MAY 13/GOLD CLOSED DOWN $31.10 TO $2336.40/SILVER CLOSED DOWN $0.04 TO $28.25/PLATINUM CLOSED UP $3.65 TO $1003.65/WHILE PALLADIUM CLOSED DOWN $13,70 TO $966.05//

363 H WELLS FARGO SEC 112 435 H SCOTIA CAPITAL 7 624 H BOFA SECURITIES 93 657 C MORGAN STANLEY 3 737 C ADVANTAGE 3 12

TOTAL: 115 115 MONTH TO DATE: 1,922

JPMorgan stopped 0/115

FOR MAY2024

GOLD: NUMBER OF NOTICES FILED FOR MAY/2024. CONTRACT: 115 NOTICES FOR 11500 OZ or 0.3571 TONNES

total notices so far: 1922 contracts for 192200 Oz (5.978 tonnes)

FOR MAY:

SILVER NOTICES: 166 NOTICE(S) FILED FOR 330,000 OZ/

total number of notices filed so far this month : 5610 for 28.050 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN 31.10

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPSIT OF 86 TONNES

/ /INVENTORY RESTS AT 831.33TONNES

INVENTORY RESTS AT 831.33 TONNES

SLV//

WITH NO SILVER AROUND AND

SILVER DOWN 4 CENTS AT THE SLV//

NO CHANGES IN SILVER INVENTORY AT THE SLV:

// INVENTORY REMAIN CONSTANT AT 422.227MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 422.227 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY SMALL SIZED 233 CONTRACTS TO 167,555 AND STALLING TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR GAIN OF $0,15 IN SILVER PRICING AT THE COMEX ON FRIDAY. WE HAD ZERO LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN SHORT COVERING BY OUR SPECS WITH THE GAIN IN PRICE. WE HAD ANOTHER HUGE SIZED 1125 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON FRIDAY NIGHT: 1125 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.15 AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD A GOOD SIZED GAIN OF 492 CONTRACTS ON OUR TWO EXCHANGES WITH THE GAIN IN PRICE OF $0.15

WE MUST HAVE HAD:

A FAIR SIZED 255 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 28.130MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 65,000 OZ

//NEW STANDING FOR SILVER//MAY IS THUS 28.475 MILLION OZ

WE HAD:

/ SMALL SIZED COMEX OI GAIN //FAIR SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1125 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED A HUGE 727CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY

TOTAL CONTRACTS for 9 DAYS, total 4595 contracts: OR 22.975 MILLION OZ (510 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 22.975 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770MILLION OZ (THIS MONTH WILL PROBABLY BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 22.975 MILLION OZ (ISSUANCE WILL BE RATHER SMALL THIS MONTH/PROBABLY MATCHING FEB 2024)

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 233 CONTRACTS WITH OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR EFP ISSUANCE CONTRACTS: 255 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAY OF 28.130 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 656,000 OZ QUEUE JUMP

//NEW TOTAL STANDING AT 28.475 MILLION OZ

WE HAVE A GOOD SIZED GAIN OF 492 OI CONTRACTS ON THE TWO EXCHANGES WITH THE GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 1125 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE FRIDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS

THE NEW TAS ISSUANCE FRIDAY NIGHT (1125 WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 66 NOTICE(S) FILED TODAY FOR 330,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

FINAL DATA

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 10,189 OI CONTRACTS TO 529,367 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 1102 CONTRACTS

WE HAD A STRONG SIZED DECREASE IN COMEX OI (10,189 CONTRACTS) OCCURRED DESPITE OUR HUGE GAIN $34.65 IN PRICE/FRIDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER TRYING TO CONTAIN GOLD’S PRICE RISE. THE LOSS IN COMEX OI WAS DUE TO SPREADER (T.A.S) LIQUIDATION. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 4.684 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY;S 0 OZ QUEUE JUMP//NEW STANDING INCREASES TO 5.7045 TONNES

NEW STANDING 5.7045 TONNES// ALL OF THIS HAPPENED DESPITE OUR $34.65 GAIN IN PRICE WITH RESPECT TO FRIDAY’S TRADING. WE HAD A STRONG SIZED LOSS OF 7189 OI CONTRACTS (22.345 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1903 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 529,367

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7184 CONTRACTS WITH10,189 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 1903 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 7184 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): ANOTHER MEGA HUMONGOUS SIZED 41,505 CONTRACTS,, THE HIGHEST EVER RECORDED FROM INCEPTION OF THIS INSIDIOUS SPREADER CONTRACT

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1903 CONTRACTS) ACCOMPANYING THE STRONG LOSS IN COMEX OI 10,189/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 8286 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 4.684TONNES FOLLOWED BY TODAY;S 11,500 OZ QUEUE JUMP

//NEW STANDING /MAY 6.062 TONNES.

/ 3) MASSIVE LONG-SHORT LIQUIDATION ALL DUE TO SPREADERS DESPITE THE HUGE GAIN IN PRICE.

// 4) STRONG SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///6: MEGA-MEGA HUMONGOUS T.A.S. ISSUANCE: 41,505 CONTRACTS/ HUGE SHORT COVERING BY OUR WRONG FOOTED SPECS WITH THE FED’S CONTINUAL FRUITLESS RAID ON THE COMEX GOLD.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY. :

TOTAL EFP CONTRACTS ISSUED: 38,413 CONTRACTS OR 3,841,300 OZ OR 119.480 TONNES IN 9 TRADING DAY(S) AND THUS AVERAGING: 4268 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES 119.48 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 119.48DIVIDED BY 3550 x 100% TONNES = 3.35% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 119.48 TONNES (WILL BE ANOTHER STRONG MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A SMALL SIZED 259 CONTRACTS OI TO 167,555 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 255 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 255 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 255 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 233 CONTRACTS AND ADD TO THE 255 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 492 CONTRACTS

THUS IN OUNCES, THE HUGE GAIN ON THE TWO EXCHANGES TOTALS 2.478 MILLION OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

MONDAY MORNING/SUNDAY NIGHT

SHANGHAI CLOSED DOWN 6,53 PTS OR 0.21% //Hang Seng CLOSED UP 131.38PTS OR 0.80%// Nikkei CLOSED DOWN 49.63 OR 0.13%//Australia’s all ordinaries CLOSED DOWN 0.04%///Chinese yuan (ONSHORE) closed DOWN TO 7,2325 CHINESE YUAN OFF SHORE CLOSED DOWN TO 7.2398/ Oil DOWN TO 78,94 dollars per barrel for WTI and BRENT DOWN AT 83.33 /Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 10,189 CONTRACTS TO 529,367 DESPITE OUR HUGE GAIN IN PRICE OF $34.65 WITH RESPECT TO FRIDAY TRADING. WE HAD ANOTHER MEGA HUMONGOUS T.A.S. LIQUIDATION YESTERDAY AS WELL AS SHORTS, DESPERATELY TRYING TO GET OUT OF THEIR NAKED SHORTS.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAY.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 1903 EFP CONTRACTS WERE ISSUED: : JUNE1903 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE:1903 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 8286 CONTRACTS IN THAT 1903 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 10,189 COMEX CONTRACTS..AND THIS STRONG LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR HUGE GAIN IN PRICE OF $34.65 FRIDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR FRIDAY NIGHT WAS ANOTHER MEGA HUMONGOUS SIZED 41,505 CONTRACTS.(4 NIGHTS IN A ROW OF HUGE ISSUANCE AND THE FRIDAY NIGHT ISSUANCE WAS THE HIGHEST EVER RECORDED WITH RESPECT TO COMEX HISTORY) WE HAD 0 EX FOR RISK ISSUANCE. MOST OF THE TRADING AND SUPPLY OF CONTRACTS ON FRIDAY WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (6.062 TONNES) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 6.062 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A HUGE $34.65 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS ALL THE LIQUIDATION CAME FROM SPREADERS (TAS)

WE HAD ANOTHER HUGE T.A.S. LIQUIDATION ON THE FRONT END OF FRIDAY’S TRADING. THE T.A.S. ISSUED ON FRIDAY NIGHT,( AND IT WAS ANOTHER DOOZY) WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS AND MOST LIKELY ON MONDAY TRADING.

WE HAVE LOST A TOTAL OI OF 22.345 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY (4.684 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 115 CONTRACTS OR 11500 OZ ( .3576 TONNES)

NEW STANDING: 5.7045 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $34.65

WE HAVE REMOVED 1102 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET LOSS ON THE TWO EXCHANGES 8286 CONTRACTS OR 828600 (25.77 TONNES)

156,059.690 OZ jpmorgan jpmorgan enhanced’ manfra loomis

.

Deposit to the Dealer Inventory in oz

00 oz

Deposits to the Customer Inventory, in oz

1704.01 brinks 55 kilobars

No of oz served (contracts) today

115 notice(s) 11500 OZ 0.3576 TONNES

No of oz to be served (notices)

27 contracts 2700 OZ 0.0839 TONNES

Total monthly oz gold served (contracts) so far this month

1922notices 192,200 oz 5.978 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: 0 oz

we have 0 customer deposits:

total deposit nil oz

total customer withdrawals: 0

TOTAL WITHDRAWALS nil 0z

Adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY

For the front month of MAY we have an oi of 142 contracts having GAINED 114 contracts.

We had 1 contracts served on FRIDAY, so we gained 115 contracts or 11,500 oz (0.3576 Tonnes).

JUNE DECREASED ITS OI BY 30,9238 CONTRACTS DOWN TO 286,052 CONTRACTS.

JULY GAINED 38 CONTRACTS TO STAND AT 204

We had 115 contracts filed for today representing 11500 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 115 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the MAY /2024. contract month, we take the total number of notices filed so far for the month (1922) x 100 oz ) to which we add the difference between the open interest for the front month of MAY ( 142 CONTRACTS) minus the number of notices served upon today (115 x 100 oz per contract( equals 194,900 OZ OR 6.062TONNES.

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (1922x 100 oz + (142 OI for the front month} minus the number of notices served upon today (115 x 100 oz which equals 194900 oz (6.062 TONNES)

TOTAL COMEX GOLD STANDING FOR MAY: 6.062 TONNES WHICH IS HUGE FOR THIS A NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,462.715.063 OZ

TOTAL REGISTERED GOLD 7,328,073,702( 227.93 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,134,641.381 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 5,761,749 oz (REG GOLD- PLEDGED GOLD)= 177.28 tonnes

179.36 tonnes/dropping like a stone

END

SILVER/COMEX

MAY 13

INITIAL

//2024// THE MAY 2025 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

621,626/420 oz brinks cnt

.

Deposits to the Dealer Inventory

nil OZ

Deposits to the Customer Inventory

972.33 oz

DELAWARE

No of oz served today (contracts)

66 CONTRACT(S) (330,000 OZ)

No of oz to be served (notices)

86 contracts (0.425 million oz)

Total monthly oz silver served (contracts)

5610 Contracts (28.050 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposit :nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i) Into delaware; 972.33 oz

total customer deposit 972.33 oz

JPMorgan has a total silver weight: 129,598million oz/297.7248 million or 43.62%

adjustment:0

Comex withdrawals: 2

i) out of Brinks 611,597.320 oz

ii out of cnt 10,029.100

total withdrawal 621,626.420 oz

TOTAL REGISTERED SILVER: 65.377MILLION OZ//.TOTAL REG + ELIGIBLE. 297.869 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF MAY/2024 OI: 151 CONTRACTS HAVING LOST 219 CONTRACT(S).

.

We had 284 notices served on FRIDAY so we GAINED 65 contracts or 325,000 oz underwent a STRONG QUEUE JUMP AS THEY WERE SET TO TAKE DELIVERY ON THIS SIDE OF THE POND.

JUNE SAW A LOSS OF 225 CONTRACTS RISING TO 1508

JULY SAW A LOSS OF 120 CONTRACTS UP TO 136,051

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 66 for 330,000 oz

CONFIRMED volume; ON friDAY 83,619 huge

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 5610 x 5,000 oz = 28.050MILLION oz

to which we add the difference between the open interest for the front month of MAY (151 and the number of notices served upon today 66x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2024 contract month: 5610 notices served so far) x 5000 oz + OI for the front month of MAY (151 number of notices served upon today minus (66x 5000 oz of silver standing for the may contract month equates to 28.475 MILLION OZ.

New total standing: 28.4575 million oz.

There are 65.377 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

MAY 13 WITH GOLD DOWN $31.10 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .86 TONNES OF GOLD INTO THE GLD////INVENTORY RISES TO 831.33 TONNES

MAY 10 WITH GOLD UP $34.65 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 9 WITH GOLD UP $18.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 8 WITH GOLD DOWN $0.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 830.47 TONNES

MAY 7 WITH GOLD DOWN $6.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 832.19 TONNES

MAY 6WITH GOLD UP $21.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .55 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 831.64 TONNES

MAY 2 WITH GOLD UP $0.20 ON THE DAY; SMAKK CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 830.47 TONNES

MAY 1 WITH GOLD UP $7.80 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNES

APRIL 29WITH GOLD UP $10,55TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNES

APRIL 26WITH GOLD UP $5.40TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.54 TONNES FROM THE GLD /INVENTORY RISES AT 832.19 TONNES

APRIL 25WITH GOLD UP $5.05 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD /INVENTORY RISES AT 833,63 TONNES

APRIL 19 WITH GOLD UP $15.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 4.32 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 831.91 TONNES

APRIL 18 WITH GOLD UP $11.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE WITHDRAWAL OF 2.59 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 827.59 TONNES

APRIL 17 WITH GOLD DOWN $17.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 830;18 TONNES

APRIL 16 WITH GOLD UP $23.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 828.45 TONNES

APRIL 15 WITH GOLD DOWN $. 80 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A HUGE WITHDRAWAL OF 1.80 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 824.84 TONNES

APRIL 12 WITH GOLD UP $2.80 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD/ INVENTORY RISESS AT 830.75 TONN

GLD INVENTORY: 830.47TONNES,

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 13 WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;

INVENTORY RESTS AT 422.227 MILLION OZ

MAY 10 WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A HUGE WITHDRAWAL OF 1.,828 MILLION OZ//INVENTORY RESTS AT 422.227 MILLION OZ

MAY 9 WITH SILVER UP 78 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 8 WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 7WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 6 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.055 MILLION OZ

MAY 3 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 2WITH SILVER UP 0.12 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/ A WITHDRAWALOF 4.471 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 1 WITH SILVER UP 0.09 TODAY: SMALLCHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF ,457 MILLION OZ INTO THE SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 29WITH SILVER UP $0.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 26WITH SILVER DOWN 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.097 MILLION OF SILVER INTO THE SLV// :SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 25WITH SILVER UP $.05 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 1.534 MILLION OF SILVER OUT OF THE SLV// :SLV INVENTORY RESTS AT 428.717 MILLION OZ

APRIL 24/WITH SILVER DOWN $.05 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 11.904MILLION OF SILVER INTO THE SLV// :SLV INVENTORY RESTS AT 428.280 MILLION OZ

APRIL 23/WITH SILVER UP $0.11TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV / :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 22/WITH SILVER DOWN $1.51 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.194 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 19/WITH SILVER UP 42 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.657 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 418.570 MILLION OZ

APRIL 18/WITH SILVER DOWN $.04TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.977 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 422.227 MILLION OZ

APRIL 17/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF .868 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 426/204 MILLION OZ

APRIL 16/WITH SILVER DOWN $0.46 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF NON EXISTENT SILVER// :SLV INVENTORY RESTS AT 427.072 MILLION OZ

APRIL 15/WITH SILVER UP $0.88 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 12/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 4.069 MILLION OZ FROM THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 11/WITH SILVER UP $0.23 TODAY: STRANGE INDEED! HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.931 MILLION OZ :SLV INVENTORY RESTS AT 437.998 MILLION OZ

CLOSING INVENTORY 422.227 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

PETER SCHIFF/SCHIFFGOLD/MIKE MAHARRAY

2.Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens/Alasdair Macleod

3. CHRIS POWELL//GATA DISPATCHES

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS /LIVE FROM THE VAULT

JAN NIEUWENHUIJS (KOOS jANSEN)

Why We Are At The Start Of A Multi-Year Gold Bull Market

Recently the dollar gold price aggressively broke a multiyear resistance level on the back of escalating wars, worrying asset bubbles, and sticky inflation. Long term indicators show gold is undervalued under these circumstances and can easily double in price over the coming years.

The past decades have been characterized by an elevated trust in credit instruments that blew the global financial system to colossal proportions. Now tensions between East and West, debt saturation and inflation are chipping away this trust, the balance between financial instruments with counterparty risk (credit) and without counterparty risk (gold) will go through a process of adjustment in favor of the gold price.

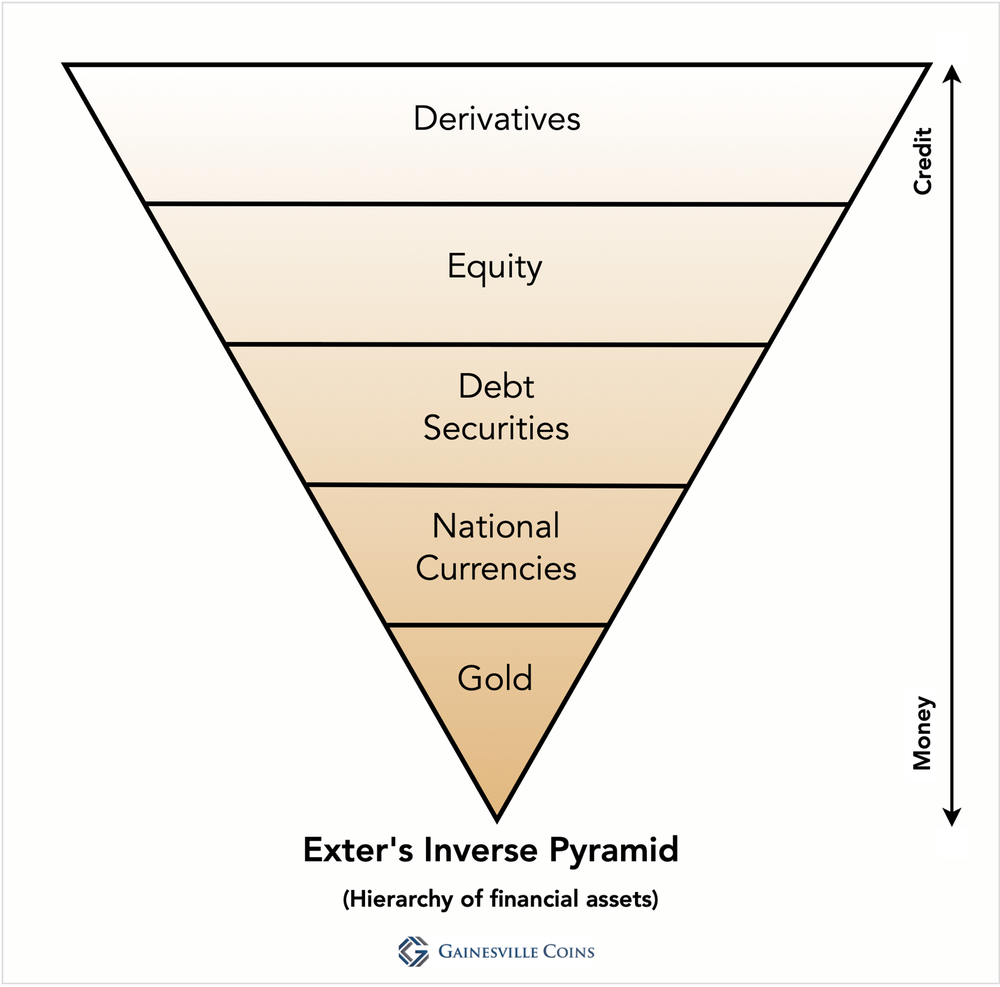

The Theory of Money and Exter’s Inverse Pyramid

“Money is gold, and nothing else.”

J.P. Morgan testimony before Congress 1912 (page 5)

Philosophically speaking all moneys are backed by trust. Because money is a social agreement it can be whatever we think it is—tobacco, salt, paper slips, silver, book entries, and so forth. Money functions as long as it is accepted by market participants.

But not all moneys are equal. Some moneys—for example tobacco and salt—are inconvenient in the modern age. Other moneys are issued by banks and therefor carry counterparty risk. Since the late 19th century gold is “officially” the only form of money that is universally accepted, has no counterparty risk, and therefore underpins the global financial system.

Below is a visualization of Exter’s inverse pyramid, whereby gold sits at the bottom, ultimately “backing” all forms of credit resting on top of it and providing indispensable trust to the financial system.

In moderation, credit is beneficial to a capitalist economy—too much credit (debt) results in lower growth, too little means foregone opportunities. But in general, and especially during a crisis, people have more trust in gold than credit.

Because everything above gold can be created out of thin air, the top of the pyramid can be easily widened. Throughout the business cycle balance sheets are extended—credit is created, the crown of the pyramid is enlarged—causing an economic boom. During a recession balance sheets shrink, the gold price increases, and the shape of the pyramid is remodeled. The overall size of the pyramid grows over time, while the pyramid’s form changes simultaneous with debt cycles.

Ratios between gold and credit assets can tell us where we are in a debt cycle. At the time of writing, we are in a boom as:

Gold as a share of global financial assets is low.

The US broad money supply relative to the gold “backing” it is overstretched.

Gold’s share of central banks’ international reserves is low.

Equity market valuations are high.

All the while trust in credit is waning, suggesting the gold price will rise (policy makers will avert outright defaults inducing a deflationary collapse).

New Multi-Year Gold Bull Market Has Begun

Let us first define what has recently happened to the gold price. From a technical perspective, as you can see in the chart below, the price of gold has broken out from a multi-year consolidation phase. If we may use history as our guide, we are now entering a multi-year bull market.

Next, we will examine the long-term fundamental indicators that display gold is undervalued under the conditions of declining trust in credit.

Unfortunately, it’s impossible to find global data on all financial assets going back 150 years to compare the value of all credit to that of gold. Though I did find estimates by Bridgewater Associates on the ratio between gold and “financial assets” (in this case gold, debt, and equity) from 1924 until 2020. I was able to roughly mimic Bridgewater’s methodology for the last two decades and could thus extend their data series.

As we can see, during periods when trust in credit is poor, in the Second World War and at the end of the 1970s, gold’s value relative to financial assets was in between 7 and 10%. Currently gold is worth 3%, which goes to show there is ample upside for gold this bull run.

Let’s also have a look at the value of the monetary gold supporting the US dollar broad money supply. What currency is more appropriate for assessing this ratio than the world reserve currency?

The value of the US monetary gold ultimately underpinning the dollars in circulation is rising from a near historic low. The two previous lows were in 1971 and 2000, after which multi-year gold bull markets followed. So, most likely a new bull market is upon us.

Making matters worse is that the dollar’s reserve currency status is slowly declining at the moment. My next measurement, therefor, is the relationship between gold and credit in the form of foreign exchange.

On the classical gold standard in the 19th century, it was mainly gold that underpinned confidence in central banks. Most of their reserves consisted of gold that literally backed the monetary base as currency could be redeemed for physical metal at a fixed parity. In the Interbellum it was agreed that foreign exchange (sterling and dollars) could substitute gold on central banks’ balance sheets to allow monetary expansion beyond the growth of the above ground stock of gold. This came to be known as the gold exchange standard. After the Second World War the US pushed the world to save in dollars and gold’s share of global international reserves declined sharply. Especially in the 1980s trust in dollars boomed.

For our final data series, we will look at the size of the US equity market versus the size of the economy (GDP) going back 120 years. Equity can be seen as a form of debt with no maturity. What the data reveals is that over time there have been cycles of easy money (credit) blowing equity bubbles, followed by the debasement of currency, reflected in a higher gold price.

The cycles can be best explained as follows: once a bubble pops, central banks ease monetary policy to stimulate the economy, but they often overshoot and plant the seeds for the next bubble—national currency (fiat) is the air that bubbles are commonly made of. This leads to a vicious cycle of bubbles and ever-easier money in which the value of currency incrementally declines, and the gold price appreciates. Cycles reminiscent of Exter’s pyramid widening (credit expands) and reshaping (gold price goes up). Time and again.

Currently the equity market (relative to GDP) is probably close to its peak, suggesting the gold price will see a significant rise in the coming years.

Conclusion

The West not only froze dollar assets owned by the Russian central bank early 2022 at the start of the war, but Congress just approved a bill to confiscate such assets and give them to Ukraine. What could speed up “de-dollarization” by BRICS members and other countries faster than this? Tensions between East and West will not be resolved quickly, telling us the gold price will continue to march higher and gold’s share of global international reserves will rise to the detriment of the dollar.

It should be noted that the Chinese central bank was a buyer of gold in the 1960s and 1990s before gold made substantial moves to the upside (see chart 1). Timothy Green writes in The World of Gold Today (1973):

In 1965 …., China bought 100 tonnes of gold … in the London market; the following year she came back for another 30 tonnes. Two years later China topped up with another 60 tonnes. The main reason behind these forays into the gold market appears to have been to divest itself of sterling [the second world reserve currency at the time]. Although no official figures of China’s reserve are available, it is likely that she substituted a good part of her holdings of sterling for gold before [the sterling] devaluation in 1967.

Dutch Newspaper NRC Handelsblad reported in 1993 that the People’s Bank of China (PBoC) was one of the buyers of a massive sale by the central bank of the Netherlands. As other European central banks sold heavily during the 1990s as well, we may assume the PBoC bought some more of that and reaped the benefits when the dollar gold price began its ascent around 2000.

The gold price can be used as an inflation expectations indicator. In the chart below one can see that a turnaround in the price of gold is often followed by surging inflation within two years. To me it would only make sense if this time around it’s no different.

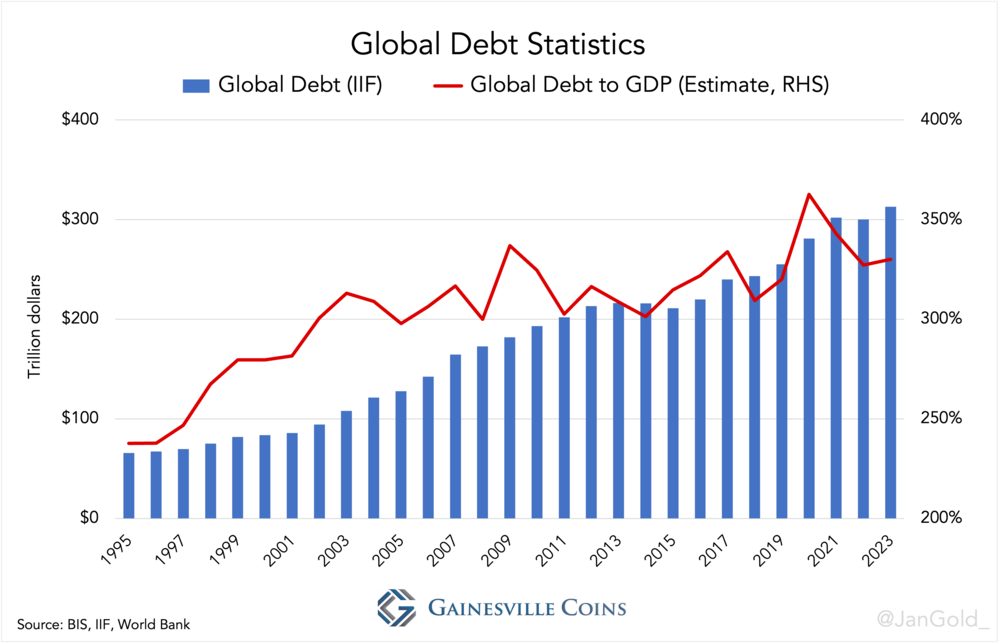

As global debt levels are near record highs and have become unsustainable, the most expedient, least well-understood, and common way of restructuring debt (credit) is inflation, according to former hedge fund manager Ray Dalio. Indeed, global debt stands at $313 trillion dollars (330% of GDP) and there are few other options to lower the debt burden. Inflation and a higher gold price would deleverage the system and restore the pyramid.

“The Thai [$35 bn] Government Pension Fund is reducing investments in assets that may be affected by war, and increasing investments in gold and oil to mitigate risk.” Notice a trend? Via

In 2023 I speculated the gold price could reach $8,000 dollars an ounce in the decade ahead. Based on all the data I came across in writing this article I still think that is a reasonable number that would stabilize the financial system by adding more trust to it.

end

BIL HOLTER

The most interesting week in MANY YEARS!

The precious metals complex had a pretty good run since early March. Gold, silver, and the miners got quite overbought and deserved to relax and digest those gains, which is what we’ve seen the past 2-3 weeks. For many years now, metals bulls have repeatedly asked “when”? It looks to me like “when” is NOW! I believe this coming week may be the most interesting week we have seen in many many years. I have pasted 3 charts, gold, silver and the HUI mining index. Before you tell me that because the metals complex is so rigged that charts are meaningless, please be patient. Something has definitely changed. That change is what we believed all along, that the physical markets would overwhelm the paper markets. This is, and has, been happening with China a huge buyer of physical gold and India the same with silver. There are now premiums on the SGE over and above COMEX and LBMA which has led to arbitrage moving physical metal from West to East and definitely tightening available supply for the paper traders to use to satisfy deliveries.

This first chart is gold which moved to all time highs. You will see a roughly 33% move up since last October, and close to a 20% move since late February. The move since February saw some serious overbought readings which you would expect to see with a move of this magnitude. If you look at the bottom of the chart, you will see the MACD (moving average convergence/divergence). This indicator can be quite useful leading up to a breakout or a breakdown. In this case, it looks to me like another push higher to further new highs is imminent. You will see a “hook” turning up, it has not crossed over yet but very close indeed!

Here we have silver. Silver has been JP Morgan’s beaten up and battered red headed stepchild. The silver market is maybe only 1/10th the size of gold, so obviously it is much easier to “manage” or manipulate. Since late February it’s had a nearly 40% move. Just as gold, it is no longer overbought but a little further advanced on the MACD “hook”. In fact, it closed Friday minutely crossing over to positive. The setup tells me that the coming week (maybe two) will be extremely telling of the future direction and do so in a huge way. “They” (the cabal) must either slam the metals complex here and now to abort the chart patterns, or suffer the consequence of a full on (and more importantly GLOBAL) “bank run” out of dollars/US Treasuries and into gold/silver/miners. $30+ silver looks like it could be only a day or a few days away. This will green light a very quick move to the $50 level where another battle will be fought …unless of course if a failure to deliver occurs, then all bets are off and the sky (floor for fiats) is the limit. I have been on the record for years that the entire fiat experiment would end in a failure to deliver physical metal. We may see this in very short order!

Lastly we have the beaten up HUI index. Same as silver, no longer overbought and the MACD infinitesimally crossed over higher on Friday. A picture perfect set up if you ask me, not severely overbought and within spitting distance of a breakout!

In conclusion, it looks like this week could be super exciting for those who have held “real money” for so many arduous years. Please remember, gold and silver do not “go up or down”, they are merely a mirror image of fiat. The real way to say the above is, this may be the week where the collapse of fiat is seen in its full nakedness! Though there are some who buy gold and silver because they believe they will “go up”, the REALLY BIG money buys metal to get out of fiat and the system as a whole. A bank run away from the system if you will? Whether or not they can find and kill Bin Laden for a 9th time remains to be seen, but they had better pull some sort of rabbit out of the hat immediately. Otherwise, we will see gold, silver, and the miners breaking out to new ground and the train fully pulled out of the station within a week or two.

There is no bull market like a gold bull market the saying goes. This is because “fear is a far greater emotion than greed”. A stampede into the metals will ultimately create a failure to deliver. When you tell a human that something is not available at any price, they only want it that much more! You are watching the canary in the coal mine, how much life is left in the empire? Stay tuned!

SHANGHAI CLOSED DOWN 6,53 PTS OR 0.21% //Hang Seng CLOSED UP 131.38PTS OR 0.80%// Nikkei CLOSED DOWN 49.63 OR 0.13%//Australia’s all ordinaries CLOSED DOWN 0.04%///Chinese yuan (ONSHORE) closed DOWN TO 7,2325 CHINESE YUAN OFF SHORE CLOSED DOWN TO 7.2398/ Oil DOWN TO 78,94 dollars per barrel for WTI and BRENT DOWN AT 83.33 /Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGSMONDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2326

OFFSHORE YUAN: DOWN TO 7.2398

SHANGHAI CLOSED DOWN 6.53 PTS OR 0.21 %

HANG SENG CLOSED UP 131.31 PTS OR 0.80%

2. Nikkei closed DOWN 49.65 PTS OR 0.12 %

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX UP TO 105.13 EURO FALLS TO 1.0789 UP 23 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +.941 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 156.22 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.512/Italian 10 Yr bond yield UP to 3.819 SPAIN 10 YR BOND YIELD UP TO 3.297%

3i Greek 10 year bond yield DOWN TO 3.321

3j Gold at $2355.00//Silver at: 28.20 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 90 100 roubles/dollar; ROUBLE AT 91.35

3m oil into the 79 dollar handle for WTI and 83 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 156.22/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.941% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9080 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9798 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.473 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.613 DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.851 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.20…(TURKEY)

10 YR UK BOND YIELD: 4.2090 UP 6 PTS

2a New York OPENING REPORT

Futures Gain With All Time Highs In Sight As Key CPI Report Looms

MONDAY, MAY 13, 2024 – 08:03 AM

US equity futures extended last week’s solid gains when they traded just about 1% below all time highs, as investors awaited key CPI later this week that will shape the Fed’s actions in coming months. As of 7:30am, contracts on the S&P 500 rose about 0.2% (but still below Friday’s highs), after the index posted a third straight week of gains; meanwhile contracts on the Nasdaq 100 climbed 0.3% even though Alphabet dropped 2% in premarket trading after Bloomberg reported that Apple is closing in on an agreement to use OpenAI’s technology on the iPhone. Treasury yields dipped and the dollar was steady. In addition to the week’s inflation data(both PPI and CPI) a handful of Fed speeches will also be in focus this week, including Cleveland Fed President Loretta Mester and Fed vice chair Philip Jefferson, who speak later in the day.

In premarket trading, Alphabet shares fall 2% as Apple is said to be closing in on an agreement to use OpenAI’s technology on the iPhone. Amusingly, GameStop shares soared and on track for the best month since March 2021 after the first (rather cryptic) tweet by Roaring Kitty after 3 years of silence on the platform, has sparked yet another massive short squeeze in the otherwise worthless company, and is allowing Keith Gil to dump stock at a huge gain.

Here are some other notable premarket movers:

AC Immune shares jump 53% after Takeda signs a worldwide option and license agreement for the biotech’s active immunotherapies targeting amyloid beta, including ACI-24.060 for the treatment of Alzheimer’s disease.

Cisco Systems shares tick 0.5% higher after losing its only negative analyst rating as BNP Paribas Exane upgrades to neutral from underperform, with limited downside now seen to consensus estimates for the networking equipment maker.

Incyte climbs 5.5% after announcing that its board approved a share repurchase authorization of $2 billion.

Intel rises 1.2% after the Wall Street Journal reports that the chipmaker is in advanced talks for a deal in which Apollo Global Management would provide more than $11 billion to help the company build a plant in Ireland, citing people familiar with the matter.

Penn Entertainment (PENN) drops 2.9% after BofA downgrades the casino and gaming company to neutral following what it describes as disappointing results.

Squarespace (SQSP) rises 13% after entering into a definitive agreement to go private with Permira in an all-cash transaction valued at approximately $6.9 billion.

Tencent Music Entertainment’s US-listed shares are up 3.5% after the online music platform reported first-quarter results that beat expectations.

Ahead of Wednesday’s all-important CPI report, all eyes will be on US producer prices due Tuesday. Data last week pointed to an economy that is slowing amid stubborn inflation, posing a challenge to the outlook for Fed policy.

“We need a catalyst to break the range on rates or change our view on risky assets,” said Mohit Kumar, Jefferies Europe chief economist. “US CPI data this week could be a potential catalyst. Even though US data has started to show some signs of moderating, inflation remains sticky, creating fears of stagflation.”

In Europe, the Stoxx Europe 600 index was little changed after posting its best weekly return since January (as we previewed just days prior) amid optimism the ECB is poised to ease policy as soon as next month. The autos and health care sectors led gains, while construction and utilities stocks were the biggest laggards. Among individual European movers, AP Moller-Maersk A/S jumped as much as 10% in Copenhagen after analysts at Citigroup Global Markets lifted their earnings estimates on the stock to reflect a recent rise in freight rates. Shell Plc rose to a record in London. Here are the most notable movers:

Maersk shares jump as much as 10% to touch a three-month high, as the shipping stock catches up after Danish markets were closed for holidays on Thursday and Friday last week. Analysts at Citi lifted their earnings estimates on the stock to reflect the recent rise in freight rates.

OX2 shares gain as much as 44% as private equity firm EQT is offering 16.4 billion kronor ($1.5 billion) for the wind park developer.

Gulf Keystone shares jump as much as 15% after the oil and gas producer operating in the Kurdistan region of Iraq demonstrated it can be profitable and generate cash from selling its output locally, according to analysts, with a key export pipeline still closed. This is reflected by the $10m share buyback announced this morning.

Diploma shares rise as much as 11% to touch a record high, the biggest gainer on the FTSE 100 index on Monday. The construction components firm reported solid results and upped its revenue and margin forecasts for the full year, while analysts noted a strong tailwind from M&A.

Nobia gains as much as 9%, the most in a month, after Nordea reinstated its coverage of the Swedish kitchen-interiors firm with a buy rating, expecting a recovery in construction market and consumer confidence to be a boon for the company.

NKT gains as much as 9% after Nordea “firmly” reiterated its buy rating for the Copenhagen-listed power-cable manufacturer, predicting that the continued electrification of society will be a huge boon for the firm in the coming years.

Almirall rises as much as 8.7% as the skin-health focused pharmaceuticals company delivers sales ahead of expectations. The beat was led by the performance of its Ilumetri psoriasis product. Meanwhile, guidance for the full year has been maintained.

Ceconomy rises as much as 6.2% after the German retailer of consumer electronics gave a better-than-expected profit forecast for the year. Baader Bank and Oddo point to Western/Southern Europe segment as a main driver.

Victrex shares drop as much as 5.6% after the polymer maker reported a 92% drop in pretax profit for the first half of the year due to high inventory levels and destocking among medical device customers. The firm has “a lot of work” to do in the second half of the year, according to Jefferies, which expects double-digit downgrades to 2024 consensus estimates.

BAE Systems shares in London fall as much as 2.9% after closing at a record high on Friday. The UK defense company was downgraded to neutral by analysts at BofA Securities, who see limited upside following the stock’s recent re-rating. That comes amid broader pressure on the European defense sector this morning.

The euro-area economy will expand more quickly than previously thought this year as the bloc’s biggest member, Germany, exits more than a year of near-stagnation, a Bloomberg poll of analysts showed. The results capture the improving mood in the region, with first-quarter GDP readings surprising to the upside and inflation is receding toward 2%.

Earlier in the session, Asian stocks were mixed with Chinese technology companies gaining ahead of earnings and the release of eco data this week. Hong Kong’s equity benchmark climbed to the highest since August, and mainland China equities also rose. But shares in South Korea, Japan and Australia fell. The MSCI Asia Pacific Index climbed as much as 0.3%, reversing earlier losses of as much as 0.2%, after reports that China is planning to issue ultra-long bonds to support its economy. TSMC, Alibaba Group and Tencent Holdings were the biggest contributors to the gauge’s gains. Mainland Chinese shares pared declines after initially falling amid concerns over an escalation of US tariffs and weak local credit data. Benchmarks in Hong Kong gained, with a gauge of technology stocks listed in the financial hub headed for its highest close since November. Taiwan shares also rose, while indexes in Japan fell.

News of the China’s plan to sell ultra-long special bonds boosted sentiment after weak data from the country published over the weekend had led to initial Asian stock losses. The specter of further US-China trade tensions also weighed on equities with a report on how much President Biden is set to increase tariffs on Chinese electric vehicles.

“You are looking at a slightly muddied growth outlook” for China, Sonal Desai, chief investment officer at Franklin Templeton, said in an interview on Bloomberg Television. Regardless of who gets elected in the US presidential election in November, we are going to see an escalation of US-China trade tensions, he said.

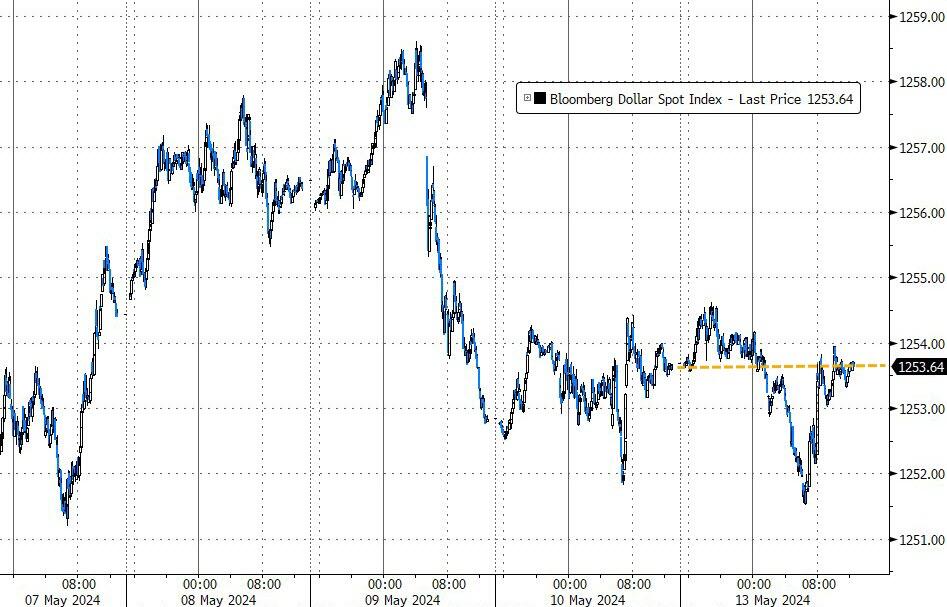

In FX, the Bloomberg Dollar Spot Index edged 0.1% lower. “After the dovish FOMC meeting and the soft April NFP sucked the momentum from the dollar’s upside, the question is whether price data can actively contribute to the dollar’s downside,” FX strategists at ING write in a note, adding that a softer PPI reading could point to a lower core PCE deflator figure, the Fed’s preferred inflation reading, due on May 31. This week’s data follows a US labour report earlier in the month which showed a slowdown in jobs growth and raised speculation that the Fed may start cutting the rate in the coming months

Traders are betting on a 73% possibility that the Fed will start cutting rates in September, little changed from late last week; roughly 40 basis points of cuts are priced in through the end of the year

In rates, treasuries are slightly richer across the curve, following similar gains for bunds and gilts during European morning. US yields richer by 1bp to 2bp across the curve with 10-year around 4.48%, about 1.5bp lower than Friday’s close, slightly underperforming bunds and gilts in the sector. Curve spreads are steeper by less than 1bp. Wednesday’s April CPI report is poised to provide the biggest test yet of the bond rally that started this month, when Jerome Powell swatted away worries that the Fed may raise interest rates; PPI data on Tuesday will also be in focus. Trading ranges narrow ahead of critical PPI and CPI reports Tuesday and Wednesday. A busy corporate new-issue slate is expected, with a weekly total of about $30 billion anticipated. The next scheduled Treasury auction is 20-year bond sale on May 22

In commodities, oil gained on optimism China’s bond plan may boost growth, and traders assessed the willingness of OPEC+ to agree to extend supply curbs at its upcoming policy meeting. Iron ore and copper extended gains

It has been a strong session for Bitcoin, climbing back up over 63k, while Ethereum is looking to reclaim USD 3k.

Looking at today’s calendar, the US economic data slate includes April New York Fed 1-year inflation expectations at 11am; retail sales and industrial production are also ahead this week. Fed officials’ scheduled speeches include Mester and Jefferson at 9am; Cook, Powell, Kashkari, Bowman, Barr, Harker, Bostic, Waller, Daly and Kugler appear later in the week

Market Snapshot

S&P 500 futures little changed at 5,251.00

STOXX Europe 600 little changed at 520.98

MXAP up 0.3% to 178.02

MXAPJ up 0.5% to 556.98

Nikkei down 0.1% to 38,179.46

Topix down 0.2% to 2,724.08

Hang Seng Index up 0.8% to 19,115.06

Shanghai Composite down 0.2% to 3,148.02

Sensex little changed at 72,722.04

Australia S&P/ASX 200 little changed at 7,750.03

Kospi little changed at 2,727.21

German 10Y yield little changed at 2.51%

Euro little changed at $1.0777

Brent Futures up 0.3% to $83.04/bbl

Gold spot down 0.7% to $2,343.69

US Dollar Index little changed at 105.30

Top Overnight News

China’s CPI rose for a third straight month in April, increasing at a pace of 0.3% compared with a year earlier, according to official data released Saturday, edging up from March’s 0.1% reading and surpassing the 0.2% growth expected by economists. Meanwhile, the PPI fell 2.5% in April from a year earlier for a 19th consecutive month of declines. WSJ

China’s credit in April shrank for the first time as government bond sales slowed, while loan expansion was worse than expected in a sign of weak demand. Aggregate financing, a broad measure of credit, decreased by almost 200 billion yuan ($27.7 billion) in April from the previous month, according to Bloomberg calculations of data released by the PBOC. That’s the first time the measure has declined since comparable data began in 2017, reflecting a contraction in financing activity. BBG

Chinese authorities have kicked off plans to sell Rmb1tn ($140bn) of long-dated bonds, as Beijing raises spending to stimulate the economy. FT

In the past three days, Russian troops, backed by fighter jets, artillery and lethal drones, have poured across Ukraine’s northeastern border and seized at least nine villages and settlements, ¬and more square miles per day than at almost any other point in the war, save the very beginning. In some places, Ukrainian troops are retreating, and Ukrainian commanders are blaming each other for the defeats. NYT

Iraq’s oil minister on Sat said the country won’t agree to any additional voluntary oil production cuts, although he expressed support for the overall OPEC+ alliance in more conciliatory comments on Sunday. RTRS

Stubbornly sticky rent is preventing the Fed from winning the “last mile” portion of its war on inflation and commencing policy easing. WSJ

Biden’s campaign considers Haley voters as a core part of its coalition in Nov, and has been heartened by the fact she continues to perform so well in GOP primaries despite being out of the race for weeks (Trump meanwhile has made little effort to court Haley or her supporters). Politico

McDonald’s is looking to launch a $5 meal plan in the US, a sign the company is becoming more aggressive on price to recapture market/mindshare as consumers dial back spending. BBG

Apple has closed in on an agreement with OpenAI to use the startup’s technology on the iPhone, part of a broader push to bring artificial intelligence features to its devices, according to people familiar with the matter. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly cautious after mixed inflation and soft financing data from China over the weekend, although Chinese markets found some solace from China’s plans to issue ultra-long treasury bonds. ASX 200 was led lower by underperformance in the energy sector and amid a tepid NAB Business survey. Nikkei 225 lacked firm direction with price action choppy amid a slew of earnings releases. Hang Seng & Shanghai Comp were initially pressured after mixed inflation data and disappointing financing data which showed a rare contraction in Aggregate Financing, while expectations of increased US tariffs on Chinese EVs also provided early headwinds. However, the Hong Kong benchmark then recovered and climbed above the 19,000 level amid tech strength, while the mainland pared the majority of its losses as the attention turned to China’s plans to issue ultra-long treasury bonds on May 17th.

Top Asian News

Chinese authorities kicked off plans to sell USD 140bln of long-dated bonds, according to the FT. It was later reported that China’s Finance Ministry is to issue ultra-long treasury bonds on May 17th in which it plans to issue 20yr, 30-year and 50-year treasuries worth CNY 300bln, CNY 600bln and CNY 100bln, respectively, while it plans to complete the issuance of long-term treasury bonds by end-November.

Country Garden (2007 HK) said it repaid onshore coupons within the grace period, according to Reuters.

BoJ offered to buy JPY 375bln in 1-3yr JGBs, JPY 425bln in 5-10yr JGBs and JPY 150bln in 10-25yr JGBs (reduced 5yr-10yr purchases from a previous JPY 475bln).

Australia’s government cut its 2024/2025 real GDP growth forecast to 2% from 2.25% and cut its 2025/2026 growth forecast to 2.25% from 2.50%, while it said inflation could slow to the RBA’s 2%-3% target range by year-end which is sooner than previously expected, according to Reuters.

Tencent Music Entertainment Group (TME) Q1 2024 (USD): EPS 0.13 (exp. 0.14), Revenue 0.94bln (exp. .91bln).

European bourses, Stoxx600 (U/C) are mixed and trading on either side of the unchanged mark, in what has been a very quiet European morning. European sectors are mixed; Autos tops the pile, with optimism potentially deriving from Chinese CPI as well as new long-dated bond sales, which will help to provide liquidity for the Chinese markets. US Equity Futures (ES +0.1%, NQ +0.1%, RTY +0.3%) are very modestly in the green, following the tentative price action also seen in Europe.

Top European News

UK PM Sunak is set to declare the UK stands ‘at a crossroads’ as he readies the Tories ahead of an election, according to FT.

Socialists were ahead in the Catalan regional election with 41 seats out of the 135-seat chamber and separatists Junts were second with 36 seats after 91% of votes were counted, according to Reuters.

S&P affirmed Poland at A-; Outlook Stable.

FX

Dollar is modestly softer, having spent much of the European morning flat, with recent EUR strength pushing the index lower, albeit marginally so. Currently, the DXY is towards the bottom end of today’s 105.36-20 range.

EUR is incrementally firmer vs the USD, catching a slight bid in recent trade though with specifics light. Currently holding around its 50DMA at 1.0786.

GBP is flat vs USD, with very modest early morning weakness petering out. Focus this week will be March’s job data, as well as potential commentary from BoE Chief Economist Pill.

USD/JPY is incrementally firmer, having wobbled very briefly after the BoJ said it reduced its purchases of 5yr-10yr JGBs. The announcement led USD/JPY to as low as 155.57, before quickly paring the move. As it stands, the pair holds above its 20DMA, with the high for today at 155.95.

Mixed trade for the Antipodeans, initially softened by the cautious risk tone in APAC trade and after the PBoC set a weaker reference rate setting. Weakness in the Kiwi, after inflation expectations, has led NZD/USD as low as 0.60.

PBoC set USD/CNY mid-point at 7.1030 vs exp. 7.2284 (prev. 7.1011).

Fixed Income

USTs are a touch firmer but near unchanged overall as the benchmark takes a slight breather from Friday’s marked bearish action but remain within a couple of ticks of the 108-21+ trough from Friday with last week’s 108-19+ base below.

Bund price action has been very contained and largely directionless. Drivers thus far have been exceptionally limited and the European docket ahead is very light.

Gilts in-fitting with the UK docket thin today with the narrative much the same as for EGBs above. Gilts themselves in a thin 20 tick range after a very contained open. Currently around the 97.75 mark above the 97.66 low.

Commodities

Crude benchmarks are on the front-foot, however action is modest and we remain within around a USD 1/bbl of Friday’s base. Focus today has been on commentary from the Iraqi Oil Minister and awaiting updates out of Rafah. Brent July current holding at USD 83/bbl.

Precious metals are slipping a touch but with the action more of a gentle decline than a pronounced fall thus far. Specifics light and impetus from broader assets limited as overall market action is fairly contained; XAU near session lows around USD 2,240.

Base metals largely followed the fortunes of China overnight with initial action bearish on the overall soft tone and weak financing data from the region.

Iraqi Oil Minister said on Saturday that Iraq has made enough voluntary production cuts and will not agree to any future reduction taken by OPEC. However, it was reported on Sunday that the Oil Minister said the voluntary oil output cut is subject to agreement between OPEC countries and any negotiable proposals may be presented at the time, while he added they are part of OPEC and it is necessary to comply with any decisions made by the organisation. The state news agency also reported the Oil Minister said Iraq is committed to voluntary output cuts made by OPEC members and is keen on cooperating with members to achieve more stability in global oil markets.

Iraqi Oil Ministry launched 29 oil and gas projects within the fifth and sixth licensing rounds.

Qatar set June marine crude OSP at Oman/Dubai plus USD 1.75/bbl and land crude OSP was set at Oman/Dubai plus USD 0.85/bbl, according to a pricing document.

QatarEnergy is to acquire two new exploration blocks offshore Egypt in which it signed a farm-in agreement with ExxonMobil (XOM) to acquire a 40% participating interest in the exploration blocks.

Russian Deputy PM Novak said Russia will be able to increase fuel output in the future, according to TASS.

Geopolitics: Middle East

Israel’s IDF said it ordered residents of additional east Rafah areas to evacuate and head to the humanitarian zone in Al-Mawasi, according to Reuters.

Israeli military spokesperson said Hamas has been trying to re-establish military capabilities in Gaza’s Jabalia and Israel is trying to prevent that, while it announced that Israeli forces in Gaza’s Zeitun killed 30 Palestinian militants. It was separately reported that Israel’s military opened a new crossing into the Gaza Strip in coordination with the US government for humanitarian aid, according to Reuters.

US State Department said Secretary of State Blinken stressed to Israeli Defence Minister Gallant the urgent need to protect civilians and aid workers in Gaza and urged to ensure humanitarian access to Gaza, while Blinken reaffirmed to Gallant US opposition to a major ground military operation in Rafah, according to Al Jazeera and Sky News Arabia.

Geopolitics: Other

Ukrainian President Zelensky said battles are ongoing at seven border villages in Kharkiv and the Donetsk situation is particularly tense, while Ukraine’s military chief said fighting is ongoing and warned of a difficult situation in the Kharkiv region, according to Reuters.

Ukrainian shelling killed at least 9 people and injured more than a dozen in an apartment block collapse in Russia’s Belgorod, according to Reuters.

Russian President Putin conducted a surprise reshuffle of top security officials whereby he removed Patrushev as head of the Security Council who will be moved to a new job and proposed that Defence Minister Shoigu become the new head of the Security Council, while he proposed economic adviser Belousov to become the new Defence Minister, according to FT.

Russian Defence Ministry said its forces have taken five settlements in Ukraine’s Kharkiv region.

Ukrainian drone attack has damaged an oil depot/power substation in Belgorod and Lipestk regions of Russia, via Reuters citing Ukrainian intelligence.

US Event Calendar

11:00: April NY Fed 1-Yr Inflation exp; prior 3.00%

Central Bank Speakers

09:00: Fed’s Mester, Jefferson Discuss Central Bank Communications

DB’s Jim Reid concludes the overnight wrap

After perusing my social media accounts, I think I’m the only person on the planet who couldn’t find the aurora borealis this weekend. All I have to show for my efforts are a few black sky pictures on my iPhone. I had more success in finding a decent song at Eurovision which is saying something.

The main thing that will light up the skies for markets this week will be US inflation data with April’s PPI (Tuesday) and CPI (Wednesday) the highlights. We’ll see if the higher-than-expected US inflation seen in Q1 extends into Q2 or not. Markets will also hear from Powell (tomorrow) and Vice Chair Jefferson (today) as the highlights of a busy Fedspeak calendar that are included in the day-by-day list at the end. The next most important US data release is Retail Sales on Wednesday.

Elsewhere China’s monthly activity numbers (Friday) are important, and staying in Asia, we also have Japanese PPI (tomorrow) and Q1 GDP (Thursday). In Europe tomorrow’s ZEW survey in Germany and UK labour market stats are highlights. Swedish CPI (Wednesday) may get a little extra attention after last week’s Riksbank cut, only the second G10 currency to ease this cycle after Switzerland earlier in the year. Earnings season quietens with only 7 S&P 500 companies and 69 Stoxx 600 companies reporting.

Previewing the main events now and let’s start chronologically with regards to US inflation. For PPI tomorrow, the headline (+0.4% DB forecast, +0.3% consensus, vs. +0.2% previously) and core (+0.3% DB, +0.2% consensus vs. +0.2% last month) are always less important than the key components that feed into the core PCE deflator – namely, health care services, portfolio management and domestic airfares. As our economists point out, whilst the March health care services print was relatively soft (+0.1%), the six-month annualised growth rate of 3.5% was still higher than at any point in the decade prior to the pandemic. They also highlight that with respect to portfolio management, the strength in asset market performance leading up to March should result in a strong print for April, given the typical lags.

With regards to CPI, our economists previewed it in full here (see “April CPI preview & webinar registration”), and think that given the 3% rise in seasonally adjusted gas prices, headline CPI (+0.37% forecast vs. +0.38% previously) should grow faster than core (+0.29% vs. +0.36%). This would lead to core YoY CPI falling two-tenths to 3.6%, and headline falling a tenth to 3.4%, both in-line with consensus. The three-month annualised rate under this scenario would fall by four-tenths to 4.1%, but the six-month annualised rate would tick up a tenth to 4.0%. As ever all eyes will be on whether rents finally respond more in keeping to the numerous models that have suggested they should already be well below where they currently are.

For Wednesday’s US Retail Sales, DB’s headline (+0.5% vs. +0.7% previously), ex-autos (+0.4% vs. +1.1%) and retail control (+0.3% vs. +1.1%) forecasts suggest some payback from a strong March release. There will be a few extra eyes on initial jobless claims this week given the spike to +231k last week after months of relative stability around the +210k level. Our economists think the spike could have been mostly due to NY school holiday dates having been shifted and would therefore expect much of the spike to reverse. We also have US housing starts and permits on Thursday which include a 2019-2024 seasonal revision which could be of note.

Various regional factory surveys are out which will help fine tune PMI forecasts. Over the weekend Chinese consumer inflation edged higher but producer prices stayed very weak. CPI came in at +0.3% YoY in April from +0.1% YoY in March and a tenth above expectations. PPI however fell -2.5% (-2.3% expected and -2.8% in March). So, deflation still remains intense in manufacturing sectors. Mainland Chinese stocks are lower with the CSI (-0.11%) and the Shanghai Composite (-0.09%) both trading slightly lower on prospects of more US trade tariffs on China across various industries with electric vehicles expected to be a particular target according to Bloomberg.

Elsewhere the KOSPI (-0.28%) and Nikkei (-0.20%) are also edging lower in early trade. Meanwhile, the Hang Seng (+0.38%) is bucking the regional negative trend. S&P 500 (+0.04%) and NASDAQ 100 (+0.07%) futures are trading just above flat with USTs fairly stable as I type.