GOLD PRICE CLOSED DOWN $13.55 TO $2341.45

SILVER PRICE UP $0.20 TO $32.17

Gold ACCESS CLOSED $2337.75

Silver ACCESS CLOSED: $31.97

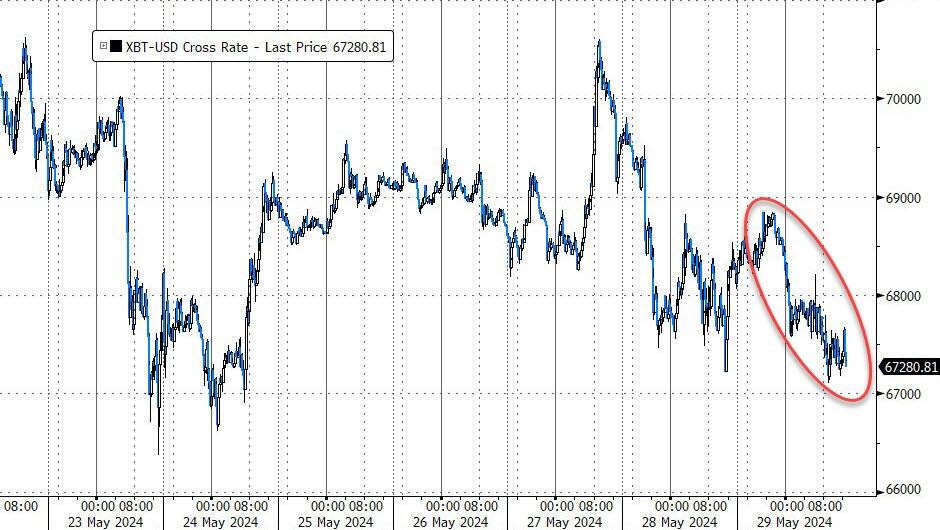

Bitcoin morning price:$67,976 DOWN 278 DOLLARS.

Bitcoin: afternoon price: $67684 DOWN 570 dollars

Platinum price closing DOWN $18.80 TO $1042.60

Palladium price; DOWN $14.75 AT $967.90

END

SHANGHAI GOLD PREMIUM 37 DOLLARS/COMEX GOLD

SHANGHAI GOLD

SHANGHAI GOLD (USD) FUTURES – QUOTES

Last Updated 29 May 2024 03:11:24 PM CT.

Market data is delayed by at least 10 minutes.

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $3206.52 DOWN 13.98 CDN dollars per oz( * NEW ALL TIME HIGH 3,305.30 CDN DOLLARS PER OZ//MAY 20 2024)

*BRITISH GOLD: 1840.55 UPDOWN 9.15 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2163.90 DOWN 10.65 Euros per oz //* (ALL TIME CLOSING HIGH: 2248.89 EUROS PER OZ//APRIL 16.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCH: COMEX

EXCHANGE: COMEX

CONTRACT: MAY 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,355.200000000 USD

INTENT DATE: 05/28/2024 DELIVERY DATE: 05/30/2024

FIRM ORG FIRM NAME ISSUED STOPPED

190 H BMO CAPITAL 4

657 C MORGAN STANLEY 11

690 C ABN AMRO 4

880 H CITIGROUP 22

905 C ADM 3

TOTAL: 22 22

MONTH TO DATE: 2,393

JPMorgan stopped 0/22

FOR MAY2024

GOLD: NUMBER OF NOTICES FILED FOR MAY/2024. CONTRACT: 22 NOTICES FOR 2200 OZ or 0.0684 TONNE

total notices so far: 2393 contracts for 239300 Oz (7.4432 tonnes)

FOR MAY:

SILVER NOTICES: 25 NOTICE(S) FILED FOR 125,000 OZ/

total number of notices filed so far this month : 6132 for 30.6600 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $13.55

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

NO CHANGES IN GOLD INVENTORY AT THE GLD:

/ /INVENTORY RESTS AT 832.21TONNES

INVENTORY RESTS AT 832.21 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER UP $.20 AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.051 MILLION OF SILVER OUT OF THE SLV

// INVENTORY LOWERS TO 417.430 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 417.430 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A FAIR SIZED 398 CONTRACTS TO 184,846 AND CONTINUING ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS FAIR SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR HUGE GAIN OF $1.64 IN SILVER PRICING AT THE COMEX ON TUESDAY. WE HAD ZERO LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN SHORT COVERING BY OUR SPECS DESPITE THE GAIN IN PRICE. WE HAD ANOTHER HUGE SIZED 889 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID LIKE TODAY.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 889 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND TODAY;S RAID.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $1.64) AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE DID HAVE A HUMONGOUS SIZED GAIN OF 1053 CONTRACTS ON OUR TWO EXCHANGES WITH THE HUGE GAIN IN PRICE OF $1.64.

WE MUST HAVE HAD:

A STRONG SIZED 655 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 28.130MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S E.F.P. JUMP TO LONDON OF 20,000 OZ

//NEW STANDING FOR SILVER//MAY IS THUS 30.655 MILLION OZ

WE HAD:

/ FAIR SIZED COMEX OI GAIN //HUGE SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 889 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED AN ENORMOUS 1535 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY

TOTAL CONTRACTS for 20 DAYS, total 24,226 contracts: OR 121.130 MILLION OZ (1211 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 115.780 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL PROBABLY BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 121.130 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

RESULT: WE HAD A FAIR SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 398 CONTRACTS WITH OUR HUGE GAIN IN PRICE OF SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG EFP ISSUANCE CONTRACTS: 889 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAY OF 29.345 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 20,000 OZ E.F.P JUMP TO LONDON

//NEW TOTAL STANDING AT 30.655 MILLION OZ

WE HAVE A HUGE SIZED GAIN OF 1053 OI CONTRACTS ON THE TWO EXCHANGES WITH THE HUGE GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG SIZED 889 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND ZERO LIQUIDATION OF SHORTS.

THE NEW TAS ISSUANCE TUESDAY NIGHT (518) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 25 NOTICE(S) FILED TODAY FOR 125,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 12,483 OI CONTRACTS TO 485,430 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE 8136 CONTRACTS

WE HAD A STRONG SIZED DECREASE IN COMEX OI (12,483 CONTRACTS) OCCURRED DESPITE OUR HUGE GAIN OF $22.00 IN PRICE/TUESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER, INITIATING THURSDAY’S RAID. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 4.684 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY;S 200 OZ E.F.P JUMP TO LONDON PLUS WE MUST ADD THAT DUBIOUS ISSUANCE OF 1084 OI EX FOR RISK CONTRACTS ISSUES ON LAST FRIDAY WHEREBY THE BUYER ASSUMES RISK OF 3.3716 TONNES OF GOLD//NEW STANDING DECREASES TO 8.5536 TONNES PLUS THE DUBIOUS 3.3716 ECH FOR RISK!

NEW STANDING 11.925 TONNES// ALL OF THIS HAPPENED WITH OUR $22.00 GAIN IN PRICE WITH RESPECT TO TUESDAY’S TRADING. WE HAD A STRONG SIZED LOSS OF 5977 OI CONTRACTS (18.59 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 6506 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 485,430

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5977 CONTRACTS WITH 12,483 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 6506 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 5977 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED 2659 CONTRACTS,,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (6506 CONTRACTS) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI 12,483/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 5977 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 4.684 TONNES FOLLOWED BY TODAY;S 200 OZ EFP JUMP PLUS 3.3716 TONNES EX FOR RISK//PRIOR

//NEW STANDING /MAY 11.925 TONNES.

/ 3) CONSIDERABLE LIQUIDATION OF CONTRACTS MOSTLY DUE TO SPREADERS ALONG WITH SOME MINOR LONG SPECS BEING WIPED OUT WITH THE LOSS IN PRICE.

// 4) STRONG SIZED COMEX OPEN INTEREST LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///STRONG T.A.S. ISSUANCE: 2659 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY. :

TOTAL EFP CONTRACTS ISSUED: 90,081 CONTRACTS OR 9,008,100 OZ OR 280.18 TONNES IN 20 TRADING DAY(S) AND THUS AVERAGING: 4504 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAY(S) IN TONNES 280/18 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 280.18 DIVIDED BY 3550 x 100% TONNES = 7.88% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 280.18 TONNES (WILL BE ANOTHER STRONG MONTH/ LARGER THAN LAST MONTH)// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A FAIR SIZED 398 CONTRACTS OI TO 184,846 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 655 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 655 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 655 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1973 CONTRACTS AND ADD TO THE 655 E.FP. ISSUED

WE OBTAIN A STRONG SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 5977 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 18.59 MILLION OZ

OCCURRED WITH OUR HUGE $1.64 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED UP 1.43 PTS OR 0.05% //Hang Seng CLOSED DOWN 344.15 PTS OR 1.83%// Nikkei CLOSED DOWN 298/50 OR 0.77%//Australia’s all ordinaries CLOSED DOWN 1.23%///Chinese yuan (ONSHORE) closed DOWN TO 7,2494 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2729/ Oil UP TO 80.43 dollars per barrel for WTI and BRENT UP AT 84.75 /Stocks in Europe OPENED ALL MOSTLY RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 12,483 CONTRACTS TO 485,430 DESPITE OUR STRONG GAIN IN PRICE OF $22.00 WITH RESPECT TO TUESDAY TRADING. WE HAD A CONSIDERABLE T.A.S. LIQUIDATION TUESDAY AS WELL AS FEW LONGS BEING CLIPPED.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAY.… THE CME REPORTS THAT THE BANKERS ISSUED A HUGE SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 6506 EFP CONTRACTS WERE ISSUED: : JUNE 6506 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE:6506 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 5977 CONTRACTS IN THAT 6506 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 12,483 COMEX CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR HUGE GAIN IN PRICE OF $22.00// TUESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A STRONG SIZED 2259 CONTRACTS. MOST OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. TODAY IS OF EXTREMELY IMPORTANCE TO OUR CROOKS IN YESTERDAY’S FALL IN PRICE

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (8.5536 TONNES+ 3.3716 EX FOR RISK/PRIOR) = 11.925 TONNES ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $22.00 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG LOSS OF 5977 CONTRACTS ON TIESDAY WITH OUR TWO EXCHANGES DESPITE THE HIGE GAIN IN PRICE. THE T.A.S. ISSUED ON TUESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE LOST A TOTAL OI OF 18.59 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY (4.684 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S SMALL E.F.P. JUMP TO LONDON OF 2 CONTRACTS OR 200 OZ ( .0060 TONNES) PLUS 3.3716 TONNES OF EX FOR RISK/PRIOR

NEW STANDING: 8.5536 TONNES PLUS 3.3716 TONNES EX FOR RISK/PRIOR = 11.925

ALL OF THIS WAS ACCOMPLISHED WITH OUR HUGE GAIN IN PRICE TO THE TUNE OF $22.00

WE HAVE REMOVED 8,136 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET LOSS ON THE TWO EXCHANGES 5977 CONTRACTS OR 597700 (18.59 TONNES)

confirmed volume TUESDAY 454,528 contracts// huge

//speculators have left the gold arena

MAY 29 MAY GOLD

/ /// THE MAY 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | NIL oz . |

| Deposit to the Dealer Inventory in oz | 32,009.658 oz ASAHI |

| Deposits to the Customer Inventory, in oz | 386.04 OZ DELAWARE |

| No of oz served (contracts) today | 22 notice(s) 2200 OZ 0.0684 TONNES |

| No of oz to be served (notices) | 357 contracts 35700 OZ 1.1104 TONNES |

| Total monthly oz gold served (contracts) so far this month | 2393 notices 239,300 oz 7.4432 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

1 dealer deposits:

(1) into ASAHI: 32009.638 oz

total dealer deposits: 32009.638 oz

we have 1 customer deposit:

i) Delaware 386.04 oz

total deposit 386.04 oz

total customer withdrawals: 0

TOTAL WITHDRAWALS nil 0z

Adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY

For the front month of MAY we have an oi of 379 contracts having LOST 2 contracts.

We had 0 contracts served on TUESDAY, so we LOST 2 contracts or 200 oz (0.00623 Tonnes).

JUNE DECREASED ITS OI BY 56,043 CONTRACTS DOWN TO 73,929 CONTRACTS. WE HAVE 2 MORE READING DAYS BEFORE FIRST DAY NOTICE

JULY GAINED 277 CONTRACTS TO STAND AT 1162

We had 22 contracts filed for today representing 2200 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 22 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the MAY /2024. contract month, we take the total number of notices filed so far for the month (2393) x 100 oz ) to which we add the difference between the open interest for the front month of MAY ( 379 CONTRACTS) minus the number of notices served upon today (22 x 100 oz per contract( equals 275,000 OZ OR 8.5536 TONNES. PLUS THE 3.3716 OF EX FOR RISK/PRIOR = 11.925 TONNES

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (2393x 100 oz + 379x OI for the front month} minus the number of notices served upon today (22) x 100 oz which equals 275,000 oz (8.5536 TONNES) PLUS 3.3716 EX FOR RISK/PRIOR = 11.925 TONNES.

TOTAL COMEX GOLD STANDING FOR MAY: 11.9250 TONNES WHICH IS HUGE FOR THIS A NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX84XXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,558,487.369 48.47 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,609,477.363 OZ

TOTAL REGISTERED GOLD 7,820,854.380 ( 243.24 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,788,618.983 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,262,367 oz (REG GOLD- PLEDGED GOLD)= 194.78 tonnes //

END

SILVER/COMEX

MAY 29

INITIAL

//2024// THE MAY 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,168,511.975 oz hsbc delaware . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 588,186.200 oz asahi |

| No of oz served today (contracts) | 25 CONTRACT(S) (125,000 OZ) |

| No of oz to be served (notices) | 1 contracts (0.050 million oz) |

| Total monthly oz silver served (contracts) | 6132 Contracts (30.660 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i) int asahi 588,186.200 oz

total customer deposit 588,186.200 oz

JPMorgan has a total silver weight: 128.497million oz/298.467 million or 43.02%

adjustment: 1

i) out of asahi 609,387.400 oz customer to dealer

Comex withdrawals: 2

i) delaware; 598,193.480 oz

i) hsbc 570,318.495 oz

ii) delaware 598,193.480 oz

total withdrawal: 1,168511.595 0z

TOTAL REGISTERED SILVER: 61.566MILLION OZ//.TOTAL REG + ELIGIBLE. 299/048 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF MAY/2024 OI: 26 CONTRACTS HAVING LOST 8 CONTRACT(S).

.

We had 4 notices served on TUESDAY so we LOST 4 contracts or 20,000 oz underwent an EFP JUMP TO LONDON AS THEY WERE SET TO TAKE DELIVERY ON THAT SIDE OF THE POND.

JUNE SAW A GAIN OF 3 CONTRACTS RISING TO 1355

JULY SAW A LOSS OF 502 CONTRACTS DOWN TO 146,411

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 25 for 125,000 oz

CONFIRMED volume; ON TUESDAY 157,986

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 6132 x 5,000 oz = 30.660 MILLION oz

to which we add the difference between the open interest for the front month of MAY ((26) and the number of notices served upon today 25x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2024 contract month: 6132 notices served so far) x 5000 oz + OI for the front month of MAY (26)x number of notices served upon today minus (25x 5000 oz of silver standing for the may contract month equates to 30.655 MILLION OZ.

New total standing: 30.655 million oz.

There are 61.566 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

MAY 29 WITH GOLD DOWN $13.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 28 WITH GOLD UP $22.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 832.21 TONNES

MAY 24 WITH GOLD DOWN $2.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 833.36 TONNES

MAY 23 WITH GOLD DOWN $53.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 22 WITH GOLD DOWN $32.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 21 WITH GOLD DOWN $12,00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 20 WITH GOLD UP $21.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.10 TONNES OF GOLD INTO THE GLD//NEW TOTAL 838.54 TONNES

MAY 17 WITH GOLD UP $31.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//NEW TOTAL 833.36 TONNES

MAY 16 WITH GOLD DOWN $7.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//NEW TOTAL 833.36 TONNES

MAY 15 WITH GOLD UP $34.90 ON THE DAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD/INVENTORY RISES TO 831.93 TONNES

MAY 14 WITH GOLD DOWN $17.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RISES TO 831.33 TONNES

MAY 13 WITH GOLD DOWN $31.10 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD////INVENTORY RISES TO 831.93 TONNES

MAY 10 WITH GOLD UP $34.65 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 9 WITH GOLD UP $18.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 8 WITH GOLD DOWN $0.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 830.47 TONNES

MAY 7 WITH GOLD DOWN $6.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 832.19 TONNES

MAY 6WITH GOLD UP $21.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .55 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 831.64 TONNES

MAY 2 WITH GOLD UP $0.20 ON THE DAY; SMAKK CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 830.47 TONNES

MAY 1 WITH GOLD UP $7.80 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNES

APRIL 29WITH GOLD UP $10,55TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNES

APRIL 26WITH GOLD UP $5.40TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.54 TONNES FROM THE GLD /INVENTORY RISES AT 832.19 TONNES

APRIL 25WITH GOLD UP $5.05 TODAY; NO CHANGES IN GOLD INVENTORY AT THE GLD /INVENTORY RISES AT 833,63 TONNES

APRIL 19 WITH GOLD UP $15.00 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 4.32 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 831.91 TONNES

APRIL 18 WITH GOLD UP $11.30 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE WITHDRAWAL OF 2.59 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 827.59 TONNES

APRIL 17 WITH GOLD DOWN $17.60 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 830;18 TONNES

APRIL 16 WITH GOLD UP $23.10 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A MASSIVE DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD/ INVENTORY RISES AT 828.45 TONNES

APRIL 15 WITH GOLD DOWN $. 80 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A HUGE WITHDRAWAL OF 1.80 TONNES OF GOLD INTO THE GLD/ INVENTORY FALLS AT 824.84 TONNES

APRIL 12 WITH GOLD UP $2.80 TODAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD //A DEPOSIT OF 2.29 TONNES OF GOLD INTO THE GLD/ INVENTORY RISESS AT 830.75 TONN

GLD INVENTORY: 832.21 TONNES, TONIGHTS TOTAL

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 29 WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 1.051 MILLION OZ INTO THE SLV//INVENTORY DECREASES TO 417.430 MILLION OZ

MAY 28 WITH SILVER UP $1.64 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 2.832 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 418.481 MILLION OZ

MAY 24 WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF .822 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 421.313 MILLION OZ

MAY 23 WITH SILVER DOWN $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.736 MILLION OZ FROM THE SLVINVENTORY INCREASES TO 420.491 MILLION OZ

MAY 22 WITH SILVER DOWN $0.66 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 21 WITH SILVER DOWN $0.41 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A DEPOSIT OF 3.792 MILLION OZ FROM THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 20 WITH SILVER UP $1.28 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 1.005 MILLION OZ FROM THE SLV// INVENTORY LOWERS TO 418.435 MILLION OZ

MAY 17 WITH SILVER UP $1.37 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 868,000 OZ FROM THE SLV// INVENTORY LOWERS TO 419.440 MILLION OZ

MAY 16 WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY REMAINS AT 420.308 MILLION OZ

MAY 15 WITH SILVER UP 101 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A WITHDRAWAL OF 1.919 MILLION OZ FROM THE SLV

INVENTORY RESTS AT 420.308 MILLION OZ

MAY 14 WITH SILVER UP 25 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;

INVENTORY RESTS AT 422.227 MILLION OZ

MAY 13 WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;NVENTORY RESTS AT 422.227 MILLION OZ

MAY 10 WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A HUGE WITHDRAWAL OF 1.,828 MILLION OZ//INVENTORY RESTS AT 422.227 MILLION OZ

MAY 9 WITH SILVER UP 78 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 8 WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 7WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 6 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.055 MILLION OZ

MAY 3 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 2WITH SILVER UP 0.12 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/ A WITHDRAWALOF 4.471 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 1 WITH SILVER UP 0.09 TODAY: SMALLCHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF ,457 MILLION OZ INTO THE SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 29WITH SILVER UP $0.13 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 26WITH SILVER DOWN 8 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.097 MILLION OF SILVER INTO THE SLV// :SLV INVENTORY RESTS AT 429.814 MILLION OZ

APRIL 25WITH SILVER UP $.05 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 1.534 MILLION OF SILVER OUT OF THE SLV// :SLV INVENTORY RESTS AT 428.717 MILLION OZ

APRIL 24/WITH SILVER DOWN $.05 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 11.904MILLION OF SILVER INTO THE SLV// :SLV INVENTORY RESTS AT 428.280 MILLION OZ

APRIL 23/WITH SILVER UP $0.11TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV / :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 22/WITH SILVER DOWN $1.51 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.194 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 416.376 MILLION OZ

APRIL 19/WITH SILVER UP 42 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.657 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 418.570 MILLION OZ

APRIL 18/WITH SILVER DOWN $.04TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.977 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 422.227 MILLION OZ

APRIL 17/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF .868 MILLION OF SILVER FROM THE SLV// :SLV INVENTORY RESTS AT 426/204 MILLION OZ

APRIL 16/WITH SILVER DOWN $0.46 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF NON EXISTENT SILVER// :SLV INVENTORY RESTS AT 427.072 MILLION OZ

APRIL 15/WITH SILVER UP $0.88 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 12/WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 4.069 MILLION OZ FROM THE SLV :SLV INVENTORY RESTS AT 433.929 MILLION OZ

APRIL 11/WITH SILVER UP $0.23 TODAY: STRANGE INDEED! HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 3.931 MILLION OZ :SLV INVENTORY RESTS AT 437.998 MILLION OZ

CLOSING INVENTORY 417.430 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

end

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS//GOLD AND SILVER COMMENTARY

END

3. CHRIS POWELL//GATA DISPATCHES

CHRIS POWELL…

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS

When Will Gold & Silver Miners Start Believing In Their Product?

WEDNESDAY, MAY 29, 2024 – 01:20 PM

Authored by Stefan Gleason via Money Metals,

Miners spend billions of dollars every year pulling precious metals out of the ground. They toil mightily for years on end to produce these stores of value – but then they turn right around and sell all their gold and silver immediately in exchange for fiat currencies.

If you stop to really think about it, this may seem strange.

These businesses quite literally mine real money. But, like nearly every other business or individual, they still seem to be stuck in the fiat currency paradigm.

It takes tremendous risk, capital, and time to find a resource, develop a mining project, and dig up and process the metals. It is extremely difficult to produce gold and silver at a profit.

Inflation constantly pushes up costs and puts pressure on the economics of the miners. They may face tremendous stumbling blocks along the way – from governments, capital markets, indigenous activists, eco-fanatics, union bosses, and many others.

All this underpins the scarcity value of the gold and silver that comes out of the ground – and provides a stark contrast to the amount of work involved in creating fiat money (i.e. none).

Of course, mining companies do need cash to pay bills. But to the extent that it’s not needed immediately, wouldn’t it make sense to hold onto some bullion to preserve purchasing power for future expenses?

Very Few Miners Hold Gold & Silver Rather Than Sell It All

If mining companies believe that gold and silver are better stores of value than fiat currency, then it would seem incumbent on them to hold onto some of their product where they can.

As far as we can tell, though, only a couple mining companies – First Majestic Silver and SilverCrest Metals – have held back a meaningful amount of their production in the past 10 years.

SilverCrest actually does more than delay sales – it has deliberately socked away more than $20 million in gold and silver bullion on its balance sheet, currently representing about 20% of its treasury assets. In other words, these folks eat their own cooking – and plan to eat more.

The company’s president, Chris Ritchie, believes holding gold and silver should become “an additional capital allocation choice that should be considered” for the mining industry.

“SilverCrest has added this choice alongside our other capital allocation opportunities because of the functionality of our product — and we want to give our investors more of what they want while also hedging against some of the risks associated with mining. The option to hold bullion is available for every individual and business that’s trying to keep up with rising cost pressures.”

“The irony is that the gold and silver mining industry spends huge sums of money over long periods of time, and yet we choose to hold fiat currencies as our preferred store of value versus the product we work so hard to get.”

Miners May Struggle to Produce Future Ounces at Today’s Prices

Discussing this idea with Money Metals, Ritchie argued that the cost to replace the gold and silver ounces sold today is likely to be much higher in the future. If companies were to include these realities in their decision-making processes, financial stability and returns could be significantly improved.

“The industry has a horrible capital allocation track record. Poor business, capital markets, and resource allocation decisions have played an enormous role in creating the lack of interest we see in the sector today,” Ritchie pointed out.

The SilverCrest president points to the undercapitalization of the mining sector more broadly to support his point. Precious metals miners represent a fraction of 1% of the global marketable investment index even though they supply a product that is the best store of value in history.

A change in mentality may take time.

One example of the prevailing mindset is when Idaho-based Money Metals reached out to Hecla, a large silver-focused miner that is likewise based in Idaho, seeking support for a 2018 sound money bill pending in the state legislature. The response: Sorry, gold and silver aren’t money.

Idaho was once the epicenter of the gold and silver mining industry. But projects have faced major obstacles in recent decades, and the Gem State’s current liberal governor seems outright hostile to the monetary metals.

In fact, Idaho Gov. Brad Little just last week vetoed a popular sound money bill in order to prevent his state treasurer from holding gold and silver bullion to help protect the state’s dollar-centric reserve funds.

In doing so, Little parted ways with his counterparts in states like Utah, Tennessee, Texas, and Ohio – and sent a terrible message to the precious metals industry in the state.

Excessive Hedging Undermines Profitability, Shareholder Interests

Barrick Gold also provides an interesting case study.

The company’s stock is the same price today as it was 20 years ago. Meanwhile, gold itself is up over 600% in the same period of time!

It doesn’t take a financial wizard to see that you would have been a lot better off investing in the end product rather than the mining process.

In fairness, mining is a tough business and Barrick is a survivor. But it’s also one of many large mining companies that has capped its upside potential by hedging exposure to metals prices via futures markets. Hedging means, in effect, selling production early – well before the metals are even brought out of the ground.

Excessive and poorly timed hedges have destroyed shareholder value over the years.

Even when hedges DO pay off in the near term, they work at cross purposes with long-term investors who buy mining stocks because they want to fully participate in a bull market for the underlying asset.

Short-Sighted Thinking Harms Long-Term Industry Health

Quarterly earnings reporting and other pressures on public companies has led to lots of short-term thinking. The benefits of holding gold and silver shine brighter the longer the time frame in which you evaluate them.

Given the years or decades necessary to discover, build, and produce from a mine, the loss of purchasing power over that journey becomes a significant financial drag that is rarely considered.

Mining companies that sell all their gold and silver ounces today usually hope to replace them at a lower cost in the future. But is that a realistic assumption?

Almost no companies hold gold on the balance sheet.

Retaining some bullion on the balance sheet adds leverage. The returns on ounces held above the ground are not burdened by rising costs. They are not exposed to operational risk. And they reliably earn a better “real” yield over the medium to longer term than cash, CDs, and bonds.

Selling every ounce of precious metals mined immediately, regardless of price, is bad business, and it’s no wonder the mining sector struggles.

A strong case can be made that no company (or person or government entity) should hold cash reserves entirely in dollars given their constant devaluation and inherent risk. But so far there are few other examples of public companies holding gold on their balance sheets. Overstock and Palantir are two of them.

If Miners Hold Back Supply, It Could Positively Impact Price

The gold market is small. The silver market is even smaller.

Whereas demand for metals can surge suddenly, the supply response will take a significant amount of time. The capital required to build new projects is large and capital availability has dwindled to a trickle.

Seizing upon supply and demand imbalances is the holy grail for investors in cyclical industries. Mining companies can add value by retaining production while they wait for up-cycles to mature.

A choice to hold back some of their production from the market – especially when spot prices are below the all-in cost of discovery, development, and production – could also positively impact the prices of gold and silver.

That’s particularly true with silver, which is dramatically undervalued versus gold on a historical basis – but now appears poised to catch up. Higher prices would ultimately improve cash flows, supporting the health of the industry.

Here’s the bottom line…

Mining companies that fail to appreciate that they are literally pulling money out of the ground may continue to disappoint metals investors. But miners that stop being kneejerk “price takers” can expect to be rewarded.

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT//COFFEE BEANS//

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

WHY BITCOIN AND NOT GOLD?

Healthcare Company Semler Soars After Adopting Bitcoin As Primary Treasury Asset

TUESDAY, MAY 28, 2024 – 10:00 PM

Healthcare company Semler Scientific (SMLR), known for pursuing remedies to chronic diseases, announced a major shift in its treasury strategy. The company’s board of directors adopted Bitcoin as its primary treasury reserve asset, alongside a substantial purchase of 581 Bitcoins for an aggregate amount of $40 million.

Subscribe

JUST IN: Healthcare product manufacturer Semler Scientific purchases 581 #Bitcoin for $40 million

·

160.6K Views

“Our bitcoin treasury strategy and purchase of bitcoin underscore our belief that bitcoin is a reliable store of value and a compelling investment,” stated Semler Scientific Chairman Eric Semler. “Bitcoin is now a major asset class with more than $1 trillion of market value. We believe it has unique characteristics as a scarce and finite asset that can serve as a reasonable inflation hedge and safe haven amid global instability. We also believe its digital, architectural resilience makes it preferable to gold, which has a market value of approximately 10 times that of bitcoin. Given the gap in value between gold and bitcoin, we believe that bitcoin has the potential to generate outsize returns as it gains increasing acceptance as digital gold.”

As Bitcoin Magazine notes, despite this strategic financial move, the tiny Semler Scientific, whose market cap is just $200 million, said it remains committed to its core mission in healthcare of delivering innovative technologies as solutions to transform the healthcare management of chronic diseases and offer providers the opportunity to reduce costs and improve long-term patient outcomes. The company will also continue to focus on its flagship product, QuantaFlo, a point-of-care test for peripheral arterial disease, while seeking expanded FDA clearance for other cardiovascular conditions.

“Furthermore, we are energized by the growing global acceptance and ‘institutionalization’ of bitcoin — reflected most recently by the Securities and Exchange Commission’s January 2024 approval of 11 bitcoin exchange-traded funds,” Mr. Semler continued. “These funds have reported more than $13 billion of net inflows, with investments from nearly 1,000 institutions, including global banks, pensions, endowments and registered investment advisors. It is estimated that more than 10% of all bitcoins are now held by institutions.”

Semler Scientific’s board and senior management shared that they have carefully considered various uses of excess cash and concluded that holding Bitcoin is the best strategy.

The market greeted the news of the company’s shift from dollars to bitcoin with excitement, and sent SMLR surging 24% higher, which the cynics would argue was the whole point of the exercise. Well, the gamble worked…

… and while not many have followed in the footsteps of bitcoin OG Microstrategy, which was one of the original companies to transition from a dollar to bitcoin reserve, the euphoric reception of Semler’s news virtually guarantees that in the coming months we will see dozens more small and micro caps ditch the dollar and embrace crypto, if only in hopes of a quick boost to the stock price. Still demand is demand, and this all bodes quite favorably for bitcoin demand for the foreseeable future.

END

ASIA TRADING//WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED UP 1.43 PTS OR 0.05% //Hang Seng CLOSED DOWN 344.15 PTS OR 1.83%// Nikkei CLOSED DOWN 298/50 OR 0.77%//Australia’s all ordinaries CLOSED DOWN 1.23%///Chinese yuan (ONSHORE) closed DOWN TO 7,2494 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2729/ Oil UP TO 80.43 dollars per barrel for WTI and BRENT UP AT 84.75 /Stocks in Europe OPENED ALL MOSTLY RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2494

OFFSHORE YUAN: DOWN TO 7.2729

SHANGHAI CLOSED UP 1.43 PTS OR 0.05 %

HANG SENG CLOSED DOWN 344.15 PTS OR 1.83%

2. Nikkei closed DOWN 298.50 PTS OR 0.77 %

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 104.66 EURO FALLS TO 1.0848 DOWN 4 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.063 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 157/29 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.6460/Italian 10 Yr bond yield UP to 3.969 SPAIN 10 YR BOND YIELD UP TO 3.389%

3i Greek 10 year bond yield UP TO 3.635

3j Gold at $2341.70//Silver at: 31.95 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 85/ 100 roubles/dollar; ROUBLE AT 89.42

3m oil into the 80 dollar handle for WTI and 84 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 157.29/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.063% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9123 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9904 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.573 UP 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.690 UP 3 BASIS PTS/

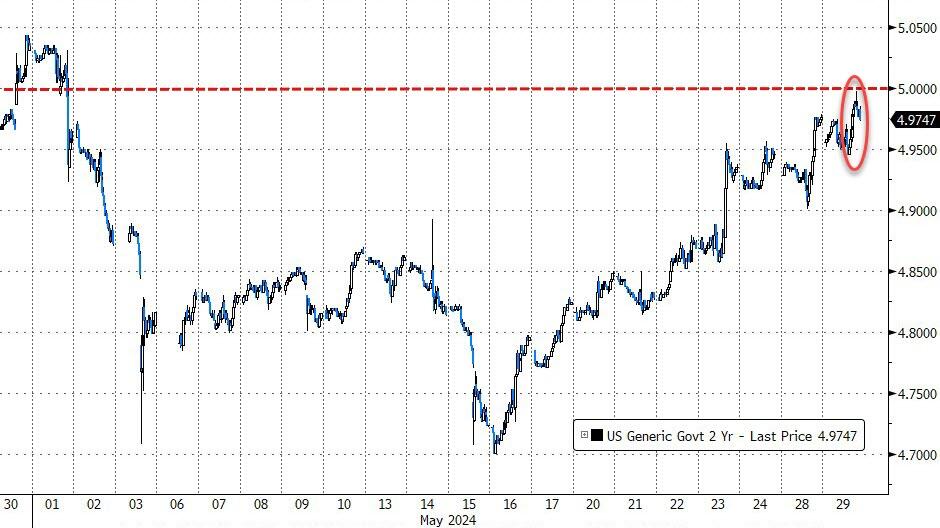

USA 2 YR BOND YIELD: 4.968 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.22…

10 YR UK BOND YIELD: 4.401 UP 12 PTS

2a New York OPENING REPORT

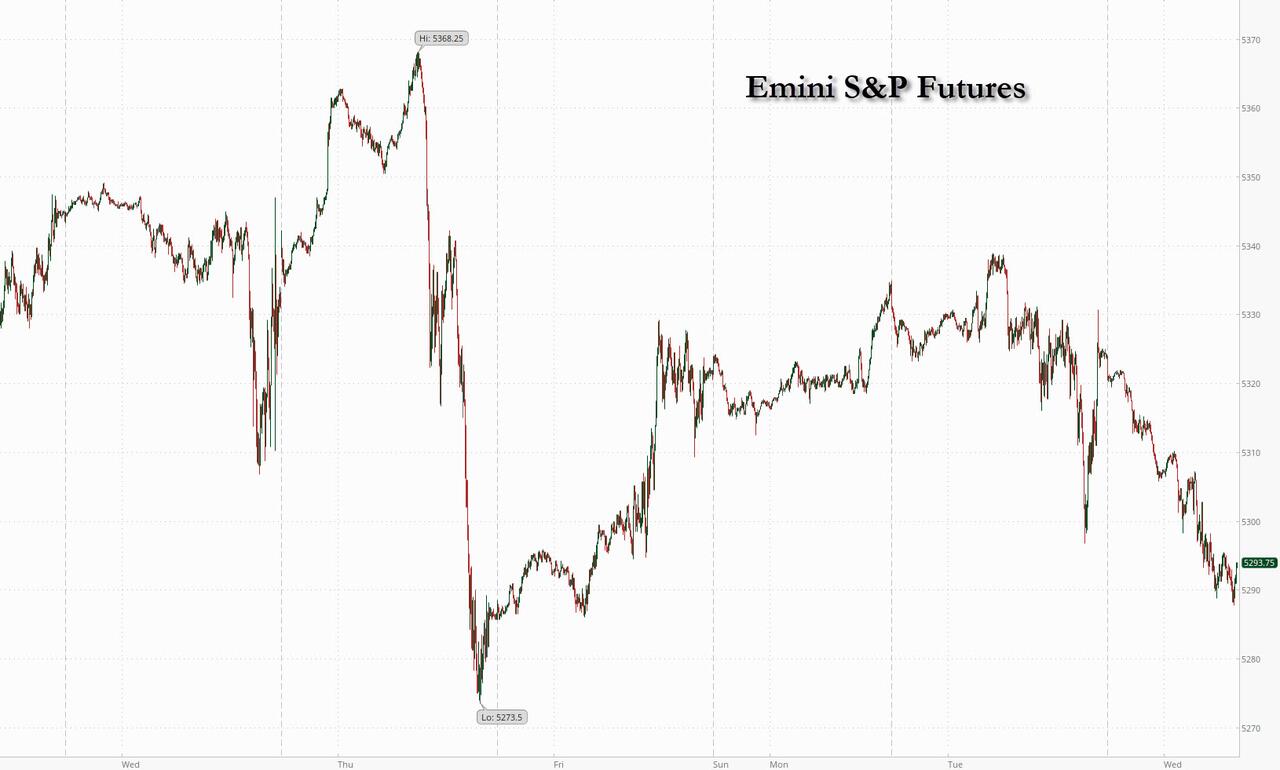

Futures Slide As Bond Yields Spike To 3 Week High

WEDNESDAY, MAY 29, 2024 – 08:18 AM

US futures are weaker with tech and small caps underperforming after the NDX made a new ATH yesterday on the back of the relentless Nvidia meltup. The weakness has been driven by surge in yields, a result of the latest batch of hawkish Fed remarks, two very weak bond auctions and stronger macro data (Consumer Sentiment; Housing Prices). Will we see more of the same today with the 7Y auction on deck? At 7:45am S&P futures are 0.6% lower while Nasdaq futures dipped 0.7% as Mag7 and Semi stocks (incl. NVDA) are all lower pre-mkt; Asian stocks fell, led by losses in Hong Kong, while Europe’s Stoxx 600 index also slipped 0.6%. Yields continued their rise, and after jumping 9 basis points on Tuesday, 10Y yields rose further to 4.57%, the highest level since May 3 when the huge payrolls miss sent yields sliding. The USD caught a bid, but commodities were a bright spot with both energy and base metals moving higher as another attack in the Red Sea added to heightened geopolitical tensions in the Middle East . It’s a light calendar: the only US eco data is the May Richmond Fed index (10am) and Dallas Fed services activity (10:30am); we also get speeches from the Fed’s Williams (1:45pm) and Bostic (7pm). Fed releases Beige book at 2pm

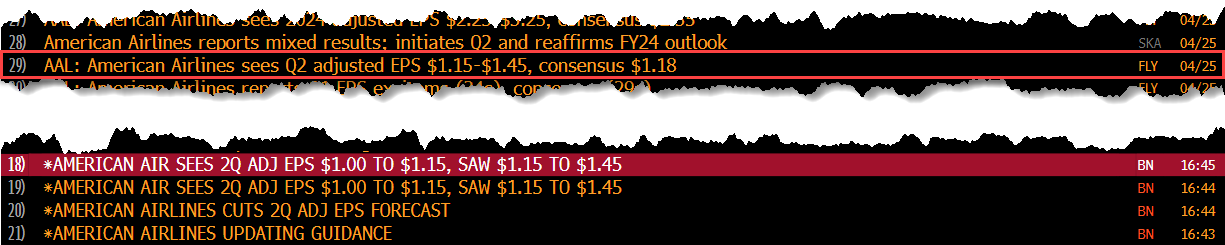

In premarket trading, Marathon Oil shares climbed 5.9% after reports that ConocoPhillips was set to acquire the E&P company, valuing the company at around $15 billion. Airline stocks on both sides of the Atlantic are under pressure after American Airlines cut its profit guidance heading into the crucial summer travel season, just one month after it published a very optimistic outlook which sent its stock price surging in a classical case of stock price manipulation.

And indeed, American Airlines shares plunged 8.3% after the airline slashed its second-quarter adjusted earnings per share outlook, taking the forecast below consensus expectations. The company also announced the departure of its chief commercial officer, Vasu Raja. Here are some other notable premarket movers:

- Bank OZK shares slip 4.4% after a downgrade to sell from buy at Citi.

- Cava (CAVA US) shares decline 3.2% despite the Mediterranean restaurant chain reporting better-than-expected 1Q same-store sales growth and boosting its outlook.

- Digital Turbine (APPS US) shares slide 8.5% after the company reported net revenue for the fourth quarter that missed estimates.

- Faraday Future (FFIE US) shares plummet 43% after the electric vehicle maker reported fourth-quarter and full-year earnings and withdrew its production target guidance for 2024.

- First Solar (FSLR US) shares fall – after a downgrade to hold from buy at DZ Bank.

- Robinhood Markets shares rise 3.3% after the board of directors approved a share repurchase program of up to $1 billion. Analysts see mostly muted effects of the buyback, with those at Keefe Bruyette & Woods calling it a “conservative approach to capital return.”

Despite solid May performance – the S&P 500 is up 5.4% in the month as of Tuesday’s close, while Europe’s Stoxx 600 is on track for a 2.2% gain in May – markets are feeling the ripples from a rough US session, after tepid demand for US note sales, resilient consumer confidence data and central bank talk fueled expectations interest rates will stay elevated. There’s an auction of seven-year Treasuries later Wednesday and an important US price growth print is in focus at the end of the week.

“The higher-for-longer bond yields risk is biting into equity valuations and short-term pressure seems to be a given,” said Leonardo Pellandini, an equity strategist at Bank Julius Baer. “Nevertheless, with inflation expectations moderating and interest-rate cuts coming soon, we think markets can continue to climb higher.”

And speaking of higher rices, Friday sees the release of the Fed’s preferred inflation gauge — the personal consumption expenditures index. Economists expect the PCE deflator to have risen in April at an annual pace of 2.7%, the same as in March.

“One potential banana skin is that major downside surprises in inflation could now bring in the view that the US economy could not be in as strong shape as previously expected — i.e. ‘bad news is bad news’,” Geoffrey Yu, strategist at Bank of New York Mellon.

European stocks also declined; the Stoxx 600 fell 0.3% with travel, financial service and consumer product shares leading declines. Major markets are all lower with France/Italy the biggest laggards. Oil and gas stocks outperformed after the price of crude hit a five-week high as another attack on a ship in the Red Sea added to heightened geopolitical tensions. Anglo American shares fell as much as 2.7% as BHP asked for more time to discuss its takeover plan and outlined a series of commitments; BHP shares meanwhile rise in London trading. Here are the biggest movers Wednesday:

- Renault rises as much as 4%, hitting highest since October 2019, as Goldman upgrades the automaker to buy from neutral in note citing its “strong product cadence”

- IDS gains as much as 4.4% after the parent company of Royal Mail agreed to a takeover by Czech billionaire Daniel Kretinsky, setting the scene for a political battle over its future ownership

- Merck KGaA shares rise as much as 2.1%, outperforming the Stoxx 600 Health Care Index, after Morgan Stanley increased its price target on the German company, citing re-rating potential

- Schibsted shares climb as much as 6% to hit levels not seen since December 2021 after analysts at Carnegie re-initiate coverage of the digital media company with a buy rating

- Xvivo Perfusion gains as much as 9.1% after SEB published a favorable note on the Swedish organ transplant technology firm, highlighting a very optimistic possible blue-sky scenario

- Saab falls as much as 5.9% after Sweden’s announcement on Tuesday that it would halt shipments of the firm’s Gripen fighter jets to Ukraine in discussion with other allies

- CD Projekt dropped as much as 7%, erasing early gains, after failing to provide new information on plans for its next Witcher game due for production phase in 2H

- RS Group falls as much as 3.5% after the industrial group was downgraded by Liberum and had its price target cut by RBC after analysts lowered their profit forecasts after recent FY results

- Mobico drops as much as 6.6% following a downgrade to hold by Berenberg, which says upside potential for the bus and rail company’s stock is still “opaque”

Earlier, Asian stocks fell, led by losses in Hong Kong, as rising bond yields and more Fedspeak saw US rate-cut bets further recede. The MSCI Asia Pacific Index fell as much as 1.4%, on track for its biggest single-day plunge since April 19. Tencent, TSMC and Samsung were among the biggest drags Wednesday. Korean stocks slid after Samsung’s labor union said it plans to carry out its first strike ever, while Australia’s key benchmark tumbled after inflation came in faster than expected in April. The regional gauge is still on course for more than 2% gain this month.

- Hang Seng and Shanghai Comp were mixed with notable losses in tech and consumer stocks front-running the declines in Hong Kong, while the mainland bucked the trend after more Chinese cities announced property support measures and the PBoC also conducted a relatively substantial liquidity injection heading into month-end.

- ASX 200 was dragged lower amid a jump in yields and after disappointing data including firmer-than-expected monthly CPI for April and a surprise contraction in Construction Work Done during Q1.

- Nikkei 225 failed to sustain an early momentum and a brief foray above 39,000 with headwinds from rising yields.

In Fx, the Dollar Index rises 0.1% while the Swedish krona is the weakest of the G-10 currencies, falling 0.3% versus the greenback. The euro fell to a near two-year low versus the pound after data showed inflation in May slowed across Germany’s regions compared to a month ago

- EUR/GBP down 0.3% to 0.84838 before halving losses, the lowest since August 2022.

- EUR/USD drops as much as 0.3% to 1.0829, hitting a fresh intraday low after the data.

- USD/JPY little changed at 157.25, versus 157.40 day high, close to the 157.52 level where Japanese officials were last suspected to have intervened to support the currency.

- AUD/USD swings between gains and losses to stand little changed at 0.6651

- Aussie gained earlier after data showed April CPI rose 3.6% year-on-year, beating estimates and bolstering the case for the Reserve Bank to keep interest rates at a 12-year high next month

In rates, the US treasury curve continues to steepen with long-end yields higher by less than 2bp on the day and front-end little changed. After jumping nine basis points on Tuesday, 10-year Treasury yields inched higher to 4.56%. Bunds pared losses during London morning after German state CPI figures suggested the national print, due at 8am New York time, might come in below forecasts. German 10-year yields rise 3bps to 2.62%. Australian bonds are among the worst performers after CPI topped estimates earlier in the session. UK 10-year yields added five basis points while those on similar-maturity German debt pulled back from a six-month high after regional inflation prints came in lower than the monthly estimate for the national figure. The US auction cycle concludes with 7-year note sale, following weak reception for 2- and 5-year notes Tuesday, and first operation of new buyback program targets shortest-maturity coupons.

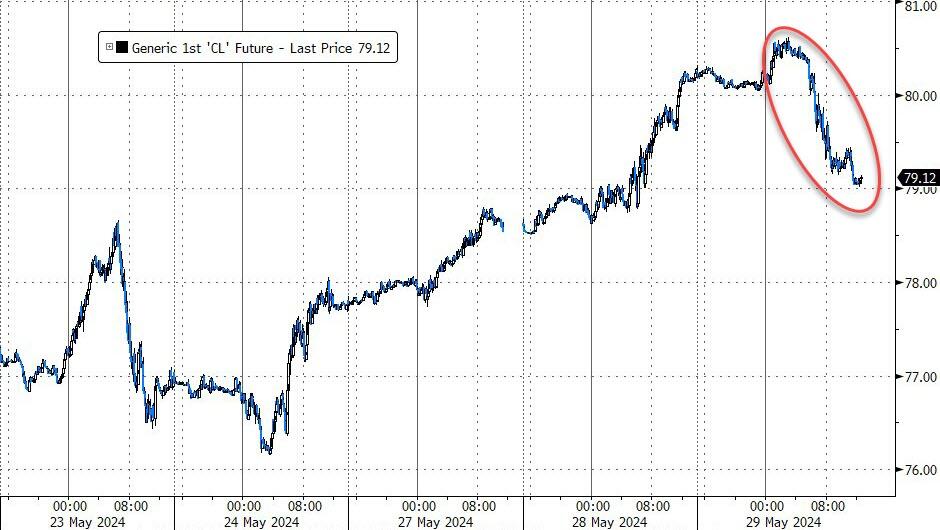

In commodities, brent crude advanced 0.8% to $84.93 per barrel as another attack in the Red Sea added to heightened geopolitical tensions in the Middle East ahead of an OPEC+ meeting on the weekend. West Texas Intermediate climbed above $80 a barrel. Spot gold falls roughly $19 to around $2,343/oz.

Bitcoin is softer and dips below $68k, whilse Ethereum holds just above $3.8k.

Looking at today’s calendar, US economic data includes May Richmond Fed manufacturing index (10am) and Dallas Fed services activity (10:30am). Fed officials’ scheduled speeches include Williams (1:45pm) and Bostic (7pm). Fed releases Beige book at 2pm

Market Snapshot

- S&P 500 futures down 0.6% to 5,294.50

- STOXX Europe 600 down 0.4% to 517.21

- MXAP down 1.4% to 178.50

- MXAPJ down 1.5% to 557.71

- Nikkei down 0.8% to 38,556.87

- Topix down 1.0% to 2,741.62

- Hang Seng Index down 1.8% to 18,477.01

- Shanghai Composite little changed at 3,111.02

- Sensex down 0.7% to 74,611.42

- Australia S&P/ASX 200 down 1.3% to 7,665.63

- Kospi down 1.7% to 2,677.30

- German 10Y yield little changed at 2.61%

- Euro down 0.2% to $1.0836

- Brent Futures up 0.7% to $84.85/bbl

- Gold spot down 0.6% to $2,347.68

- US Dollar Index up 0.14% to 104.76

Top Overnight News

- More of China’s biggest cities are easing home-buying policies, after top leaders recently signaled a shift to aggressive measures to resolve the country’s ongoing property crisis. Guangzhou and Shenzhen, two of China’s four Tier-1 cities, on Tuesday reduced the down payments required for first-home purchases by 10 and 15 percentage points, respectively. They also lowered mortgage rates for second homes and trimmed banks’ loan prime rates. WSJ

- China’s growth outlook is increased by the IMF for ’24 (from +4.6% to +5%) and ’25 (from +4.1% to +4.5%) due to a strong Q1 performance and recent policy support measures. FT

- Australia’s CPI for Apr runs hot, coming in +3.6% Y/Y (up from +3.5% in Mar and ahead of the Street’s +3.4% forecast). WSJ

- EU will move to hike tariffs on Chinese EV imports on 6/5, although it is in the interests of both sides to strike a deal and soften the blow. RTRS

- Emmanuel Macron has called for Ukraine to be allowed to use western weapons against military sites in Russia, becoming the most senior Nato leader to ask for targeting restrictions set by Kyiv’s backers to be lifted. FT

- Anglo American refused to give BHP more time to commit to a takeover offer, signaling the likely end —for now — to its $49 billion pursuit. BBG

- ConocoPhillips is reportedly in advanced talks to purchase Marathon Oil (MRO), via FT citing sources; could value the Co. at just over its current USD 15bln market cap.

- White House says Israeli strike in Rafah didn’t cross one of Biden’s red lines and will not trigger a change in US policy. NYT

- Lawyers to Plastics Makers: Prepare for ‘Astronomical’ PFAS Lawsuits. At an industry presentation about dangerous “forever chemicals,” lawyers predicted a wave of lawsuits that could dwarf asbestos litigation, audio from the event revealed. NYT

- BlackRock’s Bitcoin ETF surpassed the Grayscale Bitcoin Trust to become the world’s largest fund for the token. It attracted $16.5 billion since Jan. 11, while investors pulled $17.7 billion from Grayscale. BBG

- American Airlines (AAL) lowers guidance for adjusted operating margin by 1ppt to around 8.5%-10.5% and now expects Q2 Adj. EPS to be between USD 1.00-1.15 (prev. view USD 1.15-1.45)

- Fed Discount Rate minutes noted that all Fed reserve banks voted to hold the discount rate in April.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mostly lower after the indecisive performance stateside amid the rising yield environment. ASX 200 was dragged lower amid a jump in yields and after disappointing data including firmer-than-expected monthly CPI for April and a surprise contraction in Construction Work Done during Q1. Nikkei 225 failed to sustain an early momentum and a brief foray above 39,000 with headwinds from rising yields. Hang Seng and Shanghai Comp were mixed with notable losses in tech and consumer stocks front-running the declines in Hong Kong, while the mainland bucked the trend after more Chinese cities announced property support measures and the PBoC also conducted a relatively substantial liquidity injection heading into month-end.

Top Asian News

- IMF upgraded China’s 2024 economic growth target to 5% from 4.6% after “strong” Q1 and upgraded China’s 2025 economic growth target to 4.5% from 4.1%, while IMF’s Deputy Managing Director said they see scope for a more comprehensive policy package to address property sector issues and China’s central government resources should be deployed to assist buyers of pre-sold unfinished homes.

- China could invest some CNY 6bln in R&D of all-solid-state batteries, according to Chinese state media.

- S&P affirms India’s BBB-/A-3 rating; revises outlook to “positive” from “stable” amid robust growth and rising quality of government spending.

European bourses, Stoxx 600 (-0.4%) opened on a softer footing and continued to trundle lower as the session progressed, taking impetus from a subdued APAC session. European sectors are entirely the red, except Energy, which benefits from broader strength in the crude complex amid ongoing geopolitical uncertainty; strength which has dragged Travel & Leisure to the bottom of the pile. US Equity Futures (ES -0.6%, NQ -0.7%, RTY -0.7%) are entirely in the red, posting similar losses to that seen across European indices. As for stock specifics, American Airlines (-7.7% pre-market) sinks after it lowered its Q2 adj. EPS guidance.

Top European News

- BHP (BHP AT) update on Anglo American (AAL LN) takeover: BHP believes a further extension to the UK regulatory deadline is required to allow for further engagement on its proposal to Anglo American. Since, Anglo American (AAL LN) rejects request from BHP (BHP AT) for “put up or shut up (PUSU)” extension; unanimously reject’s BHP’s third proposal.

- Reuters Poll: ECB to cut deposit rate by 25bps to 3.75% on June 6, said all 82 economists; 55/82 economists said ECB to cut rates by 75bps in 2024 (vs. April poll 52/96)

Central Banks

- BoJ Board Member Adachi said changing monetary policy frequently to stabilise FX moves would lead to big changes in rate moves and if interest rate moves are too big, that would cause disruptions in household and corporate investment. Adachi said responding to short-term FX moves with monetary policy would affect price stability but noted if excessive yen falls are prolonged and are expected to affect the achievement of the price target, responding with monetary policy becomes an option. Adachi also commented that the BoJ must maintain accommodative financial conditions until the price goal is achieved and they are not yet at a stage where they are convinced that there is a sustained achievement of the price target, so must maintain accommodative conditions and must absolutely avoid raising interest rates prematurely. Furthermore, he said they will likely reduce JGB purchases at some stage in the future but warned reducing the BoJ’s JGB bond buying at a sharp pace could cause damage to the economy, as well as noted that if yen declines accelerate or become prolonged, inflation could re-accelerate faster than expected and may require the BoJ to quicken the interest rate hike.

FX

- USD is mixed vs. peers but DXY ultimately a touch firmer on account of EUR weakness. DXY has marginally eclipsed yesterday’s best with a 104.79 high print.

- EUR the laggard across the majors with EUR/USD nudged lower by regional German CPIs which saw M/M metrics come in broadly softer than implied by expectations for the mainland. EUR/USD has delved as low as 1.0830 vs. yesterday’s 1.0889 peak.

- Steady trade for the GBP vs. the USD with focus instead on EUR/GBP which has slipped below 0.85 for the first time since Aug’23 following the German State CPI metrics.

- USD/JPY is currently flat with limited follow-through from comments by BoJ’s Adachi. USD/JPY saw some volatility earlier in the session after tripping through stops at 157 but this was short-lived.

- AUD in focus after following hot CPI data overnight. ING notes that the high CPI print puts paid to the chances of a RBA rate cut this year. AUD/USD spiked higher from around 0.6651 to 0.6666 before fading gains.

- PBoC set USD/CNY mid-point at 7.1106 vs exp. 7.2528 (prev. 7.1101).

Fixed Income

- USTs are modestly softer, following the prior day’s soft 2yr and 5yr outings (7yr later today); Treasuries are off worst levels, in tandem with upticks in Bunds following the German State CPI figures.

- Bunds have been lifted in recent trade (though still lower by 41 ticks) after German State CPIs came in, broadly speaking, cooler than the mainland implied M/M and roughly in-line Y/Y. Bunds went as high as 129.82, before fading the initial upside and now residing around pre-release levels.

- Gilts are underperforming as the odds of a June BoE cut continue to languish around the 5% mark; Gilts down to a 95.97 base, 50 ticks below Tuesday’s trough and bringing into view 95.36 & 95.42 lows from the last week of April and first week of May respectively.

- BTPs briefly reclaimed 117.00 on the German inflation numbers though has since dipped below the level, but does fare better than European peers.

- Germany sells EUR 1.22bln vs exp. EUR 1.5bln 2.60% 2041 Bund and EUR 0.4bln vs exp. EUR 0.5bln 1.0% 2038 Bund

- UK sells GBP 1bln 0.125% 2039 I/L Gilt: b/c 3.16x (prev. 3.48x) & real yield 1.051% (prev. 1.076%)

Commodities

- Crude is firmer intraday and extending on Tuesday’s gains amid ongoing geopolitical uncertainty, in wake of Israel’s recent strikes on Rafah; Brent in a USD 84.09-84.44/bbl parameter.

- Subdued trade across precious metals after Tuesday’s rise, but with price action confined to Tuesday’s ranges with spot gold within a USD 2,346-2,361/oz parameter at the time of writing – vs USD 2,340-2,364/oz yesterday.

- Base metals are largely consolidating following Tuesday’s rally driven in part by the slew of housing market support measures announced by various Chinese cities.

- UBS forecasts end-2024 copper at USD 11.5k/MT and USD 12k/MT by mid-2025; sees higher commodity prices ahead, expects total returns of circa. 10% for broad commodity indexes over the next 6-12months.

- Caspian Pipeline Consortium says export shipments seen falling by 7% in 2024; oil exports are seen declining from expected targets.

- Norway Energy Minister says Government will not open the Nordland 6 area for Oil and Gas exploration

- Norway’s Kollsnes and Troll A platform are expected to restart today, according to the Power Exchange.

- Venezuela revoked the invitation for the EU to send electoral observers, according to the head of the electoral council.

Geopolitics: Middle East

- Algeria’s UN envoy said they will propose a draft UN Security Council resolution on Gaza “to stop the killing in Rafah”, according to Reuters.

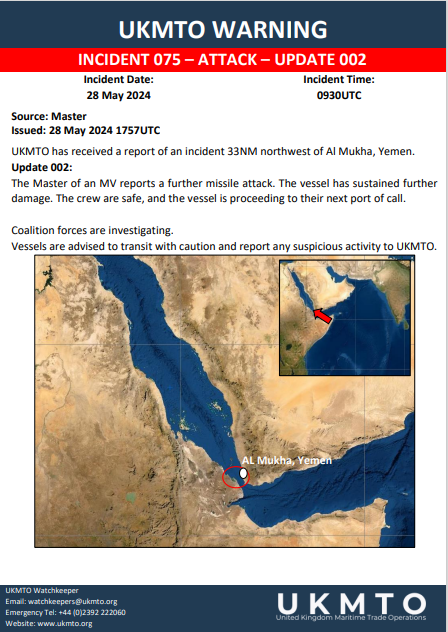

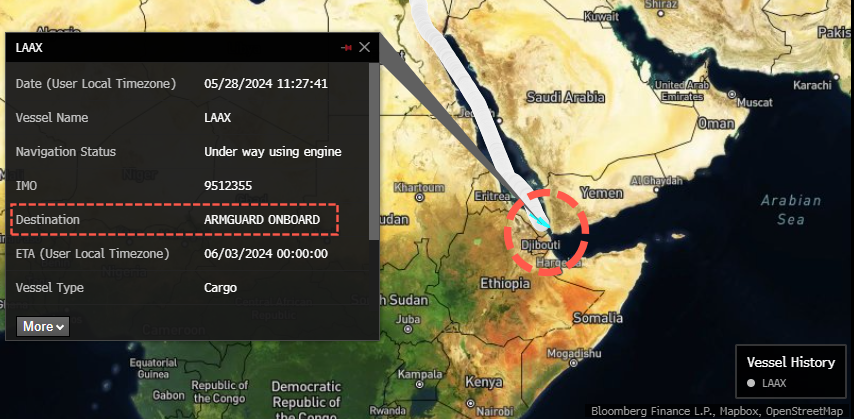

- US military said Iranian-backed Houthis launched five anti-ship ballistic missiles from Houthi-controlled areas of Yemen into the Red Sea, while M/V LAAX which is a Marshall Islands-flagged, Greek-owned and operated bulk carrier, was struck by three of the missiles but continued its voyage.

- “Israeli forces have now pushed deeper inside Rafah, mostly along the Philadelphi Corridor, and are operating in the Tal Zaroub area. This means Israel controls almost the entirety of the Philadelphi Corridor”, according to journalist Horowitz.

Geopolitics: Other

- French President Macron said Ukraine should be allowed to hit military targets in Russia, according to FT.

- North Korean leader Kim Jong Un said owning spy satellites will help the country’s self-defence capabilities against US military provocation and that the recent satellite launch failed due to abnormal operation of the first-stage engine. Kim said the satellite launch was conducted with transparency and compliance with international law, while he added they will never give up efforts to own space reconnaissance capabilities.