marginal pick up.

- JPY is trivially softer vs. the USD (compared to recent moves) with the pair briefly eclipsing the 158 mark. Focus is on today’s busy US data/FOMC docket and whether a hawkish outturn could see a revisit to 160.

- Antipodeans are both relatively steady vs. the USD after yesterday’s pronounced selling. AUD/USD marginally extended on yesterday’s low with the session trough at 0.6466 before picking up a touch.

- Click here for more details.

- Click here for OpEx for today’s NY Cut

FIXED INCOME

- USTs are flat ahead of a packed US session, holding at 107-14 which is 10 ticks above the contract low from last week. Alongside this, Quarterly refunding is due after Monday’s estimates were above exp., though coupon sizes seen unch. Q/Q with the extra need to be filled by bills.

- Gilts are softer as the benchmark catches up to the continued late-doors downside in benchmarks on Tuesday. Catalysts light thus far given the mass-European market closure for Labour Day. Gilt auction was incrementally softer than the prior but still solid overall with a few fleeting downticks to a 95.44 base.

- Click here for more details.

COMMODITIES