GOLD CLOSED UP $14.50 TO $2650.90

SILVER CLOSED UP 48 CENTS TO $30.09

Gold ACCESS CLOSED $2650.00

Silver ACCESS CLOSED: $30.03

Bitcoin morning price:$100,800 DOWN 2000 DOLLARS.

Bitcoin: afternoon price: $96,311 DOWN 6489 DOLLARS

Platinum price closing UP $22.30 TO $952.65

Palladium price; UP 8.20 TO $929.30

END

*CANADIAN GOLD: $3804.45 up 26.20 CDN dollars per oz( * NEW ALL TIME HIGH 3,872.51 CDN DOLLARS PER OZ//OCT 30 2024)

*BRITISH GOLD: 2123.40 up 17.40 Pounds per oz// *(NEW ALL TIME HIGH//CLOSING///2161.00 BRITISH POUNDS/OZ) NOV 22/2024

*EURO GOLD: 2,561.84 UP 24.59 Euros per oz //* (ALL TIME CLOSING HIGH: 2600.25 EUROS PER OZ//NOV 22 //.2024)

DONATE

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

EXCHANGE;

EXCHANGE: COMEX

CONTRACT: JANUARY 2025 COMEX 100 GOLD FUTURES

SETTLEMENT: 2,638.400000000 USD

INTENT DATE: 01/06/2025 DELIVERY DATE: 01/08/2025

FIRM ORG FIRM NAME ISSUED STOPPED

072 H GOLDMAN 3

363 H WELLS FARGO SEC 55

435 H SCOTIA CAPITAL 2

624 H BOFA SECURITIES 62

657 C MORGAN STANLEY 1

661 C JP MORGAN 6

686 C STONEX FINANCIA 5

730 C PTG DIVISION SG 1

737 C ADVANTAGE 17 2

TOTAL: 77 77

JPMorgan stopped 6/77

GOLD: NUMBER OF NOTICES FILED FOR JANUARY/2024. CONTRACT: 77 NOTICES FOR 7700 OZ 0.2372 TONNES

total notices so far: 3926 contracts for 392600 Oz (12.2115 tonnes)

FOR JANUARY

SILVER NOTICES: 184 NOTICE(S) FILED FOR 920,000 OZ/

total number of notices filed so far this month : 1488 for 7.440 million oz

XXXXXXXXXXXXXXXXXX

Click here if you wish to send a donation. I sincerely appreciate it as this site takes a lot of preparation

END

GLD/

BOTH GLD AND SLV ARE FRAUDULENT VEHICLES//THEY ARE NOW RAIDING GLD AND SLV FOR PHYSICAL

THE CROOKS ARE STEALING GOLD AND SILVER FROM THE GLD/SLV AND REPLACING THE PHYSICAL WITH PAPER DOLLARS.

WITH GOLD UP $14.50 INVESTORS SWITCHING TO SPROTT PHYSICAL (PHYS) INSTEAD OF THE FRAUDULENT GLD:

NO CHANGES IN GOLD INVENTORY AT THE GLD:

INVENTORY RESTS AT 871.08 TONNES

SLV/

WITH NO SILVER AROUND AND SILVER UP $0.48 AT THE SLV: HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A WITHDRAWAL OF 2.824 MILLION OZ OUT OF THE SLV

INVESTORS ARE SWITCHING SLV TO SPROTT’S PSLV.

CLOSING INVENTORY: 459.353 MILLION OZ

Let us have a look at the data for today

SILVER//OUTLINE

SILVER COMEX OI ROSE BY A FAIR SIZED 372 CONTRACTS TO 151,118 AND CONTINUING ON ITS MARCH TO THE RECORD HIGH OI OF 244,710, SET FEB 25/2020, AND THIS STRONG SIZED GAIN IN COMEX OI WAS ACCOMPLISHED WITH OUR GAIN OF $0,38 IN SILVER PRICING AT THE COMEX WITH RESPECT TO MONDAY’S TRADING. WE HAD A MONSTER GAIN OF 1282 TOTAL CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN IN PRICE//MONDAY’S TRADING.. WE HAD LITTLE LIQUIDATION OF T.A.S. CONTRACTS ON MONDAY COMEX TRADING AS THEY DESPERATELY TRIED TO CONTAIN SILVER’S PRICE RISE FOR THE PAST 2 WEEKS WHERE THE RAIDS WERE CALLED UPON AGAIN TO QUELL MASSIVE DERIVATIVE LOSSES BY OUR BULLION BANKS. THEY FAILED WITH //MONDAY PRICING WITH ZERO LONGS BEING KNOCKED OFF. DERIVATIVE LOSSES CONTINUE TO MOUNT. WE HAD LITTLE T.A.S. LIQUIDATION MONDAY

WE HAD A MONSTER 910 CONTRACT EXCHANGE FOR PHYSICAL ISSUANCE ACCOMPANIED BY A STRONG 660 CONTRACT T.A.S ISSUANCE WHICH WILL BE USED IN TUESDAY;S TRADING AS THEY PLAY AN INTEGRAL PART IN OUR COMEX TRADING TRYING TO CONTAIN ANY SILVER PRICE RISE. IN ESSENCE WE GAINED A HUMONGOUS SIZED 1282 CONTRACTS ON OUR TWO EXCHANGES WITH OUR GAIN IN PRICE. WE HAD LITTLE TAS LIQUIDATION THROUGHOUT MONDAY’S COMEX SESSION

PLEASE NOTE THAT THE CROOKS NEED A HIGHER SILVER/GOLD T.A.S. TO CARRY ON THEIR CROOKED MANIPULATION ON A DAILY BASIS BUT DEMAND IS JUST TOO HIGH FOR THEM. THE HIGHER ISSUANCE OF T.A.S. IS NOW USED TO TEMPER OUR SILVER/GOLD PRICE RISE OR RAID AS WHAT HAPPENED SEVERAL TIMES LAST MONTH AND AGAIN YESTERDAY.

CRAIG HEMKE HAS POINTED OUT THAT THE CROOKS USE THE MID MONTH FOR MANIPULATION AS THEY SELL THEIR BUY SIDE OF THE CALENDAR SPREAD FIRST AND THEN KEEP THE SELL SIDE TO LIQUIDATE AT A LATER DATE. THUS WE HAVE TWO VEHICLES THE CROOKS USE FOR MANIPULATION AND BOTH ARE SPREADERS: 1) AT MONTH’S END/SPREADERS COMEX AND 2/ TAS SPREADERS, MID MONTH. TOTAL TAS ISSUED ON MONDAY NIGHT: A HUGE 660 CONTRACTS. DESPITE MANY COMPLAINTS THAT THE CROOKS HAVE VIOLATED POSITION LIMITS DUE TO THE FACT THAT THE TAS ISSUED HAVE A VALUE OF ZERO (AS TO POSITION LIMITS FOR OUR CROOKED BANKERS). THE PROBLEM OF COURSE IS THAT THE CROOKS DO NOT LIQUIDATE THE TAS TOGETHER BUT SELL THE BUY SIDE FIRST AND THEN LIQUIDATE THE SELL SIDE TWO MONTHS HENCE. IT IS OBVIOUS MANIPULATION TO THE HIGHEST DEGREE BUT IT NATURALLY FELL ON DEAF EARS WITH OUR REGULATORS (OCC) WHEN THEY RECEIVED OUR COMPLAINTS. IT NOW SEEMS THAT THE OCC HAS ORDERED THE BANKS TO REDUCE ITS NEW LEVEL OF 1 TRILLION DOLLARS IN GOLD/SILVER DERIVATIVES AND THUS THE REASON FOR CONSTANT RAIDS ESPECIALLY WITH YESTERDAY’S TRADING. IT ALSO LOOKS LIKE THE FED (GOV’T) IS BEHIND EVERY DAY TRADING.

WE HAVE IN THE PAST YEAR SET ANOTHER RECORD LOW AT 114,102 CONTRACTS ///JULY 3.2023// OUR BANKERS WITH THE HELP OF SPECULATORS AND HIGH FREQUENCY TRADERS WERE UNSUCCESSFUL IN KNOCKING THE PRICE OF SILVER DOWN (IT ROSE BY $0.38) AND WERE UNSUCCESSFUL IN KNOCKING OFF ANY APPRECIABLE NET SILVER LONGS FROM THEIR PERCH AS WE HAD A STRONG GAIN IN PRICE WITH LITTLE TAS LIQUIDATION AND A HUMONGOUS GAIN IN OUR TWO EXCHANGES OF 1282 CONTRACTS.

WE HAD A 910 CONTRACT ISSUANCE OF EXCHANGE FOR PHYSICALS) iiii) AN INITIAL SILVER STANDING FOR COMEX SILVER MEASURING AT 8.110 MILLION OZ (FIRST DAY NOTICE) FOLLOWED BY TODAY’S 210,000 OZ E.F.P. TRANSFER TO LONDON//NEW STANDING REDUCES TO 8.190 MILLION OZ

// STANDING FOR SILVER//JAN RISES TO 8.1900 MILLION OZ

WE HAD:

/ FAIR SIZED COMEX OI GAIN +// A MONSTER 910 SIZED EFP ISSUANCE/ VI) STRONG SIZED NUMBER OF T.A.S. CONTRACT ISSUANCE 660 CONTRACTS)/

I AM NOW RECORDING THE DIFFERENTIAL IN OI FROM PRELIMINARY TO FINAL: REMOVED 111 CONTRACTS.

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS JAN. ACCUMULATION FOR EFP’S SILVER/JPMORGAN’S HOUSE OF BRIBES/STARTING FROM FIRST DAY/MONTH OF JAN

TOTAL CONTRACTS for 3DAYS, total 1410 contracts: OR 7.050 MILLION OZ (470 CONTRACTS PER DAY)

TOTAL EFP’S FOR THE MONTH SO FAR: 7.050 MILLION OZ

LAST 24 MONTHS TOTAL EFP CONTRACTS ISSUED IN MILLIONS OF OZ:

MAY 137.83 MILLION

JUNE 149.91 MILLION OZ

JULY 129.445 MILLION OZ

AUGUST: MILLION OZ 140.120

SEPT. 28.230 MILLION OZ//

OCT: 94.595 MILLION OZ

NOV: 131.925 MILLION OZ

DEC: 100.615 MILLION OZ

YEAR 2022:

JAN 2022-DEC 2022

JAN 2022// 90.460 MILLION OZ

FEB 2022: 72.39 MILLION OZ//

MARCH 2022: 207.140 MILLION OZ//A NEW RECORD FOR EFP ISSUANCE

APRIL: 114.52 MILLION OZ FINAL//LOW ISSUANCE

MAY: 105.635 MILLION OZ//

JUNE: 94.470 MILLION OZ

JULY : 87.110 MILLION OZ

AUGUST: 65.025 MILLION OZ

SEPT. 74.025 MILLION OZ///FINAL

OCT. 29.017 MILLION OZ FINAL

NOV: 134.290 MILLION OZ//FINAL

DEC, 61.395 MILLION OZ FINAL

TOTALS YR 2022: 1135.767 MILLION OZ (1.1356 BILLION OZ)

JAN 2023/// 53.070 MILLION OZ //FINAL

FEB: 2023: 100.105 MILLION OZ/FINAL//MUCH STRONGER ISSUANCE VS THE LATTER TWO MONTHS.

MARCH 2023: 112.58 MILLION OZ//FINAL//STRONG ISSUANCE

APRIL 111.035 MILLION OZ(SLIGHTLY GREATER THAN THAN LAST MONTH)

MAY 66.120 MILLION OZ/INITIAL (MUCH SMALLER THIS MONTH)

JUNE: 110.395 MILLION OZ//MUCH LARGER THAN LAST MONTH

JULY 85.745 MILLION OZ (SMALLER THAN LAST MONTH)

AUGUST: 171.43 MILLION OZ (THIS MONTH IS GOING TO BE HUGE //2ND HIGHEST ON RECORD

SEPT: 72.705 MILLION OZ (SMALLER THIS MONTH)

OCT: 97.455 MILLION OZ

NOV. 50.050 MILLION OZ

DEC. 66.140 MILLION OZ//

TOTAL 2023: 1,104.10 MILLION OZ/

JAN ’24 : 78.655 MILLION OZ//

FEB /2024 : 66.135 MILLION OZ./FINAL

MARCH: 143.750 MILLION OZ// 4TH HIGHEST ON RECORD.

APRIL: 161.770 MILLION OZ (THIS MONTH WILL BE A WHOPPER OF ISSUANCE OF EFPS//3RD HIGHEST EVER RECORDED FOR A MONTH)

MAY: 135.995 MILLION OZ //WILL BE A STRONG MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

JUNE 110.575 MILLION OZ ( WILL BE ANOTHER STRONG MONTH ISSUANCE)

JULY: 108.870 MILLION OZ (WILL BE A STRONG ISSUANCE MONTH/ A TOUCH OVER 100 MILLION OZ/)

AUGUST; 99.740 MILLION OZ//THIS MONTH WILL BE STRONG FOR ISSUANCE BUT LESS THAN JULY.

SEPT: 112.415 MILLION OZ//WILL BE A HUGE MONTH FOR EXCHANGE FOR PHYSICAL ISSUANCE

OCT; 97.485 MILLION OZ (WILL BE SMALLER ISSUANCE THIS MONTH )

NOV. 115.970 MILLION OZ ( HUGE THIS MONTH)

DEC: 132.54 MILLION OZ (THIS MONTH WILL BE A HUMDINGER FOR ISSUANCE BUT ISSUANCE SLOWED DRAMATICALLY THESE PAST FIVE DAYS/// WILL NOT EXCEED MARCH 2022 RECORD OF 209 MILLION OZ

YEAR 2024 TOTAL: 1363.84 MILLION OR 1.363 BILLION OZ

JANUARY 2025: 7/060 MILLION OZ///

RESULT: WE HAD AN FAIR SIZED INCREASE IN COMEX OI SILVER COMEX CONTRACTS OF 372 CONTRACTS WITH OUR STRONG GAIN IN PRICE OF SILVER PRICING AT THE COMEX//MONDAY.,. THE CME NOTIFIED US THAT WE HAD A 910 EFP ISSUANCE CONTRACTS: 910 ISSUED FOR MARCH AND 0 CONTRACTS ISSUED FOR ALL OTHER MONTHS) WHICH EXITED OUT OF THE SILVER COMEX TO LONDON AS FORWARDS. WE HAVE A GOOD INITIAL SILVER OZ STANDING FOR DEC OF 8.110 MILLION OZ ON FIRST DAY NOTICE, FOLLOWED BY TODAY’S E.F.P TRANSER TO LONDON OF 210,000 OZ

//NEW TOTAL STANDING FOR JAN REDUCES TO 8.190 MILLION OZ

WE HAVE A HUMONGOUS SIZED GAIN OF 1282 OI CONTRACTS ON THE TWO EXCHANGES WITH OUR GAIN IN PRICE…..THE TOTAL OF TAS INITIATED CONTRACTS TODAY: A STRONG 660 CONTRACTS TRYING DESPERATELY TO CONTAIN SILVER’S PRICE RISE,//LITTLE FRONT END OF THE TAS CONTRACTS WERE LIQUIDATED DURING THE MONDAY COMEX SESSION BUT THEY STILL NEED THESE ISSUANCE FOR REPLENISHMENT FOR FUTURE TRADING /THE HUGE TA.S. ISSUANCE// STRONG LIQUIDATION DISTORTS THE TOTAL OI CONTRACTS STANDING AT THE COMEX. NO NET LONG SPECULATORS WERE BURNED ON FRIDAY WITH THE GAIN IN PRICE. ALSO SOME OF OUR LONGS EXERCISED THEIR RIGHT AND TENDERED FOR PHYSICAL SILVER MUCH TO THE ANGER OF OUR BANKERS. SILVER IS NOT BASEL III COMPLIANT SO THE BANKERS CAN TAKE THEIR TIME WITH THE DELIVERY OF SILVER.

THE NEW TAS ISSUANCE MONDAY NIGHT (660) WILL BE PUT INTO “THE BANK” TO BE COLLUSIVELY USED AT A LATER DATE, AND PROBABLY NOT TODAY.

WE HAD 184 NOTICE(S) FILED TODAY FOR 920,000 OZ

THE SILVER COMEX IS NOW BEING ATTACKED FOR METAL BY LONDONERS ET AL.

GOLD//OUTLINE

IN GOLD, THE COMEX OPEN INTEREST FELL BY A FAIR SIZED 3129 OI CONTRACTS TO 464,000 AND FURTHER FROM THE RECORD (SET JAN 24/2020) AT 799,733 AND PREVIOUS TO THAT: (SET JAN 6/2020) AT 797,110, BUT WE ARE NOW GETTING CLOSER TO OUR ALL TIME LOW OF 390,000 CONTRACTS.

THE DIFFERENTIAL FROM PRELIMINARY OI TO FINAL OI IN GOLD TODAY: ADDED A HUGE SIZED 175 CONTRACTS//

WE HAD A FAIR SIZED DECREASE IN COMEX OI (3129 CONTRACTS) OCCURRED WITH OUR LOSS OF $4.90 IN PRICE MONDAY. THE FRBNY SUPPLIED THE NECESSARY SHORT PAPER.. WE ALSO HAD A GOOD INITIAL STANDING IN GOLD TONNAGE FOR JAN AT 10.1331 TONNES FOLLOWED BY TODAY’S MONSTER QUEUE JUMP OF 876 CONTRACTS OR 87,600 OZ TO WHICH WE ADD THE FIRST ISSUANCE FOR 2025 OF EXCHANGE FOR RISK TOTALLING 1700 CONTRACTS OR 170,000 OZ (5.28775 TONNES) ISSUED JAN 6/2025 . NEW STANDING FOR JAN ADVANCES TO 18.068 TONNES + 5.28775 TONNES EX FOR RISK/PRIOR = 23.3558 TONNES

/NEW STANDING 23.3558 TONNES

/ ALL OF THIS HAPPENED WITH OUR $4.90 LOSS IN PRICE WITH RESPECT TO MONDAY’S COMEX ///. WE HAD A FAIR GAIN OF 2642 OI CONTRACTS (8.2177 PAPER TONNES) ON OUR TWO EXCHANGES, WITH MANY LONGS, REMAINING AT THE END OF THE DAY, TENDERING FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE, MUCH TO THE ANGER AND HORROR EXHIBITED BY OUR MAJOR BANKER, THE FEDERAL RESERVE BANK OF NEW YORK. THE HORROR INTENSIFIED ONCE LONDON STARTED TO TRADE LAST WEEK, AND THROUGHOUT THE WEEK WITH MAJOR TENDERING FOR PHYSICAL VIA THE EXCHANGE FOR PHYSICAL ROUTE! YOU CAN VISUALIZE THIS WITH THE VIOLENT ACTION AT THE COMEX WITH RESPECT TO QUEUE JUMPING AND EXCHANGE FOR RISK ISSUANCE.

E.F.P. ISSUANCE

THE CME RELEASED THE DATA FOR EFP ISSUANCE AND IT TOTALED A HUGE SIZED 5771 CONTRACTS:

The NEW COMEX OI FOR THE GOLD COMPLEX RESTS AT 463,825

IN ESSENCE WE HAVE A FAIR SIZED INCREASE IN TOTAL CONTRACTS ON THE TWO EXCHANGES OF 2642 CONTRACTS WITH 3129 CONTRACTS DECREASED AT THE COMEX// AND A HUGE SIZED 5771 EFP OI CONTRACT ISSUANCE WHICH NAVIGATED OVER TO LONDON. THUS TOTAL OI GAIN ON THE TWO EXCHANGES OF 2642 CONTRACTS.. WE HAD THE FOLLOWING TAS CONTRACTS INITIATED (ISSUED): A STRONG SIZED BUT CRIMINAL 1789 CONTRACTS ISSUED. WE HAD A SOME LIQUIDATION OF T.A.S CONTRACTS WITH OUR LOSS IN PRICE MONDAY AS THE NEED FOR REPLENISHMENT WAS STILL IN ORDER TO CARRY OUT ITS PRICE CONTAINMENT STRATEGY IN FUTURE TRADING.

CALCULATIONS ON GAIN/LOSS ON OUR TWO EXCHANGES

WE HAD A STRONG SIZED ISSUANCE IN EXCHANGE FOR PHYSICALS (5771 CONTRACTS) ACCOMPANYING THE FAIR SIZED DECREASE IN COMEX OI OF 3129 CONTRACTS/TOTAL GAIN FOR OUR THE TWO EXCHANGES: 2642 CONTRACTS..WE HAVE 1) NOW RETURNED TO OUR FORMER FORMAT OF BANKERS GOING LONG AND SPECULATORS GOING SHORT ,2.) STRONG INITIAL STANDING AT THE GOLD COMEX FOR JAN 10.1331 TONNES FOLLOWED BY TODAY’S QUEUE JUMP OF 876 CONTRACTS OR 87600 OZ (2.724 TONNES) TO WHICH WE ADD THAT CRAZY “DELIVERY” CALLED EXCHANGE FOR RISK// NEW STANDING FOR JAN ADVANCES TO: 23.3558 TONNES

//NEW STANDING JAN: 23.3558 TONNES

/ 3) SOME T.A.S. LIQUIDATION TRYING TO LOWER GOLD’S PRICE MONDAY WITH SOME SUCCESS IN REMOVING SPECULATOR LONGS, AS WE HAD A 1) $4.90 PRICE LOSS, BUT 2) ZERO NET LONG SPECS BEING CLIPPED AS WE HAD A TOTAL GAIN OF 2467 CONTRACTS ON OUR TWO EXCHANGES. ALSO, 3)STICKY GOLD’S LONGS WERE REWARDED MONDAY EVENING AS THEY EXERCISED EFP’S FROM LONDON TO TAKE DELIVERY OF BADLY NEEDED PHYSICAL.

4) FAIR SIZED COMEX OPEN INTEREST DECREASE 5) HUGE ISSUANCE OF EXCHANGE FOR PHYSICAL PAPER///STRONG T.A.S. ISSUANCE: 1789 T.A.S.CONTRACTS//

HISTORICAL ACCUMULATION OF EXCHANGE FOR PHYSICALS IN 2023-2024 INCLUDING TODAY

JAN

ACCUMULATION OF EFP’S GOLD AT J.P. MORGAN’S HOUSE OF BRIBES: (EXCHANGE FOR PHYSICAL) FOR THE MONTH OF JAN :

TOTAL EFP CONTRACTS ISSUED: 12,556 CONTRACTS OF 1,255,600 OZ OR 39.054 TONNES IN 3 TRADING DAY(S) AND THUS AVERAGING: 4185 EFP CONTRACTS PER TRADING DAY

TO GIVE YOU AN IDEA AS TO THE SIZE OF THESE EFP TRANSFERS : THIS MONTH IN 3 TRADING DAY(S) IN TONNES 39.054 TONNES

TOTAL ANNUAL GOLD PRODUCTION, 2023, THROUGHOUT THE WORLD EX CHINA EX RUSSIA: 3555 TONNES

THUS EFP TRANSFERS REPRESENTS 39.054 DIVIDED BY 3550 x 100% TONNES = 1.098% OF GLOBAL ANNUAL PRODUCTION

ACCUMULATION OF GOLD EFP’S YEAR 2021 TO 2023

JANUARY/2021: 265.26 TONNES (RAPIDLY INCREASING AGAIN)

FEB : 171.24 TONNES ( DEFINITELY SLOWING DOWN AGAIN)..

MARCH:. 276.50 TONNES (STRONG AGAIN/

APRIL: 189..44 TONNES ( DRAMATICALLY SLOWING DOWN AGAIN//GOLD IN BACKWARDATION)

MAY: 250.15 TONNES (NOW DRAMATICALLY INCREASING AGAIN)

JUNE: 247.54 TONNES (FINAL)

JULY: 188.73 TONNES FINAL

AUGUST: 217.89 TONNES FINAL ISSUANCE.

SEPT 142.12 TONNES FINAL ISSUANCE ( LOW ISSUANCE)_

OCT: 141.13 TONNES FINAL ISSUANCE (LOW ISSUANCE)

NOV: 312.46 TONNES FINAL ISSUANCE//NEW RECORD!! (INCREASING DRAMATICALLY)//SIGN OF REAL STRESS//SURPASSING THE MARCH 2021 RECORD OF 276.50 TONNES OF EFP

DEC. 175.62 TONNES//FINAL ISSUANCE//

TOTALS: 2,578.08 TONNES/2021

JAN:2022 247.25 TONNES //FINAL

FEB: 196.04 TONNES//FINAL

MARCH/2022: 409.30 TONNES //FINAL( THIS IS NOW A RECORD EFP ISSUANCE FOR MARCH AND FOR ANY MONTH.

APRIL: 169.55 TONNES (FINAL VERY LOW ISSUANCE MONTH)

MAY: 247.44 TONNES FINAL//

JUNE: 238.13 TONNES FINAL

JULY: 378.43 TONNES FINAL/SECOND HIGHEST ON RECORD

AUGUST: 180.81 TONNES FINAL

SEPT. 193.16 TONNES FINAL

OCT: 177.57 TONNES FINAL ( MUCH SMALLER THAN LAST MONTH)

NOV. 223.98 TONNES//FINAL ( MUCH LARGER THAN PREVIOUS MONTHS//comex running out of physical)

DEC: 185.59 tonnes // FINAL

TOTAL: 2,847,25 TONNES/2022

JAN 2023: 228.49 TONNES FINAL//HUGE AMOUNT OF EFP’S ISSUED THIS MONTH!!

FEB: 151.61 TONNES/FINAL

MARCH: 280.09 TONNES/INITIAL (ANOTHER STRONG MONTH FOR EFP ISSUANCE)

APRIL: 197.42 TONNES

MAY: 236.67 TONNES (A VERY STRONG ISSUANCE FOR THIS MONTH)

JUNE: 172.667 TONNES (WEAKER ISSUANCE THIS MONTH)

JULY: 151.69 TONNES (WEAKER THAN LAST MONTH)

AUGUST: 195.28 TONNES (A STRONGER MONTH)//FINAL

SEPT: 254.709 TONNES (WILL BE LARGER THAN LAST MONTH AND A STRONG MONTH)

OCT. 248.09 TONNES. LIKE SILVER, THIS MONTH IS GOING TO BE A STRONG E.F.P. ISSUANCE.

NOV. 239.16 TONNES//WILL BE STRONG THIS MONTH,

DEC. 213.704 TONNES. A STRONG MONTH//

TOTAL FOR YEAR 2023: 2,569.57 TONNES VS 2578 TONNES LAST YEAR

JAN ’24: 291.76 TONNES (WILL BE MUCH GREATER THAN LAST MONTH.//3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL)

FEB’24: 201.947 TONNES

MARCH 2024: 352.21 TONNES//2ND HIGHEST EVER RECORDED EFP ISSUANCE.

APRIL: 267.05TONNES (WILL BE AN EXTREMELY STRONG MONTH BUT LESS THAN MARCH 2024)

MAY; 316.606 TONNES (WILL BE ANOTHER STRONG MONTH// 3RD HIGHEST RECORDED EFP ISSUANCE )// NOTICE THE HUGE INCREASES IN EX FOR PHYSICAL THESE PAST FEW MONTHS. THESE CONTRACTS ARE CIRCLED BACK FROM LONDON WHEREBY METAL IS REMOVED FROM THE COMEX.

JUNE 175.11 tonnes HEADING FOR A WEAKER MONTH AND MUCH LESS THAN THE THREE PREVIOUS MONTHS

JULY: 351. 65 TONNES (3RD HIGHEST EVER RECORDED EXCHANGE FOR PHYSICAL AND THE HIGHEST EVER RECORDED POST BASEL III)

AUGUST: 274.79 TONNES//THIS MONTH WILL NO DOUBT BE A STRONG ISSUANCE OF EFP’S BUT MUCH LESS THAN LAST MONTH.

SEPT: 335 .104 TONNES//IF THIS CONTINUES WE WILL HAVE A HUMDINGER OF AN EFP ISSUANCE. WE WILL PROBABLY END JUST SHORT OF THE 3RD HIGHEST ISSUANCE EVER RECORDED.

OCT. 277.71 TONNES (THIS WILL BE A GOOD ISSUANCE THIS MONTH)

NOV: 393.875 TONNES ( A HUGE MONTH////NOW SURPASSED THE PREVIOUS 3RD AND 2ND HIGHEST EVER RECORDED EX FOR PHYSICAL ISSUANCE TO BECOME THE 2ND HIGHEST EVER RECORDED

DEC 360.03 TONNES THIRD HIGHEST EVER RECORDED FOR EFP ISSUANCE

TOTAL 2024 YEAR.3,597.846

JAN. 39.054 TONNES

SPREADING OPERATIONS

(/NOW SWITCHING TO GOLD) FOR NEWCOMERS, HERE ARE THE DETAILS

SPREADING LIQUIDATION HAS NOW COMMENCED AS WE HEAD TOWARDS THE NEW ACTIVE FRONT MONTH OF FEB. WE ARE NOW INTO THE SPREADING OPERATION OF GOLD

HERE IS A BRIEF SYNOPSIS OF HOW THE CROOKS FLEECE UNSUSPECTING LONGS IN THE SPREADING ENDEAVOUR ;MODUS OPERANDI OF THE CORRUPT BANKERS AS TO HOW THEY HANDLE THEIR SPREAD OPEN INTERESTS:HERE IS HOW THE CROOKS USED SPREADING AS WE ARE NOW INTO THE NON ACTIVE DELIVERY MONTH OF NOV HEADING TOWARDS THE ACTIVE DELIVERY MONTH OF FEB., FOR GOLD: AND MARCH FOR SILVER

YOU WILL ALSO NOTICE THAT THE COMEX OPEN INTEREST STARTS TO RISE BUT SO IS THE OPEN INTEREST OF SPREADERS. THE OPEN INTEREST IN WILL CONTINUE TO RISE UNTIL ONE WEEK BEFORE FIRST DAY NOTICE OF AN UPCOMING ACTIVE DELIVERY MONTH (OCT), AND THAT IS WHEN THE CROOKS SELL THEIR SPREAD POSITIONS BUT NOT AT THE SAME TIME OF THE DAY. THEY WILL USE THE SELL SIDE OF THE EQUATION TO CREATE THE CASCADE (ALONG WITH THEIR COLLUSIVE FRIENDS) AND THEN COVER ON THE BUY SIDE OF THE SPREAD SITUATION AT THE END OF THE DAY. THEY DO THIS TO AVOID POSITION LIMIT DETECTION. THE LIQUIDATION OF THE SPREADING FORMATION CONTINUES FOR EXACTLY ONE WEEK AND ENDS ON FIRST DAY NOTICE.”

WHAT IS ALARMING TO ME, ACCORDING TO OUR LONDON EXPERT ANDREW MAGUIRE IS THAT THESE EFP’S ARE BEING TRANSFERRED TO WHAT ARE CALLED SERIAL FORWARD CONTRACT OBLIGATIONS AND THESE CONTRACTS ARE LESS THAN 14 DAYS. ANYTHING GREATER THAN 14 DAYS, THESE MUST BE RECORDED AND SENT TO THE COMPTROLLER, GREAT BRITAIN TO MONITOR RISK TO THE BANKING SYSTEM. IF THIS IS INDEED TRUE, THEN THIS IS A MASSIVE CONSPIRACY TO DEFRAUD AS WE NOW WITNESS A MONSTROUS TOTAL EFP’S ISSUANCE AS IT HEADS INTO THE STRATOSPHERE.

The crooks also use the spread in the TAS account (trade at settlement). They buy the spot TAS (e.g. June) and sell the future TAS two months out (e.g. August). Then they unload the front month (i.e. unload the buy side first so the price of gold/silver falls. This occurs in the middle of the front delivery month cycle. They unload the sell side of the equation, two months down the road. The crooks violate position limits as the OCC refuse to hear our complaints.

First, here is an outline of what will be discussed tonight:

1.TODAY WE HAD THE OPEN INTEREST AT THE COMEX IN SILVER ROSE BY A FAIR SIZED 372 CONTRACTS OI TO 151,229 AND CLOSER TO THE COMEX HIGH RECORD //244,710( SET FEB 25/2020). THE LAST RECORDS WERE SET IN AUG.2018 AT 244,196 WITH A SILVER PRICE OF $14.78/(AUGUST 22/2018)..THE PREVIOUS RECORD TO THAT WAS SET ON APRIL 9/2018 AT 243,411 OPEN INTEREST CONTRACTS WITH THE SILVER PRICE AT THAT DAY: $16.53). AND PREVIOUS TO THAT, THE RECORD WAS ESTABLISHED AT: 234,787 CONTRACTS, SET ON APRIL 21.2017 OVER 7 YEARS AGO. HOWEVER WE HAVE NOW SET A NEW RECORD LOW OF 114,102 CONTRACTS JULY 3.20233EFP ISSUANCE 200 CONTRACTS

OUR CUSTOMARY MIGRATION OF COMEX LONGS CONTINUE TO MORPH INTO LONDON FORWARDS AS OUR BANKERS USED THEIR EMERGENCY PROCEDURE TO ISSUE:

MAR 910 and ALL OTHER MONTHS: ZERO. TOTAL EFP ISSUANCE: 910 CONTRACTS. EFP’S GIVE OUR COMEX LONGS A FIAT BONUS PLUS A DELIVERABLE PRODUCT OVER IN LONDON. IF WE TAKE THE COMEX OI GAIN OF 483 CONTRACTS AND ADD TO THE 910 E.FP. ISSUED

WE OBTAIN A HUMONGOUS SIZED GAIN OF OPEN INTEREST CONTRACTS FROM OUR TWO EXCHANGES OF 1282 CONTRACTS

THUS IN OUNCES, THE GAIN ON THE TWO EXCHANGES TOTALS A HUGE 6.410 MILLION OZ OCCURRED WITH OUR $0.38 GAIN IN PRICE

OUTLINE FOR TODAY’S COMMENTARY

1a/COMEX GOLD AND SILVER REPORT

(report Harvey)

b, ) Gold/silver trading overnight Europe,//GOLD COMMENTARIES

(Peter Schiff)

c) Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

ii a) Chris Powell of GATA provides to us very important physical commentaries

b. Other gold/silver commentaries

c. Commodity commentaries//

d)/CRYPTOCURRENCIES/BITCOIN ETC

2.ASIAN AFFAIRS/TUESDAY MORNING MONDAY NIGHT

ASIA TRADING TUESDAY MORNING/MONDAY NIGHT

SHANGHAI CLOSED UP 22.72 PTS OR 0.71%

//Hang Seng CLOSED DOWN 240.71 PTS OR 1.97%

// Nikkei CLOSED UP 776.25 OR 1.97%//Australia’s all ordinaries CLOSED UP 0.65%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.3394 CHINESE YUAN OFFSHORE CLOSED UP TO 7.3392// Oil DOWN TO 74.16 dollars per barrel for WTI and BRENT DOWN AT 76.49 Stocks in Europe OPENED ALL MOSTLY GREEN

ONSHORE USA/ YUAN TRADING AT LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

A)NORTH KOREA/SOUTH KOREA

outline

b) REPORT ON JAPAN/

OUTLINE

3 CHINA

OUTLINE

4/EUROPEAN AFFAIRS

OUTLINE

5. RUSSIAN AND MIDDLE EASTERN AFFAIRS

OUTLINE

6.Global Issues//COVID ISSUES/VACCINE ISSUES

OUTLINE

7. OIL ISSUES

OUTLINE

8 EMERGING MARKET ISSUES

9. USA

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

1. COMEX DATA//AMOUNTS STANDING//VOLUME OF TRADING/INVENTORY MOVEMENTS

GOLD

LET US BEGIN:

THE TOTAL COMEX GOLD OPEN INTEREST FELL BY A FAIR SIZED 3129 CONTRACTS TO 464,000 WITH OUR LOSS IN PRICE OF $4.90 WITH RESPECT TO MONDAY’S TRADING. WE LOST ZERO NET LONGS DESPITE OUR PRICE LOSS FOR GOLD AS WE HAD, AS YOU WILL SEE BELOW, A VERY STRONG NUMBER OF EXCHANGE FOR PHYSICAL ISSUED (5771) . THE CME ISSUED ZERO ISSUANCE OF EXCHANGE FOR RISK: (0 CONTRACTS FOR 0 OZ) . THUS IN TOTAL WE HAD A FAIR GAIN ON OUR TWO EXCHANGES OF 2642 CONTRACTS DESPITE OUR LOSS IN PRICE. OUR FRIENDLY PHYSICAL LONDON BOYS HAD ANOTHER FIELD DAY AGAIN ON FRIDAY NIGHT AS THEY WERE READY FOR THE FRBNY.S CONTINUED ORCHESTRATED RAID AS THEY ABSORBED EVERYTHING IN SIGHT FROM THE DAILY ATTACKS WITH THE CONTINUAL LIQUIDATION OF T.A.S. CONTRACTS. LONDONERS EXERCISED THEIR BOUGHT CONTRACTS FOR PHYSICAL GOLD VIA THE EXCHANGE FOR PHYSICAL ROUTE AND THANKED THE FRBNY FOR THE THOUGHTFULNESS.

THE LIQUIDATION OF T.A.S. CONTRACTS THROUGHOUT LAST MONTH CONTINUES TO DISTORT OPEN INTEREST NUMBERS GREATLY AND IT SURELY WAS ON DISPLAY THIS ENTIRE PAST WEEK. WE HAD CONSIDERABLE T.A.S. LIQUIDATION DURING THE MONDAY COMEX SESSION. WE HAD A STRONG 1789 T.A.S. ISSUANCE MONDAY NIGHT.

THE FED IS THE MAJOR SHORT OF AROUND 82+ TONNES OF GOLD OWING TO THE B.I.S. THE FED NEEDS TO COVER AS THEY ARE VERY WORRIED ABOUT WHAT IS GOING TO HAPPEN TO GOLD PRICES ONCE THE BRICS BEGIN THEIR INITIATIVE AND ABANDON THE US DOLLAR. THIS WAS SCHEDULED TO HAPPEN LATE OCT 2024/(AS OUTLINED IN OUR GOLD PHYSICAL COMMENTARIES//VIEW ANDREW MAGUIRE LATEST LIVE FROM VAULT PODCAST 197 , 199, 2001, AND FRIDAY NIGHTS 202, 203 AND 204 AS HE TACKLES THIS IMPORTANT TOPIC). THE FOUR OR FIVE BANKS ARE ALSO WORRIED ABOUT THEIR HUGE PRECIOUS METAL DERIVATIVE EXPOSURE (NORTH OF ONE TRILLION DOLLARS) AND THIS IS PROBABLY THE MAJOR REASON FOR GOLD/SILVER’S RISE THESE PAST TWO MONTHS. THEY ARE TOTALLY TRAPPED., AND THEIR FAILURE TO STOP CENTRAL BANK PURCHASES OF PHYSICAL GOLD IS THE MAJOR ISSUE OF THE DAY!

OUR PHYSICAL LONDONERS BOUGHT NEW MASSIVE QUANTITIES OF LONGS AT ANY PRICE AND THIS GOLD BOUGHT WILL BE TENDERED FOR PHYSICAL ON A T + 1 BASIS. BECAUSE GOLD IS BASEL III COMPLIANT, GOLD MUST BE DELIVERED IN A VERY TIMELY ONE DAY. CENTRAL BANKS AROUND THE WORLD, BEING REPRESENTED BY OUR LONDONERS, ARE THE REAL PURCHASERS OF THIS GOLD.

THE PROBLEM FOR THOSE PROVIDING THE SHORT PAPER IS THE SHOCK TO THEM ON RECEIVING NOTICE THAT THE LONGS WANT THE PHYSICAL GOLD AS THEY TENDER FOR THAT SHINY YELLOW METAL. THE HIGH LIQUIDATION OF THE SPREADERS // T.A.S DURING THE LAST WEEK OF DECEMBER IS SURELY DISTORTING COMEX OPEN INTEREST BUT THAT DOES NOT STOP LONDON’S ACCUMULATION OF PHYSICAL! YOU CAN ALSO VISUALIZE THAT PERFECTLY WITH THE HUGE AMOUNTS OF QUEUE JUMPING ORCHESTRATED BY CENTRAL BANKERS BOLTING AHEAD OF ORDINARY LONGS AS THEIR NEED FOR PHYSICAL IS GREAT AS THEY SCOUR THE PLANET LOOKING FOR GOLD. AS YOU WILL SEE BELOW, WE HAD ANOTHER HUGE QUEUE JUMPING SESSION.

EXCHANGE FOR PHYSICAL ISSUANCE

WE ARE NOW DEEP INTO THE NON ACTIVE DELIVERY MONTH OF JANUARY.… THE CME REPORTS THAT THE BANKERS ISSUED A STRONG SIZED TRANSFER THROUGH THE EFP ROUTE AS THESE LONGS RECEIVED A DELIVERABLE LONDON FORWARD TOGETHER WITH A FIAT BONUS.,

THAT IS A VERY STRONG SIZED 5771 EFP CONTRACTS WERE ISSUED: : /FEB 5771 & ZERO FOR ALL OTHER MONTHS:

TOTAL EFP ISSUANCE: 5771 CONTRACTS. THESE EFP;S CIRCLE AROUND LONDON ON A 13 DAY BASIS AND ARE NOW USED BY GLOBAL CENTRAL BANKS TO EXERCISE FOR PHYSICAL GOLD WITH THE OBLIGATION TO DELIVER BEING FORCED ONTO COMEX BANKS. THE GOLD DELIVERED COMES FROM LONDON.

ON A NET BASIS IN OPEN INTEREST WE GAINED THE FOLLOWING TODAY ON OUR TWO EXCHANGES: A FAIR SIZED TOTAL OF 2642 CONTRACTS IN THAT 5771 CONTRACT LONGS WERE TRANSFERRED AS EXCHANGE FOR PHYSICALS TO LONDON AND WE HAD A FAIR LOSS OF 3129 COMEX CONTRACTS..AND THIS FAIR GAIN ON OUR TWO EXCHANGES HAPPENED WITH OUR LOSS IN PRICE OF $4.90 MONDAY// COMEX. THE EXCHANGE FOR PHYSICALS WILL BE USED BY CENTRAL BANKS, TO EXERCISE FOR PHYSICAL GOLD AT THE COMEX AS MENTIONED ABOVE.

AS PER OUR NEWBIE TRADE AT SETTLEMENT (TAS) MANIPULATION OPERATION (WHICH CRAIG HEMKE HAS POINTED OUT HAPPENS USUALLY DURING MID MONTH IN THE DELIVERY CYCLE), BUT NOW ON A DAILY BASIS, THE CME REPORTS THAT THE TOTAL T.A.S. ISSUANCE FOR MONDAY NIGHT WAS A STRONG SIZED SIZED 1789 CONTRACTS, AND THESE WILL BE USED TO REPLENISH SUPPLIES.. ALMOST ALL OF THE TRADING AND SUPPLY OF CONTRACTS WAS ORCHESTRATED BY GOVERNMENT (FEDERAL RESERVE BANK OF NEW YORK).

THROUGHOUT THE PAST SEVERAL WEEKS, THE BANKERS CONTINUE TO SELL OFF THE LONG SIDE OF THE SPREAD (T.A.S.) WHICH OF COURSE CONTINUES TO MANIPULATE THE PRICE OF GOLD SOUTHBOUND. (THEY KEEP THE SHORT SIDE OF THE CALENDAR/T.A.S. SPREAD WHICH WILL BE LIQUIDATED IN DAYS HENCE//. IT SEEMS THAT OUR CROOKS ORCHESTRATED, ON DEC. 27, THEIR HUGE RAID TO LOWER THE PRICE OF GOLD TO MAKE THEIR COMEX BETS WHOLE ON OPTIONS EXPIRY WEEK AND THUS THE NEED FOR CONTINUAL STRONG T.A.S. ISSUANCE AND THEN LIQUIDATION. THIS WAS COUPLED WITH THE LIQUIDATION OF CALENDAR SPREADERS . THE USE OF OUR TWO SPREADER MECHANISMS WERE OF EXTREME IMPORTANCE TO OUR CROOKS IN LATE DECEMBER’S OPTIONS EXPIRY TRADING. T.A.S. LIQUIDATION WAS EVIDENT IN MONDAY’S COMEX TRADING//RAID.

// WE HAVE A STRONG AMOUNT OF GOLD TONNAGE STANDING: JAN (23.3558 TONNES) WHICH IS HUGE FOR OUR NON ACTIVE JAN DELIVERY MONTH.

JANUARY: 10.1331 TONNES

HERE ARE THE AMOUNTS THAT STOOD FOR DELIVERY IN THE PRECEDING 49 MONTHS OF 2021-2024:

DEC 2021: 112.217 TONNES

NOV. 8.074 TONNES

OCT. 57.707 TONNES

SEPT: 11.9160 TONNES

AUGUST: 80.489 TONNES

JULY 7.2814 TONNES

JUNE: 72.289 TONNES

MAY 5.77 TONNES

APRIL 95.331 TONNES

MARCH 30.205 TONNES

FEB ’21. 113.424 TONNES

JAN ’21: 6.500 TONNES.

TOTAL YEAR 2021 (JAN- DEC): 601.213 TONNES

YEAR 2022:

JANUARY 2022 17.79 TONNES

FEB 2022: 59.023 TONNES

MARCH: 36.678 TONNES

APRIL: 85.340 TONNES FINAL.

MAY: 20.11 TONNES FINAL

JUNE: 74.933 TONNES FINAL

JULY 29.987 TONNES FINAL

AUGUST:104.979 TONNES//FINAL

SEPT. 38.1158 TONNES

OCT: 77.390 TONNES/ FINAL

NOV 27.110 TONNES/FINAL

Dec. 64.000 tonnes

(TOTAL YEAR 656.076 TONNES)

2023:

JAN/2023: 20.559 tonnes

FEB 2023: 47.744 tonnes

MAR: 19.0637 TONNES

APRIL: 75.676 tonnes

MAY: 19.094 TONNES + 1.244 tonnes of exchange for risk = 20.338

JUNE: 64.354 TONNES

JULY: 10.2861 TONNES

AUGUST: 38.855 TONNES(INCLUDING .6842 EXCHANGE FOR RISK)

SEPT: 15.281 TONNES FINAL

OCT. 35.869 TONNES + 1.665 EXCHANGE FOR RISK =37.0355 tonnes

NOV: 18.7122 TONNES + 16.2505 EX. FOR RISK = 34.9627 TONNES

DEC. 47.073 + 4.634 TONNES OF EXCHANGE FOR RISK = 51.707 TONNES

TOTAL 2023 YEAR : 436.546 TONNES

2024

JAN ’24. 22.706 TONNES

FEB. ’24: 66.276 TONNES (INCLUDES 1.723 TONNES EX. FOR RISK)

MARCH: 18.8398 TONNES + 1.1695 EX FOR RISK = 20.093 TONNES

APRIL: 2024: 53.673TONNES FINAL

MAY/ 2024 8.5536 TONNES + 3.3716 TONNES EX FOR RISK/= 11.9325

JUNE; 95.578 TONNES. + 1.045 TONNES EXCHANGE FOR RISK =96.623 THIS IS THE HIGHEST RECORDED GOLD STANDING SINCE AUGUST 2022

JULY: 11.692 TONNES

AUGUST 69.602 TONNES//FINAL STANDING

SEPT. 13.164 TONNES.

OCT 39.474 TONNES + + 20.917 TONNES EXCHANGE FOR RISK =60.391 TONNES

NOV . 11.265 TONNES +4.665 TONNES EXCHANGE FOR RISK/TUESDAY + 3.11 TONNES OF EX. FOR RISK/PRIOR = 19.0425 TONNES

DEC: 80.4230 TONNES PLUS DEC MONTH EXCHANGE FOR RISK TOTAL 14.6836 TONNES EQUALS 95.1066 TONNES

total year: 540.30 tonnes

January 2025: 18.068 TONNES + 5.28775 EX FOR RISK/PRIOR = 23.3558 TONNES

THE SPECS/HFT WERE SUCCESSFUL IN LOWERING GOLD’S PRICE( IT FELL BY $4.90/)//BUT WERE UNSUCCESSFUL IN KNOCKING OFF ANY NET SPECULATOR LONGS AS WE DID HAVE A FAIR GAIN IN OUR TWO EXCHANGES. AS EXPLAINED ABOVE WE HAD CONSIDERABLE T.A.S. SPREADER LIQUIDATION MONDAY

THE CROOKS COULD NOT STOP CENTRAL BANK LONGS, SEIZING THE MOMENT, THEY EXERCISED AGAIN FOR PHYSICAL IN A BIG WAY TENDERING FOR PHYSICAL MONDAY EVENING.

EXCHANGE FOR RISK EXPLANATION/DECEMBER TRADING AND NOW JANUARY!!

36 DAYS AGO, FRIDAY NIGHT (EARLY SATURDAY MORNING NOV 30) THE CME ANNOUNCED ANOTHER OF THOSE CRAZY DELIVERIES: THE ISSUANCE OF 250 EXCHANGE FOR RISK CONTRACTS WHICH TOTAL 25000 OZ (.7776 TONNES. HERE THE BUYER ASSUMES THE RISK THAT HE WILL BE DELIVERED UPON IN PHYSICAL METAL. THIS IS ABSOLUTELY INSANE AND A HUGE VIOLATION OF THE TRUE DISCOVERY PRICE MECHANISM WHICH IS THE COMEX MANTRA!. AND THEN GUESS WHAT? THE CME ANNOUNCED ANOTHER EXCHANGE FOR RISK, LATE TUESDAY EVENING/ EARLY WEDNESDAY MORNING, (DEC 5) OF 617 CONTRACTS FOR 61,700 OZ OR GOLD (1.919 TONNES). THEN MUCH TO MY ANGER, THE CME ANNOUNCED A THIRD ISSUANCE FRIDAY NIGHT DEC 7 FOR A MONSTROUS 2254 EXCHANGE FOR RISK CONTRACTS OR 225,400 OZ OR 7.0108 TONNES. NOT TO BE UNDONE, THE CROOKS CONTINUED WITH THEIR NONSENSE WITH ANOTHER 50 CONTRACT EXCHANGE FOR RISK THE MORNING OF DEC 12 FOR 5000 OZ OR .1555 TONNES. AND THIS BRINGS US TO THIS EARLY FRIDAY MORNING (DEC 13) WHERE I WAS SHOCKED TO SEE FOR THE FIFTH TIME THIS MONTH AN ENTRY FOR 250 CONTRACTS OF EXCHANGE FOR RISK FOR 25000 OZ OR .7776 TONNES.THUS ALL FIVE OF THESE ISSUANCES WILL BE ADDED TO THE TOTAL GOLD BEING “DELIVERED UPON”. THIS BRINGS US TO EARLY SATURDAY MORNING DEC 21 WHERE TO MY SHOCK AGAIN WE HAD OUR 6TH ISSUANCE OF EXCHANGE FOR RISK TOTALLING 1300 CONTRACTS FOR AN ASTOUNDING 4.043 TONNES. THIS BRINGS THE TOTAL ISSUANCE FOR THE MONTH OF DEC TO 14.6836 TONNES. THE COMEX IS TOTALLY SHATTERED TO PIECES.

WE NOW BEGIN OUR NEW MONTH OF JANUARY AND LO AND BEHOLD, THE CROOKS ISSUED ANOTHER MONSTER 1700 CONTRACTS FOR EXCHANGE FOR RISK TOTALLING 170,000 OZ OR 5.28775 TONNES ON MONDAY JAN 6/2025. THIS TONNAGE WILL BE ADDED TO OUR REGULAR DELIVERIES.

TOTAL DELIVERIES JANUARY TRADING

WE HAVE GAINED A TOTAL OF 8.2177 PAPER TONNES FROM OUR TWO EXCHANGES, ACCOMPANYING OUR INITIAL GOLD TONNAGE STANDING FOR JAN (10.133TONNES) ON FIRST DAY NOTICE FOLLOWED BY TODAY’S MONSTER QUEUE JUMP OF 876 CONTRACTS OR 87,600 OZ (2.724 TONNES) TO WHICH WE MUST ADD OUR 5.28775 TONNES OF EXCHANGE FOR RISK WHERE THE BUYERS ASSUMES THE RISK FOR DELIVERY.(ISSUED JAN 6/2025)

NEW STANDING FOR JAN: 18.068 TONNES + 5.28775 TONNES EX FOR RISK/PRIOR = 23.3558 TONNES (WHICH IS HUGE FOR OUR VERY ACTIVE DELIVERY MONTH)

ALL OF THIS WAS ACCOMPLISHED DESPITE OUR LOSS IN PRICE TO THE TUNE OF $4.90

WE HAD 175 CONTRACTS ADDED TO THE COMEX TRADES TO OPEN INTEREST (CROOKS)//PRELIMINARY TO FINAL.

NET GAIN ON THE TWO EXCHANGES 2642 CONTRACTS OR 264,200 OZ (8.2177 TONNES)

confirmed volume MONDAY 196,652 contracts: weak ////nobody wishes to play with the crooks

//speculators have left the gold arena

END

/ /// THE JAN 2024 GOLD CONTRACT

JAN 7

INITIAL

| Gold | Ounces |

| Withdrawals from Dealers Inventory in oz | nil |

| Withdrawals from Customer Inventory in oz | . NIL |

| Deposit to the Dealer Inventory in oz | NIL |

| Deposits to the Customer Inventory, in oz | NIL |

| No of oz served (contracts) today | 77 notice(s) 7700 OZ 0.2372 TONNES |

| No of oz to be served (notices) | 1883 contracts 188300 OZ 5.856 TONNES |

| Total monthly oz gold served (contracts) so far this month | 3926 notices 392600 oz 12.2115 TONNES |

| Total accumulative withdrawals of gold from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of gold from the Customer inventory this month | x |

dealer deposits: 0

total dealer deposits: end

we have 0 customer deposit

total deposit NIL oz

withdrawals: 0

adjustments:0

CALCULATIONS FOR THE AMOUNT OF GOLD STANDING FOR JAN.

For the front month of JAN: we have an oi of 1960 contracts having GAINED A HUGE 293 contracts. We had a strong 583 contract issuance on MONDAY. Thus a MONSTER QUEUE JUMP (GAIN) of 876 contracts on our two exchanges. (87,600 oz or 2.724 tonnes)

FEBRUARY LOST 7680 CONTRACTS TO 322,286 .

MARCH HAD A GAIN OF 71 CONTRACTS UP TO 136

APRIL HAD A GAIN OF 2971 CONTRACTS UP TO 74,908 CONTRACTS

We had 77 contracts filed for today representing 7700 oz

This is a huge major assault on the comex for gold and this time it is physical that will be requested.

Today, 0 notice(s) were issued from J.P.Morgan dealer and 0 notices issued from their client or customer account. The total of all issuance by all participants equate to 77 contract(s) of which 0 notices were stopped (received) by j.P. Morgan dealer and 6 notice(s) was (were) stopped (received) by J.P.Morgan//customer account

To calculate the INITIAL total number of gold ounces standing for JAN /2025. contract month, we take the total number of notices filed so far for the month (3926 x 100 oz ) to which we add the difference between the open interest for the front month of JAN(1960 CONTRACTS) minus the number of notices served upon today (77 x 100 oz per contract( equals 580,900 OZ OR 18.068 TONNES. to which we add those criminal exchange for risk issuance of 5.28775 tonnes/PRIOR = 23.3558 tonnes

thus the INITIAL standings for gold for the JAN contract month: No of notices filed so far (3926 x 100 oz +we add the difference for front month of JAN (1960 OI} minus the number of notices served upon today (77 x 100 oz which equals 580,900 oz (18.068 TONNES) + 5.28775 tonnes ex for risk/PRIOR = 23.3558

TOTAL COMEX GOLD STANDING FOR JAN.: 23.3558 TONNES WHICH IS HUGE FOR THIS NON ACTIVE DELIVERY MONTH IN THE CALENDAR.

XXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXXX

COMEX GOLD INVENTORIES/CLASSIFICATION

NEW PLEDGED GOLD:

241,794.285 oz NOW PLEDGED /HSBC 5.94 TONNES

204,937.290 OZ PLEDGED MANFRA 3.08 TONNES

83,657.582 PLEDGED JPMorgan no 1 1.690 tonnes

265,999.054, oz JPM No 2

1,152,376.639 oz pledged Brinks/

Manfra: 33,758.550 oz

Delaware: 193.721 oz

International Delaware:: 11,188.542 oz

total pledged gold: 2,122,692.639 oz 66.02 tonnes

TOTAL OF ALL GOLD ELIGIBLE AND REGISTERED GOLD: 21,972,508.258 OZ

TOTAL REGISTERED GOLD 9,043,231.170 oz or 281.28 tonnes

TOTAL OF ALL ELIGIBLE GOLD: 12,929,227.088 OZ

REGISTERED GOLD THAT CAN BE SERVED UPON: 6,920,539 oz (REG GOLD- PLEDGED GOLD)= 215.25 tonnes //

JPMorgan enhanced inventory is 3.592 million oz/1,877,000 oz = 19.15% of entire inventory..

END

SILVER/COMEX

JAN 7. 2025

INITIAL

//2024// THE JAN 2025 SILVER CONTRACT//INITIAL

| Silver | Ounces |

| Withdrawals from Dealers Inventory | NIL oz |

| Withdrawals from Customer Inventory | 2 i) Out of BRINKS 30,912.730 oz ii) Out of DELAWARE 199,205.223 oz total withdrawal: 230,117.653 oz . |

| Deposits to the Dealer Inventory | NIL |

| Deposits to the Customer Inventory | i) Into CNT; 598,886.960 oz ii) Into Brinks 133,978.800 oz iii) Into Loomis 1198,321.77 oz iv) Into JPM 4008.400 oz v) into Brinks addition: 635,480.000 oz total deposit 2,570,675.930 |

| No of oz served today (contracts) | 184 CONTRACT(S) (920,000 OZ) |

| No of oz to be served (notices) | 150 contracts (0.750 MILLION oz) |

| Total monthly oz silver served (contracts) | 1488 Contracts (7.440 oz) |

| Total accumulative withdrawal of silver from the Dealers inventory this month | NIL oz |

| Total accumulative withdrawal of silver from the Customer inventory this month |

i) 0 dealer deposit/

total dealer deposit : nil oz

i) We had 0 dealer withdrawal

total dealer withdrawals: 0 oz

deposits:5

i) Into CNT 598,886.960 oz

ii)Into Brinks 133,978.800 oz

iii) Into Loomis 1198,321.77 oz

iv) Into JPM 4008.400 oz

v0 Into Brinks added 635,480.000 oz

total deposit: 2,570.675.930 oz

We had 2 withdrawals

i) Out of Brinks: 30,912.430 oz

ii) Out of Delaware 199,205.223 oz

total withdrawal: 230,117.653 oz

JPMorgan has a total silver weight: 135.532million oz/320.047million or 42.34%

adjustments:1 customer to dealer: CNT 740,789.400 oz

TOTAL REGISTERED SILVER: 73,242 MILLION OZ//.TOTAL REG + ELIGIBLE. 320.047 million oz

CALCULATIONS FOR THE NEW STANDING FOR SILVER FOR JANUARY

silver open interest data:

FRONT MONTH OF JAN /2024 OI: 334 OPEN INTEREST FOR A LOSS OF 45 CONTRACT(S).

WE HAD ONLY 3 CONTRACT ISSUANCE ON MONDAY. THUS WE LOST 42 CONTRACTS, THAT IS WE HAD A 42 CONTRACT EXCHANGE FOR PHYSICAL TRANSFER TO LONDON FOR 210,000 OZ AS THE BOYS COULD NOT FIND ANY SILVER OVER HERE SO THEY DECIDED TO TRY THEIR LUCK OVER IN LONDON

FEBRUARY SAW A LOSS 0F 45 CONTRACTS TO STAND AT 669

MARCH SAW A LOSS OF 647 CONTRACTS DOWN TO 119,375

TOTAL NUMBER OF NOTICES FILED FOR TODAY: 3 for 15,000 oz

CONFIRMED volume; ON FRIDAY 67,755 awful//

To calculate the number of silver ounces that will stand for delivery in JAN we take the total number of notices filed for the month so far at 1488x 5,000 oz = 7.440 MILLION oz

to which we add the difference between the open interest for the front month of JAN (334) and the number of notices served upon today (184)x (5000 oz)

Thus the standings for silver for the JAN 2025 contract month: 1488 Notices served so far) x 5000 oz + OI for the front month of JAN(334) minus number of notices served upon today (184)x 5000 oz equals silver standing for the JAN contract month equating to 8.1900 MILLION OZ.

New total standing: 8.190 million oz.

There are 73.242 million oz of registered silver.

The record level of silver open interest is 234,787 contracts set on April 21./2017 with the price on that day at $18.42. The previous record was 224,540 contracts with the price at that time of $20.44.

Now that we have surpassed $28.40 the next big line in the sand for silver is $34.76. After that the moon

END

BOTH GLD AND SLV ARE MASSIVE FRAUDS!

GLD AND SLV INVENTORY LEVELS//

JAN 7 WITH GOLD DOWN $14.50 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

JAN 6 WITH GOLD DOWN $4.90 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

JAN 3 WITH GOLD DOWN $14.00 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

JAN 2 WITH GOLD UP $29.40 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

DEC 31 WITH GOLD UP $20.60 ON THE DAY; NO CHANGES IN GOLD AT THE GLD:: ///INVENTORY RESTS AT 872.52 TONNES

DEC 30 WITH GOLD DOWN $11.95 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 0.28 TONNES OF GOLD FROM THE GLD : ///INVENTORY RESTS AT 872.52 TONNES

DEC 27 WITH GOLD DOWN $17.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 1.15 TONNES OF GOLD FROM THE GLD : ///INVENTORY RESTS AT 872.80 TONNES

DEC 26 WITH GOLD UP $17.55 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: : ///INVENTORY RESTS AT 873.95 TONNES

DEC 24 WITH GOLD UP $6.10 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.45 TONNES OF GOLD OUT OF THE GLD. / // : .///INVENTORY RESTS AT 873.95 TONNES

DEC 23 WITH GOLD DOWN $13,75 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A DEPOSIT OF 16.66 TONNES OF GOLD VAPOUR GOLD INTO THE GLD. / // : .///INVENTORY RESTS AT 877.40 TONNES

DEC 20 WITH GOLD UP $29,75 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF 3.16 TONNES OF GOLD FROM THE GLD. / // : .///INVENTORY RESTS AT 860.74 TONNES

DEC 19 WITH GOLD DOWN $45.00 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD:A WITHDRAWAL OF .29 TONNES OF GOLD FROM THE GLD. / // : .///INVENTORY RESTS AT 863.90 TONNES

DEC 18 WITH GOLD DOWN $8.40 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: / // : .///INVENTORY RESTS AT 864.19 TONNES

DEC 17 WITH GOLD DOWN $6.85 ON THE DAY; SMALL CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 0.23 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 864.19 TONNES

DEC 16 WITH GOLD DOWN $2.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.70 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 863.90 TONNES

DEC 13 WITH GOLD DOWN $24.55 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A WITHDRAWAL OF 4.78 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 868.60 TONNES

DEC 12 WITH GOLD DOWN $34.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD: A DEPOSIT OF 2.59 TONNES INTO THE GLD / // : .///INVENTORY RESTS AT 873.38 TONNES

DEC 11 WITH GOLD UP $29.75 ON THE DAY; NO CHANGES IN GOLD AT THE GLD: // : .///INVENTORY RESTS AT 870.79 TONNES

DEC 9 WITH GOLD UP $31.10 ON THE DAY; NO CHANGES IN GOLD AT THE GLD. // : .///INVENTORY RESTS AT 871.94 TONNES

DEC 6 WITH GOLD UP $6.60 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD. A WITHDRAWAL OF 1.71 TONNES OF GOLD FROM THE GLD// : .///INVENTORY RESTS AT 871.94 TONNES

DEC 5 WITH GOLD DOWN $26.80 ON THE DAY; NO CHANGES IN GOLD AT THE GLD./ : .///INVENTORY RESTS AT 873.65 TONNES

DEC 4 WITH GOLD UP $6.15 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.31 TONNES OF GOLD FROM THE GLD./ : .///INVENTORY RESTS AT 873.65 TONNES

DEC 3 WITH GOLD UP $10.30 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD A WITHDRAWAL OF 2.59 TONNES OF GOLD FROM THE GLD./ : .///INVENTORY RESTS AT 875.96 TONNES

DEC 2 WITH GOLD DOWN $20.20 ON THE DAY; NO CHANGES IN GOLD AT THE GLD : .///INVENTORY RESTS AT 878.55 TONNES

NOV 29 WITH GOLD UP $16.00 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD : Z WITHDRAWAL OF .86 TONNES OF GOLD FROM THE GLD . .///INVENTORY RESTS AT 878.55 TONNES

NOV 27 WITH GOLD UP $18.05 ON THE DAY; NO CHANGES IN GOLD AT THE GLD : . .///INVENTORY RESTS AT 879.41 TONNE

NOV 26 WITH GOLD UP $3.80 ON THE DAY; HUGE CHANGES IN GOLD AT THE GLD : A DEPOSIT OF 1.44 TONNES OF GOLDINTO THE GLD. .///INVENTORY RESTS AT 879.41 TONNES

GLD INVENTORY: 872.52 TONNES, TONIGHTS TOTAL

SILVER

JAN 7 WITH SILVER UP 48 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.709 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 463.837 MILLION OZ

JAN 6 WITH SILVER UP 38 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.709 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 463.837 MILLION OZ

JAN 3 WITH SILVER UP 17 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.709 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 463.837 MILLION OZ

JAN 2 WITH SILVER UP 45 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: A DEPOSIT OF 1.616 MILLION OZ INTO THE SLV//INVENTORY AT SLV RESTS AT 462.128 MILLION OZ

DEC 31 WITH SILVER DOWN 14 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV//INVENTORY AT SLV RESTS AT 460.512 MILLION OZ

DEC 30 WITH SILVER DOWN 39 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV: // A WITHDRAWAL OF 1.13 MILLION OZ FROM THE SLV//INVENTORY AT SLV RESTS AT 460.512 MILLION OZ

DEC 27 WITH SILVER DOWN 24 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV: // //INVENTORY AT SLV RESTS AT 461.651 MILLION OZ

DEC 24 WITH SILVER UP 2 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV// //INVENTORY AT SLV RESTS AT 463.747 MILLION OZ

DEC 23 WITH SILVER UP 19 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV/////A DEPOSIT OF 6.15 MILLION OZ INTO THE SLV //INVENTORY AT SLV RESTS AT 463.747 MILLION OZ

DEC 20 WITH SILVER UP 43 CENTS //SMALL CHANGES IN SILVER INVENTORY AT THE SLV/////A DEPOSIT OF 183,000 OZ INTO THE SLV //INVENTORY AT SLV RESTS AT 457.597 MILLION OZ

DEC 19 WITH SILVER DOWN 25 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV///// //INVENTORY AT SLV RESTS AT 457.414 MILLION OZ

DEC 18 WITH SILVER DOWN 19 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 1.094 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 457.414 MILLION OZ

DEC 17 WITH SILVER DOWN 12 CENTS //SMALL CHANGES IN SILVER INVENTORY AT THE SLV A DEPOSIT OF 0.456 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 458.052 MILLION OZ

DEC 16 WITH SILVER DOWN 0 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF 4.84 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 458.052 MILLION OZ

DEC 13 WITH SILVER DOWN 46 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A WITHDRAWAL OF .536 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 462.892 MILLION OZ

DEC 12 WITH SILVER DOWN 94 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 5.787 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 463.428 MILLION OZ

DEC 11 WITH SILVER UP 10 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 2.597 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 469.215 MILLION OZ

DEC 10 WITH SILVER DOWN 8 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 1.868 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 471.812 MILLION OZ

DEC 9 WITH SILVER UP $0.91 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE WITHDRAWAL OF 1.367 MILLION OZ FROM THE SLV/// //INVENTORY AT SLV RESTS AT 473.680 MILLION OZ

DEC 6 WITH SILVER DOWN $0.00 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV A MASSIVE DEPOSIT OF 4.329 MILLION OZ/// //INVENTORY AT SLV RESTS AT 475.047 MILLION OZ

DEC 5 WITH SILVER DOWN $0.23 //NO CHANGES IN SILVER INVENTORY AT THE SLV” /// //INVENTORY AT SLV RESTS AT 470.718 MILLION OZ

DEC 4 WITH SILVER UP 26 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV”: A WITHDRAWAL OF 2.206 MILLION OZ FORM THE SLV. /// //INVENTORY AT SLV RESTS AT 470.718 MILLION OZ

DEC 3 WITH SILVER UP 59 CENTS //NO CHANGES IN SILVER INVENTORY AT THE SLV /// //INVENTORY AT SLV RESTS AT 472.924 MILLION OZ

DEC 2 WITH SILVER DOWN 19 CENTS //HUGE CHANGES IN SILVER INVENTORY AT THE SLV. A WITHDRAWAL OF 1,458,000 OZ FROM THE SLV. /// //INVENTORY AT SLV RESTS AT 472.924 MILLION OZ

NOV 29 WITH SILVER UP 51 CENTS //SMALL CHANGES IN SILVER INVENTORY AT THE SLV. A WITHDRAWAL OF 365,000 OZ FROM THE SLV. /// //INVENTORY AT SLV RESTS AT 474.382 MILLION OZ

NOV 27 WITH SILVER DOWN $0.25 //NO CHANGES IN SILVER INVENTORY AT THE SLV.. /// //INVENTORY AT SLV RESTS AT 474.747 MILLION OZ

NOV 26 WITH SILVER UP $0.10 //HUGE CHANGES IN SILVER INVENTORY AT THE SLV:.A WITHDRAWAL OF 1.094 MILLION OZ FROM THE SLV./.. /// //INVENTORY AT SLV RESTS AT 474.747 MILLION OZ

CLOSING INVENTORY 463.837 MILLION OZ//

PHYSICAL GOLD/SILVER COMMENTARIES

1/ PETER SCHIFF/SCHIFF GOLD/MIKE MAHARRY

END

2/ Commentaries from: Egon von Greyerz///Matthew Piepenburg via GoldSwitzerland.com, Pam and Russ Martens

Alasdair Macleod

END

3. CHRIS POWELL AND GATA DISPATCHES

4. OTHER GOLD COMMENTARIES/

END

ANDREW MAGUIRE AND ALASDAIR MACLEOD//LIVE FROM THE VAULT 204

end

5 B GLOBAL COMMODITY ISSUES/FOOD IN GENERAL//FREIGHT/COMMODITIES: COMMODITY/EGGS

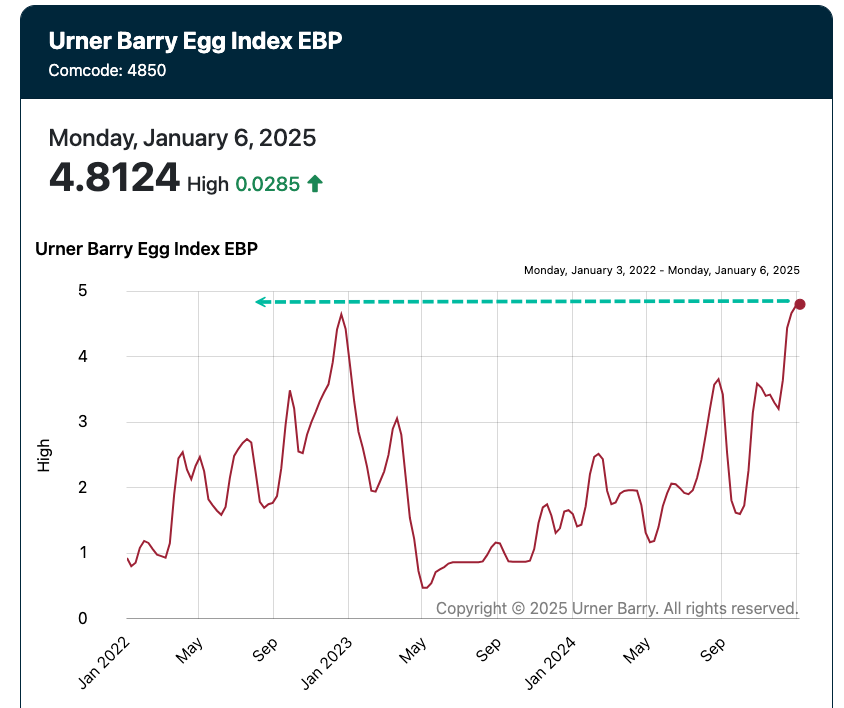

Wholesale Egg Prices Hit Record, Shortages Reported At Supermarkets

Tuesday, Jan 07, 2025 – 01:05 PM

Wholesale egg prices, as tracked by the Urner Barry Egg Index, have reached record highs at the start of the new year. This surge is mostly driven by the ongoing devastating impact of Highly Pathogenic Avian Influenza (HPAI), which has crushed commercial flocks and dented the nation’s egg-laying capacity.

Three weeks ago, new data from Expana showed that a dozen eggs at Midwest supermarkets averaged around $5.67, a record high that eclipsed the prior high of $5.46 set in December 2022.

Expana’s managing editor for eggs in the Americas, Karyn Rispoli, told Bloomberg last month that a “potent combination of avian flu-related production losses and heightened retail demand throughout the holiday baking season” catapulted prices to record highs.

Rispoli said 17 million egg-laying hens and younger birds known as pullets had been culled since mid-October amid a surge in bird flu cases, adding that was one of the worst stretches in the current bird flu outbreak since the virus first emerged in the nation’s flock in February 2022.

Last week, the USDA released a report showing the nation’s egg production totaled 8.92 billion, down 4% from the same period last year. Sliding production has sparked egg shortages at supermarkets in certain regions across the US.

The Google Search trend “egg shortage” has erupted to the highest levels since late 2022.

In California alone, USDA data showed the price of a dozen large white eggs spiked to as high as $8.97 last week, up from $5.23 in late November – a 70% increase.

end

6 CRYPTOCURRENCY NEWS

END

ASIA TRADING TUESDAY MORNING MONDAY NIGHT

SHANGHAI CLOSED UP 22.72 PTS OR 0.71%

//Hang Seng CLOSED DOWN 240.71 PTS OR 1.97%

// Nikkei CLOSED UP 776.25 OR 1.97%//Australia’s all ordinaries CLOSED UP 0.65%

//Chinese yuan (ONSHORE) CLOSED DOWN TO 7.3394 CHINESE YUAN OFFSHORE CLOSED UP TO 7.3392// Oil DOWN TO 74.16 dollars per barrel for WTI and BRENT DOWN AT 76.49 Stocks in Europe OPENED ALL MOSTLY GREEN

ONSHORE USA/ YUAN TRADING AT LEVEL OF OFFSHORE YUAN/ONSHORE YUAN TRADING WEAKER AGAINST US DOLLAR/OFFSHORE YUAN WEAKER

xxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxxx

1.YOUR EARLY CURRENCY VALUES/GOLD AND SILVER PRICING/ASIAN AND EUROPEAN BOURSE MOVEMENTS/AND INTEREST RATE SETTINGS TUESDAY MORNING.7:30 AM

ONSHORE YUAN: CLOSED DOWN AT 7.3394

OFFSHORE YUAN: DOWN TO 7.3392

SHANGHAI CLOSED CLOSED UP 22.72 PTS OR 0.71%

HANG SENG CLOSED CLOSED DOWN 240.71 PTS OR 1.22%

2. Nikkei closed UP 776.25PTS OR 1.22%

3. Europe stocks SO FAR: ALL MOSTLY GREEN

USA dollar INDEX DOWN TO 108.04 EURO RISES TO 1.0401 UP 18 BASIS PTS

3b Japan 10 YR bond yield: RISES TO. +1.120 Japan buying 100% of bond issuance)/Japanese YEN vs USA cross now at 157.75…… JAPANESE YEN NOW FALLING AS WE HAVE NOW REACHED THE RE EMERGING OF THE YEN CARRY TRADE AGAIN AFTER DISASTROUS POLICY ISSUED BY UEDA

3c Nikkei now ABOVE 17,000

3d USA/Yen rate now well ABOVE the important 120 barrier this morning

3e Gold UP /JAPANESE Yen UP CHINESE ONSHORE YUAN: UP OFFSHORE: UP

3f Japan is to buy INFINITE TRILLION YEN worth of BONDS. Japan’s GDP equals 5 trillion USA

Japan to buy 100% of all new Japanese debt and NOW they will have OVER 50% of all Japanese debt.

3g Oil DOWN for WTI and DOWN FOR UP this morning

3h European bond buying continues to push yields lower on all fronts in the EMU. German 10yr bund YIELD UP TO +2.4495 Italian 10 Yr bond yield UP to 3.592 //SPAIN 10 YR BOND YIELD UP TO 3.112

3i Greek 10 year bond yield UP TO 3.213

3j Gold at $2652.50/Silver at: 30.25 1 am est) SILVER NEXT RESISTANCE LEVEL AT $50.00//AFTER 28.40

3k USA vs Russian rouble;// Russian rouble UP 0 AND 50/100 roubles/dollar; ROUBLE AT 107.00

3m oil into the 74 dollar handle for WTI and 76 handle for Brent/

3n Higher foreign deposits moving out of China// huge risk of outflows and a currency depreciation. This can spell financial disaster for the rest of the world/

JAPAN ON JAN 29.2016 CONTINUES NIRP. THIS MORNING RAISES AMOUNT OF BONDS THAT THEY WILL PURCHASE UP TO .5% ON THE 10 YR BOND///YEN TRADES TO 157.75 10 YEAR YIELD AFTER FIRST BREAKING .54% LAST YEAR NOW EXCEEDS THAT LEVEL TO 1.120% STILL ON CENTRAL BANK (JAPAN) INTERVENTION//YEN CARRY TRADE IS NOW UNWINDING.

30 SNB (Swiss National Bank) still intervening again in the markets driving down the FRANC. It is not working: USA/SF this 0.9073 as the Swiss Franc is still rising against most currencies. Euro vs SF: 0.9435 well above the floor set by the Swiss Finance Minister. Thomas Jordan, chief of the Swiss National Bank continues to purchase euros trying to lower value of the Swiss Franc.

USA 10 YR BOND YIELD: 4.697 UP 3 BASIS PTS…

USA 30 YR BOND YIELD: 4.869 UP 3 BASIS PTS/

USA 2 YR BOND YIELD: 4.277 UP 1 BASIS PTS

USA DOLLAR VS TURKISH LIRA: 35.31…

10 YR UK BOND YIELD: 4.6945 UP 5 PTS

10 YR CANADA BOND YIELD: 3.285 UP 3 BASIS PTS

5 YR CANADA BOND YIELD: 3.000 UP 1 PTS.

2a New York OPENING REPORT

US Futures Rise With NVDA At New All-Time High

Tuesday, Jan 07, 2025 – 08:29 AM

US equity futures are up small this morning as yields continue to rise (SPX +17bps; NDX +5bps; US 10 year yield higher at 4.64%). As a reminder equities typically struggle when rates rise by 2 standard deviations in a given month, which in today’s terms is ~60bps. Stocks remain wobbly after yesterday’s performance which saw big tech \the standout, vs the Dow and S&P equal weight down on the day. Nvidia rose 1.9% in premarket trading to a new record high after CEO Jensen Huang announced a raft of new chips, software and services. Uber also gained on news about a collaboration with Nvidia for autonomous driving technology. Overnight, Europe is broadly higher with Eurozone inflation coming in line with forecasts, though ECB survey shows consumer inflation expectations picked up. Asia closed mixed (Shanghai +71bps/Hang Seng -1.22%/Nikkei +1.97%) with Japan leading the way driven by tech strength (Tokyo Electron +11%). The yen weakened to a 6-month low in the morning before verbal intervention from Finance Minister Kato. The macro focus for today will be Richmond Fed President Barkin (voter) speaks (8am est), JOLTS (10am est, GS 7,750k, consensus 7,745k, last 7,744k), ISM Services Index (10am, GS 53.5, consensus 53.5, last 52.1), & Treasury selling $39B of 10-year notes.

In premarket trading, mag 7 names are mixed: Apple (AAPL) -1%, Nvidia (NVDA) +2%, Microsoft (MSFT) +0.3%, Alphabet (GOOGL) -0.2%, Amazon (AMZN) is flat, Meta Platforms (META) -0.7% and Tesla (TSLA) -1%. Nvidia rises 2% after CEO Huang announced a raft of new chips, software and services, aiming to stay at the forefront of artificial intelligence computing. Apple dropped 1% as MoffettNathanson downgrades the iPhone maker, citing high valuation, antitrust overhang and weakening position in China. Tesla (TSLA) slips 1% after BofA stepped away from its bullish rating, citing valuation and execution risks. Here are some other notable premarket movers:

- Arbe Robotics jumps 11% after the robotics systems maker announced a collaboration with Nvidia to enhance radar-based free space mapping.

- Aurora Innovation soars 43% as the self-driving technology company partners with Continental and Nvidia to deploy driverless trucks at scale.

- Micron rises 3% after Nvidia CEO Jensen Huang said the company is providing memory chips for its new GPUs.

- Moderna gains 3%, along with other vaccine developers, as seasonal flu cases across the country continue to increase.

- Uber rises 2% after the ride-hailing company said it’s teaming up with Nvidia in order to accelerate the development of autonomous driving technology.

European stocks gained after money markets shrugged off an uptick in regional inflation and kept expectations for European Central Bank interest-rate cuts steady. The Stoxx 600 rose 0.2%, clawing back earlier losses of as much as 0.4% led by gains in financial services, retail and real estate. Data showed euro-area consumer prices rose 2.4% from a year ago in December, up from 2.2% in November and matching the median estimate in a Bloomberg poll. The increase was largely driven by energy costs, which climbed for the first time since July, Eurostat said. Swaps pricing points to just over 100 basis points of ECB easing by year-end. Here are the biggest movers Tuesday:

- European retail stocks outperform on Tuesday after UK clothing seller Next boosted its profit forecast, driven by a strong showing from its international online business

- Kion shares rose as much as 10% in Frankfurt trading after the company said it’s working with Accenture to optimize supply chains using Nvidia’s AI and simulation technologies

- BE Semiconductor shares rise as much as 5.4% to the highest since July after UBS raises its recommendation to buy from neutral, saying 2025 could mark the turning point for the company, with demand for mainstream chip packaging equipment recovering

- Boliden gains as much as 4.1% after UBS raised the stock to neutral from sell, seeing a more balanced risk/reward ratio after the acquisition of Lundin Mining’s operations in Nerves-Corvo in Portugal and Zinkgruvan in Sweden

- Next shares advance as much as 4.3%, after the UK clothing retailer boosted its full-year earnings forecast. Sales to date are ahead of previous guidance, driven by the strength of international online operations, RBC analysts said

- Deutsche Lufthansa shares rally as much as 2.4% after Citi double upgraded the airline to buy. Analysts say 2024 was likely a trough year for the German flagship airline and see potential for capacity growth and greater productivity

- Sodexo drops as much as 9.5%, the most since late September, after delivering a first-quarter performance below analyst expectations. The French catering company maintained its organic growth target for the full year

- Alstom falls as much as 6.1%, after Goldman Sachs downgraded the French rolling-stock manufacturer to sell from neutral, projecting the company’s 94% surge in 2024 will be “difficulty to sustain”

- Pennon slides as much as 5.1%, the most in over five months, after Deutsche Bank downgrades to give the water company its only sell recommendation, citing the likelihood of a large equity raise

- Sika declines drop as much as 2.3% after Barclays downgrades the building materials company by two notches to underweight from overweight and slashes its price target to CHF215 from CHF330

For European markets, “a lot of bad news is priced in already,” Florian Ielpo, head of macro reserach at Lombard Odier Asset Management, told Bloomberg TV. “You have a recovery that is only starting and that recovery can come with a tad more inflation. European equities could be capturing some of that in the next 12 months.”

Asian stocks gained, boosted by the technology sector as Nvidia chief Jensen Huang’s speech fueled optimism in artificial intelligence. The MSCI Asia Pacific Index rose as much as 0.8%, with chip stocks TSMC and Tokyo Electron among the biggest contributors. Japan led gains among regional markets, followed by Taiwan. Hong Kong shares fell after the US blacklisted Tencent and other companies. Optimism for global AI-related stocks was heightened as Huang unveiled new products featuring Nvidia’s Blackwell chips at the CES trade show in Las Vegas. Shares of chipmakers and related companies have been benefitting from robust public and private investment into AI infrastructure, as well as hopes for improvement in broader tech demand.

In FX, the Bloomberg Dollar Spot Index is down 0.3%, falling for a third day as investors keep a close eye on trade tensions after US President-elect Trump denied a report that he might moderate plans for across-the-board tariffs. Washington’s move to blacklist some Chinese companies, including Tencent Holdings, served as another reminder of growing frictions. Prior to this week’s pullback, the dollar had surged more than 7% over a three-month period as traders’ anticipated that future US policies would dent global trade and boost the local economy. That said, the greenback’s retreat over the past couple of days doesn’t constitute a lasting trend, said Jacques Henry, head of cross-asset research at Silex in Geneva. “The dollar is in a rising cycle due to the resilience of its economy that’s likely to last,” he said. Meanwhile, the Canadian dollar continued its advance following Prime Minister Justin Trudeau’s resignation as head of the Liberal Party. The yen edged off a six-month low after Japan’s finance minister warned about “excessive” FX movements. Monday’s political headlines triggered the most hectic trading day in nearly two months in the currency options markets. Volumes surged to $108 billion by the close of trade, surpassing the activity seen on the Federal Reserve and Bank of Japan monetary policy announcement days last month, according to data from Depository Trust and Clearing Corp.

Treasuries are lower with front-end yields richer by around 1bp and long-end yields slightly cheaper. The Treasury curve extends steepening trend with 2s10s and 5s30s spreads wider by more than 1bp on the day; US 10-year yield around 4.63% is little changed after touching 4.64%, the highest level since May. German yield curve has more pronounced steepening move following euro-area inflation figures for December and bond sales by Germany and Austria. Gilts lag after soft demand for a UK 30-year auction. Focal points of US session include November JOLTS job openings, December ISM services index and 10-year note auction that may draw highest yield since 2007. Meanwhile, the UK’s long-term borrowing costs surged to the highest level since 1998 as investors grapple with a flood of bond sales this year. The yield on 30-year gilts climbed four basis points to 5.22% after a sale of same-maturity securities.

In commodities, oil prices advance, with WTI up 0.2% to $73.70. Spot gold adds $7 to $2,644/oz.

Market Snapshot

- S&P 500 futures little changed at 6,024.00

- STOXX Europe 600 little changed at 513.38

- MXAP up 0.6% to 182.34

- MXAPJ up 0.2% to 572.71

- Nikkei up 2.0% to 40,083.30

- Topix up 1.1% to 2,786.57

- Hang Seng Index down 1.2% to 19,447.58

- Shanghai Composite up 0.7% to 3,229.64

- Sensex up 0.3% to 78,201.48

- Australia S&P/ASX 200 up 0.3% to 8,285.10

- Kospi up 0.1% to 2,492.10

- German 10Y yield up 1.5 bps at 2.46%

- Euro up 0.4% to $1.0428

- Brent Futures little changed at $76.35/bbl

- Gold spot up 0.2% to $2,642.55

- US Dollar Index down 0.31% to 107.93

Top Overnight News

- Fed Governor Bowman is reportedly the top candidate to replace Fed’s Barr as Vice Chair of Supervision: Semafor.

- New York judge denied US President-elect Trump’s request to delay sentencing in hush money case: RTRS

- US President-elect Trump commented on Truth Social that many people in Canada love being the 51st state and the US can no longer suffer the massive trade deficits and subsidies Canada needs to stay afloat. Furthermore, he stated if Canada merged with the US, there would be no tariffs, taxes would go down, and they would be completely secure from the threat of Russian and Chinese ships constantly surrounding them.

- Canada reportedly considers an early release of retaliatory tariffs against the US: Globe and Mail.

- China Foreign Ministry on US President-elect Trump talking to President Xi through aides, about the exchanges between China/US, says China attaches importance to the remarks of Trump.

- Chinese-state sponsored hackers penetrated the executive branch of the Philippines government and stole sensitive data as part of a years-long campaign, people familiar said. BBG

- The yen retreated from a six-month low. Japan Finance Minister Katsunobu Kato reiterated Tokyo’s discomfort over excessive foreign exchange moves and put speculators on notice that authorities are ready to act to stabilize a faltering yen. RTRS

- Eurozone CPI for Dec was right inline w/the Street at +2.4% headline (up from +2.2% in Nov) and +2.7% core (flat vs. Nov) BBG.

- Eurozone inflation expectations rise according to the latest ECB survey, climbing from 2.5% to 2.6% over 12 months and from 2.1% to 2.4% over 36 months (the 2.4% is the highest since Jul 2024). ECB

- Nvidia shares rose premarket (~+2%) after it unveiled a new lineup including gaming chips and a $3,000 desktop computer. The chipmaker also announced partnerships with Toyota and Uber, showcasing its vision for AI-powered robots, factories and self-driving vehicles. BBG

- MU (Micron) +4.82% after Jensen Huang disclosed that Micron is providing the memory chips for NVDA’s newest GPUs. BBG

- Mark Carney said he’s considering entering the race to replace Justin Trudeau as Canada’s PM. The former BOC and BOE chief, who is chair of Bloomberg Inc. and Brookfield Asset Management, joins a list of possible contenders with ex-Finance Minister Chrystia Freeland. BBG

- US corporate bankruptcies have hit their highest level since the aftermath of the global financial crisis as elevated interest rates and weakened consumer demand punish struggling groups. At least 686 US companies filed for bankruptcy in 2024, up about 8 per cent from 2023 and higher than any year since the 828 filings in 2010. FT

- Congress won’t be able to dial back portions of Biden’s 2021 infrastructure law to pay for other priorities according to a memo, dealing a blow to the GOP’s fiscal ambitions. Politico

A more detailed look at global markets courtesy of Newsquawk

APAC stocks were mostly higher following the tech strength stateside where Nvidia briefly reclaimed the largest market cap title and closed at a fresh record. ASX 200 eked mild gains as strength in tech and telecoms picked up the slack from the weakness in the utilities, miners and materials sectors, while advances were limited amid disappointing Building Approvals data which showed a wider-than-expected contraction. \Nikkei 225 outperformed on a break above the 40,000 level with the index propelled by a weaker currency. Hang Seng and Shanghai Comp were pressured from early in the session with heavy losses in Hong Kong after the Pentagon added several companies including Tencent (700 HK) and CATL to the US list of firms alleged to help Beijing’s military, while the downside in the mainland was gradually cushioned following the announcement that China is to hold a briefing on consumer goods trade-in program on Wednesday involving officials from the PBoC, MoF and NDRC.

Top Asian news

- US Treasury Secretary Yellen spoke with Chinese Vice Premier He Lifeng and discussed economic developments, while she raised issues of concern including China’s non-market policies and industrial overcapacity, as well as expressed serious concern about ‘malicious’ cyber activity by Chinese state-sponsored actors. Furthermore, she underscored ‘significant consequences’ facing Chinese companies for material support to Russia, according to Reuters.

- Japanese Finance Minister Kato said they are seeing one-sided and sudden FX moves. He reiterated that it is important for currencies to move in a stable manner reflecting fundamentals. Kato said he is alarmed over FX moves including those driven by speculators and will take appropriate action against excessive moves, while he also commented that they cannot rule out the chance of Japan going back to deflation.

- Japan’s Keizai Doyukai (business lobby) Chief Ninami says wage growth this year at big firms will likely match levels similar to that of last year.

- Japan’s Chamber of Commerce and Industry Head says the number of small/medium-sized firms which will raise wages should rise slightly this year.

European bourses opened mostly in the red, but sentiment lifted slowly as the morning progressed to display a more mixed picture in Europe. European sectors began the morning with a slight negative bias, but now display a more mixed picture. Financial Services takes the top spot, joined closely by Retail and then by Basic Resources to complete the top 3. The latter is buoyed by gains in underlying metals prices. Banks sit at the foot of the pile, but with losses to a similar magnitude as Insurance and Healthcare.

Top European news

- Barclays UK December consumer spending was flat Y/Y compared to December 2023.

- ECB Consumer Expectations Survey (Nov): See inflation in next 12 months at 2.6% (prev. 2.5%); 3y ahead sees 2.4% (prev. 2.1%). Economic growth expectations for the next 12 months became more negative, to stand at -1.3% in November, compared with -1.1% in October.

FX

- USD is softer vs. all peers with DXY down for a third consecutive session. Recent price action for the Greenback has been dictated by the recent Washington Post report that Trump’s tariff plans may not be as bad as initially feared. Whilst Trump did later attempt to downplay this, ING is of the view that “there is no smoke without fire”. For today’s docket, attention will be on ISM services PMI and JOLTS data ahead of NFP on Friday. DXY has been as low as 107.84 but is holding above yesterday’s 107.75.

- EUR remains supported after being catapulted from a 1.0294 base yesterday in the wake of reports that the Trump tariff programme may be less stringent than initially feared. The macro focus has been on the December Eurozone inflation report which showed headline HICP advancing to 2.4% from 2.2% as expected and the super-core rate holding steady at 2.7%. Some minor softness was observed in EUR/USD amid expectations of a potentially hotter figure given the outturn for Germany yesterday; currently 1.0430.

- JPY is flat vs. the USD after USD/JPY reached its highest level since July during APAC trade at 158.41. This subsequently triggered some jawboning from Japan’s Finance Minister Kato who noted they are recently seeing one-sided, rapid moves and reiterated to take appropriate action against excessive moves. Elsewhere, Barclays have shifted their BoJ view and now see the Bank hiking in March and October vs. previous forecast of January and July

- GBP has extended on yesterday’s tariff-induced gains vs. the USD with major fresh macro drivers for the UK on the light side today. As such, Cable has eclipsed yesterday’s peak at 1.2550 but has failed to sustain a move above its 21DMA at 1.2573.

- Antipodeans are both at the top of the G10 leaderboard with markets continuing to deliberate the prospect of a potentially more friendly tariff programme by the Trump regime.

- CHF is a touch softer vs. the EUR post-Swiss CPI metrics. Y/Y headline CPI fell to 0.6% from 0.7% as expected, whilst the core rate fell to 0.7% from 0.9% (expected 0.8%). The 0.6% outturn means that the average across Q4 as a whole came in around 0.63% and is shy of SNB’s 0.7% projection for Q4. EUR/CHF moved back onto a 0.94 handle following the data and is eyeing the 30th December peak at 0.9441.

- PBoC set USD/CNY mid-point at 7.1879 vs exp. 7.2994 (prev. 7.1876)

Fixed Income

- USTs are flat, in a narrow 108-13+ to 108-20 band. Complex awaits US data incl. JOLTS and ISM Services alongside Fed’s Barkin (expected to reiterate remarks from 3rd Jan.) before 10yr supply. Last night’s 3yr auction was soft overall and weighed on USTs into settlement.

- Bunds pressured in-fitting with the above and the tentatively constructive European risk tone ahead of Flash HICP. Before that, the December HICP Y/Y figure for France came in cooler than newswire consensus though hotter than the prior.

- Thereafter, EGBs saw fleeting upside on the EZ data which came in in-line for the headline though with services and core slightly hot, upside perhaps driven by expectations for a hotter headline post-Germany; though, the Bunds upside proved shortlived.

- Gilts are underperforming. UK specifics light aside from Construction PMI which spurred no move and a strong BRC Retail Sales report for December, the latter perhaps weighing on Gilts. Given the pressure, which has taken Gilts to a 91.68 trough just above last week’s 91.65 base and the contract low a tick below at 91.64, yields are firmer across the curve with the 30yr above 5.21% and at its highest since 1998. A slightly soft, but robust overall, UK auction spurred little move in Gilts.

- UK sells GBP 2.25bln 4.375% 2054 Gilt: b/c 2.75x (prev. 3.0x), average yield 5.198% (prev. 4.747%) & tail 0.3bps (prev. 0.4bps).

- Germany sells EUR 3.472bln vs exp. EUR 4.5bln 2.00% 2026 Schatz: b/c 2.30x (prev. 2.30x), average yield 2.18% (prev. 1.94%) & retention 22.8% (prev. 19.84%).

Commodities

- A relatively choppy start to the session for the crude complex, though benchmarks currently resides near the bottom end of the day’s ranges. Macro developments have been light thus far, so focus will likely be on US ISM Services PMI alongside JOLTS Job Openings. Brent’Mar currently towards the lower end of a USD 75.91-76.36/bbl range.

- Gold is firmer but only modestly so. Upside as a result of the soft USD and relatively tepid risk tone thus far. Furthermore, a modest bullish reaction was seen on China’s monthly reserves figures, which showed the second consecutive monthly increase in gold reserves. At the upper-end of USD 2632-2646/oz parameters, which is entirely within but towards the top-end of Monday’s parameters.

- Copper is modestly firmer, taking impetus from the softer USD and perhaps from the European risk tone, though that has been slightly more tentative thus far. 3M LME Copper holding above the USD 9k handle.

- BofA says natgas balances likely to tighten in 2025 as 2.5 BCF/D of demand growth outruns the 2.1 BCF/D of supply growth, supporting the bullish outlook

Geopolitics: Middle East

- Senior Israeli Foreign Ministry official says Israel is fully committed to conclude a hostage deal; the only way to get a deal is to put pressure on Hamas

- Israeli army said it bombed a cell of militants in the town of Tammun, south of Tubas, in the northern West Bank, according to Al Jazeera.

- Hamas leader said they asked for maps outlining the withdrawal process and the atmosphere pointing to an integrated deal to end the war in Gaza, according to Asharq News.

- “Iranian media report that the first phase of manoeuvres to test the defense systems of the Natanz nuclear facility has begun”, according to journalist Elster.

Geopolitics: Other

- North Korea confirmed Monday’s launch of a new hypersonic missile, while it was separately reported that North Korea plans to launch an ICBM before the Trump inauguration, according to Chosun Ilbo. In relevant news, South Korean acting President Choi said they are to respond sternly to North Korean provocation and that North Korea missile test poses a significant security threat.

US Event Calendar

- 08:30: Nov. Trade Balance, est. -$78.3b, prior -$73.8b

- 10:00: Nov. JOLTs Job Openings, est. 7.74m, prior 7.74m

- Nov. JOLTS Layoffs Rate, prior 1.0%

- Nov. JOLTS Layoffs Level, prior 1.63m

- Nov. JOLTS Quits Rate, prior 2.1%

- Nov. JOLTS Quits Level, prior 3.33m

- Nov. JOLTS Job Openings Rate, est. 4.6%, prior 4.6%

- 10:00: Dec. ISM Services Index, est. 53.5, prior 52.1

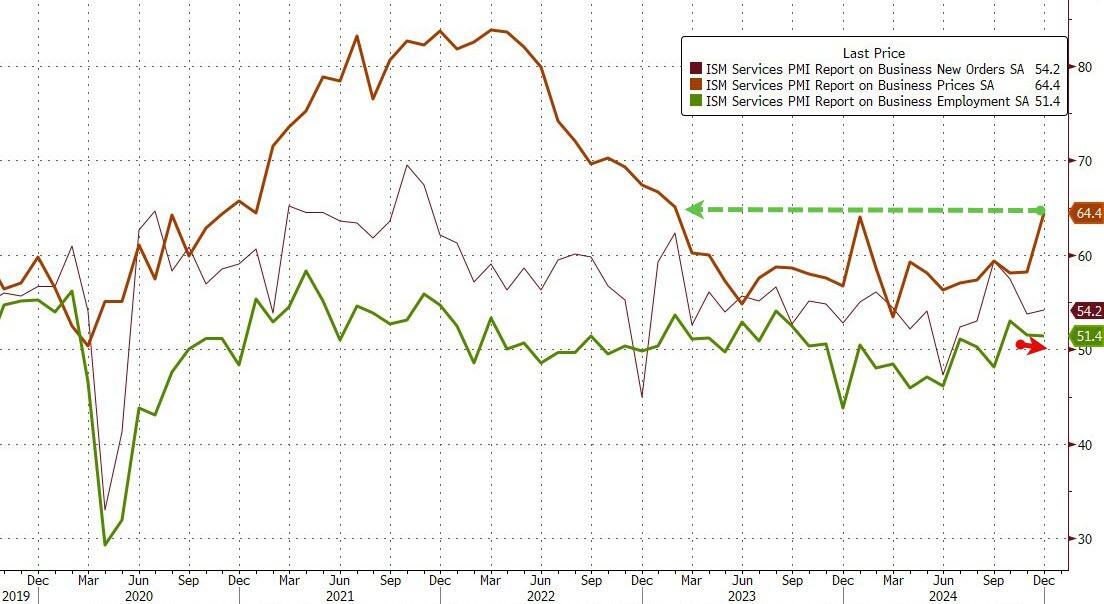

- Dec. ISM Services Employment, est. 51.4, prior 51.5

- Dec. ISM Services New Orders, est. 54.2, prior 53.7

- Dec. ISM Services Prices Paid, est. 57.5, prior 58.2

DB’s Jim Reid concludes the overnight wrap

Morning from Helsinki where I’ve started my work year pretty much every year (ex-Covid) for the last 25. It’s cold but I’m acclimatised as I’m just back from a very snowy ski trip in the Alps which unfortunately coincided with a pretty dreadful bout of flu or perhaps Covid. My wife and I spent the entire two weeks drained and coughing and spluttering 24/7 which wasn’t fun in the cold. The kids and Brontë didn’t adjust their demands accordingly though so it was hard work. I could do with a fresh two week holiday to recover.