GOLD PRICE CLOSED UP $17.25 TO $2331.70

SILVER PRICE UP $0.21 TO $29.57

Gold ACCESS CLOSED $2330.40

Silver ACCESS CLOSED: $29.54

Bitcoin morning price:$65,406 DOWN 1340 DOLLARS.

Bitcoin: afternoon price: $64,437 DOWN 2339 dollars

Platinum price closing UP $7.15 TO $976.40

Palladium price; UP $1.20 AT $893.35

END

SHANGHAI GOLD PREMIUM 48 DOLLARS/COMEX GOLD//JULY TO JULY

SHANGHAI GOLD (USD) FUTURES – QUOTES

SHANGHAI GOLD (USD) FUTURES – QUOTES

Last Updated 18 Jun 2024 09:34:00 AM CT.

Market data is delayed by at least 10 minutes.

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $3195.70 UP 13.10 CDN dollars per oz( * NEW ALL TIME HIGH 3,305.30 CDN DOLLARS PER OZ//MAY 20 2024)

*BRITISH GOLD: 1833.16 UP 7.80 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2169.53 UP 8.77 Euros per oz //* (ALL TIME CLOSING HIGH: 2248.89 EUROS PER OZ//APRIL 16.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCH: COMEX

ACCESS MARKET

EXCHANGE: COMEX

CONTRACT: JUNE 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,312.400000000 USD

INTENT DATE: 06/17/2024 DELIVERY DATE: 06/20/2024

FIRM ORG FIRM NAME ISSUED STOPPED

435 H SCOTIA CAPITAL 5

661 C JP MORGAN 65

661 H JP MORGAN 21

685 C RJ OBRIEN 1

686 H STONEX FINANCIA 100

690 C ABN AMRO 1

732 C RBC CAP MARKETS 1

737 C ADVANTAGE 55 7

880 H CITIGROUP 12

905 C ADM 3

991 H CME 71

TOTAL: 171 171

JPMorgan stopped 76/171

FOR JUNE 2024

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2024. CONTRACT: 171 NOTICES FOR 17.100 OZ or 0.5318 TONNES

total notices so far: 30, 121 contracts for 3,012,100 Oz (93.157 tonnes)

FOR JUNE:

SILVER NOTICES: 0 NOTICE(S) FILED FOR nil

OZ/

total number of notices filed so far this month :1244 for 6.220 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $17.25 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/

: NO CHANGES IN GOLD INVENTORY AT THE GLD/

/ /INVENTORY RESTS AT 825.31TONNES

INVENTORY RESTS AT 825.31 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER UP $0.21 AT THE SLV//

SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF .730 MILLION OZ INTO THE SLV

// INVENTORY DECREASES TO 429.775 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 429.775 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY AN ULTRA HUGE SIZED 1396 CONTRACTS TO 176,357 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR TINY LOSS OF $0.10 IN SILVER PRICING AT THE COMEX ON MONDAY’S TRADING ON SILVER. WE HAD SOME LONG LIQUIDATION AS WE HAD A NET LOSS OF 813 CONTRACTS ON OUR TWO EXCHANGES. WE, AGAIN HAD SHORT COVERING BY OUR SPECS WITH THE SMALL LOSS IN PRICE AS WELL AS MASSIVE T.A.S. LIQUIDATION. WE HAD ANOTHER FAIR SIZED 231 T.A.S ISSUANCE,

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED LAST TUESDAY AND AGAIN ON FRIDAY, JUNE 7

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 230 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND TODAY;S TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.10) AND WERE SUCCESSFUL IN KNOCKING SOME SILVER LONGS FROM THEIR PERCH AS WE DID HAVE A STRONG SIZED LOSS OF 813 CONTRACTS ON OUR TWO EXCHANGES WITH THE LOSS IN PRICE OF $0.10.

WE MUST HAVE HAD:

A STRONG SIZED 583 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.830 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 80,000 OZ E.F.P JUMP TO LONDON

//NEW STANDING FOR SILVER//JUNE IS THUS 6.255 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI LOSS //STRONG SIZED EFP ISSUANCE/ VI) FAIR SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 230 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED 137 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE

TOTAL CONTRACTS for 12 DAYS, total 13,100 contracts: OR 65.500 MILLION OZ (1091 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 65.500 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 65.500 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

RESULT: WE HAD A GIGANTIC SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1396 CONTRACTS DESPITE OUR SMALL LOSS IN PRICE OF SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A STRONG EFP ISSUANCE CONTRACTS: 583 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.830 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 80,000 OZ E.F.P. JUMP TO LONDON

//NEW TOTAL STANDING FOR JUNE 6.255 MILLION OZ

WE HAVE A STRONG SIZED LOSS OF 813 OI CONTRACTS ON THE TWO EXCHANGES WITH THE LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A FAIR SIZED 230 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND SOME NET LIQUIDATION OF LONGS.

THE NEW TAS ISSUANCE MONDAY NIGHT (230) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 0 NOTICE(S) FILED TODAY FOR nil OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 2839 OI CONTRACTS TO 439,211 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 380 CONTRACTS

WE HAD A FAIR SIZED DECREASE IN COMEX OI (2839 CONTRACTS) OCCURRED WITH OUR LOSS OF $18.25 IN PRICE/MONDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 89.94 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 3500 OZ QUEUE JUMP AS BANKERS SCOUR THE PLANET LOOKING FOR GOLD ON THE THIS SIDE OF THE POND

NEW STANDING 94.233 TONNES// ALL OF THIS HAPPENED WITH OUR $18.25 LOSS IN PRICE WITH RESPECT TO MONDAY’S TRADING. WE HAD A VERY SMALL SIZED LOSS OF 900 OI CONTRACTS (2.799 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1939 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 439,211

IN ESSENCE WE HAVE A VERY SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 900 CONTRACTS WITH 2839 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 1939 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 900 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 1493 CONTRACTS,,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1939 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI OF 2839 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 900 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 88.761 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 0.1088 TONNES

//NEW STANDING /JUNE 94.329 TONNES.

/ 3) HUGE T.A.S. LIQUIDATION OF CONTRACTS WITH SOME NET LONG SPECS BEING CLIPPED,

4) FAIR SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1493 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE. :

TOTAL EFP CONTRACTS ISSUED: 39,887 CONTRACTS OR 3,988,700 OZ OR 124.066 TONNES IN 12 TRADING DAY(S) AND THUS AVERAGING: 3988 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES 124.066 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 124.066 DIVIDED BY 3550 x 100% TONNES = 3.49% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 124,009 tonnes HEADING FOR A STRONG MONTH

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 1396 CONTRACTS OI TO 176,357 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 583 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 583 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 583 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1396 CONTRACTS AND ADD TO THE 583 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 813 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 4.065 MILLION OZ

OCCURRED WITH OUR $0.10 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED UP 14.36 PTS OR 0.48% //Hang Seng CLOSED DOWN 20.57 PTS OR 0.11%// Nikkei CLOSED UP 379.67 OR 1.00%//Australia’s all ordinaries CLOSED UP 0.91%///Chinese yuan (ONSHORE) closed DOWN TO 7,2561 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2760/ Oil UP TO 80.18 dollars per barrel for WTI and BRENT UP AT 84.06 /Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 2839 CONTRACTS TO 439,211 WITH OUR STRONG LOSS IN PRICE OF $18.25 WITH RESPECT TO MONDAY’S TRADING. WE HAD A HUGE T.A.S. LIQUIDATION ON MONDAY WITH SOME LONGS BEING CLIPPED.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE.… THE CME REPORTS THAT THE BANKERS ISSUED A GOOD SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 1939 EFP CONTRACTS WERE ISSUED: : AUGUST 1939 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1939 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY SMALL SIZED TOTAL OF 900 CONTRACTS IN THAT 1939 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A FAIR SIZED LOSS OF 2839 COMEX CONTRACTS..AND THIS SMALL SIZED L;OSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR HUGE LOSS IN PRICE OF $18.25

////MONDAY COMEX. AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT WAS A GOOD SIZED 1493 CONTRACTS. MOST OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN YESTERDAY’S TRADING

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (94.329 TONNES)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 94.329 TONNES. THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $18.25 //// AND WERE SUCCESSFUL IN KNOCKING A FEW SPECULATOR LONGS AS WE HAD A VERY SMALL SIZED LOSS OF 520 CONTRACTS ON MONDAY WITH OUR TWO EXCHANGES DESPITE THE HUGE LOSS IN PRICE. THE T.A.S. ISSUED ON MONDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE LOST A TOTAL OI OF 1.617 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE (89.94 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 35 CONTRACTS OR 3500 OZ (0.1088 TONNES)

NEW STANDING FOR JUNE: 94.329 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR HUGE LOSS IN PRICE TO THE TUNE OF $18.25

WE HAVE REMOVED 380 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET LOSS ON THE TWO EXCHANGES 900 CONTRACTS OR 90000 OZ (2.065TONNES)

confirmed volume MONDAY 128,720 contracts//AWFUL

//speculators have left the gold arena

JUNE 18 JUNE GOLD CONTRACT

/ /// THE JUNE 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 482.265 oz JPMORGAN 15 KILOBARS . |

| Deposit to the Dealer Inventory in oz | 0 oz |

| Deposits to the Customer Inventory, in oz | 0 OZ//BRINKS |

| No of oz served (contracts) today | 171 notice(s) 17,100 OZ 0.5318 TONNES |

| No of oz to be served (notices) | 206 contracts 20600 OZ 0.6407 TONNES |

| Total monthly oz gold served (contracts) so far this month | 30,121 notices 3,012,100 oz 93.69 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: NIL oz

we have 0 customer deposit:

total deposit nil oz

customer withdrawals: 1

i) Out of JPMorgan: 482.265 oz (15 kilobars)

TOTAL WITHDRAWALS 482.265 0z

Adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE

For the front month of JUNE we have an oi of 377 contracts having LOST 502 contracts. We had 537 contracts served on Monday so we gained 35 contracts or 3500 oz additional ounces will stand for gold at the comex as they underwent a queue jump to take delivery on this side of the pond.

JULY LOST 37 CONTRACTS TO STAND AT 2418

AUGUST LOST 3199 CONTRACTS DOWN TO 356,024 CONTRACTS

We had 171 contracts filed for today representing 17100 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notice was issued from their client or customer account. The total of all issuance by all participants equate to 171 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 76 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for June /2024. contract month, we take the total number of notices filed so far for the month (30,121) x 100 oz ) to which we add the difference between the open interest for the front month of JUNE (377 CONTRACTS) minus the number of notices served upon today (171 x 100 oz per contract( equals 3,032,700 OZ OR 94.329 TONNES.

thus the INITIAL standings for gold for the JUNE contract month: No of notices filed so far (30,121 x 100 oz +we add the difference for front month of June (377// , OI} minus the number of notices served upon today (537) x 100 oz which equals 3,032,700 oz (94.329 TONNES)

TOTAL COMEX GOLD STANDING FOR JUNE: 94.329 TONNES WHICH IS ABSOLUTELY HUGE FOR THIS VERY ACTIVE DELIVERY MONTH IN THE CALENDAR. JUNE IS TRADITIONALLY THE 2ND HIGHEST DELIVERY MONTH OF THE YEAR. FROM THIS POINT WE WILL GAIN IN GOLD TONNAGE WILLING TO STAND AT THE COMEX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,680,714.128 52.27 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,615,692.269 OZ

TOTAL REGISTERED GOLD 8,151,711.327( 246.13 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,463,981.042 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,470,997 oz (REG GOLD- PLEDGED GOLD)= 201.28 tonnes //

END

SILVER/COMEX

JUN 18/2024

INITIAL

//2024// THE JUNE 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 274,078/210 oz Brinks . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 297,950.000 oz ASAHI |

| No of oz served today (contracts) | 0 CONTRACT(S) (nil OZ) |

| No of oz to be served (notices) | 7 contracts (0.035 million oz) |

| Total monthly oz silver served (contracts) | 1244 Contracts (6.220 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 customer deposit:

i) Into ASAHI 297,950.000 oz

total customer deposit 297,950/000.oz

JPMorgan has a total silver weight: 127.822million oz/296.338million or 43.17%

adjustment: 0

Comex withdrawals: 1

i) out of Brinks: 276,078.210 oz

total withdrawal: 276.078.210 0z

TOTAL REGISTERED SILVER: 63.074MILLION OZ//.TOTAL REG + ELIGIBLE. 296.358

million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE:

silver open interest data:

FRONT MONTH OF JUNE/2024 OI: 7 CONTRACTS HAVING LOST 16 CONTRACT(S).

WE HAD 0 NOTICES SERVED UP ON MONDAY, SO WE LOST 16 CONTRACTS OR AN ADDITIONAL 80,000 OZ WILL NOT STAND AT THE COMEX VIA A CONSIDERABLE E..F.P. JUMP TO LONDON TO WHERE THEY WILL TAKE DELIVERY ON THAT SIDE OF THE POND

JULY SAW A LOSS OF 3922 CONTRACTS DOWN TO 76,051

AUG, SAW A GAIN OF 41 CONTRACTS TO 384

SEPT SAW A GAIN OF 2450 CONTRACTS TO 81,035

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

CONFIRMED volume; ON MONDAY 62,920 strong

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1244 x 5,000 oz = 6.220 MILLION oz

to which we add the difference between the open interest for the front month of JUNE ((7) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2024 contract month: 1244 notices served so far) x 5000 oz + OI for the front month of JUNE (7)x number of notices served upon today minus (0)x 5000 oz of silver standing for the JUNE contract month equates to 6.255 MILLION OZ.

New total standing: 6.255 million oz.

There are 63.074 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

JUNE 18 WITH GOLD UP $17.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/://NEW TOTAL TONIGHT 825.31 TONNES

JUNE 17 WITH GOLD DOWN $18.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.03 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 825.31 TONNES

JUNE 13 WITH GOLD DOWN$35.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.89 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 830.78 TONNES

JUNE 12 WITH GOLD UP $28.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.89 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 830.78 TONNES

JUNE 11 WITH GOLD DOWN $0.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 10 WITH GOLD UP $2,00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 7 WITH GOLD DOWN $64.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 3.56 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 837.11 TONNES

JUNE 6 WITH GOLD UP $16.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.34 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 833.55 TONNES

JUNE 5 WITH GOLD UP $32.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 4 WITH GOLD DOWN $20.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 3 WITH GOLD UP $22.85 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 31 WITH GOLD DOWN $19.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 30 WITH GOLD UP $3.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 29 WITH GOLD DOWN $13.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 28 WITH GOLD UP $22.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 832.21 TONNES

MAY 24 WITH GOLD DOWN $2.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 833.36 TONNES

MAY 23 WITH GOLD DOWN $53.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 22 WITH GOLD DOWN $32.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 21 WITH GOLD DOWN $12,00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 20 WITH GOLD UP $21.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.10 TONNES OF GOLD INTO THE GLD//NEW TOTAL 838.54 TONNES

MAY 17 WITH GOLD UP $31.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//NEW TOTAL 833.36 TONNES

MAY 16 WITH GOLD DOWN $7.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//NEW TOTAL 833.36 TONNES

MAY 15 WITH GOLD UP $34.90 ON THE DAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD/INVENTORY RISES TO 831.93 TONNES

MAY 14 WITH GOLD DOWN $17.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RISES TO 831.33 TONNES

GLD INVENTORY: 825.31 TONNES, TONIGHTS TOTAL

SILVER

JUNE 17. WITH SILVER UP $0.21//SMALL CHANGES IN SILVER INVENTORY’ A WITHDRAWAL .730 MILLION OZ INTO THE SLV/// /INVENTORY FALLS TO 429.775 MILLION OZ.

JUNE 14. WITH SILVER DOWN $0.10//NO CHANGES IN SILVER INVENTORY/ /INVENTORY REMAINS AT 429.083 TONNES

JUNE 13. WITH SILVER DOWN $1.10//HUGE CHANGES IN SILVER INVENTORY/ A HUGE DEPOSIT OF 1.958 MILLION OZ/INVENTORY RISES TO 429.083 TONNES

JUNE 12 WITH SILVER UP $0.97 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 5.983 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 427.125 MILLION OZ

JUNE 11 WITH SILVER DOWN $0.59 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.644 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 422.786 MILLION OZ

JUNE 10 WITH SILVER UP $0.30 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 3.198 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 421.142 MILLION OZ

JUNE 7 WITH SILVER DOWN $1.93 TODAY: NO CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY AT 417.944 MILLION OZ

JUNE 6 WITH SILVER UP $1.27 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 417.944 MILLION OZ

JUNE 5 WITH SILVER UP 0.38 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.52 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 415.295 MILLION OZ

JUNE 4 WITH SILVER DOWN $1.08 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

JUNE 3 WITH SILVER UP $0.35 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

MAY 31 WITH SILVER DOWN $1.09 TODAY: HUGE CHANGES IN SILVER INVENTORY: A MASSIVE WITHDRAWAL OF 3.655 MILLION OZ FROM THE SLV//INVENTORY LOWERS TO 413.775 MILLION OZ

MAY 30 WITH SILVER DOWN $0.80 TODAY: NO CHANGES IN SILVER INVENTORY//INVENTORY REMAINS AT 417.430 MILLION OZ

MAY 29 WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 1.051 MILLION OZ INTO THE SLV//INVENTORY DECREASES TO 417.430 MILLION OZ

MAY 28 WITH SILVER UP $1.64 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 2.832 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 418.481 MILLION OZ

MAY 24 WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF .822 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 421.313 MILLION OZ

MAY 23 WITH SILVER DOWN $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.736 MILLION OZ FROM THE SLVINVENTORY INCREASES TO 420.491 MILLION OZ

MAY 22 WITH SILVER DOWN $0.66 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 21 WITH SILVER DOWN $0.41 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A DEPOSIT OF 3.792 MILLION OZ FROM THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 20 WITH SILVER UP $1.28 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 1.005 MILLION OZ FROM THE SLV// INVENTORY LOWERS TO 418.435 MILLION OZ

MAY 17 WITH SILVER UP $1.37 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 868,000 OZ FROM THE SLV// INVENTORY LOWERS TO 419.440 MILLION OZ

MAY 16 WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY REMAINS AT 420.308 MILLION OZ

MAY 15 WITH SILVER UP 101 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A WITHDRAWAL OF 1.919 MILLION OZ FROM THE SLV NVENTORY RESTS AT 420.308 MILLION OZ

MAY 14 WITH SILVER UP 25 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;INVENTORY RESTS AT 422.227 MILLION OZ

CLOSING INVENTORY 429.775 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/GOLD AND SILVER COMMENTARY

CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES

Alasdair Macleod: The physical drivers of gold and silver

Submitted by admin on Mon, 2024-06-17 20:03 Section: Daily Dispatches

By Alasdair Macleod

GoldMoney, Toronto

Friday, June 14, 2024

Gold and silver steadied this week, at the lower end of their current trading ranges. In European trade this morning, gold was $2,317, up $22, while silver was $29.07, down 8 cents. Comex volumes in gold were low, while silver’s were high.

The trading dynamics in the two metals are dissimilar, as our two charts show.

Note the divergence between gold’s open interest and the price, and how it contrasts with silver, where open interest and the price correlate as one normally expects in a bull market.

In other words, the gold price has been rising without an increase in buying interest, while in silver a more normal relationship exists between rising prices and buying interest.

Pricing is being taken away from paper markets, with significant premiums developing in Shanghai. …

… For the remainder of the analysis:

https://www.goldmoney.com/research/gold-and-silvers-physical-drivers

* * *

end

Jim Rickards: No, the Saudis didn’t just kill the dollar

Submitted by admin on Mon, 2024-06-17 19:55 Section: Daily Dispatches

By James G. Rickards

The Daily Reckoning, Baltimore

Monday, June 17, 2024

There has been a lot of talk over the past several days that Saudi Arabia is ending the petrodollar deal it has had with the United States for 50 years. This story has been highly exaggerated. Today I want to address the misinformation you’re seeing and show you what really happened.

News services of dubious accuracy reported that Saudi Arabia had ended the petrodollar deal on June 9, after 50 years. This report was quickly followed by claims that oil would now be priced in everything from Chinese yuan to Indian rupees, Russian rubles, and other currencies without strong claims to being reserve currencies.

The implication of these stories was that the U.S. dollar’s long reign as the leading global reserve currency was over. New reserve currencies would come to the fore, most prominently the BRICS planned currency.

The crypto crowd wasn’t far behind shouting that the demise of the dollar proved that cryptocurrencies were the way of the future. The internet was on fire with these and other histrionic claims.

In fact, almost everything you just read is nonsense. …

… For the remainder of the analysis:

* * *

end

Jan Nieuwenhuijs: Thailand joins China in driving gold bull market

Submitted by admin on Mon, 2024-06-17 11:10 Section: Daily Dispatches

By Jan Nieuwenhuijs

Gainesville Coins, Lutz, Florida

Monday, June 17, 2024

Shedding its long-standing price sensitivity to the price of gold, Thailand is a gold buyer driving the price up, just like China.

Present changes in the global gold market, in which pricing power is shifting East, could be a precursor to a transformation in the international monetary order. Possibly, trade in the East will settle through a system connecting local central bank digital currencies, while any remaining imbalances are transferred in gold.

Until 2021 many countries in Asia were gold price sensitive for nearly a century. They bought when the gold price was steady or declining but swiftly turned into sellers when the price increased. During this period the price of gold was set in the West and the East dampened volatility, best demonstrated in my article “The West–East Ebb and Flood of Gold Revisited.”

After the war in Ukraine broke out in 2022 things started changing in the global gold market. …

… For the remainder of the analysis:

https://www.gainesvillecoins.com/blog/thailand-joins-china-driving-gold-bull-market

* * *

end

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS/

2024 Central Bank Gold Reserves Survey Results

The World Gold Council has completed the 2024 Central Bank Gold Reserves Survey. Central banks have been significant buyers of gold in recent years amid both economic and geopolitical uncertainty. Our survey, which received responses from a record-high 70 central banks, shows that:Central bank sentiment towards gold remains very high, with 29% saying they will add more gold in the next 12 months and 81% saying that official sector gold reserves overall will grow in the same period.

Optimism towards gold’s future role in global reserves continues to grow, with 69% saying that gold’s share of reserves will be higher in five years compared to 62% last year.

Gold’s role as a long-term store of value is the most highly rated reason for central banks to hold gold, followed by gold’s performance during times of crisis.

There has been a notable uptick in how advanced economy central banks view the role of gold, with their perspectives now much more closely aligned with those of emerging market central banks…

https://www.gold.org/goldhub/data/2024-central-bank-gold- reserves-survey-END-

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT//

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

ASIA TRADING//TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED UP 14.36 PTS OR 0.48% //Hang Seng CLOSED DOWN 20.57 PTS OR 0.11%// Nikkei CLOSED UP 379.67 OR 1.00%//Australia’s all ordinaries CLOSED UP 0.91%///Chinese yuan (ONSHORE) closed DOWN TO 7,2561 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2760/ Oil UP TO 80.18 dollars per barrel for WTI and BRENT UP AT 84.06 /Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2561

OFFSHORE YUAN: UP TO 7.2760

SHANGHAI CLOSED UP 14.36 PTS OR 0.48 %

HANG SENG CLOSED DOWN 20.57 PTS OR 0.11%

2. Nikkei closed UP 379.67 PTS OR 1.00 %

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 105.12 EURO FALLS TO 1.0716 DOWN 24 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +0.937 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 158.10 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.4175/Italian 10 Yr bond yield DOWN to 3.904 SPAIN 10 YR BOND YIELD DOWN TO 3.332%

3i Greek 10 year bond yield UP TO 3.648

3j Gold at $2309.35//Silver at: 29.16 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 1 AND 72/ 100 roubles/dollar; ROUBLE AT 87.99

3m oil into the 80 dollar handle for WTI and 84 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 158.10/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.937% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8876 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9512 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.290 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.420 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.771 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.65…

10 YR UK BOND YIELD: 4.1380 UP 2 PTS

2a New York OPENING REPORT

Futures Flat As Tech Stocks Rise For 7th Consecutive Day

TUESDAY, JUN 18, 2024 – 08:10 AM

Futures are flat with gigatech naturally outperforming into today’s retail sales print where the expectations are for beats to resume after last month’s sharp miss. As of 8:00am ET, S&P futures were completely flat, while Nasdaq futures were up for the 7th day in a row as it nudges toward the 20,000 mark, with semi shares higher of course, while Mag7 names are also up small. European stocks rise for a second session as political premium fades while French government bonds drift as investors keep a close eye on political developments. Bond yields are up 1-2 bps across the curve after falling Monday amid a flurry of high-grade corporate bond sales that exceeded $21 billion. A gauge of the dollar was higher with EUR, GBP, and JPY weaker. Commodity markets are mostly lower, but WTI remains above $80/bbl with CTAs now set to buy over $30BN. The macro data focus is on Retail Sales but there is another batch of Fedspeakers; yesterday’s speakers indicated a still strong economy with no consensus among the path of inflation with risks tilted more towards a growth slowdown rather than another inflation spike.

In premarket trading, Broadcom rose 2.4%, putting the stock on track for an eighth consecutive session of gains, a rally that has added more than $200 billion to the stock’s market capitalization. Chegg jumped 20% after the online-education firm announced a cut to its workforce and a growth plan that includes developing a “single platform” with artificial-intelligence tools. Here are some other notable premarket movers:

- La-Z-Boy (LZB) rises 9.4% after the furniture company reported quarterly profit and sales that topped estimates.

- Lennar (LEN) slips 2.7% after the homebuilder’s orders outlook missed estimates.

- NextEra Energy (NEE) falls 4.3% on plans to sell $2 billion of equity to raise money for new energy projects and to pay down its short-term debt.

- Philip Morris (PM) declines 2.9% after the company stopped online sales of its popular nicotine pouch brand Zyn in the US after an affiliate received a subpoena in the District of Columbia.

- Rocket Lab USA (RKLB) rises 7.4% after the space systems company signed the largest Electron launch agreement in the firm’s history.

- Silk Road Medical (SILK) rallies 23% after Boston Scientific agreed to acquire the medical device maker.

- Zentalis Pharma (ZNTL) drops 28% after the FDA placed a partial hold on azenosertib studies.

Optimism over a resilient economy and improving corporate earnings have helped push US equities up about 15% this year. Ahead of Wednesday’s holiday in the US, traders geared up for retail-sales data and a slew of Federal Reserve speakers for more pointers on the potential start of rate cuts.

“The picture being painted is that despite the fading prospects of sizeable interest rate cuts from the Fed this year, the economic outlook remains upbeat and this means that corporate earnings should continue to hold up,” said Stuart Cole, the head macro economist at Equiti Capital UK Ltd. “But everybody – the Fed, the markets, etc. – is in ‘data dependency’ mode, and this sentiment could potentially sour if we get a soft set of retail sales data from the US this afternoon.”

Europe’s Stoxx 600 benchmark staged a modest rebound and rose for a second session, up 0.5% last with travel and leisure and banks are the best performing sectors while mining and consumer stocks lag behind. Whitbread Plc rose following a trading update. Danish biotech company Novonesis (Novozymes) B jumped after lifting its outlook for the year. Carrefour SA fell after a report that France’s finance ministry is seeking a €200 million civil fine from the supermarket chain. The CAC 40 adds 0.3% amid lingering concern about political turmoil in France. European stocks have retreated since French President Emmanuel Macron called a snap legislative ballot following a drubbing by Marine Le Pen’s National Rally in the European Parliament elections. The two-round election will conclude on July 7. Here are some of the biggest movers on Tuesday:

- Whitbread shares gain as much as 5% after it reported mild growth in total sales in 1Q and said it remains confident about its outlook for the full year.

- DocMorris shares jump as much as 7.6% after Zuercher Kantonalbank raised the stock to outperform, saying the risks around data protection and mobilization of doctors for the Swiss pharmaceutical products retailer are “significantly reduced.”

- Novonesis shares rise as much as 6.4% after the Danish company increased its outlook for the year. Novonesis is holding a capital markets day in London on Tuesday.

- SAF-Holland shares rise as much as 6.1%, extending Monday’s gain, as several analysts boost their price targets on the German truck parts manufacturer.

- Qiagen shares rise as much as 2.5%, extending Monday’s gains, after the German life sciences and diagnostics firm set 2024-2028 guidance above market expectations.

- Moncler shares fall as much as 4% after analysts at Oddo BHF trimmed their price target and earnings estimates due to concerns the luxury company will see a sharp slowdown in 2Q.

- Ashtead shares fall as much as 5.1% to hit a three-month low, after the equipment rental giant’s earnings fell short of expectations in the fourth quarter due to an unexpected provision booked after one of its customers went bankrupt.

- Coloplast shares drop as much as 3.5% after Nordea downgraded the stock to sell from hold, citing a “negatively skewed” risk/reward.

- Komax shares fall as much as 8%, touching the lowest since June 2020, after the Swiss machinery manufacturer issued a warning, saying its 2024 revenue will decline by about 20%.

- Paradox Interactive drops as much as 8.3%, the most since October, after the Swedish game publisher decided to cease further operations in the wholly-owned studio Paradox Tectonic.

“A portion of the recent risk-off moves has been driven by fears of ‘Frexit’ and euro-area breakup. In our view, those fears are overblown, and we would be fading the fear-driven moves,” said Mohit Kumar, a strategist at Jefferies. “We remain positive on risky assets, but would skew our positions more toward the US in view of the coming French elections.”

Asian stocks advanced on Tuesday, led by gains in Japanese equities while chip-related shares followed US peers higher. The MSCI Asia Pacific Index rose as much as 0.8%, on track for its best day in more than a week, with TSMC and Samsung among the biggest contributors. Most markets in the region advanced, with notable gains in Taiwan and South Korea. Australian stocks mostly held gains after the nation’s central bank left its key interest rate unchanged at a 12-year high. Hong Kong equities edged lower. Chip stocks rose after the Philadelphia Semiconductor Index climbed 1.6% to a record high. Locally, TSMC gained after a number of brokers raised their price targets for the Taiwanese foundry. Samsung and SK Hynix advanced on bullishness over AI-related demand for memory.

Investors will keep a close watch on the implications of China’s latest move in its trade tensions with Brussels, after Beijing launched an anti-dumping probe on pork imports from the European Union. That comes as the bloc looks at Chinese subsidies across a range of industries and will impose tariffs on electric car imports from July.

In FX, the Bloomberg Dollar Spot Index inched higher, with economists estimating month-on-month growth in American retail sales rebounded in May; the Swiss franc tops the G-10 FX pile, rising 0.2% against the greenback. The Aussie dollar also edges up after the RBA stood pat on interest rates but revealed they did discuss a hike; the EUR, GBP, and JPY are all weaker. USD/JPY rose 0.2% to 158.11 and back to intervention territory after BOJ governor Ueda said that the reduction in bond buying and a policy rate hike are separate issues.

In rates, treasuries dip ahead of retail sales and a busy day for Fedspeak. US 10-year yields rise 2bps to 4.30% broadly in line with German counterpart while French outperforms by ~3bp. Gilts yields are richer on the day with the curve flatter. French government bonds drift as investors keep a close eye on political developments. OATs are slightly outperforming their German counterparts, tightening the 10-year spread by 2bps to ~77bps. Gilts are steady. US session includes several Fed speakers, May retail sales data and 20-year bond auction. Coupon issuance resumes with $13b 20-year bond reopening at 1pm; WI 20-year yield at around 4.540% is 9.5bp richer than last month’s auction, which stopped through by 0.2bp

In commodities, oil held the biggest advance in a week Monday as risk-on sentiment in wider markets countered a mixed outlook for crude. Brent last traded around $84.25 and erasing an earlier loss. Copper rose from its lowest close since mid-April. Spot gold falls ~$7 to around $2,312/oz.

Looking at today’s economic calendar, we will get the June New York Fed services business activity, May retail sales (8:30am), May industrial production (9:15am), April business inventories (10am) and April TIC flows (4pm). Fed officials scheduled to speak include Barkin (10am), Collins (11:40am, 4:40pm), Logan and Kugler (1pm), Musalem (1:20pm) and Goolsbee (2pm)

Market Snapshot

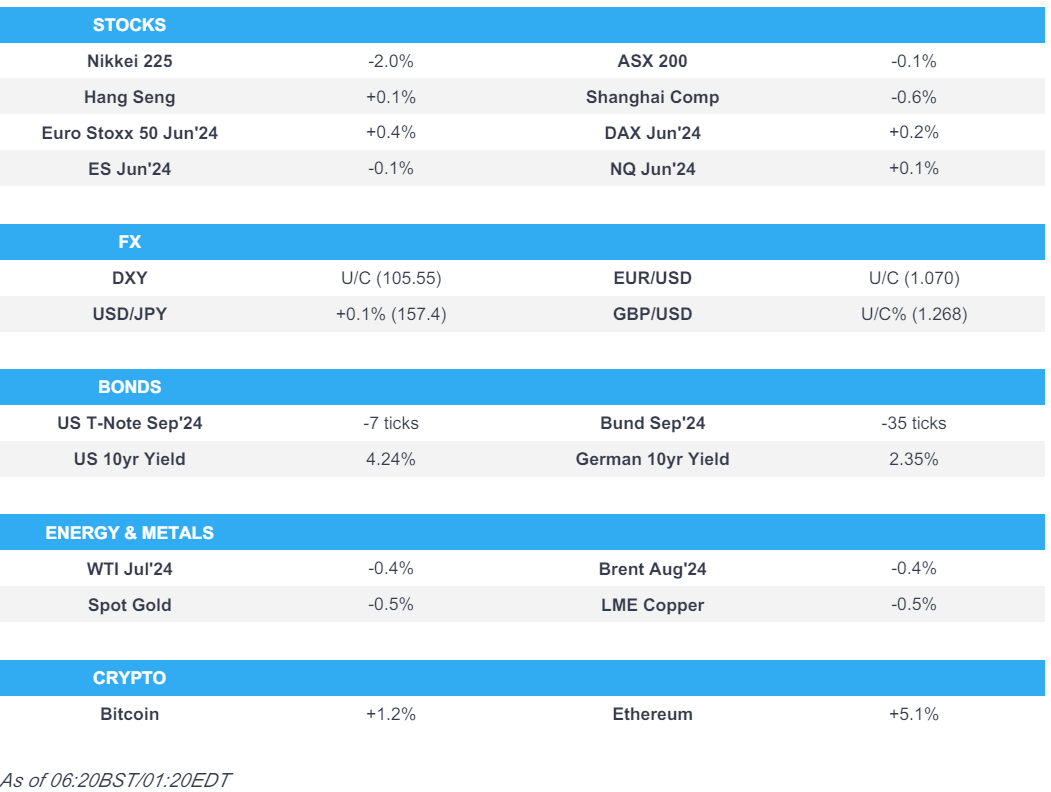

- S&P 500 futures little changed at 5,475.25

- STOXX Europe 600 up 0.2% to 512.41

- MXAP up 0.6% to 178.99

- MXAPJ up 0.6% to 565.12

- Nikkei up 1.0% to 38,482.11

- Topix up 0.6% to 2,715.76

- Hang Seng Index down 0.1% to 17,915.55

- Shanghai Composite up 0.5% to 3,030.25

- Sensex up 0.3% to 77,255.02

- Australia S&P/ASX 200 up 1.0% to 7,778.08

- Kospi up 0.7% to 2,763.92

- German 10Y yield little changed at 2.43%

- Euro down 0.1% to $1.0719

- Brent Futures down 0.5% to $83.86/bbl

- Gold spot down 0.3% to $2,312.38

- US Dollar Index up 0.18% to 105.51

Top Overnight News

- Elon Musk plans a Venmo-like payments feature for X across the US, documents show. Users will be able to store money on their accounts, pay other users or businesses, and even buy goods in physical stores. BBG

- Australia’s central bank kept interest rates at a 12-year high and highlighted sticky inflation, suggesting it’ll be some time before it’s ready to signal easing. BOJ chief Kazuo Ueda kept the door open to a possible rate increase in July. BBG

- Bank of Japan Governor Kazuo Ueda said the central bank could raise interest rates next month depending on economic data available at the time, underscoring its resolve to steadily push up borrowing costs from current near-zero levels. RTRS

- France’s corporate bosses are racing to build contacts with Marine Le Pen after recoiling from the radical tax-and-spend agenda of the rival leftwing alliance in the country’s snap parliamentary elections. FT

- Petrobras agreed to pay 19.8 billion reais ($3.5 billion) in back taxes, boosting Brazilian President Luiz Inacio Lula da Silva’s efforts to balance the budget. BBG

- UK grocery inflation declined for the 16th consecutive month to 2.1 per cent in June, according to data that will come as welcome news to consumers hit by the cost of living crisis. FT

- Biden to announce an initiative Tues whereby undocumented immigrants married to US citizens will be able to apply for legal residency. WaPo

- Apartment rents are starting to firm in several Northwest and Midwest cities, creating complications for the Fed (this is a situation where elevated rates might be helping to fuel inflation by dampening demand for home purchases). WSJ

- Last week’s benign US inflation data reinforced our view that the Q1 spike was an aberration. Meanwhile, the labor market stands at a potential inflection point where a further softening in labor demand would hit actual jobs, not just open positions, and could therefore push up the unemployment rate more significantly. Goldman

A more detailed look at global markets

APAC stocks took impetus from the gains in the US where the S&P 500 and the Nasdaq notched record highs once again despite the lack of any major fresh macros drivers and as a deluge of Fed rhetoric looms. ASX 200 was underpinned with financials and defensives front-running the broad advances seen across sectors, while attention turned to the RBA decision where the central bank provided no surprises and kept the Cash Rate target unchanged at 4.35%. Nikkei 225 recovered some of the prior day’s notable losses amid the rising tide across global equity markets and was unfazed by the latest comments from BoJ Governor Ueda who suggested the potential for a July rate hike depending on the data. Hang Seng and Shanghai Comp. were ultimately mixed as the Hong Kong benchmark later deteriorated after failing to sustain the 18,000 level, while the mainland conformed to the positive mood after the PBoC upped its liquidity efforts.

Top Asian News

- Hong Kong will start to permit trading through typhoons from September 25th.

- BoJ Governor Ueda said underlying inflation is to gradually accelerate and they must be vigilant to financial market moves and the impact on the economy, while he added that they need to scrutinise data a bit more to judge whether underlying inflation will heighten on a firm note and if they become more convinced that underlying inflation will accelerate towards the price target, they will adjust the degree of monetary easing by raising the short-term policy rate. Furthermore, Ueda said they cannot say now how much the BoJ will trim bond buying and they will not send a strong policy message by cutting JGB purchases, while he added that depending on economic, price and financial data and information available at the time, there is a chance we could raise interest rates at July meeting.

- China’s latest property support measures have boosted transactions in the largest cities, but activity in smaller localities struggles get off the ground which suggests more pain ahead for most of the country’s real estate market, according to Reuters.

- China Output (May) Gasoline 13.8mln/MT, +2.9% Y/Y; Diesel 17.35mln/MT, -6.4%; Crude Iron Ore 88.48mln/MT, +9.0%; Refiner Copper +0.6%.

- China’s Securities Regulator says they will enrich policy tools to manage market fluctuations, will resolutely prevent abnormal stock market volatility. To strengthen strategic reserves and market stabilisation mechanism

European bourses, Stoxx 600 (+0.2%) began the session entirely in the green, taking impetus from a positive APAC session overnight, continuing the strength seen in the US on Monday. Since, stocks have slipped off best levels though remain modestly firmer. European sectors are mostly in the green, and hold a risk on bias, with Travel & Leisure topping the pile, whilst Consumer Products lags. US Equity Futures (ES U/C, NQ +0.1%, RTY -0.3% are mixed, taking a breather from the prior day’s strength which saw the S&P 500 and the Nasdaq notch record highs once again.

Top European News

- EU leaders concluded their summit with no agreement on key political positions, while EU’s Michel said EU leaders will continue to work in the coming days for a deal on top jobs and that they need to agree on a program for the next five years at EU summit next week.

RBA

- Cash Rate Target unchanged at 4.35%, as expected, while it reiterated that the Board remains resolute in its determination to return inflation to the target and inflation remains high and is above target which is proving persistent. RBA said inflation is easing but has been doing so more slowly than previously expected and the Board expects that it will be some time yet before inflation is sustainably in the target range, while it added the path of interest rates that will best ensure that inflation returns to the target in a reasonable timeframe remains uncertain and the Board is not ruling anything in or out.

- Bullock: need to a lot to go our way too bring inflation back to range; board discussed whether to hike rates at this meeting, board decided to stay the course on policy. Wanted to make the point that they are alert to upside risks on inflation. Need to look across the economy, not just at Q2 CPI. Difficult to get a read on CPI with only quarterly data. Would not say the case for a rate hike is increasing, board did not consider the case for a rate cut at the gathering

FX

- Dollar is on a firmer footing today, benefiting from the slightly higher yield environment, and trading towards the upper end of today’s 105.25-47 range. Next up, US Retail Sales, with headline M/M expected at 0.3%.

- EUR is slightly softer vs the Dollar, with some of the political concerns out of France subsiding in recent trade. The Single-currency currently holds towards the bottom end of today’s 1.0715-41 range, and more resilient to the recent Dollar strength than other G10 peers.

- GBP began the session on a 1.27 handle, before succumbing to Dollar-led pressure, dragging the Pound down to lows of 1.2676. UK-specifics have been light today, though the docket picks up tomorrow in the form of UK CPI, ahead of the BoE a day later.

- A stronger session for the USD/JPY, breaching 158.00 to the upside, finding slight resistance at 158.10, before taking another leg higher towards the session’s best at 158.22; a level just shy of the 14th June high at 158.25.

- Differing performances for the Antipodeans today, on RBA day. The Bank kept rates unchanged though some upside was seen after Governor Bullock said that rate hikes were discussed at the meeting. The Kiwi is the G10 underperformer, which has been dragged lower by the AUD/NZD cross, which is currently at 1.0830.

Fixed Income

- USTs are softer by only a handful of ticks and resides just off today’s lows, ahead of US Retail Sales and a slew of Fed speakers. USTs in a narrow 110-08+ to 110-16 band, which has edged to a new WTD base by a tick.

- Bunds are also slightly subdued, in-fitting with the initial bias on Monday. Specifics light aside from ZEW, which came in softer than expected with the Current Conditions surprisingly falling and printing below the forecast range. Data lifted Bunds back to the unchanged mark, but markedly shy of their 132.68 overnight peak. Thereafter, a poor German auction prompted some modest EGB pressure.

- Gilts are flat awaiting impetus from Wednesday’s CPI and then Thursday’s BoE. Supply this morning came via a 2029 DMO tap which was well received and spurred a very modest move higher for Gilts, though the move proved shortlived.

- UK sells GBP 4bln 4.125% 2029 Gilt: b/c 3.59x (prev. 3.2x), average yield 4.083% (prev. 4.199%), tail 0.3bps (prev. 0.6bps)

- Germany sells EUR 3.36bln vs exp. EUR 4bln 2.10% 2029 Bobl: b/c 2.1x (prev. 2.8x), average yield 2.45% (prev. 2.56%) & retention 16.00% (prev. 16.75%)

Commodities

- Crude benchmarks are just underwater with specifics light, largely at the whim of the firmer Dollar, with the complex taking a breather from yesterday’s geopolitics driven gains. Brent currently just shy of USD 84/bbl.

- Precious metals are contained with specifics light and the mentioned USD strength weighing on the space. At the low end of thin USD 2313-2325/oz parameters, a low which holds just above Monday’s USD 2310/oz.

- Base metals are weighed on by the USD which is overshadowing any support for the complex from the PBoC’s latest liquidity measures.

Geopolitics: Middle East

- Israeli negotiator said tens of Gaza hostages are alive with certainty, according to AFP News Agency.

- US National Security Adviser Sullivan said they need to give and take in negotiations, as well as bridge the differences between Hamas and Israel, while he added that the current proposal represents a roadmap for a ceasefire in Gaza.

- Top US Democrats approve massive arms sales to Israel including 50 F-15 fighter jets, according to Washington Post.

- “US President Biden’s senior adviser Amos Hochstein’s paper seeks a truce agreement with Israel after removing Hezbollah forces from the border”, via Al Hadath citing Lebanese press

Geopolitics: Other

- US National Security Adviser Sullivan said their approval of Kyiv’s use of US weapons inside Russia extends to any place used by Russian forces to strike Ukraine, according to Al Jazeera.

- Russian President Putin said Russia and North Korea will develop trade and mutual settlements mechanism uncontrolled by the West and will jointly resist sanctions, while he added that Russia highly appreciates North Korea’s support in Moscow’s special operation in Ukraine and that the West is pushing Ukraine to strike Russia’s territory, according to TASS.

- South Korea’s military fired warning shots after North Korean soldiers crossed the military demarcation line, while the North Korean military suffered multiple casualties due to the explosion of land mines within the demilitarized zone, according to Yonhap.

- Chinese spokesperson criticised the Philippines’ submission on its undersea shelf in the South China Sea, claiming it infringes on China’s sovereign rights, violates international law and contradicts the Declaration on Conduct of Parties in the South China Sea.

US Event Calendar

- 08:30: June New York Fed Services Business, prior 3.0

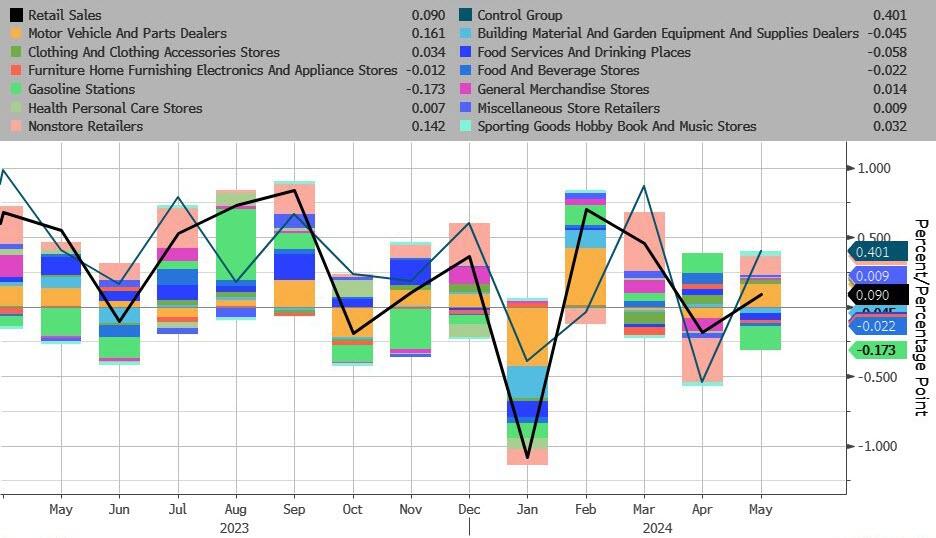

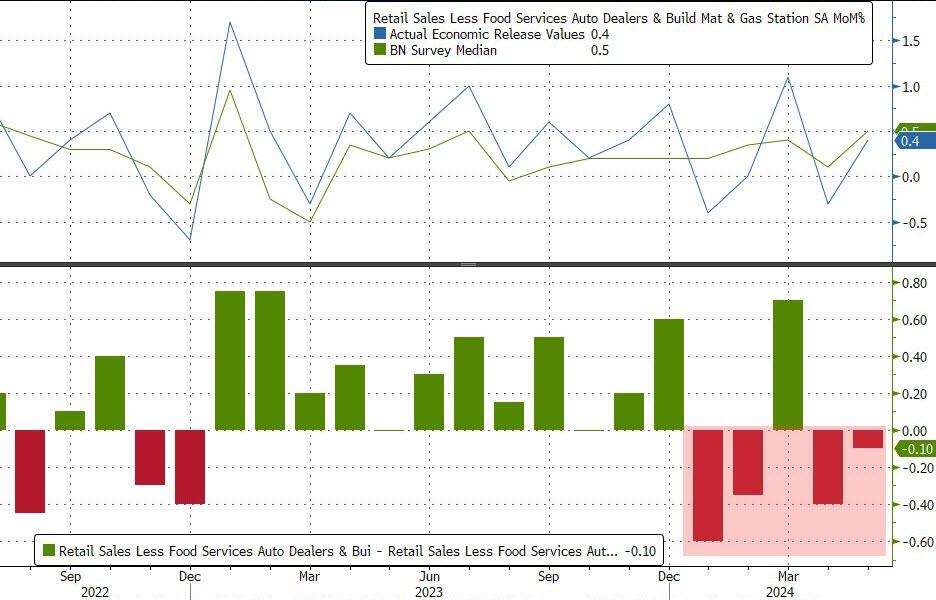

- 08:30: May Retail Sales Advance MoM, est. 0.3%, prior 0%

- May Retail Sales Ex Auto MoM, est. 0.2%, prior 0.2%

- May Retail Sales Control Group, est. 0.5%, prior -0.3%

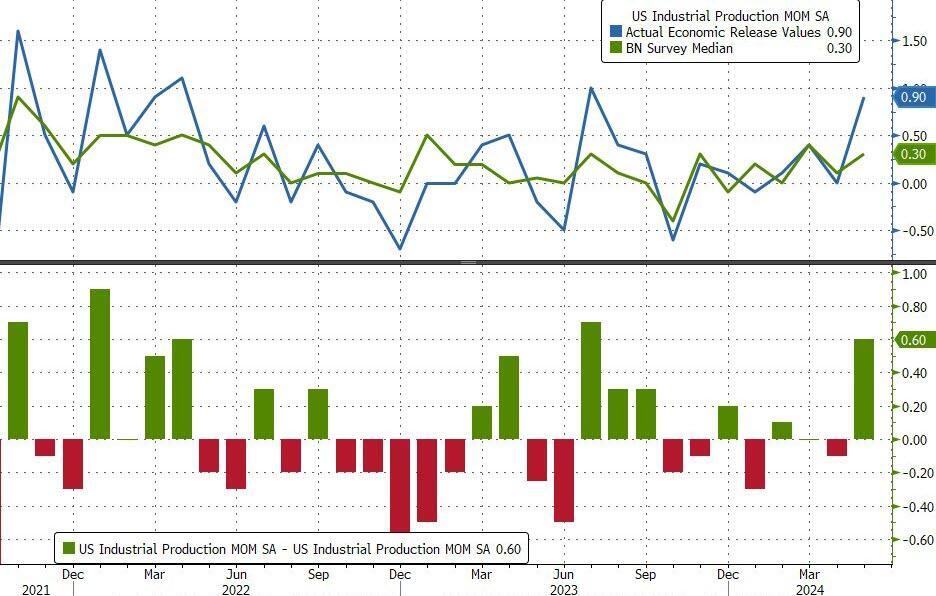

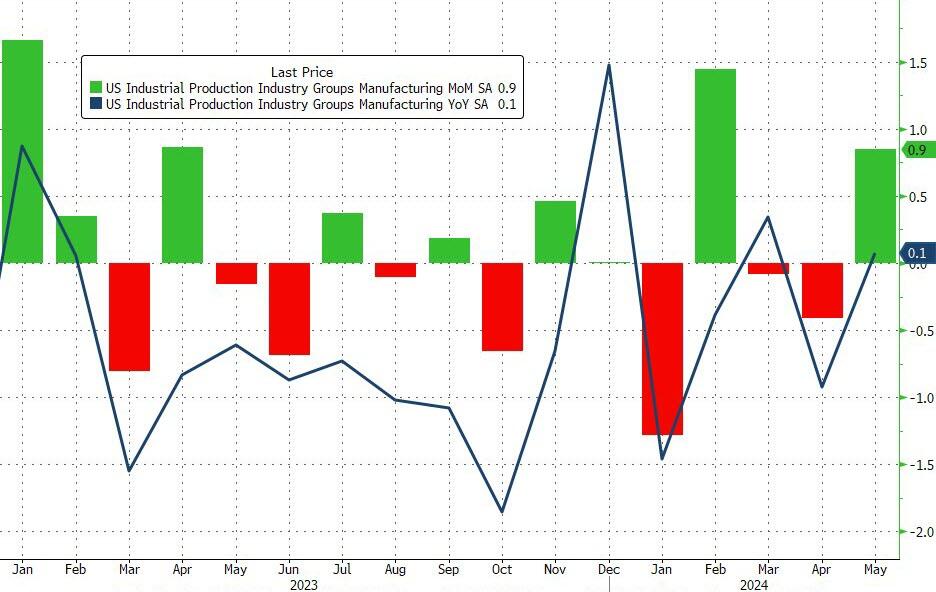

- 09:15: May Industrial Production MoM, est. 0.3%, prior 0%

- May Manufacturing (SIC) Production, est. 0.3%, prior -0.3%

- May Capacity Utilization, est. 78.6%, prior 78.4%

- 10:00: April Business Inventories, est. 0.3%, prior -0.1%

- 16:00: April Total Net TIC Flows, prior $102.1b

DB’s Jim Reid concludes the overnight wrap

Risk assets put in a stronger performance over the last 24 hours, with the S&P 500 (+0.77%) advancing to yet another record high, while European markets also stabilised after last week’s slump. That included France’s CAC 40 (+0.91%), which posted a recovery following its worst weekly performance in over two years, and sovereign bond spreads also narrowed across Europe. But even as risk assets managed to recover, the risk-on tone meant that sovereign bonds lost ground again, and comments from central bank officials meant investors dialled back the amount of rate cuts they expected over the rest of the year.

In terms of the situation in France, the Franco-German 10yr spread finally tightened again yesterday, having risen every single day over the previous week. By the close, it was down by -2.8bps, and alongside that, the Euro strengthened by +0.29% against the US Dollar. Equities also recovered, despite some weakness in the middle of the day, and the CAC 40 was supported by an outperformance among financials. That included AXA (+1.87%), BNP Paribas (+1.25%) and Société Générale (+1.17%), all of whom had experienced double-digit losses last week. And when it came to the politics, a poll out from Ifop yesterday showed that Marine Le Pen’s RN party was on 33% for the first round on June 30, the left-wing New Popular Front was in second place on 28%, and President Macron’s group was on 18%.

With increasing attention on the first round vote, we also heard from some ECB policymakers on the situation, although they didn’t seem too perturbed by the recent moves. For instance, ECB President Lagarde said that “ We are attentive to the good functioning of financial markets, and I think that today in any case we’re continuing to be attentive, but it’s limited to that.” Elsewhere, chief economist Lane said that this was “a repricing” and said it was not in “the world of disorderly market dynamics.” For more from DB Research on the developments in France, yesterday saw Chief European economist Mark Wall look at what this could mean from an economic and policy perspective (link here), while I took a look at some of the broader market takeaways (link here). Our rates strategists have also written about the OAT-bund spread (link here).

When it comes to the ECB, investors also got a reminder that they may not be in a hurry to cut rates rapidly, despite the turmoil in markets last week. For instance, chief economist Lane pointed out that the ECB wouldn’t know much more by the time of its July meeting, and Croatia’s Vujcic said that “July is always an option, but much more data will be available in September. Everything is open at that meeting”. That backdrop and the stabilisation in French assets saw investors very slightly dial back their expectations for ECB rate cuts, with the amount priced in by the December meeting falling by -0.3bps on the day to 43bps. Alongside that, yields on 10yr bunds (+5.3bps), OATs (+2.5bps) and BTPs (+1.5bps) all moved higher as well.

Over in the US, Treasuries saw an even larger selloff, with the 10yr yield up +6.0bps on the day to 4.28%. That came amidst some better-than-expected data, with the Empire State manufacturing survey up to a four-month high of -6.0 in June (vs. 10.0 expected). A sizeable amount of corporate issuance on Monday, which tends to lead to increased hedging activity, may have also contributed to the rise in yields. The data flow will continue today, as we’ve got retail sales, industrial production and capacity utilisation for May, so that will give us a better sense of economic performance into the middle of Q2. However, yields have reversed course overnight, with the 10yr Treasury yield (-1.4bps) back down to 4.27%.

In the meantime, the rally in US equities showed no sign of abating yesterday, as the S&P 500 (+0.77%) closed at an all-time high for the fifth time in six sessions (and for the 30th time this year), taking itsYTD gains to +14.75%. The advance was once again led by tech stocks, with the Magnificent 7 (+1.16%) extending its YTD gains to +36.47%. Broadcom (+5.41%) and Tesla (+5.30%) were two of the three top performers in the S&P 500 on the day. The equity rally was fairly broad, with the equal-weighted S&P 500 up +0.66% yesterday. But the equal-weighted index is still only up +4.04% YTD, so there’s a gap of more than ten percentage points with the market-cap weighted index, while the Russell 2000 is still in the red on a YTD basis (-0.25% despite a +0.79% gain yesterday). For European equities, it was France that led the way, and Italy’s FTSE MIB (+0.74%) also put in a solid performance. However, the broader STOXX 600 was only up +0.09%.

In the commodity space, oil prices extended last week’s advance, with Brent (+1.97% to $84.25/bbl) and WTI (+2.40% to $80.33/bbl) crude closing the session at their highest levels since April.

Overnight, the Reserve Bank of Australia left their policy rate unchanged at 4.35%, in line with expectations. Their statement acknowledged ongoing inflationary pressures, saying that labour market conditions “ remain tighter than is consistent with sustained full employment and inflation at target ”, whilst it said wage growth was “still above the level that can be sustained given trend productivity growth.” Later on, they kept their options open for policy, saying that “the Board is not ruling anything in or out”. Yields on 10yr Australian government bonds are just over a basis point higher since the decision was announced, and are currently up +3.2bps on the day to 4.14%.

Elsewhere overnight, markets in Asia have put in a strong performance, following the lead from Wall Street. That includes gains for the Nikkei (+0.90%), the KOSPI (+0.79%), the Shanghai Comp (+0.36%) and CSI 300 (+0.27%), although the Hang Seng (-0.18%) has fallen back. Looking forward, US equity futures are basically flat this morning, with those on the S&P 500 only down -0.02%.

To the day ahead now, and data releases include US retail sales, industrial production and capacity utilization for May, along with the German ZEW survey for June. From central banks, we’ll hear from the Fed’s Barkin, Collins, Logan, Kugler, Musalem and Goolsbee, ECB Vice President de Guindos, and the ECB’s Knot, Vujcic, Cipollone and Villeroy.

2B EUROPE OPENING/TRADING

APAC stocks benefit from a strong US close, DXY flat & AUD unreactive to RBA – Newsquawk Europe Market Open

TUESDAY, JUN 18, 2024 – 01:42 AM

- APAC stocks took impetus from the gains in the US where the S&P 500 and the Nasdaq notched record highs

- DXY steady, AUD unreactive to RBA while the JPY was unphased by Ueda

- RBA rate decision where the central bank kept rates unchanged and reiterated the Board remains resolute in its determination to return inflation to the target and it is not ruling anything in or out.

- Fixed benchmarks nursed some of Monday’s pressure but were largely rangebound into numerous Fed speakers

- Crude paused for breath after its geopolitical rally

- Looking ahead, highlights include German ZEW, EZ HICP (F), US Retail Sales & Industrial Production, NBH Policy Announcement, Comments from RBA’s Bullock, RBNZ’s Conway, ECB’s Cipollone & de Guindos, Fed’s Barkin, Collins, Logan, Kugler, Musalem & Goolsbee, UK, German & US supply.

- Click for the Newsquawk Week Ahead.

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

US TRADE

EQUITIES

- US stocks were firmer to start the week with gains led by outperformance in the large-cap sectors of Consumer Discretionary and Technology in which the latter was buoyed by strength in Micron (MU) (+4.5%) after BofA and Susquehanna raised PTs for the stock ahead of earnings next week, while there was no specific headline driving the upside in stocks which also shrugged off higher yields ahead of a deluge of Fed commentary.

- SPX +0.77% at 5,473, NDX +1.24% at 19,903, DJIA +0.49% at 38,778, RUT +0.79% at 2,022.

- Click here for a detailed summary.

NOTABLE HEADLINES

- Fed Chair Powell is to give semi-annual monetary policy testimony at the Senate Banking Committee on July 9th.

- Fed’s Harker (non-voter) said if his economic forecast plays out, he thinks one rate cut would be appropriate by year-end but added that two cuts or none are also quite possible and it depends on data. Furthermore, Harker said that more data is essential to come to a decision on rate cuts given the choppiness so far this year and noted the latest inflation data is quite promising, but falls short of the confidence needed and has not quite dissipated uncertainty.

- WSJ’s Timiraos posted on X that with PPI and import price data in hand for May, the inflation modellers who map the CPI/PPI into the PCE now expect the core PCE index rose around 0.08%-0.13% in May which would translate to a 2.6% year-on-year core PCE inflation rate and is down from 2.8% in April. Furthermore, he said this would hold the 6-month annualised core PCE rate around 3.2% (or 3.3%) in May and the 3-month annualised rate would drop back below 3% for the first time since January.

APAC TRADE

EQUITIES