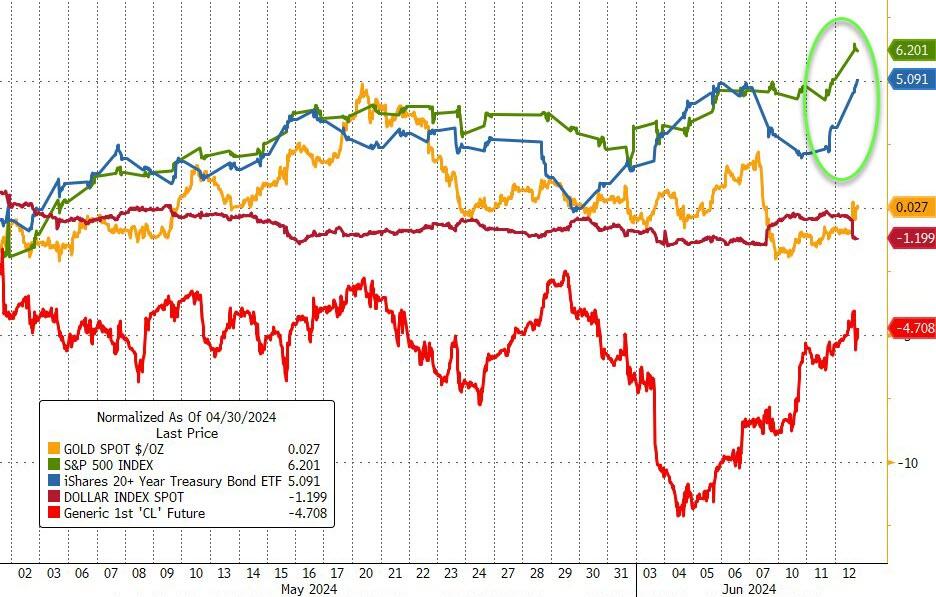

GOLD PRICE CLOSED UP $28.30 TO $2337.80

SILVER PRICE UP 0.97 TO 30.12

Gold ACCESS CLOSED $2323.15

Silver ACCESS CLOSED: $29.64

Bitcoin morning price:$67,800 UP 625 DOLLARS.

Bitcoin: afternoon price: $68,441 UP 1266 dollars

Platinum price closing UP $13.05 TO $969.75

Palladium price; UP $20.45 AT $911..60

END

there is no question we have a derivative problem especially with the high numbers of Exchange for physicals issued for gold and silver.. Andrew Maguire will address this on Friday.

SHANGHAI GOLD PREMIUM 36 DOLLARS/COMEX GOLD//JULY TO JULY

SHANGHAI GOLD

SHANGHAI GOLD (USD) FUTURES – QUOTES

Market data is delayed by at least 10 minutes.

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $3187.52 UP 3.24 CDN dollars per oz( * NEW ALL TIME HIGH 3,305.30 CDN DOLLARS PER OZ//MAY 20 2024)

*BRITISH GOLD: 1814.94 DOWN 2.90 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2149.88 DOWN 6.79 Euros per oz //* (ALL TIME CLOSING HIGH: 2248.89 EUROS PER OZ//APRIL 16.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCH: COMEX

ACCESS MARKETEXCHANGE: COMEX

CONTRACT: JUNE 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,307.500000000 USD

INTENT DATE: 06/11/2024 DELIVERY DATE: 06/13/2024

FIRM ORG FIRM NAME ISSUED STOPPED

099 H DB AG 2

190 H BMO CAPITAL 48

363 H WELLS FARGO SEC 85

435 H SCOTIA CAPITAL 190

657 C MORGAN STANLEY 2

657 H MORGAN STANLEY 361

661 C JP MORGAN 25 3

661 H JP MORGAN 7

686 H STONEX FINANCIA 3

690 C ABN AMRO 8

732 C RBC CAP MARKETS 2

737 C ADVANTAGE 5 13

880 H CITIGROUP 9

905 C ADM 2 21

TOTAL: 393 393

MONTH TO DATE: 28,995

JPMorgan stopped 10/393

FOR JUNE 2024

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2024. CONTRACT: 393 NOTICES FOR 39,300 OZ or 1.2222 TONNES

total notices so far: 2,899,500 contracts for 2,899,500 Oz (90.1866 tonnes)

FOR JUNE:

SILVER NOTICES: 0 NOTICE(S) FILED FOR nil

OZ/

total number of notices filed so far this month :1114 for 5.570 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $29.30 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : HUGE CHANGE IN GOLD INVENTORY AT THE GLD’ A MASSIVE WITHDRAWAL OF 4.89 TONNES OF GOLD FROM THE GLD//

/ /INVENTORY RESTS AT 830.78TONNES

INVENTORY RESTS AT 830.78 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER UP $.97 AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSIVE DEPOSIT OF 5.983 MILLION OZ INTO THE SLV

// INVENTORY INCREASES TO 427.125 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 427.125 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY AN ULTRA HUGE SIZED 2987 CONTRACTS TO 176,036 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR LOSS OF $0.59 IN SILVER PRICING AT THE COMEX ON TUESDAY’S TRADING ON SILVER. WE HAD CONSIDERABLE LIQUIDATION AS WE HAD A NET LOSS OF CONTRACTS ON OUR TWO EXCHANGES. WE, AGAIN HAD SHORT COVERING BY OUR SPECS WITH THE STRONG LOSS IN PRICE AS WELL AS MASSIVE T.A.S. LIQUIDATION. WE HAD ANOTHER MEGA HUMONGOUS SIZED 5,561 T.A.S ISSUANCE, THE 3ND HIGHEST EVER RECORDED FOR SILVER, AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED LAST TUESDAY AND AGAIN LAST FRIDAY.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 5561 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND TODAY;S TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.59) AND WERE SUCCESSFUL IN KNOCKING SOME SILVER LONGS FROM THEIR PERCH AS WE DID HAVE A HUGE SIZED LOSS OF 2787 CONTRACTS ON OUR TWO EXCHANGES WITH THE LOSS IN PRICE OF $0.59

WE MUST HAVE HAD:

A SMALL SIZED 200 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.830 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 15,000 OZ QUEUE JUMP

//NEW STANDING FOR SILVER//JUNE IS THUS 6.305 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI LOSS //SMALL SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 5561 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED 442 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE

TOTAL CONTRACTS for 8 DAYS, total 7424 contracts: OR 37.120 MILLION OZ (928 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 36.120 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 37.120 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2787 CONTRACTS WITH OUR LOSS IN PRICE OF SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL EFP ISSUANCE CONTRACTS: 200 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.830 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 15,000 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR JUNE 6.305 MILLION OZ

WE HAVE A HUGE SIZED LOSS OF 2787 OI CONTRACTS ON THE TWO EXCHANGES WITH THE LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A MEGA HUMONGOUS SIZED 5561 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND STRONG NET LIQUIDATION OF LONGS.

THE NEW TAS ISSUANCE TUESDAY NIGHT (5561) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 0 NOTICE(S) FILED TODAY FOR nil OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 1854 OI CONTRACTS TO 436,857 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED 20 CONTRACTS

WE HAD A FAIR SIZED INCREASE IN COMEX OI (1854 CONTRACTS) OCCURRED WITH OUR LOSS OF $0.30 IN PRICE/TUESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 89.94 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE 35,000 OZ QUEUE JUMP AS BANKERS SCOUR THE PLANET LOOKING FOR GOLD ON THE THIS SIDE OF THE POND

NEW STANDING 91.611 TONNES// ALL OF THIS HAPPENED WITH OUR $0.30 LOSS IN PRICE WITH RESPECT TO TUESDAY’S TRADING. WE HAD A FAIR SIZED GAIN OF 2632 OI CONTRACTS (8.186 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A SMALL SIZED 755 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 436,857

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2632 CONTRACTS WITH 1854 CONTRACTS INCREASED AT THE COMEX// AND A SMALL SIZED 775 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 2609 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL SIZED 775 CONTRACTS,,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (775 CONTRACTS) ACCOMPANYING THE FAIR SIZED GAIN IN COMEX OI OF 1854 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 2632 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 88.761 TONNES FOLLOWED BY TODAY’S QUEUE JUMP TO 1.0886 TONNES

//NEW STANDING /JUNE 90.522 TONNES.

/ 3) HUGE T.A.S. LIQUIDATION OF CONTRACTS WITH ZERO LONG SPECS BEING CLIPPED,

4) FAIR SIZED COMEX OPEN INTEREST GAIN 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///STRONG T.A.S. ISSUANCE: 2891 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE. :

TOTAL EFP CONTRACTS ISSUED: 27,899 CONTRACTS OR 2,789,900 OZ OR 86.777 TONNES IN 8 TRADING DAY(S) AND THUS AVERAGING: 3487 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAY(S) IN TONNES 86.777 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 86.777 DIVIDED BY 3550 x 100% TONNES = 2.44% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 86.777 tonnes HEADING FOR A STRONG MONTH

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 2987 CONTRACTS OI TO 176,036 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 200 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 200 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 200 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2987 CONTRACTS AND ADD TO THE 200 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2787 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 13.935 MILLION OZ

OCCURRED WITH OUR HUMONGOUS $0.59 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED UP 9.42 PTS OR 0.31% //Hang Seng CLOSED DOWN 238.08 PTS OR 0.66%// Nikkei CLOSED DOWN 258.08 OR 0.66%//Australia’s all ordinaries CLOSED DOWN 0.63%///Chinese yuan (ONSHORE) closed UP TO 7,2536 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2689/ Oil UP TO 78.80 dollars per barrel for WTI and BRENT UP AT 82.70 /Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 1844 CONTRACTS TO 436,857 DESPITE OUR LOSS IN PRICE OF $0.30 WITH RESPECT TO TUESDAY’S TRADING. WE HAD A HUGE T.A.S. LIQUIDATION ON TUESDAY WITH ZERO LONGS BEING CLIPPED.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE.… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A SMALL SIZED 775 EFP CONTRACTS WERE ISSUED: : AUGUST 775 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 775 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2632 CONTRACTS IN THAT 775 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A FAIR SIZED GAIN OF 1854 COMEX CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $0.30

/ /TUESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A GOOD SIZED 2891 CONTRACTS. MOST OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. TUESDAY IS OF EXTREME IMPORTANCE TO OUR CROOKS IN YESTERDAY’S TRADING

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (90.617 TONNES)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 90.617 TONNES. THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $0.30 //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR SIZED GAIN OF 2632 CONTRACTS ON TUESDAY WITH OUR TWO EXCHANGES DESPITE THE LOSS IN PRICE. THE T.A.S. ISSUED ON TUESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 8.115 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE (89.94 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 47 CONTRACTS OR 4700 OZ (0.8979 TONNES)

NEW STANDING FOR JUNE: 91.617 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $0.30

WE HAVE ADDED 20 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET GAIN ON THE TWO EXCHANGES 2632 CONTRACTS OR 263200 (8.186 TONNES)

confirmed volume TUESDAY 153,853 contracts//poor

//speculators have left the gold arena

JUNE 12 JUNE GOLD CONTRACT

/ /// THE JUNE 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 6017.560 oz brinks real gold leaving . |

| Deposit to the Dealer Inventory in oz | 0 oz |

| Deposits to the Customer Inventory, in oz | 0 OZ//BRINKS |

| No of oz served (contracts) today | 393 notice(s) 39,300 OZ 1.2222 TONNES |

| No of oz to be served (notices) | 458 contracts 45,800 OZ 1.424 TONNES |

| Total monthly oz gold served (contracts) so far this month | 28,995 notices 2,899,500 oz 90.1866 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: NIL oz

we have 0 customer deposit:

total deposit nil oz

customer withdrawals: 1

brinks; 6017.560 oz

this is a real gold transfer out of the comex

TOTAL WITHDRAWALS 6017.50 0z

Adjustments: 5/dealer to customer account

when we see this, it general means the comex is in stress

a) Brinks 3665.214 oz

b) HJSBC 24,454.665 oz

c) JPMorgan: 2121,966 oz

d) Loomis: 3279.402 oz

e) Manfra: 12,986.099 oz

total 46,508.299 oz or 1.44 tonnes

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE

For the front month of JUNE we have an oi of 851 contracts having GAINED 322 contracts. We had 28 contracts served on Tuesday so we gained a huge 350 contracts or 35,000 oz additional ounces will stand for gold at the comex as they underwent a MASSIVE queue jump to take delivery on this side of the pond.. We saw a dubious small kilobar entry gold leaving the comex on TUESDAY. Thus despite the huge 91 PLUS tonnes of gold standing at the comex little gold is arriving and hardly any gold is leaving.

JULY GAINED 186 CONTRACTS TO STAND AT 2474

AUGUST GAINED 509 CONTRACTS UP TO 357,221 CONTRACTS

We had 393 contracts filed for today representing 39300 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 25 notice was issued from their client or customer account. The total of all issuance by all participants equate to 393 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 10 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for June /2024. contract month, we take the total number of notices filed so far for the month (28,995) x 100 oz ) to which we add the difference between the open interest for the front month of JUNE (851 CONTRACTS) minus the number of notices served upon today (393 x 100 oz per contract( equals 2,945,300 OZ OR 91.617 TONNES.

thus the INITIAL standings for gold for the JUNE contract month: No of notices filed so far (28,995 x 100 oz +we add the difference for front month of June (851 OI} minus the number of notices served upon today (393) x 100 oz which equals 2,945,300 oz (91.617 TONNES)

TOTAL COMEX GOLD STANDING FOR JUNE: 91.617 TONNES WHICH IS ABSOLUTELY HUGE FOR THIS VERY ACTIVE DELIVERY MONTH IN THE CALENDAR. JUNE IS TRADITIONALLY THE 2ND HIGHEST DELIVERY MONTH OF THE YEAR. FROM THIS POINT WE WILL GAIN IN GOLD TONNAGE WILLING TO STAND AT THE COMEX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,680,714/128 52.27 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,662,910 OZ

TOTAL REGISTERED GOLD 7,951,205.990 ( 247.31 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,705,686.663 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,270,491 oz (REG GOLD- PLEDGED GOLD)= 195.03 tonnes //

END

SILVER/COMEX

JUN 12/2024

INITIAL

//2024// THE JUNE 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 582.684.867 oz Delaware . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 1,182,296.529 oz Asahi Manfra |

| No of oz served today (contracts) | 0 CONTRACT(S) (nil OZ) |

| No of oz to be served (notices) | 147 contracts (0.735 million oz) |

| Total monthly oz silver served (contracts) | 1114 Contracts (5.570 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 deposits customer account:

i) into Ashai: 587,731.200 oz

ii) into Manfra: 594,565.329

total customer deposit 1,182,296.529 oz

JPMorgan has a total silver weight: 128.416million oz/297/190million or 43.20%

adjustment: 0//

Comex withdrawals: 1

i) out of Delaware: 582,684.867 oz

total withdrawal: 582,684.867 0z

TOTAL REGISTERED SILVER: 62.494MILLION OZ//.TOTAL REG + ELIGIBLE. 297.190

million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE:

silver open interest data:

FRONT MONTH OF JUNE/2024 OI: 147 CONTRACTS HAVING GAINED 2 CONTRACT(S).

WE HAD 1 NOTICE SERVED UP ON TUESDAY, SO WE GAINED 3 CONTRACTS OR AN ADDITIONAL 15,000 OZ WILL STAND AT THE COMEX VIA A SMALL QUEUE JUMP

JULY SAW A LOSS OF 9547 CONTRACTS DOWN TO 102,752

AUG, SAW A GAIN OF 16 CONTRACTS TO 237

SEPT SAW A GAIN OF 6255 CONTRACTS TO 55,335

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for 0 oz

CONFIRMED volume; ON TUESDAY 108,931 GIGANTIC

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1114 x 5,000 oz = 5.570 MILLION oz

to which we add the difference between the open interest for the front month of JUNE ((147) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2024 contract month: 1114 notices served so far) x 5000 oz + OI for the front month of JUNE (147)x number of notices served upon today minus (0)x 5000 oz of silver standing for the JUNE contract month equates to 6.305 MILLION OZ.

New total standing: 6.305 million oz.

There are 62.494 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

JUNE 12 WITH GOLD UP $28.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.89 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 830.78 TONNES

JUNE 11 WITH GOLD DOWN $0.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 10 WITH GOLD UP $2,00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 7 WITH GOLD DOWN $64.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 3.56 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 837.11 TONNES

JUNE 6 WITH GOLD UP $16.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.34 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 833.55 TONNES

JUNE 5 WITH GOLD UP $32.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 4 WITH GOLD DOWN $20.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 3 WITH GOLD UP $22.85 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 31 WITH GOLD DOWN $19.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 30 WITH GOLD UP $3.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 29 WITH GOLD DOWN $13.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 28 WITH GOLD UP $22.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 832.21 TONNES

MAY 24 WITH GOLD DOWN $2.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 833.36 TONNES

MAY 23 WITH GOLD DOWN $53.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 22 WITH GOLD DOWN $32.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 21 WITH GOLD DOWN $12,00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 20 WITH GOLD UP $21.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.10 TONNES OF GOLD INTO THE GLD//NEW TOTAL 838.54 TONNES

MAY 17 WITH GOLD UP $31.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//NEW TOTAL 833.36 TONNES

MAY 16 WITH GOLD DOWN $7.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//NEW TOTAL 833.36 TONNES

MAY 15 WITH GOLD UP $34.90 ON THE DAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD/INVENTORY RISES TO 831.93 TONNES

MAY 14 WITH GOLD DOWN $17.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RISES TO 831.33 TONNES

MAY 13 WITH GOLD DOWN $31.10 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD////INVENTORY RISES TO 831.93 TONNES

MAY 10 WITH GOLD UP $34.65 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 9 WITH GOLD UP $18.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD////INVENTORY REMAINS CONSTANT AT 830.47 TONNES

MAY 8 WITH GOLD DOWN $0.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 830.47 TONNES

MAY 7 WITH GOLD DOWN $6.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RISES AT 832.19 TONNES

MAY 6WITH GOLD UP $21.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .55 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 831.64 TONNES

MAY 2 WITH GOLD UP $0.20 ON THE DAY; SMAKK CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.17 TONNES IF FGOLD FROM THE GLD//INVENTORY FALLS AT 830.47 TONNES

MAY 1 WITH GOLD UP $7.80 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD:INVENTORY RISES AT 832.19 TONNES

GLD INVENTORY: 835.67 TONNES, TONIGHTS TOTAL

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 12 WITH SILVER UP $0.97 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 5.983 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 427.125 MILLION OZ

JUNE 11 WITH SILVER DOWN $0.59 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.644 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 422.786 MILLION OZ

JUNE 10 WITH SILVER UP $0.30 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 3.198 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 421.142 MILLION OZ

JUNE 7 WITH SILVER DOWN $1.93 TODAY: NO CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY AT 417.944 MILLION OZ

JUNE 6 WITH SILVER UP $1.27 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 417.944 MILLION OZ

JUNE 5 WITH SILVER UP 0.38 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.52 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 415.295 MILLION OZ

JUNE 4 WITH SILVER DOWN $1.08 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

JUNE 3 WITH SILVER UP $0.35 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

MAY 31 WITH SILVER DOWN $1.09 TODAY: HUGE CHANGES IN SILVER INVENTORY: A MASSIVE WITHDRAWAL OF 3.655 MILLION OZ FROM THE SLV//INVENTORY LOWERS TO 413.775 MILLION OZ

MAY 30 WITH SILVER DOWN $0.80 TODAY: NO CHANGES IN SILVER INVENTORY//INVENTORY REMAINS AT 417.430 MILLION OZ

MAY 29 WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 1.051 MILLION OZ INTO THE SLV//INVENTORY DECREASES TO 417.430 MILLION OZ

MAY 28 WITH SILVER UP $1.64 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 2.832 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 418.481 MILLION OZ

MAY 24 WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF .822 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 421.313 MILLION OZ

MAY 23 WITH SILVER DOWN $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.736 MILLION OZ FROM THE SLVINVENTORY INCREASES TO 420.491 MILLION OZ

MAY 22 WITH SILVER DOWN $0.66 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 21 WITH SILVER DOWN $0.41 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A DEPOSIT OF 3.792 MILLION OZ FROM THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 20 WITH SILVER UP $1.28 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 1.005 MILLION OZ FROM THE SLV// INVENTORY LOWERS TO 418.435 MILLION OZ

MAY 17 WITH SILVER UP $1.37 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 868,000 OZ FROM THE SLV// INVENTORY LOWERS TO 419.440 MILLION OZ

MAY 16 WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY REMAINS AT 420.308 MILLION OZ

MAY 15 WITH SILVER UP 101 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A WITHDRAWAL OF 1.919 MILLION OZ FROM THE SLV NVENTORY RESTS AT 420.308 MILLION OZ

MAY 14 WITH SILVER UP 25 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;INVENTORY RESTS AT 422.227 MILLION OZ

MAY 13 WITH SILVER DOWN 4 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;NVENTORY RESTS AT 422.227 MILLION OZ

MAY 10 WITH SILVER UP 15 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A HUGE WITHDRAWAL OF 1.,828 MILLION OZ//INVENTORY RESTS AT 422.227 MILLION OZ

MAY 9 WITH SILVER UP 78 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 8 WITH SILVER DOWN 11 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 7WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/INVENTORY RESTS AT 424.055 MILLION OZ

MAY 6 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.055 MILLION OZ

MAY 3 WITH SILVER DOWN 12 CENTS TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF 0.338MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 2WITH SILVER UP 0.12 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/ A WITHDRAWALOF 4.471 MILLION OZ OUT OF THE SLV INVENTORY RESTS AT 424.695 MILLION OZ

MAY 1 WITH SILVER UP 0.09 TODAY: SMALLCHANGES IN SILVER INVENTORY AT THE SLV/ A DEPOSIT OF ,457 MILLION OZ INTO THE SLV INVENTORY RESTS AT 429.814 MILLION OZ

CLOSING INVENTORY 427.125 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

China’s real estate sector has been in trouble for years and it is taking its toll on their economy

(Peter Schiff)

China’s Real Estate Crisis: A New Experiment In State Intervention

TUESDAY, JUN 11, 2024 – 07:40 PM

The real estate market is responsible for anywhere from 20% to over 30% of China’s GDP (depending on who you ask). And with the latest meltdown that began with the implosion of Evergrande, the situation just keeps getting worse, inspiring a slew of government interventions beyond the scope of what would be possible in a country like the US.

It’s a test of China’s authority, and its ability to micromanage what was mismanaged from the start. With China’s real estate stocks down 20% since May can the CCP, in all its centralized power, prevent a full meltdown?

China may succeed in kicking the can down the road, but it can’t save the real estate market — or economy — in the long term. Either way, history indicates that the current drawdown likely still has a long way down to go.

This chart shows a run-up to the current route, not long before the liquidation calls began for Evergrande and Country Garden and set the latest RE spiral into motion:

You will find more infographics at Statista

The People’s Bank of China can directly inject liquidity into a struggling sector. But state-owned companies also get to buy properties at government-set prices. The state and central bank can also change mortgage rates and payment requirements directly, unlike in the US where banks react to the federal funds rate set by the Fed. China is also loosening general restrictions on who is allowed to buy a home, hoping to juice the market and reduce vacancies, but there’s a potential catch-22 inherent to all such historic-level interventions:

If they stoke concerns among consumers and investors that the crisis is something to be deeply worried about, this can fuel a self-fulfilling feedback loop that worsens investor confidence even further.

Meanwhile, home buyers who fit the previously stringent criteria for buying homes feel duped now that those restrictions have been eased, devaluing their social status and the work they put into the home-buying process. With many complexes now having their unsold buildings turned into public housing, citizens who saved up their whole lives to become homeowners in these areas are becoming enraged to discover that their complexes will now be subsidized. Not only does that mean they paid too much, but their home’s attractiveness as a longer-term investment could drop.

According to Goldman Sachs, the current interventions still aren’t enough. A recent report calls for more liquidity to the tune of $276 billion (¥2 trillion yuan) to stabilize housing in major mainland cities, with ¥20 trillion yuan worth of real estate in need of a savior.

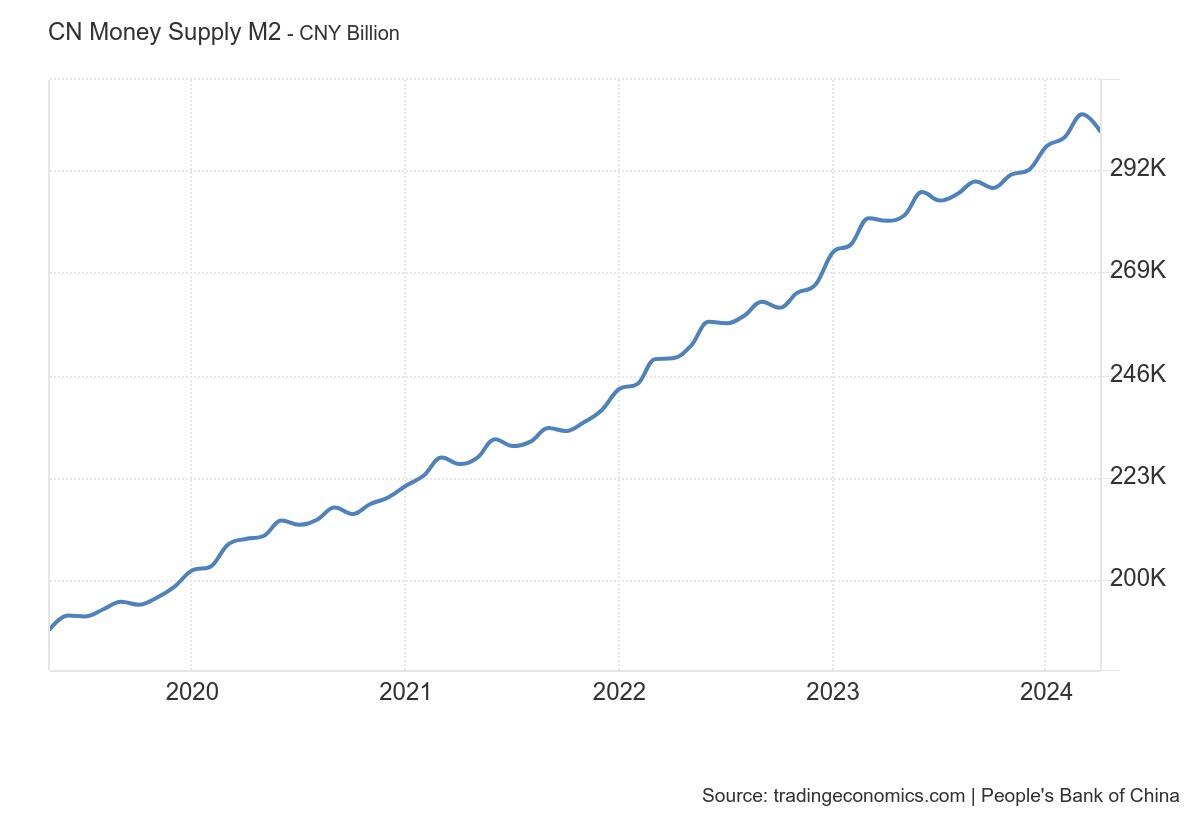

This liquidity would be meant to stop prices from continuing to plummet and allow over-indebted developers to pay back loans and interest. But in a market in need of such an intervention, even once prices stop plummeting, many become rightfully hesitant to become buyers. The below chart of China’s M2 money supply shows a dip in April 2024. It will be interesting to take another look after China’s intervention floods the economy with $500 billion yuan worth of relending programs.

To make matters worse in the longer term, declining birthrate and an aging population both indicate that demand is not going to pick back up enough to fill the apartments and houses built during China’s decades-long urbanization frenzy. This is a generational problem that goes beyond a single crash, liquidation, or bankruptcy — and can’t be properly fixed with centralized market interventions. Beyond that, even people in their prime home-buying age are more worried about future earnings than they used to be, without the feverish demand for urban homes that characterized so much of China’s rise to a global economic power.

In a free market, nature determines the winners and losers. But in a command-and-control economy, the State gets to decide. And when the interventions brazenly defy economic reality, as central banks always do, everyone ends up losing in the end. That is, except for the central bank, the government, and their preferred cronies, who will be the ones who get the free money and the bailouts when it all comes crashing down.

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/GOLD AND SILVER COMMENTARY

end

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS/

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT//COFFEE BEANS //ROBUSTA

Brewing Storm: World’s Top Robusta Coffee Producer Reports Smallest Export Since 2009

WEDNESDAY, JUN 12, 2024 – 04:15 AM

More troubling news is brewing for coffee lovers from the world’s top-producing country in Southeast Asia.

New export data reveals a sharp decline in robusta beans, commonly used in instant coffee and espresso and as a filler in various ground coffee blends. This development is part of a broader trend of tightening global supplies and soaring bean prices, exacerbating food inflation and hitting cash-strapped working poor consumers.

Bloomberg data shows Vietnam’s coffee exports plunged to the smallest volume in at least 15 years in May. Low exports are expected to persist for several months, which will only pressure prices higher.

Shipments from the world’s biggest producer of the robusta variety slumped to less than 80,000 tons in May, down 47% from a year ago, customs data show. That’s the lowest amount of beans exported for the month since 2009. -Bloomberg

Do Ha Nam, chairman of top shipper Intimex Group and deputy head of the Vietnam Coffee Cocoa Association, said monthly export data would be “insignificant” until the harvest of new beans begins in October. He warned stockpiles are quickly being depleted by farmers.

Tightening global supplies have rocketed robusta futures in London to the highest in 16 years.

About a third of the world’s robusta beans come from Vietnam.

Companies, such as J.M. Smucker Co., whose brands include Folgers, Dunkin’, Café Bustelo, Pilon, and Medaglia d’Oro, recently warned of imminent price hikes across its brands due to the surge in bean prices.

The coffee category continues to experience commodity volatility and overall meaningful inflation. In response to recent higher green coffee costs that we will begin to incur during the first quarter, we are taking a list price increase across parts of our portfolio in early June. As always, we will continue to manage our coffee business through a strategy that demonstrates a balance between recovering inflationary input costs, while providing consumers with attractive options ranging from value to premium.

Translation: Supermarket prices for coffee, especially J.M. Smucker’s brands, are set to move higher, if not already, thus raising food inflation for consumers.

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

ASIA TRADING//WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED UP 9.42 PTS OR 0.31% //Hang Seng CLOSED DOWN 238.08 PTS OR 0.66%// Nikkei CLOSED DOWN 258.08 OR 0.66%//Australia’s all ordinaries CLOSED DOWN 0.63%///Chinese yuan (ONSHORE) closed UP TO 7,2536 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2689/ Oil UP TO 78.80 dollars per barrel for WTI and BRENT UP AT 82.70 /Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2534

OFFSHORE YUAN: UP TO 7.26899

SHANGHAI CLOSED UP 9.42 PTS OR 0.31 %

HANG SENG CLOSED DOWN 238.50 PTS OR 1.31%

2. Nikkei closed DOWN 258.08 PTS OR 0.66 %

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 104.72 EURO RISES TO 1.0759 DOWN 48 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +0.974 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 157.34 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.67490/Italian 10 Yr bond yield UP to 4.150 SPAIN 10 YR BOND YIELD UP TO 3.513%

3i Greek 10 year bond yield DOWN TO 3.689

3j Gold at $2312.95//Silver at: 29.35 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 0/ 100 roubles/dollar; ROUBLE AT 89.10

3m oil into the 77 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 157.15/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.974% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8937 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9638 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.399 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.534 DOWN 0 BASIS PTS/

USA 2 YR BOND YIELD: 4.838 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.37…

10 YR UK BOND YIELD: 4.283 DOWN 5 PTS

2a New York OPENING REPORT

Futures Set For New Record High Ahead Of CPI, Fed Double Header

WEDNESDAY, JUN 12, 2024 – 08:13 AM

Futures are up modestly after another record close on Wall Street heading into today’s double whammy of CPI, and FOMC Dot Plot update, with Nasdaq leading and small-caps lagging. As of 8:00am, S&P futures are up 0.1% to 5,390 and set to extend the stretch of record highs as traders position for the potential disruption from US inflation data landing just hours ahead of Federal Reserve’s interest rate decision on Wednesday; Nasdaq futures rose 0.2%. Bond yields are flat to down 1bp after a stellar 10Y auction yesterday; the Bloomberg Dollar index rose again after four days of gains. Commodities are higher, led by Energy, despite with metals lagging. Today’s focus will be on the doubleheader of CPI and the Fed (our previews can be found here and here).

In premarket trading, Mag7 and semis names are mostly positive thanks to Oracle shares surging 8.7% to a new record high after the infrastructure software company announced a cloud infrastructure partnership with Google Cloud, as well as one with Microsoft and OpenAI. Oracle also reported fourth-quarter results that featured better-than-expected Cloud Infrastructure revenue, even as it missed on total revenue and earnings. PetMed shares drop 11% after the online pet pharmacy reported results.

Investors are preparing for a rare double-whammy of US CPI data and Fed announcements that have the potential to upend markets.

“Today is a big day in terms of economic data and Fed announcement,” said Ipek Ozkardeskaya, an analyst at Swissquote Bank. “It could determine the global market mood for the rest of the month, and a good part of summer.”

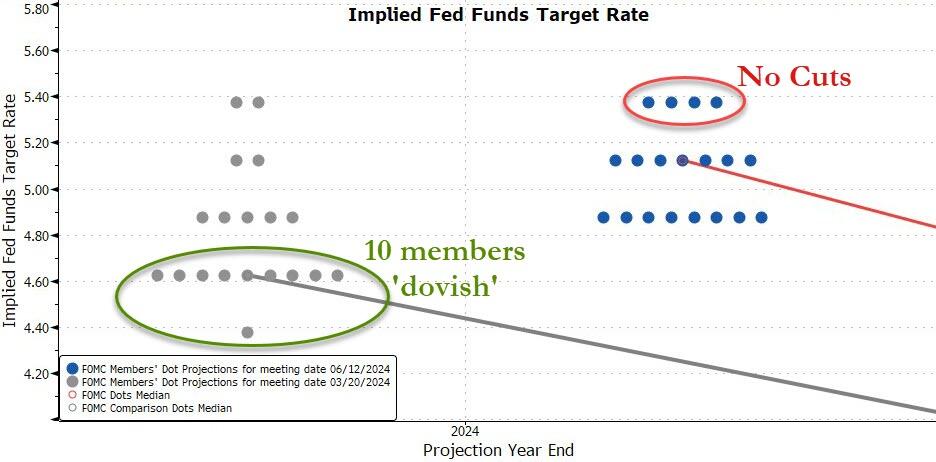

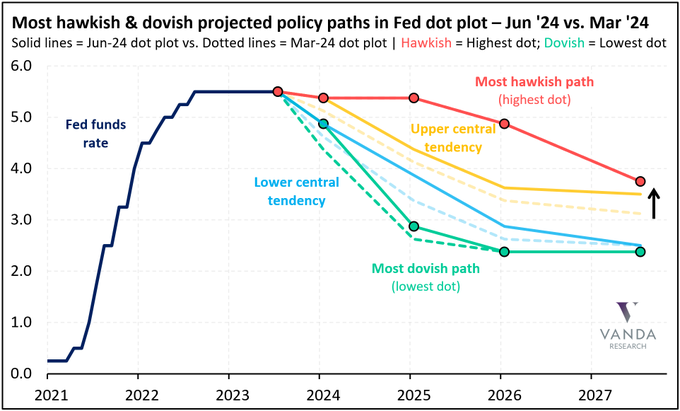

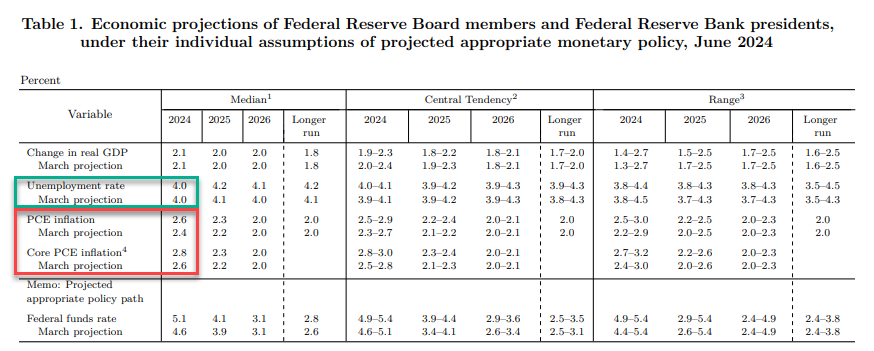

While policymakers are widely expected to hold borrowing costs at a two-decade high, there’s less certainty on officials’ quarterly rate projections, also known as the dot plot, where most expect the Fed to revise its dot plot from three rate cuts for the balance of 2024 to two, but a hawkish surprise of just one rate cut can not be excluded (see preview here). In any case, Fed voters already have the CPI print for May and it will feature prominently in their deliberations.

“If it’s two, I think the market reaction can be quite positive and would support new highs in the S&P 500,” Grace Peters, head of investment strategy for Europe, Middle East and Africa at JPMorgan Private Bank, said on Bloomberg TV.

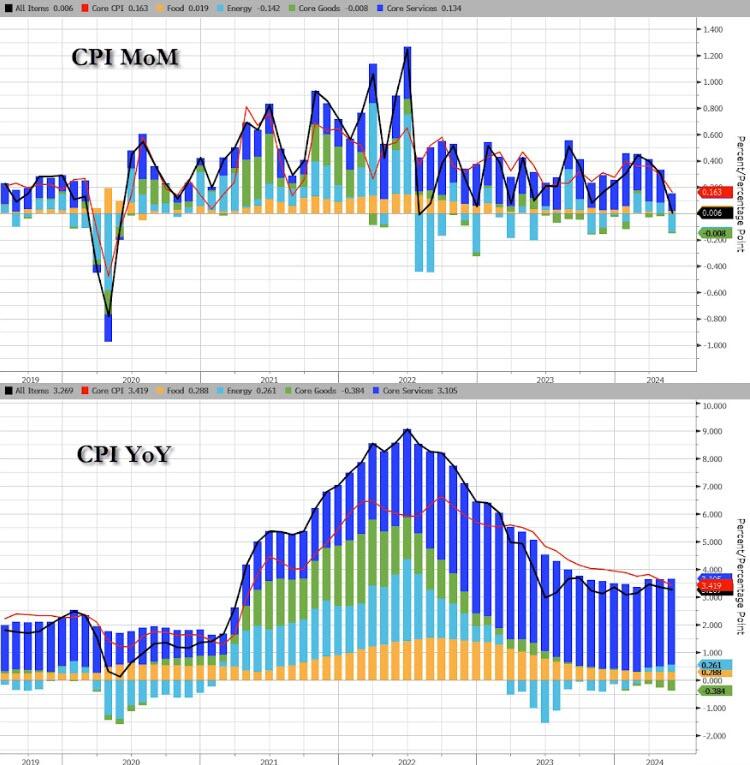

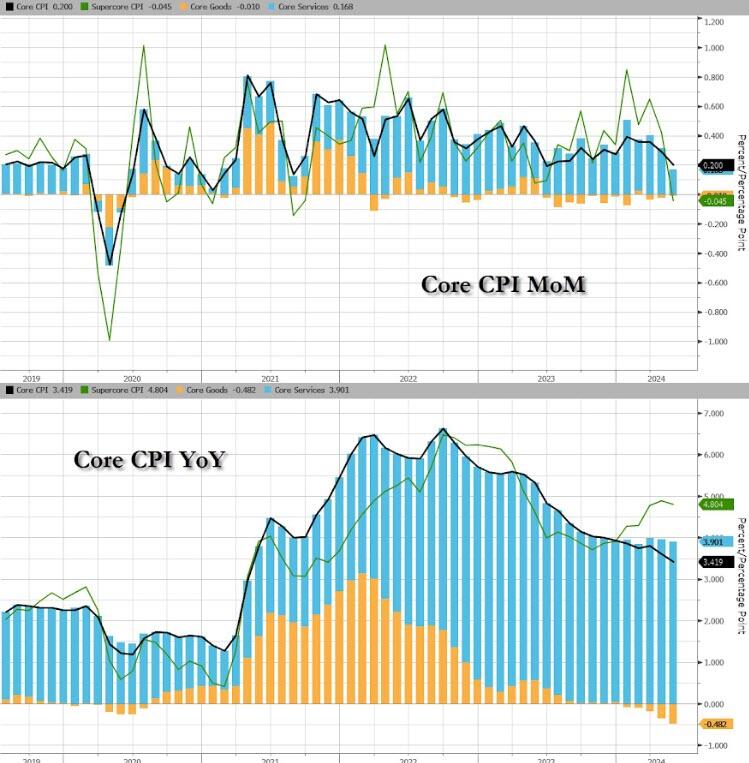

Ahead of the Fed, the May consumer price index reading is due at 8:30 a.m. and is supposed to show another modest slowdown in inflation, with Goldman’s trading desk saying that it is optimistic for a low print. Here is JPM’s core CPI MoM market reaction matrix (more details here).

- Above 0.4%. The first tail-risk scenario, this outcome is likely achieved by an increase in both Core Goods and Core Services, with Core Goods flipping from deflationary to inflationary MoM. Within Core Services, we would likely see shelter inflation increase. The bond market reaction would likely be a 12-15bps increase as part of a bear flattening. Equities would react negatively to this repricing. Given the acceleration higher in inflation, rate cut bets for 2024 would evaporate and we will see the return of views of a rate hike. This would be exacerbated by any comments from Powell suggesting rates are not restrictive enough. Probability 5%, SPX falls 1.5% to 2.5%.

- Between 0.35% – 0.40%. This outcome is likely achieved by a smaller than expected disinflationary impulse from Core Goods with Shelter remaining flat. Bonds react negatively as Sept/Nov rate cut views decrease. With market fixings pricing in ~0.26% for Core MoM, the bond market reaction could be larger than expected with many Equity investors focused on the surveyed number of 0.3%. Probability 15%, SPX falls 1% to 1.25%.

- Between 0.30% – 0.35%. This scenario has the widest range of outcomes since the low end of the range supports the disinflationary trend and the higher end of the range the stickier inflation argument. Feroli’s forecast for 0.33% would keep the YoY number flat from last month’s print. The biggest drivers are weak disinflation in shelter, increases in vehicle, medical, and communication prices. Given the move in bond yields on Friday (+14.6bps to 4.43%), there is likely a more muted response to a hotter print. Also referencing Friday, it was surprising to see stocks slough off the bond market move with the SPX falling only 11bps instead of 1%+ as we have seen over the last couple years in response to significant and sudden moves in bond yields. Probability 40%, SPX loses 0.75% to gains 0.75%.

- Between 0.25% – 0.30%. As mentioned, the market fixing implies a 0.26% core reading and the move in yields may not be as strong as one would expect on a beat where one would expect ~15bps move in the 10Y yield but this is a positive outcome for risk assets as this print would likely restart the Goldilocks narrative with 24Q1 data being viewed as an anomaly. Probability 25%, SPX gains 0.75% to 1.25%.

- Between 0.20% – 0.25%. The immediate reaction would be a surge in September rate cut expectations with some likely pointing to July for a surprise, insurance cut given the move by the ECB. While July sees highly unlikely, putting September back on the table would be view favorably by risk assets and we could see some yield curve steepening to aid the Cyclicals/Value trade. Probability 12.5%, SPX gains 1.25% to 1.75%.

- Below 0.20%. Another tail-risk scenario, likely fueled by a material decline in shelter inflation with goods disinflation supporting the print. Look for a collapse in yields, a material increase in July cut expectations, and a rally across all risk assets ex-commodities. In Equities, this would look like an “everything rally” with both NDX and RTY outperforming the SPX. This outcome, if confirmed in the July print, would trigger a reset in thinking about which stage of the economic cycle we currently reside as well as talks of the Fed having achieved a No Landing/Soft Landing scenario. Probability 2.5%, SPX gains 1.75% to 2.50%.

In Europe, the volatility of the past two days is subsiding investors were caught unprepared for French far-right gains in the weekend’s European Parliament elections; European stocks are on course to rise for the first time in four sessions, led by gains in banks, insurance and financial services. The CAC 40 is higher but underperforming its regional peers as political uncertainty continues to linger. Here are the biggest European movers:

- UCB shares gain as much as 5.6%, the most since February and to a record high, after JPMorgan raised its recommendation for the Brussels-listed biotech to neutral from underweight.

- Credit Agricole shares rise as much as 3.2% after Jefferies upgrades to buy, saying that the pullback in French banks since President Emmanuel Macron called a snap election presents an opportunity.

- Rentokil shares jump as much as 16% after US investor Nelson Peltz’s Trian Fund Management amassed a stake that made it one of the ten biggest shareholders in the pest controller.

- Richter shares gain as much as 1.5% after Hungarian pharmaceutical company agreed to buy some assets from Mithra Pharmaceuticals and its subsidiary late Tuesday.

- RWS Holdings shares rise as much as 6% after the translation services company’s interim results, with Berenberg saying growth returned in the second quarter and should now continue into 2H.

- Lonza shares dip as much as 3.2%, weighed down by speculation that a potentially beneficial US bill may be excluded from the National Defense Authorization Act due to a tight pre-election schedule.

- Legal & General shares fall as much as 4.7%, most since April 25, after the UK financial services firm forecast a slowdown in dividend-per-share growth.

- Colruyt shares plunge as much as 14% after the retailer issued cautious guidance because of increased competition and promo pressure.

- Umicore shares drop as much as 9.1%, to their lowest intraday since 2011, as the Belgian materials technology firm downgraded its guidance.

- Camurus shares fall as much as 6.1% after holder Sandberg Development offers 1.35m shares at SEK550 apiece, representing approximately an 8.6% discount to the last close.

- Stabilus shares fall as much as 17%, the steepest decline on record, after the German machinery maker sent out a profit warning last night, cutting its revenue and Ebit margin guidance.

- Safestore shares drop as much as 3.1% after the self-storage company’s interim results showed a drop in adjusted earnings, while warning full-year EPS will be at the lower-end of consensus.

Earlier, stocks in Asia fell for a second day, led by weakness in Japanese and offshore Chinese shares. The MSCI Asia Pacific Index declined as much as 0.4%, with Alibaba and Toyota among biggest drags. Benchmark in China was flat while that in Hong Kong closed at the lowest level since late April. Shares in Japan fell, while those in Korea were among the top gainers. In China, consumer prices rose less than expected in May and factory prices dropped for the 20th month in a row, fueling concerns over persistently weak demand. “Asian markets waded through murky waters today, with investors on edge ahead of a double-dose eventful day,” said Hebe Chen, an analyst at IG Markets. Also, specific headwinds are raising alarms for traders in China, Hong Kong, and Japan, she said.

In Hong Kong, the Hang Seng index slipped below the “crucial 18,000 level” due to the lackluster China’s CPI data and fresh speculation about looming US chip restrictions, Chen said, adding that Japanese stocks tumbled as hot PPI muddles the outlook for the Bank of Japan’s monetary policy decision due this Friday.

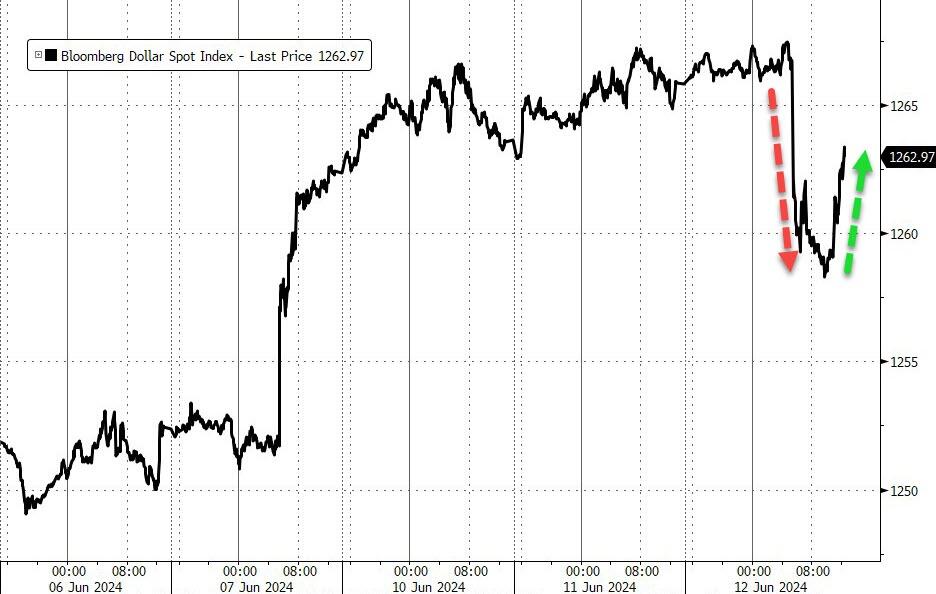

In FX, the Bloomberg Dollar Spot Index gained 0.1%, edging up for a fifth straight day as Treasury futures positioning data suggested the Fed will likely keep borrowing costs elevated. “A higher-than-expected US CPI will make the tone of the FOMC meeting more hawkish and result in USD strength,” said Richard Grace, a senior currency analyst at InTouch Capital Markets in Sydney. “Conversely, a lower-than-expected CPI will see the USD depreciate as Fed Chair Powell maintains the optimism for eventual rate cuts”

In rates, treasuries are also slightly higher ahead of US consumer prices and the Federal Reserve decision, with US 10-year yields falling 1bps to 4.40%. Traders are pricing an 80% possibility that the Fed may cut rates in November, while they price a total of 39 basis points of easing by the end of the year. French 10-year yields are flat at 3.22%. Gilts rise, with little reaction shown to a slight beat for UK GDP in April.

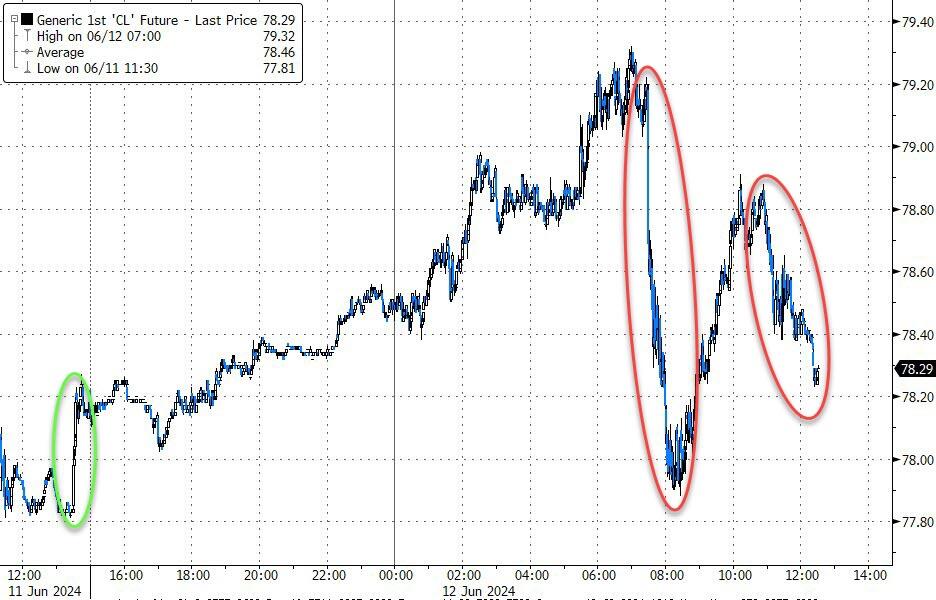

In commodities, oil prices are higher, with WTI rising 1.3% to trade near $78.90 a barrel. Spot gold falls ~$3 to around $2,314/oz.

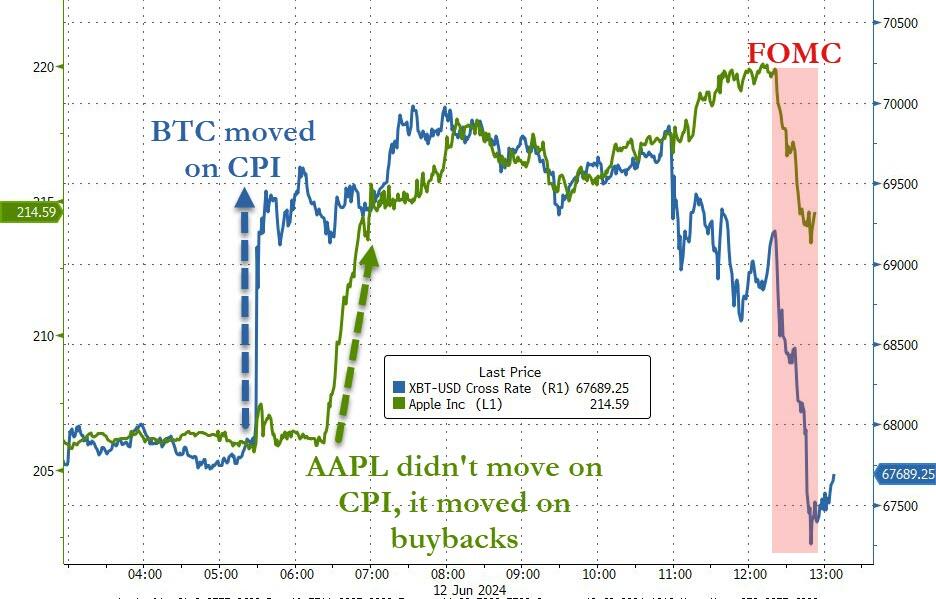

Bitcoin in consolidation mode in-fitting with broader markets; currently sitting just above USD 67k.

Today’s economic calendar includes includes May CPI (8:30am), monthly budget statement and FOMC rate decision (2pm). Fed officials scheduled to speak after the FOMC meeting include Powell (2:30pm news conference), Williams (Thursday), Goolsbee and Cook (Friday)

Market Snapshot

- S&P 500 futures little changed at 5,387.00

- STOXX Europe 600 up 0.5% to 519.79

- MXAP little changed at 178.98

- MXAPJ up 0.3% to 559.05

- Nikkei down 0.7% to 38,876.71

- Topix down 0.7% to 2,756.44

- Hang Seng Index down 1.3% to 17,937.84

- Shanghai Composite up 0.3% to 3,037.47

- Sensex up 0.4% to 76,762.03

- Australia S&P/ASX 200 down 0.5% to 7,715.51

- Kospi up 0.8% to 2,728.17

- German 10Y yield little changed at 2.61%

- Euro up 0.1% to $1.0752

- Brent Futures up 0.8% to $82.61/bbl

- Gold spot down 0.2% to $2,312.95

- US Dollar Index little changed at 105.19

Top Overnight News

- China’s May inflation is essentially inline (but still soft), with the CPI +0.3% (vs. +0.3% in Apr and vs. the Street +0.4%) and the PPI -1.4% (vs. -2.5% in Apr and vs. the Street -1.5%). RTRS

- Brussels will impose tariffs of up to almost 50 per cent on Chinese electric vehicles, brushing aside German government warnings that the move risks starting a costly trade war with Beijing. The European Commission notified carmakers on Wednesday that it will provisionally apply additional duties of between 17 and 38 per cent on imported Chinese EVs from next month. FT

- The US Treasury is expected to roll out a big expansion of its secondary sanctions program on Russia this week, treating any foreign financial institution transacting with a sanctioned Russian entity as though it is working directly with the Kremlin’s military-industrial base. FT

- The world faces a “staggering” surplus of oil equating to millions of barrels a day by the end of the decade, as oil companies increase production, undermining the ability of Opec+ to manage crude prices, the International Energy Agency has warned. FT

- Israel/Hezbollah tensions spike after an Israeli strike killed the most senior Hezbollah commander since the start of the war in Gaza (Hezbollah fired a barrage of rockets toward Israel in response). Jerusalem Post

- Emmanuel Macron said he won’t resign if his party suffers a poor result in snap French parliamentary elections, saying that’s absurd. “I will kill this idea, which never actually existed.” The French president said he’ll appoint a PM as the constitution demands but that doesn’t mean handing control to the far right. BBG

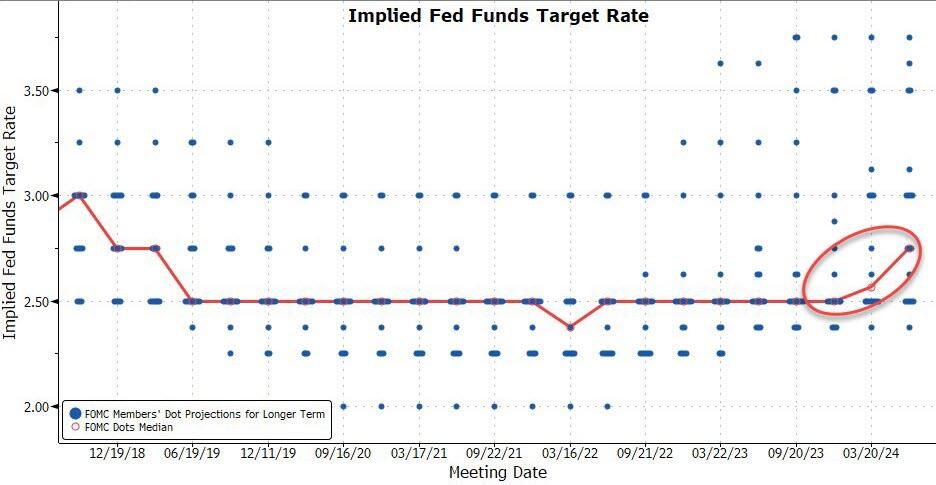

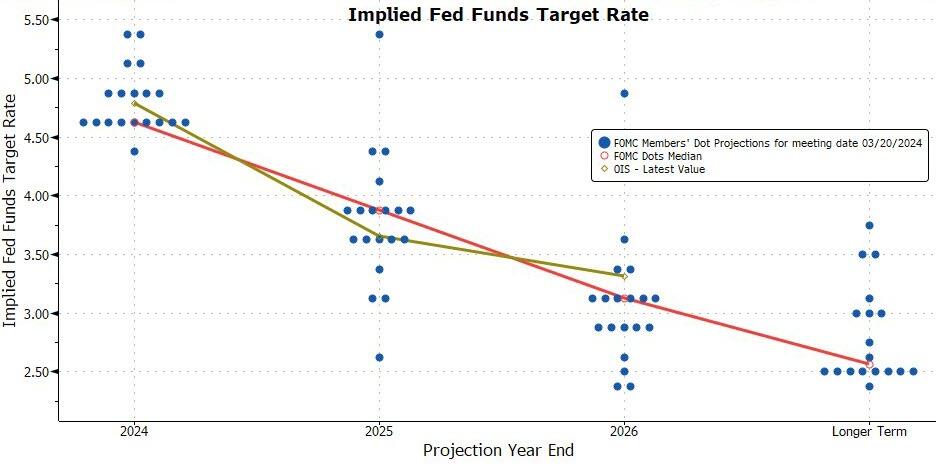

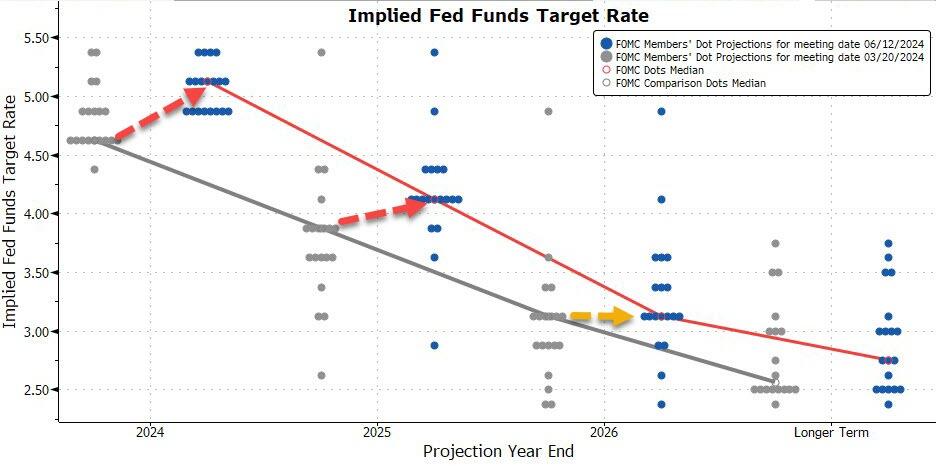

- Today’s Fed meeting looks set to be one of the year’s most pivotal with Jerome Powell potentially offering his clearest hints yet to the rate path. Bloomberg Economics expects the new dot plot will probably indicate two 25-bp cuts this year, compared with three previously. BBG

- US crude inventories resumed their downward trajectory, led by a 1.9 million barrel decline at Cushing, API data is said to show. That would be the biggest drop in more than four months if confirmed by the EIA today. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly subdued after the mixed handover from US peers as markets braced for the incoming US CPI data and the FOMC announcement. ASX 200 was pressured amid weakness in mining, tech, and the defensive sectors. Nikkei 225 retreated beneath the 39,000 level as participants digested firmer-than-expected PPI data which rose at the fastest annual pace in 9 months. Hang Seng and Shanghai Comp. were somewhat varied with underperformance in Hong Kong as China Evergrande New Energy Vehicle shares dropped around 20% amid the threat of losing key assets after local administrative bodies demanded repayment of CNY 1.9bln in subsidies by its units. Meanwhile, the mainland was cautious amid frictions with the US and after mixed Chinese inflation data including softer-than-expected CPI and a narrower deflation in factory gate prices.

Top Asian news

- US President Biden’s administration is to widen sanctions on Wednesday on the sale of semiconductor chips and other goods to Russia, according to Reuters sources. US will change export controls to include US-branded goods and not just those made in the US, while the measures are aimed at targeting third-party sellers in China and Hong Kong that are supplying Russia.

- China reportedly weighs a ban on bank distribution of hedge fund products, according to Bloomberg.

- Chinese Foreign Ministry says EU tariffs on Chinese EVs violate market economy principles and international trade rules; China will take all measures to firmly defend interests.

- EU intends to impose provisional tariffs on Chinese EV’s of 21% for cooperating companies, 38.1% for those which have not

European bourses, Stoxx 600 (+0.4%) are entirely in the green, attempting to trim some of this week’s significant losses, sparked by political uncertainty in Europe. European sectors hold a strong positive bias, with Banks taking the top spot as the sector finds its footing after this week’s weakness. Autos is the clear laggard, after news that the European Commission will notify carmakers that it will provisionally impose additional duties of up to 25% on imported Chinese EVs from next month. US Equity Futures (ES +0.1%, NQ +0.1%, RTY -0.1%) are trading on either side of the unchanged mark with price action tentative ahead of today’s key risk events, which includes US CPI and the FOMC Policy announcement.

Top European News

- ECB’s Kazaks sees hopes of further rate cuts this year. Need to be convinced that inflation will not return.

- ECB’s Villeroy says inflation will be below 2% in France starting next year, even at 1.7%.

- ECB Schnabel says the economy is recovering gradually, last mile of disinflation is proving bumpy; first indications of easing wage growth.

- UBS expects BoE to start cutting interest rates in August (prev. forecast June)

- French President Macron says they have not been able to form lasting coalitions. EU vote clear, could not be ignored.

FX

- USD is flat and in a narrow range as participants await the double dose of US risk events in the form of CPI and the FOMC; DXY resides within 105.21-32 parameters, well within yesterday’s 105.09-46 range.

- EUR price action has been uneventful thus far awaiting today’s key risk events; EUR/USD in a 1.0733-47 range thus far.

- GBP has also been trading sideways finding intraday resistance at 1.2750 (vs low 1.2729) with little immediate move seen in the wake of in-line GDP which ultimately resulted in little change in BoE pricing.

- JPY is very modestly softer irrespective of the overnight risk aversion and firmer-than-expected PPI data; USD/JPY currently trading within a 157.03-37 range.

- Antipodeans are both modestly firmer facilitated by an attempted recovery in base metals, but with gains capped as the risk tone remains cautious ahead of the aforementioned risk events.

- PBoC set USD/CNY mid-point at 7.1133 vs exp. 7.2558 (prev. 7.1135).

Fixed Income

- USTs are flat ahead of US CPI for one final read into the FOMC meeting where market pricing currently has a 99% chance of an unchanged rate. Currently holding near a fresh WTD high at 109-20, sparked by Tuesday’s strong US auction.

- Bunds are firmer with initial impetus stemming from Tuesday’s strong US auction and perhaps some marginal follow through from UK GDP numbers. Bunds are within a 130.21-130.50 bound, and have edged down towards the mid-point of the range after a poorly received Bund auction.

- Gilts are firmer, in tandem with broader strength in EGBs/USTs; amidst this, the morning’s UK GDP metrics were broadly in-line but the internals around Construction/Manufacturing were soft and sparked a very modest dovish move to BoE pricing.

- Germany sells EUR 3.3bln vs exp. EUR 4bln 2.20% 2034 Bund: b/c 2.0x (prev. 2.8x), average yield 2.6% (prev. 2.53%) & retention 16.75% (prev. 17.9%).

- UK sells GBP 900mln 0.625% I/L Gilt 2045: b/c 3.88x real yield 1.304%

Commodities

- Crude is firmer and at session highs, continuing to build on yesterday’s bullish private inventory data which saw a larger than expected draw in crude and gasoline. Additionally, geopolitical updates out of Israel/Hezbollah point towards recent escalations within the region. Brent Aug currently around USD 82.85/bbl.

- Precious metals are flat/mixed as traders look ahead to the US CPI and FOMC; XAU sits in a USD 2,310.60-2,317.70/oz range.

- Base metals are attempting a recovery from the recent slide in prices induced by Fed expectations following Friday’s NFP data. Chinese inflation did little to sway prices as trades await upcoming US macro events.

- IEA Oil Market Report: lowers 2024 demand growth forecast by 100k BPD to 960k BPD; 2025 oil demand growth seen at 1mln BPD amid a muted economy and clean energy tech deployment; major oil surplus seen this decade as demand peaks.

- UBS says on Gold “we have raised our 2024 avg. forecast and year-end target by 8% to USD 2365 and USD 2600 respectively”

- US Private Inventory Report (bbls): Crude -2.4mln (exp. -1.05mln), Cushing -1.9mln, Distillate +1mln (exp. +1.6mln), Gasoline -2.5mln (exp. +0.9mln).

- Azerbaijan oil production was 62.1k/T day in May.

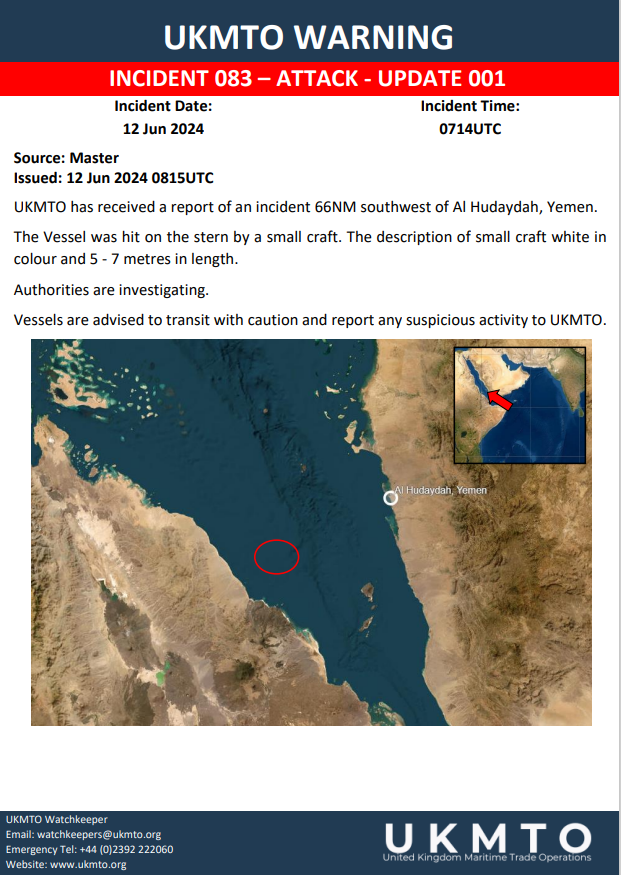

Geopolitics: Middle East

- Rocket sirens are reportedly sounding over several towns in Northern Israel, according to Horowitz on X; Israeli media says “Heavy bombardment from Lebanon towards northern Israel, and sirens activated in Tiberias, Safed, and Galilee” via Sky News Arabia.

- IDF Radio reports “More than 100 rockets fired from the south Lebanon on Safed, Tiberias and their surroundings in a few minutes”.

- Hamas official said their response to the Gaza ceasefire deal is responsible, serious, and positive, while the official added the response opens a wide way to reach an agreement.

- Israeli official said Hamas has rejected the proposal for a hostage release presented by US President Biden, while the official added that Israel received the Hamas response via mediators and that Hamas changed the proposal’s main parameters.

- Israeli airstrike on south Lebanon killed four people including a senior Hezbollah field commander, according to three security sources cited by Reuters. It was later noted that the Hezbollah commander killed in an Israeli airstrike on Tuesday was the most senior member killed in the last 8 months.

- US Pentagon said Secretary of Defense Austin discussed with his Israeli counterpart by phone efforts to calm tensions along the Israeli-Lebanese border, according to Sky News Arabia.

- Rocket sirens are reportedly sounding over several towns in Northern Israel, according to Horowitz on X; Israeli media says “Heavy bombardment from Lebanon towards northern Israel, and sirens activated in Tiberias, Safed, and Galilee” via Sky News Arabia; IDF Radio reports “More than 100 rockets fired from the south Lebanon on Safed, Tiberias and their surroundings in a few minutes”.

Geopolitics: Other

- EU is proposing to sanction Russian oil-shipping giant Sovcomflot, according to Bloomberg.

- EU is pushing ahead with Chinese electric vehicle tariffs that are set to bring in more than EUR 2bln a year, despite opposition from Germany, according to FT. European Commission will notify carmakers that it will provisionally impose additional duties of up to 25% on imported Chinese EVs from next month. Note, it was reported that yesterday Chinese Auto Industry Association CPCA said the EU could impose a 20% tariff on Chinese EVs, which is an understandable trade practice.

- Japan mulls sanctioning groups including Chinese firms for aiding Russia’s invasion of Ukraine, according to NHK.

US Event Calendar

- 07:00: June MBA Mortgage Applications +15.6%, prior -5.2%

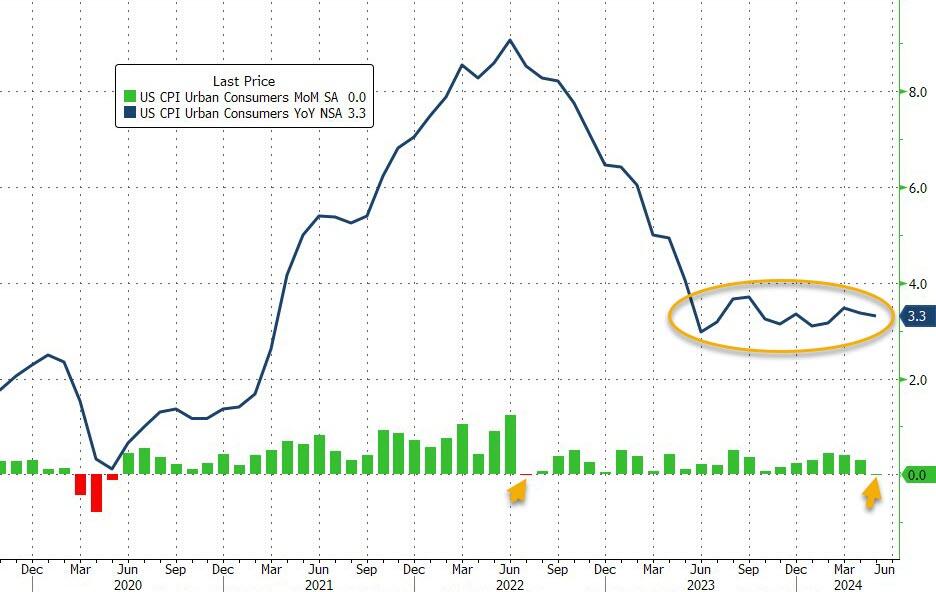

- 08:30: May CPI MoM, est. 0.1%, prior 0.3%

- May CPI YoY, est. 3.4%, prior 3.4%

- May CPI Ex Food and Energy MoM, est. 0.3%, prior 0.3%

- May CPI Ex Food and Energy YoY, est. 3.5%, prior 3.6%

- May Real Avg Hourly Earning YoY, prior 0.5%

- May Real Avg Weekly Earnings YoY, prior 0.5%, revised 0.6%

- 14:00: June FOMC Rate Decision

- 14:00: May Monthly Budget Statement, est. -$276.5b, prior -$240.3b

DB’s Jim Reid concludes the overnight wrap

Forgive me for feeling a touch melancholy this morning as I type this at 5am as a 50 year old. I’ll be celebrating by giving the opening speech this morning at DB’s 28th annual European LevFin conference featuring over 1000 investors and issuers. See you there if you’re attending. The highlights from my 40s were 3 kids I didn’t know if I’d ever have, 4 costly renovation projects, 6 knee surgeries, several inner ear surgeries, one back surgery and several trapped nerves. On the plus side of my mid-life crisis, my golf handicap has gone from 6 to 1.9 in my 40s which partly explains some of the ailments above. Let’s hope by the time I’m 60 I’ll have a few AI generated artificial limbs to help me hit the golf ball further.

It’s been another challenging 24 hours for European markets, with risk assets hacking out of the rough thanks to the ongoing political uncertainty in Europe. Meanwhile in a different universe, the S&P 500 (+0.27%) sailed down the middle of the fairway and hit a fresh all time with Apple (+7.26%) having its best day since November 2022 and returning above $3tn market cap and to an all time high itself after a difficult first 3-4 months of the year.

In terms of the European market moves, it was another difficult day for French assets. For instance, the 10yr Franco-German spread widened by another +5.0bps to 60bps, and the CAC 40 (-1.33%) fell to its lowest level in almost four months. Banks were among the worst affected again, with fresh losses for Société Générale (-5.02%), Crédit Agricole (-3.90%) and BNP Paribas (-3.89%). The three banks are now down -12.11%, -7.34% and -8.47% respectively since Monday’s open. At the height of the selloff yesterday, there were even unconfirmed press reports (later denied) that President Macron could resign after the election, before yields came off from their highs later on in the session.

President Macron is set to speak at a press conference today, but in the meantime, there have been growing questions about the political landscape his centrist alliance will be facing at the elections. On the left, an alliance was formed on Monday night between the Greens, Socialists, Communists and La France Insoumise. But on the right of the political spectrum there’s still uncertainty, as Éric Ciotti, who leads Les Républicains party, called for an alliance with Marine Le Pen’s Rassemblement National. Other figures in the party sternly rejected those suggestions, but the historic divisions between the traditional right-wing parties and the RN are becoming increasingly blurred as the latter has come to dominate the right-wing of the political spectrum in France . Later in the day, we heard that talks on forming an alliance between RN and the smaller far-right Reconquest party had broken down. In terms of the latest polls, an Ifop survey out yesterday had Marine Le Pen’s party on 35%, an alliance of four left-wing parties on 25%, and Macron’s alliance on 18%.

This political uncertainty weighed on markets across the continent. That included a third day of losses for the STOXX 600 (-0.93%), with the Stoxx banks index (-2.66%) seeing its largest decline since August. Equities slumped in several countries, with particularly sharp declines in southern Europe, including Italy’s FTSE MIB (-1.93%) and Spain’s IBEX (-1.60%). Sovereign bonds mostly rallied given the risk-off tone, and yields on 10yr bunds came down -4.8bps. But there was still a clear widening in spreads, with 10yr French yields (+0.2bps) just closing at their highest level of 2024 so far. Italian yields (-0.1bps) were also broadly flat despite the core rates rally.