GOLD PRICE CLOSED UP $1.90 TO $2392.10

SILVER PRICE DOWN $0,27 TO $26.85

Gold ACCESS CLOSED $2387.15

Silver ACCESS CLOSED: $26.75

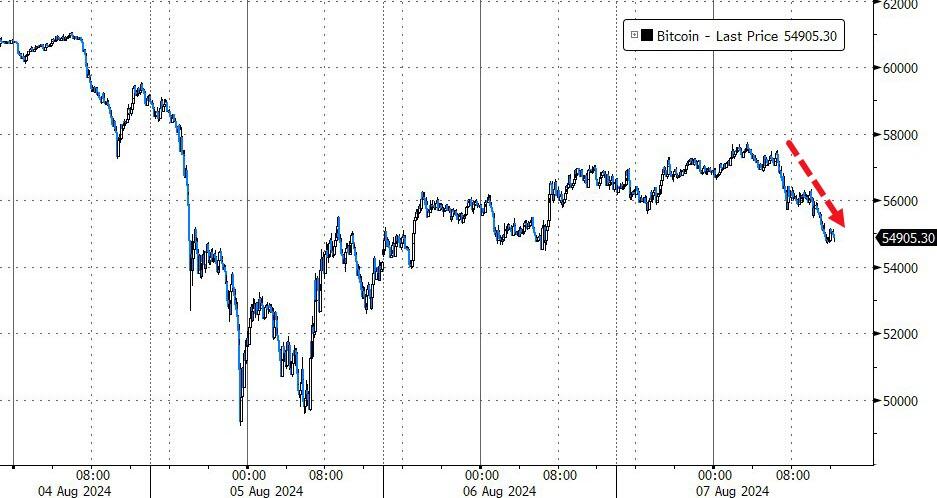

Bitcoin morning price:$57,285 UP 638 DOLLARS.

Bitcoin: afternoon price: $54,926 DOWN 1721 DOLLARS

Platinum price closing UP $6.75 TO $923.35

Palladium price; UP $17.60 TO $897.00

END

SHANGHAI GOLD PREMIUM 58 DOLLARS/COMEX GOLD//august to august

SHANGHAI GOLD (USD) FUTURES – QUOTES

Last Updated 07 Aug 2024 04:30:16 AM CT.

Market data is delayed by at least 10 minutes.

*CANADIAN GOLD: $3281.66 DOWN 5.89 CDN dollars per oz( * NEW ALL TIME HIGH 3,390.26 CDN DOLLARS PER OZ//AUG 1 2024)

*BRITISH GOLD: 1,880.74 DOWN 1.44 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1933.24 BRITISH POUNDS/OZ) APRIL 19/2024

*EURO GOLD: 2,185.70 UP 3.64 Euros per oz //* (ALL TIME CLOSING HIGH: 2.264.61 EUROS PER OZ//AUGUST 1 //.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE: COMEX

ACCESS MARKET

EXCHANGE: COMEX

CONTRACT: MARCH 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,157.300000000 USD

INTENT DATE: 03/15/2024 DELIVERY DATE: 03/19/2024

FIRM ORG FIRM NAME ISSUED STOPPED

132 C SG AMERICAS 15

435 H SCOTIA CAPITAL 6

661 C JP MORGAN 62 70

686 C STONEX FINANCIA 1

737 C ADVANTAGE 2

TOTAL: 78 78

MONTH TO DATE: 5,25

JPMorgan stopped 3/5

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2024. CONTRACT: 5 NOTICES FOR 500 OZ or 0.01555 TONNES

total notices so far: 17,075 contracts for 1,707500 Oz (53.1104 tonnes)

FOR AUGUST:

SILVER NOTICES: 102 NOTICE(S) FILED FOR 510,000

OZ/

total number of notices filed so far this month : 680 for 3.4000 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $1.90 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.16 TONNES OF GOLD INTO THE GLD//

/ /INVENTORY RESTS AT 848.06 TONNES

INVENTORY RESTS AT 848.06 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $0.27 AT THE SLV

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 4.552 MILLION OZ INTO THE SLV/

// INVENTORY AT 462.502 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 462.502 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUMONGOUS SIZED 2299 CONTRACTS TO 147,537 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH HUGE LIQUIDATION OF OI FROM OUR SPREADERS/TAS DESPITE OUR TINY GAIN OF $0.05 IN SILVER PRICING AT THE COMEX ON TUESDAY’S TRADING // //RAID. SOME OF OUR OI LIQUIDATION ACCOMPANIED OUR HUGE NET LOSS OF 1046 CONTRACTS ON OUR TWO EXCHANGES AS WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS DURING TUESDAY’S RAID. WE HAD SOME ZERO COVERING BY OUR SPECS WITH THE SMALL GAIN IN PRICE AS WE HAD A HUGE 1255 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY A HUMONGOUS 2375 CONTRACT T.A.S ISSUANCE. IN ESSENCE WE LOST 1044 CONTRACTS ON OUR TWO EXCHANGES DESPITE THE SMALL GAIN IN PRICE.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN YESTERDAY. THE DEMAND FOR SILVER WAS JUST TOO GREAT FOR OUR BANKERS TO CONTAIN AND THUS THE STEEP RISE IN OI ON OUR TWO EXCHANGES DESPITE THE TINY GAIN IN PRICE.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: 964 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS.IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1/2 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS BUT TO NO AVAIL. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.05) BUT WERE SUCCESSFUL IN KNOCKING SOME SILVER LONGS FROM THEIR PERCH AS WE HAD A HUGE SIZED LOSS OF 1044 CONTRACTS ON OUR TWO EXCHANGES.

WE HAD A HUMONGOUS 1255 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.005 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 505,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 3.950 MILLION OZ

//NEW STANDING FOR SILVER//AUGUST IS THUS 3.950 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI LOSS //HUGE SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 964 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED 98 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JUNE ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST

TOTAL CONTRACTS for 5 DAYS, total 9140 contracts: OR 39.425 MILLION OZ (1971 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 45.700 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 45.70 MILLION OZ//THIS MONTH WILL PROBABLY BE A DOOZY FOR ISSUANCE.

RESULT: WE HAD A MEGA HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 2299 CONTRACTS DESPITE OUR TINY GAIN IN PRICE OF SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 1255 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 3.005 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 505,000 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR JULY 3.950 MILLION OZ

WE HAVE A HUGE SIZED LOSS OF 1044 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE TINY GAIN IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 964 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX TRADING WHICH ACCOUNTS FOR THE MAJOR PORTION OF THE HIGH COMEX OI LOSS DESPITE THE TINY GAIN IN PRICE//// MINOR SHORT COVERING FROM OUR SPEC SHORTS AND SOME LIQUIDATION OF LONGS. ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER.

THE NEW TAS ISSUANCE TUESDAY NIGHT (946) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 102 NOTICE(S) FILED TODAY FOR 510,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GOOD SIZED 7204 OI CONTRACTS TO 480,645 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE AND CRIMINAL 2385 CONTRACTS

WE HAD A STRONG SIZED DECREASE IN COMEX OI (7204 CONTRACTS) OCCURRED WITH OUR LOSS OF $13.10 IN PRICE/TUESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER. AS WELL AS ORCHESTRATING THE RAID. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR AUGUST AT 65.55 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 600 OZ EXCHANGE FOR PHYSICAL TRANSFER TO LONDON WHERE THESE GUYS TOOK IMMEDIATE DELIVERY OF GOLD IN LONDON.

NEW STANDING REDUCES TO 65.259 TONNES

/ ALL OF THIS HAPPENED WITH OUR $23.75 LOSS IN PRICE WITH RESPECT TO TUESDAY’S TRADING. WE HAD A FAIR SIZED LOSS OF 2628 OI CONTRACTS (8.174 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 4576 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 480,645

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 241 CONTRACTS WITH 7204 CONTRACTS DECREASED AT THE COMEX// AND A HUGE SIZED 4576 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 2628 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 1888 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A HUGE SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4576 CONTRACTS) ACCOMPANYING THE STRONG SIZED LOSS IN COMEX OI OF 7204 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 2628 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR AUGUST AT 65.55 TONNES FOLLOWED BY TODAY’S 600 OZ EXCHANGE FOR PHYSICAL TRANSFER TO LONDON WHERE THESE BOYS NEEDED IMMEDIATE DELIVERY OF PHYSICAL GOLD ON THAT SIDE OF THE POND AS CENTRAL BANKS CONTINUED ON THE GOLD BUYING SPREE!

//NEW STANDING REDUCES TO: /AUGUST 65.259 TONNES.

/ 3) HUGE T.A.S. LIQUIDATION//SPREADER CONTRACTS WITH ZERO NET LONG SPECS BEING CLIPPED,

4) STRONG SIZED COMEX OPEN INTEREST LOSS 5) HUGE ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1888 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST. :

TOTAL EFP CONTRACTS ISSUED: 35,281 CONTRACTS OF 3,528,100 OZ OR 109.73 TONNES IN 5 TRADING DAY(S) AND THUS AVERAGING: 7056 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAY(S) IN TONNES 109.73 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 109.73 DIVIDED BY 3550 x 100% TONNES = 3.09% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 109.73 TONNES//THIS MONTH WILL NO DOUBT BE A HUGE ISSUANCE OF EFP’S SIMILAR TO SILVER. QUITE POSSIBLY WILL BE A RECORD ISSUANCE

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUG), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 2299 CONTRACTS OI TO 147,635 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1255 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 1255 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1255 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 2299 CONTRACTS AND ADD TO THE 1255 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 946 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 5.220 MILLION OZ OCCURRED DESPITE OUR SMALL $.05 GAIN IN PRICE

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED UP 2.55 PTS OR 0.09% //Hang Seng CLOSED UP 230.52 PTS OR 1.35% // Nikkei CLOSED UP 414.16 OR 1.19%//Australia’s all ordinaries CLOSED UP .29%///Chinese yuan (ONSHORE) CLOSED DOWN TO 7,1810 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.1837/ Oil UP TO 74.48 dollars per barrel for WTI and BRENT DOWN AT 77.91 Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 7204 CONTRACTS TO 480,645 WITH OUR LOSS IN PRICE OF $13.10 WITH RESPECT TO TUESDAY’S TRADING//RAID. WE LOST A HUGE NUMBER OF SPREADER/T.A.S. CONTRACTS AS SHORTS PANICKED QUITE EARLY IN THE SESSION AND COVERED AT MUCH HIGHER PRICES. THEN THE FED ORCHESTRATED ANOTHER HUGE RAID AGAIN AS THEY TRIED TO COVER THEIR MASSIVE GOLD SHORTFALL OWING TO THE BIS. THIS EVENT CAME IN CONTACT WITH MANY CENTRAL BANKS EXERCISING THEIR CONTRACTS VIA THE EXCHANGE FOR PHYSICAL ROUTE AND TENDERING FOR PHYSICAL GOLD. SEEMS THAT THE FED WILL BE HELL-BENT TRYING TO COVER. THE FIRST RAID ATTEMPT FAILED WITH THE PRICE OF GOLD RISING ABOVE 2400. THE SECOND ATTEMPT SUCCEEDED AS WE ENDED THE SESSION AT AROUND 2387.00

OUR LONDONERS ALSO BOUGHT NEW MASSIVE QUANTITIES OF LONGS AND THIS WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY I.E. WEDNESDAY MORNING. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD A STRONG T.A.S. LIQUIDATION ON TUESDAY’S LOSS IN PRICE WITH ZERO LONGS BEING CLIPPED (AS YOU WILL SEE BELOW) BUT WE DID HAVE MAJOR SHORT COVERING. THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE ACTIVE DELIVERY MONTH OF AUGUST.… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 4576 EFP CONTRACTS WERE ISSUED: : OCT/DEC 4576 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4576 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2628 CONTRACTS IN THAT 4576 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 2628 COMEX CONTRACTS..AND THIS SMALL LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR CONSIDERABLE FALL IN PRICE OF $13.10/TUESDAY COMEX RAID. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AS MENTIONED ABOVE.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT A FAIR SIZED 1888 CONTRACTS. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN LAST WEEK’S TRADING//RAIDS AS WELL AS THIS WEEK AND ESPECIALLY ON TUESDAY’S TRADING/RAID.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: AUGUST (65.259 TONNES)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 65.259 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $13.10 //// BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE DID HAVE A SMALL LOSS IN OUR TWO EXCHANGES. CENTRAL BANK LONGS , EXERCISED FOR PHYSICAL. WE HAD A HUGE SIZED T.A.S. LIQUIDATION TUESDAY/COMEX

WE HAVE LOST A TOTAL OI OF 0.765 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST (65.55 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 600 OZ E.F.P. JUMP TO LONDON//NEW STANDING: 65.259 TONNES.

NEW STANDING FOR AUGUST: 65.284 TONNES

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE TO THE TUNE OF $13.10

WE HAVE REMOVED A HUGE 2385 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET LOSS ON THE TWO EXCHANGES 2628 CONTRACTS OR 262800 OZ (8.174

TONNES)

confirmed volume TUESDAY 199,,716 contracts//

fair

//speculators have left the gold arena

AUGUST 7 AUGUST GOLD CONTRACT

/ /// THE AUG 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 104,683.656 oz OZ Brinks: 761 kilobars HSBC 497 kilobars JPMorgan 1998 kilobars . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | NIL oz |

| No of oz served (contracts) today | 5 notice(s) 500 OZ 0.01555 TONNES |

| No of oz to be served (notices) | 3906 contracts 390,600 OZ 12.149 TONNES |

| Total monthly oz gold served (contracts) so far this month | 17,075 notices 1,707,500 oz 53.1104 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: nil oz

we have 0 customer deposits

total deposits NIL oz

withdrawals: 3

i) Out off Brinks 24,466.911 oz 761 kilobars

ii) Out of HSBC 15,979.047 oz 497 kilobars

iii) Out of JPMorgan: 64,237.698 oz (1998 kilobars

TOTAL WITHDRAWALS 104,683.656 oz 3256 kilobars//

actually physical gold from London is used and an identical transfer re kilobars from comex is recorded.

adjustments: two

dealer to customer Brinks 21,123.207 oz

ii) dealer to customer JPMorgan 217,124.221 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JULY

For the front month of AUGUST we have an oi of 3911 contracts having LOST 20 contracts.

We had 14 contracts served on Tuesday, so we LOST an additional 6 contracts or 600 oz will NOT stand for gold at the comex as they were immediately ferried over to London to take delivery of gold via the exchange for physical route.

SEPT. GAINED 82 CONTRACTS TO STAND AT 5334 CONTRACTS.

OCTOBER LOST 867 CONTRACTS UP TO 51,435 CONTRACTS

We had 14 contracts filed for today representing 1400 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 5 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 3 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for AUGUST /2024. contract month, we take the total number of notices filed so far for the month (17,075) x 100 oz ) to which we add the difference between the open interest for the front month of August 3911( CONTRACTS) minus the number of notices served upon today (5 x 100 oz per contract( equals 2,098,100 OZ OR 65.259 TONNES.

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (17075 x 100 oz +we add the difference for front month of AUGUST (3911 X// , OI} minus the number of notices served upon today (5) x 100 oz which equals 2,098,100 oz (65.259 TONNES)

TOTAL COMEX GOLD STANDING FOR AUGUST: 65.259 TONNES WHICH IS HUGE FOR THIS VERY ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,653,477.242 oz 51.43 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,729,527.234 OZ

TOTAL REGISTERED GOLD 7954,841.143 ( 247.42 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,774, 686.091 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,301,364 oz (REG GOLD- PLEDGED GOLD)= 195.99 tonnes //

END

SILVER/COMEX

AUGUST 7/2024

INITIAL

//2024// THE AUG 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2877 OZ Delaware . |

| Deposits to the Dealer Inventory | |

| Deposits to the Customer Inventory | nil |

| No of oz served today (contracts) | 102 CONTRACT(S) (514,000 OZ) |

| No of oz to be served (notices) | 110 contracts (0.555 million oz) |

| Total monthly oz silver served (contracts) | 680 Contracts (3.40000 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit/

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 0 customer deposits:

total customer deposit nil oz

JPMorgan has a total silver weight: 134,771million oz/303.102million or 44.44%

adjustment:1;dealer to customer HSBC 413,214.830 oz

withdrawals:

i) Delaware 2877.556 oz

total customer withdrawals: 2877.556 oz

TOTAL REGISTERED SILVER: 70.185 MILLION OZ//.TOTAL REG + ELIGIBLE. 303.106 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR AUGUST:

silver open interest data:

FRONT MONTH OF AUGUST/2024 OI: 212 CONTRACTS HAVING GAINED 82 CONTRACT(S).

WE HAD 19 NOTICES SERVED ON TUESDAY, SO WE GAINED 101 CONTRACTS OR AN ADDITIONAL 505,000 OZ WILL STAND FOR SILVER AT THE COMEX. SEEMS GOLD IS SCARCE AS THE COMEX BUT NOT SILVER.

SEPT SAW A LOSS OF 3456 CONTRACTS TO 93,889. SEPT NOW BECOMES THE NEW FRONT MONTH

OCTOBER SAW ANOTHER GAIN OF OPEN INTEREST CONTRACTS OF 9 CONTRACTS AND THUS WE HAVE 147 OPEN INTEREST CONTRACTS FOR OCTOBER.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 102 for 510,000 oz

CONFIRMED volume; ON TUESDAY 79 746 strong

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 680 x 5,000 oz = 3.400 MILLION oz

to which we add the difference between the open interest for the front month of AUGUST( 212) and the number of notices served upon today 102 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST/2024 contract month: 680 notices served so far) x 5000 oz + OI for the front month of AUGUST (212)x number of notices served upon today minus (102)x 5000 oz of silver standing for the AUGUST contract month equates to 3.950 MILLION OZ.

New total standing: 3.950 million oz.

There are 70.185 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD

AUGUST 7 WITH GOLD UP $1.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.16 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 848.06 TONNES

AUGUST 6 WITH GOLD DOWN $13.10 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD” A WITHDRAWAL OF .57 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 844.90 TONNES

AUGUST 2 WITH GOLD DOWN $9.95 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.58 TONNES OF GOLD OUT OF THE GLD//INVENTORY RESTS AT 845.47 TONNES

AUGUST 1 WITH GOLD UP $9.15 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 846.05 TONNES

JULY 30 WITH GOLD UP $26.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// A /////INVENTORY RESTS AT 843.17 TONNES

JULY 29 WITH GOLD UP $27.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD// A WITHDRAWAL OF 1.98 TONNES OF GOLD OUT OF THE GLD/////INVENTORY RESTS AT 843.17 TONNES

JULY 26 WITH GOLD UP $27.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD// A DEPOSIT OF 3.45 TONNES OF GOLD INTO THE GLD/////INVENTORY RESTS AT 845.19 TONNES

JULY 25 WITH GOLD DOWN $60.45 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 841.74 TONNES

JULY 24 WITH GOLD UP $12.75 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1,73 TOONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 841.74 TONNES

JULY 23 WITH GOLD UP $12.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 22 WITH GOLD DOWN $4.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 19 WITH GOLD DOWN $56.10 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;:A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 18 WITH GOLD DOWN $2.20 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;: ///INVENTORY RESTS AT 842.02 TONNES

JULY 17 WITH GOLD DOWN $6.60 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A MASSIVE DEPOSIT OF 5.49 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 842.02 TONNES

JULY 16 WITH GOLD UP $38.60 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 836.53 TONNES

JULY 15 WITH GOLD UP $8.15 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;: /INVENTORY RESTS AT 835.09 TONNES

JULY 12 WITH GOLD DOWN $0.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 835.09 TONNES

JULY 11 WITH GOLD UP $43.05 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;:INVENTORY RESTS AT 833.37 TONNES

JULY 10 WITH GOLD UP $12.00 ON THE DAY; HUUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.44 TONNES OF GOLD VAPOUR FROM THE GLD//.//:INVENTORY RESTS AT 833.37 TONNES

JULY 9 WITH GOLD UP $5.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD.//:INVENTORY RESTS AT 834.81 TONNES

JULY 8 WITH GOLD DOWN $26.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD.//:INVENTORY RESTS AT 834.81 TONNES

JULY 5 WITH GOLD UP $29.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD..A DEPOSIT OF 1.10 TONNES OF GOLD VAPOUR INTO THE GLD//:INVENTORY RESTS AT 833.37 TONNES

JULY 3 WITH GOLD UP $35.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD..A MASSIVE DEPOSIT OF 5.76 TONNES OF GOLD VAPOUR INTO THE GLD//:INVENTORY RESTS AT 833.37 TONNES

JULY 2 WITH GOLD DOWN $4.45 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD../:INVENTORY RESTS AT 827.61 TONNES

JULY 1 WITH GOLD DOWN $.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

GLD INVENTORY: 848,06 TONNES, TONIGHTS TOTAL

SILVER

AUGUST 7//WITH SILVER DOWN $0.27//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.552 MILLION OZ INTO THE SLV////./// /INVENTORY AT 462.502 MILLION OZ

AUGUST 6//WITH SILVER UP $0.05//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 458.851 MILLION OZ

AUGUST 2//WITH SILVER DOWN $0.01//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 1.243 MILLION OZ OF SILVER OUT OF THE SLV ///./// /INVENTORY AT 460.961 MILLION OZ

AUGUST 1//WITH SILVER DOWN $0.46//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.608 MILLION OZ OF SILVER VAPOUR INTO THE SLV///./// /INVENTORY AT 462.204 MILLION OZ

JULY 31//WITH SILVER UP $0.45//NO CHANGES IN SILVER INVENTORY: /./// /INVENTORY REMAINS AT 460.596 MILLION OZ

JULY 30//WITH SILVER UP $0.61//SMALL CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 0.456 MILLION OZ OF SILVER VAPOUR INTO THE SLV/./// /INVENTORY RISES AT 460.596 MILLION OZ

JULY 29//WITH SILVER DOWN $0.07//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.382 MILLION OZ OF SILVER VAPOUR INTO THE SLV/./// /INVENTORY RISES AT 461.052 MILLION OZ

JULY 26//WITH SILVER DOWN $0.07//NO CHANGES IN SILVER INVENTORY./// /INVENTORY REMAINS AT 456.670 MILLION OZ

JULY 25 WITH SILVER DOWN $1.37//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 3.124 MILLION OZ OF SILVER OUT OF THE SLV./// /INVENTORY FALLS TO 456.670 MILLION OZ

JULY 24 WITH SILVER UP 3 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 15.880 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 23 WITH SILVER UP 3 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 15.880 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 22 WITH SILVER UP 2 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 3.920 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 19 WITH SILVER DOWN 94 CENTS//NO CHANGES IN SILVER INVENTORY/// /INVENTORY REMAINS AT 435.854 MILLION OZ

JULY 18 WITH SILVER DOWN 13 CENTS//HUGE CHANGES IN SILVER INVENTORY” A DEPOSIT OF 2.374 MILLION OZ INTO THE SLV/// /INVENTORY RISES TO 435.854 MILLION OZ

JULY 17. WITH SILVER DOWN 75 CENTS//NO CHANGES IN SILVER INVENTORY// /INVENTORY REMAINS AT 433.480 MILLION OZ.

JULY 16. WITH SILVER UP 30 CENTS//NO CHANGES IN SILVER INVENTORY// /INVENTORY REMAINS AT 433.480 MILLION OZ.

JULY 15. WITH SILVER DOWN 24 CENTS//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 2.145 MILLION OZ FROM THE SLV.// /INVENTORY LOWERS T0 AT 433.480 MILLION OZ.

JULY 12. WITH SILVER DOWN $.65 CENTS//NO CHANGES IN SILVER INVENTORY /INVENTORY REMAINS CONSTANT AT 435.625 MILLION OZ.

JULY 11. WITH SILVER UP $.72 CENTS//HUGE CHANGES IN SILVER INVENTORY A WITHDRAWAL OF 0.731 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 435.625 MILLION OZ.

JULY 10. WITH SILVER DOWN $.04 CENTS//HUGE CHANGES IN SILVER INVENTORY A MAMMOTH WITHDRAWAL OF 3.744 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 436.356 MILLION OZ.

JULY 9. WITH SILVER UP 13 CENTS//HUGE CHANGES IN SILVER INVENTORY A MAMMOTH WITHDRAWAL OF 3.744 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 436.356 MILLION OZ.

JULY 8. WITH SILVER DOWN $0.73//SMALL CHANGES IN SILVER INVENTORY A MAMMOTH DEPOSIT OF 3,292,000 OZ OF SILVER VAPOUR INTO THE SLV.: /INVENTORY RISES T0 440.100 MILLION OZ.

JULY 4. WITH SILVER UP $0.85//SMALL CHANGES IN SILVER INVENTORY A MAMMOTH DEPOSIT OF 3,292,000 OZ OF SILVER VAPOUR INTO THE SLV.: /INVENTORY RISES T0 440.100 MILLION OZ.

JULY 3. WITH SILVER UP $1.08//SMALL CHANGES IN SILVER INVENTORY A SMALL WITHDRAWAL OF 639,000 OZ: /INVENTORY LOWERS T0 436,808 MILLION OZ.

JULY 2. WITH SILVER UP $0.19//NO CHANGES IN SILVER INVENTORY: /INVENTORY REMAINS AT 437.447 MILLION OZ./

JULY 1. WITH SILVER UP $0.05//XXX CHANGES IN SILVER INVENTORY: A DEPOSIT OF 182,000 OZ OF SILVER INTO THE SLV./.// /INVENTORY RISES AT 437.447 MILLION OZ./

CLOSING INVENTORY 462.502 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

I Thought Gold Was A Safe Haven! Why Did It Tank With Stocks?

WEDNESDAY, AUG 07, 2024 – 01:25 PM

Authored by Mike Maharrey via Money Metals,

And in the blink of an eye, the expectation of a “soft” landing turned into worries about a crash landing!

It was a bloody Monday in the stock market as analysts digested the dreary jobs report released Friday and suddenly discovered the rot in the economy’s foundation.

They fretted that the Federal Reserve waited too long to cut interest rates and worried its lallygagging would tip the economy into a recession.

(I have argued for months that the problem started long before the first Fed rate hike. It began when the central bank decided to keep the easy money spigot wide open for more than a decade. You can read more about that HERE.)

The carnage in the U.S. stock market was widespread.

- Dow Jones: -1033.99/ -2.6 percent

- NASDAQ: -576.08/ -3.43 percent

- S&P 500: -160.23/ -3 percent

- Russell 2000: -70.15/ -3.33 percent

The selloff wasn’t limited to the U.S. Markets around the globe bled red ink. Some $6.4 trillion was wiped off global stock markets. For instance, Japan’s Nikkei 225 Index plunged 13.2 percent as investors absorbed the recent interest rate hike.

It just goes to show how quickly market sentiment can shift.

The reasons for the global selloff went beyond worries about the U.S. economy. As a Bloomberg article put it, investors are coming to terms with the fact that they were operating under a lot of erroneous assumptions.

“One thing is clear: the pillars that had underpinned financial-market gains for years — a series of key assumptions that investors across the world were banking on — have been shaken.

They look, in hindsight, a bit naïve: the U.S. economy is unstoppable; artificial intelligence will quickly revolutionize business everywhere; Japan will never hike interest rates — or not enough to really matter.”

So, What Happened to Gold?

Gold and silver didn’t escape the carnage.

At its low, the price of gold was down 3.2 percent before rallying later in the day to recover the $2,400 an ounce level. Nevertheless, the yellow metal finished down 1.3 percent on the day.

Silver got pounded even harder, dropping as much as 7.2 percent at its intraday low. Worries about an economic slowdown and an ensuing decrease in silver demand hammered the silver price down.

You might be wondering why gold – supposedly a safe haven – dropped during the broader selloff. Shouldn’t a good haven do well amid market chaos?

In fact, the plunge in the price of gold was perfectly normal given the market conditions. Gold often sells off early in a bear market for stocks.

In 2020, gold had a 3 percent decline multiple times in the early days of the pandemic selloff. In October 2008, gold plunged by more than 7 percent in the early days of the financial crisis.

But why?

Precisely because gold serves as a hedge.

Investors often liquidate winning gold positions during a sharp downturn to cover stock losses. But gold generally falls less sharply and recovers more quickly – exactly the scenario that played out on Monday.

Here’s how an analyst explained it to Bloomberg:

“Virtually every time there is marked equities weakness, investors who hold gold as a risk hedge will liquidate part of their holdings to raise liquidity against any potential margin calls. When the dust settles, they almost invariably buy it back.”

Margin calls are a big problem for investors during a sharp stock market downturn.

When an account falls below a certain threshold, brokers demand additional deposits of money or securities to bring the account balance up to a required minimum level.

Given gold’s liquidity, investors can quickly sell to raise the cash necessary to cover margin calls.

It’s important to put Monday’s gold selloff into perspective. Even with the downturn, gold hit a record just a few weeks ago, and the yellow metal is still up well over 15 percent on the year with bullish factors firmly in place.

A recession would likely mean deeper and quicker interest rate cuts. As a non-yielding asset, the mainstream tends to view lower interest rates as positive for gold.

And of course, a return to easy money is a surrender to inflation. In other words, the inflation dragon will likely be resurrected (if you actually believe he is dead).

As far as silver, an economic downturn would temper industrial demand, and the white metal is much more volatile than gold.

But silver is fundamentally a monetary metal, and it tends to track with gold over time. In fact, silver has historically outperformed gold in a gold bull market. For example, during the pandemic, gold increased by about 40 percent, while silver increased by 141 percent.

Whether Monday’s selloff was just a tremor before the earthquake, or the beginning of the great unwind, there are plenty of reasons to be bullish on both gold and silver.

These price dips could be viewed as a buying opportunity.

end

Central Bank Gold Buying Through First Half of 2024 Sets Record

Despite central bank gold buying slowing moderately in the second quarter, it set a record through the first half of 2024.Central banks globally added a net 483 tons of gold through the first six months of the year, 5 percent above the record of 460 tons in H1 2023.In the second quarter, central bank gold demand totaled 183 tons, according to the latest data compiled by the World Gold Council. That was up 6 percent year-on-year, but about 39 percent lower than the Q1 buying pace.With gold at or near record price levels in most currencies, it’s unsurprising that central bank buying slowed in the second quarter.China primarily drove the Q2 slowdown in central bank demand.

The People’s Bank of China reported no additions to its gold reserves in May or June and only officially added 2 tons in April.Prior to the pause in May, China had increased its gold holding for 18 straight months.Many analysts believed the Chinese paused officially adding gold to their reserves in an effort to push gold prices lower.When the Chinese reported no changes to their official reserves in May, it precipitated a panicked gold selloff. Despite the kneejerk reaction, it seems unlikely that the Chinese are finished adding gold to their reserves. There is also some speculation that China is adding a significant amount of gold to its reserves off the books.Even with the pause, China still added nearly 30 tons of gold to its reserves through the first half of 2024.

Turkey was the biggest buyer through the first half of the year, adding 45 tons to its gold hoard. The bulk of its buying was in Q1, with the pace slowing to 15 tons in the second quarter.The Turkish central bank has bought gold for 12 straight months after liquidating 160 tons of gold in the spring of 2023.India ranks as the second-biggest gold buyer through the first half of the year.

The Reserve Bank of India has added gold to its reserves every month this year totaling 37 tons.In 2022, the Indian central bank added 33 tons of gold to its reserves followed by a 16-ton increase last year.The Reserve Bank of India has been buying gold since 2017. Over that period, the RBI has increased its gold holding by over 260 tons.An Indian economist told the Times of India that the push to accumulate gold was based on both political and economic reasons. He said that the “reliability” of the U.S. dollar has “diminished.” He noted the “noticeable decline” in the confidence in U.S. dollar assets.Another economist told the Times,”It makes a lot of sense (to invest in gold), given the increased volatility in the FX market, elevated interest rates in the U.S., and, of course, also as the central banks in each economy would like to diversify the asset classes in which they are parking their reserves.”India recently transported 100 tons of its gold from the UK back into India.Poland was the biggest gold buyer in the second quarter, increasing its holding by 19 tons. The country currently holds about 13 percent of its reserves in gold. At a news conference in early June, National Bank of Poland Governor Adam Glapinski reiterated his plan to increase gold’s share of total reserves to 20 percent.Poland was the second-biggest gold buyer in 2023. The Polish central bank bought 130 tons of gold last year, increasing its holdings by 57 percent, to 359 tons.In 2021, Glapinski announced a plan to expand the country’s gold reserves by 100 tons. The central bank reached that goal in September of ’23 and kept buying.When he announced the plan to expand its gold reserves, Glapinski said holding gold was a matter of financial security and stability.”Gold will retain its value even when someone cuts off the power to the global financial system, destroying traditional assets based on electronic accounting records. Of course, we do not assume that this will happen. But as the saying goes – forewarned is always insured.And the central bank is required to be prepared for even the most unfavorable circumstances. That is why we see a special place for gold in our foreign exchange management process.”Other notable buyers in the second quarter included:

Uzbekistan – 7 tons

Czech Republic – 6 tons

Qatar – 4 tonsSingapore – 4 tons

Russia – 3 tons

Iraq – 3 tonJordan – 1 ton

Kyrgyz Republic – 1 ton

Notably, Singapore had been a consistent buyer this year before selling 12 tons of gold in June.Uzbekistan has also been a frequent seller this year, turning back to buying in May. It is not uncommon for banks that buy from domestic production – such as Uzbekistan and Kazakhstan – to switch between buying and selling.The Philippines has been the biggest seller through the first half of the year, decreasing its gold reserves by about 25 tons. Thailand was another notable seller, decreasing its holdings by just under 10 tons.Despite the modest colling of central bank gold demand in Q2, there is no indication that they are souring on the yellow metal. According to the most recent World Gold Council survey, 29 percent of central banks plan to add more gold to their reserves in the next 12 months. The WGC said it was the highest level since the survey began in 2018.Only 3 percent said they had plans to decrease gold reserves.Earlier this year, the World Gold Council said the continuation of gold buying supports its expectation that “2024 will be another solid year of central bank gold demand.””Last year central banks placed great emphasis on gold’s value in crisis response, diversification attributes, and store-of-value credentials. A few months into 2024 the world seems no less uncertain meaning those reasons for owning gold are as relevant as ever.”Last year, central bank gold buying fell just 45 tons short of 2022’s multi-decade record.According to the World Gold Council, central banks net gold purchases totaled 1,037 tons in 2023. It was the second straight year central banks added more than 1,000 tons to their total reserves.Central bank gold buying in 2023 built on the prior record year. Total central bank gold buying in 2022 came in at 1,136 tons. It was the highest level of net purchases on record dating back to 1950, including since the suspension of dollar convertibility into gold in 1971.China was the biggest buyer in 2023.Analysts at ANZ Bank recently said they expect central bank gold buying to remain hot for at least the next six years.According to these analysts, “Depleted trust in the U.S. fixed-income assets and the rise of non-reserve currencies are other themes that could support central bank gold buying.”

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY

lio.

3.CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES

4. GOLD PODCASTS//LIVE FROM THE VAULT/no 184 with Craig Hemke/Andrew Maguire

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COCOA

6 CRYPTOCURRENCY NEWS

END

ASIA TRADING/WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED UP 2.55 PTS OR 0.09% //Hang Seng CLOSED UP 230.52 PTS OR 1.35% // Nikkei CLOSED UP 414.16 OR 1.19%//Australia’s all ordinaries CLOSED UP .29%///Chinese yuan (ONSHORE) CLOSED DOWN TO 7,1810 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.1837/ Oil UP TO 74.48 dollars per barrel for WTI and BRENT DOWN AT 77.91 Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1810

OFFSHORE YUAN: DOWN TO 7.11837

SHANGHAI CLOSED UP 2.55 PTS OR 0.09 %

HANG SENG CLOSED UP 230.52 PTS OR 1.38%

2. Nikkei closed UP 414.16 PTS OR 1.19%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 102.95 EURO FALLS TO 1.0920 DOWN 5 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +0.903 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147,12…… JAPANESE YEN NOW RISING AS WE HAVE NOW REACHED THE REIGNITING OF THE YEN CARRY TRADE AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.2825/Italian 10 Yr bond yield UP to 3.720 SPAIN 10 YR BOND YIELD UP TO 3.139%

3i Greek 10 year bond yield UP TO 3.384

3j Gold at $2399.50//Silver at: 27.09 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 33/ 100 roubles/dollar; ROUBLE AT 85.99

3m oil into the 74 dollar handle for WTI and 77 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.12/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.903 % STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8630 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9425 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.930 UP 5 BASIS PTS…

USA 30 YR BOND YIELD: 4.224 UP 4 BASIS PTS/

USA 2 YR BOND YIELD: 4.022 UP 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 33.53…

10 YR UK BOND YIELD: 3.998 UP 8 PTS

10 YR CANADA BOND YIELD: 3.185 UP 7 BASIS PTS

2a New York OPENING REPORT

Futures Soar, Yields And Oil Jump After BOJ Capitulation Nukes Yen, Restarts Carry Trade

WEDNESDAY, AUG 07, 2024 – 08:10 AM

And just like that, the great carry trade freak out – which started exactly one week ago when the BOJ hiked rates by a huge 0.15% – is over, because as we had expected, the BOJ got cold feet and capitulated on its rate hiking cycle on Wednesday morning when BOJ deputy governor Shinichi Uchida sent dovish U-turn signal in the wake of historic financial market volatility by pledging to refrain from hiking interest rates when the markets are unstable. In kneejerk reaction to his comments – which were the first public remarks by a BOJ board member since the bank raised rates on July 31 – the yen, which had strengthened by a record amount in the past week as the carry trade careened sending deflationary shockwaves around the globe, weakened by more than 2%, bond yields rose and stocks soared. As of 7:30am ET, S&P 500 jumped by 1.2% with both Tech and small-caps outperforming as the BOJ capitulation relief rally continues;’ Nasdaq 100 futures gained more than 1.5% after the underlying indexes rebounded more than 1% on Tuesday following a wave of dip buying. The Stoxx Europe 600 index climbed more than 1%, with mixed earnings reports from some of the region’s biggest companies doing little to dampen the risk-on mood. Japanese stocks led a broad rally in Asia. Bond yields are higher by 4-5bps, and the USD is higher, looking to erase its weekly loss. Commodities have also caught a bid as the carry trade is reestablished with WTI, base metals, and Ags all seeing strength. Mtge Applications and 10Y bond auction are the major macro data pts. Is the panic unwind finished? Are detailed thoughts are below.

In the premarket, Mag7 are all higher and semis are shrugging off SMCI (-12%) catastrophic margin collapse as NVDA, AVGO, AMD, and QCOM lead the group higher each up 1%+. Super Micro Computer crashed 14% reversing a 20% earlier spike, as the computer hardware maker’s disappointing gross margins overshadowed an otherwise strong 2025 net sales forecast. Airbnb also tumbled 14% after the company gave a disappointing outlook for a third consecutive quarter and warned of slowing demand from US vacationers. Here are some other notable premarket movers:

- Emergent BioSolutions slumps 34% after the company forecast 3Q revenue with a midpoint that fell short of analyst estimates.

- Fortinet rises 16% after the cyber-security company posted a strong margin performance in the 2Q.

- Lumen Technologies soars 24% after the company boosted its full-year free cash flow forecast.

- Porch Group sinks 19% after the home-services software company reported 2Q results that missed expectations, with severe weather weighing.

- Rivian drops 7% after the electric vehicle startup warned of a looming plant shutdown next year to prepare for a new vehicle launch.

- Novo Nordisk A/S shares dropped as much as 5% after the Danish drugmaker cut its profit forecast for the year.

- Shopify gains 17% after posting 2Q results that exceeded analysts’ estimates, suggesting that the Canadian e-commerce company is managing to navigate cautious consumer spending.

- Trex falls 17% after the manufacturer of decking cut its year revenue forecast as 2Q sales fell short of estimates.

- TripAdvisor tumbles 19% after the online travel company reported 2Q revenue that missed consensus estimates.

- Upstart soars 25% after the AI lending marketplace firm gave a 3Q forecast that is stronger than expected.

Volatility is waning as the S&P 500 recovers from its worst one-day drop since September 2022. The VIX plunged another 17% on Wednesday following its biggest plunge since 2010. The biggest event overnight was Uchida’s surprising U-turn, and capitulation, which came less than a week after the BOJ’s historic and unexpected rate hike which unleashed a carry trade unwind and pushed the VIX as high as 65, its biggest increase since the covid crash.

“I wouldn’t underestimate importance of what the Bank of Japan has been saying overnight,” Jennison Associates Managing Director Raj Shant said on Bloomberg TV. “I think that’s really helpful. This carry trade has been many, many years in the making, and probably indirectly affects a lot of asset classes around the world.”

Still, the recent market turmoil was a “stark reminder of how quickly things can change,” said Justin Onuekwusi, chief investment officer at St James Place. “While overall corporate balance sheets are healthy and recession risks are low, we are starting to see earnings tail off a bit and companies’ guidance is outlining a more uncertain future.”

European stocks follow US futures and Asian counterparts higher after the BOJ capitulation. The Stoxx 600 adds 1.1% with auto, construction and bank names leading gains. Novo Nordisk A/S shares dropped as much as 5% after the Danish drugmaker cut its profit forecast for the year. German lender Commerzbank AG, sportswear maker Puma SE and skin-care products maker Beiersdorf AG also slumped after earnings misses. On the other end, shares in Continental AG rose after the German manufacturer posted improving returns at its struggling car-parts unit, which it may spin off in its biggest-ever restructuring. Dutch lender ABN Amro Bank NV gained after the Dutch lender raised its outlook for lending income, showing how Europe’s high interest rates continue to provide tailwind for the banking industry. The banks sub-index outperformed the benchmark. Here are the biggest European movers:

- Glencore shares climb 1.5%, reversing earlier losses. The company decided to retain its coal and carbon steel materials business after shareholder consultations, a move analysts welcome given its profitability.

- Continental shares rise as much as 5.5% after the German automotive parts maker’s second-quarter results showed what Bernstein called some “rays of hope,” though this was dampened by the cut to the FY24 sales guidance.

- Sampo rises as much as 2.5% following the insurance brokerage firm’s second-quarter earnings report. DNB Markets expects small upgrades to full-year consensus and notes the company’s positive growth momentum.

- GEA Group shares rise as much as 4.4%, the most in five months, after the mechanical engineering firm reported earnings ahead of consensus in the latest quarter.

- Sixt shares fall as much as 1.6%, fluctuating after the vehicle rental firm reported in-line earnings and warned full-year profits will be at the lower-end of its full year guidance.

- Novo Nordisk shares drop as much as 7.7%, the most in two years, after the Danish drugmaker reported weaker-than-expected sales for its Wegovy blockbuster in the second quarter.

- Beiersdorf shares drop as much as 5.9%, to the lowest intraday since November 2023, after the maker of personal-care products reported second-quarter results that missed estimates.

- Puma shares drop as much as 14% after the sportswear brand reported second-quarter revenue in constant currency that missed consensus estimates and narrowed its full-year Ebit forecast.

- Maersk shares fall as much as 4.5% after the marine shipping company’s second quarter Ebitda missed estimates. Morgan Stanley notes that the buyback is not being reinstated and says freight rates are starting to move lower.

- Evotec slumps as much as 39%, to the lowest since November 2016, after the German pharmaceutical company announced material cuts to its full-year guidance and also postponed a planned capital markets day in October to evaluate its next strategic steps.

Earlier in the session, Asian equities advanced for a second session following Monday’s global rout, after the Bank of Japan said it won’t raise interest rates if financial markets are unstable. The MSCI Asia Pacific Index climbed as much as 2.1%. Japan’s Topix index pared earlier gains to close 2.3% higher as Bank of Japan Deputy Governor Shinichi Uchida noted the recent volatility in the nation’s markets and said its rate path will shift if there’s an impact on the policy outlook. Benchmarks in South Korea and Taiwan also climbed, with the Taiex index logging its biggest single-day rally since May 2021. Technology stocks led gains across the region as concerns about further unwinding of the yen carry trade eased, with the Japanese currency weakening more than 2% against the dollar. Still, some market watchers remained cautious.

In FX, the Bloomberg index rose for a second day while the yen is around 2% weaker against the dollar with the cross topping just short of 148.00. The weaker yen boosted higher-yielding currencies. The Mexican peso, a carry trade target that tumbled after the BOJ rate hike, rose more than 1% against the dollar Wednesday. The Swiss franc also underperforms with a 1.1% fall. The kiwi outperforms, rising 1% after the unemployment rate rose less than expected.

In rates, treasuries are cheaper across the curve following the deeper selloff in core European rates after Bank of Japan Deputy Governor Shinichi Uchida pledged to refrain from hiking interest rates while markets are unstable. Treasury yields cheaper by 4bp-5bp with curve spreads little changed; 10-year around 3.94% with bunds underperforming by roughly 4.5bp in the sector. Supply is also a factor for Wednesday’s session, with 10-year note auction at 1pm New York time: the auction cycle continues with $42b 10-year new issue, following good result for Tuesday’s $58b 3-year note sale; it ends Thursday with $25b 30-year bond sale. The WI 10-year yield at ~3.93% is roughly 35bp richer than last month’s, which stopped through by 1bp.

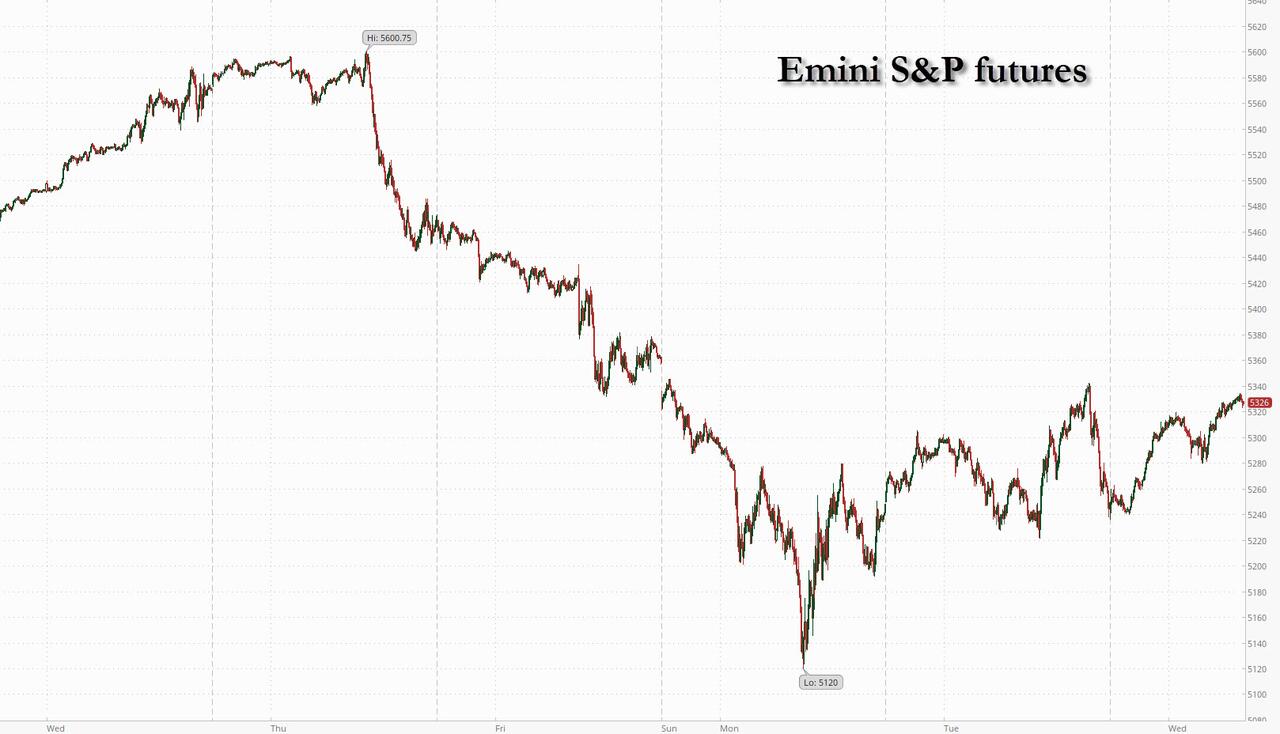

In commodities, oil prices advance, with WTI rising 0.8% to trade near $73.80 a barrel. Spot gold is steady around $2,393/oz. Bitcoin adds 1.7%.

Looking at today’s calendar, US economic data slate includes June consumer credit at 3pm. Scheduled Fed speakers include Collins at 12pm.

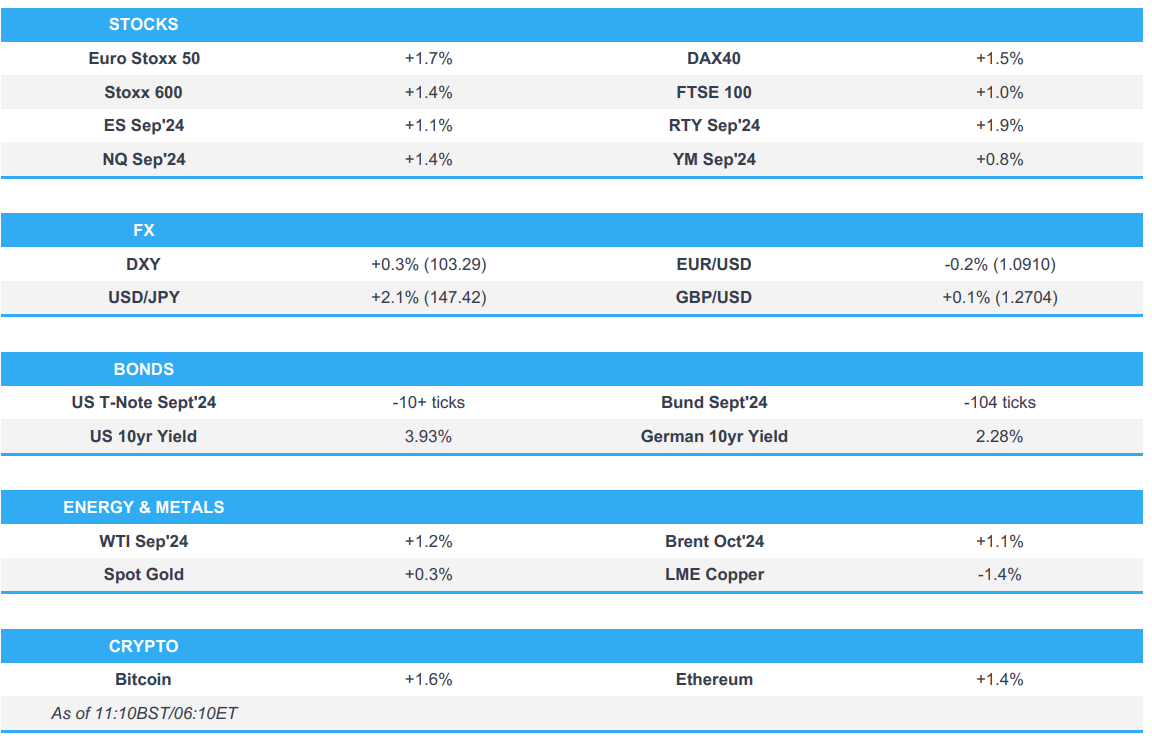

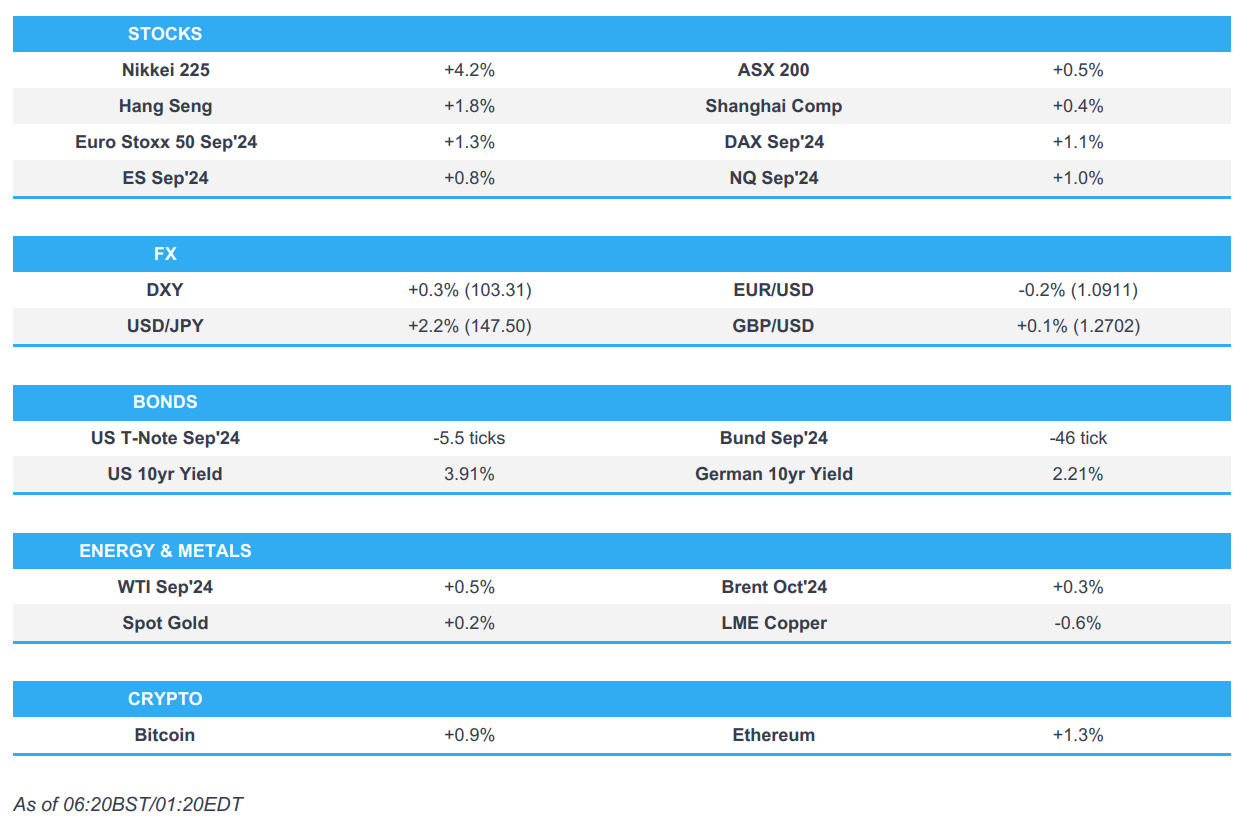

Market Snapshot

- S&P 500 futures up 0.8% to 5,306.75

- STOXX Europe 600 up 0.8% to 492.13

- MXAP up 1.5% to 174.18

- MXAPJ up 1.8% to 546.30

- Nikkei up 1.2% to 35,089.62

- Topix up 2.3% to 2,489.21

- Hang Seng Index up 1.4% to 16,877.86

- Shanghai Composite little changed at 2,869.83

- Sensex up 0.8% to 79,192.71

- Australia S&P/ASX 200 up 0.2% to 7,699.83

- Kospi up 1.8% to 2,568.41

- Brent Futures up 0.4% to $76.80/bbl

- Gold spot up 0.1% to $2,393.03

- US Dollar Index up 0.14% to 103.12

- German 10Y yield +7.5bps at 2.28%

- Euro little changed at $1.0925

Top Overnight News

- Japanese stocks rallied on Wednesday and the yen fell after a central bank official appeared to play down the immediate prospects of further interest rate rises in the face of volatile global trade. The Bank of Japan’s deputy governor Shinichi Uchida noted the sharp volatility in domestic and overseas financial markets and said “it is necessary to maintain current levels of monetary easing for the time being”. FT

- China is to impose controls on the production of critical chemicals for the manufacture of fentanyl, in a sign of rising co-operation between Beijing and Washington over efforts to crack down on the deadly synthetic opioid. FT

- SoftBank announced a buyback of as much as ¥500 billion ($3.4 billion), an outlay that still leaves founder Masayoshi Son with a substantial pile of cash as he gears up to make more aggressive investments. The outlay comes as CEO Son is preparing for what appears to be a large-scale push into artificial intelligence and semiconductor investments. BBG

- Iran may be reconsidering a plan for major retaliation against Israel following intensive diplomatic and military pressure from Washington while Netanyahu moves towards the US-brokered ceasefire deal in Gaza. WaPo

- Crude stockpiles at Cushing rose by more than 1 million barrels last week, API data is said to show, the biggest surge in more than two months if confirmed by the EIA. Total inventory also rose. In China, July imports fell to the slowest pace in almost two years. BBG

- Harris is up 3 points over Trump both head-to-head and when 3rd party candidates are considered according to a new Marist poll. The Hill

- Supermicro reported a miss on FQ4 EPS at 6.25 (vs. the Street 8.25) as soft margins (11.3% gross margins vs. the Street 14%) offset inline sales and while the revenue guide is bullish, investors have persistent worries about profitability. RTRS

- Novo plummeted as Wegovy sales missed estimates and it cut its full-year profit outlook. While the drug’s miss will be in focus in the short term, volume trends are strengthening. BBG

- Airbnb reported decent Q2 results, w/revenue +11% FXN to $2.75B (vs. the Street $2.73B), EBITDA +10% FXN to $894MM (vs. the Street $862.3MM), and bookings +12% FXN to $21.2B (about inline), although nights/experiences were a bit light (+9% to 125.1M vs. the Street 126.3M) and the guidance is soft (the Q3 revenue range mid-point is $3.7B vs. the Street’s $3.83B). “We are seeing shorter booking lead times globally and some signs of slowing demand from U.S. guests”. RTRS

A more detailed look at global markets courtesy of newsquawk

APAC stocks continued their recent rebound but with some of the gains capped as markets digested mixed Chinese trade data. ASX 200 was positive albeit with the upside limited as participants reflected on the key data from Australia’s largest trading partner. Nikkei 225 saw two-way price action in which initially suffered losses but then staged a gradual recovery and was further boosted following comments from BoJ Deputy Governor Uchida who said they won’t hike rates when markets are unstable. Hang Seng and Shanghai Comp. conformed to the upbeat mood although the advances in the mainland are limited after the PBoC refrained from injecting funds and the latest Chinese trade data printed mixed.

Top Asian News

- BoJ Deputy Governor Uchida said their interest rate path will obviously change if as a result of market volatility, economic forecasts, view on risks, and likelihood of achieving the projection change, while he added that they won’t hike rates when markets are unstable and they must maintain the current degree of monetary easing for the time being. Uchida said Japan is not in an environment where they would be behind the curve unless they hike rates at a set pace, as well as noted that a weak yen and subsequent rise in import costs pose upside risks to inflation. Furthermore, Uchida said if the economy and prices move in line with projections, it is appropriate to adjust the degree of monetary easing but also commented that Japan’s real interest rate is very low, monetary conditions are very accommodative and that the scheduled tapering of bond buying likely won’t cause major changes in the degree of monetary easing.

- BoJ’s Uchida says market volatility is very large, will be keeping a close eye on moves and the impact on the economy and prices. Real rates remain low, will underpin the economy. There is no gap in views between Ueda and Uchida, recent Uchida remarks reflect changes in the latest market developments following the last meeting.

- Honda (7267 JT) Q1 (JPY): Net 394bln (exp. 343bln), Operating 484bln (exp. 472bln), PBT 559bln (exp. 508bln). FY Guidance: Downgraded group sales guidance; sees GY global retail sales at 3.9mln vehicles (prev. guided 4.1mln). N. American sales 1.675mln vehicles (prev. guided 1.675mln)

European bourses are firmer intraday, Euro Stoxx 50 +1.7%, with the Stoxx 50 outperforming the Stoxx 600 +1.1% as the latter is weighed on by post-earnings downside in heavyweight Novo Nordisk -3.0%. Given this, Healthcare lags after Novo missed on several key metrics incl. Wegovy sales and downgraded some components of its FY guidance. Banks outperform as yields rise and after strong numbers from ABN AMRO. Breakdown has the DAX 40 +1.5% supported by Continental, which is lifting the broader Auto sector; Commerzbank bucks the banking trend after missing on numerous metrics. Stateside, futures in the green and grinding higher throughout the morning, ES +1.0%, NQ +1.1%; though, action has been choppy at times with newsflow light thus far ex-earnings. Elsewhere, Maersk earnings were mixed with the name lower despite noting market demand has been strong but warns of slower global container demand ahead.

Top European News

- Novo Nordisk (NOVOB DC) Q2 (DKK): Sales 68.06bln (exp. 68.65bln), EBIT 25.94bln (exp. 26.85bln), Wegovy Sales 11.66bln (exp. 13.54bln). CEO: Wegovy prescriptions in the US more doubled vs the start of the year; CFO says negative impact of net impact to net sales of Wegovy in Q2 is due to rebate adjustments; Competitive dynamics will not have an impact on Wegovy sales in the near future. FY Guidance: Sales growth 22-28% at CER (prev. guided 19-27%); Operating Profit growth 20-28% at CER (prev. view 22-30%), CAPEX ~45bln. FCF 59-69bln

- Maersk (MAERSKB DC) Q2 (USD): EBITDA 2.1bln (exp. 2.27bln), EBIT 963mln (exp. 810mln), EPS 51 (exp. 55.5). Market demand has been strong, Red Sea situation remains entrenched. CEO says they could see some pulling forward of demand, most notably within the US due to the upcoming election and associated uncertainty around future import tariffs. Adds, industrial action following pending union talks in the US could lead to further supply chain disruptions.

- UK Chancellor Reeves aims to follow a “Canadian model” to consolidate GBP 360bln of smaller local government pension schemes to aid in boosting investment and “fire up the economy”, according to The Times.

FX

- USD supported with the DXY bid and above 103.00 but off overnight best levels of 103.37. Strength which came as USD/JPY soared above 147.50 after remarks from BoJ’s Uchida that they won’t hike when markets are unstable.

- As such, JPY is the clear laggard but followed relatively closely by the CHF as the positive tone means haven demand is waning and as yields rally and weigh on the likes of CHF and JPY.

- Sterling modestly firmer, but has been below 1.27 in a 1.2681-1.2718 band. Specifics light but strength coming via EUR downside and associated pressure in EUR/GBP to back below 0.86.

- EUR/USD itself holding around 1.0905 and is close to, but yet to test, the figure to the downside; no real reaction to mixed German data this morning.

- Antipodeans benefit from the risk tone with NZD outperforming after encouraging employment data and as the AUD takes a slight breather from RBA-inspired strength; nonetheless, it remain underpinned with strong Chinese imports assisting.

- PBoC set USD/CNY mid-point at 7.1386 vs exp. 7.1481 (prev. 7.1318).

- Japan’s currency intervention amounted to JPY 5.92tln on April 29th and JPY 3.87tln on May 1st, while the April 29th intervention was a single-day record and surpassed the previous record of JPY 5.62tln on 21st October 2002, according to Ministry of Finance data.

Fixed Income

- Benchmarks continue to falter despite opening the European morning with modest gains. Downside which has pushed Bunds below the 134.00 mark vs. a 136.28 peak on Monday.

- Supply was uneventful in terms of reaction from Germany and the UK, though the latter was a touch softer than recent taps; reminder, US 10yr later.

- Gilts pressured but to a slightly lesser magnitude with little by way of specific driver to note. Further downside brings the 99.00 mark into view and then numerous recent lows below this.

- Amidst this, USTs are also softer but only modestly so with the docket ahead thin ex-earnings until 10yr supply which follows an unremarkable 3yr tap on Tuesday.

- Chinese regulators are reportedly restricting the duration of new bond funds, restrictions target mutual fund managers, according to Reuters sources.

- UK sells GBP 4bln 4.125% 2029 Gilt: b/c 2.87x (prev. 3.10x), average yield 3.854% (prev. 4.023%) & tail 0.9bps (prev. 0.9bps)

- Germany sells EUR 0.407bln vs exp. EUR 0.5bln 1.00% 2038 Bund & EUR 1.199bln vs exp. EUR 1.5bln 2.60% 2041 Bund

Commodities

- Crude benchmarks began with a mild positive tilt and have been gradually extending on this throughout the morning. WTI and Brent at the top-end of parameters and are holding around USD 74.11/bb and USD 77.42/bbl respectively.

- Benchmarks aided by the USD being slightly off best (though still firmer) and with gepol. risk still a key factor alongside the recent production halt at El Sharara.