GOLD PRICE CLOSED DOWN $2.25 TO $2333.75

SILVER PRICE UP $0.10 TO $30.33

Gold ACCESS CLOSED $2334.30

Silver ACCESS CLOSED: $30.34

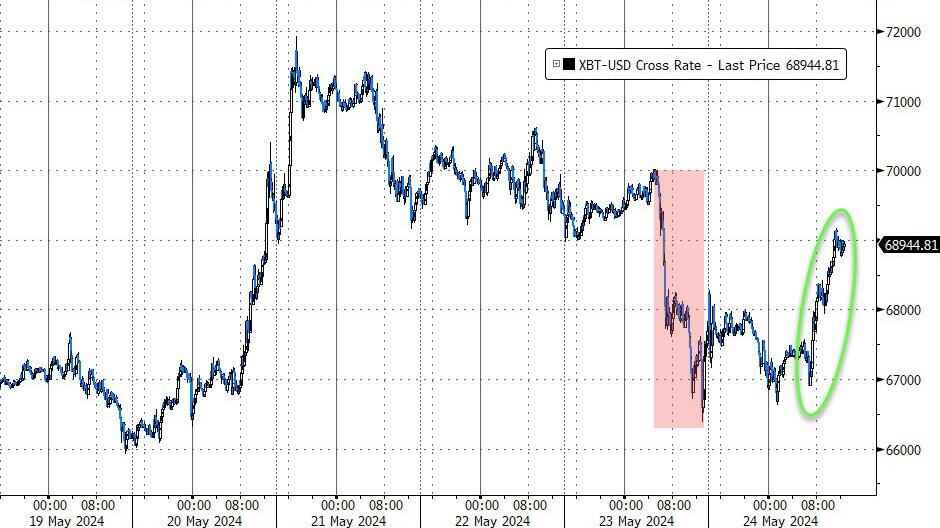

Bitcoin morning price:$67,477 DOWN 28 DOLLARS.

Bitcoin: afternoon price: $69,040 UP 1563 dollars

Platinum price closing UP 7.15 TO $1030.95

Palladium price; DOWN $1.70 AT $969.90

END

SHANGHAI GOLD PREMIUM 21 DOLLARS/COMEX GOLD

SHANGHAI GOLD

SHANGHAI GOLD (USD) FUTURES – QUOTES

Last Updated 24 May 2024 09:10:39 AM CT.

Market data is delayed by at least 10 minutes.

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $3189.54 DOWN 12.82 CDN dollars per oz( * NEW ALL TIME HIGH 3,305.30 CDN DOLLARS PER OZ//MAY 20 2024)

*BRITISH GOLD: 1839.54 UP 2.29 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2151.61 DOWN 5.14 Euros per oz //* (ALL TIME CLOSING HIGH: 2248.89 EUROS PER OZ//APRIL 16.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCH: COMEX

EXCHANGE: COMEX

CONTRACT: MAY 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,335.000000000 USD

INTENT DATE: 05/23/2024 DELIVERY DATE: 05/28/2024

FIRM ORG FIRM NAME ISSUED STOPPED

737 C ADVANTAGE 4

880 H CITIGROUP 4

TOTAL: 4 4

MONTH TO DATE: 2,371

ACCESS MARKET

TOTAL: 162 162

JPMorgan stopped 0/4

FOR MAY2024

GOLD: NUMBER OF NOTICES FILED FOR MAY/2024. CONTRACT: 4 NOTICES FOR 400 OZ or 0.0124 TONNE

total notices so far: 2371 contracts for 237,100 Oz (7.374 tonnes)

FOR MAY:

SILVER NOTICES: 87 NOTICE(S) FILED FOR 435,000 OZ/

total number of notices filed so far this month : 6103 for 30.515 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $2.25

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

BIG CHANGES IN GOLD INVENTORY AT THE GLD: A HUGE WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD

/ /INVENTORY RESTS AT 833.36TONNES

INVENTORY RESTS AT 833.36 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER UP $0.10 AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF .822 MILLION OF SILVER INTO THE SLV

// INVENTORY LOWERS TO 421.313 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 421.313 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI SHOCKINGLY FELL BY SMALL SIZED 180 CONTRACTS TO 184,732 AND CONTINUING ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS SMALL SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR HUGE LOSS OF $1.00 IN SILVER PRICING AT THE COMEX ON THURSDAY. WE HAD CONSIDERABLE LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN SHORT COVERING BY OUR SPECS WITH THE LOSS IN PRICE. WE HAD ANOTHER HUMONGOUS SIZED 741 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID LIKE TODAY.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 741 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND TODAY;S RAID.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $1.00) BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE DID HAVE A HUMONGOUS SIZED GAIN OF 859 CONTRACTS ON OUR TWO EXCHANGES DESPITE THE HUGE LOSS IN PRICE OF $1.00.

WE MUST HAVE HAD:

A HUGE SIZED 1039 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 28.130MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE JUMP OF 340,000 OZ

//NEW STANDING FOR SILVER//MAY IS THUS 30.680 MILLION OZ

WE HAD:

/ SMALL SIZED COMEX OI LOSS //HUMONGOUS SIZED EFP ISSUANCE/ VI) HUMONGOUS SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 741 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED AN ENORMOUS 2038 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY

TOTAL CONTRACTS for 18 DAYS, total 23,156 contracts: OR 115.780 MILLION OZ (1286 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 115.780 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL PROBABLY BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 115.780 MILLION OZ //WILL BE A STRONG MONTH FOR EX FOR PHYSICAL ISSUANCE

RESULT: WE HAD A SMALL SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 180 CONTRACTS DESPITE OUR LOSS IN PRICE OF SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 1039 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAY OF 29.345 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 340,000 OZ QUEUE JUMP

//NEW TOTAL STANDING AT 30.680 MILLION OZ

WE HAVE A HUGE SIZED GAIN OF 859 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 741 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND ZERO LIQUIDATION OF SHORTS.

THE NEW TAS ISSUANCE THURSDAY NIGHT (741) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 87 NOTICE(S) FILED TODAY FOR 435,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 9004 OI CONTRACTS TO 505,445 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 1042 CONTRACTS

WE HAD A STRONG SIZED DECREASE IN COMEX OI (9004 CONTRACTS) OCCURRED WITH OUR LOSS OF $53.00 IN PRICE/THURSDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER, INITIATING THURSDAY’S RAID. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 4.684 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY;S 3700 OZ QUEUE JUMP PLUS WE MUST ADD THAT DUBIOUS ISSUANCE OF 1084 OI EX FOR RISK CONTRACTS ISSUES ON LAST FRIDAY WHEREBY THE BUYER ASSUMES RISK OF 3.3716 TONNES OF GOLD//NEW STANDING INCREASES TO 8.5598 TONNES PLUS THE DUBIOUS 3.3716 ECH FOR RISK!

NEW STANDING 11.8961 TONNES// ALL OF THIS HAPPENED WITH OUR $53,00 LOSS IN PRICE WITH RESPECT TO THURSDAY’S TRADING. WE HAD A VERY FAIR SIZED GAIN OF 1381 OI CONTRACTS (4.245 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUMONGOUS SIZED 10,385 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 505,445

IN ESSENCE WE HAVE A VERY FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1381 CONTRACTS WITH 9004 CONTRACTS DECREASED AT THE COMEX// AND A HUMONGOUS SIZED 10,385 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1381 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED 2999 CONTRACTS,,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A HUGE SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (10,385 CONTRACTS) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI 9004/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 1381 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 4.684 TONNES FOLLOWED BY TODAY;S 3700 OZ QUEUE JUMP PLUS 3.3716 TONNES EX FOR RISK//PRIOR

//NEW STANDING /MAY 11.8961 TONNES.

/ 3) CONSIDERABLE LIQUIDATION OF CONTRACTS MOSTLY DUE TO SPREADERS ALONG WITH SOME MINOR LONG SPECS BEING WIPED OUT WITH THE LARGE LOSS IN PRICE.

// 4) STRONG SIZED COMEX OPEN INTEREST LOSS 5) HUGE ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///STRONG T.A.S. ISSUANCE: 2999 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY. :

TOTAL EFP CONTRACTS ISSUED: 78,921 CONTRACTS OR 7,892,100 OZ OR 245.48 TONNES IN 18 TRADING DAY(S) AND THUS AVERAGING: 4031 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAY(S) IN TONNES 245.48 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 245.48 DIVIDED BY 3550 x 100% TONNES = 6.90% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 245.48 TONNES (WILL BE ANOTHER STRONG MONTH/MAYBE LARGER THAN LAST MONTH)// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A SMALL SIZED 180 CONTRACTS OI TO 184,732 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1039 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1858 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1039 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 180 CONTRACTS AND ADD TO THE 1039 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 859 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 4.295 MILLION OZ

OCCURRED DESPITE OUR $1.00 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING/THURSDAY NIGHT

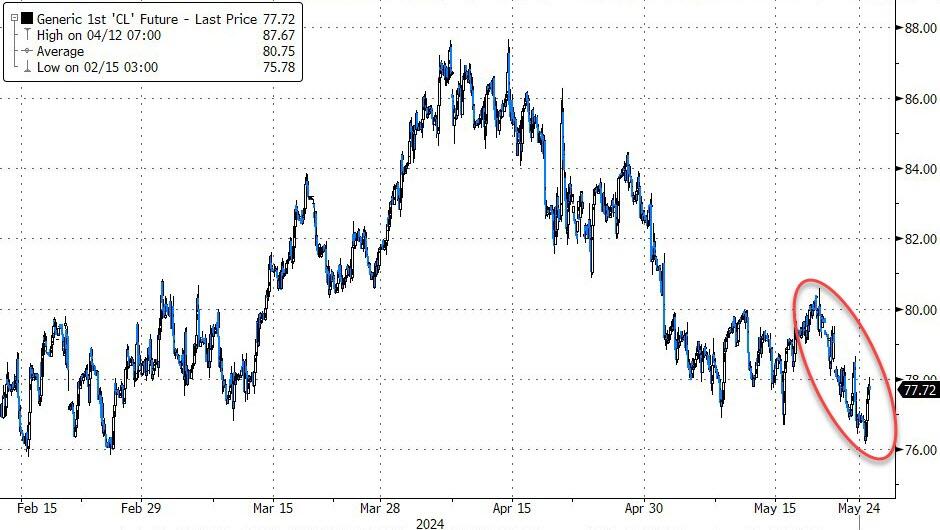

SHANGHAI CLOSED DOWN 27.52 PTS OR 0.88% //Hang Seng CLOSED DOWN 259.77 PTS OR 1.39%// Nikkei CLOSED DOWN 457.11 OR 1.17%//Australia’s all ordinaries CLOSED DOWN 1.04%///Chinese yuan (ONSHORE) closed DOWN TO 7,2438 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2587/ Oil DOWN TO 76.25 dollars per barrel for WTI and BRENT DOWN AT 80.82 /Stocks in Europe OPENED ALL RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 9004 CONTRACTS TO 505,445 WITH OUR HUGE LOSS IN PRICE OF $53.00 WITH RESPECT TO THURSDAY TRADING. WE HAD A CONSIDERABLE T.A.S. LIQUIDATION THURSDAY AS WELL AS LONGS BEING CLIPPED.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAY.… THE CME REPORTS THAT THE BANKERS ISSUED A HUGE SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A HUGE SIZED 10,385 EFP CONTRACTS WERE ISSUED: : JUNE 10,385 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE:10,385 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY FAIR SIZED TOTAL OF 1381 CONTRACTS IN THAT 10,385 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 9004 COMEX CONTRACTS..AND THIS SURPISING GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR HUGE LOSS IN PRICE OF $53.00// THURSDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT WAS A STRONG SIZED 2999 CONTRACTS. MOST OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. TODAY IS OF EXTREMELY IMPORTANCE TO OUR CROOKS IN YESTERDAY’S RAID

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (8.5398 TONNES+ 3.3716 EX FOR RISK/PRIOR) = 11.8961 TONNES ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5398 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.8961

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A MASSIVE $53.00 //// BUT WERE QUITE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A VERY FAIR GAIN OF 2333 CONTRACTS ON THURSDAY WITH OUR TWO EXCHANGES DESPITE THE LOSS IN PRICE. THE T.A.S. ISSUED ON THURSDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 4.245 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY (4.684 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 37 CONTRACTS OR 3700 OZ ( .1150 TONNES) PLUS 3.3716 TONNES OF EX FOR RISK/PRIOR

NEW STANDING: 8.5598 TONNES PLUS 3.1716 TONNES EX FOR RISK/PRIOR = 11.8961

ALL OF THIS WAS ACCOMPLISHED WITH OUR HUGE LOSS IN PRICE TO THE TUNE OF $53.00

WE HAVE REMOVED 1042 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET GAIN ON THE TWO EXCHANGES 1381 CONTRACTS OR 138100 (4.245 TONNES)

confirmed volume THURSDAY 349,121 contracts// strong

//speculators have left the gold arena

MAY 24 MAY GOLD

/ /// THE MAY 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | nil OZ . |

| Deposit to the Dealer Inventory in oz | 00 oz |

| Deposits to the Customer Inventory, in oz | 8680.770 OZ BRINKS 270 KILOBARS |

| No of oz served (contracts) today | 381 notice(s) 38100 OZ 1.185 TONNES |

| No of oz to be served (notices) | 25 contracts 2500 OZ 0.0777 TONNES |

| Total monthly oz gold served (contracts) so far this month | 2371 notices 237100 oz 7.374 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: 0 oz

we have 0 customer deposit:

total deposit nil oz

total customer withdrawals: 0

TOTAL WITHDRAWALS nil 0z

Adjustments: 1 brinks dealer to customer….289.359 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY

For the front month of MAY we have an oi of 385 contracts having GAINED 198 contracts.

We had 162 contracts served on THURSDAY, so we gained A STRONG 36 contracts or 3600 oz (0.1150 Tonnes). BANKERS USED THE RAID YSTERDAY TO OBTAIN THIS BADLY NEEDED PHYSICAL

JUNE DECREASED ITS OI BY 24,188 CONTRACTS DOWN TO 152,197 CONTRACTS.

JULY GAINED 102 CONTRACTS TO STAND AT 671

We had 4 contracts filed for today representing 400 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 4 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the MAY /2024. contract month, we take the total number of notices filed so far for the month (2371) x 100 oz ) to which we add the difference between the open interest for the front month of MAY ( 385 CONTRACTS) minus the number of notices served upon today (4 x 100 oz per contract( equals 275,200 OZ OR 8.559 TONNES. PLUS THE 3.3716 OF EX FOR RISK/PRIOR = 11.8961 TONNES

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (2371x 100 oz + (385 OI for the front month} minus the number of notices served upon today (4) x 100 oz which equals 275,200 oz (8.559 TONNES) PLUS 3.3716 EX FOR RISK/PRIOR = 11.8961 TONNES.

TOTAL COMEX GOLD STANDING FOR MAY: 11.8961 TONNES WHICH IS HUGE FOR THIS A NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX84XXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,548,842.069 48.17 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,563,550.534 OZ

TOTAL REGISTERED GOLD 7,314,146.996 ( 227.50 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,249,403.530 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 5,765,304 oz (REG GOLD- PLEDGED GOLD)= 179.33 tonnes //dropping like a stone

END

SILVER/COMEX

MAY 24

INITIAL

//2024// THE MAY 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 303,844.550 oz brinks delaware . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | nil |

| No of oz served today (contracts) | 87 CONTRACT(S) (435,000 OZ) |

| No of oz to be served (notices) | 33 contracts (0.165 million oz) |

| Total monthly oz silver served (contracts) | 6103 Contracts (30.515 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 0 deposits customer account:

total customer deposit nil oz

JPMorgan has a total silver weight: 128.997million oz/298.514 million or 43.28%

adjustment: 0

Comex withdrawals: 2

i)brinks 297,788.150 oz

ii delaware 6056.400 oz

TOTAL REGISTERED SILVER: 61.566MILLION OZ//.TOTAL REG + ELIGIBLE. 298.514 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF MAY/2024 OI: 120 CONTRACTS HAVING GAINED 61 CONTRACT(S).

.

We had 7 notices served on THURSDAY so we GAINED A HUGE 68 contracts or 340,000 oz underwent a STRONG QUEUE JUMP AS THEY WERE SET TO TAKE DELIVERY ON THIS SIDE OF THE POND.

JUNE SAW A GAIN OF 189 CONTRACTS RISING TO 1720

JULY SAW A LOSS OF 543 CONTRACTS DOWN TO 146,685

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 87 for 435,000 oz

CONFIRMED volume; ON THURSDAY 118,603 mammoth

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 6103 x 5,000 oz = 30.515 MILLION oz

to which we add the difference between the open interest for the front month of MAY ((120) and the number of notices served upon today 87x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2024 contract month: 6103 notices served so far) x 5000 oz + OI for the front month of MAY (120)x number of notices served upon today minus (87x 5000 oz of silver standing for the may contract month equates to 30.680 MILLION OZ.

New total standing: 30.680 million oz.

There are 61.566 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

MAY 24 WITH GOLD DOWN $2.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 833.36 TONNES

MAY 23 WITH GOLD DOWN $53.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 22 WITH GOLD DOWN $32.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 21 WITH GOLD DOWN $12,00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 20 WITH GOLD UP $21.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.10 TONNES OF GOLD INTO THE GLD//NEW TOTAL 838.54 TONNES

MAY 17 WITH GOLD UP $31.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//NEW TOTAL 833.36 TONNES

MAY 16 WITH GOLD DOWN $7.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//NEW TOTAL 833.36 TONNES

MAY 15 WITH GOLD UP $34.90 ON THE DAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD

///INVENTORY RISES TO 831.93 TONNES

MAY 14 WITH GOLD DOWN $17.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//

///INVENTORY RISES TO 831.33 TONNES

MAY 13 WITH GOLD DOWN $31.10 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD////INVENTORY RISES TO 831.93 TONNES

MAY 10 WITH GOLD UP $34.65 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 9 WITH GOLD UP $18.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 8 WITH GOLD DOWN $0.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 830.47 TONNES

MAY 7 WITH GOLD DOWN $6.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 832.19 TONNES

MAY 6WITH GOLD UP $21.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .55 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 831.64 TONNES

MAY 2 WITH GOLD UP $0.20 ON THE DAY; SMAKK CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 830.47 TONNES

MAY 1 WITH GOLD UP $7.80 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNES

APRIL 29WITH GOLD UP $10,55TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNES

APRIL 26WITH GOLD UP $5.40TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.54 TONNES FROM THE GLD /INVENTORY RISES AT 832.19 TONNES

APRIL 25WITH GOLD UP $5.05 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD /INVENTORY RISES AT 833,63 TONNES

APRIL 19 WITH GOLD UP $15.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 4.32 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 831.91 TONNES

APRIL 18 WITH GOLD UP $11.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE WITHDRAWAL OF 2.59 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 827.59 TONNES

APRIL 17 WITH GOLD DOWN $17.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 830;18 TONNES

APRIL 16 WITH GOLD UP $23.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 828.45 TONNES

APRIL 15 WITH GOLD DOWN $. 80 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A HUGE WITHDRAWAL OF 1.80 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 824.84 TONNES

APRIL 12 WITH GOLD UP $2.80 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD/ INVENTORY RISESS AT 830.75 TONN

GLD INVENTORY: 833.36 TONNES, TONIGHTS TOTAL

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 24 WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF .822 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 421.313 MILLION OZ

MAY 23 WITH SILVER DOWN $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.736 MILLION OZ FROM THE SLVINVENTORY INCREASES TO 420.491 MILLION OZ

MAY 22 WITH SILVER DOWN $0.66 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 21 WITH SILVER DOWN $0.41 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A DEPOSIT OF 3.792 MILLION OZ FROM THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 20 WITH SILVER UP $1.28 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 1.005 MILLION OZ FROM THE SLV// INVENTORY LOWERS TO 418.435 MILLION OZ

MAY 17 WITH SILVER UP $1.37 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 868,000 OZ FROM THE SLV// INVENTORY LOWERS TO 419.440 MILLION OZ

MAY 16 WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY REMAINS AT 420.308 MILLION OZ

MAY 15 WITH SILVER UP 101 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A WITHDRAWAL OF 1.919 MILLION OZ FROM THE SLV

INVENTORY RESTS AT 420.308 MILLION OZ

MAY 14 WITH SILVER UP 25 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;

INVENTORY RESTS AT 422.227 MILLION OZ

MAY 13 WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;NVENTORY RESTS AT 422.227 MILLION OZ

MAY 10 WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A HUGE WITHDRAWAL OF 1.,828 MILLION OZ//INVENTORY RESTS AT 422.227 MILLION OZ

MAY 9 WITH SILVER UP 78 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 8 WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 7WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 6 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.055 MILLION OZ

MAY 3 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 2WITH SILVER UP 0.12 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/ A WITHDRAWALOF 4.471 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 1 WITH SILVER UP 0.09 TODAY: SMALLCHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF ,457 MILLION OZ INTO THE SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 29WITH SILVER UP $0.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 26WITH SILVER DOWN 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.097 MILLION OF SILVER INTO THE SLV// :SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 25WITH SILVER UP $.05 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 1.534 MILLION OF SILVER OUT OF THE SLV// :SLV INVENTORY RESTS AT 428.717 MILLION OZ

APRIL 24/WITH SILVER DOWN $.05 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 11.904MILLION OF SILVER INTO THE SLV// :SLV INVENTORY RESTS AT 428.280 MILLION OZ

APRIL 23/WITH SILVER UP $0.11TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV / :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 22/WITH SILVER DOWN $1.51 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.194 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 19/WITH SILVER UP 42 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.657 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 418.570 MILLION OZ

APRIL 18/WITH SILVER DOWN $.04TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.977 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 422.227 MILLION OZ

APRIL 17/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF .868 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 426/204 MILLION OZ

APRIL 16/WITH SILVER DOWN $0.46 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF NON EXISTENT SILVER// :SLV INVENTORY RESTS AT 427.072 MILLION OZ

APRIL 15/WITH SILVER UP $0.88 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 12/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 4.069 MILLION OZ FROM THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 11/WITH SILVER UP $0.23 TODAY: STRANGE INDEED! HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.931 MILLION OZ :SLV INVENTORY RESTS AT 437.998 MILLION OZ

CLOSING INVENTORY 421.313 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

Schiff: Silver has New Support At $30

FRIDAY, MAY 24, 2024 – 01:00 PM

In this episode, Peter recounts silver’s notable rise above $30/oz and addresses the latest FOMC minutes that were released this week, in which the Fed signaled that rate cuts could be delayed even further. Peter also calls out the SchiffGold Silver Breakout Sale to celebrate the metal’s long-awaited breakout.

Silver’s rise to $32.50 on Monday has established a new support level at $30/oz:

“Silver is back down at $30.73. That’s a pretty substantial pullback—about $1.80 or so— from the $32.50 that it traded for on Monday. …That doesn’t mean Silver can’t go below $30, but I think $30 is to silver what $2,000 was to gold. Once we broke up $2,000, $2,000 became support, and yes, every once in a while we dip below $2,000, but we never stayed below it for long, and it quickly came back.”

While the Fed is uncertain about when rate cuts are likely, it’s still signaling a loosening of monetary policy later this year. The market mistakenly sold off gold and silver in response:

“The traders who are selling gold and silver still don’t understand why the prices are rising in the first place. It doesn’t matter when the Fed cuts rates. It doesn’t even matter if they do cut rates. They never have to cut rates. The Fed could leave rates right where they are, and gold and silver prices should skyrocket. Why is that? Because they’re too low. The Fed aborted the hiking campaign too soon, and so it doesn’t matter if they cut rates.”

The Fed pays lip service to raising rates if needed but fails to see that rate hikes are long overdue:

“They said that they were prepared to raise rates if the economic data supported that. But that’s not true either, because the economic data already supports that. They’re saying, ‘If the data changes, if something happens and we get new data that shows that higher rates would be appropriate, well, then we’ll raise rates.’ … The data that they’re looking at right now shows that interest rates need to go up. The fact that they’re ignoring that data— and they’re not only not hiking rates, but they’re still talking about when they’re going to cut rates— that proves that they’re never going to hike rates, because if they were going to hike rates, they would be hiking it right now.”

Fed officials think economic growth contributes to inflation, but this betrays a fundamental misunderstanding of how growth works:

“The faster an economy grows, the more prices go down. That’s what economic growth does. That’s why it’s a good thing. It lowers prices. Real economic growth means the economy is producing more stuff, right? That’s the economic growth: we get more goods and more services out of the economy because that’s what a growing economy is supposed to deliver— a higher standard of living. … How can economic growth make prices go up? How can a big increase in the supply of goods and services make those goods and services more expensive? It’s not. It’s going to make them less expensive!”

Peter closes by recounting the history of the U.S. government taking silver out of coins. In the 1960s, Uncle Sam went to a great deal of effort to hide the fact that he was ripping off American citizens:

“Why not just make dimes and quarters with these smooth edges just like pennies and nickels? Because they were counterfeiting the coins! You see, early on, they didn’t tell anybody that they took the silver out. They wanted people to think that the dimes and quarters that they were getting were still made out of silver. That’s why they put the nickel on the copper. That’s why they put mill marks on these copper-clad coins— because they wanted them to look like the coins they used to work with. That’s counterfeit. That is fraud! That is what went on in this country. The government defrauded American citizens out of their lawful silver money.”

In other news, the price of copper has exploded recently. Check out Peter’s Blog for an analysis of copper’s all-time high price.

end

Indian Central Bank Goes on Gold Buying Spree

Mike Maharrey

May 24, 2024

The Reserve Bank of India has followed the lead of China and other Eastern central banks and ramped up its accumulation of gold.

According to the latest data released by the RBI, the Indian central bank increased its gold reserves by 24 tons through the first four months of the year. The RBI added 16 tons of gold to its holdings through the entirety of 2023.

The Reserve Bank of India currently holds just over 827 tons of gold in its reserves. India ranks ninth in the world in total gold holdings.

According to a report by FirstPost.com, India is increasing its gold holdings “as a hedge against volatility amid geopolitical tensions and in challenging times,” and gold is “a component of strategic reserve diversification.”

Diversification has become a common theme in the world of central banking. As the U.S. has increasingly used the dollar’s status as the reserve currency as a foreign policy weapon, many countries have elected to minimize their exposure to dollars.

This has driven a broader trend of gold moving from the West to the East and into emerging markets.

The RBI noted this trend in a recent bulletin.

“The heightened global uncertainty is sending emerging market central banks on a spree of buying gold, adding 290 tonnes in the first quarter of 2024 and accounting for a quarter of overall global gold demand. Amid geopolitical developments and a slowing global economy, these central banks are signaling that living in challenging times calls for strategic diversification”

India went on a big gold-buying spree in 2022, adding about 200 tons of gold to its reserves before slowing purchases later in mid-2023. Since resuming purchases late last year, the RBI’s gold holdings have increased from 7.8 percent of its total reserves to 8.7 percent. On top of physical gold purchases, India’s gold holdings are increasing in both dollar and rupee terms thanks to the rising price of gold.

Central banks globally have been gobbling up gold. Last year, central bank gold buying fell just 45 tons short of 2022’s multi-decade record.

According to the World Gold Council, central banks net gold purchases totaled 1,037 tons in 2023. It was the second straight year central banks added more than 1,000 tons to their total reserves.

Central bank gold buying in 2023 built on the prior record year. Total central bank gold buying in 2022 came in at 1,136 tons. It was the highest level of net purchases on record dating back to 1950, including since the suspension of dollar convertibility into gold in 1971.

end

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS//GOLD AND SILVER COMMENTARY

Bullion prices pause…

This pullback in prices might provide the best opportunity buy gold and silver before China’s continuing demand drives them far higher.

| MACLEODFINANCEMAY 24∙PAID |

Gold and silver corrected sharply this week, with gold down $85 from last Friday’s close at $2342 in European trade this morning. And silver was off $1.30 at $30.56 over the same time period. While nominally these appear to be large numbers, in percentage terms and given their recent rises these corrections should be regarded as to be expected.

It is now widely accepted that both metals are being drained out of western vaults to satisfy demand in China. In particular, silver’s volatility indicates that there is an alarming lack of liquidity in western vaults, especially when one bears in mind that the large majority of vaulted gold and silver is custodial and therefore not available to market makers and bullion banks to cover their positions.

Many goldbugs suspect that earmarked reserves of both metals are being tapped into by bullion banks as part of their suppression schemes. Whether that is conspiracy or fact should not concern us. The problem for the paper establishment used to controlling forwards and futures values is that pricing is being taken away from them. For example, at one point this week, silver was trading in Shanghai at the equivalent of $36, a premium of $4 or 11% over spot. Clearly, Chinese and other banks are strongly incentivised to arbitrage these differentials by sourcing silver in London and Comex for delivery in Shanghai.

It is no exaggeration to claim that prices are no longer being set in the West’s paper markets. This is something that goldbugs have been praying for, but perhaps do not yet appreciate. So where does this leave the bullion bank establishment?

Comex Swaps’ short positions in silver have become alarming, as the next chart shows:

At net short 37,522 contracts, this represents 187,610,000 ounces, equivalent to over 20% of global mine output. It is also the largest net short position since April 2017 when silver was only $17.40 so the financial commitment (damage) at current prices is far greater. Furthermore, this year a further 78,975,000 silver ounces have stood for delivery, which didn’t happen in 2017.

As an illiquid market, the establishment’s silver position is worrying to say the least. Either of two events might tip it over the edge: if gold continues to rise in value, silver is bound to go with it at twice the rate; and if public demand for ETFs, coin, and bars begin to reflect bullishness the squeeze on the establishment will intensify.

Both these appear to be likely. The chart for gold in USD looks very bullish, and in this context the current correction is perfectly normal taking the price back to possibly test the 55-day moving average, currently at $2290:

The point about paper markets losing control over pricing is made clear by assessing the potential demand and behaviour of China’s household savers. Their annual savings run at about 46 trillion yuan ($6.3 trillion) which is the equivalent of 85,000 tonnes of gold. With property and the stock market out of fashion, most of this is going into bank deposits. Undoubtedly, it won’t take much for a gold-loving Chinese population to start bidding prices higher. In fact, it has already started.

END

3. CHRIS POWELL//GATA DISPATCHES

CHRIS POWELL…

India’s central bank buys 1.5 times more gold in January-April than in all of 2023

Submitted by admin on Wed, 2024-05-22 22:47 Section: Daily Dispatches

By Gayatri Nayak

The Times of India, Mumbai

Thursday, May 23, 2024

The Reserve Bank of India added 24 tonnes of gold to its stock of reserves in four months from January to April this year as a hedge against volatility amid geopolitical tensions. This is reckoned to be a part of strategic diversification of reserves in challenging times.

This is almost 1 1/2 times the volume it did during the whole of 2023 when it added 16 tonnes to its reserves, an analysis of the Reserve Bank data indicates.

The Reserve Bank held 827.69 tonnes worth of gold as a part of its foreign exchange reserves as of April 26,2024, up from 803.6 tonnes as of end December according to the latest Reserve Bank of India data

Though India has been one of the largest consumers of gold as far as the Indian household is concerned, the country’s central bank was rarely active in piling up its gold reserves.

The bank came in for heavy criticism when it had pledged a part of its gold reserves in 1991 when it faced a foreign-exchange crisis. Though all the gold is back in the central bank’s coffers, it started adding to its stocks from market purchases only from December 2017.

Though it was seen actively buying from the markets in 2022, it was laying low in 2023 only to come back aggressively since January this year. …

… For the remainder of the report:

* * *

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS /

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT//COFFEE BEANS//

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

ASIA TRADING//FRIDAY MORNING/THURSDAY NIGHT

SHANGHAI CLOSED DOWN 27.52 PTS OR 0.88% //Hang Seng CLOSED DOWN 259.77 PTS OR 1.39%// Nikkei CLOSED DOWN 457.11 OR 1.17%//Australia’s all ordinaries CLOSED DOWN 1.04%///Chinese yuan (ONSHORE) closed DOWN TO 7,2438 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2587/ Oil DOWN TO 76.25 dollars per barrel for WTI and BRENT DOWN AT 80.82 /Stocks in Europe OPENED ALL RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2438

OFFSHORE YUAN: DOWN TO 7.2587

SHANGHAI CLOSED DOWN 27.52 PTS OR 0.88 %

HANG SENG CLOSED DOWN 259.77 PTS OR 1.39%

2. Nikkei closed DOWN 457.11 PTS OR 1.17 %

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 104.77 EURO RISES TO 1.0841 UP 30 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.01 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 156.95 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.590/Italian 10 Yr bond yield DOWN to 3.844 SPAIN 10 YR BOND YIELD DOWN TO 3.343%

3i Greek 10 year bond yield DOWN TO 3.590

3j Gold at $2340.45//Silver at: 30.56 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 40/ 100 roubles/dollar; ROUBLE AT 89.61

3m oil into the 76 dollar handle for WTI and 80 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 156.95/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.010% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9147 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9918 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.477 UP 0 BASIS PTS…

USA 30 YR BOND YIELD: 4.581 UP 0 BASIS PTS/

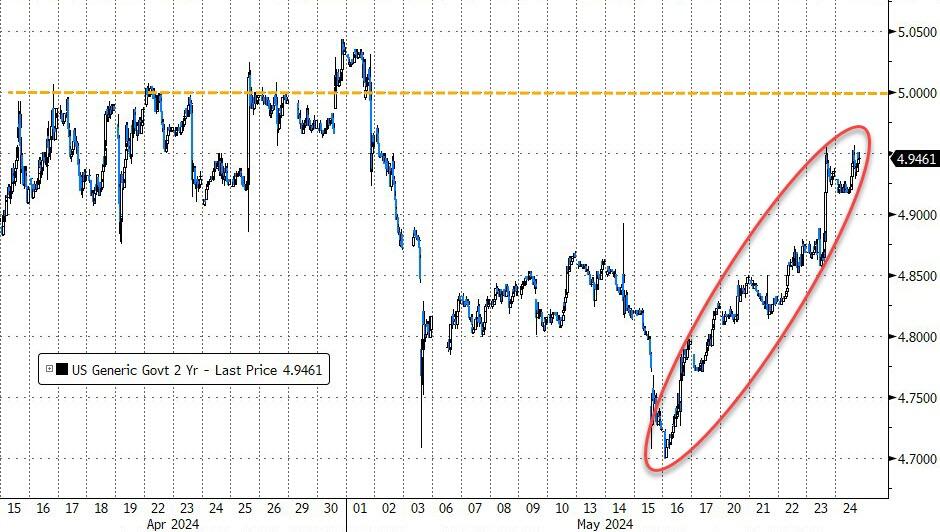

USA 2 YR BOND YIELD: 4.929 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.24…(TURKEY)

10 YR UK BOND YIELD: 4.2906 UP 4 PTS

2a New York OPENING REPORT

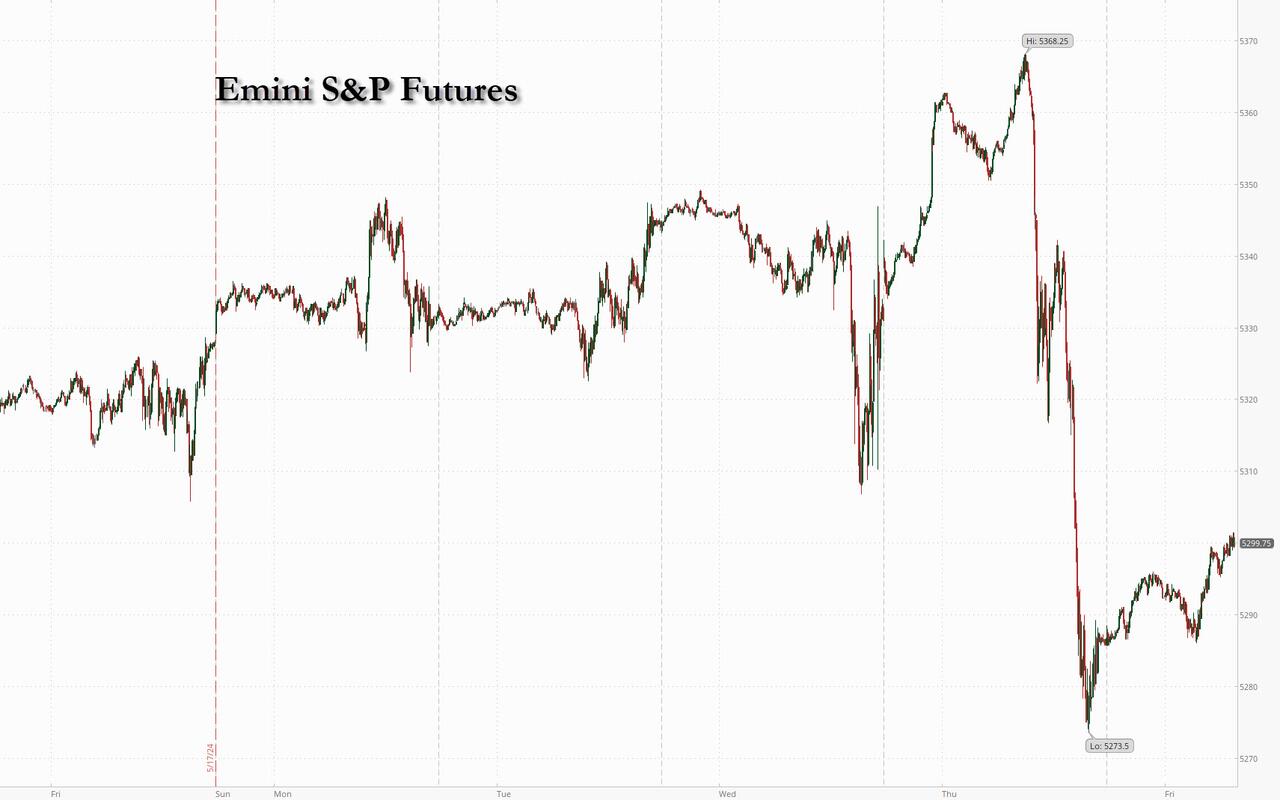

Futures Rebound After Thursday Rout As Rate Cut Expectations Fade

FRIDAY, MAY 24, 2024 – 07:56 AM

After Thursday’s rout, which saw the overbought S&P first hit an all time high before traders suddenly dumped everything (following hotter than expected PMI and Initial claims reports has further delayed expectations for the Fed’s first rate hike ostensibly to December) to buy Nvidia, whose market cap soared by over $200 billion to a record $2.55 trillion, on Friday US equity futures and treasuries have staged a modest rebound. As of 7:30am, S&P 500 and Nasdaq 100 futures rose 0.3%, led by premarket gains at Micron, Microchip Technology and Advanced Micro Devices all of which continue to benefit from bullish sentiment around artificial intelligence following Nvidia’s blockbuster earnings. Europe’s Stoxx 600 index slipped 0.4%, playing catch-up with Wednesday’s Wall Street drop, which was the biggest this month. 10Y yields dropped 1bp to 4.47% after surging the previous session by as much as 8bps ahead of a half-day trading session for the US bond market; the Bloomberg Dollar Spot Index was headed for its first drop in five days, but still on track to post its best weekly gain since April 12. Oil continued its decline despite the signal from macro data that the economy is actually growing quite strong, in what appears to be accelerating CTA liquidations. Today’s macro events includes the April prelim Durable Goods report, the Kansas City Fed and the May final UMich report.

In premarket trading, Apple shares ticked 0.7% higher after the technology firm’s price target is raised to a Street-high view of $275 from $250 at Wedbush, a move that reflects “iPhone demand turning the corner into an AI driven iPhone 16 supercycle.” Tesla was flat after a report that Elon Musk’s SpaceX has initiated discussions about selling existing shares at a price that could value the company at roughly $200 billion. Here are some other notable premarket movers:

- Bilibili (BILI US) shares fluctuate between gains and losses as analysts debate the outlook for the Chinese online entertainment firm’s goal toward reaching breakeven, with Barclays upgrading the stock to equal weight from underweight.

- Domo (DOMO US) shares slide 11% after the enterprise software firm’s second-quarter revenue forecast came in below estimates.

- DuPont (DD US) shares climb 1.8% after an upgrade to overweight at Wells Fargo.

- Exact Sciences (EXAS US) slip 2.0% after rival Guardant Health’s Shield blood test to screen for colorectal cancer received the support of an FDA advisory panel Thursday.

- Intuit (INTU US) shares are down 6.2% after the tax-preparation software company gave a forecast for adjusted fourth-quarter earnings that is weaker than expected. However, it raised its full-year revenue forecast. The company also said the CEO of its Credit Karma business will retire by the end of the year.

- Summit Theraputics (SMMT US) shares tumble 20% after trial data on Hong Kong-listed biopharmaceutical company Akeso’s lung cancer drug was seen as disappointing. Summit acquired exclusive rights for development and commercialization of the drug in the US, Canada, EU and Japan from Akeso for $500 million in late 2022.

- Workday (WDAY US) shares fall 12% after the software company cut its full-year subscription revenue forecast. The company also reported 1Q results, which analysts said were mixed. Peer Salesforce (CRM US) also decline 1.4%

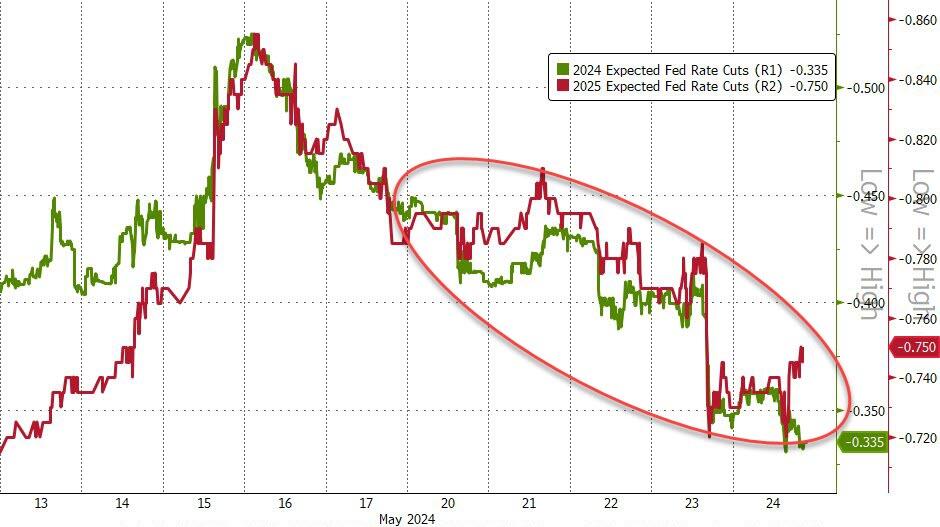

The market mood turned more sombre after stronger-than-expected US business activity data forced traders to push back rate-cut expectations by a month. The change put Bloomberg’s dollar index on track for its biggest weekly gain since early April, while rate-sensitive Treasury two-year yields traded just off the three-week highs above 4.95% hit on Thursday. Separately, the latest FOMC minutes showed policymakers are in no rush to cut rates, with some even seeing a need for more restrictive policy.

To that point, this morning Goldman pushed back its forecast of the Fed’s first rate cut back one meeting, from July to September: “Earlier this week, we noted that comments from Fed officials suggested that a July cut would likely require not just better inflation numbers but also meaningful signs of softness in the activity or labor market data. After the stronger May PMIs and lower jobless claims, this does not look like the most likely outcome” wrote Goldman economist Jan Hatzius.

“What we have is this repricing of rate cuts,” said Kenneth Broux, a strategist at Societe Generale. “Two-year yields are again within touching distance of 5%, so the debate on whether US yields have peaked is still alive.” For now, profits at larger US companies appear resilient to the higher-for-longer rates backdrop, offering encouragement to equity bulls. For broader positive momentum to reverse, “we’ll need to see if there’s a repricing of Fed cuts to hikes but the bar for that is still very high,” Broux said.

The Fed minutes and robust data have put MSCI’s global benchmark on track for its first weekly decline in five, and some strategists, including BofA’s Michael Hartnett are warning the rally is at risk of overheating. Barclays strategists said stock gains are starting to “look tired.”

European stocks followed their US and Asian counterparts lower after traders pushed back expectations of Fed interest rate cuts. The Stoxx 600 fell 0.5% with almost all subindexes in the red, with only retail and auto stocks rising. The tech sector leads declines, breaking a two-day advance fueled by sentiment around Nvidia. In company news, drugmakers GSK and Boehringer win the first US Zantac cancer case to go to trial. Here are some of the biggest European movers Friday:

- GSK rises after winning the first US Zantac cancer case to go to trial. It’s another positive step, according to Jefferies analysts

- Drugmakers GSK and Boehringer Ingelheim persuaded a Chicago jury to reject a woman’s claim that the blockbuster heartburn drug Zantac caused her cancer

- Pepco Group surges as much as 13%, after reporting gross margin improvement in 1H ended March 31 and guided for 20% increase of underlying Ebidta in FY

- DNB Bank rises as much as 2.4% after a Barclays double-upgrade as analysts grow more constructive on Norway versus other Nordic countries in a rate-cut environment

- Gerresheimer rises as much as 0.4% after being upgraded to buy by analysts at Hauck & Aufhaeuser following its deal to buy the holding company of Bormioli Pharma

- Renault gains as much as 3.2% as UBS upgrades to hold from sell, saying cash return expectations are now building due to factors including the cancellation of Ampere’s IPO

- Julius Baer gains as much as 3.4% after higher-than-expected assets under management outweighed concerns over weak net new money

- Acciona Energia falls as much as 8.5% after cutting its Ebitda guidance for 2024. Analysts say it’s “perplexing” the company failed to fully quantify its new outlook

- Zealand Pharma drops as much as 7.1% after reporting topline results from a trial investigating dapiglutide as an obesity treatment, which analysts called underwhelming

- Celon Pharma drops as much as 7.4% after announcing a venture with US life science fund Tang Capital for the development of depression drugs

- Hargreaves Lansdown falls as much as 5%, with Liberum analysts highlighting the opportunity to take profits after the investment platform rebuffed a £4.7 billion offer

In FX, the Bloomberg Dollar Spot Index was headed for its first drop in five days, but still on track to post its best weekly gain since April 12. The Norwegian krone topped the G-10 FX leaderboard while cable was steady at 1.2696 after falling earlier as UK retail sales missed forecasts; GBPUSD is poised for its best monthly gain since November on view the Bank of England will take longer to cut interest rates. USD/JPY rose 0.1% to 157.01, up a third day; Japan’s inflation cooled for a second month while staying above the Bank of Japan’s price target as the yen’s recent depreciation fuels concerns that cost-push inflationary pressures may be here to stay

“Fed cuts are likely at least four months away barring a sudden growth shock, while other central banks are starting to cut, albeit only gradually,” Wells Fargo strategists led by Michael Schumacher wrote in a research note. “And if there is a further repricing in global rate expectations, that would likely only serve to weigh on global growth expectations, tilting the balance in favor of US dollar strength”

In rates, Treasuries edge higher, with US 10-year yields falling 1bp to 4.47%. Gilts gain, led by the short end after UK retail sales fell at the fastest pace this year. UK two-year yields fall 4bps. SIFMA recommend early close for cash bond market Friday at 2pm New York, ahead of Memorial Day weekend. US yields richer by up to 1bp across front-end of the curve with 2s10s spread wider by almost 1bp as long-end yields remain close to Thursday’s closing levels. In UK 2-year gilts richer by around 2bp, outperforming across front-end of the curve

In commodities, oil prices decline, with WTI falling 0.9% to trade near $76.20. Spot gold rises 0.5%.

In crypto, Bitcoin is modestly softer and holds just above $67k, while Ethereum trades around $3.7k after the SEC approved plans from NYSE, CBOE and Nasdaq for the listing of spot Ethereum ETFs.

Looking at today’s calendar, US economic data includes April durable goods orders (8:30am), May University of Michigan sentiment (10am) and Kansas City Fed services activity (11am). Fed officials’ scheduled speeches include Waller at 9:20am, giving a keynote address at a Central Bank of Iceland event in Reykjavík on R*.

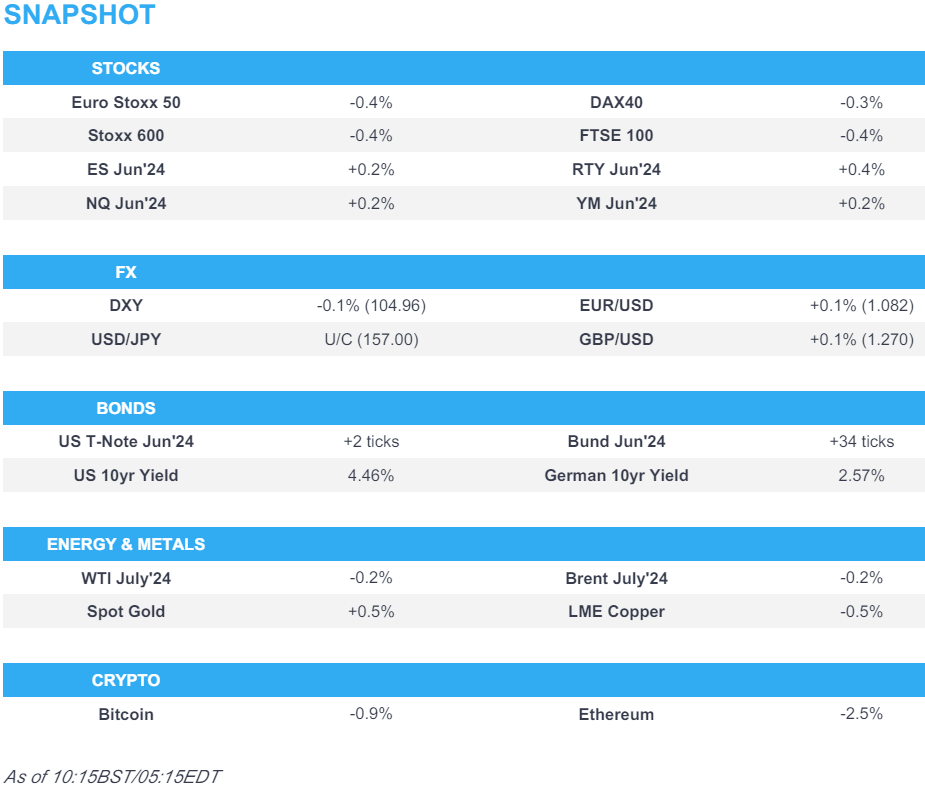

Market Snapshot

- S&P 500 futures up 0.2% to 5,295.50

- STOXX Europe 600 down 0.5% to 519.01

- MXAP down 0.8% to 179.35

- MXAPJ down 0.9% to 561.72

- Nikkei down 1.2% to 38,646.11

- Topix down 0.4% to 2,742.54

- Hang Seng Index down 1.4% to 18,608.94

- Shanghai Composite down 0.9% to 3,088.87

- Sensex up 0.1% to 75,526.60

- Australia S&P/ASX 200 down 1.1% to 7,727.59

- Kospi down 1.3% to 2,687.60

- German 10Y yield little changed at 2.58%

- Euro little changed at $1.0820

- Brent Futures down 0.3% to $81.13/bbl

- Gold spot up 0.4% to $2,338.61

- US Dollar Index little changed at 105.02

Top Overnight News

- European stocks followed New York and Asia lower after traders pushed back expectations of interest rate cuts by the Federal Reserve to later in 2024 following strong US economic data.

- Chinese President Xi Jinping urged deeper reforms for some of the country’s key sectors as investors look for hints on major policy shifts to be revealed at the upcoming party conclave.

- UK retail sales fell at the fastest pace this year as consumers delayed spending due to rainy weather, underlying the hurdles facing the Conservative government’s bid for reelection.

- Overseas issuers sold yen bonds at the fastest pace in five years this month, chasing cheap funds before an expected interest rate hike by the Bank of Japan pushes up borrowing costs.

- Tesla (TSLA) to cut Model Y output at Shanghai plant by at least 20% during March-June 2024, via Reuters citing sources

- US Treasury Secretary Yellen said many Americans are still struggling with inflation, while she expressed concern over ‘substantial’ increases in living costs, according to FT.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks followed suit to the selling on Wall St where the initial NVIDIA-related euphoria was soured after strong US PMI data lifted the dollar and yields. ASX 200 declined with underperformance seen in the consumer and rate-sensitive sectors. Nikkei 225 gapped down at the open beneath the 39,000 level amid the headwinds from the US, while participants digested mixed inflation data which slowed in pace from the prior month. Hang Seng and Shanghai Comp were lower with the former weighed on by losses in the property sector and with tech stocks pressured by mixed earnings, while the downside was limited in the mainland amid a lack of catalysts.

Top Asian News

- RBNZ Deputy Governor Hawkesby said while near-term inflation risks are to the upside, he is confident medium-term inflation is returning to the target. Hawkesby said no single data point will cause a rate hike and he is watching domestic inflation pressures and expectations, while he added that cutting interest rates is not part of the near-term discussion and there is a lot of uncertainty about tradable inflation going forward.

- RBNZ Assistant Governor Silk said RBNZ is concerned about near-term inflation risks and adjusts its models after underestimating domestic inflation.

European bourses, Stoxx 600 (-0.5%), are entirely in the red, though off worst levels, with Europe playing catch-up to the risk-off sentiment which reverberated from the Wall Street afternoon session. European sectors hold a strong negative bias; Banks and Tech reside as the laggards whilst Retail, Autos & Parts, and Media are among the better performers, albeit still mostly in the red. US Equity Futures (ES +0.2%, NQ Unch, YM +0.2%, RTY +0.3%) are marginally firmer attempting to pare back some of yesterday’s hefty losses.

Top European News

- ECB’s Schnabel says some elements of inflation are proving persistent; would caution against moving too fast on rates

- UK Ofgem Energy Price Cap (GBP): 1,568 (exp. 1,574; prev. 1,690), -7% (exp. -7%) for dual-fuel households.

- Barclays expects the BoE to begin lowering rates in August with rate cuts to follow in November and December.

FX

- DXY is marginally softer vs. some peers but ultimately still around yesterday’s PMI-inspired best levels which saw DXY tick above the 105 mark; trough thus far at 104.92.

- EUR is a touch firmer vs. the USD after finding support above the 1.08 mark. Price action this week has largely been at the whim of the USD with yesterday’s EZ PMI data overshadowed by the equivalent US release. overshadowed by the equivalent US release.

- GBP is steady vs. the USD after yesterday’s PMI-induced downside, and brushes off initial pressure following the softer-than-expected Retail Sales figures. Cable currently trades on either side of 1.27.

- JPY is marginally softer vs. the USD following mixed Japanese inflation metrics overnight which warrant a cautious stance from the BoJ and an unchanged rate at the June meeting. For now, the pair is contained within yesterday’s 156.50-157.19 range.

- Antipodeans are both contained vs. the USD in quiet trade. AUD/USD has been unable to launch much of a recovery from recent losses. NZD/USD is steady vs. the USD having performed much better than its antipodean counterpart this week on account of a hawkish RBNZ.

- PBoC set USD/CNY mid-point at 7.1102 vs exp. 7.2539 (prev. 7.1098).

Fixed Income

- USTs are marginally firmer with prices unable to launch much in the way of a meaningful recovery after yesterday’s PMI-induced losses and awaiting impetus from US Durable Goods. Today’s range is well contained within yesterday’s 108.17+ to 109.06 parameters.

- Bunds are attempting to claw back some of the lost ground seen yesterday in the wake of encouraging EZ PMI metrics, which were then followed up by an uptick in EZ wages and a particularly hot US PMI release.

- Gilts are attempting to atone for yesterday’s downside which followed the broader dynamics within global fixed income markets. Gains are smaller than their German counterpart despite disappointing UK retail sales metrics which saw a M/M contraction of -2.3% vs. exp. -0.4%.

Commodities

- Crude is modestly softer in what has been a catalyst-thin session thus far; Brent sits in a USD 81.05-81.55/bbl.

- Spot gold and silver attempt to recover from yesterday’s steep losses in the absence of fresh catalysts this morning; XAU sits in a USD 2,325.47-2,340.69/oz intraday range.

- Mixed/contained trade across base metals as prices consolidate from this week’s choppiness which saw 3M LME copper print record highs on Monday before tumbling over USD 700/t throughout the week.

- OPEC+ to meet virtually on June 2nd, according to statement (prev. June 1st)

Geopolitics

- China on Friday sent multiple bombers to conduct mock missile strikes in the Taiwanese drills, with dozens of missiles used in the drills, according to Chinese state media.

- Israel’s PM and ministers decided to expand the mandate of the negotiating team during the war cabinet meeting on Wednesday night, according to Axios’ Ravid citing an Israeli senior official, although the official noted that it is not certain that it will be possible to achieve a breakthrough in the talks on abductees.

- American and British aircraft launched two raids on Hodeidah Airport in Yemen. It was later reported that a Yemeni official said about ten Houthi leaders and experts were killed and wounded in the marches and missiles as the coalition targeted an operations room in Hodeidah, according to Sky News Arabia.

- Russian President Putin is reportedly ready to halt the war in Ukraine with a negotiated ceasefire which recognises current battlefield lines, according to Reuters sources; but is prepared to fight on if Ukraine and the West do not respond

- Ukrainian President Zelensky is set to attend the G7 leaders meeting in a fresh push for aid, according to Bloomberg. It was separately reported that House Speaker Johnson said they would soon host Israeli PM Netanyahu for a joint session of Congress.

- Japan imposed sanctions against Russian-related entities and an individual. It was separately reported that South Korea imposed sanctions on seven North Korean individuals and two Russian vessels.

- China’s Defence Ministry said military drill exercises around Taiwan continued and they will test the ability to jointly seize power, strike jointly, and occupy and control key areas.

- US, Australia, Britain, Canada, Japan, Czech Republic, Lithuania and German offices in Taipei issued a joint statement supporting Taiwan’s participation at the WHO meeting.

- Azerbaijan takes control of four villages on the border with Armenia, according to Tass

US Event Calendar

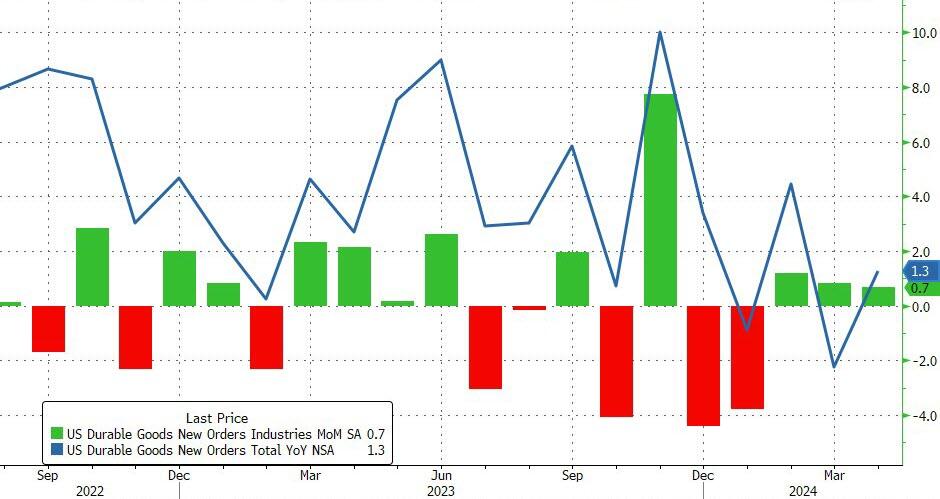

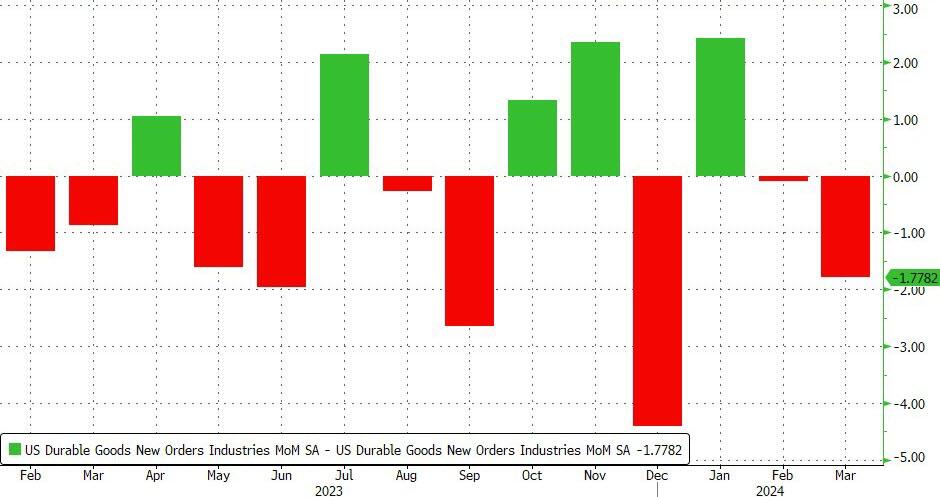

- 08:30: April Durable Goods Orders, est. -0.8%, prior 2.6%, revised 0.9%

- April Durables Less Transportation, est. 0.1%, prior 0.2%, revised 0%

- April Cap Goods Orders Nondef Ex Air, est. 0.1%, prior 0.1%, revised -0.2%

- April Cap Goods Ship Nondef Ex Air, est. 0.1%, prior 0%, revised -0.1%

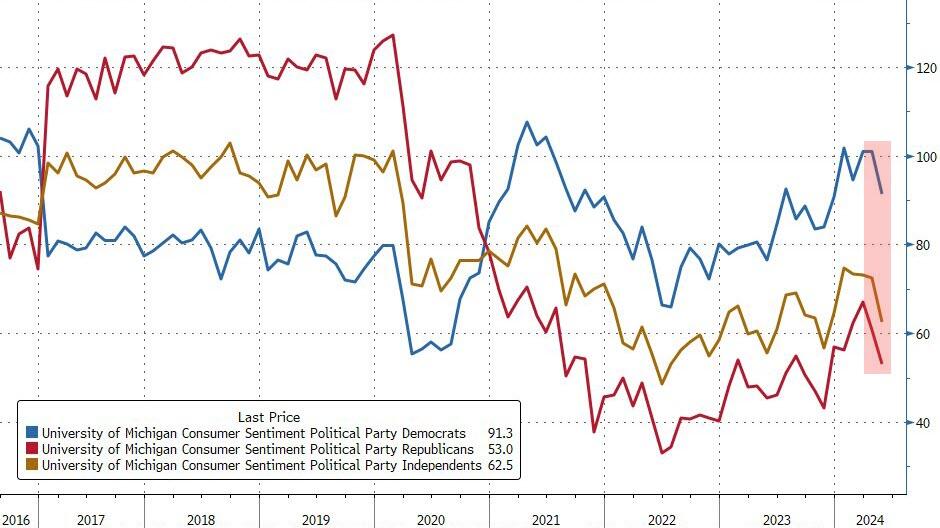

- 10:00: May U. of Mich. Sentiment, est. 67.7, prior 67.4

- May U. of Mich. Current Conditions, est. 68.8, prior 68.8

- May U. of Mich. Expectations, est. 67.0, prior 66.5

- May U. of Mich. 1 Yr Inflation, est. 3.4%, prior 3.5%

- May U. of Mich. 5-10 Yr Inflation, est. 3.1%, prior 3.1%

- 11:00: May Kansas City Fed Services Activ, prior 9

Central Bank Speakers

- 09:20: Fed’s Waller Gives Keynote Address on R*

DB’s Jim Reid concludes the overnight wrap

It was a fascinating day yesterday as a barnstorming reaction to Nvidia’s results (+9.32%) clattered headfirst into stronger data and rising yields (UST 10yr +5.5bps), with the negative impact of the latter winning out with the S&P 500 (-0.74%) and the NASDAQ (-0.39%) seeing their worst day of May so far.

After Nvidia’s results the night before it felt like nothing could derail the market and at the open the S&P had initially hit an all-time intraday high (+0.66% on the day at the peak) and the VIX index of volatility hit its lowest intraday level since the pandemic, falling as low as 11.52pts.

The momentum had started to shift as US weekly initial jobless claims fell back to 215k (vs. 220k expected). That’s a second weekly decline, and suggests that the spike to 232k a couple of weeks ago was just a blip. And shortly afterwards, that theme was cemented by the flash composite US PMI for May, which rose to its strongest in over two years, at 54.4 (vs. 51.2 expected). That was led by a strong rebound in services activity (from 51.3 to 54.8), while manufacturing also ticked up (from 50.0 to 50.9). So the data yesterday suggests there’s little urgency for the Fed to cut rates anytime soon, and the odds of a cut by the September meeting were slashed to 56% by the close, down from 72% the previous day.

With investors pricing out rate cuts, that led to a sovereign bond selloff on both sides of the Atlantic. For US Treasuries, this pushed the 10yr yield up +5.5bps to 4.48%, whilst the 2yr yield was up +6.6bps to 4.94%. In addition that move left the 2s10s yield curve at -46.3bps by the close, which is the most inverted it’s been so far this year. So as it stands, there’s little sign that the longest 2s10s inversion on record is coming to an end. This morning in Asia, yields on 2 and 10yr Treasuries are back down -1.5bps and -1bps respectively.

Meanwhile in Europe, yields on 10yr bunds (+6.1bps), OATs (+5.8bps) and BTPs (+6.3bps) all moved higher yesterday, which was cemented by their own PMI numbers earlier in the day. Indeed, the Euro Area composite PMI was up from 51.7 to 52.3 on the flash reading, which is its strongest level in a year.

Staying on Europe, there was also some interesting wage data from the ECB yesterday, which showed that negotiated pay accelerated from +4.5% to +4.7% year-on-year in Q1. Together with the PMI data, that supported a decent move lower in rate cut expectations, with the amount of rate cuts priced by the December meeting down -4.7bps to just 59bps, which is the fewest so far this year. However, the general consensus remains that they’re still likely to cut rates in June (which is 91% priced), and the ECB’s Villeroy said that they “should not over-interpret”, and that “we are very probably, barring a surprise, going to have a first rate cut in our next Governing Council meeting”. A little earlier in the year, the ECB had been telling us how crucial this wage data is, and then when it was released they downplayed it citing the role of one-off payments. Read their blog here. Our European economists note that realised wage data has been sticky of late, providing potential ammunition for the hawks, though the forward looking indicators of wages are pointing to a clear slowing.