NOV 13/ANOTHER RAID AS THE COMEX IS IN CHAOS//GOLD CLOSED DOWN $19.30 TO $2580.80//SILVER CLOSED 16 CENTS TO $30.54 //PLATINUM CLOSED $9.00 TO $938.45 WHILE PALLADIUM CLOSED DOWN $10.95 TO $937.40//FOR THE 4TH CONSECUTIVE DAY OVER 33,000 T.A.S. CONTRACTS WERE INITIALTED (SPREADERS)//GOLD COMMENTARY TONIGHT FROM ALASDAIR MACLEOD//NETHERLANDS INITIATES BORDER CONTROLS AFTER THE SOCCER GAME FIASCO//ISRAEL VS HAMAS/ISRAEL VS HEZBOLLAH UPDATES//EXCELLENT COMMENTARY TONIGHT FROM EUROPEAN EXPERT TOM LUONGO//USA CPI OUT AND STILL REMAINS HIGH/ TRUMP PICKS CONSERVATIVES FOR HIS CABINET YET THE SENATE PICKS RINO THUNE//SWAMP STORIES FOR YOU TONIGHT//

*CANADIAN GOLD: $3605,74 DOWN 18.78 CDN dollars per oz( * NEW ALL TIME HIGH 3,872.51 CDN DOLLARS PER OZ//OCT 30 2024)

*BRITISH GOLD: 2026,53 DOWN 13.91 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///2148.36 BRITISH POUNDS/OZ) OCT 30/2024

*EURO GOLD: 2,437,93 DOWN 9.93 Euros per oz //* (ALL TIME CLOSING HIGH: 2565.55 EUROS PER OZ//OCT 30 //.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE;

JPMorgan stopped 0/0

GOLD: NUMBER OF NOTICES FILED FOR NOV/2024. CONTRACT: 0 NOTICES FOR 0 OZ 0.0 TONNES

total notices so far: 2548 contracts for 254,800 Oz (7.925 tonnes)

FOR NOV

SILVER NOTICES: 0 NOTICE(S) FILED FOR 0 MILLION OZ/

total number of notices filed so far this month : 870 for 4.350 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $19.30 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

HUGE CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD./

/ /INVENTORY RESTS AT 870.53 TONNES

INVENTORY RESTS AT 870.53 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $0.16 AT THE SLV

HUGE CHANGES IN SILVER INVENTORY OUT OF THE SLV: A WITHDRAWAL OF 1,274,000 OZ OUT OF THE SLV//

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 475.157 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI SURPRISINGLY FELL BY A SMALL SIZED 173 CONTRACTS TO 147,526 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS SMALL SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR GAIN OF $0.16 IN SILVER PRICING AT THE COMEX WITH RESPECT TO MONDAY’S TRADING. WE HAD A HUGE GAIN OF 977 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN OF $0.16 IN PRICE. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS ON TUESDAY COMEX TRADING AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S CONTINUAL PRICE RISE FOR THE PAST 2 WEEKS AND FAILED. THEY HAD CONSIDERABLE SUCCESS MONDAY BUT FAILED YESTERDAY AND TODAY/. WE HAD ATTEMPTED SHORT COVERING BY OUR SPECS DURING THE COMEX TIME ZONE TUESDAY BUT TO NO AVAIL.. WE HAD A HUMONGOUS 1150 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY A MEGA HUMONGOUS 3946 CONTRACT T.A.S ISSUANCE WHICH WILL BEING USED IN FUTURE TRADING AS THEY PLAY AN INTEGRAL PART DURING RAIDS TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A HUMONGOUS 2015 CONTRACTS ON OUR TWO EXCHANGES WITH OUR SMALL GAIN IN PRICE. WE HAD MAJOR TAS LIQUIDATION THROUGHOUT MONDAY AND TUESDAY’S COMEX SESSIONS.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN ON LAST FRIDAY YESTERDAY AND AGAIN TODAY. THE ACCUMULATED T.A.S. IS BEING USED TO MANIPULATE PRICES AT THE COMEX NOW EVERY DAY..

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESSDAY NIGHT: A MEGA HUMONGOUS 3946 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS BUT TO NO AVAIL TODAY. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.16) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SILVER LONGS FROM THEIR PERCH AS WE HAD A HUMONGOUS NET GAIN OF 2015 CONTRACTS ON OUR TWO EXCHANGES.

WE HAD A HUGE 1150 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 2.810 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP//NEW STANDING REMAINS AT 4.535 MILLION OZ

// STANDING FOR SILVER//NOV AT 4.535 MILLION OZ

WE HAD:

/ SMALL SIZED COMEX OI LOSS//HUMONGOUS SIZED EFP ISSUANCE/ VI) MEGA HUMONGOUS SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 3946 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED A HUGE 1038 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS NOV. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF NOV

TOTAL CONTRACTS for 9DAYS, total 12,790 contracts: OR 63.950 MILLION OZ (1421 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 63.950 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 63.95 MILLION OZ (WILL BE HUGE THIS MONTH)

RESULT: WE HAD A SMALL SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 183 CONTRACTS WITH OUR GAIN OF $0.16 IN PRICE OF SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 1150 ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR NOV OF 2.810 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 0 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR NOV AT 4.565 MILLION OZ

WE HAVE A HUMONGOUS SIZED GAIN OF 977 OI CONTRACTS ON THE TWO EXCHANGES WITH OUR GAIN IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A MEGA HUMONGOUS SIZED 3946 CONTRACTS TRYING DESPERATE TO CONTAIN SILVER’S PRICE RISE,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION THUS THE NEED FOR REPLENISHMENT AND THAT IS WHAT THEY DID IN A BIG WAY TODAY!

/ ZERO NET SHORT COVERING FROM OUR SPEC SHORTS WITH THE GAIN IN PRICE TUESDAY/ . ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE TUESDAY NIGHT (3946) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND LATELY ON A DAILY BASIS INCLUDING YESTERDAY AND TODAY.

WE HAD 0 NOTICE(S) FILED TODAY FOR 0.0 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 4557 OI CONTRACTS TO 535,981 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED A HUGE 3591 CONTRACTS//

WE HAD A STRONG SIZED DECREASE IN COMEX OI (4557 CONTRACTS) OCCURRED WITH OUR LOSS OF $11.40 IN PRICE TUESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A GOOD INITIAL STANDING IN GOLD TONNAGE FOR NOV AT 2.488 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 7100 OZ QUEUE JUMP//NEW STANDING ADVANCES TO 10.357 TONNES

NEW STANDING FOR NOVEMBER: 10.357 TONNES

/ ALL OF THIS HAPPENED WITH OUR $11.40 LOSS IN PRICE WITH RESPECT TO TUESDAY’S COMEX RAID///. WE HAD A STRONG GAIN OF 5602 OI CONTRACTS (17.42 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THIS WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! YOU CAN VISUALIZE THIS WITH THE DAILY QUEUE JUMPING WE ARE WITNESSING (AND TODAY’S QUEUE JUMP OF 7100 OZ)

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 10,199 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 535,981

IN ESSENCE WE HAVE A STRONG SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 5602 CONTRACTS WITH 4597 CONTRACTS DECREASED AT THE COMEX// AND A HUGE SIZED 10,199 EFP OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 5602 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A MEGA MEGA HUMONGOUS SIZED AND CRIMINAL 33,535 CONTRACTS ISSUED AND THIS IS THE FOURTH DAY IN A ROW FOR A MEGA ISSUANCE OF GREATER THAN 30,000 T.A.S. CONTRACTS. WE HAD HUGE LIQUIDATION OF T.A.S CONTRACTS WITH OUR LOSS IN PRICE MONDAY AND TUESDAY AS THE NEED FOR REPLENISHMENT WAS GREAT IN ORDER TO CARRY OUT ITS RAID OPERATION. SEEMS THAT THEY WERE EXHAUSTED WEDNESDAY AS THERE WAS NO RAID.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A HUGE SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (10,199 CONTRACTS) ACCOMPANYING THE STRONG SIZED DECREASE IN COMEX OI OF 4557 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 5602 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR NOV 2.488 TONNES FOLLOWED BY TODAY’S 7100 OZ QUEUE JUMP

//NEW STANDING NOVEMBER: 10.357 TONNES

/ 3) HUGE T.A.S. LIQUIDATION (TRYING TO LOWER GOLD’S PRICE WITH GREAT SUCCESS MONDAY AND TUESDAY. TODAY, TAS USED TO CONTAIN GOLD’S RISE. WE HAD CONSIDERABLE NET LONG SPECS BEING CLIPPED. STICKY GOLD’S LONGS HOWEVER ARE NOT FOOLED BY THE RAID AS THEY WERE REWARDED MONDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL.

4) STRONG SIZED COMEX OPEN INTEREST DECREASE 5) HUGE ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///MEGA MEGA HUMONGOUS T.A.S. ISSUANCE: 33,535 T.A.S.CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

NOV

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV :

TOTAL EFP CONTRACTS ISSUED: 63,331 CONTRACTS OF 6,333,100 OZ OR 196.99 TONNES IN 9 TRADING DAY(S) AND THUS AVERAGING: 6641 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 9 TRADING DAY(S) IN TONNES 196.99 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 196.99 DIVIDED BY 3550 x 100% TONNES = 5.54% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END UP WITH THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 196.99 TONNES (WILL PROBABLY BE A HUGE MONTH/MAYBE A RECORD ISSUANCE MONTH)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPTEMBER. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A SMALL SIZED 173 CONTRACTS OI TO 147,526 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 6 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 1150 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 1150 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1150 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 173 CONTRACTS AND ADD TO THE 1150 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 977 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 10.075 MILLION OZ OCCURRED DESPITE OUR SMALL $0.16 GAIN IN PRICE

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING TUESDAY NIGHT

ASIA TRADING/WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED UP 17.31 PTS OR 0.51%

//Hang Seng CLOSED DOWN 23.54 PTS OR 0.12%

// Nikkei CLOSED DOWN 654.43 OR 1.66%//Australia’s all ordinaries CLOSED DOWN 0.76%///Chinese yuan (ONSHORE) CLOSED UP TO 7.2091 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2197// Oil DOWN TO 68.14 dollars per barrel for WTI and BRENT UP AT 71.94 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 4,557 CONTRACTS TO 535,981 WITH OUR LOSS IN PRICE OF $11.40 WITH RESPECT TO TUESDAY’S TRADING. , WE LOST ZERO NET IN NUMBER LONGS DESPITE THE LOWER PRICE FOR GOLD AS YOU WILL SEE BELOW. WE HAD A HUMONGOUS NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (10,199).

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY THIS ENTIRE WEEK AND ESPECIALLY DURING YESTERDAY’S LOSS IN PRICE/

THE FED IS THE MAJOR SHORT OF AROUND 93+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS IS SCHEDULED TO HAPPEN LATE OCT 2024/(AS OUTLINED IN OUR GOLD PHYSICAL COMMENTARIES//VIEW ANDREW MAGUIRE LATEST LIVE FROM VAULT 197 AS HE TACKLES THIS IMPORTANT TOPIC). THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST TWO MONTHS. THEY ARE TOTALLY TRAPPED. THUS THE REASON FOR THE CONTINUAL RAIDING OF OUR PHYSICAL ANCIENT METAL OF KINGS LIKE YESTERDAY, AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY! ACTUALLY THE FED HAS COAXED THE SPECULATORS TO GO MASSIVELY SHORT WHILE THEY TAKE THE LONG SIDE AFTER THEY COMMENCE THE AVALANCHE IN LOWERING PRICE OF GOLD

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD A HUGE T.A.S. LIQUIDATION THROUGHOUT LAST WEEK’S TRADING AND AGAIN WITH THIS WEEKS TRADING, MONDAY AND TUESDAY..

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF THE SPREADERS // T.A.S DURING LAST WEEK AND THIS WEEK IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE NON ACTIVE DELIVERY MONTH OF NOV.… THE CME REPORTS THAT THE BANKERS ISSUED A HUMONGOUS SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A HUGE SIZED 10,199 EFP CONTRACTS WERE ISSUED: : /DEC 10,199 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 10,199 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A STRONG SIZED TOTAL OF 5602 CONTRACTS IN THAT 10,199 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 4557 COMEX CONTRACTS..AND THIS STRONG GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $11.40 TUESDAY// COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AS MENTIONED ABOVE.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT, A MEGA MEGA SIZED 33,535 CONTRACTS, WILL BE USED TO REPLENISH SUPPLIES.. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK). THIS IS THE FOURTH CONSECUTIVE 30,000 + DAY ISSUANCE OF T.A.S BY THE CROOKS.

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ARE HAVING A HARD TIME TRYING TO CONTROL THE PRICE OF GOLD AND THUS THE NEED FOR STRONG T.A.S. ISSUANCE (AND SPREADERS LATE IN THE MONTH). THE USE OF T.A.S. IS OF EXTREME IMPORTANCE TO OUR CROOKS IN LAST WEEK’S AND THIS WEEK’S TRADING AND ESPECIALLY WITH THIS WEEK’S TWO CONSECUTIVE RAIDS.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: NOV (10.357 TONNES) WHICH IS HUGE FOR OUR NON ACTIVE NOV DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 47 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/PRIOR= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK PRIOR =60.391 TONNES

NOV . 10.357 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $11.40/)//BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A FAIR GAIN IN OUR TWO EXCHANGES. WE DID HAVE HUGE T.A.S. SPREADER LIQUIDATION MONDAY TUESDAY AND AGAIN TODAY AS THE NEED FOR REPLENISHMENT WAS IN FULL FORCE. THIS COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING

WE HAVE GAINED A TOTAL OF 6.379 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR NOV (2.488TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S STRONG QUEUE JUMP OF 71 CONTRACTS OR 700 OZ (0.2208 TONNES). THESE GUYS UNDERWENT A QUEUE JUMP BOLTING AHEAD OF OTHER LONGS TO OBTAIN BADLY NEEDED PHYSICAL GOLD. MOSTLY LIKELY THIS IS THE FRBNY DESPERATELY TRYING TO EXTINGUISH ITS MASSIVE PHYSICAL SHORT FALL OF 93 TONNES

//NEW STANDING FOR NOV 10.357 TONNES

NEW STANDING FOR NOVEMBER: 10.357 TONNES (WHICH FOR A NON ACTIVE DELIVERY MONTH)

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE TO THE TUNE OF $11.40

WE HAD 502 CONTRACTS ADDED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES 2051 CONTRACTS OR 205,100 OZ (6.379 TONNES)

400.825 oz one good London delivery bar leaves London vault.

.

Deposit to the Dealer Inventory in oz

NIL

Deposits to the Customer Inventory, in oz

73,947.30 OZ BRINKS 2300 KILOBARS

No of oz served (contracts) today

0 notice(s) 0 OZ 0.000 TONNES

No of oz to be served (notices)

782 contracts 78,200 OZ 2.243 TONNES

Total monthly oz gold served (contracts) so far this month

2548 notices 254,800oz 7.925 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

dealer deposits: 0

total dealer deposits: nil oz

we have 1 customer deposits

into Brinks 73,947.300 oz

total deposits 73,947.300 oz

withdrawals: 1

i) Out of London/JPMorgan enhanced: 400.85 oz

or one London good delivery bars leaves London England vaults

TOTAL WITHDRAWALS: 400.85 oz

adjustments: 1

JPMorgan: 14,034.972 oz leaves customer account and enters registered acct.

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR NOV.

For the front month of NOV: we have an oi of 782 contracts having GAINED 60 contracts. We had 11 contracts served on TUESDAY so we gained 71 contract as these guys underwent a HUGE queue jump of 7100 oz (0.2208 TONNES OF GOLD)

DECEMBER, THE BIGGEST DELIVERY MONTH LOST 18,564 CONTRACTS TO 280,647

JANUARY GAINED 37 CONTRACTS TO STAND AT 347

FEBRUARY GAINED 12,134 CONTRACTS TO 183,282 .

We had 0 contracts filed for today representing 0 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 0 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for NOV /2024. contract month, we take the total number of notices filed so far for the month (2548 x 100 oz ) to which we add the difference between the open interest for the front month of NOV(782 CONTRACTS) minus the number of notices served upon today (0 x 100 oz per contract( equals 333,000 OZ OR 10.357 TONNES.

thus the INITIAL standings for gold for the NOV contract month: No of notices filed so far (2548 x 100 oz +we add the difference for front month of NOV (782 OI} minus the number of notices served upon today (0 x 100 oz which equals 333,000 oz (10.357 TONNES) +

TOTAL COMEX GOLD STANDING FOR NOV.: 10.357 TONNES WHICH IS HUGE FOR THIS NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,417,876.837 OZ

TOTAL REGISTERED GOLD 7,829,907.182/// 243.54tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,597,969.,155 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,199,652 oz (REG GOLD- PLEDGED GOLD)= 182.84 tonnes //

END

SILVER/COMEX

NOV 13. 2024

INITIAL

//2024// THE NOV 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

1,423,970.109 oz CNT ASAHI HSBC

.

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

28,211.656 oz

Delaware

No of oz served today (contracts)

0 CONTRACT(S) (0 OZ)

No of oz to be served (notices)

37 contracts (185,000oz)

Total monthly oz silver served (contracts)

870 Contracts (4.350 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit/

total dealer deposit : NIL oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 customer deposit

i) Into Delaware 28,211.656 oz

total customer deposits 595,475.100oz

We had 3 withdrawals

i) Out of CNT 209,679.03 oz

ii) Out of ASAHI 615,308.300 oz

iii) Out of Brinks 598,982.779 oz

total withdrawal 1,423,970.100 oz

JPMorgan has a total silver weight: 134.401million oz/311.292million or 43,04%

adjustment 0

TOTAL REGISTERED SILVER: 70.073MILLION OZ//.TOTAL REG + ELIGIBLE. 311.292 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR NOV

silver open interest data:

FRONT MONTH OF NOV /2024 OI: 37 OPEN INTEREST FOR A LOSS OF 37 CONTRACTS

WE HAD 37 NOTICES FILED ON TUESDAY SO WE GAINED 0 CONTRACTS OR 0 OZ UNDERWENT A QUEUE JUMP

DECEMBER SAW A LOSS OF 7718 CONTRACTS DOWN TO 78,053 CONTRACTS

JANUARY SAW A LOSS OF 25 CONTRACTS DOWN TO 1110

.

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for 0.0 MILLION oz

CONFIRMED volume; ON TUESDAY 94,945 huge// t.a.s. enhanced

To calculate the number of silver ounces that will stand for delivery in NOV we take the total number of notices filed for the month so far at 870x 5,000 oz = 4.350 MILLION oz

to which we add the difference between the open interest for the front month of NOV (37) and the number of notices served upon today (0)x (5000 oz)

Thus the standings for silver for the NOV 2024 contract month: 870 Notices served so far) x 5000 oz + OI for the front month of NOV(37) number of notices served upon today minus (0)x 5000 oz of silver standing for the NOV contract month equates to 4.535 MILLION OZ.

New total standing: 4.535 million oz.

There are 70.073 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS//

GLD

NOV 13 WITH GOLD DOWN $19.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 870.63 TONNES

NOV 12 WITH GOLD DOWN $11.40 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.88 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 871,97 TONNE

NOV 11 WITH GOLD DOWN $75.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.74 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 876.85 TONNES

NOV 8 WITH GOLD DOWN $11.85 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.87 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 883.46 TONNES

NOV 7 WITH GOLD UP $30.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.45 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 883.46 TONNES

NOV 6 WITH GOLD DOWN $72.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 886.91 TONNES

NOV 5 WITH GOLD UP $4.05 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:.// . // .///INVENTORY RESTS AT 888.63 TONNES

NOV 4 WITH GOLD DOWN $2.45 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.16 TONNES OF GOLD OUT OF THE GLD.// . // .///INVENTORY RESTS AT 888.63 TONNES

NOV 1 WITH GOLD UP 0.15 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.86 TONNES OF GOLD INTO THE GLD.// . // .///INVENTORY RESTS AT 891 TONNES

OCT 31 WITH GOLD DOWN $49.55 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD.// . // .///INVENTORY RESTS AT 892.65 TONNES

OCT 30 WITH GOLD UP $20.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD INTO THE GLD.// . // .///INVENTORY RESTS AT 889,78 TONNES

OCT 29 WITH GOLD UP $25.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD.// . // .///INVENTORY RESTS AT 891.50 TONNES

OCT 28 WITH GOLD UP $1.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.02 TONNES OF GOLD FROM THE GLD.// . // .///INVENTORY RESTS AT 889.78 TONNES

OCT 25 WITH GOLD UP $6.40 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: // . // .///INVENTORY RESTS AT 893.80 TONNES

OCT 24 WITH GOLD UP $19.60 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES // // . // .///INVENTORY RESTS AT 893.80 TONNES

OCT 23 WITH GOLD DOWN $29.40 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.45 TONNES // // . // .///INVENTORY RESTS AT 895.24 TONNES

OCT 21 WITH GOLD UP $9.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.277 TONNES // // . // .///INVENTORY RESTS AT 888.63 TONNES

OCT 18 WITH GOLD UP $22.30 ON THE DAY; NO CHANGES IN GOLD AT THE GLD // // . // .///INVENTORY RESTS AT 884.59 TONNES

OCT 17 WITH GOLD UP $17.30 ON THE DAY; NO CHANGES IN GOLD AT THE GLD // // . // .///INVENTORY RESTS AT 884.59 TONNES

OCT 16 WITH GOLD UP $13.60 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD //A MONSTER DEPOSIT OF 4.02 TONNES OF GOLD INTO THE GLD.; // . // .///INVENTORY RESTS AT 884.59 TONNES

OCT 15 WITH GOLD UP $2.85 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD //A MONSTER DEPOSIT OF 4.31 TONNES OF GOLD INTO THE GLD.; // . // .///INVENTORY RESTS AT 880.57 TONNES

OCT 11 WITH GOLD UP $36.55 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 10 WITH GOLD UP $14.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 9 WITH GOLD DOWN $8.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 8 WITH GOLD DOWN $28,.95 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 7 WITH GOLD DOWN $1.85 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD; A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD// . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 4 WITH GOLD DOWN $11.20 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD; A DEPOSIT OF 12.57 TONNES OF GOLD INTO THE GLD// . // .///INVENTORY RESTS AT 877.41 TONNES

OCT 3 WITH GOLD DOWN $8.95 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; . // .///INVENTORY RESTS AT 874.82 TONNES

OCT 2WITH GOLD DOWN $20.05 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD; A DEPOSIT OF 2.88 TONNES OF GOLD INOT THE GLD. // .///INVENTORY RESTS AT 874.82 TONNES

OCT 1 WITH GOLD UP $28,55 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // .///INVENTORY RESTS AT 871.94 TONNES

SEPT 30 WITH GOLD DOWN $6.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD; A WITHDRAWAL OF 5.18 TONNES OF GOLD FROM THE GLD// .///INVENTORY RESTS AT 871.94 TONNES

SEPT 27 WITH GOLD DOWN $26.60 ON THE DAY; NO CHANGES IN GOLD AT THE GLD .///INVENTORY RESTS AT 877,12 TONNES

SEPT 26 WITH GOLD UP $11.20 ON THE DAY; NO CHANGES IN GOLD AT THE GLD .///INVENTORY RESTS AT 877,12 TONNES

SEPT 25WITH GOLD UP $9.25 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD ./// /:// A DEPOSIT OF 1.73 TONNES OF GOLD INTO THE GLD//////INVENTORY RESTS AT 877,12 ONNES

SEPT 24WITH GOLD UP $23.60 ON THE DAY; NO CHANGES IN GOLD AT THE GLD ./// /:// //////INVENTORY RESTS AT 875.39 ONNES

SEPT 23 WITH GOLD UP $6.65 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1,43 TONNES OF GOLD INTO THE GLD../// /:// //////INVENTORY RESTS AT 875.39 ONNES

SEPT 20 WITH GOLD UP $32.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1,73 TONNES OF GOLD INTO THE GLD../// /:// //////INVENTORY RESTS AT 873,96ONNES

SEPT 19 WITH GOLD UP $17,05 ON THE DAY; NO CHANGES IN GOLD AT THE GLD/// /:// //////INVENTORY RESTS AT 872.23TONNES

SEPT 18 WITH GOLD UP $5.95 ON THE DAY; NO CHANGES IN GOLD AT THE GLD/// /:// //////INVENTORY RESTS AT 872.23TONNES

SEPT 17WITH GOLD DOWN $15.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A HUGE DEPOSIT OF 1.52 TONNES INTO THE GLD /:// //////INVENTORY RESTS AT 872.23TONNES

GLD INVENTORY: 870.53 TONNES, TONIGHTS TOTAL

SILVER

NOV 13 WITH SILVER DOWN $0.16 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1,274,000 OZ OUT OF THE SLV. /// //INVENTORY AT SLV RESTS AT 475.157 MILLION OZ

NOV 12 WITH SILVER UP $0.16 //SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 576,000 OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 476.000 MILLION OZ

NOV 11 WITH SILVER DOWN $0.79 //SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 374,000 OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 477.527 MILLION OZ

NOV 8 WITH SILVER DOWN $0.43 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 2.005 MILLION OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 477.846 MILLION OZ

NOV 7 WITH SILVER UP $0.11 //NO CHANGES IN SILVER INVENTORY AT THE SLV: /// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 6 WITH SILVER DOWN $1.41 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.692 MILLION OZ FROM THE SLV/.//// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 5 WITH SILVER UP 0.18 :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.109 MILLION OZ FROM THE SLV/.//// //INVENTORY AT SLV RESTS AT 479,533 MILLION OZ

NOV 4 WITH SILVER DOWN $0.08 :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 547,000 OZ.//// //INVENTORY AT SLV RESTS AT 480.642 MILLION OZ

NOV 1 WITH SILVER DOWN $0.10 : NO CHANGES IN SILVER INVENTORY AT THE SLV:.//// //INVENTORY AT SLV RESTS AT 481.189 MILLION OZ

OCT 31 WITH SILVER DOWN $1.26 : HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.647 MILLION OZ OF SILVER INTO THE SLV//.//// //INVENTORY AT SLV RESTS AT 481.189 MILLION OZ

OCT 30 WITH SILVER DOWN 38 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV.//// //INVENTORY AT SLV RESTS AT 477.542 MILLION OZ

OCT 29 WITH SILVER UP 49 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV’ A WITHDRAWAL OF 0.628 MILLION OZ OUT OF THE SLV..//// //INVENTORY AT SLV RESTS AT 477.542 MILLION OZ

OCT 28 WITH SILVER UP 15 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV’ A WITHDRAWAL OF 1.431 MILLION OZ OUT OF THE SLV..//// //INVENTORY AT SLV RESTS AT 478.180 MILLION OZ

OCT 25 WITH SILVER DOWN $0,02 : HUGE CHANGES IN SILVER INVENTORY AT THE SLV’ A DEPOSIT OF 3.06 MILLION OZ INTO THE SLV..//// //INVENTORY AT SLV RESTS AT 480.281 MILLION OZ

OCT 24 WITH SILVER UP $0,01 : SMALL CHANGES IN SILVER INVENTORY AT THE SLV’ A WITHDRAWAL OF 0.684 MILLION OZ OF SILVER OUT OF THE SLV..//// //INVENTORY AT SLV RESTS AT 477.177 MILLION OZ

OCT 23 WITH SILVER DOWN $1.15 : SMALL CHANGES IN SILVER INVENTORY AT THE SLV’ A WITHDRAWAL OF 0.228 MILLION OZ OF SILVER OUT OF THE SLV..//// //INVENTORY AT SLV RESTS AT 477,861 MILLION OZ

OCT 22 WITH SILVER $0.93 : HUGE CHANGES IN SILVER INVENTORY AT THE SLV’ A DEPOSIT OF 3.329 MILLION OZ OF SILVER INTO THE SLV..//// //INVENTORY AT SLV RESTS AT 478.089 MILLION OZ

OCT 18 WITH SILVER $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//// //INVENTORY AT SLV RESTS AT 473.483 MILLION OZ

OCT 17 WITH SILVER DOWN 18 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 3.419 MILLION OZ INTO THE SLV// //INVENTORY AT SLV RESTS AT 473.483 MILLION OZ

OCT 16 WITH SILVER UP 25 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV// //INVENTORY AT SLV RESTS AT 470.064 MILLION OZ

OCT 15 WITH SILVER DOWN 2 CENTS : SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 456,,000 OZ FORM THE SLV. //INVENTORY AT SLV RESTS AT 470.064 MILLION OZ

OCT 11 WITH SILVER UP 53 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 932,000 OZ FORM THE SLV. //INVENTORY AT SLV RESTS AT 470.520 MILLION OZ

OCT 9 WITH SILVER UP 7 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.964 MILLION OZ FORM THE SLV..: /INVENTORY AT SLV RESTS AT 471.432 MILLION OZ

OCT 8 WITH SILVER DOWN $1.41 : HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.007 MILLION OZ FORM THE SLV..: /INVENTORY AT SLV RESTS AT 468.468 MILLION OZ

OCT 7 WITH SILVER DOWN 39 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 684,000 OZ FORM THE SLV..: /INVENTORY AT SLV RESTS AT 466.461 MILLION OZ

OCT 4 WITH SILVER UP 0 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV.: /INVENTORY AT SLV RESTS AT 465.777MILLION OZ

OCT 3WITH SILVER UP 69 CENTS :HUGE CHANGES IN SILVER INVENTORY A WITHDRAWAL OF 1.643 MILLION OZ FORM THE SLV//.: /INVENTORY AT SLV RESTS AT 467.555MILLION OZ

OCT 2WITH SILVER DOWN $0.23 : NO CHANGES IN SILVER INVENTORY: /INVENTORY AT SLV RESTS AT 469.198MILLION OZ

OCT 1 WITH SILVER UP $0.30 : HUGE CHANGES IN SILVER INVENTORY: A WITHDRAWAL OF 1.368 MILLION OZ INTO THE SLV/. /: .///./// /INVENTORY AT SLV 469.198MILLION OZ

SEPT30 WITH SILVER DOWN $0.33 : HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 1.094 MILLION OZ INTO THE SLV/. /: .///./// /INVENTORY AT SLV 470.566MILLION OZ

SEPT27WITH SILVER DOWN $0.58 : HUGE CHANGES IN SILVER INVENTORY: A DEPOSIT OF 4.653 MILLION OZ INTO THE SLV/. /: .///./// /INVENTORY AT SLV 469.472MILLION OZ

SEPT26WITH SILVER UP $0.29 : NO CHANGES IN SILVER INVENTORY:/. /: .///./// /INVENTORY AT SLV 464.819 MILLION OZ

SEPT25WITH SILVER DOWN $0.26 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 2.281MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 464,819 MILLION OZ

SEPT24 WITH SILVER UP $1.26 : HUGE CHANGES IN SILVER INVENTORY:. A DEPOSIT OF 9,305 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 467,100 MILLION OZ

SEPT23 WITH SILVER DOWN $0.39 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 1.824MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 457.795MILLION OZ

SEPT20 WITH SILVER UP $0.08 : NO CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 1.46 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 459,619 MILLION OZ

SEPT19 WITH SILVER UP $0.85 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 1.46 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 459,619 MILLION OZ

SEPT18 WITH SILVER DOWN $0.29 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWAL OF 1,551 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 461.079 MILLION OZ

SEPT17 WITH SILVER DOWN $0.13 : HUGE CHANGES IN SILVER INVENTORY:. A WITHDRAWALOF 5.976 MILLION OZ FROM THE SLV/. /: .///./// /INVENTORY AT SLV 462MILLION OZ

CLOSING INVENTORY 475.157 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY//BILL HOLTER:

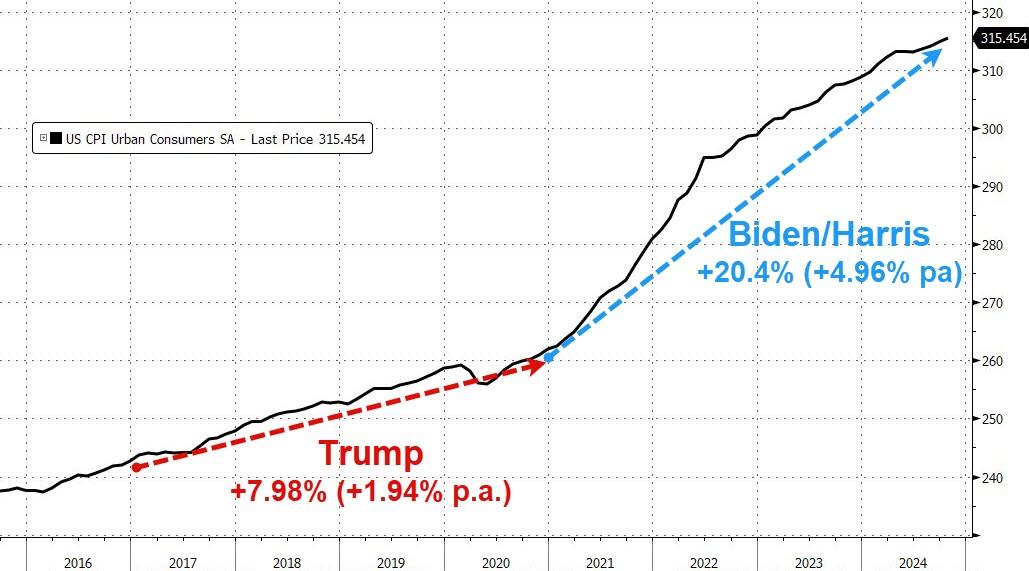

The shakeout in gold and silver markets was triggered by Trump’s landslide. All US markets are responding with conventional confusion, ignoring the contradictions and dangers in Trump’s polices

To put gold’s $200 decline in perspective, the technical chart above shows a normal bull market consolidation testing the 55-day moving average which has generally provided support since 2023. Will this support hold? We look at the dynamics behind current events.

Clearly, with a strong case for higher inflation being made by Trump’s trade tariff policies, we can say with a high degree of certainty that bond yields are going to rise. Here is the chart of the UST 10-year note:

Once it clears 5%, it looks set to run considerably higher.

There is a convenient myth that rising interest rates and bond yields are bad for gold. This error stems from the 1981—2002 bear market in gold, when physical gold bearing a leasing rate of less than 2% was used as the basis of a carry trade leveraging up into US Treasury bills yielding multiples of that. Indeed, the legacy of this gold trade, which has gone missing into markets, is still likely to come back and bite participating governments who were glad of the leasing income at the time.

When gold is in a bull market, it is an entirely different matter. Back in 2020, T-bills yielded close to zero and gold was $1500. Today, 3-month T-bills yield 4.54%, which demolishes the yield relation myth. Furthermore, between 1970—1981 prime rates soared from about 6.5% to 20%, while gold rose 24 times from $35 to $850.

So we know that the hit on the gold price is based on a myth. But so long as the myth persists, paper markets will attempt to behave accordingly. But those that don’t buy the myth are foreign central banks and their governments, particularly in Asia but also in Eastern Europe and elsewhere who are grabbing all the physical that comes available. For them, this is a heaven-sent opportunity to take in more physical — if it is available. This is a problem, for all the action is in paper markets being driven by those with a different agenda: establishment actors with no experience of current market conditions.

Interestingly, the strain between bullion and forms of gold credit are already showing. Comex stands-for-delivery this year so far amount to 129,335 gold contracts, or 402.27 tonnes. Clearly, while the bullion banks, swaps, and hedge funds play their games increasingly other players see mounting dangers.

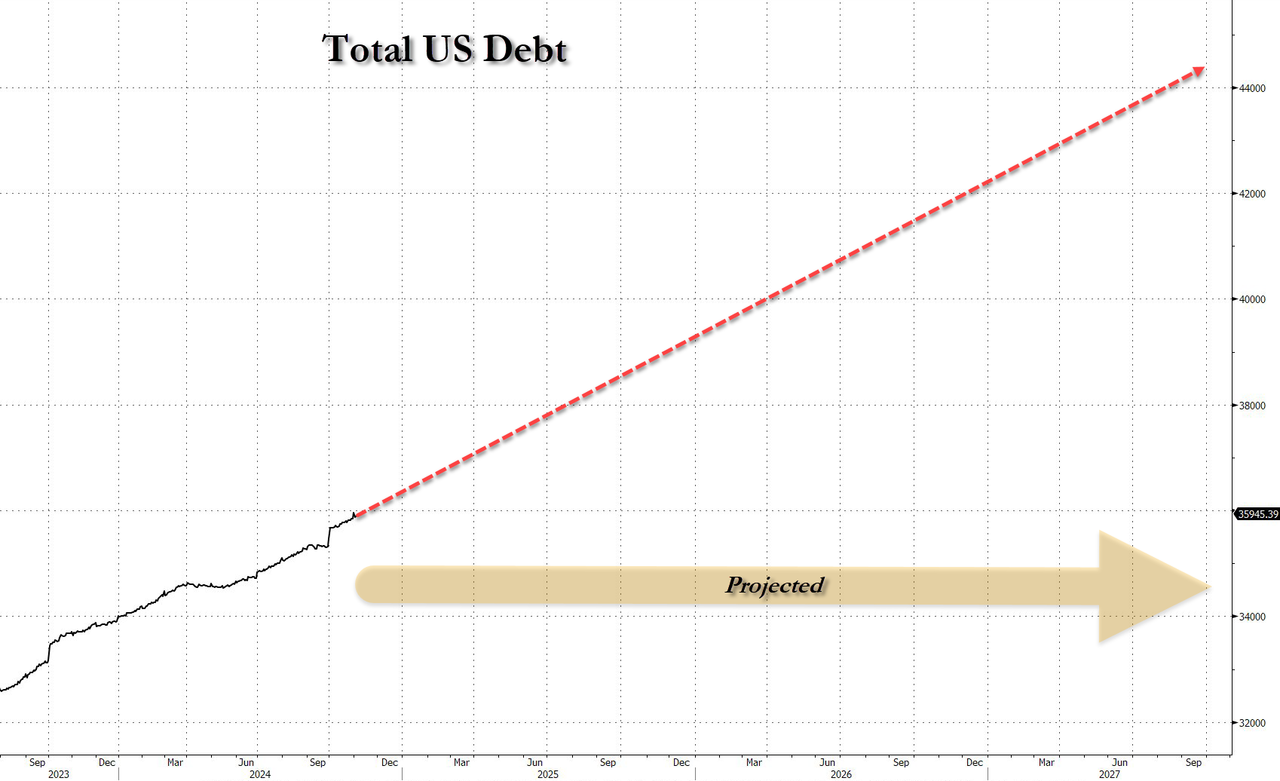

The real problem for the dollar is the enormous mountain of Federal debt, currently at just under $36 trillion. Combine that with a new inflation problem driven by higher tariffs, rapidly, shortening average maturities, and an outlook for rising (not falling) interest rates and bond yields, and the US Government faces escalating funding costs. In other words, it is in a debt trap from which the only escape is to not cut interest rates, but the budget deficit.

Cutting the deficit is easier said than done. Libertarians and others make the mistake of thinking it is simple: it’s not. Political reality, even for Trump aided by Elon Musk makes it very difficult, and as a best case it will take time and legislation which has to pass through both houses driven by vested interests.

Meanwhile, foreign holders of some $32 trillion and underlying dollar-denominated financial assets are far from convinced about Trump, who they see as bringing uncertainty to the world economy, not resolution. The fact of the matter is they see not just the US$, which Steve Hanke describes as the least dirty shirt, but debt traps emerging in the euro, yen, and sterling taking out all of the G7’s currencies.

So what are these sceptics doing? They are getting the hell out of currencies, which are credit, into the sanctity of real money, which is gold. And far from higher interest rates being a headwind against the gold price, they threaten an increasingly imminent decline and collapse of all credit denominated in these currencies and the currencies themselves.

I return to the technical chart at the head of this post. Gold could go lower towards the longer-term moving average, of course, but these are paper prices leading to an increasing squeeze on bullion liquidity. Given what lies ahead, only a fool would sell bullion to the desperadoes seeking to close their shorts.

3. CHRIS POWELL AND GATA DISPATCHES

4. OTHER GOLD COMMENTARIES//LIVE FROM THE VAULT/no 198 ANDREW MAGUIRE WITH PETER KRAUTH

TOPIC SILVER SUPPLY CRUNCH!!

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES: ALUMINA

.

6 CRYPTOCURRENCY NEWS

END

ASIA TRADING WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED UP 17.31 PTS OR 0.51%

//Hang Seng CLOSED DOWN 23.54 PTS OR 0.12%

// Nikkei CLOSED DOWN 654.43 OR 1.66%//Australia’s all ordinaries CLOSED DOWN 0.76%///Chinese yuan (ONSHORE) CLOSED UP TO 7.2091 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2197// Oil DOWN TO 68.14 dollars per barrel for WTI and BRENT UP AT 71.94 Stocks in Europe OPENED ALL MIXED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 7.2091

OFFSHORE YUAN: UP TO 7.2197

SHANGHAI CLOSED CLOSED UP 17.31 PTS OR 0.51%

HANG SENG CLOSED CLOSED DOWN 23.43 PTS OR 0.12%

2. Nikkei closed DOWN 654/43 PTS OR 1.66%

3. Europe stocks SO FAR: ALL MIXED

USA dollar INDEX DOWN TO 105.88 EURO RISES TO 1.0626 UIP 9 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.034 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 154.84…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.3880 Italian 10 Yr bond yield UP to 3.654 //SPAIN 10 YR BOND YIELD UP TO 3.119

3i Greek 10 year bond yield UP TO 3.241

3j Gold at $2610.10 /Silver at: 30.85 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 0 AND 35/100 roubles/dollar; ROUBLE AT 98.60

3m oil into the 68 dollar handle for WTI and 71 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 154.84 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.034% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8822 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9376 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.414 DOWN 2 BASIS PTS…

USA 30 YR BOND YIELD: 4.551 DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.349 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 34.36…

10 YR UK BOND YIELD: 4.560 UP 6 PTS

10 YR CANADA BOND YIELD: 3.286 UP 2 BASIS PTS

5 YR CANADA BOND YIELD: 3.138 UP 2 PTS.

2a New York OPENING REPORT

Futures, Global Stocks Slide Ahead Of Key Inflation Report

Wednesday, Nov 13, 2024 – 08:23 AM

US equity futures, and global markets dropped for the second day in a row on Wednesday as rising yields and a stronger dollar dented the euphoric sentiment behind the Trump rally, and as investors awaited key US inflation data amid concerns that Trump’s proposed America-First policies will reignite price growth. As of 8:00am S&P500 futures and Nasdaq 100 futures slipped 0.2% into the CPI print which is expected to rise for the fourth month (full preview here). Pre-mkt, Mag7 is mixed, and semis are lower; Banks, Energy, Industrials, and Healhcare are seeing a bid. Treasuries steadied after a renewed selloff Tuesday while the dollar was flat after earlier rising beyond 155 per dollar for the first time since July, raising the risk that Japan will intervene to slow the depreciation; the EURUSD briefly dropped to 1.0594 the lowest in a year. Commodities are higher led by Energy and Precious Metals. CPI and five Fed speakers are the macro focus for today as the earnings calendar thins out.

In premarket trading, Cava Group surged 15% after the Mediterranean restaurant chain increased its annual projections for comparable sales. Chegg tumbles 15% after the education technology company gave a fourth-quarter forecast that was weaker than expected. Tesla (TSLA) gains 1.6% and Roivant (ROIV) rises 3% after President-elect Donald Trump picked billionaire Elon Musk and entrepreneur Vivek Ramaswamy to lead a new department that will aim to make the government more efficient. Here are some other notable premarket movers:

Dave Inc. (DAVE) rises 34% after the financial services firm boosted its full-year revenue outlook.

Groupon (GRPN) tumbles 20% after the shopping deals website cut its adjusted Ebitda guidance for the full year.

Instacart (CART) falls 7% after the online grocery delivery company gave a weaker-than-expected fourth-quarter Ebitda forecast.

Rivian (RIVN) rises 8% after Volkswagen raised investment plans in the electric-vehicle maker by $800 million.

Rocket Lab USA (RKLB) jumps 24% after providing a 4Q revenue forecast that beat estimates, fueled by more Electron launches scheduled in November and December.

Rocket Cos. (RKT) tumbles 13% after the mortgage lender issued a weaker-than-anticipated adjusted revenue forecast for the current quarter.

Spirit Airlines (SAVE) slumps 70% as the company is closing in on a deal with creditors that would restructure its crushing debt load in bankruptcy court after discussions for a tie-up with rival Frontier Group Holdings fell apart.

Spotify (SPOT) rise 8% after the audio-streaming company reported 3Q results that beat expectations on both margins and users.

ZoomInfo Technologies (ZI) drops 14% after the infrastructure software company gave a revenue forecast that disappointed analysts.

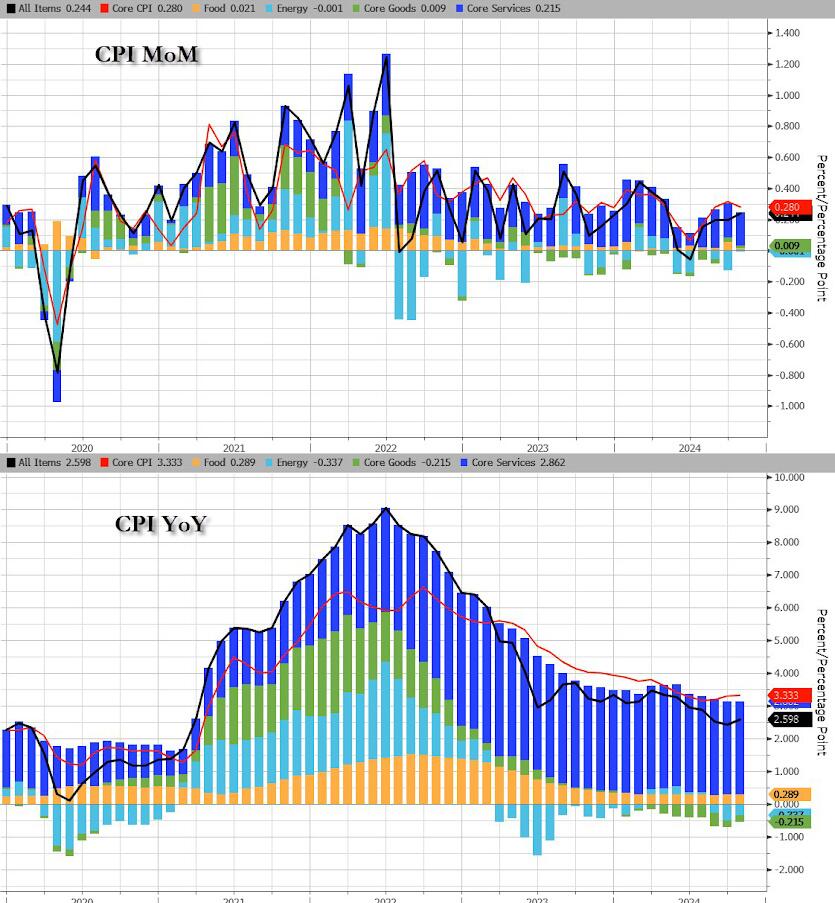

According to Bloomberg, traders are adding inflation hedges and pricing in fewer interest-rate cuts next year amid the threat that Trump’s pro-growth agenda could unleash price pressures. Today’s US data is expected to show the overall consumer price index rose by 0.2% for a fourth month.

“We’ve been pouring our way into long-dated inflation linked bonds in the US where I see the inflation risk as the highest,” Freddie Lait, managing partner at Latitude Investment Management in London, said in an interview with Bloomberg TV. “I would look at the Trump win and think that became more likely.”

The president elect’s anti-trade stance is already taking a toll on assets in the developing world. An MSCI gauge of equities excluding the US is posting its worst day in three months, while an index of emerging market currencies is close to erasing this year’s gains. China’s yuan hit a three-month low Tuesday, forcing authorities to set the currency’s reference rate higher.

European stocks are flat in early trading Wednesday, pausing after a selloff in the previous session; the Stoxx 600 is flat at 502.01. Siemens Energy and Just Eat Takeaway both rose more than 20%. Smiths Group and Dowlais rallied by a similiar amount before paring the surge. Here are the biggest movers Wednesday:

Siemens Energy surges as much as 21%, the most since 2020, taking the stock to a record high. The company increased its medium-term targets, boosted by demand in its grid tech business

AstraZeneca shares gain as much as 3.2%, continuing a recovery into a fourth day following last week’s slump, after Nordea and Intron Health both upgrade their ratings to buy

Just Eat Takeaway shares soar as much as 23% after the food delivery company announced it’s selling Grubhub to Marc Lore’s Wonder Group for an enterprise value of $650 million

RWE jumps as much as 8.9%, the most in over two years, after the German energy company announced a €1.5 billion buyback, which Citi sees as the most positive element in today’s earnings

Smiths Group briefly surged to a record high on Wednesday as the more than 150-year-old British engineering firm reported a strong quarter and increased its revenue guidance

Dowlais shares rise as much as 21%, the most ever, after the British auto engineering specialist published results that were described as much better than feared by analysts at Jefferies

SoftwareOne shares gain as much as 14% after the Swiss IT service provider announced a step-up in cost savings and gave investors a February deadline for its take-private discussions

Babcock International shares jump as much as 19%, briefly touching their highest level since 2020, after the support services provider delivered stronger earnings growth than expected

Lundbeck shares rise as much as 7.2%, the most in almost six months, after the Danish pharmaceuticals firm reported revenue and net income for 3Q that beat market expectations

Ypsomed drops as much as 5.9% after the supplier of auto-injectors reported 1H Ebit which missed estimates. The company also said it has initiated the sale process of its diabetes care business

Jenoptik drops as much as 6.1% after Hauck & Aufhaeuser downgrades the German optoelectronics firm to hold from buy and slashes its price target to a Street-low

Earlier in the session, Asian equities slumped again, headed for their lowest close since September, amid continued selling in the region’s technology stocks. The MSCI Asia Pacific Index declined as much as 1.3%, with TSMC and Samsung Electronics the biggest laggards. A guage of the region’s technology stocks fell as much as 1.4%. The region’s stocks tracked US peers lower after Treasury yields spiked ahead of data expected to show an uneven path of easing consumer price pressures. South Korea led losses in the region as global funds sold shares in companies that are vulnerable to Trump’s protectionist trade policy. Benchmarks in India, Japan, Australia and Taiwan also declined. Stocks in China were volatile before closing higher. The onshore CSI 300 index rose 0.6%, while a gauge of Chinese shares listed in Hong Kong erased a drop of as much as 1.3% to close little changed. Worries over an escalating trade war with the US and China’s unclear prospects for recovery remain as headwinds for investors.

In FX, a gauge of the dollar was little changed Wednesday near two-year highs. Dollar strength has pushed the yen beyond 155 per dollar for the first time since July, raising the risk that Japan will intervene to slow the depreciation. The EURUSD briefly dropped to a new one-year low below 1.06 before rebounding.

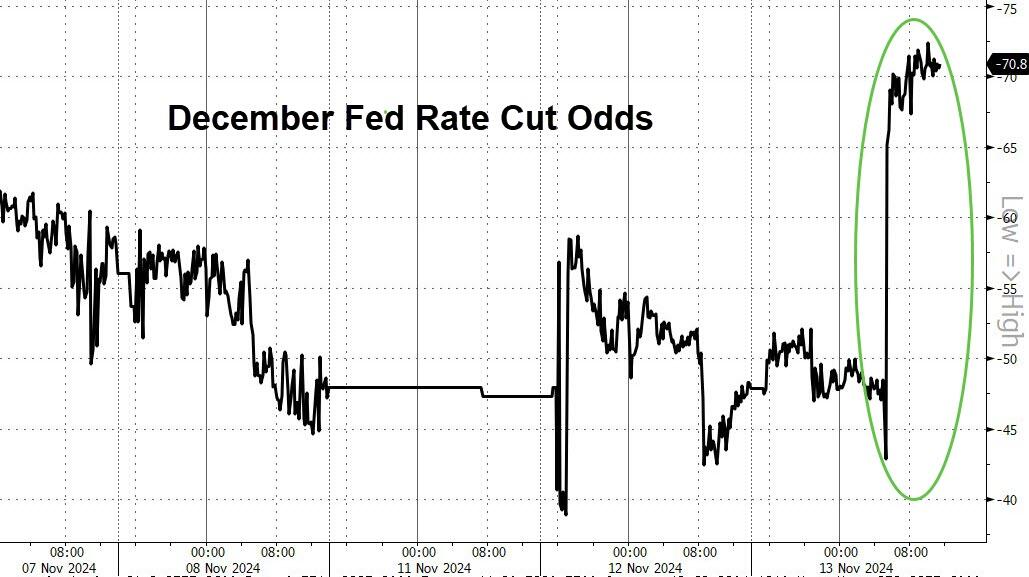

In rates, treasuries staged a minor rebound from Tuesday’s sharp selloff ahead of key US inflation data due later on Wednesday. US 10-year yields fall 1 bp to 4.41%. That’s put the brakes on the recent dollar rally with the Bloomberg Dollar Spot Index near flat. Yields are 1bp-2bp richer on the day from belly to long-end with front-end little changed, flattening 2s10s spread by ~2bp; it steepened 3.5bp in Tuesday’s selloff. The 10-year yield around 4.42% is less than 2bp richer on the day, outperforming bunds and gilts in the sector by 4bp and 3bp. Treasuries have been pummeled by the prospect that Trump’s vowed policies, like tax cuts and tariffs, could fuel price pressures and force the Federal Reserve to keep rates elevated. Traders are pricing in just over a 50% chance of another quarter-point cut in December, after yields on two- and five-year Treasuries surged to their highest levels since July.

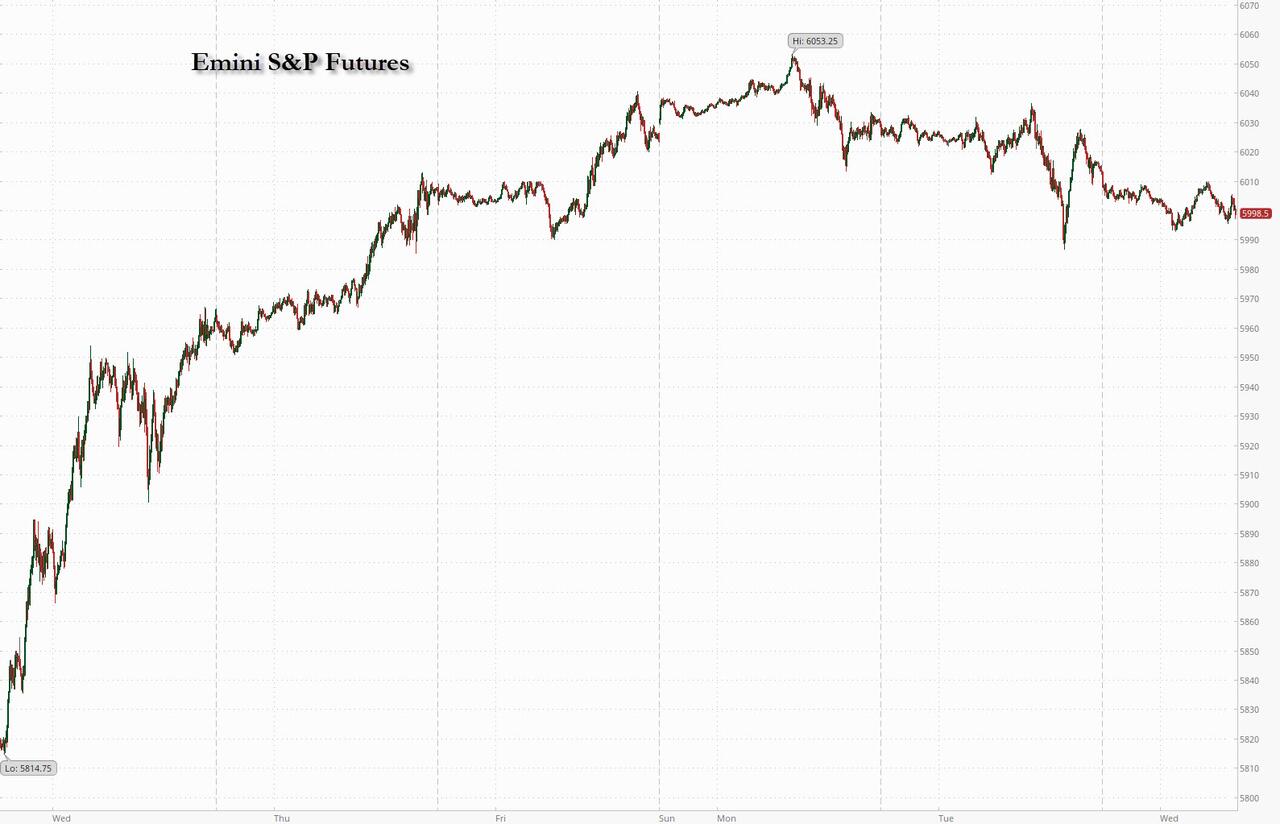

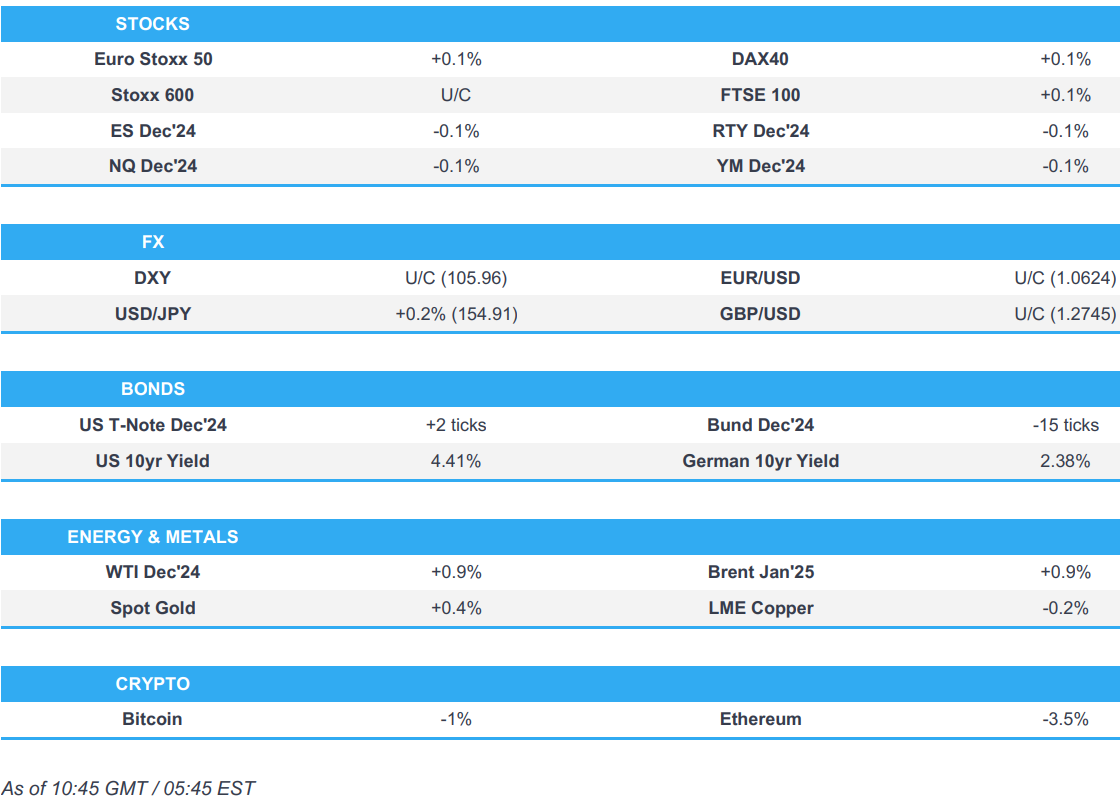

In commodities oil prices advance, with WTI rising 0.7% to $68.60 a barrel. Spot gold climbs $9 to $2,608/oz.

Bitcoin fell 1% after a chart-busting rally took the digital asset to almost $90,000.

Looking at today’s event calendar, US economic data calendar includes October CPI (8:30am) and federal budget balance (2pm). The Fed speaker slate includes Kashkari (8:30am), Williams (9:30am), Logan (9:45am), Musalem (1pm) and Schmid (1:30pm)

Market Snapshot

S&P 500 futures little changed at 6,007.25

STOXX Europe 600 little changed at 502.63

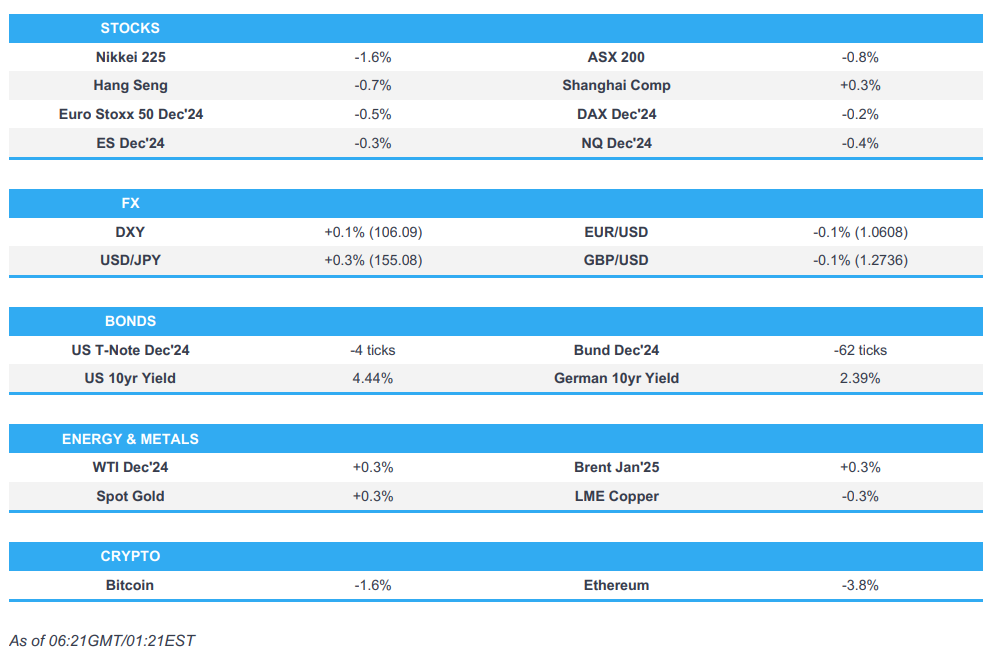

MXAP down 1.0% to 183.07

MXAPJ down 0.8% to 579.96

Nikkei down 1.7% to 38,721.66

Topix down 1.2% to 2,708.42

Hang Seng Index down 0.1% to 19,823.45

Shanghai Composite up 0.5% to 3,439.28

Sensex down 1.4% to 77,555.88

Australia S&P/ASX 200 down 0.8% to 8,193.36

Kospi down 2.6% to 2,417.08

German 10Y yield little changed at 2.36%

Euro little changed at $1.0626

Brent Futures up 0.8% to $72.50/bbl

Gold spot up 0.5% to $2,610.45

US Dollar Index little changed at 105.94

Top Overnight News

China is relieved by Trump’s national security staffing decisions as Beijing feels they could have been worse. WSJ

China needs more stimulus to revive domestic copper demand according to a major importer. BBG

The PBOC signaled its unease with the yuan’s weakness by setting a stronger-than-expected reference rate. Separately, China’s securities regulator increased the frequency of its interactions with global banks, people familiar said. BBG

The FTC under Trump could sustain Biden’s aggressive approach to tech regulations/enforcement based on the frontrunners to replace Lina Khan. FT

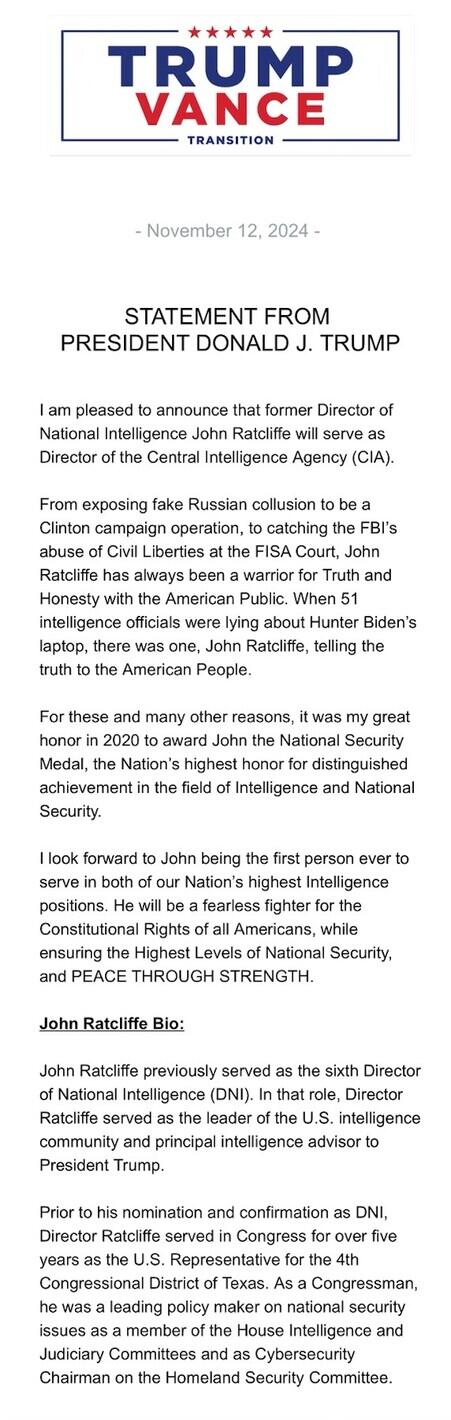

Donald Trump picked John Ratcliffe for CIA Director and will nominate Pete Hegseth for Defense Secretary, while it was also reported that Trump told allies he wants Robert Lighthizer as his trade czar.

Donald Trump’s former trade chief, Robert Lighthizer, and those close to him are preparing to aggressively sell their plans for massive new tariffs on imports that will go far beyond anything seen in Trump’s first term. Politico

Donald Trump picked Elon Musk and Vivek Ramaswamy to lead a new Department of Government Efficiency — DOGE — tasked with slashing bureaucracy, regulation and spending. The structure may allow Musk to avoid resigning from his companies. BBG

Punchbowl News notes that the GOP is planning to pass a major tax bill in the first 100 days of the new Trump presidency. Sources add that conversations between Republicans from the House and Senate Budget Committees yesterday were largely a big-picture discussion about what Republicans are looking at for reconciliation.

SoftBank will be the first to build a supercomputer with chips using Nvidia’s new Blackwell design. BBG

Spirit Airlines is preparing to file for bankruptcy protection after failing to reach a merger deal w/ULCC (Frontier). WSJ

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly subdued following the negative lead from the US amid higher yields and cautiousness ahead of US CPI data, while the region also digested a slew of earnings releases. ASX 200 was dragged lower by underperformance in the mining-related stocks and with the top-weighted financial industry also pressured in the aftermath of CBA’s earnings which posted a flat Y/Y cash profit of AUD 2.5bln for Q1. Nikkei 225 retreated following the hotter-than-expected PPI data, while losses were initially stemmed by recent currency weakness and with Sharp and Tokyo Electron among the best performers post-earnings, although selling eventually worsened. Hang Seng and Shanghai Comp were mixed amid light catalysts and as participants await Chinese tech earnings, while US President-elect Trump’s first picks for his administration included China hawks such as Waltz, Rubio and Lighthizer, although he also named China-friendly Elon Musk to lead the department of government efficiency with Vivek Ramaswamy.

Top Asian News

China cuts taxes for home purchases in fiscal support effective December 1st; MOF says tax cuts targets boosting the property market

China is to release its homebuying tax cut plans soon and will likely cut taxes for home purchases by end-2024, according to China Securities Times.

China’s Taiwan Affairs Office said in response to the TSMC (2330 TT) chip curbs that the US is playing the Taiwan card to raise tensions in the Taiwan Straits and these chip curbs ultimately undermine the interests of Taiwan’s companies, while it added that restrictions also cause Taiwan companies to miss further opportunities for industrial development.

Tencent (700 HK) Q3 (CNY): Revenue 167.19bln (exp. 167.93bln). Net Income 53.23bln (exp. 45.33bln). EPS 5.6444 (prev. 3.752 Y/Y)

Japan’s government is considering restarting electricity and gas price subsidies from Jan-March

European bourses, Stoxx 600 (+0.2%) initially opened very modestly lower across the board, in a continuation of the subdued price action seen in Asia overnight. However, sentiment soon improved just after the cash open to display a more positive picture in Europe. European sectors are mixed, having initially opened with a slight negative bias. Energy takes the top spot, lifted by significant gains in Siemens Energy after it raised its mid-term targets; gains in oil prices in recent trade may also be propping up the sector. Basic Resources follows closely behind, attempting to pare back some of the prior day’s losses. Tech is found at the foot of the pile. US Equity Futures are very modestly lower across the board, with price action tentative ahead of US CPI.

Top European News

BoE’s Mann says headline CPI “is not telling us whether underlying inflation dynamics have been vanquished”. UK services inflation is pretty sticky. Energy prices are more likely to go up than down. Sees more volatility and upward bias to some inflation drivers. Will focus on how much UK financial conditions are affected by BoE actions vs moves in the US. Better for the BoE to lean against risk that inflation is higher than expected, than to wait and see. Ready to cut rates in bigger steps when inflation risks have gone. Still sees a desire from workers and firms to catch up on lost wages and margin caused by past high inflation. Some evidence that hospitality firms are finding it harder to pass on cost increases.

ECB’s Villeroy says he expects more rate cuts. Regarding France, expects inflation to remain moderate and the unemployment rate to increase to ~8% before easing back down to 7%. US election result risks lifting inflation. Bitcoin remains a risky asset.

ECB’s Kazaks says ECB should not deliberately set out to undershoot or overshoot its 2% inflation target, via Econostream. ECB’s best bet was therefore to aim strictly for 2% at all times, so, it should continue to follow its current cautious approach. ECB should proceed with a ‘measured pace, step by step’, avoiding ‘sharp moves’ but retaining ‘full optionality and flexibility. Economic activity was ‘still within the confines of the baseline scenario’. Kazaks said the analysis underlying the Governing Council’s monetary policy decision next month should more heavily weight what it projected would happen next year rather than in 2027, for which an initial set of projections would be unveiled.

ECB’s Nagel says core inflation rate is still quite high; there is still noticeable price pressures, particularly in services. Trump’s proposed tariffs could cost Germany 1% in economic output

UK grocery sales growth slows as consumers wait for Christmas and Black Friday, according to NIQ; says UK has a polarised consumer with half the households feeling pressure on personal finances.

German Chemical Association VCI says in Q3, production rose 0.1% Y/Y or +3.3% without pharma; Q3 producer prices -0.3% amid weak demand and falling raw material costs

FX

DXY started the session off on the front foot once again as the ramifications of a Trump Presidency remain at the forefront of investor sentiment, but is now flat and holding around 105.98. Focus ahead will no doubt be on US CPI, and then a slew of Fed speakers thereafter.

EUR started the session on the backfoot vs. the USD and briefly made a fresh YTD low at 1.0594. The pair has since moved back onto a 1.06 handle. However, the ramifications of a Trump Presidency continue to act as a drag for the Eurozone outlook.

JPY’s run of losses since the start of the week has continued with USD/JPY crossing the 155 threshold for the first time since 30th July (155.21 was the high that day); this may spark some further jawboning from Japanese officials.

GBP steady vs. the USD and EUR with fresh macro drivers for the UK on the quiet side aside from commentary from MPC-hawk Mann. She kept her hawkish-tone and noted that inflation has “definitely not been vanquished”, adding that UK services inflation is pretty sticky.

AUD/USD initially extended on its recent run of losses with sentiment surrounding China acting as a drag on the pair. NZD is steadier than its Antipodean peers vs. the USD and is currently caged within yesterday’s 0.5909-72 range.

PBoC set USD/CNY mid-point at 7.1991 vs exp. 7.2305 (prev. 7.1927).

Fixed Income

USTs are incrementally firmer. Specifics so far have been light with USTs coming under modest pressure overnight, to a 109-9 trough, on a soft 30yr JGB tap and above-forecast Japanese corporate good prices. Docket ahead is headline by CPI, after which we hear from numerous Fed speakers. USTs at a 109-17+ peak, resistance some way off at yesterday’s 110-04+ best before 110-07+ from Monday.

Bunds are softer, printed a 131.62 base in the early European morning with drivers at the time light. Since, the benchmark has been gradually making its way off that trough but is struggling to make real ground above 132.00; current high 132.08. US CPI is the highlight, but for Germany specifically, Chancellor Scholz is set to speak at 12:00GMT, remarks which follow him seemingly accepting calls for an early confidence-vote with December 16th touted.

Gilts are once again the underperformer. Gapped lower as the benchmark caught up with overnight UST action and then extended further below yesterday’s 93.30 trough to a 93.19 base. BoE’s Mann kept her hawkish-tone and noted that inflation has “definitely not been vanquished”, adding that UK services inflation is pretty sticky. This sparked some very modest pressure in Gilts. UK auction was well received, but had little impact on price action.

UK sells GBP 4bln 4.375% 2028 Gilt Auction; b/c 3.12x, average yield 4.499%, tail 1.0bps.

Modest gains across the crude complex this morning after a relatively flat settlement on Tuesday as the initially heightened Middle East rhetoric was later offset by the broad Buck bid. Brent Jan trades towards the upper end of 71.78-72.63/bbl.

Mild gains across precious metals as DXY pulls back from best levels (105.88-106.21 parameter) with newsflow light and with traders gearing up for US CPI. Spot gold resides in a current USD 2,597.72-2,613.28/oz range

Copper futures hold a modest downward bias after lacking direction in APAC trade in a continuation of price action seen from the disappointing NPC Standing Committee announcement on Friday.

Iran reportedly made plans to keep oil exports stable under a Trump presidency, according to local press Shana.

Citi revised its 0-3M copper price target to USD 8,500/t (prev. USD 9,500/t); revised Q4 2024 average to USD 9,000/t (prev. USD 9,500/t)

Oil output at Kazakhstan’s Tengiz field -21% since Oct 26th to 496,200 BPD, according to Reuters sources.

Russia’s seaborne oil product exports in October -7% on the month, according to data and Reuters calculations.

Geopolitics: Middle East

Lebanon is reportedly awaiting concrete ceasefire proposals, according to Reuters citing Parliamentary speaker Berri, after a senior US official said he saw a shot at a truce soon

Israel conducted raids on the Haret Hreik and Lilaki areas in the southern suburbs of Beirut, according to Al Jazeera.

US envoy to the UN told the Security Council that Israel has taken some important steps to address the undisputed humanitarian crisis in Gaza and that it is of urgent importance that Israel pause implementation of legislation targeting UNRWA, while the envoy added Israel must ensure its actions are fully implemented and improvements are sustained over time.Syrian media reported air strikes targeting the outskirts of the city of Albu Kamal on the Syrian-Iraqi border, while the US military later confirmed that it conducted strikes against an Iranian-backed militia group’s weapons storage facility in Syria.

Geopolitics: Other

Chinese military organised naval and air forces to patrol the territorial waters and airspace of Scarborough Shoal in the South China Sea and surrounding areas on November 13th.

US sanctions agency OFAC conducts an inquiry into Russian clients UBS (UBSG SW) took over with Credit Suisse, according to Reuters sources.

S Event Calendar

07:00: Nov. MBA Mortgage Applications +0.5%, prior -10.8%

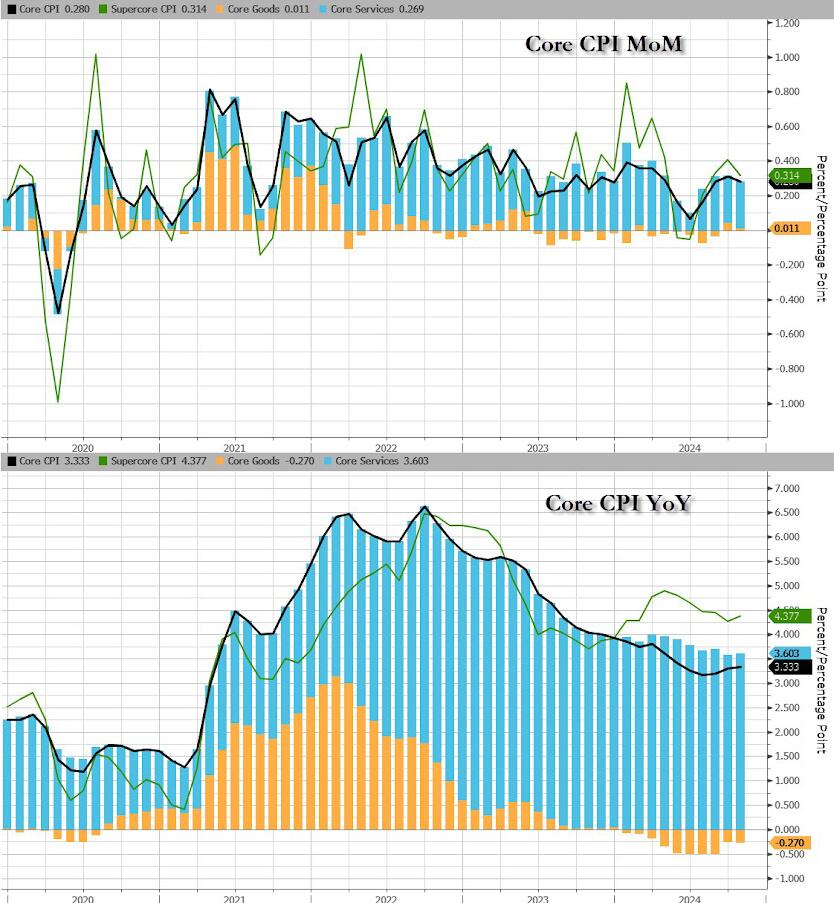

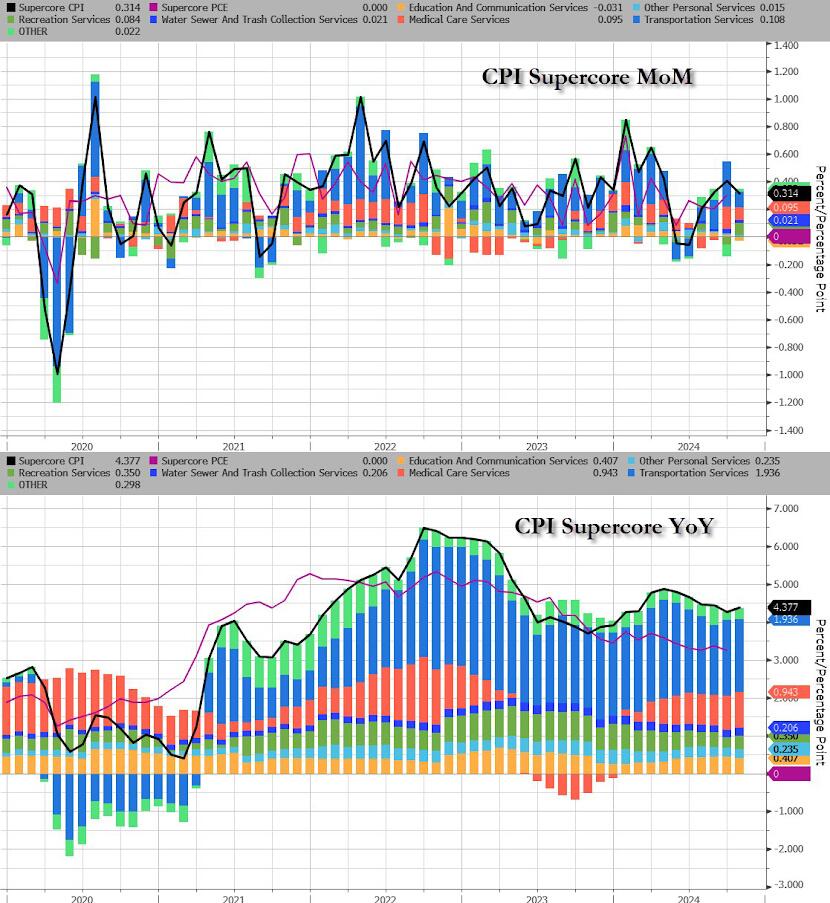

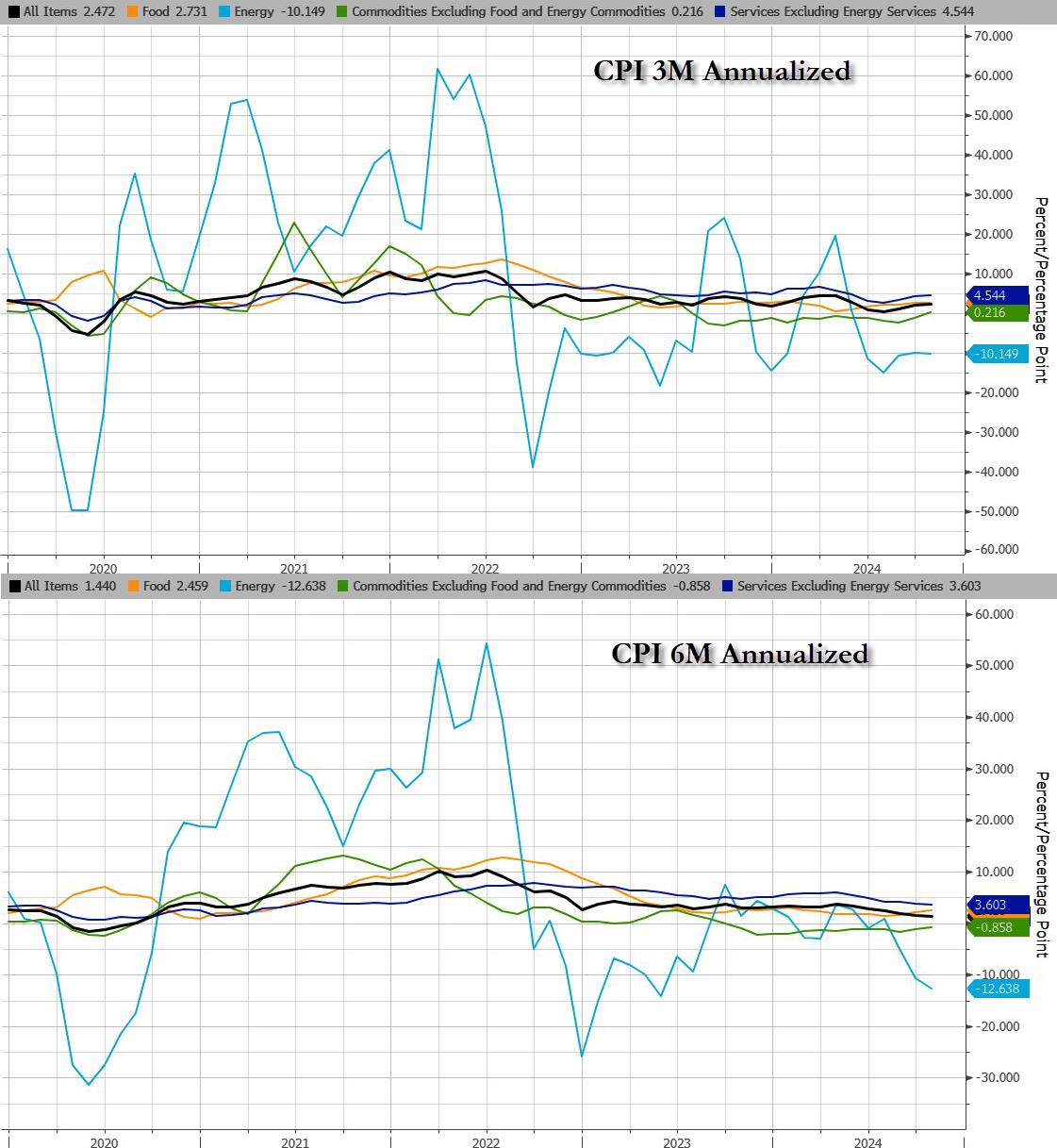

08:30: Oct. CPI MoM, est. 0.2%, prior 0.2%

Oct. CPI YoY, est. 2.6%, prior 2.4%

Oct. CPI Ex Food and Energy MoM, est. 0.3%, prior 0.3%

Oct. CPI Ex Food and Energy YoY, est. 3.3%, prior 3.3%

Oct. Real Avg Hourly Earning YoY, prior 1.5%, revised 1.4%

Oct. Real Avg Weekly Earnings YoY, prior 0.9%, revised 1.1%

14:00: Oct. Federal Budget Balance, est. -$225b, prior $64.3b

Central Bank Speakers

08:30: Fed’s Kashkari Appears on Bloomberg Television