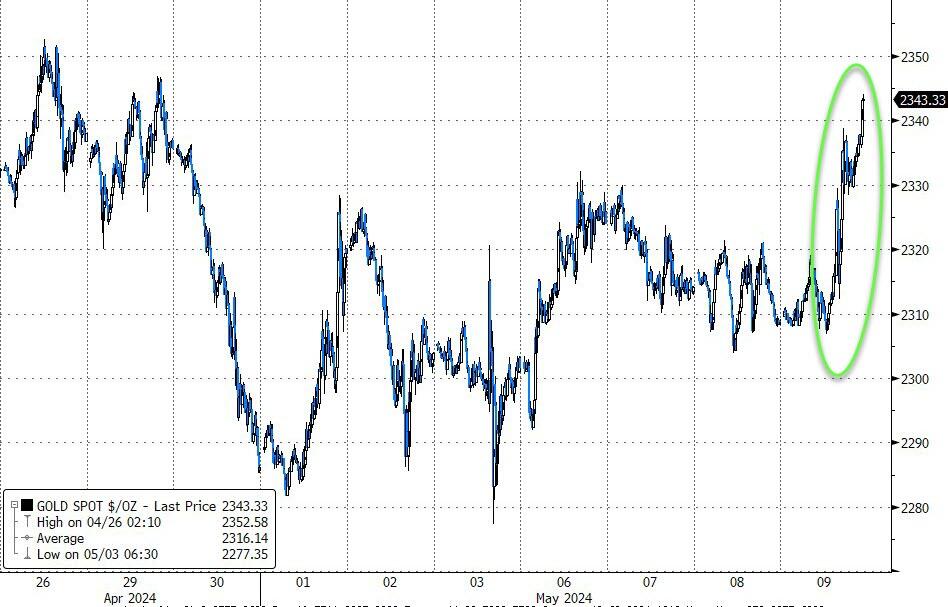

MAY 9 BLOG//GOLD CLOSED UP $18.25 TO $2333.35/SILVER CLOSED UP $0.78 TO $28.14/PLATINUM CLOSED UP $6.10 TO $984.60//PALLADIUM CLOSED DOWN $2.55 $ TO $970.25//GOLD COMMENTARY TONIGHT FROM PETER SCHIFF////ALSO AN EXCELLENT SILVER COMMENTARY ON A LOST SILVER HOARD///BIDEN VS ISRAEL ERUPTS AS USA WITHHOLDS MUNITIONS TO ISRAEL//LINDSAY GRAHAM QUESTIONS LLOYD AUSTIN IN A MUST VIEW AS BIDEN’S TEAM IMPLODES//OTHER ISRAEL VS HAMAS COMMENTARIES//COVID UPDATES/VACCINE INJURY//SLAY NEWS//REAL ESTATE TYCOON CLAIMS THAT THERE WILL BE TWO BANK FAILURES PER WEEK//SWAMP STORIES FOR YOU TONIGHT

363 H WELLS FARGO SEC 1 624 H BOFA SECURITIES 3 737 C ADVANTAGE 4

TOTAL: 4 4 MONTH TO DATE: 1,806

JPMorgan stopped 0/4

FOR MAY2024

GOLD: NUMBER OF NOTICES FILED FOR MAY/2024. CONTRACT: 4 NOTICES FOR 400 OZ or 0.01244 TONNES

total notices so far: 1806 contracts for 180600 Oz (5.617 tonnes)

FOR MAY:

SILVER NOTICES: 174 NOTICE(S) FILED FOR 870,000 OZ/

total number of notices filed so far this month : 5260 for 26.300 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $18.25

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

NO CHANGES IN GOLD INVENTORY AT THE GLD:

/ /INVENTORY RESTS AT 830.47TONNES

INVENTORY RESTS AT 830.47 TONNES

SLV//

WITH NO SILVER AROUND AND

SILVER UP 78 CENTS AT THE SLV//

NO CHANGES IN SILVER INVENTORY AT THE SLV

// INVENTORY DECREASES T0 424.055MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 424.055 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A FAIR SIZED 302 CONTRACTS TO 162,170 AND ASCENDING TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR LOSS OF $0,11 IN SILVER PRICING AT THE COMEX ON WEDNESDAY. WE HAD ZERO LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN SHORT COVERING BY OUR SPECS WITH THE LOSS IN PRICE. WE HAD A HUGE SIZED 1102 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 1102 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.11 BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A GOOD SIZED GAIN OF 467 CONTRACTS ON OUR TWO EXCHANGES DESPITE THE LOSS IN PRICE OF $0.11

WE MUST HAVE HAD:

A SMALL SIZED 165 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 28.130MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 480,000 OZ

//NEW STANDING FOR SILVER//MAY IS THUS 26.695 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI GAIN //SMALL SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1102 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED A STRONG 740CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY

TOTAL CONTRACTS for 7 DAYS, total 3675 contracts: OR 18.375 MILLION OZ (525 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 17.550 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770MILLION OZ (THIS MONTH WILL PROBABLY BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 18.375 MILLION OZ

RESULT: WE HAD A GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 302 CONTRACTS DESPITE OUR LOSS IN PRICE OF SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 165 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAY OF 28.130 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 480,000 OZ QUEUE JUMP

//NEW TOTAL STANDING AT 26.695 MILLION OZ

WE HAVE A GOOD SIZED GAIN OF 467 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE SMALL LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 1102 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (1102 WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//PROBABLY TODAY., .

WE HAD 174 NOTICE(S) FILED TODAY FOR 870,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 2947 OI CONTRACTS TO 526,888 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED 1023 CONTRACTS

WE HAD A FAIR SIZED DECREASE IN COMEX OI (2947 CONTRACTS) OCCURRED WITH OUR $0.90 LOSS IN PRICE/WEDNESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER TO WHACK GOLD’S PRICE. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 4.684 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY;S 400 OZ QUEUE JUMP//NEW STANDING 5.7045 TONNES

NEW STANDING 5.7045 TONNES// ALL OF THIS HAPPENED DESPITE OUR $0.90 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A FAIR SIZED GAIN OF 2947 OI CONTRACTS (3.391 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4034 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 526,888

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1087 CONTRACTS WITH3970 CONTRACTS DECREASED AT THE COMEX// AND A GOOD SIZED 4034 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1087 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A MEGA HUMONGOUS SIZED 32,526 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4034 CONTRACTS) ACCOMPANYING THE LOSS IN COMEX OI 2974/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 1087 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 4.684TONNES FOLLOWED BY TODAY;S 400 OZ QUEUE JUMP

//NEW STANDING /MAY 5.7045 TONNES.

/ 3) ZERO LONG LIQUIDATION DESPITE THE LOSS IN PRICE.

// 4) GOOD SIZED COMEX OPEN INTEREST LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: MEGA HUMONGOUS T.A.S. ISSUANCE: 32,526 CONTRACTS/ HUGE SHORT COVERING BY OUR WRONG FOOTED SPECS WITH THE FED’S CONTINUAL RAID ON THE COMEX GOLD.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY. :

TOTAL EFP CONTRACTS ISSUED: 30,123 CONTRACTS OR 3,012,300 OZ OR 93.69 TONNES IN 7 TRADING DAY(S) AND THUS AVERAGING: 4304 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAY(S) IN TONNES 93.69 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 93.69DIVIDED BY 3550 x 100% TONNES = 2.64% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 93.69 TONNES (WILL BE ANOTHER STRONG MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A FAIR SIZED 302 CONTRACTS OI TO 162,170 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 165 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 165 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 165 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 302 CONTRACTS AND ADD TO THE 165 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 467 CONTRACTS

THUS IN OUNCES, THE HUGE GAIN ON THE TWO EXCHANGES TOTALS 2.335 MILLION OZ

OCCURRED DESPITE OUR SMALL $0.11 LOSS IN PRICE …..

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED UP 25.84 PTS OR 0.83% //Hang Seng CLOSED UP 223.95PTS OR 1.22%// Nikkei CLOSED DOWN 128.39 OR 0.34%//Australia’s all ordinaries CLOSED DOWN 1.02%///Chinese yuan (ONSHORE) closed UP TO 7,2265 CHINESE YUAN OFF SHORE CLOSED UP TO 7.2331/ Oil UP TO 79.56 dollars per barrel for WTI and BRENT DOWN AT 84.11 /Stocks in Europe OPENED ALL MOSTLY MIXED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 2947 CONTRACTS TO 526,888 DESPITE OUR TINY LOSS IN PRICE OF $0.90 WITH RESPECT TO WEDNESDAY TRADING. WE HAD HUGE T.A.S. LIQUIDATION AS WELL AS SHORTS, DESPERATELY TRYING TO GET OUT OF THEIR NAKED SHORTS.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAY.… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 4034 EFP CONTRACTS WERE ISSUED: : JUNE4034 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE:4034 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 1087 CONTRACTS IN THAT 4034 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A GOOD SIZED LOSS OF 2947 COMEX CONTRACTS..AND THIS TINY GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $0.90 WEDNESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT WAS ANOTHER MEGA HUMONGOUS SIZED 32,526 CONTRACTS. WE HAD 0 EX FOR RISK ISSUANCE. MOST OF THE TRADING AND SUPPLY OF CONTRACTS ON WEDNESDAY WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (5.7045 TONNES) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 5.7045 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A SMALL $0.90 //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR SIZED GAIN OF1087 TOTAL CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR LOSS IN PRICE 0F $0.90

WE HAD A HUGE T.A.S. LIQUIDATION ON THE FRONT END OF WEDNESDAY’S TRADING. THE T.A.S. ISSUED ON WEDNESDAY NIGHT,( AND IT WAS ANOTHER DOOZY) WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 3.381 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY (4.684 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 4 CONTRACTS OR 400 OZ ( .0199 TONNES)

NEW STANDING: 5.7045 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $0.90

WE HAVE ADDED 1023 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET GAIN ON THE TWO EXCHANGES 1087 CONTRACTS OR 108,700(3.381 TONNES)

confirmed volume WEDNESDAY 287,902 contracts//fair/ to good

Total monthly oz gold served (contracts) so far this month

1806notices 180,600 oz 5.617 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: 0 oz

we have 0 customer deposits:

total deposit nil oz

total customer withdrawals: 1

i) Brinks 32/151 oz 1 kilobars

TOTAL WITHDRAWALS 32.151 0z

Adjustments: 1

brinks: dealer to customer: 675.171 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY

For the front month of MAY we have an oi of 32 contracts having LOST 14 contracts.

We had 18 contracts served on WEDNESDAY, so we gained 4 contracts or 400 oz (,0199onnes).

JUNE DECREASED ITS OI BY 25,216 CONTRACTS DOWN TO 325,959 CONTRACTS.

JULY LOST 26 CONTRACTS TO STAND AT 166

We had 4 contracts filed for today representing 400 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 4 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the MAY /2024. contract month, we take the total number of notices filed so far for the month (1806) x 100 oz ) to which we add the difference between the open interest for the front month of MAY ( 32 CONTRACTS) minus the number of notices served upon today (4 x 100 oz per contract( equals 183,000 OZ OR 5.8095TONNES.

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (1806x 100 oz + (32 OI for the front month} minus the number of notices served upon today (4 x 100 oz which equals 183,400 oz (5.7045 TONNES)

TOTAL COMEX GOLD STANDING FOR MAY: 5.7045 TONNES WHICH IS HUGE FOR THIS A NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,617,070.745 OZ

TOTAL REGISTERED GOLD 7,343,795.541( 228.42 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,273,275.204 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 5,766,572 oz (REG GOLD- PLEDGED GOLD)= 179.36 tonnes

179.36 tonnes/dropping like a stone

END

SILVER/COMEX

MAY 9

INITIAL

//2024// THE MAY 2025 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

407,840.721 oz Delaware Brinks

.

Deposits to the Dealer Inventory

00OZ

Deposits to the Customer Inventory

1,214,855.640 oz

ASAHI Loomid

No of oz served today (contracts)

174 CONTRACT(S) (870,000 OZ)

No of oz to be served (notices)

79 contracts (0.395 million oz)

Total monthly oz silver served (contracts)

5260 Contracts (26.300 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposit :nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 deposits customer account:

i) Into ASAHI: 612,411.900 oz

ii) Into Loomis: 602,444.240 oz

total customer deposits 1,214,855.640 oz

JPMorgan has a total silver weight: 129,598million oz/297.785 million or 43.64%

adjustment: 1/customer to dealer

a)Manfra 161,571.300 ox

Comex withdrawals: 2

i) out of Delaware 11,737.741 oz ii) out of Brinks 396,102.980 oz

total withdrawal 407,840.721 oz

TOTAL REGISTERED SILVER: 65.131MILLION OZ//.TOTAL REG + ELIGIBLE. 297.785 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF MAY/2024 OI: 253 CONTRACTS HAVING LOST 354 CONTRACT(S).

.

We had 450 notices served on WEDNESDAY so we GAINED 96 contracts or 480,000 oz underwent a STRONG QUEUE JUMP AS THEY WERE SET TO TAKE DELIVERY ON THIS SIDE OF THE POND.

JUNE SAW A GAIN OF 138 CONTRACTS RISING TO 1906

JULY SAW A GAIN OF 462 CONTRACTS UP TO 132,305

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 174 for 870,000 oz

CONFIRMED volume; ON WEDNESDAY 57,419 good

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 5260 x 5,000 oz = 26.300MILLION oz

to which we add the difference between the open interest for the front month of MAY (253 and the number of notices served upon today 174x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2024 contract month: 5260 notices served so far) x 5000 oz + OI for the front month of MAY (253 number of notices served upon today minus (174x 5000 oz of silver standing for the may contract month equates to 26.695 MILLION OZ.

New total standing: 26.695 million oz.

There are 62.355 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

MAY 9 WITH GOLD UP $18.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 8 WITH GOLD DOWN $0.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 830.47 TONNES

MAY 7 WITH GOLD DOWN $6.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 832.19 TONNES

MAY 6WITH GOLD UP $21.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .55 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 831.64 TONNES

MAY 2 WITH GOLD UP $0.20 ON THE DAY; SMAKK CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 830.47 TONNES

MAY 1 WITH GOLD UP $7.80 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNES

APRIL 29WITH GOLD UP $10,55TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNES

APRIL 26WITH GOLD UP $5.40TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.54 TONNES FROM THE GLD /INVENTORY RISES AT 832.19 TONNES

APRIL 25WITH GOLD UP $5.05 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD /INVENTORY RISES AT 833,63 TONNES

APRIL 19 WITH GOLD UP $15.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 4.32 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 831.91 TONNES

APRIL 18 WITH GOLD UP $11.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE WITHDRAWAL OF 2.59 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 827.59 TONNES

APRIL 17 WITH GOLD DOWN $17.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 830;18 TONNES

APRIL 16 WITH GOLD UP $23.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 828.45 TONNES

APRIL 15 WITH GOLD DOWN $. 80 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A HUGE WITHDRAWAL OF 1.80 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 824.84 TONNES

APRIL 12 WITH GOLD UP $2.80 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD/ INVENTORY RISESS AT 830.75 TONN

GLD INVENTORY: 830.47TONNES,

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 9 WITH SILVER UP 78 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 8 WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 7WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 6 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.055 MILLION OZ

MAY 3 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 2WITH SILVER UP 0.12 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/ A WITHDRAWALOF 4.471 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 1 WITH SILVER UP 0.09 TODAY: SMALLCHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF ,457 MILLION OZ INTO THE SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 29WITH SILVER UP $0.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 26WITH SILVER DOWN 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.097 MILLION OF SILVER INTO THE SLV// :SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 25WITH SILVER UP $.05 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 1.534 MILLION OF SILVER OUT OF THE SLV// :SLV INVENTORY RESTS AT 428.717 MILLION OZ

APRIL 24/WITH SILVER DOWN $.05 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 11.904MILLION OF SILVER INTO THE SLV// :SLV INVENTORY RESTS AT 428.280 MILLION OZ

APRIL 23/WITH SILVER UP $0.11TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV / :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 22/WITH SILVER DOWN $1.51 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.194 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 19/WITH SILVER UP 42 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.657 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 418.570 MILLION OZ

APRIL 18/WITH SILVER DOWN $.04TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.977 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 422.227 MILLION OZ

APRIL 17/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF .868 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 426/204 MILLION OZ

APRIL 16/WITH SILVER DOWN $0.46 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF NON EXISTENT SILVER// :SLV INVENTORY RESTS AT 427.072 MILLION OZ

APRIL 15/WITH SILVER UP $0.88 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 12/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 4.069 MILLION OZ FROM THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 11/WITH SILVER UP $0.23 TODAY: STRANGE INDEED! HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.931 MILLION OZ :SLV INVENTORY RESTS AT 437.998 MILLION OZ

Peter notes that April’s losses in the stock market were in part created by doubt about the Fed’s future rate cuts:

“The reason for that was heightened talk not just about the Fed not cutting rates, but for the first time, I heard people discussing the possibility that the Fed might have to raise rates, that the next move may in fact be a hike and not a cut. Now that‘s the first time that I’ve heard any mainstream discussion of that possibility. … I’ve been saying that that is the correct policy. If the Fed really is data-dependent, and if the Fed really wants to fight inflation, based on the data, they should resume their hikes.”

Despite this possibility, markets are unduly optimistic. The Fed’s historical record is not very successful, even decades ago when America’s fiscal health was much better:

“The markets believe that the Fed is going to succeed. This is pure nonsense! I look back at the inflation statistics for the 40 years before the 2008 financial crisis— so 2008, 2007, going back to 1968, those 40 years— there were only 3 years where inflation was 2% or lower. The average inflation rate over those 40 years was 4.8%. … If the Fed wasn’t able to come close to 2% during those 40 years, why does anybody think it’s going to come anywhere near it over the next 30 years?”

Fed Chair Jerome Powell still refuses to criticize federal fiscal policy, despite the apparent need for rate hikes:

“Not only is he allowed to do it, he’s really required to do it! That’s the whole point of an independent central bank…

…so you can criticize the government when it makes a mistake, not hide behind your independence and fail to criticize the government. Paul Volker was Congress’s biggest critic!”

After stock prices plummeted last week for large companies like Starbucks, Peter sees the declines as a sign of future stagflation:

“I think that this is the beginning of a trend. I think Starbucks is going to have a hard time with sales in the stagflation environment that Jerome Powell doesn’t want to acknowledge. And Starbucks wasn’t the only company! I remember Clorox came out and warned it had a big drop. Remember Peloton! Peloton missed as well.”

Peter also mentions some highlights from his Bitcoin debate on Friday. He argues again that “Know Your Customer” (KYC) and anti-money laundering (AML) regulations are primarily used to prevent tax evasion, not violent terrorism:

“If they can catch a few terrorists, ok fine, that’s the icing on the cake. The cake is tax evasion. That’s what all these governments are trying to prevent when they require all these AML KYC rules at banks. How many terrorists do you think there are in the world? Out of a hundred people, how many of them are going to be a terrorist? Very few. … I don’t think there was ever a point where a terrorist tried to deposit money at my bank.”

U.S. tax policy has strayed quite far from that of the country’s Founding era:

“The country was founded by tax protesters. The country was founded by people who didn’t want to pay a tiny tax to the British crown! There’s no way King George would’ve ever imposed an income tax on the colonists. He would never do something that draconian. No! He’s talking about excise taxes. Taxes on tea, taxes on stamps, little things! We had a whole revolutionary war because of those tiny little taxes. … No government has the right to take half of what somebody earns.”

While Peter agrees on a lot with his debate opponent Erik Voorhees, they still disagree on Bitcoin’s importance to the free market movement:

“I just don’t think that Bitcoin is part of the solution. Ultimately, it’s going to be part of the problem. Part of the solution to reigning in government is a return to sound money, a return to real money, and unfortunately, Bitcoin doesn’t fit that bill. But gold does.”

2.Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens/Alasdair Macleod

3. CHRIS POWELL//GATA DISPATCHES

Gold bars sell fast in South Korea’s convenience stores and vending machines

Submitted by admin on Wed, 2024-05-08 12:12 Section: Daily Dispatches

By Lee Ying Shan CNBC, New York Tuesday, May 7, 2024

Aside from ramen and sausages, South Korea’s convenience stores have a new popular item on the menu — gold bars.

The country’s largest convenience store chain, CU, has been collaborating with the Korea Minting and Security Printing Corp. to offer customers mini gold bars — and they’re selling like hotcakes.

A variety of fingernail sized gold bars weighing between 0.1 gram and 1.87 gram have been up for sale at CU outlets since April. A 1.87 gram bar sells for 225,000 won ($165.76) and a 0.5 gram bar sells for 77,000 won.

Priced at 113,000 won each, 1-gram bars were sold out within two days, according to local news reports. The bars come with congratulatory messages, birthday wishes, and even designs for personality types. …

Submitted by admin on Wed, 2024-05-08 21:36 Section: Daily Dispatches

By Brien Lundin Gold Newsletter / Golden Opportunities Metairie, Louisiana Wednesday, May 8, 2024

The question I got more than any other at the recent Deutsche Goldmesse conference in Frankfurt was: Why haven’t gold stocks responded to gold’s big run higher?

I had two answers for them:

1) The rally in gold had been so quick and dramatic that it took everyone by surprise. Investors felt they’d been left behind, and were waiting for a pull-back to get into the mining equities.

2) No one really understood why gold was rallying so hard. We’d been expecting a Fed pivot to be the big catalyst, but that was being postponed ever further ahead.

If we didn’t understand what’s driving gold, we couldn’t get a feel for how long the move might last. No one wanted to jump in headfirst just before a big slam back downward.

The good news, I told these investors, was that these factors were already starting to change. …

*end

Remember gold and silver are money; everything else is credit

(Stefan Gleason)

U.S. Rep. Mooney introduces bill to end federal taxation on gold and silver

Submitted by admin on Wed, 2024-05-08 21:47 Section: Daily Dispatches

From Money Metals News Service Eagle, Idaho Wednesday, May 8, 2024

U.S. Rep. Alex Mooney, R-West Virginia, has re-introduced sound-money legislation to remove all federal income taxation from gold and silver coins and bullion.

The Monetary Metals Tax Neutrality Act (H.R. 8279), backed by the Sound Money Defense League, Money Metals Exchange, and free-market activists, would clarify that the sale or exchange of precious metals bullion and coins is not to be included in capital gains, losses, or any other type of federal income calculation. Gold and silver would be treated as a non-entity for tax purposes, putting it on par with the U.S. dollar.

Reps. Scott Perry, R-Pennsylvania, and Randy Weber, R-Texas, joined as original cosponsors.

“My view, which is backed up by language in the U.S. Constitution, is that gold and silver coins are money and are legal tender,” Rep. Mooney said.

“If they’re indeed U.S. money, it seems there should be no taxes on them at all. So why are we taxing these coins as collectibles?” …

Hedge Fund Boss Loses Legal Fight Over 2,364 Silver Bars Found In WWII Shipwreck

WEDNESDAY, MAY 08, 2024 – 11:35 PM

An undersea exploration company backed by a top hedge fund boss in the United Kingdom lost a major legal fight over the salvage of $40 million worth of silver bars from the wreck of a ship lost to a Japanese submarine in World War II.

On Wednesday, Bloomberg reported that the UK’s Supreme Court ruled that the South African government could declare state immunity in a suit by hedge fund chief Paul Marshall’s Argentum Exploration Ltd.

Argentum Exploration argued in court that it was owed a ‘substantial salvage fee’ and wanted a court to ‘fix an award.’ However, the judges were informed that the two sides had agreed to a settlement.

Here’s more from Bloomberg:

The South African government had argued that that it not only still owns the silver, but insisted that it shouldn’t have to submit to the lawsuit at all.

The Supreme Court judges agreed, saying that the silver was a non-commercial cargo and the government was entitled to immunity.

The ruling overturned two prior court decisions, with a judge previously saying that the government had probably “forgotten” about the bullion. UK Companies House filings record that Marshall controls Argentum.

In 1942, the SS Tilawa was sailing from Mumbai on its way to Durban, South Africa, when two torpedoes from an Imperial Japanese Navy submarine sunk the passenger-cargo ship. On board were 2,364 bars of silver destined for the South African Mint. For seven decades, the ship resided more than two and a half kilometers below the surface of the Indian Ocean until Marshall’s exploration company discovered it.

In markets, the Bloomberg Precious Metal Subindex shows a multi-decade ‘cup and handle’ bullish formation.

We wonder if the settlement involved physical silver bars… Some analysts expect a “powerful silver bull market” ahead.

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT

SHANGHAI CLOSED UP 25.84 PTS OR 0.83% //Hang Seng CLOSED UP 223.95PTS OR 1.22%// Nikkei CLOSED DOWN 128.39 OR 0.34%//Australia’s all ordinaries CLOSED DOWN 1.02%///Chinese yuan (ONSHORE) closed UP TO 7,2265 CHINESE YUAN OFF SHORE CLOSED UP TO 7.2331/ Oil UP TO 79.56 dollars per barrel for WTI and BRENT DOWN AT 84.11 /Stocks in Europe OPENED ALL MOSTLY MIXED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGSTHURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2265

OFFSHORE YUAN: DOWN TO 7.2331

SHANGHAI CLOSED UP 25.84 PTS OR 0.83 %

HANG SENG CLOSED UP 25.84 PTS OR 0.83%

2. Nikkei closed DOWN 128.39 PTS OR 0.34 %

3. Europe stocks SO FAR: ALL MOSTLY MIXED

USA dollar INDEX UP TO 105.57 EURO FALLS TO 1.0727 DOWN 19 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.913 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 155.86 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.4865/Italian 10 Yr bond yield UP to 3.831 SPAIN 10 YR BOND YIELD UP TO 3.276%

3i Greek 10 year bond yield UP TO 3.512

3j Gold at $2316.70//Silver at: 27.70 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 0 100 roubles/dollar; ROUBLE AT 91.95/

3m oil into the 79 dollar handle for WTI and 84 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 155.86/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.913% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9096 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9758 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.510 UP 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.668 UP 4 BASIS PTS/

USA 2 YR BOND YIELD: 4.843 UP 0 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.22…(TURKEY)

10 YR UK BOND YIELD: 4.1870 UP 5 PTS

2a New York OPENING REPORT

Futures Drop As Treasury Yields Extend Gains

THURSDAY, MAY 09, 2024 – 08:19 AM

US equity futures are weaker as yields resume their rise and the USD strengthens after the BOE signaled it was ready to cut rates. As of 7:45am, S&P futures were down 0.2% and Nasdaq futures dipped 0.3% as all Mag7 names and most semis were red in the premarket. Most European markets are lower, tracking US futures and Asian stocks in what appears to be de-risking in a catalyst-light week. 10Y treasuries ticked lower for a second day, pushing the yield about 2bps higher to 4.51% after a $42 billion sale of 10-year notes received tepid demand. Commodities are stronger with Ags/Energy outperforming Metals. Jobless data is not expected to be market moving but keep an eye on the 30Y bond auction.

In premarket trading, US-listed shares of Arm Holdings plunged 8.5% after the chip-design company gave a full-year forecast that is seen as mixed relative to consensus, especially given the market’s high expectations. Airbnb shares also tumbled 8.7% after the home-rental company’s Q2 revenue forecast trailed the average analyst estimate, ahead of the peak summer season. Here are some other notable premarket movers:

AppLovin shares are up 15% after the software maker’s quarterly sales and earnings came in comfortably above forecasts.

Bumble shares jump 12% after the online dating company affirmed its full-year forecast, which Citi said offset a weak second-quarter guide.

Cardlytics shares drop 27% after the application software company reported revenue for the first quarter that missed the average analyst estimate.

Cheesecake Factory shares rise 1.6% after the restaurant chain operator reported adjusted earnings per share for the first quarter that beat the average analyst estimate. Raymond James raised the recommendation on the stock to outperform from market perform.

Compass stock climbs 13% after the real estate technology firm delivered a revenue forecast range for the second-quarter that beat the average analyst estimate at the midpoint.

Duolingo shares fall 12% after the education software provider’s daily active user growth cooled. Analysts note that it was about time for the company’s growth to normalize after years of upside.

Magnite shares rise 11% after the advertising technology firm posted 1Q profit and revenue that beat estimates.

Robinhood shares gain 5.0% after the fintech’s results beat expectations thanks to strength in crypto trading.

SolarEdge shares plunge 9.1% after the solar power company reported a wider-than-expected 1Q loss and provided guidance for 2Q that came in below even the most pessimistic forecasts, according to analysts.

Trade Desk shares are up 1.1% after the advertising technology company reported first-quarter results that beat expectations and gave an outlook that is above the analyst consensus.

Warner Bros. shares rise 3.3% after Chief Executive Officer David Zaslav ordered his lieutenants to find additional opportunities for cost-cutting in order to hit financial targets for the next couple years.

Zai Lab ADRs soar 19% after the Chinese biopharmaceutical company reported estimate-beating sales.

The recent stock bounce is fading as the earnings season winds down, leaving investors to wait for new data – especially next week’s CPI report – for clues to gauge how fast policymakers will be able to begin cutting rates. The pound fell against all of its Group of 10 peers after the Bank of England edged closer to cutting interest rates from a 16-year high, with two of the nine committee members voting for lower borrowing costs. US initial jobless claims data later Thursday will be another focal point for investors seeking more evidence that the labor market is finally softening, allowing the Federal Reserve to begin lowering rates by the end of the year. Prospects for a Fed rate cut improved after softer-than-expected US payrolls last week.

“We still see potential rate cuts to be some months out and with no probable actions occurring prior to September,” Louise Dudley, portfolio manager for global equities at Federated Hermes, said in a note to clients. “US economy figures have generally been hot.”

The CPI figures due next week will offer fresh insights about the US economy after recent employment data showed the labor market is cooling. Fed Bank of Boston President Susan Collins signaled Wednesday that interest rates will likely need to be held at a two-decade high for longer than previously thought to damp demand and reduce price pressures.

European stocks fell 0.2%, hovering near record highs after rising in the prior four sessions. The energy sector outperformed, while autos were the worst laggards. Markets in Denmark, Finland, Norway, Sweden and Switzerland are closed for a holiday. Banco de Sabadell SA rose after Banco Bilbao Vizcaya Argentaria SA commenced a $12 billion hostile bid for the lender. Here are the most notable movers:

BAE Systems shares rise as much as 0.9% in a fourth day of gains after the defense and aerospace systems manufacturer delivered results in line with expectations.

Prysmian shares gain as much as 1.3%, pushing the stock to a record high, after narrowing its guidance to the upper end of the range and producing first-quarter results which analysts view as solid.

Banco de Sabadell shares rise as much as 7.1% after BBVA made an €11.5 billion hostile bid for its smaller Spanish banking rival, days after having an initial approach rejected. BBVA drops.

BE Semiconductor shares jump as much as 8% after the Dutch chip equipment maker said it receives an order for 26 hybrid bonding systems from a “leading semiconductor logic manufacturer.”

Nexi shares rise as much as 7.7% after the payments firm reported estimate-beating results, helped by a stronger card issuing business and cost controls.

IMI shares rise as much as 1.4%, on track to close at a fresh record high, after the engineering group delivered a solid trading update and reiterated its full-year guidance.

ITV shares rise as much as 3% after the UK broadcaster issued stronger-than-expected advertising guidance for 2Q, leading brokers to raise their price targets on the stock.

Harbour Energy shares rise as much as 6.2%, the most in four months, after the oil and gas company’s update showed it remains on track to meet expectations this year.

Balfour Beatty shares rise as much as 1.7% after the group released a short trading update confirming trading has been in line with expectations since the start of 2024.

3i shares fall as much as 3.6% after total return for the full year missed the average analyst estimate, with RBC analysts noting misses in operating cash profit and net debt at year-end coming in a little above forecasts.

Argenx shares fall as much as 10%, the steepest drop this year, after first-quarter results from the biotech firm failed to provide much in the way of fresh catalysts.

BPER Banca shares decline as much as 6.1% in Milan as the bank’s key trends look weaker, according to Deutsche Bank analysts.

Wood shares fall as much as 3.5%, paring Wednesday’s rally after the Scottish engineering firm rejected a preliminary 205p/share acquisition proposal from Sidara.

Asian stocks resumed gains on Thursday, lifted by optimism around key offshore Chinese tech companies as they report earnings next week. The MSCI Asia Pacific Index climbed as much as 0.4% after its four-day winning streak was halted in the previous session. Hong Kong-listed shares were among the best performers in the region, with Tencent giving the biggest boost to the index ahead of earnings next week. Meituan shares jumped nearly 5% after Citi raised its price target on expectation that earnings will show growth in the food delivery business. Japan’s Topix gained nearly 0.9% after BOJ Minutes revealed a desire from at least one member to sell all ETFs and an acknowledgement that a weaker JPY may lead to more inflation; the Australian benchmark fell after rising for five consecutive sessions. Stocks in Korea traded lower. Earnings of top Chinese technology companies will be key for the bounce-back in the nation’s stocks from their multi-year lows to continue. Tencent and Alibaba both publish results next Tuesday, followed by JD.com and Baidu two days later.

Hang Seng & Shanghai Comp were underpinned amid resilience in the tech sector and after China’s eastern city of Hangzhou lifted all home purchase restrictions, although there were headwinds from default concerns as Country Garden Holdings (2007 HK) failed to make coupon payments on a yuan-denominated bond due today but still has a grace period.

Nikkei 225 recovered from an early dip with trade contained as participants digested BoJ rhetoric and soft wages.

ASX 200 was dragged lower by underperformance in consumer stocks and financials with the latter pressured after Australia’s largest lender CBA reported a decline in profits.

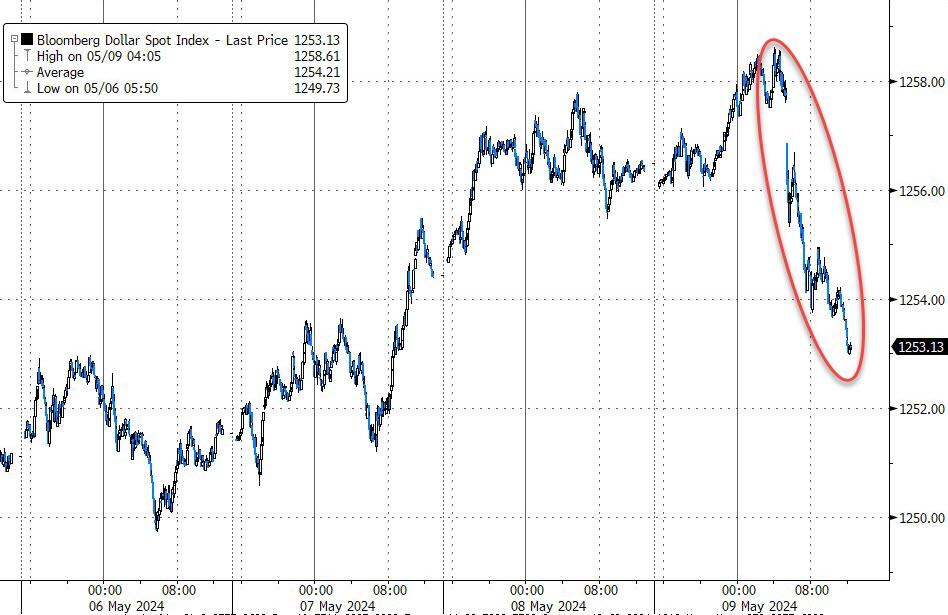

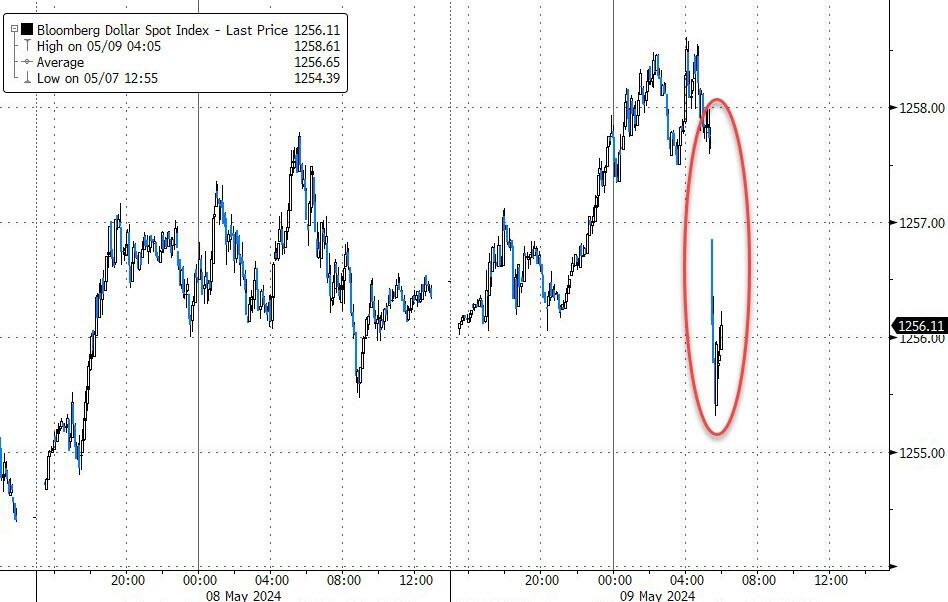

In FX, the Bloomberg Dollar Spot Index rose 0.1% as the greenback gained against all Group-of-10 peers; Treasury yields rose 1-3bps across the curve.

USD/JPY rose as much as 0.3% as the Japanese yen led losses against the dollar, earlier in the Asian session the currency pair fell 0.2%; a BOJ April meeting summary indicated the weak yen is being closely watched and could result in a faster pace of rate hikes

GBP/USD steadied around 1.2480 after falling as much as 0.4% to 1.2450 after the BOE kept rates unchanged but signaled that the time for cuts is approaching

Treasuries are lower on the day, but have pared declines as gilts jump on Bank of England’s 7-2 vote to keep rates on hold, with Ramsden joining Dhingra in supporting a cut. UK curve steepens with 2-year yields dropping around 3bp on the day. US long-end yields remain cheaper by about 3bp with front-end outperforming slightly. 10-year around 4.51%, also cheaper by 3bp on the day; gilt yields reached day’s lows and GBP/USD fell as much as 0.4% to 1.245% after BOE policy announcement. US session includes weekly jobless claims and $25b 30-year bond sale, last of week’s three auctions.

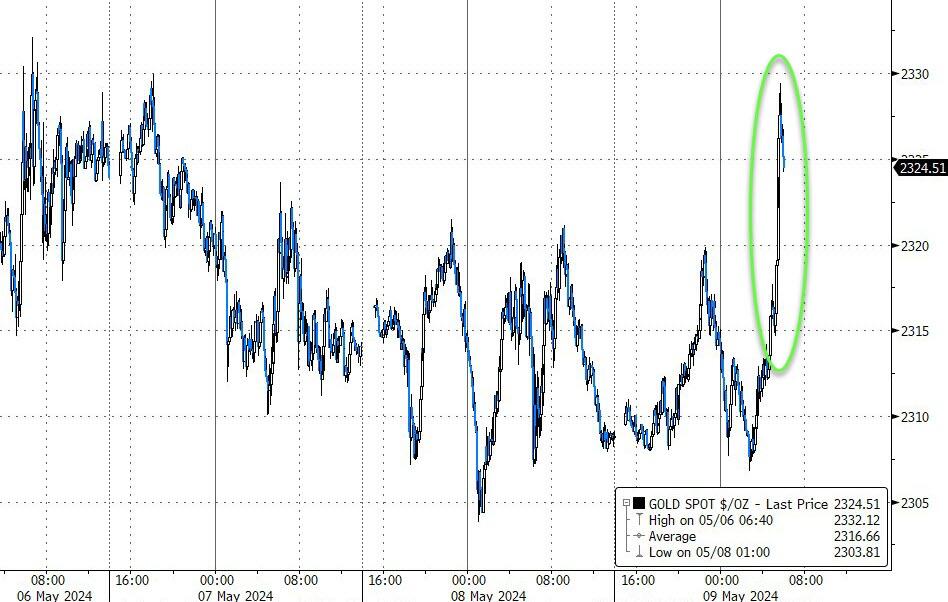

In commodities, oil prices advance, with WTI rising 0.6% to trade near $79.40. Spot gold is little changed.

Bitcoin softer on the session and holds just shy of USD 61k, whilst Ethereum unable to climb back above USD 3k.

To the day ahead now, and the main highlight will be the Bank of England’s latest policy decision and Governor Bailey’s press conference. Other speakers will include ECB Vice President de Guindos, the ECB’s Cipollone, Bank of Canada Governor Macklem, the Fed’s Daly, and BoE chief economist Pill. Otherwise in the US, we’ll get the weekly initial jobless claims, and there’s a 30yr Treasury auction taking place.

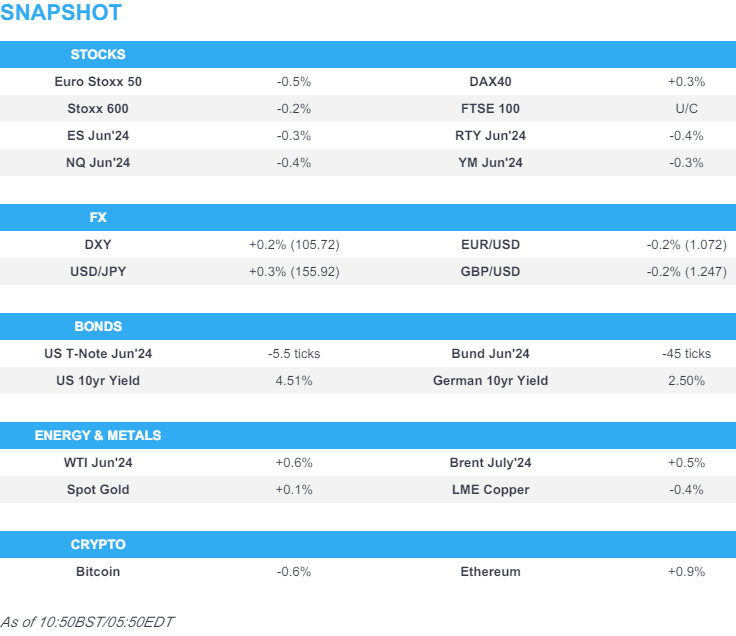

Market Snapshot

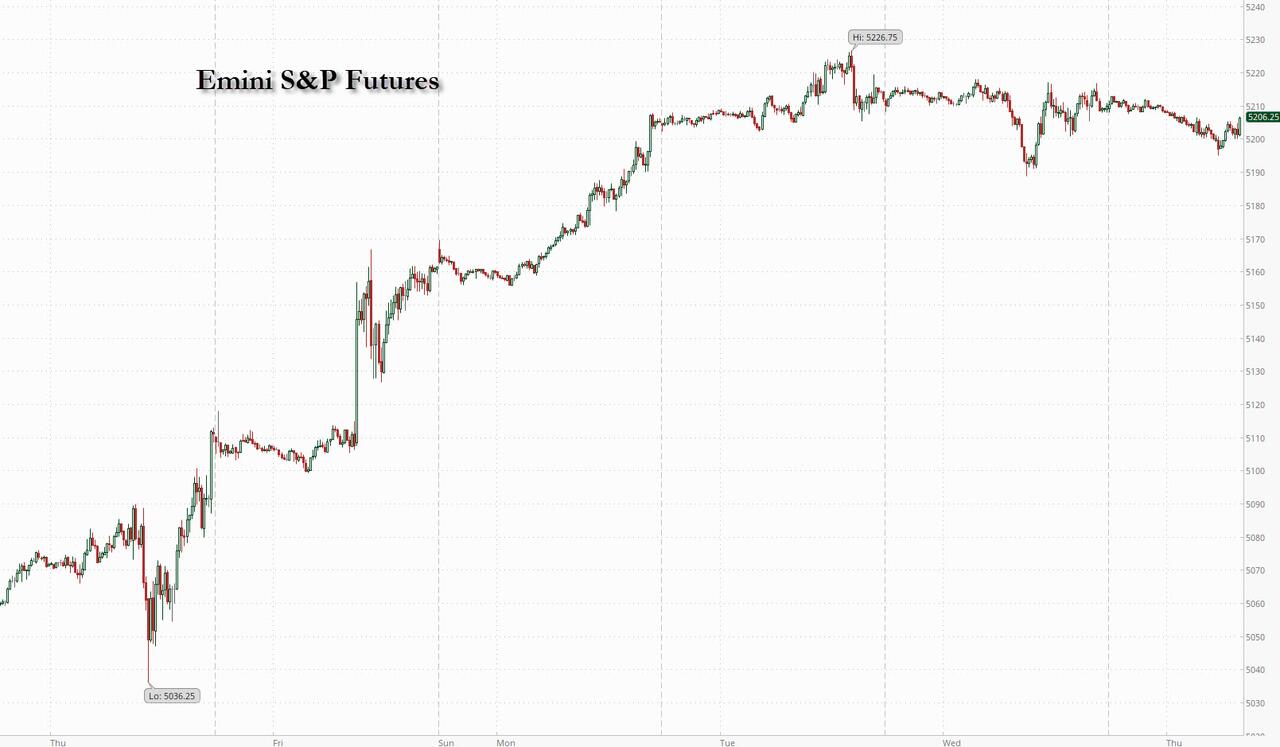

S&P 500 futures down 0.2% to 5,201.50

STOXX Europe 600 down 0.1% to 515.19

MXAP down 0.2% to 176.15

MXAPJ down 0.3% to 549.14

Nikkei down 0.3% to 38,073.98

Topix up 0.3% to 2,713.46

Hang Seng Index up 1.2% to 18,537.81

Shanghai Composite up 0.8% to 3,154.32

Sensex down 1.1% to 72,646.43

Australia S&P/ASX 200 down 1.1% to 7,721.64

Kospi down 1.2% to 2,712.14

Brent Futures up 0.6% to $84.11/bbl

Gold spot up 0.1% to $2,311.61

US Dollar Index up 0.16% to 105.71

German 10Y yield little changed at 2.50%

Euro down 0.2% to $1.0728

Brent Futures up 0.6% to $84.12/bbl

Top Overnight News

China’s efforts to revive homebuyer demand gathered steam on Thursday when two major cities scrapped all their remaining curbs on residential property purchases, a move that more local governments are expected to follow. Developer stocks surged after Hangzhou, the capital of eastern Zhejiang province, said it will remove eight-year-old restrictions on residential property purchases and no longer review the qualifications of homebuyers. Xi’an, the capital of Shaanxi province, announced similar steps hours later. BBG

China’s central bank seems very likely to make a bond purchase in the secondary market for the first time in two decades. SCMP

The BOJ’s board is becoming more concerned about the inflation outlook as a sharply weaker yen threatens to drive up import prices, a summary of its latest meeting showed. WSJ

EU countries have agreed to use an estimated €3bn in profits arising from Russia’s frozen state assets to jointly buy weapons for Ukraine. The deal struck by the bloc’s 27 ambassadors on Wednesday only targets profits made by Belgium’s central securities depository Euroclear, where about €190bn of Russian central bank assets are held. Western nations immobilized Russia’s state assets abroad in 2022, in response to its full-scale invasion of Ukraine. FT

President Biden trails former President Trump by roughly 1pp in national polling and by around 2pp in the swing state that would currently provide the winning electoral vote. Prediction markets imply around a 52% chance of a Democratic win. Biden’s lead over Trump in some prediction markets has retraced somewhat this month and Biden’s approval rating has ticked down to 38%, not far off the 37% low and below Trump’s average approval in the six months before he lost the 2020 election. GIR

Speaker Mike Johnson on Wednesday easily batted down an attempt by Representative Marjorie Taylor Greene of Georgia to oust him from his post, after Democrats linked arms with most Republicans to fend off a second attempt by G.O.P. hard-liners to strip the gavel from their party leader. NYT

Roughly one in 37 US homes is now considered seriously underwater, real estate data firm ATTOM said. That share is much higher — and growing at a faster pace — across a swath of southern states. But nationally, it’s still lower than before the pandemic. BBG

Tim Cook will likely stay AAPL’s CEO for at least another three years and his most likely successor at that time would be John Ternus, the current head of hardware engineering. BBG

A more detailed look at global markets courtesy of Newqsuawk

APAC stocks were mixed as the region took its cue from the indecisive performance stateside owing to mixed earnings and as markets await the next major catalysts, while the somewhat mixed but improved Chinese trade data had little impact. ASX 200 was dragged lower by underperformance in consumer stocks and financials with the latter pressured after Australia’s largest lender CBA reported a decline in profits. Nikkei 225 recovered from an early dip with trade contained as participants digested BoJ rhetoric and soft wages. Hang Seng & Shanghai Comp were underpinned amid resilience in the tech sector and after China’s eastern city of Hangzhou lifted all home purchase restrictions, although there were headwinds from default concerns as Country Garden Holdings (2007 HK) failed to make coupon payments on a yuan-denominated bond due today but still has a grace period.

Top Asian News

PBoC said it could either buy or sell treasury bonds in the secondary market depending on market conditions, as such trades can be used to manage liquidity, according to Reuters.

China’s eastern city of Hangzhou lifted all home purchase restrictions, according to its housing authority.

Country Garden Holdings (2007 HK) said it cannot make payments on a yuan-denominated bond, while it aims to pay onshore coupons due today and additional interests by May 13th. Furthermore, it stated that if it fails to make payments within the grace period, China Bond Insurance Co. will undertake credit enhancement obligations and it is still raising funds due to sales recovery lagging expectations.

US Commerce Secretary Raimondo said the US could ban Chinese-connected vehicles or impose guardrails, while it was separately reported that US Senator Brown is seeking a US ban on all Chinese internet-connected vehicles, according to Bloomberg.

Hong Kong and Saudi Arabia are exploring an ETF to track Hong Kong stock indices, while Hong Kong is working with several financial institutions to develop the ETF and the government is considering establishing an economic and trade office in Riyadh.

BoJ Summary of Opinions from the April meeting noted that a member stated if trend inflation accelerates, the BoJ will adjust the degree of monetary easing but an accommodative financial environment is likely to continue for the time being and a member said if forecasts under quarterly report are met, interest rates might rise to levels higher than markets currently price in. It was also stated that one option would be to hike rates moderately in accordance with economic, price and financial developments to avoid a shock from an abrupt policy shift. Furthermore, a member said they must hike rates at an appropriate time as the likelihood of achieving forecasts heightens and a member said the BoJ must deepen the debate on the timing and pace of a future rate hike.

BoJ Governor Ueda said a low real rate supports the economy and inflation, while he added that they need to monitor FX and oil for real wages. Ueda also stated the BoJ could adjust the degree of monetary accommodation via rate hikes if trend inflation accelerates gradually, as well as noted that a sharp, one-sided yen fall is undesirable and bad for the economy. Furthermore, he reiterated if FX volatility affects or risks affecting trend inflation, the BoJ must respond with monetary policy and will scrutinise the recent weak yen in guiding monetary policy.

Japanese Finance Minister Suzuki said it is important for currencies to move in a stable manner reflecting fundamentals and rapid FX moves are undesirable, while they are closely watching FX moves and will take thorough response in forex. Suzuki also stated they will take all necessary measures and continue to analyse the FX impact on the economy and livelihoods and take appropriate action.

Japanese top currency diplomat Kanda said no comment on intervention and if necessary, they will take appropriate action and are ready for currency intervention at any time, while he added that comments about Japan’s limitations are wrong when asked about FX intervention reserves.

Nissan (7201 JT) FY23/24 (JPY): Net Profits 426.65bln (+92.3% Y/Y), Operating Profit 568.72bln (+50.8%), Recurring Profits 702.16bln (+36.2%); Sees FY24 global retail sales at 3.7mln and North America sales of 1.43mln.

China is said to be considering a proposal to exempt individual investors from paying dividend taxes on Hong Kong stocks bought via Stock Connect, Bloomberg sources say

European bourses, Stoxx600 (-0.2%) are mixed and unable to find direction, taking lead from an indecisive session in APAC trade with newsflow somewhat light thus far on account of Ascension Day. European sectors are mixed and with the breadth of the market fairly narrow, though with the exception of Autos, which has been weighed on by Mercedes-Benz (-5.5%). Energy is found at the top of the pile, propped up by broader strength in crude prices. US Equity Futures (ES -0.2%, NQ -0.3%, RTY -0.5%) are in the red, with slight underperformance in the RTY continuing the weakness seen in the prior session. In terms of stock specifics, Arm (-9%) is lower in the pre-market, despite beating on top/bottom line, though its guidance failed to impress investors & Tesla (-1.5%) on reports around China job reductions. Goldman Sachs raises 12-month FTSE 100 cash target to 8,800 from 8,200 (last close 8,354)

Top European News

FX

USD is firmer vs. all peers in quiet newsflow with the DXY eclipsing yesterday’s 105.64 best. Interim resistance ahead of the 106 mark comes via the 2nd May high at 105.89.

EUR is once again on the backfoot vs. the USD in a third consecutive session of losses. Currently trading within a 1.0751-27 range.

Pound is softer vs. the broadly stronger USD but flat vs. the EUR. BoE looming large for the pair with markets on the lookout for any hints of a move in June. If this materialises, yesterday’s low sits at 1.2468 with the MTD low just below at 1.2466. To the upside, 1.25 would be the immediate target with the 200DMA at 1.2542.

JPY unaffected by ongoing jawboning from Japanese officials and is the marginal laggard across the majors. 155.84 the session high thus far for USD/JPY.

Antipodeans are both relatively contained vs. the USD with macro drivers on the light side. AUD/USD is consolidating around its 100DMA after two sessions of losses and respecting yesterday’s 0.6557-99 range. NZD/USD a touch softer.

PBoC set USD/CNY mid-point at 7.1028 vs exp. 7.2238 (prev. 7.1016).

Brazil Central Bank cut the Selic rate by 25bps to 10.50%, as expected, whereby 5 members voted in favour of a 25bps cut and 4 members voted for a 50bps reduction. The committee unanimously judged that the uncertain global scenario and the domestic scenario, marked by resilient economic activity and de-anchored expectations, require greater caution. It also stated that monetary policy should continue being contractionary until the consolidation of both the disinflation process and the anchoring of expectations around the targets.

Fixed Income

USTs are softer, in a continuation of the general bearish tone that was in place yesterday and one that appears to be driven by a pause-for-breath from the post-NFP move, lack of geopolitical escalation, relatively average 10yr before today’s 30yr and an increase in corporate issuance activity.

Gilts are pressured ahead of the BoE policy announcement. Gilts are toward the 97.50 trough and are underperforming EGBs somewhat, underperformance that appears to be a function of the UK catching up to the relatively average US 10yr auction late on Tuesday.

Bunds are softer, with action and drivers perhaps a touch thinner thus far on account of Ascension Day. Bunds down to a 130.90 base which marks a new low for the week and has taken the 10yr yield back to the 2.50% mark

Commodities

Firmer trade across energy contracts after futures settled with modest gains on Wednesday amid tailwinds from crude stocks drawing more than anticipated. Brent Jul’24 sits at the upper end of a USD 83.71-84.25/bbl range.

Mixed trade across precious metals with spot silver the outperformer, spot palladium the laggard, and spot gold flat. XAU is contained to a current USD 2,307.59-2,319.85/oz intraday range, within yesterday’s USD 2,303.75-2,321.53/oz range.

Base metals have turned lower since European traders entered the fray amid the cautious risk tone coupled with a rising Dollar.

Iraq sets the June 2024 Basrah medium crude OSP to Asia at USD +1.00/bbl vs Oman/Dubai, via SOMO; to North and South America at -0.65/bbl vs ASCO; to Europe at -3.35/bbl vs dated Brent

Geopolitics: Middle East

Yemeni Houthis targeted two ships with rockets in the Gulf of Aden yesterday, according to the spokesperson.

“Israel Broadcasting Corporation quoting a military source: Israel must reconsider its military plans in Rafah after Biden’s statements”, according to Sky News Arabia

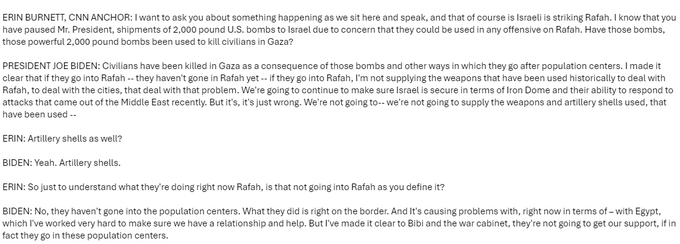

US President Biden said if Israel goes into Rafah, he won’t supply them with weapons and artillery shells, while he added that Israel will not get their support if they go into those population centres and that bombs the US had supplied to Israel and now paused have been used to kill civilians. Biden also commented that Israel has not gone over the red line yet, while he is working with Arab states that are prepared to build Gaza and prepared to help transition to a two-state solution.

Hamas senior official said the movement sticks to its approval of the truce proposal.

Egyptian media said Israel deleted the phrase ‘permanent ceasefire’ and kept it ‘sustainable’, while Hamas, Islamic Jihad and Popular Front are participating in negotiations and are open to maturing and succeeding the Egyptian effort to reach a deal. Furthermore, work is underway to overcome the controversial points during the negotiations, which will be completed on Thursday, according to Asharq News.

Israeli senior officials warned their US counterparts that the Biden administration’s decision to pause a weapons shipment to Israel could jeopardise hostage negotiations, according to two sources briefed on the issue told Axios’ Ravid.

Syria shot down Israeli missiles fired from Golan Heights towards Damascus’s surroundings.

Adviser to Iran’s Supreme Leader said Tehran will have to change its nuclear doctrine if its existence is threatened and has the capability to build a nuclear weapon, according to SNN.

Geopolitics: Other

Ukraine drone attack sparked a fire and damaged oil tanks at a refinery in Russia’s Krasnodar, according to regional officials.

Russian President Putin says tactical nuclear weapon drills are planned, according to Interfax.

Russia’s Gazprom says its Salavat plant was attacked by a drone but the plant is working normally, according to Ria

US Event Calendar

08:30: April Continuing Claims, est. 1.78m, prior 1.77m

08:30: May Initial Jobless Claims, est. 212,000, prior 208,000

Central Bank Speakers

14:00: Fed’s Daly Participates in Fireside Chat

DB’s Jim Reid concludes the overnight wrap

Morning from an early morning taxi to Heathrow en route to Madrid. After a remarkable Champions League semi-final last night I’m expecting a party in half the city at least today!

A little like Bayern last night, markets finally ran out of steam yesterday, with the S&P 500 (-0.00%) narrowly ending its run of four consecutive gains. If you’re looking for the dullest stat ever then the -0.03 points move was the smallest in either direction since the -0.02 points decline in September 2018.

The pause for breath was partly due to some disappointing earnings releases, but it also comes on the back of its strongest 4-day rally since November, so it was always going to be hard to maintain that pace. It was much the same story for sovereign bonds too, as the 10yr Treasury yield (+3.7bps) moved higher after a run of five consecutive declines. However, it wasn’t all bad news, as Europe’s STOXX 600 (+0.34%), the UK’s FTSE 100 (+0.49%) and Germany’s DAX (+0.37%) all hit fresh record highs.

Amidst all this, there were fresh signs that rate cuts were moving back into fashion yesterday, as the Swedish Riksbank became the second central bank with a G10 currency to cut rates in this cycle. The move was expected, but it was the first rate cut they’d delivered since 2016, so it was a big milestone, which took the policy rate down by 25bps to 3.75%. In addition, their statement signalled that more cuts were likely ahead, saying that if the inflation outlook held up, then they expected two more cuts in the second half of this year. It’s also worth noting that they’re in a better position than some other central banks, as their preferred measure of inflation (CPIF) was at 2.2% in March, so just above their 2% target.

The Riksbank’s decision follows the Swiss National Bank’s cut back in March, and it comes with mounting anticipation that the larger central banks are soon about to follow. In particular, the focus is turning to the ECB, who are increasingly expected to cut rates in four weeks’ time, marking the first cut since before the pandemic. Likewise, investors are now pricing in a 68% chance the Bank of Canada will cut at their next meeting in June. So it’s plausible that within a couple of months, we could have several central banks easing policy, with the global monetary policy cycle in easing mode with the considerable exception of the US. Yesterday’s CoTD (here) stretching back nearly 7 decades shows how rare it is for Europe to be easing before the US so we’ll have to see the implications in the months ahead. The obvious one is for dollar strength to continue.

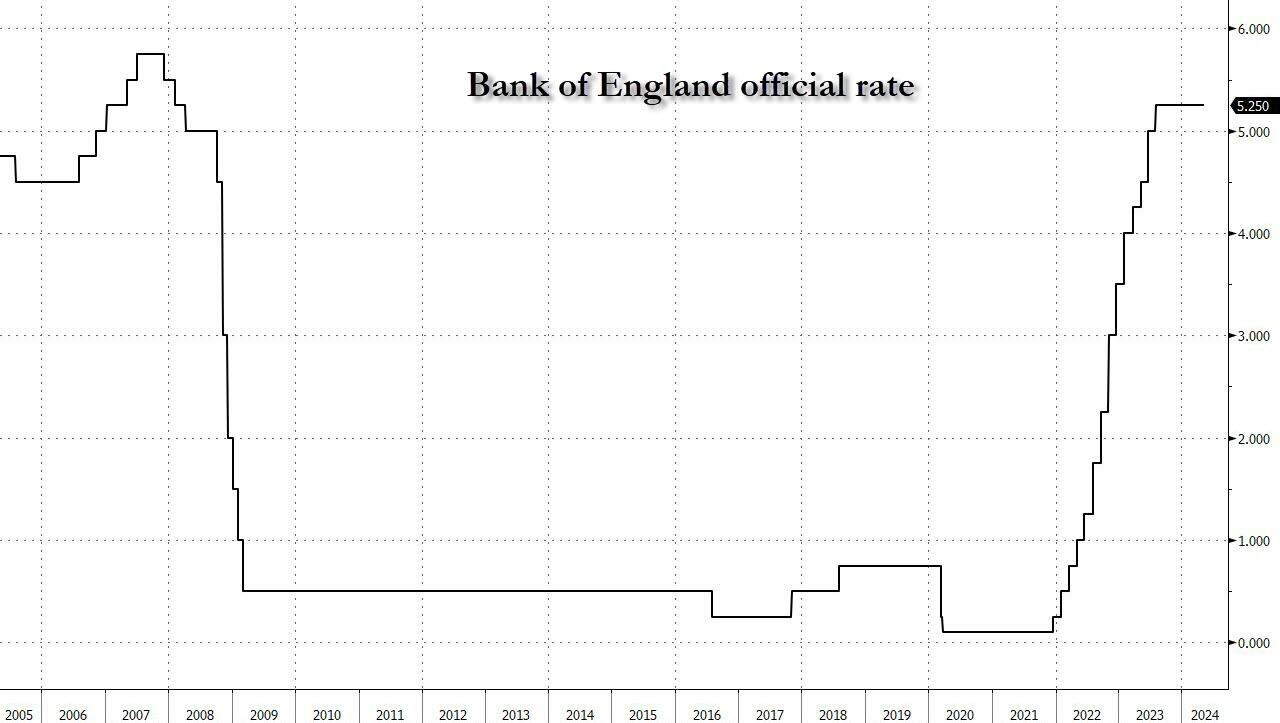

Central banks will remain in focus today, as we’ve got the Bank of England’s latest policy decision at 12:00 London time. In terms of what to expect, it’s widely anticipated they’ll leave rates unchanged at 5.25%, where they’ve been since August. So the focus will instead be on the vote split, their new forecasts, and what their forward guidance signals about potential cuts in the future. DB’s UK economist thinks the vote will be 7-2 to remain on hold, with 2 voting to cut, and he also expects a further dovish tilt in the forward guidance, which would set the stage for a June rate cut. See his full preview here

But even as central banks are pivoting towards rate cuts, yesterday saw sovereign bonds lose ground on both sides of the Atlantic, ending a run of gains since the Fed’s decision last week. For instance, the 10yr US Treasury yield was back up +3.7bps to 4.495% and is trading at 4.515% as I type in Asia hours. Marginally adding to the bond sell-off was the latest 10yr Treasury auction, that saw $42bn of bonds issued at 4.48%, 1bp above the pre-sale yield. And over in Europe, yields on 10yr bunds (+4.3bps), OATs (+4.1bps) and BTPs (+3.6bps) all moved higher, whilst Swedish 10yr yields (+3.5bps) saw a similar move despite the rate cut.

For equities, there was a more divergent performance on either side of the Atlantic, with those in Europe holding up and seeing the fresh records mentioned above and those in the US losing a touch of momentum. The S&P 500 was essentially flat on the day (-0.00%). Moderate losses from the Magnificent 7 (-0.29%) were counterbalanced by advances among sectors including utilities (+1.05%) and banks (+1.22%). But the overall tone was titled to the negative side with 7 of the 11 S&P 500 sector groups down on the day and the small cap Russell 2000 underperforming (-0.46%).

Elsewhere, it was a volatile day for oil prices, which reversed their earlier losses to leave Brent crude up +0.51% at $83.58/bbl ($83.95 overnight). At first they had seen a sharp decline, hitting an intraday low of $81.71/bbl, which is the lowest they’ve been in almost a couple of months. But then we had the latest weekly data from the EIA showing that US crude oil inventories were down by 1.36m barrels, leading to a recovery in prices.

Asian equity markets are notably higher this morning even if US futures are edging slightly lower. Chinese stocks are outperforming with the Hang Seng (+1.23%) leading gains followed by the CSI (+1.03%) and the Shanghai Composite (+0.91%) after Chinese property stocks surged after Hangzhou removed home buying restrictions, in a move that created speculation that other cities might follow. Elsewhere, the Nikkei (+0.33%) is reversing its previous session losses while the KOSPI (-1.05%) is retreating, bucking the regional trend. S&P 500 (-0.09%) and NASDAQ 100 (-0.16%) futures are trading slightly lower.

Coming back to China, export growth surpassed market expectations in April with exports rebounding +1.5% y/y (v/s +1.3% expected) after falling -7.5% in March, its first contraction since November. Imports increased +8.4% (v/s +4.7% expected), reversing the prior month’s -1.9% decline. April trade surplus stood at US$72.4 billion, compared with US$58.6 billion in March.

Moving to Japan, the latest salary data showed that real wages fell -2.5% y/y in March (v/s -1.4% expected), notching the sharpest drop in four months and extending the streak of declines to exactly 24 months. It followed the previous month’s -1.8% drop, as the rising cost of living outpaced nominal wages. Nominal wages rose +0.6% y/y in March, slowing from a downwardly revised +1.4% increase seen in February.

Elsewhere, government bonds are seeing losses in Asia with yields notably higher in Australia, New Zealand and Japan. As I type, 10yr government bond yields are over +7bps higher in Australia and New Zealand with 10yr JGB yields is +2.9bps higher at +0.90%, not far from the multi-year highs seen briefly in January.

There wasn’t much data yesterday, although German industrial production fell by -0.4% in March (vs. -0.7% expected), whilst Italian retail sales were unchanged (vs. +0.1% expected). Separately in the US, weekly data from the MBA showed that the contract rate on a 30yr mortgage was down -11bps to 7.18% over the week ending May 3, ending a run of four consecutive weekly increases.

To the day ahead now, and the main highlight will be the Bank of England’s latest policy decision and Governor Bailey’s press conference. Other speakers will include ECB Vice President de Guindos, the ECB’s Cipollone, Bank of Canada Governor Macklem, the Fed’s Daly, and BoE chief economist Pill. Otherwise in the US, we’ll get the weekly initial jobless claims, and there’s a 30yr Treasury auction taking place.

2B European Opening Report

US equity futures lower, Gilts pressured ahead of the BoE and USD/JPY nears 156 – Newsquawk US Market Open

THURSDAY, MAY 09, 2024 – 05:57 AM

European equities are mixed, Stateside futures lower with slight underperformance in the RTY

Dollar is firmer, G10s in the red and USD/JPY now just shy of 156.00

Bonds pressured in a continuation of recent action; Gilts underperform slightly ahead of the BoE

Crude is firmer, XAU flat and base metals mostly lower

Looking ahead, US IJC, NZ Manufacturing PMI, BoE Policy Announcement, BoE DMP, Banxico Policy Announcement, Comments from Fed’s Daly, BoE’s Bailey & Pill, ECB’s Cipollone & de Guindos

2. Listen to this report in the market open podcast (available on Apple and Spotify)