SEPT 5/GOLD CLOSED UP $18.00 TO $2512.90//SILVER WAS UP 55 CENTS TO $28.73//PLATINUM WAS UP $17.95 TO $928.10/PALLAIDUM WAS UP $1.25 TO $943.50//RUSSIA ANNOUNCES ITS ITS GOING TO BUY MORE MUCH PHYSICAL GOLD//ANOTHER GERMAN STABBING//VOLKSWAGEN MAY HAVE TO DDECLARE BANKRUPTCY BECAUSE OF HIGH LABOUR COSTS//ISRAEL VS HAMAS/HEZBOILLAH UPDATES/RUSSIA VS UKRAINE UPDATES//COVID UPDATES/VACCINE INJURY REPORTS/SLAY NEWS ETC//USA DATA: ADP WHICH IS GENERALLY QUITE BULLISH ANNOUNCES WEAK PRIVATE WAGE GAINS//SWAMP STORIES FOR YOU TONIGHT//

323 C HSBC 2 363 H WELLS FARGO SEC 6 661 C JP MORGAN 4 737 C ADVANTAGE 14 2

TOTAL: 14 14 MONTH TO DATE: 2,926

JPMorgan stopped 4/14

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2024. CONTRACT: 14 NOTICES FOR 1400 OZ or 0.0435 TONNES

total notices so far: 2926 contracts for 292600 Oz (9.1011 tonnes)

FOR SEPT:

SILVER NOTICES: 247 NOTICE(S) FILED FOR 1.235,000

OZ/

total number of notices filed so far this month : 4,658 for 23,340,000 oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $18.00 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ NO CHANGES IN GOLD INVENTORY AT THE GLD:

/ /INVENTORY RESTS AT 862.74 TONNES

INVENTORY RESTS AT 862.74 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $.55 AT THE SLV

SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 0.193 MILLION OZ INTO THE SLV..

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 466.234 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A FAIR SIZED 415 CONTRACTS TO 130,453 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS FAIR LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR GAIN OF $0.17 IN SILVER PRICING AT THE COMEX ON WEDNESDAY’S TRADING. WE LOST ZERO NET LONGS DESPITE THE GAIN IN PRICE. WE HAD A SMALL GAIN OF 32 CONTRACTS ON OUR TWO EXCHANGES. WE HAD AGAIN A HUGE LIQUIDATION OF T.A.S. CONTRACTS DURING WEDNESDAY’S TRADING//. WE HAD CONSIDERABLE SHORT COVERING BY OUR SPECS WITH THE GAIN IN PRICE. WE HAD A FAIR 350 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY ANOTHER STRONG 419 CONTRACT T.A.S ISSUANCE. IN ESSENCE WE LOST 125 CONTRACTS ON OUR TWO EXCHANGES DESPITE THE GAIN IN PRICE. ALL OF THE LOSS IN COMEX OI WAS DUE TO OUR SPREADER T.A.S. LIQUIDATION.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN YESTERDAY. THE ACCUMULATED T.A.S. IS BEING USED TO MANIPULATE PRICES AT THE COMEX NOW EVERY DAY..

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 419 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS.IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1/2 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS BUT TO NO AVAIL. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.17) AND WERE UNSUCCESSFUL IN KNOCKING ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A TINY LOSS OF 125 TOTAL OI CONTRACTS ON OUR TWO EXCHANGES ,

WE HAD A FAIR 350 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 22.765 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 840,000 OZ QUEUE JUMP//NEW STANDING ADVANCES TO 23.710 MILLION OZ

//NEW STANDING FOR SILVER//SEPT ADVANCES TO 23.710 MILLION OZ

WE HAD:

/ GOOD SIZED COMEX OI LOSS //FAIR SIZED EFP ISSUANCE/ VI) GOOD SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 419 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED 125 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT

TOTAL CONTRACTS for 3 DAYS, total 1531 contracts: OR 7.655 MILLION OZ (510 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 7.655 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL PROBABLY BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 7.655 MILLION OZ//

RESULT: WE HAD A FAIR SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 318 CONTRACTS DESPITE OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR EFP ISSUANCE CONTRACTS: 350 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 22.765 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE 840,000 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR SEPT ADVANCES TO 23.710 MILLION OZ

WE HAVE A TINY GAIN OF 32 OI CONTRACTS ON THE TWO EXCHANGES WITH THE GAIN IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A FAIR SIZED 350 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX TRADING//// MASSIVE ATTEMPTED SHORT COVERING FROM OUR SPEC SHORTS WITH THE GAIN IN PRICE WEDNESDAY/ AND ZERO LIQUIDATION OF LONGS. ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER.

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (419) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND FOR SURE TODAY., .

WE HAD 247 NOTICE(S) FILED TODAY FOR 1.235 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A TINY SIZED 415 OI CONTRACTS TO 510,721 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 481 CONTRACTS//

WE HAD A TINY SIZED DECREASE IN COMEX OI (415 CONTRACTS) OCCURRED DESPITE OUR GAIN OF $3.45 IN PRICE/WEDNESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT AT 12.885 TONNES ON FIRST DAY NOTICE FOLLOWED BY WEDNESDAYS GIGANTIC 29,400 OZ E.F.P. JUMP TO LONDON WHERE THESE BOYS TOOK IMMEDIATE DELIVERY OVER IN LONDON ON A T + 1 BASIS.

NEW STANDING REDUCES TO 11.940 TONNES

/ ALL OF THIS HAPPENED WITH OUR $3.45 GAIN IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A STRONG SIZED GAIN OF 7346 OI CONTRACTS (22.85 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 7761 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 511,202

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 7827 CONTRACTS WITH 415 CONTRACTS DECREASED AT THE COMEX// AND A HUGE SIZED 7761 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 7346 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL SIZED 498 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A HUGE SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (7761 CONTRACTS) ACCOMPANYING THE TINY SIZED DECREASE IN COMEX OI OF 415 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 7827 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT 12.885 TONNES FOLLOWED BY TODAY’S MASSIVE 29,400 OZ E.F.P. JUMP TO LONDON

//NEW STANDING REDUCES TO: /SEPT 11.940 TONNES.

/ 3) CONSIDERABLE T.A.S. LIQUIDATION WITH ZERO NET LONG SPECS BEING CLIPPED,

4) TINY SIZED COMEX OPEN INTEREST GAIN 5) HUGE ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///SMALL T.A.S. ISSUANCE: 498 CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

AUGUST

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

TOTAL EFP CONTRACTS ISSUED: 19,266CONTRACTS OF 1,926,600 OZ OR 59.925 TONNES IN 3 TRADING DAY(S) AND THUS AVERAGING: 6422 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAY(S) IN TONNES 59.925 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 59.925 DIVIDED BY 3550 x 100% TONNES = 1.69% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 59.925 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPTEMBER. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A FAIR SIZED 475 CONTRACTS OI TO 130,928 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 350 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

SEPT 350 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 350 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 415 CONTRACTS AND ADD TO THE 350 E.FP. ISSUED

WE OBTAIN A TINY SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 125 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 0.625 MILLION OZ OCCURRED WITH OUR $0.17 GAIN IN PRICE

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED UP 4.04 PTS OR 0.14% //Hang Seng CLOSED DOWN 13.04 PTS OR 0.07% // Nikkei CLOSED DOWN 390.52 OR 1.05%//Australia’s all ordinaries CLOSED UP 0.38%///Chinese yuan (ONSHORE) CLOSED UP TO 7,0953 CHINESE YUAN OFFSHORE CLOSED UP TO 7.0961/ Oil DOWN TO 68.40 dollars per barrel for WTI and BRENT DOWN AT 73.02 Stocks in Europe OPENED ALL MIXED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A TINY SIZED 475 CONTRACTS TO 510,721 WITH OUR GAIN IN PRICE OF $3.45 WITH RESPECT TO WEDNESDAY’S TRADING. WE LOST A FEW IN NUMBER OF /T.A.S. CONTRACTS AS SHORTS TRIED TO, THROUGHOUT THE SESSION, COVER WHAT THEY COULD AT HIGHER PRICES.

THE FED IS THE MAJOR SHORT OF AROUND 148 TONNES+ OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS IS SCHEDULED TO HAPPEN LATE SEPT 2024/BEGINNING OF OCTOBER. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER CONTAINMENT.

OUR PHYSICAL LONDONERS ALSO BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT THESE PRICES AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD SOME T.A.S. LIQUIDATION ON WEDNESDAY’S SMALL GAIN IN PRICE WITH ZERO LONGS WERE CLIPPED (AS YOU WILL SEE BELOW) BUT WE DID HAVE MAJOR SHORT COVERING. THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF THE SPREADERS // T.A.S IS SURELY DISTORTING COMEX OPEN INTEREST.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE NON ACTIVE DELIVERY MONTH OF SEPTEMBER.… THE CME REPORTS THAT THE BANKERS ISSUED A HUGE SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A MEGA HUGE SIZED 7761 EFP CONTRACTS WERE ISSUED: : OCT/DEC7761 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 7761 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 7827 CONTRACTS IN THAT 7761 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A TINY LOSS OF 415 COMEX CONTRACTS..AND THIS STRONG GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR SMALL GAIN IN PRICE OF $3.45/WEDNESDAY COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AS MENTIONED ABOVE. THE RAIDS ON LAST WEDNESDAY, FRIDAY AND THIS PAST TUESDAY WERE ORCHESTRATED BY THE FRBNY AS WE ARE NOW FINISHED WITH OPTIONS EXPIRY FOR THE OTC/LONDON LBMA BETS ENDING FRIDAY AFTERNOON. DESPITE THE FED’S HUGE SHORT PREDICAMENT THEY STILL HAVE TIME AND ENERGY TO RAID OUR PRECIOUS METALS. SUCH CROOKS!

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT A SMALL SIZED 498 CONTRACTS. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE (AND SPREADERS LATE IN THE MONTH). THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN LAST WEEK’S AND THIS WEEK’S TRADING//RAIDS

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: SEPT (11.940 TONNES) WHICH IS HUGE FOR A NON DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 44 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 11.940 TONNES.

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $3.45 ////AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE DID HAVE A STRONG GAIN IN OUR TWO EXCHANGES. WE HAD SOME T.A.S. SPREADER LIQUIDATION. BUT CENTRAL BANK LONGS, SEIZING THE MOMENT, EXERCISED FOR PHYSICAL IN A BIG WAY.

WE HAVE GAINED A TOTAL OI OF 24.345 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPT (12.885 TONNES) ON FIRST DAY NOTICE FOLLOWED BY WEDNESDAY’S E..F.P. JUMP TO LONDON OF A HUGE 29,400 OZ AS THESE BOYS WERE IN IMMEDIATE NEED OF PHYSICAL GOLD AND THUS TOOK DELIVERY ON THAT SIDE OF THE POND.

//NEW STANDING FOR SEPT REDUCES TO: 11.940 TONNES.

NEW STANDING FOR SEPT: 11.940 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $3.45

WE HAVE REMOVED 481 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL. THIS IS THE LARGEST ADJUSTMENT TO DATE.

NET GAIN ON THE TWO EXCHANGES 7346 CONTRACTS OR 734,600 OZ (22.85

Total monthly oz gold served (contracts) so far this month

2926 notices 292600 oz 9.1011 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: nil oz

we have 1 customer deposits

i) Into Brinks 27,701.480 oz

total deposits 27,701.48 oz

withdrawals:2

i) Out of Loomis: 21,509.019 669 kilobars)

ii) Out of JPMorgan 25,823.746

TOTAL WITHDRAWALS 47,332.765 oz 1.47 tonnes

adjustments: 1

JPM: dealer to customer: 85,502.069 oz

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPTEMBER

For the front month of SEPT. we have an oi of 927 contracts having LOST 479 contracts. We had 185 notices filed on Wednesday so we LOST 294 contracts or 29,400 oz will NOT stand at the comex as these boys were ferried over to London where they are taking immediate delivery of physical gold over there. This is a huge amount of gold and our bankers must be in trouble.

OCTOBER LOST 915 CONTRACTS DOWN TO 42,702 CONTRACTS

NOVEMBER GAINED another 13 CONTRACTS TO STAND AT 31

DECEMBER, THE BIGGEST DELIVERY MONTH LOST 446 CONTRACTS TO 410,344.

We had 14 contracts filed for today representing 1400 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notice issued from their client or customer account. The total of all issuance by all participants equate to 14 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 4 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for SEPT /2024. contract month, we take the total number of notices filed so far for the month (2926) x 100 oz ) to which we add the difference between the open interest for the front month of SEPT 927( CONTRACTS) minus the number of notices served upon today (14x 100 oz per contract( equals 383,900 OZ OR 11.940 TONNES.

thus the INITIAL standings for gold for the SEPTEMBER contract month: No of notices filed so far (2926 x 100 oz +we add the difference for front month of SEPT (927 X// , OI} minus the number of notices served upon today (14) x 100 oz which equals 383,90 oz (11.940 TONNES)

TOTAL COMEX GOLD STANDING FOR SEPT.: 11.940 TONNES WHICH IS HUGE FOR THIS NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

total pledged gold: 1,770,778.600 oz 55.078 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,011,410.520 OZ

TOTAL REGISTERED GOLD 7,425,642.244 ( 230.96 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,585,268.276 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 5,654,864 oz (REG GOLD- PLEDGED GOLD)= 175.89 tonnes //

END

SILVER/COMEX

SEPT 5/2024

INITIAL

//2024// THE SEPT 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

204,947.921 OZ CNT Delaware

.

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

nil oz

No of oz served today (contracts)

247 CONTRACT(S) (1.235 MILLION OZ)

No of oz to be served (notices)

84 contracts (0.420 million oz)

Total monthly oz silver served (contracts)

4658 Contracts (23.340 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit/

total dealer deposit : NIL oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 0 customer deposits:

total customer deposit nil oz

JPMorgan has a total silver weight: 134.996million oz/306.007 million or 44.08%

adjustment:2

a) dealer to customer ASAHI 603,344.540 oz

b) dealer to customer Brinks: 72,626.190 oz

withdrawals: 2

i) Out of Delaware 1974.756 oz

ii) Out of CNT 202,973.065 oz

total customer withdrawals: 204,947.921 oz

TOTAL REGISTERED SILVER: 77.743 MILLION OZ//.TOTAL REG + ELIGIBLE. 306.017 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR SEPTEMBER:

silver open interest data:

FRONT MONTH OF SEPT/2024 OI: 331 CONTRACTS HAVING GAINED 89 CONTRACT(S).

WE HAD 79 NOTICES FILED ON WEDNESDAY, SO WE GAINED 168 CONTRACTS OR 840,000 OZ

UNDERWENT A MASSIVE QUEUE JUMP TO TAKE DELIVERY OF SILVER OVER ON THIS SIDE OF THE POND..

THERE MUST BE ENOUGH SILVER OVER HERE.

OCTOBER SAW ANOTHER LOSS OF 53 OF OPEN INTEREST CONTRACTS AND THUS WE HAVE 1411 OPEN INTEREST CONTRACTS FOR OCTOBER.

NOVEMBER SAW ITS ANOTHER GAIN OF 1 CONTRACTS TO STAND AT 9.

DECEMBER SAW A LOSS OF 727 CONTRACTS UP TO 116,167.

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 247 for 1.235 MILLION oz

CONFIRMED volume; ON WEDNESDAY 49,552 weak

To calculate the number of silver ounces that will stand for delivery in SEPT. we take the total number of notices filed for the month so far at 4658 x 5,000 oz = 23.340 MILLION oz

to which we add the difference between the open interest for the front month of SEPT(331) and the number of notices served upon today 2477 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT/2024 contract month: 4658 notices served so far) x 5000 oz + OI for the front month of SEPT (3312)x number of notices served upon today minus (247)x 5000 oz of silver standing for the SEPT contract month equates to 23.740 MILLION OZ.

New total standing: 23.740 million oz.

There are 77,743 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS//

GLD

SEPT 5 WITH GOLD UP $18.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 4 WITH GOLD UP $3.45 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 3 WITH GOLD DOWN $4.25 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 5,47 TONNES OF GOLD INTO THE GLD/:/ //////INVENTORY RESTS AT 862.74 TONNES

AUGUST 30 WITH GOLD DOWN $31.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD/:/ //////INVENTORY RESTS AT 857.27 TONNES

AUGUST 29 WITH GOLD UP $23.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 28 WITH GOLD DOWN $14.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 27 WITH GOLD DOWN $1.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 26 WITH GOLD UP $9.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD VAPOUR GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 23 WITH GOLD UP $29.70 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER WITHDRAWAL OF 8.88 TONNES OF GOLD VAPOUR GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 857.85 TONNES

AUGUST 22 WITH GOLD DOWN $28.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 9.43 TONNES OF GOLD VAPOUR GOLD INTO THE GLD./ //////INVENTORY RESTS AT 866.70 TONNES

AUGUST 21 WITH GOLD DOWN $1.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER WITHDRAWAL OF 1.73 TONNES OF GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 857.27 TONNES

AUGUST 20 WITH GOLD UP $9.40 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 4.03 TONNES OF GOLD VAPOUR INTO THE GLD./ //////INVENTORY RESTS AT 859.00 TONNES

AUGUST 19 WITH GOLD UP $3.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 7.19 TONNES OF GOLD VAPOUR INTO THE GLD./ //////INVENTORY RESTS AT 854.97 TONNES

AUGUST 16 WITH GOLD UP $44.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: //////INVENTORY RESTS AT 847.78 TONNES

AUGUST 15 WITH GOLD UP $13,70 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD OUT OF THE GLD//////INVENTORY RESTS AT 847.78 TONNES

AUGUST 14 WITH GOLD DOWN $26.20 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.03 TONNES OF GOLD OUT OF THE GLD//////INVENTORY RESTS AT 845.76 TONNES

AUGUST 13 WITH GOLD UP $3.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//////INVENTORY RESTS AT 849.79 TONNES

AUGUST 12 WITH GOLD UP $30.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ////INVENTORY RESTS AT 846.91 TONNES

AUGUST 9 WITH GOLD UP $10.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 846.91 TONNES

AUGUST 8 WITH GOLD UP $31.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.02 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 844.04 TONNES

AUGUST 7 WITH GOLD UP $1.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.16 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 848.06 TONNES

AUGUST 6 WITH GOLD DOWN $13.10 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD” A WITHDRAWAL OF .57 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 844.90 TONNES

AUGUST 2 WITH GOLD DOWN $9.95 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.58 TONNES OF GOLD OUT OF THE GLD//INVENTORY RESTS AT 845.47 TONNES

AUGUST 1 WITH GOLD UP $9.15 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 846.05 TONNES

GLD INVENTORY: 862.74 TONNES, TONIGHTS TOTAL

SILVER

SEPT 5//WITH SILVER UP $.55//SMALL CHANGES IN SILVER INVENTORY A WITHDRAWAL OF 0.193 MILLION OZ OF SILVER INTO THE SLV/: .///./// /INVENTORY AT 466.234 MILLION OZ

SEPT 4//WITH SILVER UP $.17//SMALL CHANGES IN SILVER INVENTORY A DEPOSIT OF 0.456 MILLION OZ OF SILVER INTO THE SLV/: .///./// /INVENTORY AT 466.427 MILLION OZ

SEPT 3//WITH SILVER DOWN $.74//HUGE CHANGES IN SILVER INVENTORY A DEPOSIT OF 1.278 MILLION OZ OF SILVER INTO THE SLV/: .///./// /INVENTORY AT 465.971 MILLION OZ

AUGUST30//WITH SILVER DOWN $.42//NO CHANGES IN SILVER INVENTORY: .///./// /INVENTORY AT 464.693 MILLION OZ

AUGUST 29//WITH SILVER UP $.37//SMALL CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 0.558 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 464.693 MILLION OZ

AUGUST 28//WITH SILVER DOWN $0.76//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 2.301 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 465.281 MILLION OZ

AUGUST 27//WITH SILVER DOWN $0.03//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 2.921 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 462.959 MILLION OZ

AUGUST 26//WITH SILVER UP $0.23//SMALL CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 45,000 OZ OUT OF THE SLV. .///./// /INVENTORY AT 465.880 MILLION OZ

AUGUST 23//WITH SILVER UP $0.72//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 1.506 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 465.925 MILLION OZ

AUGUST 22//WITH SILVER DOWN $0.44//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 0.943 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 468.344 MILLION OZ

AUGUST 21//WITH SILVER $0.03//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 1..552 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 468.344 MILLION OZ

AUGUST 20//WITH SILVER $0.24//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 1.369 MILLION OZ FROM THE SLV. .///./// /INVENTORY AT 466.792 MILLION OZ

AUGUST 19//WITH SILVER $0.39//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 1.506 MILLION OZ FROM THE SLV. .///./// /INVENTORY AT 465.423 MILLION OZ

AUGUST 16//WITH SILVER $0.49//NO CHANGES IN SILVER INVENTORY: .///./// /INVENTORY AT 466.929 MILLION OZ

AUGUST 15//WITH SILVER $1.14//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.186 MILLION ON INTO THE SLV.///./// /INVENTORY AT 466.929 MILLION OZ

AUGUST 14//WITH SILVER DOWN $0.40//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 13//WITH SILVER DOWN $0.19//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 12//WITH SILVER UP $.37//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 9//WITH SILVER DOWN $.03//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 8//WITH SILVER UP $.70//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 3.241 MILLION OZ INTO THE SLV////./// /INVENTORY AT 462.502 MILLION OZ

AUGUST 7//WITH SILVER DOWN $0.27//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.552 MILLION OZ INTO THE SLV////./// /INVENTORY AT 462.502 MILLION OZ

AUGUST 6//WITH SILVER UP $0.05//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 458.851 MILLION OZ

AUGUST 2//WITH SILVER DOWN $0.01//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 1.243 MILLION OZ OF SILVER OUT OF THE SLV ///./// /INVENTORY AT 460.961 MILLION OZ

AUGUST 1//WITH SILVER DOWN $0.46//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.608 MILLION OZ OF SILVER VAPOUR INTO THE SLV///./// /INVENTORY AT 462.204 MILLION OZ

CLOSING INVENTORY 466.243 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

end

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY//BILL HOLTER:

3.CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES

Russia is going to buy gold exponentially and sell lots of oil

(Jerusalem post)

Russia to sell lots more oil for gold

Submitted by admin on Thu, 2024-09-05 09:13 Section: Daily Dispatches

By Tim Zyla Jerusalem Post Wednesday, September 4, 2024

The Russian Finance Ministry announced it will exponentially increase its gold purchases beginning Friday.

— the government will increase its gold purchases from 1.12 billion rubles per day to 8.2 billion rubles per day for the next month.

The report states the finance ministry expects a significant oil and gas revenue of 162 billion rubles in September, a huge jump compared to the 10.9 billion rubles generated in August.

With that money, Russia plans to purchase more gold. …

Stefan Gleason: Blundering miners are dumping every ounce they produce

Submitted by admin on Wed, 2024-09-04 20:31 Section: Daily Dispatches

By Stefan Gleason Money Metals Exchange, Eagle, Idaho Tuesday, September 3, 2024

On an annual basis, global silver supply generated by mines seems to have run into a ceiling of about 1 billion ounces. Supply has essentially flat-lined over the past several years.

At the same time, explosive growth in demand from photovoltaics (solar panels) and electric vehicles is driving widening projected supply deficits for physical silver.

Rising silver prices will, in theory, incentivize more production. But the costs of extraction are rising sharply. …

4. OTHER GOLD COMMENTARIES/LIVE FROM THE VAULT: TODAY ANDREW MAGUIRE WITH BILL HOLTER

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COPPER

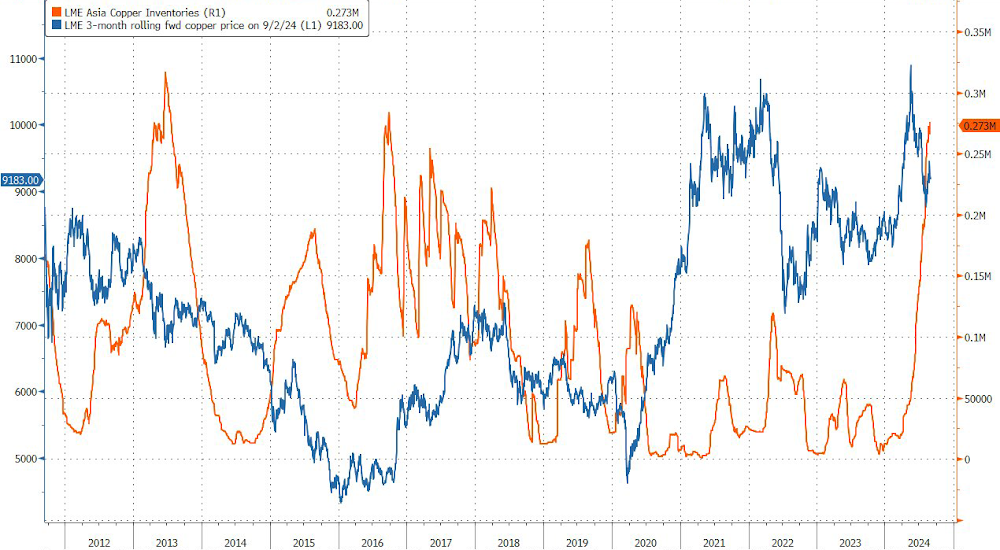

Gloom Surrounds Jeff Currie’s Super-Bull Copper Thesis As China Woes Cap Prices At $9,500

Wednesday, Sep 04, 2024 – 05:20 PM

Veteran commodities analyst Jeff Currie appeared on Bloomberg TV on Tuesday to explain how his bullish thesis for copper, which he called “the most compelling trade I’ve seen in my 30-year career” in mid-May, has been completely derailed or delayed by mounting economic woes in China.

Let’s begin with Currie, who led commodities research at Goldman Sachs for nearly three decades and now serves as the chief strategy officer of the energy pathways team at Carlyle Group, appeared on Bloomberg’s Odd Lots on May 17 to discuss why copper was the best trade he has seen in his entire career.

At the time, when copper was trading at the all-time high of $11,104.50 a ton on the LME, Currie was all googly-eyed about being the biggest copper bull cheerleader:

You know, it is the most compelling trade I have ever seen in my 30 plus years of doing this. You look at the demand story, it’s got green CapEx, it’s got AI, remember AI can’t happen without the energy demand and the constraint on the electricity grid is going to be copper.

And then you have the military demand. So unprecedented demand growth against unprecedented weakness in supply growth because we have not been investing, it’s teed you up for what I would argue is the most bullish commodity that I actually, I just quote many of our clients and other market participants say, you know, it’s the highest conviction trade they’ve ever seen.

Fast-forward 3.5 months, and LME copper is trading just below $9,000 a ton. He joined Bloomberg TV on Tuesday to explain soaring inventories in Asia and a property market downturn in the world’s second-largest economy were some of the key reasons behind copper’s fall from grace.

How did Currie not see the property market downturn 3.5 months ago? Oh, do we have questions for him…

Copper “still has a floor based upon that strong structural supply story, but it has a cap on the upside based upon that weakness in demand,” he said, adding, “I would say $8,500 on the bottom, $9,500 on the top until we start to see the policy begin to create some strength in China.”

Currie top-ticked the copper market in his bull call in May.

Meanwhile, earlier this week, Goldman revealed to clients that it exited its long-term bullish position on the base metal and slashed its 2025 price forecast by nearly $5,000. This seismic shift comes amid overwhelmingly weak economic data from China this summer and elevated levels of refined copper production being exported from the world’s second-largest economy into global markets.

Goldman’s Samantha Dart and Daan Struyven told clients:

“Copper rally delayed. In copper we’ve observed significant price elasticity of both supply and demand this summer. As a result, the sharp copper inventory depletion we had expected will likely come much later than we previously thought.”

SHANGHAI CLOSED UP 4.04 PTS OR 0.14% //Hang Seng CLOSED DOWN 13.04 PTS OR 0.07% // Nikkei CLOSED DOWN 390.52 OR 1.05%//Australia’s all ordinaries CLOSED UP 0.38%///Chinese yuan (ONSHORE) CLOSED UP TO 7,0953 CHINESE YUAN OFFSHORE CLOSED UP TO 7.0961/ Oil DOWN TO 68.40 dollars per barrel for WTI and BRENT DOWN AT 73.02 Stocks in Europe OPENED ALL MIXED

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.0953

OFFSHORE YUAN: UP TO 7.0961

SHANGHAI CLOSED UP 4.04 PTS OR 0.14 %

HANG SENG CLOSED DOWN 13.04 PTS OR 0.07%

2. Nikkei closed DOWN 390.52 PTS OR 1.05%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 101.02 EURO RISES TO 1.1106 UP 27 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +0.880 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 143.57…… JAPANESE YEN NOW RISING AS WE HAVE NOW REACHED THE COLLAPSING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.2320/Italian 10 Yr bond yield DOWN to 3.5721 SPAIN 10 YR BOND YIELD DOWN TO 3.028%

3i Greek 10 year bond yield DOWN TO 3.249

3j Gold at $2516.00//Silver at: 28.68 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 2 AND 74/ 100 roubles/dollar; ROUBLE AT 90.23

3m oil into the 68 dollar handle for WTI and 73 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 143.15/ 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.880 % STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8462 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9393 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.771 DOWN 0 BASIS PTS…

USA 30 YR BOND YIELD: 4.071 DOWN 0 BASIS PTS/

USA 2 YR BOND YIELD: 3.8710 UP 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 34.00…

10 YR UK BOND YIELD: 3.9710 UP 4 PTS

10 YR CANADA BOND YIELD: 3.039 UP 2 BASIS PTS

2a New York OPENING REPORT

Futures Flat Ahead Of Key Data As Global Market Rout Eases

Thursday, Sep 05, 2024 – 08:13 AM

After several days of rollercoaster volatility and uniform pain across global equity markets for bulls, US equity futures are flat as the global sell-off stabilizes into the most important macro data releases. As of 8:00am ET S&P futures are up 0.1% and Nasdaq futs are flat, with NVDA +40bps premarket, TSLA rising 2.3% while the balance of Mag7 is weaker and Semis under pressure, too. Europe’s Stoxx 600 index dropped 0.3%, with China-facing luxury stocks such as LVMH again among the biggest losers. Asian equities erased most gains after declines in Hong Kong and Japan. Bond yields are 1bps higher, but the USD is weaker as the yen gained overnight following unexpectedly strong – if transitory – Japanese wage data. Commodities are stronger led by Energy and precious metals while iron ore slumped to its lowest level since 2022 and traded near $90 a ton as China’s main steel industry group advised mills to be cautious in boosting output too quickly to avoid snuffing out a post-summer recovery. Looking at the coming FOMC decision, 50bps bets are increasing, rising as high as 50% after yesterday’s dismal JOLTS report, as the growth component of the Goldilocks narrative is challenged. ISM-Services today and NFP tomorrow are key facets of the narrative and we should leave for the weekend with a stronger sense of 25bps or 50bps.

In premarket trading, Frontier Communications fell 9.9% after agreeing to be purchased in a take under by Verizon Communications. Tesla gained 3% on plans to launch the advanced driver assistance system that it calls Full Self Driving technology in China and Europe in the first quarter of next year, pending regulatory approvals. Meanwhile, the company with the luckiest ticker,C3.ai (better known for its AI ticker) was not so lucky, and tumbled 19% to a new 2024 low after the software company reported 1Q subscription revenue that’s weaker than expected. Here are some other premarket movers:

ChargePoint (CHPT) falls 7.7% as the operator of the largest electric vehicle charging network in the US plans to cut 15% of its workforce after missing revenue forecasts.

Copart (CPRT) slips 5.7% after posting 4Q operating income that missed estimates.

Frontier Communications (FYBR) falls 9.9% after agreeing to be purchased by Verizon Communications.

Fortive (FTV) rises 4% after confirming plans to pursue a spinoff of its Precision Technologies segment.

JetBlue (JBLU) rises 5% after boosting its revenue forecast for the third quarter.

PagSeguro (PAGS) and StoneCo (STNE) fall after Morgan Stanley downgraded the Brazilian digital payments companies, saying the market has likely reached saturation. PagSeguro declines 8.5% and StoneCo drops 8.3%.

Hewlett Packard Enterprise (HPE) slips 3% after the computer hardware and storage company reported weaker-than-expected margins.

NIO ADRs (NIO) gain 3.5% after the automaker reported 2Q gross margin that came ahead of estimates.

Verint (VRNT) tumbles 11% after the customer-service software firm reported second-quarter profit and revenue that fell short of estimates.

After yesterday’s catastrophic JOLTS report, traders will look to weekly jobless claims data due later today and Friday’s nonfarm payrolls reports to assess whether the US economy is heading for a soft-landing as the Fed prepares to start easing policy. Global stocks suffered their worst losses earlier this week since the Aug. 5 meltdown, with VIX remaining elevated at 20. Swap traders have ramped up bets on the pace of rate cuts after a Wednesday reading on US job openings trailed estimates and the Fed’s Beige Book survey showed flat or declining economic activity. Rates pricing foresees at least 100 basis points of easing this year, including one jumbo cut of 50 basis points.

“We think that the US soft landing scenario is intact but acknowledge that the next two-three months could be a tricky period,” Eddy Loh, chief investment officer at Maybank Group Wealth Management, said on Bloomberg Television. “If the Fed were to cut 50 basis points, the market could perceive it as a negative because that means the Fed is seeing something in the economy.”

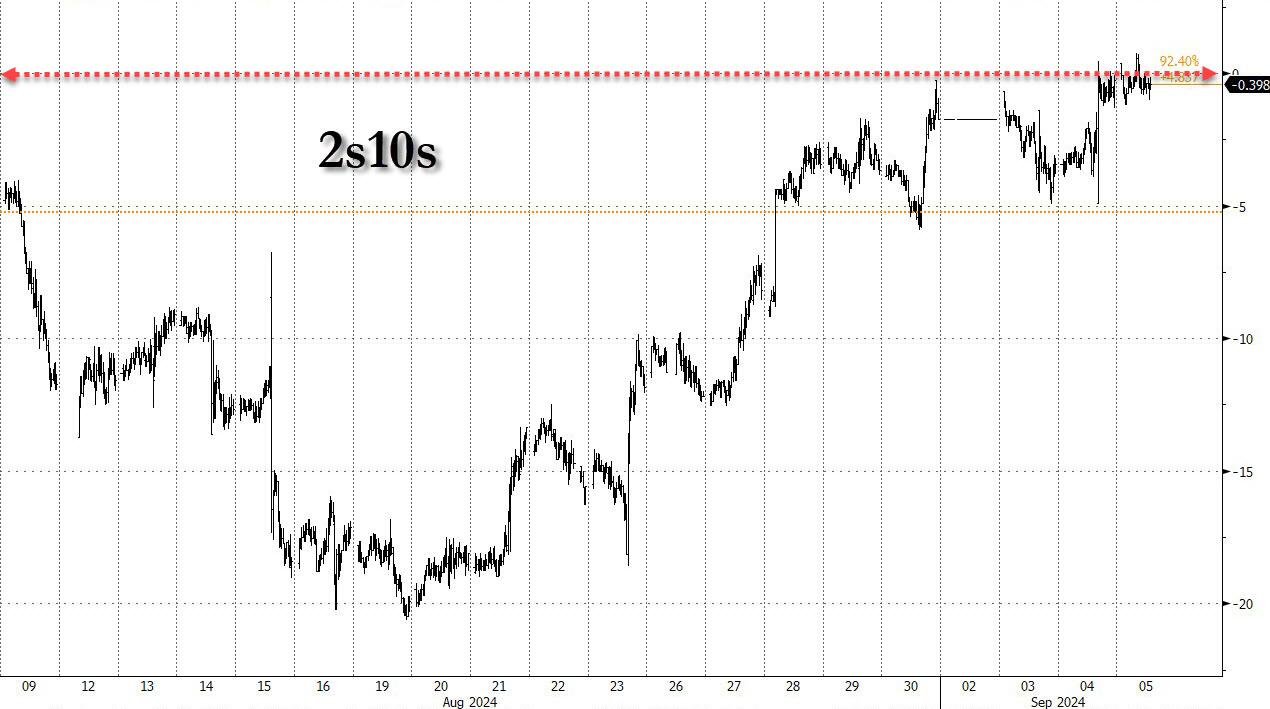

The yield on 2-year Treasuries rose 2bps after tumbling Wednesday on the data showing a slowdown in the US labor market and leading to the first 2s10s yield curve disinversion in 27 months. This morning the 2s10s flirted with the unchanged level, and was last 0.4bps.

US interest rates will settle in a range of between 3% and 4%, according to Oaktree Capital Management LP’s Howard Marks.

“The Fed will back off from the emergency rate of five and a quarter, five and a half and get down into the threes,” Marks, the co-chairman and co-founder of Oaktree said at a conference in Melbourne Thursday. “But my point to you, my belief is that we’re going to stay there in the threes and we’re not going back to zero or a half or one.”

European stocks fell to their lowest in around two weeks as global growth concerns continue to dampen investor sentiment ahead of the US jobs report on Friday. The Stoxx 600 was down 0.2%, led by losses in luxury stocks such as LVMH; consumer product, industrial and technology names also slumped. Here are the biggest movers Thursday:

Asos shares jump as much as 19%, the most intraday since January 2023, after agreeing to sell control of its Topshop and Topman brands to a company controlled by Denmark’s Holch Povlsen family. The online fashion retailer also announced refinancing moves

BioMerieux gains as much as 5.5% after the French medical technology firm slightly boosted its guidance

Lanxess shares rise as much as 4.4% as the German specialty chemicals firm was double-upgraded by Morgan Stanley, which cited investment de-gearing and lower gas prices

Ashmore rises as much as 4.6%, reversing an earlier decline, as analysts note a more positive outlook for the emerging-markets specialist fund house

Vistry Group shares rise as much as 7.1%, the most since March 14, after the UK housebuilder reported 1H revenue and profit growth following a shift in strategy

Jet2 shares rise as much as 2.1%, reversing losses in earlier trading, as analysts are positive about the trajectory of bookings of the package holiday provider

European luxury stocks slide after Bloomberg reported that LVMH’s Tiffany brand is planning to downsize a flagship store in Shanghai, fueling broader conserns about a slowdown in luxury demand in China. LVMH, Hermes and Kering fell

Grifols Class B shares slumped after a report that Brookfield will seek to pay less for that series of stock in its planned takeover offer for the Spanish blood-plasma company

AB Foods drops as much as 5.8%, the most since April 2023, after the company warned sales growth at Primark was negatively impacted by poor weather conditions

Tomra falls as much as 10%, the most since October 2023, after the Norwegian recycling technology firm published new financial targets

Genus drops as much as 5.1% after the livestock breeding specialist releases its full-year results, with the company only cautiously guiding for improving markets

Earlier in the session, Asian equities erased most gains after declines in Hong Kong and Japan even as key chipmaker shares rebounded from a Wednesday selloff sparked by concerns the artificial intelligence rally is overheating. The MSCI Asia Pacific Index rose 0.1%, with Nvidia suppliers TSMC and SK Hynix among the biggest boosts. It had added as much as 0.8% earlier in the session before erasing the advance. Taiwan’s Taiex index added 0.5% while Japanese stocks slumped as the yen strengthened. Asian stocks are “seeing flows out of Japan into other markets as hot wage data increases the likelihood of further tightening by the Bank of Japan,” said Matthew Haupt, a portfolio manager at Wilson Asset Management. A bigger divergence between the Fed and BOJ may spark “some more volatility,” he added.

In FX, the Bloomberg Dollar Spot Index falls 0.1%. The Norwegian krone tops the G-10 FX leader board, rising 0.3%. The Japanese yen is not far behind, with a 0.2% gain.

In rates, treasuries dip, paring some of Wednesday’s post-JOLTS rally with US 10-year yields rising 1 basis point to 3.76%; the US lags little-changed bunds and gilts during European morning. Yields are higher by 1bp-2bp across the curve with front-end and belly underperforming slightly, leaving 2s10s spread around -0.5bp after disinverting Wednesday for only the second time since 2022. Focal points of US session include weekly jobless claims, August ADP employment change and August ISM services gauge.

In commodities, brent crude futures were heading for the first day of gains in five, with OPEC+ getting closer to an agreement on delaying an increase in oil production. WTI rose 1% to $69.90 while Brent was trading just above $73. Iron ore slumped to its lowest level since 2022 and traded near $90 a ton as China’s main steel industry group advised mills to be cautious in boosting output too quickly to avoid snuffing out a post-summer recovery. Spot gold rises $20 to around $2,516/oz.

Looking at the calendar, US economic data calendar includes August Challenger job cuts (7:30am), ADP employment change (8:15am), 2Q final nonfarm productivity and weekly jobless claims (8:30am), August final S&P Global US services PMI (9:45am) and ISM services index (10am). No Fed speakers are scheduled; Williams and Waller are slated to speak Friday

Market Snapshot

S&P 500 futures little changed at 5,534.75

STOXX Europe 600 down 0.1% to 514.22

MXAP up 0.1% to 181.97

MXAPJ up 0.4% to 563.99

Nikkei down 1.1% to 36,657.09

Topix down 0.5% to 2,620.76

Hang Seng Index little changed at 17,444.30

Shanghai Composite up 0.1% to 2,788.31

Sensex down 0.1% to 82,245.54

Australia S&P/ASX 200 up 0.4% to 7,982.38

Kospi down 0.2% to 2,575.50

German 10Y yield unchanged at 2.22%

Euro up 0.1% to $1.1094

Brent Futures up 0.7% to $73.23/bbl

Brent Futures up 0.7% to $73.21/bbl

Gold spot up 0.7% to $2,513.92

US Dollar Index down 0.16% to 101.20

Top Overnight News

President in absentia Joe Biden is due to speak on economic policy on Thursday 5th September at 16:00 ET

Japan-US business council says they are very alarmed by any attempts to politicise the committee on foreign investments in the US review process, regarding US Steel and Nippon Verizon to acquire Frontier Communications; deal valued at USD 20bln, all-cash

Japan’s wage numbers for July cool vs. June, but come in ahead of expectations (the real wage figure came in at +0.4% for Jul, down from +1.1% in June but above the Street’s -0.6% forecast). RTRS

BOJ official says the central bank must be mindful of avoiding undue market volatility as it proceeds with its tightening agenda. RTRS

China still sees some room to lower the amount of cash banks must hold as reserves, a central bank official said on Thursday, adding that the lender will continue to implement policies to support the economic recovery. RTRS

AstraZeneca staff were detained in China over potential illegal activities involving data collection and drug imports. BBG

Russia has been forced to start storing gas from Vladimir Putin’s flagship Arctic project, in a sign that western sanctions are deterring buyers. According to ship-tracking data and satellite images, three vessels have shipped liquefied natural gas from the Arctic LNG 2, which is under US sanctions, since it started loading operations last month. FT

Hostage killings and irreconcilable demands complicate Gaza cease-fire talks. Frustrated mediators are now putting together what they have described as a “final offer,” but significant concessions on both sides are needed for agreement, said a U.S. official. WaPo

US crude stockpiles slumped by 7.4 million barrels last week, API data is said to show, pushing oil prices higher. That would bring holdings to the lowest in 11 months, if confirmed by the EIA. Crude may benefit further if OPEC+ delays its plan to to boost output. BBG

Rate options traders stepped up wagers that the Fed will start its easing cycle with a 50-bp cut. Oaktree’s Howard Marks said rates will settle in a 3-4% range, but won’t go lower. Rate reductions are needed to keep the labor market healthy, according to the Fed’s Mary Daly. BBG

Auto sales in the US cooled in Aug vs. Jul due to difficult comparisons (Jul was boosted from a recovery from an industry-wide cyberattack) and elevated interest rates. Marketwatch

A more detailed look at global markets courtesy of Newsquawk

APAC stocks eventually traded mixed following the earlier mild regional gains, with the overall market tone tentative ahead of a slew of US data ahead of NFP on Friday. ASX 200 was kept afloat by its Tech and Real Estate sectors whilst Energy resided at the bottom. Nikkei 225 was choppy on either side of 37k as it saw initial pressure amid the stronger JPY, with the index later entirely trimming losses, only to falter once again. Hang Seng and Shanghai Comp were mixed for most of the session, Hang Seng initially saw modest gains with Banks and Real Estate initially supported following reports China mulls cutting mortgage rates in two steps to shield banks, via Bloomberg sources. That being said, the mood later waned despite a lack of catalysts, although pre-market reports suggested JPMorgan cut China stocks to Neutral from Overweight.

Top Asian news

PBoC official says there is still some room for cutting the RRR. Face some constraints in further cutting deposit/lending rates. Will reasonably set the strength and pace of policy adjustments based on the economic recovery.

JPMorgan cut China stocks to Neutral from Overweight.

PBoC injected CNY 63.3bln via 7-day Reverse Repo at maintained rate of 1.70%

BoJ Board Member Takata said Japan’s economy is recovering moderately, though some weak signs are evident; notes significant volatility in stock and FX markets but maintains that achieving the inflation target remains within reach, and BoJ must be vigilant to the chance of renewed wave of price hikes, while taking into account impact of yen rise in early August, according to Reuters. He noted it is hard to debate at this stage to what degree BoJ can shrink its balance sheet, and hard to pin down the precise level of Japan’s natural rate of interest. He said Japan’s current real interest rate is below the estimated natural rate of interest, which means monetary conditions remain accommodative and the fallout from market turbulence in early August remains, “so we must scrutinize the impact for the time being”. He noted the BoJ must adjust monetary conditions by ‘another gear’ if we can confirm that firms will continue to increase capex, wages and prices, and won’t hike policy rates with a pre-set level of neutral interest rate in mind. BoJ’s decision to reduce bond buying won’t hugely affect the impact of monetary easing, but marks a big turning point from when the central bank had YCC in place, and markets stabilizing after some turbulence, but must watch market developments with a very strong sense of urgency.

BoJ to hold meeting on market operations on October 16th from 17:30 local time, according to Reuters.

RBA Governor Bullock repeated that it is premature to be thinking about rate cuts; as of now, the board does not expect to be in a position to cut rates in the near term. She noted the RBA’s highest priority has been and remains to bring inflation down, and the Board remains vigilant to upside risks to inflation, whilst the RBA’s full employment goal is not served by letting inflation stay above target indefinitely. She noted substantial uncertainty around the central outlook, with risks on both sides and if circumstances change, the board will respond accordingly. Bullock said the labour market remains relatively tight, expected to ease gradually, and labour cost growth is strong reflecting wage increases, and weak productivity. She warned key drivers of elevated inflation are housing costs, market services, and CPI rents inflation is likely to be high for some time. Bullock said need to see results on inflation before lowering rates; board is not going to focus on one inflation number, and slightly elevated AUD is positive for inflation fight.

European bourses, Stoxx 600 (U/C) began the session entirely in the red, but sentiment improved soon after the cash open, with indices now displaying more of a mixed picture. European sectors are mixed, having opened with a negative bias. Utilities takes the top spot, alongside Real Estate whilst Consumer Products lags. US Equity Futures (ES U/C, NQ -0.1%, RTY -0.1%) are mixed, but with sentiment seemingly stabilising after this week’s glum price action. Today’s docket is packed with key US data; jobs (Challenger Layoffs, ADP, IJC), activity (PMIs, ISM Services).

Top European news

ASML (ASML NA) CEO repeated 2024 and 2025 guidance and said the chip market recovery is uneven.

BoE Monthly Decision Maker Panel data August 2024; inflation expectations 1-yr 2.7% (prev. 2.7%); 3-yr 2.7% (prev. 2.7%)

FX

DXY is slightly lower and trading within a narrow 101.14-35 range and towards the bottom end of the prior day’s confines. A busy US data slate ahead; US Challenger Layoffs kicks things off, ahead of ADP Employment, IJC, PMI (F) and the key ISM Services data

EUR is incrementally firmer and trading towards the upper end of today’s 1.1076-1.11 range. Today’s much stronger-than-expected Industrials Orders sparked modest strength in the Single-Currency, whilst EZ Construction PMIs passed through without having an impact.

GBP is trading on a slightly firmer footing and near today’s high at 1.3172; UK-specific newsflow light.

JPY is slightly firmer, having pared most of its early morning strength, largely a factor of a more improved risk-tone vs the prior 2 sessions. Overnight strength was also a factor of a higher-than-expected Labour Cash Earnings print.

Antipodeans are flat/firmer, in what has been a lacklustre session for the pair thus far.

PBoC set USD/CNY mid-point at 7.0989 vs exp. 7.1010 (prev. 7.1148); strongest level since Apr 15th

Reuters Poll, FX: bullish bets have increased for most Asian FX.

Fixed Income

USTs are flat ahead of a packed and potentially pivotal afternoon agenda. From which, the labour market data points will take centre stage and be scrutinised in the context of Friday’s Payrolls. USTs are just off Wednesday’s JOLTS-driven highs at 114-18.

Bunds ultimately trade lower, but with price action choppy. Modest two-way action was seen on the latest German Industrial Orders, which came in significantly above forecasts. Bunds are yet to make much headway above the 134.00 mark, current high at 134.26.

Gilts are slightly firmer, but ultimately rangebound ahead of the busy data docket. A strong UK auction had little impact on the benchmark. Gilts are holding just above Wednesday’s 99.53 high.

OATs were weighed on by a hefty supply docket from both France and Spain; both passed without any real reaction.

France sells EUR 11.99bln vs exp. 10-12bln 3.0% 2034, 1.25% 2036, 0.5% 2040 and 3.25% 2055 OATs:

Commodities

Crude is firmer, having found a bit of a floor from the marked declines WTD. A slight recovery was assisted by the private inventory report last night. Brent’Nov as high as USD 73.46/bbl.

Spot gold is back above USD 2500/oz, benefitting from pressure in the USD and the relatively contained yield environment/risk tone in western markets; notable, further support stemming from China where yields are pressured by RRR talk from the PBoC.

Base metals are benefitting from the steady risk tone and softer USD. Though, as with precious peers, it remains to be seen what the macro backdrop will be following the afternoon’s US data deluge.

Russian President Putin on expiration of deal on Russian gas to Europe via Ukraine after Dec 31 2024, “we do reject this transit, seek to maintain gas supply contracts, if Ukraine ditches this transit we cannot force it to keep it”

UAE’s ADNOC sets the October Murban OSP at USD 77.94/bbl.

Geopolitics

White House reportedly scrambling to put forward a new Israel-Hamas proposal; draft accord could come next week or sooner; there is a strong perception that a ceasefire is slipping away, according to Reuters sources.

US Event Calendar

07:30: Aug. Challenger Job Cuts YoY 1.0%, prior 9.2%

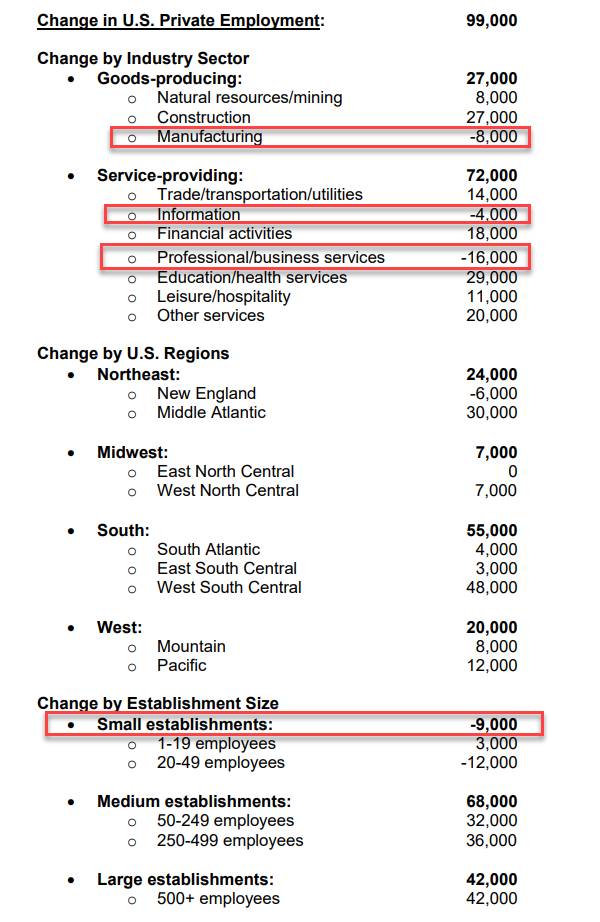

08:15: Aug. ADP Employment Change, est. 145,000, prior 122,000

08:30: 2Q Unit Labor Costs, est. 0.8%, prior 0.9%

2Q Nonfarm Productivity, est. 2.5%, prior 2.3%

08:30: Aug. Initial Jobless Claims, est. 230,000, prior 231,000

Aug. Continuing Claims, est. 1.87m, prior 1.87m

09:45: Aug. S&P Global US Services PMI, est. 55.1, prior 55.2

09:45: Aug. S&P Global US Composite PMI, est. 54.0, prior 54.1

10:00: Aug. ISM Services New Orders, est. 51.9, prior 52.4

DB’s Jim Reid concludes the overnight wrap

A cloud has lifted over our house as the kids were all back to school yesterday after a long and feral summer. To be fair Maisie is a wonderful girl and the twins are good boys individually. However together at home the twins are never more than 20 minutes away from a fight, bruises, scratches, and manic tears. 2 minutes later it’s high pitched laughter and co-scheming. Repeat to fade. It is draining. At school they all behave impeccably so I’m lobbying for it to become a boarding school asap.

Clouds continue over markets though with global bond yields continuing to tumble yesterday, as another batch of weak US data fuelled expectations that the Fed might cut rates by 50bps in just under two weeks. That led to some very significant market moves, with the 2s10s curve ending the day around the zero level for the first time in the last 2 years. We briefly traded in positive territory yesterday but haven’t closed above zero since July 2022. This is the longest ever inversion for the 2s10s curve in available data stretching back well over 60 years. Given that inversions have historically been a leading indicator of recessions, the re-steepening has previously led to suggestions that removing such an environment means a recession would now be less likely to happen. But sadly, the historic precedent isn’t particularly favourable on this front, as in previous cycles the final stage before the recession was actually a re-steepening of the curve back into positive territory. So we have to be cautious in being too optimistic about waving bye to an inversion. Henry wrote about this pattern last year, with a few charts on how this played out in previous cycles (link here).

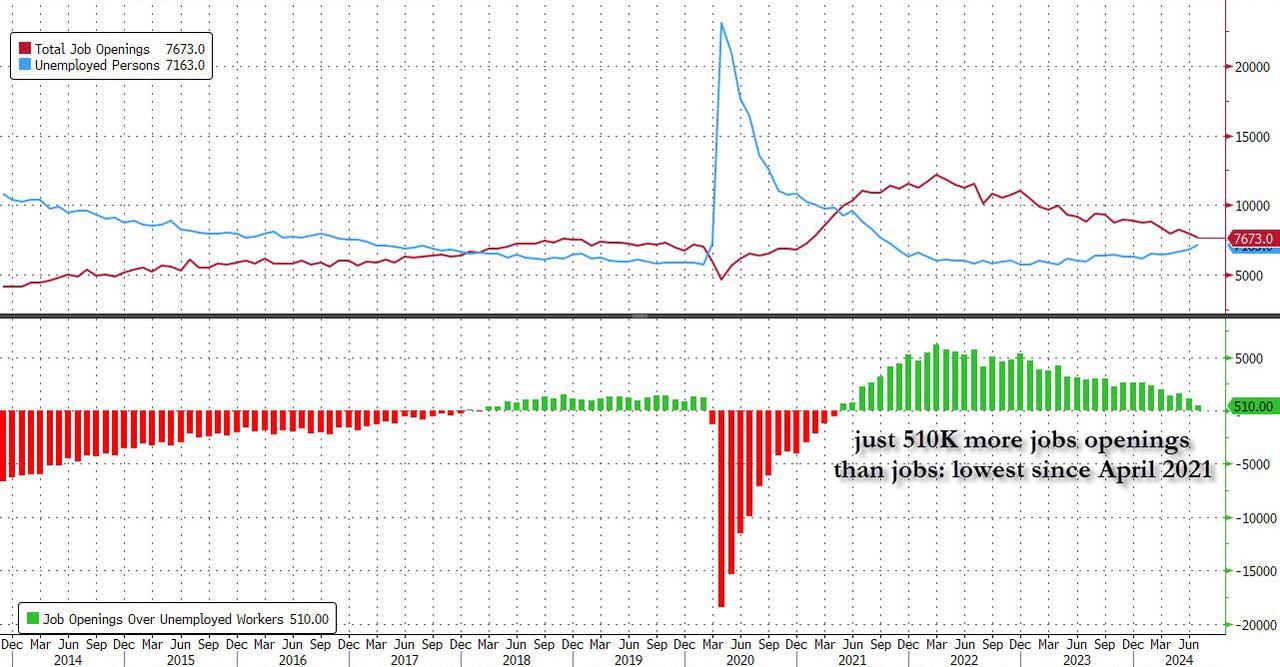

The trigger for yesterday’s moves was the latest US JOLTS report of job openings, which showed that the labour market was weakening faster than previously thought. For instance, the number of job openings fell to a three-and-a-half year low of 7.673m in July (vs. 8.1m expected). And if you look at the ratio of job openings per unemployed individuals, that also fell back to 1.07, which is now beneath its pre-Covid levels in 2019. So there’s growing evidence that the labour market is still weakening, backing up Chair Powell’s point at Jackson Hole that “labor market conditions are now less tight than just before the pandemic in 2019”.

To be fair, it wasn’t all bad news from the report. The hires rate ticked back up to 3.5% in July, and the quits rate of those voluntarily leaving their jobs also rose to 2.1%. Moreover, we should bear in mind that this is still covering July, the same month as with the underwhelming jobs report a month ago, rather than a new period since then. So all eyes will remain on tomorrow’s jobs report for August to see if that deterioration continues, or whether the weaker July numbers look like more of a blip. Ahead of that today’s services ISM will take on added significance given the nerves around at the moment.

After the JOLTS report, investors dialled up the chance that the Fed would cut by 50bps in September, and futures were giving that a 44% chance by the close (up +7pps). That’s the highest probability on 50bps since August 13 and is now back close to a 50-50 call. Investors also moved to price in a more dovish rates path over the months ahead as well. For example, there are now 111bps of cuts priced in by the December meeting, up from 102bps the previous day.

With more rapid cuts being priced in, US Treasury yields fell across the curve, and the 2yr yield (-10.9bps) fell to 3.76%, which is its lowest closing level since September 2022. The 10yr yield (-7.6ps) also fell to 3.76% also, which is its lowest close since July 2023 and marks the first time since July 2022 that the 2s10s slope has uninverted. Breakevens led the decline in yields with the 10yr (-5.2bps) ending the day at 2.06%, less than 1bp above its early August lows and otherwise its lowest level since January 2021. Over in Europe it was much the same story as well, with yields on 10yr bunds (-5.3bps), OATs (-6.7bps) and BTPs (-8.8bps) all falling back.

Alongside the JOLTS report, a few other factors supported that move to price in faster rate cuts. The first was the continued fall in oil prices, which is taking away one source of inflationary pressure. Indeed, yesterday saw Brent crude oil prices (-1.42%) fall for the fourth day in a row to $72.70/bbl, which is their lowest level since June 2023. This decline came even as Reuters reported that OPEC+ was close to agreeing a delay to the increase in oil production planned for October. The second came from the Bank of Canada, who cut rates by 25bps for a third consecutive meeting, in line with expectations. Significantly, Governor Macklem also said that “if we need to take a bigger step, we will take a bigger step.” So there was an explicit acknowledgement that such an outcome was possible. Last but not least, the Fed’s Beige Book review of regional economic conditions added to the dovish mood, as 9 of the 12 regional Fed districts “reported flat or declining activity”.

Against this backdrop, US equities held up relatively well, with the S&P 500 posting a modest -0.16% decline. In part, that was driven by the hope that the Fed would now deliver a larger 50bp cut. But unlike the original jobs report, the news from the JOLTS report didn’t lead to a sudden reassessment on how the economy was doing, given it was covering July anyway, where we’ve already got plenty of data for. Indeed, with the other data releases yesterday, the Atlanta Fed’s GDPNow estimate actually ticked up slightly to an annualised +2.1% rate for Q3. So with those various releases in hand, US equities held broadly steady. Energy (-1.42%) and information technology (-0.48%) stocks led the decline for the S&P 500, but its downside was limited by gains for defensive and rate sensitive sectors, notably utilities (+0.85%) and consumer staples (+0.52%). The Magnificent 7 were flat on the day (-0.00%), even as Nvidia (-1.66%) again declined after seeing the largest market cap fall of any global stock in history the previous day.

Over in Europe, the picture was quite a bit more negative, but that mostly reflected a catchup to the slump later in the US session the previous day. That was evident by the STOXX 600 immediately falling lower after the open, but basically staying around that range for the rest of the day, closing -0.97% lower. Even so, that’s still a third consecutive decline for the STOXX 600, so that’s another index where September is living up to its reputation as a poor one for equities. Sentiment wasn’t exactly helped by the final August PMIs either, as the final composite PMI for the Euro Area was revised down two-tenths from the flash reading to 51.0.

Asian equity markets are maintaining the risk-off start to the month with the Nikkei (-1.22%), Hang Seng (-0.45%) and KOSPI (-0.36%) also lower. Elsewhere, mainland Chinese stocks have held on to their minor gains with the CSI (+0.10%) and the Shanghai Composite (+0.04%) both trading in the green. S&P (-0.16%) and NASDAQ 100 (-0.28%) futures are both slipping.

Early morning data showed that Japan’s real wages in July unexpectedly rose +0.4% y/y (v/s -0.6% expected), advancing for the second consecutive month, boosted by pay hikes and summer bonuses. It followed a +1.1% gain in June, the first gain in 27 months. Nominal wages grew by +3.6% y/y in July, a deceleration from June’s +4.5% but surpassing market expectations of +2.9% gain. This strong performance is adding to speculation that the BOJ may look to hike again before the end of 2024 and perhaps helps explain the weak performance of Japanese equities overnight.

To the day ahead now, and data releases from the US include the ISM services index for August, the ADP’s report of private payrolls for August, and the weekly initial jobless claims. Meanwhile in Europe, there’s German factory orders for July, Euro Area retail sales for July, and the August construction PMIs from Germany and the UK. From central banks, we’ll hear from the ECB’s Holzmann.

2B) European report

Tentative price action ahead of today’s US data deluge including ADP Employment & ISM Services – Newsquawk US Market Open

Thursday, Sep 05, 2024 – 06:24 AM

European equities are mixed; US futures trade tentatively on either side of the unchanged mark

Dollar is slightly lower, JPY once again on a firmer footing, EUR saw modest strength on strong German Industrial Orders

USTs are flat ahead of today’s US data deluge, Bunds edge lower

Crude is firmer, XAU benefits from the softer Dollar and base metals are mixed

Looking ahead, US Challenger Layoffs, ADP National Employment, IJC, ISM Services

2. Listen to this report in the market open podcast (available on Apple and Spotify)

3. Trial Newsquawk’s premium real-time audio news squawk box for 7 days

EUROPEAN TRADE

EQUITIES

European bourses, Stoxx 600 (U/C) began the session entirely in the red, but sentiment improved soon after the cash open, with indices now displaying more of a mixed picture.

European sectors are mixed, having opened with a negative bias. Utilities takes the top spot, alongside Real Estate whilst Consumer Products lags.

US Equity Futures (ES U/C, NQ -0.1%, RTY -0.1%) are mixed, but with sentiment seemingly stabilising after this week’s glum price action. Today’s docket is packed with key US data; jobs (Challenger Layoffs, ADP, IJC), activity (PMIs, ISM Services).

DXY is slightly lower and trading within a narrow 101.14-35 range and towards the bottom end of the prior day’s confines. A busy US data slate ahead; US Challenger Layoffs kicks things off, ahead of ADP Employment, IJC, PMI (F) and the key ISM Services data