GOLD PRICE CLOSED DOWN $35.30 TO $2302.50

SILVER PRICE DOWN 1.10 TO 29.00

Gold ACCESS CLOSED $2303.15

Silver ACCESS CLOSED: $28.93

Bitcoin morning price:$67,899 DOWN 542 DOLLARS.

Bitcoin: afternoon price: $68,441 UP 1266 dollars

Platinum price closing DOWN $11.25 TO $954.40

Palladium price; DOWN $15.30 AT $896.30

END

SHANGHAI GOLD PREMIUM 66 DOLLARS/COMEX GOLD//JULY TO JULY

SHANGHAI GOLD (USD) FUTURES – QUOTES

VENUE:

- GLOBEX

AUTO-REFRESH IS OFF

Last Updated 13 Jun 2024 03:46:27 PM CT.

Market data is delayed by at least 10 minutes.

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $3165.63 DOWN 18.40 CDN dollars per oz( * NEW ALL TIME HIGH 3,305.30 CDN DOLLARS PER OZ//MAY 20 2024)

*BRITISH GOLD: 1804.47 DOWN 8.89 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2144.15 DOWN 16.79 Euros per oz //* (ALL TIME CLOSING HIGH: 2248.89 EUROS PER OZ//APRIL 16.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCH: COMEX

ACCESS MARKET

EXCHANGE: COMEX

CONTRACT: JUNE 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,336.000000000 USD

INTENT DATE: 06/12/2024 DELIVERY DATE: 06/14/2024

FIRM ORG FIRM NAME ISSUED STOPPED

099 H DB AG 1

190 H BMO CAPITAL 14

323 C HSBC 31

363 H WELLS FARGO SEC 25

435 H SCOTIA CAPITAL 87

624 C BOFA SECURITIES 1

624 H BOFA SECURITIES 185

657 C MORGAN STANLEY 16

661 C JP MORGAN 1

661 H JP MORGAN 2

686 H STONEX FINANCIA 1

690 C ABN AMRO 10 7

726 C PLUS500US FINAN 1

732 C RBC CAP MARKETS 1

737 C ADVANTAGE 11 18

880 H CITIGROUP 2

905 C ADM 5

991 H CME 55

TOTAL: 237 237

MONTH TO DATE: 29,232

JPMorgan stopped 17/237

FOR JUNE 2024

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2024. CONTRACT: 237 NOTICES FOR 23,700 OZ or 0.7371 TONNES

total notices so far: 29,232 contracts for 2,923,200 Oz (90.920 tonnes)

FOR JUNE:

SILVER NOTICES: 119 NOTICE(S) FILED FOR 595,000

OZ/

total number of notices filed so far this month :1233 for 6.165 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $35.30 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : NO CHANGESIN GOLD INVENTORY AT THE GLD/

/ /INVENTORY RESTS AT 830.78TONNES

INVENTORY RESTS AT 830.78 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER DOWN $1.10 AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MASSIVE DEPOSIT OF 1.958 MILLION OZ INTO THE SLV

// INVENTORY INCREASES TO 429.683MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 429.683 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY AN ULTRA HUGE SIZED 1371 CONTRACTS TO 177,407 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR STRONG GAIN OF $0.97 IN SILVER PRICING AT THE COMEX ON WEDNESDAY’S TRADING ON SILVER. WE HAD ZERO LONG LIQUIDATION AS WE HAD A NET GAIN OF CONTRACTS ON OUR TWO EXCHANGES. WE, AGAIN HAD SHORT COVERING BY OUR SPECS WITH THE STRONG GAIN IN PRICE AS WELL AS MASSIVE T.A.S. LIQUIDATION. WE HAD ANOTHER MEGA HUMONGOUS SIZED 4,806 T.A.S ISSUANCE, THE 4TH HIGHEST EVER RECORDED FOR SILVER, AND THESE WILL BE USED FOR MANIPULATION LATER THIS MONTH/AS WELL AS TODAY. PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED LAST TUESDAY AND AGAIN LAST FRIDAY.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 4806 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND TODAY;S TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.97) AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS FROM THEIR PERCH AS WE DID HAVE A HUGE SIZED GAIN OF 3111 CONTRACTS ON OUR TWO EXCHANGES WITH THE GAIN IN PRICE OF $0.97

WE MUST HAVE HAD:

A HUGE SIZED 1740 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.830 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 30,000 OZ QUEUE JUMP

//NEW STANDING FOR SILVER//JUNE IS THUS 6.275 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI GAIN //HUGE SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 4806 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED 267 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE

TOTAL CONTRACTS for 9 DAYS, total 9164 contracts: OR 45.820 MILLION OZ (1018 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 45.820 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 45.820 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

RESULT: WE HAD A GIGANTIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1371 CONTRACTS WITH OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 1740 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.830 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 30,000 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR JUNE 6.275 MILLION OZ

WE HAVE A HUGE SIZED GAIN OF 3111 OI CONTRACTS ON THE TWO EXCHANGES WITH THE GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A MEGA HUMONGOUS SIZED 4806 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND ZERO NET LIQUIDATION OF LONGS.

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (4806) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 119 NOTICE(S) FILED TODAY FOR 595,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 294 OI CONTRACTS TO 436,569 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 15 CONTRACTS

WE HAD A SMALL SIZED DECREASE IN COMEX OI (294 CONTRACTS) OCCURRED WITH OUR GAIN OF $28.30 IN PRICE/WEDNESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 89.94 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 6500 OZ QUEUE JUMP AS BANKERS SCOUR THE PLANET LOOKING FOR GOLD ON THE THIS SIDE OF THE POND

NEW STANDING 91.689 TONNES// ALL OF THIS HAPPENED WITH OUR $28.30 GAIN IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A GOOD SIZED GAIN OF 3982 OI CONTRACTS (12.385 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4276 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 436,569

IN ESSENCE WE HAVE A GOOD SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3982 CONTRACTS WITH 294 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 4276 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3982 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 1845 CONTRACTS,,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4276 CONTRACTS) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI OF 294 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 3982 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 88.761 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 0.2021 TONNES

//NEW STANDING /JUNE 90.689 TONNES.

/ 3) HUGE T.A.S. LIQUIDATION OF CONTRACTS WITH ZERO LONG SPECS BEING CLIPPED,

4) SMALL SIZED COMEX OPEN INTEREST LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1845 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE. :

TOTAL EFP CONTRACTS ISSUED: 32,175 CONTRACTS OR 3,217,500 OZ OR 100.07 TONNES IN 9 TRADING DAY(S) AND THUS AVERAGING: 3575 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES 100.07 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 100.07 DIVIDED BY 3550 x 100% TONNES = 2.81% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 100.07 tonnes HEADING FOR A STRONG MONTH

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE SIZED 1371 CONTRACTS OI TO 177,407 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1740 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1740 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1740 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1638 CONTRACTS AND ADD TO THE 1740 E.FP. ISSUED

WE OBTAIN AN ULTRA HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 3111 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 15.555 MILLION OZ

OCCURRED WITH OUR HUMONGOUS $0.97 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 8.55 PTS OR 0.28% //Hang Seng CLOSED UP 174.79 PTS OR 1.19%// Nikkei CLOSED DOWN 156.34 OR 0.40%//Australia’s all ordinaries CLOSED UP 0.47%///Chinese yuan (ONSHORE) closed UP TO 7,2526 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2675/ Oil DOWN TO 77.96 dollars per barrel for WTI and BRENT UP AT 81.95 /Stocks in Europe OPENED ALL RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 294 CONTRACTS TO 436,569 DESPITE OUR HUGE GAIN IN PRICE OF $28.30 WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A HUGE T.A.S. LIQUIDATION ON WEDNESDAY WITH ZERO LONGS BEING CLIPPED.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE.… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 4276 EFP CONTRACTS WERE ISSUED: : AUGUST 4276 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4276 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 3982 CONTRACTS IN THAT 4276 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A SMALL SIZED LOSS OF 294 COMEX CONTRACTS..AND THIS GOOD SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR HUGE GAIN IN PRICE OF $28.30

////WEDNESDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT WAS A GOOD SIZED 1895 CONTRACTS. MOST OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. WEDNESDAY IS OF EXTREME IMPORTANCE TO OUR CROOKS IN YESTERDAY’S TRADING

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (90.689 TONNES)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 90.689 TONNES. THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $28.30 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A GOOD SIZED GAIN OF 3982 CONTRACTS ON WEDNESDAY WITH OUR TWO EXCHANGES WITH THE GAIN IN PRICE. THE T.A.S. ISSUED ON WEDNESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 12.385 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE (89.94 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 65 CONTRACTS OR 6500 OZ (0.2021 TONNES)

NEW STANDING FOR JUNE: 91.689 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $28.30

WE HAVE REMOVED 15 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET GAIN ON THE TWO EXCHANGES 3982 CONTRACTS OR 398,200 (12.385 TONNES)

confirmed volume WEDNESDAY 248,379 contracts//FAIR

//speculators have left the gold arena

JUNE 13 JUNE GOLD CONTRACT

/ /// THE JUNE 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | NIL oz . |

| Deposit to the Dealer Inventory in oz | 0 oz |

| Deposits to the Customer Inventory, in oz | 0 OZ//BRINKS |

| No of oz served (contracts) today | 237 notice(s) 23700 OZ 0.7371 TONNES |

| No of oz to be served (notices) | 246 contracts 24,600 OZ 0.7651 TONNES |

| Total monthly oz gold served (contracts) so far this month | 29232 notices 2,823,200 oz 90.92 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: NIL oz

we have 0 customer deposit:

total deposit nil oz

customer withdrawals: 0

TOTAL WITHDRAWALS NIL 0z

Adjustments: dealer to customer account

when we see this, it general means the comex is in stress

a) Brinks NIL oz

b) HSBC 2990.043 oz

c) JPMorgan: 35,012.439oz

d) Loomis: NILoz

e) Manfra: NIL oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE

For the front month of JUNE we have an oi of 523 contracts having LOST 328 contracts. We had 393 contracts served on Wednesday so we gained 65 contracts or 6500 oz additional ounces will stand for gold at the comex as they underwent a queue jump to take delivery on this side of the pond.

JULY GAINED 2 CONTRACTS TO STAND AT 2476

AUGUST LOST 1028 CONTRACTS DOWN TO 356,193 CONTRACTS

We had 237 contracts filed for today representing 23700 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notice was issued from their client or customer account. The total of all issuance by all participants equate to 237 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 17 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for June /2024. contract month, we take the total number of notices filed so far for the month (29,232) x 100 oz ) to which we add the difference between the open interest for the front month of JUNE (523 CONTRACTS) minus the number of notices served upon today (237 x 100 oz per contract( equals 2,947,800 OZ OR 91.689 TONNES.

thus the INITIAL standings for gold for the JUNE contract month: No of notices filed so far (29.232 x 100 oz +we add the difference for front month of June (523 OI} minus the number of notices served upon today (237) x 100 oz which equals 2,947,800 oz (91.689 TONNES)

TOTAL COMEX GOLD STANDING FOR JUNE: 91.689 TONNES WHICH IS ABSOLUTELY HUGE FOR THIS VERY ACTIVE DELIVERY MONTH IN THE CALENDAR. JUNE IS TRADITIONALLY THE 2ND HIGHEST DELIVERY MONTH OF THE YEAR. FROM THIS POINT WE WILL GAIN IN GOLD TONNAGE WILLING TO STAND AT THE COMEX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,680,714/128 52.27 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,662,910 OZ

TOTAL REGISTERED GOLD 7,913,203.508( 246.13 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,743,687.145 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,232,489 oz (REG GOLD- PLEDGED GOLD)= 193.86 tonnes //

END

SILVER/COMEX

JUN 13/2024

INITIAL

//2024// THE JUNE 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | NIL oz . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | NIL oz |

| No of oz served today (contracts) | 119 CONTRACT(S) (595,000 OZ) |

| No of oz to be served (notices) | 22 contracts (0.110 million oz) |

| Total monthly oz silver served (contracts) | 1233 Contracts (6.165 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 0

i

total customer deposit NIL..oz

JPMorgan has a total silver weight: 128.416million oz/297/690million or 43.20%

adjustment: 1 CUSTOMER TO DEALER MANFRA 594,565.329 OZ/

Comex withdrawals: 0

total withdrawal: NIL 0z

TOTAL REGISTERED SILVER: 62.494MILLION OZ//.TOTAL REG + ELIGIBLE. 297.690

million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE:

silver open interest data:

FRONT MONTH OF JUNE/2024 OI: 141 CONTRACTS HAVING LOST 6 CONTRACT(S).

WE HAD 0 NOTICES SERVED UP ON WEDNESDAY, SO WE LOST 6 CONTRACTS OR AN ADDITIONAL 30,000 OZ WILL NOT STAND AT THE COMEX VIA A SMALL E.F.P JUMP TO LONDON WHERE THEY WILL TAKE DELIVERY ON THAT SIDE OF THE POND

JULY SAW A LOSS OF 8275 CONTRACTS DOWN TO 94,477

AUG, SAW A GAIN OF 42 CONTRACTS TO 279

SEPT SAW A GAIN OF 8956 CONTRACTS TO 64,291

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for 0 oz

CONFIRMED volume; ON WEDNESDAY 138,178GIGANTIC

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1233 x 5,000 oz = 6.165 MILLION oz

to which we add the difference between the open interest for the front month of JUNE ((141) and the number of notices served upon today 119 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2024 contract month: 1233 notices served so far) x 5000 oz + OI for the front month of JUNE (141)x number of notices served upon today minus (119)x 5000 oz of silver standing for the JUNE contract month equates to 6.275 MILLION OZ.

New total standing: 6.275 million oz.

There are 62.494 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

JUNE 13 WITH GOLD DWN$35.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.89 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 830.78 TONNES

JUNE 12 WITH GOLD UP $28.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.89 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 830.78 TONNES

JUNE 11 WITH GOLD DOWN $0.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 10 WITH GOLD UP $2,00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 7 WITH GOLD DOWN $64.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 3.56 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 837.11 TONNES

JUNE 6 WITH GOLD UP $16.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.34 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 833.55 TONNES

JUNE 5 WITH GOLD UP $32.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 4 WITH GOLD DOWN $20.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 3 WITH GOLD UP $22.85 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 31 WITH GOLD DOWN $19.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 30 WITH GOLD UP $3.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 29 WITH GOLD DOWN $13.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 28 WITH GOLD UP $22.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 832.21 TONNES

MAY 24 WITH GOLD DOWN $2.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 833.36 TONNES

MAY 23 WITH GOLD DOWN $53.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 22 WITH GOLD DOWN $32.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 21 WITH GOLD DOWN $12,00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 20 WITH GOLD UP $21.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.10 TONNES OF GOLD INTO THE GLD//NEW TOTAL 838.54 TONNES

MAY 17 WITH GOLD UP $31.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//NEW TOTAL 833.36 TONNES

MAY 16 WITH GOLD DOWN $7.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//NEW TOTAL 833.36 TONNES

MAY 15 WITH GOLD UP $34.90 ON THE DAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD/INVENTORY RISES TO 831.93 TONNES

MAY 14 WITH GOLD DOWN $17.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RISES TO 831.33 TONNES

GLD INVENTORY: 835.67 TONNES, TONIGHTS TOTAL

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 13. WITH SILVER DOWN $1.10//HUGE CHANGES IN SILVER INVENTORY/ A HUGE DEPOSIT OF 1.958 MILLION OZ/INVENTORY RISES TO 429.083 TONNES

JUNE 12 WITH SILVER UP $0.97 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 5.983 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 427.125 MILLION OZ

JUNE 11 WITH SILVER DOWN $0.59 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.644 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 422.786 MILLION OZ

JUNE 10 WITH SILVER UP $0.30 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 3.198 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 421.142 MILLION OZ

JUNE 7 WITH SILVER DOWN $1.93 TODAY: NO CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY AT 417.944 MILLION OZ

JUNE 6 WITH SILVER UP $1.27 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 417.944 MILLION OZ

JUNE 5 WITH SILVER UP 0.38 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.52 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 415.295 MILLION OZ

JUNE 4 WITH SILVER DOWN $1.08 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

JUNE 3 WITH SILVER UP $0.35 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

MAY 31 WITH SILVER DOWN $1.09 TODAY: HUGE CHANGES IN SILVER INVENTORY: A MASSIVE WITHDRAWAL OF 3.655 MILLION OZ FROM THE SLV//INVENTORY LOWERS TO 413.775 MILLION OZ

MAY 30 WITH SILVER DOWN $0.80 TODAY: NO CHANGES IN SILVER INVENTORY//INVENTORY REMAINS AT 417.430 MILLION OZ

MAY 29 WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 1.051 MILLION OZ INTO THE SLV//INVENTORY DECREASES TO 417.430 MILLION OZ

MAY 28 WITH SILVER UP $1.64 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 2.832 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 418.481 MILLION OZ

MAY 24 WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF .822 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 421.313 MILLION OZ

MAY 23 WITH SILVER DOWN $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.736 MILLION OZ FROM THE SLVINVENTORY INCREASES TO 420.491 MILLION OZ

MAY 22 WITH SILVER DOWN $0.66 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 21 WITH SILVER DOWN $0.41 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A DEPOSIT OF 3.792 MILLION OZ FROM THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 20 WITH SILVER UP $1.28 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 1.005 MILLION OZ FROM THE SLV// INVENTORY LOWERS TO 418.435 MILLION OZ

MAY 17 WITH SILVER UP $1.37 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 868,000 OZ FROM THE SLV// INVENTORY LOWERS TO 419.440 MILLION OZ

MAY 16 WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY REMAINS AT 420.308 MILLION OZ

MAY 15 WITH SILVER UP 101 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A WITHDRAWAL OF 1.919 MILLION OZ FROM THE SLV NVENTORY RESTS AT 420.308 MILLION OZ

MAY 14 WITH SILVER UP 25 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;INVENTORY RESTS AT 422.227 MILLION OZ

CLOSING INVENTORY 427.125 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/GOLD AND SILVER COMMENTARY

| Interest rates, inflation, and gold |

ALASDAIR MACLEOD

JUN 13

∙

It’s now increasingly assumed that the US economy is not performing as well as the statistics suggest, and that the Fed must cut interest rates and keep on cutting. The assumption is based on a mixture of Keynesian hope and market experience of the last three or four decades, which cover the work-experience of today’s investment managers. Last week I quoted from an article by Ambrose Evans-Pritchard in The Daily Telegraph of 5 June, who wrote that “Citigroup says that the Fed will have to cut interest rates in July and at every meeting until mid-2025”. Therefore, a research report from one of the largest banks in the US is evidence of this view.

It must be admitted that in the short term, such a strong consensus over interest rates can become self-fulfilling. Perhaps the ECB led the way last week with the first cut in its deposit rate, which suggests that the back chat between leading central banks confirms that the ECB will not be alone and that we can expect the Fed to follow as soon as it decently can, though officially it is still fence-sitting. And perhaps the Bank of England will cut after the UK’s general election.

Unfortunately, the problem for central banks is that inflation is proving to be sticky, and the prospect of it returning to their 2% target and remaining there is remote. To understand why this is the case requires an understanding of what inflation represents: it is a decline in the currency’s purchasing power. It’s just that evidence of the decline is reflected in a higher level for prices generally.

The origin is in the expansion of unproductive credit, which with a fiat currency comes in two basic forms: a government’s budget deficit not financed by an increase in consumer savings, and the expansion of bank credit financing consumption. Both lead to a dilution of the purchasing power of pre-existing currency units. The reason that an expansion of bank credit for productive purposes does not lead to a higher general level of prices is that it leads to an expansion of output whose supply has the opposite effect, counteracting the dilutive price effect of extra currency units in circulation.

Why has this not been apparent since the 1980s? Well, it has been if you look at the relationship between currencies and gold, which is real, legal, internationally accepted money with no counterparty risk, as the chart below illustrates:

Admittedly, gold only represents an indirect indication of changes in a currency’s purchasing power. But despite official and unofficial price intervention in bullion markets, and in view of continuing systemic suppression of CPI inflation statistics a currency’s price in gold is the best indication of changes to its purchasing power.

The chart shows that since the end of Bretton Woods the dollar has lost 98.5% of its purchasing power, the euro (and its prior constituents) 98.9%, the yen 96.5%, and sterling has fallen below the bottom of our chart at 99.2%. This decline has occurred in three phases: the 1970s, between 2000—2012, and more recently from 2016.

The current phase of currency depreciation measured in real money is at odds with the macroeconomic consensus, that inflation will continue to decline. Importantly, it’s also at odds with the role of interest rates, which are used by central banks to manage inflation.

This is not the economic role of interest rates, as Gibson’s paradox demonstrated. The correlation was and remains between interest rates and the general level of prices, not its rate of change (i.e. inflation). Despite Gibson’s paradox being statistically proven and known to Keynes (he actually named it after AH Gibson) he and his followers were unable to explain it so simply dismissed it as a relic of the gold standard. This is a convenient error.

To illustrate Gibson’s point, assume that you are asked to invest in a foreign government’s debt. You would only consider buying the debt if the yield was sufficient with a margin to compensate for your expectation of its loss of purchasing power over the duration of the loan. In other words, interest rates are compensation for loss of purchasing power reflected in an increase in the general level of prices.

The currency’s future purchasing power is discounted in order to determine an acceptable yield on a government bond, which today not only involves an assessment of monetary debasement but of the overall debt position of the government, the volume of its funding requirements, and other risk factors. Obviously, there is a high degree of subjectivity, or faith involved in this calculation. A foreign investor is almost certainly not interested in a domestic market’s estimates of last month’s CPI.

With fiat currencies, faith matters

The risk to a currency’s purchasing power is not solely due to the rate of credit expansion as monetarists posit. Monetarists don’t make any distinction between productive and non-productive use. Nor have they modified their theories which were put forward by David Ricardo in the early nineteenth century when a gold or silver standard were the norm, and a permanent fiat currency outside wartime was inconceivable. The fact of the matter is that the value of a fiat currency depends upon the faith its creditors have in it. Erode that faith and the value declines, irrespective of changes in its circulating quantity.

In examining the entrails of the US economy, economists miss the importance of faith entirely. But the proof is that you can have a decent economy backed by good government finances and a weak currency.

Who would buy Russia’s rouble? Yet, war finance has only led to a government debt to GDP of about 22%, and a primary budget surplus remains. Income taxes of 13%—15% is the stuff of which free market economists can only dream. Yet, the Central Bank of Russia is forced to maintain a 16% deposit rate to sustain faith in the currency.

Contrast that with King Dollar, which has a government debt to GDP of about 130%, an unsustainable budget deficit, and ever higher taxes hampering production.

The first to lose faith in a currency are never its domestic users, who in their day-to-day transactions firmly believe a dollar is a dollar, or a euro is a euro, and that price negotiation is entirely centred on the value of goods and services being exchanged. Almost the entire population, which sadly includes politicians, bankers, and economists, fall into the same trap. They don’t understand that rising prices reflect the currency’s decline.

It’s foreign creditors who are the first to make the correct assessment. If they are not compensated sufficiently for the credit risk in a foreign currency, they will not buy it until the interest rate is raised to the correct level to reimburse them for that risk. But within the fiat framework a reserve currency which acts as the international pricing medium has a special role in setting the relative values of all other currencies.

This is why despite the deterioration in US Government finances, foreigners have retained large dollar balances. Alternative currencies are less secure, which is why a positive case can be argued for the dollar. But it is a relative valuation, not an ultimate one. For that, the dollar’s value must be compared with that of gold.

While domestic Americans are blind to the threat faced by the dollar, foreigners are not. They are selling dollars for gold, which is why gold appears to be rising. Gold is no more rising than consumer prices are rising: it is the dollar, along with the other western alliance currencies falling in value, reflected in goods’ and services’ prices. It explains why Americans and Europeans are ignoring the rise in the gold price measured in their own currencies, but it is being looked at differently in Asia, particularly in China. Admittedly, there are geopolitical factors involved, but it all amounts to the same thing: there are foreigners who own dollar- and euro-denominated credit who want out.

Another source of confusion for western capital markets is over the rise in the gold price at a time of higher interest rates. The origin of this error was in the establishment of the carry trade in the 1980s, when gold had peaked and was in a declining trend against the dollar as a general belief took hold that the dollar had sidelined gold. This allowed bullion banks to lease gold typically at 2% or less and invest the proceeds in US T-bills yielding 6% or more. The relationship between gold and the dollar became sensitive to this interest rate differential. But before the carry trade, this correlation didn’t exist, as the chart below of the 1970s shows.

The chart confirms that higher interest rates lead to higher gold prices which is a decline in the dollar, and for good reason. It is entirely consistent with Gibson’s paradox. Dollar credit declining in its purchasing power is also declining against gold. And it requires recompense for holders of dollars to offset the loss of their purchasing power. That compensation is in the form of an increase in the interest rate. It boils down to what a foreign holder of a fiat currency requires not to turn seller.

This simple but fundamental truth is why almost every fiat currency collapse is initiated by foreign selling. We see this today with increasing numbers of central banks reducing their dollar reserves for gold, which with no counterparty risk is true international money. Yet it is not admitted by the core of them: the Fed, ECB, BOJ, and the Bank of England. Being wedded to their own domestic illusions, they appear to be genuinely clueless of the danger to their currencies.

It doesn’t auger well for interest rate policies, which as demonstrated in this article fly in the face of the established relationships captured by Gibson’s paradox. It also explains why the populations of these nations ignore the signals from gold, which measured in their declining currencies is hitting record levels. But belatedly, these 1,200 million or so individuals will eventually realise that it’s their currencies going down and not prices rising, and that far from being a speculation gold and silver are safe havens at any price.

end

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS/

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT//COFFEE BEANS //

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

ASIA TRADING//THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 8.55 PTS OR 0.28% //Hang Seng CLOSED UP 174.79 PTS OR 1.19%// Nikkei CLOSED DOWN 156.34 OR 0.40%//Australia’s all ordinaries CLOSED UP 0.47%///Chinese yuan (ONSHORE) closed UP TO 7,2526 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2675/ Oil DOWN TO 77.96 dollars per barrel for WTI and BRENT UP AT 81.95 /Stocks in Europe OPENED ALL RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2526

OFFSHORE YUAN: UP TO 7.2675

SHANGHAI CLOSED DOWN 8.55 PTS OR 0.28 %

HANG SENG CLOSED UP 174,79 PTS OR 1.19%

2. Nikkei closed DOWN 156.24 PTS OR 0.86 %

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 104.51 EURO FALLS TO 1.0789 DOWN 48 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +0.959 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 157.19 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.5490/Italian 10 Yr bond yield UP to 3.967 SPAIN 10 YR BOND YIELD UP TO 3.392%

3i Greek 10 year bond yield UP TO 3.659

3j Gold at $2307.95//Silver at: 29.12 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 0/ 100 roubles/dollar; ROUBLE AT 88.24

3m oil into the 77 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 157.19/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.959% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8963 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9672 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.309 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.478 UP 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.756 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.30…

10 YR UK BOND YIELD: 4.2140 DOWN 7 PTS

2a New York OPENING REPORT

S&P Set For 29th Record High Of 2024 As Futures Continue Relentless Grind Higher

BY TYLER DURDEN

THURSDAY, JUN 13, 2024 – 08:14 AM

Futures are higher, again, with Tech leading, again, and small-caps lagging, the same trend that we saw after the Powell press conference despite small-caps leading the way most of the session. As of 8:00am, S&P futures were up 0.1% and set for the 29th all time high print this year, while Nasdaq futures outperform, rising 0.6% and set to gain for a fourth straight session after another record close on Wednesday as Mag7 and Semi stocks push higher, with AVGO +13.6%, TSLA +6.3%, and NVDA +2.4% all notably higher. Many of the other Mag7 names are lower pre-mkt, but elements of the AI ecosystem are up pre-mkt, e.g., VRT +1.9%. Bond yields are ranging from -1bps to +1bps, the 10Y TSY yield last trading around 4.31%, while the dollar rebounded from the post-CPI drop to rise ahead of US data on producer prices, supported by the view that the Fed may deliver just one interest rate cut this year. Commodities are mostly higher despite crude and precious metals lower. Today’s macro data focus is on PPI, Jobless Claims; investors will also look to an event featuring New York Fed President John Williams and Treasury Secretary Janet Yellen later in the day.

In premarket trading, Tesla surged after Elon Musk said shareholder resolutions to re-ratify his pay package and moving the company’ s legal home to Texas were passing by “wide margins.”

Here are some other notable premarket movers:

- Broadcom (AVGO) gains 14% after the chip supplier reported second-quarter results that beat expectations and gave a positive forecast.

- Dave & Buster’s (PLAY) slides 10% after the restaurant chain reported first-quarter revenue and earnings per share that missed consensus estimates.

- Stellantis (STLA) falls 2.2% ahead of its investor day on Thursday that Stifel analysts previously said would carry a lot of weight in rebuilding trust with the market.

- Virgin Galactic (SPCE) drops 9% after the space tourism firm’s board approved a 1-for-20 reverse split of the company’s common stock.

Risk assets rallied on Wednesday after the latest US inflation report showed core CPI fell to the lowest in more than three years, spurring bets on faster policy easing. However, just a few hours later, the Fed penciled in just one quarter point interest-rate cut this year, down from three seen in March. That, however, did not dent bullish sentiment and one day later, swap traders are currently pricing in a 25-basis-point rate cut by November, with a 75% likelihood of a similar reduction by year-end. That compares with a 50% chance of a second cut two days ago. US producer prices may offer more signals later on Thursday.

“The Fed dot plot was marginally on the hawkish side, causing some pullback in the markets,” said Mohit Kumar, chief economist for Europe at Jefferies International. Any selloff in stocks would be a buying opportunity, he said.

European stocks erased an earlier gain, with the Stoxx 600 dropping 0.9% after advancing the most in a month following the softer US inflation print. Adding to the caution, ECB Governing Council member Joachim Nagel warned that consumer price growth in the euro zone is proving stubborn. “We are on a bumpy road, but we all know that the last mile is the most complicated one,” the Bundesbank president said. Here are the most notable European movers:

- Halma shares gain as much as 5.2%, hitting the highest in a year, after the health and safety sensor technology group releases its full-year results.

- Valmet shares advance as much as 3.9%, the most in three weeks, after Carnegie upgraded its view on the Finnish energy and paper industry equipment manufacturer to buy from hold.

- Lotus Bakeries shares rise as much as 4.8% after Mondelēz agreed to make and sell the Belgian company’s Biscoff cookies in India.

- Wise shares fall as much as 23%, the most ever, after the money transfer firm’s revenue growth forecasts missed expectations on the back of price reductions implemented at start of FY2025.

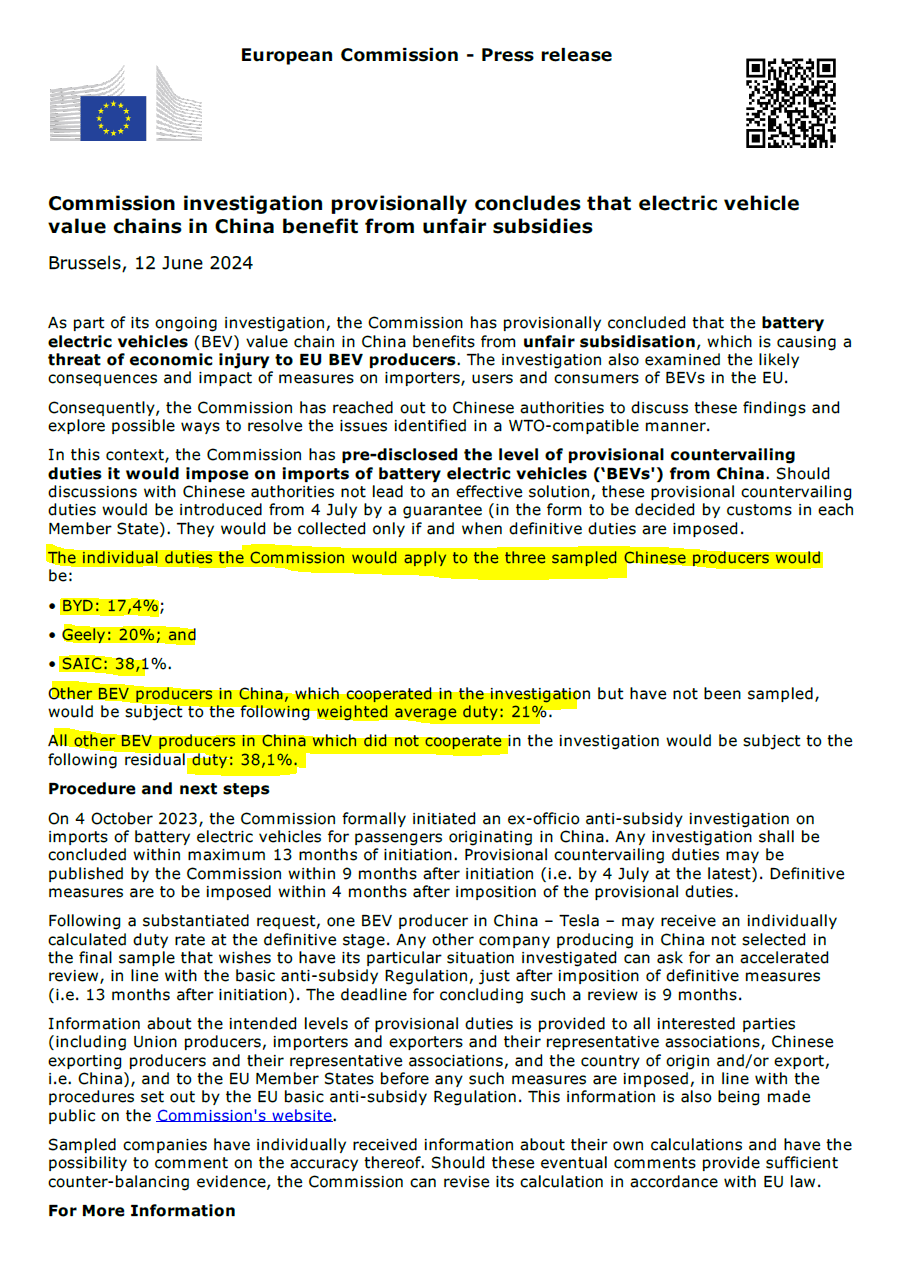

- Volvo Car shares drop 5.2%, bringing their two-day decline to more than 10% since the EU announced Wednesday that it will impose tariffs of as much as 48% on EV imports from China.

- Stellantis shares fall as much as 1.6% ahead of its investor day on Thursday that Stifel analysts previously said would carry a lot of weight in rebuilding trust with the market.

- Ericsson shares drop as much as 2.8% after Nordea downgrades the Swedish 5G gear maker to hold from buy following strong share-price performance since the company’s first-quarter results in April.

- Lufthansa shares slide as much as 7.1%, to the lowest price since October 2022, as JPMorgan analysts open a negative catalyst watch, seeing potential for further downward revisions to guidance.

- Telefonica shares slip as much as 1.9% after a downgrade to sell from hold at Deutsche Bank. The broker notes that the firm’s stock is now one of the most expensive in its sector.

- LPP shares drop as much as 3.7% even as the Polish fashion retailer reported an improved first-quarter gross margin and guided for a “significantly higher” margin in the current period.

- Synsam shares decline as much as 11%, the most since March, in reaction to a column published by Swedish business daily Dagens Industri.

- Crest Nicholson shares slide as much as 12.7% to hit a one-month low after the housebuilder’s first-half profit fell short of expectations and full-year guidance was cut.

Asian stocks fluctuated, with weakness in Japan countering advances in technology shares triggered by lowered concerns on Federal Reserve policy. The MSCI Asia Index swung between a loss of as much as 0.2% and gain of 0.4%. Tencent and TSMC were among the biggest boosts while Toyota fell. South Korea’s benchmark Kospi gained 1% and Taiwan’s main index rose more than 1.2% as tech stocks followed US peers higher. Key gauges also climbed in Hong Kong and Australia. Cooler-than-expected consumer price data reduced concerns on US interest rates, even after the Fed dialed back expectations for cuts this year to just one.

In FX, theBloomberg Dollar Spot Index edged up 0.1%, recovering after the previous day’s fall, when a weak US CPI reading had triggered selling in the currency before the Fed announcement “The market got it wrong last night and reacted more strongly to the data print than to the Fed update, and I think over the long term it should be the other way around,” said Nick Twidale, chief analyst at ATFX Global Markets

In rates, Treasuries are steady as investors continue to dissect the latest messaging from the Federal Reserve. US 10-year yields are little changed at 4.30%. In a separate development, the European Union’s bonds fell after MSCI Inc. said it won’t add the bloc’s debt to its range of government bond indexes. Bunds and gilts also fell. The week’s Treasury coupon auction cycle concludes with $22b 30-year bond reopening at 1pm New York time, following strong demand for Tuesday’s 10-year sale. WI 30-year yield at ~4.468% is roughly 17bp richer than May’s, which stopped 0.7bp through.

In commodities, crude traded near session lows, continuing the pressure sparked by the prior day’s bearish inventory data. Geopol updates out of the Middle East have been thin today, though elsewhere Reuters reports that unidentified assailants attacked soldiers guarding the Niger-Benin gas pipeline. Brent trades around $82/bbl, the lower end of a narrow overnight range. Softer trade across precious metals with deeper losses seen in spot silver and palladium vs gold, with the complex pressured by the attempted recovery in the Dollar post-FOMC with gold looking ahead to this afternoon’s US PPI and IJCs. Base metals are lower across the board, again as a function of the attempted Dollar recovery and following the cautious mood in APAC and early European markets.

Bitcoin is slightly softer and holds just below $67.5k, whilst Ethereum dips below $3.5k.

To the day ahead now, and data releases include the US PPI reading for May and the weekly initial jobless claims, along with Euro Area industrial production for April. From central banks, we’ll hear from the ECB’s Muller and the Fed’s Williams. In the political sphere, the G7 leaders summit will get underway in Italy.

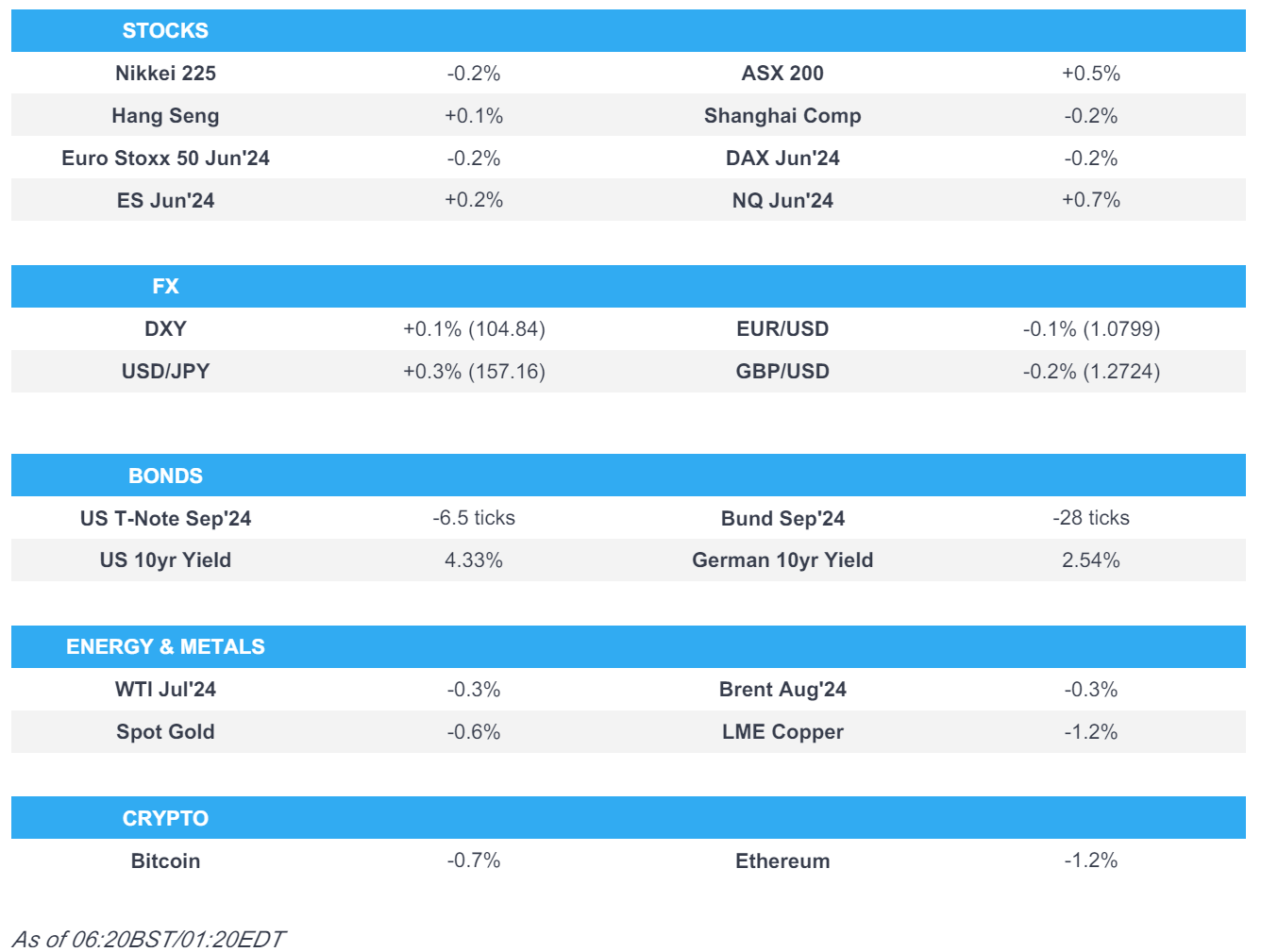

Market Snapshot

- S&P 500 futures up 0.2% to 5,436.00

- STOXX Europe 600 down 0.6% to 519.90

- MXAP little changed at 179.66

- MXAPJ up 0.7% to 564.28

- Nikkei down 0.4% to 38,720.47

- Topix down 0.9% to 2,731.78

- Hang Seng Index up 1.0% to 18,112.63

- Shanghai Composite down 0.3% to 3,028.92

- Sensex up 0.3% to 76,830.04

- Australia S&P/ASX 200 up 0.4% to 7,749.70

- Kospi up 1.0% to 2,754.89

- German 10Y yield little changed at 2.56%

- Euro little changed at $1.0808

- Brent Futures down 0.2% to $82.45/bbl

- Gold spot down 0.4% to $2,316.02

- US Dollar Index up 0.12% to 104.78

Top Overnight News

- Tesla shares jumped premarket after Elon Musk said preliminary results for proposals to re-ratify his $56 billion package and move Tesla’s legal home to Texas were passing by “wide margins” late yesterday. BBG

- Across China, 16 or more cities have allowed companies to test driverless vehicles on public roads, and at least 19 Chinese automakers and their suppliers are competing to establish global leadership in the field. No other country is moving as aggressively. The government is providing the companies significant help. In addition to cities designating on-road testing areas for robot taxis, censors are limiting online discussion of safety incidents and crashes to restrain public fears about the nascent technology. NYT

- BOJ could dial back its QE intensity at tonight’s meeting, taking the monthly pace from JPY6T to JPY5T. Nikkei

- Mexico’s peso gained after the country paid off a dollar bond due next year in a bid to calm a market selloff. It also said it’ll refinance local debt due in 2025. Banxico said it’s ready to intervene in the peso if volatility becomes “extreme.” BBG

- Washington set to sign a 10-year security agreement w/Ukraine that will commit the US to supplying Kyiv with weapons and other military assistance (although future American presidents will have the ability to withdraw from the pact). WaPo

- Blackstone and Ares-backed private credit funds have found a cheap place to raise money: the IG corporate bond market. They’re among funds that have raised over $13.4 billion in the US market so far this year — nearly double the $8 billion raised over the entirety of 2023. BBG

- OpenAI is building an international team of lobbyists as it seeks to influence politicians and regulators who are increasing their scrutiny over powerful artificial intelligence. The San Francisco-based start-up told the Financial Times it has expanded the number of staff on its global affairs team from three at the start of 2023 to 35. The company aims to build that up to 50 by the end of 2024. FT

- U.S. passenger railroad Amtrak said on Wednesday it expects ridership to top pre-COVID 2019 levels this year for the first time and reach a record high even though it has less capacity. Ridership was 20% higher in the first seven months of Amtrak’s budget year that began Oct. 1, and ticket revenue was up 10% versus the same period in 2023. RTRS

- Apple isn’t paying OpenAI to use its chatbot as it believes promoting ChatGPT’s brand and tech is just as valuable, people familiar said. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were somewhat mixed following the key developments stateside where the S&P 500 and Nasdaq extended to fresh record levels after softer-than-expected CPI data, although participants also digested the latest FOMC meeting and hawkish dot plots which suggested just one rate cut this year vs. prev. view of three cuts. ASX 200 was led higher by outperformance in tech amid a softer yield environment and with stronger-than-expected jobs data. Nikkei 225 failed to sustain early gains and dipped back below the 39,000 level as the BoJ kick-started its two-day policy meeting, while Nikkei reported the BoJ will consider gradually reducing its JGB holdings at this meeting. Hang Seng and Shanghai Comp. diverged in rangebound trade with the mood in Hong Kong positive as several automakers weathered the EU announcement of tariffs on Chinese EVs and HKMA maintained its base rate at 5.75% in lockstep with the Fed, while the mainland was lacklustre despite the PBoC’s latest efforts to support the property industry.

Top Asian News

- Hong Kong Monetary Authority maintained its base rate at 5.75%, in lockstep with the Fed.

- China hopes the EU will make some serious reconsideration on tariffs for China EVs and stop going further in the wrong direction, according to state media.

- BoJ will reportedly consider gradually reducing its Japanese government bond holdings at this week’s two-day policy meeting, according to Nikkei.

- South Korea’s government and ruling party are to increase fines and punishment for illegal short-selling, while the stock short-selling ban will be extended until March, according to Yonhap.

- Japanese Banking Association Chairman says under rising interest rates, banks’ business models are moving towards prioritising deposits.

- Chow Tai Fook (1929 HK) FY (HKD) Op profit 12.16bln (exp. 8.58bln), +28.9% Y/Y, Revenue 108.71bln (exp. 108.45bln), +14.8% Y/Y

European bourses, Stoxx 600 (-0.6%) began the session on a modestly softer footing, and continued to trundle lower as the morning progressed. European sectors hold a strong negative bias, with a slight defensive tilt. Autos is towards the bottom of the pile, continuing the losses seen this week. Chemical names, Covestro (-2.6%) and BASF (-1.5%) are also under pressure, after wholesale chemical products fell 13.9% Y/Y vs -0.9% in April. US Equity Futures (ES +0.1%, NQ +0.7%, RTY -0.4%) are mixed, with the NQ the clear outperformer, propped up by several pre-market movers within the index. Firstly, Tesla (+6.2%) gains on reports that shareholders have voted in favour of Musk’s USD 56bln pay package. Elsewhere, Broadcom (+14.8%) surges post-earnings, and Nvidia (+2.2%) continues to march forward.

Top European News

- UK opposition Labour Party leader Starmer said they are not looking at bringing in wealth taxes.

- Sky News/YouGov poll found that 64% of respondents thought Labour Party leader Starmer did better in the Sky News Leaders TV interviews, while 36% thought UK PM Sunak did better.

- ECB’s Vasle says there is a risk that the disinflation process could slow. Will be data dependent. Wage momentum is still relatively strong. More 2024 cuts probable, if the baseline holds.

- ECB’s Muller says ECB has not yet achieved inflation target; possible that inflation could temporarily rise again; services inflation still relatively high; wage growth still strong

FX

- USD is attempting to recoup more of the slump seen after US CPI yesterday, which took the index to a low of 104.25 with hawkish FOMC dot plots and Fed Chair Powell’s cautious tone also helping. The DXY has been trading within a busy 104.67-85 range throughout the London session, awaiting impetus from PPI & IJC.

- EUR straddled 1.0800 throughout APAC hours before finding some support at the level. The Single-currency was little changed to the cooler German Wholesale data, with price action tentative thus far.

- GBP is flat with Cable attempting a test of 1.2800 but failed, with the pair within a 1.2774-99. UK-specific newsflow light today, as focus remains on the UK election and awaiting the Labour manifesto.

- JPY stands as the current G10 laggard, albeit marginally, as US yields came off best levels post-FOMC. Markets will await the BoJ policy announcement due on Friday, but for now, sits in a 156.57-157.30 range.

- Antipodeans are modestly softer amid the cautious mood in Europe whilst better-than-expected Australian jobs data only provided a brief tailwind for AUD/USD.

- PBoC set USD/CNY mid-point at 7.1122 vs exp. 7.2384 (prev. 7.1133).

Fixed Income

- USTs are slightly softer as desks digest the FOMC and as market pricing pivots away from September and towards November for the first cut. Currently trading lower by a handful of ticks ahead of PPI, which will help to form the consensus for PCE.

- Bunds are on the backfoot as participants continue to pare the post-CPI rally with the bearish action driven by Wednesday’s FOMC. A handful of ECB speakers today have had little impact on price action, whilst a further cooling in German wholesale price index spurred a brief bid in Bunds to a 131.11 peak.

- Gilts gapped lower by just a handful of ticks to 97.97 which marks the current session high. Currently trading well within the prior day’s 96.84-98.23 range, awaiting the Labour manifesto and US PPI.

- Italy sells EUR 9bln vs exp. EUR 7.5-9bln 3.45% 2027, 3.45% 2031, 4.15% 2039, 3.85% 2049 BTP:

Commodities

- Crude is subdued and towards session lows, continuing the pressure sparked by the prior day’s bearish inventory data. Geopol updates out of the Middle East have been thin today, though elsewhere Reuters reports that unidentified assailants attacked soldiers guarding the Niger-Benin gas pipeline. Brent Aug towards the lower end of an 82.07-55/bbl parameter.

- Softer trade across precious metals with deeper losses seen in spot silver and palladium vs gold, with the complex pressured by the attempted recovery in the Dollar post-FOMC with gold looking ahead to this afternoon’s US PPI and IJCs.

- Base metals are lower across the board, again as a function of the attempted Dollar recovery and following the cautious mood in APAC and early European markets.

- Chevron Australia has started repair works on the Wheatstone platform – expected to be completed in the coming weeks; LNG and domestic gas production to resume following safe completion of repairs.

- Unidentified assailants attack soldiers guarding Niger-Benin gas pipeline, via Reuters citing sources; pipeline not damaged. In reference to the 110k BPD pipeline which concluded construction works in March/April 2024.

Geopolitics: Middle East

- Hamas’s request in advance for a guarantee of a permanent ceasefire complicates Gaza truce negotiations and the main sticking point in the hostage negotiation is the demand for an explicit pledge by Israel to end the war, according to The Times of Israel. it was also reported that Hamas hardened some of its positions on the truce proposal and demanded the inclusion of China, Russia and Turkey as guarantors of the agreement, according to the Israel Broadcasting Corporation.

- Hamas statement said it showed positivity in all stages of negotiations to stop the aggression, while it urged the US administration to direct its pressure on Israel which it said wants to pursue the Gaza war.

- Lebanese army chief is visiting Washington this week to discuss the situation at the border, according to Al-Monitor.

- US military said its forces successfully destroyed three anti-ship cruise missile launchers in a Houthi-controlled area of Yemen and one uncrewed aerial system launched from a Houthi-controlled area of Yemen. However, it stated that one Iranian-backed Houthi unmanned surface vessel struck M/V Tutor which is a Liberian-flagged, Greek-owned and operated vessel in the Red Sea, while the impact caused severe flooding and damage to the engine room.

- Iran is responding to last week’s IAEA resolution against it by expanding uranium-enrichment capacity at two underground sites although the escalations are not as large as many feared, according to diplomats cited by Reuters.

Geopolitics: Other

- Russian nuclear-powered submarine and other naval vessels arrived in Cuba for a five-day visit to the communist island in a show of force amid spiralling US-Russian tensions, according to AFP News Agency.

US Event Calendar

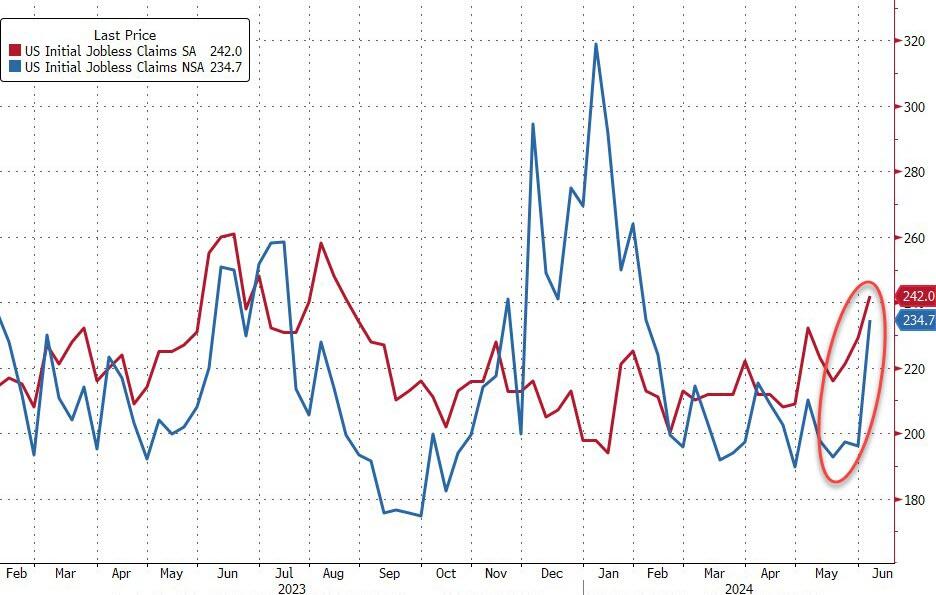

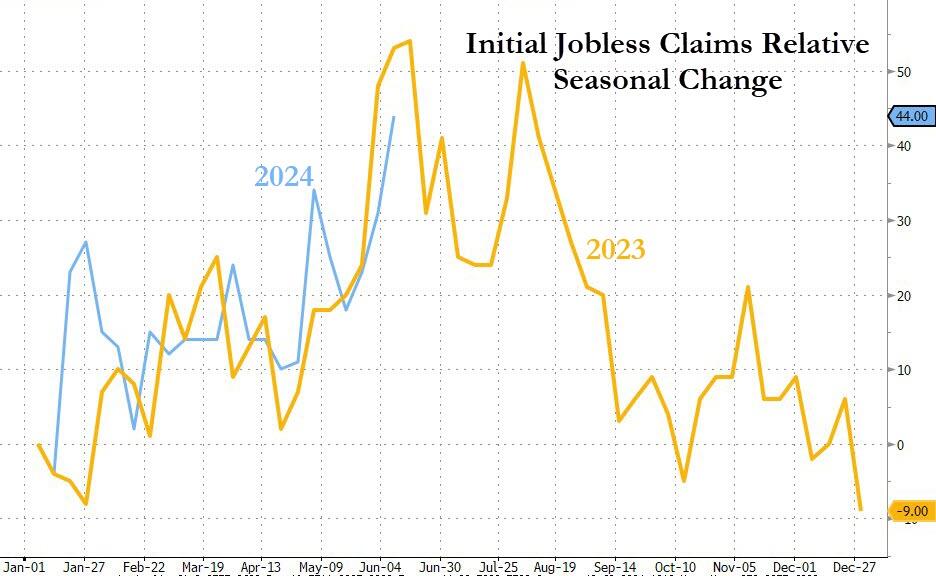

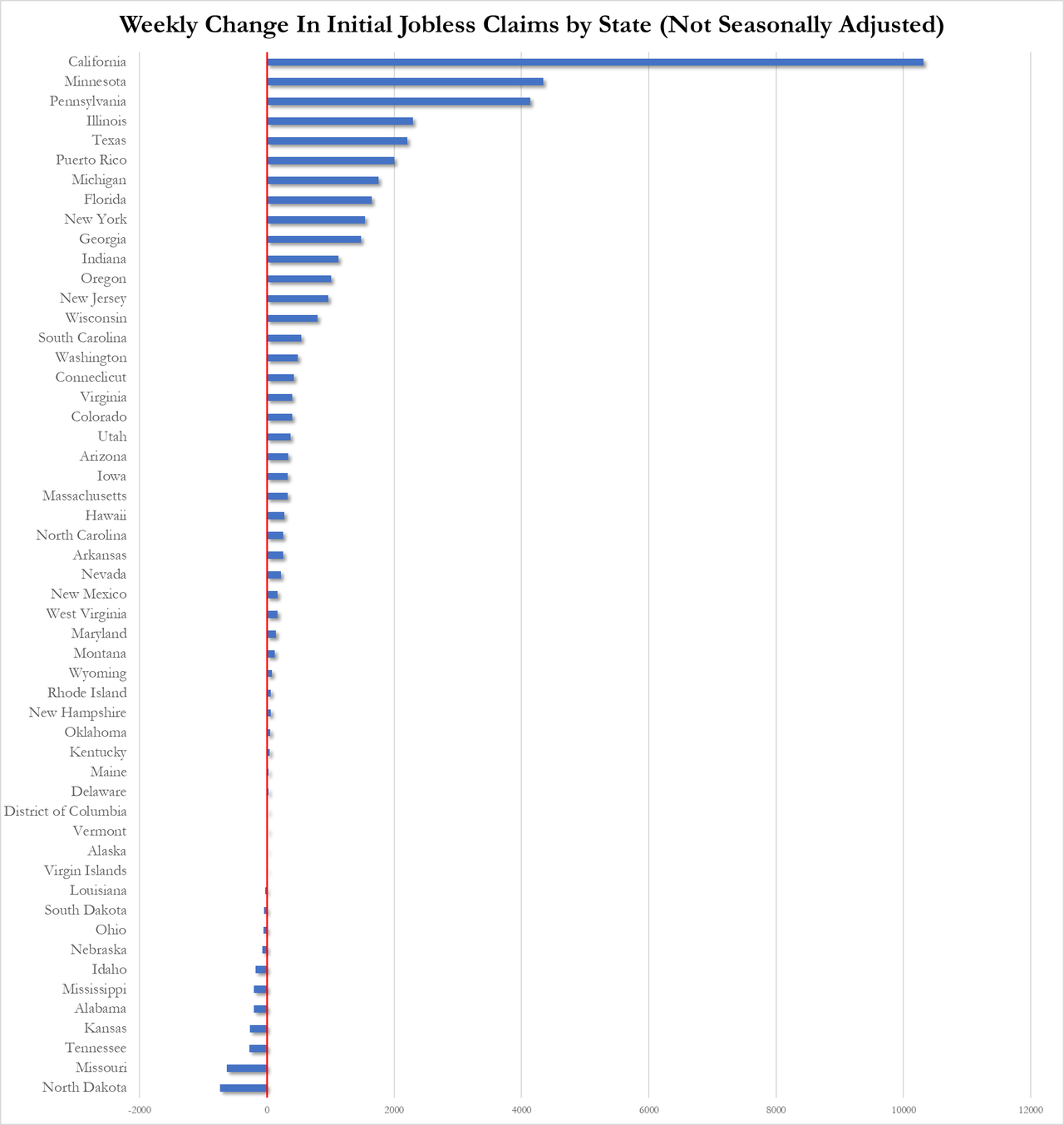

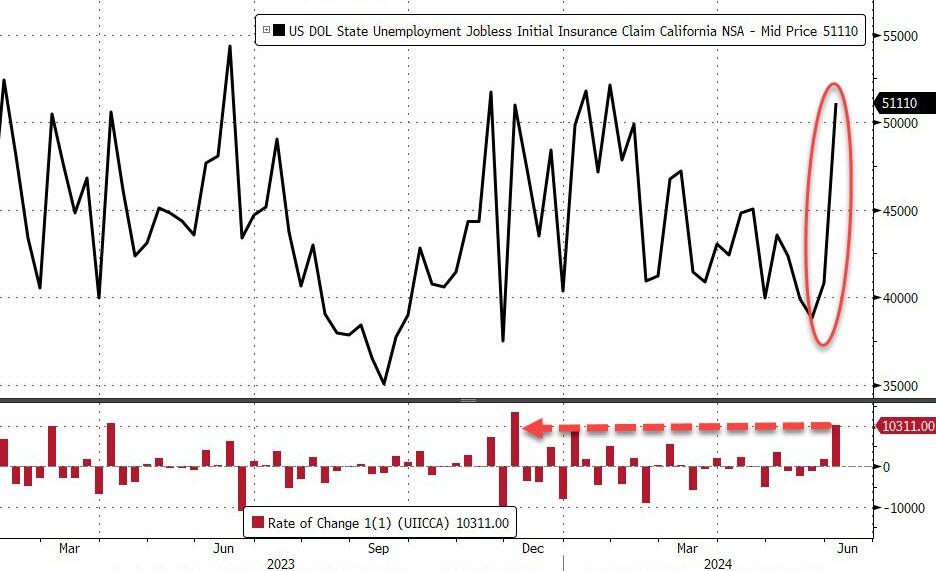

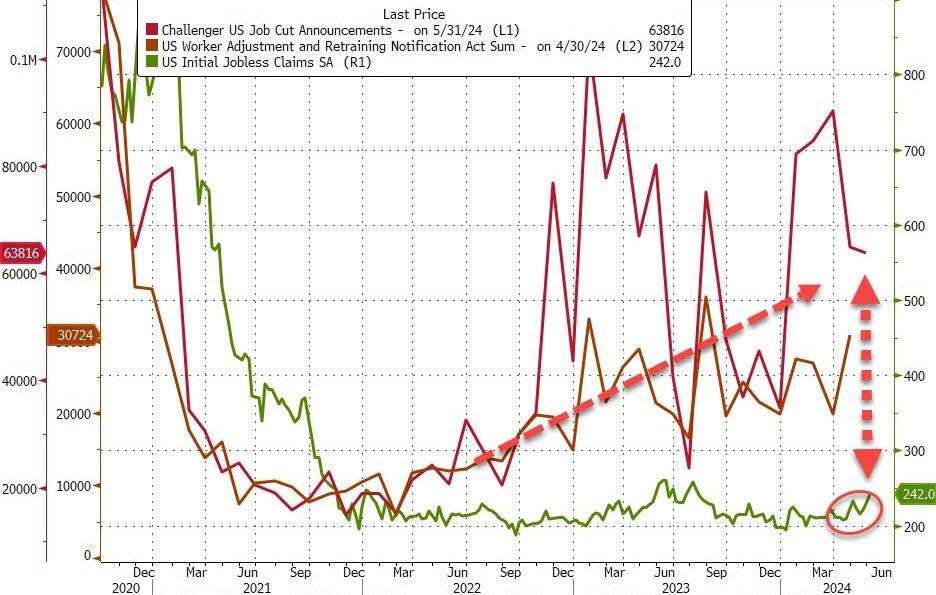

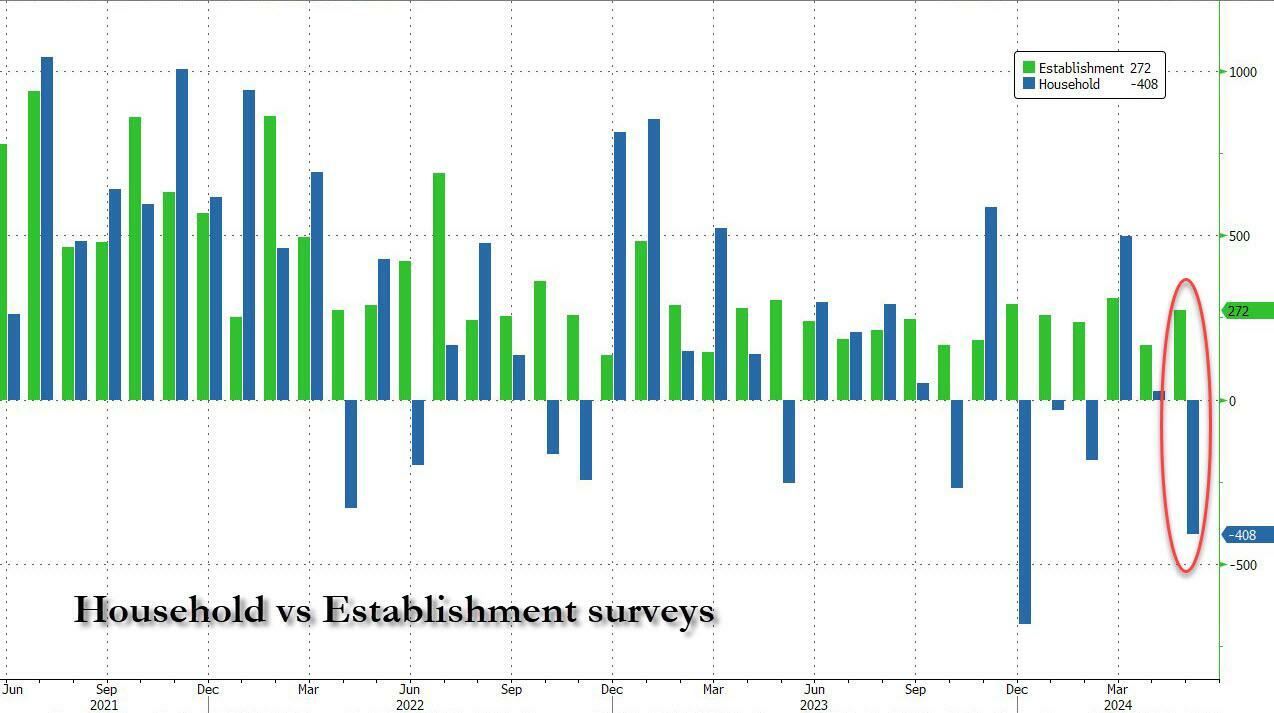

- 08:30: June Initial Jobless Claims, est. 225,000, prior 229,000

- June Continuing Claims, est. 1.8m, prior 1.79m

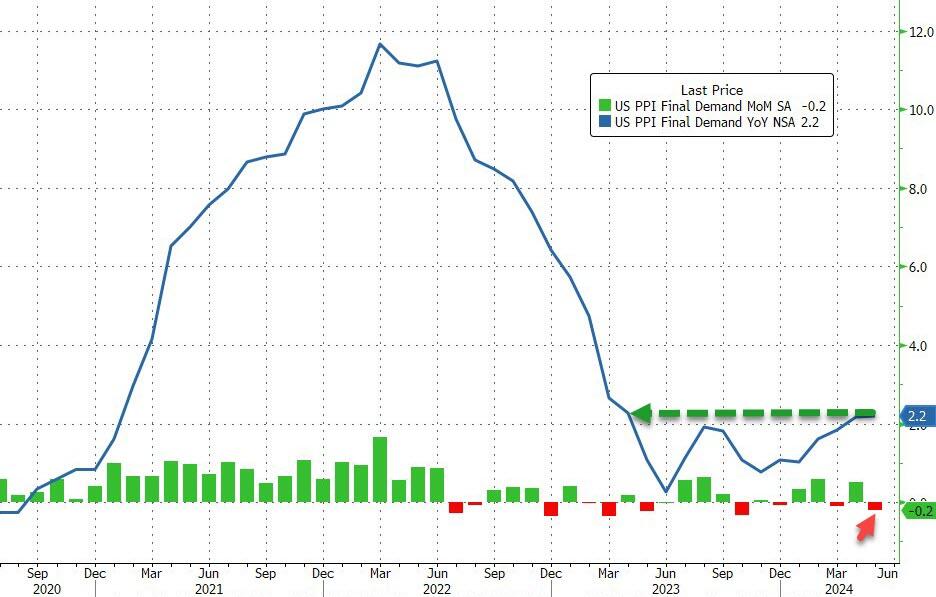

- 08:30: May PPI Final Demand MoM, est. 0.1%, prior 0.5%

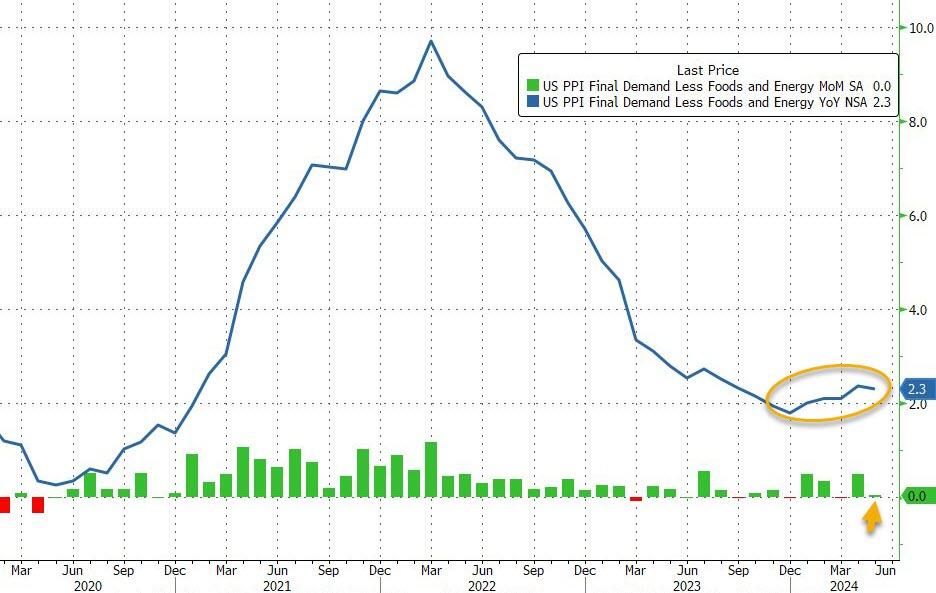

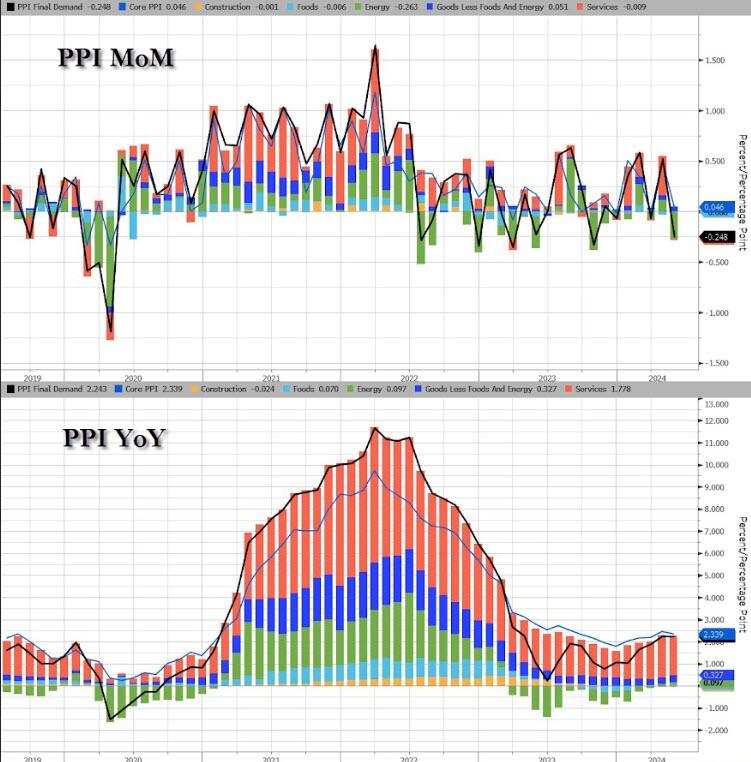

- May PPI Final Demand YoY, est. 2.5%, prior 2.2%

- May PPI Ex Food and Energy MoM, est. 0.3%, prior 0.5%

- May PPI Ex Food and Energy YoY, est. 2.5%, prior 2.4%

- 12:00: Fed’s Williams Interviews Treasury Sec. Yellen

DB’s Jim Reid concludes the overnight wrap

Markets have continued to reach new heights over the last 24 hours, with the S&P 500 (+0.85%) at another record after the US CPI report and the Fed’s latest decision. The CPI release was the main catalyst for that, as it featured the slowest month of core inflation since August 2021, and led investors to dial up the chance that the Fed would still cut rates twice this year. Later on, the Fed was then a bit more hawkish than expected, and only pencilled in one rate cut over the rest of the year. But that only unwound a part amount of the rally, with investors much more focused on the positive inflation news, with the hope that further prints like that one will open the door to faster cuts.

When it came to that US CPI release, it was one of the best prints in a long time from the Fed’s point of view. Specifically, the monthly core CPI was at just +0.16% in May, which is the slowest core inflation since August 2021, and it was also clearly beneath the +0.3% print expected by the consensus. In turn, that took the year-on-year core CPI print to +3.4% (vs. +3.5% expected), which is the lowest since April 2021. That softness was evident among headline inflation too, which was running at a monthly pace of just +0.01% in May, and the slowest since July 2022. Clearly the Fed will want to see a run of more favourable prints like this one, but there was little doubt that this was a very good number. Indeed, looking at the Cleveland Fed’s trimmed mean (which excludes the biggest outliers in either direction), it was the slowest monthly print since January 2021 at +0.13%. So it was clear this was a broad-based move lower for inflation, and it wasn’t just driven by a few outlier categories.

Overall, the report added to the sense that the faster inflation numbers from Q1 were an aberration, rather than the start of a more concerning trend of faster inflation. Indeed, if you look at the last 12 months of core CPI readings, the three fastest months were all in Q1. Moreover, it comes on the back of some softer data in recent days, particularly with the unemployment rate ticking up to 4.0%. So it cemented the idea that the Fed were getting closer to a place where they’d be able to cut rates, and led to a phenomenal market rally. Indeed, at the height of the moves after the CPI but before the Fed, the 10yr Treasury yield was down by -15.6bps intraday, and investors were fully pricing in two 25bp rate cuts from the Fed this year.

However, that rally began to unwind a bit after the Fed, who struck a more hawkish tone than had been expected. In terms of the main headlines, they kept rates unchanged, but their dot plot now pointed to just one rate cut over the rest of 2024, having signalled three cuts back in March. So that was clearly a more hawkish profile, and the consensus had still been expecting they’d show two cuts. Alongside that, the median dot for 2025 was up by 25bps as well, and the longer-run estimate of neutral moved up to 2.75%. The inflation forecasts were also revised up a bit for this year and next, with the core PCE inflation projection up two-tenths to 2.8% in 2024, whilst 2025 was up one-tenth to 2.3%.

In the press conference, Chair Powell did not emphasise the hawkish dot plot shift and noted in his prepared remarks that “the most recent inflation readings have been more favorable”. But he also downplayed the CPI print earlier in the day as only one data point and highlighted the solid performance of the economy and the labour market. For our US economists, they think the softer CPI print opens the door more widely to a September rate cut, but they think that would require more tame inflation readings over the next few months, and possible some softening in the growth and labour market data. Their baseline remains that the Fed is still likely to cut rates once this year in December. See their full reaction note here .

After the combination of the very dovish CPI, and then a somewhat hawkish Fed decision, Fed funds futures ended the day pricing in a more dovish path than they’d started. For instance, the amount of cuts priced in by December was up +5.1bps to 44bps, although that was down from a peak above 50bps before the Fed’s decision. Treasury yields followed a similar path, with 2yr yields down -16.6bps intraday before giving up around half of those gains by the close (-8.2bps to 4.75%). And 10yr yields were down -8.8bps to 4.32%, having traded at a two-month low of 4.25% intra-day. The decline in US rates weighed on the dollar, with the broad dollar index down -0.56% by the close, while the euro (+0.63%) had its strongest performance against the dollar so far this year.

For risk assets, the prospect of more rate cuts led to a major rally as well, and the S&P 500 (+0.85%) posted another record that took it above the 5400 mark for the first time. Tech stocks led the gains, with the Magnificent 7 (+1.93%) advancing for the seventh time in eight sessions. However, the gains were more moderate elsewhere, with the equal-weighted S&P 500 posting a smaller +0.53% gain, whilst the Dow Jones (-0.09%) saw a modest decline. Nevertheless, the VIX index of volatility (-0.81pts) fell to just 12.04pts, not far off from its post-Covid low of 11.86pts last month. And US HY spreads tightened -8bps on the day to 302bps.