GOLD PRICE UP $26.65 TO $2719.40

SILVER PRICE UP $0.10 TO $31.98

Gold ACCESS CLOSED $2719.65

Silver ACCESS CLOSED: $31.99

Bitcoin morning price:$98325 UP 1876 DOLLARS.

Bitcoin: afternoon price: $101,314 UP 4865 DOLLARS

Platinum price closing DOWN $5.45 TO $939.45

Palladium price; UP $15.90 TO $989.40

END

*CANADIAN GOLD: $3848.80 UP 27.20 CDN dollars per oz( * NEW ALL TIME HIGH 3,872.51 CDN DOLLARS PER OZ//OCT 30 2024)

*BRITISH GOLD: 2132.24 UP 22.70 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///2161.00 BRITISH POUNDS/OZ) NOV 22/2024

*EURO GOLD: 2,590.12UP 30.28 Euros per oz //* (ALL TIME CLOSING HIGH: 2600.25 EUROS PER OZ//NOV 22 //.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE;

EXCHANGE: COMEX

CONTRACT: DECEMBER 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,697.600000000 USD

INTENT DATE: 12/10/2024 DELIVERY DATE: 12/12/2024

FIRM ORG FIRM NAME ISSUED STOPPED

118 C MACQUARIE FUT 327

132 C SG AMERICAS 200

152 C DORMAN TRADING 4

190 H BMO CAPITAL 9

363 H WELLS FARGO SEC 160

435 H SCOTIA CAPITAL 63

555 H BNP PARIBAS SEC 5

624 H BOFA SECURITIES 91

657 C MORGAN STANLEY 12

661 C JP MORGAN 20 75

661 H JP MORGAN 7

686 C STONEX FINANCIA 53 96

690 C ABN AMRO 17 22

737 C ADVANTAGE 11 18

880 C CITIGROUP 3

880 H CITIGROUP 59

905 C ADM 4

TOTAL: 628 628

MONTH TO DATE: 18,152

JPMorgan stopped 82/628

GOLD: NUMBER OF NOTICES FILED FOR DEC/2024. CONTRACT: 628 NOTICES FOR 62,800 OZ 1.9533 TONNES

total notices so far: 18,152 contracts for 1,815,200 Oz (56.460 tonnes)

FOR DEC

SILVER NOTICES: 586 NOTICE(S) FILED FOR 2,930,000 OZ/

total number of notices filed so far this month : 7976 for 39.88 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $26.65 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 870..79 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.10 AT THE SLV

HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.597 MILLION OZ OUT OF THE SLV/.

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 469.215 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A HUMONGOUS SIZED 3811 CONTRACTS TO 151,096 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS EXTRA HUMONGOUS SIZED GAIN IN COMEX OI WAS ACCOMPLISHED DESPITE OUR LOSS OF $0,08 IN SILVER PRICING AT THE COMEX WITH RESPECT TO TUESDAY’S TRADING. WE HAD A MEGA HUMONGOUS GAIN OF 7137 TOTAL CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR LOSS IN IN PRICE. WE HAD ZERO LIQUIDATION OF T.A.S. CONTRACTS ON TUESDAY COMEX TRADING AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 2 WEEKS TO WHICH THEY SUCCEEDED WITH YESTERDAY’S SLIGHT SILVER’S LOSS IN PRICING.

WE HAD A MEGA HUGE 3326 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY A HUGE 586 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN WEDNESDAY;S TRADING AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A MEGA HUMONGOUS SIZED 7137 CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR LOSS IN PRICE. WE HAD A ZERO TAS LIQUIDATION THROUGHOUT TUESDAY’S COMEX SESSION. MONDAY MORNING (INSTEAD OF SATURDAY MORNING) WE RECEIVED NOTICE OF .5000 OZ ISSUANCE OF EXCHANGE FOR RISK/ THIS WILL BE ADDED TO THE PREVIOUS EXCHANGE FOR RISK ISSUANCE OF .66 MILLION OZ/NEW EXCHANGE FOR RISK TOTALS: 1.16 MILLION OZ.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN ON LAST WEEK. THE ACCUMULATED T.A.S. WAS BEING USED TO MANIPULATE PRICES AT THE COMEX AND THAT THAT CONTINUED ON MONDAY TO NO AVAIL.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: A HUGE 586 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS BUT TO NO AVAIL TODAY. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT FELL BY $0.08) BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SILVER LONGS FROM THEIR PERCH AS WE HAD AN EXTRA HUMONGOUS GAIN IN OI ON OUR TWO EXCHANGES OF 7137 OI. CONTRACTS.

WE HAD A HUGE 3326 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 40.435 MILLION OZ (FIRST DAY NOTICE) TO WHICH WE MUST ADD ANOTHER OF THOSE STUPID “DELIVERIES” CALLED EXCHANGE FOR RISK THURSDAY NIGHT (NOV 29). THE CME ISSUED 132 NOTICES OF EXCHANGE FOR RISK FOR .66 MILLION OZ WHERE HERE THE BUYER TAKES THE RISK THAT HE WILL EVER BE DELIVERED UPON. WHAT A CROCK OF NONSENSE! SHOCKINGLY,MONDAY MORNING DEC 9, WE HAD ANOTHER 100 CONTRACTS OF EXCHANGE FOR RISK ISSUED. TOTAL FOR MONTH 1.16 MILLION OZ. WE ALSO HUGE 402 CONTRACT QUEUE JUMP FOR 2.010 MILLION OZ AS THESE BOYS WILL TRY THEIR LUCK IN TAKING DELIVERY OVER ON THIS SIDE OF THE PLANET.

// STANDING FOR SILVER//DEC INCREASES TO 41.125 MILLION OZ + .1.16 MILLION OZ EX FOR RISK = 42.285 MILLION OZ

WE HAD:

/ MEGA HUMONGOUS SIZED COMEX OI GAIN +//HUGE SIZED EFP ISSUANCE/ VI) HUGE SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 586 CONTRACTS)/ TO WHICH WE ADD 1.16 MILLION OZ EX. FOR RISK //

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 16 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS NOV. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF DEC

TOTAL CONTRACTS for 8 DAYS, total 17,970 contracts: OR 89.850 MILLION OZ (2246 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 89.850 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 89.85 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE/ MAY EXCEED MARCH 2022 RECORD OF 209 MILLION OZ)

RESULT: WE HAD AN EXTRA HUGE SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 3811 CONTRACTS DESPITE OUR SMALL LOSS IN PRICE OF SILVER PRICING AT THE COMEX//TUESDAY.,. THE CME NOTIFIED US THAT WE HAD A HUMONGOUS EFP ISSUANCE CONTRACTS: 3326 ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR DEC OF 40.435 MILLION OZ ON FIRST DAY NOTICE, FOLLOWED BY TODAY’S 2.010 MILLION OZ QUEUE JUMP TO WHICH WE ADD .66 MILLION OZ OF EXCHANGE FOR RISK/PRIOR + .500 MILLION OZ EX FOR RISK MONDAY//NEW TOTAL; 42.285 MILLION OZ

//NEW TOTAL STANDING FOR DEC AT 42.285 MILLION OZ

WE HAVE A MEGA HUMONGOUS SIZED GAIN OF 7137 OI CONTRACTS ON THE TWO EXCHANGES DESPITE OUR LOSS IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE 586 CONTRACTS TRYING DESPERATELY TO CONTAIN SILVER’S PRICE RISE,//ZERO FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE TUESDAY COMEX SESSION. BUT THEY STILL NEED THESE ISSUANCE FOR REPLENISHMENT FOR FUTURE TRADING /THE STRONG TA.S. ISSUANCE//LIQUIDATION DISTORTS THE TOTAL OI CONTRACTS STANDING AT THE COMEX. NO NET LONG SPECULATORS WERE BURNED ON MONDAY

/ ZERO NET SHORT COVERING FROM OUR SPEC SHORTS DESPITE THE LOSS IN PRICE TUESDAY/ . ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE TUESDAY NIGHT (586) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE, PROBABLY TODAY.

WE HAD 586 NOTICE(S) FILED TODAY FOR 2, 930,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST ROSE BY A STRONG SIZED 7227 OI CONTRACTS TO 483,346 AND CLOSER TO THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A HUGE SIZED 71 CONTRACTS//

WE HAD A STRONG SIZED INCREASE IN COMEX OI (7227 CONTRACTS) OCCURRED WITH OUR GAIN OF $29.75 IN PRICE TUESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A GOOD INITIAL STANDING IN GOLD TONNAGE FOR DEC AT 57.284 TONNES ON FIRST DAY NOTICE. FOLLOWED BY 245 CONTRACT QUE JUMP FOR 24,500 OZ ( .7620 TONNES) PLUS OUR 3 ISSUANCES OF 9.7074 TONNES OF EXCHANGE FOR RISK

/NEW STANDING 67.7534 TONNES

/ ALL OF THIS HAPPENED WITH OUR $29.75 GAIN IN PRICE WITH RESPECT TO TUESDAY’S COMEX ///. WE HAD A HUGE GAIN OF 12m282 OI CONTRACTS (38.202 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! YOU CAN VISUALIZE THIS WITH THE VIOLENT ACTION AT THE COMEX WITH RESPECT TO 245 CONTRACT QUEUE JUMP TODAY (24500 OZ) ALONG WITH THE 9.77074 EXCHANGE FOR RISK ISSUANCE THIS MONTH //NEW TOTAL TONNES OF DELIVERY: 67.7534.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 5055 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 482,346

IN ESSENCE WE HAVE A HUGE SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 12,282 CONTRACTS WITH 7227 CONTRACTS INCREASED AT THE COMEX// AND A HUMONGOUS SIZED 5055 EFP OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 12,282 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A HUGE SIZED BUT CRIMINAL 2307 CONTRACTS ISSUED. WE HAD A ZERO LIQUIDATION OF T.A.S CONTRACTS WITH OUR GAIN IN PRICE TUESDAY AS THE NEED FOR REPLENISHMENT WAS STILL IN ORDER TO CARRY OUT ITS PRICE CONTAINMENT STRATEGY IN FUTURE TRADING.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A HUMONGOUS SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5505 CONTRACTS) ACCOMPANYING THE STRONG SIZED INCREASE IN COMEX OI OF 7227 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 12,282 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR DEC 55.117 TONNES FOLLOWED BY TODAY.S 24500 OZ QUEUE JUMP TO WHICH WE ADD THOSE CRAZY EXCHANGE FOR RISK ON 3 PRIOR OCCASIONS OF 9.7074 TONNES//NEW STANDING 67,7534 TONNES

//NEW STANDING DECEMBER: 67.7534 TONNES

/ 3) ZERO T.A.S. LIQUIDATION (TRYING TO LOWER GOLD’S PRICE TUESDAY WITH ZERO SUCCESS AS WE HAD A $29.75 PRICE GAIN. BUT WE HAD ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A STRONG GAIN IN OI ON OUR TWO EXCHANGES. STICKY GOLD’S LONGS ARE NOT FOOLED BY THE RAID IN PRICE AS THEY WERE REWARDED TUESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL.

4) STRONG SIZED COMEX OPEN INTEREST INCREASE 5) HUGE ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///HUGE T.A.S. ISSUANCE: 2307 T.A.S.CONTRACTS///245 CONTRACT QUEUE JUMP OR 24500 OZ WILL STAND FOR DELIVERY AT THE COMEX.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

DEC

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC :

TOTAL EFP CONTRACTS ISSUED: 55,540 CONTRACTS OF 5,554,000 OZ OR 172.75 TONNES IN 8 TRADING DAY(S) AND THUS AVERAGING: 6943 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 8 TRADING DAY(S) IN TONNES 172.75 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 172.75 DIVIDED BY 3550 x 100% TONNES = 4.87% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 172.75 TONNES (we will also have a humdinger of an ex for physical issuance for this month/maybe this time we will surpass March 22 record of 409 tonnes for the month)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A HUMONGOUS SIZED 3811 CONTRACTS OI TO 151,096 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 3326 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 3326 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 3326 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 3811 CONTRACTS AND ADD TO THE 3326 E.FP. ISSUED

WE OBTAIN A HUGE SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 7137 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS 35.685 MILLION OZ OCCURRED DESPITE OUR $0.08 LOSS IN PRICE

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS/WEDNESDAY MORNING TUESDAY NIGHT

ASIA TRADING TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED UP 9.88 PTS OR 0.29%

//Hang Seng CLOSED DOWN 156.23 PTS OR 0.77%

// Nikkei CLOSED UP 4.65 OR 0.01%//Australia’s all ordinaries CLOSED DOWN .46%///Chinese yuan (ONSHORE) CLOSED DOWN TO 7.2739 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.2722// Oil DOWN TO 69.45 dollars per barrel for WTI and BRENT UP AT 72.99 Stocks in Europe OPENED ALL MOSTLY MIXED

ONSHORE USA/ YUAN TRADING BELOW LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST ROSE BY A STRONG SIZED 7227 CONTRACTS TO 483,346 WITH OUR HUGE GAIN IN PRICE OF $29.75 WITH RESPECT TO TUESDAY’S TRADING. , WE LOST ZERO NET LONGS AS WE HAVE A STRONG PRICE GAIN FOR GOLD AND WE ALSO HAD AS YOU WILL SEE BELOW A HUGE NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (5055). THUS A HUMONGOUS GAIN ON OUR TWO EXCHANGES OF 12,282 CONTRACTS WITH OUR GAIN IN PRICE AND THEREFORE NO LOSS IN NET LONGS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY THIS ENTIRE PAST WEEK. WE HAD LITTLE T.A.S. LIQUIDATION ON TUESDAY, BUT IT WAS IN FULL FORCE TODAY

THE FED IS THE MAJOR SHORT OF AROUND 93+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS IS SCHEDULED TO HAPPEN LATE OCT 2024/(AS OUTLINED IN OUR GOLD PHYSICAL COMMENTARIES//VIEW ANDREW MAGUIRE LATEST LIVE FROM VAULT PODCAST 197 , 199, 2001,AND FRIDAY NIGHTS 202, AS HE TACKLES THIS IMPORTANT TOPIC). THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST TWO MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY! ACTUALLY THE FED HAS COAXED THE SPECULATORS TO GO MASSIVELY SHORT WHILE THEY TAKE THE LONG SIDE AFTER THEY COMMENCE THE AVALANCHE IN LOWERING THE PRICE OF GOLD.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD CONSIDERABLE T.A.S. LIQUIDATION THROUGHOUT LAST WEEK’S TRADING BUT VERY LITTLE ON TUESDAY. BUT LOTS TODAY.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF THE SPREADERS // T.A.S DURING LAST WEEK AND EARLY THIS WEEK IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW DEEP INTO THE ACTIVE DELIVERY MONTH OF DECEMBER.… THE CME REPORTS THAT THE BANKERS ISSUED A HUGE SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A HUGE SIZED 5055 EFP CONTRACTS WERE ISSUED: : /DEC 5055 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5055 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A HUMONGOUS SIZED TOTAL OF 12,282 CONTRACTS IN THAT 5055 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG SIZED GAIN OF 7227 COMEX CONTRACTS..AND THIS HUGE GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR GAIN IN PRICE OF $29.75 TIESDAY// COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR TUESDAY NIGHT WAS A GOOD SIZED SIZED 2307 CONTRACTS, AND THESE WILL BE USED TO REPLENISH SUPPLIES.. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK).

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON MONDAY NOV 25, THEIR RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION (COUPLED WITH THE LIQUIDATION OF CALENDAR SPREADERS ). THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LAST WEEK’S TRADING. WE HAD CONTINUAL T.A.S. AND FINAL MONTH END SPREADER LIQUIDATION ON FRIDAY NOV 29 .THE LIQUIDATION OF T.A.S. SUBSIDED QUITE DRAMATICALLY WITH LAST FRIDAY’S TRADING, AND IT CONTINUED WITH THIS WEEK’S TRADING, ENDING TUESDAY BUT FORECEFULLY RETURNING ON WEDNESDAY.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: DEC (67,7534 TONNES) WHICH IS HUGE FOR OUR ACTIVE DEC DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 58.046 TONNES + .776 TONNES EXCHANGE FOR RISK PRIOR + 1.919 TONNES EXCHANGE FOR RISK WEDNEDAY+ 7.0108 TONNES FRIDAY NIGHT(DEC 7) /NEW TOTAL 67.7534 TONNES

THE SPECS/HFT WERE UNSUCCESSFUL IN LOWERING GOLD’S PRICE( IT ROSE BY $29.75/)//AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A HUMONGOUS GAIN IN PRICE. WE DID HAVE LITTLE T.A.S. SPREADER LIQUIDATION MONDAY. WE ALSO HAD A GOOD T.A.S. ISSUANCE, TUESDAY NIGHT, AS THE NEED FOR REPLENISHMENT WAS STILL EVER PRESENT. THIS COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL TUESDAY EVENING.

LATE 10 DAYS AGO, FRIDAY NIGHT (EARLY SATURDAY MORNING NOV 30) THE CME ANNOUNCED ANOTHER OF THOSE CRAZY DELIVERIES: THE ISSUANCE OF 250 EXCHANGE FOR RISK CONTRACTS WHICH TOTAL 25000 OZ (.7776 TONNES. HERE THE BUYER ASSUMES THE RISK THAT HE WILL BE DELIVERED UPON IN PHYSICAL METAL. THIS IS ABSOLUTELY INSANE AND A HUGE VIOLATION OF THE TRUE DISCOVERY PRICE MECHANISM WHICH IS THE COMEX MANTRA!. AND THEN GUESS WHAT? THE CME ANNOUNCED ANOTHER EXCHANGE FOR RISK, LATE TUESDAY EVENING/ EARLY WEDNESDAY MORNING, (DEC 5) OF 617 CONTRACTS FOR 61,700 OZ OR GOLD (1.919 TONNES). THEN MUCH TO MY ANGER, THE CME ANNOUNCED A THIRD ISSUANCE FRIDAY NIGHT DEC 7 FOR A MONSTROUS 2254 EXCHANGE FOR RISK CONTRACTS OR 225,400 OZ OR 7.0108 TONNES THUS ALL THREE OF THESE ISSUANCES WILL BE ADDED TO THE TOTAL GOLD BEING “DELIVERED UPON”. (9.7074 TONNES).

WE HAVE GAINED A TOTAL OF 38.202 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR DEC (55.167TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 24,500 OZ OR 0.7620 TONNES TO WHICH WE ADD 9.7074 TONNES OF EXCHANGE FOR RISK.

THUS TOTAL EXCHANGE FOR RISK/PRIOR = : 9.7074 TONNES + NORMAL GOLD TONNES STANDING OF 57.284 = DELIVERY TOTALS OF 67.7534 TONNEES

/ STANDING FOR DEC INCREASES TO 67.7534 TONNES

NEW STANDING FOR DECEMBER: 67.7534 TONNES (WHICH IS HUGE FOR OUR VERY ACTIVE DELIVERY MONTH)

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR GAIN IN PRICE TO THE TUNE OF $31.10

WE HAD 731 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES 12,282 CONTRACTS OR 1,228,200 (38.202 TONNES)

confirmed volume TUESDAY 200,529 contracts: poor //// T.A.S. ENHANCED TO A MUCH LESSER EXTENT.

//speculators have left the gold arena

END

/ /// THE DEC 2024 GOLD CONTRACT

DEC 11

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | NIL OZ . |

| Deposit to the Dealer Inventory in oz | NIL OZ |

| Deposits to the Customer Inventory, in oz | 257,208.000 OZ JPMorgan/Brinks 8,000 kilobars |

| No of oz served (contracts) today | 628 notice(s) 62,800 OZ 1.9533 TONNES |

| No of oz to be served (notices) | 510 contracts 51000 OZ 1,5863 TONNES |

| Total monthly oz gold served (contracts) so far this month | 18,152 notices 1,815,200 oz 56.460 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

dealer deposits: 0

total dealer deposits: NIL oz

we have 2 customer deposit

i) Into JPMorgan 160,755.000 oz (5,000 kilobars)’

ii) Into Brinks: 96,453.000 oz (3000 kilobars)_

total deposits 257,208.000 oz 8,000 kilobars

strictly a paper gold entry.

withdrawals: 0

TOTAL WITHDRAWALS: oz

adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR DEC.

For the front month of DEC: we have an oi of 1138 contracts having LOST 177 contracts. We had

422 contracts were served on TUESDAY, so we GAINED 245 contracts or 24,500 oz underwent a MASSIVE queue jump bolting ahead of others to take delivery of gold over on this side of the planet.

JANUARY GAINED 64 CONTRACTS TO STAND AT 2160

FEBRUARY GAINED 6177 CONTRACTS TO 368,854 .

We had 422 contracts filed for today representing 42,200 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 20 notices issued from their client or customer account. The total of all issuance by all participants equate to 628 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 82 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for DEC /2024. contract month, we take the total number of notices filed so far for the month (18,152 x 100 oz ) to which we add the difference between the open interest for the front month of DEC(1138 CONTRACTS) minus the number of notices served upon today (628 x 100 oz per contract( equals 1,866,200 OZ OR 58.046 TONNES. to which we add 9.7074 tonnes of exchange for risk/PRIOR equals 67.7534

thus the INITIAL standings for gold for the DEC contract month: No of notices filed so far (18,152 x 100 oz +we add the difference for front month of DEC (1138 OI} minus the number of notices served upon today (628 x 100 oz which equals 1,866,200 oz (58.046 TONNES) + 9.7074 tonnes of ex. for risk PRIOR //new total 67.7534 TONNES

TOTAL COMEX GOLD STANDING FOR DEC.: 67.7534 TONNES WHICH IS HUGE FOR THIS ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,887,512.376 oz 58.71 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 18,339.010.539 OZ

TOTAL REGISTERED GOLD 8097,306.492/// 251.86 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,241,704.087 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,209,794 oz (REG GOLD- PLEDGED GOLD)= 193.15 tonnes //

JPMorgan enhanced inventory is 3.592 million oz/17.833 million oz = 20.14% of entire inventory..

END

SILVER/COMEX

DEC 11. 2024

INITIAL

//2024// THE DEC 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | nil . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 206,859.056 oz Manfra |

| No of oz served today (contracts) | 586 CONTRACT(S) (2,930,000 OZ) |

| No of oz to be served (notices) | 249 contracts (1.245 MILLION oz) |

| Total monthly oz silver served (contracts) | 7976 Contracts (39.880 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit/

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 1 customer deposits

i) Into Manfra 206,859.056

total customer deposits 206,859.056 oz

We had 0 withdrawals

total withdrawal nil oz

JPMorgan has a total silver weight: 134.401million oz/307.615million or 43.83%

adjustment 0

TOTAL REGISTERED SILVER: 76.529MILLION OZ//.TOTAL REG + ELIGIBLE. 307.822 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DEC

silver open interest data:

FRONT MONTH OF DEC /2024 OI: 835 OPEN INTEREST FOR A LOSS OF 41 CONTRACTS. WE HAD

473 CONTRACTS ISSUED ON TUESDAY SO WE HAD A HUGE 402 CONTRACT OR A 2.01 MILLION OZ QUEUE JUMP WHERE THESE BOYS WILL TRY THEIR LUCK AND TAKE DELIVERY OF PHYSICAL SILVER OVER HERE.

JANUARY SAW A GAIN OF 71 CONTRACTS DOWN TO 2523

FEBRUARY SAW A GAIN OF 68 CONTRACTS TO STAND AT 136

MARCH SAW A GAIN OF 898 CONTRACTS UP TO 123,261

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 586 for 2,930,000 oz

CONFIRMED volume; ON TUESDAY 71,773 huge// t.a.s. reduced

To calculate the number of silver ounces that will stand for delivery in DEC we take the total number of notices filed for the month so far at 7976x 5,000 oz = 39.880 MILLION oz

to which we add the difference between the open interest for the front month of DEC (835) and the number of notices served upon today (586)x (5000 oz)

Thus the standings for silver for the DEC 2024 contract month: 7976 Notices served so far) x 5000 oz + OI for the front month of DEC(935) minus number of notices served upon today (586)x 5000 oz equals silver standing for the DEC contract month equating to 41.125 MILLION OZ. + to which we add .66 million oz of exchange for risk PRIOR// + .5000 EXCHANGE FOR PHYSICAL MONDAY MORNING//new total 42.285

New total standing: 42.285 million oz.

There are 76,529 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS//

DEC 11 WITH GOLD UP $26.65 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: / // : .///INVENTORY RESTS AT 870.79 TONNES

DEC 11 WITH GOLD UP $29.75 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: // : .///INVENTORY RESTS AT 870.79 TONNES

DEC 9 WITH GOLD UP $31.10 ON THE DAY; NO CHANGES IN GOLD AT THE GLD. // : .///INVENTORY RESTS AT 871.94 TONNES

DEC 6 WITH GOLD UP $6.60 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD. A WITHDRAWAL OF 1.71 TONNES OF GOLD FROM THE GLD// : .///INVENTORY RESTS AT 871.94 TONNES

DEC 5 WITH GOLD DOWN $26.80 ON THE DAY; NO CHANGES IN GOLD AT THE GLD./ : .///INVENTORY RESTS AT 873.65 TONNES

DEC 4 WITH GOLD UP $6.15 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD./ : .///INVENTORY RESTS AT 873.65 TONNES

DEC 3 WITH GOLD UP $10.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.59 TONNES OF GOLD FROM THE GLD./ : .///INVENTORY RESTS AT 875.96 TONNES

DEC 2 WITH GOLD DOWN $20.20 ON THE DAY; NO CHANGES IN GOLD AT THE GLD : .///INVENTORY RESTS AT 878.55 TONNES

NOV 29 WITH GOLD UP $16.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD : Z WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD . .///INVENTORY RESTS AT 878.55 TONNES

NOV 27 WITH GOLD UP $18.05 ON THE DAY; NO CHANGES IN GOLD AT THE GLD : . .///INVENTORY RESTS AT 879.41 TONNE

NOV 26 WITH GOLD UP $3.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD : A DEPOSIT OF 1.44 TONNES OF GOLDINTO THE GLD. .///INVENTORY RESTS AT 879.41 TONNES

NOV 25 WITH GOLD DOWN $91.60 ON THE DAY; NO CHANGES IN GOLD AT THE GLD :. .///INVENTORY RESTS AT 877.97 TONNES

NOV 21 WITH GOLD UP $23.85 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 3.16 TONNES OF GOLD INTO THE GLD/:. .///INVENTORY RESTS AT 875,39 TONNES

NOV 20 WITH GOLD UP $22.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.58 TONNES OF GOLD INTO THE GLD/:. .///INVENTORY RESTS AT 872.23 TONNES

NOV 19 WITH GOLD UP $13.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/:. .///INVENTORY RESTS AT 871.65 TONNES

NOV 18 WITH GOLD UP $44.20 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.56 TONNES OF GOLD INTO THE GLD/:. .///INVENTORY RESTS AT 869.93 TONNES

NOV 15 WITH GOLD DOWN $1.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.25 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 867.37 TONNES

NOV 14 WITH GOLD DOWN $12.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.91 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 868.62 TONNES

NOV 13 WITH GOLD DOWN $19.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 870.63 TONNES

NOV 12 WITH GOLD DOWN $11.40 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.88 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 871,97 TONNE

NOV 11 WITH GOLD DOWN $75.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.74 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 876.85 TONNES

NOV 8 WITH GOLD DOWN $11.85 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.87 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 883.46 TONNES

NOV 7 WITH GOLD UP $30.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.45 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 883.46 TONNES

NOV 6 WITH GOLD DOWN $72.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 886.91 TONNES

NOV 5 WITH GOLD UP $4.05 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:.// . // .///INVENTORY RESTS AT 888.63 TONNES

GLD INVENTORY: 870.79 TONNES, TONIGHTS TOTAL

SILVER

DEC 11 WITH SILVER UP 10 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.597 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 469.215 MILLION OZ

DEC 11 WITH SILVER UP 10 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.597 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 469.215 MILLION OZ

DEC 10 WITH SILVER DOWN 8 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 1.868 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 471.812 MILLION OZ

DEC 9 WITH SILVER UP $0.91 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 1.367 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 473.680 MILLION OZ

DEC 6 WITH SILVER DOWN $0.00 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 4.329 MILLION OZ/// //INVENTORY AT SLV RESTS AT 475.047 MILLION OZ

DEC 5 WITH SILVER DOWN $0.23 //NO CHANGES IN SILVER INVENTORY AT THE SLV” /// //INVENTORY AT SLV RESTS AT 470.718 MILLION OZ

DEC 4 WITH SILVER UP 26 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV”: A WITHDRAWAL OF 2.206 MILLION OZ FORM THE SLV. /// //INVENTORY AT SLV RESTS AT 470.718 MILLION OZ

DEC 3 WITH SILVER UP 59 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV /// //INVENTORY AT SLV RESTS AT 472.924 MILLION OZ

DEC 2 WITH SILVER DOWN 19 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV. A WITHDRAWAL OF 1,458,000 OZ FROM THE SLV. /// //INVENTORY AT SLV RESTS AT 472.924 MILLION OZ

NOV 29 WITH SILVER UP 51 CENTS //SMALL CHANGES IN SILVER INVENTORY AT THE SLV. A WITHDRAWAL OF 365,000 OZ FROM THE SLV. /// //INVENTORY AT SLV RESTS AT 474.382 MILLION OZ

NOV 27 WITH SILVER DOWN $0.25 //NO CHANGES IN SILVER INVENTORY AT THE SLV.. /// //INVENTORY AT SLV RESTS AT 474.747 MILLION OZ

NOV 26 WITH SILVER UP $0.10 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:.A WITHDRAWAL OF 1.094 MILLION OZ FROM THE SLV./.. /// //INVENTORY AT SLV RESTS AT 474.747 MILLION OZ

NOV 25 WITH SILVER DOWN $0.96 //NO CHANGES IN SILVER INVENTORY AT THE SLV:. . /// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 22 WITH SILVER UP $0.40 //NO CHANGES IN SILVER INVENTORY AT THE SLV:. . /// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 21 WITH SILVER DOWN $0.06 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.729 MILLION OZ FORM THE SLV. . /// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 20 WITH SILVER DOWN $0.22 //NO CHANGES IN SILVER INVENTORY AT THE SLV: . /// //INVENTORY AT SLV RESTS AT 477.572 MILLION OZ

NOV 19 WITH SILVER UP $0.10 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 5,742,000 OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 477..572 MILLION OZ

NOV 18 WITH SILVER UP $0.68 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 1,277,000 OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 471,830 MILLION OZ

NOV 15 WITH SILVER DOWN $0.09 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 3,100,000 OZ OUT OF THE SLV. /// //INVENTORY AT SLV RESTS AT 471,830 MILLION OZ

NOV 14 WITH SILVER DOWN $0.07 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1,504,000 OZ OUT OF THE SLV. /// //INVENTORY AT SLV RESTS AT 473.653 MILLION OZ

NOV 13 WITH SILVER DOWN $0.16 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1,274,000 OZ OUT OF THE SLV. /// //INVENTORY AT SLV RESTS AT 475.157 MILLION OZ

NOV 12 WITH SILVER UP $0.16 //SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 576,000 OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 476.000 MILLION OZ

NOV 11 WITH SILVER DOWN $0.79 //SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 374,000 OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 477.527 MILLION OZ

NOV 8 WITH SILVER DOWN $0.43 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 2.005 MILLION OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 477.846 MILLION OZ

NOV 7 WITH SILVER UP $0.11 //NO CHANGES IN SILVER INVENTORY AT THE SLV: /// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 6 WITH SILVER DOWN $1.41 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.692 MILLION OZ FROM THE SLV/.//// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 5 WITH SILVER UP 0.18 :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.109 MILLION OZ FROM THE SLV/.//// //INVENTORY AT SLV RESTS AT 479,533 MILLION OZ

CLOSING INVENTORY 471.812 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

2/ Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

Alasdair Macleod

3. CHRIS POWELL AND GATA DISPATCHES

Robert Lambourne: BIS gold swaps fell 13% in November as debt problems grew

Submitted by admin on Tue, 2024-12-10 21:24 Section: Daily Dispatches

By Robert Lambourne

Wednesday, December 11, 2024

The November statement of account for the Bank for International Settlements was published this week —

— and it indicates that the volume of gold swaps undertaken by the BIS fell from 93 tonnes on October 31 to 81 tonnes on November 29, a decline of 12 tonnes or 13%.

Table 1 below sets out the historical level of monthly gold swaps estimated by GATA since August 2018. As is evident from the table there is still a considerable level of gold being traded via these swaps. While gold swaps are down significantly from the 501 tonnes estimated in January 2022, the level seemingly remains quite volatile, suggesting the use of swaps to cover shorter-term trading requirements.

To repeat the point made regularly in these reports, it seems that these swaps are undertaken by the BIS for one or more of its central bank customers with the swapped gold being accounted for as being held in a BIS-registered sight account at a central bank. Given what is happening in the gold market more generally with regular central bank buying, it appears reasonable to assume that the Federal Reserve is the BIS’ customer for the swaps transactions.

The evidence strongly suggests that bullion banks are the source of this gold and that the supply comes from gold registered as being held by gold exchange-traded funds (ETFs).

The 2023-24 annual report for the BIS —

— confirms GATA’s estimate of the bank’s gold swaps as of March 31 shown in Table 1 below: 72 tonnes.

The recently published BIS interim report for the six months to September 30 contains information that also confirms certain assumptions used to estimate the swap volumes. This includes confirmation that the BIS continued to hold 102 tonnes of its own gold. The interim report also provides strong support, via its reporting on transactions with related parties, that the swapped gold comes from bullion banks rather than central banks.

However, the BIS continues to offer no explanation for why it is undertaking gold swaps.

The BIS first reported gold swaps in its annual report for 2009-10, so gold swaps have been provided by the BIS for its customer central banks for more than 15 years. See Table 2 below for the year-end level of gold swaps reported by the BIS in its annual reports since March 2010.

* * *

Table 1 — Gold swaps estimated by GATA from BIS monthly statements of account

Month …. Swaps

& year … in tonnes

Nov-24 …. /81

Oct-24 …. /93

Sep-24 …. /112

Aug-24 …. /157

Jul-24 …. /148

Jun-24 …. /116

May-24 …. /109

Apr-24 …. /78

Mar-24 …. /72

Feb-24 …. /68

Jan-24 …. /117

Dec-23 …. /121

Nov-23 …./100

Oct-23 …./68

Sep-23 …./96

Aug-23 …./129

Jul-23 …. /103

Jun-23…. /87

May-23 …. /188

Apr-23 …. /135

Mar-23 …. /77

Feb-23 … /136

Jan-23 … /103

Dec-22 … /0

Nov-22 … /105

Oct-22 ….. /7

Sep-22 …../57

Aug-22 ….. /75

Jul-22 ….. /56

Jun-22 ….. /202

May-22 ….. /270

Apr-22 ….. /315

Mar-22 …. /358

Feb-22 …. /472

Jan-22 ….. /501

Dec-21…. /414

Nov-21…. /451

Oct-21…. /414

Sep-21 …. /438

Aug-21 …. /464

Jul-21 …. /502

Jun-21 …./471

May-21 …./517

Apr-21 …. /472

Mar-21…. /490

Feb-21 …../552

Jan-21 …. /523

Dec-20 …. /545

Nov-20 …. /520

Oct-20 …. /519

Sep-20…../ 520

Aug-20…../ 484

Jul-20 ….. / 474

Jun-20 …. / 391

May-20 … / 412

Apr-20 …. / 328

Mar-20 …. / 326

Feb-20 …. / 326

Jan-20 …. / 320

Dec-19 …. / 313

Nov-19 …. / 250

Oct-19 …. / 186

Sep-19 …. / 128

Aug-19 …. / 162

Jul-19 ….. / 95

Jun-19 …. / 126

May-19 …. / 78

Apr-19 ….. / 88

Mar-19 …. / 175

Feb-19 …. / 303

Jan-19 …. / 247

Dec-18 …. / 275

Nov-18 …. / 308

Oct-18 …. / 372

Sep-18 …. / 238

Aug-18 …. / 370

GATA uses gold prices quoted by USAGold.com to estimate the level of gold swaps held by the BIS at month-ends.

* * *

There seem to be no reasons to alter the assumption that the BIS is continuing to enter these swaps on behalf of the Federal Reserve. There is no evidence to suggest that any other major central bank is actively trading this much gold, and many central banks are still accumulating physical gold.

As noted above, the basic transaction that the BIS is believed to undertake is to swap dollars for gold that is transferred from a bullion bank, then to deposit this gold in a gold sight account at a central bank, presumed to be the Fed but almost certainly being the central bank that is using the BIS to execute the gold swap on its behalf.

Given the recent volatility in BIS gold swaps, it seems likely that most are of a short duration. Why a central bank needs the BIS to undertake gold swaps isn’t clear. The swaps are likely connected with short-term trading needs and perhaps are being used to aid suppression of the gold price via the futures markets.

The volatility in the volume of swaps is clear from a review of Table 1 above. Volumes of swaps in 2023 and so far in 2024 remain well below the average seen in the preceding four years, but they remain significant. The gold price decreased from $2,744 at October 31 to $2,651 at November 30 (per USAGold.com).

Using the November 30 gold price, the 81 tonnes of gold swaps outstanding via the BIS at the month-end are valued at about $6.9 billion.

So the recent trading in BIS gold swaps has high dollar value and shows that gold remains a significant monetary asset still actively traded on behalf of at least one central bank, presumably the Fed.

As ever with the BIS, it remains unlikely that more information about why it undertakes these transactions will be provided. No such information was provided in the bank’s recently published annual report, which covered the year ending March 31, 2024.

*

Summary of GATA research on gold price suppression

GATA’s research on gold price suppression indicates that an active policy of price suppression was implemented around 30 years ago and was primarily intended to hold down interest rates. A recent update on this research is provided by the presentation GATA Secretary/Sreasurer Chris Powell made in November 2024 at the New Orleans Investment Conference:

This influential report from 2005 about “Gibson’s Paradox” remains relevant and highlights work in this area by former U.S. Treasury Secretary and Harvard University President Lawrence Summers:

It also remains relevant to highlight the following remarks made in a speech by Summers on September 8, 1999, as reported in the book “The Wealth of Progressive Nations: The Collected Lectures of Lawrence Summers.” The remarks below are an extract of a section of the speech titled “A New Economic Paradigm.”

“Most important of all, the Clinton-Gore administration has established a new paradigm for the management of our nation’s budget, with enormous cumulative benefits for our economy and our citizens. It has become a commonplace to remark on how exceptional today’s 4.2% unemployment rate is relative to any expectation at the beginning of the decade. It is no less remarkable that today, after 8.5 years of expansion, long-term interest rates are around 2 percentage points lower than they were at its start.”

From this it is reasonable to conclude that keeping interest rates lower was considered a priority by the Clinton-Gore administration and succeeding at it was thought to be “remarkable.” While this is not proof that gold price suppression was undertaken specifically to reduce interest rates, it demonstrates that reducing interest rates was a priority for the U.S. government.

Further evidence of this priority is provided by an interview with former Treasury Secretary Robert Rubin about his time working in the Clinton administration after January 1993. In answer to a question on the initial decision to prioritize federal deficit reduction, Rubin remarks: “On the other hand, if interest rates go down as a result, then that will stimulate growth, and we thought that the beneficial effect of lower interest rates would outweigh the contractionary impact of the deficit reduction”:

Hence there is plenty of evidence that keeping interest rates low was a major goal of the Clinton administration.

In the context of gold price suppression being used to reinforce efforts to reduce interest rates, the following report issued by GATA in 2007 with an analysis of the gold market by Frank Veneroso is a notable reference as it confirms that GATA’s primary assertions about gold price suppression were plausible, including under-reported sales of official gold:

Here is an excerpt from the report: “I find it extremely annoying that there is a hell of a lot of obvious evidence out there that something is happening in the gold market — that there are very large supplies coming into the market — larger than the consensus would claim — and no one is willing to discuss it.” He further notes that maybe as much as 10,000 tonnes to 16,000 tonnes of gold may have been lent out starting in the 1980s and going on into the 1990s. This extra supply of gold will have acted to suppress gold prices and resulted in double counting of official gold, which having been lent out, may have been used, for example, to satisfy jewelry demand.

An interesting and entirely separate point about the surprising developments in the mid-1990s with subdued interest rates and relatively low inflation has come to the attention of this writer and is set out in a wide ranging article by professor Russell Napier:

Within this highly informative article there is a reference to the impact caused by Chinese exports of manufactured goods since 1994 on the rate of inflation around the world. Professor Napier considers that these goods were sold at below economic value for many years and were responsible for the change toward a lower rate of inflation for most of the next 30 years in the developed world.

It seems quite a coincidence that this impact from Chinese exports happened when gold price suppression started in earnest with plausible reasons to believe this was of an intentional effort by the U.S. authorities to suppress interest rates. This may suggest that in addition to gold price suppression there was a deliberate policy to allow China to export goods at low prices as part of the effort to reduce inflation and keep real interest rates low.

In light of the efforts to suppress gold prices, this extra dimension of support for sustained lower inflation seems to this writer to provide a much more complete explanation of why this dramatic change in interest rates has happened in the last 30 years.

*

More recent trends in U.S. federal government deficits

The remarks by Rubin and Summers on the U.S. government’s priorities in the 1990s are reminders of how much the financial positions of Western nations have worsened since then.

The worsening trend for Western nations, especially the United States, probably reduces the appeal to the BIS of undertaking gold swaps on behalf of any central bank where a liability to return swapped gold is incurred. The trend possibly also reduces the appeal of any such swaps to the central bank or banks for which the BIS has been acting.

A report issued by GATA in 2012 is worth revisiting as it highlights the acknowledgment of gold price suppression by a former chairman of the BIS, Jelle Zijlstra, a Dutch politician, economist, and central banker. So it seems likely that BIS management understands what the swaps are being used for and why no reasons for the transactions are given:

The conundrum facing the Federal Reserve about dollar interest rates has seemingly been resolved for now with the Fed’s recent decisions to reduce rates with further cuts suggested for December and into 2025. What will happen after the Trump administration takes control is difficult to guess. A recent stream of announcements on a wide range of topics from efforts to cut federal spending by $2 trillion to the introduction of punitive tariffs on imports from Canada, Mexico, and China highlights the uncertain outlook.

The current federal government debt of $36.2 trillion, including $7.3 trillion of special debt, as of December 6 is already $0.7 trillion higher than at September 30, the end of the last fiscal year. This current trend seems unsustainable and unless there is a rapid change it seems inevitable that gold prices will rise substantially, either via a deliberate gold price reset or by a substantial decline in the market price of the dollar. Clearly at this level of debt a substantial increase in interest rates would hasten recognition that federal government finances are unsustainable.

The direction of oil prices after the election might prove to be an important influence on the timing of a gold price reset, if it is being considered. A strong recovery in oil prices would be damaging.

The report at the following link, which reviews the possible connection between hedge funds’ basis trades in U.S. Treasuries and the Fed’s program of quantitative tightening in 2022, could be read as another sign of how difficult it is to find purchasers of U.S. Treasuries at current prices:

Perhaps the easiest way to picture this apparent correlation is to view this chart:

This further link contains a commentary on the apparent enrichment of certain hedge funds and the individuals involved as a result of the apparent support from the Fed to the hedge fund basis trade used to effect “quantitative tightening”:

It also seems that the incentives for foreigners to own U.S. Treasuries are diminishing as efforts to confiscate Russian assets appear to be moving forward. Saudi Arabia has apparently warned that any such confiscation may cause it to sell its holding of U.S. Treasuries.

Again, it seems appropriate to note that a report titled “Living with High Public Debt,” authored by Serkan Arslanalp and Barry Eichengreen, was published in August 2023 by the Federal Reserve Bank of Kansas City. This report reinforces just how difficult it is to handle high federal government debt with spending far in excess of revenue.

The report can be found at the Kansas City Fed’s internet site and at GATA’s:

Here is an excerpt from the conclusions:

“Looking forward, the challenges are daunting. Given aging populations, governments will have to find additional finance for healthcare and pensions. They will have to finance spending on defense, climate change abatement, and adaptation, and the digital transition. A growing number of low-income countries are already in debt distress.

“Living with high public debt therefore means avoiding steps that make a bad situation worse. This means minimizing unproductive public spending. It means targeting social transfers as a way of limiting pressures on the expenditure side. It means limiting contingent liabilities by, inter alia, adequately regulating banks and avoiding recapitalization costs.

“It means contemplating tax increases where revenues are low by international standards. It means further developing financial markets where markets are underdeveloped and where a diverse population of local investors in debt securities is absent. It means embracing legal and procedural changes that streamline and speed restructuring for countries whose debts are unsustainable.

“This modest medicine does not make for a happy diagnosis. But it makes for a realistic one.”

In the circumstances, vividly described in the report, it seems unsurprising that the price of gold has increased substantially so far in 2024. The report offers yet more reason to question whether gold swaps undertaken via the BIS, probably on behalf of the Fed, are being used as part of a mechanism to suppress the dollar gold price and may even represent double-counted gold supposedly held by exchange-traded funds.

*

Debt problems in China and other countries

In recent reports the International Monetary Fund has highlighted the high level of non-financial debt in many countries, and data recently reported by the BIS for non-financial debt to gross domestic product include as of Q2 2024: Japan 394%, France 319%, China 292%, U.S. 249%, UK 229%, Germany 200%, and India 183%. Both the IMF and the BIS are clearly signaling their concerns over the debt overhang.

Recent reports in Western media on efforts by the Chinese government to stimulate its economy, especially its property sector, are relevant to supporters of gold. At least one experienced observer of the Chinese economy believes that China needs to devalue its debt and possibly achieve this by way of a gold price revaluation. Even last week saw new reports on efforts to refinance the debt of local authorities in China.

Professor Russell Napier, the author of the article cited above, published in American Affairs, includes his insights into the debt situation in China and his view that much of this debt needs to be written off. An unsaid consequence of his conclusion is that gold will rise in price in yuan (and dollars) as a result of this debt write-off, which could in theory be achieved by a gold price reset by the Chinese government. Professor Napier is the author of “The Asian Financial Crisis 1995-98” and a well-known investment adviser and economic historian.

In recent YouTube videos Napier goes further and suggests in the video that Chinese President Xi Jinping has the ability to decide when to trigger a gold price reset and that it will change global trade dramatically. A decision by China to devalue the yuan versus gold would almost certainly force the United States to follow and would probably lead to bans or extremely high tariffs on Chinese exports to the United States.

If Professor Napier is correct, then any attempts by President-elect Donald Trump to introduce substantial tariffs on Chinese exports might trigger a decision by the Chinese to reset the yuan gold price, since one of the major adverse consequences of a unilateral Chinese decision to trigger a gold price reset — namely the loss of their export trade to the U.S. — would have already happened.

So the price of gold could soar if Trump carries out what he has said he will do. There is plenty of recent evidence that the Chinese intend to take measures against the U.S. if punitive tariffs are introduced on imports from China. Efforts are being made by the Chinese to stop exports of certain minerals such as gallium to the U.S. and to diversify their purchases of soybeans, formerly sourced mainly from the U.S. Also, China is seeking to adopt sanctions similar to those used by the U.S. on third parties to stop them rerouting materials to the U.S.

If Trump acts more cautiously, then maybe an agreed joint U.S.-China gold price reset might occur in 2025. The chances that the U.S. federal deficit will continue to be willingly funded by foreigners in 2025 seem really bleak, not only because of the possible adverse implications of Trump’s tax plans and the likely difficulty in cutting federal government spending by the target of $2 trillion, but especially as hedge funds have already been used and seemingly are really holding Treasuries only as a stopgap for maybe two years, a term that will start running out later in 2025.

In the opinion of this writer, Napier’s ideas on a new financial system are credible, especially if two separate spheres of influence develop based around China and the U.S.

*

Historical context of the gold swaps

The BIS rarely comments publicly on its gold activities, but its first use of gold swaps was considered important enough to cause the bank to give some background information to the Financial Times for an article published on July 29, 2010, coinciding with publication of the bank’s 2009-10 annual report.

The general manager of the BIS at the time, Jaime Caruana, said the gold swaps were “regular commercial activities” for the bank, and he confirmed that they were carried out with commercial banks and so did not involve central banks. It also seems highly likely that the BIS’ remaining swaps are still all made with commercial banks, because the BIS annual report has never disclosed a gold swap between the BIS and a major central bank.

The swap transactions potentially created a mismatch at the BIS, which may have ended up being long unallocated gold (the gold held in BIS sight accounts at major central banks) and short allocated gold (the gold required to be returned to swap counterparties). This possible mismatch has not been reported by the BIS.

The gold banking activities of the BIS have been a regular part of the services it offers to central banks since the bank’s establishment 90 years ago. The first annual report of the BIS explains these activities in some detail:

http://www.bis.org/publ/arpdf/archive/ar1931_en.pdf

A June 2008 presentation made by the BIS to potential central bank members at its headquarters in Basel, Switzerland, noted that the bank’s services to its members include secret interventions in the gold and foreign exchange markets:

The use of gold swaps to take gold held by commercial banks and then deposit it in gold sight accounts held in the name of the BIS at major central banks doesn’t appear ever to have been as large a part of the BIS’ gold banking business as it has been in recent years, although the recent declines suggest this may be changing.

As of March 31, 2010, excluding gold owned by the BIS, there were 1,706 tonnes held in the name of the BIS in gold sight accounts at major central banks, of which 346 tonnes or 20% were sourced from gold swaps from commercial banks.

If the BIS was adopting the level of disclosure made by publicly held companies, such as commercial banks, some explanation of these changes probably would have been required by the accounting regulators. This irony may not be lost on those dealing with regulatory activities at the BIS. Presumably the shrinkage of the BIS’ gold banking business shows that even central banks now prefer to hold their own gold or hold it in earmarked form — that is, as allocated gold.

Table 2 below highlights recent BIS activity with gold swaps, and despite the recent declines, the recent positions estimated from the BIS monthly statements have regularly been large, especially in early 2022, and the volume of trading has been significant.

Table 2 Year-End BIS Gold Swap Volumes

March 2010: 346 tonnes

March 2011: 409 tonnes

March 2012: 355 tonnes

March 2013: 404 tonnes.

March 2014: 236 tonnes.

March 2015: 47 tonnes.

March 2016: 0 tonnes.

March 2017: 438 tonnes.

March 2018: 361 tonnes.

March 2019: 175 tonnes

March 2020: 326 tonnes

March 2021: 490 tonnes

March 2022: 358 tonnes

March 2023: 77 tonnes

March 2024: 72 tonnes

—–

Robert Lambourne is a retired business executive in the United Kingdom who consults for GATA about the involvement of the Bank for International Settlements in the gold market and about U.S. government debt.

END

4. OTHER GOLD COMMENTARIES/

END

LIVE FROM THE VAULT/ANDREW MAGUIRE KINESIS 202

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES: beef

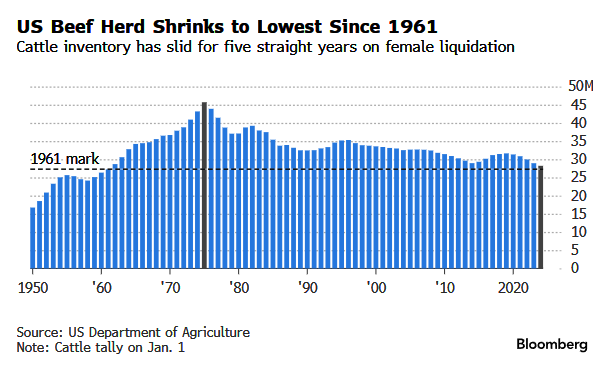

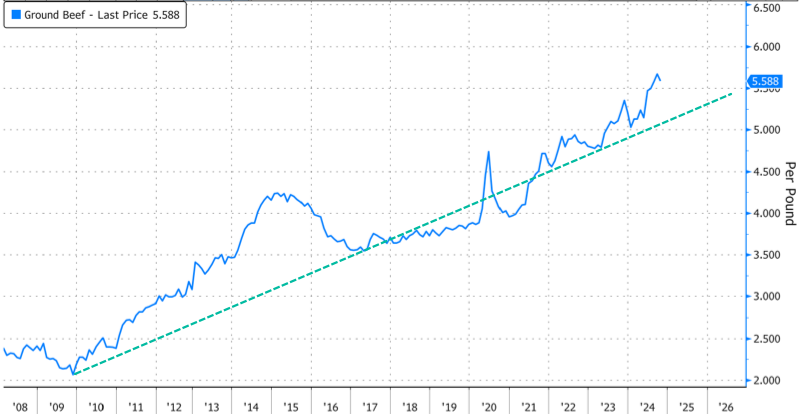

US Cattle Crisis Worsens As Nation’s Herd Size Continues Alarming Side Into Abyss

Tuesday, Dec 10, 2024 – 09:20 PM

America’s beef cow inventory has steadily declined over the last half-decade, reaching 64-year lows and signaling a deepening crisis across the cattle industry. As the cattle crisis worsens, consumers should brace for higher ground beef prices.

The shrinking beef supply has pushed the nation’s herd size to its smallest level since 1961. With severe droughts, high interest rates, costly feed prices, sliding farm income, surging farm debt, and a shifting consumer preference toward cheaper chicken, struggling ranchers have been culling heifers, preventing any meaningful recovery in the number of calves necessary to expand the nation’s herds.

As Bloomberg reports, the nation’s cattle crisis is set to worsen with new pressures: first, President-elect Trump’s anticipated tariff war 2.0, which is expected to tighten domestic beef supplies, and second, immigration reform.

“All of the things he is talking about have potentially negative consequences more so than anything positive,” Derrell Peel, a professor of agricultural economics at Oklahoma State University, told Bloomberg, adding, “Our fate’s pretty well determined in the cattle industry in the U.S. for the next two to four years” – and it’s not looking good.”

In February, the United States Department of Agriculture projected that the cattle herd could begin rebuilding by 2025. However, that timeline has since shifted to 2027. The reason is primarily because of high interest rates and poor pasture conditions in the Midwest.

“Even as the beef industry has experienced periods of growth over the past decades, the animal count has dropped almost 40% since a peak in 1975. During the current downcycle, which started in 2020, the herd has been shrinking at the fastest pace since the big farm crisis of the 1980s,” Bloomberg noted.

If Trump introduces new tariffs, it could disrupt the flow of imported beef, further tightening domestic supplies. However, as Bill Bullard, CEO of R-CALF USA—a group representing cow-calf producers nationwide—explained, this move will drive up beef prices while encouraging investment in rebuilding the nation’s cattle herd.

Bullard said, “Tariffs will provide our industry an opportunity to invest in expansion and to begin rebuilding the herd that has been shrinking at an alarming rate,” adding, “Over the long term, consumers are going to be better served because we will no longer have such a dependency on imported products.”

America’s beef supply relies heavily on small producers raising calves, but with herd levels at half-century lows—combined with new factors like tariffs and immigration reform that could drive prices even higher—consumers need to recognize that food inflation will likely remain sticky through the decade’s end.

Earlier this year, Tyson Foods CEO Donnie King told the BMO Global Farm to Market Conference that he wasn’t even sure when the nation’s collapsing herd size would reverse.

end

COFFEE

Bean Mania: Arabica Coffee Hits New High, Cocoa Jumps To 7-Month High

Tuesday, Dec 10, 2024 – 08:30 PM

Cash-strapped US consumers should be deeply concerned about rising food inflation. It’s ‘stickier’ than ever as coffee and cocoa prices surge.

Arabica coffee futures in New York hit a record high on Tuesday, driven by ongoing fears of a global supply crunch. Prices surged nearly 5% during the session, reaching their highest level in data dating back to 1972. At that time, coffee prices soared due to the disastrous Black Frost, which devastated Brazilian yields.

“Concerns over Brazil’s 2025-26 arabica crop grew this week,” said Steve Pollard, an analyst at Marex Group, as quoted by Bloomberg.

Pollard added, “Recent crop tours point to production in the mid-30 million bags,” which would result in yet another supply shortfall.

Major agricultural trader Volcafe Ltd. recently slashed Brazil’s arabica production outlook due to severe drought conditions. The trader projected that South America would produce just 34.4 million bags of arabica coffee in the next growing season, down 11 million bags from the prior September estimate, according to Bloomberg.

Volcafe also forecasted a global coffee production shortfall of 8.5 million bags for the 2025-26 season, marking the fifth consecutive year of deficits.

“We are currently experiencing a strong fundamental phase in the coffee market, which we expect to sustain the elevated price levels,” said Viktoria Kuszak, a research associate at Sucden Financial.

In the cocoa market, the most active contract in New York jumped to the highest level in seven months over West Africa’s dismal production outlook, yet another crop experiencing dwindling global supplies.

The most-active cocoa contract has jumped 58% to $10,500 per metric ton since late October, the highest since June. This comes as adverse weather dents supplies from top growers in Ivory Coast and Ghana.