GOLD PRICE DOWN $6.85 TO $2646.40

SILVER PRICE DOWN $0.12 TO $30.46

Gold ACCESS CLOSED $2644.00

Silver ACCESS CLOSED: $30.50

Bitcoin morning price:$106,870 UP 740 DOLLARS.

Bitcoin: afternoon price: $106,670 UP 540 DOLLARS

Platinum price closing UP $1.30 TO $940.55

Palladium price; DOWN $7.10 TO $937.95

END

*CANADIAN GOLD: $3784.21 UP 6,82 CDN dollars per oz( * NEW ALL TIME HIGH 3,872.51 CDN DOLLARS PER OZ//OCT 30 2024)

*BRITISH GOLD: 2080.94 DOWN 8.86 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///2161.00 BRITISH POUNDS/OZ) NOV 22/2024

*EURO GOLD: 2,521.20 DOWN 2.08 Euros per oz //* (ALL TIME CLOSING HIGH: 2600.25 EUROS PER OZ//NOV 22 //.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE;

EXCHANGE: COMEX

CONTRACT: DECEMBER 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,651.400000000 USD

INTENT DATE: 12/16/2024 DELIVERY DATE: 12/18/2024

FIRM ORG FIRM NAME ISSUED STOPPED

072 H GOLDMAN 88 563

118 C MACQUARIE FUT 6

190 H BMO CAPITAL 247

363 H WELLS FARGO SEC 77

365 C MAREX CAPITAL M 1

435 H SCOTIA CAPITAL 42

555 H BNP PARIBAS SEC 1

624 H BOFA SECURITIES 46

657 H MORGAN STANLEY 566

661 C JP MORGAN 193 95

661 H JP MORGAN 1

686 C STONEX FINANCIA 34 38

690 C ABN AMRO 1

737 C ADVANTAGE 1 3

880 H CITIGROUP 1

TOTAL: 1,002 1,002

JPMorgan stopped 96/1002

GOLD: NUMBER OF NOTICES FILED FOR DEC/2024. CONTRACT: 1002 NOTICES FOR 100,200 OZ 3.117 TONNES

total notices so far: 23,161 contracts for 2,316,100 Oz (72.040 tonnes)

FOR DEC

SILVER NOTICES: 9 NOTICE(S) FILED FOR 0.045 MILLION OZ/

total number of notices filed so far this month : 8522 for 42.610 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $6.85 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A DEPOSIT OF 0.29 TONNES OF GOLD INOT THE GLD

INVENTORY RESTS AT 864.19 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $0.12 AT THE SLV

SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 0.456 MILLION OZ OUT OF THE SLV/.

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 458.508 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI SHOCKINGLY FELL BY A HUMONGOUS SIZED 1918 CONTRACTS TO 147,750 AND STALLING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR ZERO GAIN OF $0,00 IN SILVER PRICING AT THE COMEX WITH RESPECT TO MONDAY’S TRADING. WE HAD A HUMONGOUS LOSS OF 1719 TOTAL CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR ZERO GAIN IN PRICE//MONDAY’S TRADING.. WE HAD HUGE LIQUIDATION OF T.A.S. CONTRACTS ON MONDAY COMEX TRADING AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 2 WEEKS. THE RAID WAS CALLED UPON AGAIN TO QUELL MASSIVE DERIVATIVE LOSSES BY OUR BULLION BANKS. THEY FAILED //MONDAY SO THEY TRIED AGAIN TUESDAY.

WE HAD A FAIR 210 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY A STRONG 497 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN TUESDAY;S TRADING AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE LOST A HUMONGOUS SIZED 1708 CONTRACTS ON OUR TWO EXCHANGES WITH OUR ZERO GAIN IN PRICE. WE HAD A HUGE TAS LIQUIDATION THROUGHOUT MONDAY’S COMEX SESSION. LAST MONDAY MORNING WE RECEIVED NOTICE OF .5000 MILLION OZ ISSUANCE OF EXCHANGE FOR RISK/ THIS WILL BE ADDED TO THE PREVIOUS EXCHANGE FOR RISK ISSUANCE OF .66 MILLION OZ/NEW EXCHANGE FOR RISK TOTALS FOR THE MONTH: 1.16 MILLION OZ.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN YESTERDAY.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: A HUGE 497 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS BUT TO NO AVAIL TODAY. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER FLAT (IT FELL BY $0.00) BUT WERE SUCCESSFUL IN KNOCKING OFF APPRECIABLE NET SILVER LONGS FROM THEIR PERCH AS WE HAD A HUMONGOUS LOSS IN OI ON OUR TWO EXCHANGES OF 1719 OI. CONTRACTS.

WE HAD A FAIR 210 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 40.435 MILLION OZ (FIRST DAY NOTICE) TO WHICH WE MUST ADD THOSE STUPID “DELIVERIES” CALLED EXCHANGE FOR RISK , TOTALLING 1.16 MILLION OZ. WE ALSO HAD A HUGE 23 CONTRACT QUEUE JUMP FOR 0.115 MILLION OZ AS THESE BOYS WILL TRY THEIR LUCK IN TAKING DELIVERY OVER ON THIS SIDE OF THE PLANET.

// STANDING FOR SILVER//DEC INCREASES TO 43.750 MILLION OZ + .1.16 MILLION OZ EX FOR RISK = 44.910 MILLION OZ

WE HAD:

/ HUMONGOUS SIZED COMEX OI LOSS +// HUGE SIZED EFP ISSUANCE/ VI)MEGA STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 497 CONTRACTS)/ TO WHICH WE ADD 1.16 MILLION OZ EX. FOR RISK //

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 569 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS NOV. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF DEC

TOTAL CONTRACTS for 12 DAYS, total 23,375 contracts: OR 116.875 MILLION OZ (1948 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 116.875 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 116.875 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE/ MAY EXCEED MARCH 2022 RECORD OF 209 MILLION OZ)

RESULT: WE HAD AN HUGE SIZED DECREASE IN COMEX OI SILVER COMEX CONTRACTS OF 1918 CONTRACTS DESPITE OUR ZERO GAIN IN PRICE OF SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A FAIR EFP ISSUANCE CONTRACTS: 210 ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR DEC OF 40.435 MILLION OZ ON FIRST DAY NOTICE, FOLLOWED BY TODAY’S 0.115 MILLION OZ QUEUE JUMP TO WHICH WE ADD 1.16 MILLION OZ OF EXCHANGE FOR RISK/PRIOR EQUALS 44.910 MILLION OZ

//NEW TOTAL STANDING FOR DEC AT 44.910 MILLION OZ

WE HAVE A HUMONGOUS SIZED LOSS OF 1708 OI CONTRACTS ON THE TWO EXCHANGES WITH OUR LOSS IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A HUGE 497 CONTRACTS TRYING DESPERATELY TO CONTAIN SILVER’S PRICE RISE,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION. BUT THEY STILL NEED THESE ISSUANCE FOR REPLENISHMENT FOR FUTURE TRADING /THE STRONG TA.S. ISSUANCE//LIQUIDATION DISTORTS THE TOTAL OI CONTRACTS STANDING AT THE COMEX. FEW NET LONG SPECULATORS WERE BURNED ON MONDAY

/ SOME NET SHORT COVERING FROM OUR SPEC SHORTS DESPITE ZERO LOSS IN PRICE MONDAY/ . ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE MONDAY NIGHT (497) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE, AND CERTAINLY TODAY.

WE HAD 9 NOTICE(S) FILED TODAY FOR 0.045 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A VERY STRONG SIZED 6969 OI CONTRACTS TO 471,098 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A SMALL SIZED 270 CONTRACTS//

WE HAD A STRONG SIZED DECREASE IN COMEX OI (6969 CONTRACTS) OCCURRED DESPITE OUR SMALL LOSS OF $2.80 IN PRICE MONDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A GOOD INITIAL STANDING IN GOLD TONNAGE FOR DEC AT 57.284 TONNES ON FIRST DAY NOTICE. FOLLOWED BY A HUGE 689 CONTRACT QUE JUMP FOR 68,900 OZ ( 2.1430 TONNES). WE MUST NOW ADD 10.6406 TONNES OF EXCHANGE FOR RISK ISSUED ON 5 OCCASIONS IN THIS ACTIVE DECEMBER CONTRACT MONTH.

/NEW STANDING 85.555 TONNES

/ ALL OF THIS HAPPENED WITH OUR SMALL $2.80 LOSS IN PRICE WITH RESPECT TO MONDAY’S COMEX ///. WE HAD A FAIR LOSS OF 2274 OI CONTRACTS (7.07 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! YOU CAN VISUALIZE THIS WITH THE VIOLENT ACTION AT THE COMEX WITH RESPECT TO 689 CONTRACT QUEUE JUMP TODAY (68,900 OZ) ALONG WITH THE 10.6406 EXCHANGE FOR RISK ISSUANCE THIS MONTH //NEW TOTAL TONNES OF DELIVERY: 85.555

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 4695 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 471,368

IN ESSENCE WE HAVE A FAIR SIZED DECREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2274 CONTRACTS WITH 6969 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 4695 EFP OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI LOSS ON THE TWO EXCHANGES OF 2274 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED BUT CRIMINAL 1382 CONTRACTS ISSUED. WE HAD A HUGE LIQUIDATION OF T.A.S CONTRACTS WITH OUR LOSS IN PRICE MONDAY AS THE NEED FOR REPLENISHMENT WAS STILL IN ORDER TO CARRY OUT ITS PRICE CONTAINMENT STRATEGY IN FUTURE TRADING.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (4695 CONTRACTS) ACCOMPANYING THE STRONG SIZED DECREASE IN COMEX OI OF 6969 CONTRACTS/TOTAL LOSS FOR OUR THE TWO EXCHANGES: 2274 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR DEC 55.117 TONNES FOLLOWED BY TODAY.S HJUGE 68,900 OZ QUEUE JUMP TO WHICH WE ADD THOSE CRAZY EXCHANGE FOR RISK ON 5 PRIOR OCCASIONS OF 10.6406 TONNES//NEW STANDING 85.555 TONNES

//NEW STANDING DECEMBER: 85.555 TONNES

/ 3) HUGE T.A.S. LIQUIDATION TRYING TO LOWER GOLD’S PRICE MONDAY WITH SOME SUCCESS AS WE HAD A $2.80 PRICE LOSS. WE HAD SOME NET LONG SPECS BEING CLIPPED AS WE HAD A SMALL LOSS IN OI ON OUR TWO EXCHANGES. HOWEVER, STICKY GOLD’S LONGS ARE NOT FOOLED BY THE RAID IN PRICE AS THEY WERE REWARDED MONDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL.

4) STRONG SIZED COMEX OPEN INTEREST DECREASE 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1382 T.A.S.CONTRACTS///689 CONTRACT QUEUE JUMP OR AN ADDITIONAL 68,900 OZ WILL STAND FOR DELIVERY AT THE COMEX.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

DEC

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC :

TOTAL EFP CONTRACTS ISSUED: 83,465 CONTRACTS OF 8,346,500 OZ OR 259.61 TONNES IN 12 TRADING DAY(S) AND THUS AVERAGING: 6955 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 12 TRADING DAY(S) IN TONNES 259.61 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 259.61 DIVIDED BY 3550 x 100% TONNES = 7.32% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 259.61 TONNES (we will also have a humdinger of an ex for physical issuance for this month/maybe this time we will surpass March 2022 record of 409 tonnes for the month)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER FELL BY A HUGE SIZED 1918 CONTRACTS OI TO 147,750 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 210 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 210 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 500 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI LOSS OF 1918 CONTRACTS AND ADD TO THE 210 E.FP. ISSUED

WE OBTAIN A HUGE SIZED LOSS OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1708 CONTRACTS

THUS IN OUNCES, THE LOSS ON THE TWO EXCHANGES TOTALS A HUGE 8.540 MILLION OZ OCCURRED DESPITE OUR $0.00 LOSS IN PRICE

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS/TUESDAY MORNING MONDAY NIGHT

ASIA TRADING TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED DOWN 24.85 PTS OR 0.783%

//Hang Seng CLOSED DOWN 95.01 PTS OR 0.48%

// Nikkei CLOSED DOWN 92.81 OR 0.24%//Australia’s all ordinaries CLOSED UP .76%///Chinese yuan (ONSHORE) CLOSED UP TO 7.2880 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2880// Oil DOWN TO 69.83 dollars per barrel for WTI and BRENT UP AT 73.04 Stocks in Europe OPENED ALL MOSTLY RED

ONSHORE USA/ YUAN TRADING AT LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A STRONG SIZED 6969 CONTRACTS TO 471,098 WITH OUR SMALL LOSS IN PRICE OF $2.80 WITH RESPECT TO MONDAY’S TRADING. , WE LOST SOME NET LONGS WITH OUR PRICE LOSS FOR GOLD. WE HAD, AS YOU WILL SEE BELOW A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (4695). THUS WE HAD A FAIR LOSS ON OUR TWO EXCHANGES OF 2274 CONTRACTS WITH OUR LOSS IN PRICE. OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOHER FIELD DAY AGAIN ON MONDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED RAID AS THEY ABSORBED FULLY THE MONDAY ATTACK AND OFFERED A THANK YOU NOTE TO THE FED FOR THEIR WONDERFUL LARGESSE. THE LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY THIS ENTIRE PAST WEEK. WE HAD A HUGE T.A.S. LIQUIDATION ON MONDAY.

THE FED IS THE MAJOR SHORT OF AROUND 82+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS IS SCHEDULED TO HAPPEN LATE OCT 2024/(AS OUTLINED IN OUR GOLD PHYSICAL COMMENTARIES//VIEW ANDREW MAGUIRE LATEST LIVE FROM VAULT PODCAST 197 , 199, 2001,AND FRIDAY NIGHTS 202, AND 203 AS HE TACKLES THIS IMPORTANT TOPIC). THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST TWO MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY! ACTUALLY THE FED HAS COAXED THE SPECULATORS TO GO MASSIVELY SHORT WHILE THEY TAKE THE LONG SIDE AFTER THEY COMMENCE THE AVALANCHE IN LOWERING THE PRICE OF GOLD LIKE THESE PAST THREE DAYS OF RAIDS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD CONSIDERABLE T.A.S. LIQUIDATION THROUGHOUT LAST WEEK’S TRADING CONTINUING ON THIS WEEK.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF THE SPREADERS // T.A.S DURING LAST WEEK IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW DEEP INTO THE ACTIVE DELIVERY MONTH OF DECEMBER.… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 4695 EFP CONTRACTS WERE ISSUED: : /DEC 4695 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 4695 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE LOST THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2274 CONTRACTS IN THAT 4695 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A STRONG LOSS OF 6969 COMEX CONTRACTS..AND THIS STRONG LOSS ON OUR TWO EXCHANGES HAPPENED WITH OUR SMALL LOSS IN PRICE OF $2.80 MONDAY// COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT WAS A FAIR SIZED SIZED 1382 CONTRACTS, AND THESE WILL BE USED TO REPLENISH SUPPLIES.. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK).

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON MONDAY NOV 25, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION (COUPLED WITH THE LIQUIDATION OF CALENDAR SPREADERS ). THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE NOVEMBER’S OPTIONS EXPIRY TRADING. WE HAD CONTINUAL T.A.S. AND FINAL MONTH END SPREADER LIQUIDATION ESPECIALLY ON FRIDAY NOV 29 .THE LIQUIDATION OF T.A.S. SUBSIDED QUITE DRAMATICALLY DURING THE FIRST WEEK AND A HALF OF DECEMBER BUT THAT DRAMATICALLY CHANGED WITH CONSIDERABLE LIQUIDATION YESTERDAY WITH MONDAY’S COMEX RAID AND IT CONTINUED ON WITH TODAY’S TRADING AS WELL.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: DEC (85.555 TONNES) WHICH IS HUGE FOR OUR ACTIVE DEC DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 74.4914 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 10.6406 TONNES EQUALS 85.555 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $2.80/)//AND WERE SUCCESSFUL IN KNOCKING OFF SOME NET SPECULATOR LONGS AS WE DID HAVE A LOSS IN OUR TWO EXCHANGES. AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION MONDAY. WE ALSO HAD A FAIR T.A.S. ISSUANCE MONDAY NIGHT (TUESDAY MORNING), AS THE NEED FOR REPLENISHMENT WAS STILL EVER PRESENT. THIS COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING.

17 DAYS AGO, FRIDAY NIGHT (EARLY SATURDAY MORNING NOV 30) THE CME ANNOUNCED ANOTHER OF THOSE CRAZY DELIVERIES: THE ISSUANCE OF 250 EXCHANGE FOR RISK CONTRACTS WHICH TOTAL 25000 OZ (.7776 TONNES. HERE THE BUYER ASSUMES THE RISK THAT HE WILL BE DELIVERED UPON IN PHYSICAL METAL. THIS IS ABSOLUTELY INSANE AND A HUGE VIOLATION OF THE TRUE DISCOVERY PRICE MECHANISM WHICH IS THE COMEX MANTRA!. AND THEN GUESS WHAT? THE CME ANNOUNCED ANOTHER EXCHANGE FOR RISK, LATE TUESDAY EVENING/ EARLY WEDNESDAY MORNING, (DEC 5) OF 617 CONTRACTS FOR 61,700 OZ OR GOLD (1.919 TONNES). THEN MUCH TO MY ANGER, THE CME ANNOUNCED A THIRD ISSUANCE FRIDAY NIGHT DEC 7 FOR A MONSTROUS 2254 EXCHANGE FOR RISK CONTRACTS OR 225,400 OZ OR 7.0108 TONNES. NOT TO BE UNDONE, THE CROOKS CONTINUED WITH THEIR NONSENSE WITH ANOTHER 50 CONTRACT EXCHANGE FOR RISK THE MORNING OF DEC 12 FOR 5000 OZ OR .1555 TONNES. AND THIS BRINGS US TO THIS EARLY FRIDAY MORNING WHERE I WAS SHOCKED TO SEE FOR THE FIFTH TIME THIS MONTH AN ENTRY FOR 250 CONTRACTS OF EXCHANGE FOR RISK FOR 25000 OZ OR .7776 TONNES.THUS ALL FIVE OF THESE ISSUANCES WILL BE ADDED TO THE TOTAL GOLD BEING “DELIVERED UPON”. TOTAL EXCHANGE FOR RISK ISSUANCES FOR THE MONTH NOW TOTALS 10.6406 TONNES. NO EXCHANGE FOR RISK WAS ISSUED EARLY TUESDAY MORNING.

WE HAVE LOST A TOTAL OF 6.233 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR DEC (55.167TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 68900 OZ OR 2.1430 TONNES, TO WHICH WE MUST ADD OUR 5 ISSUANCES OF EXCHANGE FOR RISK FOR A TOTAL OF 10.6406 TONNES. THUS TAKEN TOGETHER,, THE TOTAL GOLD STANDING FOR THIS VERY ACTIVE DELIVERY MONTH OF DECEMBER IS:

74.4914 TONNES (NORMAL DELIVERY) +

10.6406 TONNES (EX FOR RISK)

EQUALS: 85.555 TONNES

/ STANDING FOR DEC INCREASES TO 85.555 TONNES

NEW STANDING FOR DECEMBER: 85.555 TONNES (WHICH IS HUGE FOR OUR VERY ACTIVE DELIVERY MONTH)

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $2.80

WE HAD 85 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET LOSS ON THE TWO EXCHANGES 2274 CONTRACTS OR 227,400 (7.07 TONNES)

confirmed volume MONDAY 127,573 contracts: very weak //// T.A.S. ENHANCED TO A MUCH GREATER EXTENT.

//speculators have left the gold arena

END

/ /// THE DEC 2024 GOLD CONTRACT

DEC 17

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | nil . |

| Deposit to the Dealer Inventory in oz | 54,592.398 OZ brinks 1498 kilobars |

| Deposits to the Customer Inventory, in oz | 144,429.292 OZ a)BRINKS 9709.602 oz 302kilobars b) HSBC 64,302.000 2000 kilobars c) Manfra 70,410.690 0z 2190 kilobars 4492 kilobars |

| No of oz served (contracts) today | 1002 notice(s) 100,200 OZ 3.117 TONNES |

| No of oz to be served (notices) | 788 contracts 78,800 OZ 2.4510 TONNES |

| Total monthly oz gold served (contracts) so far this month | 23,161 notices 2,316,100 oz 72.040 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

dealer deposits: 1

into dealer Brinks: 54,592.396 oz (1698 kilobars)

total dealer deposits: 54,592.398 oz

we have 3 customer deposit

i) Into BRINKS 9709.602 oz (302 kilobars)

ii) Into Manfra: 70,410.690 oz (2190 kilobars)

iii) Into HSBC 64,302.000 oz (2,000 kilobars)

total deposits 144,422.292 oz 4492 kilobars

strictly a paper gold entry.

withdrawals: 0

i

TOTAL WITHDRAWALS: oz

adjustments: 2

a) out of JPMorgan: customer to dealer: 178,443.103 oz

b) out of Loomis 482.265 oz 15 kilobars dealer to customer

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR DEC.

For the front month of DEC: we have an oi of 1790 contracts having GAINED 120 contracts. We had A HUGE 569 contracts served on MONDAY, so we GAINED a HUGE 689 contracts or 68,900 oz (2.1430 TONNES) underwent a MASSIVE queue jump bolting ahead of others to take delivery of gold over on this side of the planet.

JANUARY GAINED 429 CONTRACTS TO STAND AT 4072

FEBRUARY LOST 6288 CONTRACTS TO 350,681 .

We had 1002 contracts filed for today representing 100,200 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 193 notices issued from their client or customer account. The total of all issuance by all participants equate to 1002 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 96 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for DEC /2024. contract month, we take the total number of notices filed so far for the month (23,161 x 100 oz ) to which we add the difference between the open interest for the front month of DEC(1790 CONTRACTS) minus the number of notices served upon today (1002 x 100 oz per contract( equals 2,394,900 OZ OR 74.4914 TONNES. to which we add 10.6406 tonnes of exchange for risk WHICH EQUALS 85.555 TONNES

thus the INITIAL standings for gold for the DEC contract month: No of notices filed so far (23,161 x 100 oz +we add the difference for front month of DEC (1790 OI} minus the number of notices served upon today (1002 x 100 oz which equals 2,394,000 oz (74.4914 TONNES) + 10.6406 tonnes of ex. for risk MONTH OF DEC //new total GOLD STANDING 85.555 TONNES

TOTAL COMEX GOLD STANDING FOR DEC.: 85.555 TONNES WHICH IS HUGE FOR THIS ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 1,891,343.356 oz 58.83 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 18,675,121.278 OZ

TOTAL REGISTERED GOLD 8,545,350.934/// 265.79 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,328,785.036 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,654,007 oz (REG GOLD- PLEDGED GOLD)= 206.96 tonnes //

JPMorgan enhanced inventory is 3.592 million oz/1,877,000 oz = 19.15% of entire inventory..

END

SILVER/COMEX

DEC 17. 2024

INITIAL

//2024// THE DEC 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | nil OZ . |

| Deposits to the Dealer Inventory | nil |

| Deposits to the Customer Inventory | 1,098,638.045 oz Brinks Manfra |

| No of oz served today (contracts) | 13 CONTRACT(S) (65,000 OZ) |

| No of oz to be served (notices) | 228 contracts (1.140 MILLION oz) |

| Total monthly oz silver served (contracts) | 8522 Contracts (42.610 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit/

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 2 customer deposits

a) Into Brinks 599,163.300 oz

b) Into Manfra: 499,474.745 oz

total customer deposits 1098,637.045 oz

We had 0 withdrawals

total withdrawal nil oz

JPMorgan has a total silver weight: 135.000million oz/310.025million or 43.54%

adjustment 1 added into Brinks eligible inventory 1,201,542.150 oz

TOTAL REGISTERED SILVER: 76.737MILLION OZ//.TOTAL REG + ELIGIBLE. 310/025 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DEC

silver open interest data:

FRONT MONTH OF DEC /2024 OI: 237 OPEN INTEREST FOR A GAIN OF 10 CONTRACTS. WE HAD

13 CONTRACTS ISSUED ON MONDAY SO WE HAD A HUGE 23 CONTRACT OR 115,000 OZ QUEUE JUMP WHERE THESE BOYS WILL TRY THEIR LUCK AND TAKE DELIVERY OF PHYSICAL SILVER OVER HERE.

JANUARY SAW A LOSS OF 45 CONTRACTS DOWN TO 2252

FEBRUARY SAW A GAIN OF 2 CONTRACTS TO STAND AT 184

MARCH SAW A LOSS OF 1710 CONTRACTS DOWN TO 118,969

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 9 for 45,000 oz

CONFIRMED volume; ON MONDAY 37,577 weak// t.a.s. enhanced

To calculate the number of silver ounces that will stand for delivery in DEC we take the total number of notices filed for the month so far at 8522x 5,000 oz = 42.610 MILLION oz

to which we add the difference between the open interest for the front month of DEC (237) and the number of notices served upon today (9)x (5000 oz)

Thus the standings for silver for the DEC 2024 contract month: 8522 Notices served so far) x 5000 oz + OI for the front month of DEC(237) minus number of notices served upon today (9)x 5000 oz equals silver standing for the DEC contract month equating to 43.750 MILLION OZ. + to which we add 1.16 million oz of exchange for risk PRIOR////new total 44.91 MILLION OIOZ

New total standing: 44.910 million oz.

There are 76,737 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS//

DEC 17 WITH GOLD DOWN $6.85 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.23 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 864.19 TONNES

DEC 16 WITH GOLD DOWN $2.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.70 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 863.90 TONNES

DEC 13 WITH GOLD DOWN $24.55 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.78 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 868.60 TONNES

DEC 12 WITH GOLD DOWN $34.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.59 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 873.38 TONNES

DEC 11 WITH GOLD UP $29.75 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: // : .///INVENTORY RESTS AT 870.79 TONNES

DEC 9 WITH GOLD UP $31.10 ON THE DAY; NO CHANGES IN GOLD AT THE GLD. // : .///INVENTORY RESTS AT 871.94 TONNES

DEC 6 WITH GOLD UP $6.60 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD. A WITHDRAWAL OF 1.71 TONNES OF GOLD FROM THE GLD// : .///INVENTORY RESTS AT 871.94 TONNES

DEC 5 WITH GOLD DOWN $26.80 ON THE DAY; NO CHANGES IN GOLD AT THE GLD./ : .///INVENTORY RESTS AT 873.65 TONNES

DEC 4 WITH GOLD UP $6.15 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD./ : .///INVENTORY RESTS AT 873.65 TONNES

DEC 3 WITH GOLD UP $10.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.59 TONNES OF GOLD FROM THE GLD./ : .///INVENTORY RESTS AT 875.96 TONNES

DEC 2 WITH GOLD DOWN $20.20 ON THE DAY; NO CHANGES IN GOLD AT THE GLD : .///INVENTORY RESTS AT 878.55 TONNES

NOV 29 WITH GOLD UP $16.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD : Z WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD . .///INVENTORY RESTS AT 878.55 TONNES

NOV 27 WITH GOLD UP $18.05 ON THE DAY; NO CHANGES IN GOLD AT THE GLD : . .///INVENTORY RESTS AT 879.41 TONNE

NOV 26 WITH GOLD UP $3.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD : A DEPOSIT OF 1.44 TONNES OF GOLDINTO THE GLD. .///INVENTORY RESTS AT 879.41 TONNES

NOV 25 WITH GOLD DOWN $91.60 ON THE DAY; NO CHANGES IN GOLD AT THE GLD :. .///INVENTORY RESTS AT 877.97 TONNES

NOV 21 WITH GOLD UP $23.85 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 3.16 TONNES OF GOLD INTO THE GLD/:. .///INVENTORY RESTS AT 875,39 TONNES

NOV 20 WITH GOLD UP $22.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.58 TONNES OF GOLD INTO THE GLD/:. .///INVENTORY RESTS AT 872.23 TONNES

NOV 19 WITH GOLD UP $13.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/:. .///INVENTORY RESTS AT 871.65 TONNES

NOV 18 WITH GOLD UP $44.20 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.56 TONNES OF GOLD INTO THE GLD/:. .///INVENTORY RESTS AT 869.93 TONNES

NOV 15 WITH GOLD DOWN $1.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.25 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 867.37 TONNES

NOV 14 WITH GOLD DOWN $12.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.91 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 868.62 TONNES

NOV 13 WITH GOLD DOWN $19.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 870.63 TONNES

NOV 12 WITH GOLD DOWN $11.40 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.88 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 871,97 TONNE

NOV 11 WITH GOLD DOWN $75.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.74 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 876.85 TONNES

NOV 8 WITH GOLD DOWN $11.85 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.87 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 883.46 TONNES

NOV 7 WITH GOLD UP $30.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.45 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 883.46 TONNES

NOV 6 WITH GOLD DOWN $72.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 886.91 TONNES

NOV 5 WITH GOLD UP $4.05 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:.// . // .///INVENTORY RESTS AT 888.63 TONNES

GLD INVENTORY: 864.19 TONNES, TONIGHTS TOTAL

SILVER

DEC 17 WITH SILVER DOWN 12 CENTS //SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.456 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 458.052 MILLION OZ

DEC 16 WITH SILVER DOWN 0 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 4.84 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 458.052 MILLION OZ

DEC 13 WITH SILVER DOWN 46 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF .536 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 462.892 MILLION OZ

DEC 12 WITH SILVER DOWN 94 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 5.787 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 463.428 MILLION OZ

DEC 11 WITH SILVER UP 10 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.597 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 469.215 MILLION OZ

DEC 10 WITH SILVER DOWN 8 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 1.868 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 471.812 MILLION OZ

DEC 9 WITH SILVER UP $0.91 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 1.367 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 473.680 MILLION OZ

DEC 6 WITH SILVER DOWN $0.00 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 4.329 MILLION OZ/// //INVENTORY AT SLV RESTS AT 475.047 MILLION OZ

DEC 5 WITH SILVER DOWN $0.23 //NO CHANGES IN SILVER INVENTORY AT THE SLV” /// //INVENTORY AT SLV RESTS AT 470.718 MILLION OZ

DEC 4 WITH SILVER UP 26 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV”: A WITHDRAWAL OF 2.206 MILLION OZ FORM THE SLV. /// //INVENTORY AT SLV RESTS AT 470.718 MILLION OZ

DEC 3 WITH SILVER UP 59 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV /// //INVENTORY AT SLV RESTS AT 472.924 MILLION OZ

DEC 2 WITH SILVER DOWN 19 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV. A WITHDRAWAL OF 1,458,000 OZ FROM THE SLV. /// //INVENTORY AT SLV RESTS AT 472.924 MILLION OZ

NOV 29 WITH SILVER UP 51 CENTS //SMALL CHANGES IN SILVER INVENTORY AT THE SLV. A WITHDRAWAL OF 365,000 OZ FROM THE SLV. /// //INVENTORY AT SLV RESTS AT 474.382 MILLION OZ

NOV 27 WITH SILVER DOWN $0.25 //NO CHANGES IN SILVER INVENTORY AT THE SLV.. /// //INVENTORY AT SLV RESTS AT 474.747 MILLION OZ

NOV 26 WITH SILVER UP $0.10 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:.A WITHDRAWAL OF 1.094 MILLION OZ FROM THE SLV./.. /// //INVENTORY AT SLV RESTS AT 474.747 MILLION OZ

NOV 25 WITH SILVER DOWN $0.96 //NO CHANGES IN SILVER INVENTORY AT THE SLV:. . /// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 22 WITH SILVER UP $0.40 //NO CHANGES IN SILVER INVENTORY AT THE SLV:. . /// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 21 WITH SILVER DOWN $0.06 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.729 MILLION OZ FORM THE SLV. . /// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 20 WITH SILVER DOWN $0.22 //NO CHANGES IN SILVER INVENTORY AT THE SLV: . /// //INVENTORY AT SLV RESTS AT 477.572 MILLION OZ

NOV 19 WITH SILVER UP $0.10 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 5,742,000 OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 477..572 MILLION OZ

NOV 18 WITH SILVER UP $0.68 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 1,277,000 OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 471,830 MILLION OZ

NOV 15 WITH SILVER DOWN $0.09 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 3,100,000 OZ OUT OF THE SLV. /// //INVENTORY AT SLV RESTS AT 471,830 MILLION OZ

NOV 14 WITH SILVER DOWN $0.07 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1,504,000 OZ OUT OF THE SLV. /// //INVENTORY AT SLV RESTS AT 473.653 MILLION OZ

NOV 13 WITH SILVER DOWN $0.16 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1,274,000 OZ OUT OF THE SLV. /// //INVENTORY AT SLV RESTS AT 475.157 MILLION OZ

NOV 12 WITH SILVER UP $0.16 //SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 576,000 OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 476.000 MILLION OZ

NOV 11 WITH SILVER DOWN $0.79 //SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 374,000 OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 477.527 MILLION OZ

NOV 8 WITH SILVER DOWN $0.43 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 2.005 MILLION OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 477.846 MILLION OZ

NOV 7 WITH SILVER UP $0.11 //NO CHANGES IN SILVER INVENTORY AT THE SLV: /// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 6 WITH SILVER DOWN $1.41 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.692 MILLION OZ FROM THE SLV/.//// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 5 WITH SILVER UP 0.18 :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.109 MILLION OZ FROM THE SLV/.//// //INVENTORY AT SLV RESTS AT 479,533 MILLION OZ

CLOSING INVENTORY 458.508 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

2/ Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

Alasdair Macleod

3. CHRIS POWELL AND GATA DISPATCHES

Looks like Barrick picked the wrong jurisdiction to have a gold mine

(Reuters)

Barrick Gold threatens to suspend Mali operations over blocked exports

Submitted by admin on Mon, 2024-12-16 14:03 Section: Daily Dispatches

From Reuters

Monday, December 16, 2024

Barrick Gold will suspend operations in Mali if gold shipments continue to be blocked, the company said today as it struggles to reach agreement with authorities on a new mining code in the West African country.

Conditions at the miner’s Loulo-Gounkoto complex have “deteriorated significantly,” Barrick said, adding that employees have been imprisoned without cause and shipments of bullion have been blocked.

“If shipments remain suspended, Barrick will be compelled to suspend operations, further impacting the viability of this critical economic driver for Mali,” the company said. …

… For the remainder of the report:

end

Assad leaves the 26 tonnes of gold inside Syria

(Reuters)

Assad stole what he could but Reuters says he left Syria’s gold in central bank’s vault

Submitted by admin on Mon, 2024-12-16 16:08 Section: Daily Dispatches

Syria Retains 26 Tons of Gold Reserves After Assad’s Fall, Sources Tell Reuters

By Timour Azhari and Libby George

Reuters

Monday, December 16, 2024

DAMASCUS — The vault of Syria’s central bank holds nearly 26 tons of gold, the same amount it had at the start of the country’s bloody civil war in 2011, even after the chaotic fall of Bashar al-Assad’s despotic regime, four people familiar with the situation told Reuters.

But the country has only a small amount of foreign currency reserves in cash, the same people said.

Syria’s gold reserves stood at 25.8 tons in June 2011, according to the World Gold Council, which cites the Central Bank of Syria as its data source. That is worth $2.2 billion at current market prices, according to Reuters calculations.

But the central bank’s foreign exchange reserves amount to just around $200 million in cash, one of the sources told Reuters, while another said the U.S. dollar reserves were “in the hundreds of millions.”

While not all reserves would be held in cash, the drop is substantial compared with before the war. At the end of 2011 Syria’s central bank reported $14 billion in foreign reserves, according to the International Monetary Fund. In 201, the IMF had estimated Syria’s foreign reserves to stand at $18.5 billion. …

Syria’s new government, led by former rebels, is still taking stock of the country’s assets after Assad fled to Russia on Dec. 8. Looters briefly accessed parts of the central bank, taking Syrian pounds with them, but did not breach the main vault, Reuters reported.

Some of what was stolen was then returned by Syria’s new rulers, Syrian officials told Reuters.

The vault is bomb-proof and requires three keys, each held by a different person, and a combination code to be opened, said one of the sources.

The vault was inspected by members of Syria’s new administration last week, two sources said, days after the rebels took control of the Syrian capital Damascus in a lightning offensive that ended more than 50 years of rule by the Assad family. …

… For the remainder of the report:

* * *

4. OTHER GOLD COMMENTARIES/

END

LIVE FROM THE VAULT/ANDREW MAGUIRE KINESIS 203

youtube.com/watch?v=5hHeh2mnvXg&list=PLE1y8hGSqr8ar1gKUdfqFDK5ygLIlrdmz&index=1

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES: COMMODITY; cattle

6 CRYPTOCURRENCY NEWS

END

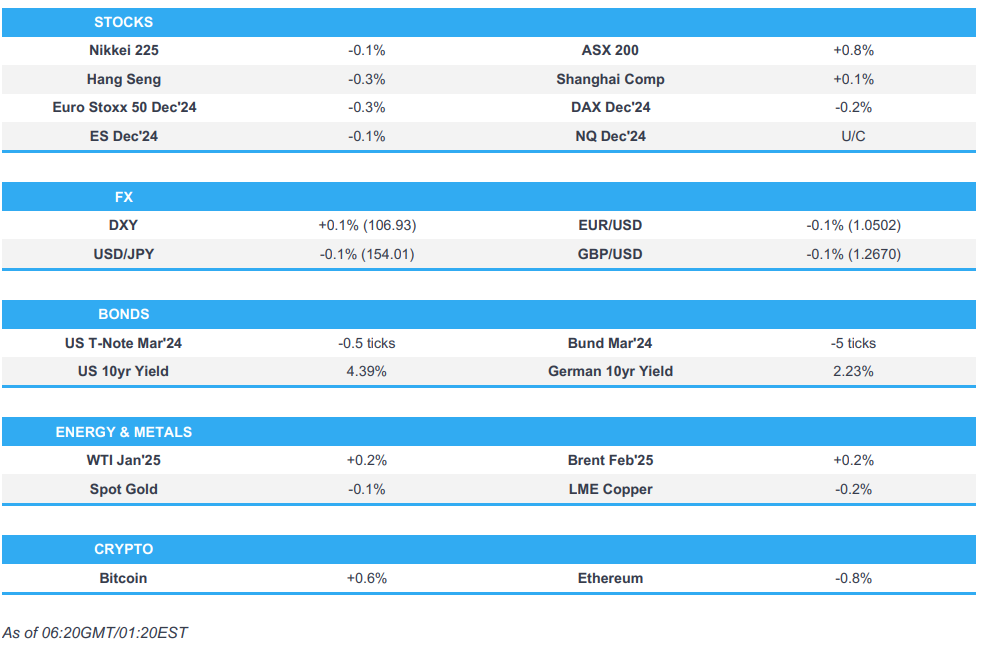

ASIA TRADING TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED DOWN 24.85 PTS OR 0.783%

//Hang Seng CLOSED DOWN 95.01 PTS OR 0.48%

// Nikkei CLOSED DOWN 92.81 OR 0.24%//Australia’s all ordinaries CLOSED UP .76%///Chinese yuan (ONSHORE) CLOSED UP TO 7.2880 CHINESE YUAN OFFSHORE CLOSED UP TO 7.2880// Oil DOWN TO 69.83 dollars per barrel for WTI and BRENT UP AT 73.04 Stocks in Europe OPENED ALL MOSTLY RED

ONSHORE USA/ YUAN TRADING AT LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING STRONGER AGAINST US DOLLAR/OFFSHORE YUAN STRONGER

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED UP AT 7.2880

OFFSHORE YUAN: UP TO 7.2880

SHANGHAI CLOSED CLOSED DOWN 24.45 PTS OR 0.73%

HANG SENG CLOSED CLOSED DOWN 95.01 PTS OR 0.48%

2. Nikkei closed DOWN 92.81 PTS OR 0.24%

3. Europe stocks SO FAR: ALL MOSTLY RED

USA dollar INDEX UP TO 106.67 EURO FALLS TO 1.0492 DOWN 25 BASIS PTS

3b Japan 10 YR bond yield: RISWS TO. +1.075 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 153.88…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold DOWN /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.2460 Italian 10 Yr bond yield UP to 3.419 //SPAIN 10 YR BOND YIELD UP TO 2.943

3i Greek 10 year bond yield UP TO 3.089

3j Gold at $2644.50/Silver at: 30.31 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 85/100 roubles/dollar; ROUBLE AT 102.75

3m oil into the 69 dollar handle for WTI and 73 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 153.88 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.075% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8964 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9410 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.436 UP 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.632 UP 2 BASIS PTS/

USA 2 YR BOND YIELD: 4.282 UP 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 34.99…

10 YR UK BOND YIELD: 4.5695 UP 12 PTS

10 YR CANADA BOND YIELD: 3.214 UP 3 BASIS PTS

5 YR CANADA BOND YIELD: 2.992 UP 2 PTS.

2a New York OPENING REPORT

Futures Drop As Global Selloff Reaches The US

Tuesday, Dec 17, 2024 – 08:26 AM

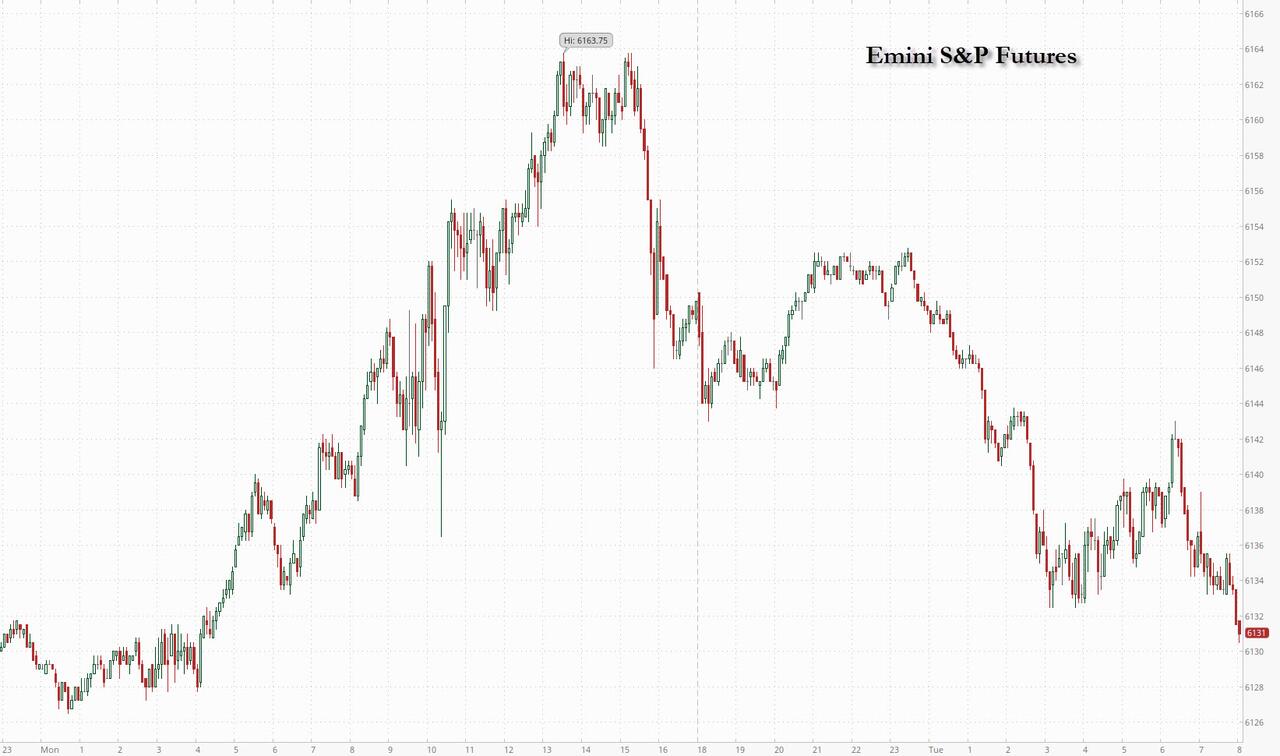

There is only so much the US can “exceptionally” decouple from the rest of the world, and on Tuesday US futures finally succumbed to the persistent selling in markets around the world, as traders awaited the Federal Reserve’s final interest-rate decision for 2024 and its monetary policy forecasts. As of 8:00am, S&P futures dropped 0.3%, while Nasdaq 100 futs eased back 0.2% after the relentless rally in tech stocks pushed the gauge to a fresh all-time high on Monday as AAPL/GOOGL/AMZN/TSLA/AVGO all reached new ATHs. TSLA (+3% pre-mkt) on an u/g away while NVDA (-1.5% pre mkt) continues to be under pressure. Europe’s Stoxx 600 fell 0.4% as weaker crude prices weighed on oil-related stocks (FTSE -70bps/DAX +15bps/CAC +30bps). A key Asian gauge dropped 0.5% after erasing gains as concerns over China’s economy persist (Shanghai -73bps/Hang Seng -48bps/Nikkei -24bps). US rates rose with 10Y TSY yields rising +4bps @ 4.43%. The Bloomberg Dollar Spot Index adds 0.1%. The Aussie dollar is the weakest of the G-10 currencies, losing 0.5%. The yen outperforms with a 0.2% gain. Crude oil extended its drop as WTI dropped 0.8% to $70.15. Meanwhile, Bitcoin adds another +90bps to $107,040 as global equities chop around ahead of a slew of central bank rate decisions the next few days (FOMC tomorrow). There is a busy macro calendar today with retail sales, industrial/mfg production, business inventories and the NAHB housing index all on deck.

In premarket trading, Pfizer rose 2% after the company forecast 2025 sales and earnings in line with analysts’ projections, a step toward fending off an activist investor’s claims that the drugmaker is being mismanaged. Here are some other notable premarket movers:

- Mitek (MITK) rallies 15% after the identity verification software company reported fourth quarter revenue and earnings that beat the average analyst estimate.

- Pacs Group (PACS) slips 3% as JPMorgan issued a downgrade after nursing home operator said it received investigative demands over its reimbursement and referral practices.

- Rockwell Medical (RMTI) climbs 14% after the manufacturer of hemodialysis products entered into a supply pact with a provider of dialysis products and services.

- Shoals Technologies (SHLS) climbs 8% as Morgan Stanley upgraded the renewable energy equipment company to overweight citing increased confidence in the earnings outlook heading into 2025.

- Tesla shares rise as much as 3.4% in premarket trading on Tuesday as Mizuho Securities upgrades to outperform from neutral citing an improved outlook under the new administration.

- Shares in electric-vehicle and charging station companies may be active on Tuesday after Reuters reported that Donald Trump’s transition team plans changes that would redirect funding from EV and charging stations markers to national-defense priorities.

As equity markets head into the final weeks of 2024, US stocks have significantly outperformed their peers for the year as optimism about artificial intelligence and falling rates fuel investor confidence. Traders are now focusing on Wednesday’s Fed announcement, with Chair Jerome Powell widely expected to deliver a quarter-point of easing.

What happens in the following months remains less clear. While the US economy is resilient, the prospect of inflationary import tariffs threatened by the incoming administration of Donald Trump may give Fed officials pause about the pace of further moves. Money markets are seeing an 80% chance of three cuts next year, compared to the small probability of a fourth reduction seen at the start of the month. “There is also the Fed, which stirs some uncertainty,” said Alexandre Baradez, chief market analyst at IG in Paris. “My scenario is for a hawkish cut with a much more cautious narrative.”

Bank of America strategists cautioned that fund managers have been reducing cash holdings to a record low and pouring money into US stocks, triggering a metric that could be a signal to sell global equities. Cash as a percentage of total assets under management fell below 4%, a move that in the past has been followed by stock market losses.

In Europe, the Stoxx 600 fell for a fourth consecutive session, as political upheaval in the region weighs on sentiment, with traders also bracing for Eurozone inflation data and a US rate decision due tomorrow. Technology and automakers are among gainers while energy and telecom sectors lead declines. Here are some of the biggest movers on Tuesday:

- Airbus shares rise as much as 1.9% after Deutsche Bank upgraded the planemaker to buy from hold, saying it is better positioned for 2025 and is trading at a relatively affordable valuation.

- Jungheinrich gains as much as 4.9% after Citi upgrades the intralogistics solutions provider to buy from neutral, saying the stock is too cheap to ignore after prolonged underperformance.

- Goodwin shares rise as much as 18% after the UK mechanical and refractory engineering company reports what Shore Capital describes as “excellent” interim results.

- Thyssenkrupp Nucera shares gain as much as 9.3% after full-year earnings from the German green hydrogen technology firm revealed encouraging developments in the pipeline and funding potential, according to Citi.

- Hollywood Bowl shares drop as much as 11%, their worst day in over four years, after the bowling center operator reported a slide in pretax profit as well as flagging an impact of £1.2 million when UK National Insurance changes are implemented next year.

- Bunzl drops as much as 5.7% after the year-end trading update reports revenue that fell below consensus as Jefferies analyst says the update flags “continued top-line weakness.”

- Capita drops as much as 11% after the outsourcing specialist issued a trading update that showed an 8% adjusted-revenue decline and flagged a further slide in revenue growth next year.

- Chemring shares fall as much as 11% as the British defense firm decided not to renew its share buyback program and said its margin has fallen due to operational challenges.

- JDE Peet’s falls as much as 5% to hit a record low, after Goldman Sachs re-initiated coverage of the Dutch coffee and tea company with a sell rating, noting that a sharp uptick in coffee prices could hit sales, potentially putting at risk its presence in equity indexes.

- UCB shares slip as much as 3.6% after a proof-of-concept study for its experimental drug minzasolmin developed in partnership with Novartis for Parkinson’s disease didn’t meet primary and secondary clinical endpoints.

Earlier in the session, HK/China closed lower despite a midday spike following a Reuters headline that placed China’s 2025 GDP growth and fiscal deficit targets at the upper bound of investor expectations. Small caps caught the most weakness today, suggesting that retail investors are taking a breather after being better buyers over the past few sessions. Meanwhile, Samsung Electronics 00597230 KS caught selling after GIR cut its price targets, while ASIC names in Taiwan were well bid after Broadcom AVGO US rallied again overnight.

- Australia: S&P/ASX 200 +0.78%, snapping a five-day losing streak. The index took cues from Wall Street, where Tech shares delivered strong performance, bolstering sentiment. Investors are bracing for an expected interest rate cut from the US Fed Reserve later this week, with much of the focus shifting to the Fed’s outlook for 2025. Notable performers were Commonwealth Bank CBA AU +1.6%, NA Bank NAB +1.5%.

- Taiwan: TAIEX -0.09%. Market opened higher but gradually lost steam over the day. TSMC 2330 TT retreated 0.9% and is just 3 ticks short of another A-T-H. United Microelectronics Corp UMC + 2.7% after the biggest morning headlines were focused on their reported securing advanced packaging orders from Qualcomm. The ASIC theme was also very strong again, as Broadcom gained another 11% overnight with the local ASIC names benefiting again, including Alchip limit up, GUC 3443 TT +8.8%, and Faraday 3035 TT +5.2%.

- Korea: KOSPI -1.29%. It opened weak and dipped lower further into the afternoon on accelerated foreign outflows with the bulk of the selling coming from program trades which indicated passive, systematic driven selling while locals (institutios, retail) were on the receiving end of the supply. Tech was an underperformer today whereas within semis – Samsung and Hynix saw divergence again while the EV names were notably weaker following potential tariff headwinds.

- Japan: Nikkei 225 -0.23%. Market opened with risk on mode led by momentum trades. Investors preferred popular themes like defense names, AI related names. Investors shifted their positions from cyclicals to defensives, from high vol names to low vol names, value names to growth names. Shares of Advantest 6857 JP tumbled 9.1% as the unveiling of its latest testing solutions for advanced applications. Meanwhile, SoftBank Group 9984 JP +4.3% after CEO Masayoshi Son announced plans to invest $100 bn in the US.

- China: SHSZ300 +0.26% but A-shares in other indices took another leg lower weighed weighed by small and micro cap names. Headlines from Reuters that China GDP growth target set at 5% for next year, and budgeted fiscal deficit 4% hit the tape at noon. Growth target is in line (and deemed aggressive by many; GSe: 4.5%), and fiscal target to the upper bound of expectation. The news spurred a quick spike in the PM session, but tapered soon.

- Hong Kong: HSI -0.22%. Markets saw a sharp spike in PM inline with onshore, but soon faded marking the 3rd straight session of losses as most sectors retreated – particularly property, consumers, and tech. Sluggish activity data for Nov in China continued to weigh on sentiment, with retail sales growth unexpectedly slowing while industrial output rose at a relatively similar pace to October. Notable decliners include Techtronic Inds. 669 HK -2.4%, JD Logistics 2618 HK -1.58%, Wuxi Biologics 2269 HK -2.66%.

In FX, Bloomberg’s dollar gauge was little changed. An index of Asian currencies fell to the lowest in more than two years amid pessimism over China’s economic outlook and expectations that Trump policies will drive gains in the greenback. The yen snapped a six-day losing streak after weakening beyond the 154 level versus the dollar overnight. The yen’s rapid decline in the past week had strategists warning that further weakness may trigger verbal intervention from authorities and add pressure on the Bank of Japan to hike rates. Traders are pricing in a less than 20% chance of a rate hike in December, according to swaps market pricing. The pound erased a small loss while gilt yields rose as traders scaled back bets on Bank of England rate cuts after UK wage growth accelerated for the first time in more than year. The implied chance of three quarter-point cuts in 2025 fell to around 55%, down from 90% before the report. The yuan was little changed in both onshore and overseas trading, as markets shrugged off news that Chinese leaders were planning to set an annual growth goal of about 5% for next year and raise the budget deficit.

In rates, yields on US Treasuries advanced across the curve, with the US 10-year yield rising 3bps to 4.432%, cheapest since Nov. 21. UK government bonds fall as traders pare bets on interest-rate cuts by the Bank of England after UK wage growth accelerated for the first time in more than a year. UK 10-year yields rise 6 bps to 4.50% although the pound has given back its earlier advance versus the dollar. OIS swaps price in about 60bps of easing through December 2025 vs around 75bp at Monday’s close. The US Treasury sells $13 billion of 20-year bonds in a reopening at 1pm New York time; WI yield near 4.72% is ~4bp cheaper than November’s new-issue sale, which tailed by 1.5bp.

The 10Y yield may climb to 6% as US fiscal woes worsen and Trump’s policies help keep inflation elevated, according to T. Rowe Price. “Is a 6% 10‑year Treasury yield possible? Why not? But we can consider that when we move through 5%,” Arif Husain, chief investment officer of fixed-income, wrote in a report. “The transition period in US politics is an opportunity to position for increasing longer‑term Treasury yields and a steeper yield curve.”

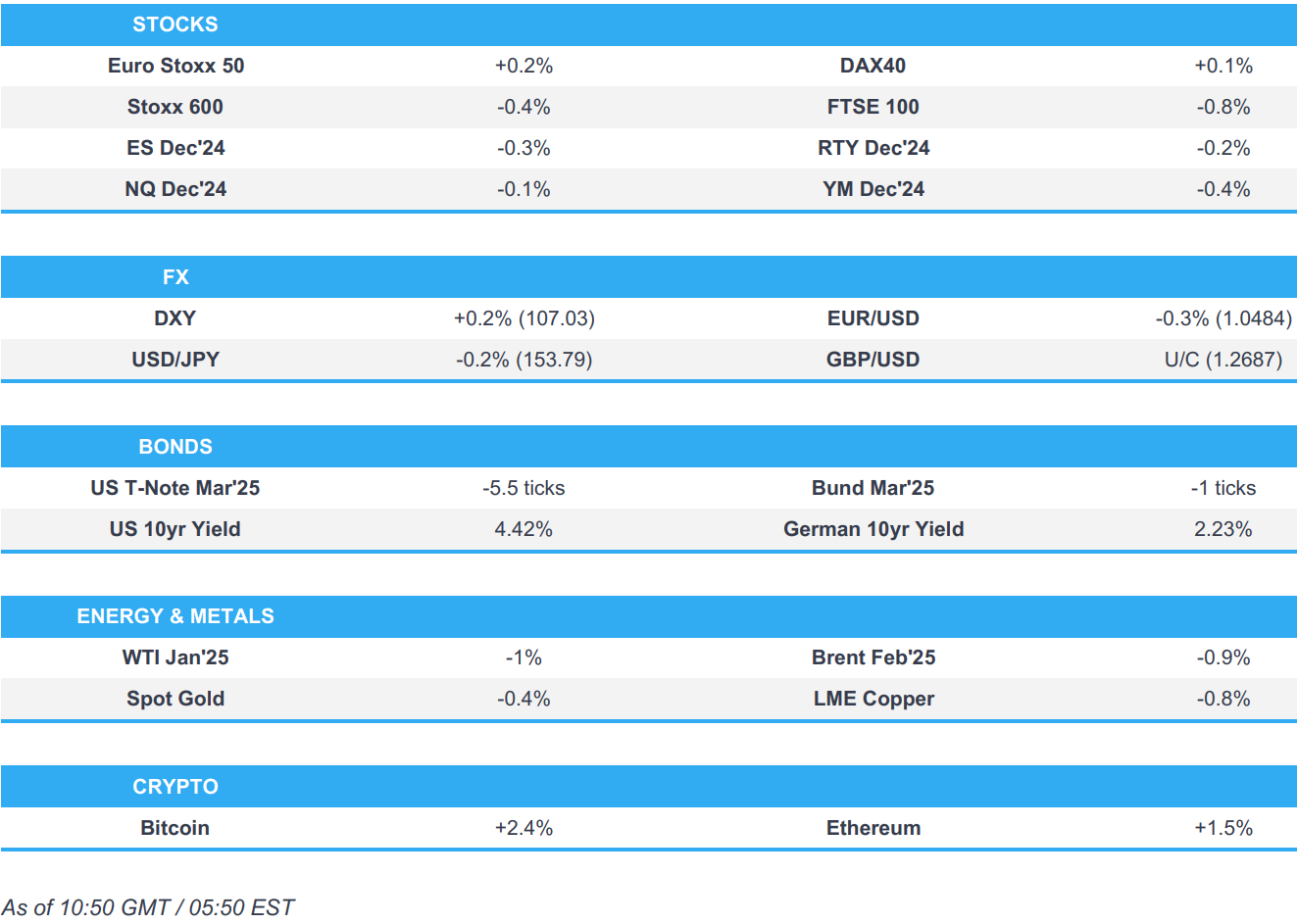

In commodities, oil prices dropped with WTI falling 1% to $70 a barrel. Spot gold drops $11 to around $2,641/oz.

The US economic data calendar includes November retail sales and December New York Fed services business activity (8:30am), November industrial production (9:15am), and October business inventories and December NAHB housing market index (10am)

Market Snapshot

- S&P 500 futures down 0.3% to 6,062.00

- STOXX Europe 600 down 0.4% to 513.83

- MXAP down 0.5% to 183.86

- MXAPJ down 0.6% to 579.67

- Nikkei down 0.2% to 39,364.68

- Topix down 0.4% to 2,728.20

- Hang Seng Index down 0.5% to 19,700.48

- Shanghai Composite down 0.7% to 3,361.49

- Sensex down 1.2% to 80,747.70

- Australia S&P/ASX 200 up 0.8% to 8,314.00

- Kospi down 1.3% to 2,456.81

- German 10Y yield down 2 bps at 2.23%

- Euro down 0.3% to $1.0482

- Brent Futures down 0.6% to $73.47/bbl

- Brent Futures down 0.6% to $73.47/bbl

- Gold spot down 0.4% to $2,641.97

- US Dollar Index up 0.18% to 107.05

Top Overnight News

- China suffered the biggest outflow on record from its financial markets last month as the prospect of higher US tariffs posed more risks for the world’s second-largest economy. Domestic banks wired a net $45.7 billion of funds overseas on behalf of their clients for securities investment. BBG

- China will keep its growth target of about 5% next year and agreed to increase its fiscal deficit target to 4% of GDP in 2025, up 1% from 2024’s 3% goal and consistent with the recent pledge to adopt a more proactive fiscal policy. RTRS

- BABA (Alibaba) to book a $1B loss on the sale of its department-store chain Intime. WSJ

- Ukraine said it killed a senior Russian general in a Moscow bombing after a device planted in a scooter exploded early Tuesday, a rare targeted assassination of a high-profile military official in the capital. Ukraine accuses the general of committing chemical weapons crimes. WSJ

- The White House reiterated its position that it’s up to Volodymyr Zelenskiy to choose the timing and terms of talks with Russia, after Trump said Kyiv must make a deal to end the war. BBG

- Senior U.S. officials say Turkey and its militia allies are building up forces along the border with Syria, raising alarm that Ankara is preparing for a large-scale incursion into territory held by American-backed Syrian Kurds

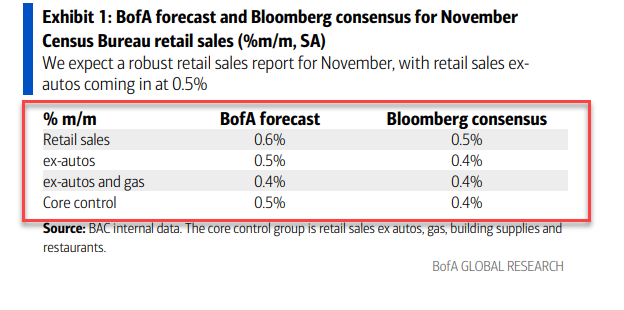

- US retail sales are expected to rise 0.6% in November, compared with 0.4% the prior month, as companies lured bargain-hunters with discounts and tariff-wary shoppers pulled forward big-ticket purchases. BBG

- Fund managers have been reducing cash holdings to a record low and pouring money into US stocks. Cash as a percentage of total AUM fell below 4%, a move that in the past has been followed by losses. BBG

- Ten-year Treasury yields may climb to 6% for the first time since 2000 on Donald Trump’s inflationary policies. The benchmark may reach 5% in the first quarter. BBG

A more detailed look at global markets courtesy of Newsquawk

APAC stocks eventually traded mixed after the region initially showed a positive bias, taking cues from Wall Street, and in the absence of macro newsflow with looming risk events. ASX 200 firmed with banks underpinning the index, with Westpac among the gainers while its CFO announced plans to retire. Nikkei 225 trimmed earlier upside as traders were cautious ahead of the BoJ, with the decision contingent on the FOMC’s announcement hours beforehand. Hang Seng and Shanghai Comp traded within narrow parameters in uneventful trade amid quiet newsflow, with participants remaining non-committal ahead of major risk events.

Top Asian News

- China is to maintain a growth target of “around 5%” for 2025, according to Reuters sources. China is to target a budget deficit of 4% in 2025 (vs 3% initially). More stimulus will be funded through issuing off-budget special bonds, sources added.

- New Zealand sees 2024/25 operating balance before gains, losses at NZD -17.32 bln (budget NZD -13.37 bln), according to Reuters.

- New Zealand Debt Management Office says 2024/25 gross bond issuance increases to NZD 40 bln from NZD 38 bln in May, according to Reuters.

- Alibaba Group (9988 HK/ BABA) sells Intime; Expected gross proceeds to Alibaba from Intime sale is approximately RMB 7.4bln; Alibaba expects to record losses of approximately RMB 9.3bln as a result of the sale of Intime.

- PBoC injected CNY 355.4 bln via 7-day reverse repos with the rate maintained at 1.50%, according to Reuters.

- South Korean acting President Han says South Korea is to implement the budget on Jan 1st; South Korea to allocate budget promptly for economic revitalisation, according to Reuters.

- Magnitude 7.4 quake has struck Port-Vila in the Vanuatu region, according to USGS.

European bourses began the session entirely in the red and have mostly resided in negative territory throughout the European morning, but have attempted to edge a little higher in recent trade, with some indices managing to climb incrementally into the green. German Ifo data confirmed the dire situation in the region, whilst ZEW surprised to the upside; metrics which sparked little price action. European sectors are almost entirely in the red, given the slip in risk sentiment in today’s session thus far. Tech is marginally in positive territory, alongside Consumer Products and Services. Energy is the clear underperformer joined by Basic Resources, attributed to the losses seen in underlying commodity prices today. US equity futures are modestly in negative territory, in-fitting with the losses seen in Europe and the general risk tone; a slight turn in fortunes in comparison to the gains seen in the prior session.

Top European News

- French Central Bank Forecasts: 2024 Growth seen at 1.1% (unchanged), 2025 seen at 0.9% (prev. 1.2% in Sept.); 2026 at 1.3% (prev. 1.5%), 2027% at 1.3%. HICP inflation 1.6% in 2025, 1.7% in 2026 and 1.9% in 2027.

- ECB’s Rehn says data to decide speed and scale of rate cuts; scale and speed of rate cuts will be determined in each meeting on the basis of incoming data and comprehensive analysis; Euro area inflation starting to stabilise at ECB’s 2% target. Monetary policy will cease to be restrictive in the later winter, early spring period (i.e. between January and June 2025)

- ECB’s Kazimir says inflation risks are well balanced, via Bloomberg. Will discuss the neutral rate when they approach 2.5%.

- ECB keeps capital requirements broadly steady for 2025, reflecting strong bank performance amid heightened geopolitical risks

FX

- DXY is on a firmer footing and topped 107.00 in early European trade, to currently trade at the top-end of a 107.05-106.69 range. Should the upside continue, the Dollar index could see a potential test of the prior day’s best at 107.16, and then 107.18 from Friday 13th December. The North American day sees the release of US retail sales, which are expected to rise +0.5% M/M in November.