GOLD PRICE CLOSED DOWN $20.60 TO $2327.90

SILVER PRICE DOWN $1.08 TO $29.55

Gold ACCESS CLOSED $2327,25

Silver ACCESS CLOSED: $29.54

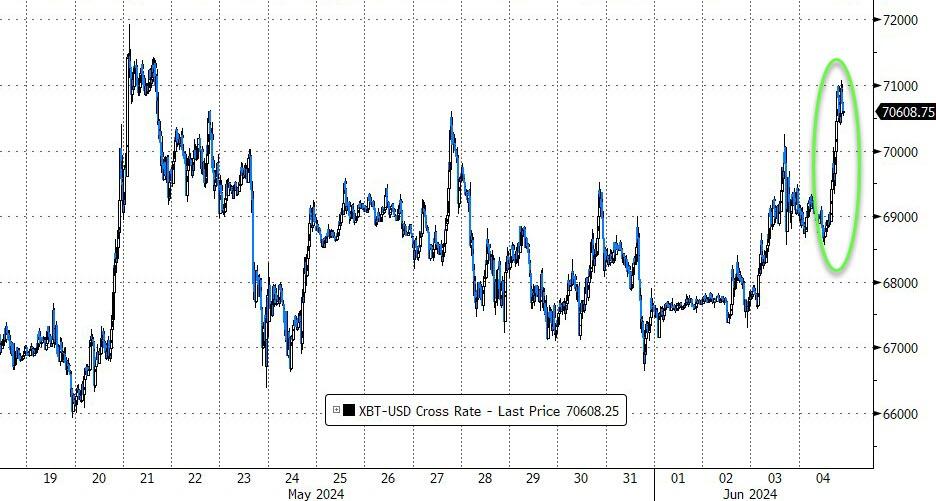

Bitcoin morning price:$68,885 DOWN 1795 DOLLARS.

Bitcoin: afternoon price: $70,587 DOWN 93 dollars

Platinum price closing DOWN $24.60 TO $995.90

Palladium price; UP $2.80 AT $919.70

END

SHANGHAI GOLD PREMIUM 43 DOLLARS/COMEX GOLD

SHANGHAI GOLD

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $3182.79 DOWN 20,77 CDN dollars per oz( * NEW ALL TIME HIGH 3,305.30 CDN DOLLARS PER OZ//MAY 20 2024)

*BRITISH GOLD: 1822.24 DOWN 12.46 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2139,07 DOWN 15.91 Euros per oz //* (ALL TIME CLOSING HIGH: 2248.89 EUROS PER OZ//APRIL 16.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCH: COMEX

EXCHANGE: COMEX

CONTRACT: JUNE 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,346.600000000 USD

INTENT DATE: 06/03/2024 DELIVERY DATE: 06/05/2024

FIRM ORG FIRM NAME ISSUED STOPPED

099 H DB AG 97

118 H MACQUARIE FUT 39

132 C SG AMERICAS 515

167 C MAREX 1

323 C HSBC 3

363 H WELLS FARGO SEC 12

435 H SCOTIA CAPITAL 48

657 C MORGAN STANLEY 9

661 C JP MORGAN 160

661 H JP MORGAN 169

685 C RJ OBRIEN 1

686 C STONEX FINANCIA 8 11

690 C ABN AMRO 43 3

732 C RBC CAP MARKETS 6

737 C ADVANTAGE 51 2

880 H CITIGROUP 61

905 C ADM 1

TOTAL: 620 620

MONTH TO DATE: 27,481

JPMorgan stopped 329/620

FOR JUNE 2024

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2024. CONTRACT: 620 NOTICES FOR 62,000 OZ or 1.9284 TONNES

total notices so far: 27,481 contracts for 2,748,100 Oz (85.477 tonnes)

FOR JUNE:

SILVER NOTICES: 120 NOTICE(S) FILED FOR 600,000 OZ/

total number of notices filed so far this month : 875 for 4.575 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $20.60

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

NO CHANGES IN GOLD INVENTORY AT THE GLD:

/ /INVENTORY RESTS AT 832.21TONNES

INVENTORY RESTS AT 832.21 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER DOWN $1.08 AT THE SLV//

NO CHANGES IN SILVER INVENTORY AT THE SLV:

// INVENTORY LOWERS TO 413.775 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 413,775 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 1464 CONTRACTS TO 181,898 AND CONTINUING ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR GAIN OF $0.35 IN SILVER PRICING AT THE COMEX ON MONDAY’S TRADING ON SILVER. WE HAD ZERO LONG LIQUIDATION AS WE HAD A NET GAIN OF 2104 CONTRACTS ON OUR TWO EXCHANGES. WE, AGAIN HAD SHORT COVERING BY OUR SPECS WITH THE GAIN IN PRICE AS WELL AS MASSIVE T.A.S. LIQUIDATION. WE HAD ANOTHER HUGE SIZED 755 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 755 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND TODAY;S TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.35) BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS AS WE DID HAVE A HUGE SIZED GAIN OF 2104 CONTRACTS ON OUR TWO EXCHANGES WITH THE GAIN IN PRICE OF $0.35

.

WE MUST HAVE HAD:

A STRONG SIZED 640 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.830MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 765,000 OZ QUEUE JUMP

//NEW STANDING FOR SILVER//JUNE IS THUS 4.685 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI GAIN //HUGE SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 755 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL ADDED A MONSTEROUS 468 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE

TOTAL CONTRACTS for 2 DAYS, total 1805 contracts: OR 9.025 MILLION OZ (903 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 9.025 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL PROBABLY BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 9.025 MILLION OZ

RESULT: WE HAD A HUMONGOUS SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 996 CONTRACTS WITH OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 640 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.830 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 765,000 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR JUNE 4.685 MILLION OZ

WE HAVE A HUGE SIZED GAIN OF 2104 OI CONTRACTS ON THE TWO EXCHANGES WITH THE GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 755 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND ZERO LIQUIDATION OF LONGS.

THE NEW TAS ISSUANCE MONDAY NIGHT (755) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 120 NOTICE(S) FILED TODAY FOR 600,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 4165 OI CONTRACTS TO 455,086 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 237 CONTRACTS

WE HAD A STRONG SIZED DECREASE IN COMEX OI (4165 CONTRACTS) OCCURRED DESPITE OUR GAIN OF $22.45 IN PRICE/MONDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNED AT 89.804 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 12,800 OZ QUEUE JUMP AS BANKERS SCOUR THE PLANET LOOKING FOR GOLD ON THIS SIDE OF THE POND

NEW STANDING 88.761 TONNES// ALL OF THIS HAPPENED WITH OUR $22.45 GAIN IN PRICE WITH RESPECT TO MONDAY’S TRADING. WE HAD A SMALL SIZED LOSS OF 27 OI CONTRACTS (0.0839 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1438 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 455,086

IN ESSENCE WE HAVE A VERY SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 27 CONTRACTS WITH 4,165 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 4138 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 27 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 1438 CONTRACTS,,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4138 CONTRACTS) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI OF 4,165 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 27 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 88.761 TONNES

//NEW STANDING /JUNE 88.761 TONNES.

/ 3) STRONG LIQUIDATION OF CONTRACTS MOSTLY DUE TO TAS ALONG WITH ZERO LONG SPECS BEING CLIPPED,

.

// 4) STRONG SIZED COMEX OPEN INTEREST LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1438 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE. :

TOTAL EFP CONTRACTS ISSUED: 7505 CONTRACTS OR 750,500 OZ OR 23.343 TONNES IN 2 TRADING DAY(S) AND THUS AVERAGING: 3752 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAY(S) IN TONNES 23,343 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 23.343 DIVIDED BY 3550 x 100% TONNES = 0.648% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 23.343 tonnes

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUMONGOUS SIZED 1464 CONTRACTS OI TO 181,898 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 640 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 640 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 640 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1464 CONTRACTS AND ADD TO THE 640 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2104 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 10.50 MILLION OZ

OCCURRED WITH OUR $0.35 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING/MONDAY NIGHT

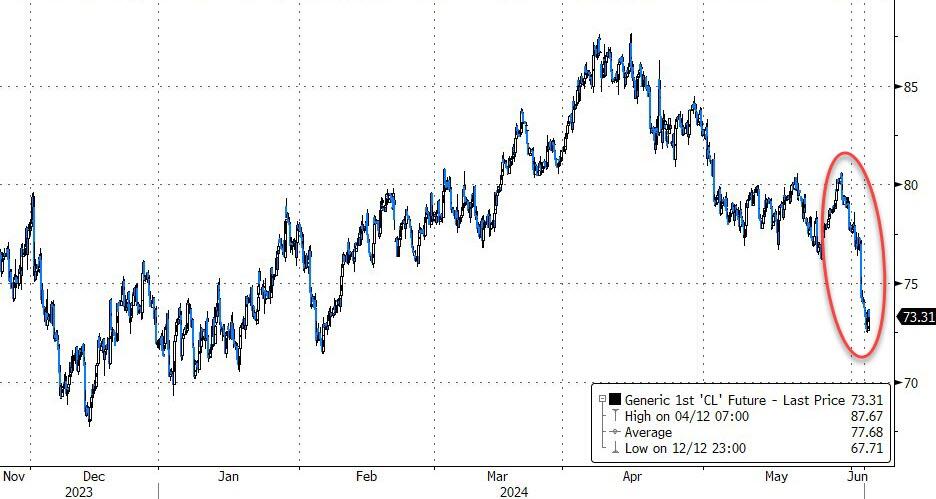

SHANGHAI CLOSED UP 12.71 PTS OR 0.41% //Hang Seng CLOSED UP 41.07 PTS OR 0.22%// Nikkei CLOSED DOWN 85.57 OR 0.22%//Australia’s all ordinaries CLOSED DOWN .31%///Chinese yuan (ONSHORE) closed UP TO 7,2394 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2456/ Oil DOWN TO 72.87 dollars per barrel for WTI and BRENT DOWN AT 77.03 /Stocks in Europe OPENED ALL RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 4,138 CONTRACTS TO 455,086 DESPITE OUR HUGE GAIN IN PRICE OF $22.45 WITH RESPECT TO MONDAY TRADING. WE HAD CONSIDERABLE T.A.S. LIQUIDATION ON MONDAY WITH ZERO LONGS BEING CLIPPED.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE.… THE CME REPORTS THAT THE BANKERS ISSUED A HUGE SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 4138 EFP CONTRACTS WERE ISSUED: : AUGUST 4138 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE:4138 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A TINY SIZED TOTAL OF 27 CONTRACTS IN THAT 4138 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A GOOD SIZED LOSS OF 4165 COMEX CONTRACTS..AND THIS SMALL LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR HUGE GAIN IN PRICE OF $22.45// MONDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT WAS A FAIR SIZED 1438 CONTRACTS. MOST OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. TODAY IS OF EXTREME IMPORTANCE TO OUR CROOKS IN YESTERDAY’S TRADING

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (88.712 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 88.712 TONNES. THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $22.45 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A TINY LOSS OF 27 CONTRACTS ON MONDAY WITH OUR TWO EXCHANGES DESPITE THE HUGE GAIN IN PRICE. THE T.A.S. ISSUED ON MONDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 0.6532 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE (89.804 TONNES) ON FIRST DAY NOTICE FOLLoWED BY TODAY’S QUEUE JUMP OF 128 CONTRACTS OR 12,800 OZ (0.398 TONNES)

NEW STANDING FOR JUNE: 88.712 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR HUGE GAIN IN PRICE TO THE TUNE OF $22.45

WE HAVE REMOVED 237 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET LOSS ON THE TWO EXCHANGES 27 CONTRACTS OR 2700 (0.0839 TONNES)

confirmed volume MONDAY 180,431 contracts// poor

//speculators have left the gold arena

JUNE 4 JUNE GOLD CONTRACT

/ /// THE JUNE 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | NIL oz . |

| Deposit to the Dealer Inventory in oz | 0 oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today | 620 notice(s) 62000 OZ 1.9284 TONNES |

| No of oz to be served (notices) | 1040 contracts 104,000 OZ 3.2348 TONNES |

| Total monthly oz gold served (contracts) so far this month | 27481 notices 2,748,100 oz 85.477 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: NIL oz

we have 0 customer deposit:

total deposit nil oz

total customer withdrawals: 0

TOTAL WITHDRAWALS nil 0z

Adjustments: 1

dealer to customer Brinks 4,843,932 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE

For the front month of JUNE we have an oi of 1660 contracts having LOST 5,319 contracts. We had 5447 contracts served on Monday so we gained 128 contracts or 12,800 oz additional oz will stand for gold at the comex as a queue jump.

JULY LOST 48 CONTRACTS TO STAND AT 2083

AUGUST GAINED 638 CONTRACTS UP TO 379,458 CONTRACTS

We had 620 contracts filed for today representing 62,000 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 620 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 329 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for June /2024. contract month, we take the total number of notices filed so far for the month (27,481) x 100 oz ) to which we add the difference between the open interest for the front month of JUNE (1660 CONTRACTS) minus the number of notices served upon today (620 x 100 oz per contract( equals 2,852,100 OZ OR 88.712 TONNES.

thus the INITIAL standings for gold for the JUNE contract month: No of notices filed so far (27,481 x 100 oz +we add the difference for front month of June (1660 OI} minus the number of notices served upon today (620) x 100 oz which equals 2,852,100 oz (88.712 TONNES)

TOTAL COMEX GOLD STANDING FOR JUNE: 88.712 TONNES WHICH IS ABSOLUTELY HUGE FOR THIS VERY ACTIVE DELIVERY MONTH IN THE CALENDAR. JUNE IS TRADITIONA;LLLY THE 2ND HIGHEST DELIVERY MONTH OF THE YEAR. FROM THIS POINT WE WILL GAIN IN GOLD TONNAGE WILLING TO STAND AT THE COMEX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX84XXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,558,487.369 48.47 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,673,584.310 OZ

TOTAL REGISTERED GOLD 7,968,033.348 ( 247.83 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,705,550.992 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,409 548 oz (REG GOLD- PLEDGED GOLD)= 199.36 tonnes //

END

SILVER/COMEX

JUN 4/2024

INITIAL

//2024// THE JUNE 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 583,936 473 oz cnt delaware . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 120 CONTRACT(S) (600,000 OZ) |

| No of oz to be served (notices) | 62 contracts (0.310 million oz) |

| Total monthly oz silver served (contracts) | 875 Contracts (4.575 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 0 deposits customer account:

total customer deposit nil oz

JPMorgan has a total silver weight: 128.167million oz/298.167 million or 42.95%

adjustment: 0//

Comex withdrawals: 0

total withdrawal: nil 0z

TOTAL REGISTERED SILVER: 62.494MILLION OZ//.TOTAL REG + ELIGIBLE. 298.167

million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE:

silver open interest data:

FRONT MONTH OF JUNE/2024 OI: 182 CONTRACTS HAVING GAINED 108 CONTRACT(S).

WE HAD 45 NOTICES SERVED UP ON MONDAY, SO WE GAINED 153 CONTRACTS OR AN ADDITIONAL 765,000 OZ WILL STAND AT THE COMEX VIA A QUEUE JUMP

JULY SAW A LOSS OF 911 CONTRACTS DOWN TO 136,718

AUG, SAW A GAIN OF 25 CONTRACTS TO 53

SEPT SAW A GAIN OF 1933 CONTRACTS TO 30,448.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 120 for 600,000 oz

CONFIRMED volume; ON MONDAY 93,525 huge

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 875 x 5,000 oz = 4.575 MILLION oz

to which we add the difference between the open interest for the front month of JUNE ((182) and the number of notices served upon today 120 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2024 contract month: 875 notices served so far) x 5000 oz + OI for the front month of JUNE (182)x number of notices served upon today minus (120)x 5000 oz of silver standing for the JUNE contract month equates to 4.685 MILLION OZ.

New total standing: 4.685 million oz.

There are 62.494 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

JUNE 4 WITH GOLD DOWN $20.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 3 WITH GOLD UP $22.85 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 31 WITH GOLD DOWN $19.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 30 WITH GOLD UP $3.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 29 WITH GOLD DOWN $13.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 28 WITH GOLD UP $22.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 832.21 TONNES

MAY 24 WITH GOLD DOWN $2.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 833.36 TONNES

MAY 23 WITH GOLD DOWN $53.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 22 WITH GOLD DOWN $32.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 21 WITH GOLD DOWN $12,00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 20 WITH GOLD UP $21.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.10 TONNES OF GOLD INTO THE GLD//NEW TOTAL 838.54 TONNES

MAY 17 WITH GOLD UP $31.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//NEW TOTAL 833.36 TONNES

MAY 16 WITH GOLD DOWN $7.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//NEW TOTAL 833.36 TONNES

MAY 15 WITH GOLD UP $34.90 ON THE DAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD/INVENTORY RISES TO 831.93 TONNES

MAY 14 WITH GOLD DOWN $17.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RISES TO 831.33 TONNES

MAY 13 WITH GOLD DOWN $31.10 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD////INVENTORY RISES TO 831.93 TONNES

MAY 10 WITH GOLD UP $34.65 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 9 WITH GOLD UP $18.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 8 WITH GOLD DOWN $0.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 830.47 TONNES

MAY 7 WITH GOLD DOWN $6.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 832.19 TONNES

MAY 6WITH GOLD UP $21.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .55 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 831.64 TONNES

MAY 2 WITH GOLD UP $0.20 ON THE DAY; SMAKK CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 830.47 TONNES

MAY 1 WITH GOLD UP $7.80 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNES

GLD INVENTORY: 832.21 TONNES, TONIGHTS TOTAL

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 4 WITH SILVER DOWN $1.08 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

JUNE 3 WITH SILVER UP $0.35 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

MAY 31 WITH SILVER DOWN $1.09 TODAY: HUGE CHANGES IN SILVER INVENTORY: A MASSIVE WITHDRAWAL OF 3.655 MILLION OZ FROM THE SLV//INVENTORY LOWERS TO 413.775 MILLION OZ

MAY 30 WITH SILVER DOWN $0.80 TODAY: NO CHANGES IN SILVER INVENTORY//INVENTORY REMAINS AT 417.430 MILLION OZ

MAY 29 WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 1.051 MILLION OZ INTO THE SLV//INVENTORY DECREASES TO 417.430 MILLION OZ

MAY 28 WITH SILVER UP $1.64 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 2.832 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 418.481 MILLION OZ

MAY 24 WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF .822 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 421.313 MILLION OZ

MAY 23 WITH SILVER DOWN $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.736 MILLION OZ FROM THE SLVINVENTORY INCREASES TO 420.491 MILLION OZ

MAY 22 WITH SILVER DOWN $0.66 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 21 WITH SILVER DOWN $0.41 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A DEPOSIT OF 3.792 MILLION OZ FROM THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 20 WITH SILVER UP $1.28 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 1.005 MILLION OZ FROM THE SLV// INVENTORY LOWERS TO 418.435 MILLION OZ

MAY 17 WITH SILVER UP $1.37 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 868,000 OZ FROM THE SLV// INVENTORY LOWERS TO 419.440 MILLION OZ

MAY 16 WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY REMAINS AT 420.308 MILLION OZ

MAY 15 WITH SILVER UP 101 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A WITHDRAWAL OF 1.919 MILLION OZ FROM THE SLV NVENTORY RESTS AT 420.308 MILLION OZ

MAY 14 WITH SILVER UP 25 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;INVENTORY RESTS AT 422.227 MILLION OZ

MAY 13 WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;NVENTORY RESTS AT 422.227 MILLION OZ

MAY 10 WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A HUGE WITHDRAWAL OF 1.,828 MILLION OZ//INVENTORY RESTS AT 422.227 MILLION OZ

MAY 9 WITH SILVER UP 78 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 8 WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 7WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 6 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.055 MILLION OZ

MAY 3 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 2WITH SILVER UP 0.12 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/ A WITHDRAWALOF 4.471 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 1 WITH SILVER UP 0.09 TODAY: SMALLCHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF ,457 MILLION OZ INTO THE SLV INVENTORY RESTS AT 429.814 MILLION OZ

CLOSING INVENTORY 413.775 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/GOLD AND SILVER COMMENTARY

END

3. CHRIS POWELL//GATA DISPATCHES

CHRIS POWELL…

Vietnam does its gold price rigging in the open, unlike ‘free market’ nations

Submitted by admin on Tue, 2024-06-04 12:15 Section: Daily Dispatches

Vietnamese Central Bank Moves to Lower Domestic Gold Prices

By Jimmy Choi

Central Banking, London

Monday, June 3, 2024

The State Bank of Vietnam started selling gold directly to four state-owned commercial banks today, aiming to lower the metal’s domestic price.

A senior SBV official recently said the domestic gold price may be affected by illicit factors, but an independent analyst cast doubt on this theory. The SBV will sell gold bars to the state-owned Saigon Jewelry Co. and lenders Agribank, Vietcombank, BIDV and VietinBank. The institutions will then sell the gold bars to the public.

The central bank will sell the bars, branded by the SJC, at 78.98 million dong ($3,107) a tael, which is equivalent to 37.5 grams. SJC gold bars dominate the domestic gold bullion market and have been considered national gold bars since the government monopolised their production since 2012.

The government tightly controls the supply of gold bars and gold trading. …

… For the remainder of the report:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS/

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT//

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

ASIA TRADING//TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED UP 12.71 PTS OR 0.41% //Hang Seng CLOSED UP 41.07 PTS OR 0.22%// Nikkei CLOSED DOWN 85.57 OR 0.22%//Australia’s all ordinaries CLOSED DOWN .31%///Chinese yuan (ONSHORE) closed UP TO 7,2394 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2456/ Oil DOWN TO 72.87 dollars per barrel for WTI and BRENT DOWN AT 77.03 /Stocks in Europe OPENED ALL RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2397

OFFSHORE YUAN: UP TO 7.2456

SHANGHAI CLOSED UP 12.71 PTS OR 0.41 %

HANG SENG CLOSED UP 41.07 PTS OR 0.22%

2. Nikkei closed DOWN 85.57 PTS OR 0.22 %

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 104.24 EURO FALLS TO 1.0866 DOWN 42 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.009 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 155.16 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.5570/Italian 10 Yr bond yield DOWN to 3.886 SPAIN 10 YR BOND YIELD DOWN TO 3.289%

3i Greek 10 year bond yield DOWN TO 3.590

3j Gold at $2327.55//Silver at: 29.77 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 24/ 100 roubles/dollar; ROUBLE AT 88.85

3m oil into the 72 dollar handle for WTI and 77 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 155.16/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.009% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8935 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9713 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.383 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.537 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.806 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.45…

10 YR UK BOND YIELD: 4.246 UP 2 PTS

2a New York OPENING REPORT

US Futures Slide As Oil Extends Plunge, India Stocks Tumble

TUESDAY, JUN 04, 2024 – 08:07 AM

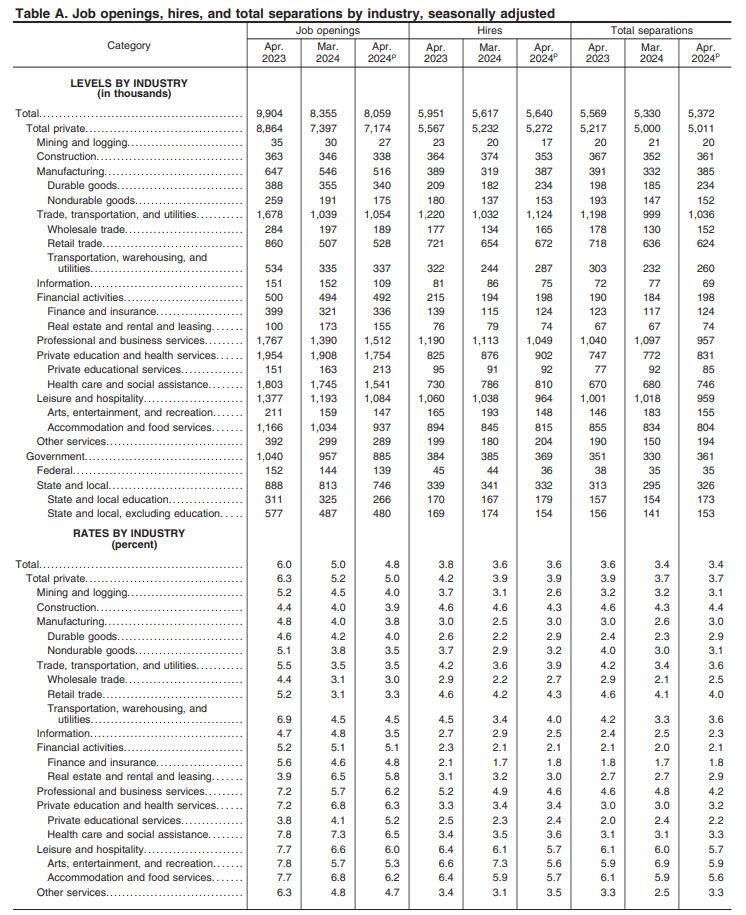

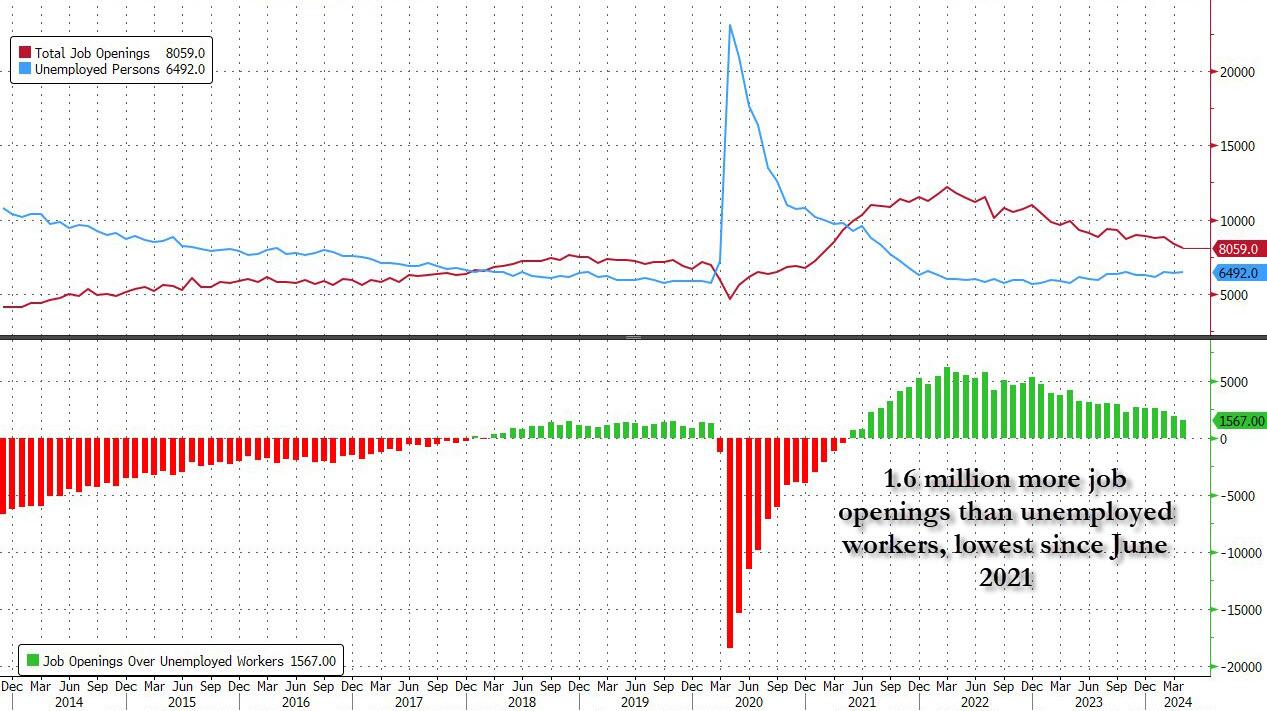

US stock futures are lower with tech and small-caps underperforming as oil extends its recent rout, bond yields are slightly lower and the USD catches a bid. As of 7:45am, S&P and Nasdaq futures are down 0.4%, as investors weigh concerns about America’s economic health against optimism that the Federal Reserve will cut rates in the fourth quarter, i.e. is “bad news bad news” again; meanwhile Indian stocks crashed the most in 4 years as election results showed a much closer results than exit polls predicted. Commodities are also getting hit again with this global risk-off tone though base metals and grains are bright spots. “What has changed overnight” asks JPMorgan’s trading desk and answers that it seems like some de-risking as investors await to see if macro data this week changes the narrative to one of a recession. After figures Monday showed that factory output came close to stagnating in May, while sent the 30-year Treasury yield held near 4.53%, the lowest level since May 23, attention is now turning to the latest JOLTS report which is forecast to indicate a monthly drop in job openings; we also get final readings for Cap Goods/Durable Goods. More important will be tomorrow’s ISM-Services data and Friday’s NFP.

In premarket trading, the Mag7 stocks are all lower by up to 78bps and Semis are weaker ex-INTC. KO, PEP, SBUX, ITW, WMT, and BMY are notable outperformers pre-mkt. Here are all the other premarket movers:

- Annexon jumps 25% after saying its phase 3 trial of blocking antibody Anx005 in Guillain-Barre Syndrome met its primary endpoint.

- Core Scientific surges 40% after the Bitcoin miner signed 12-year contracts with AI startup CoreWeave.

- FibroGen rises 12% after the pharmaceutical company entered a clinical trial supply agreement with Regeneron.

- GitLab declines 2% after the application software company’s revenue forecast for the second quarter came in weaker than anticipated.

- HealthEquity gains 5% after the company raised its full-year forecast and reported forecast-beating first-quarter results.

- Intel advances 1.6% after CEO Pat Gelsinger took the stage at the Computex show in Taiwan to talk about new products he expects will help turn back the tide of share losses to peers, including AI leader Nvidia.

- Viking Therapeutics rises 7% after saying its experimental liver disease drug VK2809 met its Phase 2b second

“At some point weak data should become bad news for risky assets, but we would argue that some point is a few weeks or a couple of months away,” Mohit Kumar, chief strategist for Europe at Jefferies, wrote in a note to clients. “We still remain long risky assets. Initially weaker data could be interpreted as good for risky assets as it increases the probability of a Fed cut.”

Swap contracts tied to upcoming Fed meetings continue to fully price in a quarter-point rate cut in December, with the odds of a move as soon as September edging up to around 50% and November also given high odds. Later Tuesday, economists expect figures to show a third consecutive monthly drop in US job openings, while Friday’s payroll numbers loom as crucial in the search for clues about the outlook for the world’s No. 1 economy and interest rates.

Meanwhile, oil extended losses from its lowest settlement in almost four months after OPEC+’s plan to return barrels to the market earlier than expected raised concerns about oversupply. Brent fell below $78 a barrel after the August contract tumbled 3.4% on Monday, while West Texas Intermediate was under $74. The move also hurt the shares of supermajors, with BP and TotalEnergies dropping more than 2%

Elsewhere, Indian stocks plummeted, erasing $386 billion in market value, as tallies signaled that Prime Minister Narendra Modi’s ruling party was struggling to win a majority of seats in national elections, a stunning result after exit polls showed he was on pace for a landslide victory. The NSE Nifty 50 Index tumbled as much as 8.5% in Mumbai, the biggest intra-day drop in more than four years, while the rupee and sovereign bonds also fell.

European shares also declined, led lower by banking and oil stocks as crude prices fall for a fifth consecutive session while health care and food beverage stocks lead outperformers. BP Plc and TotalEnergies SE dropped at least 3%, dragging Europe’s Stoxx 600 Index down 0.7%. Here are the biggest movers Tuesday:

- Maersk shares climb as much as 3.7% after the Danish shipping giant boosted its guidance. Nordea says the market may not be “fully cognizant” of the company’s earnings potential in 2024

- Klepierre advances as much as 2.8%, hitting highest since March 2020, after Citi double-upgrades to buy, saying that rental and cyclical prospects now look positive for the French property management company

- Burckhardt Compression shares jump as much as 7.3%, the most since May 2023, to hit a record high after the world’s largest piston compressor manufacturer exceeded FY consensus expectations

- Ceres Power shares jump as much as 6.5% after the fuel cell technology company was awarded a further contract for the second phase of its collaboration with Shell on green hydrogen

- Nibe falls as much as 7.4%, the most since May 17, and Tuesday’s worst performer on the Stoxx 600 regional benchmark, after Barclays cut its recommendation on the Swedish heat-pump firm to underweight from equal weight

- Allianz falls as much as 3.6% on Tuesday after Citi cuts its recommendation on the German insurer to neutral from buy, with analysts saying that Generali and Axa have greater capital optionality on a 3-year view that is expected to be at least partly realized

- British American Tobacco shares slip as much as 1.8%, the most in over two months, after the company’s trading update showed it is “on track” to deliver FY24 guidance, but with revenue growth weighted to the latter half of the year

- DS Smith, falls as much as 1.9% after Bloomberg News reported that Brazilian pulp producer Suzano is working on a revised offer to buy International Paper, a deal that would threaten to derail International Paper’s plan to acquire DS Smith

- Shelf Drilling declines as much as 7.3%, the most in two months, after announcing that the Norwegian Ocean Industry Authority did not accept its application related to a jack-up rig

- Chemring Group shares fall as much as 3.2%, easing further away from recent 12-year highs, as analysts greeted the defense firm’s reiterated guidance and its target of generating £1b in annual revenue by 2030

In Europe, strong economic data and vocal ECB hawks are pushing some analysts and investors to waver in their expectations for rate cuts this year. While most economists still foresee quarterly reductions following an initial move this week, some reckon sticky inflation, rapid wage growth and surprisingly robust euro-zone output will constrain loosening. The region’s equities are still in line for a boost from rate cuts and an improving corporate earnings outlook, according to Citigroup Inc. strategists led by Beata Manthey. If rates settle at pre-global financial crisis levels — as expected by the bank’s economists — that would be a longer-lasting tailwind for stocks, according to the Citi team.

Earlier, Asian stocks declined after weak US manufacturing data triggered concerns of slowing growth in the world’s largest economy. Indian shares led losses as signs emerged that Narendra Modi’s party may secure a narrower victory in India’s elections than previously expected. The MSCI Asia Pacific Index fell as much as 1.4%, with India’s Reliance among the biggest drags along with TSMC and ICICI Bank. Declines were also notable in the Philippines and Taiwan, while benchmarks gained in Indonesia and mainland China. Fears of slower growth in the US set in after data that showed American factory activity shrank at a faster pace in May. While the soft numbers helped revive bets on Federal Reserve policy easing, it also raised concerns about the potential drag on Asian economies.

Key Indian equity gauges fell more than 8% before paring losses. They rose more than 3% Monday on hopes for a landslide win for the Modi-led Bharatiya Janata Party. A stronger majority for the party is seen helping the prime minister push through market reforms.

“After the sharp run-up some profit booking is also expected,” said Kranthi Bathini, a strategist at WealthMills Securities. “While not many investors are expecting a defeat for the BJP-led alliance, if the ruling party gets significantly less seats than initially expected, we may see a sharp reversal.”

In FX, the Bloomberg Dollar Spot Index rises 0.2%. The Norwegian krone, Australian dollar and Swedish krona led Group-of-10 losses on sapped risk appetite, after Monday’s US ISM data showed signs the US economy is cooling. The Japanese yen is the best performer among the G-10 currencies, rising 0.5% against the greenback. USD/JPY dropped as much as 0.7% to 155.04, the lowest level since mid-May after Bloomberg reported that the BOJ is likely to discuss the reduction of bond purchases as early as its policy meeting next week (which doesn’t mean it will actually8 do anything). The Swiss franc edges higher after inflation held at its fastest pace this year. EUR/CHF fell as much as 0.5% to 0.97223, the lowest level since April 23; Swiss inflation held at its fastest pace this year, eroding the case for an SNB interest-rate cut when officials meet later this month

In rates, treasuries reversed earlier losses, with US 10-year yields dropping to 4.38% as traders awaited US JOLTS data for an indication of the health of the labor market. Treasuries were slightly richer across the curve supported by bigger gains for European bonds where German 10-year yields are more than 2bp lower on the day. Yields are less than 1bp richer on the day with 10-year around 4.39%, lagging bunds and gilts by 2.5bp and 1.5bp; curve spreads are likewise within 1bp of Monday’s close while in Europe, gilt curve is notably flatter as front-end lags. In front-end, Fed-dated OIS have resumed fully pricing in a 25bp rate cut in November. Fed swaps continue to shift back toward pricing in rate cuts this year, with 25bp of easing priced by November and 42bp for December FOMC vs 34bp at Friday’s close

In commodities, WTI is down 2.2%, trading near $72.60 a barrel. Spot gold falls ~$21 to around $2,329/oz.

US economic data includes April JOLTS job openings and factory orders and April revised durable goods orders (10am). Fed officials are expected to refrain from commenting until after their June 12 policy announcement

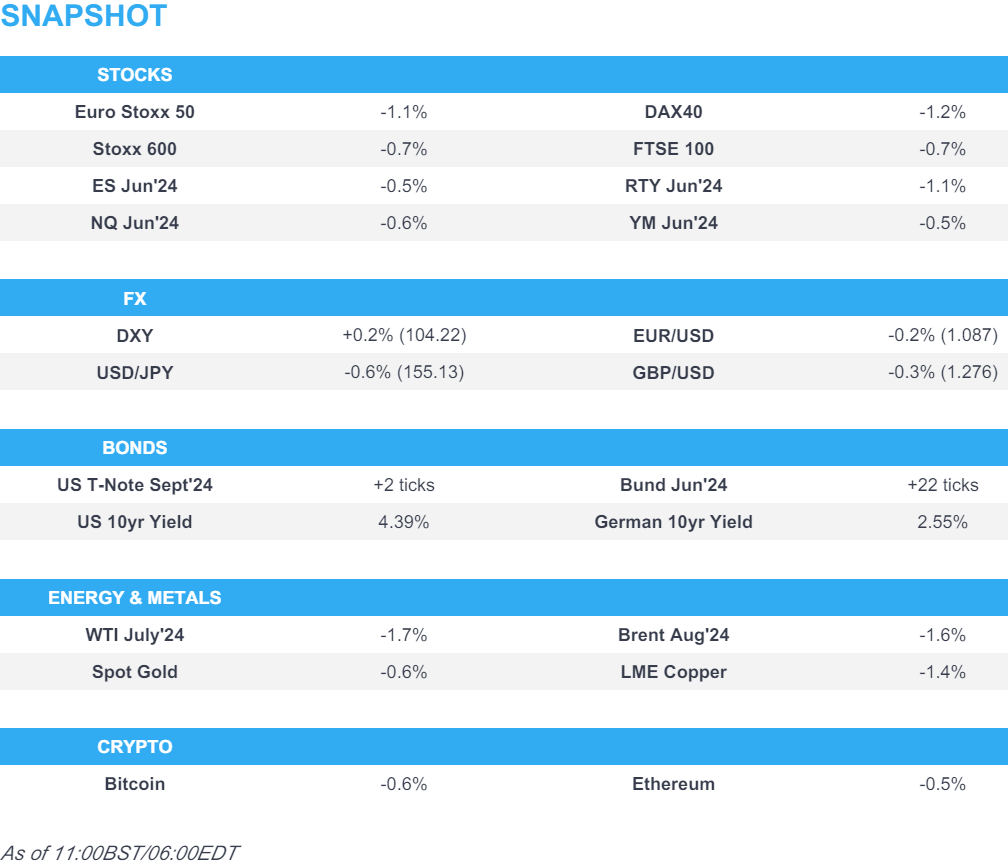

Market Snapshot

- S&P 500 futures down 0.3% to 5,280.75

- STOXX Europe 600 down 0.5% to 517.01

- MXAP down 0.7% to 178.90

- MXAPJ down 1.2% to 552.34

- Nikkei down 0.2% to 38,837.46

- Topix down 0.4% to 2,787.48

- Hang Seng Index up 0.2% to 18,444.11

- Shanghai Composite up 0.4% to 3,091.20

- Sensex down 4.7% to 72,887.88

- Australia S&P/ASX 200 down 0.3% to 7,737.06

- Kospi down 0.8% to 2,662.10

- German 10Y yield little changed at 2.55%

- Euro down 0.2% to $1.0880

- Brent Futures down 1.2% to $77.44/bbl

- Gold spot down 0.6% to $2,335.75

- US Dollar Index little changed at 104.22

Top Overnight News

- European stocks slipped, led by a tumble in energy stocks, while Treasuries steadied after Monday’s rally prompted by signs the US economy is cooling.

- The Bank of Japan is likely to discuss the reduction of bond purchases as early as its policy meeting next week, according to people familiar with the matter.

- German unemployment rose more than anticipated — underscoring expectations that Europe’s biggest economy will recover only gradually this year.

- Japan’s finance minister defended the government’s record intervention in the currency market in his first acknowledgment of the action.

- Strong economic data and vocal European Central Bank hawks are pushing some analysts and investors to waver in their expectations for interest-rate cuts this year.

- Swiss inflation held at its fastest pace this year, eroding the case for a Swiss National Bank interest-rate cut when officials meet later this month.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed following a similar performance from Wall Street in the absence of any fresh overnight catalysts, with the tone tilting lower towards the end of the session. ASX 200 saw losses in the energy sector being countered by gains among gold names. Nikkei 225 was the regional laggard with losses among energy names, whilst autos slipped after a safety test scandal among some Japanese automakers widened on Monday, with Toyota Motor and Mazda both halting shipments of some vehicles. Hang Seng and Shanghai Comp were mixed with modest gains in the former amid upside in healthcare and properties, whilst the Mainland was flat/slightly softer albeit within tight ranges. India’s Nifty 50 slipped as election results are being counted and PM Modi’s lead fluctuated, with early weakness in Indian markets attributed to a narrowing lead.

Top Asian News

- BoJ Gov Ueda said if underlying inflation moves as BoJ projects, BoJ will adjust the degree of monetary support. If economic and price projections and assessment of risks change, that will also be a reason to change interest rate levels. The policy goal is price stability, so will not guide policy to fund fiscal spending. The basic stance is to allow markets to set long-term interest rates. Ready to conduct nimble market operations if there are sharp rises in long-term rates.

- Japanese Finance Minister Suzuki said forex intervention had certain effects; intervention was intended to respond to speculative moves; will continue to respond appropriately

- Japan’s economy is recovering moderately but consumption is stalling, and wages are not rising enough to offset rising prices, according to a draft roadmap; Japan’s govt to call on the need for vigilance to impact of weak yen on households’ purchasing power in long-term.

- Japanese PM Kishida not to call a snap election during the current parliament session, according to Asahi newspaper.

- ANZ-Roy Morgan Australian Consumer Confidence changed little, increasing 0.3pts to 80.5pts. Overall confidence is very weak. The series has been below neutral for over 2yrs. Inflation expectations rose 0.1pts to 5.0%.

- The Bank of Korea said inflation is expected to ease gradually as projected in May.

- PBoC injected CNY 2bln via 7-day reverse repos with the rate at 1.80%.

- TSMC (2330 TT/TSM) said they have had conversations with customers about whether to move TSMC’s fabs out of Taiwan amid China tensions; added it is impossible to move TSMC’s fabs out of Taiwan as 80%-90% of production capacity is in Taiwan.

- BoJ’s Himino says firms will likely have more freedom in setting prices flexibly when prices and wages are rising moderately in tandem. In economy facing effect zero lower bound, asset price moves such as FX, stocks and property prices are likely to serve as key transmission channel of monpol. Guiding monpol to attain a situation where underlying inflation moves to around 2%; several measures have underlying inflation short of this figure, but gradually accelerating towards it. Need to look at price data and various factors such as wages and firm activity when judging underlying inflation. Inappropriate for monetary policy to target FX. FX fluctuations have various impacts, not just through import costs but on activity as well. Must be very vigilant to FX action. Must look at various aspects in guiding policy, should not automatically respond to FX moves in setting rates. Need to consider the whole economy and prices when considering what to do with the balance sheet. Desirable for market forces to set long-term rates. Must avoid abrupt bond market moves.

- BoJ is said to mull reducing bond buys as early as the June meeting, via Bloomberg.

European bourses, Stoxx 600 (-0.5%) began the session modestly in the red and have continued to slip throughout the morning as post-ISM demand concerns weigh alongside a marked deterioration in India’s performance (NIFTY 50 -5.9%) as the ongoing vote count for Modi is much less favourable than the exit poll implied. European sectors hold a strong negative bias; Energy and Basic Resources are found at the foot of the pile, given the broad weakness in the commodities complex. Banks are also weighed on by the relatively lower yield environment. US Equity Futures (ES -0.6%, NQ -0.6%, RTY -1.1%) are entirely in the red, conforming to the sentiment seen in Europe/India. Nvidia (-0.8%) is softer in the pre-market after reports that the TSMC new Chair has hinted that the Co. could increase the price of AI chip production services.

Top European News

- Airbus (AIR FP) is reportedly in discussions to sell over 100 widebody jets to China, via Bloomberg

FX

- DXY is attempting to claw back some of yesterday’s ISM-induced losses which sent the index down as low as 103.99 during APAC trade. Interim resistance is provided by the 200DMA at 104.39 and 100DMA at 104.40. Next up, US JOLTS.

- EUR/USD ventured as high as 1.0915 during APAC trade but the pair’s move above 1.09 proved to be short-lived, and currently holds around 1.087.

- GBP is on the backfoot vs. the USD and steady vs. the EUR. Cable went as high as 1.2817 in APAC trade in an extension of yesterday’s price action before succumbing to broader Dollar strength, taking the pair back down to c.1.276.

- JPY is benefitting vs. peers amid its safe-haven appeal, narrowing yield differentials and jawboning from various Japanese officials. USD/JPY down as low as 155.21 with not much in the way of support ahead of the 155 figure.

- Antipodeans are both suffering in the current risk environment but AUD more so alongside declines in iron ore prices and ANZ suggesting that Australian consumer confidence remains weak.

- EUR/CHF was initially slightly choppy following Swiss inflation metrics before lifting from 0.9744 to 0.9781 over the course of five minutes. The odds of a 25bp cut at the June meeting have increased to circa. 51% from around 40% earlier in the week. Move has since pared given haven allure for CHF.

- INR is pressured amid some concern over the results of the Indian elections, as while the BJP-led NDA alliance is ahead and on course for victory the margin of result looks to be much less than initial exit polls had suggested and potentially indicative of BJP alone not hitting the 272 simple majority level as they have previously done.

- Reuters reports that the RBI is likely on offer near 83.50 in USD/INR via state-run banks, citing traders; offers described as “mild”.

- PBoC set USD/CNY mid-point at 7.1083 vs exp. 7.2297 (prev. 7.1086)

- Brazil’s Finance Ministry to announce fiscal measures on Tuesday, according to a statement cited by Reuters.

Fixed Income

- USTs are firmer and continue to extend on the the post-ISM upside, with additional bullishness stemming from a well received JGB sale overnight and the general risk tone. Since, Bloomberg reported that the BoJ is said to mull bond buys as early as the June meeting, sparking some modest pressure across the fixed income complex; as such, USTs are off best levels but still in the green.

- Bunds are in-fitting with Treasury action; German employment data led to very modest upside due to the higher-than-expected unemployment change. Bunds as high as 130.48, just about above last Tuesday’s best, though has since pulled off best.

- Gilts are tracking the broader tone and as such entered the morning’s auction with upside of almost 40 ticks. An auction which sparked a pullback of around 10 ticks given the chunky tail but still leaves Gilts comfortably in the green and broadly in-fitting with peers.

- UK sells GBP 2bln 4.00% 2063 Gilt: b/c 3.10 (prev. 2.92x), average yield 4.557% (prev. 4.518%), tail 1.3bps (prev. 0.6bps)

- Germany sells EUR 3.689bln vs exp. EUR 4.5bln 2.90% 2026 Schatz: b/c 2.7x (prev. 2.5x) & avg. yield 3.01% (prev. 2.93%) and retention 18.02% (prev. 18.00%)

- Saudi’s PIF gives initial price guidance of circa. Gilts +135bps for its GBP 5yr note and Gilts +145bps for GBP 15yr notes, via IFR

- Japan sold JPY 2.6tln in 10-year JGB, b/c 3.66x (prev. 3.15x), average yield 1.048% (prev. 0.857%), tail 0.02 (prev. 0.05).

Commodities

- Crude continues to slump following the OPEC+ ‘roadmap’ and the growth concerns triggers by Monday’s US ISM Manufacturing print. Benchmarks at lows of USD 72.63/bbl and 76.89/bbl for WTI Jul’24 and Brent Aug’24 respectively.

- Nat gas futures were initially only taking a breather from Monday’s marked upside after issues to a Norwegian-Britain pipeline. Thereafter, more significant pressure emerged as Gassco announced that the work to repair the crack is a matter of days not weeks.

- Precious metals have come under increasing pressure as the European morning progresses; specifics light, although Dollar has been edging higher in today’s session.

- Base metals are also suffering on the demand angle post-PMIs, USD strength and a deterioration in the broader risk tone driven by India alongside negative updates regarding Nvidia.

- Coalition of over 400 Japanese firms is poised to set up a USD 1bln fund as early as the fiscal half ending Sept to boost hydrogen supply chains, according to Nikkei.

- HSBC said their Brent price assumption remains USD 82/bbl for 2024, including USD 80/bbl in H2 2024, falling to USD 76.50/bbl from 2025 onwards.

- UBS on OPEC+ announcements: Expects some near-term volatility on supply concerns, but retains modestly positive outlook for crude prices; says “does not think plan to unwind output cuts will tilt markets into oversupply”. Expects Brent to trade around USD 87/bbl at year-end.

- Gassco says we have received a repair schedule from the operator of the Sleipner riser platform and is expected to take 2 days to repair; repairs may take longer than 2 days or could go faster; not a matter of weeks to repair

- Chevron Australia confirms full LNG production has resumed at the Gorgon gas facility after a temporary outage on Monday, 3rd June, according to a spokesperson.

Geopolitics

- “A Hamas official told Al-Mayadeen that no delegation from the group went to Cairo, and that it did not accept what was offered by the mediators”, via Guy Elster on X

- “Media close to Hezbollah: Diplomatic letters have arrived in Beirut in recent days warning of the threat of an imminent Israeli strike”, according to Sky News Arabia

- “Major differences between Israel and the United States over the second phase of the truce deal”, according to Sky News Arabia quoting an Israeli official cited by local press.

- Hamas is slated to send a delegation to Cairo today to discuss the latest Israeli hostage deal proposal, according to Times of Israel sources.

- “Lebanese media: Renewed fires in the forests of several border towns in southern Lebanon as a result of the throwing of Israeli phosphorus bombs”, according to Sky News Arabia.

- Israeli PM Netanyahu’s office said “No date has yet been set for Prime Minister Netanyahu’s speech to both houses of Congress. In any case, the speech will not take place on June 13 due to the second holiday of Shavuot”.

- UK, France and Germany have formally submitted a draft resolution against Iran to the IAEA Board of Governors, according to Reuters citing diplomats.

US Event Calendar

- 10:00: April Cap Goods Ship Nondef Ex Air, prior 0.4%

- 10:00: April Cap Goods Orders Nondef Ex Air, est. 0.3%, prior 0.3%

- 10:00: April -Less Transportation, est. 0.4%, prior 0.4%

- 10:00: April JOLTs Job Openings, est. 8.35m, prior 8.49m

- 10:00: April Factory Orders Ex Trans, est. 0.5%, prior 0.5%, revised 0.4%

- 10:00: April Factory Orders, est. 0.6%, prior 1.6%, revised 0.8%

- 10:00: April Durable Goods Orders, est. 0.7%, prior 0.7%

DB’s Jim Reid concludes the overnight wrap

Over the last week we’ve had three sessions now where for a lot of the day weaker economic news has meant bad news for markets rather than bad news automatically being good news due to more dovish rate expectations. However in the last two sessions the pullback has failed to stick before dip buyers have come in. Yesterday, the rates market saw a major rally after the ISM manufacturing print was noticeably weaker than expected. That led to a fresh round of anticipation that the Fed would still cut rates this year, and it meant the 10yr Treasury yield (-11.1bps) fell for a 3rd consecutive day to 4.39%, whilst the 10yr bund yield was down a slightly lesser -8.4bps. The S&P 500 gained +0.11% after being down -0.8% at its lows.

In terms of the details of that manufacturing ISM print, the headline measure fell back to 48.7 (vs. 49.5 expected), marking a second consecutive decline for the measure. But importantly, the new orders subcomponent also fell to a 12-month low of 45.4 (vs. 49.4 expected), so there was little respite from the details either. The one bright spot came from the employment numbers, which did hit a 21-month high of 51.1 (vs. 48.5 expected). But apart from that, the report was definitely one that dampened optimism about the state of the US economy right now. And it follows a run of weaker US data over recent days, including the spending data on Friday and the negative Q1 GDP revisions on Thursday.

Given the worse-than-expected numbers, investors dialled up their expectations for rate cuts this year. For example, the amount priced in by the Fed’s December meeting rose by +5.1bps on the day to 41.4bps. That trend got further support from the prices paid component of the ISM, which fell to 57.0 (vs. 59.0 expected), so it added to the sense that the worst of the recent inflation spike had now passed.

Whilst the ISM was the main catalyst for yesterday’s moves, they got fresh momentum thanks to the latest decline in oil prices, as Brent crude closed beneath $80/bbl for the first time since February. In fact, it was its 4th consecutive daily decline, and the move yesterday left it down by -4.26% at $78.14/bbl. Oil had largely ignored the OPEC+ meeting on Sunday but started selling off sharply half an hour before the US data prints but then seemed to accelerate through the ISM. The initial move lower coincided with the timing of news that Israeli Prime Minister Netanyahu would meet with more right-wing members of his coalition on the current cease-fire proposal, with the market potentially giving the current negotiations more credence. The drop helped to further ease fears about inflationary pressures, and added to the sense that rate cuts were getting closer. Indeed, that rate cut theme is something we could hear a lot more about by the end of the week, as we’ve got the Bank of Canada’s decision tomorrow, followed by the ECB on Thursday.

With rate cut speculation mounting again, sovereign bonds rallied strongly across the world. In the US, it meant the 2yr Treasury yield fell -6.5bps to 4.808%, whilst the 10yr yield was down -11.0bps to 4.388%. That’s the biggest move lower in 10yr yields since January 31st and same with the combined 3-day move (-22.3bps lower). Over in Europe, yields on 10yr bunds (-8.4bps), OATs (-8.4bps) and BTPs (-9.5bps) also fell back, which came as the final manufacturing PMIs for May were revised marginally weaker than the flash prints. For instance, the Euro Area manufacturing PMI was revised down a tenth from the flash print to 47.3, and the UK number was also revised down a tenth from the flash print to 51.2.

For equities, the second half of the US session proved much more optimistic than the first, with the S&P 500 (+0.11%) eventually, after a big struggle, reacting more to the rate cut hopes than the weak growth data. The last three hours of trading in New York saw a +0.94% rally reverse the earlier losses. The rally was built on strong outperformance from the Magnificent 7 (+1.40%) and growth sectors that enjoy lower rates such as semiconductors (+2.4%), biotech (+1.1%), and tech (+0.6%), while energy (-2.6%) saw heavy losses on the move in oil and cyclicals like industrials (-1.3%) and materials (-0.6%) were unable to shake off the weaker growth backdrop. Europe outperformed with the STOXX 600 (+0.32%) advancing for a third consecutive session, alongside the DAX (+0.60%) with the CAC 40 just better than unchanged (+0.06%).

Asian equity markets are struggling to gain momentum this morning though with the KOSPI (-0.46%), Nikkei (-0.45%) and the S&P/ASX 200 (-0.22%) edging lower this morning while Chinese stocks have managed to tick up with the Hang Seng (+0.36%) and the CSI (+0.38%) eking out gains. US stock futures are fairly flat with 10yr US yields back up a couple of bps to 4.41%.

Japan’s Finance minister Shunichi Suzuki has admitted in an overnight speech that the government did intervene in the FX market in late April and early May. He suggested that it likely had some impact in stabilising the currency after the authorities on Friday disclosed that it spent 9.8 trillion yen ($62.7 billion) intervening in the market to prop up the yen. The yen is -0.20% to trade at 156.40 per dollar as we go to print.

In India, early election counting has hinted at a less substantial win for Modi’s ruling alliance than the exit polls suggested on Sunday night. After climbing more than 3% yesterday, Indian stocks have dropped around 2% this morning in early trading. We’ll have a lot more info as the count progresses today.

Here in the UK, the general election is now exactly a month away, and there was significant news yesterday as Nigel Farage announced that he would become leader of the right-wing Reform UK party. Farage was previously the leader of UKIP for many years, and played a significant role in the Brexit campaign of 2016. He previously said that he wouldn’t stand for Parliament at this election, but reversed course yesterday and said he’d be standing in the Essex seat of Clacton, which was the only seat won by UKIP in the 2015 general election. This could pose a big problem for the governing Conservatives, since if they lose votes to Reform in key seats, it would mean that the opposition Labour Party are able to win many more seats. In terms of the latest polls (taken before Farage’s announcement), the latest seat projection from YouGov suggests that Labour will win a majority of 194, taking 422 seats in the House of Commons. That would exceed their landslide victory in 1997 under Tony Blair. In the meantime, the Conservatives would fall back to just 140 seats, down from 365 at the 2019 election.

To the day ahead now, and data releases include German unemployment for May, whilst in the US there’s the JOLTS job openings and factory orders for April.

2B EUROPE OPENING/TRADING

Risk sentiment pressured and benefiting havens ex-precious metals; US JOLTS due – Newsquawk US Market Open

TUESDAY, JUN 04, 2024 – 06:09 AM

- Risk sentiment generally pressured to the benefit of havens ex-precious metals as the latest bearish driver stems from India’s election count

- Equities are entirely in the red; Energy and Basic Resources are the clear laggards, given the underperformance in the underlying commodity prices

- Dollar is firmer and attempting to claw back post-ISM losses, JPY bid with USD/JPY nearing 155, AUD slips given the risk sentiment

- Bonds are firmer in continuation of the prior day’s gains, though now off best levels following source reports relating to the BoJ’s bond buys

- Crude continues to slip, XAU and base metals suffer from USD strength, risk tone & India’s performance

- Looking ahead, US Durable Goods R, US JOLTS, US RCM/TIPP Economic Optimism Supply, UK election debate

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses, Stoxx 600 (-0.5%) began the session modestly in the red and have continued to slip throughout the morning as post-ISM demand concerns weigh alongside a marked deterioration in India’s performance (NIFTY 50 -5.9%) as the ongoing vote count for Modi is much less favourable than the exit poll implied.

- European sectors hold a strong negative bias; Energy and Basic Resources are found at the foot of the pile, given the broad weakness in the commodities complex. Banks are also weighed on by the relatively lower yield environment.

- US Equity Futures (ES -0.6%, NQ -0.6%, RTY -1.1%) are entirely in the red, conforming to the sentiment seen in Europe/India. Nvidia (-0.8%) is softer in the pre-market after reports that the TSMC new Chair has hinted that the Co. could increase the price of AI chip production services.

- Click here for the sessions European pre-market equity newsflow and here for additional news.

- Click here for more details.

FX

- DXY is attempting to claw back some of yesterday’s ISM-induced losses which sent the index down as low as 103.99 during APAC trade. Interim resistance is provided by the 200DMA at 104.39 and 100DMA at 104.40. Next up, US JOLTS.

- EUR/USD ventured as high as 1.0915 during APAC trade but the pair’s move above 1.09 proved to be short-lived, and currently holds around 1.087.

- GBP is on the backfoot vs. the USD and steady vs. the EUR. Cable went as high as 1.2817 in APAC trade in an extension of yesterday’s price action before succumbing to broader Dollar strength, taking the pair back down to c.1.276.

- JPY is benefitting vs. peers amid its safe-haven appeal, narrowing yield differentials and jawboning from various Japanese officials. USD/JPY down as low as 155.21 with not much in the way of support ahead of the 155 figure.

- Antipodeans are both suffering in the current risk environment but AUD more so alongside declines in iron ore prices and ANZ suggesting that Australian consumer confidence remains weak.

- EUR/CHF was initially slightly choppy following Swiss inflation metrics before lifting from 0.9744 to 0.9781 over the course of five minutes. The odds of a 25bp cut at the June meeting have increased to circa. 51% from around 40% earlier in the week. Move has since pared given haven allure for CHF.

- INR is pressured amid some concern over the results of the Indian elections, as while the BJP-led NDA alliance is ahead and on course for victory the margin of result looks to be much less than initial exit polls had suggested and potentially indicative of BJP alone not hitting the 272 simple majority level as they have previously done.

- Reuters reports that the RBI is likely on offer near 83.50 in USD/INR via state-run banks, citing traders; offers described as “mild”.

- PBoC set USD/CNY mid-point at 7.1083 vs exp. 7.2297 (prev. 7.1086)

- Brazil’s Finance Ministry to announce fiscal measures on Tuesday, according to a statement cited by Reuters.

- Click here for more details.

- Click here for OpEx details.

FIXED INCOME