GOLD PRICE CLOSED DOWN $0.30 TO $2329.20

SILVER PRICE UP $0.5 TO $29.27

Gold ACCESS CLOSED $2332.10

Silver ACCESS CLOSED: $29.41

Bitcoin morning price:$62,821 UP 2430 DOLLARS.

Bitcoin: afternoon price: $60,391 DOWN 1176 dollars//

Platinum price closing DOWN $21.45 TO $979.15

Palladium price; UP $0.80 AT $979.75

END

SHANGHAI GOLD PREMIUM 32 DOLLARS/COMEX GOLD//JULY TO JULY

SHANGHAI GOLD (USD) FUTURES – QUOTES

SHANGHAI GOLD (USD) FUTURES – QUOTES

SHANGHAI GOLD (USD) FUTURES – QUOTES

Last Updated 01 Jul 2024 12:34:45 PM CT.

Market data is delayed by at least 10 minutes.

*CANADIAN GOLD: $3203.79 UP 23.20 CDN dollars per oz( * NEW ALL TIME HIGH 3,305.30 CDN DOLLARS PER OZ//MAY 20 2024)

*BRITISH GOLD: 1844.80 UP 6.80 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2172,41 UP 4.08 Euros per oz //* (ALL TIME CLOSING HIGH: 2248.89 EUROS PER OZ//APRIL 16.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCH: COMEX

EXCHANGE: COMEX

CONTRACT: JULY 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,327.700000000 USD

INTENT DATE: 06/28/2024 DELIVERY DATE: 07/02/2024

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 12

365 C MAREX CAPITAL M 1

624 H BOFA SECURITIES 18

661 C JP MORGAN 2

690 C ABN AMRO 7

726 C PLUS500US FINAN 3

737 C ADVANTAGE 23 2

TOTAL: 34 34

JPMorgan stopped 2/34

FOR JULY 2024

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2024. CONTRACT: 34 NOTICES FOR 3400 OZ or .1056 TONNES

total notices so far: 1592 contracts for 159,200 Oz (4.9517 tonnes)

FOR JULY:

SILVER NOTICES: 724 NOTICE(S) FILED FOR 3.620 million

OZ/

total number of notices filed so far this month : 4591 for 22.955 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $0.30 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/

: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/ A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/

/ /INVENTORY RESTS AT 827,61TONNES

INVENTORY RESTS AT 827.61 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.05 AT THE SLV//

SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 182,000 OZ INTO THE SLV.

// INVENTORY RISES TO 437.447 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 437.447 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUMONGOUS SIZED 3222 CONTRACTS TO 155,366 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS SURPRISINGLY ACCOMPLISHED WITH OUR GAIN OF $0.27 IN SILVER PRICING AT THE COMEX ON FRIDAY’S TRADING ON SILVER. WE HAD SOME LONG LIQUIDATION AS WE HAD A NET LOSS OF 1972 CONTRACTS ON OUR TWO EXCHANGES. WE, AGAIN HAD MAJOR SHORT COVERING BY OUR SPECS DESPITE THE GAIN IN PRICE AS WELL AS MASSIVE T.A.S. LIQUIDATION WHICH ACCOUNTS FOR THE LOSS ON THE TWO EXCHANGES. WE HAD ANOTHER GOOD SIZED 468 T.A.S ISSUANCE,

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED TUESDAY JUNE 4 AND AGAIN ON FRIDAY, JUNE 7 AND AGAIN ON YESTERDAY’S TRADING

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON FRIDAY NIGHT: 468 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS.IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1/2 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.27) BUT WERE SUCCESSFUL IN KNOCKING SOME SILVER LONGS FROM THEIR PERCH AS WE DID HAVE A HUGE SIZED LOSS OF 1972 CONTRACTS ON OUR TWO EXCHANGES DESPITE THE GAIN IN PRICE OF $0.27.

WE MUST HAVE HAD:

A HUMONGOUS SIZED 1250 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 28.490 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S E.F.P. TRANSFER TO LONDON OF 510,000 OZ

//NEW STANDING FOR SILVER//JUNE IS THUS 28.350 MILLION OZ

WE HAD:

/ HUMONGOUS SIZED COMEX OI LOSS //HUMONGOUS SIZED EFP ISSUANCE/ VI) STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 468 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED 344 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE

TOTAL CONTRACTS for 1 DAYS, total 1250 contracts: OR 6.250 MILLION OZ (1250 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 6.250 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 6.250 MILLION OZ

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3222 CONTRACTS DESPITE OUR STRONG GAIN IN PRICE OF SILVER PRICING AT THE COMEX//FRIDAY.,. THE CME NOTIFIED US THAT WE HAD A HUMONGOUS EFP ISSUANCE CONTRACTS: 1250 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JULY OF 28.496 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 510,000 OZ E.F.P. TRANSFER TO LONDON

//NEW TOTAL STANDING FOR JULY 28.350 MILLION OZ

WE HAVE A HUGE SIZED LOSS OF 1972 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE STRONG GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG SIZED 468 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX TRADING/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND SOME LIQUIDATION OF LONGS.

THE NEW TAS ISSUANCE FRIDAY NIGHT (468) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 724 NOTICE(S) FILED TODAY FOR 3.620 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A SMALL SIZED 268 OI CONTRACTS TO 448,354 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 548 CONTRACTS

WE HAD A SMALL SIZED INCREASE IN COMEX OI (268 CONTRACTS) OCCURRED WITH OUR GAIN OF $3.80 IN PRICE/FRIDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 7.5645 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 2300 OZ QUEUE JUMP

NEW STANDING 7.6360 TONNES/ ALL OF THIS HAPPENED WITH OUR $3.80 GAIN IN PRICE WITH RESPECT TO FRIDAY’S TRADING. WE HAD A FAIR SIZED GAIN OF 2520 OI CONTRACTS (7.838 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2252 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 448,354

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2520 CONTRACTS WITH 268 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 2252 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2520 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL SIZED 832 CONTRACTS,,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2252 CONTRACTS) ACCOMPANYING THE SMALL SIZED GAIN IN COMEX OI OF 268 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 2520 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 7,5645 TONNES FOLLOWED BY TODAY’S 2300 OZ QUEUE JUMP

//NEW STANDING /JULY 7.6360 TONNES.

/ 3) HUGE T.A.S. LIQUIDATION OF CONTRACTS WITH ZERO NET LONG SPECS BEING CLIPPED,

4) SMALL SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///SMALL T.A.S. ISSUANCE: 832 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY. :

TOTAL EFP CONTRACTS ISSUED: 2252 CONTRACTS OR 225,200 OZ OR 7.004 TONNES IN 1 TRADING DAY(S) AND THUS AVERAGING: 2252 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAY(S) IN TONNES 7.004 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 7.004 DIVIDED BY 3550 x 100% TONNES = 0.197% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 7.004 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUG), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUMONGOUS SIZED 3222 CONTRACTS OI TO 155,336 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1250 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 1250 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1250 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 3222 CONTRACTS AND ADD TO THE 1250 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1972 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 9.8600 MILLION OZ

OCCURRED DESPITE OUR $0.27 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

MONDAY MORNING/SUNDAY NIGHT

SHANGHAI CLOSED UP 27,33 PTS OR 0.92% //Hang Seng CLOSED // Nikkei CLOSED UP 47.98 OR 0.12%//Australia’s all ordinaries CLOSED DOWN 0.27%///Chinese yuan (ONSHORE) closed DOWN TO 7,2682 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2996/ Oil DOWN TO 82.00 dollars per barrel for WTI and BRENT DOWN AT 85.52 /Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 268 CONTRACTS TO 448,354 WITH OUR GAIN IN PRICE OF $3.80 WITH RESPECT TO FRIDAY’S TRADING. WE HAD A HUGE T.A.S. LIQUIDATION ON FRIDAY’S GAIN IN PRICE WITH ZERO LONGS BEING CLIPPED AND SOME SHORT COVERING.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE NON ACTIVE DELIVERY MONTH OF JULY.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 2252 EFP CONTRACTS WERE ISSUED: : AUGUST 2252 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2252 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2520 CONTRACTS IN THAT 2252 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A SMALL SIZED GAIN OF 268 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR SMALL GAIN IN PRICE OF $3.80/FRIDAY COMEX.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR FRIDAY NIGHT WAS A SMALL SIZED 832 CONTRACTS. MOST OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN FRIDAY’S TRADING

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JULY (7.6360 TONNES)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 7.6360 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $3.80 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR SIZED GAIN OF 2520 CONTRACTS ON OUR TWO EXCHANGES ACCOMPANYING THE SMALL GAIN IN PRICE. THE T.A.S. ISSUED ON FRIDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 7.838 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY (7.5645 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 2300 OZ QUEUE JUMP//NEW STANDING 7.6360 TONNES

NEW STANDING FOR JULY: 7.6360 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $3.80

WE HAVE REMOVED 548 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET GAIN ON THE TWO EXCHANGES 2520 CONTRACTS OR 252,000 OZ (7.838 TONNES)

confirmed volume FRIDAY 145,350contracts//poor

//speculators have left the gold arena

JULY 1 JULY GOLD CONTRACT

/ /// THE JULY 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 14,298.742 IZ Malca Manfra . |

| Deposit to the Dealer Inventory in oz | |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today | 34 notice(s) 3400 OZ 0.1057 TONNES |

| No of oz to be served (notices) | 863 contracts 86300 OZ 2.6849 TONNES |

| Total monthly oz gold served (contracts) so far this month | 1592 notices 159,200 oz 4.9517 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: nil oz

we have 0 customer deposit:

total deposit: nil oz

customer withdrawals: 2

i) Out of Malca 14,202.293 oz

‘ii) Out of Manfra; 94.453 oz

TOTAL WITHDRAWALS 14,298.746 oz

Adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE

For the front month of JULY we have an oi of 897 contracts having LOST 1535 contracts. We had 1558 notices filed on Friday so we gained 23 contracts or an additional 2300 oz will stand at the comex (0.0715 tonnes)

AUGUST LOST 1563 CONTRACTS DOWN TO 347,095 CONTRACTS

SEPT. GAINED ITS FIRST CONTRACT TO STAND AT ONE.

OCTOBER GAINED 149 CONTRACTS UP TO 20,272 CONTRACTS

We had 34 contracts filed for today representing 3400 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 34 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 2 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for July /2024. contract month, we take the total number of notices filed so far for the month (1592) x 100 oz ) to which we add the difference between the open interest for the front month of JULY (897 CONTRACTS) minus the number of notices served upon today (34 x 100 oz per contract( equals 245,500 OZ OR 7.6360 TONNES.

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (1592 x 100 oz +we add the difference for front month of JULY (897// , OI} minus the number of notices served upon today (34) x 100 oz which equals 245,500 oz (7.6360 TONNES)

TOTAL COMEX GOLD STANDING FOR JULY: 7,6360 TONNES WHICH IS HUGE FOR THIS NOT VERY ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,682,975.981 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,566,511.560 OZ

TOTAL REGISTERED GOLD 7,834,327.184( 243.68 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,732m184.376 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,151,352 oz (REG GOLD- PLEDGED GOLD)= 191.332 tonnes //

END

SILVER/COMEX

JULY 1/2024

INITIAL

//2024// THE JULY 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 598,820.640 oz LOOMIS . |

| Deposits to the Dealer Inventory | nil OZ |

| Deposits to the Customer Inventory | NIL |

| No of oz served today (contracts) | 724 CONTRACT(S) (3,620,000 OZ) |

| No of oz to be served (notices) | 1079 contracts (5.395 million oz) |

| Total monthly oz silver served (contracts) | 4591 Contracts (22.955 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 0 customer deposits:

total customer deposit NIL oz

JPMorgan has a total silver weight: 128.402million oz/297.662million or 43.23%

adjustment: 2 customer to dealer

a)customer to dealer brinks 10,020,360 oz:

b) customer to dealer CNT: 305,787.840 oz

customer withdrawals:1

ii) Out of loomis: 598,820.640 0z

total withdrawal: 598,820.640 0z

TOTAL REGISTERED SILVER: 74.544MILLION OZ//.TOTAL REG + ELIGIBLE. 297.662

million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF JULY/2024 OI: 1803 CONTRACTS HAVING LOST 3969 CONTRACT(S). WE HAD 3867 NOTICES FILED ON FRIDAY SO WE LOST 102 CONTRACTS OR 510,000 OZ WERE E.F.P’D TO LONDON TO TAKE IMMEDIATE DELIVERY OVER THERE. THEY NEEDED THE REAL PHYSICAL STUFF AND NEEDED THE SUPPLY IN A HURRY.

AUG, SAW A LOSS OF 174 CONTRACTS TO 144

SEPT SAW A GAIN OF 136 CONTRACTS TO 129,532

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 724 for 3.620 oz

CONFIRMED volume; ON FRIDAY 56,510 strong

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 4591 x 5,000 oz = 22.955 MILLION oz

to which we add the difference between the open interest for the front month of JULY ((1803) and the number of notices served upon today 724 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY/2024 contract month: 4591 notices served so far) x 5000 oz + OI for the front month of JULY (1803)x number of notices served upon today minus (724)x 5000 oz of silver standing for the JULY contract month equates to 28.350 MILLION OZ.

New total standing: 28.350 million oz.

There are 74.859 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

JULY 1 WITH GOLD DOWN $.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD///:INVENTORY RESTS AT 827.61 TONNES

JUNE 28 WITH GOLD UP $3.80 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 27 WITH GOLD DOWN $16.95 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 26 WITH GOLD UP $23.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 25 WITH GOLD DOWN $13.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A STRONG WITHDRAWAL OF 2.88 TONNES OF GOLD FROM THE GLD INVENTORY RESTS AT 829.05 TONNES

JUNE 24 WITH GOLD UP$14.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A STRONG WITHDRAWAL OF 1.72 TONNES OF GOLD/NEW TOTAL TONIGHT 831.93 TONNES

JUNE 21 WITH GOLD DOWN $37.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A MAMMOTH 8.34 TONNES OF GOLD VAPOUR DEPOSIT/NEW TOTAL TONIGHT 833.65 TONNES

JUNE 20 WITH GOLD UP $23.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/://NEW TOTAL TONIGHT 825.31 TONNES

JUNE 18 WITH GOLD UP $17.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/://NEW TOTAL TONIGHT 825.31 TONNES

JUNE 17 WITH GOLD DOWN $18.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.03 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 825.31 TONNES

JUNE 13 WITH GOLD DOWN$35.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.89 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 830.78 TONNES

JUNE 12 WITH GOLD UP $28.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.89 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 830.78 TONNES

JUNE 11 WITH GOLD DOWN $0.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 10 WITH GOLD UP $2,00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 7 WITH GOLD DOWN $64.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 3.56 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 837.11 TONNES

JUNE 6 WITH GOLD UP $16.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.34 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 833.55 TONNES

JUNE 5 WITH GOLD UP $32.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 4 WITH GOLD DOWN $20.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 3 WITH GOLD UP $22.85 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 31 WITH GOLD DOWN $19.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 30 WITH GOLD UP $3.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 29 WITH GOLD DOWN $13.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 28 WITH GOLD UP $22.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 832.21 TONNES

GLD INVENTORY: 827.61 TONNES, TONIGHTS TOTAL

SILVER

JULY 1. WITH SILVER UP $0.05//SMALL CHANGES IN SILVER INVENTORY: A DEPOSIT OF 182,000 INTO THE SLV./.// /INVENTORY RISES AT 437.447 MILLION OZ./

JUNE 28. WITH SILVER UP $0.27//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 913,000 OZ FROM THE SLV./.// /INVENTORY REMAINS AT 437.265 MILLION OZ./

JUNE 27. WITH SILVER UP $0.01//NO CHANGES IN SILVER INVENTORY: .// /INVENTORY REMAINS AT 438.178 MILLION OZ.//

JUNE 26. WITH SILVER UP $0.03//HUGE CHANGES IN SILVER INVENTORY: A HUGE WITHDRAWAL OF 2.512 MILLION OZ OF SILVER FROM THE SLV.// /INVENTORY FALLS TO 438.178 MILLION OZ.//

JUNE 25. WITH SILVER DOWN $0.63//HUGE CHANGES IN SILVER INVENTORY: A MAMMOTH DEPOSIT OF 7.835 MILLION OZ OF SILVER VAPOUR INTO THE SLV.// /INVENTORY RISE TO 440.69 MILLION OZ.//WHAT AN ABSOLUTE FRAUD.

JUNE 24. WITH SILVER DOWN $0.05//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 2.104 MILLION OZ FROM THE SLV.// /INVENTORY LOWERS TO 432.835 MILLION OZ.

JUNE 21. WITH SILVER DOWN $1.15//NO CHANGES IN SILVER INVENTORY’// /INVENTORY REMAINS AT 434.935 MILLION OZ.

JUNE 20. WITH SILVER UP $1.17//HUGE CHANGES IN SILVER INVENTORY’ A DEPOSIT OF 5.164 MILLION OZ INTO THE SLV/// /INVENTORY RISES TO 434.929 MILLION OZ.

JUNE 18. WITH SILVER UP $0.21//NOCHANGES IN SILVER INVENTORY’ A WITHDRAWAL .730 MILLION OZ INTO THE SLV/// /INVENTORY FALLS TO 429.775 MILLION OZ.

JUNE 17. WITH SILVER UP $0.21//SMALL CHANGES IN SILVER INVENTORY’ A WITHDRAWAL .730 MILLION OZ INTO THE SLV/// /INVENTORY FALLS TO 429.775 MILLION OZ.

JUNE 14. WITH SILVER DOWN $0.10//NO CHANGES IN SILVER INVENTORY/ /INVENTORY REMAINS AT 429.083 TONNES

JUNE 13. WITH SILVER DOWN $1.10//HUGE CHANGES IN SILVER INVENTORY/ A HUGE DEPOSIT OF 1.958 MILLION OZ/INVENTORY RISES TO 429.083 TONNES

JUNE 12 WITH SILVER UP $0.97 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 5.983 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 427.125 MILLION OZ

JUNE 11 WITH SILVER DOWN $0.59 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.644 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 422.786 MILLION OZ

JUNE 10 WITH SILVER UP $0.30 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 3.198 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 421.142 MILLION OZ

JUNE 7 WITH SILVER DOWN $1.93 TODAY: NO CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY AT 417.944 MILLION OZ

JUNE 6 WITH SILVER UP $1.27 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 417.944 MILLION OZ

JUNE 5 WITH SILVER UP 0.38 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.52 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 415.295 MILLION OZ

JUNE 4 WITH SILVER DOWN $1.08 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

JUNE 3 WITH SILVER UP $0.35 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

MAY 31 WITH SILVER DOWN $1.09 TODAY: HUGE CHANGES IN SILVER INVENTORY: A MASSIVE WITHDRAWAL OF 3.655 MILLION OZ FROM THE SLV//INVENTORY LOWERS TO 413.775 MILLION OZ

MAY 30 WITH SILVER DOWN $0.80 TODAY: NO CHANGES IN SILVER INVENTORY//INVENTORY REMAINS AT 417.430 MILLION OZ

MAY 29 WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 1.051 MILLION OZ INTO THE SLV//INVENTORY DECREASES TO 417.430 MILLION OZ

MAY 28 WITH SILVER UP $1.64 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 2.832 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 418.481 MILLION OZ

CLOSING INVENTORY 437.447 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY

CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES

end

4. other gold commentaries/podcasts/live from the vault Andrew Maguire 179

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COPPER

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

ASIA TRADING//MONDAY MORNING/SUNDAY NIGHT

SHANGHAI CLOSED UP 27,33 PTS OR 0.92% //Hang Seng CLOSED // Nikkei CLOSED UP 47.98 OR 0.12%//Australia’s all ordinaries CLOSED DOWN 0.27%///Chinese yuan (ONSHORE) closed DOWN TO 7,2682 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2996/ Oil DOWN TO 82.00 dollars per barrel for WTI and BRENT DOWN AT 85.52 /Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS MONDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2682

OFFSHORE YUAN: DOWN TO 7.2996

SHANGHAI CLOSED UP 27,33 PTS OR 0.92 %

HANG SENG CLOSED

2. Nikkei closed UP 47.98 PTS OR 0.12 %

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 105.33 EURO RISES TO 1.0747 UP 50 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1,055 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 161.11 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.5640/Italian 10 Yr bond yield DOWN to 4.071 SPAIN 10 YR BOND YIELD UP TO 3.434%

3i Greek 10 year bond yield DOWN TO 3.720

3j Gold at $2337.30//Silver at: 29.30 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 56/ 100 roubles/dollar; ROUBLE AT 86.99

3m oil into the 82 dollar handle for WTI and 85 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 161.11/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.055% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9011 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9685 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.418 UP 8 BASIS PTS…

USA 30 YR BOND YIELD: 4.576 UP 7 BASIS PTS/

USA 2 YR BOND YIELD: 4.760 UP 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.69…

10 YR UK BOND YIELD: 4.260 UP 8 PTS

2a New York OPENING REPORT

Futures Rise, European Markets Relief Rally After No Surprises From French Election

MONDAY, JUL 01, 2024 – 08:16 AM

US equity futures are higher boosted by a relief rally in French stocks and European bonds, where the result of the French parliamentary election (no outright majority for Le Pen) was not as bad as some had feared. As of 8:00am ET, S&P futures are up 0.3, trading near session highs,while Nasdaq futures gained 0.2% with Nvidia dropping as much as 2.8%, but off the lows. Major European markets are higher led by France and Italy after Le Pen’s National Rally led the first round of snap polls but failed to secure an absolute majority as some polls had suggested; CAC +1.4%. On macro data, Germany regional CPI suggests some cooling. We will receive the national German CPI at 8am ET. In Asia, PBOC signals possible government bond sales to cool market rally which pushed Chinese bond yields to record lows. Meanwhile bond yields in the US are 1-2bp higher, the 10Y TSY trading at 4.41%, following higher EU yields; the USD is lower. Commodities are higher led by oil and base metals. Today, the macro focus will be June ISM-Mfg where consensus expects a modest increase to 49.1 vs. 48.7 prior.

In premarket trading, Spirit AeroSystems rallied 6.3% after Boeing agreed to buy back the supplier in an all-stock deal that values it at $4.7 billion. Chewy shares soared 29% after influential investor Keith Gill disclosed a 6.6% passive stake in the online pet food and product retailer. Mega cap tech (ex. NVDA) are modestly higher: AMZN +39bp, GOOG/L +28bp, MSFT +26bp; Semis are weaker: NVDA -2.8%, MU -74bp, AMD -52bp. Her are some other notable premarket movers:

- Birkenstock rises 3% after UBS boosted its rating to buy, saying that the company can achieve stronger sales and margins over the long term.

- NIO ADRs climbs 4% after the Chinese EV maker reported a rise in June deliveries.

European stocks snapped a four-day losing streak and the euro rose as French election results suggested there’s a smaller probability of extreme policies coming from Le Pen’s RN. Traders interpreted the first round of legislative voting as an indication that Marine Le Pen’s party faces a tougher-than-expected road to overall victory, reducing the risks of spending plans that would rattle financial markets. The 10-year spread on French-German debt narrowed to a two-week low.

“Markets are quite content there’s no apparent absolute majority,” said Claudia Panseri, chief investment officer for France at UBS Wealth Management. “The most extreme scenarios for the spread have been excluded.”

France’s second round of voting will be held on July 7. The French political world is now embarking on a period of horse-trading. In constituencies where three people qualified for the runoffs, the third-placed candidate can withdraw to boost the chances of another mainstream party defeating the far right.

“It’s hard to argue that you’ve got a good outcome,” Sebastian Raedler, head of European equity strategy at Bank of America, said on Bloomberg Television. “Maybe you block a majority by the hard right. But in the best-case scenario, you get a hung parliament. That effectively means very little decision making, no ability to deal with a very wide budget deficit, and also the European integration story effectively put on hold.”

In any case, the kneejerk reaction was a clear relief rally as France’s CAC 40 Index jumped as much as 2.8% before retracing some gains. Banking stocks led the advance in Europe’s Stoxx 600 Index, as French lenders Societe Generale SA, BNP Paribas SA and Credit Agricole SA all surged by more than 5%. The euro climbed to its strongest level since mid June. Here are the biggest movers Monday:

- Renault rises as much as 4.1%, buoyed by Saudi Aramco’s decision to acquire a 10% stake in Horse Powertrain, the French carmaker’s joint venture with China’s Geely

- Zalando gains as much as 6.6%, the most since May 7, as JPMorgan (neutral) reiterates its positive catalyst watch on the German online clothing retailer, ahead of August’s quarterly results

- Aurubis shares rise as much as 6.4% after analysts at Bankhaus Metzler raised their price target for the German copper smelter to €91, the highest among analysts tracked by Bloomberg, citing higher metal prices

- Gubra jumps as much as 21% after the Danish pharmaceuticals firm announced it and partner Boehringer Ingelheim have started clinical testing of BI 3034701, a long-acting triple agonist peptide with a potential to become a next-generation and first-in-class obesity treatment

- Matas shares gain as much as 5.2%, the most since May 28, after Swedish business daily Dagens Industri recommends the Nordic cosmetics retailer in its stockpick-of-the-week column

- Clariant gains as much as 4.7% after Goldman Sachs raised its recommendation to buy from neutral, saying the Swiss chemical company’s new consumer-focused strategy should allow it to close its valuation gap with peers

- Aperam shares gain as much as 5.5% after Morgan Stanley says the steelmaker’s market update points to “modest upside” to the second quarter adjusted Ebitda on small inventory valuation gains

- Anglo American drops as much as 4% in London after a fire halts production at its Grosvenor site, the company’s biggest metallurgical coal project in Australia. The miner said it will take months for the blaze to be extinguished

- Bechtle shares fall as much as 5.7% to the lowest since October, after Exane downgraded the stock to underperform from neutral, saying the IT firm likely faces continued weak demand among small- and medium-sized firms in Germany

Meanwhile, back in the US, investors prepare for the second-quarter reporting season, Goldman Sachs strategists said Corporate America faces the highest earnings bar in almost three years. Single-stock analysts predict profits at S&P 500 firms rose 9% on average in the April-June period — the biggest year-over-year increase since the fourth quarter of 2021, Goldman strategists led by David Kostin wrote in a note.

“The magnitude of earnings-per-share beats is likely to diminish as consensus forecasts set a higher bar than in previous quarters,” Kostin said. “We expect the outperformance ‘reward’ for stocks beating estimates will be smaller than average again this quarter.”

Earlkier, Asian equities started the week on a positive note after a rally in Japanese stocks and as Chinese shares reversed earlier losses. The MSCI Asia Pacific Index climbed as much as 0.3%, with Hitachi, Mitsubishi Corp. and BHP Group contributing the most. Stock benchmarks gained in Taiwan and South Korea, while they fell in Australia. Japanese shares rallied as the decimation of the yen resumed. Financial companies were among big gainers in the country, boosted by bets on a Bank of Japan rate hike. Shares also were helped by survey data that showed confidence among the country’s large manufacturers rose from a quarter ago. The survey “confirmed that an inflationary trend is in place, with business sentiment strong and manufacturing passing on rising costs,” said Kohei Onishi, a senior investment strategist at Mitsubishi UFJ Morgan Stanley Securities Co. Companies’ yen exchange rate assumptions suggest earnings will likely be upgraded, he said. In China, mainland equities reversed earlier losses after a private gauge of factory activity rose to a three-year high, even as data showed that confidence among manufacturers is sagging. Hong Kong stock trading was closed for a holiday.

In emerging markets, South African assets rallied after President Cyril Ramaphosa announced a new cabinet that includes members of the opposition Democratic Alliance, considered business-friendly by investors.

In FX, the Bloomberg Spot Dollar Index was little changed while the euro outperformed most of its G10 peers on signs Marine Le Pen’s far-right party appeared to win the first round of France’s legislative election with a smaller margin of victory than some polls had indicated.

- EUR/USD climbed as much as 0.6% to 1.0776, the highest since June 12. One-month implied volatility in USD/JPY rises above 10% for the first time since May 6 as the tenor now captures the July 31 policy decisions by the Federal Reserve and the Bank of Japan.

- EUR/CHF rose as much as 0.5%, in a sign investors took heart in the French voting result. The franc is typically the preferred haven play for political risk in Europe

Treasuries slightly cheaper from belly out to long-end of the curve which underperforms, adding to Friday’s aggressive steepening that accelerated into the month-end close. European bonds lag significantly as haven demand is unwound with the first round of voting in France pointing to no single party gaining an absolute majority. US session highlights include ISM manufacturing gauge, while Fed Chair Powell is scheduled to speak in Sintra Tuesday.

In rates, US long-end yields cheaper on the day by about 1.5bp, steepening 2s10s, 5s30s spreads; 10-year yields around 4.41% with bunds and gilts lagging by 6bp and 3.5bp in the sector. French bonds outperform in Europe after Marine Le Pen’s National Rally failed to record a decisive win in the first round of France’s snap parliamentary elections. European bonds elsewhere lag significantly as haven demand is unwound with the first round of voting in France pointing to no single party gaining an absolute majority.

In commodities, oil rose as traders assessed economic outlook and geopolitical risks in Europe and the Middle East. Iron ore rose amid tentative signs of recovery in China’s steel-intensive property market, and speculation that Beijing could do more to support the sector.

Looking at today’s calendar, US economic data slate includes S&P Global June final manufacturing PMI (9:45am), May construction spending and June ISM manufacturing (10am). JOLTS, ADP employment change, ISM services gauge and June jobs report are ahead this week, No Fed speakers scheduled for the session; Powell talks Tuesday on a panel with ECB President Christine Lagarde and Brazil’s Roberto Campos Neto in Sintra

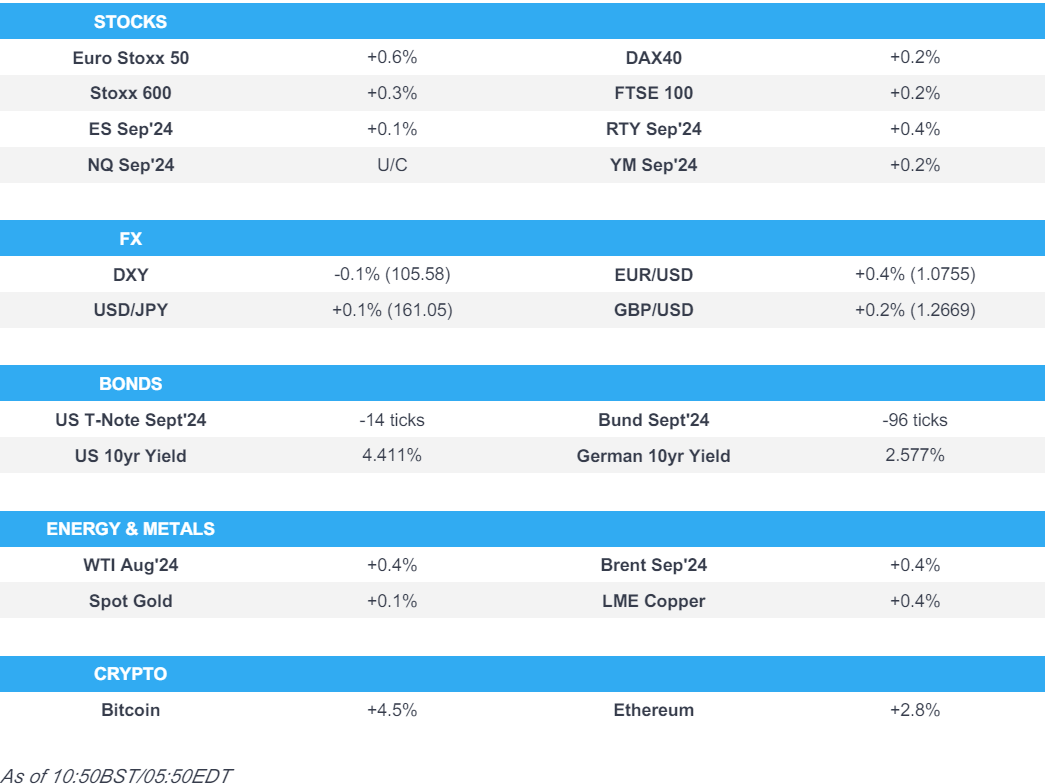

Market Snapshot

- S&P 500 futures up 0.2% to 5,532.75

- STOXX Europe 600 up 0.6% to 514.68

- MXAP up 0.2% to 180.89

- MXAPJ little changed at 567.36

- Nikkei up 0.1% to 39,631.06

- Topix up 0.5% to 2,824.28

- Hang Seng Index little changed at 17,718.61

- Shanghai Composite up 0.9% to 2,994.73

- Sensex up 0.5% to 79,457.06

- Australia S&P/ASX 200 down 0.2% to 7,750.74

- Kospi up 0.2% to 2,804.31

- Brent Futures up 0.7% to $85.60/bbl

- Gold spot down 0.1% to $2,324.93

- US Dollar Index down 0.34% to 105.51

- German 10Y yield little changed at 2.57%

- Euro up 0.5% to $1.0765

- Brent Futures up 0.7% to $85.60/bbl

Top Overnight News

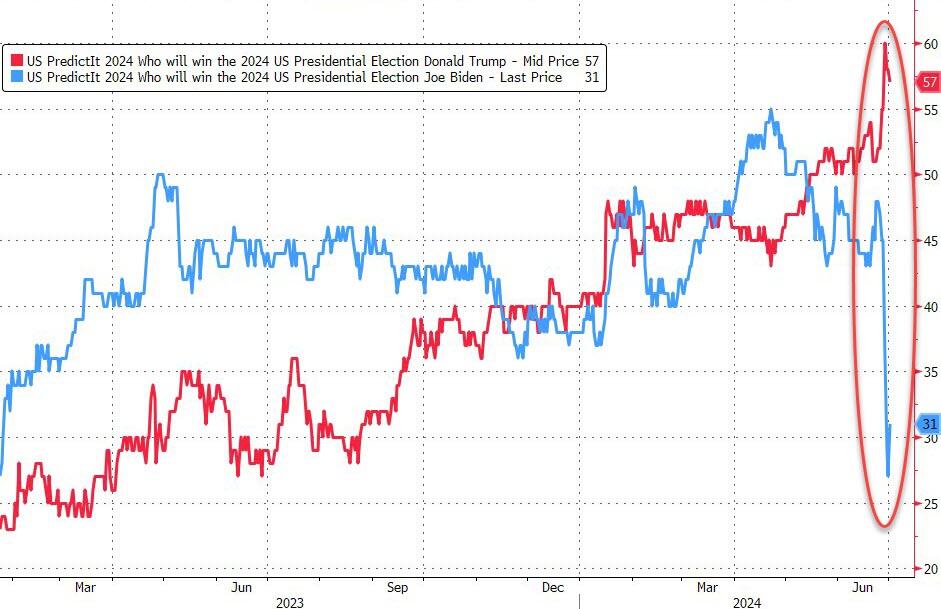

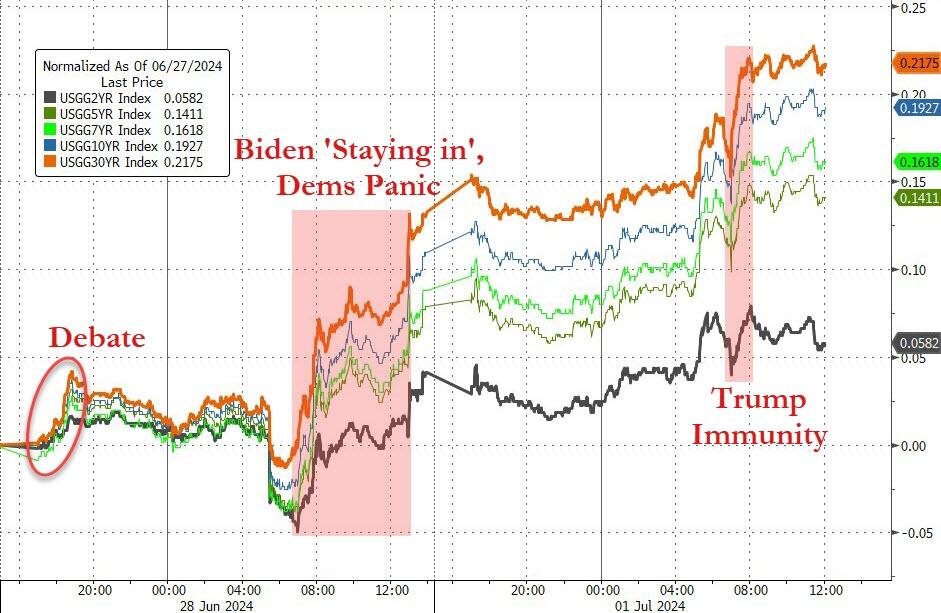

- US President Biden’s family is urging him to stay in the race and keep fighting despite last week’s disastrous debate performance, according to NYT.

- European stocks and the euro rallied on speculation Marine Le Pen’s far-right party will struggle to win an outright majority in French elections, easing investor concern that the region’s second-largest economy was headed for a radical policy shift.

- French President Emmanuel Macron’s centrist alliance and the left-wing New Popular Front are weighing whether to pull candidates from the second round of the legislative election on Sunday to keep the ascendant far-right National Rally out of power.

- French markets rebounded after Marine Le Pen’s National Rally party finished with a smaller margin of victory than indicated by polls, spurring a relief rally across the nation’s assets.

- President Joe Biden’s campaign is going on the attack against a chorus of donors, consultants, officials and media voices calling on him to drop out of the 2024 race after his devastating debate performance.

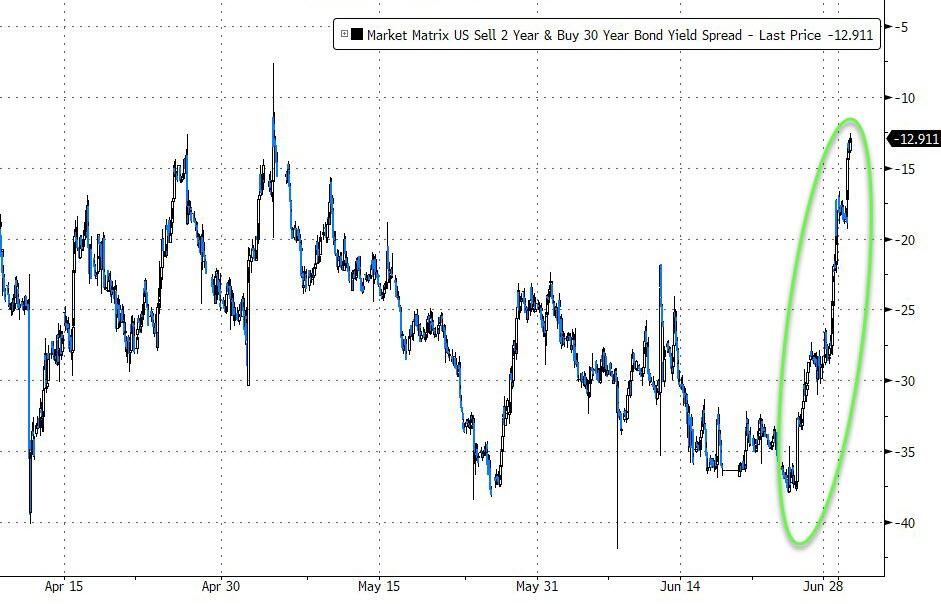

- The growing prospect of a Trump presidential victory is making yield curve steepeners an attractive bet as growth will likely slow and inflation quicken under such a scenario, according to Morgan Stanley.

- The People’s Bank of China said it will borrow government bonds from primary dealers, a sign it may be contemplating selling securities to cool down a market rally.

- Boeing Co. agreed to buy back Spirit AeroSystems Holdings Inc. for $37.25 a share in an all-stock deal that values the supplier at $4.7 billion, unwinding a two-decade separation as the embattled US planemaker tries to fix is manufacturing defects.

- EU plans to charge Meta Platforms over its ‘pay or consent’ model, FT reports citing sources; regulators are concerned the model offers consumers a misleading choice, potentially forcing consent to personal data tracking for ads due to financial barriers. Penalties could reach 10% of global turnover, rising to 20% for repeat violations.

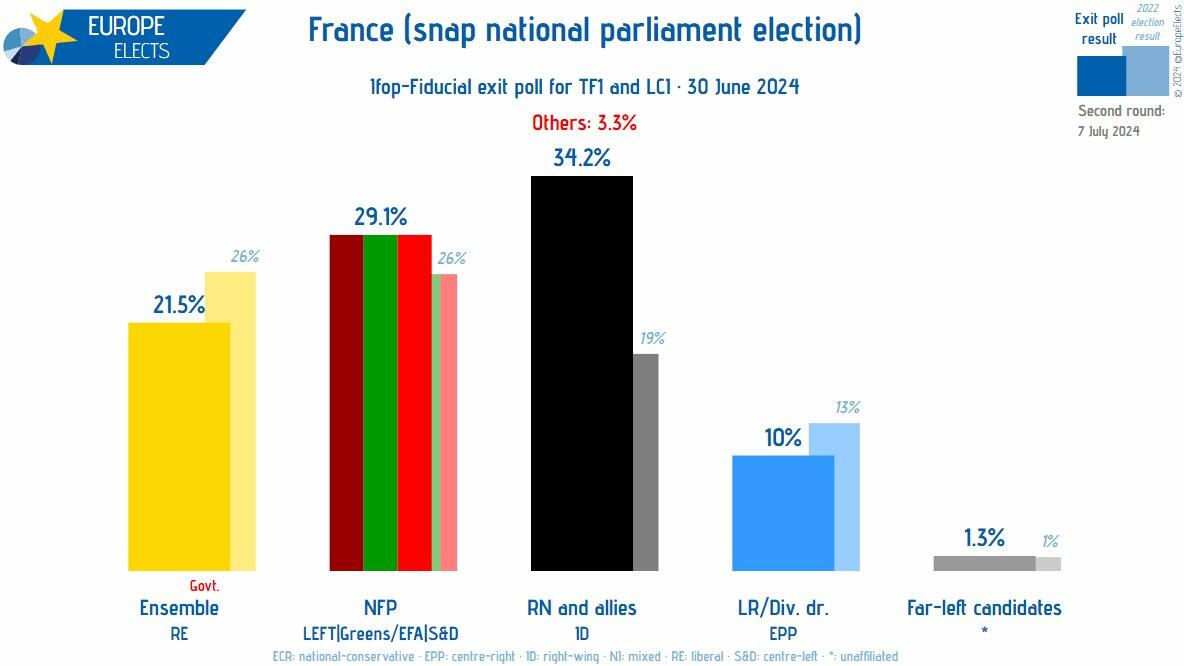

French Election

- French Election 1st Round: National Rally makes significant gains but the odds of another hung parliament have likely increased.

- Exit polls have National Rally (RN) on 34.5%, the New Popular Front (NFP) on 29%, Macron’s Ensemble (ENS) on 21-23% and Les Republicans (LR) on 10%. When extrapolated into seat projections, there is a slight discrepancy between vendors with the forecast range for RN not encapsulating the 289 majority mark via the IFOP survey and France Televisions-Radio’s calculations; however, estimates from Elabe have an RN majority within the forecast range.

- Immediately after the exit polls dropped, PM Attal outlined a broad call to the centre and left-wing. Calling for voters to prevent RN from winning a second-round majority, to facilitate this he has pledged to stand down ENS candidates who have no chance of winning in the second round to give the non-RN candidate the best chance of victory.

- Into the second round, there are now three main points to look for: Whether Macron shows any sign of wavering from his pledge to stay as President irrespective of the result; The reception of NFP to the call from ENS to cooperate to prevent an RN outright majority, i.e. if they demand the appointment of an ENS PM or similar; Any signs of the non-RN friendly contingent of LR wavering from their position and joining forces with RN, as the addition of their 41-61 projected seats could be enough to secure an outright RN majority.

- Reminder, the second round occurs on 7th July. Exit polls are to be released from 19:00BST/14:00ET with official results emerging from some constituencies immediately but the full picture will not be known until early-Monday.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks began the new quarter somewhat varied as participants digested key data releases and markets braced for a busy week ahead culminating in the latest NFP report on Friday. ASX 200 was led lower by underperformance in tech amid headwinds from firmer yields although the index was off worst levels owing to resilience in mining stocks. Nikkei 225 gained at the open amid initial currency weakness although some of the gains were then faded as participants digested a mixed BoJ Tankan survey. Shanghai Comp. swung between gains and losses with price action choppy in early trade after mixed PMI data from China which showed official Manufacturing PMI remained in contraction territory and Non-Manufacturing PMI missed estimates, but Chinese Caixin Manufacturing PMI topped forecasts to print its highest in three years. Meanwhile, Hong Kong markets were shut for a holiday which also meant the absence of Stock Connect flows.

Top Asian News

- Indonesia is to impose safeguard duties of 100% to 200% on imports ranging from footwear to ceramics, while it mainly imports apparel and clothing accessories from China, Vietnam and Bangladesh, according to Nikkei.

- India’s government source said it is monitoring cheap Chinese imports, while India’s steel ministry is in talks with the commerce ministry over rising imports and the industry has sought a probe.

- China’s Vice Premier is to hold a symposium related to foreign investments on Monday, according to State Media; says China will further expand market access and break unreasonable limit for foreign investments.

CAC 40 (+1.8%) is the marked outperformer after the 1st round of the French legislative election, with the rally coming despite marked RN gains as the projections potentially point to increased odds of another hung parliament i.e. no RN majority. Though, initial upside has trimmed somewhat given we have another week of political uncertainty ahead and the fiscal situation remains tense and unfavourable for France. Stoxx 600 (+0.3%) and European generally are firmer, but have also trimmed modestly off best levels with newsflow ex-France light or not having much impact. Sectors much the same with the breakdown largely a reflection of the respective weighting of French stocks within the sectors as opposed to a broad trend. Stateside, futures are generally in the green (ES +0.1%, NQ -0.1%, RTY +0.3%) as we began a holiday shortened week that is firmly weighted towards NFP on Friday; note, NQ has slipped just into the red amid relatively pronounced pre-market pressure in Nvidia (-2.5%) though seemingly without a fresh fundamental driver.

Top European News

- European Commission President von der Leyen said European companies are signing deals or MOUs worth over EUR 40bln at the Egypt-EU investment conference, according to Reuters.

- Austria’s far-right Freedom Party chief Kickl said they are forming a new political alliance with Orban’s Fidesz in Hungary and Babis’s Czech ANO party, according to Reuters.

- The Sunday Times newspaper endorsed the Labour Party for the upcoming UK election.

FX

- DXY weighed on by the firmer EUR. Index down to a 105.42 base, holding above the 25th June low at 105.37. Docket for today is features ISM Manufacturing PMI and Fed’s Williams, the pricing component from the PMI and any commentary from Williams on PCE will be keenly sought.

- EUR the outperformer, in a relief-rally after the weekends’ French results which show that the far-right may struggle to form a Parliamentary majority, EUR/USD at a 1.0776 peak ahead of the 1.08 figure, a point it has been below since 14th June. Hefty OpEx features on today’s NY Cut.

- Cable benefitting from the encouraging risk environment and strengthening to a 1.2689 peak into this week’s UK election; however, GBP is softer vs the EUR.

- USD/JPY holding just above 161.00 with havens generally struggling in the morning’s risk environment. Last week’s multi-year peak stands at 161.28.

- Antipodeans firmer continuing the upside seen in the tail-end of last week, no real follow-through from Chinese PMIs overnight.

- PBoC set USD/CNY mid-point at 7.1265 vs exp. 7.2558 (prev. 7.1268).

- South African President Ramaphosa reappointed Enoch Godongwana as Finance Minister, while he appointed John Steenhuisien as Agriculture Minister and Ronald Lamola as Minister of International Relations and Cooperation, according to Reuters.

Fixed Income

- OATs saw gains in excess of 20 ticks at best which alongside pressure in Bunds saw the OAT-Bund 10yr yield spread narrow to 72.4bps from an 80.1bp close on Friday. However, OATs have since come under pressure and are lower by around 20 ticks as the initial relief rally dissipates, a move which has re-widened the spread somewhat to 75bps.

- Bunds pressured as they trim recent strength seen into the French election, down to a 130.55 base. No real reaction to the numerous data points from Germany, with state CPIs broadly chiming with the mainland consensus.

- Gilts weighed on in-line with the above, at an initial low point of 97.14 which printed around the Final Manufacturing PMI that was revised lower and provided some support. Though, internal commentary factored on the hawkish side and has seen the benchmark slip to a fresh 97.07 base.

- US Treasuries are directionally in-fitting with other core players; just off a 109-15 base but remain towards the low-end of a 10 tick range

Commodities

- Crude bid across the board given the broader risk appetite and weaker USD. Crude-specific newsflow has been light this morning but as the US hurricane season nears, the desk is keeping an eye on Hurricane Beryl.

- WTI August trades within a USD 81.38-82.29/bbl range, Brent September sits in a USD 84.54-85.74/bbl parameter.

- Saudi Aramco’s strategic gas expansion reportedly progresses with USD 25bln of contract awards.

- Mixed trade across precious metals with spot gold biding time ahead of this week’s macro risk events whilst spot silver is underpinned by the softer Dollar.

- Base metals are mostly firmer, though off best, with the softer USD and risk tone assisting, though the magnitude of gains has trimmed alongside a moderation in broader risk appetite.

- NHC says Hurricane Beryl is taking aim at the windward islands, with life-threatening winds and storm surge expected to begin this morning.

Geopolitics – Middle East

- US proposed new language in an effort to reach a Gaza hostage-ceasefire deal, according to Reuters.

- Hamas officials said there is no progress in ceasefire talks with Israel but it is still ready to deal positively with any ceasefire proposal that ends the war in Gaza, according to Reuters.

- Iraq’s Islamic Resistance reportedly hit an Israeli port with a drone, according to IRNA.

- Israel’s Finance Minister extended the waiver allowing cooperation between Israeli and Palestinian banks in the West Bank for four months, according to a spokesperson cited by Reuters.

- Iran’s UN mission said an obliterating war will ensue if Israel attacks Lebanon and that all options including the full involvement of resistance fronts are on the table.

- Iran will hold a presidential election run-off on July 5th as no candidate secured 50% of votes.

- Israeli Media reports “The end of the war in its current form within 10 days”, via Sky News Arabia citing Channel 13.

Geopolitics – Other

- Russia took control of the settlement of Shumy in Ukraine, while Russian forces also took over Spirne and Novooleksandrivka in Ukraine’s Donetsk region, according to RIA citing the Defence Ministry. It was separately reported that a Ukrainian drone attack killed five people in Russia’s borderline Kursk region, while Russia’s Emergency Ministry said four of its employees were injured in Ukraine’s shelling of Donetsk.

- North Korea condemned ‘Freedom Edge’ joint military drills by the US, South Korea and Japan as provocation, while it said it will make an important announcement and will protect regional peace with an aggressive and overwhelming response, according to KCNA. It was also reported that North Korea conducted a missile launch of a short-range ballistic missile and another ballistic missile, according to Yonhap citing the South Korean military.

- US military raised the alert level of several bases in Europe to its second-highest level, according to the Times of Israel citing multiple American media outlets.

US Event Calendar

- 09:45: June S&P Global US Manufacturing PM, est. 51.7, prior 51.7

- 10:00: May Construction Spending MoM, est. 0.2%, prior -0.1%

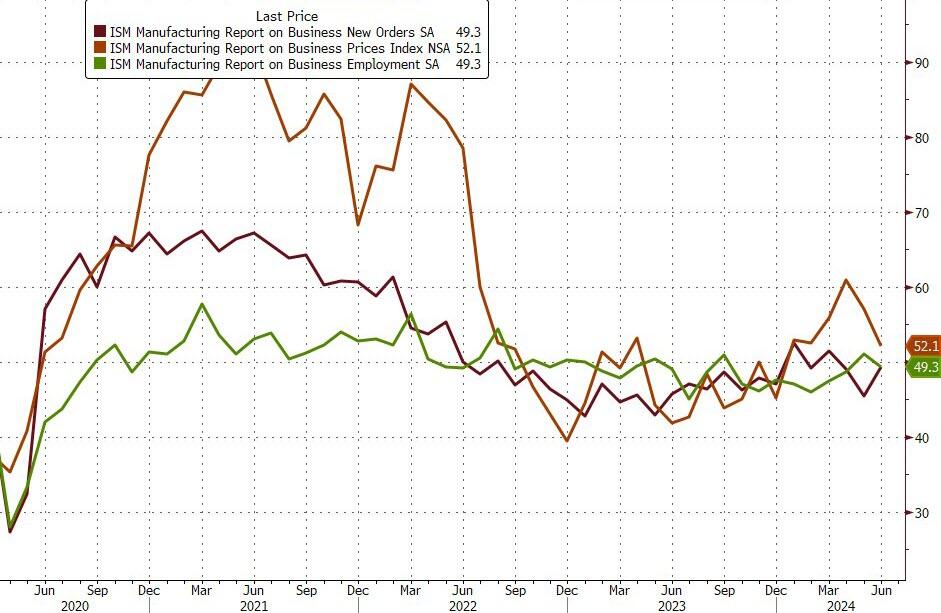

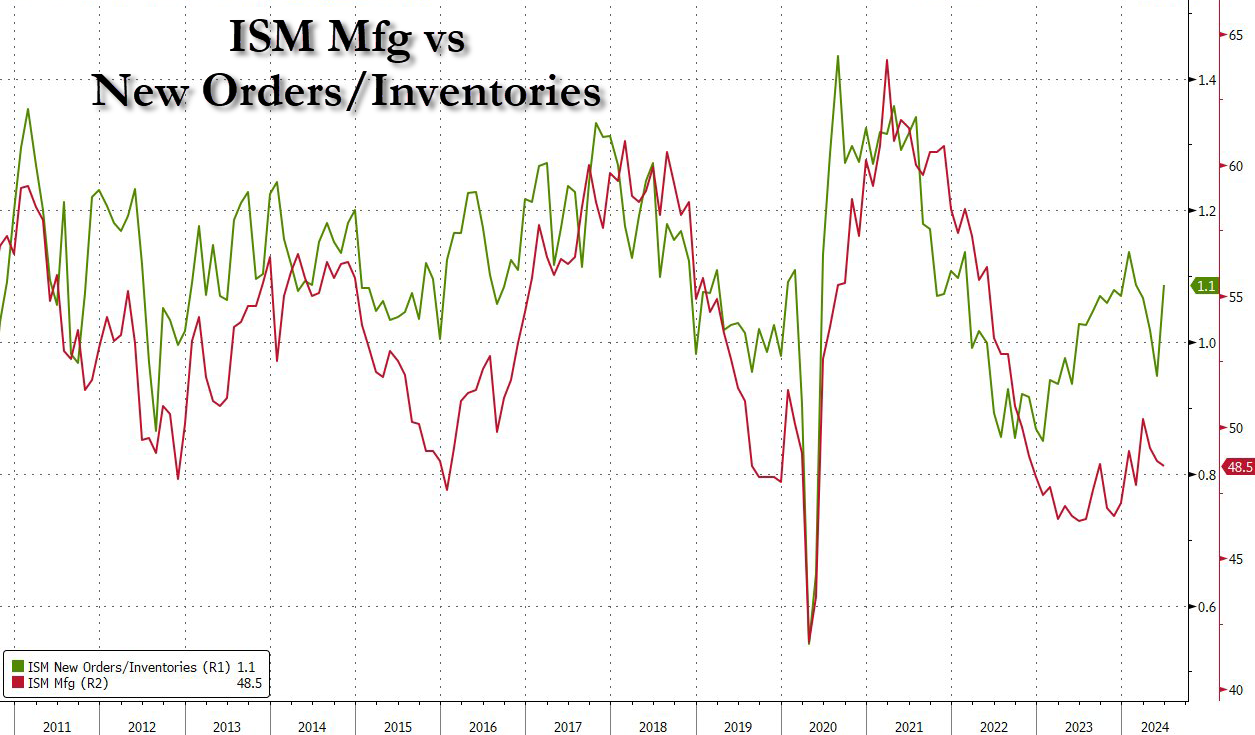

- 10:00: June ISM Manufacturing, est. 49.1, prior 48.7

- June ISM Employment, est. 50.0, prior 51.1

- June ISM New Orders, est. 49.0, prior 45.4

- June ISM Prices Paid, est. 55.8, prior 57.0

DB’s Jim Reid concludes the overnight wrap

The biggest shock in Europe on Sunday, after a hugely anticipated battle, was that England football team managed to find a way of winning through to the last 16 in what was one of the most woeful and undeserved victories of all time. As this was unfolding the first round of the French elections perhaps delivered a slightly less convincing victory for the far-right than final polls suggested and with other parties now seemingly open to form alliances in the second round, this is likely to further reduce the far-right’s chance of an overall majority in parliament. This has helped the Euro to move +0.40% higher overnight to trade at 1.0756 against the dollar, with Euro Stoxx futures climbing +1.2% as I type.

To recap, Le Pen’s National Rally look set to win around 34.2% of the vote, slightly underperforming the final poll of polls which had them at 36.2%. The left-wing NPF coalition are expected to be at around 29% slightly outperforming their final poll of polls of 28.3%. Macron’s party is on track for around 21% also a bit above the final poll of polls of 20.4%.

In terms of what happens next, all those candidates that have an absolute majority of votes and a vote greater than 25% of the electorate is elected. For those not crossing the threshold, the second round this coming Sunday is a run-off between the top two candidates plus any other candidates who polled more than 12.5% of registered voters. Then the one with the most votes is elected.

The left alliance has said it will remove candidates that are in third place which will be problematic to the Far Right’s chances of a majority. Over half the 577 parliamentary seats, a historically very high number, are expected to go to the second round with lots of tactical voting now likely. The deadline for filing papers to accept the opportunity to be on Sunday’s second round is at 6pm tomorrow. So we’ll have a good idea of tactical alliances then.

Our economics and rates strategy teams, alongside our traders, will be doing a webinar this morning at 10am London time to discuss the implications of these election results. Register Here to watch.

Moving on and as it’s the start Q3 today, we’ll shortly be releasing our performance review for the quarter just gone. On the plus side, Q2 saw equities continue to advance, and the S&P 500 hit many more fresh new highs thanks to further gains for the Magnificent 7. But the gains remained narrow, with the equal-weighted S&P 500 actually losing ground in Q2. Meanwhile, sovereign bonds struggled in Q2 as investors generally priced in slower rate cuts, even as the ECB cut for the first time since the pandemic in a June that saw a more dovish pricing for rate expectations. Politics and geopolitics were also back in focus, not least in France where there was a notable selloff after the snap election announcement. See the full report in your inboxes shortly.

In terms of this week, it will be quite a busy one considering its a US holiday. Thursday is Independence Day which means Friday will likely see a skeleton staffing for the latest employment report with the all-important payrolls number.

Elsewhere on a day-by-day basis the main highlights are as follows. Today brings the US ISM and German CPI and the start of the annual ECB Sintra central bank conference with Lagarde speaking for the first amongst many appearances this week. Tomorrow brings the US JOLTS report, Eurozone CPI and both Powell and Lagarde on a panel at Sintra. Wednesday brings US services ISM, the ADP report, initial jobless claims a day earlier than usual and the trade balance data. The FOMC minutes are also released. We’ll also see China’s Caixin services PMI and the Eurozone PPI. Thursday sees the UK election and Swiss CPI with Friday seeing German and French IP, Eurozone and Italian retail sales and the Canadian job report to go alongside the US equivalent.

Previewing the US employment report on Friday, our economists expect headline (+225k forecast vs. +272k previously) and private (+195k vs. +229k) payrolls to be above the +190k and +163k expected by the consensus. The three-month averages are +249k and +206k, respectively. Our economists and consensus expect unemployment to stay at 4% although our economists think the risk is more skewed to rounding down to 3.9%. Remember last month saw the first print above 4% in nearly 2 and a half years but there is more uncertainty over the current accuracy of the household survey which the unemployment rate comes from than their establishment survey which payrolls comes from. Remember as ever that the JOLTS data (tomorrow) should be a better gauge of how tight the labour market is but as always is a month behind the employment report.

Asian equity markets are relatively quiet this morning after mixed Chinese PMIs. As I check my screens, the Nikkei (+0.18%), the KOSPI (+0.20%) and the Shanghai Composite (+0.30%) are seeing minor gains while the CSI (-0.19%) is edging lower. Hong Kong is closed for a public holiday. S&P 500 (+0.27%) and NASDAQ 100 (+0.35%) futures are trading higher, likely helped by news from the French election. Meanwhile, yields on the 10yr USTs are around a basis point lower, standing at 4.39% as we go to print, after a surprise month-end surge on Friday that we’ll discuss below.

Over the weekend, data showed that the official Chinese manufacturing PMI contracted for a second consecutive month at 49.5, flat with the figure in May and inline with expectations while the official non-manufacturing PMI came in at 50.5 in June (v/s 51.0 expected) as against a reading of 51.1 in May. But by contrast the private Caixin manufacturing PMI rose to 51.8 in June (v/s 51.5 expected) from 51.7 in May, the fastest pace for more than 3 years.

Before we review last week, Adrian Cox recently held a webinar on “how can you use AI and machine learning in financial decision-making?” This gave an overview on how to separate the fact from the hype, followed by our Equity Quantitative Investment Solutions team explaining how Deutsche Bank is putting AI and machine learning to work in systematic strategies. Watch the replay here. ***

Now recapping last week, new data on Friday added to the amassing evidence of inflation cooling in Q2. The headline PCE index moved sidewards in May (+0.0% as expected) month-on-month, bringing the year-on-year rate to +2.6% (as expected) from +2.7%. Core PCE decelerated to +0.1% on the month, in line with consensus but a soft +0.08% unrounded. The +2.6% year-on-year core PCE pace (also as expected) was the lowest since April 2021. The data also sent a mostly healthy signal on the US consumer, with the personal income indicator rising to 0.5% (vs 0.4% expected) while real personal spending rose from -0.1% to 0.3% (as expected).

While markets initially rallied following Friday’s encouraging data, US Treasuries ended up seeing a sizeable month-end sell-off. 10yr yields were up +11.0bps to 4.40% (and +14.0bps over the week), while 30yr yields rose +13.3bps on Friday, their sharpest daily increase since November. The move was more muted on the front-end, with 2yr yields up +4.2bps (and +2.1bps on the week). So very much one of those unexplainable month-end moves.

Month-end moves also saw US equities end the week on a soft footing, with the S&P 500 sliding -0.41% (-0.08% on the week). This actually made Friday its worst day of June, a month in which the S&P 500 was still up +3.47%. Tech stocks led Friday’s correction, with the NASDAQ down -0.71% and the Magnificent 7 down -1.41%, but these were still +0.24% and +1.55% higher on the week respectively. Nvidia was -0.36% lower on Friday and -2.39% on the week.

In Europe, fixed income struggled in the lead up to the first round of the French election that took place Sunday. The 10yr French OAT yield was up +8.9bps (and +3.0bps on Friday) to 3.30%, its highest level since mid-November. Yields were up elsewhere in Europe, with yields on 10yr bunds and 10yr gilts also up by +8.9bps on the week (+4.9bps and +4.2bps on Friday respectively).

European equities underperformed over the week. The French CAC 40 fell -1.96% (and -0.68% on Friday) to its lowest level since late January. The selloff was not solely reserved for French stocks, as the STOXX 600 index also fell -0.72% (and -0.23% on Friday),though Germany’s DAX posted a gain of +0.40% (+0.14% Friday).

2B EUROPE OPENING/TRADING

Relief in Europe after the French 1st round has pared somewhat, ISM & Williams due – Newsquawk US Market Open

MONDAY, JUL 01, 2024 – 06:25 AM

- French Election 1st round saw National Rally make significant gains but the odds of another hung parliament have likely increased

- Sparking outperformance in French-related assets with OATs, CAC 40 & EUR all supported, though the magnitude of this has trimmed into another week of political uncertainty and a still challenging fiscal backdrop

- US futures generally firmer but with some slight pressure in chip names led by Nvidia

- EUR the FX outperformer weighing on DXY, USD/JPY holds above 161.00

- Fixed benchmarks in the red, initial OAT strength has faded with the OAT-Bund spread narrowing on the open to 72bps before re-widening modestly to 75bps

- Crude bid across the board, precious metals mixed while base peers track the broad tone

- Looking ahead, highlights include US Manufacturing Final PMI (June), German Prelim. CPI, US ISM Manufacturing PMI, Comments from ECB’s Lagarde & Fed’s Williams

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

FRENCH ELECTION

- French Election 1st Round: National Rally makes significant gains but the odds of another hung parliament have likely increased.

- Exit polls have National Rally (RN) on 34.5%, the New Popular Front (NFP) on 29%, Macron’s Ensemble (ENS) on 21-23% and Les Republicans (LR) on 10%. When extrapolated into seat projections, there is a slight discrepancy between vendors with the forecast range for RN not encapsulating the 289 majority mark via the IFOP survey and France Televisions-Radio’s calculations; however, estimates from Elabe have an RN majority within the forecast range.

- Immediately after the exit polls dropped, PM Attal outlined a broad call to the centre and left-wing. Calling for voters to prevent RN from winning a second-round majority, to facilitate this he has pledged to stand down ENS candidates who have no chance of winning in the second round to give the non-RN candidate the best chance of victory.

- Into the second round, there are now three main points to look for: Whether Macron shows any sign of wavering from his pledge to stay as President irrespective of the result; The reception of NFP to the call from ENS to cooperate to prevent an RN outright majority, i.e. if they demand the appointment of an ENS PM or similar; Any signs of the non-RN friendly contingent of LR wavering from their position and joining forces with RN, as the addition of their 41-61 projected seats could be enough to secure an outright RN majority.

- Reminder, the second round occurs on 7th July. Exit polls are to be released from 19:00BST/14:00ET with official results emerging from some constituencies immediately but the full picture will not be known until early-Monday.

- Click for the French Election 1st round summary/analysis

EUROPEAN TRADE

EQUITIES

- CAC 40 (+1.8%) is the marked outperformer after the 1st round of the French legislative election, with the rally coming despite marked RN gains as the projections potentially point to increased odds of another hung parliament i.e. no RN majority. Though, initial upside has trimmed somewhat given we have another week of political uncertainty ahead and the fiscal situation remains tense and unfavourable for France.

- Stoxx 600 (+0.3%) and European generally are firmer, but have also trimmed modestly off best levels with newsflow ex-France light or not having much impact. Sectors much the same with the breakdown largely a reflection of the respective weighting of French stocks within the sectors as opposed to a broad trend.

- Stateside, futures are generally in the green (ES +0.1%, NQ -0.1%, RTY +0.3%) as we began a holiday shortened week that is firmly weighted towards NFP on Friday; note, NQ has slipped just into the red amid relatively pronounced pre-market pressure in Nvidia (-2.5%) though seemingly without a fresh fundamental driver.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX