MAY 30//BLOG/GOLD CLOSED UP $3.60 TO 2345.45 WHILE SILVER WAS DOWN 80 CENTS AND THIS SETS UP OPTIONS EXPIRY TOMORROW ON FIRST DAY NOTICE//PLATINUM WAS DOPWN $10.75 TO $1031.85 WHILE PALLADIUM WAS DOWN $11.75 TO $955.85//GOLD COMMENTARY TONIGHT FROM PETER SCHIFF//ECONOMIC COMMENTARY FROM MICHAEL EVERY OF RABOBANK//CHINA BLOCKS IMPORTS OF BEEF FROM ONE MAJOR DISTRIBUTOR//FRANCE CALLS FOR A STRIKES INSIDE RUSSIA//UKRAINE TARGETS EARLY WARNING RADAR SYSTEMS INTO RUSSIA MUCH TO THE ANGER OF THE RUSSIANS//ISRAEL VS HAMAS//HOUTHIS VS WEST//CHAOS IN MEXICO HAS THE ISRAELI EMBASSY FIREBOMBED//ISRAEL ATTACKS SYRIA AND HITS A MAJOR MUNITIONS DUMP//COVID UPDATES/ VACCINE INJURY REPORTS//DR PAUL ALEXANDER//SLAY NEWS/EVOL NEWS ETC/USA NEWS JOBLESS CLAIMS RISE//REVISED FIRST QUARTER GDP FALLS TO ONLY 1.3%//MAJOR PROBLEMS FOR BOSTON AND SEATTLE/ECOMONIC REPORT ON OUR REGIONAL BANKS//SWAM NEWS FOR YOU TONIGHT

435 H SCOTIA CAPITAL 1 624 H BOFA SECURITIES 357 880 H CITIGROUP 356

TOTAL: 357 357 MONTH TO DATE: 2,750

JPMorgan stopped 0/357

FOR MAY2024

GOLD: NUMBER OF NOTICES FILED FOR MAY/2024. CONTRACT: 357 NOTICES FOR 35,700 OZ or 1.1104 TONNE

total notices so far: 2750 contracts for 275000 Oz (8.553 tonnes)

FOR MAY:

SILVER NOTICES: 1 NOTICE(S) FILED FOR 5,000 OZ/

total number of notices filed so far this month : 6133 for 30.6650 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $3.60

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

NO CHANGES IN GOLD INVENTORY AT THE GLD:

/ /INVENTORY RESTS AT 832.21TONNES

INVENTORY RESTS AT 832.21 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER DOWN $0.80 AT THE SLV//

NO CHANGES IN SILVER INVENTORY AT THE SLV:

// INVENTORY LOWERS TO 417.430 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 417.430 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUMONGOUS SIZED 2031 CONTRACTS TO 186,877 AND CONTINUING ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR GAIN OF $0.20 IN SILVER PRICING AT THE COMEX ON WEDNESDAY. WE HAD ZERO LONG LIQUIDATION AT THE COMEX SESSION WITH AGAIN SHORT COVERING BY OUR SPECS DESPITE THE GAIN IN PRICE. WE HAD ANOTHER HUGE SIZED 638 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID LIKE TODAY.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 638 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND TODAY;S RAID.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.20) AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE DID HAVE A HUMONGOUS SIZED GAIN OF 3456 CONTRACTS ON OUR TWO EXCHANGES WITH THE GAIN IN PRICE OF $0.20

.

WE MUST HAVE HAD:

A HUMONGOUS SIZED 1425 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 28.130MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 0 QUEUE JUMP TO LONDON OF NIL OZ

//NEW STANDING FOR SILVER//MAY IS THUS 30.655 MILLION OZ

WE HAD:

/ HUMONGOUS SIZED COMEX OI GAIN //HUGE SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 638 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED AN ENORMOUS 992 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY

TOTAL CONTRACTS for 21 DAYS, total 25,651 contracts: OR 128.255 MILLION OZ (1211 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 128.255 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL PROBABLY BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 128.255 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

RESULT: WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2031 CONTRACTS WITH OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUMONGOUS EFP ISSUANCE CONTRACTS: 1425 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR MAY OF 29.345 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0 OZ//QUEUE// E.F.P JUMP TO LONDON

//NEW TOTAL STANDING REMAINS AT 30.655 MILLION OZ

WE HAVE A HUGE SIZED GAIN OF 3456 OI CONTRACTS ON THE TWO EXCHANGES WITH THE GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG SIZED 638 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND ZERO LIQUIDATION OF SHORTS.

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (638) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 1 NOTICE(S) FILED TODAY FOR 5,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 10,239 OI CONTRACTS TO 476,805 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE 1614 CONTRACTS

WE HAD A STRONG SIZED DECREASE IN COMEX OI (10,239 CONTRACTS) OCCURRED WITH OUR LOSS OF $13.55 IN PRICE/WEDNESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER, INITIATING WEDNESDAY’S RAID. WE ALSO HAD A RATHER LARGE INITIAL STANDING IN GOLD TONNAGE FOR MAY AT 4.684 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY;S 0 OZ QUEUE JUMP// E.F.P JUMP TO LONDON PLUS WE MUST ADD THAT DUBIOUS ISSUANCE OF 1084 OI EX FOR RISK CONTRACTS ISSUES ON LAST FRIDAY WHEREBY THE BUYER ASSUMES RISK OF 3.3716 TONNES OF GOLD//NEW STANDING DECREASES TO 8.5536 TONNES PLUS THE DUBIOUS 3.3716 ECH FOR RISK!

NEW STANDING REMAINS AT 11.925 TONNES// ALL OF THIS HAPPENED WITH OUR $13.55 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A FAIR SIZED LOSS OF 2771 OI CONTRACTS (8.618 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 7168 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 476,805

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2771 CONTRACTS WITH 10,239 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 7468 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 2771 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 1206 CONTRACTS,,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (7468 CONTRACTS) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI 8625/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 2771 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR MAY AT 4.684 TONNES FOLLOWED BY TODAY;S 0 OZ EFP JUMP/QUEUE JUMP, PLUS 3.3716 TONNES EX FOR RISK//PRIOR

//NEW STANDING /MAY 11.925 TONNES.

/ 3) CONSIDERABLE LIQUIDATION OF CONTRACTS MOSTLY DUE TO SPREADERS ALONG WITH SOME MINOR LONG SPECS BEING WIPED OUT WITH THE LOSS IN PRICE.

// 4) STRONG SIZED COMEX OPEN INTEREST LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1206 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY. :

TOTAL EFP CONTRACTS ISSUED: 97,549 CONTRACTS OR 9,754,900 OZ OR 303.41 TONNES IN 21 TRADING DAY(S) AND THUS AVERAGING: 4645 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 21 TRADING DAY(S) IN TONNES 303.41 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 303.41 DIVIDED BY 3550 x 100% TONNES = 8.53% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 303.41 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUMONGOUS SIZED 2031 CONTRACTS OI TO 187,869 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1425 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1425 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1425 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 2031 CONTRACTS AND ADD TO THE 1425 E.FP. ISSUED

WE OBTAIN A STRONG SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 3456 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 17.28 MILLION OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 19.34 PTS OR 0.62% //Hang Seng CLOSED DOWN 246.82 PTS OR 1.34%// Nikkei CLOSED DOWN 502.74 OR 1.30%//Australia’s all ordinaries CLOSED DOWN 0.50%///Chinese yuan (ONSHORE) closed UP TO 7,2355 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2529/ Oil DOWN TO 79.28 dollars per barrel for WTI and BRENT DOWN AT 83.50 /Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 10,239 CONTRACTS TO 475,191 WITH OUR STRONG LOSS IN PRICE OF $13.55 WITH RESPECT TO WEDNESDAY TRADING. WE HAD A CONSIDERABLE T.A.S. LIQUIDATION WEDNESDAY AS WELL AS FEW LONGS BEING CLIPPED.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE NON ACTIVE DELIVERY MONTH OF MAY.… THE CME REPORTS THAT THE BANKERS ISSUED A HUGE SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 7468 EFP CONTRACTS WERE ISSUED: : JUNE7468 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE:7468 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2771 CONTRACTS IN THAT 7468 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 10,239 COMEX CONTRACTS..AND THIS LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $13.55// WEDNESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT WAS A FAIR SIZED 1206 CONTRACTS. MOST OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. TODAY IS OF EXTREMELY IMPORTANCE TO OUR CROOKS IN YESTERDAY’S FALL IN PRICE

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: MAY (8.5536 TONNES+ 3.3716 EX FOR RISK/PRIOR) = 11.925 TONNES ( NON ACTIVE MONTH)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 24 MONTHS OF 2021-2023:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $13.55 //// AND WERE SUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD A FAIR LOSS OF 2771 CONTRACTS ON WEDNESDAY WITH OUR TWO EXCHANGES WITH THE LOSS IN PRICE. THE T.A.S. ISSUED ON WEDNESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE LOST A TOTAL OI OF 8.618 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR MAY (4.684 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S ZERO JUMP//EFP JUMP PLUS 3.3716 TONNES OF EX FOR RISK/PRIOR

NEW STANDING: 8.5536 TONNES PLUS 3.3716 TONNES EX FOR RISK/PRIOR = 11.925

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $13.55

WE HAVE REMOVED 8,136 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET LOSS ON THE TWO EXCHANGES 2771 CONTRACTS OR 277,100 (8.618 TONNES)

Total monthly oz gold served (contracts) so far this month

2750 notices 275000 oz 8.559 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

1 dealer deposits:

(1) into ASAHI: 32,348.89 oz

total dealer deposits: 32,348.89 oz

we have 0 customer deposit:

total deposit nil oz

total customer withdrawals: 1

i. out of Ashai 32,335.930 oz

TOTAL WITHDRAWALS 32,335.930 0z

Adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR MAY

For the front month of MAY we have an oi of 379 contracts having LOST 2 contracts.

We had 0 contracts served on WEDNESDAY, so we LOST 2 contracts or 200 oz (0.00623 Tonnes).

JUNE DECREASED ITS OI BY 44,630 CONTRACTS DOWN TO 29,291 CONTRACTS. WE HAVE 1 MORE READING DAYS BEFORE FIRST DAY NOTICE

JULY GAINED 687 CONTRACTS TO STAND AT 1869

We had 357 contracts filed for today representing 35700 oz

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 22 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for the MAY /2024. contract month, we take the total number of notices filed so far for the month (2750) x 100 oz ) to which we add the difference between the open interest for the front month of MAY ( 357 CONTRACTS) minus the number of notices served upon today (357 x 100 oz per contract( equals 275,000 OZ OR 8.5536 TONNES. PLUS THE 3.3716 OF EX FOR RISK/PRIOR = 11.925 TONNES

thus the INITIAL standings for gold for the MAY contract month: No of notices filed so far (2750x 100 oz + 357 OI for the front month} minus the number of notices served upon today (357) x 100 oz which equals 275,000 oz (8.5536 TONNES) PLUS 3.3716 EX FOR RISK/PRIOR = 11.925 TONNES.

TOTAL COMEX GOLD STANDING FOR MAY: 11.9250 TONNES WHICH IS HUGE FOR THIS A NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,641,822.253 OZ

TOTAL REGISTERED GOLD 7,885,539.2 ( 245.27 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,756,283.053 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,327,052 oz (REG GOLD- PLEDGED GOLD)= 196.79 tonnes //

END

SILVER/COMEX

MAY 30

INITIAL

//2024// THE MAY 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

1,163,269.238 oz

hsbc delaware

.

Deposits to the Dealer Inventory

nil OZ

Deposits to the Customer Inventory

606,050.300 oz asahi

No of oz served today (contracts)

1 CONTRACT(S) (5,000 OZ)

No of oz to be served (notices)

0 contracts (0.000 million oz)

Total monthly oz silver served (contracts)

6133 Contracts (30.665 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i) into asahi 606,050.300 oz

total customer deposit 606,050.300 oz

JPMorgan has a total silver weight: 128.497million oz/297.910 million or 43.23%

adjustment: 0

Comex withdrawals: 2

i) delaware; 594,869.738 oz

i) hsbc 568,399 oz

ii) delaware 598,193.480 oz

total withdrawal: 1,163,269.238 0z

TOTAL REGISTERED SILVER: 62.175MILLION OZ//.TOTAL REG + ELIGIBLE. 297.910 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DECEMBER:

silver open interest data:

FRONT MONTH OF MAY/2024 OI: 1 CONTRACTS HAVING LOST 25 CONTRACT(S).

.

We had 25 notices served on WEDNESDAY so we LOST 0 contracts or 0 oz underwent an EFP JUMP TO LONDON/QUEUE JUMP

JUNE SAW A LOSS OF 217 CONTRACTS RISING TO 1138

JULY SAW A GAIN OF 510 CONTRACTS UP TO 145,196

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 1 for 5,000 oz

CONFIRMED volume; ON WEDNESDAY 94,172 huge

To calculate the number of silver ounces that will stand for delivery in MAY we take the total number of notices filed for the month so far at 6133 x 5,000 oz = 30.665 MILLION oz

to which we add the difference between the open interest for the front month of MAY ((1) and the number of notices served upon today 1x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the MAY/2024 contract month: 6133 notices served so far) x 5000 oz + OI for the front month of MAY (1)x number of notices served upon today minus (1x 5000 oz of silver standing for the may contract month equates to 30.655 MILLION OZ.

New total standing: 30.655 million oz.

There are 61.566 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

MAY 30 WITH GOLD UP $3.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 29 WITH GOLD DOWN $13.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 28 WITH GOLD UP $22.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 832.21 TONNES

MAY 24 WITH GOLD DOWN $2.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 833.36 TONNES

MAY 23 WITH GOLD DOWN $53.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 22 WITH GOLD DOWN $32.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 21 WITH GOLD DOWN $12,00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 20 WITH GOLD UP $21.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.10 TONNES OF GOLD INTO THE GLD//NEW TOTAL 838.54 TONNES

MAY 17 WITH GOLD UP $31.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//NEW TOTAL 833.36 TONNES

MAY 16 WITH GOLD DOWN $7.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//NEW TOTAL 833.36 TONNES

MAY 15 WITH GOLD UP $34.90 ON THE DAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD/INVENTORY RISES TO 831.93 TONNES

MAY 14 WITH GOLD DOWN $17.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RISES TO 831.33 TONNES

MAY 13 WITH GOLD DOWN $31.10 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD////INVENTORY RISES TO 831.93 TONNES

MAY 10 WITH GOLD UP $34.65 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 9 WITH GOLD UP $18.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 8 WITH GOLD DOWN $0.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 830.47 TONNES

MAY 7 WITH GOLD DOWN $6.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 832.19 TONNES

MAY 6WITH GOLD UP $21.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .55 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 831.64 TONNES

MAY 2 WITH GOLD UP $0.20 ON THE DAY; SMAKK CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 830.47 TONNES

MAY 1 WITH GOLD UP $7.80 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNES

GLD INVENTORY: 832.21 TONNES, TONIGHTS TOTAL

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 30 WITH SILVER DOWN $0.80 TODAY: NO CHANGES IN SILVER INVENTORY//INVENTORY REMAINS AT 417.430 MILLION OZ

MAY 29 WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 1.051 MILLION OZ INTO THE SLV//INVENTORY DECREASES TO 417.430 MILLION OZ

MAY 28 WITH SILVER UP $1.64 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 2.832 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 418.481 MILLION OZ

MAY 24 WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF .822 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 421.313 MILLION OZ

MAY 23 WITH SILVER DOWN $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.736 MILLION OZ FROM THE SLVINVENTORY INCREASES TO 420.491 MILLION OZ

MAY 22 WITH SILVER DOWN $0.66 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 21 WITH SILVER DOWN $0.41 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A DEPOSIT OF 3.792 MILLION OZ FROM THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 20 WITH SILVER UP $1.28 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 1.005 MILLION OZ FROM THE SLV// INVENTORY LOWERS TO 418.435 MILLION OZ

MAY 17 WITH SILVER UP $1.37 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 868,000 OZ FROM THE SLV// INVENTORY LOWERS TO 419.440 MILLION OZ

MAY 16 WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY REMAINS AT 420.308 MILLION OZ

MAY 15 WITH SILVER UP 101 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A WITHDRAWAL OF 1.919 MILLION OZ FROM THE SLV

INVENTORY RESTS AT 420.308 MILLION OZ

MAY 14 WITH SILVER UP 25 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;

INVENTORY RESTS AT 422.227 MILLION OZ

MAY 13 WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;NVENTORY RESTS AT 422.227 MILLION OZ

MAY 10 WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A HUGE WITHDRAWAL OF 1.,828 MILLION OZ//INVENTORY RESTS AT 422.227 MILLION OZ

MAY 9 WITH SILVER UP 78 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 8 WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 7WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 6 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.055 MILLION OZ

MAY 3 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 2WITH SILVER UP 0.12 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/ A WITHDRAWALOF 4.471 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 1 WITH SILVER UP 0.09 TODAY: SMALLCHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF ,457 MILLION OZ INTO THE SLV INVENTORY RESTS AT 429.814 MILLION OZ

Central bank gold buying has been a significant factor in the yellow metal’s spectacular run-up to new record highs. But with its recent small correction downward, it’s a good time to look at which central banks are selling — and why.

Gold vs USD, 1-Month Chart, Source: Bloomberg

For one, Thailand has been selling the gold top to help rebalance its reserves. However, the biggest central bank gold seller by far is currently Uzbekistan, and has been for some time. The country has better reasons than most to sell the top and pull in some revenue: Uzbekistan bought a lot of gold when prices were lower, but even more importantly, they’re one of the world’s top 10-12 producers and exporters of gold in the world.

Being a producer helps reduce some of the pressure to hold as much gold as possible as global inflation continues to run hot, conflict in the Middle East drags on, and the ongoing war continues to rage between nearby Russia and Ukraine.

However, Uzbekistan’s major problem with gold is one of overdependence — they don’t have a lot of other revenue sources, are heavily indebted, and have leaned on gold sales to replenish their treasury without any major economic reforms to reduce the degree to which it has to lean on gold exports. If gold crashes, the central bank and government have few solid resources to soften the blow. Thankfully, if you zoom out, gold always trends up as central banks devalue their currencies — but Uzbekistan doesn’t have other tools to work with during gold’s major drawdowns.

Likewise, if there are disruptions around Uzbekistan’s gold mining industry that hamper its discovery, production, or export, the Uzbekistan central bank is left without equally effective measures to prop up the som, its troubled national currency. With gold’s rise, becoming one of the world’s biggest sellers allowed Uzbekistan to prop up the som against the US dollar — but without its stash of gold, the country’s economy and currency would be in a huge heap of trouble.

UZS vs USD as Uzbekistan Sells Gold, Source: Bloomberg

With gold currently raging, there’s also less incentive for the government to push to innovate and fix its more fundamental issues, since it can lean on high gold prices to keep itself afloat and pay back debtors, like the $1 billion that just came due on a 2019 Eurobond.

One major reform effort was a new rule allowing anyone to look for gold, in an effort to increase gold production and overall employment. And while it has helped somewhat, making fewer Uzbekis dependent on Russia for jobs, it only increases the country’s broader gold dependence.

Luckily for Uzbekistan, inflation will continue to worsen as central banks and governments scramble (and fail) to contain it, which will push commodities like gold higher. Meanwhile, countries like China continue their massive buying sprees and help prop up bull markets further. That means that Uzbekistan will probably continue to sell and reap the benefits of profit-taking, likely remaining one of the world’s major sellers in the coming months and years.

Without other economic tools, however, it can’t just rely on selling gold as a shortcut to prosperity on the global stage. Then again, if major currencies start to fall due to central bank hubris and out-of-control debt, perhaps gold will soar high enough that an overdependent country like Uzbekistan will have a (literal) golden opportunity to invest heavily into other areas, building itself up from the ashes of the self-destruction of Western fiat currencies.

For now, however, all that glistens in Uzbekistan’s economy is gold.

end

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS//GOLD AND SILVER COMMENTARY

END

3. CHRIS POWELL//GATA DISPATCHES

CHRIS POWELL…

In uncertain times, gold jewellery offers financial security

Submitted by admin on Wed, 2024-05-29 15:21 Section: Daily Dispatches

When gold is remonetized, India may be the richest country in the world.

* * *

By Yumna Iftikhar The Globe and Mail, Toronto Tuesday, May 28, 2024

As a child Adiba Ahmed didn’t understand why her mother loved gold jewellery. But when her family came under financial stress and her mother sold the gold to keep them afloat, Ahmed realized that gold jewellery could be a reliable emergency fund.

Gifting gold jewellery on special occasions is a prominent tradition in many South Asian countries, including Bangladesh, from where Ahmed’s family moved to Canada. Other countries where gold gifting is popular include Pakistan and India.

According to a 2023 report by the World Gold Council, Indian households own approximately 25,000 tonnes of gold, or roughly 12% of all the gold that has been mined globally. …

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT//ALUMINUM//

Aluminum Prices Hit Two-Year High On Smelter Output Limits In China

THURSDAY, MAY 30, 2024 – 03:05 PM

Aluminum prices in London reached their highest in two years as the industrial metals rebound theme continued, driven by a combination of supply constraints and the prospect of increased demand in China and the US.

The latest driver for the silvery-white, lightweight metal, used in everything from vehicles to aircraft to window frames to soda cans, comes as China, the world’s top producer, signaled overnight aggressive emission-cutting targets for smelters, in return, tighter metal capacity.

In a further boost for the bulls, China’s State Council pledged to strengthen capacity limits in industries from steel to alumina in a work plan for energy conservation and carbon reduction in 2024-25. The move to constrain additional supply comes at a time when the transition to greener energy is boosting demand for copper and aluminum.

The country will strictly control new capacity for copper smelters and alumina output, and take a reasonable approach in allocating fresh capacity for silicon, lithium and magnesium, the government said late Wednesday.

The government also reiterated strict implementation of the “aluminum swap scheme,” or the requirement for any new smelter to be matched by closure of an existing one. New capacity for aluminum, alumina, polysilicon and lithium batteries must meet advanced levels of energy efficiency, it added. –Bloomberg

With the US economy chugging along with the US government spending $1 trillion every 100 days, i.e., stealth stimulus, demand for metals and other commodities has increased. Easing in China has also boosted the prospect of demand increases for industrial metals. However, Chaos Ternary Research Institute wrote in a note that a near-term pullback in aluminum prices is quite possibly because of inventories in China and deliveries to the London Metal Exchange, which remain elevated.

In markets, aluminum prices on the LME rose 1.4% to $2,734 a ton.

The historic squeeze in New York copper futures fizzled this week, trading below the record high.

Industrial metals tracked by Bloomberg have soared to a 1.5-year high.

As tracked by Bloomberg, spot commodity prices have risen this year to 1.5-year highs.

In a note titled “The 5D Bull Makret,” Goldman analysts led by Daan Struyven and Samantha Dart wrote, “We remain selectively bullish commodities because 1) demand growth remains solid, 2) we see more structural upside in industrial metals and gold, and 3) oil’s geopolitical risk premium has shrunk. We expect commodity total returns to rise from 13% YTD to 18% by year-end.”

The analysts provided more insight into the 5D trends:

Disinvestment: low investment in commodities induces select tightness

Decarbonization & climate change: require higher prices to attract green capex

De-risking (hedging): geopolitical de-risking and strategic restocking support demand for gold and critical commodities

Datacenters & AI: support demand via power and via higher incomes

Defense spending: support demand for metals and distillate fuels

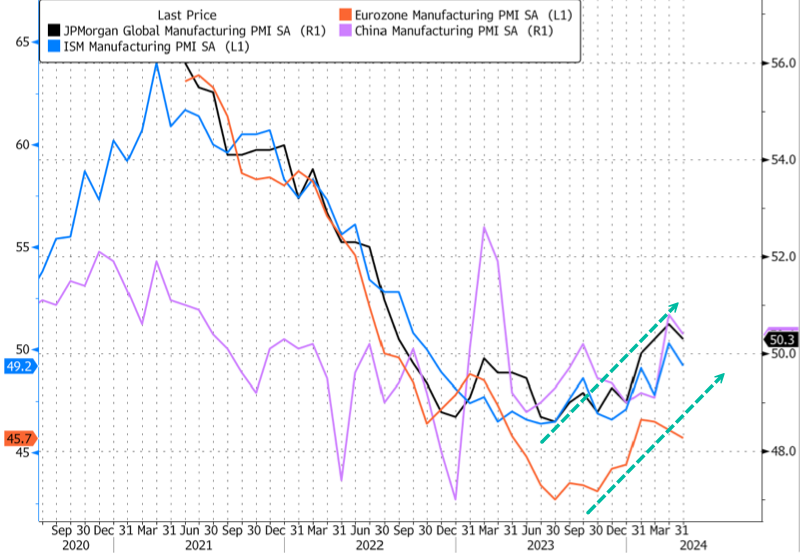

This comes as global Purchasing Managers’ Index data has turned up.

To sum up, rising commodity prices are yet more troubling signs for Jerome Powell & the gang in their attempt to slay the wicked inflation monster.

SHANGHAI CLOSED DOWN 19.34 PTS OR 0.62% //Hang Seng CLOSED DOWN 246.82 PTS OR 1.34%// Nikkei CLOSED DOWN 502.74 OR 1.30%//Australia’s all ordinaries CLOSED DOWN 0.50%///Chinese yuan (ONSHORE) closed UP TO 7,2355 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2529/ Oil DOWN TO 79.28 dollars per barrel for WTI and BRENT DOWN AT 83.50 /Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGSTHURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2355

OFFSHORE YUAN: DOWN TO 7.2529

SHANGHAI CLOSED DOWN 19.34 PTS OR 0.62 %

HANG SENG CLOSED DOWN 246.82 PTS OR 1.34%

2. Nikkei closed DOWN 502.74 PTS OR 1.30 %

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 104.54 EURO RISES TO 1.0819 UP 18 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.046 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 156.84 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and UPDOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.6770/Italian 10 Yr bond yield UP to 3.987 SPAIN 10 YR BOND YIELD UP TO 3.412%

3i Greek 10 year bond yield UP TO 3.680

3j Gold at $2335.45//Silver at: 31.29 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 24/ 100 roubles/dollar; ROUBLE AT 89.78

3m oil into the 79 dollar handle for WTI and 83 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 156.84/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.046% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9073 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9816 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.595 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.720 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.960 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.28…

10 YR UK BOND YIELD: 4.4285 UP 3 PTS

2a New York OPENING REPORT

Futures, Rates Drop As Salesforce Implosion Sours Mood

THURSDAY, MAY 30, 2024 – 08:09 AM

US equity futures are weaker despite lower bond yields, breaking away from this week’s narrative of Equity/Yields negative correlation, after Salesforce plunged 15% due to disappointing guidance. Small-caps are poised to outperform but have failed to hold gains this week. As of 7:45am, S&P futures are down 0.4%, pointing to a second day of declines but off the session’s worst levels as Nasdaq futures drop 0.3% while Europe’s Stoxx 600 benchmark was led higher by telecom and banking stocks. Premarket, the Mag7 names are mostly lower, ex-AAPL, while NVDA is -0.8%, weighing on Semis, dragged lower by the read through from Salesforce. 10Y yields are down 2 basis points after jumping about 15 bps in the past two days. The US dollar is seeing its weakest start to the day for this week; commodities and bitcoin are weaker, too. Today’s macro data focus will be on Jobless Claims, Retail Inventories, Pending Home Sales, and revisions to the 24Q1 GDP print including the GDP Price Index and Core PCE Price Index. Tomorrow we receive the monthly PCE data which should be more market moving.

In premarket trading, Salesforce shares crashed 16% after the software maker said sales growth in the current quarter will stall to its slowest in history. The miss sparked concerns about the sector more broadly, and hit other software names: Oracle (ORCL) -2%, ServiceNow (NOW) -3%, MongoDB (MDB) -1%. Here are some of the biggest US movers before the opening bell:

Agilent tumbles 13% after the life-sciences company cut its profit and sales forecast for the full year.

American Eagle drops 7% after the apparel retailer’s first-quarter net revenue narrowly missed consensus estimates. Morgan Stanley flagged the underperformance of the firm’s Aerie brand as a major negative.

Birkenstock jumps 8% after the sandal maker’s revenue forecast for the year came ahead of analyst expectations.

C3.ai climbs 10% after the software company forecast 2025 revenue well above the average analyst estimate, supported by demand for artificial intelligence features.

Foot Locker gains 13% after posting earnings that surpassed expectations as the sneaker retailer tries to get back on pace with its turnaround plan.

HP Inc. rises 5% after the company reported net revenue for the second quarter that beat estimates.

Moderna advances 2% after the Financial Times reported that the US government is nearing an agreement to bankroll a late-stage trial of the biotech firm’s mRNA pandemic bird flu vaccine.

Nutanix drops 12% after the infrastructure software company gave a fourth-quarter revenue forecast that trailed analyst estimates.

Okta climbs 4% after the security software company raised its full-year forecast.

Pure Storage gains 9% after the cloud storage provider’s results beat estimates and its second-quarter revenue forecast topped expectations, spurring a round of price target hikes.

Global equities are headed for their worst week since mid-April as US rate-cut expectations dwindle and tepid US auctions stir worries about funding the US deficit. The S&P 500 has advanced for 23 of the last 30 weeks, marking a joint record since 1989, but yesterday it fell -0.74%, and futures this morning are down again so it’s clear that the momentum is now more negative.

As DB’s Henry Allen writes, “markets have had another rough 24 hours, with no sign of the negative momentum letting up overnight. The latest selloff has been driven by a range of factors, but bonds took a particular hit after a weak US Treasury auction yesterday, along with mounting concern about inflationary pressures, which sent European yields up to their highest levels in months.”

BlackRock is sticking to the front end and the belly of the US Treasuries curve as optimism over US easing fades, according to Karim Chedid, the firm’s investment strategy head for EMEA.

“We see that as the area where you’re still getting the most bang for buck in terms of income for stability,” he said in an interview with Bloomberg Television. While the scorching rally in tech companies is underpinned by fundamentals and remains one of BlackRock’s “key sector overweights,” Chedid says he’s seeing growing inflows into European and Japanese equities.

The prospect of a rate cut from the European Central Bank at its June meeting is helping, as is “a bottoming out in the macro data in Europe, which investors are liking,” Chedid said. “Earnings have seen a significant upgrade in Europe over the past 12 months.”

And speaking of the coming ECB rate cut, European stocks are in the green after two days of losses, with telecommunication and bank shares leading gains. Major markets are all higher with Spain the notable outperformer. While some inflation prints have disappointed, the ECB remains on track to launch its easing cycle next week. Regional bonds are seeing a relief rally with Gilts curve the largest mover, seeing bull steepening. Banks among the biggest beneficiaries in EU while UK is seeing add’l support from Cyclicals. Here are the biggest movers Thursday:

Auto Trader rises as much as 14%, hitting a record high, after the online car marketplace posted FY revenue and profit that beat expectations and said the new financial year has started well

European renewables stocks are lifted by a renewed focus on M&A after Brookfield announced it is in exclusive talks to acquire a majority stake in French renewable energy developer Neoen

BW LPG gains as much as 12% and to a fresh record high after the Norwegian LPG shipper reported a “solid” first-quarter beat and provided “positive” second-quarter guidance, DNB says

Dr Martens rises as much as 11% after the bootmaker reported full-year results. While revenue and Ebitda for the period missed estimates, the company announced a cost savings plan

YIT rises as much as 12%, hitting the highest since April 2023, as Danske Bank double-upgrades the Finnish construction services firm, giving the stock its sole buy rating

De La Rue shares climb as much as 9.2% after the banknote maker said it’s in talks with potential buyers for some of its business divisions, but also said there is no certainty of a deal

Telecom Italia shares fall as much as 9.2% as the telecom operator reported results that showed still challenging trends in Italy as pace of its mobile and broadband subscriber loss quickened

NKT falls as much as 4.5%, the most since April 22, after Carnegie cut its recommendation for the Danish power cable manufacturer to hold from buy, awaiting “the next leg in the case to unfold”

Pirelli shares fell as much as 5.8% in Milan trading after shareholder China’s state-backed Silk Road Fund Co. disposed of its stake in the Italian tiremaker

European software stocks drop after US peer Salesforce gave a weak outlook, spurring worries over a slowdown in the sector more broadly and the firm’s relevance amid the advancement of AI

South Africa’s main stock index falls 1.8%, the most in more than six weeks, as initial projections of results in Wednesday’s election show a marked decline in support for the ruling ANC party

Asian stocks extended declines into a third session, led by drops in Japanese and Korean equities, as higher US Treasury yields sapped the appeal of riskier assets. The MSCI Asia Pacific Index fell as much as 1.2% to touch its lowest level in three weeks, with TSMC, Samsung and Toyota among the biggest drags. The regional tumble comes after another weak sale of Treasuries reinforced concerns about the impact of higher yields. Japan’s key benchmarks retreated as the country’s long-term yields continued to rise. The yen briefly fell through a level that prompted the latest round of suspected action by Japan to prop up the currency. The Kospi dropped, dragged by losses in Samsung after the firm’s labor union said Wednesday it plans to carry out its first strike ever.

“Asian markets are clearly taking a cue from the US session marked by higher correlation and volatility,” said Homin Lee, a senior macro strategist at Lombard Odier. “We see signs that investors are still nervous about major policy innovations in Japan and China where the recent attempts to tackle the respective macro challenges – real estate in China and currency weakness in Japan – seem to have underwhelmed the markets and need to be ramped up even further,” Lee said.

In rates, treasuries pare some of their recent decline. US 10-year yields are down 2bps at 4.59%, having risen almost 15bps in the prior two sessions; they remain near the highest levels this year as optimism over US rate cuts fades. Gains were led by gilts as European bonds also recoup some of Wednesday’s losses. 2s10s and 5s30s curves remain notably steeper on the week.

In FX, the dollar erased earlier gains to fall modestly, paring Wednesday’s 0.5% advance; the Japanese yen rebounds after falling through a level that prompted the latest round of intervention by authorities. USD/JPY is down 0.5% near 156.88 after hitting a four-week high late Wednesday at 157.71. The Swiss franc is the strongest in G-10 FX, rising 0.7% against the greenback after SNB President Jordan warned a weaker currency is currently the most likely source of higher inflation and could be offset with FX sales. The rand extended losses and banking stocks fell as South Africa’s election vote count gathers pace. The ruling party looks set to fall well short of obtaining a parliamentary majority for the first time since it came to power.

In commodities, crude slipped as traders look to US stockpile data and an OPEC+ meeting on the weekend for more clarity on the supply and demand outlook. WTI traded near $79.10 while Brent was at $83.50. Spot gold falls $3 to around $2,335/oz.

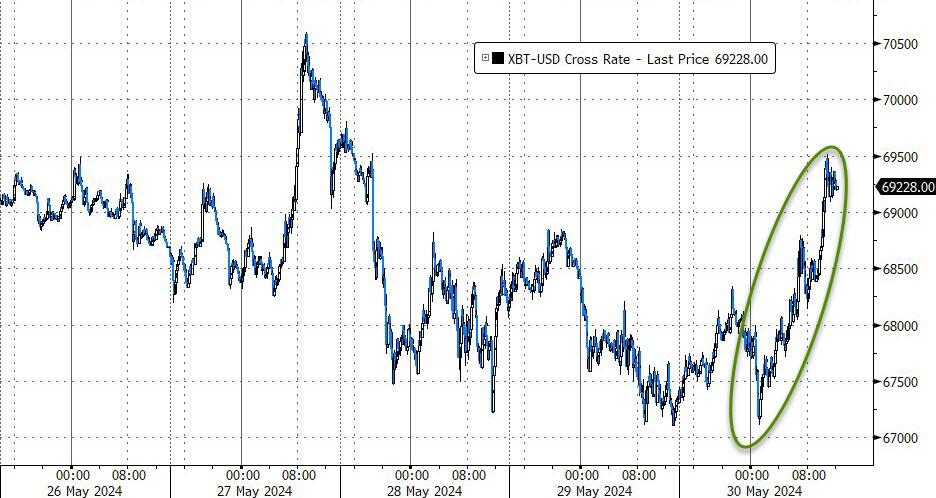

Bitcoin is modestly firmer and holds around $68k, while Ethereum continues to lose ground.

Looking to the day ahead now, US economic data includes second estimate of 1Q GDP, initial jobless claims, April wholesale inventories, advance goods trade balance (8:30am) and pending home sales (10am). Fed officials’ scheduled speeches include Williams (12:05pm) and Logan (5pm)

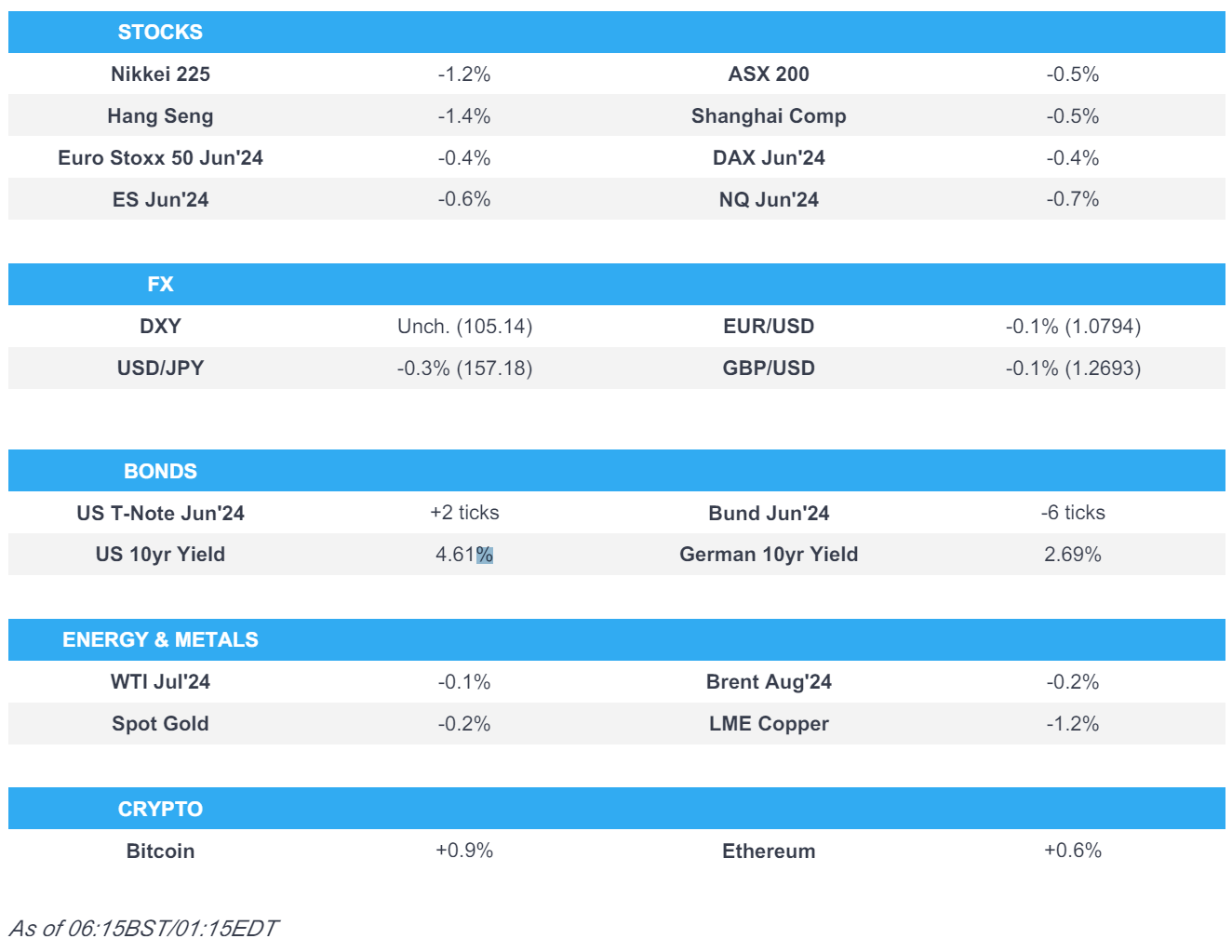

Market Snapshot

S&P 500 futures down 0.5% to 5,260.00

STOXX Europe 600 up 0.2% to 514.64

MXAP down 1.0% to 176.44

MXAPJ down 1.2% to 550.15

Nikkei down 1.3% to 38,054.13

Topix down 0.6% to 2,726.20

Hang Seng Index down 1.3% to 18,230.19

Shanghai Composite down 0.6% to 3,091.68

Sensex down 0.6% to 74,021.56

Australia S&P/ASX 200 down 0.5% to 7,628.20

Kospi down 1.6% to 2,635.44

German 10Y yield little changed at 2.66%

Euro little changed at $1.0809

Brent Futures down 0.3% to $83.36/bbl

Gold spot down 0.2% to $2,333.60

US Dollar Index down 0.11% to 105.01

Top Overnight News

Market pressure is growing on the PBOC to allow the renminbi to weaken, as traders bet that the yawning gap with US borrowing costs will lead more investors to sell out of the Chinese currency. China’s central bank has maintained a strong yuan policy so far this year, keeping its daily fixing — or reference rate around which the currency is allowed to trade — within an unusually narrow range of 7.09 to 7.11 against the US dollar. FT

China is poised to impose a record fine on PwC of at least 1 billion yuan ($138 million) and suspend some of its local operations over its role in the alleged fraud at Evergrande, people familiar said. BBG

Global sovereign bond markets are facing the biggest month of supply so far this year in June ($340B worth of net paper needs to be absorbed from the US, EU, and UK next month). RTRS

Spain’s EU harmonized CPI for May came in at +3.8%, a 40bp acceleration vs. +3.4% in Apr and higher than the Street’s +3.7% forecast (the rise was driven by an electricity tax increase). RTRS

Washington is concerned about Ukrainian strikes against Russian radar systems used by Moscow to detect nuclear weapons attacks (the Pentagon is worried this could upset the strategic balance between the US and Russia). WaPo

UBS appointed investment bank head Rob Karofsky to run its US business and jointly oversee the wealth unit with Iqbal Khan, in a management shakeup that may make them prime contenders vying to succeed CEO Sergio Ermotti. BBG

The Fed’s Raphael Bostic said many inflation measures are moving back to their target range. He said if prices and the labor market move to a more “stable-growth stance,” officials may be prepared to cut rates in the fourth quarter. BBG

US crude inventories fell by 6.5 million barrels last week, the API is said to have reported. That would be the largest drop since January, if confirmed by the EIA today. BBG

AMZN has added the Grubhub food delivery service directly to its app and website, deepening an existing partnership between the two companies (Amazon Prime members already have a free Grubhub+ membership). RTRS

Fed’s Bostic (voter) said the inflation path will be bumpy but the general trend is down and the path to 2% inflation is not assured, while he added that the Fed is vigilant and the job market is tight but not as tight. Furthermore, he said the breadth of price gains is still pretty significant and less inflation breadth would add to confidence for a cut.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were on the back foot amid spillover selling from Wall St owing to the further upside in yields. ASX 200 was pressured with underperformance in miners after recent declines in underlying commodity prices. Nikkei 225 slumped at the open and briefly fell beneath the 38,000 level but is well off worse levels. Hang Seng and Shanghai Comp conformed to the uninspiring mood in which the Hong Kong benchmark gradually weakened with notable losses in mining and property stocks, while the mainland was rangebound following another substantial liquidity injection by the PBoC and after the central bank also vowed several support efforts including promoting trade and investment facilitation.

Top Asian News

PBoC Deputy Governor Tao Ling said they will coordinate the relationship between short-term tasks and long-term goals, stable growth and risk prevention, and internal and external balances, as well as accelerate implementation and effectiveness of a relending facility for science and technology innovation. Tao said they will promote trade and investment facilitation, support the development of the offshore yuan market and support small- and medium-sized tech firms’ first-time loans and equipment upgrades in key areas with big efforts.

Chinese President Xi said at the China-Arab States Cooperation Forum that China is willing to build China-Arab relations as a benchmark for maintaining world peace and stability, while China is ready to work with the Arab side to explore ways to resolve hotspot issues conducive to upholding fairness, justice and achieving long-term peace and stability. Furthermore, he said China will accelerate the building of a China-Arab community of a shared future, as well as build a larger-scale investment and finance landscape with the Arab side.

US officials reportedly escalated a crackdown on the controversial customs exemption that Temu, Shein and other e-commerce firms use to send cheap items from overseas to American shoppers without paying tariffs, according to The Information.

RBA chief economist Hunter said they agree with the Treasury forecast on inflation and noted that CPI confirmed there was strength in some price sectors. Hunter added the Board is focused on inflation staying out of the band and there is strength in the inflation.

PBoC says it is playing close attention to current bond market changes and potential risks; will sell low risk bonds including govt bonds when necessary.

Some of China’s regional authorities reportedly are guiding firms to slow purchases of foreign currencies in a sign the nation is taking further measures to discourage capital outflows amid yuan weakness, according to Bloomberg.

European bourses, Stoxx 600 (+0.2%) began the session on a mostly softer footing, continuing the price action seen in APAC trade overnight; however, sentiment improved as the morning progressed, with indices climbing modestly into the green. European sectors hold a positive bias; Tech is the clear laggard, with sentiment in the sector hit following weak guidance from Salesforce (-16% pre-market), which has weighed on peers such as SAP. Basic Resources is hampered by broader weakness in metals prices. US Equity Futures (ES -0.4%, NQ -0.4%, RTY +0.1%) are mixed, though have been edging higher in recent trade, in tandem with the broader pick-up in European stocks.

Top European News

UK PM Sunak promises interest rate cuts if he wins the election, according to The Times. PM Sunak said the economy was ‘heading in the right direction’ and that a vote for the Tories is a vote for cuts to interest rates as he set out a vision for a “more prosperous, more secure, more united country” if he wins the election.

British Chambers of Commerce business lobby group said the next UK government must forge better trade relations with Europe and warned that companies face ever higher costs stemming from Brexit, according to FT.

ECB is to impose the first-ever fines on banks for climate failures.

FX

DXY is lower and sitting just beneath the 105 mark after popping above its 50DMA at 105.09 and advancing to a 105.18 peak. US yields have been viewed as one of the main drivers for the USD’s rise this week, as attention turns to the second reading of US Q1 GDP, PCE and Initial Jobless Claims later today.

EUR/USD has moved back onto a 1.08 handle and in close proximity to its 100 DMA (1.0807) after slipping as low as 1.0789; which is just above the 200DMA at 1.0786.

Cable is currently hugging the 1.27 mark, whilst EUR/GBP has moved back onto an 0.85 handle. Newsflow for the UK remains light aside from noise surrounding the general election.

JPY is the best performer across the majors with some pinning the move on the recent bout of risk-aversion. USD/JPY continues to pullback from yesterday’s 157.71 peak which was the highest since May 1st.

Antipodeans are both muted vs. the USD. AUD/USD has been oscillating around the 0.66 mark in quiet trade with focus in part on fluctuations around the CNY (see below); today’s 0.6591 was the lowest print since 14th May.

USD/CNY is moving ever closer to the 7.25 mark with increasing speculation over how long the PBoC will keep the USD/CNY fix steady.

ZAR has lost ground vs the Dollar as models predict that the ruling ANC party could lose its outright parliamentary majority. Further reports that suggest ANC is likely to get around 45% (prev. reports of 42.3%) helped to spark some modest upside for the ZAR; SARB Policy Announcement is also due today.

PBoC set USD/CNY mid-point at 7.1111 vs exp. 7.2623 (prev. 7.1106).

SNB’s Jordan said there is a small upward risk to the SNB’s inflation forecast and reasons to believe the natural rate of interest has increased or might rise, while he added that a weak CHF is the most likely source of inflation.

South African Election Commission: Governing African National Congress (ANC) is on 42.3% of the vote with 10% of polling stations reported; thereafter, South Africa’s ruling ANC party could win 41.5% of votes, according to Bloomberg citing a model.

Most recently, South African Broadcaster ENCA says ANC is likely to get around 45% of the national vote and will fall short of a majority

Fixed Income

USTs have bounced modestly following Wednesday’s soft 7yr auction, in part thanks to a robust JGB auction. USTs are near highs of 108-09+ vs Wednesday’s 107-31 post-auction WTD base.

Bunds are following USTs/JGBs but with magnitudes slightly more contained; Spanish harmonised inflation metrics Y/Y ticked up slightly, though was unable to spark any material move. Bunds up to a 129.23 peak.

Gilt price action is following peers, going as high as 95.81 but someway to go before a retest of 96.43, 97.09 and 97.32 highs from earlier in the week.

Italy to sell EUR 7.5bln vs exp. EUR 6-7.5bln 3.35% 2029, 3.85% 2029, 3.85% 2034 BTP and EUR 2bln vs exp. EUR 1.5-2bln 2029, 2032 CCTeu

Commodities

Subdued trade for the crude complex as prices continue to trim the gains seen earlier this week and as attention turns to the OPEC+ confab on Sunday; Brent Aug sits between a 82.94-83.58/bbl range.

Another downbeat session for precious metals despite the softer Dollar amid an intraday pullback in yields. Spot gold sees its losses more cushioned vs silver and palladium after the yellow metal found support near its 50 DMA; XAU trades within a USD 2,322.66-2,339.95/oz parameter.

A devastating session for base metals thus far following the recent rise in yields and the Dollar, whilst the downbeat mood across Chinese markets overnight only added the pessimism in the complex.

US Private Energy Inventory Data: Crude -6.5mln (exp. -2mln), Cushing -1.7mln, Distillates +2mln (exp. -0.2mln), Gasoline -0.5mln (exp. -0.5mln).

Geopolitics

Israel’s army said Hamas is in Rafah and is holding Israeli hostages, so they are launching military operations there and will not stop fighting in Rafah until the hostages are freed.

US official said the US is to boycott UN tribute to Iran’s late President Raisi on Thursday, according to Reuters.

“Hearing from sources that American resistance to the E3 censure resolution (on Iran) is fading; recognising the reality that E3 are pushing ahead”, according to WSJ’s Norman

Russian Foreign Minister Lavrov said China could arrange a peace conference in which Russia and Ukraine would participate, while he added that Russia regards planned supplies of F-16 fighters to Ukraine as a “signal action” by NATO in a nuclear area, according to RIA.

North Korea fired what was suspected to be a ballistic missile which fell shortly after the launch announcement and appeared to have landed outside of Japan’s exclusive economic zone, according to the Japanese Coast Guard and press. It was later reported that South Korea said North Korea fired what appeared to be multiple short missiles that flew about 350km.

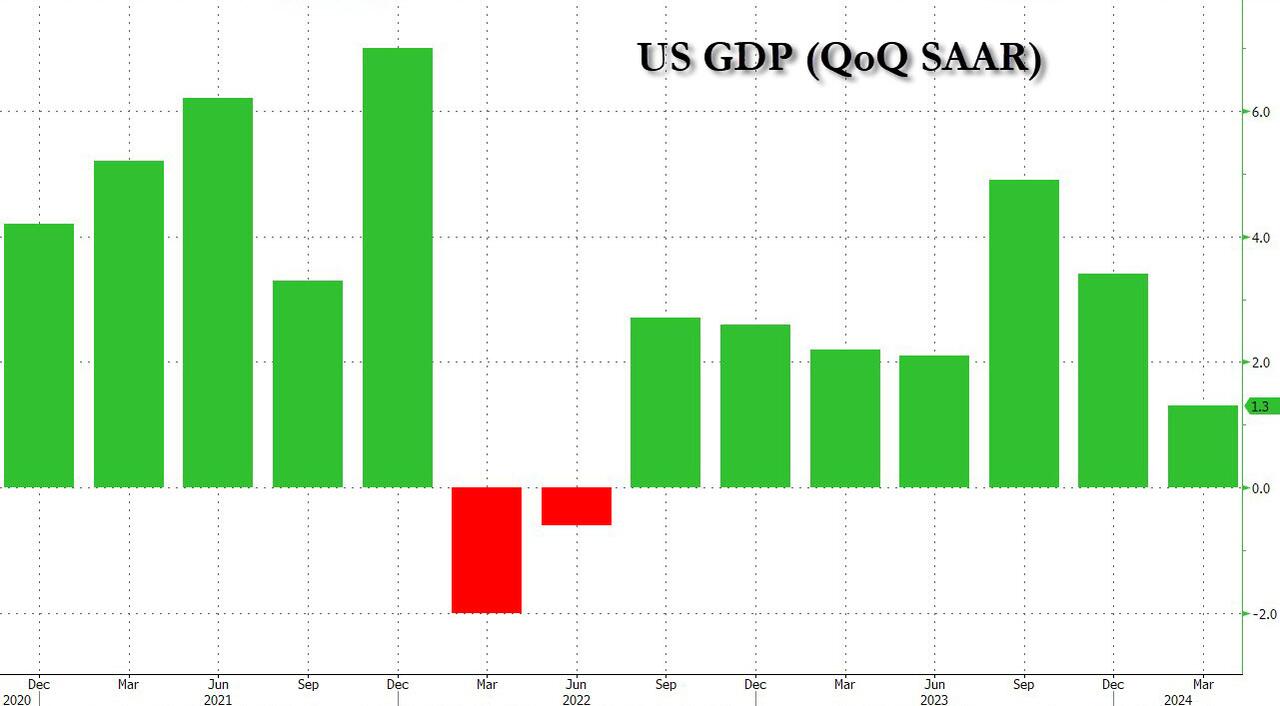

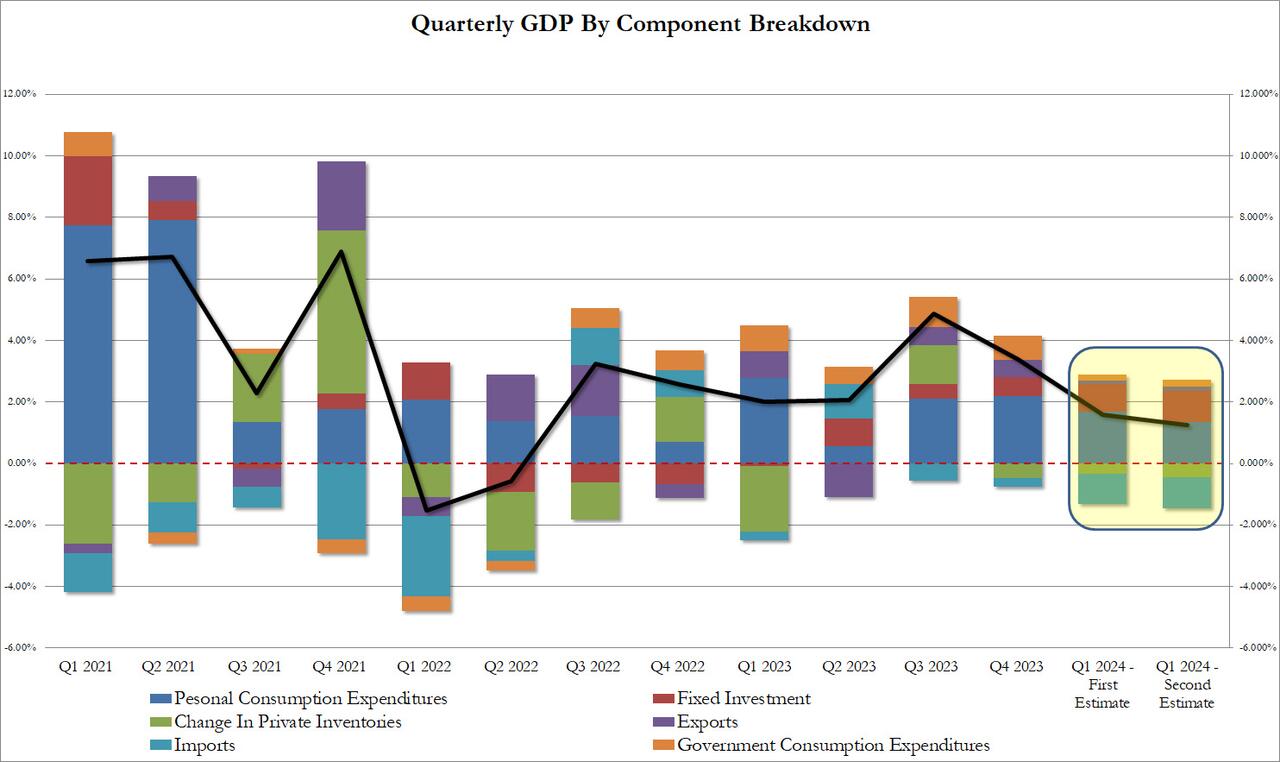

08:30: 1Q GDP Annualized QoQ, est. 1.3%, prior 1.6%

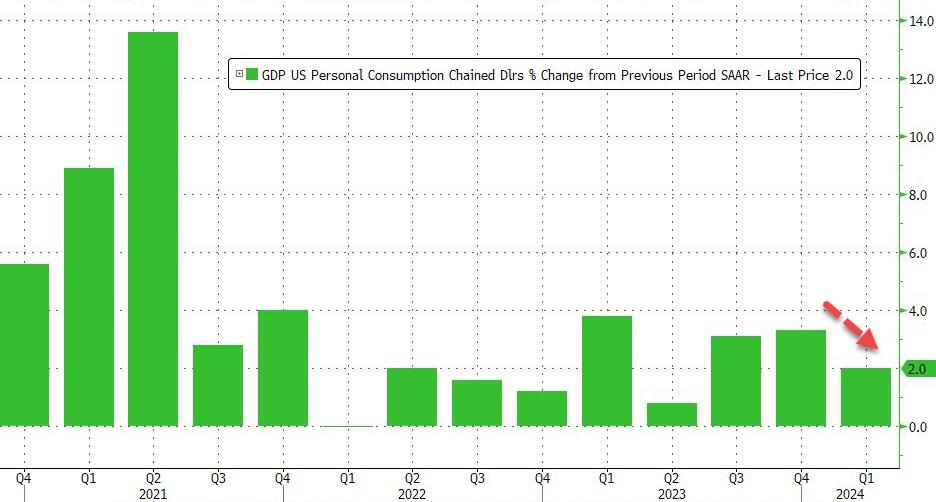

1Q Personal Consumption, est. 2.2%, prior 2.5%

1Q Core PCE Price Index QoQ, est. 3.7%, prior 3.7%

1Q GDP Price Index, est. 3.1%, prior 3.1%

08:30: May Initial Jobless Claims, est. 217,000, prior 215,000

May Continuing Claims, est. 1.8m, prior 1.79m

08:30: April Wholesale Inventories MoM, est. 0.1%, prior -0.4%

April Retail Inventories MoM, est. 0.3%, prior 0.3%

April Advance Goods Trade Balance, est. -$92.3b, prior -$91.8b

10:00: April Pending Home Sales (MoM), est. -1.0%, prior 3.4%

April Pending Home Sales YoY, est. -2.0%, prior -4.5%

Central Bank speakers

12:05: Fed’s Williams Speaks at Economic Club of New York

17:00: Fed’s Logan Speaks in Moderated Q&A

DB’s Jim Reid concludes the overnight wrap

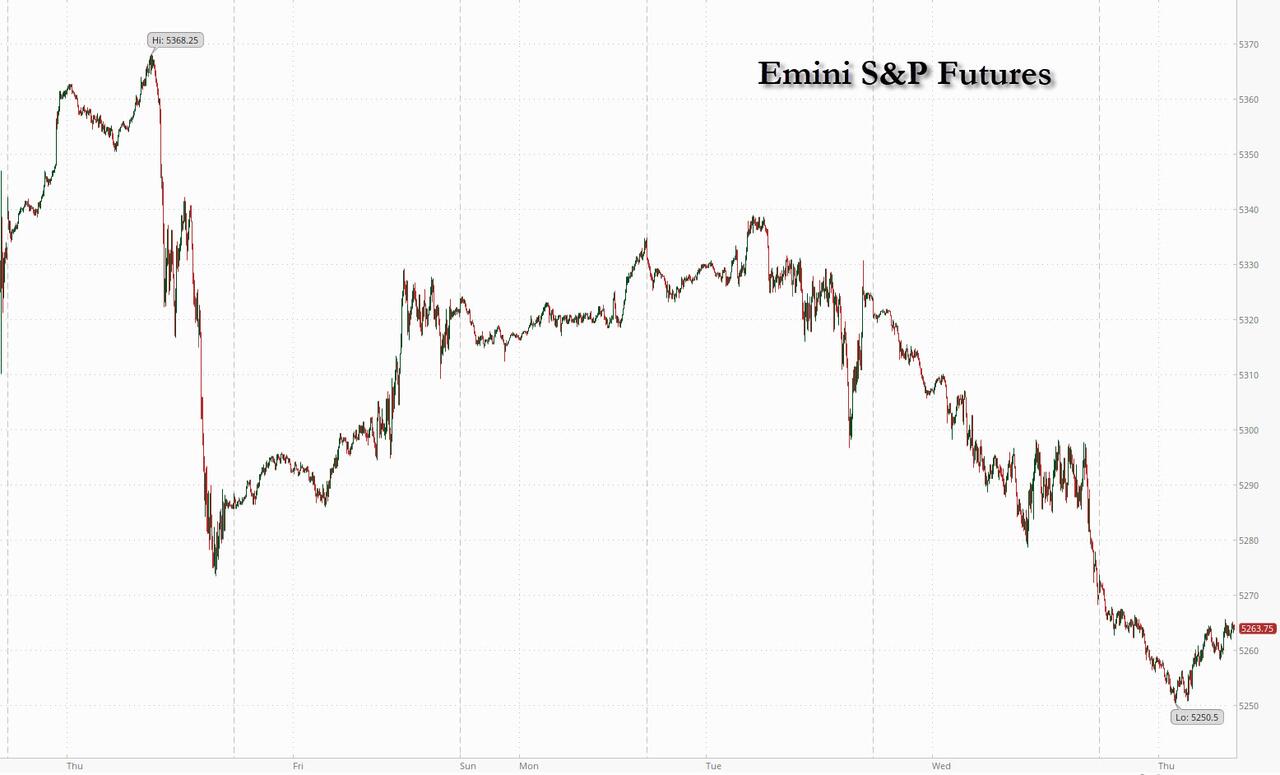

Markets have had another rough 24 hours, with no sign of the negative momentum letting up overnight. The latest selloff has been driven by a range of factors, but bonds took a particular hit after a weak US Treasury auction yesterday, along with mounting concern about inflationary pressures, which sent European yields up to their highest levels in months. That followed on from a hawkish set of headlines the previous day, where stronger-than-expected data led investors to price in that rates would stay higher for longer. So it was a tough backdrop for markets across several asset classes, and there had already been a relentless run of gains in recent weeks that was always going to be tough to maintain. Indeed, the S&P 500 has advanced for 23 of the last 30 weeks, marking a joint record since 1989, but yesterday it fell -0.74%, and futures this morning are down -0.56%. So it’s clear that the momentum is now more negative, and Asian markets are also falling across the board as we go to press this morning.

This negative tone was set from the outset yesterday after the Australian CPI report was higher than expected. But that was compounded by the German flash CPI print for May, which was also a bit above consensus. So that helped to deepen the selloff, adding to concerns that rates were set to remain at higher levels for longer than anticipated. In terms of the details, German inflation came in at +2.8% on the EU-harmonised measure, which was a tenth above expectations, and an increase from the +2.4% print in April. That was partly down to base effects, but the main significance of the release was that it cast doubt on how aggressively the ECB would cut rates over the coming months. Indeed, the amount of ECB rate cuts priced by April 2025 came down by -8.0bps to 75bps, so markets are now pricing in a shallower easing cycle after the release. We’ll get more European inflation data over the next couple of days, including from Spain today, before we get the Euro Area-wide release tomorrow.

The stronger inflation prints affected sovereign bonds across the world, but the impact was particularly noticeable in Europe ahead of the ECB’s decision next week. For instance, the 10yr bund yield was up +9.8bps to a 6-month high of 2.69%. But that wasn’t just confined to Germany, as the 10yr yield in France (+10.2bps) was also up to a 6-month high of 3.17%, and the UK 10yr gilt yield (+11.9bps) hit a 6-month high of 4.40%. Meanwhile at the front-end of the curve, the German 2yr yield (+4.3bps) hit a 7-month high of 3.10%, moving closer to its March 2023 peak (just before the SVB turmoil) at 3.33%.

That pattern was repeated in other regions, and the 1 0yr Treasury yield ended the day up +6.2bps at 4.61%. In fact, over the last two weeks, the 10yr yield is now up +27.3bps, so there’s been a big turnaround since the rally that followed the US CPI print. At the same time, the 2yr yield (-0.4bps) closed at 4.97%, just below the 5% mark again, whilst the 2yr real yield moved as high as 2.70% intraday before ending up +1.7bps at 2.68%. This came as there was weak demand for US Treasuries for a second straight day. The US sold $44bn of 7-yr notes at 4.65%, which was higher than the pre-auction level of 4.637%, as concerns over funding the US deficit in a higher rate world continued to percolate. Additionally, Fed pricing suggested that higher rates were set to persist, and this morning futures are putting a 48.5% probability on a rate cut by the September meeting. There was also a modest support from the Richmond Fed’s manufacturing index, which rose to 0 in May (vs. -7 expected), which is the strongest it’s been in 7 months.

This rise in longer-dated yields proved bad news for global risk assets. For equities, it meant the S&P 500 fell -0.74%, which currently puts the index on track to end a run of 5 consecutive weekly gains. Moreover, that decline was cushioned by a stronger performance for the Magnificent 7 (-0.08%), which only fell modestly from its all-time high the previous sessio n. So if you look at the equal-weighted S&P 500 instead, that actually fell by a larger -1.17%. So this continues the theme from last year where the equity rally is a very narrow one, as the overall S&P 500 is up +10.42% year-to-date, but the equal-weighted version is only up +2.96%. Every industry group in the index was lower by the close, with energy stocks (-1.76%) as the main underperformer after oil prices fell back (Brent Crude -0.74%). Meanwhile in Europe, the losses were even larger, and the STOXX 600 fell -1.08%, alongside declines for the DAX (-1.10%), the CAC 40 (-1.52%) and the FTSE 100 (-0.86%).

Overnight in Asia, this weakness for risk assets has continued, with losses for the KOSPI (-1.41%), the Nikkei (-1.37%), the Hang Seng (-1.22%), the CSI 300 (-0.16%) and the Shanghai Comp (-0.12%). Futures are also pointing to losses in other regions, with those on the DAX down -0.38%, and those on the S&P 500 down -0.56%.

To the day ahead now, and data releases include the Euro Area unemployment rate for April, and in the US we’ll get the second estimate of Q1 GDP, along with the weekly initial jobless claims, the advance goods trade balance for April, and pending home sales for April. From central banks, we’ll hear from the Fed’s Williams and Logan, along with the ECB’s Makhlouf.

2B EUROPE OPENING/TRADING

Yields continue to drive action after another soft US auction – Newsquawk Europe Market Open

THURSDAY, MAY 30, 2024 – 01:23 AM

APAC stocks were on the back foot amid spillover selling from Wall St owing to the further upside in yields; Nikkei 225 slumped at the open and briefly fell beneath the 38,000 level.

DXY traded flat but held on to the prior day’s gains above the 105.00 level after benefitting from higher yields, USD/JPY gradually eased back from its recent peak amid mild haven flows.

10-year UST futures were contained after the recent continued bear-steepening owing to a weak 7-year auction, Bund futures remained subdued.

European equity futures indicate a lower open with the Euro Stoxx 50 future -0.4% after the cash market closed lower by 1.3% on Wednesday.

Looking ahead, highlights include Spanish CPI, Swiss GDP, EZ Sentiment, EZ Unemployment Rate, Italian Producer Prices, US GDP Estimates, US PCE (Q1), IJC, Advance Goods Trade Balance, SARB Policy Announcement, Comments from Fed’s Williams, Logan & RBNZ Governor Orr, Supply from Italy, Earnings from Marvell, Dollar General & Best Buy.

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

US TRADE

EQUITIES

US stocks declined amid a lack of fresh macro catalysts and as yields edged higher again following another weak US auction, while the calendar was quiet with German inflation the main highlight which printed in line with estimates and participants continue to await looming key events. Futures were also pressured after-hours, especially Dow futures as Salesforce shares slumped around 17% post-earnings.

SPX -0.74% at 5,267, NDX -0.70% at 18,737, DJI -1.06% at 38,442, RUT -1.48% at 2,036

Fed’s Beige Book stated national economic activity continued to expand from early April to mid-May. However, conditions varied across industries and districts as most Districts reported slight or modest growth, while two noted no change in activity. Furthermore, retail spending was flat to up slightly, reflecting lower discretionary spending and heightened price sensitivity among consumers.

Fed’s Bostic (voter) said the inflation path will be bumpy but the general trend is down and the path to 2% inflation is not assured, while he added that the Fed is vigilant and the job market is tight but not as tight. Furthermore, he said the breadth of price gains is still pretty significant and less inflation breadth would add to confidence for a cut.

APAC TRADE

EQUITIES

APAC stocks were on the back foot amid spillover selling from Wall St owing to the further upside in yields.

ASX 200 was pressured with underperformance in miners after recent declines in underlying commodity prices.

Nikkei 225 slumped at the open and briefly fell beneath the 38,000 level but is well off worse levels.

Hang Seng and Shanghai Comp conformed to the uninspiring mood in which the Hong Kong benchmark gradually weakened with notable losses in mining and property stocks, while the mainland was rangebound following another substantial liquidity injection by the PBoC and after the central bank also vowed several support efforts including promoting trade and investment facilitation.

US equity futures were pressured with Dow futures the worst hit as Salesforce shares fell 16% post-earnings.

European equity futures indicate a lower open with the Euro Stoxx 50 future -0.4% after the cash market closed lower by 1.3% on Wednesday.

FX

DXY traded flat but held on to the prior day’s gains above the 105.00 level after benefitting from higher yields.

EUR/USD trickled to just below 1.0800 but with further losses stemmed amid large option expiries at that level.

GBP/USD was lacklustre after struggling to sustain the 1.2700 status and with little pertinent catalysts.

USD/JPY gradually eased back from its recent peak amid mild haven flows into the Japanese currency.

Antipodeans were contained amid the mostly downbeat mood and after mixed Building Approvals and Capex data from Australia, while the PBoC also continued to marginally weaken the CNY reference rate.

PBoC set USD/CNY mid-point at 7.1111 vs exp. 7.2623 (prev. 7.1106).