OCT 24/GOLD PRICE ROSE BY $19.60 TO $2735.80//SILVER WAS UP ONE CENT TO $33.67PLATINUM WAS UP $7.50 TO $1026.80 WHILE PALLADIUM WAS UP A HUGE $99.15 AFTER THE USA INITIATED SANCTIONS OF PALLADIUM FROM RUSSIA/GOLD COMMENTARY TONIGHT FROM ALSDAIR MACLEOD//ISRAEL VS HEZBOLLAH UPDATES//ISRAEL VS HAMAS UPDATES//COVID UPDATES/VACCINE INJURY REPORT/DR PAUL ALEXANDER//IN USA NEWS DENNYS PLANS TO CLOSE 150 STORES//USA PMI MANUFACTURING SCORES ITS 3RD STRAIGHT MONTH OF DECLINE//SWAMP STORIES FOR YOU TONIGHT//

190 H BMO CAPITAL 4 363 H WELLS FARGO SEC 1 686 C STONEX FINANCIA 3 737 C ADVANTAGE 3 905 C ADM 7 991 H CME 10

TOTAL: 14 14

JPMorgan stopped 0/14

GOLD: NUMBER OF NOTICES FILED FOR OCT/2024. CONTRACT: 14 NOTICES FOR 1400 OZ or 0.0435 TONNES

total notices so far: 12,580 contracts for 1,258,000 Oz (39.129 tonnes)

FOR OCT

SILVER NOTICES:2 NOTICE(S) FILED FOR 10,000 OZ/

total number of notices filed so far this month : 1428 for 7.140 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $19.60 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD OUT OF THE GLD..

/ /INVENTORY RESTS AT 893.80 TONNES

INVENTORY RESTS AT 893.80 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.01 AT THE SLV

SMALL CHANGES IN SILVER INVENTORY INTO THE SLV: A WITHDRAWAL OF .684 MILLION OZ OF SILVER OUT OF THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 477.177 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUGE SIZED 1075 CONTRACTS TO 156,189 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR HUGE LOSS OF $1.15 IN SILVER PRICING AT THE COMEX ON WEDNESDAY’S TRADING. WE HAD A SMALL GAIN OF 75 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH THE LOSS OF $1.15 IN PRICE. WE HAD CONSIDERABLE LIQUIDATION OF T.A.S. CONTRACTS ON WEDNESDAY AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S CONTINUAL PRICE RISE. THIS LASTED ONE DAY AS SILVER IS ON THE RISE AGAIN ON THURSDAY. //. WE HAD SOME MIMINAL SHORT COVERING BY OUR SPECS DURING THE COMEX TIME ZONE WEDNESDAY.. WE HAD A HUGE 1150 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY A HUGE 754 CONTRACT T.A.S ISSUANCE WHICH WILL BEING USED IN FUTURE TRADING. IN ESSENCE WE GAINED A SMALL 75 CONTRACTS ON OUR TWO EXCHANGES WITH OUR LOSS IN PRICE

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN ON LAST FRIDAY AND AGAIN THIS WEEK. THE ACCUMULATED T.A.S. IS BEING USED TO MANIPULATE PRICES AT THE COMEX NOW EVERY DAY..

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: A HUGE 754 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS BUT TO NO AVAIL. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $1.15) BUT WERE UNSUCCESSFUL IN KNOCKING ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A SMALL GAIN OF 75 TOTAL OI CONTRACTS ON OUR TWO EXCHANGES

WE HAD A HUGE 1150 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 3.355 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY;S 0 OZ QUEUE JUMP+ .195 MILLION OZ ISSUANCE OF EXCHANGE FOR RISK PRIOR//NEW TOTAL 7.345 MILLION OZ

//NEW STANDING FOR SILVER//OCT AT 7.345 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI LOSS//HUGE SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 754 CONTRACTS)/PLUS THAT STUPID ISSUANCE OF .195 MILLION OZ OF EXCHANGE FOR RISK THURSDAY, OCT 10

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: removed 67 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS OCT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT

TOTAL CONTRACTS for 17 DAYS, total 13,762 contracts: OR 68,810 MILLION OZ (809 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 68.810 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 68.810 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH)

RESULT: WE HAD A HUMONGOUS SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1075 CONTRACTS WITH OUR $1.15 LOSS IN PRICE OF SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 1150 ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR OCT OF 5.355 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S QUEUE JUMP OF 0 OZ TO WHICH WE ADD .195 MILLION OZ OF EXCHANGE FOR RISK ISSUANCE/PRIOR

//NEW TOTAL STANDING FOR OCT AT 7.345 MILLION OZ

WE HAVE A SMALL GAIN OF 75 OI CONTRACTS ON THE TWO EXCHANGES WITH OUR GAIN IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE SIZED 754 CONTRACTS ( WILL BE USED FOR WEDNESDAY’S TRADING),//ZERO FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX SESSION, AS OUR CROOKS STILL COULD NOT CONTAIN SILVER’S PRICE AS IT ROSE APPRECIABLY ON THURSDAY AS THE RAID ON WEDNESDAY FAILED MISERABLY.

/ ZERO SHORT COVERING FROM OUR SPEC SHORTS WITH THE LOSS IN PRICE WEDNESDAY/ . ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE FRIDAY NIGHT (754) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND LATELY ON A DAILY BASIS INCLUDING TODAY.

WE HAD 2 NOTICE(S) FILED TODAY FOR 10,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 8391 OI CONTRACTS TO 565,369 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE 882 CONTRACTS//

WE HAD A STRONG SIZED DECREASE IN COMEX OI (8,391 CONTRACTS) OCCURRED WITH OUR LOSS OF $29.10 IN PRICE WEDNESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A HUGE INITIAL STANDING IN GOLD TONNAGE FOR OCT AT 33.655 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 500 OZ QUEUE JUMP

NEW STANDING ADVANCES TO 39.2348 TONNES+ + 20.917 TONNES EXCHANGE FOR RISK/PRIOR// = 60.1518 TONNES

/ ALL OF THIS HAPPENED WITH OUR $29.10 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S COMEX TRADING///. WE HAD A SMALL SIZED LOSS OF 1202 OI CONTRACTS (3.738 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST THURSDAY MORNING AND THIS CONTINUED ON FRIDAY, AND THROUGHOUT THIS WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! YOU CAN VISUALIZE THIS WITH THE DAILY QUEUE JUMPING WE ARE WITNESSING AND THE STEEP RISE IN PRICE AFTER ONLY ONE DAY OF A RAID.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 7189 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 566,251

IN ESSENCE WE HAVE A SMALL SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 1202 CONTRACTS WITH 8391 CONTRACTS DECREASED AT THE COMEX// AND A HUGE SIZED 7189 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 1202 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED 1132 CONTRACTS, WE HAD ZERO LIQUIDATION OF T.A.S CONTRACTS WITH OUR LOSS IN PRICE WEDNESDAY AS WE ALSO HAD MONTH END SPREADER LIQUIDATION.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A HUGE SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (8391 CONTRACTS) ACCOMPANYING THE STRONG SIZED DECREASE IN COMEX OI OF 8391 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 1202 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR OCT 33.651 TONNES FOLLOWED BY TODAY’S 500 OZ QUEUE JUMP + 20.917 ISSUANCE OF EXCHANGE FOR RISK/PRIOR.

//NEW STANDING ADVANCES TO TO: /OCT 39.2348 TONNES. + 20.917 EX, FOR RISK/PRIOR = 60.1518 TONNES

/ 3) CONSIDERABLE T.A.S. LIQUIDATION AND SPREADER LIQUIDATION (TRYING TO CONTAIN GOLD’S PRICE RISE TO NO AVAIL AND WITH ZERO NET LONG SPECS BEING CLIPPED. STICKY GOLD’S LONGS WERE NOT FOOLED AND THEY WERE REWARDED THURSDAY AS GOLD RESUMES ITS ATMOSPHERIC RISE.

4) STRONG SIZED COMEX OPEN INTEREST DECREASE 5) HUGE ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1136 T.A.S.CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

OCT

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT :

TOTAL EFP CONTRACTS ISSUED: 61,000 CONTRACTS OF 6,100,000 OZ OR 189.73 TONNES IN 17 TRADING DAY(S) AND THUS AVERAGING: 3588 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 17 TRADING DAY(S) IN TONNES 189.73 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 189.73 DIVIDED BY 3550 x 100% TONNES = 5.32% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END UP WITH THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 189.73 TONNES (THIS WILL BE A WEAKER ISSUANCE THIS MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPTEMBER. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 1075 CONTRACTS OI TO 156,189 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1150 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 1150 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1150 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1075 CONTRACTS AND ADD TO THE 1150 E.FP. ISSUED

WE OBTAIN A SMALL SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 75 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 0.375 MILLION OZ OCCURRED WITH OUR $1.15 LOSS IN PRICE

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING WEDNESDAY NIGHT

ASIA TRADING/THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 22.54 PTS OR 0.63%

//Hang Seng CLOSED DOWN 270.53 PTS OR 1.53%

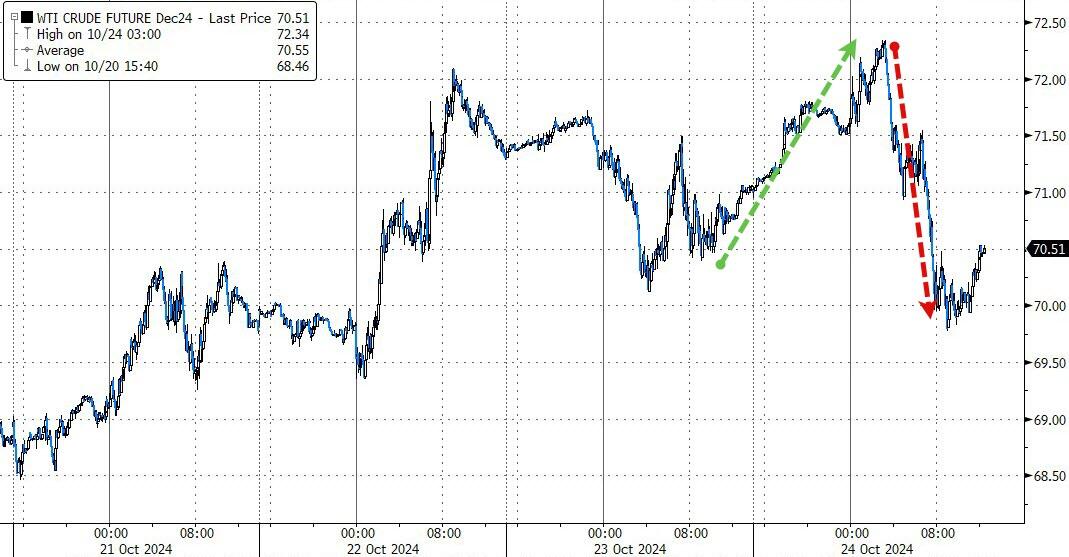

// Nikkei CLOSED UP 38.43 PTS OR 0.10%//Australia’s all ordinaries CLOSED DOWN 0.26%///Chinese yuan (ONSHORE) CLOSED UP TO 7.1151 CHINESE YUAN OFFSHORE CLOSED UP TO 7.1222// Oil UP TO 71.45 dollars per barrel for WTI and BRENT UP AT 75.39 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 8391 CONTRACTS TO 565,369 WITH OUR STRONG LOSS IN PRICE OF $29.10 WITH RESPECT TO WEDNESDAY’S TRADING.HOWEVER, WE LOST ZERO IN NUMBER LONGS WITH THE LOWER PRICE FOR GOLD AS YOU WILL SEE BELOW. WE HAD A HUGE NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (7189). AND THINGS MUST BE DESPERATE AS FIRSTLY ON TUESDAY, OCT 2, WE HAD THE FIRST ISSUANCE IN OVER 3 MONTHS FOR THAT STUPID EXCHANGE FOR RISK, WHEREBY THE BUYER ASSUMES THE RISK FOR DELIVERY. WHY ON EARTH WOULD A BUYER ASSUME SOMETHING LIKE THIS WHEN YOU ARE GUARANTEED DELIVERY VIA AN EXCHANGE FOR PHYSICAL VIA LONDON? UNLESS FOR HUGE MONEY! WELL, ON THURSDAY, OCT 10 WE RECEIVED NOTICE OF A SECOND ISSUANCE OF EXCHANGE FOR RISK, AT 239 NOTICES OR 23,900 OZ (.7433 TONNES). LAST NIGHT ZERO EXCHANGE FOR RISK WAS ISSUED. THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT THIS MONTH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY THIS ENTIRE WEEK

THE FED IS THE MAJOR SHORT OF AROUND 157+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS IS SCHEDULED TO HAPPEN LATE OCT 24 2024/. THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE. THESE PAST TWO MONTHS. THEY ARE TOTALLY TRAPPED. THUS THE REASON FOR THE CONTINUAL RAIDING OF OUR PHYSICAL ANCIENT METAL OF KINGS AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY! THIS WEEK HAS BEEN A STELLAR WEEK FOR GOLD PRICE INCREASES.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD A HUGE T.A.S. LIQUIDATION THROUGHOUT LAST WEEK’S GAIN IN PRICE AND AGAIN WITH THIS WEEKS TRADING, WITH ZERO LONGS BEING CLIPPED (AS YOU WILL SEE BELOW). THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF THE SPREADERS // T.A.S DURING LAST WEEK AND THIS WEEK IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE ACTIVE DELIVERY MONTH OF OCT.… THE CME REPORTS THAT THE BANKERS ISSUED A HUGE SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A HUGE SIZED 7189 EFP CONTRACTS WERE ISSUED: : /DEC 7189 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 7189 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A VERY SMALL SIZED TOTAL OF 320 CONTRACTS IN THAT 7189 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG LOSS OF 8391 COMEX CONTRACTS..AND THIS SMALL LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR STRONG LOSS IN PRICE OF $29.10 WEDNESDAY// COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AS MENTIONED ABOVE.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT, A FAIR SIZED 1132 CONTRACTS, WAS USED TO REPLENISH SUPPLIES.. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE (AND SPREADERS LATE IN THE MONTH). THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN LAST WEEK’S AND THIS WEEK’S TRADING.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: OCT (60.1518 TONNES) WHICH IS HUGE FOR OUR OCT DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 46 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.2348 TONNES + + 20.917 TONNES EXCHANGE FOR RISK PRIOR =60.1518 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $29.10/)//BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A TINY SIZED LOSS IN OUR TWO EXCHANGES. WE DID HAVE CONSIDERABLE T.A.S. SPREADER LIQUIDATION WEDNESDAY COUPLED WITH MONTH END SPREADER LIQUIDATION BUT TO NO AVAIL IN STOPPING GOLD’S ADVANCE AS YOU WILL SEE GOLD’S ADVANCE IN THURSDAY PRICING. CENTRAL BANK LONGS, SEIZING THE MOMENT, EXERCISED FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING.

WE HAVE LOST A TOTAL OF 0.9953 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR OCT (33.651TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 500 OZ QUEUE JUMP PLUS + 20.917 TONNES OF EXCHANGE FOR RISK//PRIOR

//NEW STANDING FOR OCT 39.2348 TONNES.+ + 20.917 TONNES (EXCHANGE FOR RISK

NEW STANDING FOR OCT 39.2348 TONNES + 20.917 TONNES EXCHANGE FOR RISK/PRIOR= 60.1518 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR STRONG LOSS IN PRICE TO THE TUNE OF $29.10

WE HAD 882 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET LOSS ON THE TWO EXCHANGES 1202 CONTRACTS OR 120,200 OZ (3.738 TONNES)

Total monthly oz gold served (contracts) so far this month

12,580 notices 1,258,000oz 39.129 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

dealer deposits:0

total dealer deposits: nil oz

we have 0 customer deposits

total deposits nil oz

withdrawals: 1

i) Out of Loomis: 482.265 oz (15 kilobars)

TOTAL WITHDRAWALS: 482.265 oz

adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR OCT.

For the front month of OCT: we have an oi of 48 contracts having LOST 21 contracts

We had 26 contracts filed on WEDNESDAY so we GAINED 5 contracts on our two exchanges or 5 CONTRACTS underwent a 500 oz queue jump. This is central bank action grabbing all the physical they can.

NOVEMBER LOST 231 CONTRACTS TO STAND AT 1083

DECEMBER, THE BIGGEST DELIVERY MONTH LOST 11,588 CONTRACTS TO 439,647

We had 14 contracts filed for today representing 1400 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 15 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for OCT /2024. contract month, we take the total number of notices filed so far for the month (12,580 x 100 oz ) to which we add the difference between the open interest for the front month of OCT(48 CONTRACTS) minus the number of notices served upon today (14 x 100 oz per contract( equals 1,261,400 OZ OR 39.234 TONNES. TO WHICH WE ADD THAT STUPID 20.917 TONNES OF EXCHANGE FOR RISK PRIOR, NEW TOTAL = 60.1518 TONNES

thus the INITIAL standings for gold for the OCTOBER contract month: No of notices filed so far (12,580 x 100 oz +we add the difference for front month of OCT (48 OI} minus the number of notices served upon today (14 x 100 oz which equals 1,261,400 oz (39.234 TONNES) + 20.917 EX. FOR RISK DELIVERY /PRIOR = 60.1518 TONNES

TOTAL COMEX GOLD STANDING FOR OCT.: 60.1518 TONNES WHICH IS HUGE FOR THIS ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,043,006,171 OZ

TOTAL REGISTERED GOLD 7,746,692.833/// 240.95tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,296,313.338 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,093,822 oz (REG GOLD- PLEDGED GOLD)= 189.54 tonnes //

END

SILVER/COMEX

OCT 24 2024

INITIAL

//2024// THE OCT 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

574.863.762 oz

Brinks CNT

.

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

1,200,760.070 oz

Loomis

No of oz served today (contracts)

2 CONTRACT(S) (10,000 OZ)

No of oz to be served (notices)

2 contracts (10,000oz)

Total monthly oz silver served (contracts)

1428 Contracts (7.140 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit/

total dealer deposit : NIL oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 customer deposits

i) Into CNT: 14,783.920 oz

ii) Into Brinks 560,079.843 oz

total customer deposits 1,200.760.070 oz

We had 2 withdrawals

i) out of CNT 14,783.920 oz

ii) out of Brinks 560,079.843 oz

total withdrawal 574,868,762 oz

JPMorgan has a total silver weight: 134.401million oz/307.778million or 43.53%

adjustment 0

TOTAL REGISTERED SILVER: 68.449MILLION OZ//.TOTAL REG + ELIGIBLE. 307.778million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR OCT

silver open interest data:

FRONT MONTH OF OCT /2024 OI: 4 OPEN INTEREST FOR A LOSS OF 68 CONTRACTS

WE HAD 68 CONTRACTS SERVED ON WEDNESDAY SO WE GAINED 0 CONTRACTS OR WE ENTERTAINED A 0 OZ QUEUE JUMP

NOVEMBER SAW A LOSS OF 58 CONTRACTS TO STAND AT 841

DECEMBER SAW A LOSS OF 2046 CONTRACTS UP TO 127,540 CONTRACTS

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 2 for 10,000 oz

CONFIRMED volume; ON WEDNESDAY 107,919 huge

To calculate the number of silver ounces that will stand for delivery in OCT we take the total number of notices filed for the month so far at 1428x 5,000 oz = 7.140 MILLION oz

to which we add the difference between the open interest for the front month of OCT (4) and the number of notices served upon today (2)x (5000 oz) to which we add 195,000 oz of exchange for risk/PRIOR equals the number of ounces standing.

Thus the standings for silver for the OCT2024 contract month: 1428 Notices served so far) x 5000 oz + OI for the front month of OCT(4) number of notices served upon today minus (2)x 5000 oz of silver standing for the OCT contract month + .195 million oz ex. for risk/PRIOR equates to 7.345 MILLION OZ.

New total standing: 7.345 million oz.

There are 69.742 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS//

GLD

OCT 24 WITH GOLD DOWN $19.60 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES // // . // .///INVENTORY RESTS AT 893.80 TONNES

OCT 23 WITH GOLD DOWN $29.40 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.45 TONNES // // . // .///INVENTORY RESTS AT 895.24 TONNES

OCT 21 WITH GOLD UP $9.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.277 TONNES // // . // .///INVENTORY RESTS AT 888.63 TONNES

OCT 18 WITH GOLD UP $22.30 ON THE DAY; NO CHANGES IN GOLD AT THE GLD // // . // .///INVENTORY RESTS AT 884.59 TONNES

OCT 17 WITH GOLD UP $17.30 ON THE DAY; NO CHANGES IN GOLD AT THE GLD // // . // .///INVENTORY RESTS AT 884.59 TONNES

OCT 16 WITH GOLD UP $13.60 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD //A MONSTER DEPOSIT OF 4.02 TONNES OF GOLD INTO THE GLD.; // . // .///INVENTORY RESTS AT 884.59 TONNES

OCT 15 WITH GOLD UP $2.85 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD //A MONSTER DEPOSIT OF 4.31 TONNES OF GOLD INTO THE GLD.; // . // .///INVENTORY RESTS AT 880.57 TONNES

OCT 11 WITH GOLD UP $36.55 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 10 WITH GOLD UP $14.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 9 WITH GOLD DOWN $8.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 8 WITH GOLD DOWN $28,.95 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 7 WITH GOLD DOWN $1.85 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD; A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD// . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 4 WITH GOLD DOWN $11.20 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD; A DEPOSIT OF 12.57 TONNES OF GOLD INTO THE GLD// . // .///INVENTORY RESTS AT 877.41 TONNES

OCT 3 WITH GOLD DOWN $8.95 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; . // .///INVENTORY RESTS AT 874.82 TONNES

OCT 2WITH GOLD DOWN $20.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD; A DEPOSIT OF 2.88 TONNES OF GOLD INOT THE GLD. // .///INVENTORY RESTS AT 874.82 TONNES

OCT 1 WITH GOLD UP $28,55 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // .///INVENTORY RESTS AT 871.94 TONNES

SEPT 30 WITH GOLD DOWN $6.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD; A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// .///INVENTORY RESTS AT 871.94 TONNES

SEPT 27 WITH GOLD DOWN $26.60 ON THE DAY; NO CHANGES IN GOLD AT THE GLD .///INVENTORY RESTS AT 877,12 TONNES

SEPT 26 WITH GOLD UP $11.20 ON THE DAY; NO CHANGES IN GOLD AT THE GLD .///INVENTORY RESTS AT 877,12 TONNES

SEPT 25WITH GOLD UP $9.25 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD ./// /:// A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD//////INVENTORY RESTS AT 877,12 ONNES

SEPT 24WITH GOLD UP $23.60 ON THE DAY; NO CHANGES IN GOLD AT THE GLD ./// /:// //////INVENTORY RESTS AT 875.39 ONNES

SEPT 23 WITH GOLD UP $6.65 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1,43 TONNES OF GOLD INTO THE GLD../// /:// //////INVENTORY RESTS AT 875.39 ONNES

SEPT 20 WITH GOLD UP $32.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD../// /:// //////INVENTORY RESTS AT 873,96ONNES

SEPT 19 WITH GOLD UP $17,05 ON THE DAY; NO CHANGES IN GOLD AT THE GLD/// /:// //////INVENTORY RESTS AT 872.23TONNES

SEPT 18 WITH GOLD UP $5.95 ON THE DAY; NO CHANGES IN GOLD AT THE GLD/// /:// //////INVENTORY RESTS AT 872.23TONNES

SEPT 17WITH GOLD DOWN $15.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 1.52 TONNES INTO THE GLD /:// //////INVENTORY RESTS AT 872.23TONNES

SEPT 16 WITH GOLD DOWN $1.25 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:// //////INVENTORY RESTS AT 870,71 TONNES

SEPT 13 WITH GOLD UP $30.45 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD /:/A DEPOSIT OF 14.54TONNES OF GOLD VAPOUR INTO THE GLD/ //////INVENTORY RESTS AT 870,71 TONNES

SEPT 12 WITH GOLD UP $37.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD /:/A DEPOSIT OF 1.74 TONNES OF GOLD INTO THE GLD/ //////INVENTORY RESTS AT 866.18 TONNES

SEPT 11 WITH GOLD DOWN $0.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD /:/A DEPOSIT OF 1.70 TONNES OF GOLD INTO THE GLD/ //////INVENTORY RESTS AT 864.44 TONNES

SEPT 10 WITH GOLD UP $12.00ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 9 WITH GOLD UP $12.95 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 6 WITH GOLD DOWN $17.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

SEPT 5 WITH GOLD UP $18.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD /:/ //////INVENTORY RESTS AT 862.74 TONNES

GLD INVENTORY: 893.80 TONNES, TONIGHTS TOTAL

SILVER

OCT 24 WITH SILVER UP $0,01 : SMALL CHANGES IN SILVER INVENTORY AT THE SLV’ A WITHDRAWAL OF 0.684 MILLION OZ OF SILVER OUT OF THE SLV..//// //INVENTORY AT SLV RESTS AT 477.177 MILLION OZ

OCT 23 WITH SILVER DOWN $1.15 : SMALL CHANGES IN SILVER INVENTORY AT THE SLV’ A WITHDRAWAL OF 0.228 MILLION OZ OF SILVER OUT OF THE SLV..//// //INVENTORY AT SLV RESTS AT 477,861 MILLION OZ

OCT 22 WITH SILVER $0.93 : HUGE CHANGES IN SILVER INVENTORY AT THE SLV’ A DEPOSIT OF 3.329 MILLION OZ OF SILVER INTO THE SLV..//// //INVENTORY AT SLV RESTS AT 478.089 MILLION OZ

OCT 18 WITH SILVER $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//// //INVENTORY AT SLV RESTS AT 473.483 MILLION OZ

OCT 17 WITH SILVER DOWN 18 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 3.419 MILLION OZ INTO THE SLV// //INVENTORY AT SLV RESTS AT 473.483 MILLION OZ

OCT 16 WITH SILVER UP 25 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV// //INVENTORY AT SLV RESTS AT 470.064 MILLION OZ

OCT 15 WITH SILVER DOWN 2 CENTS : SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 456,,000 OZ FORM THE SLV. //INVENTORY AT SLV RESTS AT 470.064 MILLION OZ

OCT 11 WITH SILVER UP 53 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 932,000 OZ FORM THE SLV. //INVENTORY AT SLV RESTS AT 470.520 MILLION OZ

OCT 9 WITH SILVER UP 7 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.964 MILLION OZ FORM THE SLV..: /INVENTORY AT SLV RESTS AT 471.432 MILLION OZ

OCT 8 WITH SILVER DOWN $1.41 : HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.007 MILLION OZ FORM THE SLV..: /INVENTORY AT SLV RESTS AT 468.468 MILLION OZ

OCT 7 WITH SILVER DOWN 39 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 684,000 OZ FORM THE SLV..: /INVENTORY AT SLV RESTS AT 466.461 MILLION OZ

OCT 4 WITH SILVER UP 0 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV.: /INVENTORY AT SLV RESTS AT 465.777MILLION OZ

OCT 3WITH SILVER UP 69 CENTS :HUGE CHANGES IN SILVER INVENTORY A WITHDRAWAL OF 1.643 MILLION OZ FORM THE SLV//.: /INVENTORY AT SLV RESTS AT 467.555MILLION OZ

OCT 2WITH SILVER DOWN $0.23 : NO CHANGES IN SILVER INVENTORY: /INVENTORY AT SLV RESTS AT 469.198MILLION OZ

OCT 1 WITH SILVER UP $0.30 : HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 1.368 MILLION OZ INTO THE SLV/. /: .///./// /INVENTORY AT SLV 469.198MILLION OZ

SEPT30 WITH SILVER DOWN $0.33 : HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.094 MILLION OZ INTO THE SLV/. /: .///./// /INVENTORY AT SLV 470.566MILLION OZ

SEPT27WITH SILVER DOWN $0.58 : HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.653 MILLION OZ INTO THE SLV/. /: .///./// /INVENTORY AT SLV 469.472MILLION OZ

SEPT26WITH SILVER UP $0.29 : NO CHANGES IN SILVER INVENTORY:/. /: .///./// /INVENTORY AT SLV 464.819 MILLION OZ

SEPT25WITH SILVER DOWN $0.26 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 2.281MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 464,819 MILLION OZ

SEPT24 WITH SILVER UP $1.26 : HUGE CHANGES IN SILVER INVENTORY:. A DEPOSIT OF 9,305 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 467,100 MILLION OZ

SEPT23 WITH SILVER DOWN $0.39 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 1.824MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 457.795MILLION OZ

SEPT20 WITH SILVER UP $0.08 : NO CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 1.46 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 459,619 MILLION OZ

SEPT19 WITH SILVER UP $0.85 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 1.46 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 459,619 MILLION OZ

SEPT18 WITH SILVER DOWN $0.29 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 1,551 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 461.079 MILLION OZ

SEPT17 WITH SILVER DOWN $0.13 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWALOF 5.976 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 462MILLION OZ

SEPT16//WITH SILVER UP $0.10 : HUGE CHANGES IN SILVER INVENTORY:. ADEPOSIT OF 958,000 OZ INTO THE SLV/. /: .///./// /INVENTORY AT SLV 468.606MILLION OZ

SEPT13//WITH SILVER UP $1.13/ NO CHANGES IN SILVER INVENTORY:./. /: .///./// /INVENTORY AT SLV 467.648MILLION OZ

SEPT 11//WITH SILVER UP $0.33/SMALL CHANGES IN SILVER INVENTORY: A HUGE DEPOSIT OF 2.099 MILLION OZ INTO THE SLV/ OZ OF SILVER FROM THE SLV./. /: .///./// /INVENTORY AT 467.648MILLION OZ

SEPT 10//WITH SILVER DOWN $.06/SMALL CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 639,000 OZ OF SILVER FROM THE SLV./. /: .///./// /INVENTORY AT 465.549MILLION OZ

SEPT 9//WITH SILVER UP $0.45//SMALL CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 46,000 OZ OF SILVER FROM THE SLV./. /: .///./// /INVENTORY AT 466.188 MILLION OZ

SEPT 6//WITH SILVER DOWN $.84//NO CHANGES IN SILVER INVENTORY /: .///./// /INVENTORY AT 466.234 MILLION OZ

SEPT 5//WITH SILVER UP $.55//SMALL CHANGES IN SILVER INVENTORY A WITHDRAWAL OF 0.193 MILLION OZ OF SILVER INTO THE SLV/: .///./// /INVENTORY AT 466.234 MILLION OZ

CLOSING INVENTORY 477.177 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY//BILL HOLTER:

Last Friday, President Putin ruled out a new BRICS currency for now saying that it is not under consideration, promoting trade settlement in national currencies instead.

The idea of a common BRICS gold-backed currency was first mooted over a year ago, with the Russian embassy in Nairobi leaking that it would be on the Johannesburg summit agenda in August 2023. It didn’t make it, with India firmly opposed, and China seemingly lukewarm. Clearly, disagreements have continued through the Russian presidency. And the larger BRICS becomes, the less likely a currency will be agreed upon.

But then, why is the gold price still rising? I’ll come to that later.

I think we can now rule out a BRICS trade settlement currency. Putin’s follow-up statement about exploring the use of digital currencies in mutual trade and investments is utterly meaningless. A currency is a currency digital in form already. It is credit which can be created by any bank, so long as it has access to an interbank settlement facility to keep its books balanced. Central banks already issue it to commercial banks, and the idea that central banks should issue it to invest and finance commercial enterprises as the Bank for International Settlements proposes, with or without a blockchain, is not just inflationary but preposterous.

Instead, Putin confirmed that BRICS nations would continue to use national currencies to settle trade. This is inevitable while India says that it is not interested in the de-dollarisation agenda and will continue to use dollars as it sees fit. It highlights a reality, that the diversity of national agendas under the BRICS umbrella makes agreement on virtually anything other than access to markets increasingly difficult as the membership expands. For this reason, it seems sensible to introduce a class of associate membership, or partnerships, for the 30-odd nations seeking to join, only offering them full membership in due course when circumstances and opportunities permit.

In his statement, Putin didn’t rule out a trade settlement currency entirely — only that it was premature. The mood music out of Moscow tells us that he is in favour of it with gold backing, perhaps for political reasons. He surely understands that to return gold backing to any currency is a frontal attack on the dollar and by crippling the US’s financing machinery it could call a halt to attacks on Russia.

The Americans are highly sensitive to this issue: Ask Colonel Ghaddafi’s or Sadam Hussein’s ghosts if your séance session permits, both of which reputedly expressed interest in remonetising gold. Not being a national currency identifiable with an attackable jurisdiction, a gold-backed trade settlement currency for BRICS might have been harder for the US to counteract. And the damage to the unclothed fiat emperor might be lightly less obvious at first.

China is likely to see consistent deficits on raw material imports offset by consumer product sales and outward investment. Russia’s imports from BRICS are unlikely to be material, instead being a net exporter particularly of energy and therefore a net receiver of weak currencies. Doubtless, this was one reason behind Russia’s desire to introduce a sound trade settlement currency. Instead, the de-dollarisation policy will depend on BRICS Pay or similar, a replacement for SWIFT with the added feature of matching currency settlements directly without the interposition of the dollar. That is still in development.

The dollar’s danger

We now turn our attention to the dollar, which is undeniably in a debt trap, increasingly plain for its creditors to see. China has been dumping dollars, we have assumed to be the consequence of her de-dollarisation policies. But the movers and shakers in Beijing are not fools: they can see the dollar’s debt trap, understand that there is nothing they can do about it, and if anything their de-dollarisation is only bringing forward the date of the dollar’s crisis. Japanese private sector investors are now the largest foreign group holding dollars, and some of them are trying to limit their losses and get out as well.

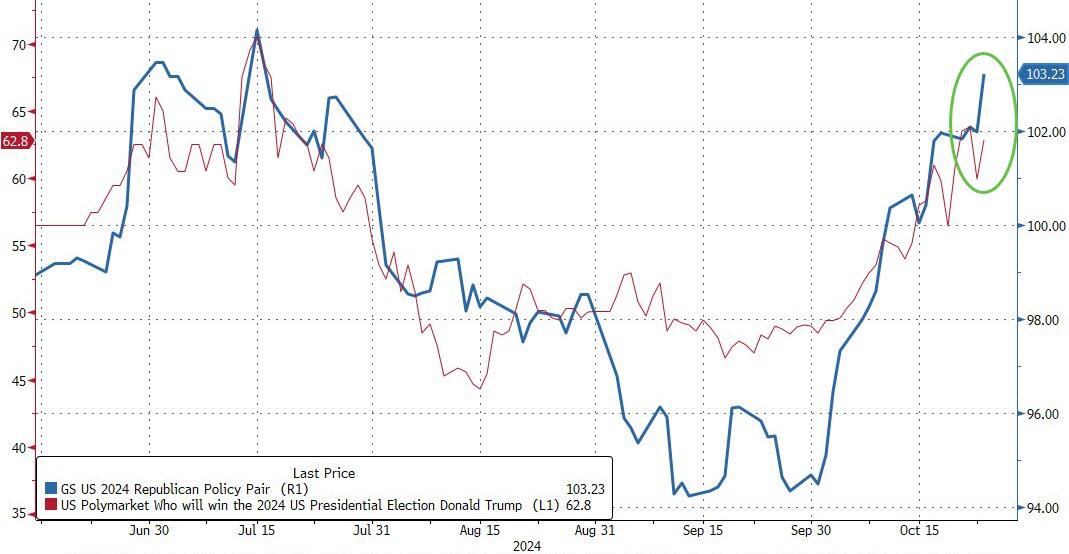

Increasingly Japanese banks, pension funds, and insurance companies can now foresee a US funding crisis, likely to be considerably worse if Trump gets elected as the bookies now predict (Trump 11/18 on, Harris 13/8 against). Whichever way you look at it, his protectionist plans will increase consumer price inflation. And the larger budget deficit will undermine the currency, leading to higher not lower interest rates. It promises a trainwreck for the dollar, and we can be sure that this prospect is accelerating the current surge out of dollars into gold.

Gold’s current bullish move started just over a year ago from $1840. The acceleration in recent days has been notable, accompanying Trump’s improvement in the opinion polls. Let’s look at this from the Asian hegemons and their close allies’ point of view. The chart below, of the dollar gold price inverted is actually of the dollar’s loss of value relative to gold, which as we know is real money while the dollar is credit depending for its value on no more than foreigners’ collective faith in the US Government:

That’s one sick dollar and the acceleration of this decline is alarming. Do foreigners really want to keep $32 trillion locked up in this failing fiat currency?

We now turn our attention to the supply of gold to meet this demand. It so happens that Ross Norman, a well-informed London-based analyst, commentator, and CEO of Metals Daily provided us with some numbers only this week. *

Norman assesses bullion supply as being the sum of 2,125 tonnes mined plus 720 tonnes of scrap since 1 March, totalling 2,850 tonnes. He can only account for demand of 1,480 tonnes, leaving a mystery over the buyers of the remaining 1,370 tonnes.

I am convinced the answer is simple. According to the World Gold Council, the combined mine output of the Asian hegemons, the ex-Soviet CIS states in central Asia, and other associated states last year was 1,232 tonnes. Throw in their portion of scrap and there are about 1,400—1,500 tonnes of supply, most of which is withheld from western capital markets and therefore not reflected in the statistics available. This excess supply simply satisfies a continuation of Asian demand which has been supplied by western sources for the last two decades — longer if you include Chinese stealth buying from the mid-eighties onwards.

Some of this demand should be evident in customs statistics for non-monetary gold. That it is not suggests that it is either not recorded or being booked as monetary gold for which no customs returns are made. If the latter is the case, then the buyers of this missing gold supply are central banks and governments.

It raises an important point. Despite the absence of a much-mooted BRICS gold settlement currency, which they would have known about for months, Asian governments and their central banks are still buying gold and continuing to do so even after President Putin told us the new currency was premature. There can only be one reason: Asian governments and those close to them are bailing out of western paper.

There are also early signs of a flight out of risk developing in western capital markets. Against the principal foreign currencies, including China’s yuan, the dollar has been rising at the same time as falling against gold. And despite the supposed downward trend in US interest rates, term yields for US Treasury notes and bonds are rising sharply. It is consistent with US capital markets themselves reflecting growing credit risk and a flight out of duration. And with a record valuation disparity relative to bonds, US equities are set to see substantial falls as well.

In conclusion, the BRICS meeting in Kazan is very important, but in a geopolitical rather than a financial sense. A rising dollar gold price is less about event-driven bullish speculation about the reintroduction of gold by BRICS for trade settlement purposes, and more about a paradigm shift in the relationship between fiat credit and real money, which is physical gold. And with big Asian players now panicking out of dollars and its fiat dependents while their opposite numbers in the west are selling lesser currencies should tell us that the entire structure of unattached western credit is at risk of collapse much sooner than even those who see these dangers might think.

We are unlikely to ever see a BRICS trade settlement currency before a dollar crisis changes the international landscape, so can assume the idea is stillborn. Instead, all that gold in Asian government hands is likely to be used defensively to stop their currencies from being dragged down with the dollar’s collapse — which though we might not know it yet, is already underway.

Central Asian countries like Kazakhstan, Uzbekistan, and Tajikistan are emerging as key players in the rare earth mineral market.

These countries offer vast reserves, political stability, and a willingness to develop their resources, attracting interest from Western powers, China, and Russia.

Securing access to rare earth minerals is crucial for countries to achieve their clean energy goals and reduce dependence on China, which currently dominates the market.

Securing reliable and strategic supply chains for rare earth minerals has become a geopolitical battleground for world superpowers in the intensifying context of the global clean energy transition. Decarbonizing the global economy will require unfathomable amounts of clean energy infrastructure from solar panels and wind turbines to lithium-ion batteries for energy storage and to power electric vehicles. All of these are going to require a whole heck of a lot of primary materials, and especially metals, many of which fall under the category of ‘rare earths.’

The term rare earth mineral is a bit of a misnomer, as these elements are not really that scarce. But global production capacity is relatively limited compared to demand, as the need for these materials has only recently skyrocketed as the world finally gets serious about a major energy pivot. Shoring up reliable and affordable access to these minerals is therefore a critical step in staying competitive in a fast-growing and fast-changing sector. And so far, China is setting the pace for such acquisitions and, in doing so, blowing its competition away.

Beijing has been eagerly acquiring rare earth reserves and contracts in emerging markets across the world for years now, resulting in what is currently an effective chokehold on global supply chains.

Today, China is home to 34% of the world’s rare earths, carried out 70% of global rare earth mining in 2022, and represents at least 85% of global capacity to process rare earth ores into manufacturing materials. What is more, China has managed to hold its distinction as the only large-scale producer of heavy rare earth ores on the planet thanks to “decades of state investment, export controls, cheap labour and low environmental standards,” the Oxford Institute of Energy Studies asserts in its 2023 report on China’s rare earths dominance and policy responses.

China’s outsized role has led to a dangerous level of international reliance on Chinese exports to meet global and national energy and climate goals. Becoming competitive with China and easing this imbalance will therefore require other global powers to ramp up their own efforts to secure supply contracts for these elements in the places where they are naturally occurring and where their extraction is relatively affordable.

The United States and China have already faced off for rare earth dominance in Latin America, but the U.S. has been relatively unsuccessful to get a significant toehold in the so-called ‘lithium triangle’ of Argentina, Chile and Bolivia. Africa has significant reserves of rare earth minerals, but is generally characterized by political instability and corruption which dampen its appeal to would-be investors. As a result, the hottest new battleground for rare earth contracts is currently emerging in Central Asia.

Kazakhstan, Uzbekistan and Tajikistan are home to vast quantities of valuable rare earth minerals, and seem to have the political and economic conditions that the West is looking for.

“Unlike in the West, Central Asian governments are enthusiastic about the prospect of turning their vast deposits of [rare earth minerals and rare metals] into a new source of revenue for the local economies,” The Interpreter recently reported.

Kazakhstan is already “taking strategic steps to strengthen its position in the global electric vehicle (EV) battery market by increasing the output of critical metals,” according to reporting from Dario, and the Kazakh President Kassym-Jomart Tokayev has even referred to these materials as the “new oil”.

The massive central Asian nation has already signed deals with the European Union and the United Kingdom, and could potentially be an amenable trading partner for the United States as well.

The only problem is that Western powers are not the only major economies with their sights set on Central Asian resource riches.

China and Russia are also eager to tap into these nascent markets, and have certain competitive advantages over the West.

“By virtue of history, geography, and regional and cultural particularities and dependencies, Central Asian countries are bound with Russia and China,” the Interpreter reports.

By the same token, however, these former soviet republics are navigating the solidification of their national identities, and a move away from Russian control could also serve as a point of strategic interest.

END

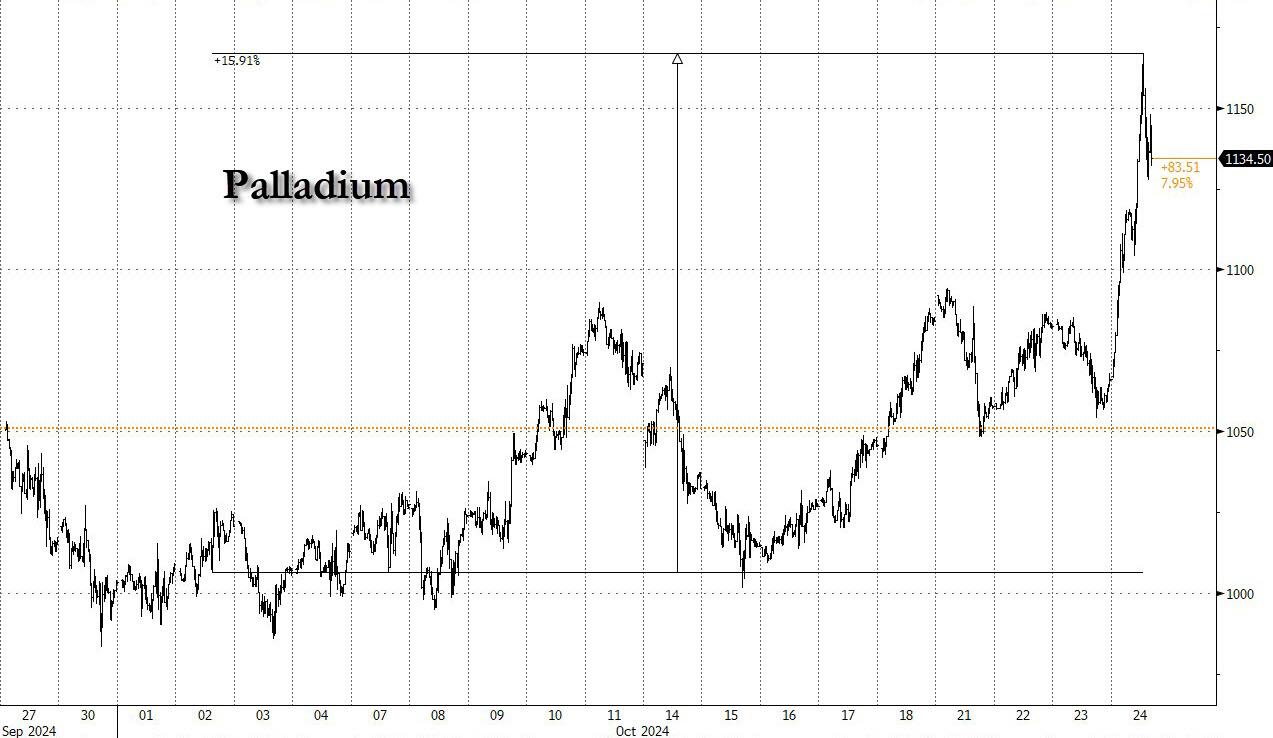

PALLADIUM….

Palladium Soars After US Seeks Sanctions On Russian Exports, Goldman Warns Of Gamma Squeeze

Thursday, Oct 24, 2024 – 11:20 AM

Three weeks ago, when the world was still enthralled by China’s latest attempt to stimulate the economy, we pointed out that one commodity that stood to gain the most should China’s momentum accelerate, was palladium which unlike gold and silver had barely moved in recent years and was trading around $1000 after rising as high as $3500 in early 2022, a time when it was called the “meme stonk” of the commodity market.

To be sure it wasn’t just China that would server as an upside catalyst: at roughly the same time, we learned that Russia’s Federal Budget outlined plans to significantly add to its holdings in precious metals over the coming years, including buying gold, platinum, silver and yes, palladium.

Fast forward to today when Palladium soared as much as 16% higher since our original observation, outperforming both gold and silver over the time period…

As we noted last night, the reason for the powerful spike is that Russia produces 38% of the Palladium in the world (25% of total supply if you take recycling into account), while China is the biggest source of demand. Remove the biggest supplier while stimulating the biggest buyer and well you get a price surge.

So what does this mean for further price gains, and is a repeat of the 2022 meltup – when palladium doubled in price in just a few months – possible?

For the answer we go to Goldman commodity trader Gerald Tan who writes this morning that “short covering started during the second half of the summer but Palladium remains quite short and sensitive to headlines per the extreme moves we saw at the beginning of this year.“

Now one of the reasons why the shorts haven’t panicked yet, and sent the price surging far higher, is because is Palladium is relatively easy to transport and store – Russia produce 2.7mm ounces or 85 MT of Palladium which only represents 7m3 – making it one of the easiest and cheapest commodity to ship and store. Additionally, while the LPPM removed Russian-produced metal from its good deliver list in April 2022, the market reaction was similar at the time but we saw no evidence of tightness in the subsequent months following this announcement.

That may change this time if the G7 indeed follows through with Russian palladium sanctions.

And while we wait, the Goldman trader notes that flow wise while his desk had seen a renewed interest from the bank’s investor franchise, consumers haven’t reacted yet: “Vols are up 10v in the front and forwards are 50 bps tighter across Cal25.”

The bottom line: Goldman is watching the 1-year highs at $1225 where dealers are short some gamma and Rhodium as a proxy for non-spec reaction and genuine tightness.

In other words should palladium rise another 8% from here, we may see the next massive gamma squeeze…

More in the full Goldman note available to pro subs.

.

6 CRYPTOCURRENCY NEWS

END

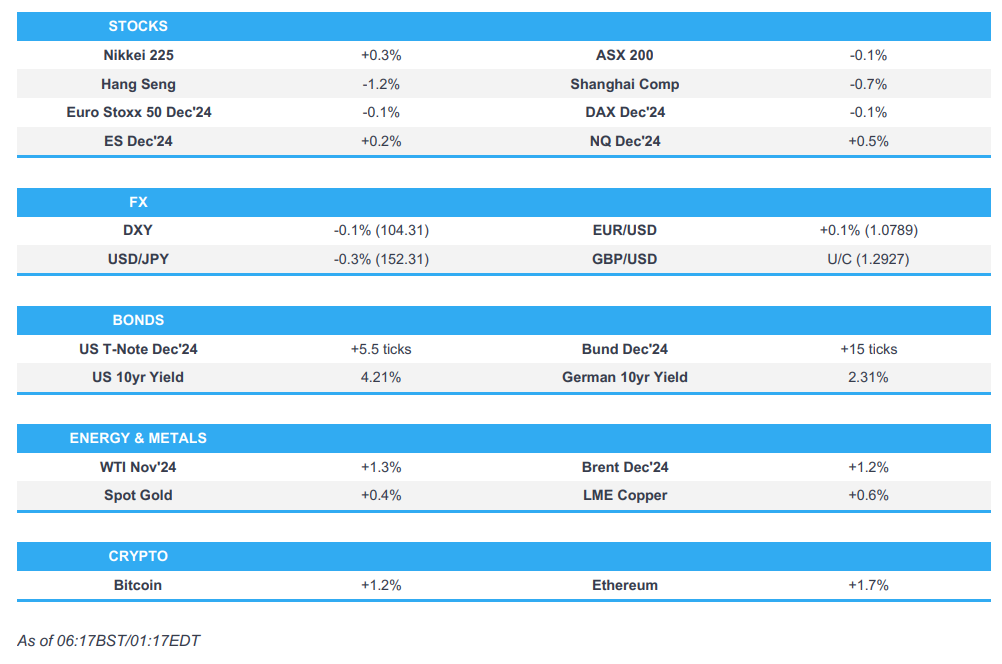

ASIA TRADING THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 22.54 PTS OR 0.63%

//Hang Seng CLOSED DOWN 270.53 PTS OR 1.53%

// Nikkei CLOSED UP 38.43 PTS OR 0.10%//Australia’s all ordinaries CLOSED DOWN 0.26%///Chinese yuan (ONSHORE) CLOSED UP TO 7.1151 CHINESE YUAN OFFSHORE CLOSED UP TO 7.1222// Oil UP TO 71.45 dollars per barrel for WTI and BRENT UP AT 75.39 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 7.1151

OFFSHORE YUAN: UP TO 7.1222

SHANGHAI CLOSED CLOSED DOWN 22.54 PTS OR 0.63%

HANG SENG CLOSED CLOSED DOWN 270.53 PTS OR 1.53%

2. Nikkei closed UP 38.43 POINTS OR 0.10%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 104.06 EURO RISES TO 1.0795 UP 14 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +0.946 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 160.86…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR UP this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.620 Italian 10 Yr bond yield DOWN to 3.466 //SPAIN 10 YR BOND YIELD DOWN TO 2.956

3i Greek 10 year bond yield DOWN TO 3.105

3j Gold at $2738.30 /Silver at: 34.08 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 92/100 roubles/dollar; ROUBLE AT 96.85

3m oil into the 71 dollar handle for WTI and 75 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 151.97 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.946% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8657 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9346 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.194 DOWN 5 BASIS PTS…

USA 30 YR BOND YIELD: 4.473 DOWN 4 BASIS PTS/

USA 2 YR BOND YIELD: 4.051 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 34.24…

10 YR UK BOND YIELD: 4.2715 UP 4 PTS

10 YR CANADA BOND YIELD: 3.249 DOWN 4 BASIS PTS

5 YR CANADA BOND YIELD: 3.006 DOWN 3 PTS.

2a New York OPENING REPORT

Futures Rebound After 3 Day Slide As Tesla Surge Lifts Tech, Yields Slide

Thursday, Oct 24, 2024 – 08:20 AM

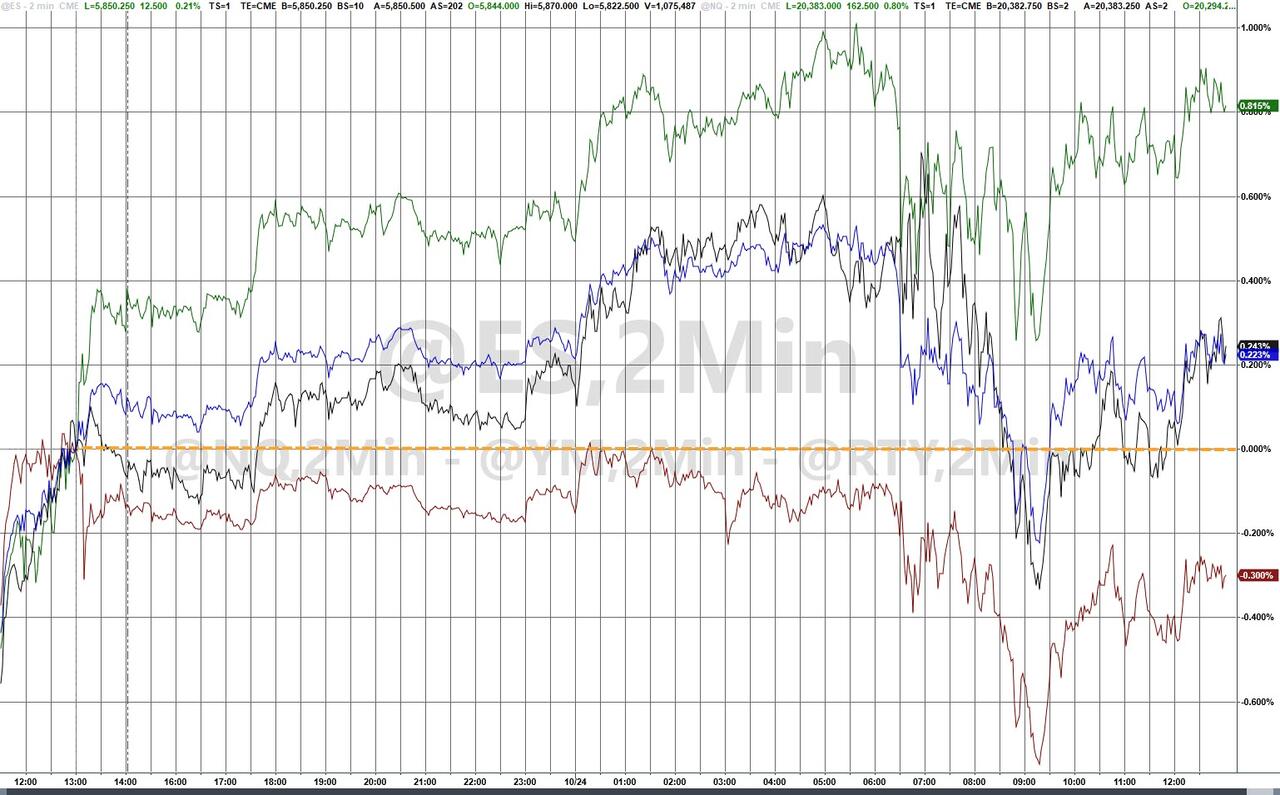

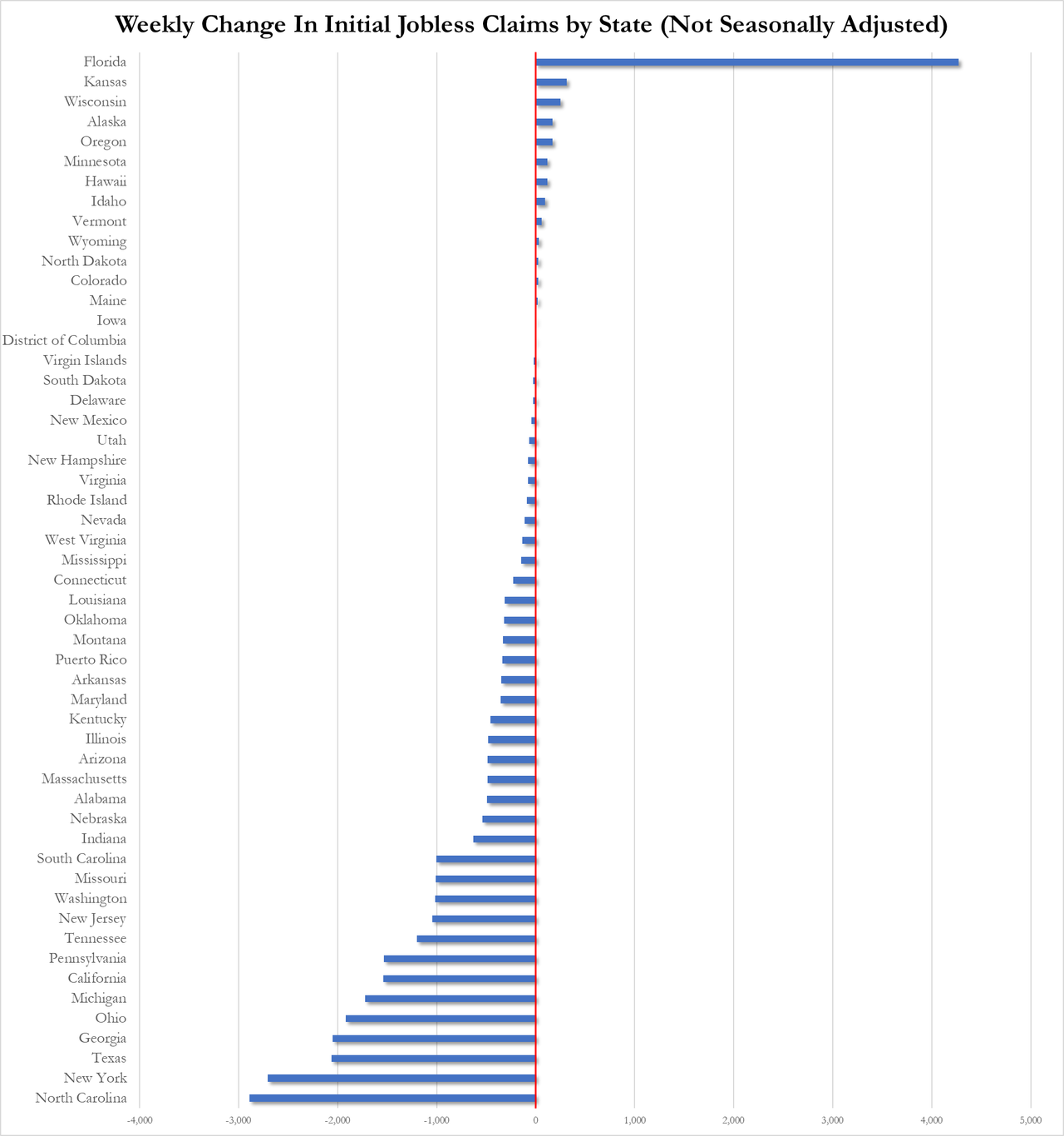

After three straight days of selling, US equity futures are higher with tech stocks leading gains as Tesla surged 13% in premarket trading after it posted its biggest quarterly profit in more than a year. Contracts on the S&P 500 rose 0.5% as of 8:00 a.m. in New York, while futures on the Nasdaq 100 advanced 0.8%, setting up the tech index to rebound from its sharpest decline in almost seven weeks as traders look ahead to earnings from the rest of the “Magnificent Seven,” kicked off by Tesla’s strong performance. The benchmark has yet to fully claw back a summer slump. Overnight, NVDA supplier SK Hynix posted record profit amid strong AI demand; BA fell 2.7% as its bid to end strikes fails while IBM slumped after the it posted underwhelming revenue in the third quarter. Bond yields are lower and the USD is weaker; 2-, 5-, 10-year yields are 3bp, 5bp, 5bp lower. Commodities, including oil, metals and Ags, are mostly higher: Oil +1.9%, Silver +1.8%, Aluminum +1.8% but Palladium is the standout, surging 10% on news the US may impose sanctions on Russian palladium exports (the country produces 38% of global palladium). The main data highlight will be the October flash PMIs from around the world. In the US, we’ll also get the weekly initial jobless claims, along with new home sales for September.

In premarket trading, Tesla soared 13%, its biggest post-earnings jump since Q3 2019, after the EV maker reported its biggest quarterly profit in over a year and issued upbeat 2025 targets. IBM slumped 4% after reporting underwhelming revenue in the third quarter. Weakness in the company’s consulting and infrastructure businesses weighed on the results. Boeing slipped 3% as factory workers rejected a new labor contract that would have increased their wages by 35% over four years. NVDA supplier SK Hynix posted record profit amid strong AI demand; NVDA +1.0%. BA fell 2.7% as its bid to end strikes fails. Here are some other notable premarket movers:

Harley-Davidson (HOG) drops 2% as motorcycle shipments fell in the latest quarter on lower overall demand and fewer sales of its highest-margin bikes.

Honeywell (HON) falls 3% after the industrial conglomerate lowered its revenue outlook for the year.

Lam Research (LRCX) rises 6% after the semiconductor equipment maker reported better-than-expected 1Q results. Investors will welcome this report after ASML’s weak report, analysts said.

Newmont shares (NEM) drops 5% after the gold miner reported 3Q profit that missed amid higher costs.

Seadrill (SDRL) surges 10% after Bloomberg reported the offshore drilling contractor is in talks to merge with rival Transocean, citing people familiar with the matter.

T-Mobile (TMUS) advances 2% after reporting more monthly mobile-phone and broadband subscribers that analysts expected.

United Parcel Service (UPS) jumps 7% after the company returned to sales and profit growth for the first time in nearly two years

Today’s market gains mark a resumption of the rally that took the S&P 500 to its 47th record high last week. Traders are bracing for more results from US tech giants, a turbulent US presidential race and the Federal Reserve’s next rate decision. With Alphabet, Amazon.com and Meta reporting next week “I would be hesitant to say we are through this earnings season,” said Colin Graham, head of multi-asset strategies at Robeco. “Earnings expectations have been downgraded more this quarter than in previous quarters and the bar to beat them was really low this time.”

Investors also have a flurry of US economic data to parse Thursday for clues on the Federal Reserves’s next move on interest rates. The latest snapshot of the health of the labor market is likely to get the most attention.

“If today’s initial jobless claims come in much below consensus forecasts of 242,000, that could send a further signal to rate setters not to overdo it on the loosening front,” said Derren Nathan, head of equity research at Hargreaves Lansdown

European stocks rise as good earnings reports from a range of companies boost the market after three days of declines. Retail stocks are the only sector in the red. The travel and leisure sub-sector is the strongest performer, boosted by Evolution which rallied after in-line results lay investor concerns to rest after a major strike. Miners and personal-care stocks also outperform. Stoxx 600 rises 0.6% to 521.73 with 159 members down, 430 up, and 11 little changed. The purchasing managers’ numbers did little to ease fears that the region’s economy is slipping back into stagnation and the probability of a half-point rate reduction by the European Central Bank in December is now a coin toss. Here are the biggest European movers:

Hermes shares rise as much as 3.4% after the French maker of high-end goods saw its sales beat estimates, signaling that companies catering to wealthy clients are weathering a luxury slowdown.

Unilever shares gain as much as 3.1% after the consumer-goods company reported third-quarter underlying sales growth that came ahead of consensus estimates.

Evolution shares gain as much as 14%, the biggest jump since April 2021, after the gaming firm delivered in-line results in the third quarter, offering relief in the wake of a major strike.

Danone shares advance as much as 2.6% after the French yogurt maker reported third-quarter like-for-like sales growth that beat consensus expectations.

Barclays shares jump as much as 4.3% to a 9-year high after it reported a surprise increase in 3Q fixed-income trading and total income that beat estimates, while upgrading guidance for UK NII.

Orange shares rise as much as 2.3% after the French telecom operator reported revenue that beat expectations in its home market, easing concerns about rising competition.

Dassault Systemes shares slip as much as 3.2% after the software firm delivered results for the third quarter which came in toward the bottom end of the guided range.

Michelin shares drop as much as 8.1%, the most since March 2022, after the French tiremaker lowered its full-year segment operating income target, although lifted guidance for free cash flow.

Kone shares fall as much as 3.9% after the Finnish elevator firm’s 3Q earnings arrived “mixed,” with Jefferies noting weaker demand in China and soft pricing key negatives in the report.

SEB shares decline as much as 5.6% after missing expectations on the key net interest income (NII) metric, a disappointment following strong prints from its Nordic peers earlier, according to analysts.

Edenred shares slide as much as 18%, the most on record, after the French payment-service provider said it faces a hit on Ebitda should a proposal to cap commisions in Italy go ahead.

Hemnet shares slump as much as 14%, the most since August 2022, after the Swedish real estate listings platform saw results come in below analyst expectations in the third quarter.

Earlier in the session, Asian equities headed for a fourth day of declines, dragged down by Chinese stocks. Technology shares slid following few key earnings reports. The MSCI Asia Pacific Index fell 0.2% to its lowest level in a month after swinging between gains and losses earlier in the day. Benchmark heavyweight TSMC erased gains while Alibaba and Tencent declined. Korean memory maker SK Hynix advanced after posting record quarterly profit, while Asian EV stocks were mixed after strong results from Tesla. Key gauges in Hong Kong and China were the region’s worst performers, resuming this month’s losses after September’s big gains. Traders continue to assess Beijing’s commitment to delivering stimulus, with few details so far on its plans to boost the economy and markets.

In FX, Bloomberg gauge of the dollar fell alongside Treasury yields, paring gains seen over the previous three sessions, ahead of claims and PMI releases. The euro edged higher after a slate of mixed PMI figures. The yen outperforms most G-10 peers, rising 0.6% against the greenback after the finance minister warned he is raising the level of urgency for monitoring currency moves.

EUR/USD rises 0.1% to 1.0796; common currency higher for first day in four

USD/JPY down 0.5% to 151.97 after Finance Minister Katsunobu Kato warned over “one-sided, rapid moves” in FX after a G-20 meeting in Washington

GBP/USD rises 0.4% to 1.2977, just above pair’s 100-DMA at 1.2966; Gilt yields rise on report Chancellor Rachel Reeves will give herself an extra £53 billion of borrowing headroom in next week’s budget

In bonds, treasuries hold gains in early US session, paring losses that pushed yields for several tenors to multimonth highs Wednesday. US yields are richer by 3bp-6bp across the curve led by long end, leaving 2s10s spread ~2bp flatter on the day; 10-year, down 5bp at 4.19% near session low, outperforms UK 10-year by 8bp. European government bonds climbed on rate-cut expectations as data showed a downtrend in private-sector activity extended into a second month. German 10-year yields fall 3 bps to 2.27%. Most euro-zone yields also are lower while UK bonds fall after reports Chancellor Rachel Reeves will look to significantly increase borrowing in next week’s budget. UK 10-year yields rise 4 bps to 4.24%; gilts failed to match a rally in their US and European peers following reports Chancellor Rachel Reeves will be looking to significantly increase her ability to borrow in next week’s budget. Bunds extended gains after weak French PMI data as traders increased bets on a 50 bps interest-rate cut by the ECB in December. US session includes weekly jobless claims and S&P Global PMIs, following mixed European PMI readings.

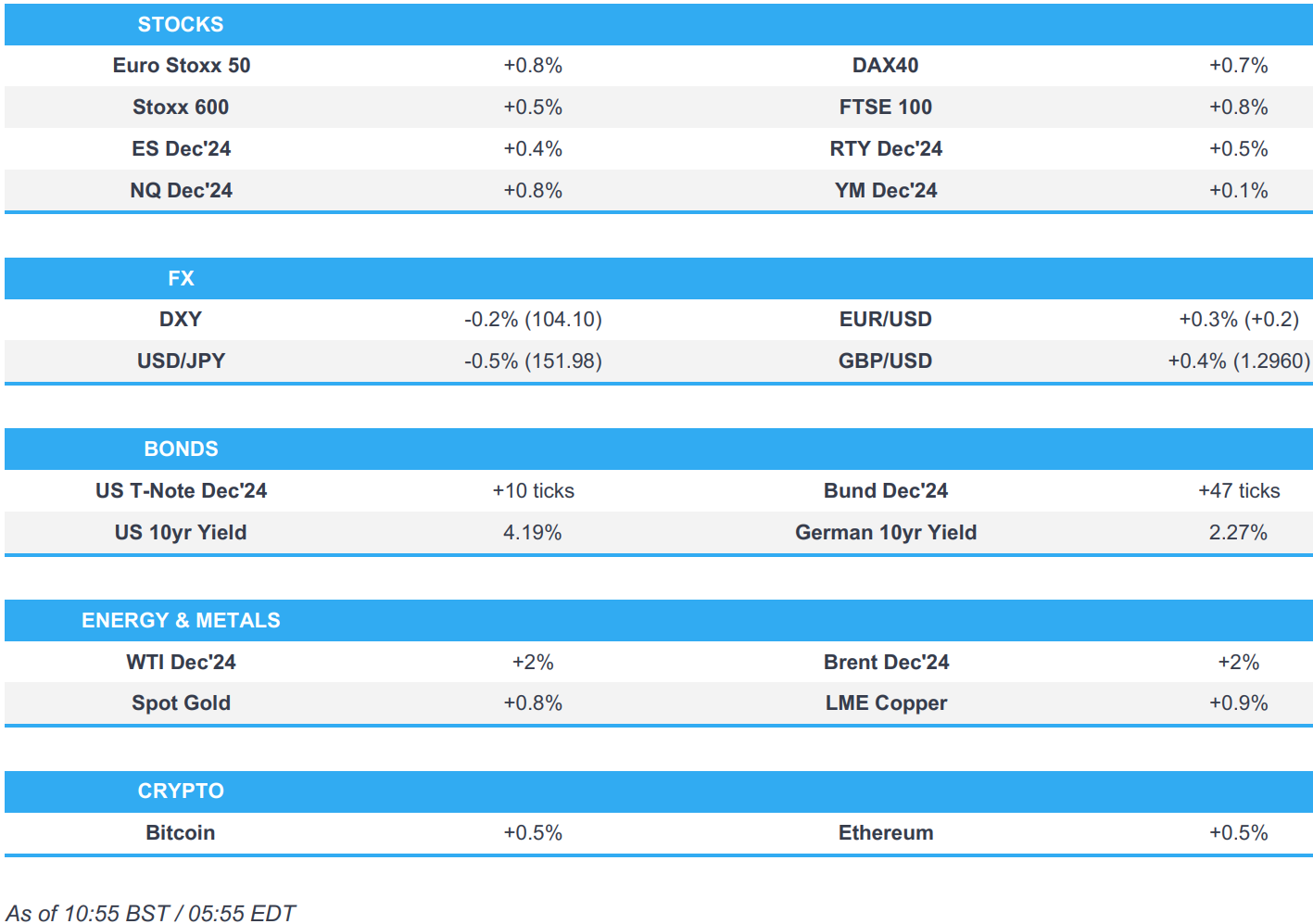

In commodities, oil prices rebounded with WTI rising 1.9% to $72 a barrel as traders continued to await a retaliatory Israeli strike on Iran.. Spot gold rises $22 to around $2,737/oz.

Looking ahead, US economic data calendar includes September Chicago Fed national activity index and weekly initial jobless claims (8:30am), October preliminary S&P Global US manufacturing and services PMIs (9:45am), September new home sales (10am) and October Kansas City Fed manufacturing activity (11am). Fed speaker slate includes Cleveland Fed’s Hammack at 8:45am

Market Snapshot

S&P 500 futures up 0.5% to 5,865.25

STOXX Europe 600 up 0.7% to 522.34

MXAP down 0.2% to 186.97

MXAPJ down 0.6% to 599.84

Nikkei up 0.1% to 38,143.29

Topix little changed at 2,635.57

Hang Seng Index down 1.3% to 20,489.62

Shanghai Composite down 0.7% to 3,280.26

Sensex little changed at 80,013.97

Australia S&P/ASX 200 down 0.1% to 8,206.26

Kospi down 0.7% to 2,581.03

German 10Y yield down 3 bps at 2.27%

Euro up 0.1% to $1.0798

Brent Futures up 1.5% to $76.08/bbl

Gold spot up 0.8% to $2,736.77

US Dollar Index down 0.22% to 104.20

Top Overnight News

Japan’s Finance Minister Katsunobu Kato said he is raising the level of urgency for monitoring currency moves, after the yen hit an almost three-month low against the dollar. BBG

China is pressuring automakers to pause EU expansion plans due to its escalating EV tariff spat with Brussels, people familiar said. That’s already led to Dongfeng halting potential plans to make cars in Italy. BBG

Eurozone flash PMIs are mixed for Oct, with a shortfall on Services (51.2 vs. the Street 51.5 and down from 51.4 in Sept) and modest beat on Manufacturing (45.9 vs. the Street 45.1 and up from 45 in Sept). RTRS

Barclays shares climb in European trading after the company reported solid Q3 results, w/upside on pre-tax income (GBP2.2B vs. the Street ~GBP2B), and the company raised its full-year NII guide. RTRS

BOE Governor Bailey says UK inflation is cooling faster than expected, although he warned that services inflation still needs to come down. FT

Global bond sales will climb 17% this year to about $9 trillion after robust third quarter activity, S&P Global said, as it raised its previous estimate. Issuance may moderate to a 4% gain next year. BBG

Trump takes a 2-point lead over Harris in a new WSJ national poll (47-45%), a shift from the last survey in Aug which had Harris up 2 points. WSJ

Tesla shares jumped on its blowout results, buoyed by a profit-turning Cybertruck, and Elon Musk’s promise of 20% to 30% delivery growth next year. Uber and Lyft stock fell on Musk’s aim to roll out ridesharing in Texas and California in 2025. BBG

Boeing’s largest union rejected a new labor deal Wednesday, extending a six-week strike that has plunged the jet maker into increasing financial peril. Members of the machinist union voted 64% against a proposed contact that would have delivered a 35% wage increase over four years, union leaders said. WSJ

A more detailed look at global markets courtesy of Newsquawk