NOV 27/LAST DAY BEFORE FIRST DAY NOTICE: GOLD CLOSED UP $18.05 TO $2639.70 WITH SILVER LOSING 25 CENTS TO $30.11//PLATINUM WAS UP $2.80 TO $930.40 WHILE PALLADIUM WAS DOWN $5.30 TO $979.10//EXCELLENT GOLD COMMENTARIES TONIGHT FROM ALASDAIR MACLEOD AND PETER SCHIFF//FASCINATING STORY OF NATO SHIPS SURROUNDING CHINESE SHIP SUSPECTED OF CUTTING SEA CABLES//HUGE GERMAN STEEL COMPANY THYSSEN KRUPP LAYING OFF 11,000 WORKERS AND THEY SEEM TO BE IN FINANCIAL TROUBLE//CHINESE REAL ESTATE BUBBLE SET TO BURST WITH MANY HUGE REAL ESTATE CONGLOMERATES ALREADY BLOWING UP//FRENCH BOND YIELDS RISE MUCH ABOVE GERMAN BUNDS CREATING PANIC IN THE FRENCH MARKETS//ISRAEL VS HEZBOLLAH: CEASEFIRE HOLDS//MANY UPDATES ON THIS MAJOR TOPIC//NOW HAMAS DESIRES A CEASEFIRE WITH ISRAEL//COVID UPDATES/VACCINE INJURY REPORT/ MARK CRISPIN MILLER//DR PAUL ALEXANDER//SLAY NEWS ETC//CANADA FURIOUS WITH TRUMP’S 25% TARIFF AND MAY RETALIATE//COMMENTARY TONIGHT FROM BRANDON SMITH ON THE RUSSIA VS UKRAINE VS USA WAR//UPDATES ON RUSSIA VS UKRAINE//MANY USA DATA RELEASES WITH THE BIG ONE: FED’S FAVOURITE INDICATOR FOR INFLATION RISING//SWAMP STORIES FOR YOU TONIGHT//

624 H BOFA SECURITIES 43 690 C ABN AMRO 5 737 C ADVANTAGE 36 905 C ADM 2

TOTAL: 43 43 MONTH TO DATE: 3,622

JPMorgan stopped 0/43

GOLD: NUMBER OF NOTICES FILED FOR NOV/2024. CONTRACT: 43 NOTICES FOR 4300 OZ 0.1337 TONNES

total notices so far: 3622 contracts for 362,200 Oz (11.265 tonnes)

FOR NOV

SILVER NOTICES: 0 NOTICE(S) FILED FOR NIL OZ/

total number of notices filed so far this month : 935 for 4.675 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $18.05 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 879.41 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $0.25 AT THE SLV

NO CHANGES IN SILVER INVENTORY AT THE SLV:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 474.747 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI SURPRISINGLY FELL BY A MEGA GIGANTIC SIZED 4705 CONTRACTS TO 134,590 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS GIGANTIC SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR SMALL GAIN OF $0.10 IN SILVER PRICING AT THE COMEX WITH RESPECT TO TUESDAY’S TRADING. WE HAD A HUGE LOSS OF 4055 TOTAL CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR GAIN OF $0.10 IN PRICE. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS ON TUESDAY COMEX TRADING (COUPLED WITH LIQUIDATION OF CALENDAR SPREADERS) AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S CONTINUAL PRICE RISE FOR THE PAST 2 WEEKS AND THEY FAILED ON TUESDAY WITH SILVER’S RISE.

WE HAD A STRONG 650 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY A HUGE 999 CONTRACT T.A.S ISSUANCE WHICH WILL BEING USED IN TODAY’S TRADING AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING (ESPECIALLY TODAY) TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE LOST A HUMONGOUS SIZED 4055 CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR GAIN IN PRICE. WE HAD MAJOR TAS LIQUIDATION THROUGHOUT TUESDAY’S COMEX SESSION ALONG WITH MONTH END SPREADER LIQUIDATION.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN ON LAST WEEK. THE ACCUMULATED T.A.S. WAS BEING USED TO MANIPULATE PRICES AT THE COMEX BUT THAT ENDED MONDAY..

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: A HUGE 999 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS BUT TO NO AVAIL TODAY. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.10) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SILVER LONGS FROM THEIR PERCH AS WE DID HAVE A SMALL GAIN JN PRICE

WE HAD A STRONG 650 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 2.810 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 55,000 OZ QUEUE JUMP//NEW STANDING ADVANCES TO 4.750 MILLION OZ

// STANDING FOR SILVER//NOV AT 4.750 MILLION OZ

WE HAD:

/ HUGE SIZED COMEX OI LOSS (DESPITE MASSIVE T.A.S. LIQUIDATION + MONTH END SPREADER LIQUIDATION)//STRONG SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 999 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: ADDED A SMALL 37 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS NOV. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF NOV

TOTAL CONTRACTS for 20DAYS, total 22,219 contracts: OR 111.095 MILLION OZ (1110 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 111.095 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 111.085 MILLION OZ (WILL BE HUGE THIS MONTH)

RESULT: WE HAD A HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 4705 CONTRACTS DESPITE OUR GAIN OF $0.10 IN PRICE OF SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUGE EFP ISSUANCE CONTRACTS: 999 ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR NOV OF 2.810 MILLION OZ ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 55,000 OZ QUEUE JUMP

//NEW TOTAL STANDING FOR NOV AT 4.730 MILLION OZ

WE HAVE A HUGE SIZED LOSS OF 4055 OI CONTRACTS ON THE TWO EXCHANGES DESPITE OUR GAIN IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUMONGOUS 999 CONTRACTS TRYING DESPERATE TO CONTAIN SILVER’S PRICE RISE,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESSDAY COMEX SESSION ALONG WITH CALENDAR SPREADER LIQUIDATION. THUS THE NEED FOR REPLENISHMENT /THE STRONG TA.S. ISSUANCE//LIQUIDATION DISTORTS THE TOTAL OI CONTRACTS STANDING AT THE COMEX. NO NET LONG SPECULATORS WERE BURNED ON TUESDAY

/ ZERO NET SHORT COVERING FROM OUR SPEC SHORTS DESPITE THE MASSIVE LOSS IN PRICE MONDAY/ . ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE TUESDAY NIGHT (999) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE AND LATELY ON A DAILY BASIS INCLUDING YESTERDAY AND TODAY.

WE HAD 0 NOTICE(S) FILED TODAY FOR 0.000 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A STRONG SIZED 78501 OI CONTRACTS TO 472,660 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A FAIR SIZED 814 CONTRACTS//

WE HAD A STRONG SIZED DECREASE IN COMEX OI (8501 CONTRACTS) OCCURRED DESPITE OUR GAIN OF $3.80 IN PRICE TUESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A GOOD INITIAL STANDING IN GOLD TONNAGE FOR NOV AT 2.488 TONNES ON FIRST DAY NOTICE FOLLOWED BY TODAY’S 4300 OZ QUEUE JUMP. BUT WE HAD ANOTHER OF THAT CRAZY ISSUANCE OF 1500 CONTRACTS ISSUED TUESDAY NIGHT FOR DELIVERY OF EXCHANGE FOR RISK OR 4.665 TONNES OF GOLD TO WHICH WE ADD 3.11 TONNES OF GOLD ISSUED ON AN EXCHANGE FOR RISK ON NOV 15.//NEW STANDING ADVANCES TO 11.265 TONNES +4.665 TONNES (EX FOR RISK TUESDAY NIGHT+ 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

NEW STANDING FOR NOVEMBER: 19.0425 TONNES

/ ALL OF THIS HAPPENED WITH OUR $3.80 IN PRICE WITH RESPECT TO TUESDAY’S COMEX ///. WE HAD A FAIR LOSS OF 3440 OI CONTRACTS (8.167 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT MONDAY AND TUESDAY WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! YOU CAN VISUALIZE THIS WITH THE DAILY QUEUE JUMPING WE ARE WITNESSING (AND TODAY’S QUEUE JUMP OF 4300 OZ)

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5061 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 472,660

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 3440 CONTRACTS WITH 8501 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 5061 EFP OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 3440 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED BUT CRIMINAL 1531 CONTRACTS ISSUED. WE HAD A HUGE LIQUIDATION OF T.A.S CONTRACTS DESPITE OUR GAIN IN PRICE TUESDAY AS THE NEED FOR REPLENISHMENT WAS STILL IN ORDER TO CARRY OUT ITS PRICE CONTAINMENT STRATEGY. THEY FAILED MISERABLY ON FRIDAY WITH GOLD’S PRICE RISE ABOVE THE $2700 PRICE LEVEL BUT SUCCEEDED MONDAY ON COMEX OPTIONS EXPIRY TO RAID GOLD. THEY FAILED MISERABLY TUESDAY.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5061 CONTRACTS) ACCOMPANYING THE STRONG SIZED DECREASE IN COMEX OI OF 7687 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 3440 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR NOV 2.488 TONNES FOLLOWED BY TODAY’S 4300 OZ QUEUE JUMP BUT WE MUST ADD THE NEW AND CRIMINAL ISSUANCE OF 1500 CONTRACTS OF EX. FOR RISK ISSUED TUESDAY NIGHT WHERE BY THE BUYER ASSUMES RISK FROM THE SELLER THAT THAT CONTRACT WOULD BE DELIVERED TO HIM. WHAT A JOKE! TOTAL EXCHANGE FOR RISK =150,000 OZ OR 4.665 TONNES. FROM THAT WE MUST ADD 3.11 TONNES OF GOLD ISSUED FOR EX. FOR RISK ON NOV 15.

//NEW STANDING NOVEMBER: 11.265 TONNES +4.665 EX FOR RISK TUESDAY + 3.11 TONES EX FOR RISK//PRIOR = 19.0425 TONNES.

/ 3) HUGE T.A.S. LIQUIDATION (TRYING TO LOWER GOLD’S PRICE RISE PM TUESDAY WITH NO SUCCESS AS WE HAD A SMALL $3.80 PRICE GAIN . WE HAD ZERO NET LONG SPECS BEING CLIPPED. STICKY GOLD’S LONGS HOWEVER ARE NOT FOOLED BY THE RAID AS THEY WERE REWARDED MONDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL.

4) STRONG SIZED COMEX OPEN INTEREST DECREASE 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///STRONG T.A.S. ISSUANCE: 1531 T.A.S.CONTRACTS

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

NOV

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF NOV :

TOTAL EFP CONTRACTS ISSUED: 118,431 CONTRACTS OF 1,1843,100 OZ OR 368.370 TONNES IN 20 TRADING DAY(S) AND THUS AVERAGING: 5921 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 20 TRADING DAY(S) IN TONNES 368.370 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 368.30 DIVIDED BY 3550 x 100% TONNES = 10.36% OF GLOBAL ANNUAL PRODUCTION

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 368.30 TONNES (WILL PROBABLY BE A HUGE MONTH/MAYBE A RECORD ISSUANCE MONTH///NOW SURPASSED THE PREVIOUS 3RD HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 3RD HIGHEST EVER RECORDED AND CLOSING IN ON THE SECOND HIGHEST RECORDED ISSUANCE..//HIGHEST EVER RECORDED ISSUANCE MARCH 2022 OF 409 TONNES.)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF SEPTEMBER. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A MONSTER SIZED 4705 CONTRACTS OI TO 134,553 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 650 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 650 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 1025 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 4705 CONTRACTS AND ADD TO THE 650 E.FP. ISSUED

WE OBTAIN A MONSTER SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 4055 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS 20.275 MILLION OZ OCCURRED DESPITE OUR $0.10 GAIN IN PRICE

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS//

WEDNESDAY MORNING TUESDAY NIGHT

ASIA TRADING WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED UP 50.02 PTS OR 1.53%

//Hang Seng CLOSED UP 443.93 PTS OR 2.32%

// Nikkei CLOSED DOWN 307.03 OR 0.80%//Australia’s all ordinaries CLOSED UP 0.55%///Chinese yuan (ONSHORE) CLOSED DOWN TO 7.2411 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2569// Oil DOWN TO 69.08 dollars per barrel for WTI and BRENT DOWN AT 73.16 Stocks in Europe OPENED ALL MOSTLY RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A HUGE SIZED8501 CONTRACTS TO 472,660 DESPITE OUR GAIN IN PRICE OF $3.80 WITH RESPECT TO TUESDAY’S TRADING. , WE LOST A NEGLIGIBLE NET IN NUMBER LONGS AS WE HAD A SMALL PRICE GAIN FOR GOLD AS YOU WILL SEE BELOW. WE HAD A HUGE NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (5061).

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY THIS ENTIRE WEEK AND ESPECIALLY DURING MONDAY’S HUGE LOSS IN PRICE. WE LOST ALSO A HUGE NUMBER OF CONTRACTS TUESDAY AS WELL. WE HAD A HUGE TA.S. LIQUIDATION COUPLED WITH A CONTINUAL HUGE MONTH END LIQUIDATION OF CALENDAR SPREADERS WHICH IS WHY WE LOST SO MANY COMEX OI CONTRACTS. SOME OF THE REMAINING LONGS REMAIN STICKY AS THEIR AIM IS TO TAKE DELIVERY OF PHYSICAL GOLD NOT WORRYING TOO MUCH ON RAIDS.

THE FED IS THE MAJOR SHORT OF AROUND 93+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS IS SCHEDULED TO HAPPEN LATE OCT 2024/(AS OUTLINED IN OUR GOLD PHYSICAL COMMENTARIES//VIEW ANDREW MAGUIRE LATEST LIVE FROM VAULT PODCAST 197 , 199, AND FRIDAY NIGHTS 200 AS HE TACKLES THIS IMPORTANT TOPIC). THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST TWO MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY! ACTUALLY THE FED HAS COAXED THE SPECULATORS TO GO MASSIVELY SHORT WHILE THEY TAKE THE LONG SIDE AFTER THEY COMMENCE THE AVALANCHE IN LOWERING THE PRICE OF GOLD. THIS WAS SURELY ON DISPLAY TUESDAY.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD A STRONG T.A.S. LIQUIDATION THROUGHOUT LAST WEEK’S TRADING AND AGAIN TODAY.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF THE SPREADERS // T.A.S DURING LAST WEEK AND THIS WEEK IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW ENTERING INTO THE NON ACTIVE DELIVERY MONTH OF NOV.… THE CME REPORTS THAT THE BANKERS ISSUED A HUGE SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A HUGE SIZED 5061 EFP CONTRACTS WERE ISSUED: : /DEC 5061 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5061 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 3,440 CONTRACTS IN THAT 5061 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG SIZED LOSS OF 7687 COMEX CONTRACTS..AND THIS EVERY LARGE LOSS ON OUR TWO EXCHANGES HAPPENED DESPITE OUR GAIN IN PRICE OF $3.80 TUESDAY// COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AS MENTIONED ABOVE. HOWEVER I AM EXTREMELY SAD TO REPORT THAT THE CROOKS ISSUED FOR THE SECOND TIME THIS MONTH A STUPID EXCHANGE FOR RISK OF A GIANT 1,500 CONTRACTS TO GO ALONG WITH THE NOV 15 ISSUANCE. IN THIS ISSUANCE A BUYER IS TAKING THE RISK THAT THEY WILL DELIVER TO HIM 4.665 TONNES (TODAY’S ISSUANCE) OF GOLD AND WE MUST ADD THE 3.110 TONNES OF GOLD (311,000 OZ) PURCHASE ON NOV 15. WE WISH THE BUYER ALL THE LUCK IN THE WORLD. TOTAL ISSUANCE THIS MONTH OF EXCHANGE FOR RISK: 2500 OI CONTRACTS FOR 250,000 OZ OR 7.7760 TONNES. I AM AFRAID THAT THE COMEX HOUSE IS BURNING DOWN!

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY WAS A NORMAL SIZED SIZED 1531 CONTRACTS, AND THESE WILL BE USED TO REPLENISH SUPPLIES.. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK).

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON MONDAY, THEIR RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE (COUPLED WITH THE LIQUIDATION OF CALENDAR SPREADERS ). THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN MONDAY’S RAID. WE HAD CONTINUAL T.A.S. AND MONTH END SPREADER LIQUIDATION TUESDAY.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: NOV (19.0425 TONNES) WHICH IS HUGE FOR OUR NON ACTIVE NOV DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 47 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY A $3.80/)//AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A GAIN IN PRICE WITH OUR TWO EXCHANGES, WE DID HAVE SOME T.A.S. SPREADER LIQUIDATION TUESDAY AND THIS WAS MAGNIFIED WITH MONTH END SPREADER LIQUIDATION. WE ALSO HAD A NORMAL T.A.S. ISSUANCE AS THE NEED FOR REPLENISHMENT WAS STILL PRESENT. THIS COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING

WE HAVE LOST A TOTAL OF 10.699 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR NOV (2.488TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S GOOD SIZED QUEUE JUMP OF 43 CONTRACTS OR 4300 OZ (0.1337 TONNES). THESE GUYS UNDERWENT A QUEUE JUMP BOLTING AHEAD OF OTHER LONGS TO OBTAIN BADLY NEEDED PHYSICAL GOLD. MOSTLY LIKELY THIS IS THE FRBNY DESPERATELY TRYING TO EXTINGUISH ITS MASSIVE PHYSICAL SHORT FALL OF 93 TONNES. HOWEVER WE MUST ADD THAT CRAZY “DELIVERY” OF 1500 CONTRACTS OF EXCHANGE FOR RISK OR 150,000 OZ OR 4.665 TONNES OF GOLD ISSUED ON TUESDAY NIGHT. AND THEN WE MUST ADD THE NOV 15 ISSUANCE OF 3.11 TONNES OF GOLD THROUGH ITS EXCHANGE FOR RISK.

//NEW STANDING FOR NOV 11.265 TONNES + 4.665 TONNES EX FOR RISK (TUESDAY NIGHT) + 3.11 TONNES EX FOR RISK/ PRIOR= 19.0425 TONNESES

NEW STANDING FOR NOVEMBER: 19.0425TONNES (WHICH FOR A NON ACTIVE DELIVERY MONTH)

ALL OF THIS WAS ACCOMPLISHED WITH OUR GAIN IN PRICE TO THE TUNE OF $3.80

WE HAD X814 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET LOSS ON THE TWO EXCHANGES 2626 CONTRACTS OR 262600 OZ (8.167 TONNES)

(consists of: 112,498.794 oz Asahi and 98,046.325 oz JPMorgan Enhanced bars or 245 400 oz bars.)

No of oz served (contracts) today

43 notice(s) 4300 OZ 0.1377TONNES

No of oz to be served (notices)

0 contracts 0 OZ 0.0 TONNES

Total monthly oz gold served (contracts) so far this month

3622 notices 362200 oz 11.265 TONNES

Total accumulative withdrawals of gold from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of gold from the Customer inventory this month

x

dealer deposits: 1

i) Into Brinks 32,427.23 oz

total dealer deposits: 32,427.23 oz

we have 0 customer deposits

total deposits 0 oz

withdrawals: 1

Out of Brinks: 32.151 oz one kilobar

TOTAL WITHDRAWALS: 32.151 oz

adjustments: 3

a)Brinks/dealer to customer:

13,274.549 oz

b)Loomis: dealer to customer: 63,948.379 oz

c)Malca; dealer to customer 4,147.479

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR NOV.

For the front month of NOV: we have an oi of 43 contracts having LOST 813 contracts. We had 856 contracts served on TUESDAY so we gained A STRONG 43 contracts as these guys underwent a queue jump of 4300 oz (0.1377 TONNES OF GOLD) to which we add the 4.665 tonnes of exchange for risk delivery/TUESDAY AND THEN ADD THE 3.11 TONNES OF EX. FOR RISK/NOV 15

DECEMBER, THE BIGGEST DELIVERY MONTH LOST 40,267 CONTRACTS TO 35,615.. WE HAVE 1 MORE READING DAYS BEFORE FIRST DAY NOTICE FRIDAY NOV 29, THE OPEN INTEREST DESPITE THE HUGE TAS LIQUIDATION IS STILL HIGH AND THUS WE WILL NO DOUBT HAVE A HUGE AMOUNT OF GOLD STANDING FOR DELIVERY WHEN I RECEIVE WEDNESDAY’S NIGHT FINAL OI READING WHICH WILL REVEAL THE INITITAL AMOUNT OF GOLD STANDING FOR THE LARGEST DELIVERY MONTH FOR COMEX, THE DECEMBER CONTRACT MONTH.

JANUARY GAINED 1084 CONTRACTS TO STAND AT 2137

FEBRUARY GAINED 28,837 CONTRACTS TO 341,805 .

We had 43 contracts filed for today representing 4300 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 43 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 0 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for NOV /2024. contract month, we take the total number of notices filed so far for the month (3622 x 100 oz ) to which we add the difference between the open interest for the front month of NOV(43 CONTRACTS) minus the number of notices served upon today (43 x 100 oz per contract( equals 362,200 OZ OR 11.265 TONNES.+ to which we add 4.665 tonnes of exchange for risk delivery AND then add the 3.11 tonnes of exchange for risk//PRIOR //new totals 19.0425 tonnes

thus the INITIAL standings for gold for the NOV contract month: No of notices filed so far (3622 x 100 oz +we add the difference for front month of NOV (43 OI} minus the number of notices served upon today (43 x 100 oz which equals 362,700 oz (11.265 TONNES) + 4.665 exchange for risk/Tuesday +3.11 tonnes (ex. for risk/PRIOR) = 19.0425

TOTAL COMEX GOLD STANDING FOR NOV.: 19.0425 TONNES WHICH IS HUGE FOR THIS NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 17,789,832.141 OZ

TOTAL REGISTERED GOLD 7,928.752.528/// 246.66tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 9,861,079.613 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,175,041 oz (REG GOLD- PLEDGED GOLD)= 192.06 tonnes //

JPMorgan enhanced inventory is 111.737 tonnes and thus 30.24% of entire inventory.

END

SILVER/COMEX

NOV 27. 2024

INITIAL

//2024// THE NOV 2024 SILVER CONTRACT//INITIAL

Silver

Ounces

Withdrawals from Dealers Inventory

NIL oz

Withdrawals from Customer Inventory

1,202,626.920 oz

DELAWARE Loomis

.

Deposits to the Dealer Inventory

nil oz

Deposits to the Customer Inventory

1,318,891.400 oz Brinks Delaware

No of oz served today (contracts)

0 CONTRACT(S) (0 OZ)

No of oz to be served (notices)

00 contracts (0,000oz)

Total monthly oz silver served (contracts)

935 Contracts (4.675 MILLION oz)

Total accumulative withdrawal of silver from the Dealers inventory this month

NIL oz

Total accumulative withdrawal of silver from the Customer inventory this month

i) 0 dealer deposit/

total dealer deposit : NIL oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 customer deposits

i) Into Brinks: 1,315,189.900 oz

ii) Into Delaware: 2999.500 oz

total customer deposits 1,318.891.400 oz

We had 2 withdrawals

i) Out of Loomis: 1,198,726.870 oz

ii) Out of Delaware 3900.100 oz

total withdrawal 1,202,626.970 oz

JPMorgan has a total silver weight: 134.401million oz/307.876million or 43.52%

adjustment 1

Brinks/customer to dealer 2,159,,445.600 oz

TOTAL REGISTERED SILVER: 80.035MILLION OZ//.TOTAL REG + ELIGIBLE. 307.976 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR NOV

silver open interest data:

FRONT MONTH OF NOV /2024 OI: 11 OPEN INTEREST FOR A LOSS OF 1 CONTRACT

WE HAD 12 NOTICE(S) FILED ON TUESDAY SO WE GAINED 11 CONTRACTS OR 55,000 OZ UNDERWENT A QUEUE JUMP

DECEMBER SAW A LOSS OF 13,952 CONTRACTS DOWN TO 12,475 CONTRACTS. WE HAVE 1 MORE READING DAYS BEFORE FIRST DAY NOTICE. TAS ISSUANCE HAS BEEN HIGH ALL WEEK AND THUS IT IS STILL TOO DIFFICULT TO SAY HOW MANY WILL REMAIN TO STAND ON FIRST DAY NOTICE WITH TONIGHT’S FINAL READING.

JANUARY SAW A GAIN OF 583 CONTRACTS UP TO 2449

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 0 for 0.000 MILLION oz

CONFIRMED volume; ON TUESDAY 109,297- huge// t.a.s. enhanced

To calculate the number of silver ounces that will stand for delivery in NOV we take the total number of notices filed for the month so far at 935x 5,000 oz = 4.675 MILLION oz

to which we add the difference between the open interest for the front month of NOV (11) and the number of notices served upon today (0)x (5000 oz)

Thus the standings for silver for the NOV 2024 contract month: 935 Notices served so far) x 5000 oz + OI for the front month of NOV(11) number of notices served upon today minus (0)x 5000 oz of silver standing for the NOV contract month equates to 4.7300 MILLION OZ.

New total standing: 4.7300 million oz.

There are 77.825 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS//

NOV 27 WITH GOLD UP $18.05 ON THE DAY; NO CHANGES IN GOLD AT THE GLD : . .///INVENTORY RESTS AT 879.41 TONNE

NOV 26 WITH GOLD UP $3.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD : A DEPOSIT OF 1.44 TONNES OF GOLDINTO THE GLD. .///INVENTORY RESTS AT 879.41 TONNES

NOV 25 WITH GOLD DOWN $91.60 ON THE DAY; NO CHANGES IN GOLD AT THE GLD :. .///INVENTORY RESTS AT 877.97 TONNES

NOV 21 WITH GOLD UP $23.85 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 3.16 TONNES OF GOLD INTO THE GLD/:. .///INVENTORY RESTS AT 875,39 TONNES

NOV 20 WITH GOLD UP $22.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.58 TONNES OF GOLD INTO THE GLD/:. .///INVENTORY RESTS AT 872.23 TONNES

NOV 19 WITH GOLD UP $13.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/:. .///INVENTORY RESTS AT 871.65 TONNES

NOV 18 WITH GOLD UP $44.20 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.56 TONNES OF GOLD INTO THE GLD/:. .///INVENTORY RESTS AT 869.93 TONNES

NOV 15 WITH GOLD DOWN $1.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.25 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 867.37 TONNES

NOV 14 WITH GOLD DOWN $12.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.91 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 868.62 TONNES

NOV 13 WITH GOLD DOWN $19.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 870.63 TONNES

NOV 12 WITH GOLD DOWN $11.40 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.88 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 871,97 TONNE

NOV 11 WITH GOLD DOWN $75.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.74 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 876.85 TONNES

NOV 8 WITH GOLD DOWN $11.85 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.87 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 883.46 TONNES

NOV 7 WITH GOLD UP $30.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.45 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 883.46 TONNES

NOV 6 WITH GOLD DOWN $72.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 886.91 TONNES

NOV 5 WITH GOLD UP $4.05 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:.// . // .///INVENTORY RESTS AT 888.63 TONNES

NOV 4 WITH GOLD DOWN $2.45 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 3.16 TONNES OF GOLD OUT OF THE GLD.// . // .///INVENTORY RESTS AT 888.63 TONNES

NOV 1 WITH GOLD UP 0.15 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 0.86 TONNES OF GOLD INTO THE GLD.// . // .///INVENTORY RESTS AT 891 TONNES

OCT 31 WITH GOLD DOWN $49.55 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.87 TONNES OF GOLD INTO THE GLD.// . // .///INVENTORY RESTS AT 892.65 TONNES

OCT 30 WITH GOLD UP $20.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.72 TONNES OF GOLD INTO THE GLD.// . // .///INVENTORY RESTS AT 889,78 TONNES

OCT 29 WITH GOLD UP $25.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD.// . // .///INVENTORY RESTS AT 891.50 TONNES

OCT 28 WITH GOLD UP $1.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.02 TONNES OF GOLD FROM THE GLD.// . // .///INVENTORY RESTS AT 889.78 TONNES

OCT 25 WITH GOLD UP $6.40 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: // . // .///INVENTORY RESTS AT 893.80 TONNES

OCT 24 WITH GOLD UP $19.60 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 1.44 TONNES // // . // .///INVENTORY RESTS AT 893.80 TONNES

OCT 23 WITH GOLD DOWN $29.40 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 3.45 TONNES // // . // .///INVENTORY RESTS AT 895.24 TONNES

OCT 21 WITH GOLD UP $9.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 1.277 TONNES // // . // .///INVENTORY RESTS AT 888.63 TONNES

OCT 18 WITH GOLD UP $22.30 ON THE DAY; NO CHANGES IN GOLD AT THE GLD // // . // .///INVENTORY RESTS AT 884.59 TONNES

OCT 17 WITH GOLD UP $17.30 ON THE DAY; NO CHANGES IN GOLD AT THE GLD // // . // .///INVENTORY RESTS AT 884.59 TONNES

OCT 16 WITH GOLD UP $13.60 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD //A MONSTER DEPOSIT OF 4.02 TONNES OF GOLD INTO THE GLD.; // . // .///INVENTORY RESTS AT 884.59 TONNES

OCT 15 WITH GOLD UP $2.85 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD //A MONSTER DEPOSIT OF 4.31 TONNES OF GOLD INTO THE GLD.; // . // .///INVENTORY RESTS AT 880.57 TONNES

OCT 11 WITH GOLD UP $36.55 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 10 WITH GOLD UP $14.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 9 WITH GOLD DOWN $8.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 8 WITH GOLD DOWN $28,.95 ON THE DAY; NO CHANGES IN GOLD AT THE GLD; // . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 7 WITH GOLD DOWN $1.85 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD; A WITHDRAWAL OF 1.15 TONNES OF GOLD OUT OF THE GLD// . // .///INVENTORY RESTS AT 876.26 TONNES

OCT 4 WITH GOLD DOWN $11.20 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD; A DEPOSIT OF 12.57 TONNES OF GOLD INTO THE GLD// . // .///INVENTORY RESTS AT 877.41 TONNES

GLD INVENTORY: 879.41 TONNES, TONIGHTS TOTAL

SILVER

NOV 27 WITH SILVER DOWN $0.25 //NO CHANGES IN SILVER INVENTORY AT THE SLV.. /// //INVENTORY AT SLV RESTS AT 474.747 MILLION OZ

NOV 26 WITH SILVER UP $0.10 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:.A WITHDRAWAL OF 1.094 MILLION OZ FROM THE SLV./.. /// //INVENTORY AT SLV RESTS AT 474.747 MILLION OZ

NOV 25 WITH SILVER DOWN $0.96 //NO CHANGES IN SILVER INVENTORY AT THE SLV:. . /// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 22 WITH SILVER UP $0.40 //NO CHANGES IN SILVER INVENTORY AT THE SLV:. . /// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 21 WITH SILVER DOWN $0.06 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.729 MILLION OZ FORM THE SLV. . /// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 20 WITH SILVER DOWN $0.22 //NO CHANGES IN SILVER INVENTORY AT THE SLV: . /// //INVENTORY AT SLV RESTS AT 477.572 MILLION OZ

NOV 19 WITH SILVER UP $0.10 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 5,742,000 OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 477..572 MILLION OZ

NOV 18 WITH SILVER UP $0.68 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 1,277,000 OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 471,830 MILLION OZ

NOV 15 WITH SILVER DOWN $0.09 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 3,100,000 OZ OUT OF THE SLV. /// //INVENTORY AT SLV RESTS AT 471,830 MILLION OZ

NOV 14 WITH SILVER DOWN $0.07 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1,504,000 OZ OUT OF THE SLV. /// //INVENTORY AT SLV RESTS AT 473.653 MILLION OZ

NOV 13 WITH SILVER DOWN $0.16 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1,274,000 OZ OUT OF THE SLV. /// //INVENTORY AT SLV RESTS AT 475.157 MILLION OZ

NOV 12 WITH SILVER UP $0.16 //SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 576,000 OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 476.000 MILLION OZ

NOV 11 WITH SILVER DOWN $0.79 //SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 374,000 OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 477.527 MILLION OZ

NOV 8 WITH SILVER DOWN $0.43 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 2.005 MILLION OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 477.846 MILLION OZ

NOV 7 WITH SILVER UP $0.11 //NO CHANGES IN SILVER INVENTORY AT THE SLV: /// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 6 WITH SILVER DOWN $1.41 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.692 MILLION OZ FROM THE SLV/.//// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 5 WITH SILVER UP 0.18 :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.109 MILLION OZ FROM THE SLV/.//// //INVENTORY AT SLV RESTS AT 479,533 MILLION OZ

NOV 4 WITH SILVER DOWN $0.08 :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 547,000 OZ.//// //INVENTORY AT SLV RESTS AT 480.642 MILLION OZ

NOV 1 WITH SILVER DOWN $0.10 : NO CHANGES IN SILVER INVENTORY AT THE SLV:.//// //INVENTORY AT SLV RESTS AT 481.189 MILLION OZ

OCT 31 WITH SILVER DOWN $1.26 : HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 3.647 MILLION OZ OF SILVER INTO THE SLV//.//// //INVENTORY AT SLV RESTS AT 481.189 MILLION OZ

OCT 30 WITH SILVER DOWN 38 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV.//// //INVENTORY AT SLV RESTS AT 477.542 MILLION OZ

OCT 29 WITH SILVER UP 49 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV’ A WITHDRAWAL OF 0.628 MILLION OZ OUT OF THE SLV..//// //INVENTORY AT SLV RESTS AT 477.542 MILLION OZ

OCT 28 WITH SILVER UP 15 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV’ A WITHDRAWAL OF 1.431 MILLION OZ OUT OF THE SLV..//// //INVENTORY AT SLV RESTS AT 478.180 MILLION OZ

OCT 25 WITH SILVER DOWN $0,02 : HUGE CHANGES IN SILVER INVENTORY AT THE SLV’ A DEPOSIT OF 3.06 MILLION OZ INTO THE SLV..//// //INVENTORY AT SLV RESTS AT 480.281 MILLION OZ

OCT 24 WITH SILVER UP $0,01 : SMALL CHANGES IN SILVER INVENTORY AT THE SLV’ A WITHDRAWAL OF 0.684 MILLION OZ OF SILVER OUT OF THE SLV..//// //INVENTORY AT SLV RESTS AT 477.177 MILLION OZ

OCT 23 WITH SILVER DOWN $1.15 : SMALL CHANGES IN SILVER INVENTORY AT THE SLV’ A WITHDRAWAL OF 0.228 MILLION OZ OF SILVER OUT OF THE SLV..//// //INVENTORY AT SLV RESTS AT 477,861 MILLION OZ

OCT 22 WITH SILVER $0.93 : HUGE CHANGES IN SILVER INVENTORY AT THE SLV’ A DEPOSIT OF 3.329 MILLION OZ OF SILVER INTO THE SLV..//// //INVENTORY AT SLV RESTS AT 478.089 MILLION OZ

OCT 18 WITH SILVER $1.46 : NO CHANGES IN SILVER INVENTORY AT THE SLV//// //INVENTORY AT SLV RESTS AT 473.483 MILLION OZ

OCT 17 WITH SILVER DOWN 18 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV//A DEPOSIT OF 3.419 MILLION OZ INTO THE SLV// //INVENTORY AT SLV RESTS AT 473.483 MILLION OZ

OCT 16 WITH SILVER UP 25 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV// //INVENTORY AT SLV RESTS AT 470.064 MILLION OZ

OCT 15 WITH SILVER DOWN 2 CENTS : SMALL CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 456,,000 OZ FORM THE SLV. //INVENTORY AT SLV RESTS AT 470.064 MILLION OZ

OCT 11 WITH SILVER UP 53 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 932,000 OZ FORM THE SLV. //INVENTORY AT SLV RESTS AT 470.520 MILLION OZ

OCT 9 WITH SILVER UP 7 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.964 MILLION OZ FORM THE SLV..: /INVENTORY AT SLV RESTS AT 471.432 MILLION OZ

OCT 8 WITH SILVER DOWN $1.41 : HUGE CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 2.007 MILLION OZ FORM THE SLV..: /INVENTORY AT SLV RESTS AT 468.468 MILLION OZ

OCT 7 WITH SILVER DOWN 39 CENTS : HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 684,000 OZ FORM THE SLV..: /INVENTORY AT SLV RESTS AT 466.461 MILLION OZ

OCT 4 WITH SILVER UP 0 CENTS : NO CHANGES IN SILVER INVENTORY AT THE SLV.: /INVENTORY AT SLV RESTS AT 465.777MILLION OZ

CLOSING INVENTORY 474.747 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

Schiff Vs. Breedlove: Gold Will Thrive In A Digital Future

Last week, Peter participated in a ZeroHedge debate moderated by Keith Knight (who also interviewed Peter recently). He faced off against Bitcoin advocate Robert Breedlove on his show, “What is Money?” Peter and Robert discuss the future use cases of Bitcoin and gold, the philosophy and economics behind money, and what it would take for each other to change their minds and renounce their preferred sound money.

The effect of that [inflation] is that prices go up. It offsets the decline in prices that might otherwise have resulted from an efficient, growing, free-market economy, where the tendency is for prices to come down over time. Governments can rob people of those benefits by creating inflation. Inflation is not just how much prices go up, and that’s not just the result. It’s how much they might have otherwise gone down, had the government not created the inflation that caused them to go down less or to go up.

As they move into the debate, Peter presents the Austrian school of economics’ explanation for the origin of money. Notably, precious metals needed some non-monetary use before they were used as a medium of exchange:

Before money, people traded goods, but it was cumbersome because you needed a coincidence of needs. … But man eventually found out that they could have one commodity that could be used in exchange for all other commodities. And gold was basically the commodity that ended up being money. Other commodities have been money, and they can be money, but gold just fulfills that role very well for a lot of the properties that Bitcoin copied. … And what gives gold value is the fact that it’s a precious metal that we need because it, you know, it does a lot of things.

Peter contends that even if cryptocurrencies are eventually used as money, there’s no good reason to think Bitcoin will out-compete other coins, especially in the future:

There’s nothing unique about Bitcoin. You say Bitcoin is the only thing. There’s tens of thousands of other tokens that I could create, that have been created, that will be created. There is nothing special about Bitcoin that anybody else can’t copy or replicate.

All that it has is that it has more people who believe in it right now. You have more computer capacity behind it. But that could change.

The odds that anyone’s even going to care about Bitcoin in 10 years, I think, are pretty low.

The fervor around Bitcoin today is driven by speculation. Most retail investors in Bitcoin are not Bitcoin maximalists who actually expect it to function as a medium of exchange:

The main driver is speculation. In fact, the main buying right now for Bitcoin is coming from ETFs. … They’re buying it because they think the price of this ETF is going to go up.

It has got nothing to do with Bitcoin as money… It’s just that people are buying that particular speculative asset in their brokerage accounts instead of some other speculative asset because, for the moment, they think there’s upside.

Robert raises the problem of counterparty risk, which Bitcoin solves under some circumstances. Peter counters by pointing out counterparty risk is inherent in a market economy. Even Robert tolerates counterparty risk, and market forces tend to minimize its effect:

Your main problem then with gold … is you’re saying that you don’t trust the custodian. That the custodian is going to loan out or embezzle my gold, or they’re going to do something. And so gold can’t work in the electronic world of the future because you can’t trust counterparties, that we’re all criminals, and capitalism doesn’t really work in that respect because there’s no way to know who’s honest and who’s a crook. And you can’t trust counterparties. Let me ask you, Rob, do you have any insurance at all? Like life insurance, fire insurance, health insurance, auto insurance—do you have any insurance?

In Peter’s closing segment, he argues that future technology will enhance gold’s monetary properties rather than supplant them. Moving back to metals, not crypto, is the path forward:

Gold, you know, has worked for thousands of years, and the technology associated with digitization, the internet, and computers doesn’t make gold obsolete or diminish its role in any way. In fact, it makes gold perform all of the functions it has performed so successfully over the centuries that much better. Rather than trying to reinvent the wheel and getting people to think, ‘Oh, let’s just create this new money out of thin air and pretend it has value,’ like Bitcoin, efforts and resources should be spent trying to move the world back to a gold standard and away from fiat money.

2. ALASDAIR MACLEOD/JIM RICKARDS/PAM AND RUSS MARTENS/ JAMES RICKARDS/ VON GREYERZ//GOLD AND SILVER COMMENTARY//BILL HOLTER:

3. CHRIS POWELL AND GATA DISPATCHES

Jan Nieuwenhuijs: Chinese central bank just bought 60 tonnes of gold secretly

Submitted by admin on Tue, 2024-11-26 14:11 Section: Daily Dispatches

By Jan Nieuwenhuijs Money Metals Exchange, Eagle, Idaho Tuesday, November 26, 2024

The People’s Bank of China is covertly buying very large amounts of gold, adding upward pressure to a tense gold market.

An explosive cocktail of Western institutional investors and central banks in the East buying gold this year is making the gold price rise sharply. Interest rate cuts and geopolitical strain will sustain this bull marke

Last July I published an analysis proving how the Chinese central bank covertly buys gold in the London Bullion Market through bullion banks.

All “non-monetary” gold (privately owned metal) in China is traded over the Shanghai Gold Exchange. However, since the war in Ukraine began, there has been more supply in the Chinese market than sold through the SGE; the “surplus” reflects what the PBoC buys. …

Alasdair Macleod: U.S. dollar on a gold standard? Not if the gold is gone

Submitted by admin on Tue, 2024-11-26 14:52 Section: Daily Dispatches

2:53p ET Tuesday, November 26, 2024

Dear Friend of GATA and Gold:

Market analyst Alasdair Macleod’s commentary yesterday at his proprietary internet site at Substack, headlined “U.S. Dollar on a Gold Standard?,” seemed so compelling to your secretary/treasurer that he asked permission to share it with you, which Macleod has kindly granted, so it is appended.

Macleod’s insights may make you want to consider subscribing to his Substack letter, which comes out every few days. A seven-day free trial subscription is available. Rates are $10 per month or $120 per year. To subscribe, please visit:

CHRIS POWELL, Secretary/Treasurer Gold Anti-Trust Action Committee Inc. CPowell@GATA.org

* * *

U.S. Dollar on a Gold Standard?

Judy Shelton recently proposed a long bond convertible into gold. She obviously believes in the integrity of U.S. gold reserves. I don’t.

By Alasdair Macleod Monday, November 25, 2024

Judy Shelton is a well-known sound-money advocate and former economic adviser to President Trump. This month she set everyone buzzing with a proposal to issue a new 50-year Treasury bond redeemable in gold. If her plan is to be followed through, it would not be gold convertibility for the dollar but merely an alternative to inflation-linked TIPS bonds.

We can argue about how things for the dollar would evolve from there and the likelihood that this would be the first step to a new gold standard for the dollar, but that is a separate debate. Anyway, dollar-centric Fed and Treasury officials would dismiss it as providing too much uncertainty to government financial obligations, because they would argue that gold is unpredictably volatile and they would not want to see a revived debate about its monetary role.

But there is a far greater problem in the background, and that is the integrity of the U.S. Treasury’s gold reserves. Do they actually exist, and, if so, to what extent?

And here we come back to the findings of analyst Frank Veneroso more thqan 20 years ago.

Famously, in a speech in Lima, Peru, in 2002, Veneroso wrote:

“Now we have a conservative set of gold lending numbers and we have a more aggressive set of such numbers. Our range of estimates implies that somewhere between 10,000 and 16,000 tonnes of the official-sector gold position has left those vaults by way of the lending process.”

The full speech can be found on GATA’s website here:

By the way, the higher figure is 50% of the official gold reserves reported (32,412.8 tonnes) when Veneroso spoke.

As a side note, Veneroso said he embarked on his analysis following a speech by Terry Smeeton, who he said was head of the Bank of England’s gold department. In fact, Smeeton was head of foreign exchange operations, which included gold. I got to know him in the late 1980s when we lunched together occasionally at the Banker’s Club, just behind the bank. And what Veneroso wrote about Smeeton I can confirm as being consistent with the man I knew.

Returning to our subject, from the end of Bretton Woods in 1971 the U.S. Treasury embarked on a policy of displacing gold with the dollar, a policy that involved virulent anti-gold propaganda and actions, like the birth of the gold carry trade, whereby central bank gold was leased or swapped for interest rates of 1%, sold for dollars, and invested in U.S. T-bills yielding considerably more.

T-bill rates declined from over 10% in the early ’80s to 4% in 1998.

As Veneroso put it, this leased and swapped gold ended up adorning the necks of Asian women and was never going to return.

Accounting for this was simple.

Replacing the lease or swap agreement would be a debt obligation on the part of the lessee in perpetuity, presumably at the official rate of $42.22 per ounce. Under the International Monetary Fund’s rules, the missing gold is accounted for as an asset in the Treasury’s (or central bank’s) reserves, even though it is not in possession.

Note the distinction.

And from the Banker’s Club in Lothbury, security trucks — often two or three at a time, moving gold back and forth from the bank’s rear entrance — could be observed most days of the week.

While the Bank of England continues to lease and swap gold (I believe more by book entry nowadays, rather than by delivery), there is no doubt that the U.S. Treasury and the Federal Reserve Bank of New York Fed (which stores foreign central bank gold) are severely short of the physical, as was revealed when Germany’s Bundesbank asked for some of its gold back. Not only were BuBa officials not permitted to visit and audit their holdings supposedly held under earmark, but they were quoted seven years to return just a fraction of their property.

No, Ms. Shelton. It’s a nice idea but the gold isn’t there to back a long bond convertible into it.

We should know that U.S. officials lie and cheat when it comes to real, legal money. No surprise there.

But a more interesting question is the fate of all those open-ended commitments owed by operators like Goldman Sachs (which wasn’t a bank at the time but a trading operation). If these obligations are properly accounted for, not only are the U.S. Treasury and the Fed bust, but so too are members of the bullion banking community owing these obligations.

—–

Alasdair Macleod is of head of research for GoldMoney.

END

Ronan Manly: Dubai’s record-breaking 300-kg gold bar

Submitted by admin on Tue, 2024-11-26 20:06 Section: Daily Dispatches

By Ronan Manly Tuesday, November 26, 2024

In a city famous for setting records such as the world’s tallest building, the Burj Khalifa, a new record-breaking gold bar weighing an incredible 300 kilograms (9,600 troy ounces) has just been produced in Dubai, United Arab Emirates.

At current gold prices, this 300-kg bar is valued at more than US$ 25 million.

Manufactured by Dubai-based Emirates Minting Facility LLC, the massive new gold bar was officially certified as record breaking by Guinness World Records on November 10 and officially unveiled at the Dubai Precious Metals Conference on November 19. …

Falling gold prices revive physical demand in key markets

Submitted by admin on Tue, 2024-11-26 23:22 Section: Daily Dispatches

By Polina Devitt and Rajendra Jadhav Reuters Tuesday, November 26, 2024

A drop in gold prices this month has drawn in buyers of the metal who had been waiting for the market’s lightning rally this year to subside, industry players and analysts said.

Spot gold prices hit a record $2,790.15 per troy ounce on Oct. 31, but are down some 4% so far in November in response to a Republican Party clean sweep in the U.S. election.

“Physical demand has picked up quite a bit since October and especially after the sharp November price drop as there has been a change in the market sentiment,” Robin Kolvenbach, co-CEO of Swiss-based refinery Argor-Heraeus, told Reuters. …

4. OTHER GOLD COMMENTARIES//LIVE FROM THE VAULT/no 200 ANDREW MAGUIRE

LIVE FROM THE VAULT/ANDREW MAGUIRE KINESIS 199

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES:

6 CRYPTOCURRENCY NEWS

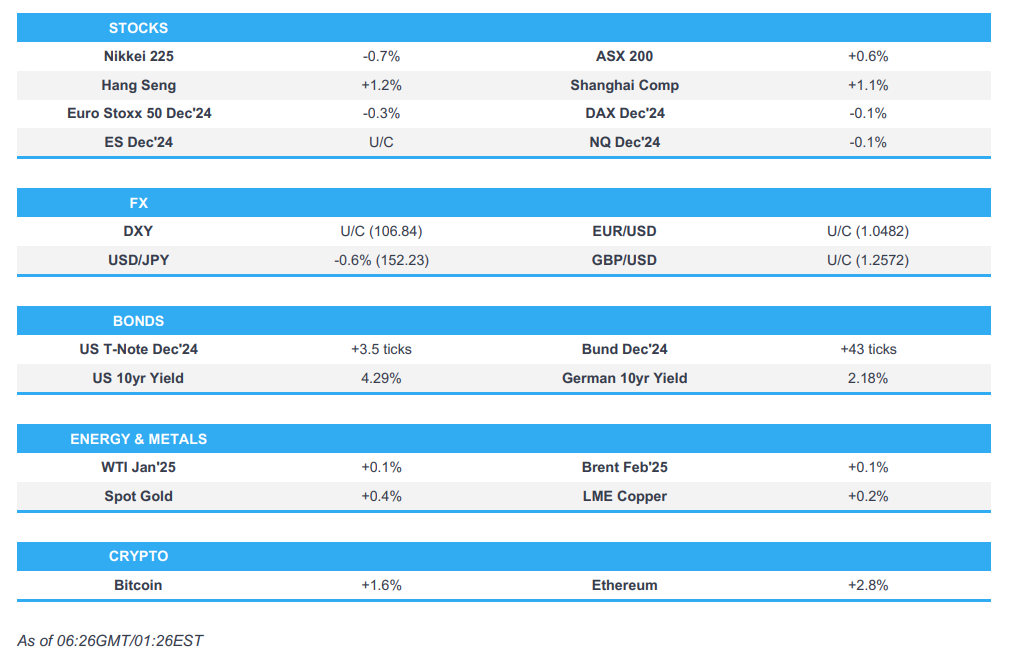

ASIA TRADING WEDNESDAY MORNING/TUESDAY NIGHT

SHANGHAI CLOSED UP 50.02 PTS OR 1.53%

//Hang Seng CLOSED UP 443.93 PTS OR 2.32%

// Nikkei CLOSED DOWN 307.03 OR 0.80%//Australia’s all ordinaries CLOSED UP 0.55%///Chinese yuan (ONSHORE) CLOSED DOWN TO 7.2411 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2569// Oil DOWN TO 69.08 dollars per barrel for WTI and BRENT DOWN AT 73.16 Stocks in Europe OPENED ALL MOSTLY RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS WEDNESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.2521

OFFSHORE YUAN: DOWN TO 7.2569

SHANGHAI CLOSED CLOSED UP 50.02 PTS OR 1.53%

HANG SENG CLOSED CLOSED UP 443.93 PTS OR 2.32%

2. Nikkei closed DOWN 307.03 PTS OR 0.80%

3. Europe stocks SO FAR: ALL MOSTLY RED

USA dollar INDEX DOWN TO 106.34 EURO RISES TO 1.0533 UP 30 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.054 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 151.33…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD DOWN TO +2.1625 Italian 10 Yr bond yield DOWN to 3.423 //SPAIN 10 YR BOND YIELD DOWN TO 2.901

3i Greek 10 year bond yield DOWN TO 3.031

3j Gold at $2650.80 /Silver at: 30.42 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble DOWN 7 AND 40/100 roubles/dollar; ROUBLE AT 112.50

3m oil into the 69 dollar handle for WTI and 73 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 151.33 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.054% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8830 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9300 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.263 DOWN 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.448 DOWN 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.201 DOWN 4 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 34.61…

10 YR UK BOND YIELD: 4.350 DOWN 5 PTS

10 YR CANADA BOND YIELD: 3.271 DOWN 3 BASIS PTS

5 YR CANADA BOND YIELD: 3.117 DOWN 3 PTS.

2a New York OPENING REPORT

Stock Futures Drop Ahead Of Data Barrage After Trump Unveils Trade Picks

Wednesday, Nov 27, 2024 – 08:22 AM

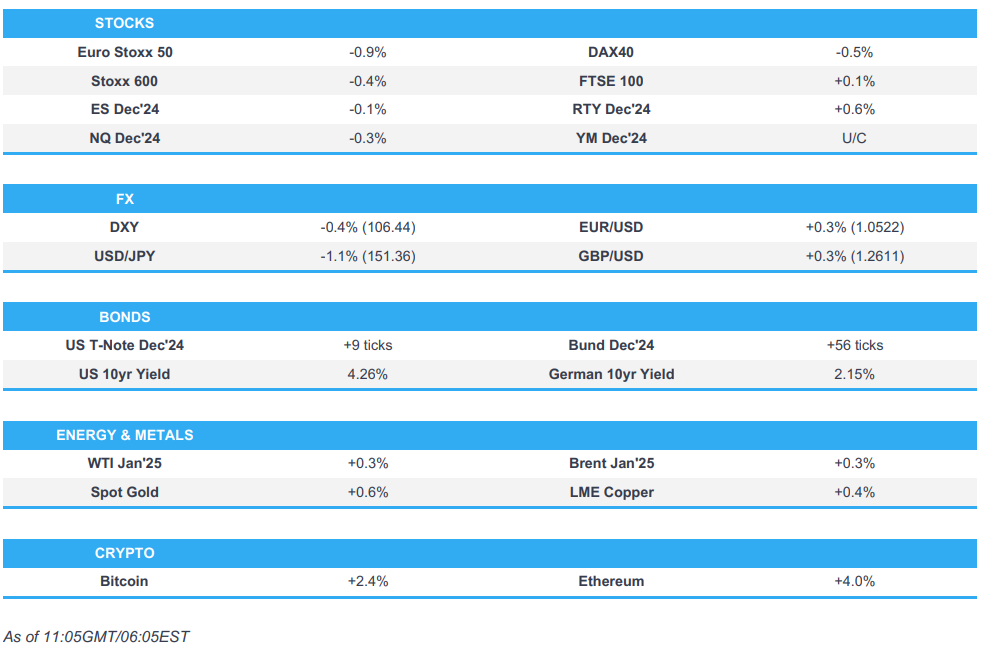

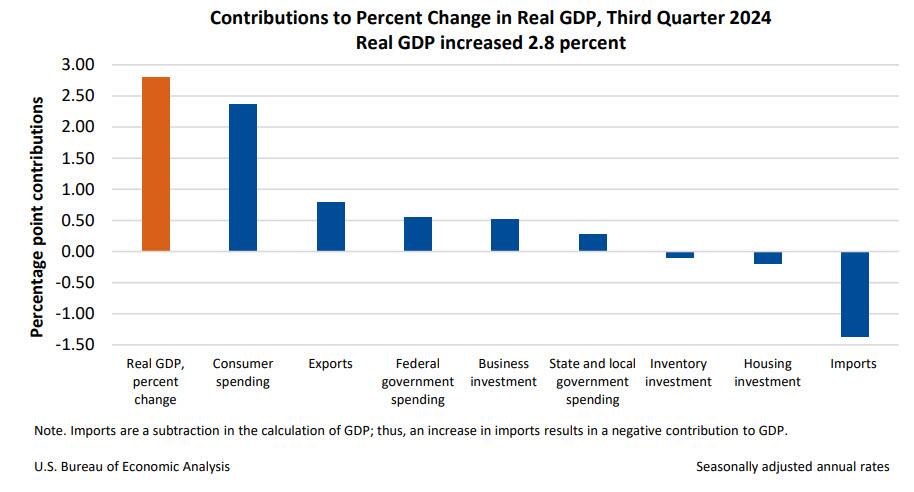

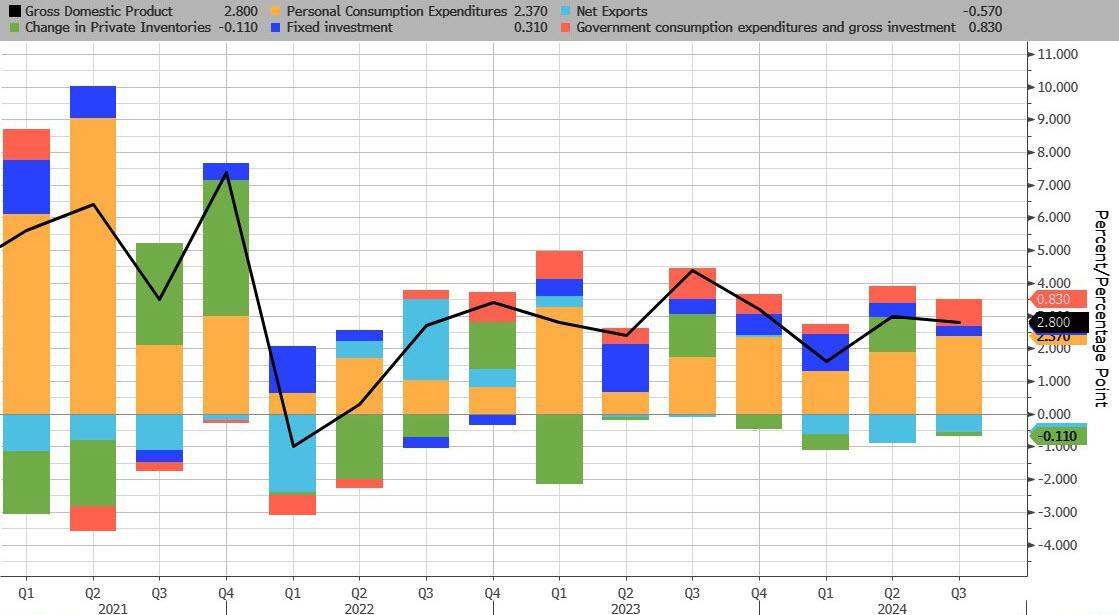

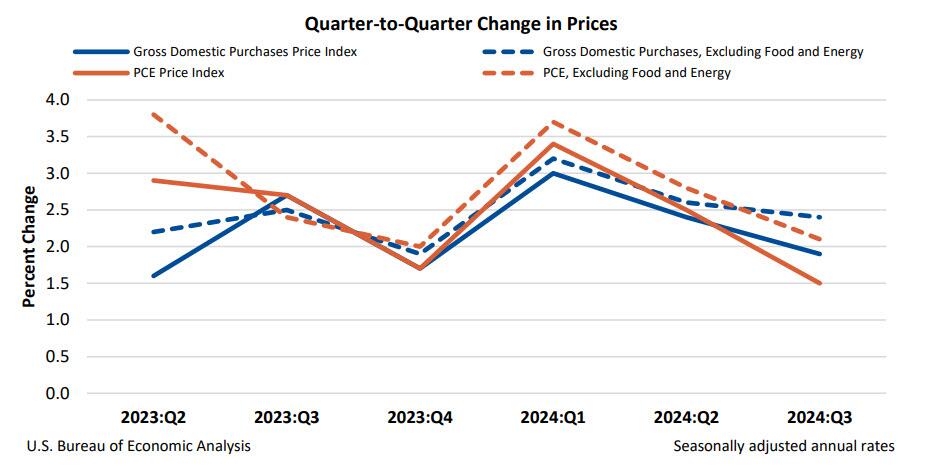

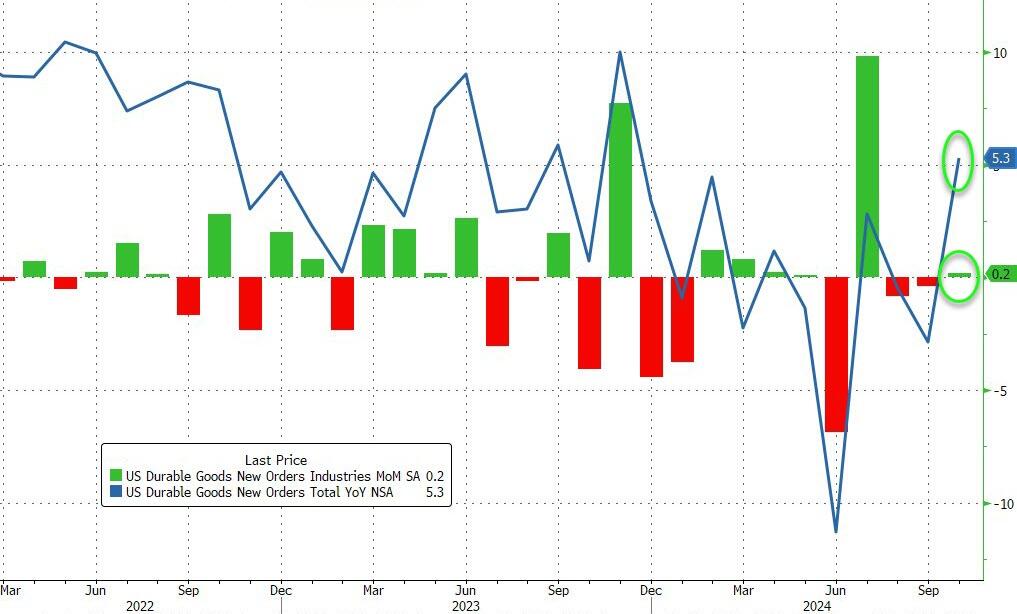

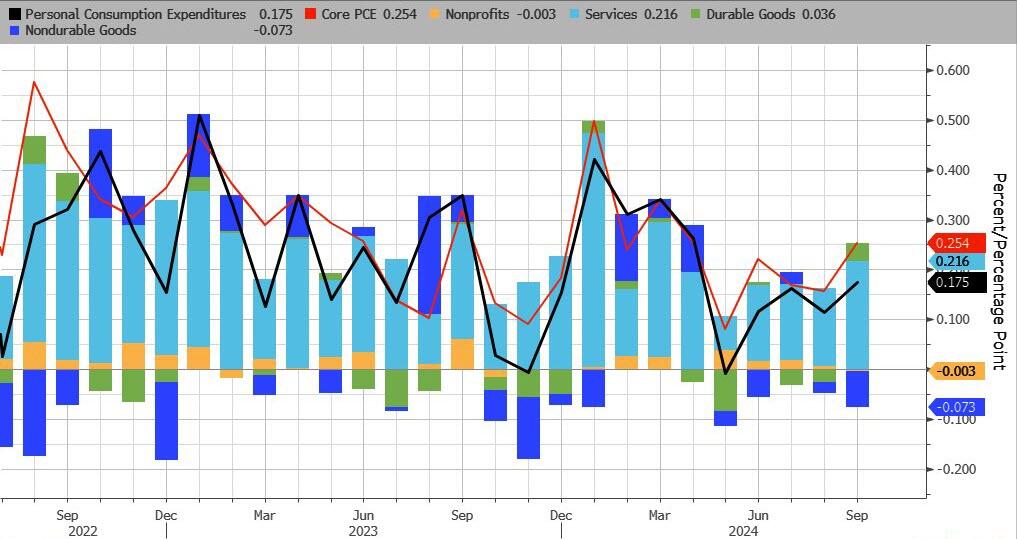

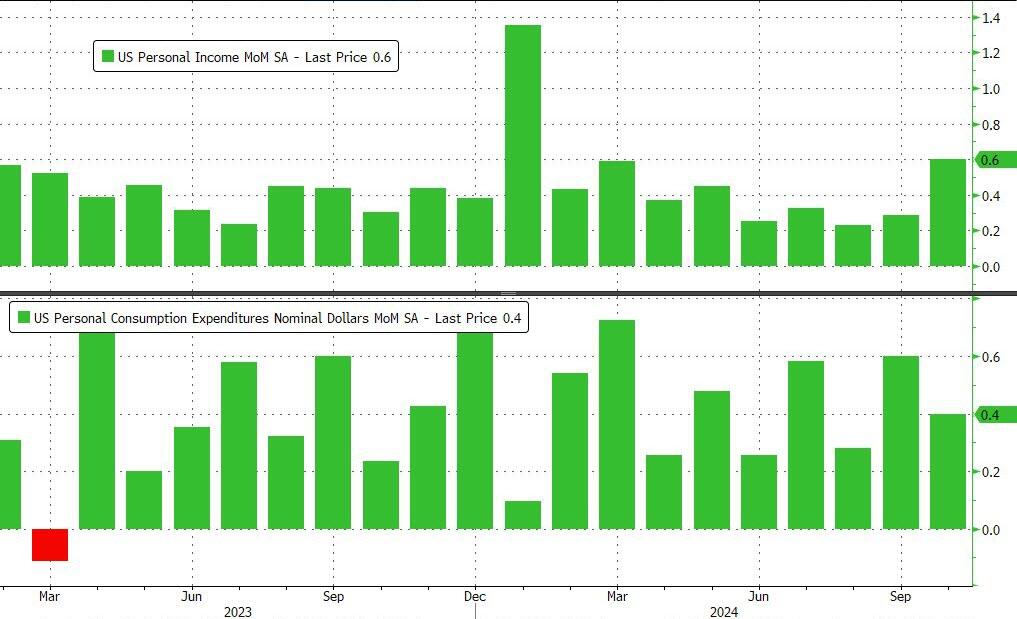

Futures are lower as markets digested Trump’s latest cabinet appointments and looked ahead to a barrage of macroeconomic data ahead of the Thanksgiving holiday for clues on the outlook for interest rates. As of 8:00am ET, Nasdaq 100 futures dropped 0.3% while the S&P 500 slipped 0.1% with Mag 7 names mostly lower (NVDA -1.2% and MSFT -0.6%). Treasuries advanced, pushing the 10-year benchmark yield down by five basis points to 4.26% with a slew of pre-Thanksgiving holiday US data expected, including the Fed’s preferred inflation gauge and an update on economic growth. The dollar fell versus all Group-of-10 peers amid month-end flows while the euro rose to a fresh day high after hawkish comments from ECB Board member Isabel Schnabel. Commodities are mixed with precious metals and oil higher, while base metals are lower. Today, the main macro focus will be PCE release and Durable/Cap Goods Orders.

Among individual premarket movers, Dell shares tumbles 12% as revenue generated by the company’s PC business declined 1% in the fiscal third quarter, falling short of estimates. Peer HP also slumped 8% after sales in its PC unit missed the average analyst estimate. Similar to its peer Dell, the firm flagged a delayed PC refresh cycle. Here are some other notable premarket movers:

Ambarella (AMBA) climbs 21% after the semiconductor device company issued a stronger-than-anticipated revenue forecast for the current quarter.

Autodesk (ADSK) slides 7% after the software company posted third-quarter adjusted operating margin that fell short of expectations.

CrowdStrike (CRWD) drops 3% after the cybersecurity firm’s issued a weaker-than-expected earnings forecast. The outlook disappointing investors who have been watching for signs that the company has recovered from a flawed update that crashed computers around the world.

Guess (GES) slides 11% after the clothing company cut its full year guidance.

Nutanix (NTNX) gains 5% after the infrastructure software company reported first-quarter results that beat expectations.

Symbotic (SYM) sinks 22% after filing to delay its 10-K report.

Urban Outfitters (URBN) jumps 12% after the clothing retailer reported stronger-than-expected quarterly sales growth. Citi upgraded the stock to buy.

Workday (WDAY) drops 11% after the software company provided a forecast that is seen as disappointing. Analysts noted that investor confidence will likely be affected by slowing subscription growth.

Trump’s tariffs agenda gathered further momentum, after the president-elect named Jamieson Greer as the US Trade Representative and Kevin Hassett to direct the National Economic Council. Greer was intimately involved in Trump’s first-term trade policy decisions.

“If we get close to a place where we are talking about across-the-board tariffs, I think that would be a wake-up call for risk assets, equities and credit alike,” Wei Li, global chief investment strategist at BlackRock Inc., said in an interview with Bloomberg TV. “We’re risk-on for now, but things could change.”

Investors have plowed money into US stocks this year, with inflows on course for a record and have been rewarded with a gain of 26% in the S&P 500, vindicating bets on American exceptionalism. European stocks are trading at a record 40% discount to the S&P 500 with the region’s benchmark gauge up just 5% this year. That divergence is making global stock market performance ever more polarized and that’s unlikely to change anytime soon, JPMorgan’s strategist Mislav Matejka wrote.

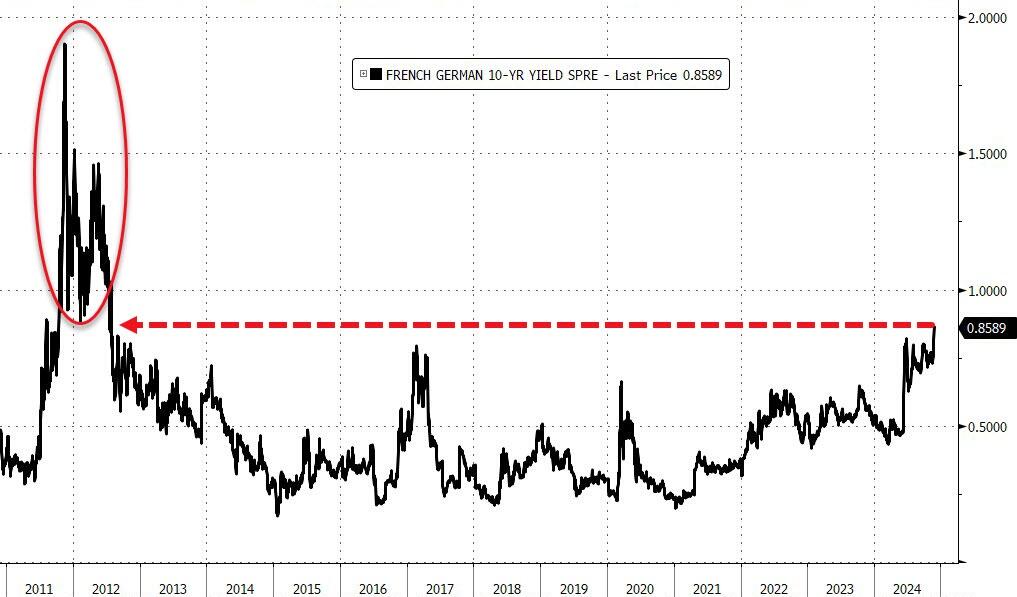

European stocks fall for a second day as traders trim their ECB interest rate cut bets after Governing Council member Isabel Schnabel warned against lowering borrowing costs too far. The Stoxx 600 is down 0.3% with underperformance in auto shares suggesting tariff risks from the US are also still providing a drag. In France, a measure of risk on the country’s bonds rose to levels last seen during the euro-area debt crisis as a political standoff over the budget threatens to bring down the government. The market nerves reflect investor concerns over Prime Minister Michel Barnier’s ability to pass a budget for next year. French bank stocks underperform following the country’s political standoff over budget. Real estate and mining stocks are the strongest-performing sectors. Among individual stocks, EasyJet gains as the airline proposed to more than double its dividend payout for this year amid robust demand for its holiday package offerings. Here are some of the most notable premarket movers:

Henkel shares climb as much as 4.1% after the chemicals company was upgraded by analysts at JPMorgan, highlighting the stock trades at a sizable discount to peers despite a rebound in earnings this year.

Anglo American shares rise as much as 2.9% in London after the miner raised 9.6 billion rand ($530 million) from the sale of a 6.6% stake in Anglo American Platinum, a move aimed at increasing the South African unit’s free float ahead of a full exit.

Ackermans & Van Haaren shares gain as much as 3.1%, rallying from an almost three-month low closing price yesterday, as Berenberg slightly lifts its Street-high target on the Belgian industrial holding company.

EasyJet shares rise as much as 4.4% to the highest intraday level since April. The travel company more than doubled its annual dividend on the back of a strong demand outlook for next year.

Idorsia shares soar as much as 28% after announcing talks with an undisclosed party for the global rights to its aprocitentan (Tryvio) drug. The deal would result in a fee of $35 million.

French bank stocks fall as the risk premium for the country’s government bonds soared to 2012 highs amid a political standoff over the budget, which threatens to bring down the government.

Grifols shares slide as much as 11% after Bloomberg reported that Brookfield Asset Management is preparing to walk away from a plan to acquire the Spanish drug maker over disagreements on valuation.

CD Projekt shares drops as much as 3.9% in early trading as 3Q earnings triggered profit taking after strong gains on stock seen in last days.

Frontline shares fall as much as 12% after the Oslo-listed crude-oil shipper reported 3Q earnings described by DNB as soft on account of a weak 4Q outlook that’s likely to lead to estimate cuts.

Johnson Matthey shares drop as much as 7%, to the lowest since July 2009, following results from the British specialty chemicals firm which analysts see as mixed.

Elekta shares fall as much as 7.8% after the Swedish medical technology firm’s 2Q report fell short of expectations on most key metrics. While guidance was reiterated, it requires a big effort from the company in its 2H, analysts note.

Pets at Home shares slump as much as 9.8% to the lowest level since July 2020 after the company warned that the pet retail market will remain subdued for the rest of the financial year.

Earlier in the session, Asian stocks gained as Chinese shares rebounded after a recent rout, while traders continued to digest the potential impact of US president-elect Donald Trump’s policy plans. The MSCI Asia Pacific Index rose as much as 0.5%, lifted by Chinese tech giants such as Tencent and Meituan. An index of Chinese stocks in Hong Kong gained 2.6% amid speculation that authorities will unveil more stimulus at key meetings that are expected to take place next month. Elsewhere, stocks dropped in Japan and Taiwan, while Australia and New Zealand saw gains. Korean chipmaker stocks fell after one of Trump’s picks to lead the Department of Government Efficiency called Chips Act subsidies to the industry “wasteful.” Japanese automakers extended declines as the yen strengthened and after US peers fell on Trump’s tariff threats.

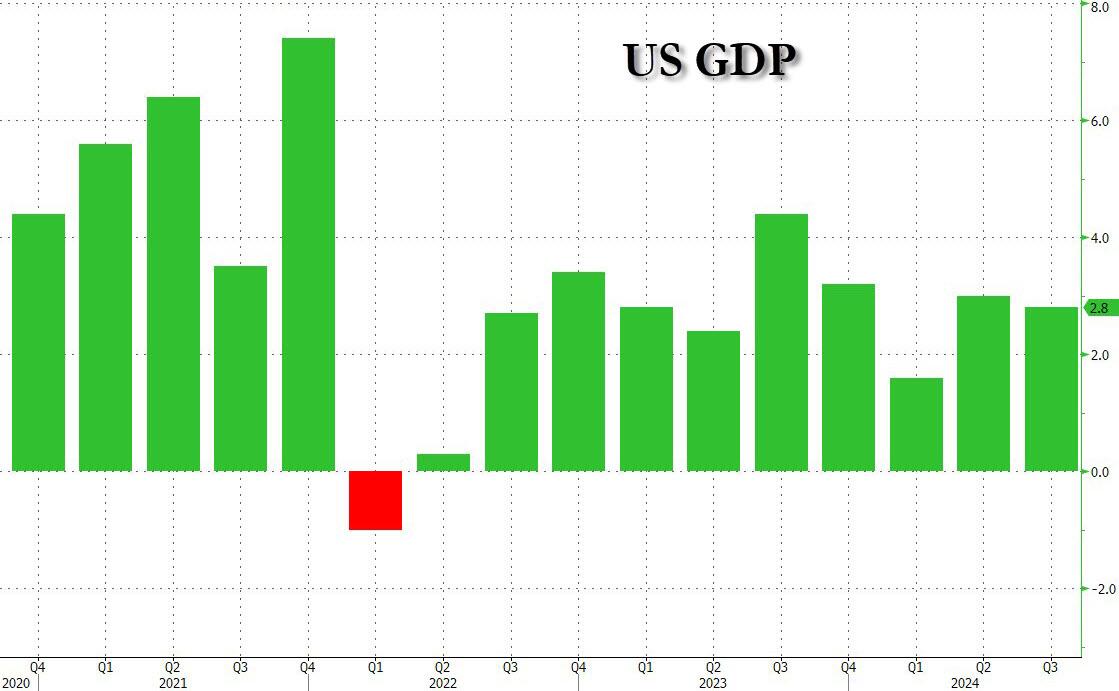

In rates, treasuries climb, with US 10-year yields falling 4 bps to 4.27%. Gilts and bunds also gain, although the Schnabel comments did dent German shorter-dated bonds while lifting the euro. French bond spreads widen again, hitting a yield gap to Bunds of 89bps, the widest since the 2012 European debt crisis as a political standoff over the budget threatens to bring down the government. The market nerves reflect investor concerns over Prime Minister Michel Barnier’s ability to pass a budget for next year. Back to Treasuries which hold most of their advance that sent yields toward the low end of two-week ranges, led by UK bond market, the outperformer in core European rates so far. Rally precedes a packed slate of US economic data including 3Q GDP revision, weekly jobless claims and PCE price indexes. A $44 billion 7-year note auction at 11:30am New York time concludes this week’s Treasury supply cycle, which has been well received.

In FX, the Bloomberg dollar index fell to the lowest this week, snapping a rally that’s propelled eight straight weeks of gains through Friday. The dollar is seen as one of the biggest beneficiaries of Trump’s pro-growth agenda. The euro rose after ECB Executive Board member Isabel Schnabel warned against cutting interest rates too far. The currency has been singled out as one of the most vulnerable to Trump’s tariff agenda by strategists at Goldman, JPMorgan and Citigroup. The yen tops the G-10 FX leader board, rising 1.1% against the greenback and pulling USD/JPY down to 151.40. The kiwi dollar is not far behind even after the RBNZ cut rates by 50 bps.

In commodities, oil prices advanced as traders monitor the cease-fire agreement between Israel and Hezbollah. WTI is up 0.3% at $69 a barrel. Middle East tensions abated somewhat as President Joe Biden said Israel reached a cease-fire deal with the Lebanese militant group Hezbollah after weeks of talks mediated by the US. Spot gold adds $15 to $2,648/oz. Bitcoin rises above $93,000.

The US economic data calendar is busy and includes second estimate of 3Q GDP, October durable goods orders and weekly jobless claims (8:30am), November MNI Chicago PMI (9:45am, several minutes earlier for subscribers), October personal income/spending with PCE price indexes and October pending home sales (10am). The Fed speaker slate blank.

Market Snapshot

S&P 500 futures down 0.2% to 6,026.00

STOXX Europe 600 down 0.4% to 503.87

MXAP up 0.4% to 183.22

MXAPJ up 0.5% to 579.48

Nikkei down 0.8% to 38,134.97

Topix down 0.9% to 2,665.34

Hang Seng Index up 2.3% to 19,603.13

Shanghai Composite up 1.5% to 3,309.78

Sensex up 0.3% to 80,232.67

Australia S&P/ASX 200 up 0.6% to 8,406.67

Kospi down 0.7% to 2,503.06

German 10Y yield little changed at 2.15%

Euro up 0.2% to $1.0515

Brent Futures up 0.5% to $73.20/bbl

Gold spot up 0.7% to $2,650.62

US Dollar Index down 0.46% to 106.53

Top Overnight News

Chinese stocks rallied on Wed as investors speculate a critical upcoming gov’t meeting could result in more stimulus support as Beijing looks to mitigate the fallout from Trump 2.0 trade restrictions. BBG

China places its defense minister under investigation for corruption (this is the third consecutive serving or former defense minister to face an investigation), although the country’s foreign ministry denied the news. FT