GOLD PRICE CLOSED DOWN $9.55 TO $2427.15

SILVER PRICE DOWN $0,01 TO $28.28

Gold ACCESS CLOSED $2436.20

Silver ACCESS CLOSED: $28.50

right after London’s afternoon gold fix, the crooks used a massive amount of hypothecated paper gold (sold short) to drive gold’s price from $2474 down to $2415 where the good guys were waiting to pick up cheap gold.

Bitcoin morning price:$64,782 UP 1381 DOLLARS.

Bitcoin: afternoon price: $62,914 down 557

dollars//

Platinum price closing DOWN $4.75 TO $959.25

Palladium price; DOWN $12.70 TO $891.55

END

SHANGHAI GOLD PREMIUM 0 DOLLARS/COMEX GOLD//august to august

*CANADIAN GOLD: $3378.31 DOWN 12.50 CDN dollars per oz( * NEW ALL TIME HIGH 3,390.26 CDN DOLLARS PER OZ//AUG 1 2024)

*BRITISH GOLD: 1,902.35 DOWN 16.41 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2,232,96 DOWN 34.45 Euros per oz //* (ALL TIME CLOSING HIGH: 2.264.61 EUROS PER OZ//AUGUST 1 //.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCH: COMEX

EXCHANGE: COMEX

CONTRACT: AUGUST 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,435.000000000 USD

INTENT DATE: 08/01/2024 DELIVERY DATE: 08/05/2024

FIRM ORG FIRM NAME ISSUED STOPPED

099 H DB AG 4470

118 H MACQUARIE FUT 177

152 C DORMAN TRADING 25

190 H BMO CAPITAL 1348

323 C HSBC 204

323 H HSBC 1188

363 H WELLS FARGO SEC 9

435 H SCOTIA CAPITAL 2

555 H BNP PARIBAS SEC 360

624 H BOFA SECURITIES 11

657 C MORGAN STANLEY 133

661 C JP MORGAN 2230

661 H JP MORGAN 1233

686 C STONEX FINANCIA 4

690 C ABN AMRO 6

709 C BARCLAYS 245

726 C PLUS500US FINAN 1

732 C RBC CAP MARKETS 2 11

737 C ADVANTAGE 4 23

880 H CITIGROUP 276

905 C ADM 2

DLV615-T CME CLEARING

BUSINESS DATE: 08/01/2024 DAILY DELIVERY NOTICES RUN DATE: 08/01/2024

PRODUCT GROUP: METALS RUN TIME: 21:33:48

TOTAL: 5,982 5,982

JPMorgan stopped 3463/5982

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2024. CONTRACT: 5982 NOTICES FOR 598,200 OZ or 18.606 TONNES

total notices so far: 16,455 contracts for 1,645,500 Oz (51.182 tonnes)

FOR AUGUST:

SILVER NOTICES: 6 NOTICE(S) FILED FOR 30,000

OZ/

total number of notices filed so far this month : 428 for 2.140 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $9.95 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.58 TONNES OF GOLD OUT OF THE GLD

/ /INVENTORY RESTS AT 845.47 TONNES

INVENTORY RESTS AT 845.47 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $0.01 AT THE SLV

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.243 MILLION OZ OF SILVER VAPOUR INTO THE SLV//

// INVENTORY AT 460.961 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 460.961 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 988 CONTRACTS TO 152,276 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH HUGE LIQUIDATION OF OI FROM OUR SPREADERS/TAS DESPITE OUR HUGE LOSS OF $0.46 IN SILVER PRICING AT THE COMEX ON THURSDAY’S TRADING ON SILVER. OUR HUGE LIQUIDATION ACCOMPANIED OUR HUMONGOUS NET GAIN OF 1638 CONTRACTS ON OUR TWO EXCHANGES AS THE MASSIVE LIQUIDATION OF T.A.S. CONTRACTS ACCOUNTS FOR THE EXTREME OI GAIN SIMILAR TO THE COMEX GOLD TRADING (DESPITE THE HUGE LOSS IN PRICE). WE, AGAIN HAD MAJOR SHORT COVERING BY OUR SPECS WITH THE HUGE LOSS IN PRICE AS WELL AS THE MASSIVE T.A.S. LIQUIDATION MENTIONED ABOVE. WE HAD A HUGE 650 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY A HUGE 611 CONTRACT T.A.S ISSUANCE,

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN YESTERDAY. THE DEMAND FOR SILVER WAS JUST TOO GREAT FOR OUR BANKERS TO CONTAIN AND THUS THE STEEP RISE IN OI DESPITE THE HUGE LOSS IN PRICE.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 611 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS.IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1/2 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS BUT TO NO AVAIL. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.46) BUT WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS FROM THEIR PERCH AS WE HAD A HUMONGOUS SIZED GAIN OF 1638 CONTRACTS ON OUR TWO EXCHANGES.

WE HAD A 650 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.005 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 30,000 OZ E.F.P. JUMP TO LONDON//NEW STANDING REDUCES TO 3.040 MILLION OZ

//NEW STANDING FOR SILVER//AUGUST IS THUS 3.040 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI GAIN //HUGE SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 611 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL removed 60 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST

TOTAL CONTRACTS for 2 DAYS, total 1500 contracts: OR 7.5000 MILLION OZ (750 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 7.5 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 7.50 MILLION OZ//

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 988 CONTRACTS DESPITE OUR HUGE LOSS IN PRICE OF SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 650 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 3.005 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 30,000 OZ E.F.P JUMP TO LONDON

//NEW TOTAL STANDING FOR JULY 3.040 MILLION OZ

WE HAVE A HUGE SIZED GAIN OF 1638 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE HUGE LOSS IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 611 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX TRADING WHICH ACCOUNTS FOR THE MAJOR PORTION OF THE HIGH COMEX OI GAIN DESPITE THE HUGE LOSS IN PRICE//// MAJOR SHORT COVERING FROM OUR SPEC SHORTS AND ZERO LIQUIDATION OF LONGS. ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER.

THE NEW TAS ISSUANCE THURSDAY NIGHT (611) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 6 NOTICE(S) FILED TODAY FOR 30,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 8125 OI CONTRACTS TO 512,329 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HGE 5150 CONTRACTS

WE HAD A STRONG SIZED INCREASE IN COMEX OI (8125 CONTRACTS) OCCURRED WITH OUR GAIN OF $9.15 IN PRICE/THURSDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR AUGUST AT 65.55 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 4700 OZ EXCHANGE FOR PHYSICAL TRANSFER TO LONDON WHERE THESE GUYS TOOK IMMEDIATE DELIVERY OF GOLD IN LONDON.

NEW STANDING REDUCES TO 65.378 TONNES

/ ALL OF THIS HAPPENED WITH OUR $9.15 GAIN IN PRICE WITH RESPECT TO THURSDAY’S TRADING. WE HAD A HUGE SIZED GAIN OF 11,024 OI CONTRACTS (34.29 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 2899 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 512,329

IN ESSENCE WE HAVE A HUMONGOUS SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 11,024 CONTRACTS WITH 8125 CONTRACTS INCREASED AT THE COMEX// AND A GOOD SIZED 2899 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 11,024 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG 2955 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2899 CONTRACTS) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI OF 8125 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 11,024 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR AUGUST AT 65.55 TONNES FOLLOWED BY TODAY’S 4700 OZ EXCHANGE FOR PHYSICAL TRANSFER TO LONDON WHERE THESE BOYS NEEDED IMMEDIATE DELIVERY OF PHYSICAL GOLD ON THAT SIDE OF THE POND.

//NEW STANDING REDUCES TO: /AUGUST 65.378 TONNES.

/ 3) HUGE T.A.S. LIQUIDATION//SPREADER CONTRACTS WITH ZERO NET LONG SPECS BEING CLIPPED,

4) STRONG SIZED COMEX OPEN INTEREST GAIN 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///STRONG T.A.S. ISSUANCE: 2955 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST. :

TOTAL EFP CONTRACTS ISSUED: 4152 CONTRACTS OF 415,200 OZ OR 12.914 TONNES IN 2 TRADING DAY(S) AND THUS AVERAGING: 2076 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 2 TRADING DAY(S) IN TONNES 12.914 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 12.914 DIVIDED BY 3550 x 100% TONNES = 0.360% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 12.914 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUG), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE SIZED 988 CONTRACTS OI TO 152,276 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 650 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 650 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 850 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 988 CONTRACTS AND ADD TO THE 650 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1638 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 8.190 MILLION OZ OCCURRED DESPITE OUR HUGE $.46 LOSS IN PRICE

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING/THURSDAY NIGHT

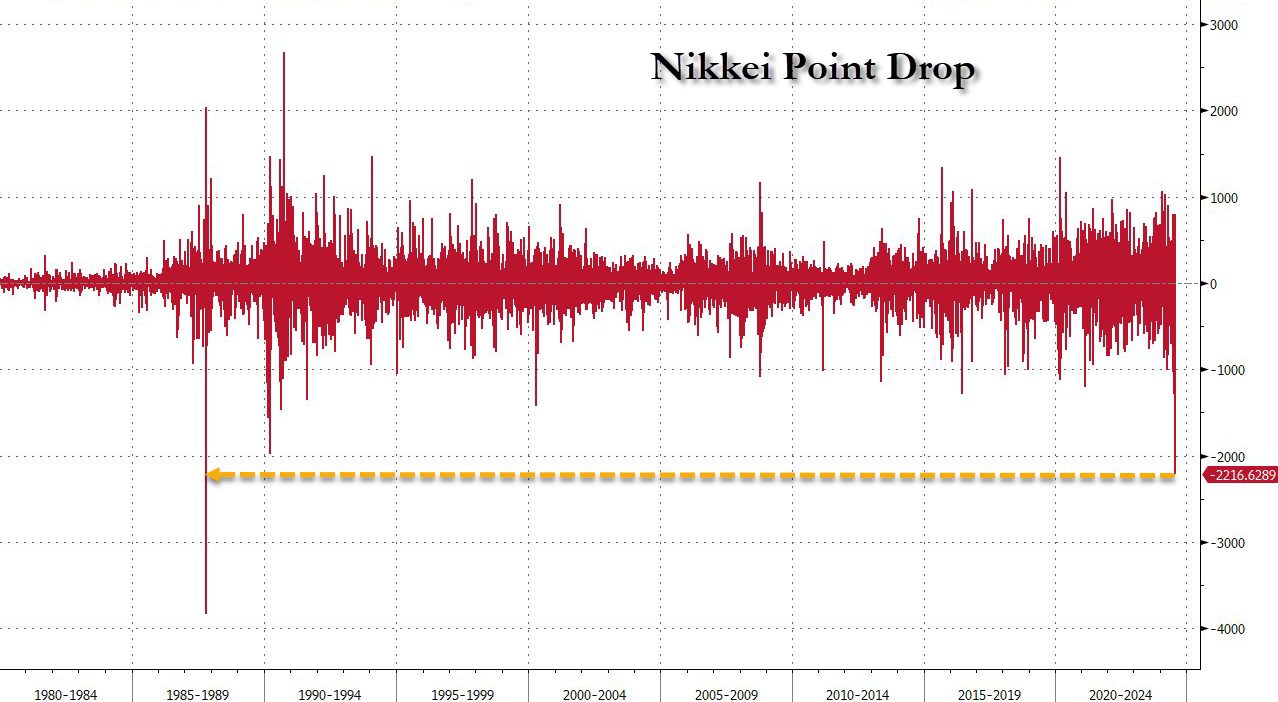

SHANGHAI CLOSED DOWN 27.05 PTS OR 0.92% //Hang Seng CLOSED DOWN 359.45 PTS OR 2.08% // Nikkei CLOSED DOWN 2216.67 OR 5.81%//Australia’s all ordinaries CLOSED DOWN 2.08%///Chinese yuan (ONSHORE) CLOSED UP TO 7,2058 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2072/ Oil DOWN TO 76,24 dollars per barrel for WTI and BRENT DOWN AT 79.,35 Stocks in Europe OPENED ALL RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 8,125 CONTRACTS TO 512,329 WITH OUR GAIN IN PRICE OF $9.15 WITH RESPECT TO THURSDAY’S TRADING. WE LOST A HUGE NUMBER OF SPREADER/T.A.S. CONTRACTS AS SHORTS PANICKED AND COVERED AT MUCH HIGHER PRICES.

OUR LONDONERS BOUGHT MASSIVE QUANTITIES OF LONGS AND THEN TENDERED FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY T PLUS ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD A STRONG T.A.S. LIQUIDATION ON THURSDAY’S GAIN IN PRICE WITH ZERO LONGS BEING CLIPPED BUT WE DID HAVE MAJOR SHORT COVERING. THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE ACTIVE DELIVERY MONTH OF AUGUST.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A GOOD SIZED 2899 EFP CONTRACTS WERE ISSUED: : AUGUST 1753 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2899 CONTRACTS.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A HUGE SIZED TOTAL OF 11,024 CONTRACTS IN THAT 2899 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG SIZED GAIN OF 8125 COMEX CONTRACTS..AND THIS HUMONGOUS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR RISE IN PRICE OF $9.15/THURSDAY COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT A GOOD SIZED 2899 CONTRACTS. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN LAST WEEK’S TRADING//RAIDS AS WELL AS THIS WEEK.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: AUGUST (65.378 TONNES)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 65.378 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $9.15 //// AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE DID HAVE A HUMONGOUS GAIN IN OUR TWO EXCHANGES. CENTRAL BANK LONGS , EXERCISED FOR PHYSICAL. WE HAD A FAIR SIZED T.A.S. LIQUIDATION THURSDAY NIGHT

WE HAVE GAINED A TOTAL OI OF 34.29 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST (65.55 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 4700 OZ E.F.P. JUMP TO LONDON//NEW STANDING: 65.378 TONNES.

NEW STANDING FOR AUGUST: 65.524 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $9.15

WE HAVE REMOVED 5150 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET GAIN ON THE TWO EXCHANGES 11,024 CONTRACTS OR 1,102,400 OZ (34.29

TONNES)

confirmed volume THURSDAY 239,230 contracts//fair

//speculators have left the gold arena

AUGUST 2 AUGUST GOLD CONTRACT

/ /// THE AUG 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 64.302 OZ brinks 2 kilobars . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | NIL oz |

| No of oz served (contracts) today | 5982 notice(s) 598,200 OZ 18.606 TONNES |

| No of oz to be served (notices) | 4564 contracts 456,400 OZ 14.19 TONNES |

| Total monthly oz gold served (contracts) so far this month | 16,455 notices 1,645,500 oz 51.182 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: nil oz

we have 0 customer deposits

total deposits NIL oz

withdrawals: 1

i)out of Brinks: 64.302 oz

2 kilobars

TOTAL WITHDRAWALS 64.302 oz

adjustments 3

1)Adjustment dealer to customer; Asahi 31,323.028 oz

ii) adjustment dealer to customer: Brinks 27,682.011 oz

iii) adjustment customer to dealer HSBC 118,751.658 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY

For the front month of AUGUST we have an oi of 10,546 contracts having LOST 1296 contracts.

We had 1249 contracts served on Thursday, so we lost 47 contracts or 4700 oz was ferried over to London via the exchange for physical route to take immediate delivery over in London.

SEPT. GAINED 128 CONTRACTS TO STAND AT 5362 CONTRACTS.

OCTOBER LOST 204 CONTRACTS DOWN TO 54,958 CONTRACTS

We had 5982 contracts filed for today representing 528,200 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 5982 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 3463 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for AUGUST /2024. contract month, we take the total number of notices filed so far for the month (16,455) x 100 oz ) to which we add the difference between the open interest for the front month of August 10,546( CONTRACTS) minus the number of notices served upon today (5982 x 100 oz per contract( equals 2,101,900 OZ OR 65.378 TONNES.

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (16,455 x 100 oz +we add the difference for front month of AUGUST (10,546 X// , OI} minus the number of notices served upon today (5982) x 100 oz which equals 2,101,900 oz (65.378 TONNES)

TOTAL COMEX GOLD STANDING FOR AUGUST: 65.378 TONNES WHICH IS HUGE FOR THIS VERY ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,661,466.962 oz 51.67 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,868,105.099 OZ

TOTAL REGISTERED GOLD 8,214,323.287 ( 255.49 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,653,782.712 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,552857 oz (REG GOLD- PLEDGED GOLD)= 203.82 tonnes //

END

SILVER/COMEX

AUGUST 2/2024

INITIAL

//2024// THE AUG 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 554,,146.100 OZ oz Asahi . |

| Deposits to the Dealer Inventory | |

| Deposits to the Customer Inventory | 1,133,361.400 oz JPM Manfra |

| No of oz served today (contracts) | 6 CONTRACT(S) (30,000 OZ) |

| No of oz to be served (notices) | 180 contracts (0.900 million oz) |

| Total monthly oz silver served (contracts) | 428 Contracts (2.140 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit/

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 customer deposits:

i) into JPMorgan:554,146.100 oz

ii) Into Manfra 579,215.310 oz

total customer deposit 1,133,361.400 oz

JPMorgan has a total silver weight: 134,771million oz/302.727million or 44.59%

adjustment:0;

customer withdrawals: 1

i) Out of DELAWARE 554,146.100 oz

total withdrawal: 554,146.100 0z

TOTAL REGISTERED SILVER: 70.019 MILLION OZ//.TOTAL REG + ELIGIBLE. 302.723 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR AUGUST:

silver open interest data:

FRONT MONTH OF AUGUST/2024 OI: 186 CONTRACTS HAVING LOST 9 CONTRACT(S).

WE HAD 3 NOTICES SERVED ON THURSDAY, SO WE LOST 6 CONTRACTS OR AN ADDITIONAL 30,000 OZ WILL NOT STAND FOR SILVER AT THE COMEX AS THEY WERE EFP’d OVER TO LONDON WHERE THEY WILL TAKE IMMEDIATE DELIVERY OVER THERE. SEEMS THAT GOLD AND SILVER ARE SCARCE OVER ON THIS SIDE OF THE POND.

SEPT SAW A LOSS OF 1072 CONTRACTS TO 103,135. SEPT NOW BECOMES THE NEW FRONT MONTH

OCTOBER SAW ANOTHER GAIN OF OPEN INTEREST CONTRACTS OF 35 CONTRACT AND THUS WE HAVE 36 OPEN INTEREST CONTRACTS FOR OCTOBER.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 6 for 30,000 oz

CONFIRMED volume; ON THURSDAY 85,751 very good

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 428 x 5,000 oz = 2.140 MILLION oz

to which we add the difference between the open interest for the front month of AUGUST( 186) and the number of notices served upon today 6 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST/2024 contract month: 428 notices served so far) x 5000 oz + OI for the front month of AUGUST (186)x number of notices served upon today minus (6)x 5000 oz of silver standing for the AUGUST contract month equates to 3.040 MILLION OZ.

New total standing: 3.040 million oz.

There are 70.019 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD

AUGUST 2 WITH GOLD DOWN $9.95 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.58 TONNES OF GOLD OUT OF THE GLD//INVENTORY RESTS AT 845.47 TONNES

AUGUST 1 WITH GOLD UP $9.15 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 846.05 TONNES

JULY 30 WITH GOLD UP $26.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// A /////INVENTORY RESTS AT 843.17 TONNES

JULY 29 WITH GOLD UP $27.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD// A WITHDRAWAL OF 1.98 TONNES OF GOLD OUT OF THE GLD/////INVENTORY RESTS AT 843.17 TONNES

JULY 26 WITH GOLD UP $27.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD// A DEPOSIT OF 3.45 TONNES OF GOLD INTO THE GLD/////INVENTORY RESTS AT 845.19 TONNES

JULY 25 WITH GOLD DOWN $60.45 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 841.74 TONNES

JULY 24 WITH GOLD UP $12.75 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1,73 TOONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 841.74 TONNES

JULY 23 WITH GOLD UP $12.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 22 WITH GOLD DOWN $4.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 19 WITH GOLD DOWN $56.10 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;:A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 18 WITH GOLD DOWN $2.20 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;: ///INVENTORY RESTS AT 842.02 TONNES

JULY 17 WITH GOLD DOWN $6.60 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A MASSIVE DEPOSIT OF 5.49 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 842.02 TONNES

JULY 16 WITH GOLD UP $38.60 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 836.53 TONNES

JULY 15 WITH GOLD UP $8.15 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;: /INVENTORY RESTS AT 835.09 TONNES

JULY 12 WITH GOLD DOWN $0.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 835.09 TONNES

JULY 11 WITH GOLD UP $43.05 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;:INVENTORY RESTS AT 833.37 TONNES

JULY 10 WITH GOLD UP $12.00 ON THE DAY; HUUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.44 TONNES OF GOLD VAPOUR FROM THE GLD//.//:INVENTORY RESTS AT 833.37 TONNES

JULY 9 WITH GOLD UP $5.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD.//:INVENTORY RESTS AT 834.81 TONNES

JULY 8 WITH GOLD DOWN $26.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD.//:INVENTORY RESTS AT 834.81 TONNES

JULY 5 WITH GOLD UP $29.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD..A DEPOSIT OF 1.10 TONNES OF GOLD VAPOUR INTO THE GLD//:INVENTORY RESTS AT 833.37 TONNES

JULY 3 WITH GOLD UP $35.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD..A MASSIVE DEPOSIT OF 5.76 TONNES OF GOLD VAPOUR INTO THE GLD//:INVENTORY RESTS AT 833.37 TONNES

JULY 2 WITH GOLD DOWN $4.45 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD../:INVENTORY RESTS AT 827.61 TONNES

JULY 1 WITH GOLD DOWN $.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

GLD INVENTORY: 845.47 TONNES, TONIGHTS TOTAL

SILVER

AUGUST 2//WITH SILVER DOWN $0.01//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 1.243 MILLION OZ OF SILVER OUT OF THE SLV ///./// /INVENTORY AT 460.961 MILLION OZ

AUGUST 1//WITH SILVER DOWN $0.46//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.608 MILLION OZ OF SILVER VAPOUR INTO THE SLV///./// /INVENTORY AT 462.204 MILLION OZ

JULY 31//WITH SILVER UP $0.45//NO CHANGES IN SILVER INVENTORY: /./// /INVENTORY REMAINS AT 460.596 MILLION OZ

JULY 30//WITH SILVER UP $0.61//SMALL CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 0.456 MILLION OZ OF SILVER VAPOUR INTO THE SLV/./// /INVENTORY RISES AT 460.596 MILLION OZ

JULY 29//WITH SILVER DOWN $0.07//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.382 MILLION OZ OF SILVER VAPOUR INTO THE SLV/./// /INVENTORY RISES AT 461.052 MILLION OZ

JULY 26//WITH SILVER DOWN $0.07//NO CHANGES IN SILVER INVENTORY./// /INVENTORY REMAINS AT 456.670 MILLION OZ

JULY 25 WITH SILVER DOWN $1.37//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 3.124 MILLION OZ OF SILVER OUT OF THE SLV./// /INVENTORY FALLS TO 456.670 MILLION OZ

JULY 24 WITH SILVER UP 3 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 15.880 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 23 WITH SILVER UP 3 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 15.880 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 22 WITH SILVER UP 2 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 3.920 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 19 WITH SILVER DOWN 94 CENTS//NO CHANGES IN SILVER INVENTORY/// /INVENTORY REMAINS AT 435.854 MILLION OZ

JULY 18 WITH SILVER DOWN 13 CENTS//HUGE CHANGES IN SILVER INVENTORY” A DEPOSIT OF 2.374 MILLION OZ INTO THE SLV/// /INVENTORY RISES TO 435.854 MILLION OZ

JULY 17. WITH SILVER DOWN 75 CENTS//NO CHANGES IN SILVER INVENTORY// /INVENTORY REMAINS AT 433.480 MILLION OZ.

JULY 16. WITH SILVER UP 30 CENTS//NO CHANGES IN SILVER INVENTORY// /INVENTORY REMAINS AT 433.480 MILLION OZ.

JULY 15. WITH SILVER DOWN 24 CENTS//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 2.145 MILLION OZ FROM THE SLV.// /INVENTORY LOWERS T0 AT 433.480 MILLION OZ.

JULY 12. WITH SILVER DOWN $.65 CENTS//NO CHANGES IN SILVER INVENTORY /INVENTORY REMAINS CONSTANT AT 435.625 MILLION OZ.

JULY 11. WITH SILVER UP $.72 CENTS//HUGE CHANGES IN SILVER INVENTORY A WITHDRAWAL OF 0.731 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 435.625 MILLION OZ.

JULY 10. WITH SILVER DOWN $.04 CENTS//HUGE CHANGES IN SILVER INVENTORY A MAMMOTH WITHDRAWAL OF 3.744 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 436.356 MILLION OZ.

JULY 9. WITH SILVER UP 13 CENTS//HUGE CHANGES IN SILVER INVENTORY A MAMMOTH WITHDRAWAL OF 3.744 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 436.356 MILLION OZ.

JULY 8. WITH SILVER DOWN $0.73//SMALL CHANGES IN SILVER INVENTORY A MAMMOTH DEPOSIT OF 3,292,000 OZ OF SILVER VAPOUR INTO THE SLV.: /INVENTORY RISES T0 440.100 MILLION OZ.

JULY 4. WITH SILVER UP $0.85//SMALL CHANGES IN SILVER INVENTORY A MAMMOTH DEPOSIT OF 3,292,000 OZ OF SILVER VAPOUR INTO THE SLV.: /INVENTORY RISES T0 440.100 MILLION OZ.

JULY 3. WITH SILVER UP $1.08//SMALL CHANGES IN SILVER INVENTORY A SMALL WITHDRAWAL OF 639,000 OZ: /INVENTORY LOWERS T0 436,808 MILLION OZ.

JULY 2. WITH SILVER UP $0.19//NO CHANGES IN SILVER INVENTORY: /INVENTORY REMAINS AT 437.447 MILLION OZ./

JULY 1. WITH SILVER UP $0.05//XXX CHANGES IN SILVER INVENTORY: A DEPOSIT OF 182,000 OZ OF SILVER INTO THE SLV./.// /INVENTORY RISES AT 437.447 MILLION OZ./

CLOSING INVENTORY 460.961 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY

special thanks to Robert H for sending this to us:

JIM WILLIE

Willie on silver

https://youtu.be/4yumZ1liuhw?si=38-jEpsHLOIsyLDu

end

ALASDAIR MACLEOD…

When prices rise overnight, or they rise into London’s morning fix we know that China and possibly India are buying again.

| ALASDAIR MACLEODAUG 2 |

This week has been a tale of diversity, with gold close to challenging new high ground, but silver lagging, evident in our headline chart. In European trade this morning, gold was $2466, up $80 from last Friday’s close, and Silver at $28.93 was up 95 cents. Looking at the relationship between price and open interest, their performance on Comex has been different as well:

MacleodFinance Substack is a reader-supported publication. To receive new posts and support my work, consider becoming a free or paid subscriber.

Note how gold’s Open Interest has declined remarkably while the price has held close to all-time highs. This indicates impressive underlying strength. The relationship in silver is more normal, with both the price and OI trending in the same direction. In both cases, speculator interest appears average, as opposed to excessive, indicating that there is room for buyer demand to drive prices higher before a consolidation is due. In the case of gold, this would be into new highs over $2500 spot (the active Comex contract is at $2507 already), and silver should have significant catch-up potential indicated by a gold/silver ratio at 85:

The chart doesn’t tell us much other than to remind us just how far from being valued as money silver has become. In these times of growing credit risk, physical silver looks badly out of kilter, and the relationship should already be reflecting its return to a role as the poor man’s gold.

Overnight demand for gold has been in evidence this week, draining already diminished western gold liquidity. We see this when prices rise overnight and when they firm up ahead of London’s morning fix. It should be noted that some of this demand is speculative, with aggressive positions being adopted in Shanghai futures. That has the potential to create some volatility, but clearly the gold price is being set not in London or Comex but in Shanghai.

It is Chinese, and also Indian demand through Dubai to which we must pay attention. Interestingly, when India recently cut the tax on imported gold to 5%, the price discount in Mumbai was replaced with a small premium.

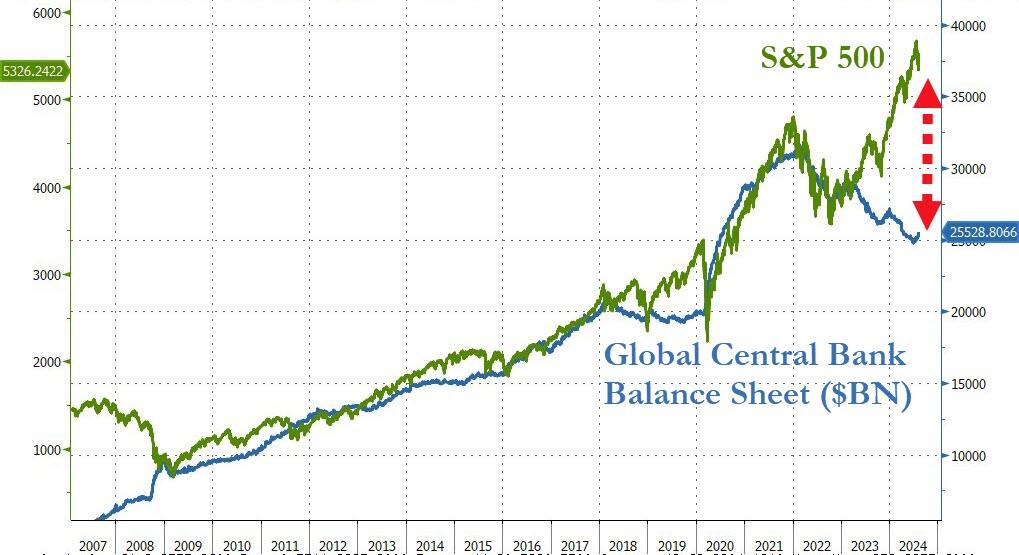

There are also tectonic plates shifting in the background. There is more evidence that global equities have entered a bear market, and we could see further substantial falls in the coming weeks. At the same time, US Treasury yields have declined sharply, partly due to growing confidence that the Fed funds rate will be reduced in September. Additionally, poor earnings from top tech stocks and growing evidence of a faltering US economy are reducing the valuation gap between bonds and equities, indicated by the double-headed arrow in the chart below.

This is probably the most excessive relative overvaluation of equities in US financial history, certainly in the last forty years, even greater than during the dot-com bubble, following which the S&P halved.

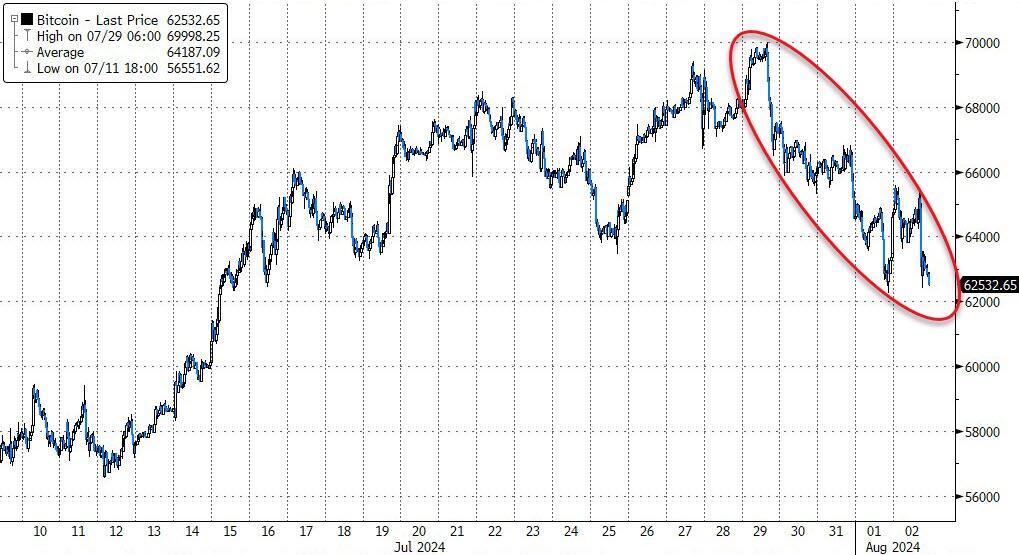

In the past, such as in 2008—2009 gold was initially seen as a source of funds in an equity market crisis. But physical gold has already gone to China, with ETF holdings having been sold down over the last three years. This time, bitcoin and other cryptos appear to be a likely source of funds if markets crash.

And finally, we cannot ignore developments in the Middle East. Israel assassinating a Hamas leader in Tehran and increasing attacks from Hezbollah are major escalations’. A deteriorating situation seems likely to flare up into a full-scale war. It could be the only way an increasingly desperate Israel can persuade America and NATO to back her against Iran.

3.CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES

Robert Lambourne’s figures are very accurate: he confirms that the BIS increased its gold swaps by 7 tonnes to 116 tonnes. There is only one central bank that is engaged in this: THE FED or its trading arm: THE FRBNY.

(Robert Lambourne/GATA)

BIS annual report again confirms GATA’s accuracy with bank’s gold swaps

Submitted by admin on Thu, 2024-08-01 15:11 Section: Daily Dispatches

3:08p ET Thursday, August 1, 2024

Dear Friend of GATA and Gold:

GATA consultant Robert Lambourne today provides below his monthly report on the gold swaps maintained by the central bank of the central banks, the Bank for International Settlements, and superficially the report may seem ordinary, disclosing a small increase in BIS gold swaps from May to June, 7 tonnes, from 109 to 116.

Lambourne is too modest to highlight the most important development with the BIS’ accounts. That is, the bank’s annual report, dated March 31 —

— has again confirmed the accuracy of his calculations of the bank’s gold swaps, which constitute the bank’s intervention in the gold market on behalf of member central banks. The BIS gives a gold swaps total only once a year, in its annual report, even as Lambourne strives to calculate the monthly changes. At the bottom of Page 194 this year’s annual report shows 72 tonnes of gold swaps as of March 31, and Lambourne had estimated 71.

The BIS’ constant trading in gold swaps is perhaps the best proof that surreptitious gold market manipulation by at least one central bank continues as a matter of policy. Maybe that’s why no mainstream financial news organizations report about the swaps, or, indeed, about anything the BIS does. Only GATA’s Lambourne does.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

———

BIS gold swaps rose from 109 to 116 tonnes in June

By Robert Lambourne

Thursday, August 1, 2024

The June statement of account for the Bank for International Settlements has recently been published:

From this it is possible to estimate the volume of gold swaps undertaken by the BIS at the month end. The estimated swap volume is 116 tonnes at June 30. This compares to an estimate of 109 tonnes for May 31, for an increase of seven tonnes.

Table 1 below sets out the historical level of monthly gold swaps estimated since August 2018. As is evident from Table 1 there is still a considerable level of gold being traded via these swaps. The level of gold swaps is down significantly from the 501 tonnes estimated in January 2022 but seemingly remains quite volatile, suggesting their use to cover shorter term trading requirements.

To repeat the point made in these GATA reports, it seems that these swaps are undertaken by the BIS for one or more of its central bank members with the swapped gold being accounted for as being held in a BIS-registered sight account at a central bank. Given what is happening in the gold market generally, it appears reasonable to assume that the U.S. Federal Reserve is the BIS customer for these gold swap transactions.

The evidence strongly suggests that the source of this gold is bullion banks and the likelihood is that the metal comes from gold registered as being held by gold exchange-traded funds.

A more detailed report on the use of gold swaps was published to cover transactions in December 2023: It covers some of the history in more detail:

https://www.gata.org/node/23016

The recently published 2023-24 BIS annual report —

— supports GATA’s estimate of gold swaps as of March 31 as shown in Table 1. The BIS said it had undertaken 72 tonnes in gold swaps. GATA’s original estimate was 71 tonnes.

The BIS Annual Report contains information that also confirms certain assumptions used to estimate the swap volumes. This includes confirmation that the BIS continues to hold 102 tonnes of its own gold. The annual report also provides strong support, via its reporting on transactions with related parties, that the source of the swapped gold is bullion banks rather than central banks.

However, the BIS continues to offer no explanation for why it is still undertaking gold swaps. The GATA report from December 2023 cited above offers some comments on possible reasons and historical comments made by the BIS when it first reported gold swaps being made, in its annual report for 2009-10.

Table 1 — Gold swaps estimated by GATA

from BIS monthly statements of account

Month ….. Swaps

& year … in tonnes

June-24 …. /116

May-24 …. /109

Apr-24 … /78

Mar-24 …. /72

Feb-24 …. /68

Jan-24 …. /117

Dec-23 … /121

Nov-23 …./100

Oct-23 …./68

Sep-23 …./96

Aug-23 …./129

Jul-23 …. /103

Jun-23…. /87

May-23 …. /188

Apr-23 …. /135

Mar-23 …. /77*

Feb-23 … /136

Jan-23 … /103

Dec-22 … /0

Nov-22 … /105

Oct-22 ….. /7

Sep-22 …../57

Aug -22 ….. /75

Jul-22 ….. /56

Jun-22 ….. /202

May-22 ….. /270

Apr-22 ….. /315

Mar-22 …. /358

Feb-22 …. /472

Jan-22 ….. /501

Dec-21…. /414

Nov-21…. /451

Oct-21…. /414

Sep-21 …. /438

Aug-21 …. /464

Jul-21 …. /502

Jun-21 …./471

May-21 …./517

Apr-21 …. /472

Mar-21…. /490±

Feb-21 …../552

Jan-21 …. /523

Dec-20 …. /545

Nov-20 …. /520

Oct-20 …. /519

Sep-20…../ 520

Aug-20…../ 484

Jul-20 ….. / 474

Jun-20 …. / 391

May-20 …. / 412

Apr-20 …. / 328

Mar-20 …. / 326**

Feb-20 …. / 326

Jan-20 …. / 320

Dec-19 …. / 313

Nov-19 …. / 250

Oct-19 …. / 186

Sep-19 …. / 128

Aug-19 …. / 162

Jul-19 ….. / 95

Jun-19 …. / 126

May-19 …. / 78

Apr-19 ….. / 88

Mar-19 …. / 175

Feb-19 …. / 303

Jan-19 …. / 247

Dec-18 …. / 275

Nov-18 …. / 308

Oct-18 …. / 372

Sep-18 …. / 238

Aug-18 …. / 370

* The estimate originally reported by GATA was 78 tonnes, but the BIS annual report states 77 tonnes. It is believed that slightly different gold prices account for the difference.

+ The estimate originally reported by GATA was 487 tonnes, but the BIS annual report states 490 tonnes, It is believed that slightly different gold prices account for the difference.

** The estimate originally reported by GATA was 332 tonnes, but the BIS annual report states 326 tonnes. It is believed that slightly different gold prices account for the difference.

GATA uses gold prices quoted by USAGold.com to estimate the level of gold swaps held by the BIS at month-ends.

—–

Robert Lambourne is a retired business executive in the United Kingdom who consults for GATA about the involvement of the Bank for International Settlements in the gold market and U.S. government debt.

* * *

Ronan Manly: Elections and political uncertainty help drive gold demand and price

Submitted by admin on Thu, 2024-08-01 23:22 Section: Daily Dispatches

By Ronan Manly

Bullion Star, Singapore

Thursday, August 1, 2024

This year is shaping up to be a perfect storm for political risk and uncertainty, given that in addition to the upcoming US presidential and Congress elections, we have already seen major shifts in the political landscapes of two other G7 countries, France, and the United Kingdom.

While often underappreciated, elections and changes in governments in major economies like the U.S., U.K., and France create political uncertainty that can have a significant impact on financial market stability, investor sentiment, and on macro factors such as interest rates, U.S. dollar strength, and geopolitical risk — all of which are key influences on the gold price.

This is because the run-up to elections leads to uncertainty about election outcomes and who will be in power, and the outcome of elections often leads to new parties and leaders assuming power who have different agendas to their predecessors. New governments and leaders assuming power with new agendas then usually implement different economic policies compared to their predecessors. This phenomenon is known as policy shift. …

… For the remainder of the analysis:

end

Bill to create U.S. bitcoin reserve would finance it with gold revaluation

Submitted by admin on Wed, 2024-07-31 09:12 Section: Daily Dispatches

U.S. Strategic Bitcoin Reserve to Be Funded Partly by Revaluing Fed’s Gold, Draft Bill Shows

By Bradley Keoun

CoinDesk, New York

Tuesday, July 30, 2024

U.S. Senator Cynthia Lummis’ plan for a new Strategic Bitcoin Reserve would finance purchases of the cryptocurrency partly by revaluing gold certificates held by the Federal Reserve System, according to a draft of the legislation obtained by CoinDesk.

Lummis, a Wyoming Republican known for her Bitcoin-friendly policy stance, announced her intention to propose the reserve on Saturday at the Bitcoin Nashville conference. She came onstage just minutes after former U.S. President Donald Trump, the Republican nominee in this year’s presidential race, delivered a speech on blockchain policy before the cheering room, filled to its 8,500-person capacity. …

… For the remainder of the report:

4. GOLD PODCASTS//LIVE FROM THE VAULT/no 184 with Craig Hemke/Andrew Maguire

Weak hands Fed running out of time Feat.…

In this week’s episode of Live from the Vault, Andrew…

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COCOA

6 CRYPTOCURRENCY NEWS

END

ASIA TRADING/FRIDAY MORNING/THURSDAY NIGHT

SHANGHAI CLOSED DOWN 27.05 PTS OR 0.92% //Hang Seng CLOSED DOWN 359.45 PTS OR 2.08% // Nikkei CLOSED DOWN 2216.67 OR 5.81%//Australia’s all ordinaries CLOSED DOWN 2.08%///Chinese yuan (ONSHORE) CLOSED UP TO 7,2058 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2072/ Oil DOWN TO 76,24 dollars per barrel for WTI and BRENT DOWN AT 79.,35 Stocks in Europe OPENED ALL RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.2058

OFFSHORE YUAN: UP TO 7.2072

SHANGHAI CLOSED DOWN 27.06 PTS OR 0.92 %

HANG SENG CLOSED DOWN 359.45 PTS OR 2.08%

2. Nikkei closed DOWN 2216.67 PTS OR 5.81%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX DOWN TO 103.86 EURO RISES TO 1.0833 DOWN 22 BASIS PTS

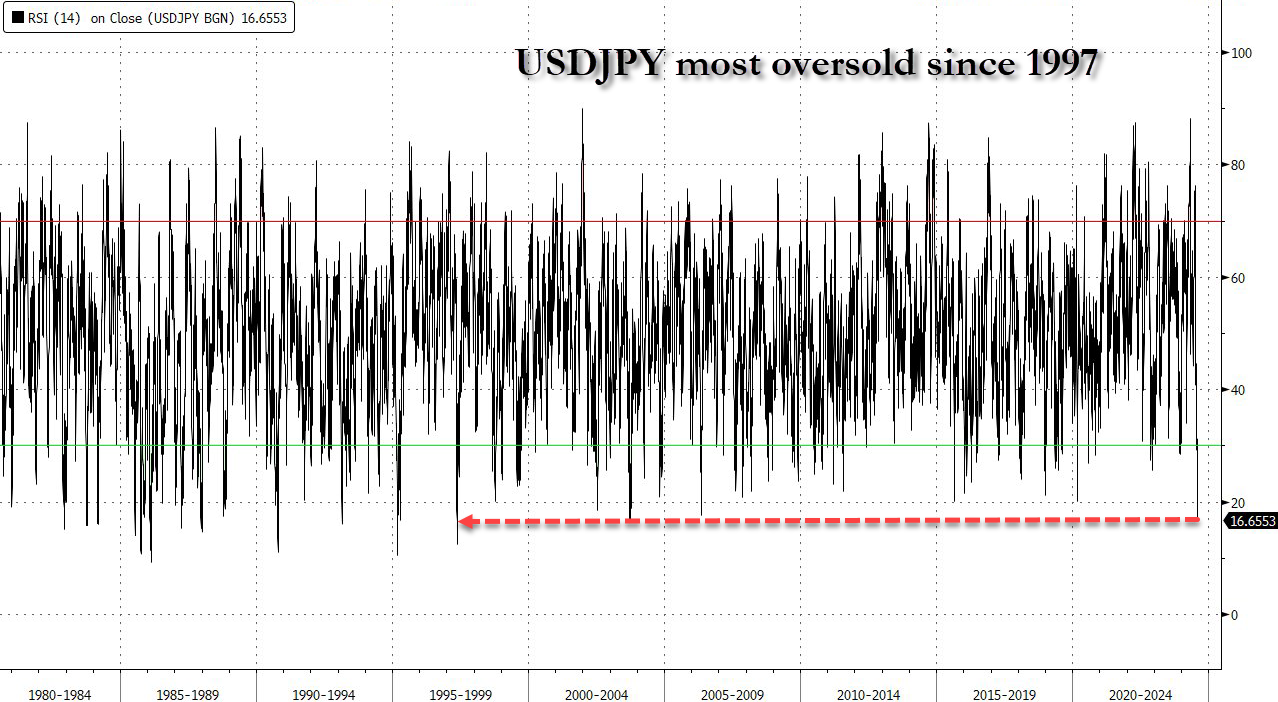

3b Japan 10 YR bond yield: FALLS TO. +0.946 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 148.99…… JAPANESE YEN NOW RISING AS WE HAVE NOW REACHED THE END OF THE YEN CARRY TRADE

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

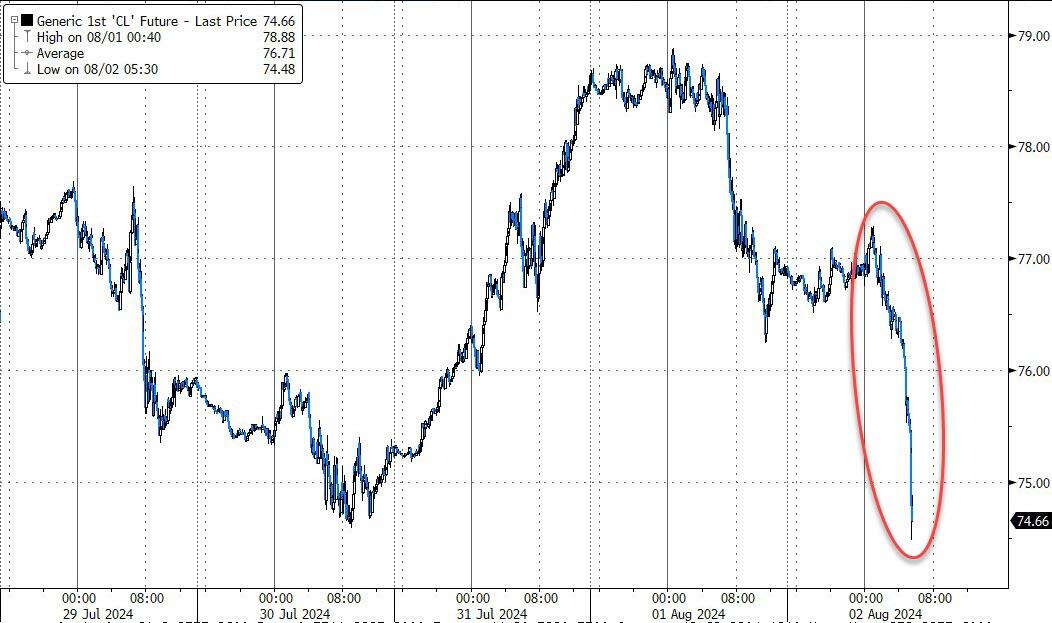

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.2084/Italian 10 Yr bond yield DOWN to 3.641 SPAIN 10 YR BOND YIELD DOWN TO 3.070%

3i Greek 10 year bond yield DOWN TO 3.297

3j Gold at $2466.50//Silver at: 28.77 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 32/ 100 roubles/dollar; ROUBLE AT 85.82

3m oil into the 76 dollar handle for WTI and 79 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 148.99/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.946 % STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8656as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9428 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

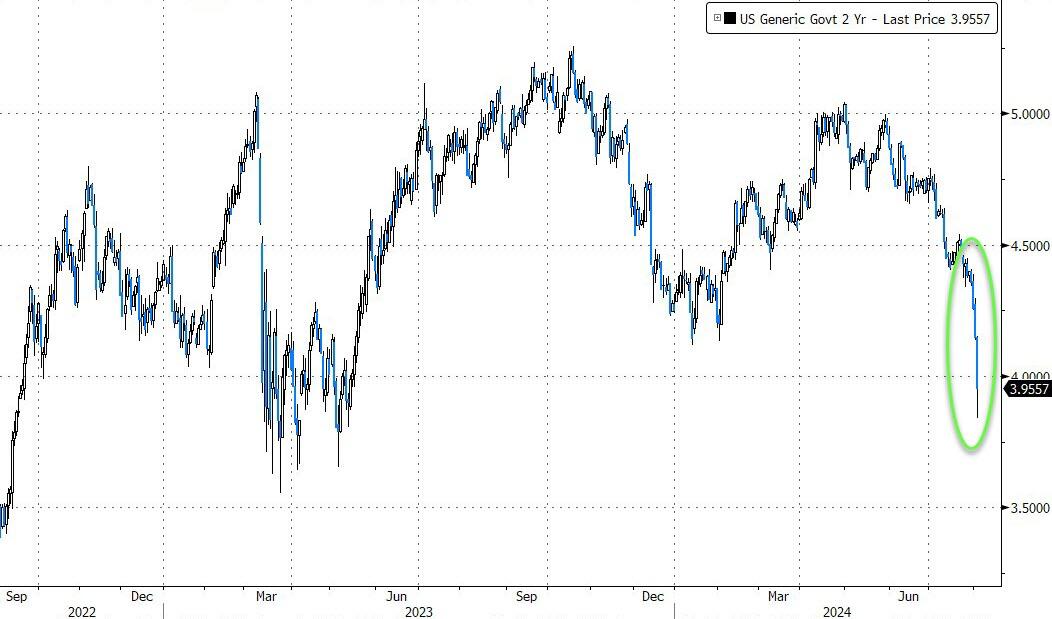

USA 10 YR BOND YIELD: 3.928 DOWN 5 BASIS PTS…

USA 30 YR BOND YIELD: 4.230 DOWN 4 BASIS PTS/

USA 2 YR BOND YIELD: 4.118 DOWN 5 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 33.17…

10 YR UK BOND YIELD: 3.88 DOWN 1 PTS

10 YR CANADA BOND YIELD: 3.077 DOWN 5 BASIS PTS

2a New York OPENING REPORT

US Futures, Global Stocks Tumble, Japan Crashes Amid Panic Fed Is Now Behind The Curve

FRIDAY, AUG 02, 2024 – 08:03 AM

It is a global selling carnage this morning, as risk-off extends across worldwide equity markets but nowhere more so than Japan where the point (if not percentage point) drop in the Nikkei has surpassed Black Monday 1987.

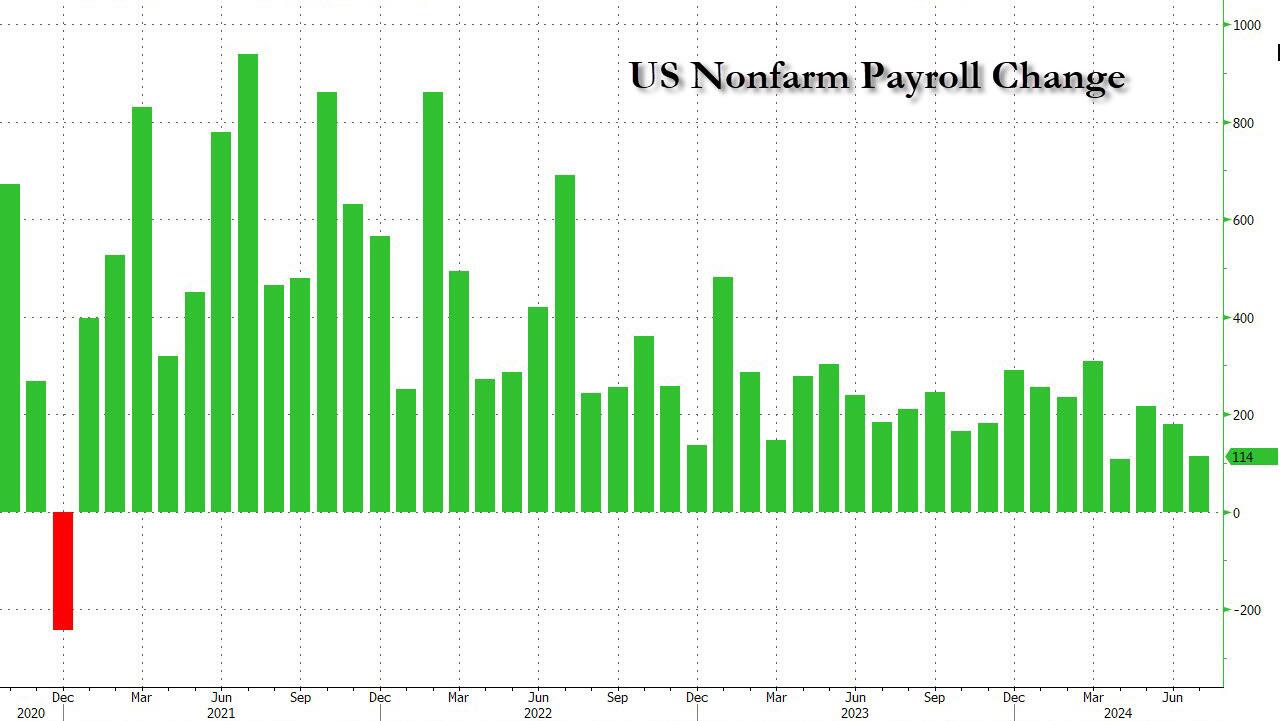

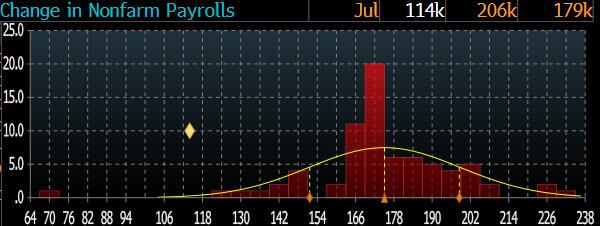

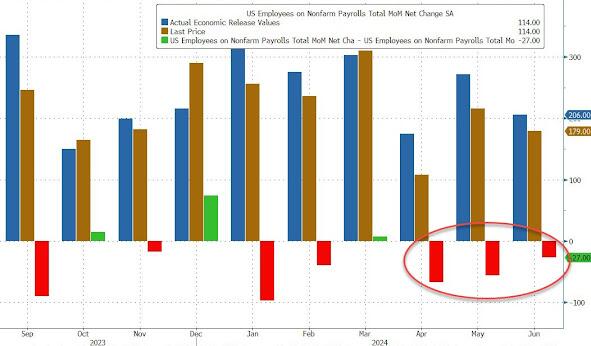

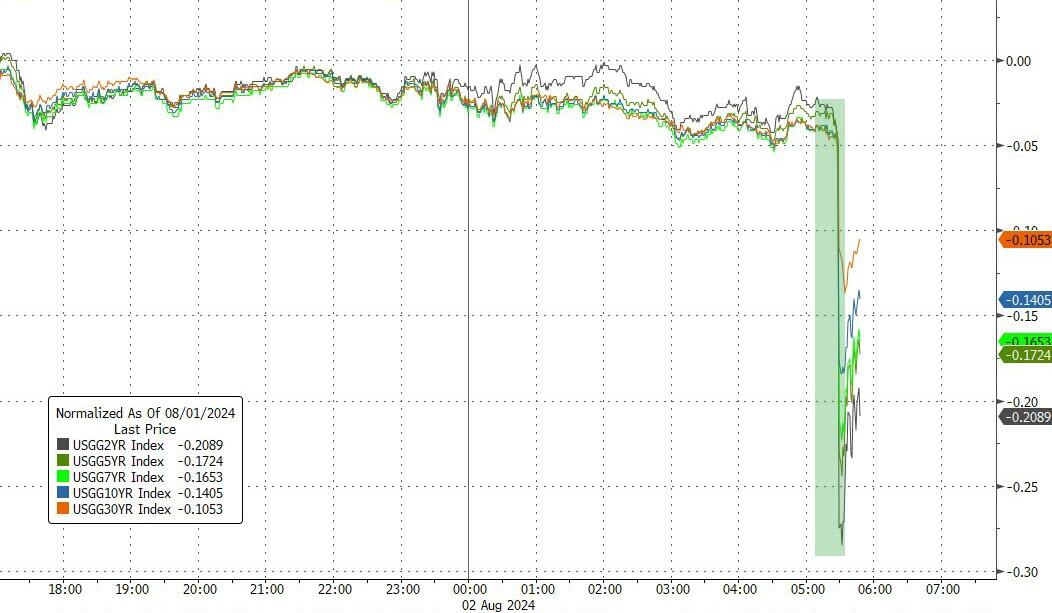

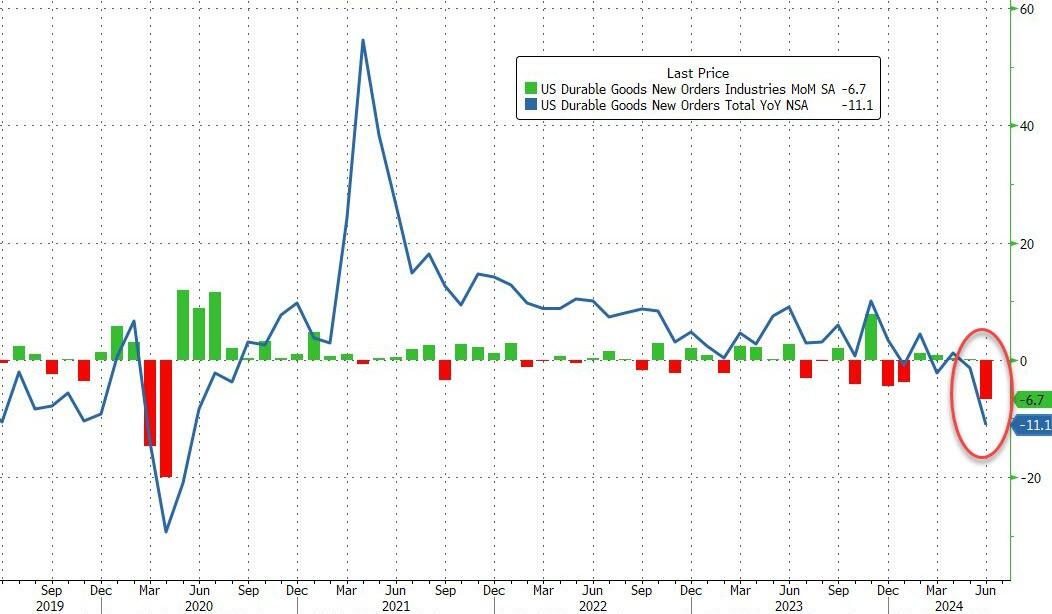

As of 7:45am, S&P futures are down 1.2% as traders worried that the Federal Reserve has been too slow to cut interest rates, and technology earnings disappointed, pushing Nasdaq futures 1.7% lower as Amazon’s Q3 earnings forecast disappointed and Apple reported a surprise plunge in Chinese revenues. While Europe is a sea of red, it is nothing compared to what took place in Asia, where the Topix index crashed 6.1%, the biggest one-day selloff since 2016, as a result of the continued meltup in the yen after the BOJ’s idiotic rate hike – which took place just as Japan’s economy slumped back into contraction and inflation peaked – and given poor risk sentiment in the US. US rates are continuing their downside momentum with the OIS market now pricing in 88bp of rate cuts in 2024. A rally in Treasuries extended into a seventh straight day, with the two-year yield slumping to its lowest in 14 months. The dollar weakened. In FX, low yielding currencies are leading the rally against USD with CNH and JPY up 0.7% and 0.3%, respectively, while higher beta currencies like MXN and NOK are both down 0.6%. Today we get the jobs report (exp. 175K) and the final Factory/Durable Orders report out of the US.

In premarket trading, Exxon Mobil jumped after it exceeded profit expectations after the $63 billion acquisition of Pioneer Natural Resources Co. pushed oil and natural gas output to a record. Chevron shares slid in premarket trading after reporting earnings per share that missed the average analyst estimate. The company also said its headquarters would move to Texas from California. Amazon plunged 8% on concern costs are rising quickly to meet demand for AI services. Intel cratered more than 20% after giving a grim growth forecast and laying out plans to slash 15,000 jobs. Snap dropped 17% as revenue undershot estimates. Here are some other notable movers:

- Intel shares plunge 22% after the chipmaker’s forecast for third-quarter revenue undershot the average analyst estimate. In a string of startling announcements, the company said it would slash 15,000 jobs and suspended its dividend starting in the fourth quarter.

- Snap shares plunge 18% after the social media company’s revenue undershot estimates and its third-quarter outlook also disappointed amid weakness in brand spending. The update prompted brokers to cut their price targets on the stock, citing the volatile nature of Snap’s business.

- Ardelyx shares rise 8.5% Friday after the company reported total revenue for the second quarter that beat the average analyst estimate.

- Block shares gain 3% in premarket trading on Friday after the payments company boosted its adjusted Ebitda guidance for the full year, beating the average analyst estimate.

- Coinbase shares advance 0.13% after the cryptocurrency trading platform reported second-quarter revenue that beat estimates. Jefferies highlighted the strength in subscription and services revenue, while Canaccord Genuity said Coinbase’s performance underscored the company’s diversifying revenue base.

- Cloudflare shares gain 9% after the cybersecurity company’s earnings and outlook surpassed analyst expectations, prompting price target hikes as brokers pointed to a strong performance and execution in a difficult environment. Some analysts also noted that the company is benefiting from Generative AI.

- Lexicon Pharma shares fall 15% after the company reported a second-quarter loss of 17c per share.

- Microchip Technology drops 6.7% as BofA downgrades the chipmaker to neutral from buy following its results, based on limited catalysts for a short-term recovery. The company also receives a number of price-target cuts from other brokers.

- Twilio shares are up 5.7% after the infrastructure-software company reported second-quarter results that beat expectations and gave an outlook that is seen as positive.

The next big data point for the market is Friday’s monthly jobs report, which is expected to show that US employers added workers at a slower pace last month (see our preview here). Forecasters anticipate the monthly US jobs numbers will show moderating job and wage growth in July, underscoring a further softening in the labor market. Payrolls probably rose by 175,000 last month following June’s 206,000 increase, according to the median estimate in a Bloomberg survey.

While Fed Chair Jerome Powell has signaled that rates are likely to be lowered in September, some investors have argued they should move faster to prevent a deeper economic slowdown. Indeed, amid the rout, jumpy markets now see the Fed delivering three consecutive quarter-point cuts in September, November and December — and are pricing a roughly 50% chance that one of those reductions will be 50 basis points. The policy-sensitive two-year yield slumped to its lowest in 14 months, while rates on the benchmark 10-year security held below 4% after falling to that level on Thursday for the first time since February.

“The data is really starting to show signs of concern and that is what’s coming back to bite the Fed,” said Daniela Hathorn, a senior market analyst at Capital.com. “They kept signaling they’d wait for the data, and that was fine until Wednesday, but yesterday’s data has investors fearing whether it waited for too long.”

Risk assets have taken a beating in recent sessions for other reasons too. Lackluster earnings from Microsoft Corp. to Amazon.com Inc. have hurt sentiment that is also being weighed down by concern about the sluggish Chinese economy and a weakening of the earlier euphoria over artificial intelligence. Middle East tensions have also multiplied after the assassination of Hamas’ political chief in Tehran.

It’s all added up to a volatile week for markets, with the VIX Index on track for the highest closing level in nine months. The Nasdaq 100 recorded swings of at least 1.4% over the past three days. A gauge for the Magnificent Seven big tech companies was up 0.3% for the week through Thursday.

The sharp recalibration in expectations for US rates came after the Fed held rates again this week. While Chair Jerome Powell signaled that central bank officials are on course to pare rates at their next meeting, economic reports on Thursday showed rising jobless claims and weaker manufacturing, spooking investors. Ahead of the Fed meeting, former New York Fed President William Dudley and Mohamed El-Erian warned that the Fed risks making a mistake by holding rates too high for too long and are once again behind the curve. That narrative has started to take hold in the past 24 hours. But bond market exuberance means that if Friday’s employment report shows signs of unexpected strength, there’s a risk some traders will dump bullish wagers en masse. According to Bloomberg, a $12 million wager has emerged in options linked to the Secured Overnight Financing Rate, which closely tracks Fed policy expectations, targeting some 225 basis points of easing by the middle of 2025. Even with the recent explosion of bets, the market is pricing in about 160 basis points by then.

“In coming days there may be even a discussion about whether the Fed will have to cut by 50 basis points at the next meeting in order to catch up with the loss of momentum in the economy,” Gary Dugan, chief executive officer of the Global CIO Office, said in an interview on Bloomberg Television. “From the peak a 10%-to-15% correction wouldn’t be strange in this huge change in shift in sentiment in the markets as central banks look well behind the curve.”

The shift in pricing “reflects investors’ growing concern that the FOMC might need to cut rates more quickly than the 25-basis-point quarterly cadence as economic headwinds continue to mount,” said Ian Lyngen, head of US rates strategy at BMO Capital Markets. Powell repeated on Wednesday that the Fed is data dependent when deciding when to lower interest rates, and emphasized that policymakers are mindful of the risk to the the labor market of waiting too long.

“We suggest investors brace for renewed volatility, but avoid overreacting to short-term shifts in market sentiment,” said Mark Hafele, chief investment officer at UBS Global Wealth Management.

European markets are all deep in the red, with the Stoxx 600 tumbling over 1% with technology and finance shares leading the declines. Among industry groups, utilities were the only category of stocks to rise. Europe’s semiconductor sector slumps, following an extended retreat among global tech stocks. Among chip-equipment stocks: ASML -5.2%, ASMI -7.9%, BE Semiconductor -6.5%, VAT Group -7.3%. Among chipmakers, Infineon -3.8%, STMicro -3.8%, Melexis -2.1%, Nordic Semiconductor -4.5%. Here are the other biggest movers:

- AXA shares gain as much as 2.7%, as the French insurer’s first-half profit beat estimates and the firm announced the sale of its asset management unit to BNP Paribas

- Engie gains as much as 4.4%, the most in a month, after the French energy company reported a strong 2024 guidance upgrade, according to Morgan Stanley

- IMCD rises as much as 9% after the Dutch chemicals provider’s first-half results were better than expected, according to KBC

- IAG shares rise as much as 6.4%, the most since March, after the British Airways-parent delivered a strong profit beat in the second quarter, helping soothe investors’ concerns after outlook downgrades from sector peers

- Ferragamo shares rise as much as 4.7% after the Italian luxury goods maker’s earnings beat estimates

But if Europe was bad, Asia was a disaster: here stocks crashed as sentiment was hit by a triple whammy of a selloff in Japanese equities, a global tech rout and signs of weakness in the US economy. The MSCI Asia Pacific Index plunged as much as 3.6%, the most since February 2021, with Taiwan Semiconductor Manufacturing Co., Mitsubishi UFJ Financial Group and Samsung Electronics Co. among the biggest drags. Japan’s Topix Index entered a technical correction in its worst two-day rout since 2011, while benchmarks in the tech-heavy markets of South Korea and Taiwan fell about 4%. Traders took risk off the table amid signs the investment landscape is shifting. Japanese stocks are falling out of favor as the prospect of further interest-rate hikes by the country’s central bank supports the yen, hitting exporters’ shares. Meanwhile, disappointing earnings from US tech behemoths has cooled optimism over artificial intelligence, triggering a rout that has ensnared Asian chip giants

“The recent strengthening of the Japanese yen coupled with tech sector weakness is poised to significantly impact the Asian stock market,” said Manish Bhargava, a fund manager at Straits Investment Holdings in Singapore. “Given the substantial weight of tech stocks in Asian indices, disappointing results from tech giants could trigger a broader market downturn in Asian markets.”

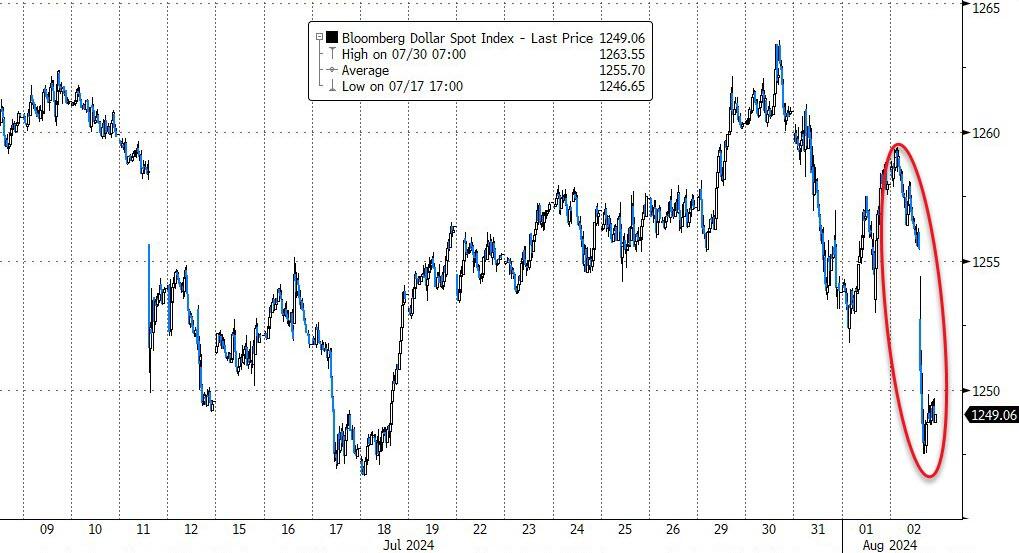

In FX, the Bloomberg Dollar Spot Index falls 0.1%. The euro and yen top the G-10 FX leaderboard, rising 0.3% a piece against the greenback. The offshore yuan climbs to the highest since May.

- GBP/USD fell 0.3% to $1.2707, with the pound headed for its biggest weekly drop since April, following the BOE’s decision to ease policy on Thursday

- USD/CHF fell 0.3% to 0.8706 and EUR/CHF was little changed around 0.94189, Swiss inflation held steady in July with a headline of 1.3% matching economist estimates

- USD/JPY fell as much as 0.5% to 148.63, with the yen on course for its biggest weekly gain since May after the BOJ’s interest-rate hike on Wednesday

In rates, a rally in Treasuries extended into a seventh straight day ahead of the US jobs report. US 10-year yields fall 3bps to 3.95% – the lowest since early February – ahead of June employment data investors are counting on to reinforce the case for aggressive Fed rate cuts this year. European bonds follow suit. Fed-dated OIS contracts price in around 32bp of easing for the next policy meeting in September, or roughly 32% odds that the central bank’s first move will be a half-point rate cut rather than 25bp.

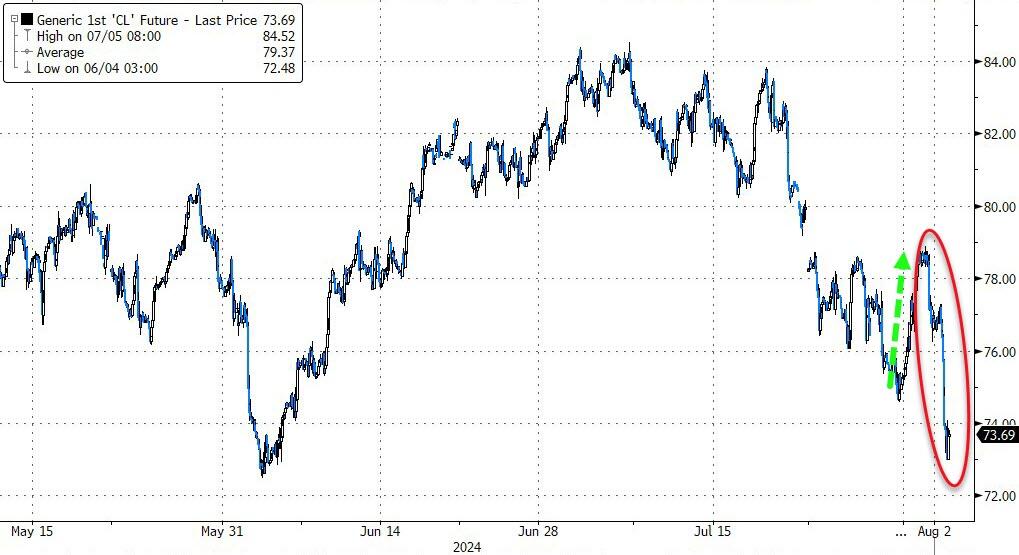

In commodities oil prices advance, with WTI rising 0.4% to $76.60 a barrel. Spot gold jumps $16 to around $2,462/oz.

Today’s economic data slate includes July employment report (8:30am) and June factory orders (10am). Scheduled Fed speaker slate includes Goolsbee (12pm) and Barkin (8:30pm)

Market Snapshot

- S&P 500 futures down 0.9% to 5,428.25

- STOXX Europe 600 down 1.4% to 504.81

- MXAP down 3.4% to 176.04

- MXAPJ down 2.4% to 554.23

- Nikkei down 5.8% to 35,909.70

- Topix down 6.1% to 2,537.60

- Hang Seng Index down 2.1% to 16,945.51

- Shanghai Composite down 0.9% to 2,905.34

- Sensex down 0.8% to 81,198.44

- Australia S&P/ASX 200 down 2.1% to 7,943.24

- Kospi down 3.7% to 2,676.19

- German 10Y yield little changed at 2.22%

- Euro up 0.2% to $1.0812

- Brent Futures up 0.6% to $79.98/bbl

- Gold spot up 0.7% to $2,464.31

- US Dollar Index down 0.22% to 104.19

Top Overnight News

- Chevron plans to relocate its headquarters to Houston, Texas from San Ramon, California. The stock fell premarket after it missed profit estimates, adding to pressure on its efforts to acquire Hess. BBG

- China’s efforts to boost household spending are expected to help the economy hit the government’s 2024 growth target of roughly 5%, but the authorities may have to do more for consumers from next year or accept slower growth. Trade tensions and local government debt risks leave Beijing few alternatives to revving up consumer stimulus in coming years, but vague promises of “incremental measures” look likely to fall short, analysts say. RTRS

- An influential PBOC adviser delivered a rare critique of China’s economic policy for being overly conservative. Huang Yiping urged the government to ramp up fiscal stimulus and set a hard target for inflation. BBG

- Once seen as a cautious policy dove, Bank of Japan Governor Kazuo Ueda is now presenting himself as a determined hawk who’s not afraid to lift interest rates a few more times, even in the face of a weakening economy. RTRS

- The US has declared Venezuela opposition candidate Edmundo González the winner of the July 28 presidential election, describing the official results favouring President Nicolás Maduro as “deeply flawed”. Antony Blinken, US secretary of state, said on Thursday that “given the overwhelming evidence, it is clear to the United States and . . . to the Venezuelan people that Edmundo González Urrutia won the most votes” and congratulated him on his “successful campaign”. FT

- For today’s jobs print GIR is calling for: +165k NFP (+175k consensus, +206k prior), U/E Rate of 4.1% (4.1% consensus, 4.1% prior) and MoM AHE +.3% (+.3% consensus, +.3% prior). The playbook on how to trade stocks around economic data prints that we have been using for most of 2024 has officially flipped as evidenced by the stock market’s reaction to the weak ISM print yesterday. We are no longer in a bad data is good for stocks environment. The fed showed its hand. Cuts are happening. Stocks do NOT want growth scare convos resurfacing. Good econ data is now good for the stock market and vice versa.

- AMZN (-8% pre mkt) reported a small miss on total sales at +10%/$148B (vs. the Street $148.7B) but op. income outperformed expectations at $14.7B (vs. the Street $13.5B). The outlook for Q3 falls short of the consensus – the guidance mid-points for Q3 work out to $156.25B on sales (below the Street’s $158.4B forecast) and $13.25B on op. income (below the Street’s $15.6B forecast).

- AAPL (+1% pre mkt) reported FQ3 upside on both sales ($85.8B vs. the Street $84.4B) and EPS (1.40 vs. the Street 1.35). China fell short, with sales of $14.72B (vs. the Street $15.2B), but they outperformed in the Americas, Europe, and Asia ex-Japan/China. The FQ4 guide is a bit ahead of the Street – they see sales up 5% (vs. the Street +4.1%) and GMs of 46% (vs. the Street 45.9%). RTRS

- INTC (-22% pre mkt) reported a miss on Q2 EPS/revenue, the guidance is very weak (the Q3 sales guidance mid-point is $13B vs. the Street $14.3B), the company is slashing its headcount by 15%, and the dividend is being suspended. BBG

Earnings

- Apple Inc (AAPL) Q3 2024 (USD): EPS 1.40 (exp. 1.35), revenue 85.78bln (exp. 84.53bln), Products rev. USD 61.56bln (exp. 60.63bln), iPhone rev. USD 39.30bln (exp. 38.95bln), iPad revenue USD 7.16bln (exp. 6.63bln), Mac rev. USD 7.01bln (exp. 6.98bln), Wearables, home and accessories rev. USD 8.10bln (exp. 7.79bln), Service rev. USD 24.21bln (exp. 23.96bln), Greater China rev. USD 14.73bln (exp. 15.26bln). Shares -0.3% in the pre-market.

- Amazon.com Inc (AMZN) Q2 2024 (USD): EPS 1.26 (exp. 1.03), rev. 148bln (exp. 148.56bln). Shares -8.3% in the pre-market.

- Intel Corp (INTC) Q2 2024 (USD): Adj. EPS 0.02 (exp. 0.10), rev. 12.83bln (exp. 12.94bln). Shares -21% in the pre-market.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks suffered firm losses following the bloodbath and flight-to-quality stateside which was triggered by weak ISM Manufacturing data, while geopolitical concerns and mixed earnings added to the downbeat sentiment. ASX 200 declined amid the broad weakness and with firm losses seen across all sectors. Nikkei 225 fell beneath 37,000 for the first time since April, while the Topix index followed the benchmark into correction territory. Hang Seng and Shanghai Comp. were pressured which saw the former give up the 17,000 status and the mainland index also retreated, while there were bearish comments on trade from a Mofcom official who stressed the seriousness of difficulties and challenges in foreign trade. SK Hynix (000660 KS) was pressured by over 10% in APAC trade as chip stocks continued to sell off.

Top Asian news

- China MOFCOM official said the complexity of the foreign trade environment is rising and we should take into full account the seriousness of the difficulties and challenges in foreign trade, as well as noted that they will use many bilateral mechanisms to help enterprises actively respond to unreasonable trade restrictions.

- Japanese Finance Minister Suzuki said they will analyse the impact of forex volatility on the economy and respond appropriately. Suzuki added that stock prices are determined in the market based on various factors such as economic conditions and he is closely watching stock moves with a sense of urgency.

- Japanese Industry Minister Saito said economic fundamentals aren’t bad when asked about the sharp fall in the stock market, while he added that a strong movement is seen in investment and wage hikes are continuing.

- BoJ’s Uchida to hold a press conference following on from a local business leaders meeting in Hakodate on 7th August

- PBoC advisor reportedly said that China should ramp up fiscal stimulus to generate growth and set a firm inflation target, via Reuters citing remarks from advisor Yiping.

- Nintendo (7974 JT) Q1 (JPY) Net 80.9bln (exp. 79bln), Operating 54.5bln (exp. 83bln), Recurring Profit 113bln, -55.3%. Switch: Sold 2.1mln units (prev. 3.91mln Y/Y); maintains FY sales forecast of 13.5mln units (prev. 15.7mln)