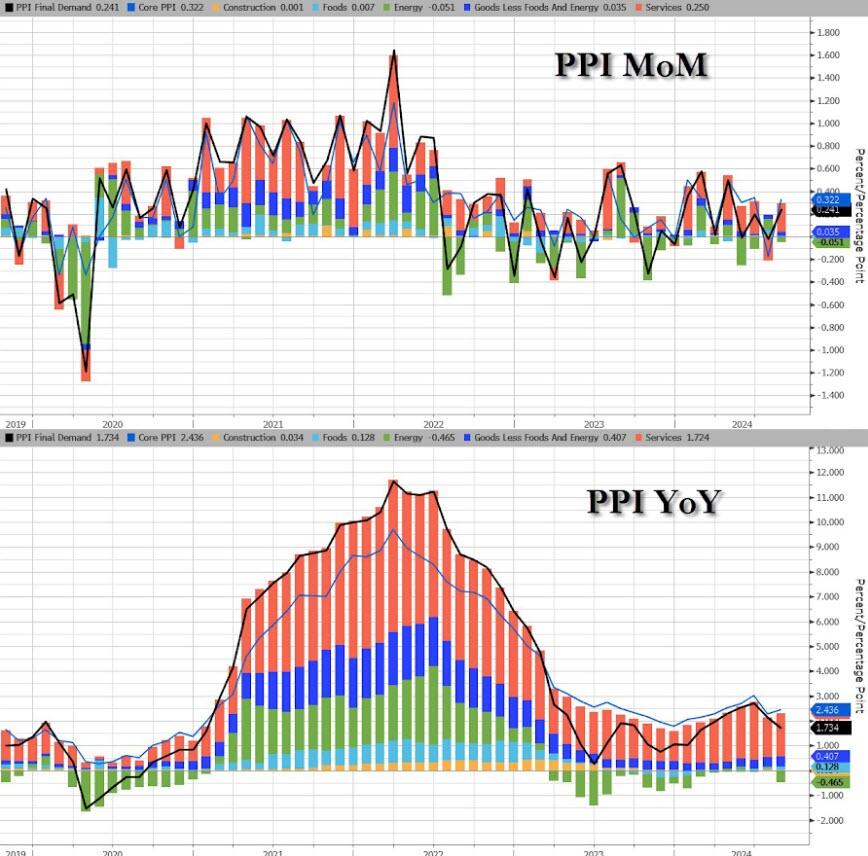

SEPT 12//HIGHER PPI AND ECB RATE CUT PROPELS OUR PRECIOUS METALS TODAY; GOLD CLOSED UP $37,80 TO $2552,05//SILVER CLOSED UP $1,13 TO $29,74//PLATINUM CLOSED UP $24,80 TO $980,50 WHILE PALLADIUM JUMPED 33.25 TO $1045,95//TWO GOLD COMMENTARIES TODAY FROM MIKE MAHARRAY: A MUST READ!// ISECB LOWERS RATE BY .25% AS EXPECTED/GERMANY SUSPENDS SCHENGEN WITH OTHER COUNTRIES TO FOLLOW DUE TO MIGRANT INFLUX//ISRAEL VS HAMAS/HEZBOLLAH UPDATES/RUSSIA VS UKRAINE: RUSSIA BEGINS OFFENSIVE IN KURSK//COVID UPDATES/VACCINE INJURY REPORT/DR PAUL ALEXANDER/SLAY NEWS ETC//USA NEWS: PPI ELEVATED AGAIN/GREAT COMMENTARY FROM RICHARD PORTER; KAMOFLAGE:HARRIS POLICY..” TEXAS CITY HAS A HUGE PROBLEM AS A VENEZUELAN GANG TOOK CONTROL OF A HOTEL//SWAMP STORIES FOR YOU TONIGHT AS WE LOOK TO ANOTHER GOVERNMENT SHUTDOWN “WAR”

323 C HSBC 1 363 H WELLS FARGO SEC 4 657 C MORGAN STANLEY 3 661 C JP MORGAN 1 737 C ADVANTAGE 15 7 905 C ADM 1

TOTAL: 16 16 MONTH TO DATE: 3,918

JPMorgan stopped 1/16

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2024. CONTRACT: 16 NOTICES FOR 1600 OZ or 0.0497 TONNES

total notices so far: 3918 contracts for 391,800 Oz (12.187 tonnes)

FOR SEPT:

SILVER NOTICES: 12 NOTICE(S) FILED FOR 60,000 OZ/

total number of notices filed so far this month : 4,826 for 24.120 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $37.80 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD

/ /INVENTORY RESTS AT 866.18 TONNES

INVENTORY RESTS AT 866.18 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $1.13 AT THE SLV

NO CHANGES IN SILVER INVENTORY AT THE SLV: ..

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 467.648 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUGE SIZED 1116 CONTRACTS TO 130,075 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR GAIN OF $0.33 IN SILVER PRICING AT THE COMEX ON WEDNESDAY’S TRADING. WE LOST ZERO NET LONGS WITH THE STRONG GAIN IN PRICE. WE HAD A HUMONGOUS GAIN OF 1321 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD AGAIN A HUGE LIQUIDATION OF T.A.S. CONTRACTS DURING WEDNESDAY’S TRADING//. WE HAD CONSIDERABLE SHORT COVERING BY OUR SPECS WITH THE STRONG GAIN IN PRICE. WE HAD A FAIR 205 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY ANOTHER HUGE 713 CONTRACT T.A.S ISSUANCE. IN ESSENCE WE GAINED A HUMONGOUS 1321 CONTRACTS ON OUR TWO EXCHANGES WITH THE GAIN IN PRICE.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN YESTERDAY. THE ACCUMULATED T.A.S. IS BEING USED TO MANIPULATE PRICES AT THE COMEX NOW EVERY DAY..

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 713 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS.IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1/2 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS BUT TO NO AVAIL. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.33) AND WERE UNSUCCESSFUL IN KNOCKING ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A HUMONGOUS GAIN OF 1321 TOTAL OI CONTRACTS ON OUR TWO EXCHANGES.

WE HAD A FAIR 205 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 22.765 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 80,000 OZ QUEUE JUMP//NEW STANDING ADVANCES TO 24.415 MILLION OZ

//NEW STANDING FOR SILVER//SEPT ADVANCES TO 24.415 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI GAIN //FAIR SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 713 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED 204CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS AUGUST ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT

TOTAL CONTRACTS for 8 DAYS, total 5446contracts: OR 27.230 MILLION OZ (680 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 27.230 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL PROBABLY BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 27.23 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1116 CONTRACTS WITH OUR GAIN IN PRICE OF SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS:713 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 22.765 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE 80,000 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR SEPT ADVANCES TO 24.415 MILLION OZ

WE HAVE A HUMONGOUS GAINOF 1321 OI CONTRACTS ON THE TWO EXCHANGES WITHTHE GAIN IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 713 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX TRADING//// MASSIVE ATTEMPTED SHORT COVERING FROM OUR SPEC SHORTS WITH THE SLIGHT LOSS IN PRICE TUESDAY/ AND ZERO LIQUIDATION OF LONGS. ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER.

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (713) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND FOR SURE TODAY., .

WE HAD 12 NOTICE(S) FILED TODAY FOR 60,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A FAIR SIZED 1868 OI CONTRACTS TO 513,469 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE 6446 CONTRACTS//

WE HAD A FAIR SIZED INCREASE IN COMEX OI (1968 CONTRACTS) OCCURRED DESPITE OUR TINY LOSS OF $0.95 IN PRICE /WEDNESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT AT 12.885 TONNES ON FIRST DAY NOTICE FOLLOWED BY WEDNESDAYS STRONG 2800 OZ QUEUE JUMP

NEW STANDING ADVANCES TO 12.432 TONNES

/ ALL OF THIS HAPPENED WITH OUR $0.95 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A STRONG SIZED GAIN OF 4627 OI CONTRACTS (14.391 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A GOOD SIZED 2659 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 519,915

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4627 CONTRACTS WITH 1968 CONTRACTS INCREASED AT THE COMEX// AND A GOOD SIZED 2659 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 4627 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A HUGE SIZED 3304 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A GOOD SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (2659 CONTRACTS) ACCOMPANYING THE FAIR SIZED INCREASE IN COMEX OI OF 1968 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 4627 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT 12.885 TONNES FOLLOWED BY TODAY’S 2800 OZ QUEUE JUMP

//NEW STANDING ADVANCES TO: /SEPT 12.432 TONNES.

/ 3) ZERO T.A.S. LIQUIDATION WITH ZERO NET LONG SPECS BEING CLIPPED,

4) FAIR SIZED COMEX OPEN INTEREST INCREASE 5) GOOD ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///HUGE T.A.S. ISSUANCE: 3304 T.A.S.CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

SEPT.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

TOTAL EFP CONTRACTS ISSUED: 37,955 CONTRACTS OF 3,795,500 OZ OR 118.055 TONNES IN 8 TRADING DAY(S) AND THUS AVERAGING: 4749 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAY(S) IN TONNES 118.055 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 118.055 DIVIDED BY 3550 x 100% TONNES = 3.32% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 118.055 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPTEMBER. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE SIZED 1116 CONTRACTS OI TO 130,075 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 205 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 205 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 205 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1116 CONTRACTS AND ADD TO THE 205 E.FP. ISSUED

WE OBTAIN A HUMONGOUS SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1321 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 6.605 MILLION OZ OCCURRED WITH OUR $0.33 GAIN IN PRICE

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 4.67 PTS OR 0.17% //Hang Seng CLOSED UP 131,68 PTS OR 0.71% // Nikkei CLOSED UP 1213.50 OR 3.41%//Australia’s all ordinaries CLOSED UP 1.20%///Chinese yuan (ONSHORE) CLOSED DOWN TO 7,1206 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.1273/ Oil UP TO 68.38dollars per barrel for WTI and BRENT UP AT 71.62 Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A FAIR SIZED 1968 CONTRACTS TO 513,469 DESPITE OUR TINY LOSS IN PRICE OF $0.95 WITH RESPECT TO WEDNESDAY’S TRADING. WE LOST ZERO IN NUMBER LONGS WITH THE LOWER PRICE FOR GOLD. THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THE MONTH DISTORTS OPEN INTEREST NUMBERS.

THE FED IS THE MAJOR SHORT OF AROUND 157+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS IS SCHEDULED TO HAPPEN LATE SEPT 2024/BEGINNING OF OCTOBER. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER CONTAINMENT.

OUR PHYSICAL LONDONERS ALSO BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT THESE PRICES AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD A ZERO T.A.S. LIQUIDATION ON WEDNESDAY’S LOSS IN PRICE WITH ZERO LONGS BEING CLIPPED (AS YOU WILL SEE BELOW) BUT WE DID HAVE MAJOR SHORT COVERING. THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF THE SPREADERS // T.A.S DURING LAST WEEK AND THIS WEEK IS SURELY DISTORTING COMEX OPEN INTEREST.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE NON ACTIVE DELIVERY MONTH OF SEPTEMBER.… THE CME REPORTS THAT THE BANKERS ISSUED A FAIR SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A FAIR SIZED 2659 EFP CONTRACTS WERE ISSUED: : OCT/DEC2659 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 2659 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 4627 CONTRACTS IN THAT 2659 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A FAIR GAIN OF 1968 COMEX CONTRACTS..AND THIS VERY STRONG GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $0.95/WEDNESDAY COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AS MENTIONED ABOVE. THE RAIDS ON LAST WEDNESDAY, FRIDAY AND THIS PAST TUESDAY AND FRIDAY WERE ORCHESTRATED BY THE FRBNY AS WE ARE NOW FINISHED WITH OPTIONS EXPIRY FOR THE OTC/LONDON LBMA BETS ENDING LAST FRIDAY AFTERNOON. DESPITE THE FED’S HUGE SHORT PREDICAMENT THEY STILL HAVE TIME AND ENERGY TO RAID OUR PRECIOUS METALS. SUCH CROOKS!

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT A HUGE SIZED 3304 CONTRACTS. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE (AND SPREADERS LATE IN THE MONTH). THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN LAST WEEK’S AND THIS WEEK’S TRADING//RAIDS

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: SEPT (12.432 TONNES) WHICH IS HUGE FOR A NON DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 44 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 12.432 TONNES.

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $0.95////BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE DID HAVE A STRONG GAIN IN OUR TWO EXCHANGES. WE HAD ZERO T.A.S. SPREADER LIQUIDATION. BUT CENTRAL BANK LONGS, SEIZING THE MOMENT, EXERCISED FOR PHYSICAL IN A BIG WAY.

WE HAVE GAINED A TOTAL OI OF 14.391 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPT (12.885 TONNES) ON FIRST DAY NOTICE FOLLOWED BY TUESDAY’S QUEUE JUMP OF A HUGE SIZED 2800 OZ

//NEW STANDING FOR SEPT ADVANCES TO: 12.432 TONNES.

NEW STANDING FOR SEPT: 12.432 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $0.95

WE HAVE REMOVED 6446CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES 4627 CONTRACTS OR 462,700 OZ (14,391

Total monthly oz gold served (contracts) so far this month

3918 notices 391,800oz 12.187 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: nil oz

we have 0 customer deposits

i

total deposits niloz

withdrawals: 2

i) Out of Brinks 11,109,971 oz

ii) Out of JPMorgan 17,792,063 oz

TOTAL WITHDRAWALS: 28,902,034 oz

adjustments:

0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPTEMBER

For the front month of SEPT. we have an oi of 95 contracts having GAINED 7 contracts. We had 21 notices filed on WEDNESDAY so we GAINED 28 contracts or 2800 oz will stand at the comex as these boys seek metal on this side of the pond.

OCTOBER LOST 834 CONTRACTS UP TO 40,960 CONTRACTS

NOVEMBER GAINED 23 CONTRACTS TO STAND AT 140

DECEMBER, THE BIGGEST DELIVERY MONTH GAINED 2239 CONTRACTS TO 413,342

We had 16 contracts filed for today representing 1600 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notice issued from their client or customer account. The total of all issuance by all participants equate to 16 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 1notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for SEPT /2024. contract month, we take the total number of notices filed so far for the month (3918 x 100 oz ) to which we add the difference between the open interest for the front month of SEPT 95 CONTRACTS) minus the number of notices served upon today (16x 100 oz per contract( equals 399,700 OZ OR 12.432 TONNES.

thus the INITIAL standings for gold for the SEPTEMBER contract month: No of notices filed so far (3918x 100 oz +we add the difference for front month of SEPT (95/ , OI} minus the number of notices served upon today (16 x 100 oz which equals 399,700oz (12.432 TONNES)

TOTAL COMEX GOLD STANDING FOR SEPT.: 12.432 TONNES WHICH IS HUGE FOR THIS NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

total pledged gold: 1,780,327.447 oz 55.375 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,038,434.827OZ

TOTAL REGISTERED GOLD 7,414,839.770 ( 230.63 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,623,595.051 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 5,634.503 oz (REG GOLD- PLEDGED GOLD)= 175.25 tonnes //

END

SILVER/COMEX

SEPT 12/2024

INITIAL

//2024// THE SEPT 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

399,055.259 OZ

Delaware

CNT HSBC

.

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

603,374.500oz loomis

No of oz served today (contracts)

12 CONTRACT(S) (60,000 OZ)

No of oz to be served (notices)

57 contracts (0.285 million oz)

Total monthly oz silver served (contracts)

4826 Contracts (24.120 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit/

total dealer deposit : NIL oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 customer deposits:

i) Into Loomis 603,374,5000 oz

total customer deposit 603,374,500 oz

JPMorgan has a total silver weight: 134.996million oz/306.156 million or 44.13%

adjustment:1

brinks//customer to dealer 50,696,479 oz

withdrawals: 3

i) Out of Delaware 113,834,632oz

ii) HSBC 80,685.600 oz

III) CNT 204,535.027

total customer withdrawals: 399,055.259oz

TOTAL REGISTERED SILVER: 76,117 MILLION OZ//.TOTAL REG + ELIGIBLE. 306.156 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR SEPTEMBER:

silver open interest data:

FRONT MONTH OF SEPT/2024 OI: 69 CONTRACTS HAVING GAINED 3 CONTRACT(S).

WE HAD 13 NOTICES FILED ON WEDNESDAY, SO WE GAINED 16 CONTRACTS OR 80,000 OZ

UNDERWENT A QUEUE JUMP TO TAKE DELIVERY OF SILVER OVER ON THIS SIDE OF THE POND..

THERE MUST BE ENOUGH SILVER OVER HERE.

OCTOBER SAW ANOTHER GAIN OF 65 OF OPEN INTEREST CONTRACTS AND THUS WE HAVE 1447 OPEN INTEREST CONTRACTS FOR OCTOBER.

NOVEMBER SAW ITS ANOTHER GAIN OF 2 CONTRACTS TO STAND AT 20

DECEMBER SAW A GAIN OF 1035 CONTRACTS UP TO 114,411

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 12 for 60,000 oz

CONFIRMED volume; ON WEDNESDAY 73,447 good

To calculate the number of silver ounces that will stand for delivery in SEPT. we take the total number of notices filed for the month so far at 4826 x 5,000 oz = 24.120 MILLION oz

to which we add the difference between the open interest for the front month of SEPT(69) and the number of notices served upon today 12 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT/2024 contract month: 4826 notices served so far) x 5000 oz + OI for the front month of SEPT (69)x number of notices served upon today minus (12)x 5000 oz of silver standing for the SEPT contract month equates to 24.415 MILLION OZ.

New total standing: 24.415 million oz.

There are 76m168million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS//

GLD

SEPT 12 WITH GOLD UP $37.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD /:/A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD/ //////INVENTORY RESTS AT 866.18 TONNES

SEPT 11 WITH GOLD DOWN $0.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD /:/A DEPOSIT OF 1.70 TONNES OF GOLD INTO THE GLD/ //////INVENTORY RESTS AT 864.44 TONNES

SEPT 10 WITH GOLD UP $12.00ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 9 WITH GOLD UP $12.95 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 6 WITH GOLD DOWN $17.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 5 WITH GOLD UP $18.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 4 WITH GOLD UP $3.45 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 3 WITH GOLD DOWN $4.25 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 5,47 TONNES OF GOLD INTO THE GLD/:/ //////INVENTORY RESTS AT 862.74 TONNES

AUGUST 30 WITH GOLD DOWN $31.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD/:/ //////INVENTORY RESTS AT 857.27 TONNES

AUGUST 29 WITH GOLD UP $23.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 28 WITH GOLD DOWN $14.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 27 WITH GOLD DOWN $1.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 26 WITH GOLD UP $9.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD VAPOUR GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 23 WITH GOLD UP $29.70 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER WITHDRAWAL OF 8.88 TONNES OF GOLD VAPOUR GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 857.85 TONNES

AUGUST 22 WITH GOLD DOWN $28.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 9.43 TONNES OF GOLD VAPOUR GOLD INTO THE GLD./ //////INVENTORY RESTS AT 866.70 TONNES

AUGUST 21 WITH GOLD DOWN $1.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER WITHDRAWAL OF 1.73 TONNES OF GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 857.27 TONNES

AUGUST 20 WITH GOLD UP $9.40 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 4.03 TONNES OF GOLD VAPOUR INTO THE GLD./ //////INVENTORY RESTS AT 859.00 TONNES

AUGUST 19 WITH GOLD UP $3.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 7.19 TONNES OF GOLD VAPOUR INTO THE GLD./ //////INVENTORY RESTS AT 854.97 TONNES

AUGUST 16 WITH GOLD UP $44.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: //////INVENTORY RESTS AT 847.78 TONNES

AUGUST 15 WITH GOLD UP $13,70 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD OUT OF THE GLD//////INVENTORY RESTS AT 847.78 TONNES

AUGUST 14 WITH GOLD DOWN $26.20 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.03 TONNES OF GOLD OUT OF THE GLD//////INVENTORY RESTS AT 845.76 TONNES

AUGUST 13 WITH GOLD UP $3.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//////INVENTORY RESTS AT 849.79 TONNES

AUGUST 12 WITH GOLD UP $30.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ////INVENTORY RESTS AT 846.91 TONNES

AUGUST 9 WITH GOLD UP $10.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 846.91 TONNES

AUGUST 8 WITH GOLD UP $31.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.02 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 844.04 TONNES

AUGUST 7 WITH GOLD UP $1.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.16 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 848.06 TONNES

AUGUST 6 WITH GOLD DOWN $13.10 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD” A WITHDRAWAL OF .57 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 844.90 TONNES

AUGUST 2 WITH GOLD DOWN $9.95 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.58 TONNES OF GOLD OUT OF THE GLD//INVENTORY RESTS AT 845.47 TONNES

AUGUST 1 WITH GOLD UP $9.15 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 846.05 TONNES

GLD INVENTORY: 866.18 TONNES, TONIGHTS TOTAL

SILVER

SEPT12//WITH SILVER UP $1.13/ NOCHANGES IN SILVER INVENTORY:./. /: .///./// /INVENTORY AT SLV 467.648MILLION OZ

SEPT 11//WITH SILVER UP $0.33/SMALL CHANGES IN SILVER INVENTORY: A HUGE DEPOSIT OF 2.099 MILLION OZ INTO THE SLV/ OZ OF SILVER FROM THE SLV./. /: .///./// /INVENTORY AT 467.648MILLION OZ

SEPT 10//WITH SILVER DOWN $.06/SMALL CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 639,000 OZ OF SILVER FROM THE SLV./. /: .///./// /INVENTORY AT 465.549MILLION OZ

SEPT 9//WITH SILVER UP $0.45//SMALL CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 46,000 OZ OF SILVER FROM THE SLV./. /: .///./// /INVENTORY AT 466.188 MILLION OZ

SEPT 6//WITH SILVER DOWN $.84//NO CHANGES IN SILVER INVENTORY /: .///./// /INVENTORY AT 466.234 MILLION OZ

SEPT 5//WITH SILVER UP $.55//SMALL CHANGES IN SILVER INVENTORY A WITHDRAWAL OF 0.193 MILLION OZ OF SILVER INTO THE SLV/: .///./// /INVENTORY AT 466.234 MILLION OZ

SEPT 4//WITH SILVER UP $.17//SMALL CHANGES IN SILVER INVENTORY A DEPOSIT OF 0.456 MILLION OZ OF SILVER INTO THE SLV/: .///./// /INVENTORY AT 466.427 MILLION OZ

SEPT 3//WITH SILVER DOWN $.74//HUGE CHANGES IN SILVER INVENTORY A DEPOSIT OF 1.278 MILLION OZ OF SILVER INTO THE SLV/: .///./// /INVENTORY AT 465.971 MILLION OZ

AUGUST30//WITH SILVER DOWN $.42//NO CHANGES IN SILVER INVENTORY: .///./// /INVENTORY AT 464.693 MILLION OZ

AUGUST 29//WITH SILVER UP $.37//SMALL CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 0.558 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 464.693 MILLION OZ

AUGUST 28//WITH SILVER DOWN $0.76//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 2.301 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 465.281 MILLION OZ

AUGUST 27//WITH SILVER DOWN $0.03//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 2.921 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 462.959 MILLION OZ

AUGUST 26//WITH SILVER UP $0.23//SMALL CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 45,000 OZ OUT OF THE SLV. .///./// /INVENTORY AT 465.880 MILLION OZ

AUGUST 23//WITH SILVER UP $0.72//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 1.506 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 465.925 MILLION OZ

AUGUST 22//WITH SILVER DOWN $0.44//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 0.943 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 468.344 MILLION OZ

AUGUST 21//WITH SILVER $0.03//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 1..552 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 468.344 MILLION OZ

AUGUST 20//WITH SILVER $0.24//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 1.369 MILLION OZ FROM THE SLV. .///./// /INVENTORY AT 466.792 MILLION OZ

AUGUST 19//WITH SILVER $0.39//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 1.506 MILLION OZ FROM THE SLV. .///./// /INVENTORY AT 465.423 MILLION OZ

AUGUST 16//WITH SILVER $0.49//NO CHANGES IN SILVER INVENTORY: .///./// /INVENTORY AT 466.929 MILLION OZ

AUGUST 15//WITH SILVER $1.14//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.186 MILLION ON INTO THE SLV.///./// /INVENTORY AT 466.929 MILLION OZ

AUGUST 14//WITH SILVER DOWN $0.40//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 13//WITH SILVER DOWN $0.19//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 12//WITH SILVER UP $.37//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 9//WITH SILVER DOWN $.03//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 8//WITH SILVER UP $.70//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 3.241 MILLION OZ INTO THE SLV////./// /INVENTORY AT 462.502 MILLION OZ

AUGUST 7//WITH SILVER DOWN $0.27//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.552 MILLION OZ INTO THE SLV////./// /INVENTORY AT 462.502 MILLION OZ

AUGUST 6//WITH SILVER UP $0.05//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 458.851 MILLION OZ

AUGUST 2//WITH SILVER DOWN $0.01//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 1.243 MILLION OZ OF SILVER OUT OF THE SLV ///./// /INVENTORY AT 460.961 MILLION OZ

AUGUST 1//WITH SILVER DOWN $0.46//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.608 MILLION OZ OF SILVER VAPOUR INTO THE SLV///./// /INVENTORY AT 462.204 MILLION OZ

CLOSING INVENTORY 467.648 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

Bad Data And Bad Models: How The Fed Has Shattered Confidence

This has been an ongoing pattern. The BLS releases a report. The media trumpets the greatness of the labor market. And then the BLS quietly revises the numbers down a month or two later and you hardly hear a peep.

The BLS struck again last week when it released revisions to its June Job Openings and Labor Turnover Survey (JOLTS) report. It initially reported 8.18 million job openings. The media reported this as great news — better than expected. The revised number came in at 7.910 million job openings.

That was a miss.

But as a post on X by ZeroHedge put it, “Of course, nobody cares one month later. This is how the Kamala/Biden Department of Labor has operated for the past 4 years.”

You might be tempted to laugh this off as “politics as usual,” but when you consider that the central bankers at the Federal Reserve use this data to make monetary policy decisions, it’s not funny.

Federal Reserve Chairman Jerome Powell and his fellow central bankers constantly talk about their “data dependence.” Kansas City Fed president Jeff Schmid recently said he wants to see “more data,” before deciding on a rate cut.

They wear data dependence like a badge of honor. After all, it does sound “sciency.” But given the reliability of the data, maybe they should rethink the approach.

Prior to Jerome Powell’s speech at Jackson Hole, Independent Institute Senior Fellow Judy Shelton appeared on Fox Business to talk about Fed monetary policy. Shelton is an economist and the author of several books, including Good as Gold How to Unleash the Power of Sound Money.

Shelton made a strong case against this data-dependent approach at the Fed. After all, bad data is going to lead to bad decision-making. As Shelton said, “There’s good reason for all of us to be skeptical about that data, especially when it gives us conflicting results,” pointing out that “there have long been discrepancies between the payroll jobs numbers and the household survey.”

“You end up getting these conflicting numbers that on the one hand said that we had tremendous job growth, and now we’re wondering if that was all a mirage.”

That leads to the logical conclusion.

“The fact that the Fed is so data-dependent should not give us confidence.”

During his Jackson Hole speech, Powell effectively surrendered to inflation, saying that the “balance of risk” has moved away from inflationary pressures to shakiness in the jobs market. But given the revisions to the data, it appears the Fed is behind the curve. The job market has been shakier than advertised for quite a while.

It gets worse.

Not only is the Fed using bad data, it plugging it into a bad model.

Shelton pointed out, “It’s ironic that on its own website, the Fed admits it can’t have much impact on the labor market and that it tends to be driven more by structural variables.”

The Federal Reserve primarily relies on curtailing demand. That’s the whole point of rate hikes. But as Shelton noted, the Fed can only impact demand on the consumer side of the economy. It has little to no impact on government spending, and that’s a big part of the equation.

“I sometimes wonder – how is the Fed going to explain why inflation came down at all? Is it just because they made the cost of capital so expensive for private business that they couldn’t hire people? They couldn’t expand?”

Meanwhile, government spending has gone on unabated. The Biden administration is blowing through half a trillion dollars every single month and running massive budget shortfalls in the process. But Powell refuses to even talk about it, instead insisting that the central bank just takes the fiscal situation “as given.”

Shelton drove home an important point. The central bank should at least acknowledge the contribution of government debt and spending to the inflation situation.

“It’s not clear that they’re really accomplishing their goal, and yet they stick with that model and claim that they have responsibility for price stability no matter what the government does.”

At least some people at the Federal Reserve know they can’t control inflation alone. A paper co-authored by Leonardo Melosi of the Federal Reserve Bank of Chicago and John Hopkins University economist Francesco Bianchi and published by the Kansas City Federal Reserve argues that central bank monetary policy alone can’t control inflation. U.S. government fiscal policy contributes to inflationary pressure and makes it impossible for the Fed to do its job.

“Trend inflation is fully controlled by the monetary authority only when public debt can be successfully stabilized by credible future fiscal plans. When the fiscal authority is not perceived as fully responsible for covering the existing fiscal imbalances, the private sector expects that inflation will rise to ensure sustainability of national debt. As a result, a large fiscal imbalance combined with a weakening fiscal credibility may lead trend inflation to drift away from the long-run target chosen by the monetary authority.”

If the monetary policy alone can’t control inflation, and the government has no intention of getting its fiscal house in order, why should we have any confidence that the Fed really has beaten inflation?

As Shelton pointed out, this also raises questions about the future.

“What if inflation starts ramping up again because of the government spending? Won’t the Fed have to go back to its model and its only tool to curtail demand is to raise interest rate?”

When you put it all together, it’s clear we shouldn’t have any confidence in the Federal Reserve. It is plugging bad data into a faulty model. This isn’t exactly a recipe for success.

end

ING Bank: This Gold Rally Is “Just Getting Started”

The Dutch financial group cites the prospect of a Federal Reserve rate-cutting cycle, geopolitical risks, and uncertainty going into the presidential election as potential catalysts to drive gold to new record highs. The report also noted several bullish trends supporting the gold price.

ING now projects gold to average $2,700 an ounce in 2025.

According to ING, the “most anticipated” Federal Reserve rate cut in decades is by far the biggest factor driving the current gold market.

During his recent Jackson Hole speech, Federal Reserve Chairman Jerome Powell gave the clearest indication yet that rate cuts are on the horizon saying, “The time has come for policy to adjust. The direction of travel is clear.”

The ING report says the only question remaining is the pace of cuts.

ING analysts note that gold is a non-yielding asset and tends to benefit from a low interest rate environment.

Lowering interest rates and ending balance sheet reduction will increase the money supply, and the expansion of the money supply is, by definition, inflation.

The Fed has tightened things up just enough to slow rising prices, but it hasn’t come close to wringing the pandemic-era inflation out of the economy. The central bank pumped nearly $5 trillion into the economy through quantitative easing alone. That was on top of the credit expansion incentivized by artificially low interest rates. It has only shrunk the balance sheet by about $1.8 trillion.

In fact, the Fed never substantively shrank the balance sheet after the 2008 financial crisis despite Ben Bernanke saying, “Ultimately, at the right time, the Federal Reserve will normalize its balance sheet,” in February of 2011.

Today, most of the inflation created during the pandemic and the Great Recession is still sloshing around in the economy.

And now, by slowing balance sheet reduction and signaling interest rate cuts, the Fed is telling you it plans to ramp up the inflation machine.

ING doesn’t mention any of this, and yet it still projects a bullish future for gold!

Bullish Indicators

ING analysts do note some other factors supporting gold, including election uncertainty in the U.S. and geopolitics. They anticipate further safe-haven demand due to the ongoing war in Ukraine and tensions in the Middle East.

Meanwhile, there are several strong and getting stronger demand sources in the gold market.

Globally, central banks added a net 37 tons of gold to their holdings in July, according to the latest data compiled by the World Gold Council (WGC). It was a 206 percent month-on-month increase and the highest level of central bank gold purchases since January.

This came on the heels of record central bank gold purchases through the first half of the year.

The report also pointed out that gold has started flowing into gold-backed ETFs. Funds in every region reported an increase in gold holdings in August with Western-based ETFs leading the way. It was the fourth straight month of global net inflows. According to ING, “Investor holdings in gold ETFs generally rise when gold prices gain, and vice versa. However, gold ETF holdings have been in decline for much of 2024, while spot gold prices have hit new highs. ETF flows finally turned positive in May.”

COMEX total net longs have also continued to rise, charting a 17 percent month-on-month increase as of the end of August. It was the highest month-end level since February 2020.

Given all of these bullish factors, ING projects gold to average $2,580 in the fourth quarter. That would boost the 2024 average to $2,388, with that average rising by more than 13 percent next year.

ING Bank photo from Wikimedia Commons and used under a Creative Commons License.

end

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY//BILL HOLTER:

The Fed Just Kicked the Capital Increases for the Dangerous Megabanks and their Derivatives Down the Road for Years

by Pam Martens and Russ Martens: September 12, 2024

~Federal Reserve Building, Washington, D.C.

When the next megabank blows up from its derivative exposure, you can add the names Jamie Dimon and Patick McHenry to former Republican Congressmen Randy Hultgren and Kevin Yoder as four of the men who greased the skids for another derivatives banking crisis. (For our report on the role played by Hultgren and Yoder, see our 2021 report here.)Dimon and McHenry are the latest lead players in the disastrous history of derivative regulation in the U.S.Dimon is the Chair and CEO of the riskiest and largest bank in the United States, JPMorgan Chase. After his bank lost $6.2 billion gambling in derivatives in London in 2012 – using deposits from his federally-insured bank – Dimon would, to rational minds, seem like the least qualified candidate to be giving advice to his banking regulators on how much capital megabanks need to hold to offset their gargantuan trading and derivatives risks. (See All the Devils from 2008 Are Back at the Megabanks: Leverage, Off- Balance-Sheet Debt, Over $192 Trillion in Derivatives, Shaky Capital Levels.)Unfortunately, rational thought holds no weight in a kleptocracy. (If it did, America would not have a 34-count indicted felon as the Republican candidate for the Presidency and safekeeper of the nuclear codes.) For the same reason that Dimon’s Board of Directors gave him a $50 million bonus after he settled his bank’s fourth and fifth criminal felony counts, Dimon is still able to throw his weight around and intimidate federal banking regulators into becoming his lapdogs.

A little background on Dimon’s battle with his banking regulators on the issue of adequate capital is in order:

On July 27 of last year, the Federal Reserve, FDIC and Office of the Comptroller of the Currency (OCC) released a proposal to require higher capital levels at banks with $100 billion or more in assets. Many of these banks had demonstrated quite clearly in the spring of 2023, via bank runs on deposits, that they could spread systemic contagion throughout the U.S. banking system.T

The three federal bank regulators provided a very generous public comment period of 120 days on the proposal. The megabanks had to only begin transitioning to the new rules on July 1, 2025, with full compliance not due for a preposterously long five years – on July 1, 2028.On September 12, 2023 the megabank cartel made its anger and intention to push back known in a 7-page letter that assaulted the proposal. The cartel demanded that the three federal agencies turn over all “evidence and analyses the agencies relied on” in making the proposal.

One of the signatories to the letter was the Bank Policy Institute (BPI), whose Board of Directors consists of the CEOs of the megabanks on Wall Street. BPI is Chaired by none other than Jamie Dimon.

BPI then launched an ad campaign that grossly distorted what the increase in capital would do, claiming that it would harm working families. (These are the same megabanks that blew up the U.S. economy in 2008, put millions of Americans out of work, left millions of working families in foreclosure and got a secret $29 trillion bailout from the Fed – because they had inadequate capital. These megabanks then formed their own coalition to battle in court against the Fed releasing the details of the trillions of dollars in revolving loans these banks had received from December 2007 to the middle of 2010. They lost that battle.

The Bank Policy Institute then hired Eugene Scalia, a law partner at Big Law firm Gibson, Dunn, to weigh options for potentially suing the Federal Reserve and the other bank regulators over the proposed higher capital rules. Scalia was expected to argue, if the case went to court, that the banking regulators did not do a proper cost benefit analysis prior to proposing the capital rule.Scalia is the son of the late Supreme Court Justice Antonin Scalia, who didn’t see anything wrong with accepting lots of free vacations from private interests while he sat on the high court. Eugene Scalia is also the lawyer who previously wielded a hatchet to gut key elements of the Dodd-Frank financial reform legislation of 2010.

The very suggestion that the Fed could end up in an embarrassing, headline-grabbing court battle with the very banks it regulates – with appeals dragging the case out for years – had the intended effect of intimidation.Fed Chair Jerome Powell appeared before the Senate Banking Committee on March 7 of this year for his regularly scheduled Semiannual Monetary Policy Report.

After Republicans on the Committee gushed over Powell’s willingness to rethink, redraft or repropose the capital rules, it came time for Senator Elizabeth Warren (D-MA) to question Powell.Warren was incensed that after Powell had promised in 2023 to support the Fed’s Vice Chair for Supervision, Michael Barr, in making capital reforms to prevent more bank runs and systemic contagion, Powell was now caving to pressure from the banking industry.

Senator Warren said the 37 largest banks that would be impacted by the higher capital rules have “spent tens of millions of dollars running ads during Sunday night football and millions more for an army of lobbyists to try to twist arms here in Congress.”Warren told Powell this: “Despite all you said last year when the banks failed about supporting Vice Chair Barr’s recommendations to strengthen rules for big banks, public reporting now says that you are driving efforts inside the Fed to weaken the capital rule. You even told the House Financial Services Committee representatives yesterday that you think it’s ‘very plausible’ that you withdraw the rule.”Warren concluded with this:”You are the leader of the Fed and when the heat was on last year, you talked a lot about getting tougher on the banks.

But now the giant banks are unhappy about that and you’ve gone weak-kneed on this. The American people need a leader at the Fed who has the courage to stand up to these banks and protect our financial system.”Dimon received assistance in his effort to bully and intimidate federal banking regulators to back off the capital proposals by Patrick McHenry, the Republican Chair of the House Financial Services Committee.According to a report in the Financial Times on Tuesday, McHenry threatened that if the Fed didn’t overhaul its capital proposal, Congress would invoke the Congressional Review Act, which gives Congress the ability to reverse federal agency rules.

The long and short of this bullying and intimidation campaign is that Michael Barr, the Fed’s Vice Chair for Supervision, addressed an audience at the Hutchins Center on Fiscal and Monetary Policy at the Brookings Institution on Tuesday and formally capitulated on the proposed capital reforms. The capital increase for the megabanks is now being proposed by the Fed at a 9 percent increase, down by more than half from the original proposal submitted for public comment in July 2023.As for those dodgy trillions of dollars in derivatives, it appears that the Fed intends to let the megabanks continue to use their own internal models to assess that risk.

The bank regulators will now need to resubmit their new capital proposal for public comment; negotiate for months or years to issue a final rule; and then offer a multi-year phase-in period – meaning this can is being indefinitely kicked down the road.At present, it’s not clear if the FDIC and the OCC are going along with the Fed’s capitulation to the demands of the Wall Street megabanks. We will report more on that as we obtain clarifying information.

3.CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHE

4. OTHER GOLD COMMENTARIES/:l

New Scandal: Watch Tor These Bullion Dealer And Depository Red Flags

One of the best tips anyone can offer when it comes to investing in physical bullion is to choose your dealer well.

The wrong choice can mean a total loss for clients who are caught as an unreputable dealer took their money and disappeared before delivering their metal.

This is, of course, also true for people putting bullion into their self-directed IRA accounts.

But these investors have an additional imperative; they must also choose well when deciding where their IRA metal will be stored.

First State Depository in Delaware recently failed after it was discovered the vault owner had absconded with much of the metal that was supposed to be held for safekeeping.

When it comes to IRAs, the term “self-directed” has an important legal connotation. The account holders will be responsible for the choices they make.

Up until now at least, IRA custodians have generally tried to be hands off and avoid making recommendations as to which dealers or depositories might be best. They have interpreted IRS guidelines to mean they should be neutral and simply serve as a record keeper. After all, these IRAs are “self-directed.”

Oxford Gold Group Scandal Tars IRA Provider

Equity Trust Company, a provider of self-directed IRAs, was named in a class-action lawsuit last month. An unscrupulous metals dealer, Oxford Gold Group, had utilized Equity Trust as the custodian when clients purchased metal for their retirement accounts.

When Oxford collapsed, news reports indicated a great number of orders had been paid for from client IRA funds held at Equity Trust. But the precious metals purchased were never delivered to the IRA holders’ chosen depository.

Oxford Gold Group’s unfortunate victims seek to hold Equity Trust liable too, specifically for not warning them about Oxford’s failures to deliver.

It will be some time before a resolution is reached. Regardless of the lawsuit’s outcome, however, one thing is clear for self-directed investors…

Nobody should rely on a dealer list or depository list provided by the IRA custodian as anything more than a starting point.

The fact that an IRA custodian has listed a particular dealer or depository as “approved” does not mean the dealer or depository has been fully vetted by the custodian. It does not mean the dealer or depository provide fast delivery or great customer service.

These lists just mean some minimal setup has been completed. Conducting additional due diligence makes sense.

One way is to look at customer reviews online.

The reality, though, is that shady precious metals dealers have managed to create seemingly good reputations online using fake or paid reviews. (And bad reviews can also be fake, planted by a company’s unethical competitors.)

In our estimation, the Better Business Bureau (BBB) is the only reasonably credible review site out there. Buyers should watch out for BBB reports of delivery delays – just as they should carefully monitor delivery speed, communication, and service as to their own orders.

Dealer Delivery Delays Are a Red Flag

Rising numbers of complaints about delays receiving delivery of orders have been a reliable indication of trouble ahead for a dealer. It was for Oxford Gold Group and for many others in the past several years.

It could even be running a Ponzi scheme; i.e., money coming from most recent orders is being used to purchase the inventory needed to fulfill other orders placed weeks earlier.

The depository you select should be able to provide independent audits of the company’s financials and the metal they store. They should also be able to furnish a Cover Note of Insurance or similar document showing that stored metals are fully insured.

Money Metals Exchange has an A+ rating with BBB and lots of happy clients leaving reviews. Meanwhile, Money Metals Depository readily provides disclosures, audits, and insurance information.

Investors who choose Money Metals when buying, selling, or storing their gold and silver can have peace of mind.

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES: IRON ORE

Goldman Predicts Iron Ore ‘Short Covering Rally’ Amid Structurally Bearish Outlook

Wednesday, Sep 11, 2024 – 08:10 PM

Despite Goldman analysts highlighting the latest gloomy high-frequency economic data out of China, and others at the bank noting that iron ore’s “fundamental outlook remains bleak” with prices hovering around a multi-year low of $93/ton, a trader from the bank told clients on Tuesday that the base metal could be primed for a ‘short covering rally.’

“The desk turn slightly more constructive in the next couple of weeks, but remain structurally bearish for longer-term outlook,” Goldman’s commodity trader Mark Ma wrote in a weekly update on iron ore and steel markets, which was featured in a note distributed to clients by Thomas Evans.

Ma said, “We expect to see short covering led rally before the long weekend and the Golden Week, after bears have gained >10% within a week only,” adding, “Pre-holiday restocking from steel mills would also add fuel to the rebound. Having said that, we still believe iron ore would remain structurally oversupplied in the long term on abundant shipment and poor Chinese demand. We don’t think the market could rebalance itself until we see production cut from mining juniors, which hasn’t materialized yet. Market sentiment can’t be more pessimistic. 9 out of 10 people in the market are bearish. Positioning wise, CTA is almost max short. Hedge ratio is high for large trading houses.”

He expects any squeeze in the base metal could “trigger a 5% short covering bounce from here” and that clients should “be ready to sell at the $95-100” level.

Ma continued, “Macro bears, CTA and discretionary money managers can’t wait for the peak demand season to pass to go short. Iron ore slumps for 5 consecutive days in a row to end the week 12% lower WoW.”

The trader summarizes the driving forces behind the iron ore market, including there is elevated supply and soft demand for steel in China, and elsewhere:

Market looks pass the seasonal demand recovery and continues to trade the longer term structural surplus in Fe content resulted from robust IO supply and lackluster domestic steel demand.

Pig iron output has bottomed out at 2.2mtpd and gradually picks up on marginal margin expansion due to lower met coke and IO price. There is more room for pig iron output to grow sequentially from here to 2.3mtpd if margin could hold or further improve.

Portside inventory stays at elevated level on back of strong shipment from Brazil and lack of production cut from mining juniors. Import arb stays slightly negative owing to the inventory overhang. 2/3 of 150mnt+ inventory is held by traders, which leaves very little room for trading houses to speculate.

Index-setting tons are well supplied in both port and seaborne market. MNPJ premium all stays in negative territory. SGX curve has shifted to contango from Sep to Dec, as a result of weak premium market and poor pricing.

Not only MNPJ premium, but also LP and 65/62 are sold off. LP retraces to 14c/dmtu upon traders puking and MOC offering down. 65/62 is compressed to the lowest level of the year, as mills continuously switch from high grade to low grade IO consumption to reduce productivity.

Steel mills take the tumble as a good opportunity to restock ahead of the long weekend and upcoming golden week in early Oct. Miners and traders are also keen to sell into the pre-holiday restocking flows, and thus transaction volumes grow at lower prices.

Hot metal production across China has slumped to a seasonal low amid high inventory levels at ports.

As for the steel market, the trader said prices touched a “7-year low upon the continuation of distressed property demand and slowing infra demand, in spite of a resilient steel export push.”

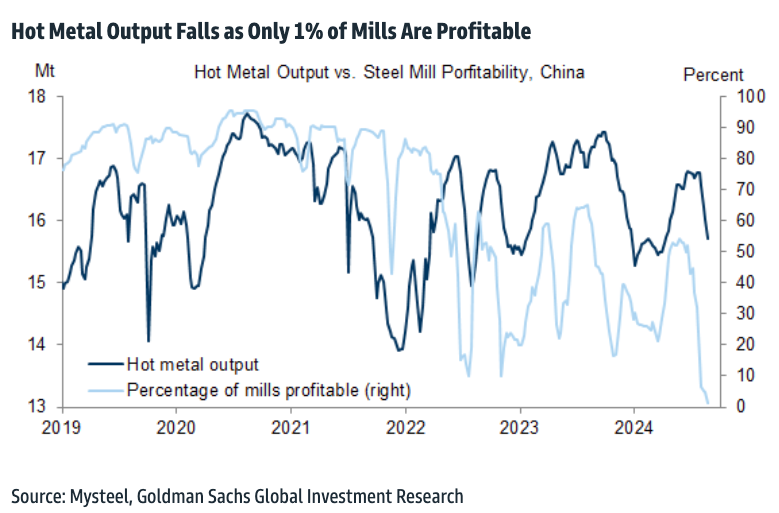

In a separate note, a team of Goldman analysts led by Aurelia Waltham and Daan Struyven said that iron ore’s “fundamental outlook remains bleak” as prices traded at a two-year low.

This was the most stunning chart from the analysts’ report: Only 1% of steel mills are profitable in the world’s second-largest economy. As profitability collapses, hot metal output declines.

Earlier this month, Goldman’s Rich Privorotsky told clients, “Iron ore is dropping to 90, China will continue to struggle, and commodities as a whole, I think, are reflecting the downgrade to growth expectations in the geography.”

A memo released by the China Iron & Steel Association to industry insiders also noted, “There will be a certain degree of recovery in steel demand through September and October, which is favorable for the steel market.”

“However, we need to be cautious of the impulse to restart production,” the association said, adding the risk of too much steelmaking material output could dampen “any improvement in the situation will end up a flash in the pan.”

China’s steel industry has been under pressure amid a severe property market downturn and weak economic recovery.

Last month, Baowu Steel Group Chairman Hu Wangming warned that economic conditions in the world’s second-largest economy felt like a “harsh winter.”

As the world’s largest steel producer, Baowu Steel’s chairman said the steel industry’s downturn could be “longer, colder, and more difficult to endure than expected,” potentially mirroring the severe downturns of 2008 and 2015.

Another team of Goldman analysts, led by Yuting Yang and Lisheng Wang, published high-frequency economic indicators, including consumption and mobility; production and investment; other macro activity, and markets and policy, that revealed there was no imminent recovery in China.

END

STEEL

Falling Chinese Steel Prices Send Ripples Through Global Markets

Weak domestic demand in China has led to a significant drop in steel rebar and h-beam steel prices, impacting global steel markets.

The US construction industry, hampered by high interest rates, is preparing for a potential resurgence in demand as the Federal Reserve signals rate cuts in late 2024.

While interest rate cuts are expected to stimulate the US construction sector, the recovery may not be immediate.

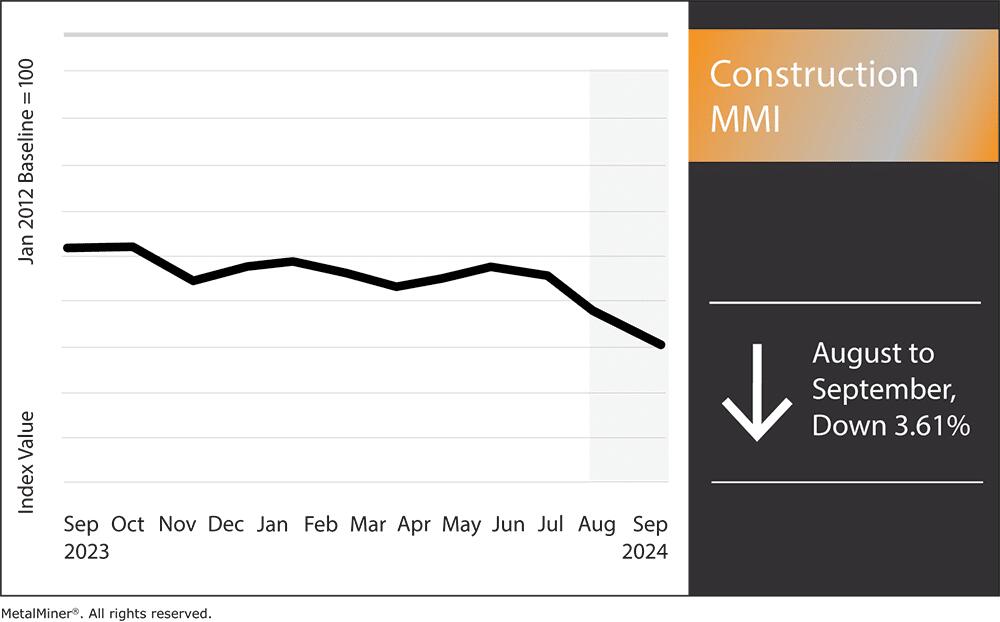

The Construction MMI (Monthly Metals Index) broke further out of its sideways trend, dipping by 3.61%. The main culprits driving the index down month-over-month were falling steel rebar and h-beam steel prices, compelled by weak domestic demand within China. With China’s property sector not anticipated to strengthen in the short term, steel prices could continue to witness bearish pressure. This, in turn, could impact the steel and construction industries far beyond China’s borders.

H-Beam and Steel Rebar Prices Drop Amid Weak Chinese Demand

The global steel market took a turn over the past month as h-beam and steel rebar prices dropped in response to weakened domestic demand in China. This drop, a direct result of China’s ongoing construction slowdown and tightening restrictions on financing for real estate developers, continues to create ripple effects across global steel markets.

Slowing Demand, Sliding Steel Prices

China’s real estate sector, which accounts for a significant portion of steel consumption, witnessed a decline in new projects as government-imposed restrictions on developer financing weigh heavily on the market. This has significantly reduced demand for h-beam steel and steel rebar, essential components for heavy-duty construction.

For Chinese steel rebar, prices dropped by about 7% through August and early September. Meanwhile, the ongoing weak domestic demand is causing an oversupply situation that has spilled into global markets.

The h-beam steel market has experienced a similar downturn, with Chinese prices dropping approximately 7-8% from August to September. This, too, reflects the broader slowdown in infrastructure and construction in China’s property sector.

Global Impact of China’s Steel Slowdown on Steel Prices

China’s weakened steel demand continues to impact global demand as well. This is mainly because China is responsible for more than half of the world’s steel production. As Chinese suppliers flood international markets with excess steel products, other major economies are seeing downward price pressure on both h-beam and rebar steel.

This means that countries that rely heavily on steel imports are now witnessing price decreases in construction materials, which could benefit industries like real estate and infrastructure. However, this trend also risks creating imbalances in global trade. With the Chinese government showing no signs of loosening financing restrictions for developers, the construction sector is unlikely to see a rapid recovery.

Source: MetalMiner Insights, which offers both short-term and long-term h-beam steel and steel rebar prices forecasts.

Meanwhile, the outlook for steel rebar and h-beam steel remains similar. Without a clear resurgence in infrastructure projects within China, the oversupply of steel in the global market will likely persist, keeping prices low through the end of the year and further threatening domestic producers of steel in other countries, who can’t compete with such low prices.

U.S. Construction Industry Prepares for Anticipated Interest Rate Drops

The U.S. construction industry currently finds itself in a precarious, yet hopeful situation. For over a year, high interest rates set by the Federal Reserve have cast a shadow over the sector, dampening new residential and commercial projects and pushing developers to the sidelines. However, the anticipation of rate cuts—projected to begin in the latter half of 2024—recently sparked a wave of preparation across the industry.

For the past 18 months, high borrowing costs have slowed the pace of U.S. construction. As high mortgage rates deterred buyers, developers, facing skyrocketing financing costs, significantly scaled back on projects. In fact, construction spending fell for the first time in over a year in mid-2024, signaling a growing weariness across the industry.

The business sector endured the most hardship, as expenditures on retail stores, medical facilities, and offices declined. Meanwhile, the rising cost of mortgages discouraged both developers and potential homeowners, negatively impacting residentialbuilding.

The Fed’s Shift in Strategy

The construction industry is already adjusting its strategy in light of signals from Federal Reserve officials that interest rate reductions may start by late 2024. Builders are preparing to profit from a drop in borrowing rates, which could spur demand for residential and commercial real estate once again.

Still, project planning acceleration is one of the tactics. Many developers delayed starting new projects to wait for anticipated rate decreases that will lower the cost of financing, hoping to capitalize on the surge of fresh demand.

How Will Interest Rate Cuts Impact the Construction Industry?

The Federal Reserve’s decision to start cutting interest rates will behoove the construction sector in several ways. First, developers will find it easier to finance new projects as borrowing costs drop. Both residential and commercial building will probably see a resurgence due to this, especially in the housing industry, which suffered significantly under high borrowing rates.?

Also, lower interest rates in the commercial real estate market will make borrowing less expensive for companies wishing to grow or restore real estate. This would revive the market for commercial buildings, shopping centers, and industrial sites, reversing some of the declines seen in recent months. However, while interest rate cuts will undoubtedly have a positive impact, the recovery may not be immediate.

6 CRYPTOCURRENCY NEWS

END

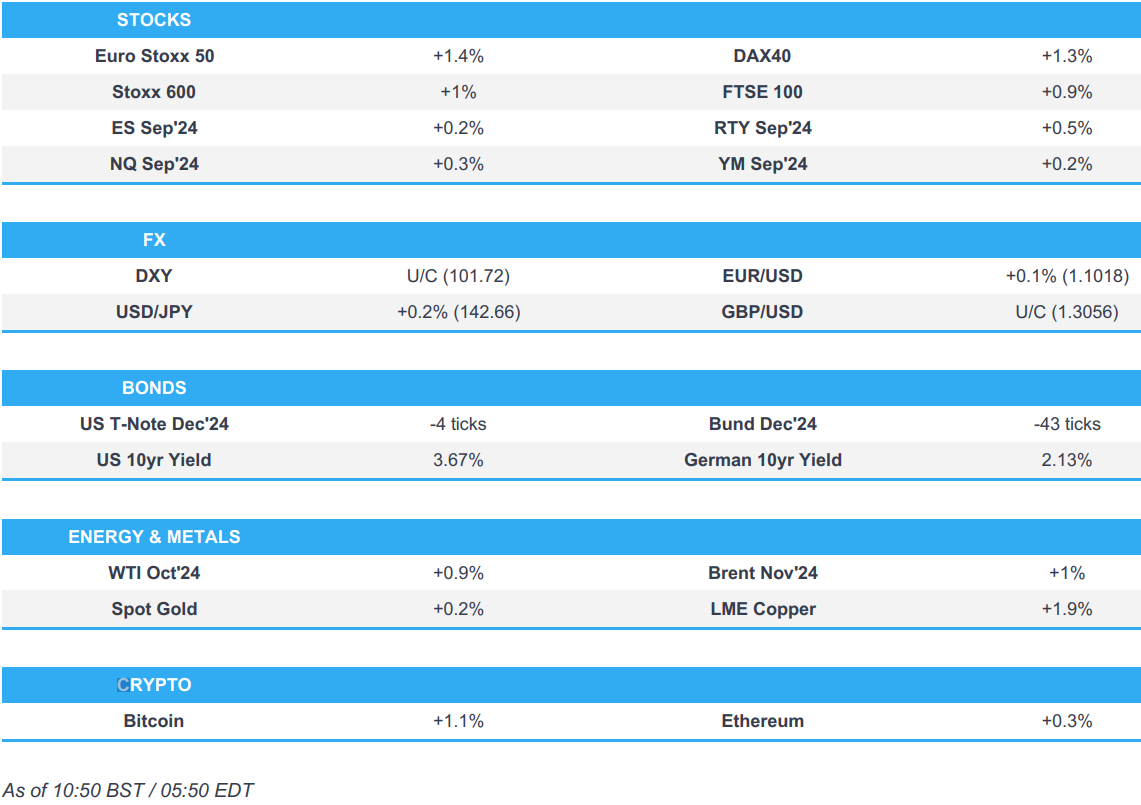

ASIA TRADING/THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 4.67 PTS OR 0.17% //Hang Seng CLOSED UP 131,68 PTS OR 0.71% // Nikkei CLOSED UP 1213.50 OR 3.41%//Australia’s all ordinaries CLOSED UP 1.20%///Chinese yuan (ONSHORE) CLOSED DOWN TO 7,1206 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.1273/ Oil UP TO 68.38dollars per barrel for WTI and BRENT UP AT 71.62 Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN TO 7.1206

OFFSHORE YUAN: DOWN TO 7.1273

SHANGHAI CLOSED DOWN 4.67 PTS OR 0.17 %

HANG SENG CLOSED UP 131.68 PTS OR 0.71%

2. Nikkei closed UP 1213.50PTS OR 3.41%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 101.71 EURO RISES TO 1.1018 UP 6 BASIS PTS

3b Japan 10 YR bond yield: FALL TO. +0.871 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 142.47…… JAPANESE YEN NOW RISING AS WE HAVE NOW REACHED THE COLLAPSING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.1270Italian 10 Yr bond yield UP to 3.527SPAIN 10 YR BOND YIELD DOWN TO 2,935

3i Greek 10 year bond yield DOWN TO 3.115

3j Gold at $2520.95/Silver at: 28.80 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 5/ 100 roubles/dollar; ROUBLE AT 91.50

3m oil into the 68 dollar handle for WTI and 71 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 142.47 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.871 % STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8535 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9402 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

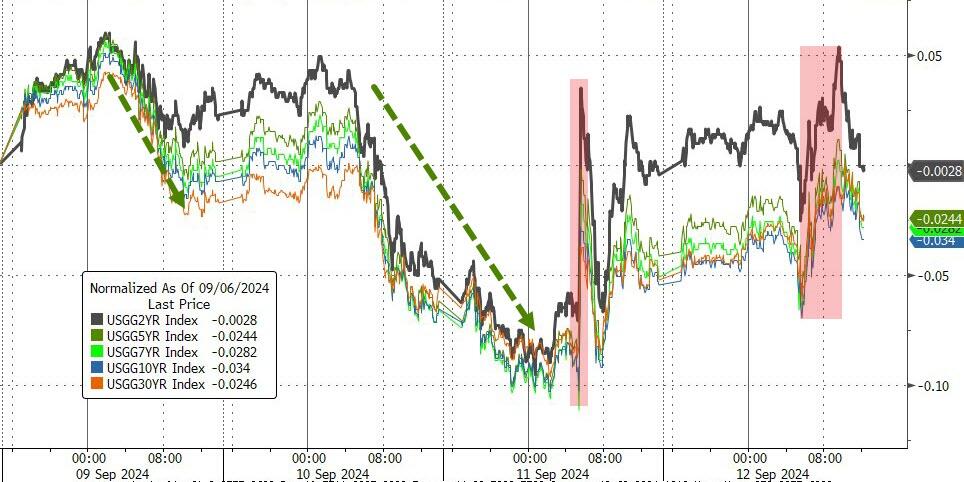

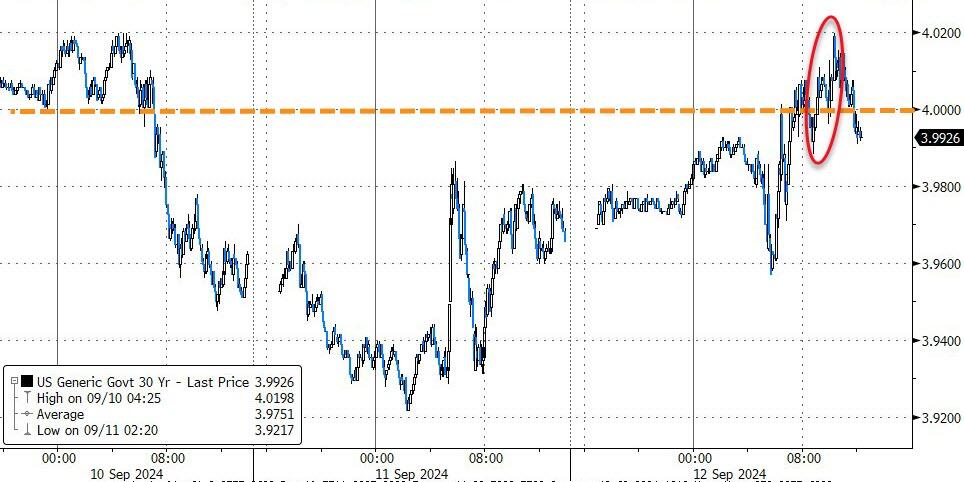

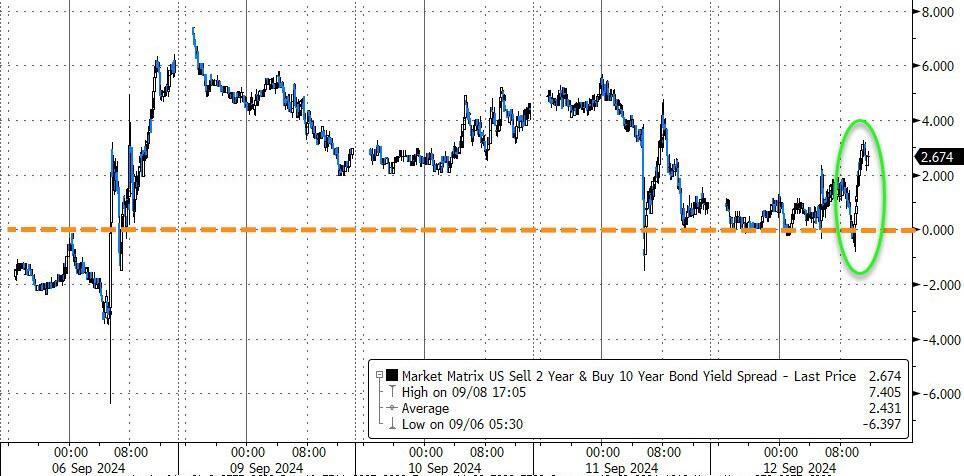

USA 10 YR BOND YIELD: 3.667 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 3.983 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 3.658 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 33,95…

10 YR UK BOND YIELD: 3.8090 UP 5 PTS

10 YR CANADA BOND YIELD: 2.939 UP 2 BASIS PTS

5 YR CANADA BOND YIELD: 2.778 UP 2 PTS.

2a New York OPENING REPORT

Futures Gain As Post-Nvidia Tech Rally Goes Global, ECB Cuts

Thursday, Sep 12, 2024 – 08:25 AM