JULY 11/BLOG//USA CPI PLUMMETS TO -.1%M/M AND THAT PROPELS OUR PRECIOUS METALS: GOLD ROSE $43.05 TO $2416.15//SILVER ROSE 72 CENTS TO $31.47//PLATINUM ROSE $9.45 TO $1004.55 WHILE PALLADIUM CLOSED UP $8.25 TO $998.15//GOLD AND SILVER COMMENTARY TODAY FROM J.MAVERICK//GOOD COMMODITY REVIEW ON COCOA//POLAND IS NOW PREPARING FOR A FULL SCALE WAR//SWEDEN ASKS NATO TO FACE CHINA AND NOT RUSSIA//ISRAEL VS HAMAS UPDATES//COVID UPDATES/VACCINE INJURY REPORT//SLAY NEWS//EVOL NEWS/NEWS ADDICTS//USA DATA: CPI FALLS INTO NEGATIVE TERRITORY ON A MONTH/MONTH BASIS/SWAMP STORIES FOR YOU TONIGHT//

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2024. CONTRACT: 1 NOTICES FOR 100 OZ or 0.00311 TONNES

total notices so far: 2723 contracts for 272,300 Oz (8.4696 tonnes)

FOR JULY:

SILVER NOTICES: 75 NOTICE(S) FILED FOR 0.375 million

OZ/

total number of notices filed so far this month : 5828 for 29.125 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $43.05 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/

: NO CHANGES IN GOLD INVENTORY AT THE GLD/

/ /INVENTORY RESTS AT 833.37 TONNES

INVENTORY RESTS AT 833.37 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP 72 CENTS AT THE SLV//

BIG CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 731,000 OZ FROM THE SLV//

// INVENTORY LOWERS TO 435.625 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 435.625 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 769 CONTRACTS TO 164.014 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR SMALL LOSS OF $0.04 IN SILVER PRICING AT THE COMEX ON WEDNESDAY’S TRADING ON SILVER. WE HAD ZERO LIQUIDATION AS WE HAD A HUGE NET GAIN OF 1697 CONTRACTS ON OUR TWO EXCHANGES. WE, AGAIN HAD CONSIDERABLE SHORT COVERING BY OUR SPECS WITH THE LOSS IN PRICE AS WELL AS MASSIVE T.A.S. LIQUIDATION WHICH ACCOUNTS FOR THE STRONG GAIN ON THE TWO EXCHANGES. WE HAD ANOTHER STRONG SIZED 472 T.A.S ISSUANCE,

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 472 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS.IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1/2 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.04) BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS FROM THEIR PERCH AS WE DID HAVE A HUMONGOUS SIZED GAIN OF 1697 CONTRACTS ON OUR TWO EXCHANGES DESPITE THE LOSS IN PRICE OF $0.04.

WE MUST HAVE HAD:

A HUGE SIZED 1000 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 28.490 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE JUMP OF 495,000 OZ

//NEW STANDING FOR SILVER//JUNE IS THUS 30.045 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI GAIN //HUMONGOUS SIZED EFP ISSUANCE/ VI) HUGED SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 472 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL ADDED 5 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY

TOTAL CONTRACTS for 8 DAYS, total 8432 contracts: OR 42.160 MILLION OZ (1054 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 42.160 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 42.160 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 697 CONTRACTS DESPITE OUR LOSS IN PRICE OF SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 1000 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JULY OF 28.496 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 495,000 OZ QUEUE JUMP WHERE THEY WILL TRY AND TAKE DELIVERY ON THIS SIDE OF THE POND.

//NEW TOTAL STANDING FOR JULY 30.085 MILLION OZ

WE HAVE A HUGE SIZED GAIN OF 1769 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG SIZED 472 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX TRADING/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND ZERO LIQUIDATION OF LONGS.

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (472) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 75 NOTICE(S) FILED TODAY FOR 0.375 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A HUGE SIZED 12,417 OI CONTRACTS TO 528,741 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 1009 CONTRACTS

WE HAD A HUGE SIZED INCREASE IN COMEX OI (12,417 CONTRACTS) OCCURRED WITH OUR GAIN OF $12.00 IN PRICE/WEDNESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 7.5645 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 300 OZ QUEUE JUMP

NEW STANDING 8.5723 TONNES

/ ALL OF THIS HAPPENED WITH OUR $12.00 GAIN IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A HUGE SIZED GAIN OF 15,234 OI CONTRACTS (47.39 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2667 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 528,741

IN ESSENCE WE HAVE A HUGE SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 16,249 CONTRACTS WITH 12,417 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 2617 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 166,243 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): ANOTHER MEGA MEGA HUMONGOUS SIZED 27,051 CONTRACTS,,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2617 CONTRACTS) ACCOMPANYING THE HUGE SIZED GAIN IN COMEX OI OF 12,417 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 15,234 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 7,5645 TONNES FOLLOWED BY TODAY’S 300 OZ QUEUE JUMP

//NEW STANDING /JULY 8.5723 TONNES.

/ 3) HUGE T.A.S. LIQUIDATION OF CONTRACTS WITH ZERO NET LONG SPECS BEING CLIPPED,

4) HUGE SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///MEGA HUMONGOUS T.A.S. ISSUANCE: 27,051 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY. :

TOTAL EFP CONTRACTS ISSUED: 36,939 CONTRACTS OR 3,693,900 OZ OR 114.89 TONNES IN 8 TRADING DAY(S) AND THUS AVERAGING: 4903 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAY(S) IN TONNES 114.89 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 114.89 DIVIDED BY 3550 x 100% TONNES = 3.23% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 114.89 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUG), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A STRONG SIZED 769 CONTRACTS OI TO 164,014 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1000 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 1000 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1000 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 769 CONTRACTS AND ADD TO THE 1000 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1769 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 8.845 MILLION OZ

OCCURRED DESPITE OUR SMALL $0.04 LOSS IN PRICE …..

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED UP 31.02 PTS OR 1.06% //Hang Seng CLOSED UP 360.46 PTS OR 2.06% // Nikkei CLOSED UP 392.03 OR 0.94%//Australia’s all ordinaries CLOSED UP 0.93%///Chinese yuan (ONSHORE) closed UP TO 7,2657 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2782/ Oil UP TO 82.40 dollars per barrel for WTI and BRENT UP AT 85.38/Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A HUGE SIZED 12,617 CONTRACTS TO 529,950 WITH OUR GAIN IN PRICE OF $12.00 WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A HUGE T.A.S. LIQUIDATION ON WEDNESDAY’S GAIN IN PRICE WITH ZERO LONGS BEING CLIPPED AND SOME ATTEMPTED SHORT COVERING.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE NON ACTIVE DELIVERY MONTH OF JULY.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 2617 EFP CONTRACTS WERE ISSUED: : AUGUST2617 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2617 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A HUGE SIZED TOTAL OF 15,234 CONTRACTS IN THAT 2617 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A HUGE SIZED GAIN OF 13,626 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $12.00/WEDNESDAY COMEX.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS ANOTHER MEGA MEGA HUMONGOUS SIZED 27,051 CONTRACTS. MOST OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN YESTERDAY’S TRADING. TODAY’S ISSUANCE WAS ANOTHER WHOPPER.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JULY (8.5723 TONNES)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 8.5723 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $12.00 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A HUGE SIZED GAIN OF 16,243 CONTRACTS ON OUR TWO EXCHANGES ACCOMPANYING THE GAIN IN PRICE. THE T.A.S. ISSUED ON WEDNESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 47.39 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY (7.5645 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 300 OZ QUEUE JUMP//NEW STANDING 8.5723 TONNES

NEW STANDING FOR JULY: 8.5723 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $12.00

WE HAVE REMOVED 1009 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET GAIN ON THE TWO EXCHANGES 15,234 CONTRACTS OR 1,523,400 OZ (47.39 TONNES)

Total monthly oz gold served (contracts) so far this month

2723 notices 272,300 oz 8.4696 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: nil oz

we have 0 customer deposit:

total deposit: nil oz

customer withdrawals: 0

TOTAL WITHDRAWALS NIL

Adjustment 1 DEALER TO CUSTOMER JPMORGAN: 7619.787 IZ

2. CUSTOMER TO DEALR ASAHI: 96.453 OZ

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JUNE

For the front month of JULY we have an oi of 34 contracts having LOST 2 contracts. We had 5 notices filed on Tuesday so we gained 3 contracts or an additional 300 oz will stand at the comex (0.00933 tonnes)

AUGUST lost 8724 CONTRACTS DOWN TO 292,348 CONTRACTS

SEPT. GAINED 19 CONTRACTS TO STAND AT 231.

OCTOBER GAINED 831 CONTRACTS UP TO 30,480 CONTRACTS

We had 1 contract filed for today representing 100 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 1 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for July /2024. contract month, we take the total number of notices filed so far for the month (2723) x 100 oz ) to which we add the difference between the open interest for the front month of JULY 34( CONTRACTS) minus the number of notices served upon today (1 x 100 oz per contract( equals 275,600 OZ OR 8.5723 TONNES.

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (2723 x 100 oz +we add the difference for front month of JULY (34 X// , OI} minus the number of notices served upon today (1) x 100 oz which equals 275,600 oz (8.5723TONNES)

TOTAL COMEX GOLD STANDING FOR JULY: 8.5723 TONNES WHICH IS HUGE FOR THIS NOT VERY ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,699,809.607 OZ

TOTAL REGISTERED GOLD 7,815,808.208 ( 243.10 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,884,001.399 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,136,593oz (REG GOLD- PLEDGED GOLD)= 190.87 tonnes //

END

SILVER/COMEX

JULY 11/2024

INITIAL

//2024// THE JULY 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

1,586,806.211oz

ASAHI CNT Delaware HSBC

.

Deposits to the Dealer Inventory

Deposits to the Customer Inventory

JPMorgan: 594,348.600 oz

No of oz served today (contracts)

75 CONTRACT(S) (.375 million OZ)

No of oz to be served (notices)

189 contracts (0.945 million oz)

Total monthly oz silver served (contracts)

5828 Contracts (29.125 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit/

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 customer deposits:

i)Into JPMorgan; 594,348.600 oz

total customer deposit 594,348.600 oz

JPMorgan has a total silver weight: 129.587million oz/297.503million or 43.52%

adjustment: 1 dealer to customer

i) Brinks 1,200,190.100 oz

customer withdrawals: 4

i) out of Delaware 596,486.241 oz

ii) out of Ashai: 594,348,600 oz

iii) Out of Delaware 596,486.241 0z

iv) Out of HSBC 90,183.930 oz

total withdrawal: 1,586,806.211 0z

TOTAL REGISTERED SILVER: 69.360 MILLION OZ//.TOTAL REG + ELIGIBLE. 297.503

million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF JULY/2024 OI: 264 CONTRACTS HAVING LOST 23 CONTRACT(S). WE HAD 121 NOTICES FILED ON WEDNESDAY SO WE GAINED A 98 CONTRACTS OR AN ADDITIONAL 490,000 OZ WILL STAND AT THE COMEX VIA A QUEUE JUMP TO TAKE DELIVERY OVER HERE.

AUG, SAW A LOSS OF 9 CONTRACTS TO 1359

SEPT SAW A GAIN OF 214 CONTRACTS TO 132,015

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 75 for 0.375 MILLION oz

CONFIRMED volume; ON WEDNESDAY 54,718 large

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 5828 x 5,000 oz = 29.125 MILLION oz

to which we add the difference between the open interest for the front month of JULY( 264) and the number of notices served upon today 75 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY/2024 contract month: 5828 notices served so far) x 5000 oz + OI for the front month of JULY (264)x number of notices served upon today minus (75)x 5000 oz of silver standing for the JULY contract month equates to 30.095 MILLION OZ.

New total standing: 30.095 million oz.

There are 69.360 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

JULY 11 WITH GOLD UP $43.05 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;:INVENTORY RESTS AT 833.37 TONNES

JULY 10 WITH GOLD UP $12.00 ON THE DAY; HUUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.44 TONNES OF GOLD VAPOUR FROM THE GLD//.//:INVENTORY RESTS AT 833.37 TONNES

JULY 9 WITH GOLD UP $5.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD.//:INVENTORY RESTS AT 834.81 TONNES

JULY 8 WITH GOLD DOWN $26.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD.//:INVENTORY RESTS AT 834.81 TONNES

JULY 5 WITH GOLD UP $29.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD..A DEPOSIT OF 1.10 TONNES OF GOLD VAPOUR INTO THE GLD//:INVENTORY RESTS AT 833.37 TONNES

JULY 3 WITH GOLD UP $35.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD..A MASSIVE DEPOSIT OF 5.76 TONNES OF GOLD VAPOUR INTO THE GLD//:INVENTORY RESTS AT 833.37 TONNES

JULY 2 WITH GOLD DOWN $4.45 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD../:INVENTORY RESTS AT 827.61 TONNES

JULY 1 WITH GOLD DOWN $.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 28 WITH GOLD UP $3.80 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 27 WITH GOLD DOWN $16.95 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 26 WITH GOLD UP $23.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 25 WITH GOLD DOWN $13.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A STRONG WITHDRAWAL OF 2.88 TONNES OF GOLD FROM THE GLD INVENTORY RESTS AT 829.05 TONNES

JUNE 24 WITH GOLD UP$14.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A STRONG WITHDRAWAL OF 1.72 TONNES OF GOLD/NEW TOTAL TONIGHT 831.93 TONNES

JUNE 21 WITH GOLD DOWN $37.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A MAMMOTH 8.34 TONNES OF GOLD VAPOUR DEPOSIT/NEW TOTAL TONIGHT 833.65 TONNES

JUNE 20 WITH GOLD UP $23.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/://NEW TOTAL TONIGHT 825.31 TONNES

JUNE 18 WITH GOLD UP $17.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/://NEW TOTAL TONIGHT 825.31 TONNES

JUNE 17 WITH GOLD DOWN $18.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.03 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 825.31 TONNES

JUNE 13 WITH GOLD DOWN$35.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.89 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 830.78 TONNES

JUNE 12 WITH GOLD UP $28.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.89 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 830.78 TONNES

JUNE 11 WITH GOLD DOWN $0.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 10 WITH GOLD UP $2,00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 7 WITH GOLD DOWN $64.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 3.56 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 837.11 TONNES

JUNE 6 WITH GOLD UP $16.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.34 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 833.55 TONNES

JUNE 5 WITH GOLD UP $32.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 4 WITH GOLD DOWN $20.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 3 WITH GOLD UP $22.85 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 31 WITH GOLD DOWN $19.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 30 WITH GOLD UP $3.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 29 WITH GOLD DOWN $13.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 28 WITH GOLD UP $22.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 832.21 TONNES

GLD INVENTORY: 833.37 TONNES, TONIGHTS TOTAL

SILVER

JULY 11. WITH SILVER UP $.72 CENTS//HUGE CHANGES IN SILVER INVENTORY A WITHDRAWAL OF 0.731 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 435.625 MILLION OZ.

JULY 10. WITH SILVER DOWN $.04 CENTS//HUGE CHANGES IN SILVER INVENTORY A MAMMOTH WITHDRAWAL OF 3.744 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 436.356 MILLION OZ.

JULY 9. WITH SILVER UP 13 CENTS//HUGE CHANGES IN SILVER INVENTORY A MAMMOTH WITHDRAWAL OF 3.744 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 436.356 MILLION OZ.

JULY 8. WITH SILVER DOWN $0.73//SMALL CHANGES IN SILVER INVENTORY A MAMMOTH DEPOSIT OF 3,292,000 OZ OF SILVER VAPOUR INTO THE SLV.: /INVENTORY RISES T0 440.100 MILLION OZ.

JULY 4. WITH SILVER UP $0.85//SMALL CHANGES IN SILVER INVENTORY A MAMMOTH DEPOSIT OF 3,292,000 OZ OF SILVER VAPOUR INTO THE SLV.: /INVENTORY RISES T0 440.100 MILLION OZ.

JULY 3. WITH SILVER UP $1.08//SMALL CHANGES IN SILVER INVENTORY A SMALL WITHDRAWAL OF 639,000 OZ: /INVENTORY LOWERS T0 436,808 MILLION OZ.

JULY 2. WITH SILVER UP $0.19//NO CHANGES IN SILVER INVENTORY: /INVENTORY REMAINS AT 437.447 MILLION OZ./

JULY 1. WITH SILVER UP $0.05//XXX CHANGES IN SILVER INVENTORY: A DEPOSIT OF 182,000 OZ OF SILVER INTO THE SLV./.// /INVENTORY RISES AT 437.447 MILLION OZ./

JUNE 28. WITH SILVER UP $0.27//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 913,000 OZ FROM THE SLV./.// /INVENTORY REMAINS AT 437.265 MILLION OZ./

JUNE 27. WITH SILVER UP $0.01//NO CHANGES IN SILVER INVENTORY: .// /INVENTORY REMAINS AT 438.178 MILLION OZ.//

JUNE 26. WITH SILVER UP $0.03//HUGE CHANGES IN SILVER INVENTORY: A HUGE WITHDRAWAL OF 2.512 MILLION OZ OF SILVER FROM THE SLV.// /INVENTORY FALLS TO 438.178 MILLION OZ.//

JUNE 25. WITH SILVER DOWN $0.63//HUGE CHANGES IN SILVER INVENTORY: A MAMMOTH DEPOSIT OF 7.835 MILLION OZ OF SILVER VAPOUR INTO THE SLV.// /INVENTORY RISE TO 440.69 MILLION OZ.//WHAT AN ABSOLUTE FRAUD.

JUNE 24. WITH SILVER DOWN $0.05//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 2.104 MILLION OZ FROM THE SLV.// /INVENTORY LOWERS TO 432.835 MILLION OZ.

JUNE 21. WITH SILVER DOWN $1.15//NO CHANGES IN SILVER INVENTORY’// /INVENTORY REMAINS AT 434.935 MILLION OZ.

JUNE 20. WITH SILVER UP $1.17//HUGE CHANGES IN SILVER INVENTORY’ A DEPOSIT OF 5.164 MILLION OZ INTO THE SLV/// /INVENTORY RISES TO 434.929 MILLION OZ.

JUNE 18. WITH SILVER UP $0.21//NOCHANGES IN SILVER INVENTORY’ A WITHDRAWAL .730 MILLION OZ INTO THE SLV/// /INVENTORY FALLS TO 429.775 MILLION OZ.

JUNE 17. WITH SILVER UP $0.21//SMALL CHANGES IN SILVER INVENTORY’ A WITHDRAWAL .730 MILLION OZ INTO THE SLV/// /INVENTORY FALLS TO 429.775 MILLION OZ.

JUNE 14. WITH SILVER DOWN $0.10//NO CHANGES IN SILVER INVENTORY/ /INVENTORY REMAINS AT 429.083 TONNES

JUNE 13. WITH SILVER DOWN $1.10//HUGE CHANGES IN SILVER INVENTORY/ A HUGE DEPOSIT OF 1.958 MILLION OZ/INVENTORY RISES TO 429.083 TONNES

JUNE 12 WITH SILVER UP $0.97 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 5.983 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 427.125 MILLION OZ

JUNE 11 WITH SILVER DOWN $0.59 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.644 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 422.786 MILLION OZ

JUNE 10 WITH SILVER UP $0.30 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 3.198 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 421.142 MILLION OZ

JUNE 7 WITH SILVER DOWN $1.93 TODAY: NO CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY AT 417.944 MILLION OZ

JUNE 6 WITH SILVER UP $1.27 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 417.944 MILLION OZ

JUNE 5 WITH SILVER UP 0.38 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.52 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 415.295 MILLION OZ

JUNE 4 WITH SILVER DOWN $1.08 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

JUNE 3 WITH SILVER UP $0.35 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

MAY 31 WITH SILVER DOWN $1.09 TODAY: HUGE CHANGES IN SILVER INVENTORY: A MASSIVE WITHDRAWAL OF 3.655 MILLION OZ FROM THE SLV//INVENTORY LOWERS TO 413.775 MILLION OZ

MAY 30 WITH SILVER DOWN $0.80 TODAY: NO CHANGES IN SILVER INVENTORY//INVENTORY REMAINS AT 417.430 MILLION OZ

MAY 29 WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 1.051 MILLION OZ INTO THE SLV//INVENTORY DECREASES TO 417.430 MILLION OZ

MAY 28 WITH SILVER UP $1.64 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 2.832 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 418.481 MILLION OZ

CLOSING INVENTORY 435.625 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY

3.CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES

JB Maverick comments on our work exposing the price manipulation of gold and silver.

Well worth reading..

J.B. Maverick: The end of gold and silver price manipulation

Submitted by admin on Thu, 2024-07-11 10:56 Section: Daily Dispatches

10:55a ET Thursday, July 11, 2024

Dear Friend of GATA and Gold:

Financial writer J.B. Maverick, a former commodities trader, credits GATA and draws heavily on its work with his essay published this week, “The End of Gold and Silver Price Manipulation.”

Maverick writes that the “the manipulators were so brazen in their efforts that, despite their constant denials of engaging in price manipulation, their actions were so heavy-handed that they became apparent to nearly everyone. As time went on, both individual traders and organizations such as the Gold Anti-Trust Action Committee complained more and more loudly to financial regulatory authorities, eventually forcing them to take some action.”

Maverick’s analysis is posted at the internet site of Miami-based monetary metals dealer True Gold Republic here:

With cocoa prices hovering over $8,000 a ton in New York, the long-anticipated demand destruction for cocoa is finally approaching. New estimates indicate that global bean processing likely declined in the second quarter.

According to six analysts and traders tracked by Bloomberg, second-quarter global grindings—where cocoa transforms into butter and powder used in food products—likely fell from a year earlier. Estimates from European grindings likely fell 2% in the quarter, hitting lows not seen since early 2020. All of the analysts forecasted much larger declines in the second half of the year.

“The cheap stuff is beginning to drop off, and the expensive stuff is coming in,” said Jonathan Parkman, head of agricultural sales at broker Marex Group.

Parkman said, “The worst of input inflation will affect the second half of this year.”

The grinding numbers are nowhere near the deterioration to end elevated cocoa prices, but the estimates suggest emerging demand destruction.

“We are more likely to see a significant change in the grind number in the second half of the year,” said Darren Stetzel, vice president of soft commodities for Asia at broker StoneX.

Stetzel noted that the market has been forced to adapt to the scarcity of beans, which should alleviate some demand pressure. He pointed out that chocolate makers are increasingly using substitutes like palm oil.

Grinding data from Europe is due on Thursday, and Asia and North America will report next week.

Last month, the KitKat-maker warned ‘cocoaflation‘ will soon send candy bar prices higher.

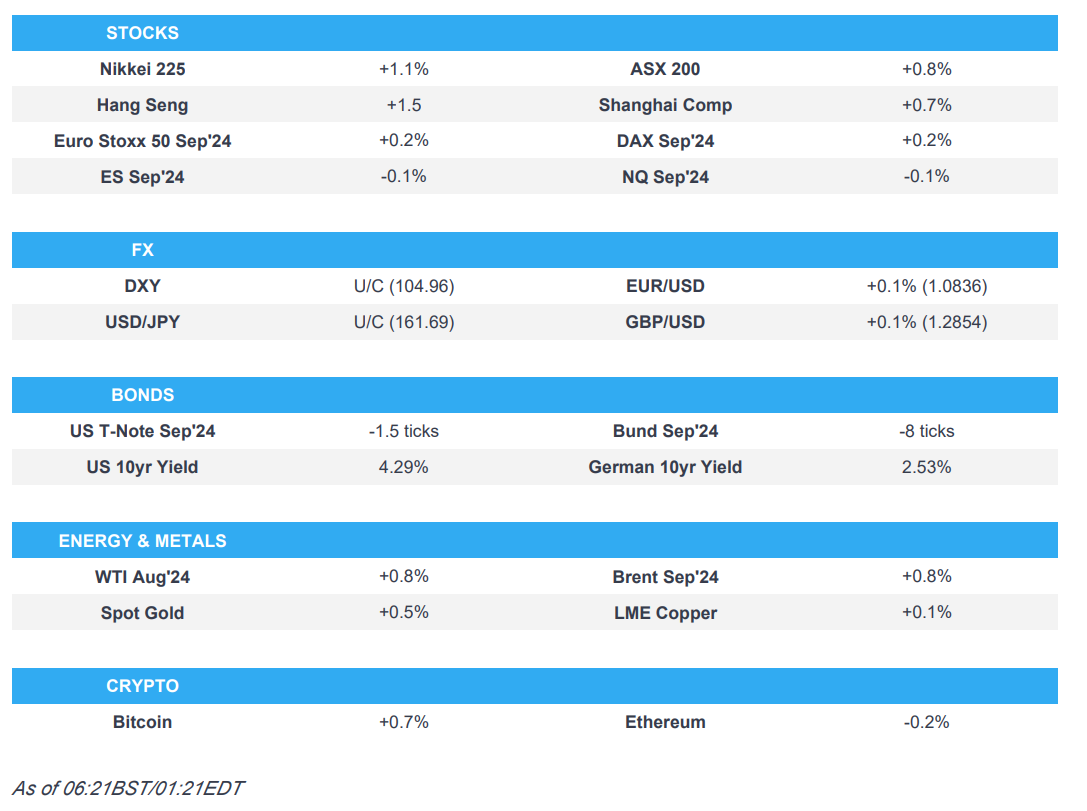

SHANGHAI CLOSED UP 31.02 PTS OR 1.06% //Hang Seng CLOSED UP 360.46 PTS OR 2.06% // Nikkei CLOSED UP 392.03 OR 0.94%//Australia’s all ordinaries CLOSED UP 0.93%///Chinese yuan (ONSHORE) closed UP TO 7,2657 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2782/ Oil UP TO 82.40 dollars per barrel for WTI and BRENT UP AT 85.38/Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGSTHURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2657

OFFSHORE YUAN: UP TO 7.2782

SHANGHAI CLOSED UP 31.02 PTS OR 1.06 %

HANG SENG CLOSED UP 360.46 PTS OR 2.06%

2. Nikkei closed UP 392.03 PTS OR 0.94%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 104.59 EURO RISES TO 1.0851 UP 17 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1,083 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 161.59 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.536/Italian 10 Yr bond yield DOWN to 3.875 SPAIN 10 YR BOND YIELD DOWN TO 3.307%

3i Greek 10 year bond yield DOWN TO 3.535

3j Gold at $2381.60//Silver at: 30.98 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 70/ 100 roubles/dollar; ROUBLE AT 87.25

3m oil into the 82 dollar handle for WTI and 85 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 161.59/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.083% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8981 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9745 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.280 UP 0 BASIS PTS…

USA 30 YR BOND YIELD: 4.473 UP 0 BASIS PTS/

USA 2 YR BOND YIELD: 4.626 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.89…

10 YR UK BOND YIELD: 4.1995 UP 7 PTS

2a New York OPENING REPORT

Futures Dip Ahead Of “Very Good” CPI

THURSDAY, JUL 11, 2024 – 08:00 AM

After the S&P closed up the first 7 trading days of July, US equity futures are down small following yesterday’s last hour meltup rally and into today’s CPI. As of 7:45am ET, S&P futures down 0.1% after the underlying index gained more than 1% to fresh all-time highs, with Nasdaq futures lagging the same as Mag7 names are mixed pre-market with AMZN/NVDA higher even as Goldman publishes another note warning that at some point the hyperscalers will have to “show investors the money” for all their AI capex investments. Bond yields are flat to down 1bps pushing the USD lower for a second day. In commodities, all 3 complexes are seeing strength. CPI and Fedspeak will dominate today’s headlines but also keep an eye on jobless claims as another Powell input.

In premarket trading, Pfizer rose more than 3% after moving forward with a new wieght-loss pill. Costco climbed after hiking its membership fee for the first time since 2017; the news helped move other staples such as WMT higher. Here are other notable premarket movers:

Albemarle drops 1.7% after Wells Fargo downgrades the stock to equal-weight in a second-quarter preview for the chemicals sector.

Airline stocks drop in premarket after Delta Air Lines issued a forecast for third-quarter adjusted earnings per share that missed consensus expectations.

Alcoa shares rise 2.7% after the aluminum producer’s preliminary adjusted Ebitda for the second quarter came in ahead of estimates.

Costco shares rise 3.0% after the warehouse-club chain announced plans to boost annual membership fees for the first time since 2017, which Jefferies said would be a positive catalyst for the stock. Additionally, the company’s US comparable sales, excluding fuel and currencies, surpassed consensus estimates.

PepsiCo shares fall 2.3% after the snack and soft-drink giant reported weaker-than-expected revenue for the second quarter and tempered its full-year outlook. The company reiterated its annual profit forecast.

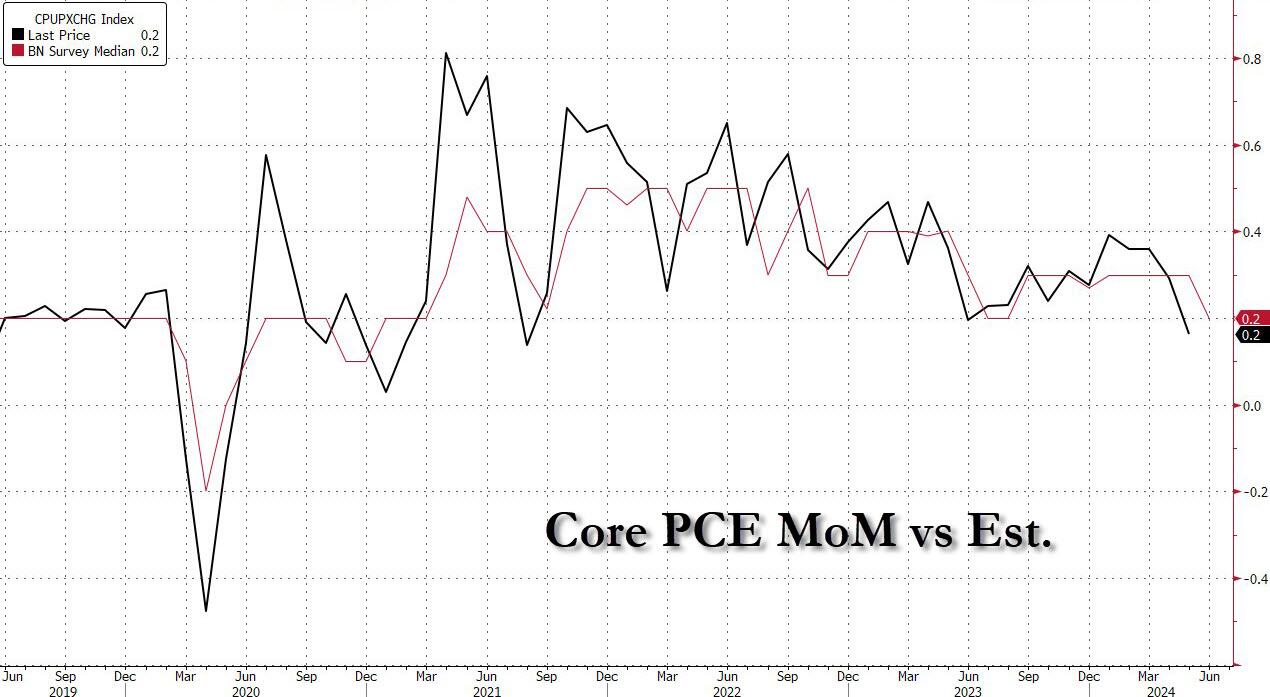

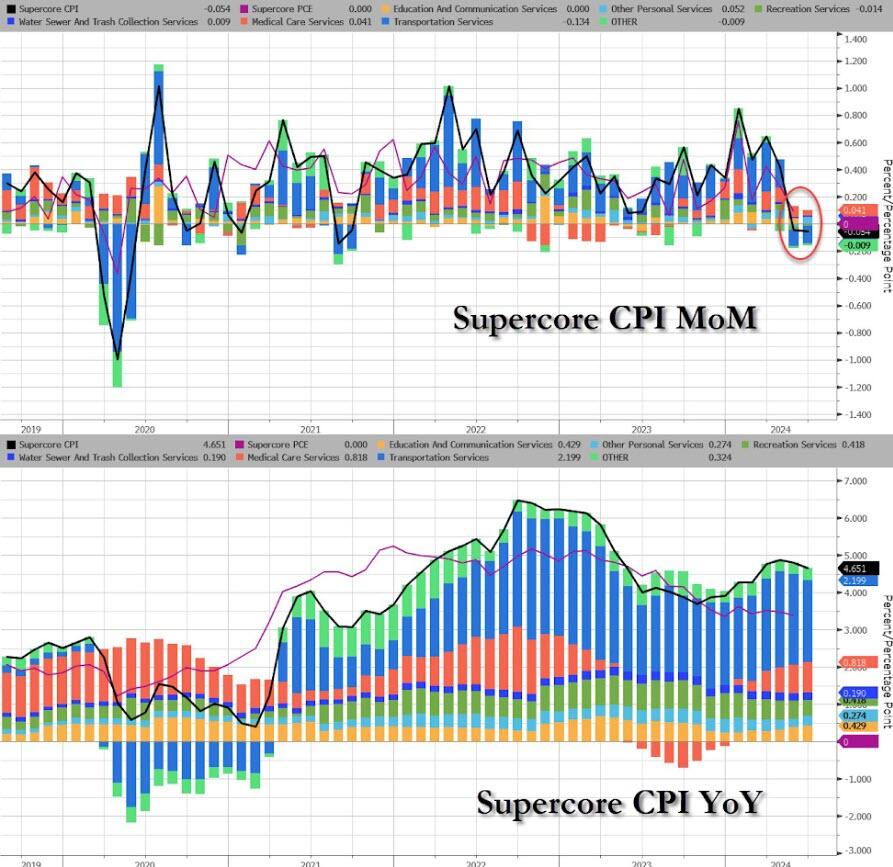

The core CPI reading Thursday is expected to rise 0.2% in June for a second month. That would mark the smallest back-to-back gains since August — a pace seen as palatable for Fed officials. Our full preview can be found here.

Swaps are pricing in two Fed cuts in 2024, with a strong chance of the first coming in September. Traders are also eyeing reports from JPMorgan Chase & Co., Wells Fargo & Co. and Citigroup Inc. tomorrow to cap off the week.

“June’s CPI report looks to be another ‘very good’ report that should boost the FOMC’s confidence about the inflation trajectory,” said Anna Wong at Bloomberg Economics. “That should set the stage for the Fed to start cutting rates in September.”

Meanwhile, Goldman strategists doubled down on their warning about the AI bubble, saying that investors are growing increasingly concerned that US technology megacaps are spending too much on artificial intelligence. Valuations could be due for a painful de-rating unless revenue and earnings rise to justify the capex spending, they said.

Investors broadly expect the frenzy to remain a key feature of a rally in the second half, although some are betting on sectors such infrastructure providers and utilities to lead gains for the remainder of 2024, the Goldman strategists said. One measure, though, signals that the rally may be losing momentum: market breadth has contracted in recent months, with the share of S&P 500 members trading above their 200-day moving average hovering around its lowest in 2024.

Europe’s Stoxx 600 advanced 0.3%, with consumer products, construction and utilities leading gains. DNB Bank ASA surged the most since Nov. 2020 after the Norwegian lender reported earnings that beat analysts’ estimates. Swiss chocolate maker Barry Callebaut AG dropped more than 10% after disappointing results affected by high cocoa-bean prices. Here are the biggest European movers:

DNB jumps as much as 6.4%, the most since November 2020, after the Norwegian lender reported an “impressive” 2Q print, Citi writes, with strong beats to net interest income (NII) and fees

Bayer shares rise as much as 2.9% after securing US FDA fast track designation for AB-1005, which is being developed for moderate Parkinson’s disease

Ambu rises as much as 6.8%, the most since May 15, after the Danish medical device firm predicted full-year revenue gains and said preliminary 3Q results indicated a jump on revenue

Husqvarna gains as much as 6.9% as Nordea upgrades its rating on the Swedish outdoor and garden equipment maker to buy based on expectations for improved earnings momentum

Vivendi gains as much as 3.4%, to the highest price in over two years, as JPMorgan places the French conglomerate on positive catalyst watch and highlights it as a top pick

UK water stocks are trading higher this morning after regulator Ofwat outlined draft determinations regarding the industry’s investment plans

Barry Callebaut slumps as much as 11% after the Swiss chocolate producer reported 9-month sales that Vontobel says show “significant exogenous, unprecedented market headwinds”

Galp declines as much as 4.9% and is the weakest performer on the Stoxx 600 energy index on Thursday as Morgan Stanley downgrades to underweight due to a “rich” valuation

Suedzucker falls as much as 5.1%, to the lowest level since April, after the German sugar producer reported operating profit for the first quarter that missed estimates

Evotec shares fall as much as 6.6% after the German pharmaceutical company was downgraded to hold by Deutsche Bank, which expects soft second-quarter results and sees guidance at risk

DocMorris drops as much as 19%, most since October, after the Swiss pharmacy’s sales came below expectations and its ramp up dynamics of electronic prescriptions could be stronger, ZKB says

Earlier, Asian stocks rose, as Taiwan Semiconductor traded at record levels after the sole supplier of the most-advanced chips for Nvidia and Apple said second-quarter sales grew the fastest since 2022. Sony, Tencent Holdings and Korean chipmaker SK Hynix which traded at its highest levels since 2000, were among top contributors to the climb in the regional stock index. The iPhone maker said it aims to ship 10% more new devices after a bumpy 2023. The S&P 500 has advanced in each of the past seven sessions, its longest winning streak since November. MSCI Inc.’s global stocks index is at a record high.

In FX, the Bloomberg Dollar Spot Index fell for a second day to a one-month low. The British pound rose to its strongest level against the dollar since March after data showed the UK economy expanded in May at twice the pace expected. Gross domestic product rose 0.4% month-on-month after the flat reading in April. That compares with the 0.2% pace economists had expected, reflecting the fastest expansion in construction in almost a year. Cable is up 0.2% and set to log its ninth gain in eleven sessions.

In rates, treasuries were steady with price action muted ahead of June CPI data at 8:30am New York time. European bonds lag, led by gilts after UK GDP rose 0.4% in May, double the median estimate. Yields are mixed across the curve but within 1bp of Wednesday’s closing levels. 10-year is around 4.28% with bunds and gilts lagging by 2bp and 3bp in the sector. Along with CPI, US session includes 30-year bond auction at 1pm, following good results earlier this week for 3- and 10-year offerings.

In commodities, oil climbed for a second day with WTI trading near $82.20 a barrel as a decline in US crude inventories countered the IEA’s call that demand growth is slowing. Gold edged higher for a third day, adding $12 to around $2,383/oz.

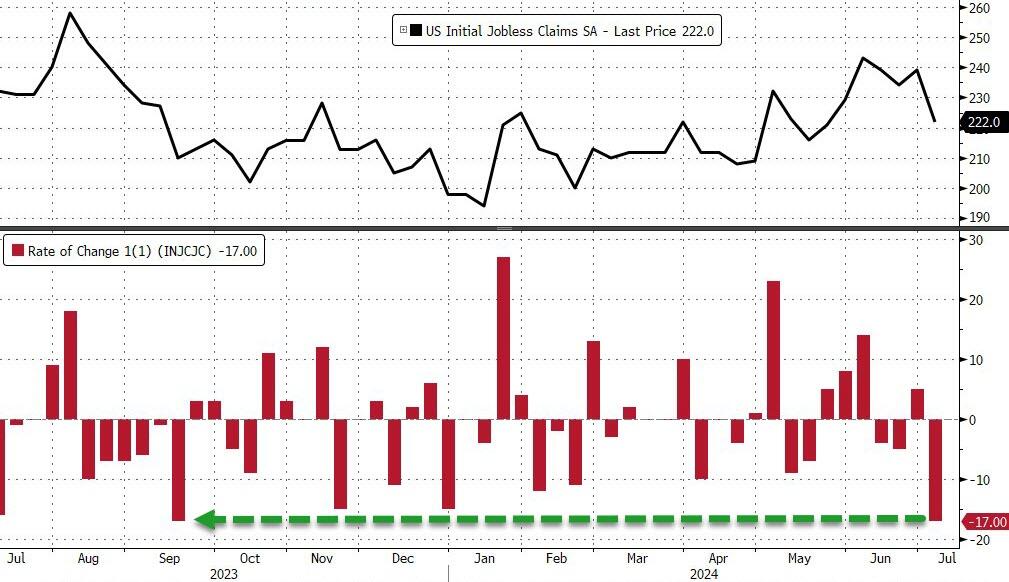

Looking at the calendar, US economic data slate includes the CPI report and initial jobless claims (8:30am) and monthly budget statement (2pm). Fed members scheduled to speak include Bostic (11:15am) and Musalem (1pm)

Market Snapshot

S&P 500 futures little changed at 5,684.75

STOXX Europe 600 up 0.5% to 519.14

MXAP up 1.1% to 187.17

MXAPJ up 1.3% to 585.57

Nikkei up 0.9% to 42,224.02

Topix up 0.7% to 2,929.17

Hang Seng Index up 2.1% to 17,832.33

Shanghai Composite up 1.1% to 2,970.39

Sensex little changed at 79,916.84

Australia S&P/ASX 200 up 0.9% to 7,889.64

Kospi up 0.8% to 2,891.35

German 10Y yield +1.5bps at 2.55%

Euro up 0.1% to $1.0841

Brent Futures up 0.4% to $85.46/bbl

Gold spot up 0.4% to $2,380.86

US Dollar Index down 0.12% to 104.92

Top Overnight News

Democratic donors have warned that funding for the November election effort is “drying up” because of President Joe Biden’s refusal to step aside, threatening to undermine the party’s effort to defeat Donald Trump. FT

The United States will start deploying long-range fire capabilities in Germany in 2026 in an effort to demonstrate its commitment to NATO and European defense, the United States and Germany said in a joint statement. RTRS

China cracks down further on short selling, with higher margin requirements for the activity (while the country’s largest stock lending provider will suspend its business of lending securities to brokerages). BBG

NATO dramatically ratcheted up its criticism of China’s support for Russia, calling Beijing a “decisive enabler” of Putin’s war, language that could open the door to sanctions against the Xi government. NYT

Global oil demand growth slowed to its weakest in more than a year last quarter, with consumption rising by just 710,000 barrels a day as China slipped into a marginal contraction, the IEA said. Demand remains on track to grow by less than 1 million b/d this year and next. BBG

The NBA has finalized an 11-year TV rights deal worth $76B with NBC, Amazon, and ESPN, although it’s not clear if TNT will retain a few games for itself. The Athletic

Apple has avoided the threat of fines from European Union regulators by agreeing to open up its mobile wallet technology to other providers free of charge for a decade. BBG

PEP reported solid EPS upside in FQ2 at 2.28 (vs. the Street 2.15), but organic revenue growth of 1.9% fell short by ~100bp (the Street was modeling +2.9%). RTRS

Since the start of 2023, 97% of NVDA’s return has been driven by greater earnings (vs. just 3% from valuation expansion). However, year to date, NVDA’s NTM P/E ratio has increased from 25x to 42x (+70%), accounting for 56% of the 165% YTD price return: Goldman

Fed’s Cook (voter) said the baseline outlook is for a continued fall in inflation without a significant increase in unemployment and US data is consistent with a soft landing. Cook added they are very attentive to what is happening with the unemployment rate and would be responsive if the situation changes quickly.

US Senate Majority Leader Schumer is privately signalling to donors he is open to a democratic presidential ticket that isn’t led by President Biden, according to Axios.

A more detailed look at global markets courtesy of Newquawk

APAC stocks took impetus from Wall St where the major indices rallied as outperformance in tech spear-headed the S&P 500 and Nasdaq to fresh record highs once again following TSMC’s record quarterly sales and as Apple aims to boost iPhone shipments. ASX 200 gained with all sectors in the green and notable strength in tech, real estate, and heavy industries. Nikkei 225 continued its record-setting streak and advanced above the 42,000 level for the first time. Hang Seng and Shanghai Comp. conformed to the broad constructive mood amid the rising tide across equities despite NATO’s firm rhetoric on China which it called a decisive enabler of Russia’s war effort in Ukraine, while sentiment was also unfazed by reports that Germany is to cut Huawei from its mobile networks.

Top Asian News

BoK kept its base rate unchanged at 3.50%, as expected, with the decision made unanimously. BoK said it will maintain a restrictive policy stance for a sufficient period of time and will examine the timing of a rate cut, while it dropped the phrase that ‘upside risks to inflation forecasts have increased’ in its policy statement and said inflation could be slower than forecast. BoK Governor Rhee said they need to assess how a rate cut would affect financial stability and that a cut could adversely affect financial stability. Furthermore, he commented “time to prepare pivot rate cuts” and that two board members said they could consider a rate cut within the next three months, although he added that market expectations for policy rate cuts are a little excessive.

Fast Retailing (9983 JT) – 9M (JPY): Net Profit 312.84bln (+31.2% Y/Y), operating profit 410.8bln (+21.5%); Sees FY operating income at 475bln (prev. 450bln)

European bourses, Stoxx 600 (+0.4%) are entirely in the green, in a continuation of the strength seen on Wall St. in the prior session, which also helped to prop up sentiment in APAC trade. European sectors hold a strong positive bias; Consumer Products takes the spot, propped up by gains in the Luxury sector. Energy is found at the foot of the pile, though with marginal losses. US Equity Futures (ES -0.1%, NQ -0.1%, RTY U/C) are flat/lower, taking a breather from the significant gains seen in the prior session.

Top European News

Goldman Sachs raises UK’s 2024 GDP growth forecast to 1.2% (prev. 1.1%)

UK PM Starmer said the special relationship with the US is so important and stronger than ever.

India warned the UK not to impose a deadline on trade talks, while India’s Commerce Minister said India and the UK are ‘on board’ on the major details, according to FT.

FX

DXY is back onto a 104 handle with all eyes on US CPI which takes place in the context of last week’s “dovish NFP” and “dovish” comments from Fed Chair Powell.

EUR/USD has marginally built on yesterday’s gains and incrementally surpassed Monday’s 1.0845 peak. For today, fate for the EUR/USD pair will likely be dictated by events stateside.

GBP is extending its run as the best performing G10 currency YTD. Strong GDP metrics have followed up recent hawkish rhetoric from Haskel, Pill and Mann. Cable as high as 1.2876 with the next target coming via the March 8th YTD peak at 1.2893.

JPY clawed back some ground vs. the USD after climbing as high as 161.75 overnight and backing away from the multi-decade 161.95 high seen on the 3rd July.

Antipodeans are both near the top of the G10 leaderboard, benefiting from the constructive risk tone. NZD/USD is attempting to atone for Wednesday’s RBNZ induced losses which saw the pair relinquish the 0.61 handle.

PBoC set USD/CNY mid-point at 7.1339 vs exp. 7.2730 (prev. 7.1342).

Fixed Income

USTs are flat in a very narrow 3+ tick range ahead of US CPI. A data point that will be scrutinised to see if it favours a September cut; within Wednesday’s 110-10 to 110-20 parameters, a hawkish CPI print could bring into play the WTD 110-07 base.

Bunds are incrementally softer with specifics light and attention entirely on US CPI. Recent very modest bout of downside came in tandem with a slight pick-up in the crude complex.

Gilts are the incremental underperformer after strong growth data for May which caused Gilts to open lower by a handful of ticks before dipping further to a 97.81 base. Gilts remain comfortably within existing 97.64-98.38 WTD parameters. Gilts caught a slight bid following a well received 7yr auction.

UK sells GBP 3.75bln 4.00% 2031 Gilt: b/c 3.29x (prev. 2.97x), average yield 4.074% (prev. 4.218%), tail 1.9bps (prev. 1.4bps).

Italy sells EUR 8.5bln vs exp. EUR 7.25-8.5bln 3.45% 2027, 1.10% 2027, 3.45% 2031, 0.90% 2031, 4.45% 2043 BTP. A well received auction which sparked modest upside in BTPs, lifting them to incremental session peaks of 117.26; though not all to surprising given the reduced auction amount.

Commodities

Crude futures hold a modest upward bias but trade off best levels after WTI Aug hit an overnight peak of USD 82.87/bbl. Elsewhere, the IEA monthly oil market report had no bearing on prices. Brent September currently sits around USD 85.30/bbl.

Mixed price action in the precious metals complex with spot palladium underperforming after yesterday’s rebound, whilst spot gold and silver hold a mild upward bias heading into the US CPI metrics. Spot gold currently sits in a USD 2,371.34-2,384.14/oz range.

Base metals are mixed with the breadth of the market also narrow. Copper prices remain subdued following a large build (+11.3k tons) in LME inventories after jumping to the highest level since 2021 yesterday.

Azerbaijan oil production at 65.597k tons per day in June (vs 62.118k in May), according to the energy ministry.

IEA OMR: Sees 2024 and 2025 oil demand growth forecasts little changed from the prior month at just below 1mln BPD; Global oil demand growth slows further at China cools; China’s oil demand growth eased to 710k BPD in Q2, IEA say. IEA sees oil demand growth at 970k BPD in 2024 (prev. 960k BPD), 980k BPD in 2025 (prev. 1mln BPD). Iran’s crude oil production rises to six-year high. Global oil stockpiles fell 18.1mln bbl in June in prelim data. Subpar economic growth, efficiencies, EVs are oil headwinds

Geopolitics: Middle East

The Gaza cease-fire agreement framework is reportedly agreed, and the parties are now “negotiating details of how it will be implemented”, according to a senior US official cited by Washington Post’s Ignatius. “US officials say the framework of a three-stage deal is down to implementation details.” “Officials caution that although the framework is in place, a final pact probably isn’t imminent, and the details are complex and will take time to work through.” “A final possible bonus of a Gaza cease-fire is that Saudi Arabia has signaled it is prepared to ‘move forward on normalization’ of relations with Israel”, according to a US official.

White House’s Kirby says he is cautiously optimistic things are moving in the right direction on Gaza ceasefire talks, according to CNN.

Geopolitics: Other

China’s mission to the EU said the declaration of the NATO summit in Washington is full of ‘Cold War mentality and belligerent rhetoric,’ and the China-related content is full of provocations, ‘lies, incitement, and smears’

Taiwan is to strengthen its civil defence to prepare against China’s threat with the government working to prepare public services and infrastructure to function in wartime as China’s aggressive stance fuels concerns about the risk of open conflict, according to FT.

Russian Deputy Foreign Minister says US and Germany’s decision to deploy long-range missiles in Germany is aimed at harming Russia’s security; says Russia will respond “in a military manner”, according to RIA

US Event Calendar

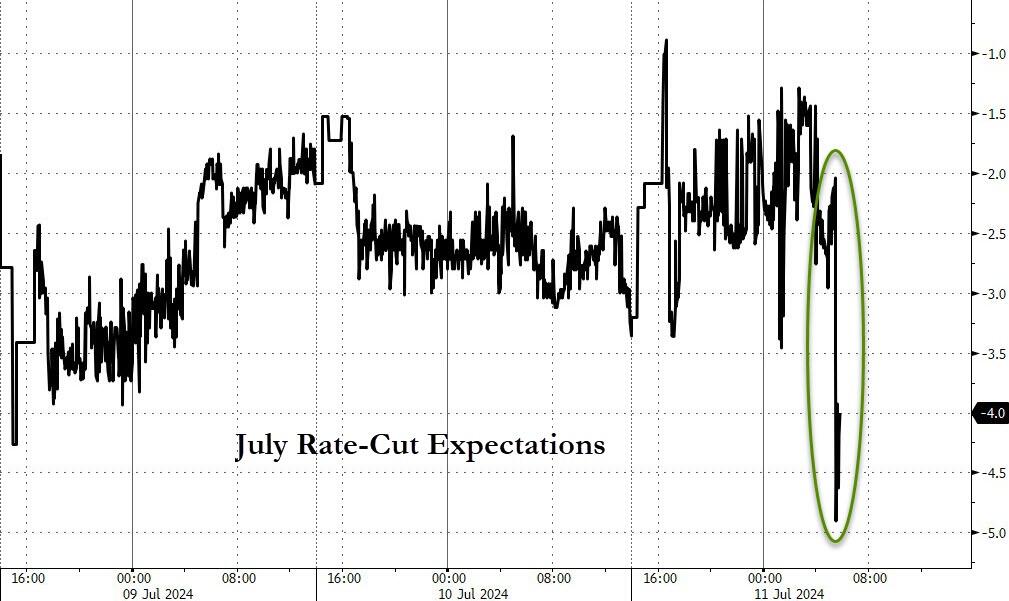

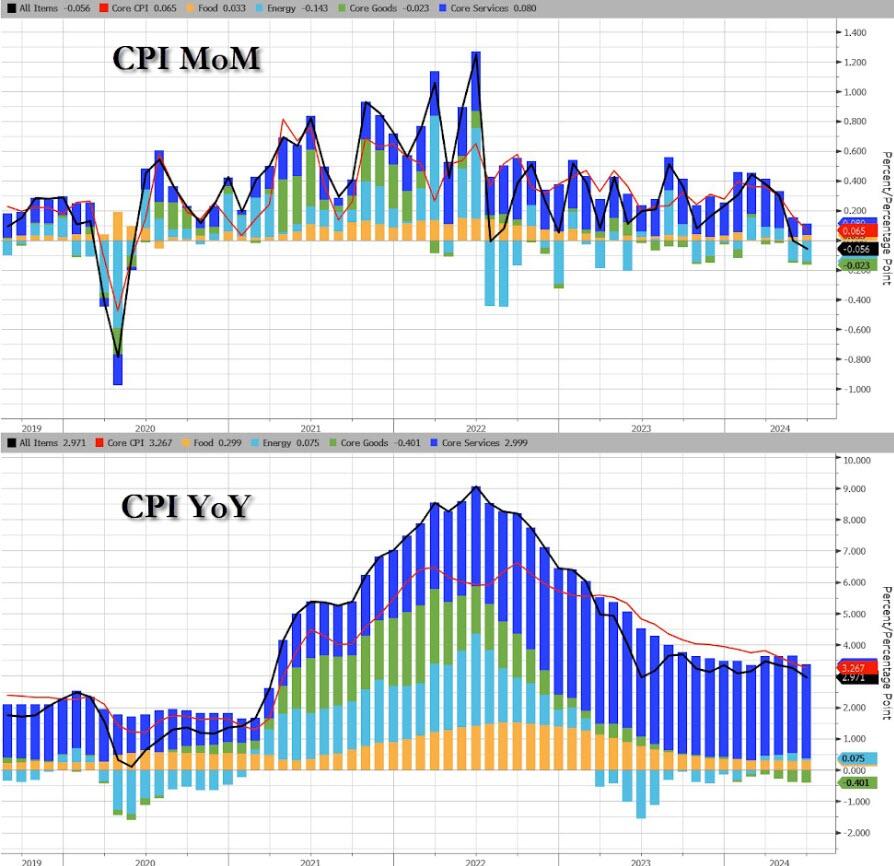

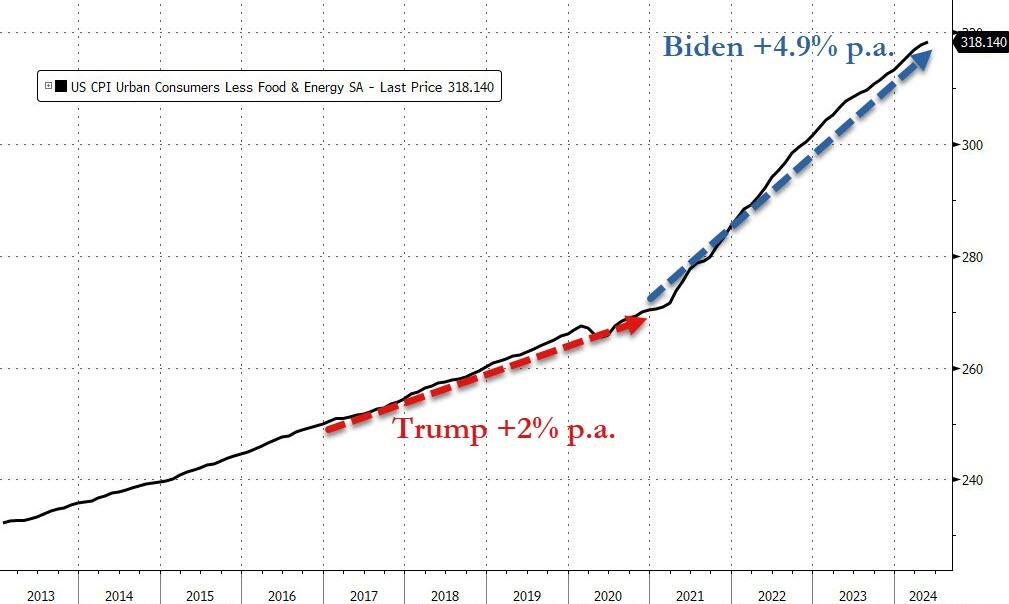

08:30: June CPI MoM, est. 0.1%, prior 0%

June CPI YoY, est. 3.1%, prior 3.3%

June CPI Ex Food and Energy MoM, est. 0.2%, prior 0.2%

June CPI Ex Food and Energy YoY, est. 3.4%, prior 3.4%

June Real Avg Hourly Earning YoY, prior 0.8%, revised 0.7%

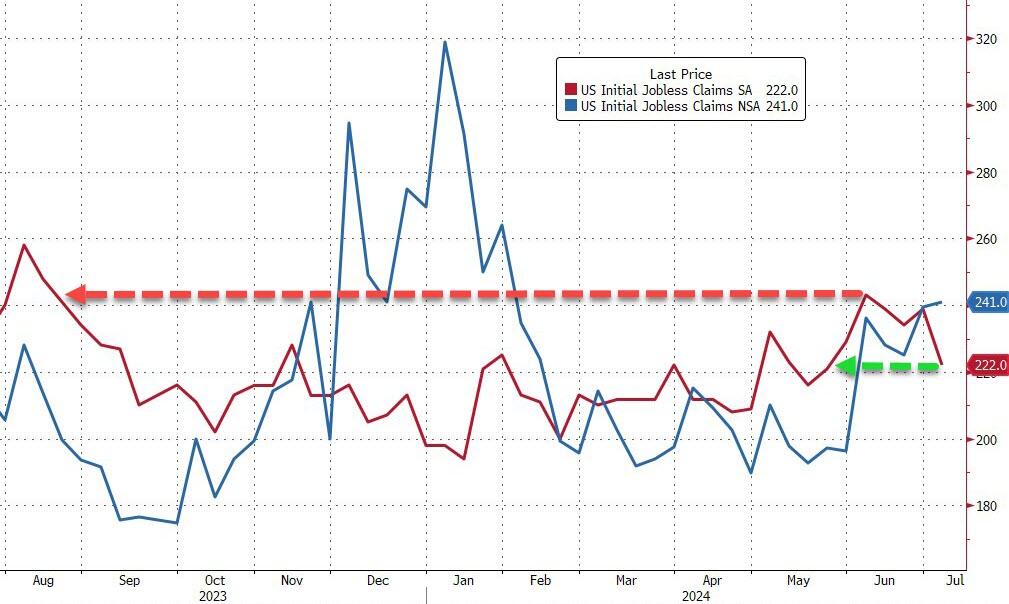

08:30: July Initial Jobless Claims, est. 235,000, prior 238,000

June Continuing Claims, est. 1.86m, prior 1.86m

14:00: June Monthly Budget Statement, est. -$76.1b, prior -$347.1b

DB’s Jim Reid concludes the overnight wrap

After telling you earlier this week that I hoped my current trip to Cape Town would be less eventful than my last 20 years ago, it is fair to say it’s not been without incident. Yesterday due to a historically bad run of weather, the mayor of Cape Town told everyone to work from home and today schools are closed with people urged to stay off the roads and remain indoors. So thanks to the many who braved the storm to meet us yesterday. Being forced to stay inside and watch England play in the current Euros would have been worse than any storm but miracles have happened and they reached the final last night. I’m not expecting Spain to be quaking in their boots this morning.

There are few storms in the US at the moment, with markets continuing to power forward over the last 24 hours, with the S&P 500 (+1.02%) advancing to its 37th record this year with the Mag-7 (+1.26%) now surpassing +50% YTD. These moves are becoming increasingly relentless now, as the S&P rose for a 7th consecutive day for the first time since November, and it’s also the first time since late-2021 that it’s managed 10 out of 11 gains in a row. So not the sort of rally you see every day, and if we can make it to 11 out of 12 gains today, that would be the first time that’s happened since April 2019. Over those 10 days the rally is +3.4% so steady and relentless rather than spectacular, at least prior to yesterday. This continued strength has been echoed across different asset classes though, but it’s now going to face several important tests, as the US CPI release is coming out today and earnings season is about to kick off in earnest, with several US banks reporting tomorrow.

That CPI release is in particular focus, because there’s been mounting anticipation that the Fed might still deliver two rate cuts this year, with September and December seen as the most likely dates. It’s true that their dot plot in June only signalled one cut this year, but since then we’ve had some weaker jobs reports, and the unemployment rate has ticked up to 4.1%, which is the highest since November 2021. So if there is positive news on inflation and we get another soft print, then that momentum for a rate cut is likely to build further.

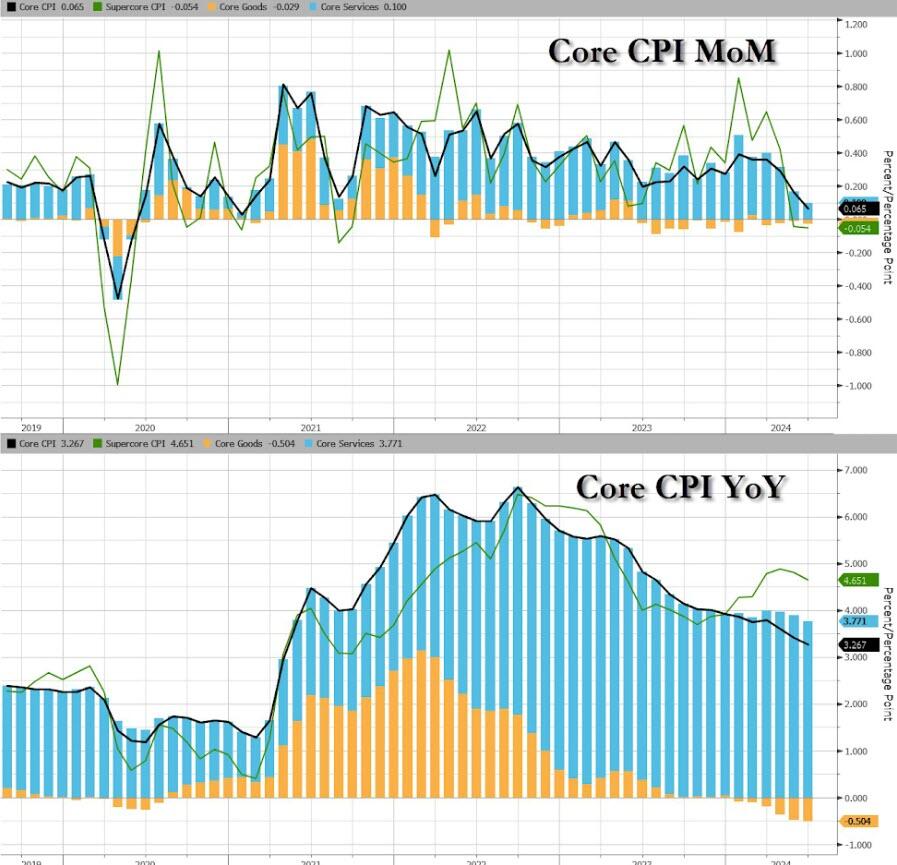

Back in Q1, the inflation numbers were much stronger than expected, which meant that market pricing for rapid rate cuts this year proved wide of the mark. But since then, the April inflation numbers eased a bit, and the latest print from May was even better from the Fed’s perspective. Indeed, the monthly core CPI reading was down to just +0.16%, the weakest since August 2021. So with more numbers like those, the Fed could feel a lot more confident that inflation was heading durably back to their 2% target.

In terms of today, our US economists are expecting that both headline and core will be a bit firmer than last month, with headline at a monthly +0.09%, and core at +0.25%. In turn, that would push the year-on-year measure down to 3.1% for headline CPI, although the core CPI measure would tick up a tenth to 3.5%. When it comes to the Fed, it’ll also be worth keeping an eye on tomorrow’s PPI report as well, since several components in that feed into the PCE measure of inflation that they officially target. So over the next couple of days we’ll get a better idea of where that’s likely to land and if the Fed have the space to cut rates. Our US economists point out that the median forecast for core PCE in the June SEP was at +2.8% on a Q4/Q4 basis, so to achieve that we need to see monthly core PCE at an average pace of 20bps a month for the rest of the year. So for them, that’s the primary test for whether the Fed can cut earlier than their baseline, which sees a first cut in December. For more details on their CPI forecast and how to sign up for their subsequent webinar, click here.

Ahead of that, Fed Chair Powell was continuing his semiannual congressional testimony yesterday, appearing at the House Financial Services Committee. But there weren’t really any fresh headlines from that, and T reasury yields were largely steady on the day, with the 2yr yield (-0.6bps) and the 10yr yield (-1.2bps) both slightly lower. It was a similar story for Fed pricing, with the amount of cuts priced by the December meeting (+0.4bps) also little changed at 51bps.

On the equity side, the S&P 500 (+1.02%) posted its biggest gain in over a month, with the advance once again led by the tech mega caps. The Mag-7 (+1.26%) extended its YTD gain to +50.9%, led by Nvidia (+2.69%) and Apple (+1.88%) on the day. That said, the session saw broad gains with all top level sector groups within the S&P 500 up by at least 0.4% on the day.

Meanwhile in Europe, markets staged a recovery yesterday, with the S TOXX 600 (+0.91%), the DAX (+0.94%) and the CAC 40 (+0.86%) all advancing. It was the same story for sovereign bonds, with spreads tightening as yields on 10yr bunds (-4.7bps), OATs (-5.9bps) and BTPs (-8.8bps) all came down as well. However, UK gilts (-3.3bps) saw a smaller decline in yields, which followed comments from BoE chief economist Pill that were perceived a bit more hawkishly. He said that “It’s still an open question of whether the time for that cut is now or not,” which seemingly cast doubt on the prospect of a cut when they announce their next decision on August 1. Indeed, investors moved to dial back the chance in response, with the probability of a cut down from 64% the previous day to 56% by the close. The next important data print will be the CPI release next week, but Pill also pointed out that “we have to be realistic about how much any one or two releases can add to our assessment.”

Asian equity markets are all higher this morning as the globa l risk move gathers momentum . Across the region, Chinese stocks are outperforming with the Hang Seng (+1.45%) leading gains while the CSI (+0.99%) and the Shanghai Composite (+0.77%) are also higher. Elsewhere, the Nikkei (+0.94%) is being powered by technology stocks and crossing 42,000 for the first time. The KOSPI (+0.75%) is also higher as the Bank of Korea kept interest rates steady at 3.5% for the 12th consecutive meeting, as widely expected. In overnight trading, US stock futures are pausing for a breather at the moment and are broadly flat alongside Treasury yields.

Early morning data showed that Japanese core machinery orders unexpectedly fell sharply again in May (-3.2% m/m v/s +0.8% expected) dampening expectations for a recovery in Japanese investment in Q2/Q3. It followed a -2.9% decline in April.

In the geopolitical space, today will see the final day of this year’s NATO summit in Washington. The summit has been somewhat overshadowed by lingering questions over President Biden’s candidacy for the November US election. These re-intensified yesterday, initially triggered by an interview from former House Speaker Nancy Pelosi, who avoided unequivocally supporting Biden, saying “it’s up to the president to decide” if he should stay on in the race. Later on Peter Welch of Vermont became the first Democratic senator to call on Biden to withdraw from the race, while Axios reported that Democrat Senate Majority Leader Chuck Schumer was privately open to replacing Biden as the presidential nominee.

To the rest of the day ahead now, and data releases include the US CPI reading for June, the weekly initial jobless claims, and UK GDP for May. From central banks, we’ll hear from the Fed’s Bostic and Musalem.

.

2B EUROPE OPENING/TRADING

Another set of record highs stateside ahead of US CPI – Newsquawk Europe Market Open

THURSDAY, JUL 11, 2024 – 01:30 AM

APAC stocks took impetus from Wall St where the S&P 500 and Nasdaq rose to fresh record highs once again.

European equity futures indicate a mildly positive open with Euro Stoxx 50 future +0.2% after the cash market closed up by 1.1% on Wednesday.

DXY sits just below the 105 mark, antipodeans lead, Cable has held onto recent gains and USD/JPY continues to edge higher.

BoE’s Mann said that wage growth is still far away from being consistent with the inflation target.

Looking ahead, highlights include UK GDP, US CPI, IJC, Comments from Fed’s Bostic & Musalem, Supply from UK, US & Italy.

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

US TRADE

EQUITIES

US stocks rallied in which the S&P 500 and Nasdaq printed fresh record highs again with gains led by outperformance in tech after semis were buoyed by strong TSMC sales and Apple caught a bid on reports it aims to boost iPhone 16 shipments. Attention was also on Fed Chair Powell’s second day of testimony to Congress where he largely stuck to the script and noted more good data was needed to be convinced inflation is returning to the target in a sustainable way, as well as repeated that risks to both sides of the mandate have come back into better balance.

SPX +1.02% at 5,633, NDX +1.09% at 20,675, DJI +1.09% at 39,721, RUT +1.10% at 2,051.

Fed’s Cook (voter) said the baseline outlook is for a continued fall in inflation without a significant increase in unemployment and US data is consistent with a soft landing. Cook added they are very attentive to what is happening with the unemployment rate and would be responsive if the situation changes quickly.

WSJ’s Timiraos wrote “Federal Reserve Chair Jerome Powell made the beginning of a pivot on interest rates that might prove more durable than one that sparked a big market rally at the end of last year”.

A senior Biden team is to brief US senators at lunch on Thursday, according to Reuters citing a senate democratic leadership source. It was later reported that the meeting between Biden’s advisers and Senate Democrats on Thursday is for Senate Democrats to express to the Biden team their reservations about the President, according to Fox News.

US Senate Majority Leader Schumer is privately signalling to donors he is open to a democratic presidential ticket that isn’t led by President Biden, according to Axios.

US House Oversight Panel subpoenaed top Biden aides over his mental fitness, according to Axios.

US House Democrat Leader Jeffries told lawmakers he will relay their concerns about Biden’s electability, according to Politico.

APAC TRADE

EQUITIES

APAC stocks took impetus from Wall St where the major indices rallied as outperformance in tech spear-headed the S&P 500 and Nasdaq to fresh record highs once again following TSMC’s record quarterly sales and as Apple aims to boost iPhone shipments.

ASX 200 gained with all sectors in the green and notable strength in tech, real estate, and heavy industries.

Nikkei 225 continued its record-setting streak and advanced above the 42,000 level for the first time.

Hang Seng and Shanghai Comp. conformed to the broad constructive mood amid the rising tide across equities despite NATO’s firm rhetoric on China which it called a decisive enabler of Russia’s war effort in Ukraine, while sentiment was also unfazed by reports that Germany is to cut Huawei from its mobile networks.

US equity futures plateaued after yesterday’s tech-driven advances and with CPI data on the horizon.

European equity futures indicate a mildly positive open with Euro Stoxx 50 future +0.2% after the cash market closed up by 1.1% on Wednesday.

FX

DXY traded uneventfully and languished just beneath the 105.00 level as participants braced for CPI data.

EUR/USD continued its gradual rebound from this week’s floor near 1.0800 as the ECB enters a quiet period.

GBP/USD held onto its recent gains as attention in the UK turns to monthly GDP and output data.

USD/JPY traded indecisively after mixed Machinery Orders although found support at the 161.50 level.

Antipodeans benefitted in tandem with the positive risk environment and mild CNY strength.

PBoC set USD/CNY mid-point at 7.1339 vs exp. 7.2730 (prev. 7.1342).

FIXED INCOME

10-year UST futures lacked direction after yesterday’s indecision heading into US CPI and a 30-year auction.

Bund futures were contained after having recently pulled back from resistance near the 131.50 level.

10-year JGB futures traded rangebound following mixed Machinery Orders data and with only brief support seen following the stronger results at the latest 20-year JGB auction.

COMMODITIES

Crude futures extended on gains amid the positive risk sentiment and following recent inventory data.

US Energy Department announced a new solicitation for up to 4.5mln barrels of oil for delivery to the Strategic Petroleum Reserve’s Bayou Choctaw site from October through December.

Spot gold gradually edged higher but remained within the prior day’s parameters ahead of inflation data.

Copper futures were little changed and only slightly benefitted from the mostly constructive mood.

CRYPTO

Bitcoin traded indecisively and ultimately faded an initial rally above the USD 58,000 level.

NOTABLE ASIA-PAC HEADLINES

US Treasury Undersecretary Shambaugh said the US may need to take further action to protect US industries from China’s industrial overcapacity and more creative approaches beyond Section 301 tariff adjustments may be necessary against China’s overproduction and exports.

BoK kept its base rate unchanged at 3.50%, as expected, with the decision made unanimously. BoK said it will maintain a restrictive policy stance for a sufficient period of time and will examine the timing of a rate cut, while it dropped the phrase that ‘upside risks to inflation forecasts have increased’ in its policy statement and said inflation could be slower than forecast. BoK Governor Rhee said they need to assess how a rate cut would affect financial stability and that a cut could adversely affect financial stability. Furthermore, he commented “time to prepare pivot rate cuts” and that two board members said they could consider a rate cut within the next three months, although he added that market expectations for policy rate cuts are a little excessive.

DATA RECAP

Japanese Machinery Orders MM (May) -3.2% vs. Exp. 0.8% (Prev. -2.9%)

Japanese Machinery Orders YY (May) 10.8% vs. Exp. 7.2% (Prev. 0.7%)

GEOPOLITICAL

MIDDLE EAST

Israeli Defence Minister Gallant and IDF Chief of the General Staff Halevi both said they are in favour of a hostage deal with Hamas, according to Kann News.

Israel is close to agreeing to withdraw from the Rafah crossing and there are attempts to open the Rafah crossing by the end of July after the full Israeli withdrawal. However, there are sticking points regarding the identification of the Palestinian parties that will operate the Rafah crossing, according to Al Arabiya citing Arabic sources.

Tel Aviv agreed in the Cairo meeting that Palestinian parties would take over the management of the Rafah crossing, according to Israeli media. Solutions proposed during the Cairo meeting do not include an Israeli presence on the ground in Gaza, while Tel Aviv requested guarantees from Washington that it could attack the Gaza Strip again if it was proven that militants had returned to its north.

White House’s Kirby says he is cautiously optimistic things are moving in the right direction on Gaza ceasefire talks, according to CNN.

US is to begin shipping 500-pound bombs to Israel, according to a report by WSJ.

OTHER