MAY 3//GOLD CLOSED DOWN $0.80 TO $2300.//SILVER WAS DOWN $0.12 TO $20.47/PLATINUM WAS DOWN $2.75 TO $955.15/WHILE PALLADIUM WAS UP $7.15 T0 $939.HE50//MUST VIEW PODCAST FROM ANDREW MAGUIRE TALKING ABOUT REAL PHYSICAL GOLD VS PHONY PAPER//USA RELEASES ANOTHER PHONY JOBS REPORT//BIDEN WANTS GAZAN MIGRANTS BUT REPUBLICANS ARE ATTEMPTING TO BLOCK THIS MOVE..OTHER USA DATA RELEASES//ISRAEL GIVES HAMAS ONE WEEK TO AGREE TO A HOSTAGE SETTLEMENT//OTHER ISRAEL VS HAMAS COMMENTARIES//UKRAINE ATTACKS RUSSIA AND THEN RUSSIA ATTACKS UKRAINE/COVID UPDATES/COVID INJURIES//DR PAUL ALEXANDER/ SLAY NEWS ETC//SWAMP STORIES FOR YOU TONIGHT//

The defense of $2300 gold is now upon us and surpassed. Next up $2400 gold//Silver’s next line is $28.42. Then $34.76 …

Gild and silver held quite nicely even though China has been absent these past few days due their holiday. When Monday arrives, gold will continue its continue on its upward trajectory

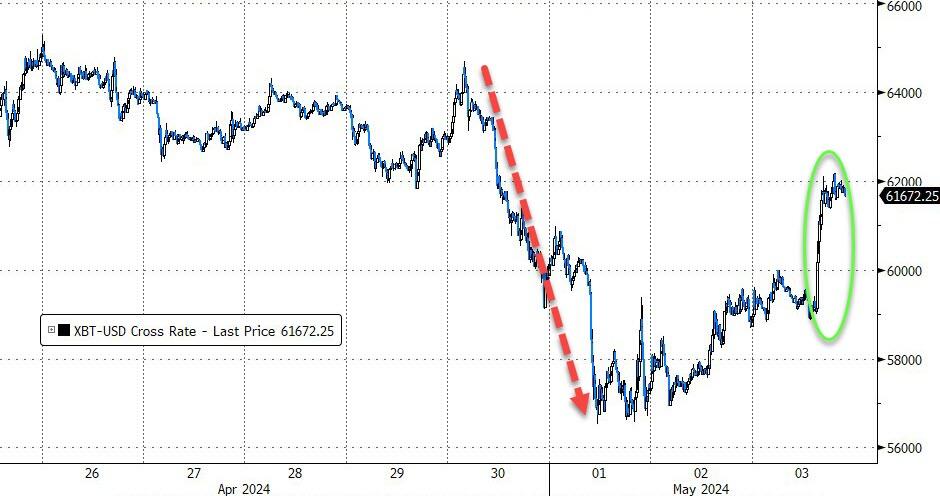

Bitcoin morning price:$59,200 UP 220DOLLARS.

Bitcoin: afternoon price: $61,727 UP 2307 dollars

Platinum price closing DOWN $2.25 TO $955.15

Palladium price; UP $7.15 AT $946.65

END

SHANGHAI GOLD PREMIUM 55 DOLLARS/COMEX GOLD

SHANGHAI GOLD…

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $3148.08 UP 12.64 CDN dollars per oz( * NEW ALL TIME HIGH 3,301.52 CDN DOLLARS PER OZ//APRIL 16 2024)

*BRITISH GOLD: 1833.72 DOWN 3.82pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2137.55 DOWN 9.81Euros per oz //* (ALL TIME CLOSING HIGH: 2248.89 EUROS PER OZ//APRIL 16.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCGE: COMEX

REPORT THIS AD

JPMorgan stopped 1/35

FOR MAY2024

GOLD: NUMBER OF NOTICES FILED FOR MAY/2024. CONTRACT: 35 NOTICES FOR 3500 OZ or 0.1088 TONNES

total notices so far: 1590 contracts for 159000 Oz (4,945 tonnes)

FOR MAY:

SILVER NOTICES: 19 NOTICE(S) FILED FOR 95,000 OZ/

total number of notices filed so far this month : 4474 for 22.370 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $0.80

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL 0F 1.80 TONNES OF GOLD FROM THE GLD

/ /INVENTORY RESTS AT 829.84 TONNES

INVENTORY RESTS AT 831.64TONNES

SLV//

WITH NO SILVER AROUND AND

SILVER DOWN 12 CENTS AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 0.338 MILLION OZ INTO THE SLV//

// INVENTORY INCREASES T0 424.512MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 424.512 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A FAIR SIZED 207 CONTRACTS TO 165,639 AND CLOSING IN AT CLOSING IN ON THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR SMALL GAIN OF $0,12 IN SILVER PRICING AT THE COMEX ON THURSDAY. WE HAD ZERO LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN SHORT COVERING BY OUR SPECS WITH THE GAIN PRICE. WE HAD A HUGE SIZED 663 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 663 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.12 AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A FAIR SIZED GAIN OF 357 CONTRACTS ON OUR TWO EXCHANGES WITH THE GAIN IN PRICE OF $0.12

WE MUST HAVE HAD:

A SMALL SIZED 150 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 28.130MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 105,000 OZ

//NEW STANDING FOR SILVER//MAY IS THUS 26.195 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI GAIN //SMALL SIZED EFP ISSUANCE/ VI) STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 663 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED A STRONG 648CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS APRIL ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY

TOTAL CONTRACTS for 3 DAYS, total 2150 contracts: OR 10.750 MILLION OZ (717 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 10.750 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770MILLION OZ (THIS MONTH WILL PROBABLY BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 10.75 MILLION OZ

RESULT: WE HAD A FAIR SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 207 CONTRACTS WITH OUR SMALL GAIN IN PRICE OF SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL EFP ISSUANCE CONTRACTS: 150 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAY OF 28.130 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAYS 105,000 OZ QUEUE JUMP

//NEW TOTAL STANDING AT 26.195 MILLION OZ

WE HAVE A FAIR SIZED GAIN OF 357 OI CONTRACTS ON THE TWO EXCHANGES WITH THE SMALL GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 663 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS

THE NEW TAS ISSUANCE THURSDAY NIGHT (472 WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 19 NOTICE(S) FILED TODAY FOR 95,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 3509 OI CONTRACTS TO 526,097 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 768 CONTRACTS

WE HAD A FAIR SIZED INCREASE IN COMEX OI (3509 CONTRACTS) OCCURRED WITH OUR $0.20 GAIN IN PRICE//THUSDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER TO WHACK GOLD’S PRICE. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 4.684 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY;S 2800 OZ QUEUE JUMP//NEW STANDING 5,.135 TONNES

NEW STANDING 5.135 TONNES// ALL OF THIS HAPPENED DESPITE OUR TINY $0.20 GAIN IN PRICE WITH RESPECT TO THURSDAY’S TRADING. WE HAD A VERY STRONG SIZED GAIN OF 10,745 OI CONTRACTS (34.043 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 7430 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 526,097

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 10,945 CONTRACTS WITH6400 CONTRACTS INCREASED AT THE COMEX// AND A HUGE SIZED 7430 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 10,945 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED 4431 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A HUGE SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (7430 CONTRACTS) ACCOMPANYING THE GAIN IN COMEX OI 3509/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 10,945 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 4.684TONNES FOLLOWED BY TODAY;S 2800 OZ QUEUE JUMP

//NEW STANDING /MAY 5.135 TONNES.

/ 3) ZERO LONG LIQUIDATION WITH THE GAIN IN PRICE.

// 4) STRONG SIZED COMEX OPEN INTEREST GAIN 5) HUGE ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: STRONG T.A.S. ISSUANCE: 2031 CONTRACTS/ HUGE SHORT COVERING BY OUR WRONG FOOTED SPECS WITH THE FED’S CONTINUAL RAID ON THE COMEX GOLD.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY. :

TOTAL EFP CONTRACTS ISSUED: 20,016CONTRACTS OR 2,001,600 OZ OR 62.26 TONNES IN 3 TRADING DAY(S) AND THUS AVERAGING: 6672EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAY(S) IN TONNES 62.26 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 62.26 DIVIDED BY 3550 x 100% TONNES = 1.74% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 62.26 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF APRIL. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A FAIR SIZED 207 CONTRACTS OI TO 165,639 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 150 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 150 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 150 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 644CONTRACTS AND ADD TO THE 150 E.FP. ISSUED

WE OBTAIN A FAIR SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 357 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 1.785 MILLION OZ

OCCURRED DESPITE OUR SMALL $0.12 GAIN IN PRICE …..

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

REPORT

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING/THURSDAY NIGHT

SHANGHAI CLOSED //Hang Seng CLOSED UP 268.79OR 1.48%// Nikkei CLOSED//Australia’s all ordinaries CLOSED UP 0.61%///Chinese yuan (ONSHORE) closed UP CHINESE YUAN CLOSED UP TO 7.1934/Oil DOWN TO 79.23 dollars per barrel for WTI and BRENT DOWN AT 84.710/Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING XXX LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 3509 CONTRACTS TO 526,097 WITH OUR GAIN IN PRICE OF $0.20 WITH RESPECT TO THURSDAY TRADING. WE HAD CONSIDERABLE T.A.S. LIQUIDATION AS WELL AS SHORTS, DESPERATELY TRYING TO GET OUT OF THEIR NAKED SHORTS.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAY.… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A HUGE 7430 EFP CONTRACTS WERE ISSUED: : JUNE7430 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE:7430 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG SIZED TOTAL OF 10,945 CONTRACTS IN THAT 7430 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A FAIR SIZED GAIN OF 3509 COMEX CONTRACTS..AND THIS STRONG GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR TINY GAIN IN PRICE OF $0.20 THURSDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT WAS A STRONG SIZED 4431 CONTRACTS. WE HAD 0 EX FOR RISK ISSUANCE. MOST OF THE TRADING AND SUPPLY OF CONTRACTS ON THURSDAY WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (5.135 TONNES) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

REPORT THIS AD

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2023 5.135TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A TINY $0.20 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG SIZED GAIN OF10,945 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN IN PRICE 0F $0.20

WE HAD A STRONG T.A.S. LIQUIDATION ON THE FRONT END OF THURSDAY’S TRADING. THE T.A.S. ISSUED ON THURSSDAY NIGHT, WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 34.043 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY (4.684 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 26 CONTRACTS OR 2800 OZ ( .0871 TONNES)

NEW STANDING: 5.135 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $0.20

WE HAVE REMOVED 2891 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET GAIN ON THE TWO EXCHANGES 10,945 CONTRACTS OR 1,094500 (34.043 TONNES)

Total monthly oz gold served (contracts) so far this month

1590notices 159,000oz 4.945TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: 0 oz

we have 0 customer deposits:

i

total deposit 0 oz

total customer withdrawals: 0

TOTAL WITHDRAWALS 0

Adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY

For the front month of MAY we have an oi of 96 contracts having GAINED 14 contracts.

We had 14 contracts served on Thursday, so we gained 28 contracts or 2800 oz (,08709tonnes).

JUNE DECREASED ITS OI BY 5733 CONTRACTS DOWN TO 390,122CONTRACTS.

JULY LOST 71 CONTRACTS TO STAND AT 163

We had 35 contracts filed for today representing 3500 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 135contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 1 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the MAY /2024. contract month, we take the total number of notices filed so far for the month (1590 ) x 100 oz ) to which we add the difference between the open interest for the front month of MAY ( 96 CONTRACTS) minus the number of notices served upon today (35 x 100 oz per contract( equals 165,100 OZ OR 5.135 TONNES.

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (1590x 100 oz + (96)OI for the front month} minus the number of notices served upon today (35 x 100 oz which equals 165,100 oz (5.135 TONNES)

TOTAL COMEX GOLD STANDING FOR MAY: 5.135 TONNES WHICH IS HUGE FOR THIS A NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,720,789.868 OZ

TOTAL REGISTERED GOLD 7,533,615.645( 234.327 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,187,767.594 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 5,951,095 oz (REG GOLD- PLEDGED GOLD)

185.10 tonnes/dropping like a stone

END

SILVER/COMEX

MAY 3

INITIAL

//2024// THE MAY 2025 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

118,481.470oz

asahi

.

Deposits to the Dealer Inventory

00OZ

Deposits to the Customer Inventory

579,123.400 oz

Manfra

No of oz served today (contracts)

19 CONTRACT(S) (95,000OZ)

No of oz to be served (notices)

746contracts (3.730 million oz)

Total monthly oz silver served (contracts)

4493Contracts (22.465 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposit :nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i) Into Manfra 579,123,400 oz

total customer deposits 579,123,400oz

JPMorgan has a total silver weight: 129,598million oz/295.648million or 43.64%

adjustment: 1

dealer to customer: 404,330.870 oz

Comex withdrawals: 1

i) out of ASAHI 118,481.470 oz

total withdrawal 118,481,470 oz

TOTAL REGISTERED SILVER: 61.951MILLION OZ//.TOTAL REG + ELIGIBLE. 295.648million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF MAY/2024 OI: 765 CONTRACTS HAVING LOST 378 CONTRACT(S).

.

We had 399 notices served on THURSDAY so we GAINED 21 contracts or 105,000 oz underwent a strong queue jump.

JUNE SAW A GAIN OF 146 CONTRACTS RISING TO 1999

JULY SAW A gain OF 10 CONTRACTS UP TO 135,754

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 19 for 95,000 oz

CONFIRMED volume; ON THURSDAY 68,762huge

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 4493 x 5,000 oz = 22.465MILLION oz

to which we add the difference between the open interest for the front month of MAY (765 and the number of notices served upon today 19x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2024 contract month: 4493 notices served so far) x 5000 oz + OI for the front month of MAY (765 number of notices served upon today minus (19x 5000 oz of silver standing for the may contract month equates to 26.195 MILLION OZ.

New total standing: 26.195 million oz.

There are 62.355 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

MAY 23WITH GOLD UP $0.20 ON THE DAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .55 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 831.64 TONNES

MAY 2 WITH GOLD UP $0.20 ON THE DAY; SMAKK CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .55 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 831.64 TONNES

MAY 1 WITH GOLD UP $7.80 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNES

APRIL 29WITH GOLD UP $10,55TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNES

APRIL 26WITH GOLD UP $5.40TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.54 TONNES FROM THE GLD /INVENTORY RISES AT 832.19 TONNES

APRIL 25WITH GOLD UP $5.05 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD /INVENTORY RISES AT 833,63 TONNES

APRIL 19 WITH GOLD UP $15.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 4.32 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 831.91 TONNES

APRIL 18 WITH GOLD UP $11.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE WITHDRAWAL OF 2.59 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 827.59 TONNES

APRIL 17 WITH GOLD DOWN $17.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 830;18 TONNES

APRIL 16 WITH GOLD UP $23.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 828.45 TONNES

APRIL 15 WITH GOLD DOWN $. 80 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A HUGE WITHDRAWAL OF 1.80 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 824.84 TONNES

APRIL 12 WITH GOLD UP $2.80 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD/ INVENTORY RISESS AT 830.75 TONN

APRIL 10 WITH GOLD DOWN $14.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 0.86 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 828.71 TONNES

APRIL 9 WITH GOLD UP $11.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 827,85 TONNES

APRIL 8 WITH GOLD UP $7.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A WITHDRAWAL OF 6.02 TONNES OF GOLD INTO THE GLD/ INVENTORY REMAINS AT 826.41 TONNES

APRIL 5 WITH GOLD UP $38.65 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/ INVENTORY REMAINS AT 832.45 TONNES

APRIL 4 WITH GOLD DOWN $3.35 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD/ INVENTORY REMAINS AT 830.73 TONNES

APRIL 3 WITH GOLD UP $33,85 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD // INVENTORY REMAINS AT 829.00 TONNES

APRIL 2 WITH GOLD UP $23.90 TODAY; HUG CHANGES IN GOLD INVENTORY AT THE GLD A WITH DRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD.:// INVENTORY REMAINS AT 829.00 TONNES

APRIL 1 WITH GOLD UP $18.70 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:// INVENTORY REMAINS AT 830.15 TONNES

MARCH 28 WITH GOLD UP $26.30 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:// INVENTORY REMAINS AT 830.15 TONNES

MARCH 27 WITH GOLD UP $15.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// INVENTORY FALLS TO 830.15 TONNES

MARCH 26 WITH GOLD UP $1.40 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 835.33 TONNES

MARCH 25 WITH GOLD UP $17.05 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 838.50 TONNES

MARCH 22 WITH GOLD DOWN $23.75 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD INVENTORY RISES TO 838.50 TONNES

GLD INVENTORY: 831.64 TONNES,

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 3 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 2WITH SILVER UP 0.12 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/ A WITHDRAWALOF 4.471 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 1 WITH SILVER UP 0.09 TODAY: SMALLCHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF ,457 MILLION OZ INTO THE SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 29WITH SILVER UP $0.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 26WITH SILVER DOWN 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.097 MILLION OF SILVER INTO THE SLV// :SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 25WITH SILVER UP $.05 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 1.534 MILLION OF SILVER OUT OF THE SLV// :SLV INVENTORY RESTS AT 428.717 MILLION OZ

APRIL 24/WITH SILVER DOWN $.05 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 11.904MILLION OF SILVER INTO THE SLV// :SLV INVENTORY RESTS AT 428.280 MILLION OZ

APRIL 23/WITH SILVER UP $0.11TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV / :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 22/WITH SILVER DOWN $1.51 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.194 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 19/WITH SILVER UP 42 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.657 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 418.570 MILLION OZ

APRIL 18/WITH SILVER DOWN $.04TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.977 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 422.227 MILLION OZ

APRIL 17/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF .868 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 426/204 MILLION OZ

APRIL 16/WITH SILVER DOWN $0.46 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF NON EXISTENT SILVER// :SLV INVENTORY RESTS AT 427.072 MILLION OZ

APRIL 15/WITH SILVER UP $0.46 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 12/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 4.069 MILLION OZ FROM THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 11/WITH SILVER UP $0.23 TODAY: STRANGE INDEED! HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.931 MILLION OZ :SLV INVENTORY RESTS AT 437.998 MILLION OZ

APRIL 10/WITH SILVER UP $0.04 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV:SLV INVENTORY RESTS AT 441.929 MILLION OZ

APRIL 9/WITH SILVER UP $0.15 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.549 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 441.929 MILLION OZ

APRIL 8/WITH SILVER UP $0.33 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.320 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 441.328 MILLION OZ

APRIL 5/WITH SILVER UP $0.61 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.748 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 441.060 MILLION OZ

APRIL 4/WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.671 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 437.312 MILLION OZ

APRIL 3/WITH SILVER UP $1.14 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 2.835 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 433.641 MILLION OZ

APRIL 2/WITH SILVER UP 84 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 6.721 MILLION OZ INTO THE SLV// SLV INVENTORY RESTS AT 430.806 MILLION OZ

APRIL 1/WITH SILVER UP 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// SLV INVENTORY RESTS AT 424.085 MILLION OZ

MARCH 28/WITH SILVER UP 20 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 1.005 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 424.085 MILLION OZ

MARCH 27/WITH SILVER UP 14 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A A DEPOSIT OF 1.691 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 423.079 MILLION OZ

MARCH 26/WITH SILVER DOWN 24 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV A A DEPOSIT OF 0.366 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 421.388 MILLION OZ

MARCH 25/WITH SILVER UP 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE WITHDRAWAL OF 3.887 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 421.022 MILLION OZ

MARCH 22/WITH SILVER DOWN 9 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A HUGE DEPOSIT OF 1.1899 MILLION OZ INTO THE SLV: SLV INVENTORY RESTS AT 424.909 MILLION OZ

Gold and silver consolidated this week, with gold testing support at $2300 and silver at $26. In European trade this morning, gold was $2302, down $35, and silver $26.56, down 66 cents. Volumes on Comex in both metals declined as the consolidation has progressed.

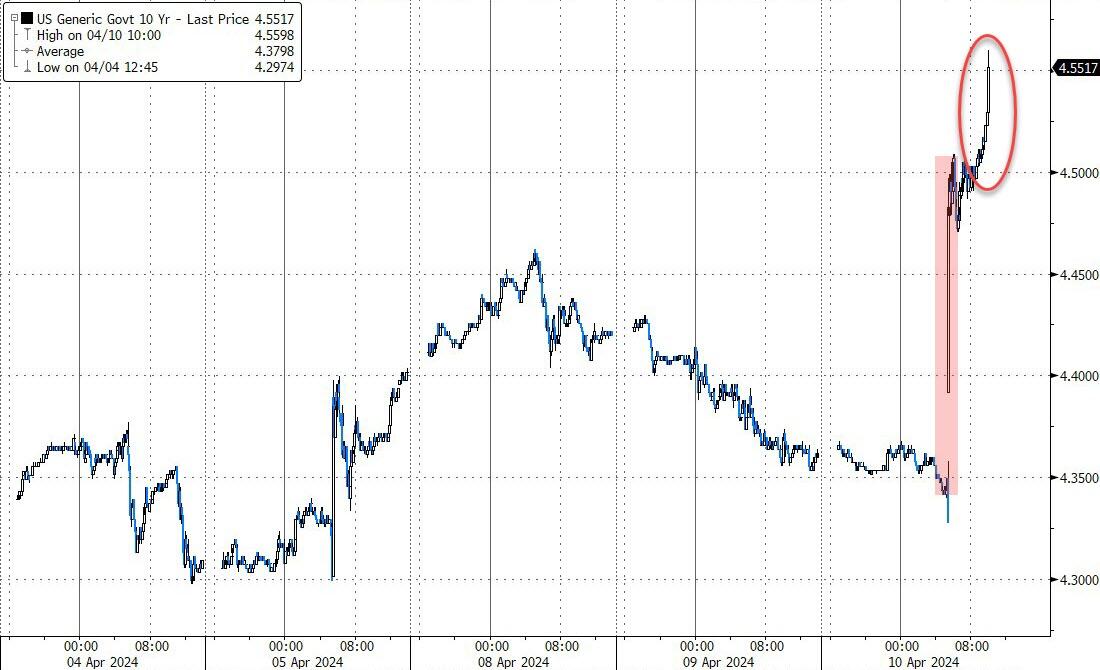

The highlight of the week was the FOMC meeting and statement. As it turned out, there was little surprise, other than the pace of quantitative tightening which persuaded optimists that pressure on yields along the curve would be reduced. Consequently, yields ticked marginally lower, as the chart of the 10-year UST note shows:

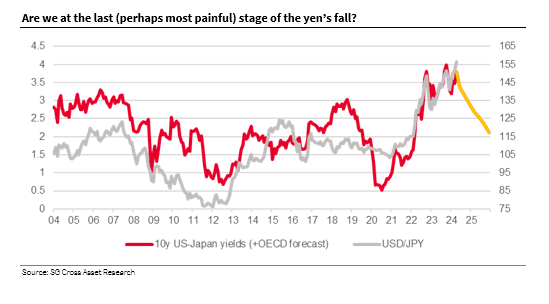

The golden cross on 7 March told us that the fall in yields from last October was over, and that instead of lower bond yields in time they were heading higher instead. This is consistent with the likely funding difficulties which the US Government faces with its $3+ trillion deficit. This problem is destabilising the entire fiat currency system, leading to a relatively strong dollar, whose trade weighted index is next.

As long as the $TWI is in a bull trend, it is bad news for other currencies, typified by the Japanese yen, which this week made a break for the downside as the yield on the 10-year JGB rose to over 0.9%. Clearly, the developing debt trap for the dollar is undermining the Bank of Japan’s monetary policy.

The determination of the Bank of Japan to sit on JGB yields only encourages the carry trade, whereby the expansion of yen bank credit feeds directly into US Treasuries. The consequences for the currency and bond yields are next:

Instability in fiat currencies is what’s driving them lower valued in gold. It is worth putting the relationship by pricing fiat currencies in gold instead of gold priced in fiat to emphasise that it is less of a question of gold rising, and more one of the dollar and other currencies falling. It is a situation which can rapidly drift into crisis.

There could be a crisis developing in silver. The next chart shows that the Swaps’ shorts are drifting out of control.

The net short position amounts to the paper equivalent of nearly 9,750 tonnes, or $8.2 billion spread between 17 traders. They are part of the same cohort which is short of $63bn in Comex paper gold.

Falling fiat currency values is putting the squeeze on the banking establishment. And it doesn’t help that longs are standing for delivery. In silver, a further 696 tonnes were stood for delivery, and in gold a further 7.6 tonnes in the first four days of this week.

How long will it be before a bullion bank defaults? We should start thinking this way. The problem in gold is bad enough, but with India scrambling for silver for its photovoltaic cell production, silver’s short position is becoming potentially explosive. When this consolidation phase ends, the next leg of rising prices could well develop into the mother of all bear squeezes — on the establishment!

3. CHRIS POWELL//GATA DISPATCHES

end

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS /LIVE FROM THE VAULT 171

GATA) Gordon Brown’s decision to sell Britain’s gold looks ever more disastrous

By Philip Pilkington

The Telegraph, London

Thursday, May 2, 2024

According to the latest estimates, taxpayers will be on the hook to cover L85 billion in losses stemming from the unwinding of the Bank of England’s quantitative easing (QE) policy. The scheme is set to lose about L20bn a year until the early 2030s — a yearly figure worth more than a third of our current defence budget.

And these estimates may, if anything, be too optimistic. Until very recently, it was widely assumed that the Federal Reserve would lower interest rates in the United States in the run-up to the election. The Bank was no doubt hoping that it could follow suit.

But inflation seems to be sticking around and it is widely anticipated that the Fed will now maintain interest rates where they are. If interest rates are kept high for a longer period — or worse if they must rise again due to an uptick in inflation — it will mean even heavier losses for the taxpayer to fund.

Meanwhile, as the BoE frets over the consequences of its funny money programme, other countries are bolstering their gold reserves. The Chinese central bank, the Peoples’ Bank of China, is now in its 17th straight month of rapacious gold-buying. Chinese gold reserves have risen from roughly 1,950 tonnes in the third quarter of 2022 to 2,260 tonnes today — an increase of 1 4%. …

SHANGHAI CLOSED //Hang Seng CLOSED UP 268.79OR 1.48%// Nikkei CLOSED//Australia’s all ordinaries CLOSED UP 0.61%///Chinese yuan (ONSHORE) closed UP CHINESE YUAN CLOSED UP TO 7.1934/Oil DOWN TO 79.23 dollars per barrel for WTI and BRENT DOWN AT 84.710/Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING XXX LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED

OFFSHORE YUAN: UP TO 7.1934

SHANGHAI CLOSED

HANG SENG CLOSED UP 268.79PTS OR 1.48%

2. Nikkei closed

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 105.97 EURO RISES TO 1.0746 UP 17 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.894 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 153.22JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: XX/ OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.5305/Italian 10 Yr bond yield UP to 3.858 SPAIN 10 YR BOND YIELD UP TO 3.303

3i Greek 10 year bond yield UPTO 3.511

3j Gold at $2298.85//Silver at: 26.41 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 1 AND 40 100 roubles/dollar; ROUBLE AT 91.65/

3m oil into the 79 dollar handle for WTI and 84 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 153.22/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.894% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9069 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9746 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.561 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.713 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.868 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.34…(TURKEY)

10 YR UK BOND YIELD: 4.316DOWN 1 PTS

2a New York OPENING REPORT

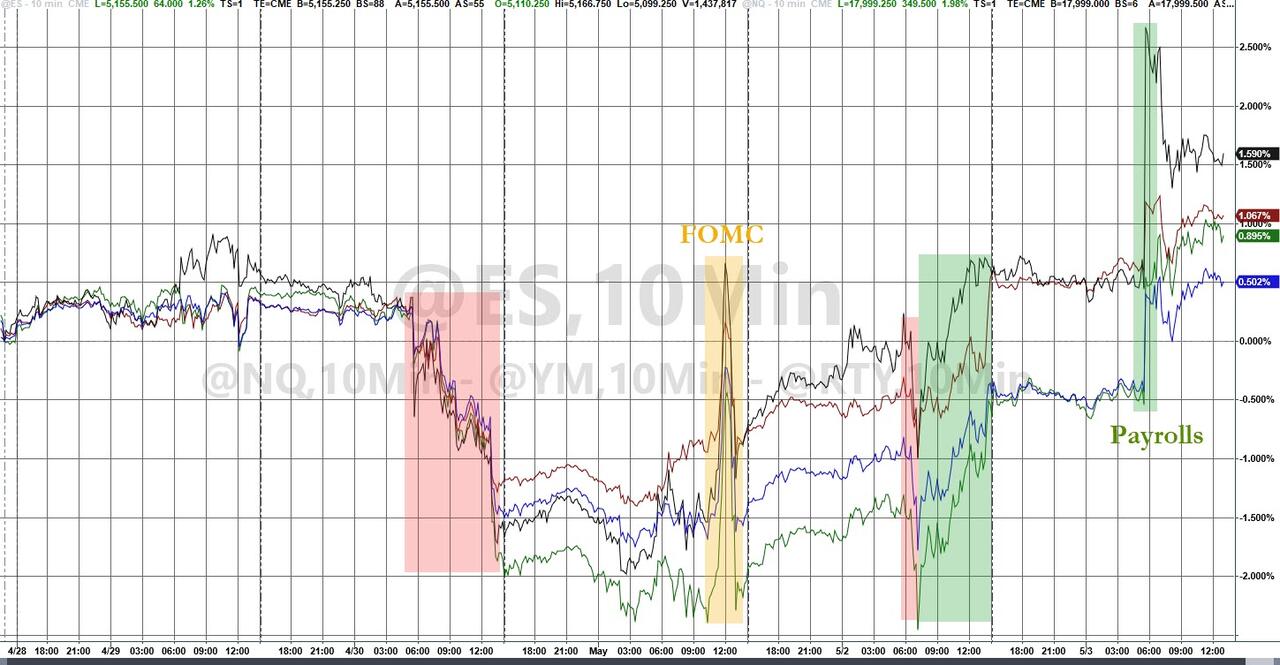

Futures Gain Boosted By Apple’s Blowout Buyback, Dollar Drops Ahead Of Payrolls

FRIDAY, MAY 03, 2024 – 08:23 AM

US stock futures pointed to further strength on Wall Street ahead of the April jobs report after solid earnings and a record buyback announcement from Apple As of 8:00am, S&P futures rise 0.3% while Nasdaq 100 contracts add 0.6% thanks to a 6% surge in Apple in premarket trading. The dollar weakened for a third day, while Treasuries were steady. The US 10-year yield is down about 9 basis points this week at 4.57%, its first weekly drop since March, after Powell struck a less hawkish tone than feared. Traders have also pulled forward expectations for the Fed’s first full interest-rate cut by a month to November.

In premarket trading Apple jumped .2% after the company posted stronger-than-expected sales last quarter and predicted a return to growth in the current period, sparking optimism that a slowdown is easing. Amgen soared 14% after its CEO said he was “very encouraged” by early results from a study of the company’s experimental obesity drug, MariTide. Here are some other notable premarket movers:UnmuteAdvanced SettingsFullscreenPauseRewind 10 SecondsUp Next

Alignment Healthcare gains 9% after the company forecast revenue for the 2Q that beat the average analyst estimate.

Ardelyx (ARDX) soars 18% after the pharma company’s Xphozah and Ibsrela drugs drove a strong 1Q revenue beat, which Jefferies expects will boost confidence in the company’s management.

BigBear.ai (BBAI) falls 14% the AI software company reported a wider-than-expected first-quarter loss.

Block (SQ) rises 7.2% after Jack Dorsey’s payments technology company forecast adjusted Ebitda for the full year above analysts’ estimates.

Cloudflare (NET) sinks 13% after the cloud security firm provided a 2Q revenue forecast that fell slightly short of estimates.

Fortinet (FTNT) falls 8% as the cybersecurity company reported a miss in first-quarter billings due to weakness in Europe.

FuboTV (FUBO) rises 8.4% after the internet television service provider reported revenue for the first quarter that beat the average analyst estimate.

ImmunityBio (IBRX) gains 8% on a deal with the Serum Institute of India for Bacillus Calmette-Guerin supply.

Live Nation Entertainment (LYV) rises 3% after the operator of Ticketmaster reported first-quarter results that beat expectations.

OneSpan (OSPN) rises 15% after the software services company reported first-quarter results that are seen as strong.

Open Text (OTEX) slips 13% after the application software company gave an outlook that is seen as weak, prompting a downgrade.

WideOpenWest (WOW) climbs 17% after shareholder Crestview says it and DigitalBridge submitted a joint, preliminary non-binding proposal to buy the cable service provider for $4.80 per Class A share.

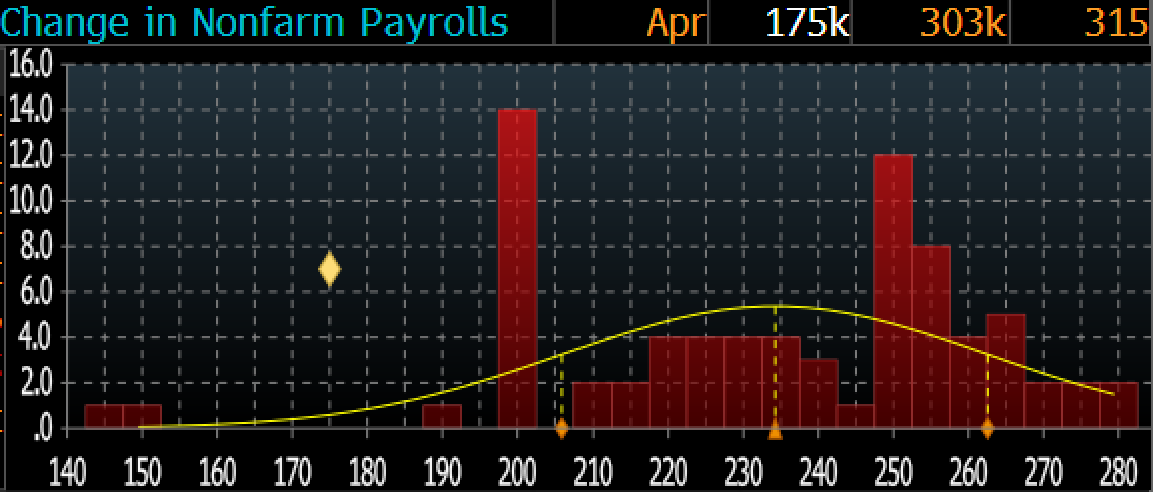

Traders will be watching this morning’s jobs report for clues about renewed slowing in the economy (full preview here). Non-farm payrolls data is the next big trigger for markets after Federal Reserve chief Jerome Powell effectively laid concerns about a potential rate hike to rest. The forecast gain of 240,000 jobs would be the weakest since November.

“NFP gains have likely slowed, but to a level that has remained strong,” wrote Credit Agricole CIB strategists led by Sébastien Barbé. “The ‘higher for longer’ narrative should remain well in place, but is largely priced in by the market at this stage.”

If the Labor Department’s report shows fewer than 125,000 jobs were added in April, and the average hourly earnings rose more than 0.4% from the previous month, that would be a “stagflation risk-off print,” according to Bank of America Corp. strategist Michael Hartnett. On the other hand, if payrolls were to rise by more than 225,000 and average hourly earnings by less than 0.2%, it would be interpreted as “Goldilocks back on and risk back on,” he wrote.

European stocks have tracked a tech-driven rally in Asia after Apple forecast a return to sales growth and announced the largest stock buyback plan in US history. The Stoxx 600 is up 0.4% as it looks to snap a three-day losing streak. While tech stocks led gains, pharmaceuticals lagged with Novo Nordisk A/S retreating more than 5% on competition concerns. Here are the most notable European movers:

Henkel jumps as much as 6.6%, the biggest gainer on the Stoxx 600 benchmark, after the German chemicals firm boosted its organic sales and adjusted Ebit margin forecasts for the full year

Credit Agricole shares rise as much as 4.2% to a fresh six-year high after the French bank delivered a big net income beat in the first quarter, according to analysts

Novonesis shares rise as much as 5.7%, the most since Oct. 26, after the Danish company reaffirmed its organic revenue forecast for the full year, rebounding from a recent slump

JCDecaux shares jump as much as 13% to the highest in more than a year after the outdoor advertising firm set a second-quarter revenue growth target that were ahead of expectations

Trainline gains as much as 9% after the online ticket retailer posted an earnings beat and upgraded its 2025 Ebitda forecast. It also announced a new £75 million share buyback program

Siemens Energy gains as much as 3.3% after Deutsche Bank raised the recommendation on the German renewable energy company to buy from hold, citing its newly-listed peer GE Vernova

Hensoldt, Renk and Rheinmetall gain as Hauck & Aufhaeuser initiates coverage of the defense contractors at buy, seeing quality in the sector and noting their resilient business model

Novo Nordisk falls as much as 4.9% after Amgen’s CEO said he was “very encouraged” by early results from a study of the US company’s experimental obesity drug, MariTide

Danske Bank falls as much as 5.7%, the most since March, after the Danish lender’s NII for the first quarter was weaker than expected, which also weighed on overall revenues in the period

Aurubis drops as much as 12%, the most since September, as UBS cuts its recommendation on the copper smelting firm to sell from buy, saying material market tightness is likely to persist

Daimler Truck declines as much as 7.3%, the most since July 2022, after the German truckmaker warned that it was seeing an increasingly difficult environment in its key European market

Bpost falls as much as 9%, the most since January, after the courier service released results that missed expectations on Ebit as M&A costs weighed, according to Jefferies

Earlier in the session, Asian stocks gained with the Hang Seng Index surging 1.5% to cap a ninth straight session of gains, the longest winning streak since 2018. Chinese technology giants Alibaba Group Holding Ltd. and Tencent Holdings Ltd. were among the top contributors to the advance.

In FX, the dollar declined 0.2% against all its Group-of-10 peers, with the Bloomberg dollar index heading for a 0.9% loss this week as traders pulled forward expectations for the first Fed rate cut to November ahead of today’s jobs report. its worst since early March. The yen strengthened as traders mulled news that authorities had likely spent about $23 billion in their second suspected currency intervention this week; Japan markets were shut for a local holiday. The Norwegian krone climbed after the nation’s central bank said tight policy may be needed somewhat longer, as it held the key interest rate steady at 4.5%, in line with expectations.

Treasuries are narrowly mixed with the yield curve flatter ahead of the April jobs report, holding most of the past two days’ steepening rally. 7- to 30-year yields are lower by ~1bp with shorter tenors little changed; 2s10s spread flattens ~2bp, unwinding less than half of Thursday’s steepening move. 5s30s spread remains near top of Thursday’s range at ~15bp. 10-year yield 4.57%, slightly outperforming bunds and gilts in the sector.

Oil prices are flat, with WTI trading near $79 a barrel. Spot gold falls 0.2% to around $2,300/oz.

Looking at today’s calendar, US economic data slate includes April jobs report (8:30am), S&P Global US services PMI (9:45am) and ISM services (10am). Fed members’ scheduled speeches include Chicago’s Goolsbee (10:30am and 7:45pm) and New York’s Williams (7:45pm)

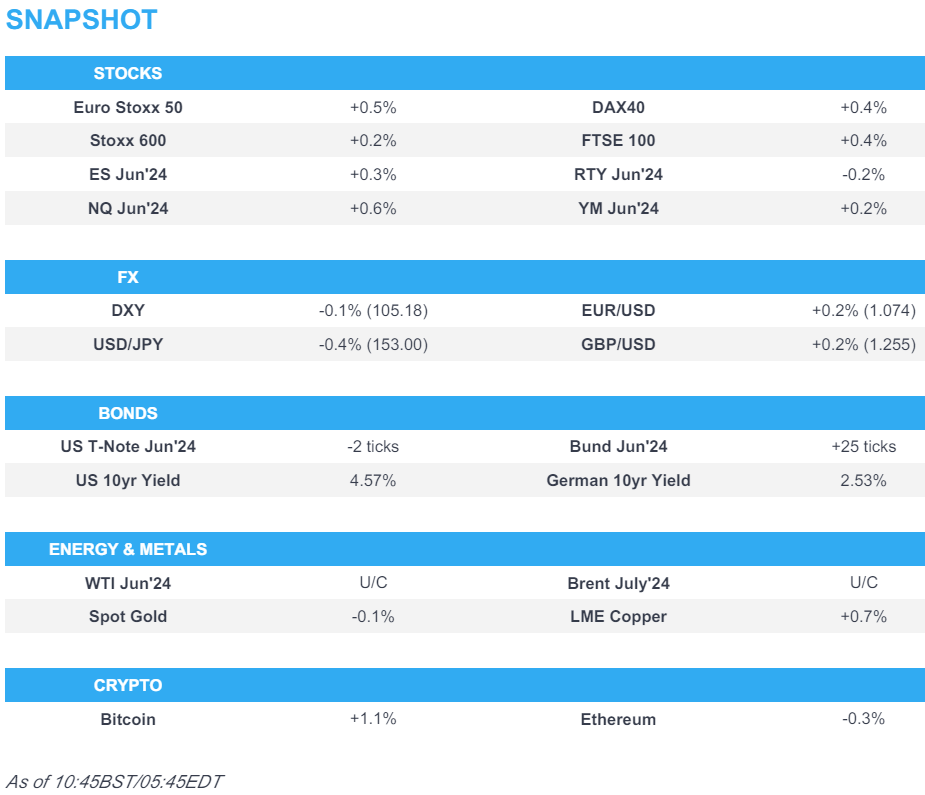

Market Snapshot

S&P 500 futures up 0.3% to 5,106.00

STOXX Europe 600 up 0.2% to 504.33

MXAP up 0.7% to 177.18

MXAPJ up 0.8% to 546.84

Nikkei little changed at 38,236.07

Topix little changed at 2,728.53

Hang Seng Index up 1.5% to 18,475.92

Shanghai Composite down 0.3% to 3,104.82

Sensex down 1.4% to 73,569.19

Australia S&P/ASX 200 up 0.6% to 7,628.97

Kospi down 0.3% to 2,676.63

German 10Y yield little changed at 2.54%

Euro up 0.1% to $1.0741

Brent Futures up 0.2% to $83.80/bbl

Gold spot down 0.2% to $2,298.75

US Dollar Index little changed at 105.22

Top Overnight News

Four Chinese generative artificial intelligence start-ups have been valued at between $1.2bn and $2.5bn in the past three months, leading a pack of more than 260 companies vying to emulate the success of US rivals such as OpenAI and Anthropic. The newly minted unicorns — Zhipu AI, Moonshot AI, MiniMax and 01.ai — have gained significant backing from a largely domestic pool of investors and are fighting to hire the best talent to develop the most popular AI products. FT

Across China and among the global scientific community, Friday’s launch of a Chinese mission to collect samples from the moon’s far side has been hailed for its potential for a scientific breakthrough. But in the U.S., lawmakers and the National Aeronautics and Space Administration are closely watching the expedition with trepidation: as a milestone in a rival’s campaign to build a base on the moon’s most strategic location. WSJ

Norway’s central bank leaves rates unchanged (as expected) and says “the policy rate will likely be kept at today’s level for some time ahead”. RTRS

Britain’s Conservative Party suffered striking early setbacks on Friday in local elections that are viewed as a barometer for how the party will perform in a coming general election and a key test for the embattled prime minister, Rishi Sunak. NYT

The OPEC+ group of countries could extend their production cuts beyond June if demand fails to improve, creating upside risks for oil prices. RTRS

The NBA is targeting $76 billion in TV rights over 11 years, three times its current deal, people familiar said. Disney and Amazon have agreed to the framework, while Warner Bros. is racing Comcast for a third package. BBG

Dated Brent has seen record trading volumes in both physical and derivative markets since WTI Midland was added to the grades that determine its price. It’s eliminated decades-long concerns over the benchmark’s viability amid shrinking North Sea production. BBG

AAPL +6% beat … “guided up LSD. Upside on Services, China revs, iPhone revs .. $110bn BUYBACK .. Revenues $90.33bn vs cons $90.3b (-4.8% y/y). iPhone revenues $45.96bn vs cons $45.76bn (-11% y/y). Services revenues $23.87bn vs cons $23.28bn (+11.4% y/y. China revenues $16.37 (-8% y/y) vs cons $15.9bn. Inventories $6.232bn (vs $6.5bn last qtr). EPS $1.53 vs cons $1.50. GS Trading

Earnings

Apple Inc (AAPL) Q2 2024 (USD): EPS 1.53 (exp. 1.50), Revenue 90.75bln (exp. 90.01bln); to buy back additional 110bln of shares and boosts quarterly dividend 4% to 0.25/shr, Revenue breakdown: Products 66.89bln (exp. 66.95bln), iPhone 45.96bln (exp. 45.76bln), Mac 7.45bln (exp. 6.79bln), iPad 5.56bln (exp. 5.91bln), Wearables, home and accessories 7.91bln (exp. 8.29bln), Service 23.87bln (exp. 23.28bln), Greater China revenue 16.37bln (exp. 15.87bln). Shares +5.9% in pre-market trade

Amgen Inc (AMGN) Q1 2024 (USD): Adj. EPS 3.96 (exp. 3.87), Revenue 7.45bln (exp. 7.44bln); Still sees share buyback up to 500mln. Shares +14.9% in pre-market trade

A more detailed look at global market courtesy of Newsquawk

APAC stocks took impetus from Wall St where equities extended on post-FOMC gains and futures were also lifted by Apple’s earnings beat, but with upside capped in the region amid key market closures including in Japan and Mainland China. ASX 200 traded higher as real estate led the outperformance in the rate-sensitive sectors. Hang Seng extended its rally after having recently entered a bull market and following stronger GDP data.

Top Asian News

China May Day railway travel reached a record high of around 20.7mln trips, according to Xinhua.

US FCC said roughly 40% of US telecom companies cannot replace Huawei or ZTE equipment in US networks without additional government funding.

European bourses, Stoxx600 (+0.2%) are entirely in the green, and with price action fairly muted as participants await the US Employment report at 13:30 BST / 08:30 EDT. European sectors hold a strong positive tilt, with Media taking the top spot, lifted by post-earning gains in JCDecaux (+12.5%) and UMG (+2.5%). Healthcare is found at the foot of the pile, dragged lower by Novo Nordisk (-4.5%), after recent Amgen updates. US Equity Futures (ES +0.3, NQ +0.6%, RTY -0.2%) are mixed, with clear outperformance in the NQ lifted by pre-market gains in Apple (+5.7%) after its earnings.

Top European News

Norges Bank maintains its Key Policy Rate at 4.50% as expected; the data so far could suggest that a tight monetary policy stance may be needed for somewhat longer than previously envisaged. Click here for more details. Norges Bank Chief Bache says Norges has not decided when to cut rates.

UK opposition Labour party wins Blackpool South by-election, taking the seat from the Conservatives in a blow for PM Sunak, according to BBC. It was also reported that the Labour party gained Hartlepool from no overall control in the local elections and they also claimed a win for Thurrock Council which the Tories won last year but had moved to no overall control after defections. Thus far, only around 30 of the 107 councils have declared but the swing as it stands is to Labour at the expense of the Conservatives. As a reminder, there have been reports in recent days that a bad result at the local elections could see MPs put in a no-confidence vote in PM Sunak in the next week or so.

ECB’s Lane said given the lags in transmission, the tightening effects from past interest rate hikes are still unfolding, while he noted expectations of future inflation normalising further and that leaving nominal rates unchanged implies a mechanical increase in real interest rates. Lane said moving from one meeting to the next meeting and from one projection round to the next projection round allows for the accumulation of further data that can help inform the rate decision. Furthermore, Lane said inflation has declined more quickly than expected and noted the more the data validates inflation coming back to the target, the more they will be able to remove restrictions this year and next year.

ECB’s Stournaras said three ECB rate cuts are more likely this year and the latest euro-area GDP figures were a positive surprise, according to comments made to Liberal cited by Bloomberg.

German Engineering Orders -17% Y/Y in March (Domestic -23%; Foreign Orders -15%), Jan-Mar orders -13% (Domestic -16%; Foreign -12%), according to VDMA

FX

DXY is modestly lower on NFP day and within 105.16-37 confines after dipping under yesterday’s trough (105.29) in APAC hours as with the next downside level the 11th April low (105.03) before the round figure.

Sideways trade for the EUR against the Dollar amid a lack of drivers, whilst dovish ECB commentary continues with ECB’s Lane yesterday. EUR/USD trades within a narrow 1.0725-45 parameter at the time of writing.

Yen stands as one of the G10 outperformers despite a lack of fresh headlines following this week’s double suspected intervention. USD/JPY trades in a 152.76-153.75 intraday band with potential support at the 12th April low (152.59).

Antipodeans are modestly firmer and holding on to recent spoils and remained afloat amid the constructive mood but with price action quiet amid a lack of drivers. AUD/USD briefly topped its 100 DMA (0.6581).

NOK came under some modest pressure as policy settings were maintained by Norges Bank but then appreciated slightly on the line that “the data so far could suggest that a tight monetary policy stance may be needed for somewhat longer than previously envisaged.”

Fixed Income

USTs are flat/incrementally softer with the curve flattening on the margin as the post-FOMC steepening settles into NFP and Fed speak. Currently within a busy 114’25-155’04 range.

Bunds are firmer but only modestly so with overnight action sparse on account of Japan’s holiday and EZ-specific drivers limited thus far; docket very much focused on US NFP & ISM Services alongside a handful of Fed speakers.

Gilt price action has been in-fitting with EGBs after Thursday’s session of outperformance. UK specifics light before Monday’s bank holiday and then a packed week incl. the BoE on Thursday.

Commodities

Crude is modestly firmer intraday but consolidating in the grander scheme after futures were relatively flat yesterday following a choppy session as participants await developments on the Israel-Hamas front after reports noted of “positive” spirit in talks. Brent July trades in a USD 83.77-84.15/bbl range.

Precious metals are subdued but contained ahead of key US data and amid the absence of updates on the geopolitical front. XAU sits in a narrow USD 2,297.85-2,308.80/oz parameter.

Base metals are mostly firmer across the board, but more so consolidation after yesterday’s weakness, with sentiment not helped by the absence of Chinese markets.

Geopolitics

Israeli air strike hit a security building outside the Syrian capital of Damascus, according to a security source cited by Reuters, while Syrian state media later reported that 8 soldiers were injured in the Israeli airstrike on the outskirts of Damascus.

Hezbollah announced it targeted the headquarters of Israel’s 91st Division in the Branet barracks with rocket-propelled grenades, according to Sky News Arabia.

Islamic Resistance in Iraq launched attacks on targets in Israel with Arqab-type cruise missiles from Iraqi territory which was the first attack targeting Israel’s Tel Aviv by the Islamic Resistance in Iraq, according to a source in the group.

Israel National Security Minister Gvir called on PM Netanyahu to remove Defence Minister Galant from office as he is not fit to continue his work as the defence minister.

Israel’s Foreign Minister said Turkish President Erdogan is breaking agreements by blocking ports for Israeli imports and exports.

Russian military personnel entered an air base in Niger that is hosting US troops which follows a decision by Niger’s Junta to expel US forces from the country, according to Reuters citing a US official. However, US Defense Secretary Austin later commented that Russians do not have access to US forces or equipment in Niger and they will continue to watch the presence of Russian forces in Niger.

US event calendar

08:30: April Labor Force Participation Rate, est. 62.7%, prior 62.7%

08:30: April Average Weekly Hours All Emplo, est. 34.4, prior 34.4

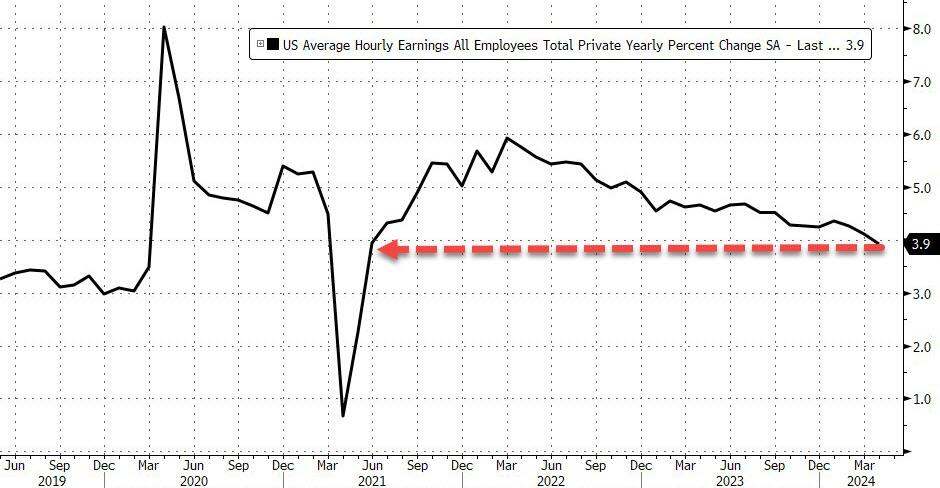

08:30: April Average Hourly Earnings YoY, est. 4.0%, prior 4.1%

08:30: April Average Hourly Earnings MoM, est. 0.3%, prior 0.3%

08:30: April Change in Manufact. Payrolls, est. 5,000, prior zero

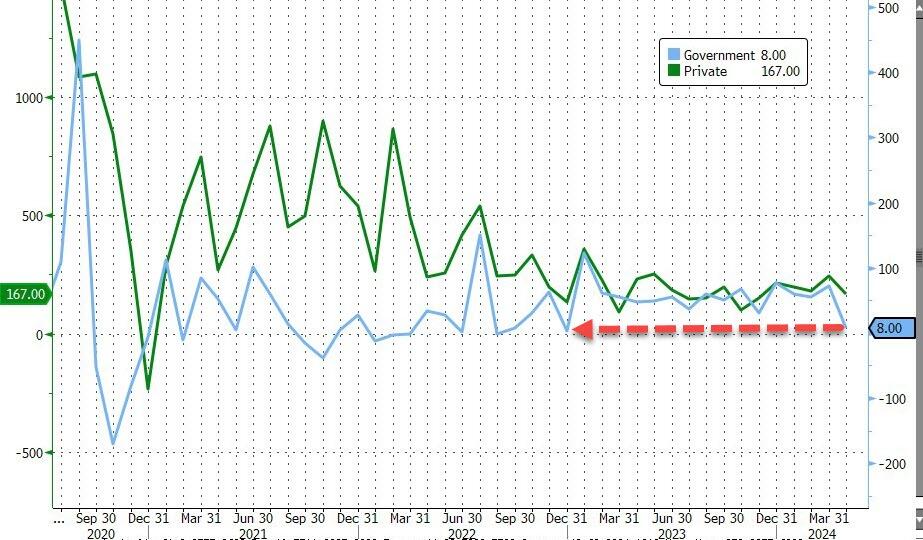

08:30: April Change in Private Payrolls, est. 195,000, prior 232,000

08:30: April Unemployment Rate, est. 3.8%, prior 3.8%

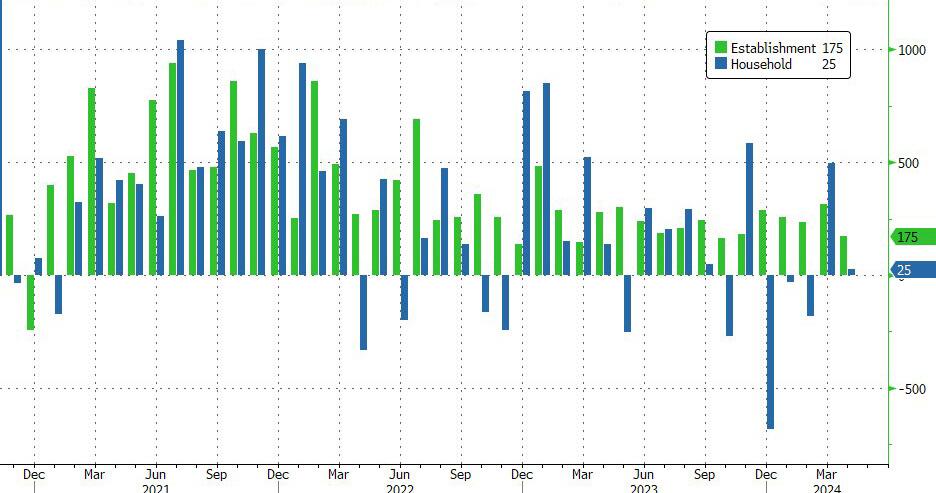

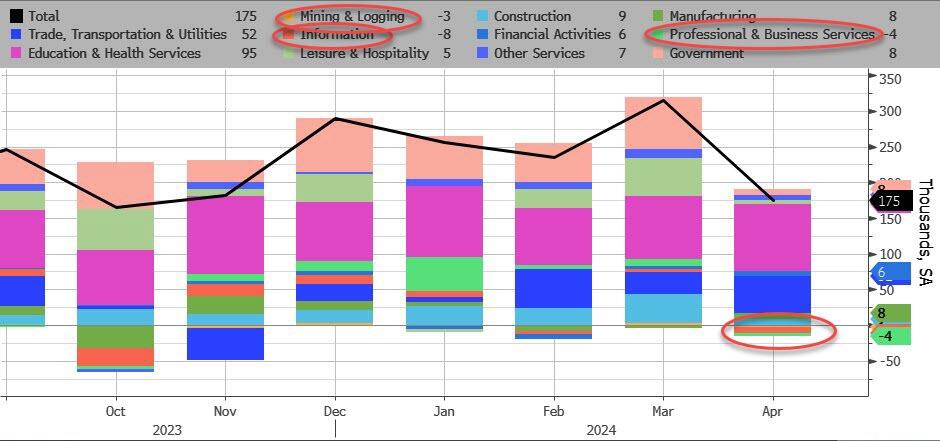

08:30: April Change in Nonfarm Payrolls, est. 240,000, prior 303,000

09:45: April S&P Global US Composite PMI, est. 51.0, prior 50.9

09:45: April S&P Global US Services PMI, est. 51.0, prior 50.9

10:00: April ISM Services Index, est. 52.0, prior 51.4

Speaking at a campaign rally in Wisconsin on Wednesday, Donald Trump urged that Europe has “opened its doors to jihad” and as a result, cities including London and Paris are sacrificing their own culture and tradition.

We’ve seen what happened when Europe opened their doors to jihad,” Trump told the large crowd, adding “Look at Paris, look at London – they’re no longer recognisable.”

“I’m going get myself into a lot of trouble with the folks in Paris and the folks in London, but you know what, that’s the fact,” he continued.

“They are no longer recognisable and we can’t let that happen to our country,” Trump urged, adding “We have incredible culture, tradition – nothing wrong with their culture, their tradition – we can’t let that happen here.”

“I’ll never let it happen to the United States of America,” he further promised.

Trump also referred to the pro-Palestine/Anti-Israel encampments and University occupations in several US cities.

“To every college president, I say remove the encampments immediately,” he said, adding “Vanquish the radicals and take back our campuses for all of the normal students who want a safe place from which to learn.

The protests have followed from regular demonstrations in Europe, particularly in London where they have been ongoing every week since late last year.

Trump has previously slammed London and Paris, noting in 2016 that “London and other places… are so radicalised that the police are afraid for their own lives.”

In Paris, the police have just conducted a fresh round of “social cleansing” illegal migrants off the street and sending them to other areas of the country ahead of the Summer Olympics.

The French government wouldn’t want the city to look “unrecognisable,” to the world, right?

Trump’s comments also come on the heels of Austrian MEP Harald Vilimsky warning that Europe risks becoming “a second Arabia or Africa” and that governments are importing migrants who create security problems then offering ‘solutions’ that only punish native populations.

Your support is crucial in helping us defeat mass censorship. Please consider donating via Locals or check out our unique merch. Follow us on X @ModernityNews.

END

Macron Says He’d Send Troops To Ukraine If Russians Advance & If Zelensky Asks

FRIDAY, MAY 03, 2024 – 02:25 PM

French President Emmanuel Macron has once again brought the possibility of Western ‘boots on the ground’ in Ukraine back into international headlines, after first controversially floating that the idea can’t be ruled out months ago.

In a fresh interview with The Economist, Macron said the possibility of injecting NATO troops into the conflict would “legitimately” arise in the scenario the Russia broke through the front lines and if the Zelensky government specifically made such a request.

Macron explained to the magazine that “if Russia decided to go further, we will in any case all have to ask ourselves this question” of sending troops. He called his prior words before NATO-member defense ministers in Paris urging them to not rule out troops a “strategic wake-up call for my counterparts.”

ays ago in a speech he dramatically declared that Europe is “mortal” and could “die” if Russia wins in Ukraine and continues on an expansionist, destructive path (an assumption that many knowledgeable analysts have rejected as a real aim of Putin’s).

Speaking to the The Economist, Macron further called Russia “a power of regional destabilization” and “a threat to Europeans’ security”.

“I have a clear strategic objective: Russia cannot win in Ukraine,” Macron continued. “If Russia wins in Ukraine, there will be no security in Europe.”

“Who can pretend that Russia will stop there? What security will there be for the other neighboring countries: Moldova, Romania, Poland, Lithuania and the others?” he posed theoretically.

A key problem and danger for escalation posed by Macron’s words is that Russian forces are already breaking through front linesin some key areas in the east.

As expected, these fresh and provocative remarks drew swift condemnation from the Kremlin, with Putin spokesman Dmitry Peskov saying “The statement is very important and very dangerous.”

Macron “continues to constantly talk about the possibility of direct involvement on the ground in the conflict around Ukraine. This is a very dangerous trend,” Peskov emphasized.

Peskov also called out remarks by UK Foreign Secretary David Cameron, who has also traveled to Kiev. He said the hawkish stance of France and the UK “potentially pose a danger to European security, to the entire European security architecture.”

“We see a dangerous tendency towards escalation in official statements. This is raising our concern,” he concluded.

5. RUSSIA AND MIDDLE EASTERN AFFAIRS.

ISRAEL/HAMAS

ISRAEL/SYRIA

Israeli Warplanes Strike Damascus As Iran Tensions Still On Edge

THURSDAY, MAY 02, 2024 – 04:50 PM

Israeli aircraft have reportedlyattacked a location on the outskirts of the Syrian capital of Damascus late Thursday (local), a security source told Reuters.

Widely circulating images have emerged on social media showing plumes of smoke rising high over buildings which were struck. Syrian state media subsequently said that eight army soldiers were injured in the attack

Pictures coming from Damascus after the Israeli airstrikes.

·

The fresh Israeli aggression could be another targeted assassination operation against Iranian generals or IRGC officers, and certainly would also be intended to signal Israel remains undeterred by Iran’s April 13th attack, which was in retaliation for the prior Israeli attack on Iran’s embassy in Damascus.

According to unverified social media reports:

The Israeli attack against Syria targeted the building of the Syrian State Security branch in the “Najha” area in the Damascus countryside.

There has been some speculation that this is an Israeli response to the launch of rockets from the Syrian side towards the Golan Heights earlier in the day and week.

END

LEBANON/HEZBOLLAH

Lebanese political leader sounds the alarm on Hezbollah

Lebanon may be tired of the excesses of Hezbollah and how it is dragging the country into conflict.

Lebanese army members stand near a poster of Fadi Bejjani who died during exchange of fire at the area where a truck was overturned the previous night, in the town of Kahaleh, Lebanon August 10, 2023.(photo credit: MOHAMED AZAKIR/REUTERS)

The leader of the Lebanese Forces, a Christian political party in Lebanon, sounded the alarm on Hezbollah and the low-level conflict with Israel that it has brought on Lebanon. His comments were published by the Associated Press this week and represent an important development in the Lebanese political landscape.

They coincide with a BBC report that also revealed how the ongoing clashes have led some areas in southern Lebanon to be deserted.

Hezbollah pretends that it is waging a successful war on Israel. In Israel, there is concern that this is the new normal, and there are discussions and disputes reported in Ynet on Thursday among the security establishment about how best to deal with Hezbollah.

END

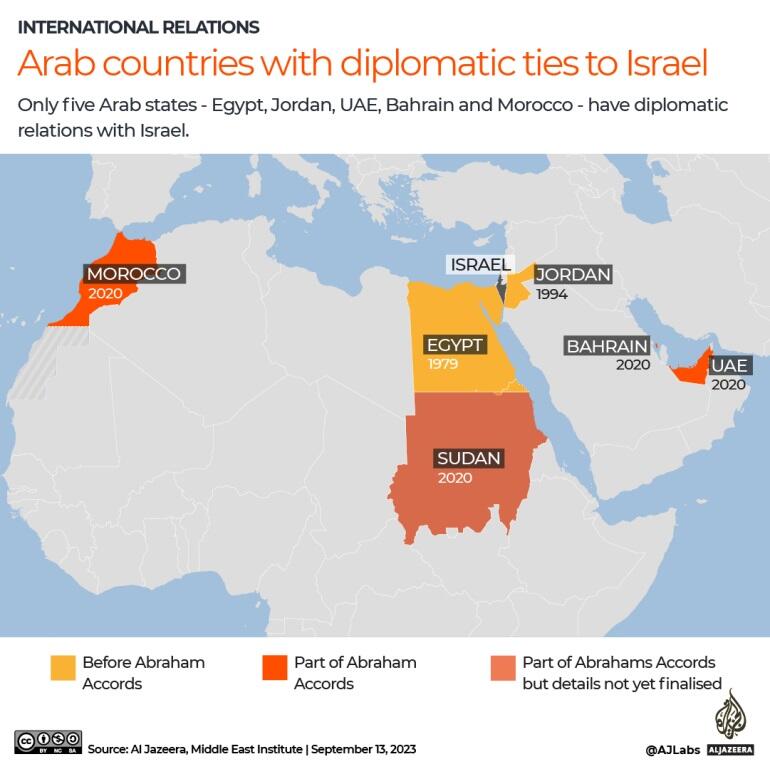

ISRAEL BAHRAIN

“Islamic Resistance In Bahrain” Claims First Ever Attack On Israel

FRIDAY, MAY 03, 2024 – 04:15 AM

Previously we detailed the ongoing Saudi crackdown on the potential for an ‘Islamist uprising’ in response to Arab Gulf countries normalizing relations with Israel. So far, the UAE has normalized, and Bahrain too, and now Saudi Arabia is said to be on the cusp.

On Thursday there emerged reports of an unprecedented first: a group by the name of the “Islamic Resistance in Bahrain” has claimed its first ever attack on Israel in retaliation for Israeli military operations in Gaza.

The Islamic Resistance in “Bahrain ?!!” “Saraya Al-Ashtar,” has released footage of a drone attack on the headquarters of the Trucknet transport company in Umm al-Rashrash (Eilat),

The group identifying itself in Arabic as Saraya al-Ashtar or al-Ashtar Brigades launched drones against the southern Israeli port city of Eilat. It reportedly happened on Saturday, but has only late this week been announced by the relatively unknown group.

The group announced that it “targeted the headquarters of the company responsible for land transportation in the Zionist entity [Trucknet] in the city of Umm al-Rashrash [Eilat] in occupied Palestine” – as cited in Al Jazeera. Eilat has been a frequent target of Yemen’s Houthis amid the ongoing Red Sea crisis.

The Israeli land transport company ‘Trucknet” is very active in Arab Gulf countries and is seen as a vital element in restoring Israel-Gulf ties. It is as yet unclear from where the Bahraini group launched the attack. There’s a likelihood it was operating from Yemeni territory.

This attack is likely intended to disrupt both diplomatic and economic ties between Bahrain and Israel:

Trucknet, which is an Israeli transport company, signed an agreement in March to transfer oil between Israel and Arab countries. Saraya al-Ashtar is designated as a “terrorist” organisation by the US, which says it has ties with Iran.

In September Israel took the unprecedented step of opening an embassy in Bahrain based on Abraham Accords talks. However the Gaza war in the wake of Oct.7 disrupted things, and Bahrain recalled its ambassador from Israel. Yet later, by December, Bahrain signaled that it remains committed to normalized ties with Israel.

The wealthy island-nation which sits just off the Saudi coast plays host to the US Naval Forces Central Command (NAVCENT), as well as the US 5th Fleet and others.

Bahrain’s Shia population and activist groups during the period of the so-called Arab Spring sought to lead large demonstrations toward toppling the Sunni monarchy, however, the Saudis sent tanks across the lengthy causeway to help quell the uprising.

Bahrain was largely left out of Washington’s ‘freedom rhetoric’ during the Arab Spring while the media spotlight was focused on places like Egypt, Libya and Syria. This is because the US needs strong Sunni Gulf rulers willing to host the Pentagon and keep the oil and gas contracts, and to clamp down on the restive Shia population in the region.

Also on Thursday there have been reports that Iran-linked groups in Iraq launched fresh cruise missile attacks on Israel, but there’s been no confirmation that projectiles made it to Israeli airspace.

END

GAZANS/USA

These are the last people on earth that you need to come to the USA

(zerohedge)

Republicans Move To Prevent Biden Resettling Palestinian Refugees In The US

Republican lawmakers are moving to prevent the Biden administration resettling Palestinian refugees in the United States, asserting that it represents a “national security threat” since large numbers of them support Hamas.

Earlier this week, it was revealed that the White House is considering using the United States Refugee Admissions Program to hand Palestinians permanent residency and “resettlement benefits like housing assistance and a path to American citizenship.”

Although CBS News reported that the “eligible population is expected to be relatively small,” European natives were given similar assurances before the 2015 refugee crisis that ended up with millions of migrants flooding the continent.

In a letter to House Appropriators, Reps. Andy Ogles (R-TN), Tom Tiffany (R-WI), and Scott Perry (R-PA) have asked that a provision be included in the Fiscal Year 2025 spending bill that prevents expenditures “of any funds to issue a visa or grant parole to any alien holding a passport issued by the Palestinian Authority.”

“Whatever fanciful leftist notion to the contrary, the United States of America cannot be expected to absorb the rest of the world’s problems. It would make much more sense for states in the region to take in those in need. If the administration is indeed working in concert with our allies in the region to pave the way for peace, that should come with the expectation that those allies are working in good faith to “do their part,” states the letter.

35 Senate Republicans are also demanding more specifics on the resettlement program, asserting that it represents “a national security risk to the United States.”

“With more than a third of Gazans supporting the Hamas militants, we are not confident that your administration can adequately vet this high-risk population for terrorist ties and sympathies before admitting them into the United States,” said the Senators.

A leaked Israeli intelligence document revealed in late October last year revealed a plan to ‘expel’ 2.2 million Palestinian refugees and send them to Europe, Canada and the United States.

The document, produced by Israel’s Intelligence Ministry, stated that one of the goals of the war with Gaza was to encourage western countries to facilitate the “absorption and settlement” of Gazan refugees.

Back in March, Jared Kushner said it was “unfortunate” that Europe isn’t taking in more Palestinian refugees, suggesting that the “cleaning up” of Palestinians from the Gaza Strip should be accelerated.

Meanwhile, as we highlight in the video below, while Americans could be set to see yet another influx of migrants thanks to Israel’s destruction of Gaza, criticizing the Middle Eastern country could technically become illegal under the draconian Antisemitism Awareness Act.

* * *

Your support is crucial in helping us defeat mass censorship. Please consider donating via Locals or check out our unique merch. Follow us on X @ModernityNews.

end

Israel gives Hamas one week to accept hostage deal before Rafah op. will begin – WSJ report

Yahya Sinwar, Hamas’s Gaza chief, has yet to make his response known, further complicating the situation.

(L-R) Prime Minister Benjamin Netanyahu; Hamas leader Yahya Sinwar(photo credit: REUTERS)

Israel gave Hamas a week to agree to a cease-fire deal, or the invasion of Rafah will begin, Egyptian officials told the Wall Street Journal on Friday.

Egyptian officials claimed that Hamas is seeking a long-term truce and guarantees from the US that a cease-fire will be respected by Israel.

Hamas expressed concern that the latest proposal is still too vague and gives Israel room to restart the fighting.