MAY 16/BLOG//GOLD CLOSED DOWN $7.90 TO $2381.00/SILVER CLOSED UP 14 CENTS TO $23.65//PLATINUM CLOSED DOWN $0.70/WHILE PALLADIUM CLOSED DOWN $18.85 TO $991.25//

363 H WELLS FARGO SEC 19 435 H SCOTIA CAPITAL 11 624 H BOFA SECURITIES 8 726 C PLUS500US FINAN 1 737 C ADVANTAGE 1

TOTAL: 20 20 MONTH TO DATE: 1,956

JPMorgan stopped 0/20

FOR MAY2024

GOLD: NUMBER OF NOTICES FILED FOR MAY/2024. CONTRACT: 20 NOTICES FOR 2000 OZ or 0.0622 TONNES

total notices so far: 1956 contracts for 195600 Oz (6.0835 tonnes)

FOR MAY:

SILVER NOTICES: 18 NOTICE(S) FILED FOR 90,000 OZ/

total number of notices filed so far this month : 5759 for 28.795 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $7.90

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD

/ /INVENTORY RESTS AT 833.36TONNES

INVENTORY RESTS AT 833.36 TONNES

SLV//

WITH NO SILVER AROUND AND

SILVER UP $0.14 AT THE SLV//

NO CHANGES IN SILVER INVENTORY AT THE SLV:

// INVENTORY REMAIN CONSTANT AT 420.308 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 420.308 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY MEGA MEGA HUMONGOUS SIZED 4038 CONTRACTS TO 175,409 AND CONTINUING TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR GAIN OF $1.01 IN SILVER PRICING AT THE COMEX ON WEDNESDAY. WE HAD ZERO LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN SHORT COVERING BY OUR SPECS WITH THE GAIN IN PRICE. WE HAD ANOTHER HUGE SIZED 1115 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 1115 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND ALL OF THESE TRADES.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $1.01 AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE HAD AN ULTRA HUMONGOUS SIZED GAIN OF 9393 CONTRACTS ON OUR TWO EXCHANGES WITH THE GAIN IN PRICE OF $1.01. THIS IS THE HIGHEST GAIN IN OUR 2 CONTRACTS IN MANY YEARS

WE MUST HAVE HAD:

A HUGE SIZED 5365 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 28.130MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 135,000 OZ

//NEW STANDING FOR SILVER//MAY IS THUS 29.750 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI GAIN //HUGE SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1115 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED 1327 214CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY

TOTAL CONTRACTS for 12 DAYS, total 12,974 contracts: OR 64.870 MILLION OZ (1081 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 64.870 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770MILLION OZ (THIS MONTH WILL PROBABLY BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 64.870 MILLION OZ

RESULT: WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4038 CONTRACTS WITH OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 5355 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAY OF 29.345 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 135,000 OZ QUEUE JUMP

//NEW TOTAL STANDING AT 29.750 MILLION OZ

WE HAVE A HUMONGOUS SIZED GAIN OF 9393 OI CONTRACTS ON THE TWO EXCHANGES WITH THE GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 1115 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (1115 WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 18 NOTICE(S) FILED TODAY FOR 90,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 9323 OI CONTRACTS TO 532,275 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED 2058 CONTRACTS

WE HAD A STRONG SIZED INCREASE IN COMEX OI (9323 CONTRACTS) OCCURRED WITH OUR HUGE GAIN $34.90 IN PRICE/WEDNESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER TRYING TO CONTAIN GOLD’S PRICE RISE. THE GAIN IN COMEX OI WAS DUE TO SPREADER (T.A.S) LIQUIDATION. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 4.684 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY;S 1800 OZ QUEUE JUMP//NEW STANDING INCREASES TO 6.112 TONNES

NEW STANDING 6.112 TONNES// ALL OF THIS HAPPENED WITH OUR $34.90 GAIN IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A STRONG SIZED GAIN OF 9972 OI CONTRACTS (31.04 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 649 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 532,275

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 9972 CONTRACTS WITH 9323 CONTRACTS INCREASED AT THE COMEX// AND A SMALL SIZED 649 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 9972 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED 7911 CONTRACTS,,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A SMALL SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (649 CONTRACTS) ACCOMPANYING THE STRONG GAIN IN COMEX OI 9323/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 9972 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 4.684 TONNES FOLLOWED BY TODAY;S 1800 OZ QUEUE JUMP

//NEW STANDING /MAY 6.112 TONNES.

/ 3) MASSIVE LONG-SHORT LIQUIDATION MOSTLY DUE TO SPREADERS WITH THE HUGE GAIN IN PRICE.

// 4) STRONG SIZED COMEX OPEN INTEREST GAIN 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///STRONG T.A.S. ISSUANCE: 7199 CONTRACTS/ HUGE SHORT COVERING BY OUR WRONG FOOTED SPECS WITH THE FED’S CONTINUAL FRUITLESS RAID ON THE COMEX GOLD.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY. :

TOTAL EFP CONTRACTS ISSUED: 46,792 CONTRACTS OR 4,679,200 OZ OR 145.54 TONNES IN 12 TRADING DAY(S) AND THUS AVERAGING: 3899 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES 145.54 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2022, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 145.54 DIVIDED BY 3550 x 100% TONNES = 4.08% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 145.54 TONNES (WILL BE ANOTHER STRONG MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUMONGOUS SIZED 4038 CONTRACTS OI TO 175,409 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 5355 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 5355 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 5355 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 5365 CONTRACTS AND ADD TO THE 5355 E.FP. ISSUED

WE OBTAIN AN ULTRA HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 9972 CONTRACTS

THUS IN OUNCES, THE HUGE GAIN ON THE TWO EXCHANGES TOTALS 46.97 MILLION OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED UP 2.50 PTS OR 0.08% //Hang Seng CLOSED UP 302.82 PTS OR 1.09%// Nikkei CLOSED UP 534.53 OR 1.39%//Australia’s all ordinaries CLOSED UP 1.51%///Chinese yuan (ONSHORE) closed UP TO 7,2170 CHINESE YUAN OFF SHORE CLOSED UP TO 7.2179/ Oil DOWN TO 78,32 dollars per barrel for WTI and BRENT DOWN AT 82.60 /Stocks in Europe OPENED MOSTLY RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 9323 CONTRACTS TO 532,275 WITH OUR HUGE GAIN IN PRICE OF $34.90 WITH RESPECT TO WEDNESDAY TRADING. WE HAD A HUMONGOUS T.A.S. LIQUIDATION YESTERDAY AS WELL AS SHORTS, DESPERATELY TRYING TO GET OUT OF THEIR NAKED SHORTS.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAY.… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A SMALL SIZED 649 EFP CONTRACTS WERE ISSUED: : JUNE649 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE:649 CONTRACTS

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 9972 CONTRACTS IN THAT 649 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG SIZED GAIN OF 9323 COMEX CONTRACTS..AND THIS STRONG GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR HUGE GAIN IN PRICE OF $34.90 WEDNESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT WAS A HUGE SIZED 7199 CONTRACTS. WE HAD 0 EX FOR RISK ISSUANCE. MOST OF THE TRADING AND SUPPLY OF CONTRACTS ON TUESDAY WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (6.112 TONNES) ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 6.112 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A HUGE $34.90 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG GAIN OF 7914 CONTRACTS ON OUR TWO EXCHANGES.

WE HAD ANOTHER HUGE T.A.S. LIQUIDATION ON THE FRONT END OF WEDNESDAY’S TRADING. THE T.A.S. ISSUED ON WEDNESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS AND MOST LIKELY ON TUESDAY TRADING.

WE HAVE GAINED A TOTAL OI OF 31.02 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY (4.684 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 18 CONTRACTS OR 200 OZ ( .0599 TONNES)

NEW STANDING: 6.112 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $34.90

WE HAVE ADDED 2058 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET GAIN ON THE TWO EXCHANGES 9972 CONTRACTS OR 997,200 (31.02 TONNES)

confirmed volume WEDNESDAY 284,298 contracts// fair to good

Total monthly oz gold served (contracts) so far this month

1956 notices 195600 oz 6.0835 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: 0 oz

we have 0 customer deposits:

total deposit nil oz

total customer withdrawals: 0

TOTAL WITHDRAWALS NIL 0z

Adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY

For the front month of MAY we have an oi of 45 contracts having GAINED 16 contracts.

We had 2 contracts served on WEDNESDAY, so we gained 18 contracts or 1800 oz (0.0559 Tonnes).

JUNE INCREASED ITS OI BY 2523 CONTRACTS UP TO 254,070 CONTRACTS.

JULY GAINED 51 CONTRACTS TO STAND AT 268

We had 20 contracts filed for today representing 2000 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 20 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the MAY /2024. contract month, we take the total number of notices filed so far for the month (1956) x 100 oz ) to which we add the difference between the open interest for the front month of MAY ( 45 CONTRACTS) minus the number of notices served upon today (20 x 100 oz per contract( equals 196,500 OZ OR 6.112TONNES.

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (1956x 100 oz + (45 OI for the front month} minus the number of notices served upon today (20 x 100 oz which equals 196500 oz (6.112 TONNES)

TOTAL COMEX GOLD STANDING FOR MAY: 6.112 TONNES WHICH IS HUGE FOR THIS A NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,459,628.558 OZ

TOTAL REGISTERED GOLD 7,328,073,702 ( 227.93 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,131,554.628.178 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 5,761,749 oz (REG GOLD- PLEDGED GOLD)= 177.28 tonnes

179.36 tonnes/dropping like a stone

END

SILVER/COMEX

MAY 16

INITIAL

//2024// THE MAY 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

588,508.700 oz

JPMORGAN

.

Deposits to the Dealer Inventory

nil OZ

Deposits to the Customer Inventory

567,140.920 OZ JPMORGAN

No of oz served today (contracts)

18 CONTRACT(S) (90,000 OZ)

No of oz to be served (notices)

191 contracts (0.955 million oz)

Total monthly oz silver served (contracts)

5759 Contracts (28.795 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposit :nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

(i) into jpmorgan 567,140.920 oz

total customer deposit 567,140.920 oz

JPMorgan has a total silver weight: 129,598million oz/297.817 million or 43.48%

adjustment: 0

Comex withdrawals: 1

i) out of jpmorgan 588,508.750 oz

total withdrawal 588,508.750 oz

TOTAL REGISTERED SILVER: 65.149MILLION OZ//.TOTAL REG + ELIGIBLE. 297.817 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF MAY/2024 OI: 209 CONTRACTS HAVING GAINED 8 CONTRACT(S).

.

We had 11 notices served on WEDSDAY so we GAINED 19 contracts or 95,000 oz underwent a STRONG QUEUE JUMP AS THEY WERE SET TO TAKE DELIVERY ON THIS SIDE OF THE POND.

JUNE SAW A LOSS OF 11 CONTRACTS FALLING TO 1403

JULY SAW A GAIN OF 3773 CONTRACTS UP TO 142,579

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 18 for 90,000 oz

CONFIRMED volume; ON WEDNESDAY 125,473 mammoth

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 5759 x 5,000 oz = 28.795 MILLION oz

to which we add the difference between the open interest for the front month of MAY (209 and the number of notices served upon today 18x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2024 contract month: 5759 notices served so far) x 5000 oz + OI for the front month of MAY (209 number of notices served upon today minus (18x 5000 oz of silver standing for the may contract month equates to 29.750 MILLION OZ.

New total standing: 29.750 million oz.

There are 65.149 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

MAY 16 WITH GOLD DOWN $7.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//NEW TOTAL 833.36 TONNES

MAY 15 WITH GOLD UP $34.90 ON THE DAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD

///INVENTORY RISES TO 831.93 TONNES

MAY 14 WITH GOLD DOWN $17.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//

///INVENTORY RISES TO 831.33 TONNES

MAY 13 WITH GOLD DOWN $31.10 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD////INVENTORY RISES TO 831.93 TONNES

MAY 10 WITH GOLD UP $34.65 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 9 WITH GOLD UP $18.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 8 WITH GOLD DOWN $0.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 830.47 TONNES

MAY 7 WITH GOLD DOWN $6.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 832.19 TONNES

MAY 6WITH GOLD UP $21.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .55 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 831.64 TONNES

MAY 2 WITH GOLD UP $0.20 ON THE DAY; SMAKK CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 830.47 TONNES

MAY 1 WITH GOLD UP $7.80 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNES

APRIL 29WITH GOLD UP $10,55TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNES

APRIL 26WITH GOLD UP $5.40TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.54 TONNES FROM THE GLD /INVENTORY RISES AT 832.19 TONNES

APRIL 25WITH GOLD UP $5.05 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD /INVENTORY RISES AT 833,63 TONNES

APRIL 19 WITH GOLD UP $15.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 4.32 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 831.91 TONNES

APRIL 18 WITH GOLD UP $11.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE WITHDRAWAL OF 2.59 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 827.59 TONNES

APRIL 17 WITH GOLD DOWN $17.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 830;18 TONNES

APRIL 16 WITH GOLD UP $23.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 828.45 TONNES

APRIL 15 WITH GOLD DOWN $. 80 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A HUGE WITHDRAWAL OF 1.80 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 824.84 TONNES

APRIL 12 WITH GOLD UP $2.80 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD/ INVENTORY RISESS AT 830.75 TONN

GLD INVENTORY: 833.36 TONNES,

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 16 WITH SILVER UP 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY REMAINS AT 420.308 MILLION OZ

MAY 15 WITH SILVER UP 101 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A WITHDRAWAL OF 1.919 MILLION OZ FROM THE SLV

INVENTORY RESTS AT 420.308 MILLION OZ

MAY 14 WITH SILVER UP 25 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;

INVENTORY RESTS AT 422.227 MILLION OZ

MAY 13 WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;

INVENTORY RESTS AT 422.227 MILLION OZ

MAY 10 WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A HUGE WITHDRAWAL OF 1.,828 MILLION OZ//INVENTORY RESTS AT 422.227 MILLION OZ

MAY 9 WITH SILVER UP 78 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 8 WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 7WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 6 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.055 MILLION OZ

MAY 3 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 2WITH SILVER UP 0.12 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/ A WITHDRAWALOF 4.471 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 1 WITH SILVER UP 0.09 TODAY: SMALLCHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF ,457 MILLION OZ INTO THE SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 29WITH SILVER UP $0.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 26WITH SILVER DOWN 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.097 MILLION OF SILVER INTO THE SLV// :SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 25WITH SILVER UP $.05 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 1.534 MILLION OF SILVER OUT OF THE SLV// :SLV INVENTORY RESTS AT 428.717 MILLION OZ

APRIL 24/WITH SILVER DOWN $.05 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 11.904MILLION OF SILVER INTO THE SLV// :SLV INVENTORY RESTS AT 428.280 MILLION OZ

APRIL 23/WITH SILVER UP $0.11TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV / :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 22/WITH SILVER DOWN $1.51 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.194 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 19/WITH SILVER UP 42 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.657 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 418.570 MILLION OZ

APRIL 18/WITH SILVER DOWN $.04TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.977 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 422.227 MILLION OZ

APRIL 17/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF .868 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 426/204 MILLION OZ

APRIL 16/WITH SILVER DOWN $0.46 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF NON EXISTENT SILVER// :SLV INVENTORY RESTS AT 427.072 MILLION OZ

APRIL 15/WITH SILVER UP $0.88 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 12/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 4.069 MILLION OZ FROM THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 11/WITH SILVER UP $0.23 TODAY: STRANGE INDEED! HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.931 MILLION OZ :SLV INVENTORY RESTS AT 437.998 MILLION OZ

CLOSING INVENTORY 420.308 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

2.Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens/Alasdair Macleod//JAMES RICKARDS

I’ve previously said that gold could reach $15,000 by 2026. Today, I’m updating that forecast.

My latest forecast is that gold may actually exceed $27,000.

I don’t say that to get attention or to shock people. It’s not a guess; it’s the result of rigorous analysis.

Of course, there’s no guarantee it’ll happen. But this forecast is based on the best available tools and models that have proved accurate in many other contexts.

Here’s how I reached that price level forecast…

This analysis begins with a simple question: What’s the implied non-deflationary price of gold under a new gold standard?

No central banker in the world wants a gold standard. Why would they? Right now, they control the machinery of global currencies (also called fiat money).

They have no interest in a form of money they can’t control. It took about 60 years from 1914–1974 to drive gold out of the monetary system. No central banker wants to let it back in.

Still, what if they have no choice? What if confidence in command currencies collapses due to some combination of excessive money creation, competition from Bitcoin, extreme levels of dollar debt, a new financial crisis, war or natural disaster?

In that case, central bankers may return to gold not because they want to, but because they must in order to restore order to the global monetary system.

What’s the Proper Gold Price?

That scenario begs the question: What is the new dollar price of gold in a system in which dollars are freely exchangeable for gold at a fixed price?

If the dollar price is too high, investors will sell gold for dollars and spend freely. Central banks will have to increase the money supply to maintain equilibrium. That’s an inflationary result.

If the dollar price is too low, investors will line up to redeem dollars for gold and then hoard the gold. Central banks will have to reduce the money supply to maintain equilibrium. That reduces velocity and is deflationary.

Something like the latter case happened in the U.K. in 1925 when it returned to a gold standard at an unrealistically low price. The result was that the U.K. entered the Great Depression several years ahead of other developed economies.

Something like the former case happened in the U.S. in 1933, when FDR devalued the dollar against gold. Citizens weren’t allowed to own gold, so there was no mass redemption of gold. But other commodity prices rose sharply.

That was the point of the devaluation. Resulting inflation helped lift the U.S. out of deflation and gave the economy a boost from 1933–1936 in the midst of the Great Depression. (The Fed caused another severe recession in 1937–1938 with their customary incompetence.)

The policy goal obviously is to get the price “just right” by maintaining the proper equilibrium between gold and dollars. The U.S. is in an ideal position to do this by selling gold from U.S. Treasury reserves, about 8,100 metric tonnes (261.5 million troy ounces), or buying gold in the open market using freshly printed Fed money.

The goal would be to maintain the dollar price of gold in a narrow range around the fixed price.

What price is just right? This question is easy to answer, subject to a few assumptions.

$27,533 Gold

U.S. M1 money supply is $17.9 trillion. (I use M1, which is a good proxy for everyday money).

What is M1? This is the supply that is the most liquid and money that is the easiest to turn into cash.

It contains actual cash (bills and coins), bank reserves (what’s actually kept in the vaults) and demand deposits (money in your checking account that can be turned into cash easily).

One needs to make an assumption about the percentage of gold backing for the money supply needed to maintain confidence. I assume 40% coverage with gold. (This was the legal requirement for the Fed from 1913–1946. Later it was 25%, then zero today).

Applying the 40% ratio to the $17.9 trillion money supply means that $7.2 trillion of gold is required.

Applying the $7.2 trillion valuation to 261.5 million troy ounces yields a gold price of $27,533 per ounce.

That’s the implied non-deflationary equilibrium price of gold in a new global gold standard. Of course, money supplies fluctuate; lately they’ve been going up sharply, especially in the U.S.

There’s room for debate about whether a 40% backing ratio is too high or too low. Still, my assumptions are moderate based on monetary economics and history. A dollar price of gold of over $25,000 per ounce in a new gold standard is not a stretch.

Obviously, you get around $12,500 per ounce if you assume 20% coverage. There are many variables in play.

The Fundamental Model

This model is also straightforward. It relies on factors we learned about in our first week of Intro to Economics — supply and demand.

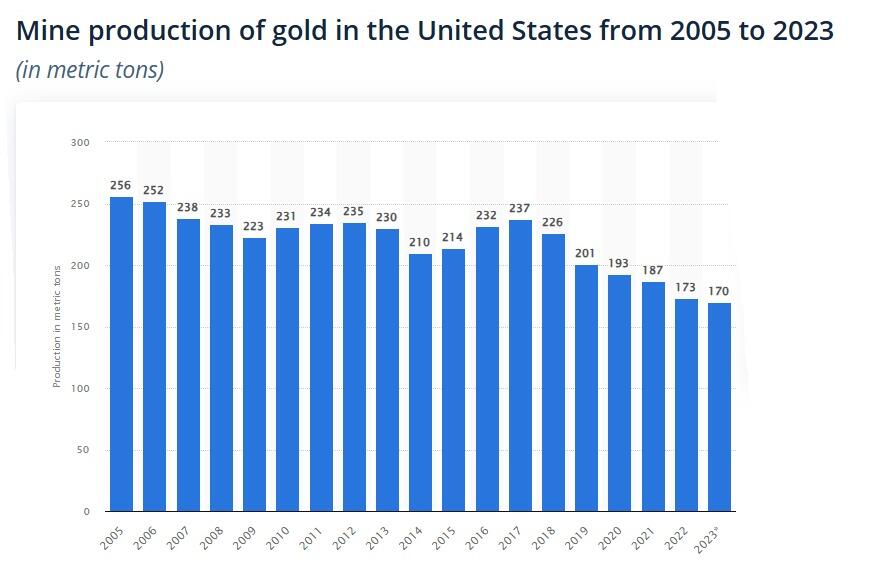

The most significant development on the supply side is the decrease of new mining output. As the chart shows below, mine production of gold in the U.S. has been decreasing steadily since 2017.

These figures reveal a 28% decrease over seven years, at the same time gold prices were rising and miners were motivated to expand output.

That’s not to argue that the world has reached “peak gold,” (output could expand in future for a variety of reasons). Still, my contacts in the mining community consistently report that gold is becoming more difficult to source and the quality of newly discovered ore is low-to-medium at best.

Flat output, all things equal, tends to put a floor under prices and to support higher prices based on other factors.

The Demand Side

The demand side is driven largely by central banks, ETFs, hedge funds and individual purchases. Traditional institutional investors are not large investors in gold. Much of the demand from hedge funds is conducted in derivatives such as gold futures.

Derivatives generally don’t involve physical delivery of gold. They involve “paper gold” that far exceeds the actual, physical gold supply. It’s this paper gold market that accounts for volatility in the gold market, not gold itself.

Meanwhile, central bank demand for gold has surged from less than 100 metric tonnes in 2010 to 1,100 metric tonnes in 2022, a 1,000% increase in 12 years. Central bank gold demand remained strong in 2023 with 800 metric tonnes acquired through Sept. 30.

That puts central bank gold demand on track for a new record. There’s no sign of that demand slowing in 2024.

Overall, the picture is one of flat supply and increasing demand, mostly in the form of official purchases by central banks.

A Math Lesson

Finally, a bit of elementary math is helpful in understanding how the dollar price of gold can move past $25,000 per ounce in the next two years. For this purpose, we’ll assume a baseline price of $2,000 per ounce (although gold has been in the $2,300 range lately with no signs of falling back to the $2,000 level).

But for our purposes, we’ll keep it simple.

A move from $2,000 per ounce to $3,000 per ounce is a heavy lift. That’s a 50% increase and could easily take a year or more. Beyond that, a further increase from $3,000 to $4,000 is a 33% increase: another large rally. A further gain from $4,000 per ounce to $5,000 per ounce is a further gain of 25%.

But notice the pattern. Each gain is $1,000 per ounce, but the percentage increase drops from 50% to 33% to 25%. That’s because the starting point is higher while the $1,000 gain is constant. Each $1,000 jump represents a smaller (and easier) percentage gain than the one before.

This pattern continues. Moving from $9,000 per ounce to $10,000 per ounce is only an 11% gain. Moving from $14,000 per ounce to $15,000 per ounce is only a 7% gain. Gold can move 1% in a single trading day, sometimes 2% or more.

As an extreme example, a move from $99,000 per ounce to $100,000 per ounce is about a 1% move. Those $1,000 pops get even easier as we approach my calculated gold price of $27,533.

The lesson for you as an investor is to buy gold now.

As prices continue to rally, you’ll get more gold for your money at the outset and high-percentage returns as gold rallies from a lower base. Toward the end of the long march past $25,000 per ounce, you’ll have bigger dollar gains because you started with more gold.

Others will jump on the bandwagon, but you’ll already have a comfortable seat.

3. CHRIS POWELL//GATA DISPATCHES

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS /LIVE FROM THE VAULT

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT//COPPER

Goldbugs Waited Years For A Massive Comex Short Squeeze, And Finally Got It… Just In The Wrong Metal

THURSDAY, MAY 16, 2024 – 02:45 PM

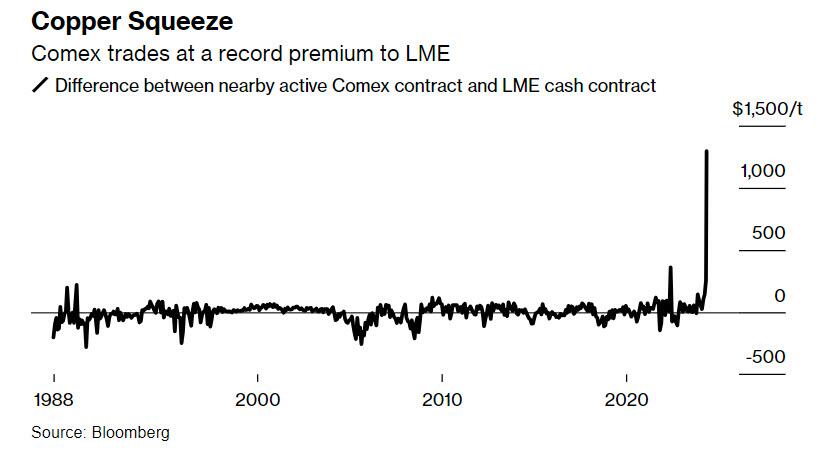

For much of the past decade, gold bugs religiously tracked the physical gold inventory located in the various gold vaults that make up the Comex system, eagerly awaiting the day when there would be more deliverables (via paper shorting of gold) than physical in storage, sparking a historic short squeeze. Well, the day of a historic Comex short squeeze finally arrived… only it wasn’t in gold but in the far less precious metal that is copper.

It all started one month ago, when we reported that in an attempt to enforce sanctions against Russia that actually worked (as opposed to the joke that is the western “oil embargo” now openly breached by absolutely everyone), the “US, UK Banned Deliveries Of Russian Copper, Nickel And Aluminum To Western Metals Exchanges.” There, in our conclusion, we wrote that “history has taught us that the market will price in some “full-sanction” risk premium which when combined with the current macro bid (reflation narrative, electrification, “copper is the first AI commodity” etc.) means we expect a complex wide rally.” Little did we know how truly historic said rally would be just one month later.

As anyone who has been following the recent moves in the price of copper – which is hitting daily record highs – knows by now, a massive dislocation between the prices for copper traded in New York and other commodity exchanges has rocked the global market for the metal and prompted a frantic dash for supplies to ship to the US.

The source of the disruption, as Bloomberg reports, is a record short squeeze that has driven up copper prices on the Comex exchange to the point where the premium for New York copper futures above the London Metal Exchange price has rocketed to an unprecedented level of over $1,200 per ton, compared with a typical differential of just a few dollars.

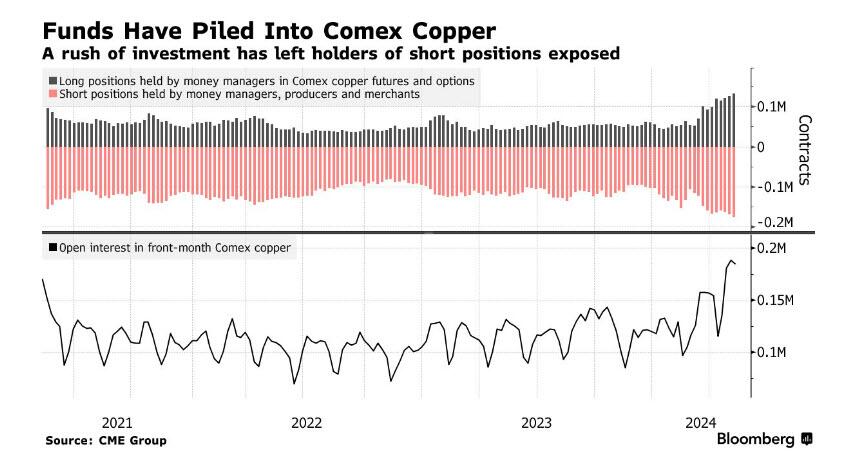

The blowout in that price spread has wrong-footed major players from Chinese traders to quant hedge funds, all of whom are now scrambling for metal that they can deliver against expiring futures contracts!

Adding fuel to the fire, the surge in the price is not just driven by technicals but also reflects the surge of interest from speculators after forecasts that long-term copper mine production will struggle to keep pace with demand. We have discussed the fundamental case for copper in “The Copper Supply Shortage Is Here“, and most notably in “the Next AI Trade” where we said that copper is starting to show signs of what Goldman has called “AI exposure” considering it is an essential material to produce power, and added that Goldman recently has gone full-bore pushing for copper (see the following note from Goldman S&T “Turning Copper into Gold” available to professional subs).

While less important than the LME, Comex, which is part of the CME Group, is a key playground for investors, some of whom have used the exchange to build up large bullish bets on copper in recent months

“The broader story is that there are new investment funds that are boosting their exposure to copper for a multitude of reasons, and while that’s a global trend, a huge amount of that investment has been heading to Comex,” said Matthew Heap, a portfolio manager at Orion Resource Partners, the largest metals-focused fund manager.

As shown in the charts above, while copper prices had been rising for months, this week’s spike was specific to the Comex and the most-active futures contract for July delivery. By Wednesday, the July price had soared as much as 10%, touching a record high for that contract, even as the global benchmark contract on the LME traded broadly flat. The move, Bloomberg reports citing numerous traders and brokers, was a classic short squeeze as market participants who had placed bets on the Comex contract moving back into line with prices on the LME and in Shanghai, the other global copper benchmark, were forced to buy those positions back as prices rose, creating a vicious cycle and sending the price to a record.

Indeed, as Colin Hamilton, managing director for commodities research at BMO Capital Markets, said the spread of more than $1,000 a ton between Comex and London was “something never seen previously,” adding that “there has been a squeeze on short positions into contract expiry, exacerbating the move.”

In yet another example of hedge funds and other traders being too smart for their own good (i.e. a replay of the original GameStop short squeeze), they had taken the other side of the bullish trades on Comex, betting on narrowing differentials between the contracts in New York, London and Shanghai, or between New York contracts for different delivery dates, often with massive leverage. With prices on the Shanghai Futures Exchange relatively depressed, some Chinese physical market participants had also sold on the LME and Comex, with plans to export.

Putting this all together, and on Wednesday morning, the July Comex copper contract soared to a record $5.128 a pound ($11,305 a ton), also trading at a record premium above the September Comex contract — a monster backwardation that is hallmark of a short squeeze.

While the spike was driven by short covering rather than any overall physical shortage, traders and brokers say, but it has shined a light on relatively tight supplies in the US copper market, just as we warned a month ago in “The Copper Supply Shortage Is Here. Case in point, inventories tracked by the Comex currently total 21,066 short tons, while LME inventories in the US are just 9,250 tons. For comparison, annual US copper demand is almost 2 million tons. Traders say solid demand, and shipping issues at the Panama and Suez canals, have left the market tight. Indeed, US copper imports year-to-date are down 15%, according to consultancy CRU Group.

“We continuously monitor our markets, which are operating as designed as market participants manage copper risk and uncertainty,” the CME said in a statement.

Of course, as our readers know too well, short squeezes are nothing new in commodity markets, and they often prompt a mad scramble to find supplies of raw materials that underpin paper contracts. The most recent and vivid example is the Nickel short squeeze of March 2022, when the Russian invasion of Ukraine led to a huge shortage in the market, and a staggering surge in the price which nearly bankrupted one of China’s biggest commodity traders and the LME itself.

A similar squeeze took place in 2020, when Covid locked down much of the world, and gold traders raced to ship metal to address a similar dislocation between New York and London bullion prices. And in 1988, a short squeeze in aluminum led some traders to load the metal into jumbo jets — a highly unusual and costly mode of transport for industrial raw materials — in order to get it on to the LME as soon as possible.

The current Comex copper squeeze has triggered a similar dash to send copper to the US: Chinese traders have spent the past 24 hours calling around shipping companies to try to secure transit to the US, according to people familiar with the matter.

Traders and miners in South America have also raced to boost their US shipments. According to Bloomberg, Chilean copper-mining giant Codelco is directing all of its available volumes to the market and also negotiating with customers to postpone some sales so that it can maximize deliveries.

That said, there are tentative signs that the squeeze is easing: the July copper contract edged lower on Thursday morning after coming off its highs from Wednesday, while the premium over cash copper on the LME narrowed to $573 a ton — although still a historically elevated level.

There may be further relief ahead, as investors with bullish positions via commodity indexes are set to start rolling their copper positions in early June, providing an opportunity for traders with short positions to defer delivery, potentially easing the backwardation. Still, it remains unclear if that will be enough to resolve the squeeze ahead of the expiry of the July contract, which goes into delivery at the start of that month. And any attempts to provide further metal to the US to ease the squeeze may face challenges: Chinese traders seeking to transport metal to the US have found that shipping schedules are fully booked, with the earliest available shipping slots from Shanghai to New Orleans at the beginning of July, said Gong Ming, analyst with Jinrui Futures Co.

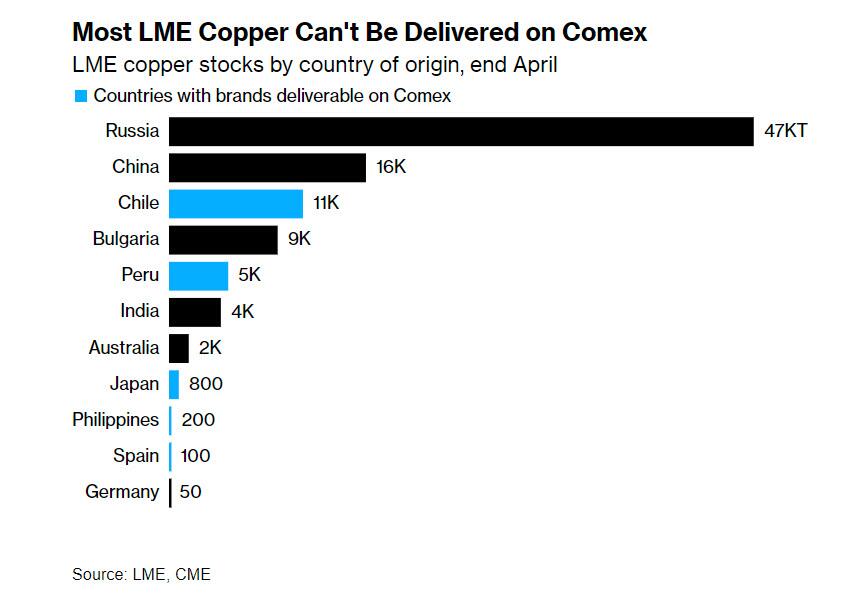

Adding to the plight of those caught out by the squeeze is the fact that much of the copper inventories outside the US is from brands that aren’t deliverable against Comex futures. For example, more than 80% of the 94,700 tons of copper on the LME at the end of April was produced in Russia, China, Bulgaria or India — countries whose copper isn’t deliverable on Comex as we reported a month ago, in a development that has eventually cascaded into today’s historic squeeze.

And while substantial inventories have built up in China in recent months, traders estimate that only about 15,000 to 20,000 tons of that could be delivered against Comex futures.

“We do not think the physical arbitrage activity will be sufficient by the July expiry to close the arb on the near month. There is not enough material and not enough time,” said Anant Jatia, chief investment officer at Greenland Investment Management, a hedge fund specializing in commodity arbitrage trading.

“However, physical traders are currently heavily incentivized to move copper into the US and over time the arb market will stabilize.”

As for gold bugs, watching with sheer shock – and outright jealousy – the epic squeeze roiling the less precious metal, all they can hope for is that one day the massive paper shorts on the comex will lead to a similar meltup in gold. All that may be needed is a pair of enterprising Hunt Brothers for the new millennium to pull it off.

SHANGHAI CLOSED UP 2.50 PTS OR 0.08% //Hang Seng CLOSED UP 302.82 PTS OR 1.09%// Nikkei CLOSED UP 534.53 OR 1.39%//Australia’s all ordinaries CLOSED UP 1.51%///Chinese yuan (ONSHORE) closed UP TO 7,2170 CHINESE YUAN OFF SHORE CLOSED UP TO 7.2179/ Oil DOWN TO 78,32 dollars per barrel for WTI and BRENT DOWN AT 82.60 /Stocks in Europe OPENED MOSTLY RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGSTHURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2170

OFFSHORE YUAN: DOWN TO 7.2179

SHANGHAI CLOSED UP 2.50 PTS OR 0.08 %

HANG SENG CLOSED UP 302.82 PTS OR 1.59%

2. Nikkei closed UP 534.53 PTS OR 1.38 %

3. Europe stocks SO FAR: MOSTLY RED

USA dollar INDEX UP TO 104.18 EURO FALLS TO 1.0872 DOWN 16 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +.918 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 154.47 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.4295/Italian 10 Yr bond yield DOWN to 3.725 SPAIN 10 YR BOND YIELD DOWN TO 3.186%

3i Greek 10 year bond yield UP TO 3.431

3j Gold at $2376.00//Silver at: 29.49 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 33 100 roubles/dollar; ROUBLE AT 90.95

3m oil into the 78 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 154.97/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.918% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9024 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9812well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.336 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.489 DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.745 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.22…(TURKEY)

10 YR UK BOND YIELD: 4.110 DOWN 3 PTS

2a New York OPENING REPORT

Futures Flat At All Time High As Markets Mull Next Move

BY TYLER DURDEN

THURSDAY, MAY 16, 2024 – 07:47 AM

US index futures are flat after notching new record highs on the S&P 500 and Nasdaq 100, spurred on by a miss in the US CPI print and retail sales data on Wednesday, which also boosted bets the Federal Reserve will ease policy. That inflation data, which the market was feverishly anticipating, was inadvertently published 30 minutes early the BLS reported, raising fresh questions about how some of the world’s most sensitive economic information is released. As of 7:30am, S&P and Nasdaq futs are up 0.1% with small caps underperforming, potentially on growth fears, so it will be interesting if this morning’s stronger than expected WMT earnings can ease those fears. With the main data point of the week now past, investors will turn to Fed speakers and jobless claims data for new clues on the path of interest rates. Bond yields are moving +/-1 bp as the curve twists flatter. The US dollar looks to rally for the first time this week. Commodities are higher led by base metals with copper soaring for another day because of a short squeeze on the Comex exchange. The macro data focus is on Housing Starts/Building Permits, Import/Export Prices, and Industrial Production. NVDA reports next week so may see investors begin positioning for that.

In pre-market trading, Mag7 and Semis are higher while the meme-stock craze continued to fizzle out, with GameStop Corp. and AMC Entertainment Holdings Inc. plunging more than 10% in the pre-market. Chubb shares jumped after Berkshire Hathaway unveiled a $6.7 billion stake in the insurer. Cisco Systems Inc. gained on a higher revenue forecast. Here are the other notable premarket movers:

AST Spacemobile shares soar 36%, putting them on track for the biggest jump since March 2022, after AT&T said had it moved from a memorandum of understanding to signing a “definitive commercial agreement” with the company for a space-based broadband network.

Chubb shares jump 9.5%, putting the stock on track for its sharpest gain since November 2008, after Warren Buffett’s Berkshire Hathaway unveiled a $6.7 billion stake in the insurer.

Cisco Systems shares rise 4.5% after the communications equipment company raised its full-year revenue forecast, indicating that businesses are starting to spend on their computer networks again.

Coupang shares gain 3.2% after UBS raised its recommendation on the stock to buy.

GameStop and AMC shares fall, putting the stocks on track for a second consecutive session of losses, as the latest meme-stock rally fizzles. GameStop -16%, AMC Entertainment (AMC US) -12%

Grab Holdings shares gain 3.3% after the ride-hailing and food delivery company reported first-quarter revenue came ahead of estimates. Additionally, the company boosted its Ebitda guidance for the year.

ZTO Express ADRs jump 11% after the Chinese delivery company reported estimate-beating earnings. The firm said it’s shoring up profitability by keeping loss-making parcels outside of its network, as price competition heats up.

On the data front, stock-market bulls will be hoping for jobless claims to give an indication of slack in the labor market that would give the Fed room to ease monetary policy. A raft of central bank officials are due to speak today as well. Investors currently expect about two rate cuts this year, according to futures markets.

“Slowdowns are not bearish equities, recessions are. I think on the body of evidence we are still miles from that. Although another rise in claims /confirmatory data from Philly Fed like we saw in Empire would keep inching us toward GDP downgrades” wrote Goldman trader Rich Privorotsky. “Now we’ll trade slowdown and the SPX is taking out the highs. The mix of leadership will change and I think the NDX (secular growth proxy) which has actually lagged most things ytd has a good chance to run particularly into the end of the month”

In Europe, the Estoxx 50 trades lower by 0.2%, threatening to end a streak of ten straight day of gains as insurance and real estate stocks outperform while energy and energy and autos lag behind. Local bourses were dragged down by energy names while German industrials continue to grapple with weak demand from China. Siemens AG dropped on lowered guidance for its key digital industries unit. Italy’s FTSE MIB outperforms peers while CAC 40 lags after reaching a fresh record. Traders were also watching direction from European Central Bank speakers on whether interest rates might start falling next month. So far, swap contracts have almost fully priced in the likelihood of three cuts in 2024. Here are some of the biggest movers on Thursday:

WOSG jumps as much as 19% after the watch retailer’s sales grew faster than expected in the final quarter of its financial year and guidance for the year ahead impressed, according to analysts. The stock is on course for its biggest gain in more than six months.

BT shares surge as much as 11% after the telecom operator unexpectedly boosted its dividend, citing an improved outlook for cash flow.

NIBE gains as much as 7.7% with the Swedish heat-pump maker guiding for improving demand in the second half, largely offsetting a weaker-than-expected 1Q report, which was weighted down by the firm’s key Climate Solutions division.

Roche shares rise as much as 4.8%, the most since Aug. 23, after the Swiss pharma company reported positive early-stage results for its experimental drug to treat obesity and type-2 diabetes.

Snam shares rise as much as 3.1%, the most in six months, after the Italian natural gas distributor delivered a strong set of results and lifted its annual earnings guidance, which analysts at Citi say will push up consensus estimates.

Sage shares slumped as much as 20%, their biggest drop since 1993, after the accounting software provider’s earnings undershot expectations.

Ubisoft shares fall as much as 15% after the French video-game maker’s guidance suggests operating profits will likely grow slower than bookings in FY25.

EasyJet shares fall as much as 7.8%, the biggest drop in seven months. Analyst say management views on revenue per seat in the fourth quarter seem softer than previous comments.

Siemens shares drop as much as 4.4% after the German industrial giant reported mixed earnings, with its key digital industries division missing already-low expectations.

Deutsche Telekom shares fall as much as 1.4% as the German company’s results fail to answer questions around union wage negotiations and the potential government stake sale in Germany.

ConvaTec shares fall as much as 4.5% after the medical device company lowered its guidance for its Advanced Wound Care division due to uncertainty stemming from proposals outlined last month concerning coverage of skin substitute grafts and cellular and tissue-based products.

Earlier in the session, in Asia stocks also pushed toward a new peak. Shares of Chinese developers soared on optimism that Beijing will provide policy support for the purchase of unsold homes from distressed builders.

Hang Seng and Shanghai Comp were positive with developers front-running the advances in Hong Kong on return from holiday as they reacted to the recent property support proposal, while the upside was capped in the mainland amid little fresh pertinent catalysts aside from Russian President Putin arrival in China where he seeks to deepen the strategic partnership with Chinese President Xi.

ASX 200 was led by strength in the rate-sensitive sectors such as real estate and tech amid a drop in yields.

Nikkei 225 gained but was off today’s best levels as participants digested a firmer currency, steeper-than-expected contraction in Japanese GDP and mega bank earnings.

In FX, the Bloomberg Dollar Spot Index rebounded after slipping as much as 0.3% to a five-week low; USD/JPY fell 0.1% at 154.90, after sliding as low as 153.60. The yen rose for a second day, shrugging off GDP data that showed a contraction in Japan’s economy as investors chose to focus on long dollar liquidation. JPY and CHF are the strongest performers and only gainers in G-10 FX. AUD and NOK fall the most.

In rates, Treasuries are mixed with the curve flatter on the day, pivoting around a near-unchanged 10-year sector as post-CPI price action consolidates around Wednesday’s session highs. US yields are cheaper by around 2bp across front-end of the curve and richer by 1bp across long-end, flattening 2s10s and 5s30s spreads by 2.2bp and 2bp on the day. 10-year yields are little changed on the day trading around 4.335% with the two-year yield rose 1bps to 4.73%, bouncing off 4.70% hit in earlier trading. Bunds and gilts both lagging by 1bp in the sector. Swaps imply an 86% chance of a quarter-point rate cut from the Fed in September, compared with 73% earlier in the week; around 49bps of cuts are priced in total through the end of the year, up from around 43bps before the CPI print on Wednesday. US session focus includes data releases at 8:30am New York along with five scheduled Fed speakers.

In commodities, crude futures and spot gold are steady. Most base metals trade in the green; LME copper rises 1.5%, outperforming peers.

Looking at today’s calendar, US economic data slate includes initial jobless claims, April housing starts/building permits, May New York services business activity, Philadelphia Fed business outlook, April import/export price index (8:30am) and April industrial production (9:15am). Fed officials’ scheduled speeches include Barr, Barkin (10am), Harker (10:30am), Mester (12pm) and Bostic (3:50pm)

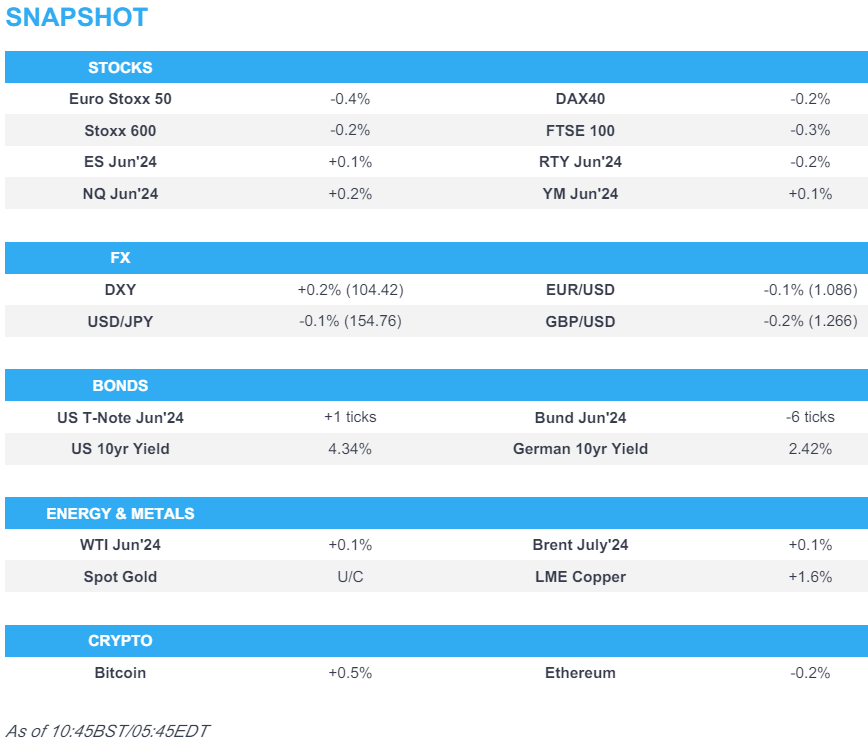

Market Snapshot

S&P 500 futures little changed at 5,336.00

STOXX Europe 600 down 0.1% to 523.95

MXAP up 1.1% to 181.64

MXAPJ up 1.3% to 568.91

Nikkei up 1.4% to 38,920.26

Topix up 0.2% to 2,737.54

Hang Seng Index up 1.6% to 19,376.53

Shanghai Composite little changed at 3,122.40

Sensex down 0.3% to 72,748.60

Australia S&P/ASX 200 up 1.6% to 7,881.29

Kospi up 0.8% to 2,753.00

German 10Y yield little changed at 2.42%

Euro down 0.1% to $1.0872

Brent Futures up 0.4% to $83.07/bbl

Brent Futures up 0.4% to $83.05/bbl

Gold spot up 0.0% to $2,386.10

US Dollar Index little changed at 104.38

Top Overnight News

Chinese property developers spike as expectations grow that local governments around the country will continue buying up excess housing units to bolster the property market. WSJ

China renews call for political end to Ukraine war as Xi Jinping rolls out red carpet for Russia’s Vladimir Putin. Any settlement must respect security and sovereignty of all parties, Chinese president says after talks Sino-Russian relationship has withstood international ‘storms and changes’ and sets a model for mutual respect and cooperation, he says. SCMP

Chinese goods are still getting into the US despite rising trade tensions between the two nations, although increasingly they are being funneled in via Vietnam. RTRS

MSFT asks hundreds of employees in China working on cloud computing and AI to transfer outside the country as tensions rise between Beijing and Washington. WSJ

Japan’s Q1 GDP came in weaker than expected at -2% (vs. the Street’s -1.5% forecast) and revisions were negative, scrambling BOJ plans to proceed with further tightening steps. RTRS

The ECB published its Financial Stability Review for May and provided a slightly improved outlook on the macro landscape – “Euro area financial stability conditions have improved as recession risks decline, but markets remain exposed to possible adverse macro-financial and geopolitical surprises”. ECB

Biden’s political team feels the president’s poll numbers are sagging because the country isn’t yet focused on the election and the prospect of a second Trump term, which is why they pushed for an early debate (Biden and Trump will face off against each other on June 27). NYT

Israeli Defense Minister Yoav Gallant criticized Netanyahu’s indecision on figuring out a post-war governance structure for Gaza (Gallant warned that the present course will result in one of two undesirable scenarios: continued Hamas rule or IDF control over Gaza’s civilian population). Jerusalem Post

Ray Dalio has warned that the US government’s rising debt levels could hit Treasury bonds, arguing that investors should move some of their money to foreign markets. FT

A more detailed look at global markets courtesy of Newsquawk

APAC stocks took impetus from the gains on Wall St where the major indices rallied to fresh record highs after softer CPI data boosted Fed rate cut bets. ASX 200 was led by strength in the rate-sensitive sectors such as real estate and tech amid a drop in yields. Nikkei 225 gained but was off today’s best levels as participants digested a firmer currency, steeper-than-expected contraction in Japanese GDP and mega bank earnings. Hang Seng and Shanghai Comp were positive with developers front-running the advances in Hong Kong on return from holiday as they reacted to the recent property support proposal, while the upside was capped in the mainland amid little fresh pertinent catalysts aside from Russian President Putin arrival in China where he seeks to deepen the strategic partnership with Chinese President Xi.

Top Asian News

Japanese Economy Minister Shindo said regarding GDP that the economy is expected to continue moderate recovery, while he added that they need to pay close attention to risks related to forex fluctuations that would push up domestic prices.

European bourses, Stoxx600 (-0.3%) are mostly lower, unable to continue the US CPI-induced gains from the prior session. Bourses initially opened marginally in the red, and continued to edge lower as the morning progressed. European sectors are mixed; Insurance is the clear outperformer, propped up by post-earning gains in Swiss Re and Zurich Insurance. Energy is found at the foot of the pile, hampered by broader weakness in crude prices over the past few days. US Equity Futures (ES +0.1%, NQ +0.2%, RTY -0.2%) are mixed, with some of the post-CPI optimism seemingly fizzling out. Stock specifics today include Cisco (+4.5% pre-market), which beat on its top/bottom lines.

Top European News

ECB’s de Guindos says price falls in CRE market to continue but at a slower pace than last year; rise in NPLs and rise in funding costs to weigh on bank profits this year

Statistics Swiss says domestic GDP likely 0.2% in Q1.

Bank of Spain says to start process to establish bank’s countercyclical buffer in Q4; plans to establish countercyclical buffer at 0.5%.

Norges Bank Expectations Survey Q2’24. The economists expect goods and services inflation 12 months ahead to be 3.6%, down 0.1pp from the previous quarter. The economists expect the average rise in real wages will be 1.2% in 2024, up 0.3pp from the previous quarter.

FX

DXY is attempting to recoup lost ground after the fallout from yesterday’s CPI and retail sales saw the index make a low at 104.07; next up, US IJC & Philly Fed data.

EUR/USD is marginally softer vs. the USD after EUR/USD ran out of steam ahead of 1.09. IJC could see the pair retest 1.09 given the reaction to last week’s jump in claims.

GBP is a touch softer vs. the USD in quiet trade but holding onto a bulk of yesterday’s notable gains. Cable went as high as 1.27 before running into resistance. If Cable manages to resume its ascent higher and breach 1.27, the April high sits just above at 1.2709.

JPY remains one of the main beneficiaries from yesterday’s post-data dollar selling as US-Japanese rate differentials turn in Japan’s favour. USD/JPY down as low as 153.61 before scaling back losses to around 154.75 currently.

Antipodeans are both softer vs. the USD following yesterday’s session of chunky gains. AUD/USD saw mixed jobs data overnight and has currently scaled back from a 0.6714 peak (highest since Jan) and retreated back onto a 0.66 handle.

Fixed Income

USTs are steady thus far with benchmarks slightly shy of this morning’s peak but still in the green. A relative pullback which is being led by the short-end with the 2yr basically unchanged and lagging a touch, with an unusually sizeable for the time block trade perhaps impacting; USTs in slim 109-24 to 109-31+ bounds.

Gilt price action is similar to that seen in USTs, with Gilts just shy of today’s WTD 98.76 peak with nothing of note until 99.00 and then 99.10 from mid-April.

Bund have also drifted back towards the unchanged mark with Bunds going as low as 131.63; overall unreactive to Spanish/French auctions.

France sells EUR 11.998bln vs exp. EUR 10.5-12bln 2.50% 2027, 2.75% 2029, 2.75% 2030, 2.50% 2030 Bond

Commodities

Crude benchmarks were in the green, though now off best levels (now flat) as the Dollar attempts to pare back some of its recent CPI-induced losses; Brent July hovers around USD 83/bbl, whilst WTI trades around USD 79/bbl.

Precious metals are mixed; spot gold is flat whilst spot silver sees mild losses. XAU topped out at USD 2397/oz after failing to breach USD 2400/oz.

Base metals hold little bias as the post-CPI move pauses for breath into more US data and Fed speak. In addition to pressure emanating from modest USD strength.

Azerbaijan Oil production at 476k in April (prev. 481k M/M)

LME says daily stock data has been delayed; investigating the situation

Geopolitics: Middle East

Israeli PM Netanyahu rejected US calls for a post-war plan in Gaza, while Arab governments have rejected the idea of establishing an Arab-led civilian administration in Gaza, according to WSJ.

Hamas’s chief said the fate of truce talks is uncertain as Israel insists on occupying Rafah crossing, according to AFP News Agency.

Lebanon’s Hezbollah launched drones at a military base west of Israel’s Tiberias in the deepest strike into Israeli territory thus far.

Massive Israeli airstrikes were reported in Baalbek, Lebanon, according to Kann’s Amichai Stein.

Islamic Resistance in Iraq said it launched a drone attack on a “vital” target in Eilat, southern Israel, according to Iran International.

Geopolitics: Other

Chinese President Xi said in a meeting with Russian President Putin that China will always be a good neighbour, friend, and partner of mutual trust with Russia, while he added China is ready to work together with Russia to achieve development and rejuvenation of our respective countries and uphold world equity and justice. Furthermore, Russian President Putin said Moscow and Beijing have acquired solid baggage of practical cooperation and Russia-China cooperation stands as a stabilising factor for the world.

Ukrainian military said “intensive” enemy fire prompted the move of some troops to new positions in the Kupiansk direction, east of Kharkiv.

US Event Calendar

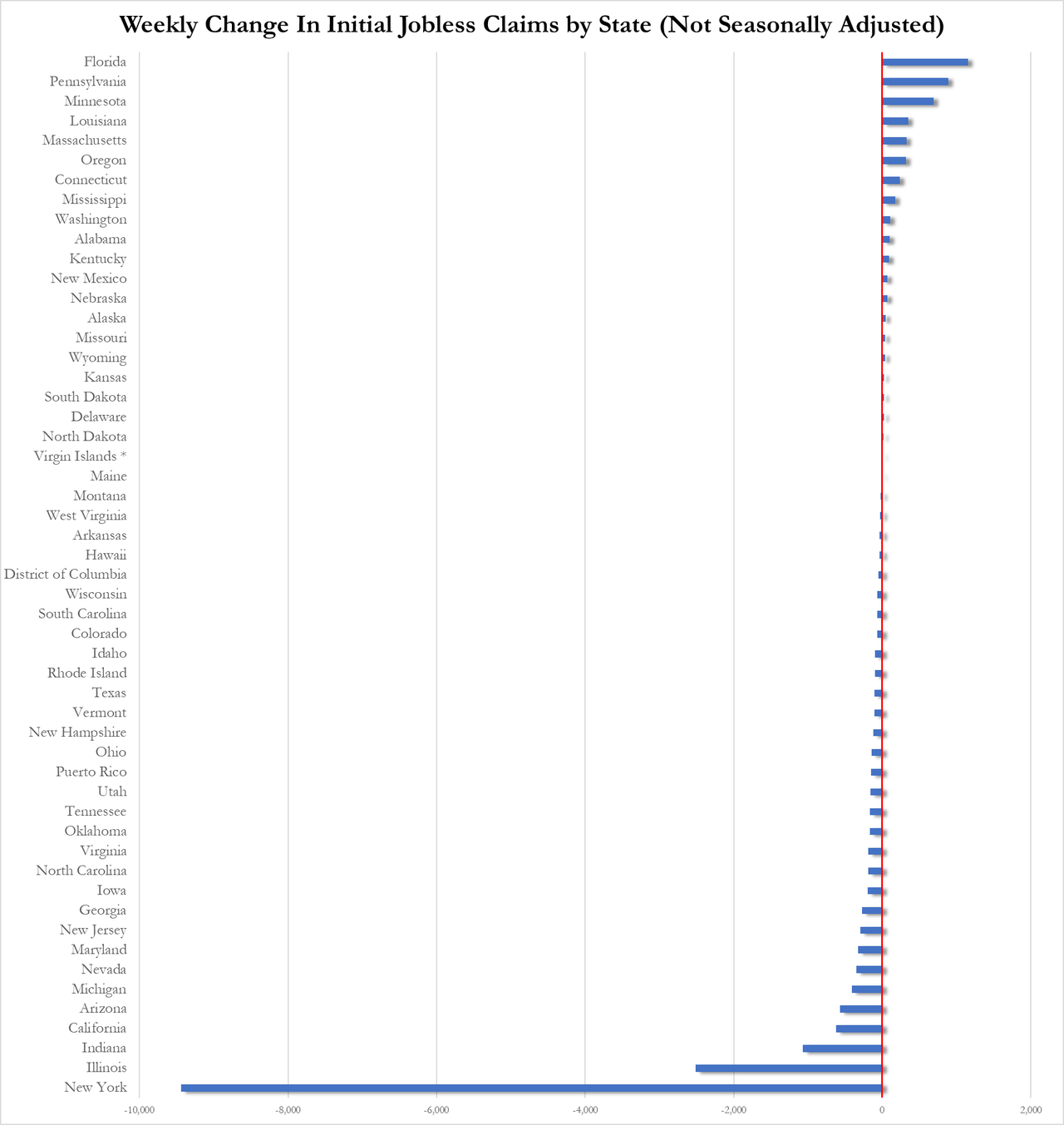

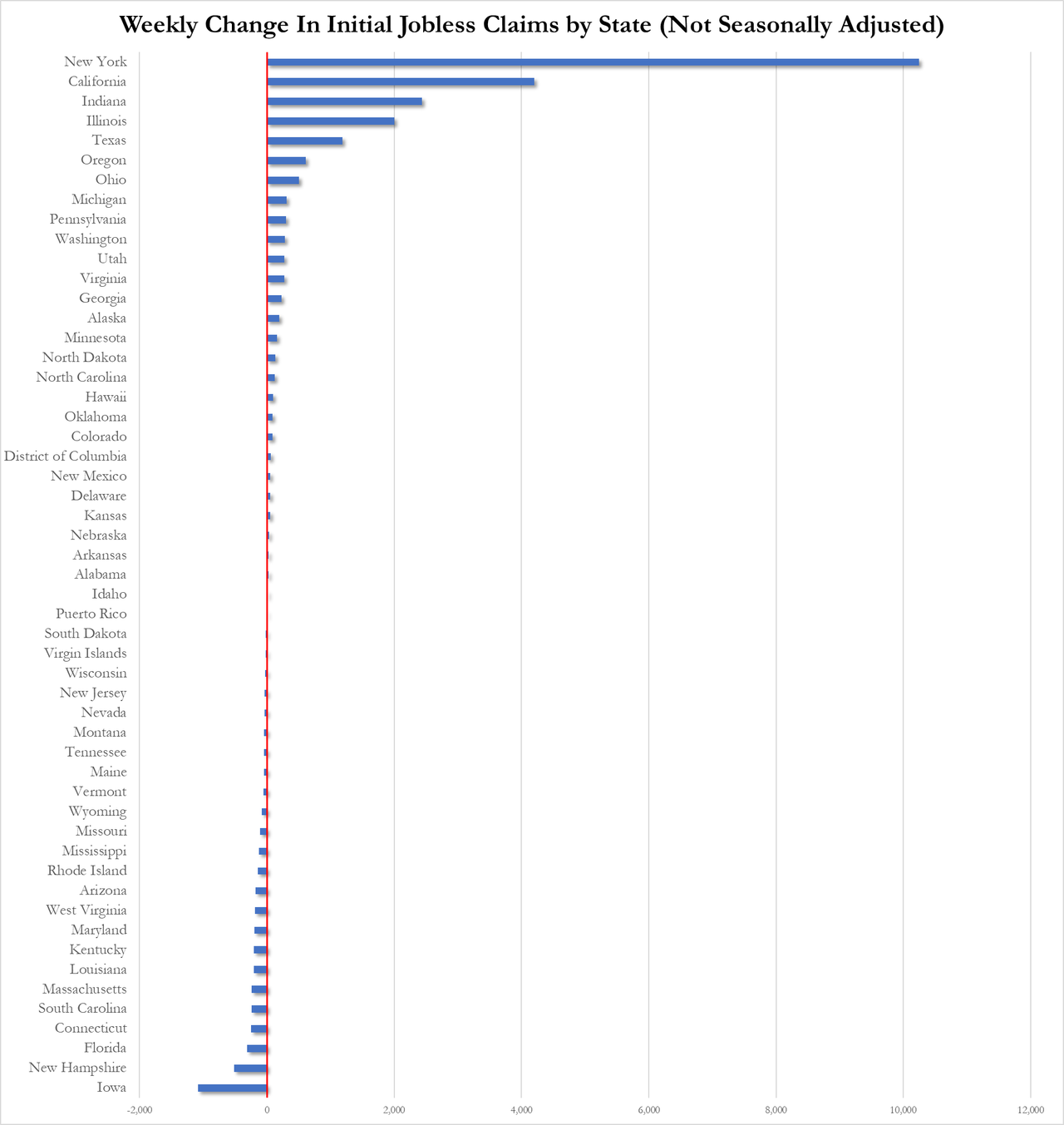

08:30: May Initial Jobless Claims, est. 220,000, prior 231,000

May Continuing Claims, est. 1.78m, prior 1.79m

08:30: April Import Price Index MoM, est. 0.3%, prior 0.4%

April Import Price Index YoY, est. 0.4%, prior 0.4%

April Export Price Index YoY, est. -1.1%, prior -1.4%

April Export Price Index MoM, est. 0.2%, prior 0.3%

08:30: May New York Fed Services Business, prior -0.6

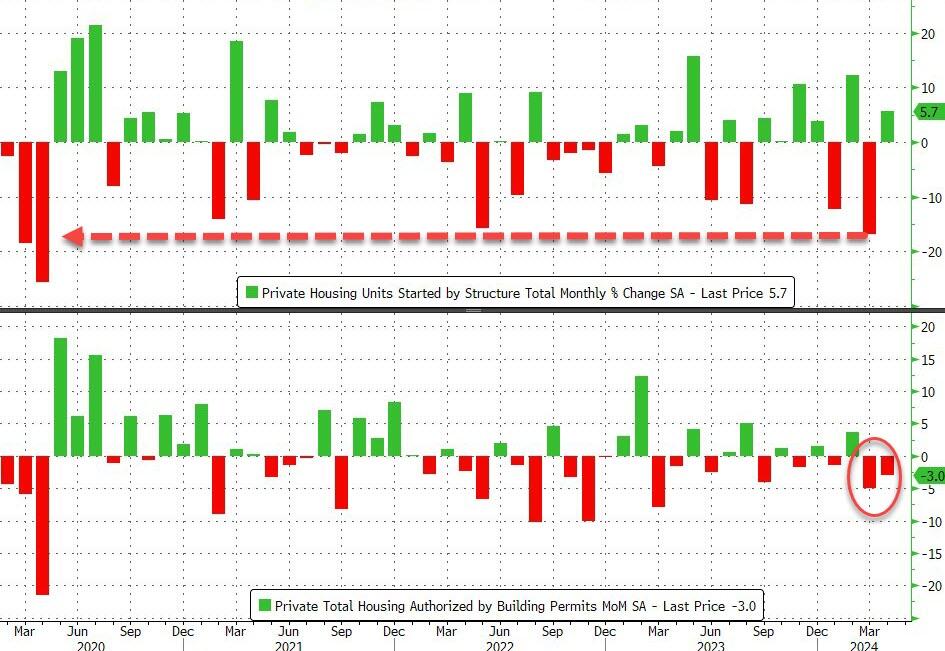

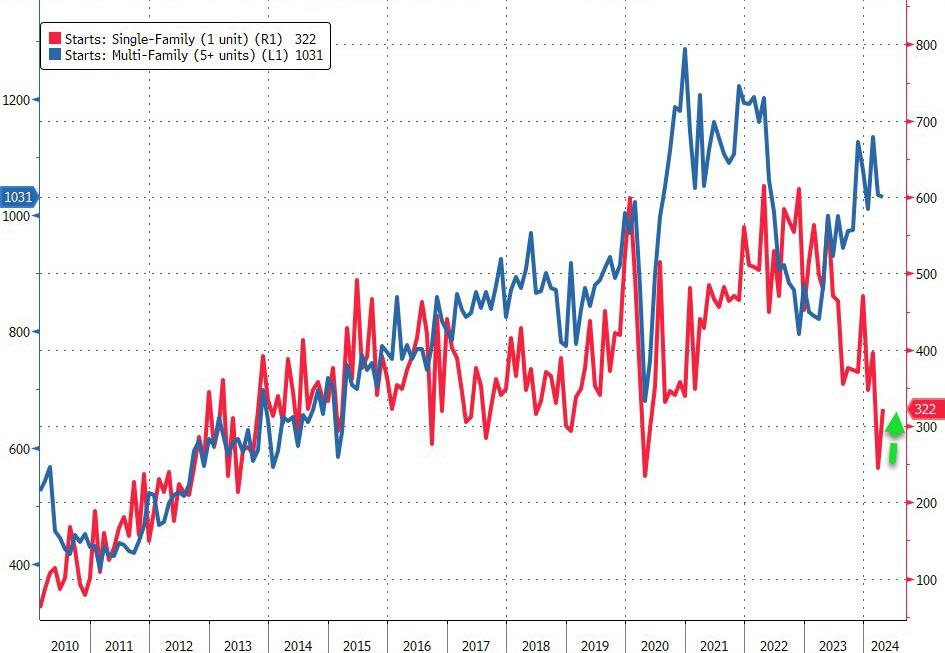

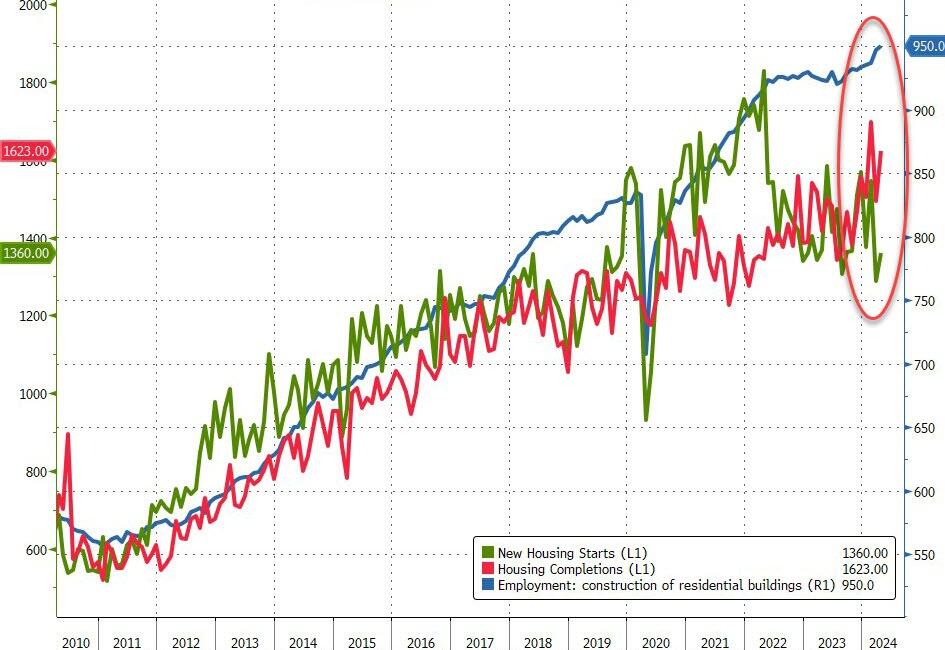

08:30: April Housing Starts MoM, est. 7.6%, prior -14.7%

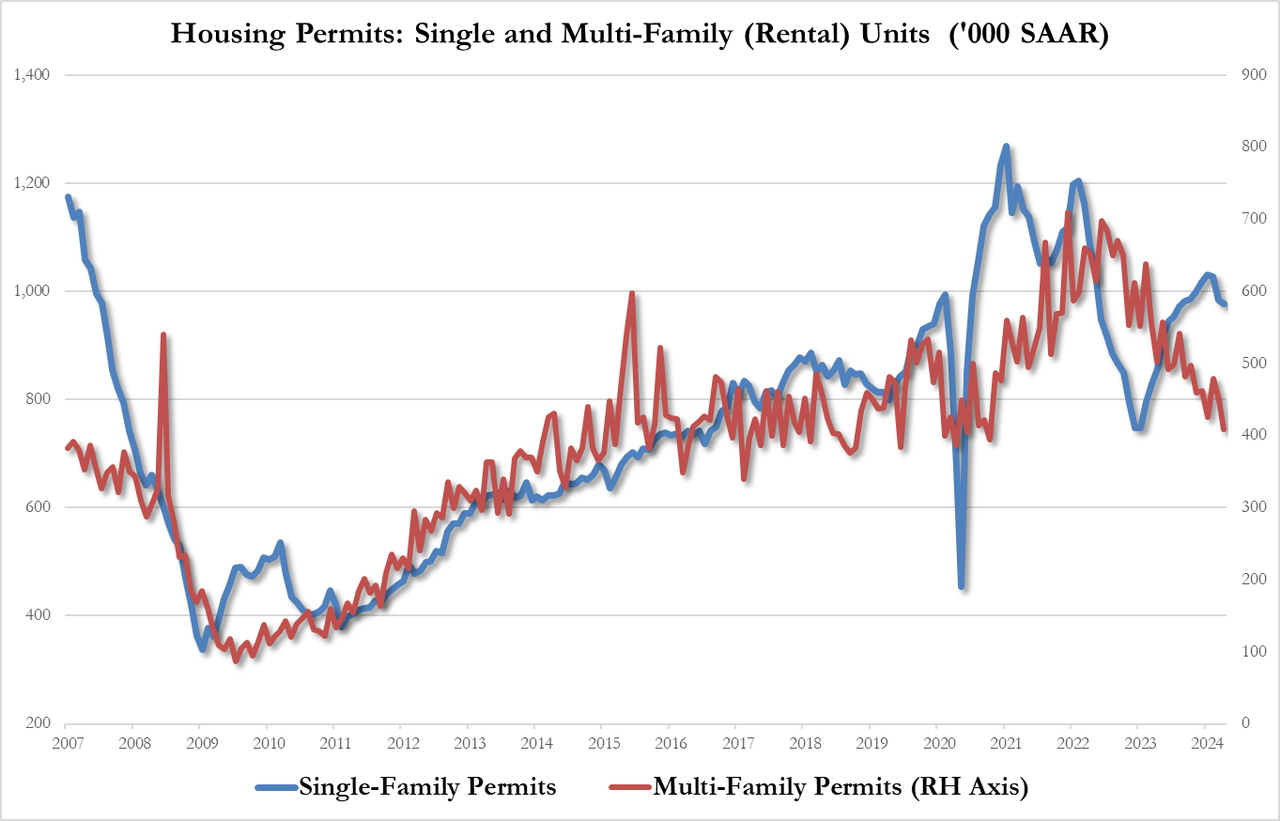

April Housing Starts, est. 1.42m, prior 1.32m

April Building Permits MoM, est. 0.9%, prior -4.3%, revised -3.7%

April Building Permits, est. 1.48m, prior 1.46m, revised 1.47m

08:30: May Philadelphia Fed Business Outl, est. 8.0, prior 15.5

09:15: April Industrial Production MoM, est. 0.1%, prior 0.4%

April Manufacturing (SIC) Production, est. 0.1%, prior 0.5%

April Capacity Utilization, est. 78.4%, prior 78.4%

Central Bank Speakers

10:00: Fed’s Barr Testifies to Senate Banking

10:00: Fed’s Barkin on CNBC

10:30: Fed’s Harker Speaks on Higher Education, Healthcare

12:00: Fed’s Mester Gives Remarks on Economic Outlook

15:50: Fed’s Bostic Speaks in Moderated Chat on Economy

DB’s Jim Reid concludes the overnight wrap

There was the slightest hint of stagflation in what was a big day in global macro yesterday but markets were in no mood to countenance such a view as a small miss in headline CPI helped ignite a rates rally, helping the S&P 500 (+1.17%) and STOXX 600 (+0.59%) to both hit fresh all time highs. Today the highlight might be to see if last week’s surprising spike in US initial jobless claims, after months of calm, was a one-off or not. Our economists think it may have been due to changes in the NY school holiday dates. We will see.

In terms of the details of the April CPI report, the headline came in at a monthly +0.3% (vs +0.4% expected). The year-on-year rate fell from +3.5% to +3.4% as expected, so it was a pretty marginal miss. Core CPI came in at +0.29% (vs. +0.3% expected), with the year-on-year rate falling to +3.6% from +3.8% (as expected). This marks the lowest annual core inflation print in two years but still at uncomfortable levels for the Fed. Digging deeper, monthly core services inflation slowed from +0.5% to +0.4%, and core goods inflation remained negative at -0.1%. A welcome development was the deceleration in shelter rents, which fell from +0.5% to +0.4%. But as markets celebrated the miss on headline CPI, core services excluding shelter, otherwise known as supercore, increased from +4.8% year-on-year in March, to +4.9% year-on-year. This measure has been rising consistently since last October in year-on-year terms, so one to watch for in the months ahead, even as the month-on-month rate slowed from +0.6% to +0.4%. Overall, our US economists see the CPI print as a step in the right direction after the hot Q1 prints, but with further progress needed over the coming months to give the Fed enough confidence to cut rates on declining inflation alone. See their full reaction here