GOLD PRICE DOWN $45 TO $2595.00

SILVER PRICE DOWN $0.25 TO $29.02

Gold ACCESS CLOSED $2596.10

Silver ACCESS CLOSED: $29.06

Bitcoin morning price:$103,600 UP 610 DOLLARS.

Bitcoin: afternoon price: $96,839 down 6151 DOLLARS

Platinum price closing DOWN $8.45 TO $924.35

Palladium price; DOWN $20.30 TO $909.50

END

*CANADIAN GOLD: $3736.77 DOWN 10.12 CDN dollars per oz( * NEW ALL TIME HIGH 3,872.51 CDN DOLLARS PER OZ//OCT 30 2024)

*BRITISH GOLD: 2071.12 UP 10.20 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///2161.00 BRITISH POUNDS/OZ) NOV 22/2024

*EURO GOLD: 2,505.20 UP 4.96 Euros per oz //* (ALL TIME CLOSING HIGH: 2600.25 EUROS PER OZ//NOV 22 //.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE;

EXCHANGE: COMEX

CONTRACT: DECEMBER 2024 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,636.500000000 USD

INTENT DATE: 12/18/2024 DELIVERY DATE: 12/20/2024

FIRM ORG FIRM NAME ISSUED STOPPED

072 H GOLDMAN 382

190 H BMO CAPITAL 23

323 C HSBC 21

363 H WELLS FARGO SEC 43

435 H SCOTIA CAPITAL 384

523 H INTERACTIVE BRO 1

624 H BOFA SECURITIES 4

657 C MORGAN STANLEY 8

661 C JP MORGAN 28 11

686 C STONEX FINANCIA 12

905 C ADM 7

TOTAL: 462 462

JPMorgan stopped 11/462

GOLD: NUMBER OF NOTICES FILED FOR DEC/2024. CONTRACT: 462 NOTICES FOR 46,200 OZ 1.4370 TONNES

total notices so far: 24,277 contracts for 2,427,700 Oz (75.511 tonnes)

FOR DEC

SILVER NOTICES: 193 NOTICE(S) FILED FOR 0.965 MILLION OZ/

total number of notices filed so far this month : 8967 for 44.835 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD DOWN $45.00 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

SMALL CHANGES IN GOLD INVENTORY AT THE GLD: A WITHDRAWAL OF .29 TONNES OF GOLD FROM THE GLD//

INVENTORY RESTS AT 863.90 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER DOWN $0.25 AT THE SLV

NO CHANGES IN SILVER INVENTORY AT THE SLV:

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 457.414 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI SURPRISINGLY ROSE BY A FAIR SIZED 401 CONTRACTS TO 147,339 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS HUGE SIZED LOSS IN COMEX OI WAS ACCOMPLISHED DESPITE OUR LOSS OF $0,19 IN SILVER PRICING AT THE COMEX WITH RESPECT TO WEDNESDAY’S TRADING. WE HAD A GOOD GAIN OF 466 TOTAL CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR LOSS IN PRICE//WEDNESDAY’S TRADING.. WE HAD CONSIDERABLE LIQUIDATION OF T.A.S. CONTRACTS ON WEDNESDAY COMEX TRADING AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 2 WEEKS. THE RAID WAS CALLED UPON AGAIN TO QUELL MASSIVE DERIVATIVE LOSSES BY OUR BULLION BANKS. THEY SUCCEEDED QUITE A BIT WITH //WEDNESDAY PRICING BUT FAILED TO KNOCK OFF ANY SPECULATOR LONGS.

WE HAD A SMALL 65 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY A GOOD 361 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN THURSDAY;S TRADING AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A GOOD SIZED 466 CONTRACTS ON OUR TWO EXCHANGES DESPITE OUR LOSS IN PRICE. WE HAD A CONSIDERABLE TAS LIQUIDATION THROUGHOUT WEDNESDAY’S COMEX SESSION AND ACCESS TRADING. LAST MONDAY MORNING WE RECEIVED NOTICE OF .5000 MILLION OZ ISSUANCE OF EXCHANGE FOR RISK/ THIS WILL BE ADDED TO THE PREVIOUS EXCHANGE FOR RISK ISSUANCE OF .66 MILLION OZ/NEW EXCHANGE FOR RISK TOTALS FOR THE MONTH: 1.16 MILLION OZ.

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN YESTERDAY.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON TUESDAY NIGHT: A GOOD 361 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS ESPECIALLY WITH YESTERDAY’S TRADING. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE SUCCESSFUL IN KNOCKING THE PRICE OF SILVER FLAT (IT FELL BY $0.19) BUT WERE BASICALLY UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SILVER LONGS FROM THEIR PERCH AS WE HAD A JUST A GOOD GAIN IN OI ON OUR TWO EXCHANGES OF 438 OI. CONTRACTS.

WE HAD A SMALL 65 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 40.435 MILLION OZ (FIRST DAY NOTICE) TO WHICH WE MUST ADD THOSE STUPID “DELIVERIES” CALLED EXCHANGE FOR RISK , TOTALLING 1.16 MILLION OZ. WE ALSO HAD A HUGE 179 CONTRACT QUEUE JUMP FOR 0.895 MILLION OZ AS THESE BOYS WILL TRY THEIR LUCK IN TAKING DELIVERY OVER ON THIS SIDE OF THE PLANET.

// STANDING FOR SILVER//DEC INCREASES TO 45.135 MILLION OZ + .1.16 MILLION OZ EX FOR RISK = 46.295 MILLION OZ

WE HAD:

/ GOOD SIZED COMEX OI GAIN +// SMALL SIZED EFP ISSUANCE/ VI) GOOD SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 361 CONTRACTS)/ TO WHICH WE ADD 1.16 MILLION OZ EX. FOR RISK //

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: added 28 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS NOV. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF DEC

TOTAL CONTRACTS for 14 DAYS, total 24,165 contracts: OR 120.825 MILLION OZ (1726 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 120.825 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 120.825 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE/ WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ)

RESULT: WE HAD AN GOOD SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 401 CONTRACTS DESPITE OUR LOSS IN PRICE OF SILVER PRICING AT THE COMEX//WEDNESDAY.,. THE CME NOTIFIED US THAT WE HAD A SMALL EFP ISSUANCE CONTRACTS: 65 ISSUED FOR DEC AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR DEC OF 40.435 MILLION OZ ON FIRST DAY NOTICE, FOLLOWED BY TODAY’S 0.895 MILLION OZ QUEUE JUMP TO WHICH WE ADD 1.16 MILLION OZ OF EXCHANGE FOR RISK/PRIOR EQUALS 46.295 MILLION OZ

//NEW TOTAL STANDING FOR DEC AT 46.295 MILLION OZ

WE HAVE A GOOD SIZED GAIN OF 466 OI CONTRACTS ON THE TWO EXCHANGES DESPITE OUR LOSS IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A GOOD 361 CONTRACTS TRYING DESPERATELY TO CONTAIN SILVER’S PRICE RISE,//HUGE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE WEDNESDAY COMEX SESSION + ACCESS. BUT THEY STILL NEED THESE ISSUANCE FOR REPLENISHMENT FOR FUTURE TRADING /THE STRONG TA.S. ISSUANCE//LIQUIDATION DISTORTS THE TOTAL OI CONTRACTS STANDING AT THE COMEX. NO NET LONG SPECULATORS WERE BURNED ON WEDNESDAY

/ LITTLE NET SHORT COVERING FROM OUR SPEC SHORTS WITH OUR LOSS IN PRICE WEDNESDAY/ . ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE WEDNESDAY NIGHT (361) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE, AND CERTAINLY TODAY.

WE HAD 193 NOTICE(S) FILED TODAY FOR 0.965 MILLION OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A GOOD SIZED 4695 OI CONTRACTS TO 461,876 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW MUCH FURTHER FROM OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: REMOVED A SMALL SIZED 376 CONTRACTS//

WE HAD A GOOD SIZED DECREASE IN COMEX OI (4695 CONTRACTS) OCCURRED WITH OUR LOSS OF $8.40 IN PRICE WEDNESDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A GOOD INITIAL STANDING IN GOLD TONNAGE FOR DEC AT 57.284 TONNES ON FIRST DAY NOTICE. FOLLOWED BY A HUGE 407 CONTRACT QUEUE JUMP FOR 40700 OZ ( 1.266 TONNES). WE MUST NOW ADD 10.6406 TONNES OF EXCHANGE FOR RISK ISSUED ON 5 OCCASIONS IN THIS ACTIVE DECEMBER CONTRACT MONTH.

/NEW STANDING 88.3856 TONNES

/ ALL OF THIS HAPPENED WITH OUR $8.40 LOSS IN PRICE WITH RESPECT TO WEDNESDAY’S COMEX ///. WE HAD A SMALL GAIN OF 469 OI CONTRACTS (1.458 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! YOU CAN VISUALIZE THIS WITH THE VIOLENT ACTION AT THE COMEX WITH RESPECT TO 407 CONTRACT QUEUE JUMP TODAY (40,700 OZ) ALONG WITH THE 10.6406 EXCHANGE FOR RISK ISSUANCE THIS MONTH //NEW TOTAL TONNES OF DELIVERY: 88.3856

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A STRONG SIZED 5164 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 461,876

IN ESSENCE WE HAVE A SMALL SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 469 CONTRACTS WITH 4695 CONTRACTS DECREASED AT THE COMEX// AND A STRONG SIZED 5164 EFP OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 469 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A FAIR SIZED BUT CRIMINAL 1163 CONTRACTS ISSUED. WE HAD A STRONG LIQUIDATION OF T.A.S CONTRACTS WITH OUR LOSS IN PRICE WEDNESDAY AS THE NEED FOR REPLENISHMENT WAS STILL IN ORDER TO CARRY OUT ITS PRICE CONTAINMENT STRATEGY IN FUTURE TRADING.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5164 CONTRACTS) ACCOMPANYING THE GOOD SIZED DECREASE IN COMEX OI OF 4695 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 469 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR DEC 55.117 TONNES FOLLOWED BY TODAY.S HJUGE 40,700 OZ QUEUE JUMP TO WHICH WE ADD THOSE CRAZY EXCHANGE FOR RISK ON 5 PRIOR OCCASIONS OF 10.6406 TONNES//NEW STANDING 88.3856 TONNES

//NEW STANDING DECEMBER: 88.3856 TONNES

/ 3) STRONG T.A.S. LIQUIDATION TRYING TO LOWER GOLD’S PRICE WEDNESDAY WITH LITTLE SUCCESS IN REMOVING SPECULATOR LONGS, AS DESPITE OUR $6.85 PRICE LOSS, WE HAD ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A SMALL GAIN IN OI ON OUR TWO EXCHANGES. HOWEVER, STICKY GOLD’S LONGS ARE NOT FOOLED BY THE RAID IN PRICE AS THEY WERE REWARDED WEDNESDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL.

4) GOOD SIZED COMEX OPEN INTEREST DECREASE 5) STRONG ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///FAIR T.A.S. ISSUANCE: 1163 T.A.S.CONTRACTS///407 CONTRACT QUEUE JUMP OR AN ADDITIONAL 40,700 OZ WILL STAND FOR DELIVERY AT THE COMEX.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

DEC

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF DEC :

TOTAL EFP CONTRACTS ISSUED: 96,457 CONTRACTS OF 9,645,700 OZ OR 300.02 TONNES IN 14 TRADING DAY(S) AND THUS AVERAGING: 6889 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 14 TRADING DAY(S) IN TONNES 300.02 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 300.02 DIVIDED BY 3550 x 100% TONNES = 8.45% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 300.02 TONNES (we will also have a humdinger of an exchange for physical issuance for this month/maybe this time we will surpass March 2022 record of 409 tonnes for the month)

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A GOOD SIZED 401 CONTRACTS OI TO 147,339 AND FURTHER FROM THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.2023

EFP ISSUANCE 65 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

DEC 65 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 65 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 401 CONTRACTS AND ADD TO THE 65 E.FP. ISSUED

WE OBTAIN A GOOD SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 466 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS A GOOD 2.33 MILLION OZ OCCURRED WITH OUR $0.19 LOSS IN PRICE

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS/THURSDAY MORNING WEDNESDAY NIGHT

ASIA TRADING THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 12.17 PTS OR 0.36%

//Hang Seng CLOSED DOWN 112.04 PTS OR 0.56%

// Nikkei CLOSED DOWN 268.17 OR 0.69%//Australia’s all ordinaries CLOSED DOWN 1.68%///Chinese yuan (ONSHORE) CLOSED DOWN TO 7.3124 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.3127// Oil DOWN TO 70.42 dollars per barrel for WTI and BRENT DOWN AT 73.12 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A GOOD SIZED 4695 CONTRACTS TO 461,876 WITH OUR LOSS IN PRICE OF $8.40 WITH RESPECT TO WEDNESDAY’S TRADING. , WE SURPRISINGLY LOST ZERO NET LONGS WITH OUR PRICE LOSS FOR GOLD AS WE HAD, AS YOU WILL SEE BELOW, A STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (5164). THUS WE HAD A SMALL GAIN ON OUR TWO EXCHANGES OF 469 CONTRACTS DESPITE OUR LOSS IN PRICE. OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON WEDNESDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED MONSTER RAID AS THEY ABSORBED EVERYTHING IN SIGHT FROM THE WESNESDAY ATTACK AND AGAIN OFFERED A THANK YOU NOTE TO THE FED FOR THEIR WONDERFUL LARGESSE. THE LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY THIS ENTIRE PAST WEEK. WE HAD CONTINUED HUGE T.A.S. LIQUIDATION ON WEDNESDAY.

THE FED IS THE MAJOR SHORT OF AROUND 82+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS IS SCHEDULED TO HAPPEN LATE OCT 2024/(AS OUTLINED IN OUR GOLD PHYSICAL COMMENTARIES//VIEW ANDREW MAGUIRE LATEST LIVE FROM VAULT PODCAST 197 , 199, 2001,AND FRIDAY NIGHTS 202, AND 203 AS HE TACKLES THIS IMPORTANT TOPIC). THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST TWO MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY! ACTUALLY THE FED HAS COAXED THE SPECULATORS TO GO MASSIVELY SHORT WHILE THEY TAKE THE LONG SIDE AFTER THEY COMMENCE THE AVALANCHE IN LOWERING THE PRICE OF GOLD LIKE THESE PAST 4 DAYS OF RAIDS.

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

WE HAD CONSIDERABLE T.A.S. LIQUIDATION THROUGHOUT LAST WEEK’S TRADING CONTINUING ON THIS WEEK.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF THE SPREADERS // T.A.S DURING LAST WEEK IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW DEEP INTO THE ACTIVE DELIVERY MONTH OF DECEMBER.… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A STRONG SIZED 5164 EFP CONTRACTS WERE ISSUED: : /DEC 5164 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5164 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A SMALL SIZED TOTAL OF 469 CONTRACTS IN THAT 5164 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A GOOD LOSS OF 4695 COMEX CONTRACTS..AND THIS SMALL GAIN ON OUR TWO EXCHANGES HAPPENED DESPITE OUR LOSS IN PRICE OF $8.40 WEDNESDAY// COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR WEDNESDAY NIGHT WAS A FAIR SIZED SIZED 1163 CONTRACTS, AND THESE WILL BE USED TO REPLENISH SUPPLIES.. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK).

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON MONDAY NOV 25, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION (COUPLED WITH THE LIQUIDATION OF CALENDAR SPREADERS ). THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE NOVEMBER’S OPTIONS EXPIRY TRADING. WE HAD CONTINUAL T.A.S. AND FINAL MONTH END SPREADER LIQUIDATION ESPECIALLY ON FRIDAY NOV 29 .THE LIQUIDATION OF T.A.S. SUBSIDED QUITE DRAMATICALLY DURING THE FIRST WEEK AND A HALF OF DECEMBER BUT THAT DRAMATICALLY CHANGED WITH CONSIDERABLE LIQUIDATION YESTERDAY WITH TUESDAY’S COMEX RAID AND IT CONTINUED ON WITH YESTERDAY’S (WEDNESDAY) TRADING AS WELL.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: DEC (88.3856 TONNES) WHICH IS HUGE FOR OUR ACTIVE DEC DELIVERY MONTH.

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 48 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 77.745 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 10.6406 TONNES EQUALS 88.3856 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $8.40/)//BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A GAIN IN OUR TWO EXCHANGES. AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION WEDNESDAY. WE ALSO HAD A FAIR T.A.S. ISSUANCE WEDNESDAY NIGHT (THURSDAY MORNING), AS THE NEED FOR REPLENISHMENT WAS STILL EVER PRESENT. THIS COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING.

19 DAYS AGO, FRIDAY NIGHT (EARLY SATURDAY MORNING NOV 30) THE CME ANNOUNCED ANOTHER OF THOSE CRAZY DELIVERIES: THE ISSUANCE OF 250 EXCHANGE FOR RISK CONTRACTS WHICH TOTAL 25000 OZ (.7776 TONNES. HERE THE BUYER ASSUMES THE RISK THAT HE WILL BE DELIVERED UPON IN PHYSICAL METAL. THIS IS ABSOLUTELY INSANE AND A HUGE VIOLATION OF THE TRUE DISCOVERY PRICE MECHANISM WHICH IS THE COMEX MANTRA!. AND THEN GUESS WHAT? THE CME ANNOUNCED ANOTHER EXCHANGE FOR RISK, LATE TUESDAY EVENING/ EARLY WEDNESDAY MORNING, (DEC 5) OF 617 CONTRACTS FOR 61,700 OZ OR GOLD (1.919 TONNES). THEN MUCH TO MY ANGER, THE CME ANNOUNCED A THIRD ISSUANCE FRIDAY NIGHT DEC 7 FOR A MONSTROUS 2254 EXCHANGE FOR RISK CONTRACTS OR 225,400 OZ OR 7.0108 TONNES. NOT TO BE UNDONE, THE CROOKS CONTINUED WITH THEIR NONSENSE WITH ANOTHER 50 CONTRACT EXCHANGE FOR RISK THE MORNING OF DEC 12 FOR 5000 OZ OR .1555 TONNES. AND THIS BRINGS US TO THIS EARLY FRIDAY MORNING WHERE I WAS SHOCKED TO SEE FOR THE FIFTH TIME THIS MONTH AN ENTRY FOR 250 CONTRACTS OF EXCHANGE FOR RISK FOR 25000 OZ OR .7776 TONNES.THUS ALL FIVE OF THESE ISSUANCES WILL BE ADDED TO THE TOTAL GOLD BEING “DELIVERED UPON”. TOTAL EXCHANGE FOR RISK ISSUANCES FOR THE MONTH NOW TOTALS 10.6406 TONNES. NO EXCHANGE FOR RISK WAS ISSUED EARLY THURSDAY MORNING.

WE HAVE GAINED A TOTAL OF 1.458 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR DEC (55.167TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S HUGE QUEUE JUMP OF 40,700 OZ OR 1.266 TONNES, TO WHICH WE MUST ADD OUR 5 ISSUANCES OF EXCHANGE FOR RISK FOR A TOTAL OF 10.6406 TONNES. THUS TAKEN TOGETHER,, THE TOTAL GOLD STANDING FOR THIS VERY ACTIVE DELIVERY MONTH OF DECEMBER IS:

77.745 TONNES (NORMAL DELIVERY) +

10.6406 TONNES (EX FOR RISK)

EQUALS: 88.3856 TONNES

/ STANDING FOR DEC INCREASES TO 88.3856 TONNES

NEW STANDING FOR DECEMBER: 88.3856 TONNES (WHICH IS HUGE FOR OUR VERY ACTIVE DELIVERY MONTH)

ALL OF THIS WAS ACCOMPLISHED WITH OUR LOSS IN PRICE TO THE TUNE OF $6.85

WE HAD 376 CONTRACTS REMOVED FROM THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES 469 CONTRACTS OR 46,900 (1.458 TONNES)

confirmed volume WEDNESDAY 168,297 contracts: very weak //// T.A.S. ENHANCED TO A LITTLE LESSER EXTENT.

//speculators have left the gold arena

END

/ /// THE DEC 2024 GOLD CONTRACT

DEC 19

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | nil . |

| Deposit to the Dealer Inventory in oz | NIL |

| Deposits to the Customer Inventory, in oz | 6,430.200 OZ (200 KILOBARS) a)BRINKS oz 200 kilobars 200 KILOBARS |

| No of oz served (contracts) today | 462 notice(s) 46,200 OZ 1.4370 TONNES |

| No of oz to be served (notices) | 718 contracts 71800 OZ 2.233 TONNES |

| Total monthly oz gold served (contracts) so far this month | 24,277 notices 2,427,700 oz 75.511 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

dealer deposits: 0

total dealer deposits: nil oz

we have 1 customer deposit

i) Into BRINKS 6,430.200 oz (200 kilobars)

total deposits 6430.200.000 oz 200 kilobars

strictly a paper gold entry.

withdrawals: 0

TOTAL WITHDRAWALS: oz

adjustments: 0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR DEC.

For the front month of DEC: we have an oi of 1180 contracts having LOST 247 contracts. We had A HUGE 654 contracts served on WEDNESDAY, so we GAINED a HUGE 407 contracts or 40,700 oz (1.266 TONNES) underwent a MASSIVE queue jump bolting ahead of others to take delivery of gold over on this side of the planet.

JANUARY GAINED 177 CONTRACTS TO STAND AT 4198

FEBRUARY LOST 4066 CONTRACTS TO 342,914 .

We had 462 contracts filed for today representing 46,200 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 28 notices issued from their client or customer account. The total of all issuance by all participants equate to 462 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 11 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for DEC /2024. contract month, we take the total number of notices filed so far for the month (24,277 x 100 oz ) to which we add the difference between the open interest for the front month of DEC(1180 CONTRACTS) minus the number of notices served upon today (462 x 100 oz per contract( equals 2,499,500OZ OR 77.745 TONNES. to which we add 10.6406 tonnes of exchange for risk WHICH EQUALS 88,3856 TONNES

thus the INITIAL standings for gold for the DEC contract month: No of notices filed so far (24,277 x 100 oz +we add the difference for front month of DEC (1180 OI} minus the number of notices served upon today (462 x 100 oz which equals 2,499,500 oz (77.745 TONNES) + 10.6406 tonnes of ex. for risk MONTH OF DEC //new total GOLD STANDING 88.3856 TONNES

TOTAL COMEX GOLD STANDING FOR DEC.: 88.3856 TONNES WHICH IS HUGE FOR THIS ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2292,357.555 oz 65.06 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 19,266,378.168 OZ

TOTAL REGISTERED GOLD 8,535,302.134/// 265.48 tonnes).

TOTAL OF ALL ELIGIBLE GOLD: 10,771,076.034 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,442,945 oz (REG GOLD- PLEDGED GOLD)= 200.40 tonnes //

JPMorgan enhanced inventory is 3.592 million oz/1,877,000 oz = 19.15% of entire inventory..

END

SILVER/COMEX

DEC 19. 2024

INITIAL

//2024// THE DEC 2024 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | NIL OZ . |

| Deposits to the Dealer Inventory | NIL |

| Deposits to the Customer Inventory | 1,781.821.800 oz Loomis ASAHI Manfra |

| No of oz served today (contracts) | 193 CONTRACT(S) (965,000 OZ) |

| No of oz to be served (notices) | 60 contracts (0.300 MILLION oz) |

| Total monthly oz silver served (contracts) | 8967 Contracts (44.835 MILLION oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit/

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

We had 3 customer deposits

a) Into Loomis: 598,445.180 oz

b) Into Asahi: 604,402.000 oz

c) Into Manfra: 578,974.700 oz

total customer deposit 1,781,821.800oz

We had 0 withdrawals

total withdrawal nil oz

JPMorgan has a total silver weight: 135.000million oz/312.399million or 43.21%

adjustments 0

TOTAL REGISTERED SILVER: 78.078MILLION OZ//.TOTAL REG + ELIGIBLE. 312.399 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR DEC

silver open interest data:

FRONT MONTH OF DEC /2024 OI: 253 OPEN INTEREST FOR A LOSS OF 73 CONTRACTS. WE HAD

252 CONTRACTS ISSUED ON WEDNESDAY SO WE HAD A HUGE 179 CONTRACT QUEUE JUMP I.E. 895,000 ADDITIONAL OZ WILL STAND AT THE COMEX WHERE THESE BOYS WILL TRY THEIR LUCK AND TAKE DELIVERY OF PHYSICAL SILVER OVER HERE.

JANUARY SAW A GAIN OF 98 CONTRACTS UP TO 2284

FEBRUARY SAW A GAIN 0F 25 CONTRACTS TO STAND AT 206

MARCH SAW A LOSS OF 71 CONTRACTS DOWN TO 118,170

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 193 for 965,000 oz

CONFIRMED volume; ON WEDNESDAY 53,071 good// HUGE, t.a.s. enhanced

To calculate the number of silver ounces that will stand for delivery in DEC we take the total number of notices filed for the month so far at 8967x 5,000 oz = 44.835 MILLION oz

to which we add the difference between the open interest for the front month of DEC (253) and the number of notices served upon today (193)x (5000 oz)

Thus the standings for silver for the DEC 2024 contract month: 8967 Notices served so far) x 5000 oz + OI for the front month of DEC(253) minus number of notices served upon today (193)x 5000 oz equals silver standing for the DEC contract month equating to 45.135 MILLION OZ. + to which we add 1.16 million oz of exchange for risk PRIOR////new total 46.295 MILLION OIOZ

New total standing: 46.295 million oz.

There are 78.078 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS//

DEC 19 WITH GOLD DOWN $45.00 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF .29 TONNES OF GOLD FROM THE GLD. / // : .///INVENTORY RESTS AT 863.90 TONNES

DEC 18 WITH GOLD DOWN $8.40 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: / // : .///INVENTORY RESTS AT 864.19 TONNES

DEC 17 WITH GOLD DOWN $6.85 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.23 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 864.19 TONNES

DEC 16 WITH GOLD DOWN $2.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.70 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 863.90 TONNES

DEC 13 WITH GOLD DOWN $24.55 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.78 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 868.60 TONNES

DEC 12 WITH GOLD DOWN $34.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.59 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 873.38 TONNES

DEC 11 WITH GOLD UP $29.75 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: // : .///INVENTORY RESTS AT 870.79 TONNES

DEC 9 WITH GOLD UP $31.10 ON THE DAY; NO CHANGES IN GOLD AT THE GLD. // : .///INVENTORY RESTS AT 871.94 TONNES

DEC 6 WITH GOLD UP $6.60 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD. A WITHDRAWAL OF 1.71 TONNES OF GOLD FROM THE GLD// : .///INVENTORY RESTS AT 871.94 TONNES

DEC 5 WITH GOLD DOWN $26.80 ON THE DAY; NO CHANGES IN GOLD AT THE GLD./ : .///INVENTORY RESTS AT 873.65 TONNES

DEC 4 WITH GOLD UP $6.15 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD./ : .///INVENTORY RESTS AT 873.65 TONNES

DEC 3 WITH GOLD UP $10.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.59 TONNES OF GOLD FROM THE GLD./ : .///INVENTORY RESTS AT 875.96 TONNES

DEC 2 WITH GOLD DOWN $20.20 ON THE DAY; NO CHANGES IN GOLD AT THE GLD : .///INVENTORY RESTS AT 878.55 TONNES

NOV 29 WITH GOLD UP $16.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD : Z WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD . .///INVENTORY RESTS AT 878.55 TONNES

NOV 27 WITH GOLD UP $18.05 ON THE DAY; NO CHANGES IN GOLD AT THE GLD : . .///INVENTORY RESTS AT 879.41 TONNE

NOV 26 WITH GOLD UP $3.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD : A DEPOSIT OF 1.44 TONNES OF GOLDINTO THE GLD. .///INVENTORY RESTS AT 879.41 TONNES

NOV 25 WITH GOLD DOWN $91.60 ON THE DAY; NO CHANGES IN GOLD AT THE GLD :. .///INVENTORY RESTS AT 877.97 TONNES

NOV 21 WITH GOLD UP $23.85 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 3.16 TONNES OF GOLD INTO THE GLD/:. .///INVENTORY RESTS AT 875,39 TONNES

NOV 20 WITH GOLD UP $22.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 0.58 TONNES OF GOLD INTO THE GLD/:. .///INVENTORY RESTS AT 872.23 TONNES

NOV 19 WITH GOLD UP $13.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 1.72 TONNES OF GOLD INTO THE GLD/:. .///INVENTORY RESTS AT 871.65 TONNES

NOV 18 WITH GOLD UP $44.20 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A DEPOSIT OF 2.56 TONNES OF GOLD INTO THE GLD/:. .///INVENTORY RESTS AT 869.93 TONNES

NOV 15 WITH GOLD DOWN $1.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.25 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 867.37 TONNES

NOV 14 WITH GOLD DOWN $12.90 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.91 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 868.62 TONNES

NOV 13 WITH GOLD DOWN $19.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.44 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 870.63 TONNES

NOV 12 WITH GOLD DOWN $11.40 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 4.88 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 871,97 TONNE

NOV 11 WITH GOLD DOWN $75.35 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.74 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 876.85 TONNES

NOV 8 WITH GOLD DOWN $11.85 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.87 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 883.46 TONNES

NOV 7 WITH GOLD UP $30.50 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 3.45 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 883.46 TONNES

NOV 6 WITH GOLD DOWN $72.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 1.72 TONNES OF GOLD FROM THE GLD/:. .///INVENTORY RESTS AT 886.91 TONNES

NOV 5 WITH GOLD UP $4.05 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:.// . // .///INVENTORY RESTS AT 888.63 TONNES

GLD INVENTORY: 863.90 TONNES, TONIGHTS TOTAL

SILVER

DEC 19 WITH SILVER DOWN 25 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV///// //INVENTORY AT SLV RESTS AT 457.414 MILLION OZ

DEC 18 WITH SILVER DOWN 19 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.094 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 457.414 MILLION OZ

DEC 17 WITH SILVER DOWN 12 CENTS //SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.456 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 458.052 MILLION OZ

DEC 16 WITH SILVER DOWN 0 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 4.84 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 458.052 MILLION OZ

DEC 13 WITH SILVER DOWN 46 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF .536 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 462.892 MILLION OZ

DEC 12 WITH SILVER DOWN 94 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 5.787 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 463.428 MILLION OZ

DEC 11 WITH SILVER UP 10 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.597 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 469.215 MILLION OZ

DEC 10 WITH SILVER DOWN 8 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 1.868 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 471.812 MILLION OZ

DEC 9 WITH SILVER UP $0.91 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 1.367 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 473.680 MILLION OZ

DEC 6 WITH SILVER DOWN $0.00 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 4.329 MILLION OZ/// //INVENTORY AT SLV RESTS AT 475.047 MILLION OZ

DEC 5 WITH SILVER DOWN $0.23 //NO CHANGES IN SILVER INVENTORY AT THE SLV” /// //INVENTORY AT SLV RESTS AT 470.718 MILLION OZ

DEC 4 WITH SILVER UP 26 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV”: A WITHDRAWAL OF 2.206 MILLION OZ FORM THE SLV. /// //INVENTORY AT SLV RESTS AT 470.718 MILLION OZ

DEC 3 WITH SILVER UP 59 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV /// //INVENTORY AT SLV RESTS AT 472.924 MILLION OZ

DEC 2 WITH SILVER DOWN 19 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV. A WITHDRAWAL OF 1,458,000 OZ FROM THE SLV. /// //INVENTORY AT SLV RESTS AT 472.924 MILLION OZ

NOV 29 WITH SILVER UP 51 CENTS //SMALL CHANGES IN SILVER INVENTORY AT THE SLV. A WITHDRAWAL OF 365,000 OZ FROM THE SLV. /// //INVENTORY AT SLV RESTS AT 474.382 MILLION OZ

NOV 27 WITH SILVER DOWN $0.25 //NO CHANGES IN SILVER INVENTORY AT THE SLV.. /// //INVENTORY AT SLV RESTS AT 474.747 MILLION OZ

NOV 26 WITH SILVER UP $0.10 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:.A WITHDRAWAL OF 1.094 MILLION OZ FROM THE SLV./.. /// //INVENTORY AT SLV RESTS AT 474.747 MILLION OZ

NOV 25 WITH SILVER DOWN $0.96 //NO CHANGES IN SILVER INVENTORY AT THE SLV:. . /// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 22 WITH SILVER UP $0.40 //NO CHANGES IN SILVER INVENTORY AT THE SLV:. . /// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 21 WITH SILVER DOWN $0.06 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1.729 MILLION OZ FORM THE SLV. . /// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 20 WITH SILVER DOWN $0.22 //NO CHANGES IN SILVER INVENTORY AT THE SLV: . /// //INVENTORY AT SLV RESTS AT 477.572 MILLION OZ

NOV 19 WITH SILVER UP $0.10 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 5,742,000 OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 477..572 MILLION OZ

NOV 18 WITH SILVER UP $0.68 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 1,277,000 OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 471,830 MILLION OZ

NOV 15 WITH SILVER DOWN $0.09 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 3,100,000 OZ OUT OF THE SLV. /// //INVENTORY AT SLV RESTS AT 471,830 MILLION OZ

NOV 14 WITH SILVER DOWN $0.07 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1,504,000 OZ OUT OF THE SLV. /// //INVENTORY AT SLV RESTS AT 473.653 MILLION OZ

NOV 13 WITH SILVER DOWN $0.16 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 1,274,000 OZ OUT OF THE SLV. /// //INVENTORY AT SLV RESTS AT 475.157 MILLION OZ

NOV 12 WITH SILVER UP $0.16 //SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 576,000 OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 476.000 MILLION OZ

NOV 11 WITH SILVER DOWN $0.79 //SMALL CHANGES IN SILVER INVENTORY AT THE SLV:A WITHDRAWAL OF 374,000 OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 477.527 MILLION OZ

NOV 8 WITH SILVER DOWN $0.43 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:A DEPOSIT OF 2.005 MILLION OZ INTO THE SLV. /// //INVENTORY AT SLV RESTS AT 477.846 MILLION OZ

NOV 7 WITH SILVER UP $0.11 //NO CHANGES IN SILVER INVENTORY AT THE SLV: /// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 6 WITH SILVER DOWN $1.41 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 3.692 MILLION OZ FROM THE SLV/.//// //INVENTORY AT SLV RESTS AT 475.841 MILLION OZ

NOV 5 WITH SILVER UP 0.18 :SMALL CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 1.109 MILLION OZ FROM THE SLV/.//// //INVENTORY AT SLV RESTS AT 479,533 MILLION OZ

CLOSING INVENTORY 457.414 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

Peter Schiff: World’s Central Banks Are Starting Inflation Again

by Tyler Durden

Thursday, Dec 19, 2024 – 06:30 AM

On the latest episode of the Peter Schiff Show, Peter dives into a week of new inflation data. He calls out the shaky foundations of the so-called “strong” economy, criticizes foreign central bank policy, and explains how inflation masks the benefits of economic growth.

To start, Peter reports alarming deficit numbers for the 2025 fiscal year:

During the first two fiscal months of 2025, because we’re already in that fiscal year, the budget deficit in those two months alone was six hundred and twenty four billion dollars. That’s a 65% increase over the same two months a year ago. In fact, the first time that the United States government ran a six hundred and twenty four billion dollar deficit for an entire year, not just for two months, but for an entire year, was 2009, right after the 2008 financial crisis.

These figures clash with the official narrative that the economy is doing well. If that’s really the case, why do the American people disagree?

If consumers were in the greatest shape ever, according to this Wall Street analyst, they would have voted for Kamala. They wouldn’t have tried to get rid of her because things are supposedly so awful, and they’re hoping that Trump would change things. … It’s like you’re lying in a hospital bed, plugged into all kinds of artificial life support, tubes in your mouth, tubes in your nose, blood going intravenously into your body, and you ask the doctor, ‘What’s going on?’ ‘You’re in great shape, absolutely perfectly healthy, except if we unplug anything you’re going to drop dead.’

A hotter-than-expected inflation report released on Thursday practically demands rate hikes from the Fed, but the market still predicts the Fed will cut rates at its December meeting:

All these numbers confirm is that inflation is bottoming out and is headed much higher, and it never got anywhere near 2%. Especially if you look at the PPI (Producer Price Index), which is a leading indicator for the CPI, because generally businesses have their prices go up first and then they pass it on to the consumer second. … The expectation for the increase in November producer prices was 0.3%, and we got 0.4%. That was double the increase from the prior month of 0.2%, so we’re heading in the wrong direction fast.

Current predictions place the likelihood of the Fed cutting rates again at over 95%. This is sadly aligned with the inflationary monetary policy being implemented in Europe and the rest of the world:

Yet the Fed is going to cut rates by another 25 basis points. By the way, the ECB (European Central Bank) cut rates 25 basis points this week, and the Swiss National Bank went for a super-sized 50 basis point cut… Inflation is going to rear its head in a big way all over the world: the Eurozone, Japan, all these countries that are cutting rates should not be cutting rates. Inflation is going to roar back stronger than ever, worse than what we had in 2001, 2002.

Central banks hoodwink their citizens with inflation, obscuring economic progress for the sake of their own policy goals:

Let’s assume that all else being equal the government doesn’t create any inflation and productivity is so good that prices would have fallen by 5. Well, that’s great. That’s a huge economic benefit for the economy. … Now the government creates inflation and instead of prices going down by 5 percent they go up by 2 percent. Now you’re going to say oh well, there’s no inflation now because now we’re at the fed’s 2 target. No! Prices are 7% higher than they otherwise would have been. We didn’t get all that inflation for free. The government robbed us of that increase in our standard of living. They took away the benefit of those price cuts.

For more analysis of last week’s economic numbers, check out Joel’s analysis on the SchiffGold Gold Wrap Podcast.

2/ Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

Alasdair Macleod

Currency and bond chaos ahead

The Fed’s signal that further interest rates cuts are not a given is roiling currencies and foreign bond markets. This mega-credit bubble is popping…

| Alasdair MacleodDec 19∙Paid |

First, let’s look at the euro and yen (inverted).

Clearly, these currencies are under pressure from US interest rate policy, which is also reflected in bond yields. Quite why France’s 10-year OAT only yields 3.1% when France is in political turmoil and heading for a 7% budget deficit illustrates how far it is from reality. And as for Japan, with the 10-year JGB yielding only 1.09%, it’s hardly surprising that the yen is plunging.

Both these currencies and their debt markets are getting a nasty wake-up call, not just from the US Fed, but also global bond markets. The yield on the leading supposedly risk-free 10-year US Treasury Note is rising as I have recently forecast:

It recently ticked back to find support on a golden cross and has subsequently risen, with price and the moving averages pointing higher. You can hardly have a clearer signal of its future direction, which is to challenge the 5% level. When or before that happens, the disparity between equity and bond values will lead to an equity bear market, which may have already started.

Given the US debt trap and its faltering economy, it won’t stop there. Yesterday, I posted an alarming chart of the 2017 long sterling gilt, which I repeat here updated for today’s price action:

UK pension funds will have bought this gilt in 2020/2021, when they could have paid £160. Now it is only £41 per £100 of stock. This is signalling a disaster for the UK economy, which is also reflected in sterling’s exchange rate:

This sterling chart is immensely bearish, with a death cross forming above the exchange rate. That it has recently rallied to the 55-day MA before being sent sharply south suggests that foreign exchange traders will short it heavily. More so, given the collapsing gilt market.

Does the average Brit expect this? Despite their grumbling at the damage the Labour government is inflicting on the economy, their disinterest in gold suggests not. But with gold looking ready to rise in dollar terms, it will rise even faster in sterling.

A final word for gold’s naysayers, who think that higher bond yields will be bad for gold. They fail to appreciate that it is not gold rising, but their currency falling. And unless their central bank aggressively raises rates high enough to stabilise their currency, it will continue to decline relative to real legal money, which is gold. But if the Fed, the ECB, the BoE, or the BoJ attempt to raise rates enough to stabilise their fiat currencies, they will bankrupt their governments, businesses, and banking systems. As a deliberate policy, it can be ruled out.

Get out of credit!

3. CHRIS POWELL AND GATA DISPATCHES

4. OTHER GOLD COMMENTARIES/

END

LIVE FROM THE VAULT/ANDREW MAGUIRE KINESIS 203

youtube.com/watch?v=5hHeh2mnvXg&list=PLE1y8hGSqr8ar1gKUdfqFDK5ygLIlrdmz&index=1

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES: COMMODITY; cattle

6 CRYPTOCURRENCY NEWS

END

ASIA TRADING THURSDAY MORNING/WEDNESDAY NIGHT

SHANGHAI CLOSED DOWN 12.17 PTS OR 0.36%

//Hang Seng CLOSED DOWN 112.04 PTS OR 0.56%

// Nikkei CLOSED DOWN 268.17 OR 0.69%//Australia’s all ordinaries CLOSED DOWN 1.68%///Chinese yuan (ONSHORE) CLOSED DOWN TO 7.3124 CHINESE YUAN OFFSHORE CLOSED DOWN TO 7.3127// Oil DOWN TO 70.42 dollars per barrel for WTI and BRENT DOWN AT 73.12 Stocks in Europe OPENED ALL RED

ONSHORE USA/ YUAN TRADING ABOVE LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS THURSDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.3124

OFFSHORE YUAN: UP TO 7.3127

SHANGHAI CLOSED CLOSED DOWN 12.17 PTS OR 0.36%

HANG SENG CLOSED CLOSED DOWN 112.04 PTS OR 0.56%

2. Nikkei closed DOWN 268.17 PTS OR 0.69%

3. Europe stocks SO FAR: ALL RED

USA dollar INDEX UP TO 107.70 EURO RISES TO 1.0404 UP 54 BASIS PTS

3b Japan 10 YR bond yield: FALLS TO. +1.056 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 156.88…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen DOWN CHINESE ONSHORE YUAN: DOWN OFFSHORE: DOWN

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil UP for WTI and UP FOR BRENT this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.2875 Italian 10 Yr bond yield UP to 3.4587 //SPAIN 10 YR BOND YIELD UP TO 2.9890

3i Greek 10 year bond yield UP TO 3.148

3j Gold at $2604.45/Silver at: 29.32 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 1 AND 31/100 roubles/dollar; ROUBLE AT 103.06

3m oil into the 70 dollar handle for WTI and 73 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 156.88 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.036% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.8956 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9317 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.537 UP 4 BASIS PTS…

USA 30 YR BOND YIELD: 4.712 UP 5 BASIS PTS/

USA 2 YR BOND YIELD: 4.329 DOWN 3 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 35.08…

10 YR UK BOND YIELD: 4.6005 UP 4 PTS

10 YR CANADA BOND YIELD: 3.294 UP 7 BASIS PTS

5 YR CANADA BOND YIELD: 3.092 UP 4 PTS.

2a New York OPENING REPORT

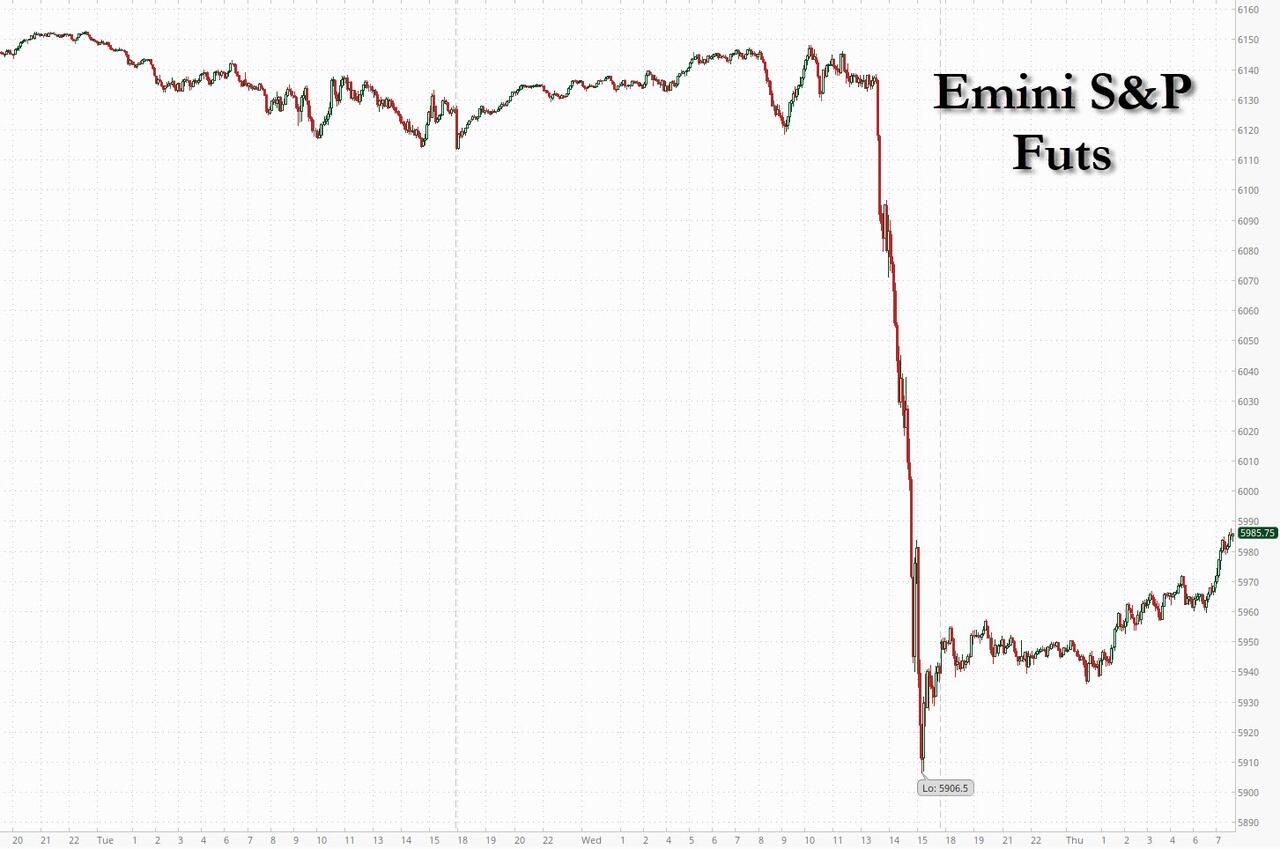

Futures Rebound After Powell’s Hawkish Pivot Plunge

Thursday, Dec 19, 2024 – 08:23 AM

US futures staged a partial recovery on Thursday after the worst Fed day rout since the 2013 Taper Tantrum, suggesting the selloff after the Federal Reserve’s hawkish pivot was overdone, even as stock indexes in Europe and Asia retreated as equity markets caught up with post-Fed moves in the US. As of 8:00am, S&P futures advanced 0.5% following the US benchmark’s biggest lost for a scheduled Fed decision day since 2001. Nasdaq 100 contracts rose 0.4% even as chip leader Micron crashed 13% on disappointing guidance. 10Y yields rose again, hitting 4.53%, the highest level since May and nearly 100bps higher than the 2024 lows reached in September. The dollar retreated after soaring on Monday even as the yen cratered after the Bank of Japan left rates unchanged, disappointing a lot of generally clueless strategists who were expecting a hike. Oil and bitcoin also rebounded after sliding on Wednesday. Key events today include the latest GDP revision, initial and continuing claims, existing home sales as well as the October TIC flows data.

In premarket trading, Micron Technology tumbles 13% after its revenue forecast missed projections, hurt by sluggish demand for smartphones and personal computers. Baidu dropped 2% after Reuters reports that Apple is in talks with Tencent and Bytedance to integrate their AI models into iPhones sold in China. Here are some other notable premarket movers:

- IonQ (IONQ) rises 5% as DA Davidson initiates with a buy recommendation, saying the stock “is positioning itself as the leader in quantum computing.”

- Lamb Weston (LW) slides 20% after the French-fry supplier cut its sales and adjusted earnings per share guidance for the full year.

- Lennar Corp. (LEN) drops 10% after the homebuilder forecast new orders for the first quarter that missed the average analyst estimate.

- Sangamo Therapeutics (SGMO) rises 8% after the biotech reached a license agreement with Astellas, under which Sangamo will receive a $20 million upfront license fee.

- Vertex Pharmaceuticals (VRTX) falls 12% after the the company’s nonaddictive drug helped patients with lower back pain in a mid-stage trial, but performed similar to a placebo, causing shares to decline.

- Worthington Steel (WS) declines 5% after posting fiscal 2Q revenue that dropped 9% from the year-ago quarter, hurt by lower volumes and selling prices.

The Fed scaled back the number of 2025 cuts it sees from four to two as Powell said future easing would require fresh progress on inflation. The reaction interrupted this year’s stellar rally in US stocks, with S&P 500 still on course to notch more than 20% of gains due to optimism about artificial intelligence and the outlook for the economy under a Donald Trump administration. While the severity of Wednesday’ reaction showed that equity markets were less prepared for the Fed’s announcement, the shift implied that profits could be stronger than anticipated in the near term, said Florian Ielpo, head of macro research at Lombard Odier Investment Managers.

“What we have seen is a little cold water poured on what is otherwise a decent economy,” John Bilton, JPMorgan Asset Management’s head of global multi-asset strategy, told Bloomberg TV. “I am constructive about next year. If I’m a bull, I have got to love a healthy pullback.” Money markets are now pricing in fewer than two quarter-point reductions for the entirety of 2025, even less than what was implied in the Fed’s so-called dot plot on Wednesday. In the SOFR options market one large block trade placed Wednesday afternoon bet on the start of another hiking cycle next year.

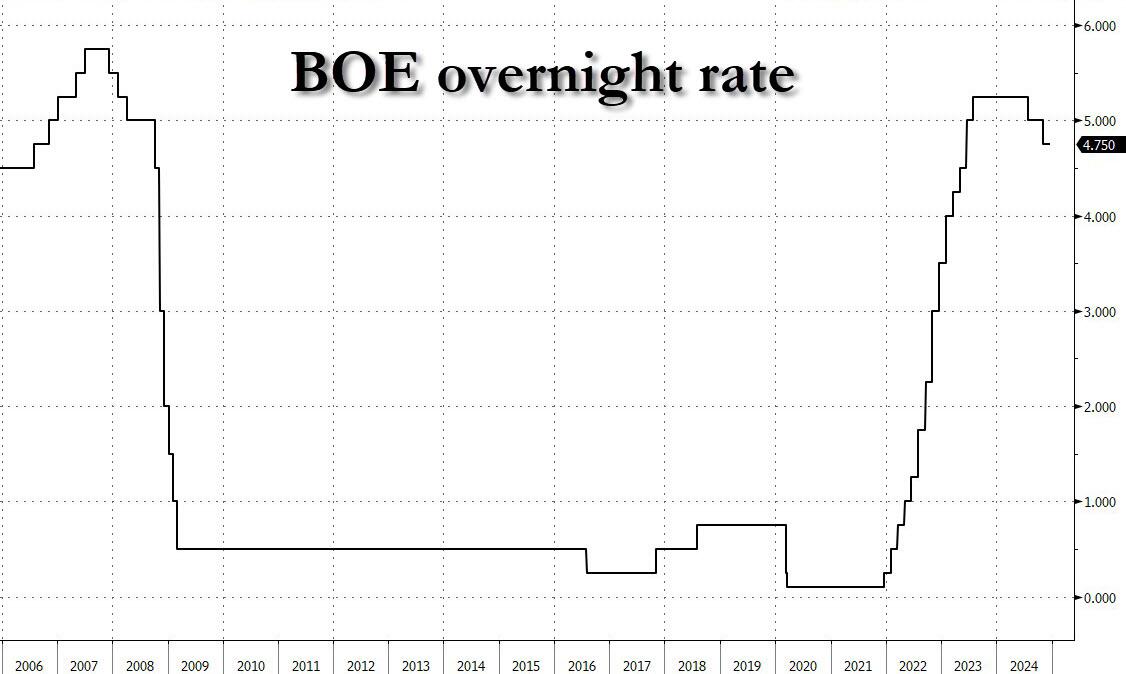

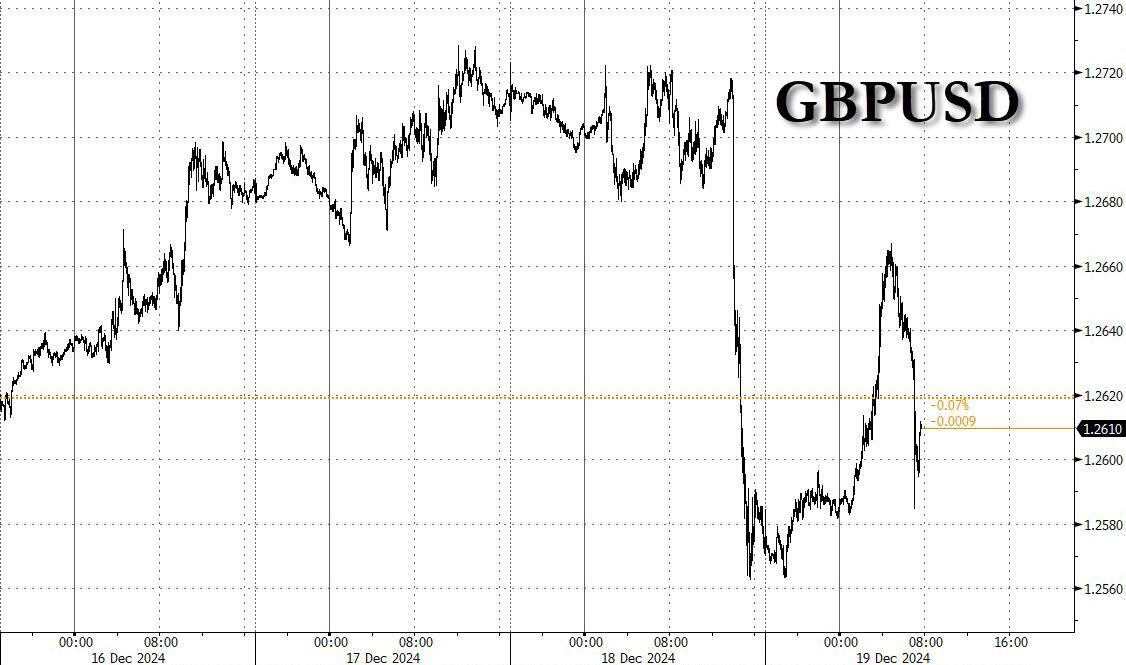

Elsewhere in central banks, the Norges Bank stood pat while the Riksbank cut their policy rate by 25 bps, both as expected. The Norwegian krone and Swedish krona both held higher on the day. The pound dropped after the Bank of England’s dovish hold.

In Europe, the Stoxx 600 dropped 1.2% after the surprisingly hawkish Fed messaging sparked the biggest rout in US stocks since early August. Semiconductor stocks fall after Micron Technology posted disappointing revenue forecast. Here are some of the biggest movers on Thursday:

- SoftwareOne shares rise as much as 13%, while Crayon drops 8.1% after the Swiss firm offers to buy the Norwegian IT services firm for a total of 144 kroner/share.

- Pharming shares gain as much as 11%, the top performer in the Euronext Amsterdam AEX Health Care Index, after RBC analysts boosted their price target on the Dutch biopharma company to a Street high.

- UK Water providers are among best performers in Europe on Thursday as industry regulator Ofwat announces details of a hike to bills. It’s a “major clearing event,” according to Barclays. Severn Trent is up as much as 2.1%, Pennon Group +3.5%.

- Saipem shares gained, reversing earlier losses, as a consortium including the Italian construction and drilling services co. won an offshore contract in Nigeria, which Mediobanca expects will push year-to-date book-to-bill ratio to highest in a decade.

- European semiconductor stocks slide in early Thursday trading, hit by a weak revenue outlook by memory chipmaker Micron and a Federal Reserve that signaled less urgency to lower rates further. ASML -3.7%, Infineon -3.8%, STMicro -4.7%.

- Roche shares drop as much as 2.2% after a mid-stage study of the pharmaceutical company’s prasinezumab missed its primary endpoint.

- Zurich Insurance Group falls as much as 2.3% after UBS cuts its recommendation to sell, saying the valuation leaves “limited margin for maneuver.” Munich Re is cut to neutral from buy and falls as much as 1.4%.

- Netcompany slumps as much as 11% after Carnegie downgrades its rating on the Danish IT company to hold from buy.

- Tessenderlo falls as much as 8% to its lowest intraday value in ten years, after the firm cut its adjusted Ebitda outlook for the full year, according to a statement. KBC says the valuation is still attractive due to the company’s sizable free cash flow.

Asian stocks recorded their biggest decline in over two month after the Federal Reserve dialed back expectations for rate cuts next year. The MSCI Asia Pacific Index fell as much as 1.7%, with TSMC, Samsung and Commonwealth Bank of Australia the biggest contributors to the decline. Benchmarks of South Korea and Australia were among the worst performers in the region. Indian stocks also dropped. China erased earlier declines amid expectations the government will maintain a loose policy in 2025.

“Investors need to be pretty agile, bob-and-weave as we always say,” Thomas Taw, head of APAC investment strategy at Blackrock, said in a Bloomberg TV interview. Interest rates are likely going to be higher for longer and the rest of market will take a little time to digest that, Taw said.

In FX, the Bloomberg Dollar Spot Index fell 0.1% after soaring on Wednesday; the yen tumbled 1.4% – just as we told our premium subscribers – after comments by BOJ Governor Kazuo Ueda cast doubt on whether the bank could hike interest rates in January, or even beyond that, instead signaling that more information is needed on wages and the policies of Donald Trump before making a decision. USD/JPY has topped 157, a level where the BOJ will have to start jawboning verbal intervention only this time nobody will believe it. In China, authorities ramped up support for the currency via its daily reference rate after the Fed’s caution over future rate cuts sent the offshore yuan to a fresh one-year low.

In rates, treasuries are mixed with the curve steeper as long-end yields rise an additional 3.5bp while front-end of the curve rallies as traders continue to digest Wednesday’s market reaction to the Fed policy announcement and revised dot-plot forecasts. The yield curve steepened further with 10-year borrowing costs rising another 1 bp to 4.52% while two-year yields pull back. Into the steepening move the 2s10s spread tops at the widest level since Sept. 26. Treasury 2-year yields richer by around 3bp on the day while 30-year yields rise around 3.5bp, steepening 2s10s and 5s30s spreads by 5.5bp and 4bp on the day; US 10-year yields trade around 4.535%, just off session highs and at cheapest levels since May. Gilts outperform Treasuries slightly after UK bonds rallied in the aftermath of Bank of England voted 6-3 to keep rates unchanged at 4.75%.

In commodities, oil held within its recent range as expectations for fewer interest-rate cuts by the Federal Reserve next year boosted the dollar. Gold staged a partial recovery after tumbling more than 2% in the previous session.

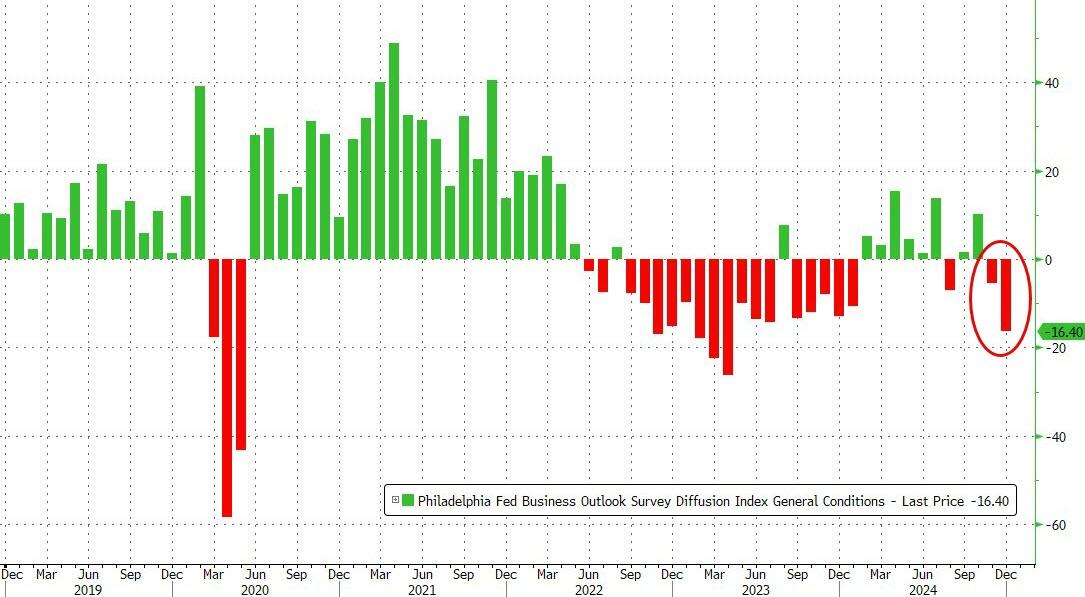

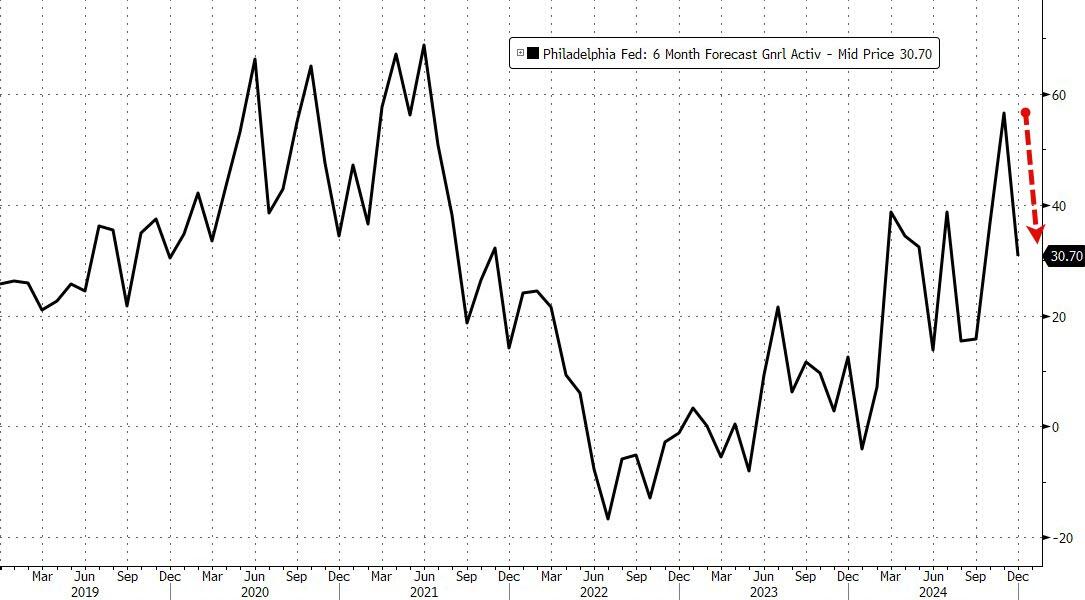

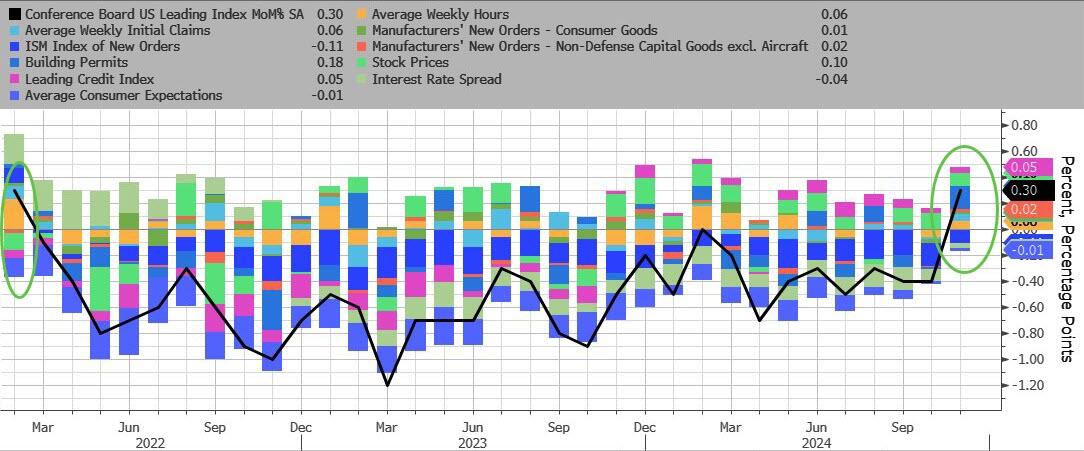

US economic data calendar includes 3Q GDP, December Philadelphia Fed business outlook, initial jobless claims (8:30am), November Leading index, existing home sales (10am), December Kansas City Fed manufacturing activity (11am) and October TIC flows (4pm)

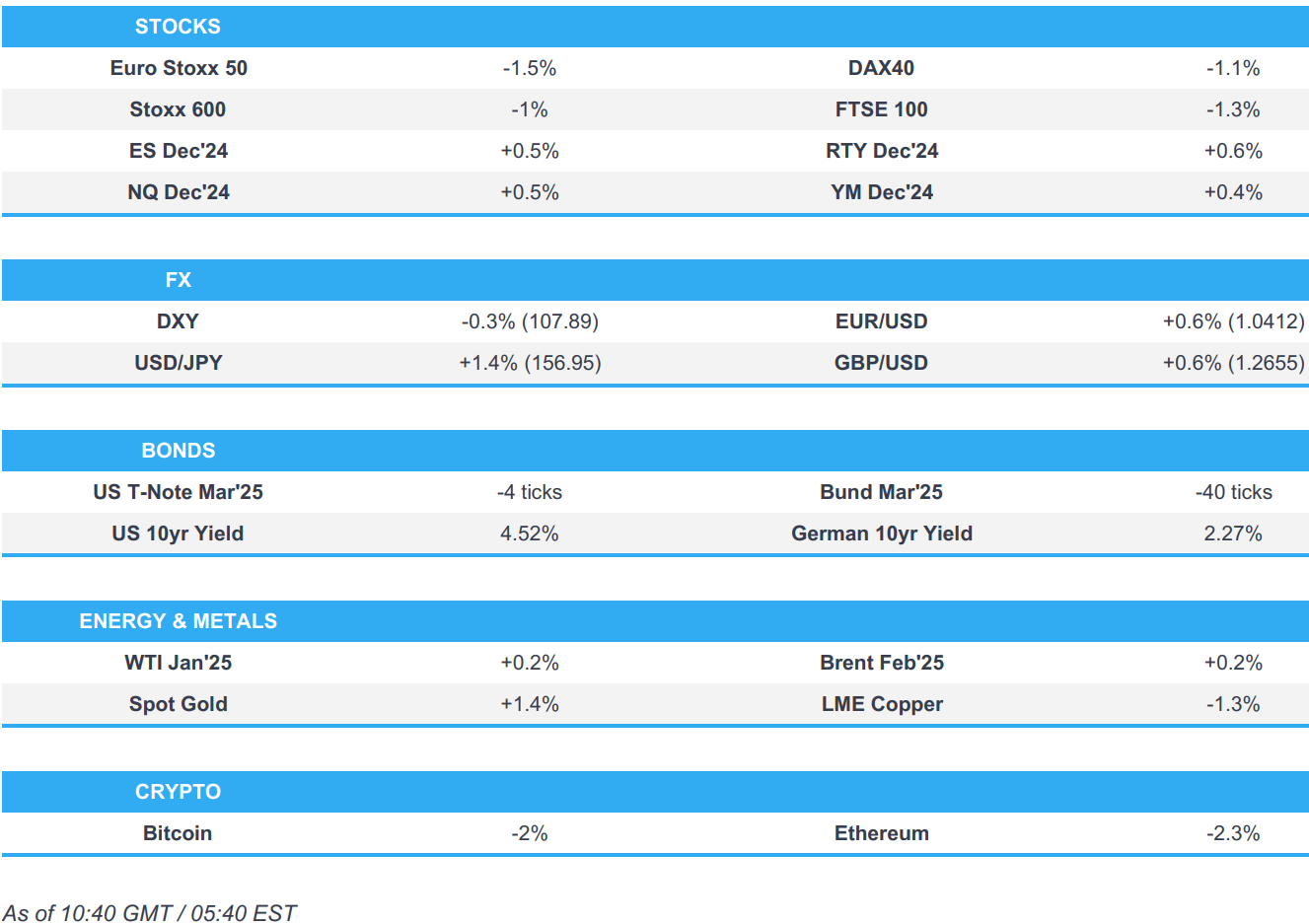

Market Snapshot

- S&P 500 futures up 0.4% to 5,894.50

- STOXX Europe 600 down 1.2% to 508.26

- MXAP down 1.6% to 180.90

- MXAPJ down 1.4% to 572.89

- Nikkei down 0.7% to 38,813.58

- Topix down 0.2% to 2,713.83

- Hang Seng Index down 0.6% to 19,752.51

- Shanghai Composite down 0.4% to 3,370.03

- Sensex down 1.2% to 79,248.34

- Australia S&P/ASX 200 down 1.7% to 8,168.22

- Kospi down 2.0% to 2,435.93

- German 10Y yield up 4 bps at 2.29%

- Euro up 0.6% to $1.0417

- Brent Futures little changed at $73.35/bbl

- Gold spot up 1.4% to $2,621.03

- US Dollar Index down 0.16% to 107.85

Top Overnight News

- A stopgap funding deal to keep the US government running collapsed following opposition from Trump and Elon Musk. The president-elect wants lawmakers to include an increase to the debt ceiling in the package — which needs to happen before the summer to avoid a default — so that it would be raised under Joe Biden’s watch. BBG

- Trump said he’s totally against stopgap bill, and instead he and JD Vance called for a temporary funding bill without “Democrat giveaways” combined with an increase in the debt ceiling; Congress should debate the debt limit now: Fox News

- The drive to force Justin Trudeau to step aside as Canadian PM gained momentum. About a third of the 153-person Liberal contingent in the House of Commons want him out, according to one lawmaker. BBG

- The yen sank more than 1% as BOJ Governor Kazuo Ueda cast doubt on the prospect of a January rate hike after the central bank stood pat. Inflationary trends are slow and rate-setters want a fuller picture on wages and Donald Trump’s policies, he said. BBG

- Chinese banks raised mortgage rates for the first time since 2021, according to research firm Data Motion. The average for buyers’ first homes in 42 big cities inched up to 3.08% in November from a record low of 3.05% in the previous month. BBG

- Sweden’s Riksbank lowers its policy rate by 25bp to 2.5% (as expected), but the forward guidance is tweaked in a modestly hawkish direction, with the central bank saying it would “carefully evaluate the need for future rate adjustments” given recent easing measures (it said it’s possible that just one 25bp reduction occurs in H1). Riksbank

- Norway’s Norges Bank kept its policy rate unchanged at 4.5% (as expected), but the forward guidance was somewhat dovish, with the central bank noting that “the time to begin easing monetary policy is soon approaching” (it said a rate reduction was likely to occur in March). Norges Bank

- The BOE left the key rate unchanged at 4.75% as the Monetary Policy Committee voted 6-3 in favor of keeping its benchmark interest rate unchanged. The BOE signaled it will keep easing gradually in 2025 as a growing minority of officials set aside evidence of lingering inflation to back an immediate cut in borrowing costs. BBG

- Israeli warplanes struck Houthi sites in Yemen’s capital and elsewhere in response to new missile attacks on Tel Aviv. BBG

- Russian President Putin says he has not spoken to US President-elect Trump in four years but is ready to talk to him.

- Morgan Stanley now expects the Fed to deliver two 25 bps rate cuts in 2025 (prev. forecast of three 25 bps cuts) following the December FOMC meeting, according to Reuters.

- Apple said Meta has made 15 requests for potentially far-reaching access to Apple’s technology, and it raises concerns about users’ privacy and security as it made more requests than other firms: Reuters.

- Apple is in talks with Tencent and ByteDance to integrate their AI models into iPhones sold in the Chinese market. RTRS

- Indonesian President Prabowo has reportedly approved Apple’s $1bln investment plan: BBG

- Teamsters launched the largest strike against Amazon in US history; workers to strike nationwide on Thursday: RTRS

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded with losses across the board amid the fallout from the hawkish Fed, as sentiment from Wall Street reverberated to the region. ASX 200 was pressured by its IT and gold sectors following the post-Fed tech downside and the slide in the yellow metal. Nikkei 225 pared some losses following the BoJ’s decision to maintain rates, but choppy trade was seen thereafter ahead of Governor Ueda’s presser. Hang Seng and Shanghai Comp were both lower as China conformed to the broader post-Fed risk tone, with Fed Chair Powell also suggesting that some Fed members had taken a very preliminary step and incorporated conditional effects of coming policies in their projections – i.e. potential Trump tariffs.

Top Asian News

- BoJ’s comprehensive review of past monetary easing steps highlighted it was deemed appropriate for the bank to continue conducting monetary policy with the aim of achieving the price stability target of 2% in a sustainable and stable manner. The bank stated that no specific measures should be excluded at this point when considering the future conduct of monetary policy. Regarding the effectiveness of monetary easing, it was noted that the quantitative degree of its effects remains uncertain compared with conventional monetary policy measures. While monetary easing influenced inflation expectations to some degree, it was not sufficiently effective in anchoring inflation at 2%. In terms of its impact on interest rates and the economy, long-term interest rates were reduced by approximately 1ppt since 2016. Large-scale monetary easing contributed to GDP growth by an estimated 1.3% to 1.8%, while its effect on CPI was between 0.5 and 0.7ppts. Note, the policy review was initiated by Ueda when he took office in April 2023.

- Honda (7267 JT) and Nissan (7201 JT) talks to start as early as next week, according to Nikkei.

- HKMA cut its base rate by 25bps to 4.75%, as expected in lockstep with the Fed.

- South Korean Finance Minister said market-stabilising measures will be taken if volatility is deemed excessive; will prepare FX stability and liquidity measures in 2025 policy plan, according to Reuters.

- South Korean financial regulator said it has asked banks to flexibly adjust FX transactions and loan maturity for firms, according to Reuters.

- South Korea’s National Pension Service (NPS) and BOK to extend and expand their FX swap agreement, according to Reuters.

- Indonesia’s central bank said it is committed to stabilising the IDR in case of any excessive volatility, according to Reuters.

- Westpac now forecasts the RBNZ to cut the cash rate to 3.25% by May 2025 following the NZ GDP data.