GOLD PRICE CLOSED DOWN $31.30 TO $2495.70 * ALL TIME HIGH CLOSING

SILVER PRICE DOWN $.42 TO $28.75

Gold ACCESS CLOSED $2502..60

Silver ACCESS CLOSED: $28.86

Friday is OTC/London LBMA options expiry which is much bigger than comex.

Bitcoin morning price:$59,574 DOWN 11 DOLLARS.

Bitcoin: afternoon price: $59,220 DOWN 385 DOLLARS

Platinum price closing DOWN $16.95 TO $928.50

Palladium price; DOWN $17.15 TO $966.75

END

*CANADIAN GOLD: $3373/50 DOWN 28.88 CDN dollars per oz( * NEW ALL TIME HIGH 3,431.95 CDN DOLLARS PER OZ//AUG 16 2024)

*BRITISH GOLD: 1,905.43 DOWN 8.26 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///1937.75 BRITISH POUNDS/OZ) AUGUST 16/2024

*EURO GOLD: 2,2693.93 DOWN 10.00 Euros per oz //* (ALL TIME CLOSING HIGH: 2.276.65 EUROS PER OZ//AUGUST 29 //.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE: COMEX

EXCHANGE: COMEX

CONTRACT: AUGUST 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,501.000000000 USD

INTENT DATE: 08/29/2024 DELIVERY DATE: 08/30/2024

FIRM ORG FIRM NAME ISSUED STOPPED

624 H BOFA SECURITIES 24

737 C ADVANTAGE 24

TOTAL: 24 24

MONTH TO DATE: 22,377

this completes August 2237700 oz or 69.602 tonnes

EXCHANGE: COMEX

CONTRACT: SEPTEMBER 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,525.700000000 USD

INTENT DATE: 08/29/2024 DELIVERY DATE: 09/03/2024

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 303

132 C SG AMERICAS 52

190 H BMO CAPITAL 222

DLV615-T CME CLEARING

BUSINESS DATE: 08/29/2024 DAILY DELIVERY NOTICES RUN DATE: 08/29/2024

PRODUCT GROUP: METALS RUN TIME: 20:43:15

323 C HSBC 288

363 H WELLS FARGO SEC 1640

435 H SCOTIA CAPITAL 946

555 C BNP PARIBAS SEC 10

624 H BOFA SECURITIES 1042

657 C MORGAN STANLEY 15 96

661 C JP MORGAN 497

661 H JP MORGAN 53

686 C STONEX FINANCIA 3

690 C ABN AMRO 3

726 C PLUS500US FINAN 1

737 C ADVANTAGE 80

905 C ADM 35

TOTAL: 2,643 2,643

MONTH TO DATE: 2,643

JPMorgan stopped 3/2643

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2024. CONTRACT: 2643 NOTICES FOR 264300 OZ or 8.2208 TONNES

total notices so far: 264300 contracts for 264,300 Oz (8.2208 tonnes)

FOR SEPT:

SILVER NOTICES: 5 NOTICE(S) FILED FOR 25,000

OZ/

total number of notices filed so far this month : 1035 for 5,175,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $31.30 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ HUGE CHANGES IN GOLD INVENTORY AT THE GLD:A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD//

/ /INVENTORY RESTS AT 857.27 TONNES

INVENTORY RESTS AT 857.27 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $0.42 AT THE SLV

NO CHANGES IN SILVER INVENTORY AT THE SLV:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 464.693 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A MEGA MEGA GIGANTIC SIZED 3203 CONTRACTS TO 134,412 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS MEGA HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR STRONG GAIN OF $0.37 IN SILVER PRICING AT THE COMEX ON THURSDAY’S TRADING. WE LOST ZERO LONGS WITH THE GAIN IN PRICE. WE HAD A HUGE LOSS OF 2778 CONTRACTS ON OUR TWO EXCHANGES. WE HAD AGAIN A HUGE LIQUIDATION OF T.A.S. CONTRACTS AS WELL AS MONTH END SPREADERS DURING THURSDAY’S TRADING//. WE HAD CONSIDERABLE SHORT COVERING BY OUR SPECS WITH THE GAIN IN PRICE. WE HAD ANOTHER GOOD 425 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY ANOTHER GOOD 337 CONTRACT T.A.S ISSUANCE. IN ESSENCE WE LOST 2514 CONTRACTS ON OUR TWO EXCHANGES DESPITE THE GAIN IN PRICE. ALL OF THE LOSS IN OI WAS DUE TO OUR TWO SPREADER LIQUIDATIONS.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN YESTERDAY. THE ACCUMULATED T.A.S. IS BEING USED TO MANIPULATE PRICES AT THE COMEX NOW EVERY DAY..

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: 337 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS.IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1/2 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS BUT TO NO AVAIL. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.37) AND WERE SUCCESSFUL IN KNOCKING ZERO SILVER LONGS FROM THEIR PERCH AS DESPITE A STRONG LOSS OF 2514 TOTAL OI CONTRACTS ON OUR TWO EXCHANGES , ALL OF THE LOSS WAS DUE TO T.A.S AND MONTH END SPREADER LIQUIDATION.

WE HAD A GOOD 425 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 22.765 MILLION OZ (FIRST DAY NOTICE)

//NEW STANDING FOR SILVER//SEPT IS THUS 22.765 MILLION OZ

WE HAD:

/ MEGA HUGE SIZED COMEX OI LOSS //GOOD SIZED EFP ISSUANCE/ VI) GOOD SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 337 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED XXX CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF AUGUST

TOTAL CONTRACTS for 22 DAYS, total 19,948 contracts: OR 99.740 MILLION OZ (906 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 94.365 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL PROBABLY BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

RESULT: WE HAD A MEGA HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3203 CONTRACTS DESPITE OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A GOOD EFP ISSUANCE CONTRACTS: 337 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 22.765 MILLION OZ ON FIRST DAY NOTICE FOLLOWED

//NEW TOTAL STANDING FOR SEPT 22.765 MILLION OZ

WE HAVE A MEGA HUGE LOSS OF 2778 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE GAIN IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A GOOD SIZED 337 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX TRADING//// MASSIVE ATTEMPTED SHORT COVERING FROM OUR SPEC SHORTS WITH THE STRONG GAIN IN PRICE YESTERDAY/ AND ZERO LIQUIDATION OF LONGS. ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER.

THE NEW TAS ISSUANCE THURSDAY NIGHT (337) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND FOR SURE TODAY., .

WE HAD 3830 NOTICE(S) FILED TODAY FOR 19.150 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 3400 OI CONTRACTS TO 525,188 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A MASSIVE 10,251 CONTRACTS//

WE HAD A FAIR SIZED INCREASE IN COMEX OI (3400 CONTRACTS) OCCURRED DESPITE OUR GAIN OF $23.60 IN PRICE/THURSDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT AT 12.885 TONNES ON FIRST DAY NOTICE

NEW STANDING BEGINS AT 12.885 TONNES

/ ALL OF THIS HAPPENED WITH OUR $23.60 GAIN IN PRICE WITH RESPECT TO THURSDAY’S TRADING. WE HAD A STRONG SIZED GAIN OF 5221 OI CONTRACTS (16.239 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A FAIR SIZED 1821 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 525,188

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5221 CONTRACTS WITH 3400 CONTRACTS INCREASED AT THE COMEX// AND A FAIR SIZED 1821 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 5221 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALLISH 689 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A FAIR SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (1821 CONTRACTS) ACCOMPANYING THE FAIR SIZED INCREASE IN COMEX OI OF 3400 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 5221 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT AT 12.885 TONNES

//NEW STANDING BEGINS AT: /SEPT 12.885 TONNES.

/ 3) CONSIDERABLE T.A.S. LIQUIDATION AND MONTH END SPREADER CONTRACT LIQUIDATION WITH ZERO NET LONG SPECS BEING CLIPPED,

4) VERY STRONG SIZED COMEX OPEN INTEREST GAIN 5) FAIR ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///SMALL T.A.S. ISSUANCE: 689 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF AUGUST. :

TOTAL EFP CONTRACTS ISSUED: 88,345 CONTRACTS OF 8,834,500 OZ OR 274.79 TONNES IN 22 TRADING DAY(S) AND THUS AVERAGING: 4015 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 22 TRADING DAY(S) IN TONNES 274.79 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 269.13 DIVIDED BY 3550 x 100% TONNES = 7.74% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF AUGUST. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (AUG), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MEGA HUGE SIZED 3203 CONTRACTS OI TO 134,412 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 425 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 425 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 425 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 3203 CONTRACTS AND ADD TO THE 425 E.FP. ISSUED

WE OBTAIN A MEGA HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2778 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 12.570 MILLION OZ OCCURRED DESPITE OUR $0.37 GAIN IN PRICE

END

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING/THURSDAY NIGHT

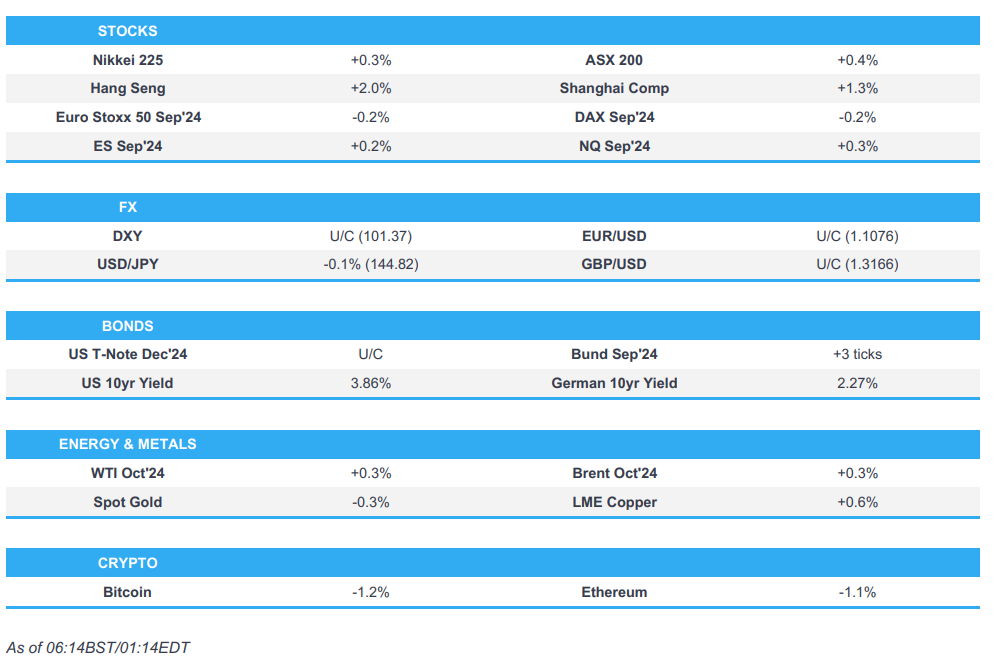

SHANGHAI CLOSED UP 19.11 PTS OR 0.68% //Hang Seng CLOSED UP 202.75 PTS OR 1/14% // Nikkei CLOSED UP 285/22 OR .74%//Australia’s all ordinaries CLOSED UP 0.64%///Chinese yuan (ONSHORE) CLOSED UP TO 7,0902 CHINESE YUAN OFFSHORE CLOSED UP TO 7.0800/ Oil UP TO 76.05 dollars per barrel for WTI and BRENT UP AT 78.86 Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 3400 CONTRACTS TO 525,188 WITH OUR GAIN IN PRICE OF $23.60 WITH RESPECT TO THURSDAY’S TRADING. WE LOST A CONSIDERABLE NUMBER OF FINAL SPREADER/T.A.S. CONTRACTS AS SHORTS TRIED TO, THROUGHOUT THE SESSION, COVER WHAT THEY COULD AT MUCH HIGHER PRICES. THE FED IS THE MAJOR SHORT OF AROUND 148 TONNES+ OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS IS SCHEDULED TO HAPPEN LATE SEPT 2024.

OUR LONDONERS ALSO BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT THESE HIGHER PRICES AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD CONSIDERABLE T.A.S. LIQUIDATION ON THURSDAY’S LOSS IN PRICE WITH ZERO LONGS WERE CLIPPED (AS YOU WILL SEE BELOW) BUT WE DID HAVE MAJOR SHORT COVERING. THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF THE SPREADERS AND T.A.S IS SURELY DISTORTING COMEX OPEN INTEREST.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE ACTIVE DELIVERY MONTH OF AUGUST.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 1821 EFP CONTRACTS WERE ISSUED: : OCT/DEC 1821 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 1821 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 5221 CONTRACTS IN THAT 1821 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A FAIR GAIN OF 3400 COMEX CONTRACTS..AND THIS HUGE GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $23.60/THURSDAY COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AS MENTIONED ABOVE. THE RAID ON WEDNESDAY WAS ORCHESTRATED BY THE FRBNY AS WE NOW ENTER OPTIONS EXPIRY FOR THE OTC/LONDON LBMA BETS ENDING THIS MORNING. DESPITE THE FED’S HUGE SHORT PREDICAMENT THEY STILL HAVE TIME AND ENERGY TO RAID OUR PRECIOUS METALS. SUCH CROOKS! THE RAID ACCOMPLISHED NOTHING BUT GRIEF TO OUR CENTRAL BANKER, THE FRBNY, AS OTHER CENTRAL BANKS TOOK THE FED’S LARGESS OF SUPPLY TO OBTAIN CONSIDERABLE PHYSICAL GOLD.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT A SMALL SIZED 689 CONTRACTS. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE (AND SPREADERS LATE IN THE MONTH). THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN LAST WEEK’S TRADING//RAIDS AS WELL AS THIS WEEK AND ESPECIALLY ON LAST THURSDAY.S HUGE /RAID AND LAST WEDNESDAY’S RAID.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: SEPT (12.885 TONNES) WHICH IS HUGE FOR A NON DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 44 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 12.885 TONNES.

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $23.60 //// AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE DID HAVE A HUGE GAIN IN OUR TWO EXCHANGES. WE HAD CONSIDERABLE FINAL SPREADER LIQUIDATION. BUT CENTRAL BANK LONGS, SEIZING THE MOMENT, EXERCISED FOR PHYSICAL IN A BIG WAY. WE HAD BOTH CONSIDERABLE T.A.S. LIQUIDATION AND FINAL SPREADER LIQUIDATION THURSDAY AT THE COMEX.

WE HAVE GAINED A TOTAL OI OF 16.239 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPT (12.885 TONNES) ON FIRST DAY NOTICE

//NEW STANDING FOR SEPT TO: 12.885 TONNES.

NEW STANDING FOR SEPT: 12.885 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR STRONG GAIN IN PRICE TO THE TUNE OF $24.60

WE HAVE REMOVED A MAMMOTH 10,251 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. THIS IS THE LARGEST ADJUSTMENT TO DATE.

NET GAIN ON THE TWO EXCHANGES 5221 CONTRACTS OR 522,100 OZ (16.239

TONNES)

confirmed volume THURSDAY 177,111 contracts poor

//speculators have left the gold arena

END

AUGUST 30 SEPTEMBER GOLD CONTRACT

/ /// THE SEPT 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | 97,199.270 oz Brinks 3.02 tones . |

| Deposit to the Dealer Inventory in oz | nil |

| Deposits to the Customer Inventory, in oz | NIL oz |

| No of oz served (contracts) today | 2643 notice(s) 264300 OZ 0.2364 TONNES |

| No of oz to be served (notices) | 1499 contracts 149900 OZ 4.6625 TONNES |

| Total monthly oz gold served (contracts) so far this month | 2643 notices 264300 oz 8.2208 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

0 dealer deposits:

total dealer deposits: nil oz

we have 0 customer deposits

total deposits NIL oz

withdrawals:1

i) Out of Brinks 97,199.270 oz (3.02 tonnes)

TOTAL WITHDRAWALS 97,199.270 oz

adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPTEMBER

For the front month of SEPT. we have an oi of 4142 contracts having LOST 969 contracts.

Thus by definition, the initial amount of gold standing for delivery in this non active delivery month of September is as follows:

4143 notices x 100 oz per notice = 414,300 oz or 12.885 tones.

OCTOBER LOST 1183 CONTRACTS DOWN TO 45,676 CONTRACTS

DECEMBER, THE BIGGEST DELIVERY MONTH GAINED 5691 CONTRACTS TO 424,455.

We had 2647 contracts filed for today representing 264,700 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notice issued from their client or customer account. The total of all issuance by all participants equate to 2643 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 3 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for SEPT /2024. contract month, we take the total number of notices filed so far for the month (2643) x 100 oz ) to which we add the difference between the open interest for the front month of SEPT 4142( CONTRACTS) minus the number of notices served upon today (2643x 100 oz per contract( equals 414,200 OZ OR 12.885 TONNES.

thus the INITIAL standings for gold for the SEPTEMBER contract month: No of notices filed so far (2643 x 100 oz +we add the difference for front month of SEPT (4142 X// , OI} minus the number of notices served upon today (2643) x 100 oz which equals 414200 oz (12.885 TONNES)

TOTAL COMEX GOLD STANDING FOR SEPT.: 12.885 TONNES WHICH IS HUGE FOR THIS NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,770,778.600 oz 55.078 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,086,712,768 OZ

TOTAL REGISTERED GOLD 7,522,254.284 ( 233.97 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,564,4458.484 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 5,751,476 oz (REG GOLD- PLEDGED GOLD)= 178.89 tonnes //

END

SILVER/COMEX

AUGUST 30/2024

INITIAL

//2024// THE SEPT 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 1,320782.180 OZ DELAWARE JPM Manfra . |

| Deposits to the Dealer Inventory | NIL |

| Deposits to the Customer Inventory | 533,345.130 oz ASAHI Brinks |

| No of oz served today (contracts) | 3830 CONTRACT(S) (19.150 MILLION OZ) |

| No of oz to be served (notices) | 723 contracts (3.615 million oz) |

| Total monthly oz silver served (contracts) | 3830 Contracts (19.150 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit/

total dealer deposit : NIL oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 customer deposits:

i) Into Delaware: 2909.73 oz

ii) Into Brinks 530,435.410 oz

total customer deposit 533,345.140 oz

JPMorgan has a total silver weight: 134.834million oz/306,367 million or 43.79%

adjustment:2

a) customer to dealer Brinks 4885.440oz

b) customer to dealer Manfra 421,392.132 oz

withdrawals: 3

i) Out of Delaware 213,079.38 oz

ii) Out of JPMorgan 501,406.200 oz

iii) Out of manfra: 606,296.600 oz

total customer withdrawals: 1,320,782.180 oz

TOTAL REGISTERED SILVER: 76.942 MILLION OZ//.TOTAL REG + ELIGIBLE. 306,367 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR SEPTEMBER:

silver open interest data:

FRONT MONTH OF SEPT/2024 OI: 4553 CONTRACTS HAVING LOST 5043 CONTRACT(S).

THUS BY DEFINITION, THE INITIAL AMOUNT OF SILVER STANDING IN THIS VERY ACTIVE DELIVERY

MONTH OF SEPTEMBER IS AS FOLLOWS:

4553 NOTICES X 5000 OZ PER NOTICE = 22.765 MILLION OZ.

OCTOBER SAW ANOTHER GAIN OF 51 OF OPEN INTEREST CONTRACTS AND THUS WE HAVE 1479 OPEN INTEREST CONTRACTS FOR OCTOBER.

DECEMBER SAW A GAIN OF 1731 CONTRACTS UP TO 117,082.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 3830 for 19.150 MILLION oz

CONFIRMED volume; ON THURSDAY 80,144 strong

To calculate the number of silver ounces that will stand for delivery in SEPT. we take the total number of notices filed for the month so far at 3830 x 5,000 oz = 19.150 MILLION oz

to which we add the difference between the open interest for the front month of SEPT(4553) and the number of notices served upon today 3830 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT/2024 contract month: 3830 notices served so far) x 5000 oz + OI for the front month of SEPT (4553)x number of notices served upon today minus (3830)x 5000 oz of silver standing for the SEPT contract month equates to 22.765 MILLION OZ.

New total standing: 22.765 million oz.

There are 76.942 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS//

GLD

AUGUST 30 WITH GOLD DOWN $31.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD/:/ //////INVENTORY RESTS AT 857.27 TONNES

AUGUST 29 WITH GOLD UP $23.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 28 WITH GOLD DOWN $14.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 27 WITH GOLD DOWN $1.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 26 WITH GOLD UP $9.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD VAPOUR GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 23 WITH GOLD UP $29.70 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER WITHDRAWAL OF 8.88 TONNES OF GOLD VAPOUR GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 857.85 TONNES

AUGUST 22 WITH GOLD DOWN $28.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 9.43 TONNES OF GOLD VAPOUR GOLD INTO THE GLD./ //////INVENTORY RESTS AT 866.70 TONNES

AUGUST 21 WITH GOLD DOWN $1.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER WITHDRAWAL OF 1.73 TONNES OF GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 857.27 TONNES

AUGUST 20 WITH GOLD UP $9.40 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 4.03 TONNES OF GOLD VAPOUR INTO THE GLD./ //////INVENTORY RESTS AT 859.00 TONNES

AUGUST 19 WITH GOLD UP $3.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 7.19 TONNES OF GOLD VAPOUR INTO THE GLD./ //////INVENTORY RESTS AT 854.97 TONNES

AUGUST 16 WITH GOLD UP $44.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: //////INVENTORY RESTS AT 847.78 TONNES

AUGUST 15 WITH GOLD UP $13,70 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD OUT OF THE GLD//////INVENTORY RESTS AT 847.78 TONNES

AUGUST 14 WITH GOLD DOWN $26.20 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.03 TONNES OF GOLD OUT OF THE GLD//////INVENTORY RESTS AT 845.76 TONNES

AUGUST 13 WITH GOLD UP $3.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//////INVENTORY RESTS AT 849.79 TONNES

AUGUST 12 WITH GOLD UP $30.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ////INVENTORY RESTS AT 846.91 TONNES

AUGUST 9 WITH GOLD UP $10.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 846.91 TONNES

AUGUST 8 WITH GOLD UP $31.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.02 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 844.04 TONNES

AUGUST 7 WITH GOLD UP $1.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.16 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 848.06 TONNES

AUGUST 6 WITH GOLD DOWN $13.10 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD” A WITHDRAWAL OF .57 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 844.90 TONNES

AUGUST 2 WITH GOLD DOWN $9.95 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.58 TONNES OF GOLD OUT OF THE GLD//INVENTORY RESTS AT 845.47 TONNES

AUGUST 1 WITH GOLD UP $9.15 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 846.05 TONNES

JULY 30 WITH GOLD UP $26.55 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// A /////INVENTORY RESTS AT 843.17 TONNES

JULY 29 WITH GOLD UP $27.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD// A WITHDRAWAL OF 1.98 TONNES OF GOLD OUT OF THE GLD/////INVENTORY RESTS AT 843.17 TONNES

JULY 26 WITH GOLD UP $27.35 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD// A DEPOSIT OF 3.45 TONNES OF GOLD INTO THE GLD/////INVENTORY RESTS AT 845.19 TONNES

JULY 25 WITH GOLD DOWN $60.45 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 841.74 TONNES

JULY 24 WITH GOLD UP $12.75 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD//A DEPOSIT OF 1,73 TOONNES OF GOLD INTO THE GLD ///INVENTORY RESTS AT 841.74 TONNES

JULY 23 WITH GOLD UP $12.75 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 22 WITH GOLD DOWN $4.40 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 19 WITH GOLD DOWN $56.10 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;:A WITHDRAWAL OF 2.01 TONNES OF GOLD FROM THE GLD// ///INVENTORY RESTS AT 840.01 TONNES

JULY 18 WITH GOLD DOWN $2.20 ON THE DAY; NO CHANGES IN GOLD INVENTORY AT THE GLD;: ///INVENTORY RESTS AT 842.02 TONNES

JULY 17 WITH GOLD DOWN $6.60 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A MASSIVE DEPOSIT OF 5.49 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 842.02 TONNES

JULY 16 WITH GOLD UP $38.60 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD;: A DEPOSIT OF 1.44 TONNES OF GOLD INTO THE GLD///INVENTORY RESTS AT 836.53 TONNES

GLD INVENTORY: 857.27 TONNES, TONIGHTS TOTAL

SILVER

AUGUST30//WITH SILVER DOWN $.42//NO CHANGES IN SILVER INVENTORY: .///./// /INVENTORY AT 464.693 MILLION OZ

AUGUST 29//WITH SILVER UP $.37//SMALL CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 0.558 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 464.693 MILLION OZ

AUGUST 28//WITH SILVER DOWN $0.76//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 2.301 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 465.281 MILLION OZ

AUGUST 27//WITH SILVER DOWN $0.03//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 2.921 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 462.959 MILLION OZ

AUGUST 26//WITH SILVER UP $0.23//SMALL CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 45,000 OZ OUT OF THE SLV. .///./// /INVENTORY AT 465.880 MILLION OZ

AUGUST 23//WITH SILVER UP $0.72//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 1.506 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 465.925 MILLION OZ

AUGUST 22//WITH SILVER DOWN $0.44//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 0.943 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 468.344 MILLION OZ

AUGUST 21//WITH SILVER $0.03//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 1..552 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 468.344 MILLION OZ

AUGUST 20//WITH SILVER $0.24//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 1.369 MILLION OZ FROM THE SLV. .///./// /INVENTORY AT 466.792 MILLION OZ

AUGUST 19//WITH SILVER $0.39//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 1.506 MILLION OZ FROM THE SLV. .///./// /INVENTORY AT 465.423 MILLION OZ

AUGUST 16//WITH SILVER $0.49//NO CHANGES IN SILVER INVENTORY: .///./// /INVENTORY AT 466.929 MILLION OZ

AUGUST 15//WITH SILVER $1.14//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.186 MILLION ON INTO THE SLV.///./// /INVENTORY AT 466.929 MILLION OZ

AUGUST 14//WITH SILVER DOWN $0.40//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 13//WITH SILVER DOWN $0.19//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 12//WITH SILVER UP $.37//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 9//WITH SILVER DOWN $.03//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 8//WITH SILVER UP $.70//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 3.241 MILLION OZ INTO THE SLV////./// /INVENTORY AT 462.502 MILLION OZ

AUGUST 7//WITH SILVER DOWN $0.27//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.552 MILLION OZ INTO THE SLV////./// /INVENTORY AT 462.502 MILLION OZ

AUGUST 6//WITH SILVER UP $0.05//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 458.851 MILLION OZ

AUGUST 2//WITH SILVER DOWN $0.01//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 1.243 MILLION OZ OF SILVER OUT OF THE SLV ///./// /INVENTORY AT 460.961 MILLION OZ

AUGUST 1//WITH SILVER DOWN $0.46//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.608 MILLION OZ OF SILVER VAPOUR INTO THE SLV///./// /INVENTORY AT 462.204 MILLION OZ

JULY 31//WITH SILVER UP $0.45//NO CHANGES IN SILVER INVENTORY: /./// /INVENTORY REMAINS AT 460.596 MILLION OZ

JULY 30//WITH SILVER UP $0.61//SMALL CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 0.456 MILLION OZ OF SILVER VAPOUR INTO THE SLV/./// /INVENTORY RISES AT 460.596 MILLION OZ

JULY 29//WITH SILVER DOWN $0.07//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.382 MILLION OZ OF SILVER VAPOUR INTO THE SLV/./// /INVENTORY RISES AT 461.052 MILLION OZ

JULY 26//WITH SILVER DOWN $0.07//NO CHANGES IN SILVER INVENTORY./// /INVENTORY REMAINS AT 456.670 MILLION OZ

JULY 25 WITH SILVER DOWN $1.37//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 3.124 MILLION OZ OF SILVER OUT OF THE SLV./// /INVENTORY FALLS TO 456.670 MILLION OZ

JULY 24 WITH SILVER UP 3 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 15.880 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 23 WITH SILVER UP 3 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 15.880 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 22 WITH SILVER UP 2 CENTS//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 3.920 MILLION OZ OF SILVER INTO THE SLV./// /INVENTORY RISES AT 439.780 MILLION OZ

JULY 19 WITH SILVER DOWN 94 CENTS//NO CHANGES IN SILVER INVENTORY/// /INVENTORY REMAINS AT 435.854 MILLION OZ

JULY 18 WITH SILVER DOWN 13 CENTS//HUGE CHANGES IN SILVER INVENTORY” A DEPOSIT OF 2.374 MILLION OZ INTO THE SLV/// /INVENTORY RISES TO 435.854 MILLION OZ

JULY 17. WITH SILVER DOWN 75 CENTS//NO CHANGES IN SILVER INVENTORY// /INVENTORY REMAINS AT 433.480 MILLION OZ.

JULY 16. WITH SILVER UP 30 CENTS//NO CHANGES IN SILVER INVENTORY// /INVENTORY REMAINS AT 433.480 MILLION OZ.

CLOSING INVENTORY 464.693 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY//BILL HOLTER:

A Look At Income And Taxation Relative To Gold

FRIDAY, AUG 30, 2024 – 10:55 AM

Authored by Clint Siegner via Money Metals,

Gold and silver prices moved higher for a second week. The odds of a September rate cut by the Federal Reserve were bolstered by dovish comments from Chairman Jerome Powell, during the central bank’s annual meeting in Jackson Hole.

The odds of a rate cut also got a boost when the Bureau of Labor Statistics announced a massive downward revision of more than 800,000 jobs last week. Turns out the unbelievable jobs reports the BLS has been publishing month after month were just what skeptics thought they were… nonsense.

Stimulus addicted markets also got a boost from the terrible jobs news.

The S&P 500 closed back near all-time highs. The Federal Reserve note dollar, on the other hand, got clobbered,and bond yields fell.

It would be hard to overstate just how profound a couple of changes made to U.S. law in 1913 have been for American society.

That year brought both the ratification of the 16th Amendment to the constitution and a federal income tax as well as passage of the Federal Reserve Act which established the privately held central bank which has managed our money and markets with such disastrous effect.

Consider what has happened in income and taxation against the yardstick of gold.

Gold was valued at a fixed exchange rate of $20.67/oz in 1916. The average annual income was roughly $600. A single household earner was able to produce that income.

In other words, a typical husband earned 30 ounces of gold per year.

The income tax, which was sold to voters as a very modest tax on wealthy households, applied only to incomes over $3,000.00 at a rate of 1%. People who earned more than the equivalent of 150 ounces of gold per year paid 1% of income in excess of that amount.

Had incomes kept up with gold, those 30 ozs per year would translate to roughly $75,000 in today’s dollars with gold at $2,500/oz. Unfortunately, they have not kept up. The average salary today is roughly $60,000 or 24 ounces, i.e. 20% below what it was all those decades ago.

It now takes two earners in most households to produce the gold equivalent income that a single earner achieved in 1913. The picture gets dramatically worse after accounting for what has happened to income taxes.

If the IRS had indexed the original threshold income tax to gold, only those earners above $360,000/year would be paying income tax. The sad reality is that anyone with even a of adjusted gross income must pay, and the income tax rates begin at 10%. Those considered wealthy as defined in 1913 pay at least 35%.

And don’t forget that 43 U.S. states have their own income taxes also, compounding the burden.

Today’s system is far from what was sold to Americans. The past century has been an economic disaster for households.

If early 20th century Americans had some way of knowing the consequences for their descendants, they would never have supported the Federal Reserve or the 16th Amendment.

3.CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES

Stefan Gleason: Holding gold yields better returns than mining for it

Submitted by admin on Thu, 2024-08-29 13:39 Section: Daily Dispatches

By Stefan Gleason

Money Metals Exchange, Eagle, Idaho

Thursday, August 29, 2024

With spot gold prices at record highs, investors might expect that shares of precious metals mining companies are also trading at record highs.

By and large, that is not the case.

Mining stocks, as represented by the HUI Gold BUGS Index, are still under water by more than 40% compared to their 2011 highs. And that’s despite being pulled up significantly this year by soaring gold and silver prices.

There are a variety of reasons why most mining shares have lagged the metals. First and foremost, mining is a tough business that is fraught with risks. Even when the value of a mine’s end product goes up, the costs of getting it out of the ground can go up even faster.

During periods when market prices for metals fall below a mining company’s all-in sustaining costs, it may choose to sell at a loss. That’s because it would be impractical for a mine to lay off all its workers and let its expensive equipment sit idle while waiting for market conditions to improve.

But there is another option available to precious metals mining companies during times when their product is being undervalued.

If the CEOs of companies that have “gold” (or “silver”) in their name truly believe in their product — which is money itself — then why don’t they hold some of it on their books as a reserve asset instead of immediately exchanging it for dollars regardless of prevailing price? …

… For the remainder of the commentary:

https://www.moneymetals.com/news/2024/08/29/holding-gold-mining-003421

END

Ghana to launch ‘monster mines’ to boost gold production

Submitted by admin on Thu, 2024-08-29 19:35 Section: Daily Dispatches

By Maxwell Akalaare Adombila

Reuters

Thursday, August 29, 2024

ACCRA, Ghana — Africa’s top gold producer, Ghana, will commission its first large-scale greenfield mine in more than a decade in November, with expected annual production of more than 350,000 ounces, the head of its mining sector regulator told Reuters.

The Cardinal Namdini mine is owned by Cardinal Resources, a unit of Shandong Gold, which received a licence for the facility in 2020.

Ghana, the world’s No. 2 two cocoa producer, has seen gold exploration slump over the past decade, limiting new projects and lowering output from big miners. …

… For the remainder of the report:

4. OTHER GOLD COMMENTARIES/LIVE FROM THE VAULT: TODAY ANDREW MAGUIRE WITH BILL HOLTER

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/

end

6 CRYPTOCURRENCY NEWS

END

ASIA TRADING/FRIDAY MORNING/THURSDAY NIGHT

SHANGHAI CLOSED UP 19.11 PTS OR 0.68% //Hang Seng CLOSED UP 202.75 PTS OR 1/14% // Nikkei CLOSED UP 285/22 OR .74%//Australia’s all ordinaries CLOSED UP 0.64%///Chinese yuan (ONSHORE) CLOSED UP TO 7,0902 CHINESE YUAN OFFSHORE CLOSED UP TO 7.0800/ Oil UP TO 76.05 dollars per barrel for WTI and BRENT UP AT 78.86 Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.0902

OFFSHORE YUAN: UP TO 7.0800

SHANGHAI CLOSED UP 19.11 PTS OR 0.68 %

HANG SENG CLOSED UP 202.75 PTS OR 1/14%

2. Nikkei closed UP 285.22 PTS OR .74%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 101.12 EURO FALLS TO 1.1098 DOWN 26 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +0.893 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 145.27…… JAPANESE YEN NOW RISING AS WE HAVE NOW REACHED THE COLLAPSING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.2570/Italian 10 Yr bond yield DOWN to 3.631 SPAIN 10 YR BOND YIELD DOWN TO 3.085%

3i Greek 10 year bond yield DOWN TO 3.290

3j Gold at $2519.50//Silver at: 29.49 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 1 AND 35/ 100 roubles/dollar; ROUBLE AT 91.25

3m oil into the 76 dollar handle for WTI and 78 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 145.27/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.893 % STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8488 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9406 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.855 DOWN 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.136 DOWN 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.902 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 34.07…

10 YR UK BOND YIELD: 4.019 DOWN 3 PTS

10 YR CANADA BOND YIELD: 3.138 DOWN 2 BASIS PTS

2a New York OPENING REPORT

Futures Rise Ahead Of Fed’s Favorite Inflation Print

Friday, Aug 30, 2024 – 07:40 AM

US equity futures were set for a stronger open to close the week after two days of wobbles, with tech stocks outperforming, paring back some of the NVIDIA-induced losses as confidence mounted that the Fed and ECB will cut interest rates in the coming months, after inflation in Europe continued to sink and with today’s core PCE expect to confirm a taming of US inflation. As of 730am, S&P futures rose 0.5% while Nasdaq 100 Index added 0.7% as traders waited to see if the Fed’s favorite inflation indicator, core PCE, confirms the picture of moderating prices. Europe’s main stock index rallied to a record high as euro-area inflation eased to a three-year low, cementing the case for the ECB to cut rates in September. The dollar was flat and 10Y yields were unchanged around 3.86% as treasuries were poised for their longest monthly winning streak in three years. Gold traded near record highs, oil was flat and bitcoin was also unchanged. Today’s macro calendar has Personal Income, Spending and core PCE as well as the UMich consumer sentiment on deck.

In premarket trading, Nvidia edged higher after tumbling 6% the previous day, while other tech names, including Marvell Technology and Dell were boosted by forecast-beating results. Here are some of the other notable premarket movers:

- Abercrombie & Fitch shares rise 2.3% after the apparel retailer was upgraded to buy from neutral at Citi, which sees several reasons as to why the investment story for the stock remains attractive.

- Autodesk shares are up 3.7% after the maker of engineering software reported second-quarter results that beat expectations. The firm raised its full-year forecast for both revenue and adjusted EPS, impressing analysts after coming under pressure from an activist investor.

- Dell Technologies shares rose 5.9% after the computer hardware company reported second-quarter results that beat expectations, with particular strength in orders for AI servers.

- Elastic shares are down 27% after the application-software company cut its full-year revenue forecast. Analysts say execution problems around sales changes made at the start of the quarter had a negative impact on the software company’s results.

- Intel shares rise 2.6% after Bloomberg News reported that the company is discussing various scenarios, including a split of its product-design and manufacturing businesses, as well as which factory projects might potentially be scrapped.

- Intuitive Machines shares soar 19% after the company said it received a $116.9 million contract from NASA to deliver six science and technology payloads, including one European Space Agency-led drill suite to the Moon’s South Pole.

- Lululemon shares rise 4.2% after the the activewear company reported second-quarter earnings. While the firm reported a top-line miss in the second quarter and reduced its full-year guidance, Morgan Stanley sees the revised guidance as achievable, noting that investors might have assigned a floor to its valuation.

- MongoDB shares rise 15.14% after the database software company reported second-quarter results that beat expectations and raised its full-year forecast. Analysts say the results suggest that growth could accelerate with an improving underlying picture.

- Ulta Beauty shares drop 8.5% after the cosmetics retailer trimmed its sales forecast following weaker-than-expected second-quarter results. Analysts flagged the impact of competition as well as the softer macroeconomic environment.

Global stocks are on track for a fourth month of gains, with most data indicating the Fed has achieved a soft-landing, by taming inflation without tipping the economy into recession. While economists expect a slight pick-up in the year-on-year PCE reading later on Friday, that’s not expected to derail prospects for a September rate cut. Bloomberg Economics sees the inflation report reviving talk of a “Goldilocks” economy that allows the Federal Reserve to start cutting rates next month.

“When rates ease, it lifts all boats,” said Florian Ielpo, head of macro research at Lombard Odier Asset Management in Geneva. “Inflation is looking better and economic growth remains decent and that’s the environment we are in.”

No matter today’s PCE print, markets expect the Fed to cut rates next month by as much as 50 basis points (but more likely 25bps after yesterday’s hot GDP and initial claims reports), and by another half-point by year-end. Ielpo said that for traders watching for monetary-policy clues, the US monthly payrolls report due next week would be even more significant than today’s PCE reading. “Inflation is a done deal so markets are more likely to pay attention to what’s happening to employment and growth,” he added, just don’t forget to keep an eye on geopolitics and the price of oil which has resumed its latest ascent and may yet throw a wrench in the Fed’s easing plans.

Expectations for central bank easing saw investors pump $20.7 billion into global bond funds this past week, with Treasuries recording the largest inflow since last October, Bank of America said, citing EPFR Global data. Treasuries were on course for their longest monthly winning streak in three years. But the wagers have weighed on the dollar, which edged lower against a basket of currencies and was set for its worst monthly performance this year.

European stocks rise for a fourth session, taking the Stoxx 600 to another record intraday high as euro-area headline and core inflation slowed as expected in August. Real estate and consumer product shares are leading gains while technology is a drag. Here are some of the biggest movers on Friday:

- Chipmaker-machinery stocks decline in Europe after a Bloomberg report saying Intel is considering splitting the design and manufacturing businesses. BE Semi falls 2.5%, ASML -2.1%, ASMI -1.3%

- Ambu shares fall as much as 14%, the most since November 2022, after the Danish health-care equipment maker reported 3Q numbers that disappointed in its key endoscopy division. Analysts also said a correction was due after the shares gained 14% in July and August.

- BlueNord falls as much 6.1%, the most since July 8, after the Norwegian fossil-fuel exploration firm said operator TotalEnergies intends to implement measures that are expected to not allow maximum technical capacity at the Tyra II field to be reached until 4Q.

Earlier in the session, Asian equities cruised to a six-week high. Hang Seng Tech Index jumps more than 3% and CSI 300 climbs almost 2%. Japanese, South Korean and Australian indexes all firmly in the green.

In FX, the Bloomberg Dollar Spot Index falls 0.1% but is poised to snap its four-week declining streak ahead of US core PCE data, with it up 0.7% on week. Tthe euro is little changed around $1.1080. USD/JPY rose above 145 after dipping back under following a post-GDP spike on Thursday. GBP/USD hovers above mid 1.31-1.32. AUD/USD consolidates around 0.68. NZD/USD grinds higher but remains below Thursday’s peak of 0.6299.

In rates, treasuries are mixed with the yield curve flatter as US trading gets under way, led by similar price action in UK and German bonds after August euro-area headline and core inflation slowed as expected. Long-end Treasury yields are richer by ~1bp curve with front-end and belly little changed, flattening 5s30s spread; the 10Y TSY yield traded 1bp lower to 3.85%. Long-end German yields richer by more than 2bps on the CPI data and held higher on the day with German 10-year yields down 2bps at 2.26%. UK’s by nearly 5bp, narrowing their curve spreads. Curve-flattening has support from anticipation of buying tied to month-end index rebalancing, which will extend the duration of the Bloomberg Treasury Index by an estimated 0.10 year as securities auctioned during the month are added to it. Also, traders anticipate flows tied to corporate bond offerings next week, a historically heavy issuance period

As noted earlier, treasuries are poised for their longest monthly winning streak in three years as traders look past US data on personal income and expenditure due Friday and prepare for the Federal Reserve to start cutting interest rates. US government bonds returned 1.5% in August through Thursday, set for a fourth month of gains that would be the longest run since July 2021, according to the Bloomberg US Treasury Total Return Index. The gauge has been rallying since the end of April, extending this year’s gain to almost 3%, as investors have grown more confident in the case for lower US borrowing costs.

In commodity markets, oil was steady with WTI trading near $76 a barrel, though the main crude benchmark is set for its first back-to-back monthly loss this year on fears that slowing economic growth, especially in China, will impact demand. Iron ore futures pulled back slightly after jumping by about 10% in 10 days to breach $100 a ton. Spot gold climbs $4 to around $2,525/oz.

Bitcoin is holding steady just above USD 59.5k, whilst Ethereum slips slightly. Elon Musk and Tesla win dismissal of lawsuit claiming they rigged Dogecoin.

The US economic data calendar includes July personal income and spending with PCE price indexes (8:30am), August MNI Chicago PMI (9:45am, several minutes earlier to subscribers) and August final University of Michigan sentiment (10am). Fed speaker slate empty for the session. Meanwhile in the Euro Area, there’s the flash CPI release for August and the unemployment rate from July. We’ll also get German unemployment for August, UK mortgage approvals for July, and Canada’s GDP for Q2. From central banks, we’ll hear from the ECB’s Schnabel, Rehn, Kazaks, Simkus and Muller.

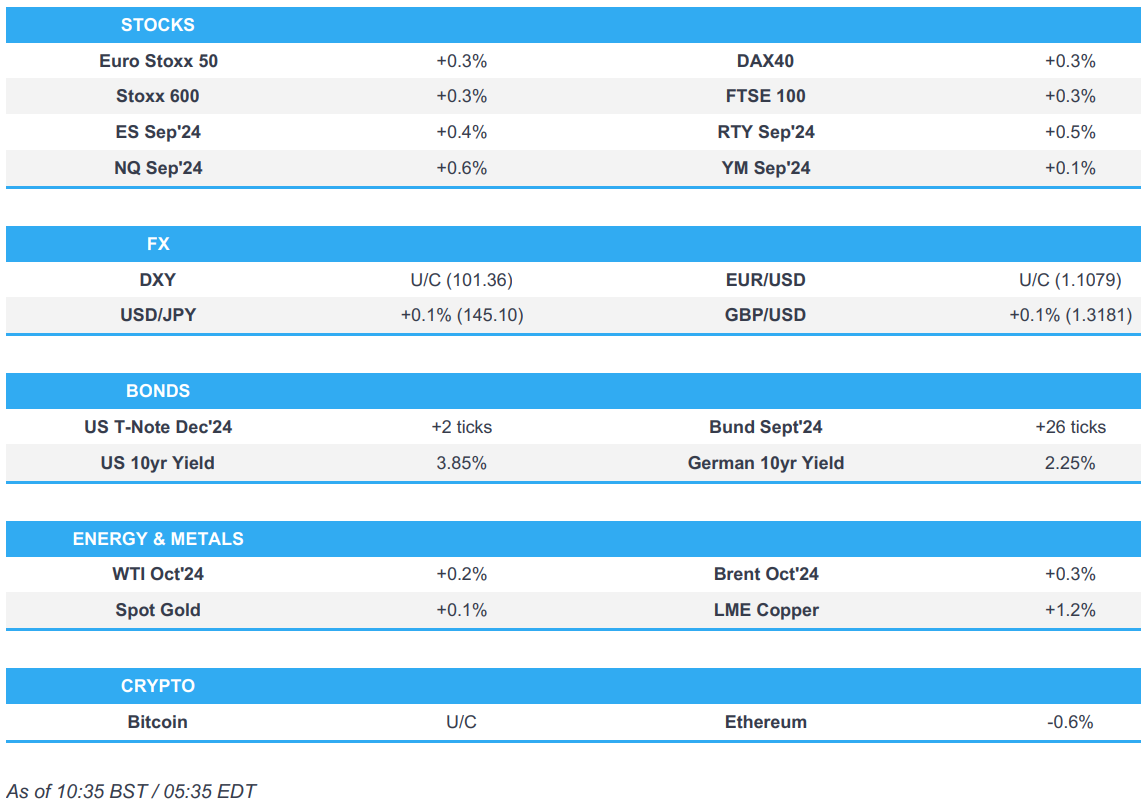

Market Snapshot

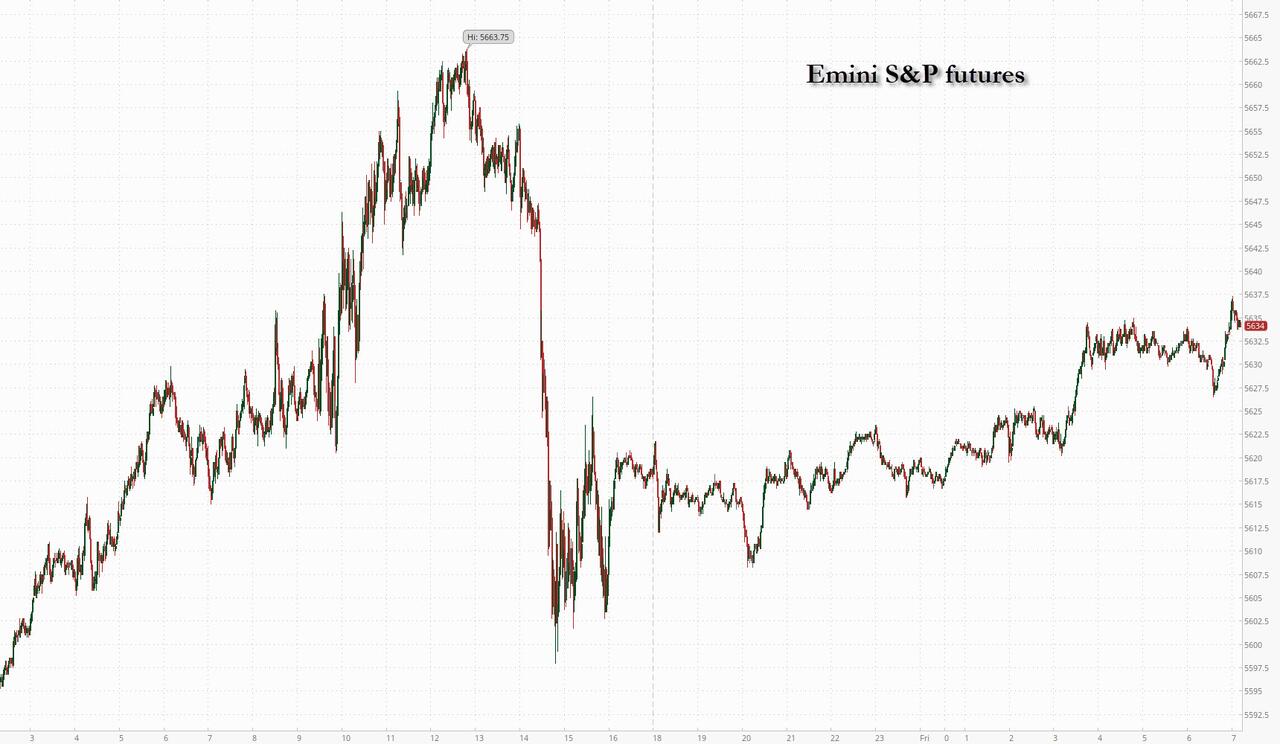

- S&P 500 futures up 0.4% to 5,633.25

- STOXX Europe 600 up 0.3% to 526.32

- MXAP up 0.8% to 186.82

- MXAPJ up 0.6% to 577.85

- Nikkei up 0.7% to 38,647.75

- Topix up 0.7% to 2,712.63

- Hang Seng Index up 1.1% to 17,989.07

- Shanghai Composite up 0.7% to 2,842.21

- Sensex up 0.4% to 82,426.55

- Australia S&P/ASX 200 up 0.6% to 8,091.85

- Kospi up 0.5% to 2,674.31

- German 10Y yield down 1.6 bps at 2.26%

- Euro up 0.2% to $1.1094

- Brent Futures up 0.6% to $80.42/bbl

- Gold spot up 0.2% to $2,526.17

- US Dollar Index little changed at 101.26

Top Overnight News

- China could allow homeowners to refinance as much as $5.4T worth of mortgages months before the process typically occurs in January, and potentially with different banks. BBG

- Offices in China’s biggest cities are emptier than they were during stringent Covid-19 lockdowns in what analysts say is a sign of how the country’s economic slowdown has hurt business confidence. FT

- Russian companies are having an increasingly difficult time transacting w/partners in China as Chinese banks become worried about running afoul of int’l restrictions and being subject to sanctions. RTRS

- Eurozone CPI is inline w/the Street for Aug, including +2.2% for headline (down from +2.6% in Jul) and +2.8% core (down from +2.9% in Aug). BBG

- Israel’s defense minister said the country should expand its war goals to ensure that the ~60K people displaced from the north by Hezbollah rocket attacks can return home. FT

- Harris is up 1 point in a head-to-head contest vs. Trump and up 2 points if all candidates are included. WSJ

- Intel is working with advisors to explore options, including potentially splitting off its manufacturing operations. BBG

- Apple and Nvidia are in talks to invest in OpenAI, a move that would strengthen their ties to a partner integral to their efforts in the artificial-intelligence race. WSJ

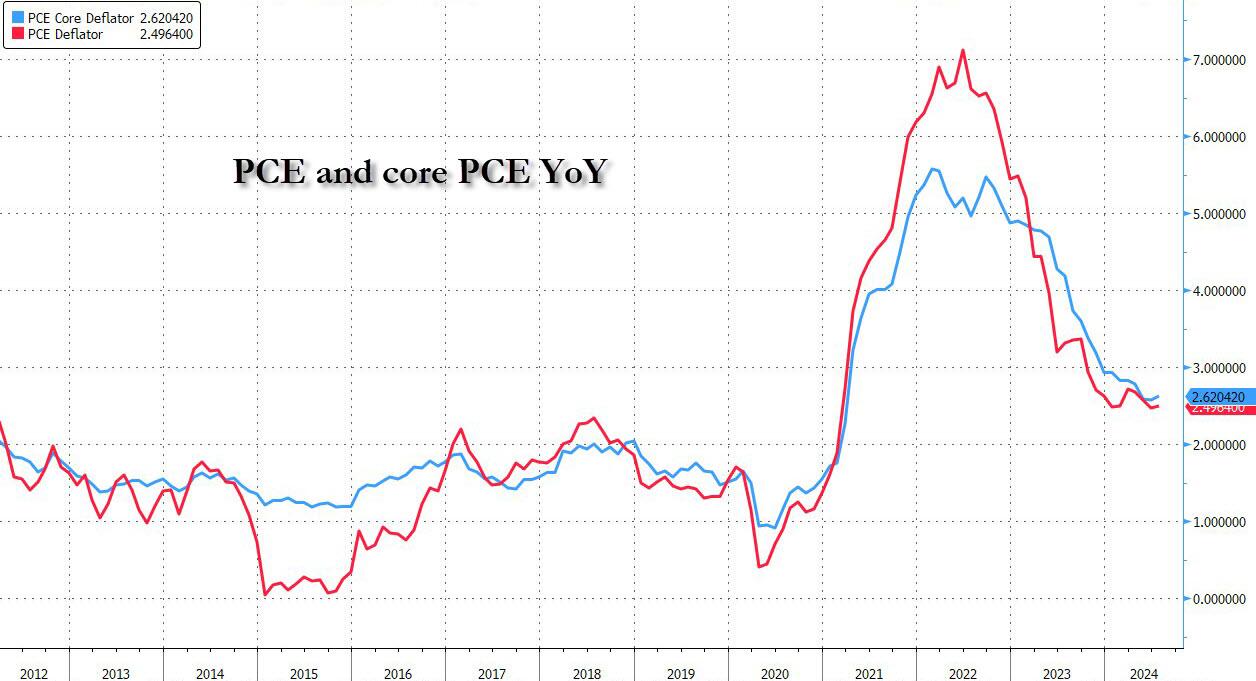

- Recent US inflation readings are “still far” from the Fed’s 2% goal, Raphael Bostic said. He may take some confidence from July’s core PCE deflator, due later. Bloomberg Economics said it probably increased at an annualized pace consistent with target, while the savings rate may have slid further. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded higher across the board despite a lack of fresh catalysts following a mixed lead from Wall Street, and ahead of US PCE and the US long weekend. ASX 200 remained in a narrow range (8,045.10-8,085.00) but was propped up by its Industrials, Energy, and Gold names. Nikkei 225 traded firmer following a choppy start after August Tokyo core CPI surprisingly ticked higher, whilst the Japanese unemployment rate surprisingly rose. Hang Seng and Shanghai Comp opened with modest gains and eventually soared despite a lack of newsflow, whilst Bloomberg suggested the CSI 300 rallied amid heavy volume. Sentiment in China could’ve also seen tailwinds from the PBoC yesterday suggesting it will step up counter-cyclical adjustments and will strengthen financial support to the real economy, whilst the mood was further lifted amid Bloomberg reports China reportedly mulls allowing refinancing on USD 5.4tln in mortgages.

Top Asian News

- China reportedly mulls allowing refinancing on USD 5.4tln in mortgages, according to Bloomberg.

- Japanese government official on industrial output, said if output falls short of plans, August production could fall M/M. September is expected to fall M/M on lower production of semiconductor production equipment and electronic component devices, although the assessment is revised upward, need to be vigilant about the outlook. The official added that the impact of Typhoon Shanshan was not taken into account in August data.

- PBoC injected CNY 30.1bln via 7-day Reverse Repo at a maintained rate of 1.70%.

- China’s major state-owned banks seen buying USD in onshore foreign exchange market to prevent CNH from appreciating too fast, via Reuters citing sources.

- China’s FX Regulator to launch foreign currency non-deliverable forwards (NDFs) on 2nd September within the interbank market.

- PBoC purchased net CNY 100bln of gov’t bonds from dealers during August, via Bloomberg.

European bourses, Stoxx 600 (+0.3%) began the session with a mixed picture, and traded tentatively on either side of the unchanged mark. As the morning progressed, indices gradually picked up and edged towards session highs. European sectors hold a strong positive bias; Real Estate is found at the top of the pile, alongside Basic Resources. Tech is found at the foot of the pile, paring back the prior day’s advances and accounting for the post-earning losses in NVIDIA. US Equity Futures (ES +0.4%, NQ +0.6%, RTY +0.5%) are entirely in the green, with the NQ outperforming, paring back some of the NVIDIA-induced losses. The docket ahead includes the Fed’s preferred measure of inflation, PCE (July).

Top European News

- ECB’s Schnabel: “while risks to growth have increased, a soft landing still looks more likely than a recession”; “Incoming data broadly confirm the baseline scenario”. “In particular, the closer policy rates get to the upper band of estimates of the neutral rate of interest – that is, the less certain we are how restrictive our policy is –, the more cautious we should be to avoid that policy itself becomes a factor slowing down disinflation.”; “In other words, the pace of policy easing cannot be mechanical. It needs to rest on data and analysis.”; “Wage pass-through may be stronger.”. In short, remarks from Schnabel are in-fitting with the data-dependent approach the ECB has been taking but with a slight hawkish skew from the ECB official, in-fitting with her general bias.

- ECB’s Kazaks says services inflation remains sticky. Open to a September discussion on policy easing.

FX

- The Dollar is broadly softer vs. peers in the run-up to US PCE metrics. DXY is currently contained within yesterday’s 100.88-101.57 range.

- EUR is steady post-EZ inflation data which was broadly in-line. However, greater concern could come via the services metric which rose to 4.2% from 4.0%. EUR/USD is contained just below the 1.11 mark and within yesterday’s 1.1055-1.1139 range.

- GBP is firmer vs. the USD but Cable is unable to reclaim the 1.32 handle with the current session high at 1.3198 and south of yesteday’s 1.3227 peak.

- JPY was a touch firmer vs. the USD following firm Tokyo inflation data overnight. In terms of price action for USD/JPY, the pair is back on a 144 handle but still some way north of yesterday’s 144.22 trough.

- AUD/USD is mildly extending on its recent uptrend which has seen the pair breach 0.68 to the upside with newsflow out of China providing support.

- USD/CNH has continued its recent move to the downside with the latest leg lower prompted by reporting from Bloomberg that China is mulling allowing refinancing on USD 5.4tln in mortgages.

- PBoC set USD/CNY mid-point at 7.1124 vs exp. 7.1116 (prev. 7.1299)

Fixed Income

- USTs are flat ahead of monthly US PCE, afterwhich conditions will likely become thinner than normal on account of Monday’s US market holiday. A few fleeting ticks higher on EGB-drivers, but not sufficient to merit a range of more than a couple of ticks; additionally, yields are pivoting the unchanged mark but with an incremental flattening bias.

- Bunds were slightly firmer after French inflation metrics and climbed above 134.00 into the EZ-wide figures. Headline cooled to 2.2% Y/Y as expected, whilst Services rose to 4.2% (prev. 4%); no real reaction was seen in Bunds.

- Gilts are firmer and specifics quite light, though the UK Nationwide House Price index saw an unexpected drop for the month. Gilts at the top-end of the session’s range but shy of the 99.00 handle.

- China’s major state-owned banks seen buying USD in onshore foreign exchange market to prevent CNH from appreciating too fast, via Reuters citing sources.

Commodities

- Crude benchmarks began with a modest upward bias and have continued to inch higher throughout the European morning despite a lack of fresh drivers.

- Thus far, WTI & Brent have been as high as USD 76.53/bbl and USD 80.60/bbl respectively, just shy of Thursday’s USD 76.87bbl and USD 80.78/bbl best.

- Spot gold is essentially unchanged, in-fitting with the tentative performance of FX into monthly US PCE; in a relatively thin USD 2512-2523/oz band, which is towards the upper-end of yesterday’s parameters.

- LME Copper is firmer but around familar levels after a choppy and shortened week; upside being driven by the modestly constructive risk tone and USD pressure.

- Liberian Environmental Protection Agency said China Union’s iron ore Bong Mines is shut down for several environmental violations, according to Reuters.

Geopolitics

- “Lebanese sources: Israeli raids on different areas in southern Lebanon”, according to Sky News Arabiya.

- Missile attack launched on US military base in eastern Syria, according to IRNA.

- There is now a planned call at the theatre commander level between the US and China, according to Fox’s Heinrich. “It comes after China bristled at US Indo-Pacific Command’s Adm. Paparo suggesting this week US forces could escort Philippine ships through the South China Sea, following a months-long series of violent confrontations between Chinese and Philippine ships”.

- Israeli military says local Hamas commander in West Bank City of Jenin killed by Israeli police.

US Event Calendar

- 08:30: July Personal Income, est. 0.2%, prior 0.2%

- July Personal Spending, est. 0.5%, prior 0.3%

- July Real Personal Spending, est. 0.3%, prior 0.2%

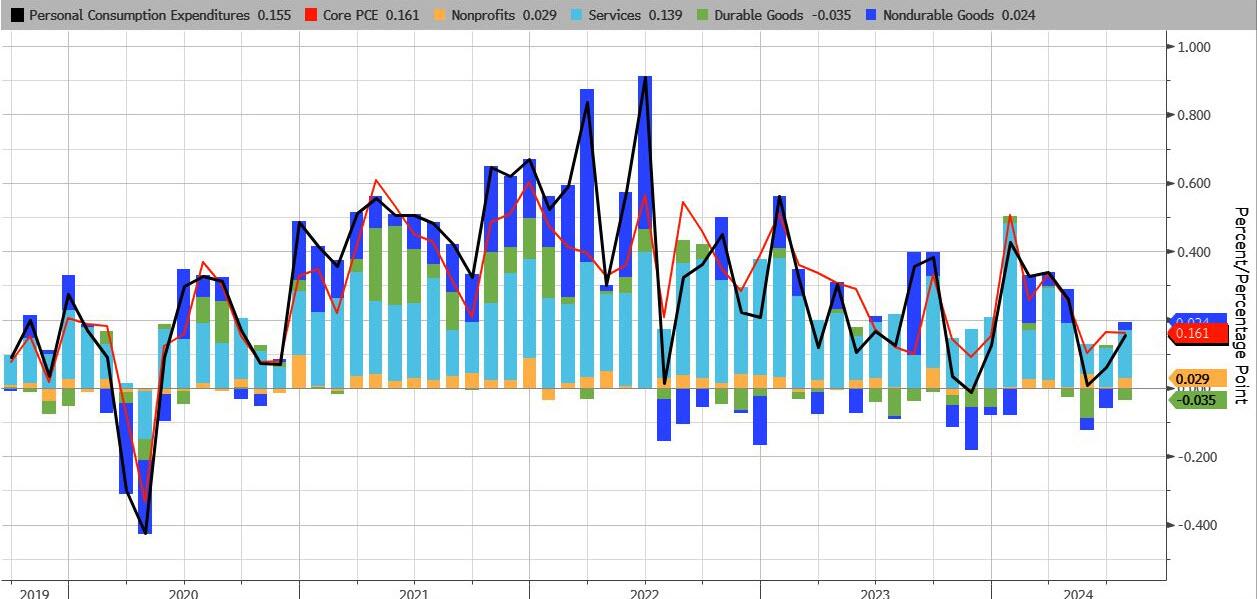

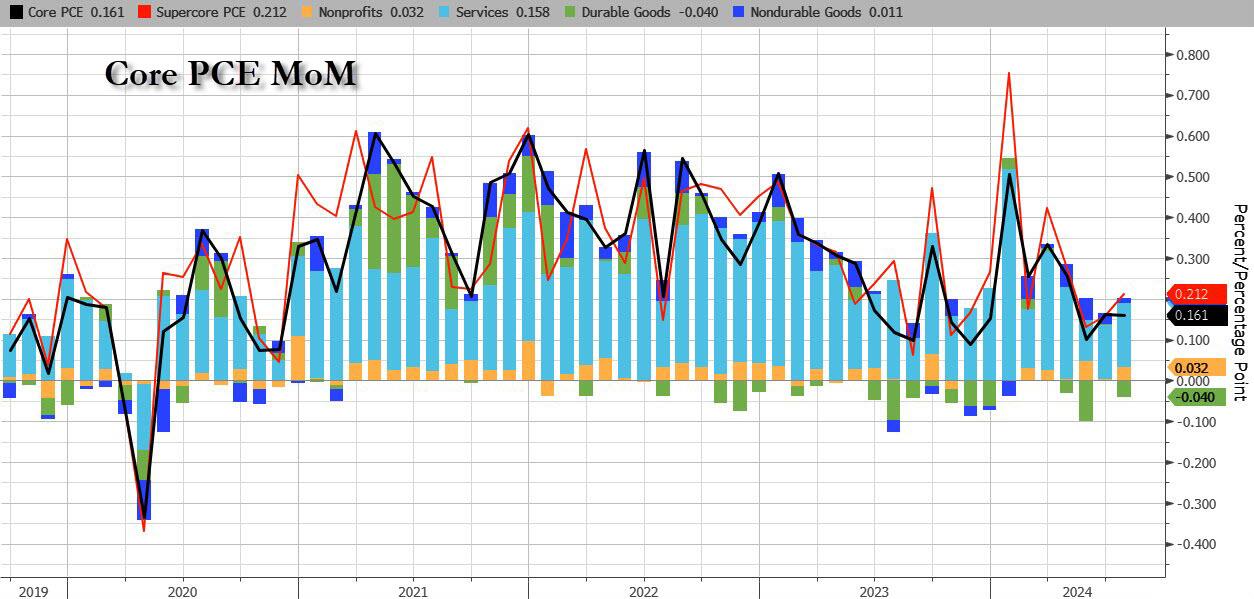

- 08:30: July Core PCE Price Index MoM, est. 0.2%, prior 0.2%

- July PCE Price Index YoY, est. 2.5%, prior 2.5%

- July PCE Price Index MoM, est. 0.2%, prior 0.1%

- July Core PCE Price Index YoY, est. 2.7%, prior 2.6%

- 09:45: Aug. MNI Chicago PMI, est. 44.8, prior 45.3

- 10:00: Aug. U. of Mich. Sentiment, est. 68.1, prior 67.8

- U. of Mich. Current Conditions, est. 61.2, prior 60.9

- U. of Mich. Expectations, est. 72.4, prior 72.1

- U. of Mich. 1 Yr Inflation, est. 2.9%, prior 2.9%

- U. of Mich. 5-10 Yr Inflation, est. 3.0%, prior 3.0%

DB’s Jim Reid concludes the overnight wrap

Risk assets put in a decent performance over the last 24 hours, as solid US data outweighed investors’ disappointment about Nvidia’s latest results. It’s true that the S&P 500 was unchanged on the day, but the index was weighed down by the Magnificent 7 (-0.72%) and the equal-weighted S&P 500 (+0.37%) moved up to a new record, as did the Dow Jones (+0.59%) and Germany’s DAX (+0.69%). So in most places it was a pretty decent performance, and overnight the Hang Seng (+1.76%) is also on track to close at a 7-week high. Other risk assets were on the stronger side, with EUR HY spreads at their tightest level in over a month, whilst oil prices moved higher as well. The main exception were sovereign bonds however, which mostly lost ground as investors dialled back the chance of a 50bp rate cut from the Fed next month.

This positivity was driven by several US data releases that collectively pointed away from a recession, leading to a fresh bout of optimism about the outlook. The key headline came from the Q2 GDP numbers. They were actually the second estimates rather than the original release, but they painted an even more positive story than the first estimate released in late July. For instance, headline GDP was revised up to show an annualised growth rate of +3.0% (vs. +2.8% previous estimate). On a year-on-year basis, that leaves real GDP up +3.1%, so these are very good numbers that really don’t look like a recession. On top of that, the GDP release included downward revisions to PCE inflation in Q2, which is the measure the Fed officially targets. Headline PCE was revised down a tenth to an annualised +2.5% rate, whilst core PCE was also revised down a tenth to +2.8%. So a bit closer to the Fed’s 2% target than we previously thought. Today we’ll get the first look at PCE inflation for the month of July, so one to keep an eye on.

On top of the GDP release, yesterday also brought the weekly initial jobless claims, which were basically in line with expectations at 231k over the week ending August 24 (vs. 232k expected). That wasn’t a shock, but it helped to bring down the 4-week moving average as well, which now stands at a two-month low of 231.5k. So again, that’s another release pointing away from a recession, with the weekly claims looking in better shape than they did at the end of July.

With all that data in hand, the general perception was that the economy was doing better than thought, and that a larger 50bp cut from the Fed was now less likely. Indeed, futures lowered the chance of a 50bp move in September from 36% to 32%. And the number of cuts priced in by December also came down from 103bps to 100bps. In turn, that led to a selloff across US Treasuries, with the 2yr yield up +2.9bps to 3.90%, whilst the 10yr yield was up +2.6bps to 3.86%.