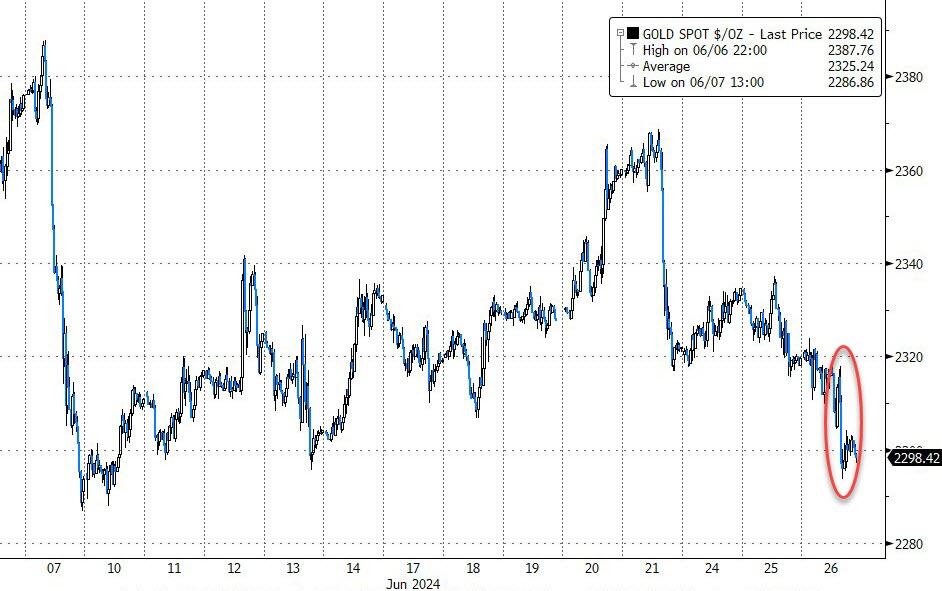

GOLD PRICE CLOSED DOWN $16.95 TO $2302.00

SILVER PRICE UP $0.03 TO $28.94

Gold ACCESS CLOSED $2298.20

Silver ACCESS CLOSED: $28.78

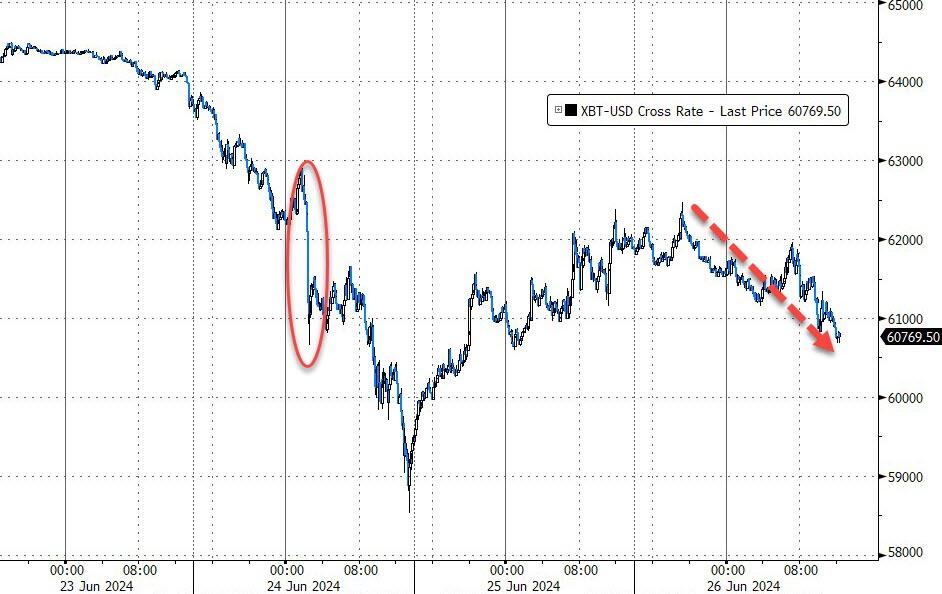

Bitcoin morning price:$61,540 DOWN 565 DOLLARS.

Bitcoin: afternoon price: $61,034 DOWN 1071 dollars//

Platinum price closing UP $35.70 TO $1021.50

Palladium price; DOWN $9.20 AT $933.80

END

SHANGHAI GOLD PREMIUM 44 DOLLARS/COMEX GOLD//JULY TO JULY

SHANGHAI GOLD (USD) FUTURES – QUOTES

SHANGHAI GOLD (USD) FUTURES – QUOTES

Last Updated 26 Jun 2024 01:04:57 AM CT.

Market data is delayed by at least 10 minutes.

*CANADIAN GOLD: $3149,41 DOWN 20.04 CDN dollars per oz( * NEW ALL TIME HIGH 3,305.30 CDN DOLLARS PER OZ//MAY 20 2024)

*BRITISH GOLD: 1820.82 DOWN 8.20 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2151.87 DOWN 14.41 Euros per oz //* (ALL TIME CLOSING HIGH: 2248.89 EUROS PER OZ//APRIL 16.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCH: COMEX

EXCHANGE: COMEX

CONTRACT: JUNE 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,316.600000000 USD

INTENT DATE: 06/25/2024 DELIVERY DATE: 06/27/2024

FIRM ORG FIRM NAME ISSUED STOPPED

737 C ADVANTAGE 76 2

905 C ADM 1 4

991 H CME 71

TOTAL: 77 77

MONTH TO DATE: 30,515

ACCESS MARKET

JPMorgan stopped 0/77

FOR JUNE 2024

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2024. CONTRACT: 77 NOTICES FOR 7700 OZ or 0.2395 TONNES

total notices so far: 30,515 contracts for 3,051,000 Oz (94.914 tonnes)

FOR JUNE:

SILVER NOTICES: 3 NOTICE(S) FILED FOR 15,000

OZ/

total number of notices filed so far this month :1339 for 6.695 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $16.95 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/

: NO CHANGES IN GOLD INVENTORY AT THE GLD/

/ /INVENTORY RESTS AT 829.05TONNES

INVENTORY RESTS AT 829.05 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.03 AT THE SLV//

HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A HUGE WITHDRAWAL OF 2/512 MILLION OZ OF SILVER OUT OF THE SLV

// INVENTORY DECREASES TO 438.178 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 438.178 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A MEGA HUMONGOUS SIZED 6629 CONTRACTS TO 166,470 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS SURPRISING HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR HUGE LOSS OF $0.63 IN SILVER PRICING AT THE COMEX ON TUESDAY’S TRADING ON SILVER. WE HAD SOME LONG LIQUIDATION AS WE HAD A NET LOSS OF 2579 CONTRACTS ON OUR TWO EXCHANGES. WE, AGAIN HAD MAJOR SHORT COVERING BY OUR SPECS WITH THE HUGE LOSS IN PRICE AS WELL AS MASSIVE T.A.S. LIQUIDATION WHICH ACCOUNTS FOR THE LOSS ON THE TWO EXCHANGES. WE HAD ANOTHER HUGE SIZED 1158 T.A.S ISSUANCE,

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED TUESDAY JUNE 4 AND AGAIN ON FRIDAY, JUNE 7 AND AGAIN ON YESTERDAY’S TRADING

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 1158 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS.IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1/2 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.63) AND WERE SUCCESSFUL IN KNOCKING SOME SILVER LONGS FROM THEIR PERCH AS WE DID HAVE A HUGE SIZED LOSS OF 2579 CONTRACTS ON OUR TWO EXCHANGES WITH THE LOSS IN PRICE OF $0.63.

WE MUST HAVE HAD:

A MEGA HUGE SIZED 4050 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.830 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 5,000 OZ QUEUE JUMP.

//NEW STANDING FOR SILVER//JUNE IS THUS 6.695 MILLION OZ

WE HAD:

/ MEGA HUGE SIZED COMEX OI LOSS //MEGA HUGE SIZED EFP ISSUANCE/ VI) HUMONGOUS SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1158 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED 619 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE

TOTAL CONTRACTS for 17 DAYS, total 21,087 contracts: OR 105.435 MILLION OZ (1240 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 85.185 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 105.435 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

RESULT: WE HAD A MEGA HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 6505 CONTRACTS WITH OUR HUGE LOSS IN PRICE OF SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 4050 ISSUED FOR JULY AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JUNE OF 3.830 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 5,000 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR JUNE 6.695 MILLION OZ

WE HAVE A MEGA HUGE SIZED LOSS OF 2455 OI CONTRACTS ON THE TWO EXCHANGES WITH THE HUGE LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUMONGOUS SIZED 1158 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX TRADING/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND SOME LIQUIDATION OF LONGS.

THE NEW TAS ISSUANCE TUESDAY NIGHT (1158) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 3 NOTICE(S) FILED TODAY FOR 15,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 1163 OI CONTRACTS TO 452,190 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 311 CONTRACTS

WE HAD A SMALL SIZED DECREASE IN COMEX OI (1163 CONTRACTS) OCCURRED WITH OUR LOSS OF $13.25 IN PRICE/TUESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 89.94 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 700 OZ E.F.P JUMP TO LONDON AS BANKERS SCOUR THE PLANET LOOKING FOR GOLD ON THE THEIR SIDE OF THE POND

NEW STANDING 94.930 TONNES// ALL OF THIS HAPPENED WITH OUR $13.25 LOSS IN PRICE WITH RESPECT TO TUESDAY’S TRADING. WE HAD A FAIR SIZED GAIN OF 1293 OI CONTRACTS (4.021 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2145 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 452,501

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 982 CONTRACTS WITH 1163 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 2145 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 982 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 1366 CONTRACTS,,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2145 CONTRACTS) ACCOMPANYING THE SMALL SIZED LOSS IN COMEX OI OF 1163 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 982 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 88.761 TONNES FOLLOWED BY TODAY’S EFP JUMP OF 0.0217 TONNES

//NEW STANDING /JUNE 94.930 TONNES.

/ 3) HUGE T.A.S. LIQUIDATION OF CONTRACTS WITH ZERO NET LONG SPECS BEING CLIPPED,

4) SMALL SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1366 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JUNE. :

TOTAL EFP CONTRACTS ISSUED: 50,896 CONTRACTS OR 5,089,600 OZ OR 158.30 TONNES IN 17 TRADING DAY(S) AND THUS AVERAGING: 2993 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAY(S) IN TONNES 158.30 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 158.30 DIVIDED BY 3550 x 100% TONNES = 4.45% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 158.30 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF JUNE. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (APRIL), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA HUGE SIZED 6629 CONTRACTS OI TO 166,534 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 4050 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

JULY 4505 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 4505 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 6629 CONTRACTS AND ADD TO THE 4050 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2579 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 12.895 MILLION OZ

OCCURRED WITH OUR STRONG $0.63 LOSS IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING/TUESDAY NIGHT

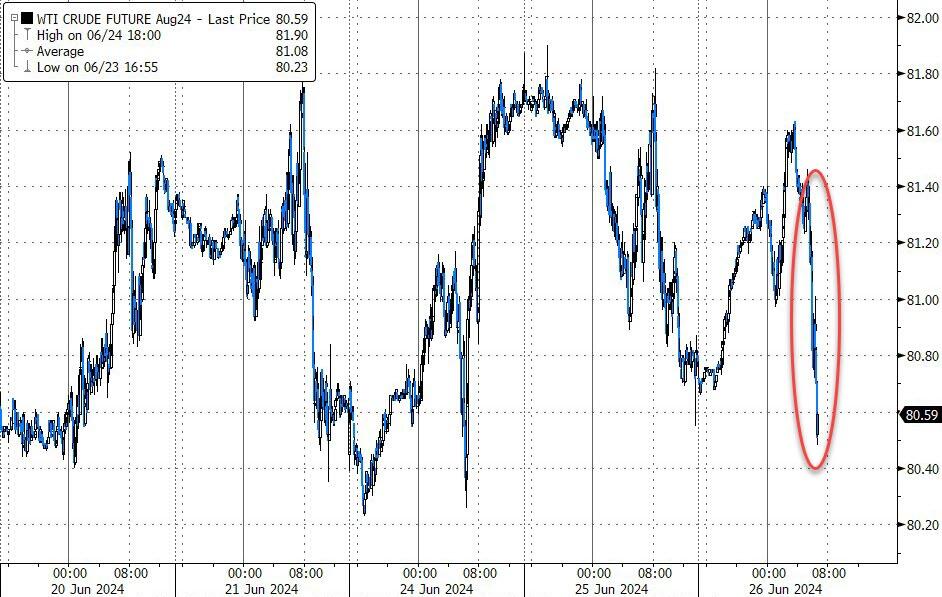

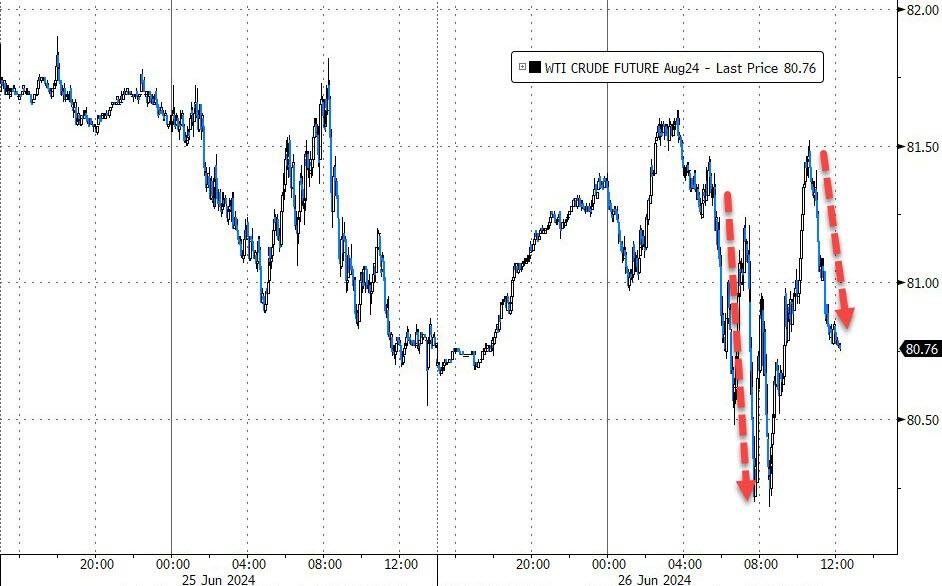

SHANGHAI CLOSED UP 22.53 PTS OR 0.76% //Hang Seng CLOSED UP 17.03 PTS OR 0.09%// Nikkei CLOSED UP 493.92 OR 1.26%//Australia’s all ordinaries CLOSED DOWN 0.67%///Chinese yuan (ONSHORE) closed DOWN TO 7,2667 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.3015/ Oil UP TO 81.42 dollars per barrel for WTI and BRENT DOWN AT 85.47 /Stocks in Europe OPENED ALL RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A SMALL SIZED 1163 CONTRACTS TO 452,190 WITH OUR STRONG LOSS IN PRICE OF $13.25 WITH RESPECT TO TUESDAY’S TRADING. WE HAD A HUGE T.A.S. LIQUIDATION ON TUESDAY’S STRONG LOSS WITH ZERO LONGS BEING CLIPPED AND MAJOR SHORT COVERING.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW IN THE ACTIVE DELIVERY MONTH OF JUNE.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 2145 EFP CONTRACTS WERE ISSUED: : AUGUST 2145 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2145 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 1293 CONTRACTS IN THAT 2145 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A SMALL SIZED LOSS OF 1163 COMEX CONTRACTS..AND THIS FAIR SIZED GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR STRONG LOSS IN PRICE OF $13.25/TUESDAY COMEX

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A GOOD SIZED 1366 CONTRACTS. MOST OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN TUESDAY’S RAID

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JUNE (94.930 TONNES)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 94.930 TONNES. THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $13.25 //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR SIZED GAIN OF 982 CONTRACTS ON OUR TWO EXCHANGES ACCOMPANYING THE STRONG LOSS IN PRICE. THE T.A.S. ISSUED ON TUESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 3.054 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JUNE (89.94 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S EFP JUMP TO LONDON OF 7 CONTRACTS OR 700 OZ (0.0217 TONNES)

NEW STANDING FOR JUNE: 94.930 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $13.25

WE HAVE REMOVED 311 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET GAIN ON THE TWO EXCHANGES 982 CONTRACTS OR 98200 OZ (3.054 TONNES)

confirmed volume TUESDAY 123,963 contracts//POOR

//speculators have left the gold arena

JUNE 26 JUNE GOLD CONTRACT

/ /// THE JUNE 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | NIL . |

| Deposit to the Dealer Inventory in oz | 22,356.76 oz ASAHI |

| Deposits to the Customer Inventory, in oz | nilOZ |

| No of oz served (contracts) today | 77 notice(s) 7700 OZ 0.2395 TONNES |

| No of oz to be served (notices) | 5 contracts 500 OZ 0.0155 TONNES |

| Total monthly oz gold served (contracts) so far this month | 30,515 notices 3,051,500 oz 94.914 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

1 dealer deposits:

i) Into ASAHI 22,356.760 oz

total dealer deposits: 22,356.760 oz

we have 0 customer deposit:

customer withdrawals: 0

TOTAL WITHDRAWALS NIL

Adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE

For the front month of JUNE we have an oi of 82 contracts having LOST 98 contracts. We had 91 contracts served on Tuesday so we lost 7 contracts or 700 oz additional ounces will not stand for gold at the comex as they underwent an EFP jump to London to take delivery on their side of the pond.

JULY LOST 401 CONTRACTS TO STAND AT 2079

AUGUST LOST 3745 CONTRACTS DOWN TO 359,069 CONTRACTS

We had 77 contracts filed for today representing 7700 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 77 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for June /2024. contract month, we take the total number of notices filed so far for the month (30,515) x 100 oz ) to which we add the difference between the open interest for the front month of JUNE (82 CONTRACTS) minus the number of notices served upon today (77 x 100 oz per contract( equals 3,052,700 OZ OR 94.952 TONNES.

thus the INITIAL standings for gold for the JUNE contract month: No of notices filed so far (30,515 x 100 oz +we add the difference for front month of June (82// , OI} minus the number of notices served upon today (77) x 100 oz which equals 3,052,000 oz (94.930 TONNES)

TOTAL COMEX GOLD STANDING FOR JUNE: 94.930 TONNES WHICH IS ABSOLUTELY HUGE FOR THIS VERY ACTIVE DELIVERY MONTH IN THE CALENDAR. JUNE IS TRADITIONALLY THE 2ND HIGHEST DELIVERY MONTH OF THE YEAR. FROM THIS POINT WE WILL GAIN IN GOLD TONNAGE WILLING TO STAND AT THE COMEX

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,682,975.981 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,598,631.903 OZ

TOTAL REGISTERED GOLD 7,834,327.184( 243.68 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,764,304.719 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,151,352 oz (REG GOLD- PLEDGED GOLD)= 191.332 tonnes //

END

SILVER/COMEX

JUN 26/2024

INITIAL

//2024// THE JUNE 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 933,445.226 oz CNT Delaware . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 3 CONTRACT(S) (15,000 OZ) |

| No of oz to be served (notices) | 0 contracts (0.000 million oz) |

| Total monthly oz silver served (contracts) | 1339 Contracts (6.695 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 0 customer deposits:

total customer deposit nil oz

JPMorgan has a total silver weight: 127.832million oz/296.265million or 43.13%

adjustment: 1

customer to dealer ASHAI: 3,862,804.700 oz

Comex withdrawals: 2

i) Out of CNT 201,049l150 oz

ii) Out of Delaware: 732,396.072 0z

total withdrawal: 933,445.225 0z

TOTAL REGISTERED SILVER: 73.156MILLION OZ//.TOTAL REG + ELIGIBLE. 296,265

million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JUNE:

silver open interest data:

FRONT MONTH OF JUNE/2024 OI: 3 CONTRACTS HAVING LOST 4 CONTRACT(S).

WE HAD 5 NOTICES SERVED UP ON TUESDAY, SO WE GAINED 1 CONTRACTS OR AN ADDITIONAL 5,000 OZ WILL STAND AT THE COMEX VIA A QUEUE JUMP

JULY SAW A LOSS OF 16,770 CONTRACTS DOWN TO 26,443

AUG, SAW A GAIN OF 121 CONTRACTS TO 854

SEPT SAW A GAIN OF 9894 CONTRACTS TO 118,246

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 3 for 15,000 oz

CONFIRMED volume; ON TUESDAY 80,020 HUGE

To calculate the number of silver ounces that will stand for delivery in JUNE we take the total number of notices filed for the month so far at 1339 x 5,000 oz = 6.695 MILLION oz

to which we add the difference between the open interest for the front month of JUNE ((3) and the number of notices served upon today 3 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JUNE/2024 contract month: 1339 notices served so far) x 5000 oz + OI for the front month of JUNE (3)x number of notices served upon today minus (3)x 5000 oz of silver standing for the JUNE contract month equates to 6.695 MILLION OZ.

New total standing: 6.695 million oz.

There are 73.156 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

JUNE 26 WITH GOLD DOWN $16.95 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:

INVENTORY RESTS AT 829.05 TONNES

JUNE 25 WITH GOLD DOWN $13.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A STRONG WITHDRAWAL OF 2.88 TONNES OF GOLD FROM THE GLD

INVENTORY RESTS AT 829.05 TONNES

JUNE 24 WITH GOLD UP$14.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A STRONG WITHDRAWAL OF 1.72 TONNES OF GOLD

/NEW TOTAL TONIGHT 831.93 TONNES

JUNE 21 WITH GOLD DOWN $37.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A MAMMOTH 8.34 TONNES OF GOLD VAPOUR DEPOSIT/NEW TOTAL TONIGHT 833.65 TONNES

JUNE 20 WITH GOLD UP $23.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/://NEW TOTAL TONIGHT 825.31 TONNES

JUNE 18 WITH GOLD UP $17.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/://NEW TOTAL TONIGHT 825.31 TONNES

JUNE 17 WITH GOLD DOWN $18.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.03 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 825.31 TONNES

JUNE 13 WITH GOLD DOWN$35.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.89 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 830.78 TONNES

JUNE 12 WITH GOLD UP $28.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.89 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 830.78 TONNES

JUNE 11 WITH GOLD DOWN $0.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 10 WITH GOLD UP $2,00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 7 WITH GOLD DOWN $64.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 3.56 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 837.11 TONNES

JUNE 6 WITH GOLD UP $16.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.34 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 833.55 TONNES

JUNE 5 WITH GOLD UP $32.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 4 WITH GOLD DOWN $20.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 3 WITH GOLD UP $22.85 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 31 WITH GOLD DOWN $19.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 30 WITH GOLD UP $3.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 29 WITH GOLD DOWN $13.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 28 WITH GOLD UP $22.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 832.21 TONNES

MAY 24 WITH GOLD DOWN $2.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 833.36 TONNES

MAY 23 WITH GOLD DOWN $53.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 22 WITH GOLD DOWN $32.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 21 WITH GOLD DOWN $12,00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: //NEW TOTAL TONIGHT 838.54 TONNES

MAY 20 WITH GOLD UP $21.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 5.10 TONNES OF GOLD INTO THE GLD//NEW TOTAL 838.54 TONNES

MAY 17 WITH GOLD UP $31.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//NEW TOTAL 833.36 TONNES

MAY 16 WITH GOLD DOWN $7.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.43 TONNES OF GOLD INTO THE GLD//NEW TOTAL 833.36 TONNES

MAY 15 WITH GOLD UP $34.90 ON THE DAY; SMALL CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF .600 TONNES OF GOLD INTO THE GLD/INVENTORY RISES TO 831.93 TONNES

MAY 14 WITH GOLD DOWN $17.10 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD//INVENTORY RISES TO 831.33 TONNES

GLD INVENTORY: 829.05 TONNES, TONIGHTS TOTAL

SILVER

JUNE 26. WITH SILVER UP $0.03//HUGE CHANGES IN SILVER INVENTORY: A HUGE WITHDRAWAL OF 2.512 MILLION OZ OF SILVER FROM THE SLV.// /INVENTORY FALLS TO 438.178 MILLION OZ.//

JUNE 25. WITH SILVER DOWN $0.63//HUGE CHANGES IN SILVER INVENTORY: A MAMMOTH DEPOSIT OF 7.835 MILLION OZ OF SILVER VAPOUR INTO THE SLV.// /INVENTORY RISE TO 440.69 MILLION OZ.//WHAT AN ABSOLUTE FRAUD.

JUNE 24. WITH SILVER DOWN $0.05//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 2.104 MILLION OZ FROM THE SLV.// /INVENTORY LOWERS TO 432.835 MILLION OZ.

JUNE 21. WITH SILVER DOWN $1.15//NO CHANGES IN SILVER INVENTORY’// /INVENTORY REMAINS AT 434.935 MILLION OZ.

JUNE 20. WITH SILVER UP $1.17//HUGE CHANGES IN SILVER INVENTORY’ A DEPOSIT OF 5.164 MILLION OZ INTO THE SLV/// /INVENTORY RISES TO 434.929 MILLION OZ.

JUNE 18. WITH SILVER UP $0.21//NOCHANGES IN SILVER INVENTORY’ A WITHDRAWAL .730 MILLION OZ INTO THE SLV/// /INVENTORY FALLS TO 429.775 MILLION OZ.

JUNE 17. WITH SILVER UP $0.21//SMALL CHANGES IN SILVER INVENTORY’ A WITHDRAWAL .730 MILLION OZ INTO THE SLV/// /INVENTORY FALLS TO 429.775 MILLION OZ.

JUNE 14. WITH SILVER DOWN $0.10//NO CHANGES IN SILVER INVENTORY/ /INVENTORY REMAINS AT 429.083 TONNES

JUNE 13. WITH SILVER DOWN $1.10//HUGE CHANGES IN SILVER INVENTORY/ A HUGE DEPOSIT OF 1.958 MILLION OZ/INVENTORY RISES TO 429.083 TONNES

JUNE 12 WITH SILVER UP $0.97 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 5.983 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 427.125 MILLION OZ

JUNE 11 WITH SILVER DOWN $0.59 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.644 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 422.786 MILLION OZ

JUNE 10 WITH SILVER UP $0.30 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 3.198 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 421.142 MILLION OZ

JUNE 7 WITH SILVER DOWN $1.93 TODAY: NO CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY AT 417.944 MILLION OZ

JUNE 6 WITH SILVER UP $1.27 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 417.944 MILLION OZ

JUNE 5 WITH SILVER UP 0.38 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.52 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 415.295 MILLION OZ

JUNE 4 WITH SILVER DOWN $1.08 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

JUNE 3 WITH SILVER UP $0.35 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

MAY 31 WITH SILVER DOWN $1.09 TODAY: HUGE CHANGES IN SILVER INVENTORY: A MASSIVE WITHDRAWAL OF 3.655 MILLION OZ FROM THE SLV//INVENTORY LOWERS TO 413.775 MILLION OZ

MAY 30 WITH SILVER DOWN $0.80 TODAY: NO CHANGES IN SILVER INVENTORY//INVENTORY REMAINS AT 417.430 MILLION OZ

MAY 29 WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 1.051 MILLION OZ INTO THE SLV//INVENTORY DECREASES TO 417.430 MILLION OZ

MAY 28 WITH SILVER UP $1.64 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 2.832 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 418.481 MILLION OZ

MAY 24 WITH SILVER UP $0.10 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A DEPOSIT OF .822 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 421.313 MILLION OZ

MAY 23 WITH SILVER DOWN $1.00 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A WITHDRAWAL OF 1.736 MILLION OZ FROM THE SLVINVENTORY INCREASES TO 420.491 MILLION OZ

MAY 22 WITH SILVER DOWN $0.66 TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 21 WITH SILVER DOWN $0.41 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A DEPOSIT OF 3.792 MILLION OZ FROM THE SLV// INVENTORY INCREASES TO 422.227 MILLION OZ

MAY 20 WITH SILVER UP $1.28 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 1.005 MILLION OZ FROM THE SLV// INVENTORY LOWERS TO 418.435 MILLION OZ

MAY 17 WITH SILVER UP $1.37 TODAY: SMALL CHANGES IN SILVER INVENTORY AT THE SLV/A WITHDRAWAL OF 868,000 OZ FROM THE SLV// INVENTORY LOWERS TO 419.440 MILLION OZ

MAY 16 WITH SILVER DOWN 14 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV/ INVENTORY REMAINS AT 420.308 MILLION OZ

MAY 15 WITH SILVER UP 101 CENTS TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV;; A WITHDRAWAL OF 1.919 MILLION OZ FROM THE SLV NVENTORY RESTS AT 420.308 MILLION OZ

MAY 14 WITH SILVER UP 25 CENTS TODAY: NO CHANGES IN SILVER INVENTORY AT THE SLV;;INVENTORY RESTS AT 422.227 MILLION OZ

CLOSING INVENTORY 438.178 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

Is China Hiding How Much Gold It Really Has?

TUESDAY, JUN 25, 2024 – 09:40 PM

Authored by Mike Maharrey via Money Metals,

A few weeks ago, gold sold off on news that the People’s Bank of China didn’t add any gold to its reserves in May.

At the time, I called it a “kneejerk reaction,” and said the news wasn’t “a particularly good reason to sell gold.”

“The fact the PBoC didn’t buy any gold in May is certainly interesting, but it hardly counts as earthshaking news. Standing pat for one month doesn’t mean “China has stopped buying gold” as some news outlets framed it.”

Before the news, China had bought gold for 18 straight months. It ranked as the biggest central bank gold buyer in 2023. Officially, the People’s Bank of China added more than 300 tons of gold to its reserves during its buying spree.

“Officially” is the keyword.

Many analysts have long thought that China has far more gold than it officially reports.

Jim Rickards pointed out on Mises Daily back in 2015 that many analysts believe that China keeps several thousand tons of gold “off the books” in a separate entity called the State Administration of Foreign Exchange (SAFE).

The Official Chinese Gold Numbers Don’t Add Up

Chen Long is the founder and lead economist for Plenum. He’s also a respected journalist who writes extensively about China’s economy, financial markets, and government policies. Long recently wrote a piece for ThinkChina, a Singapore-based news site, after he ran the numbers on China’s gold holdings.

He found the official numbers simply don’t line up.

Long starts by pointing out that Chinese central bank gold purchases are a drop in the bucket compared to the country’s gold imports. The country imported over 1,400 tons of gold in 2023. This is despite the fact that China ranks as the world’s largest gold producer. Chinese mines dug up 375 tons of gold in 2023.

In other words, there is a lot of gold flowing into China, and the country exports very little.

Only a handful of commercial banks hold licenses to import gold due to the PBoC’s tight regulation of the market. According to Long, 17 banks, including four state-owned institutions, reported gold holding of about 1,016 tons as of the end of 2023.

Interestingly, gold holdings by these commercial banks have been falling since around 2016.

Meanwhile, many commercial banks in China no longer sell gold to the public due to a commodities scandal a few years ago.

When you dig into the numbers, total official gold holdings by the PBoC, retail buyers, and the big commercial banks only rose by 431 tons last year. Total gold imports and production came in at 1,775 tons. That’s a gap of more than 1,300 tons.

Over the last two years, there have been about 2,700 tons of gold that is unaccounted for.

So, where in the world did that gold go?

Long said, “It is common to see gaps between these figures, but they are usually within a few hundred tons at most. Such a huge gap is rare.”

Where Is the Chinese Gold?

How do we account for this “missing” gold?

Long offered three possibilities.

Number one is that the People’s Bank of China bought more gold than it reported.

“If the PBoC has massively increased its gold position, it may want to withhold a full disclosure in order to avoid shocking the market.”

If all that missing gold is being held by the central bank, it would double its stated gold reserves to around 5,000 tons.

Long notes that the Chinese central bank has delayed reporting before. In June 2015, the PBoC disclosed a one-off increase in gold reserves of 621 tons. It’s highly unlikely the central bank bought all that gold in a single month.

A second possibility is China’s sovereign wealth fund holds some of that missing gold.

A sovereign wealth fund is a state-owned investment fund that holds surplus government revenues.

“After all, the sovereign wealth fund may not want to put all its money in U.S. dollars either, but the China Investment Corporation does not disclose how much gold it owns,” Long said.

A third possibility is that other numbers have been fudged. Chinese commercial banks may have overstated the reduction in their gold holdings while household gold purchases were understated.

“While the domestic banks have reported a big reduction of gold assets, some investors may have turned to the foreign banks who also have gold import licenses. They may have increased their gold holdings without making disclosures, although we doubt that such increases could completely offset the decline of gold holdings at the Chinese banks.”

With the lack of transparency in China, we’ll probably never know exactly where the gold went.

As Chris Powell recently wrote, “Mainstream financial news organizations don’t yet seem to notice that official statements about gold reserves are, to put it politely, not reliable.”

That means we’ll never know for sure just how much gold the Chinese government and its central bank hold. But you don’t have to be a wild conspiracy theorist to think they probably have far more gold than they’re letting on.

Mike Maharrey is a journalist and market analyst for MoneyMetals.com with over a decade of experience in precious metals. He holds a BS in accounting from the University of Kentucky and a BA in journalism from the University of South Florida.

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY

end

CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES

Pam and Russ Martens: Fed posts record losses as it pays 5.4% interest to banks

Submitted by admin on Wed, 2024-06-26 11:32 Section: Daily Dispatches

By Pam and Russ Martens

Wall Street on Parade

Wednesday, June 26, 2024

According to Federal Reserve data, for the first time in its history, the Fed has been losing money on a consistent monthly basis since September 28, 2022.

As of the last reporting date of June 19, 2024, those losses add up to a cumulative $176 billion. As shown by the chart posted with this report, which uses Fed data, the losses thus far in 2024 have ranged from a monthly high of $11.076 billion in February to a low of $5.674 billion in May.

These losses are separate and distinct from the unrealized losses the Fed is experiencing on the debt securities it holds on its balance sheet. It does not mark those losses to market since it intends to hold the securities to maturity and their principal is guaranteed at maturity by the U.S. government.

The losses shown in the chart are actual cash operating losses that result from the Fed’s earning significantly less interest on its debt securities than the high interest the Fed is paying to depository banks on their reserves held at the Fed; to mutual funds on its reverse repo operations; and in dividend payments to the banks that are shareowners of the 12 regional Fed banks. …

… For the remainder of the analysis:

* * *

Bank information may be at risk in Russian attempt to blackmail Fed

Submitted by admin on Mon, 2024-06-24 21:57 Section: Daily Dispatches

From Money Metals News Service, Eagle, Idaho

Monday, June 24, 2024

A Russian hacking organization appears to be in the process of blackmailing the Federal Reserve.

On June 23 the criminal organization LockBit 3.0, a Russian ransomware cybercriminal group, publicly stated that it hacked the Federal Reserve and implied it would release more than “33 terabytes of juicy banking information containing details of Americans’ banking secrets” unless a large ransom is paid.

More specifically, the cyber-terrorist organization says the Federal Reserve and the U.S. government have until this afternoon, June 24, at 4:27 p.m. ET to comply with its undisclosed monetary demands. …

… For the remainder of the report:

end

4. OTHER MAJOR GOLD COMMENTARIES/PODCASTS/

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COPPER

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

ASIA TRADING//WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED UP 22.53 PTS OR 0.76% //Hang Seng CLOSED UP 17.03 PTS OR 0.09%// Nikkei CLOSED UP 493.92 OR 1.26%//Australia’s all ordinaries CLOSED DOWN 0.67%///Chinese yuan (ONSHORE) closed DOWN TO 7,2667 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.3015/ Oil UP TO 81.42 dollars per barrel for WTI and BRENT DOWN AT 85.47 /Stocks in Europe OPENED ALL RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2634

OFFSHORE YUAN: DOWN TO 7.3015

SHANGHAI CLOSED UP 22.53 PTS OR 0.76 %

HANG SENG CLOSED UP 17.03 PTS OR 0.09%

2. Nikkei closed UP 493.92 PTS OR 1.26 %

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 105.62 EURO FALLS TO 1.0684 DOWN 26 BASIS PTS

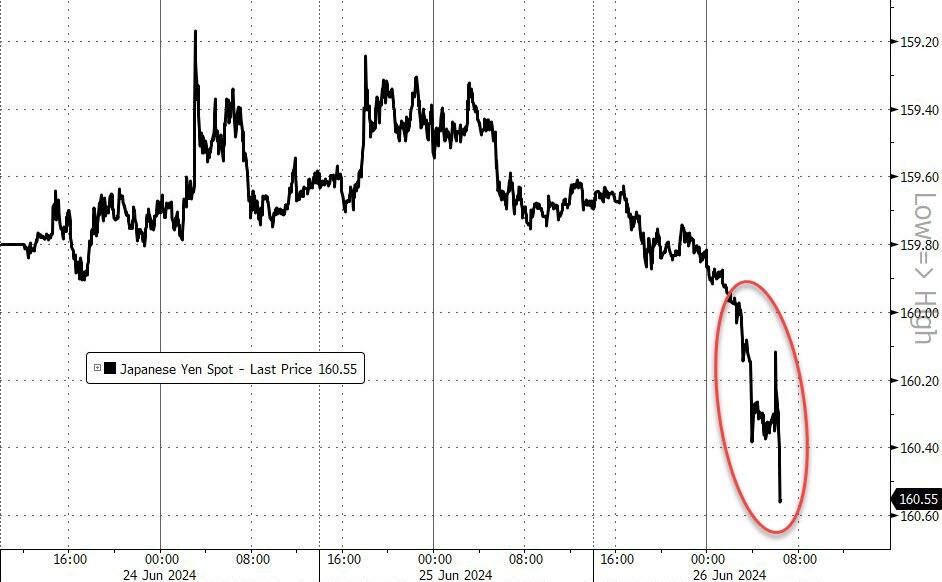

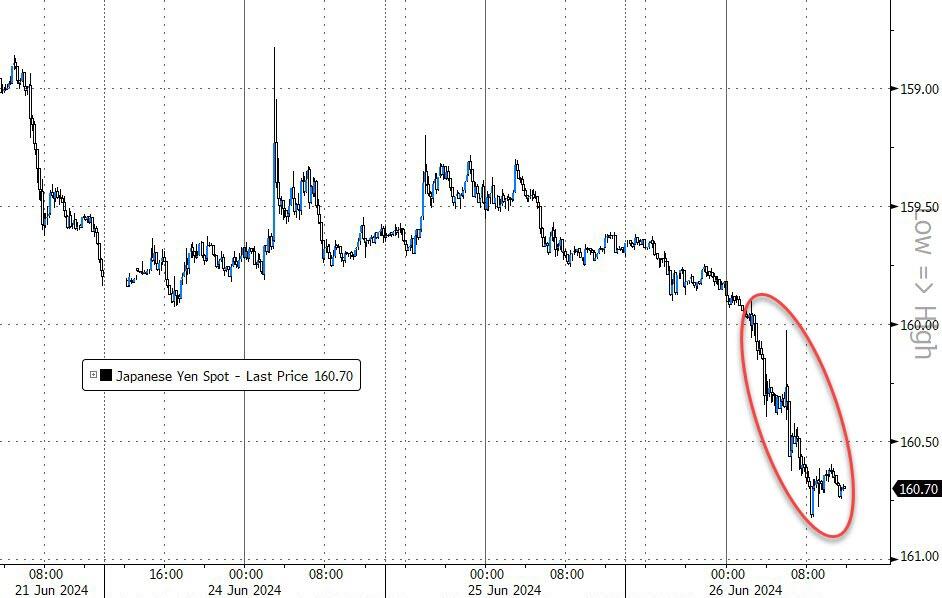

3b Japan 10 YR bond yield: RISES TO. +1,019 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 160.32 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.4355/Italian 10 Yr bond yield UP to 3.946 SPAIN 10 YR BOND YIELD UP TO 3.346%

3i Greek 10 year bond yield UP TO 3.622

3j Gold at $2308.85//Silver at: 28.86 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 99/ 100 roubles/dollar; ROUBLE AT 87,25

3m oil into the 81 dollar handle for WTI and 85 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 160..32/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.019% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8980 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9595 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.284 UP 5 BASIS PTS…

USA 30 YR BOND YIELD: 4.407 UP 4 BASIS PTS/

USA 2 YR BOND YIELD: 4.735 UP 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.94…

10 YR UK BOND YIELD: 4.1425 UP 6 PTS

2a New York OPENING REPORT

Futures Fade Despite Continued Tech Meltup, Japanese Yen Craters

WEDNESDAY, JUN 26, 2024 – 08:20 AM

Futures are trading modestly in the red near sessions lows, erasing earlier gains of as much as 0.2% even as gigacap tech stocks continue their meltup higher. At 8:00am ET, S&P futures were down 0.1%, while Nasdaq futures were still green, rising 0.1% but also fading their earlier gains in another quiet start to the day (volumes this week have been tracking down 10-15% vs 10dma), with the snapback in momentum yesterday looking to continue its rally this am (NVDA +2% in premarket). Bond yields are 2-4bp higher after Fed Governor Michelle Bowman reiterated her view that borrowing costs should remain elevated for some time; USD is higher as the yen plunges above 160 vs the USD, the lowest since 1986 with another BOJ intervention imminent. Commodities are mixed: oil and Ags are higher, while base metals are lower. Today, the key macro focus will be on MBA Mortgage Applications (up 0.8%), New Home Sales (10am, est 633k), $70bn UST 5yr note auction, Fed will release bank stress test results after the close today; Micron, Jefferies and General Mills are among companies reporting results.

Pre-mkt, Tech/Semis are continuing yesterday’s rally: Nvidia climbed more than 2% in US premarket trading, adding to Tuesday’s 7% gain. Rival Micron Technology Inc. rose more than 3% ahead of its third-quarter results later Wednesday (WTD +4.3%). Other tech names rising are QCOM +70bp, AMZN +65bp, AAPL +32bp. Here are the most notable premarket movers:

- FDX +14% pre mkt after company reported EPS upside thanks to higher op. margins and the F25 EPS outlook mid-point is slightly above plan ($21 vs. the Street $20.85). Iin addition to earnings, mgmt. outlined a plan to repurchase $2.5B in shares this FY (including $1B in FQ1) and suggested the FedEx Freight unit could be sold (the potential for a FedEx Freight sale is the key driver of the stock rally).

- Rivian Automotive shares soared 38% after Volkswagen said it plans to establish a joint venture and invest up to $5 billion until 2026 in the electric-car maker. Analysts were positive about the investment and noted that the JV is a vote of confidence for Rivian’s business. VW shares slipped.

- Aptiv shares fell 5.7% as Piper Sandler downgraded to underweight from neutral, saying that the Volkswagen-Rivian JV strikes at the core of the auto parts company’s strategy.

- Southwest Airlines shares drop as much as 10% in premarket trading after the US carrier cut its guidance for operating revenue per available seat mile for the second quarter.

- Whirlpool shares surge as much as 20% in premarket trading after Reuters reported that Robert Bosch GmbH is considering an offer for the appliance maker.

- General Mills shares fall 4.1% in premarket trading after the packaged-food company’s full-year forecast for organic net sales growth missed the average analyst estimate. The cereal maker also reported a steeper-than-expected decline in organic net sales for the fourth quarter.

- Tesla is on the verge of losing a key bragging right it’s held for the past six years: outselling all EV competitors in the US combined.

- Home Depot shares gain 0.5% in premarket trading after D.A. Davidson & Co. raised the home-improvement retailer to buy from neutral, saying a return to positive comparable sales “is in sight” with industry trends no longer getting worse.

- Grindr shares jump 5.9% in premarket trading after Dow Jones reported that the LGBTQ company raised its revenue growth forecast for the year ahead of an investor day.

- Cruise operator Carnival Corp. gained after posting a surprise quarterly profit and raising its earnings outlook.

The volatility in Nvidia shares, which account for one third of the S&P’s advance this year, has raised renewed concern about the concentration of megacap technology stocks in equity indexes.

“Nvidia’s volatility has weighed on market sentiment, but we think the structural investment case for artificial intelligence remains intact,” said Mark Haefele, chief investment officer at UBS Global Wealth Management. “We also hold a constructive outlook for broader equities amid solid fundamentals.”

Among other premarket movers, FedEx Corp. surged more than 13% after an upbeat profit forecast. Cruise operator Carnival Corp. gained after posting a surprise quarterly profit and raising its earnings outlook. Southwest Airlines Co. fell as much as 6.7% after cutting guidance.

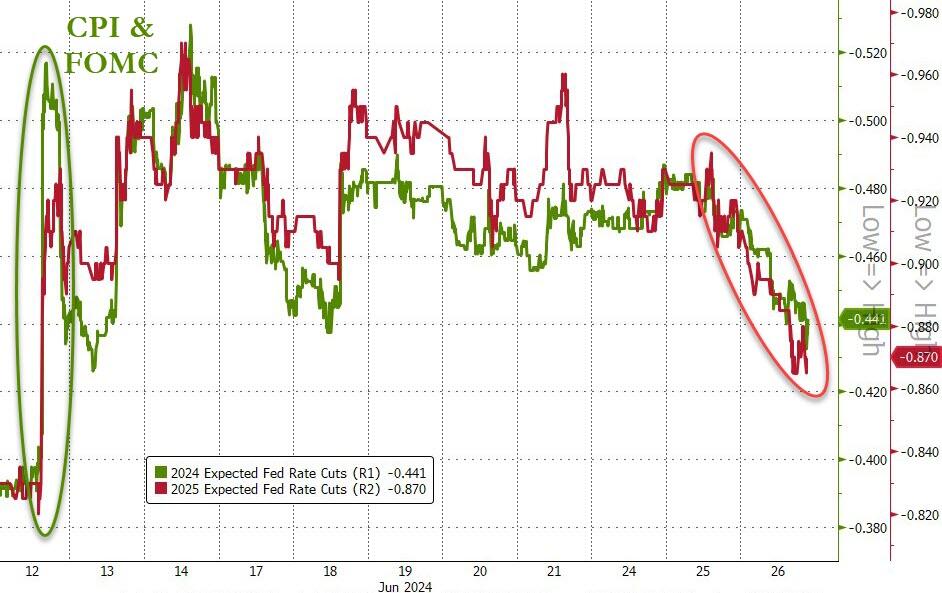

Fed officials recently forecast just 25 basis points of reductions by the end of this year and a total of 125 basis points by end-2025, while market participants are pricing in about 75 basis points by the first quarter of 2025. But some are starting to hedge against deeper and more rapid easing: positioning in the rate options market shows an increase in bets that stand to benefit if the Fed reduces its key rate to as low as 2.25% over the next nine months — a whopping 3 percentage points of cuts.

The Stoxx Europe 600 index reversed an early advance and slipped 0.4% as declines for car makers and travel and leisure stocks offset gains in the tech sector. Among individual movers in Europe, Danske Bank A/S rose as much as 2.4% after lifting its full-year outlook. Just Eat Takeaway.com NV and Delivery Hero SE fell as much as 4% each after JPMorgan forecast tepid growth for the food delivery sector. Here are the most notable European movers:

- Mail delivery stocks climb on Wednesday after US firm FedEx issued a profit forecast above Wall Street’s expectations.

- Deliveroo shares rise after Reuters reported that US food delivery firm DoorDash approached the company for takeover talks. European food delivery peers waive early gains.

- Sanofi shares rise as much as 2% after Bloomberg reported that the French pharmaceutical giant has called for initial bids for its $20 billion consumer health division ahead of a potential listing.

- Danske Bank shares gain as much as 2.4% after raising its outlook for the full year, citing the strong quality of loans it has issued.

- Philips shares rise as much as 3.3% after Italy’s billionaire Agnelli family raised its holding in the Dutch medical device manufacturer, giving it a stake worth $4.19 billion.

- Future shares gain as much as 8.1% after Jefferies double upgrades to buy, removing the media company’s only negative analyst rating, on renewed confidence over a strong return of revenue growth.

- Fincantieri shares gain as much as 8% in Milan trading, rebounding from a 9.3% drop on Tuesday, after the Italian shipbuilder launched a €400m capital increase earlier this week.

- D’Amico shares advance as much as 8.1% as Pareto adds to the clean sweep of positive ratings, starting coverage with a buy rating as notes strong re-pricing potential for the stock.

- PTWP shares rise as much as 9.2% on their first day of trading on the Warsaw Stock Exchange’s main market, after the application software firm moved its listing from the NewConnect platform for smaller companies.

- Phoenix Group shares slip as much as 1% after the UK insurer said it would explore the sale of its SunLife business.

- Volex shares slump as much as 9.3%, the most since August 2022, after the producer of interconnectors and power products reported full year results.

- Alfen shares fall as much as 43%, the most on record, after the Dutch energy infrastructure firm cuts its revenue forecast and said it expects its Ebitda margin to be mid-single digit for the full year.

In the absence of major data from the euro zone on Wednesday, traders are taking their cues from policy signals. Investor expectations for the European Central Bank to loosen monetary policy twice more this year are fair, according to Governing Council member Olli Rehn, who added that officials shouldn’t overly dampen economic activity.

Earlier, in Asia equities advanced for a second day as tech shares rebounded after Nvidia drove a rally in US peers. The MSCI Asia Pacific Index rose as much as 0.4%, with TSMC and SK Hynix among the biggest boosts. A gauge of the region’s tech shares advanced after a three-day decline. Benchmarks gained in Japan, South Korea and mainland China. Australian stocks slid as a hotter-than-expected inflation data print bolstered the case for the Reserve Bank to resume raising interest rates.

Wall Street’s tech rally overnight helped lift chip-related stocks in the region, though any bullish sentiment may be contained as uncertainties remain on the Federal Reserve’s monetary policy path. Investors are watching the central bank’s preferred inflation gauge due Friday for more clues on its path to easing. China’s 10-year bond yield fell to a more than two-decade low as investors flocked to fixed-income securities amid concern about the slowing economy and expectations for further stimulus.

In FX, it was all about the continued disintegration of the yen, which breached 160 per dollar, a level that triggered a sharp reversal on April 29 due to suspected intervention, raising speculation Japanese authorities may take steps to support the currency again. As of 8:00am, the USDJPY rose to 160.36, the lowest since 1986.

In rates, treasuries are cheaper across the curve on Wednesday, holding on to losses seen during Asian trading hours amid a selloff in Australian government bonds after the country’s May inflation reading beat estimates, raising the odds that the Reserve Bank will resume raising interest rates at its next meeting. US yields are cheaper by 2.5bp to 3.5bp across the curve, with the front and belly of the curve broadly leading losses on the day. US 10-year yields trade at around 4.28%, cheaper by 3bp on the day with bunds and gilts trading broadly in line. Aussie 2-year notes climbed 18bp following CPI data. Treasury coupon issuance resumes at 1pm New York time with $70 billion in 5-year notes, which follows a 2-year sale on Tuesday which stopped on the screws. This week’s auctions conclude Thursday with $44 billion in 7-year notes. The WI 5-year yield at around 4.305% is ~25bp richer than May’s stop-out, which tailed the WI by 1.3bp

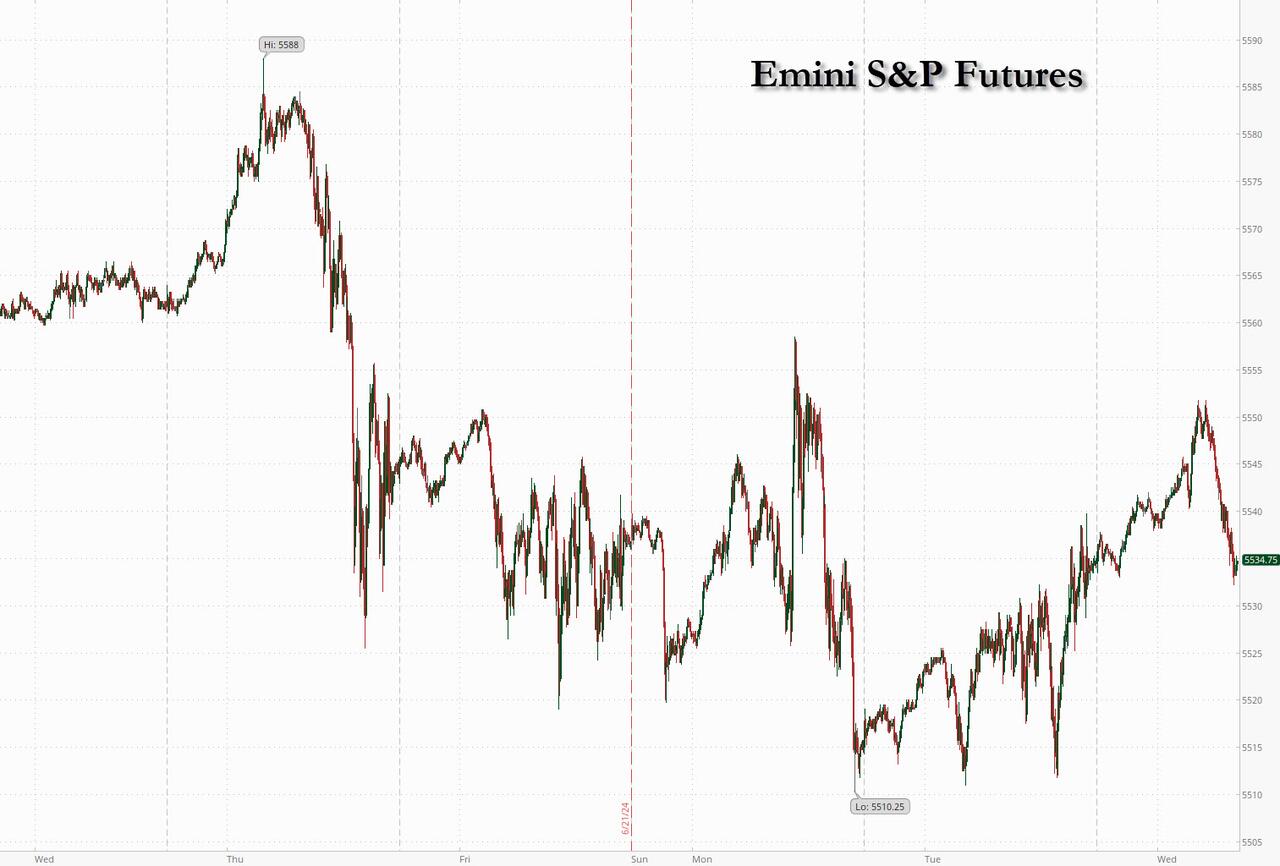

In commodities, oil rose ahead of a US government report on crude inventories and fuel demand following the release of mixed industry data. Iron ore climbed for a second day. Copper fell to the lowest in more than two months with prices facing sustained pressure from unusually weak Chinese demand. Gold was little changed. Bitcoin softer but essentially consolidating at the top-end of Tuesday’s range which itself was a consolidation of Monday’s marked Mt. Gox/technical inspired downside; at a base of USD 61.4k

The US economic data slate includes May new home sales at 10am. There are no Fed officials scheduled to speak for the session. The focus for the US session also includes a 5-year note auction, which follows solid demand for Tuesday’s 2-year sale.

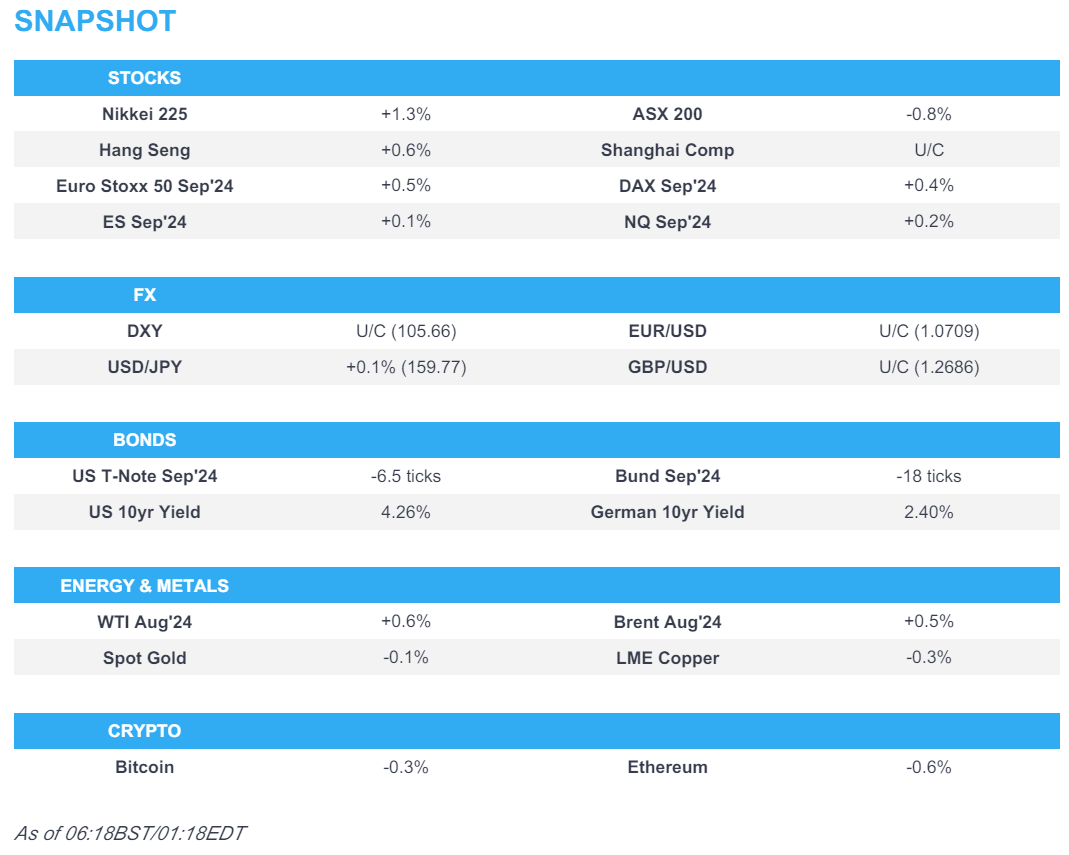

Market Snapshot

- S&P 500 futures up 0.2% to 5,549.25

- STOXX Europe 600 up 0.5% to 520.12

- MXAP up 0.3% to 180.97

- MXAPJ up 0.2% to 568.06

- Nikkei up 1.3% to 39,667.07

- Topix up 0.6% to 2,802.95

- Hang Seng Index little changed at 18,089.93

- Shanghai Composite up 0.8% to 2,972.53

- Sensex up 0.7% to 78,604.07

- Australia S&P/ASX 200 down 0.7% to 7,783.01

- Kospi up 0.6% to 2,792.05

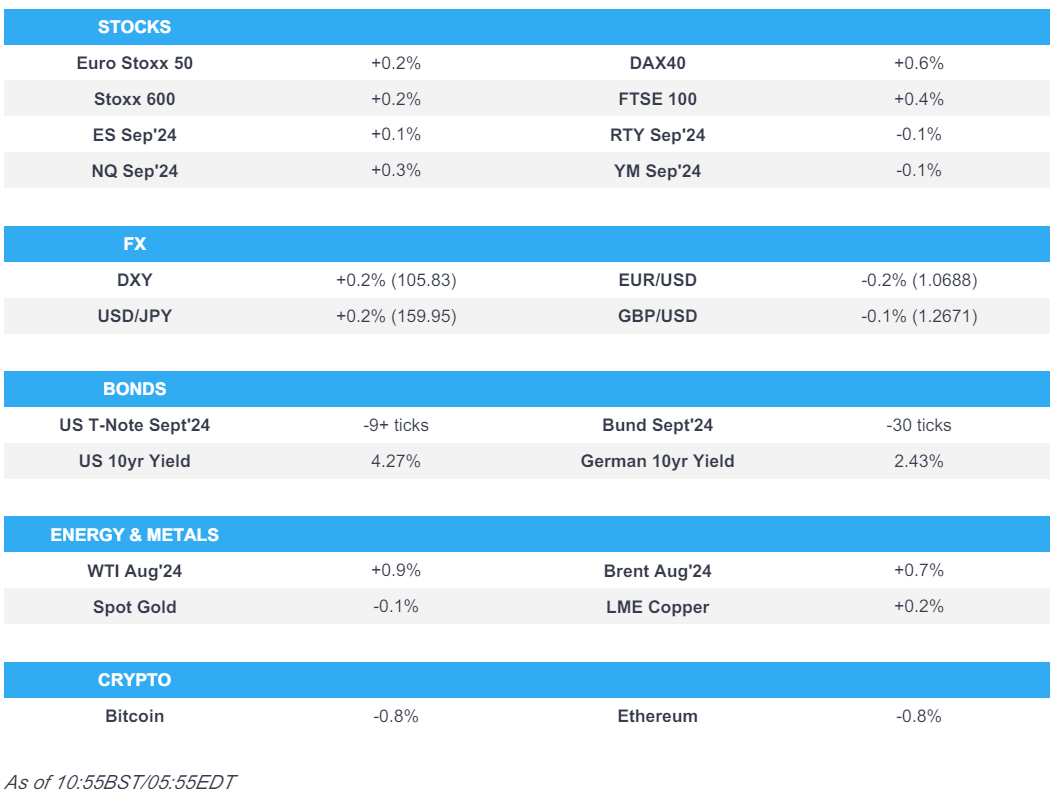

- German 10Y yield +2bps at 2.43%

- Euro down 0.2% to $1.0696

- Brent Futures up 0.1% to $85.12/bbl

- Gold spot down 0.2% to $2,315.93

- US Dollar Index up 0.18% to 105.79

Top Overnight Stories

- China’s benchmark bond yields fell to a more than two decade low, even as economists raised growth forecasts on export optimism. But adding to signs of slowing activity, vacancies are climbing at warehouses, souring global investors’ $100 billion bet. BBG

- A rare unscheduled revision to Japan’s first-quarter gross domestic product (GDP) may lead to a sharp downgrade, possibly affecting the central bank’s growth forecasts and the timing of its next interest rate hike, some analysts say. RTRS

- Rivian shares jumped 37% in premarket trading after Volkswagen agreed to invest $5 billion in a joint venture, providing a much-needed cash infusion. VW shares slipped. BBG

- Australia’s CPI came in ahead of expectations in May (+4% vs. the Street’s +3.8% forecast), which means the RBA could be forced to hike rates further in Aug. WSJ

- Switzerland dealt a surprise hit to UBS after opting to proceed with scheduling Basel III bank capital rules in January, despite wrangles over them in the US. UBS had urged the government to delay part of the rules that relate to banks’ trading books. BBG

- The ECB’s Olli Rehn said market expectations for two more cuts this year — and taking the deposit rate to as low as 2.25% in 2025 — were “reasonable,” in some of the most explicit remarks yet on the rate path from a policymaker. BBG

- US companies have been able to reprice almost $400bn of debt at lower interest rates this year due to booming investor appetite for junk loans, in an easing of financing conditions for corporate America. FT

- In New York’s 16th district, George Latimer defeated Rep. Jamaal Bowman in the most expensive congressional primary in US history. Bowman’s loss is a blow to liberals who’ve been trying to push the Democrats further left; he’s a member of the so-called “Squad” and has been critical of Israel. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks followed suit to the mixed performance stateside where the major indices reversed Monday’s price action and tech rebounded as Nvidia snapped its losing streak, while markets continue to await fresh catalysts. ASX 200 was pressured with sentiment not helped by a hot monthly CPI print which saw both Deutsche Bank and Morgan Stanley call for a 25bps hike at the next RBA meeting in August, Nikkei 225 outperforms following recent currency weakness and with tech names boosted after Nvidia’s rebound. Hang Seng and Shanghai Comp. were mixed with the former kept afloat above the 18,000 level, while the mainland was subdued despite another firm liquidity injection by the PBoC with sentiment clouded by tech and trade-related frictions as OpenAI was reportedly taking steps to block China access to its AI tools.

Top Asian News

- RBA Assistant Governor Kent said a range of measures shows that monetary policy is restrictive and policy is contributing to slower growth of demand and lower inflation, while he added that recent data reinforced the need to be vigilant to upside inflation risks and hence, they are not ruling anything in or out for interest rates.

European bourses higher across the board following the tech-led upside on Wall St.; Stoxx 600 +0.2%. Sectors mostly in the green, Tech leads while Autos lag amid pressure in Volkswagen after their investment in Rivian. Stateside, futures firmer but only modestly so, ES +0.2% & NQ +0.3% as we count down to Micron earnings after-hours; Fedex leading in the pre-market +13% post-earnings. DigiTimes reported that Nvidia (NVDA) CEO Jensen Huang was reportedly concerned about the company’s business development, with slow data centre expansion possibly impacting chip sales. Equity specifics between Volkswagen-Rivian & FedEx detailed below.

Top European News

- ECB’s Rehn said he sees bets for two more rate cuts this year as reasonable and the market’s terminal rate view of 2.25%-2.50% is also appropriate, while he sees the possibility for rate moves at any policy meeting and noted that rate cuts are contingent on additional disinflation. Rehn said he sees no disorderly market moves in France, as well as noted there is no debt crisis ahead and no need for TPI.

- ECB reportedly to begin the next strategic review once the summer break concludes, via Bloomberg; looking to present findings in H2-2025.

- Volkswagen (VOW3 GY) is to invest an initial USD 1bln in Rivian (RIVN), as part of a new, equally controlled JV to share EV architecture and software. The potential investment could rise to as much as USD 5bln by 2026 if certain milestones are achieved. The transaction could result in an unplanned cash outflow of up to EUR 2bln for Volkswagen in the current FY. Volkswagen expects FY24 net cash flow to range between EUR 2.5-4.5bln. Volkswagen will further its software-defined-vehicles plans via the JV, and transition to a pure zonal architecture. Each company will continue to separately operate their respective vehicle businesses. Rivian’s stock jumped higher by 50% in extended trading, adding around USD 6bln to its market cap. (Volkswagen).

- Switzerland is to implement Basel III trading rules as of January 1st 2025, according to Bloomberg; sees no reason to deviate from the Basel III timetable. Note, the EU has delayed it by one year to January 2026.

FX

- USD/JPY has breached 160.00 to the upside, for the first time since April 29th when it peaked at 160.20, a session which saw intervention and a large pullback in the pair; note, the breach of 160.00 this morning was accompanied by modest two-way action. Currently holding around a 160.06 session high.

- DXY continues to incrementally build on Tuesday’s advances to a current 105.86 peak but is yet to breach Monday’s 105.90 high, which essentially matches Friday’s 105.91 best.

- Action which is weighing on peers across the board; EUR/USD lost 1.07 to a 1.0686 base while Cable continues to slip from 1.27 and is approaching 12650.

- Aussie is the clear outperformer, bolstered by hot CPI which has increased the odds of a August hike to c. 33% (12% pre-release, AUD/USD to a 0.6688 peak; Kiwi softer and weighed on by the cross with NZD/USD just beneath Tuesday’s 0.6107 base.

Fixed Income

- Benchmarks in the red as the overall risk tone saps haven demand and amid a lack of fresh fundamental drivers for the complex, European docket focuses on a speech from ECB’s Lane.

- Bunds at the low-end of a 45 tick band that has seen it slip below Monday’s 132.22 base to a new WTD low, if this goes, support at 132.02 before the figure and then 131.61.

- OAT-Bund spread steady at 71bp with no fall out from an unsurprisingly fiery French election debate.

- Gilts in-fitting with only a modest uptick on the back of a robust 2038 auction, complex looks ahead to the last Sunak-Starmer debate before the election this evening.

- USTs also have a thin docket ahead with no Fed speak due and the main highlight being the 5yr auction, a tap which follows a better-than-average 2yr sale; USTs at a 110-09 fresh WTD base and holding just above last week’s 110-06+ low.

Commodities

- Initially contained trade with specifics quite light after the bearish inventory report has given way to a modest but growing bid for the crude benchmarks which are at the top-end of c. USD 1.0/bbl parameters.

- Action which comes despite a slight easing in the European risk tone (though still constructive overall) and an ongoing grind higher for the USD.

- Precious metals saw a contained start given the twin headwinds of a robust dollar and risk appetite. Yellow metal is at the low-end of a USD 2309-2323/oz band; one that sees it slip further from its 10-, 21- & 50-DMAs.

- Base metals tracking the tone but the gains capped by the dollar, overall the complex is firmer, it is yet to break the downward trend that has been in place for the likes of copper since end-May.

- US Private Inventory Data (bbls): Crude +0.9mln (exp. -2.9mln), Distillate -1.2mln (exp. -0.3mln), Gasoline +3.8mln (exp. -1.0mln), Cushing -0.4mln.

- Trading Hub Europe’s Frank remarks that German gas caverns curently show comfortable filling levels; Europe has enough LNG terminal capacities and southbound transit capacities from the north-west have been boosted.

Geopolitics: Middle East

- US Defense Secretary Austin said Hezbollah’s ‘provocations’ threaten to drag Israeli and Lebanese people into war.

- Pentagon said US Secretary of Defense Austin discussed with his Israeli counterpart efforts to de-escalate tensions on the Israeli-Lebanese border, while he warned that a war between Israel and Hezbollah would be catastrophic for Lebanon, according to Asharq News.

Geopolitics: Other

- Ukrainian President Zelensky will attend Thursday’s European Union summit in Brussels where he is expected to sign an agreement on EU security commitments for Ukraine, according to the French President’s office cited by AFP.

- Russian Defence Minister Belousov warned US Defense Secretary Austin regarding the dangers of an escalation of continued US arms supplies to Ukraine, according to the Russian Ministry.

- North Korea launched a suspected ballistic missile which was believed to have fallen outside of Japan’s EEZ shortly after with no damage reported, while Yonhap later reported that North Korea’s missile launch was believed to have failed and South Korean military said the missile used by North Korea in its failed launch was potentially a hypersonic missile.

- South Korean marines are to conduct live fire drills, according to Dong-A.

- NATO allies select Mark Rutte as the next Secretary General.

US Event Calendar

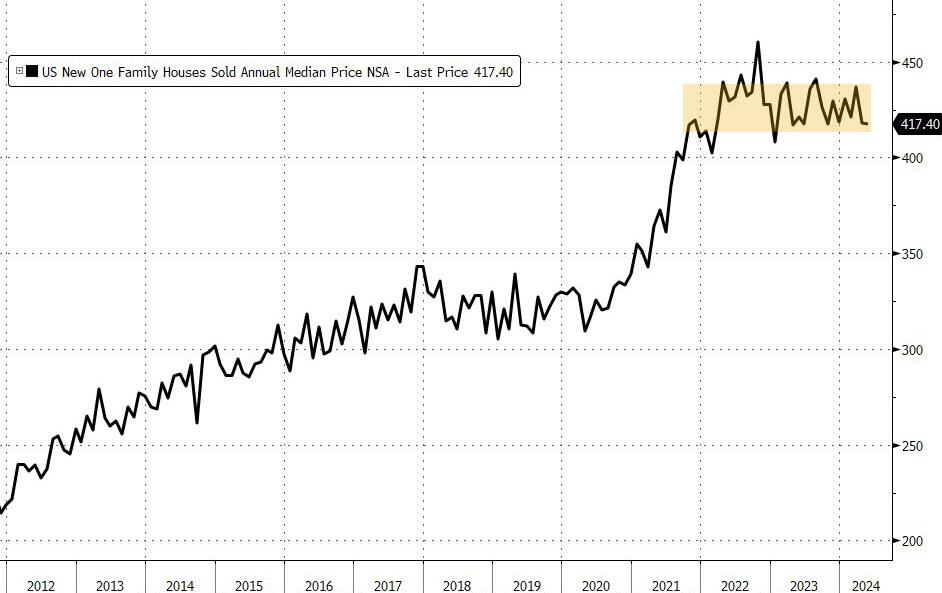

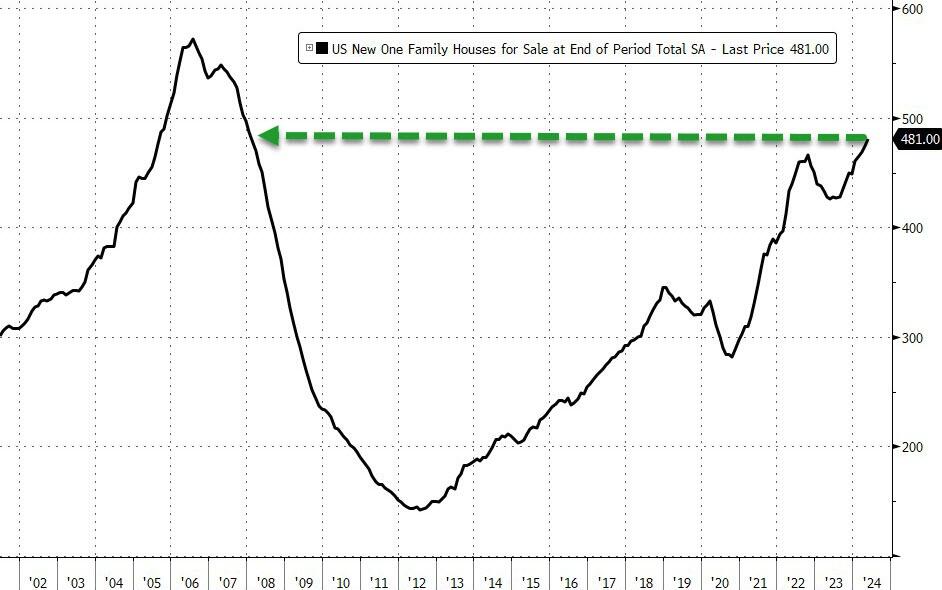

- 07:00: June MBA Mortgage Applications, prior 0.9%

- 10:00: May New Home Sales MoM, est. -0.2%, prior -4.7%

- 10:00: May New Home Sales, est. 633,000, prior 634,000

DB’s Jim Reid concludes the overnight wrap

I can safely say that this is the first time I have written the EMR from a castle. It’s in the Frankfurt countryside and quite an incredible place. This morning you need to look out at the market from the highest possible watchtower as the last 24 hours have seen a lot of differing trends from all directions.

On the plus side, tech stocks posted a decent recovery, with Nvidia (+6.76%) rebounding from its slump over recent days. But on the more negative side, several data releases were underwhelming, and multiple headlines leant on the hawkish side, i ncluding an upside surprise in both Canadian and Australian CPI. Indeed, DB have overnight changed their RBA call to a hike in August. Moreover, political events have also remained in focus, with the CAC 40 (-0.58%) and other European indices losing ground ahead of France’s election on Sunday.

We’ll start with the good news, as there was finally a bounceback for tech stocks after three consecutive declines, which helped to lift US equities more broadly. In particular, Nvidia was the second best performer in the entire S&P 500, which pushed its market cap back above the $3tn mark again. Those gains were seen amongst all the big tech stocks, with all of the Magnificent 7 (+2.40%) advancing on the day. In turn, that helped the NASDAQ (+1.26%) post a strong rebound, and it also lifted the S&P 500 up +0.39%.

But unfortunately, the good news mostly ended there, as even though the headlines pointed to a recovery for US equities, the move was dominated by the big tech stocks. In fact, over 75% of the S&P 500 actually fell yesterday, and the equal-weighted S&P 500 was down by a significant -0.72%. So as it stands with just a few days of the quarter left, the S&P 500 is up +4.09% in Q2 so far, whereas the equal-weighted index is down -2.89%. So a different story depending on which part of the market you look at, and this builds on the tech outperformance we already saw in Q1.

Matters weren’t helped by several hawkish headlines, with sovereign bonds coming under pressure after Canada’s CPI report for May. That showed headline CPI unexpectedly rising to +2.9% (vs. +2.6% expected), and the two core inflation measures followed by the Bank of Canada also rose. As it happens, the Bank of Canada did announce an initial cut at their meeting earlier this month, but after the inflation report, investors swiftly moved to dial back the chance of a follow-up move in July. Indeed, overnight index swaps had been pricing a 61% chance of a July cut on the previous day, but that was down to 16% by the close. Canadian government bonds also lost ground, with the 10yr yield up +5.0bps.

The inflation surprise has continued in Australia overnight with the latest CPI reading seeing it surge to its highest level this year. It printed at +4.0% y/y in May, above market expectations for a +3.8% gain and up from +3.6% in April. Our Aussie economist now believes the RBA will hike 25bps in August. See his report justifying the call here. Following the CPI data, the Australian dollar has risen +0.44% to trade at 0.6676 versus the dolla r while yields on the policy sensitive 3yr government bonds are currently +16.8bps higher at 4.09%, its biggest one-day gain since April, while yields on the 10yr are +11.7bps, standing at 4.32% as I type.

US Treasuries are also edging up around +1.5bps across the board after the Aussie CPI print after rising yesterday on the Canadian CPI beat. By last night’s close, 2yr Treasury yields were up +1.7bps to 4.74%, and the 10yr yield was up +1.6bps to 4.25%. Treasury yields did come slightly off their intra-day high seen around the European close following a solid 2yr auction which saw the highest bid-to-cover ratio since September. There was also some hawkish Fedspeak though, with Governor Bowman warning that “we are still not yet at the point where it is appropriate to lower the policy rate.” In addition, she said that cutting rates “ too soon or too quickly could result in a rebound of inflation, requiring further future policy rate increases to return inflation to 2 percent over the longer run.” Meanwhile, Fed Governor Cook maintained patience on rate cut prospects, saying these will be appropriate “at some point”.

Back in Europe, risk assets struggled, with the STOXX 600 (-0.23%), the CAC 40 (-0.58%) and the DAX (-0.81%) all posting losses. However, the Franco-German 10yr spread did tighten a bit, coming down by -1.1bps to 76bps, and yields came down across the continent, including on 10yr bunds (-1.1bps). With regards to politics, last night saw the debate between three potential French PM candidates though there are no immediate signs that this will materially alter the election race. Polls continue to put Marine Le Pen’s National Rally party in the lead, and yesterday’s Ifop poll had the National Rally on 36%, the left-wing alliance on 28.5%, and President Macron’s centrist group on 21%.

Asian equity markets are again mixed this morning with the Nikkei (+1.41%) sharply higher and with the KOSPI (+0.23%) edging higher. On the other hand, the S&P/ASX 200 (-0.80%) is the worst performer following the CPI data discussed above. Elsewhere Chinese stocks are also losing ground with the Hang Seng (-0.16%), the CSI (-0.39%) and the Shanghai Composite (-0.36%) all lower in morning trade. S&P 500 (+0.05%) and NASDAQ 100 (+0.08%) futures are slightly higher.