GOLD PRICE CLOSED DOWN $13.25 TO $2318.95

SILVER PRICE DOWN $0.63 TO $28.91

Gold ACCESS CLOSED $2318.75

Silver ACCESS CLOSED: $28.89

Bitcoin morning price:$61,488 DOWN UP 2109 DOLLARS.

Bitcoin: afternoon price: $62,105 DOWN 1492 dollars//

Platinum price closing DOWN $12.30 TO $985.80

Palladium price; DOWN $47.80 AT $943.00

END

SHANGHAI GOLD PREMIUM 45 DOLLARS/COMEX GOLD//JULY TO JULY

SHANGHAI GOLD (USD) FUTURES – QUOTES

SHANGHAI GOLD (USD) FUTURES – QUOTES

Last Updated 25 Jun 2024 02:37:29 AM CT.

Market data is delayed by at least 10 minutes.

I will now provide gold in Canadian dollars, British pounds and Euros

4: 15 PM ACCESS

*CANADIAN GOLD: $3167,30 DOWN 16.10 CDN dollars per oz( * NEW ALL TIME HIGH 3,305.30 CDN DOLLARS PER OZ//MAY 20 2024)

*BRITISH GOLD: 1827.75 DOWN 10.06 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2164.40 DOWN 7.30 Euros per oz //* (ALL TIME CLOSING HIGH: 2248.89 EUROS PER OZ//APRIL 16.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCH: COMEX

EXCHANGE: COMEX

CONTRACT: JUNE 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,330.000000000 USD

INTENT DATE: 06/24/2024 DELIVERY DATE: 06/26/2024

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 45

363 H WELLS FARGO SEC 11

657 C MORGAN STANLEY 47

726 C PLUS500US FINAN 3

737 C ADVANTAGE 29 3

880 H CITIGROUP 12

905 C ADM 6

991 H CME 26

TOTAL: 91 91

ACCESS MARKET

JPMorgan stopped 0/91

FOR JUNE 2024

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2024. CONTRACT: 91 NOTICES FOR 9100 OZ or 0.2830 TONNES

total notices so far: 30,438 contracts for 3,043,800 Oz (94.675 tonnes)

FOR JUNE:

SILVER NOTICES: 5 NOTICE(S) FILED FOR 25,000

OZ/

total number of notices filed so far this month :1336 for 6.680 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $13.25 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/

: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/ A STRONG 2.88 TONNES/WITHDRAWAL

/ /INVENTORY RESTS AT 829.05TONNES

INVENTORY RESTS AT 829.05 TONNES

SLV//WHAT!!!!!!

WITH NO SILVER AROUND AND SILVER DOWN $0.63 AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A MAMMOTH DEPOSIT OF 7.855 MILLION OZ OF SILVER VAPOUR INTO THE SLV//

// INVENTORY INCREASES TO 440.69 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 440.69 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUMONGOUS SIZED 1626 CONTRACTS TO 173,099 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS SURPRISING HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR TINY LOSS OF $0.05 IN SILVER PRICING AT THE COMEX ON MONDAY’S TRADING ON SILVER. WE HAD LITTLE LONG LIQUIDATION AS WE HAD A NET LOSS OF 818 CONTRACTS ON OUR TWO EXCHANGES. WE, AGAIN HAD MAJOR SHORT COVERING BY OUR SPECS WITH THE SMALL LOSS IN PRICE AS WELL AS MASSIVE T.A.S. LIQUIDATION WHICH ACCOUNTS FOR THE LOSS ON THE TWO EXCHANGES. WE HAD ANOTHER HUGE SIZED 818 T.A.S ISSUANCE,

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED TUESDAY JUNE 4 AND AGAIN ON FRIDAY, JUNE 7

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 959 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS.IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1/2 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.05) AND WERE SUCCESSFUL IN KNOCKING SOME SILVER LONGS FROM THEIR PERCH AS WE DID HAVE A HUGE SIZED LOSS OF 846 CONTRACTS ON OUR TWO EXCHANGES WITH THE LOSS IN PRICE OF $0.05.

WE MUST HAVE HAD:

A HUGED SIZED 780 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.830 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S NIL OZ QUEUE JUMP.

//NEW STANDING FOR SILVER//JUNE IS THUS 6.690 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI LOSS //HUGE SIZED EFP ISSUANCE/ VI) HUMONGOUS SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 959 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED 619 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE

TOTAL CONTRACTS for 16 DAYS, total 17,037 contracts: OR 85.185 MILLION OZ (1064 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 85.185 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 85.185 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1626 CONTRACTS DESPITE OUR TINY LOSS IN PRICE OF SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 780 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.830 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S NIL OZ QUEUE JUMP

//NEW TOTAL STANDING FOR JUNE 6.690 MILLION OZ

WE HAVE A HUGE SIZED LOSS OF 846 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE TINY LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUMONGOUS SIZED 959 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX TRADING/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND ZERO SOME LIQUIDATION OF LONGS.

THE NEW TAS ISSUANCE MONDAY NIGHT (959) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 5 NOTICE(S) FILED TODAY FOR 25,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 182 OI CONTRACTS TO 453,353 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: added 607 CONTRACTS

WE HAD A SMALL SIZED DECREASE IN COMEX OI (182 CONTRACTS) OCCURRED DESPITE OUR GAIN OF $14.30 IN PRICE/MONDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 89.94 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 6600 OZ QUEUE JUMP AS BANKERS SCOUR THE PLANET LOOKING FOR GOLD ON THE THIS SIDE OF THE POND

NEW STANDING 94.952 TONNES// ALL OF THIS HAPPENED WITH OUR $14.30 GAIN IN PRICE WITH RESPECT TO MONDAY’S TRADING. WE HAD A FAIR SIZED GAIN OF 1823 OI CONTRACTS (5.67 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2005 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 453,353

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1823 CONTRACTS WITH 182 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 2005 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 1216 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 1674 CONTRACTS,,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2005 CONTRACTS) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI OF 182 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 1823 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 88.761 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 0.2053 TONNES

//NEW STANDING /JUNE 94.952 TONNES.

/ 3) HUGE T.A.S. LIQUIDATION OF CONTRACTS WITH ZERO NET LONG SPECS BEING CLIPPED,

4) SMALL SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1674 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE. :

TOTAL EFP CONTRACTS ISSUED: 48,751 CONTRACTS OR 4,875,100 OZ OR 151.64 TONNES IN 16 TRADING DAY(S) AND THUS AVERAGING: 3116 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES 151.64 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 151.64 DIVIDED BY 3550 x 100% TONNES = 4.27% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 151.64 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 1626 CONTRACTS OI TO 173,099 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 780 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 780 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1708 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1626 CONTRACTS AND ADD TO THE 780 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 846 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 4.23 MILLION OZ

OCCURRED DESPITE OUR TINY $0.05 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED DOWN 13.10 PTS OR 0.44% //Hang Seng CLOSED UP 45.19 PTS OR 0.25%// Nikkei CLOSED UP 368.50 OR 0.95%//Australia’s all ordinaries CLOSED UP 1.28%///Chinese yuan (ONSHORE) closed DOWN TO 7,2626 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2862/ Oil UP TO 81.15 dollars per barrel for WTI and BRENT DOWN AT 85.74 /Stocks in Europe OPENED ALL RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 182 CONTRACTS TO 452,746 DESPITE OUR STRONG GAIN IN PRICE OF $14.30 WITH RESPECT TO MONDAY’S TRADING. WE HAD A HUGE T.A.S. LIQUIDATION ON MONDAY’S STRONG GAIN WITH ZERO LONGS BEING CLIPPED AND MAJOR SHORT COVERING.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 2005 EFP CONTRACTS WERE ISSUED: : AUGUST 2005 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2005 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 1823 CONTRACTS IN THAT 2005 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A SMALL SIZED LOSS OF 182 COMEX CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR STRONG GAIN IN PRICE OF $14.30/MONDAY COMEX

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT WAS A GOOD SIZED 1674 CONTRACTS. MOST OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN FRIDAY’S RAID

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (94.952 TONNES)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 94.952 TONNES. THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $14.30 //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR SIZED GAIN OF 1823 CONTRACTS ON MONDAY ON OUR TWO EXCHANGES ACCOMPANYING THE STRONG GAIN IN PRICE. THE T.A.S. ISSUED ON FRIDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 5.67 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE (89.94 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 66 CONTRACTS OR 6600 OZ (0.2053 TONNES)

NEW STANDING FOR JUNE: 94.952 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $14.30

WE HAVE ADDED 607 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET GAIN ON THE TWO EXCHANGES 1823 CONTRACTS OR 182,300 OZ (5.67 TONNES)

confirmed volume MONDAY 123,963 contracts//POOR

//speculators have left the gold arena

JUNE 25 JUNE GOLD CONTRACT

/ /// THE JUNE 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | NIL . |

| Deposit to the Dealer Inventory in oz | 0 oz |

| Deposits to the Customer Inventory, in oz | nilOZ |

| No of oz served (contracts) today | 91 notice(s) 9100 OZ 0.2830 TONNES |

| No of oz to be served (notices) | 89 contracts 8900 OZ 0.2768 TONNES |

| Total monthly oz gold served (contracts) so far this month | 30,438 notices 3,043,800 oz 94.675 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: NIL oz

we have 0 customer deposit:

customer withdrawals: 0

TOTAL WITHDRAWALS NIL

Adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE

For the front month of JUNE we have an oi of 180 contracts having LOST 0 contracts. We had 66 contracts served on Monday so we gained 66 contracts or 6600 oz additional ounces will stand for gold at the comex as they underwent a queue jump to take delivery on this side of the pond.

JULY GAINED 23 CONTRACTS TO STAND AT 2480

AUGUST LOST 2599 CONTRACTS DOWN TO 362,012 CONTRACTS

We had 91 contracts filed for today representing 9100 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 91 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for June /2024. contract month, we take the total number of notices filed so far for the month (30,438) x 100 oz ) to which we add the difference between the open interest for the front month of JUNE (180 CONTRACTS) minus the number of notices served upon today (91 x 100 oz per contract( equals 3,052,700 OZ OR 94.952 TONNES.

thus the INITIAL standings for gold for the JUNE contract month: No of notices filed so far (30,438 x 100 oz +we add the difference for front month of June (180// , OI} minus the number of notices served upon today (91) x 100 oz which equals 3,052,700 oz (94.952 TONNES)

TOTAL COMEX GOLD STANDING FOR JUNE: 94.952 TONNES WHICH IS ABSOLUTELY HUGE FOR THIS VERY ACTIVE DELIVERY MONTH IN THE CALENDAR. JUNE IS TRADITIONALLY THE 2ND HIGHEST DELIVERY MONTH OF THE YEAR. FROM THIS POINT WE WILL GAIN IN GOLD TONNAGE WILLING TO STAND AT THE COMEX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,682,975.981 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,576,275 OZ

TOTAL REGISTERED GOLD 7,811,970( 242.985 tonnes). cme CORRECTED

TOTAL OF ALL ELIGIBLE GOLD: 9,724,307.266 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,128,995 oz (REG GOLD- PLEDGED GOLD)= 190.63 tonnes //this is the lowest net registered in quite some time.

END

SILVER/COMEX

JUN 25/2024

INITIAL

//2024// THE JUNE 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 809,168,019 oz CNT . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | 592,,899.300 oz asahi |

| No of oz served today (contracts) | 5 CONTRACT(S) (25,000 OZ) |

| No of oz to be served (notices) | 2 contracts (0.010 million oz) |

| Total monthly oz silver served (contracts) | 1336 Contracts (6.680 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 customer deposits:

i) Into ASAHI 592,899.300 oz

total customer deposit 592,899.300oz

JPMorgan has a total silver weight: 127.832million oz/297.198million or 42.70%

adjustment: 0

Comex withdrawals: 1

i) Out of CNT 809,168.019 oz

total withdrawal: 809,168.019 0z

TOTAL REGISTERED SILVER: 69.293MILLION OZ//.TOTAL REG + ELIGIBLE. 297,195

million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE:

silver open interest data:

FRONT MONTH OF JUNE/2024 OI: 7 CONTRACTS HAVING LOST 13 CONTRACT(S).

WE HAD 13 NOTICES SERVED UP ON MONDAY, SO WE GAINED 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND AT THE COMEX VIA A NIL QUEUE JUMP

JULY SAW A LOSS OF 8200 CONTRACTS DOWN TO 43,213

AUG, SAW A GAIN OF 75 CONTRACTS TO 733

SEPT SAW A GAIN OF 6153 CONTRACTS TO 108,352

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 5 for 25,000 oz

CONFIRMED volume; ON MONDAY 80,020 HUGE

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1336 x 5,000 oz = 6.680 MILLION oz

to which we add the difference between the open interest for the front month of JUNE ((7) and the number of notices served upon today 5 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2024 contract month: 1336 notices served so far) x 5000 oz + OI for the front month of JUNE (7)x number of notices served upon today minus (5)x 5000 oz of silver standing for the JUNE contract month equates to 6.690 MILLION OZ.

New total standing: 6.690 million oz.

There are 63.429 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

JUNE 25 WITH GOLD DOWN $13.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A STRONG WITHDRAWAL OF 2.88 TONNES OF GOLD FROM THE GLD

INVENTORY RESTS AT 829.05 TONNES

JUNE 24 WITH GOLD UP$14.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A STRONG WITHDRAWAL OF 1.72 TONNES OF GOLD

/NEW TOTAL TONIGHT 831.93 TONNES

JUNE 21 WITH GOLD DOWN $37.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A MAMMOTH 8.34 TONNES OF GOLD VAPOUR DEPOSIT/NEW TOTAL TONIGHT 833.65 TONNES

JUNE 20 WITH GOLD UP $23.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/://NEW TOTAL TONIGHT 825.31 TONNES

JUNE 18 WITH GOLD UP $17.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/://NEW TOTAL TONIGHT 825.31 TONNES

JUNE 17 WITH GOLD DOWN $18.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.03 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 825.31 TONNES

JUNE 13 WITH GOLD DOWN$35.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.89 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 830.78 TONNES

JUNE 12 WITH GOLD UP $28.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.89 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 830.78 TONNES

JUNE 11 WITH GOLD DOWN $0.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 10 WITH GOLD UP $2,00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 7 WITH GOLD DOWN $64.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 3.56 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 837.11 TONNES

JUNE 6 WITH GOLD UP $16.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.34 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 833.55 TONNES

JUNE 5 WITH GOLD UP $32.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 4 WITH GOLD DOWN $20.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 3 WITH GOLD UP $22.85 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 31 WITH GOLD DOWN $19.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 30 WITH GOLD UP $3.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 29 WITH GOLD DOWN $13.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 28 WITH GOLD UP $22.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 832.21 TONNES

MAY 24 WITH GOLD DOWN $2.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 833.36 TONNES

MAY 23 WITH GOLD DOWN $53.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 22 WITH GOLD DOWN $32.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 21 WITH GOLD DOWN $12,00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 20 WITH GOLD UP $21.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.10 TONNES OF GOLD INTO THE GLD//NEW TOTAL 838.54 TONNES

MAY 17 WITH GOLD UP $31.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//NEW TOTAL 833.36 TONNES

MAY 16 WITH GOLD DOWN $7.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//NEW TOTAL 833.36 TONNES

MAY 15 WITH GOLD UP $34.90 ON THE DAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD/INVENTORY RISES TO 831.93 TONNES

MAY 14 WITH GOLD DOWN $17.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RISES TO 831.33 TONNES

GLD INVENTORY: 829.05 TONNES, TONIGHTS TOTAL

SILVER

JUNE 25. WITH SILVER DOWN $0.63//HUGE CHANGES IN SILVER INVENTORY: A MAMMOTH DEPOSIT OF 7.835 MILLION OZ OF SILVER VAPOUR INTO THE SLV.// /INVENTORY RISE TO 440.69 MILLION OZ.//WHAT AN ABSOLUTE FRAUD.

JUNE 24. WITH SILVER DOWN $0.05//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 2.104 MILLION OZ FROM THE SLV.// /INVENTORY LOWERS TO 432.835 MILLION OZ.

JUNE 21. WITH SILVER DOWN $1.15//NO CHANGES IN SILVER INVENTORY’// /INVENTORY REMAINS AT 434.935 MILLION OZ.

JUNE 20. WITH SILVER UP $1.17//HUGE CHANGES IN SILVER INVENTORY’ A DEPOSIT OF 5.164 MILLION OZ INTO THE SLV/// /INVENTORY RISES TO 434.929 MILLION OZ.

JUNE 18. WITH SILVER UP $0.21//NOCHANGES IN SILVER INVENTORY’ A WITHDRAWAL .730 MILLION OZ INTO THE SLV/// /INVENTORY FALLS TO 429.775 MILLION OZ.

JUNE 17. WITH SILVER UP $0.21//SMALL CHANGES IN SILVER INVENTORY’ A WITHDRAWAL .730 MILLION OZ INTO THE SLV/// /INVENTORY FALLS TO 429.775 MILLION OZ.

JUNE 14. WITH SILVER DOWN $0.10//NO CHANGES IN SILVER INVENTORY/ /INVENTORY REMAINS AT 429.083 TONNES

JUNE 13. WITH SILVER DOWN $1.10//HUGE CHANGES IN SILVER INVENTORY/ A HUGE DEPOSIT OF 1.958 MILLION OZ/INVENTORY RISES TO 429.083 TONNES

JUNE 12 WITH SILVER UP $0.97 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 5.983 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 427.125 MILLION OZ

JUNE 11 WITH SILVER DOWN $0.59 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.644 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 422.786 MILLION OZ

JUNE 10 WITH SILVER UP $0.30 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 3.198 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 421.142 MILLION OZ

JUNE 7 WITH SILVER DOWN $1.93 TODAY: NO CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY AT 417.944 MILLION OZ

JUNE 6 WITH SILVER UP $1.27 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 417.944 MILLION OZ

JUNE 5 WITH SILVER UP 0.38 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.52 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 415.295 MILLION OZ

JUNE 4 WITH SILVER DOWN $1.08 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

JUNE 3 WITH SILVER UP $0.35 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

MAY 31 WITH SILVER DOWN $1.09 TODAY: HUGE CHANGES IN SILVER INVENTORY: A MASSIVE WITHDRAWAL OF 3.655 MILLION OZ FROM THE SLV//INVENTORY LOWERS TO 413.775 MILLION OZ

MAY 30 WITH SILVER DOWN $0.80 TODAY: NO CHANGES IN SILVER INVENTORY//INVENTORY REMAINS AT 417.430 MILLION OZ

MAY 29 WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 1.051 MILLION OZ INTO THE SLV//INVENTORY DECREASES TO 417.430 MILLION OZ

MAY 28 WITH SILVER UP $1.64 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 2.832 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 418.481 MILLION OZ

MAY 24 WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF .822 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 421.313 MILLION OZ

MAY 23 WITH SILVER DOWN $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.736 MILLION OZ FROM THE SLVINVENTORY INCREASES TO 420.491 MILLION OZ

MAY 22 WITH SILVER DOWN $0.66 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 21 WITH SILVER DOWN $0.41 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A DEPOSIT OF 3.792 MILLION OZ FROM THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 20 WITH SILVER UP $1.28 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 1.005 MILLION OZ FROM THE SLV// INVENTORY LOWERS TO 418.435 MILLION OZ

MAY 17 WITH SILVER UP $1.37 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 868,000 OZ FROM THE SLV// INVENTORY LOWERS TO 419.440 MILLION OZ

MAY 16 WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY REMAINS AT 420.308 MILLION OZ

MAY 15 WITH SILVER UP 101 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A WITHDRAWAL OF 1.919 MILLION OZ FROM THE SLV NVENTORY RESTS AT 420.308 MILLION OZ

MAY 14 WITH SILVER UP 25 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;INVENTORY RESTS AT 422.227 MILLION OZ

CLOSING INVENTORY 434.935 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

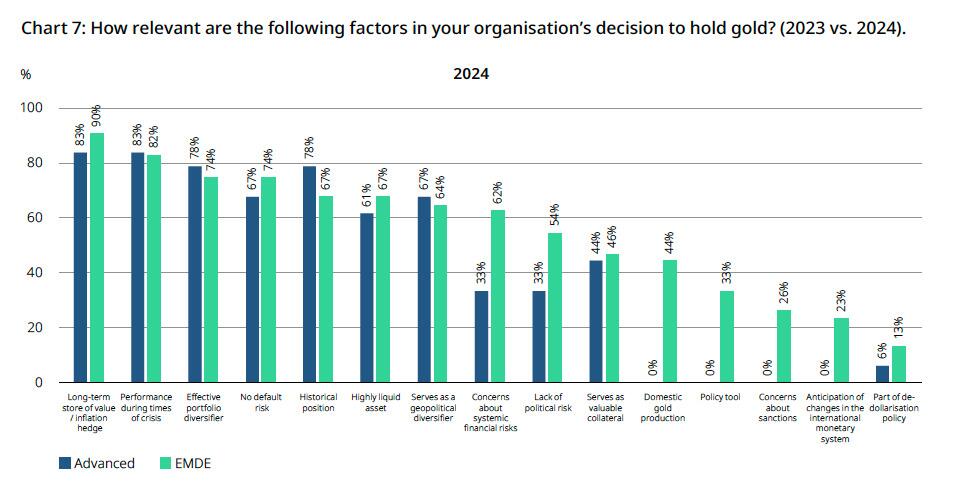

Central Banks’ Appetite For Gold Hasn’t Been Satisfied

TUESDAY, JUN 25, 2024 – 10:20 AM

Authored by Mike Maharrey via Money Metals,

Central banks have been gobbling up gold, and based on responses to the World Gold Council’s 2024 Central Bank Gold Reserves Survey, their appetites for the yellow metal aren’t going to be satisfied any time soon.

Last year, central banks added a net 1,037 tons of gold to their reserves, just slightly below the record of 1,082 tons in the previous year.

That pace of buying will likely continue.

Based on a World Gold Council survey that included 70 respondents, 29 percent of central banks plan to add more gold to their reserves in the next 12 months. The WGC said it was the highest level since the survey began in 2018.

Only 3 percent said they had plans to decrease gold reserves.

Eighty-one percent of the respondents said they expect overall global gold reserves to increase in the next 12 months. That was up from 71 percent in the 2023 survey.

Meanwhile, 69 percent of the central bankers surveyed said they think global gold reserves will be higher in five years. That was up from 62 percent in last year’s survey. In 2022, only 46 percent of the respondents thought gold reserves would be higher in five years.

The results would seem to indicate the panic and gold selloff that happened recently when China didn’t announce any change to its reserves for the first time in well over a year was probably overblown. Central banks aren’t about to stop increasing their gold reserves any time soon.

Why Gold?

Why do central banks hold gold in their reserves?

According to the World Gold Council, “[Gold] purchases are chiefly motivated by a desire to rebalance to a more preferred strategic level of gold holdings, domestic gold production, and financial market concerns including higher crisis risks and rising inflation.”

When asked about specific factors that influence overall reserve decisions, interest rate levels ranked first. Inflation concerns and geopolitical instability were the second and third biggest factors influencing reserve decisions.

A growing number of emerging market central bankers said they were concerned about shifts in global economic power. This likely reflects the growing de-dollarization trend and worries that the U.S. and other Western powers could use the dollar as a foreign policy weapon. In fact, 32 percent of the central bankers surveyed admitted that de-dollarization was a factor in their decisions to hold gold.

Central banks specifically hold gold for several reasons.

The number one reason is gold serves as a long-term store of value, and it creates a hedge against inflation.

Other key reasons given for holding gold were its performance during times of crisis, its role as a portfolio diversifier, and the fact that there is no default risk.

Emerging and developing market central banks view risks differently than those in developed markets. A higher proportion of EMDE central banks viewed the following factors as more relevant to their decision to hold gold:

- Concerns about systemic financial risks

- Lack of political risk

- Concerns about sanctions

- Anticipations of changes in the international monetary system

This likely reflects the ongoing shift of gold from the West to the East. Policymakers in the U.S. and Europe don’t seem to grasp the significance of this shift.

Mike Maharrey is a journalist and market analyst for MoneyMetals.com with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY

end

CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES

Maguire, Macleod discuss monetary metals’ future on ‘Live from the Vault’

Submitted by admin on Sat, 2024-06-22 22:11 Section: Daily Dispatches

10:11p ET Saturday, June 22, 2024

Dear Friend of GATA and Gold (and Silver):

GoldMoney research director Alasdair Macleod is the guest on this week’s edition of Kinesis Money’s “Live from the Vault” program with London metals trader Andrew Maguire.

They discuss Russia’s defeat of Western economic sanctions, the world’s diminishing fear of the United States, the possibility of de-facto gold standards in Asia, the prospects for a gold-related BRICs currency, the heavy involvement of China and India with gold, whether silver will outperform gold, and bitcoin.

The discussion is an hour and 15 minutes long and can be viewed at YouTube here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

Bank information may be at risk in Russian attempt to blackmail Fed

Submitted by admin on Mon, 2024-06-24 21:57 Section: Daily Dispatches

From Money Metals News Service, Eagle, Idaho

Monday, June 24, 2024

A Russian hacking organization appears to be in the process of blackmailing the Federal Reserve.

On June 23 the criminal organization LockBit 3.0, a Russian ransomware cybercriminal group, publicly stated that it hacked the Federal Reserve and implied it would release more than “33 terabytes of juicy banking information containing details of Americans’ banking secrets” unless a large ransom is paid

More specifically, the cyber-terrorist organization says the Federal Reserve and the U.S. government have until this afternoon, June 24, at 4:27 p.m. ET to comply with its undisclosed monetary demands. …

… For the remainder of the report:

end

Thanks, Julian Assange, for some truth about gold price suppression

Submitted by admin on Mon, 2024-06-24 21:29 Section: Daily Dispatches

9:44p ET Monday, June 24, 2024

Dear Friend of GATA and Gold:

Call us traitors if you want, but advocates of free and transparent markets in the monetary metals may be pleased by tonight’s reports that Wikileaks founder Julian Assange has a plea deal with the U.S. government that will convict him of a felony charge of conspiring to obtain and distribute classified information, sentence him to time served in the United Kingdom while resisting extradition, and allow him to return to his native Australia.

end

Pam and Russ Martens: Fed and FDIC suddenly awaken to the threat of big banks’ derivatives

Submitted by admin on Mon, 2024-06-24 11:33 Section: Daily Dispatches

By Pam and Russ Martens

Wall Street on Parade

Monday, June 24, 2024

Since the financial crash of 2008 and the Federal Reserve’s multi-trillion-dollar bank bailouts that followed, the Office of the Comptroller of the Currency has been waving a giant red flag every quarter in its Bank Trading and Derivatives Activities reports.

For 16 years the OCC has been reporting that just four megabanks are responsible for more than 80% of the trillions of dollars in bank derivatives.

As the chart published with this report shows, as of December 31, 2023, Goldman Sachs Bank, JPMorgan Chase Bank, Citigroup’s Citibank, and Bank of America held a staggering total of $168.26 trillion in derivatives out of a total of $192.46 trillion at all U.S. banks, savings associations and trust companies.

That’s four banks holding 87% of all derivatives at all 4,587 federally-insured institutions in the U.S. that existed as of December 31, 2023.

Now it would appear that some market-savvy bank examiner embedded in one of those megabanks has had an epiphany and decided to ask the question: “How is it possible that all four of these megabanks with trillions of dollars in derivatives happened to be on the correct sides of these trades during the fastest and steepest interest rate increases in 40 years?”

Multiple bank counterparties to these trades should be reporting massive losses and yet all we hear are crickets. …

… For the remainder of the analysis:

* * *

end

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS/

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COPPER

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

ASIA TRADING//TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED DOWN 13.10 PTS OR 0.44% //Hang Seng CLOSED UP 45.19 PTS OR 0.25%// Nikkei CLOSED UP 368.50 OR 0.95%//Australia’s all ordinaries CLOSED UP 1.28%///Chinese yuan (ONSHORE) closed DOWN TO 7,2626 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2862/ Oil UP TO 81.15 dollars per barrel for WTI and BRENT DOWN AT 85.74 /Stocks in Europe OPENED ALL RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2626

OFFSHORE YUAN: DOWN TO 7.2862

SHANGHAI CLOSED DOWN 13.10 PTS OR 0.44 %

HANG SENG CLOSED UP 45.19 PTS OR 0.25%

2. Nikkei closed UP 368.50 PTS OR 0.95 %

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 105.22 EURO FALLS TO 1.0717 UP 43 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +0.990 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 159.48 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.3880/Italian 10 Yr bond yield DOWN to 3.907 SPAIN 10 YR BOND YIELD UP TO 3.295%

3i Greek 10 year bond yield DOWN TO 3.592

3j Gold at $2329.25//Silver at: 29.47 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 52/ 100 roubles/dollar; ROUBLE AT 87,60

3m oil into the 81 dollar handle for WTI and 85 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 159.48/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.990% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8936 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9573 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.228 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.357 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.730 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.95…

10 YR UK BOND YIELD: 4.082 DOWN 2 PTS

2a New York OPENING REPORT

Futures Rise As Nvidia Rebound From 3-Day Rout

TUESDAY, JUN 25, 2024 – 08:17 AM

US index futures are higher, led by a rebound in the tech names in general and Nvidia in particular which rose as much as 3.5% in premarket trading after getting routed by a three-day, 13% selloff that wiped out $430 billion in market cap and saw it drop back into 3rd place behind Microsoft and Apple, after briefly becoming the world’s most valuable company last week. As of 8:00am ET, S&P futures are up 0.1% while Nasdaq futures gain 0.4%. European stocks are in the red, led lower by industrial names, while Asian equities gained, snapping a three-day losing streak, as advances in value stocks helped offset weakness in the tech sector. Bond yields reversed a modest rebound and have extended their Monday drop with 10Y TSYs trading at session lows of 4.21%, down 2bps, while the USD is at session highs. Commodities are mostly lower, particularly base metals and Ags. Overnight, the news flow was relatively quiet as investors are mostly digesting the tech correction. Today, we will receive Conf. Board Consumer Confidence data at 10am. On earnings, FDX will report after market close.

In premarket-trading, the Mag 7/Semiconductor space rebounded from yesterday’s selloff: NVDA +3.1%, MU +1.5%, AVGO +1.1%, AAPL +38bp, GOOG/L +27bp, AMZN +11bp. Spirit Aero dropped 4% after Bloomberg News reported that Boeing switched its proposed funding from an all-cash offer to a deal funded mostly by stock. Here are some other notable premarket movers:

- Birkenstock (BIRK) falls 3% after holder L. Catterton Management offered 14 million shares.

- Gap (GPS) advances 4% after TD Cowen upgraded the retailer to buy, saying the company is in the “early innings” of a transformation across all four of its brands.

- Pool Corp. (POOL) slides 11% after the distributor of swimming pool supplies slashed its earnings per share forecast for the full year, citing challenges in the discretionary parts of its business amid cautious consumer spending.

- SolarEdge Technologies (SEDG) tumbles 17% after the solar equipment maker said a customer filed for bankrupcy and the company may fail to collect the $11.4 million it is owed.

- Trump Media & Technology (DJT) climbs 8%, putting the stock on track for three straight sessions of gains.

Tech shares have been the focus of US markets this week with traders rebalancing their portfolios as the quarter draws to a close. They’ve been taking profits from the AI-driven frenzy for tech stocks and switched into value shares and other laggards. The retreat in technology shares was “purely an investor/sentiment story,” Danske Bank analysts wrote in a note. “The fundamentals remain unchanged from a week ago.”

Meanwhile, there are signs that calm is returning to French markets, with yield spreads over Germany retreating from the highest level in over a decade. Jordan Bardella, the leader of the National Rally party which is leading the polls, sought to reassure investors on Monday with assurances that he will not upend the country’s finances if his party wins an absolute majority.

Later, the US Treasury kicks off this week’s trio of bond sales with an offering of $69 billion in two-year notes. Demand for the shorter, rates-sensitive debt is expected to be stronger than at last month’s offering, coming ahead of statistics on Friday that are forecast to show a slowdown in the Fed’s favored inflation gauge.

Stocks in Europe retreated 0.3% led by weakness in materials, utilities and communications sectors; markets were weighed by a drop of more than 10% for planemaker Airbus SE, which lowered its guidance amid persistent supply-chain issues. Germany’s Merck KGaA also tumbled, following a second surprise failure of a promising medicine. Here are the most notable European movers:

- Neoen shares gain as much as 2.8% after announcing the signing of an agreement for the purchase by Brookfield of a majority stake in the renewable energy developer from Impala and other shareholders.

- Evotec shares rise as much as 3.7% as the German pharmaceutical company announced a new US Department of Defense contract for its Seattle-based subsidiary Evotec Biologics.

- Hornbach shares climb as much as 5% as a strong improvement in first-quarter earnings overshadows cautious full-year guidance from the German building materials retailer.

- Fagerhult shares gain as much as 3.2% following an initiation at buy on the lighting systems manufacturer by SEB Equities, which expects an acceleration in both growth and margins.

- Airbus shares slump as much as 9.8%, the most since Nov. 2021, after lowering both its earnings and aircraft-delivery targets, citing supply-chain issues. Deutsche Bank cuts its rating to hold.

- Merck KGaA shares drop as much as 11% after the German pharmaceutical and chemicals company discontinued late-stage trials of xevinapant in locally advanced head and neck cancer.

- Continental shares fall as much as 1.1% after analysts at Warburg Research cut the German auto supplier’s price target to €75 from €92 on a weaker-than-expected market environment.

- Fluidra shares drop as much as 7.7%. The Spanish swimming pool maker falls after after equipment distributor Pool Corp. issued a profit warning.

- Ocado shares drops as much as 4% after Morgan Stanley slashes its PT to a new Street-low of 215p, with further downside expected following the latest customer fulfillment center postponement.

- Meyer Burger shares jump as much as 27% after the Swiss solar panel maker announced it made progress regarding business relocation to the US and external financing.

- Trigano shares decline as much as 4.6% as analysts become more cautious on the motorhome maker’s prospects in FY25 due to headwinds including lower prices and excess inventory levels.

- Fincantieri shares dropped back on Milan stock exchange in early Tuesday trading, giving up some of Monday’s gains after the Italian shipbuilder launched a €400 million capital increase.

Earlier, Asian markets rebounded as advances in some value stocks helped offset weakness in the tech sector. The MSCI Asia Pacific Index rose as much as 1%, led by consumer discretionary and industrial shares. Japan and Australia were the biggest gainers in the region, while a gauge of Chinese stocks listed in Hong Kong climbed as traders moved away from semiconductors into other parts of the market. Chip-related shares extended their recent rout after Nvidia entered a technical correction amid a pause in the AI frenzy. Meanwhile, some of the biggest boosts to the Asian gauge Tuesday included auto, financial and miner stocks.

- Hang Seng and Shanghai Comp. were mixed in which the Hong Kong benchmark advanced as strength in consumer and property stocks atoned for the slack seen in some tech names, while the mainland lagged despite the PBoC’s liquidity boost with headwinds from US-China frictions as the Biden administration probes Chinese telcos. Furthermore, Premier Li flagged weak global economic momentum during his WEF address in Dalian.

- Nikkei 225 shrugged off the initial indecision and gradually reverted to above the psychological 39,000 level.

- ASX 200 outperformed with energy and real estate leading the advances amid broad optimism across sectors.

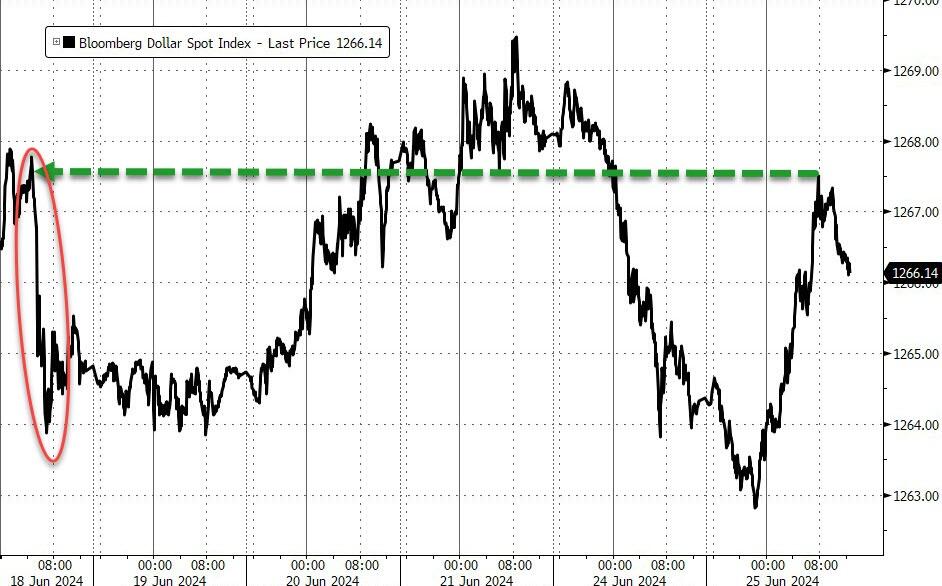

In FX, the Bloomberg Dollar Index gained 0.1%, reversing an earlier loss, with minimal moves across G-10 FX. USD/JPY was down 0.2% to 159.33 and AUD/USD little changed at 0.6659. GBP/USD rises 0.1% to 1.2695 with EUR/USD up 0.1% to 1.0740.

In rates, treasuries reverse earlier losses, with 2-year yields flat at 4.72% while 10-year yields dropped 2bps to 4.21% and 30-year yields were little changed at 4.365% as long-end outperformance deepens inversion of 2s10s spread past 50bp for first time since December. In core European rates, bunds and gilts outperform despite heavy auction slate that included Italy, UK and Germany selling a mix of linkers and bonds. French government bonds gain, outperforming their German peers and narrowing the 10-year yield spread by ~1bps to around 75.5bps. The US auction cycle begins with $69 billion 2-year note sale, followed by $70 billion 5-year and $44 billion 7-year Wednesday and Thursday. WI 2-year yield at around 4.680% is ~24bp richer than May’s, which tailed by 1bp.

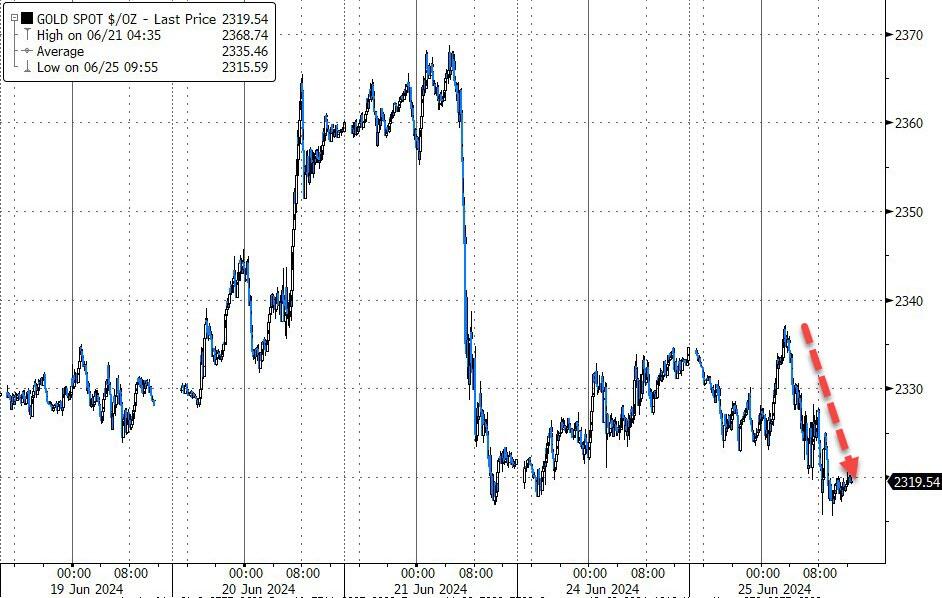

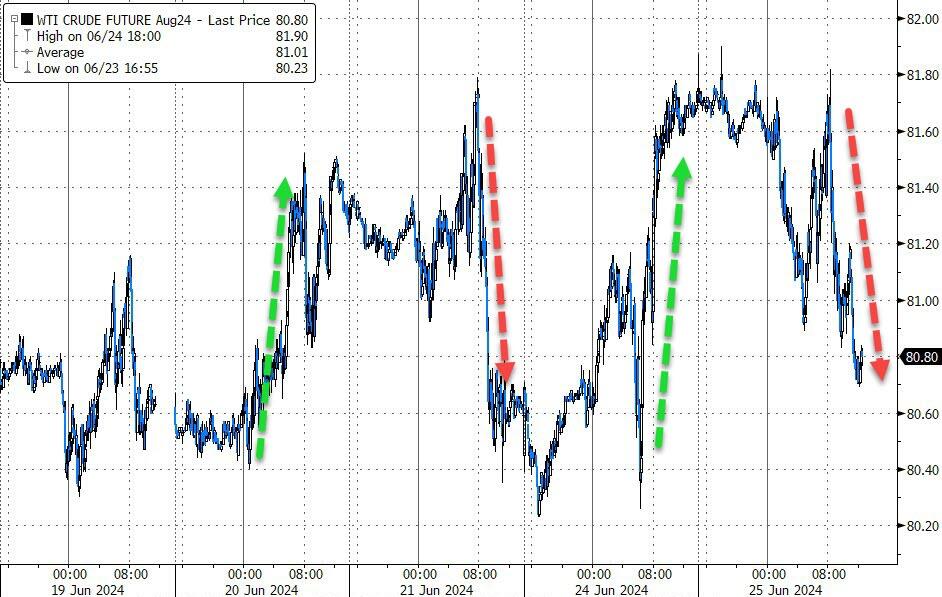

In commodities, oil prices decline, with WTI falling 0.5% to near $81.30. Spot gold falls ~$2 to around $2,333. Bitcoin rises over 2%.

Looking at today’s calendar, US economic data slate includes June Philadelphia Fed non-manufacturing activity and May Chicago Fed national activity index (8:30am), April S&P CoreLogic home prices (9am), June consumer confidence and Richmond Fed manufacturing index (10am) and June Dallas Fed services activity (10:30am). Fed officials scheduled to speak include Cook (12pm) and Bowman (2:10pm); speaking earlier Tuesday, Bowman reiterated her view that it’s too soon to cut interest rates

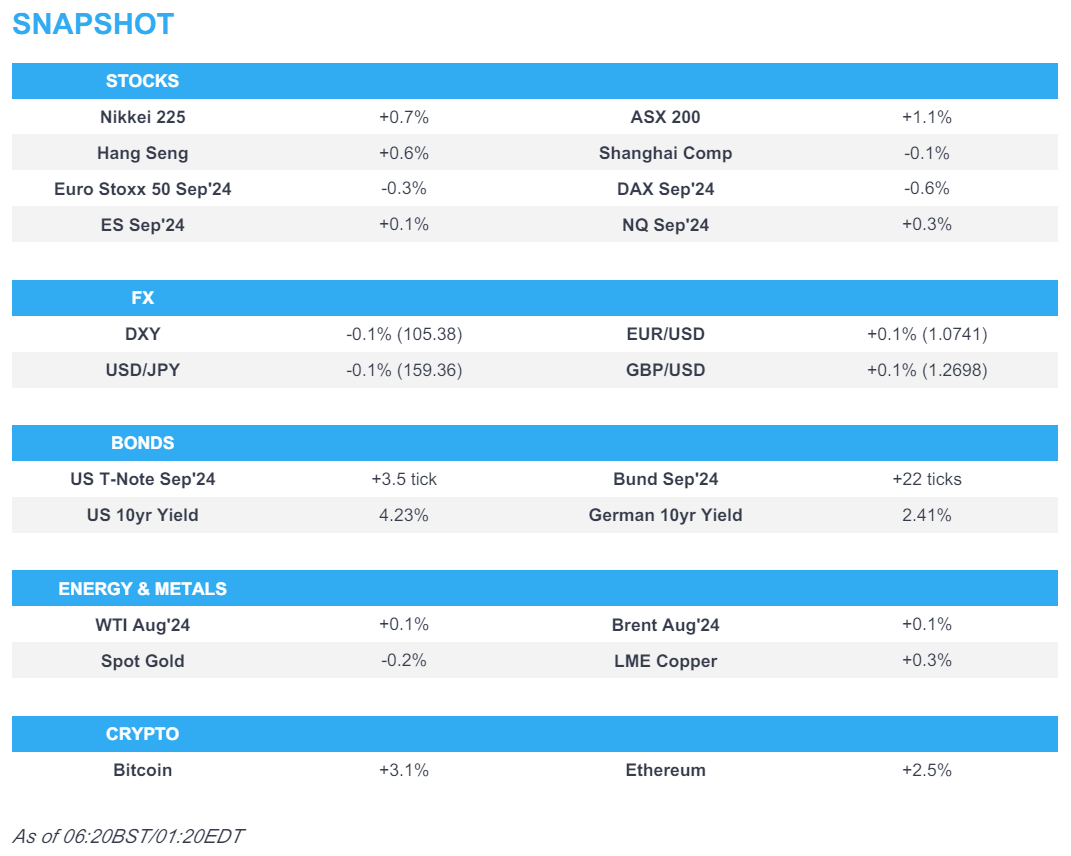

Market Snapshot

- S&P 500 futures up 0.1% to 5,523.00

- STOXX Europe 600 down 0.3% to 517.26

- MXAP up 0.9% to 180.55

- MXAPJ up 0.4% to 567.20

- Nikkei up 0.9% to 39,173.15

- Topix up 1.7% to 2,787.37

- Hang Seng Index up 0.3% to 18,072.90

- Shanghai Composite down 0.4% to 2,950.00

- Sensex up 0.8% to 77,959.91

- Australia S&P/ASX 200 up 1.4% to 7,838.79

- Kospi up 0.3% to 2,774.39

- German 10Y yield little changed at 2.41%

- Euro little changed at $1.0733

- Brent Futures little changed at $85.96/bbl

- Gold spot down 0.4% to $2,326.28

- US Dollar Index little changed at 105.47

Top Overnight News

- BOJ could be setting the stage for a “hawkish double surprise” next month with a tapering of QE coupled with a rate hike. RTRS

- Chinese telecom firms (China Mobile, China Telecom, China Unicom) face scrutiny in Washington over their access to American internet data. RTRS

- In November last year, President Biden and Chinese leader Xi Jinping agreed to boost engagement between ordinary Chinese and Americans, part of an effort to repair fraying ties ahead of a tense election year in the U.S. Instead, says Nicholas Burns, Washington’s ambassador in Beijing, China has actively undermined those ties, interrogating and intimidating citizens who attend U.S.-organized events in China, ramping up restrictions on the embassy’s social-media posts and whipping up anti-American sentiment. WSJ

- Trump considering a plan whereby the US would threaten to withhold further aid to Ukraine unless it entered into peace talks w/Russia. RTRS

- Israel’s top court told the government to begin drafting Ultra-Orthodox men for army service and stop funding seminaries whose students avoid conscription. It adds to pressure on PM Benjamin Netanyahu, whose coalition is supported by religious parties that oppose any change. BBG

- Julian Assange has left the UK after striking a plea deal with US prosecutors to end the WikiLeaks founder’s legal saga over leaked documents and allow him to walk free after years of incarceration and confinement. FT

- Brussels has accused Microsoft of anti-competitive behaviour by bundling its Teams app with its Office suite, in the first such antitrust charges brought against the tech group in more than a decade. FT

- Novo Nordisk A/S plans to invest $4.1 billion in another US factory, plowing more money into its biggest market amid rising discontent over the cost of its obesity and diabetes drugs. The project in Clayton, North Carolina, will double the company’s production footprint in the US, adding 1.4 million square feet of space for the final stages of manufacturing in which Novo’s medicines are filled into injector pens and prepared for consumers. BBG

- Boeing offered to buy Spirit AeroSystems in a mostly-stock deal that values the supplier at about $35 per share, people familiar said. The change from an all-cash bid should ease some of the squeeze on the cash-strapped planemaker. BBG

- Federal judges in Kansas and Missouri blocked parts of President Biden’s student debt relief plan, while the White House later said that it strongly disagreed with the ruling on Biden’s student loan plan,: Reuters.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly positive but with some of the gains capped following the mixed lead from Wall St where tech underperformed amid Nvidia’s continued retreat from last week’s record high into correction territory. ASX 200 outperformed with energy and real estate leading the advances amid broad optimism across sectors. Nikkei 225 shrugged off the initial indecision and gradually reverted to above the psychological 39,000 level. Hang Seng and Shanghai Comp. were mixed in which the Hong Kong benchmark advanced as strength in consumer and property stocks atoned for the slack seen in some tech names, while the mainland lagged despite the PBoC’s liquidity boost with headwinds from US-China frictions as the Biden administration probes Chinese telcos. Furthermore, Premier Li flagged weak global economic momentum during his WEF address in Dalian.

Top Asian News

- Chinese Premier Li called for facing up to the difficulty of global economic growth and said that weak global economic growth momentum was hit by Covid, high inflation and increasing debt, while he added that economic growth is becoming more difficult to achieve and noted that decoupling and protectionism will only raise economic costs for the world. Furthermore, he said they should seize the new opportunities of the tech revolution and industrial transformation and they are confident and capable of achieving the full-year growth target of around 5%, as well as noted that the Chinese economy is expected to continue to show steady improvement in Q2.

- US President Biden’s administration is investigating China Telecom (728 HK), China Mobile (941 HK) and China Unicom (762 HK) with the probe focused on potential national security risks from their US cloud and internet infrastructure, according to Reuters sources

- Japan is to revise January-March GDP to reflect corrected data on construction orders from the Land Ministry with the revised figure to be released on July 1st 00:50BST, according to the Cabinet Office.

- Japanese Finance Minister Suzuki says shared serious concerns over weakness of JPY and KRW with the South Korean Finance Minister. Will continue to respond appropriately to excessive FX moves; desirable for FX to move stably.

European bourses, Stoxx 600 (-0.3%) are almost entirely in the red, with sentiment hit following updates from Airbus (-9.8%) and Merck (-9.7%) (detailed in Notable European Headlines). European sectors are mixed; Industrials are the clear laggard after Airbus cut its 2024 delivery guidance, which has weighed on the entire sector. Tech is also towards the foot of the pile, with ASML (-2.2%) and ASM International (-2.1%) both suffering. US Equity Futures (ES +0.1%, NQ +0.3%, RTY +0.2%) are very modestly firmer, with mild outperformance in the NQ as Nvidia (+2.1% pre-market) finally edges higher after dropping around 11% over the past 5 days.

Top European News

- Airbus (AIR FP) cuts 2024 delivery guidance: now targeting around 770 (prev. 800) commercial aircraft deliveries in 2024, the production rate of 75 A320 family aircraft a month is maintained but now expected to be reached in 2027 (prev. 2026); Targets adj. EBIT of around EUR 5.5bln in 2024 (prev. 6.5-7bln). Targets FCF of EUR 3.5bln (prev. 4bln) before customer financing. To record charges of around EUR 900mln in H1’24 accounts. Facing persistent specific supply chain issues mainly in engines, aerostructures, and cabin equipment. Elsewhere, reportedly has a backlog of several undelivered wide-bodied airliners without engines parked outside its Toulouse factory; jets are reportedly waiting for seats, engines and other parts, according to Reuters citing sources. CEO says Spirit AeroSystems (SPR) situation is difficult from an industrial standpoint. Says uncertain outlook for Spirit commitments contributed to the decision to cut Airbus output targets. Supply chain is improving but not in a uniform place. (Newswires/Reuters) Shares – 9.8% in European trade

- Merck (MRK GY) ceased the Phase III TrilynX study for xevinapant in unresected locally advanced squamous cell carcinoma of the head and neck due to unlikely efficacy in extending event-free survival, despite compatible safety data. Merck KHaA will review findings for publication. Shares – 9.9% in European trade

FX

- DXY has been pivoting around the 105.50 mark after yesterday’s selling brought it down from a 105.90 high. It can be noted that month-end models point towards USD selling vs. peers. Docket ahead includes Philly Fed Nonmanufacturing Business Outlook Survey, Richmond Fed Index and speak from Fed’s Bowman and Cook.

- EUR is steady vs. the USD in quiet newsflow. Focus remains on French political risk, however, broader follow-through into the EUR is contained. For now, EUR/USD sits towards the top end of yesterday’s 1.0683-1.0746 range.

- GBP a touch firmer vs. both USD and EUR in quiet newsflow with a lack of tier 1 highlights due this week and the BoE observing its quiet period ahead of next month’s UK general election. Cable remains capped by resistance at 1.27. If breached, the 10DMA sits just above at 1.2704 with the 20th June high at 1.2724.

- JPY is edging mild gains vs. the USD after topping out yesterday at 159.93. Commentary from Finance Minister Suzuki continued to attempt to talk up the JPY, but sparked little move in the pair. Currently USD/JPY holds around 159.50 with a notable OpEx at 160.00.

- Antipodeans are mixed vs. the USD with AUD the marginal outperformer across the majors. Newsflow for AUD has been light, however, AUD/USD has been able to build on the prior day’s gains. NZD/USD is currently tucked within yesterday’s 0.6104-40 range.

- PBoC set USD/CNY mid-point at 7.1225 vs exp. 7.2587 (prev. 7.1201).

Fixed Income

- USTs are rangebound and essentially unchanged ahead of survey data, June’s Consumer Confidence and then the beginning of the week’s supply docket with a USD 69bln 2yr sale. USTs currently sits around 110-18.

- Bunds are contained with specific macro drivers sparse thus far though Bunds are at the lower-end of 132.42-65 parameters (132.47 is a 50% Fib of Monday’s move).

- Gilt price action is in-fitting with peers with the docket once again sparse as we count down to the upcoming election. Holding in a very slim 14 tick range which is entirely within Monday’s 98.38-98.76 bounds.

- UK sells GBP 1.5bln 0.75% 2033 I/L Gilt: b/c 2.89x (prev. 3.4x) and real yield 0.518% (prev. 0.440%)

- Italy sells EUR 2.5bln vs exp. EUR 2-2.5bln 3.20% 2026 Short Term BTP and EUR 2.25bln vs exp. EUR 1.25-2.25bln 0.40% 2030 & 2.40% 2039 BTPei

- Germany sells EUR 3.646bln vs exp. EUR 4.5bln 2.90% 2026 Schatz: b/c 2.4x (prev. 2.7x) & avg. yield 2.8% (prev. 3.01%) and retention 18.98%% (prev. 18.02%)

Commodities

- Crude is modestly softer on the session, having traded within a contained range for the majority of the European morning. Brent is holding just above USD 85.60/bbl.

- Precious metals are mixed, having spent much of the morning pressured; thereafter, spot gold climbed into the green, benefiting from the downbeat Dollar; the yellow metal currently sits above USD 2330/oz.

- Base metals are incrementally firmer, tracking US equity futures and the overall positive handover from the APAC session irrespective of downbeat European price action.

Geopolitics: Middle East

- Israeli media reported news about the killing of the sister of the head of Hamas’ political bureau, Ismail Haniyeh, in an Israeli bombardment that targeted the beach camp west of Gaza which killed 13 people, according to Sky News Arabia.

- US Secretary of State Blinken emphasised to Israel’s Defence Minister Gallant the need to take additional steps to protect humanitarian workers in Gaza and deliver assistance in coordination with the UN, while Blinken underscored the importance of avoiding escalation and reaching a diplomatic resolution that allows both Israeli and Lebanese families to return home, according to the State Department.

- There were initial rumours on social media that something of note occurred in the Black Sea and that a US drone had been shot down although there was no confirmation, according to Faytuks News via social media platform X. However, social media reports later noted that a US defence official said no incident involving a US surveillance drone occurred today over the Black Sea, despite claims earlier by several Russian sources

Geopolitics: Other

- Ukraine will start EU accession talks on Tuesday and will meet with EU ministers in Luxembourg to officially begin a process that is set to take years but which represents a symbolic moment, according to FT.

- Russian President Putin said in a message to North Korean leader Kim that his recent visit to North Korea raised ties to an unprecedentedly high level of partnership, while he added that Kim is an honoured guest Russia waits for, according to KCNA.

- South Korean President Yoon criticised North Korea’s balloon sending and vowed a strong response to North Korean provocation, according to Yonhap.

US Event Calendar

- 08:30: June Philadelphia Fed Non-Manufactu, prior -0.6

- 08:30: May Chicago Fed Nat Activity Index, est. -0.25, prior -0.23

- 09:00: April S&P CS Composite-20 YoY, est. 7.00%, prior 7.38%

- April S&P/CS 20 City MoM SA, est. 0.30%, prior 0.33%

- April FHFA House Price Index MoM, est. 0.3%, prior 0.1%

- 10:00: June Conf. Board Consumer Confidenc, est. 100.0, prior 102.0

- June Conf. Board Present Situation, prior 143.1

- June Conf. Board Expectations, prior 74.6

- 10:00: June Richmond Fed Index, est. -3, prior 0

- 10:30: June Dallas Fed Services Activity, prior -12.1

Fed Speakers

- 07:00: Fed’s Bowman Speaks on Monetary Policy, Bank Capital Reform

- 12:00: Fed’s Lisa Cook Speaks on Economic Outlook

- 14:10: Fed’s Bowman Gives Recorded Opening Remarks

DB’s Jim Reid concludes the overnight wrap

Nvidia has been driving markets again over the last 24 hours, as its share price came down another -6.68%, building on its -4.03% decline over the previous week and -16.1% from the intra-day high on Thursday. In turn, that held down US equity returns more broadly, as the losses for Nvidia pushed the NASDAQ (-1.09%) and the S&P 500 (-0.31%) into negative territory for the day. This decline came even as 70% of the S&P 500 constituents were higher yesterday, with the equal-weighted version of the index up +0.50%. Energy stocks (+2.73%) led on the upside, boosted by rising oil prices as Brent crude reached its highest level since April (+0.90% to $86.01/bbl).

The positive tone was more dominant in Europe, where markets continued to strengthen despite the political uncertainty as we head to the weekend French polls. For instance, the CAC 40 (+1.03%) closed at its highest level since the turmoil began, having advanced by +2.71% since its closing low on June 14. Banks were among the strongest performers, including BNP Paribas (+3.27%), Société Générale (+2.06%) and Crédit Agricole (+2.00%). And this strength was echoed among other indices across the continent, with the STOXX 600 (+0.73%), the DAX (+0.89%) and the FTSE MIB (+1.58%) all posting solid gains.

That European advance came despite another batch of weak data, as Germany’s Ifo survey for June came out. That saw the business climate indicator unexpectedly fall to 88.6 (vs. 89.6 expected), which is the second month in a row that it’s declined. Moreover, the e xpectations indicator fell back after a run of 4 consecutive monthly gains, with the measure falling to 89.0 (vs. 90.7 expected). And that follows some underwhelming flash PMI releases on Friday, where both the Euro Area and German numbers surprised on the downside.

When it comes to the politics, that will really ramp up this week, with financial markets keenly focused on the first round of the French election this Sunday. Ahead of that, an Ifop poll showed that Marine Le Pen’s National Rally was on 36%, ahead of the left-wing alliance on 29.5%, and President Macron’s centrist alliance on 20.5%. In seat terms, that would give the National Rally 220-260, short of the 289 required to win a majority in the National Assembly. The left-wing alliance would be on 185-215, and President Macron’s alliance would be on 70-100. A reminder of our joint econ/strategy webinar tomorrow at 3pm London time on the election and the market implications. Register here. Elsewhere, there are just 9 days to go until the UK’s election, and a Redfield and Wilton poll out yesterday had the opposition Labour Party in the lead on 42%, followed by Nigel Farage’s Reform UK on 19%, and the governing Conservatives on 18%.

Back to France, and the Franco-German 10yr spread tightened by -3.2bps to 77bps and away from Friday’s close which was the highest spread since 2012. That came as Jordan Bardella of the National Rally said that he would seek to repair France’s “degraded public finances”, and would “bring the country back to reasonable budgets”. Other countries’ spreads also tightened, as the 10yr bund yield rose by +1.0bps, underperforming the rest of Europe.

Meanwhile in the US, a late rally saw the 10yr Treasury yield close -2.4bps lower on the day at 4.23% where it’s stayed in Asia this morning. The rally was helped along by dovish-leaning comments from San Francisco Fed President Daly, who said that “ Future labor market slowing could translate into higher unemployment ”, adding “At this point, inflation is not the only risk we face”.

Asian equity markets are mostly trading higher this morning shrugging off the US tech weakness. The Nikkei (+0.51%), Hang Seng (+0.33%), KOSPI (+0.49%) and the S&P/ASX 200 (+0.94%) are all advancing. Elsewhere, Chinese stocks are extending recent losses with the CSI (-0.42%) and the Shanghai Composite (-0.38%) lower. S&P 500 (+0.08%) and NASDAQ 100 (+0.19%) futures are bouncing back slightly as I type.

Early morning data showed that Japan’s services producer price index climbed +2.5% y/y in May and less than the market expected gain of +3.0% as against a downwardly revised increase of +2.7% in April. The yen (+0.08%) has edged higher for a second day but at 159.51 against the dollar, it is still languishing near levels not seen since late April when the Japanese authorities intervened in the FX market. More broadly it remains very close to its 30 plus year lows.