SEPT 19/GOLD CLOSED UP $17.05 TO $2588,90 AS THE ASSAULT ON $2600 GOLD BEGINS IN EARNEST// SILVER CLOSED UP $0.85 TO $31.10/PLATINUM WAS DOWN $19.95 TO $953,20 WHILE PALLADIUM WAS UP $31,95 TO $1095,10//GOLD COMMENTARY TODAY FROM ALASDAIR MACLEOD//UPDATES ISRAEL VS HAMAS AND HEZBOLLAH//ISRAEL LAUNCHES ATTACK ON HEZBOLLAH//COVID UPDATES//VACCINE INJURY REPORTS.DR PAUL ALEXANDER. MARK CRISPIN MILLER//USA DATA EXISTING HOME SALES PLUMMET: JUST TOO EXPENSIVE FOR THE AVERAGE CITIZEN//SWAMP STORIES FOR YOU TONIGHT..

363 H WELLS FARGO SEC 2 435 H SCOTIA CAPITAL 1 624 H BOFA SECURITIES 5 657 C MORGAN STANLEY 4 686 C STONEX FINANCIA 1 737 C ADVANTAGE 6 6 905 C ADM 11

TOTAL: 18 18 MONTH TO DATE: 4,032

JPMorgan stopped 0/18

GOLD: NUMBER OF NOTICES FILED FOR SEPT/2024. CONTRACT: 18 NOTICES FOR 1800 OZ or 0.0559 TONNES

total notices so far: 4032 contracts for 403,200 Oz (12.541 tonnes)

FOR SEPT:

SILVER NOTICES: 55 NOTICE(S) FILED FOR 275,000 OZ/

total number of notices filed so far this month : 4,997 for 24.985 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $17,05 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD/ NO CHANGES IN GOLD INVENTORY AT THE GLD:

/ /INVENTORY RESTS AT 872,23 TONNES

INVENTORY RESTS AT 872,23TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP 85 CENTS AT THE SLV

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.46 MILLION OZ FROM THE SLV FROM THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 459.619 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A STRONG SIZED 523 CONTRACTS TO 141,128 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR LOSS OF $0.29 IN SILVER PRICING AT THE COMEX ON WEDNESDAY’S TRADING. WE LOST ZERO NET LONGS DESPITE THE LOSS IN PRICE. WE HAD A HUMONGOUS GAIN OF 1588 TOTAL CONTRACTS ON OUR TWO EXCHANGES. WE HAD AGAIN A HUGE LIQUIDATION OF T.A.S. CONTRACTS ESPECIALLYDURING WEDNESDAY’S AFTERNOON ACCESS TRADING//. WE HAD ATTEMPTED SHORT COVERING BY OUR SPECS WITH THE SMALL LOSS IN PRICE DURING THE COMEX HOURS AND AGAIN IN THE ACCESS TIME ZONE. WE HAD A HUGE 1065 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY A STRONG 505 CONTRACT T.A.S ISSUANCE. IN ESSENCE WE GAINED A HUMONGOUS 1588 CONTRACTS ON OUR TWO EXCHANGES DESPITE THE LOSS IN PRICE.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN YESTERDAY. THE ACCUMULATED T.A.S. IS BEING USED TO MANIPULATE PRICES AT THE COMEX NOW EVERY DAY..

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: 505 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS.IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1/2 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS BUT TO NO AVAIL. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.29) BUT WERE UNSUCCESSFUL IN KNOCKING ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A HUMONGOUS GAIN OF 1588 TOTAL OI CONTRACTS ON OUR TWO EXCHANGES.

WE HAD A STRONG 1065 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 22.765 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 255,000 OZ QUEUE JUMP//NEW STANDING ADVANCES TO 25.220MILLION OZ

//NEW STANDING FOR SILVER//SEPT ADVANCES TO 25.220 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI GAIN //HUGE SIZED EFP ISSUANCE/ VI) STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 505CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL REMOVED 485 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS SEPT, ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF SEPT

TOTAL CONTRACTS for 13DAYS, total 13,422contracts: OR 67.110 MILLION OZ (1032 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 67.110 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RDHIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 67.110 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

RESULT: WE HAD A STRONG SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 523 CONTRACTS DESPITE OUR LOSS IN PRICE OF SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS:1065 ISSUED FOR SEPT AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR AUGUST OF 22.765 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE 255,000 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR SEPT ADVANCES TO 25.220 MILLION OZ

WE HAVE A HUMONGOUS GAIN OF 1588 OI CONTRACTS ON THE TWO EXCHANGES DESPITE THE LOSS IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A GOOD SIZED 505 CONTRACTS,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX TRADING AND ACCESS TRADING//// MASSIVE ATTEMPTED SHORT COVERING FROM OUR SPEC SHORTS WITHTHE LOSS IN PRICE WEDNESDAY/ AND ZERO LIQUIDATION OF LONGS. ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER.

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (505) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE//AND FOR SURE TODAY., .

WE HAD 55 NOTICE(S) FILED TODAY FOR 275,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A SMALL SIZED 642 OI CONTRACTS TO 538,269 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 350 CONTRACTS//

WE HAD A SMALL SIZED INCREASE IN COMEX OI (642 CONTRACTS) OCCURRED WITH OUR GAIN OF $5.95 IN PRICE /WEDNESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR SEPT AT 12.885 TONNES ON FIRST DAY NOTICE FOLLOWED BY WEDNESDAYS HUGE 2300 OZ QUEUE JUMP

NEW STANDING ADVANCES TO 12.752 TONNES

/ ALL OF THIS HAPPENED WITH OUR $5.95 GAIN N PRICE WITH RESPECT TO WEDNESDAY’S COMEX TRADING. ALTHOUGH WE HAD A CONSIDERABLE TEMPORARY LOSS IN ACCESS TRADING/WEDNESDAY AFTERNOON. WE HAD A GOOD SIZED GAIN OF 4389 OI CONTRACTS (13.65 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE EARLY THURSDAY MORNING. WE ARE BEGINNING TO SIT SHIVA FOR OUR CROOKED SHORTERS

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUMONGOUS SIZED 3747 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 538,269

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 4389 CONTRACTS WITH 642 CONTRACTS INCREASED AT THE COMEX// AND A HUGE SIZED 3747 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 4389 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A SMALL SIZED 622 CONTRACTS,

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A HUGE SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (3747 CONTRACTS) ACCOMPANYING THE SMALL SIZED INCREASE IN COMEX OI OF 642 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 4389 CONTRACTS. WE HAVE ( 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR SEPT 12.885 TONNES FOLLOWED BY TODAY’S 2300 OZ QUEUE JUMP

//NEW STANDING ADVANCES TO: /SEPT 12.752 TONNES.

/ 3) CONSIDERABLE T.A.S. LIQUIDATION WITH ZERO NET LONG SPECS BEING CLIPPED, HUGE T,A,S, LIQUIDATION DURING THE ACCESS COMEX TIME ZONE

4) SMALL SIZED COMEX OPEN INTEREST INCREASE 5) HUMONGOUS ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///SMALL T.A.S. ISSUANCE: 622 T.A.S.CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

SEPT.

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF SEPT. :

TOTAL EFP CONTRACTS ISSUED: 68,440 CONTRACTS OF 6,844,000 OZ OR 212.877 TONNES IN 13TRADING DAY(S) AND THUS AVERAGING: 5264 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 13TRADING DAY(S) IN TONNES 212.877 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 212.877 DIVIDED BY 3550 x 100% TONNES = 6,00% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 212.877 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE.

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPTEMBER. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUGE SIZED 1008 CONTRACTS OI TO 141,613 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1065 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 1065 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1065 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1008 CONTRACTS AND ADD TO THE 1065 E.FP. ISSUED

WE OBTAIN A HUMONGOUS SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 2073 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 10.365 MILLION OZ OCCURRED DESPITE OUR $0.29 LOSS IN PRICE

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING/WEDNESDAY NIGHT

/ SHANGHAI CLOSED UP 18,74 PTS OR .89 %

//Hang Seng CLOSED UP 353.14 PTS OR 2,00 %

// Nikkei CLOSED UP 775.16 PTS OR 2.00%//Australia’s all ordinaries CLOSED UP 0.63%///Chinese yuan (ONSHORE) CLOSED UP TO 7,0659 CHINESE YUAN OFFSHORE CLOSED UP TO 7.0709 Oil UP TO 71.48 dollars per barrel for WTI and BRENT UP AT 74.28Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A SMALL SIZED 523 CONTRACTS TO 538,642 WITH OUR GAIN IN PRICE OF $5.95 WITH RESPECT TO WEDNESDAY’S TRADING. WE LOST ZERO IN NUMBER LONGS WITH THE HIGHER PRICE FOR GOLD. WE ALSO HAD A HUGE NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (3747). THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THIS MONTH DISTORTS OPEN INTEREST NUMBERS GREATLY.

THE FED IS THE MAJOR SHORT OF AROUND 157+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS IS SCHEDULED TO HAPPEN LATE SEPT 2024/BEGINNING OF OCTOBER. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE.THEY ARE TOTALLY TRAPPED.

OUR PHYSICAL LONDONERS ALSO BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT THESE PRICES AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD A CONSIDERABLE T.A.S. LIQUIDATION ON WEDNSDAY’S GAIN IN PRICE WITH ZERO LONGS BEING CLIPPED (AS YOU WILL SEE BELOW) BUT WE DID HAVE MAJOR ATTEMPTED SHORT COVERING AT MUCH LOWER PRICES. (AT 2:30 PM//ORCHESTRED RAID BY THE FED). THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF THE SPREADERS // T.A.S DURING LAST WEEK AND THIS WEEK IS SURELY DISTORTING COMEX OPEN INTEREST.THE RAID ORCHESTRED BY THE FED WILL NOT SHOW IN THURSDAY’S NUMBERS AS NUMBERS ARE OF 1:30 PM COMEX CLOSING. HOWEVER FRIDAY’S NUMBERS IS GOING TO BE A DILLY AS ANDREW AND HIS PHYSICAL FRIENDS WERE READY AND ANTICIPATED THE CROOKS SLAM. THEY BOUGHT HEAVY AND THEN TENDERED,

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE NON ACTIVE DELIVERY MONTH OF SEPTEMBER.… THE CME REPORTS THAT THE BANKERS ISSUED A HUMONGOUS SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A HUGE SIZED 3747 EFP CONTRACTS WERE ISSUED: : OCT/DEC 3747 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 3747 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 4389 CONTRACTS IN THAT 3747 LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A SMALL GAIN OF 642 COMEX CONTRACTS..AND THIS GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR SMALLISH GAIN IN PRICE OF $5.95/WEDNESDAY COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AS MENTIONED ABOVE

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS DURING MID MONTH IN THE DELIVERY CYCLE), THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT A SMALL SIZED 622 CONTRACTS. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE (AND SPREADERS LATE IN THE MONTH). THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN LAST WEEK’S AND THIS WEEK’S TRADING AND YESTERDAY’S SMACKDOWN/WEDNESDAY AFTERNOON AFTER THE COMEX CLOSED (DURING POWELL’S PRESSER)

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: SEPT (12.752 TONNES) WHICH IS HUGE FOR A NON DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 44 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 12.752 TONNES.

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $5.95/)//AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY SPECULATOR LONGS AS WE DID HAVE A GOOD GAIN IN OUR TWO EXCHANGES. WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION. WEDNESDAY AFTERNOON BUT CENTRAL BANK LONGS, SEIZING THE MOMENT, EXERCISED FOR PHYSICAL IN A BIG WAY. THURSDAY MORNING DURING THE LONDON PHYSICAL SESSION.

WE HAVE GAINED A TOTAL OF 14.74 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR SEPT (12.885 TONNES) ON FIRST DAY NOTICE FOLLOWED BY WEDNESDAY’S QUEUE JUMP OF A STRONG SIZED 2300 OZ

//NEW STANDING FOR SEPT ADVANCES TO: 12.752 TONNES.

NEW STANDING FOR SEPT: 12.752 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $5.95

WE HAVE REMOVED 350 CONTRACTS FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES 4799 CONTRACTS OR 479,900 OZ (.14.74

Total monthly oz gold served (contracts) so far this month

4032notices 403200oz 12.541 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

0 dealer deposits:

total dealer deposits: nil oz

we have 0 customer deposits

total deposits nil oz

withdrawals: 1

i) out of JPMorgan: 28,550.088 oz

888 kilobars

TOTAL WITHDRAWALS: 28,550.088oz

adjustments:0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR SEPTEMBER

For the front month of SEPT. we have an oi of 86 contracts having GAINED 7 contracts. We had 12 notices filed on WEDNESDAY so we GAINED 19 contracts or 1900 oz will stand at the comex as these boys seek metal on THIS side of the pond.

OCTOBER GAINED 222 CONTRACTS UP TO 41,726 CONTRACTS

NOVEMBER GAINED 94 CONTRACTS TO STAND AT 420

DECEMBER, THE BIGGEST DELIVERY MONTH GAINED 428 CONTRACTS TO 436,837

We had 18 contracts filed for today representing 1800 oz

This is a major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notice issued from their client or customer account. The total of all issuance by all participants equate to 18 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for SEPT /2024. contract month, we take the total number of notices filed so far for the month (4032 100 oz ) to which we add the difference between the open interest for the front month of SEPT 86 CONTRACTS) minus the number of notices served upon today (18x 100 oz per contract( equals 410,000 OZ OR 12.752 ONNES.

thus the INITIAL standings for gold for the SEPTEMBER contract month: No of notices filed so far (4032 x 100 oz +we add the difference for front month of SEPT (86 OI} minus the number of notices served upon today (18 x 100 oz which equals 410,000 oz (12.752TONNES)

TOTAL COMEX GOLD STANDING FOR SEPT.: 12.752 TONNES WHICH IS HUGE FOR THIS NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

total pledged gold: 1,885,944.092 oz 58.660 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 16,934,,211.150 OZ

TOTAL REGISTERED GOLD 7,486,.611 .793 232.84tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,447,599.357OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 5,600,667oz (REG GOLD- PLEDGED GOLD)= 174,18tonnes //

END

SILVER/COMEX

SEPT 19 2024

INITIAL

//2024// THE SEPT 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

84,645,880 OZ

Delaware hsbc

.

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

4141.400 oz Delaware

No of oz served today (contracts)

55 CONTRACT(S) (275,000 OZ)

No of oz to be served (notices)

47 contracts (0.235million oz)

Total monthly oz silver served (contracts)

4997 Contracts (24.985 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit/

total dealer deposit : NIL oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 customer deposits:

we had one customer deposit:

i) Into Delaware 4141.400 oz

total customer deposits 4141.400 oz

WE had 2 withdrawals

from Delaware 4141,400 oz

from HSBC 80,500.480

total withdrawal 84,645,880 oz

JPMorgan has a total silver weight: 134.996million oz/305.883million or 44.13%

adjustment:0

TOTAL REGISTERED SILVER: 74.897MILLION OZ//.TOTAL REG + ELIGIBLE. 305,883million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR SEPTEMBER:

silver open interest data:

FRONT MONTH OF SEPT/2024 OI: 102 CONTRACTS HAVING GAINED 20 CONTRACT(S).

WE HAD 31 NOTICES FILED ON WEDNESDAY, SO WE GAINED 51 CONTRACTS OR 255,000 OZ

UNDERWENT A QUEUE JUMP TO TAKE DELIVERY OF SILVER OVER ON THIS SIDE OF THE POND..

THERE MUST BE ENOUGH SILVER OVER HERE.

OCTOBER SAW A GAIN OF 29 OF OPEN INTEREST CONTRACTS AND THUS WE HAVE 1441 OPEN INTEREST CONTRACTS FOR OCTOBER.

NOVEMBER SAW A GAIN OF 2 CONTRACTS TO STAND AT 108

DECEMBER SAW A GAIN OF 428 CONTRACTS UP TO 123,435 CONTRACTS

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 55 for 275,000oz

CONFIRMED volume; ON WEDNESDAY 89,256 huge

To calculate the number of silver ounces that will stand for delivery in SEPT. we take the total number of notices filed for the month so far at 4997x 5,000 oz = 24.985 MILLION oz

to which we add the difference between the open interest for the front month of SEPT(102)and the number of notices served upon today 55 x (5000 oz) equals the number of ounces standing.

Thus the standings for silver for the SEPT/2024 contract month: 4997 notices served so far) x 5000 oz + OI for the front month of SEPT (102)x number of notices served upon today minus (55)x 5000 oz of silver standing for the SEPT contract month equates to 25.220 MILLION OZ.

New total standing: 25.220 million oz.

There are 76.168million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS//

GLD

SEPT 19 WITH GOLD UP $17,05 ON THE DAY; NO CHANGES IN GOLD AT THE GLD/// /:// //////INVENTORY RESTS AT 872.23TONNES

SEPT 18 WITH GOLD UP $5.95 ON THE DAY; NO CHANGES IN GOLD AT THE GLD/// /:// //////INVENTORY RESTS AT 872.23TONNES

SEPT 17WITH GOLD DOWN $15.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 1.52 TONNES INTO THE GLD /:// //////INVENTORY RESTS AT 872.23TONNES

SEPT 16 WITH GOLD DOWN $1.25 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:// //////INVENTORY RESTS AT 870,71 TONNES

SEPT 13 WITH GOLD UP $30.45 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD /:/A DEPOSIT OF 14.54TONNES OF GOLD VAPOURINTO THE GLD/ //////INVENTORY RESTS AT 870,71 TONNES

SEPT 12 WITH GOLD UP $37.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD /:/A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD/ //////INVENTORY RESTS AT 866.18 TONNES

SEPT 11 WITH GOLD DOWN $0.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD /:/A DEPOSIT OF 1.70 TONNES OF GOLD INTO THE GLD/ //////INVENTORY RESTS AT 864.44 TONNES

SEPT 10 WITH GOLD UP $12.00ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 9 WITH GOLD UP $12.95 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 6 WITH GOLD DOWN $17.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 5 WITH GOLD UP $18.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 4 WITH GOLD UP $3.45 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 3 WITH GOLD DOWN $4.25 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 5,47 TONNES OF GOLD INTO THE GLD/:/ //////INVENTORY RESTS AT 862.74 TONNES

AUGUST 30 WITH GOLD DOWN $31.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.15 TONNES OF GOLD INTO THE GLD/:/ //////INVENTORY RESTS AT 857.27 TONNES

AUGUST 29 WITH GOLD UP $23.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 28 WITH GOLD DOWN $14.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 27 WITH GOLD DOWN $1.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:/ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 26 WITH GOLD UP $9.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.73 TONNES OF GOLD VAPOUR GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 856.12 TONNES

AUGUST 23 WITH GOLD UP $29.70 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER WITHDRAWAL OF 8.88 TONNES OF GOLD VAPOUR GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 857.85 TONNES

AUGUST 22 WITH GOLD DOWN $28.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 9.43 TONNES OF GOLD VAPOUR GOLD INTO THE GLD./ //////INVENTORY RESTS AT 866.70 TONNES

AUGUST 21 WITH GOLD DOWN $1.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER WITHDRAWAL OF 1.73 TONNES OF GOLD OUT OF THE GLD./ //////INVENTORY RESTS AT 857.27 TONNES

AUGUST 20 WITH GOLD UP $9.40 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 4.03 TONNES OF GOLD VAPOUR INTO THE GLD./ //////INVENTORY RESTS AT 859.00 TONNES

AUGUST 19 WITH GOLD UP $3.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A MONSTER DEPOSIT OF 7.19 TONNES OF GOLD VAPOUR INTO THE GLD./ //////INVENTORY RESTS AT 854.97 TONNES

AUGUST 16 WITH GOLD UP $44.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: //////INVENTORY RESTS AT 847.78 TONNES

AUGUST 15 WITH GOLD UP $13,70 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.02 TONNES OF GOLD OUT OF THE GLD//////INVENTORY RESTS AT 847.78 TONNES

AUGUST 14 WITH GOLD DOWN $26.20 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.03 TONNES OF GOLD OUT OF THE GLD//////INVENTORY RESTS AT 845.76 TONNES

AUGUST 13 WITH GOLD UP $3.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//////INVENTORY RESTS AT 849.79 TONNES

AUGUST 12 WITH GOLD UP $30.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: ////INVENTORY RESTS AT 846.91 TONNES

AUGUST 9 WITH GOLD UP $10.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 846.91 TONNES

AUGUST 8 WITH GOLD UP $31.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.02 TONNES OF GOLD OUT OF THE GLD////INVENTORY RESTS AT 844.04 TONNES

AUGUST 7 WITH GOLD UP $1.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.16 TONNES OF GOLD INTO THE GLD////INVENTORY RESTS AT 848.06 TONNES

AUGUST 6 WITH GOLD DOWN $13.10 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD” A WITHDRAWAL OF .57 TONNES OF GOLD FROM THE GLD////INVENTORY RESTS AT 844.90 TONNES

AUGUST 2 WITH GOLD DOWN $9.95 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 0.58 TONNES OF GOLD OUT OF THE GLD//INVENTORY RESTS AT 845.47 TONNES

AUGUST 1 WITH GOLD UP $9.15 ON THE DAY; HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 2.88 TONNES OF GOLD INTO THE GLD//INVENTORY RESTS AT 846.05 TONNES

GLD INVENTORY: 872.23TONNES, TONIGHTS TOTAL

SILVER

SEPT19 WITH SILVER UP $0.85 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 1.46 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 459,619 MILLION OZ

SEPT18 WITH SILVER DOWN $0.29 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 1,551 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 461.079 MILLION OZ

SEPT17 WITH SILVER DOWN $0.13 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWALOF 5.976 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 462MILLION OZ

SEPT16//WITH SILVER UP $0.10 : HUGE CHANGES IN SILVER INVENTORY:. ADEPOSIT OF 958,000 OZ INTO THE SLV/. /: .///./// /INVENTORY AT SLV 468.606MILLION OZ

SEPT13//WITH SILVER UP $1.13/ NOCHANGES IN SILVER INVENTORY:./. /: .///./// /INVENTORY AT SLV 467.648MILLION OZ

SEPT 11//WITH SILVER UP $0.33/SMALL CHANGES IN SILVER INVENTORY: A HUGE DEPOSIT OF 2.099 MILLION OZ INTO THE SLV/ OZ OF SILVER FROM THE SLV./. /: .///./// /INVENTORY AT 467.648MILLION OZ

SEPT 10//WITH SILVER DOWN $.06/SMALL CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 639,000 OZ OF SILVER FROM THE SLV./. /: .///./// /INVENTORY AT 465.549MILLION OZ

SEPT 9//WITH SILVER UP $0.45//SMALL CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 46,000 OZ OF SILVER FROM THE SLV./. /: .///./// /INVENTORY AT 466.188 MILLION OZ

SEPT 6//WITH SILVER DOWN $.84//NO CHANGES IN SILVER INVENTORY /: .///./// /INVENTORY AT 466.234 MILLION OZ

SEPT 5//WITH SILVER UP $.55//SMALL CHANGES IN SILVER INVENTORY A WITHDRAWAL OF 0.193 MILLION OZ OF SILVER INTO THE SLV/: .///./// /INVENTORY AT 466.234 MILLION OZ

SEPT 4//WITH SILVER UP $.17//SMALL CHANGES IN SILVER INVENTORY A DEPOSIT OF 0.456 MILLION OZ OF SILVER INTO THE SLV/: .///./// /INVENTORY AT 466.427 MILLION OZ

SEPT 3//WITH SILVER DOWN $.74//HUGE CHANGES IN SILVER INVENTORY A DEPOSIT OF 1.278 MILLION OZ OF SILVER INTO THE SLV/: .///./// /INVENTORY AT 465.971 MILLION OZ

AUGUST30//WITH SILVER DOWN $.42//NO CHANGES IN SILVER INVENTORY: .///./// /INVENTORY AT 464.693 MILLION OZ

AUGUST 29//WITH SILVER UP $.37//SMALL CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 0.558 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 464.693 MILLION OZ

AUGUST 28//WITH SILVER DOWN $0.76//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 2.301 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 465.281 MILLION OZ

AUGUST 27//WITH SILVER DOWN $0.03//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 2.921 MILLION OZ OZ OUT OF THE SLV. .///./// /INVENTORY AT 462.959 MILLION OZ

AUGUST 26//WITH SILVER UP $0.23//SMALL CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 45,000 OZ OUT OF THE SLV. .///./// /INVENTORY AT 465.880 MILLION OZ

AUGUST 23//WITH SILVER UP $0.72//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 1.506 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 465.925 MILLION OZ

AUGUST 22//WITH SILVER DOWN $0.44//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 0.943 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 468.344 MILLION OZ

AUGUST 21//WITH SILVER $0.03//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 1..552 MILLION OZ INTO THE SLV. .///./// /INVENTORY AT 468.344 MILLION OZ

AUGUST 20//WITH SILVER $0.24//HUGE CHANGES IN SILVER INVENTORY:A DEPOSIT OF 1.369 MILLION OZ FROM THE SLV. .///./// /INVENTORY AT 466.792 MILLION OZ

AUGUST 19//WITH SILVER $0.39//HUGE CHANGES IN SILVER INVENTORY:A WITHDRAWAL OF 1.506 MILLION OZ FROM THE SLV. .///./// /INVENTORY AT 465.423 MILLION OZ

AUGUST 16//WITH SILVER $0.49//NO CHANGES IN SILVER INVENTORY: .///./// /INVENTORY AT 466.929 MILLION OZ

AUGUST 15//WITH SILVER $1.14//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.186 MILLION ON INTO THE SLV.///./// /INVENTORY AT 466.929 MILLION OZ

AUGUST 14//WITH SILVER DOWN $0.40//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 13//WITH SILVER DOWN $0.19//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 12//WITH SILVER UP $.37//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 9//WITH SILVER DOWN $.03//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 465.743 MILLION OZ

AUGUST 8//WITH SILVER UP $.70//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 3.241 MILLION OZ INTO THE SLV////./// /INVENTORY AT 462.502 MILLION OZ

AUGUST 7//WITH SILVER DOWN $0.27//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.552 MILLION OZ INTO THE SLV////./// /INVENTORY AT 462.502 MILLION OZ

AUGUST 6//WITH SILVER UP $0.05//NO CHANGES IN SILVER INVENTORY:///./// /INVENTORY AT 458.851 MILLION OZ

AUGUST 2//WITH SILVER DOWN $0.01//HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 1.243 MILLION OZ OF SILVER OUT OF THE SLV ///./// /INVENTORY AT 460.961 MILLION OZ

AUGUST 1//WITH SILVER DOWN $0.46//HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.608 MILLION OZ OF SILVER VAPOUR INTO THE SLV///./// /INVENTORY AT 462.204 MILLION OZ

CLOSING INVENTORY 459.619 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

end

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY//BILL HOLTER:

We’re still trying to process the latest assassination attempt on Donald Trump, which took place on Sunday in West Palm Beach. But while that’s important to dissect as the election gets closer, it’s important to consider a development I’ve been warning about for over two years.

President Trump has long been an opponent of central bank digital currencies (CBDCs) or as I call them Biden Bucks. (Now that Biden is essentially out of the picture, maybe I should rename them Kamala Bucks.)

I called them “Biden Bucks” because I wanted Biden (and his partner Kamala) to take full credit for what I consider to be crimes against American citizens. More on that shortly. For now, let’s focus on Trump.

At a New Hampshire campaign rally earlier this year, Donald Trump reiterated what he’s been saying for months: CBDCs are dangerous and he would never allow one if elected.

For too long, the average American has been squeezed by the big banks and financial elites. It’s time we take a stand — together. This would be a dangerous threat to freedom, and I will stop it from coming to America. Such a currency would give a federal government absolute control over your money. They could take your money, and you wouldn’t even know it was gone.

In fact, Trump recently pledged to ban CBDCs, promote the creation of a national crypto reserve and guarantee that the government will not sell crypto obtained through law enforcement seizures.

I’ve said it before, but I’ll say it again: “Welcome aboard, Mr. President.” Again, I’ve been sounding the alarm about Biden Bucks for over two years. I’ve been warning about Joe Biden’s plan to control your money and take away your privacy rights completely.

A Threat to Your Freedom

President Trump is right. Biden Bucks are a dangerous threat to freedom. They’re a threat to our constitutional liberties and give the government total control of our private financial information.

A change in leadership is probably our last hope in stopping this madness from continuing.

Maybe you’re a new reader who’s not familiar with Biden Bucks, or maybe you’re an existing reader who hasn’t thought of them for a while. To catch you up, here are the basics: They would replace physical cash with new electronic currencies.

These Biden Bucks would have the full backing of the U.S. Federal Reserve. To be clear, they won’t just be a complement to cash. They will entirely, or very nearly entirely, REPLACE the cash (“fiat”) dollar we have now.

In other words, the dollar will be strictly digital. This digital dollar would be the sole, mandatory currency of the United States. What does this mean for you?

It would put your money under direct government control as President Trump has said. You could use it only at the government’s discretion.

We are already seeing how many retailers are no longer accepting cash across America. What happens when physical cash is eliminated from any payment transactions?

Declined!!!

Imagine this. To further advance the Biden/Harris Green New Scam, what if the Dems and their deep state enablers decide that gasoline needs to be rationed?

Your Biden/Kamala Bucks could be rendered useless at the gas pump once you’ve purchased a certain amount of gasoline in a week. You want gas, but all you get is a one-word message: Declined.

How’s that for control? That’s just one example. Biden Bucks would create new ways for the government to control how much you can buy of an item or even restrict purchases. They would keep score of every financial decision you make.

In a world of Biden Bucks, the government will even know your physical whereabouts at the point of purchase. It’s a short step from there to putting you under FBI investigation if you vote for the wrong candidate or give donations to the wrong political party.

If any of this sounds extreme, fantastical or otherwise far-fetched, I promise you it’s not. It’s happening right now. And given all the abuses of power the government’s engaged in over the past few years, why should you be surprised that Biden/Kamala Bucks wouldn’t invite even more abuse?

Kamala Would Be Even Worse

I don’t want to exaggerate, but the U.S. is moving closer and closer to an authoritarian-style government. We’re not there yet, but things are trending in that direction. And if you thought it was bad under Biden, it’ll be worse under a possible Kamala Harris presidency.

Biden was basically a puppet of top Democratic insiders, mostly holdovers from the Obama administration.

He never had any real core beliefs, he just did what he was told to do. He just wanted to be president.

Harris is different. She’s a true believer in the progressive causes the Biden administration put forward. You’d never know that if you listened to her running for president (she’s trying to position herself as a centrist), but you just have to look at her record.

As a senator, Harris had the most liberal record, even further left than Bernie Sanders or Elizabeth Warren. Pertaining to Biden Bucks specifically, she pushed unsuccessfully in 2020 for a 400% funding increase for the U.S. Digital Service, an agency that did early work on payment technology, setting the stage for a central bank digital currency.

So Kamala is all in on Biden Bucks and the threat to your money and freedoms. With Biden Bucks, a Harris administration and the Federal Reserve would become both money printer and central bank, destroying any checks and balances to their power over Americans’ financial holdings.

You CAN Fight Back

But we can fight back against Biden/Kamala Bucks by adopting a variety of alternative currencies including cash (while it lasts), gold coins, silver coins and commodity barter.

That’s one reason the government is trying to eliminate cash and kill crypto. It may come down to gold and silver. I urge you to get yours while you still can.

The bottom line is the federal government is coming after our money and rights. Again, that’s not hyperbole or some conspiracy theory. We can already see it happening.

It’s up to us to preserve our freedoms as Americans and fight back. No one will save us but ourselves.

3.CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHE

Alasdair Macleod: The threat to commodity derivatives

Submitted by admin on Thu, 2024-09-19 14:30 Section: Daily Dispatches

2:30p ET Thursday, September 19, 2024

Dear Friend of GATA and Gold:

GoldMoney research director Alasdair Macleod today published in his proprietary letter on Substack an essay that brilliantly summarizes the longstanding Western gold price suppression policy and the dishonest philosophy behind it, with an emphasis on the use of financial derivatives against gold and all commodity prices, which another British economist, Peter Warburton, intuited back in 2001:

Once again Macleod kindly has given GATA permission to share his analysis with you below. It may make you want to consider subscribing to his letter, which comes out every few days. A seven-day free trial subscription is available. Rates are $10 per month or $120 per year.

For years, bulls of gold and silver have complained about how derivatives have been used to suppress their prices. Their dreams of the practice ending could be coming true.

If you think about it, there is a simple reason that derivatives for speculating or hedging gold is fatally flawed. It is because in nearly every nations’ common law, gold is money, and currencies are inferior credit which is where payment risk actually lies. That the western financial establishment is ignorant of this fact does not change the law.

There is good reason why this matters. Gold has lasted as legal money, and credit has been separately acknowledged to be deferred payment in money since Rome’s Twelve Tables defined them and their relationship in 449 BC. Since then, there have been many instances of governments denying these facts and promoting their currencies in the place of gold, which have always ended in their collapse.

In any price relationship involving a medium of exchange, there is an objective value and a subjective one. The objective value is always in the medium of exchange and the subjective value is in the goods or services being exchanged. Put another way, the buyer and seller will both value money or its substitute the same, but the buyer values the goods or services more highly than the seller: otherwise, the exchange won’t take place. But if gold is the money, where does that leave a fiat currency?

Clearly, if the currency is not a credible gold substitute, then it should bear the subjective value relative to gold. That it is not regarded this way is partly due to government anti-gold propaganda, but mainly due to accounting in the government’s currency for tax purposes. Furthermore, while a gold standard is always defined as a currency being exchangeable for a given weight of gold, for convenience it is referred to as so many currency units per gramme or ounce. This gives the erroneous impression that gold is being priced in the subordinate currency.

This is as may be, but in the knowledge that a fiat currency always fails while gold as money never does, the recognition of this reality will eventually kill off any derivatives in gold, and if the market in derivatives evolves without collapsing entirely, it should then refer to fiat currencies in terms of gold-grammes, or better still in a credible gold substitute instead if one exists.

That gold derivatives should not exist in the first place should be borne in mind in the context of this article.

The plan was to kill off gold as money

Following the inflationary seventies which almost destroyed the post-1971 dollar-based fiat currency system, there can be little doubt that the deep thinkers in the US Treasury thought long and hard as to how to drive inflation out of the economy while promoting the dollar to kill off gold as money. The answer they chose came in three distinct policies.

The first and most obvious was to reform the financial system so that the banks would wrest control of financial securities from the brokerage industry: this resulted in London’s big-bang, implemented by the Thatcher government in the mid-eighties at the US Treasury’s behest. A capital-starved securities industry would become turbocharged by bank finance, ensuring a perpetual bull market in financial asset values, including government debt, and ensuring everlasting demand for dollars.

The second was to reform statistical calculation for key economic indicators, such as consumer price inflation and jobless figures giving a measure of government control over them to create the illusion of currency stability. Not only was the indexation cost of pensions and welfare contained, but interest rates were thereby permitted to be lower than they would otherwise be. In fact, all economic statistics are produced by government agencies who control this information.

The third was to sanction and encourage derivative markets to expand and by doing so divert speculative demand from physical markets for gold. This was to prevent gold prices from being driven prices higher, threatening the status of the dollar as a medium of exchange. It was the basis of the massive expansion of gold trading on the LBMA, and the expansion of gold futures under the control of the large US banks which would occasionally act as conduits for the Exchange Stabilisation Fund.

In London, 44 million ounces were cleared daily in 1998 on the London Bullion Market, valued at approximately $13 billion at that time. Last May, it had dropped to a low of 16 million ounces, but at higher prices it was valued at $37 billion. It should be noted that outstanding forward commitments measured by their average duration in days are unrecorded multiples of daily settlement.

The falling settlement numbers in London forward ounces from 44 million to 16 million while the value of the settlement rose 2.8 times illustrates the problem paper markets now face. On Comex which has the same problem, this is demonstrated by the gross and net short position of the Swaps category, which is comprised mainly of bullion bank traders:

Between 2010—2018, the average gross short position was $15bn, compared with $75bn today. And the net position averaged $7bn, compared with $61bn currently.

This particularly matters because physical gold is now being drained out of London and New York directly or indirectly by a combination of central bank and wider Asian demand. While London faces a liquidity crisis of available gold bullion, Comex has a position which is proving impossible to contain, let alone drift into ever higher liabilities for bullion bank traders.

Hope that demand for physical gold will diminish allowing the bullion establishment to initiate a raid on bullish speculators is proving to be whistling into the wind, a wind blowing with increasing strength driven by a mixture of geopolitics and increasing credit risk facing the fiat dollar. In short, gold derivative markets are drifting onto the rocks of a crisis.

This matters, because gold is central to everything, more so than the illusory dollar. The reason is that gold as money in possession has no counterparty risk, while the fiat dollar with increasing counterparty risk is of uncertain future value. The central banks accumulating bullion, as well as other Asian entities and individuals, are being motivated to rid themselves of this dollar uncertainty, choosing not to encash them for other currencies which are ultimately tied to the dollar’s credibility.

The relationship between dollars and gold certainly has been a conundrum for many since the suspension of the Bretton Woods Agreement in 1971. The western financial establishment has lost all compass as to which is money and which is credit, with most actors not even aware of gold’s central importance. To illustrate this importance the chart below shows average values for a range of industrial metals priced in dollars and gold, followed by a chart of oil similarly priced.

Priced in dollars, commodity and energy prices have risen multiple times and with great volatility, while they have been remarkably steady priced in gold. The point being made is that the approaching problems in paper gold contracts will almost certainly be transmitted into higher dollar prices for commodities generally as paper hedging in the form of derivatives diminishes. And the catalyst for an implosion of commodity and energy derivatives is gold.

Just as derivatives have suppressed gold and other commodity values from the 1980s onwards, their ending is set to unleash an explosion of physical replacement demand. The contraction of outstanding commodity derivatives will not be without accidents. Banks will face enormous write-offs, and doubtless some rescues will have to be arranged by the authorities. And there’s no guarantee that other derivative markets, such as interest rate swaps and forex markets will go unscathed because of the commonality of derivative counterparties.

The rise in values for gold and commodities generally is the same thing as a decline in the value of the dollar for the purpose of dealing in commodities. Foreign holders of dollars will be acutely aware of the consequences, dumping dollars increasingly to hoard commodities.

Looking at oil and base metal values, they are already relatively cheap priced in gold. Or put the other way, being moderately expensive gold appears to have begun to discount a wider currency crisis while these commodities have not yet. Their relative cheapness is probably attributable in part to the onset of recession in western economies being discounted in derivative markets, which as yet are unaffected by a bear squeeze on the establishment already evident in gold derivatives.

Forced by global markets, as opposed to those under the control of the US authorities, the wisdom of ancient Roman lawmakers in framing the origin of all their successor nations’ common law is being reaffirmed. The error being corrected today is the accumulation of fiat currency distortions of the last fifty-three years, which looks like it is coming to a financially violent end.

4. OTHER GOLD COMMENTARIES/:live from the vault:

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:COFFEE

.

6 CRYPTOCURRENCY NEWS

END

ASIA TRADING/THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED UP 18,74 PTS OR .89 %

//Hang Seng CLOSED UP 353.14 PTS OR 2,00 %

// Nikkei CLOSED UP 775.16 PTS OR 2.00%//Australia’s all ordinaries CLOSED UP 0.63%///Chinese yuan (ONSHORE) CLOSED UP TO 7,0659 CHINESE YUAN OFFSHORE CLOSED UP TO 7.0709 Oil UP TO 71.48 dollars per barrel for WTI and BRENT UP AT 74.28Stocks in Europe OPENED ALL GREEN

ONSHORE YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP TO 7.0659

OFFSHORE YUAN: UP TO 7.0709

SHANGHAI CLOSED CLOSED UP 18.74 PTS OR .89%

HANG SENG CLOSED CLOSED 353.14 PTS OR 2.00%

2. Nikkei closed 775.16 POINTS OR 2.13%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 100.71 EURO RISES TO 1.1158 UP 44 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +0.853 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 142.89…… JAPANESE YEN NOW RISING AS WE HAVE NOW REACHED THE COLLAPSING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.1875 Italian 10 Yr bond yield UP to 3.553SPAIN 10 YR BOND YIELD UP TO 2,988

3i Greek 10 year bond yield UP TO 3.169

3j Gold at $2589.60 /Silver at: 31.20 1 am est) SILVER NEXT RESISTANCE LEVEL AT $34.40//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 75//100 roubles/dollar; ROUBLE AT 92.86

3m oil into the 71 dollar handle for WTI and 74 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 142.89 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.853% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8472 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9453 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 3.713 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.036 UP 3 BASIS PTS/

USA 2 YR BOND YIELD: 3.577 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 34.02…

10 YR UK BOND YIELD: 3.905 UP 5 PTS

10 YR CANADA BOND YIELD: 2.962 UP 3 BASIS PTS

5 YR CANADA BOND YIELD: 2.749 DOWN 1 PTS.

2a New York OPENING REPORT

Futures Rip To New All Time Highs After Fed Rate Cut, As Yields, Commodities Jump

Thursday, Sep 19, 2024 – 08:44 AM

The Fed’s first (jumbo) rate cut since the depths of the covid crash resulted in mixed reaction in markets, with initial gains for stocks fizzling and ultimately tepid moves in Treasuries, corporate bonds and commodities. However, this reversal to the kneejerk reaction has also since reversed, and US stock futures are bouncing this morning, rising to new record highs, amid gains across Europe and in Asia, while gold is heading back toward a record high and copper prices hit the strongest level in two months to lead a broad rally in base metals in what appears to be a gradual awakening of the reflation trade. As of 8:00am, S&P futures are up 1.7%, and Nasdaq futures surged more than 2.1% as part of a global risk-on trade. Similar to past rate cuts in slowing macro environments, the Nasdaq and Russell are outperforming. Pre-mkt, Mag7 names are all higher by at least 1.6%, Semis are stronger too with NVDA +3.3%. Europe’s Stoxx 600 index advanced as much as 1.4%, while Asian stocks were a sea of green, as a basket of Asian currencies notched up a 14-month high even as the Japanese yen plunged with traders once again eyeing yield differentials. The yield curve is bull steepening though 30Y is unchanged and USD is flat. Commodities are higher led by the Energy complex with precious metals outperforming base (Gold +1.3%, Silver +4.0%). The macro data today (Jobless Claims, Home Starts) will be ignored given the dovish press conference from Powell; expect multiple indices and sectors to make ATHs today.

In premarket trading, cryptocurrency-linked companies rally as Bitcoin climbs with US equity futures; Coinbase, Riot Platforms, Marathon Digital and CleanSpark all rose. Here are some other notable premarket movers:

DoorDash (DASH) gains 3.9% after BTIG upgraded the food-delivery company to buy from neutral, saying its checks signal continued strength, while touting “under-appreciated” longer term drivers.

Mobileye (MBLY) shares rise 7.6% after Intel said it does not currently have any plans to divest a majority interest in the company.

Steelcase (SCS) shares fall 6.9% after the maker of office furniture gave a third-quarter revenue forecast that fell short of the average analyst estimate.

In a move that Donald Trump called either political intervention or confirmation the US economy is doing much worse than indicated, the Fed cut rates by 50 basis points, a big move designed to preserve the strength of the US economy amid mounting risks to the labor market which has been flooded with illegal aliens. Jerome Powell said taking the step now would help to limit the chance of a full-blown downturn, while being careful to avoid committing to this as the new pace for rate reductions. Michelle Bowman dissented, voting for a 25-basis-point cut, the first time a Fed governor has done that since 2005.

Wednesday’s decision reinforced expectations that the US economy will escape a downturn. A survey of Bloomberg Terminal subscribers shows 75% expect the US to avoid a technical recession by the end of next year. At the same time, traders ramped up their bets on cuts to come from the Fed too, with more than 70 basis points of reductions seen for the rest of this year. That’s higher than the half-point of further easing implied by the Fed’s dot plot. A Citigroup trader called the jumbo cut, and so did JPMorgan, though the latter is less sure about what comes next. Mohamed El-Erian, meanwhile, saw the cut as dovish, while others on Wall Street suggested it indicated that the Fed regrets not cutting at its previous meeting.

“What we are seeing is the belief that the Fed has everything under control and they are going to engineer a soft landing and therefore risk assets are moving ahead strongly,” Jon Bell, a portfolio manager at Newton Investment Management, said on Bloomberg TV.

The Fed’s first reduction in more than four years was accompanied by projections indicating an additional 50 basis points of cuts across the remaining two policy meetings this year. Fed Chair Jerome Powell said launching the unwind of the central bank’s historic tightening campaign with a big move while the US economy is still strong would help limit the chances of a downturn.

“The Fed is embarking on what I see as a series of rate cuts,” said Stephen Jen, the chief executive at Eurizon SLJ Capital. The size of the initial move “won’t make a big difference as equities should soon stabilize, bond yields will likely drift lower for good reasons — like disinflation and not a hard landing. The dollar should continue to weaken against a broad range of currencies,” he said.

It wasn’t just the Fed making waves: the pound strengthened to the highest against the dollar since March 2022, surpassing $1.33, after the Bank of England kept rates on hold Thursday, and warned investors it won’t rush to ease policy. Government bonds retreated, money markets pared wagers on 2024 rate cuts and UK stocks trimmed an advance.

“We should be able to reduce rates gradually over time,” Governor Andrew Bailey said in a statement, stressing that such a path would depend on price pressures continuing to ease. “It’s vital that inflation stays low, so we need to be careful not to cut too fast or by too much.”

Norway’s krone led gains against the dollar after the central bank kept borrowing costs unchanged and signaled no intention to cut them before next year as it contends with inflation risks. The lira rose after the Turkey’s central bank held its main interest rate at 50%, as expected, with the statement broadly unchanged, i.e. no significant softening in language as some were hoping for.

European shares jumped 1.1% to their highest in over two-weeks and near record highs, with mining and automobile shares leading gains. Telecommunications and utilities stocks are the biggest laggards. Here are the biggest movers Thursday:

Ocado jumps as much as 16% after the grocer reported third-quarter retail sales that came ahead of consensus estimates. The company also raised its FY24 revenue guidance for Ocado Retail.

Davide Campari-Milano rise as much as 8.3%, reversing a portion of yesterday’s sharp losses, after a Campari group holding company, Lagfin, said it would buy more shares in the Italian beverage maker

Merck KGaA gains as much as 2.9%, the most since July, after Goldman Sachs initiated coverage of the German health-care group with a buy recommendation

Next shares jump as much as 6.9%, hitting a fresh record high, after the clothing retailer boosted its full-year pretax profit forecast. Additionally, the company’s first-half total group sales surpassed estimates

Babcock International climbs as much as 3.7% after the support services firm said organic revenue and underlying operating profits grew in the five months to the end of August

Bytes Technology shares rise as much as 7.1%, the biggest jump in 11 months, after reporting strong trading in the first half of the year. Analysts at Shore and Jefferies note that recent share underperformance suggests potential for re-rating

Air France-KLM shares rise as much as 4.3% after BNP Paribas Exane upgrades the stock to neutral from underperform. The broker notes that factors that weighed on the stock this year

REC Silicon rallies as much as 33% after the Norwegian silicon firm announced it will supply Sila Nanotechnologies with US-produced silane for use in the production of Sila’s anode material from its manufacturing facility in Moses Lake, Washington

Kone falls as much as 4.6% in Helsinki after announcing a new strategy for 2025-2030, including new mid-term financial targets, aiming to lead in employee and customer experience, sustainability and innovations

Note AB falls as much as 15%, the most since December, after the Swedish electronics contract manufacturer trimmed its outlook as consumer demand continued to lag

S4 Capital shares plunge as much as 15% to the lowest level in almost six months after the digital advertising company warned that annual like-for-like net revenue will decline more than previously anticipated

Earlier in the session, an Asia gauge of stocks rallied by the most in a week, while an index of Asian currencies rose to the strongest level in more than a year. The MSCI Asia Pacific Index gained 1.3%, with Japanese exporters including Toyota and Hitachi among top gainers. Both stocks jumped by the most in over a month as the yen plunged having priced in a much more dovish Fed. Hong Kong’s benchmark climbed 2% to the highest level in two months, helped by gains in technology firms. Property-developers in both China and Hong Kong gained, as the latter cut its base interest rate following the Fed’s eased policy.

“I am upbeat on Asian equities following the Fed’s 50 basis points rate cut,” said Rajeev De Mello, chief investment officer at GAMA Asset Management SA. Investors will increase their expectations of a soft landing scenario and that is beneficial for emerging markets and Asia, he added. Some of the less loved asset classes, like small caps, and emerging market equities “should really take solace” that the Fed tightening cycle is over and that monetary easing has started, he said.

On the monetary policy front, Bank of Japan Governor Kazuo Ueda faces the delicate task on Friday of making sure investors are firmly aware of rate hikes to come, without ruffling markets even as he stands pat on policy. The yen swung between gains and losses in volatile trading Thursday.

In FX, a gauge of the dollar weakened 0.4%, pulling it closer to its January lows as the Bloomberg Dollar Spot Index reversed an earlier gain to fall 0.5%. The Norwegian krone has climbed to the top of the G-10 FX leader board, rising 1.4% after the Norges Bank left rates unchanged and signaled they would remain there for the rest of the year. The Aussie dollar rises 1% after jobs data impressed. The pound is up 0.5% ahead of the Bank of England decision where borrowing costs are widely seen on hold.

In rates, the treasuries curve is steeper as US trading begins, after front-end outperformance during Asia session and London morning drove 2s10s spread above 11bp to widest level since June 2022. Treasury front-end yields are richer by nearly 3bp with longer-dated yields little changed, steepening 2s10s, 5s30s spreads by 3bp and 2bp on the day; 10-year is around 3.71% with bunds and gilts in the sector lagging by ~1bp; of note here is that the last time yields rose after a 50bps rate cut was… October 2008. Something to keep in mind. Front-end gilts pared early gains after Bank of England rate decision, with the 2-year rising from to 3.885% from around 3.86%.The Bank of England left rates unchanged at 5% and said it won’t rush to ease further. US session includes weekly jobless claims data and a 10-year TIPS reopening.

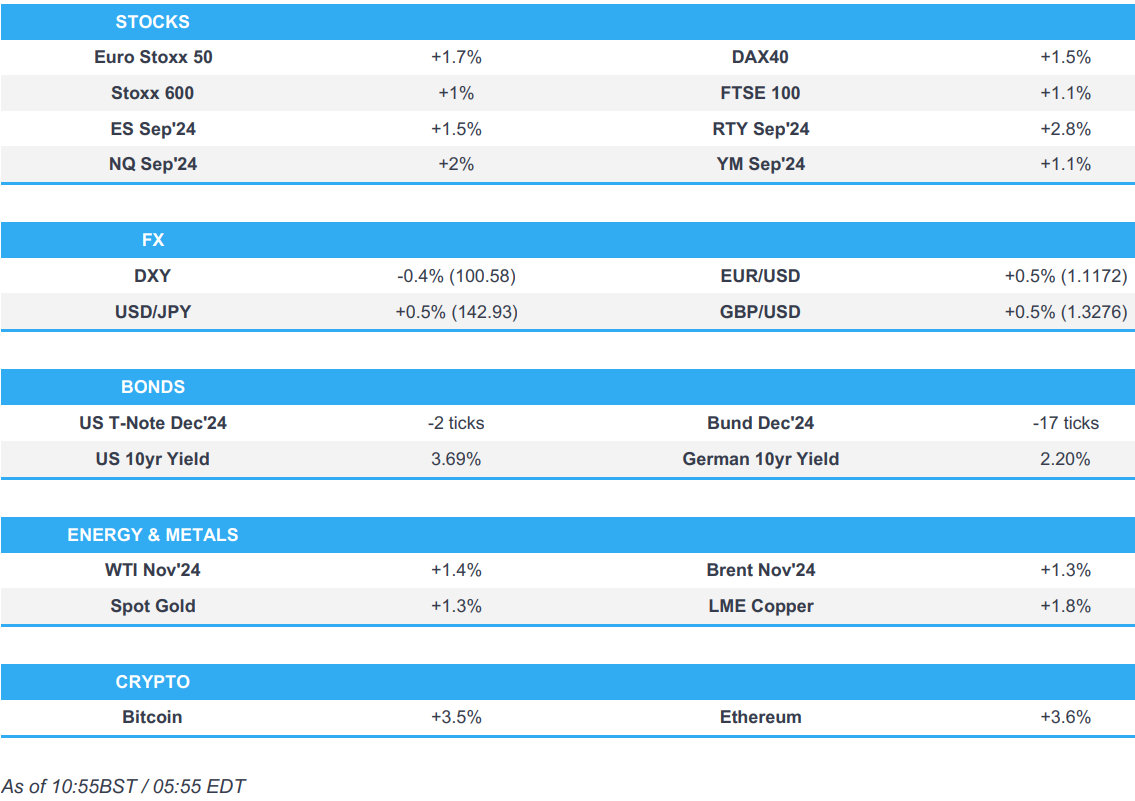

In commodities, oil advanced as the risk-on tone swept across wider markets, with traders monitoring escalating tensions in the Middle East. WTI rising 1% to $71.65 a barrel. Gold resumed its ascent back toward a record, and was last some $33 higher to around $2,592/oz; silver rallied and copper climbed to its highest level since mid-July, spurred on by the Fed’s move.

Looking at today’s calendar, the roster of Fed speakers is empty for the day and the economic agenda is thin too, with initial jobless claims top of the bill. Darden Restaurants, the owner of the Olive Garden chain, is reporting, with logistics giant FedEx set to update after the close in New York. And there’s a policy decision from the Bank of England today (where it kept rates unchanged), ahead of the Bank of Japan on Friday and after Hong Kong cut rates for the first time since 2020.

Market Snapshot

S&P 500 futures up 1.3% to 5,695.00

STOXX Europe 600 up 0.9% to 519.46

MXAP up 1.4% to 185.45

MXAPJ up 1.1% to 578.97

Nikkei up 2.1% to 37,155.33

Topix up 2.0% to 2,616.87

Hang Seng Index up 2.0% to 18,013.16

Shanghai Composite up 0.7% to 2,736.02

Sensex up 0.2% to 83,137.98

Australia S&P/ASX 200 up 0.6% to 8,191.92

Kospi up 0.2% to 2,580.80

German 10Y yield little changed at 2.20%

Euro up 0.4% to $1.1161

Brent Futures up 1.1% to $74.44/bbl

Gold spot up 0.9% to $2,583.13

US Dollar Index little changed at 100.63

Top Overnight News

US House defeated the Republican stopgap funding bill, while House Speaker Johnson said he will craft a new stopgap spending bill.

Iranian cyber actors in late June and early July sent unsolicited emails to individuals then associated with Biden’s campaign that contained excerpts taken from stolen material from Trump’s campaign, while Iranian cyber actors have continued their efforts since June to send stolen material associated with Trump’s campaign to US media organisations, according to US intelligence agencies.

China to ramp up policy steps to revive economy but no ‘bazooka’ stimulus seen. China expected to trim its Loan Prime Rate (LPR) tonight, w/the Fed’s outsized cut giving the PBOC more flexibility to ease. RTRS

Industries such as finance, consumer tech and property — key drivers of China’s growth for much of this century — are now out of favor. Instead, the most powerful Communist Party leader since Mao Zedong is funneling resources toward endeavors such as electric vehicles and chip production. “High quality” growth is the new mantra, not “high speed.” BBG

Brazil’s real looks set for a boost from carry trades after the central bank lifted its interest rate for the first time since 2022 and signaled more hikes are coming — just three months after halting an easing cycle. BBG

ECB’s Centeno says the central bank may need to accelerate the pace of easing. BBG

The BOE will probably hold its key rate at 5% today, following last month’s cut. Governor Andrew Bailey may offer more hints that it will ease again in November, though Bloomberg Economics expects officials to signal caution. BBG

Putin under growing pressure to authorize a troop mobilization as Russia’s military loses soldiers at a faster rate than it can recruit them. WSJ

Harris and Trump are tied nationally at 47%, but she’s leading by 4 points in PA according to new data published in the NYT. NYT

Microsoft is working with Anduril on combat goggles for the US Army in a project that may generate as much as $21.9 billion over a decade. BBG

Apple will face pressure from the EU to open its iOS to rivals or face sig. fines. BBG

A more detailed look at global markets courtesy of Newsquawk

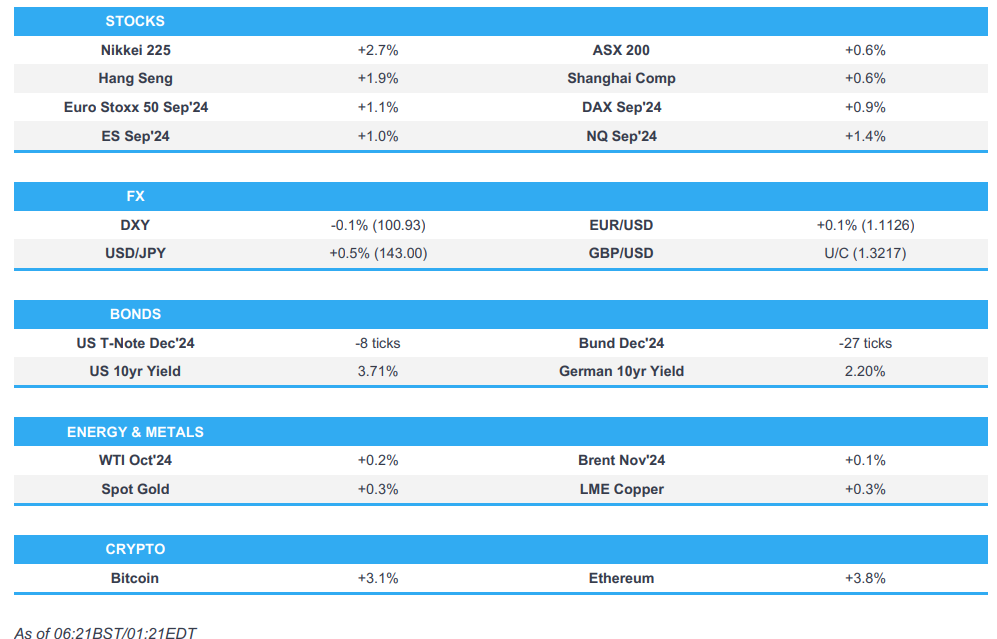

Asia-Pac stocks were in the green as the region reacted to the Fed’s oversized 50bps rate cut. ASX 200 was underpinned and printed a fresh record high albeit despite somewhat ambiguous jobs data which showed headline Employment Change topped forecast but was entirely due to Part-Time work as Full-Time jobs contracted. Nikkei 225 outperformed and surged above the 37,000 level on the back of a weaker currency. Hang Seng and Shanghai Comp conformed to the positive mood with the former led higher by strength in tech and property after the HKMA cut rates by 50bps in lockstep with the Fed, while the mainland index was also boosted following the PBoC’s continued liquidity efforts and despite the lingering EU tariff concerns.

Top Asian News

HKMA cut its base rate by 50bps to 5.25%, as expected in lockstep with the Fed, while it stated that the US interest rate cut will have a positive impact on the city’s economy and will provide some room for easing of local interest rates.

China’s Commerce Minister said regarding the EU’s electric vehicle probe that China will continue to negotiate ‘until the last minute’ and the investigation has undermined ‘confidence’ of Chinese companies in investing in Europe. It was separately reported that EU capitals will not get to vote on Chinese EV duties next week with the poll removed from the committee agenda for September 25th, according to Politico.