Says it all

SPECIAL thanks to Robert H for sending this to us:

GOLD PRICE CLOSED UP $30.50 TO $2698.70

SILVER PRICE UP $0.11 TO $31.76

Gold ACCESS CLOSED $2705.70

Silver ACCESS CLOSED: $32.00

Bitcoin morning price:$74,943 DOWN 896 DOLLARS.

Bitcoin: afternoon price: $76,919 UP 1080 DOLLARS

Platinum price closing UP $3.95 TO $993.75

Palladium price; DOWN $18.15 TO $1024.15

END

*CANADIAN GOLD: $3750.60 UP 34.77 CDN dollars per oz( * NEW ALL TIME HIGH 3,872.51 CDN DOLLARS PER OZ//OCT 30 2024)

*BRITISH GOLD: 2083.98 UP 16.26 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///2148.36 BRITISH POUNDS/OZ) OCT 30/2024

*EURO GOLD: 2,504.53 UP 22.67 Euros per oz //* (ALL TIME CLOSING HIGH: 2565.55 EUROS PER OZ//OCT 30 //.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE;

EXCHANGE: COMEX

CONTRACT: NOVEMBER 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,667.600000000 USD

INTENT DATE: 11/06/2024 DELIVERY DATE: 11/08/2024

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 390

190 H BMO CAPITAL 179

323 C HSBC 1

363 H WELLS FARGO SEC 176

435 H SCOTIA CAPITAL 1

624 H BOFA SECURITIES 9

657 C MORGAN STANLEY 16

737 C ADVANTAGE 2 9

905 C ADM 6 7

TOTAL: 398 398

MONTH TO DATE: 1,995

JPMorgan stopped 0/392

GOLD: NUMBER OF NOTICES FILED FOR NOV/2024. CONTRACT: 392 NOTICES FOR 39,200 OZ 1.348 TONNES

total notices so far: 1995 contracts for 199,500 Oz (6.205 tonnes)

FOR NOV

SILVER NOTICES: 2 NOTICE(S) FILED FOR 0.10 MILLION OZ/

total number of notices filed so far this month : 654 for 3.270 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP 30.50 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD: HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 3.45 TONNES OF GOLD FROM THE GLD./

/ /INVENTORY RESTS AT 883.46 TONNES

INVENTORY RESTS AT 883.46 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.11 AT THE SLV

NO CHANGES IN SILVER INVENTORY OUT OF THE SLV:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 475.841 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI FELL BY A HUMONGOUS SIZED 1921 CONTRACTS TO 149,205 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUMONGOUS SIZED LOSS IN COMEX OI WAS ACCOMPLISHED WITH OUR MONSTROUS LOSS OF $1,41 IN SILVER PRICING AT THE COMEX WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A SMALL GAIN OF 164 TOTAL CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR LOSS OF $1.41 IN PRICE. WE HAD CONSIDERABLE LIQUIDATION OF T.A.S. CONTRACTS ON WEDNESDAY COMEX TRADING AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S CONTINUAL PRICE RISE FOR THE PAST 2 WEEKS. THEY HAD MUCH SUCCESS YESTERDAY WITH OUR BANKER’S FRIEND OF A HUGE RAID. WE HAD ZERO SHORT COVERING BY OUR SPECS DURING THE COMEX TIME ZONE WEDNESDAY.. WE HAD A HUGE 885 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY A MEGA HUMONGOUS 1479 CONTRACT T.A.S ISSUANCE WHICH WILL BEING USED IN FUTURE TRADING AND THEY PLAY AN INTEGRAL PART DURING RAIDS PLUS TRYING TO CONTAIN ANY SILVER PRICE RISE WITH ANOTHER ABJECT FAILURE. IN ESSENCE WE LOST A HUGE 1036 CONTRACTS ON OUR TWO EXCHANGES WITH OUR LOSS IN PRICE. ALL OF THE LOSS WAS DUE TO TAS LIQUIDATION

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN ON LAST FRIDAY AND AGAIN THIS WEEK. THE ACCUMULATED T.A.S. IS BEING USED TO MANIPULATE PRICES AT THE COMEX NOW EVERY DAY..

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON WEDNESDAY NIGHT: A MEGA HUMONGOUS 1379 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS BUT TO NO AVAIL. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $1.41) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SILVER LONGS FROM THEIR PERCH AS WE HAD A SMALL GAIN OF 164 CONTRACTS ON OUR TWO EXCHANGES.

WE HAD A HUGE 885 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 2.810 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 10,000 OZ QUEUE JUMP//NEW STANDING RISES TO: 3.465 MILLION OZ

// STANDING FOR SILVER//NOV AT 3.4650 MILLION OZ

WE HAD:

/ HUMONGOUS SIZED COMEX OI LOSS//HUGE SIZED EFP ISSUANCE/ VI) MEGA HUMONGOUS SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 1379 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED A HUGE 1516 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS NOV. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF NOV

TOTAL CONTRACTS for 5 DAYS, total 6105 contracts: OR 30.525 MILLION OZ (1221 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 30.525 MILLION OZ

LAST 23 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 30.525 MILLION OZ (WILL BE QUITE LARGE THIS MONTH)

RESULT: WE HAD A GOOD SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 405 CONTRACTS WITH OUR LOSS OF $1.41 IN PRICE OF SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 885 ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR NOV OF 2.810 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 10,000 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR NOV AT 3.465 MILLION OZ

WE HAVE A HUGE LOSS OF 1921 OI CONTRACTS ON THE TWO EXCHANGES WITH OUR DISASTROUS LOSS IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A MEGA HUMONGOUS SIZED 1379 CONTRACTS ( WILL BE USED FOR THURSDAY’S TRADING),//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX SESSION

/ ZERO NET SHORT COVERING FROM OUR SPEC SHORTS DESPITE THE LOSS IN PRICE WEDNESDAY/ . ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (1379) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND LATELY ON A DAILY BASIS INCLUDING YESTERDAY AND TODAY.

WE HAD 2 NOTICE(S) FILED TODAY FOR 0.010 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 10,409 OI CONTRACTS TO 547,625 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE 1979 CONTRACTS//

WE HAD A STRONG SIZED DECREASE IN COMEX OI (10,409 CONTRACTS) OCCURRED WITH OUR LOSS OF $72.80 IN PRICE WEDNESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A GOOD INITIAL STANDING IN GOLD TONNAGE FOR NOV AT 2.488 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE 40,000 OZ QUEUE JUMP//NEW STANDING ADVANCES TO 6.534 TONNES

NEW STANDING FOR NOVEMBER: 6.534 TONNES

/ ALL OF THIS HAPPENED DESPITE OUR $72.80 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S COMEX RAID///. WE HAD A FAIR LOSS OF ONLY 3965 OI CONTRACTS (12.33 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THIS WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! YOU CAN VISUALIZE THIS WITH THE DAILY QUEUE JUMPING WE ARE WITNESSING (AND TODAY’S HUMONGOUS QUEUE JUMP OF 40,000 OZ)

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 6444 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 549,604

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3965 CONTRACTS WITH 10,409 CONTRACTS DECREASED AT THE COMEX// AND A HUGE SIZED 6444 EFP OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 3865 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED 2765 CONTRACTS, WE HAD CONSIDERABLE LIQUIDATION OF T.A.S CONTRACTS WITH OUR HUGE LOSS IN PRICE WEDNESDAY

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A HUGE SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (6444 CONTRACTS) ACCOMPANYING THE STRONG SIZED DECREASE IN COMEX OI OF 10,409 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 3965 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR NOV 2.488 TONNES FOLLOWED BY TODAY’S HUMONGOUS 40,000 OZ QUEUE JUMP

//NEW STANDING NOVEMBER: 6.534 TONNES

/ 3) CONSIDERABLE T.A.S. LIQUIDATION (TRYING TO LOWER GOLD’S PRICE RISE WITH HUGE SUCCESS WEDNESDAY , AND WITH SOME NET LONG SPECS BEING CLIPPED. STICKY GOLD’S LONGS HOWEVER ARE NOT FOOLED BY THE RAID AS THEY WERE REWARDED THURSDAY MORNING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL

4) STRONG SIZED COMEX OPEN INTEREST DECREASE 5) HUGE ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///STRONG T.A.S. ISSUANCE: 2765 T.A.S.CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

NOV

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV :

TOTAL EFP CONTRACTS ISSUED: 28,794 CONTRACTS OF 2,879,400 OZ OR 89.56 TONNES IN 5 TRADING DAY(S) AND THUS AVERAGING: 5758 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 5 TRADING DAY(S) IN TONNES 89.56 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 89.56 DIVIDED BY 3550 x 100% TONNES = 2.53% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END UP WITH THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 89.56 TONNES (WILL PROBABLY BE A HUGE MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPTEMBER. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUMONGOUS SIZED 1921 CONTRACTS OI TO 149,205 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 885 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 885 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 885 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 405 CONTRACTS AND ADD TO THE 885 E.FP. ISSUED

WE OBTAIN A HUMONGOUS SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1036 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 5.180 MILLION OZ OCCURRED DESPITE OUR $1.41 LOSS IN PRICE

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

THURSDAY MORNING WEDNESDAY NIGHT

ASIA TRADING/THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED UP 86.86 PTS OR 2.57%

//Hang Seng CLOSED UP 414.96 PTS OR 2.02%

// Nikkei CLOSED DOWN 99.26 OR 0.25%//Australia’s all ordinaries CLOSED UP 0.30%///Chinese yuan (ONSHORE) CLOSED UP TO 7.1585 CHINESE YUAN OFFSHORE CLOSED UP TO 7.1669// Oil UP TO 70.96 dollars per barrel for WTI and BRENT UP AT 74.44 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 10,409 CONTRACTS TO 547,625 WITH OUR HUGE LOSS IN PRICE OF $72.80 WITH RESPECT TO WEDNESDAY’S TRADING. , WE LOST FEW NET IN NUMBER LONGS WITH THE LOWER PRICE FOR GOLD AS YOU WILL SEE BELOW. WE HAD A HUGE NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (6444).

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY THIS ENTIRE WEEK AND ESPECIALLY DURING YESTERDAY’S HUGE RAID.

THE FED IS THE MAJOR SHORT OF AROUND 112+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS IS SCHEDULED TO HAPPEN LATE OCT 2024/(AS OUTLINED IN OUR GOLD PHYSICAL COMMENTARIES//VIEW ANDREW MAGUIRE LATEST LIVE FROM VAULT 197 AS HE TACKLES THIS IMPORTANT TOPIC). THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST TWO MONTHS. THEY ARE TOTALLY TRAPPED. THUS THE REASON FOR THE CONTINUAL RAIDING OF OUR PHYSICAL ANCIENT METAL OF KINGS AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD A HUGE T.A.S. LIQUIDATION THROUGHOUT LAST WEEK’S GAIN IN PRICE AND AGAIN WITH THIS WEEKS TRADING. HOWEVER MANY LONGS WERE CLIPPED ON LAST THURSDAY’S AND FRIDAY’S RAID AND IT CONTINUED WITH THE HUGE RAID YESTERDAY. THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF THE SPREADERS // T.A.S DURING LAST WEEK AND THIS WEEK IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE NON ACTIVE DELIVERY MONTH OF NOV.… THE CME REPORTS THAT THE BANKERS ISSUED A HUGE SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A HUGE SIZED 6444 EFP CONTRACTS WERE ISSUED: : /DEC 6444 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 6444 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 3965 CONTRACTS IN THAT 6444 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 10,409 COMEX CONTRACTS..AND THIS FAIR LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR HUMONGOUS LOSS IN PRICE OF $72.80 WEDNESDAY// COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AS MENTIONED ABOVE.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT, A STRONG SIZED 2765 CONTRACTS, WAS USED TO REPLENISH SUPPLIES.. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK)

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE (AND SPREADERS LATE IN THE MONTH). THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN LAST WEEK’S AND THIS WEEK’S TRADING.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: NOV (6.534 TONNES) WHICH IS GOOD FOR OUR NON ACTIVE NOV DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 47 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK PRIOR =60.391 TONNES

NOV . 6.534 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY A HUGE $72.80/)//AND WERE UNSUCCESSFUL IN KNOCKING OFF SOME NET SPECULATOR LONGS AS WE DID HAVE A FAIR LOSS IN OUR TWO EXCHANGES. WE DID HAVE CONSIDERABLE T.A.S. SPREADER LIQUIDATION WEDNESDAY BUT THIS COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL THURSDAY EVENING.

WE HAVE LOST A TOTAL OF 12.33 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR NOV (2.488TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUMONGOUS QUEUE JUMP OF 400 CONTRACTS OR 40,000 OZ (1.244 TONNES). THESE GUYS UNDERWENT A HUGE SIZED QUEUE JUMP BOLTING AHEAD OF OTHER LONGS TO OBTAIN BADLY NEEDED PHYSICAL GOLD.

//NEW STANDING FOR NOV 6.534 TONNES

NEW STANDING FOR NOVEMBER: 6.534 TONNES

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR HUGE LOSS IN PRICE TO THE TUNE OF $72.80

WE HAD 1979 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET LOSS ON THE TWO EXCHANGES 3965 CONTRACTS OR 396,500 OZ (12.33 TONNES)

confirmed volume WEDNESDAY 421,271 contracts//monstrous//massive t.a.s. liquidation

//speculators have left the gold arena

END

NOV 7 OCT GOLD CONTRACT

/ /// THE NOV 2024 GOLD CONTRACT

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | NIL . |

| Deposit to the Dealer Inventory in oz | NIL |

| Deposits to the Customer Inventory, in oz | 805.45 OZ BRINKS ENHANCED these 2 bars are London good delivery bars with location strictly in london. |

| No of oz served (contracts) today | 395 notice(s) 39500 OZ 1.238 TONNES |

| No of oz to be served (notices) | 106 contracts 10600 OZ 0.3297 TONNES |

| Total monthly oz gold served (contracts) so far this month | 1995 notices 199,500oz 6.205 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

dealer deposits: 0

total dealer deposits: nil oz

we have 1 customer deposits

i) Brinks 805.45 oz Bricks enhance

these are 2 London 400+ oz each, good delivery bars.

total deposits 805.45 oz

withdrawals: 0

adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR NOV.

For the front month of NOV: we have an oi of 451 contracts having GAINED 387 contracts. We had 13 contracts served on WEDNESDAY so we gained A MONSTROUS 400 contracts as they underwent a good queue jump of 40,000 oz (1.244 TONNES OF GOLD)

DECEMBER, THE BIGGEST DELIVERY MONTH LOST 16,977 CONTRACTS TO 372,338

JANUARY GAINED 56 CONTRACTS TO STAND AT 113

FEBRUARY GAINED 6542 CONTRACTS TO 113,455 .

We had 396 contracts filed for today representing 39,600 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 395 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for NOV /2024. contract month, we take the total number of notices filed so far for the month (1995 x 100 oz ) to which we add the difference between the open interest for the front month of NOV(451 CONTRACTS) minus the number of notices served upon today (396 x 100 oz per contract( equals 210,100 OZ OR 6.534 TONNES.

thus the INITIAL standings for gold for the NOV contract month: No of notices filed so far (1995 x 100 oz +we add the difference for front month of NOV (451 OI} minus the number of notices served upon today (395 x 100 oz which equals 210,100 oz (6.534 TONNES) +

TOTAL COMEX GOLD STANDING FOR NOV.: 6.534 TONNES WHICH IS HUGE FOR THIS NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,599,125.751 oz 49.74 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,134,174.442 OZ

TOTAL REGISTERED GOLD 7,619,760.679/// 237.00tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,514,413.763 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,020,635 oz (REG GOLD- PLEDGED GOLD)= 187.26 tonnes //

END

SILVER/COMEX

NOV 7. 2024

INITIAL

//2024// THE NOV 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 304,092.277 oz CNT Delaware . |

| Deposits to the Dealer Inventory | nil oz |

| Deposits to the Customer Inventory | 1,200,,023.270 oz HSBC CNT |

| No of oz served today (contracts) | 2 CONTRACT(S) (10,000 OZ) |

| No of oz to be served (notices) | 39 contracts (195,000oz) |

| Total monthly oz silver served (contracts) | 654 Contracts (3.270 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit/

total dealer deposit : NIL oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 customer deposits

i) Into HSBC 600,036.220 oz

ii) Into CNT 599,987.040 oz

total customer deposits 1,200,023.270 oz

We had 2 withdrawals

i) Out of CNT 303,,107.07 oz

ii) Out of Delaware: 985,700 oz

total withdrawal 304,092.77 ooz oz

JPMorgan has a total silver weight: 134.401million oz/311.809million or 43.10%

adjustment 0

TOTAL REGISTERED SILVER: 70.073MILLION OZ//.TOTAL REG + ELIGIBLE. 311.809 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR NOV

silver open interest data:

FRONT MONTH OF NOV /2024 OI: 41 OPEN INTEREST FOR A LOSS OF 1 CONTRACT

WE HAD 3 NOTICES FILED ON WEDNESDAY SO WE GAINED 2 CONTRACTS OR 10,000 OZ UNDERWENT A QUEUE JUMP

DECEMBER SAW A LOSS OF 4464 CONTRACTS DOWN TO 106,682 CONTRACTS

JANUARY SAW A GAIN OF 64 CONTRACTS UP TO 1058

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 1 for 0.010 MILLION oz

CONFIRMED volume; ON WEDNESDAY 139,690 monstrous//huge t.a.s. liquidation

To calculate the number of silver ounces that will stand for delivery in NOV we take the total number of notices filed for the month so far at 654x 5,000 oz = 3.270 MILLION oz

to which we add the difference between the open interest for the front month of NOV (41) and the number of notices served upon today (2)x (5000 oz)

Thus the standings for silver for the NOV 2024 contract month: 654 Notices served so far) x 5000 oz + OI for the front month of NOV(41) number of notices served upon today minus (2)x 5000 oz of silver standing for the NOV contract month equates to 3.465 MILLION OZ.

New total standing: 3.465 million oz.

There are 70.077 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS//

GLD

NOV 7 WITH GOLD UP $30.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.45 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 883.46 TONNES

NOV 6 WITH GOLD DOWN $72.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 886.91 TONNES

NOV 5 WITH GOLD UP $4.05 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:.// . // .///INVENTORY RESTS AT 888.63 TONNES

NOV 4 WITH GOLD DOWN $2.45 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.16 TONNES OF GOLD OUT OF THE GLD.// . // .///INVENTORY RESTS AT 888.63 TONNES

NOV 1 WITH GOLD UP 0.15 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.86 TONNES OF GOLD INTO THE GLD.// . // .///INVENTORY RESTS AT 891 TONNES

OCT 31 WITH GOLD DOWN $49.55 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD.// . // .///INVENTORY RESTS AT 892.65 TONNES

OCT 30 WITH GOLD UP $20.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD INTO THE GLD.// . // .///INVENTORY RESTS AT 889,78 TONNES

OCT 29 WITH GOLD UP $25.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD.// . // .///INVENTORY RESTS AT 891.50 TONNES

OCT 28 WITH GOLD UP $1.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.02 TONNES OF GOLD FROM THE GLD.// . // .///INVENTORY RESTS AT 889.78 TONNES

OCT 25 WITH GOLD UP $6.40 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: // . // .///INVENTORY RESTS AT 893.80 TONNES

OCT 24 WITH GOLD UP $19.60 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES // // . // .///INVENTORY RESTS AT 893.80 TONNES

OCT 23 WITH GOLD DOWN $29.40 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.45 TONNES // // . // .///INVENTORY RESTS AT 895.24 TONNES

OCT 21 WITH GOLD UP $9.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.277 TONNES // // . // .///INVENTORY RESTS AT 888.63 TONNES

OCT 18 WITH GOLD UP $22.30 ON THE DAY; NO CHANGES IN GOLD AT THE GLD // // . // .///INVENTORY RESTS AT 884.59 TONNES

OCT 17 WITH GOLD UP $17.30 ON THE DAY; NO CHANGES IN GOLD AT THE GLD // // . // .///INVENTORY RESTS AT 884.59 TONNES

OCT 16 WITH GOLD UP $13.60 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD //A MONSTER DEPOSIT OF 4.02 TONNES OF GOLD INTO THE GLD.; // . // .///INVENTORY RESTS AT 884.59 TONNES

OCT 15 WITH GOLD UP $2.85 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD //A MONSTER DEPOSIT OF 4.31 TONNES OF GOLD INTO THE GLD.; // . // .///INVENTORY RESTS AT 880.57 TONNES

OCT 11 WITH GOLD UP $36.55 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 10 WITH GOLD UP $14.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 9 WITH GOLD DOWN $8.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 8 WITH GOLD DOWN $28,.95 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 7 WITH GOLD DOWN $1.85 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD; A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD// . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 4 WITH GOLD DOWN $11.20 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD; A DEPOSIT OF 12.57 TONNES OF GOLD INTO THE GLD// . // .///INVENTORY RESTS AT 877.41 TONNES

OCT 3 WITH GOLD DOWN $8.95 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; . // .///INVENTORY RESTS AT 874.82 TONNES

OCT 2WITH GOLD DOWN $20.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD; A DEPOSIT OF 2.88 TONNES OF GOLD INOT THE GLD. // .///INVENTORY RESTS AT 874.82 TONNES

OCT 1 WITH GOLD UP $28,55 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // .///INVENTORY RESTS AT 871.94 TONNES

SEPT 30 WITH GOLD DOWN $6.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD; A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// .///INVENTORY RESTS AT 871.94 TONNES

SEPT 27 WITH GOLD DOWN $26.60 ON THE DAY; NO CHANGES IN GOLD AT THE GLD .///INVENTORY RESTS AT 877,12 TONNES

SEPT 26 WITH GOLD UP $11.20 ON THE DAY; NO CHANGES IN GOLD AT THE GLD .///INVENTORY RESTS AT 877,12 TONNES

SEPT 25WITH GOLD UP $9.25 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD ./// /:// A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD//////INVENTORY RESTS AT 877,12 ONNES

SEPT 24WITH GOLD UP $23.60 ON THE DAY; NO CHANGES IN GOLD AT THE GLD ./// /:// //////INVENTORY RESTS AT 875.39 ONNES

SEPT 23 WITH GOLD UP $6.65 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1,43 TONNES OF GOLD INTO THE GLD../// /:// //////INVENTORY RESTS AT 875.39 ONNES

SEPT 20 WITH GOLD UP $32.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD../// /:// //////INVENTORY RESTS AT 873,96ONNES

SEPT 19 WITH GOLD UP $17,05 ON THE DAY; NO CHANGES IN GOLD AT THE GLD/// /:// //////INVENTORY RESTS AT 872.23TONNES

SEPT 18 WITH GOLD UP $5.95 ON THE DAY; NO CHANGES IN GOLD AT THE GLD/// /:// //////INVENTORY RESTS AT 872.23TONNES

SEPT 17WITH GOLD DOWN $15.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 1.52 TONNES INTO THE GLD /:// //////INVENTORY RESTS AT 872.23TONNES

GLD INVENTORY: 883.46 TONNES, TONIGHTS TOTAL

SILVER

NOV 7 WITH SILVER UP $0.11 //NO CHANGES IN SILVER INVENTORY AT THE SLV: /// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 6 WITH SILVER DOWN $1.41 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.692 MILLION OZ FROM THE SLV/.//// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 5 WITH SILVER UP 0.18 :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.109 MILLION OZ FROM THE SLV/.//// //INVENTORY AT SLV RESTS AT 479,533 MILLION OZ

NOV 4 WITH SILVER DOWN $0.08 :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 547,000 OZ.//// //INVENTORY AT SLV RESTS AT 480.642 MILLION OZ

NOV 1 WITH SILVER DOWN $0.10 : NO CHANGES IN SILVER INVENTORY AT THE SLV:.//// //INVENTORY AT SLV RESTS AT 481.189 MILLION OZ

OCT 31 WITH SILVER DOWN $1.26 : HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.647 MILLION OZ OF SILVER INTO THE SLV//.//// //INVENTORY AT SLV RESTS AT 481.189 MILLION OZ

OCT 30 WITH SILVER DOWN 38 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV.//// //INVENTORY AT SLV RESTS AT 477.542 MILLION OZ

OCT 29 WITH SILVER UP 49 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV’ A WITHDRAWAL OF 0.628 MILLION OZ OUT OF THE SLV..//// //INVENTORY AT SLV RESTS AT 477.542 MILLION OZ

OCT 28 WITH SILVER UP 15 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV’ A WITHDRAWAL OF 1.431 MILLION OZ OUT OF THE SLV..//// //INVENTORY AT SLV RESTS AT 478.180 MILLION OZ

OCT 25 WITH SILVER DOWN $0,02 : HUGE CHANGES IN SILVER INVENTORY AT THE SLV’ A DEPOSIT OF 3.06 MILLION OZ INTO THE SLV..//// //INVENTORY AT SLV RESTS AT 480.281 MILLION OZ

OCT 24 WITH SILVER UP $0,01 : SMALL CHANGES IN SILVER INVENTORY AT THE SLV’ A WITHDRAWAL OF 0.684 MILLION OZ OF SILVER OUT OF THE SLV..//// //INVENTORY AT SLV RESTS AT 477.177 MILLION OZ

OCT 23 WITH SILVER DOWN $1.15 : SMALL CHANGES IN SILVER INVENTORY AT THE SLV’ A WITHDRAWAL OF 0.228 MILLION OZ OF SILVER OUT OF THE SLV..//// //INVENTORY AT SLV RESTS AT 477,861 MILLION OZ

OCT 22 WITH SILVER $0.93 : HUGE CHANGES IN SILVER INVENTORY AT THE SLV’ A DEPOSIT OF 3.329 MILLION OZ OF SILVER INTO THE SLV..//// //INVENTORY AT SLV RESTS AT 478.089 MILLION OZ

OCT 18 WITH SILVER $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//// //INVENTORY AT SLV RESTS AT 473.483 MILLION OZ

OCT 17 WITH SILVER DOWN 18 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 3.419 MILLION OZ INTO THE SLV// //INVENTORY AT SLV RESTS AT 473.483 MILLION OZ

OCT 16 WITH SILVER UP 25 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV// //INVENTORY AT SLV RESTS AT 470.064 MILLION OZ

OCT 15 WITH SILVER DOWN 2 CENTS : SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 456,,000 OZ FORM THE SLV. //INVENTORY AT SLV RESTS AT 470.064 MILLION OZ

OCT 11 WITH SILVER UP 53 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 932,000 OZ FORM THE SLV. //INVENTORY AT SLV RESTS AT 470.520 MILLION OZ

OCT 9 WITH SILVER UP 7 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.964 MILLION OZ FORM THE SLV..: /INVENTORY AT SLV RESTS AT 471.432 MILLION OZ

OCT 8 WITH SILVER DOWN $1.41 : HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.007 MILLION OZ FORM THE SLV..: /INVENTORY AT SLV RESTS AT 468.468 MILLION OZ

OCT 7 WITH SILVER DOWN 39 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 684,000 OZ FORM THE SLV..: /INVENTORY AT SLV RESTS AT 466.461 MILLION OZ

OCT 4 WITH SILVER UP 0 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV.: /INVENTORY AT SLV RESTS AT 465.777MILLION OZ

OCT 3WITH SILVER UP 69 CENTS :HUGE CHANGES IN SILVER INVENTORY A WITHDRAWAL OF 1.643 MILLION OZ FORM THE SLV//.: /INVENTORY AT SLV RESTS AT 467.555MILLION OZ

OCT 2WITH SILVER DOWN $0.23 : NO CHANGES IN SILVER INVENTORY: /INVENTORY AT SLV RESTS AT 469.198MILLION OZ

OCT 1 WITH SILVER UP $0.30 : HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 1.368 MILLION OZ INTO THE SLV/. /: .///./// /INVENTORY AT SLV 469.198MILLION OZ

SEPT30 WITH SILVER DOWN $0.33 : HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.094 MILLION OZ INTO THE SLV/. /: .///./// /INVENTORY AT SLV 470.566MILLION OZ

SEPT27WITH SILVER DOWN $0.58 : HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.653 MILLION OZ INTO THE SLV/. /: .///./// /INVENTORY AT SLV 469.472MILLION OZ

SEPT26WITH SILVER UP $0.29 : NO CHANGES IN SILVER INVENTORY:/. /: .///./// /INVENTORY AT SLV 464.819 MILLION OZ

SEPT25WITH SILVER DOWN $0.26 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 2.281MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 464,819 MILLION OZ

SEPT24 WITH SILVER UP $1.26 : HUGE CHANGES IN SILVER INVENTORY:. A DEPOSIT OF 9,305 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 467,100 MILLION OZ

SEPT23 WITH SILVER DOWN $0.39 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 1.824MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 457.795MILLION OZ

SEPT20 WITH SILVER UP $0.08 : NO CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 1.46 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 459,619 MILLION OZ

SEPT19 WITH SILVER UP $0.85 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 1.46 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 459,619 MILLION OZ

SEPT18 WITH SILVER DOWN $0.29 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 1,551 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 461.079 MILLION OZ

SEPT17 WITH SILVER DOWN $0.13 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWALOF 5.976 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 462MILLION OZ

CLOSING INVENTORY 475.841 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY//BILL HOLTER:

3. CHRIS POWELL AND GATA. DISPATCHES

Ronan Manly: Gold remains strong as central banks sustain upward gold buying trend in 2024

Submitted by admin on Wed, 2024-11-06 10:53 Section: Daily Dispatches

By Ronan Manly

Bullion Star, Singapore

Wednesday, November 6, 2024

As we enter the final stretch of 2024 with the international gold price having made continual new highs during the last eight months, it’s encouraging to see that central banks, on a collective basis, are still large net buyers of physical gold for their monetary gold reserves.

According to the World Gold Council’s just released Gold Demand Trend report for the third quarter of 2024, central banks (and other official sector institutions) added a net 694 tonnes of gold to their monetary gold reserves during the first nine months of 2024. This comprises net buying of 305 tonnes of gold in Q1, 203 tonnes in Q2, and 186 tonnes in Q3.

Based on World Gold Council data (which is collected by precious metals consultancy Metals Focus), January–September 2024 central bank gold purchases are below the January–September 2023 period (when central banks added a net 833 tonnes of gold), but on a par with the first nine months of 2022 (when central banks bought a combined 700 tonnes of gold).

Recalling that 2022 was a record year for central bank gold buying (with central banks net buying 1082 tonnes of gold), and 2023 was not far off that (with central banks net buying 1,049 tonnes), then 2024 is set to be a respectable year also, independent of what buying might or might not occur in the fourth quarter of 2024, and shows that the investment rationale of central banks buying gold — store of value, safe haven, no counterparty risk, no sanctions risk, diversification benefits — are still intact. …

… For the remainder of the report:

END

Junior gold miners are appealing takeover targets as bullion prices climb

Submitted by admin on Tue, 2024-11-05 18:17 Section: Daily Dispatches

By Dominique Gene and Andrew Willis

The Globe and Mail, Toronto

Monday, November 4, 2024

For the mining crowd, the annual Denver Gold Forum is a chance to swap speculation on potential deals. At this year’s gathering in September, all the takeover talk revolved around junior companies with promising properties being snapped up by larger rivals.

The country’s smallest gold miners — those developing projects that are years away from producing bullion — are becoming attractive takeover targets. Soaring gold prices have boosted the valuations of senior and intermediate mining companies and left them flush with cash, while stock prices continue to languish at exploration companies.

After hosting a series of meetings and dinners at this year’s Denver conference, mining analyst Tanya Jakusconek at Bank of Nova Scotia said in a report: “The M&A chatter this year was focused on taking out smaller-sized companies, including juniors in key mining camps, given the depressed valuations and limited access to capital.”

The price of gold soared 37% over the past year, closing Friday at US$2,736 an ounce. Last week investment bank Goldman Sachs predicted the rally will continue and the price will hit US$3,000 an ounce next year.

Takeover activity in the mining sector is picking up, with 125 deals announced in Canada in the second quarter of the year, up 34% from the previous three-month period, according to investment bank Crosbie & Co. The value of mining M&A in the most recent quarter jumped to $964 million from $328 million in the prior quarter.

So far this year, large and mid-sized mining companies focused on acquiring one another, not picking off junior companies with projects that will take years to produce gold. In a report last week, analysts at RBC Capital Markets predicted that the dynamic is about to change, as senior miners begin taking advantage of a rising tide that has only lifted a few boats.

“We think rising producer margins could start to encourage activity to backfill asset portfolios, especially if access to early-stage capital remains limited,” the RBC analysts said.

The investment bank tracked more than 100 junior mining companies, and its top stock picks based on the quality of their projects, rather than takeover potential, are Artemis Gold, Skeena Resources Ltd., and Seabridge Gold.

Brian Graves, a mergers and acquisitions lawyer at law firm Fasken, said takeover activity picked up at established producers, but not at junior companies, in part because mining executives want to see more evidence that higher bullion prices are here to stay before committing capital to projects years away from producing gold.

The higher spot gold price offers immediate benefits for senior companies that are in production, whereas the value of junior companies, which are still in the exploration or development stages, tend to be more influenced by long-term gold price forecasts, Mr. Graves said.

“There may be a concern amongst potential acquirers that the price isn’t sustainable,” he said, adding that management teams at established producers fear overpaying for projects, which they have been guilty of doing in the past.

At the 2017 Denver forum, executives at New York-based hedge fund Paulson & Co., led by long-time gold bull John Paulson, lambasted gold producers for wasting billions of dollars on value-destroying mergers and acquisitions.

M&A activity at junior miners is also being held back because the companies’ executives and boards are often reluctant to engage in takeover talks with their stock prices at relatively low valuations, Mr. Graves said. He said the management mindset at most exploration companies is to maintain control, keep raising capital, and try to reap the rewards that come from bringing a mine into production.

Juniors have found a way to bridge the gap between financings and M&A through joint ventures, Mr. Graves said. There’s an uptick in these ventures, which allows junior companies to stay involved in their assets without giving them up entirely, which they would have to do in an M&A deal.

On the other hand, senior companies can make strategic investments without fully committing to a particular junior company, Mr. Graves said.

For potential acquirers, pouncing on a junior company in the preliminary stages of launching a mine is typically the best way to make money. In a report published last month, analysts Ovais Habib and Eric Winmill at Scotiabank looked at 17 mines built over the past decade and concluded that senior mining companies “can achieve a better value proposition by pursuing earlier-stage rather than later-stage development projects when looking to make an acquisition.”

“For corporates looking to expand their growth pipeline and acquire a new project, that project will get considerably more expensive” as it gets closer to production, the Scotiabank analysts said.

* * *

4. OTHER GOLD COMMENTARIES//LIVE FROM THE VAULT/no 197 ANDREW MAGUIRE

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES: ALUMINA

.

6 CRYPTOCURRENCY NEWS

END

ASIA TRADING THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED UP 86.86 PTS OR 2.57%

//Hang Seng CLOSED UP 414.96 PTS OR 2.02%

// Nikkei CLOSED DOWN 99.26 OR 0.25%//Australia’s all ordinaries CLOSED UP 0.30%///Chinese yuan (ONSHORE) CLOSED UP TO 7.1585 CHINESE YUAN OFFSHORE CLOSED UP TO 7.1669// Oil UP TO 70.96 dollars per barrel for WTI and BRENT UP AT 74.44 Stocks in Europe OPENED ALL GREEN

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 7.1585

OFFSHORE YUAN: UP TO 7.1669

SHANGHAI CLOSED CLOSED UP 86.86 PTS OR 2.57%

HANG SENG CLOSED CLOSED UP 414.96 PTS OR 2.02%

2. Nikkei closed DOWN 99.26 PTS OR 0.25%

3. Europe stocks SO FAR: ALL GREEN

USA dollar INDEX DOWN TO 104.67 EURO RISES TO 1.0769 UP 40 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.001 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 160.86…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.4720 Italian 10 Yr bond yield UP to 3.798 //SPAIN 10 YR BOND YIELD UP TO 3.225

3i Greek 10 year bond yield DOWN TO 3.276

3j Gold at $2672/50 /Silver at: 31.28 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 55/100 roubles/dollar; ROUBLE AT 97.61

3m oil into the 70 dollar handle for WTI and 74 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 153.81 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.001% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8754 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9428 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.4942 UP 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.620 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.261 DOWN 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 34.24…

10 YR UK BOND YIELD: 4.621 UP 1 PTS

10 YR CANADA BOND YIELD: 3.341 DOWN 3 BASIS PTS

5 YR CANADA BOND YIELD: 3.156 DOWN 0 PTS.

2a New York OPENING REPORT

S&P Futures Extend Gains As Trump Trades Cool

Thursday, Nov 07, 2024 – 08:18 AM

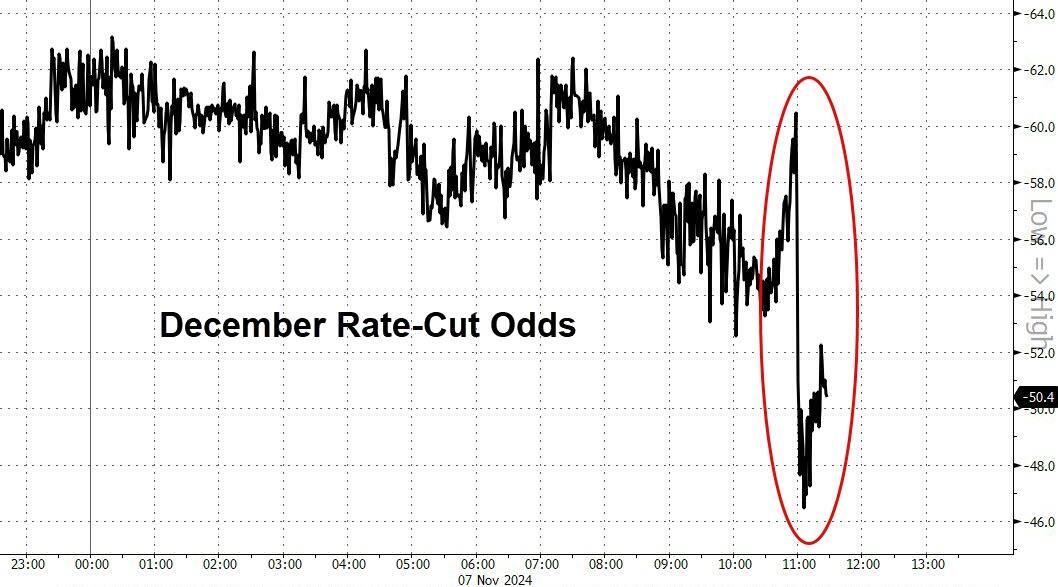

US equity futures extended their post-election gains, as S&P futures traded near session high with both Tech and small caps outperforming as the dollar eased and yields were flat, as traders continued to map out Trump’s return to the White House and what it holds for the Fed’s interest-rate path. As of 8:00am ET, S&P 500 futs traded 0.2% higher after surging in the previous session on bets that the newly elected President will boost corporates through pro-growth policies; Nasdaq futures rose 0.4% after hitting a new all time high on Wednesday; Mag7 names were mixed premarket with semis bid despite NVDA dipping -21bps. An index of the dollar retreated 0.3% following its best day since Sept 2022. Moves in US Treasury yields were muted after Wednesday’s seismic selloff; bond yields are 1-2bps lower as the curve steepens. The commodity complex is mixed with Ags higher, Energy lower, and Base metals outperforming Precious. Today’s macro data focus is on the Fed’s decision (2pm ET) and the BOE (7am ET); both CBs are expected to cut by 25bps.

In premarket trading, Lyft soared 22% after the ride-hailing company topped fourth-quarter forecast, with analysts positive about the company’s profitability path. Tinder parent Match Group tumbled 13% after the dating-app company’s fourth-quarter revenue forecast missed estimates. SolarEdge shares slumped 16% after the renewable-energy-equipment provider took a $1-billion writedown and issued underwhelming guidance for the fourth quarter. Here are some other premarket movers:

- AppLovin (APP) rises 30% after 3Q results from the mobile-gaming software company beat expectations.

- Arm Holdings (ARM) falls 6% after the chip designer issued a disappointing forecast for third-quarter revenue.

- Bumble (BMBL) drops 6% after the dating-app company posted in-line results, and analysts flagged concerns about limited visibility on the turnaround strategy.

- Corteva (CTVA) declines 7% after the company cut its net sales guidance for the year, as a reduced corn-planted area in Argentina hurt the company’s seed business in the 3Q.

- Digital Turbine (APPS) sinks 38% after the application software company cut its full-year revenue forecast.

- Dutch Bros (BROS) jumps 17% after the drive-thru coffee chain boosted its full-year total revenue forecast.

- Elf Beauty (ELF) climbs 10% after the cosmetics company boosted its full-year guidance.

- Qualcomm (QCOM) rises 6% after the world’s biggest seller of smartphone processors gave a bullish sales forecast for the current period.

- Tapestry shares (TPR) climbs 5% after the accessories company raised its annual guidance.

- Wolfspeed (WOLF) sinks 25% after the semiconductor device company gave weak second-quarter guidance below consensus.

The furious post-election rally eased on Thursday after grappling with the far-reaching consequences of a Trump presidency. His win has forced investors to come to terms with economic policies that could lead to fewer Fed rate cuts, along with a possible Republican sweep of Congress that could help fuel fiscal expansion.

“What we saw yesterday was the playbook of the Trump trade in action but it’s soon going to evolve,” said Arnaud Girod, head of economics and cross-asset strategy at Kepler Cheuvreux in Paris. “US yields can’t continue to go up with US equities on the rise, my conviction is that yields will calm down.”

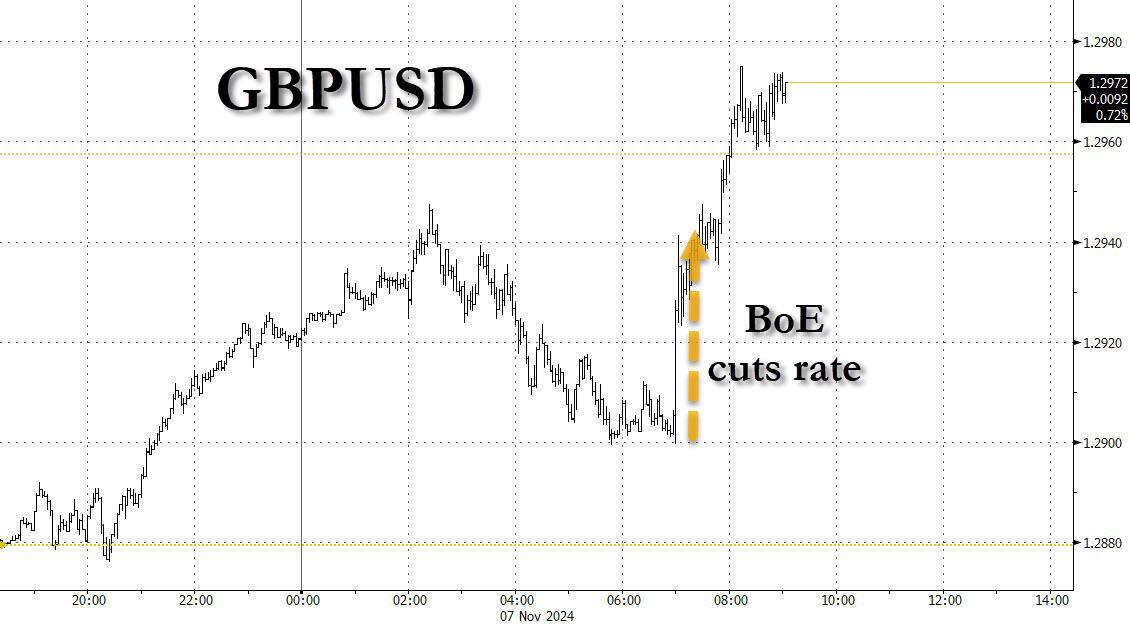

Ahead of the Fed’s rate cut at 2pm (full preview here), the Bank of England lowered borrowing costs earlier on Thursday by 25 basis points to 4.75%. Governor Andrew Bailey said that rates are likely to fall “gradually from here” and that last week’s UK budget will lift inflation by just under half a percentage point at its peak.

In Europe, stock also gained for a second day, with the Stoxx 600 rising 0.6% led by gains in basic resources after Chinese stocks closed near a one-month high as traders digested the possibility of fresh elections in Germany and whether it could help to revive growth in Europe’s biggest economy. Here are the biggest movers Thursday:

- Banco Bpm shares rise as much as 11% to the highest in almost nine years, after the Italian lender launched an all-cash takeover offer for asset manager Anima Holding SpA

- Swiss Re surges as much as 7.1%, the most in four years, after the reinsurer raised its US liability reserves by $2.4b in Property & Casualty Reinsurance in 3Q, following a comprehensive review

- Heidelberg Materials rises as much as 7.7% to their highest intraday value on record after results Jefferies called a pleasant surprise. Analysts highlighted its guidance upgrade as a positive

- ArcelorMittal shares climb as much as 5.4% after Netherlands-based mining company reported 3Q Ebitda beat that analysts attributed mainly to Brazil, Europe and mining

- PKO shares jump as much as 3% while Pekao surges as much as 6.5% following strong 3Q results by Poland’s two biggest lenders, which showed more tailwinds from the country’s high interest-rate environment

- Delivery Hero shares climb as much as 4.1% after the German delivery company narrowed its 2024 growth guidance to the upper end of the range. Analysts say the valuation is compelling

- Adyen shares fall as much as 13% after the payments firm reported net sales that missed estimates, driven by lower processing volumes, wholly driven by a single large customer

- ITV drops as much as 10% after the broadcaster gave an underwhelming forecast for a decline in total advertising revenue in 4Q, with ad bookings taking a hit from uncertainty ahead of the UK budget

- Novo Nordisk shares drop as much as 5.3% to the lowest since January as analysts weighed the drugmaker’s comments about next year’s revenue growth rate, which was slightly below market expectations

- Air France-KLM shares tumble as much as 12%, the steepest drop in two years, after reporting a third-quarter earnings before interest and tax that missed expectations

- Legrand drops as much as 6.9%, the most in a year, after the French electrical-device manufacturer released what analysts see as a “soft set” of numbers, with narrowed guidance

- Rolls-Royce shares drop as much as 4.9%, retreating from Wednesday’s record high, after the aerospace and defense firm’s engine flying hours came in toward the low-end of its guidance

Earlier in the session, Asian stocks rose, supported by a rally in China, as expectations grow that Beijing will unveil more stimulus at this week’s key policy meeting to counter potential risks from Trump’s second presidency. The MSCI Asia Pacific Index rose as much as 1%, on track to hit the highest level in more than two weeks. Toyota, TSMC and DBS were among the biggest contributors. Most major markets in the region advanced Thursday, led by mainland China, Hong Kong and Singapore. Japan’s Topix also rose, while Philippine and Indonesian stocks extended losses to a second day. Chinese shares rebounded strongly from Wednesday’s losses as robust exports data lifted sentiment. Traders are monitoring the Standing Committee meeting of the National People’s Congress, which concludes Friday, for possibly more measures to boost the economy and markets.

“The market is speculating the policymaker would announce a relatively large scale of fiscal package to stimulate domestic demand after the NPC meeting, in order to offset the potential tariff hike risk from Trump,” said Jason Chan, senior investment strategist of Bank of East Asia. “So sectors like consumer, property, Internet and SOEs are the major contributors.”

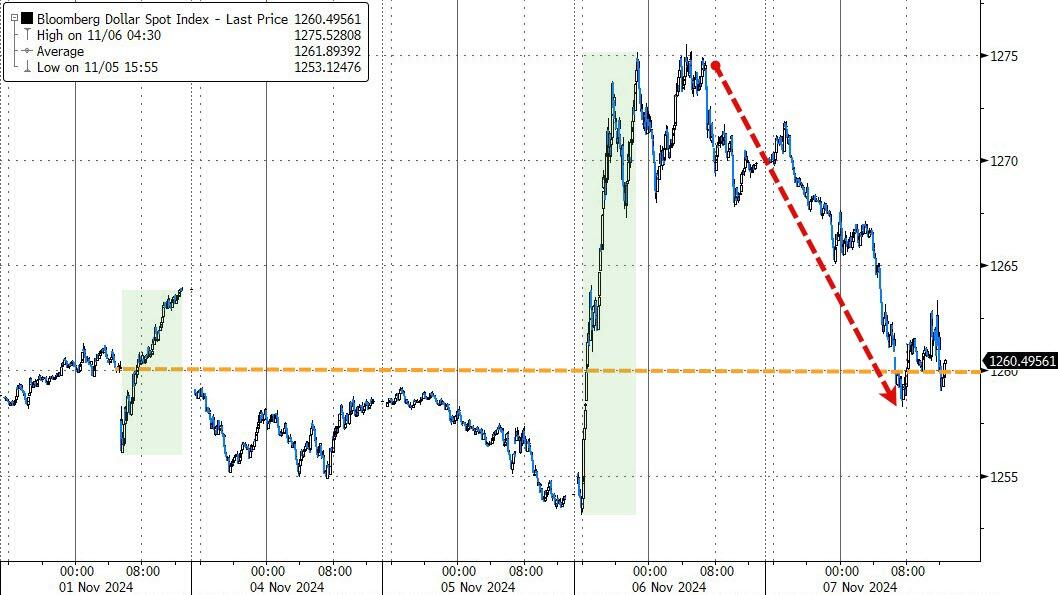

In FX, the Bloomberg Dollar Spot Index falls 0.3%. The Norwegian krone is the best performer among the G-10 currencies, rising 1.1% against the greenback after the Norges Bank repeated no imminent plans for easing. The Swedish krona adds 0.5% after the Riksbank cut interest rates by 50 bps. The pound surged 0.6% after the hawkish Bank of England rate 25bps cut with traders seeing no more rate cuts until next year.

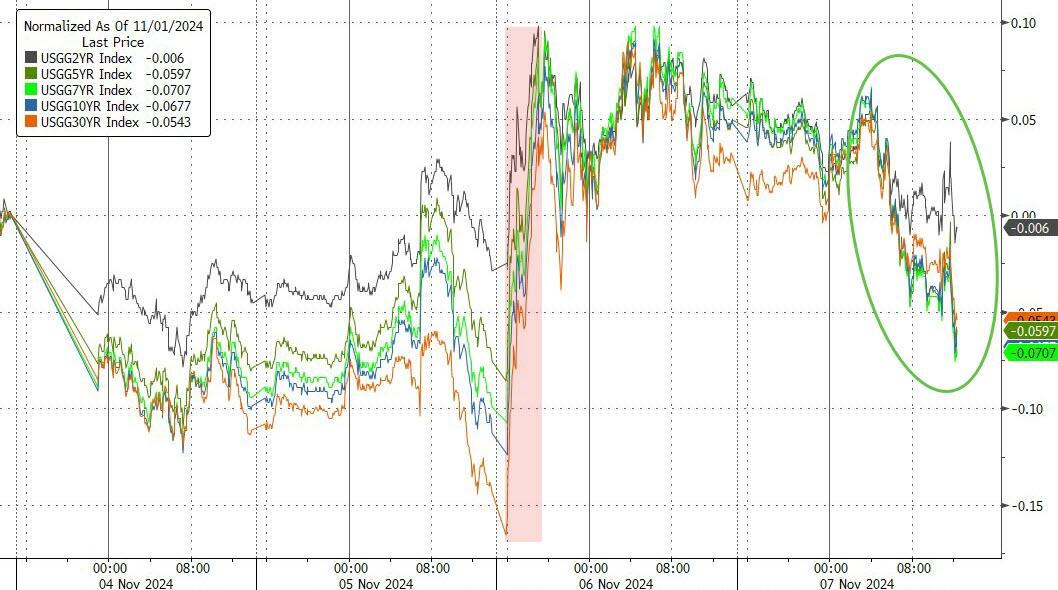

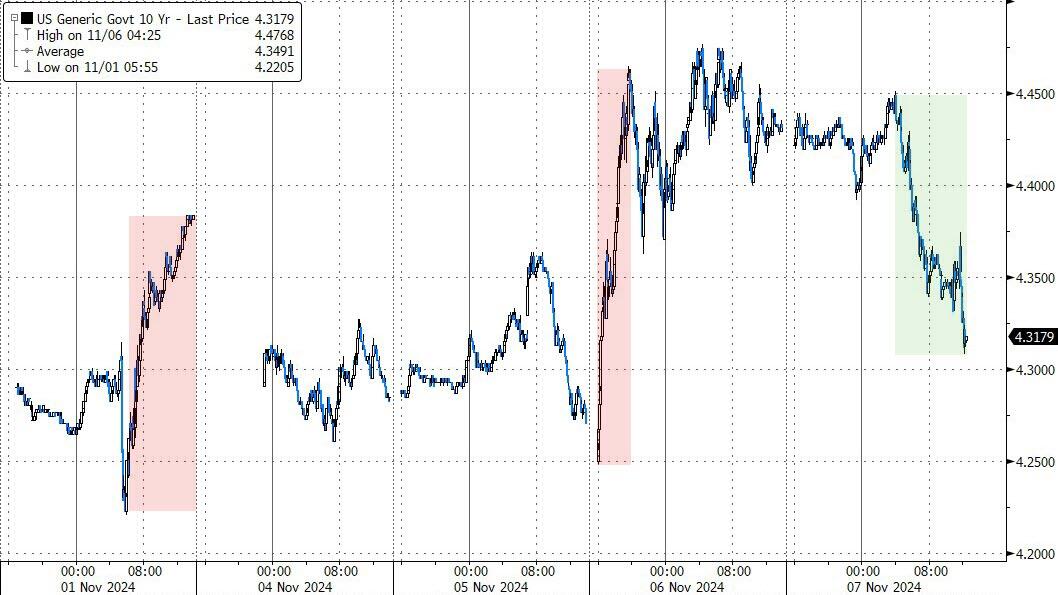

In rates, treasuries traded higher, with US 10-year yields falling less than a basis point to 4.43%. German bonds underperform their US peers, with the long end under pressure as traders brace for the possibility of more debt sales after the nation’s ruling coalition collapsed. German 10-year yields rise 8 bps and are above the equivalent swap rate for the first time as traders braced for the possibility of an administration that could be more tolerant of increasing debt.

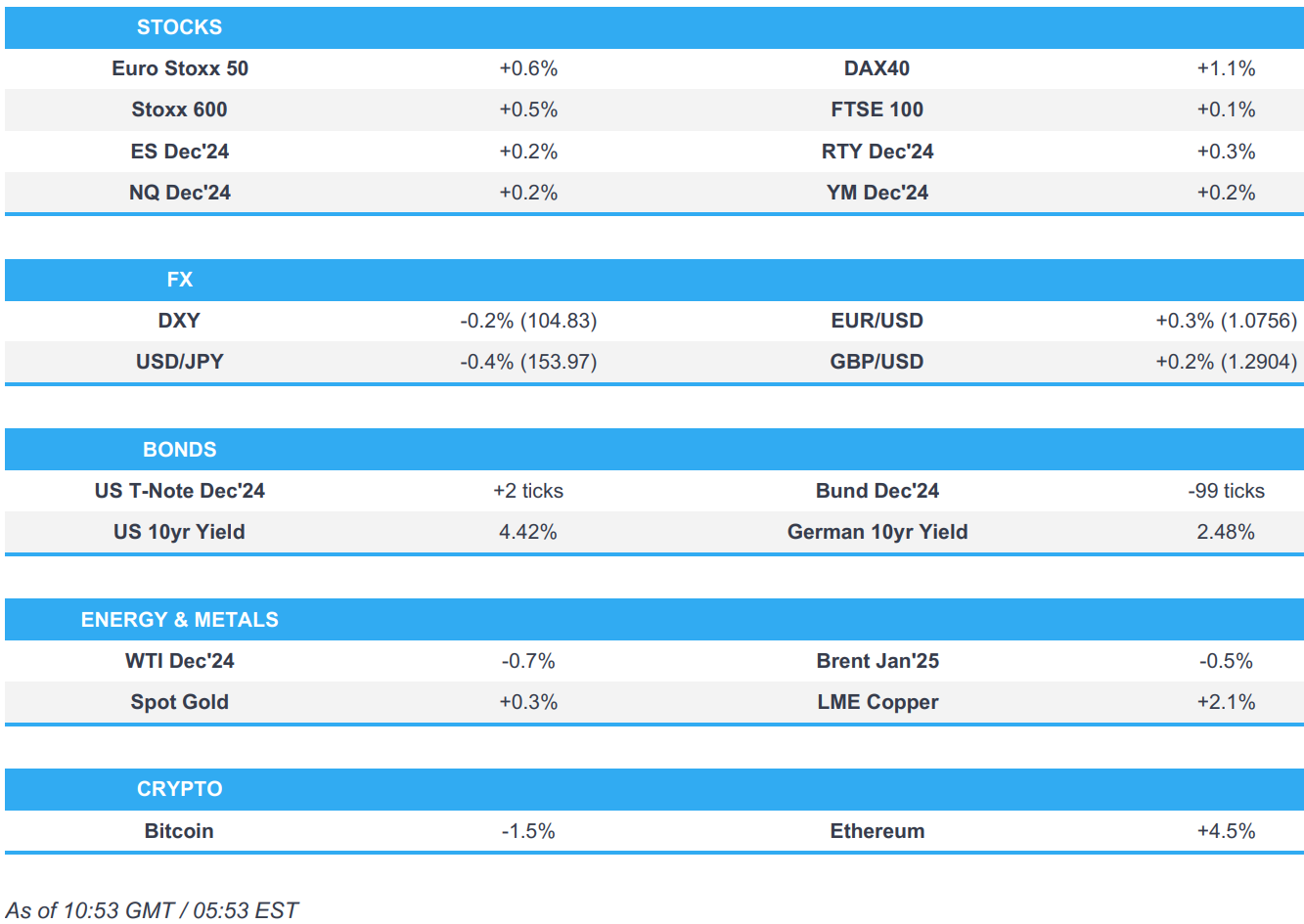

In commodities, oil prices decline, with WTI falling 0.8% to $71.10 a barrel. Spot gold rises $8 to $2,667/oz.

Looking at the US economic data calendar, the main highlight will be the Federal Reserve’s latest policy decision at 2pm ET, along with Chair Powell’s subsequent press conference. The slate also includes 3Q productivity and unit labor costs and weekly jobless claims (8:30am), September wholesale inventories (10am) and consumer credit (3pm).

Market Snapshot

- S&P 500 futures up 0.2% to 5,971.00

- STOXX Europe 600 up 0.7% to 510.21

- MXAP up 0.9% to 188.94

- MXAPJ up 0.8% to 601.67

- Nikkei down 0.3% to 39,381.41

- Topix up 1.0% to 2,743.08

- Hang Seng Index up 2.0% to 20,953.34

- Shanghai Composite up 2.6% to 3,470.66

- Sensex down 1.0% to 79,549.06

- Australia S&P/ASX 200 up 0.3% to 8,226.30

- Kospi little changed at 2,564.63

- German 10Y yield +6.5bps at 2.47%

- Euro up 0.3% to $1.0758

- Brent Futures down 0.3% to $74.70/bbl

- Gold spot up 0.2% to $2,663.91

- US Dollar Index down 0.24% to 104.84

Top Overnight News

- China’s exports surged in Oct (+12.7% vs. the Street +5% and up from +2.4% in Sept) as the government’s stimulus measures start to bear fruit, although the number means trade tensions are set to climb between Beijing and other major economies. WSJ

- BHP’s CEO says the company is finally starting to see “green shoots” in China’s economy as government stimulus efforts begin to bear fruit. FT

- Japan’s chief currency official warned of potential action against excessive yen moves. Separately, Trump’s victory may prompt a near-term rate hike if the yen weakens further, former BOJ exec Kazuo Momma said. BBG

- The BOE cut rates by 25 bps to 4.75% today. Focus will be on the path for borrowing costs beyond that, after it was thrown into doubt by the fallout from the UK budget and Trump’s victory. BBG

- GS FOMC Preview – Consecutive 25bp Cuts for Now. Fed officials have sounded more relaxed about both sides of their dual mandate than at earlier points this year. This should make a 25bp cut at the November meeting uncontroversial. We expect cuts to remain consecutive at least through December and are penciling in four more consecutive cuts in the first half of 2025 to a terminal rate of 3.25-3.5% but see more uncertainty about both the speed next year and the final destination. GIR

- The outcome of the House battle remains uncertain, with many key races still too close to call, particularly in California where absentee ballots can be counted for up to a week after the election. BBG

- President-elect Donald Trump and his senior advisers are privately assembling shortlists of candidates for top jobs in the incoming administration, from White House chief of staff to Treasury secretary. Potential Trump cabinet candidates include Chief of Staff (Susie Wiles), Treasury (Scott Bessent, John Paulson, Robert Lighthizer, Jay Clayton, Bill Hagerty), State (Marco Rubio), Defense (Mike Pompeo), Justice (Mike Lee, John Ratcliffe, Eric Schmitt, Tom Cotton), Commerce (Linda McMahon). WSJ

- Scott Bessent — a hedge fund manager and top Trump fundraiser — is positioning himself to be Treasury secretary and canvassing candidates to serve as his deputy. FT

- Companies could accelerate imports to the US in an effort to get ahead of potential Trump tariffs, providing a boost to trucking and railroad firms. WSJ

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were somewhat mixed albeit with a mostly positive bias as the dust settled from the US election and the Trump trade began to wane after reverberating across global markets with participants bracing for higher US tariffs, while participants also digested Chinese trade data as the attention turned to the incoming central bank rate decisions including from the FOMC. ASX 200 was indecisive but eventually finished positive as strength in energy, tech, industrials and financials gradually picked up the slack from weakness in real estate and defensives, while weak Australian trade data capped the upside. Nikkei 225 initially surged on the back of a weaker currency but failed to sustain the momentum and gave back its spoils. Hang Seng and Shanghai Comp shrugged off the threat of incoming blanket tariffs from the next US administration as participants continued to await a potential fiscal stimulus announcement and as the latest Chinese trade data was mostly better-than-expected with double-digit export growth. Furthermore, the PBoC held a meeting with international financial institutions and affirmed to continue its accommodative monetary policy, while China told banks to cut interbank deposit rates to boost growth.

Top Asian news

- PBoC held a meeting with international financial institutions including HSBC (5 HK), Standard Chartered (2888 HK) and Citi (C), while it affirmed to continue accommodative monetary policy stance and vowed to strengthen communication with the market. Furthermore, Governor Pan said they are to expand connectivity between domestic and overseas markets.

- China instructed banks to cut interbank deposit rates to boost growth, according to Bloomberg.

- Chinese President Xi congratulated Trump on winning the US presidential election and said he hopes that the two sides will respect each other, coexist peacefully, and achieve win-win cooperation. Furthermore, Xi said both sides should strengthen dialogue and that US-China cooperation is a long-term goal, according to Xinhua.

- Japanese top currency diplomat Mimura said they are closely watching market moves with a high sense of urgency and are ready to take appropriate actions for excess FX moves if needed.

- Nissan (7201 JT) is revising its FY24/25 operating profit forecast to JPY 150bln (prev. guided 500bln), withdraws net forecast; to sell a partial stake in Mitsubishi Motors (8058 JT). To reduce the global headcount by 9k & production capacity by 20%.

European bourses, Stoxx 600 (+0.6%) began the session on a modestly firmer footing and continued to edge higher as the morning progressed. Today’s EZ-specific docket has been relatively light, but focus ahead will lie on policy announcements from the BoE and the Fed thereafter. Region awaiting updates on China’s stimulus and also sensitive to ongoing political uncertainty in Germany. European sectors hold a strong positive bias. Basic Resources is by far the clear outperformer, lifted by strength in underlying metals prices after strong Chinese price action overnight. Telecoms is found at the foot of the pile, dragged down by losses in Telefonica (-1.5%) and BT (-5.2%), with the latter also lowering its FY25 guidance.

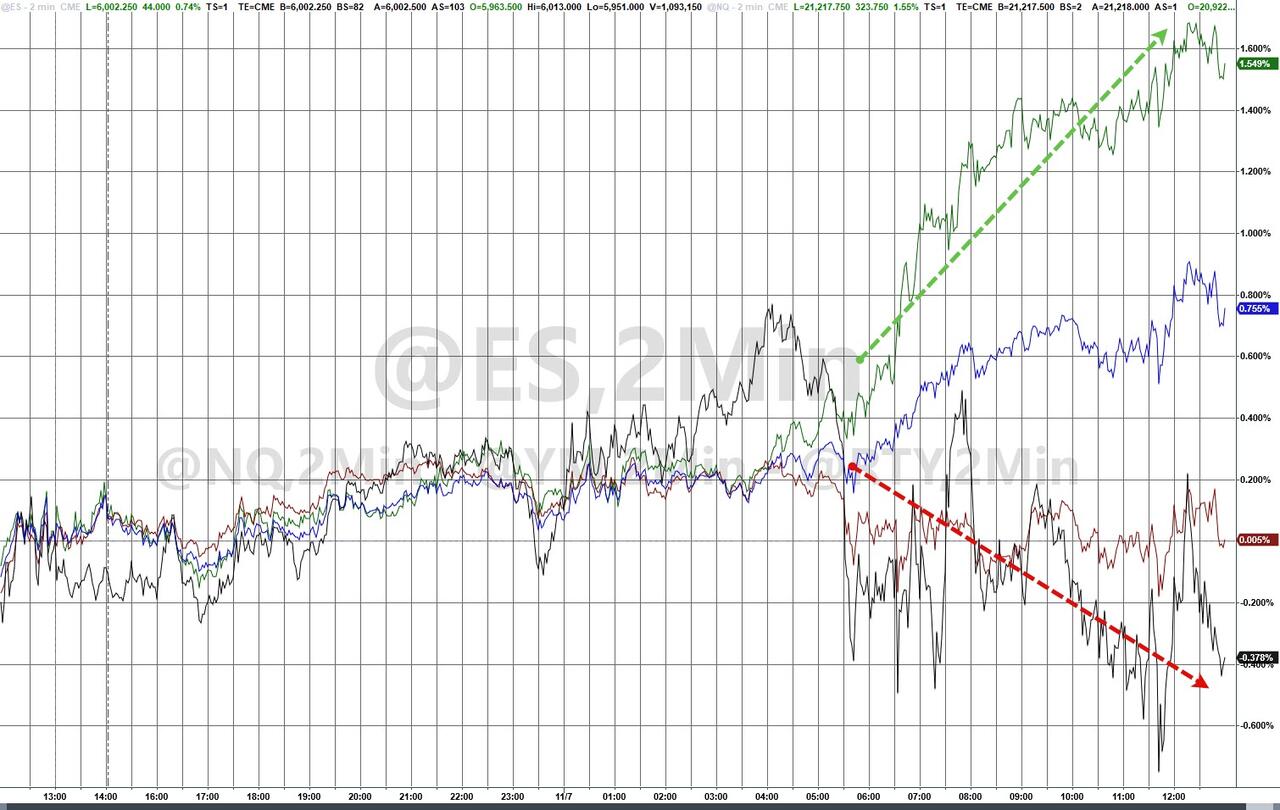

US Equity Futures (ES +0.2%, NQ +0.2%, RTY +0.3%) are modestly firmer across the board, taking a breather following the significant gains seen in the prior session, where the S&P500 soared to record highs after Trump returned to Presidency.

Top European news

- Riksbank cuts its Rate by 50bps as expected to 2.75% (prev. 3.25%); policy rate may also be lowered in December and H1 2025 (in line with what was communicated in September). Click for details.. Riksbank’s Theeden says flash CPI data for October do not change the overall picture; Crown is a risk factor “but we don’t think it will affect out inflation picture”. Says the rate path is more uncertain than usual.

- Norges Bank leaves its Key Policy Rate at 4.50% as expected; “the policy rate will most likely be kept at 4.5 percent to the end of 2024”. Click for details.

- Deutsche Bank lowers its terminal ECB rate forecast to 1.5% from 2.25%

- ECB’s Schnabel says the balance sheet reduction has not left any significant footprint in many areas, thus far.

- ECB survey on Survey on the Access to Finance of Enterprises: firms report moderate tightening of financing conditions shows cost pressures remain widespread across businesses of all sizes. Firms reported little changes regarding the availability of bank loans. However, firms’ need for bank loans has declined moderately, partly due to high internal funds. Substantially fewer firms reported rising bank interest rates on loans, although many indicated a further tightening of other conditions. Firms’ inflation expectations continued to decline, with their median expectations for annual inflation in one, three and five years all standing at 2.9%.

- Joerg Kukies has been appointed German Finance Minister, replacing Lindner.

- Maersk (MAERSKB DC) says overall freight volumes from Europe continue to report a slight 4% Y/Y increase; freight rates continue to decline. Seeing demand in Europe bounce back a lot stronger this year.

FX

- USD is giving back some ground to major peers after the DXY sky-rocketed from 103.70 to 105.44 on account of the Trump victory. Attention now turns to today’s FOMC announcement which is expected to see the Fed step down to a 25bps cadence of rate cuts.

- EUR has been able to make some headway vs. the USD. However, today’s peak at 1.0771 is some way off Wednesday’s best at 1.0936. As such, it remains to be seen how much legs the attempted recovery has, particularly given the political instability in Germany with the prospect of a general election in March next year.

- GBP is attempting to undo some of the damage seen during yesterday’s session with Cable returning to a 1.29 handle after delving as low as 1.2835. Expectations are for a 25bps cut via a 7-2 vote split.

- JPY is attempting to recoup some of the lost ground vs. the USD brought on by Trump’s victory. However, progress has been relatively limited with USD/JPY’s current low at 153.66 standing in contrast to Wednesday’s 151.27 trough.

- Antipodeans are both markedly higher and leading the charge against the USD after what was a particularly bruising session on Wednesday given exposure to China. Accordingly, AUD/USD has almost pared a bulk of yesterday’s move that dragged it down from a 0.6644 high to a 0.6511 low.

- SEK is flat following the Riksbank’s decision to cut rates by 50bps as expected (despite some outside calls for a 25bps) reduction and reiterate guidance on rates. EUR/NOK has extended on yesterday’s downside with an in-line decision from the Norges Bank underscoring the Bank’s hawkish credentials relative to most other peers.

- China state-owned banks were seen selling US dollars and buying yuan, according to traders.

- PBoC set USD/CNY mid-point at 7.1659 vs exp. 7.1679 (prev. 7.0993).

- Brazil Central Bank hiked the Selic rate by 50bps to 11.25%, as expected, with the decision unanimous. BCB stated the pace of future interest rate adjustments and total magnitude of the cycle will be determined by the firm commitment to reaching the inflation target. Furthermore, it stated the pace of future interest rate adjustments and total cycle magnitude will depend on inflation dynamics, expectations and projections, the output gap, and the balance of risks, while it added that risks to inflation scenarios are tilted to the upside.

USTs