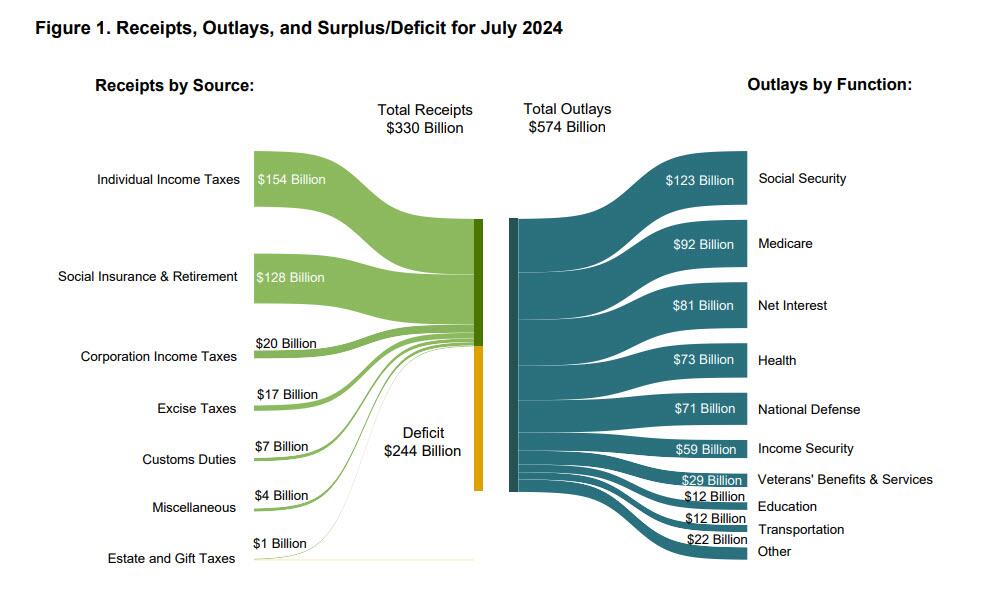

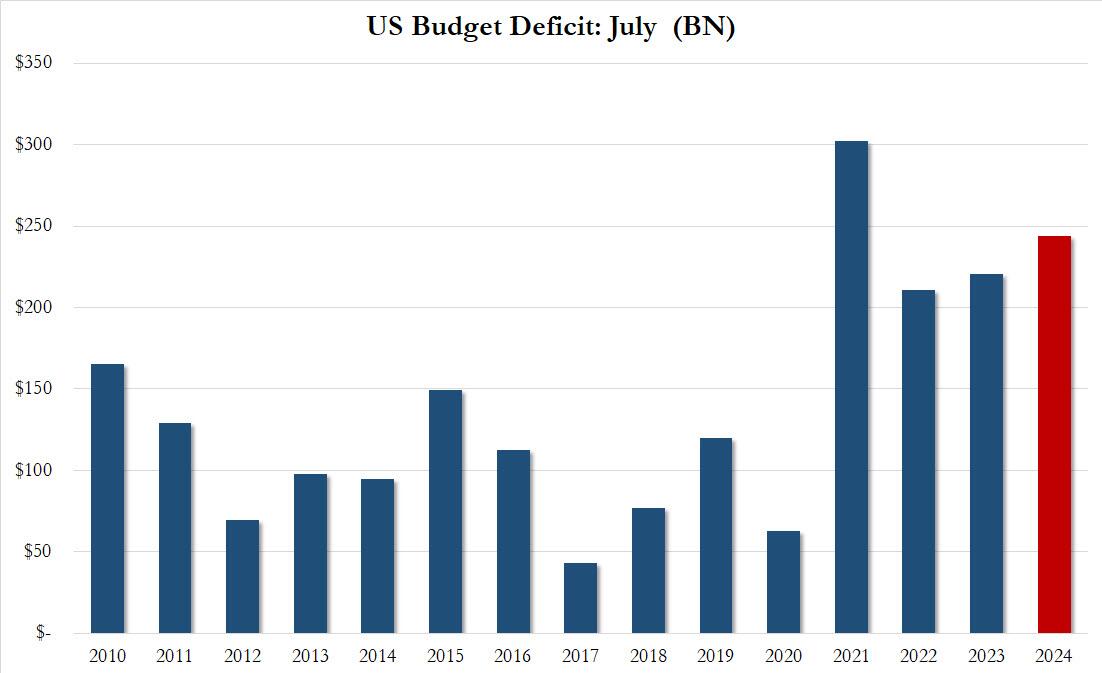

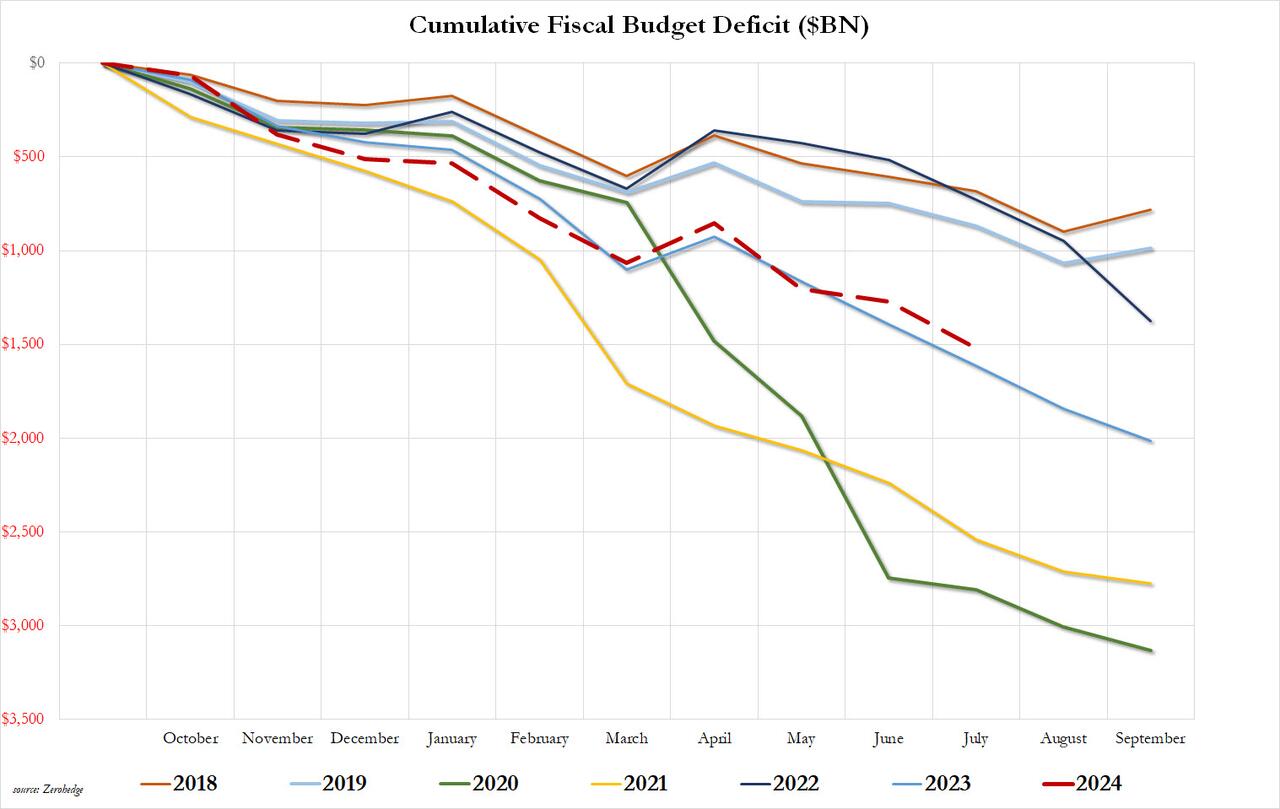

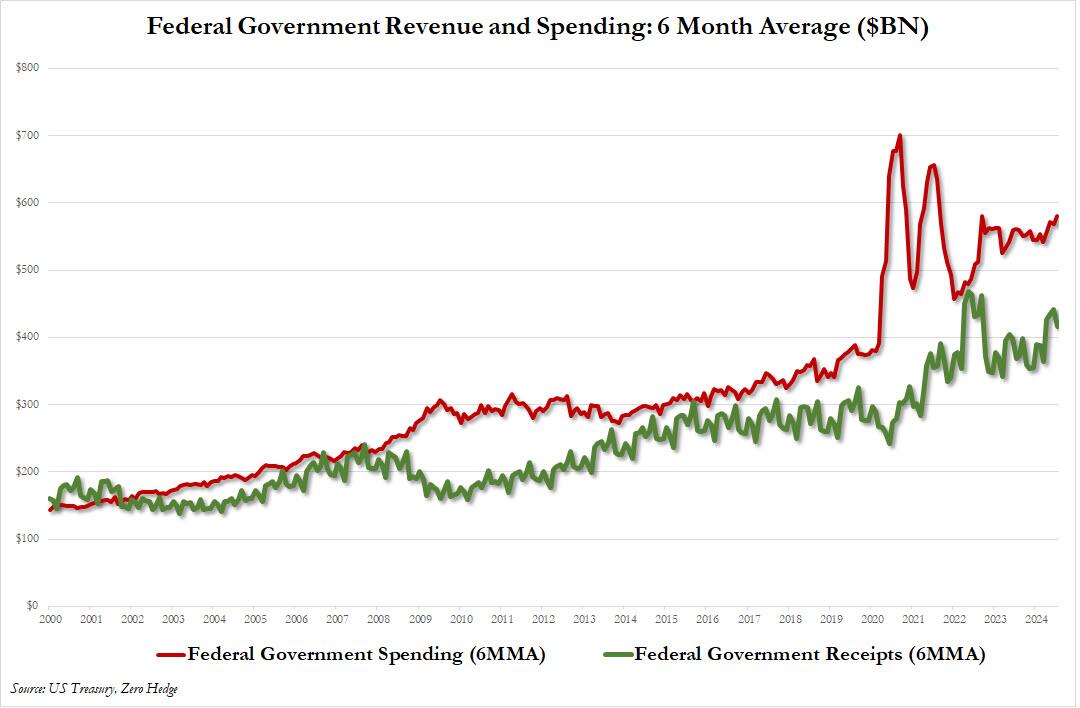

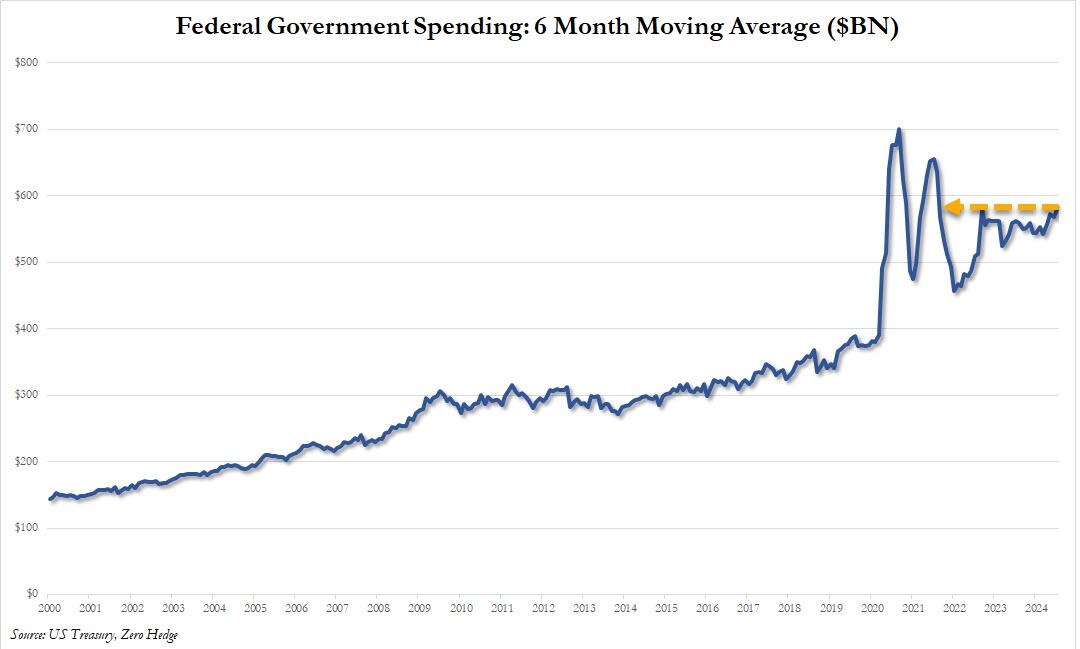

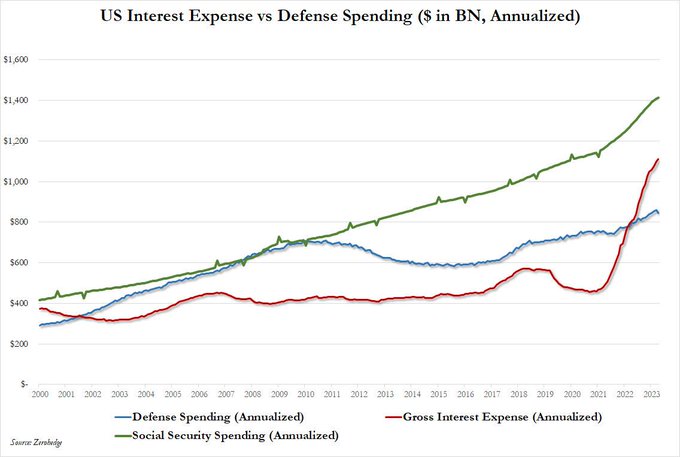

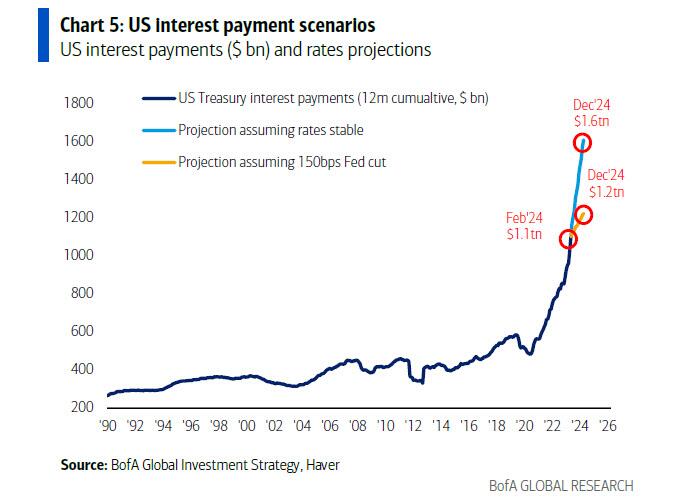

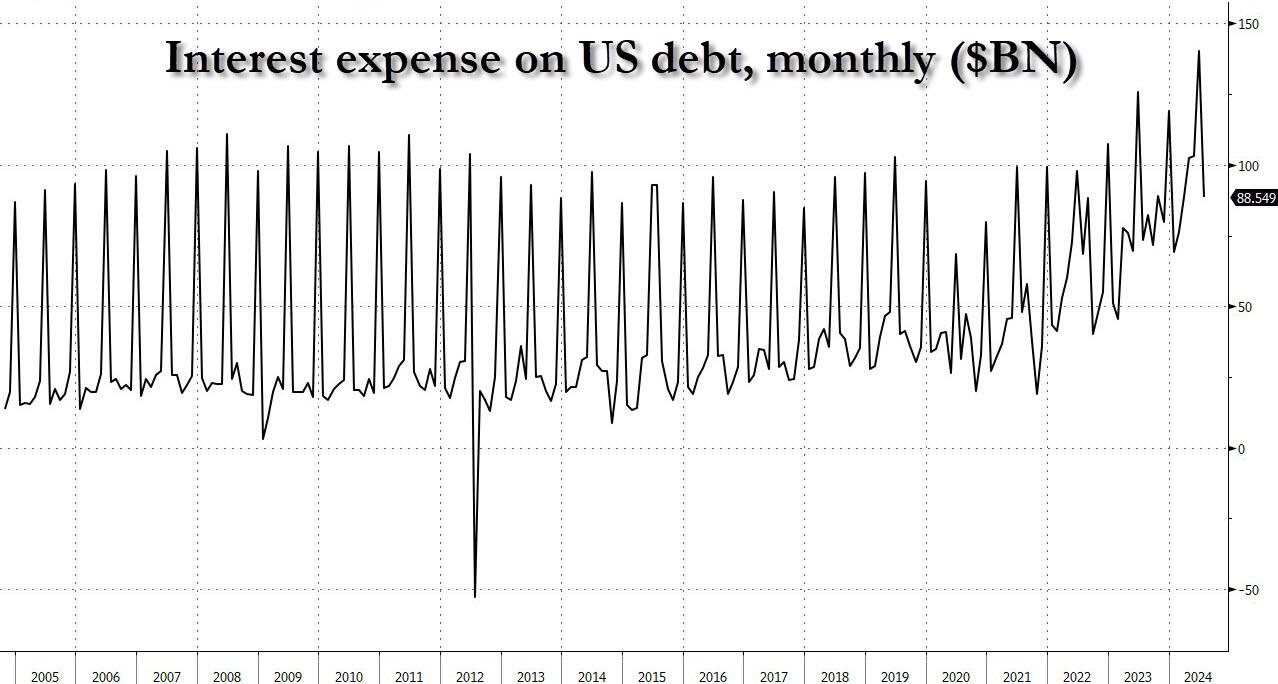

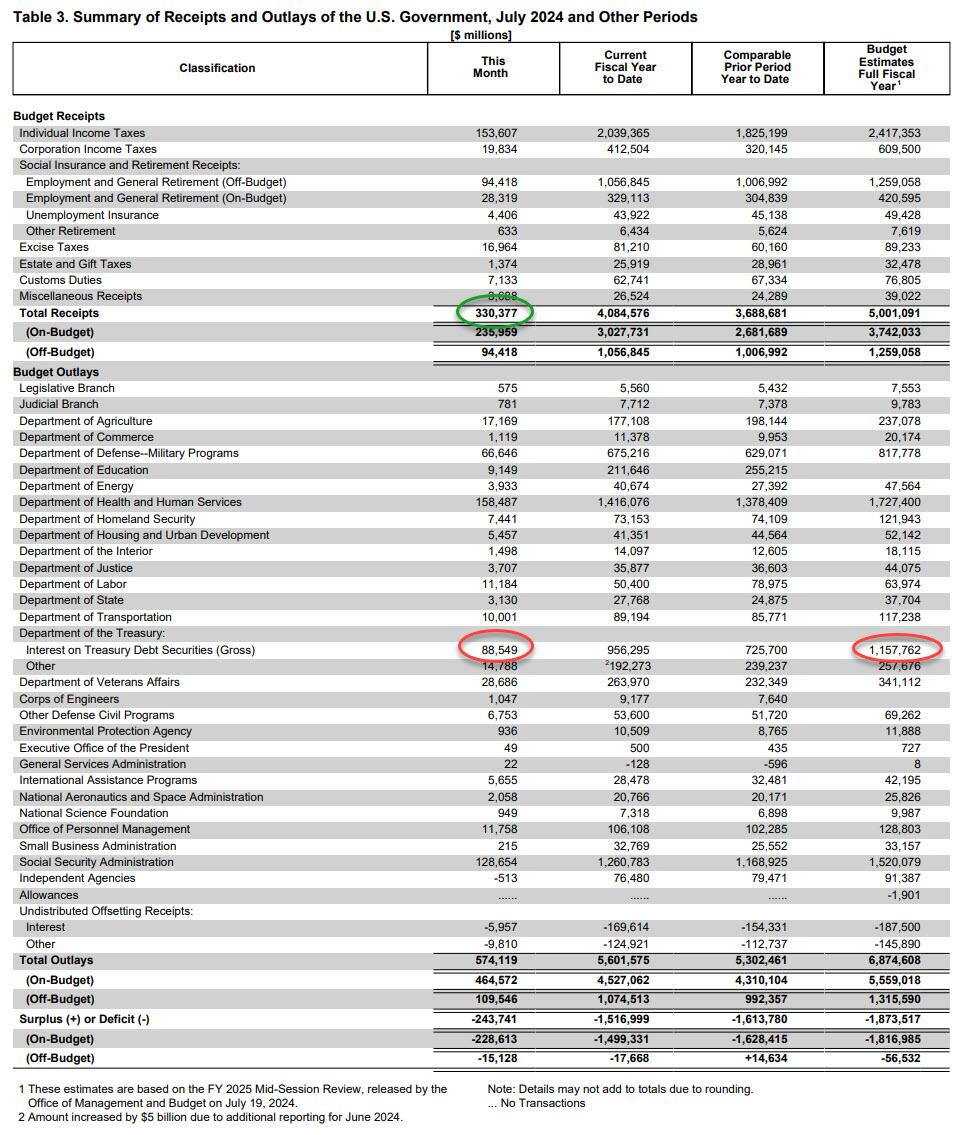

AUGUST 13/GOLD CLOSED UP $3.35 TO $2467.60//SILVER WAS DOWN 19 CENTS TO $27.70//PLATINUM WAS DOWN $3.35 TO $939.80 WHILE PALLADIUM WAS UP $18.60 TO $942.60//EXCELLENT COMMENTARY ON THE PLIGHT OF ENGLAND CAUSED BY LEFTISH GOVERNMENTS//ISRAEL VS HAMAS/IRAN UPDATES//COVID UPDATES/VACCINE INJURY REPORT/SLAY NEWS/EVOL NEWS/NEWS ADDICTS//USA RECORDS ITS 2ND HIGHEST DEFICIT IN HISTORY/INTEREST ON DEBT APPROACHES 25% OF ALL EXPENDITURES AND WILL APPROACH 1.6 TRILLION DOLARS BY DECEMBERS: THEY ARE OUT OF CONTROL/ELON MUSK AND PRES TRUMP TALK ON X AND THAT CAUSES THE LEFT TO GO BONKERS INCLUDING THE EU//SWAMP STORIESS FOR YOU TONIGHT//

118 C MACQUARIE FUT 600 118 H MACQUARIE FUT 16 190 H BMO CAPITAL 123 323 C HSBC 50 363 H WELLS FARGO SEC 3 555 H BNP PARIBAS SEC 33 624 H BOFA SECURITIES 37 657 C MORGAN STANLEY 19 661 C JP MORGAN 33 199 661 H JP MORGAN 114 685 C RJ OBRIEN 1 686 C STONEX FINANCIA 1 690 C ABN AMRO 8 709 C BARCLAYS 23 732 C RBC CAP MARKETS 1 737 C ADVANTAGE 7 905 C ADM 2

TOTAL: 635 635 MONTH TO DATE: 17,816

JPMorgan stopped 313/635

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2024. CONTRACT: 635 NOTICES FOR 63,500 OZ or 1.975 TONNES

total notices so far: 17,816 contracts for 1,781,600 Oz (55.415 tonnes)

FOR AUGUST:

SILVER NOTICES: 61 NOTICE(S) FILED FOR 330,000

OZ/

total number of notices filed so far this month : 768 for 3,840,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $3.35 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//

/ /INVENTORY RESTS AT 849.79 TONNES

INVENTORY RESTS AT 849.79 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $0.19 AT THE SLV

NO CHANGES IN SILVER INVENTORY AT THE SLV:

// INVENTORY AT 465.743+ MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 465.743 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 1056 CONTRACTS TO 147,132 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH VERY MINOR LIQUIDATION OF OI FROM OUR SPREADERS/TAS WITH OUR STRONG GAIN OF $0.37 IN SILVER PRICING AT THE COMEX ON MONDAY’S TRADING. SOME OF OUR OILIQUIDATION ACCOMPANIED OUR HUGE GAIN OF 1256 CONTRACTS ON OUR TWO EXCHANGES AS WE HAD SMALL LIQUIDATION OF T.A.S. CONTRACTS DURING MONDAY’S TRADING//. WE HAD SOME COVERING BY OUR SPECS WITH THE HUGE GAIN IN PRICE AS WE HAD A SMALL 210 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY A HUMONGOUS 4814 CONTRACT T.A.S ISSUANCE. IN ESSENCE WE GAINED 1256 CONTRACTS ON OUR TWO EXCHANGES WITH THE HUGE GAIN IN PRICE.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN YESTERDAY. THE ACCUMULATED T.A.S. IS BEING USED TO MANIPULATE PRICES TODAY.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: 4814 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS.IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1/2 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS BUT TO NO AVAIL. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.37) AND WERE UNSUCCESSFUL IN KNOCKING A ANY SILVER LONGS FROM THEIR PERCH AS WE HAD A HUGE SIZED GAIN OF 1431 CONTRACTS ON OUR TWO EXCHANGES.

WE HAD A SMALL 200 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.005 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 5,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO 4.070 MILLION OZ

//NEW STANDING FOR SILVER//AUGUST IS THUS 4.070 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI GAIN //SMALL SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 4814 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED 175 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST

TOTAL CONTRACTS for 9 DAYS, total 10,690 contracts: OR 53.450 MILLION OZ (1187 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 53.450 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 53.450 MILLION OZ//THIS MONTH WILL PROBABLY BE A VERY STRONG FOR ISSUANCE.

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1056 CONTRACTS WITH OUR STRONG GAIN IN PRICE OF SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL EFP ISSUANCE CONTRACTS: 200 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 3.005 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 5,000 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR JULY 4.070 MILLION OZ

WE HAVE A HUGE SIZED GAIN OF 1256 OI CONTRACTS ON THE TWO EXCHANGES WITH THE GAIN IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A GIGANTIC SIZED 4814 CONTRACTS,//SOME FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX TRADING WHICH ACCOUNTS FOR A PORTION OF THE COMEX OI GAIN//// SOME SHORT COVERING FROM OUR SPEC SHORTS AND ZERO LIQUIDATION OF LONGS. ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER.

THE NEW TAS ISSUANCE MONDAY NIGHT (4814) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 61 NOTICE(S) FILED TODAY FOR 330,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A HUGE SIZED 13,112 OI CONTRACTS TO 496,708 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 792 CONTRACTS

WE HAD A HUGE SIZED INCREASE IN COMEX OI (13,112 CONTRACTS) OCCURRED WITH OUR GAIN OF $30.00 IN PRICE/MONDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR AUGUST AT 65.55 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 26,100 OZ QUEUE JUMP AS FINALLY GUYS ARE STANDING FOR GOLD AT THE COMEX

NEW STANDING REDUCES TO 66.765 TONNES

/ ALL OF THIS HAPPENED WITH OUR $30.00 GAIN IN PRICE WITH RESPECT TO MONDAY’S TRADING. WE HAD A HUGE SIZED GAIN OF 16,083 OI CONTRACTS (50.02 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 2971 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 495,708

IN ESSENCE WE HAVE A HUGE SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 16,083 CONTRACTS WITH 13,112 CONTRACTS INCREASED AT THE COMEX// AND A GOOD SIZED 2971 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 16,083 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A GOOD 2688 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2971 CONTRACTS) ACCOMPANYING THE STRONG SIZED GAIN IN COMEX OI OF 13,112 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 16,083 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR AUGUST AT 65.55 TONNES FOLLOWED BY TODAY’S 17,900 OZ QUEUE JUMP AS THESE BOYS JUMP THE QUEUE TO STAND AT THE COMEX./

//NEW STANDING ADVANCES TO: /AUGUST 65.953 TONNES.

/ 3) SOME T.A.S. LIQUIDATION//SPREADER CONTRACTS WITH ZERO NET LONG SPECS BEING CLIPPED,

4) STRONG SIZED COMEX OPEN INTEREST GAIN 5) SMALL ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 2688 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST. :

TOTAL EFP CONTRACTS ISSUED: 45,619 CONTRACTS OF 4,561,900 OZ OR 141.89 TONNES IN 9 TRADING DAY(S) AND THUS AVERAGING: 5331 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES 141.89 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 141.89 DIVIDED BY 3550 x 100% TONNES = 4.00% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 141.89 TONNES//THIS MONTH WILL NO DOUBT BE A HUGE ISSUANCE OF EFP’S SIMILAR TO SILVER.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUG), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE SIZED 1056 CONTRACTS OI TO 147,132 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 200 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 75 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 200 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1056 CONTRACTS AND ADD TO THE 200 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1256 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 6.25 MILLION OZ OCCURRED WITH OUR $0.37 GAIN IN PRICE

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED UP 9.74 PTS OR 0.34% //Hang Seng CLOSED UP 62.41 PTS OR 0.36% // Nikkei CLOSED UP 1,207.51 OR 3.45%//Australia’s all ordinaries CLOSED UP 0.17%///Chinese yuan (ONSHORE) CLOSED UP TO 7,1660 CHINESE YUAN OFFSHORE CLOSED UP TO 7.1654/ Oil UP TO 79.90 dollars per barrel for WTI and BRENT UP AT 82.06 Stocks in Europe OPENED ALL MOSTLY RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A HUGE SIZED 13,112 CONTRACTS TO 495,708 WITH OUR GAIN IN PRICE OF $30.00 WITH RESPECT TO MONDAY’S TRADING. WE LOST ZERO SPREADER/T.A.S. CONTRACTS AS SHORTS CONTINUED TO PANIC THROUGHOUT THE SESSION AND COVERED AT MUCH HIGHER PRICES. THE FED IS THE MAJOR SHORT OF AROUND 116 TONNES+ OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS IS SCHEDULED TO HAPPEN LATE SEPT 2024.

OUR LONDONERS ALSO BOUGHT NEW MASSIVE QUANTITIES OF LONGS AND THIS WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD A STRONG T.A.S. LIQUIDATION ON MONDAY’S GAIN IN PRICE WITH ZERO LONGS BEING CLIPPED (AS YOU WILL SEE BELOW) BUT WE DID HAVE MAJOR SHORT COVERING. THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE ACTIVE DELIVERY MONTH OF AUGUST.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 2971 EFP CONTRACTS WERE ISSUED: : OCT/DEC2971 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2971 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A HUGE SIZED TOTAL OF 16,083 CONTRACTS IN THAT 2971 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A HUGE SIZED GAIN OF 13,112 COMEX CONTRACTS..AND THIS HUGE GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR STRONG GAIN IN PRICE OF $30.00/MONDAY COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AS MENTIONED ABOVE.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT A GOOD SIZED 2971 CONTRACTS. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN LAST WEEK’S TRADING//RAIDS AS WELL AS THIS WEEK AND ESPECIALLY ON MONDAY’S TRADING.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: AUGUST (66.8765 TONNES)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 65.953 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $30.00 //// AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE DID HAVE A HUGE GAIN IN OUR TWO EXCHANGES. CENTRAL BANK LONGS , EXERCISED FOR PHYSICAL. WE HAD A VEERY MINOR SIZED T.A.S. LIQUIDATION MONDAY/COMEX IF ANY. PROBABLY STORED FOR A TUESDAY RAID.

WE HAVE GAINED A TOTAL OI OF 52.48 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST (65.55 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE 26,100 OZ QUEUE JUMP //NEW STANDING: 66.765 TONNES.

NEW STANDING FOR AUGUST: 66.765 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $30.00

WE HAVE REMOVED 792 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET GAIN ON THE TWO EXCHANGES 16,083 CONTRACTS OR 1,608300 OZ (50.02

Total monthly oz gold served (contracts) so far this month

17,816 notices 1,781,600 oz 55.415TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: nil oz

we have 0 customer deposits

total deposits NIL oz

withdrawals: 1

i) Out of JPMorgan: 99,828.855 oz (3105 kilobars)

or 3.105 tonnes of gold transferred to London

TOTAL WITHDRAWALS 99,828.855 oz

adjustments: 1

jpmorgan: 482.265 oz customer to dealer

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST

For the front month of AUGUST we have an oi of 4284 contracts having GAINED 256 contracts.

We had 5 contracts served on MONDAY so we gained an additional 261 contracts or 26100 oz will stand for gold at the comex

SEPT. GAINED 74 CONTRACTS TO STAND AT 5577 CONTRACTS.

OCTOBER GAINED 1032 CONTRACTS UP TO 51,815 CONTRACTS

We had 635 contracts filed for today representing 63500 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 33 notices were issued from their client or customer account. The total of all issuance by all participants equate to 615 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 313 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for AUGUST /2024. contract month, we take the total number of notices filed so far for the month (17,816) x 100 oz ) to which we add the difference between the open interest for the front month of August 4284( CONTRACTS) minus the number of notices served upon today (635 x 100 oz per contract( equals 2,146,500 OZ OR 66.765 TONNES.

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (17816 x 100 oz +we add the difference for front month of AUGUST (4284 X// , OI} minus the number of notices served upon today (635) x 100 oz which equals 2,146,500 oz (66.765 TONNES)

TOTAL COMEX GOLD STANDING FOR AUGUST: 66.765 TONNES WHICH IS HUGE FOR THIS VERY ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,602,869.389 OZ

TOTAL REGISTERED GOLD 7,953,876.673 ( 247.39 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,748,379,366 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,232,543 oz (REG GOLD- PLEDGED GOLD)= 195.85 tonnes //

END

SILVER/COMEX

AUGUST 13/2024

INITIAL

//2024// THE AUG 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

558,854.257 OZ

CNT Delaware

.

Deposits to the Dealer Inventory

Deposits to the Customer Inventory

i) Asahi 593,073.000 oz

No of oz served today (contracts)

66 CONTRACT(S) (330,000 OZ)

No of oz to be served (notices)

46 contracts (0.230 million oz)

Total monthly oz silver served (contracts)

768 Contracts (3.840 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit/

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 customer deposits:

i)Into Asahi 593,073.000 oz

total customer deposit 593,073.000 oz

JPMorgan has a total silver weight: 134.771million oz/303.374million or 44.64%

adjustment:1 customer to dealer Manfra 319,275.900 oz

withdrawals: 2

i) Out of CNT 15,0911.84 oz

ii) Out of Delaware: 543,762.417 oz

total customer withdrawals:558,854.257 oz

TOTAL REGISTERED SILVER: 69.904 MILLION OZ//.TOTAL REG + ELIGIBLE. 303.374 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR AUGUST:

silver open interest data:

FRONT MONTH OF AUGUST/2024 OI: 112 CONTRACTS HAVING LOST 1 CONTRACT(S).

WE HAD 2 NOTICES SERVED ON MONDAY, SO WE GAINED 1 CONTRACT OR AN ADDITIONAL 5,000 OZ WILL STAND FOR SILVER AT THE COMEX.

SEPT SAW A LOSS OF 5335 CONTRACTS TO 71,453. SEPT NOW BECOMES THE NEW FRONT MONTH

OCTOBER SAW ANOTHER GAIN OF OPEN INTEREST CONTRACTS OF 48 CONTRACTS AND THUS WE HAVE 278 OPEN INTEREST CONTRACTS FOR OCTOBER.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 66 for 330,000 oz

CONFIRMED volume; ON MONDAY 82,956 strong

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 768 x 5,000 oz = 3.840 MILLION oz

to which we add the difference between the open interest for the front month of AUGUST( 112) and the number of notices served upon today 66 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST/2024 contract month: 768 notices served so far) x 5000 oz + OI for the front month of AUGUST (112)x number of notices served upon today minus (66)x 5000 oz of silver standing for the AUGUST contract month equates to 4.070 MILLION OZ.

New total standing: 4.070 million oz.

There are 69.585 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD

AUGUST 13 WITH GOLD UP $3.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//////INVENTORY RESTS AT 849.79 TONNES

AUGUST 12 WITH GOLD UP $30.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ////INVENTORY RESTS AT 846.91 TONNES

AUGUST 9 WITH GOLD UP $10.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 846.91 TONNES

AUGUST 8 WITH GOLD UP $31.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.02 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 844.04 TONNES

AUGUST 7 WITH GOLD UP $1.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.16 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 848.06 TONNES

AUGUST 6 WITH GOLD DOWN $13.10 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD” A WITHDRAWAL OF .57 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 844.90 TONNES

AUGUST 2 WITH GOLD DOWN $9.95 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.58 TONNES OF GOLD OUT OF THE GLD//INVENTORY RESTS AT 845.47 TONNES

AUGUST 1 WITH GOLD UP $9.15 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 846.05 TONNES

JULY 30 WITH GOLD UP $26.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// A /////INVENTORY RESTS AT 843.17 TONNES

JULY 29 WITH GOLD UP $27.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD// A WITHDRAWAL OF 1.98 TONNES OF GOLD OUT OF THE GLD/////INVENTORY RESTS AT 843.17 TONNES

JULY 26 WITH GOLD UP $27.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD// A DEPOSIT OF 3.45 TONNES OF GOLD INTO THE GLD/////INVENTORY RESTS AT 845.19 TONNES

JULY 25 WITH GOLD DOWN $60.45 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 841.74 TONNES

JULY 24 WITH GOLD UP $12.75 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1,73 TOONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 841.74 TONNES

JULY 23 WITH GOLD UP $12.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 22 WITH GOLD DOWN $4.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 19 WITH GOLD DOWN $56.10 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;:A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 18 WITH GOLD DOWN $2.20 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;: ///INVENTORY RESTS AT 842.02 TONNES

JULY 17 WITH GOLD DOWN $6.60 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A MASSIVE DEPOSIT OF 5.49 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 842.02 TONNES

JULY 16 WITH GOLD UP $38.60 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 836.53 TONNES

JULY 15 WITH GOLD UP $8.15 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;: /INVENTORY RESTS AT 835.09 TONNES

JULY 12 WITH GOLD DOWN $0.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 835.09 TONNES

JULY 11 WITH GOLD UP $43.05 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;:INVENTORY RESTS AT 833.37 TONNES

JULY 10 WITH GOLD UP $12.00 ON THE DAY; HUUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.44 TONNES OF GOLD VAPOUR FROM THE GLD//.//:INVENTORY RESTS AT 833.37 TONNES

JULY 9 WITH GOLD UP $5.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD.//:INVENTORY RESTS AT 834.81 TONNES

JULY 8 WITH GOLD DOWN $26.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD.//:INVENTORY RESTS AT 834.81 TONNES

JULY 5 WITH GOLD UP $29.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD..A DEPOSIT OF 1.10 TONNES OF GOLD VAPOUR INTO THE GLD//:INVENTORY RESTS AT 833.37 TONNES

JULY 3 WITH GOLD UP $35.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD..A MASSIVE DEPOSIT OF 5.76 TONNES OF GOLD VAPOUR INTO THE GLD//:INVENTORY RESTS AT 833.37 TONNES

JULY 2 WITH GOLD DOWN $4.45 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD../:INVENTORY RESTS AT 827.61 TONNES

JULY 1 WITH GOLD DOWN $.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

GLD INVENTORY: 849.79 TONNES, TONIGHTS TOTAL

SILVER

AUGUST 13//WITH SILVER DOWN $0.19//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 12//WITH SILVER UP $.37//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 9//WITH SILVER DOWN $.03//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 8//WITH SILVER UP $.70//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 3.241 MILLION OZ INTO THE SLV////./// /INVENTORY AT 462.502 MILLION OZ

AUGUST 7//WITH SILVER DOWN $0.27//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.552 MILLION OZ INTO THE SLV////./// /INVENTORY AT 462.502 MILLION OZ

AUGUST 6//WITH SILVER UP $0.05//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 458.851 MILLION OZ

AUGUST 2//WITH SILVER DOWN $0.01//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 1.243 MILLION OZ OF SILVER OUT OF THE SLV ///./// /INVENTORY AT 460.961 MILLION OZ

AUGUST 1//WITH SILVER DOWN $0.46//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.608 MILLION OZ OF SILVER VAPOUR INTO THE SLV///./// /INVENTORY AT 462.204 MILLION OZ

JULY 31//WITH SILVER UP $0.45//NO CHANGES IN SILVER INVENTORY: /./// /INVENTORY REMAINS AT 460.596 MILLION OZ

JULY 30//WITH SILVER UP $0.61//SMALL CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 0.456 MILLION OZ OF SILVER VAPOUR INTO THE SLV/./// /INVENTORY RISES AT 460.596 MILLION OZ

JULY 29//WITH SILVER DOWN $0.07//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.382 MILLION OZ OF SILVER VAPOUR INTO THE SLV/./// /INVENTORY RISES AT 461.052 MILLION OZ

JULY 26//WITH SILVER DOWN $0.07//NO CHANGES IN SILVER INVENTORY./// /INVENTORY REMAINS AT 456.670 MILLION OZ

JULY 25 WITH SILVER DOWN $1.37//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 3.124 MILLION OZ OF SILVER OUT OF THE SLV./// /INVENTORY FALLS TO 456.670 MILLION OZ

JULY 24 WITH SILVER UP 3 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 15.880 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 23 WITH SILVER UP 3 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 15.880 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 22 WITH SILVER UP 2 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 3.920 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 19 WITH SILVER DOWN 94 CENTS//NO CHANGES IN SILVER INVENTORY/// /INVENTORY REMAINS AT 435.854 MILLION OZ

JULY 18 WITH SILVER DOWN 13 CENTS//HUGE CHANGES IN SILVER INVENTORY” A DEPOSIT OF 2.374 MILLION OZ INTO THE SLV/// /INVENTORY RISES TO 435.854 MILLION OZ

JULY 17. WITH SILVER DOWN 75 CENTS//NO CHANGES IN SILVER INVENTORY// /INVENTORY REMAINS AT 433.480 MILLION OZ.

JULY 16. WITH SILVER UP 30 CENTS//NO CHANGES IN SILVER INVENTORY// /INVENTORY REMAINS AT 433.480 MILLION OZ.

JULY 15. WITH SILVER DOWN 24 CENTS//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 2.145 MILLION OZ FROM THE SLV.// /INVENTORY LOWERS T0 AT 433.480 MILLION OZ.

JULY 12. WITH SILVER DOWN $.65 CENTS//NO CHANGES IN SILVER INVENTORY /INVENTORY REMAINS CONSTANT AT 435.625 MILLION OZ.

JULY 11. WITH SILVER UP $.72 CENTS//HUGE CHANGES IN SILVER INVENTORY A WITHDRAWAL OF 0.731 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 435.625 MILLION OZ.

JULY 10. WITH SILVER DOWN $.04 CENTS//HUGE CHANGES IN SILVER INVENTORY A MAMMOTH WITHDRAWAL OF 3.744 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 436.356 MILLION OZ.

JULY 9. WITH SILVER UP 13 CENTS//HUGE CHANGES IN SILVER INVENTORY A MAMMOTH WITHDRAWAL OF 3.744 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 436.356 MILLION OZ.

JULY 8. WITH SILVER DOWN $0.73//SMALL CHANGES IN SILVER INVENTORY A MAMMOTH DEPOSIT OF 3,292,000 OZ OF SILVER VAPOUR INTO THE SLV.: /INVENTORY RISES T0 440.100 MILLION OZ.

JULY 4. WITH SILVER UP $0.85//SMALL CHANGES IN SILVER INVENTORY A MAMMOTH DEPOSIT OF 3,292,000 OZ OF SILVER VAPOUR INTO THE SLV.: /INVENTORY RISES T0 440.100 MILLION OZ.

JULY 3. WITH SILVER UP $1.08//SMALL CHANGES IN SILVER INVENTORY A SMALL WITHDRAWAL OF 639,000 OZ: /INVENTORY LOWERS T0 436,808 MILLION OZ.

JULY 2. WITH SILVER UP $0.19//NO CHANGES IN SILVER INVENTORY: /INVENTORY REMAINS AT 437.447 MILLION OZ./

JULY 1. WITH SILVER UP $0.05//NO CHANGES IN SILVER INVENTORY: A DEPOSIT OF 182,000 OZ OF SILVER INTO THE SLV./.// /INVENTORY RISES AT 437.447 MILLION OZ./

CLOSING INVENTORY 465.743 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY

3.CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES

A metals vault bigger than Fort Knox opens in Idaho

Submitted by admin on Mon, 2024-08-12 16:27 Section: Daily Dispatches

From Money Metals News Service, Eagle, Idaho Monday, April 12, 2024

EAGLE, Idaho — The Western United States now has its very own Fort Knox, only substantially larger.

After three years of planning and construction, Money Metals has opened its state-of-the-art 37,000-square-foot vaulting and fulfillment facility in Eagle, Idaho.

Nestled at the base of the Boise Foothills, Money Metals’ high-security gold and silver storage compound cost $28 million to construct, has the capacity to hold upwards of $100 billion in gold and silver, and can be expanded to 60,000 square feet.

Built on a 3.2-acre lot adjacent to city and county police and emergency services, the new depository offers an extremely secure location for individuals, businesses, family offices, governments, and financial institutions across the globe to store high-value precious metals assets.

Embedded into the facility are advanced security measures, around-the-clock monitoring, secure access controls, a security team composed of armed former law enforcement and military personnel, and third-party audits and insurance to ensure the highest standards of integrity and protection. …

4. GOLD PODCASTS//LIVE FROM THE VAULT/no 185 with/Andrew Maguire

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COCOA

6 CRYPTOCURRENCY NEWS

END

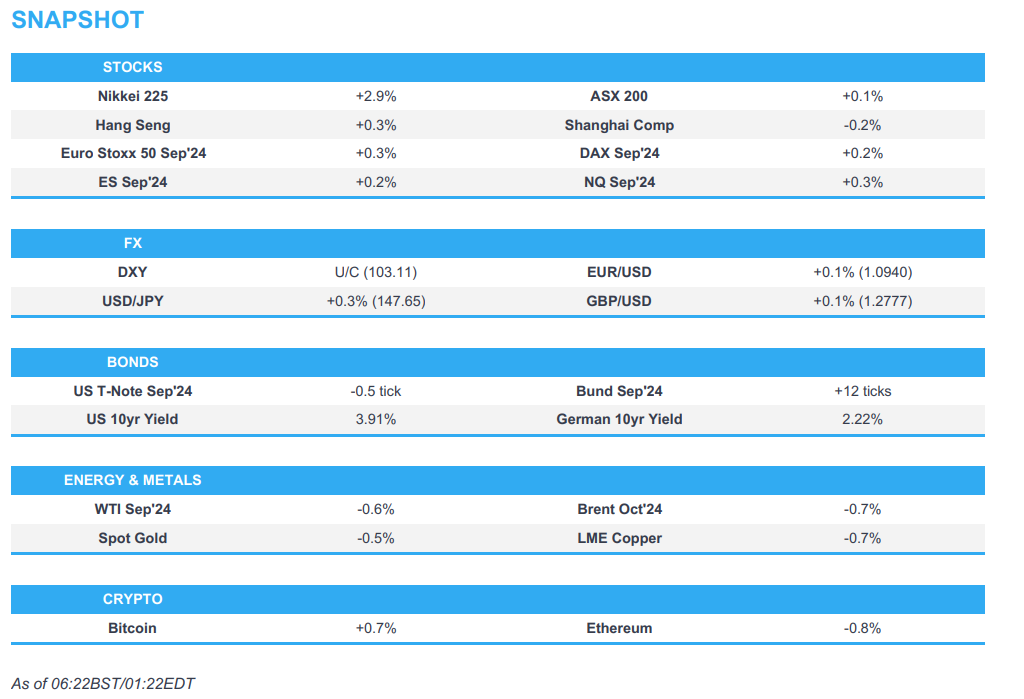

ASIA TRADING/TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED UP 9.74 PTS OR 0.34% //Hang Seng CLOSED UP 62.41 PTS OR 0.36% // Nikkei CLOSED UP 1,207.51 OR 3.45%//Australia’s all ordinaries CLOSED UP 0.17%///Chinese yuan (ONSHORE) CLOSED UP TO 7,1660 CHINESE YUAN OFFSHORE CLOSED UP TO 7.1654/ Oil UP TO 79.90 dollars per barrel for WTI and BRENT UP AT 82.06 Stocks in Europe OPENED ALL MOSTLY RED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.1660

OFFSHORE YUAN: UP TO 7.1654

SHANGHAI CLOSED UP 9.74 PTS OR 0.34 %

HANG SENG CLOSED UP 62.41 PTS OR 0.36%

2. Nikkei closed

3. Europe stocks SO FAR: ALL MOSTLY RED

USA dollar INDEX UP TO 103.00 EURO FALLS TO 1.0965 DOWN 11 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +0.851 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.52…… JAPANESE YEN NOW RISING AS WE HAVE NOW REACHED THE REIGNITING OF THE YEN CARRY TRADE AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.2035/Italian 10 Yr bond yield DOWN to 3.615 SPAIN 10 YR BOND YIELD DOWN TO 3.056%

3i Greek 10 year bond yield DOWN TO 3.287

3j Gold at $2464.35//Silver at: 27.27 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 75/ 100 roubles/dollar; ROUBLE AT 91.74

3m oil into the 79 dollar handle for WTI and 82 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.52/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.851 % STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8672 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9475 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.901 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.206 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.006 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 33.56…

10 YR UK BOND YIELD: 3.949 DOWN 2 PTS

10 YR CANADA BOND YIELD: 3.105 DOWN 3 BASIS PTS

2a New York OPENING REPORT

Futures Trim Gains After Dismal Outlook From Home Depot

TUESDAY, AUG 13, 2024 – 08:10 AM

US futures are slightly higher, although well off session highs following disappointing guidance from Home Depot while rising tension in the Middle East weighed on risk appetite. Tech leads modest gains as we receive the first batch of the week’s macro data today when PPI drops at 830am ET. As of 7:45am ET, S&P futures are 0.2% higher, paring a gain of 0.5%, after yesterday’s flat close on Wall Street; Nasdaq futs are up 0.3% with NVDA rising 1.5% as Mag7 are all higher and Semis catch a bid, following yesterday’s outperformance. European markets are lower even as Asian stocks erased last week’s sharp declines led by a bounce in Japan thanks to a drop in the yen. Bond yields are 1-2bps higher which is boosting the USD. Commodities are mostly lower with WTI reversing losses to trade around $80 and Brent at $82 as the US sees an Iranian attack against Israel as increasingly likely; Ags/Precious metals are under pressure. Fed’s Bostic speaks today, and disappointing earnings from HS may shape the market narrative. Tomorrow’s CPI and Thurs’ Retail Sales are the key catalysts.

In premarket trading, Home Depot falls 2% after the company beat lowered its same store sales forecast to a decline of 3-4% for the year, signaling that it expects consumer spending to remain soft in the coming months. Said otherwise, HD expects business to get worse in the second half of the year, which is hardly an endorsement for the strength of the US consumer. Tencent Music Entertainment plunged 6% after reporting results that showed paying users for social entertainment missing estimates. Here are some other notable premarket movers:

Dell Technologies shares climb 2.4% after being raised to equal-weight from underweight at Barclays. The bank noted that there’s less downside to the stock as much of the AI hype “has now been washed out of the share price.”

Baxter rises less than 1% after funds managed by global investment firm Carlyle agreed to buy the company’s kidney care segment for $3.8 billion.

Huya gains 7% as the board declared a special cash dividend.

On Holding slips 5% after the sneaker maker maintained its annual adjusted Ebitda forecast, despite the metric topping the consensus estimate for the second quarter.

Pacira BioSciences falls 3% after Truist downgraded the stock to sell from buy, saying a generic Exparel entry is imminent following a court ruling that canceled the drug’s patent.

Paysafe gains 10% after boosting its revenue forecast for the full year.

Rumble rises 4% after the video-network platform reported second-quarter results, with revenue topping estimates.

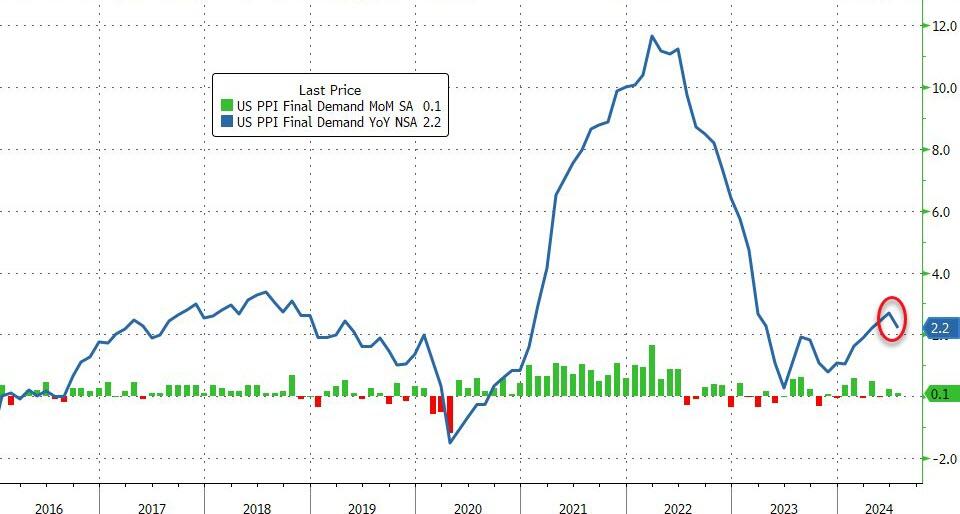

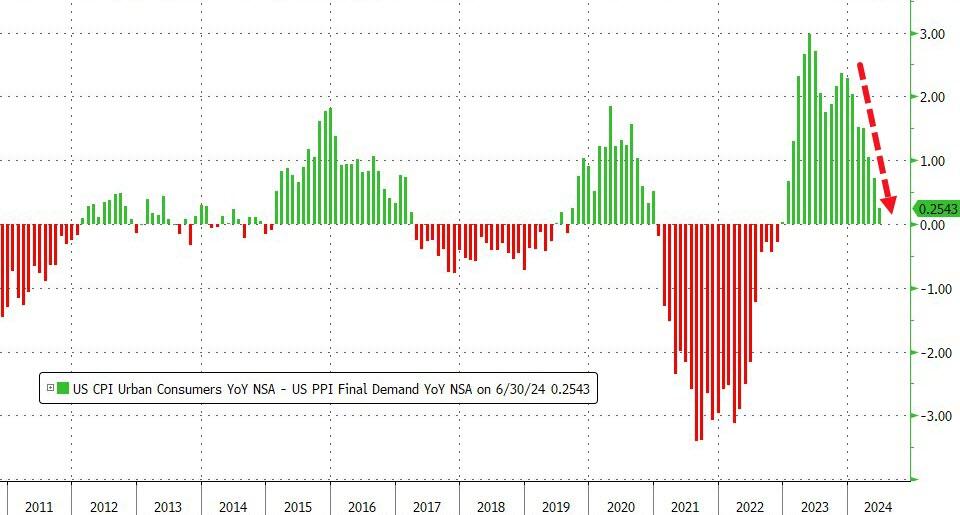

After last week’s turmoil, markets are focusing on Wednesday’s US CPI report, which may help determine whether the Fed has room to secure a soft landing for the economy. The recent rally in crude oil prices also puts the spotlight on producer-price numbers later Tuesday, as an indicator of pipeline inflationary risks. But first, there is the PPI report on deck at 830am today: economists expect core PPI to rose 0.2% last month from June, when it gained 0.4%, while the headline print is also expected to gain 0.2%.

“The US producer price index for July will give an early indication of price pressures in the month ahead of the consumer price index,” Kristina Clifton, a senior currency strategist at Commonwealth Bank of Australia, wrote in a note. “Any hints from the PPI of soft inflationary pressures in July can cause financial markets to double down on large interest rate cuts this year from the FOMC” and weigh on USD, she said.

Traders are also monitoring events in the Middle East after the US said an Iranian attack on Israel could be imminent. The implications were underscored by Fitch Ratings’ move to downgrade Israel’s sovereign debt by one notch, to A from A+, while keeping a negative outlook and citing “continued war” and geopolitical risks.

“One could argue that equity is still in recovery mode after last week’s shakeout, and holding out from really putting money to work until we get the key US data this week,” said Chris Weston, head of research at Pepperstone Group Ltd. “Pricing US growth is still the main game in town.”

The Stoxx Europe 600 erased an early advance after the ZEW gauge of German investor expectations tumbled more than economists expected (from 41.8 to 19.2, exp. 32.0). Here are the most notable European movers:

Gaztransport & Technigaz again has a clean sweep of positive analyst ratings after Berenberg moves back to a buy after five months with a hold rating, saying the pullback in the stock looks overdone. The shares gain as much as 5.4%.

Swissquote gains as much as 6.8%, hitting the highest in more than a month, after releasing first-half earnings which ZKB sees as positive even though guidance for the full year continues to be slightly below estimates.

Galderma shares rise as much as 3%, making them the biggest gainer in the Stoxx 600 Health Care Index, after the US Food and Drug Administration approved the Swiss dermatology company’s Nemluvio for the treatment of adults with prurigo nodularis, a skin disease.

PolyPeptide rises as much as 15%, extending its winning streak to a fifth day, after the Swiss biotech firm slightly lifts 2024 guidance and outlines target to double 2023’s reported revenue level by 2028.

Bilfinger shares climb as high as 6.6%, the most in six months, after the industrial services company reported faster growth in sales and earnings than expected during the second quarter, according to analysts at Oddo BHF as they nudged up their price target on the stock.

Valneva shares trade 4.3% higher after the French vaccine developer forecast “substantially lower cash burn” in the second half. The stock pared a gain of as much as 11%.

Henkel shares gain 0.3% after results from the German home products maker contained few surprises after its pre-release in July. RBC praised the firm’s 1H gross margin growth.

Tecan shares slump as much as 18%, the most since September 2004, after the Swiss laboratory-equipment maker reported weaker-than-expected results for the first half and cut its outlook for 2024.

Grifols shares dropped as much as 5.7%, worst performing stock on Spain’s IBEX 35, on a report that Brookfield, which is considering a joint takeover offer, found accounting irregularities in its due diligence.

Brenntag shares fall as much as 2% after the German chemicals distributor’s second quarter results were what Morgan Stanley called mixed, highlighting lowered guidance and softer messaging from the company.

Dowlais shares plunge as much as 17% to a record low, before paring the drop to trade 3% lower, after the automotive engineering company signaled its full year results will be below expectations, according to analysts.

Genuit Group falls as much as 5.3%, the biggest drop since June last year, after the plastic piping company suffered from soft demand and reported lower revenue and profits in the first half. Analysts note the challenging backdrop, but were impressed Genuit has grown margins and see an eventual recovery panning out next year.

Earlier in the session, Asian stocks climbed Tuesday, with a regional benchmark reclaiming levels seen before the historic August 5 selloff, as equities in Japan extended their rebound on return from a holiday. The MSCI Asia Pacific Index climbed as much as 1.2%, headed for a third-straight day of gains. Japan’s Topix jumped nearly 3% as a weaker yen was seen providing support for exporters, while benchmarks in China and South Korea also gained. Industrials and information technology were the top-performing sectors on the regional gauge. The continuation of a rebound in Japan is helping all of Asia, said Andrew Jackson, head of Japan equity strategy at Ortus Advisors Pte in Singapore. “Japan is the only market that really matters” right now, he added.

The key Asian stock gauge plunged 6.1% last Monday to mark its worst day since 2008 as fears of a deeper US economic slowdown, an extended rout in Japanese equities and a rotation away from heavyweight tech shares weighed on the market. Many investors bullish on Japan, which commands the highest weighting in the MSCI Asia gauge, have said that the recent selloff in the nation’s stocks provides a fresh reason to buy what has been one of 2024’s hottest trades.

In China, regulators told commercial banks in the Jiangxi province not to settle their purchases of government bonds, taking some of the most extreme measures yet to cool a market rally that has alarmed Beijing. The crackdown is beginning to take a toll on corporate debt markets, as the average yield for one-year corporate yuan bonds with AA ratings — typically considered junk debt in the onshore market — saw the largest jump since December 2022.

In FX, the Bloomberg Dollar Spot Index was little changed. The British pound gained and the FTSE 100 index underperformed Europe’s benchmark after data showed UK unemployment unexpectedly fell in the second quarter, complicating the Bank of England’s shift to lower interest rates.

Treasury 10-year yields erased an earlier gain to slide to a session low of 3.89%, down 1bp on the session, while US spreads also trade near prior day closing levels. Treasuries were rangebound over Asia, early London session as investors stay sidelined ahead of PPI data due 8:30am New York and then CPI print due Wednesday. Bunds marginally outperform Treasuries and gilts into the US session while S&P futures give up early gains to trade back to near unchanged on the day. Ahead of PPI data, Fed-dated swaps are still pricing in around 100bp of rate cuts for the year with approximately 36bp of cut premium priced into the Sept. 18 meeting

In commodities, WTI trades within Monday’s range, snapping a five-day streak of gains with a 0.3% decline to near $79.8. Most base metals trade in the red. Spot gold falls roughly $12 to trade near $2,460/oz.

Today’s US calendar includes only July PPI at 8:30am. CPI print is due Wednesday, Fed speakers scheduled for the session include Bostic at 1:15pm

Market Snapshot

S&P 500 futures up 0.2 to 5,381

MXAP up 1.1% to 177.48

MXAPJ up 0.1% to 556.52

Nikkei up 3.4% to 36,232.51

Topix up 2.8% to 2,553.55

Hang Seng Index up 0.4% to 17,174.06

Shanghai Composite up 0.3% to 2,867.95

Sensex down 0.8% to 79,001.72

Australia S&P/ASX 200 up 0.2% to 7,826.84

Kospi up 0.1% to 2,621.50

STOXX Europe 600 little changed at 499.36

German 10Y yield little changed at 2.23%

Euro little changed at $1.0921

Brent Futures down 0.5% to $81.85/bbl

Gold spot down 0.5% to $2,461.45

US Dollar Index little changed at 103.21

Top Overnight News

European stocks rose, tracking gains in Asia, as investors awaited US price data for guidance on the Federal Reserve’s policy path.

Chinese authorities are going to extraordinary lengths to tighten their grip on the world’s third-largest government bond market.

UK unemployment fell unexpectedly after companies stepped up hiring, a sign of underlying strength in the economy that complicates the Bank of England’s shift toward lower interest rates.

The US believes an Iranian attack against Israel has grown even more likely and may come as soon as this week, officials said, as allied leaders sought to head off all-out war and the Pentagon deployed more forces to the region.

Within the moneyed circles of the Middle East, there’s increasing talk of a shifting power dynamic in the upper echelons of high finance. Apollo, Blackstone and other big money managers are reshaping longstanding practices to win part of the $4 trillion in Gulf sovereign wealth.

MSCI Inc. continues to cull China stocks from its indexes, setting the stage for a further drop in the nation’s share of a key emerging-market benchmark.

Oil declined after a five-day advance, with a likely escalation in the Middle East conflict offset by signs of weakening global demand growth.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks followed suit to the mixed lead from the US ahead of key data and as markets continue to brace for Iran’s retaliation. ASX 200 traded indecisively after mixed data releases and as gains in financials, real estate and the commodity-related sectors were counterbalanced by losses in tech, telecoms and defensives. Nikkei 225 surged on return from the long weekend and reclaimed the 36,000 status after returning to last week’s pre-turmoil levels. Hang Seng and Shanghai Comp. were indecisive with the former supported in energy stocks after yesterday’s oil rally, while the mainland index oscillated between gains and losses in a tight range owing to the lack of fresh macro drivers.

Top Asian news

China’s Vice Premier Liu called for efforts to minimise damage to agricultural production caused by torrential rains and flooding, as well as urged efforts to improve the agricultural sector’s capacity for disaster prevention and mitigation. China’s Vice Premier also said they need to step up financial support for the restoration of agricultural production, according to Xinhua.

China’s Hesai is to be removed from the US Defence Department blacklist, according to FT.

Japan’s parliament is to hold a special session at the Lower House committee on August 23rd to discuss the BoJ rate hike, while BoJ Governor Ueda is likely to be asked to attend the special session, according to sources cited by Reuters.

China M2 (July): 6.3% (exp. 6.1%); Total Social Financing (CNY) 770bln (exp. 1.1tln)

European bourses, Stoxx 600 (+0.1%) started the session entirely in the green but succumed to some early morning pressure, which has since pared in recent trade; as it stands, indices are generally in the green. European sectors are mixed, having initially opened with a positive bias. Travel & Leisure is found at the foot of the pile, hampered by the recent advances in oil prices. Basic Resources also lags amid the weakness in the metals complex. US Equity Futures (ES +0.3%, NQ +0.5%, RTY +0.2%) are modestly firmer as traders remain mindful of today’s US PPI figures, ahead of CPI tomorrow. Firms have reportedly started testing Huawei’s new Ascend 910C chips, according to WSJ sources; Huawei in talks to secure tens of thousands of chips; framed as a “challenge” to Nvidia (NVDA) on AI hardware.

Top European news

European Gas Prices Fall as Russia Flows Take Steam Out of Rally

Fortnox Sinks to January-Low After CEO Tommy Eklund Leaves

Meta Faces Legal Challenge From Polish Billionaire Over Fake Ads

Grifols Drops on Report Brookfield Found Accounting Issues

UK Reviews Early Data Releases Traders Say Spur Volatility

Fx

DXY is a touch firmer (within a 103.08-27 range) with the USD showing a mixed performance vs. peers (softer vs. risk currencies/firmer vs. havens). Today’s focus for the greenback will fall upon PPI metrics, albeit any reaction may tempered somewhat by the fact that CPI is due out tomorrow.

EUR is softer vs. the USD with a disappointing German ZEW release adding to the woes for the region’s outlook. EUR/USD is managing to hold above yesterday’s 1.0910 low.

GBP was given a boost by UK jobs metrics which saw an unexpected fall in the unemployment rate, albeit, the usual data reliability caveats apply. BoE pricing points to a 66% chance of an unchanged rate in September.

USD is edging gains vs. JPY with the dollar firmer vs. havens alongside gains in stocks. For now, USD/JPY is respecting yesterday’s 146.41-148.22 range.

Antipodeans are both benefitting vs. the USD with the Dollar currently losing out to cyclical fx currencies.

PBoC set USD/CNY mid-point at 7.1479 vs exp. 7.1760 (prev. 7.1458)

Fixed Income

USTs are essentially unchanged and awaiting PPI before Wednesday’s US CPI for insight into PCE at the end of the month, a figure which is scheduled for the week after the Jackson Hole symposium. Into the release, USTs are in a narrow 113-04 to 113-11+ band.

Bunds are firmer but ultimately rangebound, continuing the holiday-thinned action seen on Monday. ZEW was particularly poor, with the strongest decline of expectations reported for two years, sparking a modest uptick in Bunds to re-approach their earlier 134.65 peak. No real reaction to subsequent Schatz supply.

Gilts gapped slightly higher at the open to 99.82 from a 99.72 close on Monday, despite a hawkish reaction seen in the Pound following the release. Benchmarks did pull back off these levels ahead of the regions supply, but caught another bid following the robust auction but also in tandem with Bunds, which benefited from the dire German ZEW metrics. Gilts are now back towards their 99.88 peak.

Germany sells EUR 4.038bln vs exp. EUR 5bln 2.70% 2026 Schatz: b/c 2.1x (prev. 2.0x), average yield 2.38% (prev. 2.73%) and retention 19.24% (prev. 18.08%)

Commodities

Crude is slightly subdued intraday but holding onto a bulk of yesterday’s gains amid geopolitical uncertainty. Two major risks include the threat of a retaliation against Israel from Iran and Lebanon, whilst Ukraine’s gains inside Russia could lead to increased tensions between the West and Moscow. Brent trades towards the upper end of a USD 81.50-82/bbl parameter (vs 82.40/bbl high yesterday).

Precious metals trade lower amid the rising Dollar and as newsflow remains light thus far, with participants awaiting potential geopolitical escalations before or after US CPI tomorrow.

Base metals trade lower across the board amid the cautious risk tone coupled with the firmer Dollar.

US Department of Energy said the US seeks to buy 6mln bbls of oil to help replenish the SPR.

IEA OMR: Maintains 2024 world oil demand growth forecast unchanged at 970k BPD; cuts 2025 forecast by 30k BPD; says weak growth in China now significantly drags on global gains – Chinese oil demand contracted for the third straight month. OPEC+ cuts are tightening physical markets. For now, supply is struggling to keep pace with peak summer demand – tipping the market into a deficit. Global observed oil inventories fell by 26.2mln bbls in June after four months of builds. US summer driving season set to be strongest since the pandemic.

Workers at BHP’s Escondida copper mine in Chile will begin strike action, according to the union.

Geopolitics: Middle East

Israeli forces stormed the city of Nablus in the northern West Bank from the Al-Tur military checkpoint, according to Al Jazeera.

Source close to Hezbollah said Iran expressed concern that Israel and the US may strike its nuclear program and fears they will use the outbreak of any large-scale conflict as a pretext to neutralise Iran’s nuclear deterrence, according to a report by The Washington Post.

US and Israeli officials said their assessment was that the Iranian attack wouldn’t happen on Monday night, while President Biden’s top Middle East adviser will travel to Cairo for talks on security arrangements along the Egypt-Gaza border which is critical for a hostage deal, according to Axios’s Ravid.

US State Department said Secretary of State Blinken discussed in a call with his Turkish counterpart the importance of Hamas’s return to negotiations in the middle of this month, while Blinken stressed the importance of completing the framework agreement for an immediate and permanent ceasefire in Gaza and the release of hostages, according to Al Jazeera.

FBI was reportedly investigating suspected hacking attempts by Iran in the Biden and Trump campaigns, according to Reuters and The Washington Post.

“Israeli Army Radio: Israel told allies that it would respond to any Iranian attack by hitting targets in the heart of Iran”, according to Al Jazeera.

“Hamas will participate in the round of negotiations expected next Thursday”, according to Sky News Arabia citing CNN sources

Geopolitics: Russia

Russia’s Intelligence Service suggest Ukrainian President Zelensky is taking steps that threaten escalation far beyond Ukraine, via Ria.

US Event Calendar

06:00: July SMALL BUSINESS OPTIMISM 93.7, est. 91.5, prior 91.5

08:30: July PPI Ex Food, Energy, Trade YoY, prior 3.1%

08:30: July PPI Ex Food, Energy, Trade MoM, est. 0.2%, prior 0%

08:30: July PPI Ex Food and Energy YoY, est. 2.6%, prior 3.0%

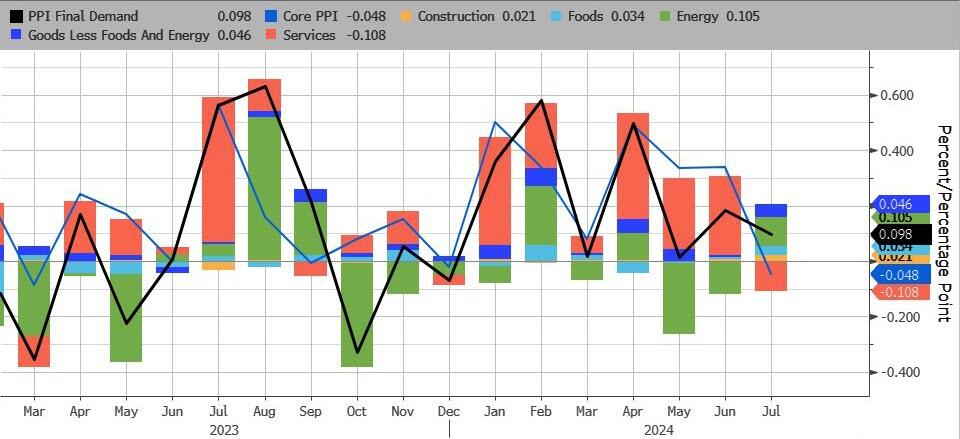

08:30: July PPI Final Demand YoY, est. 2.3%, prior 2.6%

08:30: July PPI Ex Food and Energy MoM, est. 0.2%, prior 0.4%

08:30: July PPI Final Demand MoM, est. 0.2%, prior 0.2%

2B) European report

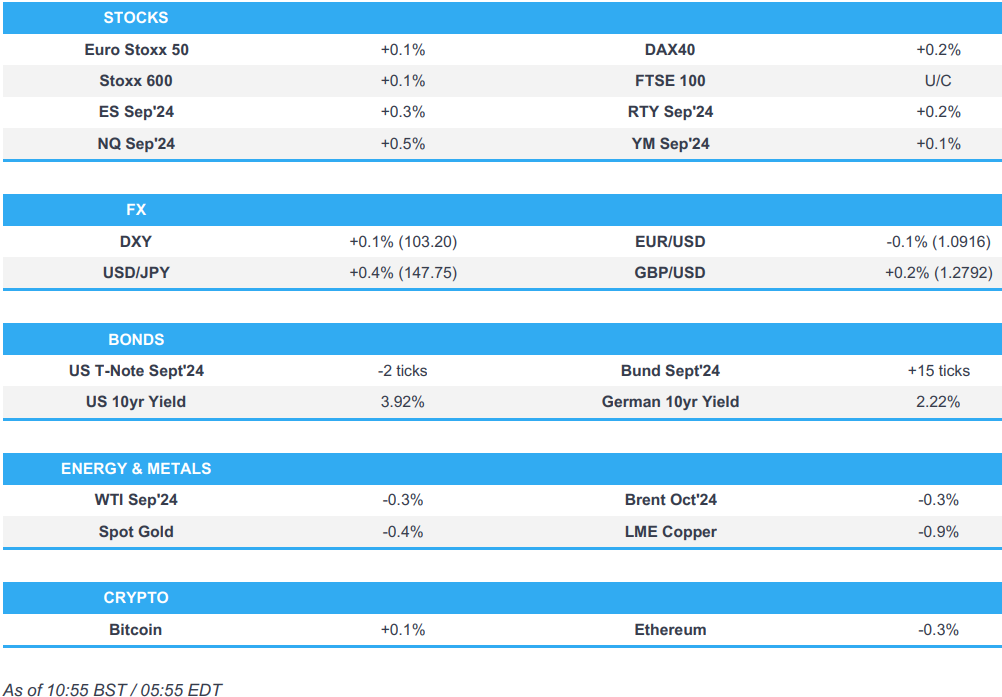

US equity futures firmer, Antipodeans lead whilst havens lag, GBP gains post-jobs data; US PPI due – US Market Open

TUESDAY, AUG 13, 2024 – 06:13 AM

A choppy session for European equities thus far, now currently modestly higher; US equity futures entirely in the green

Dollar is softer vs the Antipodeans but gains vs the typical havens, GBP benefits post-jobs data

USTs are flat awaiting today’s US PPI, Bunds benefit from dire German ZEW metrics

Crude is slightly softer, XAU is lower but within a tight range, base metals are entirely in the red

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

European bourses, Stoxx 600 (+0.1%) started the session entirely in the green but succumed to some early morning pressure, which has since pared in recent trade; as it stands, indices are generally in the green.

European sectors are mixed, having initially opened with a positive bias. Travel & Leisure is found at the foot of the pile, hampered by the recent advances in oil prices. Basic Resources also lags amid the weakness in the metals complex.

US Equity Futures (ES +0.3%, NQ +0.5%, RTY +0.2%) are modestly firmer as traders remain mindful of today’s US PPI figures, ahead of CPI tomorrow.

Firms have reportedly started testing Huawei’s new Ascend 910C chips, according to WSJ sources; Huawei in talks to secure tens of thousands of chips; framed as a “challenge” to Nvidia (NVDA) on AI hardware.

DXY is a touch firmer (within a 103.08-27 range) with the USD showing a mixed performance vs. peers (softer vs. risk currencies/firmer vs. havens). Today’s focus for the greenback will fall upon PPI metrics, albeit any reaction may tempered somewhat by the fact that CPI is due out tomorrow.

EUR is softer vs. the USD with a disappointing German ZEW release adding to the woes for the region’s outlook. EUR/USD is managing to hold above yesterday’s 1.0910 low.

GBP was given a boost by UK jobs metrics which saw an unexpected fall in the unemployment rate, albeit, the usual data reliability caveats apply. BoE pricing points to a 66% chance of an unchanged rate in September.

USD is edging gains vs. JPY with the dollar firmer vs. havens alongside gains in stocks. For now, USD/JPY is respecting yesterday’s 146.41-148.22 range.

Antipodeans are both benefitting vs. the USD with the Dollar currently losing out to cyclical fx currencies.

PBoC set USD/CNY mid-point at 7.1479 vs exp. 7.1760 (prev. 7.1458)

USTs are essentially unchanged and awaiting PPI before Wednesday’s US CPI for insight into PCE at the end of the month, a figure which is scheduled for the week after the Jackson Hole symposium. Into the release, USTs are in a narrow 113-04 to 113-11+ band.

Bunds are firmer but ultimately rangebound, continuing the holiday-thinned action seen on Monday. ZEW was particularly poor, with the strongest decline of expectations reported for two years, sparking a modest uptick in Bunds to re-approach their earlier 134.65 peak. No real reaction to subsequent Schatz supply.

Gilts gapped slightly higher at the open to 99.82 from a 99.72 close on Monday, despite a hawkish reaction seen in the Pound following the release. Benchmarks did pull back off these levels ahead of the regions supply, but caught another bid following the robust auction but also in tandem with Bunds, which benefited from the dire German ZEW metrics. Gilts are now back towards their 99.88 peak.

Crude is slightly subdued intraday but holding onto a bulk of yesterday’s gains amid geopolitical uncertainty. Two major risks include the threat of a retaliation against Israel from Iran and Lebanon, whilst Ukraine’s gains inside Russia could lead to increased tensions between the West and Moscow. Brent trades towards the upper end of a USD 81.50-82/bbl parameter (vs 82.40/bbl high yesterday).

Precious metals trade lower amid the rising Dollar and as newsflow remains light thus far, with participants awaiting potential geopolitical escalations before or after US CPI tomorrow.

Base metals trade lower across the board amid the cautious risk tone coupled with the firmer Dollar.

US Department of Energy said the US seeks to buy 6mln bbls of oil to help replenish the SPR.

IEA OMR: Maintains 2024 world oil demand growth forecast unchanged at 970k BPD; cuts 2025 forecast by 30k BPD; says weak growth in China now significantly drags on global gains – Chinese oil demand contracted for the third straight month. OPEC+ cuts are tightening physical markets. For now, supply is struggling to keep pace with peak summer demand – tipping the market into a deficit. Global observed oil inventories fell by 26.2mln bbls in June after four months of builds. US summer driving season set to be strongest since the pandemic.

Workers at BHP’s Escondida copper mine in Chile will begin strike action, according to the union.

UK ILO Unemployment Rate (Jun) 4.2% vs. Exp. 4.5% (Prev. 4.4%), Employment Change (Jun) 97k vs. Exp. 3k (Prev. 19k)

UK Average Week Earnings 3M YY (Jun) 4.5% vs. Exp. 4.6% (Prev. 5.7%); ex-Bonus 5.4% vs. Exp. 5.4% (Prev. 5.7%, Rev. 5.8%)

German ZEW Economic Sentiment (Aug) 19.2 vs. Exp. 32.0 (Prev. 41.8); Current Conditions (Aug) -77.3 vs. Exp. -75.0 (Prev. -68.9); Economic outlook for Germany is breaking down, in the current survey, we observe the strongest decline of the economic expectations over the past two years; economic expectations for the EZ, the US and China also deteriorate markedly. It is likely that economic expectations are still affected by high uncertainty. Most recently, this uncertainty expressed itself in a turmoil on international stock markets.

EU ZEW Survey Expectations (Aug) 17.9 (Prev. 43.7)

Kantar: UK Grocery Inflation 1.8% (prev. 1.6% M/M), in the four-weeks to August 4th; UK grocery price inflation warms up for the first time since March 2023.

Spanish HICP Final YY (Jul) 2.9% vs. Exp. 2.9% (Prev. 2.9%); MM -0.7% vs. Exp. -0.7% (Prev. -0.7%)

Spanish CPI YY Final NSA (Jul) 2.8% vs. Exp. 2.8% (Prev. 2.8%); MM -0.5% vs. Exp. -0.5% (Prev. -0.5%); Core YY (Jul) 2.8% (Prev. 3.0%)

GEOPOLITICS

MIDDLE EAST

Israeli forces stormed the city of Nablus in the northern West Bank from the Al-Tur military checkpoint, according to Al Jazeera.

Source close to Hezbollah said Iran expressed concern that Israel and the US may strike its nuclear program and fears they will use the outbreak of any large-scale conflict as a pretext to neutralise Iran’s nuclear deterrence, according to a report by The Washington Post.

US and Israeli officials said their assessment was that the Iranian attack wouldn’t happen on Monday night, while President Biden’s top Middle East adviser will travel to Cairo for talks on security arrangements along the Egypt-Gaza border which is critical for a hostage deal, according to Axios’s Ravid.

US State Department said Secretary of State Blinken discussed in a call with his Turkish counterpart the importance of Hamas’s return to negotiations in the middle of this month, while Blinken stressed the importance of completing the framework agreement for an immediate and permanent ceasefire in Gaza and the release of hostages, according to Al Jazeera.

FBI was reportedly investigating suspected hacking attempts by Iran in the Biden and Trump campaigns, according to Reuters and The Washington Post.

“Israeli Army Radio: Israel told allies that it would respond to any Iranian attack by hitting targets in the heart of Iran“, according to Al Jazeera.

“Hamas will participate in the round of negotiations expected next Thursday”, according to Sky News Arabia citing CNN sources

OTHER

Russia’s Intelligence Service suggest Ukrainian President Zelensky is taking steps that threaten escalation far beyond Ukraine, via Ria.

CRYPTO

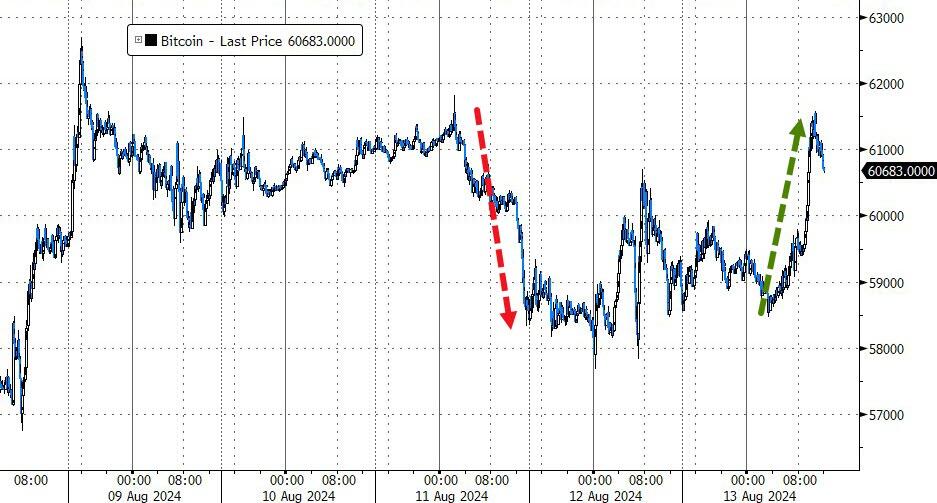

Bitcoin is trading incrementally firmer and trading just below USD 59k, whilst Ethereum slips to USD 2640.

APAC TRADE

APAC stocks followed suit to the mixed lead from the US ahead of key data and as markets continue to brace for Iran’s retaliation.

ASX 200 traded indecisively after mixed data releases and as gains in financials, real estate and the commodity-related sectors were counterbalanced by losses in tech, telecoms and defensives.

Nikkei 225 surged on return from the long weekend and reclaimed the 36,000 status after returning to last week’s pre-turmoil levels.

Hang Seng and Shanghai Comp. were indecisive with the former supported in energy stocks after yesterday’s oil rally, while the mainland index oscillated between gains and losses in a tight range owing to the lack of fresh macro drivers.

NOTABLE ASIA-PAC HEADLINES

China’s Vice Premier Liu called for efforts to minimise damage to agricultural production caused by torrential rains and flooding, as well as urged efforts to improve the agricultural sector’s capacity for disaster prevention and mitigation. China’s Vice Premier also said they need to step up financial support for the restoration of agricultural production, according to Xinhua.

China’s Hesai is to be removed from the US Defence Department blacklist, according to FT.

Japan’s parliament is to hold a special session at the Lower House committee on August 23rd to discuss the BoJ rate hike, while BoJ Governor Ueda is likely to be asked to attend the special session, according to sources cited by Reuters.

China M2 (July): 6.3% (exp. 6.1%); Total Social Financing (CNY) 770bln (exp. 1.1tln)

DATA RECAP

Japanese Corp Goods Price MM (Jul) 0.3% vs. Exp. 0.3% (Prev. 0.2%); YY (Jul) 3.0% vs. Exp. 3.0% (Prev. 2.9%)

Australian Wage Price Index QQ (Q2) 0.8% vs. Exp. 0.9% (Prev. 0.8%); YY 4.1% vs. Exp. 4.0% (Prev. 4.1%)

Australian Consumer Sentiment (Aug) 2.8% (Prev. -1.1%)

Australian NAB Business Confidence (Jul) 1.0 (Prev. 4.0); Conditions 6.0 (Prev. 4.0)

2C) ASIAN REPORT

APAC followed the mixed Wall St. lead into key data – Newsquawk Europe Market Open

TUESDAY, AUG 13, 2024 – 01:29 AM

APAC stocks followed suit to the mixed lead from the US ahead of key data.

European equity futures indicate a firmer open with the Euro Stoxx 50 future up 0.3% after the cash market finished with losses of 0.1% on Monday.

DXY is steady just above 103, havens lag vs. the USD, whilst risk currencies outperform.

White House’s Kirby said the timing of Iran’s attack on Israel could be this week and they have to be prepared for what could be significant attacks.

Looking ahead, highlights include UK Unemployment, German ZEW, US PPI, Comments from Fed’s Bostic, Supply from UK & Germany

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

US TRADE

EQUITIES

US stocks finished mixed with the Nasdaq kept afloat by tech outperformance and the small-cap Russell 2000 tumbled, while the majority of sectors took a hit and price action for the major indices was rangebound amid a lack of catalysts, lingering geopolitical risks and ahead of key data.

SPX flat at 5,344, NDX +0.16% at 18,542, DJIA -0.36% at 39,357, RUT -0.91% at 2,062.

White House official said US President Biden would sign a proposal to bar tax on tips.

APAC TRADE

EQUITIES

APAC stocks followed suit to the mixed lead from the US ahead of key data and as markets continue to brace for Iran’s retaliation.

ASX 200 traded indecisively after mixed data releases and as gains in financials, real estate and the commodity-related sectors were counterbalanced by losses in tech, telecoms and defensives.

Nikkei 225 surged on return from the long weekend and reclaimed the 36,000 status after returning to last week’s pre-turmoil levels.

Hang Seng and Shanghai Comp. were indecisive with the former supported in energy stocks after yesterday’s oil rally, while the mainland index oscillated between gains and losses in a tight range owing to the lack of fresh macro drivers.

US equity futures traded sideways as participants await the looming data releases stateside.

European equity futures indicate a firmer open with the Euro Stoxx 50 future up 0.3% after the cash market finished with losses of 0.1% on Monday.

FX

DXY traded rangebound just above the 103.00 level amid light catalysts and as participants look ahead to key data releases including US PPI on Tuesday, CPI on Wednesday and Retail Sales on Thursday.

EUR/USD remained afloat but with price action kept to within a tight range above the 1.0900 level amid a lack of drivers.

GBP/USD eked slight gains in quiet trade and as UK Unemployment and Average Earnings data releases loom.