JULY 25/BLOG:YEN CARRY TRADE COLLAPSES AND THIS CAUSES MASS LIQUIDATION OF EQUITIES THROUGHOUT THE GLOBE GOLD CLOSED DOWN $60.45 TO $2415.35 WITH SILVER DOWN $$1.37 TO $27.76 AS THE BANKERS UNLEASHED MASSIVE T.A.S. ON THE COMEX//PLATINUM CLSOED DOWN $13.50 TO $937.40 WHILE PALLADIUM CLOSED DOWN $30.35 TO $906.05//GOLD COMMENTARY TODAY FROM PETER GRANDICH AND CHRIS POWELL ON THE TOPIC OF PRECIOUS METALS MANIPULATION/COMMODITY REPORT ON COCOA STATING HIGH PRICES ARWE HERE TO STAY/IN EUROPE NESTLE’S WARNS ON EARNINGS AND GUIDANCE//ISRAEL VS HAMAS: HARRIS’ NO SHOW WILL HAUNT HER ON NOV 5 AS JEWS THAT WERE VOTING DEMOCRATIC WILL SWITCH TO REPUBLICAN//ISRAEL WARNS FRANCE THAT IRAN PLOTTING TO KILL ISRAELS AT THE SUMMER GAMES//RUSSIA VS UKRAINE UPDATE/COVID UPDATES/VACCINE INJURY REPORT/SLAY NEWS ETC/DR PAUL ALEXANDER//USA DATA: JOBLESS NUMBERS REMAIN HIGH/DURABLE GOODS ORDERS COLLAPSE//PRO PALESTINIAN EURUPTION IN WASHINGTON/BLACK LIVES MATTER FURIOUS AT HARRIS SELECTION WITHOUT HAVING A SINGLE VOTE TO HER NAME: THEY WANT A MINI PRIMARY TO SELECT THE CANDIDATE//SWAMP STORIES FOR YOU TONIGHT//

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2024. CONTRACT: 2 NOTICES FOR 200 OZ or 0.00622 TONNES

total notices so far: 3675 contracts for 367500 Oz (11.430 tonnes)

FOR JULY:

SILVER NOTICES: 3 NOTICE(S) FILED FOR 0.015 million

OZ/

total number of notices filed so far this month : 6079 for 30.395 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $60.45 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ NO CHANGES IN GOLD INVENTORY AT THE GLD

/ /INVENTORY RESTS AT 841.74 TONNES

INVENTORY RESTS AT 841.74 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $1.37 AT THE SLV/WOW!! AGAIN???//HUGE MOVEMENTS

HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 3.124 MILION OZ OF SILVER OUT OF THE SLV/

// INVENTORY FALLS TO 456.620 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 456.620 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 617 CONTRACTS TO 156,489 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR TINY LOSS OF $0.02 IN SILVER PRICING AT THE COMEX ON WEDNESDAY’S TRADING ON SILVER. WE HAD HUGE LIQUIDATION DESPITE A SMALL NET LOSS OF 200 CONTRACTS ON OUR TWO EXCHANGES WE HAD A MASSIVE LIQUIDATION OF T.A.S. CONTRACTS WHICH ACCOUNTS FOR THE OI LOSS THIS IS SIMILAR TO THE COMEX GOLD TRADING. WE, AGAIN HAD SOME SHORT COVERING BY OUR SPECS DESPITE THE SMALL LOSS IN PRICE AS WELL AS THE MASSIVE T.A.S. LIQUIDATION MENTIONED ABOVE WHICH ACCOUNTS FOR THE LOSS OF OI ON THE TWO EXCHANGES. WE HAD A FAIR SIZED 324 T.A.S ISSUANCE,

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN ON FRIDAY, ON MONDAY, TUESDAY AND AGAIN LAST NIGHT.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 324 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS.IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1/2 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.02) AND WERE BASICALLY UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS FROM THEIR PERCH AS DESPITE HAVING A SMALL SIZED LOSS OF 202 CONTRACTS ON OUR TWO EXCHANGES THE MAJORITY OF THE LOSS WAS DUE TO T.A.S. /SPREADER LIQUIDATION.

WE MUST HAVE HAD:

A GOOD SIZED 415 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 28.490 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE JUMP OF 0 OZ

//NEW STANDING FOR SILVER//JUNE IS THUS 30.730 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI LOSS //GOOD SIZED EFP ISSUANCE/ VI) FAIR SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 324 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL removed 2 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY

TOTAL CONTRACTS for 18 DAYS, total 17,448 contracts: OR 87.240 MILLION OZ (970 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 87.24 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 87.240 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 617 CONTRACTS DESPITE OUR TINY LOSSS IN PRICE OF SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD EFP ISSUANCE CONTRACTS: 415 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JULY OF 28.496 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR JULY 30.730 MILLION OZ

WE HAVE A SMALL SIZED LOSS OF 202 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE TINY LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A FAIR SIZED 324 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX TRADING WHICH ACCOUNTS FOR THE MAJOR PORTION OF THE COMEX OI LOSS/// MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND MINOR IF ANY LIQUIDATION OF LONGS.

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (415) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 3 NOTICE(S) FILED TODAY FOR 0.015 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 1365 OI CONTRACTS TO 570,941 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 1297 CONTRACTS

WE HAD A FAIR SIZED DECREASE IN COMEX OI (1365 CONTRACTS) OCCURRED DESPITE OUR GAIN OF $9.20 IN PRICE/WEDNESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 7.5645 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP

NEW STANDING 11.636 TONNES

/ ALL OF THIS HAPPENED DESPITE OUR $9.20 GAIN IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A FAIR SIZED GAIN OF 2819 OI CONTRACTS (8.768 PAPER TONNES) ON OUR TWO EXCHANGES., WITH OUR LONGS TOTALLY OBLIVIOUS TO THE RAID ORCHESTRATED BY THE STUPID BANKS AGAIN ON WEDNESDAY AFTERNOON. THEY REGROUPED ON WEDNESDAY NIGHT TO ORCHESTRATE ANOTHER VICIOUS RAID. GOLD ROSE ON WEDNESDAY AS THE SHORTS REALIZED THAT LONGS WERE EXERCISING THEIR CONTRACTS VIA THE EXCHANGE FOR PHYSICAL ROUTE FOR ACTUAL PHYSICAL METAL, MUCH TO THE SHOCK FROM THE FED (THEY ARE SHORT AT A MINIMUM 109 TONNES OF GOLD). LET US SEE HOW THEIR VICIOUS RAID FARES OUT WEDNESDAY NIGHT AND THROUGHOUT THE COMEX ON THURSDAY.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4184 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 572,238

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2819 CONTRACTS WITH 1365 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 4184 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2819 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A VERY STRONG 3914 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4184 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI OF 1365 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 2819 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 7,5645 TONNES FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP

//NEW STANDING /JULY 11.636 TONNES.

/ 3) HUGE T.A.S. LIQUIDATION//SPREADER CONTRACTS WITH ZERO NET LONG SPECS BEING CLIPPED,

4) FAIR SIZED COMEX OPEN INTEREST LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///VERY STRONG T.A.S. ISSUANCE: 3914 CONTRACTS WHICH WILL BE BADLY NEEDED IN THURSDAY’S RAID.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY. :

TOTAL EFP CONTRACTS ISSUED: 88,338 CONTRACTS OF 8,833,800 OZ OR 274.76 TONNES IN 18 TRADING DAY(S) AND THUS AVERAGING: 4907 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 18 TRADING DAY(S) IN TONNES 274.76 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 274.76 DIVIDED BY 3550 x 100% TONNES = 7.46% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 274.76 TONNES (WILL BE A VERY STRONG ISSUANCE MONTH FOR EXCHANGE FOR PHYSICALS)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUG), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 617 CONTRACTS OI TO 156,489 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 415 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 415 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 415 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 617 CONTRACTS AND ADD TO THE 415 E.FP. ISSUED

WE OBTAIN A SMALL SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 202 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 1.01 MILLION OZ OCCURRED DESPITE OUR TINY $0.02 LOSS IN PRICE …THE MAJORITY OF THE OI LOSS WAS DUE TO SPREADER/T.A.S. LIQUIDATION.

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

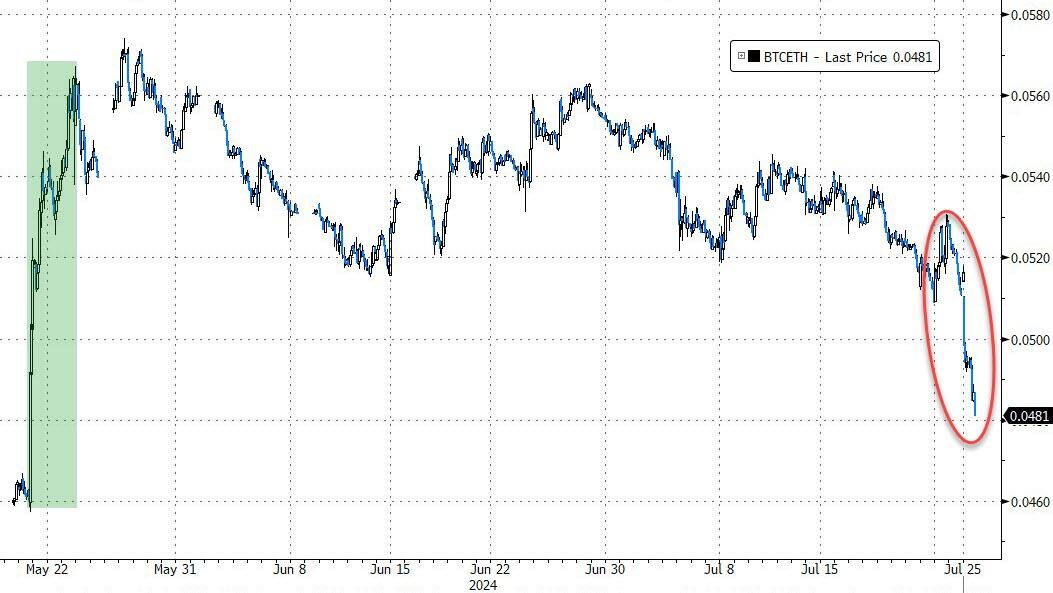

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 15.21 PTS OR 0.52% //Hang Seng CLOSED DOWN 306.08 PTS OR 1.77% // Nikkei CLOSED DOWN 1,285.34 OR 3.28%//Australia’s all ordinaries CLOSED DOWN 1.36%///Chinese yuan (ONSHORE) closed UP TO 7,184 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2187/ Oil DOWN TO 76.61dollars per barrel for WTI and BRENT DOWN AT 80.46Stocks in Europe OPENED ALL RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1365 CONTRACTS TO 570,941 DESPITE OUR STRONG GAIN IN PRICE OF $9.20 WITH RESPECT TO WEDNESDAY’S TRADING. THE LONGS COULDN’T CARE LESS WITH THE ATTEMPTED RAID ORCHESTRATED BY THE CROOKS. CENTRAL BANKS ARE PATIENT. THEY WERE WAITING FOR THE ATTACK OCCURRING EARLY WEDNESDAY MORNING AS THEY ACCUMULATED THEIR LONG PURCHASES THROUGHOUT THE DAY ESPECIALLY WHEN THE PRICE HIT BELOW 2400. THEY CONTINUED THEIR PURCHASES AND THEN TENDERED FOR PHYSICAL GOLD AT THE END OF THE WEDNESDAY SESSION. THE REASON FOR THE LOSS IN COMEX IS DUE TO SPREADERS LIQUIDATING AS WELL AS T.A.S LIQUIDATION. THUS:

WE HAD A STRONG T.A.S. LIQUIDATION ON WEDNESDAY’S GAIN IN PRICE WITH ZERO LONGS BEING CLIPPED AND MAJOR SHORT COVERING. THE SHORTS ARE ABANDONING SHIP: THEY WILL NOW REGROUP AND RAID WHEN THERE IS LITTLE COUNTERPARTY. THE RAID ORCHESTRATED FOR THURSDAY WILL BE VICIOUS.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE NON ACTIVE DELIVERY MONTH OF JULY.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 4184 EFP CONTRACTS WERE ISSUED: : AUGUST2833 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4184 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2819 CONTRACTS IN THAT 4116 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A FAIR SIZED LOSS OF 1365 COMEX CONTRACTS..AND THIS STRONG GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $9.20/WEDNESDAY COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, WEDNESDAY NIGHT TO EXERCISE FOR PHYSICAL GOLD.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT A STRONG SIZED 4184 CONTRACTS. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN LAST WEEK’S TRADING//RAIDS AS WELL AS THIS WEEK.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JULY (11.6360 TONNES)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.636 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $9.20 //// AND WERE UNSUCCESSFUL IN KNOCKING ANY SPECULATOR LONGS AS, EVEN THOUGH WE HAD A FAIR SIZED GAIN OF 2819 CONTRACTS ON OUR TWO EXCHANGES, THE LOSS IN COMEX OI WAS DUE TO EARLY SPREADER LIQUIDATION/T.A.S. LIQUIDATION AS THE SHORTS CONTINUE TO RUN FROM THE HILLS,SENSING DANGER FROM THEIR STUPID SHORTING . THE T.A.S. ISSUED ON WEDNESDAY NIGHT WILL BE “PUT INTO THE BANK” TO BE USED AT A LATER DATE AT THE COLLUSIVE CHOOSING OF OUR BANKERS.

WE HAVE GAINED A TOTAL OI OF 8.768 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY (7.5645 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP//NEW STANDING 11.636 TONNES

NEW STANDING FOR JULY: 11.636 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $9.20

WE HAVE REMOVED 1297 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET GAIN ON THE TWO EXCHANGES 2819 CONTRACTS OR 2819000 OZ (8.768 TONNES)

Total monthly oz gold served (contracts) so far this month

3675 notices 367,500 oz 11.430 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: nil oz

we have 1 customer deposits:

Into Brinks 48,766.07 oz (real gold)

total deposits 48,766.07 oz

withdrawals: 0

i

TOTAL WITHDRAWALS nil oz

Adjustment 1

b) dealer to customer Brinks : 13,599.873 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY

For the front month of JULY we have an oi of 68 contracts having LOST 16 contracts. We had 16 notices filed on WEDNESDAY so we GAINED 0 contracts or an additional NIL oz will stand at the comex (0.0000 tonnes)

AUGUST LOST 39,460 CONTRACTS DOWN TO 144,001 CONTRACTS

SEPT. GAINED 117 CONTRACTS TO STAND AT 1420.

OCTOBER GAINED 3010 CONTRACTS UP TO 51,453 CONTRACTS

We had 2 contracts filed for today representing 200 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 2 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for July /2024. contract month, we take the total number of notices filed so far for the month (3675) x 100 oz ) to which we add the difference between the open interest for the front month of JULY 68( CONTRACTS) minus the number of notices served upon today (2 x 100 oz per contract( equals 374,100 OZ OR 11.636 TONNES.

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (3675 x 100 oz +we add the difference for front month of JULY (68 X// , OI} minus the number of notices served upon today (2) x 100 oz which equals 374,100 oz (11.636 TONNES)

TOTAL COMEX GOLD STANDING FOR JULY: 11.636 TONNES WHICH IS HUGE FOR THIS NOT VERY ACTIVE DELIVERY MONTH IN THE CALENDAR.

total pledged gold: 1,677,188.801 oz 52.167 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,964,341.02 OZ

TOTAL REGISTERED GOLD 8,156,320.108 ( 253.69 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,808,020.108 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,479,132 oz (REG GOLD- PLEDGED GOLD)= 201.52 tonnes //

END

SILVER/COMEX

JULY 25/2024

INITIAL

//2024// THE JULY 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

585,095.005oz

Delaware

.

Deposits to the Dealer Inventory

Deposits to the Customer Inventory

640,766.116 oz CNT

No of oz served today (contracts)

3 CONTRACT(S) (.015 million OZ)

No of oz to be served (notices)

67 contracts (0.335 million oz)

Total monthly oz silver served (contracts)

6079 Contracts (30.395 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit/

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 customer deposits:

i) into CNT 640,766.044 oz

total customer deposit 640,766.044 oz

JPMorgan has a total silver weight: 132.563million oz/303.163million or 43.54%

adjustment:0

customer withdrawals: 1

i) Out of Delaware 585,095.005 oz

total withdrawal: 585,095.005 0z

TOTAL REGISTERED SILVER: 69.377 MILLION OZ//.TOTAL REG + ELIGIBLE. 303.163 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF JULY/2024 OI: 70 CONTRACTS HAVING LOST 15 CONTRACT(S). WE HAD 15 NOTICES FILED ON WEDNESDAY SO WE GAINED 0 CONTRACTS OR AN ADDITIONAL NIL OZ WILL STAND AT THE COMEX

AUG, SAW A LOSS OF 168 CONTRACTS TO 1106

SEPT SAW A LOSS OF 1548 CONTRACTS TO 118,259

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 3 for 0.015 MILLION oz

CONFIRMED volume; ON WEDNESDAY 60,212 good

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 6079 x 5,000 oz = 30.395 MILLION oz

to which we add the difference between the open interest for the front month of JULY( x70) and the number of notices served upon today 3 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY/2024 contract month: 6079 notices served so far) x 5000 oz + OI for the front month of JULY (70)x number of notices served upon today minus (3)x 5000 oz of silver standing for the JULY contract month equates to 30.730 MILLION OZ.

New total standing: 30.730 million oz.

There are 69.377 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

JULY 25 WITH GOLD DOWN $60.45 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 841.74 TONNES

JULY 24 WITH GOLD UP $12.75 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1,73 TOONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 841.74 TONNES

JULY 23 WITH GOLD UP $12.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 22 WITH GOLD DOWN $4.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 19 WITH GOLD DOWN $56.10 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;:A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 18 WITH GOLD DOWN $2.20 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;: ///INVENTORY RESTS AT 842.02 TONNES

JULY 17 WITH GOLD DOWN $6.60 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A MASSIVE DEPOSIT OF 5.49 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 842.02 TONNES

JULY 16 WITH GOLD UP $38.60 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 836.53 TONNES

JULY 15 WITH GOLD UP $8.15 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;: /INVENTORY RESTS AT 835.09 TONNES

JULY 12 WITH GOLD DOWN $0.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 835.09 TONNES

JULY 11 WITH GOLD UP $43.05 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;:INVENTORY RESTS AT 833.37 TONNES

JULY 10 WITH GOLD UP $12.00 ON THE DAY; HUUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.44 TONNES OF GOLD VAPOUR FROM THE GLD//.//:INVENTORY RESTS AT 833.37 TONNES

JULY 9 WITH GOLD UP $5.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD.//:INVENTORY RESTS AT 834.81 TONNES

JULY 8 WITH GOLD DOWN $26.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD.//:INVENTORY RESTS AT 834.81 TONNES

JULY 5 WITH GOLD UP $29.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD..A DEPOSIT OF 1.10 TONNES OF GOLD VAPOUR INTO THE GLD//:INVENTORY RESTS AT 833.37 TONNES

JULY 3 WITH GOLD UP $35.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD..A MASSIVE DEPOSIT OF 5.76 TONNES OF GOLD VAPOUR INTO THE GLD//:INVENTORY RESTS AT 833.37 TONNES

JULY 2 WITH GOLD DOWN $4.45 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD../:INVENTORY RESTS AT 827.61 TONNES

JULY 1 WITH GOLD DOWN $.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 28 WITH GOLD UP $3.80 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 27 WITH GOLD DOWN $16.95 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 26 WITH GOLD UP $23.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 25 WITH GOLD DOWN $13.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A STRONG WITHDRAWAL OF 2.88 TONNES OF GOLD FROM THE GLD INVENTORY RESTS AT 829.05 TONNES

JUNE 24 WITH GOLD UP$14.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A STRONG WITHDRAWAL OF 1.72 TONNES OF GOLD/NEW TOTAL TONIGHT 831.93 TONNES

JUNE 21 WITH GOLD DOWN $37.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A MAMMOTH 8.34 TONNES OF GOLD VAPOUR DEPOSIT/NEW TOTAL TONIGHT 833.65 TONNES

JUNE 20 WITH GOLD UP $23.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/://NEW TOTAL TONIGHT 825.31 TONNES

JUNE 18 WITH GOLD UP $17.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/://NEW TOTAL TONIGHT 825.31 TONNES

GLD INVENTORY: 841.74 TONNES, TONIGHTS TOTAL

SILVER

JULY 24 WITH SILVER DOWN $1.37//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 3.124 MILLION OZ OF SILVER OUT OF THE SLV./// /INVENTORY FALLS TO 456.670 MILLION OZ

JULY 24 WITH SILVER UP 3 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 15.880 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 23 WITH SILVER UP 3 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 15.880 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 22 WITH SILVER UP 2 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 3.920 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 19 WITH SILVER DOWN 94 CENTS//NO CHANGES IN SILVER INVENTORY/// /INVENTORY REMAINS AT 435.854 MILLION OZ

JULY 18 WITH SILVER DOWN 13 CENTS//HUGE CHANGES IN SILVER INVENTORY” A DEPOSIT OF 2.374 MILLION OZ INTO THE SLV/// /INVENTORY RISES TO 435.854 MILLION OZ

JULY 17. WITH SILVER DOWN 75 CENTS//NO CHANGES IN SILVER INVENTORY// /INVENTORY REMAINS AT 433.480 MILLION OZ.

JULY 16. WITH SILVER UP 30 CENTS//NO CHANGES IN SILVER INVENTORY// /INVENTORY REMAINS AT 433.480 MILLION OZ.

JULY 15. WITH SILVER DOWN 24 CENTS//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 2.145 MILLION OZ FROM THE SLV.// /INVENTORY LOWERS T0 AT 433.480 MILLION OZ.

JULY 12. WITH SILVER DOWN $.65 CENTS//NO CHANGES IN SILVER INVENTORY /INVENTORY REMAINS CONSTANT AT 435.625 MILLION OZ.

JULY 11. WITH SILVER UP $.72 CENTS//HUGE CHANGES IN SILVER INVENTORY A WITHDRAWAL OF 0.731 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 435.625 MILLION OZ.

JULY 10. WITH SILVER DOWN $.04 CENTS//HUGE CHANGES IN SILVER INVENTORY A MAMMOTH WITHDRAWAL OF 3.744 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 436.356 MILLION OZ.

JULY 9. WITH SILVER UP 13 CENTS//HUGE CHANGES IN SILVER INVENTORY A MAMMOTH WITHDRAWAL OF 3.744 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 436.356 MILLION OZ.

JULY 8. WITH SILVER DOWN $0.73//SMALL CHANGES IN SILVER INVENTORY A MAMMOTH DEPOSIT OF 3,292,000 OZ OF SILVER VAPOUR INTO THE SLV.: /INVENTORY RISES T0 440.100 MILLION OZ.

JULY 4. WITH SILVER UP $0.85//SMALL CHANGES IN SILVER INVENTORY A MAMMOTH DEPOSIT OF 3,292,000 OZ OF SILVER VAPOUR INTO THE SLV.: /INVENTORY RISES T0 440.100 MILLION OZ.

JULY 3. WITH SILVER UP $1.08//SMALL CHANGES IN SILVER INVENTORY A SMALL WITHDRAWAL OF 639,000 OZ: /INVENTORY LOWERS T0 436,808 MILLION OZ.

JULY 2. WITH SILVER UP $0.19//NO CHANGES IN SILVER INVENTORY: /INVENTORY REMAINS AT 437.447 MILLION OZ./

JULY 1. WITH SILVER UP $0.05//XXX CHANGES IN SILVER INVENTORY: A DEPOSIT OF 182,000 OZ OF SILVER INTO THE SLV./.// /INVENTORY RISES AT 437.447 MILLION OZ./

JUNE 28. WITH SILVER UP $0.27//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 913,000 OZ FROM THE SLV./.// /INVENTORY REMAINS AT 437.265 MILLION OZ./

JUNE 27. WITH SILVER UP $0.01//NO CHANGES IN SILVER INVENTORY: .// /INVENTORY REMAINS AT 438.178 MILLION OZ.//

JUNE 26. WITH SILVER UP $0.03//HUGE CHANGES IN SILVER INVENTORY: A HUGE WITHDRAWAL OF 2.512 MILLION OZ OF SILVER FROM THE SLV.// /INVENTORY FALLS TO 438.178 MILLION OZ.//

JUNE 25. WITH SILVER DOWN $0.63//HUGE CHANGES IN SILVER INVENTORY: A MAMMOTH DEPOSIT OF 7.835 MILLION OZ OF SILVER VAPOUR INTO THE SLV.// /INVENTORY RISE TO 440.69 MILLION OZ.//WHAT AN ABSOLUTE FRAUD.

JUNE 24. WITH SILVER DOWN $0.05//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 2.104 MILLION OZ FROM THE SLV.// /INVENTORY LOWERS TO 432.835 MILLION OZ.

JUNE 21. WITH SILVER DOWN $1.15//NO CHANGES IN SILVER INVENTORY’// /INVENTORY REMAINS AT 434.935 MILLION OZ.

JUNE 20. WITH SILVER UP $1.17//HUGE CHANGES IN SILVER INVENTORY’ A DEPOSIT OF 5.164 MILLION OZ INTO THE SLV/// /INVENTORY RISES TO 434.929 MILLION OZ.

JUNE 18. WITH SILVER UP $0.21//NOCHANGES IN SILVER INVENTORY’ A WITHDRAWAL .730 MILLION OZ INTO THE SLV/// /INVENTORY FALLS TO 429.775 MILLION OZ.

CLOSING INVENTORY 456.67 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

end

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY

A global equity crisis is leading at the margin to liquidation of speculative long positions in gold and silver futures. It looks like a crisis is just starting.

After declines in gold and silver prices in the second half of last week, this week started on a steady note, before heading south yesterday afternoon. In early morning trade in New York today (Thursday), gold was $2370, down $30 from last Friday, and silver at $27.60 was down $1.60.

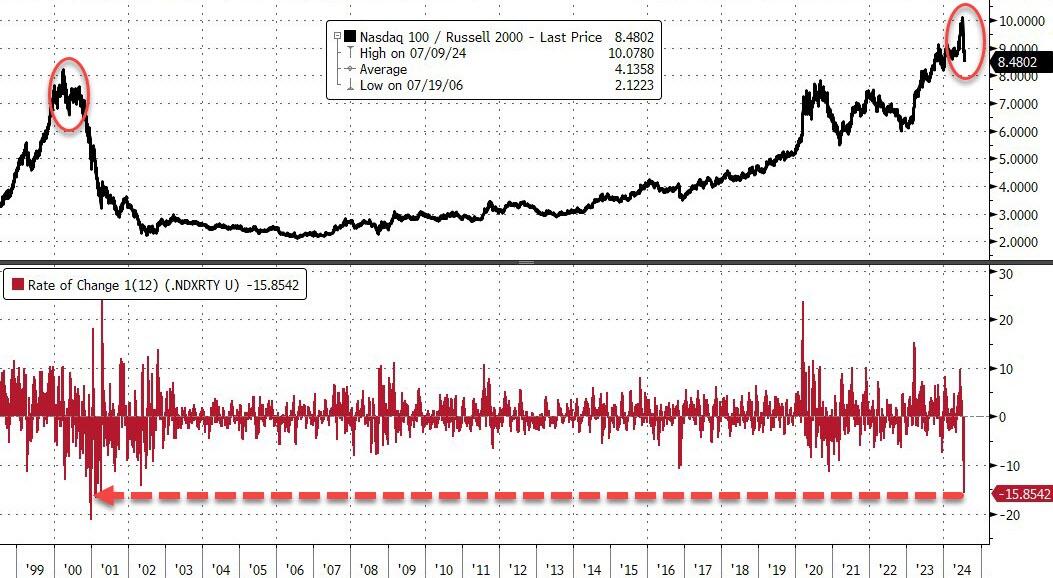

The reason for this sudden development has little to do with gold and silver per se but is due to a developing panic in equities. While the US tech bubble was running out of steam, the rot set in in Japan, with the Nikkei falling over 10% since 11 July. At the same time, the yen has rallied strongly, both moves shown in our next charts.

Japanese institutions faced substantial losses on their domestic portfolios, and the rally in the yen also imposes losses on their foreign investments. It is hardly surprising that they are panic sellers of Japanese equities and US equities alike.

Other markets Japanese investors are known to be long include France and Italy, whose major indices have also fallen, 2% and 2.5% respectively this morning.

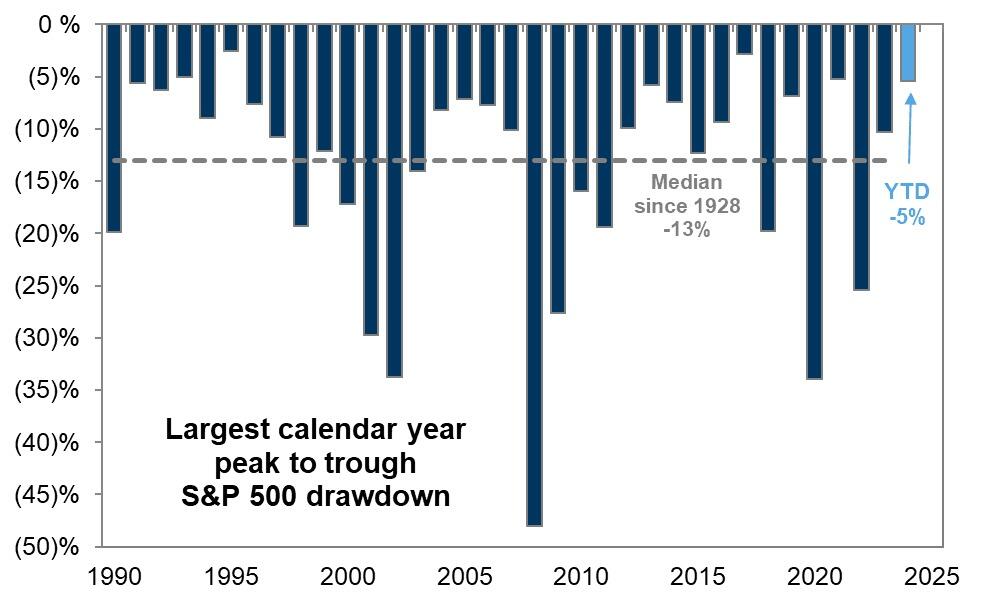

Since US equities peaked last week, the S&P 500 Index has fallen nearly 5%, with large caps badly hit. Consequently, hedge funds geared to rising tech stocks have been forced to liquidate long positions, and these are often the same players in the Managed Money category in Comex gold and silver contracts.

The first whiff of distress sees buyers vanish and the bullion banks in the Swaps category are taking the opportunity to mark paper market values down. At the same time buyers of bullion sense that this distress will provide a buying opportunity at lower prices, and at the margin will be withdrawing their bids. But when buyers do return, it is likely to turbocharge silver. The gold/silver ratio has risen to 85 on silver’s markdown (for that’s what it is). This is our next chart.

There is no knowing how long or how deep the panic in equities will go. But at a guess, it won’t be long before the gathering speculation is of crisis and that the Fed will need to reduce interest rates urgently to stop it. At that point in time, foreign holders of dollars are likely to turn sellers of dollars more aggressively, perhaps buying other major currencies (including the rising yen) but particularly gold, silver and base metals.

This is making sense of China’s policy of stockpiling commodities. The Economist and other media have recently reported buying of oil and grain beyond her consumption needs, as well as copper and other metals. Speculative explanations abound, but none have twigged that it’s about dumping dollars and euros as much, if not more than acquiring commodities.

In the very short term, for gold and silver prices it looks like being a volatile, rough ride. But perhaps this is the widely expected crisis. If so, it didn’t start with a bank run or a debt crisis, but a good old fashioned equity crash. The rest follows, and as safe havens from a major credit crisis gold and silver as money without counterparty risk will shine.

end

3.CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES

An excellent discussion on how the precious metals prices have been manipulated for over 25 years

(Chris Powell/Grandich)

Market analyst Peter Grandich discusses GATA’s work with secretary/treasurer

Submitted by admin on Wed, 2024-07-24 18:17 Section: Daily Dispatches

6:19p ET Wednesday, July 24, 2024

Dear Friend of GATA and Gold:

Market analyst and monetary metals advocate Peter Grandich today discussed with your secretary/treasurer GATA’s 25 years of exposing manipulation of the monetary metals markets, work that has led to central banks restoring and increasing their gold reserves, as well as to the disappearance of market analysts who ridiculed assertions of market rigging only to find them documented extensively year after year.

Also discussed was your secretary/treasurer’s recent compilation of evidence that the U.S. government is behind the continuing suppression of silver prices:

Why is the price of gold rising if the global economy is not in recession and inflation is under control? This is a question often heard in investment circles, and I will try to answer it.

We must begin by clarifying the question. It is true that inflation is slowly decreasing, but we cannot say that it is fully under control. Let us remember that the latest Consumer Price Index data in the United States was 3 percent annualized and that in the eurozone it is 2.6 percent, with eight countries publishing data above 3 percent, including Spain. This is why central banks are maintaining rates or lowering them very cautiously.

However, monetary policy is far from being restrictive. Money supply growth is picking up, the European Central Bank (ECB) is maintaining its “anti-fragmentation mechanism,” and the Federal Reserve is continuing to inject money through the liquidity window. We can say, without a doubt, that monetary policy is accommodative.

At the time of writing, the price of gold is above $2,400 an ounce, up 16.5 percent between January and July 19, 2024. In the same period, gold has performed better than the S&P 500, the Stoxx 600 in Europe, and the MSCI Global. In fact, over the past five years, gold has outperformed not only the European and global stock markets but also the S&P 500, with only the Nasdaq surpassing the precious metal.

This is a period of recovery and strong expansion of the stock markets. On the one hand, the market is discounting the central banks’ continued accommodative and expansionary policies, even with high debt monetization, given the elevated deficits in the United States and developed countries. That is, the market assumes that the Federal Reserve and the ECB will not be able to maintain the reduction of their balance sheets in the face of rising debt and public spending in many economies. As a result, gold protects many investors against the erosion of the currency’s purchasing power, i.e., inflation, without the extreme volatility of Bitcoin. If the market discounts further monetary expansion to cover the accumulated deficits, it is normal for the investor to seek protection with gold, which has centuries of history as an alternative to fiduciary money and offers a low-volatility hedge against currency debasement.

Another important factor is the central bank’s purchase of gold. JP Morgan is credited with the phrase, “Gold is money and everything else is credit.” All the world’s central banks include treasury bonds from countries that serve as the global reserve currency in their asset base. This allows central banks around the world to stabilize their currencies. When we read that a central bank buys or sells dollars or euros, it is not making transactions with physical currency but with government bonds. Hence, as the market price of government bonds has fallen between 2022 and 2024, many of these central banks are facing latent losses or a drop in the value of their assets. What is the best way to strengthen a central bank’s balance sheet, thereby diversifying and reducing exposure to fiat currencies? Purchase gold.

The rising purchase of gold by central banks is an essential factor justifying the recent increase in demand for the precious metal. Central banks, especially in China and India, are trying to reduce their dependence on the dollar or the euro to diversify their reserves. However, this does not mean de-dollarization. Far from it.

According to the World Gold Council, central banks accelerated their gold purchases to more than 1,000 tonnes per year in 2022 and 2023. This means that monetary authorities account for almost a quarter of the annual demand for gold during a period when supply and production have not grown significantly. The ratio of output to demand stands at 0.9 in June 2024, according to Morgan Stanley.

Global official gold reserves have increased by 290 net metric tons in the first quarter of 2024, the highest since 2000, according to the World Gold Council, 69 percent higher than the five-year quarterly average (171 metric tons).

The People’s Bank of China and the Central Bank of India are the biggest buyers as they aim to balance their reserves, adding more gold without compromising their dollar position. According to Metals Focus, Refinitiv GFMS, and the World Gold Council, China has been increasing its gold purchases for 17 months, and since 2022, it has shot up its reserves by 16 percent, coinciding with the increase in global polarization and the trade war.

That does not mean de-dollarization, as the People’s Bank of China has 4.6 percent of its total reserves in gold. U.S. Treasury bonds are the most important asset, accounting for more than 50 percent of the Chinese central bank’s assets. Its goal is to raise gold reserves to 14 percent, according to local media. This would imply a significant annual purchase of gold for years.

India’s central bank increased its gold reserves by 19 metric tons during the first quarter. Other central banks that are diversifying and buying more gold than ever are the National Bank of Kazakhstan, the Monetary Authority of Singapore, the Central Bank of Qatar, the Central Bank of Turkey, and the Central Bank of Oman, according to the sources cited above. During this period, both the Czech National Bank and the National Bank of Poland increased their gold reserves in Europe, reaching the highest level since 2021. In these cases, the aim is to balance the exposure in the asset base with more gold and less eurozone government bonds.

The goal of this central bank trend is to increase the weight of an asset that does not fluctuate with the price of government bonds. It is not about de-dollarization but about balancing the balance sheet. For years, the policy of central banks has been to reduce their gold holdings, and now they must rebalance after suffering two years of latent losses on their government bond holdings. In fact, one could say that the world’s central banks anticipate a widespread erosion of the purchasing power of reserve currencies due to the saturation of fiscal and monetary policies, and for that reason, they need more gold.

After years of thinking that money can be printed without limits and without creating inflation, monetary authorities are trying to return to logic and have more gold on their balance sheets. At the same time, many expected that the trade war between China and the United States and global polarization would be reversed in the past four years, and the opposite has happened. It has accelerated. Now the latent losses in the sovereign bond asset portfolio are leading all these central banks to buy more gold and try to protect themselves from new bursts of inflationary pressures.

In an era of high correlation between assets and perpetual monetary expansion, gold serves as a low-volatility, low-correlation, and strong return addition to any prudent portfolio.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times or ZeroHedge.

4. GOLD PODCASTS//LIVE FROM THE VAULT

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COCOA

Cocoa ,high prices still climbing and this will accentuate global slowdown

(zerohedge)

Swiss Chocolatier Warns High Cocoa Prices Resulting In Global Slowdown In Chocolate Market

THURSDAY, JUL 25, 2024 – 04:15 AM

Chocolate maker Lindt & Spruengli AG has warned the global chocolate market is under strain due to high prices. Reducing demand is necessary to prevent cocoa prices from surging once again amid persistent cocoa supply issues stemming from adverse weather conditions impacting some of the world’s largest farms in West Africa.

Bloomberg reports that Lindt CEO Adalbert Lechner told investors during an earnings call on Tuesday that the global chocolate market was experiencing a slowdown for some products due to rising cocoa prices. He said price hikes for consumers partially offset higher cocoa bean costs for the Swiss chocolatier and confectionery company, adding that cost inflation will ramp up into next year.

“It is quite difficult to predict where the futures market will go from here and how quickly we will see a further correction,” Lechner told investors.

He said, “The speed and the extent of the market correction will also depend a lot on the impact of the overall volume demand in the chocolate market.”

Cocoa futures in New York have been oscillating in what some call a ‘symmetrical triangle’ since prices peaked at $12,000 a ton in April. This followed a massive run-up early this year fueled by a historic shortage in West Africa due to poor harvests. The $8,000 level is a price magnet as traders wait for new harvest or demand data.

“It is still early in the season” to predict harvest figures, “which may keep the market in a back-and-forth pattern,” according to a Tuesday ADM Investor Services note.

Cocoa prices have been supported by better-than-expected demand and poor harvest figures. Some analysts believe prices might need to go higher to achieve proper demand destruction.

END

ASIA TRADING/THURSDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED DOWN 15.21 PTS OR 0.52% //Hang Seng CLOSED DOWN 306.08 PTS OR 1.77% // Nikkei CLOSED DOWN 1,285.34 OR 3.28%//Australia’s all ordinaries CLOSED DOWN 1.36%///Chinese yuan (ONSHORE) closed UP TO 7,184 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2187/ Oil DOWN TO 76.61dollars per barrel for WTI and BRENT DOWN AT 80.46Stocks in Europe OPENED ALL RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGSTHURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2184

OFFSHORE YUAN: UP TO 7.2187

SHANGHAI CLOSED DOWN 15.21 PTS OR 0.52 %

HANG SENG CLOSED DOWN 306.08 PTS OR 1.77%

2. Nikkei closed DOWN 1285.34 PTS OR 3.28%

3. Europe stocks SO FAR: ALL RED

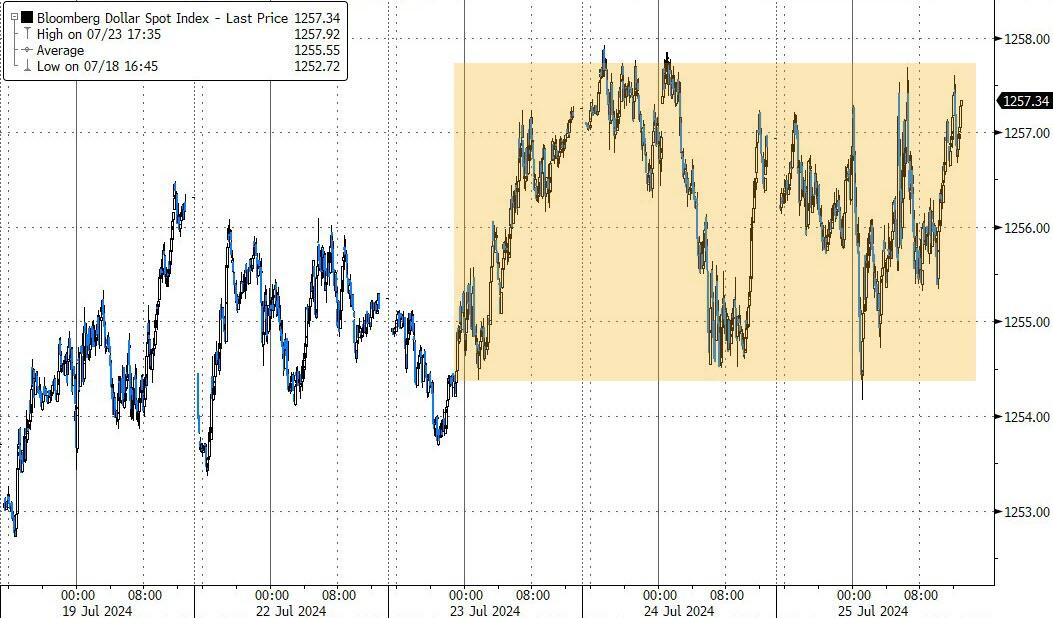

USA dollar INDEX DOWN TO 103.98 EURO RISES TO 1.0848 UP 9 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1,059 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 152.39 JAPANESE YEN NOW RISING AS WE HAVE NOW REACHED THE END OF THE YEN CARRY TRADE

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

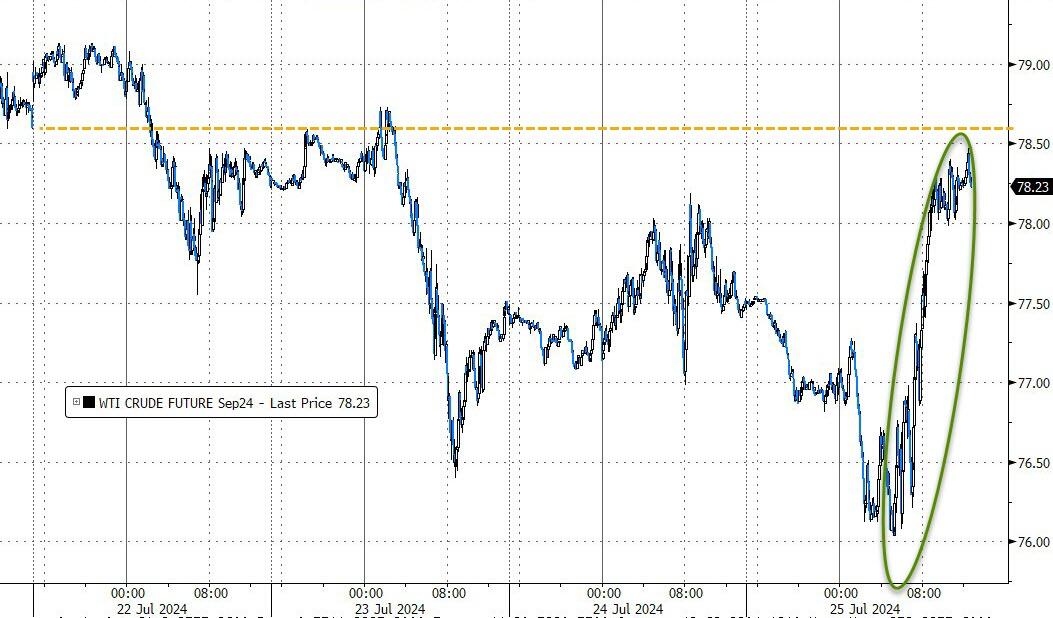

3g Oil DOWN for WTI and DOWN FOR Brent this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.4010/Italian 10 Yr bond yield DOWN to 3.778 SPAIN 10 YR BOND YIELD DOWN TO 3.236%

3i Greek 10 year bond yield DOWN TO 3.410

3j Gold at $2370.90//Silver at: 27.61 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 98/ 100 roubles/dollar; ROUBLE AT 85.25

3m oil into the 77 dollar handle for WTI and 80 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 152.39/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.059% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8781 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9522 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.223 DOWN 6 BASIS PTS…

USA 30 YR BOND YIELD: 4.496 DOWN 5 BASIS PTS/

USA 2 YR BOND YIELD: 4.361 DOWN 7 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 33.07…

10 YR UK BOND YIELD: 4.1520 DOWN 2 PTS

10 YR CANADA BOND YIELD: 3.353 DOWN 7 BASIS PTS

2a New York OPENING REPORT

Futures Drop As Japan, European Stocks Tumble On AI Bubble Bursting Fears

THURSDAY, JUL 25, 2024 – 08:19 AM

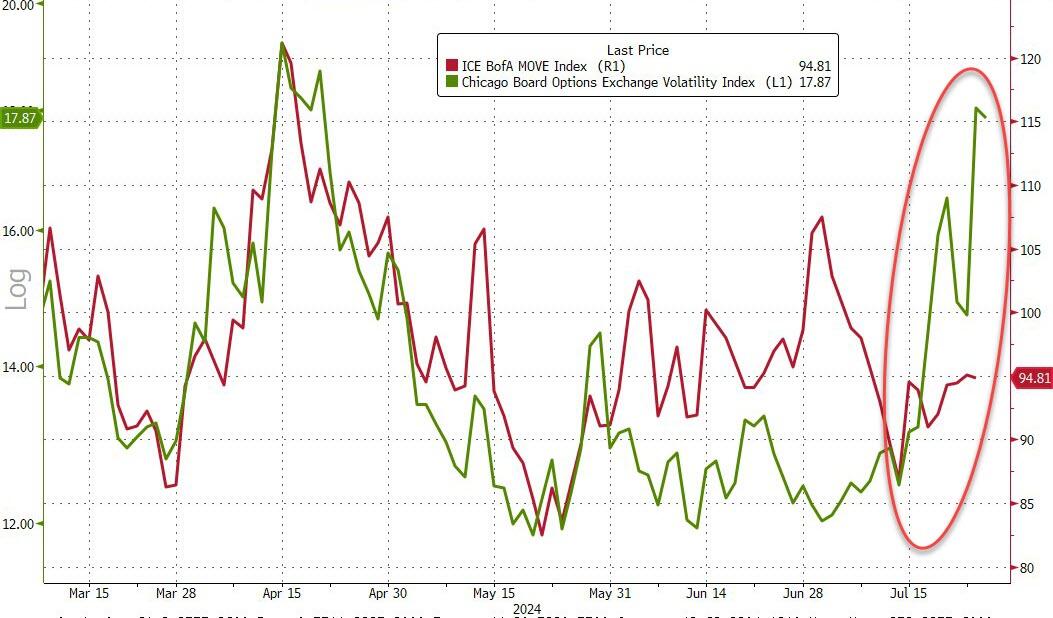

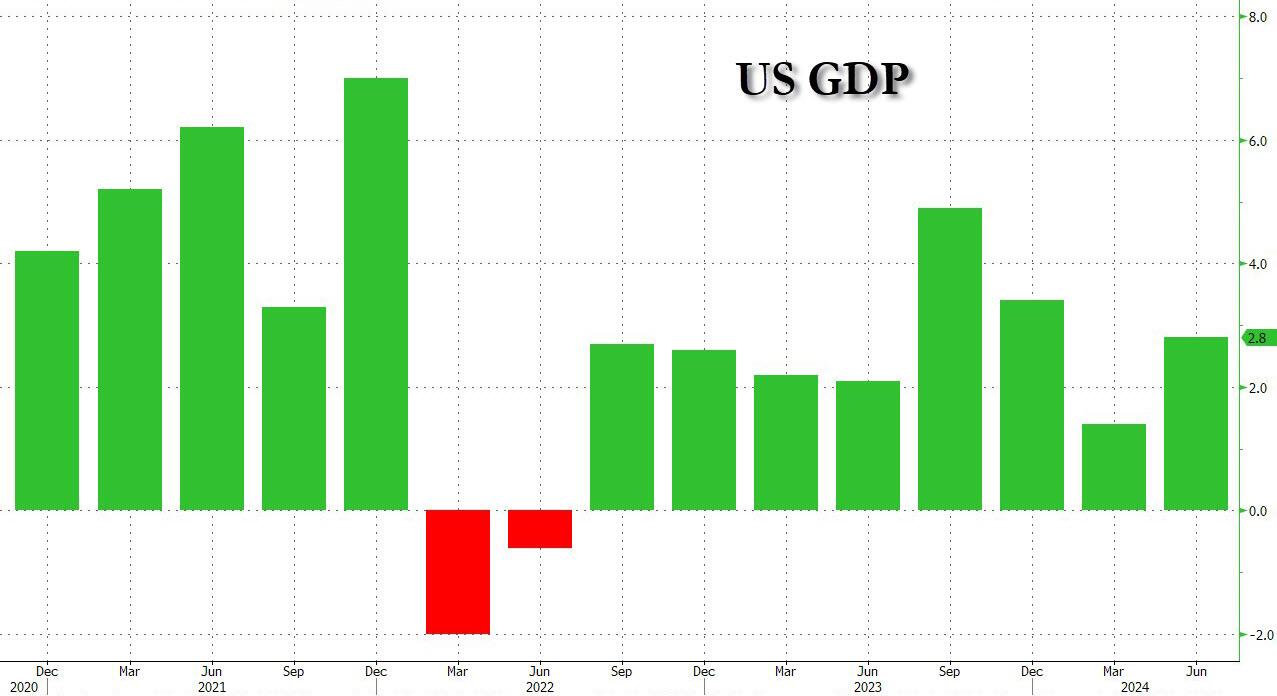

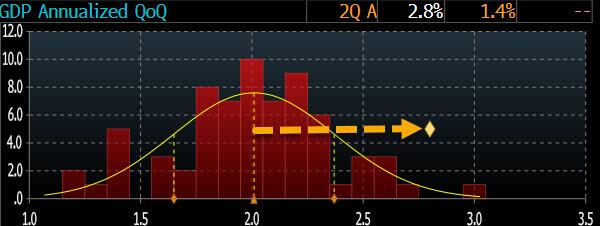

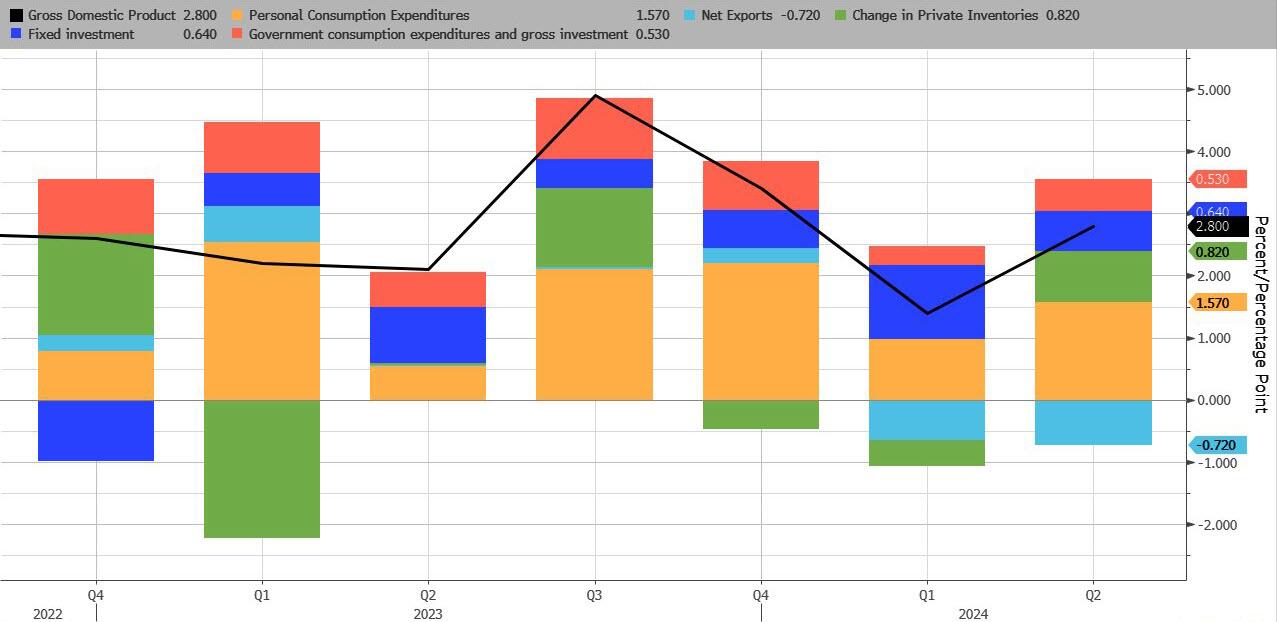

US equity futures are lower but well off their worst levels, after a rout in Japan sent the Nikkei tumbling, hammered gold and crypto as the yen carry trade unwound – if only until next week when the BOJ inevitably disappoints yet again. As of 7:50am, S&P futures were 0.1% lower, while Nasdaq futs dropped 0.2%, with tech giants are mixed pre-market trading: AAPL -43bp, NVDA -20bp, AMZN +23bp, GOOG/L +27bp. Wednesday’s session was a bloodbath: the index finally broke a 356 day streak without a down 2% (or greater) move – the longest streak since 2007, when it went 943 days without a down >2% move – as the S&P fell -2.3% (worst day since Dec ’22), NDX fell -3.7% (worst session since Oct ’22), Mag Seven -6% (worst session since Nov ’22), AI winners down -5% to -10%, and Index vol spike (VIX > 18 for first time since April). Bond yields are 5-8bp led by the front end. Commodities are weaker: WTI fell -1.8%; base metals are mostly lower. The USD is lower but also well off its worst levels. Today, the macro data focus will be 2Q data release: Consensus expects GDP to print 2.0% QoQ saar vs. 1.4% prior, driven by a rebound in personal consumption to 2.0% vs 1.5% in Q1.

In premarket trading, IBM shares rose 4.3% after the IT services company reported second-quarter results that beat expectations, with the company’s software division notably strong. IBM also said its generative AI book has grown to more than $2 billion. Ford plunged -13% after the automaker reported adjusted earnings per share for the second quarter that missed the average analyst estimate. Analysts note that unwelcome warranty headwinds drove the company’s significant miss. Chipotle shares jumped 3.5% after the burrito chain reported second-quarter comparable sales that beat consensus expectations. Analysts said traffic growth was strong, and highlighted management taking action to address negative publicity over portion size. Here are some other notable premarket movers:

Day One Biopharmaceuticals shares gain 9.2% after Ipsen enters into an exclusive ex-US licensing agreement with the biotechnology company to commercialize tovorafenib for the most common childhood brain tumor.

Edwards Life shares tumble 23% after the maker of heart valves reported sales for the second quarter that missed the average analyst estimate. The medical-devices company also said it has agreed to buy JenaValve Technology and Endotronix for about $1.2 billion.

Las Vegas Sands shares fall 3.5% after the casino operator reported net revenue for the second quarter that missed the average analyst estimate. Analysts noted weakness in Macau and disruptions caused by casino renovations as headwinds.

Lululemon shares fall 2.0% after Citigroup cut its recommendation on the athleisure apparel maker to neutral from buy. The analyst notes that the active-apparel category has slowed this year and is expected to cool further.

Viking Therapeutics shares climb 18% after the drug developer said it is advancing its weight-loss shot into a late-stage trial. The biotech also said a mid-stage trial of its obesity pill will start in the fourth quarter.

As the global economy slows, traders have also started ramping up bets that the Fed will have to cut interest rates sooner than expected to sustain the US economy. Yields on two-year Treasuries dropped seven basis points to 4.35%. The yen rallied more than 1% on bets the rate gap between Japan and the US will shrink.

“We are getting disappointment after disappointment,” said Florian Ielpo, head of macro research at Lombard Odier Asset Management. “The message is that maybe growth is weaker than the US data led us to think, and maybe it’s time to reshuffle allocations away from US large tech.”

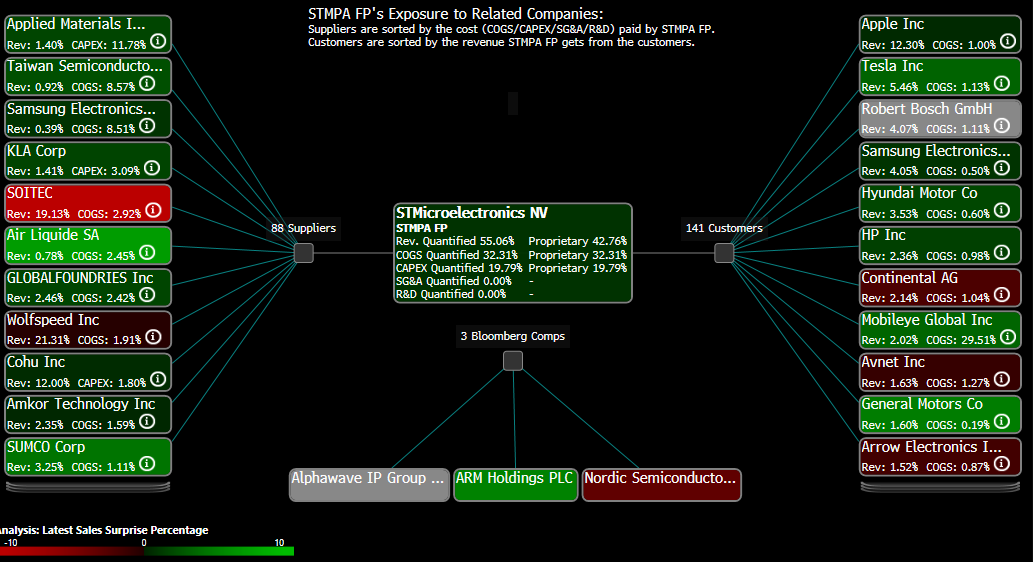

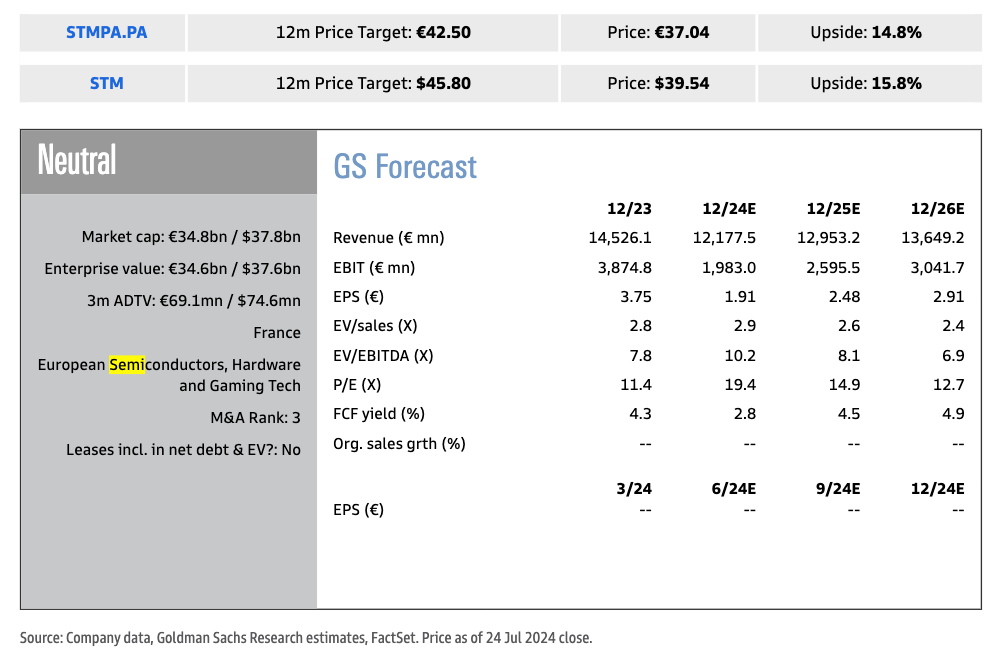

Today, the US will release GDP data for Q2 as well as initial jobless claims later on Thursday. Concern about the economy kicked into high gear on Wednesday after former New York Fed President William Dudley called for lower borrowing costs — preferably at next week’s gathering. Such a move could be worrisome as it would indicate officials rushing to avoid a recession, some analysts said. That said, the most dramatic moves have been in high-flying chipmakers, with investors taking profits after this year’s massive rally. STMicroelectronics NV and BE Semiconductor Industries NV both sank more than 10% in European trading.

“If there was a bubble in the AI and Magnificent 7-part of the market, then last night saw it pop,” said Steve Clayton, head of equity funds at Hargreaves Lansdown.

European stocks tumbled on the busiest day of the corporate earnings season, following steep declines on Wall Street and in Asia. The Stoxx 600 is down 1.4%, led lower by declines in media and technology shares after underwhelming reports from a slew of companies. Results from Nestle SA and Gucci owner Kering SA showed consumers are cutting spending on everything from food to luxury handbags. All European market are lower with French stocks on the verge of a correction. Luxury & Brands, Periphery Banks, EU Resilient Consumer and EU Semis are among the worst underperformers. The broad weakness was driven by earnings disappointments, particularly on UMG, KER and STM. Germany IFO prints 87.0 vs. 89.0 survey vs. 88.6 prior. Here are the most notable European movers:

Roche shares rise as much as 4.4% after reporting first-half results that impressed analysts, with Jefferies calling the increased guidance for the year a “positive surprise.”

Sanofi shares gain as much 4.2% after the French drugmaker reported strong 2Q earnings and raised guidance, with analysts attributing the outperformance in part to strong sales of its key drug Dupixent.

Unilever shares advance as much as 6%, reaching the highest since Nov. 2020, after the consumer-goods giant reported 1H underlying operating margin that came ahead of estimates.

Indivior shares rise as much as 19%, their best day in five months, lifted by the pharmaceutical firm’s new $100 million share buyback and a preliminary settlement related to opioid litigation.

Michelin shares gain as much as 2.3% after the tiremaker’s results were welcomed by analysts, who said pricing, mix and cost discipline were able to offset challenges in the form of lower volumes.

UCB shares gains as much as 2.2%, rising to a record high, after the Belgian biotech firm’s plaque psoriasis drug Bimzelx contributed to the strong first-half results.

Universal Music Group shares fall as much as 30%, the most on record, following second-quarter results which Citi says “undermine” what had been seen as defensive growth credentials.

Stellantis shares fall as much as 13% in Milan, the most since March 2020, after the carmaker’s earnings plunged in the first half of 2024. Morgan Stanley says free cash flow was a key disappointment.

Kering shares slump as much as 10% to a seven-year low on disappointing results, which included a warning that profit is set to plunge in the second half of the year.

Nestle shares drop as much as 4.8% to touch a four-year low, after the consumer-goods giant lowered its FY sales outlook and reported 1H organic revenue that fell short of expectations.

STMicroelectronics shares fall as much as 9.5% after reducing full-year outlook for a second consecutive quarter, citing a prolonged slump in demand for chips used in cars.

BE Semi shares slump 15% after the company missed estimates on third-quarter guidance, dragged by a slow recovery in chip assembly market, as flagged by peer ASMPT Wednesday.

J. Martins shares sink as much as 15% to a three-year low as 2Q like-for-like sales in its flagship Biedronka grocery chain in Poland declined three times faster than expected by analysts.

Earlier in the session, Asian stocks also slumped following the sell-off on Wall St where the S&P 500 and Nasdaq suffered their worst declines since late-2022 owing to disappointment following some mega-cap earnings and a surprise contraction in US Manufacturing PMI. ASX 200 was dragged lower by notable losses in tech, while miners also suffered after several quarterly production updates and lower underlying commodity prices. Nikkei 225 underperformed and briefly dipped beneath the 38,000 level after shedding over 1,000 points with pressure from currency strength and prospects of a BoJ rate hike at next week’s policy meeting. Hang Seng and Shanghai Comp. conformed to the broad selling in the region and fell towards the 17,000 level where support held, while the mainland index also retreated albeit to a lesser extent than regional peers after the PBoC’s surprise MLF operation and 20bps rate cut to the 1-year MLF rate with markets seemingly unimpressed by China’s piecemeal stimulus efforts.

In FX, the yen leads G-10 FX, rising 1% against the greenback as the USD/JPY declined as low as 152.23, the lowest since May 3. The pair has lost about 6% since its peak earlier this month as the carry trade has partially unwound as momentum has reversed. Dollar demand from Japanese importers and fix-related purchases were met with selling by leveraged accounts, while rising 2-year JGB yields and falling Treasury yields further eroded the dollar bid, according to Asia-based FX traders. The Swiss franc is not far behind with a 0.6% gain. The Aussie dollar and Norwegian krone are the weakest, falling 0.8%. The Norwegian krone dropped to its weakest level against the euro in more than a year amid falling oil prices and dampened demand for riskier assets.

In rates, treasuries were near session highs in early US trading Thursday, with US 10-year yields falling 5bps to 4.23% although tightening took place across the curve led by short-dated tenors, further steepening the curve. Front-end-led rally pushed 2-year yield to within 11.5bp of lower 10-year yield, least inverted level since October 2023, and 5-year yield as much as 43bp lower than the 30-year, widest gap since May 2023. The curve-steepening bout unleashed in late June by US presidential election outlook shift to favor Donald Trump winning in November was renewed Wednesday by mounting expectations for Fed rate cuts as US stock benchmarks slid. Weakness in stock benchmarks globally stoked haven demand, while market-implied expectations for Fed rate cuts this year increased further. Gains may complicate auction of 7-year notes at 1pm New York time. Bunds extended gains after Germany’s business outlook unexpectedly fell. The WI 7-year yield around 4.135% is lower than auction results since January and about 14bp lower than last month’s result; earlier this week, 2- and 5-year auctions drew lowest yields since January with mixed results, but both have richened from auction yield levels

In commodities, oil prices decline, with WTI falling 1.8% to trade near $76.20 a barrel. Spot gold falls $26 to around $2,371/oz.

On today’s calendar we get the first estimate of 2Q GDP, weekly jobless claims and June preliminary durable goods orders (8:30am) and July Kansas City Fed manufacturing activity (11am). Fed officials have no scheduled appearances until after the next FOMC meeting ends July 31. Over in Europe, there’s also the Ifo’s business climate indicator from Germany for July, and the Euro Area M3 money supply for June. Otherwise, central bank speakers include ECB President Lagarde, and Bundesbank President Nagel.

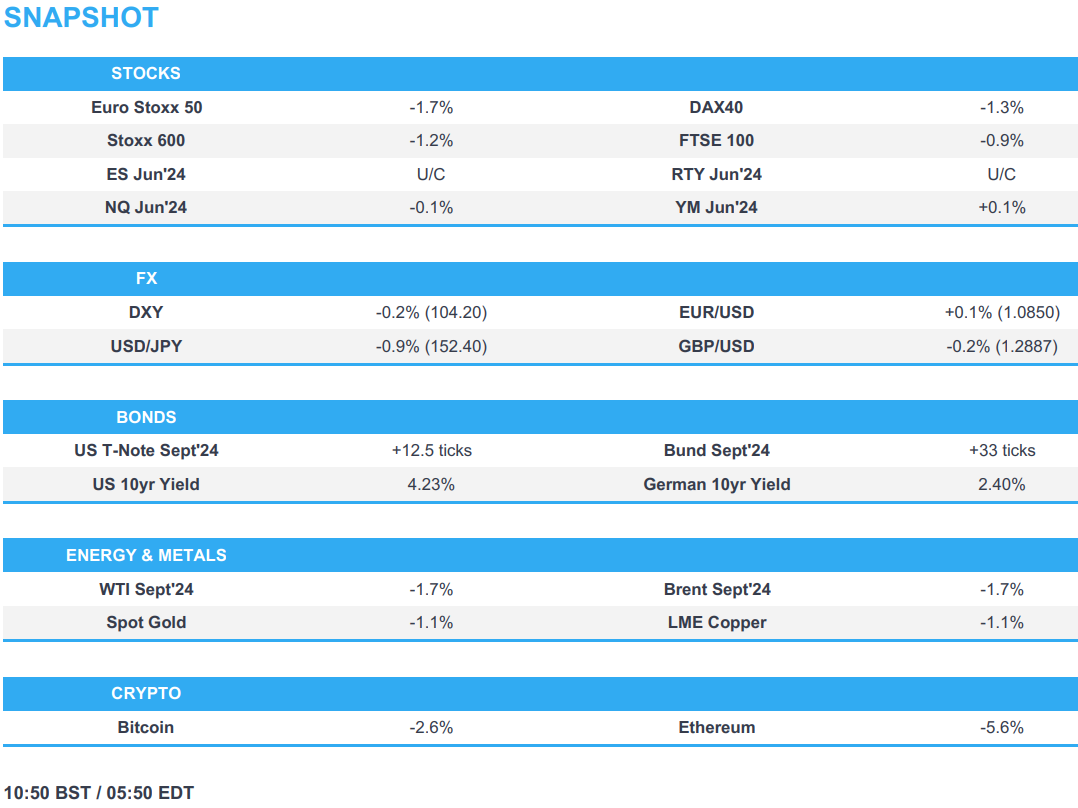

Market Snapshot

S&P 500 futures little changed at 5,470.25

STOXX Europe 600 down 1.3% to 505.72

MXAP down 1.5% to 179.71

MXAPJ down 0.9% to 559.25

Nikkei down 3.3% to 37,869.51

Topix down 3.0% to 2,709.86

Hang Seng Index down 1.8% to 17,004.97

Shanghai Composite down 0.5% to 2,886.74

Sensex little changed at 80,119.66

Australia S&P/ASX 200 down 1.3% to 7,861.21

Kospi down 1.7% to 2,710.65

German 10Y yield -3 bps at 2.41%

Euro little changed at $1.0847

Brent Futures down 0.6% to $81.20/bbl

Gold spot down 1.0% to $2,374.61

US Dollar Index down 0.19% to 104.20

Top Overnight News

US President Biden said America is to choose between hope and hate, optimism and negativity, while he added that he needs to unite the party and it is time to pass the torch but will continue his duties as President for the remainder of his term. Furthermore, he also commented that Vice President Harris is experienced, tough and capable.

China continues to lower its policy rates, taking its 1-year MLF rate down 20bp to 2.3%, as the gov’t works to bolster growth. BBG

China smartphone shipments +10% in Q2; Apple (AAPL) China sales fell 2% Y/Y in Q2, Huawei sales +41%: Canalys.

Five of China’s major state-owned banks cut deposit rates to cushion a hit to their already record low margins after this week’s surprise lowering of lending benchmarks to bolster stuttering economic growth. RTRS

The yen surged toward 152 on bets the interest-rate gap between Japan and the US is finally set to shrink. Some 90% of BOJ watchers see a risk of it hiking on July 31, even if that isn’t their base case, and the Fed faces growing calls to start cutting the same day. The move hit Japan’s Nikkei 225 and undermined assets from gold to bitcoin. BBG

Germany’s IFO survey for Jul fell a bit short of expectations, with the Expectations index coming in at 86.9 (vs. the Street 89.3 and down from 88.8 in June). BBG

Negotiations on a ceasefire-for-hostages deal in the Gaza conflict appear to be in their closing stages and U.S. President Joe Biden and Israeli Prime Minister Benjamin Netanyahu will discuss remaining gaps on Thursday, a senior U.S. official said on Wednesday. RTRS

US GDP growth probably accelerated to an annualized 2% last quarter from 1.4%. But discretionary spending growth has cooled, and demand may moderate further in the second half as the labor market weakens — tipping the Fed toward easing, Bloomberg Economics said. BBG

Harris could have her VP selection in the next two weeks, and the frontrunners remain Cooper (NC), Shapiro (PA), and Kelly (AZ). CNN

Boeing’s plea deal with the DOJ over 737 Max crashes includes at least $243.6 million in fines and three years probation. RTRS

STMicro cut its annual revenue outlook for a second time, and BE Semi issued weak third-quarter guidance. BBG

Earnings

Ford Motor Co (F) Q2 2024 (USD): Adj. EPS 0.47 (exp. 0.68), Revenue 47.8bln (exp. 44.02bln). FY adj. EBIT view 10-12bln (exp. 11.23bln). FY CapEx view affirmed between USD 8.0-9.0bln. Shares -13.5% pre-market

International Business Machines Corp (IBM) Q2 2024 (USD): Adj. EPS 2.43 (exp. 2.20), Revenue 15.77bln (exp. 15.62bln). Shares +4% pre-market

Nissan Motors (7201 JT) Q1 (JPY): Recurring profit 65.13bln (-60.9% Y/Y), Net profits 28.56bln (-72.9%); Cuts FY guidance; Cuts FY24/25 China sales forecast to 777k (prev. 800k), cuts US forecast to 1.41mln (prev. 1.43mln) Shares -6.9% in Asia trade

STMicroelectronics (STM FP) Q2 (EUR): Revenue 3.232bln (exp. 3.204bln), Q2 gross margin 40.1% (exp. 40%). Sees Q3 gross margin 38% (exp. 40.9%), sees Q3 net revenue 38% (exp. 40.9%). Cuts FY24 revenue guidance to between EUR 13.2-13.7bln (exp. 14.3bln). Shares -12.5% in European trade

Nestle (NESN SW) H1 (CHF): Sales 45bln (exp. 45.58bln), Net 5.6bln (exp. 6.08bln), EPS 2.16, +1.8%. In H1, repurchased CHF 2.4bln shares as part of the three-year CHF 20bln buyback which began in 2022. FY Guidance: Organic revenue growth of at least +3% (prev. guided +4%). Shares -4% in European trade

Roche (ROG SW) H1 (CHF): Revenue 29.8bln (exp. 29.911bln), Net Income 6.697bln (exp. 7.523bln); Outlook for 2024 earnings raised; Roche expects to further increase its dividend in CHF. Shares +2.5% in European trade

Anglo American (AAL LN) H1 (USD): Adj. EBITDA 4.9bln (exp. 4.51bln). Adj. EPS 1.06 (exp. 0.90). Adj. Profits 1.29bln (exp. 1.07bln). Decision to temporarily slowdown Woodsmith Crop nutrients project resulted in a USD 1.6bln impairment. Expect to substantially reduce overhead and other non op. costs in phases. Shares -1% in European trade

AstraZeneca (AZN LN) Q2 (USD): Revenue 12.452bln (12.628bln), Core EPS 1.98 (exp. 1.9595); Guidance for FY 2024 increased, with Total Revenue and Core EPS anticipated to grow by a mid teens % (prev. a low double-digit to low teens percentage). Shares -3% in European trade

BE Semiconductor Industries (BESI IM) Q2 (EUR): Revenue 151mln (exp. 152mln), Orders 313mln, Net 41mln. Q3 Guidance: Revenue seen flat, Gross Margin between 64-66% (prev. 65%). CEO estimates that around 50% of orders over the last 12-months were AI-related. Shares -11.5% in European trade

TotalEnergies (TTE FP) Q2 (USD): Net Income 4.7bln (exp. 4.9bln), adj. EBITDA 11.1bln (exp. 11.6bln), adj. EPS 1.98 (exp. 2.06). Refining utilisation rate is expected to be in excess of 85%. Start up of Anchor, within the Gulf of Mexico, expected in Q3. “Sales of petroleum products in the second quarter 2024 were down year-on-year by 2%, mainly due to lower diesel demand in Europe that was partially compensated by higher activity in the aviation business.” Shares -1.5% in European trade

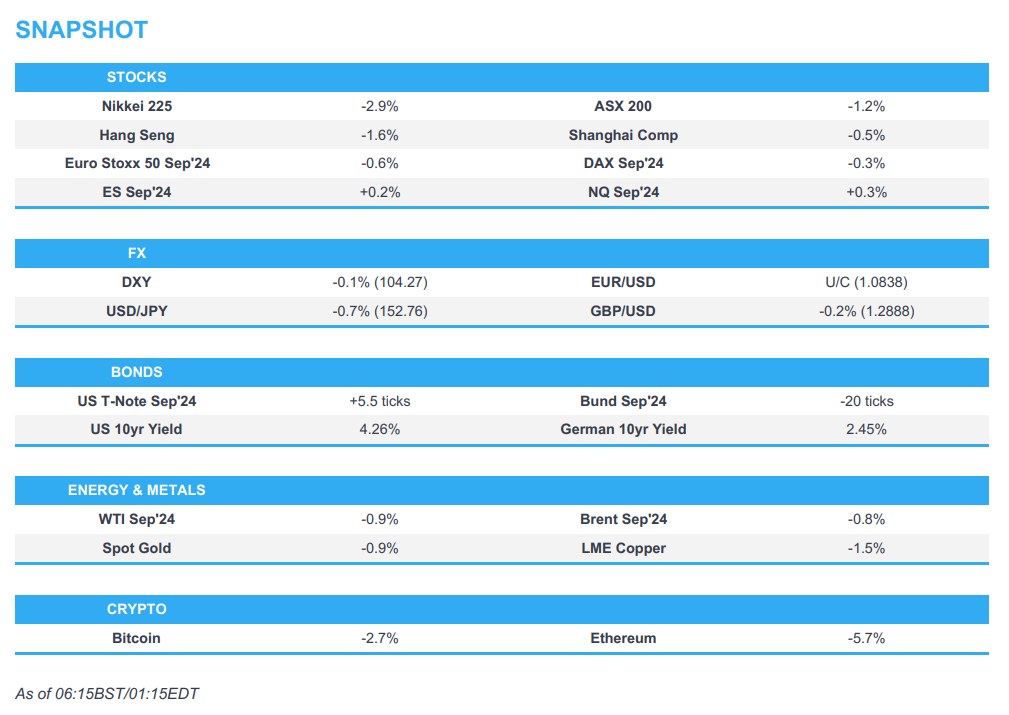

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were negative following the sell-off on Wall St where the S&P 500 and Nasdaq suffered their worst declines since late-2022 owing to disappointment following some mega-cap earnings and a surprise contraction in US Manufacturing PMI. ASX 200 was dragged lower by notable losses in tech, while miners also suffered after several quarterly production updates and lower underlying commodity prices. Nikkei 225 underperformed and briefly dipped beneath the 38,000 level after shedding over 1,000 points with pressure from currency strength and prospects of a BoJ rate hike at next week’s policy meeting. Hang Seng and Shanghai Comp. conformed to the broad selling in the region and fell towards the 17,000 level where support held, while the mainland index also retreated albeit to a lesser extent than regional peers after the PBoC’s surprise MLF operation and 20bps rate cut to the 1-year MLF rate with markets seemingly unimpressed by China’s piecemeal stimulus efforts.

Top Asian News

PBoC injected CNY 200bln via 1-year MLF loans with the rate lowered to 2.30% vs prev. 2.50%.

Japan’s Chief Cabinet Secretary Hayashi says will not comment on daily share moves; will not comment on FX moves; reiterates it is important for currencies to move in stable manner reflecting fundamental; closely watching FX moves.

China’s State Planner says it is to lower the threshold for the use of ultra-long special bond for investing in equipment upgrade projects. Issuing a notice to increase support for equipment upgrades and consumer good trade-ins. Lifts subsidies for car trade ins to up to CNY 20k/vehicle. Allocating CNY 300bln in ultra-long-term treasury bonds.

European bourses, Stoxx 600 (-1.2%) opened the session on the backfoot in fitting with the risk-averse mood seen across markets overnight. A slew of poor earnings only fuelled the pressure seen in Europe with indices heading lower since the cash open, where they currently reside. European sectors are entirely in the red. Healthcare fares better than the rest, given some of the post-earning strength in Sanofi, Roche and Lonza. Tech follows closely behind, after poor BE Semiconductor and STMicroelectronics results, but also in a continuation of the prior day’s price action. Autos are also hampered by significant losses in Renault and Stellantis. US equity futures (ES U/C, NQ -0.2%, RTY U/C) are mixed, seemingly taking a breather following the hefty losses seen in the prior session. In terms of pre-market movers, Ford (-13.5%) slips after significantly missing on the bottom line, whilst IBM (+4%) gains after strong earnings and improving guidance.

Top European News

European Stocks Hit by Weak Earnings on Busiest Reporting Day

SocGen, BofA Say Time to Buy Norway’s Krone as Rout Overdone

Julius Baer Slumps as Profit Fall Signals Tough Benko Recovery

Ipsos Slides After Full-Year Revenue Guidance Misses Estimates

German Business Expectations Fall, Deepening Rebound Concerns

Getlink Shares Rise as Citi Notes Positive Margin Performance

TotalEnergies’ Profit Drops More Than Expected on Refining

FX

Similar price action for the USD as Wednesday with the dollar softer against havens such as CHF and JPY but firmer against risk-sensitive currencies such as AUD and NZD.

EUR is a touch firmer vs. the USD but only marginally so. 1.0825 from Wednesday marks the recent base for the pair. There is a slew of DMAs to the downside in the pair with the 200 DMA at 1.0817.

GBP is seeing shallow losses vs. the USD but off worst levels after briefly breaching Wednesday’s low at 1.2878.

JPY has extended its upside vs. the USD to a 4th consecutive session with the Yen benefitting from risk-aversion, efforts by officials to guide the currency lower, an unwind of carry trades and mounting expectations of a hawkish BoJ at next week’s meeting.

AUD/USD has now extended its downtrend to a 10th consecutive session as global risk sentiment continues to suffer and questions remain over the health of the Chinese economy.

CNH edgins out gains vs. the USD in a market which is characterised by a reversal in recent popular trades with long USD/CNH having been one of them. From a fundamental standpoint, the PBoC surprised markets with a 20bps reduction to the 1yr MLF rate overnight.

Fixed Income

USTs are benefitting from the tepid risk tone with the sell-everything/deleveraging narrative not yet extending to the fixed income space. Thus far, as high as 111-04 to within half a tick of yesterday’s best. Data slate is busy today with focus on US IJCs and Q2 PCE, with a 7yr auction thereafter.

Bunds are bouncing from the US auction-induced dip that occurred late on Wednesday and benefitting from the broader macro tone. The German Ifo survey for July was weaker-than-expected, which helped to lift Bunds to a 132.78 high.

Gilts are towards session highs of 98.21; specifics for the UK light and instead Gilts have been caught up in the broader risk-off tone that is continuing from the Wall St. handover.

Commodities

A downbeat morning for the crude complex amidst the broader risk aversion seen across markets, and in a continuation of the weakness seen in prices on the back of sluggish Chinese demand, with prices unfazed by the surprise PBoC MLF rate cut overnight. Brent Sep in a USD 80.95-81.60/bbl range.

Precious metals are lower across the board despite the softer Dollar and risk aversion amid a broader downturn in metals in what is seemingly an unwind of winning trades. Spot gold slipped from a USD 2,401.31/oz high, through the psychological figure and to a current USD 2,365.91/oz low.

Base metals also trade on the backfoot amid the broader risk aversion and ongoing pessimism regarding Chinese demand.