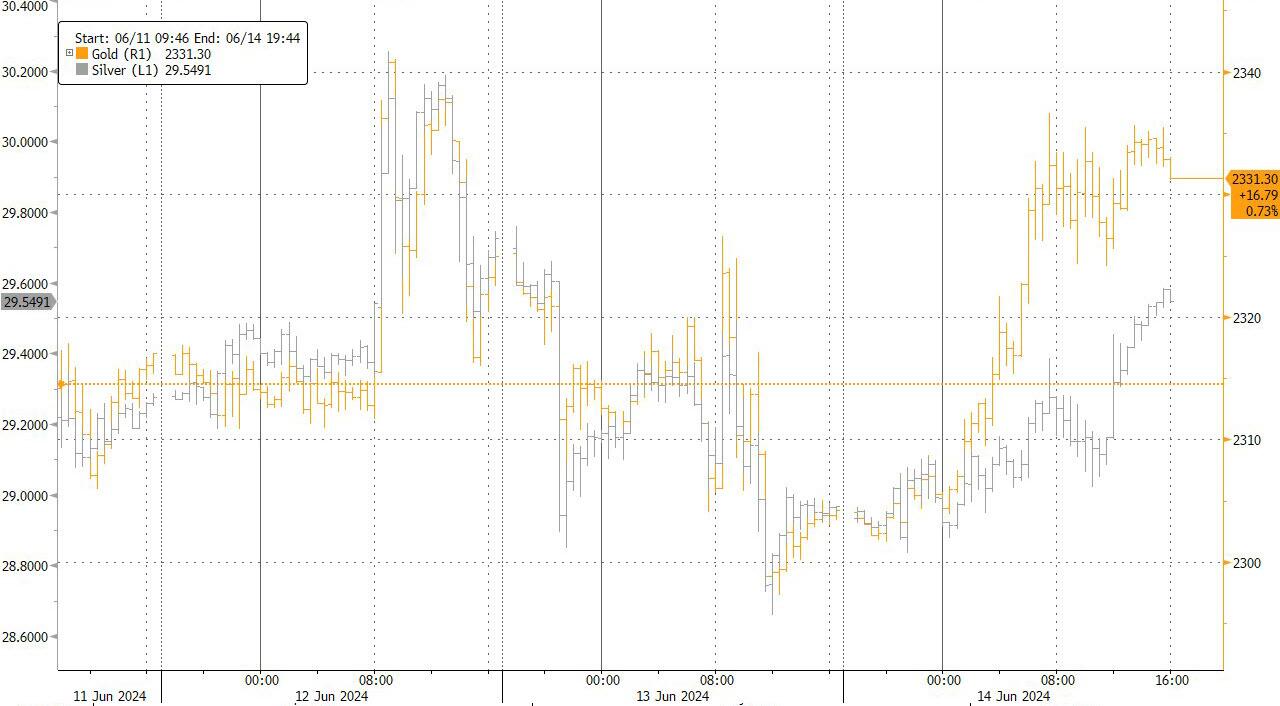

GOLD PRICE CLOSED UP $31.20 TO $2333.70

SILVER PRICE UP $0.42 TO $29.42

Gold ACCESS CLOSED $2331.25

Silver ACCESS CLOSED: $29.56

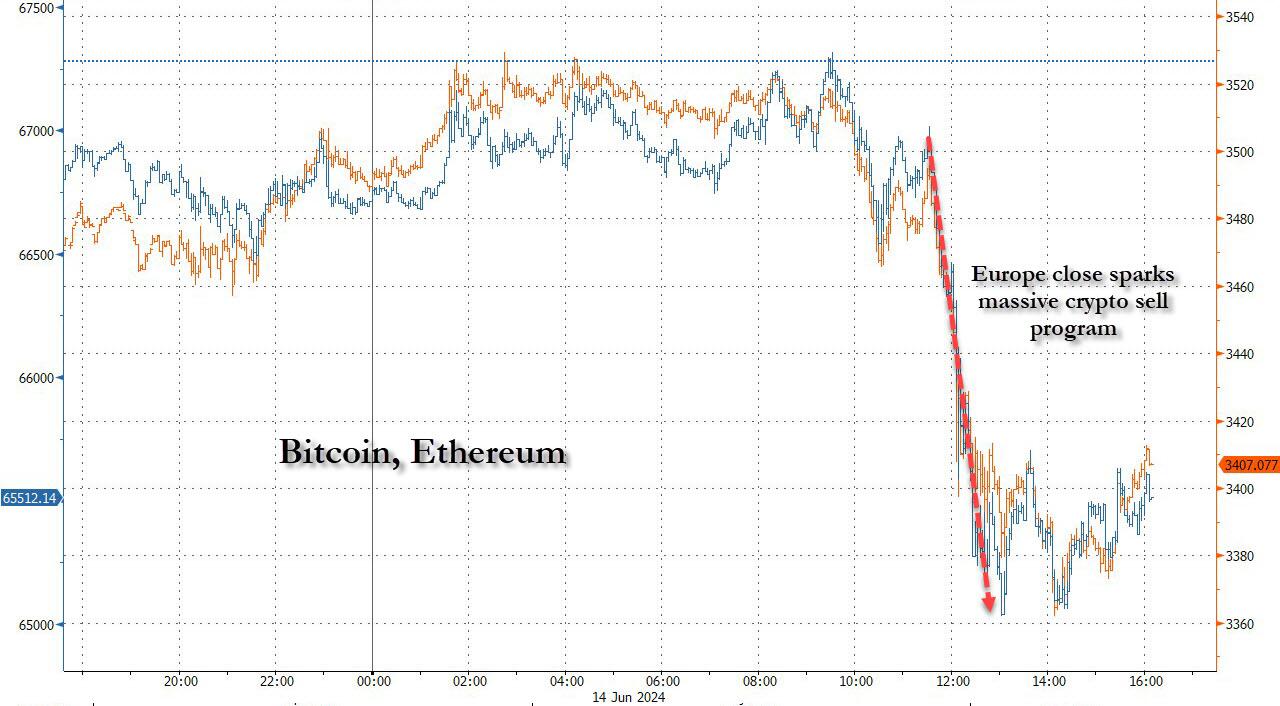

Bitcoin morning price:$66821 UP 82 DOLLARS.

Bitcoin: afternoon price: $65,376 DOWN 1363 dollars

Platinum price closing UP $2.65 TO $957.05

Palladium price; UP $0.90 AT $897.25

END

SHANGHAI GOLD PREMIUM 120 DOLLARS/COMEX GOLD//JULY TO JULY

SHANGHAI GOLD (USD) FUTURES – QUOTES

SHANGHAI GOLD (USD) FUTURES – QUOTES

Last Updated 14 Jun 2024 09:17:20 AM CT.

Market data is delayed by at least 10 minutes.

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $3201.60 UP 37.26 CDN dollars per oz( * NEW ALL TIME HIGH 3,305.30 CDN DOLLARS PER OZ//MAY 20 2024)

*BRITISH GOLD: 1837.18 UP 32.31 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2178.41 UP 33.84 Euros per oz //* (ALL TIME CLOSING HIGH: 2248.89 EUROS PER OZ//APRIL 16.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCH: COMEX

ACCESS MARKET

EXCHANGE: COMEX

CONTRACT: JUNE 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,300.200000000 USD

INTENT DATE: 06/13/2024 DELIVERY DATE: 06/17/2024

FIRM ORG FIRM NAME ISSUED STOPPED

323 C HSBC 168

435 H SCOTIA CAPITAL 60

624 H BOFA SECURITIES 87

690 C ABN AMRO 4

737 C ADVANTAGE 9 5

905 C ADM 16

991 H CME 13

TOTAL: 181 181

MONTH TO DATE: 29,413

JPMorgan stopped 0/181

FOR JUNE 2024

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2024. CONTRACT: 181 NOTICES FOR 18100 OZ or 0.5629 TONNES

total notices so far: 29,413 contracts for 2,941,300 Oz (91.486 tonnes)

FOR JUNE:

SILVER NOTICES: 11 NOTICE(S) FILED FOR 55,000

OZ/

total number of notices filed so far this month :1244 for 6.220 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $31.20 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ : HUGE CHANGES IN GOLD INVENTORY AT THE GLD/ A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/

/ /INVENTORY RESTS AT 829.34TONNES

INVENTORY RESTS AT 829.34 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER UP $0.42 AT THE SLV//

NO CHANGES IN SILVER INVENTORY AT THE SLV:

// INVENTORY INCREASES TO 429.683MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 429.683 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY AN ULTRA HUGE SIZED 1593 CONTRACTS TO 179,006 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR MONSTER LOSS OF $1.10 IN SILVER PRICING AT THE COMEX ON THURSDAY’S TRADING ON SILVER. WE HAD ZERO LONG LIQUIDATION AS WE HAD A NET GAIN OF 2890 CONTRACTS ON OUR TWO EXCHANGES. WE, AGAIN HAD SHORT COVERING BY OUR SPECS WITH THE HUGE LOSS IN PRICE AS WELL AS MASSIVE T.A.S. LIQUIDATION. WE HAD ANOTHER MEGA HUMONGOUS SIZED 3,673 T.A.S ISSUANCE,

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED LAST TUESDAY AND AGAIN LAST FRIDAY.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 3673 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND TODAY;S TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $1.10) AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS FROM THEIR PERCH AS WE DID HAVE A HUGE SIZED GAIN OF 2671 CONTRACTS ON OUR TWO EXCHANGES SESPITE THE LOSS IN PRICE OF $1.10. THE RAID SOLVED NOTHING FOR OUR CROOKS.

WE MUST HAVE HAD:

A HUGE SIZED 1078 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.830 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 10,000 OZ QUEUE JUMP

//NEW STANDING FOR SILVER//JUNE IS THUS 6.295 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI LOSS //HUGE SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 3673 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED 199 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE

TOTAL CONTRACTS for 10 DAYS, total 10,242 contracts: OR 51.210 MILLION OZ (1024 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 51.21 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 51.21 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

RESULT: WE HAD A GIGANTIC SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1593 CONTRACTS DESPITE OUR LOSS IN PRICE OF SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 3673 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.830 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 10,000 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR JUNE 6.295 MILLION OZ

WE HAVE A HUGE SIZED GAIN OF 2671 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A MEGA HUMONGOUS SIZED 3673 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND ZERO NET LIQUIDATION OF LONGS.

THE NEW TAS ISSUANCE THURSDAY NIGHT (3673) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 11 NOTICE(S) FILED TODAY FOR 55,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 2618 OI CONTRACTS TO 434,847 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 901 CONTRACTS

WE HAD A FAIR SIZED DECREASE IN COMEX OI (1593 CONTRACTS) OCCURRED WITH OUR LOSS OF $32.30 IN PRICE/THURSDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 89.94 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 16800 OZ QUEUE JUMP AS BANKERS SCOUR THE PLANET LOOKING FOR GOLD ON THE THIS SIDE OF THE POND

NEW STANDING 91.689 TONNES// ALL OF THIS HAPPENED WITH OUR $32.30 LOSS IN PRICE WITH RESPECT TO THURSDAY’S TRADING. WE HAD A SMALL SIZED LOSS OF 960 OI CONTRACTS (4.800PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4276 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 433,946

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 960 CONTRACTS WITH 1593 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 1657 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 960 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 1864 CONTRACTS,,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1657 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI OF 2617 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 901 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 88.761 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 0.5225 TONNES

//NEW STANDING /JUNE 90.689 TONNES.

/ 3) HUGE T.A.S. LIQUIDATION OF CONTRACTS WITH NEGLIGIBLE NET LONG SPECS BEING CLIPPED,

4) FAIR SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1864 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE. :

TOTAL EFP CONTRACTS ISSUED: 33,832 CONTRACTS OR 3,383,200 OZ OR 105.23 TONNES IN 10 TRADING DAY(S) AND THUS AVERAGING: 3383 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 10 TRADING DAY(S) IN TONNES 105.23 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 105.23 DIVIDED BY 3550 x 100% TONNES = 2.95% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 105.23 tonnes HEADING FOR A STRONG MONTH

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE SIZED 1593 CONTRACTS OI TO 179,000 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1078 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 1078 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1078 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1593 CONTRACTS AND ADD TO THE 1078 E.FP. ISSUED

WE OBTAIN AN ULTRA HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2671 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 14.35 MILLION OZ

OCCURRED DESPITE OUR HUMONGOUS $1.10 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING/THURSDAY NIGHT

SHANGHAI CLOSED UP 3.71 PTS OR 0.12% //Hang Seng CLOSED DOWN 170.85 PTS OR 0.99%// Nikkei CLOSED UP 94.09 OR 0.24%//Australia’s all ordinaries CLOSED UP 0.35%///Chinese yuan (ONSHORE) closed DOWN TO 7,2554 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2720/ Oil UP TO 78.70 dollars per barrel for WTI and BRENT UP AT 82.94 /Stocks in Europe OPENED ALL RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1593 CONTRACTS TO 433,946 DESPITE OUR HUGE LOSS IN PRICE OF $32.30 WITH RESPECT TO THURSDAY’S TRADING. WE HAD A HUGE T.A.S. LIQUIDATION ON THURSDAY WITH SOME LONGS BEING CLIPPED. (BUT NOT A HUGE NUMBER LOST BECAUSE OF THE RAID)

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE.… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 1657 EFP CONTRACTS WERE ISSUED: : AUGUST 1657 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1657 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 2617 CONTRACTS IN THAT 1657 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A FAIR SIZED LOSS OF 2617 COMEX CONTRACTS..AND THIS SMALL SIZED LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR HUGE LOSS IN PRICE OF $32.30

////THURSDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT WAS A GOOD SIZED 1864 CONTRACTS. MOST OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. THSOMEWHATSDAY IS OF EXTREME IMPORTANCE TO OUR CROOKS IN YESTERDAY’S TRADING

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (92.335 TONNES)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 92.335 TONNES. THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $32.30 //// AND WERE SOMEWHAT SUCCESSFUL IN KNOCKING SOME SPECULATOR LONGS AS WE HAD A SMALL SIZED LOSS OF 2617 CONTRACTS ON THURSDAY WITH OUR TWO EXCHANGES WITH THE HUGE LOSS IN PRICE. THE T.A.S. ISSUED ON THURSDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE LOST A TOTAL OI OF 0.1835 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE (89.94 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 168 CONTRACTS OR 16800 OZ (0.5225 TONNES)

NEW STANDING FOR JUNE: 92.335 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR HUGE LOSS IN PRICE TO THE TUNE OF $32.30

WE HAVE REMOVED 901 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET LOSS ON THE TWO EXCHANGES 2671 CONTRACTS OR 267,100 (4.800 TONNES)

confirmed volume THURDAY 191,355 contracts//FAIR

//speculators have left the gold arena

JUNE 14 JUNE GOLD CONTRACT

/ /// THE JUNE 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 12,984.049 oz mANFRA . |

| Deposit to the Dealer Inventory in oz | 0 oz |

| Deposits to the Customer Inventory, in oz | 0 OZ//BRINKS |

| No of oz served (contracts) today | 181 notice(s) 18100 OZ 0.5629 TONNES |

| No of oz to be served (notices) | 273 contracts 247300 OZ 0.8491 TONNES |

| Total monthly oz gold served (contracts) so far this month | 29,413 notices 2,941,300 oz 91.486 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: NIL oz

we have 0 customer deposit:

total deposit nil oz

customer withdrawals: 1

i) out of Manfra 12,984.049 oz

TOTAL WITHDRAWALS 12,984.049 0z

Adjustments: customer account to dealer

HSBC: 238,507.719 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE

For the front month of JUNE we have an oi of 454 contracts having LOST 69 contracts. We had 237 contracts served on Thursday so we gained A HUGE 168 contracts or 16,800 oz additional ounces will stand for gold at the comex as they underwent a queue jump to take delivery on this side of the pond.

JULY LOST 57 CONTRACTS TO STAND AT 2419

AUGUST LOST 3876 CONTRACTS DOWN TO 352,317 CONTRACTS

We had 181 contracts filed for today representing 18100 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notice was issued from their client or customer account. The total of all issuance by all participants equate to 181 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for June /2024. contract month, we take the total number of notices filed so far for the month (29,413) x 100 oz ) to which we add the difference between the open interest for the front month of JUNE (454 CONTRACTS) minus the number of notices served upon today (181 x 100 oz per contract( equals 2,968,600 OZ OR 92.335 TONNES.

thus the INITIAL standings for gold for the JUNE contract month: No of notices filed so far (29.413 x 100 oz +we add the difference for front month of June (454 OI} minus the number of notices served upon today (181) x 100 oz which equals 2,968,600 oz (92.335 TONNES)

TOTAL COMEX GOLD STANDING FOR JUNE: 92.335 TONNES WHICH IS ABSOLUTELY HUGE FOR THIS VERY ACTIVE DELIVERY MONTH IN THE CALENDAR. JUNE IS TRADITIONALLY THE 2ND HIGHEST DELIVERY MONTH OF THE YEAR. FROM THIS POINT WE WILL GAIN IN GOLD TONNAGE WILLING TO STAND AT THE COMEX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,680,714.128 52.27 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,643,908/604 OZ

TOTAL REGISTERED GOLD 8,151,711.227( 246.13 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,492,197.377 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,470,997 oz (REG GOLD- PLEDGED GOLD)= 201.28 tonnes //

END

SILVER/COMEX

JUN 14/2024

INITIAL

//2024// THE JUNE 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,396,802.402 oz Brinks Delaware JPMorgan . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 599,324.270 oz CNT |

| No of oz served today (contracts) | 11 CONTRACT(S) (55,000 OZ) |

| No of oz to be served (notices) | 15 contracts (0.075 million oz) |

| Total monthly oz silver served (contracts) | 1244 Contracts (6.220 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 customer deposit:

i) Into CNT 599,324.270 oz

total customer deposit 599,324.270..oz

JPMorgan has a total silver weight: 127.822million oz/296.393million or 43.17%

adjustment: 0

Comex withdrawals: 3

i) out of Brinks: 278,287.950 oz

ii) out of Delaware: 584,801.259 oz

iii) Out of JPMorgan: 583,713.200 oz

total withdrawal: 1,396,802.402 0z

TOTAL REGISTERED SILVER: 63.074MILLION OZ//.TOTAL REG + ELIGIBLE. 296.393

million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE:

silver open interest data:

FRONT MONTH OF JUNE/2024 OI: 24 CONTRACTS HAVING LOST 117 CONTRACT(S).

WE HAD 119 NOTICES SERVED UP ON THURSDAY, SO WE GAINED 2 CONTRACTS OR AN ADDITIONAL 10,000 OZ WILL STAND AT THE COMEX VIA A SMALL QUEUE JUMP TO WHERE THEY WILL TAKE DELIVERY ON THIS SIDE OF THE POND

JULY SAW A LOSS OF 8394 CONTRACTS DOWN TO 86,083

AUG, SAW A GAIN OF 59 CONTRACTS TO 338

SEPT SAW A GAIN OF 9603 CONTRACTS TO 73,895

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 11 for55,000 oz

CONFIRMED volume; ON THURSDAY 148,041 GIGANTIC

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1244 x 5,000 oz = 6.220 MILLION oz

to which we add the difference between the open interest for the front month of JUNE ((24) and the number of notices served upon today 11 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2024 contract month: 1244 notices served so far) x 5000 oz + OI for the front month of JUNE (24)x number of notices served upon today minus (11)x 5000 oz of silver standing for the JUNE contract month equates to 6.295 MILLION OZ.

New total standing: 6.295 million oz.

There are 63.074 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

JUNE 14 WITH GOLD UP$31.20 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 829,34 TONNES

JUNE 13 WITH GOLD DOWN$35.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.89 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 830.78 TONNES

JUNE 12 WITH GOLD UP $28.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.89 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 830.78 TONNES

JUNE 11 WITH GOLD DOWN $0.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 10 WITH GOLD UP $2,00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 7 WITH GOLD DOWN $64.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 3.56 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 837.11 TONNES

JUNE 6 WITH GOLD UP $16.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.34 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 833.55 TONNES

JUNE 5 WITH GOLD UP $32.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 4 WITH GOLD DOWN $20.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 3 WITH GOLD UP $22.85 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 31 WITH GOLD DOWN $19.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 30 WITH GOLD UP $3.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 29 WITH GOLD DOWN $13.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 28 WITH GOLD UP $22.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 832.21 TONNES

MAY 24 WITH GOLD DOWN $2.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 833.36 TONNES

MAY 23 WITH GOLD DOWN $53.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 22 WITH GOLD DOWN $32.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 21 WITH GOLD DOWN $12,00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 20 WITH GOLD UP $21.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.10 TONNES OF GOLD INTO THE GLD//NEW TOTAL 838.54 TONNES

MAY 17 WITH GOLD UP $31.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//NEW TOTAL 833.36 TONNES

MAY 16 WITH GOLD DOWN $7.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//NEW TOTAL 833.36 TONNES

MAY 15 WITH GOLD UP $34.90 ON THE DAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD/INVENTORY RISES TO 831.93 TONNES

MAY 14 WITH GOLD DOWN $17.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RISES TO 831.33 TONNES

GLD INVENTORY: 829.34 TONNES, TONIGHTS TOTAL

Now the SLV Inventory/( vehicle is a fraud as there is no physical metal behind them

JUNE 14. WITH SILVER UP $0.42//NO CHANGES IN SILVER INVENTORY/ /INVENTORY REMAINS AT 429.083 TONNES

JUNE 13. WITH SILVER DOWN $1.10//HUGE CHANGES IN SILVER INVENTORY/ A HUGE DEPOSIT OF 1.958 MILLION OZ/INVENTORY RISES TO 429.083 TONNES

JUNE 12 WITH SILVER UP $0.97 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 5.983 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 427.125 MILLION OZ

JUNE 11 WITH SILVER DOWN $0.59 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.644 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 422.786 MILLION OZ

JUNE 10 WITH SILVER UP $0.30 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 3.198 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 421.142 MILLION OZ

JUNE 7 WITH SILVER DOWN $1.93 TODAY: NO CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY AT 417.944 MILLION OZ

JUNE 6 WITH SILVER UP $1.27 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 417.944 MILLION OZ

JUNE 5 WITH SILVER UP 0.38 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.52 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 415.295 MILLION OZ

JUNE 4 WITH SILVER DOWN $1.08 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

JUNE 3 WITH SILVER UP $0.35 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

MAY 31 WITH SILVER DOWN $1.09 TODAY: HUGE CHANGES IN SILVER INVENTORY: A MASSIVE WITHDRAWAL OF 3.655 MILLION OZ FROM THE SLV//INVENTORY LOWERS TO 413.775 MILLION OZ

MAY 30 WITH SILVER DOWN $0.80 TODAY: NO CHANGES IN SILVER INVENTORY//INVENTORY REMAINS AT 417.430 MILLION OZ

MAY 29 WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 1.051 MILLION OZ INTO THE SLV//INVENTORY DECREASES TO 417.430 MILLION OZ

MAY 28 WITH SILVER UP $1.64 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 2.832 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 418.481 MILLION OZ

MAY 24 WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF .822 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 421.313 MILLION OZ

MAY 23 WITH SILVER DOWN $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.736 MILLION OZ FROM THE SLVINVENTORY INCREASES TO 420.491 MILLION OZ

MAY 22 WITH SILVER DOWN $0.66 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 21 WITH SILVER DOWN $0.41 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A DEPOSIT OF 3.792 MILLION OZ FROM THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 20 WITH SILVER UP $1.28 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 1.005 MILLION OZ FROM THE SLV// INVENTORY LOWERS TO 418.435 MILLION OZ

MAY 17 WITH SILVER UP $1.37 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 868,000 OZ FROM THE SLV// INVENTORY LOWERS TO 419.440 MILLION OZ

MAY 16 WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY REMAINS AT 420.308 MILLION OZ

MAY 15 WITH SILVER UP 101 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A WITHDRAWAL OF 1.919 MILLION OZ FROM THE SLV NVENTORY RESTS AT 420.308 MILLION OZ

MAY 14 WITH SILVER UP 25 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;INVENTORY RESTS AT 422.227 MILLION OZ

CLOSING INVENTORY 429.083 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

Silver Demand In The Solar Sector Could Squeeze Silver Supply In The Future

FRIDAY, JUN 14, 2024 – 02:55 PM

Authored by Mike Maharrey via Money Metals,

Silver use by the solar energy sector is one of the primary factors driving the overall demand for silver, and there is reason to believe photovoltaic silver off-take will continue to increase in the years ahead.

Not only is the demand for silver panels growing, but the amount of silver used in each panel is also increasing.

Industrial demand for silver set a record of 654.4 million ounces in 2023 and it is expected to hit new highs this year. According to the Silver Institute, ongoing structural gains from green economy applications underpinned this surge in silver demand.

“Higher than expected photovoltaic (PV) capacity additions and faster adoption of new-generation solar cells raised global electrical & electronics demand by a substantial 20 percent. At the same time, other green-related applications, including power grid construction and automotive electrification, also contributed to the gains.”

Silver is the best conductor of electricity of all metals at room temperature. That makes it a vital input in the production of solar panels.

To manufacture a solar panel, silver is formed into a paste that is applied to the front and back of silicon photovoltaic cells. The front side collects the electrons generated when sunlight strikes the cell, while the back side helps to complete the electrical circuit.

Each solar panel uses approximately 20 grams (0.643 ounces) of silver. While this is a relatively small amount, the total adds up quickly when you consider the number of panels produced each year. The solar industry used approximately 100 million ounces of silver in 2023, accounting for about 14 percent of total silver demand.

Several years ago, analysts assumed that the amount of silver used in solar panels would decline over time with the development of new technologies. However, a Saxo Bank report in 2020 disputed this claim, saying, “Potential substitute metals cannot match silver in terms of energy output per solar panel.”

“Further, due to technical hurdles, non-silver PVs tend to be less reliable and have shorter lifespans, presenting serious issues for their widespread commercial development.”

It turns out, this analysis was correct. Newer more efficient technologies use 20 to 120 percent more silver.

In 2020, Passivated Emitter and Rear Cell (PERC) technology was the standard, accounting for virtually the entire solar market. A PERC solar panel uses about 10 milligrams of silver per watt.

By 2022, PERC technology was being replaced by Tunnel Oxide Passivated Contact (TOPCon) cells. This advanced technology enhances the efficiency of solar cells by improving the way they handle electron flow. A TOPCon cell is cheaper to produce but uses more silver than a PERC solar panel. It contains about 13 milligrams of silver per watt.

Now, heterojunction (HJT) technology is beginning to dominate the solar market. HJT cells are even more efficient than TOPCon technology and can capture energy on both sides of the panel. They are also more environmentally friendly. But they use even more silver – about 22 milligrams per watt. HJT cells only made up a small part of the market in 2023, but demand for these more efficient panels is expected to grow.

With demand for solar power increasing along with the amount of silver used in each panel, analysts believe that solar panel production will consume increasingly large amounts of silver in the future.

According to a research paper by scientists at the University of New South Wales, solar manufacturers will likely require over 20 percent of the current annual silver supply by 2027.

By 2050, solar panel production will use approximately 85–98 percent of the current global silver reserves.

The green energy sector is also essentially recession-proof because it is being driven, incentivized, and in some cases directly funded by governments around the world.

The silver market is already running significant deficits with silver demand outstripping supply. The structural deficit in 2023 came in at 184.3 million ounces.

While there is still a large silver stock available, market deficits will eventually deplete the reserve of available metal. We could see a significant supply squeeze in the coming years.

Silver is not currently priced for these supply and demand dynamics.

It’s also important to remember that while industrial demand is an important factor driving the price, silver is still fundamentally a monetary metal. As such, the price tends to track with gold over time. If you are bullish on gold, you should be even more bullish on silver. In fact, silver tends to outperform gold in a gold bull market.

Given the supply and demand dynamics, the economic environment, and a historically wide gold-silver ratio that indicates silver is underpriced, there are plenty of reasons to think silver will shine in the future.

Mike Maharrey is a journalist and market analyst for MoneyMetals.com with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/GOLD AND SILVER COMMENTARY

huge story

Saudi Arabia ends 80-year petrodollar deal with U.S., boosting other currencies

Submitted by admin on Fri, 2024-06-14 08:43 Section: Daily Dispatches

By Pawan Kumar

The Times of India, Mumbai

Friday, June 14, 2024

Saudi Arabia has decided not to renew its 80-year petrodollar agreement with the United States, which expired on Sunday, June 9. This deal, signed on June 8, 1974, was a significant part of the global economic influence of the United States.

The agreement created joint commissions for economic cooperation and supported Saudi Arabia’s military needs.

At the time, American officials hoped the agreement would encourage Saudi Arabia to produce more oil and strengthen economic ties with Arab countries.

By not renewing this contract, Saudi Arabia is now free to sell oil and other goods using various currencies like the Chinese renminbi, euros, yen, and yuan rather than only U.S. dollars.

There is also talk of exploring digital currencies, such as bitcoin, for transactions.

This decision marks a major shift away from the petrodollar system, which has been in place since 1972 when the U.S. stopped linking its currency directly to gold. It is expected to speed up the global trend of using currencies other than the U.S. dollar in international trade.

Additionally, Saudi Arabia has joined Project mBridge, a collaborative effort to develop a digital currency platform shared among central banks and commercial banks.

This project aims to facilitate instant cross-border payments and foreign exchange transactions using distributed ledger technology. Project mBridge began in 2021 and involves several prominent central banks and institutions worldwide.

It has recently reached the stage of a minimum viable product, inviting private-sector firms to propose innovations and use cases to further develop the platform.

* * *

end

Hit by new U.S. sanctions, Russia halts dollar and euro trade on main bourse

Submitted by admin on Wed, 2024-06-12 20:15 Section: Daily Dispatches

By Alexander Marrow and Mark Trevelyan

Reuters

via Yahoo News, Sunnyvale, California

Wednesday, June 12, 2024

New U.S. sanctions against Russia have forced an immediate suspension of trading in dollars and euros on its leading financial marketplace, the Moscow Exchange.

The exchange and the central bank rushed out statements today — a public holiday in Russia — within an hour of Washington announcing a new round of sanctions aimed at cutting the flow of money and goods to sustain Russia’s war in Ukraine.

“Due to the introduction of restrictive measures by the United States against the Moscow Exchange Group, exchange trading and settlements of deliverable instruments in U.S. dollars and euros are suspended,” the central bank said.

The move means banks, companies, and investors will no longer be able to trade either currency via a central exchange, which offers advantages in terms of liquidity, clearing, and oversight.

Instead, they will have to trade over-the-counter, where deals are conducted directly between two parties. The central bank said it would use OTC data to set official exchange rates. …

… For the remainder of the report:

https://finance.yahoo.com/news/moscow-exchange-stop-trading-dollars-153650237.html

end

Chris Powell…..

The world will never be free if it believes official gold data

Submitted by admin on Tue, 2024-06-11 23:29 Section: Daily Dispatches

11:52p ET Tuesday, June 11, 2024

Dear Friend of GATA and Gold:

Headlines like this have been pummeling the monetary metals sector in recent days: “Gold Is Getting So Expensive That Even China’s Central Bank Stopped Buying.”

According to this particular report:

China’s central bank gold-buying streak has been a major driver of prices that hit record highs recently. However, it looks like gold has gotten so expensive that even the People’s Bank of China is taking a break

On Friday official data showed China’s gold holdings were unchanged in May from the prior month — which means the central bank did not buy gold.

The PBoC’s pause has left gold ‘vulnerable to more downside pressure,’ wrote Ewa Manthey, a commodities strategist at ING Bank, on Monday. …

China’s central bank gold buying had actually started to slow in April, when it bought just 60,000 troy ounces of the precious metal. That was down from 160,000 ounces in March and 390,000 ounces in February.

Before its pause in purchases last month, the PBoC had been snapping up gold for 18 straight months, making it the world’s largest institutional buyer. …

Mainstream financial news organizations don’t yet seem to notice that official statements about gold reserves are, to put it politely, not reliable.

That the People’s Bank of China did not report acquiring gold in May does not mean that the bank or the Chinese government did not actually acquire gold in the month. It meant only that the central bank did not report acquiring gold in May. The bank or other agencies of the Chinese government could have acquired huge amounts of gold in May and simply not reported them — perhaps because China wanted to knock the price down abruptly to make acquisitions easier and less expensive, or wanted to oblige pressure from the United States not to push the gold price up so fast.

We have been here before.

In April 2009 China caused a sensation by announcing that its gold reserves had increased by 76%, from 600 tonnes to 1,054 tonnes. For the previous six years China had been reporting to the International Monetary Fund, the compiler of official gold data, only 600 tonnes. Had China acquired those 454 new tonnes only in the year prior to the April 2009 announcement?

That’s unlikely. That much official buying in a year or less almost certainly would have manifested itself in price action or comment by market participants. It’s far more likely that China acquired the 454 tonnes reported in April 2009 over at least several years, largely by purchasing the production of China’s own fast-growing gold mining industry, but didn’t announce it or report it to the IMF. The metal may have been in the solid possession of the Chinese government but kept on the books of state-owned commercial banks or government entities other than the central bank. That would have been easy to arrange.

So for as many as six years the official gold reserve data about China was way off.

The next year, 2010, the same thing happened with Saudi Arabia. In June 2010 the World Gold Council reported that Saudi gold reserves had increased by 126%, from 143 to 323 tonnes, in just two years. That the world’s top oil exporter had made such a new commitment to gold in its foreign exchange reserves also caused a sensation. It implied a reduction of Saudi loyalty to the petrodollar.

But a few weeks after the announcement of the spurt in Saudi gold reserves, the governor of the Saudi Arabia Monetary Authority, Muhammad al Jasser, insisted to news reporters in Kuwait that Saudi Arabia had not recently purchased the gold cited in the June reports but rather had held that extra gold all along in what he called “other accounts.” That is, held the metal in accounts not reported officially — just as the true status of China’s gold accounts had not been reported officially for six years.

Official fudging about gold reserves continued this year as Federal Reserve Chairman Jerome Powell refused to answer the question posed by U.S. Rep. Alex Mooney, R-West Virginia, as to whether any foreign custodial gold recently had been repatriated from the Federal Reserve Bank of New York.

Powell ignored Mooney’s letter for a while. Eventually the Fed chairman was compelled to acknowledge it but he simply ignored the question about repatriation:

https://www.gata.org/node/23054

Comprehensively incriminating official central bank gold data and central bank intervention against gold is the secret March 1999 staff report of the International Monetary Fund that GATA obtained in December 2012. The secret IMF report says Western central banks conceal their gold swaps and loans to facilitate their secret interventions in the gold and currency markets:

http://www.gata.org/node/12016

The secret IMF report establishes not only that central banks are surreptitiously intervening in the gold market through swaps and leases but also that no official central bank gold data is any good. The IMF allows its members to count their leased and swapped gold as if it is still sitting in their vaults, unencumbered, when the gold may have left the vaults or have multiple claims on it.

That is, the secret IMF report shows that central bank gold reserves are double-counted or worse.

The exaggerated response of the gold price to the recent reports that China had stopped buying gold in May showed again that while central banks and governments have the power to create and deploy infinite amounts of money, this is not their greatest power. Their greatest power is their command of mainstream financial news organizations, which never pose or press the most obvious critical questions about gold but report only what central banks and governments want reported.

Maybe those news organizations sense, or maybe they have been frankly told, what central banks and governments know: that the true size, location, and disposition of national gold reserves are secrets far more sensitive than the true size, location, and disposition of nuclear weapons. For nuclear weapons can only destroy the world, while the control of gold means the control all financial valuations everywhere — the value of all capital, labor, goods, and services — since the value of gold is the inverse of the value of government currencies.

If it ever knew where all the official gold really was and how it was really being deployed, the world would be nearly free. Not even nominally democratic governments want that.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

this is true!!

(CNBC)

Singapore to lead gold market as it shifts east, World Gold Council says

Submitted by admin on Tue, 2024-06-11 10:25 Section: Daily Dispatches

By Lee Ying Shan

CNBC, New York

Monday, June 10, 2024

SINGAPORE — Singapore is set to become a leading gold hub as trading shifts east, according to the World Gold Council.

One key reason is that gold consumption in major emerging economies is rising, and a majority of these markets are concentrated in Asia, said Shaokai Fan, head of Asia-Pacific and global head of central banks.

Singapore’s proximity to these central banks, which are snapping up gold, is another factor, he added.

“The center of gravity of the gold market has shifted east, with Singapore, fortuitously placed as the potential fulcrum of this new balance,” Fan said at the Asia Pacific Precious Metals Conference held in Singapore. …

… For the remainder of the report:

https://www.cnbc.com/2024/06/11/singapore-to-lead-the-gold-market-said-the-world-gold-council.html

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS/LIVE FROM THE VAULT NO 177

ANDREW MAGUIRE…

Episode 177

Posted 14th June 2024

Half a $Trillion reasons gold could hit $10,000!

In this week’s episode of Live from the Vault Andrew Maguire opens by outlining how close the wrong-footed Fed came to completely imploding after gold’s recent all-time-highs.

The London whistleblower and precious metals expert answers the community’s burning questions, from where gold and silver prices could be heading in the short term, to the latest updates about the upcoming BRICS gold-backed currency.

Andrew Maguire

Host

Andrew Maguire has almost 50 years’ experience working in the precious metals industry as an independent Loco London metals trader and analyst, where he has provided Precious Metals Advisory and Trading services for international hedge fund managers, bullion banks, directors, metal traders and many of the largest global institutions.

Andrew has built strong relationships with US and UK regulatory bodies, having worked as an advisor for the Commodity Futures Trading Commission, (CFTC) and the Department of Justice, (DOJ). In the UK, Andrew is currently providing advisory services to the UK and the Financial Conduct Authority, (FCA)

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT//COCOA //

Cocoa prices rise above $10,000 per tonne

(zerohedge)

Rollercoaster: Cocoa Prices Surge Above $10,000 A Ton As Global Supply Fears Worsen

THURSDAY, JUN 13, 2024 – 03:45 PM

The great Cocoa crash from mid-April to the first half of May seems to have ended. Recall prices crashed 45% in that time after a massive multi-month run-up on global supply fears. Now, prices have surged 57% from the $6.767k/ton low, breaking over the $10k mark and printing as high as $11k during today’s intra-day session.

Commodity trader Pierre Andurand, who turned cocoa bull in March, is most likely ecstatic with the price action of the bean in New York in recent weeks, especially this week’s surge.

Andurand recently spoke with Bloomberg’s Odd Lots hosts Tracy Alloway and Joe Weisenthal about a sliding inventory-to-grinding ratio that could ignite “a real shortage of cocoa beans.” His price target for the bean is still at the $20k mark for later this year or next.

“Market volatility is also influenced by a lack of liquidity, with the number of outstanding contracts continuing to shrink. The wild daily price jumps and high margin requirements are seen making it costlier for traders to maintain their positions, prompting many to walk away,” Bloomberg noted.

Adding to global cocoa supply fears was a report from Reuters on Wednesday detailing how one of the world’s top producers, Ghana, has considered delaying delivery of up to 350,000 tons of cocoa beans for next season due to poor harvests.

Michael McDougall, managing director at Paragon Global Markets, told Bloomberg Thursday that cocoa bean arrivals date indicate “production issues continue to plague the market and lack of investment catching up as yields are suffering due to aging trees.”

McDougall warned, “It won’t be resolved quickly for sure.”

Earlier this week, Bloomberg reported that Ivory Coast, the world’s top bean producer, has begun tightening domestic bean sales to prioritize local processors as supplies dwindle due to a bad harvest across West Africa.

Here are our latest bean reports:

- Cocoa Bull Pierre Andurand Warns Of ‘Price Explosion’ If Stock-To-Grinding Ratio Collapses

- Global Cocoa Shortage Much Worse Than Previously Forecasted As Prices Surge

- Cocoa Mess: Ivory Coast Bans Some Bean Sales As Global Supplies Tighten Further

The news from West Africa is certainly worsening supply fears for the bean as prices near record highs.

However, Rabobank analyst Paul Joules recently told clients cocoa prices have likely peaked.

So, prices have peaked? Or is Andurand correct, and prices head to $20k?

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

ASIA TRADING//THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED UP 3.71 PTS OR 0.12% //Hang Seng CLOSED DOWN 170.85 PTS OR 0.99%// Nikkei CLOSED UP 94.09 OR 0.24%//Australia’s all ordinaries CLOSED UP 0.35%///Chinese yuan (ONSHORE) closed DOWN TO 7,2554 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2720/ Oil UP TO 78.70 dollars per barrel for WTI and BRENT UP AT 82.94 /Stocks in Europe OPENED ALL RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2554

OFFSHORE YUAN: UP TO 7.2720

SHANGHAI CLOSED UP 3.71 PTS OR 0.12 %

HANG SENG CLOSED DOWN 170.85 PTS OR 0.94%

2. Nikkei closed UP 94.09 PTS OR 0.24 %

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 105.18 EURO FALLS TO 1.0697 DOWN 41 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +0.925 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 157.07 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.370/Italian 10 Yr bond yield DOWN to 3.965 SPAIN 10 YR BOND YIELD DOWN TO 3.330%

3i Greek 10 year bond yield DOWN TO 3.647

3j Gold at $2329.50//Silver at: 29.23 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 44/ 100 roubles/dollar; ROUBLE AT 89.33

3m oil into the 78 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 157.07/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.925% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8934 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9557 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.2113 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.4359 DOWN 4 BASIS PTS/

USA 2 YR BOND YIELD: 4.688 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.68…

10 YR UK BOND YIELD: 4.099 DOWN 5 PTS

2a New York OPENING REPORT

Futures Slide, Yields Tumble As European Turmoil Sparks Global Risk-Off

FRIDAY, JUN 14, 2024 – 08:19 AM

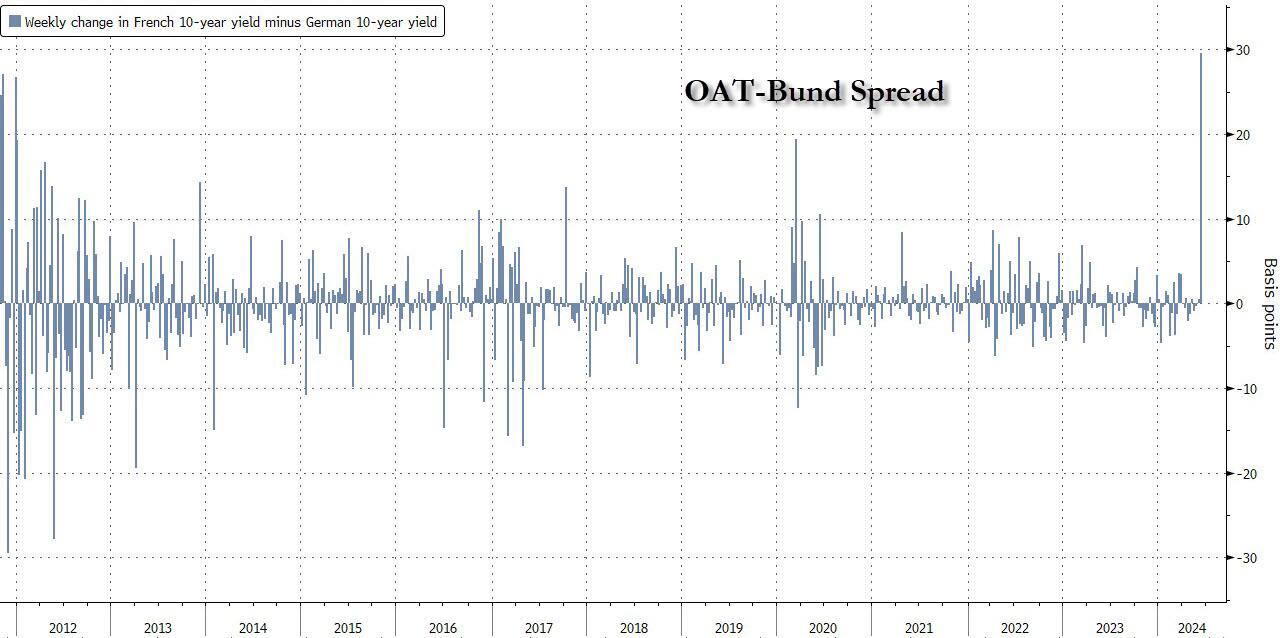

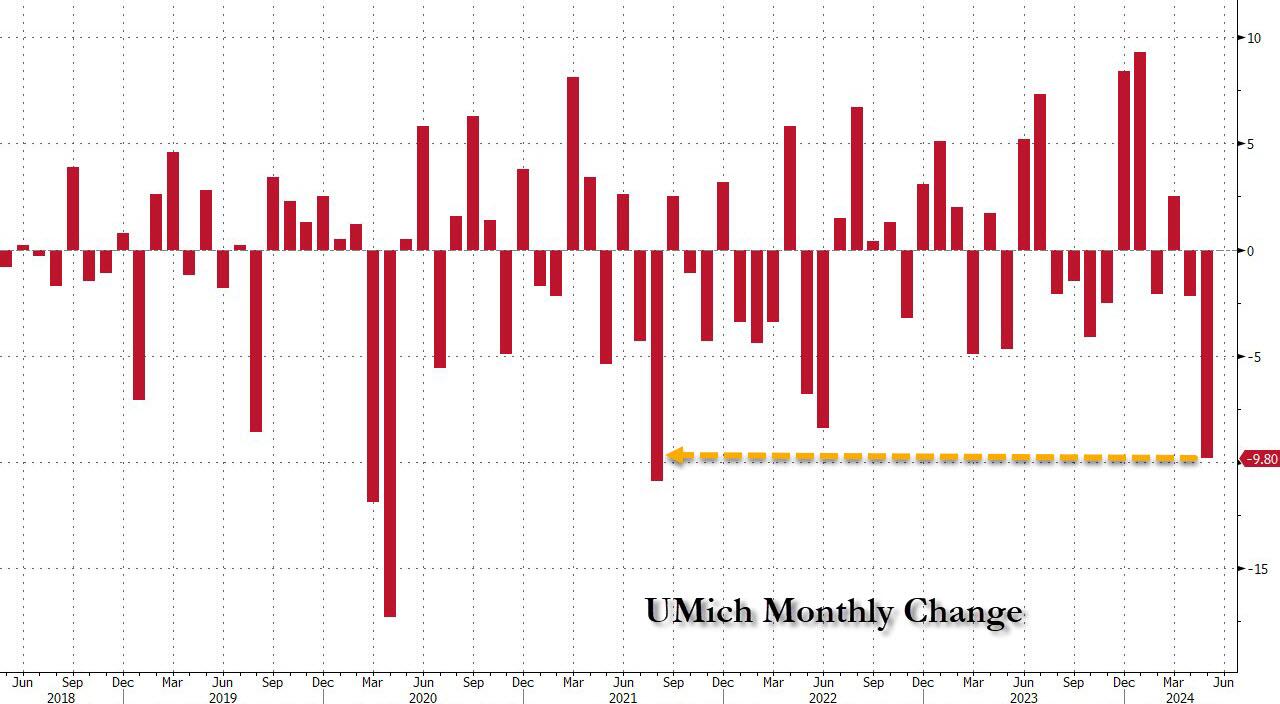

After stocks hit a 4th consecutive record and a 30th All Time High on Thursday on absolutely atrocious breadth (more than two thirds of the S&P closed red), futures traded lower as the rally finally fizzled. At 8:00am ET, S&P futures were down 0.5%, but off session lows, while Nasdaq futures outperformed, down 0.2% after closing at a fresh all time high despite more than 70% of names in the index trading lower on the session! The strong US performance – this morning notwithstanding – which delivered a 1.6% advance since last Friday, stands in contrast to a sharp decline in European stocks, which are headed for their worst week since January on growing concerns about political turmoil in France, and culminated with French public development bank SFIL SA pulling the sale of a green bond after a week that saw the country’s government debt tumble ahead of upcoming elections. Bond yields tumbled some 5bps lower, pushing the 10Y yield to 4.20%, amid an almost panicked flight to safety out of Europe, which also helped push the USD higher and EUR lower. Commodities are reversing recent losses with both oil and gold/silver are higher. Overnight, the biggest focus was BOJ’s decision, which again came in more dovish than expected: BOJ said the reduction in government bond purchases would begin after the bank’s next meeting, and sent the yen plunging initially before cross-asset flows pushed it back to unchanged. Today, the macro focus will be the Michigan sentiment and inflation expectation data at 10am.

In premarket trading, semis and giga-tech names are again in focus. Adobe soared 14% after the creative-arts software company raised its full-year forecast on key metrics. NVDA +1.2%, SMCI +33bp, AVGO +89bp. Outside NVDA/TSLA, the rest of Mag7 are lower. Here are some other notable premarket movers:

- MSC Industrial, a distributor of metalworking products, drops 13% after reporting disappointing preliminary 3Q results. Peer Fastenal slips 2%.

- Nucor falls 2% after the company provided a 2Q profit forecast that disappointed.

- Pinterest declines 3% after Piper Sandler noted a deceleration in growth in traffic to Amazon in May.

- RH tumbles 12% after the furniture retailer reported a heavier-than-expected first-quarter loss.

- Tesla rises 1.2% after investors re-approved Elon Musk’s compensation and cleared the company moving its legal home to Texas, offering votes of confidence in the chief executive despite a sales slump and falling stock price.

- ZKH Group rises 12% after the China-based firm said its board authorized a buyback program of its American depositary shares for up to $50 million.

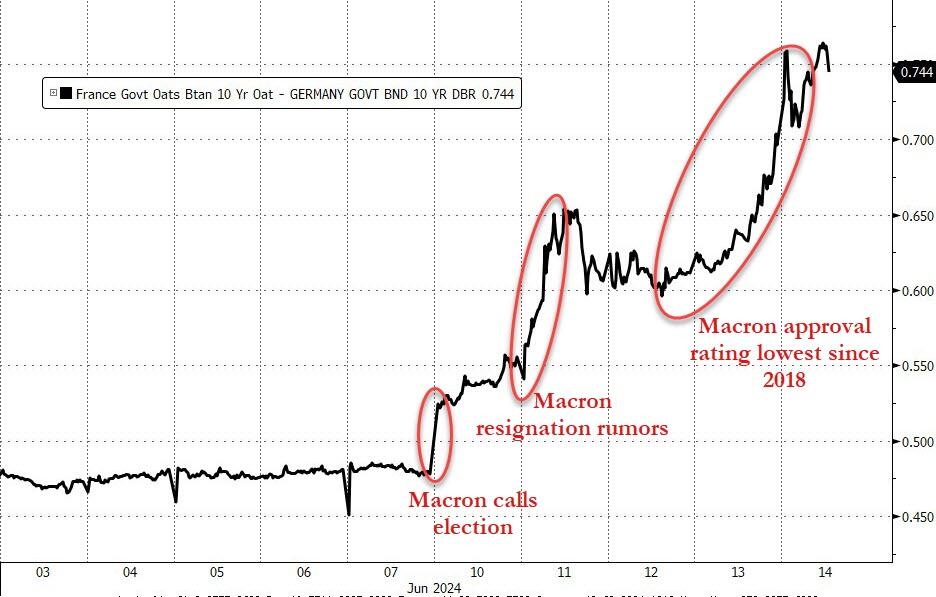

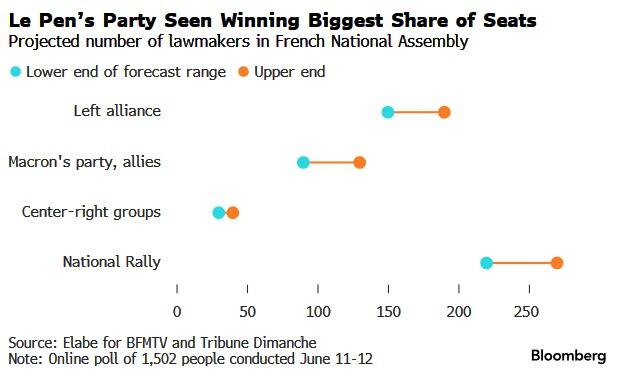

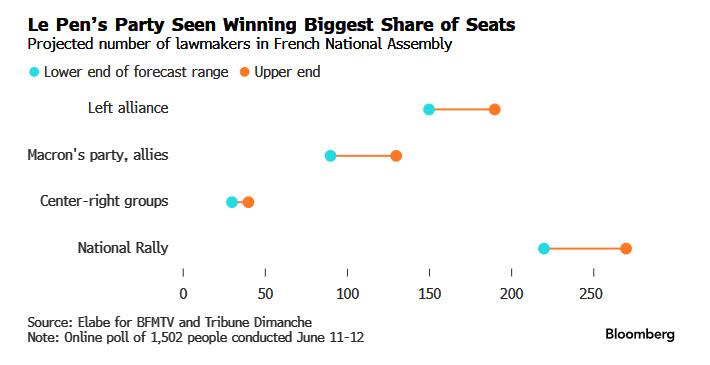

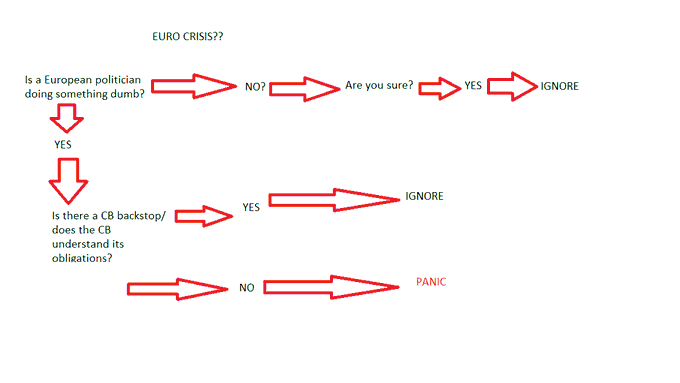

Markets are increasingly anxious after French President Emmanuel Macron announced a snap legislative election following his party’s drubbing in the European Parliament elections. Investors fear a win for Marine Le Pen’s far-right National Rally party, which leads polls by a wide margin, will usher in looser fiscal policies.

“It’s a risk-off tone with concerns over France driving the markets,” said Mohit Kumar, chief economist for Europe at Jefferies International. “Particularly going into the weekend, investors would be taking some positions off the table.”

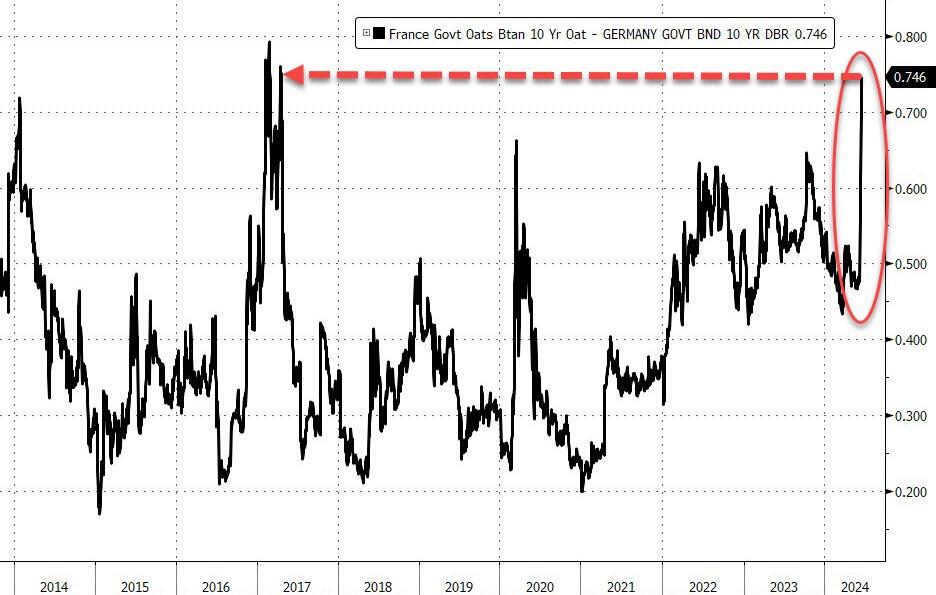

The uncertainty sent the yield spread between French and German bonds soaring this week, on pace for the most on record, while the yield on two-year debt for Germany set for the biggest drop since May 2023.

“It’s hard to ignore the parallels between our current situation and the time of the sovereign debt crisis, as there’s that familiar focus on election results, sovereign bond spreads and debt sustainability,” said Jim Reid, an analyst at Deutsche Bank AG. That’s “coupled with no obvious sign about where things are headed next.” Or as we put it…

The rising panic sent the Stoxx 600 sliding 1.2% extending losses since Monday to 2.6%; the week’s turmoil has wiped out all June’s gains for the European benchmark, with investors warning that the volatility may continue until the French vote is concluded in July. Sentiment also weighed on the Estoxx 50, which slumped nearly 2% with underperforming sectors including industrials and financials. France’s CAC 40 index plunged 2.6%, and erased its gains for the year and was on pace for its largest weekly drop since March 2022, with banking shares such as BNP Paribas SA and Societe Generale SA among the biggest losers. Here are the biggest European movers:

- H&M shares rise as much as 3.8%, the most since April 23, after UBS upgraded the Swedish fast fashion retailer to buy from neutral.

- Tesco shares rise as much as 2.3% after the grocer reported first-quarter like-for-like sales in the UK that came ahead of consensus estimates. Citi said the update was “encouraging.”

- Chemical stocks Lanxess and Wacker Chemie climb as Stifel upgrades to buy, seeing momentum.

- Keywords Studios shares rise as much as 2.8% after the video game services company extended the deadline by which EQT must announce a firm offer or walk away to June 28.

- Hilton Food Group shares rise as much as 0.4%, with analysts at Peel Hunt flagging a “helpful” update out this morning from supermarket chain Tesco, which is a major customer of the food company.

- Crest Nicholson shares gain as much as 10% after the UK homebuilder rejected an all-share offer from Bellway.

- French stocks extend their slide as political risk continues to weigh on sentiment following President Emmanuel Macron’s call for a snap legislative election.

- Kemira shares fall as much as 3.1% after being downgraded to hold from buy at Stifel, reflecting an absence of near-term catalysts.

- Opus shares drop as much as 2.1% after the Hungarian investment holding company reported a drop in first-quarter Ebitda and sales.

“Elections in France tend to be more volatile for equity markets than other developed markets,” Beata Manthey, head of European equity strategy at Citigroup Inc., told Bloomberg Television. “This volatility could continue for a bit longer.”

In Asia, MSCI’s Asia Pacific index slipped as losses in Australian and Chinese stocks offset gains in Japan’s benchmark. The Bank of Japan triggered renewed weakness in the yen after making investors wait until its July meeting for details on its paring of bond buying, a move that was also seen as a delay in the normalization in policy. Still, Governor Kazuo Ueda pushed back against the view that a rate hike was no longer possible next month.

In FX, the dollar rallied, boosted by growing political uncertainty in France, while Treasuries edged up, following gains in European bonds. The US currency also gained versus the yen after the Bank of Japan suggested it would take its time to scale back its bond-buying program. The yen fell 0.2% but was well off its worst levels, having dropped after the Bank of Japan offered little detail on its plans to reduce bond purchases. Investors await appearances later in the day by Federal Reserve speakers including Cleveland Fed President Loretta Mester and Chicago Fed President Austan Goolsbee for more clues on the outlook for US interest rates and inflation.

In rates, treasuries pushed to fresh weekly highs with futures on best levels of the day heading into early US session, following sharp gains in bunds where German 2-year yields are richer by more than 10bp on the day. Political uncertainty in Europe is weighing on sentiment, with French and Italian bond spreads aggressively wider versus bunds. Focal points of US session, include University of Michigan sentiment survey and a busy Fed speaker slate. 10-year yields tumbled to 4.19%, down around 6bp vs Thursday’s close with bunds trading 6.5bp richer in the sector vs Treasuries

Bank of Japan policy announcement overnight lacked details on its bond-buying cuts, leaving investors to wait until its July meeting for figures or a timeline, which weighed on Japan bonds overnight, leaving the yen vulnerable to further declines

In commodities, oil prices reversed an earlier drop, with Brent rising 0.5% to trade above $83. Spot gold rises ~$15 to around $2,319/oz.

In crypto, Bitcoin was back on a firmer footing and holds just of USD 67k, whilst Ethereum climbs above USD 3.5k.

Looking to the day ahead now, and data releases from the US include the University of Michigan’s preliminary consumer sentiment index for June. Central bank speakers include ECB President Lagarde, the ECB’s Vasle and Lane, along with the Fed’s Goolsbee and Cook.

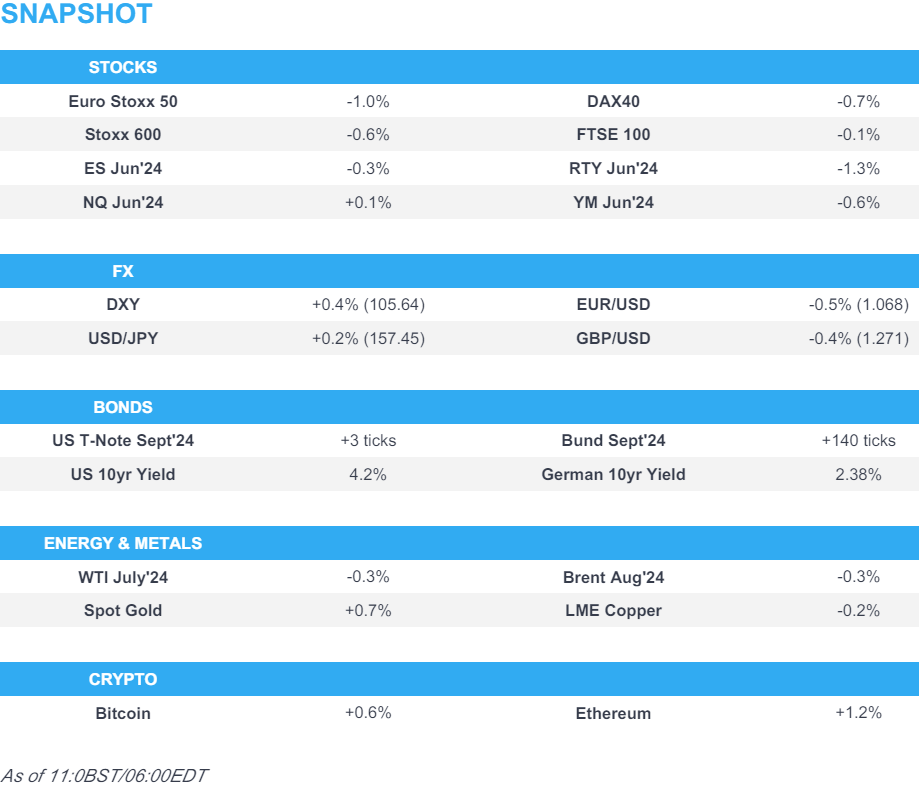

Market Snapshot

- S&P 500 futures down 0.2% to 5,429.50

- STOXX Europe 600 down 0.4% to 514.09

- MXAP down 0.2% to 179.48

- MXAPJ down 0.1% to 563.51

- Nikkei up 0.2% to 38,814.56

- Topix up 0.5% to 2,746.61

- Hang Seng Index down 0.9% to 17,941.78

- Shanghai Composite up 0.1% to 3,032.63

- Sensex up 0.1% to 76,903.15

- Australia S&P/ASX 200 down 0.3% to 7,724.26

- Kospi up 0.1% to 2,758.42

- German 10Y yield little changed at 2.41%

- Euro down 0.3% to $1.0701

- Brent Futures down 0.5% to $82.32/bbl

- Gold spot up 0.6% to $2,317.84

- US Dollar Index up 0.33% to 105.54

Top Overnight News

- The Bank of Japan said it would reduce government bond purchases in a signal of monetary tightening, as it left its policy interest rate unchanged. Monetary tightening in general should support the yen, but the Japanese currency instead weakened Friday because the central bank didn’t offer specifics on its bond plans. WSJ

- Chinese firms apply for anti-dumping probe into pork imports from the EU as trade tensions between Brussels and Beijing escalate. RTRS

- President Emmanuel Macron’s centrist alliance could be facing a wipeout in snap parliamentary elections after France’s leftwing parties struck a unity pact. New projections suggested only around 40 of Macron’s MPs would qualify for the second round vote on July 7, in run-off races that would predominantly be fought between candidates fielded by the far right or the leftwing bloc for the 589-strong assembly. FT

- Barclays was ordered by UK regulators to review its leveraged finance business as concern grows inside the BOE over how lenders are measuring their exposure to private equity. BBG

- French Finance Minister Bruno Le Maire warned that victory by a new left-wing alliance in the upcoming snap vote would lead to the country’s exit from the European Union as he put fears over the economy at the center of the campaign. BBG

- The imposition of additional sanctions on Moscow has created turmoil in Russia’s financial system, forcing the country’s main trading platform to halt dollar and euro transactions. WaPo

- CMS will recalculate the quality ratings applied to private Medicare plans, a move that could result in >$1B worth of additional payments to insurers. WSJ

- The number of people living in the streets and subways of New York City has ticked up slightly to the highest level in nearly two decades, according to results of an annual one-night field survey that the city released on Thursday. The survey, conducted in January, found an estimated 4,140 people living unsheltered, up 2.4 percent from last year’s 4,042 and the most since 2005, when the city began conducting the surveys. NYT

- Looks like “Roaring Kitty” exited his options position in GameStop. Keith Gill posted a screenshot of his portfolio that no longer included 120,000 call options and, instead, a position of more than nine million common shares. BBG

More detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly subdued after the mixed performance stateside where soft data took centre stage, while participants turned their attention to the BoJ policy announcement. ASX 200 was dragged lower by underperformance in tech and commodity-related sectors. Nikkei 225 recovered early losses and was underpinned after the BoJ policy decision in which the central bank maintained short-term rates at 0.0%-0.1% and kept bond purchases in accordance with its decision in March, while it announced to trim bond buying but will decide on a specific reduction plan for the next 1-2 years at the next policy meeting. Hang Seng and Shanghai Comp. were pressured with the former back below the 18,000 level amid tech and auto weakness, while the mainland is also lacklustre amid Western sanction threats on Chinese entities for supplying Russia’s war machine.

Top Asian News

- Japanese Finance Minister Suzuki said they will monitor the impact of China’s excess production on the Japanese economy and warned of possible deflationary pressure due to overcapacity in China, according to Reuters.

- Chinese firms have formally applied for an anti-dumping investigation into pork imports from the European Union after the EU decided to impose anti-subsidy duties on Chinese-made EVs, according to Global Times.

- China is reportedly internally moving ahead with the procedure to raise the temporary tariff rate on imported cars with large displacement engines, according to Global Times citing sources.

- China May Vehicle Sales +1.5% Y/Y vs +9.3% in April; Jan-May +8.3% Y/Y vs 11.1% Y/Y, via Industry Association

- Japan Chief Cabinet Secretary Hayashi says they will continue to closely monitor the FX market. No comment on possible market impact from the BoJ. Important for FX moves to be stable and reflect fundamentals. Expects BoJ to conduct appropriate monetary policy and working closely with the government.

European bourses, Stoxx 600 (-0.4%) are entirely in the red, with sentiment hampered amid ongoing political uncertainty; approval polls showed President Macron rating drop to the lowest in 5yrs, whilst Finance Minister Le Maire said “yes”, when asked if the current political crisis could result in a financial crisis. CAC 40 has now erased gains for the year and is flat YTD, future lower by over 2.0% on the session. European sectors hold a negative bias, with a slight defensive tilt as Healthcare tops the index. Industrials are found at the foot of the pile, with Defence names underperforming, seemingly with no clear catalyst, but potentially amid the ongoing political woes; Rheinmetall (-6.5%), Thales (-3.5%), BAE (-2.2%). Banks also lag amid the political uncertainty in Europe, with French names the most impacted as it stands. US Equity Futures (ES -0.2%, NQ +0.1%, RTY -1.1%) are mixed, with clear underperformance in the RTY, in continuation of the prior day’s hefty losses. In terms of stock specifics, Adobe (+15%) soars in the pre-market after the Co. reported a beat on headline metrics and raised its Q3 guidance above analyst expectations.

Top European News

- ECB’s Kazaks says uncertainty high but ECB on the path to lower inflation; market expectations on rates are reasonable; deviation from baseline would require sizeable and persistent data surprises.

- UK Reform Party has overtaken the Conservative party in a poll for the first time, according to a YouGov survey for The Times.

- Budget stand-off reportedly pushes Germany’s coalition to the brink, according to FT.

- Germany is said to be trying to prevent or soften EU tariffs on Chinese EVs, according to Bloomberg.

- Greek PM says they are to reshuffle the cabinet following a worse than expected EU vote result.

- Germany’s DIW Institute revises up 2024 GDP forecast to +0.3% (prev. 0%); expected to grow by 1.3% in 2025 (prev. 1.2%)

- BoE Survey: UK Public Inflation Expectation for year-ahead 2.8% (prev. 3.0%) in February.

- Draft G7 statement says they will be restricting access to financial systems for targeted entities, incl. Chinese, who support the Russian war effort. Promises additional sanctions on those engaged in deceptive practices while transporting Russian oil. Pledges to continue efforts to reduce Russian revenue from metals. Calls on China to refrain from adopting export control measures, particularly regarding critical minerals.