GOLD PRICE CLOSED UP $32.25 TO $2360.00

SILVER PRICE UP $1.08 TO $30.54

Gold ACCESS CLOSED $2355,50

Silver ACCESS CLOSED: $30.46

Bitcoin morning price:$60,363 DOWN 1674 DOLLARS.

Bitcoin: afternoon price: $60,306 DOWN 713 dollars//

Platinum price closing UP; $2.30 TO $1000.15

Palladium price; UP $15.05 AT $1034.40

END

SHANGHAI GOLD PREMIUM 39 DOLLARS/COMEX GOLD//JULY TO JULY

SHANGHAI GOLD (USD) FUTURES – QUOTES

Last Updated 03 Jul 2024 09:28:40 AM CT.

Market data is delayed by at least 10 minutes.

*CANADIAN GOLD: $3211.26 UP 26.28 CDN dollars per oz( * NEW ALL TIME HIGH 3,305.30 CDN DOLLARS PER OZ//MAY 20 2024)

*BRITISH GOLD: 1848.90 UP 12.71 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2183,75 UP 15.95Euros per oz //* (ALL TIME CLOSING HIGH: 2248.89 EUROS PER OZ//APRIL 16.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCH: COMEX

JPMorgan stopped 0/19

FOR JULY 2024

EXCHANGE: COMEX

CONTRACT: JULY 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,323.000000000 USD

INTENT DATE: 07/02/2024 DELIVERY DATE: 07/05/2024

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 6

363 H WELLS FARGO SEC 4

624 H BOFA SECURITIES 8

686 C STONEX FINANCIA 1

726 C PLUS500US FINAN 1

737 C ADVANTAGE 17 1

TOTAL: 19 19

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2024. CONTRACT: 19 NOTICES FOR 1900 OZ or 0.05909 TONNES

total notices so far: 2225 contracts for 222,500 Oz (6.920 tonnes)

FOR JULY:

SILVER NOTICES: 64 NOTICE(S) FILED FOR 0.320 million

OZ/

total number of notices filed so far this month : 4986 for 24,930 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $35.25 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/

: HUGE CHANGES IN GOLD INVENTORY AT THE GLD/A MASSIVE DEPOSIT OFF 5.76 TONNES OF GOLD VAOUR

/ /INVENTORY RESTS AT 833,37TONNES

INVENTORY RESTS AT 833.71 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $1.08 AT THE SLV//

SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 639,000 OZ OF SILVER FROM THE SLV//

// INVENTORY LOWERS TO 436.808 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 436.808 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A SMALL SIZED 77 CONTRACTS TO 154,724 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS SMALL SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR GAIN OF $0.19 IN SILVER PRICING AT THE COMEX ON TUESDAY’S TRADING ON SILVER. WE HAD SOME ZERO LIQUIDATION AS WE HAD A NET GAIN OF 1410 CONTRACTS ON OUR TWO EXCHANGES. WE, AGAIN HAD CONSIDERABLE SHORT COVERING BY OUR SPECS DESPITE THE GAIN IN PRICE AS WELL AS MASSIVE T.A.S. LIQUIDATION WHICH ACCOUNTS FOR THE STRONG GAIN ON THE TWO EXCHANGES. WE HAD ANOTHER STRONG SIZED 643 T.A.S ISSUANCE,

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED TUESDAY JUNE 4 AND AGAIN ON FRIDAY, JUNE 7 AND AGAIN ON YESTERDAY’S TRADING

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 643 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS.IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1/2 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.19) AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS FROM THEIR PERCH AS WE DID HAVE A HUMONGOUS SIZED GAIN OF 1265 CONTRACTS ON OUR TWO EXCHANGES WITH THE GAIN IN PRICE OF $0.19.

WE MUST HAVE HAD:

A HUMONGOUS SIZED 1188 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 28.490 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S EFP JUMP TO LONDON OF 196,000 OZ

//NEW STANDING FOR SILVER//JUNE IS THUS 28.735 MILLION OZ

WE HAD:

/ SMALL SIZED COMEX OI GAIN //HUMONGOUS SIZED EFP ISSUANCE/ VI) HUGED SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 653 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED 145 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JUNE

TOTAL CONTRACTS for 3 DAYS, total 2798 contracts: OR 13.990 MILLION OZ (932 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 13.990 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 13.990 MILLION OZ

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 77 CONTRACTS WITH OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUMONGOUS EFP ISSUANCE CONTRACTS: 1188 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JULY OF 28.496 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 195,000 OZ E.FP JUMP TO LONDON

//NEW TOTAL STANDING FOR JULY 28.735 MILLION OZ

WE HAVE A HUGE SIZED GAIN OF 1265 OI CONTRACTS ON THE TWO EXCHANGES WITH THE SMALL GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG SIZED 643 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX TRADING/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND ZERO LIQUIDATION OF LONGS.

THE NEW TAS ISSUANCE TUESDAY NIGHT (643) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 645 NOTICE(S) FILED TODAY FOR 0.320 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A GOOD SIZED 4358 OI CONTRACTS TO 456,066 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 516 CONTRACTS

WE HAD A GOOD SIZED INCREASE IN COMEX OI (3022 CONTRACTS) OCCURRED DESPITE OUR LOSS OF $4.45 IN PRICE/TUESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 7.5645 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 1500 OZ QUEUE JUMP

NEW STANDING 8.308TONNES

/ ALL OF THIS HAPPENED WITH OUR $4.45 LOSS IN PRICE WITH RESPECT TO TUESDAY’S TRADING. WE HAD A STRONG SIZED GAIN OF 7137 OI CONTRACTS (22.19 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4115 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 454,730

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7134 CONTRACTS WITH 3022 CONTRACTS INCREASED AT THE COMEX// AND A STRONG SIZED 4115 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 7134 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED 2435 CONTRACTS,,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4115 CONTRACTS) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI OF 3022 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 7137 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 7,5645 TONNES FOLLOWED BY TODAY’S 1500 OZ QUEUE JUMP

//NEW STANDING /JULY 8.308 TONNES.

/ 3) HUGE T.A.S. LIQUIDATION OF CONTRACTS WITH ZERO NET LONG SPECS BEING CLIPPED,

4) STRONG SIZED COMEX OPEN INTEREST GAIN 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///STRONG T.A.S. ISSUANCE: 2435 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

JUNE

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY. :

TOTAL EFP CONTRACTS ISSUED: 8972 CONTRACTS OR 897,200 OZ OR 27.906 TONNES IN 3 TRADING DAY(S) AND THUS AVERAGING: 2990 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAY(S) IN TONNES 27.906 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 27.906DIVIDED BY 3550 x 100% TONNES = 0.788% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 27.906 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUG), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A SMALL SIZED 97 CONTRACTS OI TO 154,724 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1188 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 1188 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1188 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 77 CONTRACTS AND ADD TO THE 1188 E.FP. ISSUED

WE OBTAIN A HUMONGOUS SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1410 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 7.050 MILLION OZ

OCCURRED DESPITE OUR $0.19 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED DOWN 14.64 PTS OR 0.49% //Hang Seng CLOSED UP 209.43 PTS OR 1.18% // Nikkei CLOSED UP 506.07 OR 1.26%//Australia’s all ordinaries CLOSED UP 0.33%///Chinese yuan (ONSHORE) closed DOWN TO 7,2733 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.3056/ Oil DOWN TO 82.85 dollars per barrel for WTI and BRENT DOWN AT 86,24/Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 3022 CONTRACTS TO 454,730 DESPITE OUR LOSS IN PRICE OF $4.45 WITH RESPECT TO TUESDAY’S TRADING. WE HAD A HUGE T.A.S. LIQUIDATION ON TUESDAY’S LOSS IN PRICE WITH ZERO LONGS BEING CLIPPED AND SOME SHORT COVERING.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE NON ACTIVE DELIVERY MONTH OF JULY.… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 4358 EFP CONTRACTS WERE ISSUED: : AUGUST 4358 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4358 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 7137 CONTRACTS IN THAT 4115 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG SIZED GAIN OF 3022 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $4.45/TUESDAY COMEX.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A STRONG SIZED 3684 CONTRACTS. MOST OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN FRIDAY’S TRADING

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JULY (8.308 TONNES)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 8.308 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $4.45 //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A STRONG SIZED GAIN OF 7137 CONTRACTS ON OUR TWO EXCHANGES DESPITE ACCOMPANYING THE LOSS IN PRICE. THE T.A.S. ISSUED ON TUESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 22.19 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY (7.5645 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 1500 OZ QUEUE JUMP//NEW STANDING 8.308 TONNES

NEW STANDING FOR JULY: 8.308 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $4.45

WE HAVE REMOVED 1336 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET GAIN ON THE TWO EXCHANGES 7137 CONTRACTS OR 713,700 OZ (22.19 TONNES)

confirmed volume TUESDAY 186,697 contracts//poor

//speculators have left the gold arena

JULY 3 JULY GOLD CONTRACT

/ /// THE JULY 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 64,862.002 oz Manfra . |

| Deposit to the Dealer Inventory in oz | |

| Deposits to the Customer Inventory, in oz | 14,202.283 OZ JPMorgan |

| No of oz served (contracts) today | 19 notice(s) 1900 OZ 0.05909 TONNES |

| No of oz to be served (notices) | 446 contracts 44600 OZ 1.387 TONNES |

| Total monthly oz gold served (contracts) so far this month | 2225 notices 222500 oz 6.920 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: nil oz

we have 0 customer deposit:

total deposit: oz

customer withdrawals: 1

i) Out of Manfra: 64,862.002 oz

TOTAL WITHDRAWALS 202,079.015 oz

Adjustments:

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE

For the front month of JULY we have an oi of 465 contracts having LOST 599 contracts. We had 614 notices filed on Tuesday so we gained 15 contracts or an additional 1500 oz will stand at the comex (0.0466 tonnes)

AUGUST LOST 8558 CONTRACTS DOWN TO 335,401 CONTRACTS

SEPT. GAINED I9 CONTRACTS TO STAND AT 151.

OCTOBER GAINED 742 CONTRACTS UP TO 21,439 CONTRACTS

We had 19 contracts filed for today representing 1900 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 19 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for July /2024. contract month, we take the total number of notices filed so far for the month (2225) x 100 oz ) to which we add the difference between the open interest for the front month of JULY (465 CONTRACTS) minus the number of notices served upon today (19 x 100 oz per contract( equals 265,600 OZ OR 8.2612 TONNES.

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (2225 x 100 oz +we add the difference for front month of JULY (465// , OI} minus the number of notices served upon today (19) x 100 oz which equals 267,100 oz (8.308 TONNES)

TOTAL COMEX GOLD STANDING FOR JULY: 8.308 TONNES WHICH IS HUGE FOR THIS NOT VERY ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,686,834.101 oz 52.46 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,501,649.558 OZ

TOTAL REGISTERED GOLD 7,838,185.304( 243.80 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,663,464.254 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,151351 oz (REG GOLD- PLEDGED GOLD)= 191.332 tonnes //

END

SILVER/COMEX

JULY 3/2024

INITIAL

//2024// THE JULY 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 866,067.400 oz Brinks Delaware . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | nil oz |

| No of oz served today (contracts) | 64 CONTRACT(S) (0.3200 million OZ) |

| No of oz to be served (notices) | 761 contracts (3.805 million oz) |

| Total monthly oz silver served (contracts) | 4986 Contracts (24.930 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit/

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 0 customer deposits:

total customer deposit nil oz

JPMorgan has a total silver weight: 128.402million oz/297.317million or 43.09%

adjustment: 2

a) dealer to customer ASAHI 1,149,962.100 oz

b) customer to dealer Brinks 294,963.310 oz

customer withdrawals: 2

i) Out of Delaware 7624.800 oz

ii) Out of Brinks 865,042.800

total withdrawal:866,067.400 0z

TOTAL REGISTERED SILVER: 69.059MILLION OZ//.TOTAL REG + ELIGIBLE. 297.317

million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF JULY/2024 OI: 825 CONTRACTS HAVING LOST 370 CONTRACT(S). WE HAD 331 NOTICES FILED ON MONDAY SO WE LOST 39 CONTRACTS OR 195,000 OZ WILL NOT STAND AT THE COMEX VIA AN E.F.P JUMP TO LONDON TO TAKE DELIVERY OVER ON THAT SIDE OF THE POND.

AUG, SAW A GAIN OF 110 CONTRACTS TO 1593

SEPT SAW A GAIN OF 74 CONTRACTS TO 129,132

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 64 for 0.320 MILLION oz

CONFIRMED volume; ON TUESDAY 55,738 good

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 4986 x 5,000 oz = 24.930 MILLION oz

to which we add the difference between the open interest for the front month of JULY ((825) and the number of notices served upon today 64 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY/2024 contract month: 4986 notices served so far) x 5000 oz + OI for the front month of JULY (825)x number of notices served upon today minus (64)x 5000 oz of silver standing for the JULY contract month equates to 28.735 MILLION OZ.

New total standing: 28.735 million oz.

There are 69.059 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

JULY 3 WITH GOLD UP $35.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD..A MASSIVE DEPOSIT OF 5.76 TONNES OF GOLD VAPOUR INTO THE GLD//:INVENTORY RESTS AT 833.37 TONNES

JULY 2 WITH GOLD DOWN $4.45 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD../:INVENTORY RESTS AT 827.61 TONNES

JULY 1 WITH GOLD DOWN $.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 28 WITH GOLD UP $3.80 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 27 WITH GOLD DOWN $16.95 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 26 WITH GOLD UP $23.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 25 WITH GOLD DOWN $13.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A STRONG WITHDRAWAL OF 2.88 TONNES OF GOLD FROM THE GLD INVENTORY RESTS AT 829.05 TONNES

JUNE 24 WITH GOLD UP$14.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A STRONG WITHDRAWAL OF 1.72 TONNES OF GOLD/NEW TOTAL TONIGHT 831.93 TONNES

JUNE 21 WITH GOLD DOWN $37.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A MAMMOTH 8.34 TONNES OF GOLD VAPOUR DEPOSIT/NEW TOTAL TONIGHT 833.65 TONNES

JUNE 20 WITH GOLD UP $23.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/://NEW TOTAL TONIGHT 825.31 TONNES

JUNE 18 WITH GOLD UP $17.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/://NEW TOTAL TONIGHT 825.31 TONNES

JUNE 17 WITH GOLD DOWN $18.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.03 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 825.31 TONNES

JUNE 13 WITH GOLD DOWN$35.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.89 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 830.78 TONNES

JUNE 12 WITH GOLD UP $28.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.89 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 830.78 TONNES

JUNE 11 WITH GOLD DOWN $0.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 10 WITH GOLD UP $2,00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 7 WITH GOLD DOWN $64.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 3.56 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 837.11 TONNES

JUNE 6 WITH GOLD UP $16.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.34 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 833.55 TONNES

JUNE 5 WITH GOLD UP $32.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 4 WITH GOLD DOWN $20.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 3 WITH GOLD UP $22.85 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 31 WITH GOLD DOWN $19.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 30 WITH GOLD UP $3.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 29 WITH GOLD DOWN $13.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 28 WITH GOLD UP $22.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 832.21 TONNES

GLD INVENTORY: 833.37 TONNES, TONIGHTS TOTAL

SILVER

JULY 3. WITH SILVER UP $1.08//SMALL CHANGES IN SILVER INVENTORY A SMALL WITHDRAWAL OF 639,000 OZ: /INVENTORY LOWERS T0 436,808 MILLION OZ.

JULY 2. WITH SILVER UP $0.19//NO CHANGES IN SILVER INVENTORY: /INVENTORY REMAINS AT 437.447 MILLION OZ./

JULY 1. WITH SILVER UP $0.05//XXX CHANGES IN SILVER INVENTORY: A DEPOSIT OF 182,000 OZ OF SILVER INTO THE SLV./.// /INVENTORY RISES AT 437.447 MILLION OZ./

JUNE 28. WITH SILVER UP $0.27//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 913,000 OZ FROM THE SLV./.// /INVENTORY REMAINS AT 437.265 MILLION OZ./

JUNE 27. WITH SILVER UP $0.01//NO CHANGES IN SILVER INVENTORY: .// /INVENTORY REMAINS AT 438.178 MILLION OZ.//

JUNE 26. WITH SILVER UP $0.03//HUGE CHANGES IN SILVER INVENTORY: A HUGE WITHDRAWAL OF 2.512 MILLION OZ OF SILVER FROM THE SLV.// /INVENTORY FALLS TO 438.178 MILLION OZ.//

JUNE 25. WITH SILVER DOWN $0.63//HUGE CHANGES IN SILVER INVENTORY: A MAMMOTH DEPOSIT OF 7.835 MILLION OZ OF SILVER VAPOUR INTO THE SLV.// /INVENTORY RISE TO 440.69 MILLION OZ.//WHAT AN ABSOLUTE FRAUD.

JUNE 24. WITH SILVER DOWN $0.05//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 2.104 MILLION OZ FROM THE SLV.// /INVENTORY LOWERS TO 432.835 MILLION OZ.

JUNE 21. WITH SILVER DOWN $1.15//NO CHANGES IN SILVER INVENTORY’// /INVENTORY REMAINS AT 434.935 MILLION OZ.

JUNE 20. WITH SILVER UP $1.17//HUGE CHANGES IN SILVER INVENTORY’ A DEPOSIT OF 5.164 MILLION OZ INTO THE SLV/// /INVENTORY RISES TO 434.929 MILLION OZ.

JUNE 18. WITH SILVER UP $0.21//NOCHANGES IN SILVER INVENTORY’ A WITHDRAWAL .730 MILLION OZ INTO THE SLV/// /INVENTORY FALLS TO 429.775 MILLION OZ.

JUNE 17. WITH SILVER UP $0.21//SMALL CHANGES IN SILVER INVENTORY’ A WITHDRAWAL .730 MILLION OZ INTO THE SLV/// /INVENTORY FALLS TO 429.775 MILLION OZ.

JUNE 14. WITH SILVER DOWN $0.10//NO CHANGES IN SILVER INVENTORY/ /INVENTORY REMAINS AT 429.083 TONNES

JUNE 13. WITH SILVER DOWN $1.10//HUGE CHANGES IN SILVER INVENTORY/ A HUGE DEPOSIT OF 1.958 MILLION OZ/INVENTORY RISES TO 429.083 TONNES

JUNE 12 WITH SILVER UP $0.97 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 5.983 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 427.125 MILLION OZ

JUNE 11 WITH SILVER DOWN $0.59 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.644 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 422.786 MILLION OZ

JUNE 10 WITH SILVER UP $0.30 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 3.198 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 421.142 MILLION OZ

JUNE 7 WITH SILVER DOWN $1.93 TODAY: NO CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY AT 417.944 MILLION OZ

JUNE 6 WITH SILVER UP $1.27 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 417.944 MILLION OZ

JUNE 5 WITH SILVER UP 0.38 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.52 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 415.295 MILLION OZ

JUNE 4 WITH SILVER DOWN $1.08 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

JUNE 3 WITH SILVER UP $0.35 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

MAY 31 WITH SILVER DOWN $1.09 TODAY: HUGE CHANGES IN SILVER INVENTORY: A MASSIVE WITHDRAWAL OF 3.655 MILLION OZ FROM THE SLV//INVENTORY LOWERS TO 413.775 MILLION OZ

MAY 30 WITH SILVER DOWN $0.80 TODAY: NO CHANGES IN SILVER INVENTORY//INVENTORY REMAINS AT 417.430 MILLION OZ

MAY 29 WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 1.051 MILLION OZ INTO THE SLV//INVENTORY DECREASES TO 417.430 MILLION OZ

MAY 28 WITH SILVER UP $1.64 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 2.832 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 418.481 MILLION OZ

CLOSING INVENTORY 436.808 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY

CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES

end

4. other gold commentaries/podcasts/live from the vault Andrew Maguire 179

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COPPER

END

6.CRYPTOCURRENCY//DIGITAL CURRENCY// COMMENTARIES/

END

ASIA TRADING//WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED DOWN 14.64 PTS OR 0.49% //Hang Seng CLOSED UP 209.43 PTS OR 1.18% // Nikkei CLOSED UP 506.07 OR 1.26%//Australia’s all ordinaries CLOSED UP 0.33%///Chinese yuan (ONSHORE) closed DOWN TO 7,2733 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.3056/ Oil DOWN TO 82.85 dollars per barrel for WTI and BRENT DOWN AT 86,24/Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.2733

OFFSHORE YUAN: DOWN TO 7.3056

SHANGHAI CLOSED DOWN 14.64 PTS OR 0.49 %

HANG SENG CLOSED UP 209,45 PTS OR 1.18%

2. Nikkei closed UP 506.07 PTS OR 1.26 %

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 105.31 EURO RISES TO 1.0741 UP 12 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1,103 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 161.93 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.5975/Italian 10 Yr bond yield DOWN to 4.036 SPAIN 10 YR BOND YIELD DOWN TO 3.429%

3i Greek 10 year bond yield DOWN TO 3.681

3j Gold at $2345.20//Silver at: 30.16 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 1 AND 60/ 100 roubles/dollar; ROUBLE AT 88.45

3m oil into the 82 dollar handle for WTI and 86 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 161.93/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.103% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9032 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9719 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.430 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.595 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.764 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.58…

10 YR UK BOND YIELD: 4.275 UP 2 PTS

2a New York OPENING REPORT

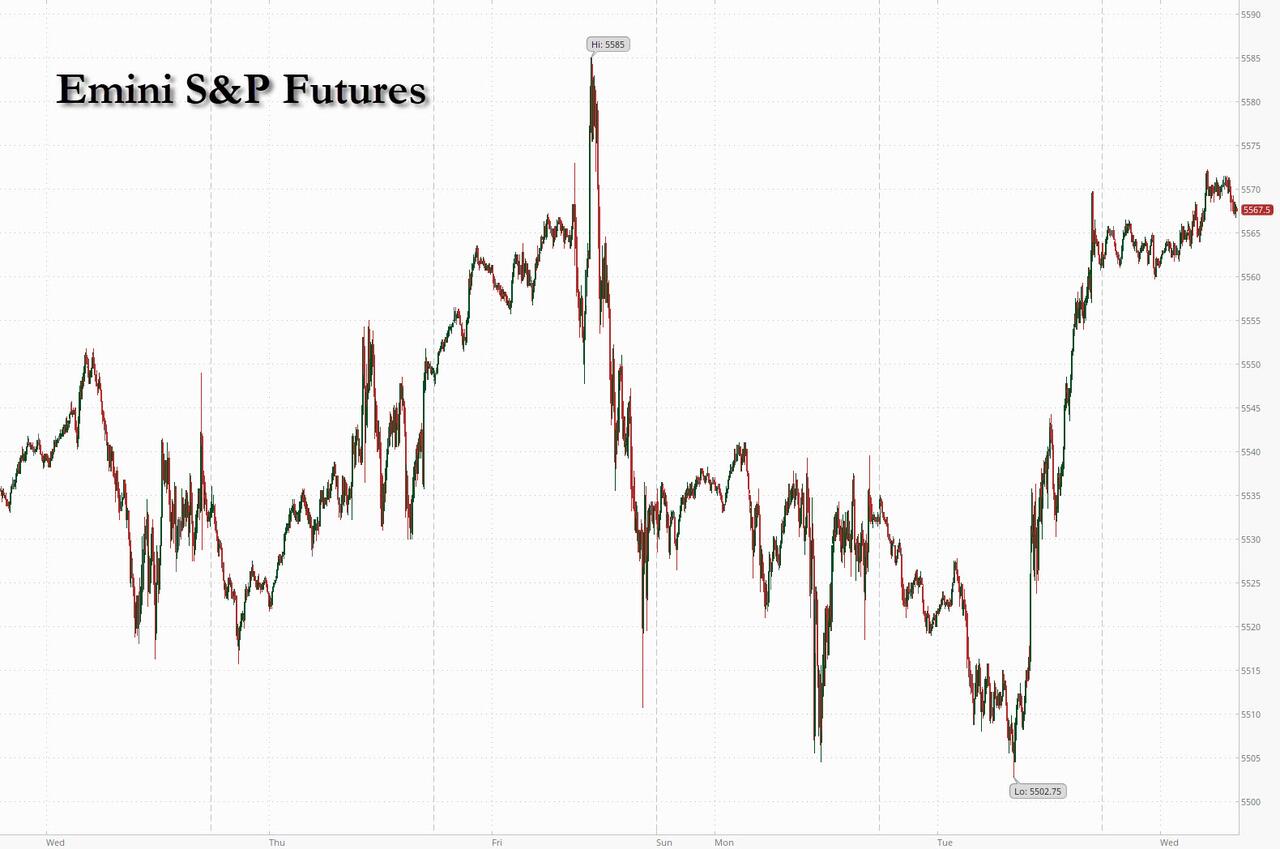

Futures Trade At Record High Ahead Of Data Flood

WEDNESDAY, JUL 03, 2024 – 08:15 AM

US futures traded at new record highs amid rising optimism a Fed rate cut is coming, perhaps as soon as the end of the month, and ignored sticky high yields which traded near the highest level in a month. As of 8:00am ET, and ahead of a data barrage later in the day which includes ADP, Trade and claims data, as well as the latest PMI, ISM, Factory orders and Durable goods reports, S&P and Nasdaq futures were flat, erasing a modest gain earlier in the session, and ahead of a shortened-session that will end at 1 p.m. because of the July 4 holiday. On Tuesday, the S&P 500 closed above 5,500 for the first time notching its 32nd record this year. Tech and small-caps are outperforming as the market received a bullish boost from Powell but now the question is whether the macro data (and earnings) can deliver with ISM Services today and NFP on Friday. European markets took heart from Wall Street’s latest all-time highs and efforts to block a right-wing majority in French elections. Bond yields are flat to +1bps as the curve is flattening; USD is lower and commodities are higher led by metals where silver is the standout. Today’s macro data focus is on ISM Services, ADP/Jobless Claims, Factory Orders, and Fed Minutes (released after the Equity close).

In premarket trading, TSLA led the Mag 7, +2.8% with NVDA weaker but broader Semis are up small. Paramount Global jumped 10% in US premarket trading after Bloomberg News reported that Skydance Media had reached a preliminary agreement to buy National Amusements Inc. and merge with Paramount. Here are some other notable premarket movers:

- Dell (DELL) advances 1.5% in premarket trading after BofA adds the personal computer maker to its US 1 list.

- Permian Resources (PR) shares advance 0.6% in premarket trading after the oil and natural gas company was upgraded to outperform from market perform at BMO Capital Markets.

With US stocks propelling higher by the day, the MSCI world index measuring both developed and emerging markets is also at a record high, evidence of the relentless euphoric sentiment toward stocks. The S&P 500 has added more than $16 trillion in value from a closing low in October 2022, thanks to solid earnings, the craze over artificial intelligence and expectations of lower borrowing costs.

After yesterday’s dovish speech by Jerome Powell at the Sintra central bank conclave, today investors will parse US initial jobless claims and ADP employment data among other readings on the economy for more clues on the policy outlook. Powell acknowledged Tuesday that the central bank has made “quite a bit of progress” in reducing inflation but emphasized officials need more evidence before lowering rates. Markets are also gearing up for the all-important US payrolls reading due Friday. Economists expect the report to show employers added about 190,000 workers in June and the unemployment rate likely held at 4%.

“We are in a situation where momentum in the US equity market is still strong, we are seeing inflation tick lower and increasing odds of a Fed cut in September, all of which should be sufficient to keep the rally going,” said Guy Miller, chief market strategist at Zurich Insurance Co.

“There are clear signs the US economy and labor markets are slowing and that should be confirmed by Friday’s payrolls data, laying the path for the Fed to cut in September,” Zurich Insurance’s Miller said.

In Europe, much of the spotlight continues to be on politics, on the eve of elections in the UK. The Stoxx 600 is up 0.7%, led by gains in technology and mining shares, while in France, the benchmark CAC 40 index rallied 1.6% as anti-National Rally parties attempt to prevent Marine Le Pen’s far-right group from achieving an absolute majority in the final round of legislative voting on Sunday. Shares of BE Semiconductor Industries NV soared 9.1% in Amsterdam after analysts wrote that Apple Inc. could adopt the Dutch chip-equipment firm’s technology as soon as next year. Here are some other notable European movers:

- Diageo shares rises as much as 3.2%, the most about five months, after Citi upgraded the spirit maker to buy, saying it is nearing an inflection point and full-year results should be a clearing event for what continues to be an “attractive compounding growth story”

- BE Semiconductor shares advance as much as 7.9% after Morgan Stanley raised its price target on the Dutch semiconductor equipment maker to a Street-high, saying that Apple could adopt the company’s hybrid bonding technology in its chips as soon as 2H next year

- Galderma shares gain as much as 2.9%, the most since May, after Vontobel initiated coverage of the Swiss skincare firm with a buy recommendation and a Street-high price target, saying its future growth will be supported by two upcoming drug launches

- BPER Banca shares gain as much as 4% after main shareholder Unipol underwrites share swap with 4.77% of the bank’s capital as underlying. Equita analysts said that Unipol’s move confirms its commitment

- Drax shares jump as much as 5.8%, the most since February, after Barclays raised its price target to a new Street high, citing the UK power utility’s “forgotten upside potential” and predicting it will get a much-needed government subsidy contract

- Grenke shares rise as much as 13%, the most since October 2022, after the German leasing finance provider reported its strongest quarter ever in terms of new business

- Text shares soar as much as 12% after the Polish chatbot tools provider reported sales rising 12% y/y in the quarter through June, fueled by higher average revenue per user

- JD Sports shares fell as much as 4.4% after the stock received its only negative analyst rating. Barclays downgraded the sports apparel retailer to underweight from equal-weight, citing its high exposure to Nike

- PostNL shares drop as much as 7.2% to the lowest in more than four years after the delivery company was downgraded by UBS, which warned that downside risks to consensus look underestimated

- Bpost shares drop as much as 11% to an all-time low after the postal delivery company gave guidance that was below expectations, prompting analysts to cut their price targets

Europe suffered the biggest reduction in overweight positions among regions globally in June, reversing the buying trend seen in May, Goldman said. Funds cut the most exposure to financial stocks, particularly banks, with net selling for that sector the largest since November 2021.

Earlier, Asian equities advanced, driven by gains in Hong Kong and Taiwan, as the region’s technology stocks saw a rally tracking a similar move in the US. The MSCI Asia Pacific Index climbed as much as 0.8% in a fourth straight day of gains, its longest stretch since May. Federal Reserve Chief Jerome Powell’s remarks that a disinflationary trend is resuming in the US boosted risk appetite in the region. A MSCI gauge of technology stocks added 1.3%. Japanese stocks climbed for the fourth session, their longest run since March. Equities also gained in South Korea, Singapore and Australia. “A bearish move in the US dollar and a halt in US Treasury yields’ upside may keep the risk environment supportive in the Asia session,” said Jun Rong Yeap, market analyst at IG Asia. Yeap expects traders to limit risk-taking ahead of a holiday-shortened session in the US later Wednesday.

In FX, the Bloomberg Dollar Spot Index eased as much as 0.1%; the US currency stumbled versus the euro, which gained for the sixth-straight day, its best run since March, on growing confidence that France’s far-right may fail to win a majority at second-round general vote later in the week USD/JPY rose 0.3% to 161.94; the yen’s slide to its weakest since 1986 raises intervention concerns

In rates, treasuries are narrowly mixed with the curve flatter. On the day long-end yields are higher by ~2bp and 2-year yields are lower by ~2bp. German and UK curves are also flatter on the day following firm services PMI readings. French government bonds rise for a second day amid reports that political parties were maneuvering to block an absolute majority for the far-right after Sunday’s second-round vote. 2s10s and 5s30s spreads are tighter by ~2bp on the day. US 10-year yield around 4.43% is little changed vs Tuesday’s close with gilts outperforming by 1.5bp in the sector, leading gains across European bonds.

The Bloomberg Dollar Spot Index is little changed. The yen is the weakest of the G-10 currencies, falling 0.2% against the greenback to a multi-decade low near 162.

In commodities, oil prices pared an earlier gain to trade little changed, with WTI near $82.90 a barrel. Spot gold adds $13 to around $2,343/oz. Crypto is under pressure this morning, with Bitcoin briefly dipping below the $60k mark as prediction markets now see Kamala replacing Joe Biden.

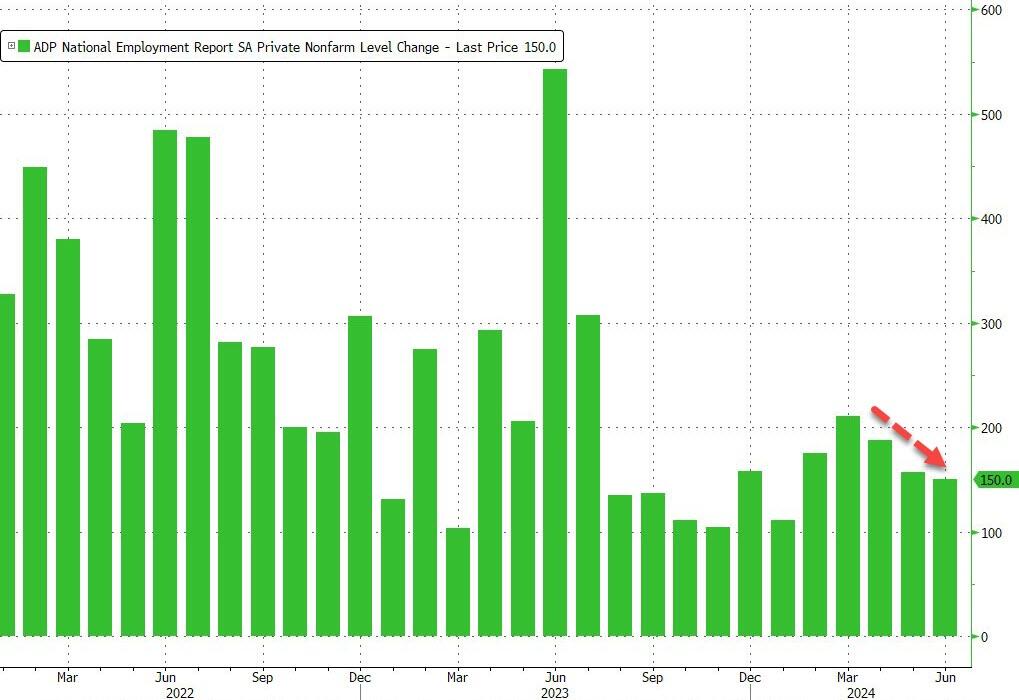

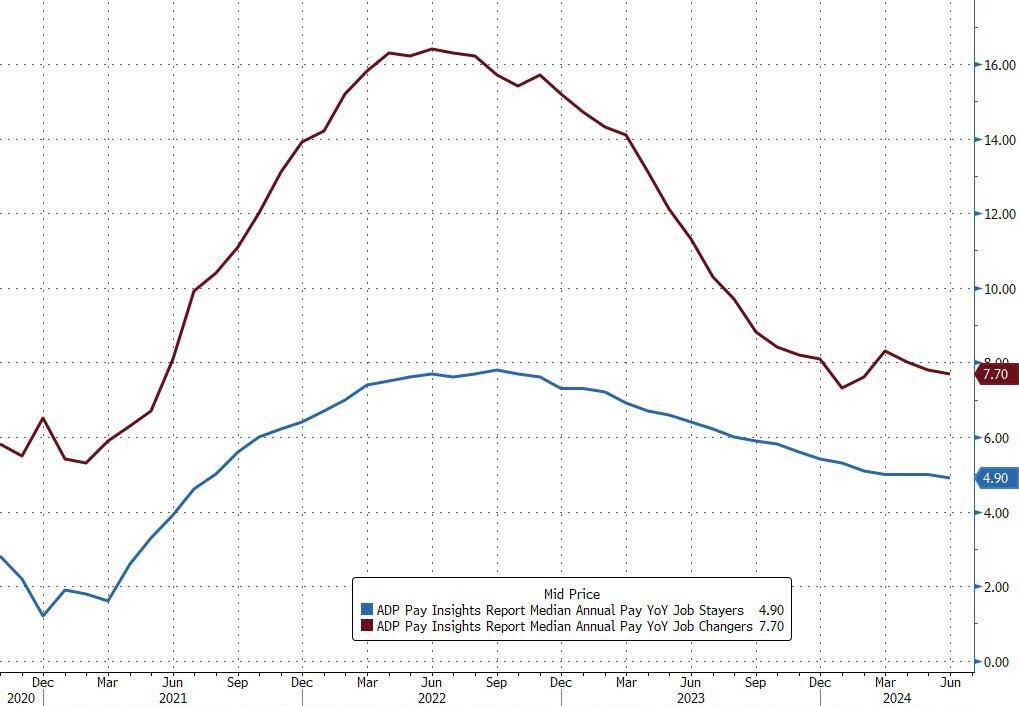

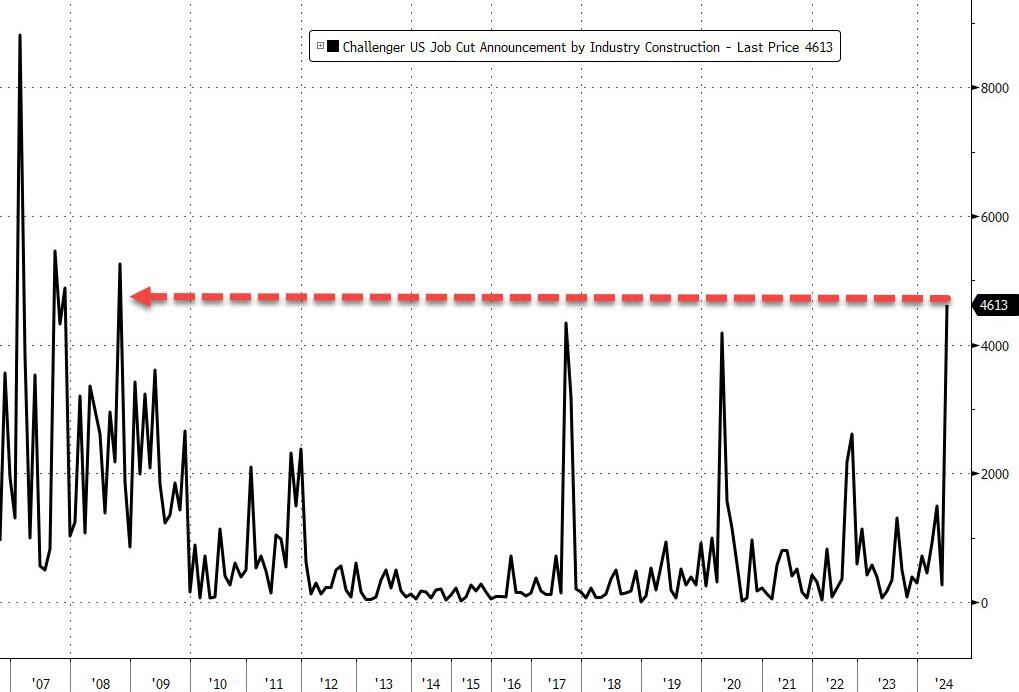

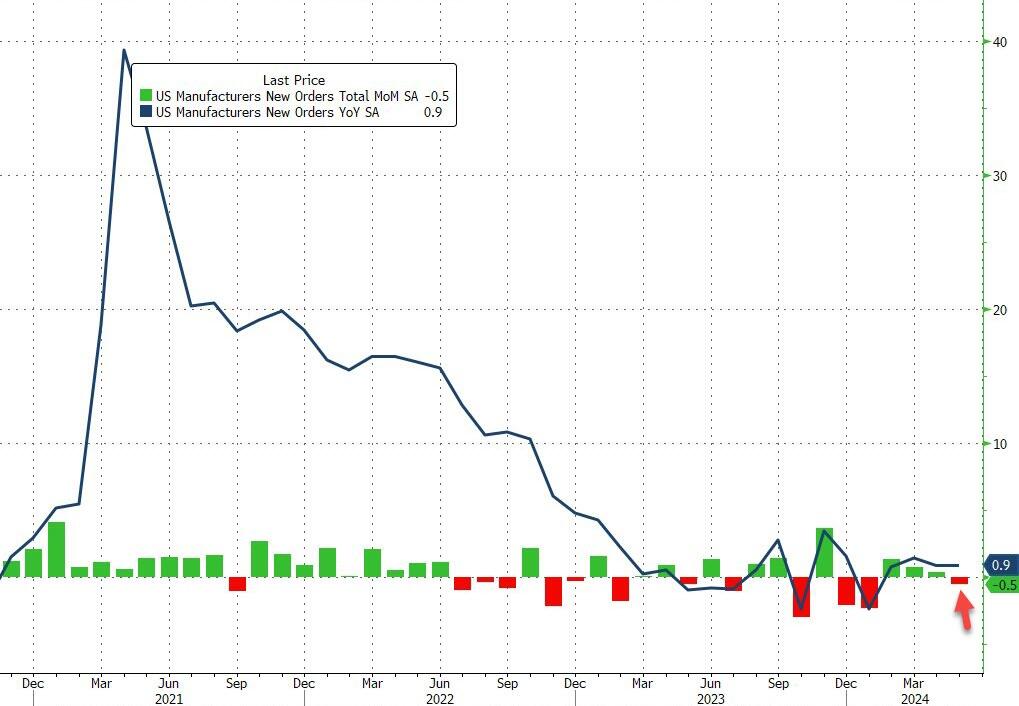

Looking at today’s barrage of data, the US economic data slate includes June Challenger job cuts (7:30am), June ADP employment change (8:15am), May trade balance, weekly jobless claims (8:30am), June final S&P Global services PMI (9:45am), May factory orders and June ISM services index (10am).

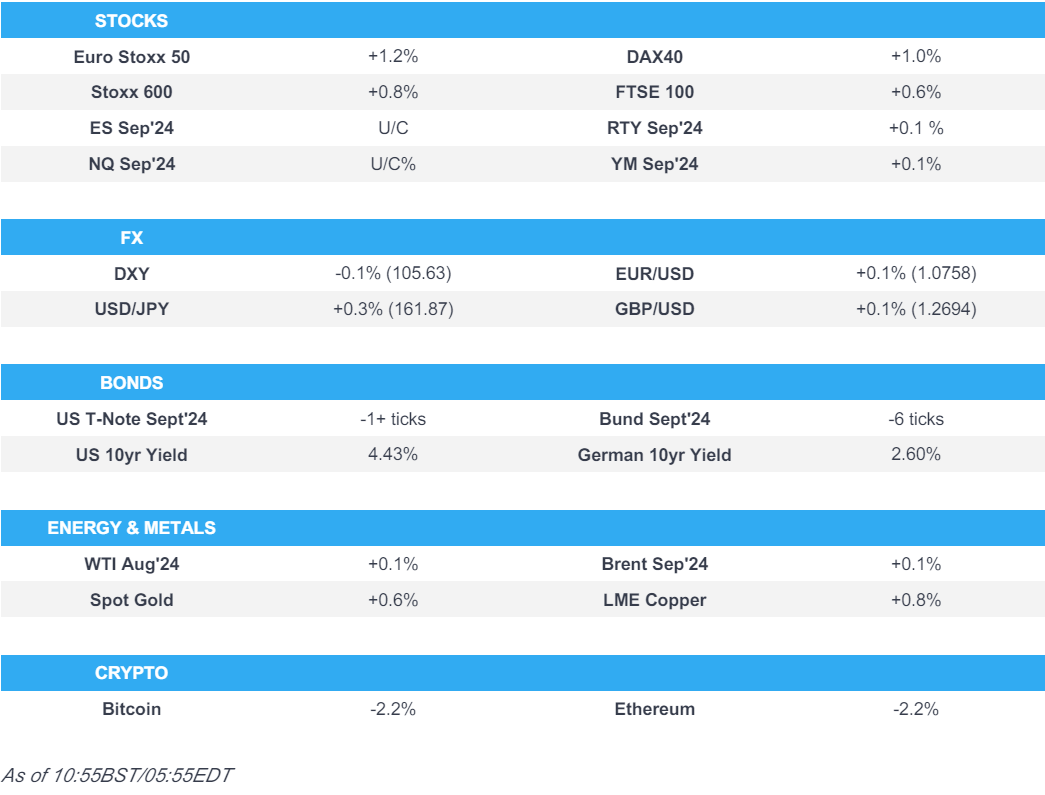

Market Snapshot

- S&P 500 futures little changed at 5,567.50

- Brent Futures up 0.3% to $86.49/bbl

- Gold spot up 0.7% to $2,345.59

- US Dollar Index down 0.10% to 105.62

- STOXX Europe 600 up 0.5% to 513.40

- MXAP up 0.7% to 182.08

- MXAPJ up 0.8% to 568.81

- Nikkei up 1.3% to 40,580.76

- Topix up 0.5% to 2,872.18

- Hang Seng Index up 1.2% to 17,978.57

- Shanghai Composite down 0.5% to 2,982.38

- Sensex up 0.6% to 79,914.27

- Australia S&P/ASX 200 up 0.3% to 7,739.88

- Kospi up 0.5% to 2,794.01

- German 10Y yield little changed at 2.63%

- Euro up 0.1% to $1.0761

- Brent Futures up 0.3% to $86.48/bbl

Top Overnight News

- European stocks rose, tracking a record S&P 500 close, on optimism about US interest-rate cuts after Federal Reserve Chair Jerome Powell said inflation is getting back on a downward path

- Marine Le Pen’s National Rally is scrambling to get an absolute majority in the final round of France’s legislative election Sunday as rival parties are maneuvering to keep the far-right party out of power

- SoftBank’s stock rose 1.5% to a new lifetime high on Wednesday, a vote of confidence in Masayoshi Son’s ambitions to ramp up investments in AI and semiconductors

- Venture dealmaking is coming back — at least, for artificial intelligence companies. Last quarter, US venture capitalists spent $55.6 billion backing startups, up by about half from a year earlier quarter and the spendiest quarter in two years, according to PitchBook data

- An activist short-seller, a New York hedge fund, a Mauritius-based investment vehicle and a broker tied to a big Indian bank: All played a role in one of the world’s most damaging short-seller attacks.

- Traders in the $27 trillion Treasury market are betting on higher long-term bond yields as Wall Street starts to adjust for Donald Trump’s potential return to the White House

- US judge postponed former President Trump’s sentencing in the hush-money case to September 18th.

- Skydance has acquired around 50% of Paramount Global’s (PARA) controlling shares at around USD 15.00/shr, CNBC reports citing sources.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks mostly took impetus from the gains on Wall St where the S&P 500 and Nasdaq posted record closes amid softer yields and dovish-leaning comments from Fed Chair Powell, although gains were capped and China lagged on weak Caixin PMI data. ASX 200 kept afloat amid strength in the commodity-related sectors and with some encouragement from the better-than-expected Retail Sales and Building Approvals data from Australia. Nikkei 225 was underpinned and further extended above the 40,000 level on the back of recent currency weakness. Hang Seng and Shanghai Comp. were mixed in which the former attempted to reclaim the 18,000 status, while the mainland bucked the trend after Caixin Services PMI data disappointed and amid lingering global frictions as European officials alleged that China is building and testing lethal attack drones for Russia.

Top Asian News

- EU reportedly targets China’s Temu and Shein with proposals for an import duty, according to FT.

- South Korean President Yoon said they have prepared KRW 25tln worth of support measures for small businesses and will provide tax benefits to companies actively raising dividend payouts, while they will address structural problems causing high local food prices.

- China’s PCA says Chinese prelim retail car sales (Jun) -8% Y/Y, 2% M/M.

European bourses are higher across the board as the region catches up to the Wall St. handover and continues generally strong APAC performance, Stoxx 600 +0.8%. CAC 40, +1.1%, the European outperformer as the agreement between ENS & NFP has seemingly held regarding candidate withdrawals into Sunday’s second round. No overarching bias or theme across the sectors; Tech gains after broker activity on ASM International & BE Semiconductor while Insurance once again lags amid the progression of Beryl. Stateside, futures flat and holding onto Tuesday’s gains into a packed and frontloaded session on account of Independence Day on Thursday, ES +0.1%, NQ +0.1%.

Top European News

- Former UK PM Boris Johnson joined the Tory election campaign and said that current PM Sunak asked him to join the campaign, while he compared their differences as “trivial” to the threat of Labour leader Starmer, according to The Sun’s Political Editor Harry Cole.

- Riksbank Minutes (Jun): Overall, the minutes chime with the tone of the last meeting which had two/three H2-2024 cuts as a possibility with the main potential headwinds being the SEK and inflation (in the context of May’s hotter print). Notably, only Breman was explicit in saying the next cut and first H2 one is likely to occur in August.

FX

- DXY under pressure and holding near the 105.59 low with peers generally firmer as the USD continues to feel the weight of Powell’s remarks and looks to the mentioned data deluge.

- Euro modestly firmer but EUR/USD yet to revisit Tuesday’s 1.0776 peak. Limited reaction to the Final PMIs and nothing noteworthy from the Sintra conference thus far; heft OpEx in EUR/USD.

- GBP similarly a touch firmer against the USD but once again looses out slightly against the EUR, Cable at its 1.2701 peak. No reaction to PMIs as we count down to Thursday’s UK election.

- USD/JPY hit another multi-decade peak of 161.97 overnight, action since limited with nothing of note from Japanese officials on the move.

- Antipodeans firmer given the risk tone, though NZD/USD us yet to re-test the 0.61 handle.

- PBoC set USD/CNY mid-point at 7.1312 vs exp. 7.2633 (prev. 7.1291).

Fixed Income

- OAT-Bund 10yr yield spread has narrowed to 67.8bps at best, though still circa. 20bps above pre-election levels; a narrowing which comes as the centre-left deal to prevent a RN majority appears to be holding with Ipsos remarking that an “absolute majority seems very unlikely” for RN.

- Bunds spent the first half of the session near the unchanged mark before fading on the PMIs and then slipping below Tusesady’s130.28 base but with still someway to go before the figure itself.

- No real reaction to the new German 2034 Bund auction, with the results perhaps marginally softer than is usually the case but not necessarily surprising given the trick environment it entered.

- Gilts await Thursday’s UK election, fleeting downticks on upwardly revised final PMIs but the benchmark is yet to meaningfully deviate from 97.00

- Stateside, Treasuries lower but above Tuesday’s 109-07 base as we enter a packed and frontloaded session on account of Thursday’s US Independence Day; data, FOMC Minutes and 3,10,30yr size announcements the highlights.

- Germany sells EUR 4.072bln vs exp. EUR 5bln 2.60% 2034 Bund: b/c 1.9 x, average yield 2.63%, retention 18.56%.

- Japanese gov’t is targeting issuing a new floating-rate note from FY26, with two- & five-year maturities seen as options, via Reuters citing sources; to mitigate investors’ risk from increasing yields.

Crude

- Crude benchmarks began the session firmer and were propped up by the much larger-than-expected draw in headline crude inventories, though this was offset somewhat by the gasoline build. Thereafter, benchmarks waned from best with specifics light into the US morning. WTI Aug and Brent Sep at lows of USD 62.77/bbl and USD 86.23/bbl respectively.

- Precious metals benefit from USD pressure and after the dovish commentary from Powell on Tuesday. XAU above the USD 2338/oz 50-DMA with the next point of significance being USD 2368/oz from 21st June.

- Base metals surged given APAC strength and the above while the likes of iron ore among the outperformers as participants cite supportive near-term demand and lingering expectations of Chinese stimulus.

- US Private Inventory Data (bbls): Crude -9.2mln (exp. -0.7mln), Distillate -0.7mln (exp. -1.2mln), Gasoline +2.5mln (exp. -1.3mln), Cushing +0.4mln.

- Lyondellbasell (LYB) Houston Refinery (268k BPD) reports flaring.

- NHC says Hurricane Beryl is expected to bring life-threatening winds and a storm surge to Jamaica later today, Cayman Islands tonight/Thursday.

Geopolitics

- Israeli army said it shelled Hezbollah positions last night in the areas of Blida, Yaron, Tair Harfa and Aitaroun in southern Lebanon, according to Al Jazeera.

- Palestinian Health Ministry said four were killed in an Israeli strike on West Bank’s Nur Shams Refugee Camp, according to Reuters.

- US State Department said it has seen disturbing reports of the Israeli army’s use of civilians as human shields and it called on Israel again to investigate quickly and ensure accountability for any abuses and violations, according to Al Jazeera.

- China is building and testing lethal attack drones for Russia with Chinese and Russian companies said to be developing an attack drone similar to an Iranian model deployed in Ukraine, according to European officials familiar with the matter cited by Bloomberg.

US Event Calendar

- 07:00: June MBA Mortgage Applications -2.6%, prior 0.8%

- 07:30: June Challenger Job Cuts YoY 19.8%, prior -20.3%

- 08:15: June ADP Employment Change, est. 165,000, prior 152,000

- 08:30: June Initial Jobless Claims, est. 235,000, prior 233,000

- June Continuing Claims, est. 1.84m, prior 1.84m

- 08:30: May Trade Balance, est. -$76.5b, prior -$74.6b

- 09:45: June S&P Global US Services PMI, est. 55.1, prior 55.1

- June S&P Global US Composite PMI, prior 54.6

- 10:00: May Factory Orders, est. 0.2%, prior 0.7%

- May Factory Orders Ex Trans, prior 0.7%

- 10:00: May Durable Goods Orders, est. 0.1%, prior 0.1%

- May Durables-Less Transportation, est. -0.1%, prior -0.1%

- May Cap Goods Orders Nondef Ex Air, est. -0.6%, prior -0.6%

- May Cap Goods Ship Nondef Ex Air, prior -0.5%

- 10:00: June ISM Services Index, est. 52.6, prior 53.8

- 14:00: June FOMC Meeting Minutes

DB’s Jim Reid concludes the overnight wrap

Markets got Q3 off to a mixed start yesterday, with a pretty divergent performance across countries and asset classes. On the positive side, there was a noticeable recovery for French assets after the election results, with the Franco-German 10yr spread (-5.8bps) seeing its biggest decline since President Macron announced the election last month. However, that came alongside more weakness in US markets after investors became increasingly focused on the fiscal outlook, with the presidential election now just four months away. That saw the 10yr Treasury yield rise a further +6.5bps to 4.461%, building on its +11.0bps move on Friday and closing +20.3bp higher than the lows that came after Friday’s soft core PCE. So had you got that data print right in advance you may have got bond markets totally wrong. I thought some of it was month-end shenanigans from Friday but a narrative has built up that due to the aftermath of the Trump/Biden debate, markets should be pricing in a higher probability of a Trump victory and larger fiscal deficits.

In terms of the French situation, the main news yesterday (as we discussed 24 hours ago) was that Marine Le Pen’s National Rally slightly underperformed the opinion polls from before the election. But DB’s economist thinks that their underperformance relative to polls likely reflected stronger participation in urban areas to some degree, in seats that the National Rally were unlikely to win anyway. He writes (link here) that the probability of a National Rally government (minority or majority) is actually now marginally higher than it was before round 1, and there is also the possibility that other MPs on the right or centre-right could implicitly support a minority government. So a slightly different view to the prevailing market narrative yesterday that a far-right majority was less likely. The house view is still a hung parliament though.

The second round will take place on Sunday, but the other parties are now attempting to keep the National Rally from gaining power, and there are negotiations on candidates standing down from districts where they wish to give another party a better chance of victory. For reference, candidates who receive more than 12.5% of registered voters can go forward to the second round, but there is a deadline tonight (6pm CET) for candidates to file papers to go forward, so it’s possible that those who did pass the threshold will withdraw, particularly if they came in third place. So once we know who’s actually standing where, we should get a better idea of the likely prospects going into Sunday’s vote.

In terms of the market reaction, there was an initial surge for equities at the open, with the CAC 40 up by +2.79% first thing. But those gains were then pared back, and the index “only” closed +1.09% higher. Other indices also advanced in Europe, but the gains were concentrated in the south, with Italy’s FTSE MIB (+1.70%) and Spain’s IBEX 35 (+1.04%) both outperforming. Meanwhile for sovereign bonds, the gap between French and German yields tightened back to 74bps, which is its tightest level in over two weeks, whilst Italian and Spanish spreads also fell. Nevertheless, yields still moved higher across the continent, and in absolute terms, the French 10yr yield (+5.1bps) was up to 3.349%, which is its highest closing level since November, whilst those on 10yr bunds were up by +10.7bps on the day. The US bond move from Friday afternoon was a big influence.

Well after the European close, ECB President Lagarde spoke at the annual retreat in Sintra, Portugal. She struck a slightly more hawkish tone, saying that Europe’s “still facing several uncertainties regarding future inflation, especially in terms of how the nexus of profits, wages and productivity will evolve and whether the economy will be hit by new supply-side shocks.” She added, “ It will take time for us to gather sufficient data to be certain that the risks of above-target inflation have passed.” There is now 38.2bps of cuts priced in by year-end, down -5.0bps from Friday’s close.

As discussed earlier, US Treasuries continued their significant last 36 hour decline from Friday as investors moved to focus on the upcoming election and the fiscal implications. That led to another fairly sharp curve steepening yesterday, with the 2s10s curve up +6.1bps to -29.9bps, having been at -49.6bps just one week earlier. For what it’s worth, this week is actually the second anniversary of the 2s10s inversion in July 2022, so we’re on track for yet more records in terms of this being the longest ever 2s10s inversion. And in terms of the specific moves, the 2yr yield was largely unchanged (+0.2bps) at 4.755%, but the 10yr yield saw a larger +6.5bps move to 4.461%. With the attention on the long end, fed futures were barely changed as the amount of cuts priced in by the December meeting was up just +1.0bps to 45bps. This morning in Asia, yields on the 10yr USTs have edged back down -2bps to around 4.44% as I type.

Risk appetite in the US was dampened by some weak data prints, with the ISM manufacturing for June falling to 48.5 (vs. 49.1 expected). Moreover, the subcomponents for new orders (49.3) and employment (49.3) were in contractionary territory as well so there was little respite in the report. The bright spot came on the inflation side, with the prices paid component down to a 6-month low of 52.1. That backdrop meant that US equities were mixed with tech once again saving the day with the Magnificent 7 surging +1.76%, even as the small-cap Russell 2000 was down -0.86%. The S&P 500 split the difference and was up +0.27%, even while 76% of the index members were lower on the day. S&P 500 (-0.23%) and NASDAQ 100 (-0.38%) futures are both trading notably lower this morning.

In Asia, the Nikkei (+0.38%) is trading higher with the Hang Seng (+0.57%) also gaining after returning from a public holiday. Elsewhere, Chinese stocks are struggling to gain traction with the CSI (-0.08%) and Shanghai Composite (+0.04%) relatively flat. Meanwhile, the KOSPI (-0.82%) is losing ground after a busy morning of inflation data. Indeed, South Korea’s inflation cooled more than expected, rising +2.4% y/y in June (v/s +2.6% expected), its slowest pace since July last year. It followed a +2.7% increase in the prior month. Meanwhile, core CPI came in +2.2% higher in June than a year before, in line with May’s reading.

In FX, the Japanese yen (-0.13%) is weakening to a fresh 38-year low of 161.68 against the dollar despite some verbal intervention from the authorities. Japanese Finance Minister Shunichi Suzuki stated that he is “closely watching FX moves with vigilance” while refraining from commenting on specific levels.

Finally, minutes from the RBA’s June monetary policy meeting indicated that board members discussed raising interest rates but eventually decided to hold rates steady at 4.35%. The board emphasized the need to remain vigilant to upside risks to inflation, noting that May’s inflation data hadn’t been enough to derail its inflation outlook of returning to target in 2026. However these minutes are slightly dated as a week after the meeting we had a strong CPI print. So our economists believe an August hike is likely.

To the day ahead now, and data releases include the Euro Area flash CPI print for June, along with the unemployment rate for May. Over in the US, there’s also the JOLTS report of job openings for May. From central banks, we’ll hear from Fed Chair Powell, ECB President Lagarde, ECB Vice President de Guindos, and the ECB’s Elderson and Schnabel

2B EUROPE OPENING/TRADING

Europe bolstered by the Wall St. handover heading into a frontloaded US docket – Newsquawk US Market Open

WEDNESDAY, JUL 03, 2024 – 06:20 AM

- European bourses are higher across the board as the region catches up to the Wall St. handover and continues generally strong APAC performance

- DXY under pressure and holding near the 105.59 low with peers generally firmer as the USD continues to feel the weight of Powell’s remarks and looks to the mentioned data deluge

- OAT-Bund 10yr yield spread has narrowed to below 68bps at best, though is still circa. 20bps above pre-election levels; largely unreactive to PMIs

- Crude benchmarks began the session firmer after the private data on Tuesday, though they have since waned; metals generally supported

- Looking ahead, highlights include US Final PMIs, US ADP, IJC, Challenger, Factory Goods, ISM Services, FOMC Minutes, NBP Policy Announcement, US Refunding (3,10,30yr), Comments from Fed’s Williams, ECB’s Lane, Lagarde, de Guindos & Knot, Earnings from Constellation Brands.

- Click for the Newsquawk Week Ahead

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses are higher across the board as the region catches up to the Wall St. handover and continues generally strong APAC performance, Stoxx 600 +0.8%.

- CAC 40, +1.1%, the European outperformer as the agreement between ENS & NFP has seemingly held regarding candidate withdrawals into Sunday’s second round.

- No overarching bias or theme across the sectors; Tech gains after broker activity on ASM International & BE Semiconductor while Insurance once again lags amid the progression of Beryl.

- Stateside, futures flat and holding onto Tuesday’s gains into a packed and frontloaded session on account of Independence Day on Thursday, ES +0.1%, NQ +0.1%.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY under pressure and holding near the 105.59 low with peers generally firmer as the USD continues to feel the weight of Powell’s remarks and looks to the mentioned data deluge.

- Euro modestly firmer but EUR/USD yet to revisit Tuesday’s 1.0776 peak. Limited reaction to the Final PMIs and nothing noteworthy from the Sintra conference thus far; heft OpEx in EUR/USD.

- GBP similarly a touch firmer against the USD but once again looses out slightly against the EUR, Cable at its 1.2701 peak. No reaction to PMIs as we count down to Thursday’s UK election.

- USD/JPY hit another multi-decade peak of 161.97 overnight, action since limited with nothing of note from Japanese officials on the move.

- Antipodeans firmer given the risk tone, though NZD/USD us yet to re-test the 0.61 handle.

- PBoC set USD/CNY mid-point at 7.1312 vs exp. 7.2633 (prev. 7.1291).

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- OAT-Bund 10yr yield spread has narrowed to 67.8bps at best, though still circa. 20bps above pre-election levels; a narrowing which comes as the centre-left deal to prevent a RN majority appears to be holding with Ipsos remarking that an “absolute majority seems very unlikely” for RN.

- Bunds spent the first half of the session near the unchanged mark before fading on the PMIs and then slipping below Tusesady’s130.28 base but with still someway to go before the figure itself.

- No real reaction to the new German 2034 Bund auction, with the results perhaps marginally softer than is usually the case but not necessarily surprising given the trick environment it entered.

- Gilts await Thursday’s UK election, fleeting downticks on upwardly revised final PMIs but the benchmark is yet to meaningfully deviate from 97.00

- Stateside, Treasuries lower but above Tuesday’s 109-07 base as we enter a packed and frontloaded session on account of Thursday’s US Independence Day; data, FOMC Minutes and 3,10,30yr size announcements the highlights.

- Germany sells EUR 4.072bln vs exp. EUR 5bln 2.60% 2034 Bund: b/c 1.9 x, average yield 2.63%, retention 18.56%.

- Japanese gov’t is targeting issuing a new floating-rate note from FY26, with two- & five-year maturities seen as options, via Reuters citing sources; to mitigate investors’ risk from increasing yields.

- Click for a detailed summary

COMMODITIES

- Crude benchmarks began the session firmer and were propped up by the much larger-than-expected draw in headline crude inventories, though this was offset somewhat by the gasoline build. Thereafter, benchmarks waned from best with specifics light into the US morning. WTI Aug and Brent Sep at lows of USD 62.77/bbl and USD 86.23/bbl respectively.

- Precious metals benefit from USD pressure and after the dovish commentary from Powell on Tuesday. XAU above the USD 2338/oz 50-DMA with the next point of significance being USD 2368/oz from 21st June.

- Base metals surged given APAC strength and the above while the likes of iron ore among the outperformers as participants cite supportive near-term demand and lingering expectations of Chinese stimulus.

- US Private Inventory Data (bbls): Crude -9.2mln (exp. -0.7mln), Distillate -0.7mln (exp. -1.2mln), Gasoline +2.5mln (exp. -1.3mln), Cushing +0.4mln.

- Lyondellbasell (LYB) Houston Refinery (268k BPD) reports flaring.

- NHC says Hurricane Beryl is expected to bring life-threatening winds and a storm surge to Jamaica later today, Cayman Islands tonight/Thursday.

- Click for a detailed summary

NOTABLE DATA RECAP

- French HCOB Composite PMI (Jun) 48.8 vs. Exp. 48.2 (Prev. 48.2); Services 49.6 vs. Exp. 48.8 (Prev. 48.8)

- German HCOB Composite Final PMI (Jun) 50.4 vs. Exp. 50.6 (Prev. 50.6); Services 53.1 vs. Exp. 53.5 (Prev. 53.5)

- EU HCOB Composite Final PMI (Jun) 50.9 vs. Exp. 50.8 (Prev. 50.8); Services 52.8 vs. Exp. 52.6 (Prev. 52.6)

- UK S&P Final PMI Composite (Jun) 52.3 vs. Exp. 51.7 (Prev. 51.7); Services 52.1 vs. Exp. 51.2 (Prev. 51.2)

- EU Producer Prices MM (May) -0.2% vs. Exp. -0.1% (Prev. -1.0%); YY -4.2% vs. Exp. -4.1% (Prev. -5.7%)

NOTABLE EUROPEAN HEADLINES

- Former UK PM Boris Johnson joined the Tory election campaign and said that current PM Sunak asked him to join the campaign, while he compared their differences as “trivial” to the threat of Labour leader Starmer, according to The Sun’s Political Editor Harry Cole.

- Riksbank Minutes (Jun): Overall, the minutes chime with the tone of the last meeting which had two/three H2-2024 cuts as a possibility with the main potential headwinds being the SEK and inflation (in the context of May’s hotter print). Notably, only Breman was explicit in saying the next cut and first H2 one is likely to occur in August.

NOTABLE US HEADLINES

- US judge postponed former President Trump’s sentencing in the hush-money case to September 18th.

- Skydance has acquired around 50% of Paramount Global’s (PARA) controlling shares at around USD 15.00/shr, CNBC reports citing sources.

GEOPOLITICS

MIDDLE EAST

- Israeli army said it shelled Hezbollah positions last night in the areas of Blida, Yaron, Tair Harfa and Aitaroun in southern Lebanon, according to Al Jazeera.

- Palestinian Health Ministry said four were killed in an Israeli strike on West Bank’s Nur Shams Refugee Camp, according to Reuters.

- US State Department said it has seen disturbing reports of the Israeli army’s use of civilians as human shields and it called on Israel again to investigate quickly and ensure accountability for any abuses and violations, according to Al Jazeera.

OTHER

- China is building and testing lethal attack drones for Russia with Chinese and Russian companies said to be developing an attack drone similar to an Iranian model deployed in Ukraine, according to European officials familiar with the matter cited by Bloomberg.

CRYPTO

- Crypto is under modest pressure thus far, with Bitcoin edging towards but still holding above the USD 60k mark ahead of numerous Tier 1 US data points.

APAC TRADE

- APAC stocks mostly took impetus from the gains on Wall St where the S&P 500 and Nasdaq posted record closes amid softer yields and dovish-leaning comments from Fed Chair Powell, although gains were capped and China lagged on weak Caixin PMI data.

- ASX 200 kept afloat amid strength in the commodity-related sectors and with some encouragement from the better-than-expected Retail Sales and Building Approvals data from Australia.

- Nikkei 225 was underpinned and further extended above the 40,000 level on the back of recent currency weakness.