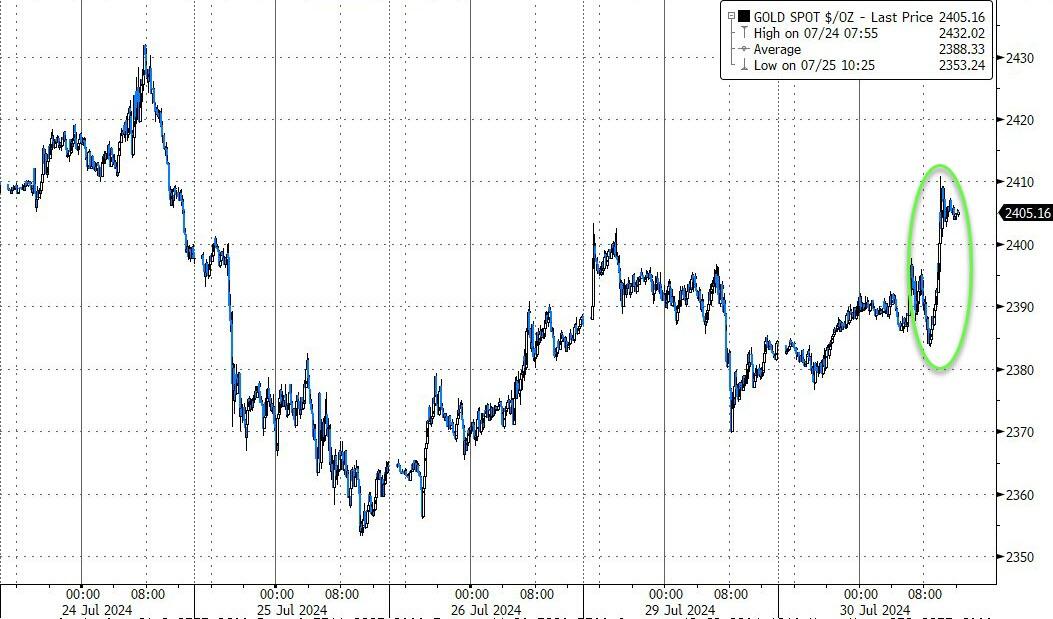

GOLD PRICE CLOSED UP $26.55 TO $2407.00

SILVER PRICE UP $0,61 TO $28.32

Gold ACCESS CLOSED $2383.35

Silver ACCESS CLOSED: $27.86

Bitcoin morning price:$65772 DOWN 664 DOLLARS. bankers doing a good job destroying the value of bitcoin

Bitcoin: afternoon price: $67,426 DOWN 490

dollars//

Platinum price closing UP $12.45 TO $964.95

Palladium price; DOWN $12.75 TO $895.05

END

SHANGHAI GOLD PREMIUM 2 DOLLARS/COMEX GOLD//august to august

*CANADIAN GOLD: $3301’90 UP 1.90 CDN dollars per oz( * NEW ALL TIME HIGH 3,375.67 CDN DOLLARS PER OZ//JULY 16 2024)

*BRITISH GOLD: 1,852.89 DOWN 1.05 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2,202.25 UP 4.38 Euros per oz //* (ALL TIME CLOSING HIGH: 2.263.98 EUROS PER OZ//JULY 16//.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCH: COMEX

EXCHANGE: COMEX

CONTRACT: JULY 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,377.300000000 USD

INTENT DATE: 07/29/2024 DELIVERY DATE: 07/31/2024

FIRM ORG FIRM NAME ISSUED STOPPED

624 H BOFA SECURITIES 8

690 C ABN AMRO 8

TOTAL: 8 8

JPMorgan stopped 0/8

GOLD: NUMBER OF NOTICES FILED FOR JUNE/2024. CONTRACT: 8 NOTICES FOR 800 OZ or 0.0249 TONNES

total notices so far: 3759 contracts for 357900 Oz (11.692 tonnes)

FOR JULY:

SILVER NOTICES: 26 NOTICE(S) FILED FOR 0.130 million

OZ/

total number of notices filed so far this month : 6175 for 30.875 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $26.55 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ NO CHANGES IN GOLD INVENTORY AT THE GLD:

/ /INVENTORY RESTS AT 843.17 TONNES

INVENTORY RESTS AT 843,17 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.61 AT THE SLV/WOW!! AGAIN???//HUGE HUGE MOVEMENTS

SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.458 MILLION OZ OF SILVER VAPOUR IOUT OF THE SLV

// INVENTORY RISES TO 460.596 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 460.596 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A FAIR SIZED 331 CONTRACTS TO 152,221 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS TINY SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OF OI FROM OUR SPREADERS/TAS WITH OUR SMALL LOSS OF $0.11 IN SILVER PRICING AT THE COMEX ON MONDAY’S TRADING ON SILVER. OUR HUGE LIQUIDATION ACCOMPANIED OUR SMALL NET GAIN OF 54 CONTRACTS ON OUR TWO EXCHANGES WE HAD A MASSIVE LIQUIDATION OF T.A.S. CONTRACTS WHICH ACCOUNTS FOR THE OI LOSS SIMILAR TO THE COMEX GOLD TRADING. WE, AGAIN HAD MAJOR SHORT COVERING BY OUR SPECS DESPITE THE SMALL LOSS IN PRICE AS WELL AS THE MASSIVE T.A.S. LIQUIDATION MENTIONED ABOVE. WE HAD A FAIR SIZED 385 EXCHANGE FOR PHYSICAL ISSUANCE AS WELL AS A HUGE 860 CONTRACT T.A.S ISSUANCE,

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN YESTERDAY.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 860 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS.IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1/2 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.11) AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS FROM THEIR PERCH AS WE HAD A SMAll SIZED GAIN OF 54 CONTRACTS ON OUR TWO EXCHANGES.

WE MUST HAVE HAD:

A FAIR SIZED 385 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 28.490 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S QUEUE JUMP OF 35,000 OZ

//NEW STANDING FOR SILVER//JUNE IS THUS 30.875 MILLION OZ

WE HAD:

/ FAIR SIZED COMEX OI LOSS //FAIR SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 860 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL removed 178 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JULY

TOTAL CONTRACTS for 21 DAYS, total 21,774 contracts: OR 108.870 MILLION OZ (1036 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 106.945 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

RESULT: WE HAD A FAIR SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 331 CONTRACTS WITH OUR SMALL LOSS IN PRICE OF SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR EFP ISSUANCE CONTRACTS: 385 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR JULY OF 28.496 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 35,000 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR JULY 30.875 MILLION OZ

WE HAVE A SMALL SIZED GAIN OF 54 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE TINY LOSS IN PRICE. THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 860 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX TRADING WHICH ACCOUNTS FOR THE MAJOR PORTION OF THE COMEX OI LOSS/// MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND ZERO LIQUIDATION OF LONGS. ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER.

THE NEW TAS ISSUANCE MONDAY NIGHT (860) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 26 NOTICE(S) FILED TODAY FOR 0.130 million OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A LARGE SIZED 10,383 OI CONTRACTS TO 509,220 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 2217 CONTRACTS

WE HAD A LARGE SIZED DECREASE IN COMEX OI (10,383 CONTRACTS) OCCURRED DESPITE OUR SMALL LOSS OF $1.80 IN PRICE/MONDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR JUNE AT 7.5645 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 800 OZ QUEUE JUMP

NEW STANDING 11.692 TONNES

/ ALL OF THIS HAPPENED DESPITE OUR $1.80 LOSS IN PRICE WITH RESPECT TO MONDAY’S TRADING. WE HAD A GOOD SIZED LOSS OF 5822 OI CONTRACTS (18.10 PAPER TONNES) ON OUR TWO EXCHANGES., WITH THOSE LONGS REMAINING, TOTALLY OBLIVIOUS TO THE SMALL RAID ORCHESTRATED BY THE STUPID BANKS ONCE LONDON WAS PUT TO BED. OUR LONGS AT THE END OF THE DAY TENDERED FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4561 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 509,220

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5822 CONTRACTS WITH 10,383 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 4561 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 5822 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A VERY STRONG 4531 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4561 CONTRACTS) ACCOMPANYING THE LARGE SIZED LOSS IN COMEX OI OF 10,383 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 5822 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JUNE AT 7,5645 TONNES FOLLOWED BY TODAY’S 800 OZ QUEUE JUMP

//NEW STANDING /JULY 11.692 TONNES.

/ 3) HUGE T.A.S. LIQUIDATION//SPREADER CONTRACTS WITH MINOR NET LONG SPECS BEING CLIPPED,

4) STRONG SIZED COMEX OPEN INTEREST LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///VERY STRONG T.A.S. ISSUANCE: 4531 CONTRACTS WHICH OUR CROOKS WILL USE PROBABLY IN WEDNESDAY’S ATTEMPTED RAID ON FIRST DAY NOTICE WHICH IS THEIR NORM.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

JULY

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JULY. :

TOTAL EFP CONTRACTS ISSUED: 107,642 CONTRACTS OF 10,764,200 OZ OR 334.81 TONNES IN 21 TRADING DAY(S) AND THUS AVERAGING: 5125 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 21 TRADING DAY(S) IN TONNES 334.81 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 334.81 DIVIDED BY 3550 x 100% TONNES = 9.40% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 334.81 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUG), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A FAIR SIZED 331 CONTRACTS OI TO 152,221 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 385 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 385 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 385 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 331 CONTRACTS AND ADD TO THE 385 E.FP. ISSUED

WE OBTAIN A SMALL SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 54 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 0.27 MILLION OZ OCCURRED DESPITE OUR SMALL $.11 LOSS IN PRICE …THE MAJORITY OF THE OI LOSS WAS DUE TO SPREADER/T.A.S. LIQUIDATION

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED DOWN 12.54 PTS OR 0.43% //Hang Seng CLOSED DOWN 236.43 PTS OR 1.37% // Nikkei CLOSED UP 57.32 OR 0.15%//Australia’s all ordinaries CLOSED DOWN 0.58%///Chinese yuan (ONSHORE) closed UP TO 7,2494 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2652/ Oil DOWN TO 75.29 dollars per barrel for WTI and BRENT DOWN AT 79.20 Stocks in Europe OPENED MOSTLY GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A LARGE SIZED 10,383 CONTRACTS TO 509,220 WITH OUR SMALL LOSS IN PRICE OF $1.80 WITH RESPECT TO MONDAY’S TRADING. WE LOST A HUGE NUMBER OF SPREADER/T.A.S. CONTRACTS WHICH ACCOUNTS FOR THE LOSS IN OI.

OUR LONDONERS BOUGHT MASSIVE QUANTITIES OF LONGS AND THEN TENDERED FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY T PLUS ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD A STRONG T.A.S. LIQUIDATION ON MONDAY’S SMALL LOSS IN PRICE WITH ZERO LONGS BEING CLIPPED BUT WE DID HAVE MAJOR SHORT COVERING. THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE NON ACTIVE DELIVERY MONTH OF JULY.… THE CME REPORTS THAT THE BANKERS ISSUED A HUGE SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 4561 EFP CONTRACTS WERE ISSUED: : AUGUST 4561 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4561 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 5822 CONTRACTS IN THAT 4561 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A LARGE SIZED LOSS OF 10,383 COMEX CONTRACTS..AND THIS FAIR LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $1.80/MONDAY COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, MONDAY NIGHT TO EXERCISE FOR PHYSICAL GOLD.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT A STRONG SIZED 4531 CONTRACTS. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN LAST WEEK’S TRADING//RAIDS AS WELL AS THIS WEEK.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JULY (11.692 TONNES)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $1.80 //// AND WERE SOMEWHAT SUCCESSFUL IN KNOCKING OFF SOME MINOR SPECULATOR LONGS. CENTRAL BANK LONGS THAT REMAINED EXERCISED FOR PHYSICAL. WE HAD A HUGE T.A.S. LIQUIDATION MONDAY NIGHT

WE HAVE LOST A TOTAL OI OF 18.10 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JULY (7.5645 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 800 OZ QUEUE. JUMP //NEW STANDING 11.692 TONNES

NEW STANDING FOR JULY: 11.692 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $1.80

WE HAVE REMOVED 2217 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET LOSS ON THE TWO EXCHANGES 5822 CONTRACTS OR 582200 OZ (18.10

TONNES)

confirmed volume MONDAY 306,592 contracts//good

//speculators have left the gold arena

JULY 30 JULY GOLD CONTRACT

/ /// THE JULY 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 160,755.000 OZ JPMorgan 5000 kilobars . |

| Deposit to the Dealer Inventory in oz | 32,023.262 asahi |

| Deposits to the Customer Inventory, in oz | NIL oz |

| No of oz served (contracts) today | 8 notice(s) 800 OZ 0.0249 TONNES |

| No of oz to be served (notices) | 0 contracts 00 OZ 0.000 TONNES |

| Total monthly oz gold served (contracts) so far this month | 3759 notices 375900 oz 11.692 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

1 dealer deposits:

i) Into ASAHI 32,023.262 oz

total dealer deposits: 32,023.262 oz

we have 0 customer deposits

total deposits NIL oz

withdrawals: 1

i)out of JPMorgan; 160,755.000 oz

5000 kilobars

TOTAL WITHDRAWALS 160,755.000 oz

Adjustment 2//customer to dealer

a) Asahi: 48,766.07 oz

ib) Brinks 157,507.767 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY

For the front month of JULY we have an oi of 8 contracts having LOST 61 contracts. We had 69 notices filed on MONDAY so we GAINED 8 contracts or an additional 800 oz will stand at the comex (0.02488 tonnes) as these guys took delivery on this side of the pond.

AUGUST LOST 33,997 CONTRACTS DOWN TO 33,806 CONTRACTS. WE HAVE 1 MORE READING DAY BEFORE THE BIG FIRST DAY NOTICE ON JULY 31. WE SHOULD HAVE A HUGE AMOUNT OF GOLD STANDING FOR AUGUST.

SEPT. GAINED 2304 CONTRACTS TO STAND AT 3865.

OCTOBER GAINED 1423 CONTRACTS UP TO 56,214 CONTRACTS

We had 8 contracts filed for today representing 800 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 8 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for July /2024. contract month, we take the total number of notices filed so far for the month (3759) x 100 oz ) to which we add the difference between the open interest for the front month of JULY 8( CONTRACTS) minus the number of notices served upon today (8 x 100 oz per contract( equals 375,900 OZ OR 11.692 TONNES.

thus the INITIAL standings for gold for the JULY contract month: No of notices filed so far (3759 x 100 oz +we add the difference for front month of JULY (8 X// , OI} minus the number of notices served upon today (8) x 100 oz which equals 375,900 oz (11.692 TONNES)

TOTAL COMEX GOLD STANDING FOR JULY: 11.692 TONNES WHICH IS HUGE FOR THIS NOT VERY ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,671,112.26 oz 51.98 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,835,609.704 OZ

TOTAL REGISTERED GOLD 8,147,698.735 ( 253,42 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,687,910.969 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,476,586 oz (REG GOLD- PLEDGED GOLD)= 201.44 tonnes //

END

SILVER/COMEX

JULY 30/2024

INITIAL

//2024// THE JULY 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,057,588.920 OZ oz Asahi Brinks CNT Delaware . |

| Deposits to the Dealer Inventory | |

| Deposits to the Customer Inventory | 1,053,669.420 CNT ASAHI |

| No of oz served today (contracts) | 26 CONTRACT(S) (.130 million OZ) |

| No of oz to be served (notices) | 0 contracts (0.000 million oz) |

| Total monthly oz silver served (contracts) | 6175 Contracts (30.875 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit/

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 customer deposits:

i) into CNT 465,557.200 oz

i) Into ASAHI 588,112.200 oz

total customer deposit 1053m669.406 oz

JPMorgan has a total silver weight: 132.563million oz/302.212million or 43.70%

adjustment:1;

customer to dealer: Asahi 591,467.800 oz

customer withdrawals: 4

i) Out of BRINKS 3092,01 oz

II) Out of Delaware 580,052.294 0z

iii) Out of Asahi 465,557.200 oz

iv) Out of CNT 8887.416 oz

total withdrawal: 1,057,588.920 0z

TOTAL REGISTERED SILVER: 68,410 MILLION OZ//.TOTAL REG + ELIGIBLE. 302.212 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JULY:

silver open interest data:

FRONT MONTH OF JULY/2024 OI: 26 CONTRACTS HAVING GAINED 1 CONTRACT(S). WE HAD 8 NOTICES FILED ON MONDAY SO WE GAINED 7 CONTRACTS OR AN ADDITIONAL 35,000 OZ WILL STAND AT THE COMEX

AUG, SAW A LOSS OF 348 CONTRACTS TO 812

SEPT SAW A LOSS OF 1970 CONTRACTS TO 107,817

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 26 for 0.130 MILLION oz

CONFIRMED volume; ON MONDAY 70,625 strong

To calculate the number of silver ounces that will stand for delivery in JULY we take the total number of notices filed for the month so far at 6175 x 5,000 oz = 30.875 MILLION oz

to which we add the difference between the open interest for the front month of JULY( 26) and the number of notices served upon today 26 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the JULY/2024 contract month: 6175 notices served so far) x 5000 oz + OI for the front month of JULY (26)x number of notices served upon today minus (26)x 5000 oz of silver standing for the JULY contract month equates to 30.875 MILLION OZ.

New total standing: 30.875 million oz.

There are 69.410 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD

JULY 30 WITH GOLD UP $26.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// A /////INVENTORY RESTS AT 843.17 TONNES

JULY 29 WITH GOLD UP $27.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD// A WITHDRAWAL OF 1.98 TONNES OF GOLD OUT OF THE GLD/////INVENTORY RESTS AT 843.17 TONNES

JULY 26 WITH GOLD UP $27.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD// A DEPOSIT OF 3.45 TONNES OF GOLD INTO THE GLD/////INVENTORY RESTS AT 845.19 TONNES

JULY 25 WITH GOLD DOWN $60.45 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 841.74 TONNES

JULY 24 WITH GOLD UP $12.75 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1,73 TOONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 841.74 TONNES

JULY 23 WITH GOLD UP $12.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 22 WITH GOLD DOWN $4.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 19 WITH GOLD DOWN $56.10 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;:A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 18 WITH GOLD DOWN $2.20 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;: ///INVENTORY RESTS AT 842.02 TONNES

JULY 17 WITH GOLD DOWN $6.60 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A MASSIVE DEPOSIT OF 5.49 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 842.02 TONNES

JULY 16 WITH GOLD UP $38.60 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 836.53 TONNES

JULY 15 WITH GOLD UP $8.15 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;: /INVENTORY RESTS AT 835.09 TONNES

JULY 12 WITH GOLD DOWN $0.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 835.09 TONNES

JULY 11 WITH GOLD UP $43.05 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;:INVENTORY RESTS AT 833.37 TONNES

JULY 10 WITH GOLD UP $12.00 ON THE DAY; HUUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.44 TONNES OF GOLD VAPOUR FROM THE GLD//.//:INVENTORY RESTS AT 833.37 TONNES

JULY 9 WITH GOLD UP $5.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD.//:INVENTORY RESTS AT 834.81 TONNES

JULY 8 WITH GOLD DOWN $26.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD.//:INVENTORY RESTS AT 834.81 TONNES

JULY 5 WITH GOLD UP $29.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD..A DEPOSIT OF 1.10 TONNES OF GOLD VAPOUR INTO THE GLD//:INVENTORY RESTS AT 833.37 TONNES

JULY 3 WITH GOLD UP $35.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD..A MASSIVE DEPOSIT OF 5.76 TONNES OF GOLD VAPOUR INTO THE GLD//:INVENTORY RESTS AT 833.37 TONNES

JULY 2 WITH GOLD DOWN $4.45 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD../:INVENTORY RESTS AT 827.61 TONNES

JULY 1 WITH GOLD DOWN $.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 28 WITH GOLD UP $3.80 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 27 WITH GOLD DOWN $16.95 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 26 WITH GOLD UP $23.70 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

JUNE 25 WITH GOLD DOWN $13.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A STRONG WITHDRAWAL OF 2.88 TONNES OF GOLD FROM THE GLD INVENTORY RESTS AT 829.05 TONNES

JUNE 24 WITH GOLD UP$14.30 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A STRONG WITHDRAWAL OF 1.72 TONNES OF GOLD/NEW TOTAL TONIGHT 831.93 TONNES

JUNE 21 WITH GOLD DOWN $37.40 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD/:/ A MAMMOTH 8.34 TONNES OF GOLD VAPOUR DEPOSIT/NEW TOTAL TONIGHT 833.65 TONNES

JUNE 20 WITH GOLD UP $23.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/://NEW TOTAL TONIGHT 825.31 TONNES

JUNE 18 WITH GOLD UP $17.25 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/://NEW TOTAL TONIGHT 825.31 TONNES

GLD INVENTORY: 843.17 TONNES, TONIGHTS TOTAL

SILVER

JULY 30//WITH SILVER UP $0.61//SMALL CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 0.456 MILLION OZ OF SILVER VAPOUR INTO THE SLV/./// /INVENTORY RISES AT 460.596 MILLION OZ

JULY 29//WITH SILVER DOWN $0.07//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.382 MILLION OZ OF SILVER VAPOUR INTO THE SLV/./// /INVENTORY RISES AT 461.052 MILLION OZ

JULY 26//WITH SILVER DOWN $0.07//NO CHANGES IN SILVER INVENTORY./// /INVENTORY REMAINS AT 456.670 MILLION OZ

JULY 25 WITH SILVER DOWN $1.37//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 3.124 MILLION OZ OF SILVER OUT OF THE SLV./// /INVENTORY FALLS TO 456.670 MILLION OZ

JULY 24 WITH SILVER UP 3 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 15.880 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 23 WITH SILVER UP 3 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 15.880 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 22 WITH SILVER UP 2 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 3.920 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 19 WITH SILVER DOWN 94 CENTS//NO CHANGES IN SILVER INVENTORY/// /INVENTORY REMAINS AT 435.854 MILLION OZ

JULY 18 WITH SILVER DOWN 13 CENTS//HUGE CHANGES IN SILVER INVENTORY” A DEPOSIT OF 2.374 MILLION OZ INTO THE SLV/// /INVENTORY RISES TO 435.854 MILLION OZ

JULY 17. WITH SILVER DOWN 75 CENTS//NO CHANGES IN SILVER INVENTORY// /INVENTORY REMAINS AT 433.480 MILLION OZ.

JULY 16. WITH SILVER UP 30 CENTS//NO CHANGES IN SILVER INVENTORY// /INVENTORY REMAINS AT 433.480 MILLION OZ.

JULY 15. WITH SILVER DOWN 24 CENTS//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 2.145 MILLION OZ FROM THE SLV.// /INVENTORY LOWERS T0 AT 433.480 MILLION OZ.

JULY 12. WITH SILVER DOWN $.65 CENTS//NO CHANGES IN SILVER INVENTORY /INVENTORY REMAINS CONSTANT AT 435.625 MILLION OZ.

JULY 11. WITH SILVER UP $.72 CENTS//HUGE CHANGES IN SILVER INVENTORY A WITHDRAWAL OF 0.731 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 435.625 MILLION OZ.

JULY 10. WITH SILVER DOWN $.04 CENTS//HUGE CHANGES IN SILVER INVENTORY A MAMMOTH WITHDRAWAL OF 3.744 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 436.356 MILLION OZ.

JULY 9. WITH SILVER UP 13 CENTS//HUGE CHANGES IN SILVER INVENTORY A MAMMOTH WITHDRAWAL OF 3.744 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 436.356 MILLION OZ.

JULY 8. WITH SILVER DOWN $0.73//SMALL CHANGES IN SILVER INVENTORY A MAMMOTH DEPOSIT OF 3,292,000 OZ OF SILVER VAPOUR INTO THE SLV.: /INVENTORY RISES T0 440.100 MILLION OZ.

JULY 4. WITH SILVER UP $0.85//SMALL CHANGES IN SILVER INVENTORY A MAMMOTH DEPOSIT OF 3,292,000 OZ OF SILVER VAPOUR INTO THE SLV.: /INVENTORY RISES T0 440.100 MILLION OZ.

JULY 3. WITH SILVER UP $1.08//SMALL CHANGES IN SILVER INVENTORY A SMALL WITHDRAWAL OF 639,000 OZ: /INVENTORY LOWERS T0 436,808 MILLION OZ.

JULY 2. WITH SILVER UP $0.19//NO CHANGES IN SILVER INVENTORY: /INVENTORY REMAINS AT 437.447 MILLION OZ./

JULY 1. WITH SILVER UP $0.05//XXX CHANGES IN SILVER INVENTORY: A DEPOSIT OF 182,000 OZ OF SILVER INTO THE SLV./.// /INVENTORY RISES AT 437.447 MILLION OZ./

JUNE 28. WITH SILVER UP $0.27//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 913,000 OZ FROM THE SLV./.// /INVENTORY REMAINS AT 437.265 MILLION OZ./

JUNE 27. WITH SILVER UP $0.01//NO CHANGES IN SILVER INVENTORY: .// /INVENTORY REMAINS AT 438.178 MILLION OZ.//

JUNE 26. WITH SILVER UP $0.03//HUGE CHANGES IN SILVER INVENTORY: A HUGE WITHDRAWAL OF 2.512 MILLION OZ OF SILVER FROM THE SLV.// /INVENTORY FALLS TO 438.178 MILLION OZ.//

JUNE 25. WITH SILVER DOWN $0.63//HUGE CHANGES IN SILVER INVENTORY: A MAMMOTH DEPOSIT OF 7.835 MILLION OZ OF SILVER VAPOUR INTO THE SLV.// /INVENTORY RISE TO 440.69 MILLION OZ.//WHAT AN ABSOLUTE FRAUD.

JUNE 24. WITH SILVER DOWN $0.05//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 2.104 MILLION OZ FROM THE SLV.// /INVENTORY LOWERS TO 432.835 MILLION OZ.

JUNE 21. WITH SILVER DOWN $1.15//NO CHANGES IN SILVER INVENTORY’// /INVENTORY REMAINS AT 434.935 MILLION OZ.

JUNE 20. WITH SILVER UP $1.17//HUGE CHANGES IN SILVER INVENTORY’ A DEPOSIT OF 5.164 MILLION OZ INTO THE SLV/// /INVENTORY RISES TO 434.929 MILLION OZ.

JUNE 18. WITH SILVER UP $0.21//NOCHANGES IN SILVER INVENTORY’ A WITHDRAWAL .730 MILLION OZ INTO THE SLV/// /INVENTORY FALLS TO 429.775 MILLION OZ.

CLOSING INVENTORY 460.596 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

Prepper Paradise: Gold’s Power When It All Goes Down

TUESDAY, JUL 30, 2024 – 06:30 AM

Society’s linear march forward is used to justify numerous seemingly innocuous lifestyle choices. The assumption that the way things have been is the way they will continue to be is the unquestionable tenet at the root of a carefree ideology that can lead to horrid unintended consequences when it all goes down.

People in developed western countries, particularly in the past 80 years, have experienced a level of stability and growth that has rarely been seen. This extremely small sample size of history has led many to bank on the success of their country as a grounding point for all other predictions of the future.

A small dive into the past could show that most nations fail or have changes of ownership fairly often. Nothing in this world is certain, but governments are particularly frail.

While governments in general should not be given our blind faith, we should be particularly wary of governments that seem to fit into historical patterns of pre-failure. The classic arc of strength to moral laxity and decadence to destruction is one to be particularly wary of, because of how many times it has occurred.

Americans and western Europeans with eyes to see could have very easily noticed how many boxes we check off when it comes to this particular type of societal degradation.

We seem to mirror the fall of Rome in particular with great accuracy.

The general carefree spirit of the enlightened “world citizen” causes little reflection when choosing investments.

The only question that is asked is, “in the circumstances of the recent past, which investments and type of investments have gained the most value?“

Stocks typically do quite well when individuals ask such a question. The gains of all stocks lose some luster when they are multiplied by the probability of societal collapse. The punishment for seeking the highest return possible will be meted out on the judgment day when returns become meaningless in comparison to food and water.

If society were to fall apart, most lucrative investments would be quick to disappear. Our society’s progression of wealth is primarily based on the fact that we have an incredible degree of specialization. The amount of communication and shipping needed to sustain this is not durable to the problems presented by any sort of collapse. The systems of commerce that we currently know are finely tuned and designed around governmental regulations. Even significant changes in regulations have proven problematic for many industries. Imagine how much more powerfully they would be impacted if they had neither the protection of the government, nor the ability to curry favor and limit competition. Some industries would be completely destroyed, such as subsidy-driven soy farming (not to mention that the demand for their crop is nearly fully based on the processing possible through intense specialization). The benefits of rapid gains in the stock market should be tempered with the knowledge that it is fundamentally a gamble on the success of our current institutions.

When the world rearranges based upon some huge shock to government or industry, few parts of our society will be recognizable. Churches and social clubs seem to be the most durable historically, because their existence is not predicated on any one type of government or industry. There’s no guarantee that any specific state will still treat a neighboring state as an ally. Shipping from farms in the central valley to the southwest could be restricted and millions would be forced to migrate or die. Depending on how much of state government remained intact, some necessary treaties could be made. City and town governments would have to step up into the sort of role the founders intended them to play. The only thing that is certain is that commerce would be much more local and specialization would be limited. More durable industry like small sustainable farms or local arts and crafts could arise in cities where property rights were enforced. All hell could break loose in cities that failed to fulfill their role as the safeguards of civilization.

In any of these scenarios, gold would provide a durable store of value. People who question its value in time of crisis have clearly never been to an unstable country. Gold is valued particularly highly when all other investments have hit the floor.

It does have use value in a way most investments don’t, yet it also is so universally accepted that it could allow for migration to other more stable countries if need be.

While some other investments may have flashy short term gains, gold can help protect against the overnight devaluation nightmares of so many assets when the world as we know it rearranges.

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY

end

3.CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES

Brien Lundin: The metals bull market has begun and NOLA conference can be your guide to it

Submitted by admin on Mon, 2024-07-29 14:44 Section: Daily Dispatches

2:47p ET Monday, July 29, 2024

Dear Friend of GATA and Gold:

Gold Newsletter editor and publisher Brien Lundin writes today that a gold, metals, and mining bull market like the one of the 1970s has begun.

“Massive buying from unexpected sources (central banks and China) has propelled gold to record heights this year,” Lundin says. “This powerful new gold bull market has come as the factor everyone was expecting to drive the gold price higher — a Fed pivot to the rate-cutting side of the cycle — has been postponed.

But the Fed is mired in a debt trap, with interest expenses on the federal debt jumping over $1 trillion and increasing rapidly, and Powell & Co. are looking for any excuse to cut rates before something breaks. This inevitable event will light another fire under the red-hot metals market.”

That’s why investors may do well to consider attending the 50th anniversary New Orleans Investment Conference, over which Lundin will preside and where GATA Chairman Bill Murphy and your secretary/treasurer will be speaking. The conference will be held Wednesday through Saturday, November 20-23.

Also speaking will be:

James Grant, George Gammon, Rick Rule, Danielle DiMartino Booth, Brent Johnson, Dominic Frisby, Jim Iuorio, Peter Boockvar, James Lavish, Adrian Day, Mike Maloney, Dave Collum, Bob Prechter, Tracy Shuchart, Avi Gilburt, Adam Taggart, Russ Gray, and Robert Helms.

And more:

Lawrence Lepard, Alex Green, Nick Hodge, David Morgan, Gerardo Del Real, Mark Skousen, Jennifer Shaigec, Lobo Tiggre, Jordan Roy-Byrne, Jeff Clark, Mary Anne and Pam Aden, Dana Samuelson, Gary Alexander, Albert Lu, Omar Ayales, Rich Checkan, and Thom Calandra.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

Jan Nieuwenhuijs: China’s gold conduit revealed, shows central bank did not stop buying in May

Submitted by admin on Mon, 2024-07-29 14:19 Section: Daily Dispatches

2:17p ET Monday, July 29, 2024

Dear Friend of GATA and Gold:

People who still believe official central bank data about gold reserves may do well to read today’s analysis from gold researcher Jan Nieuwenhuijs, who examines customs export data from the United Kingdom, where the major physical gold market is located, and discovers that plenty of gold was shipped to China in May even as the People’s Bank of China was saying it had paused its gold purchases.

END

Jan Nieuwenhuijs: China’s gold conduit revealed, shows central bank did not stop buying in May

Submitted by admin on Mon, 2024-07-29 14:19 Section: Daily Dispatches

2:17p ET Monday, July 29, 2024

Dear Friend of GATA and Gold:

People who still believe official central bank data about gold reserves may do well to read today’s analysis from gold researcher Jan Nieuwenhuijs, who examines customs export data from the United Kingdom, where the major physical gold market is located, and discovers that plenty of gold was shipped to China in May even as the People’s Bank of China was saying it had paused its gold purchases.

Nieuwenhuijs writes: “‘Unreported’ PBoC gold purchases exploded when $300 billion in foreign exchange reserves from the Russian central bank were frozen by the West early 2022 due to the war. Notably, the UK began exporting 400-ounce bars to China in huge tonnages at the same time.

“Coincidence? I think not. Ever since then China has taken over gold price control from the West and broken the gold price’s correlation with ‘real rates.'”

The UK export data, Nieuwenhuijs adds, indicates that “UK gold exports to China are destined for the PBoC — although probably not every ounce of these flows is for the Chinese central bank. Clearly, the PBoC is accumulating more gold than it wants to disclose.”

Nieuwenhuijs’ analysis is headlined “PBoC Gold Conduit Revealed — Chinese Central Bank Did Not Stop Buying Gold in May” and it’s posted at the Gainesville Coins internet site here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

END

David Morgan, Stefan Gleason discuss the future of sound money

Submitted by admin on Mon, 2024-07-29 11:29 Section: Daily Dispatches

11:30a ET Monday, July 29, 2024

Dear Friend of GATA and Gold:

In a new video at YouTube, financial letter writer David Morgan of The Morgan Report and Stefan Gleason, chairman of the Sound Money Defense League and president of Money Metals Exchange, discuss the league’s work to get the monetary metals exempted from state sales and income taxes. They also discuss the growing interest among state governments in holding gold and silver as reserve assets and the potential and difficulties involved in using gold and silver in payment systems for ordinary commerce.

The discussion is 53 minutes long and can be viewed here:

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

4. GOLD PODCASTS//LIVE FROM THE VAULT No 183 with Andrew Maguire and Craig Hemke

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COCOA

END

ASIA TRADING/TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED DOWN 12.54 PTS OR 0.43% //Hang Seng CLOSED DOWN 236.43 PTS OR 1.37% // Nikkei CLOSED UP 57.32 OR 0.15%//Australia’s all ordinaries CLOSED DOWN 0.58%///Chinese yuan (ONSHORE) closed UP TO 7,2494 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2652/ Oil DOWN TO 75.29 dollars per barrel for WTI and BRENT DOWN AT 79.20 Stocks in Europe OPENED MOSTLY GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2494

OFFSHORE YUAN: UP TO 7.2656

SHANGHAI CLOSED DOWN 12.54 PTS OR 0.43 %

HANG SENG CLOSED DOWN 235.43 PTS OR 1.37%

2. Nikkei closed UP 57.32 PTS OR 0.15%

3. Europe stocks SO FAR: ALL MOSTLY GREEN

USA dollar INDEX UP TO 104.38 EURO RISES TO 1.0829 UP 9 BASIS PTS

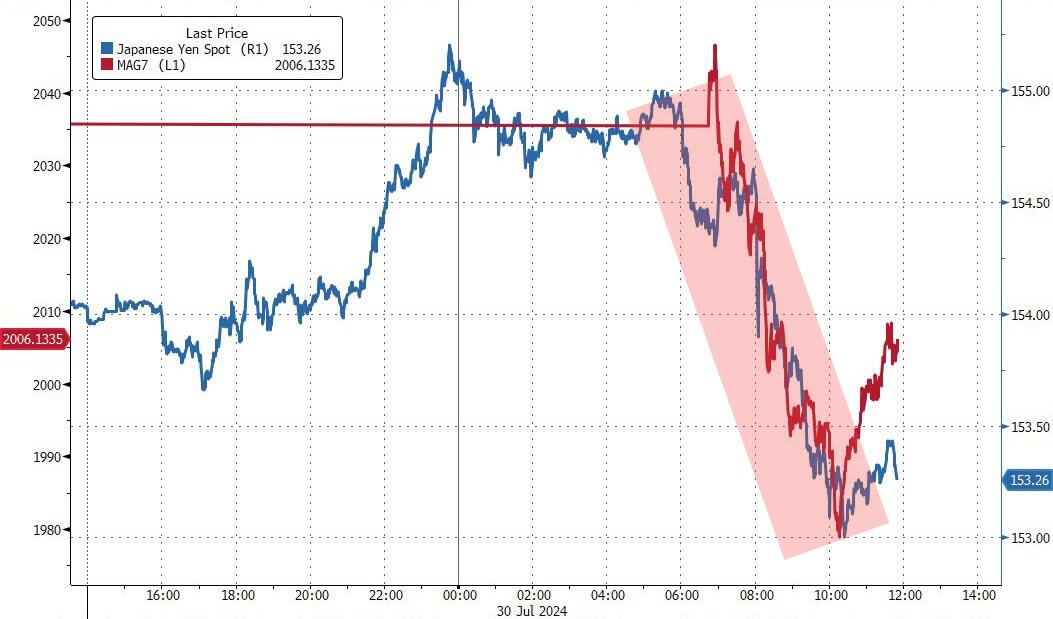

3b Japan 10 YR bond yield: FALLS TO. +1,002 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 154.82 JAPANESE YEN NOW RISING AS WE HAVE NOW REACHED THE END OF THE YEN CARRY TRADE

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and UP FOR DOWN this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.3540/Italian 10 Yr bond yield UP to 3.716 SPAIN 10 YR BOND YIELD UP TO 3.175%

3i Greek 10 year bond yield UP TO 3.363

3j Gold at $2386.70//Silver at: 27.79 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 10/ 100 roubles/dollar; ROUBLE AT 86.31

3m oil into the 75 dollar handle for WTI and 79 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 154.82/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.002% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8859as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9594 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

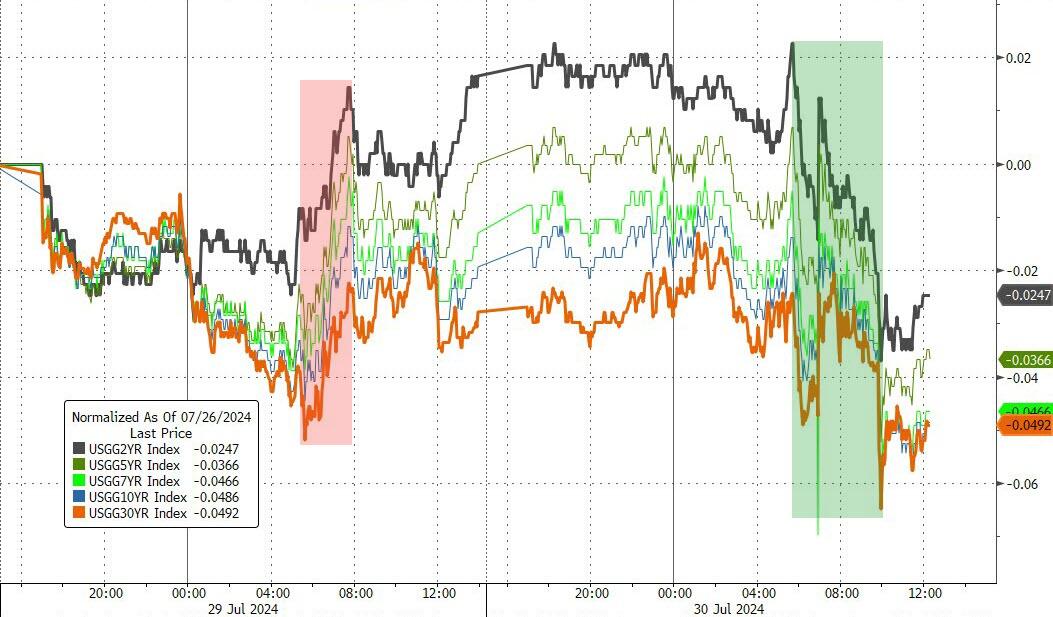

USA 10 YR BOND YIELD: 4.170 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.425 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.392 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 33.09…

10 YR UK BOND YIELD: 4.0835 UP 3 PTS

10 YR CANADA BOND YIELD: 3.296 DOWN 1/2 BASIS PTS

2a New York OPENING REPORT

Futures Rise As Microsoft Earnings, Central Bank Avalanche Looms

TUESDAY, JUL 30, 2024 – 08:15 AM

After yesterday’s market reversal, US equity futures are higher but lacking the strength seen in EU markets. As of 7:50am, S&P and Nasdaq futures are 0.2% higher, with Mag7 stocks mixed and Semis are higher despite NVDA down -63bps and MSFT flat with closely watched earnings after the close. The yield curve is twisting steeper and 10Y yield is 1bps. The dollar is flat and commodities are lower across all 3 complexes. The macro data focus is on JOLTS and Consumer Confidence in what shapes up to be a quiet session ahead of a central bank bonanza that features the BOJ and the Fed tomorrow: both could impact the yield curve though no large moves are expected. The bond market is pricing no moves tomorrow for the Fed but is not pricing a small probability of a 50bps cut in Sept.

In premarket trading, CrowdStrike dropped 4% after a CNBC report about Delta Air Lines hiring attorney David Boies to seek potential damages from the cyber security company and Microsoft following the widespread outage earlier this month. JetBlue Airways gains 4% after saying it will cut $3 billion in capital spending through 2029 and planning other measures to boost pre-tax income by as much as $900 million. Here are some of the other most notable US movers before the opening bell:

- Amkor Technology falls 6% after the chip-packaging company provided a disappointing 3Q forecast.

- Beyond Inc. climbs 7% as the household products retailer reported a smaller-than-expected adjusted loss per share for the 2Q.

- F5 jumps 13% after the communications equipment company raised its full-year revenue guidance.

- Howmet Aerospace rises 7% after the company boosted its adjusted earnings per share guidance for the full year.

- Lattice Semiconductor falls 15% after the chipmaker forecast revenue for the 3Q that came in below the average analyst estimate. Analysts note that the weak outlook is a result of a slow recovery in the auto and industrial markets.

- Merck & Co. slips 1% after the drugmaker cut its adjusted profit forecast for the full year.

- Novavax slides 8% after JPMorgan downgraded the vaccine maker, saying share levels “substantially overvalue” the potential economics and revenue to Novavax from its collaboration with Sanofi.

- PayPal rises 4% after boosting its forecast for 2024 profit as the firm remains focused on streamlining operations.

- Pfizer rises 1.5% after raising its profit expectations for the year as it seeks to rebuild credibility with investors after a plunge in Covid-related sales.

- Procter & Gamble slips 3% after reporting quarterly sales that missed analysts’ projections as the maker of Pampers diapers and Tide detergent slows its pace of price increases.

- Rambus slumps 6% after the technology company forecast product revenue for the 3Q below analyst estimates.

- Sprouts Farmers Market jumps 17% after the natural and organic food retailer boosted its full-year projections for comparable sales and profit.

- Symbotic drops 19% after the warehouse robotics and automation firm forecast revenue for the 4Q that came in below the average analyst estimate.

An index tracking the so-called Magnificent Seven technology stocks lost almost 9% in the two weeks through July 26 after investors turned skeptical about the scope for returns from investment in artificial intelligence. The gauge rebounded by 1% on Monday with focus turning again to earnings after downbeat results from Tesla and Google last week. After the close, Microsoft reports earnings which will help determine whether megacaps can turn the tide after an underwhelming start to the reporting season. Apple, Meta and Amazon are due to report later this week.

“For anything AI related, we’ve been in the investment phase but now we want to see how it translates in terms of return on investment,” said Lionel Jardin, equity sales trader at Marex in Paris.

Also in focus are central bank decisions from the Bank of Japan and the Fed on Wednesday, followed by the Bank of England a day later. US policymakers are widely expected to keep rates unchanged at a two-decade high, but will signal a move in September as risks grow of imperiling a solid but moderating job market. Swap traders are currently pricing a full cut for the September-meeting and as much as two further reductions before the end of the year. Further clues about the rate path may come from reports on US consumer confidence and jobs openings due later on Tuesday. In Japan, the yen weakened against all its Group-of-10 peers as the BOJ kicked off a two-day policy meeting on speculation that policy tightening would be too slow to dent the appeal of yen-funded carry trades.

Europe’s Stoxx 600 index advanced 0.5% after the euro-area economy expanded more than expected in the second quarter (even as Germany’s economy contracted), easing fears about the pace of an economic recovery.

Technology and retail shares leading gains, while mining and food beverage stocks are the biggest laggards; the FTSE 100 underperforms with a 0.5% fall as material names weigh on the broader market. Here are the biggest movers Tuesday:

- BP shares gain as much as 3.3%, the biggest increase since April, after the UK oil and gas company’s 2Q income beat estimates and it maintained the pace of its share buybacks

- Sika shares rise as much as 4.7%, the most since Feb. 16, with analysts saying that gross margin was the main positive surprise in the Swiss chemical company’s results

- Standard Chartered shares advance as much as 6.4% after the British lender announced a record $1.5 billion buyback that was better than analysts expected

- St James’s Place shares soar as much as 25%, the biggest intraday gain since September 2008, after the UK wealth manager reported first-half net inflows that came ahead of consensus expectations

- Allfunds shares soared as much as 8.4%, best performer on the Stoxx 600 Banks Index, after the fund distribution platform reported soaring 2Q adj. Ebitda

- Greggs shares advance as much as 6.3%, reaching the highest intraday level since January 2022, after the bakery chain reported first-half results which analysts viewed as strong.

- Poste Italiane shares gained as much as 4.3%, the most in almost two years after 2Q results beat estimates and the company raised its full-year guidance

- Diageo’s shares fall as much as 11% to a 2020 low, after the distiller’s results disappointed analysts, with RBC calling the update “grim”

- Glencore shares fall as much as 3.2%, hitting a four-month low, after production figures for some key commodities came in below expectations. Morgan Stanley warns earnings consensus could suffer hefty downgrades based on its first-half performance

- Rexel slumps as much as 8.6%, the most since March 2023, after the electrical-supplies company said it now expects full-year adjusted Ebita margin to be toward the lower end of its guided 6.3% to 6.6% range

- Sage Group shares fall as much as 8.3% as analysts said the software company’s earnings report indicates a slight slowdown in organic sales growth from the past two quarters

Earlier, Asian stocks fell as investors trimmed holdings before a number of key central bank decisions in coming days. Chinese shares extended recent losses amid weak sentiment despite the nation’s top leaders signaling more economic support. The MSCI Asia Pacific Index dropped as much as 0.9% before paring declines, with Tencent and TSMC among the biggest drags on tyhe gauge. Stocks in South Korea also fell, while Japanese benchmarks were mixed. The regional measure was on track for its first monthly decline since April. Investors took some money off the table as they braced for monetary policy decisions from the Bank of Japan and Federal Reserve on Wednesday. While traders are on alert for a potential interest-rate hike in Japan, there’s growing expectation for policy easing in the US.

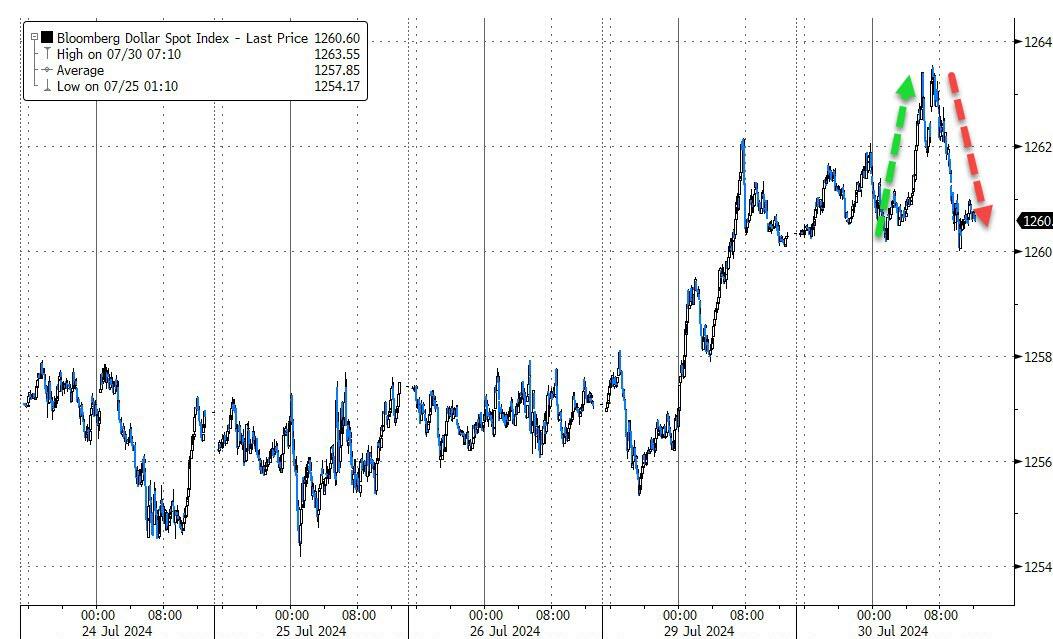

In FX, the Bloomberg Dollar Spot Index is little changed as traders awaited US employment and consumer confidence data for clues on the Federal Reserve’s policy path. The Japanese yen falls for a second day, weakening 0.5% and briefly going beyond 155 per dollar for the first time in a week as the Bank of Japan kicked off a two-day policy meeting. Overnight-indexed swaps priced in a 35% chance that the BOJ will raise its policy rate by 15 basis points this week. The wide interest-rate spread between the US and Japan “should continue to buoy the USD/JPY exchange rate as long as global macro volatility remains restrained,” Alvin Tan, head of Asia foreign-exchange strategy at Royal Bank of Canada in Singapore, wrote in a research note. “We are forecasting USD/JPY rising to 164 by early next year.” The euro is up 0.1% after showing little reaction to a flurry of data from the bloc. Euro-area GDP rose more than expected in the second-quarter despite a surprise contraction in Germany, where state CPI readings point to a steady national print later today.

In rates, Treasuries held small gains as US trading gets underway Tuesday. Yields are lower by less than 1bp, with the 10Y yield dropping to 4.17%, and with curve spreads little changed; 2s10s, 5s30s reached least-inverted or steepest levels since May 2023 last week amid declines for US stock benchmarks and increased expectations for Fed rate cuts. German 10-year yields rise 1bps to 2.37%. The Stoxx 600 rises 0.3%, led by gains in technology shares. Treasury coupon auctions resume Aug. 6, with Treasury set to unveil August-to-October issuance plans Wednesday at 8:30am; Treasury officials in May said they anticipated steady note and bond auction sizes for “at least the next several quarters,” but strategists say increases are unavoidable thereafter.

In commodities, oil prices decline, with WTI falling 0.2% to trade near $75.70. Spot gold rises 0.2%. Commodities have erased all of their gains this year as a challenging outlook in China, combined with a selloff in US natural gas and losses in foodstuffs, have weighed on raw materials.

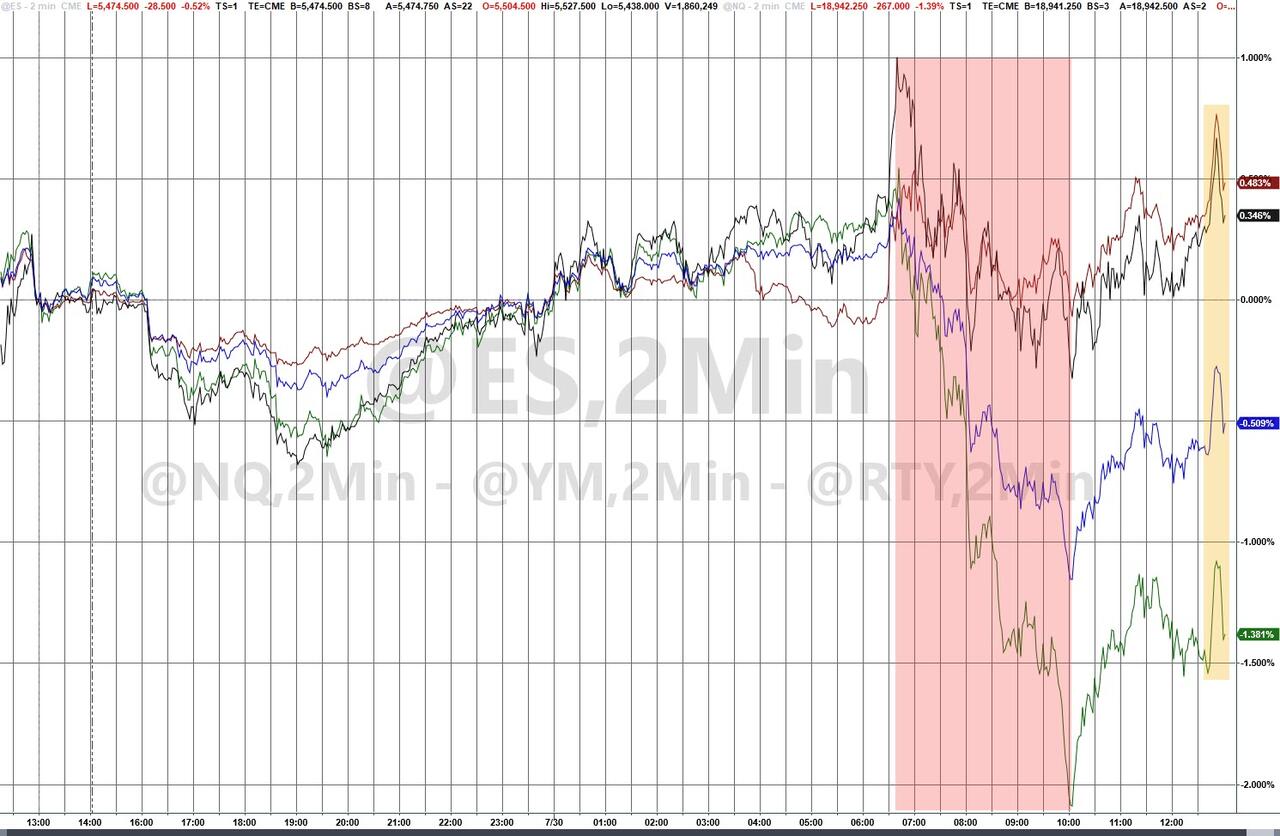

Crypto is mixed with Bitcoin under modest pressure after the weekend’s gains continued on Monday following on from Trump’s bullish commentary. Though, the downside thus far is somewhat limited with BTC currently between USD 66-67k.

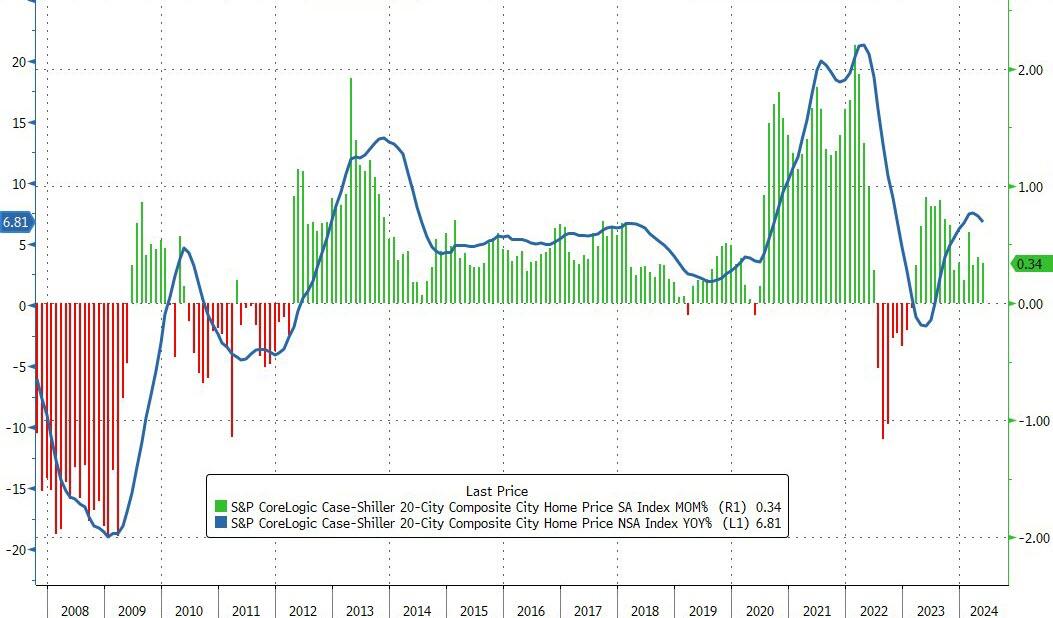

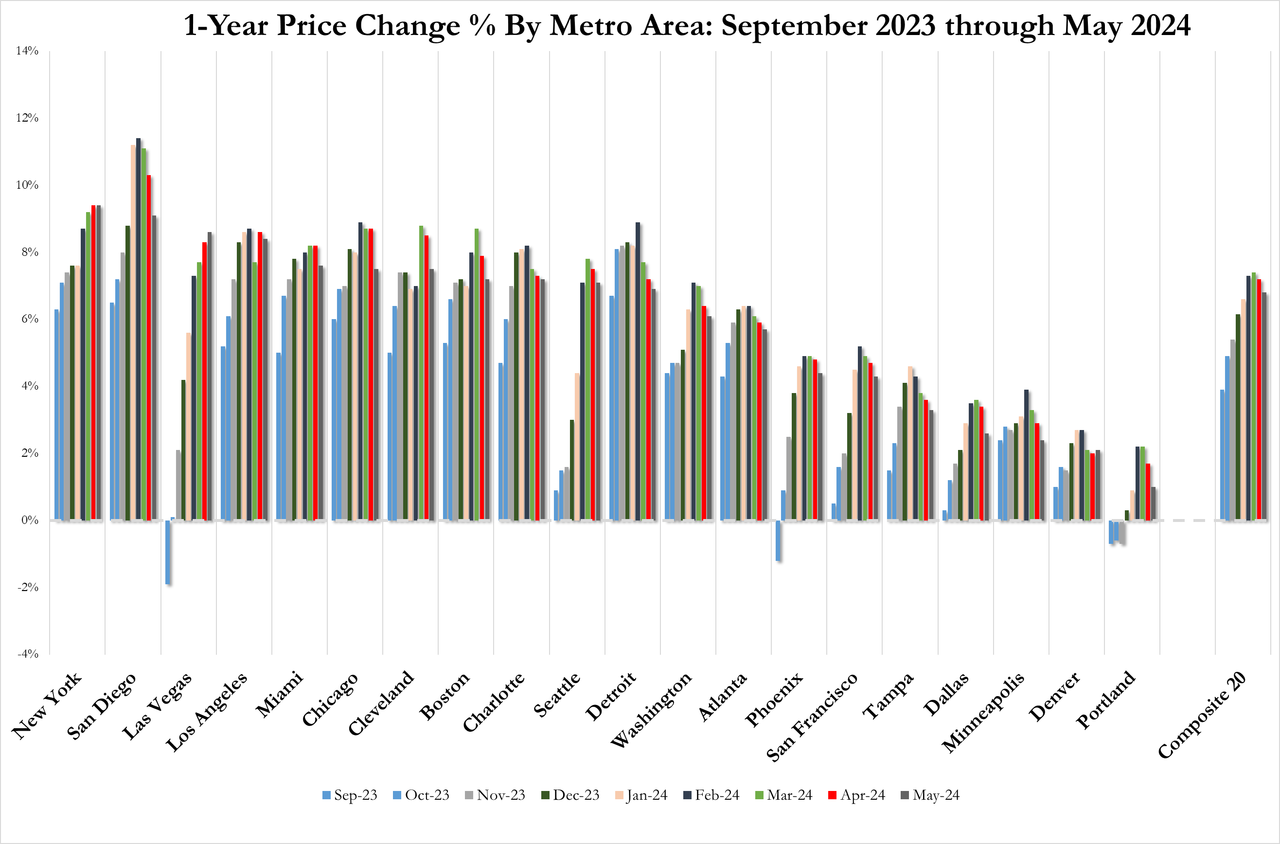

Looking at today’s calendar, US economic data calendar includes May FHFA house price index and S&P CoreLogin home prices (9am), June JOLTS job openings and July Conference Board consumer confidence (10am) and July Dallas Fed services activity (10:30am). Fed officials have no scheduled appearances until after this week’s FOMC meeting ending Wednesday

Market Snapshot

- S&P 500 futures little changed at 5,507.75

- STOXX Europe 600 up 0.1% to 512.49

- MXAP down 0.4% to 179.82

- MXAPJ down 0.4% to 559.71

- Nikkei up 0.1% to 38,525.95

- Topix down 0.2% to 2,754.45

- Hang Seng Index down 1.4% to 17,002.91

- Shanghai Composite down 0.4% to 2,879.30

- Sensex up 0.3% to 81,624.35

- Australia S&P/ASX 200 down 0.5% to 7,953.18

- Kospi down 1.0% to 2,738.19

- German 10Y yield little changed at 2.37%

- Euro up 0.1% to $1.0832

- Brent Futures up 0.2% to $79.91/bbl

- Gold spot up 0.2% to $2,389.79

- US Dollar Index little changed at 104.57

Top Overnight News

- Venezuela’s opposition said it can prove that Edmundo González won Sunday’s election by a wide margin. Leader María Corina Machado called for nationwide “citizen assemblies” in her first public statement since she was accused of plotting to sabotage the election. BBG

- German output unexpectedly shrank last quarter, casting a shadow over resilient growth in the euro region’s next three biggest economies. GDP fell 0.1%, while both France and Spain grew more than predicted and Italy slowed only slightly. Euro-area expansion was 0.3%, a tad more than expected. BBG

- Chinese leaders signaled on Tuesday that the stimulus measures needed to reach this year’s economic growth target will be directed at consumers, deviating from their usual playbook of pouring funds into infrastructure projects. RTRS

- Samsung won long-awaited approval from Nvidia for a version of its high-bandwidth HBM3 memory chips, people familiar said, helping narrow the gap with rival SK Hynix. It also expects approval for the next gen version in two to four months. BBG

- Nvidia is accelerating humanoid robotics development by offering new services, including NVIDIA NIM for robot simulation and learning, the OSMO orchestration service for robotics workloads, and a teleoperation workflow for training robots with minimal human demonstration data.

- Amazon’s Prime Video is undercutting rival Netflix on advertising pricing, as it battles for marketers’ attention in an increasingly crowded field of ad-funded streaming services. FT

- Trump says he will “probably” debate Harris, but “can also make a case for not”. ABC

- Banks and other lenders are seizing control of distressed commercial properties at the highest rate in nearly a decade, a sign that the sector’s punishing downturn is entering its next phase and approaching a bottom. In the second quarter, portfolios of foreclosed and seized office buildings, apartments and other commercial property reached $20.5 billion, according to data provider MSCI. That is a 13% increase from the first quarter and the highest quarterly figure since 2015. WSJ

- Apple utilized AI chips designed by Google to train its models instead of ones from Nvidia. RTRS

- Berkshire Hathaway further pared its stake in BofA, bringing this month’s disposal to $3 billion. It still owns $39.5 billion worth at Monday’s closing price. BBG

- Timiraos writes “The NY Fed’s measure of inflation persistence (the “multivariate core trend” rate) fell again in June, to 2.1%”, while he added “With meaningful shelter disinflation arriving in June, the declines in inflation are broadening”: WSJ

- Former US President Trump said he would probably end up debating VP Harris but added that he could also make a case for not debating.

A more detailed look at global markets courtesy of Newqsuawk

APAC stocks were mostly pressured following the mixed performance stateside and with markets cautious as this week’s major risk events drew closer. ASX 200 was dragged lower amid underperformance in mining stocks after several quarterly production updates and with heavy losses in Fortescue after an investor sought to offload as much as AUD 1.9bln of shares, while a much wider-than-expected contraction in building approvals added to the glum mood. Nikkei 225 retreated amid cautiousness as the BoJ kick-started its two-day policy meeting where it will decide on taper plans and is expected to mull lifting its policy rate by 15bps to around 0.25%. Hang Seng and Shanghai Comp. conformed to the broad negative mood in which the former tested the 17,000 level to the downside with notable weakness seen in consumer, energy and tech stocks, while the mainland was subdued with Chinese official PMI data also due tomorrow.

Top Asian News

- China customs official said China faces an increasingly uncertain trade environment and challenges to grow trade in H2.

- Japan reportedly taps brokerages to market JGBs abroad as the BoJ steps back, according to Nikkei.

- China’s Politburo has held a meeting to study the current economic situation, according to state media; has set out economic priorities for H2 2024. Domestic effective demand remains insufficient.

A mostly firmer start to the session, Euro Stoxx 50 +0.5%, with sentiment on a better footing than APAC counterparts as earnings take the spotlight ahead of this week’s risk events. Sectors have no overarching theme/bias with Autos strong and rebounding from recent pressure, Tech supported by ASML while Basic Resources have been dented by benchmark action. Breakdown dictated by earnings/data; DAX 40 +0.4% firmer but stalling after a soft Flash German GDP print and amid growing pressure in Heidelberg Materials post-earnings. FTSE 100 lags given pressure in mining and most banking names, though BP +2.2% and Standard Chartered +5.5% are strong post-earnings while Diageo -9.0% slips after warning of persisting challenges. Stateside, a modest positive bias remains in play into JOLTS and then earnings; ES +0.2% & NQ +0.2%. Stateside earnings docket has MSFT, AMD, MRK, PFE & PG.

Top European News

- German Surprise GDP Drop Casts Shadow Over Euro-Area Growth

- Indra Drops as Morgan Stanley Notes Strategic Plan Costs

- Deutsche Bank’s DWS Resurrects Corporate Titles to Mollify Staff

- BNY Mellon Cautious Against Excessive Optimism in Turkish Market

- Germany Prelim 2Q GDP Falls 0.1% Q/q, Est. +0.1%

- Diageo Hit By Latin America Slump as Drinkers Spend Less

FX

- DXY is largely contained vs. peers with specifics light into the week’s risk events; DXY is currently within yesterday’s 104.13-75 range. Upside sees the 50DMA @ 104.88 and 100DMA @ 104.89. Downside sees 10 and 200DMA both @ 104.32.

- EUR marginally firmer after a slew of data prints which have been headlined by slightly hawkish German regional CPI and a better-than-expected GDP print for the bloc. EUR/USD at the top-end of 1.0815-34 parameters.

- GBP is essentially unchanged with little follow-through from Reeves’ statement, focus remains firmly on Thursday’s BoE. Cable is currently well within yesterday’s 1.2807-1.2888 range.

- JPY on the backfoot vs. USD, though has managed to pull away marginally from the USD/JPY 155.21 high for the session. Attention firmly on Wednesday’s BoJ which could potentially be hawkish and is then followed by the FOMC’s gathering.

- NZD outperforms with nothing by way of fresh fundamental catalyst, NZD/USD is in the process of snapping an eight session losing streak; AUD essentially unchanged vs. USD.

Fixed Income

- A relatively contained start before a packed morning of data points. EGBs are under modest pressure after a slightly hawkish set of German regional CPI numbers and a stronger-than-expected EZ Flash Prelim. GDP outing.

- As such, Bunds at the low-end of a 133.09-43 range, the high printed early doors on a cooler Spanish Flash CPI release; Monday’s base at 132.72.

- Gilts steady at the low-end of yesterday’s 98.34-98.93 parameters. Supply saw the first auction for the 4.25% 2034 line post strong results after a record setting syndication in June.

- USTs are essentially flat. Holding a handful of ticks below Monday’s 111-16+ best. Docket headlined by JOLTS.

- UK sells GBP 3.75bln 4.25% 2034 Gilt: b/c 2.93x, average yield 4.082%, tail 0.5bps

- Italy sells EUR 7.75bln vs exp. EUR 6.5-7.75bln 4.10% 2029, 3.35% 2029 & 3.85% 2035 BTP and EUR 1.5bln vs exp. EUR 1.0-1.5bln 2032 CCTeu

Commodities

- Crude benchmarks are flat/choppy following APAC losses which were largely a continuation of the weakness that has plagued the complex recently.

- WTI & Brent in narrow circa. USD 0.50/bbl parameters and are currently around the mid-point of such bands.

- Nat Gas is flat but with a mild upward tilt following another session of gains for Dutch TTF which settled higher by over 4% yesterday amid hotter weather forecasts for Asia.

- Metals are mixed; precious metals are slightly firmer with gold at the top-end of a USD 20/oz band that is entirely contained by Monday’s USD 2369-2403/oz parameter; base metals pressured, but off worst.

- Adnoc announces that the Satah Al Razboot field has attained a 25% increase in production capacity due to advanced technologies, taking it to 140k BPD.

- Japan’s Eneos has restarted its 129k BPD Chiba CDU on July 28th following system issues, according to a spokesperson cited by Reuters.

- BP (BP/ LN) CEO says European refining margins are struggling due to weak gasoline and diesel demand, BP expects global fuel inventories to fall during summer driving seasons and lift refining margins.

- Ukraine is ready to resolve oil transit issues with Slovakia if Slovakia activates relevant mechanism in EU association agreement, according to the Ukrainian deputy energy minister.

Geopolitics: Middle East

- US is leading a diplomatic push to deter Israel from targeting Beirut and southern suburbs in response to the Golan strike, according to Reuters citing sources.

- Syrian Observatory said the Israeli army targeted with missiles a military site west of the city of Nawa in the western countryside of Daraa province, according to Sky News Arabia.

Geopolitics: Other

- Russia’s Navy started drills involving 20,000 personnel and 300 ships, while drills involve Russia’s Northern, Pacific and Baltic fleets and Caspian Sea flotilla, according to Interfax

- Venezuelan opposition leader Machado said the opposition has the ability to prove truth of election results, while a US senior official accused Venezuela’s Maduro government of “electoral manipulation”. It was also reported that Uruguay’s Foreign Minister said the country will never recognise Maduro’s win due to a clear victory of the opposition and Peru’s Foreign Ministry ordered Venezuelan diplomats to leave the country within 72 hours.

US Event calendar

- 09:00: May S&P CS Composite-20 YoY, est. 6.50%, prior 7.20%

- 09:00: May S&P/CS 20 City MoM SA, est. 0.30%, prior 0.38%

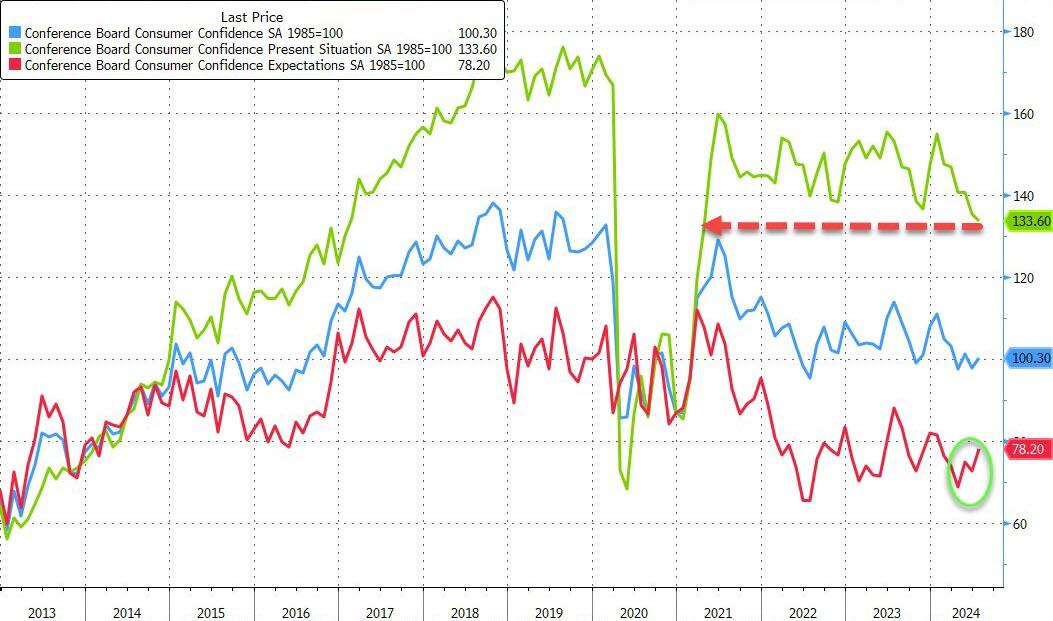

- 10:00: July Conf. Board Consumer Confidenc, est. 99.7, prior 100.4

- July Conf. Board Present Situation, prior 141.5

- July Conf. Board Expectations, prior 73.0

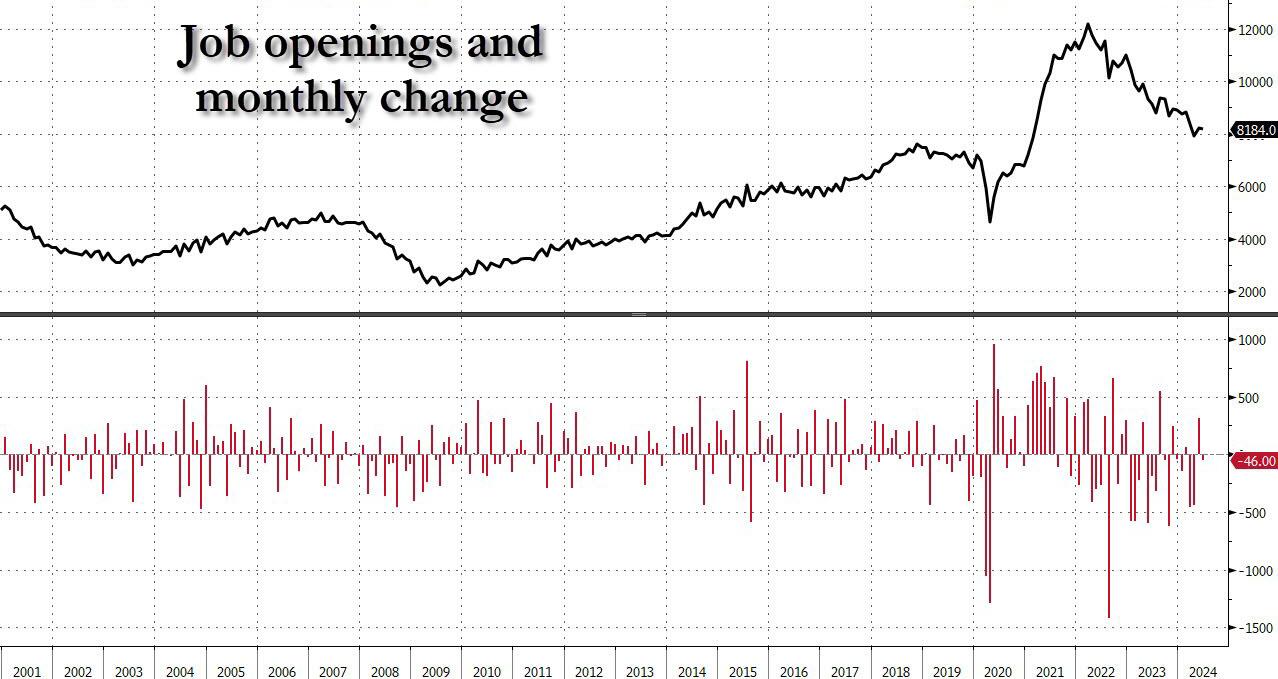

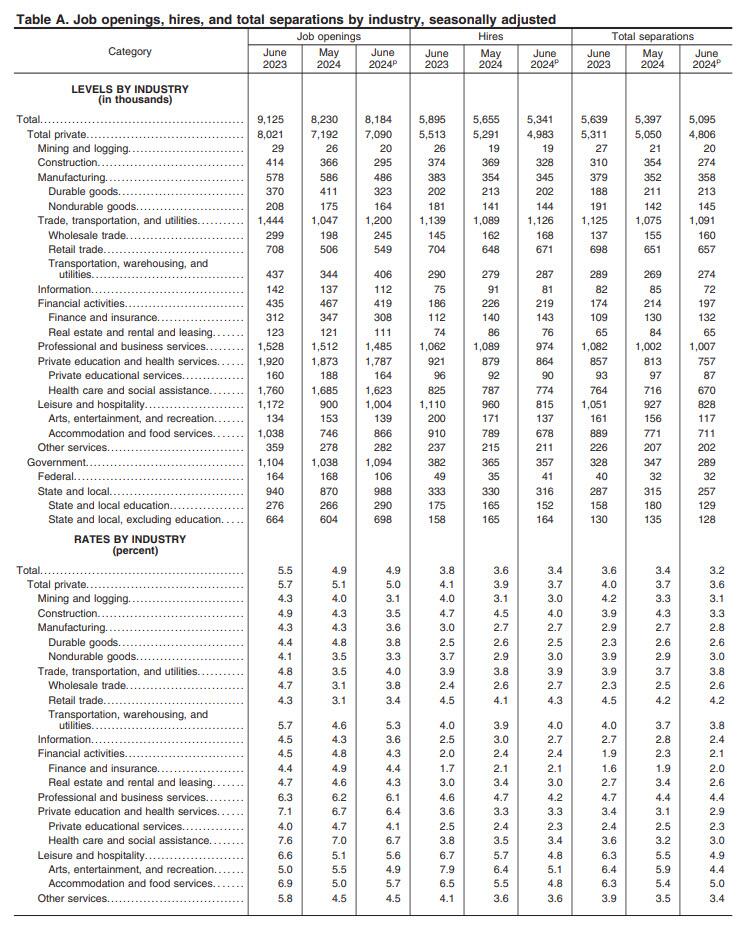

- 10:00: June JOLTs Job Openings, est. 8m, prior 8.14m

- 10:30: July Dallas Fed Services Activity, prior -4.1

DB’s Jim Reid concludes the overnight wrap

As we swelter here in London with insect bite marks building up a diversified portfolio on my body, markets are wilting a touch at the moment with Asia lower overnight and with the S&P 500 (+0.08%) just about managing to eke out a marginal gain last night after the last two weeks of declines, while bonds mostly posted modest gains. We did see a reverse rotation back into tech away from small caps as we’ll detail below. That all comes as investors face some crucial days ahead, with an array of major earnings announcements, data releases, and central bank decisions all happening that will be critical for the market narrative. That begins in earnest today, as we’ve got Microsoft’s results after the US close, along with the German and Spanish CPI prints for July, and the JOLTS report of job openings from the US. So plenty to keep us occupied as we build up to the BoJ and FOMC decision tomorrow and three additional Mag-7 earnings releases with Meta tomorrow and Amazon and Apple on Thursday.