AUGUST 22/ANOTHER ORCHESTRATE FRBNY RAID ON OUR PRECIOUS METALS: GOLD CLOSED DOWN $28.90 TO $2481.10.SILVER CLOSED DOWN 44 CENTS TOI $29.05//PLATINUM CLOSED DOWN $18.85 TO $949.60 WHILE PALLADIUM CLOSED DOWN $12.15 TO $939.90//EU TO USE ALL OF RUSSIAN FROZEN ASSETS WHICH WILL THOROUGH ANNOY RUSSIA AGAIN/ISRAEL VS HAMAS AND HEZBOLLAH//COVID UPDATES//VACCINE INJURY REPORTS//SLAY NEWS/CANADA NOW HAS A RAILWAY STRIKE WHICH WILL DAMAGE INDUSTRY//USA DATA: JOBLESSS RATE AT 33 MONTH HIGHS AND MGF PMI PLUMMETS AGAIN/SWAMP STORIES FOR YOU TONIGHT//

118 H MACQUARIE FUT 40 363 H WELLS FARGO SEC 15 661 C JP MORGAN 48 726 C PLUS500US FINAN 1 737 C ADVANTAGE 20 1 880 H CITIGROUP 96 905 C ADM 12 17 991 H CME 104

TOTAL: 177 177

JPMorgan stopped 0/177

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2024. CONTRACT: 177 NOTICES FOR 17,700 OZ or 0.5505 TONNES

total notices so far: 21,893 contracts for 2,189,300 Oz (68.096 tonnes)

FOR AUGUST:

SILVER NOTICES: 0 NOTICE(S) FILED FOR NIL

OZ/

total number of notices filed so far this month : 862 for 4,310,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $28.90 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 9.43 TONNES OF GOLD VAPOUR INTO THE GLD/

/ /INVENTORY RESTS AT 866.70 TONNES

INVENTORY RESTS AT 866.70 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.44 AT THE SLV

HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 0.913 MILLION OZ OF SILVER OUT OF THE SLV/

// INVENTORY AT 467.431 MILLION OZ/

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 467.431 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A FAIR SIZED 344 CONTRACTS TO 146,642 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS SMALL SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH SOME LIQUIDATION OF OI FROM OUR SPREADERS/TAS DESPITE OUR SMALL GAIN OF $0.03 IN SILVER PRICING AT THE COMEX ON WEDNESDAY’S TRADING. WE LOST ZERO LONGS WITH THE GAIN IN PRICE DESPITE THE FACT THAT WE HAD A FAIR LOSS OF 244 CONTRACTS ON OUR TWO EXCHANGES AS WE HAD AGAIN SOME LIQUIDATION OF T.A.S. CONTRACTS DURING WEDNESDAY’S TRADING//. WE HAD ZERO COVERING BY OUR SPECS WITH THE SMALL GAIN IN PRICE. WE HAD ANOTHER SMALL 100 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY ANOTHER STRONG 419 CONTRACT T.A.S ISSUANCE. IN ESSENCE WE LOST 244 CONTRACTS ON OUR TWO EXCHANGES DESPITE THE SMALL GAIN IN PRICE.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN YESTERDAY. THE ACCUMULATED T.A.S. IS BEING USED TO MANIPULATE PRICES AT THE COMEX NOW EVERY DAY..

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 419 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS.IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1/2 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS BUT TO NO AVAIL. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.03) AND WERE UNSUCCESSFUL IN KNOCKING ANY SILVER LONGS FROM THEIR PERCH AS WE HAD A VERY SMALL LOSS OF 27 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH ALL OF THAT LOSS DUE TO SPREADER/TAS LIQUIDATION.

WE HAD A SMALL 100 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.005 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP //NEW STANDING REMAINS AT 4.570 MILLION OZ

//NEW STANDING FOR SILVER//AUGUST IS THUS 4.570 MILLION OZ

WE HAD:

/ FAIR SIZED COMEX OI LOSS //SMALL SIZED EFP ISSUANCE/ VI) STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 419 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED 217 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST

TOTAL CONTRACTS for 16 DAYS, total 14,640 contracts: OR 73.2 MILLION OZ (915 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 73.200 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 73.200 MILLION OZ//THIS MONTH WILL PROBABLY BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

RESULT: WE HAD A TINY SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 127 CONTRACTS DESPITE OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL EFP ISSUANCE CONTRACTS: 100 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 3.005 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR AUG 4.560 MILLION OZ

WE HAVE A FAIR SIZED LOSS OF 244 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE GAIN IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG SIZED 419 CONTRACTS,//SOME FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX TRADING WHICH ACCOUNTS FOR A PORTION OF THE SMALL COMEX OI LOSS//// MASSIVE ATTEMPTED SHORT COVERING FROM OUR SPEC SHORTS AND ZERO LIQUIDATION OF LONGS. ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER.

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (419) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND MOST LIKELY TODAY., .

WE HAD 0 NOTICE(S) FILED TODAY FOR NIL OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 1168 OI CONTRACTS TO 531,699 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 1985 CONTRACTS

WE HAD A FAIR SIZED DECREASE IN COMEX OI (1168 CONTRACTS) OCCURRED WITH OUR LOSS OF $1.80 IN PRICE/WEDNESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR AUGUST AT 65.55 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 7300 OZ QUEUE JUMP AS FINALLY GUYS ARE STANDING FOR GOLD AT THE COMEX

NEW STANDING ADVANCES TO 68.590 TONNES

/ ALL OF THIS HAPPENED WITH OUR $1.80 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A SMALL SIZED GAIN OF 704 OI CONTRACTS (2.189 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1872 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 531,699

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 704 CONTRACTS WITH 1168 CONTRACTS DECREASED AT THE COMEX// AND A FAIR SIZED 1872 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2684 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR 1307 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1872 CONTRACTS) ACCOMPANYING THE FAIR SIZED LOSS IN COMEX OI OF 1168 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 704 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR AUGUST AT 65.55 TONNES FOLLOWED BY TODAY’S 7300 OZ QUEUE JUMP AS THESE BOYS JUMP THE QUEUE TO STAND AT THE COMEX./

//NEW STANDING ADVANCES TO: /AUGUST 68.5909 TONNES.

/ 3) SOME T.A.S. LIQUIDATION//SPREADER CONTRACTS WITH ZERO NET LONG SPECS BEING CLIPPED,

4) SMALL SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1307 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST. :

TOTAL EFP CONTRACTS ISSUED: 76,403 CONTRACTS OF 7,640,300 OZ OR 237,64 TONNES IN 16 TRADING DAY(S) AND THUS AVERAGING: 4775 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 16 TRADING DAY(S) IN TONNES 237.64 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 237.64 DIVIDED BY 3550 x 100% TONNES = 6.69% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 237.64 TONNES//THIS MONTH WILL NO DOUBT BE A HUGE ISSUANCE OF EFP’S BUT LESS THAN LAST MONTH.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUG), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A FAIR SIZED 344 CONTRACTS OI TO 146,642 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 100 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 100 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 100 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 344 CONTRACTS AND ADD TO THE 100 E.FP. ISSUED

WE OBTAIN A FAIR SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 244 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 1.27 MILLION OZ OCCURRED DESPITE OUR $0.03 GAIN IN PRICE

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 7.812 PTS OR 0.27% //Hang Seng CLOSED UP 249.99 PTS OR 1.44% // Nikkei CLOSED UP 259,21 OR .68%//Australia’s all ordinaries CLOSED UP 0.29%///Chinese yuan (ONSHORE) CLOSED DOWN TO 7,1388 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.1375/ Oil DOWN TO 72.32 dollars per barrel for WTI and BRENT DOWN AT 76,51 Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 1168 CONTRACTS TO 531,699 DESPITE OUR LOSS IN PRICE OF $1.80 WITH RESPECT TO WEDNESDAY’S TRADING. WE LOST A CONSIDERABLE NUMBER OF SPREADER/T.A.S. CONTRACTS AS SHORTS AGAIN PANICKED BIG TIME THROUGHOUT THE SESSION AND COVERED WHAT THEY COULD EVAN AT LOWER PRICES. THE FED IS THE MAJOR SHORT OF AROUND 148 TONNES+ OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS IS SCHEDULED TO HAPPEN LATE SEPT 2024.

OUR LONDONERS ALSO BOUGHT NEW MASSIVE QUANTITIES OF LONGS AND THIS WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD A GOOD T.A.S. LIQUIDATION ON WEDNESDAY’S SLIGHT LOSS IN PRICE WITH ZERO LONGS BEING CLIPPED (AS YOU WILL SEE BELOW) BUT WE DID HAVE MAJOR SHORT COVERING. THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE ACTIVE DELIVERY MONTH OF AUGUST.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 1872 EFP CONTRACTS WERE ISSUED: : OCT/DEC1872 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1872 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 704 CONTRACTS IN THAT 1872 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A FAIR LOSS OF 1168 COMEX CONTRACTS..AND THIS VERY SMALL GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $1.80/WEDNESDAY COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AS MENTIONED ABOVE.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT A FAIR SIZED 1307 CONTRACTS. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE. THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN LAST WEEK’S TRADING//RAIDS AS WELL AS THIS WEEK AND ESPECIALLY ON LAST FRIDAY’S HUGE TRADING DAY.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: AUGUST (68.5909 TONNES)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 42 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 68.5909 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $1.80 //// BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE DID HAVE A FAIR IN OUR TWO EXCHANGES. CENTRAL BANK LONGS , EXERCISED FOR PHYSICAL. WE HAD A CONSIDERABLE T.A.S. LIQUIDATION WEDNESDAY/COMEX.

WE HAVE GAINED A TOTAL OI OF 2.189 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST (65.55 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 7300 OZ QUEUE JUMP //NEW STANDING: 68.5909 TONNES.

NEW STANDING FOR AUGUST: 68.5909 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $1.80

WE HAVE REMOVED 1985 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL

NET GAIN ON THE TWO EXCHANGES 704 CONTRACTS OR 70400 OZ (2.189

Total monthly oz gold served (contracts) so far this month

21893 notices 2,189,300 oz 68.096 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: nil oz

we have 0 customer deposits

total deposits NIL oz

withdrawals: 2

i) Out of HSBC 42,632.226 oz

ii) Out of Manfra” 6944.666 oz (216 kilobars)

TOTAL WITHDRAWALS 49,576.842 oz 1.54 tonnes

adjustments: 1/ DEALER TO CUSTOMER

a) Manfra 18,032.362 oz

total oz moved out of registered to eligible; 58,760.927 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST

For the front month of AUGUST we have an oi of 336 contracts having LOST 68 contracts.

We had 141 contracts served on WEDNESDAY so we gained an additional 73 contracts or 7300 oz will stand for gold at the comex

SEPT. LOST 30 CONTRACTS TO STAND AT 5559 CONTRACTS.

OCTOBER LOST 317 CONTRACTS DOWN TO 54,670 CONTRACTS

We had 177 contracts filed for today representing 17700 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 48 notice issued from their client or customer account. The total of all issuance by all participants equate to 77 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for AUGUST /2024. contract month, we take the total number of notices filed so far for the month (21,893) x 100 oz ) to which we add the difference between the open interest for the front month of August 336( CONTRACTS) minus the number of notices served upon today (177 x 100 oz per contract( equals 2,205,200 OZ OR 68.5909 TONNES. Somebody was in great need of physical gold on this side of the pond today

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (21,893 x 100 oz +we add the difference for front month of AUGUST (336 X// , OI} minus the number of notices served upon today (177) x 100 oz which equals 2,205,200 oz (68.5909 TONNES)

TOTAL COMEX GOLD STANDING FOR AUGUST: 68.5909 TONNES WHICH IS HUGE FOR THIS VERY ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,259,313,949 OZ

TOTAL REGISTERED GOLD 7,788,835.885 ( 242.26 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,470,475.064 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,041,112 oz (REG GOLD- PLEDGED GOLD)= 187.90tonnes //

END

SILVER/COMEX

AUGUST 22/2024

INITIAL

//2024// THE AUG 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

1,268,817.108 OZ Ashai Delaware

HSBC

.

Deposits to the Dealer Inventory

NIL

Deposits to the Customer Inventory

1042,761.540 oz

ASAHI Delaware HSBC

No of oz served today (contracts)

0 CONTRACT(S) (NIL OZ)

No of oz to be served (notices)

50 contracts (0.250 million oz)

Total monthly oz silver served (contracts)

862 Contracts (4.310 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit/

total dealer deposit : NIL oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 3 customer deposits:

i)Into Loomis: 483,460.400 oz

ii) Into Delaware 945.54 oz

iii) Into ASHAI 608,355.600 oz

total customer deposit 1042,761.540 oz

JPMorgan has a total silver weight: 134.771million oz/306.332 million or 44.07%

adjustment:0

withdrawals: 3

i)Out of ASAHI 601,649.100 oz

ii)Out of Delaware 587m129.468 OZ

III) OUT OF HSBC 80,038.54 OZ

total customer withdrawals: 714,420.700 oz

TOTAL REGISTERED SILVER: 69.805 MILLION OZ//.TOTAL REG + ELIGIBLE. 306.332 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR AUGUST:

silver open interest data:

FRONT MONTH OF AUGUST/2024 OI: 50 CONTRACTS HAVING LOST 15 CONTRACT(S).

WE HAD 15 NOTICES SERVED ON WEDNESDAY, SO WE GAINED 0 CONTRACTs OR AN ADDITIONAL 0 OZ WILL STAND FOR SILVER AT THE COMEX.

SEPT SAW A LOSS OF 3656 CONTRACTS TO 47,441. SEPT NOW BECOMES THE NEW FRONT MONTH

OCTOBER SAW ANOTHER GAIN OF OPEN INTEREST CONTRACTS OF 55 CONTRACTS AND THUS WE HAVE 676 OPEN INTEREST CONTRACTS FOR OCTOBER.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for NIL oz

CONFIRMED volume; ON TUESDAY 66,226 strong

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 862 x 5,000 oz = 4.310 MILLION oz

to which we add the difference between the open interest for the front month of AUGUST( 50) and the number of notices served upon today 0 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST/2024 contract month: 862 notices served so far) x 5000 oz + OI for the front month of AUGUST (50)x number of notices served upon today minus (0)x 5000 oz of silver standing for the AUGUST contract month equates to 4.570 MILLION OZ.

New total standing: 4.570 million oz.

There are 69.904 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

GLD AND SLV INVENTORY LEVELS//

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD

AUGUST 22 WITH GOLD DOWN $28.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 9.43 TONNES OF GOLD VAPOUR GOLD INTO THE GLD./ //////INVENTORY RESTS AT 866.70 TONNESA

AUGUST 21 WITH GOLD DOWN $1.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER WITHDRAWAL OF 1.73 TONNES OF GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 857.27 TONNES

AUGUST 20 WITH GOLD UP $9.40 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 4.03 TONNES OF GOLD VAPOUR INTO THE GLD./ //////INVENTORY RESTS AT 859.00 TONNES

AUGUST 19 WITH GOLD UP $3.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 7.19 TONNES OF GOLD VAPOUR INTO THE GLD./ //////INVENTORY RESTS AT 854.97 TONNES

AUGUST 16 WITH GOLD UP $44.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: //////INVENTORY RESTS AT 847.78 TONNES

AUGUST 15 WITH GOLD UP $13,70 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD OUT OF THE GLD//////INVENTORY RESTS AT 847.78 TONNES

AUGUST 14 WITH GOLD DOWN $26.20 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.03 TONNES OF GOLD OUT OF THE GLD//////INVENTORY RESTS AT 845.76 TONNES

AUGUST 13 WITH GOLD UP $3.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//////INVENTORY RESTS AT 849.79 TONNES

AUGUST 12 WITH GOLD UP $30.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ////INVENTORY RESTS AT 846.91 TONNES

AUGUST 9 WITH GOLD UP $10.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 846.91 TONNES

AUGUST 8 WITH GOLD UP $31.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.02 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 844.04 TONNES

AUGUST 7 WITH GOLD UP $1.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.16 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 848.06 TONNES

AUGUST 6 WITH GOLD DOWN $13.10 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD” A WITHDRAWAL OF .57 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 844.90 TONNES

AUGUST 2 WITH GOLD DOWN $9.95 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.58 TONNES OF GOLD OUT OF THE GLD//INVENTORY RESTS AT 845.47 TONNES

AUGUST 1 WITH GOLD UP $9.15 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 846.05 TONNES

JULY 30 WITH GOLD UP $26.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// A /////INVENTORY RESTS AT 843.17 TONNES

JULY 29 WITH GOLD UP $27.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD// A WITHDRAWAL OF 1.98 TONNES OF GOLD OUT OF THE GLD/////INVENTORY RESTS AT 843.17 TONNES

JULY 26 WITH GOLD UP $27.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD// A DEPOSIT OF 3.45 TONNES OF GOLD INTO THE GLD/////INVENTORY RESTS AT 845.19 TONNES

JULY 25 WITH GOLD DOWN $60.45 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 841.74 TONNES

JULY 24 WITH GOLD UP $12.75 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1,73 TOONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 841.74 TONNES

JULY 23 WITH GOLD UP $12.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 22 WITH GOLD DOWN $4.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 19 WITH GOLD DOWN $56.10 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;:A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 18 WITH GOLD DOWN $2.20 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;: ///INVENTORY RESTS AT 842.02 TONNES

JULY 17 WITH GOLD DOWN $6.60 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A MASSIVE DEPOSIT OF 5.49 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 842.02 TONNES

JULY 16 WITH GOLD UP $38.60 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 836.53 TONNES

GLD INVENTORY: 866.70 TONNES, TONIGHTS TOTAL

SILVER

AUGUST 22//WITH SILVER DOWN $0.44//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 0.943 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 468.344 MILLION OZ

AUGUST 21//WITH SILVER $0.03//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 1..552 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 468.344 MILLION OZ

AUGUST 20//WITH SILVER $0.24//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 1.369 MILLION OZ FROM THE SLV. .///./// /INVENTORY AT 466.792 MILLION OZ

AUGUST 19//WITH SILVER $0.39//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 1.506 MILLION OZ FROM THE SLV. .///./// /INVENTORY AT 465.423 MILLION OZ

AUGUST 16//WITH SILVER $0.49//NO CHANGES IN SILVER INVENTORY: .///./// /INVENTORY AT 466.929 MILLION OZ

AUGUST 15//WITH SILVER $1.14//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.186 MILLION ON INTO THE SLV.///./// /INVENTORY AT 466.929 MILLION OZ

AUGUST 14//WITH SILVER DOWN $0.40//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 13//WITH SILVER DOWN $0.19//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 12//WITH SILVER UP $.37//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 9//WITH SILVER DOWN $.03//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 8//WITH SILVER UP $.70//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 3.241 MILLION OZ INTO THE SLV////./// /INVENTORY AT 462.502 MILLION OZ

AUGUST 7//WITH SILVER DOWN $0.27//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.552 MILLION OZ INTO THE SLV////./// /INVENTORY AT 462.502 MILLION OZ

AUGUST 6//WITH SILVER UP $0.05//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 458.851 MILLION OZ

AUGUST 2//WITH SILVER DOWN $0.01//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 1.243 MILLION OZ OF SILVER OUT OF THE SLV ///./// /INVENTORY AT 460.961 MILLION OZ

AUGUST 1//WITH SILVER DOWN $0.46//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.608 MILLION OZ OF SILVER VAPOUR INTO THE SLV///./// /INVENTORY AT 462.204 MILLION OZ

JULY 31//WITH SILVER UP $0.45//NO CHANGES IN SILVER INVENTORY: /./// /INVENTORY REMAINS AT 460.596 MILLION OZ

JULY 30//WITH SILVER UP $0.61//SMALL CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 0.456 MILLION OZ OF SILVER VAPOUR INTO THE SLV/./// /INVENTORY RISES AT 460.596 MILLION OZ

JULY 29//WITH SILVER DOWN $0.07//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.382 MILLION OZ OF SILVER VAPOUR INTO THE SLV/./// /INVENTORY RISES AT 461.052 MILLION OZ

JULY 26//WITH SILVER DOWN $0.07//NO CHANGES IN SILVER INVENTORY./// /INVENTORY REMAINS AT 456.670 MILLION OZ

JULY 25 WITH SILVER DOWN $1.37//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 3.124 MILLION OZ OF SILVER OUT OF THE SLV./// /INVENTORY FALLS TO 456.670 MILLION OZ

JULY 24 WITH SILVER UP 3 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 15.880 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 23 WITH SILVER UP 3 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 15.880 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 22 WITH SILVER UP 2 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 3.920 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 19 WITH SILVER DOWN 94 CENTS//NO CHANGES IN SILVER INVENTORY/// /INVENTORY REMAINS AT 435.854 MILLION OZ

JULY 18 WITH SILVER DOWN 13 CENTS//HUGE CHANGES IN SILVER INVENTORY” A DEPOSIT OF 2.374 MILLION OZ INTO THE SLV/// /INVENTORY RISES TO 435.854 MILLION OZ

JULY 17. WITH SILVER DOWN 75 CENTS//NO CHANGES IN SILVER INVENTORY// /INVENTORY REMAINS AT 433.480 MILLION OZ.

JULY 16. WITH SILVER UP 30 CENTS//NO CHANGES IN SILVER INVENTORY// /INVENTORY REMAINS AT 433.480 MILLION OZ.

CLOSING INVENTORY 467.433 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY//BILL HOLTER:

3.CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES

This is going to be a huge mine when it goes into production

(Barker/GATA)

‘World’s largest undeveloped gold project’ hits milestone in northwest B.C

Submitted by admin on Wed, 2024-08-21 16:53 Section: Daily Dispatches

By Thom Barker Ashcroft-Cache Creek Journal, Ashcroft, British Columbia, Canada Wednesday, August 21, 2024

It has been a banner few weeks for Seabridge Gold lately in northwestern British Columbia.

In late July, the company announced the Environmental Assessment Office had designated its flagship KSM project as “substantially started,” well in advance of its deadline.

The substantially started status makes the company’s Environmental Assessment Certificate permanent. It has been set to expire in July 2026 if Seabridge had not achieved the designation.

“This is a significant regulatory milestone for the KSM Project, positioning it to become a multigenerational economic anchor for northwestern B.C.,” said Rudi Fronk, Seabridge chair and chief executive officer.

In a press release, the company said it has spent has spent more than $1 billion since acquiring the KSM Project in 2001, of which more than $800 million was to advance the project to substantially started after KSM’s environmental assessment certificate was issued in July 2014.

The company claims that KSM, located 65 kilometres from Stewart, is the world’s largest undeveloped gold property with 88.7 million ounces of measured and indicated gold plus 71.5 million ounces inferred. The deposit also holds 19.46 billion pounds of copper resources in the measured and indicated categories plus 38.5 billion pounds in the inferred category.

Seabridge estimates when the mine goes into production, it will operate for 52 years. …

As the rich snap up gold bars, storage vaults brace for business

Submitted by admin on Wed, 2024-08-21 12:12 Section: Daily Dispatches

By Sybilla Gross and Yvonne Yue Li Bloomberg News Tuesday, August 20, 2024

Encased in sleek onyx, an enormous vault for storing precious metal soars some 32 meters (105 feet) above Singapore’s Changi Airport. For a facility that deals in secrecy and privacy, its sheer mass makes a loud statement about the sudden popularity of owning physical bullion.

The Reserve opened last month to cater to increased demand from the world’s uber wealthy for high-security storage. The six-story warehouse is designed to hold 10,000 tons of silver, more than a third of global annual supply, and 500 tons of gold — equivalent to about half of what central banks purchased in 2023.

Silver Bullion Pte Ltd. built the 180,000 square foot (16,700 square meters) facility, which it says is one of the largest in the world, after its previous vault ran out of space. Already it’s flush with inquiries from customers, it says. …

The Israel Diamond Exchange has reported a drop in its exports and membership in 2024, according to Israel media outlet Ynet news.

The exchange president, Nissim Zuaretz, said that for the first time in its history, the annual number of retirees has exceeded the exchange’s new members. “In the best years of the industry, we received 200 new members a year, in the past year only 30,” Zuaretz said.

The Israel Diamond Exchange, in the city of Ramat Gan, is the world’s largest, encompassing about 3,100 members. The country is the fifth largest global exporter of cut and uncut diamonds.

In 2024, Israel’s net exports of rough diamonds saw a six percent decrease compared to the same period in 2023, while the export of polished diamonds in the first seven months of 2024 dropped by 33 percent compared to the corresponding period in 2023.

In July 2024 alone, exports decreased by almost half compared to the previous year.

In February, the former Diamond Exchange president, Boaz Moldawsky, cited Israel’s ongoing war in Gaza and a global downturn that predated 7 October as factors driving the slump.

He said that in the weeks following October 7, the diamond market in Israel was “completely paralyzed,” but that it then returned to normal operations.

However, amid Israel’s ongoing Gaza war, buyers stopped visiting Israel, with the annual International Diamond Week in Israel, scheduled for early April, cancelled.

But according to the Rapaport Group, the slump is mainly driven by a slowdown in sales to the US and China, and collapsing diamond prices in 2023, which tumbled about 20 percent due to slowing consumer demand.

Moldawsky estimated that 80 percent of the trade’s difficulties were due to the global slump, and 20 percent to the war on Gaza.

end

6 CRYPTOCURRENCY NEWS

END

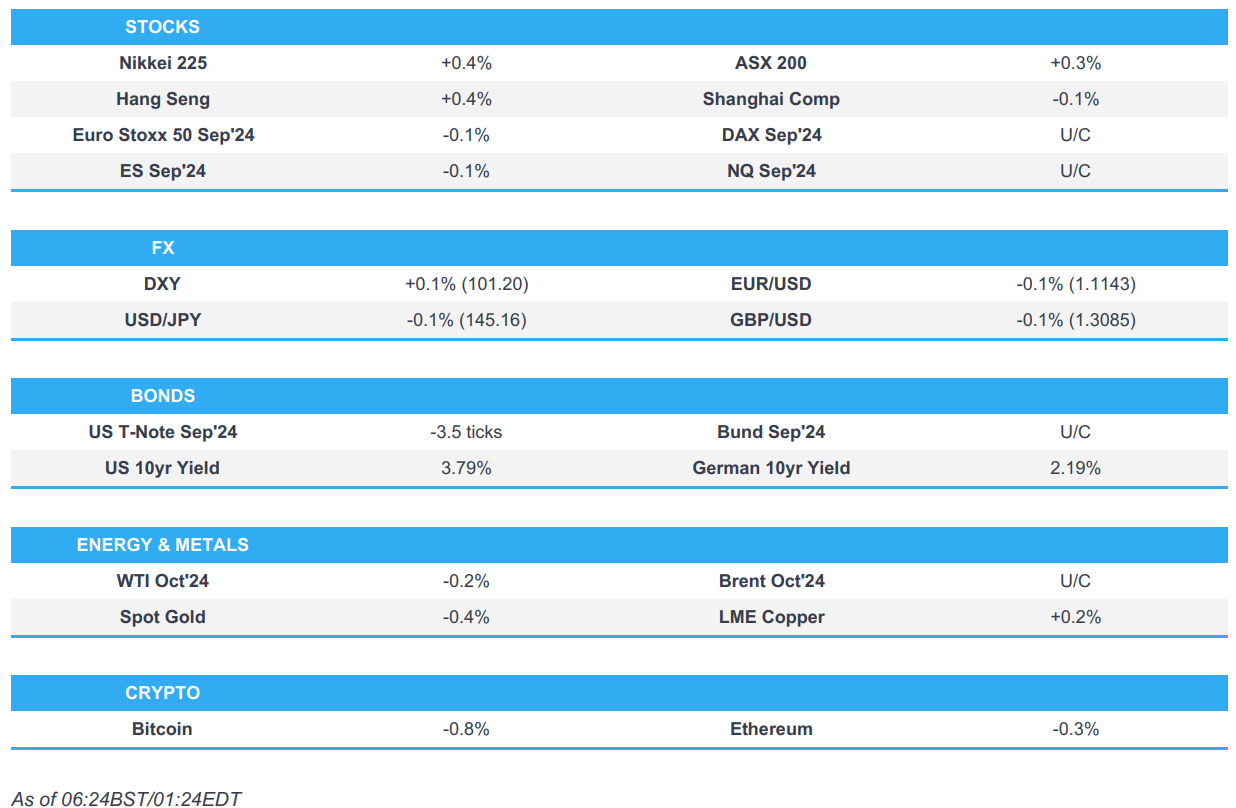

ASIA TRADING/THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 7.812 PTS OR 0.27% //Hang Seng CLOSED UP 249.99 PTS OR 1.44% // Nikkei CLOSED UP 259,21 OR .68%//Australia’s all ordinaries CLOSED UP 0.29%///Chinese yuan (ONSHORE) CLOSED DOWN TO 7,1388 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.1375/ Oil DOWN TO 72.32 dollars per barrel for WTI and BRENT DOWN AT 76,51 Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGSTHURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1388

OFFSHORE YUAN: DOWN TO 7.1375

SHANGHAI CLOSED DOWN 7.81 PTS OR 0.27 %

HANG SENG CLOSED UP 249,99 PTS OR 1.44%

2. Nikkei closed UP 259.21 PTS OR .68%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 101.23 EURO FALLS TO 1.1133 DOWN 22 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +0.885 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 146.04…… JAPANESE YEN NOW RISING AS WE HAVE NOW REACHED THE REIGNITING OF THE YEN CARRY TRADE AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE:DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.2290/Italian 10 Yr bond yield UP to 3.588 SPAIN 10 YR BOND YIELD DOWN TO 3.0290%

3i Greek 10 year bond yield UP TO 3.257

3j Gold at $2500.50//Silver at: 29.50 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 36/ 100 roubles/dollar; ROUBLE AT 91.18

3m oil into the 72 dollar handle for WTI and 76 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 146.64/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.885 % STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8521 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9488 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.838 UP 6 BASIS PTS…

USA 30 YR BOND YIELD: 4.100 UP 5 BASIS PTS/

USA 2 YR BOND YIELD: 3.966 UP 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 33.93…

10 YR UK BOND YIELD: 3.9724 UP 8 PTS

10 YR CANADA BOND YIELD: 3.065 UP 5 BASIS PTS

2a New York OPENING REPORT

Global Stocks Hit All Time High With J-Hole Expected To Preannounce Rate Cuts

THURSDAY, AUG 22, 2024 – 08:15 AM

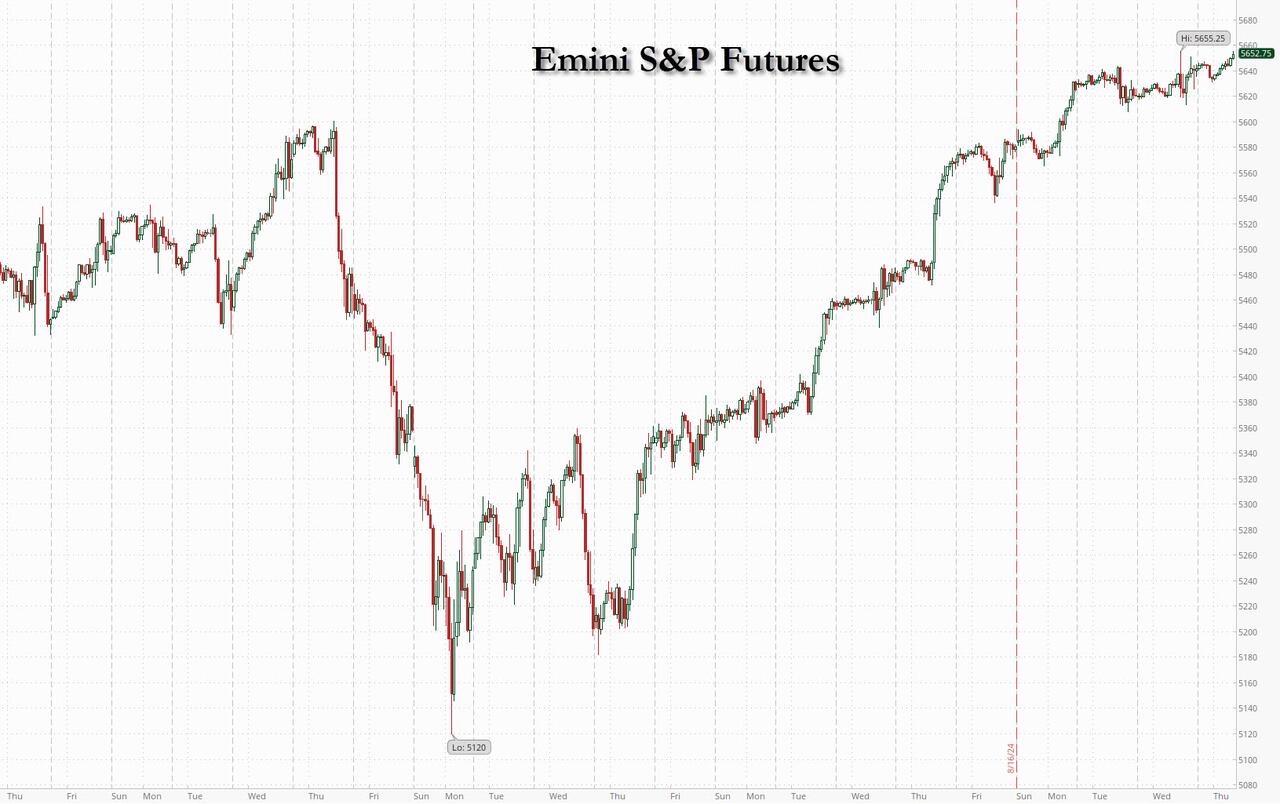

Just over two weeks after the VIX almost touched 70, the market’s freakout is completely forgotten as futures continue rising and a global gauge of stocks approached a record high as traders are now convinced the Fed will deliver its first interest-rate cuts in more than four years, which will take place with both stock and housing prices at all time highs. One can only imagine what happens next. The MSCI’s All Country World index ticked up 0.1%, trading near its all-time record close on July 16. As of 7:45am, S&P futures were 0.2% higher with the index on pace to be up 10 of the past 11 days, while Nasdaq futures gained 0.3%. Europe’s Stoxx 600 index advanced 0.5% as Deutsche Bank AG rallied after predicting a boost to third-quarter results. US futures edged higher. The Bloomberg dollar index is up after rebounding from a 5 month low, while 10Y TSY yields are higher by 3bps to 3.83% after dropping 4 days. Oil is also higher after tumbling to the lowest price of 2024 yesterday. The macro calendar is busy with Initial and jobless claims, Chicago Fed and and existing home sales for July. The Jackson Hole symposium begins tonight with Powell’s highly expected speech due tomorrow at 10am.

In premarket trading, Charles Schwab shares fall 4.3% after Toronto-Dominion Bank has raised $2.5 billion in pricing the sale of Schwab shares at $61.65 each. Paramount Global shares rose 3.7% after media investor Edgar Bronfman Jr. raised his offer to take control of thee CBS parent to $6 billion, according to Bloomberg News. Here are some other notable premarket movers:

Canadian Solar shares slip 4.2% after the company forecast revenue for the third quarter; the guidance missed the average analyst estimate.

Estee Lauder shares rise 2.3% after an upgrade to overweight at Piper Sandler.

SentinelOne shares rise 3.4% after an upgrade to overweight at Wells Fargo.

Snowflake shares drop 9.6% after the software company reported its second-quarter results and gave an outlook. While the results beat expectations on key metrics, analysts flagged some concerns.

Sprout Social shares slip 3.2% after receives its first ever sell-equivalent rating since its initial public offering in December 2019, after KeyBanc Capital Markets cut the company to underweight from sector weight and set a new Street low price target.

Synopsys shares rise 2.4% after the electronic design automation software company reported third-quarter results that beat expectations and raised its full-year forecast.

Urban Outfitters shares fall 11% after the apparel retailer reported second-quarter comparable retail segment sales growth that missed Wall Street expectations.

Zoom Video Communications shares rise 3.5% after the video-conferencing software company reported second-quarter results that beat expectations and raised its full-year forecast as new AI and contact centers products continue to deliver. It also announced that CFO Kelly Steckelberg would resign.

Expectations for US rate cuts have completely erased the market slump at the start of August that was sparked by recession fears in the US and a rapid unwind of the yen carry trade. Now, investors are focused on Powell’s speech at the Jackson Hole economic symposium on Friday for further evidence a September cut is coming, but even without it, about 100 basis points of easing are already priced in this year after some -818,000 payroll revisions reinforced the case for lower rates.

“We’ve been long Treasuries for a week now — it’s quiet and yields can grind lower from here,” said Matt Amis, investment director at Abrdn Investment Management Ltd. “Jackson Hole is obviously all the market is waiting for. Powell is desperate to cut, we don’t see why he would want to push back on current market pricing for September.”

The Stoxx 600 rises 0.6%, led by retail and travel names. Retail is the strongest-performing sector, wihle basic resources stocks are the biggest laggards. Here are the most notable European movers:

CTS Eventim shares rise 11% to an intraday record after the German events company’s first-half revenue beat estimates. The firm now expects significantly higher Ebitda and revenue for its ticketing segment compared with last year.

Swiss Re advances as much as 3.8%, the most since May, after the Swiss insurance group reported first-half earnings where all its divisions outperformed expectations. Vontobel expects Swiss Re to surpass its FY guidance this year, bar any major large claims.

JD Sports shares rise as much as 6.3% to hit their highest level since early June after the UK clothing retailer reassured investors with sales growth and increasing market share at a tough time for the broader retail space, according to analysts at Peel Hunt.

Swiss Prime shares rise as much as 2.6% to hit their highest level since June 2022 after the real estate investor reported strong rental income growth, record-low vacancy rates, an improved valuation for its portfolio and a rosier outlook, according to analysts. The stock is trading at its highest level since June 2022.

Bavarian Nordic shares rise as much as 13% after the Danish company forecast reaching the top end of its full-year guidance range following an order for its smallpox/mpox vaccine from a European country. Analysts see consensus expectations being increased for the year.

HelloFresh shares rise as much as 8.5%, hitting the highest intraday level since March, after activist investor Active Ownership disclosed a stake.

Meko gains as much as 13%, the most since May 2022, after the Swedish automotive parts retailer reported stronger-than-expected earnings, with operating income 41% ahead of Bloomberg-compiled consensus expectations.

PKO Bank Polski shares gain as much as 3% after Poland’s biggest lender reported 2Q earnings beat on interest income that rose 15% Y/y despite fresh charges on mortgage moratoriums. Analysts praise also further reduction of cost of risk and see that PKO has potential to maintain high profits in the coming quarters.

Aegon shares drop as much as 6.7% after the insurer’s first-half operating profit dropped on charges booked after the insurer updated its mortality assumptions. Analysts say this is a negative, but highlight underlying results were solid and that guidance has been reiterated.

GN Store Nord shares drop as much as 10%, the most since August 2023, after the Danish hearing-aid and audio equipment firm reported weaker-than-expected earnings for the second quarter. Morgan Stanley analysts see “modest trims” to consensus estimates for the year.

Orlen, Poland’s largest energy company, falls as much as 2.8% after it reported net loss in 2Q due to 6.3b zloty charges to finance the country’s household energy price caps. Analysts see Orlen’s plan to cut capex as well as rising profits from electricity segment as a positive signal.

Instalco falls as much as 12%, the most since November 2022, after the Swedish electrical installations group reported its latest earnings, showing an organic contraction in the quarter of 6.4% vs. 5.5% growth a year earlier.

European data showed a mixed picture for the region’s economy, despite a surprise boost from the Paris Olympics. French services expanded at the fastest pace in more than two years, while in Germany a composite PMI added to evidence that the country’s recovery has fizzled out. Britain’s private sector companies reported their strongest growth in four months alongside cooling price pressures. In company news, shares of Deutsche Bank jumped more than 3%. The lender said it expects a €430 million ($479 million) boost to pretax profit in the third quarter after reaching agreements with more than 80 plaintiffs in a long-running dispute.

Earlier in the session, Asian stocks eked out small gains. The MSCI Asia Pacific Index rose as much as 0.4% after fluctuating in early trading. Tencent contributed the most to the gauge’s increase, while AIA Group also surged after the insurer’s new business value jumped to a record in the first half of the year. Equities in Hong Kong led the gains in the region, as several major companies including Xiaomi reported upbeat results. Those in the Philippines and Japan also advanced, partly helped by expectations of US rate cuts, which may provide support to shares ranging from technology companies to machinery makers. Indonesia and Taiwan markets declined. Bank of Japan Governor Kazuo Ueda, meanwhile, faces intense market scrutiny on Friday when he speaks to lawmakers, after the central bank’s hawkish signals contributed to the global market turmoil earlier this month.

In FX, the Bloomberg Dollar Spot Index is up 0.1% while the Japanese yen falls 0.3%; the pound has risen to the top of the G-10 FX pile, climbing 0.2% against the dollar after UK manufacturing and service PMIs topped estimates. The euro falls 0.1% after more mixed readings from the bloc – manufacturing was weak but services outperformed, in part due to the Paris Olympics.

In rates, treasuries are under pressure in early US trading with the yield curve flatter as front-end yields are about 3bp higher on the day. US rates track a bigger selloff in core European bond markets sparked by August preliminary PMIs for France, Germany and euro-zone. Treasury yields are cheaper by at least 2bp across the curve with 2s10s, 5s30s spreads flatter by about 1bp on the day; 10-year is around 3.82% with comparable bunds and gilts cheaper by an additional 1.7bp and 1.5bp. German government bonds are lower and didn’t show much reaction to a slowdown in euro-zone wage growth in the second quarter.

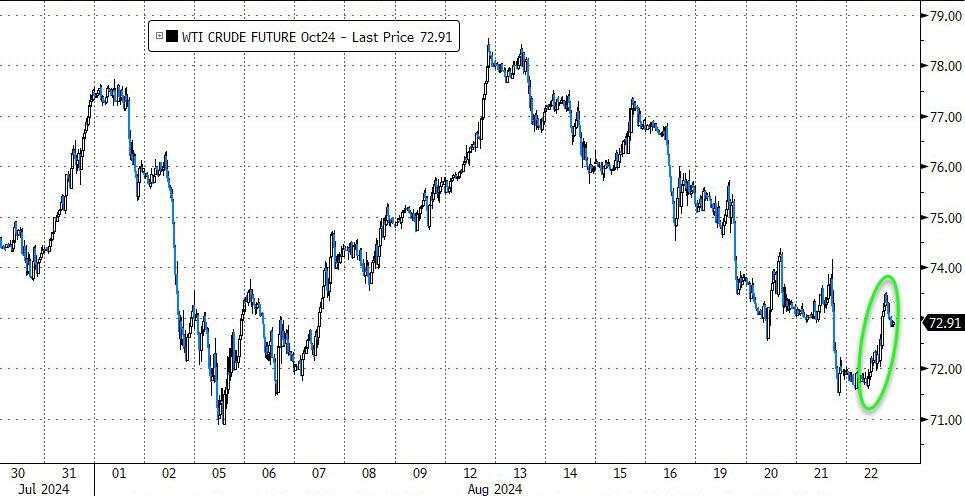

In commodities, oil prices are little changed, with WTI near $72 a barrel. Spot gold drops $8 to around $2,504/oz.

Bitcoin is flat and holds just beneath USD 61k, with Ethereum also rangebound just above USD 2.6k.

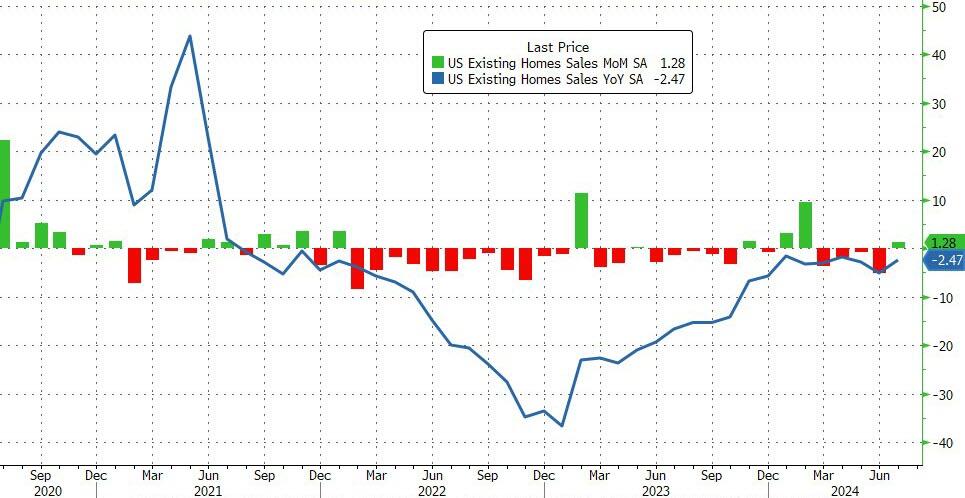

Looking at today’s calendar, the economic data includes July Chicago Fed national activity index and initial jobless claims (8:30am), August preliminary S&P Global US manufacturing and services PMIs (9:45am), July existing home sales (10am) and August Kansas City Fed manufacturing activity (11am). Fed speaker slate empty for the session

Market Snapshot

S&P 500 futures little changed at 5,645.75

MXAP up 0.3% to 185.14

MXAPJ up 0.4% to 575.40

Nikkei up 0.7% to 38,211.01

Topix up 0.2% to 2,671.40

Hang Seng Index up 1.4% to 17,641.00

Shanghai Composite down 0.3% to 2,848.77

Sensex up 0.2% to 81,091.03

Australia S&P/ASX 200 up 0.2% to 8,026.96

Kospi up 0.2% to 2,707.67

STOXX Europe 600 up 0.4% to 516.16

German 10Y yield little changed at 2.22%

Euro little changed at $1.1148

Brent Futures little changed at $76.12/bbl

Gold spot down 0.4% to $2,503.09

US Dollar Index up 0.13% to 101.17

Top Overnight News

At least three banks managed to obtain key payroll numbers Wednesday while the rest of Wall Street was kept waiting for a half-hour by a government delay that whipsawed markets and sowed confusion on trading desks.

Several Federal Reserve officials acknowledged there was a plausible case for cutting interest rates at their July 30-31 meeting before the central bank’s policy committee voted unanimously to keep them steady.

The euro’s August gains have been relentless, taking it to a one-year high against the dollar on Wednesday, but a cautious tone from Powell on Friday could turn that momentum around.

It’s arguably one of the last places you’d expect stock investors to turn as China’s economy struggles and its real estate crisis worsens.

Australia’s second-best performing hedge fund is profiting from greater market swings during earnings seasons, saying investment bank research has failed to track the ups and downs of faster-evolving industries.

French services expanded at the fastest pace in more than two years, driving Europe’s second-biggest economy as visitors from around the world flocked to Paris for the Olympic Games.

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded with a mild positive bias after the gains on Wall St where a downward payrolls revision and the FOMC Minutes further supported the consensus for a September Fed rate cut. ASX 200 edged higher but with gains capped as participants digested a slew of earnings, while data showed an improvement across Australia’s flash PMIs although manufacturing remained in contraction. Nikkei 225 marginally outperformed its peers and returned to above the key 38,000 level. Hang Seng and Shanghai Comp. wer e somewhat varied with notable strength in Hong Kong tech stocks after a solid earnings report from Xiaomi, although pharmaceutical stocks and WuXi biologics were at the other end of the spectrum after the latter reported a 24% drop in H1 net, while the mainland remained lacklustre amid growth concerns, trade frictions and a net liquidity drain.

Top Asian News

BoK kept its base rate unchanged at 3.50% as expected, with the decision made unanimously. BoK said it will examine the proper timing of rate cuts and said confidence is greater that inflation will converge on the target level, while it dropped the phrase ‘sufficient period of time’ in saying it will maintain a restrictive policy stance. BoK Governor Rhee said inflation conditions are appropriate for a cut and that four board members said room for a rate cut should remain open although Rhee also stated that rising financial stability risks warranted the BoK’s decision to hold rates today. Furthermore, Rhee said the pace and extent of an interest rate cut in South Korea will be smaller than that of the US and noted the BoK is communicating with markets using a three-month horizon forward guidance but also stated that forward guidance doesn’t guarantee a rate cut.

BoJ is considering adding wage-related items to the Tankan survey, according to Jiji News; aims to analyse wage trends in Tankan survey, reflects on monetary policy decision

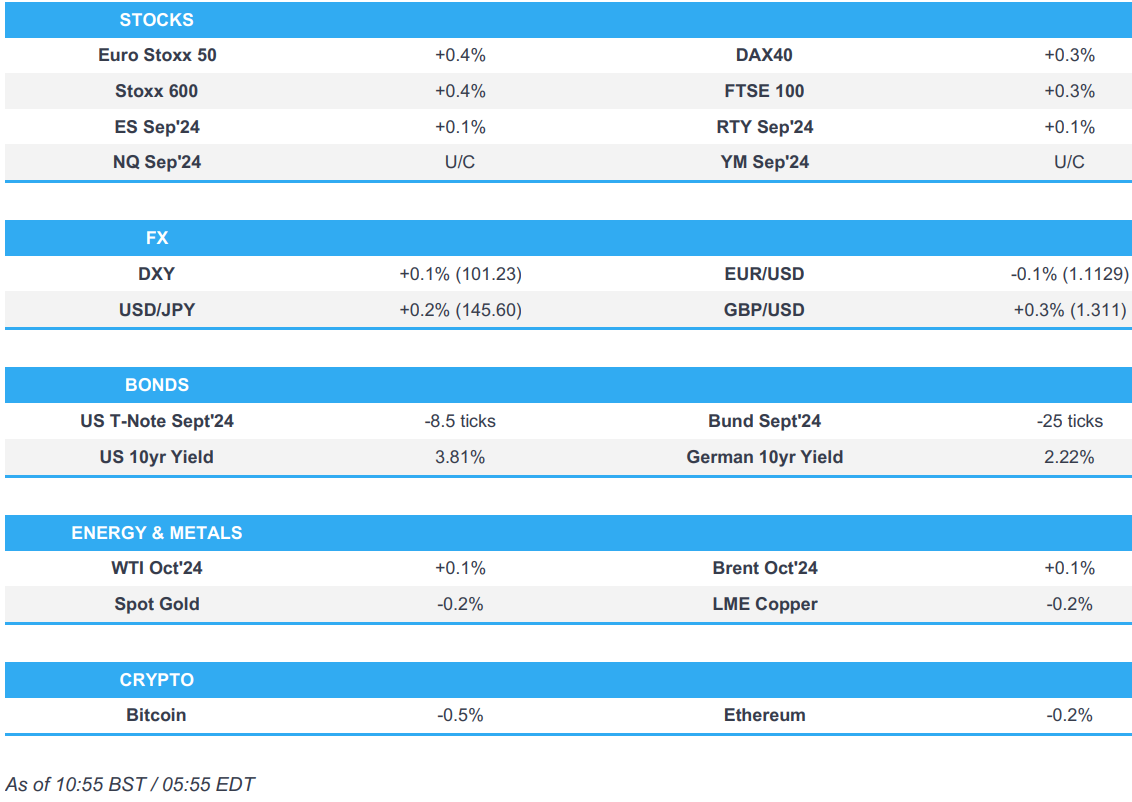

European bourses, Stoxx 600 (+0.5%) began the session flat/modestly firmer. Indices were choppy following the various PMI releases, but ultimately trudged higher as the morning progressed. European sectors hold a positive bias, albeit with the breadth of the market fairly narrow. Retail takes the top spot, propped up by post-earning strength in JD Sports (+3.1%). Basic Resources lags, paring back some of the strength seen yesterday, in line with a pullback in metals prices. US Equity Futures (ES U/C, NQ U/C, RTY U/C) are flat/firmer, with traders mindful ahead of the beginning of the Jackson Hole Symposium and Fed Chair Powell’s speech on Friday.

Top European News

UK Firms Report Faster Growth, Cooler Inflation in Boost for BOE

Private Equity Fights for UK Tax Perk While Ducking Public Ire

Norway’s Households Expect Near-Term Inflation to Accelerate

Euro-Zone Economy Handed Surprise Boost by Paris Olympics

FX

DXY is a touch higher but ultimately not showing enough of a resurgence to reverse the recent bearish run for the index. DXY went as low as 100.92 on Wednesday, but currently stands around 101.25.

EUR is marginally softer vs. the USD in the wake of a slew of EZ PMI metrics which ultimately saw continued outperformance in the service sector vs. the manufacturing industry with the former helping the composite to gain a firmer footing above the 50 mark. Elsewhere, a decline in EZ Negotiated Wages for Q2 had little sustained follow-through into the EUR. For now, EUR/USD is contained within Wednesday’s 1.1098-1.1174 range.

GBP is edging gains vs. both the USD and EUR with solid PMI metrics underpinning the pound. Cable has taken out yesterday’s 1.3119 high and therefore brought the 2023 high into view at 1.3142.

JPY is trivially softer vs. the USD with markets awaiting two potentially key inflection points for the pair tomorrow. 1) Ueda’s appearance before Parliament and 2) Powell’s appearance at Jackson Hole.

Antipodeans are both marginally firmer vs. the USD in quiet trade which is showing a mild pro-risk bias.

Fixed Income

USTs moved in tandem with the net-hawkish move seen in Bunds/Gilts on their own metrics. Docket today sees US PMIs ahead of the commencement of the Jackson Hole Symposium. At a 113-19 base, support from the last few session’s lows at 113-14+, 113-03+ and 112-31.

Bund price action today has been dictated by PMI releaes. Bunds were initially pressured by strong French PMIs, but the release is subject to extensive Olympic-related caveats, which led to the upside being mostly pared. Thereafter, German numbers were soft lifting Bunds to a 135.08 peak, spurred by the data erring towards another negative quarter and potential recession talk. Ultimately, Bunds are in the red and just below the knee-jerk base which printed on the initial French numbers.

Gilts were moving in tandem with Bunds into its own release, which was stronger across the board. Overall, a hawkish reaction was seen with GBP picking up and Gilts probing below the earlier 99.87 base; current low of 99.81.

Commodities

Relatively flat session for crude thus far following Wednesday’s losses. Brent Oct is trading within USD 75.77-76.21/bbl parameters.

Mixed trade across precious metals with slight gains in spot palladium while spot gold and silver trade subdued in what has been a quiet morning this far, and with little move seen in the metals to EZ PMIs. Spot gold trades in a USD 2,514.69-2,499.18/oz range.

Base metals are flat trade on Thursday, infitting with the broader tentative mood and following the prior day’s fluctuations, with markets seemingly on standby ahead of the Fed’s Jackson Hole symposium and Fed Chair Powell’s speech in the absence of any other macro impulses.

Russia’s Novatek has postponed launched of third line at Artic LNG 2 project to 2028, according RBC citing source.

Chinese crude steel output -9.0% Y/Y in July to 82.9mln tonnes; world steel output -4.7% Y/Y to 152.8mln tonnes.

UBS continue to expect Brent to recover into a USD 85-90/bbl range over the coming months; Reiterate a step up in Gold ETF inflows required for next leg higher toward their mid-2025 gold target of USD 2700/oz

OPEC Secretariat received updated compensation plans from Iraq and Kazakhstan.

Geopolitics

MIDDLE EAST

Ambrey reports a fire at sea approx. 58NM southwest of Salif, Yemen; likely related to the destruction of a suspected unmanned surface vessel

Israeli forces besiege Tulkarm refugee camp east of the city in the West Bank, while it was also reported that the Israeli army launched raids on 10 areas in Lebanon.

US officials said to believe that Iranian leaders have decided to postpone the response to Haniyeh’s assassination but fear that Tehran will urge Hezbollah to attack, according to The Washington Post.

US military announced on Wednesday that the USS Abraham Lincoln entered the Central Command area of responsibility in the Middle East, according to Iran International.

A fire broke out at a military facility in Russia’s Volgograd region after a drone crashed into it, according to Interfax.

US Embassy within Kyiv says they see an increased risk of Russian drone/missile attacks in the coming days, due to Ukraine’s Independence Day on 24th August

US Event Calendar

08:30: Aug. Initial Jobless Claims, est. 232,000, prior 227,000

Aug. Continuing Claims, est. 1.87m, prior 1.86m

08:30: July Chicago Fed Nat Activity Index, est. 0.03, prior 0.05

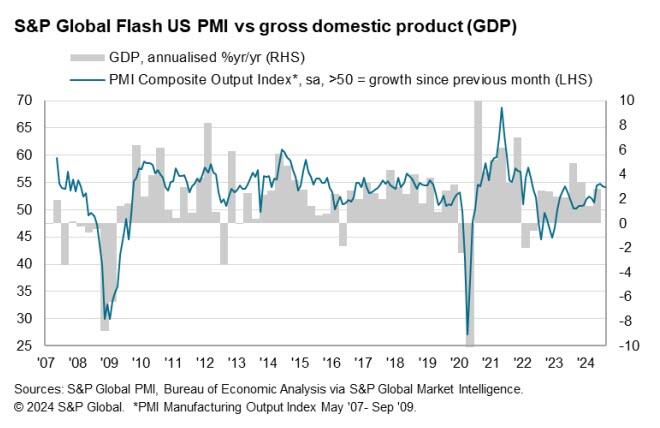

09:45: Aug. S&P Global US Manufacturing PM, est. 49.5, prior 49.6

Aug. S&P Global US Services PMI, est. 54.0, prior 55.0

Aug. S&P Global US Composite PMI, est. 53.2, prior 54.3

10:00: July Existing Home Sales MoM, est. 1.3%, prior -5.4%

11:00: Aug. Kansas City Fed Manf. Activity, est. -9, prior -13

DB’s Jim Reid concludes the overnight wrap

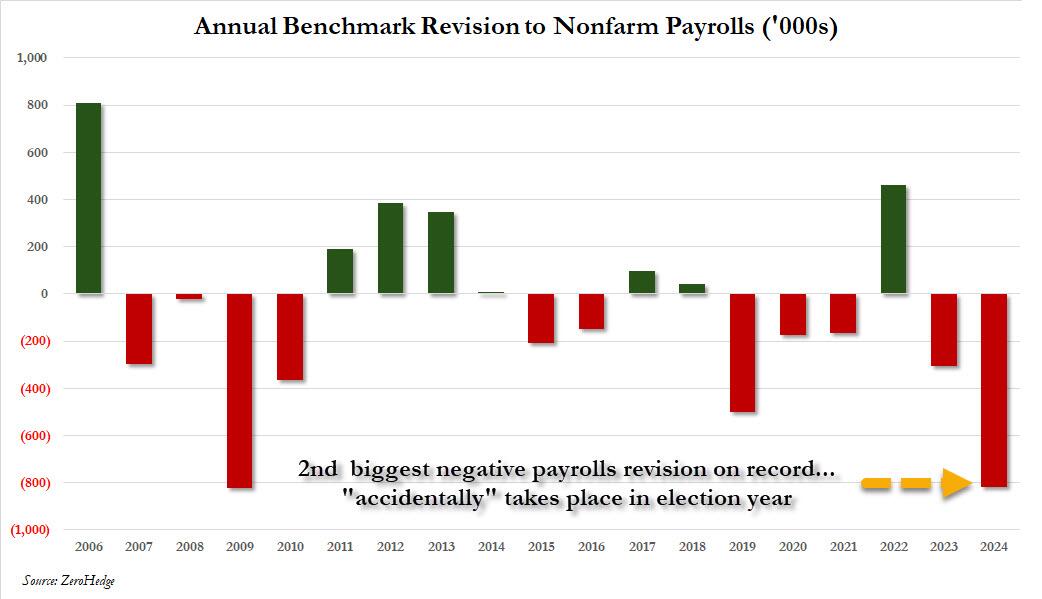

Markets put in another decent performance yesterday, as the S&P 500 (+0.42%) posted a further advance that left it less than 1% beneath its record high from July. The gains happened despite some negative revisions to US payrolls, but given the widespread expectations that they’d be revised down anyway, the news didn’t lead to a big reaction among risk assets. Plus the revisions only affect the numbers up to March, and don’t change our understanding of the more recent figures, which is ultimately what the Fed cares about. Later on in the session, we then received some dovish-leaning minutes from the Fed’s July meeting, which along with the payrolls revisions helped to cement expectations that the Fed would cut rates pretty rapidly over the coming months, with over 100bps of cuts priced in by year-end again.

In terms of the details of those revisions, what we got yesterday was the preliminary estimate for the annual benchmark revisions, which included an -818k downward revision to the March payrolls number. In other words, that means the monthly payroll numbers would be -68k lower if you assume the revisions are spread evenly across the year. Before the revisions, nonfarm payrolls had been running at an average pace of +242k per month over the year to March, so a downward revision that big would mean the pace was actually +174k instead. So these are still steady gains that are well clear of recessionary levels. But they’re noticeably less robust than previously thought, and the revisions have added to the narrative that the labour market is weakening, particularly after the jobs report at the start of the month.

The dovish mood then got a further boost from the minutes of the July FOMC meeting, which solidified the prospects of a September cut. Several FOMC participants even “observed that the recent progress on inflation and increases in the unemployment rate had provided a plausible case” for a 25bps cut at the July meeting. And while all of the FOMC supported the decision to keep rates unchanged in the end, a “vast majority” saw a September rate cut as appropriate if data came in as expected. There was also a shift in the economic assessment, as most of the FOMC “remarked that the risks to the employment goal had increased” and “some participants also noted the risk that a further gradual easing in labor market conditions could transition to a more serious deterioration”.

In response to the payroll revisions and Fed minutes, the most obvious market reaction was that investors dialled up their expectations for Fed rate cuts. For instance, futures are now pricing in 103bps of cuts by the December meeting (+4.3bps on the day). Bear in mind there’s only three meetings left this year, so that’s implicitly pricing in at least one meeting where they deliver a larger 50bp move. The chance of a 50bp move in September also ticked up from 34% to 36% by the close. Those growing expectations of a 50bp rate cut helped to weaken the dollar further, and the dollar index (-0.40%) fell back for a fourth consecutive session to its lowest since December. In turn, front-end Treasury yields moved noticeably lower with the 2yr yield (-5.3bps) down to 3.93%. This was accompanied by a sizeable steepening of the curve, with the 10yr yield (-0.6bps) down marginally and the 30yr (+1.7bps) higher on the day.

When it came to equities, there was a solid performance yesterday. The S&P 500 (+0.42%) saw a moderate but broad advance, with 80% of its constituents higher on the day and its equal-weighted version (+0.71%) posting a new all-time high. Target (+10.34%) was the second-best performer in the index after it reported that comparable sales were up +2% in Q2, ending a run of four quarterly declines. And it was a strong day for small-caps, with the Russell 2000 posting a +1.32% gain. However, there were a few signs of moderate stress, as the VIX index of volatility ticked up +0.39pts to 16.27pts.

Over in Europe it was a similar story, with moderate gains for the major equity indices that left the STOXX 600 up +0.33%. The broad dollar weakness also helped the Euro to strengthen for a fourth consecutive day, closing at a one-year high of $1.1146. At the same time, investors mirrored the US in dialling up their expectation of rate cuts from the ECB, and sovereign bond yields fell to their lowest in months across several countries. For example, yields on 10yr French OATs (-4.0bps) closed at 2.90%, their lowest since May, whilst yields on 10yr Italian BTPs (-3.4bps) closed at their lowest since December.

The dovish narrative about rate cuts got another boost from lower energy prices, which added to the sense that inflationary pressures were easing. For instance, Brent crude oil prices were down another -1.49% yesterday to $76.05/bbl, which is their lowest closing level since January. It now means that Brent crude is negative on a YTD basis again, and the effects have already been seen filtering through to lower gasoline prices. For example, the AAA’s daily tracker of US gasoline prices was down to $3.40 on Tuesday, which is its lowest level since March.

Overnight in Asia, markets have been trading more cautiously as investors look forward to Fed Chair Powell’s speech at Jackson Hole tomorrow. The Nikkei (+0.38%) has posted a decent gain, along with the Hang Seng (+0.40%). But elsewhere things have been more muted, and the CSI 300 (-0.13%), the Shanghai Comp (-0.04%) have both posted modest declines, whilst the KOSPI (+0.02%) has seen little movement after the Bank of Korea left their policy rate unchanged, in line with expectations. Looking forward, US and European equity futures are also pointing lower, with those on the S&P 500 (-0.14%) and the DAX (-0.08%) falling back slightly.

Elsewhere, one of the main highlights today will be the release of the August flash PMIs, which will offer an initial indication of how the global economy has been performing into this month. Overnight, we’ve already had some of those releases, which have painted a stronger picture so far. For instance, Australia’s composite PMI was back up to a three-month high of 51.4. And in Japan, the composite PMI was at a 15-month high of 53.0.

There was very little other data yesterday apart from the payrolls revisions. However, we did get the MBA’s weekly data on US mortgage applications. That showed the number of applications to purchase a home were down to their lowest since February, even though the contract rate fell to 6.50%, which is the lowest since May 2023.

To the day ahead now, and data releases include the August flash PMIs from Europe and the US. In addition, we’ll get the US weekly initial jobless claims and existing home sales for July, whilst in the Euro Area there’s the European Commission’s preliminary consumer confidence indicator for August. From central banks, the ECB will publish the account of their July meeting.

2B) European report

Equities gain modestly, Bonds hampered following EZ PMI metrics & GBP benefits on its own results – Newsquawk US Market Open

Thursday, Aug 22, 2024 – 06:09 AM

European bourses are mostly firmer across the board; US futures gain incrementally

Dollar is trivially higher, GBP outperforms following stronger than expected PMI metrics

Bonds are lower following the generally better than expected PMI releases, particularly in France the EZ and the UK; Germany continues to print poor metrics

Crude is flat, XAU is slightly softer but remains above USD 2500/oz

Looking ahead, US PMIs, US IJC, NZ Retail Sales, Jackson Hole Symposium, ECB Minutes, US Democratic Convention, Supply from US.

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

European bourses, Stoxx 600 (+0.5%) began the session flat/modestly firmer. Indices were choppy following the various PMI releases, but ultimately trudged higher as the morning progressed.

European sectors hold a positive bias, albeit with the breadth of the market fairly narrow. Retail takes the top spot, propped up by post-earning strength in JD Sports (+3.1%). Basic Resources lags, paring back some of the strength seen yesterday, in line with a pullback in metals prices.

US Equity Futures (ES U/C, NQ U/C, RTY U/C) are flat/firmer, with traders mindful ahead of the beginning of the Jackson Hole Symposium and Fed Chair Powell’s speech on Friday.

DXY is a touch higher but ultimately not showing enough of a resurgence to reverse the recent bearish run for the index. DXY went as low as 100.92 on Wednesday, but currently stands around 101.25.

EUR is marginally softer vs. the USD in the wake of a slew of EZ PMI metrics which ultimately saw continued outperformance in the service sector vs. the manufacturing industry with the former helping the composite to gain a firmer footing above the 50 mark. Elsewhere, a decline in EZ Negotiated Wages for Q2 had little sustained follow-through into the EUR. For now, EUR/USD is contained within Wednesday’s 1.1098-1.1174 range.

GBP is edging gains vs. both the USD and EUR with solid PMI metrics underpinning the pound. Cable has taken out yesterday’s 1.3119 high and therefore brought the 2023 high into view at 1.3142.

JPY is trivially softer vs. the USD with markets awaiting two potentially key inflection points for the pair tomorrow. 1) Ueda’s appearance before Parliament and 2) Powell’s appearance at Jackson Hole.

Antipodeans are both marginally firmer vs. the USD in quiet trade which is showing a mild pro-risk bias.

USTs moved in tandem with the net-hawkish move seen in Bunds/Gilts on their own metrics. Docket today sees US PMIs ahead of the commencement of the Jackson Hole Symposium. At a 113-19 base, support from the last few session’s lows at 113-14+, 113-03+ and 112-31.

Bund price action today has been dictated by PMI releaes. Bunds were initially pressured by strong French PMIs, but the release is subject to extensive Olympic-related caveats, which led to the upside being mostly pared. Thereafter, German numbers were soft lifting Bunds to a 135.08 peak, spurred by the data erring towards another negative quarter and potential recession talk. Ultimately, Bunds are in the red and just below the knee-jerk base which printed on the initial French numbers.

Gilts were moving in tandem with Bunds into its own release, which was stronger across the board. Overall, a hawkish reaction was seen with GBP picking up and Gilts probing below the earlier 99.87 base; current low of 99.81.

Relatively flat session for crude thus far following Wednesday’s losses. Brent Oct is trading within USD 75.77-76.21/bbl parameters.

Mixed trade across precious metals with slight gains in spot palladium while spot gold and silver trade subdued in what has been a quiet morning this far, and with little move seen in the metals to EZ PMIs. Spot gold trades in a USD 2,514.69-2,499.18/oz range.