GOLD PRICE CLOSED DOWN $19.40 TO $2325.65

SILVER PRICE DOWN $1.09 TO $30.28

Gold ACCESS CLOSED $2328.10

Silver ACCESS CLOSED: $30.36

Bitcoin morning price:$68,348 DOWN 694 DOLLARS.

Bitcoin: afternoon price: $67,730 DOWN 1312 dollars

Platinum price closing UP $5.00 TO $1036.85

Palladium price; DOWN $44.35 AT $911.50

END

SHANGHAI GOLD PREMIUM 50 DOLLARS/COMEX GOLD

SHANGHAI GOLD

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $3172.34 DOWN 25.20 CDN dollars per oz( * NEW ALL TIME HIGH 3,305.30 CDN DOLLARS PER OZ//MAY 20 2024)

*BRITISH GOLD: 1826.73 DOWN 14.63 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2145.45 DOWN 18.52 Euros per oz //* (ALL TIME CLOSING HIGH: 2248.89 EUROS PER OZ//APRIL 16.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCH: COMEX

EXCHANGE: COMEX

CONTRACT: JUNE 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,342.900000000 USD

INTENT DATE: 05/30/2024 DELIVERY DATE: 06/03/2024

FIRM ORG FIRM NAME ISSUED STOPPED

072 C GOLDMAN 127

099 H DB AG 4127

118 H MACQUARIE FUT 755

167 C MAREX 4

190 H BMO CAPITAL 2629

226 C DIRECT ACCESS 55

323 C HSBC 2560 151

323 H HSBC 500

357 C WEDBUSH 1

363 H WELLS FARGO SEC 475

365 C MAREX CAPITAL M 9

365 H MAREX CAPITAL M 2

435 H SCOTIA CAPITAL 1982

555 C BNP PARIBAS SEC 100

624 C BOFA SECURITIES 1

624 H BOFA SECURITIES 11000

657 C MORGAN STANLEY 12 355

657 H MORGAN STANLEY 774

661 C JP MORGAN 4485 5661

661 H JP MORGAN 2283

DLV615-T CME CLEARING

BUSINESS DATE: 05/30/2024 DAILY DELIVERY NOTICES RUN DATE: 05/30/2024

PRODUCT GROUP: METALS RUN TIME: 21:27:28

685 C RJ OBRIEN 2

686 C STONEX FINANCIA 79

690 C ABN AMRO 46

700 C UBS 76

732 C RBC CAP MARKETS 73

737 C ADVANTAGE 50

878 C PHILLIP CAPITAL 19

880 H CITIGROUP 4360

905 C ADM 1 74

TOTAL: 21,414 21,414

MONTH TO DATE: 21,414

JPMorgan stopped 5661/21414

FOR JUNE 2024

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2024. CONTRACT: 21,414 NOTICES FOR 21,414 OZ or 66.606 TONNES

total notices so far: 21,414 contracts for 2141400 Oz (66.606 tonnes)

FOR JUNE:

SILVER NOTICES: 710 NOTICE(S) FILED FOR 3,550,000 OZ/

total number of notices filed so far this month : 710 for 3.550 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $19.40

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

NO CHANGES IN GOLD INVENTORY AT THE GLD:

/ /INVENTORY RESTS AT 832.21TONNES

INVENTORY RESTS AT 832.21 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER DOWN $1.09 AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSIVE WITHDRAWAL OF 3.655 MILLION OZ FROM THE SLV

// INVENTORY LOWERS TO 413.775 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 413,775 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUMONGOUS SIZED 2412 CONTRACTS TO 184,465 AND STALLING FROM ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR HUGE LOSS OF $0.80 IN SILVER PRICING AT THE COMEX ON THURSDAY’S RAID ON SILVER. WE HAD LITTLE LONG LIQUIDATION AS WE HAD A NET GAIN OF 90 CONTRACTS ON OUR TWO EXCHANGES. WE, AGAIN HAD SHORT COVERING BY OUR SPECS WITH THE LOSS IN PRICE. WE HAD ANOTHER HUGE SIZED 1037 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID LIKE IN SILVER THURSDAY.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 1037 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND TODAY;S RAID.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.80) BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE DID HAVE A HUGE SIZED LOSS OF 864 CONTRACTS ON OUR TWO EXCHANGES WITH THE LOSS IN PRICE OF $0.80

.

WE MUST HAVE HAD:

A HUMONGOUS SIZED 1548 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.830MILLION OZ (FIRST DAY NOTICE)

//NEW STANDING FOR SILVER//JUNE IS THUS 3.830 MILLION OZ

WE HAD:

/ HUMONGOUS SIZED COMEX OI LOSS //HUGE SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1037 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL -REMOVED AN ENORMOUS 954 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS MAY ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF MAY

TOTAL CONTRACTS for 22 DAYS, total 27,199 contracts: OR 135.995 MILLION OZ (1236 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 135.995 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL PROBABLY BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE

RESULT: WE HAD A HUMONGOUS SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2412 CONTRACTS WITH OUR LOSS IN PRICE OF SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUMONGOUS EFP ISSUANCE CONTRACTS: 1548 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.830 MILLION OZ ON FIRST DAY NOTICE

//NEW TOTAL STANDING FOR JUNE 3.830 MILLION OZ

WE HAVE A HUGE SIZED LOSS OF 1548 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE HUGE LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG SIZED 1037 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND ZERO LIQUIDATION OF LONGS.

THE NEW TAS ISSUANCE THURSDAY NIGHT (1037) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 710 NOTICE(S) FILED TODAY FOR 3,550,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 4848 OI CONTRACTS TO 480,039 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE 2766 CONTRACTS

WE HAD A STRONG SIZED INCREASE IN COMEX OI (4848 CONTRACTS) OCCURRED WITH OUR GAIN OF $3.60 IN PRICE/THURSDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNED AT 89.804 TONNES ON FIRST DAY NOTICE

NEW STANDING 89.804 TONNES// ALL OF THIS HAPPENED WITH OUR $3.60 GAIN IN PRICE WITH RESPECT TO THURSDAY’S TRADING. WE HAD A STRONG SIZED GAIN OF 9098 OI CONTRACTS (28.267 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1368 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 482.804

IN ESSENCE WE HAVE A VERY STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 9098 CONTRACTS WITH 4848 CONTRACTS INCREASED AT THE COMEX// AND A STRONG SIZED 4240 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 9088 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 1368 CONTRACTS,,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4240 CONTRACTS) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI 4848/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 9088 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 89.804 TONNES

//NEW STANDING /JUNE 89.804 TONNES.

/ 3) CONSIDERABLE LIQUIDATION OF CONTRACTS MOSTLY DUE TO SPREADERS ALONG WITH ZER0 LONG SPECS

.

// 4) STRONG SIZED COMEX OPEN INTEREST GAIN 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1368 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF MAY. :

TOTAL EFP CONTRACTS ISSUED: 101,789 CONTRACTS OR 10,178,900 OZ OR 316.606 TONNES IN 22 TRADING DAY(S) AND THUS AVERAGING: 4626 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 22 TRADING DAY(S) IN TONNES 316.606 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 316.606 DIVIDED BY 3550 x 100% TONNES = 8.90% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUMONGOUS SIZED 2412 CONTRACTS OI TO 184,465 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1548 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1548 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1548 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2412 CONTRACTS AND ADD TO THE 1548 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 864 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 4.54 MILLION OZ

OCCURRED WITH OUR $0.80 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING/THURSDAY NIGHT

SHANGHAI CLOSED DOWN 4.06 PTS OR 0.16% //Hang Seng CLOSED DOWN 150.58 PTS OR 0.83%// Nikkei CLOSED UP 433.77 OR 1.14%//Australia’s all ordinaries CLOSED UP 0.95%///Chinese yuan (ONSHORE) closed DOWN TO 7,2411 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2587/ Oil DOWN TO 77.87 dollars per barrel for WTI and BRENT DOWN AT 81.88 /Stocks in Europe OPENED MOSTLY RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 4848 CONTRACTS TO 480,039 WITH OUR GAIN IN PRICE OF $3.60 WITH RESPECT TO THURSDAY TRADING. WE HAD A CONSIDERABLE T.A.S. LIQUIDATION THURSDAY AS WELL AS ZERO LONGS BEING CLIPPED.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE.… THE CME REPORTS THAT THE BANKERS ISSUED A HUGE SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 4240 EFP CONTRACTS WERE ISSUED: : AUGUST 4240 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE:4240 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY STRONG SIZED TOTAL OF 9088 CONTRACTS IN THAT 4240 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG SIZED GAIN OF 4848 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $3.60// THURSDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT WAS A FAIR SIZED 1368 CONTRACTS. MOST OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. TODAY IS OF EXTREME IMPORTANCE TO OUR CROOKS IN YESTERDAY’S TRADING

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (89.804 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 89.804 TONNES. THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $3.60 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A VERY STRONG GAIN OF 9088 CONTRACTS ON THURSDAY WITH OUR TWO EXCHANGES DESPITE THE SMALL GAIN IN PRICE. THE T.A.S. ISSUED ON THURSDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 28.267 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE (89.804 TONNES) ON FIRST DAY NOTICE

NEW STANDING FOR JUNE: 89.804 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR SMALL GAIN IN PRICE TO THE TUNE OF $3.60

WE HAVE REMOVED 8,136 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET GAIN ON THE TWO EXCHANGES 11,853 CONTRACTS OR 1,185,300 (36.06 TONNES)

confirmed volume THURSDAY 232,966 contracts// fair

//speculators have left the gold arena

MAY 31 MAY GOLD

/ /// THE JUNE 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 289.359 oz brinks 9 kilobars . |

| Deposit to the Dealer Inventory in oz | 32,019.295 oz ASAHI |

| Deposits to the Customer Inventory, in oz | nil |

| No of oz served (contracts) today | 21,414 notice(s) 2,141,400 OZ 66.606 TONNES |

| No of oz to be served (notices) | 7450 contracts 745000 OZ 23.197 TONNES |

| Total monthly oz gold served (contracts) so far this month | 21,414 notices 2,141,400 oz 66.606 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

1 dealer deposits:

(1) into ASAHI: 32,019.295 oz

total dealer deposits: 32,019.295 oz

we have 0 customer deposit:

total deposit nil oz

total customer withdrawals: 1

i. out of brinks 289.359 oz

TOTAL WITHDRAWALS 289.359 0z

Adjustments: 1

customer to dealer/hsbc 49,452.141

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE

For the front month of JUNE we have an oi of 28,872 contracts having LOST ONLY 427 contracts.

THUS BY DEFINITION, THE INITIAL AMOUNT OF GOLD WILLING TO STAND IN THIS VERY ACTIVE DELIVERY MONTH OF JUNE IS AS FOLLOWS:

28,872 NOTICES FILED X 100 oz per notice == 2,887,200 oz or 89.804 tonnes of gold which is absolutely huge.

JULY GAINED 216 CONTRACTS TO STAND AT 2065

AUGUST GAINED 3573 CONTRACTS UP TO 378,617 CONTRACTS

We had 21,414 contracts filed for today representing 2,141,400 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 4485 notices were issued from their client or customer account. The total of all issuance by all participants equate to 21,414 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 5661 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for June /2024. contract month, we take the total number of notices filed so far for the month (21,414) x 100 oz ) to which we add the difference between the open interest for the front month of JUNE ( 28,872 CONTRACTS) minus the number of notices served upon today (21,414 x 100 oz per contract( equals 2,887,200 OZ OR 89.804 TONNES. PLUS THE 3.3716 OF EX FOR RISK/PRIOR = 11.925 TONNES

thus the INITIAL standings for gold for the JUNE contract month: No of notices filed so far (21,414 x 100 oz + 28,872 OI for the front month} minus the number of notices served upon today (21,414) x 100 oz which equals 2,887,200 oz (89.804 TONNES)

TOTAL COMEX GOLD STANDING FOR JUNE: 89.804 TONNES WHICH IS ABSOLUTELY HUGE FOR THIS VERY ACTIVE DELIVERY MONTH IN THE CALENDAR. JUNE IS TRADITIONA;LLLY THE 2ND HIGHEST DELIVERY MONTH OF THE YEAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX84XXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,558,487.369 48.47 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,673,552.189 OZ

TOTAL REGISTERED GOLD 7,967,010.636 ( 247.80 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,706,541.553 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,408,523 oz (REG GOLD- PLEDGED GOLD)= 199.33 tonnes //

END

SILVER/COMEX

MAY 31

INITIAL

//2024// THE JUNE 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 665,132.860 oz brinks cnt . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 343,225.100 oz brinks |

| No of oz served today (contracts) | 710 CONTRACT(S) (3,550,000 OZ) |

| No of oz to be served (notices) | 56 contracts (0.280 million oz) |

| Total monthly oz silver served (contracts) | 710 Contracts (3.550 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i) into brinks 343,225.100 oz

total customer deposit 343,225.100 oz

JPMorgan has a total silver weight: 128.997million oz/297.588 million or 43.34%

adjustment: 2//both customer to dealer

i) out of delaware// 4759.400 oz

ii) 313,499.730 oz

Comex withdrawals: 2

1)out of brinks 625,127.310 oz

ii) out of cnt 40,005.550 oz

total withdrawal: 665,132.860 0z

TOTAL REGISTERED SILVER: 62.494MILLION OZ//.TOTAL REG + ELIGIBLE. 297.588 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE:

silver open interest data:

FRONT MONTH OF JUNE/2024 OI: 766 CONTRACTS HAVING LOST 372 CONTRACT(S).

THUS BY DEFINITION, THE INITIAL AMOUNT OF SILVER WILLING TO STAND FOR METAL IN THIS NON ACTIVE DELIVERY MONTH OF JUNE IS AS FOLLOWS

766 NOTICES X 5,000 OZ PER NOTICE = 3.830 MILLION OZ./

JULY SAW A LOSS OF 3920 CONTRACTS DOWN TO 142,217

SEPT SAW A GAIN OF 1642 CONTRACTS TO 27,427

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 710 for 3,550,000 oz

CONFIRMED volume; ON THURSDAY 107,360 huge

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 710 x 5,000 oz = 3.550 MILLION oz

to which we add the difference between the open interest for the front month of JUNE ((766) and the number of notices served upon today 710x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2024 contract month: 710 notices served so far) x 5000 oz + OI for the front month of JUNE (766)x number of notices served upon today minus (710)x 5000 oz of silver standing for the may contract month equates to 3.830 MILLION OZ.

New total standing: 3.830 million oz.

There are 62.494 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

MAY 31 WITH GOLD DOWN $19.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 30 WITH GOLD UP $3.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 29 WITH GOLD DOWN $13.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 28 WITH GOLD UP $22.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 832.21 TONNES

MAY 24 WITH GOLD DOWN $2.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 833.36 TONNES

MAY 23 WITH GOLD DOWN $53.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 22 WITH GOLD DOWN $32.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 21 WITH GOLD DOWN $12,00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 20 WITH GOLD UP $21.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.10 TONNES OF GOLD INTO THE GLD//NEW TOTAL 838.54 TONNES

MAY 17 WITH GOLD UP $31.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//NEW TOTAL 833.36 TONNES

MAY 16 WITH GOLD DOWN $7.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//NEW TOTAL 833.36 TONNES

MAY 15 WITH GOLD UP $34.90 ON THE DAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD/INVENTORY RISES TO 831.93 TONNES

MAY 14 WITH GOLD DOWN $17.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RISES TO 831.33 TONNES

MAY 13 WITH GOLD DOWN $31.10 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD////INVENTORY RISES TO 831.93 TONNES

MAY 10 WITH GOLD UP $34.65 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 9 WITH GOLD UP $18.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 8 WITH GOLD DOWN $0.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 830.47 TONNES

MAY 7 WITH GOLD DOWN $6.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 832.19 TONNES

MAY 6WITH GOLD UP $21.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .55 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 831.64 TONNES

MAY 2 WITH GOLD UP $0.20 ON THE DAY; SMAKK CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 830.47 TONNES

MAY 1 WITH GOLD UP $7.80 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNES

GLD INVENTORY: 832.21 TONNES, TONIGHTS TOTAL

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

MAY 31 WITH SILVER DOWN $1.09 TODAY: HUGE CHANGES IN SILVER INVENTORY: A MASSIVE WITHDRAWAL OF 3.655 MILLION OZ FROM THE SLV//INVENTORY LOWERS TO 413.775 MILLION OZ

MAY 30 WITH SILVER DOWN $0.80 TODAY: NO CHANGES IN SILVER INVENTORY//INVENTORY REMAINS AT 417.430 MILLION OZ

MAY 29 WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 1.051 MILLION OZ INTO THE SLV//INVENTORY DECREASES TO 417.430 MILLION OZ

MAY 28 WITH SILVER UP $1.64 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 2.832 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 418.481 MILLION OZ

MAY 24 WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF .822 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 421.313 MILLION OZ

MAY 23 WITH SILVER DOWN $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.736 MILLION OZ FROM THE SLVINVENTORY INCREASES TO 420.491 MILLION OZ

MAY 22 WITH SILVER DOWN $0.66 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 21 WITH SILVER DOWN $0.41 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A DEPOSIT OF 3.792 MILLION OZ FROM THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 20 WITH SILVER UP $1.28 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 1.005 MILLION OZ FROM THE SLV// INVENTORY LOWERS TO 418.435 MILLION OZ

MAY 17 WITH SILVER UP $1.37 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 868,000 OZ FROM THE SLV// INVENTORY LOWERS TO 419.440 MILLION OZ

MAY 16 WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY REMAINS AT 420.308 MILLION OZ

MAY 15 WITH SILVER UP 101 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A WITHDRAWAL OF 1.919 MILLION OZ FROM THE SLV NVENTORY RESTS AT 420.308 MILLION OZ

MAY 14 WITH SILVER UP 25 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;INVENTORY RESTS AT 422.227 MILLION OZ

MAY 13 WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;NVENTORY RESTS AT 422.227 MILLION OZ

MAY 10 WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A HUGE WITHDRAWAL OF 1.,828 MILLION OZ//INVENTORY RESTS AT 422.227 MILLION OZ

MAY 9 WITH SILVER UP 78 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 8 WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 7WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 6 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.055 MILLION OZ

MAY 3 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 2WITH SILVER UP 0.12 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/ A WITHDRAWALOF 4.471 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 1 WITH SILVER UP 0.09 TODAY: SMALLCHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF ,457 MILLION OZ INTO THE SLV INVENTORY RESTS AT 429.814 MILLION OZ

CLOSING INVENTORY 413.775 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

end

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS//GOLD AND SILVER COMMENTARY

END

3. CHRIS POWELL//GATA DISPATCHES

CHRIS POWELL…

Now this is fascinating!! The Central Bank of India is repatriating 100 tonnes from the Bank of England. If I am not mistaken, they also have some gold deposits at the BIS from which the FRBNY borrowed some of its gold, 78 tonnes none of which has been returned

India recalls 100 tonnes of gold from Bank of England, may bring back still more

Submitted by admin on Fri, 2024-05-31 09:38 Section: Daily Dispatches

From The Times of India, Mumbai

Friday, May 31, 2024

NEW DELHI — The Reserve Bank of India has moved a little more than 100 tonnes of gold from the United Kingdom to its vaults in the country, marking the first time at least since early 1991 when precious metal at this scale has been added to the stock held locally.

A similar quantity of gold may be headed in the country again in the coming months, with official sources telling the Times of India that the transfer to locations within the country was for logistical reasons as well as diversified storage.

According to the latest data, at the end of March the central bank had 822.1 tonnes of gold, of which 413.8 tonnes were overseas. The RBI is among central banks that bought gold in recent years, with 27.5 tonnes added during the last financial year.

For a large number of central banks, the Bank of England traditionally has been the storehouse and India is no different, with some the yellow metal stocks lying in London from pre-independence days.

“The RBI started purchasing gold a few years ago and decided to undertake a review of where it wants to store it, something that is done from time to time. Since stock was building up overseas, it was decided to get some of the gold to India,” an official said.

For most Indians, gold has been an emotional issue, especially after the Chandra Shekhar government pledged the precious metal to tackle the balance of payments crisis in 1991. While the RBI bought 200 tonnes of gold from the International Monetary Fund around 15 years ago, over the last few years a steady buildup in stocks has taken place through purchases by the central bank. …

… For the remainder of the report:

end

Robert Lambourne: BIS gold swaps rose 10 tonnes from February to April

Submitted by admin on Fri, 2024-05-31 07:57 Section: Daily Dispatches

By Robert Lambourne

Friday, May 31, 2024

Gold swaps undertaken by the Bank for International Settlements appear to have risen slightly in March and April, according to the bank’s monthly statements of account for those months, both published this week:

From the statements it is possible to estimate the volume of gold swaps undertaken by the BIS at the month-ends: around 71 tonnes for March and 78 for April, a total increase of 10 tonnes from the 68 tonnes of swaps estimated in February

The table below sets out the historical level of monthly gold swaps estimated since August 2018. As is evident from the table, there is still a considerable level of gold being traded via the BIS swaps.

To repeat the point long made in these reports, it seems that these swaps are undertaken by the BIS with one or more of its central bank customers, with the swapped gold being accounted for as held in a BIS-registered sight account at a central bank.

Given what is happening in the gold market generally, it seems likely that the Federal Reserve is the BIS’ customer for these gold transactions. The evidence strongly suggests that bullion banks are the source of the gold, and it probably comes from gold registered as held by gold exchange-traded funds.

A more detailed report on the use of gold swaps was published by GATA to cover transactions in December 2023:

https://www.gata.org/node/23016

—

Swaps estimated by GATA from

BIS monthly statements of account

Month …. Swaps

& year … in tonnes

Apr-24 …. 78

Mar-24 …. 71

Feb-24 …. 68

Jan-24 …. 117

Dec-23 …. 121

Nov-23 …. 100

Oct-23 …. 68

Sep-23 …. 96

Aug-23 …. 129

Jul-23 …. 103

Jun-23 …. 87

May-23 …. 188

Apr-23 …. 135

Mar-23 …. 77*

Feb-23 …. 136

Jan-23 …. 103

Dec-22 …. 0

Nov-22 …. 105

Oct-22 …. 7

Sep-22 …. 57

Aug-22 …. 75

Jul-22 …. 56

Jun-22 …. 202

May-22 …. 270

Apr-22 …. 315

Mar-22 …. 358

Feb-22 …. 472

Jan-22 …. 501

Dec-21 …. 414

Nov-21 …. 451

Oct-21 …. 414

Sep-21 …. 438

Aug-21 …. 464

Jul-21 …. 502

Jun-21 …. 471

May-21 …. 517

Apr-21 …. 472

Mar-21 …. 490±

Feb-21 …. 552

Jan-21 …. 523

Dec-20 …. 545

Nov-20 …. 520

Oct-20 …. 519

Sep-20 …. 520

Aug-20 …. 484

Jul-20 …. 474

Jun-20 …. 391

May-20 …. 412

Apr-20 …. 328

Mar-20 …. 326**

Feb-20 …. 326

Jan-20 …. 320

Dec-19 …. 313

Nov-19 …. 250

Oct-19 …. 186

Sep-19 …. 128

Aug-19 …. 162

Jul-19 …. 95

Jun-19 …. 126

May-19 …. 78

Apr-19 …. 88

Mar-19 …. 175

Feb-19 …. 303

Jan-19 …. 247

Dec-18 …. 275

Nov-18 …. 308

Oct-18 …. 372

Sep-18 …. 238

Aug-18 …. 370

* The estimate originally reported by GATA was 78 tonnes, but the BIS annual report states 77 tonnes. It is believed that slightly different gold prices account for the difference.

± The estimate originally reported by GATA was 487 tonnes, but the BIS annual report states 490 tonnes, It is believed that slightly different gold prices account for the difference.

** The estimate originally reported by GATA was 332 tonnes, but the BIS annual report states 326 tonnes. It is believed that slightly different gold prices account for the difference.

GATA uses gold prices quoted by USAGold.com to estimate the level of gold swaps held by the BIS at month-ends.

—–

Robert Lambourne is a retired business executive in the United Kingdom who consults for GATA about the involvement of the Bank for International Settlements in the gold market and U.S. government debt.

* * *

Support GATA by purchasing

Stuart Englert’s “Rigged”

“Rigged” is a concise explanation of government’s currency market rigging policy and extensively credits GATA’s work exposing it. Ten percent of sales proceeds are contributed to GATA. Buy a copy for $14.99 through Amazon —

end

Viet Nam a gold loving nation will sell gold through its state banks. The move is to quell the high inflation in the country.

Vietnam’s central bank to sell gold through state banks to quell prices

Submitted by admin on Thu, 2024-05-30 12:22 Section: Daily Dispatches

By Quynh Trang

VN Express, Hanoi

Wednesday, May 29, 2024

The State Bank of Vietnam, in a move to stabilize gold prices, will sell gold bars to four state-owned lenders so they can distribute them to retail buyers.

The sale will begin June 3 at prices determined by the central bank, bank Deputy Governor Pham Quang Dung said Wednesday.

The state-owned lenders involved are Agribank, Vietcombank, BIDV, and VietinBank, which already have extensive networks ready to sell directly to individual buyers, Dung added.

A representative of one of the banks said that they are not allowed to sell in bulk to organizations and businesses.

Some private banks have already been selling gold but only at small volume. Most retail consumers buy their gold at jewelry stores.

This is the latest effort of the central bank to bring down domestic gold prices after hosting auctions in the last several weeks to increase supply.

Although it has sold 48,500 taels (or 1.8 tons) in nine auctions, Vietnam’s Saigon Jewelry Co. gold bar price is still 20% higher than the global price.

The company has therefore decided to cease holding gold auctions. …

… For the remainder of the report:

end

a must read

gold production is now 3600 tonnes and central banks are buying 28 to 30% of that production

Ronan Manly

Ronan Manly: Trends and developments in central bank gold buying

Submitted by admin on Thu, 2024-05-30 11:59 Section: Daily Dispatches

By Ronan Manly

Bullion Star, Singapore

Thursday, May 30, 2024

As we approach mid-year 2024 in the environment of an all-time high U.S. dollar gold price, it’s notable that central bank gold buying continues to be one of the themes dominating gold market discussion.

This is because following a record year in 2022, when according to the World Gold Council central banks and official financial institutions purchased a massive 1082 tonnes of gold for their monetary gold reserves, 2023 was nearly as impressive, with central banks as a group buying a net 1,037 gonnes of gold, just shy of the 2022 total.

Given that total gold mining production was 3,625 tonnes in 2022 and 3,644 tonnes in 2023, it can be seen that central banks are now responsible for buying the equivalent of 28–30% of all newly mined gold. …

… For the remainder of the analysis:

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS/LIVE FROM THEE VAULT 174 WITH ANDREW MAGUIRE

https://www.youtube.com/watch?v=lxGge8XjGsw&list=PLE1y8hGSqr8ar1gKUdfqFDK5ygLIlrdmz&index=1

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT//COPPER

As Copper Soars, Telecoms Sitting On $7 Billion Mother Lode Of Old Cable

FRIDAY, MAY 31, 2024 – 02:00 PM

Driven by soaring demand associated with artificial intelligence, electric vehicles, power infrastructure and automation, copper prices are up around 50% in four years. Now, telecom giants are poised to cash in — by pulling their old copper lines back out from from the ground and down from poles and recycling them, according to a new report from Bloomberg.

“We’ve got all of this material, sitting redundant,” David Evans asset recovery head at UK-based TXO tells Bloomberg. The firm, which provides engineering services to telecom companies, estimates that the industry has the potential to harvest 800,000 metric tons of copper in the next 10 years. At today’s values, that would represent about $7 billion.

Still-higher copper prices may lie ahead. “You know, it is the most compelling trade I have ever seen in my 30 plus years of doing this,” Jeff Curie, chief strategy officer of the energy pathways team at Carlyle Group, recently said in an appearance on Bloomberg’s Odd Lots. “You look at the demand story, it’s got green CapEx, it’s got AI, remember AI can’t happen without the energy demand and the constraint on the electricity grid is going to be copper.“

With four US reclamation centers, AT&T’s recovery efforts are already underway, but ramping up rapidly. “With copper prices where they are, we are scaling quite significantly,” Susan Johnson, an executive vice-president at AT&T leading its copper recovery and resale efforts, tells Bloomberg.

Aside from selling the copper, telecom utilities also benefit by making more room for fiber cables and reducing the cost of ongoing maintenance. Also, as the Wall Street Journal first reported in a July 2023 exposé, when left to deteriorate, some old copper cables present a health hazard, as they’re sheathed with lead insulation, and are leaching the dangerous element into soil and water. Removing these cables — some of which go back to the late 1800s — can help mitigate liabilities.

Zerohedge.com/commodities/copper-soars-telecoms-sitting-7-billion-mother-lode-old-cable

After the cables are pulled out of the ground, they have to be stripped and cleaned to obtain the copper, which can then be sold to domestic and international buyers. At prices between $6,000 to $9,000 per ton, profit can top 30% after extraction, recovery and processing costs, said TXO’s Evans. — Bloomberg

Meanwhile, in a dog-chasing-its-tail dynamic, some premature recycling efforts are targeting the same green-energy infrastructure that’s helping to push copper prices higher:

Tesla Supercharger station in Bay Area hit by thieves with every charging cable cut

·

3.5M Views

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

ASIA TRADING//FRIDAY MORNING/THURSDAY NIGHT

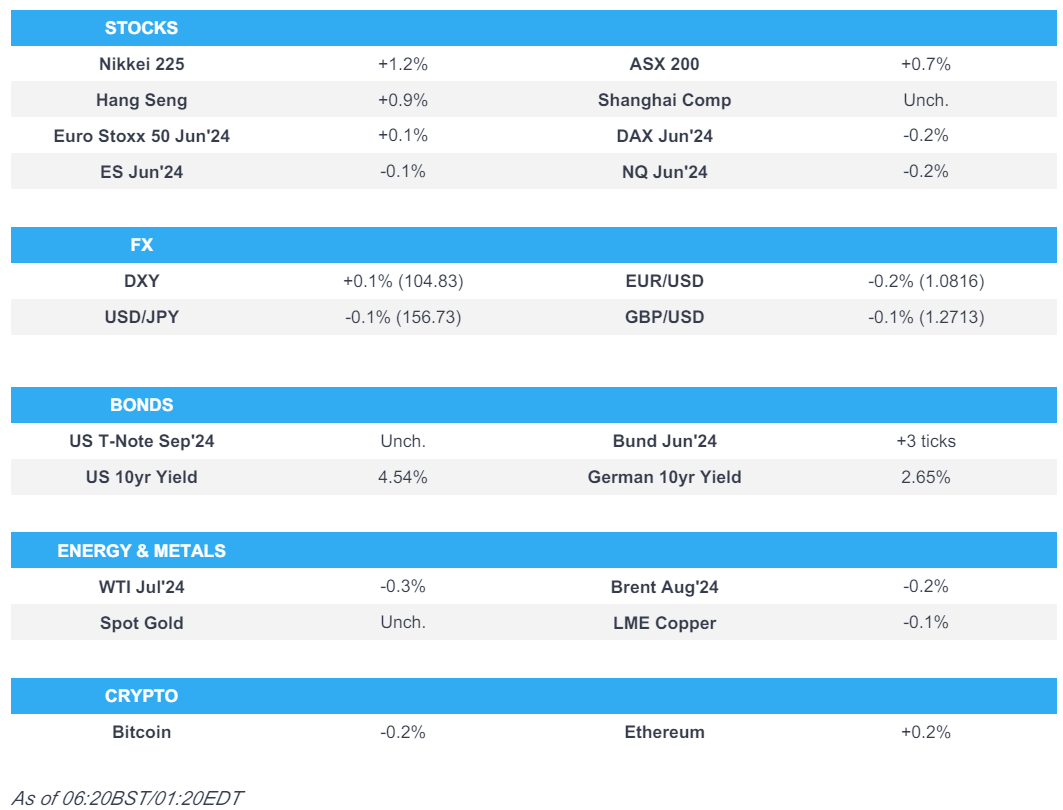

SHANGHAI CLOSED DOWN 4.06 PTS OR 0.16% //Hang Seng CLOSED DOWN 150.58 PTS OR 0.83%// Nikkei CLOSED UP 433.77 OR 1.14%//Australia’s all ordinaries CLOSED UP 0.95%///Chinese yuan (ONSHORE) closed DOWN TO 7,2411 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2587/ Oil DOWN TO 77.87 dollars per barrel for WTI and BRENT DOWN AT 81.88 /Stocks in Europe OPENED MOSTLY RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2411

OFFSHORE YUAN: DOWN TO 7.2587

SHANGHAI CLOSED DOWN 4.86 PTS OR 0.16 %

HANG SENG CLOSED DOWN 150.58 PTS OR 0.83%

2. Nikkei closed UP 433.77 PTS OR 1.14 %

3. Europe stocks SO FAR: MOSTLY RED

USA dollar INDEX DOWN TO 104.59 EURO RISES TO 1.0852 UP 21 BASIS PTS

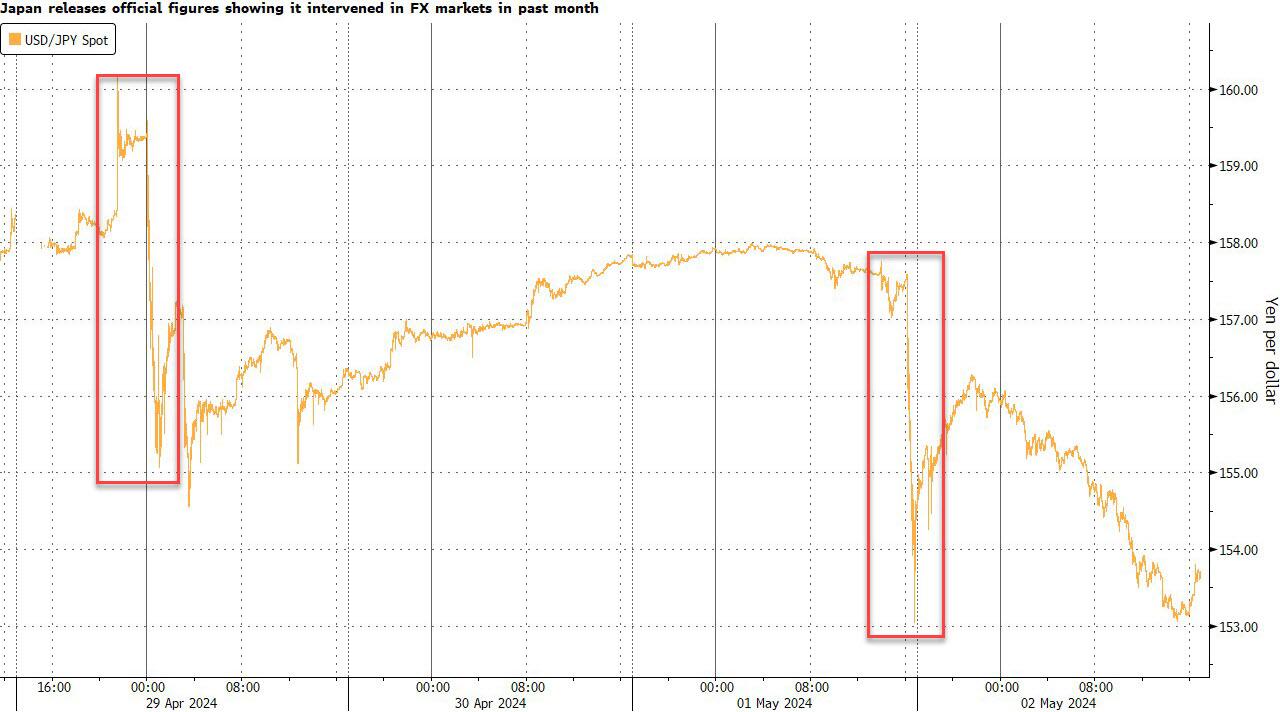

3b Japan 10 YR bond yield: RISES TO. +1.055 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 157.16 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.6950/Italian 10 Yr bond yield UP to 3.997 SPAIN 10 YR BOND YIELD UP TO 3.427%

3i Greek 10 year bond yield UP TO 3.675

3j Gold at $2343.30//Silver at: 31.25 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 31/ 100 roubles/dollar; ROUBLE AT 90.16

3m oil into the 77 dollar handle for WTI and 81 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 157.15/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.055% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9052 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9822 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.557 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.685 UP 0 BASIS PTS/

USA 2 YR BOND YIELD: 4.944 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.21…

10 YR UK BOND YIELD: 4.4185 DOWN 1 PTS

2a New York OPENING REPORT

Futures Dip On Disappointing Tech Results As Markets Brush Off Trump Verdict

BY TYLER DURDEN

FRIDAY, MAY 31, 2024 – 07:44 AM

Futs are slightly lower as bond yields rise after European inflation prints came in stronger than expected and PCE looms. As of 7:30am S&P futures are down -0.2%, off the worst levels of the session; Nasdaq futures slumped 0.5% as last night’s latest round of tech earnings disappointed: DELL plunged -14% as it failed to meet the high expectations on AI demand; MDB cratered 24% and is now down 55% below YTD highs. Indeed, most AI names (ex-NVDA) are mostly lower: AMD -1.0%, MU -78bp. Bond yields are 1-2bp higher in sympathy with the move wider in Bunds where the latest data showed European consumer prices rose more than expected; the Bloomberg dollar index dipped and commodities, energy and ags are mostly lower. Today’s macro data focus will be March PCE release; the street expects a headline and core PCE print of +0.3% MoM; on YoY basis, Core PCE is expected to rise 2.8%. Over the weekend, NVDA will host the CEO live keynote ahead of the Computex 2024 event on Sunday June 2 at 7am ET.

In premarket trading, megacap tech was mixed: NVDA +58bp, MSFT +25bp, AAPL -22bp, TSLA -53bp. Dell shares sink 15% as the personal computer maker’s strong AI server sales fail to impress investors. Analysts note that the first revenue increase since 2022 came at the cost of weaker profit margins. Here are some other notable premarket movers:

- Asana shares rise 13% as RBC says the application software company’s first-quarter results show signs of demand stabilization.

- Gap shares soar 23% after the apparel retailer reported first-quarter total comparable sales that topped Wall Street expectations, and upgraded its sales and margin projections for the full year.

- Marvell Technology shares fall 4.8% after reporting net revenue for the first quarter and July guidance in-line with average analyst estimates. Despite the match, the chipmaker’s “high share price leaves little room for error,” Morgan Stanley analysts write in a note.

- MongoDB shares plummet 25% after the database software company cut its full-year forecast, the latest in a series of disappointing software company results. DataDog -2.8%

- Nordstrom shares slide 7.4% after the apparel retailer’s first-quarter adjusted Ebitda missed estimates.

- PagerDuty shares rise 11% after the wireless applications company boosted its adjusted earnings per share forecast for the full year.

- SentinelOne shares slump 14% after the security software company cut its FY25 revenue guidance and annual recurring revenue missed the average analyst estimate. Barclays analysts trimmed their net new ARR FY25 estimates as a reflection of macro headwinds and leadership changes at the firm.

- Trump Media shares fall 6.5% after a jury found Donald Trump guilty of multiple felonies.

- Ulta shares jump 7.0% after the beauty retailer reported first-quarter earnings per share that came in ahead of estimates. The company also lowered its full-year outlook, though analysts said it was now more achievable than before.

- Zscaler shares surge 17% after the security software firm’s results beat estimates and it raised its full-year forecast as demand for its platform grows. Analysts noted that Zscaler is defying a broader slowdown in the industry, and increased their price targets on the stock.

Prior to the recent swoon in tech, and especially software names, stock gains this month were fueled by the rally in tech as well as Jerome Powell’s dovish posture on rates at the start of May. That optimism has faded over the course of the month, and Friday’s data could revive hopes for easing if there are signs inflation is returning to target.

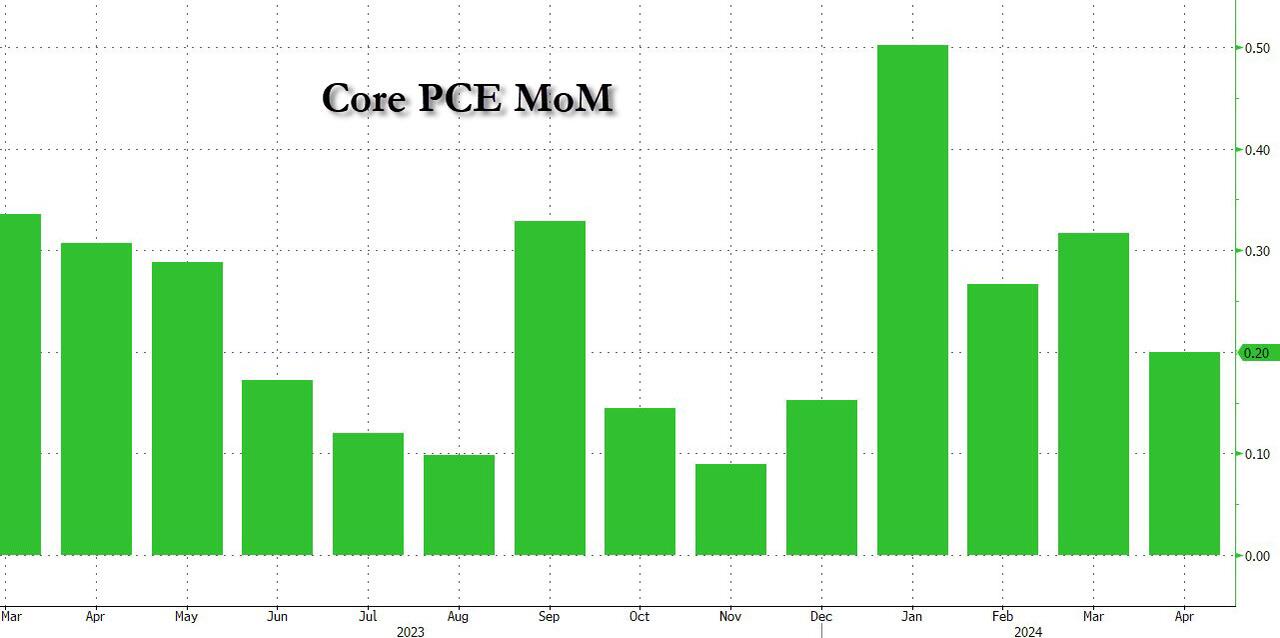

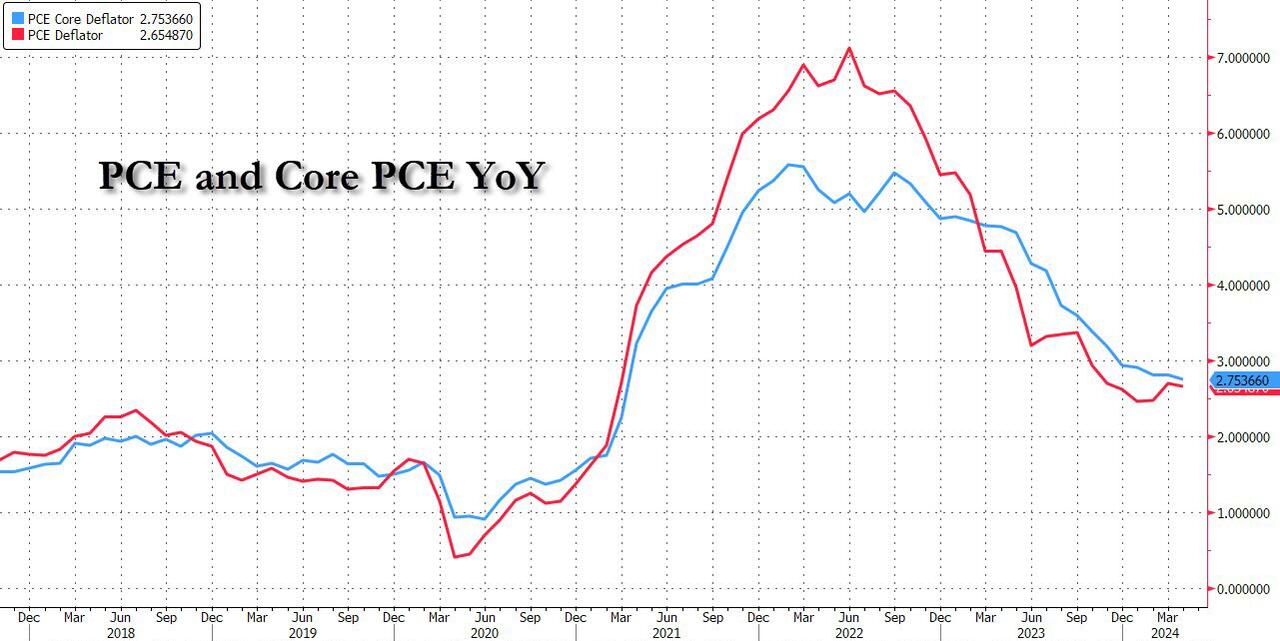

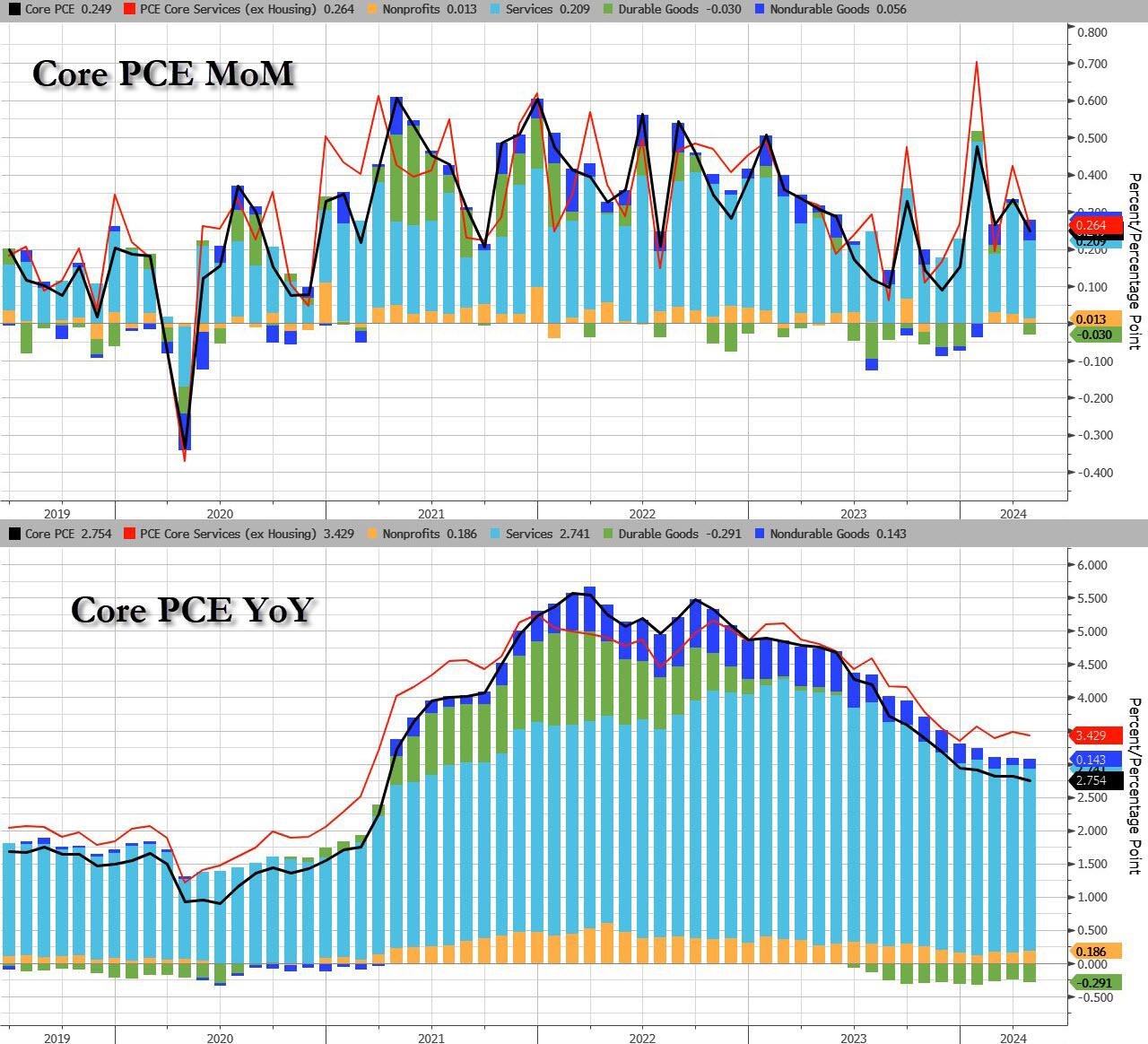

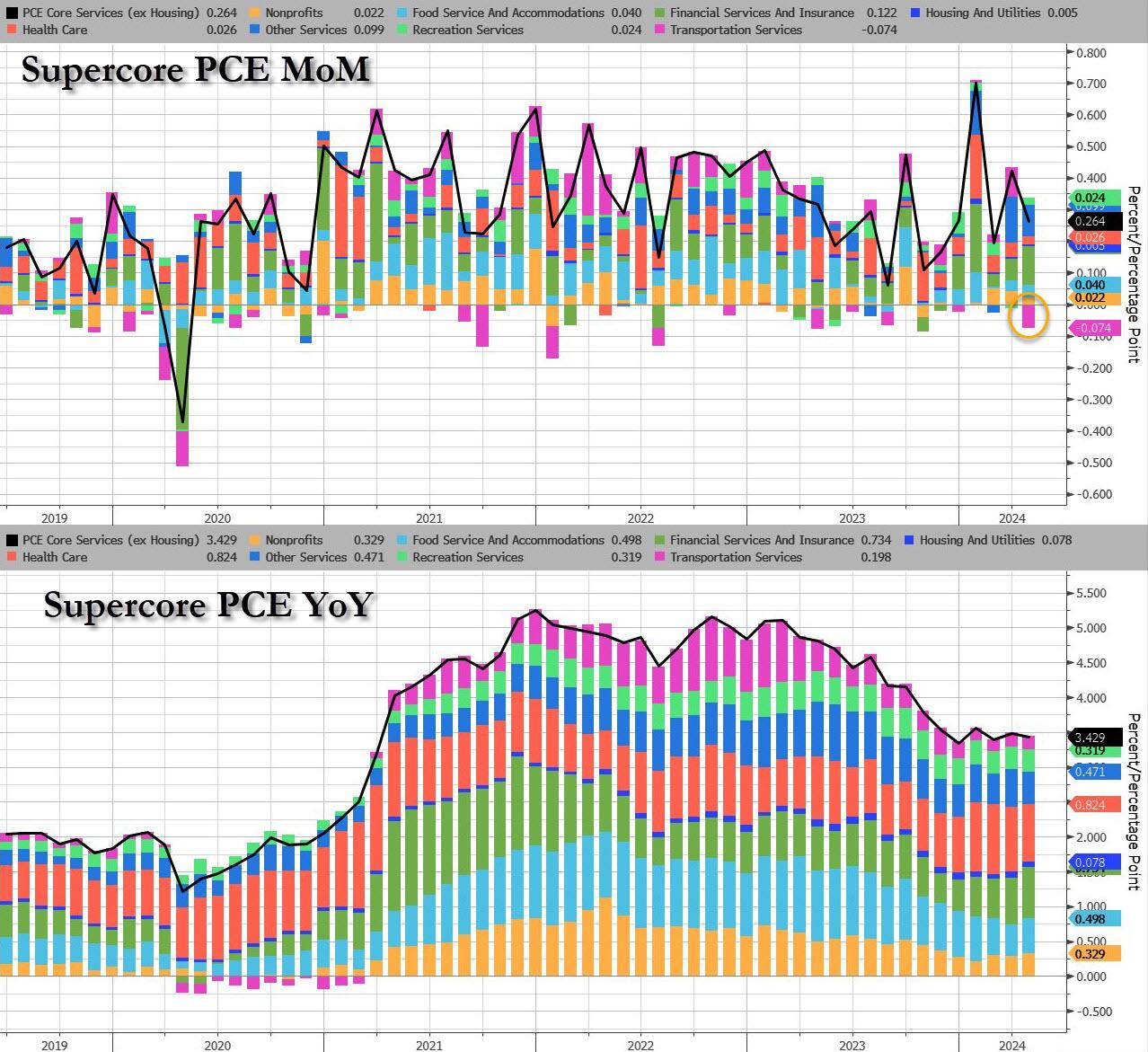

Indeed, investor attention now turns to the Federal Reserve’s preferred price-growth measure, the core PCE deflator, due at 8:30am and which likely moderated in April to the slowest monthly pace yet this year. As previewed earlier, headline PCE prices are seen rising +0.3% M/M in April (prev. +0.3%), with the annual rate expected to be unchanged at 2.7%. The core measure is seen rising +0.2% M/M (prev. +0.3%), while the core rate of annual PCE is seen unchanged at 2.8% Y/Y, although even a modest dip in the annual print would lead to the lowest annual increase in three years, since April 2021.

Elsewhere, a jury found Donald Trump guilty on all 34 counts of falsifying business records at his hush-money trial, making him the first former US president to be convicted of crimes. With Trump to due to face sentencing on July 11, the conviction creates a challenging legal and political path as he faces Biden in November as the presumptive Republican nominee. Trump Media & Technology Group traded down 12% in extended trading Thursday.

“Expectations for a guilty verdict were somewhat priced into markets,” Paresh Upadhyaya, director of fixed income and currency strategy at Amundi Asset Management in Boston. “The bigger impact to markets could be if this guilty verdict begins to turn the momentum away from Trump to Biden.”

European stocks are little changed with losses in technology shares capping any upside in the Stoxx 600. Here are the biggest movers Friday:

- Neoen share rise as much as 21% to €37.98 following news that Brookfield is in exclusive talks to acquire a majority stake at a price of €39.85 per share

- Centrica rises as much as 4.6% as analysts at RBC Capital Markets raised the British energy company to outperform, expecting further scope amid market tailwinds

- Nel gains as much as 9.5% after its Cavendish Hydrogen fueling division applied for its shares to be admitted to trading on the Oslo Stock Exchange

- Lalique Group shares climb as much as 32% to CHF 39.60 as its majority shareholder Silvio Denz intend to delist the company’s shares from the Swiss stock exchange

- Capgemini shares slide as much as 6.9% to the lowest since November after JPMorgan and Jefferies both downgraded their buy ratings on Friday

- Flutter Entertainment shares fall as much as 18% in London after the CFO announced his departure; today is also the first day Flutter’s primary listing is in the US

- JD Sports drop as much as 13%, the most in almost five months, after full-year adjusted pretax profit and sales from the sports apparel retailer missed estimates

- Pharming shares tumble as much as 12% to the lowest since June 2022 after the Dutch biopharmaceutical company noted a delay to the European regulatory review

- AB Foods fall as much as 3.8%, the most in a month, after Wittington Investments announced a sale of up to 10.3m shares at a discount of 4.1% versus Thursday’s close

Earlier, Asian stocks failed to hold initial gains to head for their second straight weekly decline, dragged by a selloff in equities in Hong Kong while contraction in factory activity weighed on Chinese shares. The MSCI Asia Pacific Index rose as much as 0.7% before trading little changed as TSMC, Tencent and Alibaba were among the biggest drags. Japan and New Zealand were among the key gainers, while a rebound in Samsung helped Korean shares higher. Shares fell about 1.5% on the week. Despite the recent decline, the Asian benchmark is still on track for a monthly gain of about 1.5% on an easing dollar and renewed expectations for help from the Fed, in addition to China’s support measures for its beleaguered property market.

In FX, the Bloomberg Dollar Spot Index is up less than 0.1% and is set to end the month 1% lower in May, after rising in the previous four months. The Swiss franc and Japanese yen are the weakest of the G-10 currencies. Euro rises 0.1% against the dollar to 1.0845 after earlier falling to 1.0811. The yen slips 0.3% to 157.27 per dollar, having risen 0.2% earlier due to a pickup in Tokyo CPI in May. In emerging markets, South Africa’s rand led declines after falling more than 3% over three days. Investors are awaiting the final results of the nation’s elections amid concern over the different permutations a coalition may take, and whether a market-friendly government will emerge.

In rates, US Treasuries slip, sending 10-year yields 1-2bps higher to 4.56%. German bund yields advanced five basis points to 2.70%, the highest since November, after the latest data showed European consumer prices rose 2.6% from a year ago in May, up from +2.4% in Apr and ahead of the Street’s +2.5% forecast. Core CPI came in +2.9%, up from +2.7% in Apr and ahead of the Street’s +2.7% forecast. Still, traders maintained bet for a cut at the ECB meeting next week, but reduced bets on easing after that. US Treasuries were also slightly cheaper across the curve with losses led by front-end, following a more aggressive selloff across bunds. Focal points of US session include PCE deflator data at 8:30am New York time. Treasuries may subsequently garner support from month-end buying flows, with a larger-than-average extension estimated for June.

In commodities, oil prices declined, with WTI falling 0.3% to trade near $77.70. Spot gold is steady near $2,343/oz.

Bitcoin has reversed earlier losses and trades just above $68k, while Ethereum has staged a rally and is trading just above $3,800.

US economic data includes April personal income and spending, including PCE deflators (8:30am) and May Chicago PMI (9:45am, 3 minutes earlier to subscribers). Fed officials’ scheduled speeches include Bostic at 6:15pm.

Market Snapshot

- S&P 500 futures little changed at 5,247.75

- STOXX Europe 600 little changed at 516.97

- MXAP up 0.1% to 176.88

- MXAPJ down 0.4% to 547.97

- Nikkei up 1.1% to 38,487.90

- Topix up 1.7% to 2,772.49

- Hang Seng Index down 0.8% to 18,079.61

- Shanghai Composite down 0.2% to 3,086.81

- Sensex up 0.6% to 74,304.07

- Australia S&P/ASX 200 up 1.0% to 7,701.74

- Kospi little changed at 2,636.52

- German 10Y yield little changed at 2.67%

- Euro little changed at $1.0834

- Brent Futures down 0.2% to $81.72/bbl

- Gold spot down 0.1% to $2,341.85

- US Dollar Index little changed at 104.78

Top Overnight News

- Former US President Trump was found guilty by a jury verdict on all 34 counts he faced at the hush money trial and will be sentenced on July 11th. Following the verdict, Trump said this was a disgrace and the real verdict will be on November 5th (US election), while he added that he is innocent and this was a rigged decision. There were also comments from House Speaker Johnson who said this was a shameful day in American history and that “President Trump will rightfully appeal this absurd verdict—and he will win”: WSJ

- China’s NBS PMIs for May fall short of expectations, coming in at 49.5 for manufacturing (vs. the Street 50.5 and down from 50.4 in Apr) and 51.1 for services (vs. the Street 51.5 and down from 51.2 in Apr). RTRS

- Japan’s Tokyo CPI for May is inline on a headline basis at +2.2% (up from +1.8% in Apr and vs. the Street +2.2%) and a tiny but cooler on core (ex-energy/food) at +1.7% (down from +1.8% in Apr and vs. the Street +1.8%). RTRS

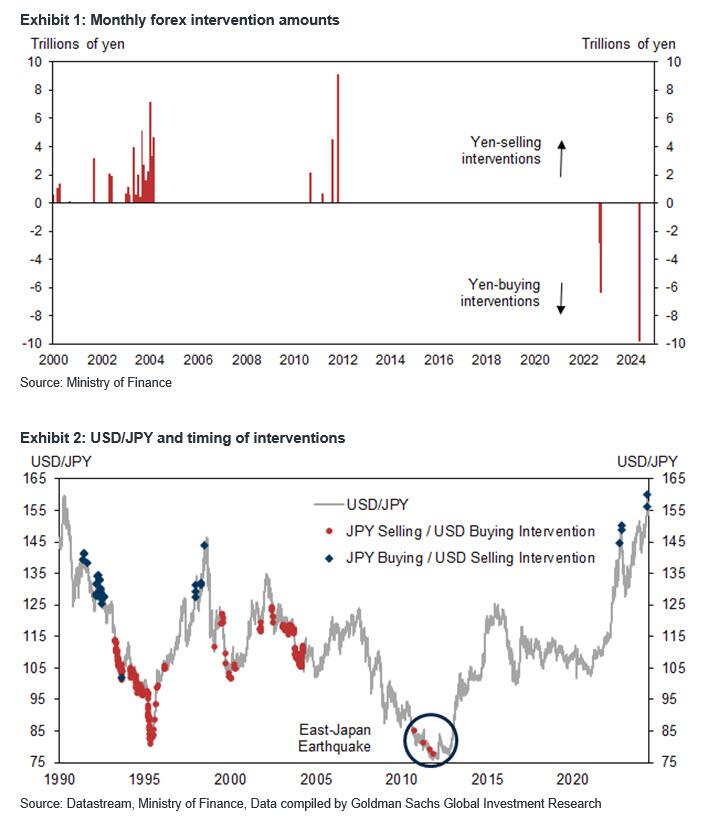

- Japan spent a record ¥9.8 trillion ($62.2 billion) in the past month to prop up the yen, surpassing the amount it used in 2022 to defend the currency. BBG

- Eurozone CPI for May runs hot, with core coming in +2.9% (up from +2.7% in Apr and ahead of the Street’s +2.7% forecast) and headline +2.6% (up from +2.4% in Apr and ahead of the Street’s +2.5% forecast). France’s CPI for May also runs a bit hot, coming in at +2.7% Y/Y on an EU harmonized basis, up from +2.4% in Apr and ahead of the Street’s +2.6% forecast. BBG

- France is seeking to assemble a coalition of European countries willing to send military trainers to Ukraine as western allies look for ways to speed up Kyiv’s recruitment efforts in the face of Russia’s renewed offensive. FT

- Trump was found guilty Thursday by a New York jury on all 34 counts in his hush-money case, concluding the first-ever criminal trial of a former president. Now voters will render their own judgment, as Trump, the presumptive GOP presidential nominee, barrels ahead to the Nov. 5 election, using the trial and other prosecutions he faces as a rallying cry for his supporters. WSJ

- Bill Ackman is planning to take his investment firm public as soon as next year, the boldest move yet by the hedge-fund manager to capitalize on his social-media fame. As a precursor to a public listing, Ackman is selling a stake in the firm, Pershing Square, to investors in a funding round expected to value the firm at about $10.5 billion, people familiar with the matter said. That deal is expected to close in the coming days. WSJ

- The Fed’s favored inflation gauge may bring some cheer to markets, with the core PCE deflator forecast to have moderated to 0.2% in April, the slowest monthly pace this year. Personal spending and income also probably cooled. But this alone won’t make the case for rate cuts, Bloomberg Economics said. BBG

- Deutsche Bank CFO James von Moltke said fixed-income trading revenue is set to drop in the second quarter. RTRS

- Fed’s Logan (non-voter) said there are good reasons to think we are still on the path to 2% inflation but it is bumpy, while she added it is too soon to think about rate cuts and policy may not be as restrictive as we might think. Furthermore, she said there are good reasons to believe the neutral rate is higher now than before the pandemic and if the neutral rate is higher than before, it suggests rates won’t go back down to pre-pandemic levels.

- Tesla is recalling 125,227 US vehicles as a seat belt warning system fails to alert occupants of an unbelted seat belt.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mostly in the green and shrugged off the weak lead from the US but with gains capped amid a deluge of data releases at month-end including disappointing official Chinese PMIs. ASX 200 traded higher with outperformance seen in gold mining stocks and the defensive sectors. Nikkei 225 advanced with the index ultimately unfazed by the mixed data mixed data from Japan including mostly in-line Tokyo CPI, a surprise contraction in Industrial Production and better-than-expected Retail Sales. Hang Seng and Shanghai Comp conformed to the positive tone albeit with gains capped in the mainland after disappointing Chinese PMI data in which Manufacturing PMI unexpectedly slipped into contraction territory

Top Asian News

- Japan’s MOF says it spent JPY 9.788tln on currency intervention between 26th April and 29th May

- Chinese state media said China has richer and more powerful countermeasures if the US continues to violate and endanger China’s sovereignty and security interests on core issues, or squeeze the development space of Chinese firms and individuals. Furthermore, it warned that in the future, whether the US will suffer greater backlash and losses depends on its sincerity and actual actions.

- Japan is to shift USD 640bln in public pension money into active investment, according to Nikkei.

- US Defence Secretary Austin says the meeting with his Chinese counterpart went well, via CNN/Pentagon Spokesperson.

- Tencent Holdings (0700 HK) has reportedly been asked by Chinese regulators to recude the mobile payment market shae of WeChat, via Nikkei citing sources; aimed at the market share of in-person payments rather than online shopping.

- Japan Business Lobby Keidanren Deputy Head Takashima says stable currency is important no matter what levels they may be at.

- Japan Business Lobby Keidanren Deputy Head Yoshida says economic strength and interest-rate differentials are among factors behind the weak Yen, so much boost investment to address this issue.

- Japan Business Lobby Keidanren Deputy Head Nagasawa says current DX levels at the mid-150 Yen range are excessively weak.

European bourses, Stoxx 600 (+0.1%) are mixed, and generally trading near the unchanged mark as focus turn to the upcoming US PCE report. Equities saw very modest pressure on the back of the hotter-than-expected EZ HICP figures. European sectors are mixed and with the breadth of the market fairly narrow; Telecoms takes the top spot, continuing to build on the prior day’s outperformance. Tech is among the worst performers, joined by Travel & Leisure. US Equity Futures (ES -0.2%, NQ -0.4%, RTY -0.3%) are entirely but modestly in the red, continuing the negative sentiment seen in the prior session; however, the price action is relatively contained given the focus around the upcoming US PCE at 13:30 BST / 08:30 EDT.

Top European News

- ECB’s Panetta says policy will remain restrictive even after several rate cuts; Monetary easing will be expected over the coming months if our forecasts are confirmed by data. Must avoid monetary policy becoming too restrictive, which could push inflation below the ECB’s symmetrical target. Euro zone inflation is expected to continue to ease in the next few quarters. Salary rises can also be expected to slow as workers recover purchasing power, firms can be expected to absorb recent salary hikes without raising prices. ECB will take account Federal Reserve’s moves, but not be bound by them. ECB’s balance sheet reduction mustn’t interfere with the monetary policy stance or create a lack of liquidity in the financial system. Larger Italian banks lag behind European peers in IT investments, must step up spending. Says the latest EZ inflation rate of 2.6% is in line with forecasts and as such is “neither good or bad”

FX

- USD is flat and trading within the middle of its weekly 104.33-105.18 range; PCE will likely determine the fate of the USD today with analysts at ING suggesting that a 0.2% M/M print could trigger a run of bond bullishness (USD weakness).

- EUR is a touch firmer vs. the USD in wake of firmer-than-expected headline and core inflation metrics from the Eurozone. Next upside target would come via the high from Wednesday at 1.0861.

- GBP is slightly softer vs. the USD in quiet trade with tier 2 data releases from the UK unable to have much sway on the pair. For now, Cable is caged within yesterday’s 1.2688-1.2747 range.

- JPY is giving back some of yesterday’s gains which saw USD/JPY dragged lower from 157.61 to 156.36. The pair has since moved back onto a 157 handle following mixed data overnight.

- Antipodeans are both a touch firmer vs. the USD. AUD/USD has made further progress on a 0.66 handle but is yet to test yesterday’s 0.6647 as the pair remains in close proximity to its 10DMA.

- South Africa’s ANC vote share drops below 42% based on results from 55.63% of polling stations; FT writes that South African President Ramaphosa’s future is in doubt after disappointing South African election, figure within the ANC notes that if the vote remains close to 40% “people will suggest he leaves”.

Fixed Income

- USTs are slightly softer as Thursday’s bounce runs out of steam and hot Tokyo headline CPI, but with price action fairly contained ahead of the key US PCE figure later today. USTs are at lows of 108-12 having dipped from Thursday’s 108-19+ peak but currently remain comfortably above the WTD base at 107-31.

- Bunds were pressured alongside USTs into Final EZ HICP, prior to this some modest two-way action was seen on German Retail Sales & Import Prices. Thereafter, hotter-than-expected prints on the three headline Y/Y metrics sent Bunds down from circa. 128.90 to a 128.74 base (matching Wednesday’s low); EGBs now back towards pre-release levels.

- Gilts are essentially unchanged with specifics light into EZ HICP, which resulted in some very modest pressure for Gilts to an incremental new session low; Gilts in a narrow 95.62-95.94 bound which itself is entirely within Thursday’s 95.54-95.99 range.

Commodities

- Crude is softer and towards session lows, continuing the overnight pressure seen following the disappointing Chinese PMI data, which saw the Manufacturing component dip into contractionary territory.

- Precious metals are flat/mixed in the run-up to US PCE and unreactive to the hotter-than-expected EZ Flash CPI figures; XAU trades in a USD 2,337-2,347.81/oz range.

- Base metals are mixed and consolidating after yesterday’s slump despite the lack of a clear driver, but amid cautiousness as yields remain elevated and US PCE nears.

- OPEC+ could extend production cuts at the June meeting, via CNBC citing sources; “demand concerns persisted until only recently”. Delegate cited notes that the US SPR release is unlikely to have an impact beyond price relief during the summer period. Three delegates cited said the 2.2mln BPD supply reduction will likely be extended, which is regarded as anticipated by the market; one noted there will probably be market tightness in H2 but added that demand concerns persisted until only recently. Gaza Strip situation is adding a little pressure to prices, but the market has absorbed the majority of this.

- Russia’s Lukoil reportedly plans to restart CDU-6 and catalytic cracker units at Norsi oil refinery (340k BPD) in June, according to Reuters sources

- Chevron (CVX) Australia has confirmed full LNG production has resumed at Gorgon gas facility, according to a spokesperson.

- Ukrainian Navy hit an oil depot in the Krasnodar region of Russia with Neptune missiles.

- Oman Crude OSP calculated at USD 83.89/bbl for July (prev. USD 89.3/bbl M/M, – USD 5.41)

Geopolitics: Middle East

- Senior Israeli Security Official says there will be no truce or any halt in fighting in Gaza which is not part-and-parcel of a hostage release deal

- US military said American and British forces conducted strikes against 13 Houthi targets in Yemen, while Houthi Al Masirah TV said one person was killed in the US-British strikes on Yemen’s Hodeidah.

- Deputy Chairman of Russia’s Security Council says the use of long-range weapons against Russia could become a reason to go to war with NATO.

- “Ukrainian media: The first attacks on the territory of the Russian Federation using US weapons may begin within hours or days”, according to Sky News Arabia

- China has told other governments it will not join the Swiss peace conference on Ukraine and said the peace conference does not meet its conditions since Russia is not attending, according to Reuters sources.

- North Korean leader Kim guided a demonstration of large-scale multiple rocket launchers, according to KCNA.

US Event Calendar

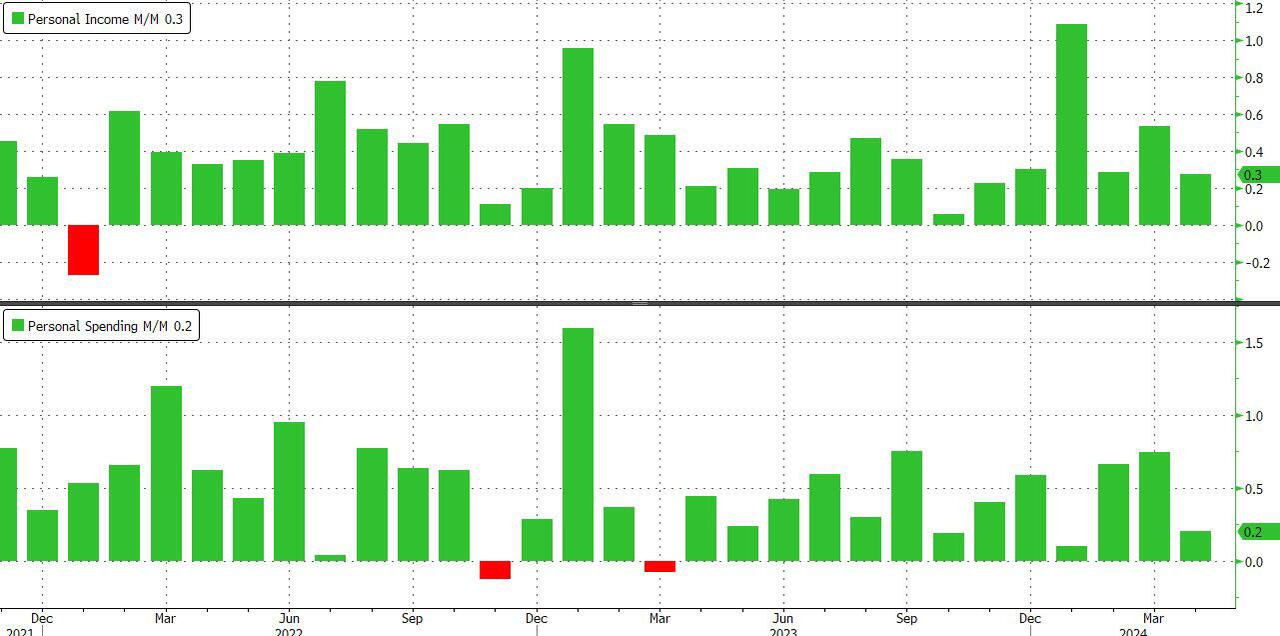

- 08:30: April PCE Deflator MoM, est. 0.3%, prior 0.3%

- April PCE Deflator YoY, est. 2.7%, prior 2.7%

- April PCE Core Deflator YoY, est. 2.8%, prior 2.8%

- April PCE Core Deflator MoM, est. 0.2%, prior 0.3%

- 08:30: April Personal Income, est. 0.3%, prior 0.5%

- April Personal Spending, est. 0.3%, prior 0.8%

- April Real Personal Spending, est. 0.1%, prior 0.5%

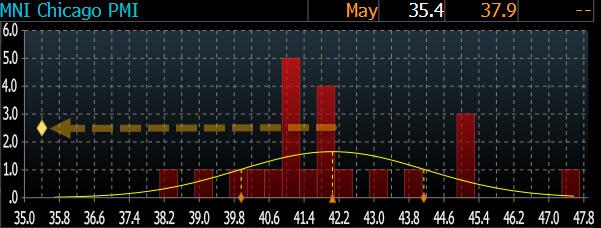

- 09:45: May MNI Chicago PMI, est. 41.5, prior 37.9

Central Bank Speakers

- 18:15: Fed’s Bostic Gives Commencement Speech

DB’s Jim Reid concludes the overnight wrap

I arrived back from NY yesterday to unexpectedly find a half-term sleepover with several noisy and excitable 8-year old girls. I ran back to the taxi to try to return to the airport but alas the driver had gone.

While I was away, the last few days have been the first for some time where good economic data (Tuesday) was a reason for markets to sell-off, and then weaker economic data (yesterday) was also seen as a reason for markets to sell-off. In recent times, both good and bad data have managed to build a bullish narrative, as bad data has been seen to raise the likelihood of rate cuts. Having said that, the sell-off this week remains pretty mild and the S&P 500 is only -1.6% beneath its record from last week, so it’s hard to get too excited about a new trend emerging.

On the plus side, sovereign bonds recovered yesterday as investors dialled up the likelihood of rate cuts this year. But on the more negative side, the S&P 500 (-0.60%) still fell back for a second day, as the data included negative revisions to consumer spending. So it encouraged the idea that the US economy had lost some momentum at the start of the year, and it means the S&P 500 has now posted its worst two-day performance (-1.33%) in four weeks.