JUNE 21 BLOG//MASSIVE RAID ON GOLD AND SILVER AS LAW AND ORDER DOES NOT EXIST IN THE USA//EUROPEAN PMI’S PLUMMET//EUROPEAN CMBS TRANCHE AAA SUFFERS SERIOUS LOSSES//UPDATES ON ISRAEL VS HAMAS, ISRAEL VS HEZBOLLAH AND VACCINE INJURY REPORTS//RUSSIA VS UKRAINE UPDATES//SWAMP STORIES FOR YOU TONIGHT//

190 H BMO CAPITAL 46 661 C JP MORGAN 10 690 C ABN AMRO 4 4 737 C ADVANTAGE 7 57 880 H CITIGROUP 73 905 C ADM 1 991 H CME 78

TOTAL: 140 140 MONTH TO DATE: 30,281

ACCESS MARKET

JPMorgan stopped 0/140

FOR JUNE 2024

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2024. CONTRACT: 140 NOTICES FOR 14,000 OZ or 0.4354 TONNES

total notices so far: 30,281 contracts for 3,028,100 Oz (94.186 tonnes)

FOR JUNE:

SILVER NOTICES: 3 NOTICE(S) FILED FOR 15,000

OZ/

total number of notices filed so far this month :1318 for 6.590 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $37.40 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/

: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/ A MAMMOTH GOLD VAPOUR DEPOSIT OF 8.34 TONNES

/ /INVENTORY RESTS AT 833.65TONNES

INVENTORY RESTS AT 833.65 TONNES

SLV//

WITH NO SILVER AROUND AND SILVER DOWN $1.15 AT THE SLV//

NO CHANGES IN SILVER INVENTORY AT THE SLV:

// INVENTORY INCREASES TO 434.939 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 434.939 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 1027 CONTRACTS TO 175,578 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS SURPRISING STRONG SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR STRONG GAIN OF $1.17 IN SILVER PRICING AT THE COMEX ON THURSDAY’S TRADING ON SILVER. WE HAD ZERO LONG LIQUIDATION AS WE HAD A NET LOSS OF 88 CONTRACTS ON OUR TWO EXCHANGES. WE, AGAIN HAD SHORT COVERING BY OUR SPECS WITH THE STRONG GAIN IN PRICE AS WELL AS MASSIVE T.A.S. LIQUIDATION. WE HAD ANOTHER HUMONGOUS SIZED 1662 T.A.S ISSUANCE,

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED TUESDAY JUNE 4 AND AGAIN ON FRIDAY, JUNE 7

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 1662 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT THUS LOOKS LIKE THE FED (GOV’T) IS BEHIND TODAY;S TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $1.17) AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS FROM THEIR PERCH AS WE DID HAVE A TINY SIZED LOSS OF 88 CONTRACTS ON OUR TWO EXCHANGES WITH THE HUGE GAIN IN PRICE OF $1.17.

WE MUST HAVE HAD:

A HUGE SIZED 939 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.830 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 75,000 OZ QUEUE JUMP.

//NEW STANDING FOR SILVER//JUNE IS THUS 6.685 MILLION OZ

WE HAD:

/ STRONG SIZED COMEX OI LOSS //HUGE SIZED EFP ISSUANCE/ VI) HUMONGOUS SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1662 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED 619 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE

TOTAL CONTRACTS for 14 DAYS, total 14,549 contracts: OR 72.745 MILLION OZ (1039 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 72.745 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 72.745 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1027 CONTRACTS DESPITE OUR STRONG GAIN IN PRICE OF SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 939 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.830 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 75,000 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR JUNE 6.685 MILLION OZ

WE HAVE A TINY SIZED LOSS OF 88 OI CONTRACTS ON THE TWO EXCHANGES WITH THE GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUMONGOUS SIZED 1662 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX SESSION/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND SOME NET LIQUIDATION OF LONGS.

THE NEW TAS ISSUANCE THURSDAY NIGHT (1662) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 3 NOTICE(S) FILED TODAY FOR 15,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A HUGE SIZED 13,078 OI CONTRACTS TO 457,423 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 1422 CONTRACTS

WE HAD A HUGE SIZED INCREASE IN COMEX OI (13,078 CONTRACTS) OCCURRED WITH OUR GAIN OF $23.60 IN PRICE/THURSDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 89.94 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 6200 OZ QUEUE JUMP AS BANKERS SCOUR THE PLANET LOOKING FOR GOLD ON THE THIS SIDE OF THE POND

NEW STANDING 94.553 TONNES// ALL OF THIS HAPPENED WITH OUR $23.60 GAIN IN PRICE WITH RESPECT TO THURSDAY’S TRADING. WE HAD A HUMONGOUS SIZED GAIN OF 15,652 OI CONTRACTS (48.68 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2574 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 457,423

IN ESSENCE WE HAVE A HUMONGOUS SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 15,652 CONTRACTS WITH 13,078 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 2574 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 15,652 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 1325 CONTRACTS,,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2574 CONTRACTS) ACCOMPANYING THE HUGE SIZED GAIN IN COMEX OI OF 13,078 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 15,652 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 88.761 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 0.1928 TONNES

//NEW STANDING /JUNE 94.553 TONNES.

/ 3) HUGE T.A.S. LIQUIDATION OF CONTRACTS WITH ZERO NET LONG SPECS BEING CLIPPED,

4) HUGE SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1325 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE. :

TOTAL EFP CONTRACTS ISSUED: 43,699 CONTRACTS OR 4,369,900 OZ OR 135.92 TONNES IN 14 TRADING DAY(S) AND THUS AVERAGING: 3121 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 14 TRADING DAY(S) IN TONNES 135.92 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 135.92 DIVIDED BY 3550 x 100% TONNES = 3.92% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 135.92 tonnes HEADING FOR A STRONG MONTH BUT LESS THAN THE THREE PREVIOUS MONTHS

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A STRONG SIZED 1027 CONTRACTS OI TO 175,578 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 939 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 939 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 939 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1027 CONTRACTS AND ADD TO THE 939 E.FP. ISSUED

WE OBTAIN A TINY SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 88 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 0.440 MILLION OZ

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING/THURSDAY NIGHT

SHANGHAI CLOSED DOWN 7.30 PTS OR 0.24% //Hang Seng CLOSED DOWN 306.80 PTS OR 1.67%// Nikkei CLOSED DOWN 36.59 OR 0.09%//Australia’s all ordinaries CLOSED UP 0.35%///Chinese yuan (ONSHORE) closed DOWN TO 7,2609 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2880/ Oil DOWN TO 81.19 dollars per barrel for WTI and BRENT DOWN AT 85.52 /Stocks in Europe OPENED ALL RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A HUGE SIZED 13,078 CONTRACTS TO 457,423 WITH OUR STRONG GAIN IN PRICE OF $23.60 WITH RESPECT TO THURSDAY’S TRADING. WE HAD A HUGE T.A.S. LIQUIDATION ON THURSDAY WITH ZERO LONGS BEING CLIPPED.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 2574 EFP CONTRACTS WERE ISSUED: : AUGUST2574 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2574 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A HUMONGOUS SIZED TOTAL OF 15,652 CONTRACTS IN THAT 2574 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A HUGE SIZED GAIN OF 13,078 COMEX CONTRACTS..AND THIS HUMONGOUS SIZED GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR STRONG GAIN IN PRICE OF $17.25/THURSDAY COMEX

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A GOOD SIZED 1325 CONTRACTS. MOST OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN THURSDAY’S TRADING

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (94.553 TONNES)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 94.553 TONNES. THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $23.60 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A HUMONGOUS SIZED GAIN OF 15,652 CONTRACTS ON THURSDAY ON OUR TWO EXCHANGES ACCOMPANYING THE STRONG GAIN IN PRICE. THE T.A.S. ISSUED ON THURSDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 48.68 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE (89.94 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 62 CONTRACTS OR 6200 OZ (0.1928 TONNES)

NEW STANDING FOR JUNE: 94.360 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAININ PRICE TO THE TUNE OF $23.60

WE HAVE REMOVED 1422 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET GAIN ON THE TWO EXCHANGES 15,652 CONTRACTS OR 1,565,200 OZ (48.68 TONNES)

Total monthly oz gold served (contracts) so far this month

30,281 notices 3,028100 oz 94,130 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: NIL oz

we have 1 customer deposit:

i) Into Brinks 2218.419 oz (69 kilobars)

total deposit 2218.491 oz

customer withdrawals: 2

i) Out of Delaware 2186.268 oz 68 kilobars

ii) Out of Brinks 3665.214 oz 114 kilobars

TOTAL WITHDRAWALS 5851.482 0z 182 kilobars

Adjustments: 4 dealer to customer:

a) HSBC 234,102.895 oz

b) JPMorgan 7716.240 oz

c) Malca 14,202.293 oz

d) Manfra 64,862.002 oz

total adjusted 340,604.880 oz and this is a sign of extreme stress//10.59 tonnes

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE

For the front month of JUNE we have an oi of 258 contracts having GAINED 42 contracts. We had 20 contracts served on Thursday so we gained 62 contracts or 6200 oz additional ounces will stand for gold at the comex as they underwent a queue jump to take delivery on this side of the pond.

JULY LOST 24 CONTRACTS TO STAND AT 2411

AUGUST GAINED 10,507 CONTRACTS UP TO 369,807 CONTRACTS

We had 140 contracts filed for today representing 14,000 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 10 notice was issued from their client or customer account. The total of all issuance by all participants equate to 1400 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for June /2024. contract month, we take the total number of notices filed so far for the month (30,281) x 100 oz ) to which we add the difference between the open interest for the front month of JUNE (258 CONTRACTS) minus the number of notices served upon today (140 x 100 oz per contract( equals 3,039,900 OZ OR 94.553 TONNES.

thus the INITIAL standings for gold for the JUNE contract month: No of notices filed so far (30,281 x 100 oz +we add the difference for front month of June (258// , OI} minus the number of notices served upon today (140) x 100 oz which equals 3,039,900 oz (94.533 TONNES)

TOTAL COMEX GOLD STANDING FOR JUNE: 94.533 TONNES WHICH IS ABSOLUTELY HUGE FOR THIS VERY ACTIVE DELIVERY MONTH IN THE CALENDAR. JUNE IS TRADITIONALLY THE 2ND HIGHEST DELIVERY MONTH OF THE YEAR. FROM THIS POINT WE WILL GAIN IN GOLD TONNAGE WILLING TO STAND AT THE COMEX

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,576,275 OZ

TOTAL REGISTERED GOLD 7,716,240( 240.006 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,764,208.266 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,043,243 oz (REG GOLD- PLEDGED GOLD)= 187.97 tonnes //this is the lowest net registered in quite some time.

END

SILVER/COMEX

JUN 21/2024

INITIAL

//2024// THE JUNE 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

587,585.506 oz

Delaware

.

Deposits to the Dealer Inventory

nil OZ

Deposits to the Customer Inventory

578m695.000 oz

manfra

No of oz served today (contracts)

3 CONTRACT(S) (15,000 OZ)

No of oz to be served (notices)

19 contracts (0.095 million oz)

Total monthly oz silver served (contracts)

1318 Contracts (6.590 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 customer deposits:

i) Into Manfra 578,695.000

total customer deposit 578,695,000oz

JPMorgan has a total silver weight: 127.832million oz/296.815million or 42.90%

adjustment: 3 all customer to dealer

a) Brinks 274,448.610 oz

b) CNT 75,997.990

c) Delaware 5104.541 oz

Comex withdrawals: 1

i) out of Delaware 587,585.504 oz

total withdrawal: 5,87,585.504 0z

TOTAL REGISTERED SILVER: 63.429MILLION OZ//.TOTAL REG + ELIGIBLE. 296.815

million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE:

silver open interest data:

FRONT MONTH OF JUNE/2024 OI: 22 CONTRACTS HAVING LOST 40 CONTRACT(S).

WE HAD 55 NOTICES SERVED UP ON THURSDAY, SO WE GAINED 15 CONTRACTS OR AN ADDITIONAL 75,000 OZ WILL STAND AT THE COMEX VIA A CONSIDERABLE QUEUE JUMP TO WHERE THEY WILL TAKE DELIVERY ON THIS SIDE OF THE POND

JULY SAW A LOSS OF 9145 CONTRACTS DOWN TO 61,183

AUG, SAW A GAIN OF 45 CONTRACTS TO 421

SEPT SAW A GAIN OF 7520 CONTRACTS TO 94,182

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 3 for 15,000 oz

CONFIRMED volume; ON THURSDAY 173,343 HUMONGOUS /EQUALS 108% OF YEARLY SILVER PRODUCITON.

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1318 x 5,000 oz = 6.590 MILLION oz

to which we add the difference between the open interest for the front month of JUNE ((22) and the number of notices served upon today 3 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2024 contract month: 1318 notices served so far) x 5000 oz + OI for the front month of JUNE (22)x number of notices served upon today minus (3)x 5000 oz of silver standing for the JUNE contract month equates to 6.685 MILLION OZ.

New total standing: 6.685 million oz.

There are 63.429 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

JUNE 21 WITH GOLD DOWN $37.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A MAMMOTH 8.34 TONNES OF GOLD VAPOUR DEPOSIT/NEW TOTAL TONIGHT 833.65 TONNES

JUNE 20 WITH GOLD UP $23.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/://NEW TOTAL TONIGHT 825.31 TONNES

JUNE 18 WITH GOLD UP $17.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/://NEW TOTAL TONIGHT 825.31 TONNES

JUNE 17 WITH GOLD DOWN $18.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.03 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 825.31 TONNES

JUNE 13 WITH GOLD DOWN$35.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.89 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 830.78 TONNES

JUNE 12 WITH GOLD UP $28.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.89 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 830.78 TONNES

JUNE 11 WITH GOLD DOWN $0.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 10 WITH GOLD UP $2,00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 7 WITH GOLD DOWN $64.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 3.56 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 837.11 TONNES

JUNE 6 WITH GOLD UP $16.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.34 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 833.55 TONNES

JUNE 5 WITH GOLD UP $32.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 4 WITH GOLD DOWN $20.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 3 WITH GOLD UP $22.85 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 31 WITH GOLD DOWN $19.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 30 WITH GOLD UP $3.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 29 WITH GOLD DOWN $13.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 28 WITH GOLD UP $22.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 832.21 TONNES

MAY 24 WITH GOLD DOWN $2.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 833.36 TONNES

MAY 23 WITH GOLD DOWN $53.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 22 WITH GOLD DOWN $32.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 21 WITH GOLD DOWN $12,00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 20 WITH GOLD UP $21.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.10 TONNES OF GOLD INTO THE GLD//NEW TOTAL 838.54 TONNES

MAY 17 WITH GOLD UP $31.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//NEW TOTAL 833.36 TONNES

MAY 16 WITH GOLD DOWN $7.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//NEW TOTAL 833.36 TONNES

MAY 15 WITH GOLD UP $34.90 ON THE DAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD/INVENTORY RISES TO 831.93 TONNES

MAY 14 WITH GOLD DOWN $17.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RISES TO 831.33 TONNES

GLD INVENTORY: 833.65 TONNES, TONIGHTS TOTAL

SILVER

JUNE 21. WITH SILVER DOWN $1.15//NO CHANGES IN SILVER INVENTORY’// /INVENTORY REMAINS AT 434.935 MILLION OZ.

JUNE 20. WITH SILVER UP $1.17//HUGE CHANGES IN SILVER INVENTORY’ A DEPOSIT OF 5.164 MILLION OZ INTO THE SLV/// /INVENTORY RISES TO 434.929 MILLION OZ.

JUNE 18. WITH SILVER UP $0.21//NOCHANGES IN SILVER INVENTORY’ A WITHDRAWAL .730 MILLION OZ INTO THE SLV/// /INVENTORY FALLS TO 429.775 MILLION OZ.

JUNE 17. WITH SILVER UP $0.21//SMALL CHANGES IN SILVER INVENTORY’ A WITHDRAWAL .730 MILLION OZ INTO THE SLV/// /INVENTORY FALLS TO 429.775 MILLION OZ.

JUNE 14. WITH SILVER DOWN $0.10//NO CHANGES IN SILVER INVENTORY/ /INVENTORY REMAINS AT 429.083 TONNES

JUNE 13. WITH SILVER DOWN $1.10//HUGE CHANGES IN SILVER INVENTORY/ A HUGE DEPOSIT OF 1.958 MILLION OZ/INVENTORY RISES TO 429.083 TONNES

JUNE 12 WITH SILVER UP $0.97 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 5.983 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 427.125 MILLION OZ

JUNE 11 WITH SILVER DOWN $0.59 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.644 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 422.786 MILLION OZ

JUNE 10 WITH SILVER UP $0.30 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 3.198 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 421.142 MILLION OZ

JUNE 7 WITH SILVER DOWN $1.93 TODAY: NO CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY AT 417.944 MILLION OZ

JUNE 6 WITH SILVER UP $1.27 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 417.944 MILLION OZ

JUNE 5 WITH SILVER UP 0.38 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.52 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 415.295 MILLION OZ

JUNE 4 WITH SILVER DOWN $1.08 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

JUNE 3 WITH SILVER UP $0.35 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

MAY 31 WITH SILVER DOWN $1.09 TODAY: HUGE CHANGES IN SILVER INVENTORY: A MASSIVE WITHDRAWAL OF 3.655 MILLION OZ FROM THE SLV//INVENTORY LOWERS TO 413.775 MILLION OZ

MAY 30 WITH SILVER DOWN $0.80 TODAY: NO CHANGES IN SILVER INVENTORY//INVENTORY REMAINS AT 417.430 MILLION OZ

MAY 29 WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 1.051 MILLION OZ INTO THE SLV//INVENTORY DECREASES TO 417.430 MILLION OZ

MAY 28 WITH SILVER UP $1.64 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 2.832 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 418.481 MILLION OZ

MAY 24 WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF .822 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 421.313 MILLION OZ

MAY 23 WITH SILVER DOWN $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.736 MILLION OZ FROM THE SLVINVENTORY INCREASES TO 420.491 MILLION OZ

MAY 22 WITH SILVER DOWN $0.66 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 21 WITH SILVER DOWN $0.41 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A DEPOSIT OF 3.792 MILLION OZ FROM THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 20 WITH SILVER UP $1.28 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 1.005 MILLION OZ FROM THE SLV// INVENTORY LOWERS TO 418.435 MILLION OZ

MAY 17 WITH SILVER UP $1.37 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 868,000 OZ FROM THE SLV// INVENTORY LOWERS TO 419.440 MILLION OZ

MAY 16 WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY REMAINS AT 420.308 MILLION OZ

MAY 15 WITH SILVER UP 101 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A WITHDRAWAL OF 1.919 MILLION OZ FROM THE SLV NVENTORY RESTS AT 420.308 MILLION OZ

MAY 14 WITH SILVER UP 25 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;INVENTORY RESTS AT 422.227 MILLION OZ

China’s recent attempt to secure a rare earth minerals stockpile ended in failure when a competitor stepped in to snag the deal…

Vital Metals, a mining firm based in Australia, announced Monday that minerals collected from its Saskatchewan-based Nechalacho Project will remain within Canadian borders.

“We were presented with a case of elevated interest for Canada,” Vital’s managing director Geordie Mark told The Northern Miner, later adding:

“This agreement highlights the strategic value and importance of the Nechalacho rare earths project and the prioritization of a rare earths value chain in Canada.”

According to Vital, the Nechalacho site in northern Canada could hold more than 200 million tons of rare earth elements (REEs), which are used in green energy production and weapons manufacturing. Right now, China dominates the industry despite its comparatively small natural stock, clinching 75% of the global market with only 35% of the global REE reserves.

“China was only able to establish such dominance over the REE industry in part because of lax environmental regulations,” said Harvard Independent Review’s Jaya Nayar.

“Low cost, high pollution methods enabled China to outpace competitors and create a stronghold in the international REE market.”

What’s pushing Canada to allow REE mining and reap the profits, despite environmental risks?

The answer lies within the Canadian critical minerals list, which includes REEs and 33 other elements/elemental groups deemed strategically and economically significant. A recent expansion of the list added high-purity iron, phosphorus, and silicon, which—like REEs and 20 other elements on the list—are key components of the green energy transition. This update, plus the last-minute swoop to protect REE supplies, gives a glimpse into the role “green” policy will play and foreshadows increasing pressure on component supply chains. If other countries follow Canada’s example, prices of related metals on that critical list—including cobalt, platinum group metals, REEs, silicon, and copper—could see significant boosts. That’s a bet Canada is placing early by securing its access to REEs while cutting China out of the deal.

The recent Canadian purchase from Vital is also part of a larger economic and political salvo led by Prime Minister Justin Trudeau, who told reporters there will be no reconciliation between Canada and China following accusations of election meddling. On the mining stage, Canada is marketing itself as a direct competitor to China, flaunting its enormous mineral reserves as an alternative source for wary European countries afraid to rely on Chinese producers. China’s dominance won’t be shaken by missing a single deal with the Australian firm, though the move certainly sends a message calculated to exacerbate already strained relations between China and the West.

As if its challenge weren’t clear enough, Canada recently joined the U.S., Japan, and the Philippines to conduct military exercises in the South China Sea. Tensions between the four countries are on the rise, and economics is the prime battlefield. With REEs as a strategic focus and green energy policies on the Western docket, nations may put pressure on each other by sanctioning or otherwise straining metals supply chains—a move strategists on both sides will surely consider. With two of the world’s largest holders of rare earths reserves vying for stockpiles, the pressure on consumer countries to pick sides is growing, and this new symptom of conflict in the metals market will likely boost REE and related metal prices as countries stock up while supplies last.

It’s not just rare earths that will see gains. Silver, though not deemed “critical,” is a component of electric vehicles and other “green” technologies that governments (and private investors) will likely snap up in anticipation of tighter supply. Stress on metals supply chains is part of gold’s lifeblood, suggesting higher prices for this metal as well.

Good news for investors looking to shoot straight for the heart: REE prices bottomed out last year, indicating they’re due for revival and primed for a low buy.

“I’ve seen forward-looking studies that … don’t even factor in demand from defense sectors that push [the global annual turnover for REEs] well over a trillion dollars by the time we reach 2050,” said Melissa Sanderson, a consultant at American Rare Earths. “It’s a good, strong market now, and it’s one that appears to have healthy legs under it.”

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/GOLD AND SILVER COMMENTARY

ALASDAIR MACLEOD…

CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES

end

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS/

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COPPER

SHANGHAI CLOSED DOWN 7.30 PTS OR 0.24% //Hang Seng CLOSED DOWN 306.80 PTS OR 1.67%// Nikkei CLOSED DOWN 36.59 OR 0.09%//Australia’s all ordinaries CLOSED UP 0.35%///Chinese yuan (ONSHORE) closed DOWN TO 7,2609 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2880/ Oil DOWN TO 81.19 dollars per barrel for WTI and BRENT DOWN AT 85.52 /Stocks in Europe OPENED ALL RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGSFRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2609

OFFSHORE YUAN: DOWN TO 7.2880

SHANGHAI CLOSED DOWN 7.34 PTS OR 0.24 %

HANG SENG CLOSED DOWN 306.80 PTS OR 1.67%

2. Nikkei closed DOWN 36.59 PTS OR 0.09 %

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 105.42 EURO FALLS TO 1.0687 DOWN 19 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +0.966 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 158.93 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.3675/Italian 10 Yr bond yield DOWN to 3.906 SPAIN 10 YR BOND YIELD DOWN TO 3.303%

3i Greek 10 year bond yield DOWN TO 3.577

3j Gold at $2361.00//Silver at: 30.20 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 24/ 100 roubles/dollar; ROUBLE AT 88,49

3m oil into the 81 dollar handle for WTI and 85 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 158.93/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.966% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8926 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9545 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.229 DOWN 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.374 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.707 DOWN 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.85…

10 YR UK BOND YIELD: 4.082 UP 2 PTS

2a New York OPENING REPORT

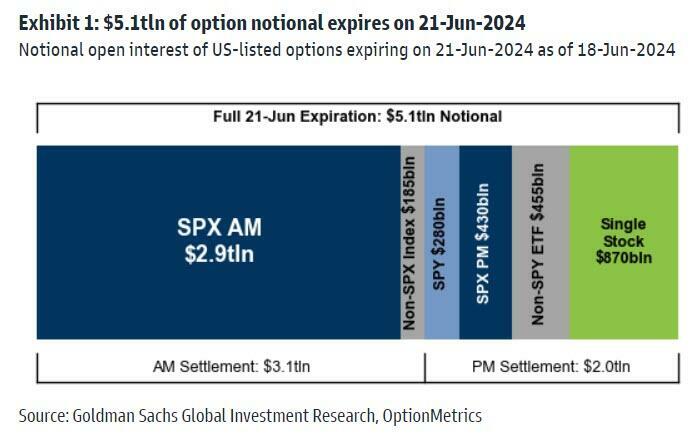

Futures Fall, Tech Rally Fades Ahead Of Record $5 Trillion OpEx

FRIDAY, JUN 21, 2024 – 08:19 AM

US futures were slightly lower, with tech companies indicating declines as the AI-fueled rally showed signs of fading, even as tech funds had their largest weekly inflow on record, which Bank of America’s Michael Harnett said hints at “AI capitulation.” As of 8:00am ET, S&P futures were down 0.1%, with Nasdaq futures also in the red.

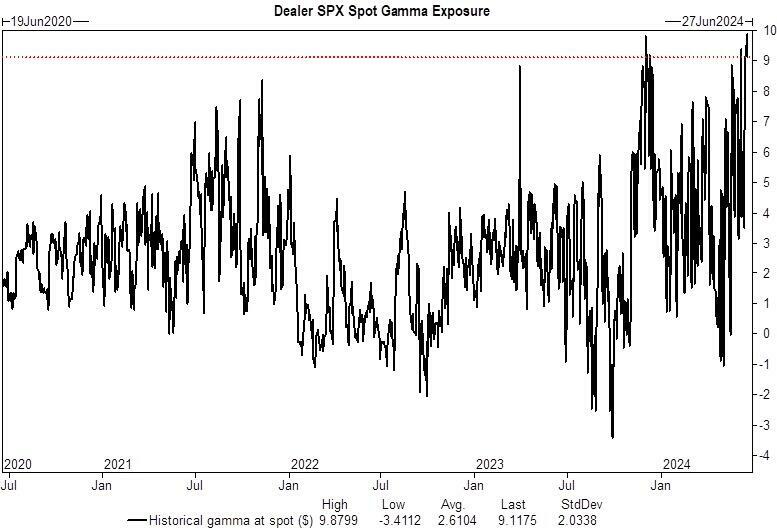

… which could “unclench” record $10 billion in dealer gamma and spark sharp market moves as “pins” expire.

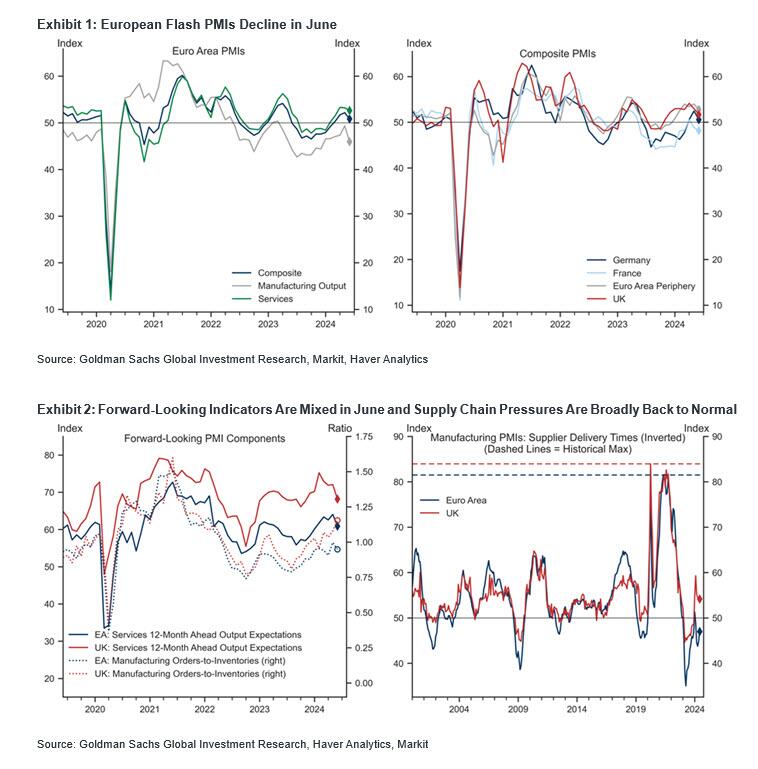

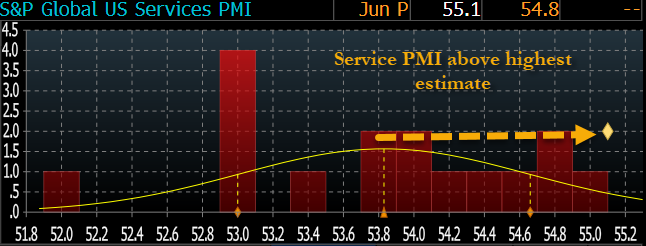

Bond yields are 2-4bp lower this morning, reversing a move higher, after Europe’s ugly PMI prints (see below) which also pushed the EUR lower and the USD higher. Commodities are mixed; oil is modestly lower; base metals are higher. Today’s macro focus will be the flash PMIs at 9.45am ET; consensus expects a mfg print of 51.0 while the PMI-Srvcs is seen printing 54.0 survey vs. 54.8 prior.

In premarket trading, tech names are mostly lower: NVDA -1.8%, QCOM -71bps, MSFT -25bps and AAPL -23bps. Spirit AeroSystems jumped 4% after Reuters reported Boeing is nearing a deal to buy back the aircraft-parts supplier. Here are the other notable premarket movers:

Abacus Life falls 21% after its offering of 10 million shares priced at $8 per share, representing an 18% discount to last close.

Gilead advances 3%, extending Thursday’s gains, after interim results from a trial of the firm’s drug lenacapavir showed 100% efficacy for the prevention of HIV in cisgender women.

Sarepta Therapeutics soars 37% after the FDA approved expanded use of the company’s gene therapy to treat children aged four and above with Duchenne muscular dystrophy.

Smith & Wesson slips 3% after the gun maker said sales in its first quarter would be about 10% lower year over year.

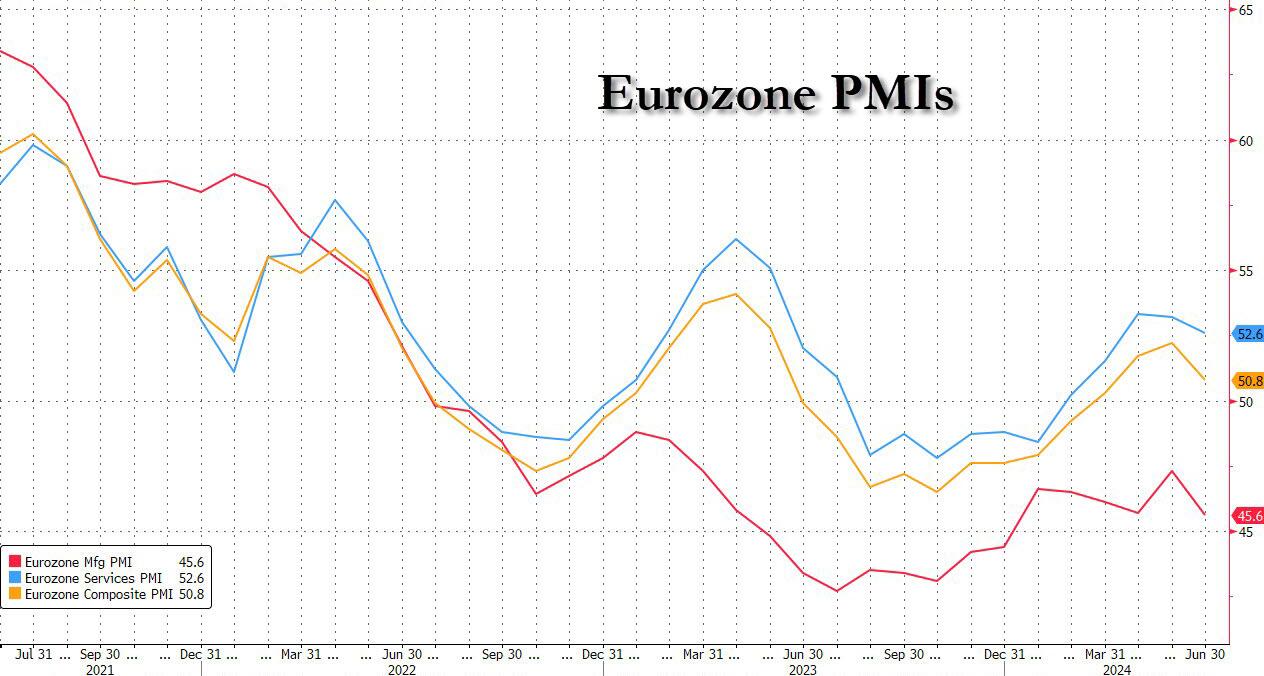

Risk-off trades were also in vogue in Europe, where the fallout from French President Emmanuel Macron’s decision to call a snap election continued to make itself felt in the region’s economy. The yield on Germany’s benchmark 10-year bonds tumbled seven basis points after manufacturing and services PMI readings for Europe’s two biggest economies fell short of expectations. The rate on US Treasuries also declined, while the dollar held near a 2024 high after the PMI data, which underscored how French political risk is dragging on growth. Traders now see a second ECB cut by October and an 80% chance of a third this year, up from about 65% on Thursday.

Key numbers:

Euro Area Composite PMI (June, Flash): 50.8, missing consensus 52.5, last 52.2.

Euro Area Manufacturing PMI (June, Flash): 45.6, missing consensus 47.9, last 47.3.

Euro Area Services PMI (June, Flash): 52.6, missing consensus 53.4, last 53.2.

France Composite PMI (June, Flash): 48.2, missing consensus 49.4, last 48.9.

UK Composite PMI (June, Flash): 51.7, missing consensus 53.0, last 53.0.

Macron’s shock call for a vote has stoked volatility in the region’s markets and left investors worried that an economic rebound could be snuffed out by far-right leaders, should they prevail in elections. European stock funds suffered their fifth week of outflows, according to Bank of America strategists, citing EPFR Global data.

“The most important problem for us is the economic outlook for the euro zone,” said Benoit Peloille, chief investment officer at Natixis Wealth Management. “It really poses a risk.”

And speaking of European stock markets, the Stoxx 600 was on course for its worst day this week, dropping 0.7%, with banks the worst performers, with construction and tech also falling. Here are the most notable European movers:

Zealand Pharma shares soar as much as 27% to a record high after the Danish drugmaker’s next-generation weight-loss compound petrelintide showed positive results in an early-stage trial, with analysts noting its impressive tolerability.

Britvic shares climb as much as 16% after its board unanimously rejected a second takeover proposal from Carlsberg. Shares in the UK beverage maker touch a record-high 1,176p, heading toward Carlsberg’s 1,250p/share offer.

RENK shares rise as much as 2.4% as analysts presented bullish takeaways from this week’s defense trade show Eurosatory, with Berenberg in particular, highlighting the strong demand outlook for the German defense company’s new ATREX transmission system.

Informa shares rise as much as 1.6% after the events and publishing firm reported 10.1% underlying revenue growth for the first five months of the year, likely beating consensus estimates that had been expecting around 8% growth in the first-half, Morgan Stanley said. The company maintained guidance that was raised in May.

ITV shares jump as much as 5.2%, most since March, as JPMorgan analysts say the British broadcaster’s advertising revenue in the current quarter will be much stronger than its previous guidance, thanks to a boost from the European Football Championship.

Kion shares fall as much as 9.7%, the steepest decline since October 2023. UBS (buy) lowers its price target on the German industrial firm, saying second-half order spikes are always tough to rely on.

REC Silicon shares drop as much as 15% after the company provided an update on its Washington facility’s delayed clean up process, which caused a setback in the delivery of product.

Intercos falls as much as 7.5% after holder Innovation Trust completed its accelerated bookbuilding offering of 6.5m shares at €15.20 a share, representing ~8.5% discount to last close.

Varta shares fall as much as 9.3%, the most in six weeks, after the company warned market conditions in the energy storage system market have deteriorated further, prompting it to lower its annual revenue goal.

Earlier in the session, Asian stocks traded lower, led by losses in Hong Kong, as a global tech-driven rally showed signs of fatigue, while concerns persist over China’s economy. The MSCI Asia Pacific Index fell as much as 0.6%, with TSMC, Samsung and Tencent among the biggest drags. Declines were also notable in South Korea and Taiwan, while a tumble in the Philippines’ main benchmark put it on course to enter a technical correction. For the week, the regional gauge is little changed. Hong Kong’s Hang Seng dropped as much as 2% while mainland gauges also slid as Beijing is seen as reluctant to step up stimulus. US stocks fell overnight as the high-flying tech group led by Nvidia came under pressure amid signs of overheating.

Canada’s Prime Minister Justin Trudeau is preparing potential new tariffs on Chinese-made electric vehicles to align the nation with actions taken by the US and European Union, Bloomberg reported. The government still has to make final decisions on how to proceed, but it’s likely to announce soon the start of public consultations on tariffs that would hit Chinese exports of EVs into Canada, according to officials. In May the US announced a plan to nearly quadruple tariffs on Chinese-manufactured electric vehicles, up to a final rate of 102.5%, while the European Union said last week it plans to increase tariffs to as high as 48% on some vehicles.

In FX, the Bloomberg Dollar Spot Index was little changed, pulling back from near this year’s high ahead of fresh data later today. Dollar demand over the Tokyo benchmark fix saw spot offers attached to 159 strikes — worth a collective $2.05 billion and expiring between today and June 26 — get taken out, according to an Asia-based FX trader. European political and fiscal risk, an easier stance from BoE and a steady slide in JPY have countered the recent run of softer US data, Tim Riddell, director of strategy at Westpac Banking Corp. wrote in a note. “Despite remaining contained within its range, the sharpness of recent DXY moves suggests that a directional move may be developing.”

EURUSD, down 0.13%, which has been under pressure since French President Emmanuel Macron’s surprise decision to call a snap election, fell to its lowest in a week.

GBPUSD +0.1% to 1.2670 after better than expected May UK retail sales data, including revisions. The gain was brief and the cable is now little changed.

In rates, treasuries hold an advance that was led by core European rates, with German bonds outperforming after soft PMI data across Europe and US PMIs due later Friday. US long-end tenors lag slightly, extending the recent steepening in 5s30s spread beyond Thursday’s highs. German 10-year yields fell 6bps to 2.38% while treasury yields were richer by 2bp to 4bp across the curve with front-end- and belly-led gains steepening 5s30s spread by around 1bp on the day; 10-year yields trade around 4.225%, richer by 3bp vs Thursday’s close with bunds outperforming by 4bp in the sector

In commodities, oil prices decline, with WTI falling 0.2% to trade near $81.15 a barrel. Spot gold rises ~$6 to $2,366/oz. Bitcoin continues to slip and now sits beneath USD 64k, with Ethereum also slipping below USD 3.5k.

Looking at today’s calendar, US economic data slate includes June S&P Global manufacturing and services PMIs (9:45am) and May Leading index and existing home sales (10am). No Fed officials scheduled to speak during the session

Market Snapshot

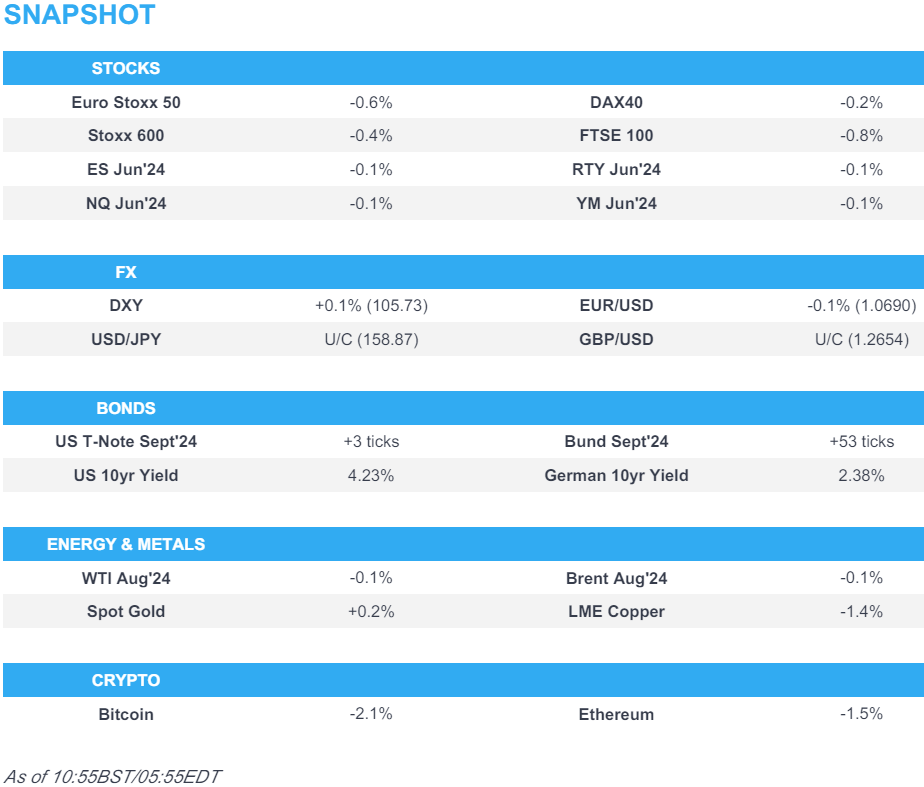

S&P 500 futures down 0.2% to 5,465.75

STOXX Europe 600 down 0.5% to 516.50

MXAP down 0.5% to 179.78

MXAPJ down 0.7% to 568.66

Nikkei little changed at 38,596.47

Topix little changed at 2,724.69

Hang Seng Index down 1.7% to 18,028.52

Shanghai Composite down 0.2% to 2,998.14

Sensex little changed at 77,422.88

Australia S&P/ASX 200 up 0.3% to 7,795.97

Kospi down 0.8% to 2,784.26

German 10Y yield -5 bps at 2.37%

Euro down 0.1% to $1.0687

Brent Futures down 0.4% to $85.33/bbl

Gold spot up 0.3% to $2,366.36

US Dollar Index up 0.15% to 105.74

Top Overnight News

Japan’s core national CPI eases to +2.1% in May, down from +2.4% in Apr and below the Street’s +2.2% forecast. RTRS

China’s 618 online shopping festival saw sales fall Y/Y for the first time, the latest indication of cooling consumer demand and price discounting. FT

Prime Minister Justin Trudeau’s government is preparing potential new tariffs on Chinese-made electric vehicles to align Canada with actions taken by the US and European Union. BBG

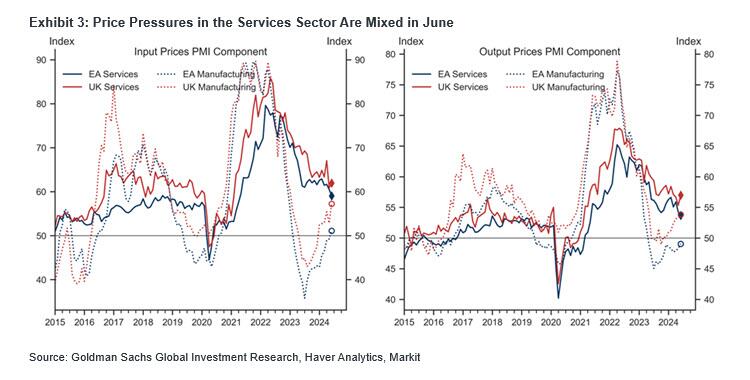

Europe’s flash PMIs show significant weakness in June, with manufacturing dropping to 45.6 (down from 47.3 in May) and services cooling to 52.6 (down from 53.2 in May), although inflationary pressures eased along with growth (which is a small silver lining). RTRS

UK retail sales for May come in solidly above expectations, rising 2.9% M/M (vs. the Street +1.8%), and Apr was revised higher. WSJ

Trump sees a surge in campaign inflows (his recent conviction helped to fuel donations), all but erasing Biden’s financial advantage. WaPo

Chicago Fed President Austan Goolsbee said policy makers will be able to cut rates if inflation continues to cool as it did last month. But Richmond Fed boss Thomas Barkin said he needs further clarity. BBG

Bank capital rules: Fed, OCC, and FDIC at odds over how to release the revised B3 endgame rules (the Fed wants to allow the industry to comment while the OCC and FDIC would prefer to just publish the rules for implementation). RTRS

Spirit is nearing a deal to be purchased by Boeing after Airbus-related work issues were resolved, and a formal announcement could arrive within days or weeks. RTRS

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly rangebound with sentiment subdued after the lacklustre handover from Wall St where tech underperformed and risk appetite was sapped as participants reflected on higher yields and soft data releases ahead of quad-witching. ASX 200 was rangebound with upside restricted after weak Australian flash PMI data including a steeper contraction in manufacturing. Nikkei 225 traded indecisively after softer-than-expected National CPI data and weakening PMIs. Hang Seng and Shanghai Comp. were pressured with underperformance in Hong Kong as the local benchmark dipped beneath 18,000 amid losses in property and tech, while the mainland conformed to the glum mood amid ongoing trade-related headwinds with Canada also preparing a tariffs plan on Chinese electric vehicles.

Top Asian News

Canada is reportedly preparing a tariffs plan on Chinese electric vehicles, according to Bloomberg.

Japanese PM Kishida is to resume utility and maintain gasoline subsidies, according to FNN. It was separately reported that Japan’s government is in final preparations to adopt additional steps to ease the burden of higher electricity and gas prices, according to NHK.

Japan’s Chief Cabinet Secretary Hayashi said the inclusion to the US monitoring list does not mean that Japan’s foreign exchange policy is a problem, while he added that stable forex levels are desirable and it is important that forex rates reflect fundamentals.

BoJ Deputy Governor Uchida says Japan’s economy recovering moderately albeit with some weak signs; underlying inflation likely to gradually accelerate. Uncertainty surrounding Japan’s economic and price outlook remains high. Must be vigilant to financial, FX market developments and their impact on Japan’s economy and prices. BoJ will decide specifics on bond tapering plan and size of reducing in bond buying will be significant. Japan’s financial system remains stable as a whole. BoJ will adjust degree of monetary easing if economy and prices move in line with forecasts.

BoJ to hold meetings with bond market participants on bond-tapering plan on July 9-10th

China’s Commerce Ministry says EU continues to escalate trade friction; may “trigger a trade war”; responsibility lies entirely with the EU side; hopes EU would meet China halfway

European bourses, Stoxx 600 (-0.4%) are lower across the board, though with price action fairly rangebound, and generally unreactive to the downbeat EZ PMI data. European sectors are mostly lower, and hold a slight defensive bias, with Utilities and Healthcare towards the top of the pile, whilst Banks are towards the bottom of the pile, alongside Tech. US Equity Futures (ES -0.1%, NQ -0.1%, RTY -0.1%) are very modestly lower, continuing some of the losses seen in the prior session, and in fitting with the broader sentiment in Europe.

Top European News

UK Conservative MPs have accused the BoE of making a “political decision” after deciding to hold rates, according to The Telegraph.

European PMIs

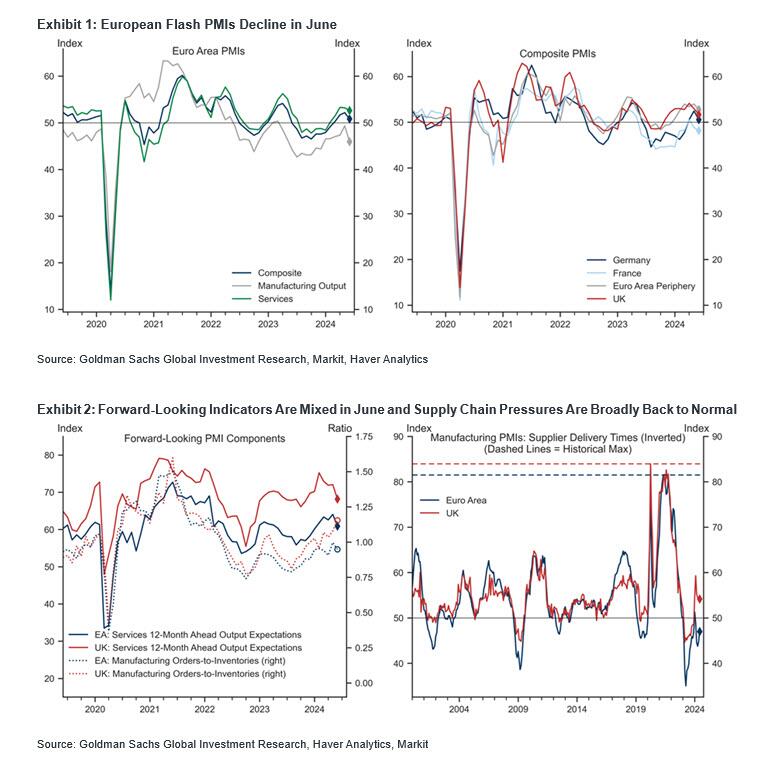

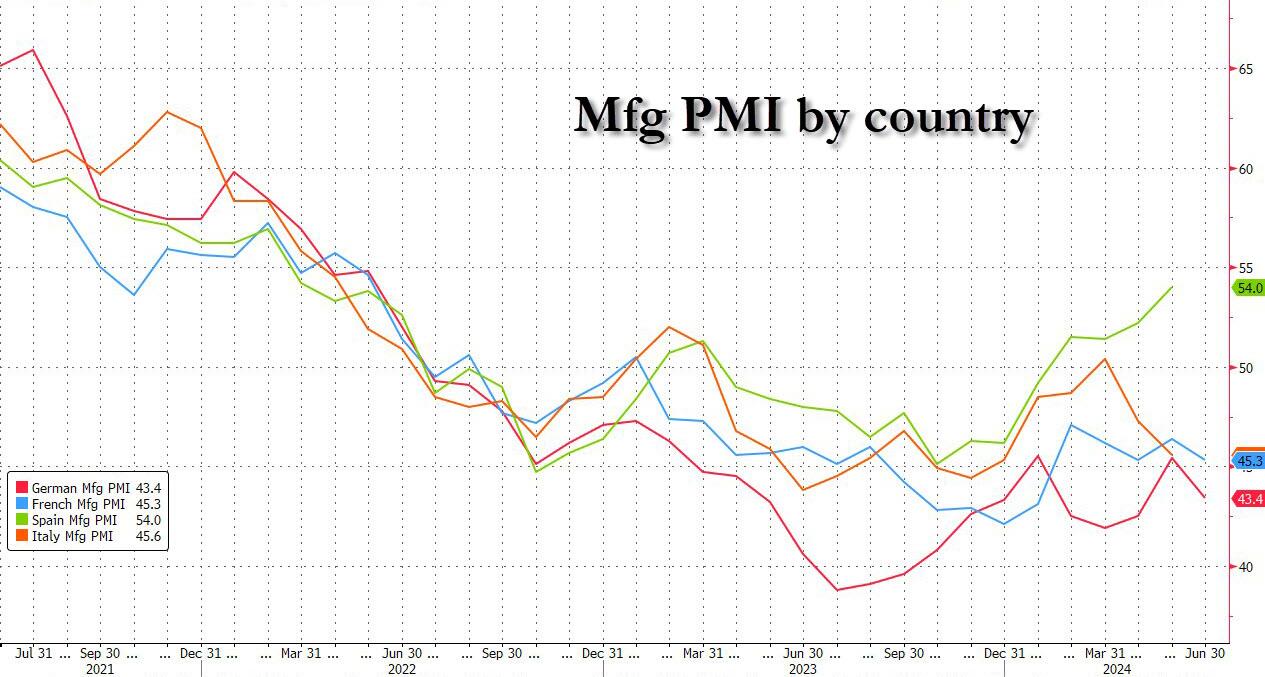

French HCOB Composite Flash PMI (Jun) 48.2 vs. Exp. 49.5 (Prev. 48.9); HCOB Services Flash PMI (Jun) 48.8 vs. Exp. 50.0 (Prev. 49.3); HCOB Manufacturing Flash PMI (Jun) 45.3 vs. Exp. 46.8 (Prev. 46.4)

German HCOB Composite Flash PMI (Jun) 50.6 vs. Exp. 52.7 (Prev. 52.4); HCOB Services Flash PMI (Jun) 53.5 vs. Exp. 54.4 (Prev. 54.2); HCOB Manufacturing Flash PMI (Jun) 43.4 vs. Exp. 46.4 (Prev. 45.4). “This should be a further reason for the ECB to proceed cautiously with interest rate cuts.”

EU HCOB Composite Flash PMI (Jun) 50.8 vs. Exp. 52.5 (Prev. 52.2); HCOB Manufacturing Flash PMI (Jun) 45.6 vs. Exp. 47.9 (Prev. 47.3); HCOB Services Flash PMI (Jun) 52.6 vs. Exp. 53.5 (Prev. 53.2)

UK Flash Manufacturing PMI (Jun) 51.4 vs. Exp. 51.3 (Prev. 51.2); Flash Services PMI (Jun) 51.2 vs. Exp. 53.0 (Prev. 52.9); Flash Composite PMI (Jun) 51.7 vs. Exp. 53.1 (Prev. 53.0). “Meanwhile, from an inflation perspective, stubbornly persistent service sector inflation – a major barrier to lower interest rates – remains evident in the survey, but should at least cool further from the current 5.7% pace in coming months. However, companies’ costs are rising, most notably in manufacturing, where shipping costs in particular are spiking again and adding to a renewed rise in inflationary pressures from goods.”

FX

DXY is slightly firmer amid the risk aversion which emanated from yesterday’s US session, with the index also benefiting from the weaker EUR following the downbeat EZ PMIs.

EUR is softer after France, Germany and the EZ all reported soft PMI figures, though with the accompanying release suggesting “the HCOB PMI do not provide ammunition for another rate cut in July by the ECB.” EUR/USD sits in a 1.0672-0720 range after testing levels near the 14th June low.

GBP is also losing vs the Dollar, with the hotter-than-expected UK Retail Sales providing fleeting upside for Cable, before edging lower ahead of the region’s own PMI data, which was mixed. Cable fell from 1.2649 to 1.2630 before paring the entirety of the move and lifting incrementally to 1.2653.

JPY is flat in the European morning following APAC weakness which saw softer-than-expected Japanese CPI and weaker PMI. USD/JPY briefly topped 159.00 to a 159.12 peak (vs low 158.68), with European strength possibly emanating from the risk aversion and a pullback in bond yields.

Mild divergence between the Antipodeans but largely flat trade with upside capped by the risk aversion (and decline in base metals).

Fixed Income

USTs are modestly firmer and at the top-end of 110-12+ to 110-23 parameters into US PMI data and Fed’s Barkin.

Bunds are firmer, with price action dominated by EZ PMIs; French numbers missed and remained in contraction with the election perhaps factoring, with Germany and the EZ-wide figure also lower than expected. The metrics have lifted Bunds from c. 132.50 to a peak of 133.00, before stabilising around 132.80.

Gilts opened modestly firmer with impetus from benchmarks more broadly somewhat capped by a hawkish UK retail sales number. Tracking EGBs into the UK’s own PMIs which came in mixed and saw a knee-jerk spike to 99.14, before swiftly paring to below 99.00.

Commodities

Crude is lower amid the stronger Dollar and the broadly downbeat risk tone across the market which reverberated from a lacklustre US performance. WTI August found some support at USD 81/bbl while Brent dipped under USD 85.50/bbl.

Mixed trade across precious metals with spot gold holding onto gains despite the stronger Dollar, with newsflow also relatively quiet this morning. Spot silver lags following yesterday’s outperformance. Spot gold resides near yesterday’s peak (USD 2,365.59/oz).

Copper futures pulled back from yesterday’s advances with demand sapped by the subdued risk tone.

Goldman Sachs sees minimal impact from new EU restrictions on Russian LNG. GS says the latest EU package of sanctions impacting Russia bans the transshipment of Russian LNG by member countries, but the measures do not block EU member states from importing Russian LNG.

Citi says crude markets are showing tightness, sees Brent picking up in Q3, but notes opportunities to sell into the strength

Global crude steel output rises 1.5% to 165.1mln tonnes in May 2024 vs May 2023; China crude steel output rises 2.7% Y/Y to 92.9mln tonnes in May 2024

Geopolitics: Middle East

“The IDF wants to declare the end of the war after the Rafah operation”, according to Sky News Arabia citing Israeli press Haaretz

Israel will reportedly step up attempts to assassinate Hamas leaders in a bid to force Hamas to accept the ceasefire deal, according to a senior Israeli official cited by The Times.

US Secretary of State Blinken underscored the importance of avoiding further escalation in Lebanon and reaching a diplomatic resolution in the meeting with Israeli officials, while he emphasised the need to take additional steps to surge humanitarian aid into Gaza and plan for post-conflict governance, security, and reconstruction, according to the State Department.

Geopolitics: Other

UK is reportedly at loggerheads with the US and Germany over Ukraine joining NATO as the US and Germany have derailed a European plan to grant Ukraine an “irreversible” path to NATO membership and instead support offering Ukraine a lighter commitment to membership of the military alliance, according to The Telegraph.

Russian President Putin said Russia is ready to start talks on a settlement of the Ukrainian conflict even as early as tomorrow but all parties should study its peace proposals and it is up to them when they bother to do it, while he added Russia never rejected the idea of negotiations and that the Ukrainian side has forbidden itself to negotiate, according to TASS.

Japan imposed sanctions against China-based companies in connection to the Ukraine war with sanctions placed on China-based Yilufa Electronics and Shenzhen 5G High-Tech Innovation Co.

South Korean military fired warning shots after North Korean soldiers crossed the border on Thursday, according to Yonhap.

US Event Calendar

09:45: June S&P Global US Services PMI, est. 54.0, prior 54.8

June S&P Global US Manufacturing PM, est. 51.0, prior 51.3

June S&P Global US Composite PMI, est. 53.5, prior 54.5

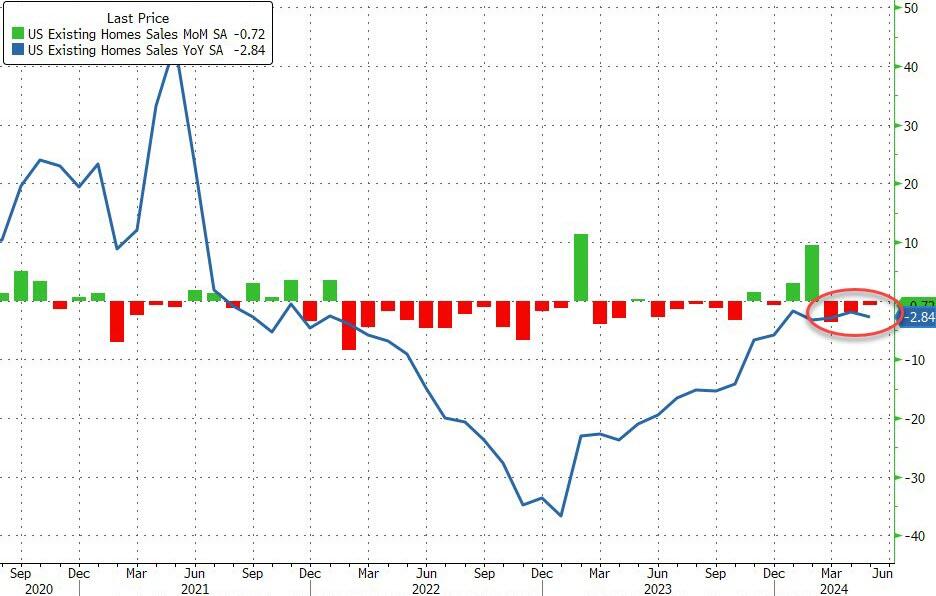

10:00: May Existing Home Sales MoM, est. -1.0%, prior -1.9%

10:00: May Leading Index, est. -0.3%, prior -0.6%

DB’s Jim Reid concludes the overnight wrap

Not to depress you but enjoy today while you can if you’re in the northern hemisphere as tomorrow will have a little less daylight as a slippery dark slope to Xmas begins. I’m currently writing this on the longest day in Watford in the middle of a large longstanding annual 2-day DB Macro conference. Maybe we should have held it at Stonehenge this year given the date.

On that theme it feels like you have to go back to the Neolithic period to find a day when the US significantly underperformed Europe but that’s what happened yesterday. The S&P 500 (-0.25%) opened around a third of a percent higher and above 5500 for the first time before slipping as the session progressed with even Nvidia, on its first day as the largest company in the world, slipping from +3.82% at the day’s early highs to close -3.54% and losing its largest company crown back to Microsoft . The recent rally in US stocks has been very narrow with only 2% of the 503 constituents currently at all-time highs and 7% at one-month lows. So we are seemingly in the hands of tech and particular Nvidia at the moment.

Over the other side of the Atlantic, sentiment was helped by a strong bond auction in France , suggesting that investors were still willing to buy OATs despite the political uncertainty. But on top of that, there was growing hope among investors about the chance of rate cuts ahead, as the Swiss National Bank marginally surprised markets by cutting rates for the second time this year, and the Bank of England made some dovish noises as well. So that offered fresh signs that the global monetary policy cycle was turning, with further rate cuts on the horizon.

That narrative got going after the SNB’s decision, where they delivered a 25bp cut in their policy rate to 1.25%. A narrow majority of economists in Bloomberg’s survey had expected them to remain on hold. They also lowered their inflation forecasts compared to March, which now see it falling from 1.3% in 2024, to 1.1% in 2025, and 1.0% in 2026. In turn, the Swiss Franc weakened by -0.80% against the US Dollar yesterday, making it the worst-performing G10 currency on the day.

That was then followed up by a dovish hold from the Bank of England. They kept the Bank Rate at 5.25% as expected, and the decision was split 7-2 with the two preferring a 25bp rate cut. But even though 7 wanted to stay on hold, the statement pointed out that for some of that group, “ the policy decision at this meeting was finely balanced ”, and investors dialled up the chance of a rate cuts in response. For instance, the chance of a cut by the next meeting in August rose from 34% the previous day to 62% by the close. That helped gilts to outperform, with the 10yr yield down -1.1bps on the day to 4.055%.

European markets got a further boost from the situation in France, where the Treasury raised €10.5bn in an auction of 3-8yr debt. That auction had been in the spotlight, as there were concerns about how much demand there’d be given the political uncertainty. But in reality it went smoothly, and the Franco-German 10yr spread came down by -2.2bps on the day to 77bps. That supportive backdrop helped French equities to recover as well, and the CAC 40 (+1.34%) posted its strongest daily performance since January.

That strength was echoed across European equities, where the STOXX 600 (+0.93%), the DAX (+1.03%) and the FTSE MIB (+1.37%) all posted solid gains. Over in the US, the S&P 500 (-0.25%) weakness after the holiday was driven by the information technology sector (-1.60%). The NASDAQ (-0.79%) and the Magnificent 7 (-0.85%) in turn posted sizeable declines. In addition to Nvidia’s reversal, Apple fell -2.15%, allowing Microsoft (-0.14%) to sneak back in as the world’s most valuable company. The equity mood was slightly more positive otherwise, with 58% of S&P 500 constituents higher on the day. Energy stocks led on the upside (+1.86%), amid a boost from the latest rise in oil prices, with Brent crude (+0.75%) closing at a 7-week high of $85.71/bbl.

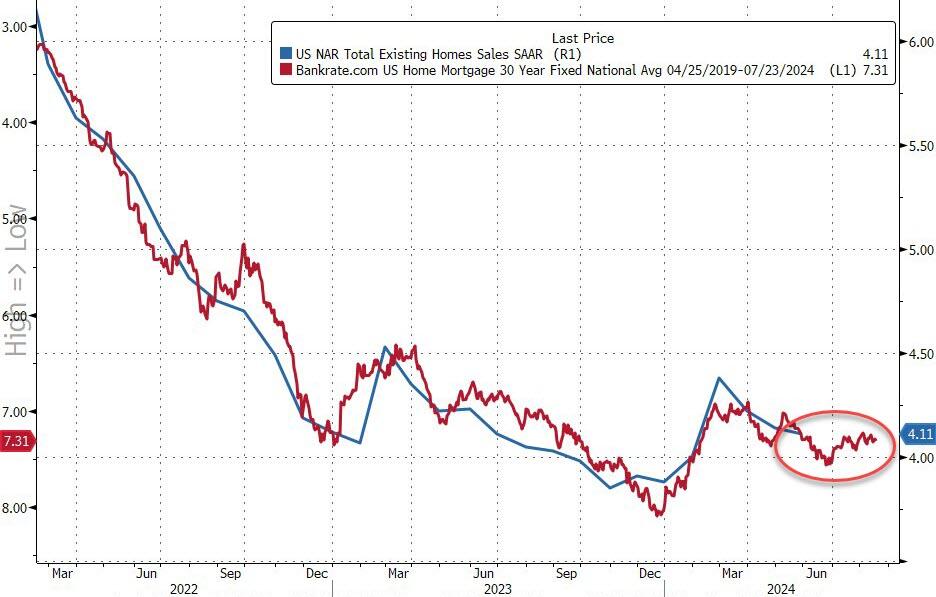

The US session was punctuated by largely weaker data releases yesterday. For example, the continuing jobless claims were up to 1.828m in the week ending June 8 (vs. 1.810m expected), which is their highest level since January. And the initial jobless claims were at 238k over the week ending June 15 (vs. 235k expected), which pushed the 4-week moving average up to a 9-month high of 232.75k. However, note that claims can be distorted this time of year by the timing of the end of the school year so we’re not yet reading too much into the recent climb. At the same time though, data also showed that housing starts fell to an annualised rate of 1.277m in May (vs. 1.370m expected), which is their lowest rate since June 2020. But even with the weaker data, the Atlanta Fed’s GDPNow estimate only ticked down a tenth in the latest update, and now points to annualised growth in Q2 at +3.0%.

That subdued data failed to stop sovereign bond yields from moving higher yesterday, which took place on both sides of the Atlantic. Indeed, yields on 10yr Treasuries were up +3.7bps to 4.26%, whilst those on bunds (+2.8bps), OATs (+0.6bps) and BTPs (+0.8bps) all moved higher as well. The only major exceptions to that were in the UK (-1.1bps) and Switzerland (-5.0bps), who both had dovish-leaning central bank decisions yesterday.

Asian equity markets are mostly trading lower this morning with Chinese stocks the major underperformers. The Hang Seng (-1.72%) is leading losses while the CSI (-0.60%) and the Shanghai Composite (-0.40%) are also edging lower. Elsewhere, the KOSPI (-0.88%) is also drifting lower in early trade with the Nikkei 225 (-0.12%) swinging between gains and losses after Japan’s inflation data (more on this below). S&P 500 (+0.02%) and NASDAQ 100 (+0.08%) futures are slightly higher.

Coming back to Japan, consumer prices ex fresh food accelerated for the first time in a couple of months, advancing +2.5% y/y in May (v/s +2.2% in April, +2.6% consensus) even if it was slightly below consensus. Headline consumer inflation also advanced at a faster pace in May, rising +2.8% y/y (+2.9% expected) and compared with the +2.5% recorded in April, partly due to higher energy bills. However, the core-core CPI, which strips away both energy and fresh food, increased +2.1% y/y in May (v/s +2.2% expected) down from a +2.4% gain in the previous month.

Separately, reports showed that Japan’s factory activity expanded for a second straight month in June but the pace of growth eased. The au Jibun Bank flash manufacturing PMI came in at 50.1 in June slightly down from 50.4 in May. Meanwhile, services sector activity contracted in June for the first time in about two years amid subdued new business as the flash services PMI slipped to 49.8 in June from 53.8 in May.

In FX, the Japanese yen (+0.03%) is trading around 159 versus the dollar, its weakest level in two-months and near the lows again, thus ramping up expectations that the authorities will again intervene in the FX market. Meanwhile, Masato Kanda, the top currency diplomat, reiterated that the authorities are prepared to take necessary measures if there are any highly volatile moves in currency markets.

To the day ahead now, and the main data highlight will be the flash PMIs for June from the US and Europe. Otherwise in the US we’ll get existing home sales for May and the Conference Board’s leading index for May, and in the UK there’s retail sales for May. From central banks, we’ll hear from the ECB’s Nagel and Simkus.

2B EUROPE OPENING/TRADING

Subdued risk tone following downbeat EZ PMIs with equities softer & bonds bid – Newsquawk US Market Open

FRIDAY, JUN 21, 2024 – 06:12 AM

Equities are subdued amid a broader risk aversion following the downbeat EZ PMI data

France, Germany and the EZ-wide figure all reported lower-than-expected PMI data, which has led to outperformance in Bunds and slight pressure in the EUR

Dollar is incrementally firmer, USD/JPY went as high as 159.12 before paring back towards 158.80 following the European data

Crude is rangebound, base metals suffer from the subdued risk tone

Looking ahead, US Manufacturing & Services PMI, Canadian Retail Sales, ECB’s Schnabel, and quad-witching

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

European bourses, Stoxx 600 (-0.4%) are lower across the board, though with price action fairly rangebound, and generally unreactive to the downbeat EZ PMI data.

European sectors are mostly lower, and hold a slight defensive bias, with Utilities and Healthcare towards the top of the pile, whilst Banks are towards the bottom of the pile, alongside Tech.

US Equity Futures (ES -0.1%, NQ -0.1%, RTY -0.1%) are very modestly lower, continuing some of the losses seen in the prior session, and in fitting with the broader sentiment in Europe.

DXY is slightly firmer amid the risk aversion which emanated from yesterday’s US session, with the index also benefiting from the weaker EUR following the downbeat EZ PMIs.

EUR is softer after France, Germany and the EZ all reported soft PMI figures, though with the accompanying release suggesting “the HCOB PMI do not provide ammunition for another rate cut in July by the ECB.” EUR/USD sits in a 1.0672-0720 range after testing levels near the 14th June low.

GBP is also losing vs the Dollar, with the hotter-than-expected UK Retail Sales providing fleeting upside for Cable, before edging lower ahead of the region’s own PMI data, which was mixed. Cable fell from 1.2649 to 1.2630 before paring the entirety of the move and lifting incrementally to 1.2653.

JPY is flat in the European morning following APAC weakness which saw softer-than-expected Japanese CPI and weaker PMI. USD/JPY briefly topped 159.00 to a 159.12 peak (vs low 158.68), with European strength possibly emanating from the risk aversion and a pullback in bond yields.

Mild divergence between the Antipodeans but largely flat trade with upside capped by the risk aversion (and decline in base metals).

USTs are modestly firmer and at the top-end of 110-12+ to 110-23 parameters into US PMI data and Fed’s Barkin.

Bunds are firmer, with price action dominated by EZ PMIs; French numbers missed and remained in contraction with the election perhaps factoring, with Germany and the EZ-wide figure also lower than expected. The metrics have lifted Bunds from c. 132.50 to a peak of 133.00, before stabilising around 132.80.

Gilts opened modestly firmer with impetus from benchmarks more broadly somewhat capped by a hawkish UK retail sales number. Tracking EGBs into the UK’s own PMIs which came in mixed and saw a knee-jerk spike to 99.14, before swiftly paring to below 99.00.

Crude is lower amid the stronger Dollar and the broadly downbeat risk tone across the market which reverberated from a lacklustre US performance. WTI August found some support at USD 81/bbl while Brent dipped under USD 85.50/bbl.

Mixed trade across precious metals with spot gold holding onto gains despite the stronger Dollar, with newsflow also relatively quiet this morning. Spot silver lags following yesterday’s outperformance. Spot gold resides near yesterday’s peak (USD 2,365.59/oz).

Copper futures pulled back from yesterday’s advances with demand sapped by the subdued risk tone.

Goldman Sachs sees minimal impact from new EU restrictions on Russian LNG. GS says the latest EU package of sanctions impacting Russia bans the transshipment of Russian LNG by member countries, but the measures do not block EU member states from importing Russian LNG.

Citi says crude markets are showing tightness, sees Brent picking up in Q3, but notes opportunities to sell into the strength

Global crude steel output rises 1.5% to 165.1mln tonnes in May 2024 vs May 2023; China crude steel output rises 2.7% Y/Y to 92.9mln tonnes in May 2024

French HCOB Composite Flash PMI (Jun) 48.2 vs. Exp. 49.5 (Prev. 48.9); HCOB Services Flash PMI (Jun) 48.8 vs. Exp. 50.0 (Prev. 49.3); HCOB Manufacturing Flash PMI (Jun) 45.3 vs. Exp. 46.8 (Prev. 46.4)

German HCOB Composite Flash PMI (Jun) 50.6 vs. Exp. 52.7 (Prev. 52.4); HCOB Services Flash PMI (Jun) 53.5 vs. Exp. 54.4 (Prev. 54.2); HCOB Manufacturing Flash PMI (Jun) 43.4 vs. Exp. 46.4 (Prev. 45.4). “This should be a further reason for the ECB to proceed cautiously with interest rate cuts.”

EU HCOB Composite Flash PMI (Jun) 50.8 vs. Exp. 52.5 (Prev. 52.2); HCOB Manufacturing Flash PMI (Jun) 45.6 vs. Exp. 47.9 (Prev. 47.3); HCOB Services Flash PMI (Jun) 52.6 vs. Exp. 53.5 (Prev. 53.2)