GOLD PRICE CLOSED DOWN $0.25 TO $2415.90

SILVER PRICE DOWN $0.65 TO $30.92

Democracy is two wolves and a lamb voting on what to have for lunch. Liberty is a well-armed lamb contesting the vote.” — Benjamin Franklin

Gold ACCESS CLOSED $2411.50

Silver ACCESS CLOSED: $30.75

Bitcoin morning price:$57,216 DOWN 349 DOLLARS. bankers doing a good job destroying the value of bitcoin

Bitcoin: afternoon price: $58,048 UP 483 dollars//

Platinum price closing DOWN $3.10 TO $1001.45

Palladium price; DOWN $22.05 AT $976.10

END

SHANGHAI GOLD PREMIUM 36 DOLLARS/COMEX GOLD//august to august

SHANGHAI GOLD (USD) FUTURES – QUOTES

Last Updated 12 Jul 2024 06:44:53 AM CT.

Market data is delayed by at least 10 minutes.

*CANADIAN GOLD: $3287.23 DOWN 3.81 CDN dollars per oz( * NEW ALL TIME HIGH 3,305.30 CDN DOLLARS PER OZ//MAY 20 2024)

*BRITISH GOLD: 1,857.04 DOWN 12.31 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2,211.25 DOWN 10.46 Euros per oz //* (ALL TIME CLOSING HIGH: 2.248.89 EUROS PER OZ//APRIL 16//.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCH: COMEX

EXCHANGE: COMEX

CONTRACT: JULY 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,415.000000000 USD

INTENT DATE: 07/11/2024 DELIVERY DATE: 07/15/2024

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 1

190 H BMO CAPITAL 18

363 H WELLS FARGO SEC 13

624 H BOFA SECURITIES 3

657 C MORGAN STANLEY 3

661 C JP MORGAN 10

726 C PLUS500US FINAN 1

737 C ADVANTAGE 3 8

905 C ADM 10 4

TOTAL: 37 37

MONTH TO DATE: 2,760

JPMorgan stopped 0/37

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2024. CONTRACT: 37 NOTICES FOR 3700 OZ or 0.1150 TONNES

total notices so far: 2760 contracts for 276,000 Oz (8.5847 tonnes)

FOR JULY:

SILVER NOTICES: 127 NOTICE(S) FILED FOR 0.635 million

OZ/

total number of notices filed so far this month : 5955 for 29.755 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $0.25 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ HUGE CHANGES IN GOLD INVENTORY AT THE GLD/A DEPOSIT OF 1.72 TONNES OF GOLD VAPOUR INTO THE GLD/

/ /INVENTORY RESTS AT 835.09 TONNES

INVENTORY RESTS AT 835.09 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN 65 CENTS AT THE SLV//

NO CHANGES IN SILVER INVENTORY AT THE SLV:

// INVENTORY LOWERS TO 435.625 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 435.625 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 1166 CONTRACTS TO 165,180 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR HUGE GAIN OF $0.72 IN SILVER PRICING AT THE COMEX ON THURSDAY’S TRADING ON SILVER. WE HAD ZERO LIQUIDATION AS WE HAD A HUGE NET GAIN OF 1948 CONTRACTS ON OUR TWO EXCHANGES. WE, AGAIN HAD CONSIDERABLE SHORT COVERING BY OUR SPECS WITH THE GAIN IN PRICE AS WELL AS MASSIVE T.A.S. LIQUIDATION WHICH ACCOUNTS FOR THE STRONG GAIN ON THE TWO EXCHANGES. WE HAD ANOTHER STRONG SIZED 516 T.A.S ISSUANCE,

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 516 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS.IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1/2 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.72) AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS FROM THEIR PERCH AS WE DID HAVE A HUMONGOUS SIZED GAIN OF 181 CONTRACTS ON OUR TWO EXCHANGES WITH THE GAIN IN PRICE OF $0.72.

WE MUST HAVE HAD:

A HUGE SIZED 715 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 28.490 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE JUMP OF 255,000 OZ

//NEW STANDING FOR SILVER//JUNE IS THUS 30.340 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI GAIN //HUMONGOUS SIZED EFP ISSUANCE/ VI) HUGED SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 516 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL removed 67 CONTRACTS //

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY

TOTAL CONTRACTS for 9 DAYS, total 9147 contracts: OR 45.735 MILLION OZ (1016 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 45.735 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 45.735 MILLION OZ

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1166 CONTRACTS WITH OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 715 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JULY OF 28.496 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 255,000 OZ QUEUE JUMP WHERE THEY WILL TRY AND TAKE DELIVERY ON THIS SIDE OF THE POND.

//NEW TOTAL STANDING FOR JULY 30.340 MILLION OZ

WE HAVE A HUGE SIZED GAIN OF 18 OI CONTRACTS ON THE TWO EXCHANGES WITH THE GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG SIZED 516 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX TRADING/// WITH MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND ZERO LIQUIDATION OF LONGS.

THE NEW TAS ISSUANCE THURSDAY NIGHT (516) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 127 NOTICE(S) FILED TODAY FOR 0.635 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A MEGA HUGE SIZED 28,226 OI CONTRACTS TO 558,833 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 1866 CONTRACTS

WE HAD A HUGE SIZED INCREASE IN COMEX OI (28,226 CONTRACTS) OCCURRED WITH OUR HUGE GAIN OF $43.05 IN PRICE/THURSDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 7.5645 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 3500 OZ QUEUE JUMP

NEW STANDING 8.6818 TONNES

/ ALL OF THIS HAPPENED WITH OUR $43.05 GAIN IN PRICE WITH RESPECT TO THURSDAY’S TRADING. WE HAD A HUGE SIZED GAIN OF 30,986 OI CONTRACTS (96.38 PAPER TONNES) ON OUR TWO EXCHANGES.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2760 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 558,833

IN ESSENCE WE HAVE A MEGA HUGE SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 30,986 CONTRACTS WITH 28,226 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 2760 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 30,986 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): ANOTHER MEGA MEGA HUMONGOUS SIZED 43,273 CONTRACTS,,(4TH DAY IN A ROW OF THESE HUMONGOUS ISSUANCES)

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2760 CONTRACTS) ACCOMPANYING THE HUGE SIZED GAIN IN COMEX OI OF 28,226 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 30,986 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 7,5645 TONNES FOLLOWED BY TODAY’S 3500 OZ QUEUE JUMP

//NEW STANDING /JULY 8.6818 TONNES.

/ 3) HUGE T.A.S. LIQUIDATION OF CONTRACTS WITH ZERO NET LONG SPECS BEING CLIPPED,

4) HUGE SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///MEGA HUMONGOUS T.A.S. ISSUANCE: 43,273 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY. :

TOTAL EFP CONTRACTS ISSUED: 39,699 CONTRACTS OR 3,969,900 OZ OR 123.48 TONNES IN 9 TRADING DAY(S) AND THUS AVERAGING: 4411 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES 123.48 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 123.48 DIVIDED BY 3550 x 100% TONNES = 3.47% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 123.48 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUG), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A STRONG SIZED 1166 CONTRACTS OI TO 165,237 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 715 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 715 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 715 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1233 CONTRACTS AND ADD TO THE 715 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1881 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 9.740 MILLION OZ

OCCURRED WITH OUR HUGE $0.72 GAIN IN PRICE …..

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING/THURSDAY NIGHT

SHANGHAI CLOSED UP 0.91 PTS OR 0.03% //Hang Seng CLOSED UP 461.05 PTS OR 2.59% // Nikkei CLOSED DOWN 1003.34 OR 2.45%//Australia’s all ordinaries CLOSED UP 0.89%///Chinese yuan (ONSHORE) closed UP TO 7,2524 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2702/ Oil UP TO 83.32dollars per barrel for WTI and BRENT UP AT 85.85/Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A MEGA HUMONGOUS SIZED 28,226 CONTRACTS TO 558,833 WITH OUR GAIN IN PRICE OF $43.05 WITH RESPECT TO THURSDAY’S TRADING.

WE HAD A HUGE T.A.S. LIQUIDATION ON THURSDAY’S GAIN IN PRICE WITH ZERO LONGS BEING CLIPPED AND SOME ATTEMPTED SHORT COVERING.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE NON ACTIVE DELIVERY MONTH OF JULY.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 2760 EFP CONTRACTS WERE ISSUED: : AUGUST 2760 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2760 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A MEGA HUGE SIZED TOTAL OF 30,986 CONTRACTS IN THAT 2760 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A HUGE SIZED GAIN OF 28,226 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR HUGE GAIN IN PRICE OF $43.05/THURSDAY COMEX.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT WAS ANOTHER MEGA MEGA HUMONGOUS SIZED 43,273 CONTRACTS. (4TH DAY IN A ROW OF THIS TYPE OF MEGA ISSUANCE) MOST OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN YESTERDAY’S TRADING. TODAY’S ISSUANCE WAS ANOTHER WHOPPER.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JULY (8.6818 TONNES)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 8.6818 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $43.05 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A MEGA MEGA HUGE SIZED GAIN OF 32,853 CONTRACTS ON OUR TWO EXCHANGES ACCOMPANYING THE GAIN IN PRICE. THE T.A.S. ISSUED ON THUTSSDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 102.186 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY (7.5645 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 3500 OZ QUEUE JUMP//NEW STANDING 8.6818 TONNES

NEW STANDING FOR JULY: 8.6818 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $43.05

WE HAVE REMOVED 1866 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET GAIN ON THE TWO EXCHANGES 30,986 CONTRACTS OR 3,098,600 OZ (96.38 TONNES)

confirmed volume THURSDAY 411,105 contracts//huge

//speculators have left the gold arena

JULY 12 JULY GOLD CONTRACT

/ /// THE JULY 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | NIL oz . |

| Deposit to the Dealer Inventory in oz | |

| Deposits to the Customer Inventory, in oz | nil OZ |

| No of oz served (contracts) today | 37 notice(s) 3700 OZ 0.1150 TONNES |

| No of oz to be served (notices) | 31 contracts 3100 OZ 0.0964 TONNES |

| Total monthly oz gold served (contracts) so far this month | 2760 notices 276,000 oz 8.5847 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: nil oz

we have 0 customer deposit:

total deposit: nil oz

customer withdrawals: 0

TOTAL WITHDRAWALS NIL

Adjustment 1 DEALER TO CUSTOMER BRINKS: 25,174.233 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY

For the front month of JULY we have an oi of 68 contracts having GAINED 34 contracts. We had 1 notices filed on Thursday so we gained 35 contracts or an additional 3500 oz will stand at the comex (0.1088 tonnes)

AUGUST lost 6187 CONTRACTS DOWN TO 286,158 CONTRACTS

SEPT. GAINED 86 CONTRACTS TO STAND AT 317.

OCTOBER GAINED 2776 CONTRACTS UP TO 33,256 CONTRACTS

We had 37 contracts filed for today representing 3700 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 10 notices were issued from their client or customer account. The total of all issuance by all participants equate to 37 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for July /2024. contract month, we take the total number of notices filed so far for the month (2760) x 100 oz ) to which we add the difference between the open interest for the front month of JULY 68( CONTRACTS) minus the number of notices served upon today (37 x 100 oz per contract( equals 279,100 OZ OR 8.6818 TONNES.

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (2760 x 100 oz +we add the difference for front month of JULY (68 X// , OI} minus the number of notices served upon today (37) x 100 oz which equals 279,100 oz (8.6818TONNES)

TOTAL COMEX GOLD STANDING FOR JULY: 8.5723 TONNES WHICH IS HUGE FOR THIS NOT VERY ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,679,117.861 oz 52.22 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,699,809.610 OZ

TOTAL REGISTERED GOLD 7,790,633.975 ( 242.32 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,909,175.635 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,111,516oz (REG GOLD- PLEDGED GOLD)= 190.20 tonnes //

END

SILVER/COMEX

JULY 12/2024

INITIAL

//2024// THE JULY 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 614,539.753oz ASAHI Delaware . |

| Deposits to the Dealer Inventory | |

| Deposits to the Customer Inventory | 2,411,830.632 oz Brinks CNT JPMorgan |

| No of oz served today (contracts) | 127 CONTRACT(S) (.635 million OZ) |

| No of oz to be served (notices) | 113 contracts (0.565 million oz) |

| Total monthly oz silver served (contracts) | 5955 Contracts (29.775 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit/

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 3 customer deposits:

i)Into Brinks 1,214,181.542 oz

ii) Into CNT 600,903.390 oz

iii) Into JPMorgan: 596,745.700 oz

total customer deposit 2,411,830.632 oz

JPMorgan has a total silver weight: 130.184million oz/302,953million or 43.52%

adjustment: 1 dealer to customer

i) CNT 9977.780 oz

i) into eligible 3342,544.630 oz acct error

customer withdrawals: 2

i) out of Delaware 596,486.241 oz

ii) out of Ashai: 596,745.700 oz

iii) Out of Delaware 12,794.053 0z

iv) Out of HSBC 90,183.930 oz

total withdrawal: 614m539.753 0z

TOTAL REGISTERED SILVER: 69.350 MILLION OZ//.TOTAL REG + ELIGIBLE. 302.943

million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF JULY/2024 OI: 240 CONTRACTS HAVING LOST 24 CONTRACT(S). WE HAD 75 NOTICES FILED ON THURSDAY SO WE GAINED 51 CONTRACTS OR AN ADDITIONAL 255,000 OZ WILL STAND AT THE COMEX VIA A QUEUE JUMP TO TAKE DELIVERY OVER HERE.

AUG, SAW A LOSS OF 75 CONTRACTS TO 1274

SEPT SAW A GAIN OF 394 CONTRACTS TO 132,409

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 127 for 0.635 MILLION oz

CONFIRMED volume; ON THURSDAY 84,952 huge

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 5955 x 5,000 oz = 29.775 MILLION oz

to which we add the difference between the open interest for the front month of JULY( 240) and the number of notices served upon today 127 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY/2024 contract month: 5955 notices served so far) x 5000 oz + OI for the front month of JULY (240)x number of notices served upon today minus (127)x 5000 oz of silver standing for the JULY contract month equates to 30.340 MILLION OZ.

New total standing: 30.340 million oz.

There are 69.360 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

JULY 12 WITH GOLD DOWN $0.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 835.09 TONNES

JULY 11 WITH GOLD UP $43.05 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;:INVENTORY RESTS AT 833.37 TONNES

JULY 10 WITH GOLD UP $12.00 ON THE DAY; HUUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.44 TONNES OF GOLD VAPOUR FROM THE GLD//.//:INVENTORY RESTS AT 833.37 TONNES

JULY 9 WITH GOLD UP $5.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD.//:INVENTORY RESTS AT 834.81 TONNES

JULY 8 WITH GOLD DOWN $26.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD.//:INVENTORY RESTS AT 834.81 TONNES

JULY 5 WITH GOLD UP $29.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD..A DEPOSIT OF 1.10 TONNES OF GOLD VAPOUR INTO THE GLD//:INVENTORY RESTS AT 833.37 TONNES

JULY 3 WITH GOLD UP $35.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD..A MASSIVE DEPOSIT OF 5.76 TONNES OF GOLD VAPOUR INTO THE GLD//:INVENTORY RESTS AT 833.37 TONNES

JULY 2 WITH GOLD DOWN $4.45 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD../:INVENTORY RESTS AT 827.61 TONNES

JULY 1 WITH GOLD DOWN $.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 28 WITH GOLD UP $3.80 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 27 WITH GOLD DOWN $16.95 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 26 WITH GOLD UP $23.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 25 WITH GOLD DOWN $13.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A STRONG WITHDRAWAL OF 2.88 TONNES OF GOLD FROM THE GLD INVENTORY RESTS AT 829.05 TONNES

JUNE 24 WITH GOLD UP$14.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A STRONG WITHDRAWAL OF 1.72 TONNES OF GOLD/NEW TOTAL TONIGHT 831.93 TONNES

JUNE 21 WITH GOLD DOWN $37.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A MAMMOTH 8.34 TONNES OF GOLD VAPOUR DEPOSIT/NEW TOTAL TONIGHT 833.65 TONNES

JUNE 20 WITH GOLD UP $23.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/://NEW TOTAL TONIGHT 825.31 TONNES

JUNE 18 WITH GOLD UP $17.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/://NEW TOTAL TONIGHT 825.31 TONNES

JUNE 17 WITH GOLD DOWN $18.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.03 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 825.31 TONNES

JUNE 13 WITH GOLD DOWN$35.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.89 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 830.78 TONNES

JUNE 12 WITH GOLD UP $28.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/: /A WITHDRAWAL OF 4.89 TONNES OF GOLD FROM THE GLD////NEW TOTAL TONIGHT 830.78 TONNES

JUNE 11 WITH GOLD DOWN $0.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 10 WITH GOLD UP $2,00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD//: / //NEW TOTAL TONIGHT 835.67 TONNES

JUNE 7 WITH GOLD DOWN $64.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 3.56 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 837.11 TONNES

JUNE 6 WITH GOLD UP $16.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD A DEPOSIT OF 1.34 TONNES OF GOLD INTO THE GLD//: / //NEW TOTAL TONIGHT 833.55 TONNES

JUNE 5 WITH GOLD UP $32.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 4 WITH GOLD DOWN $20.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

JUNE 3 WITH GOLD UP $22.85 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 31 WITH GOLD DOWN $19.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 30 WITH GOLD UP $3.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 29 WITH GOLD DOWN $13.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD: / //NEW TOTAL TONIGHT 832.21 TONNES

MAY 28 WITH GOLD UP $22.00 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD// //NEW TOTAL TONIGHT 832.21 TONNES

GLD INVENTORY: 835.09 TONNES, TONIGHTS TOTAL

SILVER

JULY 12. WITH SILVER DOWN $.65 CENTS//NO CHANGES IN SILVER INVENTORY /INVENTORY REMAINS CONSTANT AT 435.625 MILLION OZ.

JULY 11. WITH SILVER UP $.72 CENTS//HUGE CHANGES IN SILVER INVENTORY A WITHDRAWAL OF 0.731 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 435.625 MILLION OZ.

JULY 10. WITH SILVER DOWN $.04 CENTS//HUGE CHANGES IN SILVER INVENTORY A MAMMOTH WITHDRAWAL OF 3.744 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 436.356 MILLION OZ.

JULY 9. WITH SILVER UP 13 CENTS//HUGE CHANGES IN SILVER INVENTORY A MAMMOTH WITHDRAWAL OF 3.744 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 436.356 MILLION OZ.

JULY 8. WITH SILVER DOWN $0.73//SMALL CHANGES IN SILVER INVENTORY A MAMMOTH DEPOSIT OF 3,292,000 OZ OF SILVER VAPOUR INTO THE SLV.: /INVENTORY RISES T0 440.100 MILLION OZ.

JULY 4. WITH SILVER UP $0.85//SMALL CHANGES IN SILVER INVENTORY A MAMMOTH DEPOSIT OF 3,292,000 OZ OF SILVER VAPOUR INTO THE SLV.: /INVENTORY RISES T0 440.100 MILLION OZ.

JULY 3. WITH SILVER UP $1.08//SMALL CHANGES IN SILVER INVENTORY A SMALL WITHDRAWAL OF 639,000 OZ: /INVENTORY LOWERS T0 436,808 MILLION OZ.

JULY 2. WITH SILVER UP $0.19//NO CHANGES IN SILVER INVENTORY: /INVENTORY REMAINS AT 437.447 MILLION OZ./

JULY 1. WITH SILVER UP $0.05//XXX CHANGES IN SILVER INVENTORY: A DEPOSIT OF 182,000 OZ OF SILVER INTO THE SLV./.// /INVENTORY RISES AT 437.447 MILLION OZ./

JUNE 28. WITH SILVER UP $0.27//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 913,000 OZ FROM THE SLV./.// /INVENTORY REMAINS AT 437.265 MILLION OZ./

JUNE 27. WITH SILVER UP $0.01//NO CHANGES IN SILVER INVENTORY: .// /INVENTORY REMAINS AT 438.178 MILLION OZ.//

JUNE 26. WITH SILVER UP $0.03//HUGE CHANGES IN SILVER INVENTORY: A HUGE WITHDRAWAL OF 2.512 MILLION OZ OF SILVER FROM THE SLV.// /INVENTORY FALLS TO 438.178 MILLION OZ.//

JUNE 25. WITH SILVER DOWN $0.63//HUGE CHANGES IN SILVER INVENTORY: A MAMMOTH DEPOSIT OF 7.835 MILLION OZ OF SILVER VAPOUR INTO THE SLV.// /INVENTORY RISE TO 440.69 MILLION OZ.//WHAT AN ABSOLUTE FRAUD.

JUNE 24. WITH SILVER DOWN $0.05//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 2.104 MILLION OZ FROM THE SLV.// /INVENTORY LOWERS TO 432.835 MILLION OZ.

JUNE 21. WITH SILVER DOWN $1.15//NO CHANGES IN SILVER INVENTORY’// /INVENTORY REMAINS AT 434.935 MILLION OZ.

JUNE 20. WITH SILVER UP $1.17//HUGE CHANGES IN SILVER INVENTORY’ A DEPOSIT OF 5.164 MILLION OZ INTO THE SLV/// /INVENTORY RISES TO 434.929 MILLION OZ.

JUNE 18. WITH SILVER UP $0.21//NOCHANGES IN SILVER INVENTORY’ A WITHDRAWAL .730 MILLION OZ INTO THE SLV/// /INVENTORY FALLS TO 429.775 MILLION OZ.

JUNE 17. WITH SILVER UP $0.21//SMALL CHANGES IN SILVER INVENTORY’ A WITHDRAWAL .730 MILLION OZ INTO THE SLV/// /INVENTORY FALLS TO 429.775 MILLION OZ.

JUNE 14. WITH SILVER DOWN $0.10//NO CHANGES IN SILVER INVENTORY/ /INVENTORY REMAINS AT 429.083 TONNES

JUNE 13. WITH SILVER DOWN $1.10//HUGE CHANGES IN SILVER INVENTORY/ A HUGE DEPOSIT OF 1.958 MILLION OZ/INVENTORY RISES TO 429.083 TONNES

JUNE 12 WITH SILVER UP $0.97 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 5.983 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 427.125 MILLION OZ

JUNE 11 WITH SILVER DOWN $0.59 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.644 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 422.786 MILLION OZ

JUNE 10 WITH SILVER UP $0.30 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 3.198 MILLION OZ INTO THE SLV// INVENTORY RISES TO ; 421.142 MILLION OZ

JUNE 7 WITH SILVER DOWN $1.93 TODAY: NO CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY AT 417.944 MILLION OZ

JUNE 6 WITH SILVER UP $1.27 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 2.649 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 417.944 MILLION OZ

JUNE 5 WITH SILVER UP 0.38 TODAY: HUGE CHANGES IN SILVER INVENTORY: //A HUGE DEPOSIT OF 1.52 MILLION OZ INTO THE SLV// INVENTORY INCREASES TO 415.295 MILLION OZ

JUNE 4 WITH SILVER DOWN $1.08 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

JUNE 3 WITH SILVER UP $0.35 TODAY: NO CHANGES IN SILVER INVENTORY: //INVENTORY REMAINS AT 413.775 MILLION OZ

MAY 31 WITH SILVER DOWN $1.09 TODAY: HUGE CHANGES IN SILVER INVENTORY: A MASSIVE WITHDRAWAL OF 3.655 MILLION OZ FROM THE SLV//INVENTORY LOWERS TO 413.775 MILLION OZ

MAY 30 WITH SILVER DOWN $0.80 TODAY: NO CHANGES IN SILVER INVENTORY//INVENTORY REMAINS AT 417.430 MILLION OZ

MAY 29 WITH SILVER UP $0.20 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 1.051 MILLION OZ INTO THE SLV//INVENTORY DECREASES TO 417.430 MILLION OZ

MAY 28 WITH SILVER UP $1.64 TODAY: HUGE CHANGES IN SILVER INVENTORY AT THE SLV// A HUGE WITHDRAWAL OF 2.832 MILLION OZ INTO THE SLV//INVENTORY INCREASES TO 418.481 MILLION OZ

CLOSING INVENTORY 435.625 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

Is It Time To Get Bullish On Platinum?

THURSDAY, JUL 11, 2024 – 10:20 PM

Authored by Mike Maharrey via Money Metals,

Is now a good time to get bullish on platinum?

I’ve written a lot about the fact that silver appears to be underpriced given both technical factors and the supply and demand dynamics.

Platinum may be even more undervalued.

The current platinum price is hovering around $1,000 an ounce. To put that into perspective, platinum hit an all-time high of $2,213 an ounce in March 2008. This was higher than the record price gold hit in 2011.

One of the factors driving that 2008 record was a severe supply shortage due to a power crisis and labor strikes in South Africa, the world’s leading platinum producer.

Before 2011, platinum was generally more expensive than gold. In 2015, this historical trend reversed with the spread between gold and platinum growing wider.

But over the last two years, platinum has shown signs of life. In 2023, the platinum price was up a healthy 12.5 percent. So far this year, the metal has charted modest gains of about 3.8 percent.

Platinum has a long way to go to regain its historic parity with gold, but supply and demand dynamics indicate there is plenty of room for platinum to push higher.

Like silver, we’re seeing significant supply deficits in the platinum market. In 2023, there was a market deficit of over 100 million ounces, according to the World Platinum Investment Council. This was due to a combination of increasing demand and lagging mine output.

The supply shortfall continued into the first quarter of 2024.

According to the WPIC, total platinum supply in Q1 was the second lowest since the organization started tracking data.

As a result, the market deficit in Q1 came in at 369,000 ounces.

Platinum is an important component in automobile catalytic converters. Auto demand for the metal hit a 7-year high in Q1 and that pace is expected to continue through the rest of the year.

A rotation from electric vehicles to hybrids is boosting demand for platinum in the auto sector, according to the WPIC.

“Platinum demand is bolstered by stricter emissions legislation, increased hybrid vehicles that contain an internal combustion engine, and growth in the substitution of platinum for palladium. It is important to note that once platinum is substituted for palladium in specific vehicle platforms, this demand for platinum is likely to remain constant throughout the platform’s seven-year lifecycle, even if platinum prices rise to, or exceed, those of palladium for an extended period.”

Platinum jewelry demand also saw a healthy increase in the first quarter, rising by 5 percent year-on-year, driven by a 53 percent increase in Indian jewelry buying.

Overall industrial demand fell slightly from a record in 2023 but remained 17 percent above the pre-COVID average.

Investment demand is also on a positive track upward this year, supported by coin and bar purchases in China.

According to the WPIC, China’s retail investment in platinum is forecast to exhibit double-digit growth this year, driven by perceptions of the metal being undervalued relative to gold.

There is also a growing demand for platinum in the fast-growing hydrogen power sector.

“We are now seeing signs that platinum’s role in the hydrogen economy is gaining momentum, with our forecast for 2024 indicating a significant increase in demand to meaningful levels. This year will also witness the allocation and deployment of over US$300 billion in tax incentives and subsidies from various governments around the world, potentially further accelerating hydrogen’s demand for platinum,” WPIC CEO Trevor Raymond said.

Looking ahead, the WPIC projects supply will remain flat even with the weak levels seen last year. Mine supply is expected to fall by about 3 percent offset somewhat by a rebound in recycling. But with demand expected to come in at a “robust” 7.6 million ounces, the WPIC projects a 476,000-ounce market deficit.

“For the second consecutive year, the platinum market will post a meaningful deficit underscored by platinum’s sustained demand and supply vulnerability amidst global economic challenges. While we currently forecast a deficit of 476 koz, it is worth mentioning that a revision to the bar and coin investment series, based on new field research and information, could mean this deficit is potentially deeper,” Raymond said.

Above-ground stocks are forecast to decline for the second straight year, falling another 12 percent. This would mark a 4-year low in above-ground platinum supply.

Meanwhile, China is set to launch its first platinum futures contracts.

According to the South China Morning Post, the Guangzhou Futures Exchange (GFEX) “will be the first exchange to allow delivery against its contracts of platinum and palladium in a form used by the main consumers, including carmakers and other industrial sectors, and the contracts may also support platinum investment demand in China.”

According to the report, investors will be able to take delivery of platinum in both ingots and “sponge” – pure metal in powder form.

“The ability to take delivery of sponge could be transformative for industrial users of PGMs, as well as carmakers, as this is the main form typically used for their manufacturing purposes,” the WPIC said.

According to a WPIC statement, the GFEX futures will allow platinum jewelry and investment product fabricators to hedge price risk. This could reduce premiums and reduce the discount on platinum buyback, making platinum a more attractive investment.

It remains to be seen whether platinum will regain the price parity with gold we saw before the mid-2010s, but given the supply and demand dynamics, it is reasonable to be bullish on platinum in the near to mid-term. Given the price disparity with gold, this may signal a buying opportunity.

end

Gold-Silver Ratio Could Indicate The Early Stages Of A Silver Breakout

FRIDAY, JUL 12, 2024 – 07:20 AM

Authored by Mike Maharrey via Money Metals,

Two months ago, the gold-silver ratio broke an important support level, indicating the white metal could be in the early stages of closing its gap with gold.

The gold-silver ratio indicates how many ounces of silver it takes to buy one ounce of gold given the spot price of both metals. In other words, it tells you the price of gold in ounces of silver.

The current gold-silver ratio is hovering just about 76-1. That means it takes 76 ounces of silver to buy one ounce of gold.

The ratio remains historically high, meaning that silver is underpriced compared to gold, but there is some indication the trend is in the early stages of reversing.

In the modern era, the gold-silver ratio has averaged between 40-1 and 60-1. When the gold-silver ratio gets far above the high end of that historical average, it tends to return to the mean with a vengeance.

For instance, in 2020, the gold-silver ratio set a record of 123-1 as Covid hysteria gripped the world and then plunged to around 60-1 as central banks around the world cranked up the money creation machine to cope with governments shutting down economies.

In another example of this snap-back, the gold-silver ratio fell to 30-1 in 2011 after rising to over 80-1 during the money creation of the Great Recession in the wake of the 2008 financial crisis.

Three months ago, the gold-silver ratio climbed as high as 87-1. Two months ago, the ratio fell to around 73-1, below the 13-year support level. It briefly rallied, climbing back to 80-1, but it failed to regain 13-year support before dipping over the last five days to the current level.

Given that the scenario still looks bullish for gold with the likelihood of a rate hike this fall increasing, silver could be set up for a significant bull run.

Keep in mind that silver historically outperforms gold in a gold bull market. For instance, gold charted a gain of around 40 percent during the pandemic. Meanwhile, silver was up a whopping 141 percent!

The recent breakdown of the support level in the gold-silver ratio takes on more significance given the fundamentals. Demand for the metal is at record levels while supply has flatlined.

Silver demand is expected to hit 1.2 billion ounces this year. That would rank as the second-highest annual silver demand on record. Given the supply outlook, this level of demand would create a structural market deficit of 176 million ounces. That would be the fourth consecutive year of demand outstripping supply, cutting further into global silver reserves.

The structural deficit in 2023 came in at 184.3 million ounces.

Demand will likely increase in the years ahead due to the solar energy market. Not only is the demand for silver panels growing, but the amount of silver used in each panel is also increasing.

According to a research paper by scientists at the University of New South Wales, solar manufacturers will likely require over 20 percent of the current annual silver supply by 2027. By 2050, solar panel production will use approximately 85–98 percent of the current global silver reserves.

Given both the supply and demand fundamentals and the technical breakdown in the gold-silver ratio, this may be an outstanding time to buy silver in the early stages of a bull run.

END

Biden’s Student Loan Plan “SAVE” Will Cost $230 Billion

FRIDAY, JUL 12, 2024 – 03:25 PM

As student loan debt in America swells to a staggering $1.7 trillion, President Joe Biden’s new SAVE plan could actually cost $230 billion, a CBO report finds. This is not only a classic case of robbing Peter to pay Paul — it will bring more inflation, make college more expensive and give the federal government unprecedented control over higher education.

The following article was originally published by the Mises Institute. The opinions expressed do not necessarily reflect those of Peter Schiff or SchiffGold.

The federal student debt loan amount is $1.7 trillion. This debt portfolio is an installment personal loan. Payments occur monthly. Active students have loan totals not due this year. We have no idea how much of the total will be repaid.

The Saving on a Valuable Education (SAVE) plan is President Joe Biden and Secretary of Education Miguel Cardona’s reply to the Supreme Court, who ruled the administration’s original sweeping forgiveness program was unconstitutional. The SAVE plan was announced in August 2023. The White House bulletin included a table of payment amounts, indexed by the number of dependents and size of loan.

It is the greatest gift for all income-dependent student-debt payoff plans. It is a Trojan horse for the state to control higher education.

The “original” student loan program from the sixties repaid loans plus interest in a straightforward installment-style plan. A $7,500 loan might take ten years to fulfill. Larger loans received longer terms.

The federal government’s interjection into debt financing came with the Income-Contingent Repayment plan, passed in the 1993 Student Loan Reform Act signed by then-president Bill Clinton. The Student Loan Reform Act set payments at 20 percent of discretionary income. After twenty-five years of eligible payments, the plan writes off any outstanding debt. This was the first signal that the plans anticipated partial payments on student loans.

The slide toward free university accelerated in 2007 with income-based repayment. Monthly payments were calculated on what a student could pay, not what was owed, resetting Income-Contingent Repayment plan payments from 20 percent of income to 10 percent or 15 percent of discretionary income depending on the date the borrower first started borrowing student loans.

In 2010, President Barack Obama signed the Health Care and Education Reconciliation Act of 2010. Both the lending and collecting of loans was consolidated within the Department of Education (DOEd). This act nationalized the student loan process, putting it in the hands of political appointees, managed by an unprepared, non-banking-experienced staff. In 2010, student loan debt was half the 2023 total.

Income-dependent payback plans describe the four remaining options for paying student loans. SAVE is a new income-dependent plan. There are four common elements to all income-dependent plans.

Published poverty wages:

Poverty wages are deducted from adjusted gross income to produce “discretionary income.” Early plans deducted 100 percent of poverty wages. In the Affordable Care Act of 2010, poverty wage deductions became 150 percent. Later, the DOEd increased the multiplier to 200 percent. SAVE uses 225 percent of poverty wages.

Payment percentage:

Discretionary income is assessed by a fixed percentage to create a payment due. The original plan from 1993 used 20 percent of discretionary income. This changed to 15 percent of discretionary income in 2007. President (“I have my phone and a pen”) Obama issued a presidential memorandum reducing it from 15 percent to 10 percent.

Length of loan and unpaid balances:

If there is an unbroken record of payments, unpaid balances at the end of a loan term are forgiven. The DOEd waved the surrender flag for taxpayers. All loans will not be paid back to the Treasury.

Special status:

Most recently, the DOEd forgave the administration recently using extralegal authority for 1.5 million debtors with $28 billion in debts that were expunged by a department ruling of “substantial misconduct” by colleges that closed early. $45.7 billion was zeroed out by reclassifying 662,000 public service workers. This type of skullduggery is easier in the SAVE plan.

SAVE uses 225 percent of poverty wages as a deduction to reduce the subjective discretionary income. This reduced discretionary income uses a 5 percent calculation to create a payment due. The smallest amount of discretionary income assesses at the smallest percentage as calculated by the White House.

The SAVE plan is not eligible for loans in default. However, a phone call to the DOEd and enrollment in the “Fresh Start” program makes previously ineligible loans available for SAVE. Student payments that are seventy-five days delinquent will automatically enroll in the SAVE program. This can start the delinquency clock on loans greater than 270 days, erasing the record from credit reports. SAVE will eventually bring all loan payments under one process and one department, directed by the president.

We cannot be certain of the ultimate costs. With appropriate disclaimers (for static budgeting with hyperdynamic plans), the Congressional Budget Office suggests that the cost of implementing SAVE could cost $230 billion. Based on a five-year-old study, just under half of all student debt is estimated to be on income-dependent plans. The current number is likely greater based on trends. These plans have variable monthly payments during the term and have a forgiveness option, making any predictions of a final cost speculative. These plans are continually in flux. Any estimate of cost is a guess, more so after covid.

SAVE has legal challenges from attorney generals from three states. This challenge is not creating headlines. Without an injunction or congressional action, the plan would be initiated in July 2024. In June, twenty-five courts in Kansas and Missouri blocked further enrollment in the SAVE plan.

The SAVE plan fits the long-term goal of increased federal control of public higher education. The president can manipulate the plan to modify payments for a population demographic such as “dreamers” or for a major employment segment such as green energy ambassadors.

The courts’ challenge to this plan must succeed. We need a pause for a better fix on the actual debt. Both political parties have mismanaged this program. There are responsible measures in Congress to bring forward to cap this vote-buying scheme and protect taxpayers.

END

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY

3.CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES

4. GOLD PODCASTS//LIVE FROM THE VAULT EP. 181

Episode 181

Posted 12th July 2024

China’s Covert Golden War Chest

In this week’s episode of Live from the Vault, Andrew Maguire addresses the community’s burning questions, offering unmatched insights into the short-term market movements and the hidden forces shaping the precious metals landscape.

The renowned London whistleblower guides listeners through China’s covert manoeuvres influencing the price of gold, concluding with a forecast of silver’s potential for a significant rally, as we enter Q3.

Andrew Maguire

Host

Andrew Maguire has almost 50 years’ experience working in the precious metals industry as an independent Loco London metals trader and analyst, where he has provided Precious Metals Advisory and Trading services for international hedge fund managers, bullion banks, directors, metal traders and many of the largest global institutions.

Andrew has built strong relationships with US and UK regulatory bodies, having worked as an advisor for the Commodity Futures Trading Commission, (CFTC) and the Department of Justice, (DOJ). In the UK, Andrew is currently providing advisory services to the UK and the Financial Conduct Authority, (FCA).

For You

China’s Covert Golden War Chest – LFTV Ep 181

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COCOA

ASIA TRADING//FRIDAY MORNING/THURSDAY NIGHT

SHANGHAI CLOSED UP 0.91 PTS OR 0.03% //Hang Seng CLOSED UP 461.05 PTS OR 2.59% // Nikkei CLOSED DOWN 1003.34 OR 2.45%//Australia’s all ordinaries CLOSED UP 0.89%///Chinese yuan (ONSHORE) closed UP TO 7,2524 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2702/ Oil UP TO 83.32dollars per barrel for WTI and BRENT UP AT 85.85/Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2524

OFFSHORE YUAN: UP TO 7.2702

SHANGHAI CLOSED UP 0.91 PTS OR 0.03 %

HANG SENG CLOSED UP 461.05 PTS OR 2.59%

2. Nikkei closed DOWN 1003.34 PTS OR 2.45%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 104.00 EURO RISES TO 1.0890 UP 16 BASIS PTS

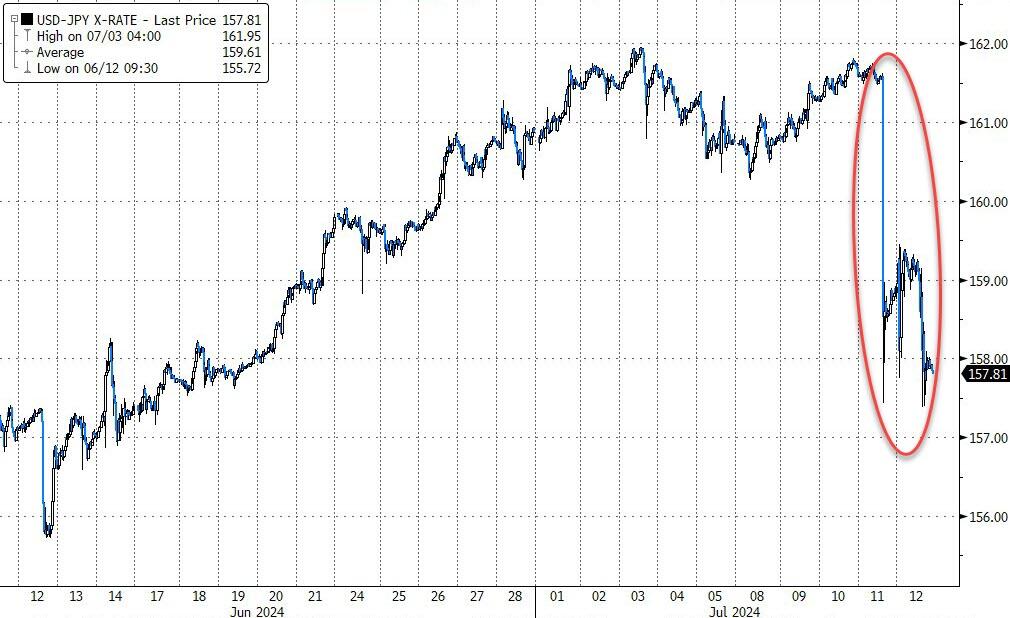

3b Japan 10 YR bond yield: RISES TO. +1,084 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 159.06 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.5060/Italian 10 Yr bond yield DOWN to 3.8080 SPAIN 10 YR BOND YIELD DOWN TO 3.269%

3i Greek 10 year bond yield DOWN TO 3.468

3j Gold at $2402.70//Silver at: 30.73 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 30/ 100 roubles/dollar; ROUBLE AT 87.69

3m oil into the 83 dollar handle for WTI and 85 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 159.06/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.084% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8956 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9755 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.217 UP 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.425 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.626 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 33.03…

10 YR UK BOND YIELD: 4.175 UP 9 PTS

2a New York OPENING REPORT

.Futures Flat After Hot PPI, Mixed Bank Earnings

FRIDAY, JUL 12, 2024 – 09:02 AM

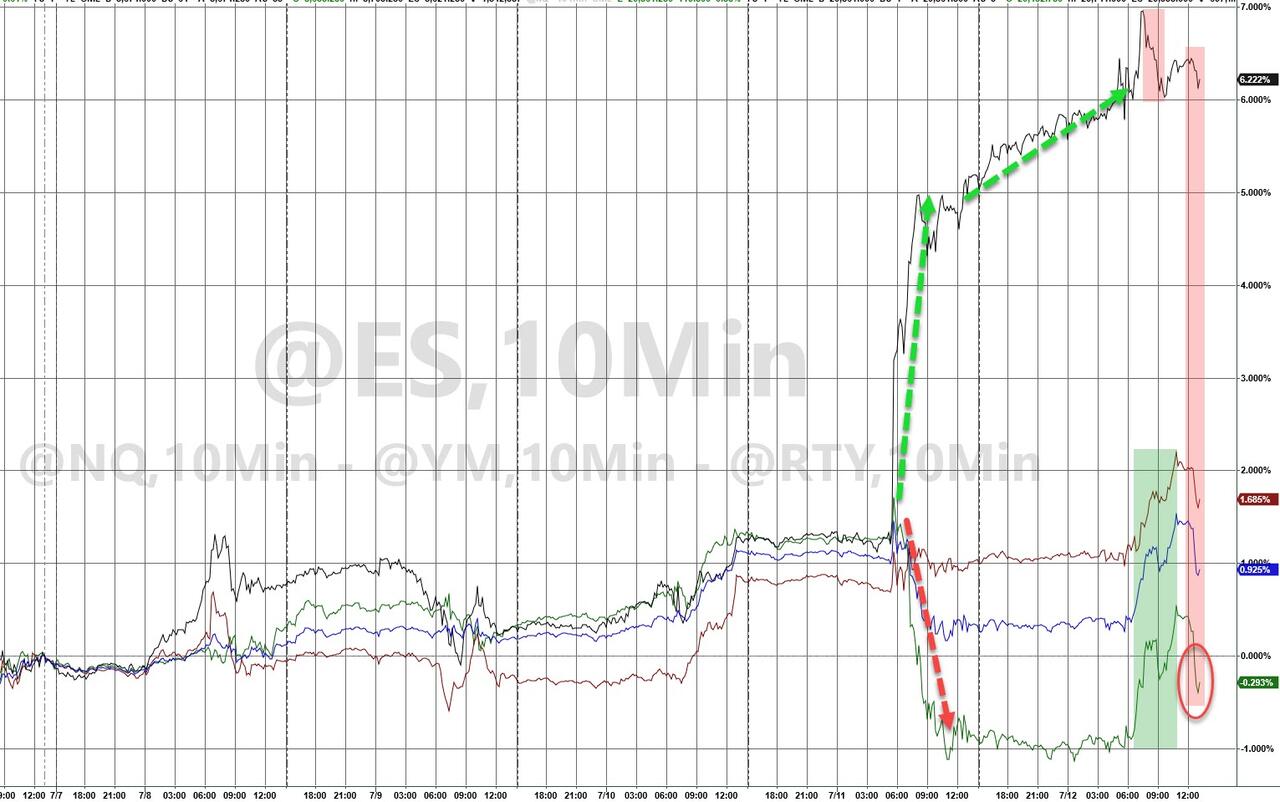

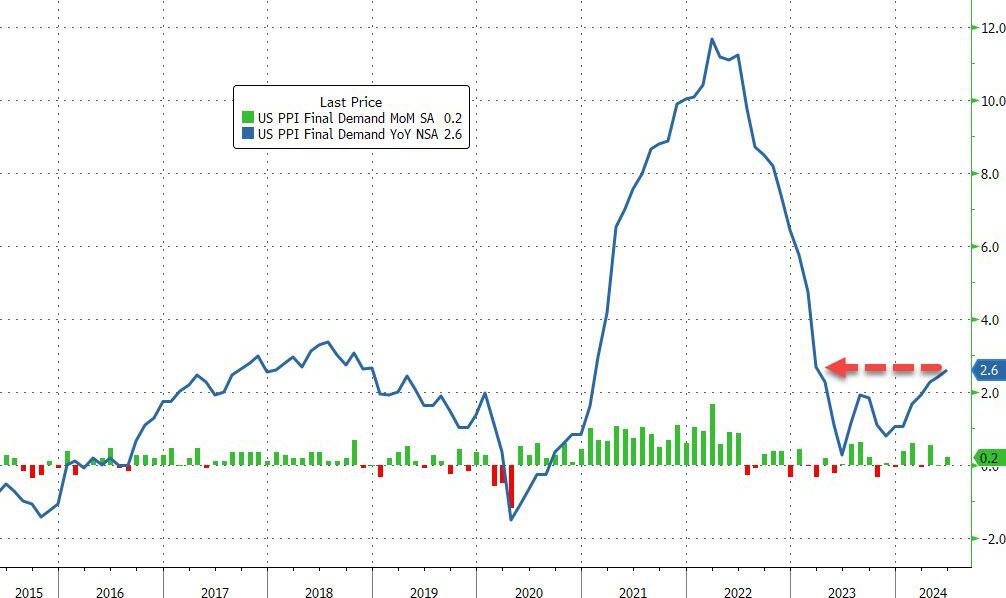

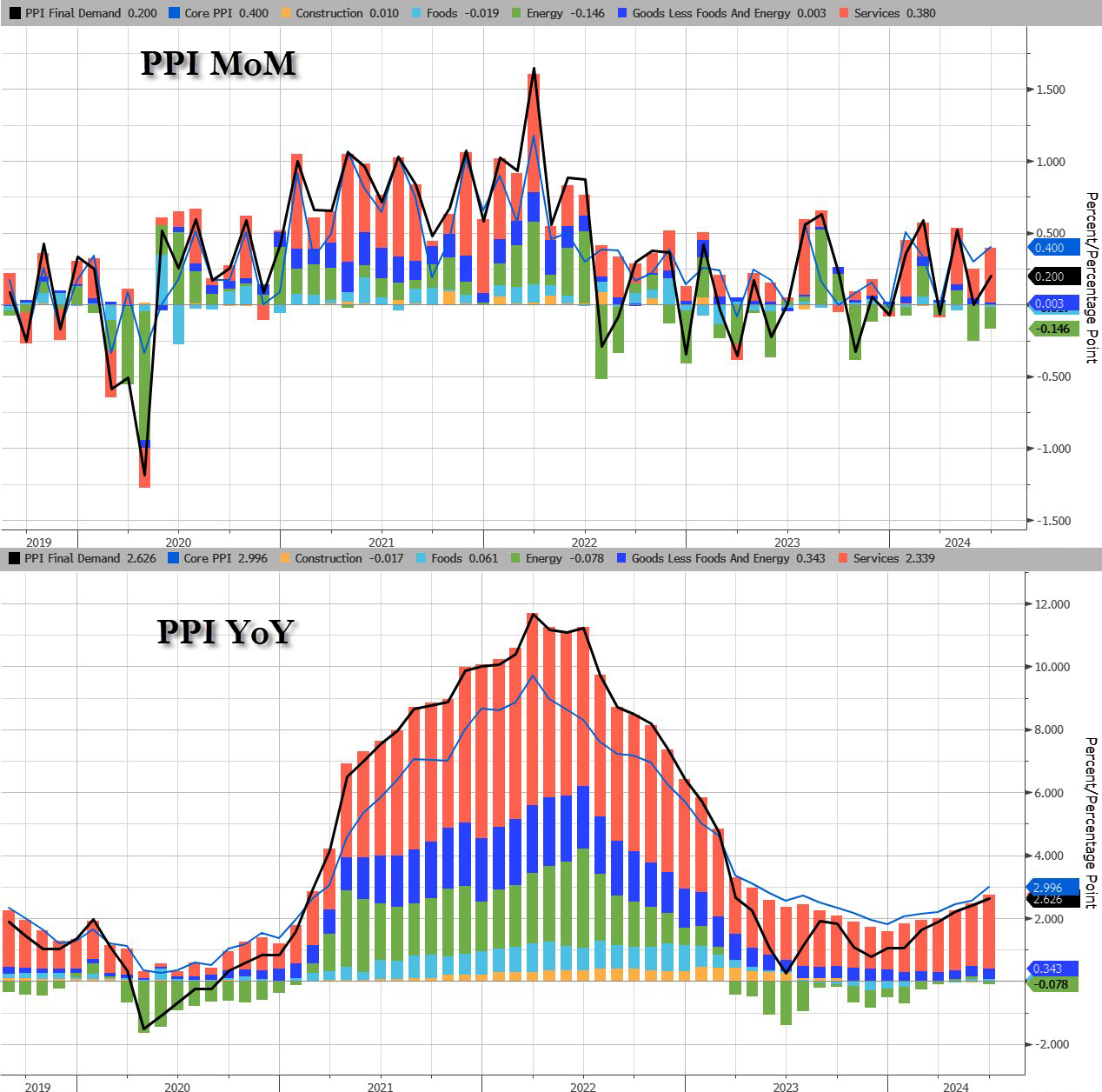

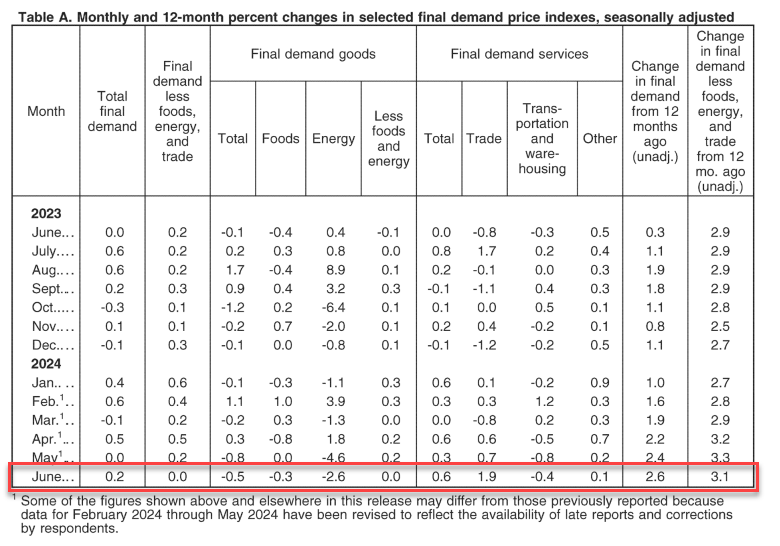

US equity futures are flat, erasing a modest earlier gain, as yesterday’s rotation continues this morning with RTY rallying +0.8% pre-mkt even as megacap tech stocks are higher (NVDA +93bp, AAPL +39bp, AMZN +19bp). As of 8:45am, S&P futures were little changed after the index fell almost 1% in the previous session. The yield on 10-year Treasuries was unchanged at 4.21% and the USD is lower despite a PPI report that came in hotter than expected. Commodities are mixed: oil is higher, base metals are lower. Today, the key focus will be PPI (which beat across the board) and banks earnings (which were mixed).

In premarket trading, Wells Fargo sank 5% after warning it won’t be able to whittle away costs as fast as forecast amid higher-than-expected expenses. JPMorgan swung between gains and losses after reporting record profit, while missing on a few key metrics, like net interest income. Citigroup climbed 3% as equity trading beat estimates even as the lender said costs for the year are likely to be at the high end of the range previously provided. Here are some other notable premarket movers:

- Tesla dropped 1% after UBS cut its rating on the electric-vehicle maker to sell, saying the stock has rallied “too much, too soon.”

- Array Technologies gains 5% after Citi raised the solar tracking equipment company to buy, touting its growth potential.

- AT&T slips 2% as the company suffered a massive hack of customer data — separate from one reported earlier this year — that included records of calls and texts for nearly all of its mobile-phone users for a six-month period in 2022.

- Bally’s ticks 1% higher after securing a funding commitment from Gaming and Leisure Properties.

- JPMorgan falls 1% despite investment banking revenue beating estimates. CEO Jamie Dimon said while there has been some progress, inflation and rates may stay higher than expected.

US producer prices climbed in June more than forecast as a pickup in margins at service providers more than offset declines in the cost of goods. Investors are also eager to hear from the largest banks about the state of the US economy and expectations for the rest of the year, including the potential impact of the presidential elections in November.

In Europe, the Stoxx 600 is up 0.2% – rising for a third day – led by gains in energy and consumer product shares. Here are the biggest movers Friday:

- Ericsson shares rise as much as 9.3% to the highest since September 2022 after the company reported stronger-than-expected sales, in part thanks to a growth revival in the key US market

- Addtech advances as much as 13%, the most since 2021 and to a record high, with DNB seeing a “solid” 1Q report from the Swedish industrial technology group, with net sales 4% ahead

- Lifco shares jump as much as 12% to hit a new record high after the maker of dental equipment, machinery and tools reported quarterly net sales above expectations in the second quarter

- Norwegian Air shares rise as much as 8.2% after 2Q Ebit surpassed expectations, leading analysts to predict upgrades to consensus forecasts, with DNB describing the report as “slightly postitive”

- Elkem shares jump as much as 11%, the most since July 2022, after the Norwegian silicon maker reported Ebitda for the second quarter that beat the average analyst estimate

- BFF Bank jumps as much as 14% to touch a two-month high after the Italian lender reported an increase in its past due exposures and risk-weighted assets, following a credit reclassification

- Volkswagen gains as much as 1% as Redburn raises its recommendation to neutral, saying the firm faces less exposure to any tariff escalations, with negotiations potentially dragging on

- European shipping companies extend their slide, with Denmark’s Maersk shedding as much as 4.6%, as economic uncertainty and excess capacity concerns continued to pressure freight rates

- Axfood falls as much as 8.8%, the most since 2022, after the Nordic retail group reported its latest earnings. DNB sees an overall week report, with its Dagab logistics unit the main drag

- EMS-Chemie shares slump as much as 7.2%, the most since 2020, after the Swiss company cut its revenue forecast and said the challenging economy and rising costs are weighing on demand

- Avanza shares drop as much as 6.5%, the most in three months, after the Swedish online bank and trading platform reported operating income for the second quarter that missed estimates

- Europris falls as much as 6.1% after DNB cut its recommendation for the Norwegian retail group to hold due to soft sales trend in its key Norwegian market and for its Swedish retail chain ÖoB

Earlier, Asian stocks declined as tech shares tracked their US peers lower after slowing inflation data. Equities in Hong Kong bucked the selloff amid prospects of lower borrowing costs. The MSCI Asia Pacific Index fell as much as 1.1%, the most in over a month, with TSMC, Samsung Electronics and Tokyo Electron among the biggest laggards. Tech-heavy markets such as Taiwan, Japan and South Korea led declines in the region. Equities in mainland China fluctuated as traders rebalanced their holdings ahead of next week’s Third Plenum. Property stocks climbed amid rising expectations for more support for the sector at the meeting. Meanwhile, shares in Hong Kong rose as soft US consumer price print boosted hopes for potential interest rate-cuts in the city. Here are the most notable movers:

- BOC Aviation shares rise as much as 5.3%, the most since April, after it closed a self-arranged club loan transaction with 25 banks globally totaling $2.3 billion.

- CK Infrastructure shares climb as much as 7.5% in Hong Kong, the most since December 2023, as the company considers a second listing on an overseas stock exchange.

- BayCurrent shares climb as much as 19%, the most since January 2022, after the Japanese IT services company reported first quarter operating income that beat analyst estimates and saw unit rates grow quarter-on-quarter.

- Chalco rises as much as 10% in Hong Kong and 6.4% on the mainland after JPMorgan upgrades the stock to overweight on expectations the company will raise its full-year payout ratio after its preliminary 2Q results beat estimates.

- Seven & I shares plunge as much as 8.4%, the most since August 2020, after the Japanese retail conglomerate reported first-quarter operating income that missed the average analyst estimates and weak performance in overseas convenience stores.

- Fast Retailing shares decline as much as 4.1%, the most since April 12, on concerns the stock’s recent gains will increase the probability that the Nikkei will reduce the company’s weighting in its benchmark average.

- Astro Malaysia Holdings shares plunge as much as 9.7% after the Inland Revenue Board served the company notices of additional tax assessment for 2019 to 2023.

- Huafon Chemical shares rise as much as 8%, the most since Feb. 7, after the company said it expects to report 1H profit rose by 1.6% to 24% y/y.

- Hanssem shares rally as much as 10% after Samsung Securities says the furniture manufacturer’s profits may get a lift from rising home sales in South Korea.

- Xtep International shares rise to the highest since June 11 as Goldman Sachs says the company’s ‘solid’ 2Q retail revenue growth is driven by online and emerging brands sales that were ahead of target.

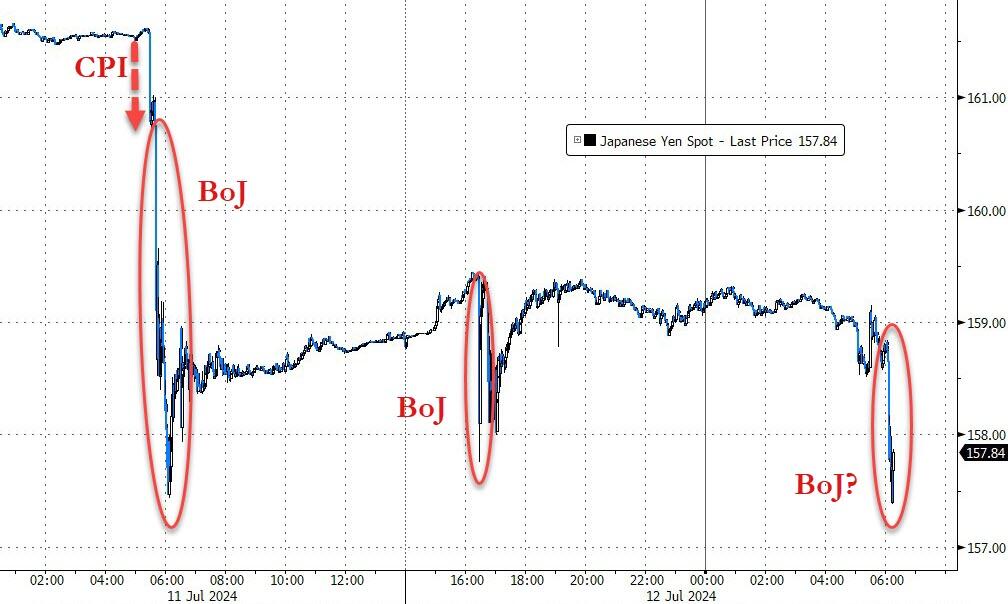

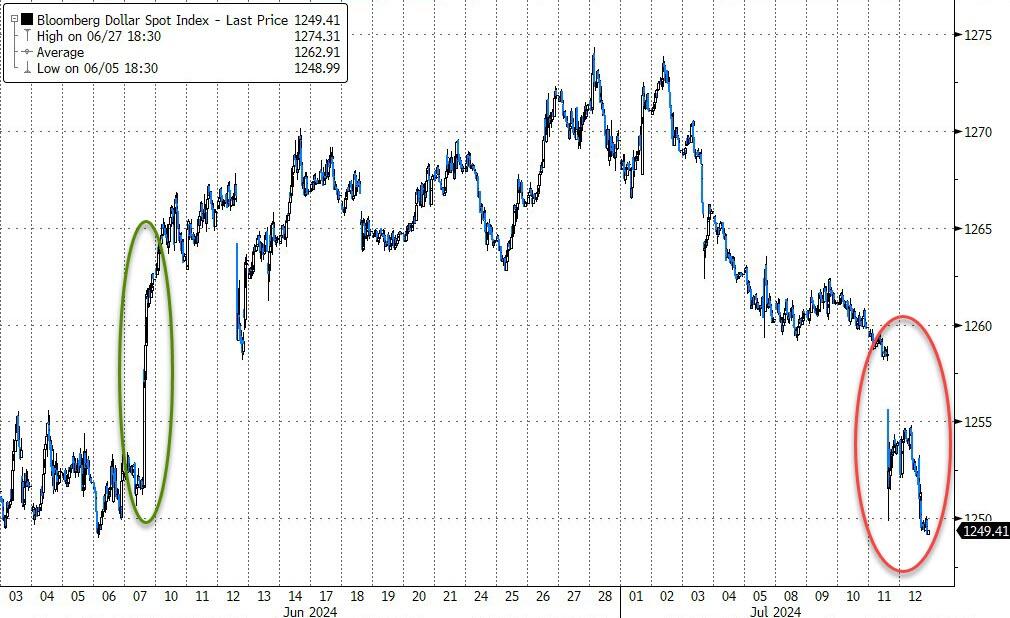

In FX, the yen initially weakened against the dollar, paring some of the sharp rally seen in the prior session, before resuming its trek higher. An analysis of Bank of Japan accounts suggests authorities did step into the markets to prop up the yen on Thursday. USD/JPY was flat at ~158.90. The Bloomberg Dollar Spot Index is down 0.1% and set for a third day of declines. The Swedish krona is the weakest of the G-10 currencies, falling 0.5% against the greenback after underlying inflation slowed more than expected.

In rates, treasuries edged lower, with US 10-year yields rising 1bps to 4.22%. Long-end yields are higher by ~1bp with 2s10s spread steeper by ~1bp; US 10-year around 4.225% outperforms bunds by ~4bp, gilts by ~6bp. European government bonds underperform their US peers.

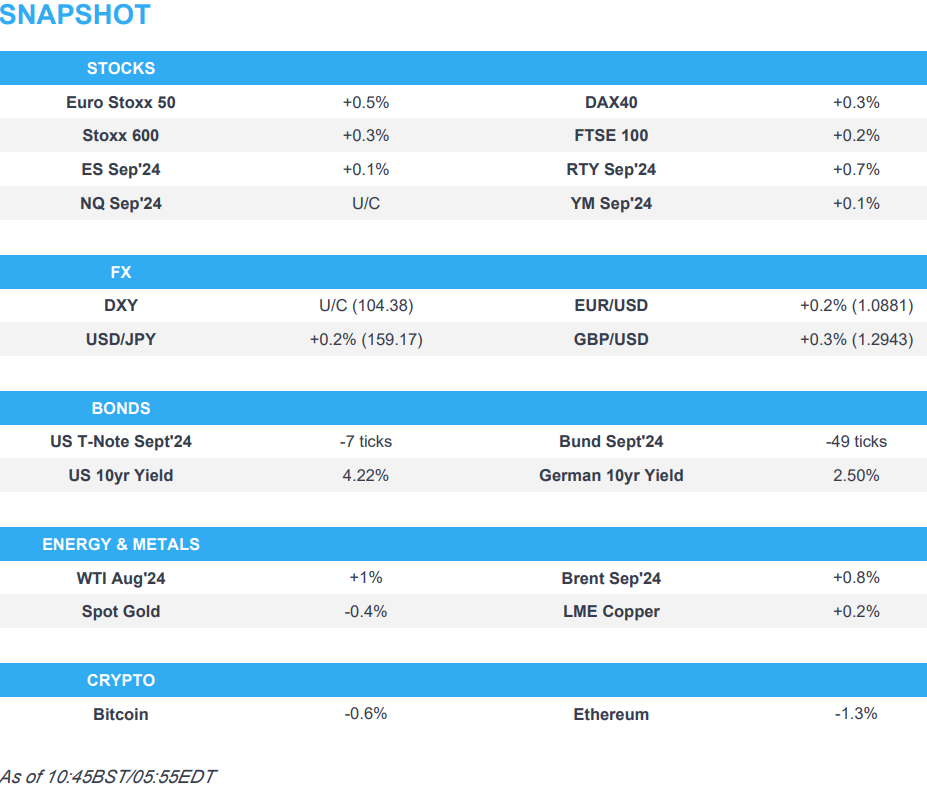

In commodities, oil prices advance, with WTI rising 1% to trade near $83.50 a barrel. Spot gold falls $12 to around $2,404/oz.

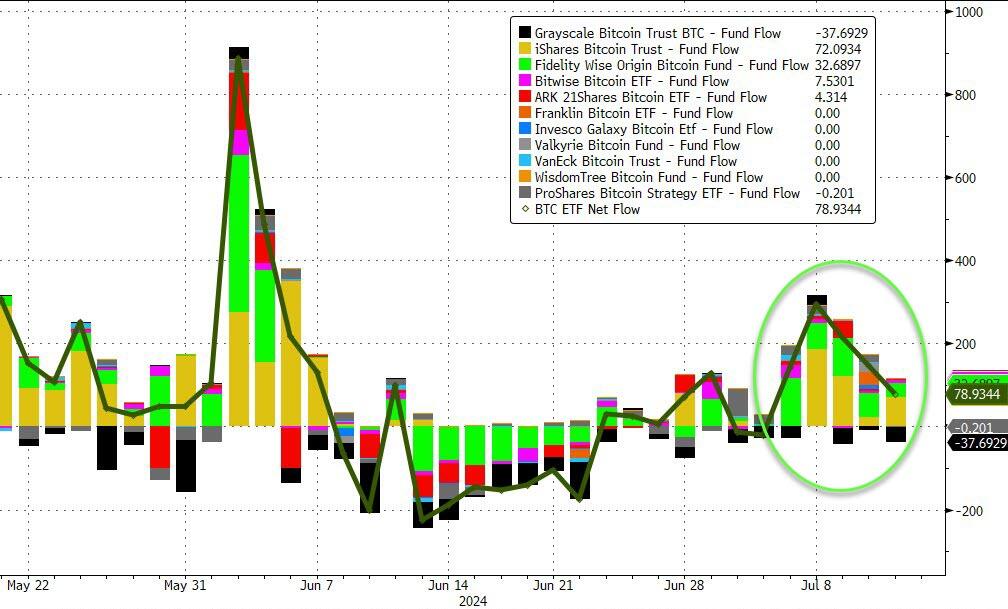

Bitcoin is incrementally softer and holds just above USD 57k, after briefly dipping below the level earlier. Ethereum remains firmly above USD 3k.

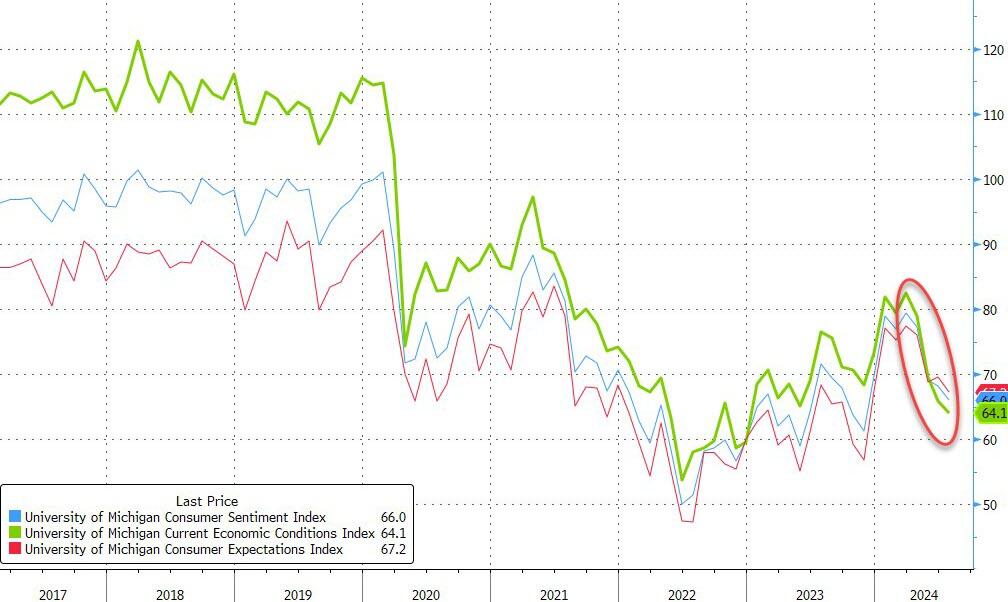

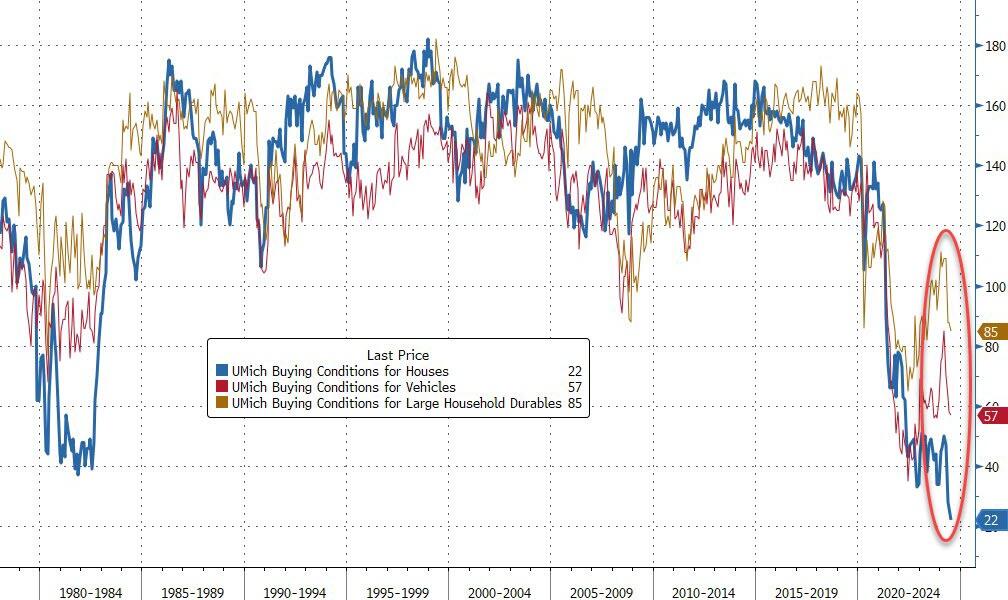

Today’s economic data slate includes June PPI (8:30am, which beat across the board) and July preliminary University of Michigan sentiment (10am). No Fed members are scheduled to speak

Market Snapshot

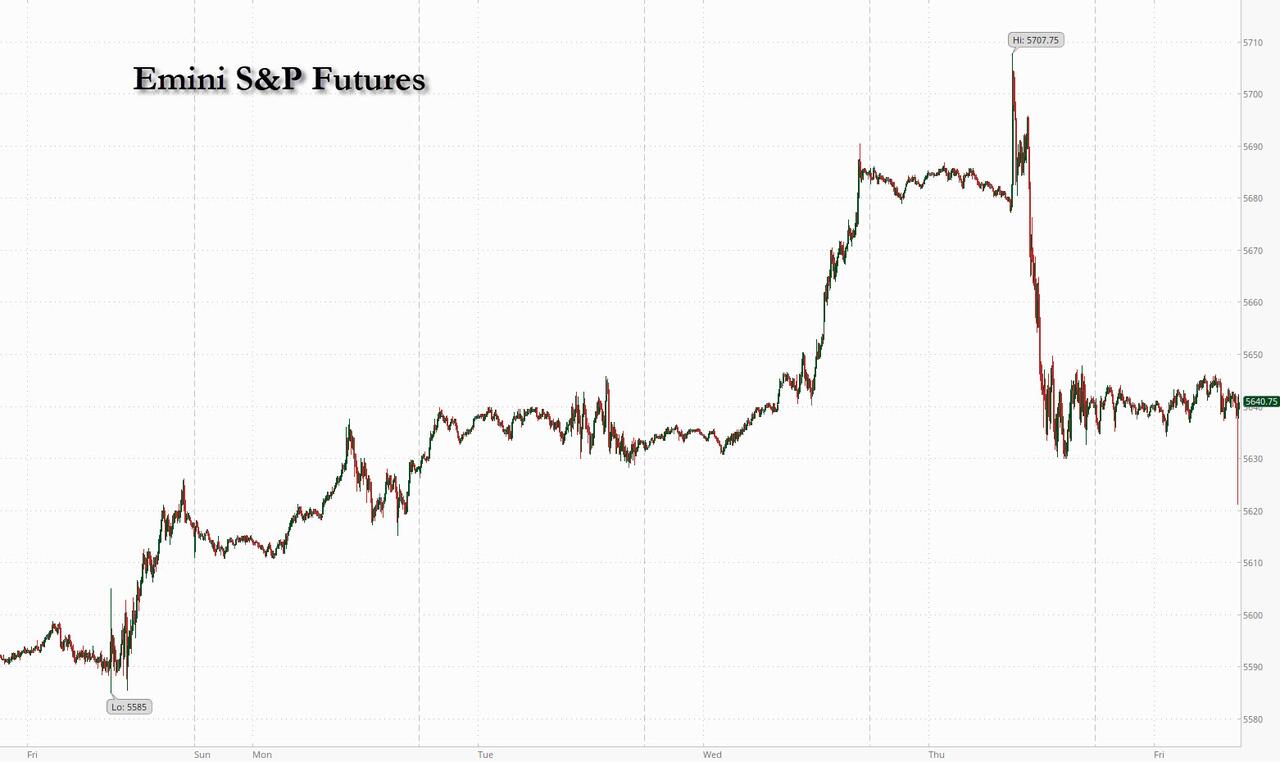

- S&P 500 futures little changed at 5,643.50

- STOXX Europe 600 up 0.3% to 521.21

- MXAP down 0.6% to 187.44

- MXAPJ up 0.1% to 587.14

- Nikkei down 2.4% to 41,190.68

- Topix down 1.2% to 2,894.56

- Hang Seng Index up 2.6% to 18,293.38

- Shanghai Composite little changed at 2,971.30

- Sensex up 1.0% to 80,665.58

- Australia S&P/ASX 200 up 0.9% to 7,959.28

- Kospi down 1.2% to 2,857.00

- German 10Y yield rose 4bps at 2.51%

- Euro up 0.1% to $1.0884

- Brent Futures up 0.9% to $86.16/bbl

- Gold spot down 0.4% to $2,406.32

- US Dollar Index little changed at 104.37

Top Overnight News

- US President Biden mistakenly referred to Ukrainian President Zelensky as President Putin before correcting himself during comments at the NATO summit, while he also mistakenly referred to Vice President Harris as Trump during his press conference. Furthermore, Biden said he has to finish the job because there is so much at stake and has taken three significant and intense neurological exams which say he is in good shape.

- US President Biden is expected to face a deluge of calls from House Democrats urging him to drop out of the presidential race regardless of his performance at the NATO press conference, according to Axios. It was also reported that dozens of Democratic lawmakers are to call for US President Biden to quit the race in the coming 48 hours: CBS.

- Three Biden officials directly involved in his re-election told NBC News that his chances of winning are zero and one said he needs to drop out, while it was also reported that some Biden advisers were discussing how to convince him to step aside: NYT.

- The Biden campaign is quietly assessing the viability of Vice President Harris’ candidacy against Donald Trump in a new head-to-head poll: MSNBC.

- Softbank has acquired U.K. semiconductor company Graphcore, the latest in a series of steps taken by the Japanese tech investment company in the artificial-intelligence field. The Bristol-based chip company, which specializes in AI, said that it is now a wholly-owned subsidiary of SoftBank Group and will continue to operate under the Graphcore name. WSJ

- Fed’s Goolsbee (non-voter) said the June CPI report is excellent and the improvement on shelter inflation is profoundly encouraging, while he added this is what a path to 2% inflation looks like and as inflation falls, leaving Fed policy rate steady means Fed is tightening policy. Goolsbee said the reason to tighten policy would be if the economy is overheating but added they are not overheating, as well as noted that he doesn’t like tying their hands on policy decisions and they need to decide when to cut rates, not trying to figure out a rate path for next seven months.

- China’s already formidable exports surged in June, China’s customs administration reported on Friday. But imports shrank, with Chinese companies and households becoming more cautious about spending money. The result was a record monthly trade surplus of just over $99 billion. NYT

- Despite billions of dollars in additional weapons and security assistance that NATO announced this week, allied officials said Ukraine would not be ready to launch a dramatic counteroffensive or retake large swaths of territory from Russia until next year. NYT

- Some American officials have grown more optimistic that a deal to release Israeli hostages held in Gaza in return for a cease-fire is at hand. But people briefed on the talks say it will be days until it is clear whether a breakthrough has been achieved because of difficulties in communication between Hamas officials in Qatar and the group’s leaders in Gaza. NYT

- Joe Biden vowed to stay in the presidential race despite new gaffes, including mixing up Volodymyr Zelenskiy and Vladimir Putin, and VP Kamala Harris and Donald Trump, during a press conference on the sidelines of the NATO summit. At least three more House Democrats, including Jim Himes, the top member from his party on the Intelligence Committee, called for Biden to drop his re-election bid. BBG

- Big bank earnings kick off today with JPMorgan, Citi and Wells Fargo as shares trounce the broader market. Investors are looking past another projected drop in net interest income, instead focusing on investment banking and a rebound in loan profits. BBG

- Boeing is said to have told some 737 Max customers that aircrafts due in 2025 and 2026 face additional delays. BBG

- U.S. Republican lawmakers are seeking a probe into Microsoft’s $1.5 billion investment in artificial intelligence firm G42, citing concerns about the transfer of advanced technology and possible ties the Abu Dhabi-based company may have with China. WSJ

- Axel Springer is considering a break-up, w/a separation of its media assets (including Politico and Business Insider) and classifieds business. FT

A more detailed look at global markets courtesy of Newquawk

APAC stocks took their cues from the mixed performance stateside where softer-than-expected CPI data boosted Fed rate cut bets and spurred a stock rotation out of large-cap tech into small-cap cyclicals. ASX 200 gained amid lower yields with gold miners, real estate, and consumer stocks leading the advances. Nikkei 225 underperformed after recently sliding back from record highs and amid speculated FX intervention. Hang Seng and Shanghai Comp. diverged as the former rallied back above the 18,000 level with strength seen in property and tech, while the mainland was lacklustre after mixed Chinese trade data in which Exports topped forecasts but Imports surprisingly contracted.

Top Asian News

- China’s Foreign Minister said in a phone call with his Dutch counterpart that China is willing to establish close ties with the new Dutch government and carry out all-around dialogue, as well as enhance mutual understanding. Furthermore, China believes the Dutch side will encourage the European side to look at China objectively and rationally and play a constructive role in maintaining a healthy and stable development of China-EU relations.

- Japanese government official said Japan conducted currency intervention to prop up the yen on Thursday, according to Mainichi citing an unidentified official. It was separately reported that the BoJ likely conducted rate checks in EUR/JPY on Friday, according to Nikkei.

- Japanese Finance Minister Suzuki said currency rates should be set by the market and rapid FX moves are undesirable, while he wouldn’t comment on FX levels, FX intervention and media reports that Japan conducted FX rate checks.

- Japanese Chief Cabinet Secretary Hayashi said no comment on FX intervention and wouldn’t comment on forex levels, while he added it is important for currencies to move in a stable manner reflecting fundamentals and they are ready to take all possible means on forex.

- Japanese top currency diplomat Kanda said no comment on FX intervention and noted recent yen moves are somewhat rapid, while he added they will take appropriate action on forex if needed. Furthermore, he is puzzled about the media report on intervention, while he did not comment on whether they intervened in the FX market and cannot think if government officials commented on forex intervention.