JUNE 11/BLOG//GOLD CLOSED DOWN $0.30 TO $2309.50/SILVER CLOSED DOWN $0.59 TO $29.15//PLATINUM CLOSED DOWN $16.75 TO $955.70//PALLADIUM CLOSED DOWN $13.30 TO $891.15//GOLD COMMENTARY TODAY BY MATHEW PIEPENBURG//GERMANY SET TO DEPORT MIGRANTS THAT VIOLATE THE LAW//ISRAEL VS HAMAS UPDATES///USA MAY WISH TO MAKE A SEPARATE DEAL WITH HAMAS TO GET BACK AMERICANS/COVID UPDATES/VACCINE INJURY REPORT SLAY NEWS, ETC//HUNTER BIDEN CONVICTED ON 3 COUNTS//RUSSIA VS UKRAINE UPDATES/SWAMP STORIES FOR YOU TONIGHT//

Bitcoin: afternoon price: $67,125 DOWN 2505 dollars

Platinum price closing DOWN $16.75 TO $956.70

Palladium price; DOWN $13.30 AT $891.15

END

SHANGHAI GOLD PREMIUM 100 DOLLARS/COMEX GOLD//JULY TO JULY

SHANGHAI GOLD

SHANGHAI GOLD (USD) FUTURES – QUOTES

Last Updated 11 Jun 2024 09:54:10 AM CT.

Market data is delayed by at least 10 minutes.

MONTH

CHART

LAST

CHANGE

PRIOR SETTLE

OPEN

HIGH

LOW

VOLUME

UPDATED

JUN 2024 SGUM4

–

–

2410.2

–

–

–

0

09:08:54 CT 11 Jun 2024

JUL 2024 SGUN4

–

–

2424.3

–

–

–

0

08:50:01 CT 11 Jun 2024

AUG 2024 SGUQ4

2353.8

-70.7 (-2.92%)

2424.5

2347.2

2355.9

2338.5

1,150

09:25:18 CT 11 Jun 2024

OCT 2024 SGUV4

–

–

2448.8

–

–

–

0

09:08:54 CT 11 Jun 2024

DEC 2024 SGUZ4

–

–

2461.3

–

–

–

0

08:50:01 CT 11 Jun 2024

FEB 2025 SGUG5

–

–

2461.9

–

–

–

0

08:50:01 CT 11 Jun 2024

APR 2025 SGUJ5

–

–

2462.5

–

–

–

0

08:50:01 CT 11 Jun 2024

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $3186.14 UP 7.74 CDN dollars per oz( * NEW ALL TIME HIGH 3,305.30 CDN DOLLARS PER OZ//MAY 20 2024)

*BRITISH GOLD: 1817.80 UP 2.90 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2156.50 UP 10.52 Euros per oz //* (ALL TIME CLOSING HIGH: 2248.89 EUROS PER OZ//APRIL 16.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCH: COMEX

JPMorgan stopped 9/73

FOR JUNE 2024

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2024. CONTRACT: 28 NOTICES FOR 2800 OZ or 0.0870 TONNES

total notices so far: 28,602 contracts for 2,860,200 Oz (88.924 tonnes)

FOR JUNE:

SILVER NOTICES: 1 NOTICE(S) FILED FOR 5,000

OZ/

total number of notices filed so far this month :1114 for 5.570 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $.30 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : NO CHANGE IN GOLD INVENTORY AT THE GLD

/ /INVENTORY RESTS AT 835.67TONNES

INVENTORY RESTS AT 835.67 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER DOWN $.59 AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 1.644 MILLION OZ INTO THE SLV

// INVENTORY INCREASES TO 422.786 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 421.142 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A FAIR SIZED 378 CONTRACTS TO 179,023 AND CONTINUING ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR GAIN OF $0.30 IN SILVER PRICING AT THE COMEX ON MONDAY’S TRADING ON SILVER. WE HAD SOME LIQUIDATION AS WE HAD A NET LOSS OF CONTRACTS ON OUR TWO EXCHANGES. WE, AGAIN HAD SHORT COVERING BY OUR SPECS WITH THE STRONG GAIN IN PRICE AS WELL AS MASSIVE T.A.S. LIQUIDATION. WE HAD ANOTHER MEGAHUMONGOUS SIZED 6358 T.A.S ISSUANCE, THE 2ND HIGHEST EVER RECORDED FOR SILVER, AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED LAST TUESDAY AND AGAIN ON FRIDAY.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 6358 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND TODAY;S TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.30) AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS FROM THEIR PERCH AS WE DID HAVE A HUGE SIZED GAIN OF 983 CONTRACTS ON OUR TWO EXCHANGES WITH THE GAIN IN PRICE OF $0.30

WE MUST HAVE HAD:

A HUGE SIZED 605 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.830 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 140,000 OZ QUEUE JUMP

//NEW STANDING FOR SILVER//JUNE IS THUS 6.44 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI GAIN //HUGE SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 6358 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED 149 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE

TOTAL CONTRACTS for 7 DAYS, total 7224 contracts: OR 36.120 MILLION OZ (1003 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 36.120 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 36.120 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

RESULT: WE HAD A FAIR SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 378 CONTRACTS WITH OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 605 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.830 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 140,000 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR JUNE 6.44 MILLION OZ

WE HAVE A HUGE SIZED GAIN OF 983 OI CONTRACTS ON THE TWO EXCHANGES WITH THE GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A MEGA HUMONGOUS SIZED 6358 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND ZERO NET LIQUIDATION OF LONGS.

THE NEW TAS ISSUANCE MONDAY NIGHT (6358) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 1 NOTICE(S) FILED TODAY FOR 5,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 6805 OI CONTRACTS TO 435,003 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 102 CONTRACTS

WE HAD A STRONG SIZED DECREASE IN COMEX OI (6805 CONTRACTS) OCCURRED WITH OUR GAIN OF $2.00 IN PRICE/MONDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 89.94 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 4700 OZ QUEUE JUMP AS BANKERS SCOUR THE PLANET LOOKING FOR GOLD ON THE THIS SIDE OF THE POND

NEW STANDING 90.522 TONNES// ALL OF THIS HAPPENED WITH OUR $2.00 GAIN IN PRICE WITH RESPECT TO MONDAY’S TRADING. WE HAD A GOOD SIZED LOSS OF 3956 OI CONTRACTS (12.304 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 2849 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 435,003

IN ESSENCE WE HAVE A GOOD SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3956 CONTRACTS WITH 6805 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 2849 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 3956 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 1668 CONTRACTS,,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2849 CONTRACTS) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI OF 6805 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 3956 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 88.761 TONNES FOLLOWED BY TODAY’S QUEUE JUMP TO 0.1461 TONNES

//NEW STANDING /JUNE 90.522 TONNES.

/ 3) HUGE T.A.S. LIQUIDATION OF CONTRACTS WITH SOME LONG SPECS BEING CLIPPED,

.

// 4) STRONG SIZED COMEX OPEN INTEREST LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///HUGE T.A.S. ISSUANCE: 3072 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

MAY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE. :

TOTAL EFP CONTRACTS ISSUED: 27,124 CONTRACTS OR 2,712,400 OZ OR 84.367 TONNES IN 7 TRADING DAY(S) AND THUS AVERAGING: 3874 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 7 TRADING DAY(S) IN TONNES 84.367 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 84.367 DIVIDED BY 3550 x 100% TONNES = 2.37% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 84.367 tonnes HEADING FOR A STRONG MONTH

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A FAIR SIZED 378 CONTRACTS OI TO 179,023 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 605 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 605 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 2075 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 527 CONTRACTS AND ADD TO THE 605 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 983 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 4.915 MILLION OZ

OCCURRED DESPITE OUR HUMONGOUS $0.30 GAIN IN PRICE …..

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED DOWN 23.23 PTS OR 0.76% //Hang Seng CLOSED DOWN 190.61 PTS OR 0.75%// Nikkei CLOSED UP 96.63 OR 1.25%//Australia’s all ordinaries CLOSED DOWN 0.76%///Chinese yuan (ONSHORE) closed UP TO 7,2543 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2704/ Oil UP TO 77.53 dollars per barrel for WTI and BRENT UP AT 81.41 /Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A HUGE SIZED 6805 CONTRACTS TO 435,003 WITH OUR GAIN IN PRICE OF $2.00 WITH RESPECT TO MONDAY’S TRADING. WE HAD A HUGE T.A.S. LIQUIDATION ON MONDAY WITH ZERO LONGS BEING CLIPPED.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE.… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A GOOD SIZED 2849 EFP CONTRACTS WERE ISSUED: : AUGUST2849 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2849 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 3956 CONTRACTS IN THAT 2849 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 6805 COMEX CONTRACTS..AND THIS FAIR SIZED LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $2.00

// MONDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT WAS A FAIR SIZED 1668 CONTRACTS. MOST OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. MONDAY IS OF EXTREME IMPORTANCE TO OUR CROOKS IN YESTERDAY’S TRADING

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (90.522 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 90.522 TONNES. THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $2.00 //// AND WERE SUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD A FAIR SIZED LOSS OF 3956 CONTRACTS ON MONDAY WITH OUR TWO EXCHANGES WITH THE GAIN IN PRICE. THE T.A.S. ISSUED ON MONDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE LOST A TOTAL OI OF 12.304 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE (89.94 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 47 CONTRACTS OR 4700 OZ (0.8979 TONNES)

NEW STANDING FOR JUNE: 90.522 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAININ PRICE TO THE TUNE OF $2.00

WE HAVE REMOVED 102 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET LOSS ON THE TWO EXCHANGES 3956 CONTRACTS OR 395600 (12.304 TONNES)

Total monthly oz gold served (contracts) so far this month

28,602 notices 2,860,200 oz 88.924 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: NIL oz

we have 0- customer deposit:

total deposit nil oz

customer withdrawals: 1

brinks; 64.32 oz (2 kilobars)

this is a paper transfer out of the comex and onto London

TOTAL WITHDRAWALS 64.32 0z

Adjustments: 1/customer to dealer//7616.240 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE

For the front month of JUNE we have an oi of 529 contracts having LOST 26 contracts. We had 73 contracts served on Monday so we gained a huge 47 contracts or 4700 oz additional oz will stand for gold at the comex as they underwent a queue jump to take delivery on this side of the pond.. We saw a dubious small kilobar entry gold leaving the comex on MONDAY. Thus despite the huge 90 tonnes of gold standing at the comex little gold is arriving and hardly any gold is leaving.

JULY GAINED 122 CONTRACTS TO STAND AT 2288

AUGUST LOST 8376 CONTRACTS DOWN TO 356,712 CONTRACTS

We had 73 contracts filed for today representing 7300 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 1 notices were issued from their client or customer account. The total of all issuance by all participants equate to 28 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 21 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for June /2024. contract month, we take the total number of notices filed so far for the month (28,652) x 100 oz ) to which we add the difference between the open interest for the front month of JUNE (529 CONTRACTS) minus the number of notices served upon today (28 x 100 oz per contract( equals 2,910,300 OZ OR 90.522 TONNES.

thus the INITIAL standings for gold for the JUNE contract month: No of notices filed so far (28,652 x 100 oz +we add the difference for front month of June (529 OI} minus the number of notices served upon today (28) x 100 oz which equals 2,910,300 oz (90.552 TONNES)

TOTAL COMEX GOLD STANDING FOR JUNE: 90.522 TONNES WHICH IS ABSOLUTELY HUGE FOR THIS VERY ACTIVE DELIVERY MONTH IN THE CALENDAR. JUNE IS TRADITIONA;LLLY THE 2ND HIGHEST DELIVERY MONTH OF THE YEAR. FROM THIS POINT WE WILL GAIN IN GOLD TONNAGE WILLING TO STAND AT THE COMEX

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,662,910 OZ

TOTAL REGISTERED GOLD 7,997,711.289 ( 248.76 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,665,198.929OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,316,997 oz (REG GOLD- PLEDGED GOLD)= 196.48 tonnes //

END

SILVER/COMEX

JUN 10/2024

INITIAL

//2024// THE JUNE 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

1007,057.045 oz

CNT

.

Deposits to the Dealer Inventory

nil OZ

Deposits to the Customer Inventory

1220,705.820 oz

Loomis

No of oz served today (contracts)

1 CONTRACT(S) (5,000 OZ)

No of oz to be served (notices)

144 contracts (0.720 million oz)

Total monthly oz silver served (contracts)

1114 Contracts (5.570 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 deposits customer account:

i) into Loomis: 1,220,705.820 oz

total customer deposit 1,220,705/820 oz

JPMorgan has a total silver weight: 128.416million oz/296.591million or 48.34%

adjustment: 0//

Comex withdrawals: 1

i) out of CNT: 1007.057 oz

total withdrawal: 1007.057 0z

TOTAL REGISTERED SILVER: 62.494MILLION OZ//.TOTAL REG + ELIGIBLE. 295.371

million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE:

silver open interest data:

FRONT MONTH OF JUNE/2024 OI: 145 CONTRACTS HAVING GAINED 20 CONTRACT(S).

WE HAD 8 NOTICES SERVED UP ON MONDAY, SO WE GAINED 28 CONTRACTS OR AN ADDITIONAL 140,000 OZ WILL STAND AT THE COMEX VIA A STRONG QUEUE JUMP

JULY SAW A LOSS OF 7252 CONTRACTS DOWN TO 112,319

AUG, SAW A GAIN OF 26 CONTRACTS TO 226

SEPT SAW A GAIN OF 7275 CONTRACTS TO 49,080

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 1 for 5,000 oz

CONFIRMED volume; ON MONDAY 90,162 GIGANTIC

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1114 x 5,000 oz = 5.570 MILLION oz

to which we add the difference between the open interest for the front month of JUNE ((145) and the number of notices served upon today 1 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2024 contract month: 1114 notices served so far) x 5000 oz + OI for the front month of JUNE (145)x number of notices served upon today minus (1)x 5000 oz of silver standing for the JUNE contract month equates to 6.440 MILLION OZ.

New total standing: 6.6440 million oz.

There are 62.494 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

JUNE 11 WITH GOLD DOWN $0.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 10 WITH GOLD UP $2,00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 7 WITH GOLD DOWN $64.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 3.56 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 837.11 TONNES

JUNE 6 WITH GOLD UP $16.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.34 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 833.55 TONNES

JUNE 5 WITH GOLD UP $32.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 4 WITH GOLD DOWN $20.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 3 WITH GOLD UP $22.85 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 31 WITH GOLD DOWN $19.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 30 WITH GOLD UP $3.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 29 WITH GOLD DOWN $13.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 28 WITH GOLD UP $22.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 832.21 TONNES

MAY 24 WITH GOLD DOWN $2.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 833.36 TONNES

MAY 23 WITH GOLD DOWN $53.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 22 WITH GOLD DOWN $32.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 21 WITH GOLD DOWN $12,00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 20 WITH GOLD UP $21.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.10 TONNES OF GOLD INTO THE GLD//NEW TOTAL 838.54 TONNES

MAY 17 WITH GOLD UP $31.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//NEW TOTAL 833.36 TONNES

MAY 16 WITH GOLD DOWN $7.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//NEW TOTAL 833.36 TONNES

MAY 15 WITH GOLD UP $34.90 ON THE DAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD/INVENTORY RISES TO 831.93 TONNES

MAY 14 WITH GOLD DOWN $17.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RISES TO 831.33 TONNES

MAY 13 WITH GOLD DOWN $31.10 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD////INVENTORY RISES TO 831.93 TONNES

MAY 10 WITH GOLD UP $34.65 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 9 WITH GOLD UP $18.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 8 WITH GOLD DOWN $0.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 830.47 TONNES

MAY 7 WITH GOLD DOWN $6.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 832.19 TONNES

MAY 6WITH GOLD UP $21.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .55 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 831.64 TONNES

MAY 2 WITH GOLD UP $0.20 ON THE DAY; SMAKK CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 830.47 TONNES

MAY 1 WITH GOLD UP $7.80 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNES

GLD INVENTORY: 835.67 TONNES, TONIGHTS TOTAL

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 11 WITH SILVER DOWN $0.59 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.644 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 422.786 MILLION OZ

JUNE 10 WITH SILVER UP $0.30 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 3.198 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 421.142 MILLION OZ

JUNE 7 WITH SILVER DOWN $1.93 TODAY: NO CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY AT 417.944 MILLION OZ

JUNE 6 WITH SILVER UP $1.27 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 417.944 MILLION OZ

JUNE 5 WITH SILVER UP 0.38 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.52 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 415.295 MILLION OZ

JUNE 4 WITH SILVER DOWN $1.08 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

JUNE 3 WITH SILVER UP $0.35 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

MAY 31 WITH SILVER DOWN $1.09 TODAY: HUGE CHANGES IN SILVER INVENTORY: A MASSIVE WITHDRAWAL OF 3.655 MILLION OZ FROM THE SLV//INVENTORY LOWERS TO 413.775 MILLION OZ

MAY 30 WITH SILVER DOWN $0.80 TODAY: NO CHANGES IN SILVER INVENTORY//INVENTORY REMAINS AT 417.430 MILLION OZ

MAY 29 WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 1.051 MILLION OZ INTO THE SLV//INVENTORY DECREASES TO 417.430 MILLION OZ

MAY 28 WITH SILVER UP $1.64 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 2.832 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 418.481 MILLION OZ

MAY 24 WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF .822 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 421.313 MILLION OZ

MAY 23 WITH SILVER DOWN $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.736 MILLION OZ FROM THE SLVINVENTORY INCREASES TO 420.491 MILLION OZ

MAY 22 WITH SILVER DOWN $0.66 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 21 WITH SILVER DOWN $0.41 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A DEPOSIT OF 3.792 MILLION OZ FROM THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 20 WITH SILVER UP $1.28 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 1.005 MILLION OZ FROM THE SLV// INVENTORY LOWERS TO 418.435 MILLION OZ

MAY 17 WITH SILVER UP $1.37 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 868,000 OZ FROM THE SLV// INVENTORY LOWERS TO 419.440 MILLION OZ

MAY 16 WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY REMAINS AT 420.308 MILLION OZ

MAY 15 WITH SILVER UP 101 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A WITHDRAWAL OF 1.919 MILLION OZ FROM THE SLV NVENTORY RESTS AT 420.308 MILLION OZ

MAY 14 WITH SILVER UP 25 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;INVENTORY RESTS AT 422.227 MILLION OZ

MAY 13 WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;NVENTORY RESTS AT 422.227 MILLION OZ

MAY 10 WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A HUGE WITHDRAWAL OF 1.,828 MILLION OZ//INVENTORY RESTS AT 422.227 MILLION OZ

MAY 9 WITH SILVER UP 78 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 8 WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 7WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 6 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.055 MILLION OZ

MAY 3 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 2WITH SILVER UP 0.12 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/ A WITHDRAWALOF 4.471 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 1 WITH SILVER UP 0.09 TODAY: SMALLCHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF ,457 MILLION OZ INTO THE SLV INVENTORY RESTS AT 429.814 MILLION OZ

CLOSING INVENTORY 422.786 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/GOLD AND SILVER COMMENTARY

end

MATHEW PIEPENBURG…

Gold & Oil: Understanding Rather Than Fearing Change

There is much legitimate (as well as dramatic) talk about the failing US, its debased currency and its identity-fractured/inflation-taxed middle-class which has been increasingly described more aptly as the working poor.

The End, or Just Change?

But is America coming to an end? Will the USD lose its world reserve currency status? Will the greenback disappear? Will gold or BTC save us from all that is breaking before our media-clouded eyes and increasingly centralized state?

Gold (now a Tier-1 asset btw…) will continue to store value (i.e., preserve wealth) better than any fiat money; and BTC will certainly make convexity headlines in the future.

And yes, we all know the Fourth Estate died long before Don Lemon or Chris Cuomo stained our screens or insulted our collective IQ.

And as for centralization, it’s not coming, but already here.

Be Prepared Rather than Emotional

So, yes there is tremendous reason for informed and genuine concern, but rather than wait for the end of the world, it would be far more effective to logically prepare for a changing world.

Rather than debate left or right, black or white, straight or trans, safe or effective, smart (Barrington Resolution) or stupid (Fauci), we’d likely serve our individual and collective minds far better by embracing the logical and tabling the emotional.

Toward that end, we’d be equally better off relying on our own judgement rather than that of the children making domestic, monetary or foreign policy decisions from DC to Belgium…

Logically speaking, the USD (and US of A) is changing.

Like its recent swath of weak leadership, the greenback and US IOU are quantifiably less loved, less trusted, less inherently strong and well…far less than they were at Bretton Woods circa 1944.

Change Is Obvious

Since our greatest generation stormed the beaches of Normandy in June of 44, we’ve gone from being the world’s leading creditor and manufacturer to the world’s greatest debtor and labor-off-shorer by June of 2024.

This is not fable but fact. A recent Normandy veteran admitted that he no longer recognizes the country he fought for—and that’s worth a pause rather than “patriotic” critique.

When the post-2001-WTO-daft policy makers weaponized what should have been a neutral world reserve currency in 2022 against a major nuclear power (i.e. stole $400B worth of Russian assets) already in economic bed with a China-driven and now growing BRICS coalition, the “payback” writing was on the wall for the greenback—as many of us understood from day-1 of the Putin of sanctions.

De-Dollarization Is a Reality, not a Headline

In short, many nations of the world, including the oil nations, quickly understood that the world wants a reserve asset that can’t be frozen/stolen at will and that simultaneously retains (rather than loses) its value.

But rather than end the USD as the world reserve currency, most of that world is simply going around (or outside of) it…

Or even more bluntly, the prior hegemony of the UST, and by extension, the USD, irrevocably changed in 2022.

Thank You Ronni & Luke

Thanks to data-focused and credit/currency-savvy thinkers like Ronnie Stoeferle and Luke Gromen, we can plainly see the facts rather than drama of these trends.

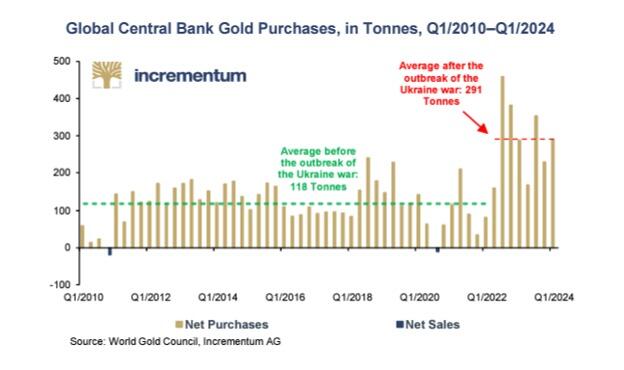

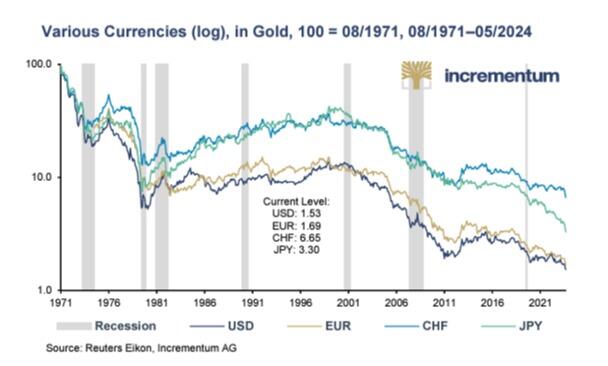

The actions rather than mere words of the BRICS+ nations and global central banks, who prefer to save in physical gold rather than US IOU’s, speak loudly for themselves, which Stoeferle’s objective charts remind.

That is, since the US weaponized its Dollar, there has been an undeniable move away from the greenback and its UST in favor of gold as a reserve asset:

The COMEX et al…

The hard facts are in, and dozens of BRICS+ countries are trading outside the USD, purchasing in local currencies for local goods, and then net settling the surpluses in physical gold, which is far better/fairer priced in Shanghai than in London or New York, two critical exchanges that are seeing more physical deliveries out of their exchanges than in.

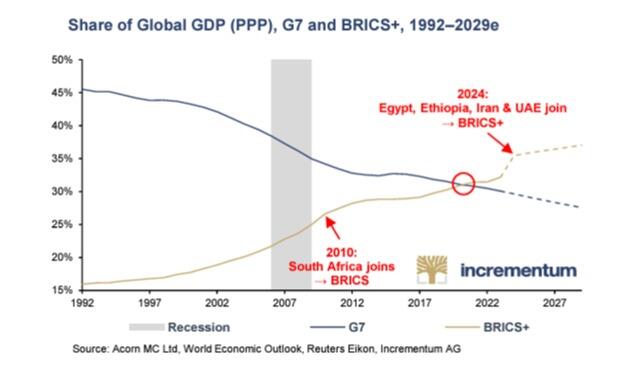

This matters, because like it or not, the rising power of the BRICS+ nations, generationally tired of being the dog wagged by the USD’s inflation-exporting tail, are growing in economic power away from a debt-driven West, which again, the facts (global share of GDP) make clear rather than sensational.

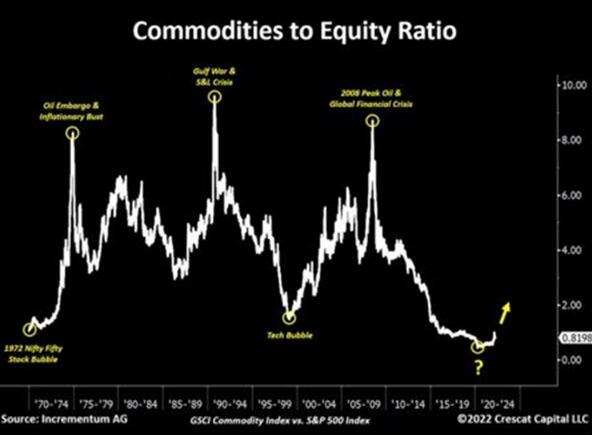

The Chart of the Decade?

Ronni posted a similarly critical chart over a year ago, asking, somewhat rhetorically, if it was not the chart of the decade?

That is, he asked if the world is moving toward a commodity super-cycle wherein real assets begin their slow rise against falling (yet currently inflated) equity markets and a falling (yet increasingly debased) USD.

As Grant Williams, would say, this should make far-sighted investors all go hmmm.

Commodity Markets: Change is Gonna Come to the Petrodollar

And as for commodities, currencies and hence gold, the changes are all around us, at least for those with eyes to see and ears to hear.

Toward this end, we can’t ignore what has been happening in the global energy markets, topics which I’ve previously (and so-far, correctly) addressed here and here.

But when it comes to understanding oil, the USD and gold, Luke Gromen leads the way in clear thinking and has informed us as well as anyone.

He reminds, for example, that oil, like any other object of international supply and demand (i.e., trade), can be equally net-settled in gold rather the UST-linked petrodollars.

(In 2023, by the way, 20% of global oil sales were outside of the USD, a fact otherwise unthinkable until the Biden White House sanctioned Russia.)

The implications of this simple observation (as well as its impact on) the USD, commodity pricing and gold are extraordinary.

Oil: The Recent Past, Prior to Sanctions…

Before the US weaponized its USD against Russia (and publicly insulted its key oil partner, Saudi Arabia), the world towed the line of both the UST and the USD-denominated oil trade, which was very, very, very convenient for Uncle Sam and his Modis Operandi of exporting US inflation to everyone else.

For example, in the past, when commodity prices got too high, nations like Saudi Arabia would absorb USTs and effectively go long the USD, which the US pumps out faster than the Saudis do oil…

This, of course, was good for stabilizing and absorbing an otherwise over-produced and debasement-vulnerable USD while simultaneously helping US government bonds stay loved and hence yield’s compressed/controlled.

In a way, this was even good for global growth, as it kept the USD stable and low enough for nations like China and other EM countries to grow.

These other nations, in turn, would keep buying the “risk-free-returning” UST’s and thus help refund (“reflate”) the US’s own debt-based “growth narrative.”

After all, if every one else is buying his IOU’s, Uncle Sam can forever go deeper and deeper into debt-financing the American Dream, right?

Oil: Present Facts, Post the Sanctions…

Well, that is true only if you assume the world never changes, and that reported–i.e., utterly dishonest inflation–makes our UST’s truly “risk-free” rather than just returning nothing but negative real yields.

Fortunately (or unfortunately), the rest of the world is seeing the changes which DC pretends to hide.

Specifically, and as of November of last year, the Saudi’s met with a bunch of BRICS+ nations looking for ways around the USD and UST when it comes to trading among themselves—and this includes the oil trade.

Think about that for a second.

This means that what has been working in favor of the USD and sovereign bond market since the early 70’s (i.e., global demand for the USD via oil) is slowly (but surely) unwinding right before Biden’s barely open eyes…

All those decades of prior support/demand for USDs and USTs is going down not up, which means unloved UST’s will have to be supported by fake (i.e., inflationary) at-home liquidity rather than immortal foreign demand.

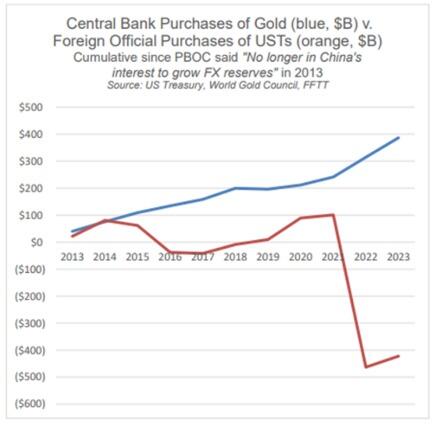

It also means that commodities, from copper to yes, even oil, can and will continue to be purchased outside the Dollar and net settled in gold, which likely explains why central banks have been net stacking gold (top line) and net-dumping USTs (bottom line) since 2014…

Again, watch what the world is actually doing rather than what your politico’s (or even bank wealth advisors) are telling you.

Gold & Oil: Impossible to Ignore?

As for gold and oil in the foregoing backdrop of a changing rather than static world, any sane investor has to give serious consideration to the changing petrodollar dynamics which Luke Gromen has been tracking with sober farsightedness.

The compressed but inevitably rising super cycle (Stoeferle chart above) in commodities this time around will differ markedly from past rallies.

As oil, for example, goes up (for any number of reasons), the old system that once recycled those costs in UST purchases can (and has) pivoted/changed to another asset.

You guessed it: GOLD.

Think it through: Russia can sell oil to China, Saudi Arabia can sell oil to China. But now in Yuan not USDs. These trading partners can then take their Yuan payments to buy Chinese “stuff” (once made in America…) and finally net settle any surpluses in gold rather than USTs.

That gold can then be converted into any EM/BRICS+ local currency (from rupees to reals) rather than Dollars to trade among themselves for other raw commodities, of which many BRICS+ nations are resource rich.

This, by the way, is not some distant possibility, but a current and ongoing reality. It can devastating to USD demand and hence strength.

When copper and other commodities, including, oil starts repricing (and stockpiling) outside the USD with increasing frequency, the Dollar’s so-called “hegemony” becomes increasingly hard to believe, telegraph or sustain.

The Ignored Gold/Oil Ratio

As Luke Gromen observes, but few wish to see…if/when gold becomes the “de facto release valve for non-USD commodity pricing and net settlement,” the impact this will have on the long-term gold price is simply a matter of math rather than debate.

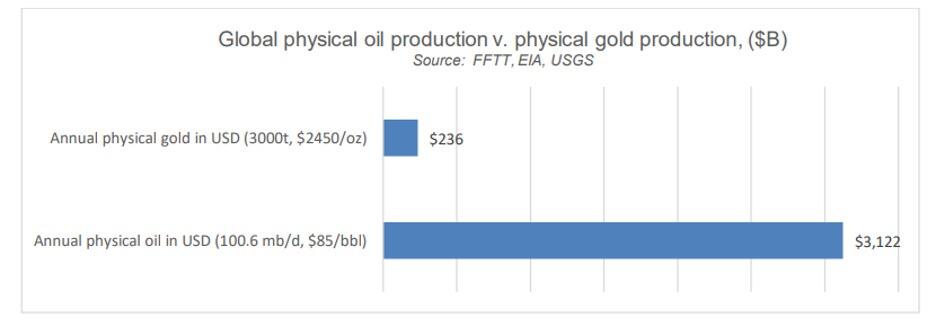

He repeatedly reminds that the global oil market is 12-15x the size of the global gold markets in physical production terms:

We thus can surmise that gold can and will be pushed higher by oil in particular and other commodities in general, a reality already in play as measured by the global gold/oil ratio, which has risen (not so coincidentally) by 4x since Moscow began stacking gold in 2008 while the Fed was preparing to mouse-click trillions of fake Dollars in DC…

The Most (Deliberately) Misunderstood Asset…

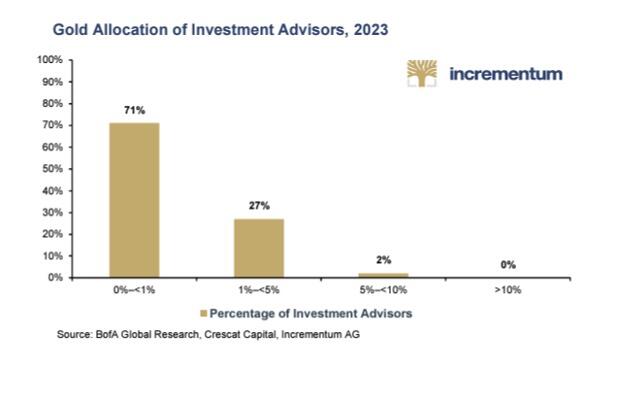

Meanwhile, as we stare in awe at the consensus-think which still places gold at only 0.5% of global asset allocations (the 40Y mean is 2%) and just barely over 1% of all family office allocations (still crawling further and further on the risk branch for yield), we have to wonder if it is human nature (or just political and monetary self-interest) to fear change, even when the evidence of it is all around us.

Yet few see gold’s real role…

For gold investors (rather than speculators) who think generations ahead rather news cycles per day, and who understand that preserving wealth is the secret to having wealth, this asset (and change) is not feared.

It is understood.

And that is how we understand gold. It preserves wealth while paper currencies destroy it.

That is why despite positive real yields, a relative strong USD and so-called contained inflation, gold is breaking away from these correlations and making all-time-highs despite their profiles as traditional gold “headwinds.”

It’s so simple.

Gold is trusted far more than broken currencies from broke countries, including the once revered USA in particular and the West and East in general:

As Ronni correctly says: “In gold we trust.”

Makes a lot of (common/historical) sense. Just do the math and read some history…

prepare accordingly to preserve our wealth. Step one is to get gold. That will see you through the storm.

3. CHRIS POWELL//GATA DISPATCHES

CHRIS POWELL…

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS/

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT//

SHANGHAI CLOSED DOWN 23.23 PTS OR 0.76% //Hang Seng CLOSED DOWN 190.61 PTS OR 0.75%// Nikkei CLOSED UP 96.63 OR 1.25%//Australia’s all ordinaries CLOSED DOWN 0.76%///Chinese yuan (ONSHORE) closed UP TO 7,2543 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2704/ Oil UP TO 77.53 dollars per barrel for WTI and BRENT UP AT 81.41 /Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGSTUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2543

OFFSHORE YUAN: DOWN TO 7.2704

SHANGHAI CLOSED DOWN 23.23 PTS OR 0.76 %

HANG SENG CLOSED DOWN 190.61 PTS OR 0.75%

2. Nikkei closed DOWN 96.63 PTS OR 1.25 %

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 104.93 EURO FALLS TO 1.0770 DOWN 34 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.007 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 157.03 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.67490/Italian 10 Yr bond yield UP to 4.150 SPAIN 10 YR BOND YIELD UP TO 3.513%

3i Greek 10 year bond yield UP TO 3.835

3j Gold at $2316.95//Silver at: 29.33 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 52/ 100 roubles/dollar; ROUBLE AT 89.05

3m oil into the 77 dollar handle for WTI and 81 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 157.03/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.007% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8965 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9621 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.426 DOWN 5 BASIS PTS…

USA 30 YR BOND YIELD: 4.564 DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.838 DOWN 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.37…

10 YR UK BOND YIELD: 4.330 UP 6 PTS

2a New York OPENING REPORT

Futures Slide Ahead Of Wednesday’s Main Event, As European Political Turmoil Sparks Bond Rout

TUESDAY, JUN 11, 2024 – 08:16 AM

US equity futures are lower with small-caps lagging, while Treasuries and the dollar rose as traders braced for a landmark day tomorrow that sees the release of both CPI data in the morning and then the Fed’s latest decision at 2pm ET. The crowded schedule sets up a crucial 36 hours for risk assets, including Bitcoin, which is currently getting hammered despite billions in ETF purchases in recent weeks, and is moving in the opposite direction to Treasury yields to an unusual degree. As of 7:50am, S&P futures were down 0.3%, near session lows while Nasdaq futures dropped 0.4%; both underlying indexes closed at record highs on Monday.

US Treasuries gained before inflation data and the Federal Reserve’s interest rate decision on Wednesday; bond yields are 3-5bps lower ahead of today’s 10Y auction and follows yesterday’s poor, tailing 3Y auction. The USD is stronger pre-mkt with both EUR and JPY weaker. French bonds tumbled the most since 2020 and the French-German yield spread blew out to October level following rumors that Macron could resign after his decision to call snap elections. Commodity markets are mostly lower with Ags finding a bid and natgas outperforming crude. Small Business Optimism is the macro data release today and even though it rose and beat expectations, coming in at 90.5, vs exp. 89.7, it will not be market-moving. As JPM notes, today’s pre-market setup is similar to yesterday but let’s see how many position adjustments are made into tomorrow’s CPI/Fed double feature as today sets up as the proverbial calm before the storm.

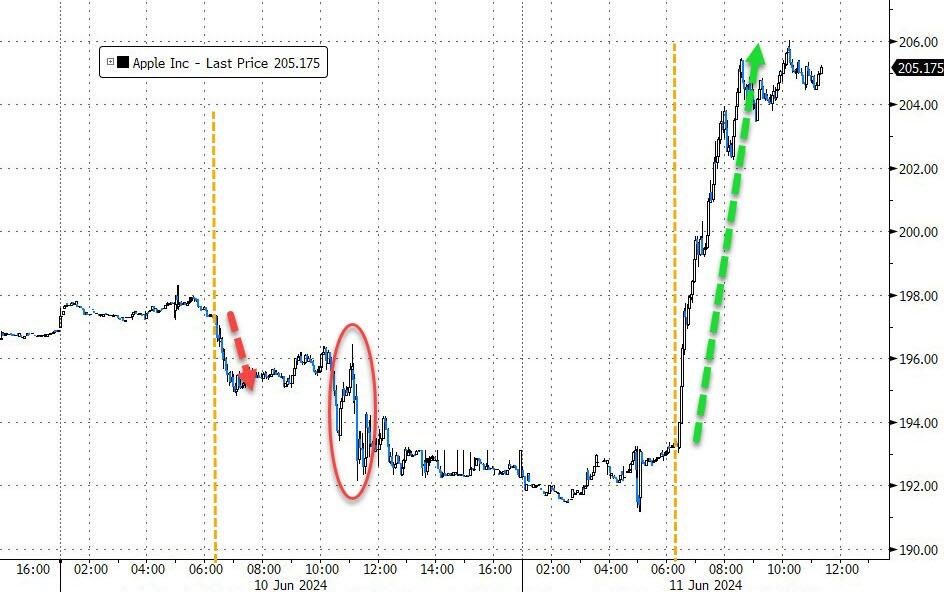

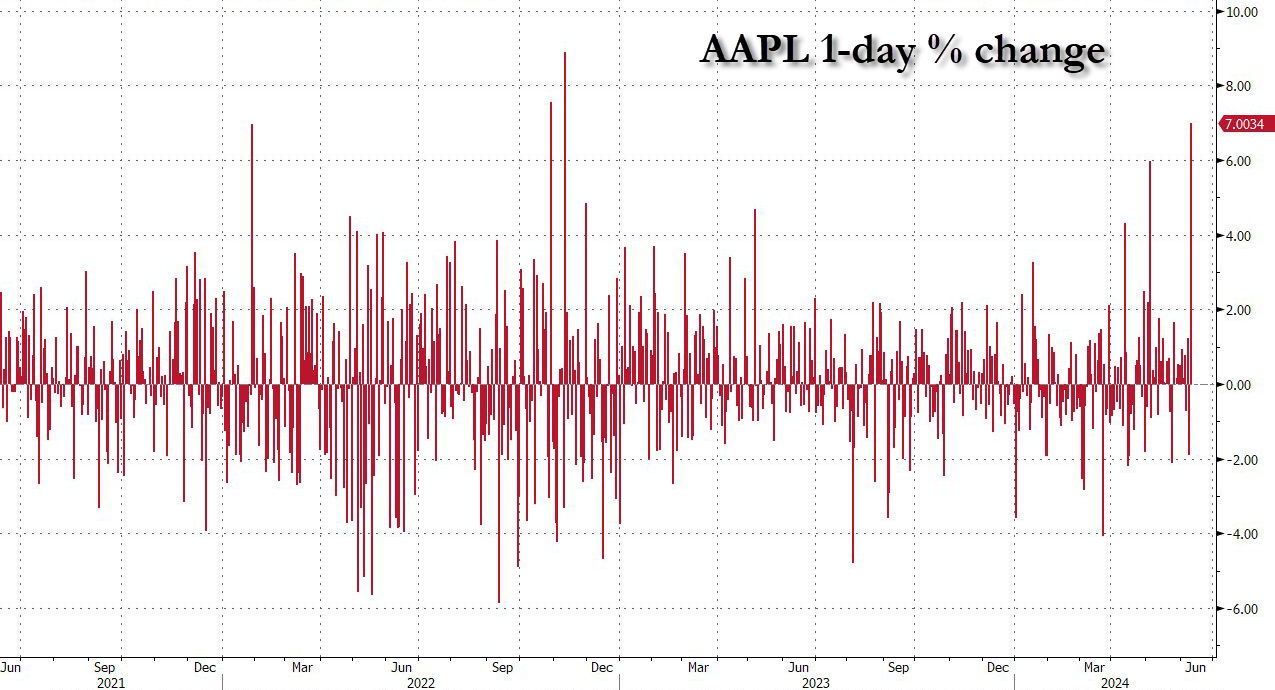

In premarket trading, Mag7 and Semi stocks were lower. Among US single stocks, Apple were set for a second day of losses, after its much-anticipated AI announcement last night saw no major surprises. The firm is making a high-stakes bid to catch up with rivals in the booming AI market, and yesterday announced a new platform called Apple Intelligence. A partnership with OpenAI — in the works for months — was only briefly mentioned at the event; it failed to inspire traders and sparked an angry backlash from Elon Musk who said he would ban Apple devices from his companies. LLY was the standout gainer, rising 2% after an FDA advisory panel deemed the firm’s Alzheimer’s drug effective and recommended US regulatory approval. Here are some of the biggest US movers before the opening bell:

Calavo Growers rises 12% after the distributor of avocados and other produce posted 2Q profit and sales that topped estimates.

Cleveland-Cliffs slips 3% after JPMorgan downgrades its rating on the steel producer to neutral, citing concerns over free cash flow and shareholder returns.

DXC Technology rises 2% after Reuters reported Apollo Global and Kyndryl Holdings are in talks for a joint bid for the information technology services company.

General Motors rises 1% after announcing a $6 billion share buyback.

Target Hospitality sinks 28% after a Wall Street Journal report that the Biden administration is closing an Immigration and Customs Enforcement detention center in Dilley, Texas, that was used to jail migrant families who crossed the border illegally.

Yext falls 13% after the digital-media technology company cut its full-year revenue forecast.

Ahead of tomorrow’s busy calendar, where the market is focused on tomorrow’s CPI/FOMC double whammy, some bond traders are already turning their attention to next year. With sticky inflation raising the prospect of higher-for-longer interest rates through 2024, the big question in the fixed-income space is how to game out 2025 and beyond, heaping more attention on the Fed’s interest rate projections, aka the dot plot.

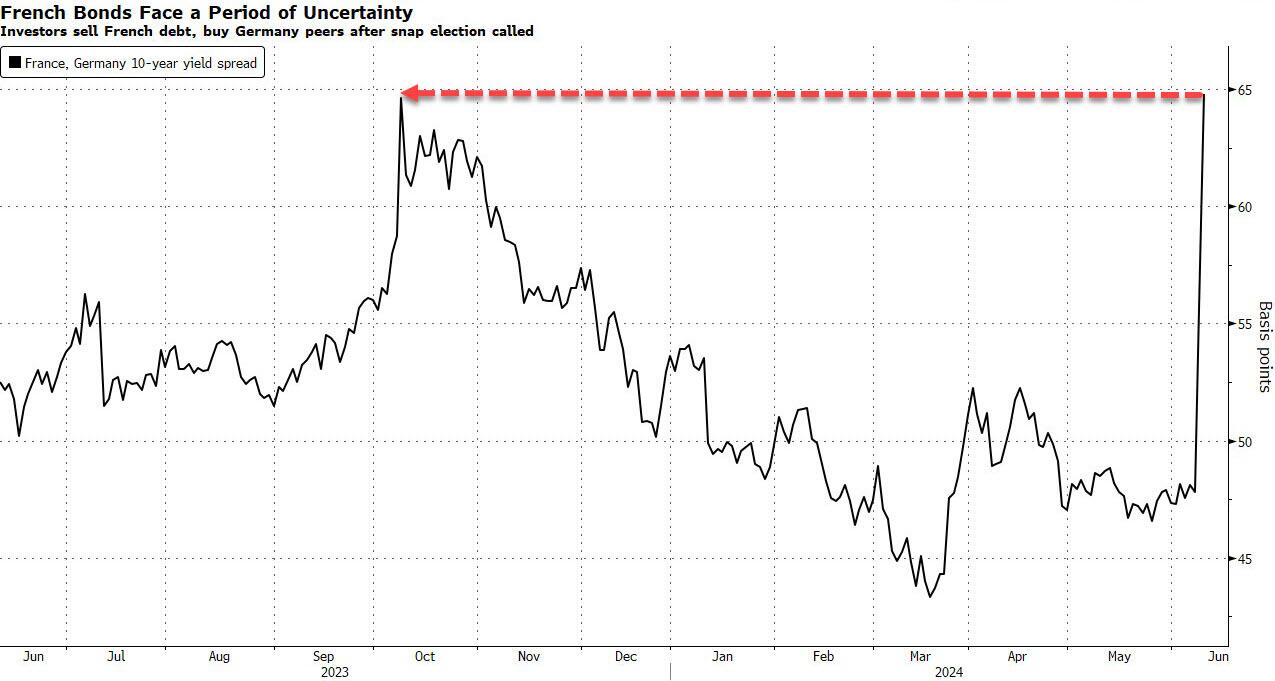

Meanwhile, European assets extended Monday’s rout as jitters over political upheaval in France continued. The euro edged lower and the Stoxx 600 fell for a third day. US equity futures dropped. Initially, it looked like some calm had returned to European markets on Tuesday after rising political risks rocked assets at the beginning of the week. But things took a turn throughout the day, with stocks sliding and French bonds remaining under pressure, pushing the 10-year spread over German bunds to the highest since October following rumors that President Emmanuel Macron was preparing to resign; while the rumorswere swiftly denied, the selling in local bonds continued…

… and appears to have quickly spread to other regions too.

SPREAD BETWEEN ITALIAN AND GERMAN 10-YEAR YIELDS WIDENS TO 150 BPS, WIDEST SINCE FEBRUARY

The biggest moves were in French markets. The yield on 10-year notes jumped as much as 10 basis points to 3.32%, putting them on course for the biggest two-day increase since March 2020. The selloff has widened the spread over equivalent German bonds to 64 basis points, the highest since October on a closing basis. European stocks were also lower with energy and industrial goods and services gain while miners are the worst performers as copper and iron ore fall. Here are some of the biggest movers on Tuesday:

UCB gains as much as 5.6%, the most since February and to a record high, after JPMorgan raised its recommendation for the Brussels-listed biotech to neutral from underweight, betting on continued strong demand for UCB’s key Bimzelx drug.

Covestro shares gain as much as 7.6% after Bloomberg News reported the German chemical company is close to granting Adnoc access to in-depth due diligence in expectation of an improved takeover bid.

Oxford Instruments shares jump as much as 12% after the instrument maker delivered annual results ahead of expectations and outlined new medium-term growth targets that should keep investors happy, according to analysts.

Idox rises as much as 4.7% as analysts at Canaccord Genuity (buy) say that the British software company continues to deliver reliable growth and forecast stability.

Maersk and European shipping peers fall after several Asian peers notched double-digit declines in Tuesday trading as traders assess the impact of revised interest-rate paths and the geopolitical impact from the latest Israel-Gaza ceasefire plan. In the US, American dockworkers halted labor talks.

European Miners were the worst performers in Europe as they followed copper and iron ore prices lower, with both commodities weakened by concerns over Chinese demand.

Naturgy shares fall as much as 13%, the most since March 2020, after Taqa and Criteria Caixa ended talks to jointly acquire the Spanish utility.

GN said it will gradually wind-down its Elite and Talk product lines and lowered its financial forecast range. The shares fell as much as 9.7% in Copenhagen.

CBrain falls as much as 14% after ABG Sundal Collier downgraded the Danish software firm to sell from hold, quoting an “excessive” near-term valuation.

In the UK, an unexpected rise in the jobless rate boosted the outlook for rate cuts later this year. Traders are fully pricing in the first quarter-point reduction by November and see around a 40% chance of a second decrease the following month. In a separate development, the country attracted over £104 billion ($132 billion) of orders for bonds in a record for gilt sales.

Earlier, Asian stocks fell, as Chinese and Australian shares led declines as markets reopened following holidays. The MSCI Asia Pacific Index fell 0.5%, with BHP Group, Samsung Electronics and China Construction Bank among the biggest drags. Benchmark in mainland China fell to their lowest closing levels since April. Korean shares were among the few gainers in Asia. Slow travel growth over the Dragon Boat Festival holiday was the latest sign of weak consumer demand in China. Property woes in the country also continued to weigh on sentiment, despite signals of additional government support measures.

Hang Seng and Shanghai Comp. were pressured amid ongoing property sector concerns after a Hong Kong court issued a wind-up order to Chinese property developer Dexin China.

ASX 200 declined amid broad weakness across sectors and as miners led the descent.

Nikkei 225 bucked the trend as it benefitted from recent currency weakness.

“The recent weekend holiday didn’t see as strong consumption as the previous May Golden Week, and weekly property sales are weak,” said Xin-Yao Ng, director of investment at abrdn.

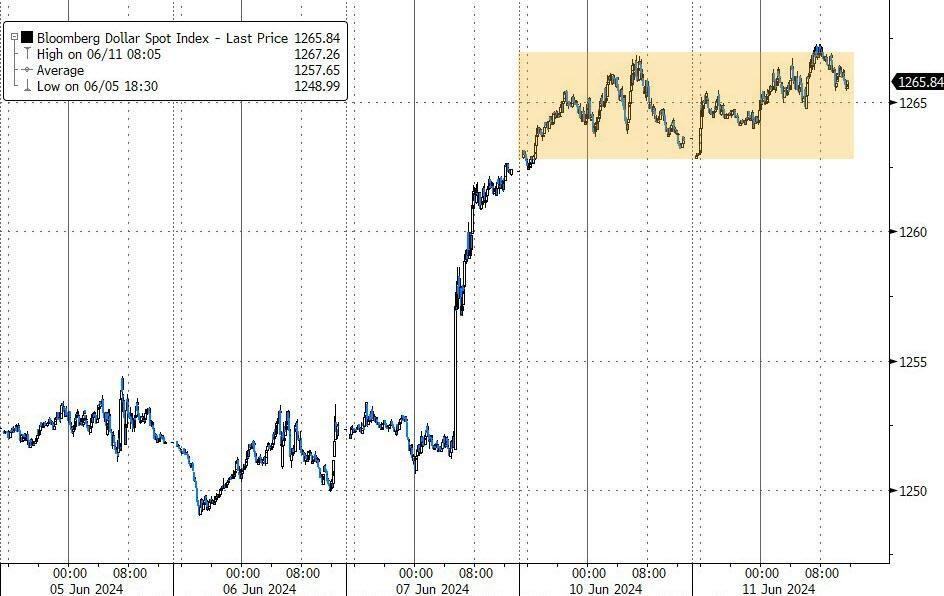

In FX, the Bloomberg Dollar Spot Index gained for a fourth day and was up 0.2% as investors positioned for the Fed’s policy decision on Wednesday at which officials are expected to scale back forecasts for a pivot; US CPI data will be released the same day.

“The US dollar has bounced back, underpinned by widening monetary policy divergences,” Elias Haddad and Win Thin, strategists at Brown Brothers Harriman & Co., wrote in a note. “We expect the Fed to deliver a hawkish hold Wednesday” Treasury 10-year yields slipped 4bps to 4.43%, tracking gains in European bond markets; the Department of the Treasury will auction $39 billion of 10-year debt on Tuesday, which follows the sale of three-year notes on Monday which drew a higher-than-expected yield. Traders see an 80% possibility that the Fed will start cutting rates in November, compared with 75% on Monday; they are pricing a total of 40bps of cuts by the end of the year

In rates, treasury futures extend advance in early US session, with yields near lows of the day, richer by up to 5bp across belly of the curve and outperforming European rates. US yields richer by 3bp to 5bp across the curve with belly-led gains steepening 5s30s spread by ~2bp vs Monday’s close. US 10-year yields around 4.43%, outperforming bunds in the sector by 2bp and French bonds by 10bps. Main focal point for Tuesday’s US session is $39 billion 10-year note auction, while in Europe French bonds continue to fall amid heightened political uncertainty following the European Parliament elections. Treasury coupon auction cycle resumes with $39b 10-year reopening at 1pm New York, concludes Thursday (after FOMC decision Wednesday) with $22b 30-year bond reopening; WI 10-year yield at around 4.425% is ~6bp richer than last month’s, which tailed by 1bp.

In commodities, oil held its biggest jump since March ahead of an OPEC report that will provide a snapshot on the market outlook. Crude surged on Monday as traders piled back into the commodity after the biggest weekly loss since early May.

The OPEC report will be followed by a Short-Term Energy Outlook from the US later on Tuesday, and a monthly release from the International Energy Agency on Wednesday.

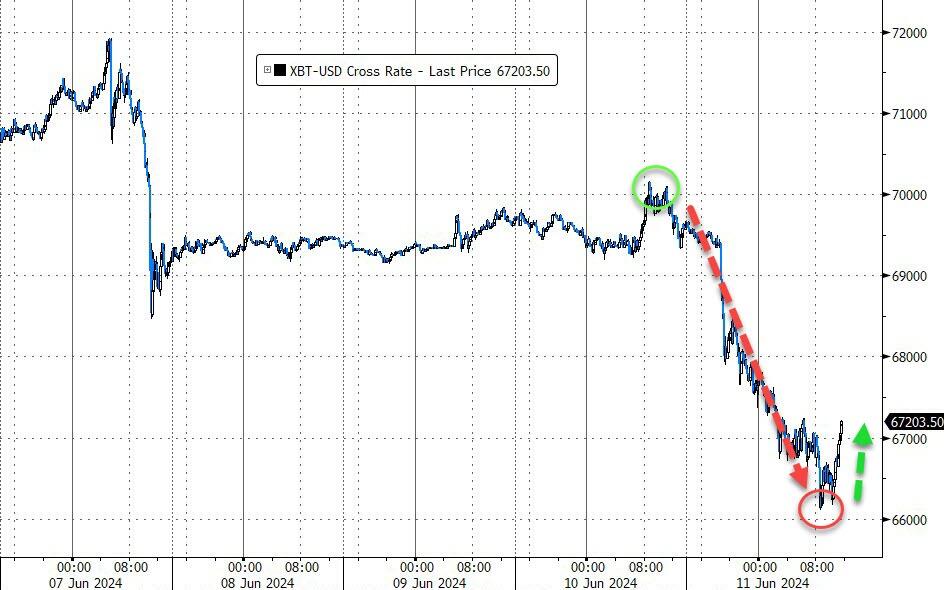

Bitcoin slumped below $68K with Ethereum also sliding towards $3.5k, giving back some of its overnight advances. Crypto insiders are said to be meeting with US Senate staffers to try to resolve a surprise crypto policy push embedded in a recent Senate spending package that cleared the intelligence committee, according to CoinDesk.

Looking at today’s calendar, US economic data is empty for the session, while Fed officials are expected to refrain from commenting until after Wednesday’s policy announcement

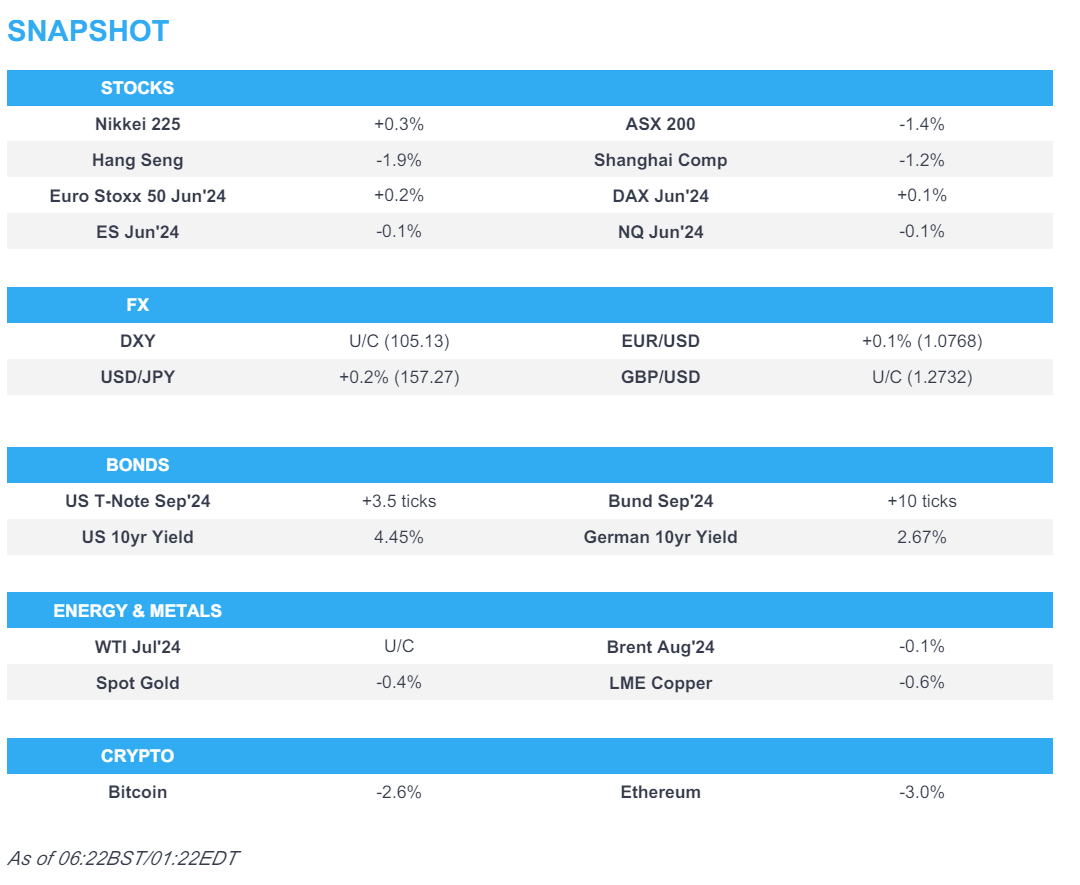

Market Snapshot

S&P 500 futures down 0.1% to 5,365.50

STOXX Europe 600 little changed at 521.82

MXAP down 0.5% to 179.29

MXAPJ down 0.5% to 558.40

Nikkei up 0.2% to 39,134.79

Topix down 0.2% to 2,776.80

Hang Seng Index down 1.0% to 18,176.34

Shanghai Composite down 0.8% to 3,028.05

Sensex up 0.2% to 76,670.09

Australia S&P/ASX 200 down 1.3% to 7,755.38

Kospi up 0.2% to 2,705.32

German 10Y yield little changed at 2.67%

Euro little changed at $1.0760

Brent Futures up 0.1% to $81.73/bbl

Gold spot down 0.1% to $2,307.44

US Dollar Index little changed at 105.20

Top Overnight News

Elon Musk isn’t a fan of Apple’s AI announcement. He said he’d ban Apple devices from his companies if OpenAI’s software is integrated at the OS level, calling the tie-up a security risk. BBG

An aggressive market grab by low-cost Chinese retailers has delivered bumper earnings for some firms but has also intensified a bruising price war, exacerbating deflationary fears in the world’s second-largest economy. From coffee to cars to clothes, China’s discount retailers have cut prices on just about everything as they chase a consumer whose confidence has been battered by a property crisis, high unemployment and a gloomy economic outlook. RTRS

France’s National Rally expected to win the upcoming election but fall short of an absolute majority. RTRS

ECB’s Lagarde repeats that policy isn’t on a preset path and rates could stay on hold for more than one consecutive meeting. FT

UK labor report showed a rise in Apr unemployment (employment fell 139K vs. the Street -98K and the UR climbed to 4.4% vs. 4.3% in the prior period) while wages stayed elevated (+5.9% vs. the Street +5.7%). WSJ

Israel is ramping strikes against Hezbollah and Hezbollah-related targets in Syria, signs the country is “gearing up for a full-scale war” against the terror group in Lebanon. RTRS

Blackstone is targeting ~$10B in Japanese deals over the next few years as the country’s economy continues improving. Nikkei

OpenAI dismissed speculation that Sarah Friar’s hiring means it is about to pursue an IPO. Market Watch

Advertising outlook increased by WPP’s GroupM to +7.8% for ’24 (ex-politics) vs. the prior estimate of +5.3% (although a big chunk of the increase was a function of how certain areas of the industry in China are measured). WSJ

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded with a negative bias after the choppy performance stateside where the S&P 500 and Nasdaq notched fresh record closes but the gains were capped ahead of the mid-week key events. ASX 200 declined amid broad weakness across sectors and as miners led the descent. Nikkei 225 bucked the trend as it benefitted from recent currency weakness. Hang Seng and Shanghai Comp. were pressured amid ongoing property sector concerns after a Hong Kong court issued a wind-up order to Chinese property developer Dexin China.

Top Asian News

China’s Auto Industry CPCA said China sold 1.72mln passenger cars in May, -2.2% Y/Y; said China’s pure EV exports saw a temporary decline in May amid Red Sea shipping issues alongside other factors; still have strong growth momentum despite disruptions in European markets.

China saw 110mln domestic tourist trips during the three-day Dragon Boat Festival holiday and official data showed that Chinese cross-border trips rose 45.1% Y/Y during the three-day holiday.

Hong Kong court issued a wind-up order to Chinese property developer Dexin China (2019 HK), while it was later reported that Dexin China suspended trading in Hong Kong.

European bourses, Stoxx 600 (-0.4%) began the session on a modestly firmer footing, though did succumb to slight selling pressure as the morning progressed, in a continuation of the downbeat mood in APAC trade overnight. European sectors are mixed, with the breadth of the market fairly narrow. Basic Resources is the standout laggard, given the broader weakness in metals prices. US equity futures (ES -0.2%, NQ -0.3%, RTY -0.7%) are modestly in the red, with price action tentative ahead of Wednesday’s key risk events, including the FOMC & US CPI.

Top European News

ECB’s Villeroy said rate reduction markets a “decisive orientation”; limited spill-over from Fed/ECB’s difference in timing. Fed policy should not greatly impact the ECB’s. Significant leeway to reduce rates before exiting restrictive territory. Monitoring actual inflation data, in particular for services but monthly figures will be volatile due to base effects on energy. “Noise” is not very meaningful and as such is more outlook driven. Will look more closely at inflation forecasts. Remains confident that the Bank will bring inflation to target by next year; will reach it with a soft, rather than hard landing.

ECB’s Simkus said it is too early to declare victory over inflation; rates can be cut more if ECB is sure the 2% inflation target will be met.

ECB’s Rehn said monetary policy has dampened price pressures; considerable progress has been made. ECB knows the inflation path is a bumpy road, but sees stabilisation ahead

France’s National Rally party and lawmaker Marion Marechal are in talks about potentially joining forces to oppose President Macron in the upcoming elections, according to Bloomberg.

Moody’s said France’s snap election is negative for France’s credit rating; said outlook and rating could move to negative if interest payments relative to revenue and GDP are seen to be significantly larger than peers.

French President Macron is said to be mulling potential resignations in the case of a possible right-wing victory in early parliamentary elections, according to News AZ.

French Elysee Palace has reportedly denied media reports suggesting that French President Macron might resign.

French President Macron is to hold a press conference on June 12 around 11:00 BST/ 06:00 EDT.

FX

USD is broadly steady vs. peers with DXY holding above the 105 mark and within yesterday’s 104.93-105.38 range; trade is contained ahead of Wednesday’s CPI/FOMC where focus will reside on the M/M core rate and any adjustments to the Fed’s FFR dots.

EUR is softer vs. the USD and ultimately still weighed on via the double-whammy of Friday’s NFP and the weekend’s EU parliamentary elections. For now, the pair is stuck on a 1.07 handle and holding above Monday’s 1.0732 low.

GBP is a touch softer vs. both the USD following UK jobs metrics which showed an unexpected uptick in unemployment, a larger-than-expected decline in employment, and mixed, but sticky wage growth. Cable ventured as low as 1.2714 but refrained from testing the 1.27 mark.

JPY is marginally building on the losses vs. the USD seen since Friday with USD/JPY now up to 157.38.

Antipodeans are both steady vs. the USD in quiet trade after managing to claw back some of Friday’s losses during yesterday’s session.

PBoC set USD/CNY mid-point at 7.1135 vs exp. 7.2724 (prev. 7.1106).

Fixed Income

USTs are firmer but ultimately unable to recoup much of the lost ground seen in the wake of Friday’s NFP release; price action has been tentative as focus lies on the US CPI and FOMC on Wednesday. The Sep’24 UST contract continues to hold above the 109 mark and did catch a recent bid in tandem with news that French President Macron is said to be mulling potential resignations in the case of a possible right-wing victory in early parliamentary elections, according to News AZ – although this was later denied. A record Gilt sale also played a factor.

European debt markets are slightly more contained, though OATs remain under pressure with Moody’s noting that the snap election called by Macron is negative for the nation’s credit rating. Sep’24 Bund sits towards the bottom end of yesterday’s 129.52-130.27 range.

Gilts are outperforming peers on account of the latest UK jobs data, which showed an unexpected uptick in unemployment and mixed, but sticky wage growth. Gilts are currently higher by around 35 ticks, taking another leg higher after UK got a record GBP 104bln in orders for its Gilt sale, via Bloomberg; beating the prior record of GBP 100bln; pricing +4bps over UKT, pricing expected later on Tuesday.

Commodities

Crude is slightly softer after spending much of the session flat in what has been a catalyst thin session, except for news that Hamas is reportedly ready to negotiate the details of the ceasefire following yesterday’s UNSC vote; oil markets were unreactive to the news. Brent Aug trades within 81.37-82.02/bbl.

Bullish price action across nat gas futures with US Henry Hub front-month back above USD 3/MMBtu for the first time since January. The rise in US prices is partly attributed to expectations of a tightening market in the medium-to-long term.

Subdued trade across precious metals despite relatively steady markets elsewhere aside from metals. Spot gold is flat/modestly lower while spot silver and spot palladium see deeper losses to the tune of -1.5 to 1.7%.

Considerable weakness across base metals with desks citing recent developments of US rate cuts expectations coupled with high Chinese inventories whilst a softer CNY also reduces the purchasing power of Chinese buyers.

India Oil Minister said India state refiners in talks for long term oil import deal with Russia.

OPEC MOMR to be released at 12:30 BST/ 07:30 EDT.

Geopolitics

Israel conducted raids on the Hosh al-Sayed Ali area of the Hermel district near the Lebanese-Syrian border, according to Al Jazeera.

US State Department said Secretary of State Blinken discussed with Israeli Defence Minister Gallant on Monday the Gaza ceasefire proposal.

“Hamas ready to implement ceasefire agreement: Senior official”, via IRNA; Senior Hamas official Mahmoud al-Mardawi said that the Hamas movement is ready to cooperate for the implementation of the ceasefire agreement. According to the Palestinian Samaa News Agency, al-Mardawi made the remarks in reaction to a United Nations Security Council (UNSC) resolution; Wider reporting: Hamas agreed to Security Council ceasefire resolution and is ready to negotiate details, according to a Hamas official cited by Reuters.

“Israeli media: About 40 rockets were launched from southern Lebanon and one landed in the Upper Galilee”, according to Sky News Arabia.

US President Biden is to lift the ban on allowing a controversial Ukrainian unit to use US weapons, according to The Washington Post.

South Korean military said it fired warning shots after North Korean soldiers briefly crossed the border on Sunday, according to Yonhap.

US Event Calendar

6:00: May small business optimism 90.5 Est. 89.7, Prior 89.7

DB’s Jim Reid concludes the overnight wrap

As I cry in a corner and hang on tight to my last day in my 40s, its fair to say its been a dramatic couple of weeks for elections with each of them having their own major surprises in a year with the largest % of the global population ever going to national elections. As we discussed yesterday the European Parliamentary elections broadly went as the polls suggested (a slight move to the right but with the centre holding) but that the big news was President Macron calling a snap legislative election. This led to sizeable losses across Europe with France at the epicentre, albeit taking Italy along for the ride. But the declines were clear across the rest of the continent, with governing parties experiencing defeats in several countries, including Germany as well.

When it came to markets, French bonds were the worst-affected, with their 10yr yield surging by +12.8bps yesterday to 3.22%. That’s their highest level since November, and the Franco-German 10yr spread also widened by +7.6bps, which is its biggest daily widening since July 2022. Moreover, equities slumped, with the CAC 40 (-1.35%) falling to its lowest level since February, though it did recover by about 1% from intra-day lows. Banks were among the worst performers, including Société Générale (-7.46%) and BNP Paribas (-4.76%). The STOXX 600 closed -0.27% lower, having traded -0.88% intra-day, while the DAX and the FTSE MIB both fell back by -0.34%. As we’ll see in more detail later, the S&P 500 (+0.26%) ignored the European noise and hit a new record high.