GOLD PRICE CLOSED UP $32.75 TO $2355.40

SILVER PRICE UP 0.38 TO $29.96

Gold ACCESS CLOSED $2353.90

Silver ACCESS CLOSED: $29.98

Bitcoin morning price:$70,785 UP 198 DOLLARS.

Bitcoin: afternoon price: $71,211 up 1050 dollars

Platinum price closing UP $0.50 TO $996.40

Palladium price; UP $13.45 AT $933.15

END

SHANGHAI GOLD PREMIUM 35 DOLLARS/COMEX GOLD

SHANGHAI GOLD

SHANGHAI GOLD (USD) FUTURES – QUOTES

Last Updated 05 Jun 2024 06:24:51 AM CT.

Market data is delayed by at least 10 minutes.

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $3222.09 UP 37.17 CDN dollars per oz( * NEW ALL TIME HIGH 3,305.30 CDN DOLLARS PER OZ//MAY 20 2024)

*BRITISH GOLD: 1840,25 UP 17.14 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2165.25 UP 25.17 Euros per oz //* (ALL TIME CLOSING HIGH: 2248.89 EUROS PER OZ//APRIL 16.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCH: COMEX

EXCHANGE: COMEX

CONTRACT: JUNE 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,325.500000000 USD

INTENT DATE: 06/04/2024 DELIVERY DATE: 06/06/2024

FIRM ORG FIRM NAME ISSUED STOPPED

099 H DB AG 42

323 C HSBC 1

363 H WELLS FARGO SEC 4

435 H SCOTIA CAPITAL 21

657 C MORGAN STANLEY 9

661 C JP MORGAN 76

661 H JP MORGAN 113

686 C STONEX FINANCIA 11

686 H STONEX FINANCIA 40

690 C ABN AMRO 42 6

732 C RBC CAP MARKETS 5

737 C ADVANTAGE 1

880 H CITIGROUP 379 121

905 C ADM 3

TOTAL: 437 437

MONTH TO DATE: 27,918

JPMorgan stopped 113/437

FOR JUNE 2024

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2024. CONTRACT: 437 NOTICES FOR 43,700 OZ or 1.3592 TONNES

total notices so far: 27,918 contracts for 2,791,800 Oz (86.876 tonnes)

FOR JUNE:

SILVER NOTICES: 30 NOTICE(S) FILED FOR 150,000 OZ/

total number of notices filed so far this month : 905 for 4.525 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $32.75

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

NO CHANGES IN GOLD INVENTORY AT THE GLD:

/ /INVENTORY RESTS AT 832.21TONNES

INVENTORY RESTS AT 832.21 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER UP $0.38 AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.52 MILLION OZ INTO THE SLV

// INVENTORY INCREASES TO 415.295 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 415.295 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 2044 CONTRACTS TO 179,854 AND STALLING ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR LOSS OF $1.08 IN SILVER PRICING AT THE COMEX ON TUESDAY’S TRADING ON SILVER. WE HAD SOME LONG LIQUIDATION AS WE HAD A NET LOSS OF 711 CONTRACTS ON OUR TWO EXCHANGES. WE, AGAIN HAD SHORT COVERING BY OUR SPECS WITH THE LOSS IN PRICE AS WELL AS MASSIVE T.A.S. LIQUIDATION. WE HAD ANOTHER MEGA– HUGE SIZED 1719 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS IN YESTERDAY

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 1719 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND TODAY;S TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $1.08) AND WERE UNSUCCESSFUL IN KNOCKING SOME SILVER LONGS FROM THEIR PERCH AS WE DID HAVE A HUGE SIZED LOSS OF 873 CONTRACTS ON OUR TWO EXCHANGES WITH THE HUGE LOSS IN PRICE OF $1.08

.

WE MUST HAVE HAD:

A HUGE SIZED 1171 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.830MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 130,000 OZ QUEUE JUMP

//NEW STANDING FOR SILVER//JUNE IS THUS 4.815 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI LOSS //HUGE SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1719 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL ADDED A 102 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE

TOTAL CONTRACTS for 3 DAYS, total 2979 contracts: OR 14.895 MILLION OZ (993 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 14.895 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL PROBABLY BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 14.895 MILLION OZ

RESULT: WE HAD A HUMONGOUS SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2044 CONTRACTS WITH OUR LOSS IN PRICE OF SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 1171 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.830 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 130,000 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR JUNE 4.815 MILLION OZ

WE HAVE A HUGE SIZED LOSS OF 873 OI CONTRACTS ON THE TWO EXCHANGES WITH THE GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A MEGA HUGE SIZED 1719 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND SOME LIQUIDATION OF LONGS.

THE NEW TAS ISSUANCE TUESDAY NIGHT (1719) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 30 NOTICE(S) FILED TODAY FOR 150,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 7598 OI CONTRACTS TO 448,650 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 1162 CONTRACTS

WE HAD A STRONG SIZED DECREASE IN COMEX OI (7598 CONTRACTS) OCCURRED WITH OUR LOSS OF $20.40 IN PRICE/TUESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 89.804 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 40,300 OZ QUEUE JUMP AS BANKERS SCOUR THE PLANET LOOKING FOR GOLD ON THIS SIDE OF THE POND

NEW STANDING 90.127 TONNES// ALL OF THIS HAPPENED WITH OUR $20.40 LOSS IN PRICE WITH RESPECT TO TUESDAY’S TRADING. WE HAD A GOOD SIZED LOSS OF 5808 OI CONTRACTS (18.06 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1798 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 447,488

IN ESSENCE WE HAVE A GOOD SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5808 CONTRACTS WITH 7598 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 1798 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 5808 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 911 CONTRACTS,,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1798 CONTRACTS) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI OF 7598 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 5808 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 88.761 TONNES FOLLWED BY TODAY’S QUEUE JUMP OF 1.2534 TONNES

//NEW STANDING /JUNE 90.127 TONNES.

/ 3) STRONG LIQUIDATION OF CONTRACTS MOSTLY DUE TO TAS ALONG WITH SOME LONG SPECS BEING CLIPPED,

.

// 4) STRONG SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 911 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE. :

TOTAL EFP CONTRACTS ISSUED: 9303 CONTRACTS OR 930,300 OZ OR 28.936 TONNES IN 3 TRADING DAY(S) AND THUS AVERAGING: 3101 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAY(S) IN TONNES 28.936 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 28.936 DIVIDED BY 3550 x 100% TONNES = 0.817% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 28.936 tonnes HEADING FOR A STRONG MONTH

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUMONGOUS SIZED 2044 CONTRACTS OI TO 179,854 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1171 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1171 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1171 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2044 CONTRACTS AND ADD TO THE 1171 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 873 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 4.365 MILLION OZ

OCCURRED WITH OUR $1.08 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED DOWN 25.90 PTS OR 0.83% //Hang Seng CLOSED DOWN 19.15 PTS OR 0.10%// Nikkei CLOSED DOWN 347.29 OR 0.89%//Australia’s all ordinaries CLOSED UP .35%///Chinese yuan (ONSHORE) closed DOWN TO 7,2470 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2550/ Oil UP TO 73.44 dollars per barrel for WTI and BRENT DOWN AT 77.77 /Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 7598 CONTRACTS TO 447,488 WITH OUR HUGE LOSS IN PRICE OF $20.60 WITH RESPECT TO TUESDAY TRADING. WE HAD CONSIDERABLE T.A.S. LIQUIDATION ON TUESDAY WITH SOME LONGS BEING CLIPPED.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 1798 EFP CONTRACTS WERE ISSUED: : AUGUST 1798 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1798 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 5808 CONTRACTS IN THAT 1798 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 7598 COMEX CONTRACTS..AND THIS STRONG LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR HUGE LOSS IN PRICE OF $20.60// TUESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A SMALL SIZED 911 CONTRACTS. MOST OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. TODAY IS OF EXTREME IMPORTANCE TO OUR CROOKS IN YESTERDAY’S RAID

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (90.127 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 90.127 TONNES. THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $20.60 //// AND WERE SUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD A GOOD SIZED LOSS OF 5808 CONTRACTS ON TUESDAY WITH OUR TWO EXCHANGES WITH THE HUGE LOSS IN PRICE. THE T.A.S. ISSUED ON TUESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE LOST A TOTAL OI OF 14.42 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE (89.804 TONNES) ON FIRST DAY NOTICE FOLLoWED BY TODAY’S QUEUE JUMP OF 403 CONTRACTS OR 40300 OZ (1.2534 TONNES)

NEW STANDING FOR JUNE: 88.712 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR HUGE LOSS IN PRICE TO THE TUNE OF $20.40

WE HAVE REMOVED 1162 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET LOSS ON THE TWO EXCHANGES 5808 CONTRACTS OR 580,800 (18.06 TONNES)

confirmed volume TUESDAY 180,431 contracts// poor

//speculators have left the gold arena

JUNE 5 JUNE GOLD CONTRACT

/ /// THE JUNE 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | NIL oz . |

| Deposit to the Dealer Inventory in oz | 0 oz |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today | 437 notice(s) 43700 OZ 1.3592 TONNES |

| No of oz to be served (notices) | 995 contracts 99,500 OZ 3.094 TONNES |

| Total monthly oz gold served (contracts) so far this month | 27981 notices 2,798,100 oz 86.836 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: NIL oz

we have 0 customer deposit:

total deposit nil oz

total customer withdrawals: 0

TOTAL WITHDRAWALS nil 0z

Adjustments: 1

dealer to customer JPMorgan 3279.402 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE

For the front month of JUNE we have an oi of 1432 contracts having LOST 217 contracts. We had 620 contracts served on Tuesday so we gained a whopping 403 contracts or 40,300 oz additional oz will stand for gold at the comex as a queue jump. (1,2534 tonnes)

JULY LOST 18 CONTRACTS TO STAND AT 2065

AUGUST LOST 7741 CONTRACTS DOWN TO 371,717 CONTRACTS

We had 437 contracts filed for today representing 43,700 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 437 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 113 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for June /2024. contract month, we take the total number of notices filed so far for the month (27,918) x 100 oz ) to which we add the difference between the open interest for the front month of JUNE (1432 CONTRACTS) minus the number of notices served upon today (437 x 100 oz per contract( equals 2,897,600 OZ OR 90.127 TONNES.

thus the INITIAL standings for gold for the JUNE contract month: No of notices filed so far (27,918 x 100 oz +we add the difference for front month of June (1432 OI} minus the number of notices served upon today (437) x 100 oz which equals 2,897,600 oz (90.127 TONNES)

TOTAL COMEX GOLD STANDING FOR JUNE: 90.127 TONNES WHICH IS ABSOLUTELY HUGE FOR THIS VERY ACTIVE DELIVERY MONTH IN THE CALENDAR. JUNE IS TRADITIONA;LLLY THE 2ND HIGHEST DELIVERY MONTH OF THE YEAR. FROM THIS POINT WE WILL GAIN IN GOLD TONNAGE WILLING TO STAND AT THE COMEX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX84XXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,558,487.369 48.47 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,673,584.310 OZ

TOTAL REGISTERED GOLD 7,964,753.946 ( 247.73 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,708,830,394 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,406.266 oz (REG GOLD- PLEDGED GOLD)= 199.26 tonnes //

END

SILVER/COMEX

JUN 5/2024

INITIAL

//2024// THE JUNE 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 881,630.807 oz cnt delaware HSBC . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 30 CONTRACT(S) (150,000 OZ) |

| No of oz to be served (notices) | 58 contracts (0.290 million oz) |

| Total monthly oz silver served (contracts) | 905 Contracts (4.525 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 0 deposits customer account:

total customer deposit nil oz

JPMorgan has a total silver weight: 128.997million oz/297.285 million or 43.43%

adjustment: 0//

Comex withdrawals: 3

i) out of CNt 208,475.900 oz

ii) out of Delaware: 592m562,987 oz

iii) Out of HSBC 80,591,920 oz

total withdrawal: 881,630.807 oz 0z

TOTAL REGISTERED SILVER: 62.494MILLION OZ//.TOTAL REG + ELIGIBLE. 297,285

million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE:

silver open interest data:

FRONT MONTH OF JUNE/2024 OI: 88 CONTRACTS HAVING LOST 94 CONTRACT(S).

WE HAD 120 NOTICES SERVED UP ON TUESDAY, SO WE GAINED 26 CONTRACTS OR AN ADDITIONAL 130,000 OZ WILL STAND AT THE COMEX VIA A QUEUE JUMP

JULY SAW A LOSS OF 5229 CONTRACTS DOWN TO 130,489

AUG, SAW A GAIN OF 14 CONTRACTS TO 67

SEPT SAW A GAIN OF 3165 CONTRACTS TO 33,613.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 30 for 150,000 oz

CONFIRMED volume; ON TUESDAY 93,525 huge

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 905 x 5,000 oz = 4.525 MILLION oz

to which we add the difference between the open interest for the front month of JUNE ((88) and the number of notices served upon today 30 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2024 contract month: 905 notices served so far) x 5000 oz + OI for the front month of JUNE (88)x number of notices served upon today minus (30)x 5000 oz of silver standing for the JUNE contract month equates to 4.815 MILLION OZ.

New total standing: 4.815 million oz.

There are 62.494 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

JUNE 5 WITH GOLD UP $32.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 4 WITH GOLD DOWN $20.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 3 WITH GOLD UP $22.85 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 31 WITH GOLD DOWN $19.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 30 WITH GOLD UP $3.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 29 WITH GOLD DOWN $13.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 28 WITH GOLD UP $22.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 832.21 TONNES

MAY 24 WITH GOLD DOWN $2.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 833.36 TONNES

MAY 23 WITH GOLD DOWN $53.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 22 WITH GOLD DOWN $32.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 21 WITH GOLD DOWN $12,00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 20 WITH GOLD UP $21.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.10 TONNES OF GOLD INTO THE GLD//NEW TOTAL 838.54 TONNES

MAY 17 WITH GOLD UP $31.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//NEW TOTAL 833.36 TONNES

MAY 16 WITH GOLD DOWN $7.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//NEW TOTAL 833.36 TONNES

MAY 15 WITH GOLD UP $34.90 ON THE DAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD/INVENTORY RISES TO 831.93 TONNES

MAY 14 WITH GOLD DOWN $17.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RISES TO 831.33 TONNES

MAY 13 WITH GOLD DOWN $31.10 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD////INVENTORY RISES TO 831.93 TONNES

MAY 10 WITH GOLD UP $34.65 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 9 WITH GOLD UP $18.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 8 WITH GOLD DOWN $0.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 830.47 TONNES

MAY 7 WITH GOLD DOWN $6.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 832.19 TONNES

MAY 6WITH GOLD UP $21.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .55 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 831.64 TONNES

MAY 2 WITH GOLD UP $0.20 ON THE DAY; SMAKK CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 830.47 TONNES

MAY 1 WITH GOLD UP $7.80 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNES

GLD INVENTORY: 832.21 TONNES, TONIGHTS TOTAL

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 5 WITH SILVER UP 0.38 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.52 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 415.295 MILLION OZ

415.295 MILLION OZ

JUNE 4 WITH SILVER DOWN $1.08 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

JUNE 3 WITH SILVER UP $0.35 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

MAY 31 WITH SILVER DOWN $1.09 TODAY: HUGE CHANGES IN SILVER INVENTORY: A MASSIVE WITHDRAWAL OF 3.655 MILLION OZ FROM THE SLV//INVENTORY LOWERS TO 413.775 MILLION OZ

MAY 30 WITH SILVER DOWN $0.80 TODAY: NO CHANGES IN SILVER INVENTORY//INVENTORY REMAINS AT 417.430 MILLION OZ

MAY 29 WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 1.051 MILLION OZ INTO THE SLV//INVENTORY DECREASES TO 417.430 MILLION OZ

MAY 28 WITH SILVER UP $1.64 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 2.832 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 418.481 MILLION OZ

MAY 24 WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF .822 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 421.313 MILLION OZ

MAY 23 WITH SILVER DOWN $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.736 MILLION OZ FROM THE SLVINVENTORY INCREASES TO 420.491 MILLION OZ

MAY 22 WITH SILVER DOWN $0.66 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 21 WITH SILVER DOWN $0.41 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A DEPOSIT OF 3.792 MILLION OZ FROM THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 20 WITH SILVER UP $1.28 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 1.005 MILLION OZ FROM THE SLV// INVENTORY LOWERS TO 418.435 MILLION OZ

MAY 17 WITH SILVER UP $1.37 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 868,000 OZ FROM THE SLV// INVENTORY LOWERS TO 419.440 MILLION OZ

MAY 16 WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY REMAINS AT 420.308 MILLION OZ

MAY 15 WITH SILVER UP 101 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A WITHDRAWAL OF 1.919 MILLION OZ FROM THE SLV NVENTORY RESTS AT 420.308 MILLION OZ

MAY 14 WITH SILVER UP 25 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;INVENTORY RESTS AT 422.227 MILLION OZ

MAY 13 WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;NVENTORY RESTS AT 422.227 MILLION OZ

MAY 10 WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A HUGE WITHDRAWAL OF 1.,828 MILLION OZ//INVENTORY RESTS AT 422.227 MILLION OZ

MAY 9 WITH SILVER UP 78 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 8 WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 7WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 6 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.055 MILLION OZ

MAY 3 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 2WITH SILVER UP 0.12 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/ A WITHDRAWALOF 4.471 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 1 WITH SILVER UP 0.09 TODAY: SMALLCHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF ,457 MILLION OZ INTO THE SLV INVENTORY RESTS AT 429.814 MILLION OZ

CLOSING INVENTORY 415.295 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/GOLD AND SILVER COMMENTARY

ALASDAIR MACLEOD…

A Keynesian window for gold buyers

A realisation that the US economy is sliding into recession persuades mainstream economists that prices, interest rates, and bond yields will fall after all. They ignore instability in the dollar

| MACLEODFINANCEJUN 5∙PAID |

The quality of mainstream economic analysis is extremely poor, evidenced by its consistent failures. The latest evidence of this paucity is a growing realisation that the US economy is in recession, particularly as yesterday’s job opening numbers (JOLTS) hit the lowest level since February 2021. Wake up folks!

Anyone who understands that a GDP number driven by government deficit spending is not economic growth is either ignorant or being informed by personal bias. But it is thinking of this ultra-low quality which dominates financial markets today.

There’s little doubt that the fall in Treasury yields is down to this hopium:

And the fall in oil prices in thin volatile paper markets is driven by the same story:

Now that there is an awakening to recession, mainstream analysts seize the opportunity to talk rates down: “Citigroup says that the Fed will have to cut interest rates in July and at every meeting until mid-2025” (Ambrose Evans-Pritchard, today’s Daily Telegraph). And others are talking of reducing exposure to equities in favour of bonds.

The simple assumption is that a recession is a period of falling demand and unsold goods. This is half true in that there is falling demand. But the error is to assume that supply won’t decline as well. In fact, supply declines first, as foretold by the JOLTS number. A recession leads to a drop in employment first, and therefore total consumer spending second.

An even more significant error is to assume that for the purpose of economic forecasting the purchasing power of the currency remains constant. If the currency was bound to gold, this would be broadly true. But today’s currencies are valued and therefore their purchasing power is determined by faith in them purely as credit.

Among America’s foreign creditors, this faith is plainly waning, though the useful idiots in America’s financial mainstream simply don’t understand the danger this presents. While domestic users of the dollar are generally clueless, it is foreign holders who will set the dollar’s value, not so much against other currencies, but in terms of its purchasing power measured in commodities.

Furthermore, foreign interests have been relied upon to be not only buyers of dollars, but buyers of US debt as well. They increasingly see the US as being ensnared in a debt trap and have begun to back off from further involvement with the dollar and its federal debt. Inevitably, there is a funding crisis looming for the US Government, which will drive bond yields higher, not lower.

The advice to invest in bonds is badly misplaced. Citibank’s reported advice that the Fed will reduce interest rates effectively to the zero bound is irresponsible.

Without massive cuts in government spending (dream on!), the dollar and its global fiat currency regime is in the early stages of a titanic decline. That’s why gold and silver as the monetary representatives of the entire commodity complex appear to be rising. But in the kingdom of the blind…

The Chinese and other Asians are not taking chances and their demand for physical metal is bound to accelerate. Meanwhile, paper gold in the west is on pause, but for how long only time will reveal. Doubtless, anyone who doesn’t take the opportunity to escape from the collapsing mountains of increasingly dodgy credit by buying gold at any price will end up kicking himself.

END

3. CHRIS POWELL//GATA DISPATCHES

CHRIS POWELL…

INTERESTING!

Customers crowd Vietnamese banks to buy gold

Submitted by admin on Tue, 2024-06-04 15:32 Section: Daily Dispatches

By Quynh Tran and Giang Huy

VN Express, Hanoi

Monday, June 3, 2024

Banks in Hanoi and Ho Chi Minh City saw up to 50 customers queuing at a time Monday to buy gold, which the banks are selling at below market rates.

At 2 p.m. an Agribank branch in HCMC’s District 1 saw dozens of customers queuing in the basement to await their turn to buy.

The bank, along with Vietcombank, VietinBank, and BIDV, bought gold from the State Bank of Vietnam at VND78.98 million ($3,107.00) per tael and sold it at no more than VND79.98 million to retail customers, 1.2% lower than market prices.

This is the latest effort of the central bank to narrow the gap between domestic and global gold prices. …

… For the remainder of the report:

https://e.vnexpress.net/photo/business/customers-fill-up-banks-to-buy-gold-4754029.html

* * *

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS/

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT//

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

ASIA TRADING//WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED DOWN 25.90 PTS OR 0.83% //Hang Seng CLOSED DOWN 19.15 PTS OR 0.10%// Nikkei CLOSED DOWN 347.29 OR 0.89%//Australia’s all ordinaries CLOSED UP .35%///Chinese yuan (ONSHORE) closed DOWN TO 7,2470 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2550/ Oil UP TO 73.44 dollars per barrel for WTI and BRENT DOWN AT 77.77 /Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2470

OFFSHORE YUAN: DOWN TO 7.2550

SHANGHAI CLOSED DOWN 25.80 PTS OR 0.83 %

HANG SENG CLOSED DOWN 19.15 PTS OR 0.10%

2. Nikkei closed DOWN 347.29 PTS OR 0.89 %

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 104.33 EURO FALLS TO 1.0862 DOWN 20 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +0.999 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 156.15 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.5250/Italian 10 Yr bond yield DOWN to 3.843 SPAIN 10 YR BOND YIELD DOWN TO 3.257%

3i Greek 10 year bond yield DOWN TO 3.547

3j Gold at $2334.55//Silver at: 29.61 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 9/ 100 roubles/dollar; ROUBLE AT 88.70

3m oil into the 73 dollar handle for WTI and 77 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 156.15/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.9999% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8925 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9695 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.341 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.481 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.789 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.49…

10 YR UK BOND YIELD: 4.2400 UP 2 PTS

2a New York OPENING REPORT

Futures Gain With Fresh S&P All-Time High Less Than 1% Away

WEDNESDAY, JUN 05, 2024 – 08:10 AM

US equity futures edged higher and were again on pace to reclaim all time highs (which again is less than 1% away away) on expectations that a slew of labor-market readings this week may support the Federal Reserve’s policy easing. As of 7:40am ET, S&P futures rose 0.25% and were at session highs with tech outperforming and small-caps keeping pace; Nasdaq futs were up 0.4% as all the Mag7 names were higher with Semis outperforming. AMD, INTC, MU, and NVDA all up at least 1% premarket. The S&P had seen three straight days of sliding in overnight trading, to then drift higher post EU close and close unchanged or green; today we start in the green so it will be interesting if in a mirror image we close red. Treasury yields were steady after their largest two-day drop for 2024, erasing an earlier yield gain of 2bps, and potentially aiding USD strength. Commodities are finally rebounding with strength in Energy, Ags, and precious metals. Oil was little changed and Bitcoin topped $70,000. In corporate news, Intel agreed to sell a stake in a venture that controls a plant in Ireland to Apollo Global for $11 billion, while activist investor Elliott is pushing SoftBank to launch a $15 billion buyback. Today’s macro data focus is ISM-Services and ADP.

In premarket trading, Hewlett Packard Enterprise and Crowdstrike were among the best performers after better-than-expected results. Meanwhile, chipmakers Intel, Nvidia and AMD were all quoted up more than 1%. Here are all the notable premarket movers:

- 3D Systems rises 15% after the 3D printing company won an orthodontics contract.

- ASML ADRs rises 3% after the semiconductor firm confirmed it will ship its latest chipmaking machine to TSMC and Samsung this year.

- CrowdStrike climbs 11% after the security software company raised its year forecast.

- Dollar Tree slips 2% after the retailer reported weaker-than-expected comparable sales for its first quarter and cut its annual EPS forecast.

- Hewlett Packard Enterprise surges 14% after the company reported revenue that beat analysts’ estimates on a big jump in sales of servers built to handle artificial intelligence work.

- Psychedelic stocks fall after the drug MDMA failed to get backing from US regulatory advisers to treat post-traumatic stress disorder.

Besides the barrage of labor market indicators which saw a disappointing JOLTS report yesterday, the ADP print and ISM Service employment today and the jobs report on Friday, investors will be focused on central banks: the ECB is expected to kick off an interest-rate cutting cycle Thursday, leapfrogging past the Fed; the Bank of Canada is likewise expected to cut rates. Meanwhile, expectations for the Fed’s first full 25 basis-point rate cut are now tilting toward November, a month ahead of earlier expectations, after the Fed’s preferred inflation gauge held steady and measures of manufacturing and spending came in softer than expected.

“We are starting to see labor market slackness, which gives the Fed more flexibility,” Justin Onuekwusi, chief investment officer at St James’s Place Management, said in an interview. “Given we have seen weakaness in labor market data this past week, all eyes will be on this number,” he said of the payrolls data.

European shares also rise a day before the European Central Bank is expected to deliver a 25bps interest-rate cut. Tech, telecom and retailers led the advance in Europe, as Zara owner Inditex SA delivered a stronger-than-expected trading update while banks and food beverages are the biggest laggards. Here are the biggest movers Wednesday:

- Inditex shares rise as much as 5.5%, the biggest advance among members of the Europe 600 Index, after the parent of Zara reported better-than-expected first-quarter earnings and offered a trading update for the current period that Jefferies says is “amply ahead”

- Voestalpine gains as much as 5.3%, the most in almost six months, with the steel producer’s solid fourth-quarter results and positive guidance outweighing a dividend miss

- Smith & Nephew shares rise as much as 4.8%, the most since Feb. 27, after UBS upgraded the medical devices company to buy from neutral, saying the stock is now “cheap and no longer a value trap”

- WH Smith shares rise as much as 3.3% after the retailer delivered sales growth in line with expectations, with analysts at RBC pointing to a “reassuring” acceleration in North America that could help improve investor sentiment toward the stock

- Clas Ohlson gains as much as 18%, the most since December, after the Swedish retail group’s fourth-quarter earnings impressed, with operating profits well ahead of expectations

- Xior Student Housing gains as much as 6.6% after Morgan Stanley starts coverage with an overweight recommendation, describing the company as a “high risk, high reward play” on the student housing sector

- Bayer shares rise as much as 2.9% after the company said a $2.25 billion Roundup verdict was reduced to $400 million by a US judge

- Centrica’s shares fall as much as 4.6% after the British energy supplier gave a trading update ahead of its AGM, saying that its performance so far has been in line with expectations

- Elekta drops as much as 16%, the most since Nov. 2019, after the Swedish medical equipment firm’s results came in below expectations, with Morgan Stanley saying that guidance suggests significant downgrades to consensus

- Lectra shares fall as much as 7.7% after American Industrial Partners sold its entire stake in the French company, which makes software and equipment used in the clothing and auto industries for cutting fabric

Earlier, Asian stocks were mixed with Indian equities leading gains in the region, while the markets in Japan and Indonesia slid. Indian stocks outperformed as an alliance partner of Prime Minister Narendra Modi’s party affirmed support to form a coalition government. The Nifty 50 Index rose more than 2%, recouping some of Tuesday’s loss when the gauge fell the most in four years. As a result, the MSCI Asia Pacific Index pared most of its losses after dropping as much as 0.5%. TSMC, Tencent and Samsung provided main support, while Toyota and Hitachi were among the biggest drags on the gauge.

In FX, the Bloomberg Dollar Spot Index is little changed while the yen was the worst-performing currency as it tumbles, falling 0.8% against the greenback toward 156.20, as carry trades reassert themselves and after a surprisingly weak print in Japanese wage growth prompted fears the BOJ may not get to further tightening of monetary conditions. The Swiss franc is also slightly lower.

- USD/JPY rose as much as 0.9% to 156.30; yen led G-10 losses against the dollar after a key measure of Japanese wage growth rose less than forecast

- USD/CAD inched up 0.1% to as high as 1.3691 ahead of the Bank of Canada’s rate decision; most analysts anticipate a cut and traders are bracing for further weakness in the Canadian dollar

In rates, treasuries gain, extending some of Tuesday’s post-JOLTS rally, with US 10-year yields dropping 1bp to 4.32%. Gilts underperform bunds and Treasuries across the curve.

Oil prices hold losses near a four-month low with WTI near $73.30 as oil halts the recent slide, rising around 0.3%. Spot gold rises $6 to around $2,333/oz. Most base metals trade in the red.

Bitcoin continues to gain and currently holds above USD 70k as Bitcoin ETF’s continue to take focus.

Looking at today’s US calendar, economic data includes May ADP employment change (8:15am), S&P Global services PMI (9:45am) and ISM services index (10am), Fed officials remain in blackout ahead of the June 12 FOMC policy announcement. Finally, we will have earnings from Dollar Tree and Lululemon.

Market Snapshot

- S&P 500 futures up 0.1% to 5,310.00

- STOXX Europe 600 up 0.5% to 519.53

- MXAP little changed at 178.67

- MXAPJ up 1.1% to 556.50

- Nikkei down 0.9% to 38,490.17

- Topix down 1.4% to 2,748.22

- Hang Seng Index down 0.1% to 18,424.96

- Shanghai Composite down 0.8% to 3,065.40

- Sensex up 2.8% to 74,071.83

- Australia S&P/ASX 200 up 0.4% to 7,769.00

- Kospi up 1.0% to 2,689.50

- German 10Y yield little changed at 2.54%

- Euro little changed at $1.0874

- Brent Futures up 0.3% to $77.73/bbl

- Gold spot up 0.3% to $2,333.82

- US Dollar Index up 0.17% to 104.29

Top Overnight News

- Treasury Secretary Yellen said the Treasury never tries to time the market in debt management. She added the issuance of Treasury Bills is in line with historical averages. Market participants believe that short-term rates will come down. She said short-term bill issuance is in line with recommendations from the TBAC. Yellen said there is nothing about issuing short-term debt that creates a ‘sugar high’ for the economy, according to Reuters.

- A group backed by BlackRock (BLK) and Citadel Securities is planning to start a new national stock exchange in Texas, according to WSJ.

- Nike has cut staff in its European HQ as part of a multiyear cost-cutting plan, according to Bloomberg.

- Bridgewater’s Dalio says Chinese assets are attractively priced, Bridgewater has done well operating in the region over the past five years.

- Dollar Tree (DLTR) is exploring the sale of Family Dollar, according to WSJ

- Bond traders are tilting dovish again, piling into wagers that would benefit from a faster pace of Federal Reserve interest rate cuts as Treasuries rally.

- Japanese workers’ base pay jumped by the largest margin since 1994 in a sign that corporate pledges to offer wage increases are starting to take effect, though market players appeared unconvinced over the strength of the trend.

- Donald Trump asked the New York judge presiding over his hush-money trial to lift his gag order in the case, arguing that the basis for limiting what the former president could say “no longer exists” after the jury convicted him of 34 felonies last week.

- Hedge funds are backpedaling on yen option trades with a sudden spate of bullish bets on the currency, according to market participants.

- Indian Prime Minister Narendra Modi is gearing up for coalition talks after his party lost its majority in parliament, forcing him to rely on allies to form a government for the first time since he stormed to power a decade ago.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed as the cautious mood from Wall Street reverberated into Asia-Pacific, with macro newsflow overnight on the lighter side. ASX 200 was modestly firmer with defensive sectors among the better performers, whilst lagging sectors include gold names, mining stocks, and energy companies. Little immediate reaction was seen on commentary from RBA Governor Bullock and the softer-than-expected Q1 GDP report. Nikkei 225 was the regional laggard and dipped under the 38,500 mark with mining and industrial firms among the losers, whilst autos continued to feel the woes of the latest safety scandal in the country. Hang Seng and Shanghai Comp varied with the former propped up by auto stocks after some firms were permitted to test out advanced levels of autonomous driving. Mainland markets shrugged off the improvement in Caixin Services PMI which also noted “China’s economy is generally stable and remains on the road to recovery.”

Top Asian News

- Some Chinese AI chip firms are reportedly designing less powerful processors to retain access to TSMC (TSM /2330 TT) production in the face of US sanctions, according to Reuters sources.

- RBA Governor Bullock expected Q1 GDP growth to be quite low; the economy is weak and that is showing up in consumption; not ruling anything in or out on policy. Looking for a soft landing for the economy. Inflation is coming down but only slowly. The board won’t hesitate to act on rates if inflation does not come down as expected. Still judges inflation risks as balanced. Q2 inflation data will be important for monetary policy, not the single most important thing.

- PBoC injected CNY 2bln via 7-day reverse repos with the rate at 1.80%.

- Fitch affirmed India at BBB-, outlook Stable.

- Fitch lowers 2024 China new home sales forecast, expects it to decline by 15-20% to CNY 8.3-8.8tln.

- Foxconn (2317 TT) May Revenue +22.1%; due to higher than expected demand from AI servers, current visibility for Q2 is expected to beat expectations.

- China May Retail Car Sales -3% Y/Y, via PCA cited by Bloomberg

European bourses, Stoxx600 (+0.4%) are modestly firmer across the board, attempting to reclaim some of the losses seen in the prior session. European sectors hold a strong positive bias, with Tech topping the index alongside Retail, with the latter lifted by post-earning strength in Inditex (+5.5%). Banks are slightly in the red. US Equity Futures (ES +0.1%, NQ +0.3%, RTY +0.2%) are very modestly firmer and contained within a tight range ahead of US ADP and ISM Services. Barclays European Equity Strategy: Upgrades Consumer Staples to Marketweight from Overweight Upgrades Real Estate to Overweight. Upgrades Retail to Overweight. Cuts Energy to Underweight. Cuts Autos to Underweight.

Top European News

- ECB’s Kazimir says inflation is on a good trajectory and the ECB is approaching its first interest rate cut. Note, these comments are being made in the ECB’s quiet period.

- YouGov/Sky News Snap Debate Poll: PM Sunak won the first head-to-head election debate (Sunak 51%, Starmer 49%). Snap YouGov poll of 1,657 viewers reveals how people feel each party leader performed, and who they think came across best.

FX

- DXY is continuing to inch higher after briefly printing a 103 handle on Tuesday. 104.32 is the high watermark for today which is in close proximity to Tuesday’s 104.33 peak.

- EUR/USD is back on a 1.08 handle after venturing as high as 1.0916 yesterday. For now, the pair is managing to hold above Tuesday’s 1.0858 low with ING of the view that the pair’s “neutral range” could be between 1.0850-1.09.

- GBP is marginally firmer vs. the USD and EUR in quiet newsflow with last night’s general election debate not having any follow-through given it is unlikely to reverse the polls. Cable remains tucked within Tuesday’s 1.2743-1.2818 range.

- USD/JPY is markedly higher and reversing a bulk of Tuesday’s selling which brought the pair as low as 154.44. Next upside level for the pair is Tuesday’s best at 156.48.

- Antipodeans remain resilient amid the recent Dollar advances helped by the recovery in risk sentiment. AUD has shrugged off the disappointing growth figures overnight. NZD/USD also firmer but ran into resistance just below the 0.62 mark.

- CAD is steady vs. the USD ahead of an expected rate reduction by the BoC (market pricing 77% probability of a cut). USD/CAD is currently tucked within yesterday’s 1.3619-99 range.

- PBoC set USD/CNY mid-point at 7.1097 vs exp. 7.2418 (prev. 7.1083)

Fixed Income

- USTs are slightly softer in a breather from this week’s upside ahead of US ISM Services and ADP National Employment. Treasuries are currently holding around the low of 109-26+ with no follow-through from the morning’s European/UK data points.

- Bunds are also incrementally softer and holding around the 131.00 mark. There was no real follow-through from the PMIs despite final EZ figure showing a slight easing of inflationary pressures in the service sector; fleeting upside on a robust 2030 tap.

- Gilt price action is in-fitting with peers, though has pulled back slightly more than EGBs. PMIs passed without reaction and was little changed to a well received UK auction; currently holding around 97.33.

- UK sells GBP 4bln 3.75% 2027 Gilt: b/c 3.27x (prev. 3.68x), average yield 4.505% (prev. 4.204%) & tail 0.6bps (prev. 0.3bps)

- Germany sells EUR 2.442bln vs exp. EUR 3bln 2.40% 2030 Bund: b/c 2.6x (prev. 2.10x), average yield 2.55% (prev. 2.30%) & retention 18.6% (prev. 18.00%)

Commodities

- Crude is modestly firmer in what has been a choppy session for the complex; initially taking a breather from the hefty WTD pressure post-OPEC/demand concerns but with price action choppy at times. Brent currently holding around USD 77.60/bbl.

- Precious metals are essentially flat, though have been attempting to nudge into the green but not making any real ground as the USD picks up and yields have an upward bias.

- Base metals are mixed, continuing the similar price action seen in APAC trade overnight.

- US Private Energy Inventory Data: Crude +4.05mln (exp. -2.3mln), Cushing +0.983mln, Distillates +4.03mln (exp. +2.5mln), Gasoline +1.98mln (exp. +2mln).

- US Energy Secretary Granholm said the global oil market is well stocked and feels comfortable that there will be no huge increase in oil and gas prices in the ‘next short while’. The US could boost the rate of replenishing the Strategic Petroleum Reserve as maintenance work at two sites winds down. Work at SPR will be finished by the end of year. Creating a Strategic Resilience Reserve for stockpiles of critical minerals with allies to help energy transition is a good idea. US talking with allies on critical minerals production, stockpile goals, could release details ‘soon’. Granholm said even OPEC countries recognize there is only so much they can do to manipulate oil prices. Granholm said ‘We should all be concerned’ about oil industry consolidation. The US aims to complete the LNG export review in Q1 2025. She doesn’t expect permitting a pause to damage US competitiveness in the global LNG market.

- UAE’s ADNOC set July Murban crude OSP at USD 83.93/bbl (prev. USD 89.14/bbl in June).

- Aluminium name Novelis has postponed its IPO due to market conditions; Novelis will continue to evaluate the timing of the offering in the future, according to PR Newswire.

Geopolitics: Middle East

- Israeli military chief of staff said Israel is prepared to shift offense along the Northern border with Lebanon, nearing a decision point.

- “Israeli tanks penetrate downtown Rafah for the first time since the start of the Israeli invasion of the area”, according to Sky News Arabia.

- Israel Ministry of Defense said it has signed an agreement with the US government for a third squadron of F-35 stealth aircraft for the Israeli Air Force, according to Reuters.

- US military said in the past 24 hours, Iranian-backed Houthis launched two anti-ship ballistic missiles (ASBM) from Houthi-controlled areas of Yemen into the Red Sea

Geopolitics: Other

- White House said US President Biden will attend the G7 leaders summit in Apulia, Italy on June 13-14. They will advance efforts to make use of Russia’s immobilised sovereign assets to help Ukraine.

- Taiwan Defence Ministry said in the past 24 hours, 26 Chinese Air Force planes were detected operating around Taiwan.

- China Maritime Safety Administration said they are to shut an area in the Northern Yellow Sea from June 5-7 due to planned live firing.

US Event Calendar

- 07:00: May MBA Mortgage Applications -5.2%, prior -5.7%

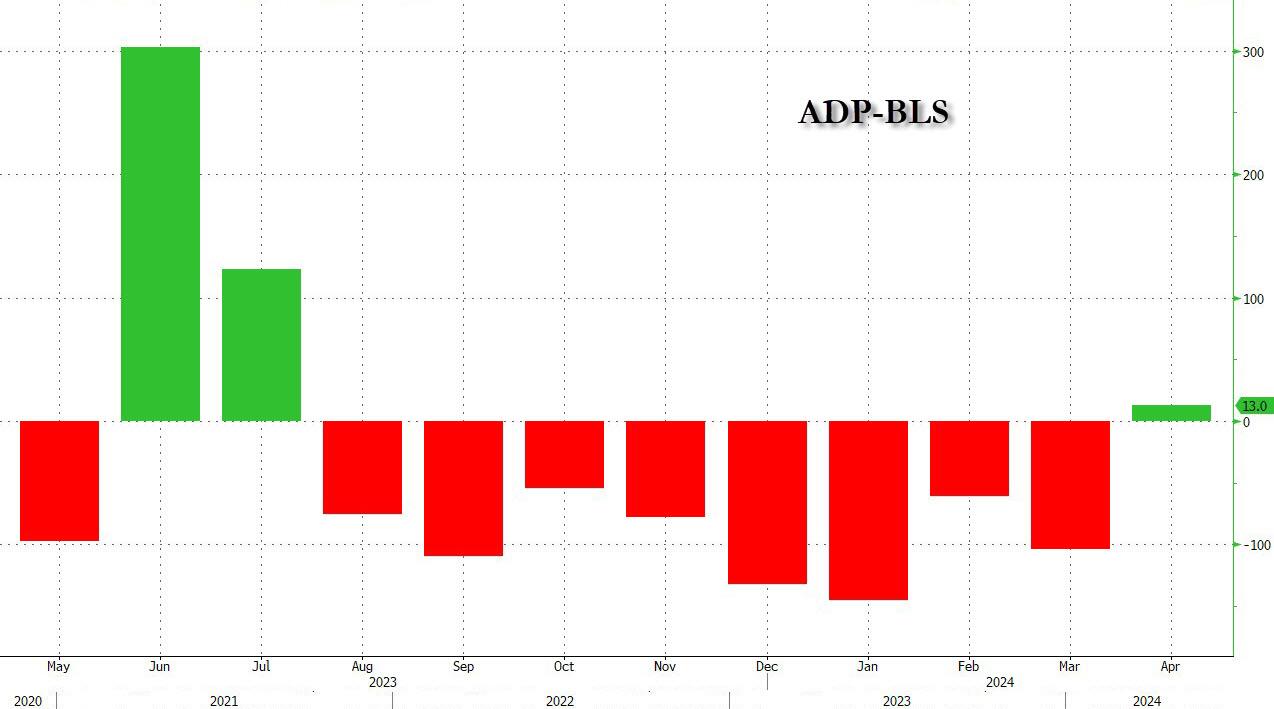

- 08:15: May ADP Employment Change, est. 175,000, prior 192,000

- 09:45: May S&P Global US Services PMI, est. 54.8, prior 54.8

- May S&P Global US Composite PMI, est. 54.2, prior 54.4

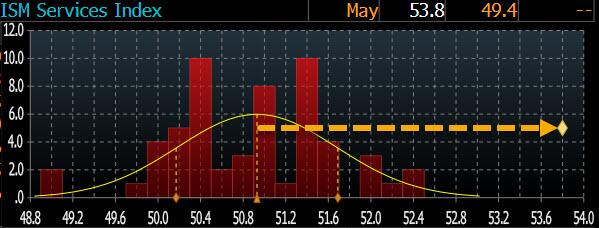

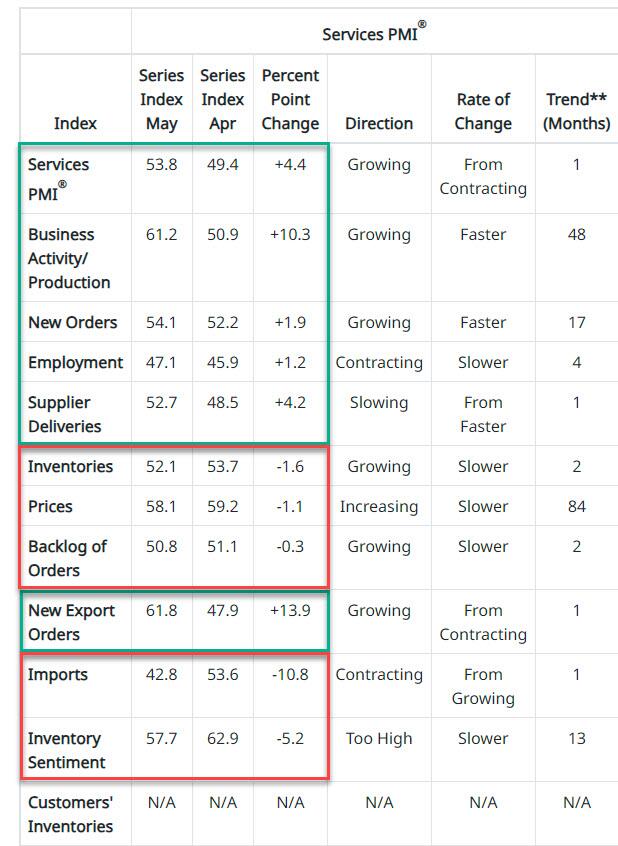

- 10:00: May ISM Services Index, est. 51.0, prior 49.4

- May ISM Services New Orders, est. 53.2, prior 52.2

- May ISM Services Employment, est. 47.2, prior 45.9

- May ISM Services Prices Paid, est. 59.0, prior 59.2

DB’s Jim Reid concludes the overnight wrap

The last week has proved to be a real challenge for markets to work out whether weaker US data is good or bad news for equities. This marks a bit of a change as in recent months both good and bad data were used as a justification for a rally. It does seem we’ve moved to a more nuanced debate. However before we get too excited about a possible change in emphasis, the S&P 500 is only down -0.25% since returning to trading after Memorial Day last Monday and keeps on bouncing off the weaker data inspired intra-day lows of the last week.

This trend continued yesterday following the April JOLTS report which encouraged another notable fixed income rally with 10yr Treasury yields (-6.3bps) falling for a fourth consecutive session. The combined -28.6bp drop over that time period is the largest such fall in yields since Mid-December. Until the last 100 minutes of US trading equities were lower but another late rally helped edge the S&P 500 (+0.15 %) higher.

In terms of the details of the JOLTS report, the openings rate came in beneath expectations at 8.06mn (vs 8.35mn expected), falling to its lowest level since February 2021. So a clear indicator of a cooling US labour market, with labour demand continuing to moderate. This also follows on from a series of generally weaker US data over the past few days.

Elsewhere in the report, the ratio of openings to unemployed workers fell to its lowest level since July 2021, to 1.2, as the labour market slackened further in April. The private sector quits rate, which measures the number of people who voluntarily leave their job, came in at 2.4%, with the previous month also revised up to 2.4%. The revision confirms the series has been flatlining since the end of 2023, at its lowest level since 2020. In terms of other data, we also had US factory orders for April, which surprised a little to the upside at 0.7% (vs 0.6% expected). But this still marked a deceleration from 1.6% last month.

Against this backdrop, markets raised their expectations for Fed rate cuts this year. For example, the number of Fed cuts expected by year-end rose for the fifth consecutive day, up +3.9bps. Supporting the prospect of more rate cuts was another fall in oil prices, which brought further relief to inflation fears. Brent crude fell -1.07% to $77.52/bbl, the 5th consecutive decline in prices and the lowest level since February. WTI crude similarly fell -1.31% to $73.25/bbl. In turn, the chance of additional rate cuts supported US Treasuries, as 2yr yields fell -3.8bps, whilst the 10yr yield slipped -6.3bps to 4.326% (4.34% overnight). From here, the next major catalyst will be the US employment report on Friday.

In Europe, the major data point of the day was German unemployment, which jumped +25k (vs +7k expected). The increase helped contribute to investors dialling up the expected number of ECB cuts through to year-end by +2.6bps. Off the back of this, German 10yr bunds rallied, with yields falling -4.6bps. Yields on OATs (-3.9bps) and BTPs (-1.3bps) also declined.

Moving on to more details on equities, the -0.5% mid-session decline followed by a late rally was typical of the last few days with the index closing +0.15% higher. The underperformers were largely the energy (-0.97%) and materials (-1.22%) sectors driven by lower commodity prices. The rebound was led by Telecoms (+1.89%), Real Estate (+0.95%) and Consumer Staples (+0.93%). The NASDAQ likewise rebounded to finish at +0.17%. The second half bounce back was not that broad-based, as the Russell 2000 index of small cap stocks underperformed, falling -1.25%. Elsewhere, other global equities were generally on the backfoot. The STOXX 600 retreated -0.54%, whilst the MSCI EM index underperformed after falling -0.66%.

Not helping sentiment was a dramatic turnaround in India as Exit Polls over the weekend proved to be very inaccurate. They suggested Modi’s NDA coalition would get 355-380 out of the 543 seats with his own BJP party on course for around 327 seats. 272 is needed for a majority. The final count is that his party looks set for 240 seats (losing their own majority from 2019’s 303 seats) and the coalition 292 (down from 353 in 2019). While Modi can still form the government if his alliance sticks together, it provides a much more uncertain environment than was anticipated as we woke up on Monday. As a result Indian equities had their worst performance in 4 years with the Nifty 50 falling -5.93% yesterday after bouncing +3.25% to an all-time high on Monday. This morning it is slightly higher as I type early in the session. Last night our economist published an initial reaction (see here) to the surprise result, one that he doesn’t see derailing India’s impressive growth prospects.

Elsewhere in Asia, there is a divergent trend in equities this morning. As I check my screens, the KOSPI (+1.08%) is leading gains across the region with the Hang Seng (+0.34%) and the S&P/ASX 200 (+0.36%) also edging higher. Chinese stocks are mixed though with the CSI (+0.03%) swinging between gains and losses while the Shanghai Composite (-0.30%) is lower. However, the Nikkei (-0.80%) is bucking the regional trend albeit trimming its opening losses as stronger wage data spurred fears of tighter monetary policy from the BoJ. S&P 500 (+0.18%) and NASDAQ 100 (+0.31%) futures are higher.

Early morning data showed that China’s Caixin services PMI accelerated at the fastest pace in 10 months jumping from 52.5 in April to 54.0 in May on improving local and overseas demand. However, the private survey data contrasted with official PMI data released last week, which showed that services sector activity grew at a slower pace in May than April. Moving to Japan, real cash earnings declined -0.7% y/y in April (v/s -0.9% expected), notching a record streak of 25 consecutive monthly declines. It followed a revised -2.1% drop in the preceding month. On the brighter side, labour cash earnings rose at the fastest pace in 10 months, increasing +2.1% y/y in April (v/s +1.8% expected) as against an upwardly revised +1.0% rise in March.

Elsewhere Australia’s first quarter 2024 GDP growth slowed to just +0.1% (v/s +0.2% expected) and slower than the revised +0.3% pace for the final three months of 2023. On an annual basis, the economy expanded +1.1% with markets expecting it to slow to +1.2% from a growth of +1.5% in the December quarter. Yields on 10yr Australian government bonds initially fell -9.76bps (half domestic and half a global story) before settling -6.7bps lower at 4.23% as we go to print.

It’s a huge week (past and present) for elections and tomorrow the European Parliamentary Elections start. We’ll preview the implications later in the week. Also of note was the -6.01% fall in the Mexican index on Monday that was followed by a +3.24% rebound yesterday. The peso fell -3.82% on Monday and then fell a further -0.97% yesterday. The overall decline is on concerns that the landslide victory for the ruling party may increase state influence on the economy. See DB’s review of the implications from the election results here.

Briefly back on commodities, oil prices were not alone in recording a fall yesterday. Copper prices pulled back -2.80% to $453.70/lb, and now officially erasing all its May gains (-11.4% from the peak). The fall comes as global inventories rise, with the Shanghai Futures Exchange recording its highest level of stockpiles since 2020. Elsewhere after a +5.23% surge on Monday following disruption to Norwegian supply, European natural gas retreated yesterday, falling -6.16% to EUR33.80/MWh following reports the outage is expected to be short-lived.

Now to the day ahead, and data releases include the US May ADP report and ISM services, the UK May new car registrations, official reserves changes, France April industrial production, Italy May services PMI, Eurozone April PPI, Canada Q1 labour productivity and the May services PMI. In terms of central banks, we have the Bank of Canada decision. Finally, we will have earnings from Dollar Tree and Lululemon.

2B EUROPE OPENING/TRADING

Mixed/cautious trade ahead of US data & the BoC – Newsquawk Europe Market Open

WEDNESDAY, JUN 05, 2024 – 01:25 AM

- APAC stocks traded mixed as the cautious mood from Wall Street reverberated into Asia-Pacific, with macro newsflow overnight on the lighter side; Tokyo underperformed.

- DXY was caged in a tight range as traders look ahead to the US ISM Services data for impetus following Monday’s dovish Manufacturing print.

- YouGov/Sky News Snap Debate Poll: PM Sunak won the first head-to-head election debate [Sunak 51%, Starmer 49%].

- European equity futures are indicative of a firmer cash open with the Euro Stoxx 50 future +0.5% after cash closed -1.0% on Tuesday.

- Looking ahead, highlights include EZ, UK, Canadian & US Services & Composite PMIs, US ADP National Employment, US ISM Services, NBP and BoC Policy Announcement, BoC’s Macklem & Rogers, and Supply from the UK and Germany.

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

US TRADE

EQUITIES

- US stocks closed mixed in overall contained trade. The risk tone throughout the session was cautious. Cash equities opened with a soft bias, and after some fleeting choppiness post-JOLTs data, resumed to the downside as growth concerns continued to weigh on traders’ minds.

- SPX +0.15% at 5,291, NDX +0.29% at 18,655, DJIA +0.36% at 38,711, RUT -1.25% at 2,034

- Click here for a detailed summary.

NOTABLE HEADLINES

- Treasury Secretary Yellen said the Treasury never tries to time the market in debt management. She added the issuance of Treasury Bills is in line with historical averages. Market participants believe that short-term rates will come down. She said short-term bill issuance is in line with recommendations from the TBAC. Yellen said there is nothing about issuing short-term debt that creates a ‘sugar high’ for the economy, according to Reuters.

- A group backed by BlackRock (BLK) and Citadel Securities is planning to start a new national stock exchange in Texas, according to WSJ.

- Tesla (TSLA) CEO Musk said his current best guess for Nvidia (NVDA) purchases by Tesla is USD 3-4bln this year, via a post on X.

- Nike (NKE) has cut staff in its European HQ as part of a multiyear cost-cutting plan, according to Bloomberg.

APAC TRADE

EQUITIES

- APAC stocks traded mixed as the cautious mood from Wall Street reverberated into Asia-Pacific, with macro newsflow overnight on the lighter side.

- ASX 200 was modestly firmer with defensive sectors among the better performers, whilst lagging sectors include gold names, mining stocks, and energy companies. Little immediate reaction was seen on commentary from RBA Governor Bullock and the softer-than-expected Q1 GDP report.

- Nikkei 225 was the regional laggard and dipped under the 38,500 mark with mining and industrial firms among the losers, whilst autos continued to feel the woes of the latest safety scandal in the country.

- Hang Seng and Shanghai Comp varied with the former propped up by auto stocks after some firms were permitted to test out advanced levels of autonomous driving. Mainland markets shrugged off the improvement in Caixin Services PMI which also noted “China’s economy is generally stable and remains on the road to recovery.”

- US equity futures held a modest upward bias (ES +0.2%) following the prior day’s cautious trade as participants look ahead to the US ADP and ISM Service today ahead of Friday’s US jobs report.