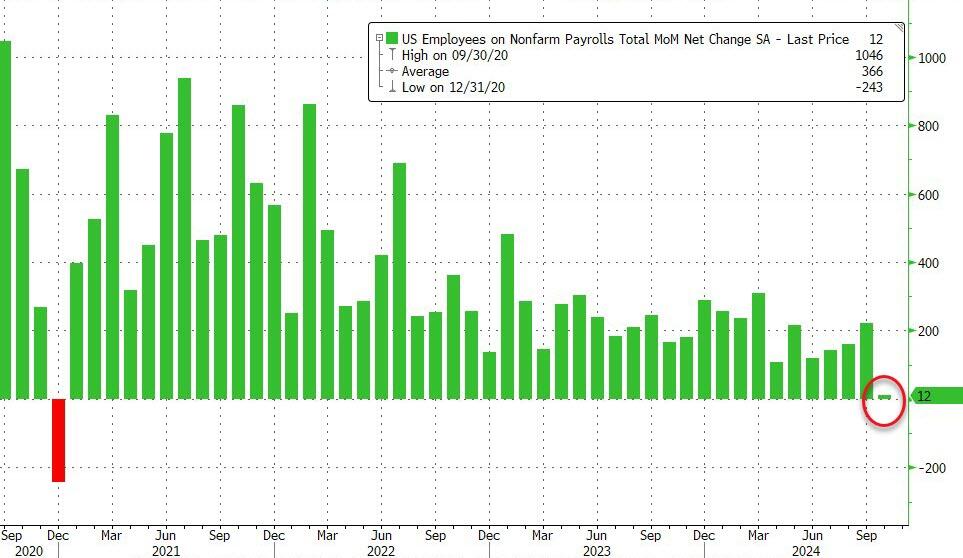

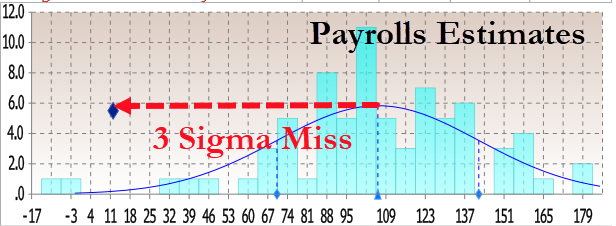

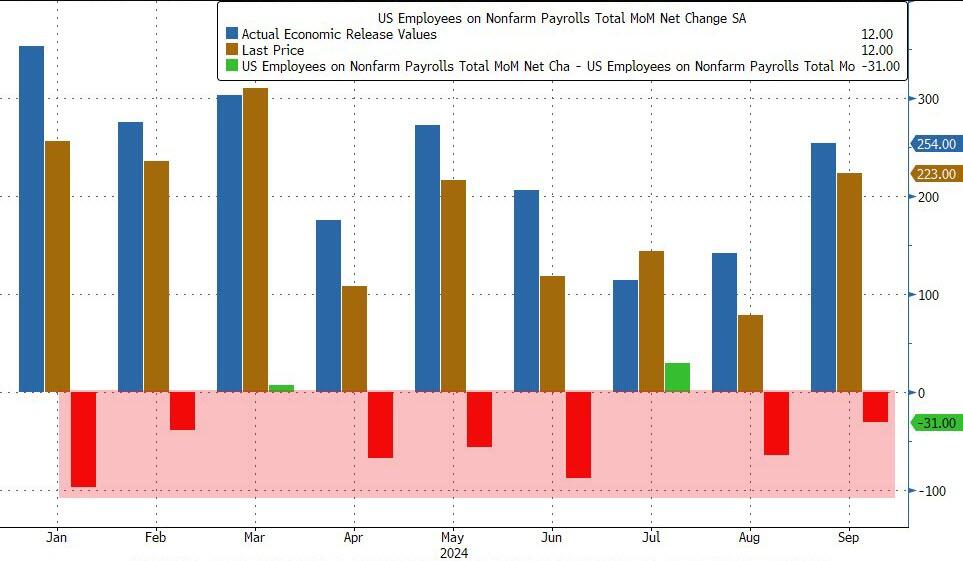

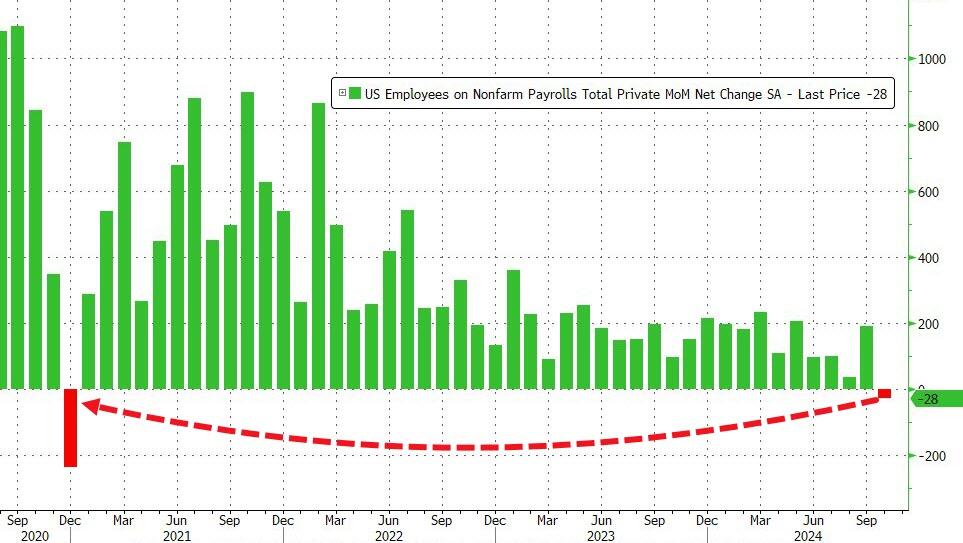

NOV 1/GOLD CLOSED UP A TINY $0.15 TO $2739.75 WHILE SILVER WAS DOWN 10 CENTS TO $32.55//PLATINUM WAS UP $0.80 TO $995.10 WHILE PALLADIUM WAS DOWN $7.05//USA JOBS REPORT FOR SEPT IS OUT AND IT SHOWED A HUGE DOWNFALL IN JOBS//GOLD COMMENTARY TONIGHT: CHRIS POWELL ON GOLD MANIPULATION/FRAUD PUBLISHED BY THE JERUSALEM POST//GOOD COMMODITY REPORT ON ALUMINA//ISRAEL VS HEZBOLLAH//LOOKS LIKE HEZBOLLAH HAS HAD ENOUGH WITH MAJOR DEPLETIONS IN ROCKETS AND MEN//ISRAEL VS HAMAS//COVID UPDATES//VACCINE INJURY REPORT//SLAY NEWS ETC/ DR PAUL ALEXANDER//USA MANUFACTURING SURVEY FALLS BADLY/JOBS REPORT/SWAMP STORIES FOR YOU TONIGHT//

072 C GOLDMAN 3 104 C MIZUHO 1 118 C MACQUARIE FUT 100 132 C SG AMERICAS 4 190 H BMO CAPITAL 79 323 C HSBC 44 363 H WELLS FARGO SEC 222 435 H SCOTIA CAPITAL 566 624 H BOFA SECURITIES 407 657 C MORGAN STANLEY 9 661 C JP MORGAN 21 23 690 C ABN AMRO 28 732 C RBC CAP MARKETS 15 737 C ADVANTAGE 78 21 905 C ADM 5

TOTAL: 813 813 MONTH TO DATE: 1,368

MONTH TO DATE: 12,670

JPMorgan stopped 23/813

GOLD: NUMBER OF NOTICES FILED FOR NOV/2024. CONTRACT: 813 NOTICES FOR 81,300 OZ 2.528 TONNES

total notices so far: 1368 contracts for 136,800 Oz (4.255 tonnes)

FOR OCT

SILVER NOTICES: 24 NOTICE(S) FILED FOR 0.120 MILLION OZ/

total number of notices filed so far this month : 551 for 2.755 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $.15 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL 0F 0.86 TONNES OF GOLD INTO THE GLD.

/ /INVENTORY RESTS AT 891.79 TONNES

INVENTORY RESTS AT 891,79 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $0.10 AT THE SLV

NO CHANGES IN SILVER INVENTORY INTO THE SLV:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 481.189 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A FAIR SIZED 495 CONTRACTS TO 155,148 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS FAIR LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR GIGANTIC LOSS OF $1.26 IN SILVER PRICING AT THE COMEX WITH RESPECT TO THURSDAY’S TRADING. WE HAD A SMALL GAIN OF 140 TOTAL CONTRACTS ON OUR TWO EXCHANGES DESPITE THE GIGANTIC LOSS OF $1.26 IN PRICE. WE HAD CONSIDERABLE LIQUIDATION OF T.A.S. CONTRACTS ON THURSDAY COMEX TRADING AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S CONTINUAL PRICE RISE WITH HUGE SUCCESS YESTERDAY. WE HAD SOME SHORT COVERING BY OUR SPECS DURING THE COMEX TIME ZONE THURSDAY.. WE HAD A HUMONGOUS 635 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY A HUMONGOUS 1595 CONTRACT T.A.S ISSUANCE WHICH WILL BEING USED IN FUTURE TRADING AND THEY PLAY AN INTEGRAL PART DURING RAIDS. IN ESSENCE WE GAINED A SMALL 140 CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR LOSS IN PRICE

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN ON LAST FRIDAY AND AGAIN THIS WEEK. THE ACCUMULATED T.A.S. IS BEING USED TO MANIPULATE PRICES AT THE COMEX NOW EVERY DAY..

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON THURSDAY NIGHT: A HUMONGOUS 1595 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS BUT TO NO AVAIL. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $1.26) BUT WERE UNSUCCESSFUL IN KNOCKING ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A SMALL GAIN OF 140 TOTAL OI CONTRACTS ON OUR TWO EXCHANGES

WE HAD A HUGE 635 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 2.810 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 155,000 OZ QUEUE JUMP//NEW STANDING: 2.965 MILLION OZ

//NEW STANDING FOR SILVER//NOV AT 2.965 MILLION OZ

WE HAD:

/ FAIR SIZED COMEX OI LOSS//HUGE SIZED EFP ISSUANCE/ VI) HUMONGOUS SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1595 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: removed 104 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS OCT. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF OCT

TOTAL CONTRACTS for 1 DAYS, total 635 contracts: OR 3.175 MILLION OZ (635 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 3.175 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 3.175 MILLLION OZ

RESULT: WE HAD A FAIR SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 495 CONTRACTS WITH OUR LOSS OF $1.26 IN PRICE OF SILVER PRICING AT THE COMEX//THURSDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 635 ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR NOV OF 2.810 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 155,000 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR NOV AT 2.965 MILLION OZ

WE HAVE A SMALL GAIN OF 140 OI CONTRACTS ON THE TWO EXCHANGES DESPITE OUR LOSS IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUMONGOUS SIZED 1595 CONTRACTS ( WILL BE USED FOR THURSDAY’S TRADING),//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE THURSDAY COMEX SESSION, AS OUR CROOKS NEEDED TO RAID TO REWARD BANKERS ON FINAL OPTIONS EXPIRY DAY

/ ZERO NET SHORT COVERING FROM OUR SPEC SHORTS DESPITE THE LOSS IN PRICE THURSDAY/ . ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE THURSDAY NIGHT (1595) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND LATELY ON A DAILY BASIS INCLUDING TODAY.

WE HAD 24 NOTICE(S) FILED TODAY FOR 0.120 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A VERY STRONG SIZED 15,853 OI CONTRACTS TO 568,592 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED 3175 CONTRACTS//

WE HAD A VERY STRONG SIZED DECREASE IN COMEX OI (15,853 CONTRACTS) OCCURRED WITH OUR LOSS OF $49.55 IN PRICE THURSDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A GOOD INITIAL STANDING IN GOLD TONNAGE FOR NOV AT 2.488 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S MONSTER 73,100 OZ QUEUE JUMP//NEW STANDING 4.762 TONNES

NEW STANDING FOR NOVEMBER: 2.488 TONNES + 2.27 TONNES = 4.762 TONNES

/ ALL OF THIS HAPPENED WITH OUR $49.55 LOSS IN PRICE WITH RESPECT TO THURSDAY’S COMEX TRADING///. WE HAD A STRONG LOSS OF 8739 OI CONTRACTS (27.181 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST THURSDAY MORNING AND THIS CONTINUED ON LAST FRIDAY, AND THROUGHOUT THIS WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! YOU CAN VISUALIZE THIS WITH THE DAILY QUEUE JUMPING WE ARE WITNESSING (AND TODAY’S MONSTER QUEUE JUMP OF 73,100 OZ)

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 7114 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 568,592

IN ESSENCE WE HAVE A STRONG SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 8739 CONTRACTS WITH 15,853 CONTRACTS DECREASED AT THE COMEX// AND A HUGE SIZED 7114 EFP OI CONTRACTS WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 8739 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED 4188 CONTRACTS, WE HAD CONSIDERABLE LIQUIDATION OF T.A.S CONTRACTS WITH OUR LOSS IN PRICE THURSDAY PLUS WE ALSO HAD FINALIZATION OF MONTH END SPREADER LIQUIDATION.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (7114 CONTRACTS) ACCOMPANYING THE VERY STRONG SIZED DECREASE IN COMEX OI OF 15,893 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 8739 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR NOV 2.488 TONNES FOLLOWED BY TODAY’S HUGE 73,100 OZ QUEUE JUMP

/ 3) CONSIDERABLE T.A.S. LIQUIDATION AND SPREADER LIQUIDATION (TRYING TO CONTAIN GOLD’S PRICE RISE WITH HUGE SUCCES THURSDAY , AND WITH CONSIDERABLE NET LONG SPECS BEING CLIPPED. STICKY GOLD’S LONGS HOWEVER ARE NOT FOOLED AS THEY WERE REWARDED THURSDAY AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL

4) VERY STRONG SIZED COMEX OPEN INTEREST DECREASE 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///STRONG T.A.S. ISSUANCE: 4188 T.A.S.CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

NOV

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF OCT :

TOTAL EFP CONTRACTS ISSUED: 7114 CONTRACTS OF 711,400 OZ OR 22.127 TONNES IN 1 TRADING DAY(S) AND THUS AVERAGING: 7114 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 1 TRADING DAY(S) IN TONNES 22.127 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 22.127 DIVIDED BY 3550 x 100% TONNES = 0.062% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END UP WITH THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV. 22.127 TONNES

NOV

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPTEMBER. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A FAIR SIZED 498 CONTRACTS OI TO 155,148 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 635 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 635 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 635 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 498 CONTRACTS AND ADD TO THE 635 E.FP. ISSUED

WE OBTAIN A SMALL SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 140 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 0.700 MILLION OZ OCCURRED DESPITE OUR $1.26 LOSS IN PRICE

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

FRIDAY MORNING THURSDAY NIGHT

ASIA TRADING/FRIDAY MORNING/THURSDAY NIGHT

SHANGHAI CLOSED DOWN 7.81 PTS OR 0.24%

//Hang Seng CLOSED UP 189.10 PTS OR 0.93%

// Nikkei CLOSED DOWN 1,027.58 PTS OR 2.63%//Australia’s all ordinaries CLOSED DOWN 0.50%///Chinese yuan (ONSHORE) CLOSED DOWN TO 7.1226 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.1275// Oil UP TO 70.60 dollars per barrel for WTI and BRENT UP AT 74.16 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A HUGE SIZED 15,853 CONTRACTS TO 568,592 WITH OUR HUGE LOSS IN PRICE OF $49.55 WITH RESPECT TO THURSDAY’S TRADING. , WE LOST CONSIDERABLE IN NUMBER LONGS WITH THE LOWER PRICE FOR GOLD AS YOU WILL SEE BELOW. WE HAD A HUGE NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (4188).

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY THIS ENTIRE WEEK

THE FED IS THE MAJOR SHORT OF AROUND 157+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS IS SCHEDULED TO HAPPEN LATE OCT 2024/(AS OUTLINED IN OUR GOLD PHYSICAL COMMENTARIES). THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE. THESE PAST TWO MONTHS. THEY ARE TOTALLY TRAPPED. THUS THE REASON FOR THE CONTINUAL RAIDING OF OUR PHYSICAL ANCIENT METAL OF KINGS AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY! THIS WEEK HAS BEEN A STELLAR WEEK FOR GOLD PRICE INCREASES.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD A HUGE T.A.S. LIQUIDATION THROUGHOUT LAST WEEK’S GAIN IN PRICE AND AGAIN WITH THIS WEEKS TRADING. HOWEVER MANY LONGS WERE CLIPPED ON THURSDAY’S RAID (AS YOU WILL SEE BELOW). THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF THE SPREADERS // T.A.S DURING LAST WEEK AND THIS WEEK IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE NON ACTIVE DELIVERY MONTH OF NOV.… THE CME REPORTS THAT THE BANKERS ISSUED A HUGE SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A HUGE SIZED 7114 EFP CONTRACTS WERE ISSUED: : /DEC 7114 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 7114 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG TOTAL OF 8739 CONTRACTS IN THAT 7114 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A HUGE SIZED LOSS OF 15,853 COMEX CONTRACTS..AND THIS STRONG LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR HUGE DROP IN PRICE OF $49.55 THURSDAY// COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AS MENTIONED ABOVE.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR THURSDAY NIGHT, A STRONG SIZED 4188 CONTRACTS, WAS USED TO REPLENISH SUPPLIES.. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE (AND SPREADERS LATE IN THE MONTH). THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN LAST WEEK’S AND THIS WEEK’S TRADING.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: NOV (2,488 TONNES) WHICH IS GOOD FOR OUR NON ACTIVE NOV DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 46 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK PRIOR =60.391 TONNES

NOV . 2.488 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $49.55/)//AND WERE SUCCESSFUL IN KNOCKING OFF SOME NET SPECULATOR LONGS AS WE DID HAVE A STRONG SIZED LOSS IN OUR TWO EXCHANGES. WE DID HAVE CONSIDERABLE T.A.S. SPREADER LIQUIDATION THURSDAY COUPLED WITH FINALIZATION OF MONTH END SPREADER LIQUIDATION BUT THIS COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING.

WE HAVE LOST A TOTAL OF 27.181 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR NOV (2.488TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S WHOPPING QUEUE JUMP OF 731 CONTRACTS OR 73,100 OZ (2.27 TONNES). THESE GUYS UNDERWENT A MASSIVE QUEUE JUMP BOLTING AHEAD OF OTHER LONGS TO OBTAIN BADLY NEEDED PHYSICAL GOLD.

//NEW STANDING FOR NOV 2.488 TONNES + 2.27 TONNES = 4.762 TONNNES

NEW STANDING FOR NOVEMBER: 2.488 TONNES + 2.27 TONNES = 4.762 TONNES

ALL OF THIS WAS ACCOMPLISHED WITH OUR HUGE LOSS IN PRICE TO THE TUNE OF $49.55

WE HAD 3175 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET LOSS ON THE TWO EXCHANGES 8739 CONTRACTS OR 873,900 OZ (27.181 TONNES)

1. INTO LOOMIS: 65,909.55 OZ 2050 KILOBARS) 2. INTO INT. DELAWARE: 1060.982 OZ (33 KILOBARS)

TOTAL; 66,970.1 OR 2083 KILOBARS

No of oz served (contracts) today

813 notice(s) 81300 OZ 2/528 TONNES

No of oz to be served (notices)

163 contracts 16300 OZ 0.5069 TONNES

Total monthly oz gold served (contracts) so far this month

1368 notices 136,800oz 4.255 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

dealer deposits: 0

total dealer deposits: nil oz

we have 2 customer deposits

i) Into Loomis: oz (2050 kilobars)

ii) Into INT. DELAWARE: 1060.982 oz (33 kilobars)

total deposits 66,970.533 oz

withdrawals: 0

adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR NOV.

For the front month of NOV: we have an oi of 976 contracts having GAINED 176 contracts. We had 555 contracts served on Thursday so we gained a huge 731 contract gain as they underwent a massive queue jump (2.27 TONNES OF GOLD)

DECEMBER, THE BIGGEST DELIVERY MONTH LOST 19,527CONTRACTS TO 418,362

JANUARY GAINED ITS FIRST 11 CONTRACTS

FEBRUARY GAINED 1922 CONTRACTS TO 91,420 .

We had 813 contracts filed for today representing 81,300 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 21 notices issued from their client or customer account. The total of all issuance by all participants equate to 813 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 23 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for NOV /2024. contract month, we take the total number of notices filed so far for the month (1368 x 100 oz ) to which we add the difference between the open interest for the front month of NOV(976 CONTRACTS) minus the number of notices served upon today (813 x 100 oz per contract( equals 153,100 OZ OR 4.762 TONNES.

thus the INITIAL standings for gold for the NOV contract month: No of notices filed so far (1368 x 100 oz +we add the difference for front month of NOV (976 OI} minus the number of notices served upon today (813 x 100 oz which equals 153,100 oz (4.762 TONNES) +

TOTAL COMEX GOLD STANDING FOR NOV.: 4.762 TONNES WHICH IS GOOD FOR THIS NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,133,368.992 OZ

TOTAL REGISTERED GOLD 7,692,100.435/// 239.25tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,441,268.557 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,087.753 oz (REG GOLD- PLEDGED GOLD)= 189.35 tonnes //

END

SILVER/COMEX

NOV 1. 2024

INITIAL

//2024// THE NOV 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

627,947.065oz BRINKS INT. DELAWARE

.

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

611,126.000 oz

asahi

No of oz served today (contracts)

24 CONTRACT(S) (120,000 OZ)

No of oz to be served (notices)

42 contracts (210,000oz)

Total monthly oz silver served (contracts)

551 Contracts (2.755 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit/

total dealer deposit : NIL oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 customer deposits

i) Into Loomis 65,909.55 oz

ii) Into Int. Delaware: 1060.983

total customer deposits 66,970.533 oz

We had 0 withdrawals

total withdrawal nil oz

JPMorgan has a total silver weight: 134.401million oz/308.581million or 43.42%

adjustment 0

TOTAL REGISTERED SILVER: 70.072MILLION OZ//.TOTAL REG + ELIGIBLE. 308.581million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR OCT

silver open interest data:

FRONT MONTH OF NOV /2024 OI: 66 OPEN INTEREST FOR A HUGE LOSS OF 496 CONTRACTS

WE HAD 527 NOTICES FILED ON THURSDAY SO WE GAINED A STRONG 31 CONTRACTS OR 155,000 OZ UNDERWENT A QUEUE JUMP IN A DESPERATE SEARCH FOR PHYSICAL METAL OVER ON THIS SIDE OF THE POND.

DECEMBER SAW A LOSS OF 2068 CONTRACTS DOWN TO 121,873 CONTRACTS

JANUARY SAW A LOSS OF 18 CONTRACTS DOWN TO 900

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 24 for 0.120 MILLION oz

CONFIRMED volume; ON THURSDAY 103,128 huge

To calculate the number of silver ounces that will stand for delivery in NOV we take the total number of notices filed for the month so far at 551x 5,000 oz = 2.755 MILLION oz

to which we add the difference between the open interest for the front month of NOV (66) and the number of notices served upon today (24)x (5000 oz)

Thus the standings for silver for the NOV 2024 contract month: 551 Notices served so far) x 5000 oz + OI for the front month of NOV(66) number of notices served upon today minus (24)x 5000 oz of silver standing for the NOV contract month equates to 2.965 MILLION OZ.

New total standing: 2.965 million oz.

There are 70.077 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS//

GLD

NOV 1 WITH GOLD UP 0.15 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.86 TONNES OF GOLD INTO THE GLD.// . // .///INVENTORY RESTS AT 891 TONNES

OCT 31 WITH GOLD DOWN $49.55 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD.// . // .///INVENTORY RESTS AT 892.65 TONNES

OCT 30 WITH GOLD UP $20.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD INTO THE GLD.// . // .///INVENTORY RESTS AT 889,78 TONNES

OCT 29 WITH GOLD UP $25.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD.// . // .///INVENTORY RESTS AT 891.50 TONNES

OCT 28 WITH GOLD UP $1.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.02 TONNES OF GOLD FROM THE GLD.// . // .///INVENTORY RESTS AT 889.78 TONNES

OCT 25 WITH GOLD UP $6.40 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: // . // .///INVENTORY RESTS AT 893.80 TONNES

OCT 24 WITH GOLD UP $19.60 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES // // . // .///INVENTORY RESTS AT 893.80 TONNES

OCT 23 WITH GOLD DOWN $29.40 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.45 TONNES // // . // .///INVENTORY RESTS AT 895.24 TONNES

OCT 21 WITH GOLD UP $9.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.277 TONNES // // . // .///INVENTORY RESTS AT 888.63 TONNES

OCT 18 WITH GOLD UP $22.30 ON THE DAY; NO CHANGES IN GOLD AT THE GLD // // . // .///INVENTORY RESTS AT 884.59 TONNES

OCT 17 WITH GOLD UP $17.30 ON THE DAY; NO CHANGES IN GOLD AT THE GLD // // . // .///INVENTORY RESTS AT 884.59 TONNES

OCT 16 WITH GOLD UP $13.60 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD //A MONSTER DEPOSIT OF 4.02 TONNES OF GOLD INTO THE GLD.; // . // .///INVENTORY RESTS AT 884.59 TONNES

OCT 15 WITH GOLD UP $2.85 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD //A MONSTER DEPOSIT OF 4.31 TONNES OF GOLD INTO THE GLD.; // . // .///INVENTORY RESTS AT 880.57 TONNES

OCT 11 WITH GOLD UP $36.55 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 10 WITH GOLD UP $14.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 9 WITH GOLD DOWN $8.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 8 WITH GOLD DOWN $28,.95 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 7 WITH GOLD DOWN $1.85 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD; A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD// . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 4 WITH GOLD DOWN $11.20 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD; A DEPOSIT OF 12.57 TONNES OF GOLD INTO THE GLD// . // .///INVENTORY RESTS AT 877.41 TONNES

OCT 3 WITH GOLD DOWN $8.95 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; . // .///INVENTORY RESTS AT 874.82 TONNES

OCT 2WITH GOLD DOWN $20.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD; A DEPOSIT OF 2.88 TONNES OF GOLD INOT THE GLD. // .///INVENTORY RESTS AT 874.82 TONNES

OCT 1 WITH GOLD UP $28,55 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // .///INVENTORY RESTS AT 871.94 TONNES

SEPT 30 WITH GOLD DOWN $6.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD; A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// .///INVENTORY RESTS AT 871.94 TONNES

SEPT 27 WITH GOLD DOWN $26.60 ON THE DAY; NO CHANGES IN GOLD AT THE GLD .///INVENTORY RESTS AT 877,12 TONNES

SEPT 26 WITH GOLD UP $11.20 ON THE DAY; NO CHANGES IN GOLD AT THE GLD .///INVENTORY RESTS AT 877,12 TONNES

SEPT 25WITH GOLD UP $9.25 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD ./// /:// A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD//////INVENTORY RESTS AT 877,12 ONNES

SEPT 24WITH GOLD UP $23.60 ON THE DAY; NO CHANGES IN GOLD AT THE GLD ./// /:// //////INVENTORY RESTS AT 875.39 ONNES

SEPT 23 WITH GOLD UP $6.65 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1,43 TONNES OF GOLD INTO THE GLD../// /:// //////INVENTORY RESTS AT 875.39 ONNES

SEPT 20 WITH GOLD UP $32.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD../// /:// //////INVENTORY RESTS AT 873,96ONNES

SEPT 19 WITH GOLD UP $17,05 ON THE DAY; NO CHANGES IN GOLD AT THE GLD/// /:// //////INVENTORY RESTS AT 872.23TONNES

SEPT 18 WITH GOLD UP $5.95 ON THE DAY; NO CHANGES IN GOLD AT THE GLD/// /:// //////INVENTORY RESTS AT 872.23TONNES

SEPT 17WITH GOLD DOWN $15.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 1.52 TONNES INTO THE GLD /:// //////INVENTORY RESTS AT 872.23TONNES

GLD INVENTORY: 891.79 TONNES, TONIGHTS TOTAL

SILVER

NOV 1 WITH SILVER DOWN $0.10 : NO CHANGES IN SILVER INVENTORY AT THE SLV:.//// //INVENTORY AT SLV RESTS AT 481.189 MILLION OZ

OCT 31 WITH SILVER DOWN $1.26 : HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.647 MILLION OZ OF SILVER INTO THE SLV//.//// //INVENTORY AT SLV RESTS AT 481.189 MILLION OZ

OCT 30 WITH SILVER DOWN 38 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV.//// //INVENTORY AT SLV RESTS AT 477.542 MILLION OZ

OCT 29 WITH SILVER UP 49 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV’ A WITHDRAWAL OF 0.628 MILLION OZ OUT OF THE SLV..//// //INVENTORY AT SLV RESTS AT 477.542 MILLION OZ

OCT 28 WITH SILVER UP 15 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV’ A WITHDRAWAL OF 1.431 MILLION OZ OUT OF THE SLV..//// //INVENTORY AT SLV RESTS AT 478.180 MILLION OZ

OCT 25 WITH SILVER DOWN $0,02 : HUGE CHANGES IN SILVER INVENTORY AT THE SLV’ A DEPOSIT OF 3.06 MILLION OZ INTO THE SLV..//// //INVENTORY AT SLV RESTS AT 480.281 MILLION OZ

OCT 24 WITH SILVER UP $0,01 : SMALL CHANGES IN SILVER INVENTORY AT THE SLV’ A WITHDRAWAL OF 0.684 MILLION OZ OF SILVER OUT OF THE SLV..//// //INVENTORY AT SLV RESTS AT 477.177 MILLION OZ

OCT 23 WITH SILVER DOWN $1.15 : SMALL CHANGES IN SILVER INVENTORY AT THE SLV’ A WITHDRAWAL OF 0.228 MILLION OZ OF SILVER OUT OF THE SLV..//// //INVENTORY AT SLV RESTS AT 477,861 MILLION OZ

OCT 22 WITH SILVER $0.93 : HUGE CHANGES IN SILVER INVENTORY AT THE SLV’ A DEPOSIT OF 3.329 MILLION OZ OF SILVER INTO THE SLV..//// //INVENTORY AT SLV RESTS AT 478.089 MILLION OZ

OCT 18 WITH SILVER $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//// //INVENTORY AT SLV RESTS AT 473.483 MILLION OZ

OCT 17 WITH SILVER DOWN 18 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 3.419 MILLION OZ INTO THE SLV// //INVENTORY AT SLV RESTS AT 473.483 MILLION OZ

OCT 16 WITH SILVER UP 25 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV// //INVENTORY AT SLV RESTS AT 470.064 MILLION OZ

OCT 15 WITH SILVER DOWN 2 CENTS : SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 456,,000 OZ FORM THE SLV. //INVENTORY AT SLV RESTS AT 470.064 MILLION OZ

OCT 11 WITH SILVER UP 53 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 932,000 OZ FORM THE SLV. //INVENTORY AT SLV RESTS AT 470.520 MILLION OZ

OCT 9 WITH SILVER UP 7 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.964 MILLION OZ FORM THE SLV..: /INVENTORY AT SLV RESTS AT 471.432 MILLION OZ

OCT 8 WITH SILVER DOWN $1.41 : HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.007 MILLION OZ FORM THE SLV..: /INVENTORY AT SLV RESTS AT 468.468 MILLION OZ

OCT 7 WITH SILVER DOWN 39 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 684,000 OZ FORM THE SLV..: /INVENTORY AT SLV RESTS AT 466.461 MILLION OZ

OCT 4 WITH SILVER UP 0 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV.: /INVENTORY AT SLV RESTS AT 465.777MILLION OZ

OCT 3WITH SILVER UP 69 CENTS :HUGE CHANGES IN SILVER INVENTORY A WITHDRAWAL OF 1.643 MILLION OZ FORM THE SLV//.: /INVENTORY AT SLV RESTS AT 467.555MILLION OZ

OCT 2WITH SILVER DOWN $0.23 : NO CHANGES IN SILVER INVENTORY: /INVENTORY AT SLV RESTS AT 469.198MILLION OZ

OCT 1 WITH SILVER UP $0.30 : HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 1.368 MILLION OZ INTO THE SLV/. /: .///./// /INVENTORY AT SLV 469.198MILLION OZ

SEPT30 WITH SILVER DOWN $0.33 : HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.094 MILLION OZ INTO THE SLV/. /: .///./// /INVENTORY AT SLV 470.566MILLION OZ

SEPT27WITH SILVER DOWN $0.58 : HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.653 MILLION OZ INTO THE SLV/. /: .///./// /INVENTORY AT SLV 469.472MILLION OZ

SEPT26WITH SILVER UP $0.29 : NO CHANGES IN SILVER INVENTORY:/. /: .///./// /INVENTORY AT SLV 464.819 MILLION OZ

SEPT25WITH SILVER DOWN $0.26 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 2.281MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 464,819 MILLION OZ

SEPT24 WITH SILVER UP $1.26 : HUGE CHANGES IN SILVER INVENTORY:. A DEPOSIT OF 9,305 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 467,100 MILLION OZ

SEPT23 WITH SILVER DOWN $0.39 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 1.824MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 457.795MILLION OZ

SEPT20 WITH SILVER UP $0.08 : NO CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 1.46 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 459,619 MILLION OZ

SEPT19 WITH SILVER UP $0.85 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 1.46 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 459,619 MILLION OZ

SEPT18 WITH SILVER DOWN $0.29 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 1,551 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 461.079 MILLION OZ

SEPT17 WITH SILVER DOWN $0.13 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWALOF 5.976 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 462MILLION OZ

On Friday, Peter dropped another episode of the Peter Schiff Show. He comments on an IMF conference in Europe, the newsworthy BRICS conference held in Russia, and the latest political proposals made in the presidential race, namely Donald Trump floating the idea of replacing income taxes with tariffs and Kamala Harris taking aim at subscription services.

First, Peter addresses the turbulence in mining stocks. Newmont suffered a major blow after missing earnings, and the sector in general was down this week:

“Even though gold was positive on the week, gold stocks got crushed. The GDX, which is the seniors, the biggest index, was down 5.3% on the week. … But the reason was Newmont Mining, the biggest gold company in the world and the only gold company in the S&P 500, which reported earnings after the bell on Wednesday. Newmont closed the day down 14%.

Despite this, Peter is optimistic that Newmont is still a valuable company. They slightly missed profit forecasts, but are setting new earnings records and matched revenue expectations:

“It was actually the best quarter in five years. And if you compare the quarter to the same quarter a year ago, they earned six times as much money—way more than the prior quarter. They’re still on a path to make the most money in the history of Newmont Mining, and they’re still going to have a record year for earnings. The reason the stock got killed was because they missed. They were supposed to earn 86 cents on the quarter, and they earned 81 cents—less than a 6% miss. The revenues were about in line.”

Turning to the aforementioned IMF conference, Peter lambasts Janet Yellen, who is deluded enough to think the country is in a sound fiscal position:

“[Yellen] is the secretary of the debt, not the secretary of the treasury, because we don’t have any treasury—the treasury is bare. All we got is debt. She’s basically in charge of managing the debt and getting people to buy it. What’s your plan? How are you going to convince people to buy this stuff? Janet Yellen’s response was, ‘We’re just going to make sure that we stay on a sound fiscal path.’ How do we stay on a path that we’re not even on? We left soundness decades ago. We can’t stay on anything.”

“I would love nothing more than to go back to that tax system, but we have to do it honestly, which means we have to cancel a lot of government. We have to eliminate agencies and departments. We have to really shrink the government in order to get back to the freedom and prosperity that we had at that time, which we could have again. I think it’s very unlikely, given the politics.”

Finally, Peter turns to the major geopolitical news of the week: the BRICS summit. After adding four new members (Iran, Ethiopia, Egypt, and the UAE), the leaders of BRICS met in Russia to plan a gradual move away from the dollar. When the US continually erodes the value of the dollar and wields it against geopolitical rivals, it does make sense to consider alternative currencies:

“First of all, it makes no sense. Why should two countries that don’t use dollars transact in the dollar? Just pick one of the currencies that’s involved. You’ve got two countries that have currencies. Why involve the United States, a third party, who’s not even involved in the transaction? Why use our dollars? Use the currencies that you’re actually transacting in. And so that is the goal, for the BRICS nations to phase out the use of the US dollar and use their own currencies.”

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY//BILL HOLTER:

3.CHRIS POWELL AND DAILY GOLD/SILVER DISPATCHES

a must read

Chris Powell/JerusalemPost

Gold’s Rise, Central Banks, and BRICS Influence with Chris Powell

Chris Powell, a veteran in the gold market, suggests that central banks are manipulating gold prices.

By PRNOVEMBER 1, 2024 15:22

Gold’s Rise, Central Banks, and BRICS Influence with Chris Powell(photo credit: PR)

In a recent interview with Sprott Money, Chris Powell, a prominent figure in the precious metals field, delved into the factors driving the surge in gold prices. Powell, known for his work with the Gold Anti-Trust Action Committee (GATA), offered a unique perspective on the role of central banks and the emerging influence of the BRICS nations.

Central Banks: A Double-Edged Sword

Powell expressed surprise at the significant rise in gold prices, particularly given the historical efforts of central banks to suppress the yellow metal. However, he noted a recent shift in their strategy. “Central banks have turned from netsellers and lenders of gold to very big net purchasers,” he explained. This shift, coupled with their potential involvement in manipulating the gold market, has contributed to the upward price trajectory.

BRICS and Gold:

The growing influence of the BRICS nations, particularly China and Russia, has also played a role in the gold market. Powell highlighted the potential for these nations to challenge the dominance of the US dollar and promote gold as an alternative reserve currency. “The world is changing,” he said. “Countries are slowly moving away from the dollar and rapidly moving into gold and silver.”

A Historical Perspective

To illustrate the historical context, Powell referenced the 1974 meeting between Henry Kissinger and Thomas O. Enders, where they discussed the need to prevent Western European allies from returning to a gold standard. This historical event underscores the enduring interest of powerful nations in controlling the gold market.

Looking Ahead

As we move forward, Powell believes that the combination of central bank activity, BRICS influence, and global economic uncertainty will continue to support gold prices. He advises investors to consider adding physical gold and silver to their portfolios as a hedge against inflation and currency devaluation.

In conclusion, Chris Powell’s insights provide valuable context for understanding the current gold market dynamics. While central banks may be attempting to influence the price, the underlying fundamentals, such as geopolitical tensions and economic uncertainty, remain strong drivers for gold.

4. OTHER GOLD COMMENTARIES//LIVE FROM THE VAULT/no 196 ANDREW MAGUIRE

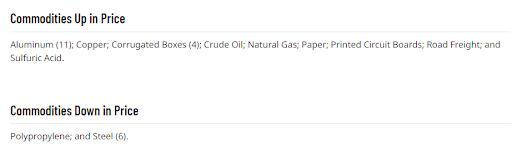

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES: ALUMINA

“No Signs Of A Turnaround”: Alumina Prices Near Record As Global Supply Chain Snarls Mount

Friday, Nov 01, 2024 – 04:15 AM

A squeezed global aluminum supply chain has sent the price of the metal’s critical ingredient, alumina, to the brink of a new record high on Wednseday of $707.59 a ton, nearly eclipsing the 2018 high of $707.75.

Since the mid-point of the year, supply chain snarls and production disruptions in major alumina-exporting countries have sparked shortages. Countries critical to the aluminum supply chain include Guinea, Australia and China.

Mounting supply chain woes from the West African country of Guinea, a top source of seaborne-traded bauxite that supplies over 70% of China’s imports, come amid continued trade disputes with local government customs officials.

Meanwhile, Australia, another large producer of bauxite and alumina, has seen exports move lower on climate change policies and sliding natural gas supplies.

“There are no signs of a turnaround in spot alumina prices within this year,” Gao Yin, an analyst with consultant Horizon Insights, said who was quoted by Bloomberg, adding that aluminum inventories at Chinese smelters have been declining, but “the market hasn’t considered output cuts as a base-case scenario yet.”

Data from Fastmarkets shows alumina prices are back to near-record highs of around $707 a ton.

Earlier this week, UBS Dominic Schnider told clients that increasing supply chain concerns surrounding “bauxite and alumina” and another round of Chinese stimulus “have provided underlying support for higher aluminum prices.”

Schnider said, “Supply challenges on the bauxite and alumina side (site closure, force majeure, and export blockages) from Australia to Guinea are likely to be a key issue into the year-end.”

Morgan Stanley recently told clients that stresses were materializing in the global aluminum supply chain, with China facing challenges in alumina and bauxite supply.

Just imagine what happens to aluminum markets if and when China fires the mega bazooka stimulus package…

.

6 CRYPTOCURRENCY NEWS

END

ASIA TRADING FRIDAY MORNING/THURSDAY NIGHT

SHANGHAI CLOSED DOWN 7.81 PTS OR 0.24%

//Hang Seng CLOSED UP 189.10 PTS OR 0.93%

// Nikkei CLOSED DOWN 1,027.58 PTS OR 2.63%//Australia’s all ordinaries CLOSED DOWN 0.50%///Chinese yuan (ONSHORE) CLOSED DOWN TO 7.1226 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.1275// Oil UP TO 70.60 dollars per barrel for WTI and BRENT UP AT 74.16 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS FRIDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.1226

OFFSHORE YUAN: DOWN TO 7.1275

SHANGHAI CLOSED CLOSED DOWN 7.81 PTS OR 0.24%

HANG SENG CLOSED CLOSED UP 189.10 PTS OR 0.93%

2. Nikkei closed DOWN 1,027.51 POINTS OR 2.63%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX UP TO 103.99 EURO FALLS TO 1.0864 DOWN 20 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +0.941 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 160.86…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and DOWN FOR UP this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.3980 Italian 10 Yr bond yield UP to 3.682 //SPAIN 10 YR BOND YIELD UP TO 3.113

3i Greek 10 year bond yield UP TO 3.304

3j Gold at $2752.80 /Silver at: 32.82 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 63/100 roubles/dollar; ROUBLE AT 98.00

3m oil into the 70 dollar handle for WTI and 72 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 152.64 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 0.941% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8674 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9424 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.294 UP 1 BASIS PTS…

USA 30 YR BOND YIELD: 4.467 DOWN 1 BASIS PTS/

USA 2 YR BOND YIELD: 4.1850 UP 2 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 34.32…

10 YR UK BOND YIELD: 4.4865 UP 3 PTS

10 YR CANADA BOND YIELD: 3.247 DOWN 3 BASIS PTS

5 YR CANADA BOND YIELD: 3.037 DOWN 3 PTS.

2a New York OPENING REPORT

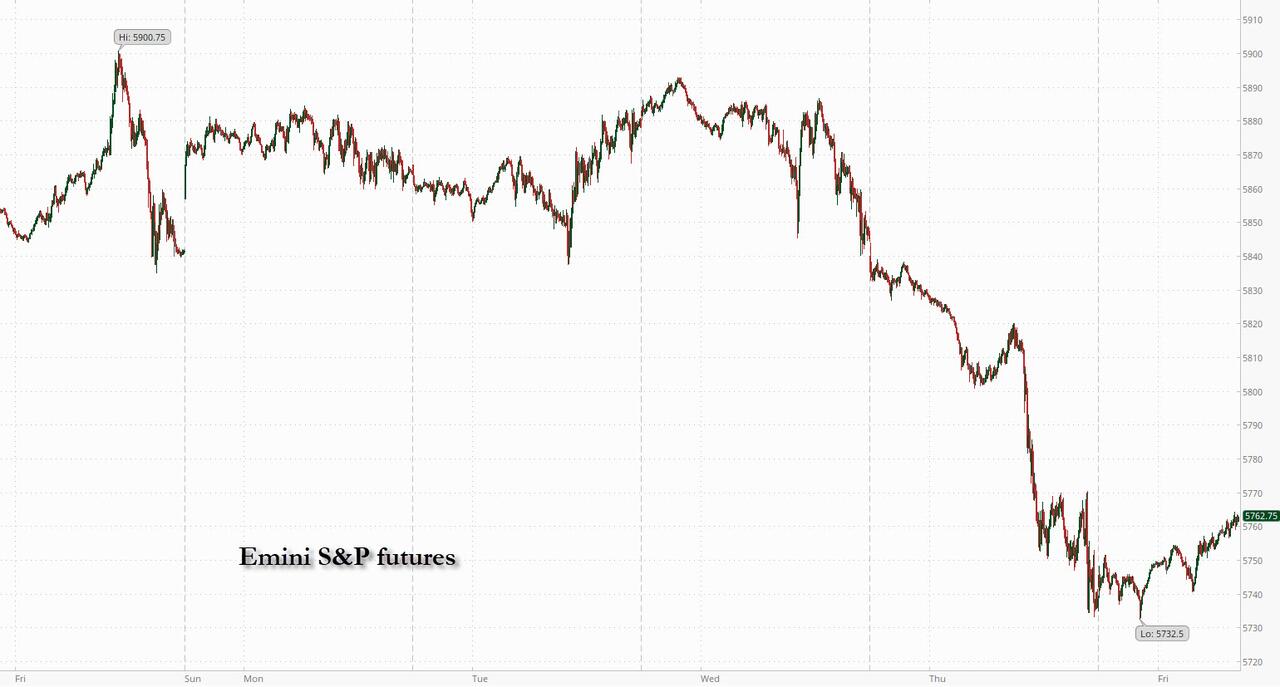

Futures Rise Ahead Of Payrolls As Tech Stocks Rebound

Friday, Nov 01, 2024 – 08:18 AM

Futures are higher on the first day of the month and ahead of what may be a very poor jobs report, with MegaCap tech leading. As of 8:00am ET, S&P futures were 0.4% with the benchmark on track for its worst weekly performance in more than a year amid unease over the outlook for artificial intelligence and cloud computing following results from Microsoft and Meta; Nasdaq futures gained 0.5%, as AMZN and INTC surged 5.8% and 5.7%, respectively, after strong earnings while AAPL is down -1% after its guidance disappointed; NVDA is rebounding and is up +2.0% this morning. Bond yields are flat, and the USD is fractionally higher. Commodities are mixed, with oil higher (WTI +2.9%) amid renewed tension in the Middle East, base metals lower, and precious metals modestly higher. The main event today is the jobs report, but we also get the Mfg ISM, US Mfg PMI, and Construction Spending.

In premarket trading, Amazon.com and Intel shares surged on optimistic earnings results, while Apple declined after reporting softer demand in China, a miss in wearables and services revenue and disappointed with its holiday quarter guidance. Oil majors Exxon Mobil and Chevron both rose after earnings beats. Boeing gained after the aircraft maker reached a tentative agreement to end a labor dispute. Here are all the notable movers this morning:

Abbott Laboratories (ABT US) shares rise 5.1% after a St. Louis jury cleared the company, along with a unit of Reckitt Benckiser, over claims they hid risks their premature-infant formulas can cause a bowel disease that severely sickened a baby boy. It was the firms’ first trial win in litigation over the products.

ADMA Biologics (ADMA) shares rise 14% after KPMG agreed to be the biotech’s auditor, according to a filing, which analysts said should remove an overhang on the stock.

Apple (AAPL) shares fall 1.7% after the iPhone maker reported fourth-quarter results that were weaker than expected on notable metrics, including its Services business and revenue in the intensely competitive China market.

Amazon.com (AMZN) shares rise 7.1% after the e-commerce and cloud computing company reported third-quarter results that beat expectations and gave a solid outlook. Analysts cited margins, AWS and the international retail business as highlights of the quarter.

Atlassian (TEAM) shares soar 21% after the enterprise software developer forecast revenue for its fiscal second quarter ahead of expectations and also beat first-quarter adjusted earnings consensus. KeyBanc Capital Markets upgraded the company to overweight, noting that it had cleared a high bar.

Globalstar (GSAT) shares surge 56% after the company agreed to deliver expanded services to Apple over a new mobile satellite services network, including a new satellite constellation, more ground infrastructure and increased global licensing.

Intel (INTC) shares gain 5.4% after the chipmaker reported third-quarter revenue that beat the average analyst estimate, raising optimism about the company’s turnaround effort. Analysts were positive about the quarter, but said that expectations were low going into the results.

PayPal (PYPL) shares dip 0.5% after Phillip Securities downgraded the payments technology company to accumulate from buy, citing recent stock performance.

Super Micro Computer (SMCI) shares fall 3.3%, putting the stock on track to drop for a third consecutive day, since Ernst & Young resigned as the company’s auditor, citing concerns about governance and transparency.

Today’s payrolls report (full preview here) could show job growth weakening, after the core PCE yesterday posted its biggest monthly gain since April. That muddied the water ahead of next week’s Fed policy meeting, with swaps pricing in 20 basis points of easing, down from 24 at the start of the week. Investors are also bracing for next week’s US election, with the VIX rising to levels last seen during the August market upheaval.

The “highly anticipated employment report, a busy week of earnings that includes a handful of the Magnificent Seven names, rising yields and, of course, next week’s U.S. election are all contributing to building angst in the market, not to mention the FOMC meeting,” said Adam Turnquist, chief technical strategist at LPL Financial. “We may need to wait until after Election Day for volatility to normalize as the VIX futures curve points to potential elevated near-term turbulence for stocks.”

In Europe, the Stoxx 600 index advanced 0.7%, snapping three straight days of declines after they posted the worst monthly drop in a year on Thursday; it remains on track for its biggest weekly drop in two months. Gains for energy stocks helped prop up the gauge, with Shell Plc, Total Energies SE and BP Plc adding more than 1%. Consumer products also gained, boosted by Reckitt after a baby formula trial win. Reckitt Benckiser soared 10% after a unit of the household goods company was cleared by a jury over claims it hid health risks of its premature-infant formula. Only the travel & leisure sector is declining. Here are some of the most notable movers:

Reckitt shares gain as much as 12%, their steepest rise since March 2000, while Abbott Labs rises in US premarket trading after a St. Louis jury cleared the companies over claims they hid risks their premature-infant formulas can cause a bowel disease that severely sickened a baby boy.

HelloFresh shares rally as much as 11% to the highest since March after JPMorgan raises recommendation to overweight from neutral, saying earnings estimates are bottoming out while the stock’s valuation has become attractive following the meal-kit provider’s strategy pivot to shore up its profitability.

Universal Music shares rise as much as 5.6% after reporting a stronger-than-expected growth in revenue generated from music subscriptions.

Scout24 shares rise as much as 4.1%, hitting a new record high. Analysts at Barclays increased their price target on the stock by 10% after the online property platform said annual revenue growth will be at the upper-end of its guidance range as it reported a beat on Thursday.

Boohoo shares gain as much as 6.7% after the online fashion retailer appointed Dan Finley, chief executive officer of the firm’s Debenhams unit, as group CEO.

Kalmar shares gain as much as 12% to reach a record high after the Finnish industrial crane firm reported blow-out earnings. DNB flagged beats on most key metrics.

Meyer Burger shares sink as much as 25% to a record low after the Swiss solar panel maker reported a wider first-half loss.

Fugro shares fall as much as 21% after the Dutch geological data firm’s third-quarter earnings missed estimates, with revenue coming under pressure amid “short-term market-driven challenges” in the Americas, as well as conflicts in the Middle East, according to a release.

Fielmann shares fall as much as 11%, the steepest intraday drop in two years, after the German eyewear firm’s third-quarter results missed estimates.

Earlier in the session, Asian stocks declined, set to cap their fifth-straight week of losses, as a stream of earnings reports failed to lift sentiment ahead of next week’s US election and a key meeting of China’s legislative body. The MSCI Asia Pacific Index fell as much as 0.8% Friday, on course for its longest weekly losing streak in more than two years. Japanese stocks fell the most since Sept. 30, after the yen strengthened against the dollar following Bank of Japan Governor Kazuo Ueda’s comments; benchmarks in Australia and South Korea also slipped. Tech megacaps including TSMC and SoftBank were among the biggest drags on the regional gauge. Equity benchmarks rose in Hong Kong after a private survey showed China’s manufacturing activity unexpectedly picked up last month, a sign of stabilization on Beijing’s stimulus blitz. Traders are awaiting a session by the Standing Committee of National People’s Congress over Nov. 4-8, where further fiscal measures may be announced.

In FX, the Bloomberg Dollar Spot Index rises 0.2%. The yen weakens 0.5%, extending declines after the DPP chief said the BOJ shouldn’t raise interest rates before March. The Swiss franc drops 0.5% after CPI surprised to the downside.

In rates, US Treasuries were steady after minor gains Thursday. But October was the worst month for Treasuries in two years after the heavy selling of the past few weeks that reflected a rethink on US interest rates given signs of resilience in the economy. Front-end yields are higher by 1bp-2bp inside Thursday’s ranges, which included the highest 2- and 5-year yields since July-August. 10-year yields around 4.29% are only slightly cheaper on the day amid similarly muted price action in bunds and gilts; 5s30s spread near 30bp is ~1bp tighter on the day, 13bp on the week UK bonds fell, extending losses this week after the Labour government’s pivotal budget and plans for additional bond sales unleashed a wave of selling. UK 10-year yields rise 2 bps to 4.47%.

In commodities, brent crude futures rose 2% to $74.30 after a report that Iran could be preparing to attack Israel from Iraqi territory in the coming days. European stocks gain for the first time in four days, led by energy and personal care names. US equity futures also rise as Amazon and Intel shares rally in premarket post-earnings, offsetting a fall in shares of Apple. Spot gold is steady around $2,746/oz.

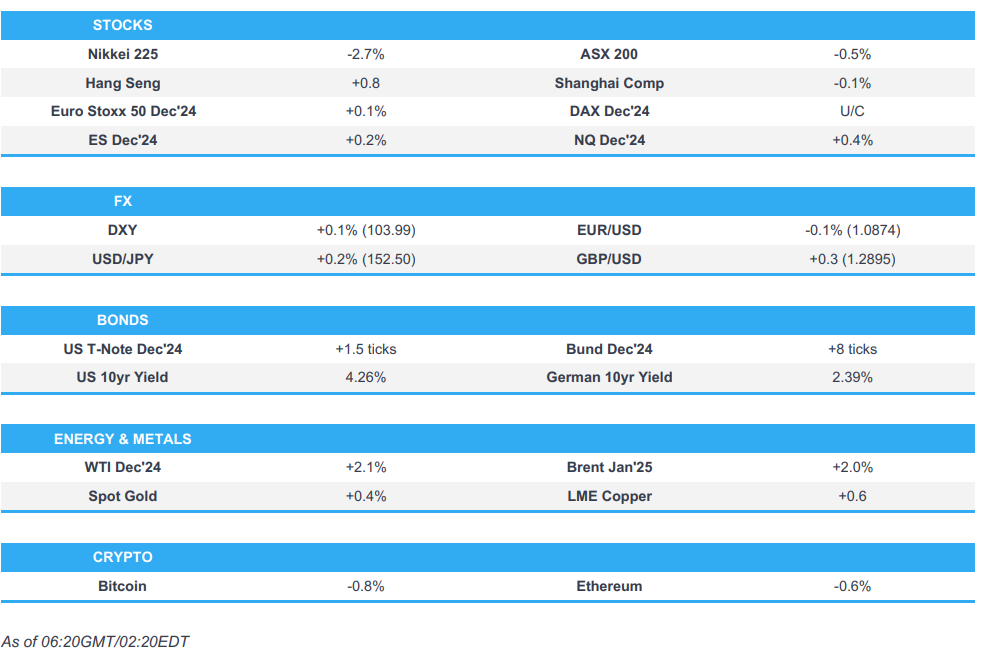

Market Snapshot

S&P 500 futures up 0.3% to 5,753.00

STOXX Europe 600 up 0.5% to 507.91

MXAP down 0.6% to 185.03

MXAPJ up 0.2% to 591.43

Nikkei down 2.6% to 38,053.67

Topix down 1.9% to 2,644.26

Hang Seng Index up 0.9% to 20,506.43

Shanghai Composite down 0.2% to 3,272.01

Sensex down 0.7% to 79,389.06

Australia S&P/ASX 200 down 0.5% to 8,118.83

Kospi down 0.5% to 2,542.36

German 10Y yield little changed at 2.41%

Euro down 0.2% to $1.0859

Brent Futures up 2.7% to $74.76/bbl

Gold spot up 0.4% to $2,754.19

US Dollar Index up 0.13% to 104.11

Top Overnight News

China’s Caixin manufacturing PMI for Oct comes in ahead of expectations at 50.3 (up from 49.3 in Sept and higher than the Street’s 49.7 forecast). WSJ

China has slashed its dependency on US food imports, putting it in a better position to withstand increased trade tensions w/Washington. RTRS

South Korea’s conservative President Yoon Suk Yeol is weighing directly providing arms to Ukraine, a potentially consequential shift in the conflict, in response to North Korea’s deployment of troops to the Russian front line. FT

Blinken says Israel and Lebanon are making progress on how to implement a UN resolution that could be the foundation for ending the present war. RTRS

Donald Trump sued CBS, alleging it engaged in election interference by airing two different versions of an interview with Kamala Harris. He’s seeking $10 billion in damages. LeBron James endorsed Harris. BBG

Apple shares fell premarket after a tepid sales forecast added to lingering concerns about the China market. Amazon reported strong results in cloud and e-commerce. Intel sparked optimism over its turnaround after its revenue outlook slightly beat. Shares jumped. BBG

We estimate nonfarm payrolls rose by 95k in October, below consensus of +105k and the three-month average of +186k. Alternative measures of employment growth were mixed, and strikes and the recent hurricanes likely weighed on payrolls growth this month. GIR

The oil and gas industry has achieved the biggest labor productivity gains of any US sector over the past decade. Crude output has risen to a record 13.3 million barrels a day, 48% more than Saudi Arabia — all with less than a third of the rigs and far fewer workers than 10 years ago. BBG

Boeing and union leaders representing 33,000 striking workers reached a tentative deal that includes a 38% wage increase over four years and a $12,000 signing bonus, though doesn’t reinstate defined-benefit pension plans. Workers will vote on the proposal Monday. Shares rose premarket. BBG

China’s residential property sales rose in October, the first year-on-year increase of 2024, as the government’s latest stimulus blitz brought back buyers. The value of new-home sales from the 100 biggest real estate companies rose 7.1% from a year earlier to 435.5 billion yuan ($61.2 billion), reversing from a 37.7% slump in September, according to preliminary data from China Real Estate Information Corp. Sales surged 73% from a month earlier. BBG

Earnings

Apple Inc (AAPL) Q4 2024 (USD): Adj. EPS 1.64 (exp. 1.58), Revenue 94.93bln (exp. 94.58bln), Products revenue 69.96bln (exp. 69.15bln), iPhone revenue 46.22bln (exp. 45.04bln), Mac revenue: 7.74bln (exp. 7.74bln), iPad revenue: 6.95bln (exp. 7.07bln), Wearables, home, and accessories revenue: 9.04bln (exp. 9.17bln), Service revenue: 24.97bln (exp. 25.27bln), Greater China revenue fell 0.3% Y/Y to 15.03bln (exp. 15.8bln), Co. expects Q1 rev. growth at low to mid-single digits.. -1.1% pre-market

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed following the tech-heavy losses stateside and heightened geopolitical concerns, while Chinese markets outperformed after further encouraging manufacturing PMI data. ASX 200 declined with nearly all industries subdued aside from the commodity-related sectors. Nikkei 225 slumped at the open after recent currency strength and the hawkish tone from BoJ Governor Ueda. Hang Seng and Shanghai Comp were underpinned after the Chinese Caixin Manufacturing PMI followed suit to yesterday’s official release with a surprise return to expansion territory, while the attention was also on recent earnings reports.

Top Asian News

China National People’s Congress Standing Committee proposed a law amendment for further refining government debt supervision, while it added the provision state council and above county-level governments should report on debt management progress.

IMF expects Asia’s economy to expand by 4.6% in 2024 and 4.4% in 2025 but noted risks to Asia’s economic outlook are tilted to the downside and that an acute risk for Asia is an escalation in tit-for-tat retaliatory tariffs between major trading partners. Furthermore, it stated that persistent downward price pressures from China can hurt countries with similar export structures and provoke trade tensions, as well as noted that China’s property sector problems have not been addressed comprehensively, leading to plummeting consumer confidence.

Japan’s Opposition, DPP Chief Tamaki says “the BoJ should not raise interest rates for at least half a year”.

European bourses, Stoxx 600 (+0.6%) are entirely in the green, with sentiment lifted following strong results from Amazon/Intel which have ultimately been able to outmuscle pre-market losses in Apple. European sectors hold a positive bias. Optimised Personal Care tops the pile, lifted by Reckitt after it received a favourable litigation decision. Energy follows close behind, with oil prices firmer amid heightened geopolitical tensions – as such, Travel & Leisure lags. US equity futures (ES +0.1%, NQ +0.4%, RTY +0.1%) are modestly firmer, and with sentiment on a stronger footing after good results from Amazon and Intel; traders await US NFP/ISM Manufacturing later in the session.

Top European News

Moody’s says the UK budget creates challenges as it warns of a muted UK growth, according to the FT.

S&P says UK fiscal position is constrained following budget announcements; new budget decisions, however, do not have an immediate impact on headline budgetary forecasts for the UK

FX

USD is broadly firmer vs. peers with DXY back above the 104 mark. Today’s main data highlight is of course the US NFP report whereby expectations are for a cooling in the headline rate to 113k amid weather and strike activity distortions; the unemployment rate is not expected to be impacted. For now, DXY is tucked within yesterday’s 103.82-104.21 range.

EUR is softer vs. the USD after a recent run of gains that have been underpinned by firmer growth and inflation metrics from the Eurozone. EUR/USD has been as low as 1.0858 but is holding above Thursday’s low at 1.0843.

After two sessions of losses vs. the USD in the wake of Wednesday’s UK budget, Cable is attempting to stabilise and has managed to make its way back onto a 1.29 handle after drifting as low as 1.2843 Thursday.

After strengthening vs. the USD in the wake of the BoJ policy announcement and subsequent hawkish Ueda press conference yesterday, JPY has returned to its recent trend of losses vs. the USD. USD/JPY has been as high as 152.83.

Antipodeans are both marginally softer vs. the USD in quiet newsflow for both countries.

CHF is the laggard across the majors following soft Swiss inflation data. The release has stoked fears that Switzerland could enter into deflation next year and therefore expectations of a 50bps cut by the SNB have heightened (currently priced at 28%).

PBoC set USD/CNY mid-point at 7.1135 vs exp. 7.1122 (prev. 7.1250).

Fixed Income

USTs are a handful of ticks lower, 110-09+ base matches the week’s opening level and is 6+ ticks clear of Thursday’s WTD base. Focus entirely on Payrolls, forecast range of -10k to +200k, with ISM Manufacturing thereafter.

Bunds are softer as the week’s bearish action continues but thus far we remain clear of the WTD 131.15 trough by around 30 ticks but still in the red for the week as a whole by over a full point.

Gilts opened lower by 21 ticks, stabilised briefly before slipping to a 93.45 trough, a low which is just above yesterday’s 93.18 contract low. As such, while the UK’s 10yr yield is elevated it remains shy of 4.5% and Thursday’s 4.52% YTD high.

UK Treasury official says the scenario currently is very different from the Truss-budget.

Commodities

Crude is on a firmer footing as recent rhetoric brings back risk-premium into the weekend. Focus on an Axios piece that Iran is reportedly preparing a major retaliatory strike from Iraq within days. Brent’Jan 25 currently near session highs of USD 74.94/bbl.

Spot gold is firmer, though action is minimal with the metal contained into NFP & ISM Manufacturing. Holding just above the USD 2750/oz mark and yet to make any real headway into recovering towards the USD 2790/oz ATH from early-doors yesterday.

Base metals are firmer, owing to the Chinese Caixin Manufacturing PMI making a surprising return to expansionary territory. 3M LME Copper above the USD 9.6k mark, though the move has paused for breath with the docket now light until the US data deluge.

Geopolitics

Lebanese Prime Minister Mikati says “the continuation of Israeli attacks is an indication of Tel Aviv’s rejection of all efforts to cease fire”, via Asharq News

Iran’s supreme leader Khamenei instructed the Supreme National Security Council on Monday to prepare for attacking Israel, according to NYT citing three Iranian officials familiar with the war planning. Khamenei was said to have made the decision after he reviewed a detailed report from senior military commanders on the extent of damage to Iran’s missile production capabilities and air defence systems around Tehran, critical energy infrastructure and a main port in the south.

Israel conducted strikes on Beirut suburbs for the first time in days, while a Lebanese news agency reported that dozens of buildings in the southern suburbs of Beirut were flattened by Israeli raids, according to Sky News Arabia.

Islamic Resistance in Iraq said it attacked with marches a vital target in the south of the occupied territories several times since dawn today, according to Al Jazeera.

US Defence Secretary Austin spoke to Israeli Defence Minister Gallant and reaffirmed the US remains fully prepared to defend US personnel and partners across the region against threats from Iran, according to the Pentagon.

US State Department issued a response to Israel’s cabinet decision on extending indemnification for correspondent banking between Israel and West Bank in which it stated the short-term extension creates another looming crisis by November 30th and called for Israel to swiftly extend indemnification for essential banking relationships for at least a year.

North Korea’s Standing Committee Chairman Choe says we need to strengthen nuclear weapons and improve readiness for a retaliatory nuclear strike.

US Event Calendar

08:30: Oct. Change in Nonfarm Payrolls, est. 100,000, prior 254,000

Oct. Change in Manufact. Payrolls, est. -30,000, prior -7,000

Oct. Change in Private Payrolls, est. 70,000, prior 223,000

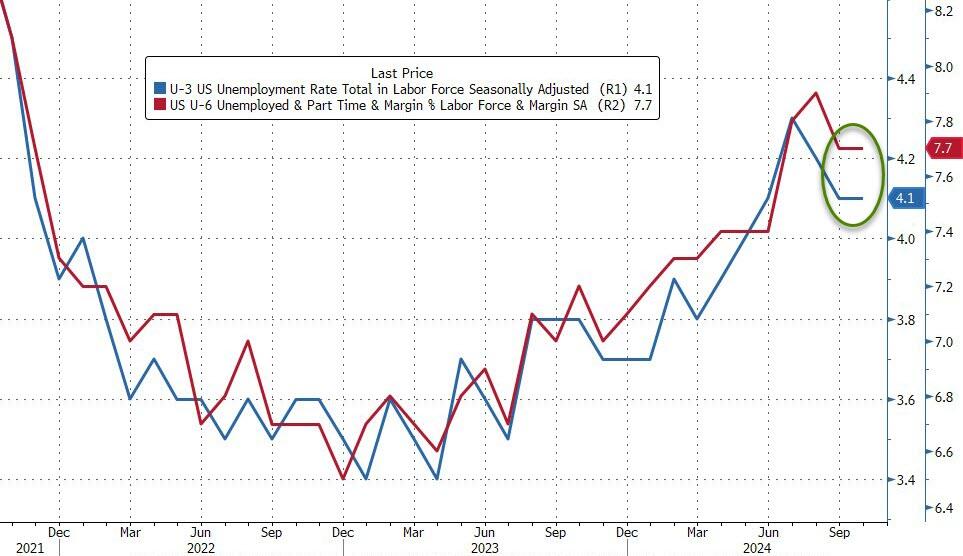

08:30: Oct. Unemployment Rate, est. 4.1%, prior 4.1%

Oct. Underemployment Rate, prior 7.7%

Oct. Labor Force Participation Rate, est. 62.7%, prior 62.7%

08:30: Oct. Average Weekly Hours All Emplo, est. 34.2, prior 34.2

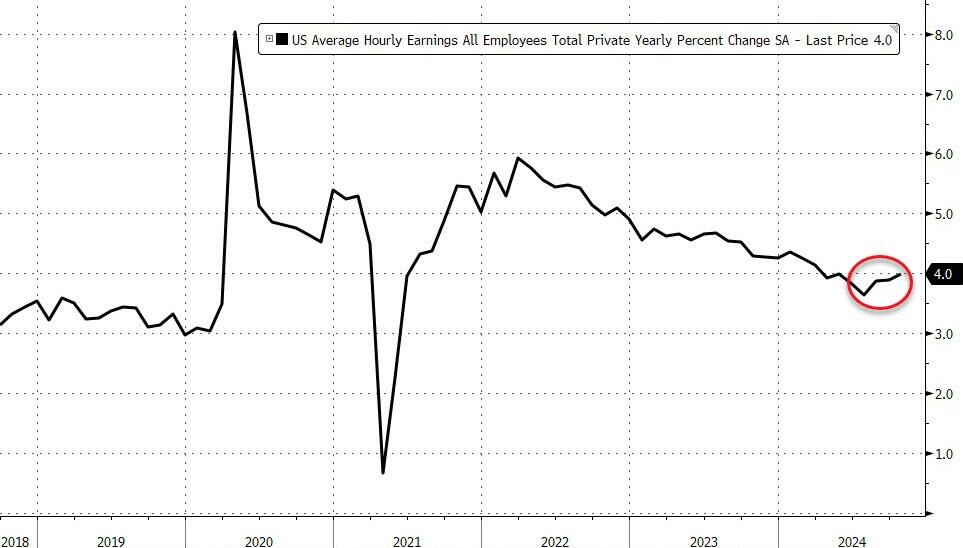

Oct. Average Hourly Earnings YoY, est. 4.0%, prior 4.0%

Oct. Average Hourly Earnings MoM, est. 0.3%, prior 0.4%

09:45: Oct. S&P Global US Manufacturing PM, est. 47.8, prior 47.8

10:00: Sept. Construction Spending MoM, est. 0%, prior -0.1%

10:00: Oct. ISM Manufacturing, est. 47.6, prior 47.2

Oct. ISM Employment, est. 45.0, prior 43.9

Oct. ISM New Orders, est. 47.0, prior 46.1

Oct. ISM Prices Paid, est. 50.0, prior 48.3

DB’s Jim Reid concludes the overnight wrap

Markets finished October on a rough note yesterday, with the S&P 500 (-1.86%) posting its biggest decline in nearly two months, whilst UK assets lost significant ground thanks to investor concerns about Wednesday’s Budget. We’ll have more to say in our monthly performance review out shortly, but the declines mean that Bloomberg’s global bond aggregate has just experienced its worst month since September 2022, back when inflation was still raging and the Fed was hiking by 75bps each meeting. And for equities it’s been a lacklustre month as well, with the S&P 500 losing ground for the first time in six months.