GOLD PRICE CLOSED UP $22.15 TO $2745.60

SILVER PRICE UP $0.93 TO $34.81

Gold ACCESS CLOSED $2747.50

Silver ACCESS CLOSED: $34.80

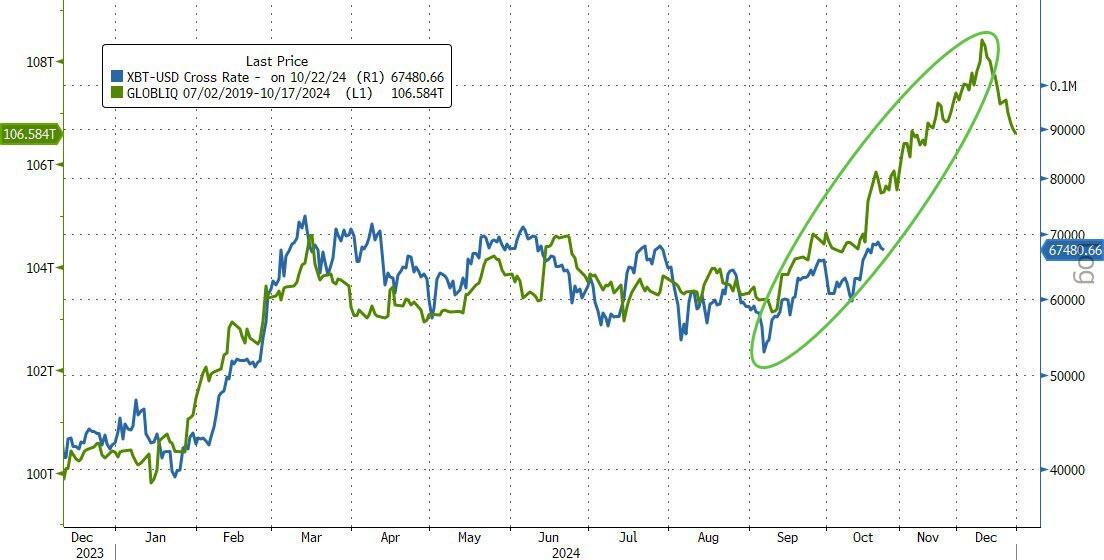

Bitcoin morning price:$67,328 down 188 DOLLARS.

Bitcoin: afternoon price: $67,537 DOWN 21 DOLLARS

Platinum price closing UP $24.96 TO $1032.10

Palladium price; UP 23.35 TO $1082.35

END

*CANADIAN GOLD: $3797.70 UP 34.50 CDN dollars per oz( * NEW ALL TIME HIGH 3,797.70 CDN DOLLARS PER OZ//OCT 22 2024)

*BRITISH GOLD: 2110.33 UP 20.62 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///2110.33 BRITISH POUNDS/OZ) OCT 22/2024

*EURO GOLD: 2,544.58 UP 10.90 Euros per oz //* (ALL TIME CLOSING HIGH: 2.544/58 EUROS PER OZ//OCT 22 //.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE

Gold ACCESS CLOSED 2036.00

Silver ACCESS CLOSED: 22.93EXCHANGE: COMEX

CONTRACT: OCTOBER 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,723.100000000 USD

INTENT DATE: 10/21/2024 DELIVERY DATE: 10/23/2024

FIRM ORG FIRM NAME ISSUED STOPPED

363 H WELLS FARGO SEC 39

661 C JP MORGAN 2

686 C STONEX FINANCIA 22

737 C ADVANTAGE 6

905 C ADM 10 1

TOTAL: 40 40

JPMorgan stopped 0/26

GOLD: NUMBER OF NOTICES FILED FOR OCT/2024. CONTRACT: 40 NOTICES FOR 4000 OZ or 0.1244 TONNES

total notices so far: 12,540 contracts for 1,254,000 Oz (39/000 tonnes)

FOR OCT

SILVER NOTICES:8 NOTICE(S) FILED FOR 40,000 OZ/

total number of notices filed so far this month : 1358 for 6.790 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $22.15 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 3.16 TONNES OF GOLD INTO THE GLD..

/ /INVENTORY RESTS AT 891.79 TONNES

INVENTORY RESTS AT 891.79 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.93 AT THE SLV

HUGE CHANGES IN SILVER INVENTORY INTO THE SLV: A DEPOSIT OF 3.329 MILLION OZ OF SILVER INTO THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 478.089 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUMONGOUS SIZED 1942 CONTRACTS TO 153,012 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS STRONG GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR HUGE GAIN OF $0.83 IN SILVER PRICING AT THE COMEX ON MONDAY’S TRADING. WE HAD A HUMONGOUS GAIN OF 2966 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH THE GAIN OF $0.83 IN PRICE. WE HAD SOME LIQUIDATION OF T.A.S. CONTRACTS ON MONDAY DESPERATELY TRYING TO CONTAIN SILVER’S PRICE RISE.. //. WE HAD ZERO SHORT COVERING BY OUR SPECS DURING THE COMEX TIME ZONE.. WE HAD A HUGE 1024 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY A HUGE 727 CONTRACT T.A.S ISSUANCE WHICH WILL BEING USED IN FUTURE TRADING. IN ESSENCE WE GAINED A HUGE 2966 CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN IN PRICE

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN ON LAST FRIDAY AND AGAIN THIS WEEK. THE ACCUMULATED T.A.S. IS BEING USED TO MANIPULATE PRICES AT THE COMEX NOW EVERY DAY..

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: A HUGE 727 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS BUT TO NO AVAIL. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.83) AND WERE UNSUCCESSFUL IN KNOCKING ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A HUMONGOUS GAIN OF 2966 TOTAL OI CONTRACTS ON OUR TWO EXCHANGES

WE HAD A HUGE 1024 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.355 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY;S 190,000 OZ QUEUE JUMP+ .195 MILLION OZ ISSUANCE OF EXCHANGE FOR RISK PRIOR//NEW TOTAL 7.150 MILLION OZ

//NEW STANDING FOR SILVER//OCT AT 7.150 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI GAIN//HUGE SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 727 CONTRACTS)/PLUS THAT STUPID ISSUANCE OF .195 MILLION OZ OF EXCHANGE FOR RISK THURSDAY, OCT 10

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL removed 200 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS OCT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT

TOTAL CONTRACTS for 15 DAYS, total 10,954 contracts: OR 54.770 MILLION OZ (730 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 54.770 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 54.770 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH)

RESULT: WE HAD A HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1942 CONTRACTS WITH OUR $0.83 GAIN IN PRICE OF SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 1024 ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR OCT OF 5.355 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 190,000 OZ TO WHICH WE ADD .195 MILLION OZ OF EXCHANGE FOR RISK ISSUANCE/PRIOR

//NEW TOTAL STANDING FOR OCT AT 7.150 MILLION OZ

WE HAVE A HUMONGOUS GAIN OF 2966 OI CONTRACTS ON THE TWO EXCHANGES WITH OUR GAIN IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 727 CONTRACTS ( WILL BE USED FOR TUESDAY’S TRADING),//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION, TRYING TO CONTAIN SILVER’S PRICE RISE.

/ ZERO SHORT COVERING FROM OUR SPEC SHORTS DESPITE THE GAIN IN PRICE MONDAY/ . ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE FRIDAY NIGHT (727) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND LATELY ON A DAILY BASIS INCLUDING TODAY.

WE HAD 8 NOTICE(S) FILED TODAY FOR 40,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A VERY SMALL SIZED 730 OI CONTRACTS TO 567,444 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE 8819 CONTRACTS//

WE HAD A VERY SMALL SIZED INCREASE IN COMEX OI (730 CONTRACTS) OCCURRED WITH OUR GAIN OF $9.30 IN PRICE MONDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR OCT AT 33.655 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 4000 OZ QUEUE JUMP

NEW STANDING ADVANCES TO 39.154 TONNES+ + 20.917 TONNES EXCHANGE FOR RISK/PRIOR// = 60.071 TONNES

/ ALL OF THIS HAPPENED WITH OUR $9.30 GAIN IN PRICE WITH RESPECT TO MONDAY’S COMEX TRADING///. WE HAD A GOOD SIZED GAIN OF 5633 OI CONTRACTS (17,52 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST THURSDAY MORNING AND THIS CONTINUED ON FRIDAY, AND THROUGHOUT THIS WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! YOU CAN VISUALIZE THIS WITH THE DAILY QUEUE JUMPING WE ARE WITNESSING.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 4903 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 567,444

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5633 CONTRACTS WITH 730 CONTRACTS INCREASED AT THE COMEX// AND A HUGE SIZED 4903 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 14,452 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 1347 CONTRACTS, WE HAD ZERO LIQUIDATION OF T.A.S CONTRACTS WITH OUR GAIN IN PRICE MONDAY.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A HUGE SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4903 CONTRACTS) ACCOMPANYING THE SMALL SIZED INCREASE IN COMEX OI OF 730 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 14,452 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR OCT 33.651 TONNES FOLLOWED BY TODAY’S 4000 OZ QUEUE JUMP + 20.9188 ISSUANCE OF EXCHANGE FOR RISK/PRIOR.

//NEW STANDING ADVANCES TO TO: /OCT 39.154 TONNES. + 20.917 EX, FOR RISK/PRIOR = 60.071 TONNES

/ 3) MINOR ATTEMPTED T.A.S. LIQUIDATION (TRYING TO CONTAIN GOLD’S PRICE RISE0 WITH ZERO NET LONG SPECS BEING CLIPPED,

4) VERY STRONG SIZED COMEX OPEN INTEREST INCREASE 5) HUGE ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1247 T.A.S.CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT :

TOTAL EFP CONTRACTS ISSUED: 54,376 CONTRACTS OF 5,437,600 OZ OR 169.13 TONNES IN 15 TRADING DAY(S) AND THUS AVERAGING: 3625 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 15 TRADING DAY(S) IN TONNES 169.13 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 169.13 DIVIDED BY 3550 x 100% TONNES = 4.76% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END UP WITH THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 169.13 TONNES (THIS WILL BE A WEAKER ISSUANCE THIS MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPTEMBER. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUMONGOUS SIZED 1942 CONTRACTS OI TO 153,212 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1024 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 1024 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1024 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 1942 CONTRACTS AND ADD TO THE 1024 E.FP. ISSUED

WE OBTAIN A HUMONGOUS SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 3,166 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 15.830 MILLION OZ OCCURRED WITH OUR $0.83 GAIN IN PRICE

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

TUESDAY MORNING MONDAY NIGHT

ASIA TRADING/TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED UP 17.76 PTS OR 0.54%

//Hang Seng CLOSED UP 20.49 PTS OR 0.10%

// Nikkei CLOSED DOWN 524.64 PTS OR 1.39%//Australia’s all ordinaries CLOSED UP 0.62%///Chinese yuan (ONSHORE) CLOSED DOWN TO 7.1240 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.1338// Oil UP TO 71.24 dollars per barrel for WTI and BRENT UP AT 74.83 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A VERY SMALL SIZED 730 CONTRACTS TO 567,444 WITH OUR STRONG GAIN IN PRICE OF $9.30 WITH RESPECT TO MONDAY’S TRADING. WE LOST ZERO IN NUMBER LONGS WITH THE HIGHER PRICE FOR GOLD AS YOU WILL SEE BELOW. WE HAD A HUGE NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (4903). AND THINGS MUST BE DESPERATE AS FIRSTLY ON TUESDAY, OCT 2, WE HAD THE FIRST ISSUANCE IN OVER 3 MONTHS FOR THAT STUPID EXCHANGE FOR RISK, WHEREBY THE BUYER ASSUMES THE RISK FOR DELIVERY. WHY ON EARTH WOULD A BUYER ASSUME SOMETHING LIKE THIS WHEN YOU ARE GUARANTEED DELIVERY VIA AN EXCHANGE FOR PHYSICAL VIA LONDON? UNLESS FOR HUGE MONEY! WELL, ON THURSDAY, OCT 10 WE RECEIVED NOTICE OF A SECOND ISSUANCE OF EXCHANGE FOR RISK, AT 239 NOTICES OR 23,900 OZ (.7433 TONNES). LAST NIGHT ZERO EXCHANGE FOR RISK WAS ISSUED. THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THIS MONTH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY THIS ENTIRE WEEK

THE FED IS THE MAJOR SHORT OF AROUND 157+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS IS SCHEDULED TO HAPPEN LATE OCT 22 -24 2024/. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE. THESE PAST TWO MONTHS. THEY ARE TOTALLY TRAPPED. THUS THE REASON FOR THE CONTINUAL RAIDING OF OUR PHYSICAL ANCIENT METAL OF KINGS AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY! THIS WEEK HAS BEEN A STELLAR WEEK FOR GOLD PRICE INCREASES.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD A HUGE T.A.S. LIQUIDATION THROUGHOUT LAST WEEK’S GAIN IN PRICE AND AGAIN WITH THIS WEEKS TRADING, WITH ZERO LONGS BEING CLIPPED (AS YOU WILL SEE BELOW). THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF THE SPREADERS // T.A.S DURING LAST WEEK AND THIS WEEK IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE ACTIVE DELIVERY MONTH OF OCT.… THE CME REPORTS THAT THE BANKERS ISSUED A HUGE SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A HUGE SIZED 4903 EFP CONTRACTS WERE ISSUED: : /DEC 3459 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4903 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A GOOD SIZED TOTAL OF 5633 CONTRACTS IN THAT 4903 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A VERY SMALL GAIN OF 730 COMEX CONTRACTS..AND THIS HUGE GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR STRONG ADVANCE IN PRICE OF $9.30 FRIDAY// COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AS MENTIONED ABOVE.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR FRIDAY NIGHT, A FAIR SIZED 1347 CONTRACTS, WAS USED TO REPLENISH SUPPLIES.. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE (AND SPREADERS LATE IN THE MONTH). THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN LAST WEEK’S AND THIS WEEK’S TRADING.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: OCT (60.071 TONNES) WHICH IS HUGE FOR OUR OCT DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 46 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.154 TONNES + + 20.917 TONNES EXCHANGE FOR RISK PRIOR =60.071 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $9.30/)//AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A GOOD SIZED GAIN IN OUR TWO EXCHANGES. WE DID HAVE CONSIDERABLE T.A.S. SPREADER LIQUIDATION MONDAY BUT TO NO AVAIL IN STOPPING GOLD’S ADVANCE. CENTRAL BANK LONGS, SEIZING THE MOMENT, EXERCISED FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING.

WE HAVE GAINED A TOTAL OF 17L52 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR OCT (33.651TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 4000 OZ QUEUE JUMP PLUS + 20.917 TONNES OF EXCHANGE FOR RISK//PRIOR

//NEW STANDING FOR OCT 39.154 TONNES.+ + 20.917 TONNES (EXCHANGE FOR RISK

NEW STANDING FOR OCT 39.154 TONNES + 20.917 TONNES EXCHANGE FOR RISK/PRIOR= 60.071 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR STRONG GAIN IN PRICE TO THE TUNE OF $9.30

WE HAD 8819 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES 5633 CONTRACTS OR 563300 OZ (17.52 TONNES)

confirmed volume MONDAY 225,540 contracts fair

//speculators have left the gold arena

END

OCT 22 OCT GOLD CONTRACT

/ /// THE OCT 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | NIL . |

| Deposit to the Dealer Inventory in oz | NIL |

| Deposits to the Customer Inventory, in oz | |

| No of oz served (contracts) today | 40 notice(s) 4000 OZ 0.1244 TONNES |

| No of oz to be served (notices) | 48 contracts 4800 OZ 0.1493 TONNES |

| Total monthly oz gold served (contracts) so far this month | 12,540 notices 1,254,000oz 39.000 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

dealer deposits:0

total dealer deposits: nil oz

we have 0 customer deposits

total deposits nil oz

withdrawals: 0

TOTAL WITHDRAWALS: NIL oz

adjustments: 2

I) 65,105.760 oz JPMorgan: dealer to customer (2025 kilobars)

II) 482.265 OZ (LOOMIS) dealer to customer (15 kilobars)

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCT: we have an oi of 88 contracts having GAINED 14 contracts

We had 26 contracts filed on MONDAY so we GAINED 40 contracts on our two exchanges or 40 CONTRACTS underwent a 4000 oz queue jump. This is central bank action grabbing all the physical they can.

NOVEMBER LOST 95 CONTRACTS TO STAND AT 1343

DECEMBER, THE BIGGEST DELIVERY MONTH GAINED 4435 CONTRACTS TO 447,540

We had 26 contracts filed for today representing 2600 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 2 notices issued from their client or customer account. The total of all issuance by all participants equate to 40 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for OCT /2024. contract month, we take the total number of notices filed so far for the month (12,540 x 100 oz ) to which we add the difference between the open interest for the front month of OCT(88 CONTRACTS) minus the number of notices served upon today (40 x 100 oz per contract( equals 1,258,800 OZ OR 39.154 TONNES. TO WHICH WE ADD THAT STUPID 20.917 TONNES OF EXCHANGE FOR RISK PRIOR, NEW TOTAL = 60.071 TONNES

thus the INITIAL standings for gold for the OCTOBER contract month: No of notices filed so far (12,540 x 100 oz +we add the difference for front month of OCT (88 OI} minus the number of notices served upon today (40 x 100 oz which equals 1,258,800 oz (39.154 TONNES) + 20.917 EX. FOR RISK DELIVERY /PRIOR = 60.071 TONNES

TOTAL COMEX GOLD STANDING FOR OCT.: 60.1071 TONNES WHICH IS HUGE FOR THIS ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,652,970.049 oz 51.41 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 16,992,783.935 OZ

TOTAL REGISTERED GOLD 7,746,692.835/// 240.95tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,246,091.100OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,093,822 oz (REG GOLD- PLEDGED GOLD)= 189.54 tonnes //

END

SILVER/COMEX

OCT 22 2024

INITIAL

//2024// THE OCT 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 664,968.710 oz DELAWARE MANFRA . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 1,270,353.310 oz Brinks Asahi Delaware |

| No of oz served today (contracts) | 8 CONTRACT(S) (40,000 OZ) |

| No of oz to be served (notices) | 32 contracts (160,000oz) |

| Total monthly oz silver served (contracts) | 1358 Contracts (6.790 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit/

total dealer deposit : NIL oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 3 customer deposits

i) Into ASAHI: 593,877.900 oz

ii) Into Brinks 675,445.010 oz

iii) Into Delaware: 1010.460 oz

total customer deposits 1,270,353.310 oz oz

We had 2 withdrawals

i) out of Delaware 1021.200 oz

ii) Out of Manfra 6004,363.380 oz

total withdrawal 664,968.730 oz

JPMorgan has a total silver weight: 134.401million oz/307.197million or 44.11%

adjustment 1

brinks/dealer to customer: 687,768.290 oz

TOTAL REGISTERED SILVER: 68.449MILLION OZ//.TOTAL REG + ELIGIBLE. 307.17million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR OCT

silver open interest data:

FRONT MONTH OF OCT /2024 OI: 40 OPEN INTEREST FOR A GAIN OF 9 CONTRACTS

WE HAD 29 CONTRACTS SERVED ON MONDAY SO WE GAINED 38 CONTRACTS OR WE ENTERTAINED A 190,000 OZ QUEUE JUMP

NOVEMBER SAW A GAIN OF 27 CONTRACTS TO STAND AT 808

DECEMBER SAW A GAIN OF 1107 CONTRACTS UP TO 126,760 CONTRACTS

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 8 for 40,000 oz

CONFIRMED volume; ON MONDAY 111,107 huge

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 1358x 5,000 oz = 6.790 MILLION oz

to which we add the difference between the open interest for the front month of OCT (40) and the number of notices served upon today (8)x (5000 oz) to which we add 195,000 oz of exchange for risk/PRIOR equals the number of ounces standing.

Thus the standings for silver for the OCT2024 contract month: 1358 Notices served so far) x 5000 oz + OI for the front month of OCT(40) number of notices served upon today minus (40)x 5000 oz of silver standing for the OCT contract month + .195 million oz ex. for risk/PRIOR equates to 7.150 MILLION OZ.

New total standing: 7.150 million oz.

the comex must be now chaotic as we received notice of exchange for risk for both gold and silver.

There are 69.742 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS//

GLD

OCT 22 WITH GOLD UP $22.15 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.16 TONNES // // . // .///INVENTORY RESTS AT 891.79 TONNES

OCT 21 WITH GOLD UP $9.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.277 TONNES // // . // .///INVENTORY RESTS AT 888.63 TONNES

OCT 18 WITH GOLD UP $22.30 ON THE DAY; NO CHANGES IN GOLD AT THE GLD // // . // .///INVENTORY RESTS AT 884.59 TONNES

OCT 17 WITH GOLD UP $17.30 ON THE DAY; NO CHANGES IN GOLD AT THE GLD // // . // .///INVENTORY RESTS AT 884.59 TONNES

OCT 16 WITH GOLD UP $13.60 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD //A MONSTER DEPOSIT OF 4.02 TONNES OF GOLD INTO THE GLD.; // . // .///INVENTORY RESTS AT 884.59 TONNES

OCT 15 WITH GOLD UP $2.85 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD //A MONSTER DEPOSIT OF 4.31 TONNES OF GOLD INTO THE GLD.; // . // .///INVENTORY RESTS AT 880.57 TONNES

OCT 11 WITH GOLD UP $36.55 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 10 WITH GOLD UP $14.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 9 WITH GOLD DOWN $8.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 8 WITH GOLD DOWN $28,.95 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 7 WITH GOLD DOWN $1.85 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD; A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD// . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 4 WITH GOLD DOWN $11.20 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD; A DEPOSIT OF 12.57 TONNES OF GOLD INTO THE GLD// . // .///INVENTORY RESTS AT 877.41 TONNES

OCT 3 WITH GOLD DOWN $8.95 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; . // .///INVENTORY RESTS AT 874.82 TONNES

OCT 2WITH GOLD DOWN $20.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD; A DEPOSIT OF 2.88 TONNES OF GOLD INOT THE GLD. // .///INVENTORY RESTS AT 874.82 TONNES

OCT 1 WITH GOLD UP $28,55 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // .///INVENTORY RESTS AT 871.94 TONNES

SEPT 30 WITH GOLD DOWN $6.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD; A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// .///INVENTORY RESTS AT 871.94 TONNES

SEPT 27 WITH GOLD DOWN $26.60 ON THE DAY; NO CHANGES IN GOLD AT THE GLD .///INVENTORY RESTS AT 877,12 TONNES

SEPT 26 WITH GOLD UP $11.20 ON THE DAY; NO CHANGES IN GOLD AT THE GLD .///INVENTORY RESTS AT 877,12 TONNES

SEPT 25WITH GOLD UP $9.25 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD ./// /:// A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD//////INVENTORY RESTS AT 877,12 ONNES

SEPT 24WITH GOLD UP $23.60 ON THE DAY; NO CHANGES IN GOLD AT THE GLD ./// /:// //////INVENTORY RESTS AT 875.39 ONNES

SEPT 23 WITH GOLD UP $6.65 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1,43 TONNES OF GOLD INTO THE GLD../// /:// //////INVENTORY RESTS AT 875.39 ONNES

SEPT 20 WITH GOLD UP $32.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD../// /:// //////INVENTORY RESTS AT 873,96ONNES

SEPT 19 WITH GOLD UP $17,05 ON THE DAY; NO CHANGES IN GOLD AT THE GLD/// /:// //////INVENTORY RESTS AT 872.23TONNES

SEPT 18 WITH GOLD UP $5.95 ON THE DAY; NO CHANGES IN GOLD AT THE GLD/// /:// //////INVENTORY RESTS AT 872.23TONNES

SEPT 17WITH GOLD DOWN $15.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 1.52 TONNES INTO THE GLD /:// //////INVENTORY RESTS AT 872.23TONNES

SEPT 16 WITH GOLD DOWN $1.25 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:// //////INVENTORY RESTS AT 870,71 TONNES

SEPT 13 WITH GOLD UP $30.45 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD /:/A DEPOSIT OF 14.54TONNES OF GOLD VAPOUR INTO THE GLD/ //////INVENTORY RESTS AT 870,71 TONNES

SEPT 12 WITH GOLD UP $37.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD /:/A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD/ //////INVENTORY RESTS AT 866.18 TONNES

SEPT 11 WITH GOLD DOWN $0.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD /:/A DEPOSIT OF 1.70 TONNES OF GOLD INTO THE GLD/ //////INVENTORY RESTS AT 864.44 TONNES

SEPT 10 WITH GOLD UP $12.00ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 9 WITH GOLD UP $12.95 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 6 WITH GOLD DOWN $17.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 5 WITH GOLD UP $18.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

GLD INVENTORY: 891.79 TONNES, TONIGHTS TOTAL

SILVER

OCT 22 WITH SILVER $0.93 : HUGE CHANGES IN SILVER INVENTORY AT THE SLV’ A DEPOSIT OF 3.329 MILLION OZ OF SILVER INTO THE SLV..//// //INVENTORY AT SLV RESTS AT 478.089 MILLION OZ

OCT 18 WITH SILVER $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//// //INVENTORY AT SLV RESTS AT 473.483 MILLION OZ

OCT 17 WITH SILVER DOWN 18 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 3.419 MILLION OZ INTO THE SLV// //INVENTORY AT SLV RESTS AT 473.483 MILLION OZ

OCT 16 WITH SILVER UP 25 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV// //INVENTORY AT SLV RESTS AT 470.064 MILLION OZ

OCT 15 WITH SILVER DOWN 2 CENTS : SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 456,,000 OZ FORM THE SLV. //INVENTORY AT SLV RESTS AT 470.064 MILLION OZ

OCT 11 WITH SILVER UP 53 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 932,000 OZ FORM THE SLV. //INVENTORY AT SLV RESTS AT 470.520 MILLION OZ

OCT 9 WITH SILVER UP 7 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.964 MILLION OZ FORM THE SLV..: /INVENTORY AT SLV RESTS AT 471.432 MILLION OZ

OCT 8 WITH SILVER DOWN $1.41 : HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.007 MILLION OZ FORM THE SLV..: /INVENTORY AT SLV RESTS AT 468.468 MILLION OZ

OCT 7 WITH SILVER DOWN 39 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 684,000 OZ FORM THE SLV..: /INVENTORY AT SLV RESTS AT 466.461 MILLION OZ

OCT 4 WITH SILVER UP 0 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV.: /INVENTORY AT SLV RESTS AT 465.777MILLION OZ

OCT 3WITH SILVER UP 69 CENTS :HUGE CHANGES IN SILVER INVENTORY A WITHDRAWAL OF 1.643 MILLION OZ FORM THE SLV//.: /INVENTORY AT SLV RESTS AT 467.555MILLION OZ

OCT 2WITH SILVER DOWN $0.23 : NO CHANGES IN SILVER INVENTORY: /INVENTORY AT SLV RESTS AT 469.198MILLION OZ

OCT 1 WITH SILVER UP $0.30 : HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 1.368 MILLION OZ INTO THE SLV/. /: .///./// /INVENTORY AT SLV 469.198MILLION OZ

SEPT30 WITH SILVER DOWN $0.33 : HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.094 MILLION OZ INTO THE SLV/. /: .///./// /INVENTORY AT SLV 470.566MILLION OZ

SEPT27WITH SILVER DOWN $0.58 : HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.653 MILLION OZ INTO THE SLV/. /: .///./// /INVENTORY AT SLV 469.472MILLION OZ

SEPT26WITH SILVER UP $0.29 : NO CHANGES IN SILVER INVENTORY:/. /: .///./// /INVENTORY AT SLV 464.819 MILLION OZ

SEPT25WITH SILVER DOWN $0.26 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 2.281MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 464,819 MILLION OZ

SEPT24 WITH SILVER UP $1.26 : HUGE CHANGES IN SILVER INVENTORY:. A DEPOSIT OF 9,305 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 467,100 MILLION OZ

SEPT23 WITH SILVER DOWN $0.39 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 1.824MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 457.795MILLION OZ

SEPT20 WITH SILVER UP $0.08 : NO CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 1.46 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 459,619 MILLION OZ

SEPT19 WITH SILVER UP $0.85 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 1.46 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 459,619 MILLION OZ

SEPT18 WITH SILVER DOWN $0.29 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 1,551 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 461.079 MILLION OZ

SEPT17 WITH SILVER DOWN $0.13 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWALOF 5.976 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 462MILLION OZ

SEPT16//WITH SILVER UP $0.10 : HUGE CHANGES IN SILVER INVENTORY:. ADEPOSIT OF 958,000 OZ INTO THE SLV/. /: .///./// /INVENTORY AT SLV 468.606MILLION OZ

SEPT13//WITH SILVER UP $1.13/ NO CHANGES IN SILVER INVENTORY:./. /: .///./// /INVENTORY AT SLV 467.648MILLION OZ

SEPT 11//WITH SILVER UP $0.33/SMALL CHANGES IN SILVER INVENTORY: A HUGE DEPOSIT OF 2.099 MILLION OZ INTO THE SLV/ OZ OF SILVER FROM THE SLV./. /: .///./// /INVENTORY AT 467.648MILLION OZ

SEPT 10//WITH SILVER DOWN $.06/SMALL CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 639,000 OZ OF SILVER FROM THE SLV./. /: .///./// /INVENTORY AT 465.549MILLION OZ

SEPT 9//WITH SILVER UP $0.45//SMALL CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 46,000 OZ OF SILVER FROM THE SLV./. /: .///./// /INVENTORY AT 466.188 MILLION OZ

SEPT 6//WITH SILVER DOWN $.84//NO CHANGES IN SILVER INVENTORY /: .///./// /INVENTORY AT 466.234 MILLION OZ

SEPT 5//WITH SILVER UP $.55//SMALL CHANGES IN SILVER INVENTORY A WITHDRAWAL OF 0.193 MILLION OZ OF SILVER INTO THE SLV/: .///./// /INVENTORY AT 466.234 MILLION OZ

CLOSING INVENTORY 478.089 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY//BILL HOLTER:

3.CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES

Clint Siegner: Regulators won’t stop big bank malfeasance

Submitted by admin on Mon, 2024-10-21 18:11 Section: Daily Dispatches

By Clint Siegner

Money Metals Exchange, Eagle, Idaho

Monday, October 21, 2024

TD Bank just made headlines for pleading guilty to the crime of money laundering and a variety of other charges.

Bankers there provided services to despicable people who needed a way to recycle the cash proceeds acquired by selling everything from drugs to children.

TD Bank, which will pay a total of $3.09 billion in fines, is yet another giant bank with a long rap sheet.

… For the remainder of the commentary:

END

James Turk says $50+ silver is days or weeks away, not months

Submitted by admin on Mon, 2024-10-21 18:02 Section: Daily Dispatches

From King World News

Sunday, October 20, 2024

Today GoldMoney founder James Turk warned King World News that $50 silver is days or weeks away, not months.

“You know what I find noteworthy about all these record highs in gold, Eric? It’s the lack of excitement normally seen at bull market tops

“Few people are paying attention. That usually means a bull market has much further to run, from which we can presume that gold at $2700 is still early in this uptrend.

“So today looks to me like the early stage of other great bull markets in gold I’ve lived through since 1971. It’s like $45 in 1971 on its way to $200 two years later, or $100 in 1976 then climbing to its 1980 high of $850, or $340 in 2002 on its way to $1900 in 2011 after the Great Financial Crisis.

“The current uptrend began in November 2023 when gold finally hurdled $2,000 into new record highs. Since then it has been stair-stepping its way higher to new records, as we can see in this chart. …

… For the remainder of the report:

Jan Nieuwenhuijs: A major shift as Western investors start buying gold

Submitted by admin on Tue, 2024-10-22 09:40 Section: Daily Dispatches

By Jan Nieuwenhuijs

Money Metals Exchange, Eagle, Idaho

Tuesday, October 22, 2024

In the past two years the East has been responsible for a momentous move upward in the gold price, decoupling it from the West’s pricing model. But Western investors have taken back the baton and have been driving gold higher since June 2024.

Tellingly, Western investors are abandoning their old pricing model too. Instead of participating in the gold market for speculative reasons, they are now buying gold as a safe haven. This is highly bullish because Wall Street has little exposure to gold.

Meanwhile, on a net basis, the East is not selling. In this tight market, the gold price is sharply rising: year-to-date, it’s up more than 30%. …

… For the remainder of the analysis:

* * *

4. OTHER GOLD COMMENTARIES//LIVE FROM THE VAULT/no 195 ANDREW MAGUIRE

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:ORANG JUICE

.

6 CRYPTOCURRENCY NEWS

END

ASIA TRADING TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED UP 17.76 PTS OR 0.54%

//Hang Seng CLOSED UP 20.49 PTS OR 0.10%

// Nikkei CLOSED DOWN 524.64 PTS OR 1.39%//Australia’s all ordinaries CLOSED UP 0.62%///Chinese yuan (ONSHORE) CLOSED DOWN TO 7.1240 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.1338// Oil UP TO 71.24 dollars per barrel for WTI and BRENT UP AT 74.83 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.1240

OFFSHORE YUAN: DOWN TO 7.1338

SHANGHAI CLOSED CLOSED UP 17.76 PTS OR 0.54%

HANG SENG CLOSED CLOSED UP 20.49 PTS OR 0.10%

2. Nikkei closed DOWN 524.64 POINTS OR 1.39%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 103.80 EURO RISES TO 1.0816 UP 6 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +0.965 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 160.86…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and DOWN FOR UP this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.3179 Italian 10 Yr bond yield UP to 3.539 //SPAIN 10 YR BOND YIELD UP TO 3.021

3i Greek 10 year bond yield UP TO 3.173

3j Gold at $2736.10 /Silver at: 34.43 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 25/100 roubles/dollar; ROUBLE AT 96.55

3m oil into the 71 dollar handle for WTI and 74 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 150.86 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.965% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8657 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9365 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.203 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.491 UP 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.052 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 34.25…

10 YR UK BOND YIELD: 4.203 UP 5 PTS

10 YR CANADA BOND YIELD: 3.278 UP 4 BASIS PTS

5 YR CANADA BOND YIELD: 3.053 UP 3 PTS.

2a New York OPENING REPORT

Futures Slide As Global Yields Surge

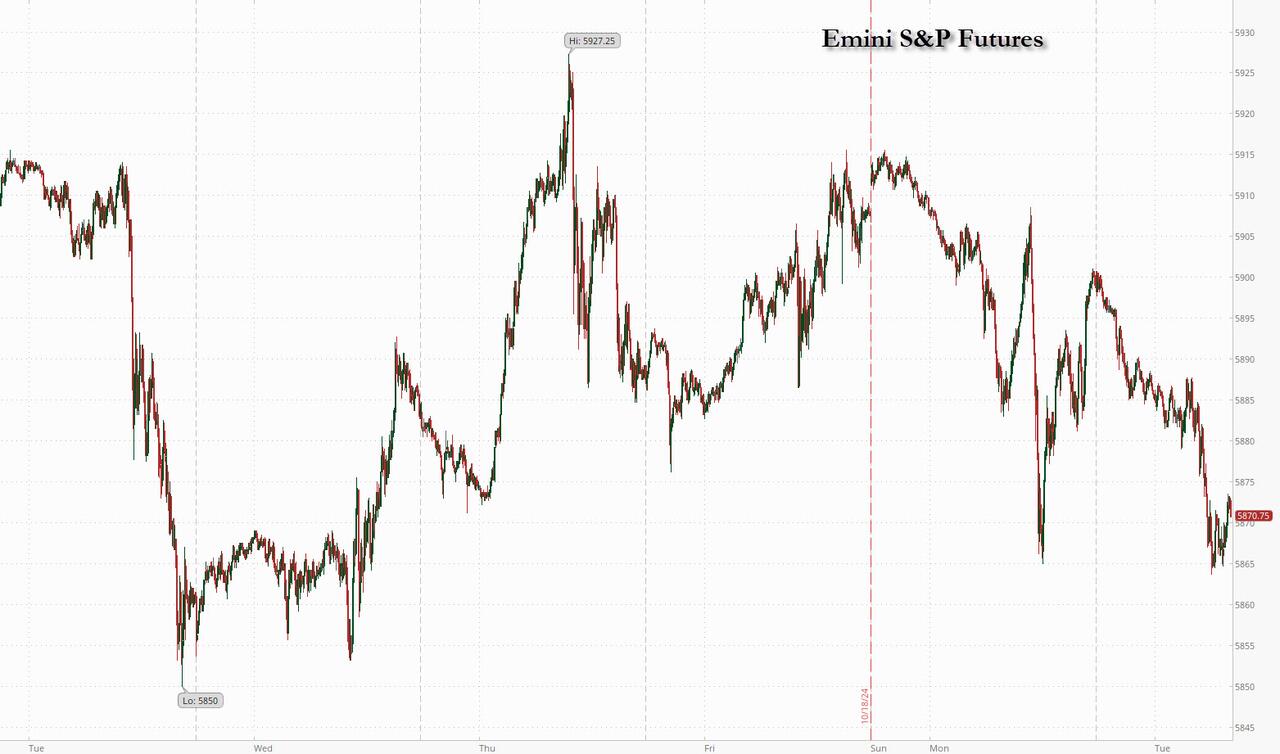

Tuesday, Oct 22, 2024 – 08:17 AM

US futures are lower, extending yesterday’s losses, as treasuries extended their recent rout sending 10Y yields surging briefly above 4.22% before retracing some of the move as traders priced in the growing probability of a red sweep. The Treasury rout has gone global, pushing interest rates across the world higher. As of 8am ET, S&P 500 futures dropped 0.3%, pointing to the first back-to-back decline in about 30 sessions for the gauge. Nasdaq 100 futures underperformed, dropping 0.4%, as tech stocks start to groan against the weight of surging rates; megacap tech all showed declines: TSLA -0.8%, GOOG -0.5%, AMZN -0.5%. The yield on 10-year Treasuries added one basis point to 4.21% after an 11 basis-point surge at the start of the week; the USD is flattish after reversing a modest earlier loss. Commodities are mixed: Oil added 0.5%, base metals are lower, and precious metals are higher: silver rises +1% to $34.5, a new 12 year high. The only macro today are the October Philly Fed and Richmond Fed reports.

In premarket trading, Philip Morris rises 2% after lifting its profit outlook amid strong sales of tobacco alternatives such as Zyn and IQOS. 3M climbed 4% after increasing the low end of its 2024 profit forecast and reporting 3Q earnings that topped analyst estimates as a push to boost productivity gained traction. Polaris tumbled 7% after the automaker lowered its full-year earnings per share and sales guidance. Here are some of the biggest US movers today:

- Cheesecake Factory (CAKE) gains 3% following a report that activist investor JCP Investment Management has built a stake in the restaurant chain.

- Danaher (DHR) rises 2% after the life-sciences firm reported 3Q profit and sales that topped the average analyst estimate.

- General Electric (GE) drops 4% as sales fell short of Wall Street’s expectations last quarter, tempering enthusiasm for its improved profit outlook as the jet engine maker grapples with supply-chain limitations that are weighing on deliveries.

- General Motors (GM) ticks 1% higher after signaling solid US demand for its highest-margin vehicles even as the broader market softens, posting better-than-expected results for the latest quarter.

- IRhythm (IRTC) jump 20% after the company said it received FDA 510(k) clearance for design updates to its Zio AT device.

- Medpace (MEDP) drops 12% after the health care services company cut its revenue forecast for the full year.

- Zions (ZION) rises 2% as 3Q earnings per share beat estimates.

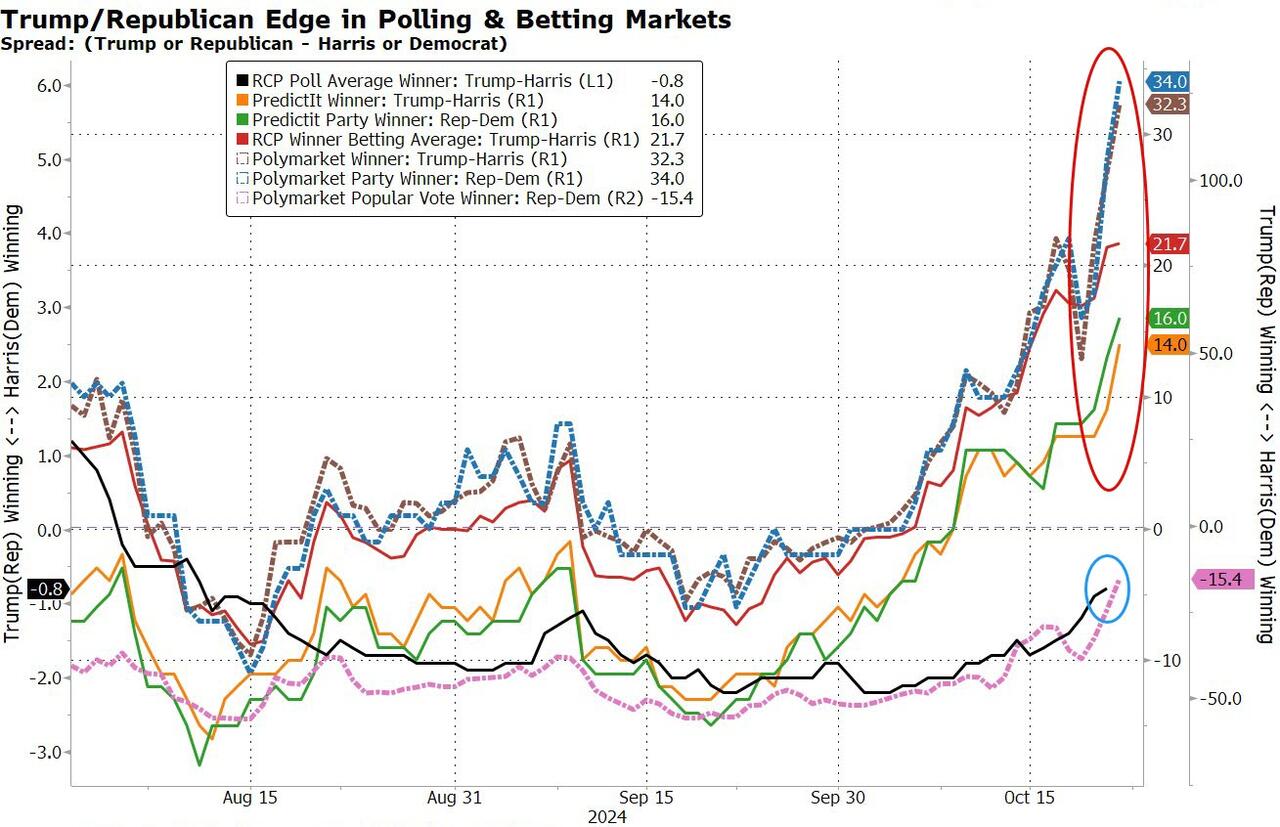

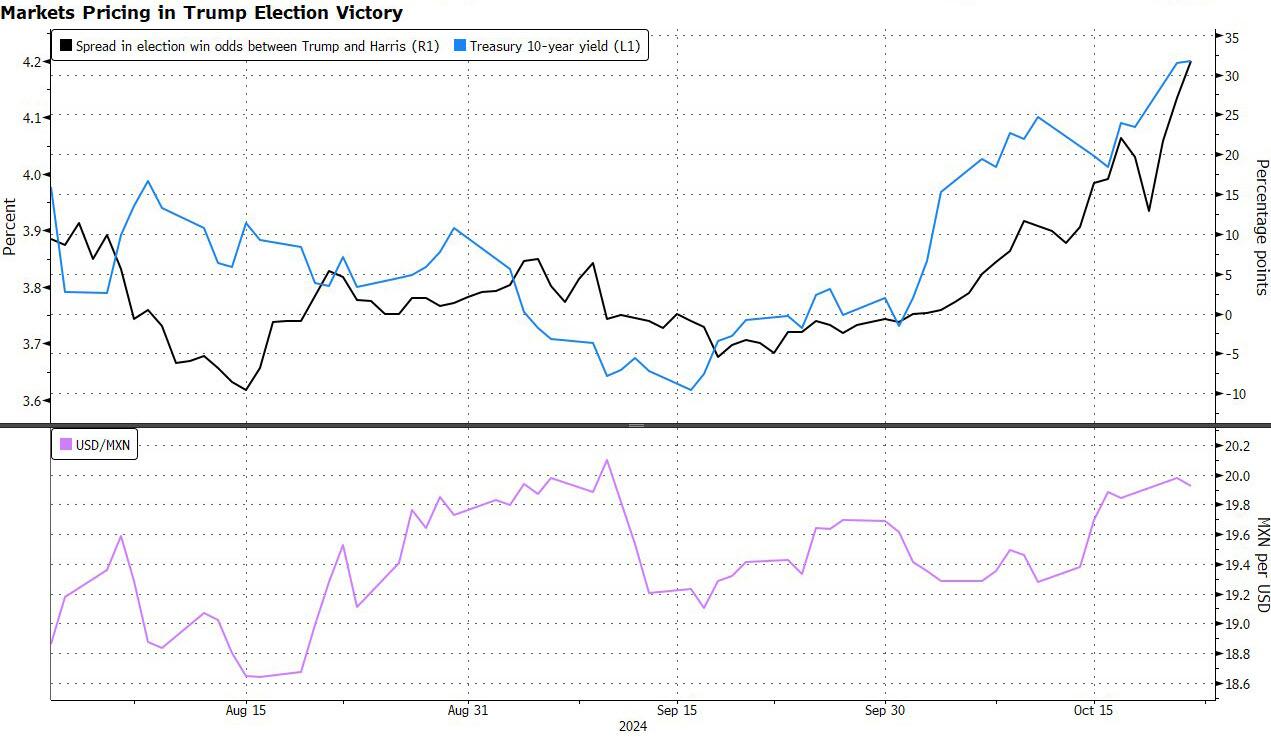

Investors further pared paring back their expectations for Fed rate cuts after central bank officials indicated a preference for reducing rates at a slower pace after recent resilient economic data. The inflationary impact of a possible Donald Trump presidential win is also weighing, given his promised tax cuts and trade tariffs could ultimately entail higher rates.

“This is very clearly linked to trading a victory of the Republicans — and therefore to an agenda which would be much more inflationist than that of the Democrats. We’re in a market that is betting on Trump,” said Christopher Dembik, senior investment adviser at Pictet Asset Management. “The rise in yields is starting to threaten equity markets.” (see more here “Wall Street Going “All-In On Trump“.”)

Elsewhere, exposure to the S&P 500 has reached levels that were followed by a 10% slump in the past, Citigroup Inc. strategists said. Still, despite the mounting risks, the current winning streak for US stocks ranks among the very best since 1928, according to data compiled by SentimenTrader. And even though US equities are expensive, going underweight is a tough call for investors in the environment where S&P 500 reached 47 record highs this year starting from January, said Vera Fehling, DWS Europe chief investment officer.

“If you said then: ‘things are looking quite stretched’ — you would have massively underperformed,” she added. “It’s difficult to explain going into the end of such a year with a significant underweight in US equities.”

European equities appear cheap by comparison and got even cheaper on Tuesday after the Stoxx 600 benchmark declined 0.8%, led by real estate and utilities sectors, which suffer when the cost of borrowing money rises. Major markets are all lower (UKX -0.6%, SX5E -0.4%, SXXP -0.7%, DAX -0.1%.) with Spain lagging. SAP is driving the tech sector to outperform after the German software giant delivered a beat on several key metrics in the third quarter and boosted some elements of its guidance for the full year. ING shares slip as Barclays downgraded the bank to equal-weight from overweight. Here are the most notable European movers:

- SAP shares gain as much as 5.9%, reaching a record high, after the software giant delivered a beat on several key metrics in 3Q and boosted some elements of its guidance for the full year.

- DNB Bank shares advance as much as 5.1% after Norway’s largest lender reported what Citi says were “impressive” quarterly results, with revenue beating estimates amid the best 3Q for fees.

- ING shares decline as much as 1.7%, the worst-performing stock on the Stoxx 600 Banks Index, as Barclays cut the recommendation on the lender to equal-weight from overweight.

- Traton shares rise as much as 5.4% after the truck maker issued preliminary third-quarter results ahead of expectations, with its International and Scania units driving the beat.

- Logitech shares gain as much as 4.2% after the Swiss maker of computer accessories boosted its operating income expectations for the full year.

- Saab shares advance as much as 5.9%, the most since June, as analysts praise the Swedish defense firm’s third-quarter order intake and cash flow.

- Boliden shares climb as much as 7.5%, after the miner reported 3Q revenue that beat the average analyst estimate, with Morgan Stanley noting mines and smelter-production volumes came in higher than expected.

- Randstad shares rise as much as 5.1% after the Dutch staffing company said that it has seen stable volumes in the first weeks of October, adding that it expects to benefit from easier 4Q comparables.

- Morgan Sindall shares rise as much as 11% after the construction and regeneration group said its annual results will be significantly ahead of expectations, driven by its Fit Out division that designs, builds and refurbishes commercial and office spaces.

- IHG shares drop as much as 2.8% after the hotel operator reported third-quarter revenue per available room that Morgan Stanley said missed consensus estimates.

- Eurofins Scientific shares drop as much as 12% after the laboratory-testing company reported third-quarter revenue that missed estimates.

- Hunting shares plunge as much as 19%, the most in over two years, after the energy services provider cut its annual earnings guidance due to challenges within its US onshore division that caused its Titan unit to disappoint, according to analysts.

So far about 47% of MSCI Europe companies reported results below expectations while only 27% delivered beats, according to data compiled by Bloomberg Intelligence. L’Oreal is set to report earnings later today, with analysts watching the impact of Chinese economic weakness on the stock.

Earlier in the session, Asian stocks fell on Tuesday, dragged by weakness in the technology and financial sectors, amid lower expectations for Federal Reserve interest-rate cuts. The MSCI Asia Pacific Index fell as much as 1.1%, with TSMC and Commonwealth Bank of Australia among the biggest drags. The decline follows comments from some US central bank officials signaling they favor a slower pace of rate reductions. Australian and Korean benchmarks were among the biggest decliners. Japanese stocks slid as uncertainty surrounding the Oct. 27 general election weighed on local markets. Stocks in India were also lower, led by automakers amid lackluster trading debut for Hyundai Motor Co.’s local unit. Stocks gained in Hong Kong after declining on Monday. China’s commitment to delivering stimulus is an ongoing focal point for traders in addition to the US presidential vote, which is about two weeks away. Focus is also turning to earnings performance this results season, which could help determine the near-term path for the MSCI Asia gauge.

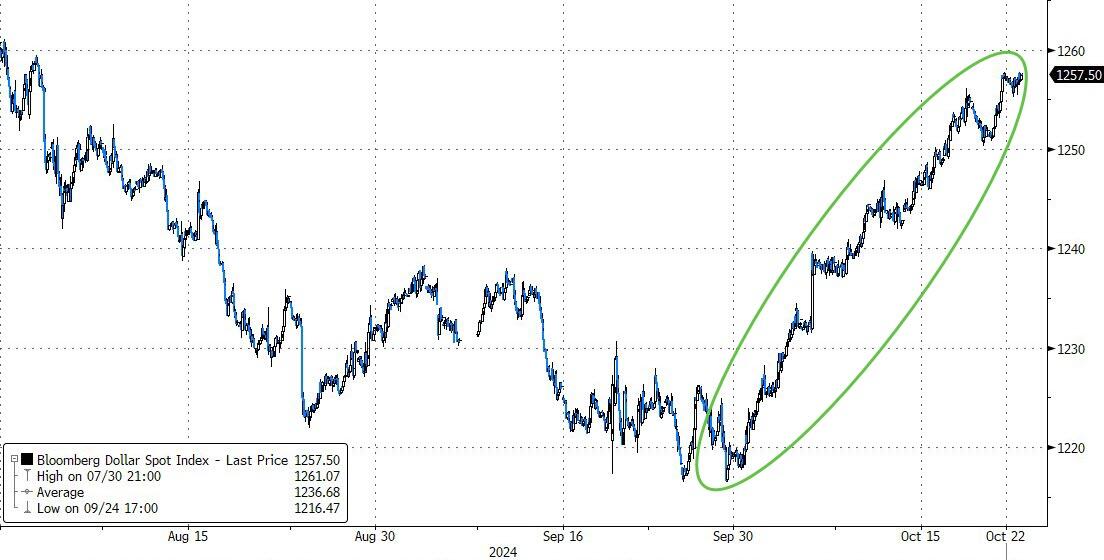

In FX, the Bloomberg Dollar Spot Index was flat after rallying 0.4% on Monday. One-month implied volatility in BBDXY stands above 9.61, fresh cycle high; risk reversals on the tenor steady around 0.5 vol The Australian and New Zealand dollars outperformed their Group-of-10 peers as higher bond yields and gains in Chinese equities boosted sentiment.

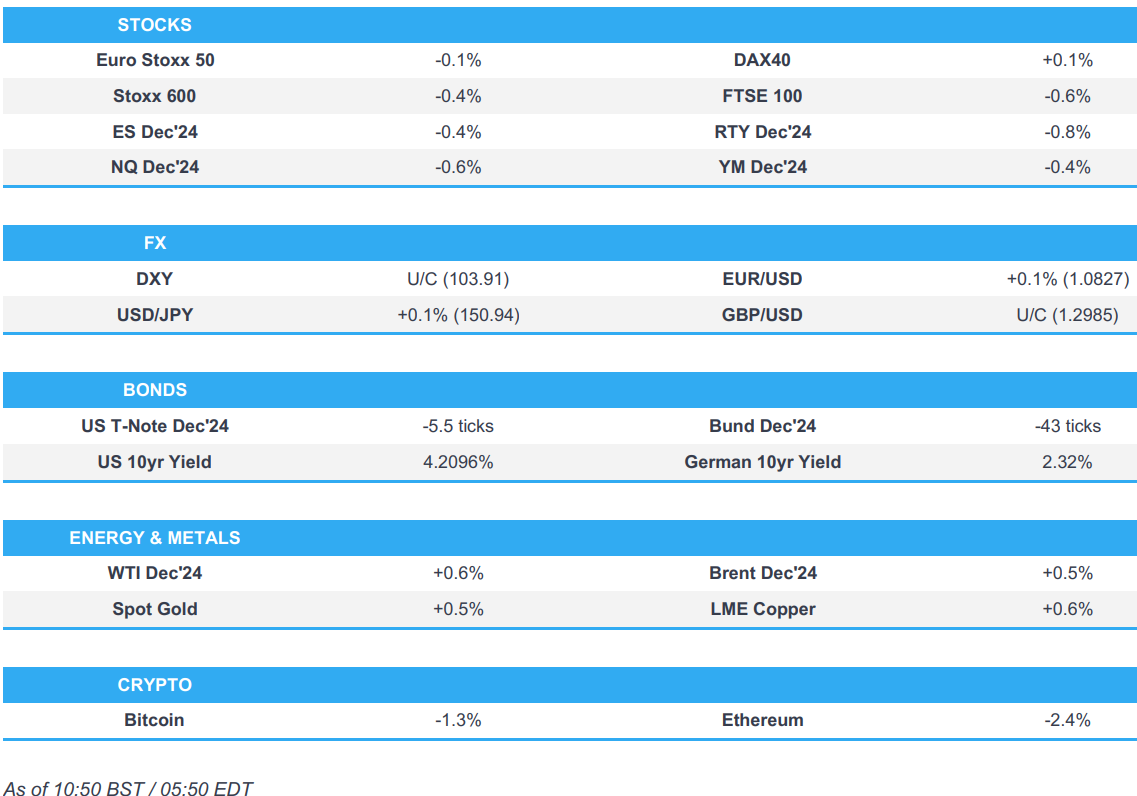

In rates, treasuries fell for a second day, adding to Monday’s steep selloff as Fed officials indicated a preference for reducing rates at a slower pace. US 10-year yields rise 2 bps, topping 4.2% for the first time since July. Oil also continues to rise, adding to upward pressure on yields from shifting Fed policy outlook and focus on next month’s US presidential election and fiscal outlook. European government bond are also lower, with UK and German 10-year borrowing costs rising 3 bps and 4 bps respectively. Italy 10-year is ~3bp cheaper vs Treasuries, underperforming amid 7- and 30-year bond syndication. Treasury auctions this week include Wednesday’s $13b 20-year bond reopening and a $24b 5-year TIPS sale Thursday.

In commodities, oil prices reversed course, with WTI now up 0.5% at $71 a barrel. Spot gold rises $13 to just below Monday’s record high. Gold rose – approaching Monday’s record high – with haven demand coming from traders focused on the conflict in the Middle East and the looming US vote. Silver jumped 1% to hit $34.50, a new 12 year high.

US economic data calendar includes October Philadelphia Fed non-manufacturing activity (8:30am) and Richmond Fed manufacturing index (10am); Fed’s Harker is scheduled to speak at 10am

Market Snapshot

S&P 500 futures down 0.3% to 5,877.00

Brent Futures down 0.5% to $73.95/bbl

Gold spot up 0.6% to $2,736.07

US Dollar Index down 0.10% to 103.90

Top Overnight News

- Share buybacks on mainland China’s biggest exchanges have soared to a record high this year as Beijing pushes for companies to return cash to shareholders as part of its efforts to revive a flagging stock market. There have been Rmb235bn ($33bn) in buybacks across mainland-listed shares so far in 2024, more than double last year’s total and far surpassing the previous record of Rmb133bn in 2022, according to Chinese financial data provider Wind. FT

- U.S. rules that will ban certain U.S. investments in artificial intelligence in China are under final review, according to a government posting, suggesting the restrictions are coming soon. RTRS

- China’s youth unemployment rate dips in Sept to 17.6%, down 120bp from 18.8% in August. CNBC

- HSBC’s cost-cutting shakeup intensified. The lender said it will combine its global commercial and institutional banking operations, and create a new International Wealth and Premier Banking business. Pam Kaur was named as CFO. BBG

- Israel is apparently considering an Egyptian proposal for a 2-week ceasefire in with Hamas in Gaza that could potentially build into a more permanent deal. NBC News

- Federal Reserve Bank of San Francisco President Mary Daly said she expected the US central bank would continue cutting interest rates to guard against further weakening in the labor market. BBG

- The US Securities and Exchange Commission’s examiners will step up scrutiny of financial firms’ use of artificial intelligence next year, the latest sign of regulators’ growing concerns about the emerging technologies. BBG

- US drinkers are continuing to cut back on their vodka, whisky and tequila intake in a sign that, despite the improved economic environment, consumers are finding higher prices hard to swallow. FT

- GM shares jumped premarket after signaling solid US demand for its highest-margin vehicles, and raising the low end of its profit forecast. GE Aerospace reported a profit jump and raised its full-year guidance as the jet-engine maker capitalizes on its strong order book. BBG

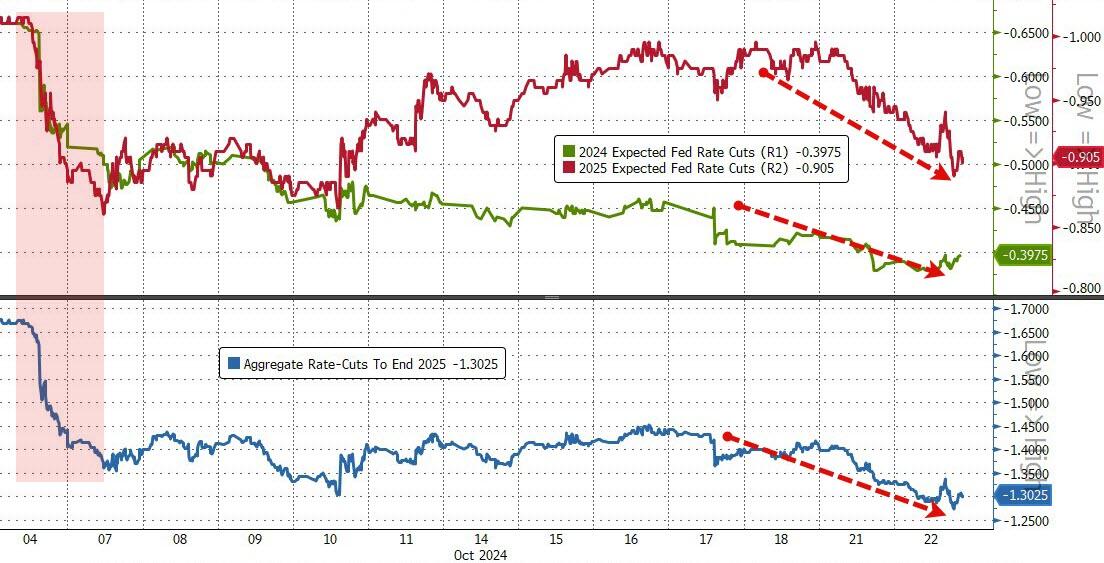

- Fed’s Daly (2024 voter) said the Fed will continue to adjust policy and a 50bps cut was to right-size policy, while she expects additional cuts going forward. Daly said the recent Fed rate cut was a close call and she came down strongly in favour of a 50bps cut, as well as noted that a 50bps cut was needed and they didn’t want to find out they had overtightened and taken jobs from people. She also said they will be data-dependent for the Fed’s November meeting and haven’t seen anything so far that would suggest they would not continue to cut rates, while she noted policy is absolutely still tight and would want to be open-minded to continue to ease policy if inflation is falling, even if the economy is strong.

- Fed’s Schmid (2025 voter) called for a cautious, gradual and deliberate approach to rate cuts, while he prefers to avoid outsized rate cuts and noted that they are seeing a normalisation of the labour market, not a deterioration. Furthermore, Schmid said current policy is restrictive, but not very restrictive, as well as noted the balance sheet is probably influencing longer-term rates and that they should be normalising the Fed’s balance sheet on both size and duration.

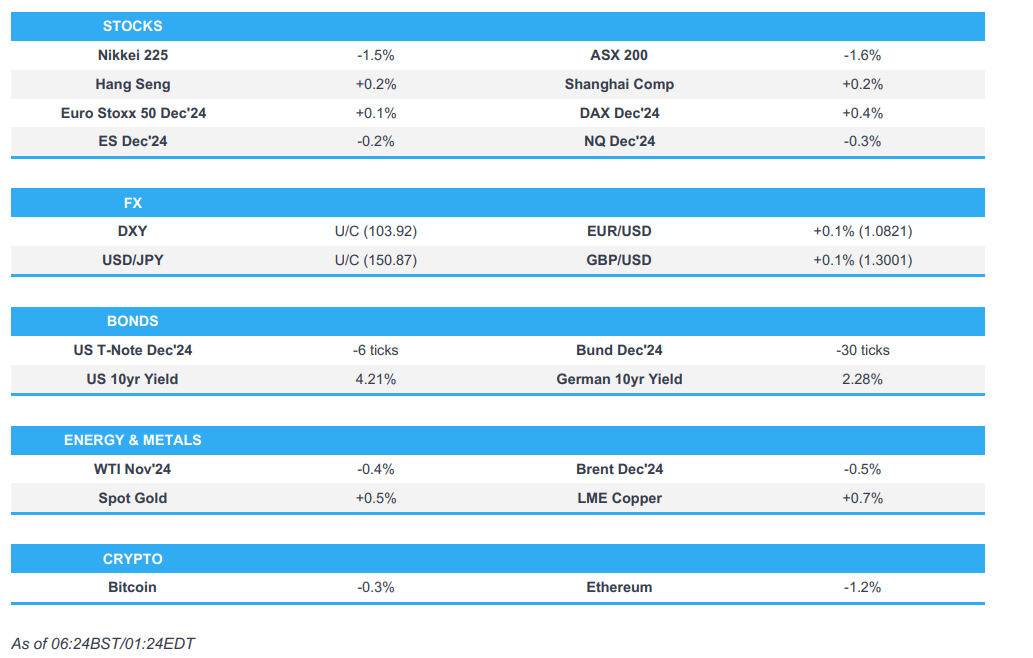

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed with participants somewhat cautious following the mostly negative bias stateside amid a lack of major catalysts, ongoing geopolitical tensions in the Middle East and a higher yield environment. ASX 200 retreated from the open with Real Estate and Healthcare leading the broad downturn seen across sectors. Nikkei 225 was pressured following its recent failure to hold on to the 39,000 level despite a weaker currency. Hang Seng and Shanghai Comp shrugged off early weakness to trade in the green albeit with price action choppy as the attention turned to earnings updates, while the PBoC conducted its first swap operation involving securities brokerages, funds and insurance companies worth CNY 50bln on Monday.

Top Asian News

- Chow Tai Fook Jewellery (1929 HK) reports same store sales down 24.3%; HY revenue decreases by 18%; HY Net profit decreases by 42%.

- China’s FX regulator said the Yuan exchange is basically stable at reasonable and balanced levels, while it added that cross-border capital turned to inflows in the first three quarters of this year and cross-border capital flow has been balanced since the start of 2024. Furthermore, it stated the FX market shows relatively strong resilience and market expectations and trading are in order overall.

- FT article suggests that there is no sign yet of determined Chinese reforms or spending to spur more household consumption, despite many agreeing that President Xi’s thinking on stimulus has changed. Focus is reportedly still largely on repairing local governments’ and banks’ balance sheets.

- China State Planner say China will continue to issue ultra long term special government bonds in 2025; and further optimise their allocation next year.

European bourses, Stoxx 600 (-0.2%) began the session mostly, but modestly on the backfoot, (ex-DAX 40 & Euro Stoxx 50; benefiting from post-earning strength in SAP) and have traded in a busy range throughout the morning; in recent trade, indicies are now broadly in the red, due to geopolitical updates out of Israel. European sectors hold a strong negative bias; Tech is by far and away the clear outperformer, lifted by post-earning strength in SAP (+5.4%). Real Estate is towards the foot of the pile, given the relatively higher yield environment. US Equity Futures (ES -0.1%, NQ -0.2%, RTY -0.4%) are modestly in the red to varying degrees and with slight underperformance in the RTY, which was subject to hefty selling pressure in the prior session. ASML (ASML NA) CEO says 2025 will be a growth year, the long term will still see growth. “Not everyone is surfing the AI wave”. “What we have seen in the last few months is people beginning to push the breaks”. “China demand is for mainstream chips, older generations of technology”. “Normal Chinese demand is for 20-25% of ASML’s sales, expect it to return to those levels”. “China may be able to produce some 5 or 3 nanometre chips, but few, using older tech”. It is clear the US will push for more export restrictions to China. “The Netherlands and Europe will start to discuss with China export restrictions make sense”

Top European News

- UK Shadow Chancellor Hunt warned Chancellor Reeves against hiking business taxes ahead of next week’s Budget, according to FT.

- Italy’s budget deficit seen at 3.9% of GDP in 2024 (exp. 3.8%); GDP expected to grow 0.8% in 2024 (exp. 0.9%) and 0.9% in 2025 (est. 1.1%)

FX

- USD is broadly slightly softer vs. peers and to varying degrees. That being said, DXY remains in close proximity to Monday’s 104.01 peak and above its 200DMA at 103.72.

- EUR is marginally firmer vs. the USD but unable to scale back much of the downside from yesterday which saw the pair match last week’s multi-month low at 1.0810. Docket ahead sees a slew of ECB speakers.

- Cable is continuing to pivot around the 1.30 mark within a 1.2980-1.3014 range. Focus today will be on today’s trio of BoE speakers with Governor Bailey being the obvious highlight, with focus on if he echoes his recent dovish rhetoric.

- JPY is unable to claw back any of the losses vs. the USD seen during yesterday’s session which brought the pair above its 100DMA at 150.73 and breifly onto a 151 handle. If upside resumes, technicians flag the 200DMA at 151.34.

- Antipodeans are both firmer vs. the USD and attempting to atone for recent losses. Overnight, AUD/USD printed a fresh low for the month at 0.6652 before paring losses (no clear fundamental driver was behind the move). NZD/USD has endured similar price action after recovering from a 0.6022 base overnight.

- Goldman Sachs says the EUR could drop as much as 10% under Trump tariff and domestic tax cuts.

Fixed Income

- Bunds are under pressure in a continuation of the action seen on Monday which was primarily a function of supply and energy upside. Bunds are around a 132.69 trough, having faded from Monday’s 133.06 low. The complex was fairly unreactive to a new German 2026 auction.

- USTs are in-fitting with the above, and in a continuation of the “Trump trade” seen in the prior session. Region awaits its own supply which comes on Wednesday with a 20yr tap, but before that, Fed’s Harker.

- Gilts are pressured in-fitting with the above and roughly in-line with peers. Docket ahead sees a Bank of England trio of Governor Bailey, Breeden and Greene. Currently just off a 96.67 base and erring back towards opening levels of 96.88.

- Orders for Italy’s new seven-year over EUR 70bln (spread at 7bps) whilst 30-year BTP tap demand is in excess of EUR 80bln (spread at 9bps), according to Reuters.

- UK sells GBP 900mln 0.625% 2045 I/L Gilt: b/c 3.57x (prev. 3.44x) & real yield 1.328% (prev. 1.20%).

- Germany sells EUR 4.162bln vs exp. EUR 5.0bln 2.00% 2026 Schatz: b/c 2.61x, average yield 2.16%, and retention 16.76%.

Commodities

- Crude oil is subdued following a firmer session on Monday despite a lack of fresh drivers but as markets still await Israel’s attack on Iran. The complex then lifted off worst levels amid reports that Israeli PM Netanyahu will hold consultations tonight with a specific number of his cabinet ministers at the headquarters of the Ministry of Defense in Tel Aviv, via Al Jazeera. Thereafer, reports that Iran was involved in the assassination attempt on Netanyahu, crude soared to session highs of USD 75.06/bbl.

- Spot gold is firmer intraday with the complex buoyed by the aforementioned geopolitics, ahead of US elections, and with extra momentum after notching fresh all-time highs. XAU resides in a current USD 2,719-2,738.50/oz range.

- Base metals are mostly firmer trade in the complex with gains in most industrial metals pinned on hopes of Chinese stimulus, although iron ore prices retreated with desks citing concerns of softening steel demand.

- US is reportedly in talks with Southeast Asian nations to deploy small modular nuclear reactors, according to Bloomberg.

- China crude steel output -6.1% Y/Y to 77.1mln tonnes in September 2024; global steel output -4.7% Y/Y to 143.6mln tonnes, according to worldsteel.

Geopolitics: Middle East

- Israeli PM Netanyahu will hold consultations tonight with a specific number of his cabinet ministers at the headquarters of the Ministry of Defense in Tel Aviv, via Al Jazeera citing Israeli media.

- “Officials at the Iranian embassy in Beirut are involved in the assassination attempt on PM Netanyahu. The Israeli investigation shows Iranian involvement in launching the drone towards Netanyahu’s house”, via Kans’ Kai on X citing Saudi Al-Hadath channel

- “Al-Arabiya correspondent: Netanyahu meets today with security leaders in Tel Aviv after meeting with Blinken”, according to Al Arabiya

- Israeli Home Front said sirens sounded in Haifa, its Gulf and dozens of cities and sites in northern Israel, while it was later reported that Israeli media and military announced sirens sounded in central Israel’s Samaria area, West Bank settlements, Acre and areas in upper Galilee.

- Israel’s Channel 14 reported that the homes of senior officials in Iran were added as possible targets for Israeli attack and the Air Force will know the exact target of the attack shortly before implementation, according to Al Jazeera. Furthermore, Israel’s Channel 14 cited Israeli sources that stated plans for the strike against Iran were presented by the military leadership and the Mossad to the Prime Minister and Minister of Defence, according to Sky News Arabia.

- US Secretary of State Blinken said he is heading to Israel and other stations in the region to discuss ending the war in Gaza, returning the hostages and alleviating the suffering of the Palestinians, according to Al Jazeera.

Geopolitics: Other

- UK is to lend Ukraine an additional GBP 2.26bln for weapons to fight Russia with the loans to be repaid using interest generated from USD 300bln of Russian frozen assets, according to The Guardian.

US Event Calendar

- 08:30: Oct. Philadelphia Fed Non-Manufactu, est. 4.1, prior -6.1

- 10:00: Oct. Richmond Fed Business Conditio, prior -3

- 10:00: Oct. Richmond Fed Index, est. -17, prior -21

Central Bank Speakers

- 09:00: ECB’s Centeno Speaks in Washington

- 10:00: Fed’s Harker Speaks at Fintech Conference

- 10:00: Fed’s Harker Gives Opening Remarks

DB’s Jim Reid concludes the overnight wrap

Only two weeks until the big day. One that I’ve been looking forward to for what seems an exceptionally long time. Yes, the kids will go back to school after an extended 2-week half-term. As predicted last week my wife was already fed up with them last night after one day of holiday yesterday. The twins are so noisy! I’m off to Center Parcs with them all for a long weekend on Friday so I won’t be spared.

With two weeks to go today until the election, markets have started the week a bit more nervously than during the last 6 where the the S&P 500 has gone up each week for only the second time since the pandemic. Yesterday it started the week -0.18% but with bigger sell-offs elsewhere and extending into the Asian session this morning. The sell-off was much more pronounced among sovereign bonds though, with the 10yr Treasury yield (+11.3bps) reaching its highest level (4.20%) since late July, shortly before the weak payroll report, the Japanese mini-crash and the associated brief market turmoil. Moreover, the move was primarily driven by higher real yields, with the 10yr real yield (+10.2bps) moving up to 1.88%, which is its highest level since the end of July. Overnight, 10yr USTs are another +1.4bps higher as we go to print.

There were several factors behind the move but none that particularly dominated yesterday. In the background there has been a rising concern about debts and deficits, particularly ahead of the US election. Indeed, the IMF pointed out in their recent Fiscal Monitor that global public debt is forecast to exceed $100 trillion this year, and rise further in the medium term, so this is a growing issue as policymakers gather for the IMF/World Bank Annual Meetings in Washington this week. Moreover, our US economists have pointed out that irrespective of who wins the presidency or congress, they could see deficits in the 7-9% area over 2026-28, which is a level unprecedented outside of major wars or massive economic shocks like the GFC and Covid-19.