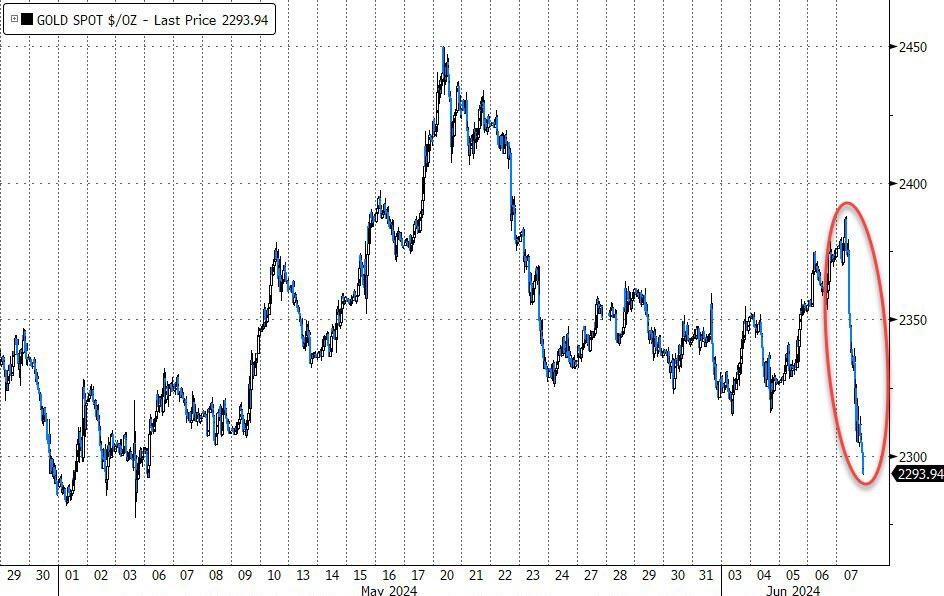

GOLD PRICE CLOSED DOWN $64.35 TO $2307.80

SILVER PRICE DOWN 1.93 TO 29.34

Gold ACCESS CLOSED $2288,60

Silver ACCESS CLOSED: $29.17

Bitcoin morning price:$71,566 UP 916 DOLLARS.

Bitcoin: afternoon price: $69070 DOWN 1580 dollars

Platinum price closing DOWN $40.25 TO $969.75

Palladium price; DOWN $19.25 AT $915.75

END

SHANGHAI GOLD PREMIUM 100 DOLLARS/COMEX GOLD//JULY TO JULY

SHANGHAI GOLD

SHANGHAI GOLD (USD) FUTURES – QUOTES

Last Updated 07 Jun 2024 01:54:43 PM CT.

Market data is delayed by at least 10 minutes.

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $3148.65 DOWN 99.90 CDN dollars per oz( * NEW ALL TIME HIGH 3,305.30 CDN DOLLARS PER OZ//MAY 20 2024)

*BRITISH GOLD: 1798.62 DOWN 59.73 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2116.90 DOWN 64.14 Euros per oz //* (ALL TIME CLOSING HIGH: 2248.89 EUROS PER OZ//APRIL 16.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCH: COMEX

EXCHANGE: COMEX

CONTRACT: JUNE 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,370.300000000 USD

INTENT DATE: 06/06/2024 DELIVERY DATE: 06/10/2024

FIRM ORG FIRM NAME ISSUED STOPPED

099 H DB AG 11

363 H WELLS FARGO SEC 25

624 H BOFA SECURITIES 1

657 C MORGAN STANLEY 1 1

661 C JP MORGAN 25 8

661 H JP MORGAN 29

686 H STONEX FINANCIA 10

732 C RBC CAP MARKETS 2 1

737 C ADVANTAGE 4 6

880 H CITIGROUP 88 30

TOTAL: 121 121

MONTH TO DATE: 28,501

JPMorgan stopped 8/121

FOR JUNE 2024

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2024. CONTRACT: 121 NOTICES FOR 12,100 OZ or 0.3763 TONNES

total notices so far: 28,501 contracts for 2,850,100 Oz (88.65 tonnes)

FOR JUNE:

SILVER NOTICES: 200 NOTICE(S) FILED FOR 1.0 MILLION OZ/

total number of notices filed so far this month :1105 for 5.525 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $64.35

INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ :

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.56 TONNES OF GOLD INTO THE GLD

/ /INVENTORY RESTS AT 833.55TONNES

INVENTORY RESTS AT 833.55 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER DOWN $1.93 AT THE SLV//

NO CHANGES IN SILVER INVENTORY AT THE SLV:

// INVENTORY REMAINS AT 417.944 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 417.944 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 595 CONTRACTS TO 180,588 AND CONTINUING ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS SMALL SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR GAIN OF $1.27 IN SILVER PRICING AT THE COMEX ON THURSDAY’S TRADING ON SILVER. WE HAD SOME ZERO LIQUIDATION AS WE HAD A NET GAIN OF 1694 CONTRACTS ON OUR TWO EXCHANGES. WE, AGAIN HAD SHORT COVERING BY OUR SPECS WITH THE HUGE GAIN IN PRICE AS WELL AS MASSIVE T.A.S. LIQUIDATION. WE HAD ANOTHER HUGE SIZED 1405 T.A.S ISSUANCE AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED ON TUESDAY

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 1405 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND TODAY;S TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $1.27) AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS FROM THEIR PERCH AS WE DID HAVE A HUGE SIZED GAIN OF 1585 CONTRACTS ON OUR TWO EXCHANGES WITH THE GAIN IN PRICE OF $1.27

.

WE MUST HAVE HAD:

A HUGE SIZED 990 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.830MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 1.26 MILLION OZ QUEUE JUMP

//NEW STANDING FOR SILVER//JUNE IS THUS 6.14 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI GAIN //HUGE SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1405 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED 109 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE

TOTAL CONTRACTS for 5 DAYS, total 4544 contracts: OR 22.720 MILLION OZ (909 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 22.72 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL PROBABLY BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 22.72 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 595 CONTRACTS WITH OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 990 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.830 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 1.27 MILLION OZ QUEUE JUMP

//NEW TOTAL STANDING FOR JUNE 6.14 MILLION OZ

WE HAVE A HUMONGOUS SIZED GAIN OF 1585 OI CONTRACTS ON THE TWO EXCHANGES WITH THE GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 1405 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND ZERO LIQUIDATION OF LONGS.

THE NEW TAS ISSUANCE THURSDAY NIGHT (1405) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 200 NOTICE(S) FILED TODAY FOR 1.0 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 2945 OI CONTRACTS TO 456,354 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 975 CONTRACTS

WE HAD A GOOD SIZED INCREASE IN COMEX OI (2945 CONTRACTS) OCCURRED WITH OUR GAIN OF $16.25 IN PRICE/THURSDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 89.94 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 2300 OZ QUEUE JUMP AS BANKERS SCOUR THE PLANET LOOKING FOR GOLD ON THE THIS SIDE OF THE POND

NEW STANDING 89.94 TONNES// ALL OF THIS HAPPENED WITH OUR $16.25 GAIN IN PRICE WITH RESPECT TO THURSDAY’S TRADING. WE HAD A STRONG SIZED GAIN OF 7883 OI CONTRACTS (24.51 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 3963 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 456,354

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 6908 CONTRACTS WITH 2945 CONTRACTS INCREASED AT THE COMEX// AND A STRONG SIZED 3963 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 6908 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED 2399 CONTRACTS,,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3963 CONTRACTS) ACCOMPANYING THE GOOD SIZED GAIN IN COMEX OI OF 2945 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 6908 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 88.761 TONNES FOLLOWED BY TODAY’S QUEUE JUMP TO OF 0.0715 TONNES

//NEW STANDING /JUNE 89.94 TONNES.

/ 3) SOME T.A.S. LIQUIDATION OF CONTRACTS WITH ZERO LONG SPECS BEING CLIPPED,

.

// 4) GOOD SIZED COMEX OPEN INTEREST GAIN 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///STRONG T.A.S. ISSUANCE: 2399 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE. :

TOTAL EFP CONTRACTS ISSUED: 14,918 CONTRACTS OR 1,491,800 OZ OR 46.40 TONNES IN 5 TRADING DAY(S) AND THUS AVERAGING: 2738 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAY(S) IN TONNES 46.40 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 46.40 DIVIDED BY 3550 x 100% TONNES = 1.30% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 46.40 tonnes HEADING FOR A STRONG MONTH

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A STRONG SIZED 595 CONTRACTS OI TO 180,585 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 990 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 990 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 990 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 595 CONTRACTS AND ADD TO THE 990 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1585 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 7.925 MILLION OZ

OCCURRED WITH OUR $1.27 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING/THURSDAY NIGHT

SHANGHAI CLOSED UP 2.49 PTS OR 0.08% //Hang Seng CLOSED DOWN 109.85 PTS OR 0.59%// Nikkei CLOSED DOWN 19.58 OR 0.05%//Australia’s all ordinaries CLOSED UP .48%///Chinese yuan (ONSHORE) closed UP TO 7,2415 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2498/ Oil UP TO 76.08 dollars per barrel for WTI and BRENT UP AT 80.32 /Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A GOOD SIZED 2945 CONTRACTS TO 456,354 WITH OUR HUGE GAIN IN PRICE OF $16.25 WITH RESPECT TO THURSDAY TRADING. WE HAD CONSIDERABLE T.A.S. LIQUIDATION ON THURSDAY WITH ZERO LONGS BEING CLIPPED.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 3963 EFP CONTRACTS WERE ISSUED: : AUGUST 3963 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3963 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 6908 CONTRACTS IN THAT 3963 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A GOOD SIZED GAIN OF 2945 COMEX CONTRACTS..AND THIS STRONG GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $16.25// THURSDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT WAS A GOOD SIZED 2399 CONTRACTS. MOST OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. TODAY IS OF EXTREME IMPORTANCE TO OUR CROOKS IN YESTERDAY’S TRADING

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (89.94 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 89.866 TONNES. THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $16.25 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG SIZED GAIN OF 6908 CONTRACTS ON THURSDAY WITH OUR TWO EXCHANGES WITH THE HUGE GAIN IN PRICE. THE T.A.S. ISSUED ON THURSDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 21.48 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE (89.94 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 23 CONTRACTS OR 2300 OZ (0.0715 TONNES)

NEW STANDING FOR JUNE: 89.94 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR HUGE GAIN IN PRICE TO THE TUNE OF $16.25

WE HAVE REMOVED 975 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET GAIN ON THE TWO EXCHANGES 6908 CONTRACTS OR 690800 (21.48 TONNES)

confirmed volume THURSDAY 179,077 contracts// poor and volumes have been dropping

//speculators have left the gold arena

JUNE 7 JUNE GOLD CONTRACT

/ /// THE JUNE 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 9806.05 oz BRINKS 305 KILOBARS . |

| Deposit to the Dealer Inventory in oz | 0 oz |

| Deposits to the Customer Inventory, in oz | 0 OZ//BRINKS |

| No of oz served (contracts) today | 121 notice(s) 12100 OZ 0.37763 TONNES |

| No of oz to be served (notices) | 416 contracts 41,600 OZ 1.2939 TONNES |

| Total monthly oz gold served (contracts) so far this month | 28,501 notices 2,850,100 oz 88.650 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: NIL oz

we have 0- customer deposit:

total deposit nil oz

customer withdrawals: 1

BRINKS; 9806.05 oz (305 kilobars)

this is a paper transfer out of the comex and onto London

TOTAL WITHDRAWALS 9806.05 0z

Adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE

For the front month of JUNE we have an oi of 537 contracts having LOST 439 contracts. We had 462 contracts served on Thursday so we gained a small 23 contracts or 2300 oz additional oz will stand for gold at the comex as they underwent a queue jump to take delivery on this side of the pond.. We saw 0 gold leaving the comex despite the high 90 tonnes standing for delivery.

JULY LOST 27 CONTRACTS TO STAND AT 1995

AUGUST GAINED 3084 CONTRACTS UP TO 380,079 CONTRACTS

We had 121 contracts filed for today representing 12100 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 25 notices were issued from their client or customer account. The total of all issuance by all participants equate to 121 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 8 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for June /2024. contract month, we take the total number of notices filed so far for the month (28,501) x 100 oz ) to which we add the difference between the open interest for the front month of JUNE (537 CONTRACTS) minus the number of notices served upon today (121 x 100 oz per contract( equals 2,891,700 OZ OR 89.94 TONNES.

thus the INITIAL standings for gold for the JUNE contract month: No of notices filed so far (28,501 x 100 oz +we add the difference for front month of June (537 OI} minus the number of notices served upon today (121) x 100 oz which equals 2,891,700 oz (89.94 TONNES)

TOTAL COMEX GOLD STANDING FOR JUNE: 89.94 TONNES WHICH IS ABSOLUTELY HUGE FOR THIS VERY ACTIVE DELIVERY MONTH IN THE CALENDAR. JUNE IS TRADITIONA;LLLY THE 2ND HIGHEST DELIVERY MONTH OF THE YEAR. FROM THIS POINT WE WILL GAIN IN GOLD TONNAGE WILLING TO STAND AT THE COMEX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX84XXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,652,260.493 51.39 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,666,253.917 OZ

TOTAL REGISTERED GOLD 7,989,995 ( 242.58 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,676,258.868OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,337,735 oz (REG GOLD- PLEDGED GOLD)= 197.13 tonnes //

END

SILVER/COMEX

JUN 7/2024

INITIAL

//2024// THE JUNE 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,186,759.200 oz Brinks HSBC JPMorgan . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 608,857.990 oz Delaware Loomis |

| No of oz served today (contracts) | 200 CONTRACT(S) (1.0 MILLION OZ) |

| No of oz to be served (notices) | 123 contracts (0.615 million oz) |

| Total monthly oz silver served (contracts) | 1105 Contracts (5.525 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 deposits customer account:

i)Into Delaware: 1006.990 oz

ii) into Loomis: 607,851.00 oz

total customer deposit 608,857.990 oz

JPMorgan has a total silver weight: 128.416million oz/295.631million or 48.34%

adjustment: 0//

Comex withdrawals: 3

i) out of Brinks 2978/100 oz

ii) out of JPMorgan: 580,672/400 oz

iii) Out of HSBC 603,108.700 oz

total withdrawal: 1,579,765.094 0z

TOTAL REGISTERED SILVER: 62.494MILLION OZ//.TOTAL REG + ELIGIBLE. 295.630

million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE:

silver open interest data:

FRONT MONTH OF JUNE/2024 OI: 323 CONTRACTS HAVING GAINED 252 CONTRACT(S).

WE HAD 0 NOTICES SERVED UP ON THURSDAY, SO WE GAINED 252 CONTRACTS OR AN ADDITIONAL 1.2600 MILLION OZ WILL STAND AT THE COMEX VIA A MASSIVE QUEUE JUMP

JULY SAW A LOSS OF 1760 CONTRACTS DOWN TO 126,719

AUG, SAW A GAIN OF 91 CONTRACTS TO 191

SEPT SAW A GAIN OF 1535 CONTRACTS TO 36,989.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 200 for 1.0 MILLION oz

CONFIRMED volume; ON THURSDAY 108,030 MEGA GIGANTIC

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1105 x 5,000 oz = 5.525 MILLION oz

to which we add the difference between the open interest for the front month of JUNE ((323) and the number of notices served upon today 200 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2024 contract month: 1105 notices served so far) x 5000 oz + OI for the front month of JUNE (323)x number of notices served upon today minus (200)x 5000 oz of silver standing for the JUNE contract month equates to 6.140 MILLION OZ.

New total standing: 4.880 million oz.

There are 62.494 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

JUNE 7 WITH GOLD DOWN $64.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 3.56 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 837.11 TONNES

JUNE 6 WITH GOLD UP $16.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.34 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 833.55 TONNES

JUNE 5 WITH GOLD UP $32.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 4 WITH GOLD DOWN $20.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 3 WITH GOLD UP $22.85 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 31 WITH GOLD DOWN $19.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 30 WITH GOLD UP $3.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 29 WITH GOLD DOWN $13.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 28 WITH GOLD UP $22.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 832.21 TONNES

MAY 24 WITH GOLD DOWN $2.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 833.36 TONNES

MAY 23 WITH GOLD DOWN $53.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 22 WITH GOLD DOWN $32.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 21 WITH GOLD DOWN $12,00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 20 WITH GOLD UP $21.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.10 TONNES OF GOLD INTO THE GLD//NEW TOTAL 838.54 TONNES

MAY 17 WITH GOLD UP $31.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//NEW TOTAL 833.36 TONNES

MAY 16 WITH GOLD DOWN $7.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//NEW TOTAL 833.36 TONNES

MAY 15 WITH GOLD UP $34.90 ON THE DAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD/INVENTORY RISES TO 831.93 TONNES

MAY 14 WITH GOLD DOWN $17.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RISES TO 831.33 TONNES

MAY 13 WITH GOLD DOWN $31.10 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD////INVENTORY RISES TO 831.93 TONNES

MAY 10 WITH GOLD UP $34.65 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 9 WITH GOLD UP $18.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 8 WITH GOLD DOWN $0.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 830.47 TONNES

MAY 7 WITH GOLD DOWN $6.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 832.19 TONNES

MAY 6WITH GOLD UP $21.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .55 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 831.64 TONNES

MAY 2 WITH GOLD UP $0.20 ON THE DAY; SMAKK CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 830.47 TONNES

MAY 1 WITH GOLD UP $7.80 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNES

GLD INVENTORY: 837.11 TONNES, TONIGHTS TOTAL

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 7 WITH SILVER DOWN $1.93 TODAY: NO CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY AT 417.944 MILLION OZ

JUNE 6 WITH SILVER UP $1.27 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 417.944 MILLION OZ

JUNE 5 WITH SILVER UP 0.38 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.52 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 415.295 MILLION OZ

JUNE 4 WITH SILVER DOWN $1.08 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

JUNE 3 WITH SILVER UP $0.35 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

MAY 31 WITH SILVER DOWN $1.09 TODAY: HUGE CHANGES IN SILVER INVENTORY: A MASSIVE WITHDRAWAL OF 3.655 MILLION OZ FROM THE SLV//INVENTORY LOWERS TO 413.775 MILLION OZ

MAY 30 WITH SILVER DOWN $0.80 TODAY: NO CHANGES IN SILVER INVENTORY//INVENTORY REMAINS AT 417.430 MILLION OZ

MAY 29 WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 1.051 MILLION OZ INTO THE SLV//INVENTORY DECREASES TO 417.430 MILLION OZ

MAY 28 WITH SILVER UP $1.64 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 2.832 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 418.481 MILLION OZ

MAY 24 WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF .822 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 421.313 MILLION OZ

MAY 23 WITH SILVER DOWN $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.736 MILLION OZ FROM THE SLVINVENTORY INCREASES TO 420.491 MILLION OZ

MAY 22 WITH SILVER DOWN $0.66 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 21 WITH SILVER DOWN $0.41 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A DEPOSIT OF 3.792 MILLION OZ FROM THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 20 WITH SILVER UP $1.28 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 1.005 MILLION OZ FROM THE SLV// INVENTORY LOWERS TO 418.435 MILLION OZ

MAY 17 WITH SILVER UP $1.37 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 868,000 OZ FROM THE SLV// INVENTORY LOWERS TO 419.440 MILLION OZ

MAY 16 WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY REMAINS AT 420.308 MILLION OZ

MAY 15 WITH SILVER UP 101 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A WITHDRAWAL OF 1.919 MILLION OZ FROM THE SLV NVENTORY RESTS AT 420.308 MILLION OZ

MAY 14 WITH SILVER UP 25 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;INVENTORY RESTS AT 422.227 MILLION OZ

MAY 13 WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;NVENTORY RESTS AT 422.227 MILLION OZ

MAY 10 WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A HUGE WITHDRAWAL OF 1.,828 MILLION OZ//INVENTORY RESTS AT 422.227 MILLION OZ

MAY 9 WITH SILVER UP 78 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 8 WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 7WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 6 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.055 MILLION OZ

MAY 3 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 2WITH SILVER UP 0.12 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/ A WITHDRAWALOF 4.471 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 1 WITH SILVER UP 0.09 TODAY: SMALLCHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF ,457 MILLION OZ INTO THE SLV INVENTORY RESTS AT 429.814 MILLION OZ

CLOSING INVENTORY 417.944 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/GOLD AND SILVER COMMENTARY

JAN NIEUWENHUIJS

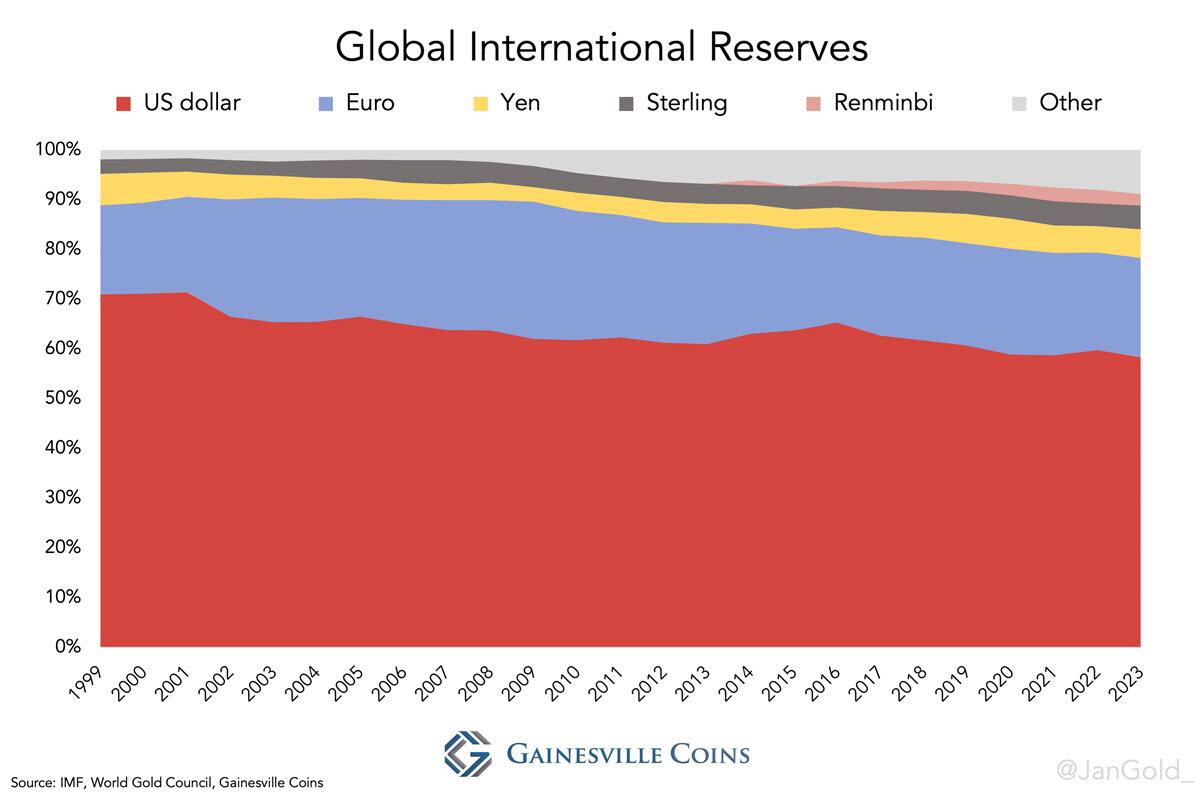

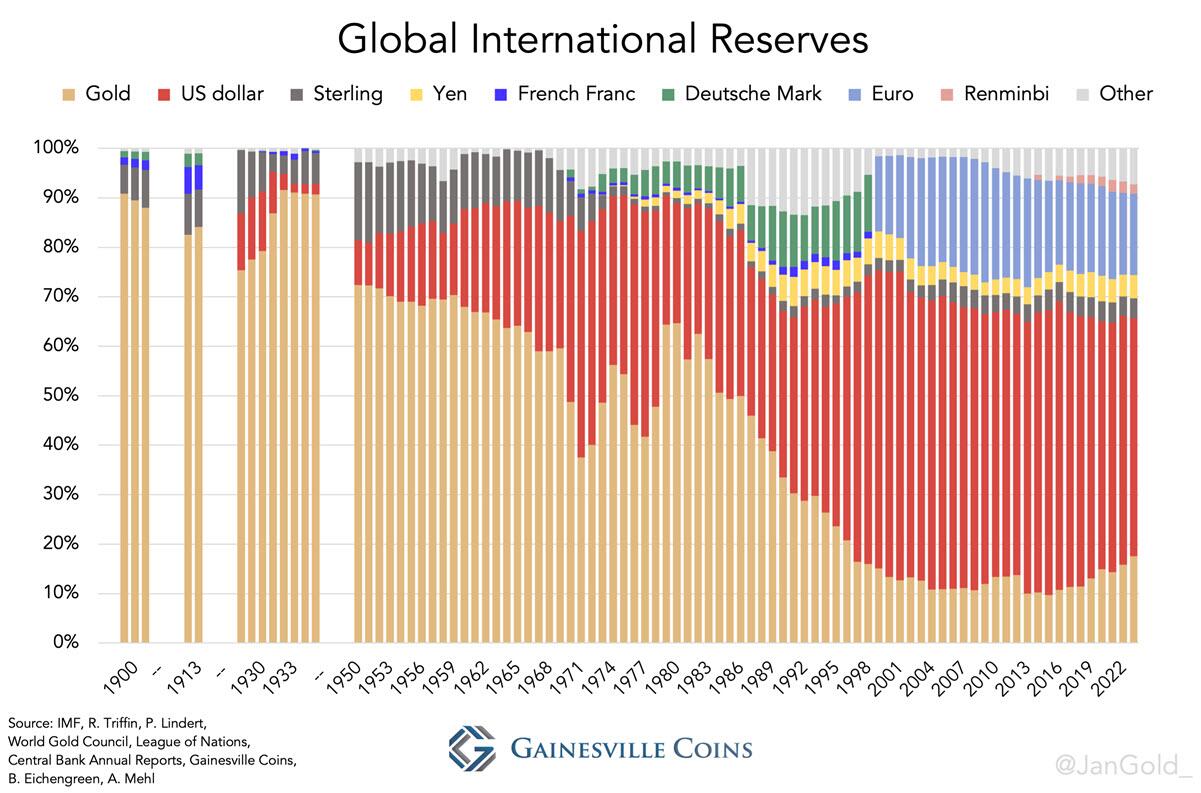

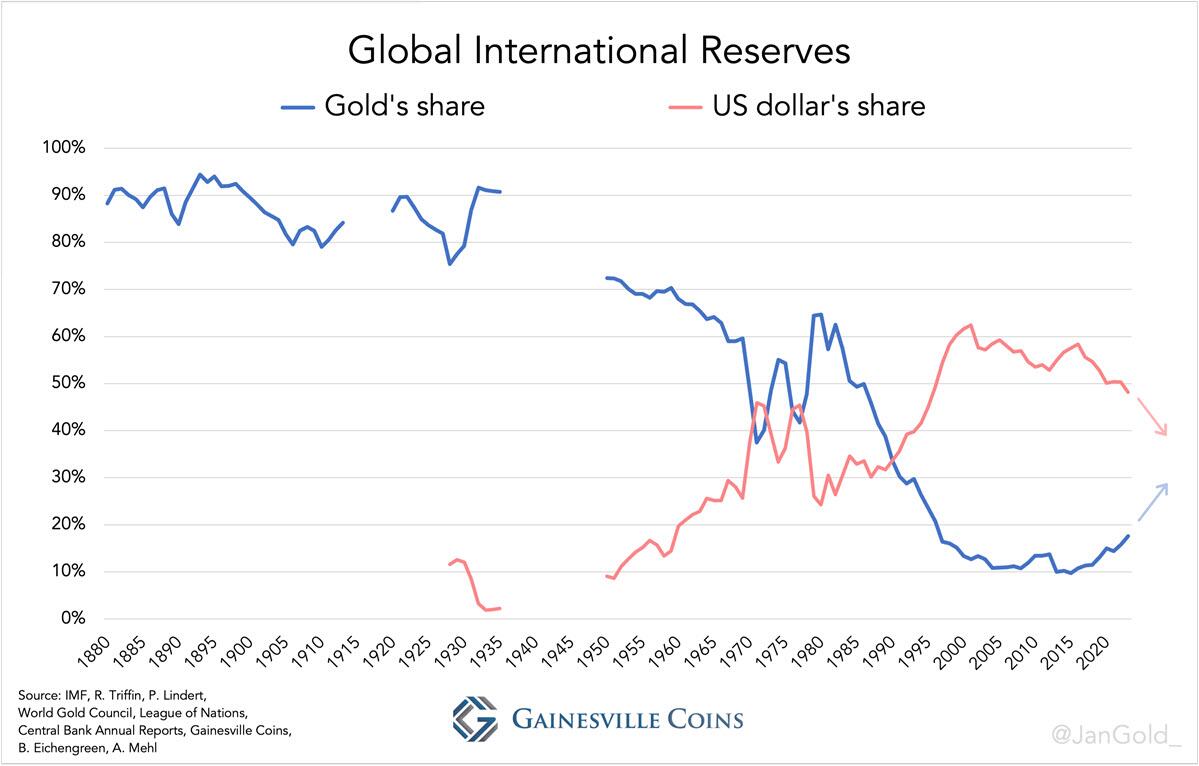

Gold Overtakes Euro in Global International Reserves

FRIDAY, JUN 07, 2024 – 06:30 AM

ByJan Nieuwenhuijs of Gainesville Coins

Sturdy central bank gold buying since 2009 and a rising gold price has grown the precious metal’s share of global international reserves to the detriment of fiat currencies. By the end of 2023 gold surpassed the euro and the next fiat currency to be challenged is the US dollar.

Often when financial analysts draw charts on the distribution of international reserves they focus on foreign exchange (omit gold) and start when the euro was introduced in 1999. Based on such charts the dollar’s share of total reserves appears to be falling slowly, from a peak of 72% in 2001 to 58% in 2023. In addition, it seems there is not one specific currency that is competing with the dollar.

But why not include gold and look back as far as possible? By combining multiple sources, we get a glimpse of the dissemination of reserve currencies from 1899 until 1935 (both fiat and gold), and a full picture starting from 1950.

This paints a whole different story. Instead of showing only the demise of the dollar at snail pace, the historic balance between gold and fiat currencies is revealed. It’s not the dollar that normally backs the international monetary system, it’s gold. Gold used to make up the majority of international reserves, even when sterling was said to be the world reserve currency before the dollar. In a chart covering more years but only gold and the dollar, the latter’s reign becomes even more relative.

The above chart displays that the dollar’s share of total reserves has fallen to 48% in 2023—caused by a declining trust in “credit assets” (fiat currencies), due to worrying asset bubbles, escalating wars, and fear of inflation—while gold is making ground.

Based on personal calculations of official gold reserves that include covert acquisitions, for example by the Chinese central bank, gold’s percentage of total reserves reached 18% in 2023, up from 11% in 2008. Gold has currently surpassed the euro, which got stuck at 16%. As the problems haunting fiat currencies won’t fade anytime soon it’s possible gold will overtake the dollar as well in the decade ahead (explained more detailed here).

Be sure not to miss the X-post below that includes a video illustrating the development of reserve assets since 1950 in a bar chart race!

Gold overtakes the euro in global international reserves. In our annual update of the chart below on global international reserves, it shows gold has a greater share than the euro since late 2023. We are of the opinion that gold is at the start of a multi-year bull market because there currently is too much confidence in “credit assets,” which will result in capital flowing from national currencies, bonds, and stocks into gold (as we explained here: https://shorturl.at/xQfzQ). Gold’s rising share in international reserves is a reflection of this trend—although we are just at the beginning. Kindly note, we calculate world official gold reserves differently than the IMF, as we take into account “unreported” purchases by China, Saudi Arabia, and other countries (more here: https://shorturl.at/U4IV1).

0:46

·

134.9K Views

end

ALASDAIR MACLEOD…

Chinese demand is driving gold and silver

Despite continuing efforts by the paper establishment in western capital markets to shake out weak gold and silver holders, they are being swamped by Chinese physical demand.

| MACLEODFINANCEJUN 7 |

This week has seen underlying firmness in gold and silver markets, with gold trading at $2351 in European trade this morning, up $25, and silver at $30.82, up 45 cents. Silver was especially volatile, falling sharply mid-week before rallying over 4% yesterday. Being Friday and China off for the weekend, the shorts are taking the opportunity to unwind some of yesterday’s rise.

Having had such strong rises since mid-February, technical analysts have been calling for more consolidation before a resumption of this bull phase. The position for gold is shown next:

So far, gold has reacted to find support at the 55-day moving average, but the longer-term 12-month average is still below $2100, suggesting that a deeper correction is possible. The technical chart for silver is next

Technicians would argue that the silver price is still too far above its moving averages for comfort. It would be wrong to dismiss these concerns out of hand, but there are more important forces at play.

The next chart shows that gold is closer to being oversold than most analysts think:

Why have I taken Comex’s open interest as the indicator? Because it encapsulates the combined positions of all categories on Comex. The solid line at 450,000 contracts clearly indicates an oversold market, strongly suggesting that we are near to a price bottom.

But the clincher is the rate at which physical metal is draining from western vaults. According to Doug Casey’s Substack latest post, huge premiums in Shanghai are draining western vaults, with LBMA’s vaulted silver stocks falling 60% this year so far, and Comex’s falling by 46%. Gold’s drain has been less dramatic perhaps, but recent days have seen record stand-for-deliveries. In the last eight trading sessions, nearly 90 tonnes of gold have been stood for delivery taking the total so far to 253 tonnes, a rate which easily exceeds this year’s US gold mine annual output estimated by Metal Focus at 166 tonnes.

In previous postings, I have pointed out that it is massive Chinese household savings with unattractive alternatives driving demand, and this was evidenced yesterday (Thursday). Changing the pattern of recent trading sessions, gold and silver prices opened higher indicating overnight demand had returned. It was less in evidence this morning, but then on a Friday Chinese futures speculators (yes, there are some!) were probably closing positions before the weekend.

In other news, the ECB lowered its benchmark deposit rate by ¼% from 4%, the first of the majors to do so. Markets are buzzing with hope that the Fed and others will follow suite. But with budget deficits continuing to run high, inflation is far from over, and in the next few months we will see how funding them progresses, bearing in mind that immediate liquidity is drying up reflected in the US’s Reverse Repo position:

Most of this has gone into T-bills, funding the deficit and being spent on non-production. Liquidity is clearly running dry and higher borrowing costs beckon.

3. CHRIS POWELL//GATA DISPATCHES

CHRIS POWELL…

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS/

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT//

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

ASIA TRADING//FRIDAY MORNING/THURSDAY NIGHT

SHANGHAI CLOSED UP 2.49 PTS OR 0.08% //Hang Seng CLOSED DOWN 109.85 PTS OR 0.59%// Nikkei CLOSED DOWN 19.58 OR 0.05%//Australia’s all ordinaries CLOSED UP .48%///Chinese yuan (ONSHORE) closed UP TO 7,2415 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2498/ Oil UP TO 76.08 dollars per barrel for WTI and BRENT UP AT 80.32 /Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2415

OFFSHORE YUAN: UP TO 7.2494

SHANGHAI CLOSED UP 2.49 PTS OR 0.08 %

HANG SENG CLOSED DOWN 109.85 PTS OR 0.59%

2. Nikkei closed DOWN 19.58 PTS OR 0.05 %

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 104.00 EURO RISES TO 1.0896 UP 5 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +0.994 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 156.15 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.5740/Italian 10 Yr bond yield UP to 3.907 SPAIN 10 YR BOND YIELD TO 3.355%

3i Greek 10 year bond yield UP TO 3.617

3j Gold at $2336.70//Silver at: 30.35 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 19/ 100 roubles/dollar; ROUBLE AT 88.60

3m oil into the 76 dollar handle for WTI and 80 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 155.61/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.994% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8896 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9695 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.298 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.447 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.748 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.27…

10 YR UK BOND YIELD: 4.224 UP 4 PTS

2a New York OPENING REPORT

Global Rally Sputters With US Futures Flat Ahead Of Payrolls

BY TYLER DURDEN

FRIDAY, JUN 07, 2024 – 08:10 AM

The global stock rally faltered as US equity futures were unchanged for the second day in a row this morning and trading right on top of the “gamma gravity” level of 5350, where as discussed yesterday there is a record $10 billion dealer long gamma pile up which has made the market “stuck” at the strike price.

As of 7:30am ET, S&P futures are down -0.1%, at session lows after trading in a narrow range all night. Nasdaq futures are a mirror image, trading about 0.1% higher as Mega tech names outperform: GOOGL +27bp, NVDA +13bp, AAPL +12bps. Bond yields are 1-2bp higher this morning, with the OIS forwards sees ~60% prob. of first cut in September. Commodities are mixed: oil/ags are slightly higher this morning reversing an earlier loss. The Bloomberg dollar gauge eased. All eyes on NFP today (preview here): both Goldman (165K) and JPM (150k) are below the Street median estimate of 180k, which suggests we beat.

In premarket trading, GameStop tumbled after surging as high as $67.5 after hours yesterday when the company confirmed that the latest meltup was another manipulative grift when it filed to sell up to 75 million shares. Tech names outperformed: Micron and Intel rose while tech giants gained (GOOGL +27bp, NVDA +13bp, AAPL +12bps). Here are some other notable premarket movers:

- Biomea Fusion shares plunge 61% after the biotech said the FDA had placed a clinical hold on its ongoing Phase I/II trials of BMF-219 in type 1 and type 2 diabetes. Analysts slashed their price targets on the stock.

- Braze shares jump 14% after the cloud-based software company boosted its revenue guidance for the full year; the guidance beat the average analyst estimate.

- Concrete Pumping shares slide 13%. William Blair analysts cut the rating on the stock to market perform from outperform.

- DocuSign shares are down 8.4% after the e-signature company forecast billings for the second quarter that fell short of the average analyst estimate.

- Geron shares rise 16% after the biopharmaceutical company secured approval for its blood disorder drug named Rytelo from the FDA.

- Lyft shares gain 3.5% after Loop Capital lifted its rating on the ride-hailing firm, citing a positive investor day and recent stock retreat.

- Samsara shares fall 6.2% despite the application software company reporting first-quarter results that beat expectations and raising its full-year forecast.

- Vail Resorts shares slump 8.5% after the ski resort operator cut its full-year Ebitda outlook. The guidance missed the average analyst estimate.

With traders wary of placing big bets either way ahead of the payrolls report, global stocks are on track to snap a two-week losing stretch. Rate-cut expectations have escalated in the past week, encouraged by a slew of weaker-than-forecast US data, as well as easing by the Bank of Canada and ECB. A Bloomberg gauge of global government bonds posted its longest rising streak since November.

“All focus on the payrolls and the potential aftermath,” said Michael Brown, senior strategist at Pepperstone Group Ltd. “A number that’s bang in line with expectations will reaffirm where current market pricing is for Fed cuts and could give the market the fuel it needs to keep moving higher.”

As previewed earlier, Friday’s report is expected to show the US added 180,000 jobs in May, slightly more than in April, with the unemployment rate seen holding steady. Swap markets are pricing a full Fed rate cut by November, with a strong likelihood of one in September. In its preview, Goldman’s trading desk wrote that the set up into the print remains favorable for stocks (“I have goldilocks zone in the low 100s as stocks continue to cheer for a palatable slowdown”), and provided the following trading framework:

- <50k S&P + 50bps

- 50k – 100k S&P +75 – 100bps

- 100k – 150k S&P +100bps

- 150k – 200k S&P + / – 50bps

- 200k – 250k S&P -50bps

- 250k – 300k S&P -75bps

- >300k S&P sells off more than 100bps

Meanwhile, as bond yields drop and as rate-cut bets build, investors are pouring money into stocks, with US equity funds getting $4.6 billion in a seventh week of inflows, BofA’s Michael Hartnett said, although the strategist warned a Fed rate cut may not be entirely good news, calling it the “first hint of trouble.” Chances of a hard landing could increase if the market grows more confident of lower borrowing costs, he added.

European stocks and bonds fall after several ECB policymakers offered wary assessments of the possibility of future interest-rate cuts. The move lower extended after the ECB’s preferred measure of pay showed acceleration at the start of 2024. The Stoxx 600 is down 0.4% with technology and retail stocks the biggest outperformers, while property and insurance stocks lagged, given the ECB’s signal that it wouldn’t rush additional rate cuts. Here are the biggest movers Friday;

- ING Groep NV shares rise as much as 1.5% after Barclays upgrades the Dutch lender to overweight from equal-weight, with models pointing to €7.5 billion more in buybacks before the end of next year

- Bellway shares rise as much as 2.1% after it delivered an upbeat trading update that shows the UK housebuilder on track to build 7,500 homes this year at a higher selling price than previously expected

- Tecnicas Reunidas climbed as much as 8.9% after Oddo BHF raised the recommendation on the Spanish company to outperform from neutral as risk/reward profile seen attractive.

- Daimler Truck drops as much as 2.5%, Volvo -2.4% after Citi says it has been a “roller coaster” for truck stocks this year, as it opens 90-day downside catalyst watches on the two companies with likely weaker orders and margins set to drive downgrades

- Rexel shares fall as much as 3.4% to hit a one-month low after the French provider of electrical supplies released new and upgraded medium-term financial targets ahead of a capital markets day on Friday

- Arcadis NV shares slip as much as 3.5% after the Dutch engineering firm is downgraded to accumulate from buy at KBC Securities, which highlights an absence of “substantial” short-term triggers for the stock

- Burckhardt Compression declines as much as 6.1%, snapping four days of gains, as Baader Helvea downgrades to reduce from add, saying it’s time to take profits with shares of the piston compressor manufacturer having surged to record highs

- C&C shares fall as much as 13% after the UK alcoholic beverage manufacturer announced an €150 million impairment charge and as CEO Patrick McMahon has resigned due to previously disclosed accounting adjustments.

Earlier, Asian stocks gained, set for their best week in three weeks, as a rally in South Korean shares tempered losses in most other markets. The MSCI Asia Pacific Index rose as much as 0.4%. South Korean equities were among the biggest advancers on the regional gauge after the market reopened from a holiday. The country’s stock markets were supported by foreign buying of local chipmakers. Indian shares also climbed, as the central bank held its benchmark interest rate while tweaking growth projection higher. Chinese stocks declined for the third straight session, with stronger-than-expected exports for May failing to boost sentiment. There are also concerns that a growing backlash among trade partners would dent overseas demand even as consumer spending remained weak at home.

While “we are constructive on Asia markets,” the second half has risks including a stronger dollar, geopolitical uncertainty and possible volatility around the US elections, Timothy Moe, an Asia equity strategist at Goldman Sachs Group Inc., told Bloomberg TV.

In FX, the Bloomberg Dollar Spot Index was little changed with focus on the US non-farm payrolls data, which is expected to show a steady unemployment rate and 180k jobs added in May, according to a Bloomberg survey of economists

- USD/JPY dropped as much as 0.3% before paring to trade unchanged at 155.59; Japanese Minister of Finance Shunichi Suzuki said authorities should resort to currency intervention only on a limited basis

- GBP/USD steadied around 1.28; Data showed the UK housing market extended its stagnation in May, a measure of property values fell 0.1% after no change the month before

- EUR/USD was little changed at 1.09; The ECB’s preferred measure of euro-zone pay showed acceleration at the start of 2024

In rates, Treasuries dipped ahead of the jobs report, with US 10-year yields rising 1bps to 4.30%. German 10-year yields rise 3bps to 2.58%.

In commodity markets, gold prices fell after the People’s Bank of China said it hadn’t added to its bullion holdings last month, pausing an 18-month long buying spree that lifted the precious metal to record highs. Brent crude futures edged up, but were set for a third weekly loss. Spot gold fell ~$37 to around $2,338 after data showed the Chinese central bank halted gold purchases in May.

Today’s focus will be on the payrolls report at 8:30am; data also includes April wholesale trade sales (10am), 1Q household change in net worth (12pm) and April consumer credit (3pm). Fed officials are expected to refrain from commenting until after their June 12 policy announcement

Market Snapshot

- S&P 500 futures little changed at 5,366.75

- STOXX Europe 600 down 0.1% to 523.93

- MXAP up 0.3% to 180.71

- MXAPJ up 0.3% to 563.66

- Nikkei little changed at 38,683.93

- Topix little changed at 2,755.03

- Hang Seng Index down 0.6% to 18,366.95

- Shanghai Composite little changed at 3,051.28

- Sensex up 1.8% to 76,403.28

- Australia S&P/ASX 200 up 0.5% to 7,860.02

- Kospi up 1.2% to 2,722.67

- German 10Y yield little changed at 2.56%

- Euro little changed at $1.0890

- Brent Futures down 0.4% to $79.59/bbl

- Gold spot down 1.0% to $2,351.54

- US Dollar Index little changed at 104.10

Top Overnight News

- Japan’s largest banks plan to sell 1.32 trillion yen ($8.5 billion) of Toyota shares, people familiar said, the strongest sign yet that the country’s big businesses are serious about unwinding their cross-shareholdings. BBG

- China’s May exports beat expectations, climbing 7.6% in dollar terms from a year earlier. Still, Bloomberg Economics said the lift from firmer overseas demand probably won’t be enough to offset domestic weakness, which showed through in May’s unexpectedly weak import growth of 1.8%. BBG

- China halts its 18-month gold purchase spree (the PBOC didn’t purchase any gold last month, the first time it hasn’t done so since Oct ’22). BBG

- The ECB’s preferred measure of euro-zone pay showed acceleration at the start of 2024, in the latest sign that price pressures in the region are proving stubborn. Compensation per employee rose by 5.1% from a year ago in the first quarter, up from a revised 4.9% in the previous three months, ECB data showed Friday. That exceeded a Bloomberg Economics forecast of 4.6%. BBG

- The European Commission has recommended that the EU start accession talks with Ukraine this month, in an effort to signal support to the war-torn country before Budapest takes over the rotating presidency of the bloc, according to people familiar with the matter. FT

- The estimated $4.6 trillion cost of extending expiring portions of Donald Trump’s 2017 tax cuts isn’t damping Republican enthusiasm for renewal next year. However, this time the nation’s debt load and interest costs are heavier burdens, requiring unprecedented budget pain to offset the lost revenue. BBG

- Moody’s warns 6 regional banks, including FRME (First Merchants), FNB (F.N.B Corp.), FULT (Fulton Financial), ONB (Old National), PGC (Peapack-Gladstone), and WAFD (WaFd), are at risk of being downgraded over their CRE exposure. BBG

- A risky style of trading is roaring back in popularity, driven by amateur traders who call themselves “degens” and pile into long-shot trades that proudly have nothing to do with conventional ways of assessing investments. Some are flinging cash at specific stocks or cryptocurrencies just to be part of a movement. Others are sticking around for the jokes and memes. Degens are part of the fuel for meme-stock mania, like the logic-defying action in GameStop shares in recent weeks. When these internet-fueled traders stick together, they have the potential to spark wild swings in assets. All it takes is for a meme to catch fire. WSJ

- A federal judge in San Francisco dismissed a proposed class action against Google (GOOG), which had alleged the company misused personal and copyrighted data to train its AI systems, including its Bard chatbot, according to Reuters.

- South African ANC Leader Ramaphosa said they have agreed that they will invite parties to form a government of national unity, according to Reuters.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed in cautious and tentative trade and macro newsflow on the quieter side ahead of the US jobs report. ASX 200 was kept afloat by gains in gold miners, alongside Resources and Materials names. while Real Estate and Healthcare lagged. Nikkei 225 was subdued following softer-than-expected household spending data. On an index level, gains in Pharma and Mining failed to counter the downside from Banking and Autos, with the latter continuing to feel the woes from its domestic safety scandal. Hang Seng and Shanghai Comp both dipped into the red after opening modestly firmer, whilst CATL shares tumbled some 7% after US lawmakers said Chinese EV battery manufacturers rely on forced labour and should be blocked from importing goods into the US. No reaction was seen on the Chinese trade data.

Top Asian News

- Japanese Foreign Reserves USD 1.2316tln at end-May (vs USD 1.2790tln at end-April), according to MOF. “Japan’s holdings of foreign securities dropped sharply in May, indicating that the government likely financed most of its recent record currency market intervention by selling Treasuries and other foreign securities and still has ample firepower to step into markets again.” – via Bloomberg.

- Japanese Finance Minister Suzuki said the drop in Japan’s foreign reserves as of end-May partially reflects FX intervention; and will take action against excessive forex moves. Forex intervention was conducted to address excessive moves. Forex intervention should be done in a restrained manner. Not taking into account the limit to reserves for forex intervention.

- BoJ offered to buy JPY 150bln in up to 1yr JGBs, JPY 375bln in 1-3yr JGBs, JPY 425bln in 5-10yr JGBs and JPY 150bln in 10yr-25yr JGBs; all unchanged.

- PBoC injected CNY 2bln via 7-day reverse repos with the rate at 1.80%.

- RBI maintained its Repo Rate at 6.50% as expected and maintained its policy stance as expected. FY25 real GDP growth was upgraded to 7.2% vs 7% previously. RBI Chief said risks to growth and inflation are evenly balanced and the RBI will remain resolute in commitment to aligning inflation to target.

- TSMC (TSM / 2330 TT) May Sales TWD 229.6bln, +30.06% Y/Y

- BoJ may drop clue on bond tapering plans next week, via Reuters citing sources; there is no consensus yet. Could trim monthly purchases or clarify plans to proceed with a slow but steady taper, according to the sources.The decision could be delayed if the bond market becomes too volatile. Focus would be to avoid abut spikes in yields.

- China extends anti-dumping duties on the imports of some chemicals from India for a five-year period as of 8th June.

European bourses, Stoxx 600 (-0.2%) began the session on a tentative footing, in what was initially directionless trade. However, as the morning progressed, sentiment quickly waned and stocks trundled lower to session lows, where they currently reside. European sectors hold a negative bias, and with the breadth of the market fairly narrow. Tech takes the spot, continuing to build on the past week’s outperformance. Real Estate is found at the foot of the pile after Morgan Stanley downgraded Vonovia (-3.7%) and Leg Immobilien (-3.8%). US Equity Futures (ES U/C, NQ +0.1%, RTY U/C) are mixed and with trade tentative ahead of today’s US employment report, where expectations are for the headline to tick higher to 185k from 175k.

Top European News

- German Economy Minister says if things go well will have 1-1.5% growth next year.

ECB Speakers

- ECB’s Kazaks says victory over inflation is not yet on hand; any further rate cuts should be gradual; the next steps are data dependent and will be meeting by meeting, via Bloomberg.

- ECB’s Muller says they need to be cautious when making decisions and should not be in a rush to cut.

- ECB’s Nagel says ECB policy is not on auto pilot when it comes to rate cuts; inflation is proving to be stubborn, especially in the case of services. Negotiated wages are expected to rise particularly sharply this year and continue to see strong growth thereafter. The decision to cut was logical, tendency is there that inflation is going down. Decision to cut was not premature. Still acting restrictively despite lowered rates. Not on autopilot, will look at the data and make a decision at each meeting. Says “well on the way” when it comes to the balance sheet reduction

- ECB’s Vasle says cannot predetermine path of ECB interest rates.

- ECB’s Simkus says more than one cut this year is a possibility. Data clearly show disinflation and inflation returning to target but the road is bumpy.

- ECB’s de Guindos says inflation will be around 2% next year, sees huge uncertainties on the economy.

- ECB’s Rehn says inflation will continue to decline, rate cuts will also bolster the economies recovery.

- ECB’s de Guindos says sometimes in order to attain cross-border merger, need to engage with national consolidation first.

- ECB’s Makhlouf says unsure how fast the ECB will carry on with rate reductions, or if at all.

- ECB’s Schanbel says the lack of fiscal consolidation, despite high debt levels may impede monetary policy and heighten the risk of fiscal dominance.

- ECB’s Holzmann says “my decision on rates was based on the latest data and forecasts; fight against inflation is not over yet”. “Currently I see little risk of a second inflation wave but inflation is stickier than expected”.

FX

- USD is steady vs. peers ahead of the crucial jobs report due at 13:30BST. Levels to the downside for DXY include; 103.99 a double bottom from overnight and Tuesday. To the upside, focus remains on whether the index can move beyond its 200 and 100DMAs at 104.40 and 104.43 respectively.

- EUR is flat vs. the USD as the dust settles on yesterday’s ECB rate cut, and unreactive to the slew of ECB speakers today. As it stands, the next 25bps reduction is not fully priced in until December. Upside for EUR/USD sees the 1.09 mark.

- GBP is flat against both USD and EUR. Cable remains within yesterday’s 1.2763-1.2809 range, which could be tested by the upcoming NFP release. Tuesday’s 1.2818 high was the highest since March 14th.

- JPY is the marginal outperformer vs the Dollar, currently within a 155.13-93 range. NFP could prove an inflection point for the pair ahead of BoJ next week.

- Antipodeans are both steady vs. the USD in quiet newsflow with not much follow-through from Chinese trade data overnight. AUD/USD for now is contained within yesterday’s 0.6633-83 range with the pair having traded on a 0.66 handle all week.

- PBoC sets USD/CNY mid-point at 7.1106 vs exp. 7.2430 (prev. 7.1108)

Fixed Income

- USTs are marginally in the red, with no real reaction to the morning’s data points or extensive ECB speak. Focus entirely on payrolls before CPI and the FOMC next Wednesday; USTs in narrow 110-06 to 110-10 bounds which are entirely contained by Thursday’s 110-03 to 110-13 parameters.

- Bunds is softer, weighed on by the softer than expected German Industrial Output data, though were unreactive to the extensive number of ECB officials this morning; speak for the most part stuck with the party script of meeting-by-meeting and data-dependency; Bunds were essentially unchanged and at the top-end of initial 130.78-131.05 parameters but dipped to a 130.65 base on the latest EZ Q1 wage number; ECB’s Q1 Key wage indicator accelerated to 5.1% Y/Y vs. prev. 4.9% (Q4’23)

- Gilts are rangebound and unreactive to the morning’s Halifax House Price data which unexpectedly declined on the month, though the note described this as essentially unchanged.

Commodities

- Crude benchmarks are marginally in the red but have essentially been pivoting the unchanged mark in limited APAC/European trade ahead of the NFP print. Brent currently around USD 79.80/bbl.

- Precious metals were relatively contained but tumbled on the release of China’s monthly gold reserves which showed they were maintained at 72.8mln/oz. XAU slipped from USD 2373/oz to USD 2358/oz over the course of five minutes; thereafter, tumbled further to a USD 2342/oz fresh low for the session.

- Base metals are entirely in the red, with sentiment hit following the Chinese gold reserves headline.

- Chinese gold reserves 72.8mln/oz vs. prev. 72.8mln/oz; The maintained figure for the China gold reserves seemingly breaks the 18-month streak of purchases for the yellow metal.

- Chinese May iron ore imports 102.03mln tons (vs 101.82mln tons in April) Jan-May iron ore imports +7% Y/Y.

- Chinese May crude oil imports 46.97mln metric tons (vs 44.72mln tons in April); Jan-May crude oil imports -0.4% Y/Y.

- SPDR Gold Trust GLD reports holdings up 0.4% to 837.10 tonnes by June 6th.

- Chile’s state-run Codelco is said to be looking for partners on a major new lithium project slated to begin production in 2030, according to documents cited by Reuters.

- Goldman Sachs said, “Even assuming comfortable European end-October 2024 storage, we still see winter global gas price risks skewed to the upside, led by TTF.”

- Natural gas flow has restarted from the UK to Norway via Langeled pipeline, according to UK national gas data.

Geopolitics

- Hamas reportedly said that it will reject the Israeli ceasefire proposal, arguing that the proposal does not ensure a permanent end to hostilities. Hamas will continue to reject proposals until it secures a “permanent ceasefire”, via Critical Threat on X

- Israeli PM Netanhayu is to address US Congress on July 24th, according to Punchbowl’s Sherman. However, Times of Israel sources suggested July 27th.

- US military said it destroyed eight Houthi drones and two Houthi uncrewed surface vessels in the Red Sea, according to Reuters.

- Philippine Coast Guard reports that the Chinese Coast Guard intentionally rammed a Philippine Navy rubber boat transporting sick personnel, according to Reuters.

US Event Calendar

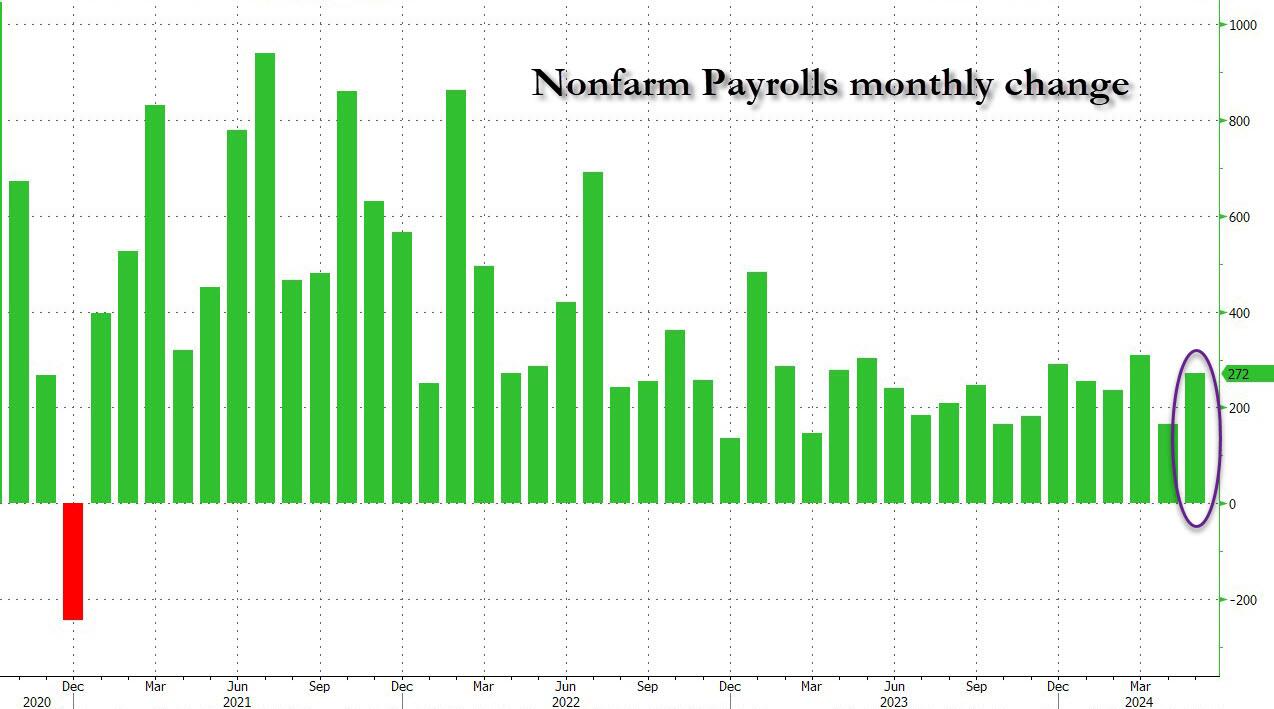

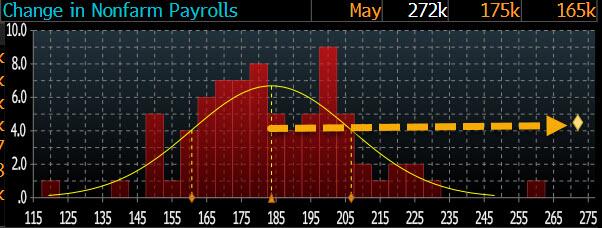

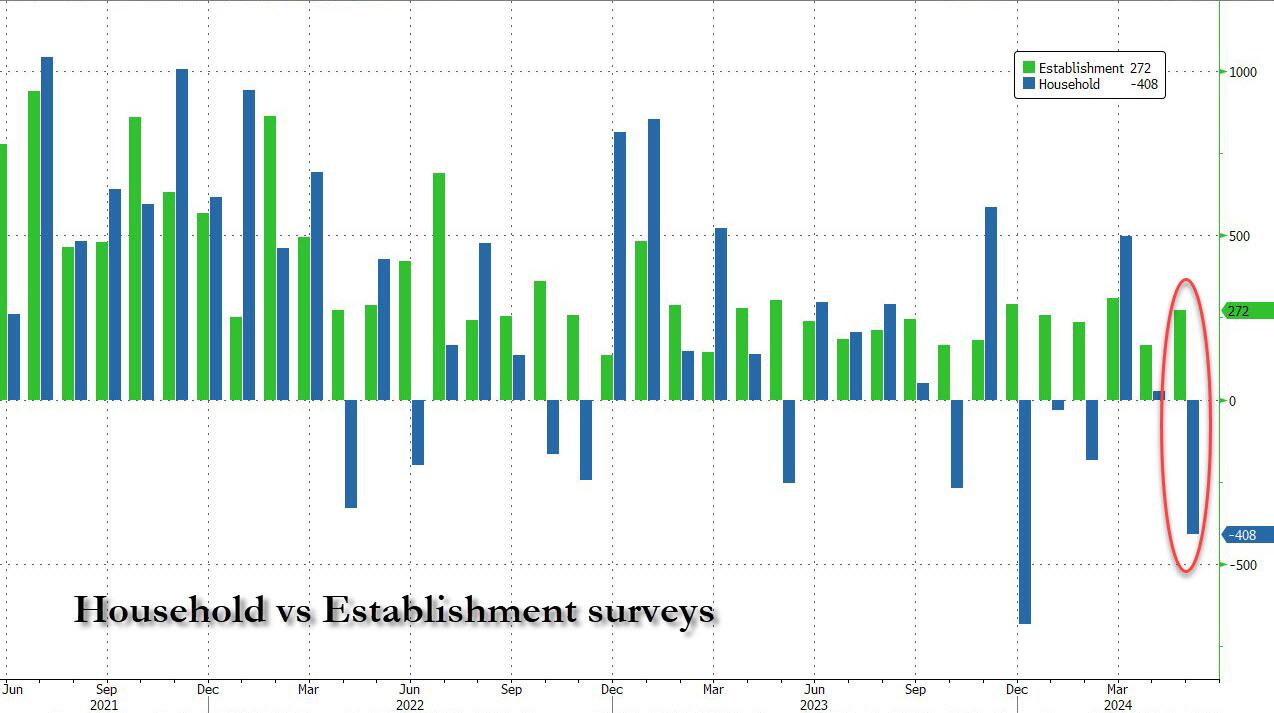

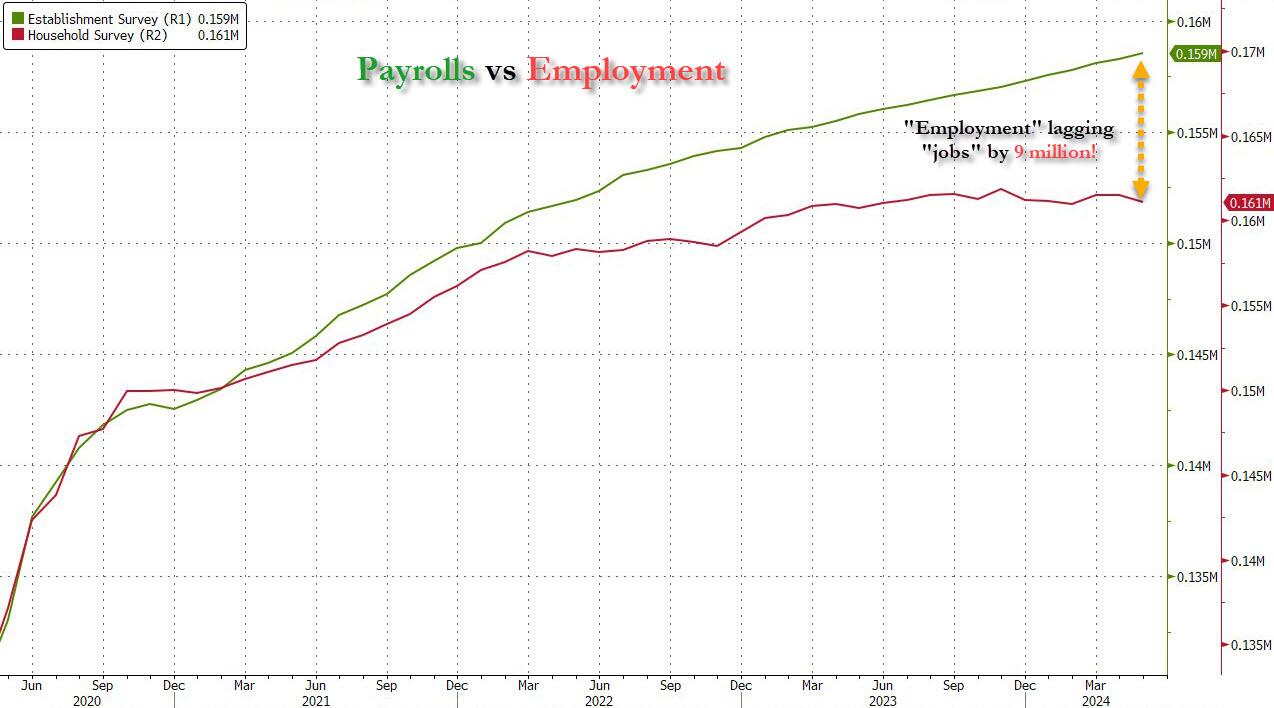

- 08:30: May Change in Nonfarm Payrolls, est. 180,000, prior 175,000

- May Change in Private Payrolls, est. 165,000, prior 167,000

- May Change in Manufact. Payrolls, est. 5,000, prior 8,000

- May Unemployment Rate, est. 3.9%, prior 3.9%

- May Underemployment Rate, prior 7.4%

- May Labor Force Participation Rate, est. 62.7%, prior 62.7%

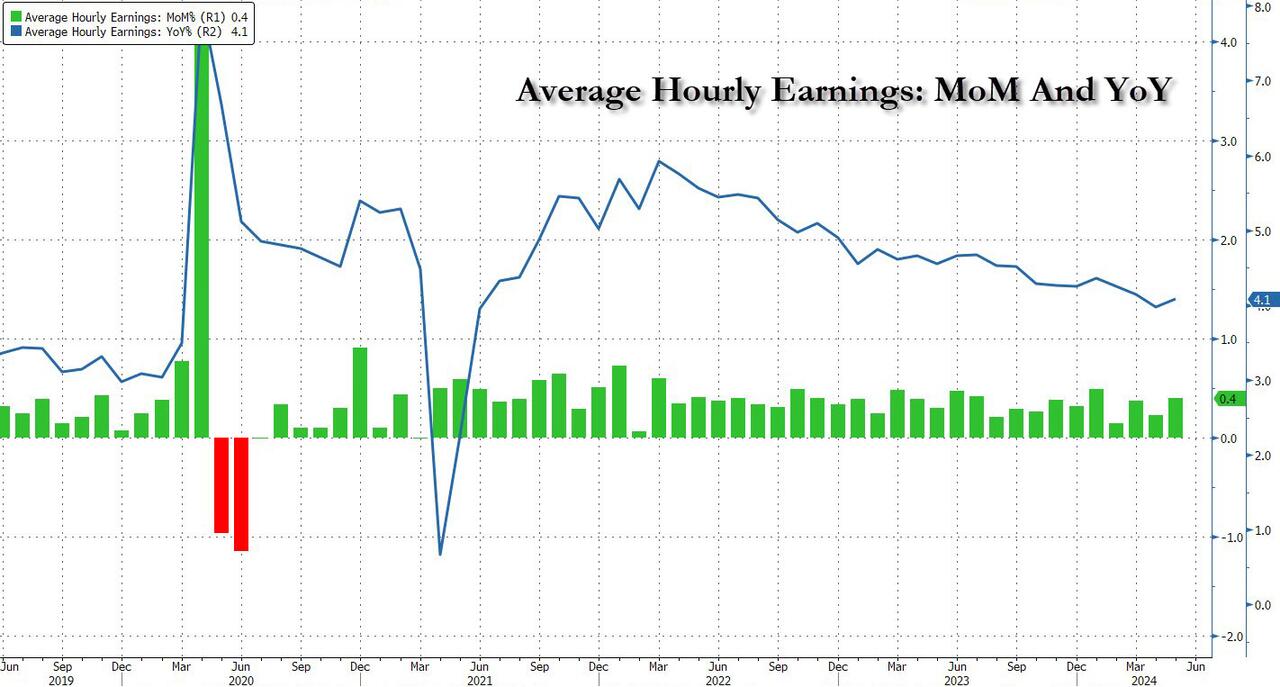

- May Average Hourly Earnings MoM, est. 0.3%, prior 0.2%

- May Average Hourly Earnings YoY, est. 3.9%, prior 3.9%

- May Average Weekly Hours All Emplo, est. 34.3, prior 34.3

- 10:00: April Wholesale Trade Sales MoM, est. 0.5%, prior -1.3%

- April Wholesale Inventories MoM, est. 0.2%, prior 0.2%

- 12:00: 1Q US Household Change in Net Wor, prior $4.84t

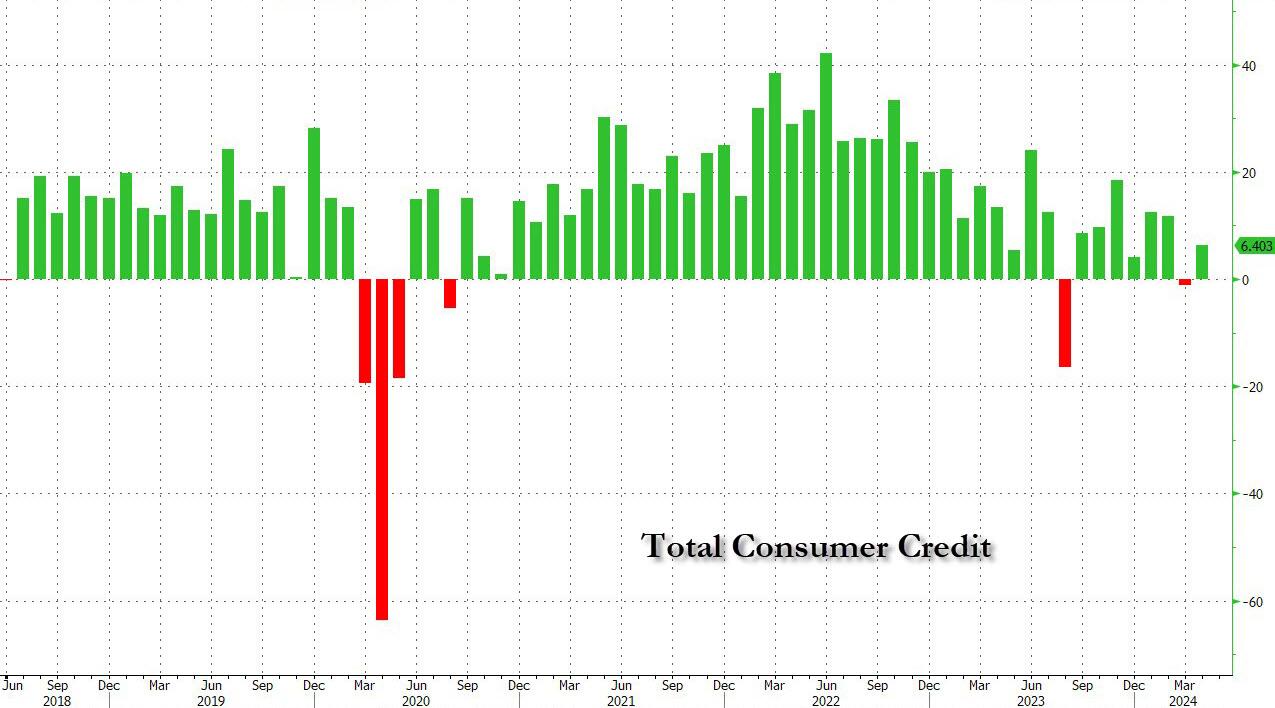

- 15:00: April Consumer Credit, est. $10b, prior $6.27b

DB’s Jim Reid concludes the overnight wrap

For markets, it was another day of milestones yesterday, with the ECB becoming the latest central bank to cut rates this cycle. They announced a 25bp cut in their deposit rate to 3.75%, which is the first cut they’ve delivered since 2019. And even though the tone was a bit hawkish in several respects, it now makes them the fourth G10 central bank to have cut rates, after Canada, Sweden and Switzerland . In turn, the move has cemented the idea that the global monetary policy cycle is moving towards an easing mode, with investors expecting further cuts on the horizon. So it marks a big shift from much of the last couple of years, when central banks were rapidly hiking rates to try to bring down inflation.

In terms of the ECB’s decision, the rate cut itself was widely expected, so didn’t come as much surprise to markets. But there were several aspects of the decision that leant in a hawkish direction. For instance, they took out the line from the last statement that “ it would be appropriate to reduce the current level of monetary policy restriction ” if their confidence grew that inflation was returning to target. Moreover, they actually upgraded their inflation forecasts, with 2024 revised up by two-tenths to 2.5%, and 2025 also up two-tenths to 2.2%. On top of that, in the press conference President Lagarde said, “Are we today moving into a dialing back phase? I wouldn’t volunteer that”. So investors grew more sceptical that this would kick off a rapid series of rate cuts.

The rate cut was supported by all but one of the ECB’s Governing Council and our European economists observe that garnering the support of most hawks came at the cost of a clear signal on the direction of travel. An implicit easing bias persists, but recent data did not give the ECB the collective confidence to present the move as the first in a series of cuts. Our economists maintain a baseline view of two more rate cuts this year (in September and December), but with a September cut not being a done deal. See their full reaction here.

This hawkish leaning was echoed in markets, and sovereign bond yields rose across the Euro Area after yesterday’s decision. By the close, yields on 10yr bunds (+3.8bps), OATs (+4.3bps) and BTPs (+4.7bps) had all moved higher, and the Euro also strengthened after the decision, ending the day up +0.17% at $1.088. Looking forward, overnight index swaps see a July cut as in the balance, with a 38% chance of a cut priced in as we go to press this morning. But a cut by September is still seen as more likely than not, with the chance of a cut by that meeting at 91%.

Looking forward, attention will now turn to the US jobs report for May, which comes at an important point ahead of the Fed’s decision on Wednesday. This report could see an important milestone, as i f the unemployment rate stays beneath 4%, then it would mark the longest stretch of sub-4% unemployment for the US since the early 1950s, at 28 months. Indeed, we pointed out several parallels with the early 1950s earlier this week (link here), including a strong performance for risk assets, a temporary burst of inflation, and heightened geopolitical risks.

When it comes to today’s report, our US economists are looking for nonfarm payrolls to come in at +200k, which would be an uptick from April, when nonfarm payrolls growth was at a 6-month low of +175k. Otherwise, they see the unemployment rate holding steady at 3.9%, and average hourly earnings ticking back up a tenth to +0.3%. See their full preview and how to sign up to their webinar afterwards here.

Ahead of the jobs report, the US weekly initial jobless claims were a bit weaker than expected yesterday, rising to 229k over the week ending June 1 (vs. 220k expected). That’s a 4-week high, but some of the other economic news was more positive. Indeed, the Atlanta Fed’s GDPNow estimate for Q2 was upgraded again to an annualised rate of 2.6%. We also had data yesterday showing the US trade deficit was a bit smaller than expected in April, at $74.6bn (vs. $76.5bn expected), even if the number was still the highest since October 2022.