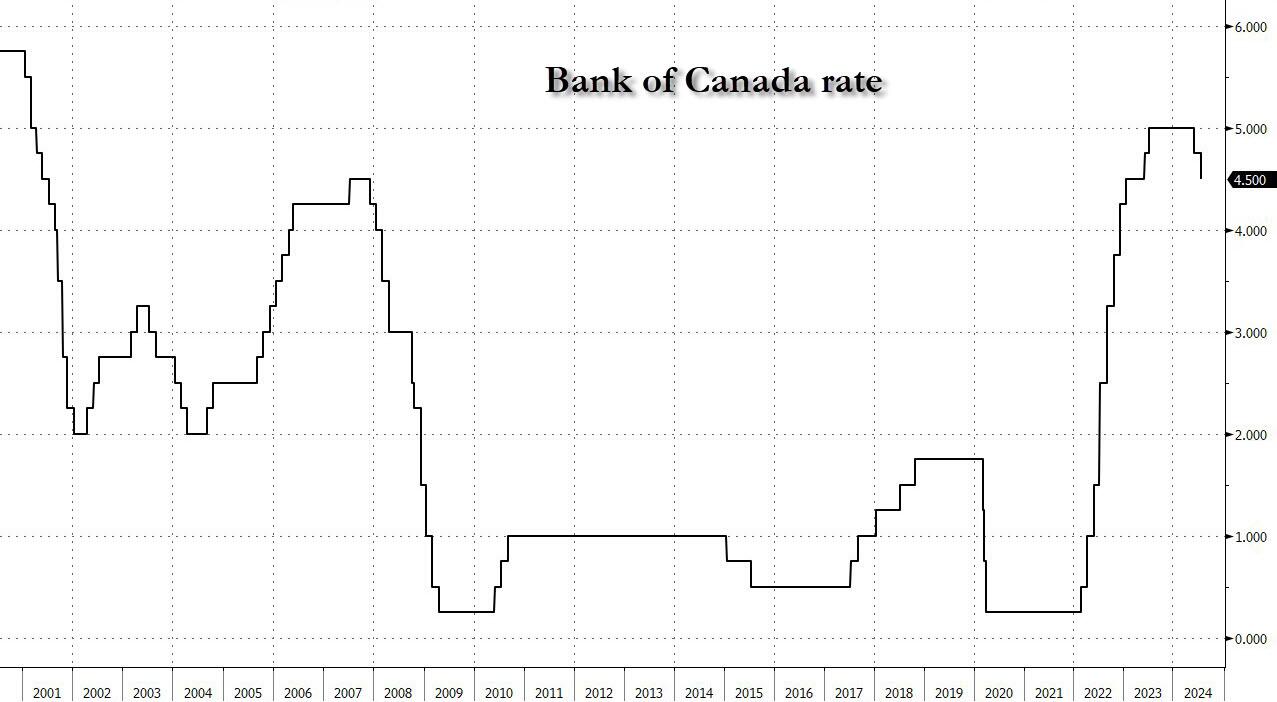

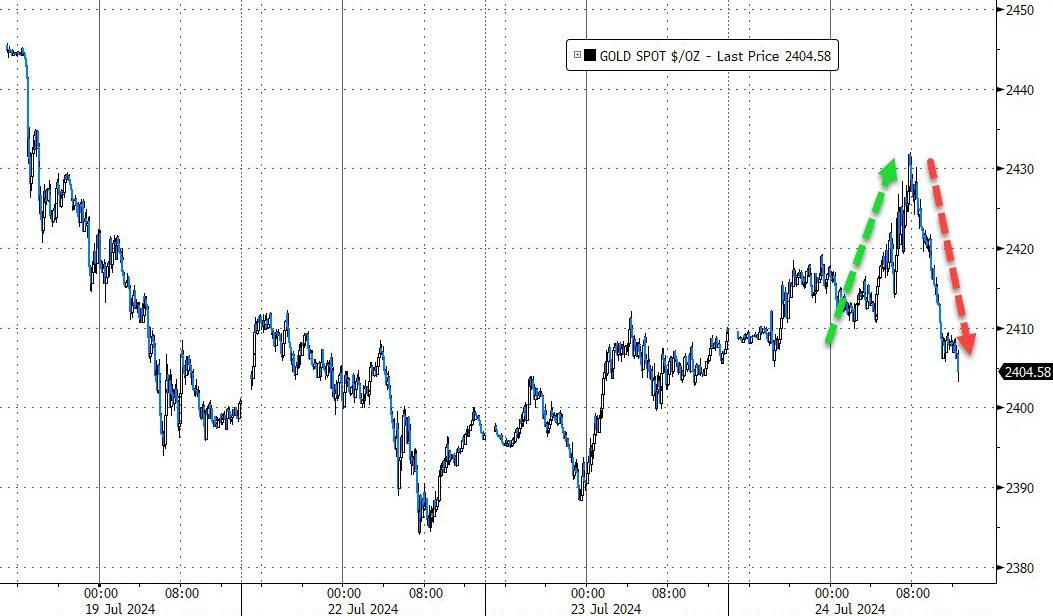

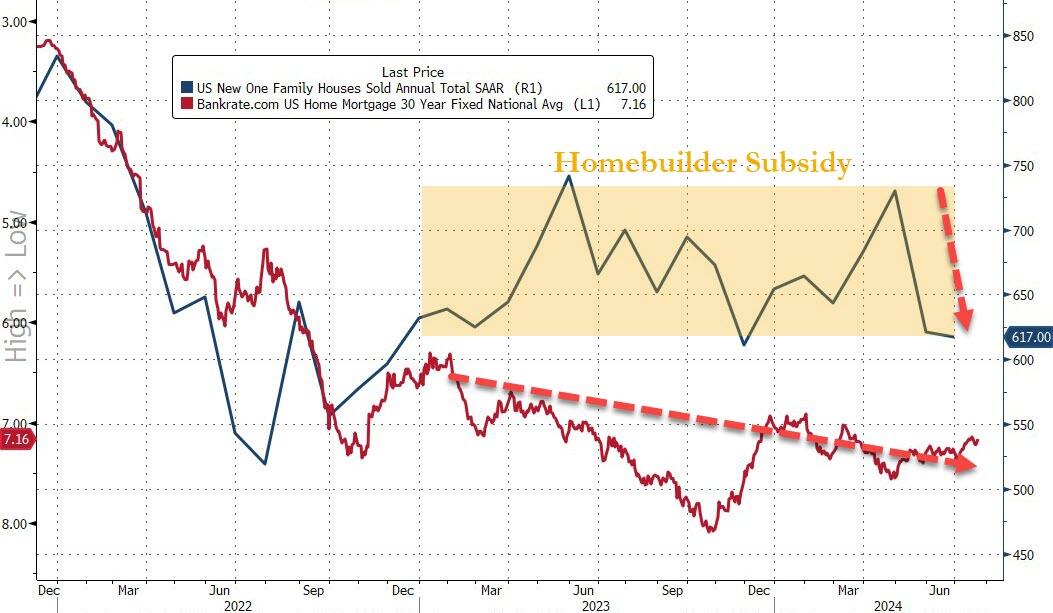

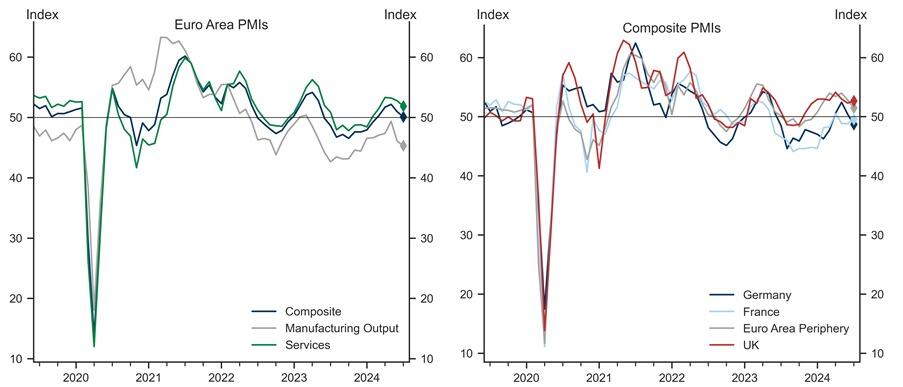

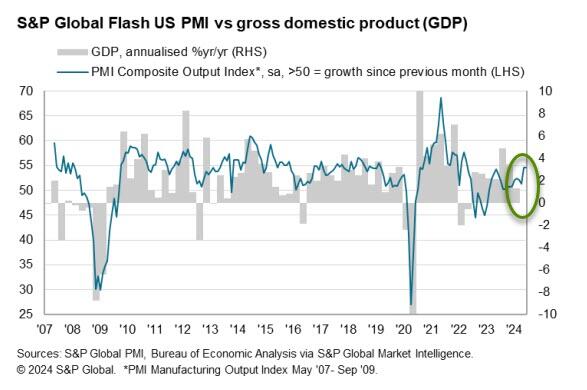

JULY 24/GOLD CLOSED UP $9.20 TO $2415,35//SILVER WAS DOWN 2 CENTS TO $29.13/PLATINUM WAS UP $8.30 TO $957.03 WHILE PALLADIUM CLSOED UP $10.6060 TO $936.40//ISRAEL VS HAMAS/HEZBOLLAH IN BRAZIL/ISRAEL VS WEST BANK/HOUTHIS VS THE WEST//COVID UPDATES/VACCINE INJURY REPORTS/SLAY NEWS ETC/CANADA CUTS ITS INTEREST RATE BY 1/4%//BLACKSTONE CUTS ITS DIVIDEND DUE TO CRE CONCERNS//USE DATA; NEW HOME SALES PLUMMET//PMI MANUFACTURING FALTERS//GOOD COMMENTARY FROM CONRAD BLACK//SWAMP STORIES FOR YOU TONIGHT///

624 H BOFA SECURITIES 11 661 C JP MORGAN 15 737 C ADVANTAGE 1 3 905 C ADM 2

TOTAL: 16 16 MONTH TO DATE: 3,673

JPMorgan stopped 0/16

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2024. CONTRACT: 16 NOTICES FOR 1600 OZ or 0.04977 TONNES

total notices so far: 3673 contracts for 367300 Oz (11.424 tonnes)

FOR JULY:

SILVER NOTICES: 15 NOTICE(S) FILED FOR 0.075 million

OZ/

total number of notices filed so far this month : 6076 for 30.380 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $9,20 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ HUGE CHANGES IN GOLD INVENTORY AT THE GLD” A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD

/ /INVENTORY RESTS AT 841.74 TONNES

INVENTORY RESTS AT 841.74 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $.02 AT THE SLV/WOW!! AGAIN???

HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 4.108 MILION OZ OF SILVER INTO THE SLV/

// INVENTORY RISES AT 459.794 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 459.774 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUMONGOUS SIZED 1035 CONTRACTS TO 157,106 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR TINY GAIN OF $0.02 IN SILVER PRICING AT THE COMEX ON TUESDAY’S TRADING ON SILVER. WE HAD HUGE LIQUIDATION DESPITE A HUGE NET LOSS OF 896 CONTRACTS ON OUR TWO EXCHANGES WE HAD A MASSIVE LIQUIDATION OF T.A.S. CONTRACTS WHICH ACCOUNTS FOR THE LARGE OI LOSS THIS IS SIMILAR TO THE COMEX GOLD TRADING. WE, AGAIN HAD SOME SHORT COVERING BY OUR SPECS DESPITE THE SMALL GAIN IN PRICE AS WELL AS THE MASSIVE T.A.S. LIQUIDATION MENTIONED ABOVE WHICH ACCOUNTS FOR THE HUGE LOSS OF OI ON THE TWO EXCHANGES. WE HAD A FAIR SIZED 366 T.A.S ISSUANCE,

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN ON FRIDAY, ON MONDAY AND LAST NIGHT.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 366 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS.IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1/2 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.02) AND WERE BASICALLY UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS FROM THEIR PERCH AS DESPITE HAVING A HUGE SIZED LOSS OF 787 CONTRACTS ON OUR TWO EXCHANGES THE MAJORITY OF THE LOSS WAS DUE TO T.A.S. /SPREADER LIQUIDATION.

WE MUST HAVE HAD:

A FAIR SIZED 248 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 28.490 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE JUMP OF 50,000 OZ

//NEW STANDING FOR SILVER//JUNE IS THUS 30.730 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI LOSS //FAIR SIZED EFP ISSUANCE/ VI) FAIR SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 366 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL added 109 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY

TOTAL CONTRACTS for 17 DAYS, total 17,033 contracts: OR 85.165 MILLION OZ (1002 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 85.165 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 85.165 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/OVER 100 MILLION OZ/)

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1035 CONTRACTS DESPITE OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR EFP ISSUANCE CONTRACTS: 248 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JULY OF 28.496 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 50,000 OZ QUEUE JUMP WHERE THEY WILL TRY AND TAKE DELIVERY ON THIS SIDE OF THE POND.

//NEW TOTAL STANDING FOR JULY 30.730 MILLION OZ

WE HAVE A HUGE SIZED LOSS OF 787 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE TINY GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A FAIR SIZED 366 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX TRADING WHICH ACCOUNTS FOR THE MAJOR PORTION OF THE COMEX OI LOSS/// MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND MINOR IF ANY LIQUIDATION OF LONGS.

THE NEW TAS ISSUANCE TUESDAY NIGHT (366) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 15 NOTICE(S) FILED TODAY FOR 0.075 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A HUGE SIZED 12,761 OI CONTRACTS TO 572,306 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 794 CONTRACTS

WE HAD A HUGE SIZED DECREASE IN COMEX OI (12,761 CONTRACTS) OCCURRED DESPITE OUR GAIN OF $12.75 IN PRICE/TUESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 7.5645 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 600 OZ QUEUE JUMP

NEW STANDING 11.636 TONNES

/ ALL OF THIS HAPPENED DESPITE OUR $12.75 GAIN IN PRICE WITH RESPECT TO TUESDAY’S TRADING. WE HAD A HUGE SIZED LOSS OF 10,728 OI CONTRACTS (33.37 PAPER TONNES) ON OUR TWO EXCHANGES., WITH OUR LONGS TOTALLY OBLIVIOUS TO THE RAID ORCHESTRATED BY THE STUPID BANKS AGAIN ON TUESDAY MORNING. GOLD ROSE AS THE SHORTS REALIZED THAT LONGS WERE EXERCISING THEIR CONTRACTS VIA THE EXCHANGE FOR PHYSICAL ROUTE FOR ACTUAL PHYSICAL METAL, MUCH TO THE SHOCK FROM THE FED (THEY ARE SHORT AT A MINIMUM 109 TONNES OF GOLD)

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2033 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 572,306

IN ESSENCE WE HAVE A HUGE SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 9934 CONTRACTS WITH 12,761 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 2033 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF10,728 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 1377 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2033 CONTRACTS) ACCOMPANYING THE HUGE SIZED LOSS IN COMEX OI OF 12,728 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 9934 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 7,5645 TONNES FOLLOWED BY TODAY’S 600 OZ QUEUE JUMP

//NEW STANDING /JULY 11.636 TONNES.

/ 3) HUGE T.A.S. LIQUIDATION//SPREADER CONTRACTS WITH ZERO NET LONG SPECS BEING CLIPPED,

4) HUGE SIZED COMEX OPEN INTEREST LOSS 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1337 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY. :

TOTAL EFP CONTRACTS ISSUED: 84,154 CONTRACTS OF 8,415,400 OZ OR 261.75 TONNES IN 17 TRADING DAY(S) AND THUS AVERAGING: 4950 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAY(S) IN TONNES 261.75 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 261.75 DIVIDED BY 3550 x 100% TONNES = 7.35% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 261.75 TONNES (WILL BE A VERY STRONG ISSUANCE MONTH FOR EXCHANGE FOR PHYSICALS)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUG), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 1035 CONTRACTS OI TO 156,997 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 248 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 248 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 248 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1035 CONTRACTS AND ADD TO THE 248 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 787 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 3.935 MILLION OZ OCCURRED DESPITE OUR TINY $0.02 GAIN IN PRICE …THE MAJORITY OF THE OI LOSS WAS DUE TO SPREADER/T.A.S. LIQUIDATION.

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING/TUESDAY NIGHT

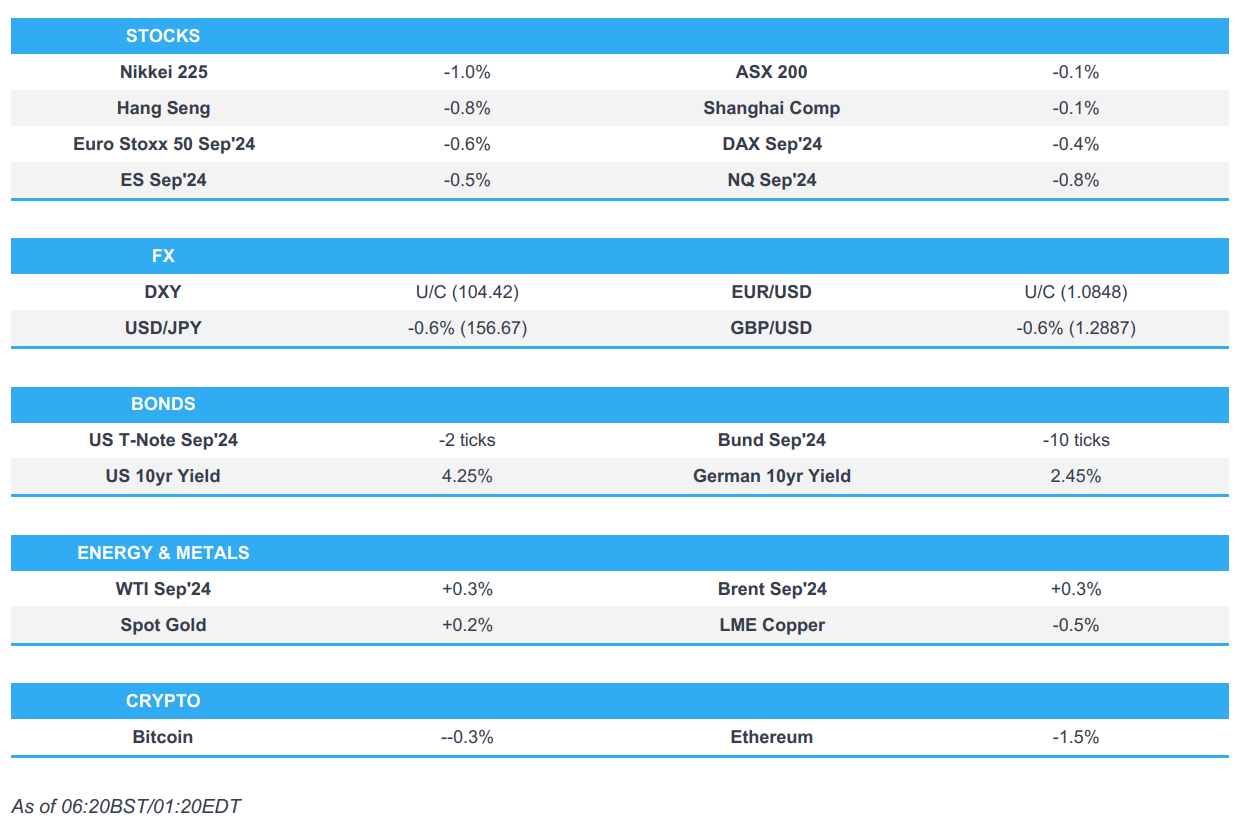

SHANGHAI CLOSED DOWN 13.42 PTS OR 0.46% //Hang Seng CLOSED DOWN 158.31 PTS OR 0.91% // Nikkei CLOSED DOWN 439.54 OR 1.11%//Australia’s all ordinaries CLOSED DOWN 0.04%///Chinese yuan (ONSHORE) closed DOWN TO 7,2769 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2860/ Oil DOWN TO 77.70dollars per barrel for WTI and BRENT DOWN AT 81.87/Stocks in Europe OPENED ALL RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A HUGE SIZED 12,761 CONTRACTS TO 572,306 DESPITE OUR STRONG GAIN IN PRICE OF $12.75 WITH RESPECT TO TUESDAY’S TRADING. THE LONGS COULDN’T CARE LESS WITH THE RAID ORCHESTRATED BY THE CROOKS. CENTRAL BANKS ARE PATIENT. THEY WERE WAITING FOR THE ATTACK OCCURRING EARLY TUESDAY MORNING AS THEY ACCUMULATED THEIR LONG PURCHASES THROUGHOUT THE DAY ESPECIALLY WHEN THE PRICE HIT BELOW 2400. THEY CONTINUED THEIR PURCHASES AND THEN TENDERED FOR PHYSICAL GOLD AT THE END OF THE TUESDAY SESSION. THE REASON FOR THE STRONG LOSS IN COMEX IS DUE TO SPREADERS LIQUIDATING AS WELL AS T.A.S LIQUIDATION. THUS:

WE HAD A HUGE T.A.S. LIQUIDATION ON TUESDAY’S GAIN IN PRICE WITH ZERO LONGS BEING CLIPPED AND MAJOR SHORT COVERING. THE SHORTS ARE ABANDONING SHIP: THEY ARE NOW SCARED.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE NON ACTIVE DELIVERY MONTH OF JULY.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 2833 EFP CONTRACTS WERE ISSUED: : AUGUST2833 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2833 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A HUGE SIZED TOTAL OF 10,728 CONTRACTS IN THAT 2033 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A HUGE SIZED LOSS OF 12,761 COMEX CONTRACTS..AND THIS STRONG LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR GAIN IN PRICE OF $12.75/TUESDAY COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TUESDAY NIGHT TO EXERCISE FOR PHYSICAL GOLD.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT A FAIR SIZED 1337 CONTRACTS. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN LAST WEEK’S TRADING//RAIDS AS WELL AS THIS WEEK.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JULY (11.6360 TONNES)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.636 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $12.75 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS, EVEN THOUGH WE HAD A HUGE SIZED LOSS OF 10,728 CONTRACTS ON OUR TWO EXCHANGES, THE LOSS IN OI WAS DUE TO EARLY SPREADER LIQUIDATION/T.A.S. LIQUIDATION AS THE SHORTS ARE RUNNING FROM THE HILLS,SENSING DANGER FROM THEIR STUPID SHORTING . THE T.A.S. ISSUED ON TUESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE LOST A TOTAL OI OF 30.898 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY (7.5645 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 600 OZ QUEUE JUMP//NEW STANDING 11.636 TONNES

NEW STANDING FOR JULY: 11.636 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $12.75

WE HAVE REMOVED 794 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET LOSS ON THE TWO EXCHANGES 10,728 CONTRACTS OR 1,072,800 OZ (33.37 TONNES)

Total monthly oz gold served (contracts) so far this month

3673 notices 367,300 oz 11.424 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: nil oz

we have 0 customer deposits:

total deposits nil

withdrawals: 1

i) Out of Brinks 3311.533 oz

311 kilobars

TOTAL WITHDRAWALS 3311,533 oz

Adjustment 2

a) Customer to dealer; JPMorgan: 294,181.650 oz

b) customer to dealer Loomis : 96,453,000 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY

For the front month of JULY we have an oi of 84 contracts having LOST 0 contracts. We had 6 notices filed on TUESDAY so we GAINED 6 contracts or an additional 600 oz will stand at the comex (0.0187 tonnes)

AUGUST LOST 26,866 CONTRACTS DOWN TO 183,461 CONTRACTS

SEPT. GAINED 157 CONTRACTS TO STAND AT 1303.

OCTOBER GAINED 1828 CONTRACTS UP TO 48,443 CONTRACTS

We had 16 contracts filed for today representing 1600 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 15 notices were issued from their client or customer account. The total of all issuance by all participants equate to 16 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for July /2024. contract month, we take the total number of notices filed so far for the month (3673) x 100 oz ) to which we add the difference between the open interest for the front month of JULY 84( CONTRACTS) minus the number of notices served upon today (16 x 100 oz per contract( equals 374,100 OZ OR 11.636 TONNES.

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (3673 x 100 oz +we add the difference for front month of JULY (84 X// , OI} minus the number of notices served upon today (16) x 100 oz which equals 374,100 oz (11.636 TONNES)

TOTAL COMEX GOLD STANDING FOR JULY: 11.636 TONNES WHICH IS HUGE FOR THIS NOT VERY ACTIVE DELIVERY MONTH IN THE CALENDAR.

total pledged gold: 1,677,188.801 oz 52.167 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,915,574.922 OZ

TOTAL REGISTERED GOLD 8,169,920.807 ( 254.18 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,745,654.665 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,492,732 oz (REG GOLD- PLEDGED GOLD)= 201.95 tonnes //

END

SILVER/COMEX

JULY 24/2024

INITIAL

//2024// THE JULY 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

2968.05oz

Delaware

.

Deposits to the Dealer Inventory

Deposits to the Customer Inventory

1,200.980.200 oz ASAHI

No of oz served today (contracts)

15 CONTRACT(S) (.075 million OZ)

No of oz to be served (notices)

70 contracts (0.385 million oz)

Total monthly oz silver served (contracts)

6076 Contracts (30.320 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit/

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 customer deposits:

i) into ASAHI 1,200,980.200 oz

total customer deposit 1,200,980/200 oz

JPMorgan has a total silver weight: 132.563million oz/303.107million or 43.54%

adjustment:0

customer withdrawals: 1

i) Out of Delaware 2968.05 oz

total withdrawal: 2968.05 0z

TOTAL REGISTERED SILVER: 69.377 MILLION OZ//.TOTAL REG + ELIGIBLE. 301.909 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF JULY/2024 OI: 85 CONTRACTS HAVING GAINED 8 CONTRACT(S). WE HAD 2 NOTICES FILED ON TUESDAY SO WE GAINED 10 CONTRACTS OR AN ADDITIONAL 50,000 OZ WILL STAND AT THE COMEX AS THEY TOOK DELIVERY ON THIS SIDE OF THE POND.

AUG, SAW A LOSS OF 32 CONTRACTS TO 1274

SEPT SAW A LOSS OF 2400 CONTRACTS TO 119,807

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 15 for 0.075 MILLION oz

CONFIRMED volume; ON TUESDAY 59,497 good

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 6076 x 5,000 oz = 30.320 MILLION oz

to which we add the difference between the open interest for the front month of JULY( 85) and the number of notices served upon today 15 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY/2024 contract month: 6076 notices served so far) x 5000 oz + OI for the front month of JULY (85)x number of notices served upon today minus (15)x 5000 oz of silver standing for the JULY contract month equates to 30.730 MILLION OZ.

New total standing: 30.730 million oz.

There are 69.377 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

JULY 24 WITH GOLD UP $12.75 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1.73 TONNES OF GOLDINTO THE GLD ///INVENTORY RESTS AT 841.74 TONNES

JULY 23 WITH GOLD UP $12.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 22 WITH GOLD DOWN $4.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 19 WITH GOLD DOWN $56.10 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;:A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 18 WITH GOLD DOWN $2.20 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;: ///INVENTORY RESTS AT 842.02 TONNES

JULY 17 WITH GOLD DOWN $6.60 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A MASSIVE DEPOSIT OF 5.49 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 842.02 TONNES

JULY 16 WITH GOLD UP $38.60 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 836.53 TONNES

JULY 15 WITH GOLD UP $8.15 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;: /INVENTORY RESTS AT 835.09 TONNES

JULY 12 WITH GOLD DOWN $0.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 835.09 TONNES

JULY 11 WITH GOLD UP $43.05 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;:INVENTORY RESTS AT 833.37 TONNES

JULY 10 WITH GOLD UP $12.00 ON THE DAY; HUUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.44 TONNES OF GOLD VAPOUR FROM THE GLD//.//:INVENTORY RESTS AT 833.37 TONNES

JULY 9 WITH GOLD UP $5.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD.//:INVENTORY RESTS AT 834.81 TONNES

JULY 8 WITH GOLD DOWN $26.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD.//:INVENTORY RESTS AT 834.81 TONNES

JULY 5 WITH GOLD UP $29.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD..A DEPOSIT OF 1.10 TONNES OF GOLD VAPOUR INTO THE GLD//:INVENTORY RESTS AT 833.37 TONNES

JULY 3 WITH GOLD UP $35.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD..A MASSIVE DEPOSIT OF 5.76 TONNES OF GOLD VAPOUR INTO THE GLD//:INVENTORY RESTS AT 833.37 TONNES

JULY 2 WITH GOLD DOWN $4.45 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD../:INVENTORY RESTS AT 827.61 TONNES

JULY 1 WITH GOLD DOWN $.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 28 WITH GOLD UP $3.80 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 27 WITH GOLD DOWN $16.95 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 26 WITH GOLD UP $23.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 25 WITH GOLD DOWN $13.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A STRONG WITHDRAWAL OF 2.88 TONNES OF GOLD FROM THE GLD INVENTORY RESTS AT 829.05 TONNES

JUNE 24 WITH GOLD UP$14.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A STRONG WITHDRAWAL OF 1.72 TONNES OF GOLD/NEW TOTAL TONIGHT 831.93 TONNES

JUNE 21 WITH GOLD DOWN $37.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A MAMMOTH 8.34 TONNES OF GOLD VAPOUR DEPOSIT/NEW TOTAL TONIGHT 833.65 TONNES

JUNE 20 WITH GOLD UP $23.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/://NEW TOTAL TONIGHT 825.31 TONNES

JUNE 18 WITH GOLD UP $17.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/://NEW TOTAL TONIGHT 825.31 TONNES

GLD INVENTORY: 841.74 TONNES, TONIGHTS TOTAL

SILVER

JULY 24 WITH SILVER UP 3 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.118 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 459.774 MILLION OZ

JULY 23 WITH SILVER UP 3 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 15.880 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 22 WITH SILVER UP 2 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 3.920 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 19 WITH SILVER DOWN 94 CENTS//NO CHANGES IN SILVER INVENTORY/// /INVENTORY REMAINS AT 435.854 MILLION OZ

JULY 18 WITH SILVER DOWN 13 CENTS//HUGE CHANGES IN SILVER INVENTORY” A DEPOSIT OF 2.374 MILLION OZ INTO THE SLV/// /INVENTORY RISES TO 435.854 MILLION OZ

JULY 17. WITH SILVER DOWN 75 CENTS//NO CHANGES IN SILVER INVENTORY// /INVENTORY REMAINS AT 433.480 MILLION OZ.

JULY 16. WITH SILVER UP 30 CENTS//NO CHANGES IN SILVER INVENTORY// /INVENTORY REMAINS AT 433.480 MILLION OZ.

JULY 15. WITH SILVER DOWN 24 CENTS//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 2.145 MILLION OZ FROM THE SLV.// /INVENTORY LOWERS T0 AT 433.480 MILLION OZ.

JULY 12. WITH SILVER DOWN $.65 CENTS//NO CHANGES IN SILVER INVENTORY /INVENTORY REMAINS CONSTANT AT 435.625 MILLION OZ.

JULY 11. WITH SILVER UP $.72 CENTS//HUGE CHANGES IN SILVER INVENTORY A WITHDRAWAL OF 0.731 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 435.625 MILLION OZ.

JULY 10. WITH SILVER DOWN $.04 CENTS//HUGE CHANGES IN SILVER INVENTORY A MAMMOTH WITHDRAWAL OF 3.744 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 436.356 MILLION OZ.

JULY 9. WITH SILVER UP 13 CENTS//HUGE CHANGES IN SILVER INVENTORY A MAMMOTH WITHDRAWAL OF 3.744 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 436.356 MILLION OZ.

JULY 8. WITH SILVER DOWN $0.73//SMALL CHANGES IN SILVER INVENTORY A MAMMOTH DEPOSIT OF 3,292,000 OZ OF SILVER VAPOUR INTO THE SLV.: /INVENTORY RISES T0 440.100 MILLION OZ.

JULY 4. WITH SILVER UP $0.85//SMALL CHANGES IN SILVER INVENTORY A MAMMOTH DEPOSIT OF 3,292,000 OZ OF SILVER VAPOUR INTO THE SLV.: /INVENTORY RISES T0 440.100 MILLION OZ.

JULY 3. WITH SILVER UP $1.08//SMALL CHANGES IN SILVER INVENTORY A SMALL WITHDRAWAL OF 639,000 OZ: /INVENTORY LOWERS T0 436,808 MILLION OZ.

JULY 2. WITH SILVER UP $0.19//NO CHANGES IN SILVER INVENTORY: /INVENTORY REMAINS AT 437.447 MILLION OZ./

JULY 1. WITH SILVER UP $0.05//XXX CHANGES IN SILVER INVENTORY: A DEPOSIT OF 182,000 OZ OF SILVER INTO THE SLV./.// /INVENTORY RISES AT 437.447 MILLION OZ./

JUNE 28. WITH SILVER UP $0.27//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 913,000 OZ FROM THE SLV./.// /INVENTORY REMAINS AT 437.265 MILLION OZ./

JUNE 27. WITH SILVER UP $0.01//NO CHANGES IN SILVER INVENTORY: .// /INVENTORY REMAINS AT 438.178 MILLION OZ.//

JUNE 26. WITH SILVER UP $0.03//HUGE CHANGES IN SILVER INVENTORY: A HUGE WITHDRAWAL OF 2.512 MILLION OZ OF SILVER FROM THE SLV.// /INVENTORY FALLS TO 438.178 MILLION OZ.//

JUNE 25. WITH SILVER DOWN $0.63//HUGE CHANGES IN SILVER INVENTORY: A MAMMOTH DEPOSIT OF 7.835 MILLION OZ OF SILVER VAPOUR INTO THE SLV.// /INVENTORY RISE TO 440.69 MILLION OZ.//WHAT AN ABSOLUTE FRAUD.

JUNE 24. WITH SILVER DOWN $0.05//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 2.104 MILLION OZ FROM THE SLV.// /INVENTORY LOWERS TO 432.835 MILLION OZ.

JUNE 21. WITH SILVER DOWN $1.15//NO CHANGES IN SILVER INVENTORY’// /INVENTORY REMAINS AT 434.935 MILLION OZ.

JUNE 20. WITH SILVER UP $1.17//HUGE CHANGES IN SILVER INVENTORY’ A DEPOSIT OF 5.164 MILLION OZ INTO THE SLV/// /INVENTORY RISES TO 434.929 MILLION OZ.

JUNE 18. WITH SILVER UP $0.21//NOCHANGES IN SILVER INVENTORY’ A WITHDRAWAL .730 MILLION OZ INTO THE SLV/// /INVENTORY FALLS TO 429.775 MILLION OZ.

CLOSING INVENTORY 459.774 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

end

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY

end

3.CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES

4. GOLD PODCASTS//LIVE FROM THE VAULT

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COCOA

ASIA TRADING/WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED DOWN 48.85 PTS OR 1.65% //Hang Seng CLOSED DOWN 166.52 PTS OR 0.94% // Nikkei CLOSED DOWN 4.61 OR 0.01%//Australia’s all ordinaries CLOSED UP 0.52%///Chinese yuan (ONSHORE) closed UP TO 7,2744 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2807/ Oil DOWN TO 78.15dollars per barrel for WTI and BRENT UP AT 82.06/Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGSWEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2744

OFFSHORE YUAN: UP TO 7.2807

SHANGHAI CLOSED DOWN 48.85 PTS OR 1;65 %

HANG SENG CLOSED DOWN 166.52 PTS OR 0.94%

2. Nikkei closed DOWN 4.61 PTS OR 0.01%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 104.15 EURO FALLS TO 1.0863 DOWN 27 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1,065 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 156,15 JAPANESE YEN NOW FALLING AS WELL AS LONG TERM 10 YR. YIELDS RISING //EVENTUALLY THIS WILL BREAK THE JAPANESE CENTRAL BANK

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.4550/Italian 10 Yr bond yield UP to 3.748 SPAIN 10 YR BOND YIELD UP TO 3.228%

3i Greek 10 year bond yield UP TO 3.405

3j Gold at $2408.50//Silver at: 29.06 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 68/ 100 roubles/dollar; ROUBLE AT 87.17

3m oil into the 78 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 156.15/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.065% STILL ON CENTRAL BANK (JAPAN) INTERVENTION

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8913 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9601 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.238 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.454 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.517 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 32.94…

10 YR UK BOND YIELD: 4.1715 UP 1 PTS

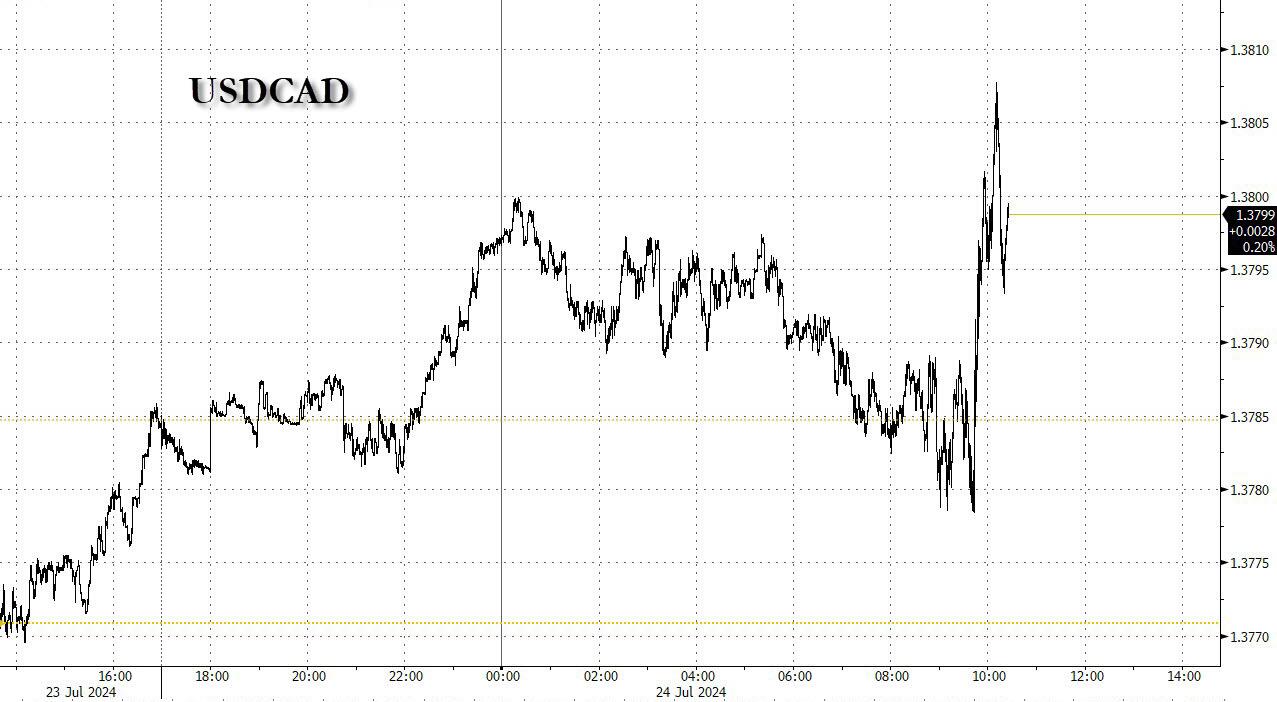

10 YR CANADA BOND YIELD: 3.421 UP 1 BASIS PTS

2a New York OPENING REPORT

2B) EUROPEAN REPORT

GOLD PRICE CLOSED UP $12.75 TO $2406.15

SILVER PRICE UP $0.03 TO $29.15

Gold ACCESS CLOSED $2408.00

Silver ACCESS CLOSED: $29.22

Bitcoin morning price:$66,803 DOWN 1003 DOLLARS. bankers doing a good job destroying the value of bitcoin

Bitcoin: afternoon price: $66,141 down 2368

dollars//

Platinum price closing DOWN $0.0 TO $949.40

Palladium price; UP $14.20 AT $925.80

END

SHANGHAI GOLD PREMIUM 13 DOLLARS/COMEX GOLD//august to august

*CANADIAN GOLD: $3318.04 UP 18.10 CDN dollars per oz( * NEW ALL TIME HIGH 3,375.67 CDN DOLLARS PER OZ//JULY 16 2024)

*BRITISH GOLD: 1,865.58 UP 13.12 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2,218.98 UP 18,91 Euros per oz //* (ALL TIME CLOSING HIGH: 2.263.98 EUROS PER OZ//JULY 16//.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCH: COMEX

JPMorgan stopped 0/6

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2024. CONTRACT: 6 NOTICES FOR 600 OZ or 0.0186 TONNES

total notices so far: 3657 contracts for 365,700 Oz (11.3748 tonnes)

FOR JULY:

SILVER NOTICES: 2 NOTICE(S) FILED FOR 0.010 million

OZ/

total number of notices filed so far this month : 6061 for 30.3748 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $12.75 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ NO CHANGES IN GOLD INVENTORY AT THE GLD

/ /INVENTORY RESTS AT 840.01 TONNES

INVENTORY RESTS AT 840.01 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $.03 AT THE SLV//WOW!!!!!

HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 15.886 MILION OZ OF SILVER INTO THE SLV/

// INVENTORY RISES AT 455.666 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 455.666 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUMONGOUS SIZED 1561 CONTRACTS TO 157,967 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR TINY GAIN OF $0.03 IN SILVER PRICING AT THE COMEX ON MONDAY’S TRADING ON SILVER. WE HAD LITTLE LIQUIDATION AS DESPITE A HUGE NET LOSS OF 811 CONTRACTS ON OUR TWO EXCHANGES WE HAD A THE MASSIVE LIQUIDATION OF T.A.S. CONTRACTS WHICH ACCOUNTS FOR THE LARGE OI LOSS. WE, AGAIN HAD SOME SHORT COVERING BY OUR SPECS DESPITE THE GAIN IN PRICE AS WELL AS THE MASSIVE T.A.S. LIQUIDATION MENTIONED ABOVE WHICH ACCOUNTS FOR THE HUGE LOSS OF OI ON THE TWO EXCHANGES. WE HAD ANOTHER HUGE SIZED 626 T.A.S ISSUANCE,

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN ON FRIDAY AND LAST NIGHT.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 624 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS.IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1/2 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.02) AND WERE BASICALLY UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS FROM THEIR PERCH AS DESPITE HAVING A HUGE SIZED LOSS OF 811 CONTRACTS ON OUR TWO EXCHANGES THE MAJORITY OF THE LOSS WAS DUE TO T.A.S. LIQUIDATION.

WE MUST HAVE HAD:

A MEGA HUGE SIZED 750 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 28.490 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S E.F.P JUMP TO LONDON OF 55,000 OZ

//NEW STANDING FOR SILVER//JUNE IS THUS 30.680 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI LOSS //HUGE SIZED EFP ISSUANCE/ VI) HUGED SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1626 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED XXX CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY

TOTAL CONTRACTS for 17 DAYS, total 16,785 contracts: OR 83.925 MILLION OZ (1049 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 83.925 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 83.925 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/OVER 100 MILLION OZ/)

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1561 CONTRACTS DESPITE OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 750 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JULY OF 28.496 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 55,000 OZ E.F.P JUMP TO LONDON WHERE THEY WILL TRY AND TAKE DELIVERY ON THEIR SIDE OF THE POND.

//NEW TOTAL STANDING FOR JULY 30.680 MILLION OZ

WE HAVE A HUGE SIZED LOSS OF 811 OI CONTRACTS ON THE TWO EXCHANGES WITH THE TINY GAIN IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 626 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX TRADING WHICH ACCOUNTS FOR THE MAJOR PORTION OF THE COMEX OI LOSS/// MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND MINOR IF ANY LIQUIDATION OF LONGS.

THE NEW TAS ISSUANCE MONDAY NIGHT (624) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 2 NOTICE(S) FILED TODAY FOR 0.010 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A TINY SIZED 394 OI CONTRACTS TO 585,067 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 4548 CONTRACTS

WE HAD A TINY SIZED INCREASE IN COMEX OI (394 CONTRACTS) OCCURRED DESPITE OUR GAIN OF $12.75 IN PRICE/TUESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 7.5645 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 100 OZ QUEUE JUMP

NEW STANDING 11.6174 TONNES

/ ALL OF THIS HAPPENED DESPITE OUR $12.75 GAIN IN PRICE WITH RESPECT TO TUESDAY’S TRADING. WE HAD A FAIR SIZED GAIN OF 3177 OI CONTRACTS (9.88 PAPER TONNES) ON OUR TWO EXCHANGES., WITH OUR LONGS TOTALLY OBLIVIOUS TO THE RAID ORCHESTRATED BY THE STUPID BANKS AGAIN ON FRIDAY AND MONDAY.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2783 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 585,067

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3177 CONTRACTS WITH 394 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 2783 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 3177 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 1062 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2783 CONTRACTS) ACCOMPANYING THE TINY SIZED GAIN IN COMEX OI OF 394 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 3177 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 7,5645 TONNES FOLLOWED BY TODAY’S 100 OZ QUEUE JUMP

//NEW STANDING /JULY 11.6174 TONNES.

/ 3) CONSIDERABLE T.A.S. LIQUIDATION OF CONTRACTS WITH ZERO NET LONG SPECS BEING CLIPPED,

4) GOOD SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1062 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY. :

TOTAL EFP CONTRACTS ISSUED: 82,121 CONTRACTS OF 8,212,100 OZ OR 255.43 TONNES IN 17 TRADING DAY(S) AND THUS AVERAGING: 5289 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAY(S) IN TONNES 255.43 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 255.43 DIVIDED BY 3550 x 100% TONNES = 7.18% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 255.43 TONNES (WILL BE A VERY STRONG ISSUANCE MONTH FOR EXCHANGE FOR PHYSICALS)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUG), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 1561 CONTRACTS OI TO 158,141 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 750 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 750 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 750 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1561 CONTRACTS AND ADD TO THE 750 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 811 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 4.055 MILLION OZ OCCURRED DESPITE OUR TINY $0.02 GAIN IN PRICE …THE MAJORITY OF THE OI LOSS WAS DUE TO SPREADER/T.A.S. LIQUIDATION.

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED DOWN 48.85 PTS OR 1.65% //Hang Seng CLOSED DOWN 166.52 PTS OR 0.94% // Nikkei CLOSED DOWN 4.61 OR 0.01%//Australia’s all ordinaries CLOSED UP 0.52%///Chinese yuan (ONSHORE) closed UP TO 7,2744 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2807/ Oil DOWN TO 78.15dollars per barrel for WTI and BRENT UP AT 82.06/Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A TINY SIZED 394 CONTRACTS TO 585,067 DESPITE OUR GAIN IN PRICE OF $12.75 WITH RESPECT TO TUESDAY’S TRADING. THE LONGS COULDN’T CARE LESS WITH THE RAID ORCHESTRATED BY THE CROOKS. CENTRAL BANKS ARE PATIENT. THEY WERE WAITING FOR THE ATTACK OCCURRING EARLY MONDAY MORNING AS THEY ACCUMULATED THEIR LONG PURCHASES THROUGHOUT THE DAY ESPECIALLY WHEN THE PRICE HIT BELOW 2400. THEY CONTINUED THEIR PURCHASES AND THEN TENDERED FOR PHYSICAL GOLD AT THE END OF THE MONDAY SESSION.

WE HAD A HUGE T.A.S. LIQUIDATION ON MONDAY’S LOSS IN PRICE WITH ZERO LONGS BEING CLIPPED AND SOME SHORT COVERING.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE NON ACTIVE DELIVERY MONTH OF JULY.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 2783 EFP CONTRACTS WERE ISSUED: : AUGUST2783 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2783 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 3177 CONTRACTS IN THAT 2783 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A TINY SIZED GAIN OF 394 COMEX CONTRACTS..AND THIS STRONG GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR GAIN IN PRICE OF $12.75/TUESDAY COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, MONDAY NIGHT TO EXERCISE FOR PHYSICAL GOLD.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT A FAIR SIZED 1062 CONTRACTS. MOST OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN LAST WEEK’S TRADING//RAIDS. + MONDAY’S TRADING.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JULY (11.6174 TONNES)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.6174 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $12.75 //// BUT WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS WE HAD A FAIR SIZED GAIN OF 3177 CONTRACTS ON OUR TWO EXCHANGES DESPITE THE LOSS IN PRICE. THE T.A.S. ISSUED ON MONDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 9.881 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY (7.5645 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 100 OZ QUEUE JUMP//NEW STANDING 11.6174 TONNES

NEW STANDING FOR JULY: 11.6174 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $4.40

WE HAVE REMOVED 4548 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET GAIN ON THE TWO EXCHANGES 3177 CONTRACTS OR 317700 OZ (9.881 TONNES)

Total monthly oz gold served (contracts) so far this month

3657 notices 365,700 oz 11.3748 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: nil oz

we have 1 customer deposits:

i) into Loomis: 96,453.000 oz

total 96,453.000 oz (3000 kilobars)

customer withdrawals: 0

TOTAL WITHDRAWALS nil oz

Adjustment 2

a) Customer to dealer; JPMorgan: 7716.240 oz

b) Dealer to customer Brinks: 10,320.470 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY

For the front month of JULY we have an oi of 84 contracts having LOST 1 contracts. We had 2 notices filed on MONDAY so we GAINED 1 contracts or an additional 100 oz will stand at the comex (0.00311 tonnes)

AUGUST LOST 19,215 CONTRACTS DOWN TO 210,327 CONTRACTS

SEPT. GAINED 61 CONTRACTS TO STAND AT 1146.

OCTOBER GAINED 64 CONTRACTS UP TO 46,515 CONTRACTS

We had 6 contracts filed for today representing 600 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 6 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for July /2024. contract month, we take the total number of notices filed so far for the month (3657) x 100 oz ) to which we add the difference between the open interest for the front month of JULY 84( CONTRACTS) minus the number of notices served upon today (6 x 100 oz per contract( equals 373,500 OZ OR 11.6174 TONNES.

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (3657 x 100 oz +we add the difference for front month of JULY (84 X// , OI} minus the number of notices served upon today (6) x 100 oz which equals 373,500 oz (11.6174 TONNES)

TOTAL COMEX GOLD STANDING FOR JULY: 11.6174 TONNES WHICH IS HUGE FOR THIS NOT VERY ACTIVE DELIVERY MONTH IN THE CALENDAR.

total pledged gold: 1,677,188.801 oz 52.167 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,918,886.525 OZ

TOTAL REGISTERED GOLD 7,779,286.157 ( 241.968 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,139,600.368 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,102,098 oz (REG GOLD- PLEDGED GOLD)= 189.80 tonnes //

END

SILVER/COMEX

JULY 24/2024

INITIAL

//2024// THE JULY 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

616,155.905oz

Delaware

.

Deposits to the Dealer Inventory

Deposits to the Customer Inventory

nil

No of oz served today (contracts)

2 CONTRACT(S) (.010 million OZ)

No of oz to be served (notices)

75 contracts (0.225 million oz)

Total monthly oz silver served (contracts)

6061 Contracts (30.305 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit/

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 customer deposits:

i) into Delaware 616,155.965 oz

total customer deposit 616,155.965 oz

JPMorgan has a total silver weight: 132.563million oz/301.909million or 43.70%

adjustment:

customer withdrawals: 0

total withdrawal: nil 0z

TOTAL REGISTERED SILVER: 69.377 MILLION OZ//.TOTAL REG + ELIGIBLE. 301.909 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF JULY/2024 OI: 77 CONTRACTS HAVING LOST 56 CONTRACT(S). WE HAD 45 NOTICES FILED ON MONDAY SO WE LOST 11 CONTRACTS OR AN ADDITIONAL 55,000 OZ WILL NOT STAND AT THE COMEX AS THEY WERE FERRIED OVER TO LONDON VIA AN E.F.P. TO TAKE IMMEDIATE DELIVERY OVER THERE.

AUG, SAW A LOSS OF 39 CONTRACTS TO 1306

SEPT SAW A LOSS OF 2605 CONTRACTS TO 122,207

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 2 for 0.010 MILLION oz

CONFIRMED volume; ON TUESDAY 66,679 good

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 6061 x 5,000 oz = 30.305 MILLION oz

to which we add the difference between the open interest for the front month of JULY( 77) and the number of notices served upon today 2 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY/2024 contract month: 6061 notices served so far) x 5000 oz + OI for the front month of JULY (77)x number of notices served upon today minus (2)x 5000 oz of silver standing for the JULY contract month equates to 30.680 MILLION OZ.

New total standing: 30.680 million oz.

There are 69.377 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

JULY 24 WITH GOLD UP $9.20 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 23 WITH GOLD UP $12.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 22 WITH GOLD DOWN $4.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 19 WITH GOLD DOWN $56.10 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;:A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 18 WITH GOLD DOWN $2.20 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;: ///INVENTORY RESTS AT 842.02 TONNES

JULY 17 WITH GOLD DOWN $6.60 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A MASSIVE DEPOSIT OF 5.49 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 842.02 TONNES

JULY 16 WITH GOLD UP $38.60 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 836.53 TONNES

JULY 15 WITH GOLD UP $8.15 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;: /INVENTORY RESTS AT 835.09 TONNES

JULY 12 WITH GOLD DOWN $0.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 835.09 TONNES

JULY 11 WITH GOLD UP $43.05 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;:INVENTORY RESTS AT 833.37 TONNES

JULY 10 WITH GOLD UP $12.00 ON THE DAY; HUUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.44 TONNES OF GOLD VAPOUR FROM THE GLD//.//:INVENTORY RESTS AT 833.37 TONNES

JULY 9 WITH GOLD UP $5.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD.//:INVENTORY RESTS AT 834.81 TONNES

JULY 8 WITH GOLD DOWN $26.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD.//:INVENTORY RESTS AT 834.81 TONNES

JULY 5 WITH GOLD UP $29.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD..A DEPOSIT OF 1.10 TONNES OF GOLD VAPOUR INTO THE GLD//:INVENTORY RESTS AT 833.37 TONNES

JULY 3 WITH GOLD UP $35.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD..A MASSIVE DEPOSIT OF 5.76 TONNES OF GOLD VAPOUR INTO THE GLD//:INVENTORY RESTS AT 833.37 TONNES

JULY 2 WITH GOLD DOWN $4.45 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD../:INVENTORY RESTS AT 827.61 TONNES

JULY 1 WITH GOLD DOWN $.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 28 WITH GOLD UP $3.80 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 27 WITH GOLD DOWN $16.95 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 26 WITH GOLD UP $23.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 25 WITH GOLD DOWN $13.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A STRONG WITHDRAWAL OF 2.88 TONNES OF GOLD FROM THE GLD INVENTORY RESTS AT 829.05 TONNES

JUNE 24 WITH GOLD UP$14.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A STRONG WITHDRAWAL OF 1.72 TONNES OF GOLD/NEW TOTAL TONIGHT 831.93 TONNES

JUNE 21 WITH GOLD DOWN $37.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A MAMMOTH 8.34 TONNES OF GOLD VAPOUR DEPOSIT/NEW TOTAL TONIGHT 833.65 TONNES

JUNE 20 WITH GOLD UP $23.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/://NEW TOTAL TONIGHT 825.31 TONNES

JUNE 18 WITH GOLD UP $17.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/://NEW TOTAL TONIGHT 825.31 TONNES

GLD INVENTORY: 840.01 TONNES, TONIGHTS TOTAL

SILVER

JULY 24 WITH SILVER DOWN 2 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 15.880 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 23 WITH SILVER UP 3 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 15.880 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 22 WITH SILVER UP 2 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 3.920 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 19 WITH SILVER DOWN 94 CENTS//NO CHANGES IN SILVER INVENTORY/// /INVENTORY REMAINS AT 435.854 MILLION OZ

JULY 18 WITH SILVER DOWN 13 CENTS//HUGE CHANGES IN SILVER INVENTORY” A DEPOSIT OF 2.374 MILLION OZ INTO THE SLV/// /INVENTORY RISES TO 435.854 MILLION OZ

JULY 17. WITH SILVER DOWN 75 CENTS//NO CHANGES IN SILVER INVENTORY// /INVENTORY REMAINS AT 433.480 MILLION OZ.

JULY 16. WITH SILVER UP 30 CENTS//NO CHANGES IN SILVER INVENTORY// /INVENTORY REMAINS AT 433.480 MILLION OZ.

JULY 15. WITH SILVER DOWN 24 CENTS//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 2.145 MILLION OZ FROM THE SLV.// /INVENTORY LOWERS T0 AT 433.480 MILLION OZ.

JULY 12. WITH SILVER DOWN $.65 CENTS//NO CHANGES IN SILVER INVENTORY /INVENTORY REMAINS CONSTANT AT 435.625 MILLION OZ.

JULY 11. WITH SILVER UP $.72 CENTS//HUGE CHANGES IN SILVER INVENTORY A WITHDRAWAL OF 0.731 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 435.625 MILLION OZ.

JULY 10. WITH SILVER DOWN $.04 CENTS//HUGE CHANGES IN SILVER INVENTORY A MAMMOTH WITHDRAWAL OF 3.744 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 436.356 MILLION OZ.

JULY 9. WITH SILVER UP 13 CENTS//HUGE CHANGES IN SILVER INVENTORY A MAMMOTH WITHDRAWAL OF 3.744 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 436.356 MILLION OZ.

JULY 8. WITH SILVER DOWN $0.73//SMALL CHANGES IN SILVER INVENTORY A MAMMOTH DEPOSIT OF 3,292,000 OZ OF SILVER VAPOUR INTO THE SLV.: /INVENTORY RISES T0 440.100 MILLION OZ.

JULY 4. WITH SILVER UP $0.85//SMALL CHANGES IN SILVER INVENTORY A MAMMOTH DEPOSIT OF 3,292,000 OZ OF SILVER VAPOUR INTO THE SLV.: /INVENTORY RISES T0 440.100 MILLION OZ.

JULY 3. WITH SILVER UP $1.08//SMALL CHANGES IN SILVER INVENTORY A SMALL WITHDRAWAL OF 639,000 OZ: /INVENTORY LOWERS T0 436,808 MILLION OZ.

JULY 2. WITH SILVER UP $0.19//NO CHANGES IN SILVER INVENTORY: /INVENTORY REMAINS AT 437.447 MILLION OZ./

JULY 1. WITH SILVER UP $0.05//XXX CHANGES IN SILVER INVENTORY: A DEPOSIT OF 182,000 OZ OF SILVER INTO THE SLV./.// /INVENTORY RISES AT 437.447 MILLION OZ./

JUNE 28. WITH SILVER UP $0.27//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 913,000 OZ FROM THE SLV./.// /INVENTORY REMAINS AT 437.265 MILLION OZ./

JUNE 27. WITH SILVER UP $0.01//NO CHANGES IN SILVER INVENTORY: .// /INVENTORY REMAINS AT 438.178 MILLION OZ.//

JUNE 26. WITH SILVER UP $0.03//HUGE CHANGES IN SILVER INVENTORY: A HUGE WITHDRAWAL OF 2.512 MILLION OZ OF SILVER FROM THE SLV.// /INVENTORY FALLS TO 438.178 MILLION OZ.//

JUNE 25. WITH SILVER DOWN $0.63//HUGE CHANGES IN SILVER INVENTORY: A MAMMOTH DEPOSIT OF 7.835 MILLION OZ OF SILVER VAPOUR INTO THE SLV.// /INVENTORY RISE TO 440.69 MILLION OZ.//WHAT AN ABSOLUTE FRAUD.

JUNE 24. WITH SILVER DOWN $0.05//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 2.104 MILLION OZ FROM THE SLV.// /INVENTORY LOWERS TO 432.835 MILLION OZ.

JUNE 21. WITH SILVER DOWN $1.15//NO CHANGES IN SILVER INVENTORY’// /INVENTORY REMAINS AT 434.935 MILLION OZ.

JUNE 20. WITH SILVER UP $1.17//HUGE CHANGES IN SILVER INVENTORY’ A DEPOSIT OF 5.164 MILLION OZ INTO THE SLV/// /INVENTORY RISES TO 434.929 MILLION OZ.

JUNE 18. WITH SILVER UP $0.21//NOCHANGES IN SILVER INVENTORY’ A WITHDRAWAL .730 MILLION OZ INTO THE SLV/// /INVENTORY FALLS TO 429.775 MILLION OZ.

CLOSING INVENTORY 455.666 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

end

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY

end

3.CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES