GOLD PRICE CLOSED UP $23,59 TO $2527.00 * ALL TIME HIGH CLOSING

SILVER PRICE UP $.37 TO $29.58

Gold ACCESS CLOSED $2504.05

Silver ACCESS CLOSED: $29.17

Friday is OTC/London LBMA options expiry which is much bigger than comex.

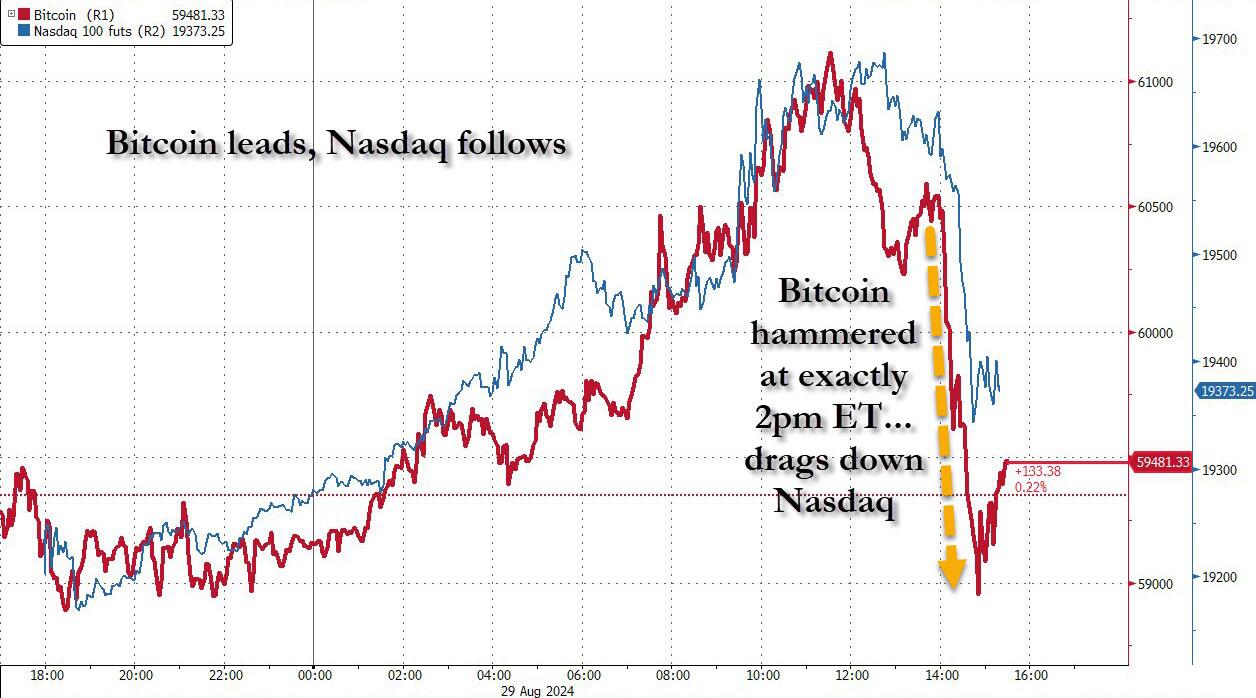

Bitcoin morning price:$59,633 UP 230 DOLLARS.

Bitcoin: afternoon price: $59,585 UP 182 DOLLARS

Platinum price closing UP $10.50 TO $945.45

Palladium price; UP $36.30 TO $983.40

END

*CANADIAN GOLD: $3400.90 UP 29.39 CDN dollars per oz( * NEW ALL TIME HIGH 3,431.95 CDN DOLLARS PER OZ//AUG 16 2024)

*BRITISH GOLD: 1,915.02 UP 14.04 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1937.75 BRITISH POUNDS/OZ) AUGUST 16/2024

*EURO GOLD: 2,276.65 UP 22.19 Euros per oz //* (ALL TIME CLOSING HIGH: 2.276.65 EUROS PER OZ//AUGUST 29 //.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE: COMEX

JPMorgan stopped 0/76

EXCHANGE: COMEX

CONTRACT: AUGUST 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,501.000000000 USD

INTENT DATE: 08/28/2024 DELIVERY DATE: 08/30/2024

FIRM ORG FIRM NAME ISSUED STOPPED

132 C SG AMERICAS 39

624 H BOFA SECURITIES 76

737 C ADVANTAGE 35

905 C ADM 2

TOTAL: 76 76

GOLD: NUMBER OF NOTICES FILED FOR AUGUST/2024. CONTRACT: 76 NOTICES FOR 7600 OZ or 0.2364 TONNES

total notices so far: 22,353 contracts for 2,235,300 Oz (69.527 tonnes)

FOR AUGUST:

SILVER NOTICES: 5 NOTICE(S) FILED FOR 25,000

OZ/

total number of notices filed so far this month : 1035 for 5,175,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $23.50 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ NO CHANGES IN GOLD INVENTORY AT THE GLD:

/ /INVENTORY RESTS AT 856.12 TONNES

INVENTORY RESTS AT 856.12 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.37 AT THE SLV

SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF .558 MILLION OZ OUT OF THE SLV/

//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 464.683 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A MEGA MEGA GIGANTIC SIZED 3998 CONTRACTS TO 137,615 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS MEGA HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR STRONG LOSS OF $0.76 IN SILVER PRICING AT THE COMEX ON WEDNESDAY’S TRADING. WE LOST CONSIDERABLE LONGS WITH THE LOSS IN PRICE. WE HAD A HUGE LOSS OF 3348 CONTRACTS ON OUR TWO EXCHANGES. WE HAD AGAIN A HUGE LIQUIDATION OF T.A.S. CONTRACTS AND MONTH END SPREADERS DURING WEDNESDAY’S TRADING//. WE HAD CONSIDERABLE COVERING BY OUR SPECS WITH THE HUGE LOSS IN PRICE. WE HAD ANOTHER STRONG 650 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY ANOTHER HUGE 669 CONTRACT T.A.S ISSUANCE. IN ESSENCE WE LOST 3348 CONTRACTS ON OUR TWO EXCHANGES WITH THE LOSS IN PRICE.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN YESTERDAY. THE ACCUMULATED T.A.S. IS BEING USED TO MANIPULATE PRICES AT THE COMEX NOW EVERY DAY..

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 669 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS.IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1/2 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS BUT TO NO AVAIL. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.76) AND WERE SUCCESSFUL IN KNOCKING A FEW SILVER LONGS FROM THEIR PERCH AS WE HAD A STRONG LOSS OF 3290 TOTAL CONTRACTS ON OUR TWO EXCHANGES. THE MAJORITY OF THE LOSS WAS DUE TO T.A.S AND MONTH END SPREADER LIQUIDATION.

WE HAD A HUGE 650 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.005 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 25,000 OZ QUEUE JUMP //NEW STANDING RISES TO 5.175 MILLION OZ

//NEW STANDING FOR SILVER//AUGUST IS THUS 5.175 MILLION OZ

WE HAD:

/ MEGA HUGE SIZED COMEX OI LOSS //HUGE SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 669 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED 58 CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST

TOTAL CONTRACTS for 21 DAYS, total 19,523 contracts: OR 97.615 MILLION OZ (930 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 94.365 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 97.615 MILLION OZ//THIS MONTH WILL PROBABLY BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

RESULT: WE HAD A MEGA HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3998 CONTRACTS WITH OUR HUGE LOSS IN PRICE OF SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 650 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 3.005 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 25,000 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR AUG 5.1750 MILLION OZ

WE HAVE A MEGA HUGE LOSS OF 3348 OI CONTRACTS ON THE TWO EXCHANGES WITH THE HUGE LOSS IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 669 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX TRADING//// MASSIVE ATTEMPTED SHORT COVERING FROM OUR SPEC SHORTS WITH THE STRONG FALL IN PRICE YESTERDAY/ AND CONSIDERABLE LIQUIDATION OF LONGS. ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER.

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (669) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND FOR SURE TODAY., .

WE HAD 5 NOTICE(S) FILED TODAY FOR 25,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A TINY SIZED 29 OI CONTRACTS TO 521,788 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A MASSIVE 3159CONTRACTS//

WE HAD A TINY SIZED INCREASE IN COMEX OI (29 CONTRACTS) OCCURRED DESPITE OUR LOSS OF $14.65 IN PRICE/WEDNESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR AUGUST AT 65.55 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE 10,000 OZ QUEUE JUMP AS THESE GUYS NEEDED BADLY PHYSICAL GOLD ON THIS SIDE OF THE PLANET.

NEW STANDING RISES TO 69.602 TONNES

/ ALL OF THIS HAPPENED WITH OUR $14.65 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A FAIR SIZED GAIN OF 2174 OI CONTRACTS (6.762 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE LOW GAIN IN COMEX OI WAS DUE TO DISTORTION FROM CONSIDERABLE T.A.S. LIQUIDATION AND MONTH END SPREADER LIQUIDATION.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 2145 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 521,788

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2174 CONTRACTS WITH 29 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 2145 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 5333 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALLISH 313 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2145 CONTRACTS) ACCOMPANYING THE TINY SIZED INCREASE IN COMEX OI OF 29 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 2174 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR AUGUST AT 65.55 TONNES FOLLOWED BY TODAY’S HUGE 10,000 OZ QUEUE JUMP AS THESE GUYS NEEDED PHYSICAL GOLD ON THIS SIDE OF THE PLANET.

//NEW STANDING ADVANCES TO: /AUGUST 69.290 TONNES.

/ 3) CONSIDERABLE T.A.S. LIQUIDATION AND MONTH END SPREADER CONTRACT LIQUIDATION WITH ZERO NET LONG SPECS BEING CLIPPED,

4) FAIR SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///SMALL T.A.S. ISSUANCE: 313 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST. :

TOTAL EFP CONTRACTS ISSUED: 86,524 CONTRACTS OF 8,652,400 OZ OR 269.125 TONNES IN 21 TRADING DAY(S) AND THUS AVERAGING: 4120 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 21 TRADING DAY(S) IN TONNES 269.13 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 269.13 DIVIDED BY 3550 x 100% TONNES = 7.58% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 269.13 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUG), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA HUGE SIZED 3998 CONTRACTS OI TO 137,615 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 650 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 650 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 650 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 3998 CONTRACTS AND ADD TO THE 650 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 3348 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 16.740 MILLION OZ OCCURRED WITH OUR $0.76 LOSS IN PRICE

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 14.32 PTS OR 0.50% //Hang Seng CLOSED UP 93.87 PTS OR 0.53% // Nikkei CLOSED DOWN 9.23 OR .02%//Australia’s all ordinaries CLOSED DOWN 0.33%///Chinese yuan (ONSHORE) CLOSED UP TO 7,0929 CHINESE YUAN OFFSHORE CLOSED UP TO 7.0896/ Oil UP TO 74.78 dollars per barrel for WTI and BRENT UP AT 78.85 Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A TINY SIZED 29 CONTRACTS TO 521,788 DESPITE OUR LOSS IN PRICE OF $14.65 WITH RESPECT TO WEDNESDAY’S TRADING. WE LOST A HUGE NUMBER OF SPREADER/T.A.S. CONTRACTS AS SHORTS TRIED TO, THROUGHOUT THE SESSION, COVER WHAT THEY COULD AT LOWER PRICES. THE FED IS THE MAJOR SHORT OF AROUND 148 TONNES+ OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS IS SCHEDULED TO HAPPEN LATE SEPT 2024.

OUR LONDONERS ALSO BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT THESE HIGHER PRICES AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD A HUGE T.A.S. LIQUIDATION ON WEDNESDAY’S LOSS IN PRICE WITH ZERO LONGS WERE CLIPPED (AS YOU WILL SEE BELOW) BUT WE DID HAVE MAJOR SHORT COVERING. THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF THE SPREADERS AND T.A.S IS SURELY DISTORTING COMEX OPEN INTEREST.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE ACTIVE DELIVERY MONTH OF AUGUST.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 2145 EFP CONTRACTS WERE ISSUED: : OCT/DEC 2145 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2145 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2174 CONTRACTS IN THAT 2145 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A TINY GAIN OF 29 COMEX CONTRACTS..AND THIS STRONG GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $14.65/WEDNESDAY COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AS MENTIONED ABOVE. THE RAID YESTERDAY WAS ORCHESTRATED BY THE FRBNY AS WE NOW ENTER OPTIONS EXPIRY FOR THE OTC/LONDON LBMA BETS. DESPITE THE FED’S HUGE SHORT PREDICAMENT THEY STILL HAVE TIME AND ENERGY TO RAID OUR PRECIOUS METALS. SUCH CROOKS! THE RAID ACCOMPLISHED NOTHING BUT GRIEF TO OUR CENTRAL BANKER, THE FRBNY, AS OTHER CENTRAL BANKS TOOK THE FED’S LARGESS OF SUPPLY TO OBTAIN CONSIDERABLE PHYSICAL GOLD.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT A SMALL SIZED 313 CONTRACTS. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE (AND SPREADERS LATE IN THE MONTH). THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN LAST WEEK’S TRADING//RAIDS AS WELL AS THIS WEEK AND ESPECIALLY ON LAST THURSDAY.S HUGE /RAID AND YESTERDAY’S RAID.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: AUGUST (69.602 TONNES)

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 44 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $14.65 //// BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE DID HAVE A FAIR GAIN IN OUR TWO EXCHANGES. WE HAD HUGE SPREADER LIQUIDATION. BUT CENTRAL BANK LONGS, SEIZING THE MOMENT, EXERCISED FOR PHYSICAL. WE HAD BOTH HUGE T.A.S. LIQUIDATION AND SPREADER LIQUIDATION WEDNESDAY AT THE COMEX.

WE HAVE GAINED A TOTAL OI OF 16.587 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR AUGUST (65.55 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE 10,000 OZ QUEUE JUMP //NEW STANDING ADVANCES TO: 69.602 TONNES.

NEW STANDING FOR AUGUST: 69.602 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $14.65

WE HAVE REMOVED A MAMMOTH 4782 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. THIS IS THE LARGEST ADJUSTMENT TO DATE.

NET GAIN ON THE TWO EXCHANGES 5333 CONTRACTS OR 533,300 OZ (16.587

TONNES)

confirmed volume WEDNESDAY 180,096 contracts poor

//speculators have left the gold arena

END

AUGUST 29 AUGUST GOLD CONTRACT

/ /// THE AUG 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | NIL oz |

| No of oz served (contracts) today | 76 notice(s) 7600 OZ 0.2364 TONNES |

| No of oz to be served (notices) | 24 contracts 2400 OZ 0.0745 TONNES |

| Total monthly oz gold served (contracts) so far this month | 22,353 notices 2,235300 oz 69.527 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: nil oz

we have 0 customer deposits

total deposits NIL oz

withdrawals:

TOTAL WITHDRAWALS nil oz

adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR AUGUST

For the front month of AUGUST we have an oi of 100 contracts having GAINED 15 contracts.

We had 85 contracts served on WEDNESDAY so we GAINED an additional 100 contracts or 10,000 oz will stand for gold at the comex as these guys needed physical gold on this side of the planet.

SEPT. LOST 199 CONTRACTS TO STAND AT 5,111 CONTRACTS.

OCTOBER GAINED 415 CONTRACTS UP TO 46,859 CONTRACTS

We had 76 contracts filed for today representing 7600 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notice issued from their client or customer account. The total of all issuance by all participants equate to 76 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for AUGUST /2024. contract month, we take the total number of notices filed so far for the month (22,353) x 100 oz ) to which we add the difference between the open interest for the front month of August 100( CONTRACTS) minus the number of notices served upon today (76x 100 oz per contract( equals 2,237,700 OZ OR 69.602 TONNES. Somebody was in great need of physical gold on THIS side of the pond today (NEW YORK)

thus the INITIAL standings for gold for the AUGUST contract month: No of notices filed so far (22,353 x 100 oz +we add the difference for front month of AUGUST (100 X// , OI} minus the number of notices served upon today (76) x 100 oz which equals 2,237,700 oz (69.602 TONNES)

TOTAL COMEX GOLD STANDING FOR AUGUST: 69.602 TONNES WHICH IS HUGE FOR THIS VERY ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,770,778.600 oz 55.078 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,183,912.038 OZ

TOTAL REGISTERED GOLD 7,522,254.284 ( 233.97 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,661,657,754 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 5,751,476 oz (REG GOLD- PLEDGED GOLD)= 178.89 tonnes //

END

SILVER/COMEX

AUGUST 29/2024

INITIAL

//2024// THE AUG 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 597,021.570 OZ DELAWARE . |

| Deposits to the Dealer Inventory | NIL |

| Deposits to the Customer Inventory | 1,239,861.472 oz ASAHI Brinks |

| No of oz served today (contracts) | 5 CONTRACT(S) (25,000 OZ) |

| No of oz to be served (notices) | 0 contracts (0.000 million oz) |

| Total monthly oz silver served (contracts) | 1035 Contracts (5.175 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit/

total dealer deposit : NIL oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 customer deposits:

i) Into ASAHI 596,614.000 oz

ii) Into Brinks 643,247.472 oz

total customer deposit 1,239.861.472 oz

JPMorgan has a total silver weight: 135.336million oz/307.154 million or 44.04%

adjustment:1

a) customer to dealer Delaware 597,021.570 oz

withdrawals: 1

iii) Out of Delaware 597,021.570 oz

total customer withdrawals: 597,021.570 oz

TOTAL REGISTERED SILVER: 76.516 MILLION OZ//.TOTAL REG + ELIGIBLE. 307.154 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR AUGUST:

silver open interest data:

FRONT MONTH OF AUGUST/2024 OI: 5 CONTRACTS HAVING LOST 73 CONTRACT(S).

WE HAD 78 NOTICES SERVED ON WEDNESDAY, SO WE GAINED 5 CONTRACTs OR AN ADDITIONAL 25,000 OZ WILL STAND FOR SILVER AT THE COMEX.

SEPT SAW A LOSS OF 10,056 CONTRACTS TO 9596. SEPT NOW BECOMES THE NEW FRONT MONTH. WE HAVE 1 MORE READING DAY BEFORE FIRST DAY NOTICE I.E. FRIDAY’S READING ON FIRST DAY NOTICE

OCTOBER SAW ANOTHER GAIN OF OPEN INTEREST CONTRACTS OF 107 CONTRACTS AND THUS WE HAVE 1428 OPEN INTEREST CONTRACTS FOR OCTOBER.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 5 for 25,000 oz

CONFIRMED volume; ON THURSDAY 98,303 strong

To calculate the number of silver ounces that will stand for delivery in AUGUST we take the total number of notices filed for the month so far at 1035 x 5,000 oz = 5.1750 MILLION oz

to which we add the difference between the open interest for the front month of AUGUST(5) and the number of notices served upon today 5 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the AUGUST/2024 contract month: 1035 notices served so far) x 5000 oz + OI for the front month of AUGUST (5)x number of notices served upon today minus (5)x 5000 oz of silver standing for the AUGUST contract month equates to 5.1750 MILLION OZ.

New total standing: 5.1750 million oz.

There are 76.516 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS//

GLD

AUGUST 29 WITH GOLD UP $23.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 28 WITH GOLD DOWN $14.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 27 WITH GOLD DOWN $1.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 26 WITH GOLD UP $9.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD VAPOUR GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 23 WITH GOLD UP $29.70 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER WITHDRAWAL OF 8.88 TONNES OF GOLD VAPOUR GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 857.85 TONNES

AUGUST 22 WITH GOLD DOWN $28.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 9.43 TONNES OF GOLD VAPOUR GOLD INTO THE GLD./ //////INVENTORY RESTS AT 866.70 TONNES

AUGUST 21 WITH GOLD DOWN $1.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER WITHDRAWAL OF 1.73 TONNES OF GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 857.27 TONNES

AUGUST 20 WITH GOLD UP $9.40 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 4.03 TONNES OF GOLD VAPOUR INTO THE GLD./ //////INVENTORY RESTS AT 859.00 TONNES

AUGUST 19 WITH GOLD UP $3.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 7.19 TONNES OF GOLD VAPOUR INTO THE GLD./ //////INVENTORY RESTS AT 854.97 TONNES

AUGUST 16 WITH GOLD UP $44.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: //////INVENTORY RESTS AT 847.78 TONNES

AUGUST 15 WITH GOLD UP $13,70 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD OUT OF THE GLD//////INVENTORY RESTS AT 847.78 TONNES

AUGUST 14 WITH GOLD DOWN $26.20 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.03 TONNES OF GOLD OUT OF THE GLD//////INVENTORY RESTS AT 845.76 TONNES

AUGUST 13 WITH GOLD UP $3.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//////INVENTORY RESTS AT 849.79 TONNES

AUGUST 12 WITH GOLD UP $30.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ////INVENTORY RESTS AT 846.91 TONNES

AUGUST 9 WITH GOLD UP $10.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 846.91 TONNES

AUGUST 8 WITH GOLD UP $31.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.02 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 844.04 TONNES

AUGUST 7 WITH GOLD UP $1.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.16 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 848.06 TONNES

AUGUST 6 WITH GOLD DOWN $13.10 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD” A WITHDRAWAL OF .57 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 844.90 TONNES

AUGUST 2 WITH GOLD DOWN $9.95 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.58 TONNES OF GOLD OUT OF THE GLD//INVENTORY RESTS AT 845.47 TONNES

AUGUST 1 WITH GOLD UP $9.15 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 846.05 TONNES

JULY 30 WITH GOLD UP $26.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// A /////INVENTORY RESTS AT 843.17 TONNES

JULY 29 WITH GOLD UP $27.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD// A WITHDRAWAL OF 1.98 TONNES OF GOLD OUT OF THE GLD/////INVENTORY RESTS AT 843.17 TONNES

JULY 26 WITH GOLD UP $27.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD// A DEPOSIT OF 3.45 TONNES OF GOLD INTO THE GLD/////INVENTORY RESTS AT 845.19 TONNES

JULY 25 WITH GOLD DOWN $60.45 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 841.74 TONNES

JULY 24 WITH GOLD UP $12.75 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1,73 TOONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 841.74 TONNES

JULY 23 WITH GOLD UP $12.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 22 WITH GOLD DOWN $4.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 19 WITH GOLD DOWN $56.10 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;:A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 18 WITH GOLD DOWN $2.20 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;: ///INVENTORY RESTS AT 842.02 TONNES

JULY 17 WITH GOLD DOWN $6.60 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A MASSIVE DEPOSIT OF 5.49 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 842.02 TONNES

JULY 16 WITH GOLD UP $38.60 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 836.53 TONNES

GLD INVENTORY: 856.12 TONNES, TONIGHTS TOTAL

SILVER

AUGUST 29//WITH SILVER UP $.37//SMALL CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 0.558 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 464.693 MILLION OZ

AUGUST 28//WITH SILVER DOWN $0.76//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 2.301 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 465.281 MILLION OZ

AUGUST 27//WITH SILVER DOWN $0.03//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 2.921 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 462.959 MILLION OZ

AUGUST 26//WITH SILVER UP $0.23//SMALL CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 45,000 OZ OUT OF THE SLV. .///./// /INVENTORY AT 465.880 MILLION OZ

AUGUST 23//WITH SILVER UP $0.72//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 1.506 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 465.925 MILLION OZ

AUGUST 22//WITH SILVER DOWN $0.44//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 0.943 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 468.344 MILLION OZ

AUGUST 21//WITH SILVER $0.03//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 1..552 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 468.344 MILLION OZ

AUGUST 20//WITH SILVER $0.24//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 1.369 MILLION OZ FROM THE SLV. .///./// /INVENTORY AT 466.792 MILLION OZ

AUGUST 19//WITH SILVER $0.39//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 1.506 MILLION OZ FROM THE SLV. .///./// /INVENTORY AT 465.423 MILLION OZ

AUGUST 16//WITH SILVER $0.49//NO CHANGES IN SILVER INVENTORY: .///./// /INVENTORY AT 466.929 MILLION OZ

AUGUST 15//WITH SILVER $1.14//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.186 MILLION ON INTO THE SLV.///./// /INVENTORY AT 466.929 MILLION OZ

AUGUST 14//WITH SILVER DOWN $0.40//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 13//WITH SILVER DOWN $0.19//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 12//WITH SILVER UP $.37//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 9//WITH SILVER DOWN $.03//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 8//WITH SILVER UP $.70//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 3.241 MILLION OZ INTO THE SLV////./// /INVENTORY AT 462.502 MILLION OZ

AUGUST 7//WITH SILVER DOWN $0.27//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.552 MILLION OZ INTO THE SLV////./// /INVENTORY AT 462.502 MILLION OZ

AUGUST 6//WITH SILVER UP $0.05//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 458.851 MILLION OZ

AUGUST 2//WITH SILVER DOWN $0.01//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 1.243 MILLION OZ OF SILVER OUT OF THE SLV ///./// /INVENTORY AT 460.961 MILLION OZ

AUGUST 1//WITH SILVER DOWN $0.46//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.608 MILLION OZ OF SILVER VAPOUR INTO THE SLV///./// /INVENTORY AT 462.204 MILLION OZ

JULY 31//WITH SILVER UP $0.45//NO CHANGES IN SILVER INVENTORY: /./// /INVENTORY REMAINS AT 460.596 MILLION OZ

JULY 30//WITH SILVER UP $0.61//SMALL CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 0.456 MILLION OZ OF SILVER VAPOUR INTO THE SLV/./// /INVENTORY RISES AT 460.596 MILLION OZ

JULY 29//WITH SILVER DOWN $0.07//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.382 MILLION OZ OF SILVER VAPOUR INTO THE SLV/./// /INVENTORY RISES AT 461.052 MILLION OZ

JULY 26//WITH SILVER DOWN $0.07//NO CHANGES IN SILVER INVENTORY./// /INVENTORY REMAINS AT 456.670 MILLION OZ

JULY 25 WITH SILVER DOWN $1.37//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 3.124 MILLION OZ OF SILVER OUT OF THE SLV./// /INVENTORY FALLS TO 456.670 MILLION OZ

JULY 24 WITH SILVER UP 3 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 15.880 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 23 WITH SILVER UP 3 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 15.880 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 22 WITH SILVER UP 2 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 3.920 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 19 WITH SILVER DOWN 94 CENTS//NO CHANGES IN SILVER INVENTORY/// /INVENTORY REMAINS AT 435.854 MILLION OZ

JULY 18 WITH SILVER DOWN 13 CENTS//HUGE CHANGES IN SILVER INVENTORY” A DEPOSIT OF 2.374 MILLION OZ INTO THE SLV/// /INVENTORY RISES TO 435.854 MILLION OZ

JULY 17. WITH SILVER DOWN 75 CENTS//NO CHANGES IN SILVER INVENTORY// /INVENTORY REMAINS AT 433.480 MILLION OZ.

JULY 16. WITH SILVER UP 30 CENTS//NO CHANGES IN SILVER INVENTORY// /INVENTORY REMAINS AT 433.480 MILLION OZ.

CLOSING INVENTORY 464.693 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/MIKE MAHARRAY

Peter Schiff: Fed’s Pivot Is Misguided

Thursday, Aug 29, 2024 – 02:35 PM

In this episode, Peter analyzes the Fed’s conference in Jackson Hole and the pivot Jerome Powell signaled in figure monetary policy. He also dives into the hot political topics from this week, namely, the Democratic National Convention and RFK Jr.’s endorsement of Donald Trump for President.

Despite what Powell says, Peter is convinced there’s not sufficient evidence to support rate cuts in September:

“And during the speech, Powell said that now, finally, after all of these months, now I’m convinced that inflation is headed back down to 2%. But why? What data have we seen that has shown a significant improvement that you would think that inflation is headed back down to 2%? It’s 3% right now. … If you look at the actual CPI, 2.9% was the last one.”

The Fed’s dual mandate to fight both inflation and unemployment is proving problematic, since improving one often worsens the other:

“He [Powell] said that any additional weakness in the labor market is unwelcome. See, before he was saying we wanted some weakness in the labor market, because that’s how we were going to bring down inflation. But now, based on all of the weak data that we got on the labor market— especially that last non-farm payroll report— he’s saying, ‘No, we can’t have any more weakness in the labor market.’ So the Fed has really pivoted now from fighting inflation to fighting unemployment, which is on the rise.”

These problems are inevitable when you tamper with interest rates, which are fundamental to a healthy economy:

“The Fed gets the economy all juiced up on cheap money. They build the entire phony recovery on a foundation of artificially low interest rates, and as a result, everybody goes into debt. And now they think they can raise interest rates without having a collapse. That’s impossible. You can’t have a foundation built on debt and then raise interest rates and expect the foundation not to collapse.”

Moving on to politics, Peter explains what stood out to him about this year’s DNC:

“I’ve watched a number of these over the years. Again, I’ve been to a couple of them— not as a delegate. I was there on a press pass. I’ve never been a delegate. But I’ve never seen a convention where they vilified the opposition and the opponent anywhere near to the degree that they vilified Trump. I thought that they would have backed off on that kind of characterization, given the fact that someone tried to kill him.”

Many of the DNC’s criticisms of Trump are outright lies:

“They spend almost all their time lying about Trump. Most of the things— almost everything, actually— that they accuse Trump of doing or wanting to do, he’s not going to do. And they repeated all these lies where they take things out of context, like the ‘bloodbath’ or ‘bad people on both sides’ or whatever it is or all these quotes that have already been proven were either not said or were taken out of context and don’t even apply to the way they’re using them.”

One silver lining from the week is RFK Jr.’s endorsement of Donald Trump for president. Constituting arguably the first true “unity campaign” in decades, the revitalized Trump ticket is a legitimate threat to the establishment, and hopefully it can take action to end wasteful wars around the world:

“At least Robert Kennedy and Donald Trump care about all these people who are dying, and they want to stop it. Now, secondarily, we’re wasting all this money so all these innocent people could die, and for what reason? Ukraine is in much worse shape now than it was two years ago. For what? For nothing. Again, there was more freedom in Russia than in Ukraine before the whole thing started. We were trying to preserve Ukrainian freedom; they’re less free now than they were before because of this war. … This has been a disaster. So at least you’ve got Kennedy and Trump that are thorns in the side of the political establishment, and that’s what we need. We need to break the stranglehold of the neocons.”

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY//BILL HOLTER:

3.CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES

4. GOLD PODCASTS//LIVE FROM THE VAULT/

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/

end

6 CRYPTOCURRENCY NEWS

END

ASIA TRADING/THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 14.32 PTS OR 0.50% //Hang Seng CLOSED UP 93.87 PTS OR 0.53% // Nikkei CLOSED DOWN 9.23 OR .02%//Australia’s all ordinaries CLOSED DOWN 0.33%///Chinese yuan (ONSHORE) CLOSED UP TO 7,0929 CHINESE YUAN OFFSHORE CLOSED UP TO 7.0896/ Oil UP TO 74.78 dollars per barrel for WTI and BRENT UP AT 78.85 Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.0929

OFFSHORE YUAN: UP TO 7.0896

SHANGHAI CLOSED DOWN 14.32 PTS OR 0.50 %

HANG SENG CLOSED UP 93.87 PTS OR 0.53%

2. Nikkei closed DOWN 9.23 PTS OR .02%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 101.12 EURO FALLS TO 1.1098 DOWN 26 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +0.894 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 144.53…… JAPANESE YEN NOW RISING AS WE HAVE NOW REACHED THE COLLAPSING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.2425/Italian 10 Yr bond yield DOWN to 3.631 SPAIN 10 YR BOND YIELD DOWN TO 3.072%

3i Greek 10 year bond yield DOWN TO 3.289

3j Gold at $2521.50//Silver at: 29.42 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 5/ 100 roubles/dollar; ROUBLE AT 90.55

3m oil into the 74 dollar handle for WTI and 78 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 144.53/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.894 % STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8437 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9364 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.838 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.119 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 3.863 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 34.03…

10 YR UK BOND YIELD: 4.031 UP 3 PTS

10 YR CANADA BOND YIELD: 3.097 DOWN 1 BASIS PTS

2a New York OPENING REPORT

Futures Rebound From NVDA Earnings Slide

Thursday, Aug 29, 2024 – 08:07 AM

Tech stocks recovered from the knee-jerk selling of Nvidia, which plunged as much as 8% after the company’s Q3 guidance disappointed some even as Q2 results met or beat analysts’ estimates on nearly every measure and showed that revenue more than doubled in the quarter, reinforcing the earnings power of artificial intelligence. As of 7:50am ET, Nasdaq 100 futures added 0.1% after sliding as much 1.4% earlier as Nvidia, which had tumbled sharply in trading after the close of US exchanges, trimmed losses to just down only 2% in pre-market trading. Intel Corp., Apple Inc. and Microsoft Corp. all posted small gains; S&P 500 futs rose 0.2%, fully reversing an earlier drop as Germany’s DAX Index hit a new record. Treasury 10-year yields and the dollar was steady. West Texas Intermediate crude rose to $75 after sliding back under $74 yesterday. On the macro calendar, we have the second 2Q GDP estimate, July trade balance and wholesale inventories and initial jobless claims (8:30am) and July pending home sales (10am).

In premarket trading, Nvidia fell 3%, reversing a much bigger plunge, after the company failed to live up to investor hopes with its latest results, delivering an underwhelming forecast and news of production snags with its much-awaited Blackwell chips. Here are some other notable premarket movers:

- Affirm Holdings soars 21% after the financial technology company’s 1Q revenue forecast came in ahead of estimates.

- Best Buy rises 6% after the company raised its annual profit guidance in a sign that demand for electronics and appliances could start to improve.

- Birkenstock falls 13% after the sandal maker reported 3Q revenue that just missed the average analyst estimate. Some analysts said expectations were high heading into results, with shares up about a third since its $1.5 billion initial public offering.

- Dollar General falls 23% after the company cut its full-year sales forecast, a sign that the discounter’s turnaround efforts may not be fending off competition.

- Five Below rises 6% after the discount retailer reported 2Q comparable sales that declined less than analysts had anticipated. While the company lowered its annual comparable sales forecast, the reduced outlook was also better than Wall Street expected.

- ILearningEngines sinks 42% after Hindenburg Research said it is short the stock.

- Nutanix gains 17% after the company gave a full-year revenue forecast that came in stronger than expected.

- Okta drops 13% after some of the application software company’s outlook disappointed.

- Salesforce rises 5% after the maker of customer management software reported 2Q results that beat expectations.

- Topgolf Callaway Brands declines 3% after Jefferies downgraded the golf equipment company to hold, saying it was “increasingly uncertain” about the company’s prospects, in particular its debt levels.

As extensively discussed yesterday, Nvidia’s Q3 earnings report, the most anticipated part of the tech industry’s earnings season, beat analysts’ estimates on nearly every measure, but Nvidia spoiled investors have grown accustomed to blowout quarters, and the latest numbers didn’t qualify especially as regards guidance which came in below some of the more optimistic estimates. NVDA revenue more than doubled to $30 billion in the fiscal second quarter, and the company said third-quarter revenue will be about $32.5 billion; while analysts had predicted $31.9 billion on average, estimates ranged as high as $37.9 billion. Of concern to investors was the fact that Nvidia’s next big cash cow — the new Blackwell processor lineup — has proved more challenging to manufacture than anticipated. The product is the next generation of the company’s dominant artificial intelligence processor.

“Fundamentally, market participants are reflecting on those Nvidia results and saying: they were actually pretty good,” said Michael Brown, a senior strategist at Pepperstone Group Ltd. “The bar for a beat was impossibly high, so the results don’t derail the bull case for the chipmakers or the equity market more broadly.”

In any case, with Q2 earnings season officially at an end, focus is turning back to the macro landscape. Money markets are wagering on 100 basis points worth of rate cuts by year-end but uncertainty remains as to whether the Federal Reserve will ease policy by a quarter-point next month or deliver a larger 50 basis-point cut. Atlanta Fed President Raphael Bostic said it “may be time to cut,” but he’s still looking for additional data to support lowering rates next month. Key to that will be a reading of the Fed’s preferred inflation gauge, the core PCE, due Friday.

“What investors are looking for now is further confirmation that if economic momentum is weakening, the Federal Reserve are going to ride to the rescue and provide a series of substantial cuts,” said Brian O’Reilly, head of market strategy at Mediolanum International Funds.

European stocks gain as traders added to their ECB interest-rate cut bets after soft inflation data from Spain and Germany which reinforced expectations for a European Central Bank rate cut in September. The Stoxx 600 rises 0.8% to the highest since mid July while Germany’s DAX gained as much as 0.7%, reaching 18,912.47 points and topping its previous peak of May 15. Here are some of the biggest movers on Thursday:

- Pernod Ricard shares extend gains to as much as 9.7%, the biggest advance in almost 16 years, after China said it won’t take any anti-dumping measures over EU brandy for the time being. The stock extended gains that were initially fueled by relief over the French distiller’s in line results. Peers Diageo, Remy Cointreau and Campari also jump.

- Delivery Hero shares rise as much as 9% in early trading, to their highest intraday value two months, after the German online food service’s second quarter results showed strength in the Middle East and North Africa region and as the firm said it was planning a Dubai initial public offering of its Talabat operations.

- Universal Music shares rise as much as 4.2% after BNP Paribas Exane raised its recommendation on the music company to outperform from neutral. The broker says streaming expectations are now “materially reset” which offers an “attractive entry point.”

- Schott Pharma shares jump as much as 12%, the most on record, after the German healthcare supplier increased its revenue forecast for the year following strong third-quarter results.

- Close Brothers jumps as much as 11%, the most since March, after RBC upgraded its recommendation on the UK financial services group to outperform from sector perform. The broker says the firm’s shares are cheap historically as well as compared to sector peers.

- DEME Group shares rise as much as 6.2% after the marine engineering provider reported turnover for the half-year that beat estimates. KBC upgraded its its recommendation on the stock, citing a higher sales growth outlook.

- Corbion shares rise as much as 5.3% after the Dutch ingredients firm is upgraded to overweight at Barclays, which sees improving growth prospects and reduced balance-sheet risk prompting a rerating.

- Teleperformance falls as much as 6.2%, after the French digital business services company’s CEO told French paper Les Echos the company is considering listing its stock in the US, frustrated by its stock performance in Paris.

- CD Projekt drops as much as 4.4% after the video game maker’s revenues development disappointed analysts. Ipopema appreciated the update to the Polish game developer’s key asset Project Polaris, a codename for the new The Witcher game, and hopes to see a game trailer by the end of 2024.

- IG Group shares fall as much as 2.6% in London after holders Tom Sosnoff and Scott Sheridan sold 6.5m shares in an offering to a limited number of institutional investors.

Earlier in the session, Asian stocks fell as tech shares declined in the wake of Nvidia Corp.’s disappointing forecast, while Chinese shares were mixed amid earnings misses. The MSCI Asia Pacific Index dropped as much as 0.6% before paring, with TSMC, Samsung Electronics and SK Hynix among the biggest drags. Asian chip shares declined as Nvidia’s less-than-outstanding outlook cooled investor sentiment on the artificial intelligence trade. Benchmarks in Taiwan and South Korea led declines in the region. “Nvidia had a good result yet share price was down on the back of big expectations for next year,” said Jun Bei Liu, a portfolio manager at Sydney-based Tribeca Investment Partners. The cooling-off in the shares after their strong performance this year “provides buying opportunities as long-term structural growth remains intact.”

In FX, the Bloomberg Dollar Spot Index slips 0.1% drop ahead of US GDP data and weekly jobless claims data; risk-sensitive currencies including the New Zealand and Australian dollars lead gains. the euro underperforms its G-10 rivals, falling 0.2% against the greenback after softer than expected inflation prints out of Germany and Spain. EUR/USD drops as much as 0.4% to 1.1072, lowest since Aug. 20 and set for its worst two-day run in more than two months. One-week risk reversals now at 12 basis points, versus Wednesday’s high at 58 basis points. The kiwi dollar is the best performer, rising 0.6% after New Zealand business confidence hit a 10-year high. The offshore yuan climbs 0.6%.

Treasuries are marginally richer across the curve following another narrow overnight trading range, keeping most yields within 1bp of Wednesday’s closing levels. US 10-year trades around 3.83% with bunds in the sector outperforming slightly while gilts keep pace. Most of the price action occurred during European morning as the German curve bull-steepened Core European rates outperform led by German front-end, where 2-year yields are lower by around 4bp on the day following domestic inflation data; German 10-year yields falling 2bps to 2.24%. This week’s Treasury coupon auction cycle concludes with $44b 7-year note sale at 1pm, following good demand for 2- and 5-year notes. WI 7-year yield near 3.73% is ~43bp richer than last month’s result and, like the earlier sales, lower than results over the past year at least

In commodities, oil prices declined, with WTI rising 1% to $75 a barrel. Spot gold rises $16 to around $2,520/oz.

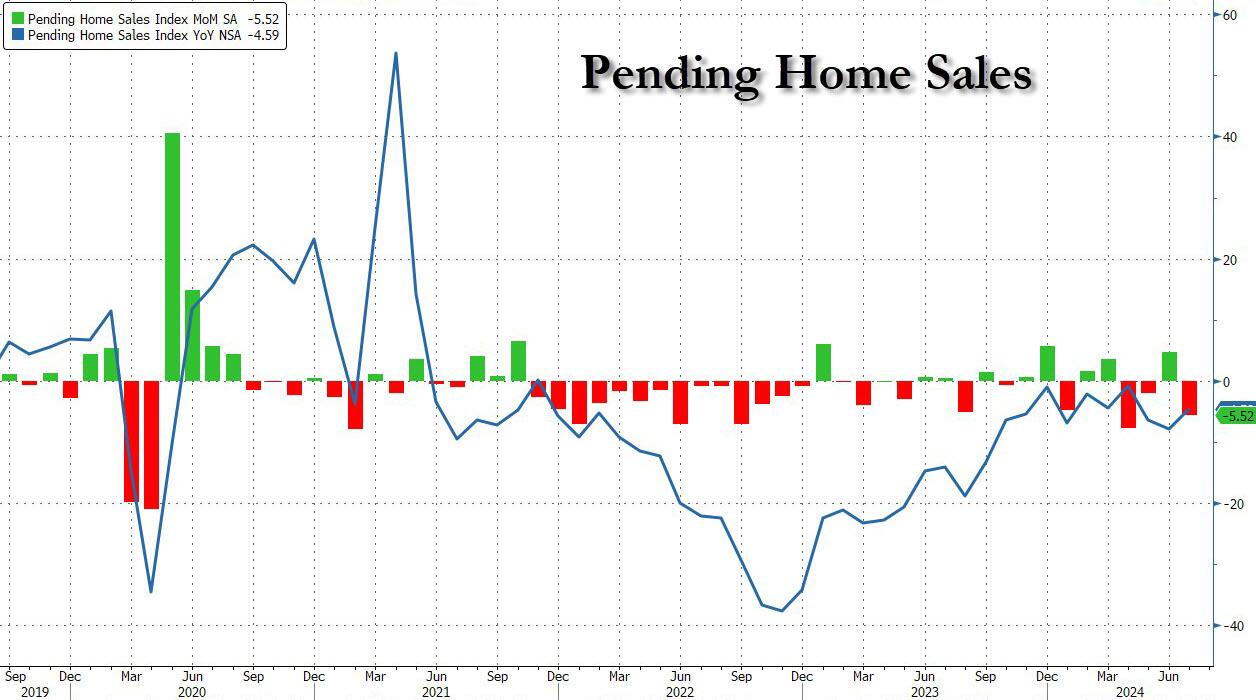

Looking at today’s US data calendar, we have the second 2Q GDP estimate, July trade balance and wholesale inventories and initial jobless claims (8:30am) and July pending home sales (10am). Fed speaker slate includes Bostic at 3:30pm.

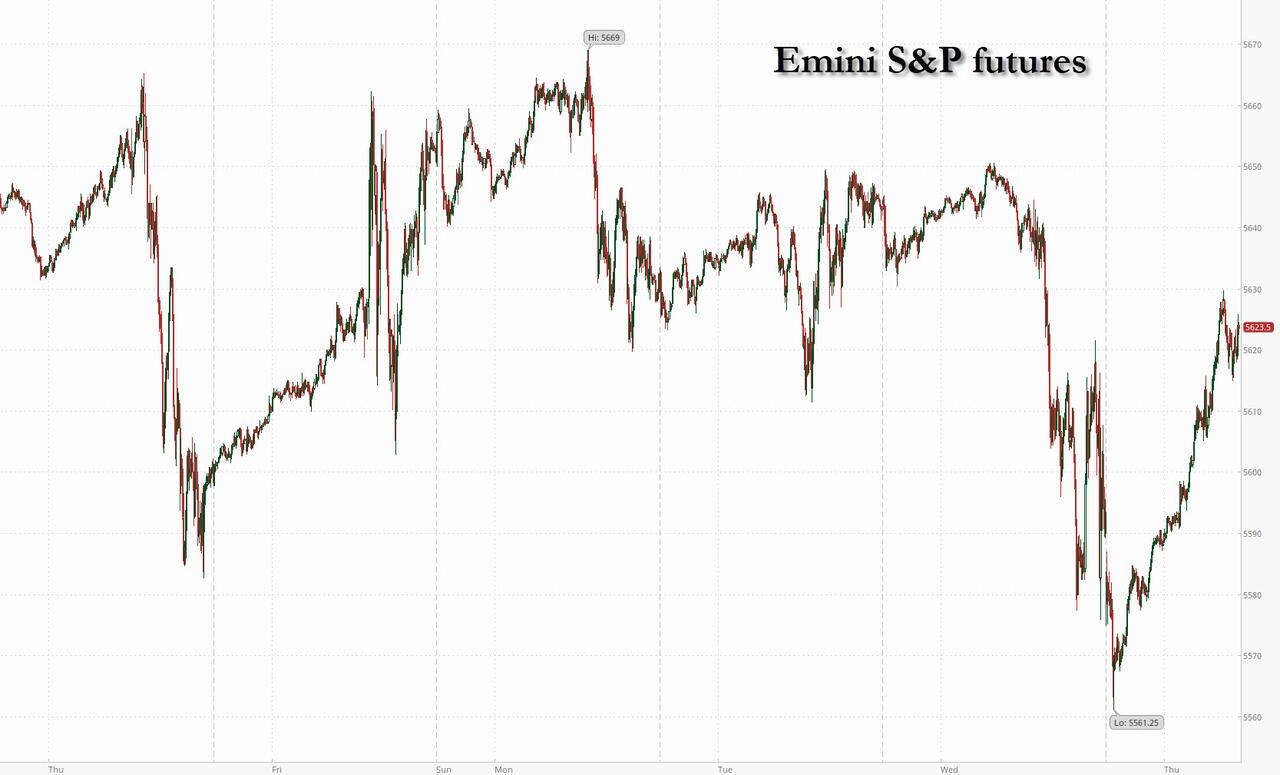

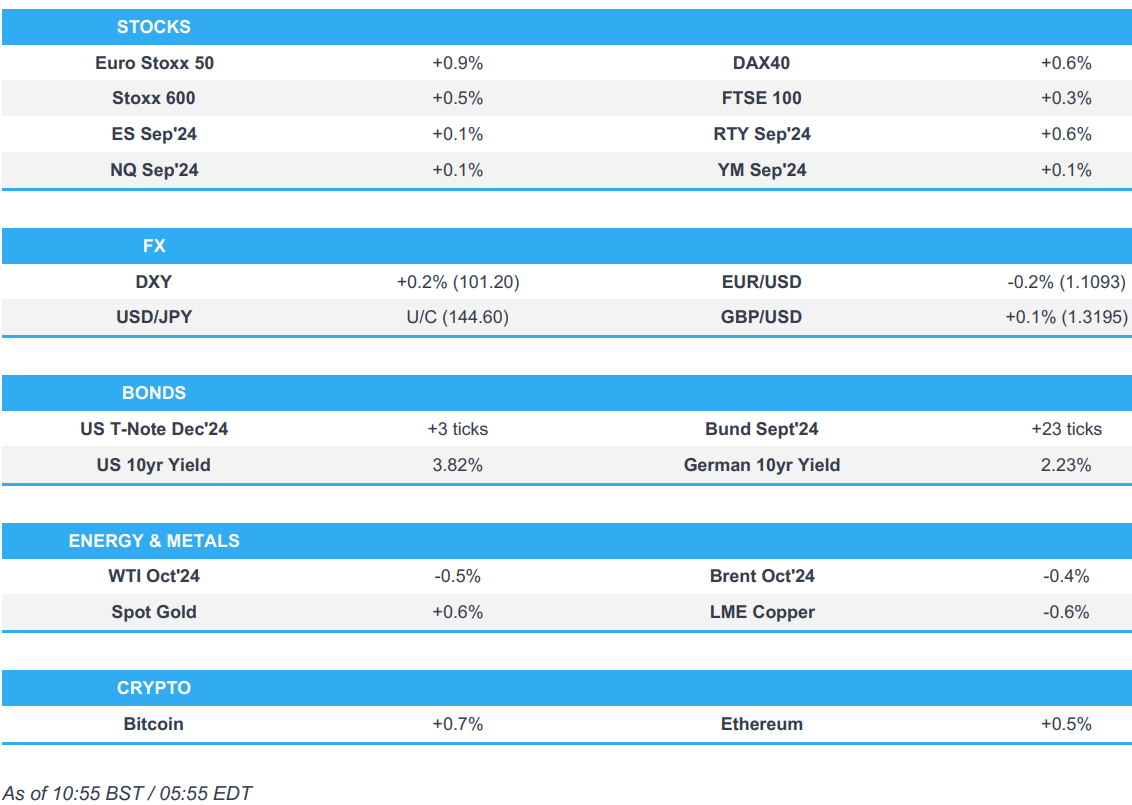

Market Snapshot

- S&P 500 futures little changed at 5,609.00

- STOXX Europe 600 up 0.5% to 522.95

- MXAP down 0.2% to 185.56

- MXAPJ down 0.3% to 573.39

- Nikkei little changed at 38,362.53

- Topix little changed at 2,693.02

- Hang Seng Index up 0.5% to 17,786.32

- Shanghai Composite down 0.5% to 2,823.11

- Sensex little changed at 81,714.16

- Australia S&P/ASX 200 down 0.3% to 8,045.13

- Kospi down 1.0% to 2,662.28

- German 10Y yield down 3.3 bps at 2.23%

- Euro down 0.3% to $1.1084

- Brent Futures down 0.5% to $78.23/bbl

- Gold spot up 0.5% to $2,517.04

- US Dollar Index up 0.18% to 101.28

Top Overnight News

- AAPL has started mass producing the new iPhone lineup in India, including the Pro model, just days after commencing the process in China. Nikkei

- China growth doubts grow as local government debt issuance falls behind schedule amid a clamp down on inefficient infrastructure investment. China’s sluggish economic performance is creating a problem for the world as the company floods the globe with goods its companies can’t sell domestically. RTRS / WSJ

- China aims to clamp down on the recent iron ore rally, saying it doesn’t have any fundamental basis. BBG

- China accuses European brandy makers of dumping, but declines to impose tariffs (for now) in a step that should help cool trade tensions between Brussels and Beijing. BBG

- Spanish inflation eased to its lowest level in a year — a retreat that’s likely to be mirrored across the euro zone, allowing the European Central Bank to continue lowering interest rates. Consumer prices advanced 2.4% from a year ago, according to data published Thursday by the national statistics agency. That’s less than the 2.5% median estimate in a Bloomberg survey of economists. BBG

- The Fed’s Raphael Bostic said it “may be time” to cut interest rates but he’s still looking for additional data to support a move next month. “I don’t want us to be in a situation where we cut and then we have to raise rates again,” he said. BBG

- Kamala Harris leads Donald Trump by one point in Arizona and by two points in Georgia and Nevada, according to a Fox News poll. Trump is ahead by one point in North Carolina. The margin of sampling error for each state is 3 ppts. Tonight, Harris and Tim Walz will have their first campaign interview, with CNN. BBG

- GOOGL is relaunching its Gemini AI tool used to create images of people after pulling it from the market in Feb following criticism. CNBC

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mostly with modest losses following the weak lead from Wall Street and in the aftermath of NVIDIA’s ill-received earnings. The tech sector was among the laggards in the region with Samsung Electronics (005930 KS), Tokyo Electron (8035 JT), and TSMC (2330 TT) all opening lower by 2-3%. ASX 200 was subdued amid the broader market mood and with Australia’s earnings season picking up in pace. Materials, energy and Tech resided as some of the lagging sectors. Nikkei 225 briefly dipped under USD 38k in early trade, with Japanese activity also affected by the approaching Typhoon Shanshan, although the index eventually eked mild gains amid gains in Industrial names. Hang Seng and Shanghai Comp both conformed to the APAC mood and later extended their losses, whilst earnings season in Hong Kong saw Meituan jump almost 10% while Li Autos slid 10.6%.

Top Asian News

- PBoC injected CNY 150.9bln via 7-day Reverse Repo at a maintained rate of 1.70%.

- South Korean President Yoon said the government will introduce an automatic stabilization tool for the long-term sustainability of pension fund and is to raise the basic monthly pension by KRW 400k within his term, according to Reuters.

- PBoC will step up counter-cyclical adjustments; will strengthen financial support to the real economy

European bourses, Stoxx 600 (+0.5%) began the session with a modest upward bias. As the session progressed, indices continued to edge higher, but most notably in the Euro Stoxx 50 (+0.9%) and AEX (+0.9%), with Tech leading, despite NVIDIA (-2.8% pre-market) slipping post-earnings (albeit. metrics were strong). European sectors hold a strong positive bias. Tech is the clear outperformer, propped up by gains in the ASM International (+2.4%) and ASML (+2%), benefiting from strong NVIDIA results, despite the Co. itself being down by around 2.8% in the pre-market. Alcohol names shot higher following an announcement that China’s Commerce Ministry will not impose provisional anti-dumping subsidy on brandy imported from the EU; Pernod Ricard (+4.5%) / Remy Cointreau (+7.6%). US Equity Futures (ES +0.1%, NQ +0.1% RTY +0.6%) are flat/mixed, with very slight outperformance in the RTY, whilst the NQ fails to find a firm direction, following NVIDIA’s results on Wednesday.

Top European News

- Riksbank’s Bunge foresees two or three further rate cuts this year, monetary policy should still be characterised by a gradual adjustment.

- China’s Commerce Ministry says it will not impose provisional anti-dumping subsidy on brandy imported from the EU.

FX

- DXY is extending the upside seen on Wednesday’s session after basing out at 100.51 on Tuesday. DXY has printed a 101.36 peak with the pre-Powell high at 101.55 coming into view.

- EUR/USD is pressured and back on a 1.10 handle after regional German CPI metrics came in softer than suggested by expectations for the mainland data. German CPI due at 13:00BST ahead of the EZ-wide data on Friday.

- GBP is flat vs. the USD with UK-specific updates once again on the light side. Cable has returned to a 1.31 handle after printing a fresh YTD peak earlier in the week at 1.3266.

- USD/JPY is flat in quiet newsflow and opting to consolidate on a 144.00 handle and within yesterday’s 143.69-145.04 range.

- NZD is the best performer across the majors after ANZ data showed NZ business confidence soaring. AUD is also firmer vs. the USD but to a lesser extent due to pressure in the AUD/NZD cross, though AUD/USD is within reach of the YTD peak.

- PBoC set USD/CNY mid-point at 7.1299 vs exp. 7.1297 (prev. 7.1216)

Commodities

- Crude is slightly softer, but with specifics light and the complex essentially in a holding pattern until there is an update to the geopolitical and/or Libya front. Brent’Oct currently near session lows at around USD 78.30/bbl, weighed on by EUR-driven USD strength.

- Spot gold is firmer and relatively unreactive to the referenced uptick in the USD as pressure in yields globally are serving as a countering impulse for the yellow metal. At the top-end of a relatively wide USD 2503-2521/oz band.

- Base metals are broadly on the backfoot, largely in continuation of the broader negative sentiment seen in APAC trade overnight.

- South32 (S32 AT) expects to see improvement in aluminium prices on USD weakness and China buying, according to Reuters.

- Russian gov’t has announced that fuel and oil production numbers are to be a state secret, via KyivPost.

US Event Calendar

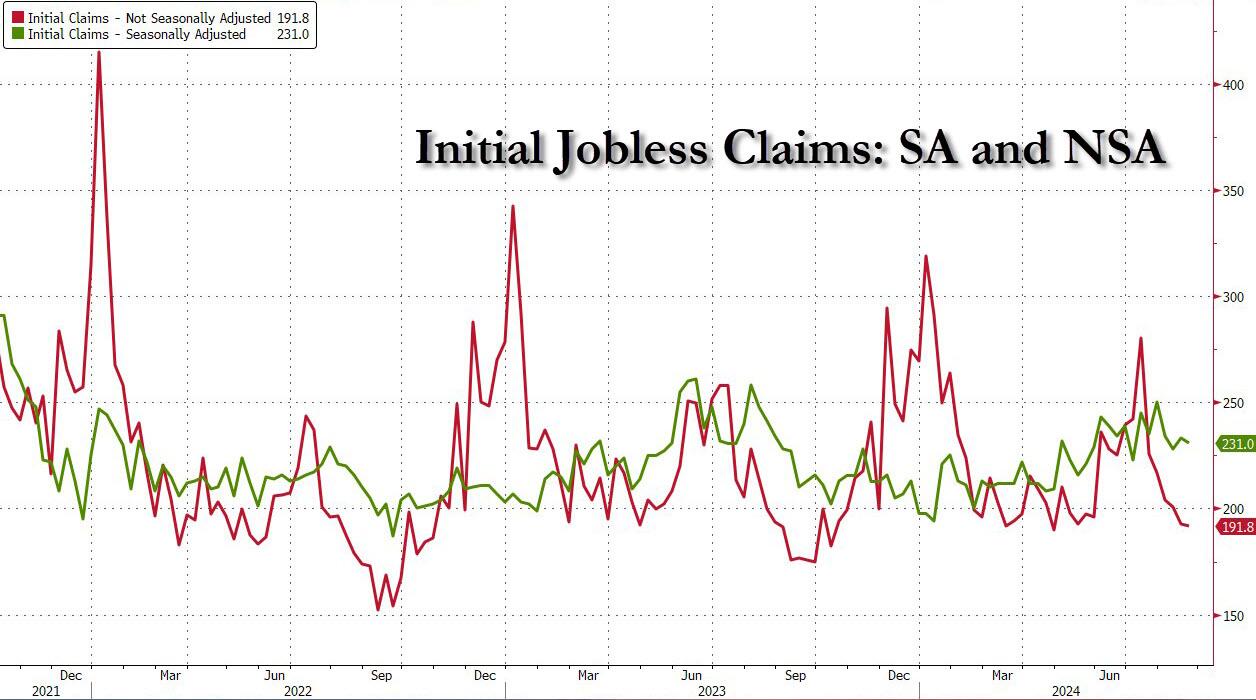

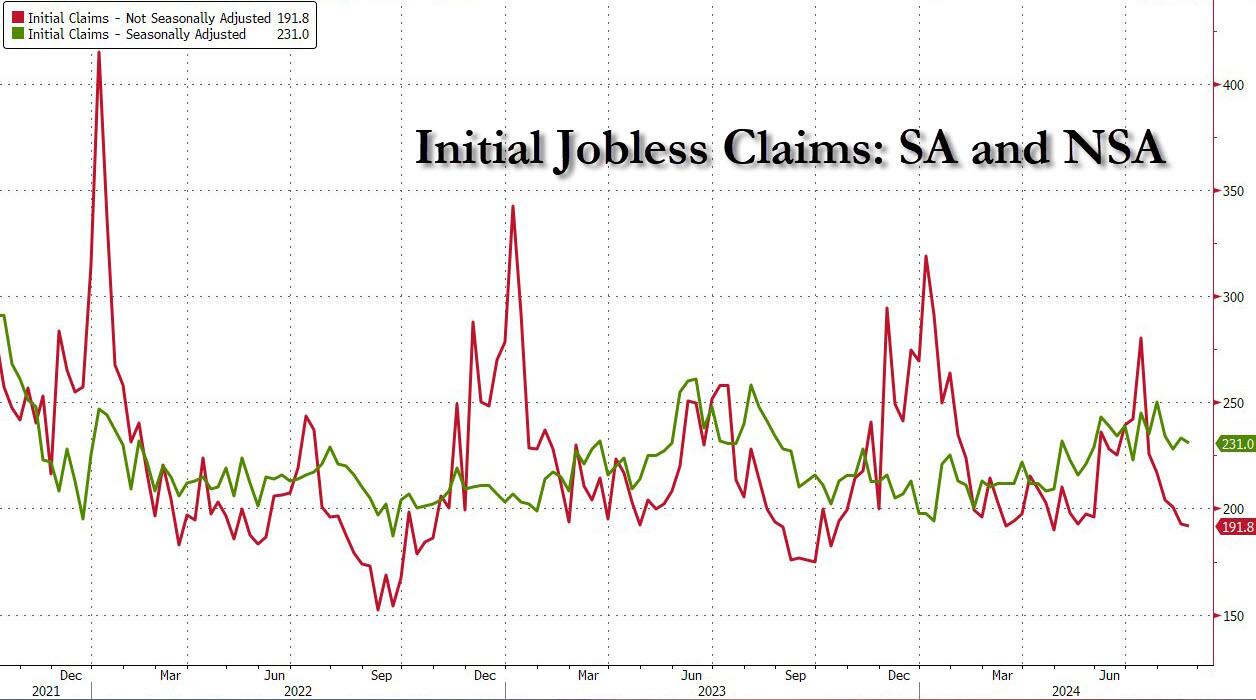

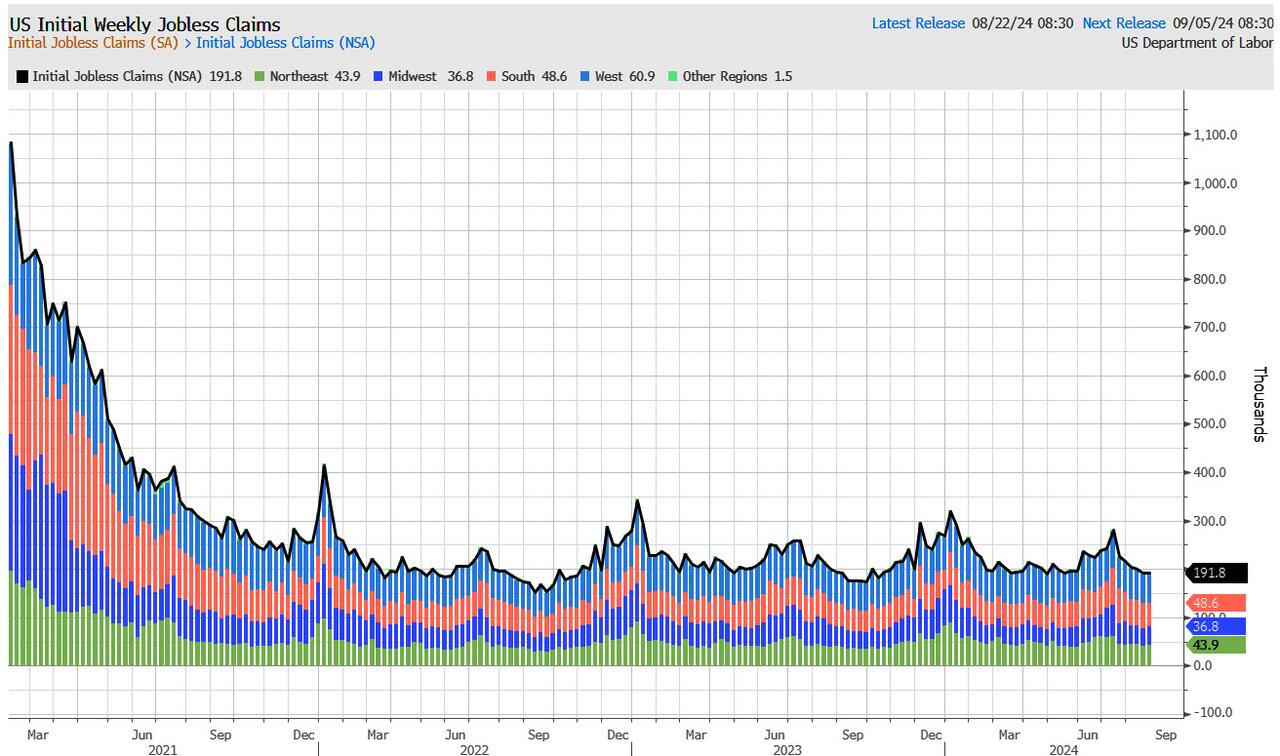

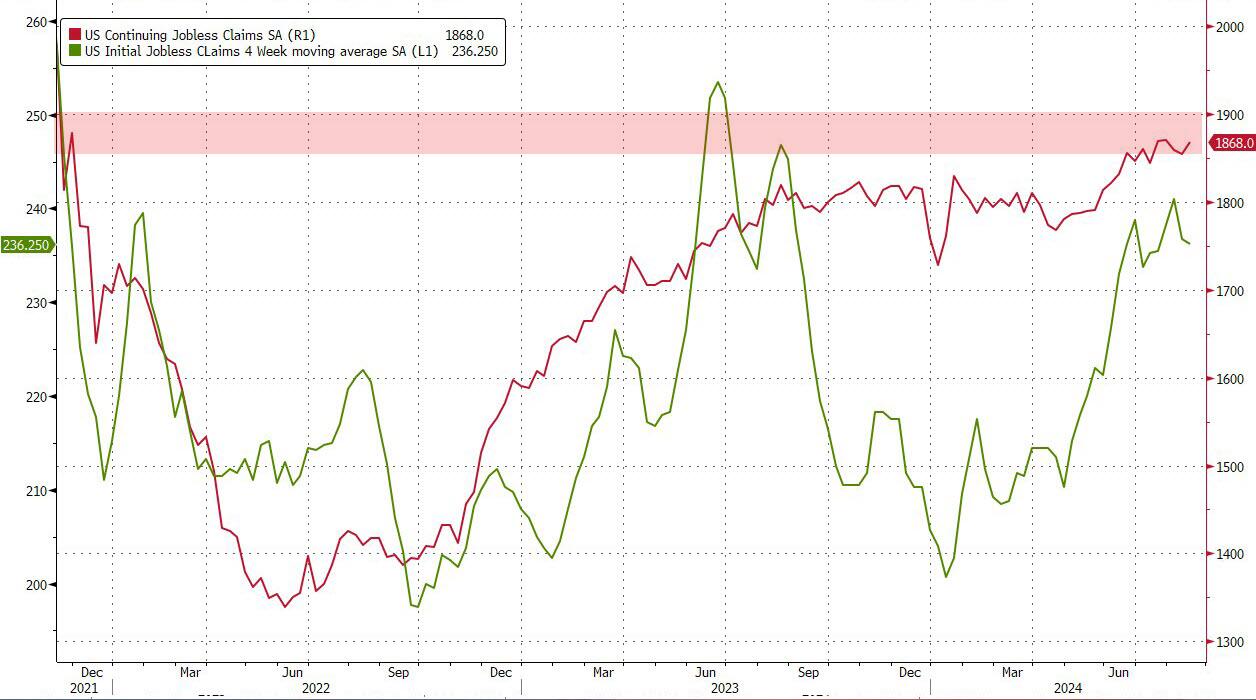

- 08:30: Aug. Initial Jobless Claims, est. 232,000, prior 232,000

- Aug. Continuing Claims, est. 1.87m, prior 1.86m

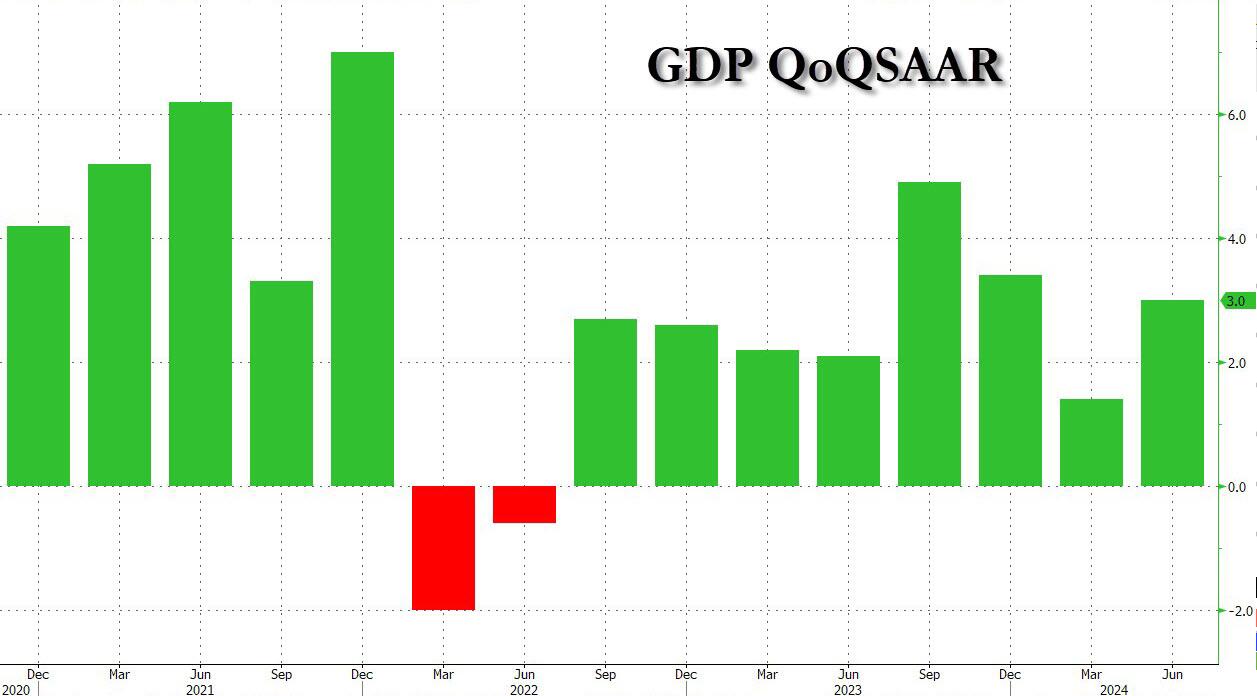

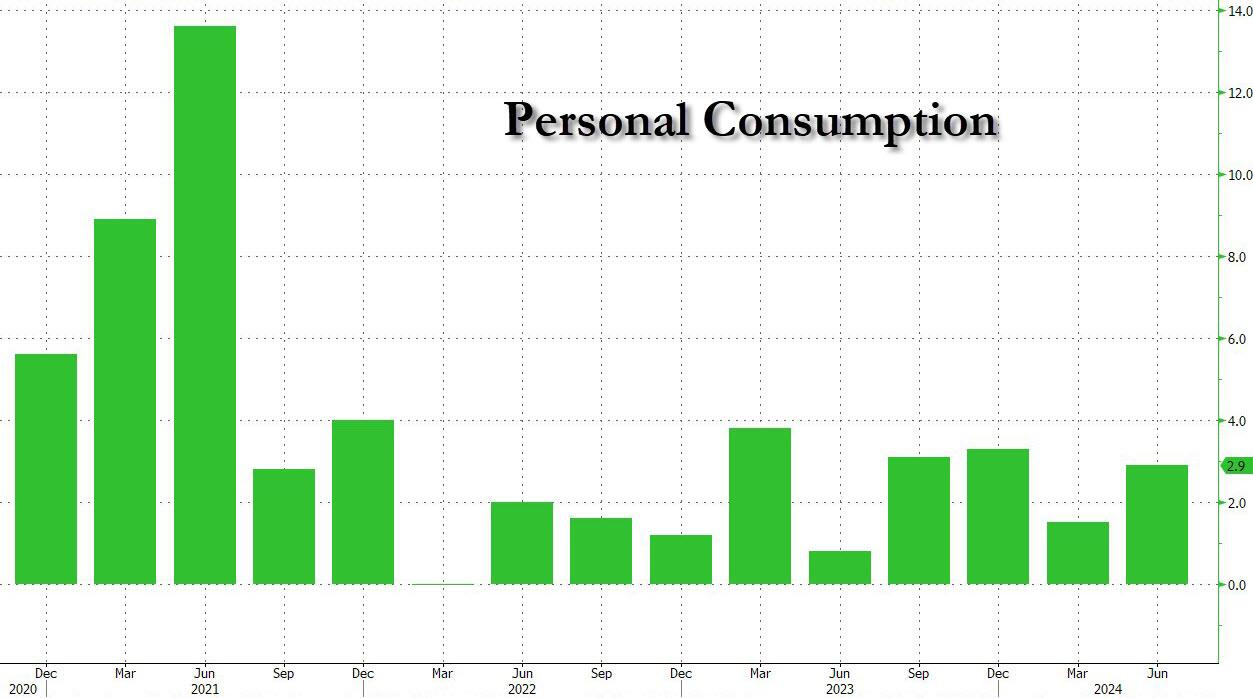

- 08:30: 2Q GDP Annualized QoQ, est. 2.8%, prior 2.8%

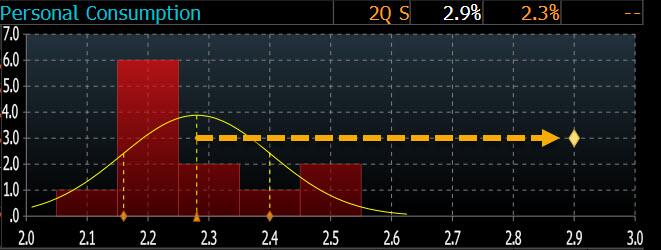

- 2Q Personal Consumption, est. 2.2%, prior 2.3%

- 2Q Core PCE Price Index QoQ, est. 2.9%, prior 2.9%

- 2Q GDP Price Index, est. 2.3%, prior 2.3%

- 08:30: July Advance Goods Trade Balance, est. -$97.8b, prior -$96.8b, revised -$96.6b

- 08:30: July Retail Inventories MoM, est. 0.5%, prior 0.7%

- July Wholesale Inventories MoM, est. 0.3%, prior 0.2%

- 10:00: July Pending Home Sales (MoM), est. 0.2%, prior 4.8%

- July Pending Home Sales YoY, est. -2.0%, prior -7.8%

DB’s Jim Reid concludes the overnight wrap

As we go to press this morning, the main market focus is on Nvidia’s latest results, which came out after the US close last night. Although the results slightly beat expectations, their share price was down around -7% in after-hours trading, partly because it fell short of some estimates that had been looking for an even stronger release. For instance, the revenue outperformance was the smallest relative to expectations in six quarters, so this wasn’t the sort of massive beat that Nvidia has often reported over the last 18 months. At the same time, the Q3 revenue guidance came in a touch above the average estimate ($32.5bn vs $31.9bn est.) but still well within the range of analysts’ views. So there’s been a pullback overnight, and that decline in after-hours trading has built on the -2.10% decline in yesterday’s session. In turn, US equity futures are lower more broadly this morning, with those on the S&P 500 (-0.33%) and the NASDAQ 100 (-0.64%) both falling back.

That more negative tone has also been evident overnight, with many of the major indices losing ground in Asia. That includes losses for the KOSPI (-0.81%), the Hang Seng (-0.65%) and the Shanghai Comp (-0.45%), alongside smaller declines for the CSI 300 (-0.07%) and the Nikkei (-0.06%).

Ahead of Nvidia’s release, US markets had already lost ground yesterday, with the S&P 500 filling -0.60%, though it did partially recover from a -1.1% fall intra-day. The decline came primarily because of losses among tech stocks, with the Magnificent 7 (-1.19%) falling back for a third consecutive day, whilst the NASDAQ also fell -1.12% to a two-week low. Sentiment around tech wasn’t helped by a -19.02% drop for Super Micro Computer, which saw the largest decline in the S&P 500 yesterday after they said they’d delay filing their annual financial disclosures. And the pick up in volatility ahead of Nvidia’s results also saw the VIX index rise +1.68pts to 17.11, its largest daily increase since the market turmoil on August 5.

To be fair, there were some relatively brighter spots, with more than 40% of the S&P 500 constituents higher on the day, while the Dow Jones (-0.39%) saw a more modest decline, having initially been on track to close at a new all-time high. It was a strong day for banks as well, with those in the S&P 500 up +0.70%. And in other news, Berkshire Hathaway (+0.86%) became the first US company that’s not in the tech sector to achieve a $1 trillion market capitalisation.

Whilst equities were losing ground, US Treasuries put in a pretty subdued performance, with the main theme being an ongoing curve steepening. While there was little data or commentary from Fed officials, the 2yr yield still fell by -3.4bps to 3.87%, its lowest closing level since May 2023. By contrast, the 10yr yield was up +1.3bps to 3.84% and the 2s10s slope ended the session at -3.4bps, only a basis point from its 2-year high on August 7. Meanwhile, we got more indication that the prospect of rate cuts was filtering through to the real economy. Specifically, data from the Mortgage Bankers Association showed that the contract rate on a 30yr mortgage was down to 6.44%, the lowest since April 2023. Bear in mind that investors are still pricing in rapid rate cuts over the months ahead, with over 100bps priced in by the December meeting. This pricing was little changed despite somewhat hawkish comments from Atlanta Fed’s Bostic later on, who said that it “may be time” to cut but that he still wanted to see additional data to support a September cut.

Today, we should start to get some more data that will help to shape investors’ views. In particular, there’s the weekly initial jobless claims out of the US, which will offer a timely indicator on the state of the labour market. We’ll also get the second estimate of Q2 GDP, and although that’s a backward-looking reading, that will include the latest revisions to core PCE inflation in Q2. Any revisions to that would add to the uncertainty when it comes to tomorrow’s core PCE print for July, so that could have implications for the 25bps vs 50bps debate depending how that looks. As of this morning, futures are placing a 35% probability on a 50bp rate cut in September, so the view remains that 25 is more likely. But it’s far from a done deal, and we’ve still got both the jobs report and CPI release for August before that meeting, so plenty of time for that to shift around still.

Over in Europe, markets put in a more robust performance, with the STOXX 600 (+0.33%) closing in on its all-time high, ending the day just -0.78% beneath its record from May. Germany’s DAX (+0.54%) was even closer to its own record, with yesterday’s advance leaving it just -0.46% beneath its peak. That optimism was also echoed among sovereign bonds, with yields on 10yr bunds (-3.0bps), OATs (-2.8bps) and BTPs (-2.1bps) all moving lower.

Europe will stay in focus today, as we’ll start to get the flash HICP prints for August, including Germany and Spain today, ahead of the Euro Area release tomorrow. Those will be important for the ECB, as even though a September cut is widely expected, markets have been pricing around a 50% chance of a second cut at the subsequent meeting in October. So the release could influence whether they cut at a quarterly pace (having already delivered an initial cut in June), or whether they speed that up and start cutting every meeting. In a mini series of notes this week, our European economists examine the factors that will determine both how far (see here) and how fast (see here) the ECB is likely to cut. When it comes to upcoming inflation data, our economists expect the Euro Area headline to slow to +2.2% in August, which would be the weakest since July 2021, with core HICP also coming down to +2.8%.

There was very little other data yesterday, although the Euro Area M3 money supply grew by +2.3% year-on-year in July (vs. +2.7% expected). Otherwise, French consumer confidence ticked up to 92 in August as expected, which is its highest level since February 2022.

To the day ahead now, and data releases include the German and Spanish CPI prints for August. In the US, we’ll also get the second estimate of Q2 GDP, the weekly initial jobless claims, and pending home sales for July. From central banks, we’ll hear from the ECB’s Lane and Nagel, as well as the Fed’s Bostic.

2B) European report

NVDA -1.8% pre-market, USD gains & EUR hampered by German State CPIs – Newsquawk US Market Open

Thursday, Aug 29, 2024 – 06:08 AM

- European bourses edge higher with Tech leading; US futures are slightly higher, NVDA -1.5% pre-market vs -4.9% after-hours

- Dollar is firmer, Antipodeans outperform given the risk-tone whilst EUR is hampered post-German State CPIs

- Bonds have been lifted after the cool German State CPIs vs mainland expectations

- Crude is lower and near session lows, XAU gains whilst base metals are broadly lower

- Looking ahead, US PCE (Q2), GDP (Q2), IJC, Fed’s Bostic, Supply from the US, and Earnings from Lulelemon, Dollar General, Best Buy, Marvell

More Newsquawk in 3 steps:

1. Subscribe to the free premarket movers reports

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

- European bourses, Stoxx 600 (+0.5%) began the session with a modest upward bias. As the session progressed, indices continued to edge higher, but most notably in the Euro Stoxx 50 (+0.9%) and AEX (+0.9%), with Tech leading, despite NVIDIA (-2.8% pre-market) slipping post-earnings (albeit. metrics were strong).

- European sectors hold a strong positive bias. Tech is the clear outperformer, propped up by gains in the ASM International (+2.4%) and ASML (+2%), benefiting from strong NVIDIA results, despite the Co. itself being down by around 2.8% in the pre-market.