GOLD PRICE CLOSED UP $13.70 TO $2455.10

SILVER PRICE UP $1.14 TO $28,34

Gold ACCESS CLOSED $2455.80

Silver ACCESS CLOSED: $28.33

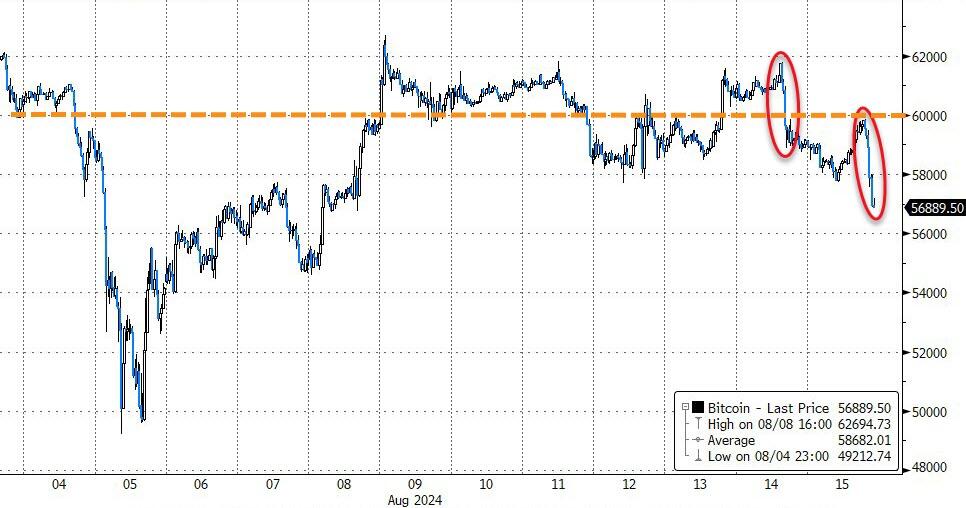

Bitcoin morning price:$58,515 DOWN 374 DOLLARS.

Bitcoin: afternoon price: $57,364 DOWN 1625 DOLLARS

Platinum price closing UP $35,60 TO $960,75

Palladium price; UP $7,50TO $941.60

END

*CANADIAN GOLD: $3372.76 UP 13.10 CDN dollars per oz( * NEW ALL TIME HIGH 3,397.10 CDN DOLLARS PER OZ//AUG 12 2024)

*BRITISH GOLD: 1,910.11 UP 1.00 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1935.68 BRITISH POUNDS/OZ) AUGUST 12/2024

*EURO GOLD: 2,233.48 UP 14.17 Euros per oz //* (ALL TIME CLOSING HIGH: 2.264.61 EUROS PER OZ//AUGUST 1 //.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: AUGUST 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,439.400000000 USD

INTENT DATE: 08/14/2024 DELIVERY DATE: 08/16/2024

FIRM ORG FIRM NAME ISSUED STOPPED

118 H MACQUARIE FUT 2

190 H BMO CAPITAL 12

323 C HSBC 8

363 H WELLS FARGO SEC 16

435 H SCOTIA CAPITAL 19

555 H BNP PARIBAS SEC 4

624 H BOFA SECURITIES 6

657 C MORGAN STANLEY 1

661 C JP MORGAN 20

661 H JP MORGAN 11

709 C BARCLAYS 2

732 C RBC CAP MARKETS 24

737 C ADVANTAGE 2

905 C ADM 5

TOTAL: 66 66

MONTH TO DATE: 18,131

JPMorgan stopped 31/66

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2024. CONTRACT: 66 NOTICES FOR 6600 OZ or 0.2053 TONNES

total notices so far: 18,131 contracts for 1,813,100 Oz (56.395 tonnes)

FOR AUGUST:

SILVER NOTICES: 30 NOTICE(S) FILED FOR 150,000

OZ/

total number of notices filed so far this month : 798 for 3,990,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $13,70 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD OUT OF THE GLD//

/ /INVENTORY RESTS AT 847.78 TONNES

INVENTORY RESTS AT 847.78 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $1.14 AT THE SLV

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.186 MILLION OZ INTO THE SLV/

// INVENTORY AT 466.929 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 466.929 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A STRONG SIZED 675 CONTRACTS TO 147,184 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS STRONG SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH MAJOR LIQUIDATION OF OI FROM OUR SPREADERS/TAS WITH OUR LOSS OF $0.40 IN SILVER PRICING AT THE COMEX ON WEDNESDAY’S TRADING. LOTS OF OUR OI LIQUIDATION ACCOMPANIED OUR STRONG LOSS OF 515 CONTRACTS ON OUR TWO EXCHANGES AS WE HAD CONSIDERABLE LIQUIDATION OF T.A.S. CONTRACTS DURING WEDNESDAY’S TRADING//. WE HAD SOME COVERING BY OUR SPECS WITH THE HUGE LOSD IN PRICE AS WE HAD A SMALL 160 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY ANOTHER HUGE 1039 CONTRACT T.A.S ISSUANCE. IN ESSENCE WE LOST 515 CONTRACTS ON OUR TWO EXCHANGES WITH THE LOSS IN PRICE.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN YESTERDAY. THE ACCUMULATED T.A.S. IS BEING USED TO MANIPULATE PRICES AT THE COMEX NOW EVERY DAY..

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 1059 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS.IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1/2 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS BUT TO NO AVAIL. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.40) AND WERE SOMEWHAT SUCCESSFUL IN KNOCKING SOME SILVER LONGS FROM THEIR PERCH AS WE HAD A STRONG SIZED LOSS OF 515 CONTRACTS ON OUR TWO EXCHANGES.

WE HAD A SMALL 160 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.005 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 150,000 OZ QUEUE JUMP //NEW STANDING RISES TO 4.220 MILLION OZ

//NEW STANDING FOR SILVER//AUGUST IS THUS 4.220 MILLION OZ

WE HAD:

/ STRONG SIZED COMEX OI LOSS //SMALL SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1059 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED 139 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST

TOTAL CONTRACTS for 11 DAYS, total 10,880 contracts: OR 54.400 MILLION OZ (989 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 54.400 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 54.400 MILLION OZ//THIS MONTH WILL PROBABLY BE STRONG FOR ISSUANCE.

RESULT: WE HAD A STRONG SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 675 CONTRACTS WITH OUR LOSS IN PRICE OF SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL EFP ISSUANCE CONTRACTS: 160 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 3.005 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 150,000 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR JULY 4.220 MILLION OZ

WE HAVE A STRONG SIZED LOSS OF 515 OI CONTRACTS ON THE TWO EXCHANGES WITH THE LOSS IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A GIGANTIC SIZED 1059 CONTRACTS,//SOME FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX TRADING WHICH ACCOUNTS FOR A PORTION OF THE COMEX OI LOSS//// SOME SHORT COVERING FROM OUR SPEC SHORTS AND SOME LIQUIDATION OF LONGS. ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER.

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (1059) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 30 NOTICE(S) FILED TODAY FOR 150,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GOOD SIZED 4,205 OI CONTRACTS TO 501,647 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 812 CONTRACTS

WE HAD A GOOD SIZED DECREASE IN COMEX OI (4,205 CONTRACTS) OCCURRED WITH OUR STRONG LOSS OF $26.20 IN PRICE/WEDNESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR AUGUST AT 65.55 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 4200 OZ QUEUE JUMP AS FINALLY GUYS ARE STANDING FOR GOLD AT THE COMEX

NEW STANDING ADVANCES TO 67.508 TONNES

/ ALL OF THIS HAPPENED WITH OUR STRONG $26.20 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A TINY SIZED LOSS OF 614 OI CONTRACTS (1.909 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 3591 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 501,647

IN ESSENCE WE HAVE A TINY SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 614 CONTRACTS WITH 4205 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 3591 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 614 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 1776 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3591 CONTRACTS) ACCOMPANYING THE GOOD SIZED LOSS IN COMEX OI OF 4205 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 614 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR AUGUST AT 65.55 TONNES FOLLOWED BY TODAY’S 4200 OZ QUEUE JUMP AS THESE BOYS JUMP THE QUEUE TO STAND AT THE COMEX./

//NEW STANDING ADVANCES TO: /AUGUST 67.508 TONNES.

/ 3) SOME T.A.S. LIQUIDATION//SPREADER CONTRACTS WITH ZERO NET LONG SPECS BEING CLIPPED,

4) GOOD SIZED COMEX OPEN INTEREST LOSS 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1766 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST. :

TOTAL EFP CONTRACTS ISSUED: 55,853 CONTRACTS OF 5,585,300 OZ OR 173.726 TONNES IN 11 TRADING DAY(S) AND THUS AVERAGING: 5077 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 11 TRADING DAY(S) IN TONNES 173.726 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 173.726 DIVIDED BY 3550 x 100% TONNES = 4.87% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 173.726 TONNES//THIS MONTH WILL NO DOUBT BE A HUGE ISSUANCE OF EFP’S SIMILAR TO LAST MONTH.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUG), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A STRONG SIZED 675 CONTRACTS OI TO 147,184 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 160 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 160 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 160 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 675 CONTRACTS AND ADD TO THE 160 E.FP. ISSUED

WE OBTAIN A STRONG SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 376 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 1.880 MILLION OZ OCCURRED WITH OUR $0.40 LOSS IN PRICE

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED UP 26.70 PTS OR 0.94% //Hang Seng CLOSED DOWN 4.22 PTS OR 0.02% // Nikkei CLOSED UP 284.21 OR 0.78%//Australia’s all ordinaries CLOSED UP 0.17%///Chinese yuan (ONSHORE) CLOSED DOWN TO 7,1583 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.1613/ Oil DOWN TO 77.49 dollars per barrel for WTI and BRENT UP AT 80.40 Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 4205 CONTRACTS TO 501,667 WITH OUR HUGE LOSS IN PRICE OF $26.20 WITH RESPECT TO WEDNESDAY’S TRADING. WE LOST A HUGE NUMBER OF SPREADER/T.A.S. CONTRACTS AS SHORTS CONTINUED TO PANIC THROUGHOUT THE SESSION AND COVERED AT MUCH LOWER PRICES. THE FED IS THE MAJOR SHORT OF AROUND 116 TONNES+ OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS IS SCHEDULED TO HAPPEN LATE SEPT 2024.

OUR LONDONERS ALSO BOUGHT NEW MASSIVE QUANTITIES OF LONGS AND THIS WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD A STRONG T.A.S. LIQUIDATION ON WEDNESDAY’S LOSS IN PRICE WITH SOME LONGS BEING CLIPPED (AS YOU WILL SEE BELOW) BUT WE DID HAVE MAJOR SHORT COVERING. THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE ACTIVE DELIVERY MONTH OF AUGUST.… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 3591 EFP CONTRACTS WERE ISSUED: : OCT/DEC 3591 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3591 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A TINY SIZED TOTAL OF 614 CONTRACTS IN THAT 3591 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A GOOD SIZED LOSS OF 4205 COMEX CONTRACTS..AND THIS TINY GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR STRONG LOSS IN PRICE OF $26.20/WEDNESDAY COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AS MENTIONED ABOVE.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT A FAIR SIZED 1766 CONTRACTS. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN LAST WEEK’S TRADING//RAIDS AS WELL AS THIS WEEK AND ESPECIALLY ON WEDNESDAY’S RAID.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: AUGUST (67.508 TONNES)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 67. TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $26.20 //// BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE DID HAVE A TINY LOSS IN OUR TWO EXCHANGES. CENTRAL BANK LONGS , EXERCISED FOR PHYSICAL. WE HAD A CONSIDERABLE T.A.S. LIQUIDATION WEDNESDAY/COMEX.

WE HAVE LOST A TOTAL OI OF 1.909 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST (65.55 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 4200 OZ QUEUE JUMP //NEW STANDING: 67.508 TONNES.

NEW STANDING FOR AUGUST: 67.508 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR HUGE LOSS IN PRICE TO THE TUNE OF $26.20

WE HAVE REMOVED 812 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET LOSS ON THE TWO EXCHANGES 674 CONTRACTS OR 67400 OZ (1.909

TONNES)

confirmed volume WEDNESDAY 198,936 contracts//poor

//speculators have left the gold arena

END

AUGUST 15 AUGUST GOLD CONTRACT

/ /// THE AUG 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 77,323.135OZ Brinks Delaware brinks 2250 kilobars Delaware 155 kilobars . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | NIL oz |

| No of oz served (contracts) today | 66 notice(s) 6600 OZ 0.2053 TONNES |

| No of oz to be served (notices) | 3573 contracts 357,300 OZ 11.11 TONNES |

| Total monthly oz gold served (contracts) so far this month | 18,131 notices 1,813,100 oz 56.395 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: nil oz

we have 0 customer deposits

total deposits NIL oz

withdrawals: 2

i) Out of Brinks 72,339.750 oz (2250 kilobars)

ii) Out of Delaware: 4983,385 oz (155 kilobars)

TOTAL WITHDRAWALS 77,323,135 oz this obligation transferred to London

adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST

For the front month of AUGUST we have an oi of 3639 contracts having LOST 207 contracts.

We had 249 contracts served on WEDNESDAY so we gained an additional 42 contracts or 4200 oz will stand for gold at the comex

SEPT. LOST 93 CONTRACTS TO STAND AT 5499 CONTRACTS.

OCTOBER LOST 682 CONTRACTS UP TO 51,818 CONTRACTS

We had 66 contracts filed for today representing 6600 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices were issued from their client or customer account. The total of all issuance by all participants equate to 66 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 31 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for AUGUST /2024. contract month, we take the total number of notices filed so far for the month (18,131) x 100 oz ) to which we add the difference between the open interest for the front month of August 3639( CONTRACTS) minus the number of notices served upon today (66 x 100 oz per contract( equals 2,170,400 OZ OR 67.508 TONNES. Somebody was in great need of physical gold on this side of the pond today

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (18,131 x 100 oz +we add the difference for front month of AUGUST (3639 X// , OI} minus the number of notices served upon today (66) x 100 oz which equals 2,170.400 oz (67.508 TONNES)

TOTAL COMEX GOLD STANDING FOR AUGUST: 67.508 TONNES WHICH IS HUGE FOR THIS VERY ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,742,209.881 oz 54.19tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,525,546.254OZ

TOTAL REGISTERED GOLD 7,877,094.495( 245.01 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,648,451.759 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,134,885 oz (REG GOLD- PLEDGED GOLD)= 190,80tonnes //

END

SILVER/COMEX

AUGUST 15/2024

INITIAL

//2024// THE AUG 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1066,946.820 OZ CNT Brinks Delaware . |

| Deposits to the Dealer Inventory | |

| Deposits to the Customer Inventory | 1,907,293.908oz i) Brinks ii)Delaware iii) Manfra |

| No of oz served today (contracts) | 30 CONTRACT(S) (150,000 OZ) |

| No of oz to be served (notices) | 46 contracts (0.230 million oz) |

| Total monthly oz silver served (contracts) | 798 Contracts (3.990 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit/

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 3 customer deposits:

i)Into Brinks 1,327,312.335 oz

ii) Into Delaware: 1038.630 oz

iii) Into Manfra: 578,942.943 oz

total customer deposit 1,907,293.908 oz

JPMorgan has a total silver weight: 134.771million oz/305,147 million or 44.36%

adjustment:

withdrawals: 3

i) Out of CNT 6993,14oz

ii) Out of Delaware: 599,085.860oz

iii) Out of Brinks 460,867,820 oz

total customer withdrawals: 1066,946.820 oz

TOTAL REGISTERED SILVER: 69.904 MILLION OZ//.TOTAL REG + ELIGIBLE. 305.147 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR AUGUST:

silver open interest data:

FRONT MONTH OF AUGUST/2024 OI: 76 CONTRACTS HAVING GAINED 30 CONTRACT(S).

WE HAD 0 NOTICES SERVED ON WEDNESDAY, SO WE GAINED 30 CONTRACTs OR AN ADDITIONAL 150,000 OZ WILL STAND FOR SILVER AT THE COMEX.

SEPT SAW A LOSS OF 2289 CONTRACTS TO 64,211. SEPT NOW BECOMES THE NEW FRONT MONTH

OCTOBER SAW ANOTHER GAIN OF OPEN INTEREST CONTRACTS OF 11 CONTRACTS AND THUS WE HAVE 319 OPEN INTEREST CONTRACTS FOR OCTOBER.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 30 for 150,000 oz

CONFIRMED volume; ON WEDNESDAY 75,684

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 798 x 5,000 oz = 3.990 MILLION oz

to which we add the difference between the open interest for the front month of AUGUST( 76) and the number of notices served upon today 30 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST/2024 contract month: 798 notices served so far) x 5000 oz + OI for the front month of AUGUST (76)x number of notices served upon today minus (30)x 5000 oz of silver standing for the AUGUST contract month equates to 4.220 MILLION OZ.

New total standing: 4.220 million oz.

There are 69.904 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD

AUGUST 15 WITH GOLD UP $13,70 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD OUT OF THE GLD//////INVENTORY RESTS AT 847.78 TONNES

AUGUST 14 WITH GOLD DOWN $26.20 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.03 TONNES OF GOLD OUT OF THE GLD//////INVENTORY RESTS AT 845.76 TONNES

AUGUST 13 WITH GOLD UP $3.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//////INVENTORY RESTS AT 849.79 TONNES

AUGUST 12 WITH GOLD UP $30.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ////INVENTORY RESTS AT 846.91 TONNES

AUGUST 9 WITH GOLD UP $10.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 846.91 TONNES

AUGUST 8 WITH GOLD UP $31.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.02 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 844.04 TONNES

AUGUST 7 WITH GOLD UP $1.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.16 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 848.06 TONNES

AUGUST 6 WITH GOLD DOWN $13.10 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD” A WITHDRAWAL OF .57 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 844.90 TONNES

AUGUST 2 WITH GOLD DOWN $9.95 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.58 TONNES OF GOLD OUT OF THE GLD//INVENTORY RESTS AT 845.47 TONNES

AUGUST 1 WITH GOLD UP $9.15 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 846.05 TONNES

JULY 30 WITH GOLD UP $26.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// A /////INVENTORY RESTS AT 843.17 TONNES

JULY 29 WITH GOLD UP $27.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD// A WITHDRAWAL OF 1.98 TONNES OF GOLD OUT OF THE GLD/////INVENTORY RESTS AT 843.17 TONNES

JULY 26 WITH GOLD UP $27.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD// A DEPOSIT OF 3.45 TONNES OF GOLD INTO THE GLD/////INVENTORY RESTS AT 845.19 TONNES

JULY 25 WITH GOLD DOWN $60.45 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 841.74 TONNES

JULY 24 WITH GOLD UP $12.75 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1,73 TOONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 841.74 TONNES

JULY 23 WITH GOLD UP $12.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 22 WITH GOLD DOWN $4.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 19 WITH GOLD DOWN $56.10 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;:A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 18 WITH GOLD DOWN $2.20 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;: ///INVENTORY RESTS AT 842.02 TONNES

JULY 17 WITH GOLD DOWN $6.60 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A MASSIVE DEPOSIT OF 5.49 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 842.02 TONNES

JULY 16 WITH GOLD UP $38.60 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 836.53 TONNES

JULY 15 WITH GOLD UP $8.15 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;: /INVENTORY RESTS AT 835.09 TONNES

JULY 12 WITH GOLD DOWN $0.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 835.09 TONNES

JULY 11 WITH GOLD UP $43.05 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;:INVENTORY RESTS AT 833.37 TONNES

JULY 10 WITH GOLD UP $12.00 ON THE DAY; HUUGE CHANGES IN GOLD INVENTORY AT THE GLD; A WITHDRAWAL OF 1.44 TONNES OF GOLD VAPOUR FROM THE GLD//.//:INVENTORY RESTS AT 833.37 TONNES

JULY 9 WITH GOLD UP $5.00 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD.//:INVENTORY RESTS AT 834.81 TONNES

JULY 8 WITH GOLD DOWN $26.60 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD.//:INVENTORY RESTS AT 834.81 TONNES

JULY 5 WITH GOLD UP $29.90 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD..A DEPOSIT OF 1.10 TONNES OF GOLD VAPOUR INTO THE GLD//:INVENTORY RESTS AT 833.37 TONNES

JULY 3 WITH GOLD UP $35.25 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD..A MASSIVE DEPOSIT OF 5.76 TONNES OF GOLD VAPOUR INTO THE GLD//:INVENTORY RESTS AT 833.37 TONNES

JULY 2 WITH GOLD DOWN $4.45 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD../:INVENTORY RESTS AT 827.61 TONNES

JULY 1 WITH GOLD DOWN $.30 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD/:INVENTORY RESTS AT 829.05 TONNES

GLD INVENTORY: 847.78 TONNES, TONIGHTS TOTAL

SILVER

AUGUST 15//WITH SILVER $1.14//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.186 MILLION ON INTO THE SLV.///./// /INVENTORY AT 466.929 MILLION OZ

AUGUST 14//WITH SILVER DOWN $0.40//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 13//WITH SILVER DOWN $0.19//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 12//WITH SILVER UP $.37//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 9//WITH SILVER DOWN $.03//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 8//WITH SILVER UP $.70//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 3.241 MILLION OZ INTO THE SLV////./// /INVENTORY AT 462.502 MILLION OZ

AUGUST 7//WITH SILVER DOWN $0.27//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.552 MILLION OZ INTO THE SLV////./// /INVENTORY AT 462.502 MILLION OZ

AUGUST 6//WITH SILVER UP $0.05//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 458.851 MILLION OZ

AUGUST 2//WITH SILVER DOWN $0.01//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 1.243 MILLION OZ OF SILVER OUT OF THE SLV ///./// /INVENTORY AT 460.961 MILLION OZ

AUGUST 1//WITH SILVER DOWN $0.46//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.608 MILLION OZ OF SILVER VAPOUR INTO THE SLV///./// /INVENTORY AT 462.204 MILLION OZ

JULY 31//WITH SILVER UP $0.45//NO CHANGES IN SILVER INVENTORY: /./// /INVENTORY REMAINS AT 460.596 MILLION OZ

JULY 30//WITH SILVER UP $0.61//SMALL CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 0.456 MILLION OZ OF SILVER VAPOUR INTO THE SLV/./// /INVENTORY RISES AT 460.596 MILLION OZ

JULY 29//WITH SILVER DOWN $0.07//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.382 MILLION OZ OF SILVER VAPOUR INTO THE SLV/./// /INVENTORY RISES AT 461.052 MILLION OZ

JULY 26//WITH SILVER DOWN $0.07//NO CHANGES IN SILVER INVENTORY./// /INVENTORY REMAINS AT 456.670 MILLION OZ

JULY 25 WITH SILVER DOWN $1.37//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 3.124 MILLION OZ OF SILVER OUT OF THE SLV./// /INVENTORY FALLS TO 456.670 MILLION OZ

JULY 24 WITH SILVER UP 3 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 15.880 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 23 WITH SILVER UP 3 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 15.880 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 22 WITH SILVER UP 2 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 3.920 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 19 WITH SILVER DOWN 94 CENTS//NO CHANGES IN SILVER INVENTORY/// /INVENTORY REMAINS AT 435.854 MILLION OZ

JULY 18 WITH SILVER DOWN 13 CENTS//HUGE CHANGES IN SILVER INVENTORY” A DEPOSIT OF 2.374 MILLION OZ INTO THE SLV/// /INVENTORY RISES TO 435.854 MILLION OZ

JULY 17. WITH SILVER DOWN 75 CENTS//NO CHANGES IN SILVER INVENTORY// /INVENTORY REMAINS AT 433.480 MILLION OZ.

JULY 16. WITH SILVER UP 30 CENTS//NO CHANGES IN SILVER INVENTORY// /INVENTORY REMAINS AT 433.480 MILLION OZ.

JULY 15. WITH SILVER DOWN 24 CENTS//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 2.145 MILLION OZ FROM THE SLV.// /INVENTORY LOWERS T0 AT 433.480 MILLION OZ.

JULY 12. WITH SILVER DOWN $.65 CENTS//NO CHANGES IN SILVER INVENTORY /INVENTORY REMAINS CONSTANT AT 435.625 MILLION OZ.

JULY 11. WITH SILVER UP $.72 CENTS//HUGE CHANGES IN SILVER INVENTORY A WITHDRAWAL OF 0.731 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 435.625 MILLION OZ.

JULY 10. WITH SILVER DOWN $.04 CENTS//HUGE CHANGES IN SILVER INVENTORY A MAMMOTH WITHDRAWAL OF 3.744 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 436.356 MILLION OZ.

JULY 9. WITH SILVER UP 13 CENTS//HUGE CHANGES IN SILVER INVENTORY A MAMMOTH WITHDRAWAL OF 3.744 MILLION OZ OF SILVER VAPOUR OUT OF THE SLV.: /INVENTORY FALLS T0 436.356 MILLION OZ.

JULY 8. WITH SILVER DOWN $0.73//SMALL CHANGES IN SILVER INVENTORY A MAMMOTH DEPOSIT OF 3,292,000 OZ OF SILVER VAPOUR INTO THE SLV.: /INVENTORY RISES T0 440.100 MILLION OZ.

JULY 4. WITH SILVER UP $0.85//SMALL CHANGES IN SILVER INVENTORY A MAMMOTH DEPOSIT OF 3,292,000 OZ OF SILVER VAPOUR INTO THE SLV.: /INVENTORY RISES T0 440.100 MILLION OZ.

JULY 3. WITH SILVER UP $1.08//SMALL CHANGES IN SILVER INVENTORY A SMALL WITHDRAWAL OF 639,000 OZ: /INVENTORY LOWERS T0 436,808 MILLION OZ.

JULY 2. WITH SILVER UP $0.19//NO CHANGES IN SILVER INVENTORY: /INVENTORY REMAINS AT 437.447 MILLION OZ./

JULY 1. WITH SILVER UP $0.05//NO CHANGES IN SILVER INVENTORY: A DEPOSIT OF 182,000 OZ OF SILVER INTO THE SLV./.// /INVENTORY RISES AT 437.447 MILLION OZ./

CLOSING INVENTORY 466.929 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1.PETER SCHIFF SCHIFF GOLD/MIKE MAHARRAY

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY//BILL HOLTER:

3.CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES

Chris Powell: is the uSA ready for a gold revaluation?

The U.S. is ready with a gold revaluation mechanism too

Submitted by admin on Thu, 2024-08-15 01:15 Section: Daily Dispatches

1:36a ET Thursday, August 15, 2024

Dear Friend of GATA and Gold:

In an interview this week with Mark Moss of Market Disruptors that is posted at YouTube —

— Luke Gromen of the Forest for the Trees financial letter notes something about the U.S. Treasury Department and Federal Reserve that gold researcher Jan Nieuwenhuijs of Gainesville Coins long has been noting about other governments and central banks.

It’s that the U.S. Treasury Department, like the governments Nieuwenhuijs has been writing about, maintains what is essentially its own gold revaluation account at the Fed, in which U.S. gold reserves could be revalued to create any amount of U.S. dollars for the Treasury to draw upon.

The U.S. gold revaluation account is called the Gold Certificate Account and is described on Page 12 of the April edition of the Fed’s Financial Accounting Manual for Federal Reserve Banks:

The manual says:

“The Secretary of the Treasury is authorized to issue gold certificates to the Reserve Banks to monetize gold held by the U.S. Department of the Treasury. At any time Treasury may reacquire the gold certificates by demonetizing the gold.

“Treasury maintains an account with the [Federal Reserve’s] Board of Governors entitled ‘Gold Certificate Fund / Board of Governors of the FR System.’ When the Treasury monetizes gold, it credits this account in return for deposit credit at the Federal Reserve Bank of New York (FRBNY). When demonetizing gold, Treasury decreases the account and authorizes the FRBNY to charge its deposit account.

“The offsetting entry in each case on FRBNY’s books is made to the Gold Certificate Account and the U.S. Treasury General Account. The FRBNY accounting staff sends an advice of these entries to the [Federal Reserve] Board [of Governors].

“Also, whenever the official price of gold is changed, Treasury adjusts the account and, simultaneously, the deposit account.”

Revaluation of government gold reserves to create money isn’t a new mechanism. It’s a mechanism whose last exercise in the United States is so old that few people are aware of it — President Franklin D. Roosevelt’s revaluation of gold from $20.67 per ounce to $35 per ounce in 1934, an event whose facilitating money creation was well described a few months ago by Money Metals News Service writer Mike Maharrey:

https://www.moneymetals.com/news/2024/05/31/did-fdr-really-confiscate-everybodys-gold-003226

Revaluation of the U.S. gold reserve to facilitate money creation was mentioned, rather remarkably, by a former member of the Fed’s Board of Governors, Lyle Gramley, during an interview with Business News Network in Canada in December 2008:

https://www.gata.org/node/6989

It was also examined at length by the U.S. economists Paul Brodsky and Lee Quaintance in 2012:

https://www.gata.org/node/11373

In his discussion this week with Market Disruptors’ Moss, Gromen remarks that a substantial official U.S. revaluation of gold — say, to $20,000 per ounce or more — might enable the creation of trillions of dollars for the U.S. government to use to repay enough of its debt to make the country’s ratio of debt to gross national product appear more plausible and sustainable.

Moss responds that such a revaluation likely would generate huge inflation, but Gromen says that only huge inflation can diminish the debt problem and that other countries have survived and adjusted to such periods.

Of course in the end gold revaluation, like the recent proposal for the Treasury to mint platinum coins with trillion-dollar denominations and turn them into cash at the Fed, is just legerdemain, accounting trickery to rationalize creation of money far out of proportion to national economic production. But that governments and central banks are so prepared for gold revaluation may be a reminder that the metal remains not just money but also the secret knowledge of the financial universe — and that the nuttiest gold bugs of all are central bankers and the elected officials whose bidding they do, creating a world financial system so crazy that only gold may be able to save it.

CHRIS POWELL, Secretary/Treasurer

Gold Anti-Trust Action Committee Inc.

CPowell@GATA.org

end

4. GOLD PODCASTS//LIVE FROM THE VAULT/no 185 with/Andrew Maguire

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/RARE EARTH

6 CRYPTOCURRENCY NEWS

END

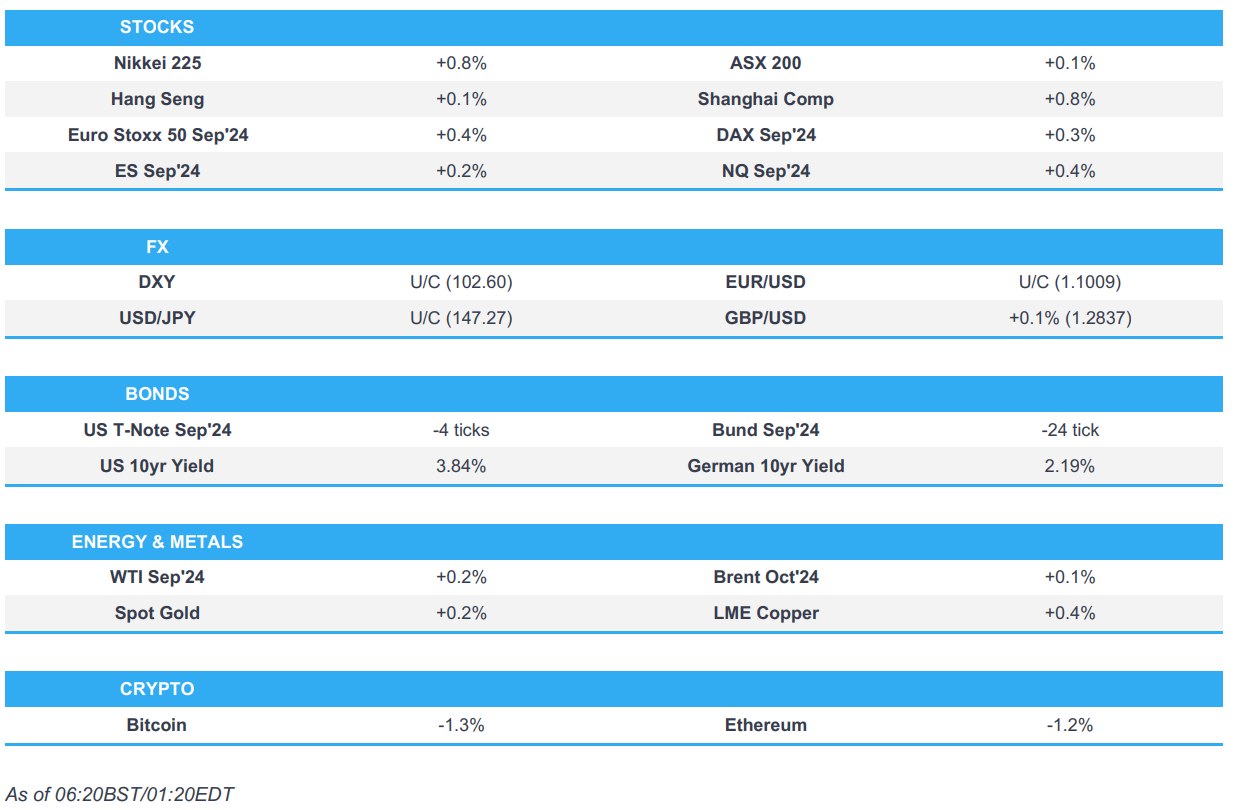

ASIA TRADING/THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED UP 26.70 PTS OR 0.94% //Hang Seng CLOSED DOWN 4.22 PTS OR 0.02% // Nikkei CLOSED UP 284.21 OR 0.78%//Australia’s all ordinaries CLOSED UP 0.17%///Chinese yuan (ONSHORE) CLOSED DOWN TO 7,1583 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.1613/ Oil DOWN TO 77.49 dollars per barrel for WTI and BRENT UP AT 80.40 Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1583

OFFSHORE YUAN: DOWN TO 7.1613

SHANGHAI CLOSED UP 26.78 PTS OR 0.94 %

HANG SENG CLOSED DOWN 4.22 PTS OR 0.02%

2. Nikkei closed UP 284.21 PTS OR .78%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 102.41 EURO RISES TO 1.1012 UP 1 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +0.845 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 147.28…… JAPANESE YEN NOW RISING AS WE HAVE NOW REACHED THE REIGNITING OF THE YEN CARRY TRADE AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.1910/Italian 10 Yr bond yield DOWN to 3.571 SPAIN 10 YR BOND YIELD DOWN TO 3.023%

3i Greek 10 year bond yield DOWN TO 3.256

3j Gold at $2462.25//Silver at: 28.18 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 68/ 100 roubles/dollar; ROUBLE AT 89.25

3m oil into the 77 dollar handle for WTI and 80 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 147.28/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.845 % STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8663 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9539 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.846 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.128 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.951 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 33.64…

10 YR UK BOND YIELD: 3.889 UP 2 PTS

10 YR CANADA BOND YIELD: 3.042 UP 2 BASIS PTS

2a New York OPENING REPORT

Futures Rise Ahead Of Data Deluge Including Key Retail Sales Report

by Tyler Durden

Thursday, Aug 15, 2024 – 07:46 AM

US equity futures are following European and most Asian stocks higher, with traders’ attention turning to today’s retail sales report (full preview here) which may support the case for the Federal Reserve to cut rates at its September meeting. As of 7:45am, S&P futures are up 0.2%, higher for the fifth day in a row, as the burst of 13-F releases overnight helps to boost some individual names; Nasdaq futures also gain 0.1% led by tech with Mag7 and Semis leading pre-mkt though NVDA is lower to start the day. Bond yields are flat to up 1bps, and USD is flat. Commodities are bid across all 3 complexes though base metals are lagging and Silver over Gold. PPI/CPI data shaped the inflation story and now Retail Sales/Jobless Claims will do the same for the Growth story, while Walmart boosting its profit outlook will help ease recessionary fears. That said, the Fed may not reveal its hand until the Sep 6 NFP print.

Walmart jumped 7.8% in premarket trading after raising its sales and profit guidance for the full year, as the chain expects to draw shoppers searching for deals. Cisco Systems rose after the networking equipment maker’s results beat expectations. Nike rallied after Pershing Square Capital Management LP disclosed a new stake in the sportswear company. Bavarian Nordic A/S, one of few companies with an approved mpox vaccine, soared 17% in Copenhagen after the World Health Organization declared a fast-spreading outbreak of the disease a global public health emergency. Here are some other notable premarket movers:

- Brinker International shares rise 1.0% after KeyBanc Capital Markets upgraded the Chili’s owner to overweight from sector weight, seeing a compelling entry point for the stock following its post-results decline.

- Cisco Systems shares rose 6.1% after the maker of computer networking equipment reported fourth-quarter results that beat expectations and gave a positive revenue forecast. It also said it plans to cut more jobs. Analysts note strong results in a tough backdrop.

- Dell Technologies rose as much 2.3% as JPMorgan added the computer maker’s stock to its analyst focus list, citing an “attractive entry point.”

- Lumentum shares jump 16% after the optical and photonic products maker reported fourth-quarter earnings per share that came ahead of consensus estimates. Morgan Stanley highlighted the announcement of an 800G transceiver customer win as “encouraging.

- Nike shares rose 4.2% after Bill Ackman’s Pershing Square Capital Management LP disclosed it had a new position of about 3 million shares worth $229 million at the end of the second-quarter.

- Robinhood Markets rises 2.5% after Deutsche Bank upgrades to buy from hold in a mid-third quarter outlook note on North American brokers, asset managers and exchanges.

- Spire Global falls 19% after the provider of space-based data analytics notified the SEC that its 10-Q filing for the quarter ended June 30 will be late.

- Titan Machinery shares slump 28% after the owner of agricultural equipment stores cut its fiscal 2025 profit guidance, saying retail demand has softened further over the last several months.

- Ulta Beauty shares climb 14% after Warren Buffett’s Berkshire Hathaway disclosed that it took a new stake in the cosmetics retailer, according to a 13F filing for the quarter ended June 30. Meanwhile, Sirius XM rose 14% as Buffett showed an increased stake in the company.

S&P 500 contracts were steady after the benchmark extended its winning streak to a fifth day Wednesday, buoyed by a benign consumer price index print. Europe’s Stoxx 600 Index rose 0.2%.

“The latest US inflation data supports our view of a gradual cooling of the US economy,” said Mark Haefele, chief investment officer at UBS Global Wealth Management. “This underlines our view that the Fed will start easing policy at its September meeting. That provides a positive backdrop for risk assets. It would also erode returns on cash, underlining our view that investors should brace for lower rates.”

In the UK, the economy maintained its muted rebound from last year’s recession, with GDP rising 0.6% in the second quarter after an 0.7% gain in the first three months. The figures are unlikely to shift the calculus of policymakers at the Bank of England, which had expected an even stronger expansion.

Norway’s central bank kept rates unchanged (as expected) for an eighth month and shed little light on when easing might begin, given risks to the inflation outlook from a weaker krone. The currency gained after the announcement.

Meanwhile, it will be another busy session for for traders tracking updates on the world’s biggest economy. Thursday brings readings on initial jobless claims and retail sales. Figures out Wednesday showed that US year-on-year core consumer prices in July rose at the slowest pace since 2021. Traders are fully pricing in one 25 basis-point cut by the Fed next month and 100 basis points of reductions through year-end.

European stocks rise for a third day, led by health care, insurance and technology names, while travel and leisure is falling the most. Here are the most notable movers:

- Bavarian Nordic shares surge as much as 17% in Copenhagen to the highest since November 2022 after the World Health Organization declared a fast-spreading mpox outbreak in Africa a global health emergency. Bavarian Nordic is one of the few companies with an approved mpox vaccine.

- Adyen shares rise as much as 8.5% after the payments firm reported estimate-beating revenue, defying a slowdown in consumer spending. Take rate — a closely watched metric that tracks the proportion Adyen charges merchants for processing each transaction — stabilized after a sharp drop in 1Q.

- Admiral shares rise as much as 12% to hit their highest level since February 2022 after the insurer reported pretax profit ahead of expectations in the first half. The company cited strong performance from its UK Motor arm.

- Zealand Pharma shares rise as much as 4.5%, best performer in the Stoxx 600 Health Care index on Thursday morning, after the Danish drugmaker released financial results. The increased investment in obesity programs is “welcome,” according to Jefferies analysts.

- Holmen shares rise as much as 7.1%, the most since April 2023, after the Swedish paper and forestry group beat estimates in the second quarter and announced buyback plans. Jefferies analysts say the results are positive in the long-term, as the board and paper division offsets weaknesses in renewable energy.

- Yubico shares surge as much as 24% to a record high, with DNB Markets describing the Swedish cybersecurity firm’s results as a “mic drop” quarter.

- HelloFresh shares rise as much as 8.7% to the highest intraday since April. Bankhaus Metzler analysts upgrade the meal-kit maker to hold from sell, noting that strength in the first half makes the company’s full-year guidance more attainable. The stock is still down 52% YTD.

- Orsted shares plunge as much as 9.3% to hit their lowest level since November after the offshore wind farm specialist reported a surprise net loss in the latest quarter, having slipped into the red after booking hefty impairments against multiple projects.

- OSB Group shares plummet as much as 20%, the worst performance in the FTSE All-Share today, to hit their lowest level since April after the bank lowered its net interest margin outlook for the year. Analysts flagged the loan book is growing more slowly than hoped amid increased competition in lending.

- Autostore slumps as much as 17%, the most on record, after order intake came in significantly below consensus in a second-quarter report which Morgan Stanley describes as “notably weak.” The Norwegian warehouse automation group says customers are acting cautiously due to a challenging economic backdrop and sustained high interest rates.

Earlier, in Asian trading Japan’s Topix index and China’s CSI 300 benchmark rose in a broadly positive reaction to data points in the two countries. Japan’s economy grew faster in the second quarter than analysts forecast. China, meanwhile, saw signs of stabilization that included slowing declines in home prices and better-than-expected retail sales.

In FX, the Bloomberg Dollar Spot Index is unchanged; the pound rises 0.1% against the dollar. The Norwegian krone has risen to the top of the G-10 FX leader board, adding 0.4% after a hawkish hold from the Norges Bank.

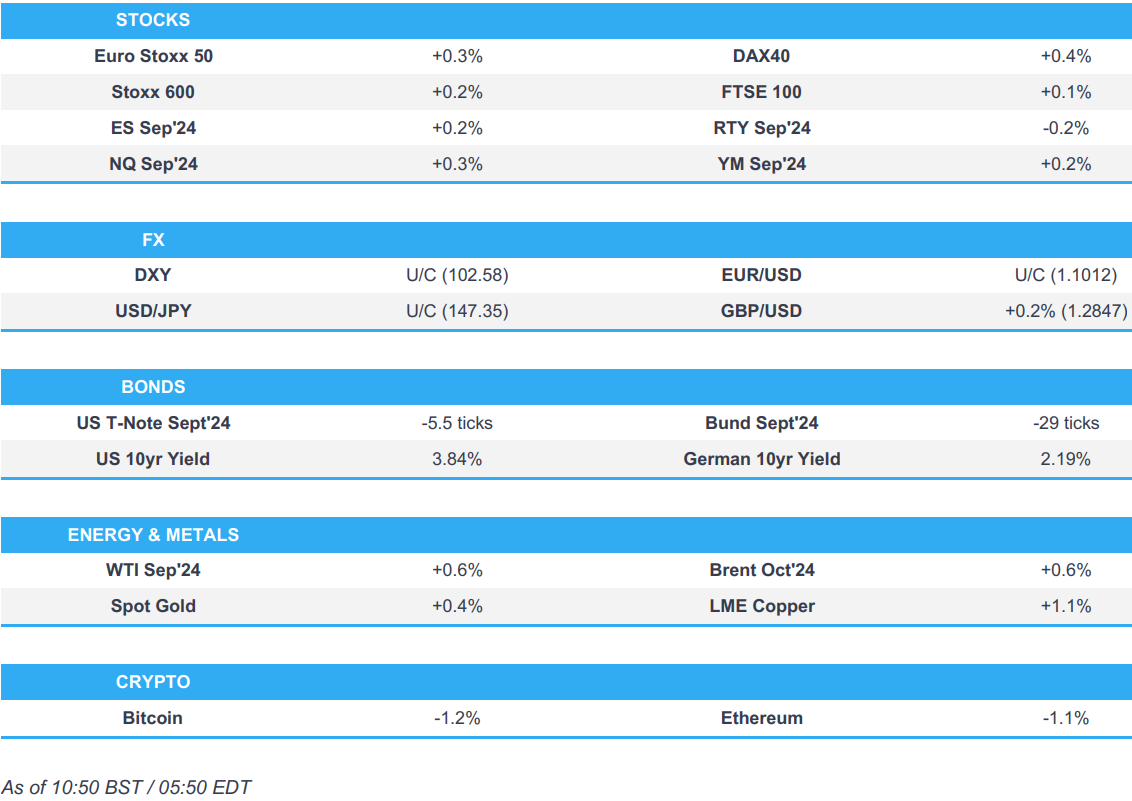

In rates, treasuries dip, with US 10-year yields rising 1bps to 3.84% while gilts underperformed after data showed the UK economy grew in line with estimates during the second-quarter and industrial production topped forecasts.

In commodities, oil prices advanced, with WTI rising 0.7% to $77.50 a barrel. Spot gold rises $9 to around $2,457/oz. Iron ore falls 1.4%.

Looking at today’s busy calendar, the US data slate includes August Empire manufacturing, July retail sales, August Philadelphia Fed business outlook, initial jobless claims, July import/export price indexes (8:30am), industrial production (9:15am), June business inventories, August NAHB housing market index (10am) and June TIC flows (4pm). Fed speakers scheduled for the session include Musalem (9:10am) and Harker (1:10pm)

Market Snapshot

- S&P 500 futures little changed at 5,478.50

- STOXX Europe 600 up 0.2% to 505.04

- MXAP little changed at 179.07

- MXAPJ down 0.1% to 558.27

- Nikkei up 0.8% to 36,726.64

- Topix up 0.7% to 2,600.75

- Hang Seng Index little changed at 17,109.14

- Shanghai Composite up 0.9% to 2,877.36

- Sensex up 0.2% to 79,105.88

- Australia S&P/ASX 200 up 0.2% to 7,865.52

- Kospi up 0.9% to 2,644.50

- German 10Y yield little changed at 2.20%

- Euro little changed at $1.1007

- Brent Futures up 0.3% to $80.00/bbl

- Gold spot up 0.3% to $2,456.27

- US Dollar Index little changed at 102.63

Top Overnight News

- Fed’s Bostic (voter) is open to a September rate cut as inflation cools and said as price pressures ease officials also need to be conscious of their mandate of maintaining full employment, while he added the labour market is weakening but is not weak: FT.

- China’s economic malaise extended into the third quarter, drawing renewed attention to the need for more fiscal stimulus as domestic demand falters under a prolonged housing downturn.

- Euro-zone productivity barely improved in the second quarter and again missed the European Central Bank’s expectations – a blow for its efforts to bring inflation back to 2%.

- Japan’s economy rebounded to growth in the second quarter on the back of an increase in private consumption, in a sign that a virtuous cycle long sought by the central bank linking rising incomes to increased spending may be starting to emerge.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks shrugged off the mixed lead from the US and gained as participants digested a slew of key data. ASX 200 traded higher but with gains capped as participants digested earnings releases and jobs data. Nikkei 225 was among the biggest gainers after GDP data topped forecasts and showed a return to growth. Hang Seng and Shanghai Comp. gradually advanced in the aftermath of mixed Chinese activity data in which industrial production disappointed but retail sales topped forecasts, while Chinese indices were also unfazed by the steeper contraction in home prices. Furthermore, the PBoC delayed its MLF operation to later in the month but announced a firm liquidity injection via 7-day reverse repos which is meant to counteract maturing MLF loans, tax payments and government bond issuance.

Top Asian News

- PBoC announced it will conduct its MLF operation on August 26th and injected CNY 577.7bln via 7-day reverse repos, while it added that the reverse repo operation today is meant to counteract maturing MLF loans, tax payments and government bond issuances.

- China’s stats bureau said China’s economic operation was generally stable in July but noted a rising negative impact from changes to China’s external environment, while it stated the economic recovery trend needs to be consolidated and expects the recovery in consumption to consolidate as policies gain traction. Furthermore, it said domestic demand is likely to improve due to policy support and Chinese foreign trade remains resilient despite rising protectionism.

- RBNZ Governor Orr addressed a parliamentary committee in which he stated that CPI is returning sustainably to the target band of 1%-3% and the current economic environment is weak with the economy weaker than anticipated six months ago. Orr added there is no talk on the committee of raising rates again and policy discussions in the future will focus on whether to maintain or reduce rates, as well as noted that they are to proceed with caution in adjusting interest rates and that removing restraint is appropriate for now.

- China’s Commerce Ministry is to impose export controls on antimony (semi-metal) and other metals from 15th September.

- Earthquake in Taiwan reported to be magnitude 5.7 (vs prelim 4.7), striking off Taiwan’s North-eastern Coast, according to Central Weather Bureau.

European bourses, Stoxx 600 (+0.2%) are modestly firmer across the board. Price action today has generally been rangebound, but some modest pressure has entered the complex in recent trade. European sectors hold a positive tilt; Healthcare takes the top spot, propped up by AstraZeneca (+0.9%). Insurance is also found near the top after Admiral (+7.3%) reported strong results. Travel & Leisure is at the foot of the pile. US Equity Futures (ES +0.1%, NQ +0.2%, RTY -0.1%) are mixed, with very slight outperformance in the NQ, ahead of a packed schedule including jobless claims, retail sales and Fed speak.

Top European News

- Norges Bank maintains its Key Policy Rate at 4.50% as expected, reiterates “policy rate will likely be kept at the current level for some time ahead”. Click for full details

- Norges Bank Governor notes of a “very high” threshold for Norges Bank to intervene in FX to support the NOK; adds a floating NOK is an advantage; no new prognosis on when the first rate cut will come. Not targeting a particular NOK level. Norges cares about the NOK due to its effects on inflation. Norges has information since the last rate meeting, but information pulling the bank in different directions. No new prognosis on when the first rate cut will come. Regarding debate on pegging NOK to EUR, says the Bank follows the mandate given.

FX

- DXY is steady and holding above 102.50 with the USD seeing a mixed performance vs. peers, ahead of key US data and Fed speak. A dovish batch of metrics could see DXY revisit the August 5th multi-month low at 102.16.

- EUR/USD is just about holding onto a 1.10 handle after pulling back from yesterday’s YTD peak at 1.1047.

- GBP is one of the better performers across the majors after Q2 GDP metrics underpinned the view that the UK economy saw a solid H1. Cable has climbed from a 1.2820 low to a 1.2843 high but is yet to challenge Wednesday’s 1.2868 best.

- USD/JPY remains within its recent 146-148 band as the recent impact of carry trade unwinding continues to recede.

- AUD leading the majors vs. the USD following strong jobs data overnight which was driven by full-time employment. AUD/USD as high as 0.6627 and back above its 200DMA at 0.6600.

- NOK experienced little follow-through from the Norges Bank’s decision to stand pat on rates as expected and reiterate guidance.

Fixed Income

- USTs are lower, but only modestly so, into a packed data docket. Headlined by Retail Sales while the weekly jobless claims data will draw particular focus as participants increase their focus on the jobs-side of the Fed’s dual mandate. USTs at a 113-18 base which is comfortably above the last two session’s 113-13+ and 113-02+ lows.

- Gilts are softer, and lagging slightly, after the morning’s GDP data for June/Q2. However, the release itself is perhaps not the driver behind the pressure, but more-so in a catch up play to the lows seen in APAC trade for USTs & Bunds.

- Bund benchmarks are in the red, with specific drivers and macro newsflow generally on the lighter side. Currently, Bunds at the low-end of 134.76-135.07 parameters.

Commodities

- Modest upward bias across crude contracts as broader market sentiment remains modestly positive and with geopolitics continuing to brew in the background as markets await the Iranian/Lebanese retaliation against Israel, with ceasefire talks due to continue in Doha (Qatar) today. Brent Oct trades in a USD 79.61-80.30/bbl parameter.

- Precious metals are firmer across the board to varying degrees despite an uneventful Dollar but against the backdrop of heightened geopolitics as Israel-Hamas ceasefire talks resume with low optimism whilst Ukraine makes ground in Russian territory. Spot gold trades in a contained USD 2,446.64-2,458.89/oz range.

- Base metals are seeing modest gains in fitting with the cautious but mildly positive sentiment across equities.

Geopolitics: Middle East

- US Secretary of State Blinken and Qatar’s PM warned all sides not to undermine Gaza ceasefire talks set to open in the Gulf nation, in a veiled warning to Iran, Hamas and Israel, according to Al Arabiya.

- US sources told Axios that former President Trump spoke with Israeli PM Netanyahu on Wednesday and encouraged Netanyahu to accept the deal to free hostages and for a ceasefire in Gaza.

- IRGC-linked hacking group APT42 has been targeting personal accounts of individuals connected to President Biden, VP Harris, and former President Trump, including current and former government officials, as well as those involved with their campaigns, according to Iran International citing Google.

- Hamas told mediators it was ready to meet them after today’s talks “if there are developments or a serious response from Israel”, via Sky News Arabia.

- “The Israeli delegation for the hostage deal talks has left Israel towards Doha”, via Kann’s Stein citing ItayBlumental.

Geopolitics: Other

- Russia conducted a missile attack on Ukraine’s Odesa which targeted port infrastructure and injured one person, according to Reuters citing the regional governor.

- South Korean President Yoon laid out the blueprint for establishing a unified Korea and said the freedoms enjoyed in the South must be extended ‘to the frozen kingdom of the North’. Yoon said they will create a North Korean human rights fund to support activists and offered to create a working-level consultation body with North Korea, while he added they are ready to begin political and economic cooperation if North Korea takes the initial step to denuclearise.

US Event Calendar

- 08:30: July Retail Sales Advance MoM, est. 0.4%, prior 0%

- July Retail Sales Ex Auto MoM, est. 0.1%, prior 0.4%

- July Retail Sales Ex Auto and Gas, est. 0.2%, prior 0.8%

- July Retail Sales Control Group, est. 0.1%, prior 0.9%

- 08:30: July Import Price Index MoM, est. -0.1%, prior 0%

- July Import Price Index YoY, est. 1.5%, prior 1.6%

- July Import Price Index ex Petroleu, est. 0.1%, prior 0.2%

- July Export Price Index MoM, est. 0%, prior -0.5%

- July Export Price Index YoY, est. 0.1%, prior 0.7%

- 08:30: Aug. Initial Jobless Claims, est. 235,000, prior 233,000

- Aug. Continuing Claims, est. 1.87m, prior 1.88m

- 08:30: Aug. Empire Manufacturing, est. -6.0, prior -6.6

- 08:30: Aug. Philadelphia Fed Business Outl, est. 5.2, prior 13.9

- 09:15: July Industrial Production MoM, est. -0.3%, prior 0.6%

- July Manufacturing (SIC) Production, est. -0.3%, prior 0.4%

- July Capacity Utilization, est. 78.5%, prior 78.8%

- 10:00: June Business Inventories, est. 0.3%, prior 0.5%

- 10:00: Aug. NAHB Housing Market Index, est. 43, prior 42

- 16:00: June Total Net TIC Flows, prior $15.8b

Central Bank Speakers

- 09:10: Fed’s Musalem Speaks on Economy, Policy

- 13:10: Fed’s Harker Gives Speech on Center at Philadelphia Fed

2B) European report

US equity futures are mixed & DXY flat ahead of US IJC/Retail Sales, AUD bid post-jobs data – US Market Open

Thursday, Aug 15, 2024 – 06:02 AM

- European bourses are modestly firmer; US futures are mixed ahead of today’s jobless claims and retail sales

- Dollar is flat and AUD outperforms post-jobs data

- Bonds are modestly lower, with slight underperformance in Gilts while USTs are contained into data

- Crude is modestly firmer, XAU gains alongside strength in base metals

- Looking ahead, US NY Fed Manufacturing, Export/Import Prices, IJC, Retail Sales, Comments from Fed’s Musalem, Harker. Earnings from Deere, Alibaba & Walmart.

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses, Stoxx 600 (+0.2%) are modestly firmer across the board. Price action today has generally been rangebound, but some modest pressure has entered the complex in recent trade.

- European sectors hold a positive tilt; Healthcare takes the top spot, propped up by AstraZeneca (+0.9%). Insurance is also found near the top after Admiral (+7.3%) reported strong results. Travel & Leisure is at the foot of the pile.

- US Equity Futures (ES +0.1%, NQ +0.2%, RTY -0.1%) are mixed, with very slight outperformance in the NQ, ahead of a packed schedule including jobless claims, retail sales and Fed speak.

- Click for the sessions European pre-market equity newsflow

- Click for the additional news

- Click for a detailed summary

FX

- DXY is steady and holding above 102.50 with the USD seeing a mixed performance vs. peers, ahead of key US data and Fed speak. A dovish batch of metrics could see DXY revisit the August 5th multi-month low at 102.16.

- EUR/USD is just about holding onto a 1.10 handle after pulling back from yesterday’s YTD peak at 1.1047.

- GBP is one of the better performers across the majors after Q2 GDP metrics underpinned the view that the UK economy saw a solid H1. Cable has climbed from a 1.2820 low to a 1.2843 high but is yet to challenge Wednesday’s 1.2868 best.

- USD/JPY remains within its recent 146-148 band as the recent impact of carry trade unwinding continues to recede.

- AUD leading the majors vs. the USD following strong jobs data overnight which was driven by full-time employment. AUD/USD as high as 0.6627 and back above its 200DMA at 0.6600.

- NOK experienced little follow-through from the Norges Bank’s decision to stand pat on rates as expected and reiterate guidance.

- Click for a detailed summary

- Click for NY OpEx Details

FIXED INCOME

- USTs are lower, but only modestly so, into a packed data docket. Headlined by Retail Sales while the weekly jobless claims data will draw particular focus as participants increase their focus on the jobs-side of the Fed’s dual mandate. USTs at a 113-18 base which is comfortably above the last two session’s 113-13+ and 113-02+ lows.

- Gilts are softer, and lagging slightly, after the morning’s GDP data for June/Q2. However, the release itself is perhaps not the driver behind the pressure, but more-so in a catch up play to the lows seen in APAC trade for USTs & Bunds.

- Bund benchmarks are in the red, with specific drivers and macro newsflow generally on the lighter side. Currently, Bunds at the low-end of 134.76-135.07 parameters.

- Click for a detailed summary

COMMODITIES

- Modest upward bias across crude contracts as broader market sentiment remains modestly positive and with geopolitics continuing to brew in the background as markets await the Iranian/Lebanese retaliation against Israel, with ceasefire talks due to continue in Doha (Qatar) today. Brent Oct trades in a USD 79.61-80.30/bbl parameter.

- Precious metals are firmer across the board to varying degrees despite an uneventful Dollar but against the backdrop of heightened geopolitics as Israel-Hamas ceasefire talks resume with low optimism whilst Ukraine makes ground in Russian territory. Spot gold trades in a contained USD 2,446.64-2,458.89/oz range.

- Base metals are seeing modest gains in fitting with the cautious but mildly positive sentiment across equities.

- Click for a detailed summary

NOTABLE DATA RECAP

- UK GDP Estimate MM (Jun) 0.0% vs. Exp. 0.0% (Prev. 0.4%); YY 0.7% vs. Exp. 0.8% (Prev. 1.4%); 3M/3M 0.6% vs. Exp. 0.6% (Prev. 0.9%, Rev. 0.8%)

- UK GDP Prelim QQ (Q2) 0.6% vs. Exp. 0.6% (Prev. 0.7%); YY 0.9% vs. Exp. 0.9% (Prev. 0.3%)

NOTABLE EUROPEAN HEADLINES

- Norges Bank maintains its Key Policy Rate at 4.50% as expected, reiterates “policy rate will likely be kept at the current level for some time ahead”. Click for full details

- Norges Bank Governor notes of a “very high” threshold for Norges Bank to intervene in FX to support the NOK; adds a floating NOK is an advantage; no new prognosis on when the first rate cut will come. Not targeting a particular NOK level. Norges cares about the NOK due to its effects on inflation. Norges has information since the last rate meeting, but information pulling the bank in different directions. No new prognosis on when the first rate cut will come. Regarding debate on pegging NOK to EUR, says the Bank follows the mandate given.

NOTABLE US HEADLINES

- Fed’s Bostic (voter) is open to a September rate cut as inflation cools and said as price pressures ease officials also need to be conscious of their mandate of maintaining full employment, while he added the labour market is weakening but is not weak, according to FT.

GEOPOLITICS

MIDDLE EAST

- US Secretary of State Blinken and Qatar’s PM warned all sides not to undermine Gaza ceasefire talks set to open in the Gulf nation, in a veiled warning to Iran, Hamas and Israel, according to Al Arabiya.

- US sources told Axios that former President Trump spoke with Israeli PM Netanyahu on Wednesday and encouraged Netanyahu to accept the deal to free hostages and for a ceasefire in Gaza.